Business Incentives and Grants Tax

21

Business Incentives and Grants Tax SAIT Webinar 18 November 2021 YOUR KEY TO THE TAX COMMUNITY

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Business Incentives and Grants Tax

Business Incentives and Grants Tax

SAIT Webinar18 November 2021

YOUR KEY TO THE TAX COMMUNITY

Presenters:• Nicole de Jager – (Senior Manager, Tax and

Government Incentive & Carbon Tax at KPMG)• Justin Shein– (Director, Head of Global

Operations at Catalyst Solutions)

Section 11D: Research and Development

YOUR KEY TO THE TAX COMMUNITY

Global R&D trends

Materials design

Disease control

Robotics Agriculture

Artificial intelligence

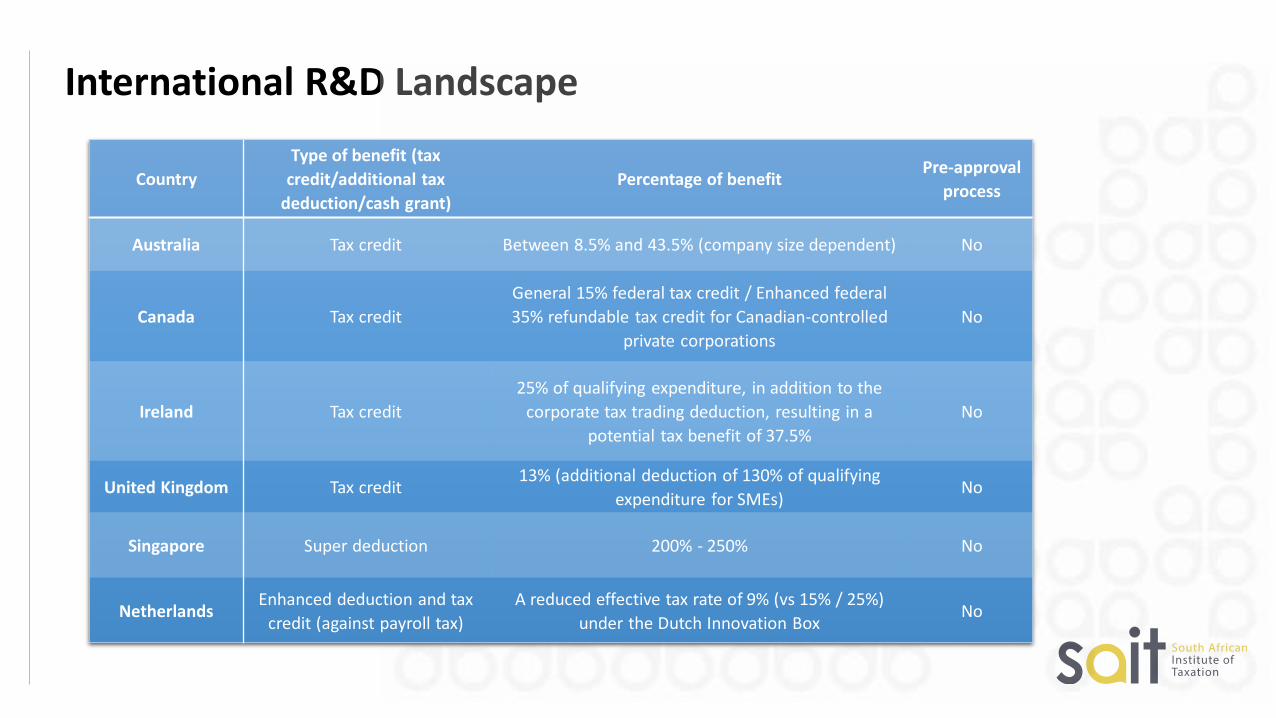

International R&D Landscape

Country

Type of benefit (tax

credit/additional tax

deduction/cash grant)

Percentage of benefitPre-approval

process

Australia Tax credit Between 8.5% and 43.5% (company size dependent) No

Canada Tax credit

General 15% federal tax credit / Enhanced federal

35% refundable tax credit for Canadian-controlled

private corporations

No

Ireland Tax credit

25% of qualifying expenditure, in addition to the

corporate tax trading deduction, resulting in a

potential tax benefit of 37.5%

No

United Kingdom Tax credit13% (additional deduction of 130% of qualifying

expenditure for SMEs)No

Singapore Super deduction 200% - 250% No

NetherlandsEnhanced deduction and tax

credit (against payroll tax)

A reduced effective tax rate of 9% (vs 15% / 25%)

under the Dutch Innovation BoxNo

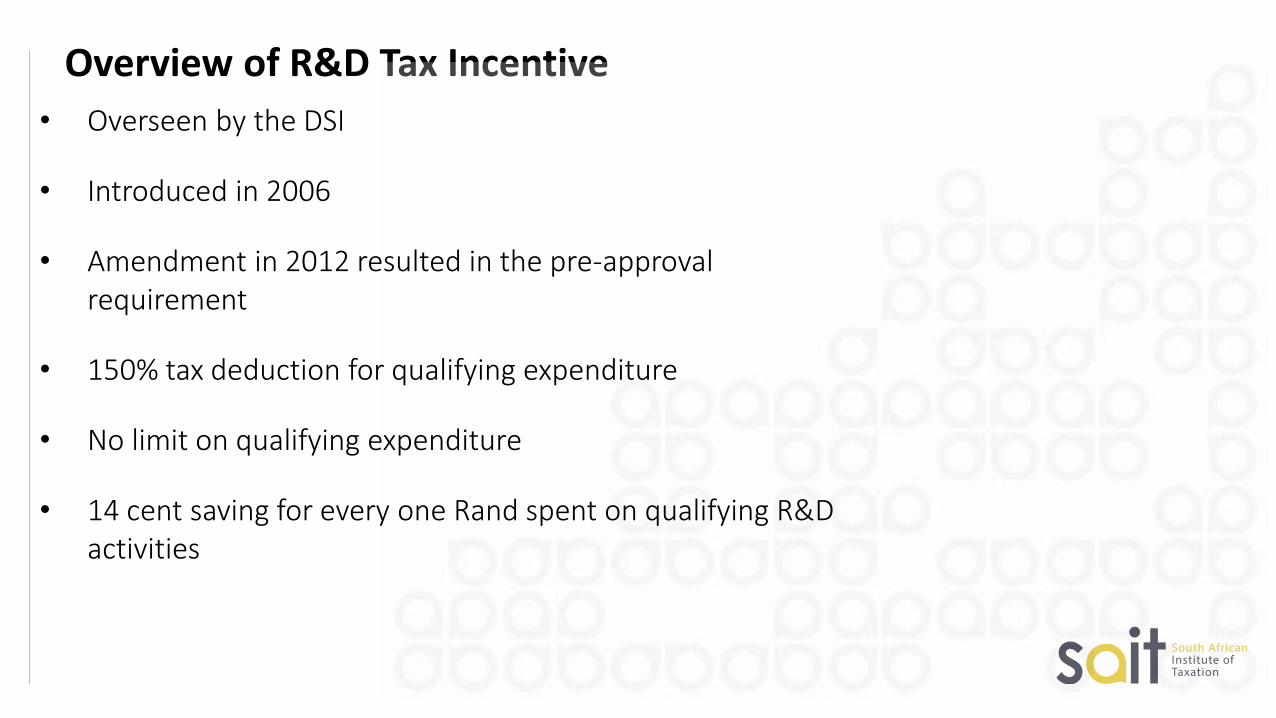

Overview of R&D Tax Incentive

• Overseen by the DSI

• Introduced in 2006

• Amendment in 2012 resulted in the pre-approval requirement

• 150% tax deduction for qualifying expenditure

• No limit on qualifying expenditure

• 14 cent saving for every one Rand spent on qualifying R&D activities

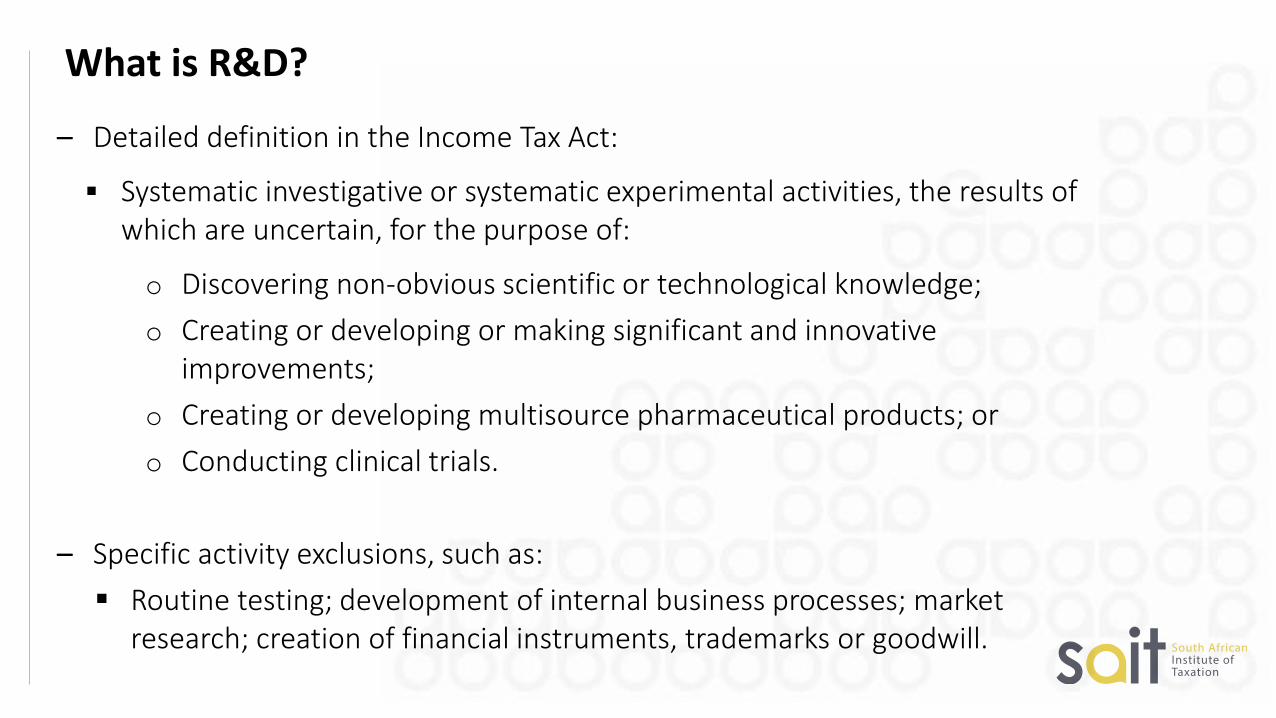

What is R&D?

– Detailed definition in the Income Tax Act:

▪ Systematic investigative or systematic experimental activities, the results of which are uncertain, for the purpose of:

o Discovering non-obvious scientific or technological knowledge;

o Creating or developing or making significant and innovative improvements;

o Creating or developing multisource pharmaceutical products; or

o Conducting clinical trials.

– Specific activity exclusions, such as:

▪ Routine testing; development of internal business processes; market research; creation of financial instruments, trademarks or goodwill.

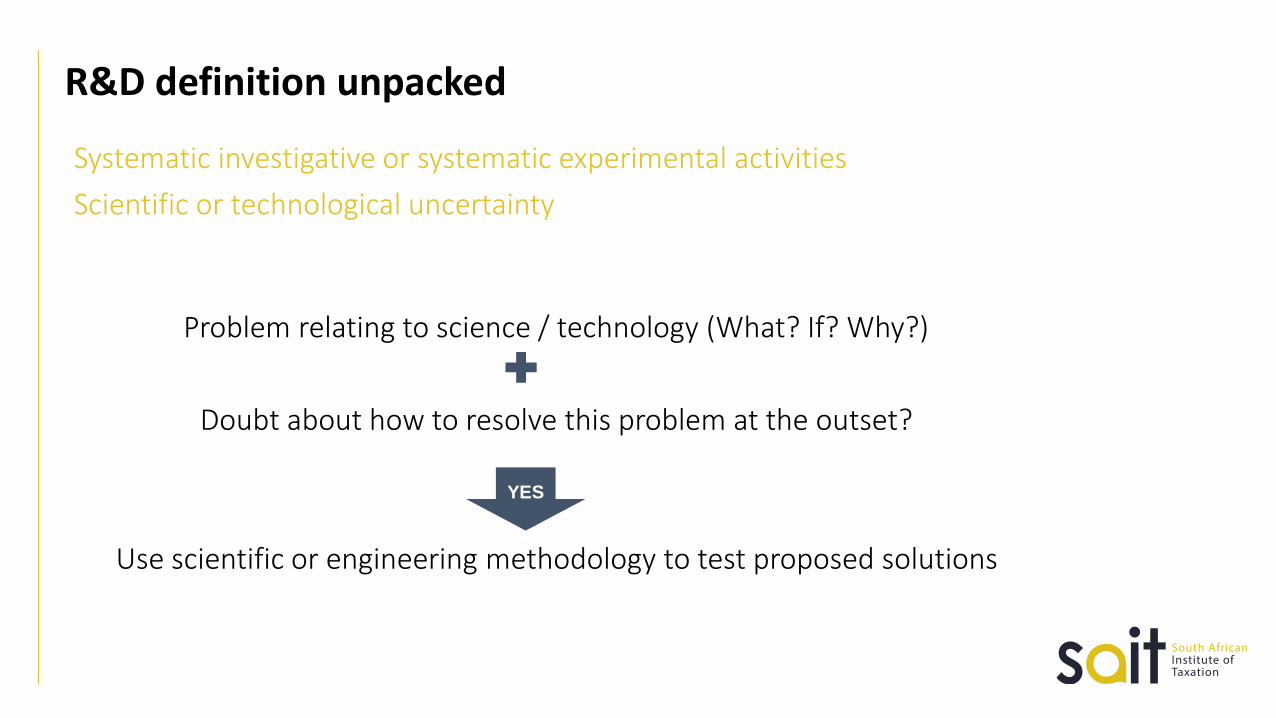

R&D definition unpacked

Systematic investigative or systematic experimental activities

Scientific or technological uncertainty

Problem relating to science / technology (What? If? Why?)

Doubt about how to resolve this problem at the outset?

Use scientific or engineering methodology to test proposed solutions

YES

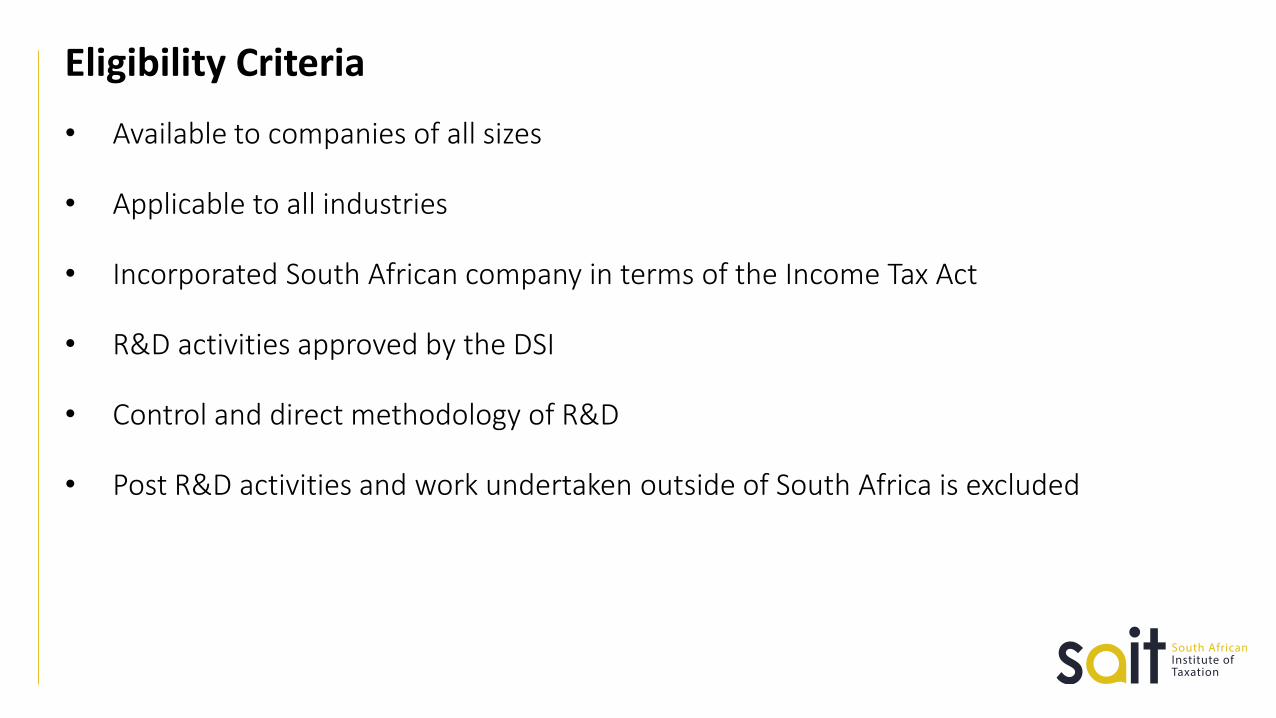

Eligibility Criteria

• Available to companies of all sizes

• Applicable to all industries

• Incorporated South African company in terms of the Income Tax Act

• R&D activities approved by the DSI

• Control and direct methodology of R&D

• Post R&D activities and work undertaken outside of South Africa is excluded

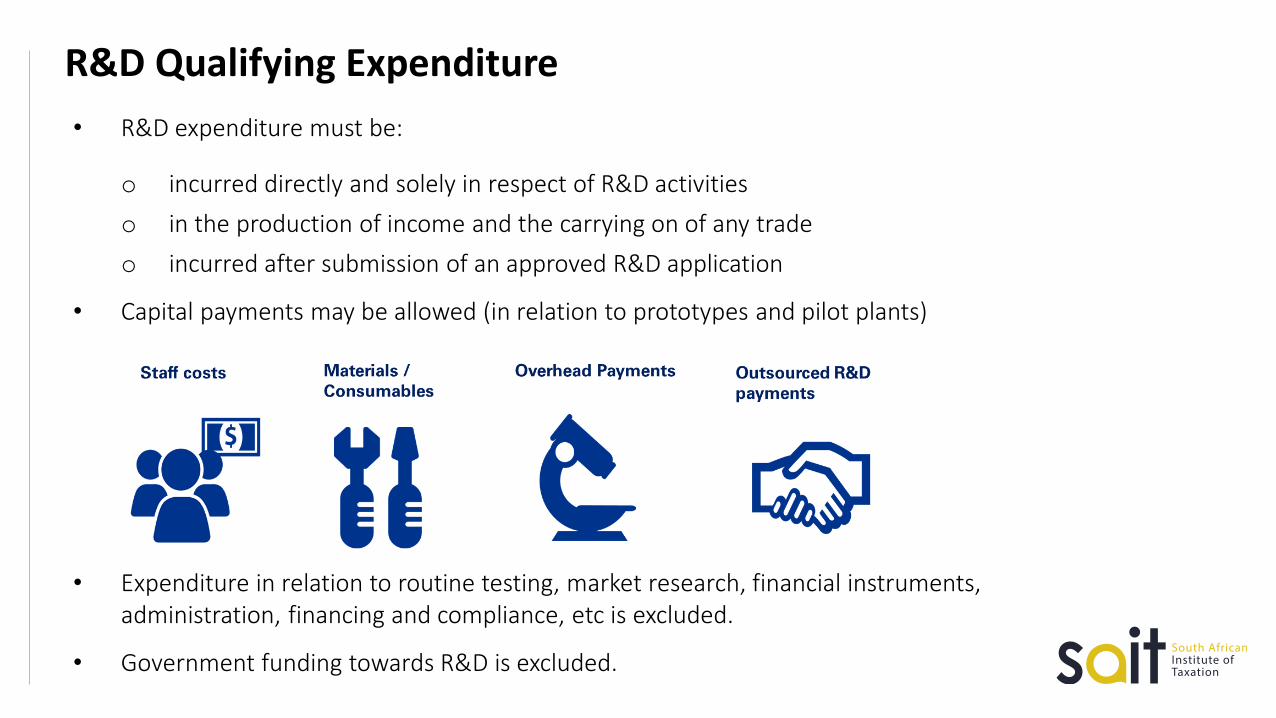

R&D Qualifying Expenditure

• R&D expenditure must be:

o incurred directly and solely in respect of R&D activities

o in the production of income and the carrying on of any trade

o incurred after submission of an approved R&D application

• Capital payments may be allowed (in relation to prototypes and pilot plants)

• Expenditure in relation to routine testing, market research, financial instruments, administration, financing and compliance, etc is excluded.

• Government funding towards R&D is excluded.

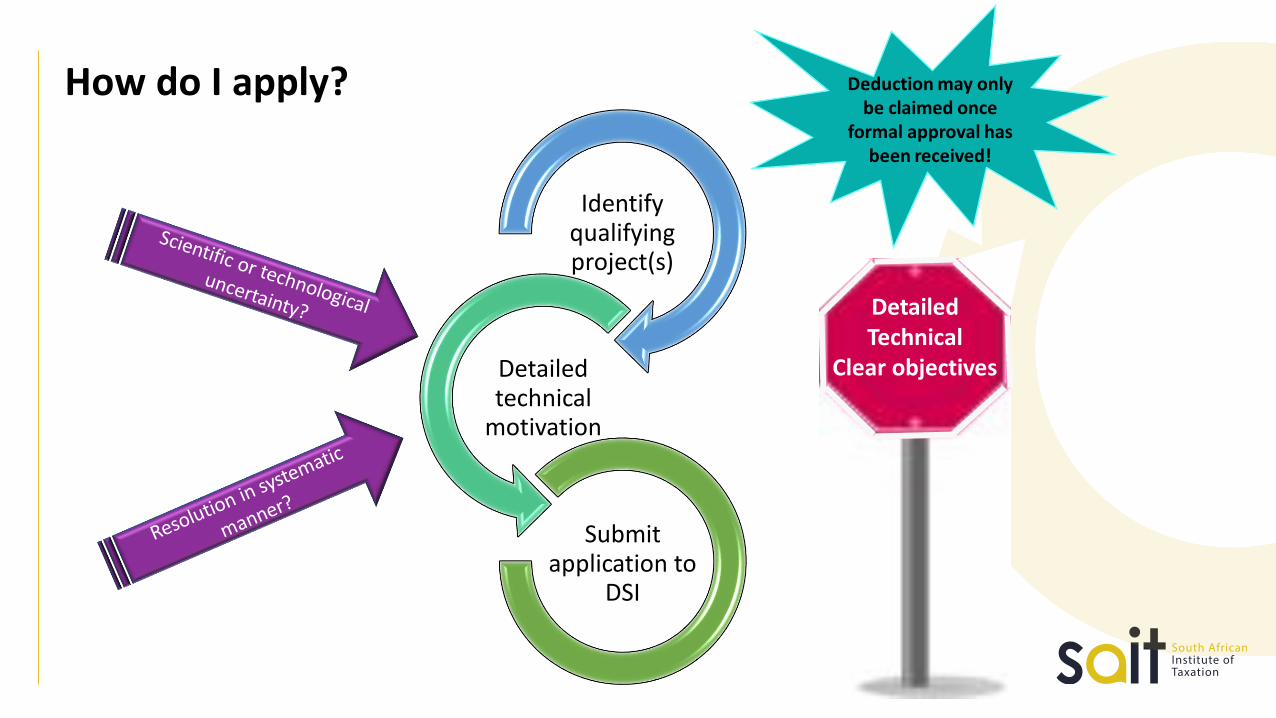

How do I apply?

Identify qualifying project(s)

Detailed technical

motivation

Submit application to

DSI

DetailedTechnical

Clear objectives

Deduction may only be claimed once

formal approval has been received!

R&D Application & Claim

• Applications are submitted to the adjudication committee consisting of:

o DSI

o SARS

o National Treasury

o Technical experts

• Decision in formal letter from the Minister

• Approved applicants:

o Submit annual progress reports to DSI

o Expenditure claimed as part of tax return submission

Practical Aspects and Common Pitfalls

IntroductionThe Research and Development (R&D) Tax Incentive (s11D) is a significant driver of innovation in SouthAfrica encouraging companies to undertake R&D activities they might not otherwise be able to fundthrough the lucrative supercharged 150% tax deduction.

The government’s tax deduction for research and development expenses have been a catalyst forinnovation and experimentation across the economy. Identifying, processing and securing the 11Dincentive and dealing with the complex regulatory issues involved, requires vast expertise and experience.However, most businesses are still either unaware of the program or underestimate its benefits.

Below are some of the pitfalls and common errors associated with the R&D Tax Incentive that you need look out for and avoid:

1. Failure to Identify R&D Undertaken2. Not submitting R&D Tax Incentive Applications

Timeously3. Claiming Ineligible Costs (over-claiming)

4. Not Claiming All The Qualifying Costs (Under-claiming)

5. Not Categorizing All The Relevant Costs6. Failure To Submit Annual Progress Reports

1. Failure to Identify R&D Undertaken Issue:

The current application process is very administratively burdensome and requires a deepunderstanding of both the qualifying criteria and the nature of R&D being done. The definition ofwhat qualifies as R&D is broad and is accessible to broad category of claimants. Many South Africancompanies don’t claim the R&D deduction because:1. they aren’t aware of its existence; or2. fail to identify that their current day to day operations constitute R&D as defined under the

incentive's guidelines.

Result:

Taxpayers that do not claim tax relief are missing out on an opportunity to reduce their taxableincome and boost their investment resources. Many firms are missing out on thousands or millions ofRands in savings under the tax incentive due to a lack of awareness and common misconceptionsabout the incentive. The reality is that the section 11D Tax Incentive is far more widely applicablethan many believe, can be secured efficiently with the right guidance, and continues to be hugelyvaluable to South African taxpayers who invest in innovation and R&D.

2. Late Project Application Submissions

Issue:

South Africa is unique in that it is one of the few countries globally that require pre-approval in orderto claim an R&D tax incentive. All projects must be pre-approved by the Department of Science andInnovation (DSI) before they are eligible to claim the s11D tax incentive. Taxpayers can claim from thedate of submission of the pre-approval application and not just the date of approval and can continueto claim until the project’s completion. Most other countries that offer an R&D incentive utilise apost-approval process in which companies claim the incentive with possible audits after utilising theincentive.

Result:

Only costs incurred after submission of the pre-approval application will qualify for the incentive. Assuch, it is best to submit applications as early as possible in the life of a project in order to maximisethe value of the deduction. Through submitting projects late in the life of a project, significant savingsare lost.

3. Claiming Ineligible Costs (Over-claiming)

Issue:

As a general rule, qualifying costs are costs that are directly solely and directly related to the R&Dactivities of the qualifying project. As such, costs do not qualify when they are incurred in respect ofindirect R&D or other supporting activities. Often times company’s mistakenly claim ineligible coststhat do not meet this requirement.

Result:

The claiming of ineligible costs in your return under the s11D deduction can lead to protracted SARSaudits, as well as interest and penalties for your business. The resulting delays, interest and penaltiescan have severe impacts on the cashflow of companies who may otherwise have been eligible toreceive a refund from SARS.

4. Not Claiming All The Qualifying Costs (Under-claiming)

Issue:

The value of the tax relief hinges on the nature and quantum of expenses incurred on research anddevelopment. It’s easy to overlook some essential expenses that are part of the R&D effort and couldqualify for tax deduction. Having a thorough understanding of the DSI incentive guidelines and s11Dof the Income Tax Act, will aid taxpayers by ensuring that they are claiming for all the relevantqualifying expenditure and thus maximising their claim.

Result:

Whilst erring on the side of caution can go a long way to avoiding the terrifying pitfalls of goingthrough a SARS audit, being too cautious can mean losing out on substantial sums of money.

5. Not Categorizing All The Relevant CostsIssue:

Once approved, costs fall into the following categories when calculating the claim value:• Labour• Subcontractors• Overheads• Materials

The above categorizations are required for the purpose of the progress reports required in terms of s11D(13) andfailing to be cognizant of these categories from the start often delay the process of submitting the progressreports.

Result:

As with any other tax-related issue, maintaining meticulous and comprehensive records for SARS is essential.Should the submission of your progress report be delayed as a result of a taxpayer struggling to categorise thequalifying expenditure, the Minister of the Department of Science and Innovation may revoke the approval forthe project(s) and the ability to claim the tax incentive will be lost.

6. Failure To Submit Annual Progress Reports TimeouslyIssue:

Annual Progress reports are an important administrative element of the incentive. Annual progressreports on the DSI approved projects are required to be submitted annually (coinciding with thecompany’s financial year-end reporting) to the DSI. These reports detail the progress made in thetaxpayers R&D activities. The report requires information relating to whether the company attainedits R&D goals, the R&D expenditure and the amount of the tax incentive benefit amongst otherthings.

Result:

Failure to timeously submit annual progress reports to the DSI, will result in the DSI issuing a non-compliance letter ordering the participant to submit a progress report within a defined period. Failureto submit the report within the grace period will result in the DSI withdrawing all approvals. If thedepartment were to issue a withdrawal, it would essentially mean that the taxpayer would not beentitled to the s11D tax incentive benefit.

YOUR KEY TO THE TAX COMMUNITY

Thank you!

Questions & Answers

Contact Persons:Justin Shein CA(SA) CFA Dov Paluch Nicole de Jager

[email protected] [email protected] [email protected]

+27 72 125 3727 +27 82 773 7947 +27 82 717 4762