Corporate tax avoidance, shareholder dividend tax policy, and ...

Scek’s Consulting

Aues Scek 23/10/08 1

Capacity Building for Tax Administration, Revenue Collection and Intergovernmental

Fiscal Relations

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

2

Contents Introduction ......................................................................................................................... 3 Current Legal Framework ................................................................................................... 4 Budgetary Process ............................................................................................................... 5

Federal Budget ................................................................................................................ 5 State Budgets .................................................................................................................. 6 District Budgets .............................................................................................................. 7

Revenue Control Procedures............................................................................................... 7 Transitional Federal Government ................................................................................... 7

Puntland .............................................................................................................................. 8 Somaliland .......................................................................................................................... 9

Financial Devolution ....................................................................................................... 9 Revenue Sharing Formula and Transfers ...................................................................... 10

Broad Implications ............................................................................................................ 10 Revenue and Tax Policy ................................................................................................... 11

Fiscal Institutions .............................................................................................................. 13 Revenue and Tax Administration ................................................................................. 14

Fiscal Function of Local Authorities ............................................................................ 16 Fiscal Relations between Local Administrative & State .............................................. 16

The Role of Federal, State, Regional, and District Authorities ................................ 18

Auditor General’s Office .............................................................................................. 18 Revenue Policy ................................................................................................................. 19

Medium-term Revenue Measures ................................................................................. 23

TFG Fiscal Policy Objective ......................................................................................... 24

Somalia’s Debt .............................................................................................................. 25 Source: Creditor Statements and World Bank Global Development Finance .................. 26

Capacity and Capability Building ..................................................................................... 26

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

3

Introduction The current tax system in Somalia is weak and has several deficiencies. One of the most

striking characteristics of the Somali tax system is its excessive reliance on customs

duties from the few actively functioning and accessible Ports and Air Ports. Almost over

80% of the total government revenue consists of taxes on imports.1 In contrast direct

taxes on income including income from public enterprises, account for less than 3% of

the total revenue for Puntland and Somaliland, while for the TFG is even less as there are

no permanent staff working for the government. This imbalance is inevitable in light of

the limited domestic resource base; it is also the result of structural and administrative

deficiencies of the tax system. Taxes on exports are estimated to be in the range or

around 10 to 15% of the total government revenue. The reason for this is the limited

export capacity coupled with the lack of a government in Somalia proper.

Another shortcoming of the tax system is its nature of being specific rather than ad-

valorem. Specific Import duties range from $0.0 for some food items to over $1000 on

imported vehicles and some luxurious items. The specific nature of the tax system on the

one hand reduces the problem of under-invoicing, but on the other hand is not responsive

to inflationary pressures, thus adversely affecting the real value of tax collections.

The customs valuation of imports is one of the weakest areas of Somalia’s tax system.

Since the collapse of the Somali state in 1991, imports are not financed with a letter of

credit through the banking system, given the fact that there are no Banks operating in the

country, except The Hawaalo (the money transfers companies) and the prices of invoices

are not reliable as they are or could be manipulated by importers. Therefore, the authority

resorts to discretionary measures of assessment and collection of taxes, which are prone

to corruptions and mismanagement.

Development partners are interested to provide assistance through budgetary support to

the Somali authorities to help jump-start the establishment of the Federal and state

institutions, but this is made dependent on the ability of the authorities to show it has the

support of the citizens by acting in a united way to collect basic revenue. Therefore the

most urgent tasks for the Federal and state authorities will be to put in place a transparent

tax system and tax administration at federal, state and local level, the earlier this is done

the better.

The objective of designing a tax system is to make it as broad as possible in terms of

administrative feasibility, while keeping the initial tax rate low in such a way that it yield

significant amount of revenue and not having any adverse impact on business activity in

the country. Toward this end a study was conducted in 2006 by Malner et. al, which

identified the major potential tax bases, including some that have not frequently been

taxed, such as money transfer companies, telecommunication and trade.

1 Besides the revenue classified under import taxes, a proportion of revenue from stamp taxes and

administrative duties is also generated by imports.

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

4

Given the weak revenue collection capacity, focus in the early stages of a totally new

revenue collection services, the tax system will have to concentrate on taxes on economic

transactions, especially imports. Another important aspect in the design of the new tax

system would be to make tax system as simple as possible in order to keep the cost of

collection to the minimal as also to keep a low cost of compliance by businesses.

While in the medium term, it is expected to have in place a reasonably effective revenue

administration, which could possibly increase indirect taxes without encountering tax

evasion.

This study review existing tax and revenue administration in the TFG, Puntland and

Somaliland and propose a broad framework on how to improve and the system to make it

simple, efficient

Current Legal Framework There are currently three separate legal frameworks that guide budgeting systems,

revenue policies, administration and intergovernmental fiscal relation with the boundaries

of the Somali Republic (Somalia Proper). These are: (i) the transitional Federal Charter

(2004); Somaliland Constitution (2001), and the Puntland Charter (1998). All the three

frameworks include guidance on decentralization system of governance, with significant

devolution of power to district level, particularly for the purpose of local services

delivery. Among the three authorities, Somaliland is the most advanced in implementing

the proposed decentralized system, it is expected the same system to evolve in Puntland

and the rest of Somalia, albeit at different pace.

The TFG strategy aims at a bottom–up approach where districts are formed before the

regions and states. This seems to be due to the wide rejection of the centralized system of

governance of the earlier Somalia’s governance system operated during the Barre’s

regime.

The framework for Puntland decentralized governance and service delivery is embedded

in the Local Government Act, which provides a significant degree of devolved power to

the districts, backed by revenue and expenditure assignments. It also outlines the

districts’ right to “domestic and international borrowing”, upon approval from the state

authorities.

However, due to extremely limited fiscal capacity, Puntland authorities had little

involvement with service delivery responsibilities. The authorities were and still are more

concerned with regulatory functions and revenue collection.

Somaliland has been increasingly devolving financial and administrative responsibilities

to the elected district councils. The shift increased the autonomy of districts and also

expected to help for better planning and budgeting, financial management and efficient

revenue generation and collection.

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

5

As for what concern intergovernmental allocation of resources the Federal, State and

districts the administrative structure varies among the three levels of governance. For the

TFG, there is a total absence of any inter-governmental fiscal relation. While for

Puntland and Somaliland there are slight differences, but they are all characterized by the

lack of objective criteria as regards to financial resource allocation to the districts. In

Somaliland they are two approaches of transferring or allocating resources to the districts.

The first approach is the shared revenues. A district which possesses customs collection

points receive 10% of the customs taxes collected in that district. In the case of Berbera

Port through which a bulk of Somaliland imports and exports go through the district of

Berbera receive 10% of the total customs revenue it collects. Thus if more money is

collected in a district the more revenue it is allowed to keep. The second approach is

whereby 12.5% of the total customs revenue collected by the Ministry of Finance, after

deducting the 10% share, is redistributed to all districts. This intergovernmental transfer

of 12.5% of total customs revenue is determined by a presidential decree and is aligned

with the size of expenditure in the district. Apparently districts are divided into three

categories. Revenue generating districts and those located along major routes are

redistributed revenue ranging from 35.6% (in the case of Hargeisa) to 1%. A second

category receives 0.95% while a third category is distributed 0.70%. Often these funds

are distributed with instructions from the President or the Ministry to spend them for

specific expenditures such as for an election outlay. Neither of these revenue transfers is

based on the needs of the population in the districts.

In Puntland there is no transfer system, although a series of surcharges are levied in

addition to the regular customs duty at the port of Bosaso. Of these, 2.5% is collected on

behalf of the Municipality of Bosaso, while another 3.5% is earmarked for the Ministry

of Local Government and Rural Development to finance the process of electing district

councils. The revenue from surcharges is never recorded in the budget and it is unclear

whether these reach the intended recipients.

It is seen from the foregoing that throughout Somalia differing levels of administrative

structures, revenue generating capacities and expenditure responsibilities are widespread

and a significant degree of harmonization will be required for decentralization to succeed.

Along with the process of decentralization, it will be necessary to have in place an

acceptable inter-governmental financial relationship which is based on objective criteria

for financial resource allocation to local administrative units.

Budgetary Process

Federal Budget

Federal Budget, the Transitional Federal Government of Somalia, established in 2004

prepared its first budget in December 2005. The total budget amounted around US$150

million; the purpose of this budget was establishing key functions of the government

through paying salaries and allowances, reconstructing facilities, and providing basic

equipment and maintenance. At the time the TFG had practically zero revenue, as there

was neither collection capacity, nor infrastructures in place to enforce taxation. The

budget was presented to international community for funding. Little financing came form

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

6

the development partners, as it was believed that due to inexistent of finance institutions

and lack of transparency budget support was considered to be inappropriate.

Development partners funded a number of activities both humanitarian and

developmental outside the government channels but through the UN and INGOs.

.

The second budget prepared by TFG was for the last quarter of 2007. In this budget the

TGF projected to be able mobilize revenues of around US$ 6,918,365 (domestic and

international) per month totaling US$20,755,095 for the remaining three months of this

year.

Domestic revenue is estimated to be US$ 3million per month and US$3.9million is

expected to come as grant from international communities. The key objectives of this

budget were strengthening government capability to functions and to deliver needed

services to community. Provide security and create an environment that is conducive to

development.

The third budget2 prepared by TFG with the assistance of The Horn Economic and Social

Policy Institute (HESPI) is the most comprehensive one. In the first instance is that the

budget is based on the government’s Interim Economic Strategy (under the RDP), which

is build in four pillars, namely: (a) revitalize the economy, (b) strengthen governance and

the rule of law, (c) rehabilitate infrastructure and basic social services delivery, and (d)

rebuild capacity of the Transitional Federal Institutions. Each of these pillars a multiyear

framework is being prepared which deals with policies and provides a costing of policy

interventions to help secure support the Somalia needs from the development partners.

Unfortunately, up to now none of these budgets got off to implementation stage, practical

terms they just remained on papers.

State Budgets

Both the states of Puntland and Somaliland have been preparing budgets for several

years now. Somaliland has been doing that since 1992 and Puntland since 1998. These

budgets are not properly classified, but they are functional in the sense that expenditures

are aggregated from the various ministries and agencies of the government. The approach

used for budget preparation processes do not take into account the needs, priorities and

lack participation of key stakeholders. Both states budgets are coded and classified alone

similar expenditures heads, with the main ones being wages and salaries, operating

expenses (services) and other general expenses amounting on average about 73% of the

total for Somaliland and 83% for Puntland. On the revenue, customs duties and direct

taxes account for about 90% of the total in both states, with government charges making

the remainder. Budget preparation is largely a mechanical exercise, that’s it increase

from one year to next with some arbitrary increments that could be linked to increase in

the size of civil services or security personnel or any other administrative expenditures.

2 The TFG: 2008 Draft Budget, Volume I The Budget Framework, March 2008

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

7

District Budgets

Local administrations exist to a varying degree throughout Somalia. In the TFG areas,

there is nevertheless far too little data available to describe the financial status or even

limited governance structures which do exist. There are governors and districts

commissioners (either appointed by the TFG or self appointed clan leaders, militias) who

collect some revenue and provide limited security services but no records are kept. In

most cases, public services are delivered either by the NGOs or private sector and

financed either through user fees or by donor support. One of the most troublesome

financial and governance problems facing districts in the TFG areas is the fact that

resources are still highly contested by various factions, thereby making it difficult to

manage them through future established district administrations.

Puntland and Somaliland have a two-tier administrative structure which is operational

below the state governments i.e. regions and districts. Under this structure region and

districts are not independent tiers of government but extended arms of the state with

responsibilities for coordination. The regions do not have their own revenue sources and

the expenditures of the governor’s establishment are incorporated in the budget of the

relevant ministries. The regions are further divided into districts and a number of them

have elected district councils. Both Puntland and Somaliland are increasingly devolving

financial and administrative responsibilities to the elected district councils. This shift will

increase stepwise the autonomy of districts and also the need for better budget planning,

financial management and efficient revenue generation and collection.

Revenue Control Procedures

Transitional Federal Government

The main source of revenue for the TFG is customs duty, even though not yet exploited

to its potential. The authorities do not have under their control of all the key ports and

airports or border points operated in the country. Other sources of income include

sometimes contributions given by the private sectors, such as the telecommunication

companies or Hawaal0 to the TFG and some bilateral donors like the Saudis and a few

Arab countries that provide budget support. In theory the Accountant General is supposed

to have the responsibility for control of all official receipts, but in practice other people

who control the Ports, airports or border points are the one who have control of the

receipts.

The TFG established receipts and payments system to manager national resources. Under

which the Accountant General has the responsibility for control of all official receipts and

the supervision of Government expenditures by ensuring that no payment is done without

proper authority and availability of funds.

The receipts are supposed to be serially numbered and controlled using registers.

Collectors (particularly Ports, Airports and local authorities, etc.) will be issued official

receipts at the time of surrendering the daily collections to the Cashier. Upon receipt of

collections, the Cashier issues a Collector’s receipt. Then the Funds are banked intact in

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

8

the Government Account at one of the three brunches (Baidoa, Mogadishu and Kismayo)

of the Central Bank.

The payments voucher is raised by the spending Ministry’s Accountant on receipt of

adequately supported payment request. The Accountant General will verify the

availability of the budget and enters the appropriate code on payment voucher. The

voucher is then reviewed and approved by the Director General of the Ministry. Once

approved it is then forwarded to the Accountant General’s office. At the Accountant

General’s office the payment voucher is checked against available funds, reviewed for

correctness in all respect and approved for payment. The voucher is then forwarded to the

Central Bank for payment, where the Central Bank Cashier makes payment and ensures

the payee signs the payment voucher for receipt of funds. In practice none of these

procedures are operational, but just on papers.

Puntland

In the case of Puntland, the main source of revenue is customs duty, which in the past

decade has been ranging at around 75% of total estimated revenue. Government charges

have been contributing at 11%. Other important sources of revenues included indirect

taxes, transfers, Government property charges and income taxes. Theoretically revenue

accounting records are maintained in the Regional Accounting Offices and a monthly

revenue report prepared and submitted to the Accountant General (AG) within the first 10

days of the close of the month.

The Accountant General is responsible for the supervision of Government expenditure

and ensuring that no payment is made without proper authority and availability of funds

on the respective vote. The AG operates through delegated authority to Regional

Accountants.

The payment voucher is prepared by the spending Ministry’s Accountant on receipt of a

payment request adequately supported and approved by the Ministry’s Director General.

It is approved by the Ministry’s Director General, recorded in the Ministry memorandum

records and forwarded to the Regional Accounting office.

The process of review and recording in the Regional Accounting office is as in the

Accountant General (Sub Accounting Units) in Puntland. Payment vouchers are recorded

in master vote books analyzed by heads and subheads. A list of all payment vouchers

approved by the Regional Accountant is compiled and together with the payment

vouchers forwarded to the Bank of Puntland for payment. On payment the Bank cashier

ensures the payee signs the payment voucher and enters the Bank stamp for payment.

Every ten days the Bank prepares a statement of payment vouchers received, paid and

unpaid, certifies it and forwards it to the Regional Accounting office together with the

paid vouchers. At the Regional Accounting office the paid vouchers are recorded in the

cashbook and filed.

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

9

Within the first ten days of the close of the month, the Regional Accounting office

prepares the monthly revenue and expenditure report and forwards it together with the

supporting analysis sheets, payment vouchers, receipt vouchers, cashbooks and vote-

books to the Accountant General’s office.

The Accountant General’s office reviews and consolidates the monthly returns. The

consolidated monthly accounts are signed by the Accountant General and forwarded to

the Auditor General within 15 to 20 days of close of the month.

Somaliland The main source of revenue for the Somaliland authorities is customs duty, which is

estimated to be on average over 85% of the total revenue. Other sources of income

include telecommunication and postage, rural development charges, court charges, water

income and fishing charges, among others.

The Accountant General is responsible for control of all official receipts. The receipts

are serially numbered and controlled using registers. The collectors account for all

official receipts issued to them at the time of surrendering the daily collections to the

Cashier. On receipt of the collections, the Cashier issues a Collector’s receipt. The funds

are banked “intact” in the Government Account in the nearest branch of the Bank of

Somaliland.

The Accountant General is supported by Sub-Accountants in 8 stations in the six regions

of Somaliland who maintain revenue accounting records. Receipts are recorded in a

cashbook analyzed by revenue subheads. On a monthly basis a revenue report is

prepared and forwarded to the Accountant General.

Financial Devolution

The states of Puntland and Somaliland have taken a series of steps toward the devolution

of financial and administrative responsibilities to the few elected district councils. In

Somaliland there are more than 20 elected district councils and in Puntland over 10. This

process did to some extend increased the fiscal and administrative autonomy of the

districts, with it also the need of the districts to strengthen their ability to perform a range

of new functions, including budget planning, prioritization, financial accountability and

revenue generation.

The districts have been granted autonomy in determining the size and composition of

their establishments, but they are constrained by the use of the state government pay and

grading structure and the fact that their budgets are forwarded through the Ministry of

Local Government and Rural Development in the case of Puntland and Ministry of

Interior in the Somaliland to the Parliament for approval. The ministries provide

instructions/guidance to the districts in the use of funds. There are several positive signs

that the devolution of responsibility in the two states could be followed by further

decentralization of resources in the near future.

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

10

Most the districts are operating under fiscal stress and face significant challenges in

finding the resources to pay for their constitutional/charter mandated responsibilities.

The key sources of district revenues are generated from immobile sources, such as

markets, but district capacity for revenue collection is limited and barely sufficient to pay

for salaries and wages, operating expenses, security and basic social services. Besides

oversized district staffing places a burden on local revenue.

In the case of the TFG the Transitional Charter does not provide specifics on the district

level functions on devolution/decentralization. While Puntland and Somaliland legal

frameworks do provide itemized long list of functions, which district councils are

expected to fulfill. On the revenue side, district councils are given broad latitude to

establish their own revenue base, included the choice of instruments and rates as long as

those don’t interfere with the state revenue collection. In practice, few of the assigned

revenue sources are being collected, this is due to lack of capacity and political control,

and districts are for the most part resorting to applying different mixes of local revenue

sources, with mixed results.

Revenue Sharing Formula and Transfers

Districts in addition to raising their own revenue, they also receive funds from the state in

the case of Somaliland. The state of Somaliland uses two approaches for this purpose,

these are:

(i) Shared revenue - in those districts where customs collection points exist,

they are entitled to receive 10 points customs taxes collected in their districts.

Funds are deposited in a separate account at the local office of the Bank of

Somaliland.

(ii) Intergovernmental transfer – a 12.5 percent of the total customs

taxes collected by the Ministry of Finance (after the 10% deduction of shared

revenue) are distributed among all districts. The formula for the distribution is

aligned with the size of district expenditures.

For Puntland there is no proper transfer system in place but there are a series of

surcharges placed at the top of regular customs duty at the Bosaso Port. Of these 2.5% is

collected on behalf of Municipality of Bosaso, while another 3.5% is collected for the

Ministry of local Government and Rural Development to finance the process of electing

and establishing district council.

Broad Implications

A number of broad implications emerge from the overview of the Somaliland and

Puntland and the TFG tax and revenue systems. Above all, it would be safe to conclude

that continuation of the present trend, namely, of

increased reliance on the tax bases which already yield the bulk of the government

revenue could be self-defeating insofar as Somalia (TFG, Puntland ands Somaliland) is

close to its taxable capacity. If anything, such an approach is likely to exacerbate the

impediments to efficient resource allocation, and eventually lead to the erosion of

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

11

existing tax bases by encouraging taxpayers’ delinquency and by diverting factor inputs

to less productive uses. The combination of relatively high import duties and widespread

discretionary practices leads not only to revenue leakages, but more importantly, to

mismanagement of resources.

The authorities in Somaliland, Puntland and the TFG should embark on a redistribution

of the tax burden as permitted by the administrative constraints. Major elements of this

policy would be a massive overhaul of the tax system, the reduction of the excessive

reliance on import duties, reduction of exemptions and arrears, and the implementation of

a broad based income tax under a unified single progressive rate structure. Over the long-

run, with sufficient time and resources to undertake administrative capacity building and

taxpayer, it may be feasible to bring about a broad matching of tax instruments and

overall policy objectives.

The existing specific duty rates must be replaced by revenue-equivalent ad-valorem rates.

The price list should be adjusted on the basis of comprehensive and reliable data on

prices, collected regularly from foreign trade journals, retail and wholesale catalogues

and other sources. Even though, under the circumstances, the use of the price list is the

best solution, every effort must be made to improve customs valuation methods so that

gradually less reliance will have to be placed on price lists and more on real transactions

values.

Revenue and Tax Policy

Public administrations attempt to use tax systems to achieve many objectives and raising

revenue is one of many and is of vital importance. An improved tax system not only

enhances tax revenues but also it simplifies the system and makes it easier and less costly

to administer. In the theory of public finance, there are generally four broad principles,

these are:

(a) The principle of equity: it focuses on horizontal and vertical equity.

Horizontal equity means that similar incomes should be taxed equally,

while vertical equity requires that a higher tax burden is placed on

individuals with greater capacity to pay. In common language it is called

the ability-to-pay principle by which the rich are taxed more than poor. In

practice taxes do little to change the overall distribution of income. Their

role in pursuit of equity is to raise the revenue to pay for distributive

expenditures such as primary education, health care, better water and

sanitation services to alleviate poverty. In Somaliland and Puntland import

duties are higher on those imported items consumed by higher income

groups such as cars, and other luxurious items, while basic food items are

taxed at lower rates. As far as income tax is concerned, in the absence of

any data it is not known how progressive the income tax structure is.

However, when the tax policy is formulated by the Federal Ministry of

Finance, the tax rationalization exercise should incorporate the principle

of equity right across Somalia. In addition, the budgetary policy should

ensure that distributive expenditures like education, health, water and

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

12

sanitation constitute a larger share of the total expenditure rather than the

current preponderance of total share going to salaries and wages, such as

in the cases Somaliland and Puntland budgets.

(b) The principle of economic efficiency: the transfer of resources to the

public sector always involves an added cost to the economy (or excess

burden) that arises out of the distortions in the price system caused by taxes.

Taxes not only reduce the size of the private sector, but also change the

prices such as wage and interest rates, prices of goods and services, etc., in

an economy which results in changes in the pattern of consumption, savings,

work effort, investment, etc. compared to the pattern that would have

prevailed without taxes. These changes in patterns or allocation of economic

resources cause an added cost on the economy. A tax structure should

therefore be designed to be relatively neutral i.e. one that generates the

necessary revenue with a minimum of economic efficiency cost or has the

least effect on the allocation of resources. Generally, high efficiency costs

are related to high tax rates and to large differentials in tax rates. The current

import duties in the case of Somaliland are too many – 13 different rates in

total and range from 2% to 75%. The tax policy for Somalia should examine

the taxes on duties and reduce the number and also the high tax rates to bring

about a minimum economic efficiency cost.

(c) The principle of administrative costs: This refers to the public sector cost

of administering the tax. The administrative costs of tax collection are

divided into two major components, these are:

Compliance cost which usually refers to costs to the private sector in

complying with the tax laws; and

Tax administration cost which usually refers to the public sector costs of

administering the tax laws.

Excessive public spending on tax administration can be wasteful, but spending too

little can also be economically wasteful. To gain broad coverage of a tax base

requires sufficient enforcement capacity. Broad coverage is generally more

equitable and allows collection of tax revenues at lower, more efficient tax rates.

Added administrative spending that make aware the taxpayer and services their

tax-paying needs can lower the economic costs of complying with the tax. If the

import duty structure is more simplified and its coverage is made as broad as

possible so that hardly any imported item is exempt, compliance cost would go

down and the tax administration would be easy. Fewer taxes and absence of

exemption would imply that tax laws would be easy to interpret and follow thus

enabling ready compliance and such laws would be easy to administer therefore

lowering administrative cost.

(d) The principle of revenue stability: introduced taxes which should produce

stable revenue flows so that budget surplus or deficits are predictable. It is

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

13

often difficult to cut public expenditures or to change tax laws or to upgrade

administrative capacity rapidly in response to revenue crisis. Hence stability

of revenue is necessary. Consequently, the taxes should be revenue elastic at

unchanged tax rates and unchanged definition of the tax base. Ad valorem

tax rates are adopted to ensure revenue elasticity. Both in Somaliland and

Puntland import and export duties are levied at specific rate and not ad

valorem rate. Thus if the value of such item increases the revenue does not

increase unless the rate of duty is also increased. Whereas if ad valorem duty

is imposed the rate of duty remains the same but the revenue increases

because the tax is based on the value of the item.

Fiscal Institutions One of the key institutions that need to be put in place or strengthened in the first instance

at the federal or state level is the Ministry of Finance with three basic vested functions: (i)

to develop a fiscal strategy and monitor its impact on the economy; (ii) to formulate

expenditure policy and implement the budget, and (iii) to formulate tax policy and ensure

revenue collection is efficient. These will require establishing a number of key

departments, which include, budget department vested with the responsibility to

coordinate the overall expenditure program and prepare fiscal projections (including tax

revenues) and budget execution and reports. This department can also have

responsibility for assessing the fiscal impact of policy measures. In the medium term, it

will be appropriate to set up a separate macroeconomic department, but at the initial stage

it could be kept under the budget department. At a late stage the macroeconomic policy

department would be responsible for formulating tax policy changes, making budge

revenue forecasts for the annual budget, monitoring monthly revenue collections and

making at least quarterly revisions of the annual revenue forecasts. It should also

monitor developments in monthly expenditure commitment payments, and any payment

arrears. Based on this analysis it should make recommendations whether any intra year

adjustments in revenue or expenditure policy appear necessary to meet the annual budget

balance objective. It may be appropriate to establish a separate unit or department

responsible for the tracking of donor aid flows, such as aid management department.

There will be a need to improve the budget law, which is part of the PFM Bill and have it

passed by parliament to serve as the basis for the operation of the Ministry of Finance. In

addition a budget and accounting manual will need to be prepared, which will provide the

appropriate guidelines and procedures to be followed by staff carrying out budgeting and

accounting functions in the Ministry of Finance and line ministries.

The second department which needs to be established or strengthened is a treasury department, vested with the responsibility for controlling spending and ensuring that it

is properly accounted for. In order to carry out the treasury function it is necessary to

establish a well-functioning cash management and payments system, which makes

expenditure payments and provides for the deposit of revenue collections into Treasury

accounts. Currently this function is performed by the Central Bank. The treasury

department also needs to establish proper accounting for external aid flows, and domestic

borrowing, if any. There is also a need for a separate unit to carry out the internal audit

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

14

function. Separate from the Ministry of Finance, strengthening the Auditor General’s

office to perform the external auditing function for all government Ministries.

Another important department is a revenue administration or agency, which could be set

up under a separate tax administration law with some degree of independence from the

MoF in its hiring and compensation polices and functions. The department’s

responsibility could include collection of customs revenue, domestic tax revenue and

administrative fees and charges among the key functions. The most important

appointment or recruitment would be that of the head of the revenue administration

department and the heads of the main departments, this should be done on merit basis and

not on the base of clan affiliation. Initially the functions could be limited to a customs

department levying duties on imports and exports and a department responsible for all

other revenue. The following section discusses the main issues which emerge with

regard to the revenue administration.

Revenue and Tax Administration

From the administrative point of view the objective should be to have a lean well-paid

revenue service, which would be part of a lean well-paid civil service. If it is politically

unacceptable to have a lean, well-paid civil service, then it may be necessary to establish

a separate independent revenue authority, which presently exists in a number of African

countries. It is important to establish a recruitment mechanism which seeks the

technically most qualified people and ignores clan affiliations. From the beginning,

principles of good governance need to be put in place promoting accountability and

transparency. It is particularly important to make clear that corrupt behavior by revenue

officials will not be tolerated and to put in place mechanisms to identify and punish

corrupt behavior. An effective police force and judiciary need to be in place at an early

stage. This is necessary to be able to punish corrupt revenue officials and taxpayers who

do not pay their taxes. It is not sufficient to simply fire corrupt officials from their jobs.

It is also necessary to have the threat of criminal prosecution and spending time in jail as

a deterrent to corruption. As soon as appropriate staff has been selected there will be a

need for effective training. Tax laws will need to be drafted, tax forms and regulations

printed, and educational material explaining the laws to the public will need to be

produced. Experts should be hired to help with this process. UNDP and the World Bank

and Development Partners will have to provide both financial and technical support with

the tasks associated with putting in place an effective revenue administration.

The option of hiring a private foreign firm to collect customs revenue, as was done for a

period in Mozambique could be one alternative, but given the fact of a relatively small

market it is likely to prove to be too expensive, and it would also undermine the strategy

of building local capacity. A better option worth pursuing is to seek assistance from

neighboring countries such as the Kenya or Uganda Revenue Authorities, or some other

African revenue authorities, with regard to a number of these tasks. They are especially

well-placed to help with the procedures for valuation of imports, because many of the

same products are imported into countries. The idea of seeking assistance from the KRA

to collect import duties on exports from Kenya to Somalia has already been discussed

between the two governments, so it should be possible to explore a wider range of

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

15

assistance form the KRA. In any event it would appear to be useful to hire a couple of

senior expatriate staff with experience in another African revenue service.

Currently there is no Federal Government tax administration in place nor is there any

federal institution established to administer taxes. At the same time there is no agreement

with Somaliland or Puntland regarding their role vis-à-vis Federal Government revenue

collections. However, in the short term laws need to be enacted governing federal tax

administration and the establishment of a lean and well paid independent customs and

inland tax revenue Departments, as well as a Department to collect revenues from

charges and fees. The need for transparency and accountability requires that a lean,

separate well paid revenue administration agency, similar to the Kenya Revenue

Authority, under a separate tax administration law, with powers to independently recruit

qualified persons be established with a policy to recruit staff on the basis of merits only.

After the Revenue department or authority is set up, staff should be recruited and

provided with training in computers and recording of trade and other revenue data

through computerized systems to replace the existing structures at the ports and airports.

Since in the short and medium terms the Department/authority will not have the capacity

for correct valuation of imports for import duty purposes and since bulk of imports into

Somalia come from Dubai and Kenya, close co-operation with the Dubai authorities and

the Kenya Revenue Authority should be initiated even though cost of freight and

insurance from these destinations to Somalia is not included in the valuation. Also

collection of duties at the main ports and airports in Somalia should commence side by

side with the commencement of correct valuation of imports for duty purposes. In

addition, recording of valuation and revenue data by detailed commodity classification,

consistent with the internationally accepted Harmonized System (HS) of commodities

should be introduced forthwith. The Harmonized System of commodities for customs

purposes should be achieved by the end of the medium term and a committee should be

established in the short term to determine how to carry out this exercise. Technical

assistance will be required to initiate and supervise this special assignment. Furthermore,

the Department/authority should introduce taxpayer unique Personal Identification No.

system (PIN) which should be used by taxpayers for making payments for imports,

exports and income tax. Finally, revenue administration should initiate training in

determining incomes and profits for income tax purposes for the medium term.

At present, 90% and 80% of total revenue in Somaliland and Puntland respectively, is

generated from customs duty alone. So the top priority in the short and medium term is to

rationalize the customs duties. Some imports are still taxed at specific rather than ad

valorem rate of duty. Also the number of ad valorem duties on imports is many. In the

case of Somaliland the number is thirteen. These are 2% on brake shoes and core plugs,

7% on tin milk, etc 10%, 15%, 18%, 20%, 25%, 30%, 35%, 40%, 50%, 55% on cars and

75% on tobacco and cigarettes. Most of the imported items carry a rate of between 10%

and 30%. In the medium term, all customs duties should be made ad valorem and the

number of duties reduced to five or six rates with the lowest rate being 5% for many food

and medicinal items and the highest 35% including the rate for khat. Export duty on

livestock should also be converted to ad valorem rate and because of the seasonal nature

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

16

of such exports, should be levied at 10%. During this period, administrative capacity and

regulations for collecting income tax from wage earners – Pay As You Earn (PAYE) -

and corporations should be developed for imposition of such taxes in the long run.

Fiscal Function of Local Authorities

At federal level decision has been made to introduce a significantly decentralized federal

system in Somali. However, much work remains to be done on assigning specific

revenue sources and expenditure responsibilities to the various levels of Government. An

important issue is work needs to be done on whether their will be a significant role for

state governments, as of now the two states Somaliland, which declared it independency

and Puntland which consider itself as an autonomous state of Somalia the limited revenue

and administrative capacity would argue for giving the district level the main local

government responsibilities. There is also an issue of whether there are too many

districts at present to facilitate efficient administration and whether some consolidation

would be useful.

Currently, there are many districts with minimal local administrative structures. A few

district administrations levy licenses, charges and fees and provide limited services but

keep hardly any records and remain unaccountable. They are not lean and remain

unviable. Therefore, some viable minimal local administrative units need to be

established and some staff recruited for them in the short term. Also staff training in

computers, record keeping, simple revenue collecting procedures and simple accounting

and budgeting should be initiated. In addition in the first year, these units should prepare

preliminary local administrative budgets for 2007 and simplified local budgets for 2008

and also plan to levy fees, charges, etc and the level of services that could be provided

with the raised revenue. In the second year, these units should begin imposing the levying

of fees, charges and begin to keep records of revenue raised and expenditure incurred in

providing services. In the medium term, such units should strengthen financial planning,

budgeting and accounting functions of staff through continuous training in financial

management, as well as progressively administer collection of revenue and social service

expenditures and start recording estimated and actual spending by donors and NGOs in

simplified annual budgets. Thus lean local administration would be in place providing

social services jointly with donors and NGOs and also progressively would be in charge

of tax revenue collection and expenditure management.

Fiscal Relations between Local Administrative & State

Whatever inter-governmental fiscal relations that exist are between the state and the

districts in Somaliland and Puntland. Such type of inter-governmental fiscal relation is

non-existent in the TFG. There is no fiscal relation either at federal level as yet. Even the

relationship in the above mentioned states and districts that exist is haphazard and

arbitrary and does not follow laid down rules. There is considerable overlap in their roles

and functions. In some security is a function of the district whereas it is the role of the

state to be in charge of security. There is also a need to establish economically viable

local administrative units with lean administration. In the short term, standardized roles

and functions of state and viable local administrative units have to be established and in

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

17

the medium term, government laws need to be harmonized with regard to expenditure

responsibilities and revenue sources that would support the decentralized services of the

local administrative units.

As far as the inter-governmental allocation of financial resources is concerned, there is no

objective criteria established for financial resource allocation to local administrative units

from states. Therefore, in the short term objective criteria for resource allocation needs to

be established and also general acceptance of these criteria needs to be obtained. In the

medium term, preliminary financial resource allocation based on acceptable criteria

should commence, to local administrative units whose roles and functions are

harmonized. Perhaps some of the objective criteria which are commonly applied for

inter-governmental allocation of financial resources and could be considered are based on

district population; level of district poverty; balanced economic development; level of

revenue collected in the district; size of district administration, etc.

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

18

The Role of Federal, State, Regional, and District Authorities

The Functions and responsibilities of the four (4) levels of the Somali governmental

authorities (federal, state, region and district) need to be clearly delineated and their

abilities to conduct fiscal operations in particular be harmonized and coordinated. A

preliminary tabulation is indicated below.

Table 1: Functions and Responsibilities at all Levels of Administrations SN Functions Federal State Region District

1

2

3

4

5

6

7

8

Macro economic policy and management

Ports, airports, roads and other infrastructure.

Postal and telecommunication.

Social services (Health & education)

Water supply

Power and electricity.

Agriculture.& industry

Natural resources e.g. water, forests, sea etc.

Yes

“

“

“

No

“

“

No

Yes

No

Yes

“

“

“

No

“

“

Yes

“

“

“

No

“

“

Yes

“

“

“

Auditor General’s Office

For accountability and transparency, an external audit of public resources and the way in

which these resources are spent is a sin qua non. To ensure that the expenditure and

revenue of government is carried out according to parliamentary approval, the task of

control is entrusted to the body known as the Auditor General’s Office. To establish such

an office an act of parliament is required to provide for the control and management of

the public finances and for the audit of public accounts. The Auditor General’s Office is

headed by the Controller and Auditor-General and the enactment also provides for the

appointment, terms of office, duties and powers of the Controller and Auditor-General.

His duties on behalf of parliament are to examine, inquire into and audit the accounts of

all accounting officers and receivers of revenue and of all persons entrusted with the

collection, receipt, custody, issue or payment of public moneys. Within a period of four

months or such longer period agreed by Parliament, after the end of each financial year,

the Treasury in the Ministry of Finance, Somalia, shall prepare and transmit to the

Controller and Auditor-General accounts showing fully the financial position at the end

of the year. On receipt of accounts, the Controller and Auditor-General shall carry out

examination and audit pf accounts and within a period of seven months after the end of

financial year to which the accounts relate certify them and prepare and transmit a report

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

19

of the examination and audit of all such accounts to the Minister. The Minister on receipt

of the report shall, within fourteen days of the receipt of the report, lay it before

parliament.

The accounts of every local authority or local administrative unit will be audited by the

Controller and Auditor-General’s or by an auditor authorized by him on his behalf. Every

local authority will prepare an annual account and submit it within six months after the

end of each financial year to which it relates, for examination and audit. The Controller

and Auditor-General will prepare a report for each local authority of his examination and

audit and a copy of each report will also be transmitted to the Minister for Local

Government.

Revenue Policy

Short-term options: While a number of donors are interested to prove budgetary support

to the TFG to help jump-start the establishment of the Somali State, the continuation of

such support will eventually be partly dependent on the ability of the TFG to show it has

the support of the Somali people by acting in a united way to collect some of its own

revenue. Thus, one of the most urgent tasks of the TFG will be to put in place a tax

system and tax administration at the federal and local government levels. It will be

desirable to put in place this revenue system within the first year.

It will be important to design a tax system, which is consistent with the basic objective of

the TFG to severely limit the role of government and to concentrate on providing a

favorable enabling environment for the private sector to prosper. Thus, the new tax

system should not be a constraint on private sector growth and development. The

objective should be to make the initial tax base as broad as administratively feasible,

while keeping the initial tax rates quite low. Such a system can yield a significant amount

of revenue in an equitable manner, while not having any serious adverse impact on any

business activity. Towards this end, it is important to identify the major potential tax

bases, including some that have not frequently been taxed, and to design effective

mechanisms to tax them.

Given the relatively weak revenue collection capacity which will be feasible in the early

stages of a totally new revenue collection service, it will be best to concentrate on taxes

on economic transactions, especially imports. Another important objective is to make the

tax system as simple as possible in order to keep the cost of collection low as well as to

keep a low cost of compliance by businesses. Consistent with these principles, Box 1

presents the revenue generation options that could be considered for short term

implementation.

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

20

Box 1: Summary of Short Term Revenue Generation Options for the TFG

Tax on Imports: The simplest and most efficient option would be to tax most imports at a uniform low ad valorem

(percentage) rate of something like 5 or 8 percent, while a few specified goods, which are either luxuries or have

harmful affects on health or the environment, are taxed at higher rates of 10 to 50 percent. The rates should be kept low

enough so as not to provide a significant incentive to try to smuggle goods to avoid payment of any duty or to seek to

bribe customs officials to undervalue the goods. Some of the goods for which a higher rate of customs duty would be

appropriate are: khat, cigarettes, petrol, diesel fuel, and motor vehicles.

Exports: It is the normal international practice not to tax exports, because it would put the country’s exporters at a

competitive disadvantage and it is usually not possible for the exporter to pass on the tax to the foreign consumer.

However, since it will not be possible to tax income for a number of years, a 5 percent tax on the following exports

might be considered: livestock, fish, frozen meat, hides and skins, fruit and vegetables. Because of the severe

environmental damage it causes, it would be best to seek to prohibit the export of charcoal from Somalia, rather than to

tax it. However, the alternative of levying an increasingly high rate of export tax on it for a transitional period might

also be considered.

Sales Tax on Domestic Production of Goods and Services: For a considerable period there is not likely to be enough

manufacturing or other value-added activity to justify a general value added tax or sales tax on goods and services.

However, consideration could be given to the levy of a 5 percent tax on sales by manufacturers of selected domestically

produced goods and the services provided by luxury hotels.

Telecommunications: Levy a 5 to 10 percent tax on the total value of airtime sold by companies for use in cell phones,

as well as charges for land lines and on the revenue received by the telephone companies from handling incoming

international calls.

Remittances: Levy a tax at a low rate of ½ to 1 percent of the value of all remittances made through money exchange

companies to individuals or businesses in Somalia. For amounts above $1,000, the rate could be cut in half.

Offshore Fishing Rights: This has been an important source of revenue in the past and should be made an important

source of revenue in the near future, along with a policy to limit the amount of fishing in offshore waters so as not to

deplete the stock of fish. However, this is an area of a possible conflict as long as there is no stable, democratic

government in place.

Tax on departing passengers on international air flights from Somalia: This could be levied at a rate of $20 on

foreigners, and $10 on Somalia passport holders. This should be considered an airport usage fee and also apply to

diplomats.

Passports and Visas: Once the TFG has become more unified, has effectively restored law and order, and has received

some international recognition, it will be desirable to issue new passports to all Somali citizens who wish to obtain

them. Passports could be issued at a price of US $50. It is also recommended that Somalia issue visas at points of entry

into the country. Non- Somali citizens could be charged a fee of something like $20 for a single entry visa and $50 for a

multiple entry visa.

Business Licenses: A dual system of issuing annual business licenses could be considered. The central government

would issue licenses for financial institutions, telecommunications companies (including telephone, TV and radio

companies), airlines, large manufacturers and firms engaged in the import and export trade. All other businesses with

fixed premises would be issued licenses by local governments.

Motor Vehicle Licenses: Motor vehicle and driving licenses should also be issued, as soon as the modalities for

issuing them can be put in place. Sources: Somali Joint Needs Assessment and Reconstruction and Development Program, Macroeconomic Policy Framework and

Data Development Cluster Report (2006)

1) Tax on imports: the simplest and most efficient option would be that most imports

be taxed at a uniform low ad valorem (percentage) rate of something like 5 or 8 %, while

a few specified goods, which are either luxuries or have harmful affects on health or the

environment, are taxed at higher rates of 10 to 50 % The rates should be kept low

enough so as not to provide a significant incentive to try to smuggle goods to avoid

payment of any duty or to seek to bribe customs officials to undervalue the goods. Some

of the goods for which a higher rate of customs duty would be appropriate are: khat,

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

21

cigarettes, alcoholic beverages, petrol, diesel fuel, and motor vehicles. While some of the

goods coming into Somalia are”transit goods”, which are smuggled into Kenya or

Ethiopia, these should also be taxed at the same rate. In the early stages of the new

revenue administration, it will not have the capacity to distinguish transit goods from

goods destined for the domestic market and to the extent that taxes can be levied on these

goods by the Somalia Government, it will discourage smuggling into neighboring

countries.

There are four important categories of goods which many countries either tax at a

relatively low rate or completely exempt from tax: necessities, medicines, agricultural

and industrial machinery, and raw materials. The pre-civil war Somalia government

provided a low customs duty rate, rather than exemptions, for all these categories.

Necessities are defined as products which account for a more important share of the

consumption of relatively poor people than of relatively better off people. This list is

usually made up almost entirely of food items. As long as the basic rate of customs duty

is only 5 or 8 percent, it would probably be best not to try to have a lower rate or

exemption for any of the four categories indicated above. Having a single rate of duty

on most imports would greatly simplify customs administration. As long as the basic

rate is low, providing an exemption from duty is not a major benefit. After a couple of

years it would be appropriate to raise the basic customs duty to 10 percent and at that

time it could be decided which products to keep at a lower rate.

With regard to exports of goods from Kenya to Somalia consideration is already being

given by the TFG to seeking agreement from the Kenyan Revenue Authority to help

collect import duties on behalf of the Somali authorities. Important goods exported from

Kenya to Somalia include Khat, cigarettes, tea, and construction materials. It might also

be worth exploring the possibility of an agreement with the United Arab Emirates Dubai

Customs authorities and Somali businessmen re-exporting goods from Dubai to Somalia

that the 5 % customs duty collected when these goods are imported into Dubai (which is

levied on most goods other than foodstuffs) be given to the Somalia government, rather

than refunded to the re-exporter. Kenya and Dubai are by far the two most important

sources of imports into Somalia, so this would greatly reduce the task of customs officials

at the main entry points into Somalia to levy import duty on goods coming from other

countries. A major reason to use the Dubai and Kenyan authorities to help with

collecting import duty is that they will be better able to carry out valuation of goods and

Somali officials could be trained in the use of their valuation procedures, some of which

could be eventually adopted for general use by Somali customs.

2) Exports: it is the normal international practice not to tax exports, because it would put

the country’s exporters at a competitive disadvantage and it is usually not possible for the

exporter to pass on the tax to the foreign consumer. However, since it will not be

possible to tax income for a number of years, a 5% tax on the following exports might be

considered: livestock, fish, frozen meat, hides and skins, fruit and vegetables. Livestock

could also be subject to this rate, or it may be easier administratively to levy a roughly

equivalent specific duty, as is currently done by Puntland and Somaliland. Because of the

severe environmental damage it causes, it would be best to seek to prohibit the export of

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

22

charcoal from Somalia, rather than to tax it. However, the alternative of levying an

increasingly high rate of export tax on it for a transitional period might also be

considered.

3) Sales tax on domestic production of goods and services: For a considerable period

there is not likely to be enough manufacturing or other value-added activity to justify a

general value added tax or sales tax on goods and services. However, consideration

could be given to the levy of a 5% tax on sales by manufacturers of selected domestically

produced goods and the services provided by luxury hotels. The list of domestically

manufactured goods which might be taxed at the stage of the sale by the manufacturer to

the wholesaler or retailer includes soft drinks, bottled water, plastic bags, detergents and

soaps, and foam mattresses and pillows. At this point, the only significant service worth

taxing appears to be the expenses of customers in luxury hotels. Given that the revenue

from the domestic sales tax is not likely to be high relative to its cost of administration,

its implementation could be delayed for a couple of years. In the meantime, some

revenue can be obtained from these sources by levying a moderately high business

license fee on them.

4) Telecommunication: levy a 5 to 10 % tax on the total value of airtime sold by

companies for use in cell phones, as well as charges for land lines and on the revenue

received by the telephone companies from handling incoming international calls. Such a

tax has been introduced in Uganda and Kenya, and this is an important economic activity

in Somalia, which is concentrated in a few firms and can be relatively easily taxed.

5) Remittances: Levy a tax at a low rate of something like ½ to 1 % of the value of all

remittances made through Hawaalo companies to individuals or businesses in Somalia.

For amounts above $1000, the rate could be cut in half. However, there should be no tax

on outward payments from Somalia, because the commissions charged on such payments

tend to be very small. The tax on inward remittances would be collected by the Hawaalo

companies from the person doing the remitting from a foreign country and would be paid

monthly by the Hawaalo companies to the Somali Government.

6) Offshore fishing rights: This has been an important source of revenue in the past and

should be made an important source of revenue in the near future, along with a policy to

limit the amount of fishing in offshore waters so as not to deplete the stock of fish.

7) Tax on departing passengers on international air flights from Somalia: At a rate of

something like $20 on foreigners, and $10 on Somalia passport holders. This should also

apply to diplomats.

8) Passports and visas: Once the TFG has become more unified, has effectively restored

law and order, and has received some international recognition, it will be desirable to

issue new passports to all Somali citizens who wish to purchase them. The existing

Somali passports, either issued by the pre-1991 government or counterfeited

subsequently, are generally not recognized for travel to foreign countries. In addition to

providing an important document to Somali citizens enabling them to travel more readily

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

23

for business, pleasure, and medical purposes, issuing new passports can be a significant

quick source of revenue. They could be issued at a price of something like US $50. It is

also recommended that Somalia issue visas at points of entry into the country. Non-

Somali citizens could be charged a fee of something like $20 for a single entry visa and

$50 for a multiple entry visa. It would probably be appropriate to follow the normal

custom of not requiring diplomats and employees of international organizations to pay a

fee for their visas.

9) Business licenses: A dual system of issuing annual business licenses could be

considered. The central government would issue licenses for financial institutions,

telecommunications companies (including telephone, TV and radio companies), airlines,

large manufacturers and firms engaged in the import and export trade. All other

businesses with fixed premises would be issued licenses by local governments. Motor

vehicle and driving licenses should also be issued, as soon as the modalities for issuing

them can be put in place. This may take a year or so. Although in some countries these

are issued by local government, in Somalia it would be best to have them issued by the

central government for the sake of ensuing uniformity.

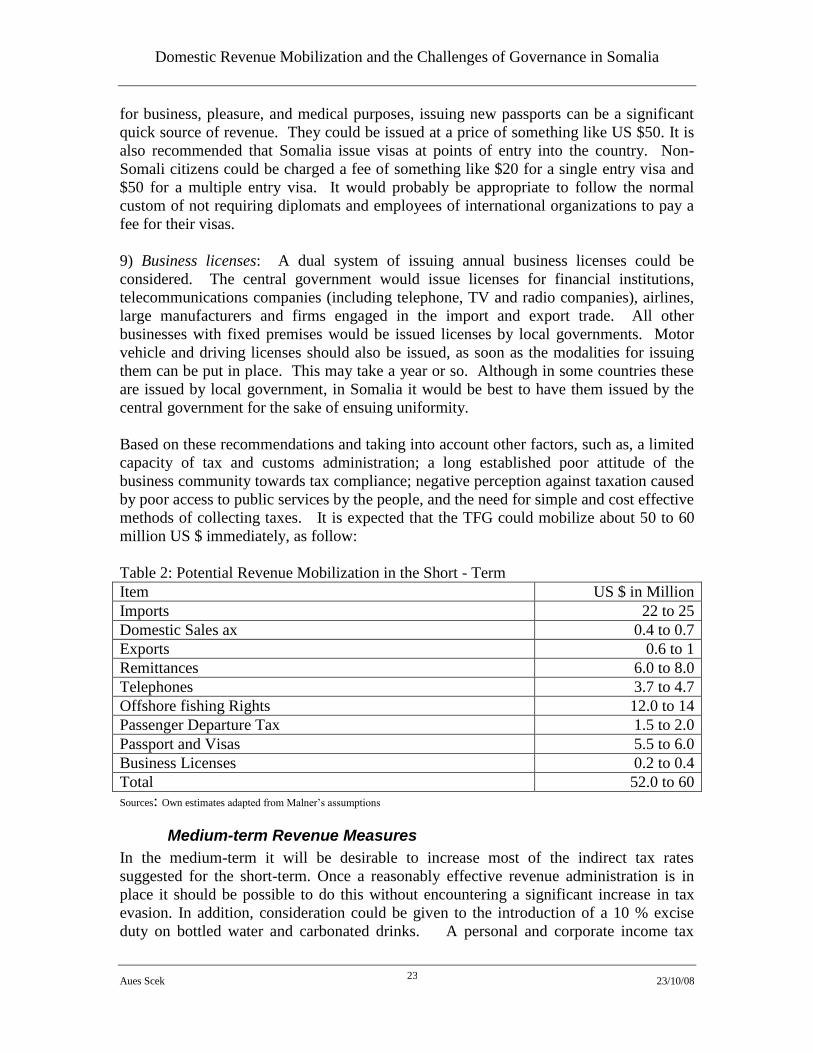

Based on these recommendations and taking into account other factors, such as, a limited

capacity of tax and customs administration; a long established poor attitude of the

business community towards tax compliance; negative perception against taxation caused

by poor access to public services by the people, and the need for simple and cost effective

methods of collecting taxes. It is expected that the TFG could mobilize about 50 to 60

million US $ immediately, as follow:

Table 2: Potential Revenue Mobilization in the Short - Term

Item US $ in Million

Imports 22 to 25

Domestic Sales ax 0.4 to 0.7

Exports 0.6 to 1

Remittances 6.0 to 8.0

Telephones 3.7 to 4.7

Offshore fishing Rights 12.0 to 14

Passenger Departure Tax 1.5 to 2.0

Passport and Visas 5.5 to 6.0

Business Licenses 0.2 to 0.4

Total 52.0 to 60

Sources: Own estimates adapted from Malner’s assumptions

Medium-term Revenue Measures

In the medium-term it will be desirable to increase most of the indirect tax rates

suggested for the short-term. Once a reasonably effective revenue administration is in

place it should be possible to do this without encountering a significant increase in tax

evasion. In addition, consideration could be given to the introduction of a 10 % excise

duty on bottled water and carbonated drinks. A personal and corporate income tax

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

24

should also be introduced in the medium or long term. Somalia had in place quite

extensive systems of taxation of business and personal income in the past. However, the

administrative apparatus to effectively implement these taxes was always weak. Their

introduction will require significant work in drafting legislation and putting in place

trained specialized tax officials.

TFG Fiscal Policy Objective

The main goal of the TFG has been to achieve peace throughout the country. In fact in

the past year or so it made several attempts to negotiate with the various opposition

groups to disarm, demobilize, rehabilitate and reintegrate ex-militia so that they can

become productive members of society and improve security. The main component of

budget expenditure for the past three has been on security. The TFG also made efforts to

establish government institutions that are vital to maintain the rule of law including a

well-vetted and managed police force, a functioning judiciary and criminal courts, and a

corrections service. In addition efforts were also made to repair of some infrastructure,

including buildings and equipment. Practically emphasis was given to the provision of

law and order as it’s considered being a pre-condition required to facilitating

humanitarian assistance, restoration of civil authority and the promotion of economic

growth and development.

For at least the first couple of years of operation of the Federal Government, the objective

should be to ensure that there is a balance in the budget, with no domestic financing. On

a yearly basis, given the experience of the pre civil war Somalia government with high

levels of domestic deficit financing through money creation, it would be prudent to avoid

budget deficits until a firm record of good fiscal management has been established.

However, there is likely to be a need for some intra year financing to balance budget

revenue and expenditure on a monthly basis. Thus, there is an important issue of what

would be the most appropriate mechanism for such temporary financing. It is unlikely to

be feasible to sell government securities to the public for many years until a track record

for prudent fiscal policy is established. It would also be unwise to do the kind of ad-hoc

borrowing from prominent businessmen which have frequently been used by the

Puntland government. It may also be unwise to have the Central Bank inject or

withdraw money from circulation on a temporary basis, because this may interfere with

achieving the price stability objective in a smooth manner. Thus, it would appear to be

desirable to establish a modest size fund in the central bank, with the use of some donor

resources. This dollar fund could be used to temporarily lend money to the government,

which would then use the money to cover a temporary budget deficit. By the end of the

year, it should be fully repaid. Since most of the government expenditure is likely to be

for wages, there will not be much short-term flexibility to adjust expenditure. By their

very nature, revenue projections are unlikely to unfold as initially envisaged and it is not

easy to make short term adjustments in revenue. Thus some flexibility in the objective of

a balance budget on a monthly basis is appropriate.

Macroeconomic policy should eventually be formulated by a macroeconomic policy

department in the Ministry of Finance and a monetary policy department in the Central

Domestic Revenue Mobilization and the Challenges of Governance in Somalia

Aues Scek 23/10/08

25

Bank. However, for the first two years, small units will be sufficient to carry out the

function. The macroeconomic policy department would be responsible for formulating

tax policy changes, making budge revenue forecasts for the annual budget, monitoring

monthly revenue collections and making at least quarterly revisions of the annual revenue