effect of information technology on tax administration and ...

82

EFFECT OF INFORMATION TECHNOLOGY ON TAX ADMINISTRATION AND PERFORMANCE BY KENYA REVENUE AUTHORITY (KRA): A STUDY OF SAMEER PARK BRANCH BY CHARITY N. KINYUA UNITED STATES INTERNATIONAL UNIVERSITY - AFRICA SUMMER 2019

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of effect of information technology on tax administration and ...

EFFECT OF INFORMATION TECHNOLOGY ON TAX

ADMINISTRATION AND PERFORMANCE BY KENYA REVENUE

AUTHORITY (KRA): A STUDY OF SAMEER PARK BRANCH

BY

CHARITY N. KINYUA

UNITED STATES INTERNATIONAL UNIVERSITY - AFRICA

SUMMER 2019

EFFECT OF INFORMATION TECHNOLOGY ON TAX

ADMINISTRATION AND PERFORMANCE BY KENYA REVENUE

AUTHORITY (KRA): A STUDY OF SAMEER PARK BRANCH

BY

CHARITY N. KINYUA

A Research Project Report Submitted to the Chandaria School of Business in Partial

Fulfillment of the Requirement for the Degree of Masters in Business

Administration (MBA)

UNITED STATES INTERNATIONAL UNIVERSITY - AFRICA

SUMMER 2019

ii

STUDENT’S DECLARATION

I, the undersigned, declare that this is my original work and has not been submitted to any

other college, institution or university other than the United States International

University - Africa in Nairobi for academic credit.

Signed: ________________________ Date: _________________________

Charity N. Kinyua (ID No: 657273)

This research project report has been presented for examination with my approval as the

appointed supervisor.

Signed: ________________________ Date: _________________________

Prof. Zachary Mosoti

Signed: ________________________ Date: _________________________

Dean, Chandaria School of Business

iii

COPYRIGHT

Copyright © Charity N. Kinyua, 2019

All Rights Reserved

No part of this research project report may be reproduced or distributed in any form or

any means electronically, mechanically or photocopy, or stored in a database or retrieval

systems, without prior permission of the author and the institution.

iv

ABSTRACT

The objective of this study was to investigate the effect of information technology on tax

administration and performance by Kenya Revenue Authority (KRA). The study was

guided by specific objectives driven to identify the effect of employees’ IT knowledge on

tax administration performance, the effect of business processes technology on tax

administration performance, and effect of taxpayers’ IT knowledge on tax administration

performance in relation to the performance of KRA and its sustainability.

The study adopted an explanatory research design. The population of the study targeted

300 members of staff working at the Sameer Park Branch along Mombasa road who were

300. The sample frame for the study was a list of the population which was obtained from

the staff members at Sameer Park Branch provided by the directors at Sameer Park. The

study used a probability sampling design known as the systematic random sampling

design. The sample size was derived using the formula suggested by Yamane (1967),

which provided the study with a sample size of 171 respondents. The study collected

primary data using questionnaires which comprised of closed-ended questions.

Cronbach’s Alpha test was used to examine the reliability of the questionnaires. The data

collected was analysed using Statistical Package for Social Science (SPSS). Descriptive

statistics of frequencies, means and standard deviations were used during analysis to

provide figures and tables. Inferential statistics including Correlation and regression

analysis were also employed in the study.

The study showed that information technology has increased productivity in the

organization, as well as help staff from different departments in the organization to

communicate without necessarily having to meet in person, enabled the employees to

meet deadlines for daily operations as well as prioritize their work in terms of need. IT

has allowed employees to access to information via a touch of a button and the automated

systems have reduced the work of printing personal and business information. KRA is

keen on ensuring all staff members are educated and trained appropriately in order for

them to operate effectively and meet their deadlines.

The study indicated that automated systems in the organization required less if any human

labour and they were cheap as compared to human labour. Social media in the

organization involves turning communication into interactions through various platforms

v

and KRA values the integration of social media into its business process. KRA employees

prefer to make their own time to work and their working behaviour has changed due to

the increasing use of IT, because, the adoption of computers in the organization has

transformed the organization.

The study revealed that technology is necessary for the tax administration activities in the

organization, it has reduced the period of time between when the tax is generated and the

moment it is paid. Technology in tax administration aims at enhancing efficiency in tax

collection and it has reduced the errors in procedures of gathering of data automatically as

well as reducing the overall cost of tax administration. Automating revenue collection has

helped taxpayers to have a better audit trail of their tax, and technology has brought about

a significant improvement in the revenue collection time for tax payers.

The study concludes that technology had distracted employees, especially social media

and entertainment sites, as well as leading to a decrease in creativity and innovation in the

workplace. However, it had also facilitated the streamlining of KRA’s administrative

process, as well as enabling the organization to reduce the need for middle managers, by

helping employees bypass traditional organizational hierarchy and menu-driven mail

repositories.

The study recommends the management of KRA at Sameer Business Park to encourage

its employees to make use of technology and become more creative and innovative in the

firm. The managers could encourage and task employees to come-up with better methods

of using technology to process and handle their tax administration which would improve

the firm’s overall tax administration performance.

vi

ACKNOWLEDGEMENT

I would like to thank my supervisor Prof. Zachary Mosoti for leading me through this

research project report journey and certifying that I have completed it in the desired

manner. Thank you for words of encouragement and support throughout my research

period for I would not have made it.

I would also wish to extend my thanks to my family and friends for their support and

encouragement throughout my study.

vii

DEDICATION

I dedicate this project to God Almighty my creator, my strong pillar, my source of

wisdom, knowledge and inspiration and understanding. He has been the source of my

strength throughout my pursuit for education and on His wings have I soared. I also

dedicate this work to my family who have encouraged me all the way and whose

encouragement has made sure that I give it all it takes to finish that which I have started.

To my child, Ryan who has been affected in every way possible by this quest. Thankyou.

My love for you all can never be quantified. God bless you.

viii

TABLE OF CONTENTS

STUDENT’S DECLARATION ........................................................................................ ii

COPYRIGHT ....................................................................................................................iii

ABSTRACT ....................................................................................................................... iv

ACKNOWLEDGEMENT ................................................................................................ vi

DEDICATION.................................................................................................................. vii

TABLE OF CONTENTS ...............................................................................................viii

LIST OF TABLES ............................................................................................................. x

LIST OF FIGURES .......................................................................................................... xi

LIST OF ABBREVIATIONS AND ACRONYMS ....................................................... xii

CHAPTER ONE ................................................................................................................ 1

1.0 INTRODUCTION........................................................................................................ 1

1.1 Background of the Study ............................................................................................... 1

1.2 Statement of the Problem ............................................................................................... 5

1.3 General Objective .......................................................................................................... 6

1.4 Specific Objectives ........................................................................................................ 7

1.5 Significance of the Study ............................................................................................... 7

1.6 Scope of Study ............................................................................................................... 8

1.7 Definition of Terms........................................................................................................ 8

1.8 Chapter Summary .......................................................................................................... 8

CHAPTER TWO ............................................................................................................. 10

2.0 LITERATURE REVIEW ......................................................................................... 10

2.1 Introduction .................................................................................................................. 10

2.2 Employees’ Information and Technology Knowledge and Tax Administration ......... 10

2.3 Business Process Technology and Tax Administration ............................................... 14

2.4 Taxpayers’ Information and Technology Knowledge and Tax Administration .......... 19

2.5 Chapter Summary ........................................................................................................ 24

CHAPTER THREE ......................................................................................................... 25

3.0 RESEARCH METHODOLOGY ............................................................................. 25

3.1 Introduction .................................................................................................................. 25

3.2 Research Design........................................................................................................... 25

ix

3.3 Population and Sampling Design ................................................................................. 25

3.4 Data Collection Methods ............................................................................................. 27

3.5 Research Procedures .................................................................................................... 28

3.6 Data Analysis Methods ................................................................................................ 29

3.7 Chapter Summary ........................................................................................................ 29

CHAPTER FOUR ............................................................................................................ 30

4.0 RESULTS AND FINDINGS ..................................................................................... 30

4.1 Introduction .................................................................................................................. 30

4.2 Demographic Information ............................................................................................ 30

4.3 Employees’ Information and Technology Knowledge and Tax Administration ......... 33

4.4 Business Process Technology and Tax Administration ............................................... 37

4.5 Taxpayers’ Information and Technology Knowledge and Tax Administration .......... 41

4.6 Chapter Summary ........................................................................................................ 46

CHAPTER FIVE ............................................................................................................. 47

5.0 DISCUSSIONS, CONCLUSIONS AND RECOMMENDATIONS ...................... 47

5.1 Introduction .................................................................................................................. 47

5.2 Summary of Findings ................................................................................................... 47

5.3 Discussions .................................................................................................................. 48

5.4 Conclusions .................................................................................................................. 55

5.5 Recommendations ........................................................................................................ 56

REFERENCES ................................................................................................................. 58

APPENDICES .................................................................................................................. 63

APPENDIX I: RESEARCH PARTICIPATION LETTER ............................................... 63

APPENDIX II: QUESTIONNAIRE .................................................................................. 64

APPENDIX III: NACOSTI PERMIT ………………………………………………...…68

x

LIST OF TABLES

Table 3.1: Population Distribution .................................................................................... 26

Table 3.2: Sample Size Distribution ................................................................................. 27

Table 4.1: Reliability Test ................................................................................................. 30

Table 4.2: Assessment of Employees’ IT Knowledge and Tax Administration ............... 34

Table 4.3: Correlations for Employees’ IT Knowledge and Tax Administration ............ 35

Table 4.4: Employees’ IT Knowledge and Tax Administration Model Summary ........... 36

Table 4.5: Employees’ IT Knowledge and Tax Administration Coefficients .................. 36

Table 4.6: Assessment of Business Process Technology and Tax Administration .......... 38

Table 4.7: Correlations for Business Process Technology and Tax Administration ........ 39

Table 4.8: Business Process Technology and Tax Administration Model Summary ....... 40

Table 4.9: Business Process Technology and Tax Administration Coefficients .............. 40

Table 4.10: Assessment of Taxpayers’ IT Knowledge and Tax Administration .............. 42

Table 4.11: Correlations for Taxpayers’ IT Knowledge and Tax Administration............ 43

Table 4.12: Taxpayers’ IT Knowledge and Tax Administration Model Summary .......... 43

Table 4.13: Taxpayers’ IT Knowledge and Tax Administration Coefficients ................. 44

Table 4.14: Correlations for Information Technology Items and Tax Administration ..... 44

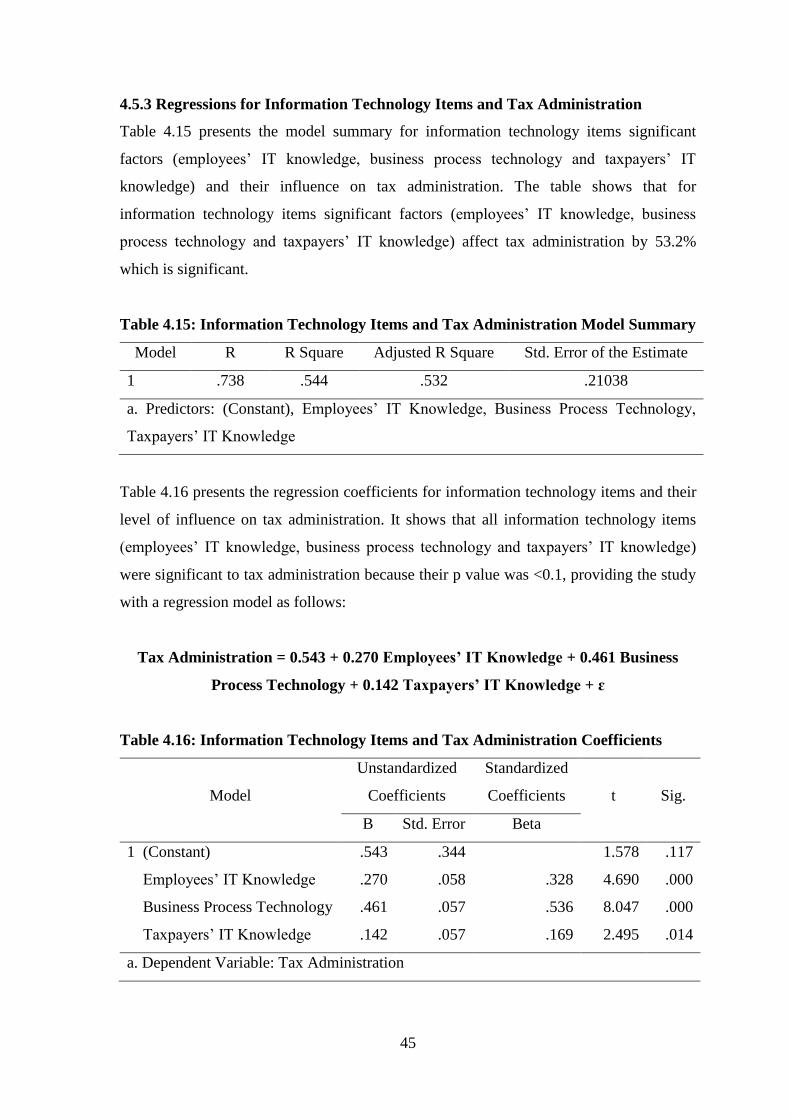

Table 4.15: Information Technology Items and Tax Administration Model Summary ... 45

Table 4.16: Information Technology Items and Tax Administration Coefficients ........... 45

xi

LIST OF FIGURES

Figure 4.1: Response Rate ................................................................................................ 30

Figure 4.2: Gender ............................................................................................................ 31

Figure 4.3: Age Bracket .................................................................................................... 31

Figure 4.4: Education Level.............................................................................................. 32

Figure 4.5: Years with KRA ............................................................................................. 32

Figure 4.6: Designation..................................................................................................... 32

xii

LIST OF ABBREVIATIONS AND ACRONYMS

CBK:

DSS:

EGMS:

EIS:

FY:

G2B:

G2C:

G2E:

G2G:

GDP:

ICT:

IRS:

IS:

IT:

KRA:

MIS:

OSBP:

PAYE:

RECTS:

SA:

TPS:

UK:

USA:

VAT:

Central Bank of Kenya

Decision Support Systems

Excisable Goods Management System

Executive Information Systems

Financial Year

Government-to-Businesses

Government-to-Citizens

Government-to-Employees

Government-to-Government

Gross Domestic Product

Information Communication and Technology

Internal Revenue Services

Information Systems

Information Technology

Kenya Revenue Authority

Management Information Systems

One Stop Border Post

Pay as You Earn

Regional Electronic Cargo Tracking System

South Africa

Transactional Processing Systems

United Kingdom

United States of America

Value-Added Tax

1

CHAPTER ONE

1.0 INTRODUCTION

1.1 Background of the Study

Over the last decade, public administration around the world has been following the goal

of increasing its efficiency and flexibility by using information technology (IT). This has

been inspired by the success of IT in other environments, especially in the private sector.

Various authors have demonstrated that IT enables improved quality and performance of

services (easier, faster, better) (Gupta, 2008), improved quality and increased operational

efficiency, reduced costs, and increased productivity (Gil-García & Pardo, 2015). Wang

and Liao (2016) stress that throughout the various efforts of understanding the use of IT

in business; the focus must be multidimensional and interdependent.

While the term “information technology in government” goes back at least to the 1970s,

the term e-government emerged in the late 1990s with the internet boom (Grönlund &

Horan, 2014). It does not rely only on the internet, but also includes other technologies

and aspects. Throughout the e-government domain a classification of areas of interactions

with citizens through government-to-citizens (G2C), government-to-businesses (G2B),

internal employee’s government-to-employees (G2E), and other institutional government

organizations government-to-government (G2G) emerged and remain (Wang & Liao,

2016). In the case of G2C, integrated information systems are needed in order to gather,

transfer, process, and store internal data, which is the foundation for the further

elaboration of electronic government services offered to external users, namely citizens,

the private sector, and other governmental organizations (Baležentis & Paražinskaitė,

2012).

According to Au and Cheng (2012), ensuring that end users are able and willing to use

advanced information systems (IS) is critical for the organization to gain operational

efficiency and user satisfaction. Many researchers have recognized user satisfaction as a

critical determinant of the success of IS. In their work DeLone and McLean (2013)

proposed that higher levels of individual satisfaction with IS usage leads to higher levels

of intention to use, which subsequently affects the use of the system. Hsieh et al. (2012)

proved that employees’ overall user satisfaction with their mandated use of IS has a

positive impact on employee service quality. Thus, IS performance, the organizational

2

environment, and the people who use the IS are crucial. Iivari (2015) also showed that IS

performance has a positive relationship with the satisfaction of the IS user.

Today, taxation-related services are among the most developed e-government services all

over the world. At the same time, e-taxation services are among those most used by

clients in many countries, sometimes even because clients are forced to use them. For

instance, the e-Europe measurement reports indicate that year after year the services

included in the income-generating cluster (income and corporate tax, social contributions

for employees, value-added tax (VAT), customs declarations) were and remain the most

developed (Baležentis & Paražinskaitė, 2012). When one explains e-taxation, they usually

refer to on-line filing and assessment of tax returns, enabling electronic payment of taxes,

sharing information on tax assessment between different government departments, and

web-based portals for educating taxpayers on taxation issues (Wang & Liao, 2016). Use

of e-taxation systems by the tax administration according to Jiménez, Sionnaigh and

Kamenov (2013) has been shown to have several advantages such as: provision of

support, automation, workflow management, and authorization management to tax

administration functions; it provides information, education, and support to taxpayers and

facilitates compliance and administration; a compliance performance system deploys risk-

based procedures to detect and deter noncompliance; and a management information

system facilitates the collection and dissemination of performance information to staff

and management.

The electronic and automated tax filing and administration were fast used in the United

States of America (USA), where her Internal Revenue Services (IRS) started offering tax

return e-filing for only tax refunds. This has seen tremendous growth to the level that

almost all the taxpayers are required to file and pay their taxes electronically. This has

been enabled by the various features and enhancements being added to the system over

the years (Muita, 2011). The electronic filing today has been adopted by many other

developed countries such as Canada, France, Germany, United Kingdom (UK), Australia,

Italy, Finland, Netherlands, Turkey, Singapore, Norway, India, China, Turkey, Malaysia

(Ramayah, Ramoo & Amlus, 2012).

3

In Slovenia, the Slovenian government introduced a special e-taxation portal soon after

the introduction of the main e-government portal. Slovenia’s e-taxation portal was

established at the end of 2003. Initially, taxpayers could find and print tax forms from the

e-taxation portal. Subsequently, form completion was possible, such that taxpayers could

complete forms and submit them to the tax administration (Iivari, 2015). As of 2015, all

communication with business taxpayers is carried out through the e-taxation system.

Several small surveys among tax administrators were carried out in Slovenia before its

establishment and they concluded from all of them that civil servants find e-taxation to

entail an improvement in their working conditions, since information is available more

quickly, less importing of different data is necessary, a finding of logical incorrectness is

available promptly, archiving documents is easier and requires less space, processing of

the calculation of tax obligations is much shorter (Muita, 2011).

Currently, the world has become a global village and the interconnection between Africa

and the rest of the world is the use of IT in, almost, every sector of its economy. For

instance, a country like Malaysia implemented the new tax system in 2005. Through the

internet, a multi-stage tax is imposed on goods and services at every delivery point to the

end customer (Booth, 2012). The objective of tax autonomy in South Africa (SA) was

mainly to increase effectiveness and efficiency and tax equality in the country (Muita,

2011). Other developing countries like Nigeria, Rwanda, Tanzania, and Uganda have also

embraced the automated electronic filing of tax documents and tax returns (Muita, 2011).

In Nigeria, Oseni (2015) deduced that tax evaders will no longer have loopholes to hide

with the usage of the modern automated tax technology and systems because all the

taxpayers have to make use of the tax system to declare all their transactions. The

objective of tax autonomy in Uganda, Zambia, Ghana, and Tanzania was to increase tax

collection. Research by Chatama (2013), Tanzania adopted technology in tax

administration in 2001. The technological tax systems adopted by Tanzania minimized

delays in filing of tax returns and reduced operational costs.

Policies on tax administration play a vital role in resulting in high tax compliance by

taxpayers. Good policies ensure good governance. High tax collections are attributed to

better technology advances and proper policies (Wang & Liao, 2016). A research by

Kiema (2017), concluded that high tax collections are evident in countries practicing

4

appropriate tax policies. Ejiaku (2014) suggested that government policies affect tax

administration, more so in developing countries.

In Kenya, taxation has been the single largest contributor to government budgetary

resources. Between 2006 and 2017, the tax revenue instituted 93% of total government

revenue. Given its major role in the government, taxation has been used to attain to meet

several objectives (KRA, 2015). First, taxation is used to raise adequate revenue to fund

the governments’ public spending without recourse to excessive borrowing. Secondly, it

has been used to collect revenue using methods that are equitable which reduce its

disincentive impacts on economic activities (Broadway, 2012). The organization in

charge with tax collection in Kenya is the Kenya Revenue Authority (KRA).

KRA was established by an Act of Parliament Cap.469 in 1995 as an Independent

organization for tax administration and autonomous from the Ministry of Finance and

Treasury. It was mandated to collect revenue on behalf of the government of Kenya to

finance service delivery to the Kenyan population of over 45million, which is estimated

to increase by one million per year (Macharia, 2016). The Ministry of Finance and

Treasury is responsible for setting tax policies and tax reforms while on the other hand

KRA is mandated to ensure that these policies relating to revenue mobilization are

undertaken. The Authority is mandated to collect these types of taxes: VAT, Pay as You

Earn (PAYE), Excise duty tax, Income Tax Corporation Taxes, Customs Duty, Import

Duty, Income Tax Individual Business Taxes among others (KRA, 2012).

The specific functions of KRA are: to govern and enforce written laws or specified

provisions of written laws which pertain to collection, assessment and accounting for

whole revenue in accordance with these laws, enhance the effectiveness and efficiency of

administration of tax, eliminate tax evasion by streamlining and simplifying procedures to

improve the compliance rates through improving taxpayer education and service delivery,

promote professionalism and ensure protection of the local industries and enable

economic growth of the country through the administration of the various tax laws

relating to trade (KRA, 2012).

5

The key mandate of KRA is revenue collection, and of the key performance indicators is

the Gross Domestic Product (GDP) ratio. In financial year (FY) 2016/2017 the tax

authority managed to collect sh. 1.365 Trillion, whereas in the FY 2015/2016 KRA had

collected sh. 1.210 trillion. This shows a growth of 13.8%. The current Tax-to-GDP ratio

is at 19.3% marking the 2nd highest in non-oil economies in Africa. This achievement is

attributed to the technological reforms that KRA has embarked on in the recent past.

These include iTax, icms, Cargo Scanner Management Solution, Regional Electronic

Cargo Tracking System (RECTS), Excisable Goods Management System (EGMS), i-

support, i-care, One Stop Border Post (OSBP), among others (KRA, 2015). These

reforms have enhanced revenue collection through reduced compliance costs, increased

tax base and efficient revenue administration. This is by providing an online platform for

the customers to account and pay their taxes. These reviews are done under the arm of

information communication and technology (ICT) which oversees the process and their

objective is to offer integrated self-service and online services to customers in an

effective and efficient way (KRA, 2015).

1.2 Statement of the Problem

Information technology forms part of individuals’ lives in the modern world. Dependency

on technology by people is increasing on a daily basis. The reason is that new innovations

in technological devices and applications are encouraged all over the world. Countries

around the world have adopted technology in matters tax (Masese, 2011). Technology

contributes to easier, faster, and more accurate tax system. Tax administration has

improved in efficiency and effectiveness as a result of information technology. Many

countries are investing heavily in the tax administration systems. Governments depend on

tax revenues to develop a country, hence the demand to improve tax administration

systems (Wang & Liao, 2016).

Research by Muita (2011) found that the electronic and automated tax filing and

administration were fast used in the USA, where her IRS started offering tax return e-

filing for only tax refunds. This has seen tremendous growth to the level that almost all

the taxpayers are required to file and pay their taxes electronically. This has been enabled

by the various features and enhancements being added to the system over the years. The

electronic filing today has been adopted by many other developed countries such as

6

Canada, France, Germany, UK, Australia, Italy, Finland, Netherlands, Turkey, Singapore,

Norway, India, China, Turkey, Malaysia (Ramayah, Ramoo & Amlus, 2012).

In Nigeria, Oseni (2015) deduced that tax evaders will no longer have loopholes to hide

with the usage of the modern automated tax technology and systems because all the

taxpayers have to make use of the tax system to declare all their transactions. Hadler

(2000) observed the objectives for tax autonomy vary between governments. The

objective of tax autonomy in SA was mainly to increase effectiveness and efficiency and

tax equality in the country. The objective of tax autonomy in Uganda, Zambia, Ghana,

and Tanzania was to increase tax collection, and the research by Chatama (2013) in

Tanzania showed that the country adopted technology in tax administration in 2001. The

technological tax systems adopted by Tanzania minimized delays in filing of tax returns

and reduced operational costs.

KRA has invested heavily in technology improvements and innovations as a strategic tool

to ensure tax compliance since 2003 (KRA, 2015). Technological automation of revenue

collection has further added a fresh touch to the once choking KRA, with tax evasion

minimized and improved business efficiency recorded. Automation has reduced the cost

of revenue collection and interaction between the taxpayer and staff, a fertile area for

corruption (Masese, 2011). The system has enhanced a seamless flow of information

between KRA, Central Bank of Kenya (CBK) and other government departments in the

areas of taxpayer registration, customer service, cargo clearance, both on air and sea,

returns processing, payments on specific tax heads and tax clearance certificates and a

copy of records. With this emergence of technology, the length of time used in filing tax

returns has condensed from 2 weeks to 30 minutes, while that of clearing cargo reduced

from between 6 to 15 days to between 2 and 6 days (Masese, 2011). However, with all

these improvements, one still finds that the voluntary compliance levels have not

increased as previously anticipated. This, therefore, calls for the question whether

technology has been efficient in enhancing tax compliance in Kenya. It is because of the

above concern that this study was therefore necessary.

1.3 General Objective

The objective of this study was to investigate the effect of information technology on the

performance of Kenya Revenue Authority’s tax administration.

7

1.4 Specific Objectives

The study was guided by the following specific objectives:

1.4.1 To identify the effect of employees’ IT knowledge on tax administration

performance.

1.4.2 To identify the effect of business process technology on tax administration

performance.

1.4.3 To identify the effect of taxpayers’ IT knowledge on tax administration

performance.

1.5 Significance of the Study

1.5.1 KRA Management and Board

The findings of the study avails recommendations to the KRA Board on the options for

improvement of its technological improvements and innovations in future so as to ensure

that the Authority is able to achieve its set revenue collection targets over the respective

financial years.

1.5.2 Taxpayers/ Customers

The findings of this study offer in details the effect of technological improvements and

automation on the performance of Kenya Revenue Authority to the taxpayers and also a

breakdown of the tax reforms already undertaken for both educational purposes and

improving awareness and service delivery to the customers.

1.5.3 Policy Makers

The findings of the study provide recommendations to the policymakers and the Treasury

on the options for improvement of its technological improvements and innovations in

future so as to ensure that the Authority is able to achieve its set revenue collection targets

over the respective financial years.

1.5.4 Future Researchers

This study forms a basis for further research in the areas of leveraging technology to

enhance increased performance by Kenya Revenue Authority. Research could be carried

out on the effects of increased automation and innovation by Kenya Revenue Authority

on product awareness.

8

1.6 Scope of Study

The study focused on KRA, in particular, the Small Taxpayers Office based in Sameer

Park Branch Mombasa road. The explanatory research design was adopted with a focus

on quantitative characteristics and status of revenue collection strategies at KRA with

regard to enhancements of revenue collection. The target population in this category was

about 300 members of staff. The data was collected between January and April 2019. In

this study, data was collected using a questionnaire which was administered through drop

and pick format.

1.7 Definition of Terms

1.7.1 Small Taxpayers

These are the taxpayers whose annual turnover ranges from one Kenyan shilling to 200

million Kenya shillings. Most of these operate under the informal sector (KRA, 2012).

1.7.2 Technological Change

This is defined as an increase in the efficiency of a process or product that results in

output growth with the input remaining constant, through three main ways which include

invention, innovation and diffusion (Crabtree, 2012).

1.7.3 Automation

This refers to the use of technological devices, programs, applications, and systems that

render human labor obsolete (Ng’ang’a, 2013).

1.7.4 E-Filing

Electronic filing/ e-filing refers to the transmission of tax data directly to the tax

administration system using technology and internet. This may be done in the comfort of

every taxpayer in their homes, offices, and malls or done by a tax agent or auditor

provided there is internet connectivity (Allink & Kommer, 2010).

1.8 Chapter Summary

Chapter one covers the introduction and background information on the research topic. It

provides information on the statement of the problem and the general objective of the

study as well as the specific objectives that guided the study. The chapter provides the

significance and scope of the study as well as the definition of key terms used in the

9

study. The second chapter provides the study’s literature review by exploring deeper into

the study research topic, while chapter three provides literature on the particular research

methodologies that were adopted in the study. Chapter four presents the study’s results

and findings and chapter five provides the study’s discussions, conclusions and

recommendations.

10

CHAPTER TWO

2.0 LITERATURE REVIEW

2.1 Introduction

This section focuses on the literature about the effect of information technology on tax

administration. This study aims at addressing three research objectives: identifying the

effect of employees’ IT knowledge on tax administration performance, the effect of

business processes technology on tax administration performance, and effect of

taxpayers’ IT knowledge on tax administration performance.

2.2 Employees’ Information and Technology Knowledge and Tax Administration

Information technology has taken over the world of business. Many institutions and

organizations have adapted to the new era of IT which involves the transmission and

storage of information in electronic formats (Rezaei et al., 2014). Businesses,

organizations, and institutions have adopted information technology. Thus, employees are

the first to be affected by the introduction of information technology. The reason is that

the employees are responsible for operating the technological systems (Berisha-Shaqiri,

2015). Information technology affects employees in both negative and positive ways.

Some employees appreciate the introduction of technology in the workplace while others

are rigid to the change (Cyr, Gehling & Gibson, 2014).

2.2.1 Increased Productivity

One of the impacts of information technology on the authority is increased productivity.

The employees use technological devices and systems in carrying out daily operations

which have led to high levels of productivity (Rezaei et al., 2014). Increased productivity

by staff is as a result of less time used in operations and accessibility to information. By a

touch of a button information, reports, and records are available with the help of

technology (Grönlund & Horan, 2014). Currently, most employees rely more on

information from the internet as compared to print media. Information is power, thus,

organizations practice storing information in servers and websites. Information

technology saves time since all information required is easily accessible and

communication is also made easier (Kaino, 2008). Staff from different departments in an

organization can communicate without necessarily having to meet in the same room.

Communication is possible between staff members in different department, regions, and

even countries via telephone, teleconferencing, email, fax, and social media. The

11

increased productivity results in high performance by the employees and in turn the

organization (Grönlund & Horan, 2014).

The manufacturing process is made faster by the use of technology. The automated

machines used to manufacture products work at an increasingly high speed without

stopping, thus, increasing the productivity in an organization that has adopted information

technology (Kaino, 2008). Information technology has increased the levels of creativity

by many employees. Through research, employees learn new ways of operations and

saving time. Multi-tasking is possible as a result of information technology. By using

simple applications such as Skype an employee can teleconference with another

employee while simultaneously sending emails, and memos to other staff members.

Increased productivity is evident from all the marketing and advertising on electronic

media (Jiménez, Sionnaigh & Kamenov, 2013). Most organizations market their products

and services via social media and electronic media. Creativity from employees uploading

marketing items is attributed to extensive research on the internet and use of various

applications such as Photoshop. Rezaei et al. (2014) states that employee’s productivity

increases with the extensive use of information technology thus improving the

performance of an organization.

2.2.2 Work Efficiency

Information technology has a vital role in work efficiency (Hadler, 2014). It is via

information technology that employees are able to meet deadlines for daily operations.

Work is done faster due to less paperwork and the accessibility of information. Due to

automated systems, most of the work that would have consumed a lot of time and

procedures can be done in seconds (Masese, 2011). Staff members are able to prioritize

work in terms of need, which ensures all operations are carried out within the required

deadlines. Information technology provides adequate information via the internet

(Peansupap & Walker, 2015). Through websites and social platforms, employees are able

to obtain information required for daily operations. Research is made easier for

employees via information technology (Hadler, 2014).

12

Work efficiency is attained as a result of fast communication processes (Mutuku &

Nyaribo, 2015). Information technology has made communication easy and cheap. By

having internet an individual is able to communicate with other people from different

countries and even continents. Communication via phone calls, emails, memos, fax, video

conferencing, text, and social media is practiced in most organizations. Good

communication between employees and departments has improves the work efficiency in

organizations (Otaghsara & Mohseni, 2012). Employees work performance has improved

also as a result of continued use of information technology to obtain information and in

communication. Communication is important in ensuring the success or failure of any

organization. According to Mutuku and Nyaribo (2015), great internal and external

communications an institution stands to make profits and grow into a big corporation.

2.2.3 Reduced Workload

Previously, information was obtained and stored in print media. Print media meant a lot

of paperwork which had to be stored for future reference. However, the new era of

information technology focusses for less paperwork, since all information is saved on

servers. Information technology allows for access to information via a touch of a button

(Rezaei et al., 2014). The reduced workload of staff is convenient, thus saving time in the

organization. Information is easily accessed, stored and retrieved by employees who use

information technology. The automated systems have reduced the work of printing

personal and business information, which is later stored in paper form. Currently, only the

required and relevant information is stored in print media. In case of any additional

information, the servers are simply updated from the office (Hsieh et al., 2012).

Information technology has simplified all the work carried out by most employees in an

organization. From communication to the actual performance of an activity, automation

has made working easier. Research is obtained straight from the internet. As Haddud,

Dugger and Gill (2016) concluded, most employees rely on the internet for information

and research. Better performance by employees is experienced as a result of the reduced

workload. The reason is that the employees are not overworked, hence able to undertake

all daily operations in due time (Hsieh et al., 2012).

13

2.2.4 Employee Education and Training

Technological devices demand skilled labor. Thus, organizations using information

technology are keen on ensuring all staff members are educated and trained appropriately.

Through education and training, employees are able to earn skills that help with daily

operations and projects (Otaghsara & Mohseni, 2012). The training equips the staff

members with the relevant knowledge and skills in operating the automated systems

efficiently. Education and training are relevant to each institution, especially when

introducing new systems. The reason is that trained staff members are able to operate

effectively and meet all deadlines (Gil-García & Pardo, 2015). Performance of employees

and organizations improve with continued emphasis on training and education. The

improving performance of organizations using information technology is partly attributed

to the education and training offered to employees (Hsieh et al., 2012).

Through training and education, employees are able to offer better and improved services

to all customers (Otaghsara & Mohseni, 2012). The knowledge on how to operate

technological applications and devices, staff members are able to concentrate in catering

to customer’s needs rather than worrying about how a system is operated. The training

offered also involves some knowledge on how to handle customers via phone and

computer. Eloquence, etiquette, and result oriented skills are equipped to all employees

throughout the training process (Gil-García & Pardo, 2015). Eloquence is of importance

since with the adoption of information technology most queries are addressed via phone

calls and emails. The training offered ensures that all staff members are in a position to

handle all customers thus providing better services at all times (Kimani, 2015). Reduced

cases of customer complaints are evidence of improved services offered by employees.

Training and education of staff members improve the performance of employees resulting

in high performance by an organization (Iivari, 2015).

2.2.5 Concentration and Innovation Levels

Information technology contributes greatly to the success of any organization. However,

information technology also destructs most employees. Information technology includes

social media and entertainment sites. Employees love to relate to other people more so via

the internet. As such, some employees easily lose concentration from work and start

chatting in the office via social media platforms (Turban, Bolloju & Liang, 2011). Some

of the social media platforms frequented by employees include Facebook, WhatsApp,

14

Twitter, and Instagram. Research shows that 77% of employees with Facebook accounts

spend one-hour daily chatting while at work (Haddud, Dugger & Gill, 2016). The easy

accessibility of such social media platforms in the workplace results in low productivity

by employees. The low productivity then results in low performance by organizations

(Hsieh et al., 2012).

Creativity and innovation form the backbone of some organizations. However, the level

of innovation of employees in the workplace is reducing with the increased use of

technology (Rubin, 2012). Since almost every innovation in available online, most

employees lack the drive to work in creating anything originals. The rate of counterfeit

product and services is increasing in Kenya with every passing day. Young people in the

workforce are highly dependent on internet searches for solutions that creativity has

become a thing of the past (Kiema, 2017). Prior to technology, the rate of creativity by

young people was high. With the accessibility of information, research, and reports

people have become reluctant to be creative (Rubin, 2012). Creativity in the past was

practiced through reading. In the 21st century reading of printed books is a rare

phenomenon. Most young people prefer playing video games, watching, and listening to

music. Some writers like Abelson et al. (2015), have warned against such activities since

they inhibit innovation (Rubin, 2012). However other writers have reported that surgeons

who play video games make less surgical errors in comparison to those who do not play

video games.

2.3 Business Process Technology and Tax Administration

Business processes and procedures have changed as a result of information technology

adoption. Organizations and institutions are using technology in daily operations and as

motivators for employees especially the millennial staff (Peansupap & Walker, 2015).

The businesses procedures that were used in the past are almost obsolete due to the

increased use of technology. The procedures are now easy to practice, save time and

money, and are not barred by geographical area. The effects of information technology on

business processes include saving time and reduced costs of production (Webley, 2014).

IT, in its nascent business world form, was generally considered a support tool. But as

time passed and technological sophistication grew, IT’s usage and impact increased

dramatically (Gupta, 2008). This pattern of progress may be due to advancement of

15

technology. But a technological diffusion or infusion may be attributable to the fact that

IT's introduction into an organization creates further technological needs and encourages

product and policy innovation to meet such needs (Peansupap & Walker, 2015).

2.3.1 Automation

Automation is the use of control processes and systems that render human labor obsolete

(Ng’ang’a, 2013). Automated systems require less if any human labor. Organizations all

over the world are turning to automated systems in place of human labor. Automated

systems include all machines that simplify work and requires little labor such as

lawnmowers, manufacturing machines, and smart cars (Kimani, 2015). Most large

corporations have adopted the use of automated systems including Coca-Cola, Apple,

Google, and Microsoft (Ng’ang’a, 2013). Automated systems are computerized and are in

electric form. Automated systems are cheap as compared to human labor thus favored by

many organizations. The initial purchase of the automated systems is expensive, however

afterward the machine works with little maintenance costs. Automated systems are also

fast in comparison to human labor, thus saving time (Kimani, 2015).

Automated machines work at a faster rate in comparison to human labor (Ng’ang’a,

2013). Humans are prone to get tired, but an automated machine does not tire thus can

work more hours. With more hours and high speed of work, automated systems increase

productivity. Organizations that use automation make large profits as a result of the

continuous productivity (Kimani, 2015). However, for an automated system to be

successful, an organization must select the best suitable automated system. An

organization stands to lose if it selects an automated system that is not compatible with

the production of products and services (Ng’ang’a, 2013).

The automated systems are different from year’s prior technology. Before technology was

invented and adopted by organizations and companies, human labor was valued by

managers (Nübler, 2016). Information technology has changed organizations from

accessing human labor to favoring machines and computers. Automation has led to the

loss of jobs, hence the increasing rates of unemployment (Jenkins, 2014). The machineis

invented daily and different codes discover, thus reducing the opportunities for human

labor. Research by Ng’ang’a (2013) when Coca-Cola was shifting to automated systems

100,000 employees lost their jobs. Kenya, however, has been slow in adopting

16

automation systems. This is despite the many advantages of automated systems. By 2002

only 33% of the textile industry had adopted automation (Ng’ang’a, 2013). However,

organizations that turned to automated systems have lowered labor costs and expenditure.

2.3.2 Social Media Use

Social media is part of information technology. Social media involves turning

communication into interactions through various platforms. Social media platforms

include; Facebook, WhatsApp, Twitter, Instagram, and LinkedIn. Social media has

invaded the workplace thus the business process practiced. The research concluded that

each of the fortune 500 companies had at least one social media platform in 2010

(Haddud, Dugger & Gill, 2016). The rise of social media use in the workplace is growing

rapidly more so with the millennials occupying the workplace. Some organizations value

the integration of social media into the business while some are rigid to the changing

times (Berisha-Shaqiri, 2015). Research by Kane et al. (2014), showed that 18% of

managers acknowledged the importance of social media in business while 63% predicted

the importance of social media in the future. With the increasing rise of information

technology, many organizations are acknowledging the use and importance of social

media.

Different research argues the correlation between social media use and work. Research by

Haddud, Dugger and Gill (2016), states that, 28% of employees spend their time

responding to emails while 20% spend time surfing the net for appropriate labor. Hence

social media plays a vital role in work especially due to the embrace of information

technology. Social media is reported to increase employees’ productivity. Most marketing

and advertising are carried out via social media platforms. However, some researches like

Turban, Bolloju and Liang (2011), argue that social media in the workplace lowers

productivity. Employees spend most of the time chatting rather than working thus

lowering organizations productivity.

2.3.3 Work Behavior Change

The work behaviors have changed with the increased use of technology. Many employees

prefer making their own time to work. Prior to technology the working hours were

stipulated and had to be followed to the letter (Haddud, Dugger & Gill, 2016). However,

with the changing times, most employees favor jobs that allow them to set their own time.

17

According to Berisha-Shaqiri (2015), working hours and places of working have changed

as a result of information technology. Most people are able to work from home and others

while on the move. Millennials prefer working from home rather than in an office. The

growth of information technology is evident more so in the United States of America,

where a quarter of the working population works from home while the other quarter is

mobile working from anywhere in the country (Berisha-Shaqiri, 2015). Working from

home or during the late hours at night is possible as a result of internet availability that

allows for communication and research. The changing working behavior is effective since

employees work with passion resulting in increased productivity.

The working behavior of employee and employers is changing with increasing use of

information technology. Due to the high rates of automation, many employees are losing

their jobs since they are being replaced by the machines (Ng’ang’a, 2013). The

fragmentation in the workplace is changing thus demanding new jobs. Some researchers

argue that with the continued innovation of technological devices more jobs will be

created while others argue that more jobs are lost (Nubler, 2016). As technology takes

charge of all aspects of life in the modern world, many employees are losing jobs on a

daily basis, reducing the income earned by a country through PAYE taxation. However,

with the new wave of innovation and creativity on matters technology, new startups are

developing, thus creating better jobs (Turban, Bolloju & Liang, 2011). The work

environment is no longer static as a result of changes in services and products offered

through information technology.

With every new innovation and invention, new jobs are created. Such is the hope of some

researchers that history will repeat itself (Nubler, 2016). Research shows that throughout

history, new inventions resulted in loss and creation of jobs. Many employees are holding

on to such optimism, that information technology will not mean the end of jobs and

sources of incomes for most people. However, some pessimistic researchers warn that the

continuing high rise of technology will mean the doom of life. Researches argue that

technology is moving at a fast rate that the human brain can comprehend (Rubin, 2012).

The technological advances are way beyond the imagination of humans.

18

2.3.4 Computer Adoption

The adoption of the computer in an organization not only enabled changes in the job

routine itself but may also lead to organization transformation. IT’s spread beyond

clerical support is characterized by IT applications such as Transactional Processing

Systems (TPS), Management Information Systems (MIS), Decision Support Systems

(DSS), and Executive Information Systems (EIS) (Ramayah, Ramoo & Amlus, 2012).

While the traditional TPS, MIS, and DSS are primarily enablers and facilitators of

business processes, they have evolved to providing organizational support that augments

basic office features such as word-processing programs with a diverse collection of

information communication systems (Evans, 2013). For example, these systems may

include e-mail, videotext, and some horizontal and vertical integration technologies. The

resulting system enables the circulation and dissemination of information to the

appropriate parties and facilitates the information flow to be at a rapid rate (Winter &

Taylor, 2015).

IT enables the bypassing of the traditional organizational hierarchy and menu-driven mail

repositories reduce information overload. Intelligence can now be included in information

systems such as data warehousing systems (Jenkins, 2014). Companies are thus

empowered to compete more efficiently and to respond internally to developments in the

external business environment more rapidly (Cyr et al., 2014). Furthermore, organizations

can apply EIS-related applications. Top executives are now enabled to make more

informed decisions, as information and knowledge are now available at a much faster

pace. On the other hand, this initiated a change in what top executives have to do and how

they do their job (Ramayah, Ramoo & Amlus, 2012). It becomes necessary to have EIS

applications developed to meet this need because, due to the availability of information,

any uninformed decision may put an organization into a competitive disadvantage or may

even be detrimental (Winter & Taylor, 2015). Furthermore, as a result, the way top

executives are making decisions is changed to require more information and analysis of

information (Cyr et al., 2014).

2.3.5 Streamlined Administrative Process

IT facilitates the streamlining of the administrative process and enables the

decentralization of the scope and scale of the business (Rubin, 2012). An unparalleled

method for processing, analyzing and communicating the information from both inside

19

and outside the organization enables the detection and understanding of the pattern and

pace of change. Furthermore, facilitation on the improvement of telecommunication has

enabled a reduction of the need for middle managers as conduits for information (Winter

& Taylor, 2015).

Organizations may become distributed as opposed to centralization. Furthermore, IT is

often recognized as a powerful agent for social and economic change. As the pace of

technological development quickens, human knowledge and understanding are likewise

exploding (Ramayah, Ramoo & Amlus, 2012). The dissemination of information and the

dissection of new discoveries take place in today's environment in a matter of seconds.

Just as IT has made communication a faster and more approachable process, it has

heightened our dependence on such forms of communication (Cyr et al., 2014).

Davenport and Short (1990) pointed out that there is a need to establish, in this context, a

more flexible, team-oriented, and communication-based working environment to take

advantage of the current climate and to maximize benefit to the whole organization.

Furthermore, organizations may become learning organizations.

2.4 Taxpayers’ Information and Technology Knowledge and Tax Administration

Technology needs to make it easier for taxpayers to comply with their tax obligations if it

increases the accessibility level as well as the amount of information available, widening

the range of payment modalities, reducing the need for taxpayers to visit the office and

shortening waiting times for those taxpayers who need help (Abelson et al., 2015).

Advanced internet options, payment via electronic banking services as well as virtual

telephone have been developed to achieve these aims. The tax administration agency

needs to see the taxpayer as a customer, not as someone who owes money to the

Administration (Holniker, 2015).

Finally it can be argued that the effective cost of tax administration, collection costs are

likely to be positively related to tax compliance. Such a relationship, however, depends

largely on the way compliance maximization is achieved (Wang & Liao, 2016). For

instance if the only target set for the tax authority is to maximize tax compliance, it will

go a long way in allocating its budget such that the last amount spent on enforcement

activities offers the same tax revenue as compared to the last amount spent on improving

taxpayer services (Abelson et al., 2015). Hence, it goes without saying that the

20

unconditional maximization of tax compliance is unlikely to reduce collection costs, as

well as the additional goal of minimizing compliance costs needs to be imposed explicitly

(Wang & Liao, 2016).

2.4.1 Tax Administration Activity

Technology is necessary for the tax administration activity as large sets of data needs to

be processed. However technology needs not be considered given that the objective, quite

the opposite needs to be regarded as a means to gain efficiency (Reinganum & Wilde,

2012). State-of-the-art technology though expensive to purchase and maintain in some

cases the results are not so brilliant from the economic point of view. In order to achieve

the excellence in the tax administration activity, organisations needs to focus on the

customer/taxpayer (Kane et al., 2014). As a consequence, the most essential concepts are

“reducing the period of time between when the tax is generated and the moment it is

paid”, “decreasing the number of the human errors by automating ordinary procedures”,

“therefore making possible to pay the tax any time and almost anywhere”, and “therefore

allowing any employee to help every customer at the office” (Reinganum and Wilde,

2012).

Bearing these objectives in mind, it is very easy to infer that indeed technology in tax

administration simply means integrated software with a one-stop-shop implementation;

comprehensive work flow systems in that every document or form is included in the

information system; easy-to-use internet websites that have online information and

payment options; customer service network which is connected by fast lines; mobility to

allow service in remote areas as well as real-time process monitoring (Andarias, 2012).

Most if not all revenue bodies have taken a unique approach to the selection, development

and deployment of information technology software applications to support the operation

and delivery of their business (Haddud, Dugger & Gill, 2016). Very little has yet been

done between revenue bodies - and between revenue bodies and the software industry - to

develop a shared and sharable model which revenue bodies and the software industry can

use to explore and develop best practice, and – most importantly – assets, providing

common solutions to common business needs (Andarias, 2012).

21

2.4.2 Technology Usage

Technology is an important tool if properly used; otherwise it can as well become a

problem that needs solving, rather than the solution. The technology used in tax

administration entails the use of computer, internet and software applications. Technology

is only regarded as efficient when handled by well-trained personnel and if embedded in

the workflow of the organization (Jiménez, Sionnaigh & Kamenov, 2013).

Good technology needs only to be applied in tax administration if it satisfies some basic

principles which also include; reducing life of tax, improving efficiency and reducing

errors in procedures, increasing multi-tasking levels of tax officers and facilitating

taxpayers in complying with tax regulations (Erard, 2012). In the reduction of the “life-

time of the tax”, proper technology needs to ensure that the time period between the date

a property or service become liable for tax and the payment of this tax or rate is reduced

to the minimum (Andarias, 2012). All technological advances in automation processing,

mass data processing and elimination of administrative challenges fall in this category

(Jiménez, Sionnaigh & Kamenov, 2013).

Technology in tax administration needs to also aim at enhanced efficiency and also the

reduction of errors in procedures, gathering of data automatically, as well as avoidance of

duplication, storage of images of documents, integration of aerial photography and digital

plans with identification data of property (Winter & Taylor, 2015). Additionally good

technology needs to increase the multitask-level of personnel, as well as the integration of

all procedures in a single information system and also the design of appropriate software

enables any employee to provide all service at a “single counter” (Gil-García & Pardo,

2015).

Technology needs to facilitate the task of taxpayers when complying with their tax

obligations, as it aids in increasing accessibility to information, widening range of means

of payment, reducing need for tax-payers to visit tax office, and by reduction in the time

taken by taxpayers waiting for assistance (Jiménez, Sionnaigh & Kamenov, 2013). All

these activities described are simply aimed at enhancing compliance.

22

2.4.3 Tax Costs

Technology use is key for the tax administration activity given that large set of data must

be processed. But the technology needs not be considered the objective, quite opposite it

needs to be regarded as a means to gain efficiency and also cost reduction in overall tax

administration (Evans, 2013). Effective tax administration is therefore desired by the tax

authority and the taxpayers. For the taxpayers, it comes with numerous advantages such

as less paperwork, rationalization as well as simplification of ancillary tax obligations,

elimination of tax audits on companies, expedition of procedures controlled by tax

administration and enhanced competitive edge with decrease in tax evasion (Winter &

Taylor, 2015).

Jenkins (2014) also emphasizes that indeed the tax system can never work better than its

tax administration, but even the best tax administration would certainly fail to turn a bad

tax system into a well-operating one. He also warns that the existence of many ambitious

tax reforms did not succeed because of the inefficient tax administration. In the absence

of permanent reorganization of the tax administration and almost daily improvements in

the methods of its management, it is not possible to expect that tax reforms will be

successfully realized (Quintana, 2016). This therefore means that tax reforms has a close

correlation between successful tax policy and efficient tax administration. In other words,

there is no good tax policy without efficient tax administration (Jenkins, 2014).

2.4.4 Tax Compliance

In terms of tax compliance, exercising this responsibility requires taxpayers to have a

systematic approach for managing tax compliance risks, aims to ensure that these risks

are properly identified, assessed, prioritised and also treated (Webley, 2014). One of the

ways through which to achieve cost effectiveness in tax administration is by use of

technology (Bird & Casangera, 2012). The use of technology not only in tax

administration but also in e-government as well as e-services already have a certain

amount of history, having developed from just simpler past levels to the more

sophisticated levels offered today (Webley, 2014).

According to Reinganum and Wilde (2012), improved technology in tax administration

alone is not entirely positive, however its benefits include features such as 24/7 access to

taxation services, services from the comfort of one’s home, lower services’ costs, reduced

23

burden on tax officers, as well as automated procedures. However, the most important

negatives include high costs, additional communication channels to be managed,

additional knowledge requirements, and the need for policies and plans (Jiménez,

Sionnaigh & Kamenov, 2013). According to Erard (2012) planning the anticipated costs

ine-tax administration, is often limited to the purchase costs for equipment, with many

parties neglecting to consider the costs of maintaining and upgrading IT, educational

costs for users both tax officers and taxpayers alike, and costs for additional human

resources, for management, and maintenance of IT (or outsourcing costs).

2.4.5 Tax Automation

Automation system helps to improve revenue collection. This is because they are based

on the electronic payment system via applications such as toll revenue collection,

automatic fare collection, bus revenue system and parking system (Gil-García & Pardo,

2015). Additionally by automating revenue collection, service providers are in better

audit trail since all transactions captured can be detailed by time, whom and where (Sani,

2016). This prevents revenue loss through abuses as all moves are recorded electronically.

Automation also provides huge transactions that need to be handled efficiently.

According to Sani (2016), automating revenue collection is key especially within the

revenue collection agencies, which therefore requires fast and efficient output, as there

will always be a trade-off between control and operational needs.

Holniker (2015) argues that the use of the system has brought about a significant

improvement in the revenue collection time for tax payers. Revenue mobilization is

considered as one of the key factors key for economic development of nations and links

into national agenda on social wellbeing, poverty reduction and economic development of

countries and their citizens. Revenue collection, according to Gil-García and Pardo

(2015) is considered as a mandatory element when it comes to the movement of goods

across borders and the procedures applied to these goods significantly influence the role

of national industry in international trade and their contribution to national economy.

The efficiency and effectiveness of revenue collection procedures has an important

influence on the economic competitiveness of nations and in the growth of international

trade and the development of the global marketplace (Holniker, 2015). As government

organizations that control revenue generation, are so much in a unique position to provide

24

increased security to the global supply chain and to contribute to socio-economic

development through revenue collection and trade facilitation (Erard, 2012).

2.5 Chapter Summary

The literature review chapter focused on identifying the effect of information technology

on employee’s performance, identifying the effect of employees’ IT knowledge on tax

administration performance, the effect of business processes technology on tax

administration performance, and effect of taxpayers’ IT knowledge on tax administration

performance in relation to the performance of KRA and its sustainability. This has been

achieved through focusing on other studies relevant to the effects of information

technology on employees, business processes, and taxpayers. The next chapter is research

methodology.

25

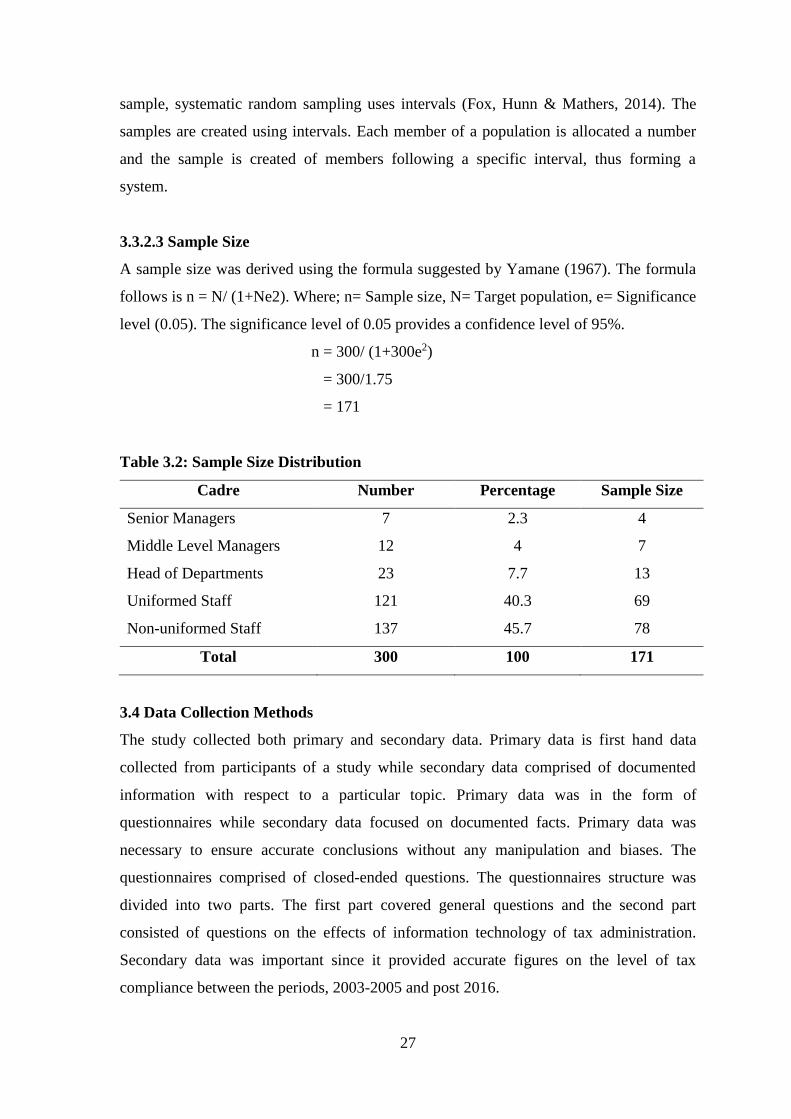

CHAPTER THREE

3.0 RESEARCH METHODOLOGY

3.1 Introduction

This chapter covers a comprehensive discussion on the research methodology that was

used to carry out the study. The research design, target population, and data collection

and analysis methods are discussed in the chapter.

3.2 Research Design

Research design refers to the direction taken in collecting information relevant to a

research study (Creswell & Clark, 2014). A research design focuses on answering the

research questions. It aims at directing the method of data collection and analysis to solve

the research problem. The study adopted an explanatory research design. An explanatory

research design has two phases in which the qualitative data explains the quantitative data

(West, 2012). Explanatory research design provides for a deeper understanding and

analysis of a particular topic. An explanatory research design is suitable for social studies

related topic.

The reason is that through explanatory design better explanations are provided for the

quantitative data available. Also, explanatory design works well with topics that have

been researched before to explain the findings of the research and identify the study gaps

available on the topic. This study required the explanation of previous quantitative data

collected on topics relevant to technology and tax administration by the Kenya Revenue

Authority, thus, an explanatory research design appropriate for the study.

3.3 Population and Sampling Design

3.3.1 Population

Sekaran and Bougie (2013) refers to the population as a group of things or people that a

researcher has interest and wants to investigate. The main aim of the population in a study

is to ensure correct conclusions are derived without biases. A study population mainly

comprise of the stakeholders to be affected by the research topic. The population of the

study targeted 300 members of staff working at the Sameer Park along Mombasa road.

The 300 employees included all the head of departments, uniformed and non-uniformed

staff at Sameer Park distributed as indicated in Table 3.1. The population of the study was

26

appropriate since all the 300 members of staff at Sameer Park had KRA pins, thus,

taxpayers and some work in the KRA small taxpayers’ officers.

Table 3.1: Population Distribution

Cadre Number Percentage

Senior Managers

Middle Level Managers

Head of Departments

Uniformed Staff

Non-uniformed Staff

7

12

23

121

137

2.3

4

7.7

40.3

45.7

Total 300 100

Population distribution 2018

3.3.2 Sampling Design

3.3.2.1 Sampling Frame

A sampling frame comprises of elements from which a sample is created and has to be

related to the population (Mukabi, 2014). A sampling frame forms the basis for sample

creation in probability sampling designs. A sampling frame is vital since it ensures only

the target population is covered by the study. Thus, the study was relevant and inclusive

of all target population. The list of the population was obtained from the staff members at

Sameer Park. The list was provided by the managers at Sameer Park.

3.3.2.2 Sampling Technique

A sample is a small number of people of things selected from a population under

investigation (Alvi, 2016). A good sample should represent the characteristics of the

larger population. Sampling, therefore describes the process in which a sample is

extracted. Sampling designs vary from probability to nonprobability sampling designs.