The Determinants of the Usage of Accounting Information ...

19

Citation: Thuan, Pham Quoc, Nguyen Vinh Khuong, Nguyen Duong Cam Anh, Nguyen Thi Xuan Hanh, Vo Huynh Anh Thi, Tieu Ngoc Bao Tram, and Chu Gia Han. 2022. The Determinants of the Usage of Accounting Information Systems toward Operational Efficiency in Industrial Revolution 4.0: Evidence from an Emerging Economy. Economies 10: 83. https://doi.org/ 10.3390/economies10040083 Academic Editor: Wadim Strielkowski Received: 27 January 2022 Accepted: 25 March 2022 Published: 1 April 2022 Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affil- iations. Copyright: © 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https:// creativecommons.org/licenses/by/ 4.0/). economies Article The Determinants of the Usage of Accounting Information Systems toward Operational Efficiency in Industrial Revolution 4.0: Evidence from an Emerging Economy Pham Quoc Thuan 1,2 , Nguyen Vinh Khuong 1,2, * , Nguyen Duong Cam Anh 1,2 , Nguyen Thi Xuan Hanh 1,2 , Vo Huynh Anh Thi 1,2 , Tieu Ngoc Bao Tram 1,2 and Chu Gia Han 1,2 1 Faculty of Accounting and Auditing, University of Economics and Law, Ho Chi Minh City 700000, Vietnam; [email protected] (P.Q.T.); [email protected] (N.D.C.A.); [email protected] (N.T.X.H.);[email protected] (V.H.A.T.); [email protected] (T.N.B.T.); [email protected] (C.G.H.) 2 Vietnam National University, Ho Chi Minh City 700000, Vietnam * Correspondence: [email protected] Abstract: The purpose of this study is to determine the factors affecting the application of accounting information systems (AIS) in small and medium enterprises (SMEs) in Vietnam. Drawing upon the Technology–Organization–Environment (TOE) theoretical framework, Diffusion of Innovations theory (DOI), and Resource-based theory (RBV), we proposed a research model to investigate the antecedents and influence of AIS usage in Vietnamese SMEs. This study used an online survey of individuals who work in Vietnamese SMEs for data collection. The result was assembled by applying the PLS-SEM model to test the proposed hypotheses based on 132 valid responses. First, the factors that have a significant impact on AIS usage are as follows: relative advantage; owner/manager commitment; and impact of COVID-19. Second, the research results also confirm that there is a positive relationship between AIS usage and AIS effectiveness; AIS performance has a positive impact on business performance. Research implications are to help business owners and leaders decide whether to use AIS to strengthen the company’s position and reduce the burden on departments, particularly the accounting department. Keywords: accounting information systems (AIS); AIS effectiveness; AIS usage; COVID-19 1. Introduction Accounting information is used by all commercial organizations, even nonprofits, to assist business stakeholders including management and outsiders such as investors, agencies, the government, and banks to attain certain objectives when making economic decisions (Hansen et al. 2007). Accurate accounting information is the foundation for assisting managers in making proper business decisions, orienting suitable operations on a regular basis, effectively operating and managing the firm, and maintaining excellent internal control. Particularly in current times, such as as IT 4.0, which is the era of digital technology, everything is connected to the Internet. The Fourth Industrial Revolution is the trend towards automation and data exchange in manufacturing technologies and life (Hermann et al. 2016). Information technology makes it easier for individuals to execute their tasks, saves money, and manages high efficiency whilst also providing timely and reliable information. As a result, with the advent of current information technology, the proper operation and management of a firm is now required. The accounting information system, in particular, is a world-class information technology tool that focuses on processing accounting data and successfully assisting managers in decision making. Many research studies on the use of AIS have been undertaken all around the world. However, no specific research has been undertaken to examine the relationship between Economies 2022, 10, 83. https://doi.org/10.3390/economies10040083 https://www.mdpi.com/journal/economies

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of The Determinants of the Usage of Accounting Information ...

�����������������

Citation: Thuan, Pham Quoc,

Nguyen Vinh Khuong, Nguyen

Duong Cam Anh, Nguyen Thi Xuan

Hanh, Vo Huynh Anh Thi, Tieu Ngoc

Bao Tram, and Chu Gia Han. 2022.

The Determinants of the Usage of

Accounting Information Systems

toward Operational Efficiency in

Industrial Revolution 4.0: Evidence

from an Emerging Economy.

Economies 10: 83. https://doi.org/

10.3390/economies10040083

Academic Editor:

Wadim Strielkowski

Received: 27 January 2022

Accepted: 25 March 2022

Published: 1 April 2022

Publisher’s Note: MDPI stays neutral

with regard to jurisdictional claims in

published maps and institutional affil-

iations.

Copyright: © 2022 by the authors.

Licensee MDPI, Basel, Switzerland.

This article is an open access article

distributed under the terms and

conditions of the Creative Commons

Attribution (CC BY) license (https://

creativecommons.org/licenses/by/

4.0/).

economies

Article

The Determinants of the Usage of Accounting InformationSystems toward Operational Efficiency in Industrial Revolution4.0: Evidence from an Emerging EconomyPham Quoc Thuan 1,2 , Nguyen Vinh Khuong 1,2,* , Nguyen Duong Cam Anh 1,2, Nguyen Thi Xuan Hanh 1,2,Vo Huynh Anh Thi 1,2, Tieu Ngoc Bao Tram 1,2 and Chu Gia Han 1,2

1 Faculty of Accounting and Auditing, University of Economics and Law, Ho Chi Minh City 700000, Vietnam;[email protected] (P.Q.T.); [email protected] (N.D.C.A.);[email protected] (N.T.X.H.); [email protected] (V.H.A.T.);[email protected] (T.N.B.T.); [email protected] (C.G.H.)

2 Vietnam National University, Ho Chi Minh City 700000, Vietnam* Correspondence: [email protected]

Abstract: The purpose of this study is to determine the factors affecting the application of accountinginformation systems (AIS) in small and medium enterprises (SMEs) in Vietnam. Drawing uponthe Technology–Organization–Environment (TOE) theoretical framework, Diffusion of Innovationstheory (DOI), and Resource-based theory (RBV), we proposed a research model to investigate theantecedents and influence of AIS usage in Vietnamese SMEs. This study used an online survey ofindividuals who work in Vietnamese SMEs for data collection. The result was assembled by applyingthe PLS-SEM model to test the proposed hypotheses based on 132 valid responses. First, the factorsthat have a significant impact on AIS usage are as follows: relative advantage; owner/managercommitment; and impact of COVID-19. Second, the research results also confirm that there is apositive relationship between AIS usage and AIS effectiveness; AIS performance has a positive impacton business performance. Research implications are to help business owners and leaders decidewhether to use AIS to strengthen the company’s position and reduce the burden on departments,particularly the accounting department.

Keywords: accounting information systems (AIS); AIS effectiveness; AIS usage; COVID-19

1. Introduction

Accounting information is used by all commercial organizations, even nonprofits,to assist business stakeholders including management and outsiders such as investors,agencies, the government, and banks to attain certain objectives when making economicdecisions (Hansen et al. 2007). Accurate accounting information is the foundation forassisting managers in making proper business decisions, orienting suitable operations ona regular basis, effectively operating and managing the firm, and maintaining excellentinternal control. Particularly in current times, such as as IT 4.0, which is the era of digitaltechnology, everything is connected to the Internet. The Fourth Industrial Revolution isthe trend towards automation and data exchange in manufacturing technologies and life(Hermann et al. 2016). Information technology makes it easier for individuals to executetheir tasks, saves money, and manages high efficiency whilst also providing timely andreliable information. As a result, with the advent of current information technology, theproper operation and management of a firm is now required. The accounting informationsystem, in particular, is a world-class information technology tool that focuses on processingaccounting data and successfully assisting managers in decision making.

Many research studies on the use of AIS have been undertaken all around the world.However, no specific research has been undertaken to examine the relationship between

Economies 2022, 10, 83. https://doi.org/10.3390/economies10040083 https://www.mdpi.com/journal/economies

Economies 2022, 10, 83 2 of 19

AIS effectiveness and company operational efficiency, particularly in the current context,the impact of external agents, the COVID-19 pandemic, and whether or not the enterprise’suse of AIS is affected. In Vietnam, there are studies on the application of accountinginformation systems, although they are still fairly limited. The majority of these studiesare concerned with the analysis of constraints in AIS development, the application of AISin enterprises, and so on, in order to make recommendations and solutions. Among thenotable overseas studies is a study on the factors influencing the use of AIS in small andmedium-sized businesses (Lutfi et al. 2017). The results reveal that the elements influencingthe implementation of AIS are as follows: organizational readiness, competitive pressure,compatibility, owner/manager commitment, and government support. In addition, there isa study on the elements influencing the effectiveness of AIS (Kouser et al. 2011) conductedin the context of Pakistan. According to the findings, there are two important drivers ofAIS effectiveness: manager participation in AIS implementation and manager accountingknowledge. Moreover, Ali et al. (2012) conducted research on the intention of small andmedium-sized businesses to continue using AIS (Ali et al. 2012). The study results showthat relative advantage is the biggest predictor of attitude toward AIS and satisfaction,both of which have significant mediation impacts on the intention to continue usingAIS. Outstanding domestic research studies the implementation of accounting informationsystems in Vietnamese small and medium firms using the core components of AIS (Tu 2020).The results that designate three elements have the largest influence on AIS usage: persons,information technology infrastructure, and internal control systems. In general, no researchhas been conducted to analyze the relationship between AIS effectiveness and a company’soperational efficiency (Tu 2020). There are a few domestic research studies on the factorsinfluencing the deployment of AIS; in particular, in the context of the COVID-19 epidemic,new technology, digitization, and automation are increasingly popular in Vietnam.

In Vietnam, achievements in accounting information systems are now more widelyused, such as Enterprise Resource Planning systems (ERP) and Cloud Computing (CISCO2020). Vietnamese business executives are aware of the need of digital transformation(Vietnam News 2021). More than 60% of SMEs use accounting software, and over 200,000enterprises employ electronic invoices (Vietnam News 2021). Accounting professionalstaking place in 22 nations around the world, including Vietnam, demonstrate that thefollowing: Trends are projected to have the greatest impact in the next three to ten years,according to up to 55% of survey respondents stating that the development of automatedaccounting systems is regarded as having the most potential (ACCA_GLOBAL 2016).Vietnamese enterprises from various businesses have all used AIS in accounting and man-agement. In recent years, the accounting software market in our country has also been fairlyactive. It is estimated that there are more than 130 accounting software suppliers legally.Moreover, as the digital economy evolves, new business forms and payment methodsemerge, and economic transactions become more complicated and diverse, resulting inongoing changes in the accounting record system promulgated and updated by the Stateto be relevant and timely with economic development. Despite the strong developmenttrend, the State’s support, and the benefits of AIS, the level of AIS usage in Vietnamesefirms remains relatively low compared with countries in the same region (CISCO 2020).

The study aim is to fill research gaps by analyzing and identifying the elementsinfluencing the implementation of AIS. The research is carried out in the context of Vietnam,a developing country with great economic achievements. Economic reforms since thelaunch of Doi Moi in 1986, coupled with beneficial global trends, have helped propelVietnam from being one of the world’s poorest nations to a middle-income economy thatleads a group of countries with similar incomes in one generation. Thanks to its solidfoundations, the economy has proven resilient through different crises, the latest beingCOVID-19 (Word Bank 2021). Vietnam was one of only a few countries to post GDP growthin 2020 when the pandemic hit (Word Bank 2021). The COVID-19 epidemic, on the otherhand, has a negative impact on the Vietnamese economy (Word Bank 2021). Due to thestrong outbreak of the epidemic wave, social distancing and stringent blockade had to be

Economies 2022, 10, 83 3 of 19

applied on a constant basis for people’s safety, severely affecting production and economicactivity in many fields (Word Bank 2021). Businesses face numerous difficulties and thepossibility of insolvency when there is little revenue while operational costs are high (WordBank 2021). Small and medium-sized businesses, in particular, play an essential role in theVietnamese economy, accounting for a large proportion. Small and micro firms make up asizable share of this total (Word Bank 2021). Because of its tiny size, this company sector isextremely vulnerable to the devastating impact of the COVID-19 pandemic, which couldforce it out of the market (Word Bank 2021). This study also makes significant theoreticalcontributions by integrating three theories: the Technology–Organization–Environmentmodel, Diffusion of Innovations theory, and Resource-based theory in building a researchmodel. PLS-SEM will be used to test and identify the factors influencing AIS usage in SMEs,as well as confirm the influence of that application on AIS effectiveness and the relationshipbetween AIS effectiveness and business operational efficiency.

The remainder of the research is organized as follows: Section 2 provides a theoreticalsummary based on prior research. Section 3 provides a thorough theoretical foundation aswell as research assumptions. Section 4 describes the research model and methodologies.Section 5 contains the outcomes of the data analysis and discussion. Section 6 then closeswith implications, limitations, and further studies.

2. Literature Review

Some studies conducted a study on the factors affecting the use of AIS and examinedthe influence of AIS use on the effectiveness of AIS in the context of small and mediumenterprises (SMEs) (A Ali and AlSondos 2020; Ali et al. 2012, 2016; Henderson et al. 2012;Khairi and Baridwan 2015; Kouser et al. 2011; Lutfi et al. 2017, 2020). The proposed researchmodel is based on Resource theory, the TOE research model and TAM. The proposedhypotheses refer to the effective use of AIS in SMEs, the relationship between them, andthe role of enterprises and identify a significant gap with previous studies when very fewstudies were able to explain the impact of AIS use on AIS effectiveness (Lutfi et al. 2020).According to the results of one study, influential factors for the use of AIS are as follows:competitive pressure, compatibility, owner/manager commitment, government support,and business benefits. The results also demonstrate that the use of AIS has a significanteffect on the effectiveness of AIS (Lutfi et al. 2017, 2020). Another study discovered two sig-nificant predictors of AIS effectiveness: management involvement in AIS implementationand management accounting knowledge (Kouser et al. 2011). Another group of authorsdeveloped more widely deployed variables from the underlying theories, such as attitude,pre-satisfaction, and intention to continue, and baseline variables deployed in the model,in addition to having the effect of money on behavior mediated by attitudes and utility anddemonstrating that relative advantage is the strongest antecedent of attitudes toward AISand satisfaction, both of which have a significant impact on the retention of intent (Ali et al.2012). Another study confirmed that having the right accounting information system inplace provides you a competitive advantage; causal relationships have been establishedbetween accounting information systems and performance; the current study’s findingswere presented; and other areas of research were also discussed (A Ali and AlSondos2020). According to the findings of a study, service quality, information quality, and systemquality are important success factors for AIS in increasing organizational performance(Ali et al. 2016). The study also shows that culture organizations help increase performanceby interacting with information quality, data quality, and system quality; thus, businessesshould create a favorable environment for employees to feel happy, which motivates themto work more diligently for the organization (Ali et al. 2016). According to one study,the following factors influence AIS adoption: management support on perceived ease ofuse, management support on perceived usefulness, self-efficacy on perceived ease of use,self-efficacy on perceived usefulness, perceived usefulness on the behavioral intention ofusing AIS, and perceived ease of use on the behavioral intention of using AIS (Khairi andBaridwan 2015).

Economies 2022, 10, 83 4 of 19

In general, these studies have shown that the factors affecting the use of AIS in SMEsinclude the relative advantages of using AIS, which will limit the problems arising andbring about higher efficiency; the readiness of the business is reflected in the relevantaspects; the commitment of the owners/managers on the future direction with the actualimpacts of AIS; the support from the government shown through the policies and regu-lations to encourage the use of AIS in business; the use and effectiveness of AIS to meetbusiness needs; the impact of COVID-19 promotes technical development to improve laborefficiency; operational effectiveness and efficiency come from the business, its employees,and customers.

3. Theoretical Framework and Hypothesis Development3.1. Theoretical Framework3.1.1. Technology–Organization–Environment (TOE)

Concerning the use of technology in organizations, the theory explains the interactionof three factors: technology context, organizational context, and environmental context,TOE (the technology–organization–environment framework) (Tornatzky et al. 1990). Thistheory has been revisited for its broad applicability (Awa et al. 2017), with the results indi-cating that the theory’s application has a direct relationship, meaning statistical significancewith the application possibilities of new technology. The paradigm emphasizes higher-levelcharacteristics rather than the specific behaviors of individuals within the organization.TOE is the foundation for studying the application of new technology to businesses, as wellas understanding the application of technology at the individual level through behavioralmodels such as theory of rational action and theory of behavior. There are plans and modelsfor integrating technologies that should be used.

3.1.2. Diffusion of Innovations (DOI)

DOI is a hypothesis that describes how a new technology advances and spreadsthroughout society as well as penetrates culture, beginning with gender identity andspreading in people’s consciousness (Rogers 2010). Product introduction in preparatorywork for the acceptance of DOI is viewed as the pioneer for explaining aspects of ICTinnovation adoption in the field of Library and Information Science (LIS) (Minishi-Majanjaand Kiplangat 2005). Theory attempts to explain why new and experimental ideas areaccepted over time and spread over long periods of time. The combination of rural andurban populations in a society, the level of education in the society, and the scale ofindustrialization and development are all factors that influence the rate of innovationdiffusion. Adoption rates may differ between societies. The diffusion of a new idea isinfluenced by four factors, according to the following theory: the level of improvement, thechannel of communication, the time of adoption, and the social system (situation).

3.1.3. Resource Based View Theory (RBV)

According to the resource-based view (RBV), each independent organization hasspecific resource structures such as physical assets, its ability to own or control its assets,which are considered separate resources arising from the organization’s history of formationand development capacity (Barney 1991). The study of RBV is a typical example of thewidespread application and demonstration of this theory in economics (Acedo et al. 2006).Over the last decade, the use of resource-based theory (RBT) in marketing research hasincreased by more than 500%, demonstrating its importance as a framework for explainingand predicting competitive advantage and performance results (Kozlenkova et al. 2014).

Material resources include finance, factories, technology, and equipment systems;(2) immaterial resources include (1) trademarks, licenses, reputations, network partnerships,and databases; and (3) competencies include knowledge, organizational ability to use fixedassets, observation of business opportunities, ability to produce new knowledge basedon existing knowledge, and ability to innovate production (Baumane-Vitolina and Cals

Economies 2022, 10, 83 5 of 19

2013). Furthermore, resources are classified into two types: knowledge-based resourcesand relationship-based resources.

3.2. Hypothesis Development

Many organizations have considered the advantages that come from using suchnovelties by using the concept of relative advantage in Diffusion of Innovation (DOI)theory when adopting new technology (Henderson et al. 2012; To and Ngai 2006). This fitis preferable to the predecessor (Rogers 2010). In the context of AIS, enterprise use of AIS ispreferable to non-use (Khairi and Baridwan 2015; Lutfi et al. 2020). It should be noted thatthe main motivation for SMEs to adopt new technologies is that the benefits are expectedto benefit the company (Ali et al. 2012; Lutfi et al. 2020). The study hypothesized, based onthe reasons given, the following.

Hypothesis 1 (H1). Relative Advantage has positive influences on the use of AIS.

The potential benefits alone are not always enough to convince an organization toadopt a new technology. According to the Technology–Organization–Environment (TOE)model theory, organizational factors influence the application of technology (Lutfi et al.2020; Maryeni et al. 2014). As a result, whether firms are willing to use new technologyeffectively is an important organizational factor to consider (Ali et al. 2012; Lutfi et al. 2020).In the case of SMEs, they may be hesitant to implement AIS if they are not prepared to facethe potential risks associated with its use (Lutfi et al. 2020; Ramdani and Kawalek 2007).Employees’ positive attitudes prior to implementing a new system are also critical duringimplementation (Ali et al. 2012). Similarly, one of the major determinants of AIS adoption isorganizational readiness (Lutfi et al. 2020; Rahayu and Day 2015). As a result, the followinghypothesis is developed:

Hypothesis 2 (H2). Organizational Readiness has positive influences on the use of AIS.

Owner or manager commitment (OMC) is another factor in the Technology–Organiza-tion–Environment (TOE) model theory, indicating that they are involved in system plan-ning and implementation. They not only ensure that such technologies are used by theiremployees, but they also have a positive impact on the success of IS/IT in SMEs (Lutfi et al.2020). Due to the natural resistance of technology use, it is critical when making decisionsto ensure that they are committed to properly implementing all available resources to makegood use of AIS (Grover and Goslar 1993; Nasiren et al. 2016; Rozzani and Rahman 2013).As a result, OMC is an important factor in the use of AIS (Al-Alawi and Al-Ali 2015). Thefollowing is our next hypothesis.

Hypothesis 3 (H3). Owner/Managers Commitment has positive influences on the use of AIS.

Another important factor that may have an impact is government support for the TOEmodel’s environmental component, which involves the government’s role in encourag-ing and promoting the use of technology in business (Tornatzky et al. 1990). The studyalso suggests that different government policies and regulations can influence businesses’adoption of AIS. Many studies have taken this factor into account, and the results consis-tently show the importance of government support in the use of technology by businesses(Al Nahian Riyadh et al. 2009; Ali et al. 2012; Lutfi et al. 2020; Zhu and Kraemer 2005). Thefollowing is the next hypothesis proposed by the study:

Hypothesis 4 (H4). Government Support has positive influences on the use of AIS.

The ultimate goal of using AIS is to improve company performance; companies thatuse AIS effectively are more likely to report positive results (Ali et al. 2012). Similarly, TOEtheory suggests that the impact of a technology is determined by how much it is used to

Economies 2022, 10, 83 6 of 19

conduct business activities (Lutfi et al. 2020; Zhu et al. 2006). As a result, a company mustfirst use AIS in order to understand its impact on the effectiveness of AIS. As a result, thefollowing hypothesis is advanced:

Hypothesis 5 (H5). AIS Usage has positive influences on the effectiveness of AIS.

We have observed the importance of technology in the difficult global COVID-19pandemic over the last two years (Beland et al. 2020; Spurk and Straub 2020; Stuerz et al.2020). Accepting new technology as part of daily routine is critical in this context (Momaniet al. 2017). Technology adoption is regarded as one of the most important success factorsfor new technology (Molino et al. 2020; Scherer et al. 2019). To meet demand, technologyhas undergone stronger transformations to keep up with the times; COVID-19 is regardedas a driving force for technological development; many new business models have emerged,and online business and e-commerce platforms are becoming more popular (Pedró 2020).Furthermore, COVID-19 promotes and upgrades technology and automation infrastructuresystems, including AIS infrastructure. Based on the data presented above, the studyhypothesizes the following.

Hypothesis 6 (H6). COVID-19 has positive influences on the effectiveness of AIS.

When it comes to customer satisfaction, an effective business can be assessed throughsatisfaction, which means that the business is operating effectively in some manner. Em-ployees’ professional ethics, on the other hand, are used to evaluate performance (A Aliand AlSondos 2020). Furthermore, in order to evaluate operational efficiency, it is necessaryto pay attention to the growth of factors such as market share, revenue, and profit of theenterprise, if even after the implementation of new technology such as AIS, these indicatorsof growth have increased. It is undeniable if the business is constantly growing (Ali et al.2016, 2020; Koli and Rawat 2011; Rozzani and Rahman 2013). We propose the followingresearch hypothesis.

Hypothesis 7 (H7). AIS effectiveness has positive influences on operational efficiency.

4. Research Design4.1. Scale and Structure of the Questionnaire

This study was conducted to briefly understand the factors affecting the application ofAIS in SMEs in Vietnam. When analyzing by the PLS-SEM method, the required samplesize is at least 80 (Hair et al. 2016). We conducted an online quantitative survey sent toindividuals who have been and are working in SMEs in Vietnam, during the period fromSeptember to November 2021. The results obtained 132 valid questionnaires, which aremore than the minimum sample size and meet the research requirements. The questionnaireconsists of 3 parts. Part 1 is personal information, part 2 is business information, and part 3is quantitative questions about factors affecting the application of AIS in SMEs in Vietnam.To determine the influence of factors in the study, we use the Google questionnaire withthree main parts with eight variables. The first variable is the relative advantage of usingAIS, which we study based on the scale (Premkumar and Roberts 1999; Rogers 2010). Next,we apply the scale of Grandon and Pearson (2004) to measure the readiness of the business(Grandon and Pearson 2004). For the commitment variable of owners/managers, we applythe scale of (Damanpour and Schneider 2006). Tornatzky et al. (1990) is the subsequentstudy for us to make the scale of the government support variable (Tornatzky et al. 1990).For the use of AIS, we relied on the do-scale of (Bhattacherjee 2001a, 2001b; Limayem andCheung 2008). For the efficiency variable using AIS, we used the scale of the (Mcmahon2001). We use the scale of (Beland et al. 2020; Nagel 2020; Pedró 2020) to measure the impactof COVID-19 on AIS performance. To measure the impact of AIS performance on business

Economies 2022, 10, 83 7 of 19

performance, we use the scale of (A Ali and AlSondos 2020). Appendix A Table A1 willcontain information on measuring scales.

4.2. Methodology

The scale of the study is built based on our research on the combination of the theoreti-cal basis of the TOE model and the results obtained from previous studies mentioned in theresearch hypotheses above, then it is adjusted to fit the actual situation. The quantitativescales built in the article will measure the perceptions of the survey subjects by using aLikert scale with five levels: 1—Strongly disagree; 2—Disagree; 3—Neutral; 4—Agree;5—Strongly agree.

Available survey samples will be processed using SPSS 20.0 and SmartPLS software toperform the analysis steps of the PLS-SEM model. PLS-SEM analysis has the advantage ofemphasizing forecasting goals while being similar in terms of data needs and relationshipcharacteristics, being able to compute combinations of observed variables using as a repre-sentative of the concepts in the study, the model is also not constrained by the identificationproblem, even when the model becomes complex (Hair et al. 2017). Furthermore, PLS-SEMcan better handle causal modeling and has advantages when the sample is relatively small(Hair et al. 2017).

PLS-SEM works efficiently with small sample sizes and complex models (Hair et al.2021). PLS-SEM can easily handle reflective and formative measurement models, as well assingle-item constructs, with no identification problems (Hair et al. 2021). It can, therefore, beapplied in a wide variety of research situations (Hair et al. 2021). When applying PLS-SEM,researchers also benefit from high efficiency in parameter estimation, which is manifestedin the method’s greater statistical power in comparison to that of CB-SEM (Hair et al. 2021).No distributional assumptions are made; PLS-SEM is a nonparametric method. Influentialoutliers and collinearity may influence the results (Hair et al. 2021).

4.3. Research Model

Based on the background theory and arguments from the research hypotheses, wepropose the research model presented in Figure 1.

Economies 2022, 10, x 7 of 19

of the business (Grandon and Pearson 2004). For the commitment variable of owners/man-agers, we apply the scale of (Damanpour and Schneider 2006). Tornatzky et al. (1990) is the subsequent study for us to make the scale of the government support variable (Tornatzky et al. 1990). For the use of AIS, we relied on the do-scale of (Bhattacherjee 2001a, 2001b; Limayem and Cheung 2008). For the efficiency variable using AIS, we used the scale of the (Mcmahon 2001). We use the scale of (Beland et al. 2020; Nagel 2020; Pedró 2020) to measure the impact of COVID-19 on AIS performance. To measure the impact of AIS performance on business performance, we use the scale of (A Ali and AlSondos 2020). Appendix A Table A1 will contain information on measuring scales.

4.2. Methodology The scale of the study is built based on our research on the combination of the theo-

retical basis of the TOE model and the results obtained from previous studies mentioned in the research hypotheses above, then it is adjusted to fit the actual situation. The quan-titative scales built in the article will measure the perceptions of the survey subjects by using a Likert scale with five levels: 1—Strongly disagree; 2—Disagree; 3—Neutral; 4—Agree; 5—Strongly agree.

Available survey samples will be processed using SPSS 20.0 and SmartPLS software to perform the analysis steps of the PLS-SEM model. PLS-SEM analysis has the advantage of emphasizing forecasting goals while being similar in terms of data needs and relation-ship characteristics, being able to compute combinations of observed variables using as a representative of the concepts in the study, the model is also not constrained by the iden-tification problem, even when the model becomes complex (Hair et al. 2017). Furthermore, PLS-SEM can better handle causal modeling and has advantages when the sample is rel-atively small (Hair et al. 2017).

PLS-SEM works efficiently with small sample sizes and complex models (Hair et al. 2021). PLS-SEM can easily handle reflective and formative measurement models, as well as single-item constructs, with no identification problems (Hair et al. 2021). It can, there-fore, be applied in a wide variety of research situations (Hair et al. 2021). When applying PLS-SEM, researchers also benefit from high efficiency in parameter estimation, which is manifested in the method’s greater statistical power in comparison to that of CB-SEM (Hair et al. 2021). No distributional assumptions are made; PLS-SEM is a nonparametric method. Influential outliers and collinearity may influence the results (Hair et al. 2021).

4.3. Research Model Based on the background theory and arguments from the research hypotheses, we

propose the research model presented in Figure 1.

Figure 1. Research model. Source: proposal from the author. Figure 1. Research model. Source: proposal from the author.

5. Results5.1. Descriptive Statistics

All qualitative variables of the survey, including personal information of surveysubjects and business information, were subjected to descriptive statistical analysis, andthe findings revealed the level of spread across all components. The survey findings aregathered, demonstrating that the survey results are unaffected by any special factor orvariable in determining the factors influencing the business using AIS. The specific resultsare presented in Table 1.

Economies 2022, 10, 83 8 of 19

Table 1. Summary of statistical results describing qualitative variables.

Category Percentage

Gender

Female 61.36%

Male 38.64%

Total 100%

Age

18–24 66.67%

24–35 26.51%

35–45 3.03%

45 and above 3.79%

Total 100%

Work experience

5 years or less 83.33%

6–10 years 9.85%

11–15 years 1.52%

More than 15 years 5.30%

Total 100%

Average income per month

Under 10 million 59.85%

10–20 million 29.55%

20–40 million 6.05%

Over 40 million 4.55%

Total 100%

Living place

Ha Noi 1.52%

TP.HCM 86.36%

Ða Nang 1.52%

Others 10.60%

Total 100%

Position

Staff 86.36%

Manager 11.36%

Chief executive officer 1.52%

Senior manager 0.76%

Total 100%

Academic level

College 5.30%

University 89.40%

Post-university 5.30%

Total 100%

Economies 2022, 10, 83 9 of 19

Table 1. Cont.

Category Percentage

Type of business

Mining industry 9.85%

Retail 23.48%

Repair of other cars and engines 0.76%

Accommodation and food service 48.48%

Water supply and waste treatment 1.52%

Energy and mining 2.27%

Transportation, warehousing, and construction 6.06%

Electronic technology 7.58%

Total 100%

Age of business

1–5 years 27.27%

6–10 years 22.73%

11–20 years 19.70%

More than 20 years 30.30%

Total 100%

Number of employees

Under 10 people 11.36%

10–99 people 27.27%

100–199 people 14.39%

200–300 people 9.10%

More than 300 people 37.88%

Total 100%Source: Author synthesized from research data.

During the entire survey process, the team obtained 132 forms with 132 valid forms.The outcomes are described in detail below. The first information about individuals inthe survey was gathered through the observation of variables such as gender, age, workexperience, average income per month, living place, position, and academic level. Forgender, males accounted for 38.64%, while females accounted for 61.36%. The samplesurvey is then sent to all age groups and collects the opinions of all subjects in the factorgroup, with the age group 18–24 receiving the highest response rate of 66.67%. Similarlywith respect to age and work experience, the proposals are dominated by groups with 5years or less, with 83.33%. The subjects’ average income per month was also distributedevenly, with income under 10 million accounting for the largest proportion (59.85%). Interms of living place, the majority of those polled (86.36%) live in Ho Chi Minh City.The majority of positions (86.36%) are held by employees, but higher-ranking positions(Manager 11.36%, Chief executive officer 1.52%, and Senior Manager 0.76%) are alsorepresented in the survey. The academic level is the final information factor. Up to 89.40%of subjects have university level education, while the rest have college and post-universityeducation equivalent to 5.30%. For business information, three items can be displayed:the type of business, the age of the business, and the number of employees. In terms ofthe age of business factor, businesses arranged at similar time levels were divided intofour groups ranging from 19.70% to 30.30%. Regarding the type of business surveyed, theresults shown in Table 1 show that there are many types of businesses surveyed, with afew types accounting for the most, such as Accommodation and food service with 48.48%

Economies 2022, 10, 83 10 of 19

and Retail with 23.48%, but these two figures account for many parts (not the majority),and the remaining types of businesses still participate in the survey with correspondingproportions. Similarly, for equally important information, the number of employees isalso diversified from the sample survey when five groups of numbers have a ratio of9.10–37.88%; there is no company in which the group is too large. We find that the samplewas overall similar, making the results more reliable, and this stems from two factors: typeof business and number of employees, which are diverse in most types and sizes, and theremaining factors do not have a single factor that is dominated by business groups.

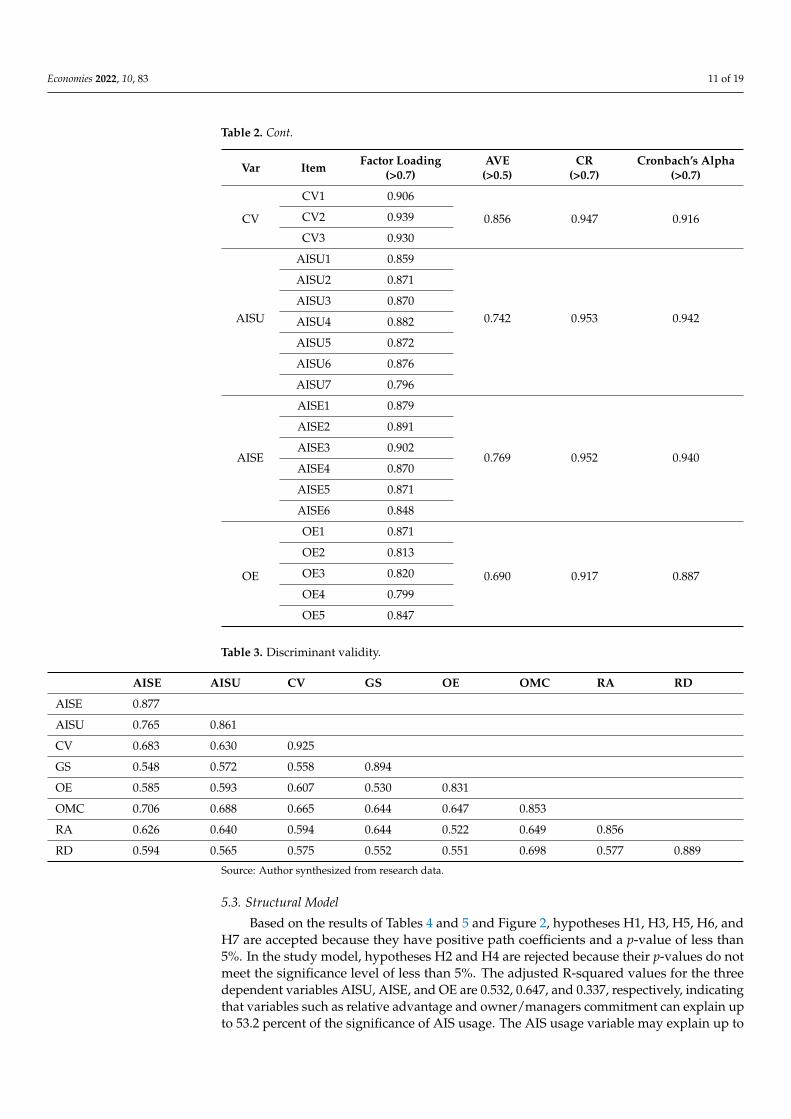

5.2. Check Measurement

The data are evaluated for convergent validity, discriminant validity, and reliability bythe measurement model. The parameters of Average Variance Extracted (AVE), CompositeReliability (CR), Cronbach’s Alpha, and Discriminant Value are highlighted in detail. Thehypothesis was given a 5 percent significance level. There was a greater than 0.70 loadfactor (Wong 2013). AVE should be more than 0.5 according to (Fornell and Larcker 1981).The AVE estimate from SmartPLS was 50% higher for all factors in this investigation.The discriminant value as the square root of AVE is also bigger than the other associatedvariables and lies on the same diagonal as the other correlated variables.

According to the study’s measurement model, the values of Composite reliability,Cronbach’s alpha reliability value, and Discriminant value determined from the collectedsurvey data are completely suitable for the inclusion of scales in structural model analysis.

Tables 2 and 3 show the findings of the survey data measurement model analysis.Table 2 shows that all of the study variables are acceptable, and the model is viable, withCronbach’s alphas ranging from 0.819 to 0.942, exceeding the threshold of 0.70 (Churchill1979). The CR value is substantially higher than the 0.7 level (Nunnally 1978), ranging from0.892 to 0.953. AVE values range from 0.690 to 0.856, far exceeding the minimum of 0.5,when evaluated for Discriminatory Values in Table 3. The square root of AVE always lieson the diagonal and is greater than all the remaining values of the correlated variables inthe model, indicating that the value here is the discriminant value, which is completelyconsistent with Fornell and Larcker’s (1981) opinion.

Table 2. Convergent validity and reliability.

Var Item Factor Loading(>0.7)

AVE(>0.5)

CR(>0.7)

Cronbach’s Alpha(>0.7)

RA

RA1 0.899

0.734 0.892 0.819RA2 0.790

RA3 0.876

RDRD1 0.900

0.790 0.918 0.869RD2 0.925

RD3 0.839

OMC

OMC1 0.841

0.727 0.941 0.924

OMC2 0.870

OMC3 0.882

OMC4 0.891

OMC5 0.857

OMC6 0.769

GS

GS1 0.871

0.799 0.923 0.874GS2 0.903

GS3 0.908

Economies 2022, 10, 83 11 of 19

Table 2. Cont.

Var Item Factor Loading(>0.7)

AVE(>0.5)

CR(>0.7)

Cronbach’s Alpha(>0.7)

CV

CV1 0.906

0.856 0.947 0.916CV2 0.939

CV3 0.930

AISU

AISU1 0.859

0.742 0.953 0.942

AISU2 0.871

AISU3 0.870

AISU4 0.882

AISU5 0.872

AISU6 0.876

AISU7 0.796

AISE

AISE1 0.879

0.769 0.952 0.940

AISE2 0.891

AISE3 0.902

AISE4 0.870

AISE5 0.871

AISE6 0.848

OE

OE1 0.871

0.690 0.917 0.887

OE2 0.813

OE3 0.820

OE4 0.799

OE5 0.847

Table 3. Discriminant validity.

AISE AISU CV GS OE OMC RA RD

AISE 0.877

AISU 0.765 0.861

CV 0.683 0.630 0.925

GS 0.548 0.572 0.558 0.894

OE 0.585 0.593 0.607 0.530 0.831

OMC 0.706 0.688 0.665 0.644 0.647 0.853

RA 0.626 0.640 0.594 0.644 0.522 0.649 0.856

RD 0.594 0.565 0.575 0.552 0.551 0.698 0.577 0.889

Source: Author synthesized from research data.

5.3. Structural Model

Based on the results of Tables 4 and 5 and Figure 2, hypotheses H1, H3, H5, H6, andH7 are accepted because they have positive path coefficients and a p-value of less than5%. In the study model, hypotheses H2 and H4 are rejected because their p-values do notmeet the significance level of less than 5%. The adjusted R-squared values for the threedependent variables AISU, AISE, and OE are 0.532, 0.647, and 0.337, respectively, indicatingthat variables such as relative advantage and owner/managers commitment can explain upto 53.2 percent of the significance of AIS usage. The AIS usage variable may explain up to

Economies 2022, 10, 83 12 of 19

64.7 percent of the AIS efficiency variable’s significance, and the AIS efficiency variable canexplain 33.7 percent of the operational efficiency variable’s significance. Almost all of thehypotheses that were established were found to be validated by the findings. However, thefindings show that there are up to two assumptions concerning two independent elements,namely organizational readiness and government support, that are not recognized in theprocess of influencing AIS adoption. Finally, the results show that only two aspects ofrelative advantage and owner/managers commitment in the proposed research modelhave an influence on the use of AIS in SMEs.

Table 4. R square adjusted.

Var R Square Adjusted

AISU AIS Usage 0.532

AISE AIS Effectiveness 0.647

OE Operational Efficiency 0.337Source: Author synthesized from research data.

Table 5. Hypothesis Results.

Hypothesis Path Coefficient T-Stat p-Values Conclusion

H1 RA → AISU 0.279 2.707 0.007 Supported

H2 RD → AISU 0.079 1.035 0.301 Not Supported

H3 OMC → AISU 0.389 3.700 0.000 Supported

H4 GS → AISU 0.098 0.948 0.344 Not Supported

H5 AISU → AISE 0.556 5.602 0.000 Supported

H6 CV → AISE 0.333 3.507 0.000 Supported

H7 AISE → OE 0.585 6.561 0.000 SupportedSource: Author synthesized from research data.

Economies 2022, 10, x 12 of 19

Because the p-value is less than 0.05, the T-stat value is more than 1.96, and the path coefficient value is positive, the proposed hypotheses H1, H3, H5, H6, and H7 are ac-cepted and have a positive effect. H1 is acceptable because the Relative Advantage factor has a positive effect on AIS use (Coefficient = 0.279, T-stat = 2.707, p-value = 0.007). For H3, there is a positive association between Owner/Managers commitment and AIS utilization (Coefficient = 0.389, T-stat = 3.700, p-value = 0.000). H5 is also approved because the data reveal that using AIS has a beneficial effect on AIS Efficiency (Coefficient = 0.556, T-stat = 5.5602, p-value = 0.000). Finally, two hypotheses H6 (Coefficient = 0.333, T-stat = 3.507, p-value = 0.000) and H7 (Coefficient = 0.585, T-stat = 6.561, p-value = 0.000) are accepted because there are satisfactory values, confirming the hypotheses H6 and H7 that AIS us-age positively affects AIS Effectiveness and AIS Effectiveness positively affects Opera-tional efficiency. Meanwhile, hypotheses H2 and H4 are rejected because the T-stat value is less than 1.96 and the p-value is greater than 0.05, implying that organizational readiness and government support have no effect on SMEs’ use of AIS.

Table 5. Hypothesis Results.

Hypothesis Path Coefficient T-Stat p-Values Conclusion H1 RA → AISU 0.279 2.707 0.007 Supported H2 RD → AISU 0.079 1.035 0.301 Not Supported H3 OMC → AISU 0.389 3.700 0.000 Supported H4 GS → AISU 0.098 0.948 0.344 Not Supported H5 AISU → AISE 0.556 5.602 0.000 Supported H6 CV → AISE 0.333 3.507 0.000 Supported H7 AISE → OE 0.585 6.561 0.000 Supported

Source: Author synthesized from research data.

Figure 2. Structural Model.

6. Discussion According to the findings, relative advantage and owner/managers commitment are

two factors that have a positive impact on AIS usage in SMEs. This means that of the four hypotheses H1–H4 about the factors influencing AIS usage, H1 and H3 are consistent with our original opinion. Regarding such findings, the relative advantage factor that influ-ences the use of AIS is consistent with the findings of (Ali et al. 2012), and this factor has a positive effect on AIS usage but this result is not consistent with the findings of (Lutfi et

Figure 2. Structural Model.

Because the p-value is less than 0.05, the T-stat value is more than 1.96, and the pathcoefficient value is positive, the proposed hypotheses H1, H3, H5, H6, and H7 are acceptedand have a positive effect. H1 is acceptable because the Relative Advantage factor hasa positive effect on AIS use (Coefficient = 0.279, T-stat = 2.707, p-value = 0.007). For H3,there is a positive association between Owner/Managers commitment and AIS utilization

Economies 2022, 10, 83 13 of 19

(Coefficient = 0.389, T-stat = 3.700, p-value = 0.000). H5 is also approved because the datareveal that using AIS has a beneficial effect on AIS Efficiency (Coefficient = 0.556, T-stat= 5.5602, p-value = 0.000). Finally, two hypotheses H6 (Coefficient = 0.333, T-stat = 3.507,p-value = 0.000) and H7 (Coefficient = 0.585, T-stat = 6.561, p-value = 0.000) are acceptedbecause there are satisfactory values, confirming the hypotheses H6 and H7 that AIS usagepositively affects AIS Effectiveness and AIS Effectiveness positively affects Operationalefficiency. Meanwhile, hypotheses H2 and H4 are rejected because the T-stat value is lessthan 1.96 and the p-value is greater than 0.05, implying that organizational readiness andgovernment support have no effect on SMEs’ use of AIS.

6. Discussion

According to the findings, relative advantage and owner/managers commitment aretwo factors that have a positive impact on AIS usage in SMEs. This means that of the fourhypotheses H1–H4 about the factors influencing AIS usage, H1 and H3 are consistent withour original opinion. Regarding such findings, the relative advantage factor that influencesthe use of AIS is consistent with the findings of (Ali et al. 2012), and this factor has a positiveeffect on AIS usage but this result is not consistent with the findings of (Lutfi et al. 2020).According to this study, the relative advantage factor has no effect on AIS usage. Concerningthe owner/managers’ commitment, which is a factor influencing enterprise adoption ofAIS, it is completely consistent with the conclusion of (Lutfi et al. 2020). The use of AIS isnot a trivial matter; therefore, businesses must consider the benefits of using AIS versus notusing it, the advantage that businesses gain from adopting A is that it outweighs the costof implementation or it increases the business’s competitive advantage. Furthermore, ifSMEs’ managers or owners believe that the benefits of implementing advanced technologysystems outweigh the risks, they are more likely to implement technology. The commitmentof managers is the motivation for employees to adopt these new technologies. This alsoimplies that the levels of commitment, active participation, and support of the businessmanagement in adopting AIS and ensuring the use of such technologies by its employeesare extremely important factors in the adoption of AIS (Ali et al. 2012; Lutfi et al. 2020).

The hypothesis that AIS usage has a positive effect on AIS use efficiency is entirelyconsistent with the conclusion reached by (Lutfi et al. 2020). In terms of AIS effectiveness,research shows that using AIS effectively helps businesses collect reports that have a greaterpositive impact on their operations than businesses that use AIS infrequently or not atall (Ali et al. 2012). When businesses use technologies such as AIS in their work, thetechnologies must undoubtedly bring efficiency and benefits to the businesses, and thebusinesses must use AIS in order to recognize a positive relationship between the use ofAIS and the effectiveness of AIS. From there, it is concluded that the more widely usedAIS is, the greater enterprises’ ability to create valuable impacts, challenge competitors toimitate, and create long-term sustainability (Lutfi et al. 2020). From here, we also observethat when using technology or anything new, we see the effect it brings.

According to the findings, the COVID-19 epidemic over the last two years has notonly not hampered the effectiveness of AIS, but it has actually had a positive impact. Theepidemic broke out during a period of technological development when all activities werecarried out via the Internet, and technological applications had the opportunity to promoteextremely optimal efficiency, including the effectiveness of AIS; this is consistent withthe findings of other studies on the positive impact of COVID-19 on AIS effectiveness,such as (Beland et al. 2020; Spurk and Straub 2020; Stuerz et al. 2020). The adoptionof new technology, such as AIS, is one of the most important success factors (Molinoet al. 2020; Scherer et al. 2019). Above all, COVID-19 promotes and upgrades technologyand automation infrastructure systems, including AIS infrastructure so that businessescan ensure that employees can use the system securely even when not using enterpriseequipment or systems. A more robust system is also a factor in the AIS’s Efficacy claim(Nagel 2020).

Economies 2022, 10, 83 14 of 19

Finally, a company that implements new technology will help improve the company’soperational efficiency. As a result, the study’s final result is not surprising and is entirelyconsistent with the proposed hypothesis. AIS efficiency has a positive impact on businessperformance. A successful company is one that has earned the trust and satisfaction ofits customers. Furthermore, an effective enterprise will be able to manage its employees,which is reflected in employee professional ethics, particularly in the field of accounting,where employee ethics is prioritized. Otherwise, ethical issues will have unpredictabilityfor businesses. The business’s performance is reflected in the rate of development, andgrowth, as well as revenue, profit, market share, and competitiveness (A Ali and AlSondos2020; Ali et al. 2016; Rozzani and Rahman 2013).

In conclusion, the research findings show that two factors, relative advantage andowner/managers commitment, have a positive influence on AIS usage; the COVID-19pandemic have a positive impact on AIS effectiveness; and AIS effectiveness has a positiveimpact on operational efficiency. The systematic influence of technological and organiza-tional factors, as well as the environment’s push, makes the Board of Directors feel moresecure in applying and expanding AIS to help businesses grow more and more. The studyis relevant for businesses in various economies, particularly SMEs, because when thesebusinesses share the characteristic of unstable financial and human resources, they needmore motivation for the application of AIS, as well as the accomplishments of the industrialrevolution (A Ali and AlSondos 2020; Lutfi et al. 2020; Nastase et al. 2020).

7. Conclusions and Implications7.1. Conclusions

After a period of research and summary, the results have brought great practicalsignificance. The implementation process proceeds through many stages: from preliminaryto detailed. First, we posed a research problem and developed a hypothetical model aswell as a preliminary survey. Thanks to the comments of the implementers, we were ableto identify many flaws in the actual survey process based on those preliminary results.Then, the questionnaire was completed, and the formal survey began. By using our ownrelationships, social networking groups, face-to-face interviews at local businesses, and soon, we actively sought out sources of access to office staff and management at all levels ofbusiness. Following the collection of sufficient samples, the survey sample is filtered. Totest the model, which is based on the TOE model, we used the PLS-SEM method. Finally,a conclusion was reached. Almost all of the proposed hypotheses have an impact on theuse of AIS. Furthermore, it has a positive impact on enterprises’ decision to use AIS ornot. It is undeniable that organizations that have implemented AIS have reaped significantbenefits such as time, cost, and labor savings, providing useful information to leadership,and improving professional qualifications. They are almost completely satisfied with thequality that AIS has provided. When survey respondents are willing to continue to use andutilize all resources, as well as encourage employees to work with AIS, it is a good thing forthe Vietnamese economy. Furthermore, AIS is demonstrated to be a superior technologycapable of managing massive amounts of data. As a result, the use of AIS will become morewidespread in the near future. As the COVID situation continues to be complicated, officeworkers in general and management, accounting, and auditing departments, in particular,are forced to work remotely and cannot communicate directly, while organizations mustalways maintain and protect data. This is a significant factor in increasing the demand forAIS use.

7.2. Theorical Contribution

This research has a number of theoretical implications. First, we use the TOE modelas the foundation and combine it with the DOI theory to provide greater clarity on thefactors influencing AIS demand in our country: specifically, the three factors of technology,organization, and environment. It expands on factors influencing AIS decision making thathave received little attention in previous research. The most notable point is to mention

Economies 2022, 10, 83 15 of 19

improving the efficiency of AIS, thereby increasing enterprise operational efficiency. Asa result, our findings have helped to supplement existing research on AIS and improvedusers’ understanding of the technology.

In the current context, the majority of Vietnamese enterprises have used softwareto support management in conjunction with the COVID-19 pandemic in recent years,emphasizing the importance of AIS in creating convenience when working from afar.The article adds critical data to the theoretical model, and the novel model serves as afoundation for future research.

7.3. Practical Implications

For practical purposes, we propose some ideas aimed at promoting AIS while alsoaddressing the concerns of businesses considering AIS.

To begin, employees who use AIS must be willing to learn and develop the ability toapply technology in order to meet the needs of the 4.0 era. Technology is becoming moreadvanced, serving as an effective assistant and shouldering a portion of the workload foremployees. The most useful information can be collected, processed, stored, and renderedby AIS. It also aids in the reduction in business and legal risks. Accountants and auditorswho use it skillfully will not only maximize the benefits but also save time and efforton manual work that requires less intelligence, allowing them to focus more on decisionmaking and dealing with real-life situations. As a result, when working with equipmentand technology, users must first equip themselves with the most fundamental computerknowledge and skills in order to comprehend it. In addition to that, the accountingand auditing team must be highly adaptable due to changes, constant updates with newversions of technology, and uncontrollable epidemiological fluctuations that cause changesin structure and working conditions, it is necessary to understand how to capitalize onopportunities and deal with challenges in order to avoid being obliterated by technologicaladvancement.

Second, in the market economy, competition for each enterprise is becoming increas-ingly fierce. Thousands of businesses have become bankrupt or been dissolved as a resultof the COVID-19 epidemic. To avoid falling behind competitors in the industry, it is nec-essary to understand how to invest in equipment and technology, including AIS, andtrain employees through periodic courses, as human resources are always the backboneof an organization. We encourage the use of AIS by focusing on the long-term benefits itbrings rather than the short-term costs; the initial investment will be offset by the increasedcapacity and work efficiency that technology brings. A developed accounting informationsystem will be a decisive factor for the overall smooth and effective operation of the ERPsystem. At that time, the operating system of the business is enhanced. Managers easilyplan and manage their resources and business activities. Senior management must haveforesight, recognize the current innovation situation, make the most of AIS, and play a rolein reaffirming their market position.

Third, because cost is likely to be a significant barrier to using AIS for small andmedium-sized businesses, the government must make efforts to encourage enterprises touse technology in business by using financial support measures and assist in the develop-ment of highly qualified human resources. They should also extend cooperation to receiveglobal scientific achievements and create opportunities for large corporations and foreigncompanies to assist and mentor domestic enterprises.

7.4. Limitations and Future Research

In addition to the new points and practical implications, we are also confronted withsome limitations. First, we only discovered two factors influencing the use of AIS (T andO—Technology and Organization), and the E factor mentioned by the GS variable hasbeen eliminated but has not been replaced by variable GS. Another point to consider isthat the term AIS is relatively new, and it creates barriers in the process of informationcommunication between the surveyor and the surveyor. Future studies can create annota-

Economies 2022, 10, 83 16 of 19

tions and explanations integrated within the survey to increase understanding and maketerms easier to understand. The study then sampled all of Vietnam’s provinces, but theresults were only obtained in Ho Chi Minh City, which is unfortunate given the short timeframe. We hope that the approach to the topic will be expanded to other provinces in thecoming years through media published on reputable search sources. Finally, more researchwill contribute to the expanding topic while also being highly practical, providing anopportunity to compare the position of AIS application in organizations across the countryand even abroad.

Author Contributions: All of the authors contributed to the conceptualization, formal analysis,investigation, methodology, and writing and editing of the original draft. All authors have read andagreed to the published version of the manuscript.

Funding: This research is funded by University of Economics and Law, Vietnam National UniversityHo Chi Minh City, Vietnam.

Institutional Review Board Statement: Not applicable.

Informed Consent Statement: Informed consent was obtained from primary data.

Data Availability Statement: The data will be made available upon request.

Conflicts of Interest: The authors declare no conflict of interest.

Appendix A

Table A1. Scale of variables.

Study Measures Measurement Items

RAAli et al. (2012)

RA1. Using AIS can reduce our operation cost.RA2. Using AIS can reduce our operation time.RA3. Using AIS can provide useful information to make decisions.

RDAli et al. (2012)

RD1. We are financially ready to use AIS.RD2. We have enough technological resources to use AIS.RD3. Our employees have adequate knowledge to use AIS.

OMCLutfi et al. (2020)

OMC1. We consider AIS adoption important.OMC2. We are active engagement in planning and using AIS.OMC3. We support the management shows regarding the deployment and the planning of AIS.OMC4. We are committed to encourage and support the AIS usage by staff.OMC5. We are committed to correctly implement every available resource to use AIS successfully.OMC6. We overcome the hurdles present due to natural resistance to technology usage.

GSLutfi et al. (2020)

GS1. Government support plays an important role in encouraging and promoting the use of AIS.GS2. Government policies and regulations vary from one industry to another that affect the use of AIS.GS3. Government policies and regulations vary from one country to another that affect the use of AIS.

AISULutfi et al. (2020)

AISU1. Information-related needs for reporting dissemination.AISU2. Non-economic information needs, information risk analysis.AISU3. Information needs related to business decisions.AISU4. Ability to respond to information related to business decisions.AISU5. The ability to respond to information related to notification dissemination.AISU6. Ability to respond to analytic risk and non-economic information.AISU7. The ability to reply to informational links to other issues.

AISELutfi et al. (2020)

AISE1. AIS is a data collection, storage, recording and processing system to generate information fordecision managers.AISE2. Minimize uncertainty in decision making improve the ability to plan and control activities.AISE3. AIS supports SMEs growth in terms of sales, revenue and customers. Provide information tointernal and external audiences.AISE4. Improve user satisfaction, reduce errors, and improve information availability.AISE5. Reduce costs, reduce time, save human resources for businesses to use.AISE6. AIS is a connection tool for management systems and operational systems.

Economies 2022, 10, 83 17 of 19

Table A1. Cont.

Study Measures Measurement Items

CVNagel (2020)

CV1. COVID-19 accelerating digital transformation work-from-anywhere (work from home, no globalbarrier, work-life balance, flexible work arrangement, time-saving as no commuting needed, . . . ).CV2. COVID-19 accelerating digital transformation provides benefits of innovative business model (runbusiness remotely, evolution of product, service and processes, online transaction improvement, drivinginnovative solutions, . . . ).CV3. COVID-19 accelerating digital transformation provides benefits of technologies, automation andcollaboration (telecommuting, virtual workplace, mobility, IT security, the wise use of scrum, . . . ).

OEA Ali and AlSondos

(2020)

OE1. Customer satisfaction.OE2. Employee Ethics.OE3. Enterprise market share.OE4. The growth of sales.OE5. Profits of the business.

ReferencesA Ali, Basel J., and Ibrahim A. Abu AlSondos. 2020. Operational Efficiency and the Adoption of Accounting Information System (Ais):

A Comprehensive Review of the Banking Sectors. International Journal of Management 11: 221–34.ACCA_GLOBAL. 2016. Professional Accountants—The Future: Drivers of Change and Future Skills. London: ACCA_GLOBAL.Acedo, Francisco José, Carmen Barroso, and Jose Luis Galan. 2006. The resource-based theory: Dissemination and main trends.

Strategic Management Journal 27: 621–36. [CrossRef]Al Nahian Riyadh, Md, Shahriar Akter, and Nayeema Islam. 2009. The adoption of e-banking in developing countries: A theoretical

model for SMEs. International Review of Business Research Papers 5: 212–30.Al-Alawi, Adel Ismail, and Faisal M. Al-Ali. 2015. Factors affecting e-commerce adoption in SMEs in the GCC: An empirical study of

Kuwait. Research Journal of Information Technology 7: 1–21. [CrossRef]Ali, Azwadi, Mohd Shaari Abdul Rahman, and WNSW Ismail. 2012. Predicting continuance intention to use accounting information

systems among SMEs in Terengganu, Malaysia. International Journal of Economics and Management 6: 295–320.Ali, B. J., Wan Ahmad Wan Omar, and Rosni Bakar. 2016. Accounting Information System (AIS) and organizational performance:

Moderating effect of organizational culture. International Journal of Economics, Commerce and Management 4: 138–58.Ali, Basel J. A., Anas A. Salameh, and Mohammad Salem Oudat. 2020. The relationship between risk measurement and the accounting

information system: A review in the commercial and islamic banking sectors. PalArch’s Journal of Archaeology of Egypt/Egyptology17: 13276–90.

Awa, Hart O., Ojiabo Ukoha, and Sunny R. Igwe. 2017. Revisiting technology-organization-environment (TOE) theory for enrichedapplicability. The Bottom Line 30: 2–22. [CrossRef]

Barney, Jay. 1991. Firm resources and sustained competitive advantage. Journal of Management 17: 99–120. [CrossRef]Baumane-Vitolina, Ilona, and Igo Cals. 2013. Theoretical framework for using resource based view in the analysis of SME innovations.

European Scientific Journal, 9.Beland, Louis-Philippe, Oluwatobi Fakorede, and Derek Mikola. 2020. Short-term effect of COVID-19 on self-employed workers in

Canada. Canadian Public Policy 46: S66–S81. [CrossRef]Bhattacherjee, Anol. 2001a. An empirical analysis of the antecedents of electronic commerce service continuance. Decision Support

Systems 32: 201–14. [CrossRef]Bhattacherjee, Anol. 2001b. Understanding information systems continuance: An expectation-confirmation model. MIS Quarterly 25:

351–70. [CrossRef]Churchill, Gilbert A., Jr. 1979. A paradigm for developing better measures of marketing constructs. Journal of Marketing Research 16:

64–73. [CrossRef]CISCO. 2020. Asia Pacific SMB Digital Maturity Study. Available online: https://www.cisco.com/c/dam/global/en_sg/solutions/

small-business/pdfs/ebookciscosmbdigitalmaturityi5-with-markets.pdf (accessed on 11 November 2021).Damanpour, Fariborz, and Marguerite Schneider. 2006. Phases of the adoption of innovation in organizations: Effects of environment,

organization and top managers. British Journal of Management 17: 215–36. [CrossRef]Fornell, Claes, and David F. Larcker. 1981. Evaluating structural equation models with unobservable variables and measurement error.

Journal of Marketing Research 18: 39–50. [CrossRef]Grandon, Elizabeth E., and J. Michael Pearson. 2004. Electronic commerce adoption: An empirical study of small and medium US

businesses. Information & Management 42: 197–216.Grover, Varun, and Martin D. Goslar. 1993. The initiation, adoption, and implementation of telecommunications technologies in US

organizations. Journal of Management Information Systems 10: 141–64. [CrossRef]Hair, Joseph F., Jr., G. Tomas, M. Hult, Christian M. Ringle, and Marko Sarstedt. 2016. A Primer on Partial Least Squares Structural

Equation Modeling, 2nd ed. Thousand Oaks: SAGE Publications, p. 390.

Economies 2022, 10, 83 18 of 19

Hair, Joseph F., Jr., Marko Sarstedt, Christian M. Ringle, and Siegfried P. Gudergan. 2017. Advanced Issues in Partial Least SquaresStructural Equation Modeling. Thousand Oaks: SAGE Publications.

Hair, Joseph F., Jr., G. Tomas, M. Hult, Christian M. Ringle, Marko Sarstedt, Nicholas P. Danks, and Soumya Ray. 2021. An introductionto structural equation modeling. In Partial Least Squares Structural Equation Modeling (PLS-SEM) Using R. Berlin/Heidelberg:Springer, pp. 1–29.

Hansen, D., M. Mowen, and L. Guan. 2007. Cost Management: Accounting & Control, 6th ed. Mason: South-Western Cengage Learning.Henderson, Dave, Steven D. Sheetz, and Brad S. Trinkle. 2012. The determinants of inter-organizational and internal in-house adoption

of XBRL: A structural equation model. International Journal of Accounting Information Systems 13: 109–40. [CrossRef]Hermann, Mario, Tobias Pentek, and Boris Otto. 2016. Design principles for industrie 4.0 scenarios. Paper presented at the 2016 49th

Hawaii International Conference on System Sciences (HICSS), Koloa, HI, USA, January 5–8.Khairi, Mohammad Shadiq, and Zaki Baridwan. 2015. An empirical study on organizational acceptance accounting information

systems in Sharia banking. The International Journal of Accounting and Business Society 23: 97–122.Koli, L. N., and B. Rawat. 2011. Measuring of operational efficiency and its impact on overall profitability. A Case Study of BPCL.

BVIMR Management Egde 4: 105–14.Kouser, Rehana, Gul Rana, and Farasat Ali Shahzad. 2011. Determinants of AIS effectiveness: Assessment thereof in Pakistan.

International Journal of Contemporary Business Studies 2: 6–21.Kozlenkova, Irina V., Stephen A. Samaha, and Robert W. Palmatier. 2014. Resource-based theory in marketing. Journal of the Academy of

Marketing Science 42: 1–21. [CrossRef]Limayem, Moez, and Christy M. K. Cheung. 2008. Understanding information systems continuance: The case of Internet-based

learning technologies. Information & Management 45: 227–32.Lutfi, Abd Alwali, Kamil Md Idris, and Rosli Mohamad. 2017. AIS usage factors and impact among Jordanian SMEs: The moderating

effect of environmental uncertainty. Journal of Advanced Research in Business and Management Studies 6: 24–38.Lutfi, Abdalwali, Manaf Al-Okaily, Adi Alsyouf, Abdallah Alsaad, and Abdallah Taamneh. 2020. The impact of AIS usage on AIS

effectiveness among Jordanian SMEs: A multi-group analysis of the role of firm size. International Journal of Sociology and SocialPolicy 40: 861–75. [CrossRef]

Maryeni, Yen Yen, Rajesri Govindaraju, Budhi Prihartono, and Iman Sudirman. 2014. E-commerce adoption by Indonesian SMEs.Australian Journal of Basic and Applied Sciences 8: 45–49.

Mcmahon, Richard G. P. 2001. Growth and performance of manufacturing SMEs: The influence of financial management characteristics.International Small Business Journal 19: 10–28. [CrossRef]

Minishi-Majanja, Mabel K., and Joseph Kiplangat ’. 2005. The diffusion of innovations theory as a theoretical framework in library andinformation science research. South African Journal of Libraries and Information Science 71: 211–24. [CrossRef]

Molino, Monica, Emanuela Ingusci, Fulvio Signore, Amelia Manuti, Maria Luisa Giancaspro, Vincenzo Russo, Margherita Zito, andClaudio G. Cortese. 2020. Wellbeing costs of technology use during COVID-19 remote working: An investigation using theItalian translation of the technostress creators scale. Sustainability 12: 5911. [CrossRef]

Momani, Alaa M., Mamoun M. Jamous, and Shadi M. S. Hilles. 2017. Technology acceptance theories: Review and classification.International Journal of Cyber Behavior, Psychology and Learning 7: 1–14. [CrossRef]

Nagel, Lisa. 2020. The influence of the COVID-19 pandemic on the digital transformation of work. International Journal of Sociology andSocial Policy. [CrossRef]

Nasiren, M. D. A., M. N. Abdullah, and Mohd Asmoni. 2016. Critical Success Factors on the BCM Implementation in SMEs. Journal ofAdvanced Research in Business and Management Studies 3: 105–22.

Nastase, Carmen Eugenia, Ancuta Lucaci, and Carmen Chas, ovschi. 2020. Circular economy: A perspective for the transformation ofrural built heritage in Europe. Paper presented at Competitiveness and Sustainable Development, Chisinău, Moldova, November20.

Nunnally, Jum C. 1978. Psychometric Theory, 2nd ed. New York: McGraw Hill.Pedró, Francesc. 2020. COVID-19 y educación superior en América Latina y el Caribe: Efectos, impactos y recomendaciones políticas.

Análisis Carolina 36: 1–15. [CrossRef]Premkumar, G., and Margaret Roberts. 1999. Adoption of new information technologies in rural small businesses. Omega 27: 467–84.

[CrossRef]Rahayu, Rita, and John Day. 2015. Determinant factors of e-commerce adoption by SMEs in developing country: Evidence from

Indonesia. Procedia-Social and Behavioral Sciences 195: 142–50. [CrossRef]Ramdani, Boumediene, and Peter Kawalek. 2007. SME adoption of enterprise systems in the Northwest of England. Paper presented

at IFIP International Working Conference on Organizational Dynamics of Technology-Based Innovation, Manchester, UK, June14–16.

Rogers, Everett M. 2010. Diffusion of Innovations. New York: Simon and Schuster.Rozzani, Nabilah, and Rashidah Abdul Rahman. 2013. Determinants of bank efficiency: Conventional versus Islamic. International

Journal of Business and Management 8: 98–109. [CrossRef]Scherer, Ronny, Fazilat Siddiq, and Jo Tondeur. 2019. The technology acceptance model (TAM): A meta-analytic structural equation

modeling approach to explaining teachers’ adoption of digital technology in education. Computers & Education 128: 13–35.

Economies 2022, 10, 83 19 of 19

Spurk, Daniel, and Caroline Straub. 2020. Flexible Employment Relationships and Careers in Times of the COVID-19 Pandemic. Amsterdam:Elsevier, p. 103435.

Stuerz, Roland, Christian Stumpf, Ulrike Mendel, and Dietmar Harhoff. 2020. Digitalisierung durch Corona?—Verbreitung undAkzeptanz von Homeoffice in Deutschland: Ergebnisse zweier bidt-Kurzbefragungen. bidt Analysen und Studien.

To, March L., and Eric W. T. Ngai. 2006. Predicting the organisational adoption of B2C e-commerce: An empirical study. IndustrialManagement & Data Systems 106: 1133–47.

Tornatzky, Louis G., Mitchell Fleischer, and Alok K. Chakrabarti. 1990. Processes of Technological Innovation. Lanham: Lexington Books.Tu, Trương Văn. 2020. Nghiên cứu áp dụng hệ thống thông tin kế toán trong các doanh nghiệp nhỏ và vừa ở Việt Nam. Tạp Chí Tài

Chính 4: 17–20.Vietnam News. 2021. Guidebook on Digital Transformation for Businesses Published. Vietnamnews, June 16.Wong, Ken Kwong-Kay. 2013. Partial least squares structural equation modeling (PLS-SEM) techniques using SmartPLS. Marketing

Bulletin 24: 1–32.Word Bank. 2021. The Word Bank in Vietnam. Washington, DC: Word Bank.Zhu, Kevin, and Kenneth L. Kraemer. 2005. Post-adoption variations in usage and value of e-business by organizations: Cross-country

evidence from the retail industry. Information Systems Research 16: 61–84. [CrossRef]Zhu, Kevin, Kenneth L. Kraemer, and Sean Xu. 2006. The process of innovation assimilation by firms in different countries: A

technology diffusion perspective on e-business. Management Science 52: 1557–76. [CrossRef]