Methanol in Energy - Applications & Experience - Stanford ...

Upload

khangminh22Category

view

1download

0

INTERNATIONAL ASSOCIATION IA FOR ENERGY ECONOMICS EE President Hoesung Lee President-Elect Peter A. Davies Immediate Past President Charles Spierer Past President Dennis J. O’Brien Treasurer Jean-Thomas Bernard Vice President for Development & International Affairs Peter C. Fusaro Vice President for Publications Hossein Razavi Vice President and Secretary Arild N. Nystad Vice President for Conferences Michelle Michot Foss Elected Council Member Michael C. Lynch Elected Council Member Hans Larsen Appointed Council Member Robert Bartels Appointed Council Member David Knapp Appointed Council Member Anthony Owen Appointed Council Member Paul J. Stevens

The Energv Journal is a publication of the Energy Economics Education Foundation, Inc., 28790

Chagrin Blvd., Suite 350, Cleveland, OH, 44122-4630, USA, anon-protit organization, in association with the Intemational Association for Energy Economics.

Membership dues for the IAEE include subscriptions to The Energy Journal and the IAEE

Newsletter. Subscriber & Membership matters should be sent to IAEE, 28790 Chagrin Blvd., Suite 350, Cleveland, OH, 44122, USA; phone (216) 464-5365, fax 464-2737. Non-member subscriptions to The Energy Journal are $175 for institutions, libraries, and individuals. Postage and handling are

paid by the publisher. Outside the United States and Canada, non-member subscriptions are $200. Articles appearing in The Energv Journal are listed in both Environmental Periodicals

Bibliography and The Journal of Economic Literafure and are indexed in SciSearch, Research Alert,

COMPENDEX*PLUS, Energy Abstracis, Ei Page One, PAIS Bulletin, Trade and Industty, DOE

Energv, Energvline, Enviroline, and Wilsonline.

Authorization to photocopy articles published in The Energy Journal for interna1 or personal use,

or the interna1 or personal use of specific clients, is granted by IAEE provided that you register with the Copyright Clearance Center, 222 Rosewood Drive, Danvers, MA 01923. CCC’s phone number is (978) 750-8400. The Energy Journal is available in referente systems (e.g. microfilm, CD-ROM,

full text etc.) produced by the Information Access Company (IAC), University Microfilms Inc. (UMI), and the H.W. Wilson Company’s Business Periodicals Index. For further information please

contact IAC at (415)-378-5000, UMI at (313)-761-4700, or H.W. Wilson Co., at (718)-588+X400.

AUTHORS: Please see back pages for information on the proper style of submissions. ADVERTISING INFORMATION: For a complete media kit, contact Marketing Department, IAEE

Headquarters, 28790 Chagrin Blvd., Ste. 350, Cleveland, OH, 44122-4630. Phone: 216-464-5365, fax: 216-464-2737. E-mail: [email protected]. Homepage: http://www.iaee.org.

Copyright 0 1999 by the International Association for Energy Economics. All rights reserved.

The editors and publisher assume no responsibility for the views expressed by the authors of articles printed in The Energv Journal.

International Standard Serial Number: 0195-6574. Printed in the U.S.A.

Editors, Adonis Yatchew, Campbell Watkins Founding Editor, Helmut J. Frank

European Editor, Yves Smeers Associate Editor, Geoffrey Pearce

Book Review Editor, Richard L. Gordon

Board of Editors

Alexander A. Arbatov Institute for Systems

Studies. Moscow

Lars Bergman Stockllolm scllool

of Economics

Fadhil J. Chalabi Centre for Global Energy

Studies, London

Caro1 Dahl Colorado School of

Mines

Dnvid Dorenfeld Exxon Ventures CIS

Joy C. Dunkerley Washington, DC.

A. Denny Ellerman MIT Center for Energy & Enviromnental Research

Michelle Michot Foss CBA Energy Institute,

University of Houston

Lawrence J. Goldstein Petroleum Industry Research Foundation, Inc.

Richard L. Gordon Pennsylvania State

University

James M. Griffin Texas A & M University

William W. Hogan Harvard University

David Huettner University of Oklahoma

Mark K.Jaccard Simon Fraser University British Columbia

Willirm A. Johnson JECOR, Saudi Arabia

J. Daniel Khazzoom San Jose State University

Jean Masseron Institut Francais du Petrole

Kenichi Matsui Institute of Energy Economics, Tokyo

Mohan Munasinghe The World Bank

Washington, DC

Peter R. Odell Erasmus Universiteit

R.K. Pachauri TATA Energy Research Institute, New Delhi

Frrncisco R. Parra F.R. Parra Inc.

Peter Pearson Imperial College of Science, Technology and

Medicine, London

Stephen Peck EPRI, Palo Alto, CA

André Plourde University of Alberta

Hossein Razavi The World Bank Washington, DC

Ali Reza Oakland California

Dieter Schmitt Universität Essen Germany

Margaret Slade University of British Columbia

James L. Smith Southern Methodist University, Dallas

Thomas Sterner Göteborg University

John Surrey University of Sussex United Kingdom

Leonard Waverman London Business School

John P. Weyant Stanford University

Franz Wirl Otto-von-Guericke

University of Magdeburg

Chi-Keung Woo Energy and Environmental

Economics. 111~.

ii

THE COSTS OF THE KYOTO PROTOCOL A MULTI-MODEL EVALUATION

A Special Issue of The Energy Journal

GUEST EDITOR

JOHN P. WEYANT Director, Energy Modeling Forum Stanford University

Assisted by

Henry Jacoby Massachusetts Institute of Technology James Edmonds Batelle Pacijk Northwest National Laboratory Richard Richels Electric Power Research Institute

Publication of this special issue was made possible by generous financia1 support from the U 3. DEPARTMENT OF ENERGY, THE U.S. ENVIRONMENTAL PROTECTION AGENCY, AND THE ELECTRIC POWER RIBEARCH INSTITUTE. The studies of the Energy Modeiing Forum are sponsored by the U.S DOE, U.S. EPA, EPRI, Mitsubishi Corporation, the New Energy and Industrial Technology Development Organization of Japan, and about 20 corporate afftliates.

. . . III

THE ENERGY JOURNAL

SPECIAL ISSUE

THE COSTS OF THE KYOTO PROTOCOL: A MULTI-MODEL EVALUATION

Table of Contents

Preface Campbell Watkins vi

Introduction and Overview John P. Weyant and Jennifer N. Hill vii

The Kyoto Protocol: A Cost-Effective Strategy for Meeting Environmental Objectives? Alan S. Manne and Richard Richels 1

The Economics of the Kyoto Protocol Christopher N. MacCracken, James A. Edmonds,

Son H, Kim, and Ronald D. Sands 25

Adjustment Time, Capital Malleability and Policy Cost Henry D. Jacoby and lan Sue Wing 73

Requiem for Kyoto: An Economic Analysis of the Kyoto Protocol William D. Nordhaus and Joseph G. Boyer 93

Kyoto, Effkiency, and Cost-Effectiveness: Applications of FUND Richard S.J. Tol 13 1

Analysis of Carbon Emission Stabilization Targets and Adaptation by Integrated Assessment Model Atsushi Kurosawa, Hiroshi Yagita, Zhou Weisheng

Koji Tokimatsu, and Yukio Yanagisawa 157

Clubs, Ceilings and CDM: Macroeconomics of Compliance with the Kyoto Protocol Johannes Bollen, Arjen Gielen, and Hans Timmer 177

iv

Analysis of Post-Kyoto Scenarios: The Asian-Pacific Integrated Model Mikiko Kainuma, Yuzuru Matsuoka, Tsuneyeki Morita 207

Effects of Restrictions on International Permit Trading: The MS-MRT Model Paul M. Bernstein, W. David Montgomery, Thomas F. Rutherford and Gui-Fang Yang 221

The Kyoto Protocol: An Economic Analysis Using GTEM Vivek Tulpulé, Stephen Brown, Jaekyu Lim,

Cain Polidano. Hom Pant and Brian S. Fisher 257

Emissions Trading, Capital Flows and the Kyoto Protocol Warwick McKibbin, Martin Ross, Robert Shackleton and Peter Wilcoxen 287

The Economic Implications of Reducing Carbon Emissions: A Cross-Country Quantitative Investigation using the Oxford Global Macroeconomic and Energy Model Adrian Cooper, Scott Livermore, Vanessa Rossi,

Alan Wilson and John Walker 335

CO, Emissions Control Agreements: Incentives for Regional Participation Stephen C. Peck and Thomas J. Teisberg 367

About the Authors

Short biographies of the contributing authors 391

Preface

The Kyoto Protocol dealing with climate change was adopted in December, 1997. Over a year later 84 countries have signed, but only eight had ratified it. Getting agreement among Protocol participants is one thing; achieving ratification is quite another.

The main culprit targeted is carbon dioxide emissions from fossil fuels. A five percent reduction from 1990 emission levels to be reached about a decade from now seems modest. Not so. Given actual economic growth since 1990 and anticipated growth, the ‘Kyoto Gap’ could be as much as 30 percent from base line emissions expected by 2010.

Implementing the Protocol will require prodigious efforts. Hence the importance of attempts to measure the magnitude, severity and incidence of meeting the Kyoto targets. This special issue of i%e Energy Journal, edited by John Weyant of Stanford University with assistance from Henry Jacoby of MIT, Jae Edmonds of Batelle and Richard Richels of EPRI, provides international simulations of implementing the Kyoto agreement using several different models. The canvas is wide. The modeling tapestry is rich. The results provide both focus and perspective.

I think I am right in saying that this volume is the longest E,yergy Journal Special Issue to date. It could not have been produced wi.thout substantial financial support from the Electric Power Research Institute, the US Department of Energy and the US Environmental Protection Agency. We are in their debt.

G. Campbell Wtztkins Joint Bditor

The Energy Journal

vi

INTRODUCTION AND OVERVIEW

John P. Weyant and Jennifer N. Hill*

This Special Issue of 27ze Energy Journal represents the first comprehensive report on a comparative set of analyses of the economic and energy sector impacts of the Kyoto Protocol on Climate Change. Organized by the Stanford Energy Modeling Forum (EMF), the objectives of this study were the same as for previous EMF studies: (1) identifying policy-relevant insights and analyses that are robust across wide ranges of models, (2) providing explanations for differences in results from different models, and (3) identifying high priority areas for future research. This study has produced a particularly rich set of results in all three areas, which is a tribute to the active participation of the modeling teams and the care each team took in preparing a paper for this volume.

The volume consists of a paper prepared by each modeling team on what it did and what it concluded from the model runs that were undertaken, proceeded by this introduction and summary paper. This summary focuses on the motivation for the study, the design of the study scenarios, and the interpretation of results for the four core scenarios, which all the teams ran. Each succeeding chapter contains ideas and insights drawn by the modeling teams from applying their models to issues they were able to address selected from a small set of important areas on which the group had mutually agreed to focus.

Ihe Energy Journal, Kyoto Special Issue. Copyright Q 1999 by the IAEE. All rights reserved.

* Department of Engineering-Economic Systems and Operations Research, Stanford University,

Stanford, CA 94305-4023. E-mail: [email protected].

The studies of the Energy Modeling Forum are sponsored by the U.S. Department of Energy, the

U.S. Environmental Protection Agency, the Electric Power Research Institute, Mitsubishi

Corporation, the New Energy and Industrial Technology Development Organization of Japan, and

about 20 corporate affiliates. Besides the authors of the other papers in this volume, we would

especially like to thank Campbell Watkins for his enthusiasm about the idea of doing this specia.1

issue and his insightful advice at each step in the production process. In addition, we would like to

thank Geoff Pearce of the Energy Journal and Dave Williams of the IAEE for going above and

beyond the call of duty in making this special issue a reality.

vii

viii / The Energy Journal

The reader is cautioned not to view the wide range of model results presented here as an expression of hapless ignorance on the part of the analysts, but as a manifestation of the uncertainties inherent in projecting how the future will unfold with and without climate change policies. The uncertainties highlighted here are endemic in the operation of our world or the result of limitations in our understanding it. The models do not produce lthese uncertainties. They make them more transparent and help assess their magnitudes. This is important in the analyses of climate policies because of the complexities and interdependencies involved.

The climate change debate is often posed as an all or nothing choice about whether or not we are serious about a problem that could have disastrous consequences. However, we know that the problem may turn out to be more or less serious than currently envisioned and that we can change our course of action in subsequent years as more is learned about the nature of the problem and its potential solutions. It is also often asserted that the models do not provide useful information because they sometimes produce different results. No thing could be further from the truth; by comparing results from alternative modeling systems we gain additional information about the relationships between assumptions and outputs that are not available when results from a single model or a single expert are considered.

This introduction starts with a brief discussion of the UN Framework Convention on Climate Change (UNFCCC); the Conference of Parties process set out in the UNFCCC, the Kyoto Protocol, and the Buenos Aires agenda. Next the scenarios designed by the group to address some of the key uncertainties about how the Protocol might be implemented are described, followed by brief overviews of mitigation economics and a structural comparison of the models included in the comparison. A summary of key common results and interpretations of model differences that were developed this from a review of results for the core scenarios follows. Finally, an overview of the papers by the participating modeling teams, stressing issues focused on and insights obtained, completes the process of setting the stage for the papers prepared by the modeling teams which follow.

A BRIEF HISTORY OF THE FCCC AND THE KYOTO PROTOCOL

The United Nations Framework Convention on Climate Change was adopted on May 9, 1992, and was opened for signature at the UN Conference on Environment and Development in June 1992. The Convention entered into force on March 21, 1994, 90 days after receipt of the 50th ratification. Currently, 176 countries have ratified it. One of the key elements of the UNFCCC was a set of voluntary commitments to stabilize carbon emissions at 1990 levels by 2000 by the developed countries listed in Annex I of the Convention document (dominantly the OECD countries, the countries in Eastern

Introduction / ,k

Europe and the states of the former Soviet Union-e.g., the Russian Federation, the Ukraine, Belarus, etc.-which, thus, became known as the “Annex I” countries).

The first meeting of the Conference of the Parties to the FCCC (COP- 1) took place in Berlin from March 28 - April 7, 1995. In addition to addressing a number of important issues related to the future of the Convention, delegates reached agreement on what many believed to be the central issue before COP- 1 -adequacy of commitments, the “Berlin Mandate” to establish binding emission limitations for Annex I countries beyond the year 2000. At that point, an open-ended Ad Hoc Group on the Berlin Mandate (AGBM) was established to begin a process toward appropriate action for the period beyond 2000, including the strengthening of the commitments of Annex I Parties through th.e adoption of a protocol or other legal instrument. COP-I also requested th.e Secretariat to make arrangements for sessions of a Subsidiary Body on Scienc:e and Technological Advice (SBSTA) and a Subsidiary Body on Implementation (SBI). SBSTA would serve as the link between scientific, technical and technological assessments, the information provided by competent international bodies, and the policy-oriented needs of the COP. During the AGBM process, SBSTA addressed several issues, including the treatment of the Intergovernmental Panel on Climate Change’s (IPCC’s) Second Assessment Report (SAR). SBI was created to develop recommendations to assist the COP in the review and assessment of the implementation of the Convention and in the preparation and implementation of its decisions.

The AGBM met eight times between August 1995 and December 1997. During the first three sessions, delegates focused on analyzing and assessing possible policies and measures to strengthen the commitments of AMeX I Parties, how Annex I countries might distribute or share new commitments and whether commitments should take the form of an amendment or Protocol. AGBM4, which coincided with COP-2 in Geneva in July 1996, completed its in-depth analysis of the likely elements of a Protocol and the participating States appeared ready to prepare a negotiating text. At AGBM-5, which met in December 1996, delegates recognized the need to decide whether or not to allow mechanisms that would provide Annex I Parties with flexibility in meeting quantified emission limitation and reduction objectives (QELROs).

As a Protocol on climate change was drafted during the sixth and seventh sessions of the AGBM, in March and August of 1997, respectively, delegates created a negotiating text by merging or eliminating some overlapping provisions within the myriad of proposals. Much of the discussion centered on a proposal from the European Union (EU) for a 15% cut in a “basket” of three greenhouse gases by the year 2010 relative to 1990 levels. In October 1997, as AGBM-8 began, U.S. President Bill Clinton made a call for “meaningful participation” by developing countries in the negotiating position he announced

x / The Energy Journal

in Washington. This statement rekindled some of the major debates that had preceded the tentative agreement reached agreement in 1995; G-77/Chins* involvement was once again linked to the level of commitment acceptable to the US. In response, the G-77/Chins distanced itself from anything that could be interpreted as new commitments.

The Third Conference of the Parties (COP-3) to the FCCC was held from December l-l 1, 1997 in Kyoto, Japan. Over 10,000 participants, including representatives from governments, intergovernmental organizations, Non- Government Organizations (NGOs) and the press, attended the Conference, which included a high-level segment featuring statements from over 125 ministers. Following a week and a half of intense formal and infalrmal negotiations, Parties to the FCCC adopted the Kyoto Protocol on December 11, 1997; it was opened for signature on March 16, 1998 at United Nations Headquarters, New York.

The Protocol is subject to ratification, acceptance, approval or acce:ssion by Parties to the Convention. It enters into force on the ninetieth day after the date on which not less than 55 Parties to the Convention, incorporating Annex I Parties which accounted in total for at least 55 percent of the total carbon dioxide emissions for 1990 from that group, have deposited their instruments of ratification, acceptance, approval or accession. As of March 15, 1999, 84 countries had signed the Kyoto Protocol, but only the Maldives, Antigua and Barbuda, El Salvador, Panama, Fiji, Tulvalu, and Trinidad and Tobago had ratified it.

The subsidiary bodies of the FCCC met from June 2-12, 1998 in BOM, Germany. These were the first formal FCCC meetings since the adoption of the Kyoto Protocol. SBSTA-8 agreed to draft conclusions on cooperation with relevant international organizations, methodological issues, and education and training. SBI-8 reached conclusions on, national communications, the financial mechanism and the second review of adequacy of Annex I Party commitments. After joint SBVSBSTA consideration and extensive contact group debates on the flexibility mechanisms, delegates could only agree to a compilation docu.ment containing proposals from the G- 77/Chins, the EU and the US on the issues for discussion and frameworks for implementation.

The Fourth Conference of the Parties to the UNFCCC (COP-4) met in Buenos Aires from November 2-13, 1998 concluding in the early hours of Saturday morning of November 141h with the adoption a ‘Buenos Aires Action Plan’ establishing deadlines for finalizing work on the Kyoto Mechanisms (joint implementation, emissions trading and the clean development mechanism), compliance issues and policies and measures.

1. The G-77 was originally a group of 77 developing countries, but now refers to a coalition of

virtually all non-Annex I countries except China which joins it in supporting positions OEI many

matters.

Introduction / xi

KEY FEATURES OF THE KYOTO PROTOCOL’

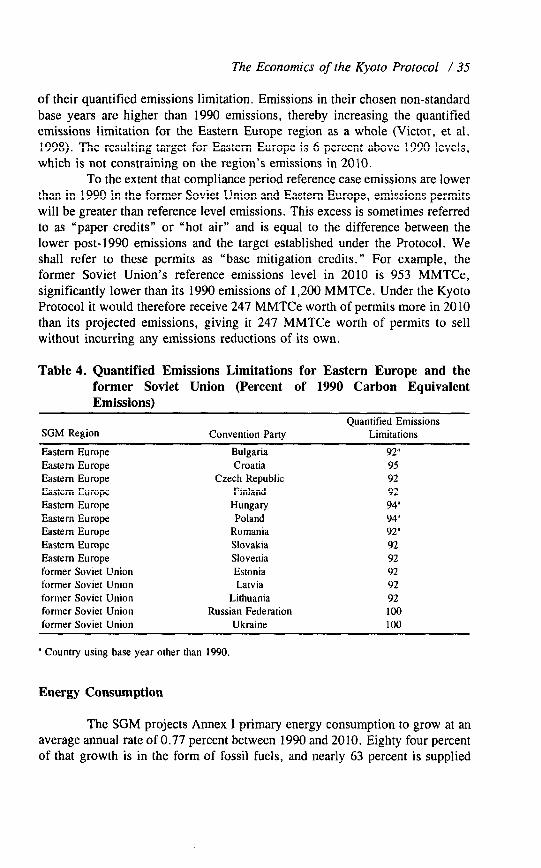

The most prominent feature of the Kyoto Protocol is the quantified emissions limitations and reduction commitments. Thirty-nine parties accepted quantified emissions limitations or reduction commitments, which would result in emissions of greenhouse gases from Annex 1 countries in 2008-2012 being about 5 percent below their 1990 level.3 We can summarize the obligations as follows.

Western European nations accepted an 8 percent reduction relative to 1990 emissions, with the exception of Iceland and Norway which were allowed 110 and 101 percent of 1990 emissions respectively.

Eastern European nations generally had the same obligation as Western European nations with some exceptions-Croatia was 95 percent, and Hungary and Poland were 94 percent of base year emissions. Note that the base year for the countries in this region need not be 1990, but could be a later date like 1995.

The Russian Federation and Ukraine were allowed 1990 emissions levels, while Latvia, Estonia and Lithuania agreed to 8 percent reductions.

Japan and Canada agreed to a 6 percent reduction from 1990 emissions levels.

The United States of America agreed to reduce emissions 7 percent below 1990 levels. And,

Australia was allowed to increase emissions 8 percent above 1990 levels and New Zealand was allowed to emit up to 1990 levels.

2. This section was provided by the group that authored MacCracken. et al. in this volume.

3. The Kyoto Protocol actually prescribes emissions limitations for countries listed in Annex 13

to the Protocol. These countries are: Australia, Austria, Belgium, Bulgaria, Canada, Croatia, Czech

Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy,

Japan, Latvia, Liechtenstein, Lithuania, Luxembourg, Monaco, Netherlands, New Zealand, Norway,

Poland, Portugal, Romania, Russian Federation, Slovakia, Slovenia, Spain, Sweden, Switzerland,

Ukraine, United Kingdom, and the United States. This list varies somewhat from the countries

contained in Annex I to the 1992 Framework Convention (FCCC). Several countries such as

Slovakia, Slovenia, Liechtenstein, and Monaco have been added, while Belarus and Turkey are listed

in Annex I of the FCCC but not Annex B of the Kyoto Protocol. In this volume we generally refer

only to Annex I. This yields results that are approximately the same as for Annex B in the

aggregate.

xii / The Energy Journal

In the Protocol, emissions are defined in terms of a basket of six gases: carbon dioxide (CO?), methane (CH,), nitrous oxide (N,O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), and sulfur hexaflouride (SF,). Gases are compared to each other using global warming potential (GWP) coefficients as developed by the IPCC. The use of GWPs allows for the aggregation of the six greenhouse gases specified in the Protocol into a single value based on the carbon equivalent of each gas. Carbon dioxide emissions lead to well over half of the increase in radiative forcing that is taking place today and that share is likely to increase in the future. Thus, although reductions in several of these gases could be significant in meeting the objectives of the Kyoto Protocol, reductions in CO, emissions will be the most significant.

Another feature of the Kyoto Protocol is the treatment of emissions of greenhouse gases from land-use change. A very complicated set of rules was developed which addresses both political and scientific concerns. They describe how nations compute their base year emissions, against which all future mitigation is measured.

The principle of international emissions trading was established in the Kyoto Protocol. However, several important issues were left unresolved. Emissions trading could occur within or between Annex I parties. Within a nation, domestic permit trading could take place among firms or other groups to which permits are allocated. Similarly, permit trading could take place among firms or governments of different nations in an international permit market. Specific arrangements under which trade would occur, however, are left to be worked out in the future. The Protocol also established the principle that, “trading shall be supplemental to domestic actions for the purpose of meeting quantified emission limitation and reduction.” Therefore, limits may be established in the use of emissions trading to satisfy a commitment.

The Protocol also established a Clean Development Mechanism (CDM). The CDM was created “to assist Parties not included in Annex I in achieving sustainable development and in contributing to the ultimate objective of the Convention, and to assist Parties included in Annex I in achieving compliance with their quantified emission limitation and reduction commitments under Article 3.” It allows emissions mitigation credits to be developed by non-Annex I parties beginning in the year 2000, as long as these activities are supplemental to activities that would have been undertaken in the normal course of events. It also identified a certification authority to insure that emissions mitigation activities were in fact real and supplemental. As with emissions trading, the rules are left to be developed in subsequent deliberations. Further, the degree to which this mechanism can capture emissions mitigation potential outside Annex I remains unclear. Unlike the Montreal Protocol, which established sanctions for non-compliance, the Kyoto Protocol establishes no such penalties.

Introduction / xiii

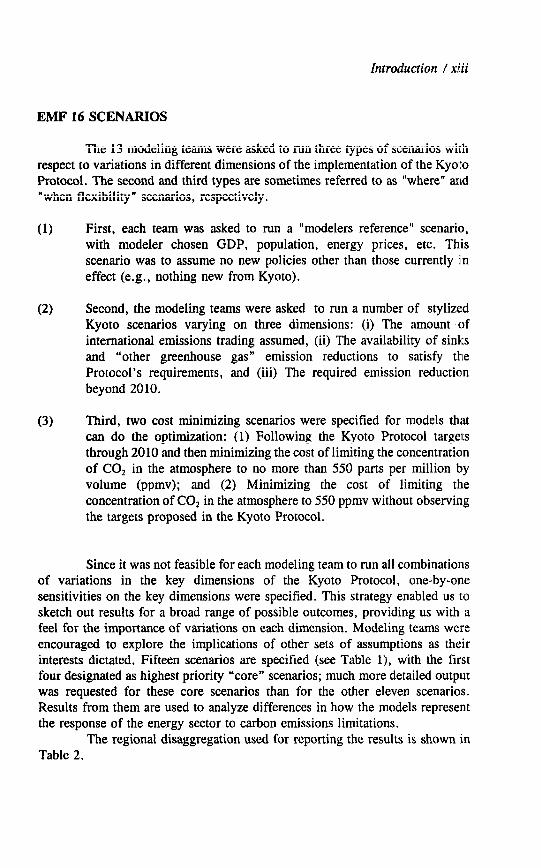

EMF 16 SCENARIOS

The 13 modeling teams were asked to run three types of scenarios with respect to variations in different dimensions of the implementation of the Kyo to Protocol. The second and third types are sometimes referred to as “where” and “when flexibility” scenarios, respectively.

(1) First, each team was asked to run a “modelers reference” scenario, with modeler chosen GDP, population, energy prices, etc. This scenario was to assume no new policies other than those currently in effect (e.g., nothing new from Kyoto).

(2) Second, the modeling teams were asked to run a number of stylized Kyoto scenarios varying on three dimensions: (i) The amount of international emissions trading assumed, (ii) The availability of sinks and “other greenhouse gas” emission reductions to satisfy the Protocol’s requirements, and (iii) The required emission reduction beyond 2010.

(3) Third, two cost minimizing scenarios were specified for models that can do the optimization: (1) Following the Kyoto Protocol targets through 2010 and then minimizing the cost of limiting the concentration of CO2 in the atmosphere to no more than 550 parts per million by volume (ppmv); and (2) Minimizing the cost of limiting the concentration of CO2 in the atmosphere to 550 ppmv without observing the targets proposed in the Kyoto Protocol.

Since it was not feasible for each modeling team to run all combinations of variations in the key dimensions of the Kyoto Protocol, one-by-one sensitivities on the key dimensions were specified. This strategy enabled us to sketch out results for a broad range of possible outcomes, providing us with a feel for the importance of variations on each dimension. Modeling teams were encouraged to explore the implications of other sets of assumptions as their interests dictated. Fifteen scenarios are specified (see Table l), with the fit% four designated as highest priority “core” scenarios; much more detailed output was requested for these core scenarios than for the other eleven scenarios. Results from them are used to analyze differences in how the models represent the response of the energy sector to carbon emissions limitations.

The regional disaggregation used for reporting the results is shown in Table 2.

xiv / The Energy Journal

Table 1. EMF 16 Kyoto Scenarios

Scenario Emissions Trading

Clean Contribution of Development Sinks and

Post-2010

Mechanism “Other Gases” Objectives

1. Modelers Reference’

2. No Emissions Trading’

3. Full Annex I Trading’

4. Full Global Trading’

5. The Double Bubble

6. Annex I Trading - Limit on Purchases

7. Annex I Trading - Limit on Sales

8. Annex 1 Trading- Limit on Purchases and Sales

9. Annex I Monopoly

10. Annex I + China & India

11. CDM (Clean Development Mechanism)

12. Supply Curves for Sinks and ‘Other GWZS.”

13. Kyoto + 550 ppm

14. Kyoto + Full Annex I Min. Cost 550 ppm Trading

15. Min. Cost Full Annex I Trading

Reference case using your preferred set of population, economic, trade flow, and energy inputs assuming the Kyoto Protocol is never implemented.

None None None Kyoto Forever

Kyoto Forever

Kyoto Forever

Kyoto Forever

Annex I Only

Global

Separate EU and Rest of Annex-I Emissions Trading Bubbles Purchases Limited to 10% of Target Sales Limited to 10% of Target Both Purchases and Sales Limited to 10% of Target Sellers Use Monopoly Power India and China Added to Annex I Trading Regime Full Annex I Trading

Full Annex I Trading

550 ppm Limit

None

None

None

None

None

None

None

None

Non Annex I countries can sell 15% of full global trading sales None

None

None

None

None

None

None

None

None

None

None

None

None

5 %tage point increase in emissions allocations None

None

Kyoto Forever

Kyoto Forever

Kyoto Forever

Kyoto Forever

Kyoto Forever

Kyoto Forever

Kyoto For,ever

Kyoto. then limit CO, ‘10 550 ppmv by any feasible program Kyoto.then min. cost of 550 ppmv Min. cost of 550 ppmv

*Core Scenarios

Introduction / xv

Table 2. EMF 16 Regional Reporting Scheme

Annex 1 Non-Annex I -

US China

OECD-Europe India

Japan Mexico & OPEC

CAN2 (Canada/Australia/New Zealand) ROW (Rest of World)

Japan Non-Annex I Total

OECD Total Non-OECD Total

EEFSU (East Europe and Former Soviet Union) (=Non-Annex I + non-OECD Annex I)

Non-OECD Annex I

Annex I Total

Global Total

INTRODUCTION TO GREENHOUSE GAS MITIGATION ECONOMICS

We can use simple supply and demand economics to introduce some of the key concepts embedded in the models used to compute mitigation costs. Figure 1 shows the supply and demand for energy. For simplicity here we assume a single energy aggregate transacted at a single point in time and space. The supply and demand curves can be the result of either a statistical analysis, an engineering process model, or a combination of the two. If we also assume a uniform carbon content of each unit of energy, this picture also represents the supply and demand for carbon in the form of energy.4

If a tax is imposed on carbon, this creates a gap between the supply and demand price and a reduction in carbon emissions. We can plot the tax/carbon reduction relationship as a marginal cost curve for carbon emission reductions as shown in Figure 2. Note that at this point, unlike the simple fixed coefficients approach used in Figure 1, we could (and will) aggregate across fuels using the more realistic multi-fuel/multi-carbon emission factor formulation actually embedded in the model to generate the aggregate supply curve shown in Figure 2. Among other refinements, this would allow fuel switching from more to less carbon intensive fuels to be considered along side other emission reduction options.

4. Note here we can use the same price/cost axis for carbon as for energy but a linealr

transformation is required.

xvi / The Energy Journal

Figure 1. Supply and Demand for Energy/Carbon

Marginal Cost/Price

($/Gj or ton)

Pe or Pc

Qe or Qc

Figure 2. Marginal Cost Curve for Carbon Emission Reductions

Carbon TaX

Won)

Tax

, Emission Reduction

Reduction In Carbon Emissions (tons)

Introduction / xvii

The carbon tax resulting from any particular policy is an imperfect measure of the welfare costs (or even the total economic costs) of a particular policy. By integrating under the marginal cost curve we can compute a total resource cost estimate that includes the loss of surplus by consumers who are no longer willing to buy the carbon intensive goods at the new price and producers who no longer find it profitable to produce them. To this we would need to add payments for carbon emission rights or receipts from the sale of them to form a simple cost measure that can be easily understood and compared acrclss models. However, this simple cost measure will generally be different from. a more comprehensive measure such as the change in welfare derived fmm changes in consumers’ utility. Divergence between these two cost measures can be attributed to changes in other components that are explicitly included in sorne models, but not in others, yet contribute to overall changes in economic welfare. Examples of such components include changes in the world price of crude oil, the effect of pre-existing energy taxes, and the manner in which carbon tax revenues are recycled. In addition, some representation of consumers’ utilities of consumption and leisure would need to be added to get a consistent and meaningful welfare measure. The size of the carbon tax required is, howeve:r, a good indicator of the size of the economic adjustments required to satisfy the requirements of the Protocol under the alternative international emissions trading regimes.

The benefits from international emissions trading result from differences in the marginal cost of reducing emissions between countries. If the marginal cost in any country participating in the trading regime is higher than in any other participating country, it is advantageous to both countries for the higher cost country to buy emissions rights from the lower cost country at a price that is between the two marginal costs.’ The resulting equilibrium for a simple two country example is shown in Figure 3. Country “a” initially has an emission reduction obligation of % and country “b” an emissions reduction obligation of R,. Without trading, the carbon tax required to meet the obligations would be T, in country a and Tb in country b, and the total cost of the emissions reductions would be A, + AZ in country a, and B, in country b. Since the tax required to meet country b’s obligation is lower than that for country a, if trading is allowed it will be possible for country b to sell emission rights 1.0 country b at a price of Tb,f = T,,,, making both countries better off than without trading. The total amount of emissions reductions must be the same with and without trading, so R,, + R,,, = R, + Rt,. Country a’s marginal cost curve -is now capped at T,,,, and country b receives Tb,l x (Rb,t - R,,) for emission reductions that cost it (Tb,t - T&/2 x (Rb,, - R,,) = B,. So the global cost of reducing emissions is reduced from A, + A2 + B, to A, + B, + B2 for a reduction of A2 - BZ.

5. This is just another example of the gains fmm trade (c.f., Bhagwatti and Scrinivasan, 1983),

albeit for a good that is not now traded.

xviii / The Energy Journal

Figure 3. Two Country Example of International Emissions

Emission

Price TT:,,

Rights

R ..I R. Em ission Reductions Rb R b.l

If we aggregate all regions participating in the trading system together, we can compute similar supply and demand schedules for emissions rights, and corresponding equilibrium emission rights price, P,, as shown in Figure 4. Besides the unconstrained equilibrium, ER, and P,, three other cases are shown in Figure 4. If the supply of emissions rights is restricted to ER,,, a higher price, P,, results. Restrictions on the demand for emission rights, ER,, leads to a lower price, P,,. Finally, if there is a single seller of emission rights or a unified block of sellers, a monopoly price, P, and quantity of emissions rights traded, ER, would result.6

Figure 4. Impact of Restrictions on Emissions Trading and Exercise of Monopoly Power by Sellers

Price of Emission Rights

($/ton)

Prs

Pm

Pu

Prd

ERrd ERrs ERm ERu Emissions Rights Traded (tons)

S=MC

6. For a more in-depth discussion of the monopoly case see Bernstein, et al. in this volume.

Introduction / xix

THE MODELS

Thirteen modeling teams participated in this exercise, with half of them based in the U.S. and half outside of it. Each team made a special effort to run the five scenarios discussed here, and selected additional scenarios to run in accordance with their interests and model capabilities. The models are identified in Table 3. For a list of principal model architects, see the individual papers in the balance of this volume.

Although each model has characteristics that are unique to it and have proven to be extremely valuable for studying certain types of issues, the structures of the models can be put into the five basic categories shown in Table 4, with many of the models now employing combinations of traditional modeling paradigms.

One category of models focuses on carbon as one key input to the economy. These models consider the cost of reducing carbon emissions from an unconstrained baseline via an aggregate cost function in each country/region which takes into account the time lags in the reduction in carbon intensity in response to increases in the price of carbon via a simple vintaging structure. In these models, all industries are aggregated together, and GDP is determined by an aggregate production function with capital, labor, and carbon inputs. These models generally omit inter-industry interactions, include trade in carbon and carbon emissions rights, but not in other goods and services, and assume full employment of capital and labor. The RICE and FUND models are examples of this category of models.

Another closely related category of models focuses heavily on the energy sector of the economy. These models consider the consumption and supplies of fossil fuels, renewable energy sources, and electric power generaticln technologies, as well as energy prices, and transitions to future energy technologies. In general, they explicitly represent capital stock turnover and new technology introduction rate constraints in the energy industries, but take a more aggregated approach in representing the rest of the economy. In these models, all industries are aggregated together, and GDP is determined by an aggregate production function with capital, labor, and energy inputs. These models generally omit inter-industry interactions and assume full employment of capital and labor. The MERGE3, CETA, and GRAPE models are examples of this category of models. MERGE3 and CETA have the same basic structure, but nine and up to four regions respectively. GRAPE includes a somewhat broader set of technology options, including especially carbon sequestration technologies.

xx / The Energy Journal

Table 3. Models Analyzing Post-Kyoto EMF Scenarios - -

Model Acronym

(Full Model Name)

ABARE-GTEM (Global Trade and Environment Model)

-

Home Institution(s)

- Australian Bureau of Agriculture and

Resource Economics

(ABARE, Australia)

AIM National Institute for Environmental -

(Asian-Pacific Integrated Model) Studies (NIES-Japan)

Kyoto University -

CETA Electric Power Research Institute

(Carbon Emissions Trajectory Assessment) Teisberg Associates -

(Climate Framework for Uncertainty,

Negotiation, and Distribution)

G-Cubed

(Global General Equilibrium Growth Model)

Vrije Universiteit Amsterdam

(Netherlands)

- Australian National University

University of Texas

U.S. Environmental Protection Agency

GRAPE Institute for Applied Energy (Japan) -

(Global Relationship Assessment to Protect the Research Institute of Innovative

Environment) Technology for Earth (Japan)

University of Tokyo -

MERGE 3.0 (Model for Evaluating Regional and Global

Stanford University

Effects of GHG Reductions Policies) Electric Power Research Institute

- MIT-EPPA

(EPPA - Emissions Projection and Policy Massachusetts Institute of Technology

Analysis Model) (MIT)

-

MSMHT Charles River Associates

(Multi-Sector - Multi-Region Trade Model) University of Colorado -

Oxford Model (Oxford Economic Forecasting)

Oxford Economic Forecasting

-

RICE

(Regional Integrated Climate and Economy Yale University

Model) -

SGM Batelle Pacific Northwest National

(Second Generation Model) Laboratory -

WorldScan Central Planning Bureau/

Rijksinstituut voor Volksgezondheid en

Milieuhygiene (RIVM) (Netherlands) -

Introduction / yxi

Table 4. Model Types

ENERGY/CARBON MODEL -

Fuel Supplies & Energy

Demands Technology Carbon

by Sector Detail Coefficients

ECONOMY

MODEL

Aggregate CETA

Production/Cost MERGE3

Function GRAPE

Multisector

General

Equilibrium

MIT-EPPA

WorldScan

G-Cubed

ABARE-GTEM

AIM

MS-MRT

SGM

Multisector

Macroeconometric

FUND

RICE

Oxford

A third category of models are those that include multiple economic sectors within a general equilibrium framework, focusing on the interactions of the firms and consumers in various sectors and industries, allowing for inter- industry interactions and international trade in non-energy goods. In these models, adjustments in energy use result from changes in the prices of energy fuels produced by the energy industries included in the inter-industry structure of the model (e.g., coal, oil, gas, electricity), and explicit energy sector capital stock dynamics are generally omitted. These multi-sector general equilibrium models tend to ignore unemployment and financial market effects. The MIT- EPPA, and WorldScan models are examples of this type of model. G-Cubed does consider some unemployment and financial effects and is, therefore, a hybrid general equilibrium/macro-econometric model, G-Cubed, MIT-EPPA, and WorldScan all include trade in non-energy goods.

A fourth basic class of models are those that combine elements of the first two categories. That is, they are multi-sector, multi-region economic models with explicit energy sector detail on capital stock turnover, energy efficiency, and fuel switching possibilities. Examples of this type of hybrid model are the AIM, ABARE-GTEM, SGM and MS-MRT models. These models include trade in non-energy goods, with AIM including energy end-use detail, GTEM and MS-MRT including some energy supply detail, and the SGM considering five separate supply sub-sectors to the electric power industry.

xvii / The Energy Journal

By including unemployment, financial markets, international capital flows, and monetary policy, the Oxford model is the only model included here that is fundamentally macro-economic in orientation. However, as shown in Table 4, the G-Cubed model does consider some unemployment and financial effects, as well as international capital flows.

Given space limitations, it is not possible to give a complete report on what was learned from the model comparisons, but we can give the reader a good feel for the kinds of insights that were developed by focusing on one issue (international emissions trading), and a small number of economic and environment variables (carbon emissions, GDP, total primary energy and carbon taxes/incremental value of carbon emissions). With this background we can also describe what happens when one looks beyond these scenarios/measures in more detail.

BASELINE EMISSION PROJECTIONS

The Kyoto Protocol constrains emissions in certain countries (the developed or Annex I countries) to specified rates in the first budget period (2008-2012). One of the major determinants of the cost of satisfying the constraint in each region is the level of emissions projected to occur in that region in the absence of the constraint during the budget period. Other things being equal, the higher the baseline emissions, the higher the cost of satisfying the constraint. In the EMF 16 study we asked each modeling team to prepare its own reference case (or baseline) projection of carbon emissions in each world region.

Reference case carbon emission projection results for Annex I (approximately the same as Annex B) in the aggregate are shown here in Figure 5. The corresponding Reference case carbon emission projection results for the four OECD regions-the United States, the European Union, Japan, and CANZ (Canada, Australia and New Zealand) are shown in Figure 6. A wide range of projected carbon emissions reveals itself by the latter part of the next century, but even by the time of the first (and only) budget period covered by the Kyoto Protocol (2008-2012), significant differences are observed.

These differences are the result of different assumptions about economic growth, fuel costs, capital stock turn over, etc. Figure 7 shows how reference case GDP, Total Primary Energy, and carbon emissions are projected to change between 1990 and 2010 in each model. These differences are analyzed more fully in EMF 16 Working Group (1999), but here simply help set the stage for the carbon tax comparison results.

Introduction / xxiii

H 5 0

xxiv / The Energy Journal

Introduction / xxv

I t 1 Y .

I \\ I , l �

(Suol qJPw UOllllW)

xxvi / The Energy Journal

l m

!i \\ ;* \\ , .’

Introduction 1 xxvii

. . f

(suoa WM u!) patmauag uoq433

xxviii / The Energy Journal

Figure 7. Comparison of Characteristics of Reference Case Projections

(a) United States

Model 2

(c)Japan

% ‘0 0

Model

Introduction / xxix

Figure 7. Comparison of Characteristics of Reference Case Projections (Continued)

M&el

(d) Canada-Australia-New Zealand

120 I

xxx / The Energy Journal

COMPARISONS OF ALTERNATIVE EMISSION TRADING REGIMES

Although the Kyoto Protocol does explicitly mention the possibility of international trading of carbon emission rights, the negotiators have yet to agree on the extent of participation in any trading regime and whether there will be constraints on how many emissions rights can be bought or sold by individual participants. In our scenario design we started with some relatively simple implementations of the trading provisions in the Protocol in order to get a rough idea for what is at stake in the determination of the rules governing the trading regime. Here we look at carbon tax results for four alternative scenarios: (1) No Trading of international emission rights, (2) full Annex 1 (or Annex B) Trading of emissions rights, (3) the Double Bubble, which considers separate EU and rest of Annex 1 emissions trading blocks, and (4) Full Global Trading of emissions rights, with the non-Annex 1 countries constrained to their reference case emissions.

Several conclusions emerged from running these scenarios. First, virtually all of the modeling teams were uncomfortable running the Full Global Trading scenario as a realistic outcome of the current negotiating process; there is simply not enough time between now and the first budget period to agree on and design a trading regime involving all the participants in the United Nat-ions Framework Convention on Climate Change. Thus, this scenario was run only as a benchmark for what ultimately might be achieved only. Second, in many of the models carbon taxes in the No Trade scenario rise to levels that make the modeling teams question whether the macro-economic constraints left out of most of the models (except the Oxford model, and parts of G-Cubed) might liead to economic impacts that are on the order of the equilibrium impacts that are considered. Despite these limitations a number of general conclusions can be drawn from the model results.

Figure 8 shows carbon tax results for the U.S., EU, Japan, and CANZ for four alternative trading regimes (here we add results for the Double Bubble scenario to those for the three “core” trading scenarios). The potential advantages of expanding the scope of the trading regime are evident in the figures. Moving from the No Trade to the Annex 1 Trading case lowers the carbon tax required in the four regions by a factor of two as a result of equalizing the marginal abatement cost across regions. This effect is particularly significant in this case because almost all models project a significant amount of “hot air” will be available from Russia. This represents reductions in Russia’s Reference Case carbon emissions by 2010 relative to its 1990 level baseline allocation. Figure 9 shows projected GDP loss results for the U.S., EU, Japan, and CANZ for the four alternative trading regimes. The GDP losses are generally adjusted for payments for the purchase of carbon emission rights (a deduction) or receipts for the sale of carbon emission rights (an addition). The pattern of these results is similar to that for the carbon tax comparisons.

Zntroduction / mxi

Figure 8. Year 2010 Carbon Tax Comparisons

(a) United States

50

0

2 Model H No Trading n Annex I Trading 0 Double Bubble q Global Trading

(4 Japan

q No Trading n Annex I Trading 0 Double Bubble q Global Trading

mii / The Energy Journal

Figure 8. Year 2010 Carbon Tax Comparisons (Continued)

(b) Euopean Union

1200 I

q No Trading n Annex I Trading 0 Double Bubble •l Global Trading

(d) Canada-Au&alla-New Zealand

2 Model

q No Trading n Annex I Trading 0 Double Bubble 0 Global Trading

Introduction / xxxi.ii

Figure 9. Comparison of Year 2010 GDP Losses

(a) United States

200

180 3 2 180

2 140

e 80 p .Z 40 g

20

WNo Trading n Annex I Trading q Double Bubble q Global Trading

(c) Japan

90 G k 80 = B 70

3: 80

Model n NO Trading Wtnnex I Trading q Double Bubble q Global Trading

xrxiv / The Energy Journal

Figure 9. Comparison of Year 2010 GDP Losses (Continued)

(b) European Union

Model

WNo Trading WAnnex I Trading 0 Double Bubble q Global Trading

(d) Canada-Australia-New Zealand

Model n No Trading Wumex I Trading q Double BubMe q Global Trading

introduction / xxxv

The advantages of Global Trading relative to Annex I Trading are also significant. They result primarily from the fact that non-Annex I countries can reduce emissions more inexpensively relative to their unconstrained allocation of emissions rights than can the Annex I countries relative to their much more tightly constrained Kyoto allocation. For example, most of the models project about a 30 percent increase in the amount of carbon emissions in the U.S. in 2010 relative to 1990. By contrast the Protocol calls for a 7 percent decline from 1990 levels, while reference case emissions in China are projected to increas,e by 100 percent or more over that time period.

Finally, it turns out that the Double Bubble, which assumes separate EU and rest of Annex I trading blocks, increases the cost of implementing the Protocol for the EEC countries and decreases it for the non-Annex 1 countries. This result occurs because Russia and the United States have lower cost emission reduction options than the EEC.

UNDERSTANDING MODEL DIFFERENCES

Although all the models show a similar pattern of results for the relative costs of the alternative trading regimes, there are significant differences in the models’ projections of the magnitude of the economic dislocations projected for each regime. Part of the explanation for these differences is the differences in reference case carbon emissions. In general, other things being equal, the higher the reference case emissions, the higher the costs of implementing the Protoco.l. However, this observation provides only an incomplete explanation of the relative cost estimates from the models.

The other reason for the observed differences is the degree of difficulty in adjusting energy demands embedded in the input assumptions and structure of each model. Important dimensions of the adjustments dynamics are the rate at which energy demands and energy inputs into production respond to pric.e changes, the rate at which the energy producing and consuming capital stock can be turned over, the rate at which new technologies can be introduced, the rate at which natural gas production can be increased, etc. We cannot discuss all these differences individually here, but we can use model results to give us an aggregate picture of how they work together in each model.

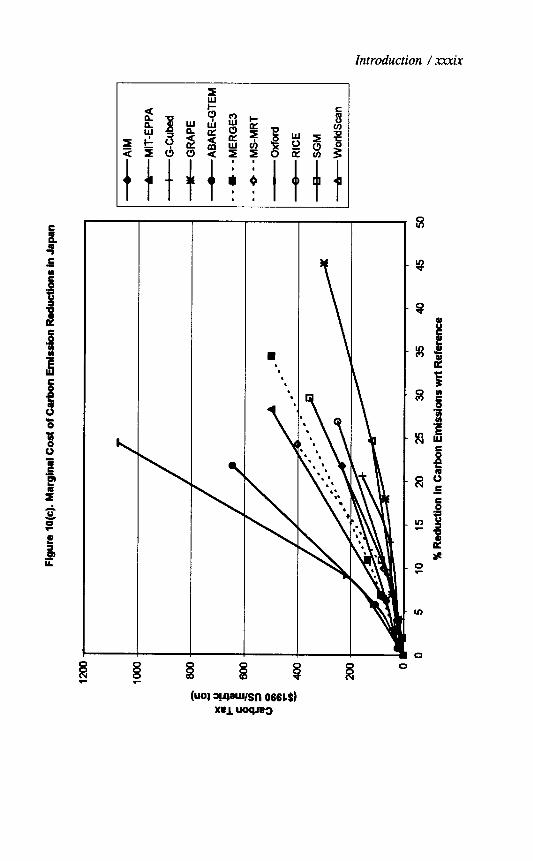

By plotting the projected carbon tax versus percentage reduction in carbon emissions for each of the trading regimes considered, we can construct an approximate marginal cost of carbon emission reductions curve for each model for each region in each year. Marginal cost curves for the four OECD regions in 2010 are shown in Figure 10. A steeper marginal cost curve for a model implies that it requires a larger price incentive to reduce carbon emissions by a given amount through energy conservation and fuel switching. That is, the steeper the marginal cost curve, the larger the carbon tax required to achieve a

mvi / The Energy Journal

given percentage reduction in reference case emissions. The steepness of .these curves depends on the reference case emissions projected by the model, the magnitude of the substitution and demand elasticities embedded in it, and the way capital stock turnover/energy demand adjustments are represented. All ithree factors work together, so one observes that models with higher baseline emissions to lead to higher adjustment costs. If the elasticities are high and the adjustment dynamics rapid, that can lead to lower adjustment costs. In addition, a relatively high adjustment cost can result from either relatively low long-run elasticities and relatively rapid adjustment dynamics, or relatively high long run elasticities and relatively slow adjustment dynamics, or both.

As in past EMF studies, it has proven difficult to anticipate differefnces in the price responsiveness of the models from published parameter values. The definitions, points of measurement, and level of aggregation of the parameters differ greatly from mode1 to model, greatly complicating the task of formulating a price sensitivity estimate analytically. Thus, the information embedded in Figure 10 is an extremely valuable starting point in the process of understanding model differences. Besides the difference in the magnitude of the response and different baseline shown in Figure 10, we also observe that some of the models exhibit a nearly linear dependence of the carbon tax on the percentage reduction in carbon emissions, while others exhibit a quadratic or even more steeply rising relationship. These differences among models in the relative contribution of energy intensity reductions and carbon intensity reductions in achieving carbon emission reductions and the implied differences in fuel share adjustments; are discussed more fully in EMF 16 Working Group, 1999.

OVERVIEW OF SPECIAL ISSUE

Since each modeling team ran and reported results for the four core scenarios, each of the thirteen papers that follow contains some discussion o-f the comparison of the different pure trading options with more depth, but basically reaches the same bottom line as that reported here. In addition to that comparison, each modeling team focused on sensitivities, additional results, and sets of scenarios (many drawn from Table 1) that seemed particularly interesting to them and that the structures of their models allowed them to address. For example, several modeling teams focused on the impact of restrictions on the amount of emissions trading that would be allowed in the Annex I Trading case (which assumes no restrictions) and the potential for a limited number of selllers to exercise monopoly power in that trading regime (i.e., no explicit restrictions, but self imposed restrictions by sellers designed to increase the price they receive and their revenues). The MS-MRT (Bernstein, et al.), SGM (MacCracken, et al.), and MERGE3 (Marme and Richels) papers deal with these issues in some depth and conclude that restrictions on Annex 1 trading could double the cost of meeting the objectives of the Protocol under unrestricted Annex I trading without the exercise of market power.

Introduction / x.xmii

.,

\

\

0 . . .

.

.

q

\

xxviii / The Energy Journnl,

Introduction 1 xxxi.x

Q 8 R O (UOJ wwsn 066LS)

ml uoqrw

xl / l%e Energy Journal

\

\

\

I

\

0

\

‘. l ,

Introduction 1 xl’i

Another group of models dealt with comparing the results of the Kyoto Protocol with those obtained for other longer-run objectives for climate policy. The RICE model (Nordhaus and Boyer), MERGE3 (Manne and Richels), FUND (Tol), and CETA (Peck and Teisberg) analyses considered a number of potential longer term objectives for climate policy-for example, stabilization of the concentration of CO? in the atmosphere, limitations on the rise in global mean temperature, match the marginal benefits of greenhouse gas reductions in each region with its marginal costs of mitigation. These studies generally show that the emissions trajectory prescribed in the Protocol is lower and the cost of emissions mitigation higher than that required to meet the long run objectives that were considered.

Other groups focused their analysis on key sensitivities that could potentially affect results for both the core and other types of scenarios. One example is the careful and insightful analysis done with the MIT-EPPA model (Jacoby and Wing) on the sensitivity of results from a multi-sector general equilibrium model to variations in the parameters represented the sectoral malleability of capital, that is the rate at which the capital stock in each sector is assumed to turn over or to have its input mix adjusted. This analysis shows both the sensitivity of the cost of meeting the Protocol to variations in these parameters, and also the extent to which the cost of meeting the emission reductions obligation specified in the Protocol for 2008-2012 increases with each year there is a delay in initiating action (this point is also made by To1 in the FUND analysis).

Another group of important sensitivities concerns the use of sinks and the “other” greenhouse gases covered by the Protocol to satisfy its emission reduction requirements. Although the core scenarios did not consider sinks and “other gases” a number of the modeling teams did. The analysis with FUND by To1 considers the potential of methane reductions to reduce the costs of satisfying the Protocol’s requirements, while the SGM analysis (MacCracken, et al.) considers the potential of both sinks and all the other gases. It is important to understand that broadening the scope to all six gases covered in the Protocol brings with it both new mitigation options and new obligations, so the key issue becomes the relative costs of reducing a unit of global radiative forcing attributable to each of the gases. That is, the other gases are not simply low cost alternatives to carbon emission reductions. They also generate additional emission reduction requirements. Nonetheless, preliminary estimates seem to show that the inclusion of sinks and other gases have the potential to reduce the total cost of meeting the obligation specified in the Protocol.

A number of teams focused on the role of technologies and technology trends in influencing the costs and energy sector impacts of satisfying the requirements of the Protocol. Although many of the models have some technology detail, the GRAPE model (Kurosawa, et al.) considered .a

xiii / The Energy Journal

particularly rich set of energy supply technologies, including carbon separation and isolation technologies. The AIM model (Kainuma, et al.) is the only model included here that represents energy demand at the end-use level. The availability of new technologies can have a significant effect on the costs of satisfying the requirements of the Protocol, although the first budget period (2008-2012) is soon enough at this point that most of the benefits of the: new technologies are felt after 2012.

Another area that is well covered in this volume and one that is sure to attract additional policy and research attention in the years ahead is the impact of any emissions reductions agreement that work through the international trade system. In early global emissions reduction modeling systems, trade in energy fuels and carbon were the only international trade possibilities considered. A number of models now represent trade in non-energy goods within a general equilibrium representation of economic activity. These analyses have generally focused on the impact of international trade considerations on the cost of the Protocol to both Annex I and non-Annex I countries (the latter commonly referred to as “spill over” effects), as well as the increase in carbon emissions from non-Annex I countries that might result from AMeX I actions to limit carbon emissions (the so called “carbon leakage” effect). The ABARE-GTEM (Tulpule, et al.), MS-MRT (Bernstein, et al.), WorldScan (Bollen, et al.), G- Cubed (McKibbin, et al), MIT-EPPA (Jacoby and Wing), and AIM (Kainuma, et al.) analyses consider international trade of non-energy goods, with the first four including detailed descriptions of trade results in this volume. In general, the models show that there can be significant positive economic impacts of Annex I action on non-AMeX I economies with the sign and magnitude depending on who the country trades with and what they trade (see Bernstein, et al.), the magnitude of international capital flows (see McKibbin, et al.), and the magnitude of the trade and substitution elasticities embedded in the models (see especially McKibbin, et al., Bernstein, et al., and Bollen, et al.). The carbon leakage projections produced by the models span a wide range and depend on many of the same factors that determine the spill over effects, with the import substitution elasticity parameter values likely the most impclrtant assumptions.

Some of the papers deal with very important issues not addressed anywhere else in the volume. For example, the Oxford model considers m.acro- economic adjustment costs (e.g., induced unemployment, inflation, and exch.ange rate adjustments) that are generally not, with the exception of the treatment in G-Cubed, included in the other analyses included in this volume. Results from this model confirm the suspicions of the other groups that these additional adjustment costs depend on assumptions about baseline monetary and fiscal policy assumptions and the assumed policy responses to the introduction of the Protocol, but can be quite significant, especially in the cases with very lirnited amounts of international emissions trading available. The G-Cubed ana:lysis

Introduction / xliii

(McKibbin, et al.) also looks in considerable depth at the impact that adjustments in capital flows could have on the costs of the Protocol to participants in the Protocol (both those that have first budget period obligations and those that do not) under alternative trading regimes. Interesting results concerning the impact of global trading on the cost of the Protocol to the non- Annex I countries emerge.

The CETA model looks at a very simple two party (Annex I and Non- Annex I) formulation of the climate policy debate, focusing on the bargaining set between the two parties (that is, the set of allocations that leads both parties to be better off (in terms of benefits less costs). This analysis is performed for the optimal emissions trajectory and then compared with the allocation suggested by the Kyoto program.

A final highlight of the analyses presented in this volume is the discussion of appropriate cost measures to use in assessing the economic impact of the Protocol. This issue is addressed explicitly or implicitly in every paper, with illuminating comparisons and analysis of results for alternative measures included in MacCracken, et al. using results from the SGM and especially in Bernstein, et al. using results from the MS-MRT. The alternative o:r complementary cost/welfare measures included in the volume include carbon taxes, total resource costs, GDP, GNP, aggregate economic consumption, discounted aggregate consumption, and intertemporal equivalent variation. Bernstein, et al. conducted a standardized comparison of projections for a number of the different measures across scenarios for the MS-MRT model. (See also MacCracken, et al., and EMF 16 Working Group, 1999) for more on this issue.

This volume contains a wide range of estimates of the cost of the Kyoto Protocol. This range of estimates reflects differing assumptions about how the Protocol will get implemented and differences in the structures of the models used to make the cost projections. The key uncertainties about how the Protocol will be implemented include the scope for carbon emission rights trading that will be permitted; the extent to which reductions in emissions of the othe:r greenhouse gases besides carbon and the development of carbon sinks will be permitted, and how the accounting will be done; and the type of post-201:! commitments that will be undertaken. The principal model differences that impact the magnitude of the cost estimates are the level of baseline emissions during the first budget period (2008-2012), the value of the substitution and demand elasticities embedded in the models, and the rate at which it is assumed that the stock of energy using equipment can be adjusted over time. However, there are also other categories of costs that are largely omitted from the models that participated in this study that could be quite significant. First, there are macro-economic adjustment costs that come through induced unemployment and financial markets that are omitted in all but the Oxford and parts of the G-Cubed

xliv / The Energy Journal

model and that could be significant, especially in the more tightly constrained scenarios. Second there are regulatory imperfections that could lead policy makers to implement much less efficient and more costly instruments than the carbon taxes that are assumed to be the instrument of preference here. Finally, there could be less or more efficient recycling of the carbon tax revenues than the lump sum recycling that is assumed in virtually all of the simulations reported here.

Despite these considerable uncertainties, a number of common results and insights emerge from the set of model results considered here. First, meeting the requirements of the Kyoto Protocol will not stop economic g:rowth anywhere in the world, but it will not be free either. In most Annex I countries, significant adjustments will need to be undertaken and costs will need to be paid. Second, unless care is taken to prevent it, the sellers of international emissions rights (dominantly the Russian Federation in the case of Annex I trading, and China and India in the case of global trading) may be able to exercise market power raising the cost of the Protocol to the other Annex I countries. Third, meaningful global trading probably requires that the non-Annex I countries take on emissions targets; without them accounting and monitoring (even Annex I monitoring and enforcement may be quite difficult) becomes almost impossible. Finally, it appears that the emissions trajectory prescribed in the Kyoto Protocol is neither optimal in balancing the costs and benefits of climate change mitigation, nor cost effective in leading to stabilization of the concentration of carbon dioxide at any level above about 500 ppmv.

With this introduction, the stage has been set for the set of papers that follows. We hope you find them as interesting and insightful as we did. That the study has produced such a rich set of results owes everything to the active participation of the modeling teams and the care each team took in preparing a paper for this volume.

REFERENCES

Bhagwatti, Jagdish N.. and T.N. Scrinivasan (1983). Lectures on International Trade. Cambridge,

MA: MIT Press.

EMF 16 Working Group (1999). ‘Economic and Energy System Impacts of the Kyoto Protocol;

Results from the Energy Modeling Forum Study,” the EMF 16 Working Group, Stanford Energy

Modeling Forum, Stanford University, Stanford, CA, July 1999.

The Kyoto Protocol: A Cost-Effective Strategy for Meeting Environmental Objectives?

Alan S. Manne* and Richard G. Richels**

This paper has three purposes: 1) to identify the near-term costs to the United States of ratifying the Kyoto Protocol; 2) to assess the significance of the Protocol ‘s ‘Iflexibility provisions “; and, 3) to evaluate the Kyoto targets in the context of the long-term goal of the Framework Convention. We find that the short-term U.S. abatement costs of implementing this Protocol are likely to be substantial. These costs can be reduced through international trade in emission rights. The magnitude of the costs will be determined by the number of countries participating in the trading market, the shape of each country’s marginal abatement cost curve, and the extent to which buyers can sari@ their obligation through the purchase of emission rights. Finally and perhaps most important: unless the ultimate concentration target is well below 550ppmv, the Protocol seems to be inconsistent with a long-term strategy for stabilizing global concentrations.

INTRODUCTION

The Kyoto Protocol represents a milestone in climate policy.’ For the first time, negotiators have attempted to lay out emission reduction targets for the early part of the 21”’ century. The goal is for Annex 1 (developed countries plus economies in transition) to reduce their aggregate anthropogenic carbon dioxide equivalent emissions by at least 5 percent below 1990 levels in the commitment period 2008 to 2012. The Protocol, however, has yet to enter into force. To do so will require ratification by 55 countries representing 55 percent of total Annex 1 CO, emissions in 1990.

?71a Energy Jolrmal, Kyoto Special Issue. Copyright Q 1999 by the IAEE. All rights reserved.

* Professor Emeritus, Engineering-Economic Systems and Operations Research, Stanford University, Terman Engineering Center, Stanford, CA 943054023 USA.

** Electric Power Research Institute, Environment Division, 3412 Hillview Avenue, P.O. Box 10412, Palo Alto, CA 94303. E-mail: rrichelsQepri.com

1. Conference of the Parties (1997). “Kyoto Protocol to the United Nations Framework Convention on Climate Change,” Third Session Kyoto. l-10 December.

1

2 / The Energy Journal

As each country considers ratification, important questions will arise. High up on the U.S. list is the issue of economic costs. The Senate, for example, has stated that “any Protocol should be accompanied by a detailed financial analysis of impacts on the economy .“* Not surprisingly, U.S. negotiators had hardly returned from Kyoto before the first hearings were scheduled on Capitol Hill. Although the issue of costs is but one of many important considerations, policy makers are keenly interested in the economic implications of ratification.

This paper is intended to help clarify our understanding of compliance costs. The focus is on three questions, which we believe to be of particular relevance: What are the near-term costs of implementation? How significant are the so-called “flexibility provisions ?” And, perhaps most importantly, is the Protocol cost-effective in the context of the long-term goals of the Framework Convention?3

Unfortunately, the answers to these questions will not come easily. It has always been difficult to calculate the economic costs of implementing climate policy. Kyoto has done little to simplify matters. Indeed, it raises at least as many questions as it resolves. These questions fall into two categories: those related to the near-term implementation of the Protocol and those related to the evolution of climate policy over the longer term.

The Protocol is unclear on a number of topics. These include the rules governing emission trading, joint implementation (JI), the Clean Development Mechanism (CDM), and the treatment of carbon sinks. In addition, there is a weak knowledge base regarding the costs of sink enhancement and of controlling several of the relevant trace gases. Until these issues are clarified, analyses will be highly speculative.

Calculating the costs of Kyoto is also complicated by the issue of “what happens next?” Energy sector investments are typically long-lived. Today’s investment decisions are not only influenced by what happens during the next decade, but also by what happens thereafter. In order to estimate the costs of implementing emission cuts in the first commitment period, assumptions are required concerning the longer-term requirements. Unfortunately, the international negotiation process offers little guidance on this issue. This further complicates the process of analysis.

We do not wish to suggest that economic analysis is premature at the present time. Uncertainty is rarely an excuse for paralysis. It does mean, however, that we must be careful to highlight the tentative nature of the projections and focus, to the extent possible, on the insights for decision making.

2. 105th Congress, 1st Session (1997), S. Res. 98. 3. Intergovernmental Negotiating Committee for A Framework Convention on Climate Change

(1992). Fifth Session, Second Part, New York, 30 April-9 May.

Kyoto Protocol: A Cost-Effective Strategy / 3

Here, sensitivity analysts can be particularly useful. For example, in the case of several of the flexibility provisions (emission trading, joint implementation and the Clean Development Mechanism), we explore a variety of scenarios regarding constraints on the purchase of carbon emission rights. While the exact magnitude of the benefits will continue to be debated, the insights, nevertheless, appear to be quite robust.

We also examine the Protocol in the context of the longer-term goal of the Framework Convention, i.e., the stabilization of greenhouse gas concentrations in the earth’s atmosphere. A particular concentration goal can be reached through a variety of emission pathways. Considerable effort has been devoted to trying to understand the characteristics of cost-effective pathways (IPCC, 1997). It is interesting to examine Kyoto in the context of this work. The price tag for moving forward may be formidable. Consistent with the Framework Convention, it is essential that “policies and measures to deal with climate change should be cost-effective so as to ensure global benefits at the lowest possible costs. ‘14

2. THE MODEL

This analysis is based on MERGE (a _model for evaluating the regional and global effects of greenhouse gas reduction policies).5 MERGE is an intertemporal market equilibrium model, It combines a bottom-up representation of the energy supply sector together with a top-down perspective on the remainder of the economy. Savings and investment decisions are modeled as though each of the regions maximizes the discounted utility of its consumption subject to an intertemporal wealth constraint. Each region’s wealth includes not only capital, labor and exhaustible resources, but also its negotiated international share in carbon emission rights.

For the present version of the model, known as MERGE 3.0, we have adopted IO-year time intervals through 2050 and 25-year intervals through 2100. Geographically, the world is divided into nine geopolitical regions: 1) the USA, 2) OECDE (Western Europe), 3) Japan, 4) CANZ (Canada, Australia and New Zealand), 5) EEFSU (Eastern Europe and the Former Soviet Union), 6) China, 7) India, 8) MOPEC (Mexico and OPEC) and, 9) ROW (the rest of world). Note that the OECD (regions 1 through 4) together with EEFSU constitute Annex 1 of the Framework Convention.

Particularly relevant for the present analyses, MERGE provides a general equilibrium formulation of the global economy. We model the possibility

4. Intergovernmental Negotiating Committee for A Framework Convention on Clirmate Change (1992).

5. See Manne, Mendelsohn and Richels (1995); and Manne and Richels (1995).

4 / The Energy Journal

of international trade in carbon emission rights. This is sometimes known as “where” flexibility. It would allow regions with high marginal abatement costs to purchase emission rights from regions with low marginal abatement costs. In addition, MERGE can be used to examine the related issue of “when” flexibility -intertemporal transfers of carbon emission rights.

We also model international trade in oil, natural gas, and energy- intensive basic materials. We are therefore able to examine issues related to “carbon leakage. ” Such leakage can occur through a variety of pathways. For example, AMeX 1 emission reductions will result in lower oil demand, which in turn will lead to a decline in the international price of oil. As a result, non- Annex 1 countries may increase their oil imports and emit more than they would otherwise.