tax policy and foreign direct investment (fdi) in nigeria

119

TAX POLICY AND FOREIGN DIRECT INVESTMENT (FDI) IN NIGERIA BY: DANLADI KAMAL MOHAMMED MEC/41616/133/DF A Thesis submitted to the College of Higher Degrees and Research in Partial Fulfillment of the Requirements for the Award of Master of Arts in Economics Of Kampala International University Kampala, Uganda May,2015

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of tax policy and foreign direct investment (fdi) in nigeria

TAX POLICY AND FOREIGN DIRECT INVESTMENT (FDI)

IN NIGERIA

BY:

DANLADI KAMAL MOHAMMED

MEC/41616/133/DF

A Thesis submitted to the College of Higher Degrees and Research in Partial Fulfillment of

the Requirements for the Award of Master of Arts in Economics

Of Kampala International University

Kampala, Uganda

May,2015

DECLARATION A

"This thesis is my original work and has not been presented for a Degree or any other academic

award in any University or Institution of learning"_

Signature~~-~ ----~---- - Name of the Candidate Danladi Kamal Mohammed

Approval

"I confinn that the work reported in this thesis was carried out by the candidate under my

supervision" .

Name of the Supervisor Dr. ISAAC MO KONO ABU GA

Sign~l;.£. .. .. . . . ... . . ~ .

Date: J~ ly eJ ~

11

DEDICATION

I dedicate this thesis to my late parents' Malam Mahammadu kado and Malama Saadatu Ali may

their soul rest in perfect peace Amin.

111

ACKNOWLEDGEMENTS

First and foremost i would like to thank the almighty God for the gift of life and health that he

has given to me to make me be able to write this research work. I would also like to acknowledge

the assistance and role played by the following personalities to the successful completion of this

study. I thank my late parents may their soul rest in peace for sacrificing the little they had, in

thick and thin and invested in my education. Thank you for looking after me and enabling me to

acquire a lifelong investment. I also thank my best friend and Brother Baffa Yahaya for his

financial assistance during my programme in Kampala International University (K.I.U).

I cannot s.1y exactly how grateful. I am to my supervisor Dr.Abuga Isaac whose guidance in this

study was beyond mensure tlrnnk you for guiding me with patience and o.lso for providing me

with professional advice.

I cannot forget the efforts of staff of Kampala International University especially lecturers of

College of Business and Management for their input and effort that made me acquire the

invaluable knowledge.

[n the same way. I \Votilcl like to thank the management and staff of Central Bank of Nigeria

(CBN) ABUJA. federal ministry of finance Abuja Nigeria National Bureau of Statistics Abuja

Nigeria for their time given to me.

L.1stly [ would like to acknowledge my wives. sons and daughters for their patience during my

study at Kampala International University Uganda.

IV

CTL

EU

FDI

FIRS

GDP

GFCF

NBS

MAT

MNEs

OECD

PAYE

PIT

FIRS

SMES

SPSS

U.K

CBN

U.S.

NRA

LIST OF ACRONYMS AND ABBREVIATIONS

Commercial Transaction Levy

European Union

Foreign Direct Investment

Federal Inland Revenue Services

Gross Domestic Product

Gross Fixed Capital Formation

National Bureau of Statistics

Minimum Alternate Tax

Multinational Enterprises

Organization for Economic Co-operation and Development

Pay As You Earn

Personal Income Tax

Federal Inland Revenue Sen,ice

Small and Medium Enterprises

Special Package for Social Scientists

United Kingdom

Central Bank of Nigeria

United States

Nigeria Revenue Authority

V

VAT

VIF

OVTEST

Value Added Tax

Variance Inflating Factor

Omitted Variable Test

VI

LIST OF TABLES

Table 4.1 Summary of All Variables Exercised in this Study

Table 4.2 Descriptive Statistics of FDI the Dependent variable and the Independent variables

Table 4.3 Trend ofFDI inflow in Nigeria between 1984 and 2014

Table 4.4Trend of Tax Incentives in Nigeria between 1984 and 2014

Table 4.5Trend of Corporate Tax Rates In Nigeria between 1984 and 2014

Table4.6The main Categories of Tax Incentives in Nigeria

Table 4.7Sumrnary ofFDI inflow. Tax Rate, Tax Incentives and GDP (1984 -2014)

Table 4.8 Pearson Correlation of the Independent Variables v-,1ith the Dependent variables

Table 4.9 Correlation value among Independent variables

Table 4.10 VIF value among Independent Variables

Table 4.11 Linktest calculation

Table 4.12 Shapiro Wilk Test on Normality Problem

Table 4.13 Regression Estimation using Robust Standard Error

Vil

LIST OF FIGURES

Figure 2.1 conceptual frame work

Figure 4.1 Trend ofFDI inflows in Nigeria 1984 to 2014

Figure 4.2 Trend of Corporate Tax Rates In Nigeria between 1984 and 2014

Figure 4.3 Trend of tax incentive in Nigeria 1984 to 2014

VIII

ABSTRACT

The study investigated the influence of tax incentives, tax rate on the foreign direct

investment in the period 1984-2014. The model is derived from eclectic paradigm

theory. It can be understood from this theory the main factors that driven FDI inflows

have been the need to receive market access, the opportunities presented by large scale

privatization process and the degree of political and economic stability. The researcher

utilized secondary data of 30 years. Data points and data have been taken from

UNICTAD Annual reports World Bank development reports, central bank of Nigeria

CBN publication on monetary policy. CBN Annual Report and statement of account

and federal ministry of finance reports. The trend of each of the above mentioned

construct variables have also been examined in the study to show their movement and

changes between (the independent variable) tax policy and foreign direct investment

(dependent variable) in Nigeria. The researcher used Pearson Linear Correlation

Coefficient (PLCC) and ordinary lenst square (OLS) regression analysis. To examine

the trend of the research variables line graphs have been employed. The study findings

showed the trend of tax incentive in Nigeria in the study period were fluctuations fi·om

time to time. Tax incentives in million of Naira has experienced a decreasing and

increasing trend. In summary form tax incentive from 1984-1986 was declining then

from 1987-1993 ,,vere a general rising trend of tax incentive in Nigeria. Fluctuations

from time as that of tax incenti\'es. [n summary form the FDI intlov, of Nigeria has

experienced an increased trends in some shorter year for instance 1992 the FDI inflmv

raised to 42, 624from 111, 730 in 1991.

The research concluded the tax policy as presented by tax incentives and tax rate ,vhich

were the main focus of this study. Based on the research finding the researcher

concluded the tax policy presented by tax incentive and tax rate have positive

significant effect on FDI ini10\v in Nigeria. The researcher also recommenclecl based on

the empirical quantitative analysis that tnx rate has a significant and negative impact on

FDI inflow accordingly. lowering tax rate accompanied by tax procedure simplification

,vill increase FDI inflow and a tax incentive policy showed be planned and managed

appropriately.

IX

TABLE OF CONTENTS

DECLARATION A

DECLARATION B

DEDICATION

ACKNOWLEDGEMENTS

LIST OF ACRONYMS AND ABBREVIATIONS

LIST OF TABLES

LIST OF FIGURES

ABSTRACT

TABLE OF CONTENTS

CHAPTER ONE

INTRODUCTION

1.0 Introduction

1.1 Background of the Study

1.1. l Historical and Global Perspectives

1.1.2 Theoretical Perspective

1.1.3 Conceptual Perspective

1.1.4 Contextual Perspective

1.2 ProblemStatement

1.3 General Objective

1.4 Objectivesof the study

1.4 .1 Specific objective

1.5 Research Questions

1.6 Research hypothesis

1.7 Research Scope

1.7.1 Geographical Scope

1.7.2 Content Scope

1. 7 .3 Theoretical Scope

1.7.4 Time Scope

1.8 Significance of the Study

1. 9 Operationa I Definition of Key Words

1.10 Study Limitations

X

Error! Bookmark not defined.

iii

iv

V

vii

viii

ix

X

1

1

1

1

1

6

6

10

12

13

13

13

13

14

14

14

14

15

15

16

16

17

CHAPTER TWO

REVIEW OF RELATED LITERATURE

2.0 Introduction

2.1 Conceptual Framework

Figure 2.1: Conceptual Framework

2.2 Theoretical Review

2.2.2.1 Foreign Direct Investment Theory

2.2.2.2 Capital Market Theory

2.2.2.3 Theories Assuming Perfect Market

2.2.2.4 Theories Assuming Imperfect Market

2.2.2.5 The Eclectic Theory

2.3Foreign Direct Investment

2.4 Tax Incentives and Foreign Direct Investment (FDI)

2.5 Policy Arguments for Tax Incentives in Attracting FDI

2.5 Tax Policy

2.7 Challenges Faced by Developing Countries in Tax System

2.8 Tax Administration and Data

2.9 Gaps in the Literature

CHAPTER THREE

METHODOLOGY

3.0 Introduction

3.1 Research Design

3.2 Data Collection Techniques

3.3 Data Analysis

3.3.1 Statistical method

3.3.2 Variables descriptions and measurement

CHAPTER FOUR

PRESENTATION ANALYSIS AND INTERPRETATION OF DATA

4.0 Introduction

4.1.1 Foreign Direct Investment (FDI) Inflow as Dependent Variable

4.1.2 Tax Incentives

4.1.3 Tax Rate

:-:1

18

18

18

18

18

19

19

20

20

22

23

24

29

36

38

40

41

45

47

47

47

47

47

49

49

51

52

52

52

53

53

53

le!

' !

lal

Ii I I, I'! II i

' Ii ·i

1

4.1.4 Gross Domestic Product (GDP) Growth

4.2 Descriptive Analysis

Source: World Bank (2015); Central Bank ofNigeria (2014)

Source: World Bank (2015); Central Bank ofNigeria (2014)

4.6 Basic Assumption Test

4.6.1 Multicollinearity

4,6.2 Omitted Variable Test

4.6.3 Normality Test

4.6.4 Autocorrelation Test

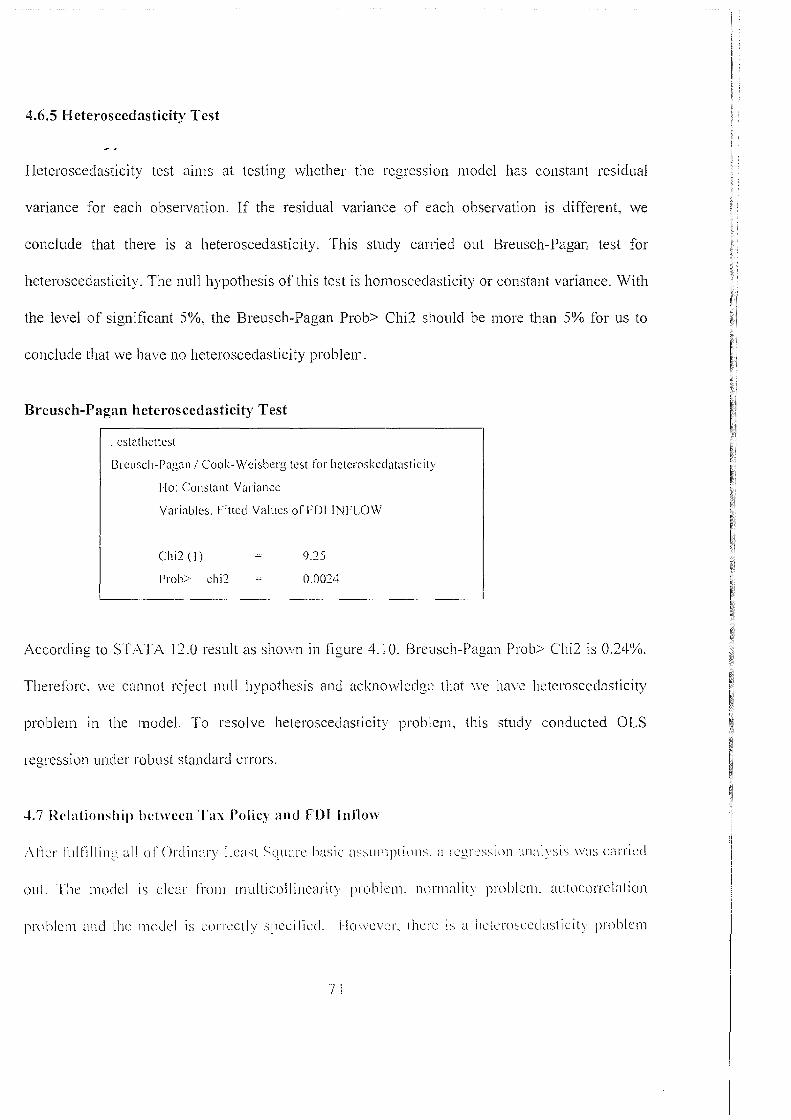

4.6.5 Heteroscedasticity Test

4. 7 Relationship between Tax Policy and FDI Inflow

4.8 Statistical Test for OLS Model

4.8.1 GDP Growth

4.8.2 Tax Rate

4.8.3 Tax Incentives

CHAPTER FIVE

SUMMARY, OF FINDINGS, CONCLUSIONS AND RECOMMENDATIONS

5.0 Introductions

5.1 Summary of Findings

5.2 Conclusions

5.3 Recommendations

REFERENCES

APPENDICES

APPENDIX 1 A: TRANSMITTAL LETTER

APPENDIX 18: TRANSMITTAL LETTER FOR THE ORGANIZATIONS

APPENDIX II: CLEARANCE FROM ETHICS COMMITTEE

APPENDIX III: INFORMED CONSENT

APPENDIX VI: TIME FRAME FOR RESEARCH PROJECT

APPENDIX VII: RESEARCH BUDGET

APPENDIX VIII: RESEARCHER'S CURRICULUM VITAE

APPENDIX IX: TREND OF FDI NET INFLOWS TO NIGERIA 1984 - 2014 (US$)

APPENDIX X: NIGERIA'S GDP GROWTH (1984-2014)

Xll

54

55

56

57

69

69

71

72

73

74

74

77

77

77

77

79

79

79

79

80

82

84

89

89

90

91

92

93

94

95

97

99

APPENDIX XI: TAX RATE IN NIGERIA 1984 - 2014 101

APPENDIX XIII: SUMMARY OF ALL VARIABLES EXERCISED IN THIS STUDY 105

XIII

1.0 Introduction

CHAPTER ONE

INTRODUCTION

Considerable effort and attention in most developing and mid-developed countries is devoted to

tax policies best suited to influencing foreign direct investment (FDI), \Nhich is believed to be

pivotal in the promotion of economic development. The major focus of these efforts is the

formulation and implementation of desirable fiscal policies ,vith considerable stress being placed

on the role of tax policies as an instrument of promoting FDI. Tax policy has always been an

important instrument for augmenting revenue. This is as true in developing countries as in

developed countries. where tax revenue is the major source of domestic revenue. This paper

empirically analyzed the relationship between Nigeria's tax policies and foreign direct

investment (FDI) in the country. Tax policy was the independent variable w"hilst FDI was

dependent variable. This chapter covers background to the study. statement of the problem,

objectives of the study. research questions Ztnd hypotheses. justification. significance and scope

of the study and limitations.

1.1 Background of the Study

I.LI Historical and Global PcrspcctiYCs

Tnxation ts an important issue today as tt was in the past and it \viii be in the future. The lirst

detailed information about taxation can be found in Ancient Egypt. This means. the origin of

taxation policies can be traced in the Ancient Egypt around 3000-2800 BC in the first dynasty of

the Old kingdom (Keen & Mansour. 20 I 0). The earliest and most widespread form of taxation

was the corvee and tithe . This was a form of forced labor provided to the state by peasants too

poor to pay other forms of taxation. Therefore, labour in ancient Egypt is a synonym for taxes).In

the earliest times, countries were confronted with similar problems as we are today. For example,

the pharaohs searched for ways to reduce corruption of their tax collectors called scribes (Adam

1993). This was inscribed the famous Rosetta Stone at around 200 B.C during the reign of

Ptolemy, which did not only help to maintain the hieroglyphic knowledge but is also the first

"tax-oriented" documentation, which reports a tax amnesty, where tax rebels were released from

prison, remitting them also the tax debts. The success of the tax amnesty increased the incentive

to use this instrument as a regular medicine to check civil disorder (Adams 1993).

Since 1980, FDI inflow in the world has rapidly increased, especially to developing counh·ies. It

reached culmination point around the year 2007 where global FDI inflows attained USD 2.3

billion. After experiencing a declining during the period of 2001 -2003 , FDI inflows began to

show an upward trend in 2005 -2007. Unfortunately, after then it showed a declining trend until

2009 . In 2010, global FDI inflow reached an estimated $1,244 billion with a little increase from

level of $1,185 billion (Sources: www.unctad.org/fdistatistics). However, there was an uneven

pattern between regions and also between sub-regions. FDl inflows to developed countries and

transitional economies contracted further in 20 I 0. In contrast. those to developing economies

recovered strongly, and together with transitional economies for the first time surpassed the 50

per cent mark of global FDI flows (UNCTAD. 2012).

In this age of globalization. most African countries seek to become integrated with the

international economy. However, they face significant challenges in this pursuit, including the

need to increase tax revenues. Hence tax policy makers have to analyze the prevailing conditions

2

in the country and determine the relevant mix of taxes that can influence FDI and thus, raise

sufficient revenue for national development. Many Sub-Saharan African (SSA) countries,

Nigeria included, have increasingly restructured their tax systems for this specific purpose.

Despite numerous tax reforms that were intended to improve the economic and social situation,

the rate of growth FDI has remained low, fragile, and the country remains on the list of the mid

developed countries in the world.

Africa's natural resources account for the uneven spread of FDI inflows across the continent and

the 24 countries in Africa classified by the World Bank as oil and mineral-dependent have on

average accounted for close to three-quarters of annual FDI flows over the past two decades

(UNCTAD, 2005). Nigeria share of net FDI in 1990 was 588 million Dollars accounting 24.19%

of African countries but this however declined in 21.07% in 1995, 14.43% in 1997, 8.22% in

1999, 5.88% in 2001 and 7.98% in 2006. In spite of the abundance of natural resources in the

country, the investment response has been poor even with the economic reforms aimed at

creating an investor-friendly environment. Col.lier and Patillo (1999) argued that FDl is lmv in

Africa because of the closed trade and unfriendly tax policies and corruption. Other scholars

have however. contended that most African countries' tax policies lack do not offer tax

incentives to effectively attract larger inflows of FDI even in the primary sector (Lall, 2004 ). Lall

sees the lack of "attractive tax incentives·• in Africa as cutting it off from the most dynamic

components of global FDl inflows in all sectors.

In order to achieve uniformity in the system of taxation throughout Nigeria. the colonial

Government set tip the Raisman Commission in 1958. This Commission recommended the

introduction of uniform basic income tax principles. for application in all the regions of Nigeria .

.,

.)

The recommendation was accepted by GovernmenL which incorporated same, into the

Constitution of the Federal Republic of Nigeria. This led to the promnlgation of the Income Tax

Management Act, 1961 and The Companies income Tax Act, 1961. These legislations were later

repealed arid re-enacted as The Personal Income Tax Act CAP P8 FN 2004 and The Companies

Income Tax Act CAP C21 FN 2004, respectively. As a result of the reassessment carried out by

the law Review Commission, these laws have been reviewed and codified, and are included in

the laws of the Federal Republic of Nigeria 2004.

The adoption of the macroeconomic programme embedded in the SAP started the process of

gradual increase in the FDI inflow in Nigeria. The period 1990 and 1993 witnessed a drop in

the rate of inflow largely due to a protracted political impasse that disrupted productive

activities and created a regime of uncertainty, which subsequently encouraged capital flight.

In 1995, in order to improve on the level of uncertainty and liberalise the investment climate

in the country, the government promulgated the Nigerian Investments Promotion Commission

Act cap n.117 ( 1995 ), LFN .(NIPC). The aftermath of the promulgation of the commission

was a momentous increase in the FDI inflow into the country especially into the non-oil

sectors.

In the recent years, government of this oil-rich Nigeria. which has for a couple of years been

hobbled by political instability. corruption, inadequate infrastructure. and poor macroeconomic

management hindering economic development and grO\vth began pursuing economic reforms.

Major interests were FDI as a means of achie,,ing economic growth. In this effort. a National

Council on Privatisation was established. in addition the Nigerian Investment Promotion Council

(NIPC) and. has been strengthened to serve as a one- stop office for clearing all the requirements

4

11

11.1.· ' i .,

! lj

fl l:I il Ei

11

for investment in Nigeria. This has been through attracting FDI through taxation policy in form

of tax incentives is an avenue bei11-g adopted.

Taxes in Nigeria can broadly be divided into two categories: direct and indirect taxes. The major

direct taxes for 2011/2012 in Nigeria were: Pay As You Earn (PA YE), corporate taxes, and

withholding taxes (Murgatroy et al., (2013). Indirect taxes include the Value Added Tax (VAT),

which is a consumption tax, as well as import duties and excise taxes imposed on international

trade and locally manufactured goods. The authors state that these taxes were introduced to meet

Nigeria's broad tax policy objectives that include: establishment of a semi-autonomous revenue

authority, enacting new laws, and rationalizing the overall tax structure.

Lyakurwa (2003) has stressed macroeconomic policy failures as deflecting FDI inflows in Africa.

According to Lyakurwa, irresponsible fiscal policies have generated unsustainable budget

deficits and inflationary pressures, raising local production costs, generating exchange rate

instability and making the region too risky a location for FDI. In addition, excessive levels of

corruption, regulation and political risk all associated with tax policies are also believed to have

further derail FDI, adding to an unattractive business climate for FDI.

Ngowi (2001) points out that the main factors preventing an increased inflow of FDI in Africa is

that most countries are regarded as high risk because they are characterized by a lack of political

and institutional stability. Additional factors that are cited as hindrances to prospective FDI

include poor access to world markets. price instability. high levels of corruption, small and

stagnant markets and inadequate infrastructure. Morrisset (2000) suggests that the most

important features of African countries successfully attracting FDI are strong economic growth

and aggressive trade liberalization. Other important factors include privatization programs. the

5

modernization of mining and investment codes, the adoption of international agreements relating

to FDI, a few large priority projects which have significant multiplier effects, and a high-profile

image-building exhibition involving the head of state.

1.1.2 Theoretical Perspective

This study was guided by the Theory of Foreign Direct Investment (FDI), Dunning (1993)

electronic paradigm as sited in Dunning (2011) suggested that the main factors that drive FDI

inflows have been the need to secure market access, the oppmtunities presented by large scale

privatization processes and the degree of political and economic stability; and the Capital Market

Theory by Greta Garbo that was fonnulatecl in 2007, which explains the dynamic

macroeconomic Foreign Direct Investment theory. It emphasizes that the timing of the

investment depends on the changes in the macroeconomic environment.These theoriesaided the

researcher to understand why companies participate in FDI, what FDisconsider when

selectingone destined country over the others, and why they prefer a specific entry mode tohost

countries (Moosa, 2002). This theory fmther enabled the researcher to understand the

relationship between tax policy incentive provisions and FDI from a host country point of view

and why one country succeed in attracting FDI while others remain stagnant in FDigrowth, what

incentives are more preferable to investors in establishing attractiveinvesting environment.

1.1.3 Conceptual Perspective

Tax policy is an administrative apparatus that is built to levy and collect tax. through applying

different tariff and basis taxation, in order lo apply policy that has built (Slemrocl, 2000). Tax

policy is concerned with the reasoning behind how much revenue the government is collecting,

6

what the revenue is being used for, and whether the government is collecting revenue in the most

appropriate way.

On the other hand, Foreign direct investment (FDI) is a direct investment into production or

business in a country by an individual or company in another country, either by buying a

company in the target country or by expanding operations of an existing business in that country

(Agosin, 2009a). Broadly, foreign direct investment includes "mergers and acquisitions, building

new facilities, reinvesting profits earned from overseas operations and intra company loans". In a

narrow sense, foreign direct investment refers just to building new facilities. It is often argued

that countries are less vulnerable to external financing difficulties when ctment account deficits

are financed largely by FDI inflows. rather than debt-creating capital flows (Dean et al.. (2011 ).

According to Nwankwo (2006), FDI creates employment and acts as a vehicle of technology

transfer, provides superior skills and management techniques, facilitates increases product

diversity. Ayanwale (2007) stated that most countries strive to attract FDI because of its

acknowledged advantages as a tool of economic development. This view is supported

by Nwankwo (2006) study on Nigeria which stated that FD I is an engine of economic grovvth and

development in Africa where its need cannot be over emphasized. Nigeria joined the rest of the

World in seeking FOi as evidenced by the [n view of the NEPAD initiative. the government is

working toward developing stronger public-private partnerships for roads, agriculture. and power

through the attraction of FOi among other measures.

Taxation is the bedrock of a Country to fulfil its responsibility and ensure its continuity.

According to Modugu, Eragbe and lzedonmi (2012), taxation goes hand in hand with economic

grow1h and lifeblood for governments to deliver essential services and to make long-term

7

investments m public goods. However, sometime, government waives taxes 111 exchange for

certain gains. This is done in form of tax incentives as a provision of the prevailing tax policy.

Therefore, as pait of the efforts to provide an enabling environment that is conducive to the

growth and incentives for various sectors of the economy. However, the tax sensitivity of FDI

has important policy implications.

Although the potential importance of the need to attract FDI in the development process cannot

be over-emphasised, two fundamental issues concerning FDI are critical. These include the

determinant factors of FDI in a typical host country, whether these factors are under the control

of the host country and not subjected to the manipulations of FDI countries.

Scholars assert that FDI inflows generally provide a more stable source of external financing

than private debt and portfolio equity flows. And there is no gainsaying the importance of FDI

inflows for its contribution to sustaining current account imbalances in countries such as

Pakistan, South Africa and Turkey, where the value of FDI inflows is estimated to have covered

their entire current account deficit in 2007. But this is only part of the story. As governments

employ some incentives in form of taxation so as to attract foreign investors, there is need to

finds out the extent to which these two variables are related especially in case of Nigeria.

FDI has played a crucial role in business internationalization. Massive changes have taken place

both in terms of size, scope. and methods of FDI in the last decade. These changes occur

because of developments in technology. relaxing restrictions on foreign investment barriers in

many countries, as well as deregulation and privatization of many industries. Development of

information technology systems, as well as. more affordable cost in global communication

allows foreign investment to be managed easier.

8

Based on the data provided by the Word Development Indicators (WDI), it is known that the FDI

inflow into Nigeria was still low tn 2005 standing at 1,-005 million Dollars. Although it happened

to increase in the subsequent years 2006, 2009 and 2012, it was still lower compared to other

countries in the same development bracket, which means that there was a capital flight.

Exercising a tax policy for instance tax incentives in enticing foreign direct investment is not a

new method. According to M01isset and Pimia (1999), when other factors such as infrastructure,

cost of production, economic and political stability are more or less equal, tax regulation may

have a significant effect on choices. This effect varies, however, depending on the tax

instrument used, the characteristics of the multinational company, and the relationship between

the tax systems of the home and recipient countries.

In a more competitive world, exercising a tax policy, tool or incentives to attract FDI has become

a global phenomenon. Some countries in Asia and Afiica rely on tax holidays and import duty

exemptions to entice FDI while those in Western Europe prefer to apply accelerated depreciation

(UNCT AD, 1995). This competition will encourage Nigeria to enact tax policy regulations that

tend to be more beneficial for FDI companies than achieving its tax revenue target. However,

there should be a balance that might lead the country to win both tax revenue target and FOi

inflow. This research sees to analyze the relationship between tax policy and FDI in Nigeria

using a quantitative method. It focused on tax policy provision as tax incentive determinant

factors in attracting FDI inflows in Nigeria. The researcher also included some other

determinant factors as control variable such as GDP growth as a proxy for market size. Gross

Fixed Capital Formation (GFCF) as a proxy for infrastructure. trade openness as a proxy for

government policy inflation as a proxy for economy stability and tax rate.

9

I

1.1.4 Contextual Perspective

Nigeria has the potential to become Sub-Saharan Africa's largest economy and a major player

in the global economy because of its rich human and material resources. With its large

reserves of human and natural resources, Nigeria has the potential to build a prosperous

economy, reduce poverty significantly, and provide the health, education, and infrastructure

services its population needs. However this has not been achieved because all major

productive sectors have considerably shrunk in size with the over dependence on oil. Income

distribution is so skewed that the country is one of the most unequal societies in the world,

with 50% of the population having only 8% of the national income (Adaora, 2006).

He futther posits that the economy remains highly uncompetitive and with an average annual

investment rate of barely I 0% of GDP, Nigeria is far behind the minimum investment rate of

about 30% of GDP required to unleash a pove1ty-reducing growth rate.Most of the FDI in

Nigeda goes into the oil and extractive sectors and the economic structure remains highly

undiversified, with oil accounting for 95% of exports (USAID 2003). However, the Nigerian

government has acted to stimulate non-oil businesses through the promotion of Small and

Medium Enterprise (SME). These effmts and the momentum provided to the nation by the

return of a democratic government are reflected in the '"Improvement and Optimism Indexes"

compiled by the World Economic Forum "s Africa Competitiveness Rep01t (2000-2001 ),

which ranks Nigeria fomth among 12 African countries in terms of improvement and first, in

terms of "'optimism'' (AFDB/OECD 2003: Ari yo 2004 ).The Federal Inland Revenue Services

(FIRS) has disclosed that the implementation of the new national tax policy for the country

10

I t

I

has commenced following the approval of the final draft of the regulation by the Federal

Government which was gazette on September 21, 2012.

Commenting on Transfer Pricing regulation in Nigeria, Bamidele noted that the regulations

gave effect to the provisions of-(a)section 17 of the Personal Income Tax Act, CAP P8, Laws of

the Federation of Nigeria, 2004 (as amended by the Personal Income Tax (Amendment) Act,

2011 );(b) section 22 of the Companies Income Tax Act, CAP C2 l, Laws of the Federation of

Nigeria, 2004 (as amended by the Companies Income Tax (Amendment} Act 2007; and (c)

section 15 of the Petroleum Profit Tax Act, CAP 13, Laws of the Federation of Nigeria. 2004.

The objectives, according to him, include: to ensure that Nigeria is able to tax on an appropriate

taxable basis corresponding to the economic activity deployed by multinational enterprises in

Nigeria, including in their transactions and dealings with associated enterprises; to provide the

Nigerian authorities the tools to fight tax evasion through over or under-pricing of controlled

transactions between associated enterprises etc.

The country has remained ahead of several other African economies in offering incentives and

creating a favorable environment for foreign investors. In spite of the discouragement caused by

the political instabilities in the n01thern part of the country. foreign investors still find Nigeria a

favorable place for investment (Fjeldstad and Moore. 2009). This has been enhanced by the

government's effo1ts to attract investors through many favorable investment policies. However,

there is a lot of concern on in the recent years that a range of factors need to be taken into

consideration to attract and sustain FOi on the Nigerian economy (Wade. 2010). Besides the

quality of labor, standard of living, skills, human resource retaining capacity of the local market,

one of the biggest issues has been that of tax policy since many of the donors have ,vithclrawn

11

- ........ - .................................................................................................... --- -------········· .. ··-·---····~·······---

their support to the country and the country has to tussle is budget through revenue generated

from local tax (Wade, 2010). It is therefore through this fact that tlris study is attempting to

investigate the relationship between tax policy and FDI in Nigeria.

1.2 ProblemStatement

A good tax policy can significantly attract FDI in any country. This can be achieved through tax

revenue reduction inform of tax incentive. This however, can be counterproductive if care is not

taken for many reasons. Adeola (2011) opined that it is note-worthy to emphasize that there is

enormous untapped investment opportunities that exist in the Nigerian economy for the

investment appetite of both local and foreign investors.

Despite Adoela's (201 I) argument, investments particularly FDI is perceived to be potentially

significant to promote economic growth. In addition, the presence of foreign capital can be a

source of technological development, expmt growth and employment. Therefore, countries like

Nigeria are very enthusiastic and eager to attract FOL One of the factors influencing FOi that is

still controversial in the country is tax policy, a policy that provides for a form of tax incentive

facilities. Accordingly, there is a need to have more empirical evidences about the relationship

between tax incentive policy and FDI. Better understanding on the issue will allow government

and policy maker to design better policies in attracting FDI. This study therefore seeks to

empirically examine the relationship between the tax policy incentive provisions and FOI inflow

in Nigeria.

12

I I

1.3 General Objective

The broad objective of this study is to analyze the relationships between tax rate, tax incentives,

GDP growth and foreign direct investment in Nigeria.

1.4 Objectives of the study

1.4.1 Specific objectives

The specific objectives are to:

1. Examine the relationship between tax incentive and foreign direct investment in Nigeria.

11. Examine the relationship between tax rates and foreign direct investment in Nigeria.

111. Examine the relationship between GDP growth and foreign direct investment in Nigeria.

1.5 Research Questions

Based on the above problem statement this study seeks to answer the following research

questions;

1. What is the relationship between tax incentive and foreign direct investment in Nigeria?

11. What is the relationship between tax rates and foreign direct investment in Nigeria?

111. What is the relationship between GDP growth and foreign direct investment in Nigeria?

13

1.6 Research hypothesis

The research study employs individual test hypotheses that identifies which of the set of

independent variables are significant predictors of dependent variable. That is it tests the

independent variables individually rather than as a unit.

Tax incentive has no significant relationship on FDI inflow in Nigeria (ie ~1 = 0)

Tax rate has no significant relationship on FOi inflow in Nigeria (ie ~1 = 0)

GDP Growth has no significant relationship on FOi inflow in Nigeria (ie B1 = 0)

1.7 Research Scope

1.7.1 Geographical Scope

This study was carried out in Nigeria, the country has been chosen for this study because it has

many foreign investors carrying out different forms of business. Thus, finding relevant and

appropriate secondary data will be much easier.

1.7.2 Content Scope

While there are many determinant factors of FD!. the present study focused on tax policy as

determinant factor in attracting FOi inflow in Nigeria. To have a robust empirical result in

14

I

I ~)

---···········~--~···········~·········~···········

pe1forming the quantitative method using Pearson's linear correlation coefficient and Ordinary

Least Square, technique the researcher consider GDP growth, Tax rate and tax incentives as the

constructs t independent variables.

1.7.3 Theoretical Scope

This research study is guided by Dunning (1987) proposed a theoretical framework to examine

the relationship between fiscal policies and the flow of investments from a foreign country to a

host country and institute as electronic theory. According to the theory, there are foreign country

to host country. There must be advantage the investor company, the host country must have a

location advantage to be able to attract investors to invest their capital and their must be a

stimulus in internalizing factor that encourages firms or foreign investors to invest directly in the

form of FDI. The study is also guided by several Garbo capital market theory (2007) explains the

dynamic Macro economic foreign direct investment theory which emphasis that the taming of

the investments depends on the charge of microeconomic environment.

1.7.4 Time Scope

Regarding the time frame of this research, in qualitative analysis of tax policy regulations. the

researcher picked out regulation from government gazette enacted in 1961 to the current one in

2004. However. in performing the quantitative estimation the researcher only included data from

period 1984 to 2014 considering the data availability.

15

I I I I

f

I i

1.8 Significance of the Study

Given that the study examines the relationship between tax policy and FDI in Nigeria, it is hoped

that the findings and recommendations may be of use to various pat1ies in different ways.

(i) To Nigeria Federal Inlands Revenue, it will provide an insight on the extent to which the

prevailing tax rate and tax incentives influence FDI in Nigeria.

(ii) To policymakers, the findings will be used as principle guide in formulating new or

amending existing tax policy provisions for including tax incentives / holidays.

(iii) To FD Investors and the entire business community in Nigeria, it will serve as an

instrument and report paper for betterment of the existing tax policy and policy

provisions that will drive them to investing in Nigeria (FDis) and growing their

businesses (local investors) thus, addressing their grievances.

(iv) To the general public, it will benefit them through improved and increased service

delivery and provision of public good either in the short or long run.

(v) To other academicians, it will add on the existing body of knowledge in the literature

relating to taxation and FDI and, for better understanding of the subject under study,

scholars will make use of the findings and recommendations of this study to carry out

further research.

1.9 Operational Definition of Key Words

Tax policy is an administrative apparatus that is built to levy and collect tax. through applying

different tariff and basis taxation, in order to apply policy that has built. Tax policy in this study

16

was measured in terms of effectiveness of tax incentives; tax administration, and tax policy

convemence.

Foreign direct investment (FD/) is a direct investment into production or business in a country

by an individual or company in another country, either by buying a company in the target country

or by expanding operations of an existing business in that country. FDI was measured through

the scope of FDI; human resource development; technological development and level of

employment opportunities.

1.10 Study Limitations

One of the major limitations of this study is cost analysis of tax policy regulation in attracting

FDI inflow due to the difficulty in both data source and complicated calculation. However, the

idea of cost analysis of tax holiday can be a subject of further research after knowing the

relationship and impact of tax policy incentives on FDI inflow.

Since the researcher did not collect the data he has no control over ·what is contained in the data

as used in the study was secondary data from both national and international organizations.

17

I I I

I I

l t

CHAPTER TWO

REVIEW OF RELATED LITERATURE

2.0 Introduction

The following chapter elaborates the theoretical review; then illustrates the conceptual

framework showing the interaction between the study variables.

2.1 Conceptual Framework

Figure 2.1: Conceptual Framework

Independent Variable

Tax Policy • Tax Incentives • Tax Rates • GDP growth

Intervening Variables • Inflation • Trade Openness • GFCF

Dependent Variable

Foreign Direct Investment

Income distribution

Government

Source: Adopted from Greta Garbo (2007): Modified by the Researcher

18

I f f

t

I !

II• . I

I I'.·,,:. ' . I·.' •

I m;

Figure 2.1 indicates the effectiveness in tax policy in regards to GDP growth tax incentive. tax

rate and other control variables (inflation, trade openness and GFCF) in influencing FDI inflow

in Nigeria. However, this relationship can be affected if cases of corruption, civil wars, and weak

government policies are not well streamlined.

2.2 Theoretical Review

A number of theories have been developed to explain the determinants of FDI. Extensive

reviews of the main FDI theories and determinants of FDI range from the FID theory. economic

theories of Vernon (1966), the internationalization theory of Rugman (1981), Dunning·s (1993)

electronic theory and Greta's capital market theory (2007).

2.2.2.1 Foreign Direct Investment Theory

The fast growing and reliability of FDI compared to other capital instruments has brought

interest to the development theory of FDI. Some FDI theories tried to explain why companies

participate in FDL what are the considerations of selecting one destined country over the others,

and why they prefer a specific entry mode to host countries. From the host country point of

views, other FDr theories explained why one country succeed in attracting FDI while others

remain stagnant in FDI growth. what incentives are more preferable to inveswrs in establishing

attractive investing environment. According to Moosa (2002), theories of FD! can be classified

into four types: (1) Theories assuming perfect market; (2) theories assuming imperfect market:

(3) other theories: ( 4) theories based on other variables. The following section will discuss in

detail each of theory.

19

2.2.2.2 Capital Market Theory

The Capital Market Theory as formulated by Greta Garbo (2007) explains the dynamic

macroeconomic Foreign Direct Investment theory. This theory emphasizes that the timing of the

investment depends on the changes in the macroeconomic environment. As taxation is an issue

connected to macroeconomics, this theory becomes relevant to this study as its variables include

tax policy and foreign direct investment.

In establishing a clear understanding between tax policy and FDI, Logue (2009) presents Capital

market theory in relation to taxation and professional investors' ability to forecast future

earnings. According to him, there is no significant difference between the average investment

performance of the well-informed and the uninformed investors. If there were, the differences in

performance between and within the two groups of investors should be due to chance. There are

tests of security prices and returns predictability based upon several explanatory variables such

as dividend yields, term-structure of interest rate, quarterly earnings reports, calendar effect, day

of-the-week effects, price-earnings ratios effect, price-to-book ratios effect, size effect. and

trading volume effect. Since this theory sets its emphasis on taxation and investors ability to

forecast the future and these are also the variables on which this study is centered on, the theory

becomes relevant principle to guide this study.

2.2.2.3 Theories Assuming Perfect Market

There are three hypotheses under this theory: (]) the differential rate of return~ (2) the

diversification of hypothesis; (3) the output and market size hypothesis.

20

The gist of differential rate of return hypothesis is that capital flows from the country with a

lower rate of return to the country \.\Tith a higher rate of return and eventually leads to equality of

the real rate of return. In this hypothesis, business risk is assumed to be neutral regardless

investing location, making real rate of return as an isolated variable in investment decision.

Business risk neutrality means that an investor considers foreign market as perfect substitution of

the domestic market. As this represents one of the first efforts in elaborating FDI theory, many

researchers have tested this hypothesis by examining the relationship between FDI inflow and

rate of return in several countries. Unfortunately, most of them failed to provide suppo1ting

evidence relevant to this hypothesis (Agarwal, 1980}.

Yang (1999) in his research on FOi in China between rich coastal area and poor inland area

attempted to adjust the role of rate of return by inputting human capital variable. The result

suggested that majority FDI in china flows to rich coastal area even though poor inland area

offers a higher rate of return. Perhaps, human capital adjusted the differential rate of return effect

between rich coastal area and poor inland area.According to Moosa (2002), the failure in

suppo1ting this hypothesis. arose from inconsistency of this hypothesis. This is because in this

hypothesis. capital only flows in one direction, which is from a lower rate of return country to a

higher rate of return country. This hypothesis fundamentally failed in explaining why countries

like Nigeria experiences inflow and outflow of FDI simultaneously even if it has a higher rate of

return than others.

In portfolio hypothesis, investors do not only consider rate of return. but also incorporate risk of

business in investment decision. This hypothesis postulates investment as a positive function on

rate of return and a negative function on risk of business. When risk of business is included. then

21

investment diversification becomes relevant. Rather than selecting countries exclusively on

-higher rate of return, capital mobility now also flows by desire to n111111mze risk by

diversification. While some scholars identified some loopholes in this theoretical hypothesis, the

theory itself is preferable to differential rate of return hypothesis for some reasons. First, it

considers business risks which constitute vital element in business decision. Second, it proposes

logical reason on the existence of cross investment intra countries.

2.2.2.4 Theories Assuming Imperfect Market

Several hypotheses fall under this theory such as the industrial organization hypothesis, the

internalization hypothesis, the location hypothesis. the eclectic theory. the product life cycle

hypothesis and the oligopolistic reaction hypothesis.

According to this theory, when a multinational company establishes a subsidiary outside its

home country, it will encounter many disadvantages when competing with domestic company.

These disadvantages derive from various differences in culture, language, the legal system. and

manyinter-country differences. For example. foreign companies more often have to pay higher

wages for the same quality workers since working with them is associated with high risk and

uncertainty. It happens to language differences as well, as foreign companies should bear extra

cost to overcome the language barrier. Therefore. in order to deal with these disadvantages,

foreign companies must possess some advantages among which are tax incentives provided by

the prevailing tax policy of a receiving country. These comparative advantages should be innate

advantages that can be easily transferred to foreign subsidiaries and large enough to surpass these

disadvantages, (LallandStreeten, I 977)

According to this theory·s internalization hypothesis. FDI emanates to substitute market

transaction with internal transaction. This theory explains why companies prefer FDI than

exporting or importing from abroad or licensing. For example if there is a problem in production

process regarding sh01i supply in raw material, a company may decide to establish a subsidiary

company abroad in producing that raw material to ensure that raw material is available. Similar

problems might arise from imperfection and failure of market for other intermediary goods or

services such as labor, knowledge. marketing, and resource endowment. Moosa (2002)

mentioned several advantages of internalization such as avoiding of time lags, bargaining and

buyer uncertainty. In association to the time lag, bargaining and uncertainty, companies replace

some of market function for intermediary goods or services with internal process such as intra

company transaction. For that reason, researchers claimed that internalization theory represents

the main body of FOi theory, and considered others as a subset of this theory.

2.2.2.5 The Eclectic Theory

Dunning (1987) proposed a theoretical framework to examine the relationship between fiscal

policies and the flovv of investments from a foreign country to a host country and institute it as

eclectic theory. Till today, this theory is still relevant. According to Dunning ( 1987), there are

three main aspects causing the flow of capital from a foreign country to host country. First there

must be ownership advantage of the investor company. This advantage is very specific in each

company and required as compensation to offset disadvantage a company might encounter

during investment in the host country. Ownership advantage can take the form of a monopoly on

a particular product or brand, a more efficient production processes, management skills and

greater knowledge about the market or marketing techniques. Out of those advantages. there are

also internal factors in the home country which stimulate companies to expand their operation

abroad such as unfavorable tax policies, high wage tates, increasingly expensive energy, limited

resources, and tight regulation on environment.

Second, the host country must have a location advantage to be able to attract foreign investors to

invest their capital. This advantage will be an enticement for potential investors to exploit the

existing potential advantages for the sake of business. Location advantage can be enormous

attractive tax incentives and lax policy regulation. Others include domestic potentials, high

growth, low inflation, cheap labor, abundant natural resources, and availability of infrastructure,

and lax regulation on environmental control. If the first condition is fulfilled, but the second

condition is not satisfied, investors, (in this term a multinational company), will choose to export

to host country as a way to exploit ownership advantage.

Third, although the first and second conditions are met, there must be a stimulus in internalizing

factor that encourages firms or foreign investors to invest directly in the form of FDI and not the

other way such as licensing, franchising or investment portfolio. Those three factors are a

representation of the previous three hypotheses consists of the industrial organization

hypotheses, the internalization hypothesis and the location hypotheses.

2.3Foreign Direct Investment

Feenstra and Hanson (2005) showed that foreign direct investment (FDI) has been one of the

principal beneficiaries of the liberalization of capital flows over recent decades, and now

constitutes the m~jor fonn of capital inflow for many developing countries, including low

income ones like Chad, Mauritania, Sudan and Zambia. But while there are reasons to celebrate

24

I

this success, the current financial turmoil does not bode well for the sustainability these flows in

2009.lt is often argued that countrie~are less vulnerable to extemal financing difficulties when

current account deficits are financed largely by FDI inflows, rather than debt-creating capital

flows (Dean et al., (201 I). The scholars assert that FDI inflows generally provide a more stable

source of external financing than private debt and portfolio equity flows. And there is no

gainsaying the impotiance of FDI inflows for its contribution to sustaining current account

imbalances in countries such as Pakistan, South Africa and Turkey, where the value of FDI

inflows is estimated to have covered their entire current account deficit in 2007. But this is only

pait of the story.

Wade (20 IO)noted that FD I might actually be one of the forms of cross-border flows that will be

privileged (as it has been in the aftermath to previous crises). Indeed, in a deleveraged world,

FDI may become one of the few ways in which low and middle-income countries can access

capital for development. But in the meanwhile policy makers in developing countries need to

monitor trends carefully and adapt policy accordingly. FDI is in itself no panacea. and can

sometimes compound problems during times of financial crisis. It is certainly no substitute for

enlarging tax bases and promoting better mobilization of domestic resources.

Nigeria has joined the rest of the world in seeking FDI and the country is deeply involved in the

attracting FDI in the country as a mqjor component (Fjelclstacl and Moore. 2009). The empirical

results like other previous studies confirmed that FDI impacts positively on Nigeria's economic

growth. Therefore. taking a peek at Kano State through the lens of FOL we can see that this

country is making bigger economic strides step by step and year by year. From the results. it was

recommended that in order to encourage and finance economic growth. the government should

25

continue striving to achieve a sound degree of infrastructural development, together with a good

cromestic labor force (Nigeria Federal Office of Statistics, 2012).

There are several problems facing all businesses; both domestic and foreign. These are

weaknesses in infrastructure provision, a lack of personal and property security, poor governance

and corruption. Without continued efforts in these areas, efforts on other fronts, however sound,

might have a limited impact. Reflecting such major constraints, Nigeria ranked below average in

the 2005 Transparency International Business Cm?fidence Survey among African countries

surveyed. Such a poor environment for business makes it difficult for Nigeria to increase the rate

of FDI inflows. While these factors are in a sense intangible in the business climate, their impact

is real in terms of its effect on foreign investment and consequently on the growth of the

economy.

Other elements like the complex regulatory environment, policy instability, the predominance of

state owned enterprises, and layers of business regulation at the state and local level, all

contribute to corruption by providing opportunities for patronage and intervention in private

business affairs (AFDB/OECD 2003; World Bank. 2002). [n spite of this, the table below

indicates that Nigeria still ranks amongst the top FOi receiving countries in Africa.

However with the transition to democracy and intense competition for FDl by other developing

countries, the Nigerian administration now shows a welcoming attitude to investors. The

government has aimed its most generous incentives at the sectors that present the greatest

obstacles to economic development particularly infrastructure. Nigeria is becoming investor

friendly, with some laws allowing for 100% foreign ownership of businesses and unhindered

repatriation of capital. In addition, the gO\·ernrnent has put in place a range of incentives

16

designed to lower the cost of doing business to offset the higher-cost operating environment

arising from factors such as deficient infrastructure (Adaora, 2006).

He fm1her states that various industries have been afforded 'pioneer status', giving start-ups a

five-year tax holiday. There are 69 industries benefiting from this incentive, including mining,

large-scale commercialised agriculture, food processing, manufacturing and tomism.

Manufacturers that add value to imp011ed inputs are eligible for a five-year 10% local VAT

concession. Manufacturers using a prescribed minimum level of local raw materials, for instance,

70% for agro-allied industries and 60% for engineering industries, are entitled to a five-year 20%

tax concession.

Investors can take advantage of an infrastructure incentive that permits a 20% tax deduction of

the cost of providing infrastructure facilities that should have been provided by the government.

Such facilities include access roads, pipe-borne water and electricity supply. There is a generous

tax allowance on research and development (R&D), with up to 120% of expenditure being tax

deductible, provided that such R&D activities are carried out in Nigeria and are related to the

business from which profits are derived. In the case of research into the use of local raw

materials, the tax-deductible allowance rises to 140%. The government is also targeting

investment into some economically disadvantaged areas, extending the tax holiday available to

'pioneer status' industries to seven years and adding a 5% capital depreciation allowance.

Additional tax breaks are available for labour-intensive modes of production (Financial Times.

2005).

According to the World Bank, Nigeria's macroeconomic performance over the last two years

has been commendable. The economic reform eff011s are showing positive results including:

27

I

• In 2005, growth continued to be strong at 7% for the economy as a whole and 8% for the

non-oil sector. In the first quaiter of 2006, the Nigerian economy grew by 8.3%.

• In January 2006, the country received its first credit rating (BB-) from Fitch and Standard

and Poor's.

• Year-on-year inflation fell from 28% in August to 12% by December 2005.

• A Fiscal Responsibility Bill has passed critical second readings in both the Senate and

House.

• The National Assembly is discussing a Public Procurement Refonn Bill.

• A bank consolidation prograin was implemented strengthening the financial sector and

enhancing its ability to provide credit to the private sector.

• The import tariff regime has been liberalized reducing the number of tariff bands from 19

to 5 and lowering the average tariff from about 29% to 12%.

With the deregulation of the telecommunication sector, Nigeria's telecommunications

sector is now in a rapid growth mode. According to the Nigerian Communications

Commission (NCC), there's enormous growth potential in the market, as demand for telecom

service has been high because of market liberalization and massive telecom investments. Over

recent years, all branches of the telecom industry have generated considerable growth and the

telecom industry has emerged as a main motor of the country's economy. rt is only the oil

sector that has seen more investment and telecom is novv seen as the most lucrative branch for

investment in Nigeria's economy.

As a result, Nigeria presently boasts Africa·s largest and most promising telecom market.

Even though Nigeria is trailing other countries in terms of providing phone technology at an

28

affordable pnce and doing so reliably, the market has taken significant strides m its

development (Ariyo 2005).

According to the studies caffied out by Chen (2011 )in Nigeria, it was noted that after the

1980s economic crisis, Nigeria, like other Sub-Saharan countries, recognized the need to

rationalize and harmonize the tax rates. The objectives were to attract and promote investment

in Nigeria, increase revenue yields, and simplify tax administration. This study shows that the

corporate income tax was lowered from 60% to 30% in 1997, and the maximum individual

tax rate was reduced from 60% in 1987/88 to 30% in 1993/94. The many wide-ranging

exemptions that have been granted to special sectors over the years -- including a number of

Minister's powers to exempt -- have been abolished. They include provisions granting tax

holidays under the Investment Code of 1991, which were repealed in 1997, and a provision in

the Customs Management Act empowering the Minister to grant specific waiver of taxes and

duties on imports, which was repealed in 2001.

2.4 Tax Incentives and Foreign Direct Investment (FOi)

According to (Easson. 2004), tax incentives can be defined as a special tax provision granted to

qualified investment projects (however determined) that represents a statutory favorable

deviation from a corresponding provision applicable to investment projects in general (projects

that receive no special tax provision). An implication of this definition it is any tax provision that

is applicable to all investment projects. As it has been defined above, according to statutory

regulation, tax incentive is a tax facility granted to specific investors that meet certain criteria as

stipulated in tax law. Those who are eligible benefit more than those who do not receive tax

incentives. According to UNCTAD (2000) there are different categories of tax incentives

29

commonly used by both developed countries and developing countries and these include reduced

corporate income tax rate, which can be set lowered by governments as an exception on common

statutory income tax rate to induce FDI into some regions or specific sectors; loss carry forward,

tax holidays, investment allowances, investment tax credits. reduced taxes on dividends and

interest paid abroad, preferential treatment of long-term capital gains, deductions for qualifying

expenses, zero or reduced tariffs and employment-based deductions.

These incentives are commonly targeted toward foreign investors. The rationale for increased

efforts to attract FDI stems from the belief that FDI have several positive effects on national

development indicators. Among these are productivity gains, technology transfers. introduction

of new processes, managerial skills and technical know-how in the domestic market, employee

training, international production networks, and access to markets. Empirical studies have

showed that a tax policy that puts incentives at forefront of attracting FDI is an important vehicle

for the transfer of technology, contributing to growth in larger measure than domestic

investment.

Therefore, in the face of inadequate resources to finance long-term development in Africa and

with pove1ty reduction looking increasingly bleak, attracting FOi has assumed a prominent place

in the strategies of African countries (Nwankwo. 2006). While contributing to the debate on FOi

and tax incentives, Fakile and Adegbile (201 I ) stated that it is on the basis of these asse1tions

about the advantages of FDI that governments have often provided special incentives to foreign

firms to set up companies in their countries.

Levying taxes on the transaction or business activity is one of the considerations to promote

economic efficiency. Tax neutrality requires that the tax provisions do not discriminate treatment

30

t

I i

I

for any activity or other economic decisions. Tax is one crucial factor for investors in

determining the decision to invest in a country. Theoretically, taxes affect investment decisions

because tax assessment influences the amount of benefits and costs. Hovvever, econometric

studies, which try to find the relationship betv,reen tax poly and FDI, ended up with inconclusive

decision smce there are many variables g1vmg influence on FDI inflow. Easson (2004)

explained the importance of tax policies in investment decision.

In the first instance. countries with high income tax rate would induce compames to invest

abroad more than countries with lower income tax rate. The logical explanation for this in te1ms

of cost of production is that high level of taxes contributes in raising labor cost and might be a

stimulus for company to dislocate its production to countries with lower cost (Easson. 2004 ).

HO\:vever, many economists refuted this explanation by claiming that taxation plays a little in

constructing the production cost. Therefore, they understate its role as the last thing to be

considered

Easson (2004) further asserts that tax provisions and tax rates factor in selecting host countries

\viii only become consiclen1tion after the decision to invest abroad has been made. However. the

main considerations for in\'estor in selecting the location are market size and political stability.

When all main considerations are relatively equal. then taxes may play important role in

investing decision.

According to Easson (2004 ), export oriented FDI is relatively more sensitive to cost factor since

international market is inherent with its high level of competitiveness. Therefore. difference in

tax rate \\1ill significantly influence investment decision. On the other hand, domestic market

31

I ,, I I

I

oriented FOi is less sensitive to tax rate difference as long as other domestic competitors bear the

same tax provision.

Majority of the studies conducted before 1990s revealed that taxation played a minor role in any

FDI decision. However, most recent studies suggested the increasingly importance of taxation in

investment decision. It seemed that the location of destination countries selected by companies

is sensitive to taxation and becoming more so over time for several explanation. According to

Easson (2004 ), there are other FDI barriers, which have been eliminated, taxation as the

remaining obstacle deserves for more consideration. Secondly, as a process of production in

multinational companies is getting globalized, it will become an international production which

involves other worldwide companies. This will increase export and import as channeling means

in the process of production. In this case, import and exp011 correspond sensitively toward tax

difference.

In support of Fakile and Adegbile (2011) and Morisset (2003) view that tax incentive is a tool to

attract FDI, Edmiston et al., (2003), opined that governments often seek to attract FDI by

offering tax incentives to firms in exchange for ce1tain benefits.

Curiously, the empirical evidence of the benefits of offering tax incentives both at the firm level

and at the national level remains ambiguous. Although trade theory expects FDI inflows to

result in improved competitiveness of host countries' exports, the pace of technological change in

the economy as a whole will depend on the innovative and social capabilities of the host country,

together with the absorptive capacity of other enterprises in the country (Carkovic and Levine,

2002).

32

Morisset (2003) asse1ts that tax incentive is a reduction in the corporate income tax rate, through

tax holidays or temporary rebates for ce1tain types of investment or companies. This is supp01ted

by Fakile and Adegbile (2011) who stated that tax incentives are pa1t of the tax policies of

developing countries and usually established and enacted by governments in order to grant

foreign investors more attractive conditions to invest in their country. Other evidence emerging

around the world suggests that tax incentives have a more apparent effect on the composition of

FDI than on its level (Morisset, 2003). Indeed, most governments use tax policies to attract

particular types of investment or to change conduct rather than to increase the overall level of

investment.

According to Morisset, the tax sensitivity of FDI has important policy implications. However, in

attracting FDI there is no doubt that more important are such factors as basic infrastructure,

political stability and the cost and availability of labour. Some empirical analysis and surveys

have confirmed that tax incentives are a poor instrument for compensating for negative factors in

but that does not mean that tax incentives have no effect on FOL

Research has shown that in recent years, there has been growing evidence that tax incentives

influence the location decisions of companies with regional economic groupings such as

European Union, North American Free Trade Area and Association of Southeast Asian Nations.

Also in the United States of America incentives can play a decisive role in the final location

decisions of foreign companies once the choices are nan-owed down to a handful of sites with

similar characteristics (Morisset. 2003 ).

In Nigeria, growing evidence shows, that tax incentives are a crucial factor for mobile firms and

firms operating in multiple markets. such as banks. insurance companies. and Internet-related

...,..., ..)..)

businesses. This is because these firms can better exploit different tax regimes across countries

FaRile and Adegbile, 2011 ). Such strategies may explain the success of tax havens in attracting

subsidiaries of global companies and the spending by multinationals on economists and

accountants to justify their transfer prices, designed to suit their tax needs. Similarly, tax rates

generally have a greater effect on the investment decisions of export-oriented companies than on

those seeking the domestic market or location-specific advantages, because such firms not only

are more mobile but also operate in competitive markets with very slim margins.

The Nigerian Government has put in place a number of investment incentives for the stimulation

of private sector investment from within and outside the country. While some of these incentives

cover all sectors, others are limited to some specific sectors. The nature and application of these

incentives have been considerably simplified. The incentives include: tax holidays, initial capital

allowance, and free duty on equipment (Fakile and Adegbile 2011 ).

Never the less, tax incentives being used to attract FDI is not the end of the story, there is the

problem of tax compliance on the part of companies. Also tax incentive has its cost. For instance

Modugu et al., (2012), expressed concern over tax compliance in their study on voluntary tax

compliance in Nigeria they opined that the need to improve voluntary tax compliance has

resulted in various tax policy reforms by various successive governments. They stated that these

reforms have not been able to stimulate the expected increase in tax revenue over the years, and

this has snowballed into a tax gap as revealed in the share of income taxes in total revenue

profile of the country.

While competition in the application of tax incentives to attract FDI already started in some

regions, most notably in Asia. the concern remains that countries may end up in a bidding war,

34

I

I I

favouring multinational firms at the expense of the state and the welfare of its citizens. This risk

has pushed governments to try to harmonize their tax policies under regional or international

agreements. Beyond the risk of a bidding war, tax incentives are likely to reduce fiscal revenue

and create frequent opportunities for illicit behaviour by companies and tax administrators.

These issues have become cmcial in developing countries, which face more severe budgetary

constraints and corruption than do industrial countries.

There is no doubt that tax incentives are costly. The first and most direct costs are those

associated with the potential loss of revenue for the host government. The second is whether or

not the new investment would have come to the country if it had offered lower incentives or

none at all. If the answer is yes, free-rider investors benefit while the treasury loses, and the

economy reaps no net gains. These examples illustrate the need to clearly evaluate the welfare

implications of tax incentives, both at the level of the firm and globally.

Tax incentives also have many other, less obvious costs. Because they influence the investment

decisions of private companies. they can distort the allocation of resources. And they can attract

investors looking exclusively for short term profits, especially in countries where the basic

fundamentals (such as political and macroeconomic stability) are not yet in place. Another

problem \Vith incentive measures relates to the cost and difficulty of administering them

effectively.

Literature expressed that incentive regimes generally impose a large administrative burden. so

they must be more than marginally effective to cover the costs of their implementation and

produce a net benefit. Discretionary regimes, which rely on case-by-case evaluations, are

especially difficult to administer. These regimes result in delay and uncertainty for investors,

35

which can increase the cost of investment. They have also led to significant corruption.

effectively screened out desirable investments, and undermined sound policymaking and the

development of competitive markets. Morisset (2003) opined that to achieve the gains of tax

incentives for national development, developing countries must structure tax policies in a way so

as to attract foreign investment, without creating a negative impact in the domestic economy.

This is to ensure that they do not fall into a harmful tax competition against other countries.

2.5 Policy Arguments for Tax Incentives in Attracting FOi

Numerous arguments have been brought fo1ward for using tax policy provisions for incentives

in attracting FDI. OECD Tax Policy Studies (2001) stated several crucial arguments for using

tax incentives which can be classified as: international competitiveness, regional development,

income distribution and, macroeconomic considerations. These tax policy arguments for tax

incentives must consider other fiscal objectives like host country needs and circumstances.

These studies argue that tax incentives designed to encourage FDI, including general host

country tax relief measures, those targeted at investment in R&D. and those tied to exports, are

oftof a country, by improving its ability to attract internationally mobile capital. This view

assumes that multinational companies take tax incentives into account when making location

decisions and that tax incentives operate at the margin to swing investment decisions in favor of

the host country.

The theory of correcting for market failureposits correcting market failure as tax incentives.