FDI IN INDIA

141

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ] ECONOMICS ASSIGNMENT “FOREIGN DIRECT INVESTMENT (FDI) IN INDIA” BY: “GROUP 6” NAVNEET CHAUDHARY NIKESH BISWAL SAGAR SINGH Fazlani Altius Business School [Batch : 2013-2015] Page 1

Transcript of FDI IN INDIA

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

ECONOMICS ASSIGNMENT“FOREIGN DIRECT INVESTMENT (FDI)

IN INDIA”

BY:“GROUP 6”

NAVNEET CHAUDHARY NIKESH BISWAL SAGAR SINGH

Fazlani Altius Business School [Batch : 2013-2015] Page 1

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

MUTHU AYYANAR JAIRAJ VAIDYA

CONTENT:

PARTICULAR PAGE NO.

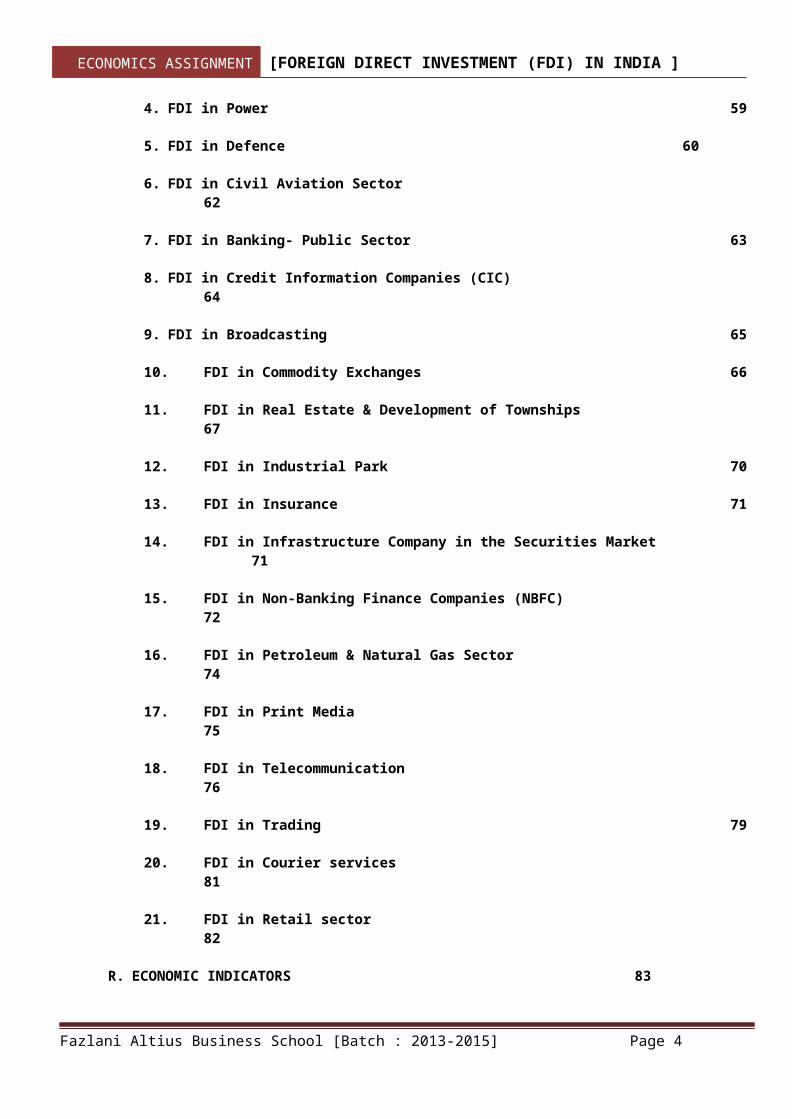

A. INTRODUCTION 4

B. FOREIGN DIRECT INVESTMENT (FDI) FLOWS TO INDIA 5

C. WHO CAN INVEST IN INDIA 6

D. ENTITIES FOR FDI 7

E. ENTRY ROUTES FOR FDI 8

F. GUIDELINES FOR CONSIDERATION OF FDI PROPOSALS BY FIPB 9

G. TREND IN FDI FLOWS 11

H. TRENDS IN FDI FLOWS TO INDIA 13

1. Cumulative FDI flows into India (2000-2013)14

2. Financial Year-Wise FDI inflow Data 20

I. STATEMENT ON COUNTRY-WISE FDI EQUITY INFLOWS 22

J. STATEMENT ON SECTOR-WISE FDI EQUITY INFLOWS 25

K. INDIAN ECONOMY1. Recent Trends in Indian Economy 27

Fazlani Altius Business School [Batch : 2013-2015] Page 2

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

2. Growth in Gross Domestic Product 28

3. Economic Survey 2012-13 29

L. POTENTIAL FOR INVESTMENT IN INDIA 30

M. ADVANTAGE IN INDIA 321. Indian Economy 33

2. Agriculture Sector 33

3. Industry Sector 33

4. Services Sector 33

N. FDI POLICY FRAMEWORK

1. FDI Policy Framework in India 34

2. FDI Policy: The International Experience37

3. Cross-Country Comparison of FDI Policies – Where does India stand?41

O. FDI FLOWS TO INDIA IN RECENT PERIOD 44

P. APPROVAL FOR FDI IN LIMITED LIABILITY PARTNERSHIP FIRM 54

Q. SECTOR FOR FDI

1. FDI in Agriculture 55

2. FDI in Mining 57

3. FDI in Manufacturing 59

Fazlani Altius Business School [Batch : 2013-2015] Page 3

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

4. FDI in Power 59

5. FDI in Defence 60

6. FDI in Civil Aviation Sector62

7. FDI in Banking- Public Sector 63

8. FDI in Credit Information Companies (CIC)64

9. FDI in Broadcasting 65

10. FDI in Commodity Exchanges 66

11. FDI in Real Estate & Development of Townships67

12. FDI in Industrial Park 70

13. FDI in Insurance 71

14. FDI in Infrastructure Company in the Securities Market71

15. FDI in Non-Banking Finance Companies (NBFC)72

16. FDI in Petroleum & Natural Gas Sector74

17. FDI in Print Media75

18. FDI in Telecommunication76

19. FDI in Trading 79

20. FDI in Courier services81

21. FDI in Retail sector82

R. ECONOMIC INDICATORS 83

Fazlani Altius Business School [Batch : 2013-2015] Page 4

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

S. TOP 10 FDI EQUITY INFLOW CASES 85

T. CONCLUSION 95

U. LIST OF INVESTMENT PROMOTION AGENCIES IN INDIA STATE-WISE 97

V. REFERENCES 106

A. INTRODUCTION

India has been ranked at the second place in global foreign directinvestments in 2010 and will continue to remain among the top fiveattractive destinations for international investors during 2010-12 period,according to United Nations Conference on Trade and Development (UNCTAD)in a report on world investment prospects titled, 'World InvestmentProspects Survey 2009-2012'.

The 2010 survey of the Japan Bank for International Cooperation releasedin December 2010, conducted among Japanese investors, continues to rankIndia as the second most promising country for overseas businessoperations.

Fazlani Altius Business School [Batch : 2013-2015] Page 5

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

A report released in February 2010 by Leeds University Business School,commissioned by UK Trade & Investment (UKTI), ranks India among the topthree countries where British companies can do better business during2012-14.

According to Ernst and Young's 2010 European Attractiveness Survey, Indiais ranked as the 4th most attractive foreign direct investment (FDI)destination in 2010. However, it is ranked the 2nd most attractivedestination following China in the next three years.

Moreover, according to the Asian Investment Intentions survey released bythe Asia Pacific Foundation in Canada, more and more Canadian firms arenow focusing on India as an investment destination. From 8 per cent in2005, the percentage of Canadian companies showing interest in India hasgone up to 13.4 per cent in 2010.

India attracted FDI equity inflows of US$ 2,014 million in December 2010.The cumulative amount of FDI equity inflows from April 2000 to December2010 stood at US$ 186.79 billion, according to the data released by theDepartment of Industrial Policy and Promotion (DIPP).

The services sector comprising financial and non-financial servicesattracted 21 per cent of the total FDI equity inflow into India, with FDIworth US$ 2,853 million during April-December 2010, whiletelecommunications including radio paging, cellular mobile and basictelephone services attracted second largest amount of FDI worth US$ 1,327million during the same period. Automobile industry was the third highestsector attracting FDI worth US$ 1,066 million followed by power sectorwhich garnered US$ 1,028 million during the financial year April-December2010. The Housing and Real Estate sector received FDI worth US$ 1,024million.

During April-December 2010, Mauritius has led investors into India withUS$ 5,746 million worth of FDI comprising 42 per cent of the total FDIequity inflows into the country. The FDI equity inflows in Mauritius isfollowed by Singapore at US$ 1,449 million and the US with US$ 1,055million, according to data released by DIPP.

Fazlani Altius Business School [Batch : 2013-2015] Page 6

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

B. FOREIGN DIRECT INVESTMENT (FDI) FLOWS TO INDIA

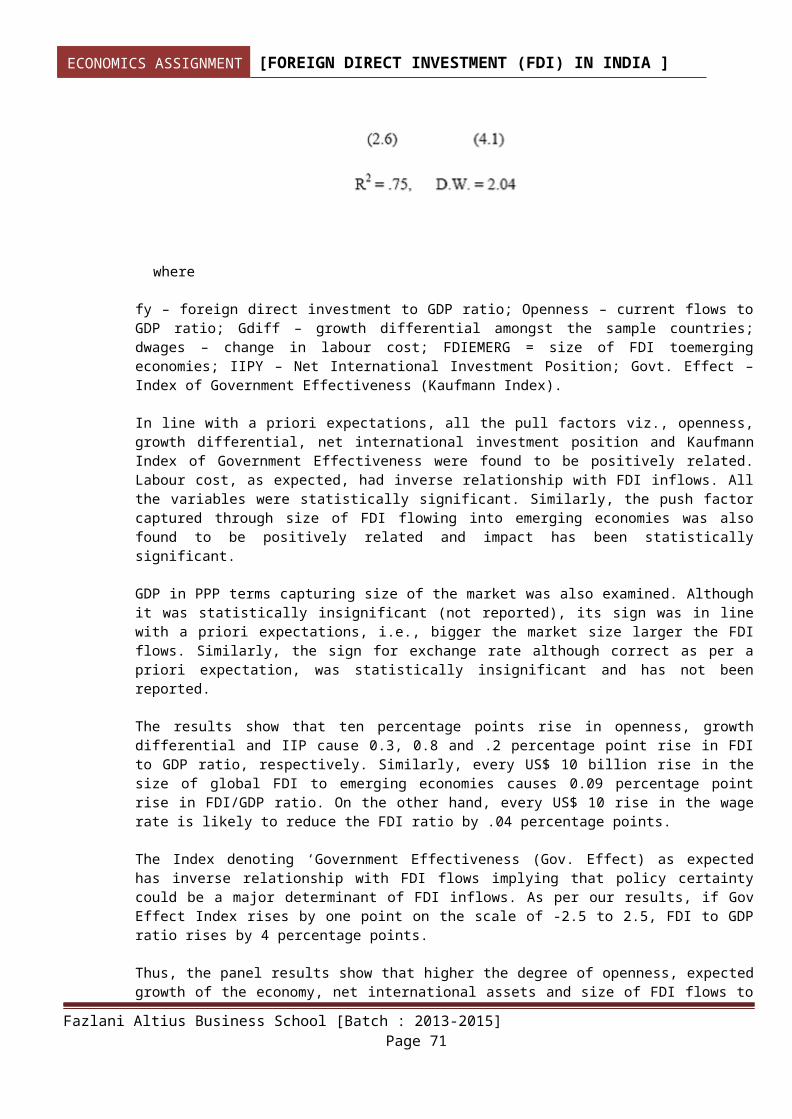

FDI inflows to India remained sluggish, when global FDI flows to EMEs hadrecovered in 2010-11, despite sound domestic economic performance ahead ofglobal recovery. The paper gathers evidence through a panel exercise thatactual FDI to India during the year 2010-11 fell short of its potentiallevel (reflecting underlying macroeconomic parameters) partly on accountof amplification of policy uncertainty as measured through Kauffmann’sIndex.

FDI inflows to India witnessed significant moderation in 2010-11 whileother EMEs in Asia and Latin America received large inflows. This hadraised concerns in the wake of widening current account deficit in Indiabeyond the perceived sustainable level of 3.0 per cent of GDP duringApril-December 2010. This also assumes significance as FDI is generallyknown to be the most stable component of capital flows needed to financethe current account deficit. Moreover, it adds to investible resources,provides access to advanced technologies, assists in gaining productionknow-how and promotes exports.

A perusal of India’s FDI policy vis-à-vis other major emerging marketeconomies (EMEs) reveals that though India’s approach towards foreigninvestment has been relatively conservative to begin with, itprogressively started catching up with the more liberalized policy stanceof other EMEs from the early 1990s onwards, inter alia in terms of wideraccess to different sectors of the economy, ease of starting business,repatriation of dividend and profits and relaxations regarding norms forowning equity. This progressive liberalization, coupled with considerableimprovement in terms of macroeconomic fundamentals, reflected in growingsize of FDI flows to the country that increased nearly 5 fold during firstdecade of the present millennium.

Though the liberal policy stance and strong economic fundamentals appearto have driven the steep rise in FDI flows in India over past one decadeand sustained their momentum even during the period of global economiccrisis (2008-09 and 2009-10),the subsequent moderation in investment flowsdespite faster recovery from the crisis period appears somewhatinexplicable. Survey of empirical literature and analysis presented in thepaper seems to suggest that these divergent trends in FDI flows could bethe result of certain institutional factors that dampened the investors‘sentiments despite continued strength of economic fundamentals. Findings

Fazlani Altius Business School [Batch : 2013-2015] Page 7

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

of the panel exercise, examining FDI trends in 10 select EMEs over thelast 7 year period, suggest that apart from macro fundamentals,institutional factors such as time taken to meet various proceduralrequirements make significant impact on FDI inflows.

This paper has been organized as follows: Section 1 presents trends inglobal investment flows with particular focus on EMEs and India. Section 2traces the evolution of India’s FDI policy framework, followed by cross-country experience reflecting on India’s FDI policy vis-à-vis that ofselect EMEs. Section 3 deals with plausible explanations of relativeslowdown in FDI flows to India in 2010-11 and arrives at an econometricevidence using panel estimation. The last section presents theconclusions.

C. WHO CAN INVEST IN INDIA

1. A non-resident entity (other than a citizen of Pakistan or an entity incorporated in Pakistan) can invest in India, subject to the FDI Policy. A citizen of Bangladesh or an entity incorporated in Bangladesh can investin India under the FDI Policy, only under the Government route.

2. NRIs resident in Nepal and Bhutan as well as citizens of Nepal and Bhutan are permitted to invest in the capital of Indian companies on repatriationbasis, subject to the condition that the amount of consideration for such investment shall be paid only by way of inward remittance in free foreign exchange through normal banking channels.

3. OCBs have been derecognized as a class of Investors in India with effect from September 16, 2003. Erstwhile OCBs which are incorporated outside

Fazlani Altius Business School [Batch : 2013-2015] Page 8

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

India and are not under the adverse notice of RBI can make fresh investments under FDI Policy as incorporated non-resident entities, with the prior approval of Government of India if the investment is through Government route; and with the prior approval of RBI if the investment is through Automatic route.

4. (i) An FII may invest in the capital of an Indian Company under the Portfolio Investment Scheme which limits the individual holding of an FII to 10% of the capital of the company and the aggregate limit forFII investment to 24% of the capital of the company. This aggregate limit of 24% can be increased to the sectorial cap/statutory ceiling, as applicable, by the Indian Company concerned by passing a resolution by its Board of Directors followed by passing of a special resolution to that effect by its General Body. The aggregate FII investment, in the FDI and Portfolio Investment Scheme, should be within the above caps.(ii) The Indian company which has issued shares to FIIs under the FDI Policy for which the payment has been received directly into company’s account should report these figures separately under item no. 5 of Form FC-GPR (Annex-1-A) (Post-issue pattern of shareholding) so that the details could be suitably reconciled for statistical/monitoring purposes.(iii) A daily statement in respect of all transactions (except derivativetrade) have to be submitted by the custodian bank in floppy / soft copy in the prescribed format directly toRBI to monitor the overall

ceiling/sectorial cap/statutory ceiling.

5. No person other than registered FII/NRI as per Schedules II and III of Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations of FEMA 1999, can invest/trade in capital of Indian Companies in the Indian Stock Exchanges directly i.e. through brokers like a Person Resident in India.

6. A SEBI registered Foreign Venture Capital Investor (FVCI) may contribute up to 100% of the capital of an Indian Venture Capital Undertaking (IVCU) and may also set up a domestic asset management company to manage the fund. All such investments can be made under the automatic route in terms of Schedule 6 to Notification No. FEMA 20. A SEBI registered FVCI can alsoinvest in a domestic venture capital fund registered under the SEBI (Venture Capital Fund) Regulations, 1996. Such investments would also be subject to the extant FEMA regulations and extant FDI policy including sectorial caps, etc. SEBI registered FVCIs are also allowed to invest under the FDI Scheme, as non-resident entities, in other companies, subject to FDI Policy and FEMA regulations.

Fazlani Altius Business School [Batch : 2013-2015] Page 9

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

D. ENTITIES FOR FDI

1. FDI in an Indian Company (i) Indian companies including those which are micro and smallenterprises (MSEs) can issue capital against FDI.

2. FDI in Partnership Firm / Proprietary Concern:

(i) A Non-Resident Indian (NRI) or a Person of Indian Origin (PIO) resident outside India can invest by way of contribution to the capital of a firm or a proprietary concern in India on non-

repatriation basis provided:(a) Amount is invested by inward remittance or out of

NRE/FCNR(B)/NRO account maintained with Authorized Dealers / Authorized banks. (b) The firm or proprietary concern is not engaged in any agricultural/plantation or real estate business or print media sector. (c) Amount invested shall not be eligible for repatriation outside India. (ii) Investments with repatriation benefits: NRIs/PIO may seek prior permission of Reserve Bank for investment in sole proprietorship concerns/partnership firms with repatriation benefits. The application will be decided in consultation with the Government of India. (iii) Investment by non-residents other than NRIs/PIO: A person resident outside India other than NRIs/PIO may make an application and seek prior approval of Reserve Bank for making

investment by way of contribution concern or any association of persons in India. The application will be decided in consultation with the Government of India. (iv) Restrictions: An NRI or PIO is not allowed to invest in a firm or proprietorship concern engaged in any and immovable property with a view to earning profit or earning income there from) or

engaged in Print Media.

3. FDI in Venture Capital Fund (VCF): FVCIs are allowed to invest in Indian Venture Capital Undertakings (IVCUs) /Venture Capital Funds (VCFs) /other companies, as stated in paragraph 3.1.6 of this Circular.If a domestic VCF is set up as a trust, a person resident outside India(non-resident entity/individual including an NRI) cannot invest in suchdomestic VCF under the automatic route of the FDI scheme and would be

Fazlani Altius Business School [Batch : 2013-2015] Page 10

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

allowed subject to approval of the FIPB. However, if a domestic VCF is set-up as an incorporated company under the Companies Act, 1956, then aperson resident outside India (non-resident entity/individual includingan NRI) can invest in such domestic VCF under the automatic route of FDI Scheme, subject to the pricing guidelines, reporting requirements, mode of payment, minimum capitalization norms, etc.

4. FDI in Trusts: FDI in Trusts other than VCF is not permitted.

5. FDI in other Entities: FDI in resident entities other than those

mentioned above is not permitted.

E. ENTRY ROUTES FOR FDI

1. Investments can be made by non-residents in the equity shares/fully, compulsorily and Mandatorily convertible debentures/ fully, compulsorily and mandatorily convertible preference shares of an Indiancompany, through two routes:

(i) The Automatic Route: under the Automatic Route, the non-resident investor or the Indian company does not require any approval fromthe RBI or Government of India for the investment.

(ii) The Government Route: under the Government Route, prior approval of the Government of India through Foreign Investment Promotion Board (FIPB) is required. Proposals for foreign investment under Government route as laid down in the FDI policy from time to time, are considered by the Foreign Investment Promotion Board (FIPB) in Department of Economic Affairs (DEA), Ministry of Finance.

Fazlani Altius Business School [Batch : 2013-2015] Page 11

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

F. GUIDELINES FOR CONSIDERATION OF FDI PROPOSALS BY FIPB:

The following guidelines are laid down to enable the FIPB to consider the proposals for FDI and formulate its recommendations.

1. All applications should be put up before the FIPB by its Secretariat within 15 days and it should be ensured that comments of the administrative ministries are placed before the Board either prior to/or in the meeting of the Board.

2. Proposals should be considered by the Board keeping in view the time frame of thirty (30) days for communicating Government decision.

Fazlani Altius Business School [Batch : 2013-2015] Page 12

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

3. In cases in which either the proposal is not cleared or further information is required in order to obviate delays presentation by applicant in the meeting of the FIPB should be resorted to.

4. While considering cases and making recommendations, FIPB should keep inmind the sectorial requirements and the sectorial policies vis-à-vis the proposal (s).

5. FIPB would consider each proposal in its totality.

6. The Board should examine the following while considering proposals submitted to it forconsideration:(i) Whether the items of activity involve industrial licence or not and if so the considerations for grant of industrial licence must be gone into.(ii) Whether the proposal involves any export projection and ifso the items of export and the projected destinations.

(iii) Whether the proposal has any strategic or defence related considerations.

7. While considering proposals the following may be prioritized:(i) Items falling in infrastructure sector.

(ii) Items which have an export potential.

(iii) Items which have large scale employment potential and especially for rural people.(iv) Items which have a direct or backward linkage with agro business/farm sector.(v) Items which have greater social relevance such as hospitals, human resource development, life saving drugs and equipment.

(vi) Proposals which result in induction of technology or infusion of capital.

8. The following should be especially considered during the scrutiny and consideration ofproposals:(i) The extent of foreign equity proposed to be held (keeping in viewsectoral caps if any.(ii) Extent of equity from the point of view whether the proposed project would amount to a holding company/wholly owned subsidiary/a company with dominant foreign investment (i.e. 76% or more) joint venture.

Fazlani Altius Business School [Batch : 2013-2015] Page 13

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

(iii) Whether the proposed foreign equity is for setting up a new project (joint venture or otherwise) or whether it is for enlargement of foreign/NRI equity or whether it is for fresh induction of foreign equity/NRI equity in an existing Indian company.

(iv) In the case of fresh induction offerings/NRI equity and/or in cases of enlargement of foreign/NRI equity, in existing Indian companies whether there is a resolution of the Board of Directors

supporting the said induction/enlargement of foreign/NRI equity and whether there is a shareholders agreement or not.

(v) In the case of induction of fresh equity in the existing Indian companies and/or enlargement of foreign equity in existing Indian companies, the reason why the proposal has been made and the modalityfor induction/enhancement (i.e. whether by increase of paid up capital/authorized capital, transfer of shares(hostile or otherwise) whether by rights issue, or by what modality.

(vi) Issue/transfer/pricing of shares will be as per SEBI/RBI guidelines.(vii) Whether the activity is an industrial or a service activity or a combination of both.(viii) Whether the items of activity involves any restriction by way of reservation for the Micro & Small Enterprises sector.

(ix) Whether there are any sectorial restrictions on the activity.

(x) Whether the proposal involves import of items which are either hazardous/banned or detrimental to environment (e.g. import of plastic scrap or recycled plastics).

9. No condition specific to the letter of approval issued to a non-resident investor would be changed or additional condition imposed subsequent to the issue of a letter of approval. This would not prohibit changes in general policies and, regulations applicable to theindustrial sector.

Fazlani Altius Business School [Batch : 2013-2015] Page 14

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

G. TREND IN FDI FLOWS

Widening growth differential across economies and gradual opening up ofcapital accounts in the emerging world resulted in a steep rise in crossborder investment flows during the past two decades. This section brieflypresents the recent trends in global capital flows particularly toemerging economies including India.

1. Global Trends in FDI Inflows

During the period subsequent to dotcom burst, there has been anunprecedented rise in the cross-border flows and this exuberance wassustained until the occurrence of global financial crisis in the year2008-09. Between 2003 and 2007, global FDI flows grew nearly four -foldand flows to EMEs during this period, grew by about three-fold. Afterreaching a peak of US$ 2.1 trillion in 2007, global FDI flows witnessedsignificant moderation over the next two years to touch US$ 1.1 trillionin 2009, following the global financial crisis. On the other hand, FDIflows to developing countries increased from US$ 565 billion in 2007 toUS$ 630 billion in 2008 before moderating to US$ 478 billion in 2009.

Fazlani Altius Business School [Batch : 2013-2015] Page 15

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

The decline in global FDI during 2009 was mainly attributed to subduedcross border merger and acquisition (M&A) activities and weaker returnprospects for foreign affiliates,which adversely impacted equityinvestments as well as reinvested earnings. According to UNCTAD, declinein M&A activities occurred as the turmoil in stock markets obscured theprice signals upon which M&As rely. There was a decline in the number ofgreen field investment cases as well, particularly those related tobusiness and financial services.

From an institutional perspective, FDI by private equity funds declined astheir fund raising dropped on the back of investors’ risk aversion and thecollapse of the leveraged buyout market in tune with the deterioration incredit market conditions. On the other hand, FDI from sovereign wealthfunds (SWFs) rose by 15 per cent in 2009. This was apparently due to therevised investment strategy of SWFs - who have been moving away frombanking and financial sector towards primary and manufacturing sector,which are less vulnerable to financial market developments as well asfocusing more on Asia.

As the world economic recovery continued to be uncertain and fragile,global FDI flows remained stagnant at US $ 1.1 trillion in 2010. Accordingto UNCTAD’s Global Investment Trends Monitor (released on January 17,2011), although global FDI flows at aggregate level remained stagnant,they showed an uneven pattern across regions – while it contracted furtherin advanced economies by about 7 per cent, FDI flows recovered by almost10 per cent in case of developing economies as a group driven by strongrebound in FDI flows in many countries of Latin America and Asia. Reboundin FDI flows to developing countries has been on the back of improvedcorporate profitability and some improvement in M&A activities withimproved valuations of assets in the stock markets and increased financialcapability of potential buyers.

Improved macroeconomic conditions, particularly in the emerging economies,which boosted corporate profits coupled with better stock marketvaluations and rising business confidence augured well for global FDIprospects. According to UNCTAD, these favourable developments may helptranslate MNC’s record level of cash holdings (estimated to be in therange of US$ 4-5 trillion among developed countries’ firms alone) into newinvestments during 2011. The share of developing countries, which nowconstitutes over 50 per cent in total FDI inflows, may increase further onthe back of strong growth prospects. However, currency volatility,sovereign debt problems and potential protectionist policies may pose somerisks to this positive outlook. Nonetheless, according to the Institute ofInternational Finance (January 2011), net FDI flows to EMEs was projectedto increase by over 11 per cent in 2011. FDI flows into select countriesare given in Table 1.

Fazlani Altius Business School [Batch : 2013-2015] Page 16

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

Table 1 : Countries with Higher Estimated Level of FDIInflows than India in 2010Amount (US$ billion) Variation

(Percent)2007 2008 2009 2010

(Estimates)

2008

2009

2010(Estimat

es)World 2100

.01770.9

1114.2

1122.0 -15.

7

-37.

1

0.7

DevelopedEconomies

1444.1

1018.3

565.9

526.6 -29.

5

-44.

4

-6.9

UnitedStates

266.0

324.6

129.9

186.1 22.0

-60.

0

43.3

France 96.2 62.3 59.6 57.4 -35.

2

-4.3

-3.7

Belgium 118.4

110.0

33.8 50.5 -7.1

-69.

3

49.4

UnitedKingdom

186.4

91.5 45.7 46.2 -50.

9

-50.

1

1.1

Germany 76.5 24.4 35.6 34.4 -68.

1

45.9

-3.4

DevelopingEconomies

564.9

630.0

478.3

524.8 11.5

-24.

1

9.7

China 83.5 108.3

95.0 101.0 29.7

-12.

3

6.3

Hong Kong 54.3 59.6 48.4 62.6 9.8 -18.

8

29.3

Russian 55.1 75.5 38.7 39.7 37. - 2.6

Fazlani Altius Business School [Batch : 2013-2015] Page 17

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

Federation 0 48.7

Singapore 35.8 10.9 16.8 37.4 69.6

54.1

122.6

Saudi Arabia 22.8 38.2 35.5 - 67.5

-7.1

-

Brazil 34.6 45.1 25.9 30.2 30.3

-42.

6

16.6

India 25.0 40.4 34.6 23.7 61.6

-14.

4

-31.5

Source: World Investment Report, 2010 and Global InvestmentTrends Monitor, UNCTAD.

H. TRENDS IN FDI FLOWS TO INDIA

With the tripling of the FDI flows to EMEs during the pre-crisis period ofthe 2000s, India also received large FDI inflows in line with its robustdomestic economic performance. The attractiveness of India as a preferredinvestment destination could be ascertained from the large increase in FDIinflows to India, which rose from around US$ 6 billion in 2001-02 toalmost US$ 38 billion in 2008-09. The significant increase in FDI inflowsto India reflected the impact of liberalisation of the economy since theearly 1990s as well as gradual opening up of the capital account. As partof the capital account liberalisation, FDI was gradually allowed in almostall sectors, except a few on grounds of strategic importance, subject tocompliance of sector specific rules and regulations. The large and stableFDI flows also increasingly financed the current account deficit over theperiod. During the recent global crisis, when there was a significantdeceleration in global FDI flows during 2009-10, the decline in FDI flows

Fazlani Altius Business School [Batch : 2013-2015] Page 18

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

to India was relatively moderate reflecting robust equity flows on theback of strong rebound in domestic growth ahead of global recovery andsteady reinvested earnings (with a share of almost 25 per cent) reflectingbetter profitability of foreign companies in India. However, when therehad been some recovery in global FDI flows, especially driven by flows toAsian EMEs, during 2010-11, gross FDI equity inflows to India witnessedsignificant moderation. Gross equity FDI flows to India moderated to US$20.3 billion during 2010-11 from US$ 27.1 billion in the preceding year.

Table 2: Equity FDI Inflows to India(Percent)

Sectors 2006-07

2007-08

2008-09

2009-10

2010-11

Sectoral shares (Percent)Manufactures 17.6 19.2 21.0 22.9 32.1Services 56.9 41.2 45.1 32.8 30.1Construction, Real estateand mining

15.5 22.4 18.6 26.6 17.6

Others 9.9 17.2 15.2 17.7 20.1Total 100.

0100.

0100.

0100.

0100.0

Equity Inflows (US$ billion)Manufactures 1.6 3.7 4.8 5.1 4.8Services 5.3 8.0 10.2 7.4 4.5Construction, Real estateand mining

1.4 4.3 4.2 6.0 2.6

Others 0.9 3.3 3.4 4.0 3.0Total Equity FDI 9.3 19.4 22.7 22.5 14.9

From a sectoral perspective, FDI in India mainly flowed into servicessector (with an average share of 41 per cent in the past five years)followed by manufacturing (around 23 per cent) and mainly routed throughMauritius (with an average share of 43 per cent in the past five years)followed by Singapore (around 11 per cent). However, the share of servicesdeclined over the years from almost 57 per cent in 2006-07 to about 30 percent in 2010-11, while the shares of manufacturing, and ‘others’ largelycomprising ‘electricity and other power generation’ increased over thesame period (Table 2). Sectoral information on the recent trends in FDIflows to India show that the moderation in gross equity FDI flows during2010-11 has been mainly driven by sectors such as ‘construction, realestate and mining’ and services such as ‘business and financial services’.Manufacturing, which has been the largest recipient of FDI in India, hasalso witnessed some moderation (Table 2).

Fazlani Altius Business School [Batch : 2013-2015] Page 19

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

I. CU M U L A T I V E FDI F LOW S IN T O IND I A (2 0 0 0 - 2 013 ) :

A. TOTAL FDI INFLOWS (from April, 2000 to March, 2013):

1. CUMULATIVE AMOUNT OF FDI INFLOWS(Equity inflows + ‘Re-invested earnings’ +‘Other capital’) *

-US$ 290,078million

2. CUMULATIVE AMOUNT OF FDI EQUITY INFLOWS(excluding, amount remitted through RBI’s-NRI

Rs. 896,38crore

US$ 193,282million

B. FDI INFLOWS DURING FINANCIAL YEAR 2012-13 (from April, 2012 to March, 2013):

1. TOTAL FDI INFLOWS INTO INDIA(Equity inflows + ‘Re-invested earnings’ + ‘Other capital’)(as per RBI’s Monthly bulletin dated:

- US$ 36,860million

2. FDI EQUITY INFLOWS Rs. 121,907crore

US$ 22,423million

C. FDI EQUITY INFLOWS (MONTH-WISE) DURING THE FINANCIAL YEAR 2012-13:

Financial Year 2012-13( April-March )

Amount of FDI Equity inflows(In Rs. Crore) (In US$ mn)

1 April, 2012 9,620 1,8572.

May, 2012 7,229 1,3273 June, 2012 6,971 1,2444 July, 2012 8,182 1,4755 August, 2012 12,578 2,2646 September, 2012 25,552 4,6797 October, 2012 10,295 1,9428 November, 2012 5,798 1,0589 December, 2012 6,012 1,1001 January, 2013 11,719 2,1571 February, 2013 9,654 1,7951 March, 2013 8,297 1,5252012-13 (up to March, 2013) # 121,907 22,4232011-12 (up to March, 2012) # 165,146 35,121

%age growth over last year ( - ) 28 % ( - ) 38 %

Fazlani Altius Business School [Batch : 2013-2015] Page 20

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

D. FDI EQUITY INFLOWS (MONTH-WISE) DURING THE CALENDAR YEAR 2013:

Calendar Year 2013(Jan.-Dec.)

Amount of FDI Equity inflows(In Rs. Crore) (In US$ mn)

1. January, 2013 11,719 2,1572. February, 2013 9,654 1,7953. March, 2013 8,297 1,525Year 2013 (up to March, 2013) 29,670 5,477Year 2012 (up to March, 2012) 29,354 5,844%age growth over last year ( + ) 01 % ( - ) 06 %

N o te : Country & Sector specific analysis is available from the year 2000 onwards, as Company-wise details are provided by RBI from April, 2000 onwards only.* Data on „Re-invested earnings‟ & „Other capital‟, are the estimates on an average basis, based upon data for the previous two years, published by RBI in monthly bulletin dated: 10.12.2012.# Figures are provisional, subject to reconciliation with RBI, Mumbai.^ Inflows for the month of March, 2012 are as reported by RBI, consequent to the adjustment made in the figures of March, „11, August,‟11 and October, „11.

Fazlani Altius Business School [Batch : 2013-2015] Page 21

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

E. SHARE OF TOP INVESTING COUNTRIES FDI EQUITY INFLOWS (Financial years):

Amount Rupees in crores(US$ in

million)

Ranks Country 2010-1 1 (April -March)

201 1 -1 2 ( April -March)

2012-1 3 (April –March)

C u m u lat i v e I n fl ows

(April ‟00– March’13)

%age tototal

Inflows (interms of US

1. MAURITIUS31,855(6,987)

46,710(9,942)

51,654(9,497)

341,125(73,666) 38 %

2. SINGAPORE7,730(1,705)

24,712(5,257)

12,594(2,308)

90,182(19,460) 10 %

3. U.K.12,235(2,711)

36,428(7,874)

5,797(1,080)

80,459(17,549) 9 %

4. JAPAN7,063(1,562)

14,089(2,972)

12,243(2,237)

70,094(14,550) 8 %

5. U.S.A.5,353(1,170)

5,347(1,115)

3,033(557)

50,923(11,121) 6 %

6. NETHERLANDS5,501(1,213)

6,698(1,409)

10,054(1,856)

42,378(8,965) 5 %

7. CYPRUS4,171(913)

7,722(1,587)

2,658(490)

32,328(6,889) 4 %

8. GERMANY908

(200)7,452(1,622)

4,684(860)

25,512(5,480) 3 %

9 FRANCE3,349(734)

3,110(663)

3,487(646)

16,865(3,573) 2 %

10. U.A.E.1,569(341)

1,728(353)

987(180)

11,307(2,422) 1 %

TOTAL FDI INFLOWSFROM

ALL COUNTRIES *

97,320(21,383)

165,146(35,121)

121,907(22,423)

896,913(193,403) -

*Includes inflows under NRI Schemes of RBI.

N o te : (i) Cumulative country-wise FDI equity inflows (from April, 2000 to March, 2013) are at – A nne x- „ A ‟

(ii) %age worked out in US$ terms & FDI inflows received through FIPB/SIA+ RBI‟s Automatic Route + acquisition of existing shares only.

Fazlani Altius Business School [Batch : 2013-2015] Page 22

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

F. SECTORS ATTRACTING HIGHEST FDI EQUITY INFLOWS: Amount in Rs. crores (US$ in million)

Ranks Sector 2010-11 (April -March)

2011-12 ( April- March)

2012-13 (April –March)

C u m u lat i v e I n fl ows

(April ‟00–

% age tototal

Inflows(In1. SERVICES SECTOR ** 15,054

(3,296)24,656(5,216)

26,306(4,833)

172,275(37,235) 19 %

2. CONSTRUCTIONDEVELOPMENT:

TOWNSHIPS, HOUSING,BUILT-UP INFRASTRUCTURE

7,590(1,663)

15,236(3,141)

7,248(1,332)

101,049(22,080) 11 %

3. TELECOMMUNICATIONS(radio paging,

cellular mobile,basic telephone

7,542(1,665)

9,012(1,997)

1,654(304)

58,732(12,856)

7 %

4. COMPUTER SOFTWARE &HARDWARE

3,551(780)

3,804(796)

2,656(486)

52,774(11,691) 6 %

5. DRUGS & PHARMACEUTICALS 961(209)

14,605(3,232)

6,011(1,123)

48,880(10,318) 5 %

6. CHEMICALS (OTHER THANFERTILIZERS)

10,612(2,354)

18,422(4,041)

1,596(292)

40,496(8,881) 5 %

7. AUTOMOBILE INDUSTRY 5,864(1,299)

4,347(923)

8,384(1,537)

39,170(8,295) 4 %

8. POWER 5,796(1,272)

7,678(1,652)

2,923(536)

36,137(7,834) 4 %

9. METALLURGICALINDUSTRIES

5,023(1,098)

8,348(1,786)

7,878(1,466)

34,814(7,507)

4 %

10 HOTEL & TOURISM 1,405(308)

4,754(993)

17,777(3,259)

33,260(6,631) 3 %

N o te : (i) ** Services sector includes Financial, Banking, Insurance, Non-Financial / Business, Outsourcing, R&D, Courier, Tech.Testing and Analysis

(ii) Cumulative Sector- wise FDI equity inflows (from April, 2000 to March, 2013) are at - A nne x- „ B ‟ .

(iii) FDI Sectoral data has been revalidated / reconciled in line with the RBI, which reflects minor changes in the FDI figures (increase/decrease) as compared to the earlier published sectoral data.

Fazlani Altius Business School [Batch : 2013-2015] Page 23

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

G. STATEMENT ON RBI’S REGIONAL OFFICES (WITH STATE COVERED) RECEIVED FDI EQUITY INFLOWS (from April, 2000 to March, 2013):

Amount Rupees in crores (US$ in million)

S.No.

RBI‟s -RegionalOffice

State covered 2010-1 1 (April

-March)

2011-1 2 ( April- March)

2012-13 (April –March)

C umu lat i v e I n fl ows

(April ‟00 –March’13)

%age tototal

Inflows(in terms

1 MUMBAI MAHARASHTRA,DADRA & NAGAR

HAVELI,DAMAN & DIU

27,669(6,097)

44,664(9,553)

47,359(8,716)

293,494(63,337)

33

2 NEW DELHI DELHI, PARTOF

UP AND

12,184(2,677)

37,403(7,983)

17,490(3,222)

168,581(36,294)

19

3 CHENNAI TAMIL NADU,PONDICHERRY

6,115(1,352)

6,711(1,422)

15,252(2,807)

52,810(11,081)

6

4 BANGALORE KARNATAKA 6,133(1,332)

7,235(1,533)

5,553(1,023)

49,445(10,784)

6

5 AHMEDABAD GUJARAT 3,294(724)

4,730(1,001)

2,676(493)

39,100(8,650)

4

6 HYDERABAD ANDHRAPRADESH

5,753(1,262)

4,039(848)

6,290(1,159)

36,891(7,968)

4

7 KOLKATA WEST BENGAL,SIKKIM,

ANDAMAN &NICOBARISLANDS

426(95)

1,817(394)

2,319(424)

10,504(2,306)

1

8 CHANDIGARH CHANDIGARH,PUNJAB,HARYANA,HIMACHALPRADESH

1,892(416)

624(130)

255(47)

5,564(1,201)

1

9 BHOPAL MADHYAPRADESH,

CHATTISGARH

2,093(451)

569(123)

1,208(220)

4,787(997)

0.5

10. KOCHI KERALA,LAKSHADWEEP

167(37)

2,274(471)

390(72)

4,321(911)

0.5

11 PANAJI GOA 1,376(302)

181(38)

47(9)

3,554(771)

0.4

12 JAIPUR RAJASTHAN 230(51)

161(33)

714(132)

3,325(685)

0.4

13 KANPUR UTTARPRADESH,

UTTRANCHAL

514(112)

635(140)

167(31)

1,614(347)

0.2

14 BHUBANESHWAR ORISSA 68(15)

125(28)

285(52)

1,617(341)

0.2

Fazlani Altius Business School [Batch : 2013-2015] Page 24

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

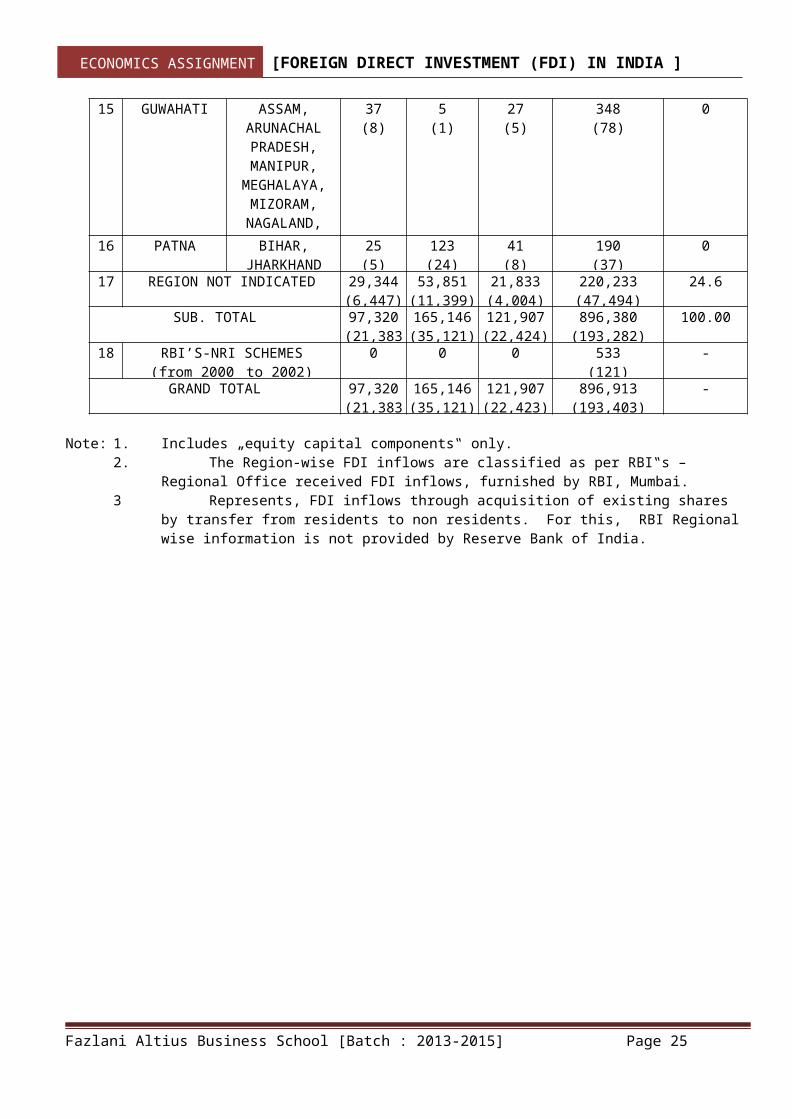

15 GUWAHATI ASSAM,ARUNACHALPRADESH,MANIPUR,

MEGHALAYA,MIZORAM,NAGALAND,TRIPURA

37(8)

5(1)

27(5)

348(78)

0

16 PATNA BIHAR,JHARKHAND

25(5)

123(24)

41(8)

190(37)

0

17 REGION NOT INDICATED 29,344(6,447)

53,851(11,399)

21,833(4,004)

220,233(47,494)

24.6

SUB. TOTAL 97,320(21,383

165,146(35,121)

121,907(22,424)

896,380(193,282)

100.00

18 RBI’S-NRI SCHEMES(from 2000 to 2002)

0 0 0 533(121)

-

GRAND TOTAL 97,320(21,383

165,146(35,121)

121,907(22,423)

896,913(193,403)

-

Note: 1. Includes „equity capital components‟ only.2. The Region-wise FDI inflows are classified as per RBI‟s –

Regional Office received FDI inflows, furnished by RBI, Mumbai.3 Represents, FDI inflows through acquisition of existing shares

by transfer from residents to non residents. For this, RBI Regional wise information is not provided by Reserve Bank of India.

Fazlani Altius Business School [Batch : 2013-2015] Page 25

Sr.No.

Financial Year(April-March)

FO R E I GN DIR E C T IN VE S T M E N T ( F DI ) I nv est m e n t

by F II ‟ s

ForeignInstitutiona l

InvestorsFund

Equity Re-investe

dearning

s+

Othercapita

l+

FDI FLOWS INTOINDIAFIPB

Route/RBI‟s

AutomaticRoute/

Acquisition Route

Equitycapital

ofunicorporated

bodies #

Tot a l F D I

F l ows

%agegrowthover

previousyear

(in US$FINANCIAL YEARS 2000-01 to 2012-13 (up to March, 2013)

1. 2000-01 2,339 61 1,350 279 4,029 - 1,8472. 2001-02 3,904 191 1,645 390 6,130 (+) 52 % 1,5053. 2002-03 2,574 190 1,833 438 5,035 (-) 18 % 3774. 2003-04 2,197 32 1,460 633 4,322 (-) 14 % 10,9185. 2004-05 3,250 528 1,904 369 6,051 (+) 40 % 8,6866. 2005-06 5,540 435 2,760 226 8,961 (+) 48 % 9,9267. 2006-07 15,585 896 5,828 517 22,826 (+) 146 3,2258. 2007-08 24,573 2,291 7,679 300 34,843 (+) 53 % 20,3289. 2008-09 31,364 702 9,030 777 41,873 (+) 20 % (-)10. 2009-10 (P) (+) 25,606 1,540 8,668 1,931 37,745 (-) 10 % 29,04811. 2010-11 (P) (+) 21,376 874 11,939 658 34,847 (-) 08 % 29,42212. 2011-12 (P) 34,833 1,022 8,206 2,495 46,556 (+) 34 % 16,81213. 2012-13 (P)

(up to March,21,825 1,059 11,025 2,951 36,860 - 27,583

CU M U L A T IVE T OT A L (from April, 2000 to

March’ 2013)

194,966 9,821 73,327 11,964 290,078 - 144,654

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

II. FI N A N C I A L Y E A R -W I S E F DI INF LOW S D A T A :

A. AS PER INTERNATIONAL BEST PRACTICES:

(Data on FDI have been revised since 2000-01 with expended coverage to approach International Best Practices)

(Amount US$ million)

Source: (i) RBI‟s Bulletin May, 2013 dt. 13.05.2013 (Table No. 34 – FOREIGN INVESTMENT INFLOWS).(ii) Inflows under the acquisition of shares in March, 2011, August,

2011 & October, 2011, include net FDI on account of transfer of participating interest from Reliance Industries Ltd. to BP

Exploration (Alpha).(iii) RBI had included Swap of Shares of US$ 3.1 billion under equity

components during December 2006.(iv) Monthly data on components of FDI as per expended coverage are

not available. These data, therefore, are not comparable with FDI data for previous years.

(v) Figures updated by RBI up to March, 2013.

Fazlani Altius Business School [Batch : 2013-2015] Page 26

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

„#‟ Figures for equity capital of unincorporated bodies for 2010-11 are estimates. (P) All figures are provisional“+” Data in respect of „Re-invested earnings‟ & „Other capital‟ for the years 2009- 10, 2010-11 & 2012-13 are estimated as average of previous two years.

B. DIPP’S – FINANCIAL YEAR-WISE FDI EQUITY INFLOWS: (As per DIPP’s FDI data base – equity capital components only):Sr.Nos

Financial Year(April – March)

Amount of FDI Inflows %age growthover

previousyear

(in terms ofUS $)

FINANCIAL YEARS 2000-01 to 2012-13(up to March, 2013)

In Rs crores In US$million

1. 2000-01 10,733 2,463 -2. 2001-02 18,654 4,065 ( + ) 65 %3. 2002-03 12,871 2,705 ( - ) 33 %4. 2003-04 10,064 2,188 ( - ) 19 %5. 2004-05 14,653 3,219 ( + ) 47 %6. 2005-06 24,584 5,540 ( + ) 72 %7. 2006-07 56,390 12,492 (+ )125 %8. 2007-08 98,642 24,575 ( + ) 97 %9. 2008-09 ‘*’ 142,829 31,396 ( + ) 28 %10. 2009-10 # 123,120 25,834 ( - ) 18 %11. 2010-11 # 97,320 21,383 ( - ) 17 %12. 2011-12 # ^ 165,146 35,121 (+) 64 %13. 2012-13 #

(from April, 2012 to March,121,907 22,423 -

CU M U L A T IV E T OT A L (from April, 2000 to March, 2013)

896,913 193,404 -

Note: (i) Including amount remitted through RBI‟s-NRI Schemes (2000-2002).(ii) FEDAI (Foreign Exchange Dealers Association of India)

conversion rate from rupees to US dollar applied, on the basis of monthly average rate provided by RBI (DEPR), Mumbai.

# Figures for the years 2009-10, 2010-11, 2011-12 & 2012-13 (from April, 2012 to August, 2012) are provisional subject to reconciliation with RBI.^ Inflows for the month of March, 2012 are as reported by RBI, consequentto the adjustment made in the figures of March, „11, August, ‟11 and October, „11.

Fazlani Altius Business School [Batch : 2013-2015] Page 27

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

*‟ An additional amount of US$ 4,035 million pertaining to the year 2008-09, since reported by RBI, has been included in FDI data base from February, 2012.

Fazlani Altius Business School [Batch : 2013-2015] Page 28

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

I. S T A T E M E NT O N C O UN T R Y -W I S E FDI E Q UI T Y INF LOW S A P R IL, 2 0 0 0 T O M A RC H , 2 0 1 3

Sr.

Country Amount of Foreign Direct %age with totalFDI Inflows (+)(In Rs crore) (In US$ million)

1 Mauritius 341,124.86 73,666.11 38.112 Singapore 90,182.32 19,460.35 10.073 United Kingdom 80,458.61 17,548.55 9.084 Japan 70,094.45 14,550.29 7.535 U.S.A 50,922.68 11,121.11 5.756 Netherlands 42,378.39 8,965.08 4.647 Cyprus 32,328.14 6,889.33 3.568 Germany 25,512.17 5,480.30 2.849 France 16,864.63 3,572.99 1.8510 UAE 11,307.02 2,422.47 1.2511 Switzerland 11,064.28 2,367.02 1.2212 Spain 6,960.69 1,463.19 0.7613 South Korea 5,821.17 1,231.55 0.6414 Italy 5,258.45 1,169.48 0.6115 Hong Kong 4,769.75 1,028.74 0.5316 Sweden 4,604.83 982.37 0.5117 Caymen Islands 3,755.52 877.74 0.4518 British Virginia 3,604.01 795.76 0.4119 Indonesia 2,825.48 610.30 0.3220 Poland 2,987.28 568.79 0.2921 Malaysia 2,730.13 549.45 0.2822 Australia 2,478.02 535.06 0.2823 The Bermudas 2,252.20 502.07 0.2624 Belgium 2,277.18 491.86 0.2525 Luxembourg 2,197.27 473.03 0.2426 Russia 2,236.55 468.17 0.2427 Canada 1,954.65 425.67 0.2228 Oman 1,622.44 352.02 0.1829 Denmark 1,645.73 342.61 0.1830 China 1,428.48 278.31 0.1431 Finland 1,301.95 273.89 0.1432 Austria 895.05 187.64 0.1033 Ireland 687.66 154.23 0.0834 Chile 654.72 141.07 0.0735 Morocco 649.65 136.99 0.0736 Norway 607.06 126.18 0.0737 South Africa 564.27 120.71 0.0638 Thailand 513.66 111.10 0.0639 British Isles 451.33 98.37 0.0540 West Indies 348.17 78.28 0.0441 Taiwan 306.60 65.70 0.0342 Mexico 345.83 64.97 0.03

Fazlani Altius Business School [Batch : 2013-2015]Page 29

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

43 Turkey 279.53 59.66 0.0344 Israel 247.93 55.69 0.0345 St. Vincent 254.02 49.67 0.0346 Saudi Arabia 193.91 40.93 0.0247 Panama 185.36 40.61 0.0248 Korea(North) 187.15 36.94 0.0249 Saint Kitts & Nevis 147.88 33.53 0.0250 New Zealand 145.92 32.62 0.0251 Philippines 168.58 31.24 0.0252 Bahamas 141.68 30.74 0.0253 Sri Lanka 138.45 29.45 0.0254 Jordan 155.03 28.57 0.0155 Portugal 119.72 25.00 0.0156 Iceland 93.72 21.14 0.0157 Kenya 98.45 21.07 0.0158 Brazil 100.43 20.97 0.0159 Virgin Islands(US) 101.10 20.83 0.0160 Gibraltar 83.67 19.51 0.0161 Seychelles 86.99 18.24 0.0162 Kuwait 84.96 17.95 0.0163 Kazakhstan 81.11 17.42 0.0164 Czech Republic 74.81 17.36 0.0165 Bahrain 130.53 29.23 0.0166 Liberia 64.54 14.56 0.0167 Malta 58.39 12.78 0.0168 Channel Islands 57.20 12.71 0.0169 Belarus 49.93 12.17 0.0170 Nigeria 49.48 10.44 0.0171 Hungary 47.86 10.30 0.0172 Argentina 46.23 10.15 0.0173 Myanmar 35.75 8.96 0.0074 Isle of Man 38.09 8.49 0.0075 Slovenia 39.07 8.24 0.0076 Liechtenstein 29.90 6.43 0.0077 Belize 25.14 5.52 0.0078 Maldives 24.72 5.49 0.0079 Slovakia 22.62 5.22 0.0080 Rep. of Fiji Islands 22.30 5.07 0.0081 Romania 23.16 4.60 0.0082 Ghana 21.13 4.46 0.0083 Tunisia 19.84 4.31 0.0084 Guersney 23.27 4.20 0.0085 Greece 18.78 3.72 0.0086 Uruguay 16.06 3.63 0.0087 Scotland 13.51 2.99 0.0088 Qatar 14.23 2.84 0.0089 West Africa 12.31 2.47 0.0090 Nepal 9.12 1.93 0.0091 Yemen 7.74 1.87 0.00

Fazlani Altius Business School [Batch : 2013-2015]Page 30

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

92 Monaco 7.49 1.52 0.0093 Egypt 7.30 1.43 0.0094 Tanzania 6.31 1.41 0.0095 Colombia 5.36 1.17 0.0096 Ukraine 5.06 1.12 0.0097 Uganda 5.06 1.10 0.0098 Cuba 4.73 1.04 0.0099 Guyana 4.60 1.00 0.0010 Vanuatu 4.41 0.94 0.0010 Bermuda 3.45 0.64 0.0010 Togolese Republic 3.08 0.60 0.0010 Congo (DR) 2.41 0.54 0.0010 Croatia 2.29 0.52 0.0010 Aruba 1.96 0.43 0.0010 Lebanon 1.87 0.39 0.0010 Bulgaria 1.69 0.36 0.0010 Estonia 1.31 0.30 0.0010 Anguilla 1.46 0.29 0.0011 Yugoslavia 1.13 0.24 0.0011 Vietnam 1.14 0.24 0.0011 Jamaica 1.00 0.22 0.0011 Iraq 0.85 0.19 0.0011 Zambia 0.67 0.15 0.0011 Iran 0.47 0.10 0.0011 Libya 0.28 0.07 0.0011 Latvia 0.27 0.06 0.0011 Mongolia 0.27 0.06 0.0011 Sudan 0.24 0.05 0.0012 Peru 0.20 0.04 0.0012 Bangladesh 0.16 0.03 0.0012 Afghanistan 0.12 0.03 0.0012 Botswana 0.13 0.02 0.0012 St. Lucia 0.06 0.01 0.0012 Georgia 0.02 0.00 0.0012 East Africa 0.02 0.00 0.0012 Bolivia 0.01 0.00 0.0012 Costa Rica 0.01 0.00 0.0012 Kyrgyzstan 0.01 0.00 0.0013 Trinidad & Tobago 0.01 0.00 0.0013 Cameroon 0.01 0.00 0.0013 Djibouti 0.00 0.00 0.0013 Venezuela 0.00 0.00 0.0013 Barbados 0.00 0.00 0.0013 Muscat 0.00 0.00 0.0013 FII's 0.25 0.06 0.0013 NRI ‘*’ 20,383.66 4,684.25 2.4213 Country Details Awaited 30,854.20 6,960.47 3.65

SUB.-TOTAL 896,379.66 193,281.91 100.0013 RBI’S- NRI SCHEMES 533.06 121.33 -

Fazlani Altius Business School [Batch : 2013-2015]Page 31

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

GRAND TOTAL 896,912.72 193,403.24 -

J. S T A T E M E NT O N SE C T O R -W I S E FDI E Q UI T Y INF LOW S A P R IL, 2 0 0 0 T O M A RC H , 2 0 1 3

Sr.

Sector Amount of FDI Inflows %age withtotal(In Rs (In US$

1 SERVICES SECTOR(Fin., Banking, Insurance, NonFin/Business, Outsourcing, R&D,

Courier, Tech.

172,275.31

37,234.60 19.26

2 CONSTRUCTION DEVELOPMENT Townships,housing, built-up infrastructureand construction-development

101,049.13

22,080.20 11.42

3 TELECOMMUNICATIONS 58,732.23 12,856.06 6.654 COMPUTER SOFTWARE & HARDWARE 52,774.07 11,691.10 6.055 DRUGS & PHARMACEUTICALS 48,879.53 10,318.17 5.346 CHEMICALS

(OTHER THAN FERTILIZERS)40,495.55 8,880.83 4.59

7 AUTOMOBILE INDUSTRY 39,169.94 8,294.85 4.298 POWER 36,136.88 7,834.22 4.059 METALLURGICAL INDUSTRIES 34,814.13 7,507.07 3.8810 HOTEL & TOURISM 33,260.03 6,631.25 3.4311 PETROLEUM & NATURAL GAS 24,808.41 5,381.48 2.7812 TRADING 18,646.51 3,955.80 2.0513 INFORMATION & BROADCASTING

(INCLUDING PRINT MEDIA)15,495.69 3,284.21 1.70

14 ELECTRICAL EQUIPMENTS 14,668.58 3,182.70 1.6515 CEMENT AND GYPSUM PRODUCTS 11,779.04 2,626.43 1.3616 NON-CONVENTIONAL ENERGY 12,901.12 2,591.22 1.3417 MISCELLANEOUS MECHANICAL &

ENGINEERING INDUSTRIES10,522.52 2,318.71 1.20

18 INDUSTRIAL MACHINERY 11,017.51 2,302.14 1.1919 CONSULTANCY SERVICES 9,692.72 2,095.13 1.0820 CONSTRUCTION (INFRASTRUCTURE)

ACTIVITIES9,741.06 2,090.41 1.08

21 FOOD PROCESSING INDUSTRIES 8,681.38 1,811.06 0.9422 PORTS 6,717.38 1,635.08 0.8523 AGRICULTURE SERVICES 7,797.73 1,608.69 0.8324 HOSPITAL & DIAGNOSTIC CENTRES 7,437.93 1,597.33 0.8325 TEXTILES

(INCLUDING DYED,PRINTED)5,689.76 1,226.02 0.63

26 ELECTRONICS 5,466.74 1,198.22 0.6227 SEA TRANSPORT 5,492.51 1,194.50 0.6228 FERMENTATION INDUSTRIES 5,095.29 1,134.63 0.59

Fazlani Altius Business School [Batch : 2013-2015]Page 32

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

29 RUBBER GOODS 5,824.46 1,134.44 0.5930 MINING 4,368.18 998.30 0.5231 PAPER AND PULP

(INCLUDING PAPER PRODUCTS)4,056.14 865.54 0.45

32 PRIME MOVER(OTHER THAN ELECTRICAL GENERATORS)

4,131.80 848.68 0.44

33 EDUCATION 3,332.97 684.35 0.3534 SOAPS, COSMETICS & TOILET

PREPARATIONS3,115.54 632.39 0.33

35 MACHINE TOOLS 2,967.09 622.99 0.3236 MEDICAL AND SURGICAL APPLIANCES 2,913.92 604.47 0.3137 CERAMICS 2,195.59 508.13 0.2638 AIR TRANSPORT (INCLUDING AIR

FREIGHT)2,022.00 449.26 0.23

39 DIAMOND,GOLD ORNAMENTS 1,810.74 390.76 0.2040 GLASS 1,942.21 389.07 0.2041 VEGETABLE OILS AND VANASPATI 1,893.72 384.94 0.2042 FERTILIZERS 1,425.53 297.90 0.1543 AGRICULTURAL MACHINERY 1,423.25 296.42 0.1544 PRINTING OF BOOKS

(INCLUDING LITHO PRINTING INDUSTRY)1,257.51 272.32 0.14

45 RAILWAY RELATED COMPONENTS 1,246.35 270.33 0.1446 COMMERCIAL, OFFICE & HOUSEHOLD

EQUIPMENTS1,181.76 254.83 0.13

47 EARTH-MOVING MACHINERY 769.05 174.95 0.0948 LEATHER,LEATHER GOODS AND PICKERS 527.88 107.43 0.0649 TEA AND COFFEE

(PROCESSING & WAREHOUSING COFFEE &RUBBER)

456.01 101.21 0.05

50 RETAIL TRADING (SINGLE BRAND) 459.55 95.36 0.05

51 SCIENTIFIC INSTRUMENTS 496.11 94.48 0.0552 TIMBER PRODUCTS 398.52 79.15 0.0453 PHOTOGRAPHIC RAW FILM AND PAPER 269.26 66.54 0.0354 INDUSTRIAL INSTRUMENTS 307.45 66.53 0.0355 BOILERS AND STEAM GENERATING PLANTS 305.75 61.83 0.03

56 SUGAR 242.32 51.82 0.0357 COAL PRODUCTION 103.11 24.78 0.0158 DYE-STUFFS 87.32 19.50 0.0159 GLUE AND GELATIN 70.56 14.55 0.0160 MATHEMATICAL,SURVEYING AND DRAWING

INSTRUMENTS39.80 7.98 0.00

61 DEFENCE INDUSTRIES 19.89 4.12 0.0062 COIR 10.37 2.17 0.0063 MISCELLANEOUS INDUSTRIES 35,469.28 7,843.68 4.10

SUB -TOTAL 896,379.6 193,283.31 10064 RBI’S- NRI SCHEMES (2000-2002) 533.06 121.33 -

GRAND TOTAL 896,912.73

193,404.64 -

Fazlani Altius Business School [Batch : 2013-2015]Page 33

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

FDI inflows data re-classified, as per segregation of data from April 2000 onwards.

+‟ Percentage of inflows worked out in terms of US$ & the above amount of inflows received through FIPB/SIA route RBI‟s automatic route & acquisition of existing shares only.FDI Sectoral data has been revalidated / reconciled in line with the RBI, which reflects minor changes in the FDI figures (increase/decrease) as compared to the earlier published sectoral data.

K. INDIAN ECONOMY

I. Recent Trends in Indian Economy

1. The Indian economy has emerged with remarkable rapidity from the slowdown caused by the global economic crisis and emerged stronger in 2011.The Indian economy is estimated to grow at 8.6 per cent in 2010-11as compared to the growth rate of 8.0 per cent in 2009-10. The growth rate of 8.6 per cent in GDP during 2010-11 has been due to the robust growth rates of over 8 per cent in the sectors of manufacturing, construction, trade, hotels, transport and communication, financing, insurance, and, real estate and business services.

2. The agriculture, forestry and fishing sector is likely to show a growthof 5.4 per cent during 2010-11, as against the previous year's growth rate of 0.4 per cent. According to the Department of Agriculture and Cooperation (DAC) of Government of India, production of food grains andoilseeds is expected to grow by 6.5 per cent and 11.9 per cent, respectively, as compared to the previous agriculture year. The production of cotton and sugarcane is also expected to rise by 41.2 percent and 15.2 per cent, respectively, in 2010-11. Among the horticultural crops, production of fruits and vegetables is expected toincrease by 4.1 per cent and 3.8 per cent, respectively, during the year 2010-11.

3. The growth in mining and quarrying and manufacturing sectors during 2010-11 is expected to be 6.2 and 8.8 per cent respectively over previous year. According to the latest estimates available of the Indexof Industrial Production (IIP), mining and manufacturing registered growth rates of 8.0 per cent and 10.0 per cent respectively during April-November, 2010. The estimated growth rate for construction sectoris 8.0 per cent in 2010-11. The key indicators of construction sector, namely, cement production and steel consumption have registered growth rates of 4.4 per cent and 8.8 per cent, respectively during April-

Fazlani Altius Business School [Batch : 2013-2015]Page 34

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

December, 2010.

4. The estimated growth in the trade, hotels, transport and communication sectors during 2010-11 is placed at 11.0 per cent, mainly on account ofgrowth of 14.9 per cent in passengers handled in civil aviation, 21.3 per cent in air cargo handled and 40.9 per cent in stock of telephone connections. The sales of commercial vehicles witnessed an increase of 34.1 per cent per cent in April-December, 2010. The financing, insurance, real estate and business services sectors are expected to show a growth rate of 10.6 per cent during 2010-11, on account of 14.0 per cent growth in aggregate deposits and 22.6 per cent growth in bank credit during April- November 2010 (against the respective growth ratesof 18.6 per cent and 10.1 per cent in the corresponding period of previous year). The growth rate of community, social and personal services during 2010-11 is estimated to be 5.7 per cent.

5. India's per capita income, often used to measure a country's standard of living, increased by 14.5 per cent during 2009-10 to US$ 1038.2 as compared to US$ 906.9 in 2008-09.

II. Growth in Gross Domestic Product

Annual growth by economic activity in Gross Domestic Product (GDP) for the year 2010-11, released by the Central Statistics office (CSO) of Government of India

S.No.

Industry GDP at FactorCost (2010-11)

Percentage change over previousyear

at 2004-05prices(US$

at currentprices (US$

at 2004-05

atcurrent

Fazlani Altius Business School [Batch : 2013-2015]Page 35

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

billion) billion) prices prices1 Agriculture, forestry &

fishing152.42 295.25 5.4 23.2

2 Mining & quarrying 24.32 40.13 6.2 18.23 Manufacturing 170.87 228.09 8.8 14.54 Electricity, gas & water

supply20.49 22.15 5.1 8.6

5 Construction 84.57 129.21 8.0 17.06 Trade, hotels, transport

& communication291.36 379.65 11.0 16.7

7 Financing, insurance, real estate & business services

187.89 285.97 10.6 26.5

8 Community, social & personal services

141.87 216.87 5.7 11.3

Total GDP 1073.79 1597.49 8.6 18.3

Source: Central Statistics Office (CSO), Ministry of Statistics & Programme Implementation, Government of India

Fazlani Altius Business School [Batch : 2013-2015]Page 36

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

III. Economic Survey 2012-13

According to the Economic Survey 2010-11, tabled in Parliament on February25, 2011 by the Union Finance Minister, Mr. Pranab Mukherjee, the economyis expected to grow at 8.6 per cent in 2010-11 and is expected to be around 9 per cent in the next fiscal year. The growth has been broad basedwith a rebound in the Agriculture sector which is expected to grow around 5.4 per cent. Manufacturing and Services sector have registered impressivegains. The Survey reports that the industrial output growth rate was 8.6 per cent while the manufacturing sector registered a growth rate of 9.1 per cent in 2010-11.

The main highlights of the survey are:

1. Economy expected to grow at 8.6 per cent in 2010-11 and 9 per cent in next fiscal.

2. Growth broad based with rebound in Agriculture, continued momentum in manufacturing and private services.

3. Fundamentals strong with savings and investments up, exports rising rapidly and inflation falling.

4. Agriculture likely to grow at 5.4 per cent in 2010-11.

5. Industrial output grows by 8.6 per cent.

6. Manufacturing sector registers 9.1 per cent growth.

7. Exports in April–December 2010 up by 29.5 per cent.

8. Imports in April–December 2010 up by 19 per cent.

9. Trade gap narrowed to US$ 82.01 billion in April-December 2010.

10. 59 per cent rise in Net Bank Credit.

11. Social programme spending stepped up by 5 percentage points of GDPover past 5 years.

Fazlani Altius Business School [Batch : 2013-2015]Page 37

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

12. 9.7 per cent growth of GDP at market prices.

13. Production of food grains estimated at 232.1 million tonnes.

14. Forex Reserves estimated at US$ 297.3 billion.

15. Gross Fiscal Deficit stands at 4.8 per cent of GDP

L. POTENTIAL FOR INVESTMENT IN INDIA

1. India presents a vast potential for overseas investment and is activelyencouraging the entrance of foreign players into the market. India is also one of the few markets in the world, which offers high prospects for growth and earning potential in practically all areas of business.

2. India’s biotechnology sector is set to become a $10 billion industry by2015, CMD of Biocon Ltd, Kiran Mazumdar-Shaw said . She expects the industry to grow to $5 billion by next year. In 2008-09 it was $2.51 billion. “India’s biotechnology industry is at an inflexion point, and has attained a critical mass, Mazumdar-Shaw said. It now has a platformfrom where it can leapfrog and deliver exponential growth, she said. India is also becoming the vaccine capital.Clinical trials, agri-biotech and bio-fuels are becoming opportunities. There are a lot of growth drivers and trigger points which, she said, will deliver in the next five years.

3. With the launch of video telephony, by BSNL and Sai Info Systems (SIS),will boost demand for broadband connection, Sam Pitroda, advisor to Prime Minister on public information, infrastructure and innovations, expects the number to hit 100 million in next five years. "The service is expected to revolutionize the telecom sector and take it to the nextlevel. Globally with video phones have become an integral part of life.

Fazlani Altius Business School [Batch : 2013-2015]Page 38

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

The service will be provided and marketed by SIS while the connectivityfor the service will be provided by BSNL. BSNL will also market it as another value added service to its large broadband customer base," saidVijay Mandora, director, SIS.

4. Tumbling voice tariffs contributing to the declining average revenue per user (ARPU) rates, will result in SMS volumes to reach 191.6 billion in India by 2013, predicts Gartner. By 2013, the country would have more than 750 million mobile connections; therefore the SMS usage per user would essentially drop. However, overall large base of mobile connections would support this SMS volume. Strong organic growth continues in Asia’s developing markets, with marginal subscribers turning to low-cost messaging as an entry-level service. In the mature markets of the Asia-Pacific region, SMS has seen sustained healthy growth as a result of steady price declines and increasingly generous SMS and data bundles," said Madhusudan Gupta, senior research analyst at Gartner. SMS contributes around 8% to value added services (VAS), which in turn contributes 10-12% of an operator’s revenue.

5. The Indian auto sector is likely to witness an overall growth of 10% - 12% in sales during 2010 and a faster recovery in expected in passengervehicle (PV) volumes of 12% - 14% compared with 5% - 6% for the commercial vehicle (CV) segment. The positive outlook for demand could result in a sharp increase in capex plans, which could offset the positive impact on credit profiles of higher volumes and lower inventories, said Fitch Ratings. The PV rebound has been supported by an improving liquidity scenario and restoration of consumer confidence;modest growth in industrial production, together with the government stimulus, has brought about stability in CV sales, though at lower levels than for PVs. Domestic CV sales grew by 22.3% during April-December 2009 compared with same period in 2008, building on the recovery in demand beginning Q4 09. However, growth trends have distinctly varied within the CV segment - depending on the tonnage capacity and end-use, as light commercial vehicles (LCVs) have been able to maintain their ground while medium and heavy commercial vehicles (M&HCVs) continued to face pressure due to the decline in industrial output. The M&HCV segment is now stabilizing with the higherindustrial production, while the LCV segment is showing a more rapid recovery. Fitch expects the full-year 2010 numbers to reveal moderate growth in the range of 5% - 6% for domestic sales, with the first few months being driven by regulatory guidelines.

Fazlani Altius Business School [Batch : 2013-2015]Page 39

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

6. The Union food processing ministry has set a target of attracting investments to the tune of Rs 1 lakh crore in the sector by 2015.SubodhKant Sahai, Union food processing minister, said: “We are expecting investments of Rs 1 lakh crore in the next five years. We are planning to increase food processing to 20% of the total fruits and vegetable produced in the country. “According to him, food processing has grown by 10% in India while value-added products have grown by 10-15% in the last five years. We are looking at a growth of 35% in value-added production by 2015,” Sahai said.

7. The 234 million tonne per annum (mtpa) Indian cement industry, which witnessed a double digit dispatch growth in December 2009 and an overall growth thanks to infrastructure and real estate projects, is set to add 43.2 mtpa capacity during the next 15 months (January 2010 to March 2011).South India, which has already started feeling the heat of oversupply, will add the maximum capacity of 17.6 million tonne during that period. The next in line is the northern region, which willadd 9.6 mt. The western, central and eastern regions will add 9 mt, 3 mt and 4 mt, respectively. “The southern market with 18 players having capacity of 1mtpa or more is the most fragmented one in India. Capacities of three new players (Raghuram Cement, Jayajyothi and JSW Cement with more than 2 mtpa each) will stabilize in the next 6-9 months. With sharp price cuts, new producers may find it difficult to break even, and this would likely to prompt some consolidation. All thethree new producers are unlikely to participate in consolidation,” J Radhakrishnan, analyst with IIFL, said in his report.

8. The healthcare industry in the country, which comprises hospital and allied sectors, is projected to grow 23% per annum to touch $77-billionmark by 2012 from the current estimated size of $35 billion, according to a Yes Bank and Assocham report. The sector has registered a growth of 9.3% between 2000-2009, comparable to the sectorial growth rate of other emerging economies such as China, Brazil and Mexico. The growth in the sector would be driven by healthcare facilities, both private and public sector, medical diagnostic and pathlabs and the medical insurance sector. Of the sum, diagnostic and pathology services would account for $2.5 billion in 2012, more than double its estimated current size of $1billion. The growth in the segment is expected to be driven by consolidation in the industry and increasing insurance penetration among the country’s population. Healthcare facilities, inclusive of public and private hospitals, the core sector, around which the healthcare sector is centered, would continue to contribute over 70% of the total sector and touch a figure of $54.7 billion by

Fazlani Altius Business School [Batch : 2013-2015]Page 40

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

2012.The medical insurance sector would account for another $ 3 billionin the next three years, up from the estimated current size of $1 billion.

9. Steve King, CEO of Zenith Optimedia Worldwide feels that new and emerging advertising markets like India and China will power the globalindustry’s recovery, on the back of positive signals from developed markets like US, Europe. “India, with an approximate 10% growth, will certainly be in the top ten advertising markets in absolute dollar terms by 2015,” he told. Zenith Optimedia, the world’s third largest media-buying agency and an enterprise under the Paris-based Publics Group is upbeat about India. It has brought fresh business worth $100 million in the country this year. India figures amongst Zenith Optimedia’s 20 largest markets globally, but over the past five years, it has been among the top three fastest growing ones. “Most of our markets are between 15 to 20 years old, so despite being here for only five years, this market has responded very well. Our focus here will beon winning local clients, apart from the international ones. By the next five years, we will have considerably closed the gap on the top two market leaders here,” King said.

M. ADVANTAGE IN INDIA

1. World's largest democracy with 1.2 billion people.

2. Stable political environment and responsive administrative set up.

3. Well established judiciary to enforce rule of law.

4. Land of abundant natural resources and diverse climatic conditions.

Fazlani Altius Business School [Batch : 2013-2015]Page 41

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

5. Rapid economic growth: GDP to grow by 8.5% in 2010-11* and 9.0% in 2011-12.

6. India's growth will start to outpace China\'s within three to five years and hence will become the fastest large economy with 9-10% growth over the next 20-25 years (Morgan Stanley).

7. Investor friendly policies and incentive based schemes.

8. Second most attractive Foreign Direct Investment (FDI) location in the world: India received a total of US$ 25.9 billion of FDI in 2009-10.

9. Healthy macro-economic fundamentals: Investment rate is expected to be 37% in 2010-11 and 38.4% in 2011-12 while Domestic Savings rate is expected to be 34% in 2010-11 and 36% in 2011-12.

10. India's economy will grow fivefold in the next 20 years (McKinsey).

11. Cost competitiveness: low labour costs.

12. Total labour force of nearly 530 million.

13. Large pool of skilled manpower; strong knowledge base with significant English speaking population.

14. Young country with a median age of 30 years by 2025: India\'s economy will benefit from this "demographic dividend".

15. The proportion of population in the working age group (15-59 years) is likely to increase from approximately 58% in 2001 to more than 64% by 2021.

16. Huge untapped market potential.

17. The urban population of India will double from the 2001 census figure of 290m to approximately 590m by 2030 (McKinsey).

18. Progressive simplification and rationalization of direct and indirect tax structures.

19. Reduction in import tariffs.

20. Full current account convertibility.

Fazlani Altius Business School [Batch : 2013-2015]Page 42

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

21. Compliance with WTO norms.

22. Robust banking and financial institutions.

"* India's financial year is from April to March. 2010-11 above means April 2010-March 2011."

I. Indian Economy

India has undergone a paradigm shift owing to its competitive stand in the world. The Indian economy is on a robust growth trajectory and boastsof a stable annual growth rate, rising foreign exchange reserves and booming capital markets among others.

Indian economy is estimated to grow at 8.6 percent in 2010-11 as comparedto the growth rate of 8.0 percent in 2009-10. These GDP figures are basedat factor cost at constant (2004-05) prices in the year 2010-11.The growth rate of 8.6 per cent in GDP during 2010-11 has been due to the robust growth rates of over 8 per cent in the sectors of manufacturing, construction, trade, hotels, transport and communication, financing, insurance, and, real estate and business services. Agriculture sector registered a growth rate of 5.4 percent in 2009-10. A growth rate of 18.3percent is estimated for GDP at current prices in the year 2010-11.

II. Agriculture Sector

The agriculture, forestry and fishing sector is likely to show a growth of 5.4 per cent in its GDP during 2010-11, as against the previous year’sgrowth rate of 0.4 per cent. The estimate of GDP from agriculture in 2010-11, according to the Department of Agriculture and Cooperation (DAC),production of food grains and oilseeds is expected to grow by 6.5 per cent and 11.9 per cent, respectively, as compared to the previous agriculture year. The production of cotton and sugarcane is also expectedto rise by 41.2 per cent and 15.2 per cent, respectively, in 2010-11. Among the horticultural crops, production of fruits and vegetables is expected to increase by 4.1 per cent and 3.8 per cent, respectively, during the year 2010-11.

III.Industry Sector

The growth in GDP for mining and quarrying and manufacturing sectors during 2010-11 is expected to be 6.2 and 8.8 percent respectively over previous year. According to the latest estimates available on the Index

Fazlani Altius Business School [Batch : 2013-2015]Page 43

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

of Industrial Production (IIP), the index of mining and manufacturing registered growth rates of 8.0 per cent and 10.0 per cent during April-November, 2010. The estimated growth rate for construction sector is 8.0 percent in 2010-11. The key indicators of construction sector, namely, cement production and steel consumption have registered growth rates of 4.4 per cent and 8.8 per cent, respectively during April- December, 2010.

IV. Services Sector

The estimated growth in GDP for the trade, hotels, transport and communication sectors during 2010-11 is placed at 11.0 per cent, mainly on account of growth during April- November, 2010-11 of 14.9 per cent in passengers handled in civil aviation, 21.3 per cent in air cargo handled and 40.9 per cent in stock of telephone connections. The sales of commercial vehicles witnessed an increase of 34.1 per cent per cent in April-December, 2010. The financing, insurance, real estate and business services sector is expected to show a growth rate of 10.6 per cent during2010-11, on account of 14.0 per cent growth in aggregate deposits and 22.6 per cent growth in bank credit during April- November 2010 (against the respective growth rates of 18.6 per cent and 10.1 per cent in the corresponding period of previous year). The growth rate of community, social and personal services during 2010-11 is estimated to be 5.7 per cent.

N. FDI POLICY FRAMEWORK

Policy regime is one of the key factors driving investment flows to acountry. Apart from underlying macro fundamentals, ability of a nation toattract foreign investment essentially depends upon its policy regime -whether it promotes or restrains the foreign investment flows. Thissection undertakes a review of India’s FDI policy framework and makes acomparison of India’s policy vis-à-vis that of select EMEs.

1. FDI Policy Framework in India

There has been a sea change in India’s approach to foreign investmentfrom the early 1990s when it began structural economic reformsencompassing almost all the sectors of the economy.

Fazlani Altius Business School [Batch : 2013-2015]Page 44

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

Pre-Liberalization Period

Historically, India had followed an extremely cautious and selectiveapproach while formulating FDI policy in view of the dominance of‘import-substitution strategy’ of industrialization. With the objectiveof becoming ‘self-reliant’, there was a dual nature of policy intention –FDI through foreign collaboration was welcomed in the areas of hightechnology and high priorities to build national capability anddiscouraged in low technology areas to protect and nurture domesticindustries. The regulatory framework was consolidated through theenactment of Foreign Exchange Regulation Act (FERA), 1973 wherein foreignequity holding in a joint venture was allowed only up to 40 per cent.Subsequently, various exemptions were extended to foreign companiesengaged in export oriented businesses and high technology and highpriority areas including allowing equity holdings of over 40 per cent.Moreover, drawing from successes of other country experiences in Asia,Government not only established special economic zones (SEZs) but alsodesigned liberal policy and provided incentives for promoting FDI inthese zones with a view to promote exports. As India continued to behighly protective, these measures did not add substantially to exportcompetitiveness. Recognising these limitations, partial liberalisation inthe trade and investment policy was introduced in the 1980s with theobjective of enhancing export competitiveness, modernisation andmarketing of exports through Trans-national Corporations (TNCs). Theannouncements of Industrial Policy (1980 and 1982) and Technology Policy(1983) provided for a liberal attitude towards foreign investments interms of changes in policy directions. The policy was characterized byde-licensing of some of the industrial rules and promotion of Indianmanufacturing exports as well as emphasizing on modernization ofindustries through liberalized imports of capital goods and technology.This was supported by trade liberalization measures in the form of tariffreduction and shifting of large number of items from import licensing toOpen General Licensing (OGL).

Post-Liberalization Period

A major shift occurred when India embarked upon economic liberalizationand reforms program in 1991 aiming to raise its growth potential andintegrating with the world economy. Industrial policy reforms graduallyremoved restrictions on investment projects and business expansion on theone hand and allowed increased access to foreign technology and fundingon the other. A series of measures that were directed towardsliberalizing foreign investment included:

(i) Introduction of dual route of approval of FDI – RBI’s automaticroute and Government’s approval (SIA/FIPB) route,

Fazlani Altius Business School [Batch : 2013-2015]Page 45

ECONOMICS ASSIGNMENT [FOREIGN DIRECT INVESTMENT (FDI) IN INDIA ]

(ii) Automatic permission for technology agreements in high priorityindustries and removal of restriction of FDI in low technologyareas as well as liberalization of technology imports,

(iii) Permission to Non-resident Indians (NRIs) and OverseasCorporate Bodies (OCBs) to invest up to 100 per cent in highpriorities sectors,

(iv) Hike in the foreign equity participation limits to 51 per centfor existing companies and liberalization of the use of foreign‘brands name’ and