Task Force on Incomes and Adjustment in the Atlantic Fishery

118

Prepared for the Task Force on Incomes and Adjustment in the Atlantic Fishery

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Task Force on Incomes and Adjustment in the Atlantic Fishery

Prepared for the

Task Force on Incomes and Adjustment in the Atlantic Fishery

Published by:

Communications Directorate Department of Fisheries and Oceans Ottawa, Ontario KlA 0E6

DF0/4937

©Minister of Supply and Services Canada 1993 Cat. No. Fs 41-40/5-1993E ISBN 0-662-21158-8

Les textes en français sont disponibles sur demande

Printed on Recycled Paper

The Fish Processing Sector in Atlantic Canada: Financial Performance and Sustainable Core

by

W. P. Moore, Debora Walsh Iona Worden, J. D. MacDonald

Coopers & Lybrand

April, 1993

The views expressed in this paper are the responsibility of the authors and do not necessarily reflect the views of the Task Force or the Government of Canada.

TABLE OF CONTENTS

RESUME ............................................. V

1. INTRODUCTION ........................................ 1

2. THE ASSIGNMENT ...................................... 2

3. FINANCIAL OVERVIEW OF TIIE ATLANTIC FISHERY ............. 4

The Peaks and Troughs of Performance in Fish Processing . . . . . . . . . . . . . . . 5 Profitability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11 Productivity ........................................... 16 Debt Service . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18 Financial Position . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20 Financial Position of Large Versus Small Companies . . . . . . . . . . . . . . . . . . 21 Financial Comparison of the Fish Processing Industry

to Other Industries .. ...... .............................. 25 Overcapacity in Fish Processing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26 Summary Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

4. THE SUSTAINABLE CORE FISHERY MODELS . • ................ 35

Sustainable Capital Investment Model (SCIM) . . . . . . . . . . . . . . . . . . . . . . 35 Direct Labour Model (DLM) ................................. 38

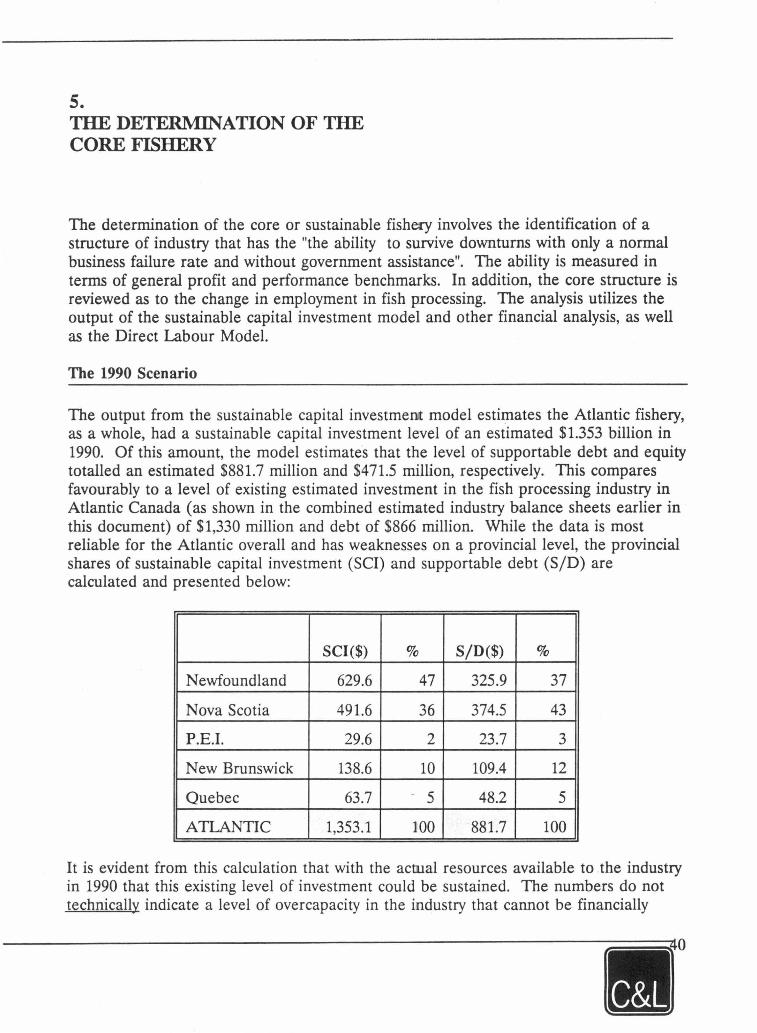

5. THE DETERMINATION OF THE CORE FISHERY . . . . . . . . . . . . . . . . 40

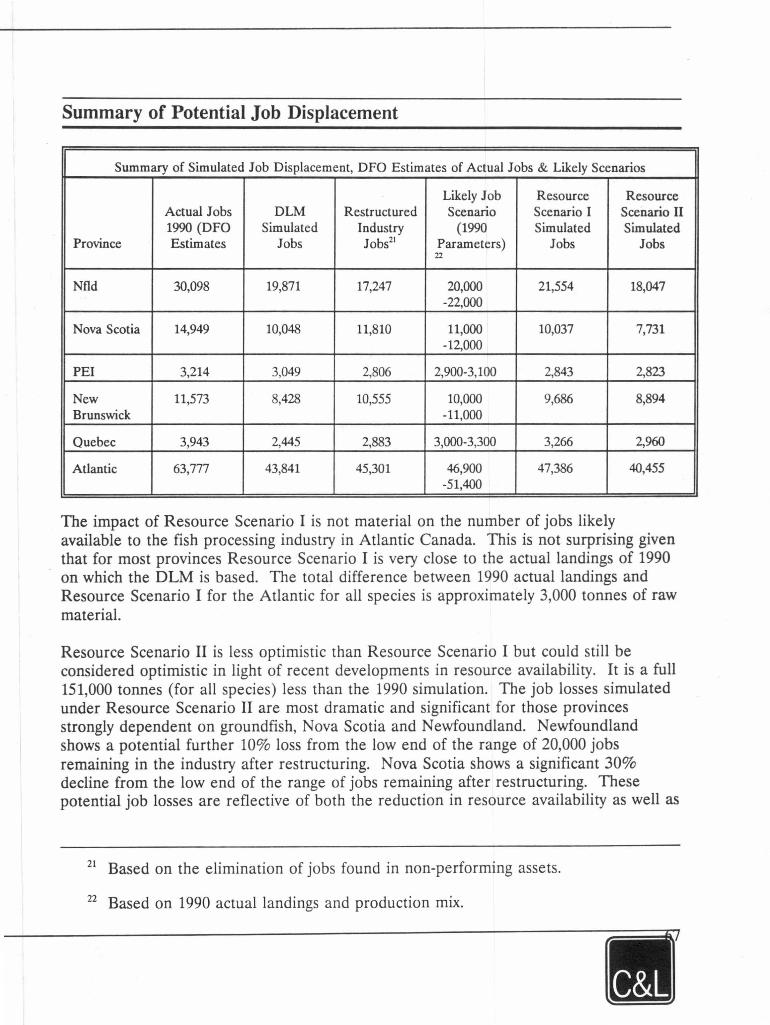

Dimensions of a Sustainable Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41 Summary of Potential Job Displacement . . . . . . . . . . . . . . . . . . . . . . . . . . 67 Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

6. THE MODIFIED CORE FISHERY . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

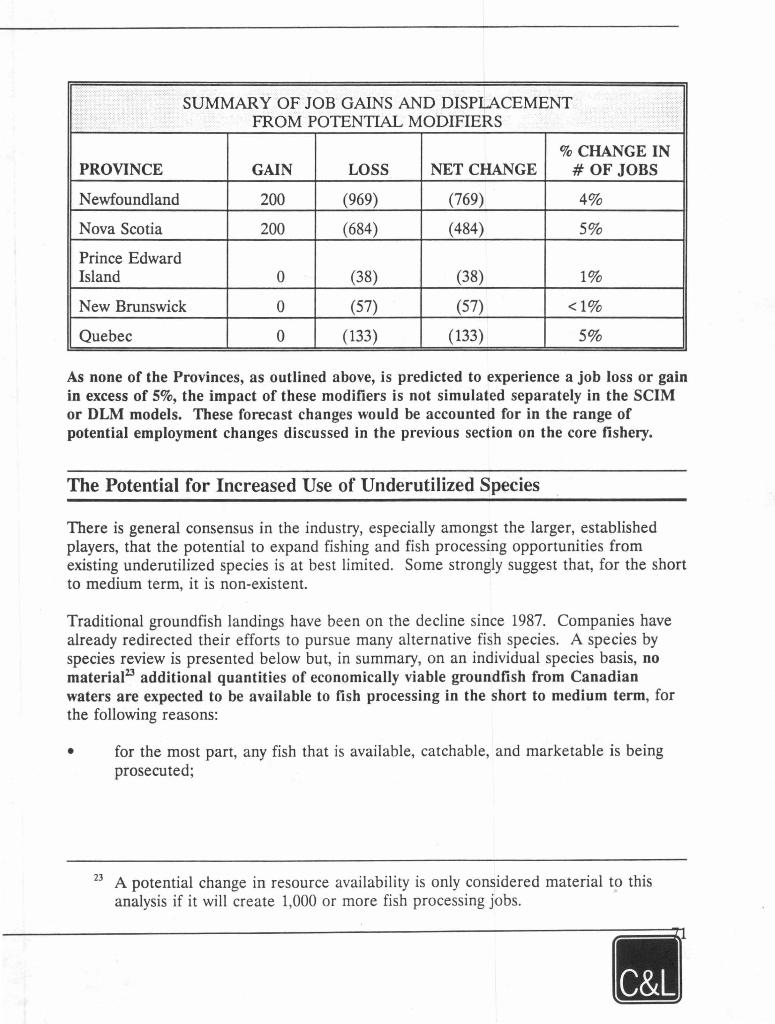

Summary of Job Gains and Displacement from Potential Modifiers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

The Potential for Increased Use of Underutilized Species .................................... 71

The Potential for Increased Imports of Fresh and Frozen Fish for Processing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

The Potential for Increased Technology Absorption . . . . . . . . . . . . . . . . . . . 80 The Potential for Increased Value Added in

Fish Processing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

APPENDICES

APPENDIX 1: TABLE OF CONTENTS FOR REPORT ONE, TWO AND THREE ... 89

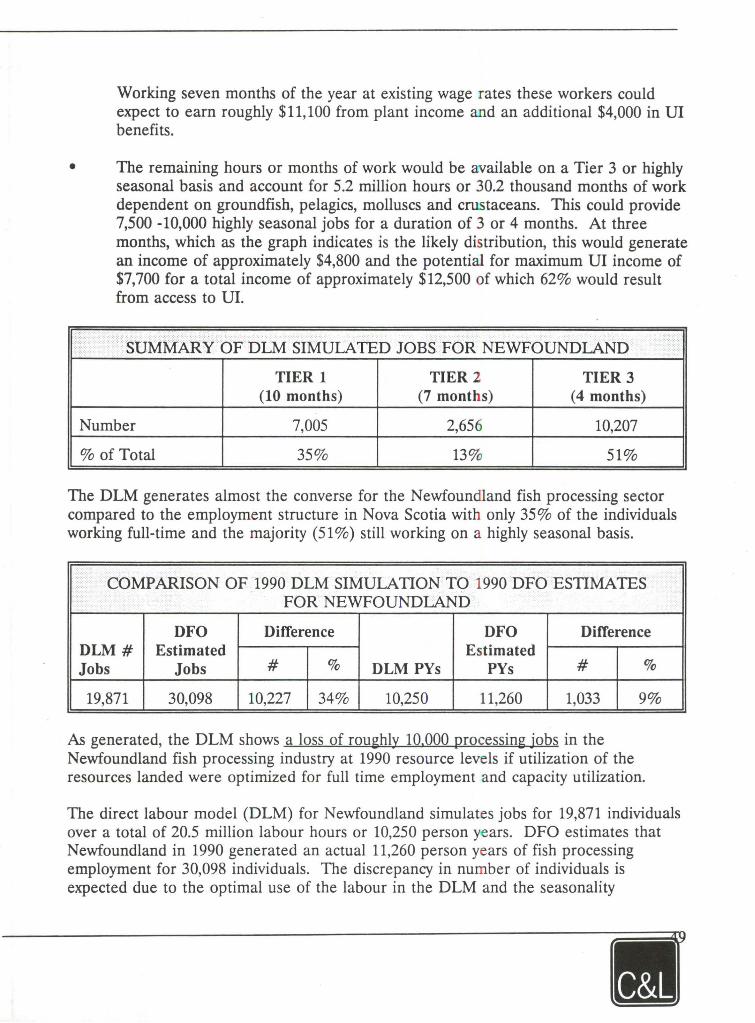

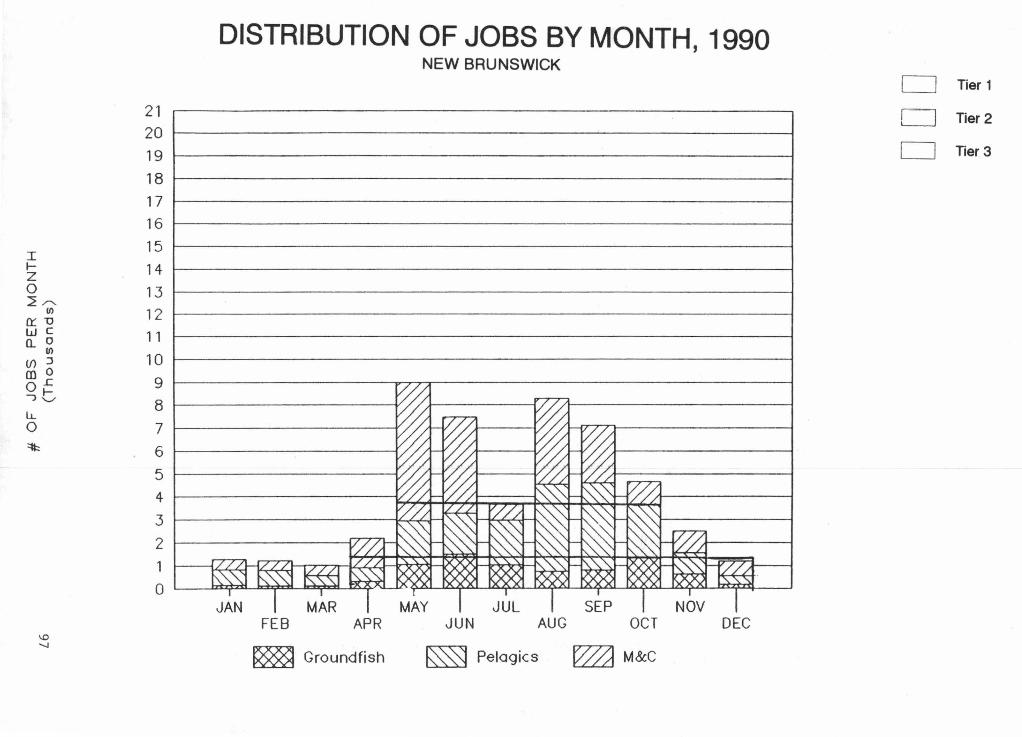

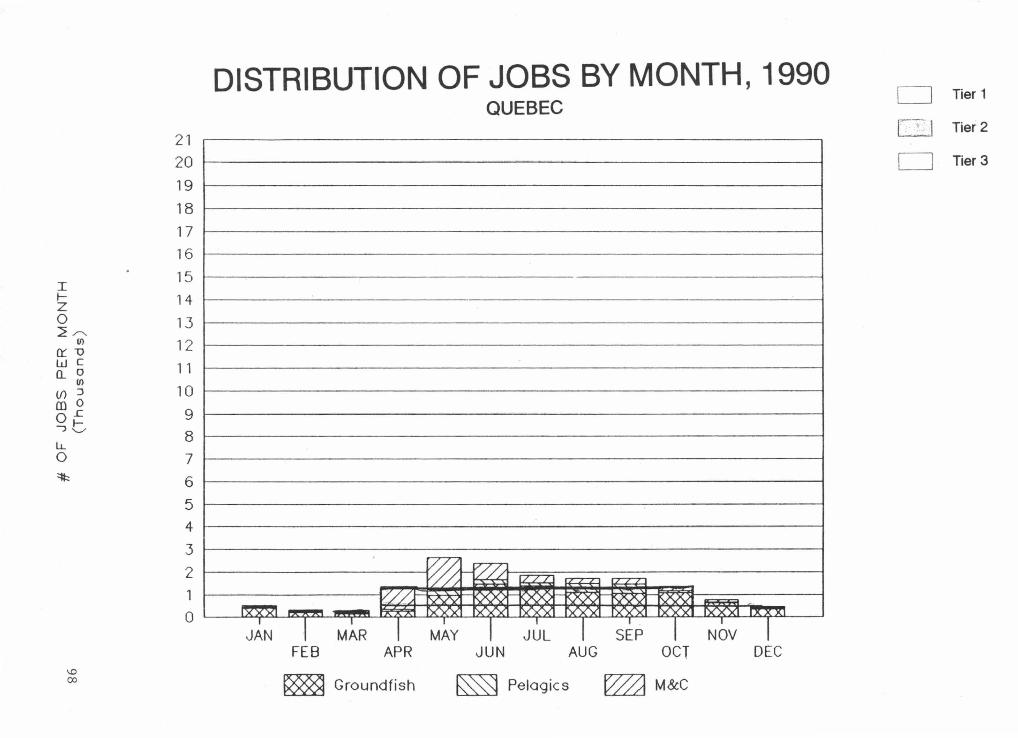

APPENDIX II: MONTHLY DISTRIBUTION OF TIER 1, 2, AND 3 JOBS, 1990 .... 93

Résumé

Cette étude analyse le rendement financier et les aspects opérationnels, ainsi que l'emploi dans le secteur de la transformation du poisson, dans l'Atlantique et au Québec, au cours de la dernière décennie.

Après avoir exposé divers facteurs qui font obstacle à la rentabilité de l'industrie et à son rendement relatif, les auteurs évaluent la surcapacité de l'ensemble de l'industrie. Ils quantifient la valeur des investissements excédentaires ou celle de l'actif non producteur, puis la capacité de l'industrie à soutenir ses immobilisations en se servant de 1990 comme année de référence. Ce modèle simule les investissements viables de l'industrie à divers niveaux de disponibilité de la ressource. Un modèle d'utilisation de la main-d'œuvre simule le nombre optimal d'emplois à temps plein, à temps partiel et saisonniers, en supposant une répartition saisonnière plus efficace des débarquements. Les deux modèles permettent ensuite de faire l'estimation des investissements et des niveaux d'emploi excédeataires, qui peuvent être appuyés au moyen d'autres mesures du rendement financier et selon certains scénarios relatifs à la ressource.

Enfin, les auteurs examinent le potentiel de gain ou de déplacement d'emplois qu'offrent l'augmentation de la transformation d'espèces sous-utilisées, l'importation de matière première, l'absorption accrue de technologies et l'augmentation de la valeur ajoutée à la transformation.

V

1. INTRODUCTION

In March 1992 the Minister of Fisheries, Mr. John Crosbie, and the Minister for Employment and Immigration, Mr. Bernard Valcourt, announced the membership and terms of reference for the Task Force on Incarnes and Adjustment in the Atlantic fishery. This action was spurred by the 1991 Atlantic groundfish catch failure which highlighted the need to address the problem of overcapacity and unstable incarnes in the fishing industry. The mandate of the Task Force, chaired by Richard Cashin and including members of the Atlantic business, legal, and academic community, is to develop a comprehensive long term strategy for the industry that will work towards stability and profitability for the industry's participants.

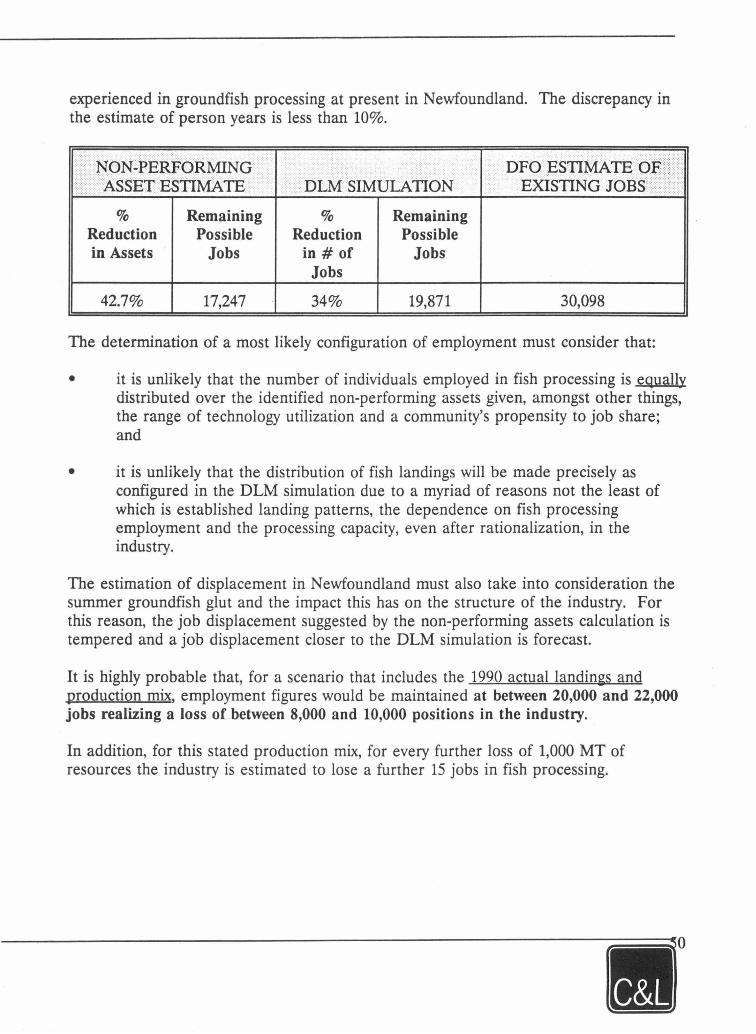

2. THE ASSIGNMENT

The Fisheries and Marine Group of Coopers & Lybrand Consulting Group were contracted by the Task Force through Fisheries and Oceans (DFO) to undertake a comprehensive review and analysis of the fish processing sector in Atlantic Canada. The principal objectives of the assignment were:

• to document and analyze the activity and performance, both financial and operational, of the fish processing industry and certain aspects of fisb harvesting for the period 1977 to 1990;

• to utilize the output of that analysis to develop two predictive models that would estimate the level of sustainable capital investment possible and optimum for the fish processing industry or the core fishery, a measure of overcapacity that the sustainable capital investment implied, and an optimal labour utilization scenario; and

• to then further modify these scenarios for possible future changes in resource availability, technology change, and increased value added which is described as the modified core.

While the work of the Task Force was precipitated by the crisis in the groundfish fishery, the analysis undertaken by Coopers & Lybrand includes all species of groundfish, pelagics, and molluscs and crustaceans.

The vast majority of the information and detailed data used in this report is data collected on a regular or special purpose basis by Fisheries and Oceans. The data has been presented here in its original form or is utilized to derive other indicators of the industry. Coopers & Lybrand is cognizant of the weaknesses of much of this data, a fact which has been confirmed by DFO, and bas highlighted potential problems or margins of error where possible. It is certain that the precision and validity of the analysis undertaken in this report is a function of, and therefore lirnited by, the quality of the original data. While no estimate is made of the margin of error overall resulting from errors and omissions in the data, Coopers & Lybrand is confident that the information presented is the best available and does not materially impede the intended output of this undertaking.

The results of this review are presented in three separate documents as follows:

• Report One, which includes the financial overview of the industry, the core fishery, and the modified core;

• Report Two, which documents the historical review of the industry, including the trends and dynarnic of the Atlantic industry and a comparison of certain aspects of the Atlantic Canadian fish processing sector with Iceland and Norway; and

• Report Three, which contains the models employed in this analysis as well as a user's guide to their structure and utilization.

A detailed Table of Contents for all three reports is found in Appendix 1. It is strongly recommended that this document be read in conjonction with the two companion reports.

Note to Reader:

Report Three was not published as a Task Force Background Study. However, several copies have been deposited with the Department of Fisheries and Oceans Library in Ottawa.

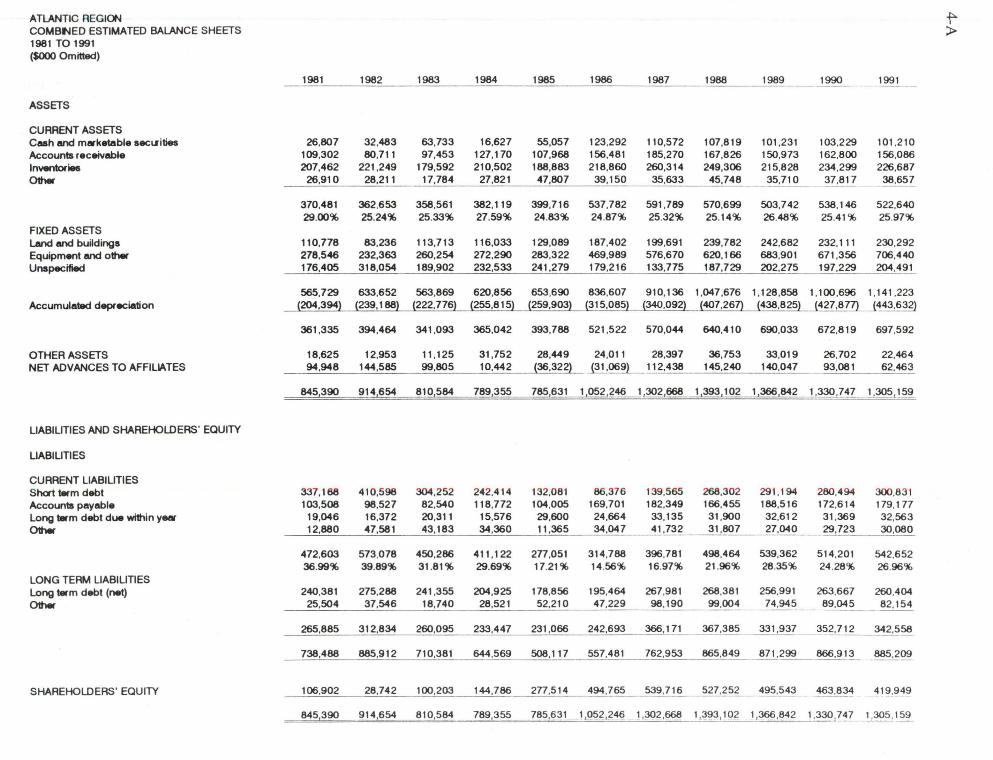

3. FINANCIAL OVERVIEW OF THE ATLANTIC FISHERY

The following analysis is based on combined industry balance sheet and incarne profiles for the eleven year period 1981 to 1991. The figures provided for the period 1981 to 1987 are based on detailed aggregated financial statement data provided by Statistics Canada for the fish processing industry. This information, based on data from 300 to 400 companies each year, captured a significant majority of the industry, ranging from 98.27% to 121.68%1

• To provide continuity, the data was adjusted to reflect the total industry.

Since 1987, however, Statistics Canada has discontinued collecting detailed financial information from the fish processing industry in the same format or the same sample size. The financial profiles from 1988 to 1991, therefore, have been generated using regression and other analysis, using data from several sources:

• Dun & Bradstreet (D&B) detailed aggregated industry financial data covering 1987 to 1991, generally dealing with small and medium-sized companies in fish processing;

• ail of Canada's major chartered banks, and any other lender or institution having a loan portfolio in the fish processing industry (data collected by survey by Coopers & Lybrand);

• lndustry, Science & Technology (ISTC) data related to capital investment and fixed asset investment, covering the period 1981 to 1991;

• Fisheries & Oceans (DFO) data dealing with production volumes, and unit values for landings and production; and,

• the financial statements for the large public companies operating in the industry, specifically covering the period 1984 to 1991.

Reference was also made to aggregated data contained in a 1992 study by Peat Marwick, related to Newfoundland companies directly affected by the Northern cod crisis.

1 The financial data utilized was known to include non-domestic activity which has been estimated and accounted for.

4

ATLANTIC REGION f'" COMBNED ESTIMATED BALANCE SHEETS > 1981 TO 1991 ($000 Omitted)

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991

ASSETS

CURRENT ASSETS Cash and market.able aecll'ities 26,807 32,483 63,733 16,627 55,057 123,292 110,572 107,819 101,231 103,229 101 ,210 Accounts receivable 109,302 80,711 97,453 127,170 107,968 156,481 185,270 167,826 150,973 162,800 156,086 Inventories 207,462 221 ,249 179,592 210,502 188,883 218,860 260,314 249,306 215,828 234,299 226,687 Other 26,910 28,211 17,784 27,821 47,807 39,150 35,633 45,748 35,710 37,817 38,657 -------

370,481 362,653 358,561 382,119 399,716 537,782 591 ,789 570,699 503,742 538,146 522,640 29.00% 25.24% 25.33% 27.59% 24.83% 24.87% 25.32% 25.14% 26.48% 25.41% 25.97%

FIXED ASSETS Land and buildings 110,778 83,236 113,713 116,033 129,089 187,402 199,691 239,782 242,682 232,111 230,292 Equipment and other 278,546 232,363 260,254 272,290 283,322 469,989 576,670 620,166 683,901 671,356 706,440 Unapecified 176,405 318,054 189,902 232,533 241,279 179,216 133,775 187,729 202,275 197,229 204,491

565,729 633,652 563,869 620,856 653,690 836,607 910,136 1,047 ,676 1,128,858 1,100,696 1,141 ,223 Accumulatlld depreciation (204,394) (239,188) (222,776) (255,815) (259,903) (315,085) (340,092) (407,26Z) (438,825) (427,87Z) 443,632

361,335 394,464 341,093 365,042 393,788 521,522 570,044 640,410 690,033 672,819 697,592

OTHER ASSETS 18,625 12,953 11, 125 31,752 28,449 24,011 28,397 36,753 33,019 26,702 22,464 NET ADVANCES TO AFFILIATES 94,948 144,585 99,805 10,442 (36,322) (31 ,069) 112,438 145,240 140,047 93,081 62,463

845,390 914,654 810,584 789,355 785,631 1,052 ,246 1,302 ,668 1,393,102 1,366 ,842 1,330 ,747 1 ,30~159

LIABILITIES AND SHAREHOLDERS' EQUITY

LIABILITIES

CURRENT LIABILITIES Short wm debt 337, 168 41 0,598 304,252 242,4 14 132,081 86,376 139,565 268,302 291 ,194 280,494 300,831 Accounts payable 103,508 98,527 82,540 118,772 104,005 169,701 182,349 166,455 188,516 172,614 179,177 Long wm debt due within YNI 19,046 16,372 20,311 15,576 29,600 24,664 33,135 31 ,900 32,612 31 ,369 32,563 Other 12,880 47,581 43,183 34,360 11,365 34,047 41,732 31,807 27,040 29,723 30,080

472,603 573,078 450,286 411 ,122 277,051 314,788 396,781 498,464 539,362 514 ,201 542,652 36.99% 39.89% 31.81% 29.69% 17.21% 14.56% 16.97% 21 .96% 28.35% 24.28% 26.96%

LONG TERM LIABILITIES Long wm debt (net) 240,381 275,288 241 ,355 204,925 178,856 195,464 267,981 268,381 256,991 263,667 260,404 Other 25,504 37,546 18,740 28,521 52,210 47,229 98,190 99,004 74,945 89,045 - 82,154

265,885 312,834 260,095 233,447 231,066 242,693 366,171 367,385 331,937 352,712 342,558

738,488 885,912 710,381 644,569 508,117 557.481 762,953 865,849 871.~ 866,913 885,209

SHAREHOLDERS' EQUITY 106,902 28,742 100,203 144,786 277,514 494,765 539,716 527,252 495,543 - 463 .~~ 419,949

845 390 914,654 810,584 789 355 785,631 1~,246 . J . 3()2 .~ 1 ,~93 , 102 1,366,842 1 , 330,7~ ~305 , 159

For the period 1981 to 1987, base financial data represented approximately 80% to 100% of actual annual industry activity based on value of revenues, and therefore required only minor annual adjustment to develop profiles covering the entire industry.

For the period 1988 to 1991, base data represented approximately 50% to 60% of actual annual industry activity, and therefore required somewhat greater adjustment.

Therefore, base data in any given year represented at least 50% of total industry activity. Further, certain bench-mark data was obtained, particularly related to fixed asset investment (ISTC) and debt (financial institutions).

The result of this analysis is a series of annual profiles, considered to be representative of the industry, and covering the period 1981 to 1991.

While these financial profiles are presented in financial statement form, they do not purport to represent the actual aggregated financial statements of the participants in the industry. Therefore, any reference to the data, taken outside the context of this analysis, may not be suitable for other purposes and may in fact be misleading.

The following will focus on providing a financial picture of the Atlantic fishery. Specifically, the analysis will review the profitability, productivity, debt service capacity, and financial position of the whole industry. This analysis will be further refined with a commentary on the distinct financial position differences between small and large companies and a financial comparison of fish processing to other industries. Finally, the issue of overcapacity will be analyzed and discussed at length with summary conclusions for the section overall.

Numbers contained within brackets represent lasses or negative amounts.

The Peaks and Troughs of Performance In Fish Processing

A detailed financial analysis for the Atlantic fishing industry is presented in this report for the eleven year period 1981 to 1991. To further the understanding of the dynamic of the industry, certain critical "windows" representing the commonly identified peaks and troughs in the industry in recent times, in particular since extension of the Canadian fishing zone to 200 miles in 1977, are highlighted. In addition to the information provided on the common drivers of

• exchange rates • interest rates • U.S. per capita consumption of seafood • resource availability (indexed to 1989)

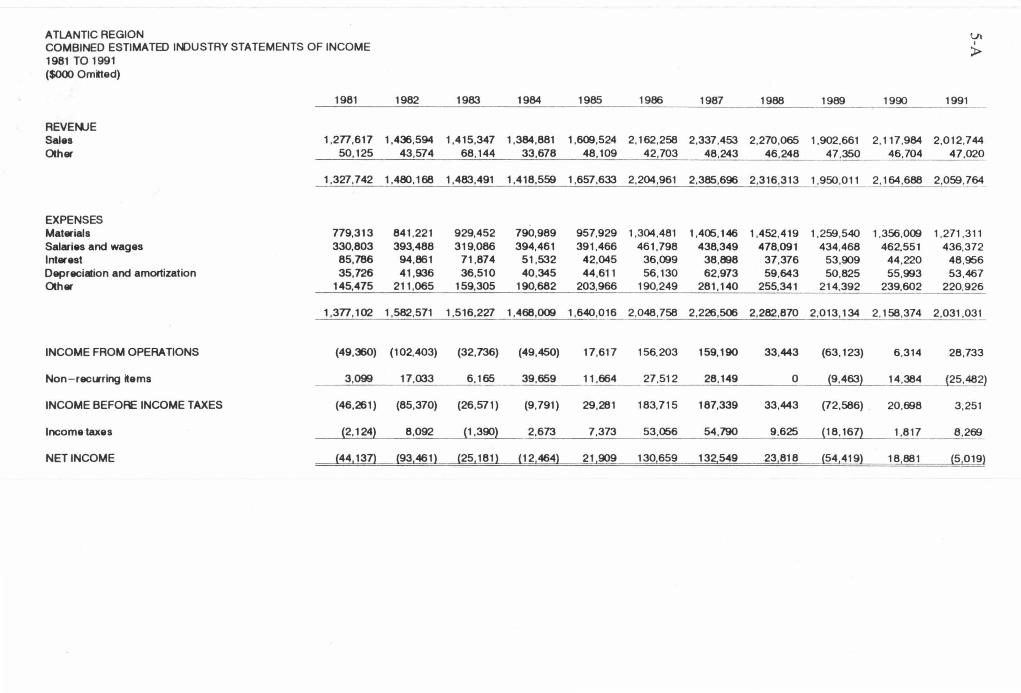

ATLANTIC REGION VI COMBINED ESTIMATED l~USTRY STATEMENTS OF INCOME 1

> 1981 TO 1991 ($000 Om~ed)

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991

REVEt>UE Sales 1.2n.611 1,436,594 1,415,347 1,384,881 1,609,524 2,162,258 2,337,453 2,270,065 1,902,661 2,117,984 2,012.744 Other 50, 125 43,574 68,144 33,678 48, 109 42,703 48,243 46,248 47,350 46,704 47,020

1,327,742 1 .4~ . 168 1,483,491 1,418,559 1,657,633 2,204,961 2,385,696 2,316,313 1,950,011 2,164,688 2,059,764

EXPENSES Materials 779,313 841 ,221 929,452 790,989 957,929 1,304,481 1,405, 146 1,452,419 1,259,540 1,356,009 1,271 ,311 Salaries and wages 330,803 393,488 319,086 394,461 391,466 461,798 438,349 478,091 434,468 462,551 436,372 Inter est 85,786 94,861 71.874 51,532 42,045 36,099 38,898 37,376 53,909 44,220 48,956 Depreciation and amortization 35,726 41,936 36,510 40,345 44,611 56,130 62,973 59,643 50,825 55,993 53,467 Other 145,475 211 ,065 159,305 190,682 203,966 190,249 281 ,140 255,341 214,392 239,602 220,926

1,3n.102 1,582,571 1,516,227 1,468,009 1,640,016 2,048,758 2,226,506 2,282,870 2,013,134 2, 158,374 2,031 ,031

INCOME FROM OPERATIONS (49,360) (102,403) (32,736) (49,450) 17,617 156,203 159,190 33,443 (63 ,123) 6 ,314 28,733

Non - recll'ring items 3 ,099 17,033 6 ,165 39,659 11 ,664 27,512 28,149 0 (9,463) 14,384 (25,482)

INCOME BEFOAE INCOME TAXES (46,261) (85,370) (26,571) (9,791) 29,281 183,715 187,339 33,443 (72 ,586) 20,698 3 ,251

lncome taxes (2, 124) 8,092 (1 ,390) 2,673 7,373 53,056 54,790 9.625 (18, 167) 1,817 8,269

NETINCOME (44, 137) (93,461) (25,181) (12,464) 21 ,909 130,659 132,549 23,818 (54,419) 18,881 (5 ,019)

information is provided on the general industry environment for these periods. It is intended to provide the reader with a more complete understanding of the industry dynamic during these periods of extreme variation in industry performance.

A Trough • The Groundfish Industry Crisis 1980 - 1981

The financial pressures that were brought to bear on the Atlantic coast fishing companies in the early 1980s were the result, in part, of the extended debt loads resulting from the industry's general overly enthusiastic response and highly optimistic expectations of extension of Canada's fishing zone to 200 miles in 1977. Spurred by government incentives (it is reported that in 1980 $46 million of the $157 million invested in fish processing was provided by government agencies), companies significantly increased their investment in fishing fleets and plants, investment that was financed largely through borrowing. It was the practice at the time to maintain, and finance, large inventories of frozen groundfish as companies aggressively harvested groundfish resources in the early part of the year to ensure as large a share of the established quota as possible. These practices, when combined with unprecedented interest rates and other unfavourable external factors, led to the financial crisis of 1980 -1981.

This financial crisis saw the closure of plants, the lay-off of thousands of workers, and the severe financial distress of many of the key industry players. In 1980 it was reported that at least 50% of fish processing companies were losing money; by 1981 the estimate had increased to 70% of the industry. For the Atlantic Canada industry the crisis was characterised by:

• severely weakened financial positions resulting from increasing costs in the face of declining market prices. The attached Combined Estimated Industry Statements of Incarne show a collective net incarne loss in 1981 of $44 million;

• increasing groundfish harvests. Total groundfish landings in 1981 were 27% higher than 1978;

• despite falling prices, labour and other costs were increasing and significantly decreasing gross margins;

• huge groundfish inventory build up as the U.S. market for groundfish, on which the industry was highly dependent, softened;

• unprecedented interest rates, nearing 20% which made the cost of doing business, especially carrying inventory, extremely high;

• significantly expanded debt load of the fishing companies due, in large part to the expansionary environment fed by the promise of the 200 mile extension, very

~·

optimistic projections on future resource availability, and the existence of several incentive programs to expand fish processing capacity;

• a competitive fishing environment that did not allow a planned harvest of fish in response to market conditions as is the case under the existing Enterprise Allocation program; and

• exchange rates that ranged between $0.855 - .834.

In response to the distress, the government struck the Kirby Commission to recommend on "how to achieve and maintain a viable Atlantic fishing industry" the result of which was an operational and financial restructuring of the industry. The Commission created two super-companies with improved balance sheets; a costly re-configuration that was intended to bolster the industry to withstand the inevitable cyclical downturns. The restructuring was completed in 1984 and the restructured companies, National Sea Products, and Fishery Products International soon entered into the heyday of the fishery, the boom period of 1986 -1987.

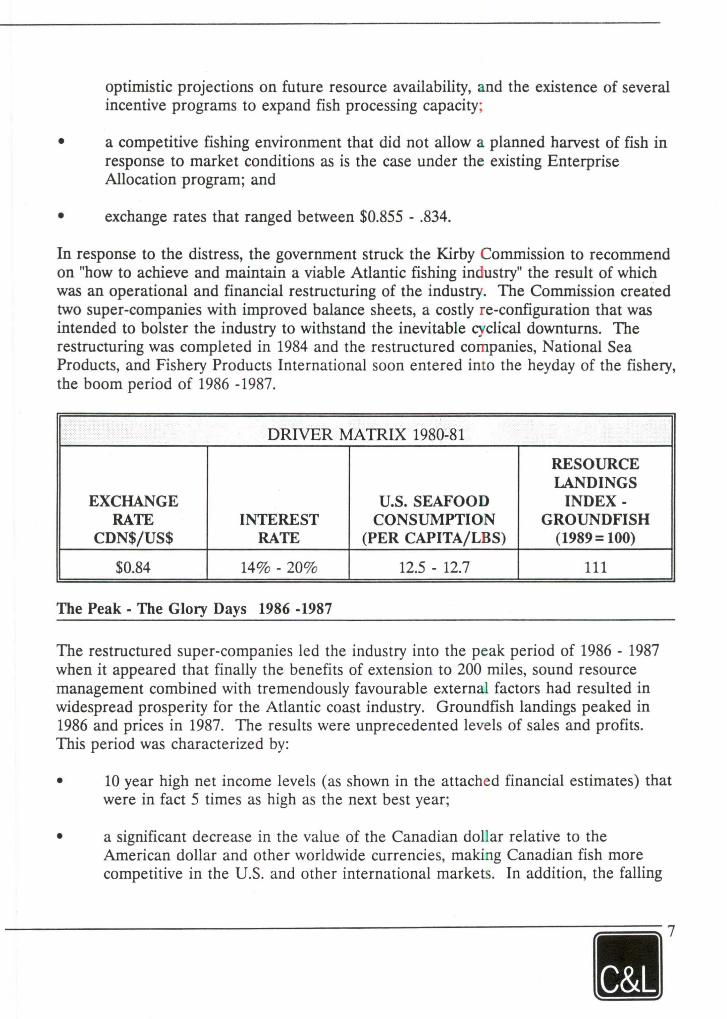

DRIVER MATRIX 1980-81

RESOURCE LANDINGS

EX CHANGE U.S. SEAFOOD INDEX· RATE INTEREST CONSUMPTION GROUNDFISH

CDN$/US$ RATE (PER CAPITA/LBS) (1989= 100)

$0.84 14% - 20% 12.5 - 12.7 111

The Peak. The Glory Days 1986 -1987

The restructured super-cornpanies led the industry into the peak period of 1986 - 1987 when it appeared that finally the benefits of extension to 200 miles, sound resource management combined with trernendously favourable external factors had resulted in widespread prosperity for the Atlantic coast industry. Groundfish landings peaked in 1986 and prices in 1987. The results were unprecedented levels of sales and profits. This period was characterized by:

• 10 year high net incarne levels (as shown in the attached financial estirnates) that were in fact 5 tirnes as high as the next best year;

• a significant decrease in the value of the Canadian dollar relative to the American dollar and other worldwide currencies, rnaking Canadian fish more cornpetitive in the U.S. and other international markets. In addition, the falling

Canadian dollar meant that processors, paid in U.S. dollars, could bank more Canadian dollars for each U.S. dollar earned;

• major expansions in international sales of seafood outside the U.S., in particular in Japan where groundfish sales alone expanded by 65% in 1986 from 15,800 tonnes to 24,000 tonnes;

• significant expansion in the food service in the U.S. that was supplied by Atlantic Canadian fish;

• tight supply situations for most groundfish species, i.e. U.S. Atlantic groundfish landings fell by 10,000 tonnes in 1986;

• increasing demand for seafood in the U.S. market. U.S. per capita seafood consumption was on the rise and increased from 15.1 in 1985 to 16.2 in 1987. With a population of 240 million this represented a staggering 3.8 billion pounds of seafood to be consumed;

• rapidly increasing market prices for most seafood products;

• an apparently healthy resource with Atlantic groundfish landings experiencing an eight year high; and

• the introduction of enterprise allocations for the offshore companies allowing controlled, market driven harvesting plans and reduced inventories.

Canadian exports of seafood totalled $2.4 billion (591 thousand tonnes) in 1986 compared to $1.8 billion (556 thousand tonnes) for 1985, an increase of 33% in value and 6% in volume. In 1986 groundfish exports totalled $988 million (285 thousand tonnes) compared to $750 million (262 thousand tonnes) in 1985, an increase of 32% in value and 5% in volume. Export prices increased, for example, on average by 30% for cod blacks, over 50% for frozen cod fillets and 15% for haddock.

Arnericans, still the primary market for Canadian seafood exports (roughly 70% of production), were eating more seafood and paying more for it. The preoccupation with healthy living, the stated benefits of fish consumption, the effects of the fifth year of sustained economic growth in the developed world buoyed seafood demand and prices despite falling prices for alternative proteins. Further support for the industry was provided when initial consumer resistance in the U.S. and Europe to increasing seafood prices was offset by decreases in supply allowing the price pbenomenon to continue into 1987.

•

~·

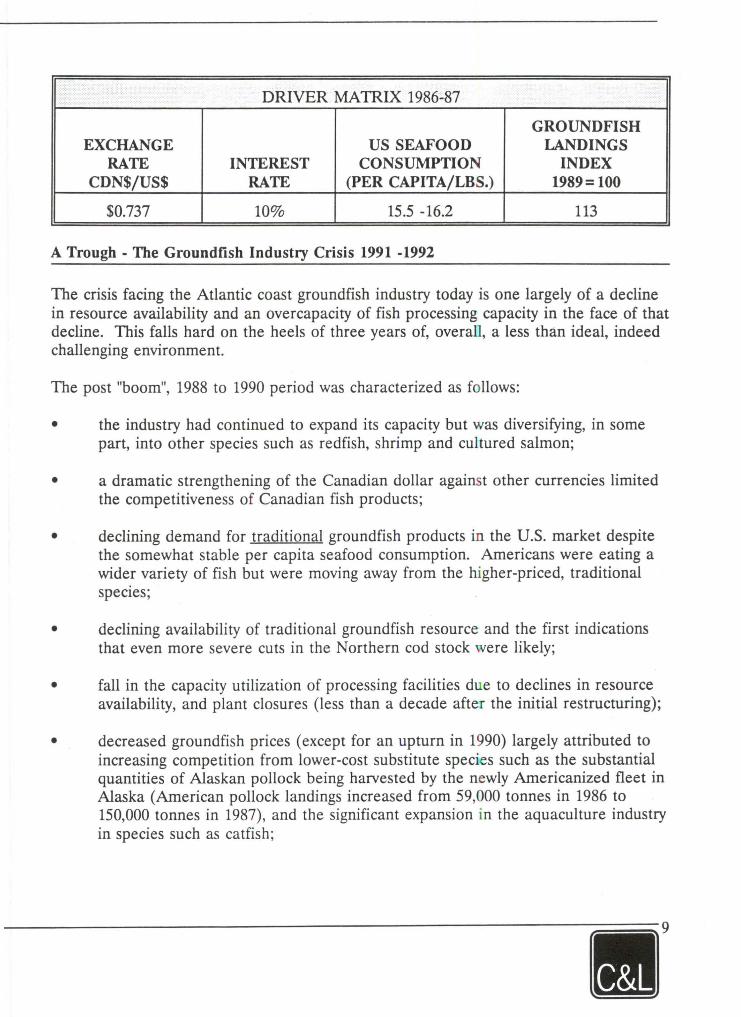

DRIVER MATRIX 1986-87

GROUNDFISH EX CHANGE US SEAFOOD LANDINGS

RATE INTEREST CONSUMPTION INDEX CDN$/US$ RATE (PER CAPITA/LBS.) 1989= 100

$0.737 10% 15.5 -16.2 113

A Trough - The Groundfish Industry Crisis 1991 -1992

The crisis facing the Atlantic coast groundfish industry today is one largely of a decline in resource availability and an overcapacity of fish processing capacity in the face of that decline. This falls hard on the heels of three years of, overall, a less than ideal, indeed challenging environment.

The post "boom", 1988 to 1990 period was characterized as follows:

• the industry had continued to expand its capacity but was diversifying, in some part, into other species such as redfish, shrimp and cultured salmon;

• a dramatic strengthening of the Canadian dollar against other currencies limited the competitiveness of Canadian fish products;

• declining demand for traditional groundfish products in the U.S. market despite the somewhat stable per capita seafood consumption. Americans were eating a wider variety of fish but were moving away from the higher-priced, traditional species;

• declining availability of traditional groundfish resource and the first indications that even more severe cuts in the Northern cod stock were likely;

• fall in the capacity utilization of processing facilities due to declines in resource availability, and plant closures (less than a decade after the initial restructuring);

• decreased groundfish prices ( except for an upturn in 1990) largely attributed to increasing competition from lower-cost substitute species such as the substantial quantities of Alaskan pollock being harvested by the newly Americanized fleet in Alaska (American pollock landings increased from 59,000 tonnes in 1986 to 150,000 tonnes in 1987), and the significant expansion in the aquaculture industry in species such as catfish;

• the beginning of real cost cutting measures in fish processing and upgrading of product mix to make the most of the fish resources available to the processing entities; and

• major realignment in the two major processing companies to rationalize harvesting and processing capacity which eliminated thousands of jobs in fish processing in Atlantic Canada.

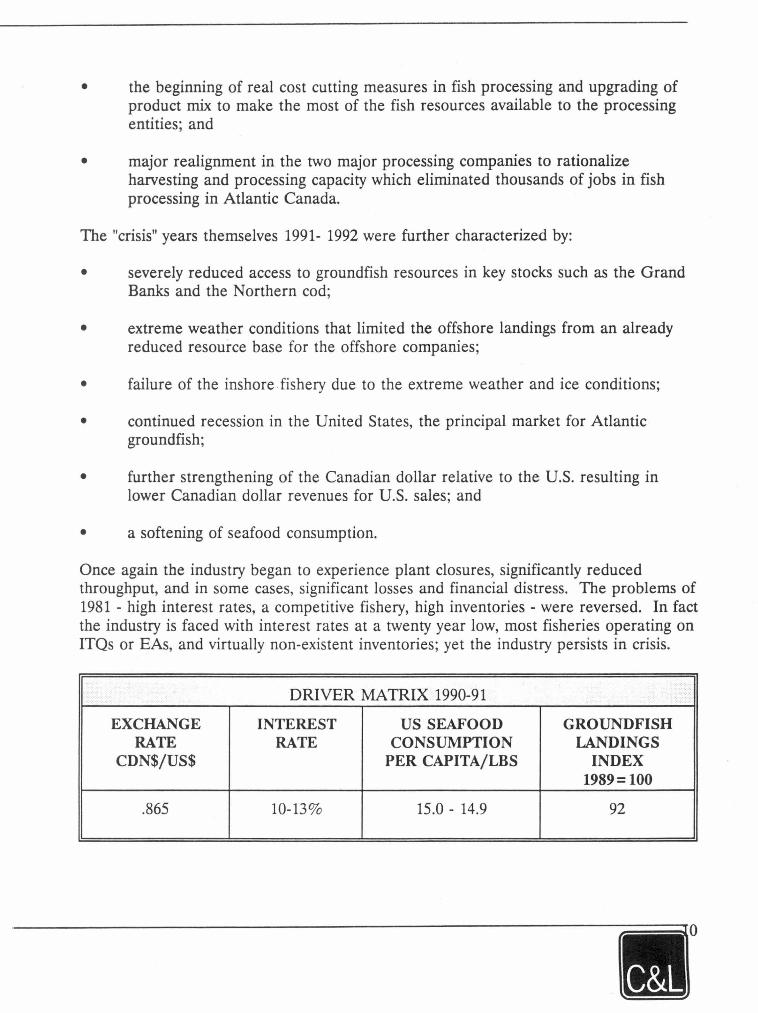

The "crisis" years themselves 1991- 1992 were further characterized by:

• severely reduced access to groundfish resources in key stocks such as the Grand Banks and the Northern cod;

• extreme weather conditions that limited the offshore landings from an already reduced resource base for the offshore companies;

• failure of the inshore . fishery due to the extreme weather and ice conditions;

• continued recession in the United States, the principal market for Atlantic groundfish;

• further strengthening of the Canadian dollar relative to the U.S. resulting in lower Canadian dollar revenues for U.S. sales; and

• a softening of seafood consumption.

Once again the industry began to experience plant closures, significantly reduced throughput, and in some cases, significant lasses and financial distress. The problems of 1981 - high interest rates, a competitive fishery, high inventories - were reversed. In fact the industry is faced with interest rates at a twenty year low, most fisheries operating on ITQs or EAs, and virtually non-existent inventories; yet the industry persists in crisis.

DRIVER MA TRIX 1990-91

EX CHANGE INTEREST US SEAFOOD GROUNDFISH RATE RATE CONSUMPTION LANDINGS

CDN$/US$ PER CAPITA/LBS INDEX 1989= 100

.865 10-13% 15.0 - 14.9 92

~·

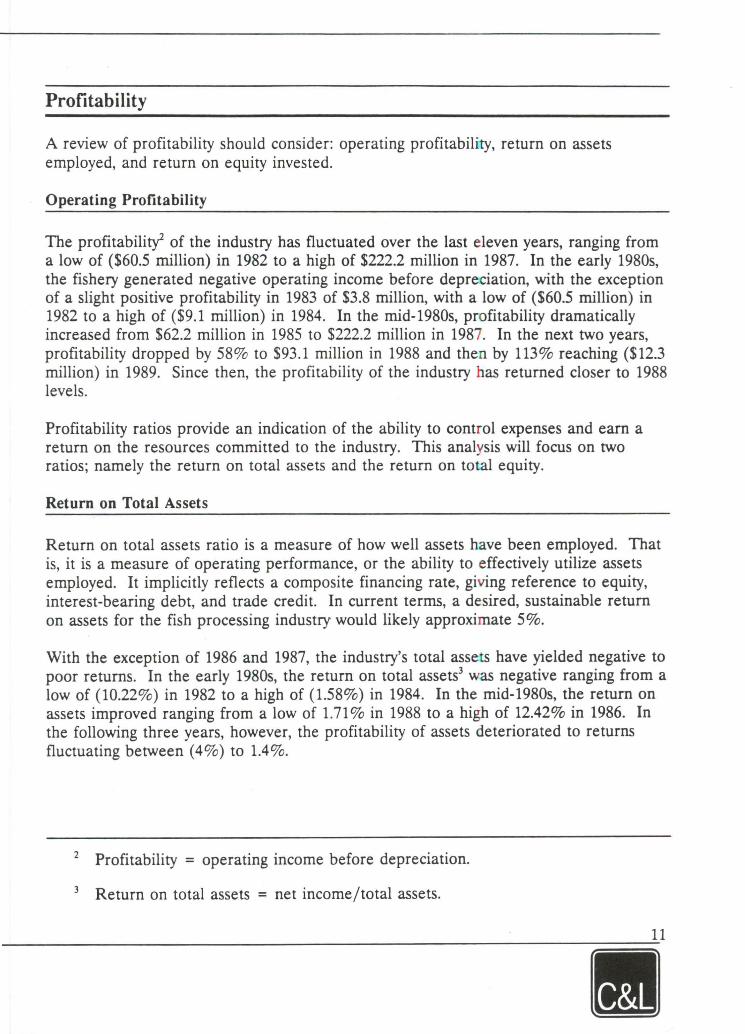

Profitability

A review of profitability should consider: operating profitability, return on assets employed, and return on equity invested.

Operating Profitability

The profitability2 of the industry has fluctuated over the last eleven years, ranging from a low of ($60.5 million) in 1982 to a high of $222.2 million in 1987. In the early 1980s, the fishery generated negative operating incarne before depreciation, with the exception of a slight positive profitability in 1983 of $3.8 million, with a low of ($60.5 million) in 1982 to a high of ($9.1 million) in 1984. In the mid-1980s, profitability dramatically increased frorn $62.2 million in 1985 to $222.2 million in 1987. In the next two years, profitability dropped by 58% to $93.1 million in 1988 and then by 113% reaching ($12.3 million) in 1989. Since then, the profitability of the industry bas returned doser to 1988 levels.

Profitability ratios provide an indication of the ability to control expenses and earn a return on the resources committed to the industry. This analysis will focus on two ratios; namely the return on total assets and the return on total equity.

Return on Total Assets

Return on total assets ratio is a measure of how well assets have been employed. That is, it is a measure of operating performance, or the ability to effectively utilize assets employed. It implicitly reflects a composite financing rate, giving reference to equity, interest-bearing debt, and tracte credit. In current terrns, a desired, sustainable retum on assets for the fish processing industry would likely approximate 5%.

With the exception of 1986 and 1987, the industry's total assets have yielded negative to poor returns. In the early 1980s, the return on total assets3 was negative ranging from a low of (10.22%) in 1982 to a high of (1.58%) in 1984. In the mid-1980s, the retum on assets improved ranging from a low of 1.71 % in 1988 to a high of 12.42% in 1986. In the following three years, however, the profitability of assets deteriorated to returns fluctuating between ( 4%) to 1.4%.

2 Profitability = operating incarne before depreciation.

3 Return on total assets = net incarne/total assets.

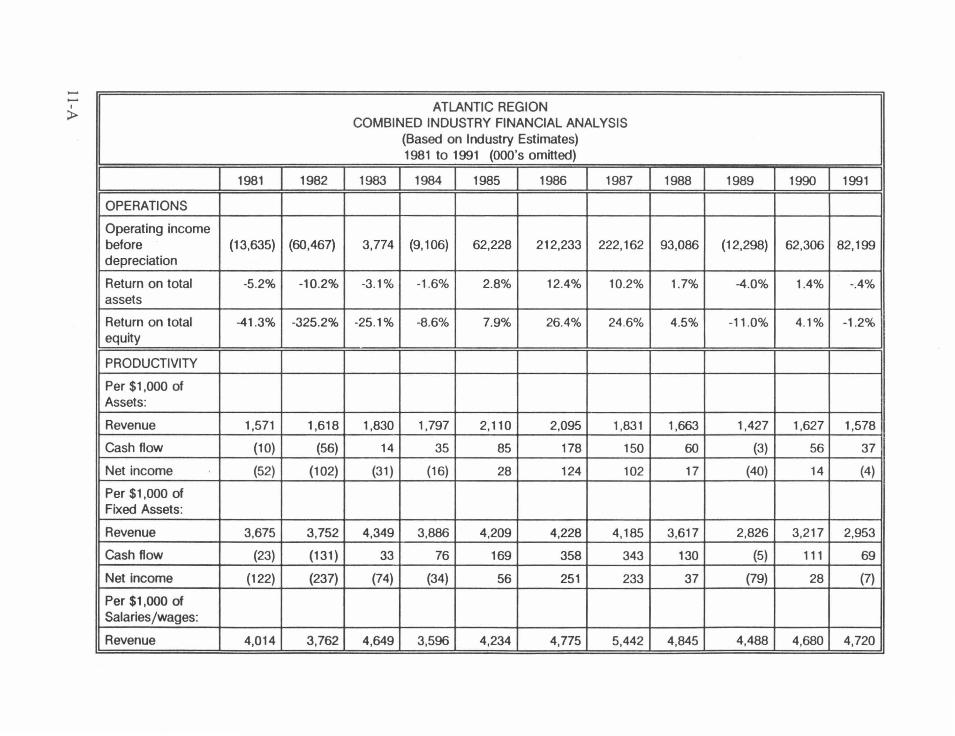

ATLANTIC REGION COMBINED INDUSTRY FINANCIAL ANALYSIS

(Based on lndustry Estimates) 1981 to 1991 (OOO's omitted)

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991

OPERATIONS

Operating income before (13,635) (60,467) 3,774 (9, 106) 62,228 212,233 222,162 93,086 (12,298) 62,306 82, 199 depreciation

Return on total -5.2% -10.2% -3.1% -1 .6% 2.8% 12.4% 10.2% 1.7% -4.0% 1.4% -.4% assets

Return on total -41 .3% -325.2% -25.1% -8.6% 7.9% 26.4% 24.6% 4.5% -11.0% 4.1% -1.2% equity

PRODUCTIVITY

Per $1 ,000 of Assets:

Revenue 1,571 1,618 1,830 1,797 2,110 2,095 1,831 1,663 1,427 1,627 1,578

Cash flow (10) (56) 14 35 85 178 150 60 (3) 56 37

Net income (52) (102) (31) (16) 28 124 102 17 (40) 14 (4)

Per $1,000 of Fixed Assets:

Revenue 3,675 3,752 4,349 3,886 4,209 4,228 4,185 3,617 2,826 3,217 2,953

Cash flow (23) (131) 33 76 169 358 343 130 (5) 111 69

Net income (122) (237) (74) (34) 56 251 233 37 (79) 28 (7)

Per $1,000 of Salaries/wages:

Revenue 4,014 3,762 4,649 3,596 4,234 4,775 5,442 4,845 4,488 4,680 4,720

In conclusion, the industry bas been relatively unsuccessful in earning a reasonable rate of return on its assets.

Return on Total Equity

The return on total equity indicates the amount earned on the equity committed to the industry, and provides an indication of investment performance, or performance on capital at risk. This ratio is often used to choose from available investment options. In current terms, a low risk investment ( term deposits, government or large company bonds, T-bills) will yield returns between 7% and 10%, depending on term and liquidity. An at-risk investment, again depending on term and liquidity, will yield anywhere from 10% to 40+ %. A desired, sustainable return on equity for the fish processing industry would likely be a minimum of 15%, given industry structure, liquidity and relative risk.

Similar to the return on total assets, the industry's total equity yielded poor returns in the early 1980s. The return on total equity4 ranged from a low of (325%) to a high of (9%). In the mid-1980s, the return fluctuated between a low of 4.5% in 1988 to a high of 26.4% in 1986. In the following three years, the profitabi ty of equity also deteriorated to returns fluctuating between ( 11 % ) to 4%.

The industry bas been successful in meeting acceptable operating returns in only two of the eleven years under review.

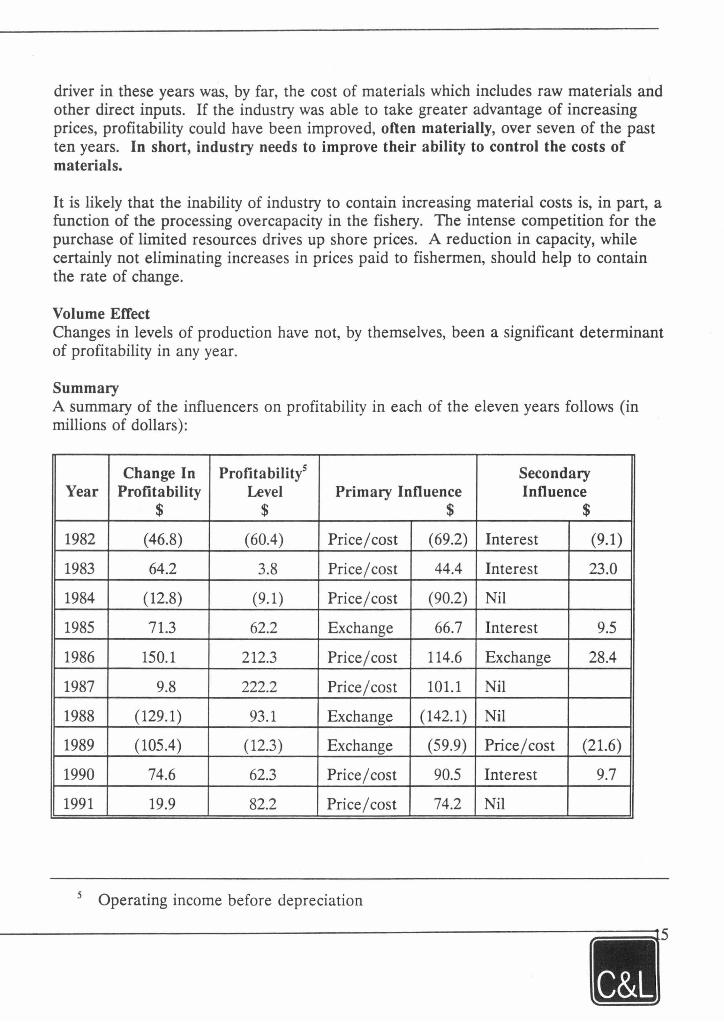

Profitability Drivers

It has been generally held that profitability in the industry has been historically driven by two factors:

• interest rates; • US dollar exchange rates.

To draw conclusions as to profitability factors, changes in profitability were analyzed over the eleven year period 1981 to 1991.

The change in profitability in any given year can be attributed to one or more of the following factors:

4 Return on total equity = net incarne/total equity.

• interest effect; • exchange eff ect; • price effect (net of exchange); • cost effect (net of interest); and • volume effect

The interest effect determines the impact of changes in interest rates on the cost of carrying short and long term debt. The analysis examined bath imputed rates (actual interest costs over actual average debt values), and actual rates based on chartered bank prime rates. It was found that imputed rates closely tracked actual rates over the eleven years.

The exchange effect measures the impact of changes in the annual average exchange rate between the United States and Canada. The analysis assumes that 80% of Atlantic production value is exported to the US.

Price, cost and volume effect are essentially the results of variance analysis. The variance calculations isolate the impact of changes in factors such as selling prices, costs, and volume of production, and determine the impact of each of these factors on overall profitability in a given year.

Analysis of these factors accounts for all of the change in profitability from one year to another.

Analysis of these factors reveals that, contrary to conventional wisdom, the impact of changes in interest and exchange rates has not been nearly as profound as other factors.

Interest Effect The interest effect has had a significant effect in only one year, 1983, but even in that year, other factors were more important. In four other years, the impact is worth noting but not significant. The impact is summarized as follows:

Year 1982

1983

1985

1989

Impact of Change in Interest Costs Interest changes contributed $9.1 million to a profitability loss of $46.8 million.

Interest changes contributed $22.9 million to a $64.2 million increase in profitability.

Interest changes contributed $9.5 million to a $71.3 million increase in profitability.

Interest changes contributed $16.5 million to a $105.4 million decline in profitability.

1990 Interest changes contributed $9.7 million to a $74.6 million increase in profitabili ty.

Exchange Effect Again, contrary to popular belief, the exchange effect bas been the predominant influencer in only three years. The impact is summarized as follows:

Y ear Impact of Change in Exchange Rates 1985 Exchange rate changes contributed $66.7 million to a profitability

improvement totalling $71.3 million.

1988 Exchange rate changes contributed $142.1 million to a total drop in profitability of $129 .1 million.

1989 Exchange rate changes contributed $59.9 million to a total drop in profitability of $105.4 million.

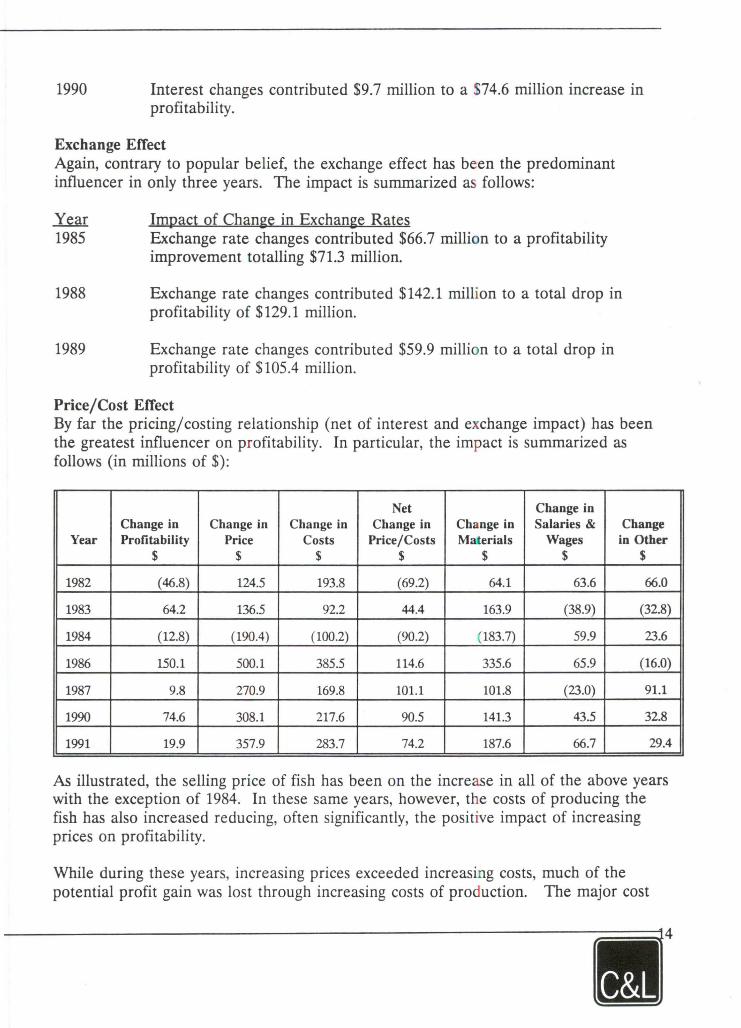

Price/Cost Effect By far the pricing/costing relationship (net of interest and exchange impact) bas been the greatest influencer on profitability. In particular, the impact is summarized as follows (in millions of$):

Net Change in Change in Change in Change in Change in Change in Salaries & Change

Year Profitability Price Costs Price/Costs Materials Wages in Other $ $ $ $ $ $ $

1982 (46.8) 124.5 193.8 (69.2) 64.1 63.6 66.0

1983 64.2 136.5 92.2 44.4 163.9 (38.9) (32.8)

1984 (12.8) (190.4) (100.2) (90.2) (183.7) 59.9 23.6

1986 150.1 500.1 385.5 114.6 335.6 65.9 (16.0)

1987 9.8 270.9 169.8 101.1 101.8 (23.0) 91.1

1990 74.6 308.1 217.6 90.5 141.3 43.5 32.8

1991 19.9 357.9 283.7 74.2 187.6 66.7 29.4

As illustrated, the selling price of fish has been on the increase in ail of the above years with the exception of 1984. In these same years, however, the costs of producing the fish has also increased reducing, often significantly, the positive impact of increasing prices on profitability.

While during these years, increasing prices exceeded increasing costs, much of the potential profit gain was lost through increasing costs of production. The major cost

driver in these years was, by far, the cost of materials which includes raw materials and other direct inputs. If the industry was able to take greater advantage of increasing prices, profitability could have been improved, often materially, over seven of the past ten years. In short, industry needs to improve their ability to control the costs of materials.

It is likely that the inability of industry to contain increasing material costs is, in part, a function of the processing overcapacity in the fishery. The intense competition for the purchase of limited resources drives up shore prices. A reduction in capacity, while certainly not eliminating increases in prices paid to fishermen, should help to contain the rate of change.

Volume EfTect Changes in levels of production have not, by themselves, been a significant determinant of profitability in any year.

Summary A summary of the influencers on profitability in each of the eleven years follows (in millions of dollars):

Change In Profitability5 Secondary Year Profitability Level Primary Influence Influence

$ $ $ $

1982 (46.8) (60.4) Price/cost (69.2) Interest (9.1)

1983 64.2 3.8 Price/cost 44.4 Interest 23.0

1984 (12.8) (9.1) Price/cost (90.2) Nil

1985 71.3 62.2 Ex change 66.7 Interest 9.5

1986 150.1 212.3 Price/cost 114.6 Ex change 28.4

1987 9.8 222.2 Price/cost 101.1 Nil

1988 (129.1) 93.1 Ex change (142.1) Nil

1989 (105.4) (12.3) Ex change (59.9) Price/cost (21.6)

1990 74.6 62.3 Price/cost 90.5 Interest 9.7

1991 19.9 82.2 Price/cost 74.2 Nil

5 Operating incarne before depreciation

In summary, changes in prices (net of exchange) have been the single most important determinant of profitability in the fish processing industry. lt is very important to note, however, that since 1985, negative changes in profitability have been caused primarily by exchange factors. It is equally important to note that current favourable exchange rates may help mitigate some of the negative consequences of the resource crisis in 1992 and early 1993.

This means that the industry's ability to control costs, in response to changing prices, is the single most important factor in achieving sustained profitability.

By way of illustration, after accounting for interest and exchange eff ect, 1990 saw a favourable price variance totalling $308.1 million. By itself, this factor should have resulted in a tremendous increase in industry profitability in that year. However, in that year, costs rose by some $217.6 million, nearly eliminating the price increase. To the extent that costs can be better controlled, then consistent profits will result. It is recognized that this is a very simplistic statement in that there many elements that contribute to increasing costs. The fact remains however, that this is likely the only area subject to ongoing contrai and improvement by the industry and deserves much more attention than it has received in the past.

Productivity

Productivity trends of the industry can be measured in terms of revenue and profitability (cash flow) versus investment in assets and utilization of human resources (salaries and wages). It should be noted that there are no benchmarks or reference points for these measures - the trends themselves determine the context for the analysis.

Productivity of Total Assets

Revenue per $1,000 of total assets has ranged from a low of $1,427 in 1989 to a high of $2,110 in 1985. In the early 1980s, revenue per $1,000 of total assets increased by nearly 20% from $1,571 in 1981 to $1,830 in 1983 thereby indicating increased asset productivity. Between 1985 and 1989, however, productivity deteriorated from a period high of $2,110 to a low of $1,427. Since then, productivity has changed very little reaching $1,578 in 1991.

Cash flow per $1,000 of total assets ranged from a low of ($56) in 1982 to a high of $178 in 1986. In the early 1980s, this productivity measure trended upwards reaching a high in 1986. Since then, cash flow per $1,000 of total assets has declined to a low of ($3) in 1989.

Productivity of Fixed Assets

Revenue per $1,000 of fixed assets followed a similar trend to that for total assets-. Productivity of fixed assets increased from $3,675 in 1981 to $4,349 in 1983. Between 1986 and 1989, however, productivity deteriorated from $4,228 to a low of $2,826. Since then, this productivity measure bas exhibited very little movement reaching $2,953 by 1991.

Cash flow per $1,000 of fixed assets reached a low of ($131) in 1982 and a high of $358 in 1986, following the same trend as that for revenue.

These two productivity measures present tangible evidence of the much discussed overcapacity which bas been present in the industry since 1986. The increasing tendency toward capital investment which began at that time continued until 1989, at which time a levelling off in investment took place. This issue is discussed in greater detail in Report Two.

Utilization of Fish Processing Employment

The utilization of fish processing employment is assessed using two measures: (1) revenue generated per $1,000 of salaries and wages and (2) an inflation-adjusted labour cost per tonne. The first measure assesses whether the per dollar investment in human resources is yielding more or less revenues. This analysis is limited as it does not isolate whether the trend is attributed to changing productivity and/or changing selling prices versus wage rates. The second measure is better in that it isolates the productivity of human resources by adjusting for the inflation of wage rates and does not take into account the impact of prices.

The revenue generated per $1,000 of salaries and wages ranged from a low of $3,596 in 1984 to a high of $5,442 in 1987. In the early 1980s, this measure fluctuated between $3,596 in 1984 and $4,649 in 1983. Following the low in 1984, the utilization of human resources followed an upward trend reaching a period high in 1987. In the subsequent years, however, the utilization of fish processing employment again fluctuated; increasing to $4,680 in 1990 and then dropping to $4,720 in 1991.

Discounting for the peaks noted above, this measure indicates that the per dollar investment in human resources is yielding 18% more revenue from 1981 to 1991. This improvement appears to be real in that it is not distorted by price improvement, as the change in prices over the period closely paralleled increases in wage rates.

This is confirmed when labour costs per tonne produced are inflation adjusted over the period. The average inflation adjusted labour cost per tonne is as follows (1986 is indexed to 100):

1981 1982 1983 1984 1985 1986 1987 1988 1989 1990

773 831 701 791 671 751 684 686 629 663

The trend in labour costs per tonne can be more clearly reflected by the following period averages:

1981 to 1985 - five year average 1986 to 1987 - two year average 1988 to 1990 - three year average

$753 717 682

1991

752

The above averages do not take into consideration 1991, as production data for 1991 is not considered to be reliable, and may thus distort the conclusion drawn on this issue.

As is depicted, the utility of human resources in the fish proœssing sector appears to be improving. In particular, labour costs have declined from $773 in 1981 to $663 in 1990 with an absolute improvement of $110. This represents an improvement of 14.2% which compares favourably with the 18% improvement noted above for the period 1981 to 1991.

It can be concluded, therefore, that labour utility has improved by some 18% over the eleven years under review.

No cause can be identified for this improvement other than the continuing investment in processing plant and equipment that has taken place in the industry. Leaving aside the issue of overcapacity, which is discussed below, this improvement is desirable and likely essential to the continuing well being of the industry. It is noted that this trend will likely result in increasingly less labour being used by the industry, a trend which is manifesting itself in almost every other manufacturing environment.

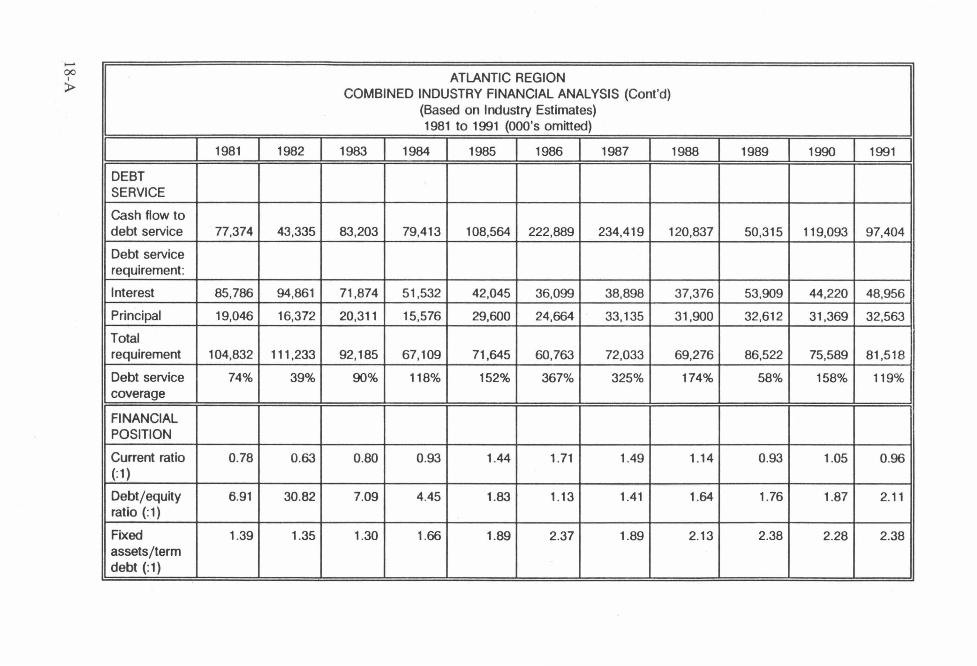

Debt Service

This analysis will focus on assessing the industry's ability to service debt, that is, ability to meet interest and principal payments.

The debt service coverage ratio6 helps assess debt service capability. It is a function of profitability and is generally used as a measure in determining how much debt can be safely carried. Depending on the nature of the business, acceptable debt service ratios range from 100% to 150%, with the higher ratios being used in industries where

6 Debt service coverage ratio = cash flow to debt service/debt service requirement.

-OO ' p

1

DEBT SERVICE

Cash flow to debt service

Debt service requirement:

lnterest

Principal

Total requirement

Debt service coverage

FI NAN CIAL POSITION

Current ratio (: 1)

Debt/equity ratio (:1)

Fixed assets/term debt (:1)

1 1981 1 1982 1

77,374 43,335

85,786 94,861

19,046 16,372

104,832 111,233

74% 39%

0.78 0.63

6.91 30.82

1.39 1.35

ATLANTIC REGION COMBINED INDUSTRY FINANCIAL ANALYSIS (Cont'd)

(Based on lndustry Estimates) 1981 to 1991 (OOO's omitted)

1983 1 1984 1 1985 1 1986 1 1987 1 1988 1 1989 1 1990 1 1991 1

83,203 79,413 108,564 222,889 234.419 120,837 50,315 119,093 97,404

71,874 51,532 42,045 36,099 38,898 37,376 53,909 44,220 48,956

20,311 15,576 29,600 24,664 33,135 31,900 32,612 31,369 32,563

92,185 67,109 71,645 60,763 72,033 69,276 86,522 75,589 81,518

90% 118% 152% 367% 325% 174% 58% 158% 119%

0.80 0.93 1.44 1.71 1.49 1.14 0.93 1.05 0.96

7.09 4.45 1.83 1.13 1.41 1.64 1.76 1.87 2.11

1.30 1.66 1.89 2.37 1.89 2.13 2.38 2.28 2.38

profitability is less predictable or consistent. A typical industrial ratio would be 125% to 130%, meaning that for every $1 required to service interest and principal payments, $1.25 to $1.30 of cash flow is required to provide reasonable comfort that the debt will indeed be serviced.

The industry did not generate adequate cash flow to service its debt requirement in 1981, 1982, 1983, and 1989. In 1982, the industry witnessed the most adverse debt position with a debt service coverage of only 39%. The low ratios of the early 1980s reflect the impact of significant debt burdens combined with high interest rates, whereas the ratio of 58% in 1989 is a result of a dramatic drop in cash flow.

The debt service coverage ratio improved substantially in the mid-1980s ranging from 118% in 1984 to 367% in 1986. Since then the ratio bas been a little more stable, with the exception of 1989, fluctuating between 119% and 174%.

Debt service coverage of 157.5% in 1990 would be considered acceptable, and 1991 would be marginally acceptable at 119.5%. This relative stability is a function of significant equity infusions in the industry in the early 1980s, primarily by governments in large offshore oriented companies. Higher than normal earnings in 1986 and 1987 also strengthened the industry's position. Finally, there bas been some additional equity invested in the late 1980s, primarily to fund operating lasses and charges related to down-sizing.

The ability of the industry to service its debt is being negatively affected by generally increasing levels of borrowing, particularly short term debt. This has been caused by two factors:

1. Significant increases in fixed asset investment from 1985 to 1989, funded to a significant extent by short term borrowings.

2. Declines in operating incarne from 1988 to 1990, with lasses being funded by short term borrowings.

The financial profiles indicate total interest-bearing debt of some $600 million in the industry by the end of 1991, excluding estimated amounts related to non-Atlantic Canadian assets and operations.

A survey of lenders with loans to the industry suggests total debt at the. end of 1992 approaching $800 million, including non-Atlantic Canadian assets. There is clear evidence of increased borrowing, in spite of significant restraint in the lending community.

It is a reasonably safe assumption that the industry will not likely be able to maintain acceptable overall debt service coverage throughout 1992 and 1993. This stress will be

concentrated in groundfish producers, particularly in N ewfoundland. There is also some weakness evident in companies relying heavily on pelagics, due primarily to weak market conditions. While there has been no evidence of significant weakness being experienced by processors of molluscs and crustaceans, very recent comments suggest significant price volatility which may prove disruptive in the short term.

Financial Position

A review of financial ratios serves as a useful indication of the industry's strength. To provide a relatively accurate financial picture of the fish processing sector, this section will review the industry's current, debt to equity, and fixed assets to debt ratios.

Current Ratio

The current ratio is based on current assets and current liabilities. A current asset is one that is cash or will turn in to cash within one year whereas a current liability is one that is due within one year. Analysis of the current ratio provides insight into the industry's ability to pay its short term debt obligations.

A review of the current ratio, reconfirms that the industry was at its strongest, financially, during the mid-1980s. In the early 1980s, the industry's current ratio was less than 1:1 and thus had limited financial capacity to service its short-term debt. Between 1982 and 1986, however, the industry witnessed an improving short-term financial situation with the current ratio increasing from .63:1 to 1.71:1. The current ratio then proceeded to decline reaching a low of .93:1 by 1989 and, in the early 1990s, the ratio hovered around the 1:1 mark.

A widely used rule of thumb is that a company or industry with a current ratio of 2: 1 or more is in good shape in terms of being able to pay maturing current liabilities. Though this ratio by itself can be misleading, the fishery, as an industry, has not in any given year reached close to 2: 1.

Debt/Equity Ratio

The debt to equity ratio7 assesses the balance between the portion of assets being financed by creditors and the portion of assets being financed by the stockholders of the industry. An acceptable debt/equity ratio for a large company is approximately 1:1, while small companies can opera te qui te easily with a ratio of 2.0: 1 to 3.0: 1. A ratio of 1.5: 1 would be considered acceptable for the industry overall.

7 Debt to equity ratio = total liabilities/equity.

~·

The industry's debt to equity ratio has been variable. In the early 1980s, the ratio was quite extreme with a high of 30.82:1 in 1982 and a low of 4.45:1 in 1984. In the mid-1980s, the ratio dramatically declined to 1.83: 1 and 1.13: 1. This trend was caused by massive infusions of government funds during the restructuring of the early 1980s, combined with the high earnings of the mid-1980s. The ratio weakened in the late 1980s, again as a result of significant borrowings to fund capital investment, and exacerbated by significantly weakened earnings. At the end of 1991, the ratio stood at 2.1:1, moving well outside acceptable levels.

Fixed Assets To Term Debt

The fixed assets to term debt ratio determines to what degree the industry is relying on long term financing to fund long term assets. It is a measure of balance within the financial structure.

The fixed assets to term debt ratio declined marginally in the early 1980s from 1.39:1 in 1981 to 1.3:1 in 1983. In the following three years, however, the ratio increased by roughly 80% to 2.37:1 in 1986. This increase indicates that the industry became less dependent on long term debt to finance fixed asset purchases, relying more on retained earnings and short term borrowings. Generally, this situation would suggest some room to increase long term borrowings which would help alleviate working capital stress. The lending community, however, is generally averse to providing term debt to the industry, as the security value of long term assets is now suspect, and weakened earnings generally do not support additional borrowing of any kind.

Financial Position of Large Versus Small Companies

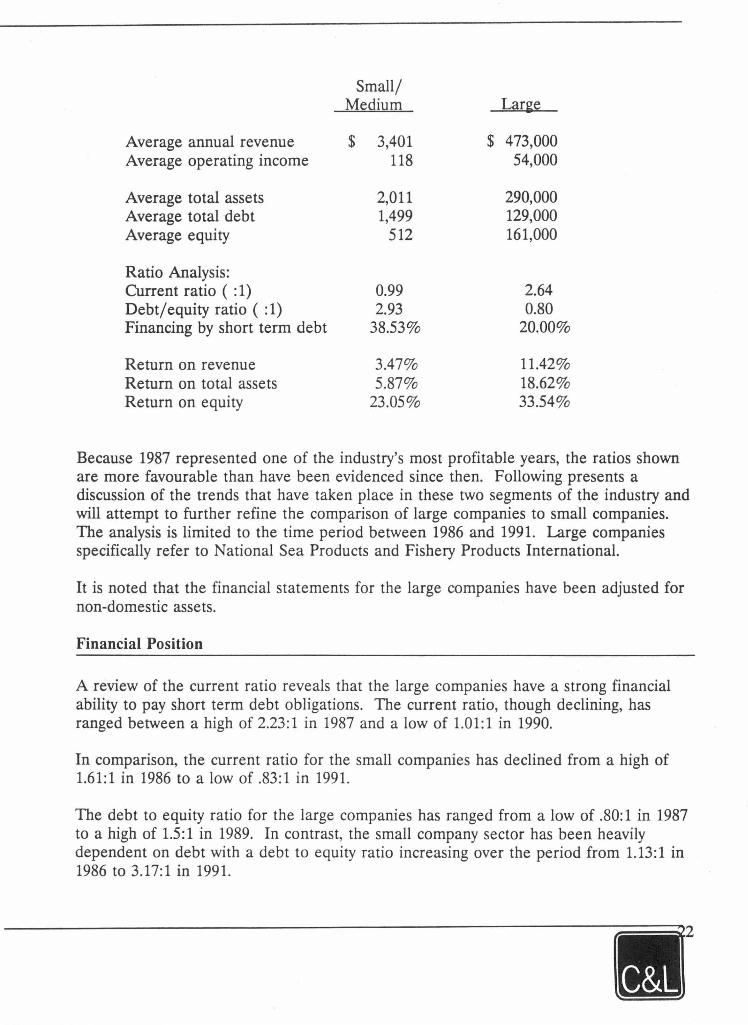

Summary Information, 1987

Based on the relatively complete financial information available for 1987, the following is a financial summary comparing large fish processing companies to small and mediumsized enterprises. While profitability and financial strength have changed since 1987, the data serves well in contrasting the two groups. It is noted that this data has not been adjusted for non-domestic assets, and some of the ratios are therefore slightly different from the trend analysis described later, where such adjustments have been made ($000 omitted):

Small/ Medium Large

Average annual revenue $ 3,401 $ 473,000 Average operating incarne 118 54,000

Average total assets 2,011 290,000 Average total debt 1,499 129,000 Average equity 512 161,000

Ratio Analysis: Current ratio ( : 1) 0.99 2.64 Debt/equity ratio ( :1) 2.93 0.80 Financing by short term debt 38.53% 20.00%

Retum on revenue 3.47% 11.42% Return on total assets 5.87% 18.62% Retum on equity 23.05% 33.54%

Because 1987 represented one of the industry's most profitable years, the ratios shown are more favourable than have been evidenced since then. Following presents a discussion of the trends that have taken place in these two segments of the industry and will attempt to further refine the comparison of large companies to small companies. The analysis is lirnited to the time period between 1986 and 1991. Large companies specifically refer to National Sea Products and Fishery Products International.

It is noted that the financial statements for the large companies have been adjusted for non-domestic assets.

Financial Position

A review of the current ratio reveals that the large companies have a strong financial ability to pay short term debt obligations. The current ratio, though declining, bas ranged between a high of 2.23:1 in 1987 and a low of 1.01:1 in 1990.

In comparison, the current ratio for the small companies has declined from a high of 1.61:1 in 1986 to a low of .83:1 in 1991.

The debt to equity ratio for the large companies bas ranged from a low of .80: 1 in 1987 to a high of 1.5:1 in 1989. In contrast, the small company sector has been heavily dependent on debt with a debt to equity ratio increasing over the period from 1.13: 1 in 1986 to 3.17:1 in 1991.

In summary, large and small company financial positions are largely a function of the ability and tendency of the larger companies to raise equity financing, as opposed to debt.

Further, there is evidence to suggest that the small company sector is more consistently profitable, within a smaller band of fluctuation, than the large companies.

Profitability

Over the six year period, the profitability8 of the large fish processing companies bas responded more to changes in the industry. Profitability of large companies bas tended to fall more during years of decline and rise more during years of prosperity. For instance, the profitability of the large companies outperformed the profitability of the small companies in the mid-1980s; however, when the fishery witnessed a downtum in 1989 and 1991, the impact was more detrimental to the profitability of the large companies than to that of the small companies.

The total assets of the large companies yielded strong returns in 1986 and 1987 but then deteriorated in the subsequent year. In the mid-1980s, the return on total assets9 was between 14% and 16%. In the next four years, however, the return on assets ranged from a low of (7.7%) in 1989 to a high of 1.53% in 1988. In contrast, the total assets of small companies yielded low, yet relatively stable, returns. The mid-1980s witnessed higher returns than the latter years; ranging from a low of .03% in 1989 to a high of 9% in 1986.

Similar to the return on total assets, the total equity of large companies yielded high returns in the mid-1980s and then lower retums in the following years. The return on total equity10 ranged from a low of (19%) in 1989 to a high of 34% in 1986.

Characteristics Of Small Companies

The following points characterize smaller enterprises in the industry:

• They tend to rely more heavily on debt financing, as is typical of smaller companies in most industries.

8 Profitability = Cash flow from operations.

9 Retum on total assets = net incarne/total assets.

10 Return on total equity = net incarne/total equity.

• They tend to pay less attention to the balance of financing and often rely on short term borrowings to finance long term assets. This often causes working capital problems, particularly when unexpected events occur requiring working capital, and short term borrowing capability has been used to finance long term assets.

• They tend not to have adequate information and control systems and often rely on rudimentary analysis to support pricing and casting.

• They tend to have limited marketing scope and market intelligence, often relying heavily on intermediaries for marketing effort and penetration. Further, the approach to marketing is often opporturustic, with less emphasis on longer term development or strategy.

• They tend to react more quickly to changing circumstances, as there are usually fewer layers of management, and decisions can be made and implemented on short notice. This does not mean that they are better decision makers, as small enterprises often do not have adequate information for proper decision making.

Conclusion

While the two segments of the industry are somewhat different in make-up and approach, they have both followed the same trends in production volume and profitability.

The larger companies are generally better capitalized, resulting primarily from sigruficant equity infusions that were made in the restructuring of the early 1980s, the benefit of which continues to this day. Accordingly, they are able to absorb financial shocks better than smaller ones. At the same time, because they respond more quickly to changing circumstances, smaller companies tend to be able to survive with less equity and less working capital.

The larger comparues have been more profitable in times of industry prosperity, but they have suffered more when faced with unfavourable conditions. Smaller comparues have generally been more consistently profitable, having better withstood the volatility experienced in recent years.

Having said that, the smaller companies are now in reasonably poor shape. The tendency to use short term debt to finance long term assets, combined with a worsening debt/ equity position, means that they are now vulnerable to continuing difficult conditions, and will likely suffer significantly as a sector in the short term.

N COMPARISON OF FISH PROCESSING INDUSTRY WITH OTHER INDUSTRIES --------- - --- ---

+>-1

>

RETURN ON EQUITY (%) 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 -- --··-·-----

FOOD MANUFACTURING 2 13.90 13.20 11 .00 13.80 13.70 12.90 13.10 16.00 14.00 11 .50 10.37 6.54 TOTAL MANUFACTURING 2 16.90 11 .40 4.50 8.90 12.00 10.20 10.00 13.10 16.10 11 .00 N/A N/A FISH PROCESSING NIA -41.29 -325.17 -25.13 -8.61 7.89 26.41 24.56 4.52 -10.98 4.07 -1.20 -

PROFIT MARGIN (%) 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 ----

FOOD MANUFACTURING 3.90 3.50 3.20 3.80 3.80 4.20 4.50 4.70 4.00 3.70 2.24 2.29 TOTAL MANUFACTURING 9.10 7.20 3.80 5.80 7.20 7.00 6.80 8.50 9.30 7.10 N/A N/A FISH PROCESSING N/A -3.48 -5.77 - 1.79 -0.69 0.02 8.33 7.85 1.44 -3.72 0.96 0.16

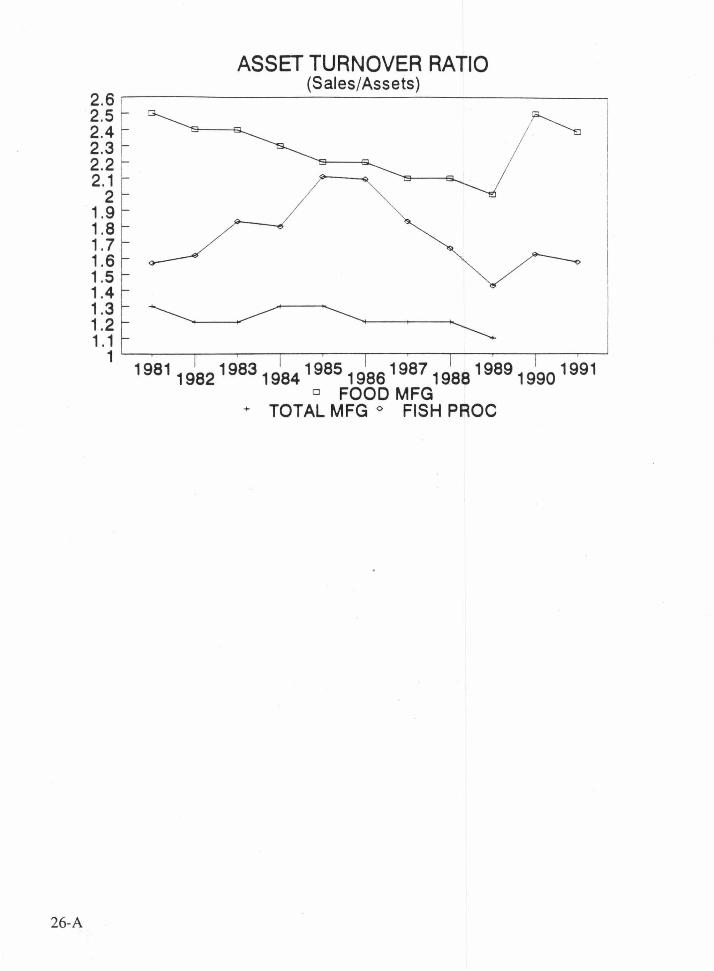

ASSET TURNOVER RATIO 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991

FOOD MANUFACTURING 2.50 2.50 2.40 2.40 2.30 2.20 2.20 2.10 2.10 2.00 2.50 2.39 TOTAL MANUFACTURING 1.40 1.30 1.20 1.20 1.30 1.30 1.20 1.20 1.20 1.10 N/A N/A FISH PROCESSING NIA 1.57 1.62 1.83 1.80 2.11 2.10 1.83 1.66 1.43 1.63 1.58

1. Due to the large negative retum on equity in 1982 for fish processing, the retum on equity graph is only presented for the period 1983 to 1991 . 2. The financial ratios presented for food manufacturing and total manufacturing comprises corporations with $10 million or more in total assets.

SOURCES: Food Market Commentary, Agriculture Canada, January 1991, p. 20. Statistics Canada, lndustrial Corporation Financial Statistics, cat. no. 61-008.

Financial Comparison of the Fish Processing Industry to Other Industries

The following comparative analysis determines the relative financial position of the fish processing industry compared to other industries. In particular, the analysis focuses on comparing the fish processing industry to the food manufacturing and total manufacturing industries.

The industries are compared on the basis of profitability and productivity. The profitability analysis focuses on two measures; namely the return on equity" and profit margin12

• The productivity analysis reviews the asset turnover ratio13• The return on

equity ratio is reviewed for the time period, 1983 and 1991, with the exception of the total manufacturing industry for which data is only available prior to 1990. The profit margin and asset turnover ratios are reviewed for the time period, 1981 to 1991 again with the exception of the total manufacturing industry.

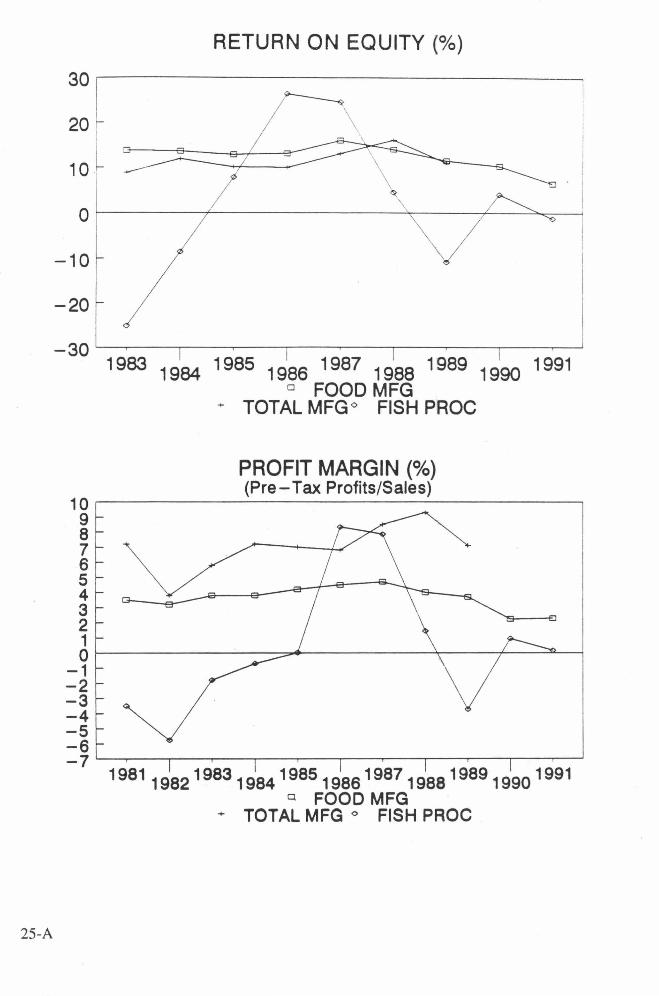

Profitability

The return on equity (%)for the food manufacturing and total manufacturing industries are relatively comparable over the period. The return on equity for the food manufacturing industry is declining from a high of 13.8 in 1983, with the exception of a large peak of 16.00 in 1987, to a low of 6.54 in 1991. In contrast the retum for the total manufacturing industry has fluctuated between a higb of 16.1 in 1988 to a low of 8.9 in 1983.

In comparison to these two sectors, the profitability, as measured by the retum on equity, of the fish processing industry bas been significantly lower, with the exception of 1986 and 1987. Specifically, the profitability of the fish processing industry bas been on average, excluding 1986 and 1987, 132% lower than the profitability of the food manufacturing sector and 170% lower than the profitability of the total manufacturing industry. In 1986 and 1987, however, the return on equity for the fish processing sector was more than double that for the total manufacturing industry and 75% more than that for the food manufacturing industry. ·

The profit margin (%)for the food manufacturing industry bas been relatively stable; increasing from 3.5 in 1981 to a high of 4.7 in 1987 and then dropping to 2.29 by 1991.

11 Return on equity (%) = net incarne/total equity.

12 Profit margin = pre-tax net incarne/total sales.

13 Asset turnover ratio = total sales/total assets.

25-A

30 [

20 1

10 l

-10

-20

RETURN ON EQUITY (%)

\,

1983 1984 1985 1986 1987 1988 1989 1990 1991 ° FOOD MFG

+ TOTAL MFG ° FISH PROC

PROFIT MARGIN (%) (Pre-Tax Profits/Sales)

10,---~~~~~~~~~~~~~~~~~-----,

9 8 7 6 5 4 3 2 1 or--~~~~~~~~~~~~~~-f-~-=-_,

-1 -2 -3 -4 -5 -6 -7'---.------.-~---.-~,------,-~-.----.~----.-~-.----.-~---.-~

19811982198319841985198619871988198919901991 ° FOOD MFG

+ TOTAL MFG ° FISH PROC

In contrast, the profit margin ( % ) for the total manufacturing industry has been higher than that of the food manufacturing industry, fluctuating from a high of 9.3 in 1988 to a low of 3.8 in 1982.

In comparison, the trend in the profit margin for the fish processing industry has dramatically differed from that of the food and total manufacturing. The industry has only managed to reach, or surpass, the level of profitability of the food manufacturing industry in 1986 and 1987.

Productivity

The productivity of an industry can be measured by the effectiveness of the utilization of assets. One such measure is the ratio of total sales to assets, or the asset turnover ratio. Specifically, this ratio measures the level of revenue generated by the industry's assets.

The productivity, as measured by the asset turnover ratio, of the food manufacturing industry declined from 2.5 in 1981 to 2.00 in 1989; rose again to 2.5 in 1990; and then slightly dropped to 2.39 in 1991.

In contrast, the productivity of the total manufacturing industry has exhibited little variation, ranging between 1.1 and 1.3.

The asset turnover ratio for the fish processing industry increased from 1.57 in 1981 to 2.11 in 1985; proceeded to decline, with a sharp drop in 1989 to 1.43, and then reaching 1.58 by 1991. Over the period, the productivity of the fish processing industry has been lower than that of the food manufacturing industry but higher than that of the total manufacturing sector. In 1985 and 1986, the productivity of the fish processing industry reached, but did not exceed, that of the food manufacturing sector.

Conclusion

In comparison to the food and total manufacturing sectors, the profitability of the fish processing sector has performed poorly with the exception of 1986 and 1987. While the productivity of the fish processing sector has outperformed the total manufacturing sector, it has never reached the productivity levels of the food manufacturing industry.

Overcapacity In Fish Processing

This topic is perhaps the most discussed issue in the industry today. It is also likely one of the most misunderstood.

26-A

ASSET TURNOVER RATIO (Sales/Assets)

2 . 6 r--~~~~~~~~~~~~~~~~~~

2.5 2.4 2.3 2.2 2.1

2 1.9 1.8 1.7 1.6 1.5 1.4 1.3 1.2 1.1 1'--~~~~~~~~~~~~~~~~~__,

19811982198319841985198619871988198919901991 D FOOD MFG

+ TOTAL MFG ° FISH PROC

By most definitions, overcapacity is a measure of non-producing investment. That is, it represents an attempt to quantify that level of investment which is in excess of that required to handle normal production levels.

The problem in quantifying the level of overcapacity in the industry lies with the notion of capacity itself. Capacity is not a fixed quantum. It is a function of all of the resources available to the industry at any given time, in terms of plant and equipment, capital, and human effort. While plant and equipment are relatively fixed at any given point, capital and human effort can be volatile.

For example, capacity is generally measured in terms of maximum throughput within a time period, eg. number of tonnes processed in month. When capacity is measured in this manner, it is generally deterrnined by individual constraints in the processing cycle, such as such as freezing capacity, or filleting capacity. We may, for instance, be able to fillet 100 tonnes per 40 hour work week, but if we can only freeze 80 tonnes, then our capacity to produce frozen fillets is limited to 80 tonnes.

The difficulty in this approach to capacity measurement is twofold:

1. Certain constraints can be expanded, thereby expanding capacity. If we increase the number of shifts worked from one to two, thereby increasing the work week to 80 hours, we potentially double capacity.

2. Production mix is not fixed. In the above example, we are lirnited to 80 tonnes of frozen fillets in a week, but we can fillet 100 tonnes. If we change our production mix to include fresh fillets, we have effectively increased capacity by 25%.

Because of these factors, approaches that deal with fixed measures of capacity are generally inadequate, and become more inadequale as time passes and variables change.

Accordingly, other approaches have been developed. One of these is used by Statistics Canada. It attempts to measure capacity utilization by equating the value of production with the value of the assets employed. In this approach, the notion of "full capacity utilization" becomes irrelevant, to be replaced by a concept that rnight be called "best capacity utilization".

A derivative of this approach has been utilized he:re. This approach renders moot the notion of overcapacity measured in percentage terms and replaces it with a quantification of the value of non-producing assets.

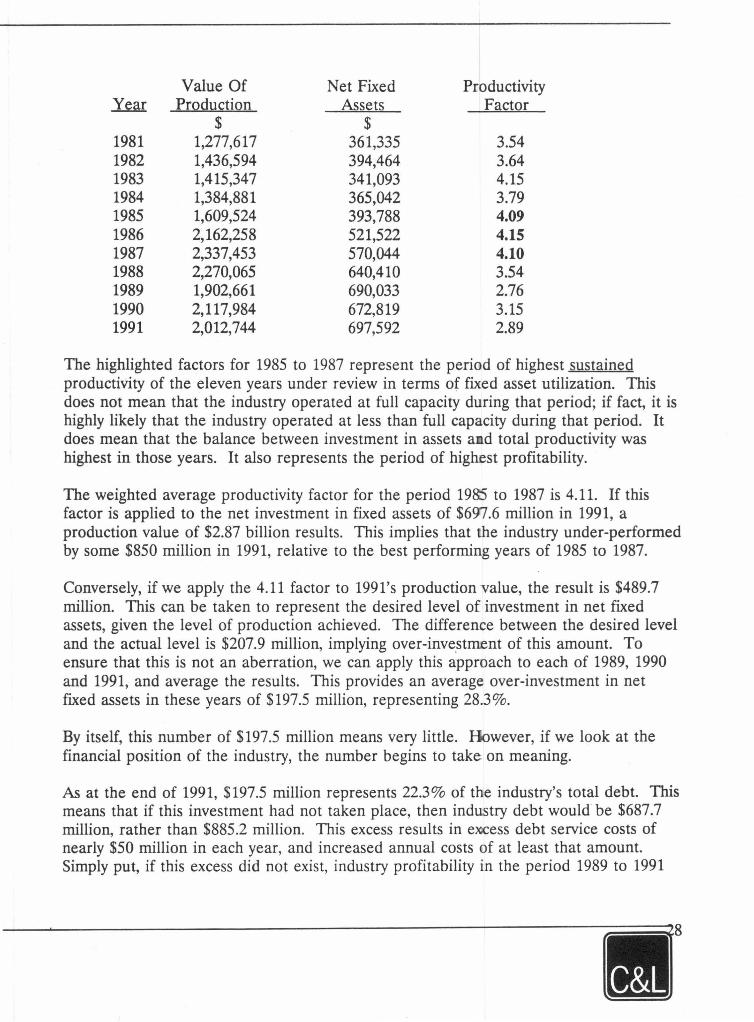

A summary of the relationship between assets and production follows ($000 ornitted):

Value Of Net Fixed Productivity Year Production Assets Factor

$ $ 1981 1,277,617 361,335 3.54 1982 1,436,594 394,464 3.64 1983 1,415,347 341,093 4.15 1984 1,384,881 365,042 3.79 1985 1,609,524 393,788 4.09 1986 2,162,258 521,522 4.15 1987 2,337,453 570,044 4.10 1988 2,270,065 640,410 3.54 1989 1,902,661 690,033 2.76 1990 2,117,984 672,819 3.15 1991 2,012,744 697,592 2.89

The highlighted factors for 1985 to 1987 represent the period of highest sustained productivity of the eleven years under review in terms of fixed asset utilization. This does not mean that the industry operated at full capacity during that period; if fact, it is highly likely that the industry operated at less than full capacity during that period. It does mean that the balance between investment in assets a d total productivity was highest in those years. It also represents the period of highest profitability.

The weighted average productivity factor for the period 1985 to 1987 is 4.11. If this factor is applied to the net investment in fixed assets of $697.6 million in 1991, a production value of $2.87 billion results. This implies that the industry under-performed by some $850 million in 1991, relative to the best performing years of 1985 to 1987.

Conversely, if we apply the 4.11 factor to 1991's production value, the result is $489.7 million. This can be taken to represent the desired level of investment in net fixed assets, given the level of production achieved. The difference between the desired level and the actual level is $207.9 million, implying over-inve.stment of this amount. To ensure that this is not an aberration, we can apply this approach to each of 1989, 1990 and 1991, and average the results. This provides an average over-investment in net fixed assets in these years of $197 .5 million, representing 28.3 %.

By itself, this number of $197.5 million means very little. However, if we look at the financial position of the industry, the number begins to take on meaning.

As at the end of 1991, $197.5 million represents 22.3% of the industry's total debt. This means that if this investment had not taken place, then industry debt would be $687.7 million, rather than $885.2 million. This excess results in exicess debt service costs of nearly $50 million in each year, and increased annual costs of at least that amount. Simply put, if this excess did not exist, industry profitability in the period 1989 to 1991

would have exceeded $70 million, as opposed to the aggregate operating loss of $28 million actually experienced for the three year peiiod.

In other terrns, this excess investment has seriously undermined the industry's ability to respond to the current crisis from a position of strength. This excess of $197.5 million represents 47% of the industry's total equity as at the end of 1991. This is effectively non-perforrning equity and this fact significantly changes the appearance of the industry's financial position.

The industry financial position at the end of 1991 is as follows (millions of dollars):

Total assets Total debt Total equity

$1,305.1 885.2 419.9

This position produces a debt/ equity ratio of 2.1: 1, which is generally acceptable as discussed earlier.

If we adjust this position for excess investment of $197.5 million, the following picture results:

Total assets Total debt Total equity

$1,107.6 885.2 222.4

We have adjusted equity rather than debt because we cannot simply make the debt go away - lenders expect to have their loans repaid and generally have the ability to force repayrnent. Under normal circumstances, we should be able to liquidate assets to pay down debt. But current industry circumstances have effectively eliminated any market for fish processing assets, making this strategy difficult if not impossible.

This adjusted picture produces a debt/ equity ratio of nearly 4: 1, which is well outside acceptable levels. A small company can likely survive with such a financial position, but an entire industry consisting of large, medium and small enterprises will have difficulty.

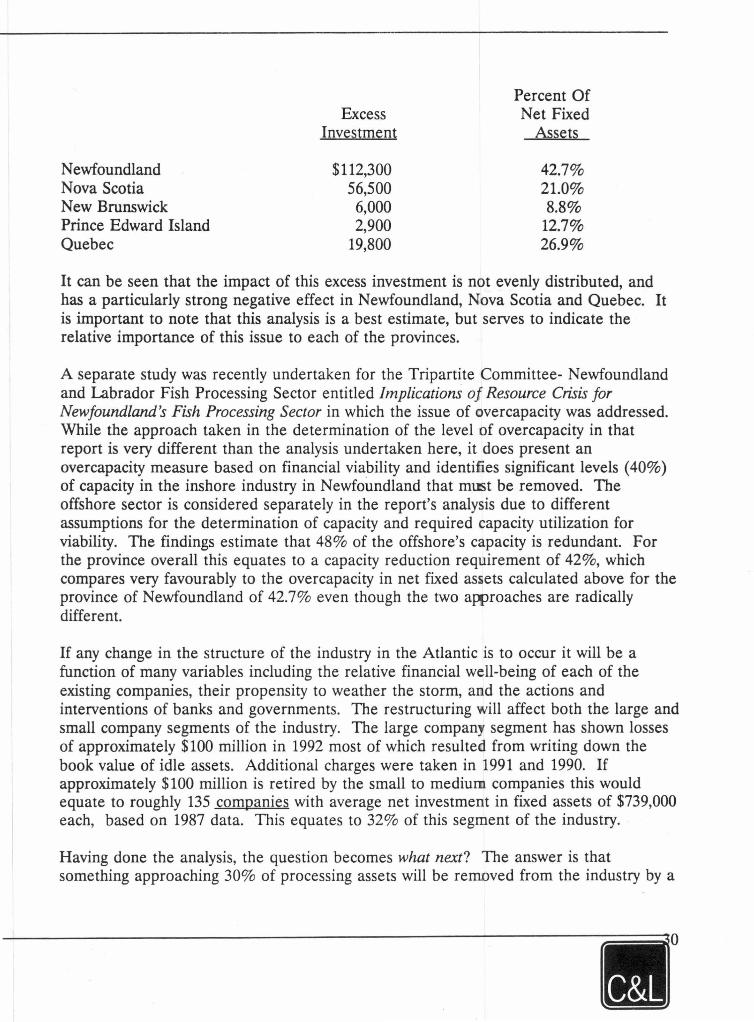

It is very difficult to accurately allocate this excess investment by province because the effects of interprovincial operations and ownership are very difficult to account for. However, using the same technique as applied to the Atlantic overall, best efforts produce the following estimated results ($000 omitted):

-. ~

N ewfoundland Nova Scotia New Brunswick Prince Edward Island Que bec

Excess Investment

$112,300 56,500

6,000 2,900

19,800

Percent Of Net Fixed

As sets

42.7% 21.0% 8.8%

12.7% 26.9%

It can be seen that the impact of this excess investment is not evenly distributed, and has a particularly strong negative effect in Newfoundland, Nova Scotia and Quebec. It is important to note that this analysis is a best estimate, but serves to indicate the relative importance of this issue to each of the provinces.

A separate study was recently undertaken for the Tripartite Committee- Newfoundland and Labrador Fish Processing Sector entitled Jmplication.5 of Resource Crisis for Newfoundland's Fish Processing Sector in which the issue of overcapacity was addressed. While the approach taken in the determination of the level of overcapacity in that report is very different than the analysis undertaken here, it does present an overcapacity measure based on financial viability and identifies significant levels ( 40%) of capacity in the inshore industry in Newfoundland that mŒt be removed. The offshore sector is considered separately in the report's analysis due to different assumptions for the determination of capacity and required capacity utilization for viability. The findings estimate that 48% of the offshore's capacity is redundant. For the province overall this equates to a capacity reduction requirement of 42%, which compares very favourably to the overcapacity in net fixed assets calculated above for the province of Newfoundland of 42.7% even though the two awroaches are radically different.

If any change in the structure of the industry in the Atlantic is to occur it will be a function of many variables including the relative financial well-being of each of the existing companies, their propensity to weather the storm, and the actions and interventions of banks and governments. The restructuring will affect both the large and small company segments of the industry. The large company segment has shown losses of approximately $100 million in 1992 most of which resulted from writing down the book value of idle assets. Additional charges were taken in 1991 and 1990. If approximately $100 million is retired by the small to medium companies this would equate to roughly 135 companies with average net investrnent in fixed assets of $739,000 each, based on 1987 data. This equates to 32% of this segment of the industry.

Having done the analysis, the question becornes what next? The answer is that something approaching 30% of processing assets wi-11 be removed from the industry by a

~·

process akin to financial attrition, unless additional equity is produced, or production volumes increase significantly - bath unlikely scenarios.

Attrition will be effected by lenders foreclosing when and if possible, by the weak selling to the strong where assets are desirable, and by the simple closure of assets which do not warrant foreclosure or merit sale. If any value is to be derived from this process, selective attrition would be desired. This would have the best assets kept in the industry, transferred from weak to strong, and deteriorating assets removed.

Summary Conclusions

Giving consideration to all of the foregoing, the following may be said about the performance of the fish processing industry in Atlantic Canada:

• The industry has not been able to achieve acceptable levels of profitability on a consistent basis. Other than 1986 and 1987, performance has been less than marginal. This is so when industry returns are examined in isolation. It is even more evident when fish processing industry returns are compared with food and other manufacturing, where returns have been higher and more consistent during the period under review. But for 1986 and 1987, combined with the government intervention of the early 1980s, the industry would not be able to sustain itself by relying on its own returns.