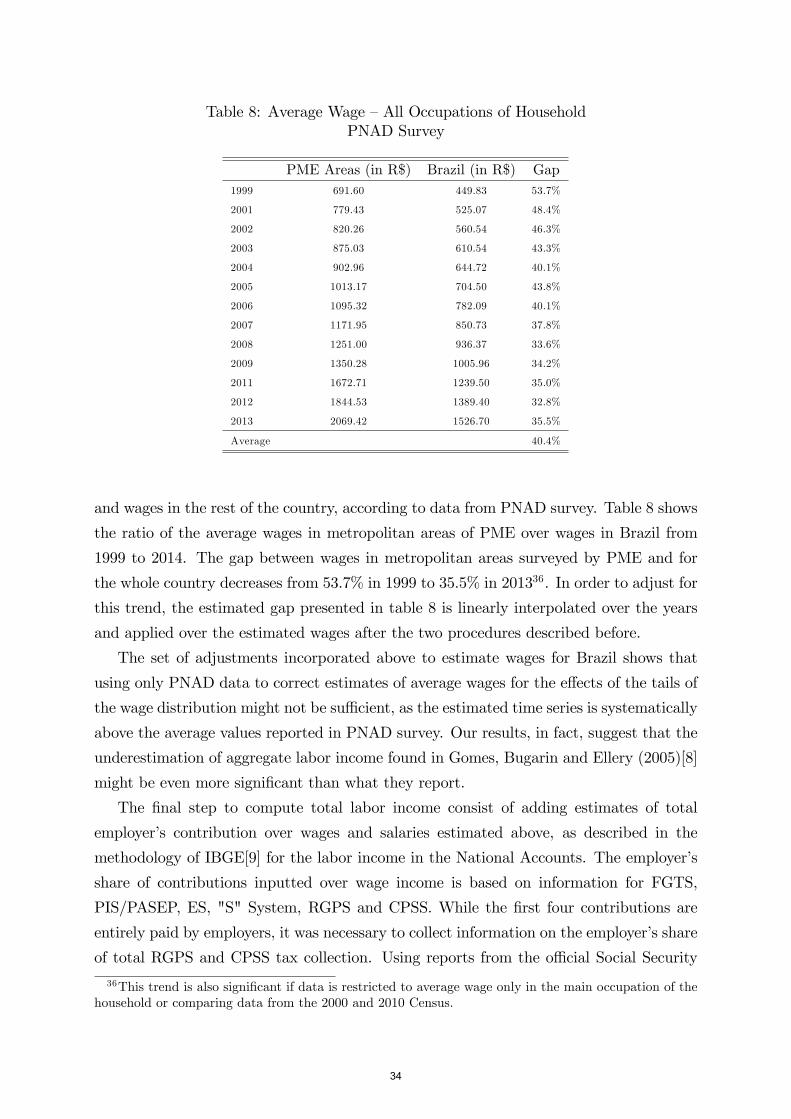

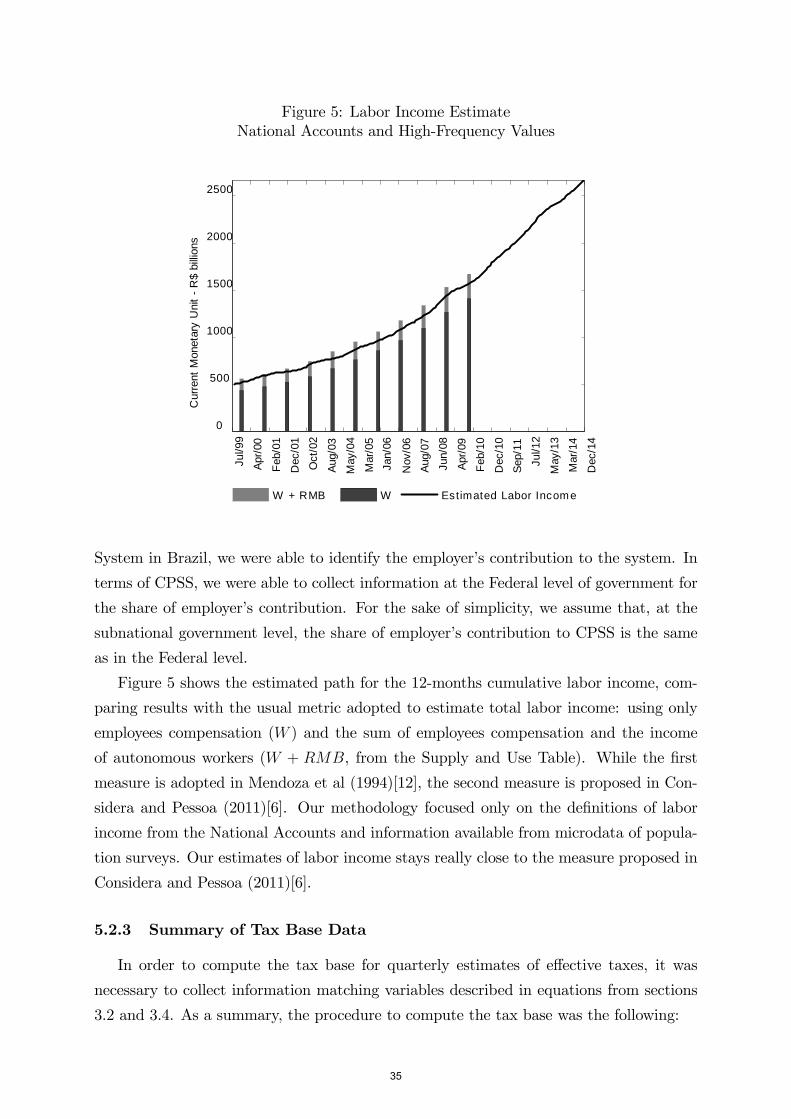

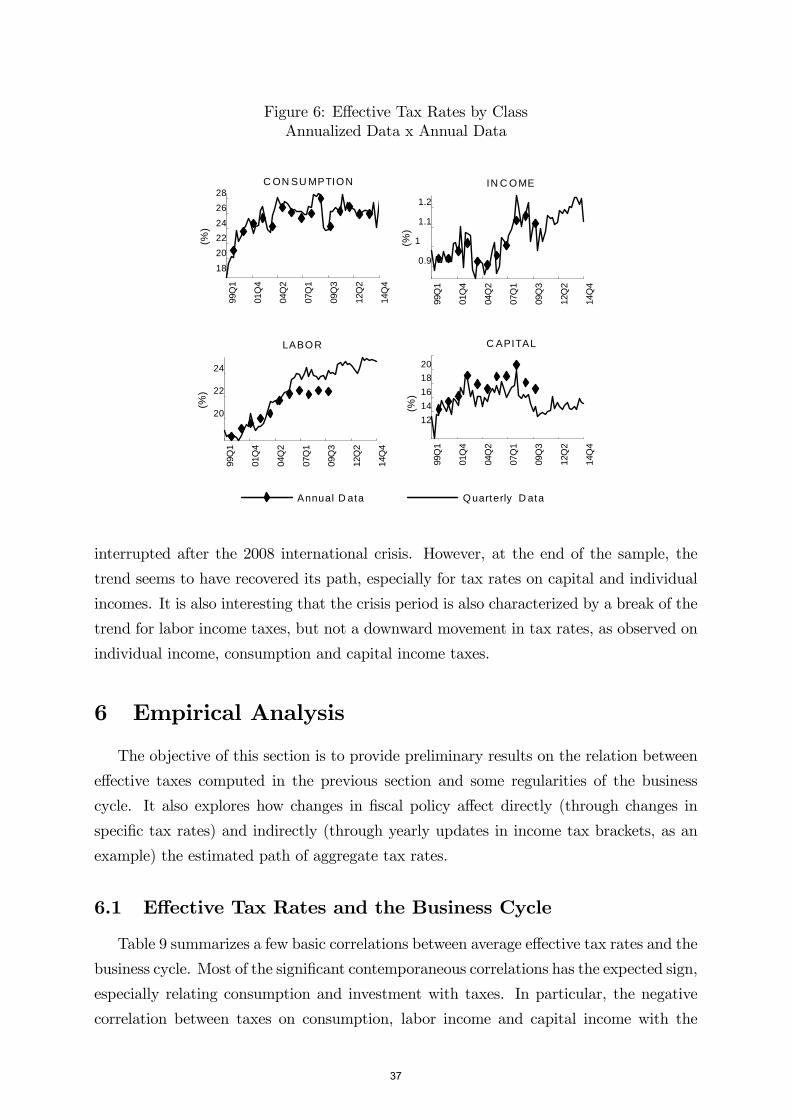

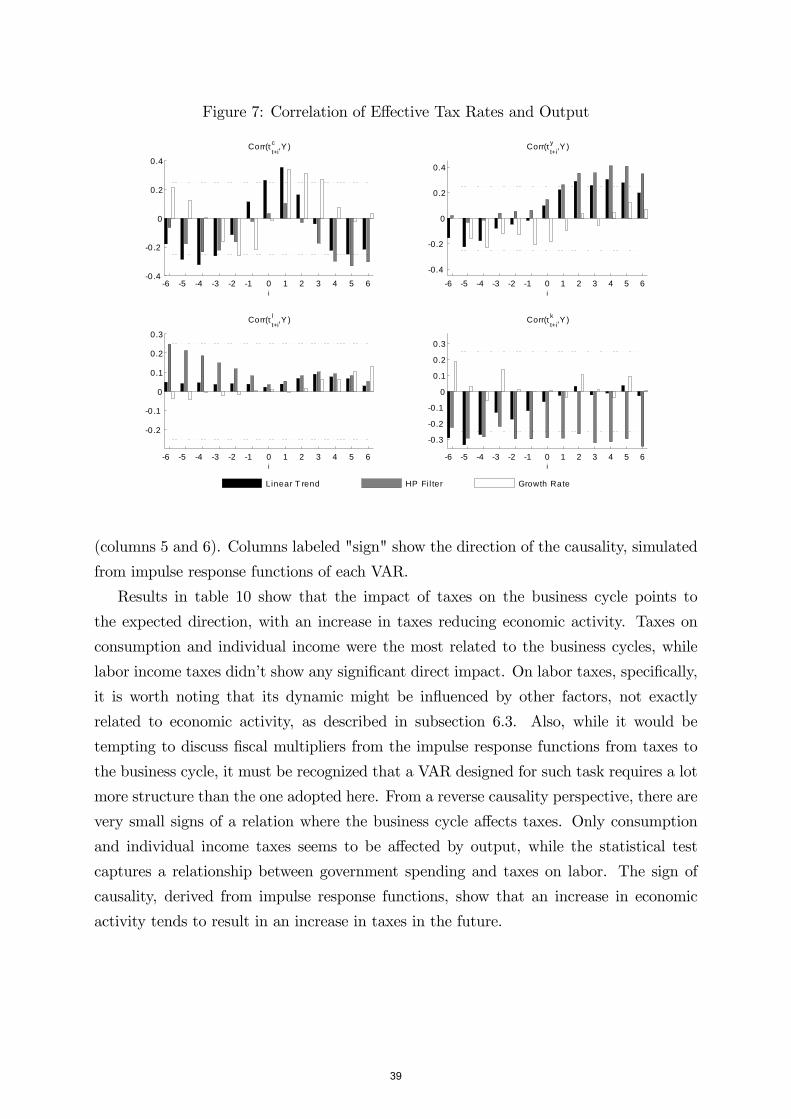

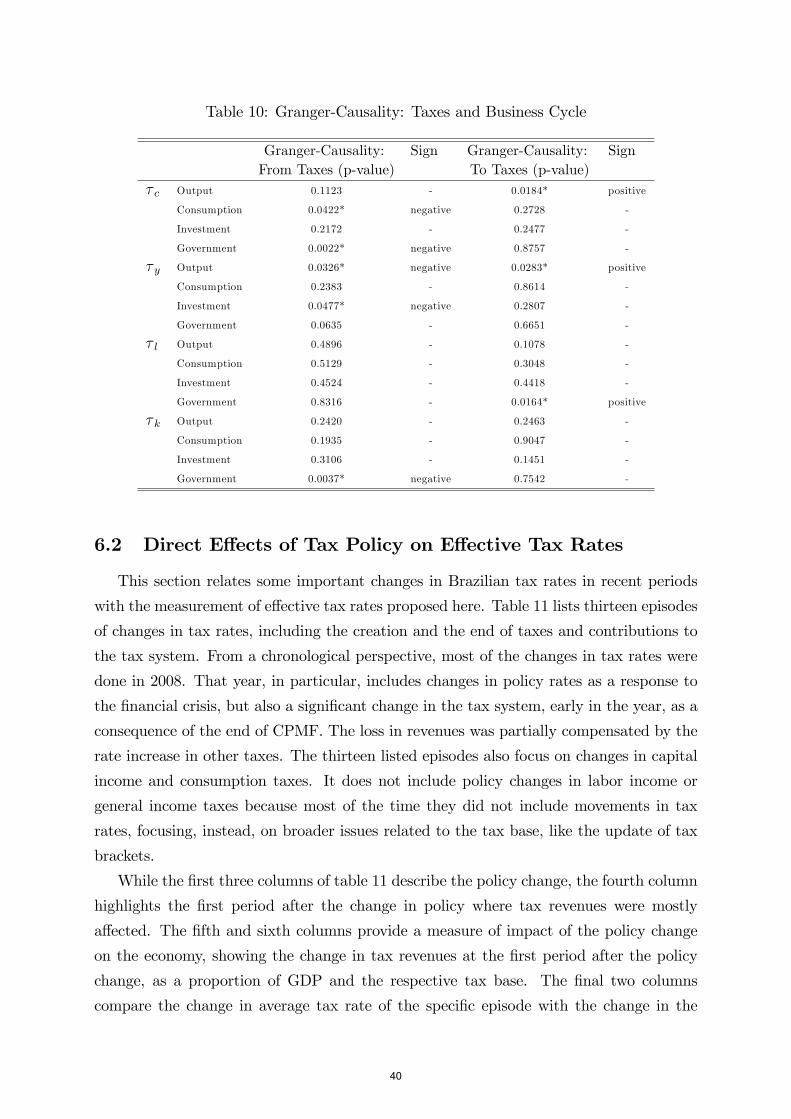

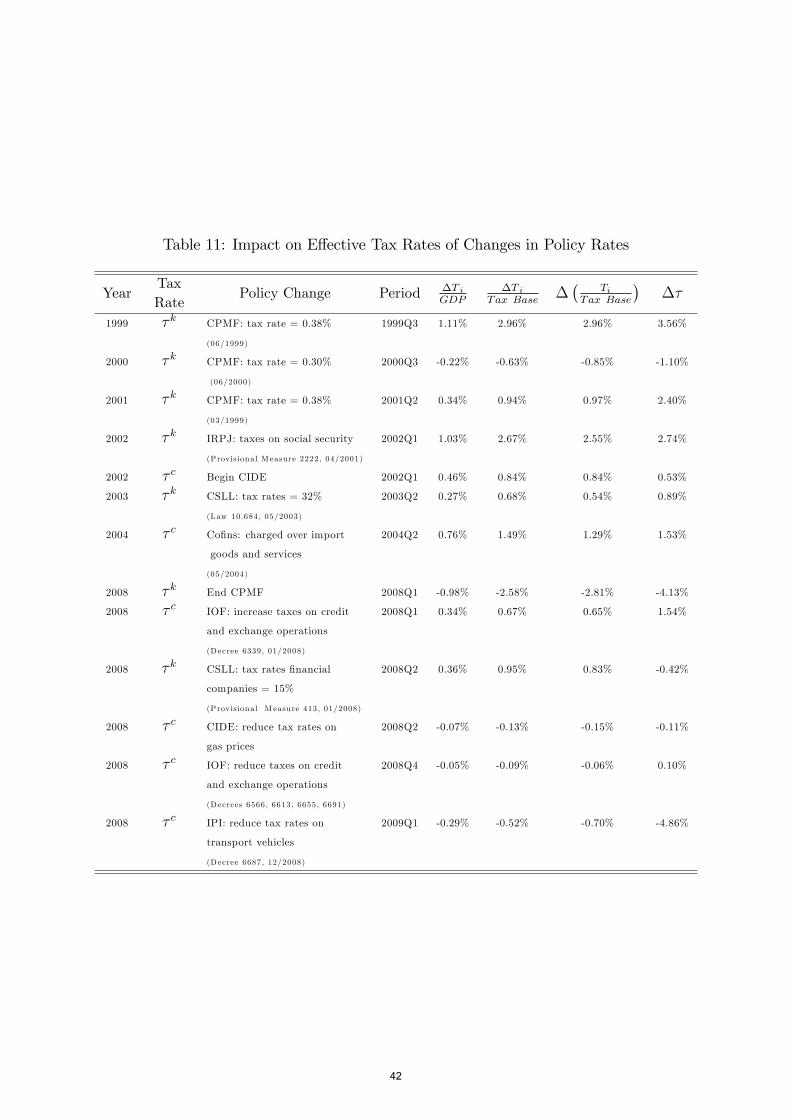

Effective Tax Rates on Consumption and Factor Incomes

57

Effective Tax Rates on Consumption and Factor Incomes: a quarterly frequency estimation for Brazil Cyntia Freitas Azevedo and Angelo Marsiglia Fasolo September, 2015 398

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Effective Tax Rates on Consumption and Factor Incomes

Effective Tax Rates on Consumption and Factor Incomes: a quarterly frequency estimation for Brazil

Cyntia Freitas Azevedo and Angelo Marsiglia Fasolo

September, 2015

398

ISSN 1518-3548 CGC 00.038.166/0001-05

Working Paper Series Brasília n. 398 September 2015 p. 1-56

Working Paper Series

Edited by Research Department (Depep) – E-mail: [email protected]

Editor: Francisco Marcos Rodrigues Figueiredo – E-mail: [email protected]

Editorial Assistant: Jane Sofia Moita – E-mail: [email protected]

Head of Research Department: Eduardo José Araújo Lima – E-mail: [email protected]

The Banco Central do Brasil Working Papers are all evaluated in double blind referee process.

Reproduction is permitted only if source is stated as follows: Working Paper n. 398.

Authorized by Luiz Awazu Pereira da Silva, Deputy Governor for Economic Policy.

General Control of Publications

Banco Central do Brasil

Comun/Dipiv/Coivi

SBS – Quadra 3 – Bloco B – Edifício-Sede – 14º andar

Caixa Postal 8.670

70074-900 Brasília – DF – Brazil

Phones: +55 (61) 3414-3710 and 3414-3565

Fax: +55 (61) 3414-1898

E-mail: [email protected]

The views expressed in this work are those of the authors and do not necessarily reflect those of the Banco Central or

its members.

Although these Working Papers often represent preliminary work, citation of source is required when used or reproduced.

As opiniões expressas neste trabalho são exclusivamente do(s) autor(es) e não refletem, necessariamente, a visão do Banco

Central do Brasil.

Ainda que este artigo represente trabalho preliminar, é requerida a citação da fonte, mesmo quando reproduzido parcialmente.

Citizen Service Division

Banco Central do Brasil

Deati/Diate

SBS – Quadra 3 – Bloco B – Edifício-Sede – 2º subsolo

70074-900 Brasília – DF – Brazil

Toll Free: 0800 9792345

Fax: +55 (61) 3414-2553

Internet: <http//www.bcb.gov.br/?CONTACTUS>

Effective Tax Rates on Consumption andFactor Incomes: a quarterly frequency

estimation for Brazil∗

Cyntia Freitas Azevedo†

Angelo Marsiglia Fasolo‡

Abstract

The Working Papers should not be reported as representing the views of the

Banco Central do Brasil. The views expressed in the papers are those of the

author(s) and do not necessarily reflect those of the Banco Central do Brasil.

This paper estimates time series of effective tax rates for consumption and factor

incomes for Brazil, following the spirit of Mendoza et al (1994)[12]. The procedure

to generate quarterly estimates of the tax base, using microdata from populational

surveys, and the tax revenues seems to be appropriate, despite its simplicity, as

the time series of the tax burden and the effective tax rates are in line with the

historical Brazilian experience on fiscal policy. The estimated tax burden identifies

a positive trend over time, despite the partial interruption after the international

crisis in 2008. The paper also provides preliminary evidence on the properties of

the computed effective tax rates and their relation with the business cycles.

Keywords: Fiscal policy; Effective tax rates; Consumption tax; Factor income

taxes

JEL Classification: E62, F41

∗We would like to thank Luis Gonzaga de Queiroz Filho, André Minella and Jeferson Luis Bittencourt

on preliminary discussions and valuable information on data sources. We also thank Pierpaolo Benigno

and members of the Research Department of the Central Bank of Brazil that contributed with helpful

comments on the first draft of this paper. We also thank the DataZoom’s website portal team, of the

Economics Department of PUC-RJ, for the codes to access microdata from IBGE. We are also indebted

to Jose Deodoro de Oliveira Filho for his help with the system to read and convert PDF files to build our

dataset. All these people provided significant support while writing this paper, but the remaining errors

are our own fault.†Research Department, Banco Central do Brasil and PUC-Rio, e-mail: [email protected]‡Research Department, Banco Central do Brasil, e-mail: [email protected]

3

1 Introduction

The main purpose of this study is to construct quarterly time series of the effective tax

rates on consumption, labor and capital for Brazil. An appropriate measure of tax rates is

central for the construction of macroeconomic models that aim at evaluating the impacts

of fiscal policy. As pointed by Mendoza et al (1994)[12], "these tax rates are necessary both

to develop quantitative applications of the theory and to help transform the theory into

a policy-making tool". However, calculating these rates, specially at a higher frequency,

has proven to be a very challenging task. In Emerging Economies, where the quality and

availability of information on tax collection and its tax base are usually questionable, the

number of strong assumptions necessary to make inference about tax rates might prove

the exercise useless.

In Brazil, particularly, there are two types of problems associated with the computation

of average effective tax rates and its use as a policy-making tool. The first problem,

associated with the computation of the tax base, is a result of the lack of timely updates in

National Accounts necessary to keep the estimates of tax rates useful for policy exercises.

The National Accounts in Brazil provide estimates of labor and capital income at annual

frequency only and with very long delays. As of today, the last information available

from the Brazilian Institute of Geography and Statistics (IBGE, in Portuguese) finishes

in 2009. Thus, the construction of estimates of the effective tax rates at a frequency

higher than annual demands additional hypotheses to replace the available information

on capital and labor returns based on the National Accounts.

The second type of problem is related to information on fiscal policy in Brazil —

more specifically, on information from subnational entities of the Federation. Data on

revenues and expenses of the Federal Government are available at monthly frequency

with very little delay. For municipalities, however, detailed information from offi cial

authorities is available at annual frequency only, mostly from a recent comprehensive

dataset published by the National Treasury Secretariat ("Secretaria do Tesouro Nacional",

in Portuguese) called FINBRA. Also, in terms of tax collection, an annual study published

by the Secretariat of the Federal Revenue ("Secretaria da Receita Federal", in Portuguese)

estimates the total tax burden over the Brazilian economy for the previous fiscal year.

Building a real time estimate of effective tax rates in Brazil demands accessing information

on tax revenues and contributions to civil servants’social security system from sources

other than offi cial National authorities responsible for conducting fiscal policy in the

country.

This paper proposes solutions for these problems, trying to overcome the issues pre-

sented above using alternative sources of information and providing a detailed method-

ology to compute effective taxes in Brazil. In order to solve problems associated with

4

information from subnational entities, we built a system capable of downloading, read-

ing and compiling information from reports that each subnational government is required

to submit bimonthly to a public access database run by a federal public bank (Caixa

Econômica Federal) together with the National Treasury Secretariat1. Each report is

submitted in a standard form, converted to PDF format when made available for public

consultation. Thus, the computational system must be capable of: 1) downloading, for

each unit of subnational government, the bimonthly reports in PDF format; 2) converting

reports to a format in which other software is able to read the information; 3) compiling,

with the support of other computational tools, a single, aggregate dataset of each variable

for the use in our exercises. The idea of using such system to calculate tax revenues from

states and municipalities is not new: Orair et al (2013)[15], in a parallel effort from the

development of this paper, built a similar system to obtain monthly estimates of the total

tax burden applied over the Brazilian economy. In this paper, we take a step further,

collecting also information on government spending and civil servants’contributions to

their social security system from the same set of reports. We also take a simpler approach

in order to estimate gaps in the information from municipalities, combining data from

FINBRA to fill the missing gaps.

To construct a quarterly series on labor and capital income, instead of relying on in-

formation from the National Accounts, we use microdata from three population surveys

available at different frequencies. These surveys provide information on employment and

average wages, from which we compute the aggregate labor compensation in the econ-

omy. The use of data from three different surveys required a detailed evaluation of the

labor income distribution profile over time. This information is taken into account when

building the time series of total labor income for the Brazilian economy.

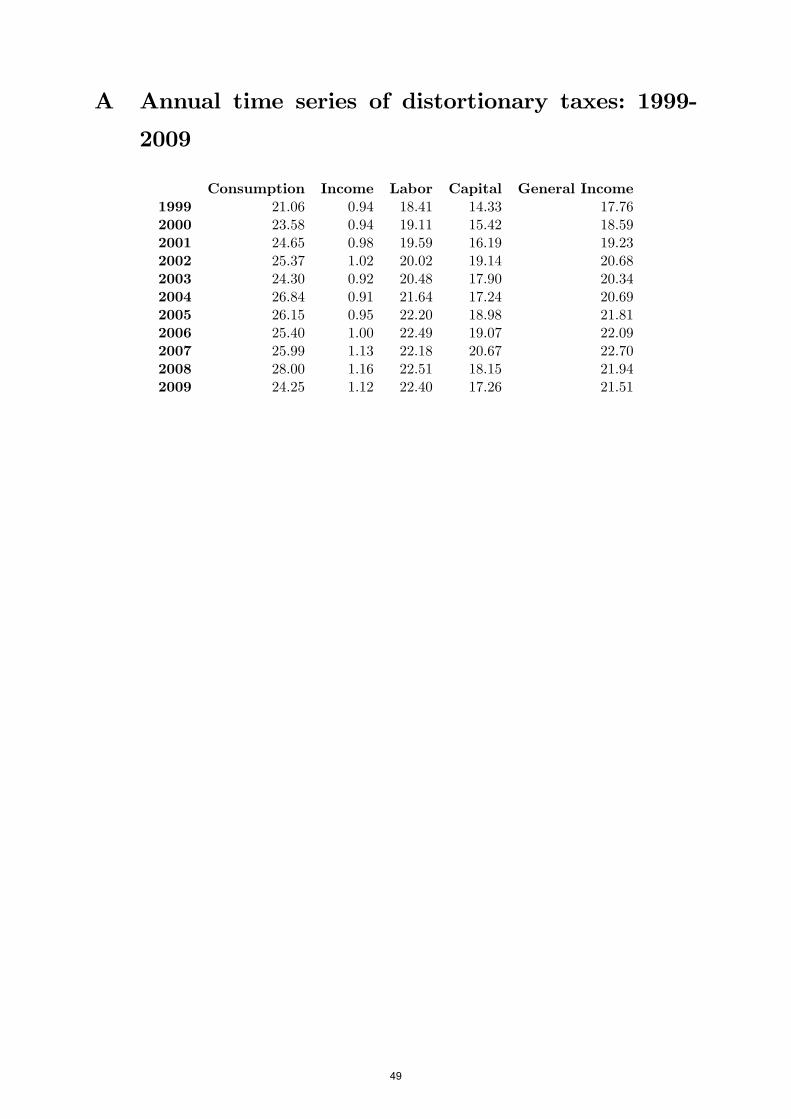

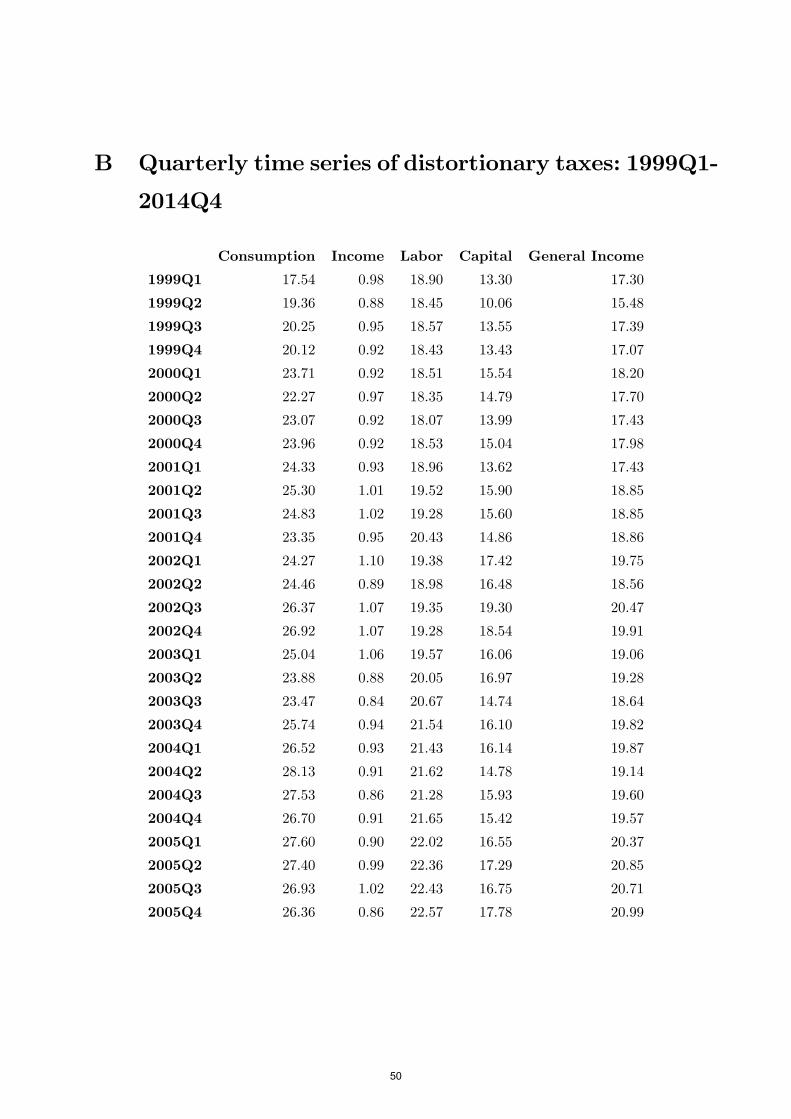

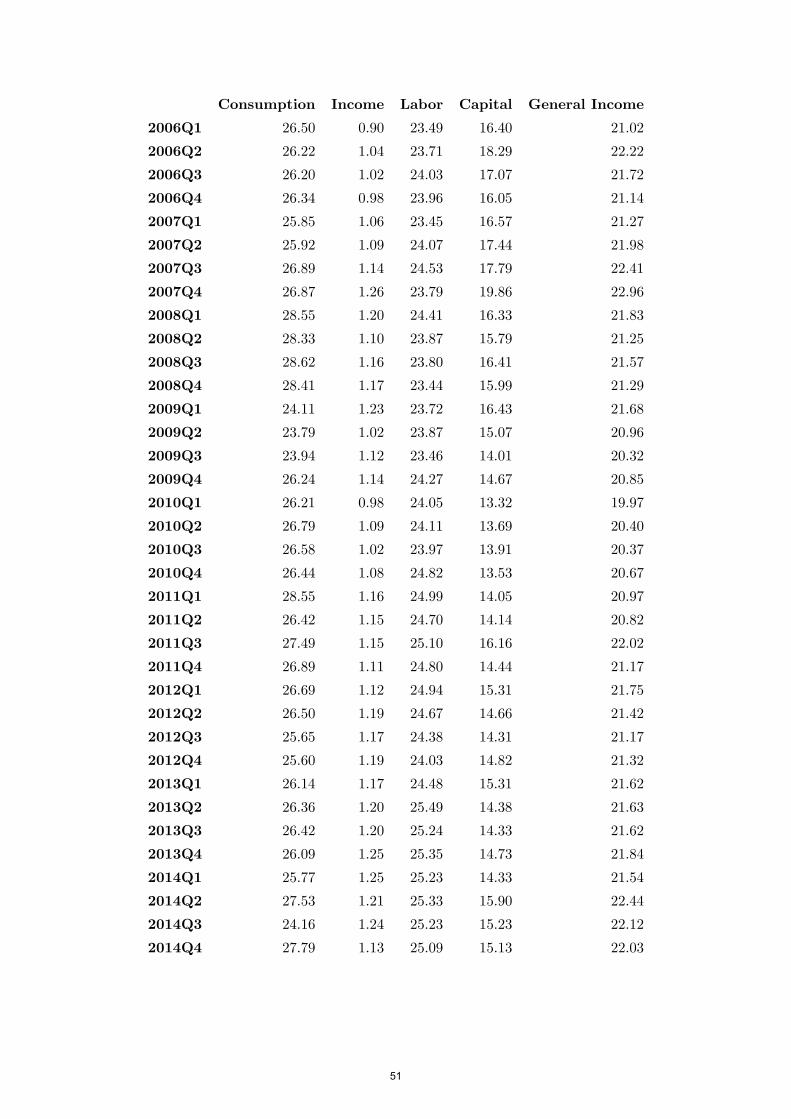

In this paper, we provide annual values of effective taxes for Brazil, from 1999 until

2009, based on information from the National Treasury Secretariat, Secretariat of the

Federal Revenue and the National Accounts. We also detail the methodology employed

to build a quarterly dataset using the reports provided by subnational governments and

population surveys. Under an additional set of assumptions, given the available amount

of information collected, we were able to construct a quarterly dataset on tax revenues

and the tax base from 1999 to 2014. The comparison of annual rates with the 4-quarter

cumulative rates computed using the high-frequency dataset shows some discrepancies,

most likely due to the quality of data provided by subnational governments. Gaps between

annual data and the high-frequency dataset mostly affects the composition between capital

1Starting in 2015, the National Treasury Secretariat introduced a new system for collecting andorganizing information on the public accounts. The new system (Siconfi) summarizes data on re-gional governments collected from both SISTN and annual data from FINBRA. It is available inhttps://siconfi.tesouro.gov.br/siconfi/index.jsf

5

and labor taxes, despite preserving the dynamics over time of both effective tax rates.

Given the final dataset on average effective tax rates, we also provide an initial analysis

on the sources of fluctuations in those rates. Changes in average effective tax rates are

associated with both changes in tax policy and changes in the overall state of the economy.

The paper is organized as follows. The next section discusses the literature on comput-

ing effective tax rates, with special focus on previous efforts documented for the Brazilian

economy. Section 3 outlines the methodology of computing average effective tax rates

for Brazil, following closely the work of Mendoza et al (1994)[12] and Lledó (2005)[10],

while also presenting the additional hypotheses necessary to move from the annual to the

quarterly estimates. Sections 4 and 5 apply the described methodology to compute effec-

tive rates at annual and quarterly frequencies, respectively, presenting all the necessary

adjustments due to the data collected —especially in terms of high-frequency database

on tax and contributions revenues and on the tax base. An empirical analysis of the

quarterly time series of effective tax rates is presented in section 6. Section 7 concludes.

2 Related Literature

The main reference on the computation of effective tax rates is the work of Mendoza

et al (1994)[12]. Their approach allows to estimate the effective tax rates on consumption

and factor incomes consistent with the tax distortions faced by a representative agent in

a general equilibrium framework. One of the advantages of their method is that it does

not require a rigorous treatment of the tax legislation. It is a simple method that requires

only data from the National Accounts and tax revenues statistics, allowing cross-country

comparisons. They point out to three objectives achieved by their approach: (i) it takes

into account the net effect of existing rules regarding credits, exemptions and deductions;

(ii) it separates taxes on labor income from taxes on capital income; and, (iii) it incor-

porates the effects of taxes not filed with individual income tax revenues, such as social

security contributions and property taxes, on factor income taxation. Given the authors

objective, it is an appropriate methodology to compute average tax rates, capturing the

effects of changes in tax deductions, tax credits and a general characterization of feed-

back effects on taxes from economic agents. It does not, however, measure important

movements in taxes with significant macroeconomic impacts, like changes in marginal tax

rates, as highlighted in Carey and Rabesona (2002)[3]. Average effective tax rates might

also be sensitive to other issues, like tax planning and the international taxation of capital

flows.

The work of Mendoza et al (1994)[12] and Carey and Rabesona (2002)[3] is focused on

the use of data compiled by OECD, usually available for large time spans, with detailed

6

definitions and good quality control of information across countries, allowing reasonably

appropriate cross-country comparisons. As mentioned in the introduction, datasets from

Emerging Economies usually show problems that might compromise the estimates of such

tax rates2. For Brazil, specifically, there is a growing literature on the evaluation of the

impacts of fiscal policies and tax reforms. In general, these studies apply some measure of

average effective tax rates in order to calibrate models or to perform econometric analysis.

Due to the problems listed here and in the introduction —namely, the lack of accurate and

updated data on fiscal variables for long periods of time, at higher frequency and with

little delay; and the lack of details and information with regular updates from the National

Accounts with respect to the returns of labor and capital for the Brazilian economy —,

the few studies that computed effective tax rates for Brazil used annual data only.

One example of a study using estimates of effective tax rates for Brazil is provided

by Araújo and Ferreira (1999)[1], who evaluate the allocative effects and welfare impacts

of a tax reform. The authors use a neoclassical model calibrated with information of

tax rates based on total tax revenues of 1995. Cavalcanti and Silva (2010)[5] use an

overlapping generations (OLG) model to study the impact of tax reforms on GDP, capital

accumulation and welfare. Simulations estimated the effects of capital and labor tax

exemption measures, compensated by increases in income tax. They compute tax rates

based on data from the National Accounts for the year of 2004.

One of the first attempts to apply the methodology from Mendoza et al (1994)[12]

for Brazil was made by Araújo Neto and Sousa (2001)[2] to study the comovements

between macroeconomic aggregates and average effective tax rates. They make a good

correspondence between the standard OECD coding for tax revenues used by Mendoza et

al (1994)[12] and the different sources of tax revenues in Brazil. The authors were able to

compute annual average tax rates on consumption, labor and capital using data on tax

revenues and the National Accounts from 1975 to 1999. They faced, however, problems to

construct the dataset due to missing data, despite still being able to provide a relatively

long time series.

Lledó (2005)[10] constructs a dynamic general equilibriummodel to analyze the macro-

economic and redistributive effects of replacing turnover and financial taxes in Brazil by

a consumption tax. He uses an OLG model calibrated with data for 2002, computing

effective tax rates based on the framework of Mendoza et al (1994)[12], modified to in-

corporate details of the Brazilian economy and features of the OLG model. Ferreira and

Pereira (2010)[7] follow the procedure presented by Lledó (2005)[10] to calibrate a simple

RBC model to analyze the impact of a tax reform in the Brazilian economy. They assume,

2Volkerink, Sturm and de Haan (2002)[18] note that even the use of OECD data might be flawed.They compute the effective tax rates for a group of OECD countries using data from local, nationalsources and find significant discrepancies in results compared to Mendoza et al (1994)[12].

7

from the first order conditions of the model, that the tax base is proportional to changes

in aggregate output, as the labor and capital shares are determined by a single parameter

of the production function.

While the previous two papers calibrate models using information from a single year,

Pereira (2009)[16] computes effective tax rates on consumption, individual income, labor

income and capital income from 2001 to 2005. The author follows the methodology pre-

sented by Mendoza et al (1994)[12], adapted to specific features of the Brazilian economy,

in order to build the dataset used to calibrate a model to analyze the impact of fiscal

policies on business cycles.

Finally, other alternatives to compute effective tax rates are based on a combination

of input-output tables and microdata, using disaggregated information to analyze the

inequality of the tax burden over the economy. While not avoiding the hypothesis of

a full pass-through of taxes to consumers, studies based on disaggregated data provide

useful information on marginal tax rates. For Brazil, Siqueira et al (2001)[17] use infor-

mation from input-output tables of 1995 to compute effective tax rates on consumption

for Brazil, disaggregating information on economic sectors and tax incidence over demand

components for Brazil. More recently, Nogueira et al (2013)[13] use microdata from two

population surveys to simulate a model, trying to estimate the tax burden inequality over

labor income for the Brazilian economy in 2009. The model simulated in Nogueira et al

(2013)[13] receives as an input not only survey data, but also information from Brazilian

legislation on tax rates. The idea of using information from the legislation as an input

for modelling purposes was adopted in Carvalho and Valli (2011)[4] to calibrate a DSGE

model for the Brazilian economy.

Previously mentioned literature worked only with annual data on tax revenues and

the National Accounts. To the best of our knowledge, the first attempt to construct a

high-frequency database on tax revenues for Brazil was made by Orair et al (2013)[15].

The authors estimate the Brazilian tax burden at monthly frequency from 2002 until

2012. Their estimation of subnational government information on taxes is very precise,

mostly by their effort on building a complex state-space model to estimate high-frequency

time series based on low-frequency information available. The compilation of a dataset

of tax revenues of subnational entities is analogous to what is done in this paper, with

the development of a system capable of reading several reports from PDF files. As said

before, the main focus of Orair et al (2013)[15] is on the evolution of the tax burden; our

paper, on the other hand, combines information on tax revenues with a high-frequency

inference on the tax base to compute effective tax rates.

8

3 Computing Effective Tax Rates

This section details the methodology employed to compute the average effective tax

rates for Brazil, both at the annual and quarterly frequencies. We closely follow the

presentation in Lledó (2005)[10], who adapted the basic methodology of Mendoza et al

(1994)[12] to Brazil, to discuss the computation of effective rates for the country. The

section starts providing some context on the way effective tax rates are computed here,

with possible applications in a general equilibrium framework. It follows with details

on the definitions of tax rates on consumption, labor and capital income, followed by

a presentation on the adjustments performed when working with quarterly data, with

the necessary adaptations to the specificities of the Brazilian tax system. A complete

description of datasets, along with a discussion on the appropriate separation of taxes

under each class, are presented in the next section.

3.1 Effective Tax Rates in General Equilibrium

This subsection relates the average effective tax rates computed in this paper with

a very broad framework of dynamic general equilibrium models. The objective is to

provide context on the incidence of taxes in theoretical models, while also outlining a few

diffi culties when dealing with Brazilian data. Despite its relevance, the general equilibrium

framework presented here does not include any form of heterogeneity on households or

firms. A few topics related to agents’ heterogeneity, like the effects of labor income

distribution on effective tax rates on labor, are discussed on section 6.

A general description of the budget constraint of a representative household includes

the total spending on consumption goods (ct), investment on capital goods (it) and gov-

ernment debt holdings (bt), on the expenses side. On the revenues side, it includes interest

received on previously held government debt (rtbt−1), returns on production factors (wthtand rkt kt as the returns on labor supply and capital rental, respectively) and firms’profits

(φt) (all variables in nominal terms). Spending on consumption goods includes the ex-

penditure on taxes levied exclusively on those goods and paid by households, τ c,h. Gross

capital and labor incomes are net of taxes paid by households —τ l,h and τ k,h, respectively.

In order to account for taxes levied on general income, that cannot be split in terms of

capital and labor, the budget constraint also includes an additional tax rate (τ y), equally

charging the household’s returns on the production factors3.

(1 + τ c,h) ct + it + bt = rtbt−1 + (1− τ l,h − τ y)wtht + (1− τ k,h − τ y) rkt kt + Φt (1)

3If the model does not allow for taxes on aggregate income, one can use (τ l,h + τy) as the effectivetax rate on labor and (τk,h + τy) as the effective tax rate on capital levied on households.

9

On the firms’side, profits are generated by the revenue of selling output, minus pay-

ments to labor and capital used during the production process. Output (yt) is consumed

by households (ct), and the government (gt) or used as investment good (it). Similar to

the equation describing the households’budget constraint, there are taxes levied on the

output sold as a consumption good4, τ c,f , on total payroll, τ l,f , and rented capital, τ k,fthat are paid by the firm.

Φt = (1− τ c,f ) (ct + gt) + it − (1 + τ l,f )wtht − (1 + τ k,f ) rkt kt (2)

yt = ct + gt + it = wtht + rkt kt (3)

In the analytical example described above, revenues from the general income tax rate

are given by5:

Ty = τ y(wtht + rkt kt

)Similarly, tax revenues on consumption, labor and capital income are computed using

the total revenues collected from households and firms:

Tc = (τ c,h + τ c,f ) (ct + gt) Tl = (τ l,h + τ l,f )wtht Tk = (τ k,h + τ k,f ) rkt kt

Once information on tax revenues is available, effective tax rates on consumption (τ c),

income (τ y), labor income (τ l) and capital income (τ k) are computed using the definition

of their respective tax bases:

τ c =Tc

ct + gtτ y =

Tywtht + rkt kt

τ l =Tlwtht

τ k =Tkrkt kt

The equations above highlight two important features of computing average effective

tax rates. First, calculating aggregate tax rates does not depend if taxes are levied on

households or firms, since, in general equilibrium, taxes levied on firms are also affecting

households’decisions, either through the pricing and production decisions of the firms, or

through the profits transferred to families. Only two pieces of information are necessary

to calculate such tax rates —tax revenues and the tax base —and this information does

not depend on the agent of the economy charged with the tax.

Second, disaggregated measures of effective tax rates are conditioned on the informa-

tion set on tax revenues. For Brazil, as sections 4 and 5 show, information on labor income

taxes allows a reasonable approximation of effective rates levied on firms and households,

τ l,h and τ l,f . Unfortunately, the same disaggregation is not possible with respect to taxes

4In this example, without loss of generality, assume that goods demanded for investment are not taxedby the government.

5For the sake of notation, define Tx as the total revenue from taxes over aggregate x. Define also τxas the effective tax rate over aggregate x.

10

on consumption and capital income.

Ideally, if data on tax revenues and the tax base were readily available, it would be

simple to compute average effective rates for a simple economy like the one described

above. The main challenge here is to build both types of datasets, specially at higher

frequency, where detailed information is scarce. The adjustments applied to Brazilian

data in order to compute the effective tax rates both at annual and quarterly frequencies

are discussed in the rest of the section.

3.2 Effective Tax Rate on Consumption

The effective average tax rate on sales of consumption goods is given by:

τ c =Tc

C +G−GW − Tc(4)

where Tc represents the total revenue from taxes on consumption of goods and services

and excise taxes. C and G are the National Accounts data on private and government

consumption, respectively. GW is the compensation of government employees. In order

to obtain the pre-tax value of consumption, which is the definition of the tax base, rev-

enues on consumption tax are discounted in the denominator, since the Brazilian National

Accounts measure consumption expenditures at post-tax prices.

For the sake of comparison, Pereira (2009)[16] does not include government consump-

tion on the tax base. Here, as in Mendoza et al (1994)[12], government consumption is

included, net of the compensation of government employees (G−GW ), as the tax revenuesstatistics include taxes paid by the government in the purchase of goods and nonfactor

services.

3.3 Effective Tax Rates on General Income

The major problem associated with the definition of tax rates on labor and capital

income is the identification of the tax burden over household’s labor and capital income.

The problem, pointed out by Mendoza et al (1994)[12] and also observed in Brazilian data,

is that information sources usually do not provide a clear breakdown of the tax incidence

over individual income. In order to overcome this problem, Mendoza et al (1994)[12]

assume that all sources of household’s income from labor supply and capital rental are

taxed at the same rate when directly taxed.

In the framework of Mendoza et al (1994)[12], the tax rate over individual income is

computed as a first step to obtain tax rates over labor and capital incomes. In the second

step, an exogenous parameter defining a constant labor share of income is used to split tax

revenues and tax base for each production factor. Lledó (2005)[10] points out that this

11

imputation assumes a symmetric tax treatment between labor and capital income. As in

Lledó (2005)[10], equation 1 allows an effective tax rate on household’s general income to

coexist with separate taxes on capital and labor. The effective tax rate on total individual

income is then given by:

τ y =Ty

W +RMB + EOB(5)

where Ty is the total revenue collected by the individual income tax rate. The denom-

inator is defined as the net domestic income, which is the sum of wages and salaries (W ),

gross mixed income6 (RMB) and the gross operating surplus (EOB), obtained from the

National Accounts. The sum W + RMB + EOB corresponds to the income households

receive from labor supply and capital rental, wtht + rkt kt.

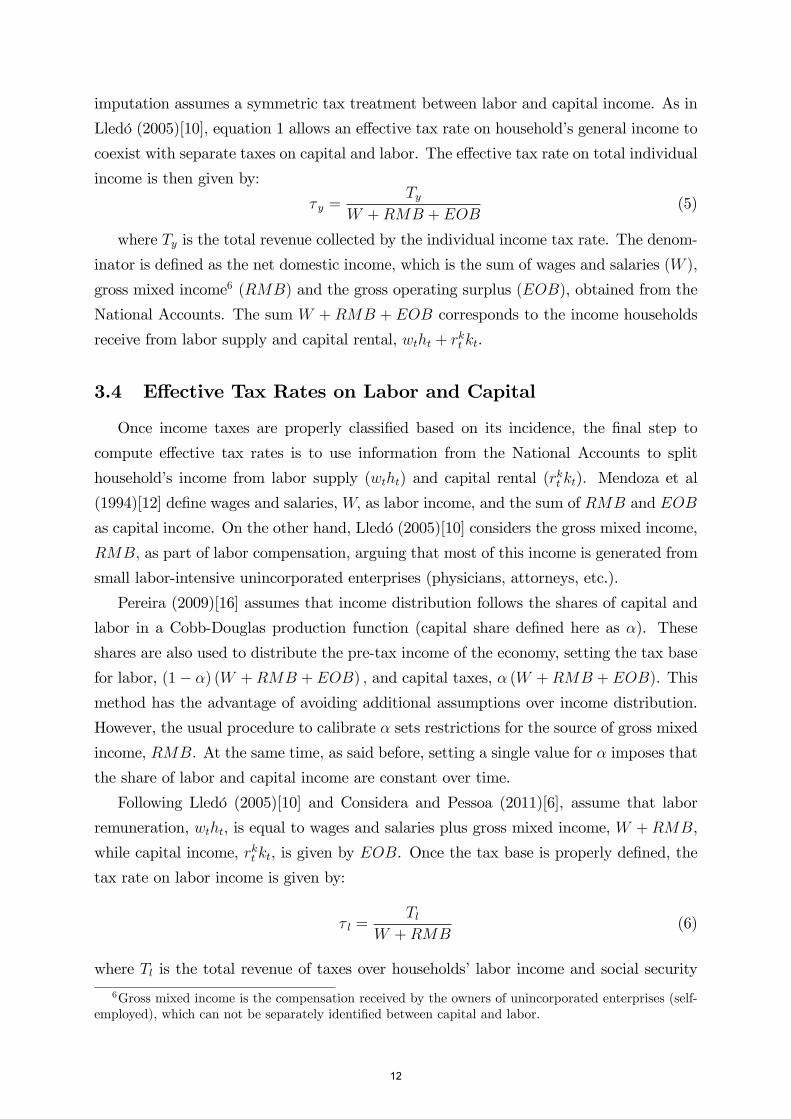

3.4 Effective Tax Rates on Labor and Capital

Once income taxes are properly classified based on its incidence, the final step to

compute effective tax rates is to use information from the National Accounts to split

household’s income from labor supply (wtht) and capital rental (rkt kt). Mendoza et al

(1994)[12] define wages and salaries, W, as labor income, and the sum of RMB and EOB

as capital income. On the other hand, Lledó (2005)[10] considers the gross mixed income,

RMB, as part of labor compensation, arguing that most of this income is generated from

small labor-intensive unincorporated enterprises (physicians, attorneys, etc.).

Pereira (2009)[16] assumes that income distribution follows the shares of capital and

labor in a Cobb-Douglas production function (capital share defined here as α). These

shares are also used to distribute the pre-tax income of the economy, setting the tax base

for labor, (1− α) (W +RMB + EOB) , and capital taxes, α (W +RMB + EOB). This

method has the advantage of avoiding additional assumptions over income distribution.

However, the usual procedure to calibrate α sets restrictions for the source of gross mixed

income, RMB. At the same time, as said before, setting a single value for α imposes that

the share of labor and capital income are constant over time.

Following Lledó (2005)[10] and Considera and Pessoa (2011)[6], assume that labor

remuneration, wtht, is equal to wages and salaries plus gross mixed income, W + RMB,

while capital income, rkt kt, is given by EOB. Once the tax base is properly defined, the

tax rate on labor income is given by:

τ l =Tl

W +RMB(6)

where Tl is the total revenue of taxes over households’labor income and social security

6Gross mixed income is the compensation received by the owners of unincorporated enterprises (self-employed), which can not be separately identified between capital and labor.

12

contributions. In an analogous way, the tax rate on capital income is given by:

τ k =Tk

EOB(7)

where Tk is the total revenue obtained by taxes over capital income, especially income

from corporations and taxes on property and financial transactions.

3.5 Effective Tax Rates at Quarterly Frequency

Computing effective tax rates at quarterly frequency is not straightforward from the

framework outlined above. While the high-frequency database on tax revenues con-

structed in section 5.1 contains the same information of the annual database (Tc, Ty, Tl and Tk),

additional steps are necessary to compute quarterly time series of the tax base used in

equations 5, 6 and 7. The tax rate on consumption, τ c, is still given by equation 4, as

every component of the tax base is also available at quarterly frequency.

In Brazil, the National Accounts provides data on total factor income only at annual

frequency. In order to overcome this problem, notice first that, using the Income Approach

of National Accounts, the gross domestic income of the economy (Y ), net of taxes paid

over production, is given by the total income received by residents from labor (wtht) and

capital (rkt kt):

Y −Net Taxes = wtht + rkt kt = W +RMB + EOB (8)

In order to build the denominator in equation 5, the left-hand side of equation 8 is

approximated by the difference between gross domestic product (GDP) and a set of taxes

classified in Orair at al (2013)[15] as part in the National Accounts of total taxes on

production7, available at quarterly frequency. In Pereira (2009)[16], this denominator is

defined as the difference between GDP and total taxes on consumption, Y − Tc. While asignificant share of the so-called "taxes on production" is classified as taxes on consump-

tion, the procedure in Pereira (2009)[16] ignores that some taxes over labor income are

also significant in the actual composition of "net taxes" in the National Accounts8. Under

this assumption, the quarterly effective tax rate on individual income is given by:

τ y =Ty

Y −Net Taxes (9)

7The lack of quarterly information in the National Accounts forces a decision to ignore the value ofthe subsidies to production. We recognize that this procedure might not be appropriate, as subsidiesrepresent, on average, 1.8% of GDP over the period analyzed.

8The actual composition of our approximation of "net taxes" and the differences in classification oftaxes with respect to other papers in the literature are presented in section 4.

13

The total pre-tax labor income, wtht, is defined in the National Accounts as the sum

of the gross wage income received by the labor force, WI, and the share of social security

contributions charged on firms’payroll, FC :

wtht ≡ WI + FC (10)

Section 5.2.2 describes the procedure based on population surveys used to construct

a quarterly time series for WI. It also shows the main sources of information to build

a dataset for FC, using only the contribution paid by employers to the social security

system. The quarterly effective labor income tax rate is, then, defined by:

τ l =Tl

WI + FC(11)

Capital income is calculated as a by-product of the estimate of pre-tax labor income,

according to equation 8:

rkt kt ≡ Y −Net Taxes−WI − FC (12)

implying the effective tax rate over capital income at quarterly frequency to be given by:

τ k =Tk

Y −Net Taxes−WI − FC (13)

4 Tax Rates at Annual Frequency

This section computes effective tax rates at annual frequency using a dataset on tax

revenues available from reports of the Secretariat of the Federal Revenue measuring the

total tax burden over the Brazilian economy9. Data on tax revenues are presented only

at annual frequency and cover the period between 1999 to 2013. Taxes and contributions

used to build the dataset in this section are exactly those with information available at

higher frequency. Under the criterion of using the same set of taxes and contributions

at both frequencies, the final dataset covers, on average, 96.83% of total tax revenues

for the period. Compared to the dataset at quarterly frequency, the major difference is

related to the concept of tax revenues: monthly time series of tax revenues, used to build

the quarterly dataset, show the gross tax revenues; on the other hand, annual reports of

the Secretariat of the Federal Revenue show net tax revenues, defined as gross revenues

minus refunds. The effects of using gross or net tax revenues are discussed in subsection

9Reports in Portuguese named "Carga Tributária no Brasil" available at:http://www.receita.fazenda.gov.br/historico/esttributarios/Estatisticas/default.htm

14

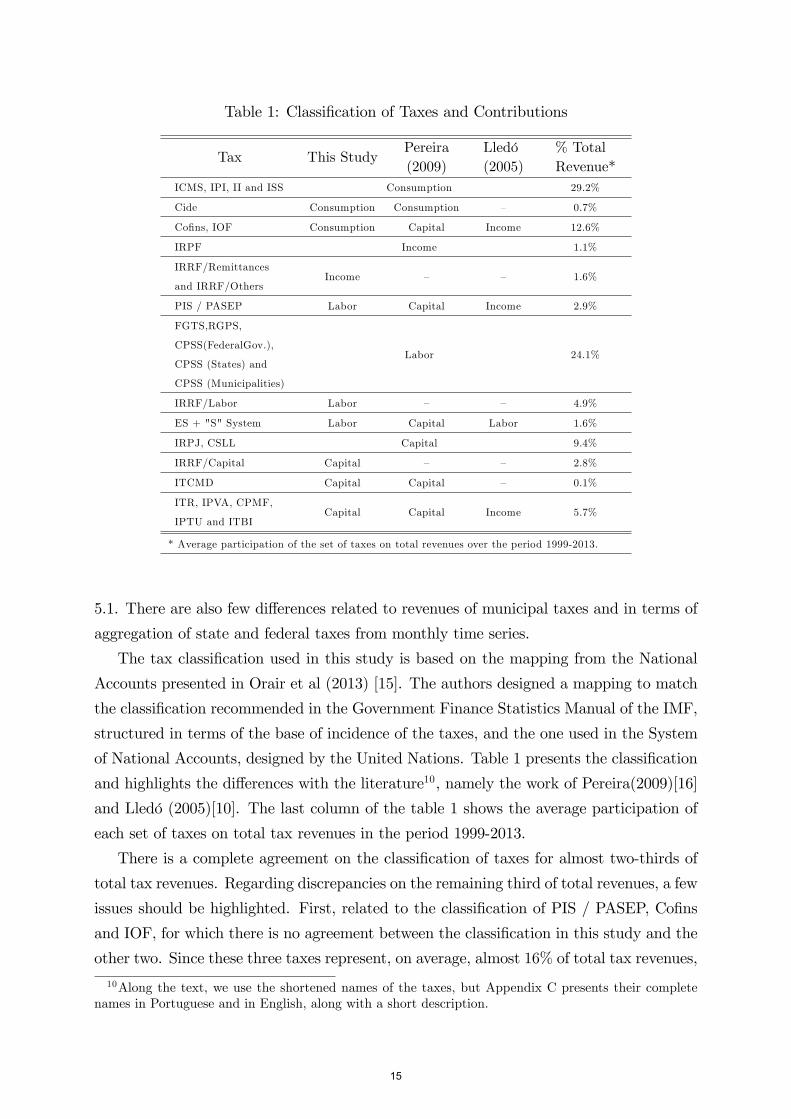

Table 1: Classification of Taxes and Contributions

Tax This StudyPereira(2009)

Lledó(2005)

% TotalRevenue*

ICMS, IPI, II and ISS Consumption 29.2%

Cide Consumption Consumption — 0.7%

Cofins, IOF Consumption Capital Income 12.6%

IRPF Income 1.1%

IRRF/Remittances

and IRRF/OthersIncome — — 1.6%

PIS / PASEP Labor Capital Income 2.9%

FGTS,RGPS,

CPSS(FederalGov.),

CPSS (States) and

CPSS (Municipalities)

Labor 24.1%

IRRF/Labor Labor — — 4.9%

ES + "S" System Labor Capital Labor 1.6%

IRPJ, CSLL Capital 9.4%

IRRF/Capital Capital — — 2.8%

ITCMD Capital Capital — 0.1%

ITR, IPVA, CPMF,

IPTU and ITBICapital Capital Income 5.7%

* Average participation of the set of taxes on total revenues over the period 1999-2013.

5.1. There are also few differences related to revenues of municipal taxes and in terms of

aggregation of state and federal taxes from monthly time series.

The tax classification used in this study is based on the mapping from the National

Accounts presented in Orair et al (2013) [15]. The authors designed a mapping to match

the classification recommended in the Government Finance Statistics Manual of the IMF,

structured in terms of the base of incidence of the taxes, and the one used in the System

of National Accounts, designed by the United Nations. Table 1 presents the classification

and highlights the differences with the literature10, namely the work of Pereira(2009)[16]

and Lledó (2005)[10]. The last column of the table 1 shows the average participation of

each set of taxes on total tax revenues in the period 1999-2013.

There is a complete agreement on the classification of taxes for almost two-thirds of

total tax revenues. Regarding discrepancies on the remaining third of total revenues, a few

issues should be highlighted. First, related to the classification of PIS / PASEP, Cofins

and IOF, for which there is no agreement between the classification in this study and the

other two. Since these three taxes represent, on average, almost 16% of total tax revenues,

10Along the text, we use the shortened names of the taxes, but Appendix C presents their completenames in Portuguese and in English, along with a short description.

15

their classification have a significant impact on the effective tax rates calculated as will

be discussed below. With respect to PIS / PASEP, those taxes are indeed social security

contributions made by firms in the name of employees. Thus, even if these contributions

directly affect firms’profits, they constitute part of the pre-tax labor income from the

perspective of the National Accounts. In the case of Cofins, despite being a very similar

contribution to PIS / PASEP, the absence of a direct link between the collection of the

revenue and the transfer to social security activities might be the reason Orair et al (2013)

[15] classified Cofins as a tax on products. The tax base of Cofins is strictly related to

firms’revenues and there is no direct return to employees, despite its name suggesting

a contribution to social security activities. Finally, IOF is a tax affecting a significant

number of financial transactions. Despite the impact on capital allocation, the effects of

IOF are mostly noted on the use of payment instruments and their effects on consumption.

As a consequence, Orair et al (2013) [15] define IOF as a tax on products, instead of a tax

affecting production. Also related to the classification of taxes, while Pereira (2009)[16]

defines contributions to the "S" System and Education Salary (ES) as taxes over capital

income, this paper follows Lledó (2005)[10] in classifying these contributions as a tax over

labor income, since both are based on firms’payroll.

The second discrepancy with respect to the literature is related to data sources: this

paper uses disaggregated data on Withholding Income Tax (IRRF), available from Sec-

retariat of the Federal Revenue and published at Ipeadata11. With this information, it is

possible to separate tax revenues in terms of its incidence over labor and capital income,

leaving those from Remittances and Others under the individual income class. Pereira

(2009)[16] only uses the aggregate numbers for IRRF, classifying it entirely under the

individual income class. Lledó (2005)[10] do not mention including IRRF on their tax

revenues classification.

Most of data used to construct the tax base comes from National Accounts, available

at the IBGE database12. Gross domestic product, private consumption and government

spending data come from the expenditures accounts, while wages and salaries (W ), gross

mixed income (RMB) and the gross operating surplus (EOB) come from the Supply

and Use Table ("Tabela de Recursos e Usos", in Portuguese). Unfortunately, the lack of

information on factor income from the National Accounts limits the analysis to a span

between 1999 and 2009. Data on the compensation of government employees (GW ) was

constructed with data for payroll and social charges for the three levels of government

(Federal, State and Municipal) from Ipeadata.

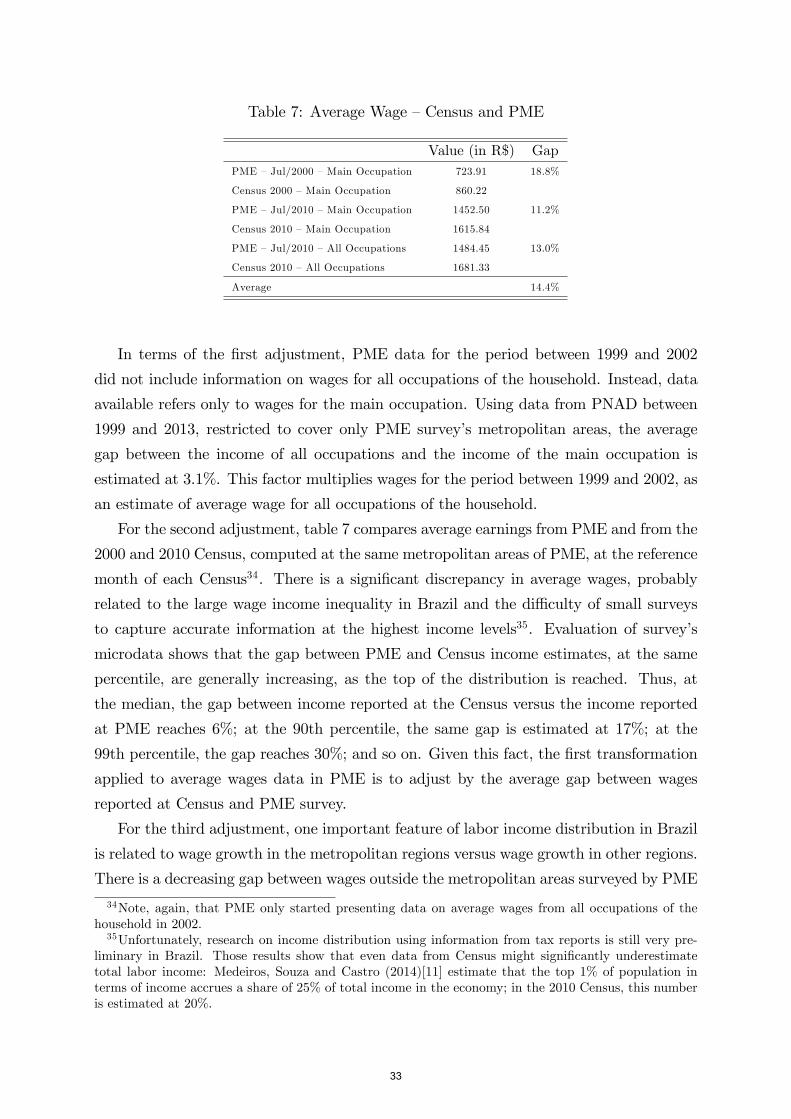

Table 2 shows average effective tax rates at annual frequency. For comparison, the

11Ipeadata is a free dataset mantained by IPEA, a thinktank in economic and social policies mantainedby the Brazilian government. The website content is available at http://www.ipeadata.gov.br/.12Available at http://www.sidra.ibge.gov.br/

16

table also includes values presented in Pereira (2009)[16] and Lledó (2005)[10], combined

with a partial sample analysis for each paper: effective tax rates are recalculated using

our own dataset, but under the tax classification and time span of each author. The

adjustment of dataset closes the gap between estimates in terms of different methodologies,

while the adjustment of time span accounts for the dynamics of tax rates.

From results at Table 2, the effective tax rate on consumption (τ c) is much higher in

our study (25.3%), mainly reflecting the classification of IOF and Cofins as consumption

taxes. These two taxes have a significant impact in terms of effective tax rates, as they

represent, on average, 12.6% of total tax revenues. Under Pereira’s (2009)[16] and Lledó’s

(2005)[10] classification, for the same time span, effective tax rates on consumption in our

database become closer to values presented in their work.

Most of the differences observed on individual income taxes (τ y) reflect different as-

sumptions regarding the tax classification, since the tax base is the same in all three

studies. To be more specific, Pereira (2009) does not present his final figures for income

tax. However, using our annual dataset, note that the estimated value for income tax

considerably increases (from 1.0% to 4.1%) by defining revenues of IRRF under that

category13. Lledó (2005)[10] obtains the highest tax rate over individual income, as he

includes under that category a significant set of taxes, like Cofins, PIS / PASEP and

CPMF, representing, on average, 21.3% of total tax revenues. Unfortunately, even after

adjusting for Lledó’s (2005)[10] classification of taxes, there is a significant gap in terms

of effective tax rates on individual income (8.5%, versus 13.4% from our estimates). Most

of this gap seems to be related to different figures in terms of total tax revenues14.

Regarding effective tax rates on labor (τ l) and capital income (τ k), there is a significant

discrepancy between our figures and the other two. Lledó’s (2005)[10] model presents a

separate tax rate for social security contributions, resulting in lower labor tax rates overall.

On average, General Social Security System (RGPS, in Portuguese) accounts for 15.9%

of total tax revenues in the period. Another difference is related to a large group of the

taxes classified as capital taxes here and under the individual income class in his work.

Even after adjusting for his classification, results in our partial sample analysis are slightly

smaller because of discrepancies in estimates of the tax base: Lledó (2005)[10] shows a

large share for EOB/Y in 2002, compared to our figures.

The comparison with Pereira (2009)[16] is a little more diffi cult, as the author do not

keep a general income tax as a separate category in the theoretical model, apart from

13From Table 1, aggregate IRRF on labor and capital correspond to approximately 7.5% of total taxrevenues.14More specifically, figures on the tax burden on individual income tax (IRPF) reported by Lledó

(2005)[10] in table A-1 do not match our estimates, suggesting that the author included WithholdingIncome Tax (IRRF) together with IRPF.

17

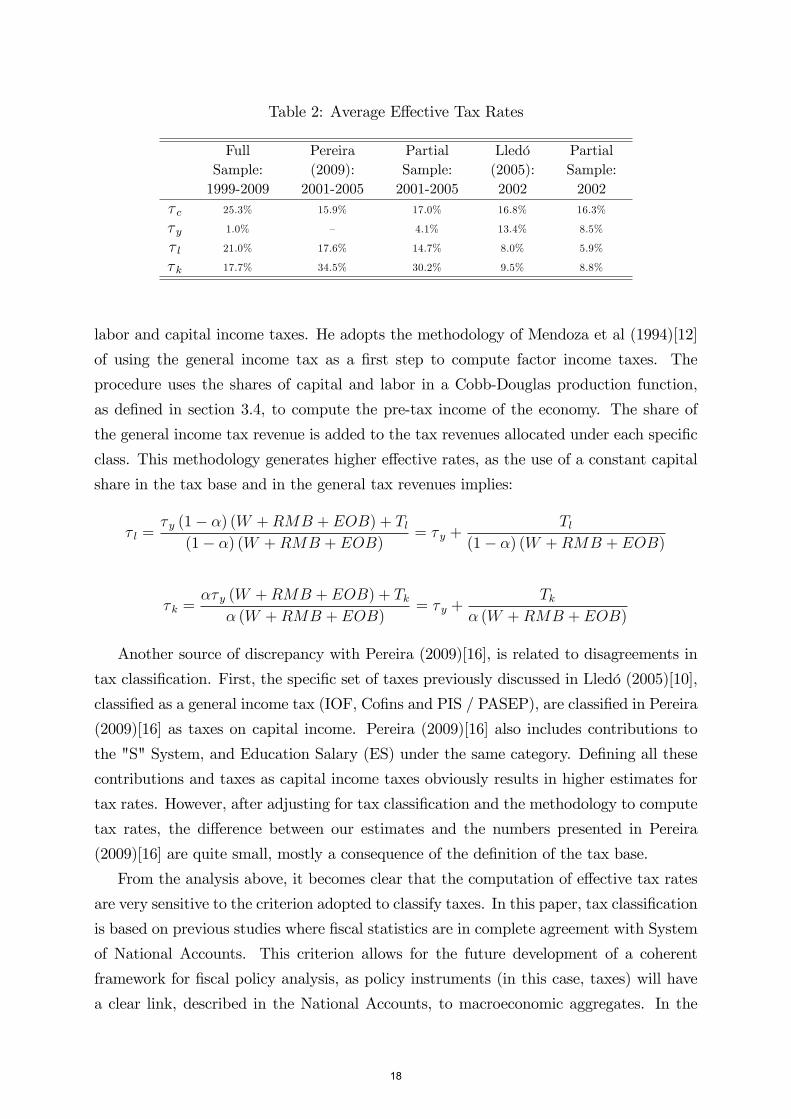

Table 2: Average Effective Tax Rates

FullSample:1999-2009

Pereira(2009):2001-2005

PartialSample:2001-2005

Lledó(2005):2002

PartialSample:2002

τ c 25.3% 15.9% 17.0% 16.8% 16.3%

τ y 1.0% — 4.1% 13.4% 8.5%

τ l 21.0% 17.6% 14.7% 8.0% 5.9%

τ k 17.7% 34.5% 30.2% 9.5% 8.8%

labor and capital income taxes. He adopts the methodology of Mendoza et al (1994)[12]

of using the general income tax as a first step to compute factor income taxes. The

procedure uses the shares of capital and labor in a Cobb-Douglas production function,

as defined in section 3.4, to compute the pre-tax income of the economy. The share of

the general income tax revenue is added to the tax revenues allocated under each specific

class. This methodology generates higher effective rates, as the use of a constant capital

share in the tax base and in the general tax revenues implies:

τ l =τ y (1− α) (W +RMB + EOB) + Tl

(1− α) (W +RMB + EOB)= τ y +

Tl(1− α) (W +RMB + EOB)

τ k =ατ y (W +RMB + EOB) + Tk

α (W +RMB + EOB)= τ y +

Tkα (W +RMB + EOB)

Another source of discrepancy with Pereira (2009)[16], is related to disagreements in

tax classification. First, the specific set of taxes previously discussed in Lledó (2005)[10],

classified as a general income tax (IOF, Cofins and PIS / PASEP), are classified in Pereira

(2009)[16] as taxes on capital income. Pereira (2009)[16] also includes contributions to

the "S" System, and Education Salary (ES) under the same category. Defining all these

contributions and taxes as capital income taxes obviously results in higher estimates for

tax rates. However, after adjusting for tax classification and the methodology to compute

tax rates, the difference between our estimates and the numbers presented in Pereira

(2009)[16] are quite small, mostly a consequence of the definition of the tax base.

From the analysis above, it becomes clear that the computation of effective tax rates

are very sensitive to the criterion adopted to classify taxes. In this paper, tax classification

is based on previous studies where fiscal statistics are in complete agreement with System

of National Accounts. This criterion allows for the future development of a coherent

framework for fiscal policy analysis, as policy instruments (in this case, taxes) will have

a clear link, described in the National Accounts, to macroeconomic aggregates. In the

18

next section, we present the main contribution of this paper, which is the estimation of

the effective tax rates at quarterly frequency.

5 Tax Rates at Quarterly Frequency

The main objective of this section is to calculate time series of effective tax rates

for consumption, individual, labor and capital incomes at quarterly frequency. While

most of the information on tax and contribution revenues at the federal level is avail-

able at monthly frequency, the main challenge to compute time series of the tax rates

were related to obtaining information on municipal taxes and the contributions for the

civil servants’social security system from subnational governments. In terms of the tax

base, data of expenditure from the National Accounts are readily available at quarterly

frequency, but the Supply and Use Table only provides delayed information at annual

frequency. As a consequence, this section also provides details on the procedures adopted

to estimate capital and labor compensations and payroll and social charges of subnational

governments.

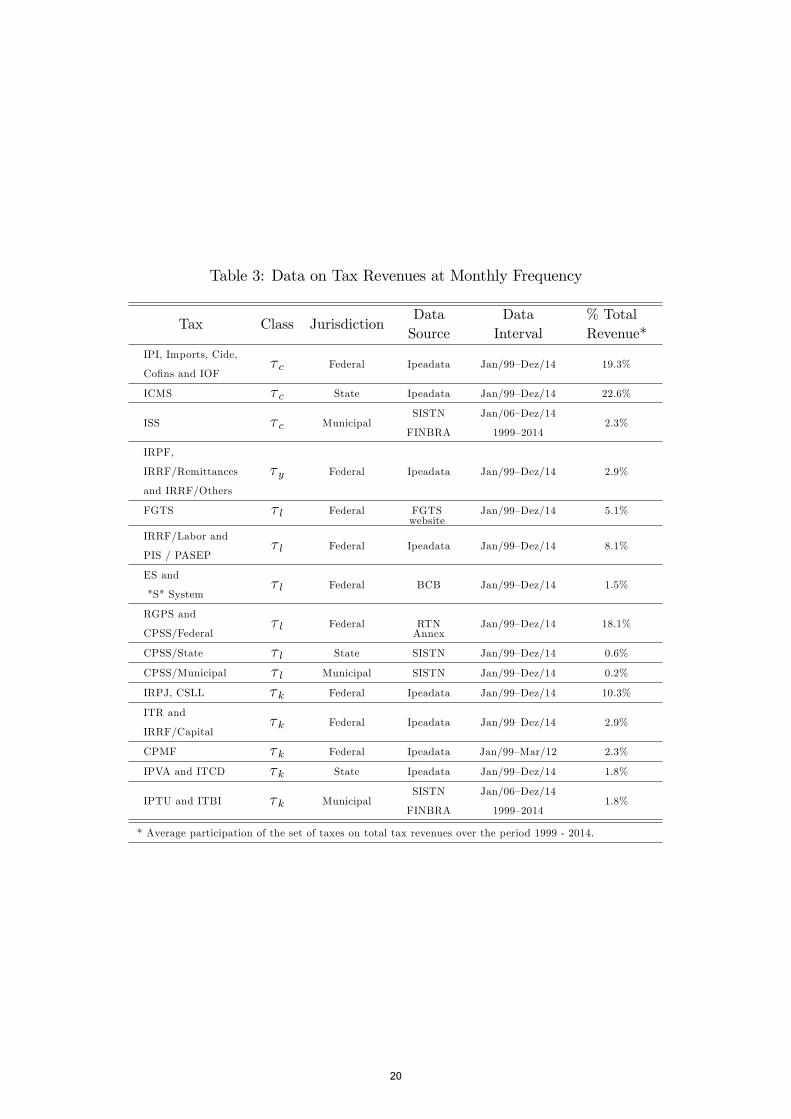

5.1 Data Sources on Tax Revenues

Table 3 presents the dataset on taxes and contributions revenues at monthly frequency

considered here, with their respective classification, jurisdiction, data sources and time

span. The last column of table 3 shows the average share of each revenue on the total

classified revenues. Again, for the sake of reference, this dataset represents 96.83% of total

tax revenues of the country. Most of data on federal and state taxes are readily avail-

able at the website of Ipeadata. The series of contributions to the FGTS was obtained

from the FGTS website15. Data on Education Salary (ES) and Contributions to the "S"

System are from the Central Bank of Brazil’s Time Series Dataset16. Data on contri-

butions to RGPS and civil servants’social security contributions of federal government

employees (CPSS/Union) are obtained from the monthly report of the National Treasury

Secretariat17.

Most of the problems related to building a dataset on tax and contributions revenues

resided on obtaining information on municipal taxes (IPTU, ITBI and ISS) and contribu-

tions to the civil servants’social security system of subnational governments —CPSS/State

15Available at http://www.fgts.gov.br.16Website: http://www.bcb.gov.br/?TIMESERIESEN. The series is called "Previdência social (Fluxos)

—Despesas —Transferências a terceiros" under the identification number 2286. These are contributionsthat the National Institute of Social Security (INSS, in Portuguese) collects and transfers to the respectiveentities.17Available at www.tesouro.fazenda.gov.br/resultado-do-tesouro-nacional.

19

Table 3: Data on Tax Revenues at Monthly Frequency

Tax Class JurisdictionDataSource

DataInterval

% TotalRevenue*

IPI, Imports, Cide,

Cofins and IOFτ c Federal Ipeadata Jan/99—Dez/14 19.3%

ICMS τ c State Ipeadata Jan/99—Dez/14 22.6%

ISS τ c MunicipalSISTN

FINBRA

Jan/06—Dez/14

1999—20142.3%

IRPF,

IRRF/Remittances

and IRRF/Others

τ y Federal Ipeadata Jan/99—Dez/14 2.9%

FGTS τ l Federal FGTSwebsite

Jan/99—Dez/14 5.1%

IRRF/Labor and

PIS / PASEPτ l Federal Ipeadata Jan/99—Dez/14 8.1%

ES and

"S" Systemτ l Federal BCB Jan/99—Dez/14 1.5%

RGPS and

CPSS/Federalτ l Federal RTN

AnnexJan/99—Dez/14 18.1%

CPSS/State τ l State SISTN Jan/99—Dez/14 0.6%

CPSS/Municipal τ l Municipal SISTN Jan/99—Dez/14 0.2%

IRPJ, CSLL τ k Federal Ipeadata Jan/99—Dez/14 10.3%

ITR and

IRRF/Capitalτ k Federal Ipeadata Jan/99—Dez/14 2.9%

CPMF τ k Federal Ipeadata Jan/99—Mar/12 2.3%

IPVA and ITCD τ k State Ipeadata Jan/99—Dez/14 1.8%

IPTU and ITBI τ k MunicipalSISTN

FINBRA

Jan/06—Dez/14

1999—20141.8%

* Average participation of the set of taxes on total tax revenues over the period 1999 - 2014.

20

and CPSS/Municipal. The next subsections discuss: (i) the details of the procedure to

reconcile the few public datasets available on subnational government spending and rev-

enues; (ii) the final information set on tax revenues at quarterly frequency.

5.1.1 Subnational Governments Data Construction Using SISTN

Every year, the National Treasury Secretariat publishes a large dataset called FIN-

BRA18, with information on the annual balance of municipalities. Municipalities are

required to report detailed information, otherwise being subject to sanctions to finance

debt in financial markets19. The dataset consolidated by the National Treasury Secretariat

provides details on tax collection, but unfortunately misses information on social security

contributions and government employees payroll. One of the main sources of information

to FINBRA is a system called SISTN ("Sistema de Coleta de Dados Contábeis dos Entes

da Federação", in Portuguese), created in 2000 and with detailed information starting in

2006. Municipalities are required by law to send periodical reports to this system, where

those reports are made available for public consultation20.

One report submitted by states and municipalities to SISTN is particularly impor-

tant for our purposes: a simplified bimonthly report called RREO (Summary Report

of Budget Execution, "Relatório Resumido de Execução Orçamentária", in Portuguese)

provides details on the main taxes and contributions collected at subnational level. Al-

though RREOs are submitted bimonthly, the information on taxes and contributions are

presented at monthly frequency for the previous 12 months. RREOs also provide in-

formation on civil servants’social security contributions, at monthly frequency, and on

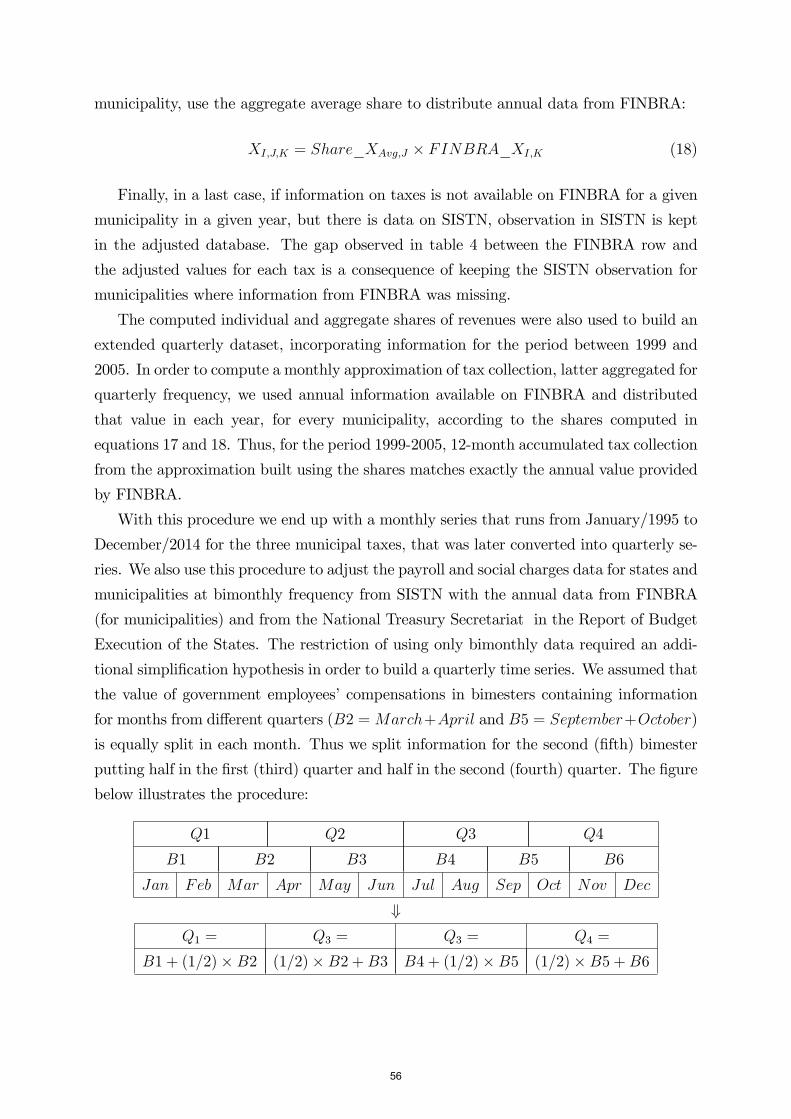

government employees payroll and social charges, at bimonthly frequency21.

Unfortunately, it is not possible to extract from SISTN a single report consolidating

information over time or across subnational entities. In order to work with SISTN, it

was necessary to build a system capable of downloading reports in PDF format for every

individual subnational government entity, for every period of time; convert the PDF

reports to a format able to read and process the information in those reports; and compile

the final dataset, summarizing information from all reports. This process demanded a

significant computational effort, where three VBA routines were developed to handle the

first two tasks. The first routine was built to download the correspondent PDF file for

18Available at http://www.tesouro.fazenda.gov.br/en/contas-anuais.19The requirement of sending reports to the Federal Government is described in sections II, III and IV

of the Fiscal Responsibility Law (Complementary Law 101, of May 4th, 2000).20Available at https://www.contaspublicas.caixa.gov.br/sistncon_internet/index.jsp . See footnote 1

about the modernized system implemented by the National Treasury.21Details on how we handle bimonthly information on payroll and social charges are presented in

subsection 5.2.1.

21

each RREO, for the 5568 municipalities, 26 states and the Federal District22, from 2006

to 201423. The second routine reads every PDF file and converts the information to TXT

files. The third routine reads the TXT files and extracts only information on tax revenues,

government spending and social security contributions to build the aggregate dataset.

In order to evaluate the quality of the data on municipal taxes revenues (IPTU, ITBI

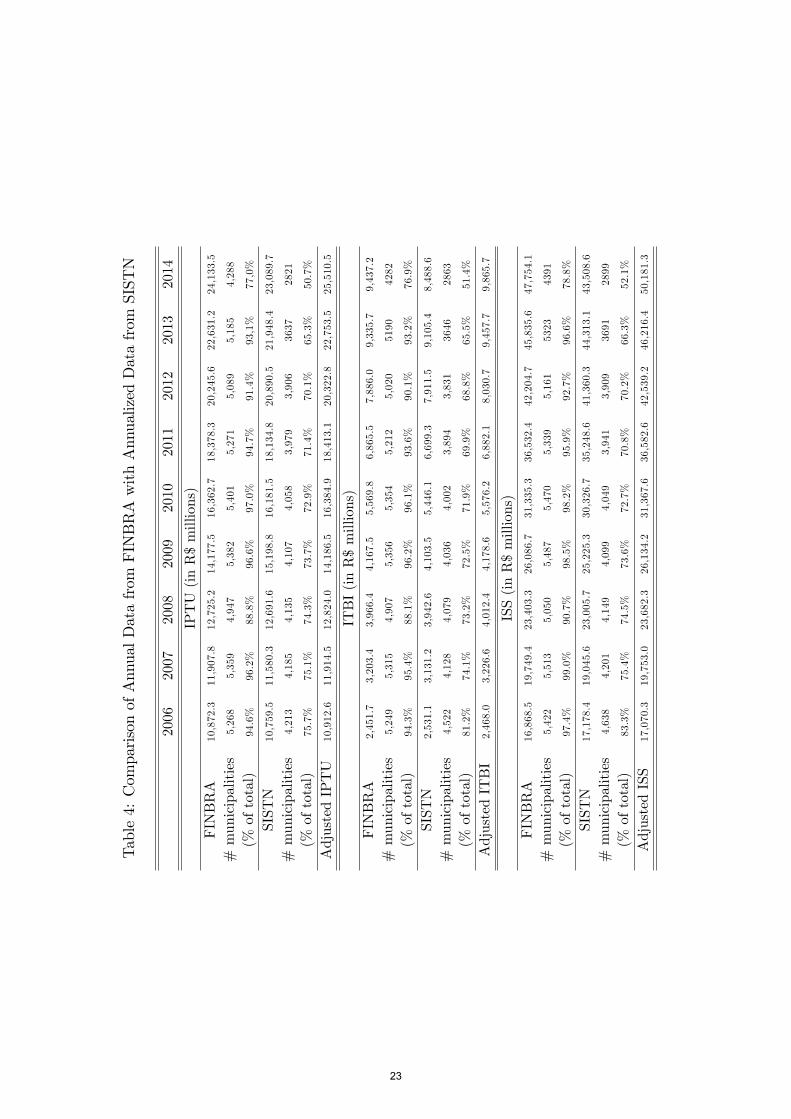

and ISS) collected from SISTN, Table 4 presents the annualized data from SISTN between

2006 and 2014 and the values reported for every year in FINBRA. It also shows the number

of municipalities, including the Federal District, that have information on FINBRA and

submitted a valid report24 on SISTN. The coverage of FINBRA database (on average,

94.8%, 94.1% and 96.5%, for IPTU, ITBI and ISS, respectively) is larger than the coverage

observed on SISTN (on average, 71.1%, 71.8% and 72.7%, for IPTU, ITBI and ISS,

respectively). In terms of number of municipalities reporting information, both databases

show a decrease in participation rate over the years, with a more accentuated fall in

SISTN.

The decline in the number of municipalities reporting information to SISTN and FIN-

BRA does not correspond to a decline in the ratio of aggregate taxes reported to SISTN

over taxes presented in FINBRA. That means, even with a significant decline in the

number of cities providing reports to SISTN, relative to those presenting information to

FINBRA, the loss in terms of aggregate taxes does not seem to be significant. The main

reason for that is the unequal distribution of tax collection across municipalities, with a

small number of large cities (in terms of population size) generating a large share of total

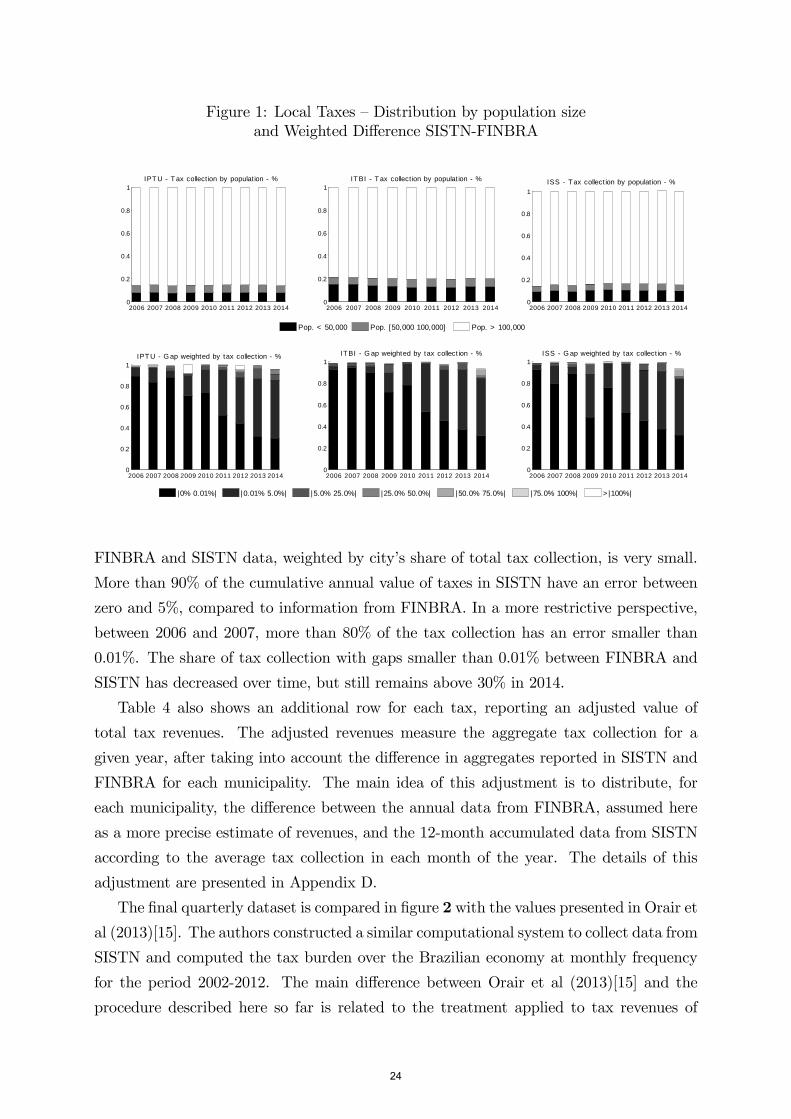

tax collection. Figure 1 summarizes the information on the distribution of taxes based on

city’s population and the precision of SISTN data, compared to data on FINBRA. The

first row of graphs in figure 1 shows that, on average, municipalities with at least 100,000

inhabitants —299 cities —collect 86% of total IPTU and ISS revenues and 80% of total

ITBI revenue. Moving one step further, municipalities with at least 50,000 inhabitants —

638 cities —collect, on average, 92% of total IPTU revenues, 91% of total ISS revenues

and 87% of total ITBI revenues.

The second row of graphs in figure 1 shows that, despite the unequal distribution of

tax collection across cities, data seem to have good quality, as the discrepancy between

22The Federal District is a special subnational entity that includes the Nation’s capital. Its organizationin terms of taxes is similar to a state without municipalities: the Federal District’s Government (GDF, inportuguese) collects all taxes that other states in the country are able to collect, plus municipal taxes likeIPTU, ITBI and ISS. GDF reports all tax revenues on its RREOs. This data was checked for consistencywith information from the annual balance of GDF.23This gaves us 192,318 reports for municipalities and 1,289 reports for the states and the Federal

District.24Here, an RREO is considered a valid report for the analysis, if there is at least a non-zero entry for

a given tax in any month of the year. If the municipality reported only zeros as the tax collection for afull year, it is considered as an invalid/missing report.

22

Table4:ComparisonofAnnualDatafrom

FINBRAwithAnnualizedDatafrom

SISTN

2006

2007

2008

2009

2010

2011

2012

2013

2014

IPTU(inR$millions)

FINBRA

10,872.3

11,907.8

12,725.2

14,177.5

16,362.7

18,378.3

20,245.6

22,631.2

24,133.5

#municipalities

5,268

5,359

4,947

5,382

5,401

5,271

5,089

5,185

4,288

(%oftotal)

94.6%

96.2%

88.8%

96.6%

97.0%

94.7%

91.4%

93,1%

77,0%

SISTN

10,759.5

11,580.3

12,691.6

15,198.8

16,181.5

18,134.8

20,890.5

21,948.4

23,089.7

#municipalities

4,213

4,185

4,135

4,107

4,058

3,979

3,906

3637

2821

(%oftotal)

75.7%

75.1%

74.3%

73.7%

72.9%

71.4%

70.1%

65.3%

50.7%

AdjustedIPTU

10,912.6

11,914.5

12,824.0

14,186.5

16,384.9

18,413.1

20,322.8

22,753.5

25,510.5

ITBI(inR$millions)

FINBRA

2,451.7

3,203.4

3,966.4

4,167.5

5,569.8

6,865.5

7,886.0

9,335.7

9,437.2

#municipalities

5,249

5,315

4,907

5,356

5,354

5,212

5,020

5190

4282

(%oftotal)

94.3%

95.4%

88.1%

96.2%

96.1%

93.6%

90.1%

93.2%

76.9%

SISTN

2,531.1

3,131.2

3,942.6

4,103.5

5,446.1

6,699.3

7,911.5

9,105.4

8,488.6

#municipalities

4,522

4,128

4,079

4,036

4,002

3,894

3,831

3646

2863

(%oftotal)

81.2%

74.1%

73.2%

72.5%

71.9%

69.9%

68.8%

65.5%

51.4%

AdjustedITBI

2,468.0

3,226.6

4,012.4

4,178.6

5,576.2

6,882.1

8,030.7

9,457.7

9,865.7

ISS(inR$millions)

FINBRA

16,868.5

19,749.4

23,403.3

26,086.7

31,335.3

36,532.4

42,204.7

45,835.6

47,754.1

#municipalities

5,422

5,513

5,050

5,487

5,470

5,339

5,161

5323

4391

(%oftotal)

97.4%

99.0%

90.7%

98.5%

98.2%

95.9%

92.7%

96.6%

78.8%

SISTN

17,178.4

19,045.6

23,005.7

25,225.3

30,326.7

35,248.6

41,360.3

44,313.1

43,508.6

#municipalities

4,638

4,201

4,149

4,099

4,049

3,941

3,909

3691

2899

(%oftotal)

83.3%

75.4%

74.5%

73.6%

72.7%

70.8%

70.2%

66.3%

52.1%

AdjustedISS

17,070.3

19,753.0

23,682.3

26,134.2

31,367.6

36,582.6

42,539.2

46,216.4

50,181.3

23

Figure 1: Local Taxes —Distribution by population sizeand Weighted Difference SISTN-FINBRA

2006 2007 2008 2009 2010 2011 2012 2013 20140

0.2

0.4

0.6

0.8

1IPT U T ax collect ion by populat ion %

Pop. < 50,000 Pop. [50,000 100,000] Pop. > 100,000

2006 2007 2008 2009 2010 2011 2012 2013 20140

0.2

0.4

0.6

0.8

1IT BI T ax collect ion by populat ion %

2006 2007 2008 2009 2010 2011 2012 2013 20140

0.2

0.4

0.6

0.8

1ISS T ax collect ion by populat ion %

2006 2007 2008 2009 2010 2011 2012 2013 20140

0.2

0.4

0.6

0.8

1IPT U G ap weighted by tax collect ion %

|0% 0.01%| |0.01% 5.0%| |5.0% 25.0%| |25.0% 50.0%| |50.0% 75.0%| |75.0% 100%| > |100%|

2006 2007 2008 2009 2010 2011 2012 2013 20140

0.2

0.4

0.6

0.8

1IT BI G ap weighted by tax collect ion %

2006 2007 2008 2009 2010 2011 2012 2013 20140

0.2

0.4

0.6

0.8

1ISS G ap weighted by tax collect ion %

FINBRA and SISTN data, weighted by city’s share of total tax collection, is very small.

More than 90% of the cumulative annual value of taxes in SISTN have an error between

zero and 5%, compared to information from FINBRA. In a more restrictive perspective,

between 2006 and 2007, more than 80% of the tax collection has an error smaller than

0.01%. The share of tax collection with gaps smaller than 0.01% between FINBRA and

SISTN has decreased over time, but still remains above 30% in 2014.

Table 4 also shows an additional row for each tax, reporting an adjusted value of

total tax revenues. The adjusted revenues measure the aggregate tax collection for a

given year, after taking into account the difference in aggregates reported in SISTN and

FINBRA for each municipality. The main idea of this adjustment is to distribute, for

each municipality, the difference between the annual data from FINBRA, assumed here

as a more precise estimate of revenues, and the 12-month accumulated data from SISTN

according to the average tax collection in each month of the year. The details of this

adjustment are presented in Appendix D.

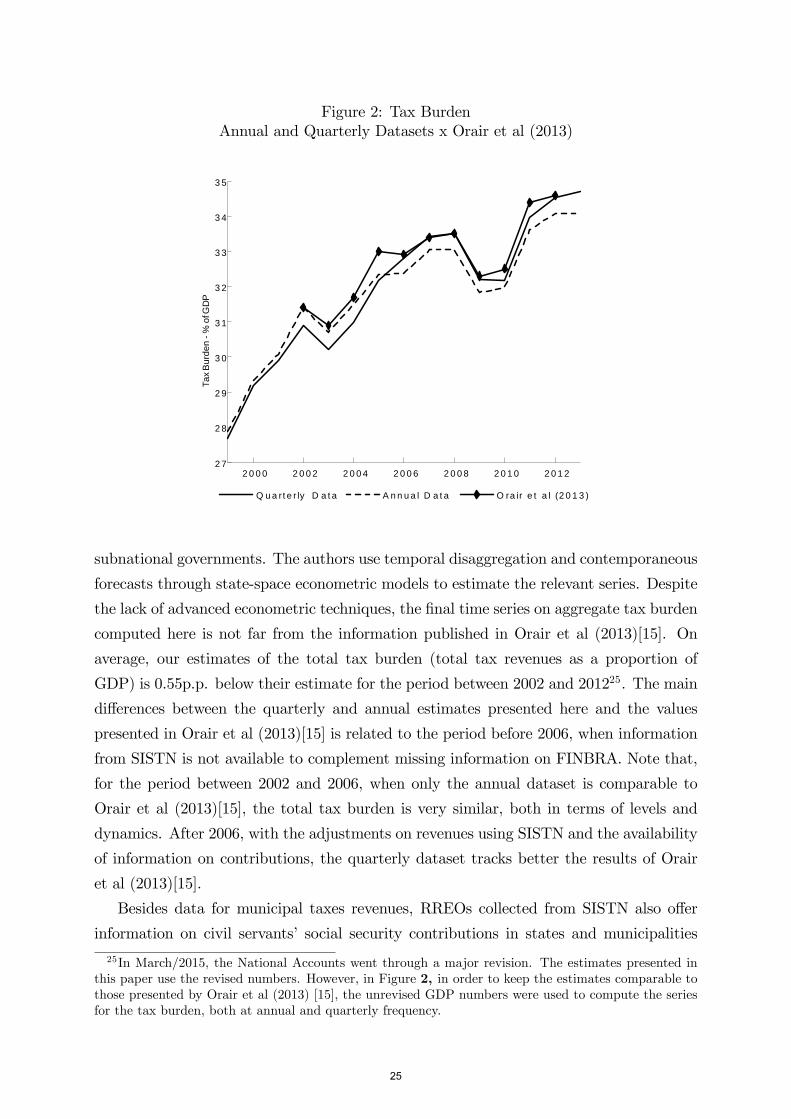

The final quarterly dataset is compared in figure 2 with the values presented in Orair et

al (2013)[15]. The authors constructed a similar computational system to collect data from

SISTN and computed the tax burden over the Brazilian economy at monthly frequency

for the period 2002-2012. The main difference between Orair et al (2013)[15] and the

procedure described here so far is related to the treatment applied to tax revenues of

24

Figure 2: Tax BurdenAnnual and Quarterly Datasets x Orair et al (2013)

2 0 0 0 2 0 0 2 2 0 0 4 2 0 0 6 2 0 0 8 2 0 1 0 2 0 1 22 7

2 8

2 9

3 0

3 1

3 2

3 3

3 4

3 5

Tax

Bur

den

% o

f GD

P

Q u a rt e r ly D a t a A n n u a l D a t a O ra ir e t a l (2 0 1 3 )

subnational governments. The authors use temporal disaggregation and contemporaneous

forecasts through state-space econometric models to estimate the relevant series. Despite

the lack of advanced econometric techniques, the final time series on aggregate tax burden

computed here is not far from the information published in Orair et al (2013)[15]. On

average, our estimates of the total tax burden (total tax revenues as a proportion of

GDP) is 0.55p.p. below their estimate for the period between 2002 and 201225. The main

differences between the quarterly and annual estimates presented here and the values

presented in Orair et al (2013)[15] is related to the period before 2006, when information

from SISTN is not available to complement missing information on FINBRA. Note that,

for the period between 2002 and 2006, when only the annual dataset is comparable to

Orair et al (2013)[15], the total tax burden is very similar, both in terms of levels and

dynamics. After 2006, with the adjustments on revenues using SISTN and the availability

of information on contributions, the quarterly dataset tracks better the results of Orair

et al (2013)[15].

Besides data for municipal taxes revenues, RREOs collected from SISTN also offer

information on civil servants’ social security contributions in states and municipalities

25In March/2015, the National Accounts went through a major revision. The estimates presented inthis paper use the revised numbers. However, in Figure 2, in order to keep the estimates comparable tothose presented by Orair et al (2013) [15], the unrevised GDP numbers were used to compute the seriesfor the tax burden, both at annual and quarterly frequency.

25

(CPSS/States and CPSS/Municipal). Unfortunately, to the best of our knowledge, there

is not an annual dataset disaggregated by states and municipalities similar to FINBRA

available to check the accuracy of reports. The only source of information on CPSS/States

and CPSS/Municipal are the annual aggregated figures published by the National Trea-

sury Secretariat and the Secretariat of Federal Revenue. Given this limitation, the ad-

justment made on tax revenues using information from FINBRA was not repeated for

contributions of civil servants. Even without the adjustment, however, the comparison

of annual values from the National Treasury with figures from SISTN shows a small gap

between the two time series. Notably, the gap observed for Municipal contributions is

much smaller than the one obtained for States.

Another problem with information from CPSS is the lack of disaggregated data for

CPSS/States and CPSS/Municipal for the period before 2006. The short time span

with information available at monthly frequency after 2006, combined with the lack of

alternative datasets to check the accuracy of the procedure, suggests that it would not

be a good strategy to distribute aggregated annual data over monthly information. The

effects of missing high-frequency information for CPSS/States and CPSS/Municipal are

discussed next.

5.1.2 Tax Revenues Series

Given the procedure described above to collect information from different datasets, we

were able to construct monthly time series on taxes and contributions revenues for each

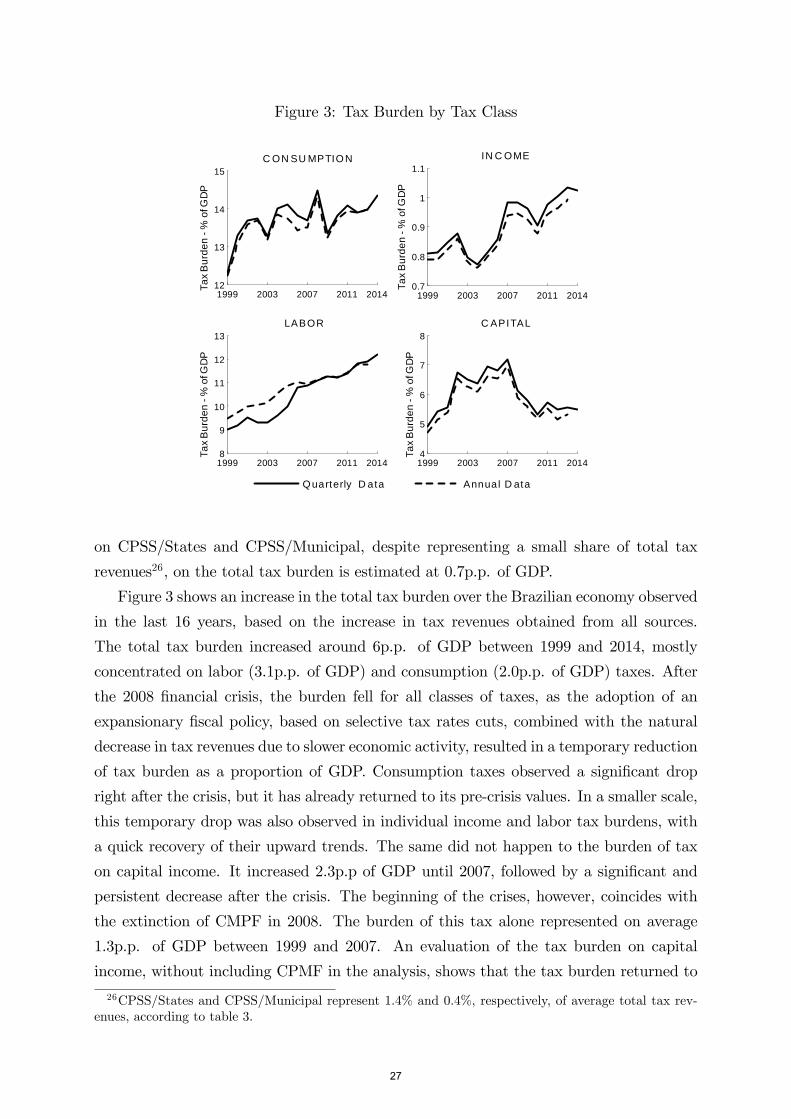

class of tax (Tc, Ty, Tl and Tk). Figure 3 compares the total tax burden for each class

of taxes as a share of GDP using annual and quarterly data. The annualized, 4-quarter

accumulated tax burden series are in general not too far from the annual series. In fact,

taxes on consumption, individual income and capital income from the quarterly dataset

are consistently above the annual estimates, with a stable gap separating time series at

different frequencies. The gap between annual and annualized time series is a consequence

of two factors: first, as briefly discussed above, the use of net taxes revenues in the annual

reports of the of the Secretariat of the Federal Revenue, instead of gross tax revenues

as published in monthly reports; second, the adjustment of SISTN data to information

from FINBRA, which usually generated higher aggregate estimates of tax revenues of

municipalities, as shown in table 4.

The most important differences between annual and quarterly estimates are related

to the estimates of labor tax revenues for the period between 1999 and 2006. This gap is

a consequence of the lack of data on CPSS/States and CPSS/Municipal at monthly fre-

quency for that period, plus some discrepancies in monthly information for contributions

to the "S" System. The average impact of missing information on these taxes, specially

26

Figure 3: Tax Burden by Tax Class

1999 2003 2007 2011 201412

13

14

15C ON SU MPTION

Tax

Bur

den

% o

f GD

P

Quarterly D ata Annual D ata

1999 2003 2007 2011 20140.7

0.8

0.9

1

1.1IN C OME

Tax

Bur

den

% o

f GD

P

1999 2003 2007 2011 20148

9

10

11

12

13LABOR

Tax

Bur

den

% o

f GD

P

1999 2003 2007 2011 20144

5

6

7

8C APITAL

Tax

Bur

den

% o

f GD

P

on CPSS/States and CPSS/Municipal, despite representing a small share of total tax

revenues26, on the total tax burden is estimated at 0.7p.p. of GDP.

Figure 3 shows an increase in the total tax burden over the Brazilian economy observed

in the last 16 years, based on the increase in tax revenues obtained from all sources.

The total tax burden increased around 6p.p. of GDP between 1999 and 2014, mostly

concentrated on labor (3.1p.p. of GDP) and consumption (2.0p.p. of GDP) taxes. After

the 2008 financial crisis, the burden fell for all classes of taxes, as the adoption of an

expansionary fiscal policy, based on selective tax rates cuts, combined with the natural

decrease in tax revenues due to slower economic activity, resulted in a temporary reduction

of tax burden as a proportion of GDP. Consumption taxes observed a significant drop

right after the crisis, but it has already returned to its pre-crisis values. In a smaller scale,

this temporary drop was also observed in individual income and labor tax burdens, with

a quick recovery of their upward trends. The same did not happen to the burden of tax

on capital income. It increased 2.3p.p of GDP until 2007, followed by a significant and

persistent decrease after the crisis. The beginning of the crises, however, coincides with

the extinction of CMPF in 2008. The burden of this tax alone represented on average

1.3p.p. of GDP between 1999 and 2007. An evaluation of the tax burden on capital

income, without including CPMF in the analysis, shows that the tax burden returned to

26CPSS/States and CPSS/Municipal represent 1.4% and 0.4%, respectively, of average total tax rev-enues, according to table 3.

27

its pre-crisis level by 2014.

5.2 Data Sources on the Tax Base

Two main sources were used to compute the tax base at quarterly frequency, given

the definitions presented in equations 4, 9, 11 and 12. First, to compute consumption

taxes, as in the case of effective taxes computed with annual data, the main source is

the National Accounts. Then, to compute factor income, population surveys are used to

make inference on total labor income. Beyond describing details of these two sources,

this section presents, first, the computation of government employee’s compensation at

quarterly frequency. After that, the details on the use of population surveys to estimate

labor and capital income are presented.

From the National Accounts perspective, beyond information on gross domestic out-

put, private consumption and government spending, it is necessary to build an estimate

of the economy’s value added at factor costs. As in the case of labor and capital income,

offi cial estimates available for the value added at factor costs are available only at annual

frequency and without constant updates. By the definition presented in equation 8, value

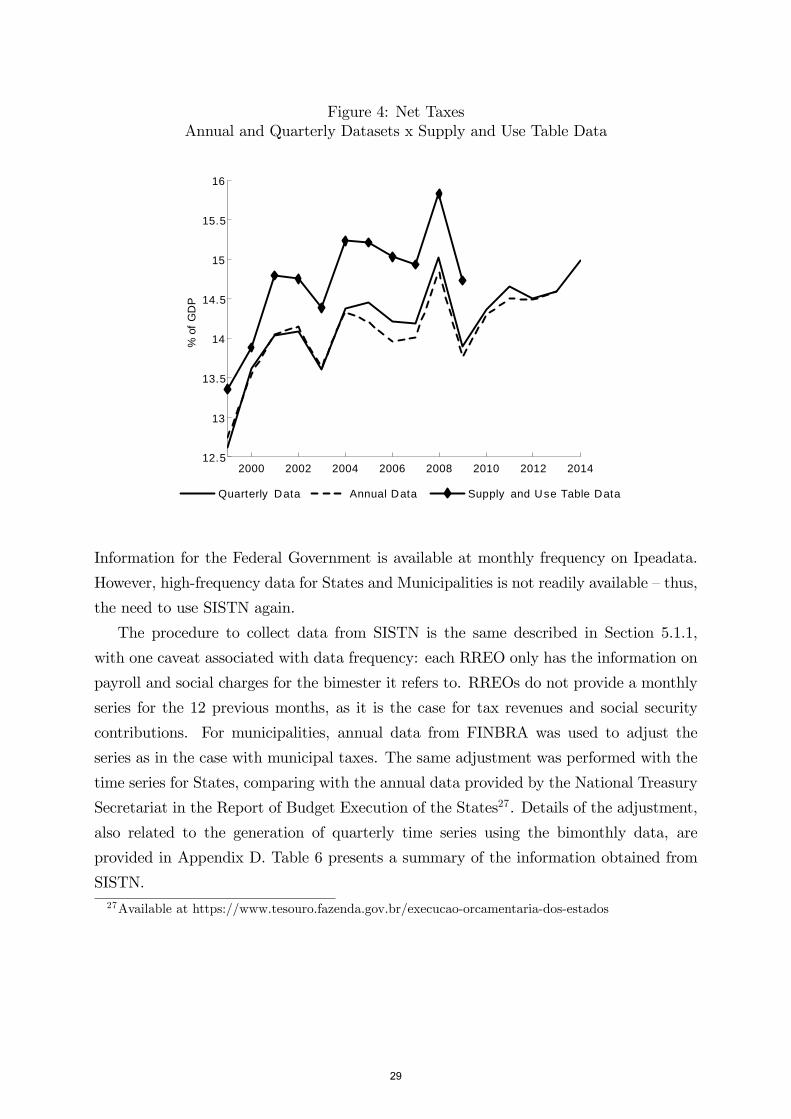

added at factor costs is computed by the difference between net domestic income and an

estimate of "net taxes on production". While estimates of the gross domestic product are

readily available, an approximation of "net taxes" is constructed, based on the definitions

of Orair et al (2013)[15], as the sum of IPI, ICMS, ISS, CIDE, II, IOF, Cofins, ES and

contributions to the "S" System. Figure 4 compares this approximation with information

on "taxes on production" from the Supply and Use Table, both measured as a proportion

of GDP. Our estimates based on quarterly data are, on average, 0.7p.p. below of the

Supply and Use Table, showing good accuracy, even with the problems reported before

on the database for quarterly data.

After generating an estimate of total factor income, W + RMB + EOB, by using

gross domestic product, Y −Net Taxes, the next two subsections show the procedure toconstruct time series for government employees’compensations, GW, and for labor and

capital income. Table 5 summarizes the data sources used to construct the series on the

tax base.

5.2.1 Constructing a Series for Government Employees’Compensations

In order to construct a quarterly time series on government employees’compensations

(GW in equation 4), information from SISTN was used to estimate figures for subna-

tional entities of the federation. Datasets from the National Treasury Secretariat pro-

vided annual information on payroll and social charges for the three levels of government.

28

Figure 4: Net TaxesAnnual and Quarterly Datasets x Supply and Use Table Data

2000 2002 2004 2006 2008 2010 2012 201412.5

13

13.5

14

14.5

15

15.5

16%

of G

DP

Quarterly Data Annual Data Supply and Use Table Data

Information for the Federal Government is available at monthly frequency on Ipeadata.

However, high-frequency data for States and Municipalities is not readily available —thus,

the need to use SISTN again.

The procedure to collect data from SISTN is the same described in Section 5.1.1,

with one caveat associated with data frequency: each RREO only has the information on

payroll and social charges for the bimester it refers to. RREOs do not provide a monthly

series for the 12 previous months, as it is the case for tax revenues and social security

contributions. For municipalities, annual data from FINBRA was used to adjust the

series as in the case with municipal taxes. The same adjustment was performed with the

time series for States, comparing with the annual data provided by the National Treasury

Secretariat in the Report of Budget Execution of the States27. Details of the adjustment,

also related to the generation of quarterly time series using the bimonthly data, are

provided in Appendix D. Table 6 presents a summary of the information obtained from

SISTN.27Available at https://www.tesouro.fazenda.gov.br/execucao-orcamentaria-dos-estados

29

Table 5: Data on Tax Base Components

Component Frequency Data Source Data IntervalY, C, G Quarterly IBGE 1999.T1 - 2014.T4

Payroll and Social Charges Monthly Ipeadata 1999.01 - 2014.12

Federal Government

Payroll and Social Charges Bimonthly SISTN 2006.B1 - 2014.B6

State Governments Annually National Treasury 1999 - 2013

Payroll and Social Charges Bimonthly SISTN 2006.B1 - 2014.B6

Municipal Governments Annually FINBRA 1999 - 2014

Labor and Capital Income Monthly PME, PNAD and Census (IBGE) 1999.01 - 2014.12

5.2.2 Constructing the Series on Labor and Capital Income

National Accounts in Brazil do not provide quarterly information on labor and capital

income28. As mentioned in subsection 3.5, in order to compute average income taxes rates

at quarterly frequency, information from population surveys in Brazil is used to build an

approximation of total labor income (WI + FC, defined in equation 10). According to

equation 12, capital income is calculated as a residual from value added at factor cost,

Y −Net Taxes, and total labor income.Total labor income is defined as the sum of wages and salaries and the employer’s

contribution to social security system29. The information on employer’s contribution to

social security system, FC, is available at monthly frequency, after a few assumptions

on the contribution of subnational governments. Hence, the major issue is related to

the estimate of wages and salaries, WI, for Brazil at a higher frequency. The procedure

adopted to build this time series is based on two steps: first, estimate the total occupied