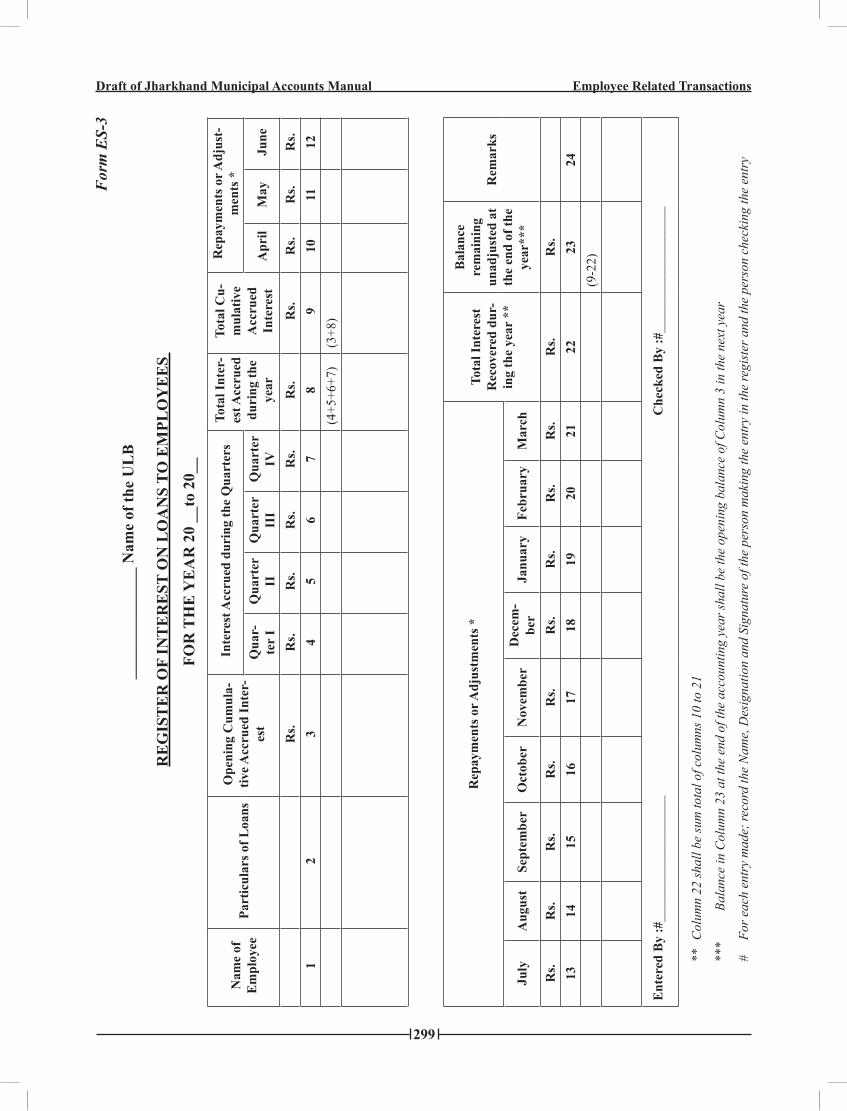

chApteR 11 RentAls, Fees &OtheR IncOMes - UDHD, Jharkhand

157

215 Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes CHAPTER 11 RENTALS, FEES &OTHER INCOMES INTRODUCTION 11.1 ULBs derive substantial portions of their revenue from Holding & other taxes, Water Tax/Water Charges and Grants. In addition, they also have certain additional sources of revenue like Rentals from Municipal Properties, Advertisement Taxes, License Fees, etc. This chapter contains the recommended accounting procedures for transactions related to such Incomes. 11.2 Some of the Incomes under these categories that may arise to ULBs are listed below: Crematorium Charges; ➢ Burial Ground Charges; ➢ Cattle Pounding Fees; ➢ Parking Fees; ➢ Fees for Pay & Use Toilets; ➢ Slaughtering Fees; ➢ Library Fees; ➢ Fire Extinguishing Service Charges; ➢ Sale & Hire Charges, for example, ➢ Sale of Scrap; • Sale of Forms & Documents; ➢ Sale of Tender Forms; • Hire Charges of Road Rollers; • Hire Charges of Tools & Equipment; • Sale of garbage/Manure; • Sale of Trees, • Sale of Fruits; • Sale of Grass; • Sale of Nursery Plants; • Sale of Flowers; etc. • 11.3 The aspects relating to Incomes to be accounted on actual receipt basis include: Collections ➢ Refunds. ➢ INCOMES TO BE ACCOUNTED ON ACCRUAL BASIS 11.4 Incomes for which demand is raised shall be accounted on accrual basis. These include the following (indicative): i. Rental Income from Municipal Properties, for example Rent from Markets/Shopping Complexes; •

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of chApteR 11 RentAls, Fees &OtheR IncOMes - UDHD, Jharkhand

215

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

chApteR 11RentAls, Fees &OtheR IncOMes

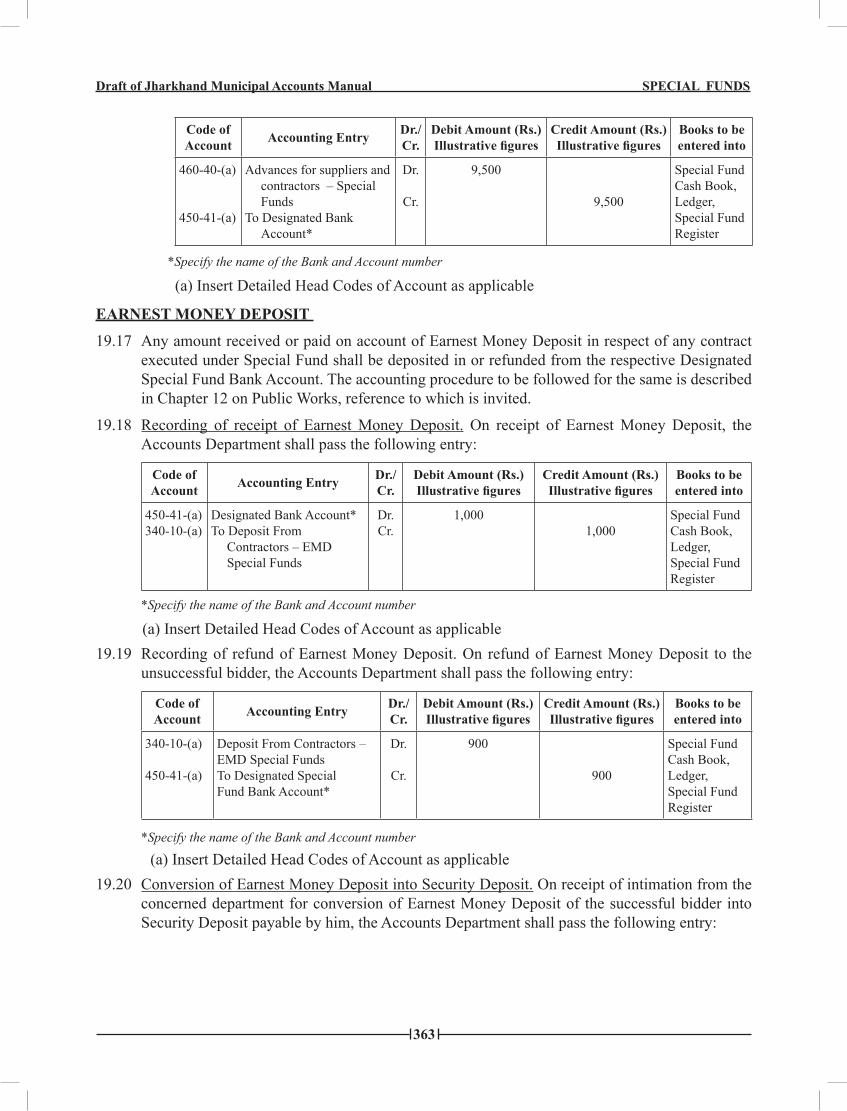

IntRODuctIOn

11.1 ULBs derive substantial portions of their revenue from Holding & other taxes, Water Tax/Water Charges and Grants. In addition, they also have certain additional sources of revenue like Rentals from Municipal Properties, Advertisement Taxes, License Fees, etc. This chapter contains the recommended accounting procedures for transactions related to such Incomes.

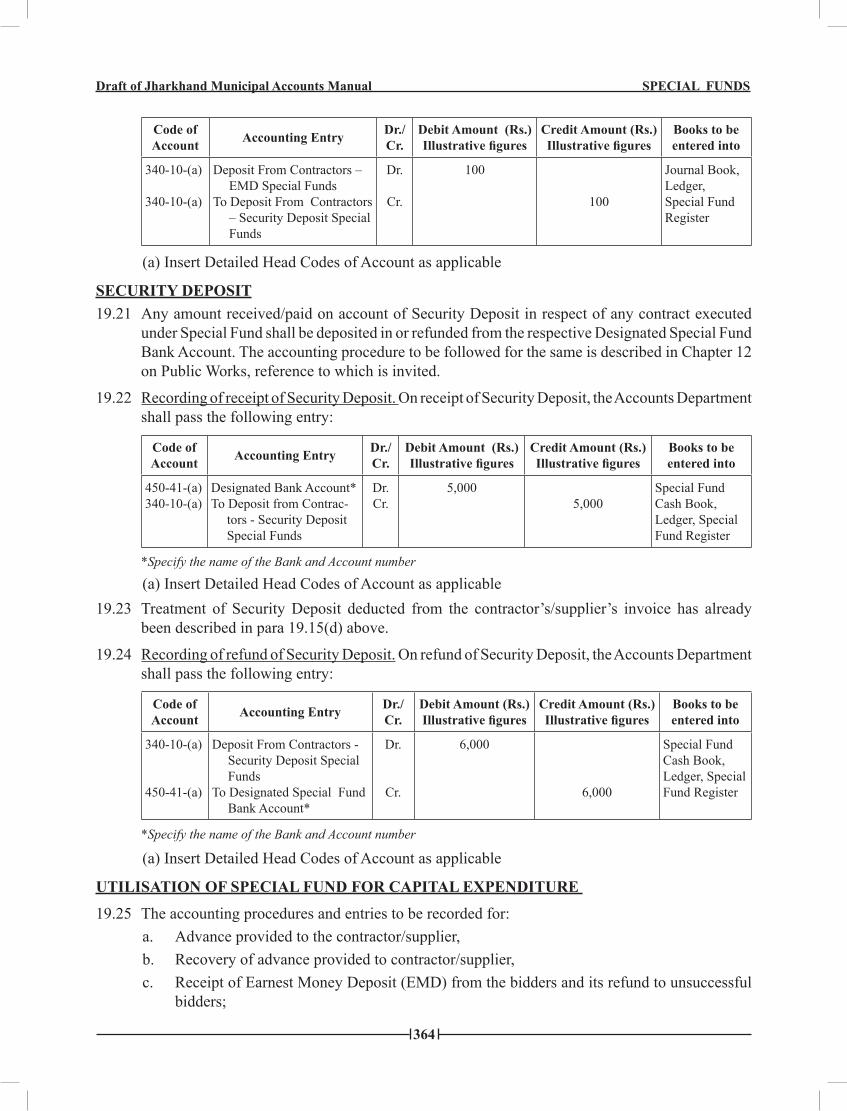

11.2 Some of the Incomes under these categories that may arise to ULBs are listed below:

Crematorium Charges; ➢

Burial Ground Charges; ➢

Cattle Pounding Fees; ➢

Parking Fees; ➢

Fees for Pay & Use Toilets; ➢

Slaughtering Fees; ➢

Library Fees; ➢

Fire Extinguishing Service Charges; ➢

Sale & Hire Charges, for example, ➢

Sale of Scrap; •Sale of Forms & Documents; ➢

Sale of Tender Forms; •Hire Charges of Road Rollers; •Hire Charges of Tools & Equipment; •Sale of garbage/Manure; •Sale of Trees, •Sale of Fruits; •Sale of Grass; •Sale of Nursery Plants; •Sale of Flowers; etc. •

11.3 The aspects relating to Incomes to be accounted on actual receipt basis include:

Collections ➢

Refunds. ➢

IncOMes tO Be AccOunteD On AccRuAl BAsIs

11.4 Incomes for which demand is raised shall be accounted on accrual basis. These include the following (indicative):

i. Rental Income from Municipal Properties, for exampleRent from Markets/Shopping Complexes; •

216

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

Rent from Office Buildings; •Rent from Guest Houses; •Rent from Auditorium, Art Galleries; •Rent/Lease from Parking Zones; etc. •Rent/Lease from Parking Zones; etc. •

ii. Trade License Feesiii. Advertisement Charges/Rightsiv. Profession Tax.

11.5 The various aspects relating to Incomes to be accounted on accrual basis include:

Entry in the Demand Register ➢

Raising of Bills ➢

Collection of dues ➢

Refunds, Remissions and write-offs. ➢

AccOuntIng pRIncIples

11.6 The following Accounting Principles shall govern the recording, accounting and treatment of transactions relating to Other Incomes:

a. Revenue in respect of Advertisement rights shall be accrued either based on Demand or based on the contract. The premium amount, if any, or the lump sum amount received shall be recognized over the period of agreement

b. Revenue in respect of Trade License Fees shall be accrued in the year to which it pertains and where the Demand is raised based on applicable Acts of the state.

c. Revenues in respect of Profession Tax on Organisations / entities shall be accrued in the year to which it pertains where the demand is raised based on applicable Acts of the state.

d. Revenues in respect of rents from properties shall be accrued based on terms of agreement.

e. Other income, in respect of which demand is ascertainable and can be raised in regular course of operations of the ULB, shall be recognised in the period in which they become due, i.e., when the bills are raised.

f. The Other Incomes, which are of an uncertain nature or for which the amount is not ascertainable or where demand is not raised in regular course of operations of the ULB, shall be recognised on actual receipt.

g. Revenue in respect of Notice Fee, Warrant Fee, Other Fees shall be recognised when the bills for the same are raised.

h. Interest element and Penalties, if any, in demand shall be reckoned only on receipt.i. In respect of the demand outstanding beyond two (2) years, provision shall be made to the

extent of income of ULB in the demand, based on the following provisioning norms:Outstanding for more than 2 year but not exceeding 3 years: 50% •Outstanding for more than 3 years: 100% (additional 50%) •

j. Any additional provision for demand outstanding required to be made during the year shall

217

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

be recognised as expenditure and any excess provision written back during the year shall be recognised as income of the ULB.

k. Refunds, remissions of Other Incomes for the current year shall be adjusted against the income and if pertain to previous years then it shall be treated as prior period item.

l. Write-offs of Other Incomes shall be adjusted against the provisions made and to that, extent recoverable is reduced.

m. Any subsequent collection or recovery of ‘Receivables of Rental, Fees and Other Incomes’ which were already written off shall be recognised as a ‘Prior Period Income’.

n. In case of Public Private Partnership where the ULB along with a private concern enters into an agreement of operation or business, revenue shall be recognised on due basis. In case of revenues generated from commercial ventures undertaken by the ULB without any private partnership, it shall also be accounted for on due basis.

o. Salami/ One time initial lump sum payment received against property shall be accounted for on receipt basis and transferred to Municipal Fund.

AccOuntIng RecORDs AnD pROceDuRes

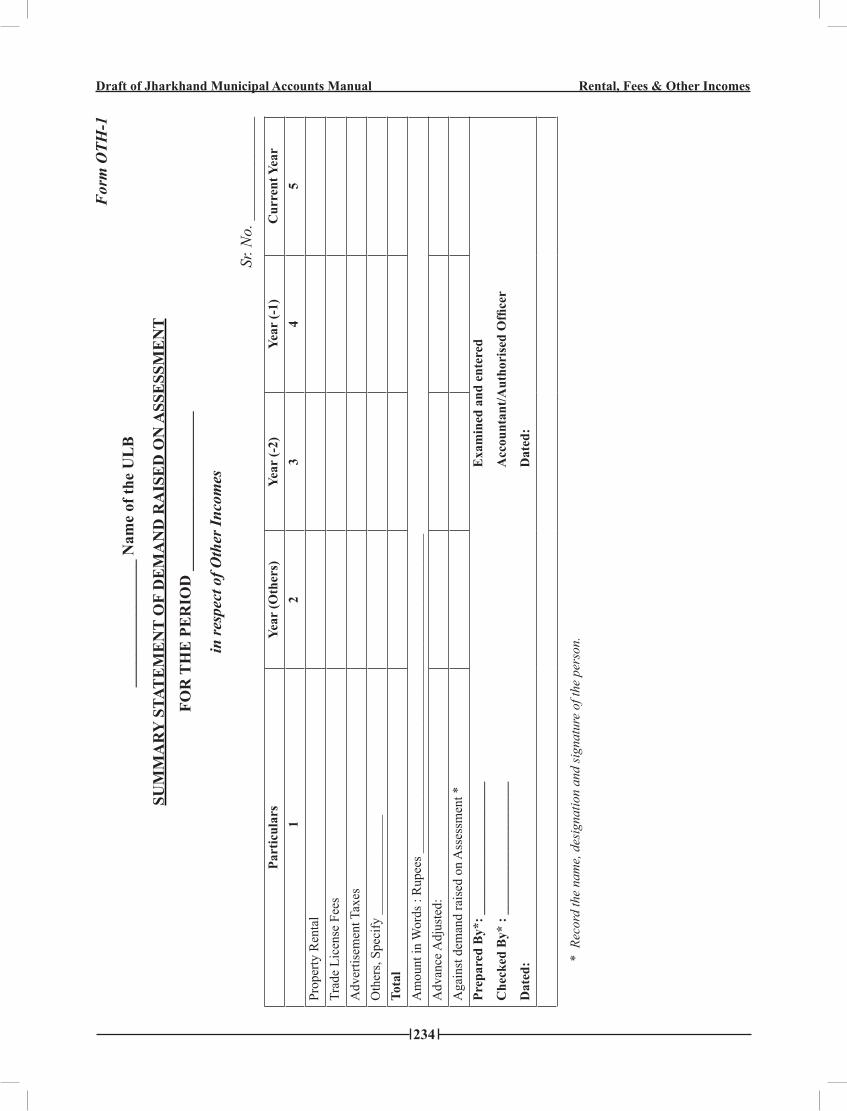

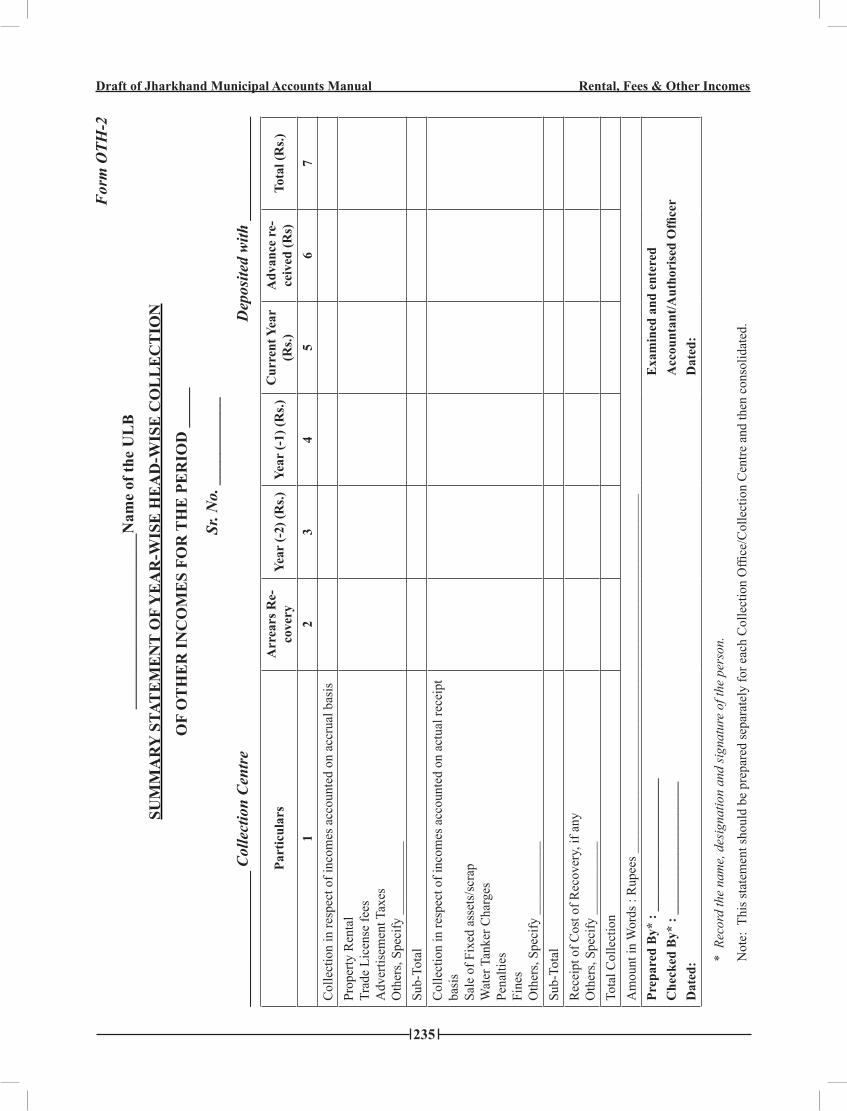

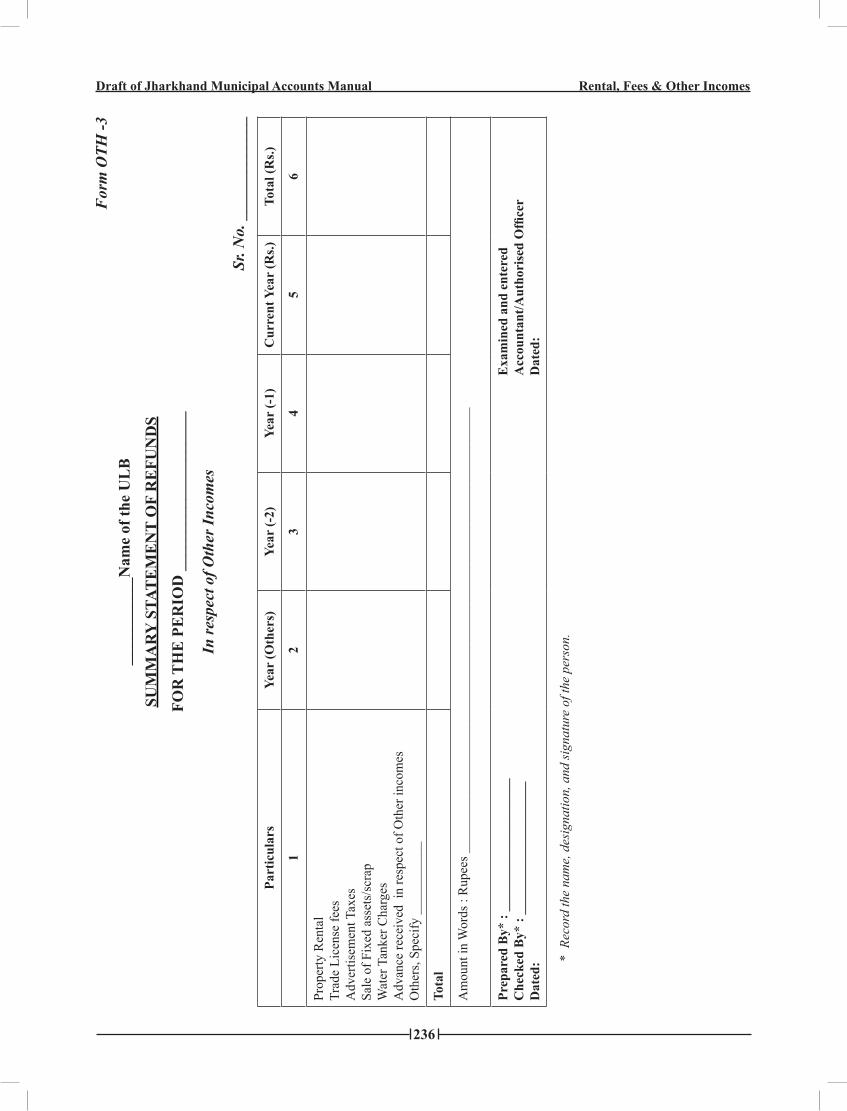

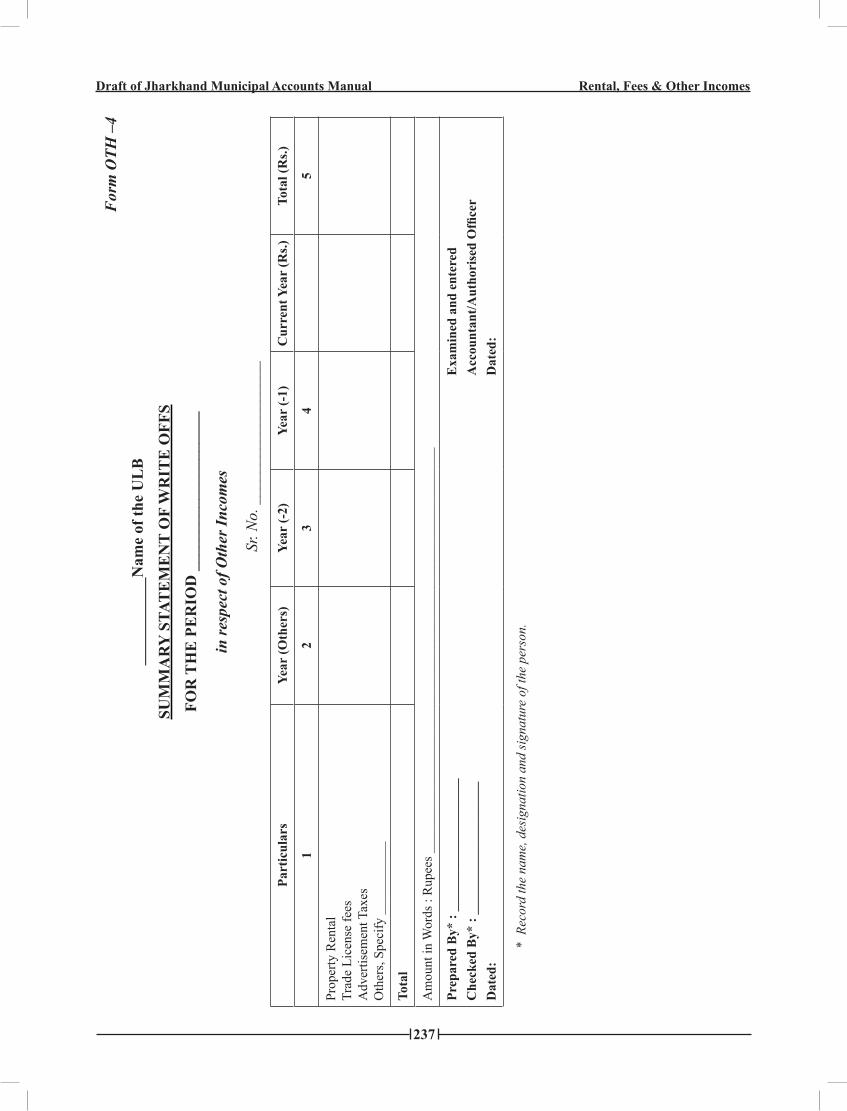

11.7 This section describes the records, registers, documents, forms, accounting entries, etc., in respect of accounting for transactions related to Rental, Fees and Other Incomes. For the purposes of accounting of Other incomes there are certain forms, registers, etc., which are specific to certain type of other incomes, e.g., Summary Statement of Year-wise Head-wise Collection of Rents or similar incomes (Form OTH-1). These Forms OTH –1 to OTH –4 are annexed to this chapter.

AccOuntIng FOR IncOMes tO Be AccOunteD On ActuAl ReceIpt BAsIs

cOllectIOn

11.8 The following shall be the procedure for accounting of the collections made in respect of these Incomes:

Recording of income. Suppose an ULB has earned income on registration charges on dogs and sale of Birth Certificate Forms - To record the income in respect of these Incomes accounted on actual receipt basis, based on the Summary of Daily Collection (Form GEN- 12) received from the various Collection Offices and Collection Centers, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.)

Illustrative figures

Books to be entered into

450-21-(a)140-10-08

150-11-08

Bank Account*To Registration on

Dogs (Fees & User) Charges

To Birth Certificate Forms (Sale & Hire) \ Charges

Dr.Cr.

Cr.

10,0007,000

3,000

Cash Book, Ledger

* Specify name of the Bank and account number

(a) Insert detailed Head codes of Account as applicable

218

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

Note: The postings in the Ledger (Form GEN-3) of “Bank” Account and “_____User Charges” Account shall be carried out as indicated in Chapter 5 – General Accounting Procedures. The postings in the Ledger shall be similarly carried out in respect of all other accounting entries described subsequently in this chapter. Whenever, the cash or the bank account is involved, there will be no entry in the Journal Book (Form GEN-2)

ReceIpt OF IncOMes In ADvAnce

11.9 In cases where the Incomes that are accounted on actual receipt basis are received in advance, i.e., before providing the services/goods, they shall be recorded as income on collection. In case the amount collected is to be refunded, the refund shall be recorded as expenditure.

11.10 For example, if a sum of Rs. 1,000/- has been received in advance for Service Charges. On receipt, the amount shall be recorded as Fees & User Charges. To record the income, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

450-21-(a)140-(b)

Bank Account*To (Fees & User)

Charges**

Dr.Cr.

1,0001,000

Cash Book, Ledger

* Specify name of the Bank and account number

(a) Insert detailed Head codes of Account as applicable(b) Insert Minor & Detailed Head Codes of Account as applicable.

11.11 In case the service is not provided and the customer demands a refund of the amount paid by him in advance. To record the refund, the Accounts Department shall pass the following entry on payment of the refund:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

140-(b)

450-21-(a)

Refund- (Fees & User) Charges *To Bank Account*

Dr.

Cr.

1,000

1,000

Cash Book, Ledger

* Specify name of the Bank

(a) Insert detailed Head Codes of Account as applicable(b) Insert Minor & Detailed Head Codes of Account as applicable.

DepOsIts

11.12 In respect of certain Incomes (including incomes accounted for on accrual basis), a deposit is taken at the time of receiving the application for providing the services/goods, e.g., Rent Deposit, etc. The accounting for the different transactions in respect of deposits received in respect of Incomes, have been discussed below, using the example of Rent Deposit.

11.13 Recording of receipt of deposits. On receipt of deposit, the same shall be treated as a liability. To record the receipt of Rent Deposit, say of Rs. 10,000/-, the Accounts Department shall pass the following entry:

219

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative

figures

Books to be entered

into

450-21-(a)340-20-(a)

Bank Account*To Deposits Revenues

– Rent

Dr.Cr.

10,00010,000

Cash Book, Ledger

* Specify Name of the Bank and account number

(a) Insert detailed Head codes of account as applicable11.14 Recording of adjustment of deposits. The ULB may adjust the deposits received against the

cost of the services rendered by it to the customer. On adjustment of deposits, the respective departments shall send the details of deposits adjusted in the Summary Statement of Deposits Adjusted (GEN- 19) to the Accounts Department on monthly basis. If Rent Deposit of Rs. 5,000/- has been adjusted against Rent Income, to record the adjustment of deposits, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

340-20-(a)130-(b)

Deposit Revenues – RentTo Rental Income from

Municipal Properties

Dr.Cr.

5,0005,000

Journal Book, Ledger

(a) Insert detailed Head codes of account as applicable(b) Insert Minor & Detailed Head Codes of Account as applicable.

11.15 Recording of refund of deposits. The deposits shall be refunded when an application is made for it as per the rules prescribed for the same. A Payment Order (GEN – 14) shall be prepared by the respective departments for the refund of the deposits. On refund of the balance Rent Deposit of Rs. 5,000, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

340-20-(a)

450-21-(a)

Deposit Revenues – Rent

To Bank Account *

Dr.

Cr.

5,000

5,000

Cash Book, Ledger

* Specify name of the Bank and account number

(a) Insert detailed Head Codes of Account as applicable

11.16 Recording of income in respect of lapsed deposit. Deposits not claimed within the period as laid down by the ULB, from the date it is due for payment, shall be considered as lapsed and shall not be repaid to the party. At the end of each accounting year, the respective departments shall prepare a list of such lapsed deposits. To recognise the income, on obtaining the approval of the Authorised Officer, the Accounts Department shall pass the following entry (assuming Rent Deposit of Rs. 1,000 has lapsed):

220

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

340-20-(a)

180-11-(a)

Deposit Revenues – Rent

To Lapsed Deposit - Rent

Dr.

Cr.

1,000

1,000

Journal Book, Ledger, Deposit Register

(a) Insert detailed Head Codes of Account as applicable

11.17 Similar entries as above shall be passed for recording the various transactions in receipt of other deposits for example deposits relating to License Fees and Advertisement Taxes.

AccOuntIng FOR IncOMes tO Be AccOunteD On AccRuAl BAsIs

11.18 The accounting of the various aspects relating to Incomes accounted on accrual basis have been discussed below in respect of Rent, License Fees, and Advertisement Taxes are explained below:

A. RentAl IncOMe

DeMAnD RAIseD

11.19 In respect of the demand raised, the Accounts Department shall do the following:

Recording of demand raised. The demand raised for Incomes shall be recognised as an income for the ULB and correspondingly as a current asset. Accordingly, based on the Summary Statement of Bills Raised (Form OTH –1) received from the respective departments, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

431-40-(a)

130-(b)

Receivables from Other Sources -Rent (Year…)**

To Rental Income from Municipal Properties

Dr.

Cr.

20,000

20,000

Journal Book, Ledger

(a) Insert detailed Head Codes of Account as applicable (b) Insert Minor & detailed Head Codes of Account as applicable

11.20 It is a normal practice for the ULB to enter the arrears of the dues while issuing the fresh demand. Entries in respect of the arrears shall have already been recorded earlier. The above entry shall be passed only in respect of the current demand of Other Incomes. The rental incomes earned out of shopping complexes, markets, office buildings, etc shall be entered in the relevant fixed assets register for E.g. Register of Immovable properties in form GEN 30 or in Register of Movable Properties in form GEN 31. The registers shall be updated periodically as per the provisions and rules of the Act governing the ULBs.

cOllectIOn OF AccRueD IncOMes

11.21 The following shall be the procedure for accounting of the collections made in respect of accrued Incomes:

221

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

11.22 Recording of Income collections. To record the income based on the Summary of Daily Collections (Form GEN-12) received from the various Collection Offices and Collection Centers, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

450-21-(a)431-80-(a)

Bank Account*To Receivables Control

Account – Rent

Dr.Cr.

15,00015,000

Cash Book, Ledger

* Specify Name of the Bank and account number

(a) Insert detailed Head Codes of Account as applicable11.23 For Other Incomes to be accounted on accrual basis, the Summary of Daily Collection (Form

GEN- 12) does not provide the break-up of the collections into arrears collected, collections received in advance and collection made in respect of the current year’s demand. Hence, the total amount collected is credited to “Consolidated Receivables of Rent” Account which shall be segregated on a monthly basis.

11.24 Recording of break-up of collections. A Summary Statement of Year-wise/ Head-wise Collection of various other incomes in Form OTH-2 shall be prepared on a monthly basis by the respective departments and sent to the Accounts Department to record the details of collection. . To record the break-up of the collections made in respect of Incomes accounted for on accrual basis, into current and arrears recovery and to record any income collected in advance, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

431-80-(a)

431-40-(a)

431-40-(a)

350-41-(a)

Receivables Control Account -Rent

To Receivables from Other Sources –Rent

(Year…)To Receivables from

Other Sources –Rent (Year…)To Advance Collection

of Revenues – Rent*

Dr.

Cr.

Cr.

Cr.

18,000

15,000

2,000

1,000

Journal Book, Ledger

* Adjustment of income collected in advance is discussed separately under section ‘Adjustment of Other Incomes received in Advance’

(a) Insert detailed Head Codes of Account as applicable

nOtIce Fee, WARRAnt Fee AnD OtheR Fees

11.25 Notices of demand and warrants shall be issued and other fees may be charged as per the relevant provisions.

11.26 Recording of demand raised. A Summary Statement of Notice Fee, Warrant Fee and Other Fees Charged in Form GEN 24 shall be prepared on a monthly basis and sent to the Accounts Department.

222

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

11.27 For recording the demand raised in respect of Notice Fee, Warrant Fee and Other Fees charged for rent not received, on the basis of the Summary Statement of Notice Fee, Warrant Fee and Other Fees Charged received from the respective departments, the Accounts Department shall pass the same entry as explained in Para 6.15 of Chapter 6 on Holding & Other Taxes.

ReFunDs AnD ReMIssIOns

11.28 All refunds and remissions arising on account of certain changes or amendments of the provisions or acts governing the revenues shall be duly recorded in the Demand Registers maintained and the details of the same shall also be communicated to the Accounts Department.

11.29 Recording of refunds/remissions payable. A Summary Statement of Refunds and Remissions in Form OTH – 3 shall be prepared on a monthly basis. Refunds / Remissions pertaining to prior period shall be identified separately from the current period based on which the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

130-90-(a)280-60-(a)

350-40-(a)

Rents Remission & Refund Prior Period Expenses Refund

of Other Revenues– Rent To Refund Payable –Rent*

Dr.Dr.

Cr.

500100

600

Journal Book, Ledger

* Refunds/Remissions arising on account of change in the applicable rules shall be either passed for ‘Payment’ or credited to the account ‘Advance Collection of Revenues- Rent’ (with account code 350-41-(a)) in accordance with the accounting principles of the ULB.

(a) Insert detailed Head Codes of Account as applicable11.30 Recording of payment of refunds/remissions granted: The Accounts Department shall prepare

a Payment Order (Form GEN-14) in respect of the refunds and communicate the details of refunds/remissions payments to the concerned departments for updating the Register of Demand and other registers. To record refunds made, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

350-40-(a)450-21-(a)

Refund Payable – RentTo Bank Account*

Dr.Cr.

500500

Cash Book, Ledger

* Specify name of the Bank and account number

(a) Insert detailed Head Codes of Account as applicable

ADJustMent OF IncOMes ReceIveD In ADvAnce

11.31 The respective departments shall intimate the Accounts Department of the advance adjusted against the subsequent bills raised through the Summary Statement of Bills Raised (Form OTH – 1).

(a) Recording of subsequent demand raised in the normal course. To record the demand raised for rent, the Accounts Department shall pass same entry as in the case of original demand as explained in Para 11.19.

223

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

(b) Recording of adjustment of advance. To record the adjustment of Other Incomes received in advance, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

350-41-(a)

431-40-(a)

Advance Collection of Revenues – Rent

To Receivables from Other Sources –Rent (Year…)

Dr.

Cr.

1,000

1,000

Journal Book, Ledger

(a) Insert detailed Head Codes of Account as applicable

DepOsIts

11.32 The accounting in respect of receipt, adjustment, refund of deposits and recognising income in respect of lapsed deposits for Incomes accounted on accrual basis shall be similar to that for Incomes accounted for on actual receipt basis. The entry for adjustment of deposit for income to be accounted on accrual basis has been given below.

11.33 Recording of adjustment of deposits. The ULB may adjust the deposits received against the cost of the services rendered by it to the customer. The respective departments shall send the details of deposits adjusted in the Summary Statement of Deposits Adjusted (Form GEN-19) to the Accounts Department on monthly basis.

11.34 If Rent Deposit of Rs. 5,000/- has been adjusted against recovery of dues towards Rent Income, to record the adjustment of deposits, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

340-20-(a)431-40-(a)

Deposit Revenues – RentTo Receivables from Other Sources - Rent (Year…)

Dr.Cr.

5,0005,000

Journal Book, Ledger

(a) Insert detailed Head Codes of Account as applicable

pROvIsIOn FOR unReAlIseD Revenue ReceIvABles

11.35 Recording of provision for unrealised Income. The demand outstanding beyond two (2) years shall be provided for as per provisioning norms given below:

Outstanding for more than 2 year but not exceeding 3 years: 50% ➢

Outstanding for more than 3 years: 100% (additional 50%) ➢

For example, provision for the year ended March 31, 2010 is as under:

a. 50% of outstanding Receivables of Rent for the year ended March 31, 2008 b. 100% of outstanding Receivables of Rent for the year ended March 31, 2007 and before.

11.36 Additional provision or reversal of excess provision for the current period shall be calculated similar to computations explained in Tables 6.1 & 6.2 in Chapter 6 for Holding & Other Taxes.

11.37 For making the provision, the following entry shall be passed by the Accounts Department:

224

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

270-10-(a)

432-40-(a)

Provision for Doubtful Receivables- RentTo Provision forOutstanding Other Receiv-ables – Rent

Dr.

Cr.

1,500

1,500

Journal Book, Ledger

(a) Insert detailed Head Codes of Account as applicable11.38 The effect of the above entry will be as follows:

a. Provision for Doubtful Receivables - Rent will be shown as a separate item under the Major expense head ‘Provisions and Write off;

b. Provision for Outstanding Other Receivables will be shown as a deduction from Receivables from Other Sources- Rent in the Balance Sheet.

11.39 To write back the provision made earlier, the following entry shall be passed:

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

432-40-(a)

180-60-(a)

Provision for Outstanding Other Receivables – Rent

To Excess Provision Written Back – Rent

Dr.

Cr.

500

500

Journal Book, Ledger

(a) Insert detailed Head Codes of Account as applicable

WRIte-OFFs

11.40 Recording of Write-offs. If for any reason, it is decided by the ULB to write-off any Other Income dues, the details of the write off has to be entered in the ‘Statement of Write off’ by the respective departments in Form OTH – 4. This form has to be prepared on a monthly basis and forwarded to the Accounts Department and based on which , the write off shall be adjusted against the provision made and the following entry will be passed:

code of Account* Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

432-40-(a)

431-40-(a)

Provision for Outstanding Other Receivables – Rent

To Receivables from Other Sources –Rent (Year…)

Dr.

Cr.

500

500

Journal Book, Ledger

(a) Insert detailed Head Codes of Account as applicable11.41 Recording of subsequent collection/ recovery of ‘Receivables of Rents/License Fees/

Advertisement Taxes’ written off: In case of a ‘Receivables of Rents/License Fees/Advertisement Taxes’ written off already were recovered/collected during the year, the accounts department shall pass the following entry:

225

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

code of Account* Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative figures

Books to be entered into

431-80-(a) 280-30-(a)

Receivables Control Account - - Rent

To Prior period Income –Recovery of Revenues written off-Rent

Dr.

Cr.

1,000

1,000

Journal Book, Ledger

(a) Insert detailed Head Codes of Account as applicable

tRAnsFeR OF AMOunt OutstAnDIng In Respect OF ARReARs FROM specIFIc yeAR-WIse AccOunt tO geneRAl AccOunt

11.42 The arrears of Other Income shall be carried forward year-wise, e.g., in “Receivables of Other Income (Year…)” account up to three years. On completion of the third year, the amount outstanding in the specific year-wise receivable account shall be transferred to a general arrears account, i.e., “Receivables of Other Income (Others)” Account. For example, the rent receivable in respect of the demand raised during the accounting year 2007-08 shall be carried forward in “Receivables of Rent (2008)” Account up to the year ending March 31, 2011. On March 31, 2011, the balance outstanding in this account shall be transferred to “Receivables of Rent (Others)” Account.

11.43 Recording of transfer of arrears to general account. To record this transfer, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

431-40-(a)

431-40-(a)

Receivables from Other Sources –Rent (Others)

To Receivables from Other Sources –Rent (Year…)

Dr.

Cr.

5,000

5,000

Journal Book, Ledger

(a) Insert detailed Head Codes of Account as applicable

RecOveRy OF OtheR IncOMes thROugh legAl pROceeDIngs

11.44 The transactions in respect of Recovery of Holding and Other Taxes have been described in Chapter 6 – Holding & Other Taxes (para 6.34 to 6.40), reference to which is invited. The transactions relating to Recovery of Other Incomes shall be accounted in similar manner.

B. lIcense Fees

11.45 The license fees charged for granting license to any trade, shops, markets etc. Similar to accruing of rental income, license fees shall also be accrued based on raising a demand in form OTH – 1. Accounting entries in respect of Demand and Collection are detailed below. However in respect of notice fees, refunds, adjustment of advances & deposits, provisions, write off and transfer outstanding from specific year to general account, reference is invited to entries explained above under Section A – Rental Income.

DeMAnD RAIseD

11.46 Recording of demand raised. The demand raised for Income shall be recognised as an income for the ULB and correspondingly as a receivable. Accordingly, based on the Summary Statement of

226

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

Bills Raised (Form OTH –1) received from the respective departments, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

431-30-(a)

140-11-(a)

Receivables for Fees & User Charges - License Fees (Year…)

To Licensing Fees - Trade

Dr.

Cr.

20,000

20,000

Journal Book, Ledger

(a) Insert detailed Head Codes of Account as applicable11.47 It is a normal practice for the ULB to enter the arrears of the dues while issuing the fresh demand.

Entries in respect of the arrears shall have already been recorded earlier. The above entry shall be passed only in respect of the current demand of Other Incomes.

cOllectIOn OF AccRueD IncOMes

11.48 The following shall be the procedure for accounting of the collections made in respect of accrued Incomes:

a. Recording of Income collections. To record the income based on the Summary of Daily Collections (Form GEN-12) received from the various Collection Offices and Collection Centres, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

450-21-(a)431-30-(a)

Bank Account*To Receivables Control

accounts - License Fees

Dr.Cr.

15,00015,000

Cash Book, Ledger

* Specify name of the Bank and account number

(a) Insert detailed Head Codes of Account as applicableb. For Other Incomes to be accounted on accrual basis, the Summary of Daily Collection (Form

GEN- 12) does not provide the break-up of the collections into arrears collected, collections received in advance and collection made in respect of the current year’s demand. Hence, the total amount collected is credited to “Consolidated Receivables of License Fees” Account which shall be segregated on a monthly basis.

c. Recording of break-up of collections. A Summary Statement of Year-wise/ Head-wise Collection of various other incomes in Form OTH-2 shall be prepared on a monthly basis by the respective departments and sent to the Accounts Department to record the details of collection. . To record the break-up of the collections made in respect of Incomes accounted for on accrual basis, into current and arrears recovery and to record any income collected in advance, the Accounts Department shall pass the following entry:

227

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

431-80-(a)

431-30-(a)

431-30-(a)

350-41-(a)

Receivables Control Account –License Fees

To Receivables for Fees & User Charges –Licens Fees (Year…)

To Receivables for Fees & User Charges – License Fees (Year…)

To Advance Collection of Revenues – License Fees *

Dr.

Cr.

Cr.

Cr.

18,000

15,000

2,000

1,000

Journal Book, Ledger

* Adjustment of income collected in advance is discussed separately under section ‘Adjustment of Other Incomes received in Advance’

(a) Insert detailed Head Codes of Account as applicable

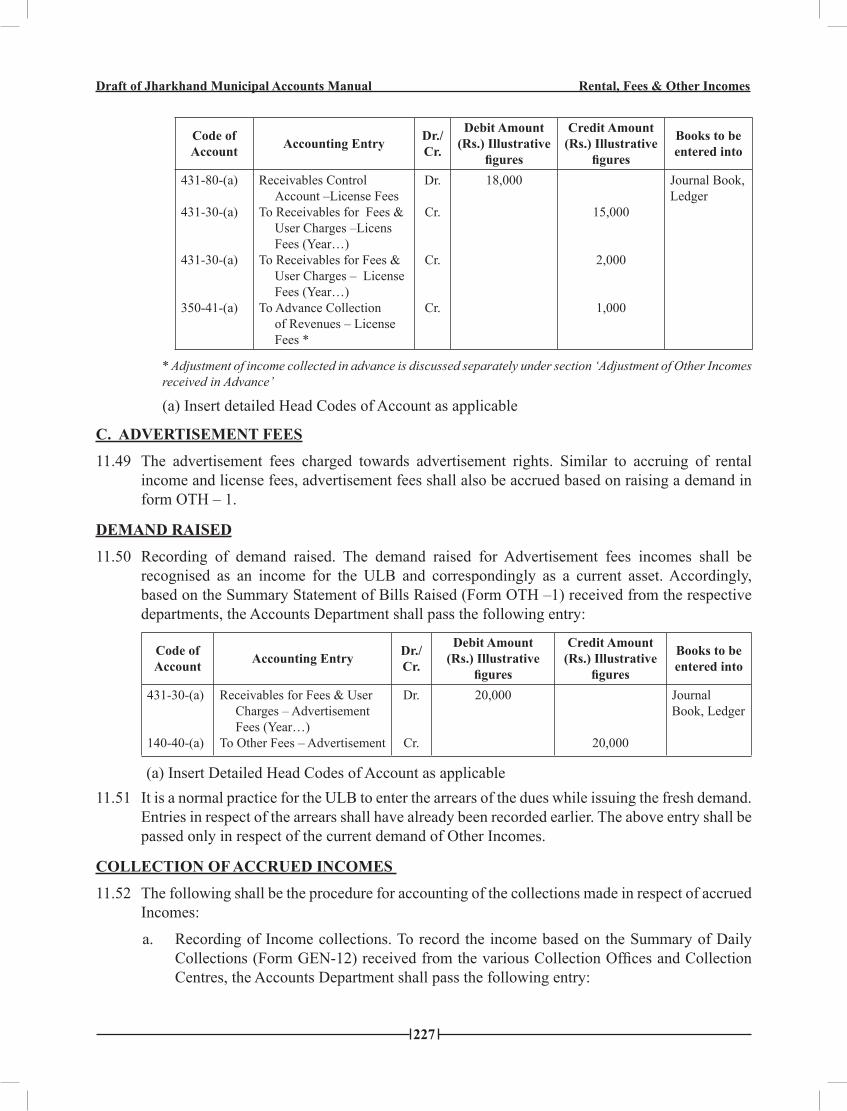

c. ADveRtIseMent Fees

11.49 The advertisement fees charged towards advertisement rights. Similar to accruing of rental income and license fees, advertisement fees shall also be accrued based on raising a demand in form OTH – 1.

DeMAnD RAIseD

11.50 Recording of demand raised. The demand raised for Advertisement fees incomes shall be recognised as an income for the ULB and correspondingly as a current asset. Accordingly, based on the Summary Statement of Bills Raised (Form OTH –1) received from the respective departments, the Accounts Department shall pass the following entry:

code ofAccount Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

431-30-(a)

140-40-(a)

Receivables for Fees & User Charges – Advertisement Fees (Year…)

To Other Fees – Advertisement

Dr.

Cr.

20,000

20,000

Journal Book, Ledger

(a) Insert Detailed Head Codes of Account as applicable11.51 It is a normal practice for the ULB to enter the arrears of the dues while issuing the fresh demand.

Entries in respect of the arrears shall have already been recorded earlier. The above entry shall be passed only in respect of the current demand of Other Incomes.

cOllectIOn OF AccRueD IncOMes

11.52 The following shall be the procedure for accounting of the collections made in respect of accrued Incomes:

a. Recording of Income collections. To record the income based on the Summary of Daily Collections (Form GEN-12) received from the various Collection Offices and Collection Centres, the Accounts Department shall pass the following entry:

228

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative figures

Books to be entered into

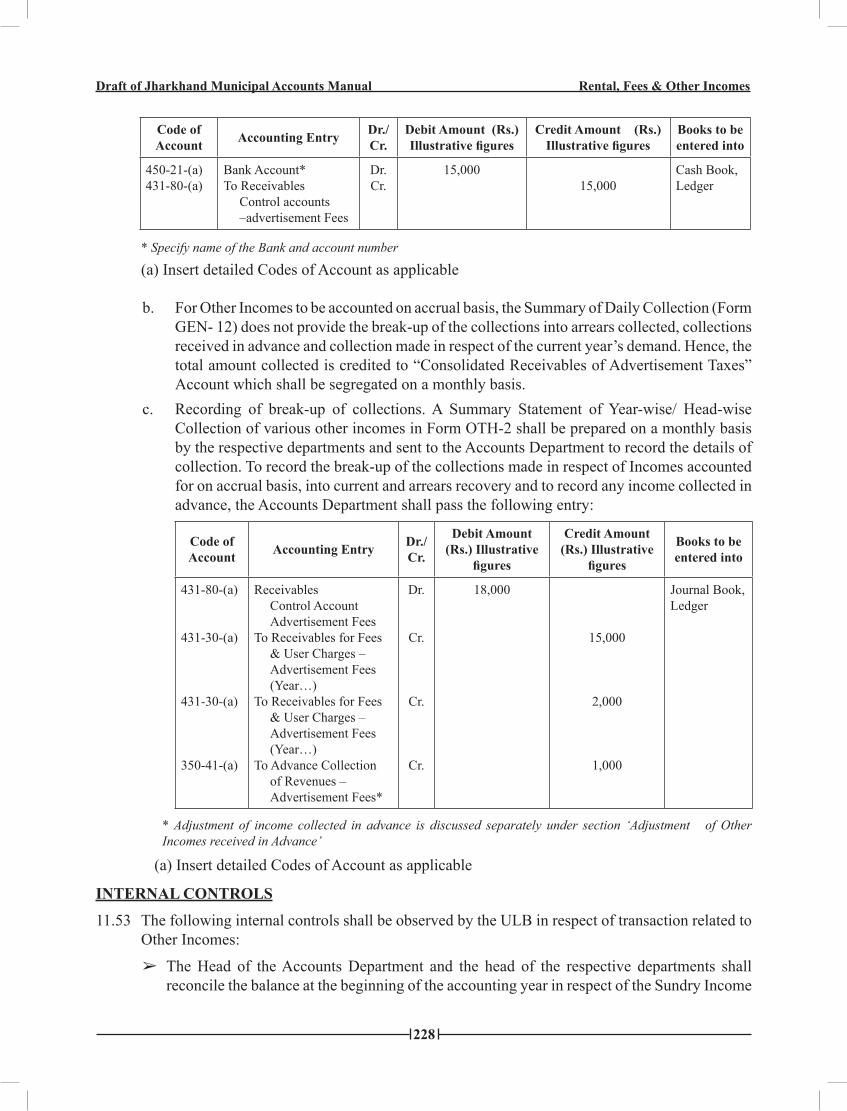

450-21-(a)431-80-(a)

Bank Account*To Receivables

Control accounts –advertisement Fees

Dr.Cr.

15,00015,000

Cash Book, Ledger

* Specify name of the Bank and account number

(a) Insert detailed Codes of Account as applicable

b. For Other Incomes to be accounted on accrual basis, the Summary of Daily Collection (Form GEN- 12) does not provide the break-up of the collections into arrears collected, collections received in advance and collection made in respect of the current year’s demand. Hence, the total amount collected is credited to “Consolidated Receivables of Advertisement Taxes” Account which shall be segregated on a monthly basis.

c. Recording of break-up of collections. A Summary Statement of Year-wise/ Head-wise Collection of various other incomes in Form OTH-2 shall be prepared on a monthly basis by the respective departments and sent to the Accounts Department to record the details of collection. To record the break-up of the collections made in respect of Incomes accounted for on accrual basis, into current and arrears recovery and to record any income collected in advance, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.

Debit Amount (Rs.) Illustrative

figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

431-80-(a)

431-30-(a)

431-30-(a)

350-41-(a)

Receivables Control Account Advertisement Fees

To Receivables for Fees & User Charges – Advertisement Fees (Year…)

To Receivables for Fees & User Charges – Advertisement Fees (Year…)

To Advance Collection of Revenues – Advertisement Fees*

Dr.

Cr.

Cr.

Cr.

18,000

15,000

2,000

1,000

Journal Book, Ledger

* Adjustment of income collected in advance is discussed separately under section ‘Adjustment of Other Incomes received in Advance’

(a) Insert detailed Codes of Account as applicable

InteRnAl cOntROls

11.53 The following internal controls shall be observed by the ULB in respect of transaction related to Other Incomes:

The Head of the Accounts Department and the head of the respective departments shall ➢

reconcile the balance at the beginning of the accounting year in respect of the Sundry Income

229

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

Receivables Arrears (as appearing in the Balance Sheet of the previous year) with the year-wise total of the arrears recorded in the Demand Registers.A quarterly reconciliation shall be carried out by the Head of the Accounts Department and ➢

the head of the respective departments in respect of the amount collected and the arrears outstanding between the balances standing in the Ledger maintained at the Accounts Department and the Demand Registers maintained at the respective departments. A monthly reconciliation shall be carried out by the Head of the Accounts Department and ➢

the head of the respective departments in respect of the various deposits collected, between the balances standing in the Ledger maintained at the Accounts Department and the Deposits Registers maintained at the respective departments. The head of the respective departments shall ensure that the Receipt / Challan for Remittance ➢

of Money prepared, provides reference to the Consolidated Collection Register.The Chief Executive Officer/Head of the ULB shall specify such appropriate calendar of ➢

returns /reports for monitoring.Levy of stallages, rents and fees in Municipal Markets, Slaughter-houses and Stock-yards; ➢

Registration of Births and Deaths Fees; ➢

Fee for grant of licence to Surveyors, Architects, Engineers, Structural Designers, Clerk of ➢

Works, and Plumbers;Professional Tax; ➢

Advertisement Charges/Rights; ➢

Development Charges; etc. ➢

Registration of Births and Deaths Fees; ➢

Fee for grant of licence to Surveyors, Architects, Engineers, Structural Designers, Clerk of ➢

Works, and Plumbers;Professional Tax; ➢

Advertisement Charges/Rights; ➢

Development Charges; etc. ➢

Registration of Births and Deaths Fees; ➢

Fee for grant of licence to Surveyors, Architects, Engineers, Structural Designers, Clerk of ➢

Works, and Plumbers;Professional Tax; ➢

Advertisement Charges/Rights; ➢

Development Charges; etc. ➢

Levy of stallages, rents and fees in Municipal Markets, Slaughter-houses and Stock-yards; ➢

11.54 All Reconciliation Statements shall be certified by the Head of the Accounts Department:

pResentAtIOn In FInAncIAl stAteMents

11.55 The various heads of account used for the accounting of Other Incomes related transactions should be reflected in the Financial Statements or in the Schedules attached to the Financial Statements of the ULB. All such Financial Statements and schedules should be affixed with signature and seal of designated authorities.

230

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

11.56 The provision against the Outstanding Rental and Other Incomes receivable is to be disclosed under the major head Accumulated Provisions as a separate line item in the Balance Sheet below the ‘Sundry Debtors’.

11.57 The Schedule of Income and Expenditure Statement in respect of Other Incomes are presented below.

schedule I-3: Rental income from Municipal properties

Minor head code particulars current year

Amount (Rs.)previous year Amount (Rs.)

1 2 3 4130-10-(a)130-20-(a)130-30-(a)130-40-(a)130-80-(a)

Rent from Civic AmenitiesRent from Office BuildingsRent from Guest HousesRent from lease of landsOther rentssub-totalLess:

130-90-(a) Rent Remission and Refunds sub-total

total Rental Income from Municipal properties

(a) Insert detailed Codes of Account as applicable

schedule I-4: schedule of Income from Fees & user charges

Detailed head code particulars current year

Amount (Rs.)previous year Amount (Rs.)

1 2 3 4140-11-(a)140-20-(a)140-40-(a)140-50-(a)140-60-(a)140-80-(a)

Licensing FeesPenalties and FinesOther Fees – Advertisement FeesUser ChargesEntry FeesOther Chargessub-totalLess:

140-90-(a) Rent Remission and Refunds sub-total

total Income of Other income to be shown as part of Fees & user charges – Income head-wise schedule

(a) Insert detailed Codes of Account as applicable

231

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

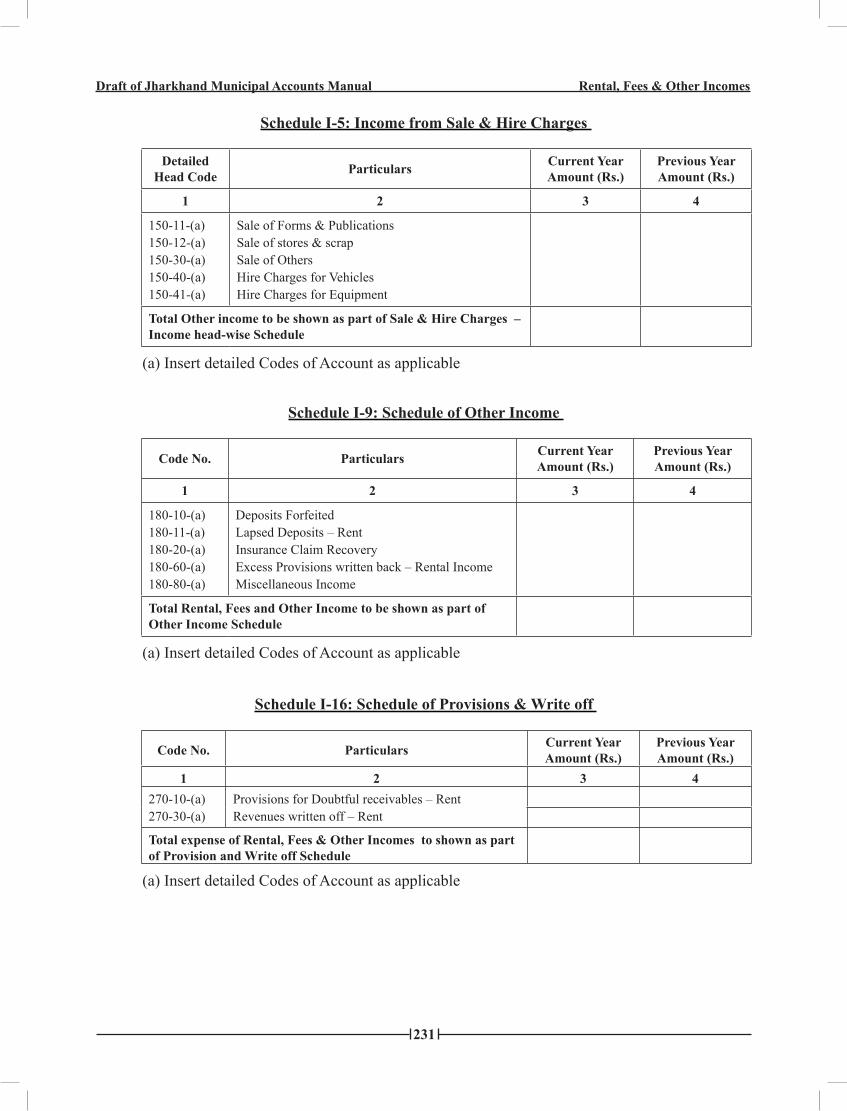

schedule I-5: Income from sale & hire charges

Detailed head code particulars current year

Amount (Rs.)previous year Amount (Rs.)

1 2 3 4

150-11-(a)150-12-(a)150-30-(a)150-40-(a)150-41-(a)

Sale of Forms & PublicationsSale of stores & scrapSale of OthersHire Charges for VehiclesHire Charges for Equipment

total Other income to be shown as part of sale & hire charges – Income head-wise schedule

(a) Insert detailed Codes of Account as applicable

schedule I-9: schedule of Other Income

code no. particulars current year Amount (Rs.)

previous year Amount (Rs.)

1 2 3 4

180-10-(a)180-11-(a)180-20-(a)180-60-(a)180-80-(a)

Deposits ForfeitedLapsed Deposits – RentInsurance Claim RecoveryExcess Provisions written back – Rental IncomeMiscellaneous Income

total Rental, Fees and Other Income to be shown as part of Other Income schedule

(a) Insert detailed Codes of Account as applicable

schedule I-16: schedule of provisions & Write off

code no. particulars current year Amount (Rs.)

previous year Amount (Rs.)

1 2 3 4270-10-(a)270-30-(a)

Provisions for Doubtful receivables – RentRevenues written off – Rent

total expense of Rental, Fees & Other Incomes to shown as part of provision and Write off schedule

(a) Insert detailed Codes of Account as applicable

232

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

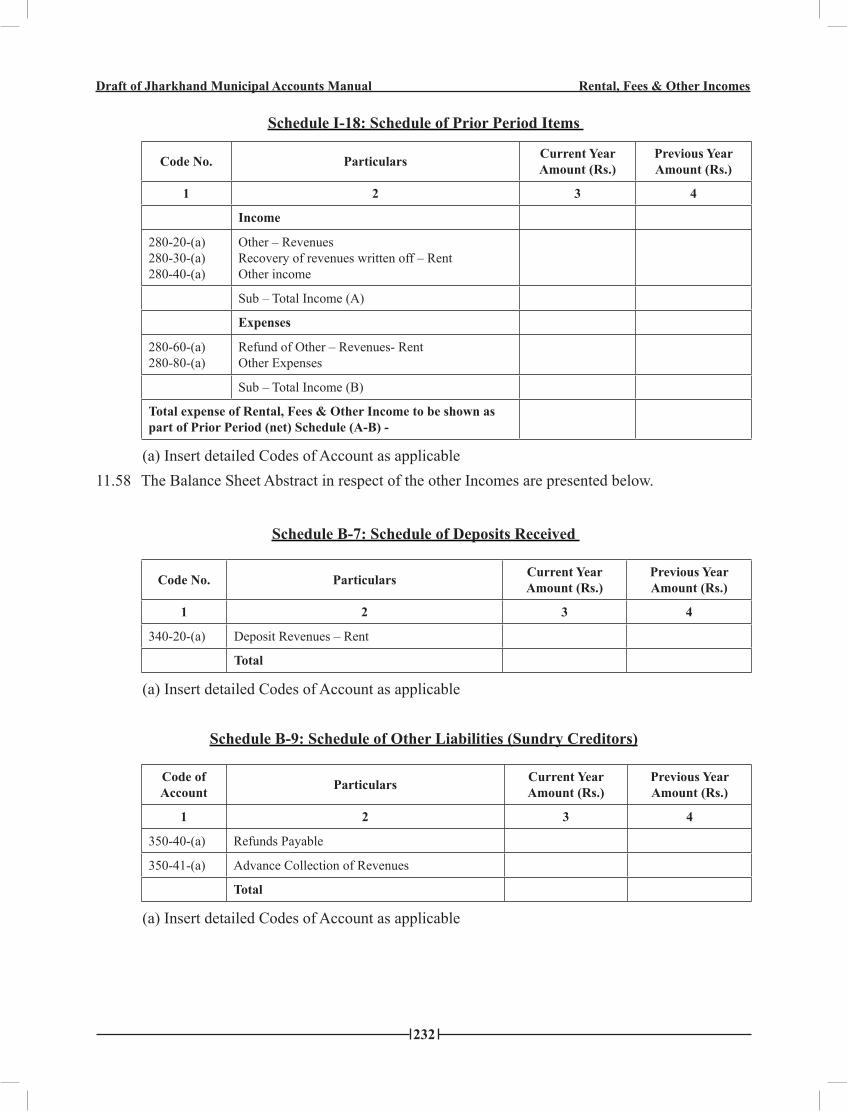

schedule I-18: schedule of prior period Items

code no. particulars current year Amount (Rs.)

previous year Amount (Rs.)

1 2 3 4

Income

280-20-(a)280-30-(a)280-40-(a)

Other – RevenuesRecovery of revenues written off – RentOther income

Sub – Total Income (A)

expenses

280-60-(a)280-80-(a)

Refund of Other – Revenues- RentOther Expenses

Sub – Total Income (B)

total expense of Rental, Fees & Other Income to be shown as part of prior period (net) schedule (A-B) -

(a) Insert detailed Codes of Account as applicable11.58 The Balance Sheet Abstract in respect of the other Incomes are presented below.

schedule B-7: schedule of Deposits Received

code no. particulars current year Amount (Rs.)

previous year Amount (Rs.)

1 2 3 4

340-20-(a) Deposit Revenues – Rent

total

(a) Insert detailed Codes of Account as applicable

schedule B-9: schedule of Other liabilities (sundry creditors)

code of Account particulars current year

Amount (Rs.)previous yearAmount (Rs.)

1 2 3 4

350-40-(a) Refunds Payable

350-41-(a) Advance Collection of Revenues

total

(a) Insert detailed Codes of Account as applicable

233

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

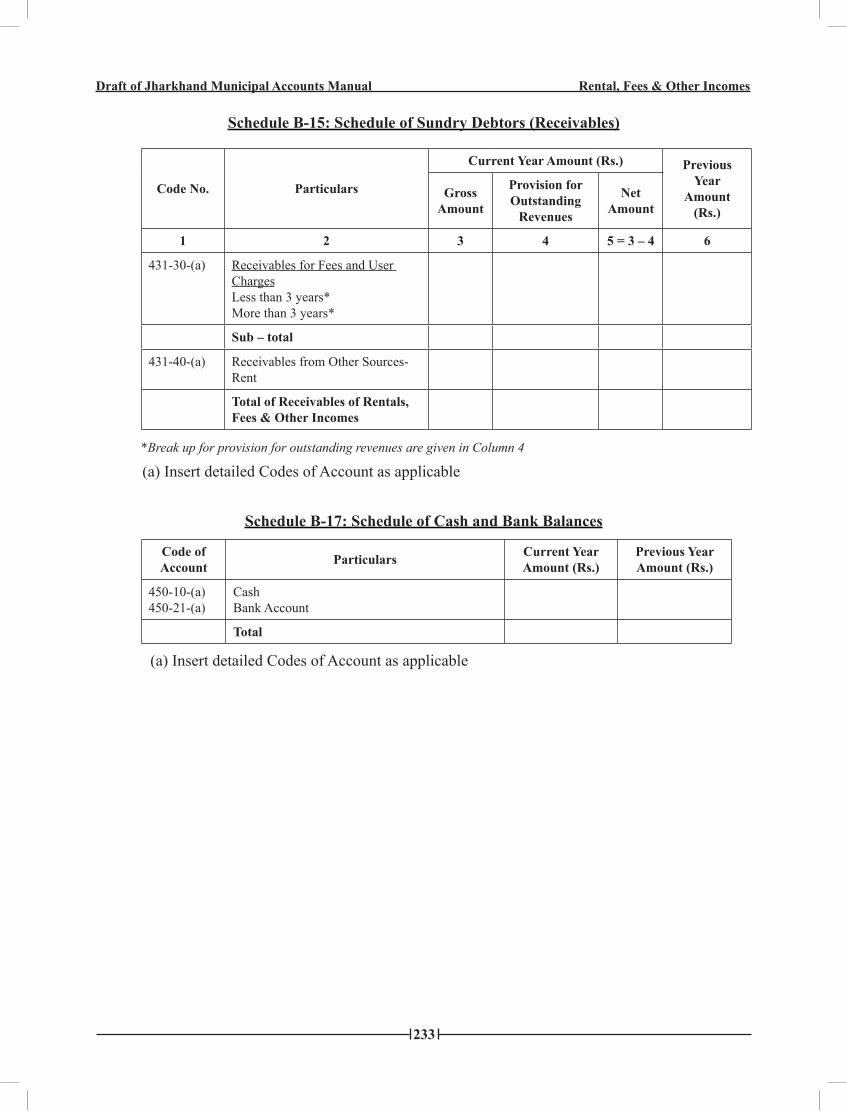

schedule B-15: schedule of sundry Debtors (Receivables)

code no. particulars

current year Amount (Rs.) previous year

Amount (Rs.)

gross Amount

provision for Outstanding

Revenues

net Amount

1 2 3 4 5 = 3 – 4 6

431-30-(a) Receivables for Fees and User ChargesLess than 3 years*More than 3 years*

sub – total

431-40-(a) Receivables from Other Sources- Rent

total of Receivables of Rentals, Fees & Other Incomes

*Break up for provision for outstanding revenues are given in Column 4

(a) Insert detailed Codes of Account as applicable

schedule B-17: schedule of cash and Bank Balances

code of Account particulars current year

Amount (Rs.)previous yearAmount (Rs.)

450-10-(a)450-21-(a)

CashBank Account

total

(a) Insert detailed Codes of Account as applicable

234

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other IncomesF

orm

OTH

-1

____

____

____

____

nam

e of

the

ul

B

suM

MA

Ry

stA

te

Me

nt

OF

De

MA

nD

RA

Ise

D O

n A

sse

ssM

en

t

FOR

th

e p

eR

IOD

___

____

____

____

____

_

in re

spec

t of O

ther

Inco

mes

S

r. N

o. _

____

____

____

part

icul

ars

year

(Oth

ers)

year

(-2)

year

(-1)

cur

rent

yea

r

1

23

45

Prop

erty

Ren

tal

Trad

e Li

cens

e Fe

esA

dver

tisem

ent T

axes

Oth

ers,

Spec

ify _

____

____

____

__to

tal

Am

ount

in W

ords

: R

upee

s ___

____

____

____

____

____

____

____

____

____

____

____

_A

dvan

ce A

djus

ted:

Aga

inst

dem

and

rais

ed o

n A

sses

smen

t *pr

epar

ed B

y*: _

____

____

____

____

___

exa

min

ed a

nd e

nter

ed

Che

cked

By*

: __

____

____

____

____

__

Acc

ount

ant/A

utho

rise

d O

ffice

r

Dat

ed:

Dat

ed:

* R

ecor

d th

e na

me,

des

igna

tion

and

sign

atur

e of

the

pers

on.

235

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other IncomesF

orm

OTH

-2

____

____

____

____

____

__n

ame

of th

e u

lB

suM

MA

Ry

stA

te

Me

nt

OF

ye

AR

-WIs

e h

eA

D-W

Ise

cO

ll

ec

tIO

n

OF

Ot

he

R In

cO

Me

s FO

R t

he

pe

RIO

D _

____

Sr. N

o. _

____

____

__

____

____

____

____

_ C

olle

ctio

n C

entr

e

Dep

osite

d w

ith _

____

____

____

part

icul

ars

Arr

ears

Re-

cove

ryye

ar (-

2) (R

s.)ye

ar (-

1) (R

s.)c

urre

nt y

ear

(Rs.)

Adv

ance

re-

ceiv

ed (R

s)to

tal (

Rs.)

12

34

56

7C

olle

ctio

n in

resp

ect o

f inc

omes

acc

ount

ed o

n ac

crua

l bas

isPr

oper

ty R

enta

l Tr

ade

Lice

nse

fees

Adv

ertis

emen

t Tax

esO

ther

s, Sp

ecify

___

____

____

Sub-

Tota

lC

olle

ctio

n in

resp

ect o

f inc

omes

acc

ount

ed o

n ac

tual

rece

ipt

basi

sSa

le o

f Fix

ed a

sset

s/sc

rap

Wat

er T

anke

r Cha

rges

Pena

lties

Fine

sO

ther

s, Sp

ecify

___

____

____

Sub-

Tota

lR

ecei

pt o

f Cos

t of R

ecov

ery,

if a

nyO

ther

s, Sp

ecify

___

____

____

Tota

l Col

lect

ion

Am

ount

in W

ords

: R

upee

s ___

____

____

____

____

____

____

____

____

____

____

____

____

___

prep

ared

By*

: __

____

____

____

____

__

exa

min

ed a

nd e

nter

edC

heck

ed B

y* :

____

____

____

____

____

A

ccou

ntan

t/Aut

hori

sed

Offi

cer

Dat

ed:

Dat

ed:

* R

ecor

d th

e na

me,

des

igna

tion

and

sign

atur

e of

the

pers

on.

Not

e: T

his s

tate

men

t sho

uld

be p

repa

red

sepa

rate

ly fo

r eac

h C

olle

ctio

n O

ffice

/Col

lect

ion

Cen

tre a

nd th

en c

onso

lidat

ed.

236

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other IncomesF

orm

OTH

-3__

____

____

_nam

e of

the

ul

B

suM

MA

Ry

stA

te

Me

nt

OF

Re

Fun

Ds

FOR

th

e p

eR

IOD

___

____

____

____

____

_

In re

spec

t of O

ther

Inco

mes

S

r. N

o. _

____

____

____

part

icul

ars

year

(Oth

ers)

year

(-2)

year

(-1)

cur

rent

yea

r (R

s.)to

tal (

Rs.)

12

34

56

Prop

erty

Ren

tal

Trad

e Li

cens

e fe

esA

dver

tisem

ent T

axes

Sale

of F

ixed

ass

ets/

scra

pW

ater

Tan

ker C

harg

esA

dvan

ce re

ceiv

ed i

n re

spec

t of O

ther

inco

mes

Oth

ers,

Spec

ify _

____

____

__

tota

l

Am

ount

in W

ords

: R

upee

s ___

____

____

____

____

____

____

____

____

____

____

____

____

____

____

____

____

prep

ared

By*

: __

____

____

____

____

__

exa

min

ed a

nd e

nter

edC

heck

ed B

y* :

____

____

____

____

____

A

ccou

ntan

t/Aut

hori

sed

Offi

cer

Dat

ed:

Dat

ed:

* R

ecor

d th

e na

me,

des

igna

tion,

and

sign

atur

e of

the

pers

on.

237

Draft of Jharkhand Municipal Accounts Manual Rental, Fees & Other Incomes

For

m O

TH –

4

____

____

___n

ame

of th

e u

lB

suM

MA

Ry

stA

te

Me

nt

OF

WR

Ite

OFF

s

FOR

th

e p

eR

IOD

___

____

____

____

____

_

in re

spec

t of O

ther

Inco

mes

Sr. N

o. _

____

____

____

____

_

part

icul

ars

year

(Oth

ers)

year

(-2)

year

(-1)

cur

rent

yea

r (R

s.)to

tal (

Rs.)

12

34

5

Prop

erty

Ren

tal

Trad

e Li

cens

e fe

esA

dver

tisem

ent T

axes

Oth

ers,

Spec

ify _

____

____

__

tota

l

Am

ount

in W

ords

: R

upee

s ___

____

____

____

____

____

____

____

____

____

____

____

____

____

____

__

prep

ared

By*

: __

____

____

____

____

__

exa

min

ed a

nd e

nter

edC

heck

ed B

y* :

____

____

____

____

____

A

ccou

ntan

t/Aut

hori

sed

Offi

cer

Dat

ed:

Dat

ed:

*

Rec

ord

the

nam

e, d

esig

natio

n an

d si

gnat

ure

of th

e pe

rson

.

238

Draft of Jharkhand Municipal Accounts Manual public Works

chApteR 12

puBlIc WORks

IntRODuctIOn

12.1 This chapter contains the recommended accounting system for Public Works transactions undertaken by the Urban Local Body (ULB). These would generally include construction/expansion/major modification of buildings, development of land, construction of roads, construction of water works, construction of drainage systems or other public utilities. Repairs and maintenance of these would also constitute Public Works. Apart from these, any non-civil contracts (e.g., for furniture) undertaken by the ULB through the Public Works Department would also be covered here. This chapter also covers the accounting treatment for ‘Deposit works’ executed by the ULB on behalf of the Government or Government Departments and recognition on revenue from these Deposit works.

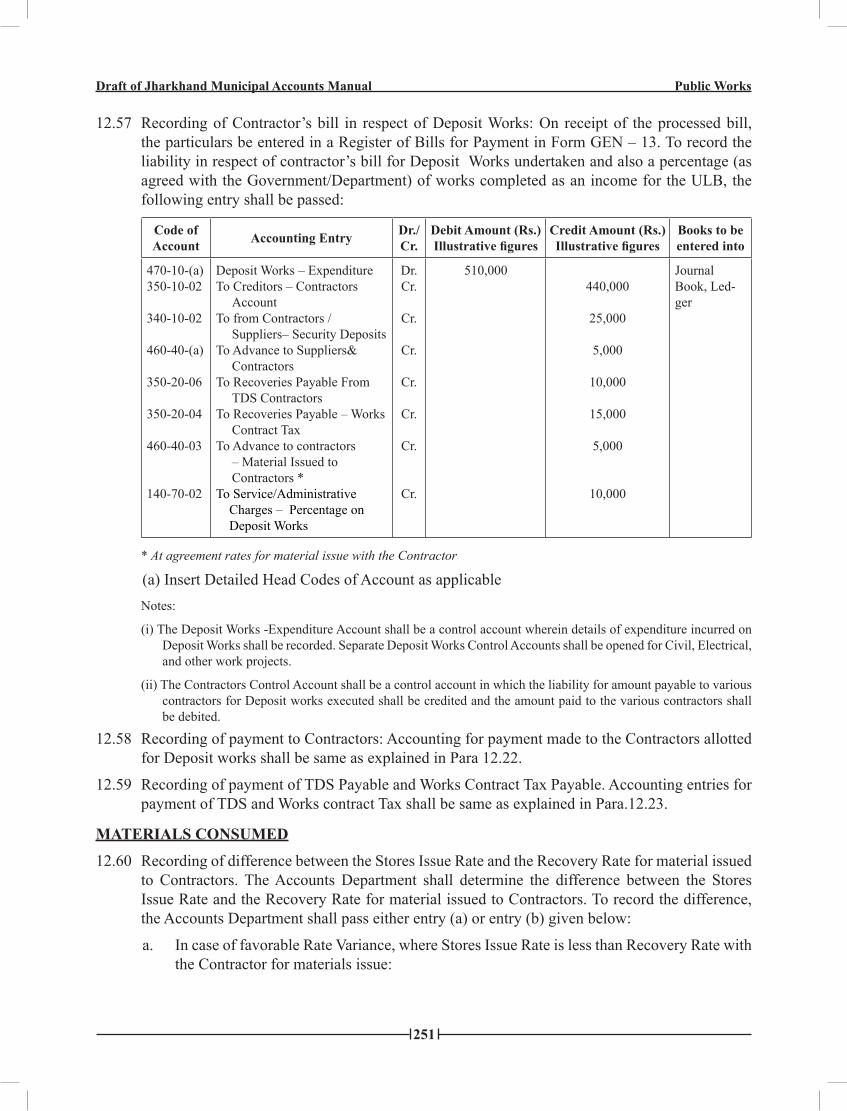

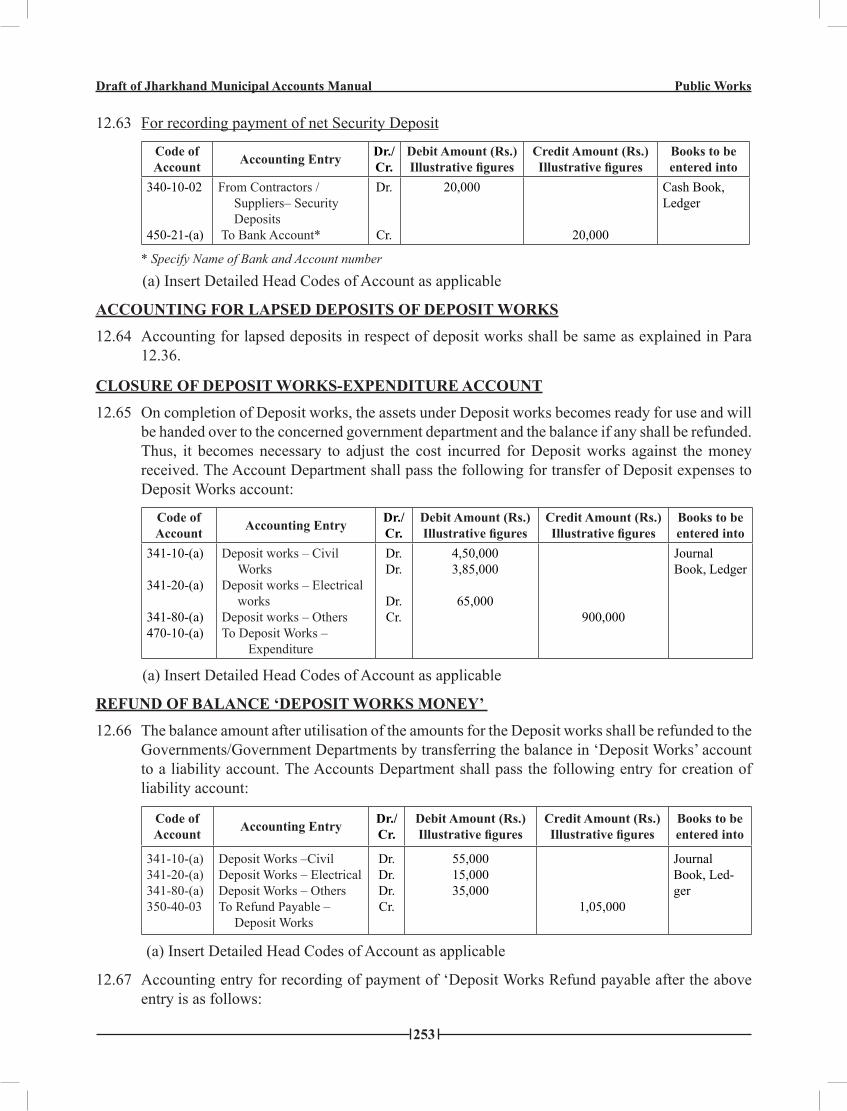

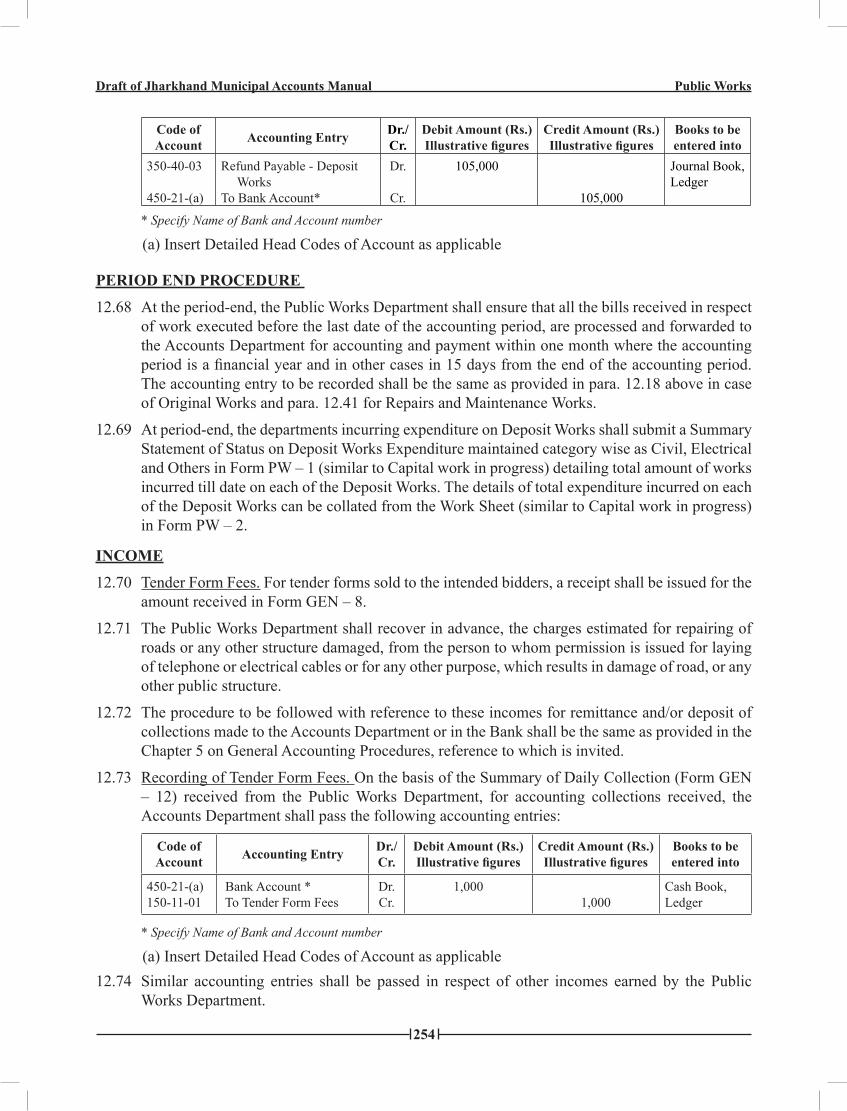

12.2 ‘Original Works’ includes all new constructions or additions and alterations to existing works. Repairs to newly purchase or previously abandoned buildings, which are required for bringing them into use, should be classified as Original Works. Where a portion of an existing structure is dismantled and replaced and if the cost of such replacement represents a genuine increase in the permanent value of the property as an asset, the work should be classified as ‘Original Works’.

12.3 ‘Repairs and Maintenance’ includes works, other than those specified under Original Works, required to maintain buildings, roads, water work assets, drainage system and other works in proper condition for ordinary use.

12.4 ‘Fees & User Charges’: Where the Public Works Department issues any permission for road digging or any other activity for private purpose; it recovers the charges incurred for repair of the damaged road or any other structure from the person seeking permission.

12.5 The Public Works may be carried out in a municipal area either from Municipal Funds or from Grants or Special Funds. The accounting procedure for dealing with the various transactions of Public Works would be similar irrespective of the source of funds. The accounting entries in respect of works executed from Grants have been described in Chapter 17 on Grants. Similarly, accounting entries in respect of works executed from Special Funds have been described in Chapter 19 on Special Funds. This chapter describes the accounting entries for works executed out of Municipal Funds of the ULB.

12.6 ‘Deposit works:’ The Governmental departments or the State Governments may use the services of ULB, for execution of certain works/schemes/approved infrastructure schemes. Money received from the Governments for the above shall be treated as ‘Deposit works’ and are accounted as a liability of an ULB. ULBs are provided certain percentage of the value of the works/scheme/project/plans completed as their service charges.

AccOuntIng pRIncIples

12.7 The following Accounting Principles shall govern the recording, accounting and treatment of transactions relating to public works:

The cost of fixed assets shall include cost incurred/money spent in acquiring or installing or a. constructing fixed asset, interest on borrowings attributable to acquisition or construction

239

Draft of Jharkhand Municipal Accounts Manual public Works

of qualifying fixed assets up to the date of commissioning of the assets and other incidental expenses incurred up to that date.Any addition to or improvement to the fixed asset that results in increasing the utility or b. capacity or useful life of the asset shall be capitalised and included in the cost of asset. Revenue expenditure in the nature of repairs and maintenance incurred to maintain the asset and sustain its functioning or the benefit of which is less than for a year, shall be charged off. However if the demarcation is difficult between Capital and Revenue Expenditure, onetime expenses which exceeds 10% of the cost of specific Fixed Asset, subject to a minimum of Rs. 5000/- will be treated as Capital Expenditure and thus capitalised.Assets under erection/installation on existing projects and capital expenditures on new c. projects (including advances for capital works and project stores) shall be shown as “Capital Work-in-Progress”.The Earnest Money Deposit and Security Deposit received if forfeited shall be recognised as d. income when the right for claiming refund of deposit has expired.Deposit received under Deposit works shall be treated as a liability till such time the projects e. for which money is received is completed. Upon completion of the projects, the cost incurred against it shall be reduced from the liability. Revenues (percentage charges) in respect of Deposit works shall be accrued along with f. expenditure of Deposit works.

AccOuntIng RecORDs AnD pROceDuRes

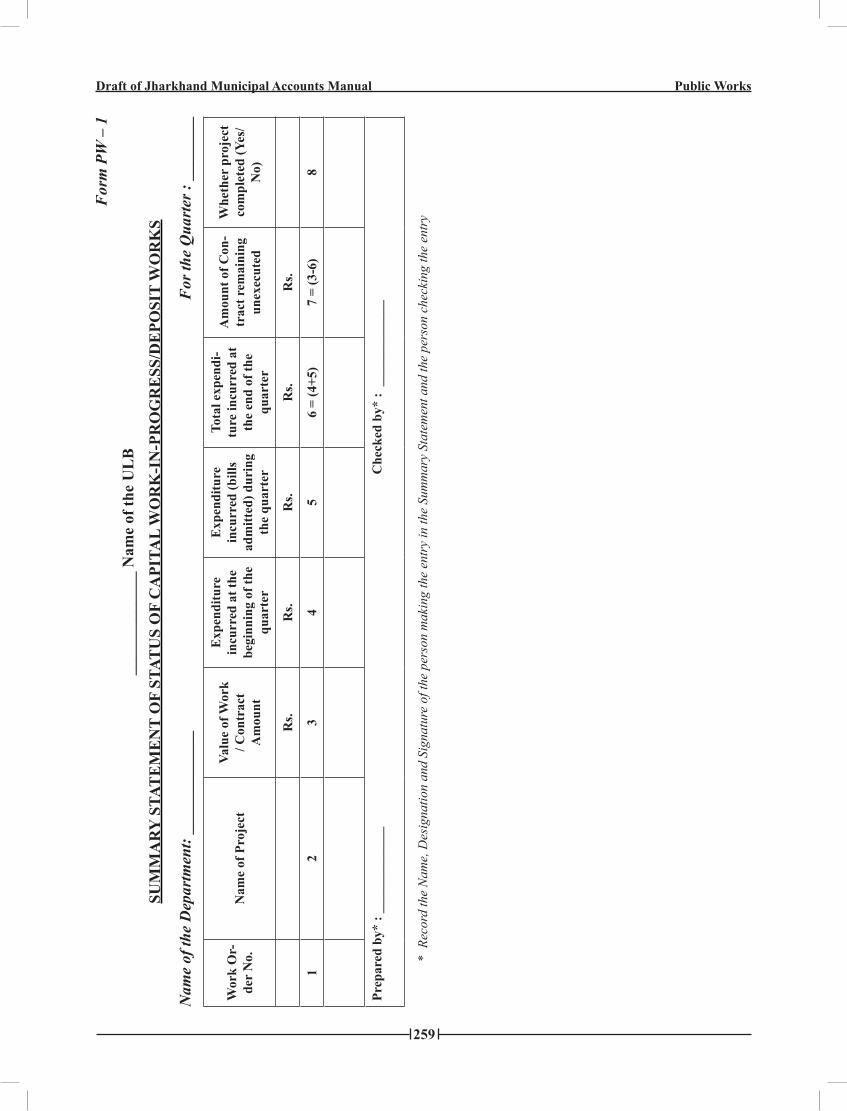

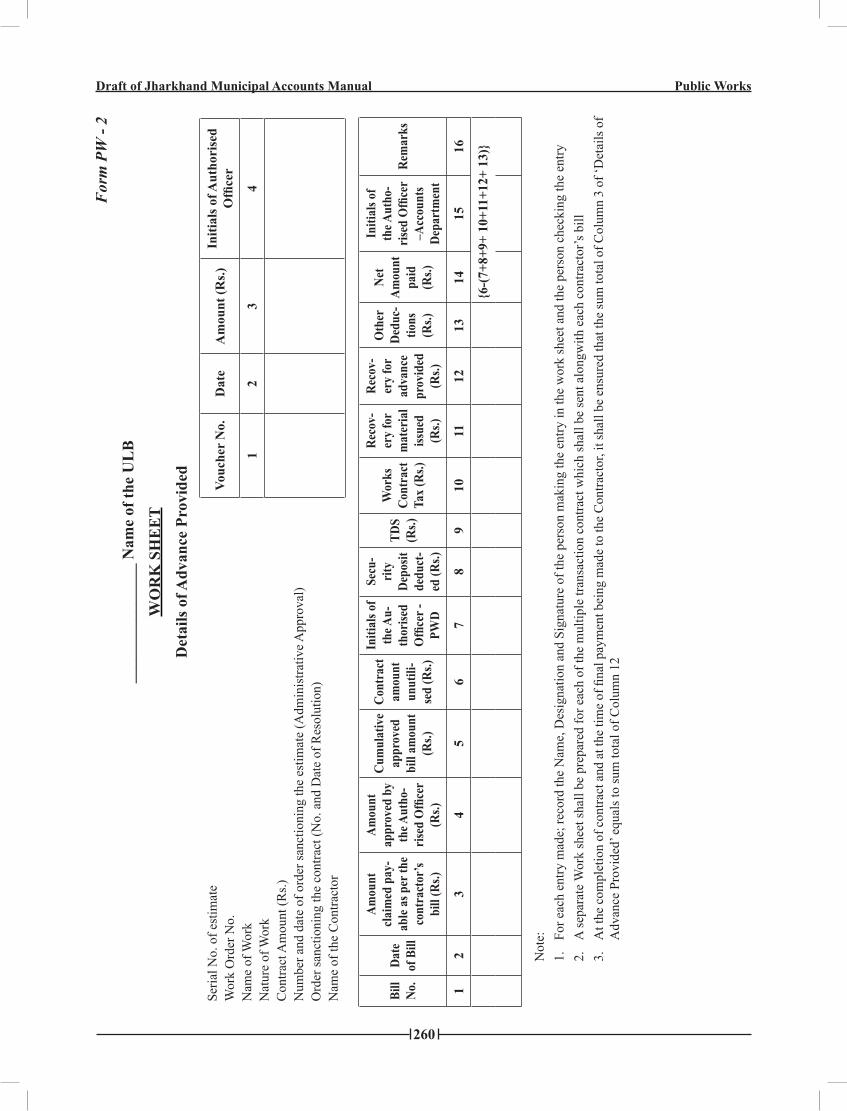

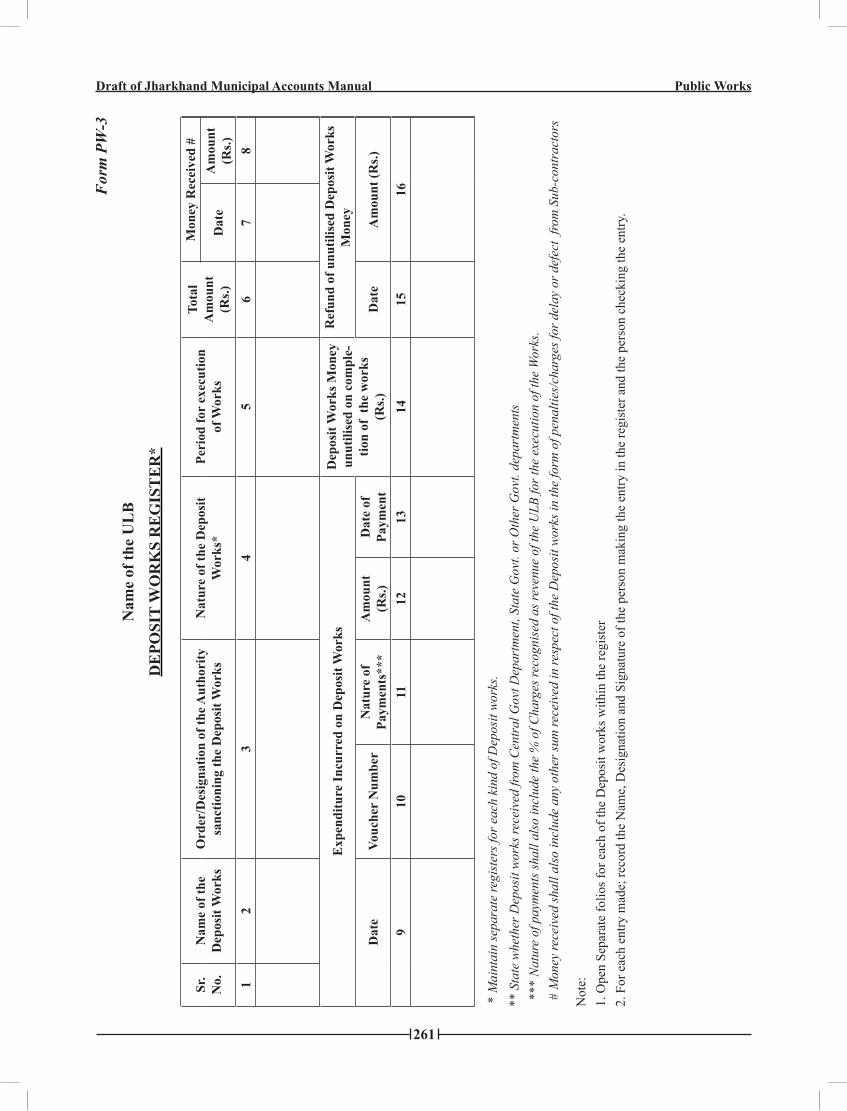

12.8 This section describes the records, registers, documents, forms, accounting entries, etc., in respect of accounting for transactions related to Public Works. For the purposes of accounting of Public Works there are certain forms, registers, etc., which are specific to Public Works, e.g., Statement of status of Capital Work-in-Progress PW – 1, etc. These Forms (Forms PW - 1 and PW - 2) are annexed to this chapter and are prefixed “PW”.

12.9 The procedure for accounting of works expenditure is briefly described below:

Earnest Money Deposit (EMD) may be received from the bidders bidding for the tender as a. per the principle and the procedures prescribed by the ULB. On tender being awarded, EMD shall be refunded to the unsuccessful bidders.

An agreement may be entered into with the successful bidder as per the terms of the Tender b. and agreement; Security Deposit may be taken in advance.

Advance may be provided to the contractor as per the terms and procedures of the ULB and c. agreement entered into with the contractor.

Payment shall be made against bill raised after deducting Security Deposit, income tax, works d. contract tax and other deductions/ recovery including advance provided, if any.

Security Deposit shall be refunded after successful completion of the work as per terms of e. agreement

In case of Original Works, the expenditure incurred shall be capitalised and disclosed as an f. asset in the Balance Sheet.

240

Draft of Jharkhand Municipal Accounts Manual public Works

AccOuntIng FOR ReceIpt OF eARnest MOney DepOsIt

12.10 The following procedure shall be followed for accounting of receipt of EMD received in respect of works executed.

The procedure to be followed for collection of EMD and its remittance and/or deposit to a. the Accounts Department or in the Bank shall be the same as provided in the Chapter 5 on General Accounting Procedures. The following entry for the amount received is passed:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative figures

Books to be entered into

450-21-(a)340-10-01

Bank Account *To FromContractors/Suppliers– EMD

Dr.Cr.

10,00010,000

Cash Book, Ledger

* Specify name of Bank and account number

(a) Insert .detailed Head Codes of Account as applicableNote: The postings in the Ledger Account of “Earnest Money Deposit - Public Works Department” Account shall

be carried out as indicated in Chapter 5 – General Accounting Procedures. The postings in the Ledger Accounts shall be similarly carried out in respect of all other accounting entries described subsequently in this chapter. Whenever, the cash or the bank account is involved, there will be no entry in the Journal Book.

AccOuntIng FOR ReFunD OF eARnest MOney DepOsIt

12.11 The procedure followed for accounting of refund shall be the same as any payment provided in Chapter 5 on General Accounting Procedures.

12.12 Recording of refund of Earnest Money Deposit. After the receipt of approval for payment and upon payment, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative figures

Books to be entered into

340-10-01

450-21-(a)

From Contractors/Suppliers– EMD

To Bank Account*

Dr.

Cr.

9,000

9,000

Cash Book, Ledger

*Specify name of Bank and account number

(a) Insert Detailed Head Codes of Account as applicable

AccOuntIng FOR cOnveRsIOn OF eARnest MOney DepOsIt IntO secuRIty DepOsIt

12.13 Recording of conversion of Earnest Money Deposit into Security Deposit. On receipt of intimation for conversion of EMD of the successful bidder into Security Deposit payable the following entry shall be passed:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative figures

Books to be entered into

340-10-01

340-10-02

From Contractors/Suppliers– EMD

To From Contractors/Suppliers-Security Deposits

Dr.

Cr.

1,000

1,000

Journal Book, Ledger

(a) Insert Detailed Head Codes of Account as applicable

241

Draft of Jharkhand Municipal Accounts Manual public Works

ReceIpt OF secuRIty DepOsIt

12.14 Recording of Security Deposit received: The procedure followed for accounting of Security Deposit is similar to that of Earnest Money Deposit. The Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative figures

Books to be entered into

450-21-(a)340-10-02

Bank Account*To From Contractors/

Suppliers– Security Deposits

Dr.Cr.

10,00010,000

Cash Book, Ledger

* Specify name of Bank and account number

(a) Insert detailed Head Codes of Account as applicable12.15 As per the terms of agreement entered into with the contractor, Security Deposit may be deducted

from the contractor’s bill. For accounting treatment for Security Deposit deducted from the contractor’s bill, refer section “Expenditure” in this chapter.

ADvAnces

12.16 Recording of payment of advance for work carried out from Municipal Fund, Grant and Special Fund. As per the terms of agreement, advance may be paid to the contractor. Advance may be provided either in cash or in kind, i.e., by way of supply of materials. On receipt of approval for payment, and on payment, entries will be made for money advanced in Cheque Issue Register in Form GEN –15 and in Register of Advance in Form GEN – 16 for the cheques issued to the contractor. The accounting entries to be passed are :

a. For recording advance sanctioned for payment

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative figures

Books to be entered into

460-40-(a)

350-10-07

350-20-06

Advance to Suppliers &Contractors

To Creditors – Contractors Advance Control Account

To Recoveries Payable – TDS from Contractors

Dr.

Cr.

Cr.

1,000

950

50

Journal Book, Ledger

(a) Insert detailed Head Codes of Account as applicable

b. For recording disbursement of advance, i. In cash/cheque:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative

figures

Books to be entered

into

350-10-07

450-21-(a)

Creditors –Contractors Advance Control Account

To Bank Account *

Dr.

Cr.

950

950

Cash Book, Ledger

*Specify name of Bank and account number

242

Draft of Jharkhand Municipal Accounts Manual public Works

(a) Insert Detailed Head Codes of Account as applicableii. Materials supplied to the Contractor:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

460-40-03

430-(b)

Advances to Contractors- Material Issued to contractors

To Stock in Hand – Purchase of Materials

Dr.

Cr.

950

950

Cash Book, Ledger

(b) Insert Minor & Detailed Head Codes of Account as applicable.Note: This entry will be passed along with other items of consumption based on valuation Statement as explained in

Para 13.24 to 13.27 of Chapter 13 on Stores Accounting.

expenDItuRe

12.17 Preparation of Bill for payment. On the basis of work completed as per governing rules, a bill shall be prepared and sent for payment. The amount of security deposit, income tax deducted at source, works contract tax and any other recovery or deduction, including recovery for supply of material by the Stores and money advanced to the contractor, should be specified in the Bill. Running bills are submitted during the progress of work and final bill is normally submitted on completion of work. The Contract Completion Certificate shall be annexed to the final bill.

12.18 Recording of Contractor’s bill in respect of Original Work On receipt of the processed bill, the particulars be entered in a Register of Bills for Payment in Form GEN – 13. To record the liability in respect of contractor’s bill for Original Works undertaken, the following entry shall be passed:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative

figures

Books to be entered

into

412-(a)350-10-02

340-10-02

460-40-(b)

350-20-06

350-20-04

460-40-03

Capital Work-in-ProgressTo Creditors – Contractors

AccountTo From Contractors /

Suppliers– Security Deposits

To Advance to Suppliers & Contractors

To Recoveries Payable from TDS Contractors

To Recoveries Payable – Works Contract Tax

To Advance to Contractors - Material Issued to Contractors *

Dr.Cr.

Cr.

Cr.

Cr.

Cr.

Cr.

50,00044,000

2,500

500

1,000

1,500

500

Journal Book, Led-ger

* At agreement rates for material issue with the Contractor

(a) Insert Minor & Detailed Head Codes of Account as applicable(b) Insert Detailed Head Codes of Account as applicable

243

Draft of Jharkhand Municipal Accounts Manual public Works

12.19 The Capital Work-in-Progress Account shall be a control account wherein details of expenditure incurred on capital projects shall be recorded. Separate Capital Work-in-Progress Control Accounts shall be opened for Civil, Electrical, Water Works and Other projects.

12.20 At period-end, the departments incurring expenditure on capital projects shall submit a Summary Statement of Status on Capital Work-in-Progress in Form PW – 1 detailing total expenditure incurred till date on each of the capital projects. The details of total expenditure incurred on each of the capital projects can be collated from the Work Sheet (Form PW – 2).

12.21 The Contractors Control Account shall be a control account in which the liability for amount payable to various contractors for work executed shall be credited and the amount paid to the various contractors shall be debited.

12.22 Recording of payment made to Contractors. The procedure to be followed for approval of a contractor’s bill for payment and making payment shall be the same as provided in Chapter 5 on General Accounting Procedures to which reference is invited. The Accounts Department shall, on receipt of Payment Order in Form GEN – 14 together with the Work Sheet and Contract Completion Certificate, where applicable, after making the payment, enter the details of the payment in the Work Sheet (Form PW – 2) and pass the following entry:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative figures

Books to be entered

into

350-10-02

450-21-(a)

Creditors – Contractors Account

To Bank Account *

Dr.

Cr.

44,000

44,000

Cash Book, Ledger

* Specify name of the Bank and Account number

(a) Insert Detailed Head Codes of Account as applicable12.23 Recording of payment of TDS Payable and Works Contract Tax Payable. The income tax and

works contract tax deducted from the bills of the contractors shall be paid by the Accounts Department to the concerned authorities as and when due as per the relevant laws in force. On payment of Income Tax and Works Contract Tax deducted, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative figures

Books to be entered into

350-20-06

350-20-04

450-21-(a)

Recoveries Payable -TDS from Contractors

Recoveries Payable -Works Contract Tax

To Bank Account*

Dr.

Dr.

Cr.

1,050

1,500

2,550

Cash Book, Ledger

*Specify name of the Bank and Account number

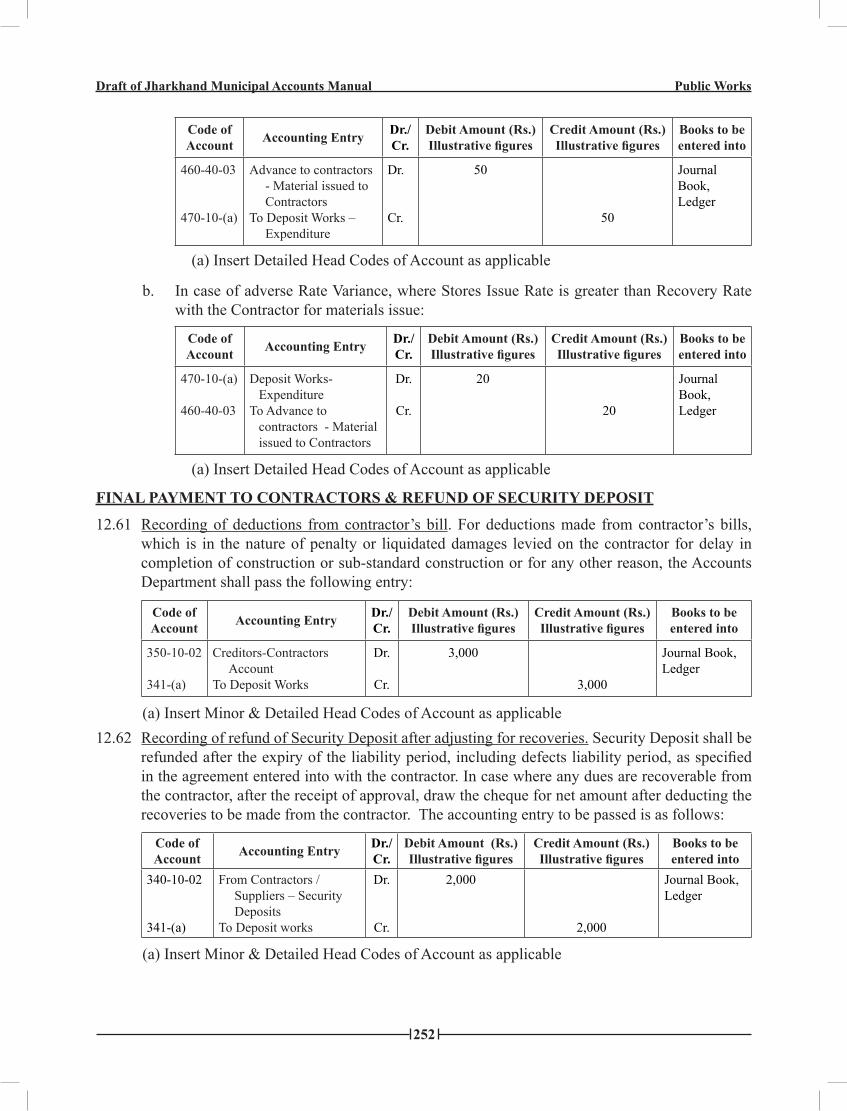

(a) Insert Detailed Head Codes of Account as applicable1224 Recording of difference between the Stores Issue Rate and the Recovery Rate for material issued

to Contractors. The Accounts Department shall determine the difference between the Stores Issue Rate and the Recovery Rate for material issued to Contractors. To record the difference, the Accounts Department shall pass either entry (a) or entry (b) given below:

244

Draft of Jharkhand Municipal Accounts Manual public Works

a. In case of favourable Rate Variance, where Stores Issue Rate is less than Recovery Rate with the Contractor for materials issue:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

460-40-03

412-(a)

Advance to Contractors - Material issued to Contractors

To Capital Work-in-Progress

Dr.

Cr.

50

50

Journal Book, Ledger

(a) Insert Minor & Detailed Head Codes of Account as applicable

b. In case of Adverse Rate Variance, where Stores Issue Rate is greater than Recovery rate from the Contractor for materials issue:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative

figures

Books to be entered into

412-(a)460-40-03

Capital Work-in-ProgressTo Advance to Contractors

Material issued to Contractors

Dr.Cr.

2020

Journal Book, Ledger

(a) Insert Minor & Detailed Head Codes of Account as applicable

WORks executeD By puBlIc WORks DepARtMent

12.25 The accounting procedure and the accounting entries to be recorded for materials purchased for works shall be the same as provided in Chapter 13 on Stores.

12.26 Recording of materials consumed in Original Works. Based on the bill received from the Public Works Department for works executed, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative figures

Books to be entered into

412-(a)430-(a)

Capital Work-in-ProgressTo Stock in Hand –Purchase of Materials

Dr.Cr.

5,0005,000

Journal Book, Ledger

(a) Insert Minor & Detailed Head Codes of Account as applicable.Note: This entry will be passed along with other items of consumption based on valuation statement as explained in

Para 13.24 to 13.27 of Chapter 13 on Stores Accounting

cApItAlIsAtIOn OF cApItAl WORk-In pROgRess

12.27 On completion of construction of the asset, the asset becomes ready for use. Thus, it becomes necessary to transfer the cost incurred for construction (which is temporarily accounted in capital work-in-progress account) to the relevant asset account. This process is called capitalisation.

12.28 Recording of capitalisation of Capital Work-in-progress. On receipt of Contract Completion Certificate, the Accounts Department shall capitalise the amount lying in the Capital Work-in-

245

Draft of Jharkhand Municipal Accounts Manual public Works

Progress Account and convert the amount pertaining to the Capital Work-in-Progress and lying in the Capital Work-in-Progress Account into a Fixed Asset. The Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative figures

Books to be entered into

410-(a)

412-(a)

Fixed Asset (Name of the Fixed Asset) (1)

To Capital Work-in-Progress (please specify)

Dr.

Cr.

1,00,000

1,00,000

Journal Book, LedgerRegister of Movable/ Immovable Assets

(a) Insert Minor & Detailed Head Codes of Account as applicable (1) Fixed Assets of a particular class shall be accounted for under one broad fixed asset

account head. For instance, ULB may have more than one hospital building and then all the hospital buildings shall be recorded under one broad head of Buildings (Code of Account 410-20-(a)). Any new hospital building constructed, though shall be recorded separately in the Register of Buildings, shall be recorded under the account head ‘Hospital Buildings’.

12.29 Recording of deductions from contractor’s bill. For deductions made from contractor’s bills, which is in the nature of penalty or liquidated damages levied on the contractor for delay in completion of construction or sub-standard construction or for any other reason, the Accounts Department shall pass the following entry:

code of Account Accounting entry Dr./

cr.Debit Amount (Rs.) Illustrative figures

credit Amount (Rs.) Illustrative figures

Books to be entered into

350-10-02

180-80-(a)

Creditors –Contractors Account

To Other Income –Miscellaneous Income

Dr.