Strategic Perspectives for Unconventional Gas in the EU

16

STRATEGIC PERSPECTIVES FOR UNCONVENTIONAL GAS IN THE EU FRANK UMBACH ASSOCIATE DIRECTOR, EUROPEAN CENTRE FOR ENERGY AND RESOURCE SECURITY (EUCERS), KING‘S COLLEGE 64 FRANK UMBACH

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Strategic Perspectives for Unconventional Gas in the EU

Strategic PerSPectiveS for Unconventional

gaS in the eU

frank Umbach

aSSociate Director, eUroPean centre for energY anD reSoUrce SecUritY (eUcerS), king‘S college

65

CASPIAN REPORT, SPRIN

G 2014

64

FRAN

k Um

bACh

IntroductIon

The U.S. shale gas development is not a technical revolution, but rather an evolution of modern techniques and the combining of two key technolo-gies – horizontal drilling and “slick water” hydraulic fracturing. Together these can crack shale rock, and have thus cracked the code with regard to opening up major North American shale gas resources.

The rapidly expanding production of shale gas has transformed the U.S. from the largest LNG import market to a self-sustaining gas producer and a net gas exporter. In 2009, the U.S. even overtook Russia as the world’s largest gas producer, and in 2010 it exceeded Qatar as the world’s largest LNG exporter by about 60%. In 2012, U.S. natural gas production increased to 681.4 billion cubic meters (bcm; 20.4% of the global production), whereas Russia’s was just 592.3 bcm (17.6% of global production).

The combination of three factors - (1) a drop in demand linked to the global economic recession, (2) a unexpected dramatic increase in incremental U.S. non-conventional shale gas production, and (3) the arrival of new LNG delivery capac-

ity - have created a sudden “gas glut”. This stems from the overcapacity of LNG, which made LNG in Europe less expensive than pipeline gas (based on long-term contracts), and contributed to the de-linkage of the gas prices from the oil prices in at least Europe at present. This could become a permanent feature of the global energy market because the remaining global unconventional gas resources are considerably big-ger than conventional ones. The U.S. could even overtake Russia as the world’s largest combined oil and gas producer by 2015.

The development of unconventional gas in the U.S. since 2006 has not only triggered a revolution in U.S. energy markets, but has also laid the groundwork for an expanded role for natural gas in the world economy. This has prompted the IEA to envis-age a “Golden Age of Gas” era with unconventional gas being a “game changer.” It has already transformed the global gas markets, which were in the past “sellers’ markets” rather than “buyers’ markets.”

meanwhile, some countries in Eu-rope (Poland, United kingdom, Ro-mania, Lithuania, Spain and Ukraine) have become very interested at the

The expanded role for natural gas in the world economy has prompted the IEA to envisage a “Golden Age of Gas” era with

unconventional gas being a “game changer.”

65

CASPIAN REPORT, SPRIN

G 2014

64

FRAN

k Um

bACh

exploitation of their own unconven-tional gas resources. Others however have adopted a moratorium (bul-garia, Czech Republic) or even a ban on the fracking technology (France) and the production of shale gas due to perceived environmental risks.

Against this background, the article analyses the different policies in re-gard to unconventional gas in the EU-member states, some of which are in favor of shale gas production (Poland, the United kingdom, Roma-nia, Lithuania and Spain) and some of which have adopted (temporary) moratoriums (Germany, bulgaria) or even a ban (France).

EuropE’s unconvEntIonal Gas rEsourcEs and thE EnErGy polIcIEs of Its MEMbEr statEs

While initial assessments of Eu-rope’s unconventional gas potential were relatively skeptical and con-servative, Europe has depositories of significant unconventional gas re-sources with estimated total recover-able reserves of 33-38 tcm. Reserves in some states are now thought to be much larger than previously esti-mated, and in others, there is grow-ing concern over the market domi-nance of the U.S. Some are also keen to break their dependence on Rus-sian conventional gas. In June 2013 the EIA published a new worldwide assessment of unconventional gas resources, which has added nine more countries to the total number

of countries with technically re-coverable shale gas resources. This number now stands at 41. For Eu-rope, some country estimates have been increased, while others have been reduced. Worldwide, the EIA has estimated 10% more shale gas resources in comparison with its pre-vious estimates of 2011.

Many of the shale gas fields in Eu-rope are situated in areas where the geology makes it much harder to ex-tract than in the U.S. They are also in places with much higher popula-tion densities, and their service in-dustries and infrastructure for the industry are much less developed. but the perceived risks are often overestimated, not very different to conventional gas drilling and often not related to the fracturing process itself.

The IEA has remained cautious and has estimated that Europe’s uncon-ventional gas production by 2035 may reach not more than 20 bcm by 2035 due to the unclear conditions, specifically, to what extent social and environmental concerns will lead to the tightening of the regulatory framework at the EU level.

New geological analyses in Germany and Great Britain have confirmed the historical experiences of fossil fuels, whereby at the beginning of their findings and exploration the estimates of reserves and resources go up for a longer time alongside of using new technologies for discover-ing and exploration of fossil fuels be-fore they are decreasing after having received their peak estimates and production levels.

manY of the Shale gaS fielDS in eUroPe are

SitUateD in areaS where the geologY makeS it

mUch harDer to extract than in the U.S.

67

CASPIAN REPORT, SPRIN

G 2014

66

FRAN

k Um

bACh

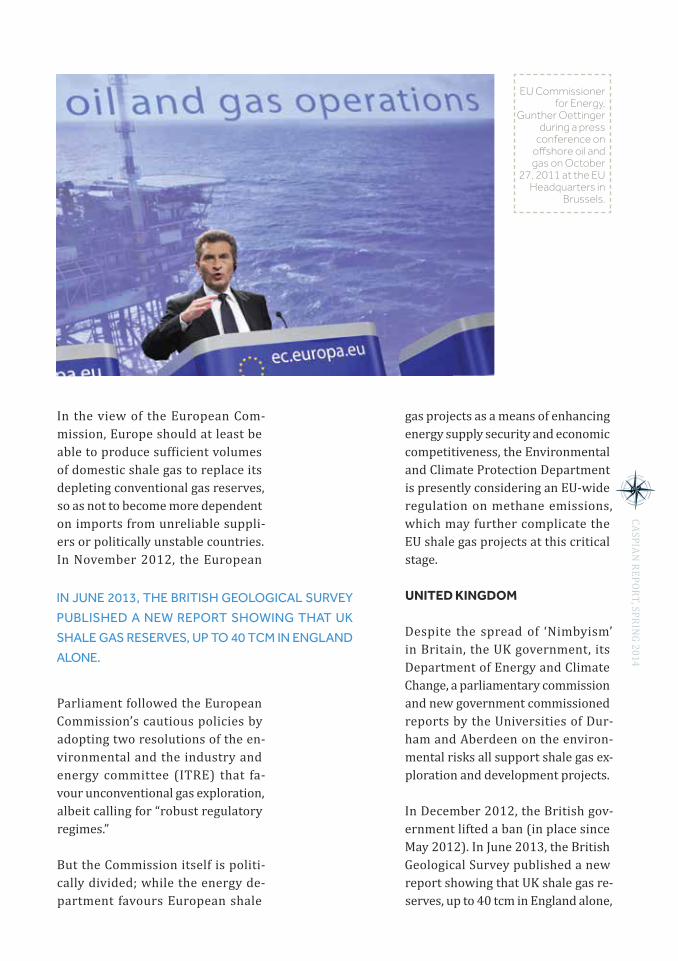

In the view of the European Com-mission, Europe should at least be able to produce sufficient volumes of domestic shale gas to replace its depleting conventional gas reserves, so as not to become more dependent on imports from unreliable suppli-ers or politically unstable countries. In November 2012, the European

Parliament followed the European Commission’s cautious policies by adopting two resolutions of the en-vironmental and the industry and energy committee (ITRE) that fa-vour unconventional gas exploration, albeit calling for “robust regulatory regimes.”

but the Commission itself is politi-cally divided; while the energy de-partment favours European shale

gas projects as a means of enhancing energy supply security and economic competitiveness, the Environmental and Climate Protection Department is presently considering an EU-wide regulation on methane emissions, which may further complicate the EU shale gas projects at this critical stage.

unItEd KInGdoM

Despite the spread of ‘Nimbyism’ in britain, the Uk government, its Department of Energy and Climate Change, a parliamentary commission and new government commissioned reports by the Universities of Dur-ham and Aberdeen on the environ-mental risks all support shale gas ex-ploration and development projects.

In December 2012, the british gov-ernment lifted a ban (in place since may 2012). In June 2013, the british Geological Survey published a new report showing that Uk shale gas re-serves, up to 40 tcm in England alone,

in JUne 2013, the britiSh geological SUrveY

PUbliSheD a new rePort Showing that Uk

Shale gaS reServeS, UP to 40 tcm in englanD

alone.

EU Commissioner for Energy,

Gunther Oettinger during a press

conference on offshore oil and gas on October

27, 2011 at the EU Headquarters in

Brussels.

67

CASPIAN REPORT, SPRIN

G 2014

66

FRAN

k Um

bACh

are considerably higher than previ-ously estimated (in fact, almost 20 times higher). Around 10-20% is es-timated as economically recoverable. These new figures were confirmed in a report by the Institute of Directors in September 2012 (a non-party po-litical organization of british indus-try with approximately 38,000 mem-bers in the Uk and overseas). The report estimated that around 35,000 jobs can be created and that onshore shale gas production in britain could produce enough gas to meet 10% of the Uk’s gas needs for the next 103 years, while decreasing carbon emis-sions by 45 million tonnes of CO2. Even if britain only gets 10% of this gas-in-place produced, it will supply the Uk for 25-50 years. The most op-timistic scenario has estimated the future shale gas production at up to 122-255 bcm per year – more than twice the present annual consump-tion of almost 100 bcm.

Unconventional gas reserves provide the foundation for the government’s newly released “Gas Generation Strategy” in December 2012, which envisages the construction of 20 new gas-fired power plants, with 9 giga-watts (GW) by 2020 and 26 GW by 2030.

The Royal Society and Royal Acad-emy of Engineering reviewed the scientific and engineering as well as

related environmental risks associ-ated with hydrofracking. The report concluded that those environmen-tal risks can be managed effec-tively and enforced through strong regulation. It also sees fracking as an unlikely cause of ground water contamination.

Energy companies expect that it will take as long as five years for produc-tion to reach a commercial scale. Like in other EU countries, public fears in regard to potential environ-mental risks have also increased and thus slowed down the planning and permissions processes for shale gas projects at the local level. An engi-neering consultancy advising the Department of Energy and Climate Change (DECC) has reduced the fig-ure of jobs that could be created by the shale gas industry from 74,000 (as Prime minister Cameron was speculating) to 15,900-24,300. but the Uk water and fossil-fuel industry lobbies have agreed to work together to minimize the environmental harm of the shale gas projects for the coun-try’s water supply.

The Uk government is currently seeking new ways to simplify the permissions process for british shale gas projects. This process has been widely criticized as too complex for prospective investors. In December 2013, the british government un-veiled its plans to reduce the tax pay-able on a proportion of profits from 62% to 30% in order to encourage investment in the shale gas indus-try. but more than half of britain’s cabinet ministers may experience shale gas projects in their constitu-encies, which may further deepen

in november 2013, the new granD coalition

government agreeD on a “temPorarilY

fracking ban”, Until environmental

iSSUeS like the USe of toxic chemicalS are

reSolveD.

69

CASPIAN REPORT, SPRIN

G 2014

68

FRAN

k Um

bACh

the political conflict over fracking, and weaken political support due to the “fear of unknown” in rural communities.

GErMany

With an annual gas consumption of around 100 bcm, Germany’s do-mestic production covers just 12% of the national gas demand. 40% of Germany’s gas consumption is sup-plied by Gazprom. Despite a morato-rium adopted by the federal states of North Rhine-Westphalia and strong opposition to shale gas drilling on environmental grounds, several companies, including Exxonmobil, have acquired exploration licenses in six of the federal states: Nord Rhine Westphalia, Thuringia, Lower Saxony, Saxony-Anhalt, hessen and baden-Wuerttemberg. The state of hessen has called for uniform practice and legal rules across the country, fear-ing a competition between federal states.

but the previous government in berlin and its ministry for Environ-ment have tried to slow down the discussions and any governmental decisions. The Environment minis-try has generally opposed fossil fuel resources and instead has always favoured heavily subsidised support for re¬new¬able energy projects.

In July 2012, the German Federal Institute for Geosciences and Natu-ral Resources (bGR) published its first estimate for domestic shale gas reserves and officially described them as “significant”. The estimates are considerably higher (up to three times) than those published by Exx-

onmobil in January 2012, and much higher than Germany’s conventional gas reserves. The bGR also concluded that environmentally friendly [frack-ing] technology is possible from a geo-scientific point of view and that

“fracking and drinking-water protec-tion are fundamentally compatible.” It also confirmed - together with the comprehensive environmental study

“hydrofracking Risk Assessment” - that the fracking risks can be con-trolled and regulated. At present, a third of Germany’s domestic produc-tion already uses fracking technolo-gies - some for more than 50 years.

Germany’s energy-intensive and manufacturing industry (i.e. bayer, bASF at al.) has begun to voice its in-creasing concern about the implica-tions of the U.S. unconventional gas revolution for its future economic competitiveness, as the reduced gas prices in the U.S. are an essential cost factor for petrochemical manu-facturing, in particular ethane. These cheap feed stocks are reshaping the global competitive landscape for pet-rochemicals with a “quite phenom-enal advantage” for the U.S. industry.

“Cracking” ethane makes ethylene, which is the major building block for plastics such as polythene.

In January 2013, the bGR criticised the lack of geo-scientific expertise on the deep underground and identi-fied many instances of inconsistency

with an annUal gaS conSUmPtion of

aroUnD 100 bcm, germanY’S DomeStic

ProDUction coverS JUSt 12% of the

national gaS DemanD 40% of germanY’S

gaS conSUmPtion iS SUPPlieD bY gazProm.

69

CASPIAN REPORT, SPRIN

G 2014

68

FRAN

k Um

bACh

and subjective argumentation as well as a trend of ignoring the broad knowledge base and modern meth-ods of geo-scientific exploration. It also pointed out that this allegation of missing data on regional assess-ments is not supported by facts. The political debate moved away from an outright national ban of hydro-fracking to the question how far to legislate environmental safeguards before the national parliamentary elections in September 2013.

GErMan fEdEral InstItutE for GEoscIEncEs and natural rEsourcEs (bGr) July 2012 – GErMany’s shalE Gas rEsErvEs:

• Total shale gas reserves: 6.8-22.6 tcm;• Technically recoverable reserves: 0.7-2.3 tcm (10% of total shale gas reserves)• ExxonMobil estimate of Germany’s exploitable reserves: 827 bcm• Conventional Gas reserves in com-parison: 150 bcm

In November 2013, the new grand coalition government agreed on a

“temporarily fracking ban”, until en-vironmental issues like the use of toxic chemicals are resolved. Until non-toxic fracking fluids are avail-able, the agreement is not a strict ban but rather a temporary mora-torium. The German EU Energy Commissioner Gunther Oettinger

repeatedly warned the previous German government against fully rejecting the shale gas exploration through fracking technology. In the summer 2013, three geologi-cal research institutes, the bGR in hannover, the German Research Centre for Geosciences (GFZ) in Potsdam and helmholtz Centre for Environmental Research in halle launched a programme to support the exploration of the country’s shale gas potential by making the shale gas industry more environ-mentally friendly and the fracking technology “greener”, by develop-ing biological alternatives to the chemicals being used for fracking, for instance.

poland

Poland itself still generates more than 90% of its power from coal, but is seeking to replace part of its coal consumption with gas. In 2012, Poland produced 5.5 bcm of conventional gas in its own coun-try. but that covered only 30% of its domestic gas consumption, 16 bcm in total. The shale gas reserve estimate from the Polish Geologi-cal Institute (PGI) in march 2012 revised downwards the estimates of national reserves to around 2 tcm, in contrast to EIA’s optimis-tic forecast of 5.3 tcm. Its techni-cally recoverable gas reserves may amount to just 346-768 bcm. but these published figures included only archival data, predominantly from exploration testing in the 1960s and 1970s. The preliminary estimate will be upgraded and re-vised on an annual basis. but even the lowest estimate of 346 bcm of

the Uk government iS cUrrentlY Seeking new

waYS to SimPlifY the PermiSSionS ProceSS for

britiSh Shale gaS ProJectS.

71

CASPIAN REPORT, SPRIN

G 2014

70

FRAN

k Um

bACh

shale gas reserves would satisfy Poland’s domestic demand for 35 years.

The government’s proposed taxes exceeding 40%, for instance, have raised concerns among energy companies as they face exception-ally capital investments. Difficult geology, a non-competitive service sector, poor infrastructure, lengthy permissions processes, an uncer-tain regulatory and tax environment as well as lack of rigs have hindered development. In addition, prelimi-nary costs per well have increased to US$15 million – nearly three times the cost in the U.S. As a result of the failure to provide an attractive in-vestment climate, the uncertainties and bureaucratic constraints as well as unrealistic expectations for the short-term future, the pace of shale gas exploration in Poland has clearly slowed down in 2013. For the indus-

try, 287 wells still remain open for exploration, but at the present rate, the exploration process may not end before 2037.

The government and Polish industry representatives still expect that do-mestic shale gas production will be significantly cheaper than Russian gas. In contrast to public opinion in Germany and France, the pro-shale gas policies are supported by more than 70%. The government has

promised to change its shale gas reg-ulations to speed up its exploration and announced last may that it will not collect taxes on the production of shale gas until 2020.

in contraSt to PUblic oPinion in germanY

anD france, the Pro-Shale gaS PolicieS

are SUPPorteD bY more than 70%.

Global shale gas map.

71

CASPIAN REPORT, SPRIN

G 2014

70

FRAN

k Um

bACh

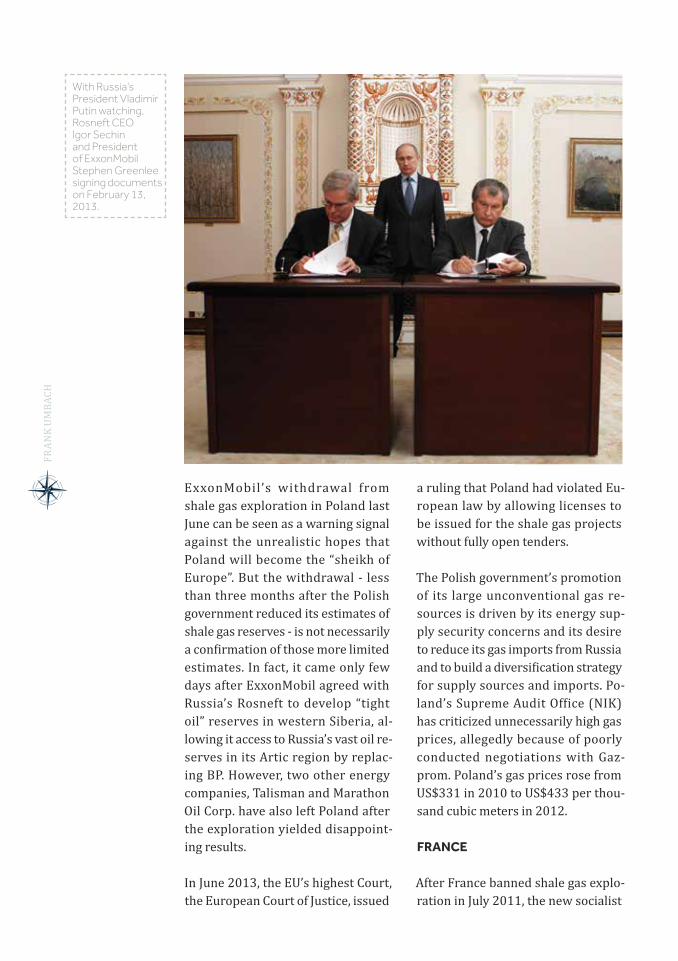

Exxonmobil’s withdrawal from shale gas exploration in Poland last June can be seen as a warning signal against the unrealistic hopes that Poland will become the “sheikh of Europe”. but the withdrawal - less than three months after the Polish government reduced its estimates of shale gas reserves - is not necessarily a confirmation of those more limited estimates. In fact, it came only few days after Exxonmobil agreed with Russia’s Rosneft to develop “tight oil” reserves in western Siberia, al-lowing it access to Russia’s vast oil re- serves in its Artic region by replac-ing bP. however, two other energy companies, Talisman and marathon Oil Corp. have also left Poland after the exploration yielded disappoint-ing results.

In June 2013, the EU’s highest Court, the European Court of Justice, issued

a ruling that Poland had violated Eu-ropean law by allowing licenses to be issued for the shale gas projects without fully open tenders.

The Polish government’s promotion of its large unconventional gas re-sources is driven by its energy sup-ply security concerns and its desire to reduce its gas imports from Russia and to build a diversification strategy for supply sources and imports. Po-land’s Supreme Audit Office (NIK) has criticized unnecessarily high gas prices, allegedly because of poorly conducted negotiations with Gaz-prom. Poland’s gas prices rose from US$331 in 2010 to US$433 per thou-sand cubic meters in 2012.

francE

After France banned shale gas explo-ration in July 2011, the new socialist

With Russia’s President Vladimir Putin watching, Rosneft CEO Igor Sechin and President of ExxonMobil Stephen Greenlee signing documents on February 13, 2013.

73

CASPIAN REPORT, SPRIN

G 2014

72

FRAN

k Um

bACh

French government has opposed any lifting of the embargo since its inau-guration in may 2012, despite having the third largest shale gas resources in Europe (after Russia and Poland) with technically recoverable shale re-serves of 3.88 tcm. however, debates have intensified and have become more polarized – even within Presi-dent hollande’s socialist party itself. Furthermore, though the “Jacob law” of 2011 banned hydraulic fracturing, other means of shale gas extractions are allowed, as well as fracking un-der certain restrictions in pursuit of

“scientific experimentation”.

The French Economy and Finance ministry want to lift the embargo. The French Commissioner for In-vestment, Louis Gallois, called for the government to revoke the ban on shale gas extraction in France in the November 2012 “Pact for the Competitiveness of French Industry”. GDF Suez SA (GSZ) and Total SA (FP) have been the most vocal industrial supporters of shale gas projects in France. Arnaud montebourg, the minister of Industrial Renewal, has also repeatedly supported a re-thinking of shale gas exploration and seeks to circumvent the present ban by developing strict guidelines. The former French Prime minister, Fran-cois Fillion, has also deplored plans to ban research into shale gas devel-opments as “criminal” and indicative of a “medieval mind set”. The IEA ex-pects a reversal of the moratorium and ban on hydrofracturing, and a subsequent rise in shale gas produc-tion after 2020 to around 8 bcm by 2035, exceeding its peak gas produc-tion back at the end of the 1970s.

While the French energy giant Total has moved forward with shale gas exploration in the U.S. and has begun or declared its intention to invest in shale gas exploration projects in Uk, Poland, Denmark, China and Argen-tina, the French policies for shale gas explorations will be determined by the progress in other European countries like Poland and the Uk

rather than by domestic develop-ments in the coming years. Even the dismissal of minister of Ecology, Sustainable Development and En-ergy, Delphine batho, in July 2013 did not change the French govern-ment’s position; President hollande made it clear that under his presi-dency no shale gas projects will be allowed in France. Furthermore, the French Constitutional Council – the country’s highest constitutional au-thority – rejected a legal challenge concerning the government’s ban on fracking after the U.S. gas com-pany Schuepbach Energy, which was originally granted two exploration licenses before the anti-shale legisla-tion was introduced in 2011, issued complaint against the legal ban. but the debates are continuing.

A report by the French bank So-ciété Génerale warned at the end of October 2013 that European shale gas could be the only answer to the poorly-functioning EU gas market in which four foreign national oil companies (Gasprom from Russia, Statoil from Norway, Qatar Petro-

PreSiDent hollanDe maDe it clear that

UnDer hiS PreSiDencY no Shale gaS

ProJectS will be alloweD in france.

73

CASPIAN REPORT, SPRIN

G 2014

72

FRAN

k Um

bACh

leum and Sonatrach from Algeria) control around 50% of the Euro-pean gas supply. France’s Académie des Sciences has recommended that further research into shale gas ex-traction be undertaken, and has also called for an “independent and mul-tidisciplinary scientific authority” to assess the methods and operating practice.

spaIn

The Spanish Energy ministry and the Autonomous Communities have granted numerous exploration per-mits in various autonomous regions (mainly in the northern part of the country) after recent discoveries of shale gas deposits. During the last three years, exploration licenses for Spain’s conventional and unconven-tional hydrocarbon resources have almost doubled in the Asturias/Cantabria/basque Country onshore and offshore areas, as well as in the offshore regions of Fuertenventura, Lanzarote in the Canary Islands. In the latter region, shale gas depos-its are reportedly much larger than in peninsular Spain. In the basque Country area, a “world-class-shale-gas play” has been identified. With the strong support of regional gov-ernments and North American ex-ploration companies, the Spanish unconventional gas industry hopes to expand exploration activities and go into the production of its shale gas reserves in the mid-term.

In August 2013, the Spanish gov-ernment prepared a project for the Law of Environmental Evaluation, which would require all projects us-ing fracking technology to submit an

“evaluation of impact” report. The government has advanced the use of fracking and given legal protection to the controversial technology. Due to the severity of Spain’s economic crisis, the concept of using cheap domestic energy resources has had greater resonance among the Span-ish population than in most other European countries.

The Superior College of mining En-gineering has estimated that Spain’s shale gas resources can provide 39 years of domestic gas consump-tion. Spanish fracking companies have formed the lobby group “Shale Gas Espana” to promote shale gas projects and to dispel myths sur-rounding suspected environmental risks of the fracking technology.

Despite its dependence on imports of hydrocarbons up to 99% - leading to an energy deficit worth 45 billion Euros (almost 4% of the national GDP) - environmental groups and dozens of Town halls and provincial governments as well as the Spanish Federation of municipalities and Provinces (FEmP) have presented 103 motions against fracking.

At the end of last October, parlia-ment passed an amendment to the country’s hydrocarbon law, which will speed up the development of unconventional gas projects in Spain. The law prevents regional governments from banning hy-draulic fracturing projects. Com-

DUring the laSt three YearS, exPloration

licenSeS for SPain’S conventional anD

Unconventional hYDrocarbon reSoUrceS

have almoSt DoUbleD.

75

CASPIAN REPORT, SPRIN

G 2014

74

FRAN

k Um

bACh

panies are obliged to submit an environmental impact assessment to pass the highest environmental approvements. however, Spain’s history of excessive bureaucracy causes doubts about future shale gas projects. but despite the coun-try’s heavy dependence on LNG im-ports, Spain is tied into relatively few long-term take-or-pay gas con-tracts for pipeline gas. This gives Spain much commercial flexibility for its shale gas projects.

lIthuanIa

For the baltic states (as with Poland), the exploration and development of shale gas projects represent an im-portant strategy for diversifying gas supplies, to reduce their gas depen-dence on Russia and to access much cheaper gas than the expensive Gaz-prom imports.

After Poland, Romania, and Ukraine, Lithuania is considered as the fourth most attractive country for shale gas production in Central Eastern. Lithuania could hold 480 bcm of unconventional gas with around recoverable 120 bcm. If these un-conventional gas reserve estimates are confirmed, Lithuania - consum-ing 3.4 bcm in 2011 (all supplied by Gazprom) - could supply its domestic gas demand for the next 30-40 years.

Lithuania was the first Baltic state to announce a shale gas tender in June 2012. In September 2013, Chevron won a tender for a license to explore shale gas resources. but few weeks afterwards, Chevron re-treated. The investment and legal regulations adopted by the Lithu-

anian government shortly after the tender included chaotic changes to the legal, fiscal and regulatory frame-works (due to a lack of governmen-tal coordination, which made the tender increasingly less attractive and commercially viable. Chevron’s withdrawal considerably damaged Lithuanian’s pursuit of energy in-dependence, or at least its aim for reducing gas imports from Russia. It has also damaged the national economy by deterring other foreign investors. but it did reveal that the government did not seek to obtain a broad base of public support. None-theless, the government remains op-timistic that a new tender will attract serious investors.

roManIa

bulgaria, Romania and hungary have around 538 bcm of technically recoverable shale gas reserves. Ro-mania’s annual gas consumption is 13-14 bcm, most of which it can cover with its own significant gas reserves – unlike many of the neigh-bouring balkan countries. In 2012, Romania imported 2.17 bcm of gas from Gazprom. Despite a tempo-rary until the beginning of 2013, the Romanian government continued its negotiations with Chevron for a shale gas exploration project in Con-stanta County. In December 2012, the hungarian energy company mOL and Canada’s East West Petroleum also obtained exploration licenses

after PolanD, romania, anD Ukraine, lithUania

iS conSiDereD aS the foUrth moSt attractive

coUntrY for Shale gaS ProDUction in central

eaStern.

75

CASPIAN REPORT, SPRIN

G 2014

74

FRAN

k Um

bACh

approved by the government. In the same month, a local referendum on the use of fracking technology for shale gas production was declared invalid because less than 50% of vot-ers participated.

At the end of January 2013, the Ro-manian government awarded Chev-ron exploration licenses to pursue unconventional gas production, de-spite environmental concerns. Prime minister Victor Ponta has warned that Romania’s economic competi-tiveness vis-à-vis Poland and other countries will suffer if shale gas is not exploited. he also hopes to re-duce the country’s dependence on Russia and Gazprom, with the fur-ther benefit of purchasing gas much more cheaply in comparison with Russia’s high prices of US$450 per 1,000 cubic meters. but he believes that the exploration and confirma-tion of existing or non-existing eco-nomically exploitable resources may take up to five years before a final decision to produce shale gas can be made by the government. Together with its newly discovered offshore conventional gas resources in the black Sea holding 42-84 bcm (which would cover its gas demand for nine years), Romania’s even higher shale gas resources could cover its net do-mestic demand and make the coun-try self-sufficient in terms of gas.

In November 2013, the European Centre for Excellence in the field of natural gas (CENTGAS) and part of the Romanian National Committee of the World Energy Council (RNC-WEC) published a study concluding that Romania’s shale gas resources could represent a real alternative

for strengthening Romania’s energy security and energy independence. Romania’s unconventional gas re-sources could transform the country into a gas exporter by the beginning of the next decade, contributing 1.5% to annual GDP, reducing gas prices by 12% in the short-term and by 33% in the long-term, creating jobs and generating more tax for the state budget with estimated annual rev-enues of US$176.2 million. New hy-draulic fracturing technologies and a responsible water management can reduce the risks of technical acci-dents and environmental impacts, as responsible water management will eliminate potential sources of water pollution.

bulGarIa

bulgaria has an annual gas consump-tion of around 3 bcm and is almost completely dependent on imports from Gazprom. The bulgarian gov-ernment adopted a moratorium on the exploration of shale gas and the fracking technology in Janu-ary 2012 as a consequence of local opposition, months of protest and pro-Russian attitudes. Legislation was amended in may 2012 to al-low the development of natural gas projects by conventional drilling technologies, for instance for the newly discovered offshore gas fields on bulgaria’s black Sea coast. how-ever, fracking technology for shale gas exploration is still not permitted. Since then, there has been a push to lift or at least review the ban by the movement for Energy Independence (DEN), parts of the government and the bulgarian President Rosen Plev-neliev. Even bulgaria’s Environment

77

CASPIAN REPORT, SPRIN

G 2014

76

FRAN

k Um

bACh

minister stated that the moratorium on hydraulic fracturing is rather a temporary measure until a review of potential environmental and health risks have been conducted and prove that those environmental risks can be controlled and managed.

Romania’s issuance of exploration li-censes for its shale gas reserves and early successful lighthouse projects will shape the future trajectory of bulgarian discussions and decisions in regard to the current moratorium on hydrofracking. however, many energy experts believe that this deci-sion is likely to be reversed once en-vironmental studies are completed.

EstIMatEd EuropEan shalE Gas rEsErvEs:

• UK: Up to 1,700 trillion cubic me-tres. Original estimates were as high as 5.3 tcm.• Germany: 6.8-22.6 tcm, with techni-cally recoverable reserves of 0.7-2.3 tcm (10% of total shale gas reserves).• ExxonMobil estimate of Germany’s exploitable reserves: 827 bcm.• German conventional gas reserves in comparison: 150 bcm.• Bulgaria, Romania and Hungary: 538 bcm of technically recoverable shale gas reserves.

conclusIons and pErspEctIvEs

Notwithstanding its own uncon-ventional gas prospects, the EU-28 stands to benefit from the expand-ing worldwide unconventional gas production in various ways. This emerging global trend will open up new sources of LNG imports, includ-

ing from the U.S. and countries for which exporting gas is an entirely new industry.

The U.S. shale gas revolution can-not be replicated in Europe with the same low costs of shale gas produc-tion; nor will it reach the same vol-umes. It will take place in an evolu-tionary (rather than ‘revolutionary’) way. Nonetheless, it is expected to become an economically competi-tive source of energy, in particular compared to imported Russian con-ventional gas from its new and very expensive gas fields in the remote regions of Yamal and Siberia, trans-ported via long distance pipelines.

With the growing use of LNG on the global gas market, traditional oil-indexed gas contracts will gradually decrease as the global gas market becomes increasingly integrated, whereas spot markets for gas will expand both in number and impor-tance. Embracing unconventional gas will keep costs lower than any future conventional production from new gas fields in remote re-gions, including the Arctic in Russia, as well as the hugely expensive new (underwater) gas pipelines. Cheaper European shale gas will help break Europe’s overdependence on very costly future Russian gas supplies.

The short and mid-term conse-quences of ignoring or denying the positive strategic dimensions of Eu-rope’s domestic unconventional gas reserves are increased gas imports from Russia, plus higher volumes of LNG from often politically un-stable producer countries outside of Europe. In 2012, the EU-27 spent

77

CASPIAN REPORT, SPRIN

G 2014

76

FRAN

k Um

bACh

€408 billion on energy imports – six times more than in 1999, and equal to 3.9% of GDP. This “alternative” not only threatens Europe’s energy supply security and economic com-petitiveness, but also creates a much bigger CO2-footprint. If lifecycle analyses are calculated based on emissions not only from the produc-tion process, but also from the long distance transport via thousands of kilometres of pipelines from Russia, CO2 emissions from domestic shale gas resources would be around 30% lower. The alternatives to domes-tically-produced shale gas would therefore lead to higher gas prices,

reduced supply security and higher CO2 emissions. In other words: the use of domestically-produced uncon-ventional gas serves all three major objectives of the “energy triangle”: supply security, economic competi-tiveness and environmental/climate protection.

With the increasingly wide price gap between the North American and the European oil and gas market (gas: US$4.5 per million british ther-mal units in the U.S. in comparison with US$9 in Europe and US$18 in Asia), a “re-industrialization” of en-ergy intensive and other industries

Shale gas drilling rig.

79

CASPIAN REPORT, SPRIN

G 2014

78

FRAN

k Um

bACh

is already underway on the U.S. side. The future economic competitive-ness of Europe and Asia towards the U.S. faces increasing challenges with much higher gas and other energy prices. Confronted with rising oil and import dependency (in contrast to the U.S.) from politically unstable or other problematic suppliers, EU energy security faces even more se-vere risks, vulnerabilities, and un-certainties in the future. Increased European efforts to maximise the potential of its own unconventional oil and gas resources could also help the EU to retain or create industrial sector jobs, contributing to its over-all future economic competitiveness.

79

CASPIAN REPORT, SPRIN

G 2014

78

FRAN

k Um

bACh