STANDARD AND POOR’S DOWNGRADES COUNTRIES IN THE EUROZONE: AN EXAMINATION OF ITS POSSIBLE...

79

APPLIED MANAGEMENT PROJECT (BSS000-6) STANDARD AND POOR’S DOWNGRADES COUNTRIES IN THE EUROZONE: AN EXAMINATION OF ITS POSSIBLE IMPLICATIONS ON THE MAJOR EXPORTS AND IMPORTS OF EUROPEAN UNION TO THE GLOBAL MARKET A Thesis submitted to the Bedfordshire Business School In partial fulfilment for the award of degree Master of Sciences In INTERNATIONAL BUSINESS AND MANAGEMENT WRITTEN AND SUBMITTED BY: BASHIR IBRAHIM DABO 1030028 4 TH MAY, 2012 1 | Page

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of STANDARD AND POOR’S DOWNGRADES COUNTRIES IN THE EUROZONE: AN EXAMINATION OF ITS POSSIBLE...

APPLIED MANAGEMENT PROJECT

(BSS000-6)

STANDARD AND POOR’S DOWNGRADES COUNTRIES IN THE EUROZONE: AN

EXAMINATION OF ITS POSSIBLE IMPLICATIONS ON THE MAJOR EXPORTS AND

IMPORTS OF EUROPEAN UNION TO THE GLOBAL MARKET

A Thesis submitted to the Bedfordshire Business School

In partial fulfilment for the award of degree

Master of Sciences

In

INTERNATIONAL BUSINESS AND MANAGEMENT

WRITTEN AND SUBMITTED BY:

BASHIR IBRAHIM DABO

1030028

4TH MAY, 2012

1 | P a g e

DEDICATION

This thesis is dedicated to Almighty Allah (SWT) for fulfilling

His covenant upon me; And also to my parents, Late Alhaji (Dr.)

Ibrahim Dabo, Wakilin Birnin Zazzau and Hajiya Asiya Mahmood for

their love, moral upbringing and support. May the positive

influence your love and lives cast on me, be restored to you from

Allah's Throne with blessings and mercy!

2 | P a g e

ACKKNOWLEDGEMENT

Glory be to Allah (SWT), The Omnipotent, The Omnipresence and The

Omniscience! With His help, all negative forces that would have

stood my way in the course of this sojourn were crushed and

defeated!

I would like to acknowledge and appreciate the support of my

siblings- Alh. Idris Dabo, Alh. Dalhatu Ibrahim Dabo, Mal.

Suleiman Ibrahim Dabo and Lawal Ibrahim Dabo; and also Hajiya

Bilkisu Nasiru Shagari, Hajiya Rabi’atu Hussaini Sambo and Halima

Suleiman Gidado for being with me in joy and in difficulty; and

special prayers goes to my three late sisters who would have been

proud of me today, Hajiya Aishatu Shehu Shagari, Hajiya Fatima

Ibrahim Dabo and Khadija Ibrahim Dabo who answered the sacred

calls back to the Almighty in 2001, 1982 and 2009 respectively.

May their souls continue to rest in the position of exalted

glory!

I am also indeed very grateful to my uncles and aunty-inlaw- Alh.

Nazeefi Abdulaziz, Alh. Dr. Gidado Idris (GCON) and Haj. Zainab

Idris.

3 | P a g e

I thank Dr. Yazid of University of Essex, whom I call my new

mentor. His guidance and attention to supervising every detail of

this work is unparalleled

A big shout out to my relatives and friends here in the UK like

Ahmed Sani, Ummi, Fauzi, Zainab Usman, Habib Gajam, Bashir

Hassan, Mal. Idris Musawa, Mal. Shehu Jallo, Afrah, Mamman and

Yakubu Doma, Feke, Joel and a host of others too numerous to be

mentioned- I identify with you all for tolerating me through

thick and thin. Same goes to my two nephews- Dr. Shehu Idris Dabo

(MBBS); and ASC Shehu Tambari- my undiluted loyalty sir! Alh.

Shehu Salisu, Umar Sani and Ibrahim Yakubu Misau,a big thank you

for your encouragements too.

My beautiful Xaarah, I love you and identify with you- thank you

for being with me always throughout this challenging period when

I needed you!

Finally, I conclude by taking my hat off to the entire deprived

and marginalised plight in the world especially those in my

country- Nigeria, be rest assured that your perseverance will

never be in vain God willing!

TABLE OF CONTENTS

TITLE PAGE……………………………………………………………………….1

DEDICATION……………………………………………………………………....2

4 | P a g e

ACKNOWLEDGEMENT…………………………………………………………..3

TABLE OF CONTENTS…………………………………………………………...4

LIST OF ABBREVIATIONS……………………………………………………….6

EXECUTIVE SUMMARY………………………………………………………….7

1.0 AIM AND OBJECTIVES……..……………………………………………….8

1.1 Aim of the Research………………...…………………………………………8

1.2 Objectives of the Research……..…………………………………………….8

1.3 Background to the Study……………………..……………………………….8

1.3.1FinancialCrisis………………………………………………..……………….8

1.3.2 Credit Rating and Rating Agency….…………….…………...……………

9

1.3.3 A Background of EU’s Exports and

Imports…………………………………..……………….…………………………10

2.0 LITERATURE REVIEW…….…………..………………………………......13

2.1 Standard and Poor’s Downgrades and affected

Countries…………………………………….……………………………………..13

2.2 Determinants of Sovereign Governments Credit Ratings

by Standard and Poor’s……………………………………………………………………………....14

2.2.1 Reasons Why These Countries Were

Downgraded……………………………………………….............................

.....16

2.3.0 Impacts of Sovereign Credit Rating

Downgrades………………………………………………….…………………….18

2.3.1 Foreign Exchange, Stock and Bond Markets versus

Imports and Exports…………………………………...…………………………………………20

5 | P a g e

2.3.2 Korea: Foreign Exchange Market versus Exports and

Imports…………………………..………………………………………………….21

2.3.3 Stock and Bond Markets versus Exports and

Imports…………………………….……………………………………………….22

3.0 ANALYSIS AND DISCUSSION………………….………………………….25

3.1 France Exports and Imports Movements and Balance Of

Trade within the Downgrades

Period…………………………………………………………….....25

3.1.2 Italy’s Exports, Imports and Balance Of Payments

within the Period of the

Downgrades…………………………………………………………………...27

3.1.3 United Kingdom……………………………………………………………..30

3.1.4 Germany’s Exports, Imports and Balance Of Trade..

…………………..32

3.2.0 An Analysis Of The Exports Of German Car Giants

Daimler- Makers Of Mercedes-Benz And The Imports From

Japan Of Toyota Cars In The Aftermath Of The Eurozone

Mass Credit Ratings Downgrades……………...35

3.2.1 Daimler……………………………….………………………………………35

3.2.2 Japanese Toyota…………………….……………………………………..37

4.0 CONCLUSIONS AND RECOMMENDATIONS...…………………………39

4.1 Conclusion……………………………………………………………………..39

4.2 Recommendations…………….……………………………………………...40

References…………………………………………………….…...................42-47

Reflective Report

6 | P a g e

LIST OF ABBREVIATIONS

EU – European Union

UK - United Kingdom

USA – United States of America

EUR – Euro Currency

USD – United States Dollar

GBP - British Pound

Won – Korea’s Currency

Yen – Japanese Currency

ECB – European Central Bank

CRA – Credit Rating Agency

CR – Credit Rating

S&P – Standard and Poor’s

7 | P a g e

EXECUTIVE SUMMARY

This research looked at the possible implication of the January 13th, 2012 mass downgrades of some nine countries in the Euro zone by the United States based credit rating agency of Standard and Poor’s in relation to the exports and imports of European Union as a whole.

It found from existing literatures that sovereign credit ratings downgrade in general has no direct implications to a country’s exports or imports. But an indirect relationship did exist because downgrades had impacted on the bond, stock and foreign exchange markets of Korea during the Asian financial crisis, as well as that of Australia and New Zealand which later on influenced the exports and imports of some of these countries especially the exchange rates movements in the foreign exchange market.

This works findings on the EU was in consistent with the literatures above, whereas the European stock and foreign exchange markets both reacted negatively sequel to S&P’s downgrades news. And the exchange rates movement would likely have negative implications to the imports of Toyota vehicles into

8 | P a g e

the E.U. However, it was established using German Daimler Group- makers of Mercedes-Benz cars as an example, in terms of exports, the company made mentioned of exchange rates movements as positive factor in within the first quarter of 2012.

The work concluded that the downgrades would likely have negativeimplications on imports of the countries that use the EUR as their currency not the E.U. as a whole if the exchange rate market continues to remain volatile. But exports would not likelybe affected.

1.0 AIM AND OBJECTIVES

1.1 Aim of the Research

The aim of this work is to try and figure out the likely implications of S&P’s downgrades vis-à-vis major exports and imports in the EU in relation to global market- by raising valid points and references in an objective and articulate way which would help in giving out some meaningful results thereafter. Thus, the researcher has chosen the recent January 13th, 2012

9 | P a g e

mass downgrades of nine countries in the Eurozone by S&P to use in meeting its aim.

1.2 Objectives of the Research

The aim of this research would be impossible to achieve without outlining the ways upon which it will be achieved. Hence the objectives of the work below:

• To evaluate the current economic crisis in the European Union

• To provide a background of credit rating

• To provide a background to EU exports and imports.

• To examine why the affected countries were downgraded and how Standard and Poor’s rates countries.

• To review a number of established academic theories that talked about the implications of downgrading.

• To use some examples in proposing the possible implications of the downgrading on EU’s ability to export and import.

The above six points will henceforth form the basis for this entire work.

1.3 Background to the Study

1.3.1 Financial Crisis

The year 2008 marked another watershed in the history of Global economy. As the world witnessed what would best be described as the year in which the global economy was relegated to shambles. The collapsed of Lehman Brothers in September, 2008 doomed the hopes and fears of international actors and individuals about thefear of experiencing another recession since after the great depression of the 1930’s (European Communities, 2009). It startedas a financial crisis from Wall Street which resulted in the loss

10 | P a g e

of a shocking and unexpected amount of nearly US $25 Trillion in stock markets value alone by the last quarter of 2008 (Naude, 2009). This collapse was immediately felt in Europe as the economy started to shrink drastically worst only to the era of the great depression. This unprecedented impact forced experts toproject a 4% decrease of the region’s GDP in 2009 (European Communities, 2009). As a result of this unprecedented dent to thehealth of the global economy, many analysts believed that the recession would be as traumatic as the pre-second world war GreatDepression of the 1930’s (Shapiro and Shultz II, 2009; and Imbs, 2010). This shocking revelation generated a lot of fear, questions, and criticisms and of course most importantly how to save the vulnerable global economy from total collapse.

Hence, Countries affected amongst many were those in the EuropeanUnion, who then started looking for alternative funds to borrow in order to bail-out their troubled economies. This then made lenders to become cautious in lending out money to borrowers due to fear that most of the troubled economies were indeed lacking the financial adequacy to repay the borrowed funds if given. Mostof these lenders, rely heavily on reports generated by reputable Credit Rating Agencies (CRA), notably Standard and Poor’s, Moody’s Investor Service and Fitch Ratings which play a “key rolein the pricing of credit risk and in the delineation of investment strategies.” (Altman and Rijken, 2005:127).

However, In order to give a clear picture to the reader regardingthe validity of further analysis, it would be expedient to give abrief and comprehensive analysis on Credit Rating, Credit Rating Agency, its modus operandi and finally a preamble of the CRA in question- Standard and Poor’s.

1.3.2 Credit Rating and Rating Agency

Credit rating is an extensive evaluation process which involves scrutinizing sensitive financial information of corporations or

11 | P a g e

governments done by independent rating agencies in order to help the public especially credit issuers in making financial decisions particularly when giving out debts to borrowers - either as mortgages, bonds, loans or promissory bills to mention some, would be able to pay back (Kronwald, 2009). Credit ratings are done by Credit Rating Agencies like Moody’s, Standard and Poor’s, Fitch Ratings amongst others. These three agencies are considered as the top three in the world according to Anand (2011). The agencies based their ratings in graded forms from ‘AAA’ down to ‘D’ grade. This grading pattern represented those of Standard and Poor’s and Fitch Ratings: whereas Moody’s Corporation graded from ‘Aaa’ down to ‘C’ grade. Regardless of the grading patterns however, they all represented similar messages. Thus, AAA or Aaa rating signifies lowest-risky of security and therefore has low interest rate as well. While grades from ‘D’ or ‘C’ passes a strongly negative message to the public as they represent default status- i.e. a status in which aborrower would not be able to pay back a loan if granted. Hence, they are of extremely high risk and of high interest rates. However, in between the highest grades and the lowest, there exists some grading status as well.

Likewise, it was in line with the above rating analysis that Standard and Poor’s recently downgraded some western countries including two major global economic powers- the United States andFrance by losing their top ‘AAA’ rating down by single notch to ‘AA+’ for the first time since 1917 and 1975 respectively. The downgrade, particularly of the US was seen as a “Historical move”by Danluy (2011). Austria also lost its “AAA” by a single notch to AA+. Others affected by stripping off one notch in their ratings were; Slovenia from “AA-” to “A+”; Slovakia from “A+” to “A”; and Malta from “A” to “A-“. In contrast, four other countries got their ratings stripped off by two notches. These countries were: Italy from “A” to “BBB+”; Spain from “AA-“to “A”;Portugal from “BBB-“to “BB”; and lastly Cyprus from “BBB” to 12 | P a g e

“BB+” (Standard and poor’s, 2012). But interestingly, despite these ugly pictures of the above countries, the EU as a whole still maintained its triple A rating from S&Ps, though with a negative outlook!

All the above countries downgraded were in the Euro zone and wereannounced by S&Ps on the 13th of January, 2011 with the exceptionof US. Hence, these countries will form the basis for this research along with other troubled countries in the Euro zone particularly Greece which had seen series of downgrading in the past and it still the most troubled economy in not only in the Euro zone but EU as a whole. Likewise, Standard and Poor’s ratingagency will be used henceforth in the course of writing this work. But others would probably be cited as a matter of reference.

1.3.3 A Background of EU’s Exports and Imports

The EU with a composition of 27 sovereign entities is the largesteconomy in the world second only to the United States of America (U.S.A.) (European Communities, 2009). These countries are Belgium, Bulgaria, Czech Republic, Denmark, Germany, Estonia, Greece, Spain, France, Ireland, Italy, Cyprus, Latvia, Lithuania,Luxembourg, Hungary, Malta, The Netherlands, Austria, Poland, Portugal, Romania, Slovenia, Slovakia, Finland, Sweden, United Kingdom (European Communities, 2009). However, Seventeen out of these countries had already debunked their default national currencies and replaced it with a common currency known as the Euro, as their legal official tender (European Central Bank, 2011). It is the second most powerful and used currency in the world behind the US dollar, and it is being used by close to 330 million people within the EU alone (Euro Stat, 2011). Amongst them were Germany, France, Austria, Italy, Spain, Portugal, Greece, Ireland, Luxemburg, Belgium, Netherlands, Slovenia and Finland. Others were Cyprus, Malta, Slovakia and finally Estonia-although, others members are still on the process of switching to13 | P a g e

the Euro (European Central Bank, 2011). Interestingly, some of these countries notably Germany, Italy and France contributed major share of EU’s major trading products; like manufactured goods, machinery and equipment, electrical appliances, and automotives amongst others (Eurostat, 2012).

The EU was the major exporter of manufactured goods in the world.The United States as at 2011 remained the major destination of almost all EU’s exports and also its major trading partner. Followed by Switzerland; then China, which was the major destination of EU’s raw materials exports. And also Russia was a major partner too (Eurostat, 2012). Additionally, other manufactured goods sector is also critical to EU’s trade, second only to machinery. Exports in this area in 2010 were 23.1% while imports stood at 24.1% ((Eurostat, 2012; Statistical Books, 2011).

Machinery and electrical appliances were the major export products for the EU and also its major industrial sector. The industry was a direct employer of close to 11 million people in 2010 with a total annual output of nearly EUR 1 trillion (Euro Machinery, 2011). It added that as at 2010, its exports stood at EUR 408 billion and conversely, imports stood at EUR 278 billion.The percentages of exports and imports in this sector stood at 42.4% and 29.5% respectively in 2010. Germany, Italy, the United Kingdom and France were the dominant actors. This sector is critical to overall EU economy as a whole. This was because its production gave life to all other sectors (Euro Machinery, 2011).

In the automotive industry, EU was the global leader as at 2010 with a global share of automotive production of 25% with Germany and France as dominant contributors! Needless to say, this percentage makes EU an important player as far international trade in this sector is concerned. In the same period, EUR 132 billion was realized from exports while close to EUR 47 billion was spent on imports (Euro Automotive, 2011). 14 | P a g e

Chemicals sector is another crucial sector that needs to be cited. The EU contributed almost 30% out of 100 of the world’s total chemicals market with Germany taking the lead by contributing 25% of EU’s total production in 2008. In the same year, the region’s chemical production was said to be worth over EUR 560 billion. Also interestingly, in 2009 its chemicals exports revolved around EUR 118 billion while imports stood at EUR 75 billion. The US again was the major destination for EU’s chemicals exports, with Canada, Switzerland, China, India and Japan following (Euro Chemical, 2011).

Raw materials sector had also it share in EU’s exports and imports. Though it was a sector that EU had trade deficit, this is to say, its imports quiet outweighed its exports. In 2010, EU’s exports stood at EUR 100 billion as against EUR 142 billion paid in terms of imports. However, this sector covered only 4.7% and 2.8% of EU’s total imports and exports respectively. Most of EU’s raw materials went to China and in contrast, imported most from the US (Euro Raw Material, 2011).

Food drinks and tobacco was another sector that covered 5.7% of EU’s total exports while imports stood at 5.4%. The main destination of these products was the US as at 2010 (Euro, 2010).

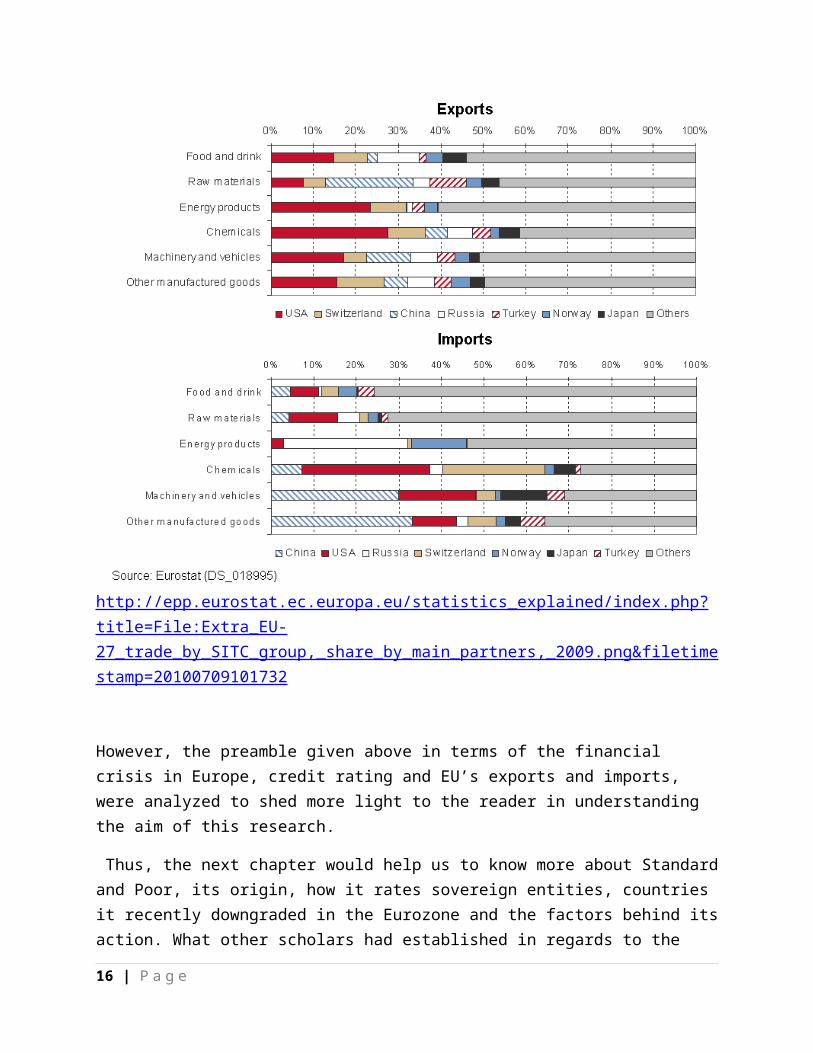

Summarily, Machinery and transport equipment, other manufactured goods, chemicals and related products, food, drinks and tobacco, mineral fuels, lubricants and related, and finally commodity transactions constituted the major exports and imports products of the EU. Albeit not all the products were detailed above, but US, Switzerland, China, Russia, Turkey, Norway and Japan remainedEU’s major trading partners. The diagram below would perhaps addmore light to the reader. Thus:

15 | P a g e

http://epp.eurostat.ec.europa.eu/statistics_explained/index.php?title=File:Extra_EU-27_trade_by_SITC_group,_share_by_main_partners,_2009.png&filetimestamp=20100709101732

However, the preamble given above in terms of the financial crisis in Europe, credit rating and EU’s exports and imports, were analyzed to shed more light to the reader in understanding the aim of this research.

Thus, the next chapter would help us to know more about Standardand Poor, its origin, how it rates sovereign entities, countries it recently downgraded in the Eurozone and the factors behind itsaction. What other scholars had established in regards to the

16 | P a g e

factors the economic implications of downgrading the credit rating of a sovereign entity will be reviewed.

17 | P a g e

2.0 LITERATURE REVIEW

2.1 Standard and Poor’s, Downgrades and affected Countries

Standard and Poor’s traces it origin in 1846, when its founder Henry Varnum Poor was appointed editor of ‘The American Railroad Journal’ (Sylla, 2001). It was this job that exposed Poor and made him and his son to form ‘the Poor Company’ which initially started with publishing of Railroad publication called the ‘The Manual of the Railroads of the United States.’. After Poor’s death in 1905, the son entered into bond rating business with thecompany in 1916 (Sylla, 2001). This continued until 1946 when thefirm merged with a company called ‘Standard Statistics’, which resulted in the change of name of the company to ‘Standard and Poor’s’ which it has maintained up till today (Sylla, 2001)! The company is based in the United States and it is currently owned by The MacGraw Hill Publishing Company and has been so since in the 1960’s (Sylla, 2001). It has a reputation of being one of thethree best and renowned credit rating agencies in the world (Anand (2011).

On 13th January, 2012, some nine Eurozone countries were dealtwith another blow to their already troubled economies or the EU economy as a whole, as Standard and Poor’s downgraded 9 countriesout of 15 that were initially issued warnings in early December 2011 of a possibility of being downgraded by S&P (Wiesmann, Spiegel and Wigglesworth, 2012). Amongst the countries affected were the Eurozone only triple A credit ratings holders; France and Austria, who saw their triple rating being downgraded by stripping off a single notch from AAA rating to AA+ (Ibid). The latter’s case was worst unlike the former’s, because it was the first time France was downgraded since 1974 (ibid). Others were

18 | P a g e

Italy, Spain, and Portugal who all lost two notches. Cyprus lost its rating by double notches too, together with Slovenia, Slovakia and Malta who albeit unlike Cyprus lost their ratings bysingle notch. The downgrades announcement by S&P went thus:

“We have lowered the long-term ratings on Cyprus, Italy, Portugal, and Spain by two notches; lowered the long-term ratingson Austria, France, Malta, the Slovak Republic, and Slovenia, by one notch; and affirmed the long-term ratings on Belgium, Estonia, Finland, Germany, Ireland, Luxembourg, and the

Netherlands. All ratings on the 16 sovereigns have been removed from

CreditWatch where they were placed with negative implications on Dec. 5, 2011

(Except for Cyprus, which was first placed on CreditWatch on Aug.12, 2011)? The outlooks on our long-term ratings on all but two of the 16 eurozone

Sovereigns are negative; the outlooks on the long-term ratings onGermany and

Slovakia is stable.” (Standard and Poor’s, 2012).

Albeit, this did not appeared to be a surprise to many, as all the countries downgraded with the exception of Cyprus who was already included on the creditwatch list, were earlier warned in a statement issued by S&P in the first week of December, 2011 of the possibilities of being downgraded if visible improvements were not sighted, as reported by Platt (2012); and Deen and Livesey (2011).

However, let us take a look at the criteria or factors upon whichS&P follow to rate a sovereign government. This would perhaps help us to see reason behind the downgrades of the nine Eurozone countries in question thereafter.

19 | P a g e

2.2 Determinants of Sovereign Governments Credit Ratings by Standard and Poor’s

Before Standard and Poor (2011) announces the downgrade or upgrade of any sovereign government, certain factors must which they termed as their “five sovereign rating scores” must first beassessed before taking an official decision (Standard and Poor’s,2011). These five factors (score) are: political score; economic score; external score; fiscal score; and monetary score. Let us look at how these scores operate independently.

Political Score: This score assesses how a sovereign government policy or decision making influences its credit fundamentals by ensuring its public finances are sustainable, promoting balanced economic growth and its ability to respond to difficult situations like economic or financial shocks. And have knowledge on it, S&P relied on three major factors namely primary, secondary and what they called potential adjustment factors (Standard and Poor’s, 2011).

The primary looks at effectiveness, stability and predictability of a sovereign government’s decision or policy making; and the secondary focuses on a government level of transparency and accountability, data and processes coupled with having reliable statistical information; while the potential adjustment factor covers the payment culture of a government, its risks of externalsecurity and lastly, the potentiality of effects of external forces e.g. the EU, IMF, UN, etcetera on a sovereign government’s policy setting (Standard and Poor’s, 2011).

Economic Score: A sovereign government economic score is being measured by S&P on three main factors, namely income level; growth prospects; and economic and diversity (Standard and Poor’s, 2011).

20 | P a g e

Income level is determined by the GDP per capita of a country, which is being established by using the up-to-date GDP per capitafigures obtained from national statistics of a sovereign entity. Standard &Poor’s (2011) noted that a country with higher GDP per capita income would have a huge potential tax and funding base todraw. They believed that it enhances the creditworthiness of a country positively. It is however important to point out that GDPper capita is normally converted to USD by S&P in measuring income level. Albeit, they acknowledged that the conversion is sometimes results in not having the exact reflection of a country’s income level due to the vulnerability and uncertainty of the currency market- which could be faced with over or under-valuation of the currency.

Growth prospects in the other hand, is being determine by what S&P reported as real per capita GDP “trend growth”. “Trend growth” according to Standard and Poor’s (2011) “refers to the rate at which GDP grows sustainably over an extended period… derived from empirical observations based on the recent past and longer-term historical trend…to look through the fluctuations of an economic cycle, smoothing for peaks and troughs in output during the period being analyzed.”

Economic and diversity score is considered to be adjustable when an industry of a country that accounts for over 20% of its GDP isbeing faced with tremendous exposure, or when economic activitiesare always being hindered sequel to problems associated to natural disasters or adverse conditions of weather. However, it would be considered in good position if over 50% of its GDP comesfrom general government liquid assets- which would serve as palliative if things turn awry (Standard and Poor’s, 2011).

External Score: This reflects the total international transactions of a sovereign entity. It includes transactions doneby players from both private and public sectors in relation to their foreign counterparts (Standard and Poor’s, 2011). This type21 | P a g e

transaction shapes the movement of a country’s currency exchange rates. The economic score is measured by three factors: currency status in international transaction; external liquidity; and external indebtedness (Standard and Poor’s, 2011).

Currency status in international transaction connotes with how a country’s local currency is being used in cross-border transactions and it is assessed by ascertaining how a sovereign government’s currency is being involved in cross-border transactions. S&P gave two categorizations in this regard. Eithercountries that have a “reserved currency” like U.S, Japan, Franceand Germany to mention a few or countries that have “actively traded currency” like New Zealand, Canada and all Eurozone countries with the exception of France and Germany that have beenmentioned earlier in the first category (Standard and Poor’s, 2011).

External liquidity is being determined by knowing the ability ofa sovereign entity in generating the requisite amount of foreign exchange needed by both private and public sectors in their cross-border transactions. Further, external liquidity is being retrieved by scrutinizing what S&P called the “ratio of external financing needs” and “usable official foreign exchange reserves”,which the information on expected imports, terms of trade and external debt structure of a country are key in determining it (Standard and Poor’s, 2011) .

External indebtedness is realizable by knowing the “narrow net external debt” in relation to a country’s current account receipts (Ibid).

Fiscal Score: This is used in examining the sustainability of a sovereign government in terms of deficit and debt burden. It is determine by looking at the fiscal flexibility, fiscal trends andvulnerabilities, debt structure and accessibility to funding, andrisks as a result of potential fiscal liabilities of sovereign

22 | P a g e

government. Fiscal performance and flexibility and debt burden are the two variables used in analyzing it (Standard and Poor’s, 2011). It added that, fiscal performance and flexibility is realized from the change in the nominal general government debt calculated as a percentage of GDP.

Debt burden focused on knowing how sustainable a government’s debt level is. Because it was observed by Standard and Poor’s (2011) that debt level and debt structure of a country, accessibility to funds and the relative cost of debt in relation to the growth of a country’s revenue were the major forces behindthat blocked it.

Monetary Score: is determine from the role played by financial regulatory authorities in supporting the continuous survival of acountry’s economic growth and also providing mechanisms of tackling anything that may cause a potential threat to the survival of that economy. This score is seen as crucial in preventing the creditworthiness of a sovereign entity from deteriorating especially when the country is in a financial or economic mess. It is being analyzed by looking at how a country uses it monetary policy in responding to domestic economic or financial challenges, the credible nature of the monetary policy using inflation changes as yardstick, and lastly how policy decisions taken are being effectively translated into meaningful actions (Standard and Poor’s, 2011).

The five points analyzed above formed the basis of S&P’s rating criteria. However, having looked at S&P’s rating criteria, now this work will try to look at the reasons behind S&P’s downgrading of these countries in the Eurozone.

2.2.1 Reasons Why These Countries Were Downgraded

23 | P a g e

On the 13th of January 2012, S&P in announcing the downgrades of the nine Eurozone countries in question, Identified five primary challenges facing the these countries and the Eurozone as a whole. These key challenges as noted by Standard and Poor’s (2012) were: tightening credit conditions; increase in risks premium for a widening group of Eurozone issuers; a simultaneous attempt to deliver by governments and households; weakening economic growth prospects and; an open and prolonged dispute among European policy makers over the proper approach to address challenges.

In line with the above, it is believed that the actions and reactions of the European policy makers were not perceived to be effective and stable in solving the identified pressing challenges (Standard and Poor’s, 2012) . This assertion became more convincing after the outcome of the EU summit on 9th December, 2011 (ibid). They believed the decision reached at the summit “has not produced a breakthrough of sufficient size and scope to fully address the euro zone’s financial problems.” Hence, these countries were downgraded (Standard and Poor’s, 2012). The downgrades focused on three scores in line with S&P’s five scores of rating criteria- political score, external score and monetary score.

The political score of the affected countries was adjusted downward. This was sequel to the belief that European policy makers and political actors were not approaching the established problems as effectively as they should, looking at the gravity ofthe crisis that bedevilled the area. Furthermore, the external score was also adjusted downward in line with S&P’s rating criteria. However, the monetary score of the parties concerned remained positive and commendable. This was attributed to the fact that the respective monetary authorities have been doing wonderful jobs in addressing the problems as they should and with

24 | P a g e

all sincerity of purpose especially the European Central Bank (ECB) (Standard and Poor’s, 2012).

Summarily, the above factors were identified by S&P as the major reasons behind their downgrades. Now this work will further look at how the euro zone reacted to these downgrades.

Reactions to the Downgrades

After the rating announcement by S&P, a lot of comments were followed by different stake holders regarding their views on the downgrades in the Euro zone. France as the second largest economybehind Germany in the Euro zone which had its triple A rating stripped off by one notch commented through its finance Minister Francois Barion that “it is not good news…but it is not a catastrophe” noted the minister. He added that “It is not rating agencies that dictate the policies of France.” (Wiesmann, Spiegeland Wigglesworth, 2012). Portugal also reacted angrily by saying that the downward review of its credit rating was “ill-founded” and was marred with massive “inconsistencies”. This also went similar with the reaction of the European Union commissioner of monetary affairs, Mr Olli Rehn, which he tagged S&P’s decision oneuroze as also “inconsistent” and should be discarded and concentrate on tackling more serious and challenging issues that surrounds the area (Wiesmann, Spiegel and Wigglesworth, 2012).

Should this be the case, one could say that the above reactions from some of the policy makers in the EU shows that the rating agency is facing credibility problem with the parties concerned. However, established academic theories that talked about the implications of credit rating downgrade will now be looked into.

2.3.0 Impacts of Sovereign Credit Rating Downgrades

This literature review will examine some theoretical works on theimplications of a downwards review of the sovereign credit ratingof an entity.

25 | P a g e

(Hill&Faff, 2010) understood that the effects of changes caused as a result of either downwards or upwards grading of the sovereign credit rating of a country is still limited in terms theoretical research. In other words, researches conducted in this area remain at its lowest ebb. In consistent with Hill and Faff, Correa (2011), believed that most of the established theoretical works in this area lacked differential implications to the general aspects of the economy rather focused mainly on the implications of sovereign rating changes on equity and stock returns as well as bond yields. This assertion was validated in the works of (Kaminsky&Schmukler, 2002); (Brooks et al., 2004); and (Gande and Parsley, 2005).

Further with the above observations,(Dallocchio et al., 2006) also noted that there are considerably low numbers of research conducted in regards to the European bond markets which he blamedit on the fact that rating activities were relatively new in the European markets. However, they established in their study on theFrench bond markets that downgrading or upgrading a country’s credit rating has no relevant impact in its financial market. Rather they concluded that changes in outlooks or watches of ratings are likely to have impacts on a country’s financial market.

In contrast to the assertion of Dallacchio et al. above, Archer, Biglaiser and De Rouen Jr. (2007) posits that a sovereign downgrading of a government by a credit rating agency (CRA) normally resulted to higher risk premia and also results in a significant upwards spread of bond and higher cost to the issuer of the bond. Reisen&von Maltzan, (1999) also conducted a study which explored the market response for 30 days before and after rating announcements. Their observation was that both downgrades and upgrades have imminent impacts on dollar bond yields. They also noted that sovereign ratings changes and changes in bond

26 | P a g e

yields are of mutual interdependence. Their finding was confirmedin the work of Cantor and Packer (1996).

Furthermore, Brooks et al., (2004) added that, although the sovereign rating changes has impacts on bond yields as observed by Reisen and Maltzan, but the changes also has significant impact on national stock markets. They specified that downgrades have a negative wealth impact in regards to stock market returns.This went in harmony with (Kaminsky&Schmukler, 2002) observationsthat change in sovereign debt rating have direct implication not only on bonds that are being rated but also the stock markets. They further added that change in sovereign rating outlook also has impact on both bond and stock markets. They also noted that these changes create a kind of cross-country shock amongst the countries affected by the rating changes, more especially negative change. Finally they were of the belief that downgrades goes hand in hand with economic downturn. This was similar to thestudy of (Creighton, Gower & Richards, 2007) where they noted that sovereign rating downgrade lagged the Australian stock market, which in turn resulted in low equity returns. So was the case in Korean stock market during the Korean financial crisis asobserved by (Joo&Pruitt, 2006).

In another study credited to (Reisen&von Maltzan, 1999), they noted that during the initial stage of the Asian financial crisis, the sovereign ratings of Asian borrowers were downgraded by moody to “Junk status” i.e. non investment grade giving by a rating agency or a low-rated bond that is too risky for investment as explained by Encyclopedia Britannica (2012). This apparent negative development contaminated the already collapsingAsian economy transit from bad to much worsen situation in many ways than one, for example the automobile, manufactured goods andraw materials industries were affected amongst others. It affected both imports and exports. As cited by Reisen&von Maltzan(1999:274) “commercial banks could no longer issue international

27 | P a g e

letters of credit for local importers and exporters; institutional investors had to offload Asian assets as they were required to maintain port folios only in investment-grade securities and foreign creditors were entitled to call in loans upon the downgrades.” In addition, they added that sovereign downgrading might also reduce capital flows as investors might likely be panic. This could translate to capital outflow or in other words money taking out of the country. Hence, chances couldbe high that capital outflow in any crisis ridden economy would most likely worsen its situation.

Horst (2007) understood that credit rating announcements generates shock which naturally has direct effect on the party the rating announcement was focused on. Further, he established that the effect could transcend to a much wider level by affecting the whole economy in a strategic way. This effect may come through “counter-play relations” which involves some important activities like borrowing and lending in the banking sector (Allen and Gale 2000). They believed that credit default news on one bank could affect other banks in the entire sector.

However, whereas there seemed to be general agreement by the authors of most of the literatures cited above in regards to the assertion that sovereign credit rating downgrades have negative effect on financial markets, but interestingly (Elayan, Wei & Meyer, 2003) came up with a complete contradictory finding on their study of the New Zealand’s stock market. They found that sovereign rating downgrade did more good than harm to the stock market, as there was significant return running in excesses in share prices during the downgrades period.

Hooper, Hume & Kim (2008) believed that the impact of sovereign credit rating downgrades does not only stop at the stock or bond markets, but it also has impact on foreign exchange markets. Albeit, their findings showed that the impact has link with the stock market. They were of the believe that sovereign credit 28 | P a g e

rating downgrade has significant negative impact on returns of stocks denominated in USD which would lead to increase in the volatility of it. Krueger (1983), in Hatemi-J&Roca, (2005:539) added more light to the findings of Hooper et al., he noted that changes in stock prices affects exchange rate itself “ …because achange in stock market prices affects domestic wealth which in turn affects the demand for money leading to a change in interestrates. This consequently impacts on capital flows, which then change exchange rates.” This went in harmony with the study of Subasi (2008), he examined the effects of sovereign credit ratingchanges on exchange rates with particular reference on the two most used and powerful currencies in the global transaction terrain i.e. the USD ($) and the EUR. He found out that downgrades amount to depreciation of the both currencies.

In similar but somehow different perception,(Bissoondoyal-Bheenick et al., 2011) purported that, albeit sovereign rating downgrades has negative impact on foreign exchange especially in terms of its volatility, but multiple downgrades of a single entity by different CRAs would be more catastrophic to the volatility of foreign exchange market than that done by one CRA.

As most of these literatures above focused on foreign exchange, bond and stock markets as the areas upon which sovereign rating downgrades had impact, thus this report discovers out from other sources whether there are relationships or linkages between theseestablished areas vis-à-vis imports and exports or foreign trade as the case may be.

2.3.1 Foreign Exchange, Stock and Bond Markets versus Imports andExports

Briggs (1994) reported that when two or more parties involved in cross-border transactions or exports and imports, and the partiesuses different currencies, then the issue of exchange rates comes

29 | P a g e

in. Because, there has to be consensus upon which currency would be used for the monetary transactions.

Foreign trade payment transactions are made through cash advance,letter of credit, open account, escrow, documents against payment/ bill of exchange, consignment sales, et al. (Sirpal, 2009). Foreign trade involves parties from different countries and in most cases they used different currencies in such transactions and thus it involves exchange rates risk (Briggs, 1994). And the risks possibility exists between the exchange rates of the exporters’ country and that of the importers’ in-between the exporter’s date of quotation and the importer’s date of (quoted price) settlement (Ibid). (Sirpal, 2009) purported further that fluctuation or movement of exchange rates has both negative and positive effect when it comes to cross-border transactions between the recipient of the foreign currency (exporter) and the importer that makes the payment. Albeit, he added that exporter can avoid the foreign exchange fluctuation risk by giving out quotation of their products in their home or local currency and by also demanding from the importer to make payment only in the quoted currency (Ibid).

Based on this, (Abor, 2005) added that sort of problem causes serious disadvantages to firms, for example the West African country of Ghana. He also noted that the fluctuation in foreign currency market in Ghana was frequent and it normally resulted inthe depreciation of Ghana’s local currency while the foreign currencies continued to appreciate. This forced their local firms(importers) to buy and save foreign currencies in advance or rather prior to making international transactions. He added that the fluctuation forced Ghanian importers to be buying goods from their foreign counterparts at disadvantaged prices, which in turnaffected the prices of goods produced and sold to the final consumers by the importing firms. (Hassan, 2009) further added

30 | P a g e

that even Islamic banking countries that are reasonably good in managing risks like Brunei faces foreign exchange risks.

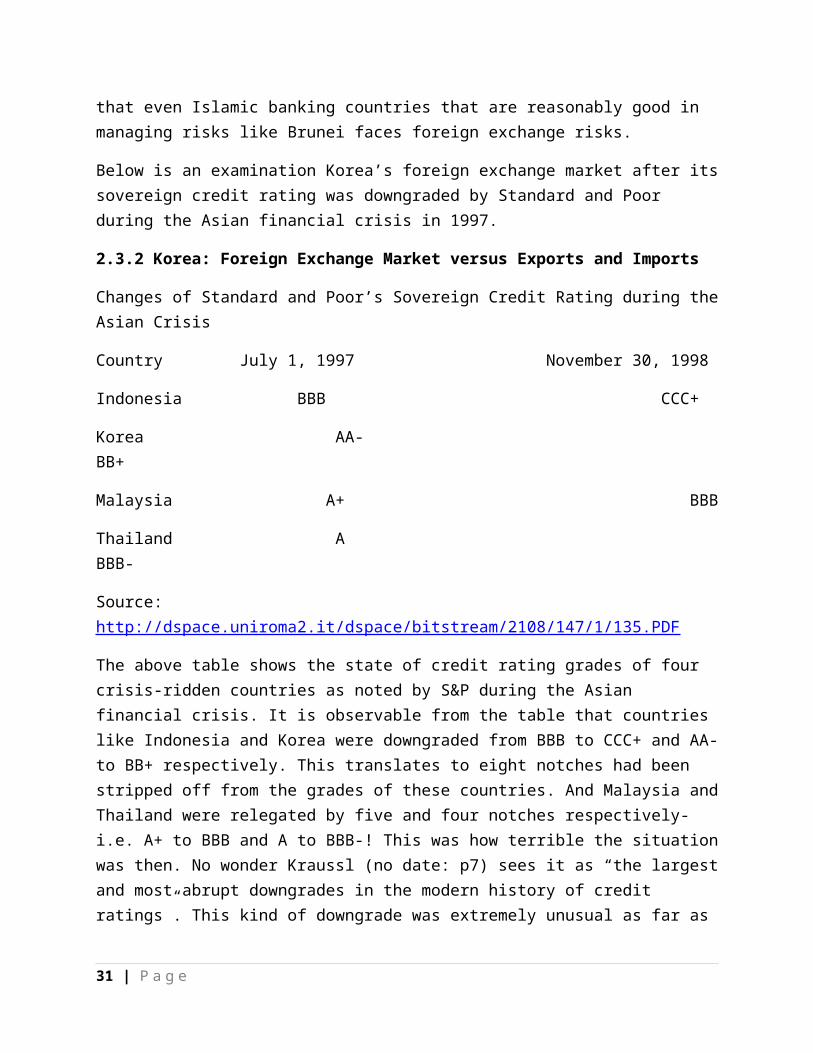

Below is an examination Korea’s foreign exchange market after itssovereign credit rating was downgraded by Standard and Poor during the Asian financial crisis in 1997.

2.3.2 Korea: Foreign Exchange Market versus Exports and Imports

Changes of Standard and Poor’s Sovereign Credit Rating during theAsian Crisis

Country July 1, 1997 November 30, 1998

Indonesia BBB CCC+

Korea AA- BB+

Malaysia A+ BBB

Thailand A BBB-

Source: http://dspace.uniroma2.it/dspace/bitstream/2108/147/1/135.PDF

The above table shows the state of credit rating grades of four crisis-ridden countries as noted by S&P during the Asian financial crisis. It is observable from the table that countries like Indonesia and Korea were downgraded from BBB to CCC+ and AA-to BB+ respectively. This translates to eight notches had been stripped off from the grades of these countries. And Malaysia andThailand were relegated by five and four notches respectively- i.e. A+ to BBB and A to BBB-! This was how terrible the situationwas then. No wonder Kraussl (no date: p7) sees it as “the largestand most abrupt downgrades in the modern history of credit ratings”. This kind of downgrade was extremely unusual as far as

31 | P a g e

rating announcements were concerned (Ferri, Liu & Stiglitz, 1999).

A lot of criticisms went on air by different observers about the actions of the rating agencies. Despite lagging in predicting thefinancial crisis in the region to investors, but they went ahead to unjustifiably downgraded countries in the region which even their pitiful economic status would not accommodate or justify (Mora, 2005). The actions of these CRAs only made the crisis of the countries in question more catastrophic (Ibid).

However, this research looks at the foreign exchange markets of these countries and vis-à-vis their exports and imports after thedowngrading that was cited above occurred. It will be looked at by examining one out of the four countries cited above.

Before the summer of 1997 as reported by Park (1998), Korea was relegated from being the 11th most powerful economy in the world to a mere struggling one surviving and being sustained with the help of the loans given to the country by international money markets. Even though the country’s economy was already hijacked by financial crisis that bedeviled the whole of South-East Asia, but credit rating agencies notably Moody’s and Standard and Poor’s made things catastrophic for the country by downgrading its sovereign credit rating ranging to four and five times respectively by December 1997.

Park (1998) observed that whenever the rating downgrade announcements were made by either of the rating agencies, the premium of Korean securities in international financial market promptly reacted by skyrocketing! This then led external lenders or foreign banks not to issue short-term loans to stakeholders inKorea’s business terrain which was central to survival of the economy (Ibid). Hence, the foreign exchange rate of the country against the USD was depreciated which immediately translated to worsening the market and trade flows. Amidst this apparent

32 | P a g e

vulnerability, the credit rating agencies made things worse by continuously downgrading the country’s sovereign rating to the extent that one could only imagine the level of damages their actions mated the Korea’s economy. Most of Korea’s exports and imports are transacted in USD, making the Korean won to be servedonly as “invoice currency” in such transactions as noted by (Kim and Suh, no date).

International trade is seen to be fading and is continuously being overtaken by foreign direct investment (FDI) which constitutes the largest source of global capital flows with closeto 450 percent increased between 1980-2003 (Abbott&De Vita, 2011), the exchange rates uncertainty does not only has effect ontrade but also on FDI (Schiavo, 2007). Further, the case could beworst to the extent that a higher volatility in exchange rates can cause an investment opportunity to be suspended or aborted. Albeit, he believed that this exchange rate volatility could be eliminated by having a currency union. This also went in harmony with the findings of (Rose, 2000).

Having examined the relationship between foreign exchange market and international trade in Korean experience, the research will now examined the linkage of stock and bond markets to exports andimports.

2.3.3 Stock and Bond Markets versus Exports and Imports

Fung, Lo and Leung (1995) in their study on Hong Kong, Korea, Singapore and Taiwan, they identified linkage between stock markets in these countries and imports and exports. The linkage was established in terms of trade flows which had serious impact on imports and exports growth of the countries in question. They also extended the relationship of the stock market returns to exchange rates.

33 | P a g e

Furthermore, there are more scholars that investigated whether there is any linkage between stock market and exchange rate; amongst them were Wen Shwo Fang and Miller (2002) who found that during the Asian financial crisis, currency depreciation in the exchange rate market that occurred impacted on the performance ofits stock market as well. Branson (1983) added that upward shift in the interest rate of local currency translates to increase in the prices of stock. This went in harmony with the findings of Nieh and Lee (2001), in their study conducted with the G7 countries as case study, they found out that increase in the stocks prices of Germany, Italy and Japan amounted to depreciation of currencies in their exchange rate markets. Dornbush and Fisher (1980), confirmed that exchange rates are determined by two factors- current account of a country and tradebalance performance (ibid); and this proves that exchange rates and stock prices are indeed related.

In contrast, Gavin and Dewald (1989) could not figure any relationship between the two variables. It believed nothing exists between them. Albeit, it acknowledged that their movementswere influenced by common forces.

Furthermore, Alexander et al. (2000) tried to find whether a relationship exist between bond and stock returns on daily basis,which was examined on individual firm-stage. Their findings showed that a relationship did exist even though it was a weak one. (Hotchkiss&Ronen, 2002) also concurred with Alexander et al;and (Norden&Weber, 2009) - though their studies introduced creditdefault swap (CDS) market.

Summarily, most of the literatures reviewed above, concur that there exist direct relationships between imports and exports and foreign exchange market. Albeit, they seem to fell short in establishing a direct relationship between stocks and bond markets with imports and exports, but studies done by Alexander et al. (2000), Wen Shwo Fang and Miller (2002) among others were 34 | P a g e

able to establish direct relationships between bond, stocks and foreign exchange markets.

Should this be the case, it would seem fair to believe that relationship exist between foreign exchange, bond and stocks markets and export and import based on these findings.

However, since this research was able to identify the relationship between export/import and foreign exchange, bond andstock markets, it will go further in the next chapter to look at the imports and exports of some countries in the European Union both the ones that were recently downgraded by Standard and Poor’s notably France and Italy; and also those that were not affected by the downgrades like Germany and the United Kingdom. This would perhaps play a role in finding out what impacts did the downgrades had on the international trade of these countries,and would lead us to establish whether or not the effects of thedowngrades in the EU would go in harmony with the findings of relevant literatures already reviewed above.

This would be achieved by employing secondary methodology of datacollection strictly. That is to say data will be collected from sources such as the newspaper articles, periodicals, internet, and magazines amongst others.

35 | P a g e

3.0 ANALYSIS AND DISCUSSION

3.1 France Exports and Imports Movements and Balance Of Trade within the Downgrades Period

Exports

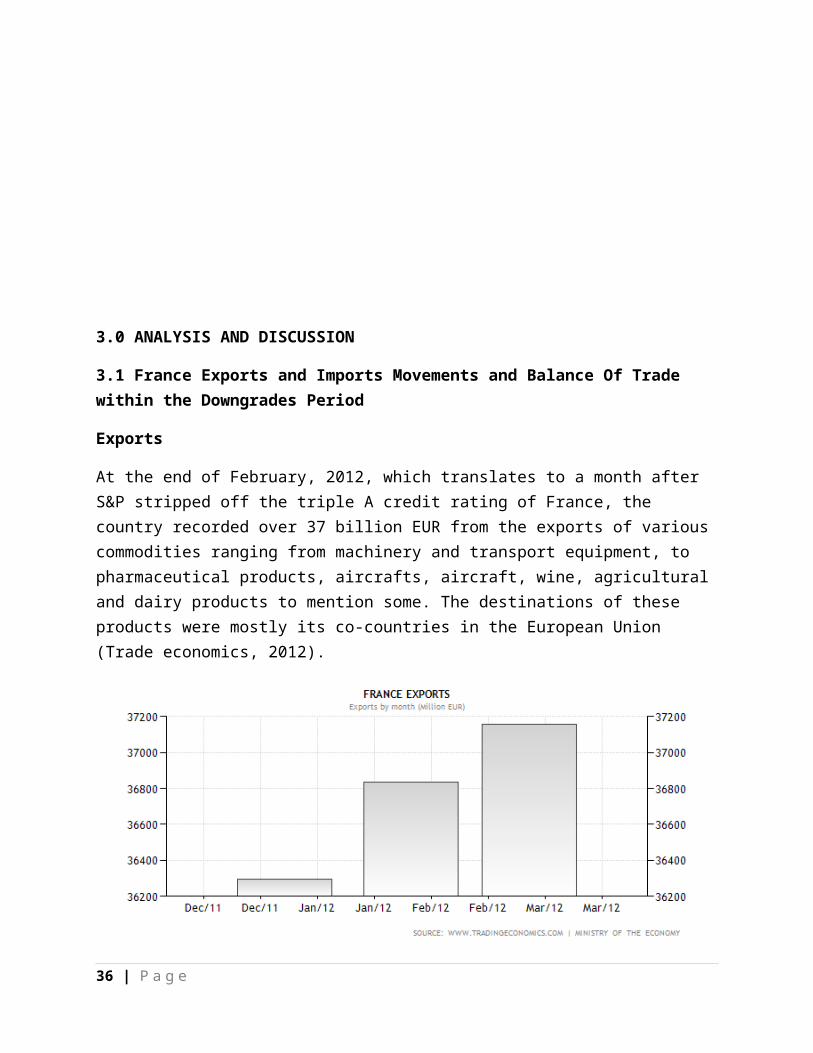

At the end of February, 2012, which translates to a month after S&P stripped off the triple A credit rating of France, the country recorded over 37 billion EUR from the exports of various commodities ranging from machinery and transport equipment, to pharmaceutical products, aircrafts, aircraft, wine, agricultural and dairy products to mention some. The destinations of these products were mostly its co-countries in the European Union (Trade economics, 2012).

36 | P a g e

Source: http://www.tradingeconomics.com/france/exports

The above graph show the amount of money realised from December 2011 to March, 2012 in the exports of France as provided by the French ministry for the economy (ibid). It shows that there had been promising rise every month from December, 2011 to March, 2012 amounting to an increase of over 1 billion EUR within three months going by the figure provided in the graph above.

This could mean that S&P’s rating downgrade announcement in January did not have any direct impact to France export.

Imports

As observed by trade economics (2012), France imports spending was not quite positive in line with the health of it economy, as imports spending figures apparently surpassed the amount realisedfrom exports within the first three months of 2012. As imports exceeds 43 billion EUR compared to 37.1 billion EUR realised fromexports during the same period (Trade economics, 2012). The primary things that were imported include crude oil, Vehicles, machinery and equipment products and plastics and chemical which mostly came in from United States, China and some countries within the European Union notably Germany, Spain, Belgium and Italy (ibid). The graph below shows the monetary movement within the period in question.

37 | P a g e

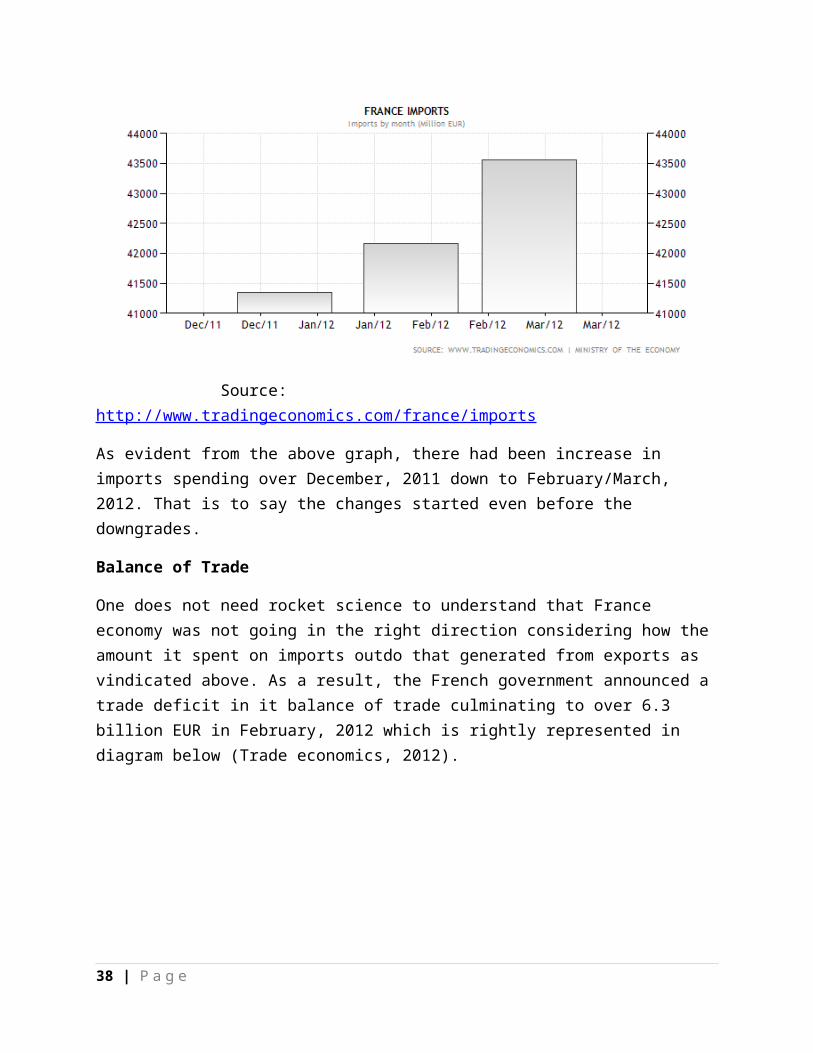

Source: http://www.tradingeconomics.com/france/imports

As evident from the above graph, there had been increase in imports spending over December, 2011 down to February/March, 2012. That is to say the changes started even before the downgrades.

Balance of Trade

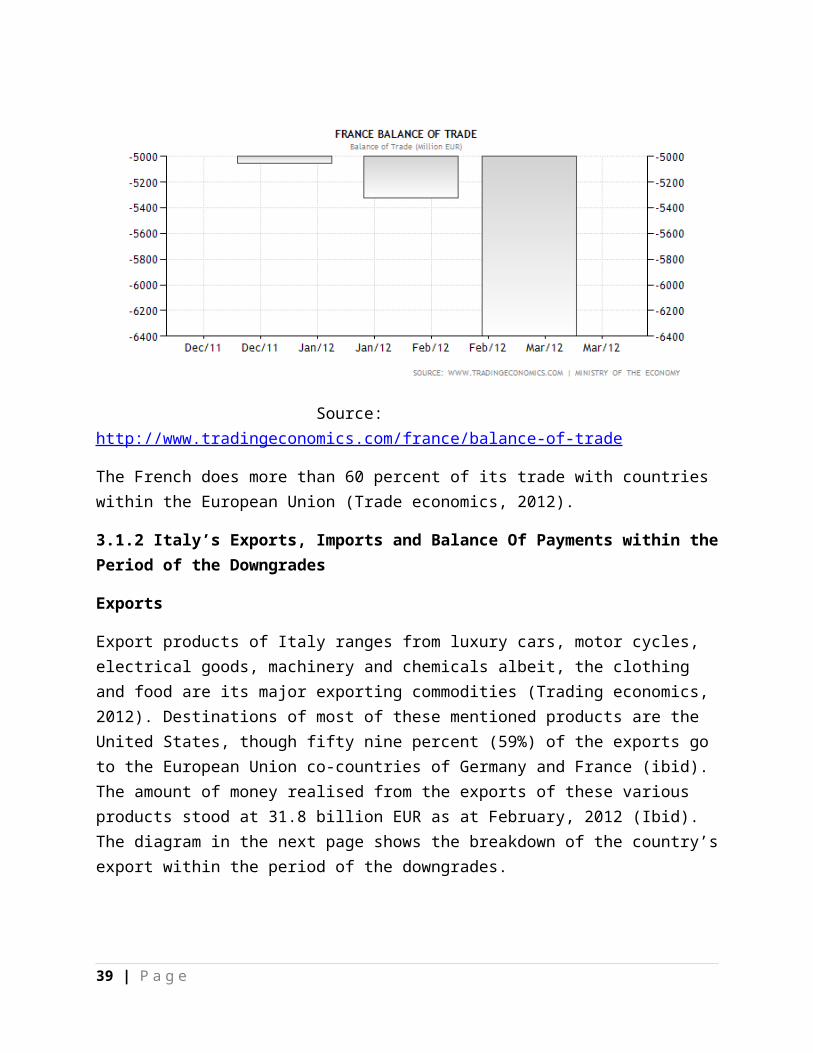

One does not need rocket science to understand that France economy was not going in the right direction considering how the amount it spent on imports outdo that generated from exports as vindicated above. As a result, the French government announced a trade deficit in it balance of trade culminating to over 6.3 billion EUR in February, 2012 which is rightly represented in diagram below (Trade economics, 2012).

38 | P a g e

Source: http://www.tradingeconomics.com/france/balance-of-trade

The French does more than 60 percent of its trade with countries within the European Union (Trade economics, 2012).

3.1.2 Italy’s Exports, Imports and Balance Of Payments within thePeriod of the Downgrades

Exports

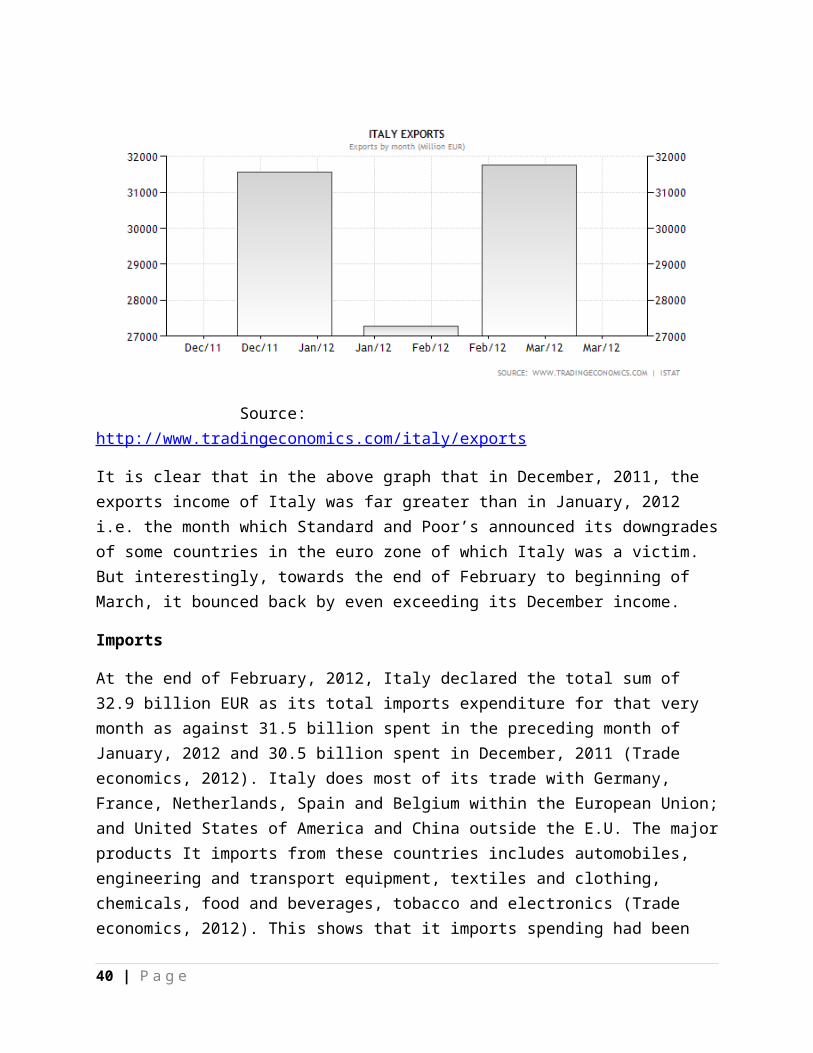

Export products of Italy ranges from luxury cars, motor cycles, electrical goods, machinery and chemicals albeit, the clothing and food are its major exporting commodities (Trading economics, 2012). Destinations of most of these mentioned products are the United States, though fifty nine percent (59%) of the exports go to the European Union co-countries of Germany and France (ibid). The amount of money realised from the exports of these various products stood at 31.8 billion EUR as at February, 2012 (Ibid). The diagram in the next page shows the breakdown of the country’sexport within the period of the downgrades.

39 | P a g e

Source: http://www.tradingeconomics.com/italy/exports

It is clear that in the above graph that in December, 2011, the exports income of Italy was far greater than in January, 2012 i.e. the month which Standard and Poor’s announced its downgradesof some countries in the euro zone of which Italy was a victim. But interestingly, towards the end of February to beginning of March, it bounced back by even exceeding its December income.

Imports

At the end of February, 2012, Italy declared the total sum of 32.9 billion EUR as its total imports expenditure for that very month as against 31.5 billion spent in the preceding month of January, 2012 and 30.5 billion spent in December, 2011 (Trade economics, 2012). Italy does most of its trade with Germany, France, Netherlands, Spain and Belgium within the European Union;and United States of America and China outside the E.U. The majorproducts It imports from these countries includes automobiles, engineering and transport equipment, textiles and clothing, chemicals, food and beverages, tobacco and electronics (Trade economics, 2012). This shows that it imports spending had been

40 | P a g e

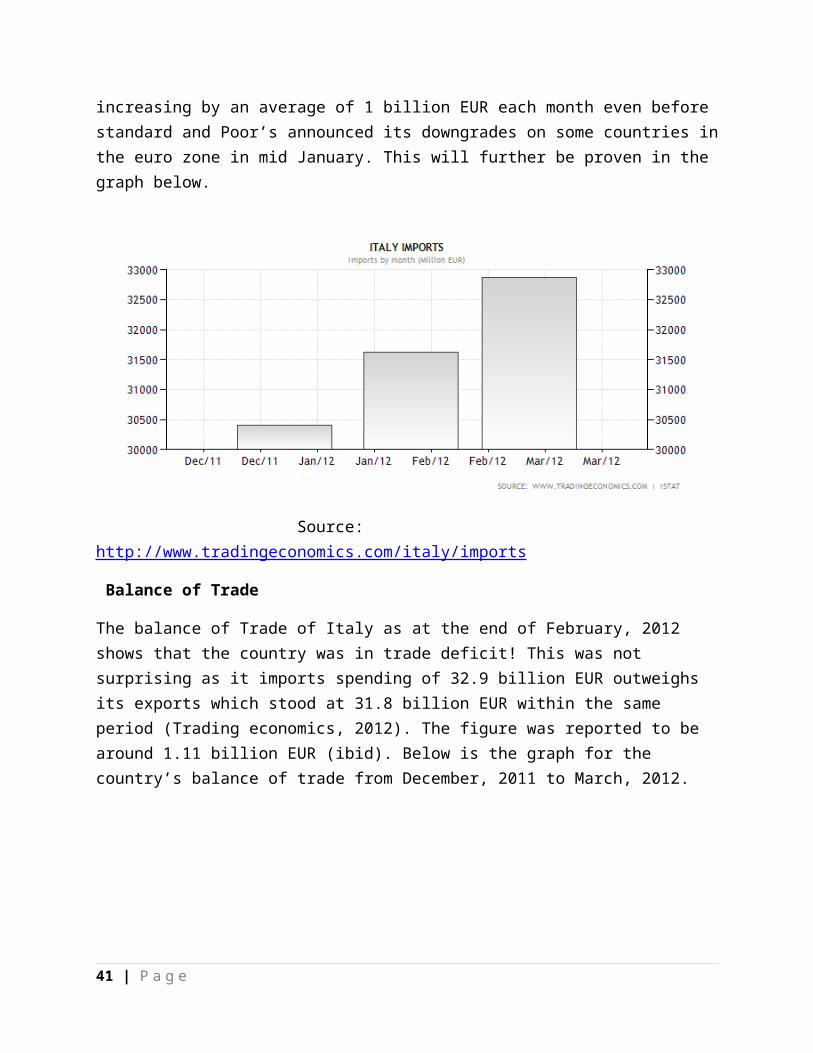

increasing by an average of 1 billion EUR each month even before standard and Poor’s announced its downgrades on some countries inthe euro zone in mid January. This will further be proven in the graph below.

Source: http://www.tradingeconomics.com/italy/imports

Balance of Trade

The balance of Trade of Italy as at the end of February, 2012 shows that the country was in trade deficit! This was not surprising as it imports spending of 32.9 billion EUR outweighs its exports which stood at 31.8 billion EUR within the same period (Trading economics, 2012). The figure was reported to be around 1.11 billion EUR (ibid). Below is the graph for the country’s balance of trade from December, 2011 to March, 2012.

41 | P a g e

Source: http://www.tradingeconomics.com/italy/balance-of-trade

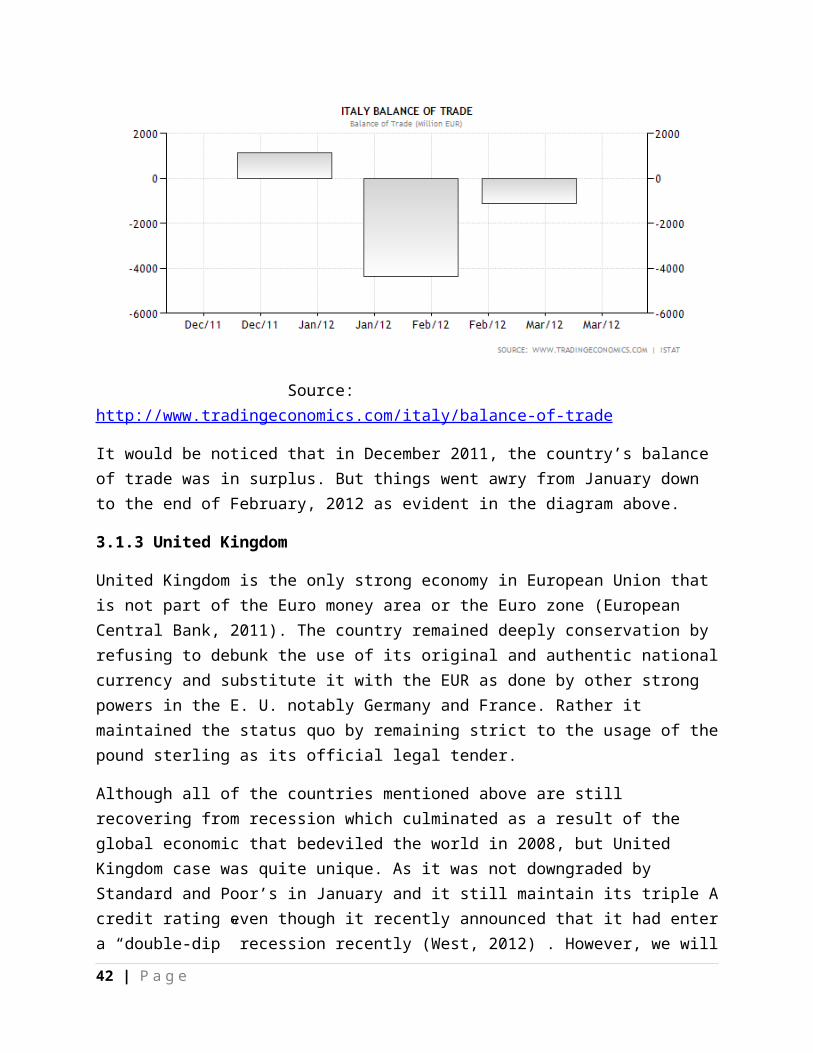

It would be noticed that in December 2011, the country’s balance of trade was in surplus. But things went awry from January down to the end of February, 2012 as evident in the diagram above.

3.1.3 United Kingdom

United Kingdom is the only strong economy in European Union that is not part of the Euro money area or the Euro zone (European Central Bank, 2011). The country remained deeply conservation by refusing to debunk the use of its original and authentic nationalcurrency and substitute it with the EUR as done by other strong powers in the E. U. notably Germany and France. Rather it maintained the status quo by remaining strict to the usage of thepound sterling as its official legal tender.

Although all of the countries mentioned above are still recovering from recession which culminated as a result of the global economic that bedeviled the world in 2008, but United Kingdom case was quite unique. As it was not downgraded by Standard and Poor’s in January and it still maintain its triple Acredit rating even though it recently announced that it had entera “double-dip” recession recently (West, 2012) . However, we will42 | P a g e

try and look at the exports, imports, balance of trade as well asthe exchange rates market of the country.

Exports

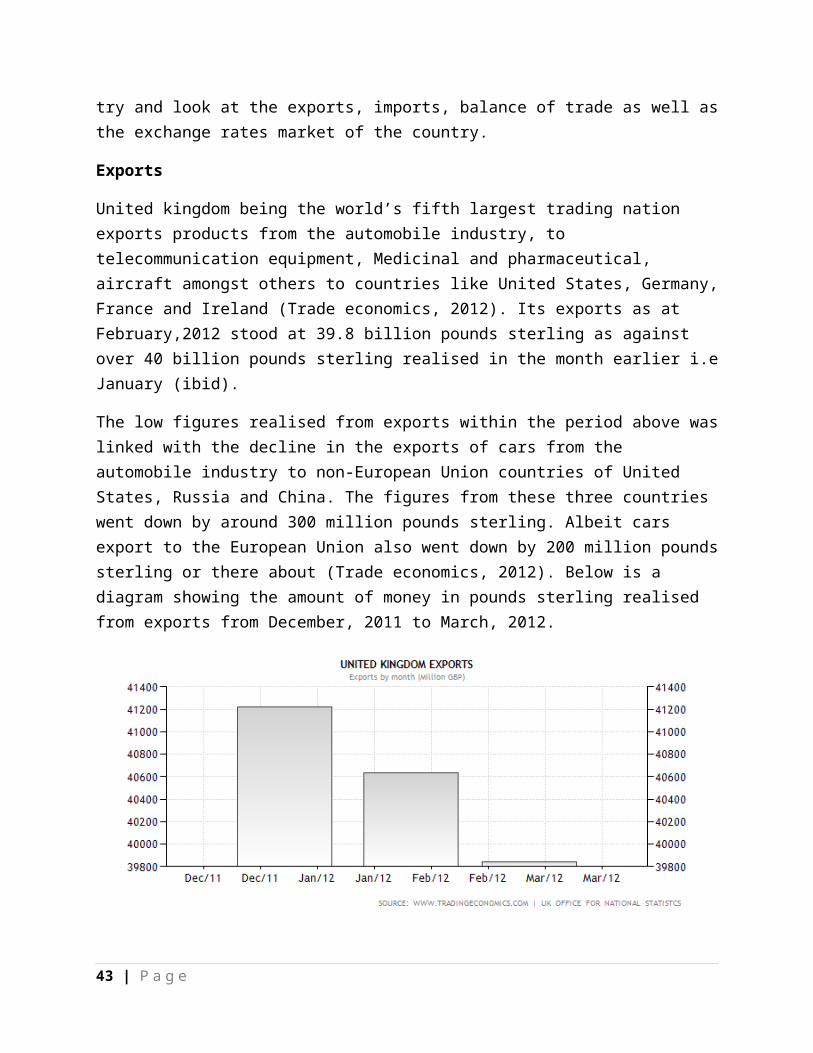

United kingdom being the world’s fifth largest trading nation exports products from the automobile industry, to telecommunication equipment, Medicinal and pharmaceutical, aircraft amongst others to countries like United States, Germany,France and Ireland (Trade economics, 2012). Its exports as at February,2012 stood at 39.8 billion pounds sterling as against over 40 billion pounds sterling realised in the month earlier i.eJanuary (ibid).

The low figures realised from exports within the period above waslinked with the decline in the exports of cars from the automobile industry to non-European Union countries of United States, Russia and China. The figures from these three countries went down by around 300 million pounds sterling. Albeit cars export to the European Union also went down by 200 million poundssterling or there about (Trade economics, 2012). Below is a diagram showing the amount of money in pounds sterling realised from exports from December, 2011 to March, 2012.

43 | P a g e

Source: http://www.tradingeconomics.com/united-kingdom/exports

The graph shows a continuous decline in exports from December, 2011 down to March, 2012 after the downgrades of U.K.’s European Union counterparts was announced by S&P.

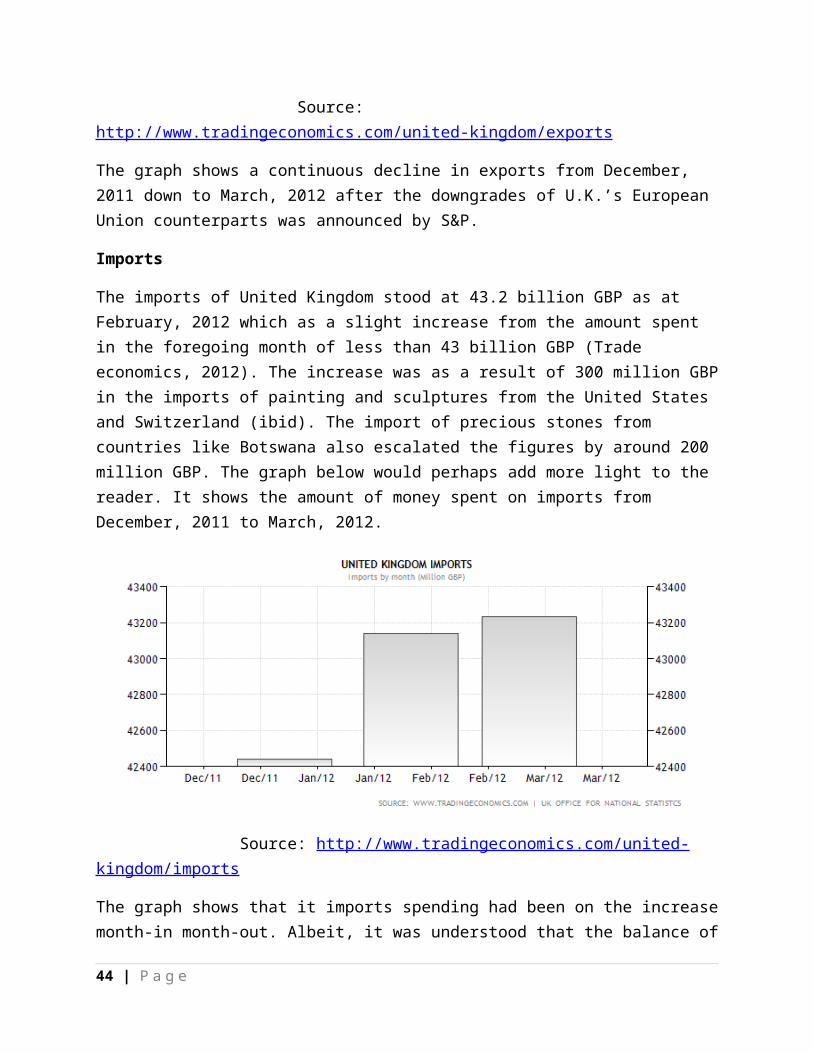

Imports

The imports of United Kingdom stood at 43.2 billion GBP as at February, 2012 which as a slight increase from the amount spent in the foregoing month of less than 43 billion GBP (Trade economics, 2012). The increase was as a result of 300 million GBPin the imports of painting and sculptures from the United States and Switzerland (ibid). The import of precious stones from countries like Botswana also escalated the figures by around 200 million GBP. The graph below would perhaps add more light to the reader. It shows the amount of money spent on imports from December, 2011 to March, 2012.

Source: http://www.tradingeconomics.com/united-kingdom/imports

The graph shows that it imports spending had been on the increasemonth-in month-out. Albeit, it was understood that the balance of

44 | P a g e

trade of the country has been on deficit for quite a long period since March, 2010, which apparently meant two years prior to S&P euro zone downgrades (Trading economics, 2010).

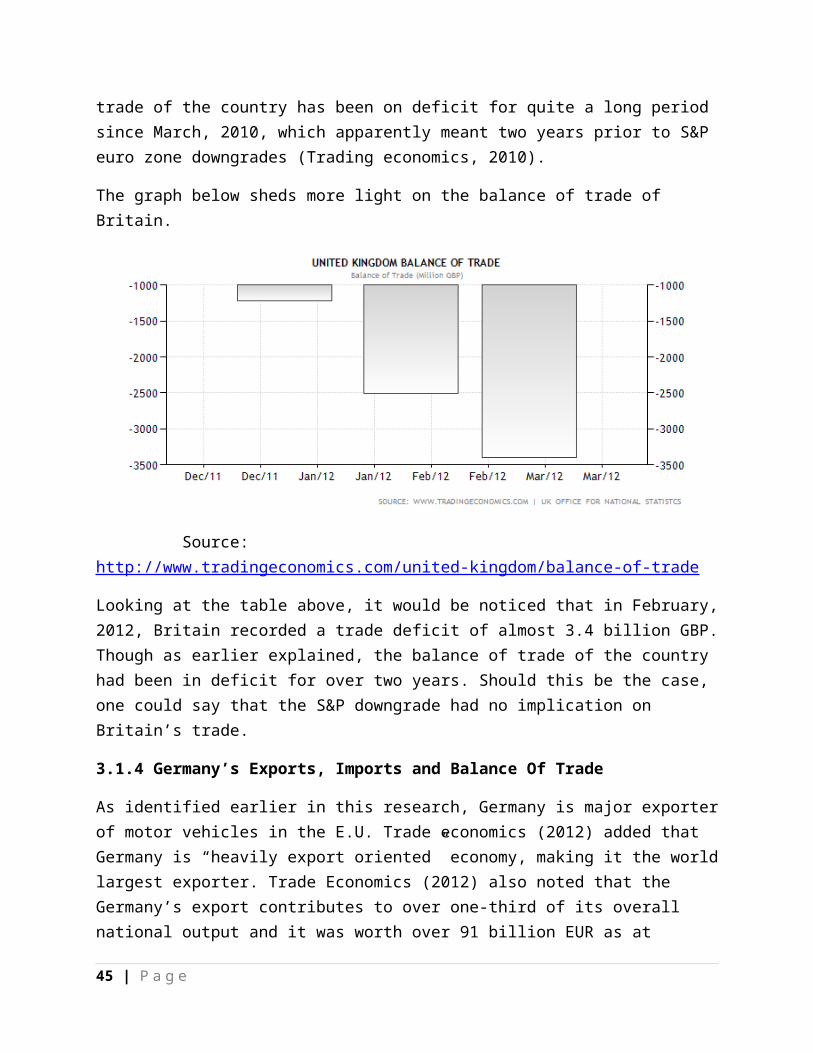

The graph below sheds more light on the balance of trade of Britain.

Source: http://www.tradingeconomics.com/united-kingdom/balance-of-trade

Looking at the table above, it would be noticed that in February,2012, Britain recorded a trade deficit of almost 3.4 billion GBP.Though as earlier explained, the balance of trade of the country had been in deficit for over two years. Should this be the case, one could say that the S&P downgrade had no implication on Britain’s trade.

3.1.4 Germany’s Exports, Imports and Balance Of Trade

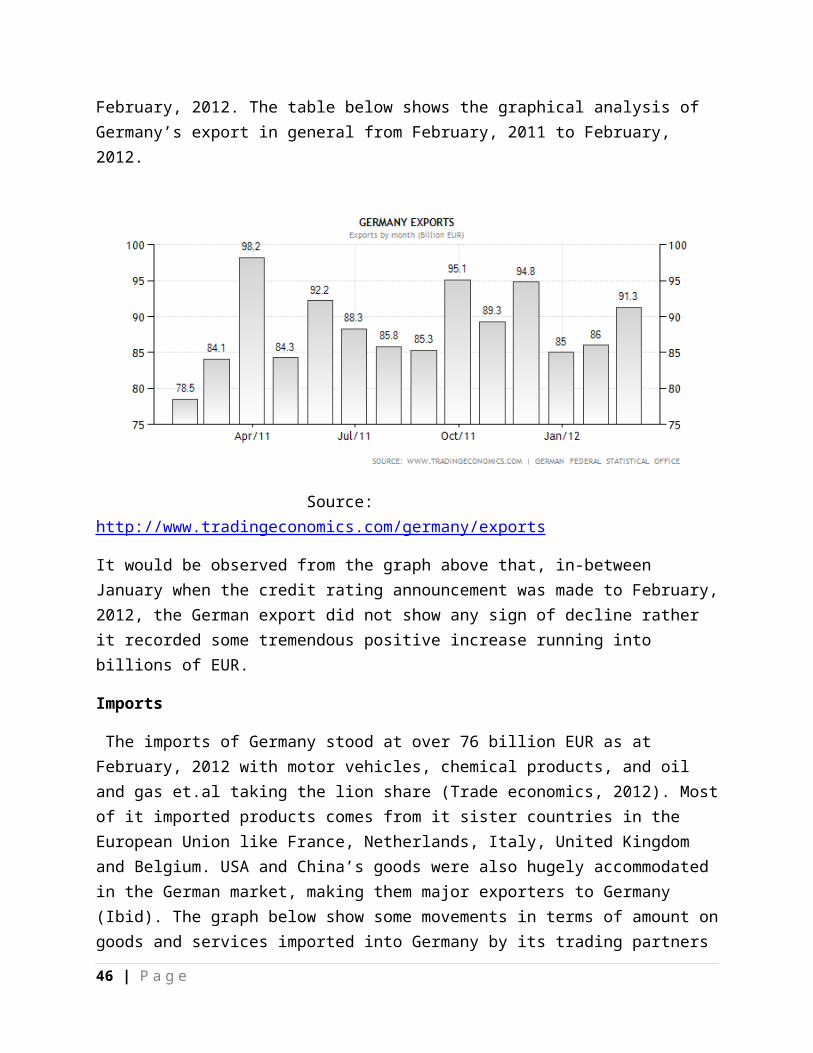

As identified earlier in this research, Germany is major exporterof motor vehicles in the E.U. Trade economics (2012) added that Germany is “heavily export oriented” economy, making it the worldlargest exporter. Trade Economics (2012) also noted that the Germany’s export contributes to over one-third of its overall national output and it was worth over 91 billion EUR as at

45 | P a g e

February, 2012. The table below shows the graphical analysis of Germany’s export in general from February, 2011 to February, 2012.

Source: http://www.tradingeconomics.com/germany/exports

It would be observed from the graph above that, in-between January when the credit rating announcement was made to February,2012, the German export did not show any sign of decline rather it recorded some tremendous positive increase running into billions of EUR.

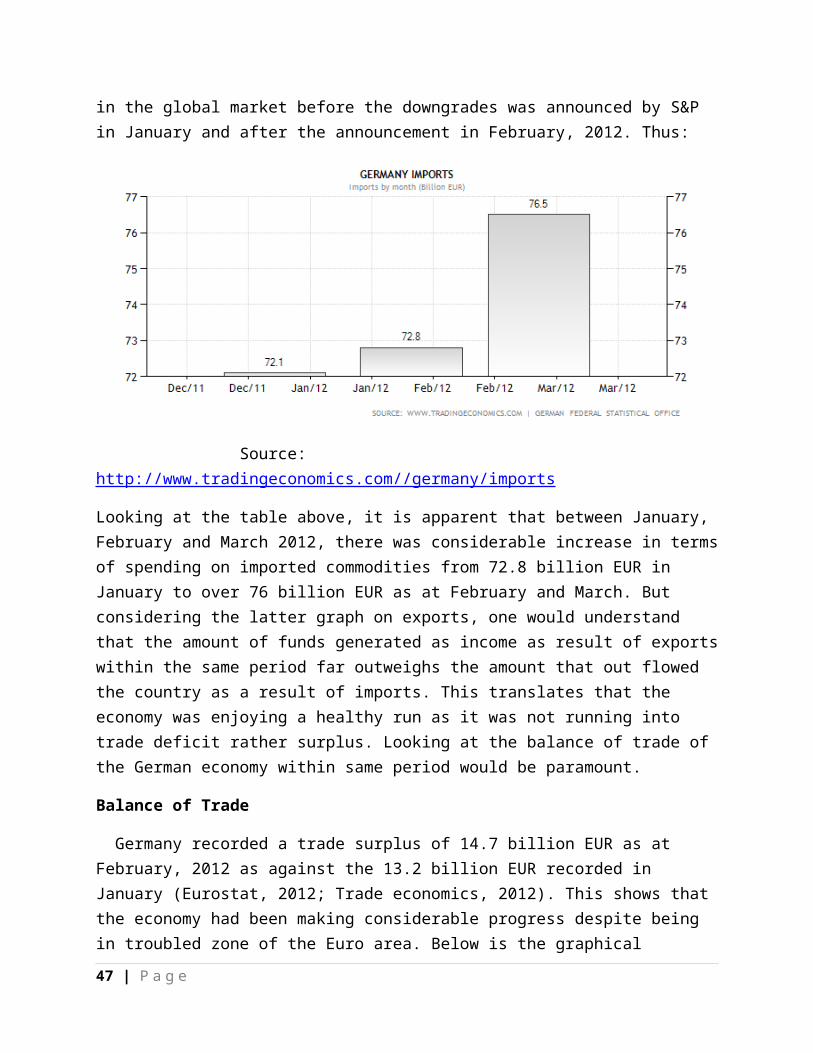

Imports

The imports of Germany stood at over 76 billion EUR as at February, 2012 with motor vehicles, chemical products, and oil and gas et.al taking the lion share (Trade economics, 2012). Mostof it imported products comes from it sister countries in the European Union like France, Netherlands, Italy, United Kingdom and Belgium. USA and China’s goods were also hugely accommodated in the German market, making them major exporters to Germany (Ibid). The graph below show some movements in terms of amount ongoods and services imported into Germany by its trading partners

46 | P a g e

in the global market before the downgrades was announced by S&P in January and after the announcement in February, 2012. Thus:

Source: http://www.tradingeconomics.com//germany/imports

Looking at the table above, it is apparent that between January, February and March 2012, there was considerable increase in termsof spending on imported commodities from 72.8 billion EUR in January to over 76 billion EUR as at February and March. But considering the latter graph on exports, one would understand that the amount of funds generated as income as result of exportswithin the same period far outweighs the amount that out flowed the country as a result of imports. This translates that the economy was enjoying a healthy run as it was not running into trade deficit rather surplus. Looking at the balance of trade of the German economy within same period would be paramount.

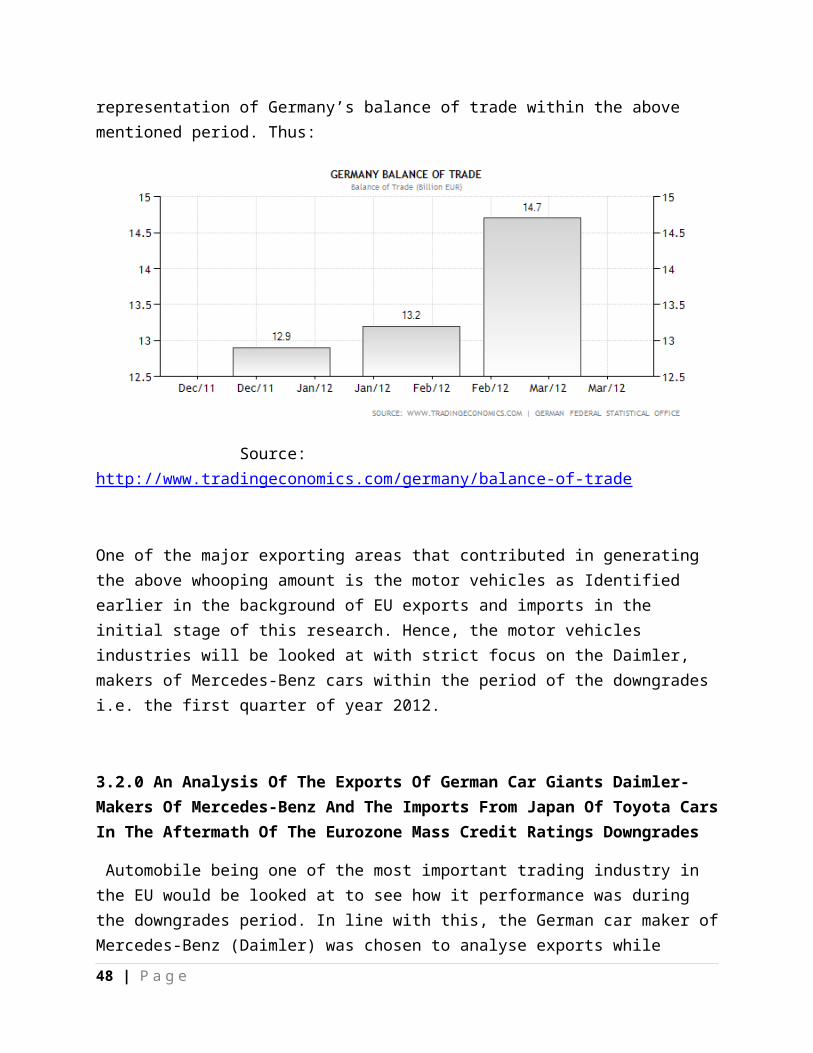

Balance of Trade

Germany recorded a trade surplus of 14.7 billion EUR as at February, 2012 as against the 13.2 billion EUR recorded in January (Eurostat, 2012; Trade economics, 2012). This shows that the economy had been making considerable progress despite being in troubled zone of the Euro area. Below is the graphical 47 | P a g e

representation of Germany’s balance of trade within the above mentioned period. Thus:

Source: http://www.tradingeconomics.com/germany/balance-of-trade

One of the major exporting areas that contributed in generating the above whooping amount is the motor vehicles as Identified earlier in the background of EU exports and imports in the initial stage of this research. Hence, the motor vehicles industries will be looked at with strict focus on the Daimler, makers of Mercedes-Benz cars within the period of the downgrades i.e. the first quarter of year 2012.

3.2.0 An Analysis Of The Exports Of German Car Giants Daimler- Makers Of Mercedes-Benz And The Imports From Japan Of Toyota CarsIn The Aftermath Of The Eurozone Mass Credit Ratings Downgrades

Automobile being one of the most important trading industry in the EU would be looked at to see how it performance was during the downgrades period. In line with this, the German car maker ofMercedes-Benz (Daimler) was chosen to analyse exports while 48 | P a g e

Japanese Toyota was as well picked as this research unit for analysis on Imports to the European Union.

3.2.1 Daimler

“Despite higher investment in future growth and a challenging market environment, we succeeded in surpassing the very good prior-year results in terms of unit sales, revenues, EBIT, and net profit” Said Dr. Dieter Zetsche, Chairman of the Board of Management of Daimler and Head of Mercedes-Benz Cars (Daimler, 2012). This statement was captured during the announcement of theGroup’s first quarter result of 2012 in April.

Going by Dr. Zetsche statement, one would assume that the companyhad recorded a positive result in its first quarter. But let us dig in to understand the true picture of the situation.

Vehicles Sales, Revenue and Net Profit

Despite the challenges in the euro zone which includes the downgrades of credit rating associated with the area, it was apparent that Daimler was not moved by such forces as it recordeda nine percent increase on the number of vehicles it sold in the global market most importantly to countries like the United States and some countries in Europe.

It sold a total of 502,100 units of vehicles of which 338,300 were Mercedes-Benz products.

Further, a total revenue of 27 billion EUR was realised as against 24.7 billion EUR realised at the end of same quarter lastyear (Daimler, 2012). Out of this total amount, almost 15 billionEUR was realised from the sales of Mercedes-Benz Cars in mostly Europe and the United States.

49 | P a g e

Hence, a net profit of 1.416 billion EUR was announced as against1.180 billion realised during the same period last year. It showsan increase of twenty percent (20%) compared to last year.

Europe’s Stock Market Impact on Daimler’s Shares and Exports

After S&P’s announcement of its decision to downgrade nine countries in the euro zone, it was reported that the European stock market reacted as share prices dropped down to five months low (Guest, 2012). This went in consistent with this work’s findings in the preceding chapter by Brooks et al. 2004; Reisen and Von Maltzan, 1999; Creighton et al., in their study on Australian stock market (2004); Joo and Pruitt in their research on Korea’s stock market (2006) amongst others.

However, going by the first quarter report of Daimler group, it was found that the shares of the company within the period of thedowngrades had more positive than negative effect to its exports,as it announced that it shares rose from 0.99 EUR to 1.25 EUR (Daimler, 2012). This confirmed the findings of Elayan et al. (2004) in their study on New Zealand stock market.

Europe’s Foreign Exchange Market after Standard and Poor’s Downgrades and Its Impact on Daimler’s Exports

After Standard and Poor’s announcement, it was observed by Steward (2012) that the Euro slipped down against the dollar, Guardian (2012) reported that the Euro dropped to 16-month low against the USD. This proved that Subasi (2008) and Bissoondoyal-Bheenick et al. (2011) were right to say that sovereign credit rating downgrade affects foreign exchange market negatively.

Interestingly, Daimler Group contradicted the above findings in its first quarter result released in April, 2012. Daimler (2012) noted that the exchange rates movements of euro against the

50 | P a g e

currencies of it partners in the global market had proved more positive than negative on it earnings during the period.

And as established by Daimler (2012), most of it vehicles were exported and sold in the United States and within Europe during the period.

Daimler’s Negativities in the First Quarter of 2012

Despite obvious positive result, it pointed out some factors thatcontributed negatively to its earning within the period in question. Firstly, it identified harsh economic condition that inLatin America and low pricing in China as part of external factors amongst others. Internally, it pointed to its expansion on the production of Daimler Trucks as another factor that impacted on the company negatively during the first quarter (Daimler, 2012)

Should this be the case, both the stock and foreign exchange markets had more positive effects on Daimler’s Exports to its market outside the European Union notably the United States basedon the analysis above.

3.2.2 Japanese Toyota

Unlike Daimler, Toyota Company was yet to make its business quarterly report public. But information gathered from other secondary sources would be used to analyse the impact of S&P’s mass downgrades of the Eurozone on the importation of Toyota carsinto Europe.

Toyota Shares and Standard and Poor’s Downgrade

The case with the stock market in Asia was similar to that of Europe following S&P’s mass downgrades in the euro zone as sharesprices fell downwards (BBC, 2012). The shares badly affected in the case of Japan were those of the Japanese exporters like Toyota which lost 1.5% of its shares value sequel to the news

51 | P a g e

(ibid). However, this was relatively not as alarming as the foreign exchange market.

Exchange Rates and Standard and Poor’s Downgrade News

Sequel to the news of the downgrades, the Japanese foreign exchange market reacted immediately as the EUR reached a record of 11-year low against the Japanese Yen (Reuters, 2012).

This became alarming as exporters like Toyota had huge reliance on demand from the Euro area (BBC, 2012). It added that a weaker EUR against the yen would translate to making Japanese products like Toyota cars more expensive in the Euro zone and therefore making the demand lower. No wonder the Japanese finance Minister Jun Azumi was quoted by Reuters (2012) saying that “I am worried because currency moves have been a little rapid. Unless Europe builds a strong firewall and provides a sense of security to markets and the world, the Eurozone crisis would become a worrying factor for global growth this year”.

Therefore, going by the facts examined and analysed, the researchwill conclude in the next chapter by submitting its finding in terms of what it believes could be the possible implications of the downgrades on EU major exports and imports in the global market. Thereafter, recommendation would be given.

52 | P a g e

4.0 CONCLUSIONS AND RECOMMENDATIONS

4.1 Conclusion

This work concludes that going by its findings especially on the two companies that were used in the automobile industry i.e. Daimler- Benz in terms of exports; and Toyota in terms of Imports, the Standard and Poor’s downgrades would perhaps have possible impact on the foreign exchange market of the Eurozone which could indirectly affect not really the exports but the importation of products into the Euro area only but not the European Union as whole so far the exchange rates market remain volatile.

Though the research found that the possible implications of the downgrades would most likely be short-term, this because the European exchange rates market reacted immediately after the downgrade but later on bounced back within few days, making the market volatility temporary. Thus, it would not also be surprising if the downgrades would have no any further impact on the capital markets of the Eurozone countries.

Further, as identified in the foregoing chapter, downgrades had affected the foreign exchange rates of the EUR against the currency of its trading partners like Japan and the USA.

53 | P a g e

Therefore, this work’s also found that the countries that are notusing the EUR as its official legal tender in the E.U. would not likely be affected by the downgrades making the E.U. as whole nota likely victim.

Further, sequel to the downgrades news, EUR had fallen drastically against the Yen especially as noted earlier. Hence, products imported into the Euro area would become more expensive and thus chances would be high that the demand for products like Toyota cars from Japan would most likely decrease which would indirectly translates to decrease in imports.

But in terms of exports this research could not figure out much impact of the S&P’s downgrades on the exports of Daimler’s cars outside the European Union. Albeit, Daimler announced that it hadgained positively as a result of exchange rates movements in terms of its vehicles sales outside the E.U. Going by this, it could be safe to say even if there would be implications it wouldbe more of a positive one that negative.

In achieving the above result, this work identified and analysed the major products which the European Union exports and Imports. It also identified a number of countries that engaged in major trading activities with the E.U. which the United States took thelead. Credit ratings agencies and how they did their ratings was analysed with particular focus on Standard and Poor’s.

The Second section reviewed a number of established academic journals that had earlier researched on the implications of sovereign credit ratings downgrade in general, as there were limited materials available to the researcher that had treated the issue of sovereign credit rating downgrade in general not to talk of its link with export and imports. However, the academic literatures used helped the researcher in achieving the aim of this research. The literatures were then linked with the main question this research aimed to answer, by examining the rating

54 | P a g e

criteria of Standard and Poor’s and also why it downgraded some countries in the Euro zone.

This takes us to the third section where the imports and exports of four countries in the European Union were studied within the period of the downgrades. These countries were United Kingdom, Germany, Italy and France. Some graphical data were presented regarding the trade of the countries to validate the analysis. Wefound that countries like U.K. that are not in the Euro area werenot moved during the period of the downgrade. Most of their trading activities remained consistent as it were before, during and after the credit ratings downgrade of the euro zone was announced by S&P.

The research went further to analyse the exports of Daimler-makers of Mercedes Benz outside the E.U. and the Imports of Toyota cars from Japan into the E.U. And exchange rates movement was identified as the major factor that would likely influence trading activities in the Euro area not the E.U. as submitted in beginning of this chapter.

Finally, this would be useful to policy makers, government organisations, businesses and business men, and also for future researchers in the field of credit rating!

4.2 Recommendations

Having successfully established this research aim and objectives by spelling out what the possible impact of S&P downgrades would be on the international trading activity of the single geographical entity known as the European Union, however, the research would remain incomplete if it fell short to proffer somerecommendations which could be useful to relevant stake holders, policy makers, researchers, and other concerned parties that may be interested in knowing more about how sovereign credit rating downgrades impacts on the major exports and imports of the EU and

55 | P a g e

how it could be avoided. Hence, this work came up with the following recommendations:

This researcher recommends that it would perhaps be in the interest of the 27 Countries that make up the EU, if the 17 EUROZONE countries would restore back the use of their default national currencies as their official legal tenders as against the EUR. This is because it was noted in the course of undertaking this research that all the countries affected by S&P’s downgrades so far were in the debt crisis area of the EUROZONE and it was also observed that the crisis in the area wasmore of a currency crisis caused one.