Investment, Technological Upgrading, and Exports in Indian ...

53

Heinz School, 2 nd Paper, Carnegie Mellon, 2008 1 | Page No Such Thing as a Free Lunch: Investment, Technological Upgrading, and Exports in Indian Pharmaceuticals Chirantan Chatterjee {[email protected]} April 2008 Draft for 2 nd Paper Requirements, H John Heinz III School of Public Policy & Management, Carnegie Mellon University Advisory Committee Professor Lee Branstetter, Carnegie Mellon Professor Ashish Arora, Carnegie Mellon Professor Irina Murtazashvili, University of Pittsburgh

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Investment, Technological Upgrading, and Exports in Indian ...

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

1 | P a g e

No Such Thing as a Free Lunch:

Investment, Technological Upgrading, and Exports in Indian Pharmaceuticals

Chirantan Chatterjee

April 2008 Draft for 2nd Paper Requirements,

H John Heinz III School of Public Policy & Management,

Carnegie Mellon University

Advisory Committee

Professor Lee Branstetter, Carnegie Mellon

Professor Ashish Arora, Carnegie Mellon

Professor Irina Murtazashvili, University of Pittsburgh

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

2 | P a g e

Abstract

The Indian pharmaceutical industry’s exports began to exceed its imports in the late 1980s.

Since then, exports have grown rapidly, and the leading Indian firms have become significant exporters

of generic drugs to the most advanced markets, including the U.S. As the Indian pharmaceutical industry

increases its R&D spending and innovative efforts, leading firms clearly hope to export new products

and processes to the U.S. and other advanced markets. Because it constitutes a (rare) example of a high

tech exporting industry in a developing country, the Indian pharmaceutical industry provides an

interesting context in which to explore the relationship between exports and technological upgrading.

We investigate these linkages in this paper. The received literature has suggested that the

exposure to advanced country technologies achieved through exports should lead to technological

improvements in the exporting firms’ products and processes. Researchers have generally tried to

measure these improvements by looking for changes in exporting firms’ measured total factor

productivity that could be ascribed to increase in exports. The conceptual association in the literature

between technological learning or upgrading through exports and increases in TFP is so strong that the

phrase “learning by exporting” has come to mean an increase in TFP following an increase in exports.

We find that there is not much learning effect (from exports) observed for the overall industry. Some

apparent learning effect is observed for a section of the industry, but only for firms who appear to be

technologically backward within the industry. The leading firms that have undertaken the most

technological upgrading and have had the most success exporting to the most advanced markets appear

to show no signs of “learning by exporting.” The concentration of apparent “learning by exporting”

effects in technologically backward firms would appear to be highly problematic. Given the narrow way

the received literature has conceptualized learning by exporting effects, we might be lead to conclude

that these either do not exist in the Indian pharmaceutical industry or are unimportant for its significant

firms.

We disagree with this assessment, and our disagreement is partly founded on our belief that the

received literature has conceptualized the “learning by exporting” phenomenon too narrowly. Exports

can induce technological upgrading even if conventionally measured TFP fails to rise after exports start.

In making this criticism, we are contributing to a stream of recent papers which also argue that past work

has looked for the effects of exporting on technological upgrading in the wrong places. Recent work by

Trefler (2008) and Javorcik et.al (2008) argue that the learning by exporting literature should take a

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

3 | P a g e

more inclusive view of the phenomenon. They argue that exporting often follows substantial (costly)

investment by the firm that allows it to raise its product/process quality to the levels required by more

advanced markets. In the Indian pharmaceutical industry, while we find only weak evidence of TFP

growth after exporting, we find strong evidence of significant increases in capital investment prior to

exporting, and this is especially true for firms exporting to the most advanced markets. We refer to this

as a “getting ready to export” effect, following Javorcik et al. (2008), and present arguments supporting

the view that these investments can be viewed as a form of costly technological upgrading.

Key Words: Indian Pharmaceuticals; learning by exporting; TFP.

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

4 | P a g e

A. Introduction

A key strand of the new international economics literature explores the impact of firm or plant level

exports on the technological upgrading of the firm as measured by total factor productivity. Dubbed

informally as the learning by exporting literature the genesis of this stream of research dates back to

Bernard and Jensen’s seminal paper on exporting and productivity in US manufacturing in the mid

1990s. Since that work, researchers have found at best mixed evidence for productivity increases, or a

learning effect that are caused by exporting by firms. On the one hand the literature has documented no

evidence from exporting on the productivity of firms in many contexts in which it might be reasonably

expected (Clerides, Lach and Tybout 1998, Bernard and Jensen 1999, 2004, Bernard and Wagner 1997,

Delgado, Farinas and Ruano 2002). More recently, a small number of researchers have found a positive

effect of exporting on firm productivity (Aw, Chung, and Roberts 2000, Baldwin and Gu 2003, Van

Biesebroeck 2004, Lileeva 2004, Hallward-Driemeier, Iarossi and Sokoloff 2005, Fernandes and Isgut

2006, Park, Yang, Shi, and Jiang 2006, Aw, Roberts and Winston 2007 and De Loecker (forthcoming)).

Given the mixed and largely inconclusive state of the evidence in the received literature, it is perhaps not

surprising that our own findings are also mixed. While at an overall level, the industry does not witness

much learning effect from exporting, certain subsections of the industry do reveal significant increases in

total factor productivity accruing from exporting. They are not, however, the industry subsections that

have experienced the most technological upgrading. Measured TFP growth in the elite firms at the

forefront of the industry – the firms that have had the most success exporting to the most advanced

markets – appears unrelated to export activity.

Recent work by Trefler (2007) and Javorcik et.al (2008) argue that the learning by exporting literature

should broaden its focus to include alternative measures of technological upgrading other than TFP.

They argue that successful exporting often requires (costly) ex ante investments in capital and more

skilled labor. These investments must often be made before any significant level of exporting occurs.

Whereas the learning by exporting literature has tended to view productivity improvements from

exporting as something that comes “for free,” the more recent work suggests that much of the upgrading

occurs before, not after exports commence. In addition, much of the technological upgrading is

embodied in new capital equipment, worker training, and quality certifications, all of which require real

outlays on the part of the firm. Furthermore, once firms enter the export market, they are often

constrained in terms of their ability to appropriate the gains from their technological upgrading. Facing

fierce competition from existing incumbents and from other foreign entrants, exporters must often accept

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

5 | P a g e

lower profit margins on export sales than on sales in their domestic market. All of this can lead to very

modest measured increases in TFP after the inception of exports. Yet the prospect of serving export

markets can induce firms to make costly investments in technological upgrading that they would not

make in the absence of the export opportunities. Trefler (2007) shows that Canadian manufacturing

firms seeking to exploit opportunities in the U.S. market are disproportionately likely to invest in

advanced manufacturing technologies. Javorcik et al. (2008) show similar results for Mexican firms

preparing to export. Following this recent work, we show that while learning effects seem negligible,

Indian pharmaceutical firm’s investments in physical capital appear to be related to future export plans.

We discuss in the text a number of reasons why these investments are likely to be driven, in part, by

technological upgrading. Evidence suggests that the leading firms within the Indian pharmaceutical

industry are getting ready to export.

Our data is an unbalanced panel of 315 publicly traded Indian drug firms from 1990 to 2005, accounting

for close to 80% of the industry’s output. We capture for these firms, annual financial information on

sales, gross fixed assets, plant and equipment, labor, materials and power and fuel expenses, R & D

expenditure and exports. Our learning effect or the lack of it is arrived in the following econometric

manner. We compute first a Cobb Douglas production function where in any year, a firm’s output (sales)

are a function of its inputs (labor, capital, materials, power and fuel expenses). The residual in this

specification is what economists have conventionally termed as total factor productivity (TFP). An

introduction of the exports variable in this Cobb Douglas equation, gives us the impact on output from

exports. If we can control for other inputs, a positively signed exports variable (we use logs, intensity,

levels and dummy for exporting), should imply the following. Output is increasing in exports and that

happens through a positive effect of exporting on the residual, in this case TFP. The sign of the exporting

variable is not always positive or even significant in our overall regressions but then, in certain

subsections they do reveal a positive impact on output through total factor productivity. These also

happen to be those firms, who are more or less technologically backward in terms of their R & D

capabilities. However, further investigation on investing-exporting linkages unearths evidences of

getting ready to export in the industry i.e. Indian pharmaceutical firms’ current investments indeed are

positively influencing its future decision to enter export markets, this while controlling for year effects

and other firm level factors (like size, technological competence, past productivity, or past export

performance).

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

6 | P a g e

The following sections are organized thus. We discuss the exporting history of the industry following up

with a review of the learning by exporting literature. The set-up used to explore learning by exporting is

then discussed followed by a section on our data and variables. Our first set of mixed findings on

learning effect from exporting are presented next. We then discuss why the traditional approaches in the

learning by exporting literature might not be best suited to understand technological upgradation and

exporting. We then summarize the getting ready to export literature and present our results on the

investing-exporting linkages. We conclude with key findings and implications of the paper. The

appendix contains discussion on industry categories, variable construction, and some additional results.

B. Background on exporting history in Indian pharmaceuticals.

Indian pharmaceutical exports have seen a quantum shift in its character as well as importance in global

trade in the last three decades. A 2003 Business Week articlei pointed out that Indian drug makers could

export drug deflation (cheaper drugs) to the world, the impact being as much as China’s impact on the

electronics industry. In 1980, total exports of drug and pharmaceuticals from India was some $ 87.9 mil,

in 1990 it reached $ 514.6 mil, and in 2000 it stood at $ 1668 mil levels. Analysts predict that

pharmaceutical exports, $ 5.7 billion in 2007, will at an annual average growth of 30% surpass domestic

sales figures by 2008. India now accounts for 8% of global drug product sales in volume terms (ranked

4th) and 1% in value terms (ranked 13th) of global pharmaceutical sales. The past decade also has seen a

shift in the nature of the drug products exported. Starting from mainly being a bulk and active

pharmaceutical ingredients (API) supplier, Indian drug firms have now moved on to becoming a major

player in the world generics and formulations marketii. Further its destinations for exports have widened

globally to more than 200 countries.

Figure 1: Exports breakup in $ mil, Indian Pharma

(Souce: CMIE data from Business Beacon provided by Professor Sudip Chaudhuri, IIM Kolkata, India. Respective year end average exchange rates have

been used from RBI Handbook to convert INR values in USD million. 2005 data comes from data cited by USITC report from World Trade Atlas. 2006 data:

http://www.sunmediaonline.com/indiachroniclejanuary/policyupdate.html. 2007 data:

http://economictimes.indiatimes.com/Pharma_exports_to_surpass_retail_sales/articleshow/2140285.cms)

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

7 | P a g e

Evolution of Indian pharmaceutical exports & some descriptive statistics

Till 1970s, the Indian pharmaceutical industry was dominated by foreign firms accounting for nearly

70% of total market share. However, three key policies, enactment of the Patent Act 1972, changes to

Foreign Exchange Regulation Act, 1973 and the introduction of the New Drug Policy, 1978iii brought

about changes in the industry structure. These policy interventions ensured that domestic firms got an

environment where they could start producing bulk drugs and active pharmaceutical ingredients for drug

products. Bulk drug production which was only about $ 115 million (in current terms) in 1975, and

reached $ 294 mil by 1985. By 2004 Indian drug firms were producing some $ 1.8 billion worth of bulk

drugs. Bulk drug exports reached close to $ 1 billion by 2001, accounting for about half of total Indian

drug product exports.

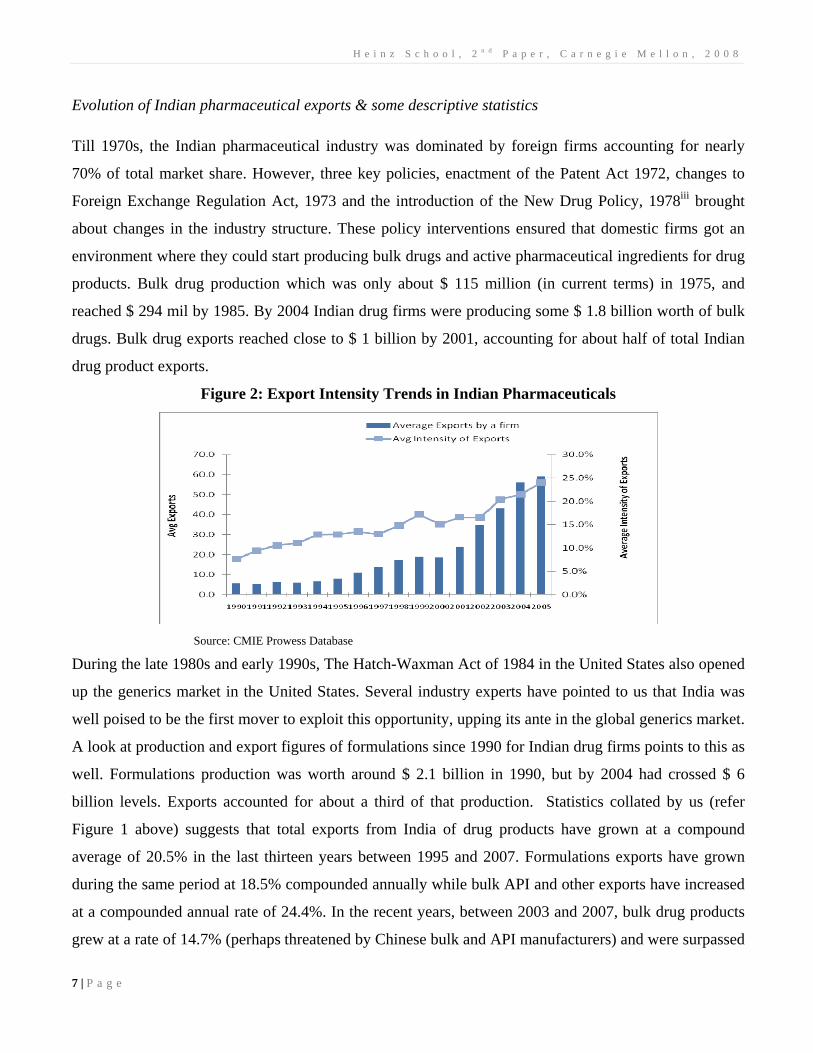

Figure 2: Export Intensity Trends in Indian Pharmaceuticals

Source: CMIE Prowess Database

During the late 1980s and early 1990s, The Hatch-Waxman Act of 1984 in the United States also opened

up the generics market in the United States. Several industry experts have pointed to us that India was

well poised to be the first mover to exploit this opportunity, upping its ante in the global generics market.

A look at production and export figures of formulations since 1990 for Indian drug firms points to this as

well. Formulations production was worth around $ 2.1 billion in 1990, but by 2004 had crossed $ 6

billion levels. Exports accounted for about a third of that production. Statistics collated by us (refer

Figure 1 above) suggests that total exports from India of drug products have grown at a compound

average of 20.5% in the last thirteen years between 1995 and 2007. Formulations exports have grown

during the same period at 18.5% compounded annually while bulk API and other exports have increased

at a compounded annual rate of 24.4%. In the recent years, between 2003 and 2007, bulk drug products

grew at a rate of 14.7% (perhaps threatened by Chinese bulk and API manufacturers) and were surpassed

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

8 | P a g e

in growth rates by formulation export growth rates of 16.2%. Intensity of total exports as a percentage of

total industry sales has risen from 8.6% in 1990 to 31.7% in 2005. The average firm was exporting some

7.7% of its sales in 1990 and this has increased to 24% by 2005. Our data also suggests that the number

of firms reporting non-zero exports had also increased to 110 by 2005 from about 46 in 1990, suggesting

considerable entry into export markets by Indian drug firms (Refer figure 2 and 3).

Figure 3: Entry into Exports in Indian pharmaceuticals

Source: CMIE Prowess Database

Export destinations

The export market for Indian drugs can be broadly classified into regulated and unregulated markets. The

former requires elaborate registration and for some countries inspection procedures to satisfy the drug

control authorities about the quality of medicines (also see appendix for a discussion on export

destinations). Such requirements are not so important and sometimes may even be absent in unregulated

markets. Regulations thus create stricter entry barriers and higher price realizations. Regulated markets

for Indian drug exports have traditionally included North America, Western Europe, Japan, Australia and

New Zealand. USA has had the strictest regulatory norms. Among unregulated markets the norms have

differed between countries. Vietnam, Syria and Jordan have been economies with far relaxed regulatory

norms in comparison to Brazil, China, Korea, Taiwan and Egypt. Regulated markets accounted for 39%

of total exports while more than half of all the bulk drugs exported has been going to regulated markets

(Chaudhuri (2005)). USA is India’s largest drug trading partner constituting about 17% of Indian bulk

drug exports and 14% of formulation exports. In bulk drugs large trading partners are Germany, China,

Hong Kong, Brazil and United Kingdom while in formulations, Russia, Nigeria, Vietnam, Nepal and Sri

Lanka account for the largest shares in exports. Our firm-level data, however, doesn’t allow us to capture

exports by product or destination type.

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

9 | P a g e

MNC firms in India have traditionally never exported with the exception of Aventis which has exported

in excess of 20% of its sales in the last few years or GlaxoSmithKline which has exported only about 3%

of its sales from its Indian unit. The exporters are thus local Indian companies and a large number of

them, especially those exporting to unregulated markets come from the pool of more than 200 small

scale bulk drug exporters. The larger Indian firms are placed both in bulks as well as formulation

exports. The share of the top five in total exports was 48% in 1990, was about 39% in 1995 and 2000

and was marginally higher at 41% in 2005. Aurobindo Pharma, Aventis, Cipla Ltd, Kopran Ltd, Ipca

Labs, Lupin Ltd, Matrix Laboratories, Orchid Chemicals, Ranbaxy Labs, Dr Reddy’s Labs and Sun

Pharmaceuticals have been the firms who have been the largest exporters of both bulk and formulations

products from India. Broadly, firms like Ranbaxy Ltd and Cipla have been exporting branded generics or

formulations in their own brands to unregulated markets and they also own their own marketing assets.

Some others like Aurobindo Pharma, Orchid Pharmaceuticals, and Matrix laboratories have exported

specialized bulk drugs to both regulated and unregulated markets. Only a few firms have moved into

exporting to the US with a broad majority still stuck in exporting to unregulated markets. The benefits of

sticking to unregulated markets are lower entry barriers in terms of requirement for product registrations

or non-inspections. The trade-off is that price realizations are low. This is not the case with regulated

markets like the US, where, while entry barriers are high, price realizations are high too. The broad

basket of firm strategies as discussed above encouraged us to classify firms into within industry

categories. We explore for learning effects within these sub-categories.

The United States Market & Entry Barriers

The United States has historically been India’s largest trading partner in pharmaceuticals exports.

Formulation marketing in the US requires Indian firms to file an Abbreviated New Drug Application

(ANDA)iv with the Food and Drug Administration (FDA) in the US. This also includes information on

the supplier of bulk drugs used to make the end product. The requirement to file an ANDA started in the

United States after the Hatch-Waxman Act of 1984. This act was implemented to spur the generic

markets with regulated proceedings on the safety and efficacy of generic drugs. If one looks at ANDA

counts or ANDA concentration counts (a single ANDA can be filed in more than one concentration) that

generic Indian firms have been required to file for a drug product to enter US generics market one can

observe a steep rise. The maximum number of ANDAs filed by an Indian drug firm has increased to 22

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

10 | P a g e

in 2008 from none in 1996. If one considers industry totals, ANDA counts in 2008 were 205 in

comparison to only 32 filed by the industry in 1990 (Refer Figure 4 below).

Figure 4: ANDA Counts at FDA by Indian Drug firms

Bulk drug exports to the US on the other hand requires filing of a Drug Master File with detailed

information to the Food and Drug Administration (FDA) about kind of equipment, location of the plant,

description of production facility, process chemistry, raw materials specification, stability and impurity

data and so on. Anecdotal evidence suggests that the cost for filing a DMF could be in the range of

$200,000 depending on the extent of information required and provided but despite that DMF filings are

also on the rise for the industry. This also points that Indian pharmaceutical firms are increasingly

becoming aggressive in terms of its entry strategies overseas. In our data on ANDA applications, we

found that there 8 such Indian drug firms, the most technologically progressive firms in the industry,

who are known to have a focus on US markets. They are the ones who have gone through the entire

experience curvev to handle the entry barriers in the US markets. Also, we observe firm strategies to

enter US markets in various combinations. There are few firms who have both DMFs and ANDAs in

their own names. A few others have DMFs but not ANDAs, these firms are tied up with marketing

partners who have ANDAs in their names (Cipla Ltd ANDA filed by US marketing partner, and JB

Chemicals has a joint venture in US). Finally there are bulk suppliers or contract manufacturers who

only have DMFs in their names.

Firm strategies in the US markets could also be classified in terms of generic products exported. Quite a

few in the industry like Lupin Ltd in anti-Tuberculosis drugs, Shasun Drugs in ibuprofen exports, USV

Ltd for metmorfin, Sri Krishna Drugs Ltd for acetaminophen, Calyx Ltd for pyrazinamide and Divis

Labs for naproxen have adopted what the industry analysts call a commodity generic exports strategy.

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

11 | P a g e

The other category would be of exports in value-added generics to the US markets. Various strategies to

enter the value-added generics segment would include non-infringing processes (as Matrix Laboratories

did for citalopram) that allow firms to use novel non-patent infringing processes for the manufacture of

generic drugs, novel drug delivery systems (Ranbaxy Ltd. developed a once-a-day version to administer

ciprofloxacin instead of the prevalent twice-a-day one), and successful Para IV ANDA application and

180-day exclusivity. 180-day exclusivity is infact a lucrative but difficult to surmount option ever since

Figure 5: Increasing International Alliances of Indian pharmaceuticals

Source: Newspaper & analyst reports, incomplete list, MERIT – CATI data provided by Geert Duysters; Also, this is

an incomplete list with 1990 numbers including ones prior to it and in 1990.

the Hatch-Waxman Act, from when generics producers have been encouraged to introduce drugs that

compete with patented products even before those patents expire. Any generic producer that can

demonstrate its competing product does not infringe on the patent earns a brief period (180 days) during

which it can exclusively market its rival product without any legal competition. During this period, the

generics producer becomes the monopoly producer of a product that is certified as biologically

equivalent to a patented product. The producer can charge a premium price during this interval. After

the 180-day exclusivity period expires, any generics producer is allowed to offer a competing product

based on the pioneers’ methods or compounds. Ranbaxy received one of these 180-day exclusivity

periods for ibuprofen and Dr Reddy’s Ltd for fluoxetime after challenging Eli Lilly’s blockbuster

Prozac. There are some other strategies emerging as well. Firms like Morepen Labs have opted to play it

safer by establishing ties with a successful para IV ANDA filer, Geneva the generics arm of Novartis Ltd.

Couple of them have opted to act aggressive, directly challenging a patented drug as Ranbaxy did for

cefuroxime axetil with a crystalline version of the salt contending GSK’s amorphous version. It must be

mentioned here that the high risk high returns US markets are being complemented by Indian firms with

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

12 | P a g e

entry into other markets as well. One can note (refer Figure 5 above) Indian drug firms adopting various

FDI instruments apart from pure exporting activity to enter other advanced markets.

C. Literature on the exporting-productivity relationship

As cited in the introduction, the literature on exporting and productivity has found mixed evidences on

the key question bothering researchers in this area. Do firms acquire better technology through exporting

activity? In the literature, this question is usually recast: after a transition to exporting, does measured

TFP grow more quickly in a manner that can be reasonably attributed to a “learning by exporting”

effect? There could be two broad effects one of which might dominate as one tries to answer that

question. The first is the market selection hypothesis, which argues that firms self select into export

markets. The reason for this is that there exists an additional cost of selling goods in foreign countries,

which might include transportation costs, distribution or marketing costs, costs involved in overcoming

country specific non-tariff barriers as mentioned above, costs for recruiting personnel with skill to

manage foreign networks, or even production costs in modifying current domestic products for foreign

consumption. These costs are a source of entry barriers that less successful firms cannot overcome.

Furthermore, the behavior of firms might be anticipatory i.e. they desiring to export tomorrow want to

improve performance today to be competitive on the foreign market in the future. Cross-section

differences between exporters and non-exporters, therefore, may in part be explained by differences ipso

facto between firms: The more productive firms become exporters. The second dominating hypothesis is

the learning effect hypothesis, which argues that a presence in export markets helps in enhancing

productivity in firms. This is not unreal too, knowledge flows from international buyers and competitors

can always aid in improving post-entry performance of export starters. Furthermore, firms participating

in international markets are exposed to more intense competition and must improve faster than firms

who sell their products domestically only. Finally, it is always possible that exporting generates

knowledge spillovers, which other domestic firms could gain from raising the productivity of the

industry as a whole. Exporting thus could have a learning effect making firms more productive.

Earliest works in the area, spearheaded by Bernard and Jensen (1995) looked at the linkages between

exports and productivity in US manufacturing and documented some interesting observations. First, they

observe, that while exports made up a small fraction of total US manufacturing output, exporting plants

had a disproportionate share in total employment and output. While they do report that good plants are

exporters, they are cautious in interpreting if on an average ‘today’s exporters will become tomorrow’s

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

13 | P a g e

success stories’, this due to the self-selection of good plants becoming tomorrow’s exporters being a

more plausible reality. In another seminal paper in the area (Clerides, Lach, and Tybout 1998), the

authors point out that in a dataset of Colombian and Moroccan plants, the causal hypothesis that

exporting leads to firm efficiencies is not econometrically validated. Current literature at large too has

observedvi, no learning effect from exporting for firms (Clerides, Lach, and Tybout 1998, Bernard and

Jensen 1999, Bernard and Wagner 1997, Delgado, Farinas and Ruano 2002, Bernard and Jensen 2004,

Trefler 2007) There are however some studies who provide evidences to the contrary i.e. there is indeed

a positive effect on productivity from exporting (Aw, Chung, and Roberts (2000), Baldwin and Gu

(2003), Van Biesebroeck (2004), Lileeva (2004), Hallward-Driemeier, Iarossi, and Sokoloff (2005),

Fernandes and Isgut (2006), Park, Yang, Shi, and Jiang (2006), Aw, Roberts, and Winston (2007) and

De Loecker (forthcoming)).

Given that the verdict is still not out on the exporting-productivity relationship, it might be worthwhile to

outline the empirical strategy for researchers in econometrically understanding the exports-productivity

relation. The most favored approach has obviously taken to observing a firm or plant performance

measure, like unit costs, labor productivity or total factor productivity and establishes its relationship

with exports, lagged or contemporaneous. Controls used are for unobserved effects, for example for firm

managerial competence taken care of with fixed effects, time dummies (to control for year to year

macroeconomic changes like exchange rate shifts) and for firm size, past productivity. This paper adopts

the total factor productivity (TFP) approach. To keep matters simple, we use a Cobb Douglas

specification to compute total factor productivity, where sales of a firm i in time t is the output measure

which is a function of some input measures, labor, capital, materials and fuel. We introduce the export

variable directly into our TFP regressions. The argument for this is as follows: First, the traditional

approach of computing estimated TFP (residuals from the first stage Cobb Douglas specifications) and

regressing them on measured export variable might lead us to potential problems in error structure.

Second, a direct one stage regression could be used such that the sign on the coefficient on the exports

variable could be interpreted as follows: sales or the output measure could be increasing or decreasing in

exports, controlling for all the other input variables. This impact of exports on output could only happen

if TFP is increasing or decreasing in exports, depending on the sign of the coefficient. A positive sign

thus on the RHS, on the export variable would mean observing a performance enhancing or a learning

effect controlling for other inputs following literature. Absence of it, or a –ve sign (we occasionally use –

ve for negative and +ve for positive all along in the paper) would imply non-observance of a learning

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

14 | P a g e

effect as a section of the literature finds. We discuss more details of our model specification in the

following section.

One key problem of this literature has been identifying if better firms self-selected into export markets or

exports enhanced productivity, in a nutshell as outlined above identifying the direction of causality. It

would be more than helpful, if one could find an instrument, for example a policy instrument that

stimulated exports but to the extent rationalisable, not productivity. One could then say, that we have

identified a policy (plant specific tariffs for example) which enhanced exports (and not productivity) and

check if that resulted in enhanced productivity. This is however easier said than done in real life,

literature much like us has struggled in identifying that policy instrument. We did try our best to identify

a policy instrumentvii. Not finding one, we instead do the following. We investigate if within sub-

samples of the industry, we could identify any substantial learning effects. Thus we check if learning

effects can be observed in the following categories of firms Principal exporters, Major exporters, FDA

firms, Modern Firms, Bulk exporters, Generic firms and firms based on whether they were domestically

or foreign owned (See appendix for approaches to firm categorisation) in Indian pharmaceuticals.

In Indian pharmaceuticals, it might further be important to understand what might be the mechanisms of

learning, whether firms learn by exporting certain particular portfolio of drug products and not others,

and whether exporting to regulated markets yields more learning effects than exporting to regulated

markets. Another interesting issue worth investigating could be to check if other forms of international

presence, like FDI instruments such as joint ventures, wholly owned subsidiaries, or overseas

acquisitions has led to an increase in firm productivity, or is it that we observe self selection in these

modes of international strategic presence as well! Unfortunately, our data limits us in investigating

product wise, destination wise, or firm international strategy wise, learning or selection effects. We

instead report our findings on learning from exporting and proceed to see if as Trefler (2008) & Javorcik

(2008) has argued, firm exporting decision in future is based on contemporaneous investments in Indian

pharmaceuticals. More details on our strategy to investigate investing and the decision to exports, in

short getting ready to exporting effects in Indian pharmaceuticals are outlined in Section H.

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

15 | P a g e

D. Set-Up & Empirical Strategy

The Production Function

Our model specification for investigating learning by exporting follows the literature closely. First, we

outline a production function of the Cobb Douglas form like below:

titi utititititi eFMKALY ,,,,,,,

+Ω= κδβα (1)

where the subscripts i, t denotes various input and output measures for the firm i in year t. Y the output

measure is normally observed through sales, revenues or value-added. L denotes labor in the firm, K is

capital stock, M materials, F energy and fuel expenses with ti ,Ω referring to the productivity shock

known to the firm but unobserved to the econometrician and tiu , an i.i.d. error referring to all other

disturbances and shocks affecting output that are unknown to the firm when making input decisions.

Taken in logs, equation (1) can be simplified as follows:

tititititititi uFMKLAY ,,,,,,, lnlnlnlnlnln +Ω+++++= κδβα (2)

Total factor productivity (TFP), could then be computed by estimating the coefficients κδβα ,,, and the

intercept term. The residual gives the value of ln TFPs or:

titititititi FMKLYTFP ,

^

,

^

,

^

,

^

,, lnlnlnlnlnln κδβα −−−−= (3)

There is obviously some level of endogeneity in this specification (Marschack and Andrews 1944), firms

based on some sort of optimizing behavior choose inputs in such a manner unknown to the

econometrician. A more productive firm could thus absorb more inputs and this could make the OLS

estimates of equation (2) above inconsistent and biased, because productivity of the firm could both be

contemporaneously and serially correlated with the inputs. Contemporaneous correlation will occur for

example, if a firm hires more workers based on its current productivity in anticipation of future

profitability while serial correlation between productivity and hiring decisions like above could upward

bias the estimate in a single-input setting, the direction of bias not being obvious in a multi-input setting

as ours. To address simultaneity as highlighted above, we estimate equation (2) adopting the Levinsohn-

Petrin approach of production function estimation following literature. This was done apart from simple

pooled OLS with time dummies, with and without fixed effects, and with first differences.

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

16 | P a g e

Identification by introducing the export variable

Our key identification comes from the introduction of the exports variable in the production function in

equation (2). The export variable was introduced in four variations, log of exports, intensity of exports as

a percent of sales, a dummy for the exporting decision which takes the value of 1 if our data on exports

showed a non-zero and a non-missing value and also level of exports. It must be mentioned here that this

meant that equation (2) would have an additional term, either as an input just like labor or capital, in this

case exports (which reduces to the variation log of exports in the final estimation), or the term would be

an exponentiated form of the export variable (for intensity of exports, dummy for exporters, level of

exports), as in Ze where Z stands for either the intensity, dummy or level of exports in the firm i at time t

and this enters the production function in (2) multiplicatively. All the variables, input, output as well as

exports are deflated using literature specified deflators as used previously in the Indian context. The

estimation approaches for all the export introduced regressions are similar to the basic TFP regressions.

The results for the contemporaneous case are similar if we instrument with lagged exports both for the 1st

and 2nd lag of the export variable, use revenues as another output measure, or use R & D expenditure

stocks as an additional input in the production function.

Searching for learning from exports

As outlined above, our basic identification comes from introducing exports into the production function

and estimation of the coefficients on the export variable. If we look at the variation of the export

variable, viz. log of exports, equation (2) would in effect look like this:

titi utitititititi eFMKLExportsAY ,,*)(** ,,,,,,

+Ω= κδβαρ (4)

One just needs to take logs of the above equation and carry out an estimation of the coefficient on

exports, ρ . If the variation of the export variable used in our analysis is intensity of exports, dummy for

exporters, or level of exports, then denoting either of them as z, Ze enters equation (2) multiplicatively:

tititi utitititi

Zti eFMKLeAY ,,, *)(** ,,,,

)(,

+Ω= κδβαρ (5)

where tiZ , in equation (5) is the relevant exports variable (intensity, dummy or level) and ρ is the

coefficient on either of them. The key contribution of this analysis comes from whether we can identify

learning effects from exports. The sign of the coefficient on the export variable ρ helps us in identifying

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

17 | P a g e

that irrespective of the nature of the export variable used (levels, logs, intensity or dummy). The

explanation would be as follows. Controlling for other inputs into the production function, a +vely

signed export variable would mean that revenues (or sales) our dependent variable, is increasing in

exports. That is only possible, if exports positively impact the residual, in this case, TFP, this in turn

showing up in increasing sales or revenues. Based on their product mix and export destinations different

categories of firms as discussed in Section B might have differential learning and even no observed

learning effects Bearing this in mind, we subdivide our sample of Indian pharmaceutical firms into

various sub-samples and search for learning evidences (See appendix for within industry firm category

classification). The empirical strategy used to identify sub-category level learning effects was as follows.

We used the group dummy and interacted that with our export variable (and all its variations). Our

regressions included the interaction term, the group dummy, and the export variable, and we report

learning effect if the linear combination of the point estimates on the export variable and the interaction

term was positive besides reporting their significance. Details are outlined in the section with results on

learning effects.

E. Data and Variables

Firm Data

Our primary source for firm data was the Prowess database from the Center for Monitoring of Indian

Economy, this database providing us a ready-made industry classification of firms. The Prowess

database is similar to Compustat database for U.S. companies providing information that incorporated

companies are required to disclose in their annual reports. Our study is conducted on a panel of 315

publicly listed Indian drugs and pharmaceutical firms (National Industrial Classification 2423) from

1990 to 2005. For these firms, the dataset provides us annual firm financial data from 1990 to 2005. The

key firm variables used were sales (deflated and its logs used as Y), exports (deflated and otherwise),

raw material expenses (deflated and its logs used as M), power and fuel expenses (deflated and its logs

used as F), salaries and wages and gross fixed assets (deflated and its logs used as capital stocks, K). We

additionally extracted data on plant and equipment expenses of firms and R & D expenditure, whose use

we outline in the section on getting ready to exports.

Exports, Capital Stocks and Labor

Some words are in order especially for the exports, capital stocks, and labor data used. The CMIE data

dictionary, defines the export variable as ‘total revenue earned from goods and services inclusive of

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

18 | P a g e

income earned in foreign currency by way of interest, dividend, or consultancy fees.’ The value is on

FOB basis and deemed export sales are also included in the data. For capital stocks, our ideal bet would

have been to follow standard best practice as here in the US, using a firm’s yearly series on new plant

and equipment investment, applying suitable depreciation rates and create stocks with a perpetual

inventory method. Unfortunately, Indian accounting standards don’t require a compulsory reporting of

new plant and equipment. Given that, we used gross fixed assets (refer appendix on capital stock

creation), deflated with the wholesale price index, as our measure of capital stocks as reported by firm

annual reports and furnished by the Prowess dataset. Admittedly, this will have limitations, given the

firm to firm accounting tricks and depreciation rates used; nonetheless for reasons mentioned in the

appendix this looks like the best measure for capital stocks. Finally, publicly traded Indian firms are not

required to report the number of employees on their annual reports. The Prowess database thus reveals

that firm reporting of yearly count of employees is inconsistent. The standard approach as used for

Indian data was thus adopted. Following previous literature on Indian manufacturing (Basant and Fikkert

1996, Kathuria 2000, and Unel 2003), we use the wage bill, salaries and wages reported by firms

annually, together with industry numbers to create a proxy for labor. We first computed ‘man days

worked’ for a firm in a year as follows: Man-days worked = (Salaries and wages for a firm-year

observation)/(Average Wage Rate). Average wage rate was obtained by dividing total emoluments of the

pharmaceutical industry to its employees by the industry’s total yearly man day employees as given in

the Annual Survey of Industries data in India. Industry codes for pharmaceuticals posed some issues

given that the National Industrial Classification (NIC) in India had undergone a change in 1997-1998.

Following previous literature on Indian manufacturing (Basant and Fikkert 1996, Hasan Mitra and

Ramaswamy 2007), we used the code 304 for drugs and pharmaceuticals till ASI 1997-1998 as per the

NIC 87 3 digit level. For ASI data from 1998-1999 till 2004-2005, the 4 digit industry code 2423 was

used to extract total emoluments and yearly man day employees data for Indian drugs and

pharmaceuticals firms.

Deflator data

All variables used in our analysis (except those used to create a proxy for labor) were deflated. A variety

of deflators have been used in the Indian context, in our case, we use the whole sale price index (WPI)

from the RBI Statistical Handbook (base year = 1993-94). Sales and material expenses were deflated

using the WPI for all commodities. It is conceivable, that given that an overall WPI exists, there should

be the existence of a price deflator for capital goods that should have been used on gross fixed assets for

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

19 | P a g e

our capital stock calculations. Our search for a capital goods price deflator however yielded

unsatisfactory results and we decided to proceed with the WPI for all commodities for deflating gross

fixed assets to create our capital stocks. We don’t here discount the fact that especially in the recent

years, WPI in India might not track trends in capital good prices all that closely, but given that we are

using time dummies and fixed effects in our regressions, this should not significantly alter our results.

WPI for fuel and power was used to deflate power and fuel expenses.

Table 2 on Descriptive Statistics of Key Variables

Variable Obs Mean Std. Dev. Min Max

log of sales 2798 -1.75243 2.001509 -9.77509 3.236235

log of labor 2765 4.103458 1.990653 -1.88585 8.857314 log of capital stocks 2843 -2.29846 1.582982 -9.21034 2.10563

log of material expenses 2673 -2.63658 1.931647 -9.83788 2.064384 log of fuel expenses 2552 -5.49542 1.905799 -10.232 -1.18332

Exports Variable

Deflated export levels 5120 0.087019 0.49943 0 15.34257

log of exports 1953 -3.46057 2.259972 -9.83789 2.730631 Intensity of Exports 2798 0.156734 0.236887 0 3 Dummy for exporter 5120 0.381445 0.485789 0 1

Industry sub-sample data

We outline above our search for learning not only at the overall industrial level in Indian

pharmaceuticals but also in industry subsections. The data used for identifying sub-samples within the

industry comes from a range of sources. We use Drug Master Files (DMF) filings available on the FDA

website to identify bulk makers (refer appendix for more details on firm categories). FDA also provides

us kindly with data on manufacturing facilities that have been granted a FDA certification in India

between 1995 and 2005. Finally, Orange Book in FDA website tracks Abbreviated New Drug

Applications, for generic products, we do a search by firm name and extract that data for our analysis.

Data for identifying modern firms comes from scanning of websites by firms, website of the Department

of Science and Technology, India and popular press searches and data provided to us by Professor Geert

Duysters at UNU-MERIT from the MERIT-CATI database.

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

20 | P a g e

F. Findings on Learning Effect

In this section, we discuss the coefficients from basic TFP regressions moving on to discuss our results

from our primary identification by introducing the exports variable in the TFP regressions. We wrap up

with our search for learning effects, the productivity-exports findings for industry sub-samples.

Basic TFP results

Table 3: Basic TFP Coefficients

Pooled OLS First Differences Fixed effects Lev-Pet

Labor 0.354 0.193 0.278 0.362

(20.98)** (8.44)** (12.61)** (12.99)**

Capital 0.035 0.051 0.026 0.403

(2.04)* (1.70) (1.32) (5.85)**

Materials 0.542 0.451 0.528 --

(49.27)** (34.53)** (43.56)** --

Fuel 0.052 0.138 0.106 --

(3.31)** (6.95)** (5.69)** -- Observations 2396 1953 2396 2396

Number of firms 302 279 302 320 R-Squared 0.93 0.60 0.77 --

Dependent Variable: log of sales. Value of z stats in parenthesis except t-stats for Fixed effects. * Significant at 5% level; ** significant at 1% level. Lev-pet Wald test of constant returns to scale: Chi2 = 16.12 (p = 0.0001)

The table above reports the point estimates from the basic TFP regressions. All regressions include time

dummies and results are for pooled OLS with and without fixed effects, first differences and Lev-Pet. At

first glance, the elasticity of sales with respect to labor is highest with the Lev-Pet approach where

materials is used an instrument to control for productivity shocks. It is significant all through, and the

labor elasticity varies between 19% to 40%, higher than 6-10% levels reported from previous studies on

overall Indian manufacturing (Unel 2003, Topalova 2004) but lower still from levels in OECD

economies (Bernard and Jones 1996). The coefficient on capital stocks, are very low, between 2% to 5%

though its performance improves in the Lev-Pet approach. Materials have close to 50% elasticity while

for fuels this varies between 5 %-14%. Materials, fuel and labor show some level of significance. The

industry seems closer to constant returns to scale though this is not observed in Lev-Pet. The coefficients

are roughly the same if one introduces R & D in the regressions as another input or one uses revenues as

the output measure. At an overall level, TFP computed from the residuals in equation (3) in Section D is

reported in the appendix for all estimation approaches.

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

21 | P a g e

Results on learning effect from introducing the export variable

As Table 4 indicates, we introduce exports in four variations in our TFP regressions for the overall

industry. We report here the results from pooled OLS with fixed effects and from the Lev-Pet approach.

When exports enter as levels, the impact of exports on productivity, controlling for other inputs, and thus

on sales is close to 0. This is negative if we use the variable intensity of exports as % of sales though one

should be cautious while introducing this variable because sales would then appear on both sides of our

estimating equation skewing the intuition behind the findings. The dummy for exporter variable appears

more realistic, it taking a value of 1 if a firm-year observation shows the firm’s export market presence.

This throws up a positive effect of exporting on productivity with the Lev-Pet approach though the point

estimates are small and insignificant, but with fixed effects, sales and productivity seem to be decreasing

in exports. With log of exports, a positive effect is observed but the sizes of the point estimate are close

to 0 while being significant. Point estimates for the other inputs into the production function follow the

broad trend as outlined in the basic TFP regressions. The results don’t change if we use revenues as an

output measure. They follow the broad trend of small size or –vely signed point estimates on the export

variable, if we instrument for exports (given the self selection problem) with 1st and 2nd lags of exports.

A word of caution is however in order here while arriving at an immediate conclusion. We must

acknowledge that there might be differential learning by firms based on the type of products that they

export (bulks/API/formulations) or the destination to where they export. Further, our basic motivation

was to investigate the link between exporting and technological upgradation, and we argue in section G

that learning by exporting might not capture all sources of enhancement of technical efficiency for a

firm from its presence in export markets. Finally, our data doesn’t permit us to capture break up of firm

exports either in terms of product or destination and this could be clouding our findings.

Searching for Learning in Industry Sub-Samples

Having failed in identifying performance enhancement from exports at the broad industrial level, we try

to do the next best thing given our data limitations in capturing exports by product or destination type.

We explore for within-industry effects of learning from exports by industry subcategories namely, in

firms that we categorized as Principal exporters, Major exporters, firms with FDA approval of

manufacturing facility, Modern Firms, Original Bulk exporters, Generic firms and firms based on

whether they were domestically or foreign owned. A short discussion is in order to discuss our estimation

approach as we search for learning within the industry.

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

22 | P a g e

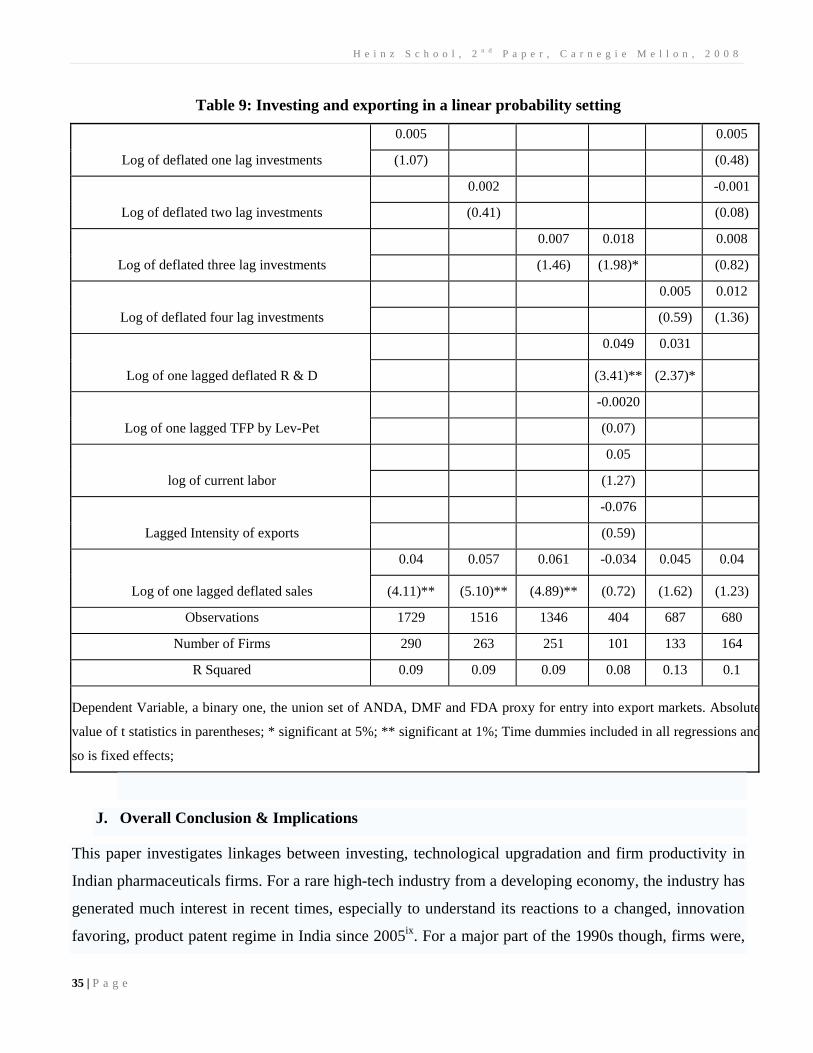

Table 4: Searching for Learning at the Overall Industry level

FIXED

EFFECTS Lev-Pet

FIXED

EFFECTS Lev-Pet

FIXED

EFFECTS Lev-Pet

FIXED

EFFECTS Lev-Pet

Log of labor: L

0.271 0.364 0.278 0.348 0.28 0.361 0.292 0.384

(12.19)** (16.77)** (12.58)** (15.92)** (12.64)** (18.62)** (13.64)** (19.59)**

Exports

0.001 0.001

(2.52)* (1.52)

Intensity of Exports

-0.003 -0.178

(0.01) (2.40)*

Dummy

for exporters

-0.024 0.037

(0.91) (1.00)

Log of exports

0.062 0.046

(10.06)** (4.15)**

K

0.021 0.385 0.026 0.427 0.026 0.398 -0.022 0.33

(1.04) (5.41)** (1.32) (5.97)** (1.29) (6.35)** (1.23) (3.37)*

M

0.528 0.528 0.53 0.583

(43.55)** (43.52)** (43.26)** (38.79)**

F

0.108 0.106 0.106 -0.017

(5.82)** (5.69)* (5.69)** (0.98)

Observations 2396 2396 2396 2396 2396 2396 1781 1781

Number of firms 302 320 302 320 302 320 249 320

R-squared 0.77 -- 0.77 -- 0.77 -- 0.84 --

Dependent variable log of sales, results don’t change when we use revenues, time dummies included. Absolute value of z statistics in

parentheses for Lev-Pet and t-stats for fixed effects;* Significant at 5%; ** significant at 1%. Results go through similarly in terms of

sign on export variable on pooled OLS and first differences. Wald test of constant returns to scale in Lev-Pet yields a p value less than

0.01 in all cases.

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

23 | P a g e

Our identification for learning effect comes from introducing the exports variable in the basic production

function. When it enters the production function just like other inputs in (4) the expression takes the

form:

titi utitititititi eFMKLExportsAY ,,*)(** ,,,,,,

+Ω= κδβαρ

A +vely signed ρ from the above specification with some level of significance will be the first evidence

of a learning effect from exporting as discussed in Section D. We find that at the broad industry level we

don’t see much learning effect due to either a –vely signed ρ or its insignificantly small size despite it

being +ve. It is however possible that learning is observed within industry, in select sub-samples of the

industry and for that we introduce group dummies to identify various categories of firms as discussed in

section C. The GroupDummy (for example the bulk exporter dummy) could then be interacted with the

exports variable as above to check if learning effects are observed. If exports enter the production

function multiplicatively like any other input (log of exports being our variable of interest), with the

interaction term the specification would be:

....)log(***)log(*loglog ,'

,, ++++= tititi ExportsGroupDummyGroupDummyExportsAY ααρ (i)

where the ‘…’ section in (i) above, includes the log of the other input variables, L, K, M and F and the

error terms as in equation (2). Partial effects of exports in an industry sub-sample are then)(log

))(log(

,

,

ti

ti

ExportsY

∂

∂ ,

a linear combination of the point estimates ρ and 'α from (i) above.

When the export variable of interest enters the production function multiplicatively, but in an

exponentiated form like in (5):

tititi utitititi

Zti eFMKLeAY ,,, *)(** ,,,,

)(,

+Ω= κδβαρ

the expanded equivalent of (i) above to identify learning comes from the following specification:

....)(***)(*loglog ',, ++++= ZGroupDummyGroupDummyZAY titi ααρ (ii)

where tiZ , is the concerned exports variable (in our case is intensity of exports, dummy for exporters, and

export level). The partial effects of exports (or Z more generally) from (ii) would be)(

))(log(

,

,

ti

ti

ZY

∂

∂ , again a

linear combination of the point estimates ρ and 'α from (ii) above. We report below the sign of these

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

24 | P a g e

partial effects for all our export variables, when we include time dummies and conduct a pooled OLS,

with and without fixed effects, and also adopt the Levinsohn-Petrin approach for the production function

estimation. The point estimates outside the braces are the linear combinations, the numbers within (.) are

the z-stats for the pooled OLS and Lev-Pet regressions and t-stats for the fixed effects regressions. The

numbers within the curly braces {.} indicates the p-value if we test the null that interaction term

)(* ZGroupDummy is 0.

Table 5 on point estimates of the partial effects in the next page reveal that the size of the point

estimates, indicating the impact of exports on productivity might be throwing up a +ve sign in some sub-

categories, but then the sizes are small and then again based on the type of export variable used or the

estimation approach adopted, they are not consistently signed. In a nutshell not much productivity

enhancement from exports is observed as any broad trend from the within-industry search for learning

among firm categories. If at all, there is some trend, it is the fringe firms (dummy for bulk exporters) in

the industry, those who could be called as the technologically backward ones (having started off

originally as downstream bulk producers), who yield a consistently +vely signed partial effect of exports

on productivity. Another category that comes close to convincingly showing some learning effects are

the Principal exporters, those exported greater than 40% of their sales any year between 1990 and 2005.

This is puzzling, especially if one expects, the industry to have shifted gears in the last decade with

stronger appropriability coming into place. Firms which are technologically progressive, the modern or

the FDA tagged firms, could be hypothesized to be the ones who would show up productivity

enhancements from exports. This however is not the case, one way to rationalize might be as follows.

Maybe, the set-up of learning by exporting doesn’t capture the entire gamut of experiences that enhances

a firm’s technical efficiency. We argue that could be a strong possibility. The learning by exporting

literature has tended to view productivity improvements from exporting as something that comes “for

free”. Yet, recent work suggests that much of the upgrading occurs before, not after exports commence.

In addition, much of the technological upgrading is embodied in new capital equipment, worker training,

and quality certifications, all of which require real outlays on the part of the firm. Furthermore, once

firms enter the export market, they are often constrained in terms of their ability to appropriate the gains

from their technological upgrading. Facing fierce competition from existing incumbents and from other

foreign entrants, exporters must often accept lower profit margins on export sales than on sales in their

domestic market. All of this can lead to very modest measured increases in TFP after the inception of

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

25 | P a g e

exports. While all of this is true, the very prospect of serving export markets can induce firms to make

costly investments in technological upgrading that they would not make in the absence of the export

opportunities. We are not convinced thus that lack of learning invalidates our basic premise, that firms

get technically more efficient with entry into export markets. It might not show up in TFP improvements,

but there might be a link between ex-ante investments and the decision to export. The motivation for this

track of investigation, the empirical strategy, and the results on this are presented next in the paper.

Table 5: Partial effects of Exports Variable

(Note: The point estimates outside the braces are the linear combinations, the numbers within (.) are the z-stats for the pooled OLS and Lev-Pet

regressions and t-stats for the fixed effects regressions. The numbers within the curly braces {.} indicates the p-value if we test the null that

interaction term )(* ZGroupDummy is 0. )

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

26 | P a g e

G. An introspection on learning by exporting

Our findings in the preceding section indicate that there are no substantial productivity enhancements or

learning effects observed in the Indian pharmaceutical industry. Infact, we are presented with a challenge

to explain learning in bulk exporters, firms who appear to be technologically non-progressive in the

industry. We believe that this is not unexpected given the methodological and data constraints. Let us

take these one by one. First, it has been well established that in the absence of detailed firm (or plant)-

product-price level data, conventional methods like learning by exporting cannot capture the full benefits

from exporting. A simple exposition as laid out in the diagram below could explain why.

Let us suppose that the firm faces a downward sloping domestic demand curve and a flat foreign demand

curve (with no global market power). Let us also assume that in this static setting, the firm is ex-ante

only present in domestic markets; entry into exports comes later on. Marginal costs for this product in

both markets are assumed to be the same for the firm. How does the firm behave in terms of its

production decisions? A domestic firm in an imperfectly competitive setting domestically produces an

amount of domesticQ till E. At E, its marginal revenue from selling one unit of the product in domestic

markets is just equal to its marginal revenue from selling that product in foreign markets (foreign

marginal revenue curve is same as the flat foreign demand curve). From E onwards, marginal revenue

from export markets exceeds it marginal revenue from domestic markets and the firm focuses on exports

till F, producing ForeignQ units for its export markets. From F onwards, the firm’s marginal cost curve

exceeds even its marginal revenues from export markets and it would then have to rethink its strategies.

The producer’s surplus for the firm till E, is given by the trapezoidal area ABCD, it’s profits from

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

27 | P a g e

domestic markets. An entry into export markets generates profits in the form of the triangular area ECF.

This diagram illustrates the shortcoming of the learning by exporting methodology, this despite being a

very informal static depiction of the situation with assumptions on the demand and marginal cost curve

of the firm. Conventional methods like TFP (that we also employ) will only indicate that profits from

entering export markets declined from its current domestic market levels, the new area ECF vis-à-vis its

old surplus, area ABCD. It however will not fully capture the impact of exporting behavior on

technology absorption by local firms, especially among firms within the same industry. This is

specifically so because the methodology fails to distinguish effectively between changes in firm profits

and changes in the technical efficiency of production for the firm.

Anecdotal evidences have shown that once the decision is taken, an entry into export markets has made a

firm inarguably more technically efficient in various industrial settings globally. An exporting firm is

able to implement process improvements, learn about employing advanced marketing techniques, or

incorporate the Western consumer tastes in its initial product that was initially geared towards a domestic

consumer. Further, in a setting as ours, these learnings by the firm could have spillover effects. Entry in

the US markets for example, of the first Indian pharmaceutical firm in a certain therapeutic category,

could bring in new knowledge on how to succeed in those categories in Western drug markets for other

firms. They could then follow suit. For these set of subsequent entrants in the export markets, entry into

foreign markets would then come almost at no cost, as if they had instant access to a “free window” to

exploit export opportunities. However profit opportunities for these firms will be minimal given the

perfectly competitive nature in global drug markets. Thus an Indian pharmaceutical firm’s entry into

global drug markets might result in a short run lowering of profits for the first moving firm or close to

non-existential profits for subsequent entrants, this registering as fall or perhaps only modest increases in

TFP. However the benefits from exports still remain raising the firm’s as well as the industry’s technical

efficiency but for the econometrician employing the TFP approach this will remain out of bounds. It is

thus well nigh possible that learning by exporting might then systematically underestimate the true

benefits for the firm from exporting. There might then be less to be discouraged about from findings on

no learning in the previous section.

What are the alternatives then for a researcher to understand technological upgradation and the true

benefits from exporting? One option as recent work suggests (Trefler 2007 and Javorcik 2008) is to

search for more detailed data at the plant or firm product-price level. One could ask plant managers (as

done in Trefler 2007) if they invested in advanced technological upgradation, before or after entering

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

28 | P a g e

export markets. Alternatively, one can use unit values of products (as in Javorcik 2008), to truly measure

a firm’s surplus generated after entering export markets. In the absence of either, we do the next best

thing. We look for our version of evidences to support what the new international economics literature

dubs as getting ready to export. We argue that an entry into export markets, more so advanced export

markets, would be preceded by ex-ante investment bumps, a hypothesis that will synchronize with our

argument, that an entry into foreign markets entails an ex-ante technological upgradation by the firm.

One can witness that in our case with bumps in investments (a proxy for substantial technological

upgradation) occurring prior to entry into export markets. We also argue (and indeed find) that

especially for entry into the most advanced markets (US generic markets with ANDA filings), the partial

effect of an investment bump on the decision to enter is quite substantial. The next section details more

on investing-exporting linkages.

H. The literature & Set-Up for Getting to Ready Export

Getting Ready to Export

Recent work in new international economics (Trefler 2007, Javorcik et.al 2008, Melitz 2003) argue that

contemporaneous investments and the future exporting decision are complementary to each other. This is

not unrealistic if investment is done as discussed in Section G for ex-ante technological upgradation by a

firm entering export markets. It is hard to imagine that without costly productivity enhancing

investments (somewhat close to what the literature dubs as fixed costs of exporting) in previous periods,

a firm is going to enter an export marketviii. We argue then that exploring linkages between investing and

exporting could help us understand the decision behind the Indian pharmaceutical firm’s entry into

export markets. This is especially relevant in our case, where we don’t witness much learning for the

industry at large. We argue learning by exporting, fails to fully capture the ex-ante enhancements in

technical efficiency of a firm before it enters export markets. This section then documents that the firm’s

decision to export is increasing in ex-ante technological upgradation as measured through year to year

firm investment bumps. We argue that this adds more evidence to our basic premise, that indeed, a

presence in export markets for Indian pharmaceutical firms is closely related to the upgradation of its

technical efficiency frontier.

The Set-Up

Closely following this literature on getting ready to export, we model the exporting decision (a binary

choice variable) as a function of lagged investments, subject to controls, time dummies, and firm fixed

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

29 | P a g e

effects in a binary choice linear probability, probit and conditional-logit setting. Our simple set up

models a firm’s entry into the exporting market conditional on a vector of firm level characteristics. Thus

the exporting decision Y is 1 if in a particular firm-year observation, one is present in the export market,

zero else. Thus:

tiititi xY ,,, ελβ ++= (6)

where the exporting decision tiY , for a firm i in time t is modeled thus:

tiY , = 1 if firm is present in the export market in a particular year

= 0 if it is absent in the export market in a particular year.

where tix , is a firm specific vector which includes lagged investments, firm size controls, in our case log

of deflated sales, lagged TFP, log of current labor, one lagged intensity of exports, and also one lagged

log of deflated R & D expenses. We also control for year-effects by including time dummies in the

regressions. Further unobserved heterogeneity is accounted for with firm level fixed effects iλ and ti,ε is

an idiosyncratic i.i.d error term. In a binary choice setting, more specifically in linear probability models,

one can take expectations of (6) and thus:

)()|()|( ,,,,,, itititiitititi ExxxExYE λβελβ +=++= (7)

Also one can show that in a binary choice setting, expectations are equal to the probability of the

dependent variable taking on the value of 1, thus:

)|1()|1(Pr)|( ,,,,,, titititititi xYPxYobxYE ==== (8)

Using (8) and (7) one can then write:

βtititi xxYP ,,, )|1( == (9)

Our objective is to see how lagged investments, subject to firm controls and year-effects influence the

conditional probability of the exporting decision )|1( ,, titi xYP = . We carry out our analysis thus with our

setup as illustrated in the equations (6) to (9), employing a linear probability setting, a pooled probit

estimator and conditional logit, following closely Trefler (2007), Javorcik et.al (2008) and Bernard and

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

30 | P a g e

Jensen (2004). We include firm effects in linear probability and group by firm in conditional logit

allowing for firm specific unobserved heterogeneity, iλ that we drop in (9).

Data & Variables

Our data comes as before from the Prowess dataset as outlined in Section E. Our key independent

variable in the vector of firm characteristics is investments. As discussed, Indian firms don’t report a

series on new plant and equipment, instead CMIE Prowess collects what is reported, figures for plant

and equipment for our panel firms. The figures that we have are of gross block, that includes plant and

equipment at the end of a financial year lumped with additions and deletions of plant and equipment

investment during a current year. We take these figures of gross block and difference gross block of year

t with year t-1 to get current year investment in plant and equipment. We deflate these figures with the

WPI of all commodities. We then use the logs of 1st, 2nd, 3rd and 4th lags of these deflated investments

(defonelaginv, deftwolaginv, defthreelaginv, deffourlaginv) in the binary choice regressions (See figure

in Appendix illustrating plant and equipment accounting norms from the annual report of Aurobindo

Pharma in 2005).

For measures of a firm’s decision to be an exporter or a non-exporter we adopt the following five

approaches. First, we use our dataset to notice if the exports variable used in our TFP regressions is non-

missing and non-zero. If it is then we say that the dummy for exporting, Dumexp is 1, if it is not it takes a

value of 0. Second, we use data of firm counts of filings with the Food and Drug Administration for

Abbreviated New Drug Application, Drug Master Files, along with the data from FDA approval of a

firm’s manufacturing plant in a certain year. We say that the fact that a firm had a non-zero or a non-

missing ANDA or DMF count in a particular year, proxies for its entry in the export markets, the ANDA

indicator, ANDAI and the DMF indicator, DMFI takes a value of 1 or 0 accordingly. We also employ this

approach if a firm had a FDA approval in a particular year, the FDA indicator, FDAI taking a value of 1,

0 otherwise. We also take a union set of the three indicator variables for exports, ANDAI, DMFI and

FDAI. That is, if a firm-year observation had a non-zero ANDA count, or a non-zero DMF count, or a

non-zero FDA approval of its manufacturing plants (one or more), the union dummy OI takes a value of

1, 0 otherwise. This is off course an informal measure to proxy for entry into export markets apart from

using the Dumexp indicator. But industry sources point out that the fact, that a firm in a particular year

has a presence in the list of US regulatory filings, should in most cases point to it having transcended the

entire exporting cycle that is in general the norm for Indian pharmaceutical firms, viz. starting off with

H e i n z S c h o o l , 2 n d P a p e r , C a r n e g i e M e l l o n , 2 0 0 8

31 | P a g e

production for domestic markets, exporting to unregulated markets, exporting to regulated markets other

than USA and then finally setting sight on US markets. To the extent that is true and in the absence of

export destination wise firm-year data, we argue that a particular firm-year observation has a non-zero

ANDA, DMF or a FDA approval count, should proxy sensibly for its presence in export markets at large.

There are 1953 firm-year observations which are 1s for Dumexp, 29 ANDA observations which are 1s,