Provisions of Interfaith Dialogue in Islamic Shari'ah - Allama ...

Upload

khangminh22Category

view

6download

0

kasneb NEWSLINE, Issue No. 1, January - March 2017 i

The Professional Journal of kasneb Issue No. 1, January - March 2017kasneb

EDUCATIVE INFORMATIVE ENTERTAINING EMPOWERING

INSIDE PORTFOLIO THEORY

FINANCE ACT 2016

THE RIGHT COLLECTION

AGENCY

STRATEGIC LEADERSHIP

BE YOUR OWN BOSS

kasneb LAUNCHES

NEW BRAND

kasneb UPDATES

PRIZE WINNERS

THEORYPORTFOLIO

NEWSLINE The Professional Journal of kasneb Issue No. 2, April - June 2017

EDUCATIVE INFORMATIVE ENTERTAINING EMPOWERING

INSIDE ISLAMIC BANKING

VALUE CURVES

MANAGEMENT ETHICS

THROUGHPUT ACCOUNTING

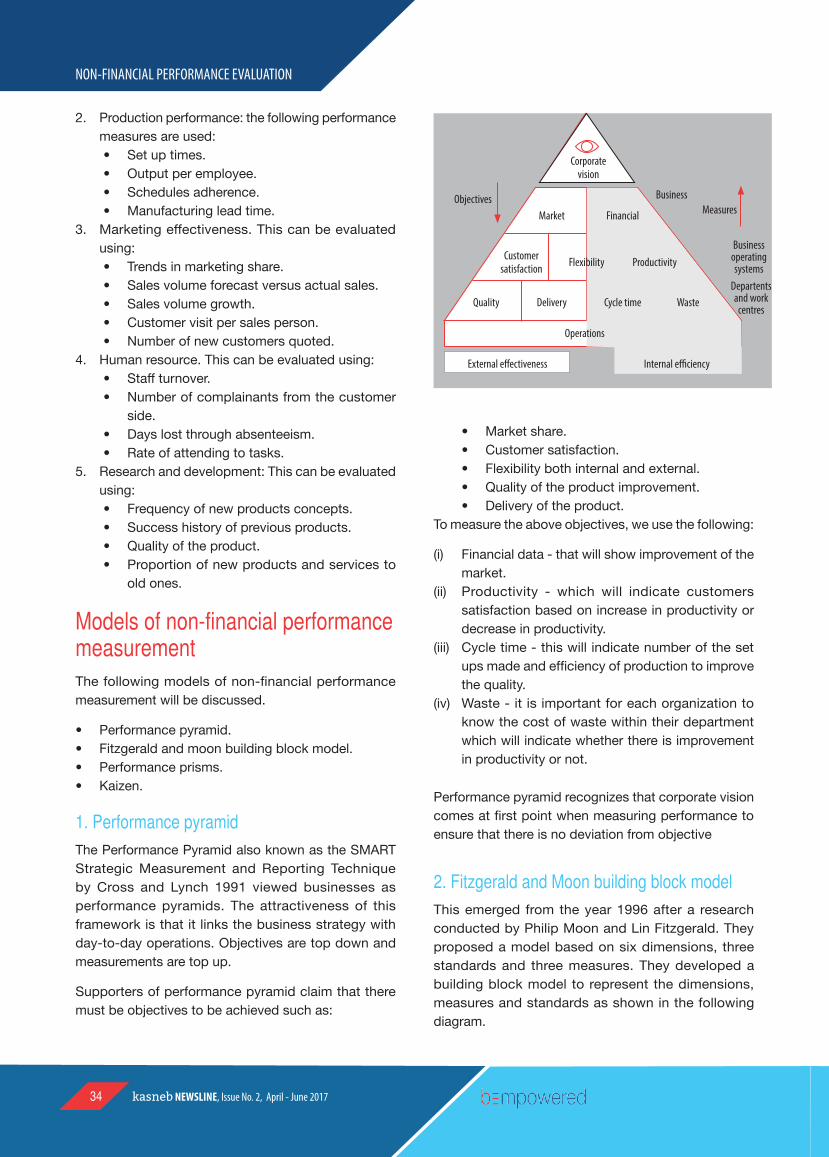

NON-FINANCIAL PERFORMANCE

EVALUATIONe-kasneb kasneb

UPDATESPRIZE

WINNERS

SHARI’AH COMPLIANT

kasneb NEWSLINE, Issue No. 2, April - June 2017ii

kasneb NEWSLINE, Issue No. 2, April - June 2017 1

XXXXXXXXXXXXXX

Editor Honoraris Pius M. Nduatih

Editorial Team Staff members of Kasneb

Circulation OfficeKasneb Towers

Hospital Road, Upper HillP.O. Box 41362 - 00100

Nairobi - KenyaTel: 254 020 4923000

Cellphone: 0722-201214/0734-600624Fax: 254 020 2712915

E-mail: [email protected]: www.kasneb.or.ke

Facebook:kasnebOfficialTwitter: @kasnebOficial

Kasneb Newsline is the professional students journal of Kasneb. The views in the articles featured in this journal

are those of the respective authors and do not necessarily reflect the views of

Kasneb or its partners.

The Editor welcomes contributions from readers especially students and trainers in

accountancy, finance, credit, governance and management, information

communication technology and cognate subjects.

The Editor reserves the right to edit articles for purposes of clarity

and brevity.Trainers and students are free to

photocopy materials contained in this journal for purposes of learning without

seeking prior consent from Kasneb.

Reproduction is allowed without charge as long as prior consent is sought and

the source acknowledged.

Correspondence should be addressed to:

The Editorkasneb Newsline

Marketing and Corporate Affairs UnitP.O. Box 41362 - 00100, Nairobi

E-mail: [email protected]

CONTRIBUTORS

TO THIS ISSUE

Abdhallah Mambo Isaac MainaKellen Kiambati

63 List of prize winners Kasneb is ISO 9001:2015 certified

Kasneb NEWSLINEIssue No.2, April - June 2017

Raymond Kiambati

3 Auditing and Shari’ah supervision of Islamic financial institutions

33 Non-financial performance evaluation

15 Management ethics

Derrick Majani

43 The Trainee Accountants Practical Experience Framework (TAPEF)

48 Kasneb updates

9 Value curves

25 Throughput accounting and the theory of constraints

CONTENTS

ETHICS

RIGHT

WRONG

kasneb NEWSLINE, Issue No. 2, April - June 20172 kasneb NEWSLINE, Issue No. 2, April - June 2017 3

Editor HonorarisPius M. Nduatih

From the CEO’s desk

The concept of Islamic banking, also referred to as Shari’ah

compliant banking, has continued to gain currency globally

over the last few years. In Kenya, for instance, the entry of new

Islamic Financial Institutions (IFIs), and the roll out by conventional

banks of Islamic financial products such as “Amanah”, ‘’Iman” and

“Lariba” is a clear testimony of the increasing popularity of this new

business niche.

In spite of the above trend, a number of players in the financial market

are unable to trace the line of demarcation between Islamic banking and

conventional banking. Principally, the underlying structures in Islamic banking

are based on the trading of assets, leasing arrangements and profit or loss

sharing. On the other hand, conventional banking is based on lending, ability to

pay and charging of interest.

The underlying uniqueness of Islamic banking poses challenges in the auditing and

supervision of Islamic Financial Institutions (IFIs). Part of the scope of audit or supervision

in this context is to ensure that an Islamic financial product or service complies with Islamic

legal precepts and principles (Shari’ah compliance).

It is in the above context that we feature a lead article in this edition of the kasneb

Newsline titled “Auditing and Shari’ah Supervision of Islamic Financial Institutions”. The

writer sheds more light on the Shari’ah audit framework, role of the Shari’ah Supervisory

Board and the challenges in the audit of IFIs.

In the second articled titled “Reading the Value Curves in Strategy”, the writer integrates

the concept of value curves with strategy development and implementation within the

background of a blue ocean strategy. According to the writer, the right value curve should

depict an organisation’s competitive advantage in terms of strategic focus, divergence

and a compelling tag line that “speaks” to the market.

This edition also features other articles in diverse areas of interest to our readers,

including on ethics management, non-financial performance evaluation, throughput

accounting and the theory of constraints.

Enjoy your reading.

Ethics must begin at the top of every organisation. It is a leadership

issue and CEO must set the example.

Edward Hennessy

kasneb NEWSLINE, Issue No. 2, April - June 2017 3

Introduction

Islamic or Shari’ah compliant banking is a fast-growing segment of the financial sector in Kenya. The industry has shown double digit growth rates although from

a relatively low absolute base. The growth of Islamic finance in Kenya is linked to the reform agenda of the Central Bank of Kenya that reviewed the banking laws more than five years ago that extended to the insurance industry and now the capital markets.

Kenya’s experience with Shari’ah compliant banking is already being shared by Tanzania and Uganda as they seek to enact similar laws. Currently, Kenya has two fully fledged Islamic banks: Gulf African Bank and First Community Bank. Conventional banks such as National Bank, Chase Bank, Barclays Bank and Standard Chartered Bank are already tapping into the Islamic financial market with their National “Amanah”, Chase “Iman”, Barclays “Lariba”, Standard Chartered

“Sadiq” accounts respectively. Other international banks like Dubai Islamic Bank (DIB), the largest Islamic bank in the United Arab Emirates, have registered interest in the Kenyan market. Financiers see a growing demand for this alternative mode of finance that widens the choice for investors and governments that have proactively created the enabling environment to promote the diversification of their financial markets.

In terms of functionality and the objectives of realising financial intermediation, Islamic banking and finance is not any different from the conventional banking and finance, only that the underlying structures are based on the trading of assets, leasing arrangements and profit and loss sharing investments as dictated by the Shari’ah principles. It is this difference that makes auditing and supervision of the Islamic Financial Institutions different from the conventional banking system.

AUDITING AND SHARI’AH SUPERVISION OF ISLAMIC FINANCIAL INSTITUTIONS

• The basic sources of Shari’ah principles are in the Quran and the Sunnah, which are followed by the consensus of the jurists and interpreters of Islamic law.

• Profit sharing and fee-based financing approaches have developed in compliance with Shari’ah laws.

• The Islamic law (Shari’ah) prohibits taking or giving interest (Riba) which is the most essential feature of Islamic banking.

• These special modes of financing have emerged in retail, private and commercial banking for debit and capital markets, insurance, asset management, structured and project financing.

Governing principles in Islamic finance

Tenets of Islamic Finance

Money as potential capital

Prohibition of interest

Sanctity of contract

Risk sharing

Shari’ah compliant activities

Prohibition on speculative

transaction

Islamic financial system

ConventionalMoney

BANK CLIENT

Money + Money (interest)

Islamic

Money

BANK CLIENTTrade

ABDHALLAH MAMBO DALLU, BBM, CPAK, CIAInternal Auditor, Umma University

kasneb NEWSLINE, Issue No. 2, April - June 20174 kasneb NEWSLINE, Issue No. 2, April - June 2017 5

AUDITING AND SHARI’AH SUPERVISION

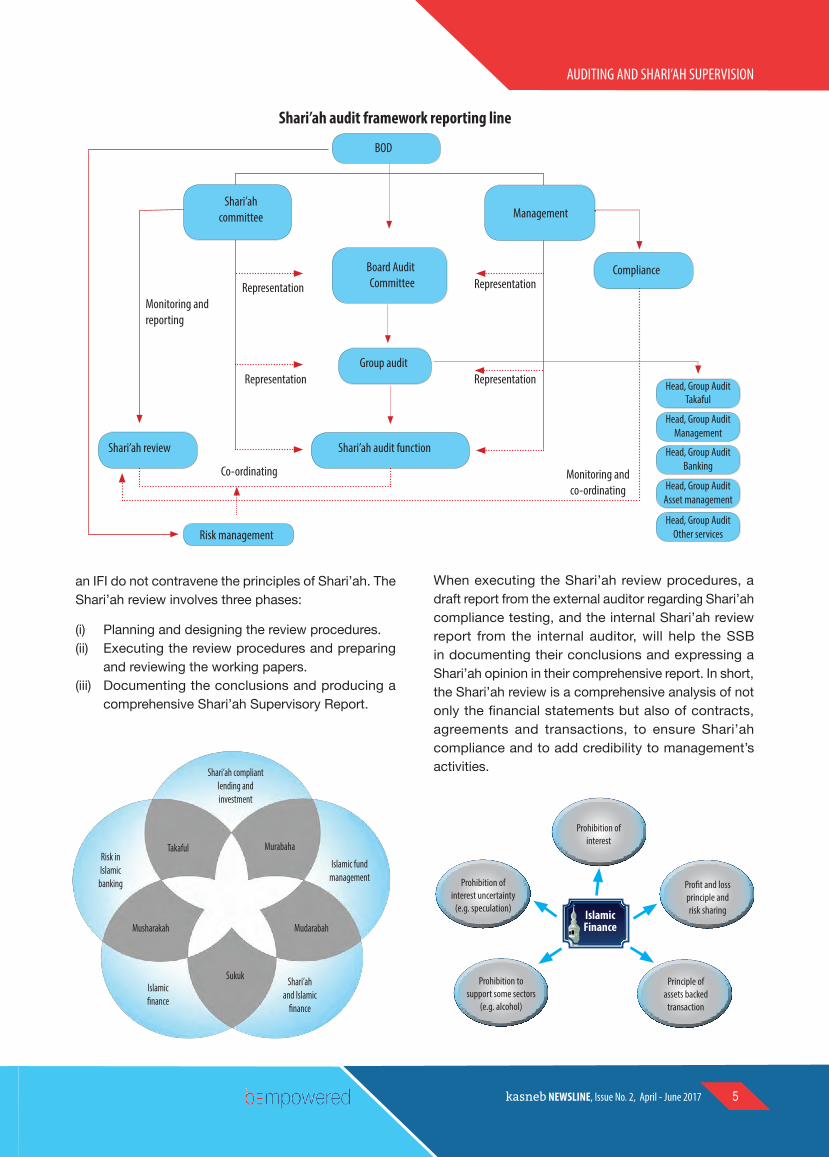

Shari`ah supervision in Islamic Financial Institutions Shari`ah supervision is the process of ensuring that a financial product or service complies with Islamic legal precepts and principles, either by its conforming (to one degree or another) to a recognised Islamic legal norm or by its not violating the same. Ideally, Shari`ah supervision will be a part of an Islamic product or service from the time of its development, to its launch, and throughout the period it is offered. At the stage of research and development or of drafting contracts or offering memorandum, Shari`ah supervision, in one form or another, should be an active participant. By including Shari`ah supervision and advice at the earliest stages, management may save costly legal fees that may be required at a later stage if elements of the proposed business/contracts need to be modified to comply with Shari`ah principles and precepts.

If Shari`ah supervisors are to certify a venture, they will insist on being a part of its development; or at least to having access to the details of whatever went into the development or structuring of the product, instrument, service or enterprise. Moreover, once a product is launched, Shari`ah supervision may take the form of ongoing monitoring through periodic audits. Such audits may be undertaken by means of site visits, document reviews, or consultation with management at regular intervals.

Role of key players in the audit of Islamic Financial Institutions (IFIs)Due to the need to ensure proper adherence to the Shari’ah principles in operations and activities, external auditors are not expected to conduct both types of audit for IFIs. This is because the criteria in deciding whether an activity complies with Shari’ah principles or not is a matter for the Shari’ah Supervisory Board (SSB) of the individual IFI to decide, as they have expert knowledge in Islamic jurisprudence. Given the accepted divergence in Shari’ah principles between, and even within, national groups, the additional attestation of Shari’ah compliance is measured against the Islamic Shari’ah rules and principles, as determined by the SSB in each IFI. The role of the external auditor with respect to Shari’ah compliance is only to test for compliance based on the outlines provided by the SSB. Besides the SSB and external auditors, the other two key players involved in the audit of IFIs are the internal auditors and the Audit and Governance Committees.

The role of Shari’ah Supervisory Board in auditing of IFIs The Shari’ah Supervisory Board (SSB) plays a key role in the overall audit and governance framework, both ex-ante and ex-post. Their role ex-ante is to formulate policy and guidelines to be followed by management in their activities, including approval of products. The ex-post role is to conduct Shari’ah review, which is an examination to ensure that the activities carried out by

Global Islamic finance

Eco-system

Islamic Financial

Services Board (IFSB)

International Liquidity

Management Corporation

(IILM)

Accounting and Auditing

Organisation of Islamic Financial

Institutions (AAOIFI)

International Islamic Financial

Market (IFM)

Islamic International

Rating Agency (IIRA)

International Islamic Fiqh

Academy (IFA)

International Islamic Centre for

Reconciliation and Arbitration

(IICRA)

Shari’ah governance: A credible Shari’ah structure that promotes integrityProper governance provides multi-layer assurance on Shari’ah compliance1. Shari’ah Advisory Council given legislative

stature as highest authority for Shari’ah matters in Islamic finance

2. Institutionalise mutual respect by recognising differences of Shari’ah interpretations in various jurisdiction

3. Accountability of Shari’ah committee of Islamic Financial Institutionds (IFIs) on decision, views and opinions related to Shari’ah matters

4. Board and senior management with sufficient expertise and capability in dealing with issues specific to Islamic financial transactions

5. Emphasise the function of Shari’ah review and Shari’ah audit to provide checks and balance

6. Timely disclosure on fatwa rulings

Shari’ah as overarching principle in Islamic finance

Shari’ah compliance functions:Shari’ah reviewShari’ah audit

MANAGEMENT SHARI’AH COMMITTEE

BOARD

kasneb NEWSLINE, Issue No. 2, April - June 2017 5

AUDITING AND SHARI’AH SUPERVISION

an IFI do not contravene the principles of Shari’ah. The Shari’ah review involves three phases:

(i) Planning and designing the review procedures. (ii) Executing the review procedures and preparing

and reviewing the working papers. (iii) Documenting the conclusions and producing a

comprehensive Shari’ah Supervisory Report.

When executing the Shari’ah review procedures, a draft report from the external auditor regarding Shari’ah compliance testing, and the internal Shari’ah review report from the internal auditor, will help the SSB in documenting their conclusions and expressing a Shari’ah opinion in their comprehensive report. In short, the Shari’ah review is a comprehensive analysis of not only the financial statements but also of contracts, agreements and transactions, to ensure Shari’ah compliance and to add credibility to management’s activities.

Co-ordinating

Group audit

Risk management

Shari’ah audit functionShari’ah review

Shari’ah committee

Monitoring and reporting

Representation

Representation

BOD

RepresentationBoard Audit Committee

Management

Compliance

Monitoring and co-ordinating

Head, Group Audit Takaful

Head, Group Audit Management

Head, Group Audit Banking

Head, Group Audit Asset management

Head, Group Audit Other services

Representation

Shari’ah audit framework reporting line

Risk in Islamic

banking

Islamic finance

Shari’ah and Islamic

finance

Islamic fund management

Shari’ah compliant lending and investment

Takaful Murabaha

Musharakah Mudarabah

Sukuk

Prohibition of interest

Prohibition to support some sectors

(e.g. alcohol)

Principle of assets backed

transaction

Profit and loss principle and risk sharing

Prohibition of interest uncertainty

(e.g. speculation)Islamic Finance

kasneb NEWSLINE, Issue No. 2, April - June 20176 kasneb NEWSLINE, Issue No. 2, April - June 2017 7

AUDITING AND SHARI’AH SUPERVISION

External AuditorOne of the unique roles played by the external auditor of an IFI, besides performing the financial statements audit, is to conduct a test of Shari’ah compliance. The audit process involves a structured, documented plan involving a series of steps beginning with planning the audit and ending with expressing an opinion in an external audit report as to whether the financial statements are prepared in accordance with the fatwa (religious opinions), rulings and guidelines issued by the SSB of the IFI and relevant accounting standards and practices in the country in which the IFI operates.

In order to provide reasonable assurance that the IFI has complied with Shari’ah rules and principles as determined by the SSB, the auditor needs to obtain sufficient and appropriate audit evidence. In order to guide the auditor in making judgement as to whether the financial statements of the IFI have been prepared in accordance with Shari’ah rules and principles, the auditor will rely on the fatwa and rulings and guidance

issued by the SSB. However, the auditor is not expected to provide interpretation of the Shari’ah rules and principles.

Hence, when conducting the audit, the auditor will include procedures in his or her examination to ensure that all new fatwa rulings and guidance and modifications to existing fatwa rulings and guidance are identified and reviewed for each period under examination. The auditor will review the reports issued by the SSB to the IFI concerning Shari’ah compliance as well as the SSB’s minutes of meetings to ensure that all types of products offered by the IFI have been subjected to a review by the SSB. The auditor must also examine the findings of all internal reviews carried out by the IFI’s management, the internal audit and the report of the internal Shari’ah review. The auditor will send his or her draft report and conclusions related to Shari’ah compliance to the SSB, and if the SSB’s draft report indicates that compliance is lacking, the auditor may modify his or her draft report, providing adequate explanation of the nature of, and reasons for, the modification.

Internal auditor - Shari’ah Review According to governance standards for IFIs No. 3 (GSIFI 3), the conduct of the internal Shari’ah review process may be undertaken by the internal audit department, provided that the reviewers are properly qualified and independent. Before the review process can take place, management prepares a charter containing a statement of purpose, authority and responsibility, and sends it to the SSB for approval. Once the charter is approved, the board of directors will send the charter to the head of the internal Shari’ah review, who will then appoint a team that has competence to carry out the task.

The reviewers will first plan each review assignment and the documentation. Then they will collect, analyse and interpret all matters related to the review objectives and scope of work, including examination of documentation, analytical reviews, inquiries, discussions with management and observations to support their review results. Working papers that document the review will be prepared by the reviewer and reviewed by the head of internal Shari’ah review, who will then discuss the conclusions and recommendations with appropriate levels of management before issuing the final written report.

Islamic Banking

Focus on investment

Emphasis on soundness of project

Coordination with partners in resource mobilisation

Apply moral criteria in investment

Emphasis on ability to repay

Dependence on borrowing in resource mobilisation

Apply only financial criteria

Conventional Banking

Focus on lending

Differences from conventional banks

kasneb NEWSLINE, Issue No. 2, April - June 2017 7

AUDITING AND SHARI’AH SUPERVISION

Audit and Governance CommitteeThe role of the Audit and Governance Committee (AGC), comprising non-executive directors, is described in detail under GSIFI No.4. It is responsible for checking the structure and internal control processes and ensuring that the activities of the IFI are Shari’ah-compliant. The duties of the AGC also include the review of the reports produced by the internal Shari’ah review and the SSB to ensure that appropriate actions have been taken.

The scope of audit for IFIs is much broader. AAOIFI defines “scope of an audit” as the audit procedures deemed necessary by the auditor in the circumstances to achieve the objective of the audit for the IFI. It further states: “The procedures required to conduct an audit in accordance with Auditing Standards for Islamic Financial Institutions (ASIFIs) should be determined by the auditor having regard to the requirements of appropriate Islamic Rules and Principles, ASIFIs, relevant professional bodies, legislation, regulations which do not contravene Islamic Rules and Principles and, where appropriate, the terms of audit engagement and reporting requirements. International Standards on Auditing (ISAs) shall apply in respect of matters not covered in detail by ASIFIs providing these do not contravene Islamic Rules and Principles.”

From the above statement, it is clear that external auditors of IFIs are expected to deal with wider rules and guidelines. Since they are expected to conduct tests of Shari’ah compliance, they will have to ensure that management has adhered to the interest-free and permissibility (halal) principles as specified by the SSBs.

Challenges on the audit of IFIsThere are currently a number of challenges with regard to the auditing of IFIs, especially in terms of Shari’ah compliance audit.

First, despite the efforts of AAOIFI in promulgating auditing standards, the focus and scope tend to be on financial statements rather than the broader concept of Shari’ah audit, which involves the audit of all activities of IFIs based on maqasid al-Shari’ah (purposes of Islamic faith). Furthermore, the use of the term “Shari’ah review” rather than “Shari’ah audit” by AAOIFI may implicate a lower level of assurance in the case of the former.

Second, based on AAOIFI’s auditing standards, the functions of Shari’ah audit or review are distributed to different entities, for example, external auditor, Shari’ah Supervisory Board (SSB), internal Shari’ah reviewer and the Audit and Governance Committee. While external auditors act as the external mechanism in monitoring compliance, their lack of competence makes them rely heavily on the SSB’s fatwa, whereas in fact they should be making an independent judgement on the issue of compliance.

Third, the independence of the SSB has been questioned as they are involved in making fatwa and in setting up the guidelines on Shari’ah compliance as well as in conducting a Shari’ah review or audit of the IFI concerned. Given the rapid growth of IFIs globally, there is the need for a proactive measure by AAOIFI to issue clear auditing standards, which will make the work distinct from supervisory boards, so as to overcome these challenges and provide a flat form for the professionalism of Shari’ah compliant auditing.

ConclusionShari’ah audit and Shari`ah supervision may be thought of as the most important distinction between a conventional and a truly Islamic financial institution. While a business may attempt to represent itself as “Islamic,” unless it has qualified Shari`ah auditors and supervisors, it has no way of certifying that its services, products and operations are actually Shari`ah-compliant. Shari`ah supervision signifies a real commitment on the part of management to the principles of transparency and accountability in the matter of Shari`ah compliance.

THE ISLAMIC FINANCE MODEL

Real economy

Financial economy

Islamic finance

= Asset

backed

Maysir = Gambling

Riba = Interest

Gharar = Uncertainty

kasneb NEWSLINE, Issue No. 2, April - June 2017 9

The quality of education am getting from

my kasneb-accredited college

is high.

Before you enroll, ask if the college is accredited by kasneb

MY FUTURE IS BRIGHT

kasneb NEWSLINE, Issue No. 2, April - June 2017 9

The strategy canvas enables companies to see the future in the present. To achieve this, companies must understand how to read value curves.

Embedded in the value curves of an industry is a wealth of strategic knowledge on the current status and future of a business.

The first question the value curves answer is whether a business deserves to be a winner. When a company’s value curve, or its competitors’, meets the three criteria that define a good blue ocean strategy; focus, divergence and a compelling tagline that speaks to the market, the company is on the right track.

These three criteria serve as an initial litmus test of the commercial viability of blue ocean ideas. On the other hand, when a company’s value curve lacks focus, its

cost structure will tend to be high and its business model complex in implementation and execution. When it lacks divergence, a company’s strategy is a me-too, with no reason to stand apart in the marketplace. When it lacks a compelling tagline that speaks to buyers, it is likely to be internally driven or a classic example of innovation for innovation’s sake with no great commercial potential and no natural take-off capability.

READING THE VALUE CURVES IN STRATEGY

A tagline that represents the brand promise

Benefits of using a compelling tagline

• It is a simple and effective way to communicate brand extension, revitalisation or a change in positioning, and can deliver a message that enhances your brand experience by promoting unique product and/or service benefits.

• Helps differentiate new or revised brands and creates effective brand awareness when launching new products and/or services to the desired market audience.

• Can be easily updated or changed to suit the organisation’s product/services marketing mix, and can be used to communicate an organisation’s broader range of products and/or services.

• One or more taglines can be used to suit various organisational product/services or business units.Aspects of a good tagline

Contains key words

Shows specific benefits

Shows what they can do

for you

DR. KELLEN KIAMBATI, Management Consultant

kasneb NEWSLINE, Issue No. 2, April - June 201710 kasneb NEWSLINE, Issue No. 2, April - June 2017 11

VALUE CURVES

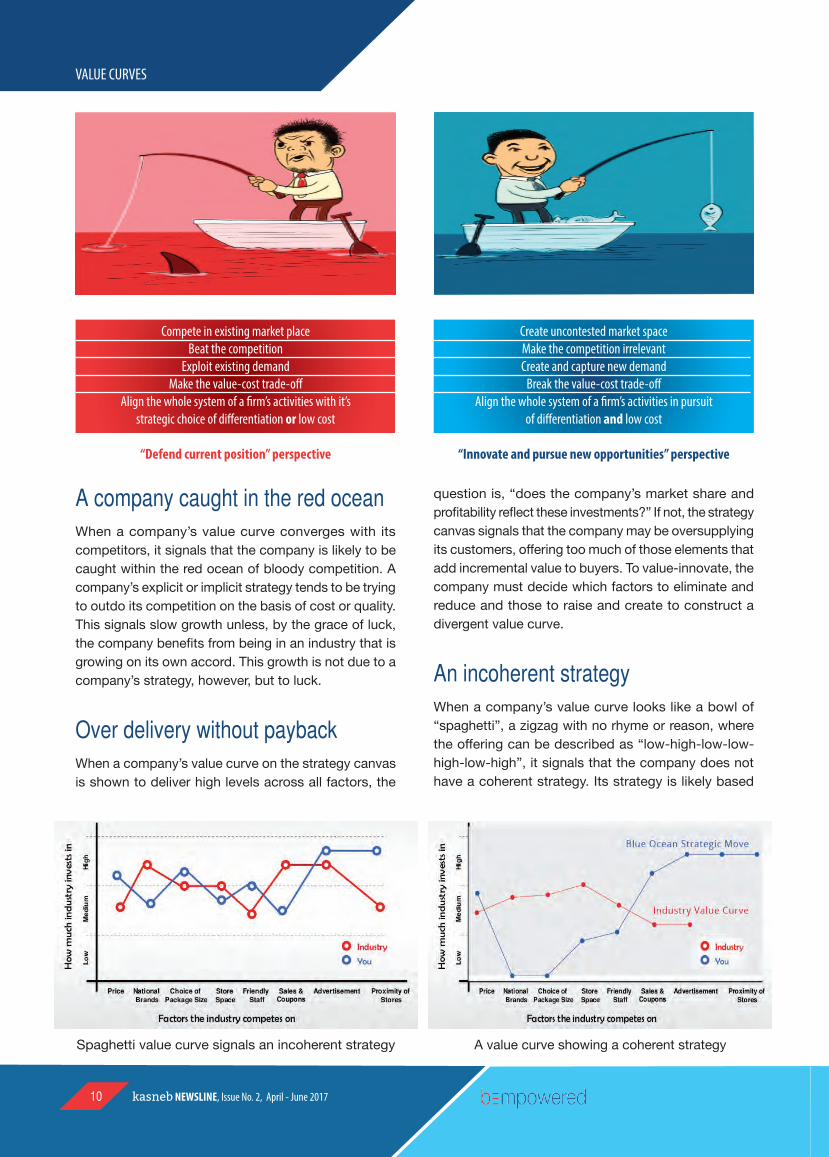

A company caught in the red oceanWhen a company’s value curve converges with its competitors, it signals that the company is likely to be caught within the red ocean of bloody competition. A company’s explicit or implicit strategy tends to be trying to outdo its competition on the basis of cost or quality. This signals slow growth unless, by the grace of luck, the company benefits from being in an industry that is growing on its own accord. This growth is not due to a company’s strategy, however, but to luck.

Over delivery without paybackWhen a company’s value curve on the strategy canvas is shown to deliver high levels across all factors, the

question is, “does the company’s market share and profitability reflect these investments?” If not, the strategy canvas signals that the company may be oversupplying its customers, offering too much of those elements that add incremental value to buyers. To value-innovate, the company must decide which factors to eliminate and reduce and those to raise and create to construct a divergent value curve.

An incoherent strategyWhen a company’s value curve looks like a bowl of “spaghetti”, a zigzag with no rhyme or reason, where the offering can be described as “low-high-low-low-high-low-high”, it signals that the company does not have a coherent strategy. Its strategy is likely based

Spaghetti value curve signals an incoherent strategy A value curve showing a coherent strategy

Compete in existing market placeBeat the competition

Exploit existing demandMake the value-cost trade-off

Align the whole system of a firm’s activities with it’s strategic choice of differentiation or low cost

“Defend current position” perspective

Create uncontested market spaceMake the competition irrelevantCreate and capture new demand

Break the value-cost trade-offAlign the whole system of a firm’s activities in pursuit

of differentiation and low cost

“Innovate and pursue new opportunities” perspective

kasneb NEWSLINE, Issue No. 2, April - June 2017 11

VALUE CURVES

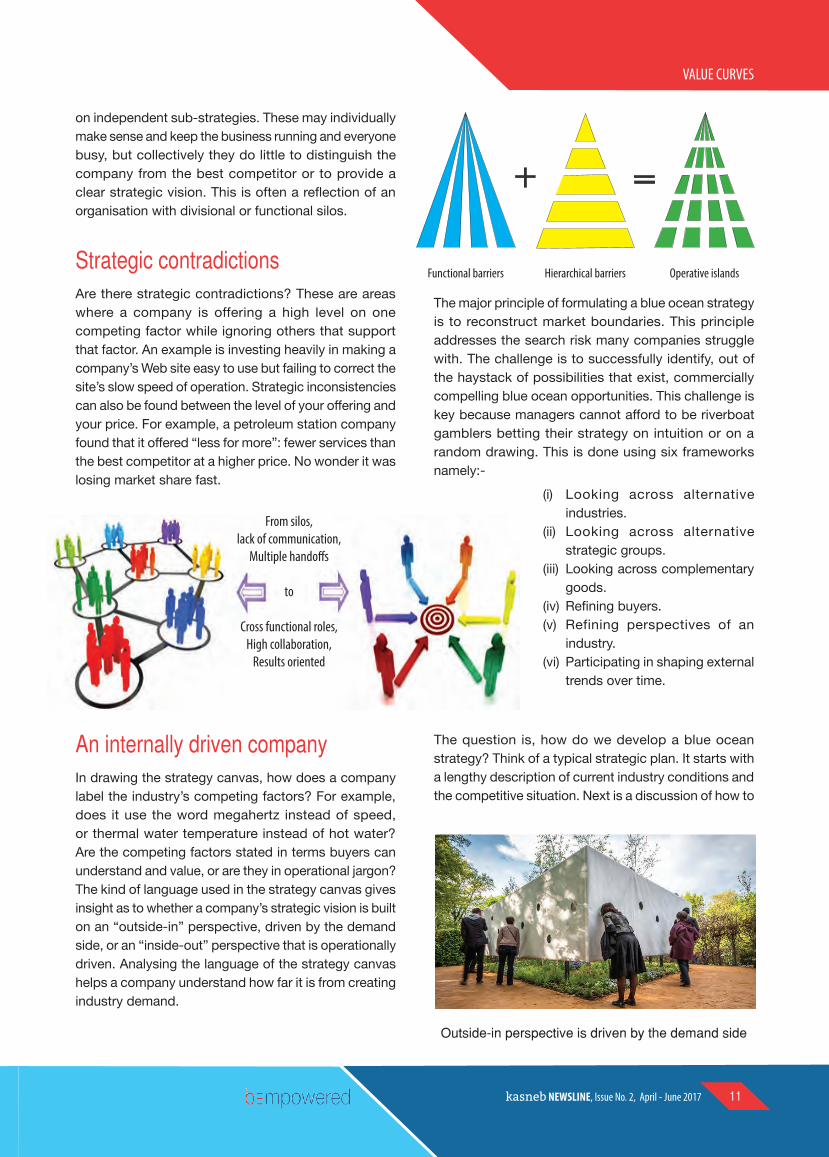

on independent sub-strategies. These may individually make sense and keep the business running and everyone busy, but collectively they do little to distinguish the company from the best competitor or to provide a clear strategic vision. This is often a reflection of an organisation with divisional or functional silos.

Strategic contradictionsAre there strategic contradictions? These are areas where a company is offering a high level on one competing factor while ignoring others that support that factor. An example is investing heavily in making a company’s Web site easy to use but failing to correct the site’s slow speed of operation. Strategic inconsistencies can also be found between the level of your offering and your price. For example, a petroleum station company found that it offered “less for more”: fewer services than the best competitor at a higher price. No wonder it was losing market share fast.

The major principle of formulating a blue ocean strategy is to reconstruct market boundaries. This principle addresses the search risk many companies struggle with. The challenge is to successfully identify, out of the haystack of possibilities that exist, commercially compelling blue ocean opportunities. This challenge is key because managers cannot afford to be riverboat gamblers betting their strategy on intuition or on a random drawing. This is done using six frameworks namely:-

Functional barriers Hierarchical barriers Operative islands

An internally driven companyIn drawing the strategy canvas, how does a company label the industry’s competing factors? For example, does it use the word megahertz instead of speed, or thermal water temperature instead of hot water? Are the competing factors stated in terms buyers can understand and value, or are they in operational jargon? The kind of language used in the strategy canvas gives insight as to whether a company’s strategic vision is built on an “outside-in” perspective, driven by the demand side, or an “inside-out” perspective that is operationally driven. Analysing the language of the strategy canvas helps a company understand how far it is from creating industry demand.

Outside-in perspective is driven by the demand side

(i) Looking across alternative industries.

(ii) Looking across alternative strategic groups.

(iii) Looking across complementary goods.

(iv) Refining buyers. (v) Refining perspectives of an

industry. (vi) Participating in shaping external

trends over time.

The question is, how do we develop a blue ocean strategy? Think of a typical strategic plan. It starts with a lengthy description of current industry conditions and the competitive situation. Next is a discussion of how to

From silos, lack of communication,

Multiple handoffs

to

Cross functional roles,High collaboration,

Results oriented

kasneb NEWSLINE, Issue No. 2, April - June 201712 kasneb NEWSLINE, Issue No. 2, April - June 2017 13

VALUE CURVES

increase market share, capture new segments, or cut costs, followed by an outline of numerous goals and initiatives. A full budget is almost invariably attached, as are lavish graphs and a surfeit of spreadsheets. The process usually culminates in the preparation of a large document culled from a mishmash of data provided by people from various parts of the organisation who often have conflicting agendas and poor communication. In this process, managers spend the majority of strategic thinking time filling in boxes and running numbers instead of thinking outside the box and developing a clear picture of how to break from the competition. If you ask companies to present their proposed strategies in no more than a few slides, it is not surprising that few clear or compelling strategies are articulated.

It is no wonder that few strategic plans lead to the creation of blue oceans or are translated into action. Executives are paralysed by the muddle. Few employees deep down in the company even know what the strategy is. And a closer look reveals that most plans do not contain a strategy at all but rather a smorgasbord of tactics that individually make sense but collectively do not add up to a unified, clear direction that sets a company apart let alone makes the competition irrelevant.

The other principle is to focus on the big picture. This principle is key to mitigating the planning risk of investing lots of effort and lots of time but delivering only tactical red ocean moves. Here, the aim is to develop an alternative approach to the existing strategic planning process that is based not on preparing a document but on drawing a strategy canvas. This approach consistently

BIG picture thinkingFocus on the big picture instead of being immersed in numbers and jargon

produces strategies that unlock the creativity of a wide range of people within an organisation, open companies’ eyes to blue oceans and are easy to understand and communicate for effective execution.

Drawing a strategy canvas not only visualises a company’s current strategic position in its marketplace but also helps it chart its future strategy. By building a company’s strategic planning process around a strategy canvas, a company and its managers focus their main attention on the big picture rather than becoming immersed in numbers and jargon and getting caught up in operational details.

Drawing a strategy canvas does three things.

(i) First, it shows the strategic profile of an industry by depicting very clearly the factors (and the possible future factors) that affect competition among industry players.

(ii) Second, it shows the strategic profile of current and potential competitors, identifying which factors they invest in strategically.

(iii) Finally, it shows the company’s strategic profile or value curve depicting how it invests in the factors of competition and how it might invest in them in the future.

The strategic profile with high blue ocean potential has three complementary qualities: focus, divergence and a compelling tag line. If a company’s strategic profile does not clearly reveal those qualities, its strategy will likely be muddled, undifferentiated and hard to communicate.

kasneb NEWSLINE, Issue No. 2, April - June 2017 13

VALUE CURVES

Visualising strategy at the corporate levelVisualizing strategy can also greatly inform the dialogue among individual business units and the corporate center in transforming a company from a red ocean to a blue ocean player. When business units present their strategy canvases to one another, they deepen their understanding of the other businesses in the corporate portfolio. Moreover, the process also fosters the transfer of strategic best practices across units.

Using the Pioneer-Migrator-Settler (PMS) MapVisualising strategy can also help managers responsible for corporate strategy predict and plan the company’s future growth and profit. All the companies that create blue oceans have been pioneers in their industries, not necessarily in developing new technologies but in pushing the value they offer customers to new frontiers. Extending the pioneer metaphor can provide a useful way of talking about the growth potential of current and future businesses. A company’s pioneers are the businesses that offer unprecedented value. These are your blue ocean strategists and they are the most powerful sources of profitable growth. These businesses have a mass following of customers. Their value curve diverges from the competition on the strategy canvas. At the other extreme are settlers—businesses whose value curves conform to the basic shape of the industry’s. These are me-too businesses. Settlers will not generally

contribute much to a company’s future growth. They are stuck within the red ocean. The potential of migrators lies somewhere in between. Such businesses extend the industry’s curve by giving customers more for less, but they don’t alter its basic shape. These businesses offer improved value, but not innovative value. These are businesses whose strategies fall on the margin between red oceans and blue oceans. A useful exercise for a corporate management team pursuing profitable growth is to plot the company’s current and planned portfolios on a pioneer-migrator-settler (PMS) map. If both the current portfolio and the planned offerings consist mainly of settlers, the company has a low growth trajectory, is largely confined to red oceans, and needs to push for value innovation. Although the company might be profitable today as its settlers are still making money, it may well have fallen into the trap of competitive benchmarking, imitation and intense price competition. If current and planned offerings consist of a lot of migrators, reasonable growth can be expected. But the company is not exploiting its potential for growth and it risks being marginalised by a company that value-innovates.

Overcoming the limitations of strategic planningManagers often express discontent, either explicitly or implicitly, with existing strategic planning, the core activity of strategy. To them, strategic planning should be more about collective wisdom building than top-down or bottom-up planning. They think that it should be

PIONEERSValue Innovation

MIGRATORSValue Improvements

SETTLERSValue Imitation

TODAY TOMORROW

Cost savings are made by eliminating and reducing the factors an industry

competes on

Buyer value is lifted by raising and creating elements the industry has

never offered

kasneb NEWSLINE, Issue No. 2, April - June 201714 kasneb NEWSLINE, Issue No. 2, April - June 2017 15

IF YOU CHANGE THE WAY YOU LOOK

AT THINGS, THE THINGS YOU LOOK AT

CHANGE.

Reconstruct market conditions

Focus on the big picture, not the numbers

Reach beyond existing demand

Get the strategic sequence right

Overcome key organisational hurdles

Execution principles

Formulation principles

Execution risk

Formulation risk

Build execution into strategy Management risk

Organisational risk

Business Model risk

Scale risk

Planning risk

Search risk

Six Principles of Blue Ocean Strategy

ConclusionRecent developments in strategy formulation and implementation call for a paradigm shift from the traditional approach. This shift should focus more on drawing a strategy canvas and open a company’s eyes to blue oceans.

Building the process around a picture addresses many of managers’ discontents with existing strategic planning and yields much better results. As Aristotle pointed out, “The soul never thinks without an image.”

more conversational than solely documentation-driven, and it should be more about building the big picture than about number-crunching exercises. It should have a creative component instead of being strictly analysis-driven and it should be more motivational, invoking willing commitment, than bargaining-driven, producing negotiated commitment. Despite this appetite for change, however, scant work exists on building a viable alternative to existing strategic planning, which is the most essential management task in the sense that almost every company in the world not only does it but often takes several grueling months each year to complete the exercise.

Some renowned taglines

VALUE CURVES

kasneb NEWSLINE, Issue No. 2, April - June 2017 15

Defining ethics

Ethics can generally be defined as the branch of philosophy that deals with morality. It is concerned with distinguishing between good and evil in the

world, between right and wrong human actions and between virtuous and non-virtuous characteristics of people. Ethics has also been defined as the moral principles that control or influence human behaviour. Given that ethics deals with an individual’s conduct, it is important that it be considered in all aspects of human life.

Others have defined ethics as a code of thinking and behaviour governed by a combination of personal, moral, legal and social standards of what is right. Although the definition of “right” varies with situations and cultures, its meaning in the context of a community intervention involves a number of guiding principles with which most community activists and service providers would probably agree.

Ethics can also be defined as the discipline, often classified as a sub-discipline of philosophy, which is concerned with what is good and just for individuals, groups, organisations and society. The discipline investigates the nature of our well-being and happiness,

ETHICS MANAGEMENT

Good versus evil in the world

ISSUES THAT CONCERN ETHICS

Right versus wrong human actions Virtuous versus non-virtuous characteristics Justice and fairness

Virtue ethical theories

Individual character ethics

Work character ethics

Professional character ethics

RAYMOND KIAMBATI, Management Consultant

kasneb NEWSLINE, Issue No. 2, April - June 201716 kasneb NEWSLINE, Issue No. 2, April - June 2017 17

Management ethics The main goal of management ethics is to treat all employees and customers justly and fairly. It is believed that by following moral and ethical codes, business will improve. When management adheres to management ethics, employees become motivated and the workplace

environment becomes motivational. Acting ethically means adhering to law, competing with others in an honest manner and performing daily tasks without any element of deceit. Many companies around the globe update written codes of conduct as a result of past corporate scandals. It is not uncommon for a company to update this document on a yearly basis. After a code of conduct document has been updated, each staff member must read and understand the document. Further, all employees must adhere to the updated codes of conduct and those that do not follow these regulations are often dismissed. Although managers must follow the same codes of conduct as employees, they have additional obligations.

Almost every decision that is made on a daily basis involves an ethical decision. Managers must keep this in mind at all times. By setting a good ethical example for their employees, managers can easily encourage all employees to follow the same ethical practices. Some companies offer managers specialised management ethics courses that must be completed prior to job acceptance.

Frequently, managers who switch companies are asked to follow a different code of conduct. This does not mean that all other management ethics should be forgotten, but it does mean that additional ethics should be learned. Ethics are not necessarily interchangeable from country to country. Sometimes, different cultures respect different ethical rules. Thus, any person who decides to move to another country may have to adapt to cultural and workplace ethical differences. In this case, management ethics is the ethical treatment of employees, stockholders, owners and the public by a company. A company, while needing to make a profit, should have good ethics. Employees should be treated well, whether they are employed locally or overseas.

Different renumeration structures for the same task No payment for overtime work Poor working conditions

HOW DO WE RELATE?

Individual

Group

Organisation

Society

Individual

Group

Organisation

Society

the appropriate pathways to our prosperity, our obligations and, related to all this, the rights that we owe to ourselves and to one another. In modern society, ethics defines how individuals, professionals, corporations and societies choose to interact with one another.

HOW DOES THE ORGANISATION RELATE WITH ITS STAKEHOLDERS

Employees

Managers

Owners

Internal Stakeholders

External Stakeholders

Suppliers

Customers

SocietyGovernment

FinanciersCompetitors

Shareholders

Organisation

They need masks

Masks? That’s an extra cost to the firm.

Thought it was CSR

We worked the whole weekend!

ETHICS MANAGEMENT

kasneb NEWSLINE, Issue No. 2, April - June 2017 17

Background information on management ethicsThe word ethics comes from the Greek word ethos which means character. The definition of ethics has been constantly developed through generations of philosophers such as Socrates, Plato, Aristotle, Plutarch, Cicero, Avicenna and the renaissance and modern philosophers. Ethics has to do with morality, principles or standards that we employ in our day-to-day activities and interactions. Whether we like it or not, we all partake in the moral reality, by thinking about moral issues and making moral choices. We do so even when the choice is to avoid making any choice on moral issues. Every time we think of what we did in the past, what we should be doing now or what we should be doing in the future, we are thinking to some extent about our morality. Morality, however, is not ethics. If morality is the lived ethical domain, then ethics is the principled investigation of that domain.

Ethics flourishes in an environment where people have confidence with one another and have mutual trust. Perceived fairness in the performance management process is essential so that it is part of the solution, not part of the problem. A culture of continuous improvement that directly faces and deals with the development needs of employees and leaders will benefit when people are able to learn from their mistakes and, therefore, develop sustainably. Fundamentally, performance management

helps develop quality leadership, which is a key element in strong ethical culture and business success.

The scope of ethics is so broad that it affects almost every decision made in our social interaction. Ethics is an integral part of individuals and management in all aspects of life, that is, from private life, social to organisation level. Ethics is as old as human race.

Leaders play a critical role in creating, sustaining and changing their organisation’s culture, through their own behaviour and through the programmes and activities they support and praise or neglect and criticise. All leaders must demonstrate behaviour that fosters an ethical environment, one that‘s conducive to ethical practices and that effectively integrates ethics into the overall organisational culture.

A key leadership responsibility is to ensure that the organisation makes it easy for employees to “do the right thing.” Leaders must foster an environment and

It is unethical to knowingly sell products that are faulty

It is unethical to do work only when under supervision

It is unethical to spend office time doing things unrelated to the office

KEY WORDS REGARDING BUSINESS ETHICS

Quick! Let’s check our facebook accounts before the

boss drops in.

Business EthicsFor interested parties that are

influenced by decision making or action of enterprises, it is regarded as

a standard for an enterprises’s decision making and action as well as ethical standard for policies, organisations

and behaviours.

Ethical Management

From CEO to staff, ethics management is a decision

standard that separates right or wrong and good or bad of personal

behaviour

ETHICS MANAGEMENT

I just unboxed the phone. I swear am not the one who broke the screen. I found it

that way.

I wonder if the boss has noticed I have not done a

thing the whole day.

I wonder if they noticed I have not done a thing the

whole day.

kasneb NEWSLINE, Issue No. 2, April - June 201718 kasneb NEWSLINE, Issue No. 2, April - June 2017 19

an organisational culture that supports doing the right thing, doing it well, and doing it for the right reasons, that is, reasons that are supported by ethical values.

A study conducted in the year 2000 by Boulstridge and Carrigan to investigate the response of consumer’s to ethical and unethical marketing behaviour concluded that most consumers lacked information to distinguish whether a company had or had not behaved ethically. Because of little awareness on the part of customers of any other socially responsible behaviour by companies, Boulstridge and Carrigan cited two multinational companies which despite being known offenders, continued having good sales. Most respondents in

the study agreed that social responsibility was not an important consideration in their purchasing behaviour. Hence even with knowledge about unethical activities by the company, some consumers still bought products from the offending company. Others argued that lack of information did mean that social responsibility was not placed high on their purchasing agenda. If they liked and regularly bought a product, they would find it hard to boycott the product over unethical behaviour. The most important purchasing criteria were price, value and quality and brand familiarity, meaning that consumers bought for personal reasons rather than societal ones.

In the business reality of the 21st century where management and intangible assets are key sources of competitive advantage, the individual behaviour of employees from top management to front-line workers can make or break an organisation’s reputation. This has a significant impact on share value, the ability to attract and retain clients, investors, employees, or customers, and the risk of compliance violations.

The Nestle boycott: Nestle aggressively pushed their breastfeeding formula in less economically developed countries (LEDCs), specifically targeting the poor. They made it seem that their infant formula was almost as good as a mother’s milk, which is highly unethical.

Rotten apples can make an otherwise ethical organisation unethical Unethical organisation can make an otherwise ethical employee unethical

All employs of Kasneb must abide by these values.

• INTEGRITY

• PROFESSIONALISM

• CUSTOMER FOCUS

• TEAMWORK

• INNOVATIVENESS

Core values of kasneb

ETHICS MANAGEMENT

kasneb NEWSLINE, Issue No. 2, April - June 2017 19

Globalisation increases the potential impact of behavioural conflicts. An organisation operating in different countries may find that the values and ethical standards of other cultures clash with its own. Each of these issues contributes to the need for every organisation to define its own principles of behaviour by clearly outlining its organisational values and creating a code of ethics and corporate conduct that provides guidance in decision making internally and in relation to external parties and compliance requirements. Such guidance is a critical element in the creation of a framework for ethical management.

Global perspective of ethicsBusiness ethics has evolved through time and across disciplines into a discipline that is one of the most important topics in the field of business today. In the global context, management ethics can be defined as decisions about what is right or wrong (acceptable or unacceptable) in the organisational context of planning and implementing business activities in a global environment.

It is clear that changing values, as influenced by global media, and changing perceptions and cultures will impact global ethics. The most challenging aspect is that the global business does not have a single definition of “fair” or “ethical.” While culture influences the definitions of those ideals, many companies are forced to navigate this sensitive area very carefully, as it impacts both their profitability and reputations.

As a result of the Enron scandal and other recent scandals, there has been a strong push to improve business ethics. This is occurring on several fronts – action began by former New York attorney general and former governor Elliot Spitzer and others who sued

companies for improper acts, Congress passing of the Oxley Bill to impose sanctions on executives who sign financial statements later found to be fraudulent.

Ethics evolves over time. It is difficult for both companies and professionals to operate within one set of accepted standards or guidelines only to see them gradually evolve or change. For example, bribery has been an accepted business practice for centuries in Japan and Korea. When these nations adjusted their practices in order to enter the global system, the questionable practices became illegal. Hence a Korean businessman who engaged in bribery ten or twenty years ago may not do so today without finding himself on the wrong side of the law. Even in the United States, regulations and laws that encouraged or supported unethical business practices such as discrimination have changed tremendously over the last several decades. Who knows what the future holds? Some of the business practices that are commonly accepted today may become irrelevant in future.

What is considered right in one place may be wrong in another place. Likewise, ethics may vary from one place to another owing to religion and culture

What is “fair” or “ethical” varies from place to place because of religion, law and culture

Sources of business ethics

Religion

LawCulture

Why is she trying to shake my

hand?Why is he bowing?

Regulations and laws that supported unethical practices like discrimination in some countries have had to change because of globalisation

ETHICS MANAGEMENT

kasneb NEWSLINE, Issue No. 2, April - June 201720 kasneb NEWSLINE, Issue No. 2, April - June 2017 21

Use of unethical means to exceed or achieve set targets

Doing business globally opens the arena for conflicts in norms. Many multinational companies have codes of ethics, mission statements and integrity policies guiding their practices. However, when operating outside their boundaries they confront different sets of norms which sometimes conflict with their home based ones. In this conflict of norms, occasionally the ethical issue is not seen to be the same by the parties concerned. Ethics in management can change and develop as human evolution continues.

The senior managers of companies are under increasing pressure from owners and shareholders to provide ever-growing returns. The historic Sarbanes-Oxley legislation was created due to the public outrage over ethical and financial misconduct by the senior

management of companies. The high demands on exceptional performance have forced some managers to use unethical means to exceed or achieve set targets.

Local perspectives of business ethicsManagement ethics is approached from a compliance perspective rather than a culture building perspective that requires leadership commitment in order for it to be effective. Management ethics is practiced widely and forms a part of the management system of many firms in Kenya. Most companies/ institutions have their internal codes of conduct. In addition to strengthening integrity, Chapter 6 of the Constitution of Kenya requires all to act ethically. However despite systems and modalities put in place, unethical practices are widespread in our society. For example, corruption remains a major issue that seriously impedes political, social and economic

Kick backs are a common unethical practice in business

Are you guided by moral values or legal compliance. The first has to do with integrity and the other with simply being right. The first is an inner quality

while the latter is an outer quality. In the first instance, you do it out of your own will and in the latter, you are forced to do it by law. We need people who can stand up against unethical practices like fraud

As you can see, we did extremely well this quarter.

ETHICS MANAGEMENT

OUR CORE VALUES

IntegrityHonestyQuality

Do you expect me to show this to

shareholders?

Are you saying what I think you

are saying..... and that?

kasneb NEWSLINE, Issue No. 2, April - June 2017 21

ETHICS MANAGEMENT

development of Kenya. Most private businesses are interested in making money irrespective of how the money is made. Making money is not wrong in itself; it is the manner in which firms conduct their businesses that raises ethical concerns.

The accounting profession has not been spared of unethical blame either. Research carried out by Kamau, C .et al (2012) shows that to achieve set goals, managers commonly practice creative accounting. These are accounting practices that are not conventionally accepted or practiced. These practices are performed with the objective of making the company appear to be financially stronger or weaker depending on the management‘s goals. Creative accounting is also known as

scholars. A study by Kamau, C. et al (2012) ascertains that tax avoidance and evasion are some of the major factors contributing to practice of creative accounting among companies in the private sector in Kenya. This raises the issue of ethical practices in accounting among Kenyan accountants and calls for accounting regulatory bodies to tighten the grip on financial reporting rules in a bid to curb creative accounting practices in Kenya.

In organisations, business ethics encompasses issues such as corporate governance, adherence to regulations, the effectiveness of board committees, accurate financial reporting auditing, executive compensation for the leadership of the organisation and the role of the CEO in setting ethical standards among others.

Instances of ethical misconduct are also seen in academia. According to the Center for Academic Integrity, 70% of students on most college campuses admit to some form of cheating. Cheating has also become a significant problem in high school, with 60% to 70% of students admitting to cheating, according to the center.

Unethical practices have led to collapse of companies, a recent example being that of Triton Kenya. Another example is that of the Kenya National Assurance Company. The once giant life assurance company collapsed due to mismanagement and theft of assets by employees.

Collusion during examinations is an unethical misconduct in academia

“Cooking” financial reports is a practice that goes against business ethics

“cooking the books”, “window dressing” or “earnings management.” Creative accounting is the transformation of accounting figures from what they actually are to what perpetrators desire by taking advantage of the existing rules or ignoring some or all of them. It may involve simple practices like window dressing as well as those which are sophisticated, such as off-balance sheet financing. The difference between creative accounting and fraud is that creative accounting is working within the regulatory framework but fraud involves breaking the law (Jones, 2011). There are four main forms of creative accounting, namely earnings management, income smoothing, aggressive accounting and big bath accounting.

Techniques, effects and detection of creative accounting has been identified and researched on by various

Don’t but me. They say figures don’t lie. Your job here is to make them lie.

But sir.....that’s unethical.

kasneb NEWSLINE, Issue No. 2, April - June 201722 kasneb NEWSLINE, Issue No. 2, April - June 2017 23

Ethical issues in managementPerformance management contributes to the success of an organisation through the alignment of values and behaviour with business goals, through employee evaluation and reward, and through employee development. The more that employee goals and organisation values are aligned, the stronger the ethical culture will be. Perceived fairness in the performance management process is essential so that it is part of the solution, not part of the problem. A culture of continuous improvement that squarely faces and deals with the development needs of employees and leaders will benefit when people are able to learn from their mistakes and, therefore, develop sustainably. Fundamentally, performance management helps develop quality leadership, which is a key element in strong ethical culture and business success.

A case study at the Zimbabwe Broadcasting Corporation found that top management and the board were corrupt. Procurement of goods and services were done without following proper tender procedures, thereby depriving the corporation of millions of dollars. There was no efficiency and effectiveness in the way service was being delivered. There was lack of accountability and transparency in the way business was being done. It was reported that employees went for over seven months without salaries yet top management and the board paid themselves handsomely. There was no relationship between the chief executive officer’s salary and performance of the organisation. Nepotism and intimidation were also reported to be high and this affected morale among employees and service delivery to the general public remained poor. It was noted that bad corporate governance and unethical conduct of top management affected both staff morale and service delivery.

Widespread and highly visible organisational misconduct and scandals such as Enron and WorldCom in the United States and in Europe, Parmalat (Italy) and Royal Ahold (Netherlands) have plagued global businesses. All four of these companies engaged in massive accounting frauds to overstate their earnings and had operated under unethical organisational cultures. Managers were involved in channel stuffing, inventory shifting strategies, deceptive sales techniques, financial fraud and other schemes to inflate earnings. Misconduct related to employees, suppliers, and consumers created discussions about right and wrong as well as the

appropriate legal consequences. Organisational ethics programmes were developed in public corporations as ethics became more institutionalised by the Federal Sentencing Guidelines for Organisations, especially the 2004 amendment.

The numerous scandals in business such as those at AIG, Tyco, WorldCom and Enron have raised many concerns about the emergence of unethical and irresponsible behaviour in organisations. The seemingly unending occurrence of instances of corruption in both business and politics has also activated consciousness about ethics in general and business ethics in particular.

Arguments are being made by governments and organisations such as Oxfam and Medecins Sans Frontieres on ethical grounds to allow cheaper access for consumers of drugs such as AZT. Pharmaceutical firms defend their pricing policies based on the consideration of other stakeholders such as shareholders, employees and the wider community who can only benefit from new product developments if high economic returns are made from existing drugs. In this situation, it is difficult to decide who should be considered most important. Is it stakeholders or consumers? Often it is difficult to make a consistent ethical judgement that achieves equal “good” or avoids harming all stakeholder interests. There remains a need for marketers to continue to seek to act with social responsibility.

Having various interests, objectives and beliefs, interest groups are involved in the public procurement system in several ways; such as lobbying legislative bodies to pass or alter procurement statutes, influencing implementation of these rules and influencing budget authorisation and appropriation processes. In addition to social and economic environment, public procurement practitioners are under other external pressures such as environmental protection movements, foreign policy commitments, politicians and other interested groups. The procurement functions are performed in a very complex environment. Both individual interest and factors in the external environment affects the extent to which managers can carry out procurement in an ethical manner.

ConclusionThere is no doubt that there are strong and persuasive reasons for managers to engage in and promote ethical behaviour within their organisations. The reasons range

ETHICS MANAGEMENT

kasneb NEWSLINE, Issue No. 2, April - June 2017 23

from normative ones (managers are expected to be ethical and ought to be ethical) to the pragmatic or instrumental (it is in their self-interest to be ethical). Management ethics has become a vital concern to organisations and society over the past several decades. The Kenyan Government has established the Ethics and Anti-Corruption Commission, ethical requirement has been promulgated in chapter six of the Constitution of Kenya and many organisations have set an ethics and Integrity department in order to fight the vice of unethical conducts. However, much remains to be done.

For the management community to turn this situation around, significant efforts are required. Part of the challenge is coming to understand what management ethics means, why it is important and how it should be integrated into decision making. Principles of ethics from moral philosophy and management theory are available to inform interested managers. One of the most formidable challenges is avoiding immoral management, and transitioning from an immoral to a moral management mode of leadership, behaviour, decision making, policies and practices. Moral management requires ethical leadership. It entails more than just “not doing wrong.” Moral management requires that managers search out those vulnerable situations in which immorality may reign if careful, thoughtful reflection is not given by management. Moral management requires that managers understand, and be sensitive to, all the stakeholders of the organisation and their stakes. If the

moral management model is to be achieved, managers need to integrate ethical wisdom with their managerial wisdom and to take steps to create and sustain an ethical climate in their organisations. If this is done, the desirable goals of moral management are achievable.

There is still much to be done to understand and improve business ethics globally. The academic community can support business ethics with more research to determine the role of both the individual and organisational culture in building an effective ethics program. Businesses need to remain open to learning more about how to build an effective ethics initiative and understanding the importance of managing the internal organisational culture to maintain a commitment to integrity and transparency.

The importance of management ethics in all aspect of life cannot be expounded. It is a key ingredient to the success of any organisation and hence the need to incorporate it into the management system. To achieve ethical conduct, institutions as well as professional bodies should develop and practice their own ethical codes. An example is the accountants code of ethics. The intent of this code of ethics is to make all accounting professionals aware of their responsibility to act as change agents within their organisations, supporting the maintenance of effective internal controls and ensuring that their organisations have considered, adopted and fully implemented ethical codes.

Characteristics of compliance strategy

Ethos Conformity with externally imposed standards

Objective Prevent criminal misconduct

Leadership Lawyer driven

Methods Education, reduced discretion, auditing and controls, penalties

Behavioural assumptions

Autonomous beings guided by material self-interest

Characteristics of integrity strategy

Ethos Self-governance according to chosen standards

Objective Enable responsible conduct

Leadership Management driven with aid of lawyers, HR, others

Methods Education, leadership, accountability, organisational systems and decision processes, auditing and controls, penalties

Behavioural assumptions

Autonomous beings guided by material self-interest

Implementation of compliance strategy

Standards Criminal and regulatory law

Staffing Lawyers

Activities Develop compliance standards Train and communicateHandle reports of misconductConduct investigationsOversee compliance auditsEnforce standards

Education Compliance standards and system

Implementation of integrity strategy

Standards Company values and aspirationsSocial obligations, including law

Staffing Executives and managers with lawyers, others

Activities Lead development of company values and standardsTrain and communicateIntegrate into company systems, provide guidance and consultationAssess value performanceIdentify and resolve problemsOversee compliance activities

Education Compliance standards and system

Strategies for ethics management

ETHICS MANAGEMENT

kasneb NEWSLINE, Issue No. 2, April - June 2017 25

kasneb NEWSLINE, Issue No. 2, April - June 2017 25

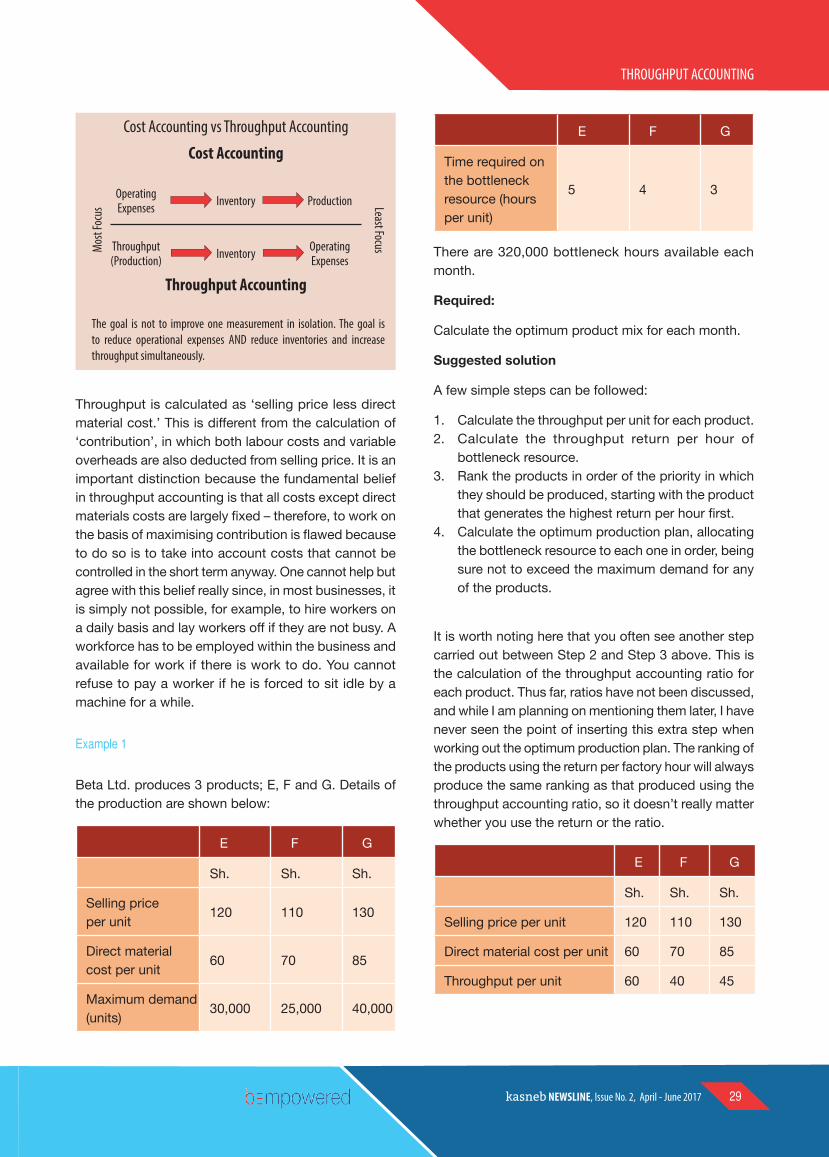

Throughput is the amount of a product or service a company can produce and deliver to a client in a specific period of time. Businesses with high

throughput levels can take market share away from lower throughput firms, because they can produce that product or service more efficiently than their competitors.

In general terms, throughput is the maximum rate of production or the maximum rate at which something can be processed. It could be the productivity of a machine, procedure, process, or system over a unit period and is expressed in a figure-of-merit or a term meaningful in the given context, such as output per hour, cash turnover, number of orders shipped.

Throughput accounting is a principle-based and simplified management accounting approach that provides managers with decision support information for enterprise profitability improvement.

Throughput accounting was proposed by Eliyahu M. Goldratt (photo below) as an alternative to traditional cost accounting.

As an approach that is relatively new in management accounting, it identifies factors that limit an organisation from reaching its goals and then focuses on simple measures that drive behaviour in key areas towards reaching organisational goals.

It is cash-focused and does not allocate all costs (variable and fixed expenses, including overheads) to products and services sold or provided by an enterprise.

THROUGHPUT ACCOUNTING AND THE THEORY OF CONSTRAINTS

3 trucks3 gas pumps

Throughput = 3/minute (no waiting)

Eliyahu M. Goldratt: “ I say an hour lost at a bottleneck is an hour out of the entire system. I say an hour saved at a non-bottleneck is worthless. Bottlenecks govern both throughput and inventory.”

CPA DERRICK MAJANI, HEAD OF FINANCE, BANDARI SACCO LTD, MOMBASA

kasneb NEWSLINE, Issue No. 2, April - June 201726 kasneb NEWSLINE, Issue No. 2, April - June 2017 27

THROUGHPUT ACCOUNTING

The idea of throughput is part of the theory of constraints in business management. The guiding ideology of the theory of constraints is that a chain is only as strong as its weakest link. Advocates of the theory attempt to minimise how weak links affect a company’s performance.

Goldratt postulated that every process has a constraint (bottleneck) and focusing improvement efforts on that constraint is the fastest and most effective path to improved profitability. By identifying and exploiting the constraint that limits any system of work, Goldratt believed that management would get control, execute well, release capacity and enjoy success.

The theory of constraints is applied within an organisation to increase throughput by following what are called ‘the five focusing steps as identified by Goldratt. These steps are methodologies that have been developed to help organisations deal with constraints, otherwise known as bottlenecks, within the system as a whole (rather than any discrete unit within the organisation).

THE FIVE FOCUSING STEPS

Step 1: Identify the system’s bottlenecks

In many scenarios, the bottleneck resource is known. If not, it is usually straight forward to work out. For example, an organisation has market demand of 50,000 units for a product that goes through three processes: cutting, heating and assembly. The total time required in each process for each product and the total hours available are shown in the table below.

Process Cutting Heating Assembly

Hours per unit 2 3 4

Total hours available 100,000 120,000 220,000

A system is as weak as its weakest link

A system typically only has one

constraint at a time

A system optimum performance is NOT the sum of local

optimization. Strengthening anything other than the weakest

link has no impact on the performance of the system.

This is the weakest link. Making it stronger will allow the chain to

carry more weight.

Systems succeed or fail as an integrated system,

not a collection of discrete tasks.

Strengthening this link will have zero impact on the chains ability to carry

more weight.

THE SYSTEM CAN CARRY ONLY 10KG

10Kg

20Kg

50Kg 5 Focusing

steps

Go back to step #1

Identify the constraint

Exploit the constraint

Elevate the constraint Subordinate

everything else to the constraint

5

1

2

34

Since the strength of the chain is determined by the weakest link, then the first step to improve an organisation must be to identify the weakest link - Goldratt Peter at the back of the line, a half

a mile behind the lead hiker

Peter at the front of the line, huffing and puffing away with

everyone behind him

Peter’s load lightened and shared; the whole troop makes good time

Ronnie: the slowest hiker

A system can produce only to the bottleneck’s capacity - max throughput is 40 units/day

BOTTLENECK

60 units per day

40 units per day

70 units per day

60 units per day

Hey, wait!

I am hurrying!

kasneb NEWSLINE, Issue No. 2, April - June 2017 27

THROUGHPUT ACCOUNTING

The total time required to make 50,000 units of the product can be calculated and compared to the time available in order to identify the bottleneck.

Process Cutting Heating Assembly

Hours per unit 2 3 4

Total hours required for 50,000 units

100,000 150,000 200,000

Total hours available 100,000 120,000 220,000

Shortfall in hours 0 30,000 0

It is clear that the heating process is the bottleneck. The organisation will in fact only be able to produce 40,000 units (120,000/3) as things stand.

Step 2: Decide how to exploit the system’s bottlenecks This involves making sure that the bottleneck resource is actively being used as much as possible and is producing as many units as possible. So, ‘productivity’ and ‘utilisation’ are the key words here. In the above case, productivity from the use of heating hours should be optimised.

Step 3: Subordinate everything else to the decisions made in Step 2 The main point here is that the production capacity of the bottleneck resource should determine the production schedule for the organisation as a whole. Idle time is unavoidable and needs to be accepted if the theory of constraints is to be successfully applied. To push more work into the system than the constraint can deal with results in excess work-in-progress, extended lead times, and the appearance of what looks like new bottlenecks, as the whole system becomes clogged up. By definition, the system does not require the non-bottleneck resources to be used to their full capacity and therefore they must sit idle for some of the time.

3. SUBORDINATE ALL ELSEAlign the whole system or organisation to support the decisions made above.

Some options:• Limit WIP of upstream to match.• Upstream do preparation work.• Upstream improve their quality.• Pair upstream with constraint staff.

1. IDENTIFY THE CONSTRAINTConstraint: The resource or policy that prevents the organisation from obtaining more of the goal.

Symptoms• Work piles up waiting to be processed by the constraint.• Resource is heavily stressed.• Resources downstream from constraint are regularly idle.

2. EXPLOIT THE CONSTRAINTGet the most capacity out of the constrained process, with only minor changes.

Some options:• Shield them from interruptions• Limit their WIP• Reduce their non value add work.Note: Do not ask them to do overtime

Activating a resource is like pressing the ON switch of a machine; it runs whether or not there is any benefit to be derived from the work it’s doing - Goldratt

Throughput accounting

Cost versus throughput accounting

Cost accountingInventory is an assetEfficiency = function/shilling (hours) Labour is a “variable” costPeople sitting idle are discarded!

Inventory is a liabilityEfficiency = function/direct costs (idle or not) Labour is a “fixed” costPeople sitting idle are a part of the system!

kasneb NEWSLINE, Issue No. 2, April - June 201728 kasneb NEWSLINE, Issue No. 2, April - June 2017 29

THROUGHPUT ACCOUNTING

Step 4: Elevate the system’s bottlenecks Elevating a bottleneck without cost is unusual. Normally, elevation will require capital expenditure. However, it is important that an organisation does not ignore Step 2 and jumps straight to Step 4, and this is what often happens. There is often untapped production capacity that can be found if you look closely enough. Elevation should only be considered once exploitation has taken place.

Step 5: If a new constraint is broken in Step 4, go back to Step 1, but do not let inertia become the system’s new bottleneck When a bottleneck has been elevated, a new bottleneck will eventually appear. This could be in the form of another machine that can now process less units than the elevated bottleneck. Eventually, however, the ultimate constraint on the system is likely to be market demand. Whatever the new bottleneck is, the message of the theory of constraints is: never get complacent. The system should be one of ongoing improvement because nothing ever stands still for long.

I am now going to have a look at an example of how a business can go about exploiting the system’s bottlenecks, that is, using them in a way so as to maximise throughput. In practice, there may be lots of options open to the organisation. In the context of an examination question, however, you are more likely to be asked to show how a bottleneck can be exploited by maximising throughput via the production of an optimum production plan. This requires an application of the simple principles of key factor analysis, otherwise known as limiting factor analysis or principal budget factor.

LIMITING FACTOR ANALYSIS AND THROUGHPUT ACCOUNTINGOnce an organisation has identified its bottleneck resource, as demonstrated in Step 1 above, it then has to decide how to get the most out of that resource. Given that most businesses are producing more than one type of product (or supplying more than one type of service), this means that part of the exploitation step involves working out what the optimum production plan is, based on maximising throughput per unit of bottleneck resource.