Sector Competitiveness Plan

156

Sector Competitiveness Plan 2017

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Sector Competitiveness Plan

Sector Competitiveness Plan

2017

NERA’s vision is to maximise the value to the Australian economy by having an energy resources sector which is globally competitive, growing, sustainable, innovative and diverse.

Registered office:Australian Resources Research Centre Level 3, 26 Dick Perry Avenue Kensington WA 6151

ABN 24 609 540 285

T: (08) 6555 8040 E: [email protected]: www.nera.org.au

@NERAnetwork NERA – National Energy Resources Australia

3National Energy Resources Australia – Sector Competitiveness Plan 2017

Contents

About NERA 4 About this Document 5 Foreword 6

1 Executive Summary 8

Executive Summary 10

Introduction to this SCP 14 Sector Themes 19

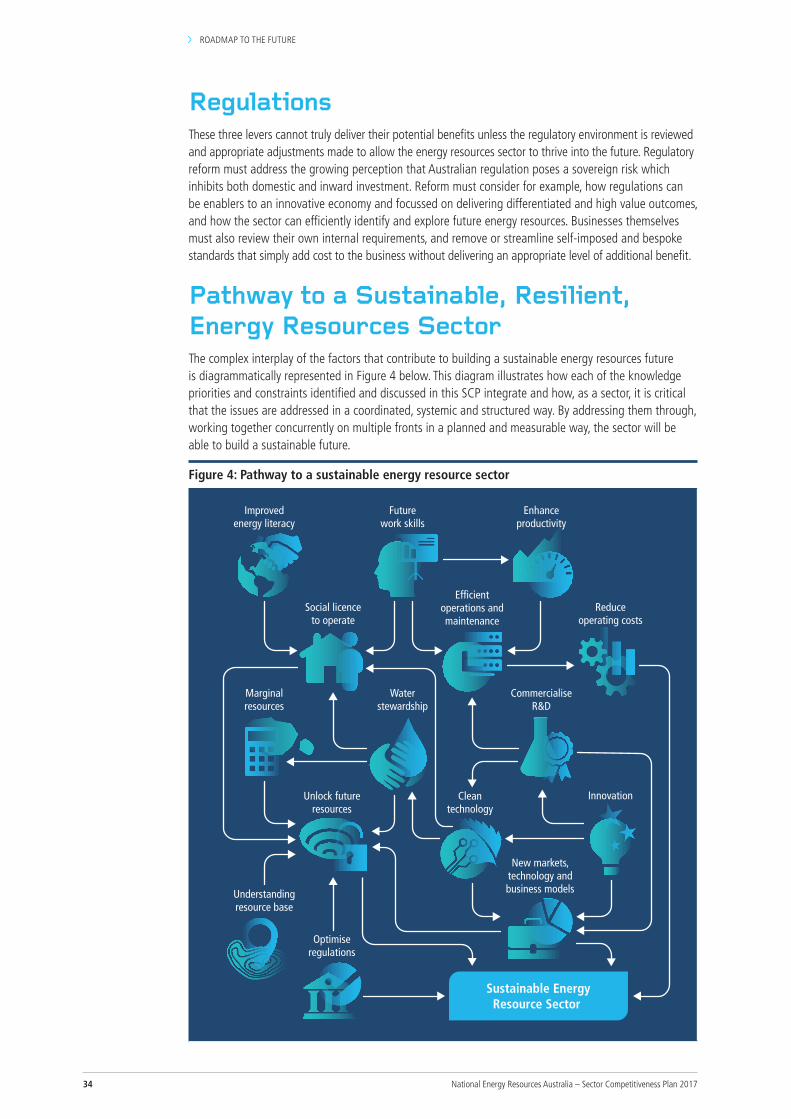

Roadmap to the Future 32 The Three Levers to a Strong Future 33 Regulations 34 Pathway to a Sustainable, Resilient, Energy Resources Sector 34 Knowledge Priorities Action Plan 35 Key Performance Indicators 40

2 Global and National Challenges 48

Global Megatrends and Implications for Australia’s Energy Resource Sector 50 Global Megatrends 51 An Emerging Megatrend – The Search for Energy Security 54 An Environment of Disruption 55 Impact of Global Megatrends on Australia 56 Australia’s Response to Sector Trends 57

Current State of the Energy Resources Sector 60 Australian Oil and Gas Industry 65 Australian Coal Industry 70 Australian Uranium Industry 74 Transition from Rapid Growth 77

Sector Benchmarking 78 Oil and Gas Industry Competitiveness Assessment 2016 80 Coal Industry Competitiveness Assessment 2016 87

3 Sector Challenges and Knowledge Priorities 94

Sector Wide Challenges and Opportunities 96 Sector Wide 97

Sector Specific Challenges, Constraints and Opportunities 98 Australian Oil and Gas Industry 98 Australian Coal Industry 101 Australian Uranium Industry 102 Cross Sector Challenges and Opportunities 103

How the Australian Energy Resource Sector Should Respond 104 The Three Levers to a Strong Future 104

Sector Knowledge Priorities 108

Capability and Leadership 114

Business and Operating Models, Technology and Services 128

Regulatory Environment 144

Glossary 149

Definitions 149 Stakeholder Consultation Process 149 Acronyms 150

Bibliography 151

4 National Energy Resources Australia – Sector Competitiveness Plan 2017

About NERA

The Australian Energy Resources Growth Centre (AERGC Ltd), trading as National Energy Resources Australia (NERA), is an industry-led, government-funded initiative, which aims, through a national focus, to improve competitiveness, collaboration and productivity by focussing on reducing cost, directing research to industry needs, improving work skills, facilitating partnerships and reducing regulatory burden.

NERA forms part of the Australian Government’s Industry Innovation and Competitiveness Agenda. It is one of six national Industry Growth Centres established to drive innovation, productivity and competitiveness in sectors of competitive strength and strategic priority for Australia, and to increase employment and opportunities for small and medium sized enterprises (SMEs).

NERA will work to support the Australian energy resources sector to identify and deliver projects and activities to enhance the sector’s innovation, competitiveness and productivity. The long-term objectives and strategic outcomes of the sector cannot be delivered by NERA alone, and will require commitment from industry leaders, government, research organisations and other key stakeholders.

NERA’s vision, mission and strategies were developed as a result of early stakeholder consultation to develop the proposal to establish NERA. Key sector themes have informed the consultation which was undertaken to develop the 10-year Sector Competitiveness Plan, including the knowledge priorities, strategic goals and focus areas for the sector.

VisionTo maximise the value to the Australian economy by having an energy resources sector which is globally competitive, growing, sustainable, innovative and diverse.

MissionThrough a national focus, grow collaboration and innovation to assist the energy resources sector manage cost structures and productivity, direct research to industry needs, deliver the future work skills required and promote proportionate fit for purpose regulation.

Six StrategiesNERA will achieve our vision though six strategies:

1. Connect industry stakeholders to promote collaboration.

2. Facilitate deeper engagement between industry and researchers.

3. Support industry growth through policy and regulation.

4. Promote industry sustainability through fostering a greater understanding of the social, environmental, economic and operational consequences of industry activity, and by promoting trusted, inclusive custodians of scientific data.

5. Develop and support initiatives to focus on work skills of the future.

6. Identify and facilitate growth of new opportunities for the energy and resources industry value chain domestically and globally.

5National Energy Resources Australia – Sector Competitiveness Plan 2017

About this Document

This Sector Competitiveness Plan (SCP) will underpin the efforts of the Australian energy resources sector to increase the competitiveness and sustainability of the Australian oil and gas, coal and uranium industries. To achieve this, the SCP sets out a strategic road map over a 10-year horizon, including key themes, knowledge priorities, goals and initiatives. These will be addressed through industry led projects.

This SCP considers the trends and influences impacting the entire Australian energy resources sector and identifies broad challenges, constraints and opportunities both at a sector-wide and industry-specific level. Many of the challenges and opportunities identified are common across all three industries of oil and gas, coal and uranium, while others are specific to one; these differences are highlighted in the body of the plan.

The SCP is a foundation document for NERA. It presents the challenges and opportunities faced by the Australian energy resources sector and describes how NERA will assist the sector to address key priorities to enhance innovation, competitiveness and productivity. This document will be updated annually. It will necessarily evolve if it is to remain relevant over the next 10 years as goals are achieved, the sector’s priorities change and the opportunities to capture change and disruption both globally and locally continue to evolve.

The document is presented in three major sections:

Section 1 comprises an executive summary to the document, highlighting the SCP’s key material and subjects, and the roadmap to the future which sets out NERA’s plan and the key performance indicators (KPIs) being used to measure the sector’s progress.

1

Section 2 discusses the global megatrends that are changing the face of the energy resources sector and how those trends are impacting Australia. It then places the Australian energy sector into perspective with both the background to each industry and the historic trends that have resulted in the current state of the industry, before presenting the results of sector benchmarking that NERA has commissioned into the oil and gas, and coal sectors.

2

Section 3 considers the sector wide and individual industry challenges and constraints, then discusses each of the NERA knowledge priorities and initiatives in detail, as well as offering some case studies that have helped inform the initiatives currently being developed.

3

6 National Energy Resources Australia – Sector Competitiveness Plan 2017

Foreword

An Industry on the Move: Navigating an Age of Innovation and DisruptionAs this document goes to print, the Australian energy resources sector is on the move, and in exciting ways.

Energy resources will continue to make a significant contribution to the economic growth of Australia for the foreseeable future. However, as the world’s energy balance continues to evolve the sector must adapt to remain competitive, productive and sustainable.

It is well understood that the sector is nearing the conclusion of an unprecedented level of investment and construction. At the same time, the sector faces a perfect storm of disruptive and significant threats and Australia as a nation must find a path to a low emissions economy whilst also securing both energy reliability and affordability for all.

In the face of this storm, it is tempting to batten down the hatches and retreat into the pursuit of individual solutions. Yet significant challenge can also trigger much needed change and unlock huge opportunities - opportunities that can only be realised to their full potential by working together to innovate, transfer knowledge and commercialise value.

As an industry, we have a long and proud history of pioneering, discovery, problem solving and invention. Over decades, the Australian energy resources sector has delivered critical infrastructure, some of the world’s newest high technology production facilities and significant high quality natural resources, while reliant on and underpinning the development of a well-educated and highly skilled workforce. Additionally, we have the advantage of proximity to the Asian economies, world leading capabilities in remote operations and low carbon emissions technologies, a strong and growing start-up community, world class research facilities and knowledge and a strong tax incentive scheme for research and development.

In recent times, faced with a volatile commodity price environment and increasing global competition, the focus of energy resource companies has necessarily been to significantly lower capital costs and improve efficiency and profitability. This focus on efficiency will ensure the sector has the fundamentals right and, combined with our existing strengths and advantages, provide a solid base on which to build for the future.

The next phase of change though is far harder. Relying on incremental changes to yesterday’s practices is a sure recipe for stagnation and ultimately decline. For the Australian energy resources sector to remain globally competitive and able to rapidly adapt in an age of disruption and innovation, we will need to seek transformational change.

It will take strong leadership and skilful navigation by all parties - governments, industry, the technology and service sector and research organisations - to find sensible and practical solutions that the community will accept, and to innovate to support a globally competitive and sustainable sector.

Transformational change requires bold and insightful leadership and a willingness to find and break through barriers. For example, if the energy resources sector is to harness the huge efficiency benefits and competitive advantages to be had from the explosive growth of technologies, including advanced manufacturing techniques, automation, 3D manufacturing (with plant able to be printed onsite to meet immediate need), drones (to take over remote, offshore exploration and significantly reduce cost), and the Internet of Things (including cloud computing, mobile computing, embedded computing and consumer electronics), then we must unlock our intellectual property and move away from a reliance on closed, single sourced and bespoke solutions. We need to commercialise our huge investment in research and knowledge, and adopt open, multi-vendor approaches that deliver improved products and capabilities to a global market.

7National Energy Resources Australia – Sector Competitiveness Plan 2017

FOREWORD

Such changes will enable operators and miners to form new relationships with technology vendors across the value chain, and for the technology vendors to collaborate with each other and bundle products and services, for example in formal clusters to lower the risks of failing and maximise the benefits that new technologies can provide for all.

This new digital environment, as well as changes to the sector’s commercial and operating models, will also result in the need for a very different mix of skills. The sector needs to build a comprehensive understanding of its future skills requirements in terms of scope, scale, skills and experience, and collaborate with governments and other skills development stakeholders to set out a clear plan for building that capability.

From an energy perspective, Australia is currently facing a number of serious challenges, and urgently needs a clear and cohesive pathway for its transition to a low emissions future and to underpin economic development. To get there will require substantial, highly funded collaboration in selected areas between industry, research institutions and government. For example, Australia could secure a strong carbon capture and storage technology advantage, and there is potential to both develop and commercialise low emissions technology and to transfer and export that knowledge and capability globally. The research has been done and the next stage is demonstration and deployment. However, for this to occur it will require funding in the order of billions of dollars, and this will be difficult to obtain without clear priorities and concerted effort by all parties.

A vibrant exploration industry is also critical to the ongoing supply, security, reliability and affordability of Australia’s energy supply. NERA’s global competitiveness benchmarking shows that in oil and gas we have an attractive environment for exploration, but we are at the lowest point in decades for exploration activity (both onshore and offshore). This low level of activity is driven by a combination of low commodity prices, high cost, government red tape and community opposition. A priority for immediate action is, that the state governments and regulators address approvals for onshore gas projects on a case by case basis, and not proceed with blanket moratoria. For the coal exploration sector, according to the 2015 Fraser Institute Survey of Mining Companies, 55 per cent of respondents in Queensland and New South Wales reported that regulation uncertainty had a negative impact on the states’ investment attractiveness, versus only 13 per cent in Western Australia. Australia must make progress in creating an attractive exploration environment across the whole energy resources sector and for new and existing firms.

Achieving a stable and high-performance regulatory environment across all jurisdictions is critical. Regulation needs to support economic development and innovation, whilst providing for independent, transparent and objective oversight of industry activities and measurable environmental performance proportionate with risk. This will assist in securing the acceptance of Australian communities. The focus needs to be on risk based, transparent and outcome focussed regulation which requires strong demonstration of and accountability for, industry performance, whilst also encouraging innovation.

In conclusion, the size of the prize is significant for everybody. NERA’s benchmarking to date has identified the potential to unlock AUD$5 billion of value in the oil and gas sector, and AUD$4.5 billion of value in the coal sector. We will be identifying the uranium sector’s potential to create value in 2017. Australia has the potential to continue to supply innovative products, capabilities and services for many years to come to meet both domestic and international energy resource needs, generate substantial revenue for the nation and grow an export orientated sector.

This Sector Competitiveness Plan represents the collective wisdom and insights of all stakeholders across the Australian energy resources sector. During our extensive consultations, it became very clear to us that there is strong commitment and passion for achieving a competitive, innovative and sustainable sector, and that the sector remains vital to Australia’s economic development and low emissions future.

NERA is committed to working with stakeholders to pursue strategic initiatives and projects that will assist the energy resources sector adapt to current and future challenges and disruption.

We would like to thank you all for your support and valuable input into this roadmap for the sector’s future, and we look forward to working with you on this journey of change.

Miranda Taylor Chief Executive Officer

Ken Fitzpatrick Chair

8 National Energy Resources Australia – Sector Competitiveness Plan 2017

9National Energy Resources Australia – Sector Competitiveness Plan 2017

EXECUTIVE SUMMARY

1

This section provides a stand-alone summary of the Sector Competitiveness Plan for the Australian energy resources sector.

It provides an executive summary, an overview of the key themes, the challenges and opportunities facing the Australian energy resources sector, and a road map to achieve a vision for innovation, improved productivity and sustainability and a globally competitive service and technology sector. The road map identifies three key business levers to a strong future, sets out nine knowledge priorities with initial key performance indicators against which the changes in the sector can be tracked over the coming decade.

10 National Energy Resources Australia – Sector Competitiveness Plan 2017

This Sector Competitiveness Plan (SCP) has been produced to provide a cohesive and comprehensive call to action for the Australian energy resources sector. It is the product of an extensive industry consultation process and review of the contemporary literature on both the sector and the broader global trends affecting the sector into the next 10 years. This SCP identifies the challenges and opportunities that the sector must navigate in the coming decade, based on the current landscape. It proposes a structured and evolving series of knowledge priorities to be addressed in order to build on the industry’s existing strengths, and create an adaptable, resilient and sustainable Australian energy resources sector.

Executive Summary

11National Energy Resources Australia – Sector Competitiveness Plan 2017

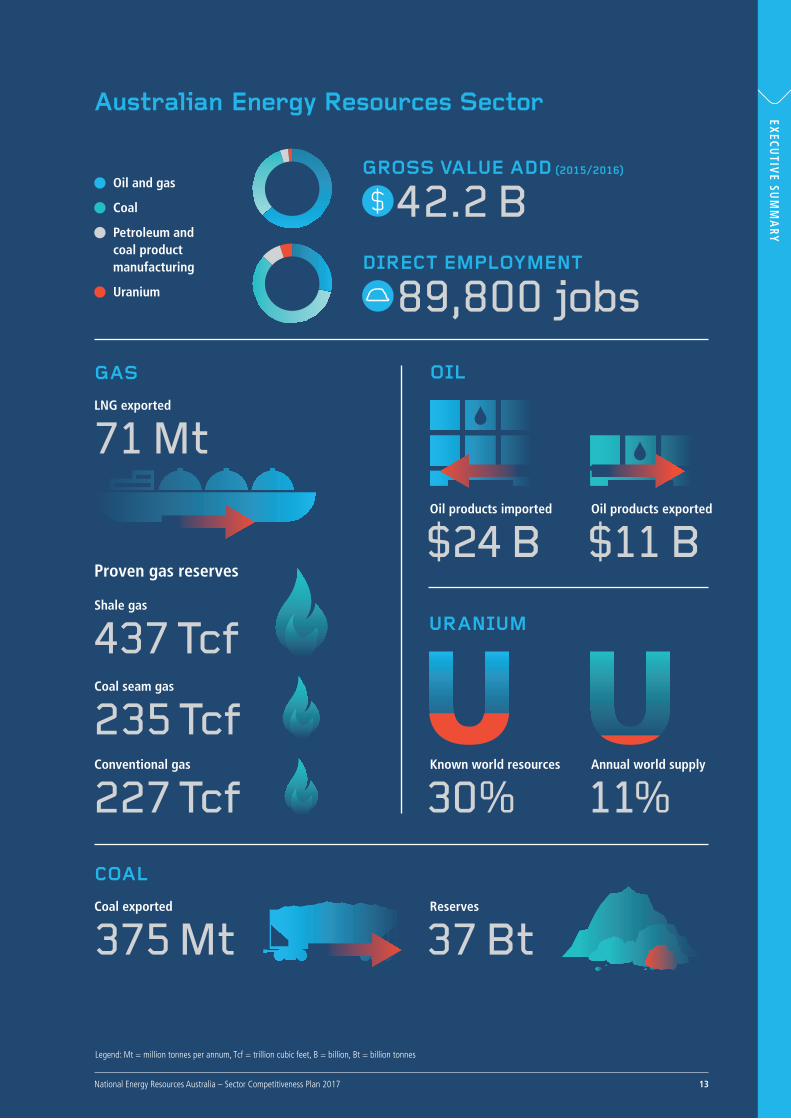

The value added to the Australia economy from the Australian energy resources sector, comprising the coal, oil and gas and uranium industries, has been and continues to be huge. Combined, the sector directly provides approximately 89,800 jobs with a gross value add of $42.2 billion (2015/2016). Coal and gas are the nation’s largest commodity exports after iron ore, providing a safe and secure energy source to our trading partners. The scale of the sector makes the nation largely self-sufficient in energy and provides the fuel needed to underpin many industries and the lifestyle of a developed nation.

After decades of capital investment, innovation and operation, the Australian energy resources sector has many strengths that it can build on, including some of the world’s newest high technology production facilities, a well-educated and highly skilled workforce and significant high quality natural resources. These attributes are supported by Australia’s proximity to the Asian economies, world leading capabilities in remote operations and low carbon emissions technologies, a strong and growing start-up community, world class research facilities and knowledge and, a strong tax incentive scheme for research and development. With these strategic advantages, the sector has the potential to continue to supply both domestic and international energy resource needs for many years to come, to continue to generate substantial revenue for the nation and to grow an export orientated service and technology sector.

However, the Australian energy resources sector is facing a number of individual and systemic challenges. How the sector reacts to them will determine whether it continues to thrive as one of the world’s principal sources of energy, or stagnates under the burden of current global and economic pressures.

Internationally and domestically, society is facing increasing energy security challenges. In the international energy market, many developed nations are seeing the end of their domestic energy supplies and are looking to international sources for the energy resources they need to fuel their economies and societies. Domestically, Australia is struggling with changing societal and political drivers, with both short and long term impacts on the security and affordability of the energy needed to attract and fuel businesses.

As set out in this SCP, the sector must react to volatile commodity prices, a rapidly evolving energy marketplace, changing societal energy expectations, an increasingly complex regulatory environment and a rapidly evolving global energy mix. Only by working together, with producers, service suppliers, research and educational communities all collaborating, will the sector be able to deliver its future potential.

To unlock this potential, the sector needs to use the three levers of building contemporary business models, enhancing operational models and technology capabilities and improving capacity, skills and culture, while also addressing the regulatory environment in which the sector operates. Through addressing these levers, the sector will remain competitive while creating future markets and customers.

• Buildingcontemporarybusinessmodels – involves building new markets, new customers and new services through the entire value chain. It requires, for example, providing turnkey solutions to customers rather than simply the resources used to generate energy, finding new export markets for our LNG operations and maintenance knowledge and expertise, and delivering clean technologies. It involves building new, collaborative relationships within the entire energy resources value chain, global partnerships to access global supply chains, and other industry sectors such as advanced manufacturing, defence and shipping.

• Enhancingoperationalmodelsandtechnologycapabilities – the sector urgently needs to reduce process complexity and waste, to standardise operating practices and to collaborate through initiatives such as research/industry precincts, multi-user technical facilities and establishment of industry and innovation clusters (clusters can force-multiply investment, reduce risk for the participants and commercial contributors, and speed innovation; vendors can achieve critical mass and collaborate to provide scale and ease of access for export opportunities). The sector could work together to optimise processes through the development and adoption of disruptive technologies such as machine learning and diagnostics, 3D printing, advanced materials and new ways to build small scale, economically viable plants which require minimal capital investment to maintain production. There are further opportunities for the sector to share non-competitive and pre-competitive information such as environmental and meteorological data.

EXECUTIVE SUMMARY

EXECU

TIVE SU

MM

ARY

12 National Energy Resources Australia – Sector Competitiveness Plan 2017

• Improvingcapacity,skillsandculture – the sector needs to find ways to maintain and build its skill base, both to operate its existing facilities and to prepare personnel to become ‘operators of the future’, with the commercial skills needed to develop new markets, customers and services. As the sector drives productivity and efficiency, companies are looking to optimise plants and work processes, and are increasingly adopting automation, digital technologies and collaborative teams. This requires industry to develop new capabilities, workforce skills and attributes.

• Addressingtheregulatoryenvironment – to facilitate innovation, improve productivity and competitiveness and secure both future investment and a sustainable economy, Australia needs a modern, best in class regulatory environment. The energy resources sector needs consistency, efficiency and flexibility to allow innovation, whilst working within a regulatory framework that provides the community with transparency on, and confidence in, regulators’ decision-making processes and the industry’s performance and where the regulations in place are proportionate to the risks being controlled. The sector itself can work collaboratively on its own internal standards to ensure alignment across the sector, and cooperatively with governments to reform regulation to focus on high performance outcomes. Australia needs to re-establish its reputation as an attractive business environment and a destination for future investment.

Moving from current operating models to those of the future will require ongoing incremental change together with more disruptive, transformational change. Incremental change, with the occasional adoption of a major technological innovation, has largely been the standard operating practice for the majority of business. While this approach provides a relatively low risk, predictable environment, it is only capable of maintaining the status quo because an incremental approach is also adopted by peers and competitors alike. Transformational change, while offering large potential opportunities created by changes to business models, operating models and culture, comes with higher risk. However, only through accepting this risk in a considered way, and pursuing the opportunities created through transformational change will the Australian energy resources sector move ahead of the competition into a sustainable and resilient future.

Business and operating models that can adopt and deploy transformative, plug-in technology or combinations of disruptive technologies offered by small to medium enterprises will accelerate cost savings, improve efficiencies and experience improved productivity. By way of example, working directly with unmanned aircraft systems, continuously collecting high-definition seismic data onshore or offshore, delivered in real-time directly into the operator, with real-time geophysics analytics, reducing seismic interpretation from many months, to a few days or even hours, adjusting as new data streams into the business. Or, building microscale plant using remote advanced manufacturing techniques, commissioned, operated and maintained remotely through onshore or offshore remotely operated vehicles.

This SCP, therefore, proposes a number of incremental and transformational changes for the energy resources sector. It offers a timeline to pursue the changes, and provides research-based benchmarking of the industries that show where the greatest opportunities can be found now and in the future. It proposes a series of Key Performance Indicators (KPIs) against which future change can be measured and adjustments made over time.

It is incumbent on all parties in the Australian energy resources sector to consider these changes and collectively work to implement them, both collaboratively and in constructive competition. The sustainability of the industry depends on the actions taken in the next few years. There is a real opportunity to transform the industry and unlock its full potential.

EXECUTIVE SUMMARY

13National Energy Resources Australia – Sector Competitiveness Plan 2017

LNG exported

Proven gas reserves

Shale gas

Oil products imported

Known world resources

Coal seam gas

Conventional gas

GAS

GROSS VALUE ADD (2015/2016)

42.2 BDIRECT EMPLOYMENT

89,800 jobs

Oil and gas

Coal

Petroleum and coal product manufacturing

Uranium

OIL

URANIUM

71 Mt

437 Tcf

$24 B

30%

Oil products exported

$11 B

235 Tcf

227 Tcf

Coal exported

COAL

375 MtReserves

37 Bt

Annual world supply

11%

EXECU

TIVE SU

MM

ARY

Legend: Mt = million tonnes per annum, Tcf = trillion cubic feet, B = billion, Bt = billion tonnes

Australian Energy Resources Sector

14 National Energy Resources Australia – Sector Competitiveness Plan 2017

Australia is one of the world’s top producers and exporters of natural gas, coal and uranium. With the combined value of exports to the Australian economy estimated to be around $60 billion 1 the sector creates valuable jobs, export income and tax revenue. The anticipated sustained growth in energy demand presents significant opportunities for Australia.

Introduction to this SCP

15National Energy Resources Australia – Sector Competitiveness Plan 2017

While Australia’s current role in the energy resources market is a strong one, the rapidly evolving global energy market, together with growing societal environmental awareness, global commitments to reduce carbon emissions and the increasing economic and technological viability of alternative energy sources require sector wide adaptation. The Australian energy resources sector represented by NERA, and comprising the oil and gas, coal and uranium industries, must embrace this change to secure its role in powering the world and contributing to a clean and sustainable future.

As a result of the significant investment in, and development of, knowledge and technical capabilities and skills, the Australian energy resources sector is well-placed to compete globally and unlock new investment, supply chain efficiencies and export opportunities. To maximise this potential, the sector must improve the efficiency and competitiveness of both exploration activity and existing operating assets as a priority. It must rapidly adapt and transform through:

Business Models

• Newmarkets

• Newcustomers(includingproviding turnkey energy solutions across the value chain)

• Newcollaborativepartnerships,acrossvalue and supply chains, with the research sector and with other industry sectors, to leverage scale and cross sector transfer of knowledge

• Technologyandcapability

Operating Models and Technology Capabilities

• Radicallyreduceprocesscomplexity and waste

• Collaborateandstandardise

• Sharelogisticsandregionalsupply bases

• Removeunnecessaryandbespokestandards and conditions

• Shareenvironmentalresearch

• Optimisethroughautomation

• Digitaltechnologyandadoption of advanced manufacturing systems and technologies (such as 3D printing and new materials)

• Developandoperateminiplants to enhance the ability to scale up and down and adapt to a more distributed world

Culture, Capabilities and Skills

• Leadershipforcollaboration

• Commercial

• Digital,automation

• Innovationandentrepreneurialrisk taking

• Baselineskillsstudies

• Commoncompetencyframeworks and future skill requirements

To be competitive in the sector, Australia will need to be:

• Atop-rankedjurisdictionforenergyresourcesinvestment;

• Acentreofinnovationacrossthelifecycleofenergyresourcese.g.exploration,development,operations and maintenance and decommissioning, and within the community of supporting technology companies and service providers; and

• Positionedtocapitaliseonthedevelopmentsinglobalandregionaleconomies,andtherapidlychanging energy mix.

INTRODUCTION TO THIS SCP

EXECU

TIVE SU

MM

ARY

16 National Energy Resources Australia – Sector Competitiveness Plan 2017

To achieve these strategic outcomes, the Australian energy resources sector must overcome the following challenges:

• Legacyofpoorproductivityperformanceduringthehighcapitalinvestmentphase,andtheneedtodrive improved asset and labour productivity in the operations phase;

• Tighteningoperatingmargins;

• Addressingthesocial,economicandenvironmentalimpactsofenergyresourceextraction,productionand use, and building community engagement with the sector and a social licence to operate;

• Adaptingtothelowcarbonemissionsenvironment,cleantechnologiesandchangingglobalenergymix;

• Complexityofgovernmentregulationandapprovals;and

• DevelopingthecapabilitiesofAustralianorganisationsatalllevelsinthevaluechainsupportingthesector, and driving deeper engagement between the research sector and SMEs within the service sector.

This SCP provides a 10-year horizon road map. It sets out the key themes and strategies, the challenges, constraints and opportunities and then identifies the knowledge priorities, focus areas and initiatives that combined can ensure the Australian oil and gas, coal and uranium industries remain globally competitive, innovative, sustainable and diverse.

The SCP examines the challenges, constraints and opportunities in three ways:

1. It considers the evolving global environment and megatrends in which the sector must operate.

2. It examines the current state of the Australian energy resources sector, both as a whole and at the individual industry sector level.

3. It provides an overview of the ‘size of the prize’ to be had for Australia from improved competitiveness, through a series of sector global competitiveness assessments. The assessments and benchmarking will provide a base for year-on-year tracking of Australia’s performance.

Knowledge priorities and focus areas:

This review, undertaken through extensive domestic and international literature research, together with data gathering and stakeholder and industry consultations, has identified a set of knowledge priorities. These knowledge priorities in turn identify focus areas, areas where the sector needs to focus its short to medium term collective efforts.

Combined, these form a 10-year road-map for the sector, building on its strong knowledge and technology capabilities and skills base to ensure the Australian energy resources sector has a strong and growing future.

Building the strong future envisioned in this SCP requires the collective effort of all stakeholders in the sector to work together for the common good.

• Majoroperatorsoftheenergyresourcesector’sprojects,facilitiesandactivitieshaveasignificant part to play to support this future.

• Thesupplychain,whichprovidesthetechnology,equipmentandservicestotheoperatorsalsoplaysa major role in helping identify, develop and deliver innovative and practical solutions.

• Universitiesandresearchorganisationshaveacriticalroleinunderpinningtheknowledgeeconomy.They explore and identify new frontiers, new technology developments, new techniques and trials, create new methodologies and provide independent sources of trusted data.

• Educationandskillsprovidersneedtotrainandequiptheindustryworkersoftodayandidentifyandprepare for future Australian energy resources sector work skill demands.

• Governmentsplayacriticalroleinsettingaconsistent,clear,fairandobjectivepolicyenvironmentand supporting robust, independent and competent regulators and regulations that provide the community with confidence that the industry is accountable to high standards, whilst in parallel giving industry the ability to innovate and adapt within a stable and supportive framework.

INTRODUCTION TO THIS SCP

17National Energy Resources Australia – Sector Competitiveness Plan 2017

In the days of the construction boom and high commodity prices, companies were able to act independently, without considering collaboration or building in options for third party access/usage in the future. Now that commodity prices have dropped significantly, and with increasing disruption in the energy mix, there is an imperative for companies to work together to develop mutually beneficial situations. This will take a change in the traditional mindset, for operators of existing assets to adopt more flexible operating regimes, and for regulators to support the new paradigm.

This SCP covers all parts of the energy resources life cycle, from exploration, development and execution, through the long production phase and into abandonment.

To address the role of all parts of the sector, this SCP outlines:

• CollaborationbetweenOperators/MinersandSupplyChain (technology and services and to build value chain opportunities).

• ResearchandInnovation (industry led, including research sector engagement with supply chain, to drive greater commercialisation).

• WorkforceSkillsandEducation.

• RegulatoryReform.

APPROACHThe SCP has been developed through a multi-step, iterative process. This process included a combination of desk top studies, industry and stakeholder consultations, meetings and workshops. Figure 1 below shows the key steps undertaken in developing the SCP.

Figure 1: Sector Competitiveness Plan development

Strategic Imperative

Strategic Engagement

Research Hypotheses Prioritise Socialise

NERA’s strategic goals

established

Early engagement with industry

Sector Competitiveness Plan knowledge priorities, strategies, projects

Identify global and national themes

Develop hypotheses,

test and refine through

workshops

Identify priorities and

initiatives

Further testing and refinement

The SCP provides an outline of priorities for the next 10 years which underpin a transformational program for the sector. While this SCP identifies plans for the Australian energy resources sector set against the challenges and opportunities in early 2017, it is an evolving document and will be updated on an ongoing annual basis to reflect changes in the marketplace.

INTRODUCTION TO THIS SCP

EXECU

TIVE SU

MM

ARY

18 National Energy Resources Australia – Sector Competitiveness Plan 2017

Figure 2 below sets out how NERA is facilitating new ways for stakeholders across the energy resources sector to work together to better adapt, drive innovation, access entrepreneurial investment, reduce costs and improve efficiency across the value chain.

Figure 2: Ten year transformation process

The transformation path: industry leadership and collaboration to deliver an energy resources sector in Australia that is innovative and adapting to a disruptive energy market

Formulating

Year 1-2Creating

Year 3-4

Participating and changing

Year 5-8

Leading and transforming

Year 9-10• FormingNERA

• Earlystakeholderengagement

• Initialalignmentwith vision, mission and strategies

• Clearvalueproposition

• Furtherstakeholderengagement on Sector Competitiveness Plan

• Identifyandbegintoconnect initiatives, organisations and networks

• Identifyopportunitiesfor industry and broad cross-sector collaboration

• Earlyindustrycollaboration focused on improving efficiency and performance

• Earlyparticipation in pilot initiatives and projects

• Growingindustryparticipation and engagement

• Earlyworkonanational work skills framework

• Beliefsandbehaviours are being challenged

• Willingnesstoshare,cooperate and challenge thinking

• Enhanceddatasharing

• Industry,innovationnetworks, entrepreneurs, researchers, value chain and venture capitalists actively collaborating

• Commoncompetency frameworks established

• Widerangeofsector stakeholders collaborating

• Newentrantstovalue chain with new capabilities

• Megadatasets/insights emerge – intelligently interrogating data and applying lessons learnt

• Workforceskillssupporting disruptive innovation and technology uptake

• Innovationsallowingthe sector to adapt more quickly

• Policyandregulationreforms supporting timely industry investment, activities and growth, whilst ensuring high industry standards e.g. social, environment and safety

• Industryisoptimistic and experiential

• Strongleadershipsupports collaboration - accepted normal way of working

• Industryableto harness entrepreneurial innovation and investment

• SCPaddressingmega trends and knowledge priorities resulted in measurable improvements to the sector’s competitiveness

• Developingnewinsights and capabilities

• Delivering‘newto the world’ operating models, markets, products, technologies and services

• Workinginnovationsystem increasing global demand for Australian value chain e.g. in areas of comparative advantage

INTRODUCTION TO THIS SCP

19National Energy Resources Australia – Sector Competitiveness Plan 2017

Sector ThemesEight key themes have been identified and adopted by NERA and supported by the Australian Government. These themes represent the key opportunities for achieving sector wide improvements in competitiveness and sustainability through greater collaboration and knowledge sharing, and provide a framework for NERA and the industry to categorise initiatives and projects for further development, review and prioritisation.

These themes are:

Theme 1: Manage cost structures and improve productivity Improve management of high cost activities and focus on increasing efficiency and asset productivity to drive value creation through innovation and collaboration. Australia’s energy resources sector must aspire to be best in class in all phases, from exploration through operations and maintenance, to closure and abandonment.

Theme 2: Adopt predictive analytics (digital technologies)Improve industry operational performance through the application of digital technologies and a collaborative approach to the identification and resolution of operational issues. Through such an approach, the Australian energy resources sector can achieve global best practice operational performance, improve productivity and international competitiveness.

Theme 3: Drive deeper engagement with the value chainEnhance collaboration amongst supply chain organisations and operators to harness existing capabilities and identify solutions that will improve the competitiveness of the sector. Through deeper engagement new ideas will be brought forward faster, allowing the sector to become increasingly innovative.

Theme 4: Develop work skills of the futureFurther develop our understanding of the skills implications associated with new technology and innovation across the energy resources sector. Through collaboration, assist the education and training sector to respond effectively to these identified skill demands, building a workforce ready to engage with tomorrow’s technologies and challenges.

Theme 5: Drive industry-led researchPromote ‘industry-led’ research through stronger engagement between industry and research organisations. Encourage a more streamlined research funding application process and support universities in placing greater value on applied research, commercialisation and mid-tier and SME participation engagement pathways. Support the development of a reliable database of research related information.

Theme 6: Improve industry sustainability (social, environmental, economic) Improve industry sustainability through identifying and supporting leading practices in stakeholder engagement, to enhance understanding of the social, environmental, economic and operational consequences of industry activity, and by identifying and supporting trusted custodians of scientific knowledge.

Theme 7: Understanding and unlocking Australia’s future resource base Improve identification, appraisal and cost effective and sustainable development of marginal resources. Develop cost-effective and sustainable means to commercialise these resources to deliver significant economic, social and community benefits.

Theme 8: Achieve proportionate, fit for purpose regulationPromote effective policy and regulation that supports energy resources industry activities and provides the Australian community with confidence and trust in industry oversight by promoting: evidence and outcomes based regulatory frameworks; greater harmonisation of regulatory requirements between states and territories, and between the states/territories and the Commonwealth; acceptance of trusted international standards; and reduction of the regulatory burden on the energy resources sector.

INTRODUCTION TO THIS SCP

EXECU

TIVE SU

MM

ARY

20 National Energy Resources Australia – Sector Competitiveness Plan 2017

GLOBAL MEGATRENDSGlobally, the energy resources sector is facing a number of megatrends. Individually, each of these trends present significant change and challenge to the sector but when combined, they are resulting in operational and market disruption to which the sector must respond and adapt. Seven current and one emerging global megatrends are considered in this SCP:

UrbanisationTechnological

evolutionAsian

centuryChanging

energy mix

Globalisation of business

Changing demographics

Low carbon future

Search for energy security (emerging)

The disruption caused by these megatrends requires the energy resources sector to find new ways of working and to work together to innovate. These trends pose challenges but also opportunities for the energy resources sector, to maximise the value from existing industry investment, to adapt to the changing landscape and to build a competitive, resilient and sustainable future for the sector.

An environment of disruptionThese multiple trends, when considered together, form one overarching ‘megatrend’ – an increasingly disrupted energy market. This one megatrend is transformative, defines the present and shapes the future by its significant impact on societies, economies, industries, and organisations. It provides significant challenges and substantial opportunities to the sector, and the pace of change is likely to continue. Industry must be agile, adaptable and innovative and needs to build the organisational skills and attributes to stay at the forefront of the wave of disruption.

Impact of global megatrends on AustraliaAs a major supplier of the world’s conventional energy and as a country with its own established energy networks, the Australian energy resources sector faces a number of major challenges to remain competitive in the increasingly complex modern energy marketplace. While the global and regional demand for our resources in the energy market continues to be strong, internal changes in each market are placing additional complexity on what has, for a long time, been a relatively stable mix of energy demand.

How the Australian energy resources sector responds to this new environment will determine its future trajectory. The sector must be prepared to undergo both incremental and transformational improvements. Incremental improvements alone will not be enough to keep pace with change. Transformational change is required for the sector to keep pace with the shifting energy paradigm and compete with global challenges. Finding ways to exploit the opportunities presented by the disruptions will be vital to the future of the Australian energy resources sector, allowing it to continue to play a significant role in the global energy mix.

INTRODUCTION TO THIS SCP

21National Energy Resources Australia – Sector Competitiveness Plan 2017

Incremental improvement

• Leaneroperations,asexemplifiedbythemanyoperatorsalreadyfocusingonincreasingassetutilisation;

• Bettermanagementofhighcostactivities,particularlyinnewprojectsandothermajorcapitalinvestments;

• Increasingmovementbyoperatorstowardsharinginfrastructurebothattheirfacilitiesandinlocations such as maintenance and supply bases;

• Collaborativeplanningoflabourandresourceintensiveplannedmaintenanceandupgradeactivitiesto avoid competition over labour and shop time;

• Staffreviewsatfacilitiesandinvariousnationalheadoffices;and

• Anincreasingdrivetoimproveproductivityfromnewandexistingassets.

Transformational improvement

• Developoperatingmodelsfocusingonnewandinnovativeapproachestoexecutionandbetterleveraging of existing capacity. Build on Australia’s highly regarded existing capabilities in areas such as remote operations and data analytics for process optimisation and decision making, to support operational and value chain optimisation;

• Expandourstrengthsinthedevelopmentofalternativeenergysourcesandactasabaselinecleanenergy source for Asia;

• Assistdevelopingnations,particularlythosetransitioningfromfossilfuels,tomeettheiremissionsreduction commitments by providing energy diversification;

• Increase‘energyliteracy’ofcommunities,governments,regulators,companiesandotherstakeholders;and

• Exportcleantechnologiestodevelopingcountries.Thiscouldincludelowcarbonemissiontechnologies,hybrid power generation, battery storage and carbon capture and storage (especially geosequestration where Australia’s geology provides a strong competitive advantage). Leading the development and adoption of these clean technologies is likely to help the sector strengthen its social licence, drive up the demand of our existing energy resource portfolio, as well as opening up new markets (i.e. gasification utilising coal deposits with low ash fusion temperatures).

An imperative to changeStanding still is not an option. The modern energy resources environment requires all sector participants to continually explore ways to change regulatory, business and operational models simply to remain competitive. As set out in this SCP, the Australian energy resources sector must find ways to:

• Collaboratemore-betweenpeerorganisations,verticallywithinvaluechains,acrossthetraditionalboundaries between industries and with research organisations, where directed and undirected findings can help lift the productivity of the industry;

• Addresstheregulatoryburdenrestrainingmanyareasoftheenergyresourcessectorfromthrivingand growing in the future, in ways that maintain and enhance community support for the industry;

• Identifyandexplorenewmarketsfortheproductsoftheenergyresourcessector,opportunitiesthatfill needs in the marketplace or displace expensive import alternatives: one example is expanding the use of LNG as a domestic source of energy.

INTRODUCTION TO THIS SCP

EXECU

TIVE SU

MM

ARY

22 National Energy Resources Australia – Sector Competitiveness Plan 2017

CHALLENGES, OPPORTUNITIES AND CONSTRAINTSGrowing energy demand in Asia, increased societal environmental awareness, and an evolving global energy mix create immense opportunity and substantial challenges for the Australian energy resources sector.

Major shifts are expected in the ways in which power is generated, distributed, controlled and consumed as the world moves to incorporate more renewable energy in the broader mix. This shift will force sector-wide adaptation, as new infrastructure needs to be built and integrated, and new operational frameworks are created. Despite these challenges, there are significant opportunities for Australian energy resources participants, particularly in meeting growing Asian demand.

Sector wideA number of challenges and constraints are sector wide and, while impacting each sector differently, there are some common causes and solutions.

Challenges

• Volatilecommoditypricesduetomajorstructuralchangesinglobalsupplyandanongoingoversupply in the global market.

• Highcapital(CAPEX)andoperational(OPEX)costsmakingAustraliauncompetitiveasaninvestmentdestination.

• Concernsassociatedwiththeongoingmanagementofwater,ensuringitisequitablyavailableforallland users including agriculture, human settlement and industry.

• Understandinghowbesttomanagecarbonemissionsfromboththeprimaryproductionofenergyresources and their consumption.

Constraints

• PerceptionthatAustraliahasgrowingsovereignriskforcapitalinvestmentduetoincreasedrestrictiveregulatory burden, frequent changes in policy and growing restrictions on development in various states. These restrictions are inhibiting both domestic exploration and the sector’s ability to develop discoveries necessary to underpin the long-term viability of the Australian energy resources sector.

• Australia’srelativelypooradoptionofinnovation,makingitdependantonimportedideasandtechnology rather than building home grown solutions. Australia was ranked twenty-sixth for innovation by the World Economic Forum in 2016 2.

In addition to these sector wide challenges, there are also a number of more discrete challenges and opportunities that will be faced by the industries making up the sector over the coming decade.

INTRODUCTION TO THIS SCP

23National Energy Resources Australia – Sector Competitiveness Plan 2017

Oil and gasThe Australian Liquefied Natural Gas (LNG) industry’s capacity has increased more than four-fold over the past five years to supply the anticipated increase in demand. This rapid growth has created a number of challenges and opportunities for the developing industry.

Challenges

• Relativelyhighoperatingcostenvironmentduetohighlabourcosts,remotenessofoperations,anddistance from global supply chains result in many aspects of the Australian oil and gas industry being substantially more expensive than other jurisdictions. For example, costs to explore and develop a shale gas well in Australia are believed to be around 250 to 300 per cent higher than to develop a similar well in the United States.

• Limitedavailabilityofprocesstechniciansandoperatorswiththehigh-levelskillsrequiredtorunincreased numbers of integrated teams and operations. Technological change will drive multiskilling into the future, requiring significant changes to current training regimes as well as articulation of skills development pathways to ensure a sufficient number of suitably skilled personnel for future needs.

• Apotentialshortageofspecialistskilledandexperiencedlabourformaintenanceandturnaroundsfor Australia’s 21 LNG trains. This could be further impacted by parallel activities in the broader energy resources sectors especially in the case of a recovery in commodity prices which will increase competition for such skills.

• Challengestotheindustry’ssociallicencetooperate,includingnegativecommunityperceptionsofthe social and environmental impacts of unconventional developments, concerns over the potential development of new offshore basins and increasing community expectations around the transition to renewable energy sources. This will require the sector to operate through high levels of community engagement, corporate transparency and exemplary social citizenship.

• Areputationasahighcost/lowproductivitymarketplace,giventhemanyprojectbudgetandschedule overruns experienced during the recent expansion phase of the industry, is contributing to operators deferring future major capital investment in Australia in favour of other jurisdictions. To help restore Australia’s reputation, the industry needs to demonstrate that it can operate and maintain the new and existing facilities to world’s best standards at competitive cost.

• Uncertaintyovercapitalandregulatorycostsofabandonment,asmanyoperatorsbegintoplanfor the end of life of their facilities; and given that, to date such abandonment activities have been relatively few, the need to establish and test an appropriate regulatory framework.

• TheemergenceoftheUnitedStatesasanewandmateriallylowcostLNGsupplierintoboththeAtlantic and Pacific basins. The United States is now seen as a low risk jurisdiction for project delivery and sovereign risk - a position which Australia held for many years.

• TheexpansionofgasexportsintoChinafromRussianandBalticnations.

• TheunknownbutpotentialriseofadomesticChineseunconventionalsourceofgassupply.

• Difficultyoflocalserviceproviderstointegrateintotheinternationalsupplychain.

INTRODUCTION TO THIS SCP

EXECU

TIVE SU

MM

ARY

24 National Energy Resources Australia – Sector Competitiveness Plan 2017

While the output capacity of the Australian oil and gas industry has grown over the past decade through the construction of additional LNG trains, the long term viability of the sector has been jeopardised by the precipitous decline in exploration. This is illustrated by the almost tenfold decline in the number of new offshore wells being drilled 3 as shown in Figure 3. There are still a number of known offshore reservoirs yet to be developed, but without an active exploration regime the long-term future of the sector remains at risk.

Figure 3: Offshore petroleum exploration wells

100

90

80

70

60

50

40

30

20

10

02008 2009 2010 2011 2012 2013 2014 2015 2016

Source: APPEA

Opportunities

• Increasingcollaborationamongstoperatorstomaximiseassetproductivity.

• Improvingcollaborationbetweenoperatorsandtechnologyandengineeringserviceproviderstoincrease innovation and productivity.

• LeveragingthecriticalmassemerginginAustralianoperationstodevelopanexport-orientedandcompetitive service and technology sector.

• Addressingcost,regulatoryandsociallicenceconcernstoensureAustraliacontinuestobeperceivedas a politically stable and economically reliable destination for future capital investment.

• Developingshaleandtightgasbasinstosupportdomesticdemand,andpotentiallyforexport.

• Emergingnewmarkets,suchasIndia,andfromtheexpandeduseofgas(LNGandcompressednatural gas) as a source of transport fuel.

INTRODUCTION TO THIS SCP

25National Energy Resources Australia – Sector Competitiveness Plan 2017

CoalIncreased pressure to reduce carbon dioxide (CO2) emissions and a switch towards renewable energy sources means that domestic demand for thermal coal is forecast to decline over the next 10 years. However, reduced domestic demand will be offset by increased export demand from Asia and an anticipated overall growing demand globally 4. Demand for metallurgical coal is expected to increase in the medium term with reinvigorated demand from China and other developing nations.

Challenges

• Sub-optimalassetproductivityandcostsinavolatilepriceenvironment.

• Highcostandinefficientinfrastructurecontractsimpactingsomeproducers.

• OverlapofcoalminingtenementswithagriculturallandinNewSouthWalesandQueensland,leading to conflicting pressures on land and water use.

• Effectivemanagementofbothsurfaceandgroundwaterconsistentwithenvironmentalrequirements.

• Increasingsocialconcernwithclimatechangeandtheenvironmentalimpactofresourceextraction,which will limit the industry’s social licence to operate.

• IncreasingGovernmentregulationand‘greentape’.

• Developmentofcoherentandcosteffectivemineclosureandrehabilitationplans.

Opportunities

• Technologicaladvancesandimplementationofoperatorassistanddecisionsupporttechnologiesused in other bulk commodities to unlock productivity improvements.

• Ongoingutilisationofhighefficiencylowemission(HELE)technologies,controloffugitiveemissionsand carbon capture and storage (CCS) to minimise carbon footprint.

• Improvedminedesignandoperationstofacilitatereducedconsumptionandcompliancewithregulatory scrutiny of water use.

• Improvingutilisationoftheserviceindustrytoleverageexistingcapacityofworkshops,skilledpersonnel and equipment.

• Productmixevolutionwiththedevelopmentofnewsuperiorproducts.

• StrategictargetingofincreasingAsiandemandforhigherqualitycoalwithahigherspecificenergyand lower ash content.

INTRODUCTION TO THIS SCP

EXECU

TIVE SU

MM

ARY

26 National Energy Resources Australia – Sector Competitiveness Plan 2017

Uranium The uranium industry will need to overcome regulatory hurdles, perceived radiation safety concerns and social licence to operate issues to participate more fully in the energy future of Australia and the world.

Challenges

• Lackofinformedpublicknowledgeandunderstandingofthescienceassociatedwithenergygeneration and the associated levels of risk with each technology.

• Limitsontheportsfromwhereuraniumcanbeexported,withonlyDarwinandAdelaidecurrentlylicensed for the export of uranium, and limits on the ability to access ports elsewhere in Australia whilst carrying cargoes of uranium. This restricts the options available to the domestic uranium industry to transport its products to international customers.

• LegislativeandpolicyrestrictionsattheFederalandState(s)levelonmininge.g.inNewSouthWales,Queensland and Victoria, and on the development of nuclear power and other parts of the uranium value chain (e.g. waste management and disposal), which limits the growth of the industry.

• Buildingacomprehensiveunderstandingofthechallengesassociatedwithprocessingchallengingore bodies in which much of the known Australian uranium is found.

• EquipmentandskillsshortageswhichlimitthecapacityofAustralianminestorespondquicklytoanincrease in demand.

• StrategicdevelopmentofuraniumproductioncapacitybyKazakhstan 5 through counter-cycle investment has positioned them ahead of Australia to respond to any increase in uranium demand (although Australian uranium is still regarded by many customers as their preferred product).

Opportunities

Given the drive to reduce carbon emissions globally, Australia’s uranium has the potential to assume a much more significant position as a source of export revenue. To realise this potential, Australia needs to take advantage of the following opportunities:

• Aspartofabroaderenergyliteracyinitiative,thesectorneedstohelpenhancetheoveralllevelofpublic understanding of how energy resources are produced, how power is generated and the role energy resources play in the nation’s economy. The sector also needs to continue to test current attitudes towards uranium mining and other aspects of the nuclear value chain.

• Reconsiderationofrestrictivelegislation,replacementwithefficient,fitforpurposeregulation.

• Testingoftechnologicalimprovementssuchasheapleachingandin-situleachingtoimproveproduction capacity with low operating expenditure.

• Improvingtheattractivenessoftheuraniumminingsectortodrawlabourbackfromotherminingsectors, both in terms of radiation safety and salaries.

INTRODUCTION TO THIS SCP

27National Energy Resources Australia – Sector Competitiveness Plan 2017

CROSS SECTOR CHALLENGES AND IMPACTSMany opportunities and challenges span two or more sectors or sit outside discrete sectors, and are likely to have a profound influence and impact on the energy resources sector in the coming years.

These will include factors such as the rapid emergence of renewable energy technologies which, when added to the global and domestic mix, may drive markets in unanticipated directions. An example of this is seen in the deployment of domestic solar power technologies to meet household electricity needs, which are causing substantial disruption to the generation and distribution networks together with increased pricing instability. The impact of the increasing uptake in solar panels, combined with emerging domestic battery storage and smart grid technology, will cause even greater disruptions in the coming years.

A further challenge facing not only the energy resources sector, but the broader Australian workforce is the ageing working population and declining numbers of students pursuing science, technology, mathematics and engineering (STEM) subjects in schools and universities. This will limit the available pool of appropriately skilled workers to pursue the next waves of innovation and to maintain the increasingly technologically challenging facilities operated by the sector 6, all of which are highly influential on the future prosperity of the nation.

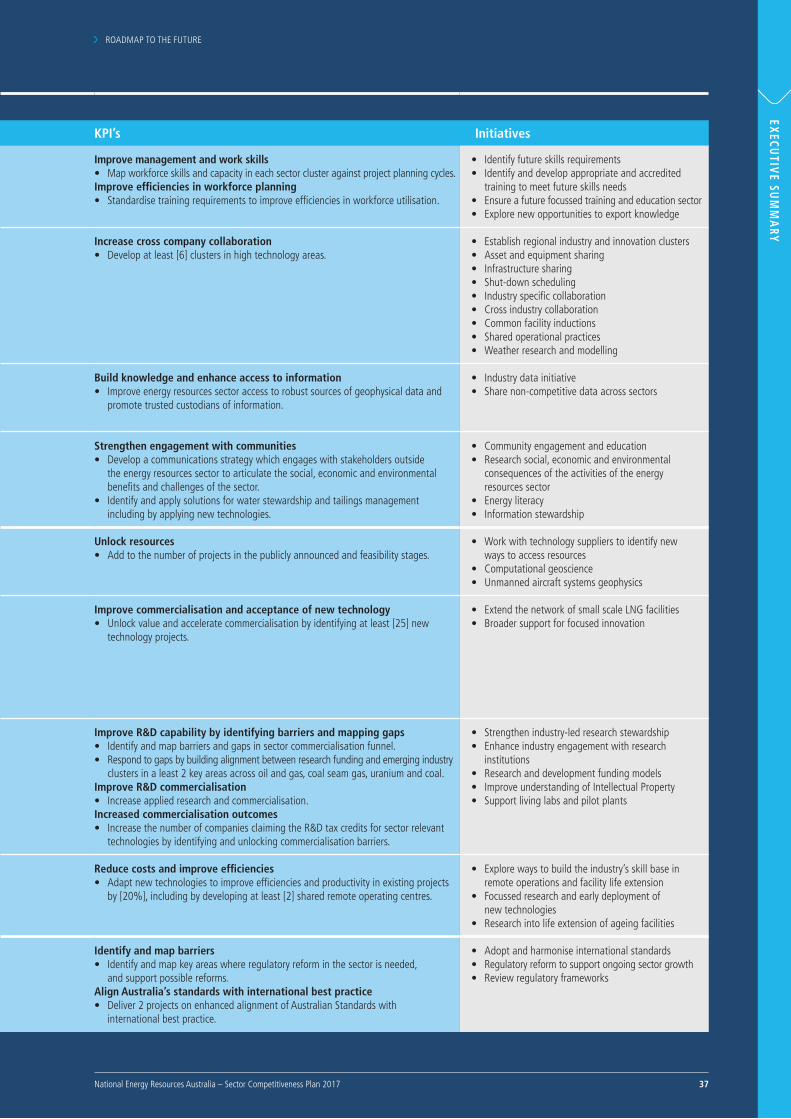

SECTOR KNOWLEDGE PRIORITIESWhile many of the actions required by the sector to address the challenges and opportunities ahead are relatively well known and understood, there are other issues which are not as well defined or where there are known gaps in knowledge – these are referred to as knowledge priorities. Many of these knowledge priorities were identified in the initial consultation period during the preparation of this SCP, and have been aligned with NERA’s key themes. The nine knowledge priorities, listed in Table 1, identify the key areas where additional work is required to understand the challenges and choices the sector faces in the current environment.

These knowledge priorities will change over time as the sector and new challenges arise. However, by systematically addressing these knowledge priorities now, the industry will maintain its globally competitive edge and thrive in the future.

The nine knowledge priorities have been grouped into three broad categories:

1. Capability and leadership;2. Business and operating models, technology and services; and3. Regulatory environment governing the industry.

Many of the knowledge priorities encompass multiple challenges and opportunities.

INTRODUCTION TO THIS SCP

EXECU

TIVE SU

MM

ARY

28 National Energy Resources Australia – Sector Competitiveness Plan 2017

Table 1: Sector knowledge priorities

Knowledge priority Focus areas

Capa

bilit

y an

d le

ader

ship

1 Work skills for the future

• Integratedoperationsofthefuture• Workforcecapability• Projectmanagementskills

2 Enabling effective collaboration

• Crosscompanycollaboration• Intergenerationalandinterdisciplinaryengagement• Industryandappliedresearchcollaboration

3

Understanding Australia’s resource base

• Developingagreaterunderstandingofprospectivebasin geology across the minerals and energy sectors

4 Social licence to operate

• Socialbenefits• Infrastructureclosureandrehabilitation• Watermanagement• Tailingsmanagement

Busi

ness

and

ope

rati

ng m

odel

s, te

chno

logy

and

ser

vice

s

5 Unlocking future resources

• Integratedgeologicalinformation• Crossindustrycollaboration• Maximisingageingassets• Environmentalsciencecollaboration

6

New markets, new technologies, new business models

• Asiantradeagreements• Developinternationaltechnologypartnerships• Commercialisationofoperationaltechnological

developments• Carboncaptureandstorage(CCS)• Lowemissionstechnologies• LNGasafuel• Hybridtechnologies• Adaptingtothechangingenergymix

7 Commercialisation of Research and Development (R&D)

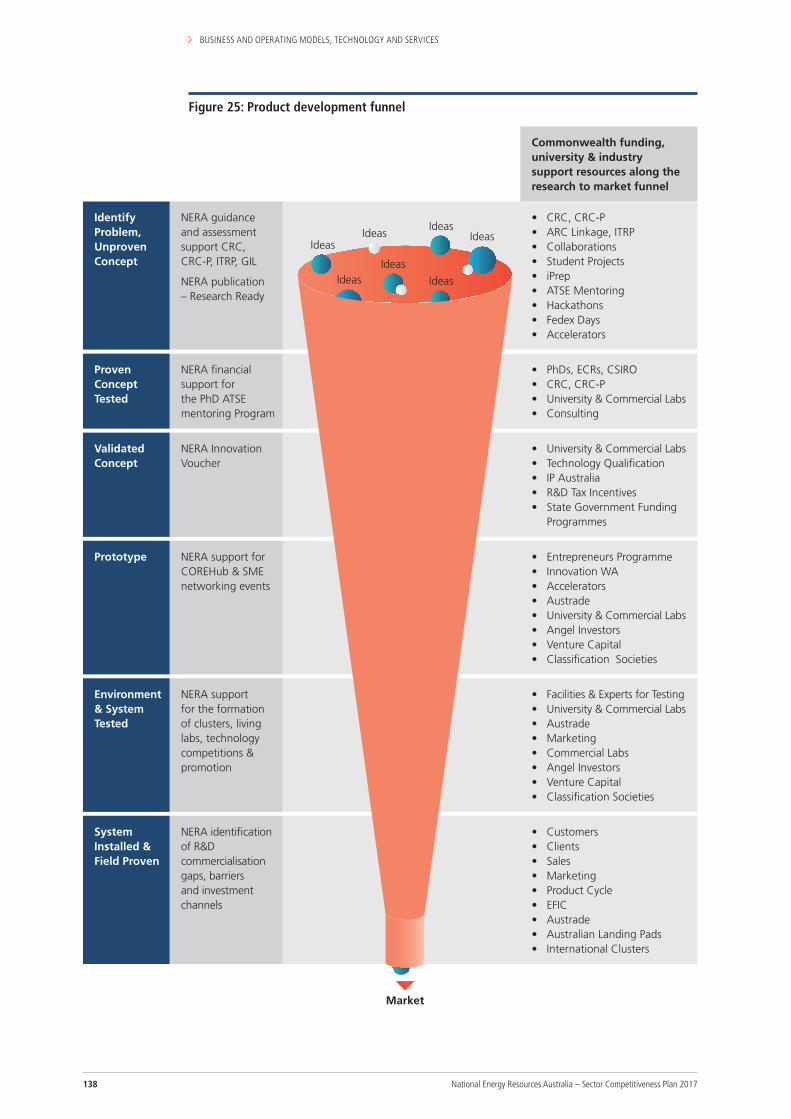

• Livinglabs• Understandinganddevelopingcommercialisation

pathways

8 Efficient operations and maintenance

• Operatingmodelsforremoteoperations• Data,digitisationandpredictiveanalytics• Robotics,sensorsandautomation• Developagreaterunderstandingofdecommissioning

techniques

Regu

lato

ry

envi

ronm

ent

9

Regulatory framework optimisation

• Encouragingsensibleregulatoryframeworkstoallowongoing exploration

• Harmonisationofstandards• Reviewofself-imposedregulations• Industrialrelationsandworkplacereform*• Resourcemanagementreformandreviewofthe

existing permitting systems

*Note:IndustrialrelationsandindustrialreformarenotpartofNERA’sscope

INTRODUCTION TO THIS SCP

29National Energy Resources Australia – Sector Competitiveness Plan 2017

LIKELY EVOLUTION OF THE SECTORFor the foreseeable future, the energy resources sector will continue to make a significant contribution to the economic stability of Australia. However, as the world’s energy balance continues to evolve, the sector must adapt to remain competitive. While the full impact of the macro changes in the sector are hard to foresee, many aspects of the sector’s evolution during the coming decade can be more easily predicted.

Asian demand

A sustained increase in Asian demand across all energy resources is expected, as India and the Association of Southeast Asian Nations (ASEAN) take up the slack from plateauing Chinese demand. Indeed, the global demand for energy is anticipated to increase by 34 per cent between 2014 and 2035 7. Australia is ideally located to service much of this growth, and can reasonably expect continued development in export volumes and revenue growth.

High capacity export industry

In the near future Australia is forecast to overtake Qatar as the world’s largest producer of LNG, though Australia could be challenged by capacity increases in the United States depending on how the United States gas market develops. Similarly, Australia already enjoys a very strong position as one of the world’s top exporters of coal and uranium. Having invested substantially in the infrastructure to achieve these rankings, the sector needs to continue to invest in their operations to ensure a strong future.

International nuclear revival

The extent and magnitude of the nuclear revival, and its impact on current uranium over-supply, could make a significant difference to Australian energy exports. In addition, an increased acceptance of uranium locally may result in other aspects of the downstream nuclear value chain being considered.

Renewable energy sources

With the increasing penetration of both wind generation and rooftop solar, electricity distribution networks are experiencing major disruptions. The impact of this change will be further deepened by the growing deployment of domestic battery storage. These technologies are exerting new pressures on the traditional coal and gas fired assets of electricity generators and distribution networks as the flow of electricity changes from purely outbound from the power stations, to a more dynamic and complex pattern.

Demand for coal

Domestically, increased commitments to reduce CO2 emissions, coupled with a move towards renewable energy sources, means that domestic demand for thermal coal may decline over the next 10 years. However, developments in clean technologies such as carbon capture and storage and increased export demand from Asia as high-quality Australian coal displaces domestic Asian production, is likely to offset this decline. Demand for metallurgical coal is expected to increase in the medium term with reinvigorated demand from China and other parts of Asia. Meeting this ongoing demand will require the timely approval of new developments to ensure adequate capacity.

Exploration challenges

The growth of the Australian energy resources sector is dependent on its ability to identify, appraise and produce from new fields and deposits cost effectively. However, the viability of exploration activities on these future and frontier assets are being placed under serious question. Exploration companies are subject to an increasingly onerous and unpredictable regulatory burden. For example, the future viability of the Australian oil and gas sector is being placed at risk by the current lack of exploration, especially because, in the current low-price environment, companies are producing from their reserves faster in order to maintain revenue but are not adding new reserves to their portfolio through exploration to ensure future production capacity.

In parallel, activist shareholders are applying growing and conflicting pressures by simultaneously demanding greater immediate returns on their investments in a traditionally long-term industry and also divesting investments in industries such as fossil fuels, which are out of favour with sections of the broader society.

INTRODUCTION TO THIS SCP

EXECU

TIVE SU

MM

ARY

30 National Energy Resources Australia – Sector Competitiveness Plan 2017

Optimisation focus on facilities

Significant capital investment in new major energy resource projects appears unlikely in the short to medium term, in view of the major expansion phase across the sector, most visible in the growth of the LNG industry, coupled with the decline in commodity prices for the sector over the last two to three years. The focus is expected to be on optimisation of new and existing facilities through productivity and efficiency improvements while maintaining capacity through smaller projects.

HELE and CCS Development

To enable industry growth to continue within required COP21 (also known as the 2015 Paris Climate Conference) emission levels, the energy resources sector will need to develop high efficiency, low emissions (HELE) technologies for coal fired power generation and CCS for both coal and gas.

Incentives for research and development

The focus on operational and social licence to operate research and development has been a strong industry-wide activity in the coal sector through the work of the Australian Coal Industry’s Research Program (ACARP) 8, where a small voluntary but sector wide levy is placed on production.

The fund generated from this levy, which qualifies under research and development tax incentive legislation, is managed by an industry body to support an ongoing list of around 200 individual and focussed research initiatives across the industry, including funding a number of PhD scholarships 9. Such an independent, industry focussed scheme could be considered for the Australian oil and gas sector to build a broad, industry wide and transparent research community to examine issues of interest to the sector, complementing the joint industry project (JIP) model more traditionally employed by the sector.

SUMMARY

The Australian energy resources sector faces major challenges to remain competitive in the increasingly complex modern global energy market.

Maintaining Australia’s current position as a world leading energy resources producer will require transformative effort by all those directly and indirectly involved across the oil and gas, coal and uranium industries.

While global and regional demand for our energy resources continues to be strong, internal disruptions in each market are placing complexity on what has, for a long time, been a relatively stable mix of energy demand. The Australian energy resources sector needs to adapt to these market disruptions and it must be prepared to undergo both incremental and transformational changes.

Incremental improvement

Incremental improvements include leaner operations, better management of high cost activities, particularly in the areas of new projects and other major capital investments, sharing infrastructure both at facilities and in locations such as maintenance and supply bases, collaborative planning of maintenance and upgrade activities to avoid competition over labour and shop time, reviews of staffing levels both at the facilities and in the various national head offices, and an increasing drive to improve productivity from new and existing assets. However, these incremental improvements alone will not be enough to keep pace with change.

Transformational improvement

Transformational change is required for the sector to keep pace with the shifting energy paradigm and meet global challenges. The sector needs to develop new operating models, focusing on new and innovative approaches to execution and better leveraging of existing capacity. Given the expected high level of automation in future operations, we need to build on Australia’s highly regarded existing capabilities in areas such as remote operations and data analytics for process optimisation and decision making, to support operational and value chain optimisation.

INTRODUCTION TO THIS SCP

31National Energy Resources Australia – Sector Competitiveness Plan 2017

Finding ways to exploit the opportunities presented by the disruptions will be vital to the future of the Australian energy resources sector, allowing it to continue to play a significant role in the global energy mix.

Opportunities exist for Australia to continue to act as a baseline energy source to meet the sustained and increasing demand from Asia. But Australia needs to build strengths in the development of alternative and renewable energy sources. Australia is well placed to assist developing nations, particularly those transitioning from fossil fuels, to meet their emissions reduction commitments by providing energy diversification and reliable electrical grids and systems.

Standing still is not an option. In the modern energy resources environment, continually exploring ways to change regulatory, business and operational models is required of all participants to simply remain competitive.

As set out in this SCP, the Australian energy resources sector must find ways to:

• Collaboratebetterinallways,betweenpeerorganisations,verticallywithinvaluechains,acrossthe traditional boundaries between industries and with research organisations where directed and undirected findings can help lift the productivity of the industry;

• Explorewaystoaddresstheregulatoryburdenthatisrestrainingmanyareasoftheenergyresourcessector from growing into the future, but in ways that maintain and enhance community support for the industry; and

• Identifyandexplorenewmarkets,createopportunitiestofillneedsinthemarketplaceordisplaceexpensive import alternatives, such as expanding the use of LNG as a domestic source of energy.

NERA is committed to working openly with stakeholders to identify and pursue strategic initiatives and projects that will assist the Australian energy resources sector to adapt to current and future challenges and disruption.

NERA will achieve this through directing research and technology development to meet the needs of operators and end-users in ways which are tied to commercial pathways. It will facilitate industry-led projects and ensure they address NERA’s strategic themes, knowledge priorities and strategic initiatives set out in this SCP and are endorsed/supported by the energy resources sector and stakeholders.

NERA is not acting alone in this endeavour, but is building on the work of many previous sector wide and specific economic and industry reports and research initiatives. Many of these previous reports have substantially similar findings, whether they investigated a single industry or jurisdiction, a specific technology or considered the broader energy resources sector in its entirety.

Achieving an Australian energy resources sector that remains globally competitive over the next 10 years and beyond will require significant innovation, growth and behavioural change. To be considered competitive, Australia needs to be:

• Atop-rankedlocationforenergyresourcesinvestment–somewhereinternationalanddomesticoperators seek to invest because it is cost competitive and has a strong reputation with a stable and supportive policy and regulatory environment, and is recognised as a centre of excellence for knowledge and skills;