Embedded Competitiveness: Taiwan's Shifting Role in ...

307

Embedded Competitiveness: Taiwan’s Shifting Role in International Footwear Sourcing Networks Lu-Lin Cheng Department of Sociology Duke University 1

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Embedded Competitiveness: Taiwan's Shifting Role in ...

Embedded Competitiveness: Taiwan’s Shifting Role in International

Footwear Sourcing Networks

Lu-Lin Cheng Department of Sociology

Duke University

1

Embedded Competitiveness:

Taiwan’s Shifting Role in International Footwear Sourcing Networks

ABSTRACT

The thesis studies Taiwan’s shifting role in international footwear sourcing networks over

the last three decades. It draws on multiple sources of data, including in-depth interview,

field observation, and published data, to construct phases and faces of the socially

embedded market. The research points to the anomalies in the comparative advantage

theory, evaluates the weakness of the state-centered and production-centered sociological

approaches in giving satisfactory explanations, and demonstrates a global commodity

chain approach which analyzes the changing institutional infrastructure, social

networking, and transaction organizations that have been shaping the changing positions

of Taiwanese footwear producers in the footwear OEM export market. The study shows

that production site transitions in the world footwear market are not universalistic.

Given similar state policy and environmental challenges on the global and local levels,

the differences between the Japan-to-Taiwan and Taiwan-to-China transitions reveal the

historically contingent and organizationally operated nature of markets.

2

TABLE OF CONTENTS

Acknowledgements............................................................................................................6

List of Tables ................................................................................................................. 7

List of Figures and Maps .............................................................................................. .9

Part I Case, Theory, and Method

Chapter 1 The Global Footwear Market and the Taiwanese Footwear Industry .......11

The World Footwear Market and the Fable of Economics................................11

Taiwan and its Miracle Economy......................................................................19

The Footwear Industry in the Industrialization of Taiwan.................................21

The Footwear Question: Taiwan’s Shifting Role in International Market........ 27

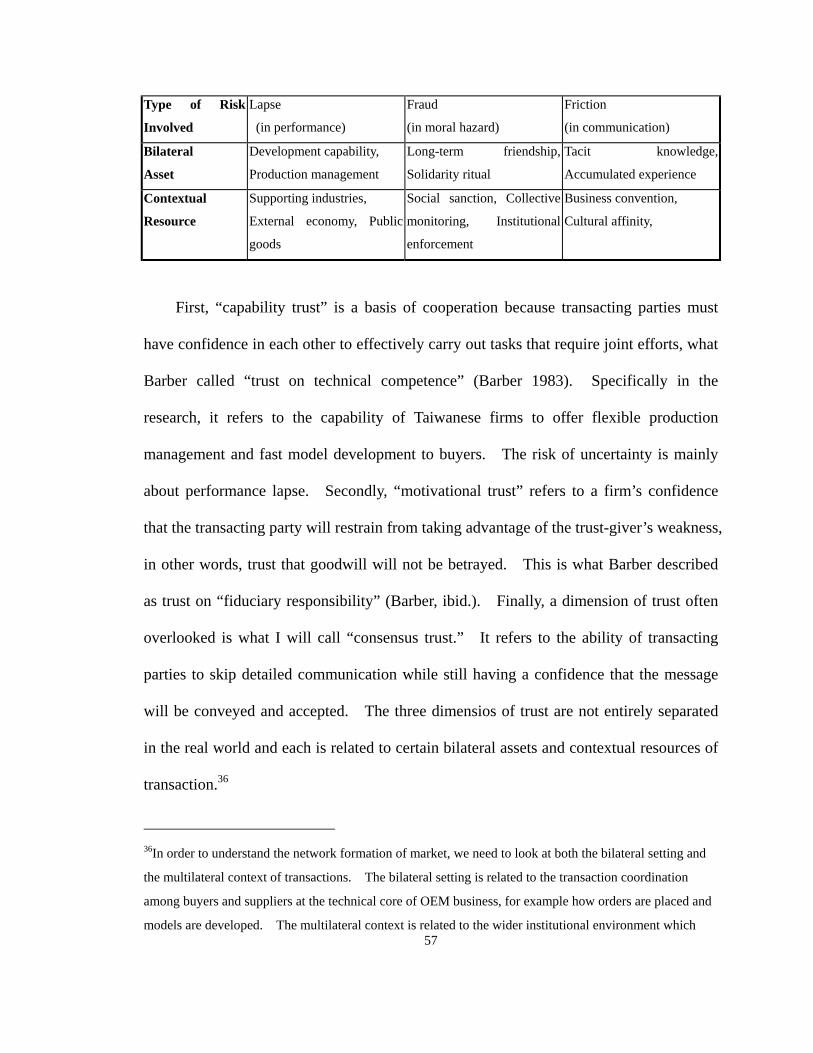

Chapter 2 Theory, Major Arguments, and Method ............................................30

Economics vs. Sociology: Fundamental Statement.......................................... 31

From Comparative Advantage to Commodity Chain........................................34

Price-Mediated Market vs. Trust-Mediated Market......................................... 44

Trust, Transaction Organization, and Institutionalized Resource ................... 51

Research Method I: Qualitative Interview.........................................................58

Research Method II: Field Observation............................................................ 64

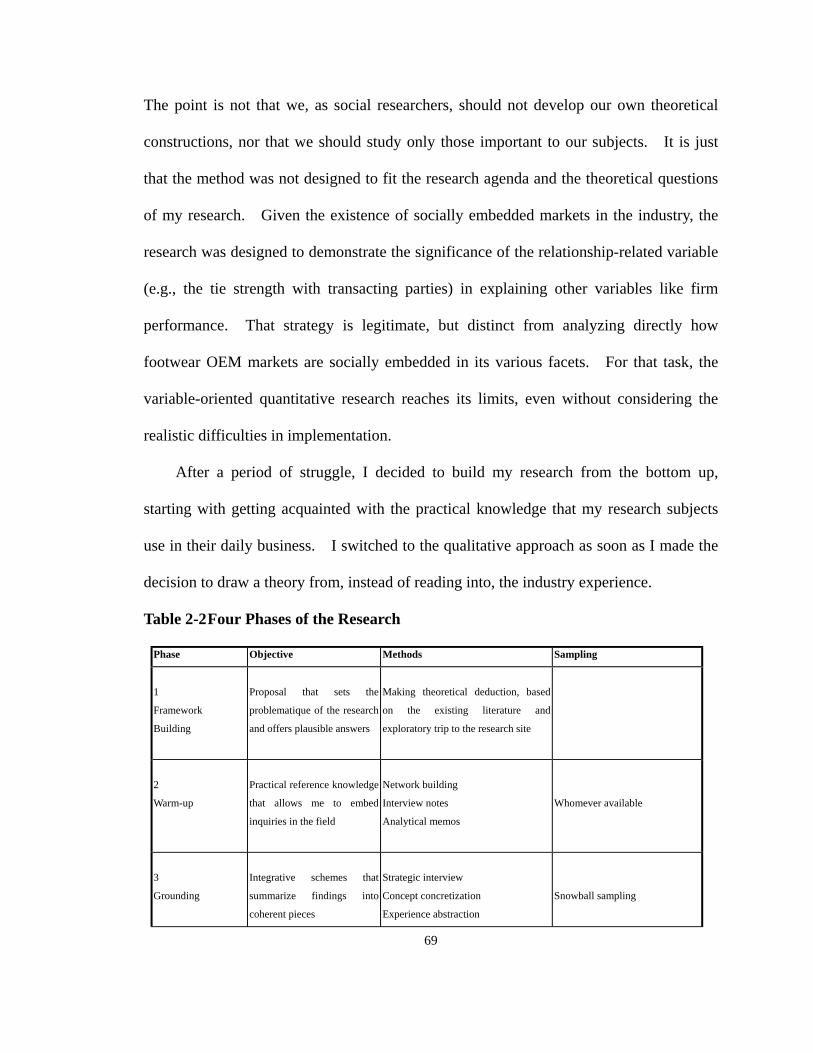

Phases of the Research...................................................................................... 68

Part II Taiwanese Footwear Industry in its Booming Years (1960-1986)

Chapter 3 Institutional Formation of the Industry: From TPSEA to TFMA..... 77

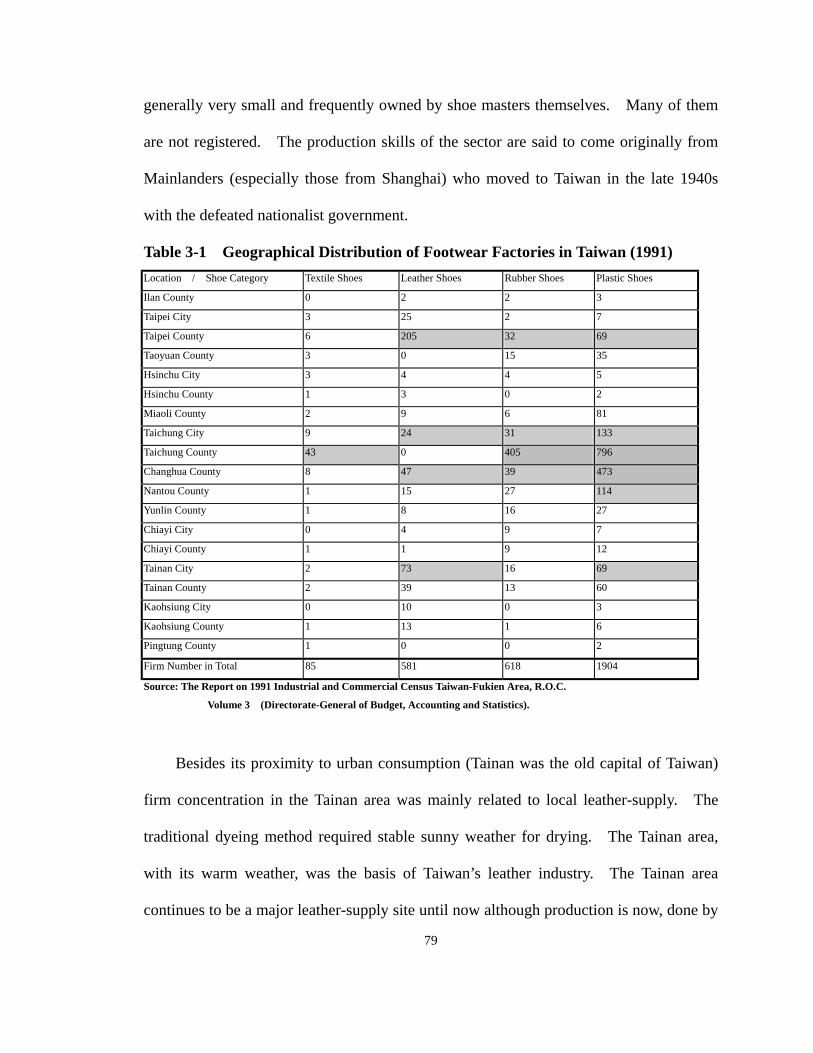

Historical Origins of the Taiwanese Footwear Industry: Straw Hat Exports.... 78

The Growth of Upstream Plastic Industry........................................................ 84

The Birth of TPSEA and the Industry Institutionalization............................... 87 3

Evaluating the Japanese Influence.................................................................... 90

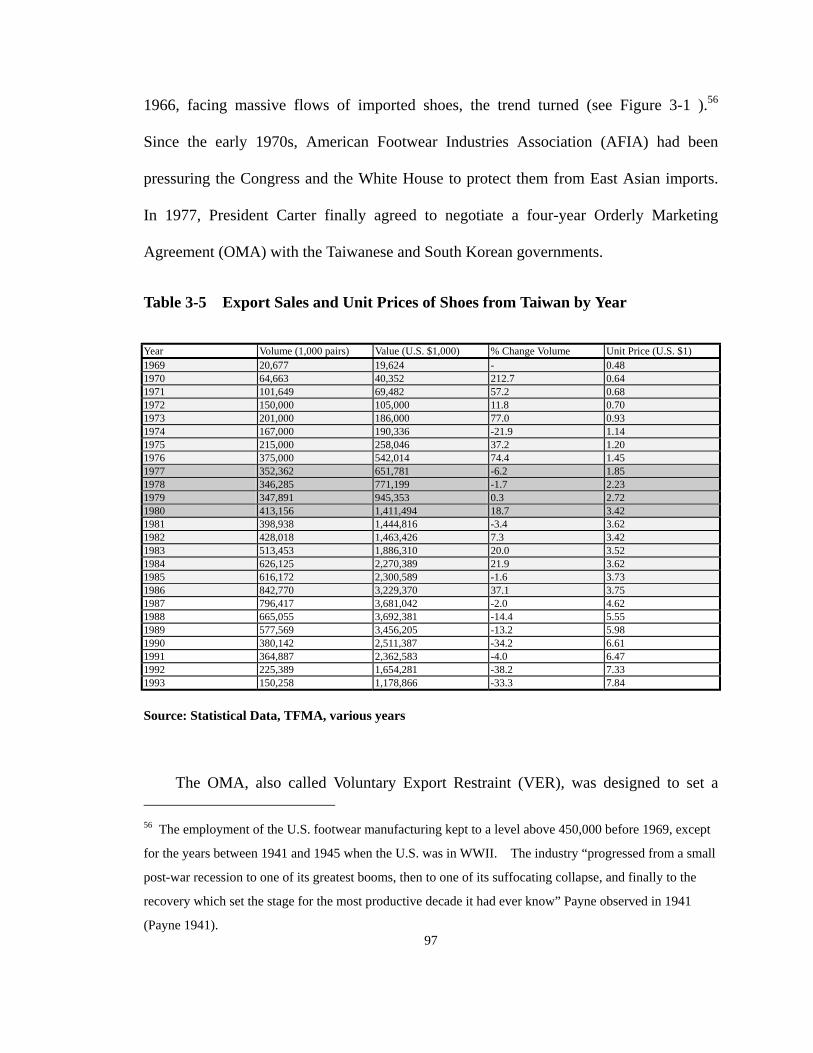

Protectionism Came After Booming Growth: OMA........................................ 96

Economics’ Evaluation on OMA.....................................................................101

Taking Advantage of OMA Institutionally: The Birth of TFMA................... 104

Taking Advantage of OMA Institutionally: Quota Management....................106

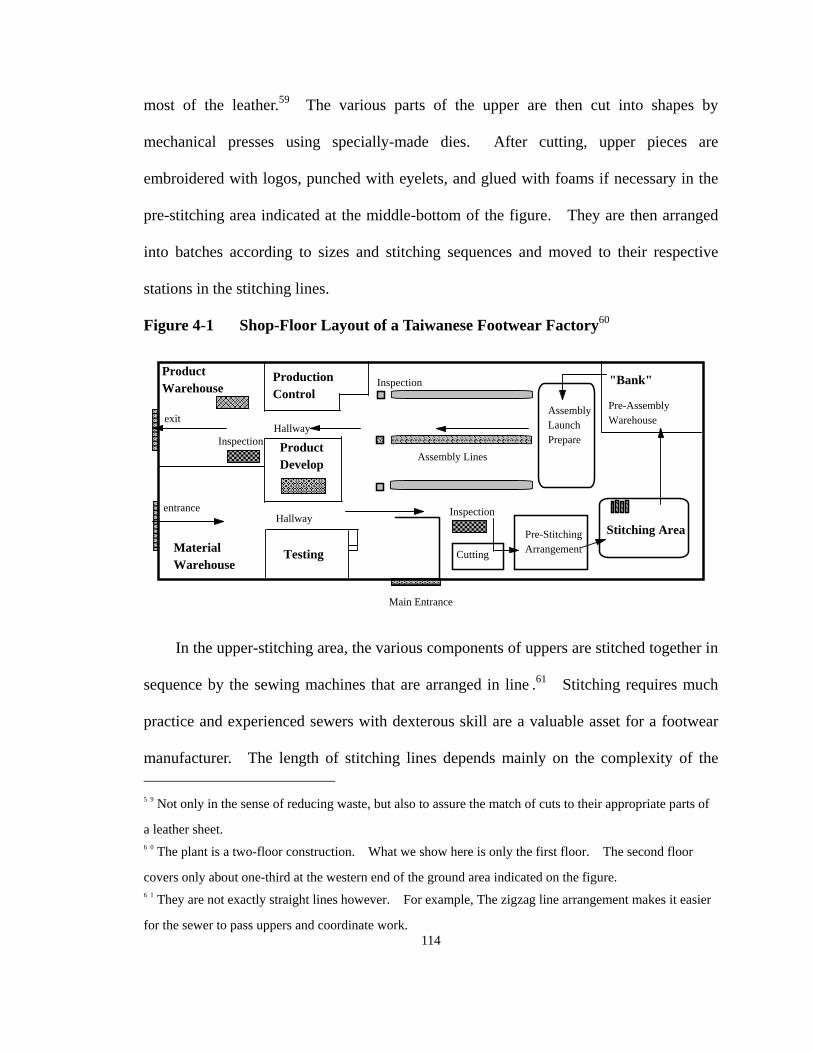

Chapter 4 The Socially Embedded Footwear Commodity Chain.......................112

Shop-floor Arrangement of a Taiwanese Footwear Factory............................113

Footwear OEM Export Network: Beyond In-house Production......................120

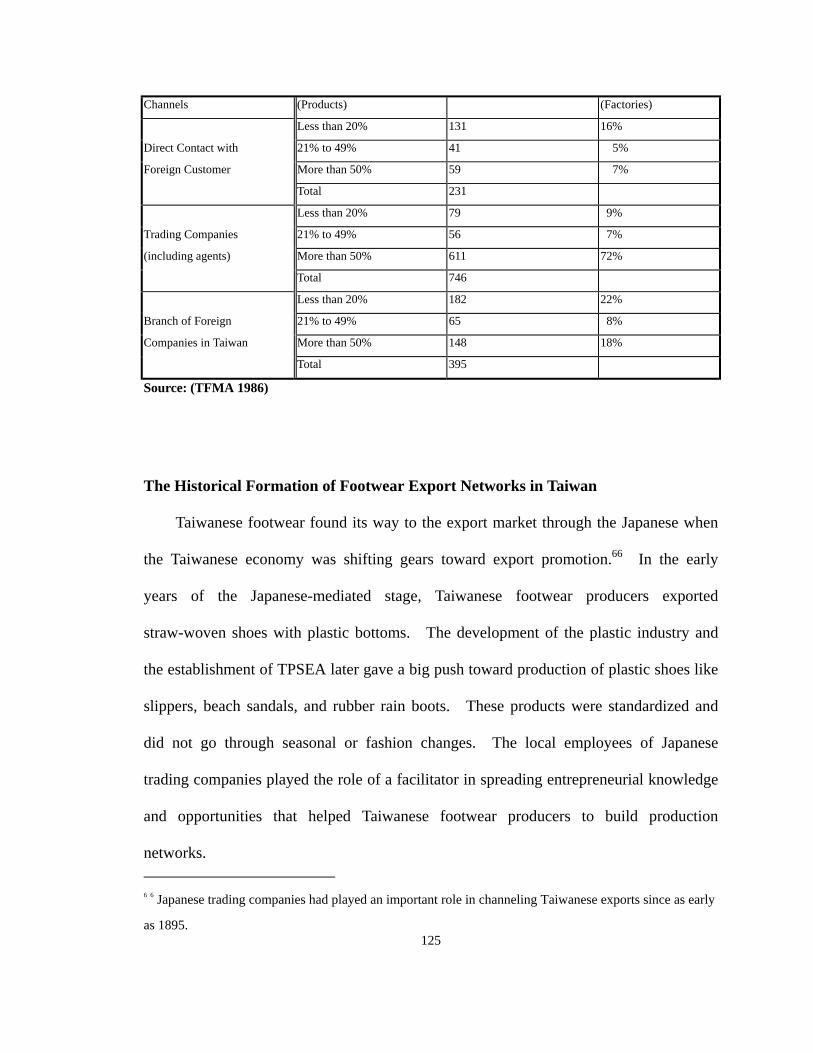

The Historical Formation of Footwear Marketing Networks in Taiwan........ 125

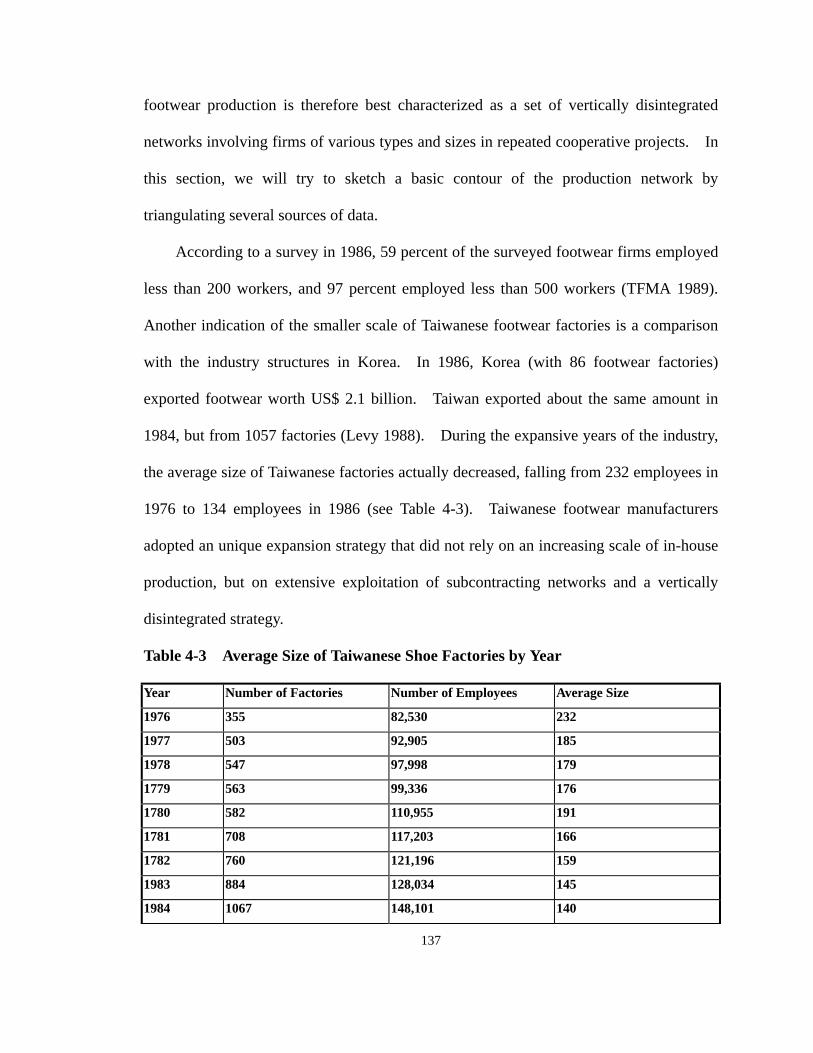

Expansion of the Production Network in Taiwanese Footwear Industry........136

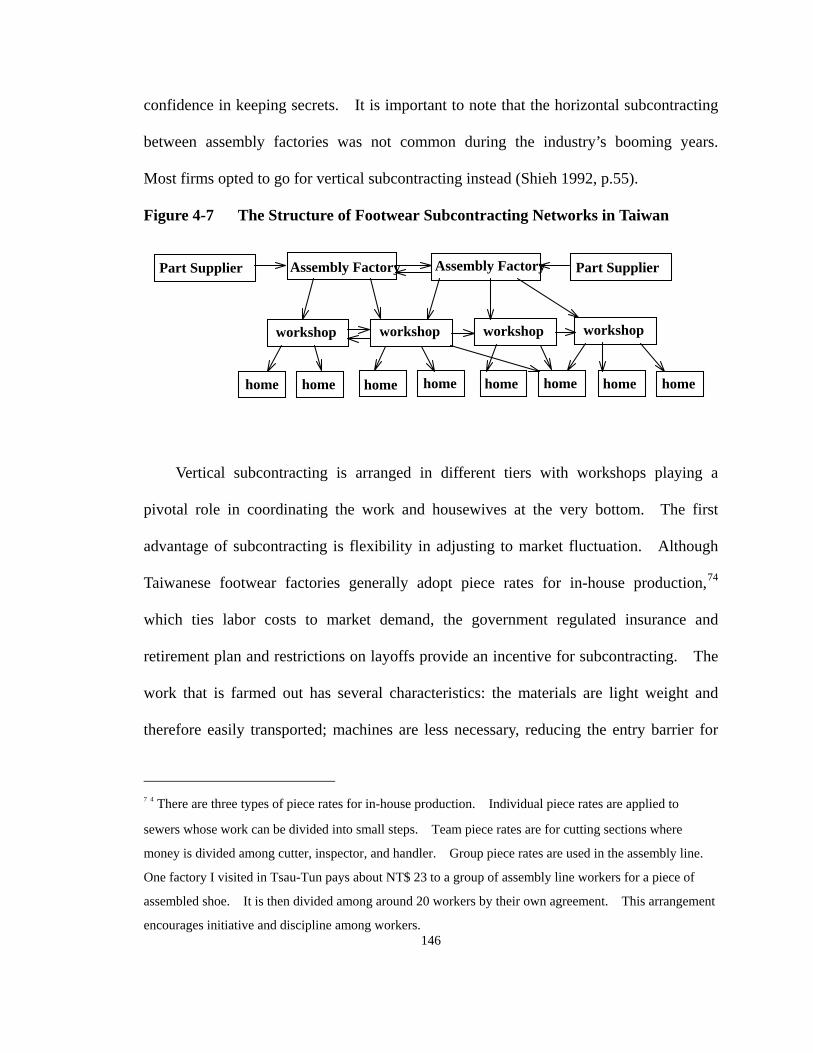

Dynamism of the Taiwanese Footwear Subcontracting Networks..................145

Chapter 5 The Design-Sensitive Market, New Competition, and Market Closure

..........................................................152

The Emergence of New Competition in the 1980s..........................................154

Design-Intensiveness and Development Uncertainty in DS Transaction....... 161

Faces of Network Closure in the DSM: Exclusive Sourcing.......................... 165

Faces of Network Closure in the DSM: Tight Coupling................................ 175

Faces of Network Closure in the DSM: Culture of Commitment.................. 179

Chapter 6 The Cost-Sensitive Market, Flexible Imitation, and Quick Response

..........................................184

Cost-Sensitive Buyers and the Follower Strategy........................................... 185

Speed, Timing of Entry, and Flexible Imitation............................................. 190

Risk, Timing of Exit, and the Use of Competition .........................................198

Quick Response and Cushion Nets in Overlapping Networks........................205

Part III Industry Internationalization (1987-1995)

4

Chapter 7 Institutional Embeddedness of FDI in China.................................. 212

Industrial Crisis of the Taiwanese Footwear Industry.....................................214

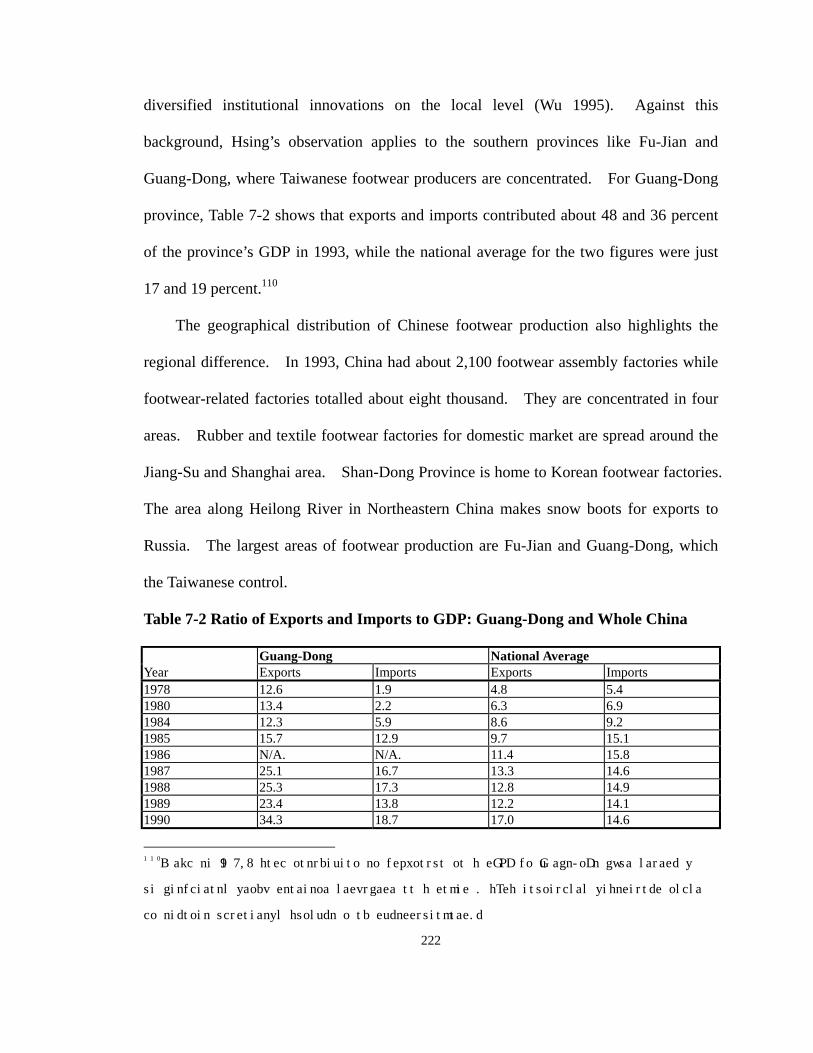

Searching for a “Second Spring” in China..................................................... 219

Dong-Guan: the Taiwanese Shoe Nest in China..............................................221

Institutional Embeddedness as Buffering: FDI in Disguise.............................227

Restructuring a Labor Regime........................................................................ 233

The Formation of a Taiwanese Footwear Industrial District...........................239

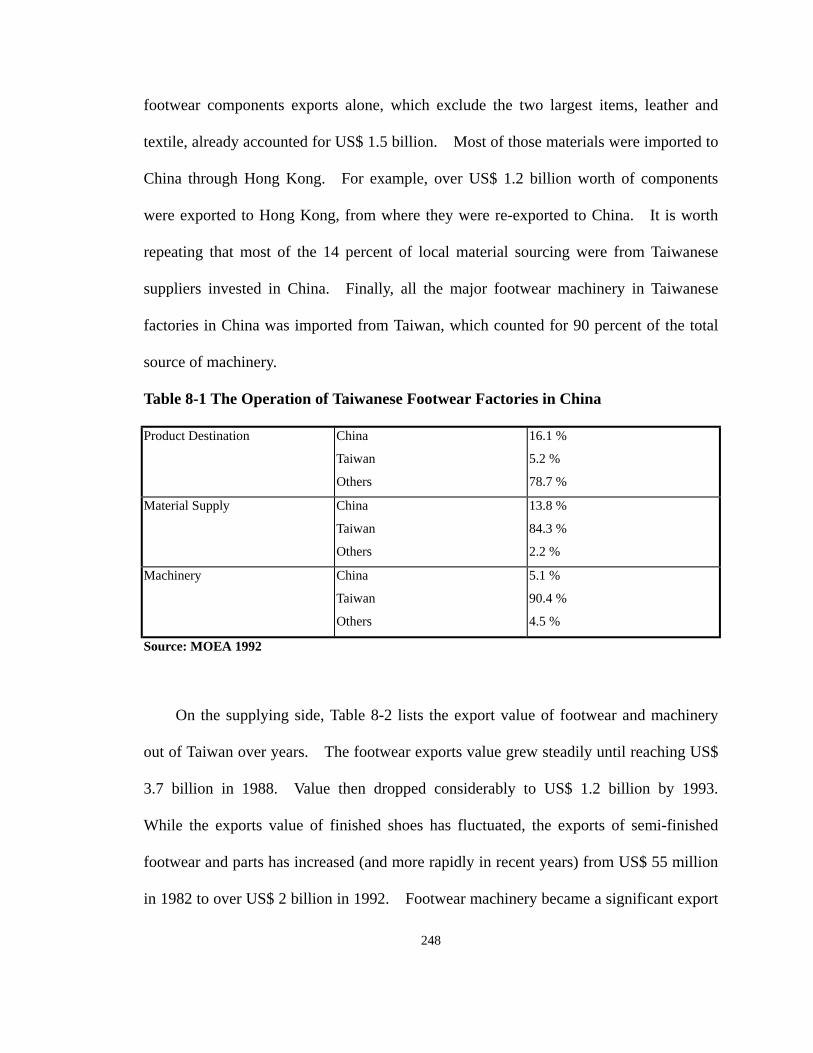

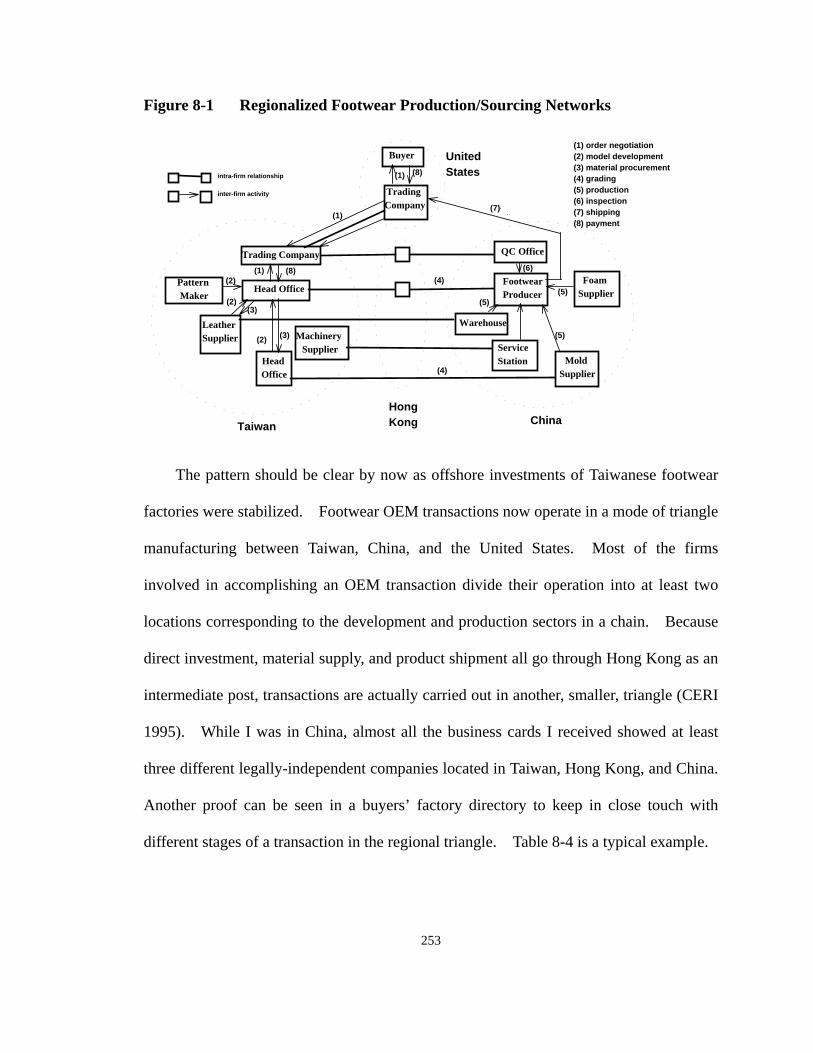

Chapter 8 Restructuring Regional Sourcing Networks in the 1990s............... 246

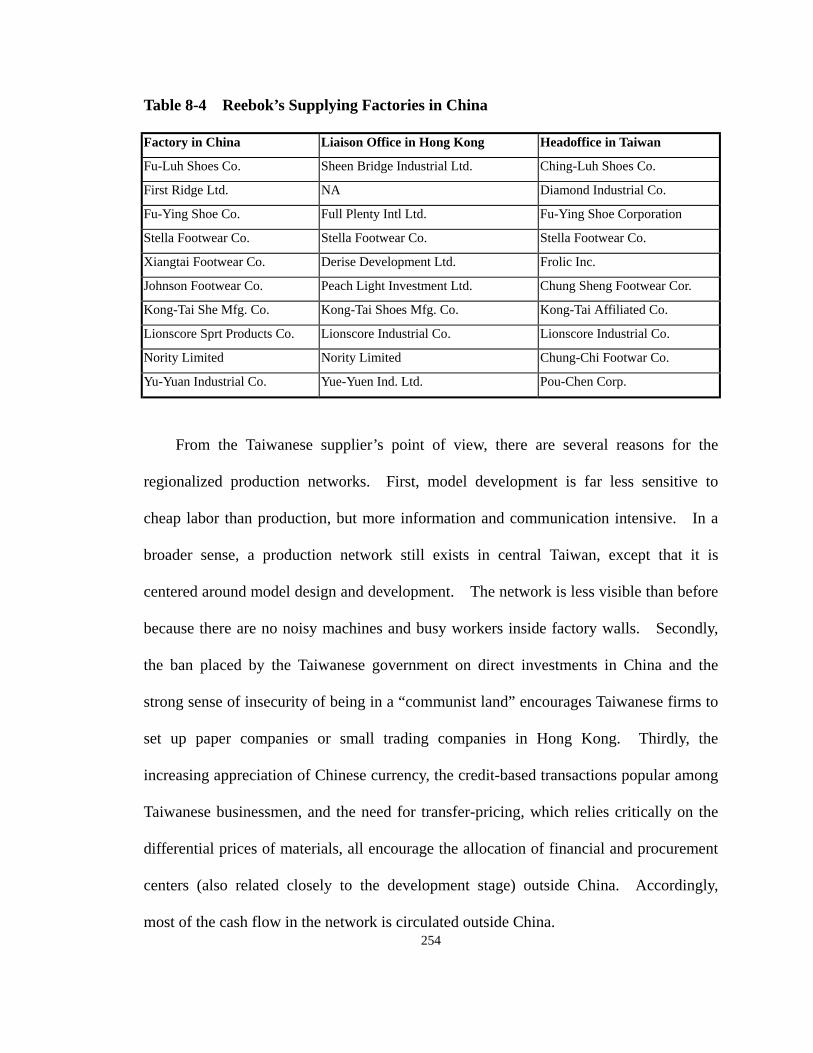

Division of Labor Regionalized: Triangle Manufacturing..............................247

Cheap Labor is Not Easy to Use: the Buyer’s First Move...............................255

Invisible Shoe Nest in Taiwan: a Strong Sourcing Arm for Buyers................260

Production Site Transition: Limits of Comparative Advantage.......................269

Reference.................................................................................................................278

Appendix I Interviewee List........................................................................................ 295

Appendix II Abbreviations and Acronyms...................................................................299

Appendix III Maps .......................................................................................................287

5

ACKNOWLEDGEMENTS The intellectual integrity and infinite patience of my advisor, Dr. Gary Gereffi, have always

been the benchmark for my learning. I hope this thesis proves worthy of the many discussions

we have conducted and the encouragement he has given me over the years. I am also indebted

to Dr. Nan Lin, Dr. John Wilson, Dr. Angela O’Rand, Dr. Thomas Janoski, Dr. Gao Bai, Dr. G. S.

Shieh, Dr. C.M. Ka, and Dr. C. Y. Wu for their comments and suggestions, which helped me

clarify my dissertation significantly. The last four professors invited me to the area of economic

sociology. I hope this thesis, as my first step, shows the same encouragement. Dr. Hsin Huang

Michael Hsiao and Dr. Cheng-Kuang Hsu were the advisors of my master thesis in the National

Taiwan University. I apreciate their continuing support during my stay at the Institute of

Ethnology.

I want to thank those friends I met during the fieldwork who not only made the research

possible but also a rich journey: Morris Lin, Popper Hsu, Michael Cooper, Kenith Luo,

Mao-Shuh Ren, Yi-Kun Lin, Justine Wang, Wei-Chin Lee, Homer Lu, You-Tsu, Jack Lin, Seio

Nakajima, Shiro Honda, James Mann, Calvin Kao, Albertto Dy, and many others who kindly

offered precious time and wisdom to my research. Many wonderful friends, An-Ru, Mei-Lin,

Latiff, Hon-Chiu, Insook, Chih-Jou, Jinn-Yuh, and Irene, to name just a few, have been

challenging me to give the thesis a better shape. I wish their research successful. Thanks also

go to two institutes: the Institute of Ethnology, Academia Sinica, which provided me a very

supportive research environment, and the Chiang Ching-kuo Foundation, which offered me a

research fellowship for my fieldwork.

My wife, I-Yin, has accompanied me over the years, especially during the most difficult

time of the research, with loving support and hard-earned money. This thesis is as much hers as

my own. It’s now time for me to support her carreer. I hope her dream will come true in the

very near future.

We thank our parents who have been encouraging us in both our family life and individual

careers. Finally, this thesis is dedicated to my grandmother, Her-Li (1909-1995), who passed

away a year ago after a year of difficult struggle with a serious stroke. We had learned from her

a fading tradition of Taiwanese culture and are still nurtured by her endless care and love.

We will always miss her.

6

LIST OF TABLES Table 1-1 Market Shares of US Non-Rubber Footwear Imports, by Volume

Table 1-2 Wage and Unit Price of Footwear Exports in Selected Countries (1990)

Table 1-3 General Features of Taiwanese Society and Economy

Table 1-4 Number of Registered Footwear Factories, 1969-1994

Table 1-5 Ranks of Taiwan’s Principle Export Industries (1981-1994)

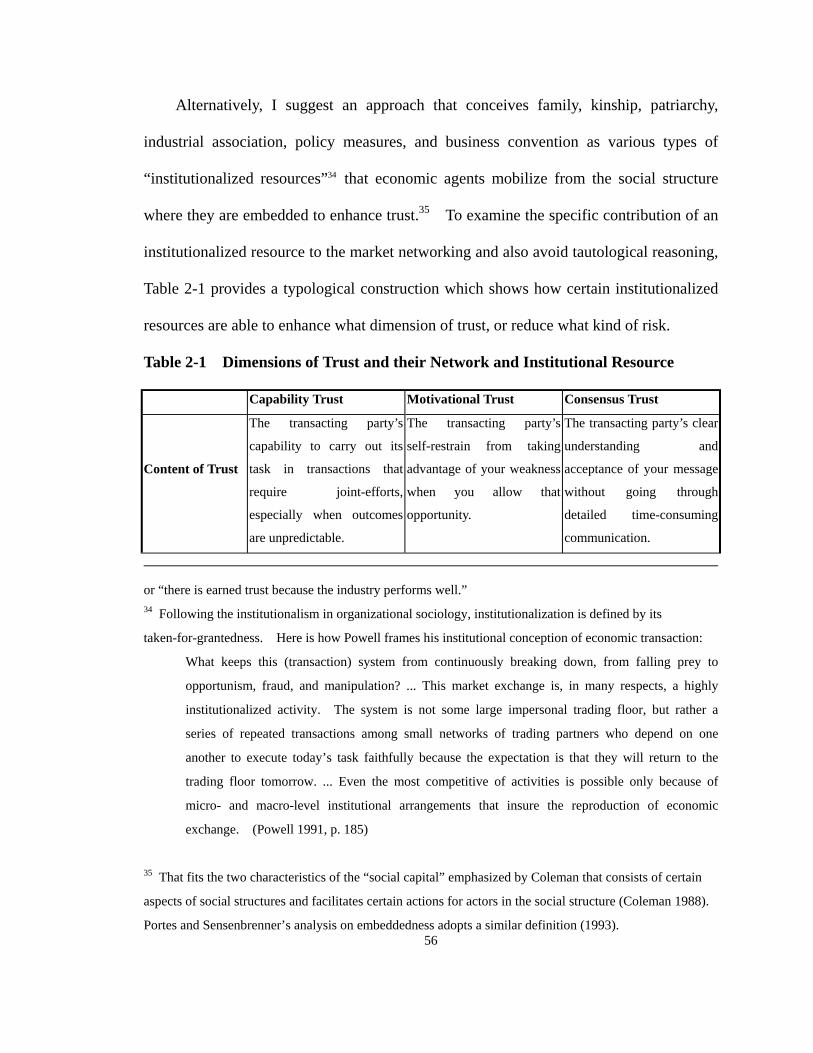

Table 2-1 Dimensions of Trust and their Network and Institutional Resource

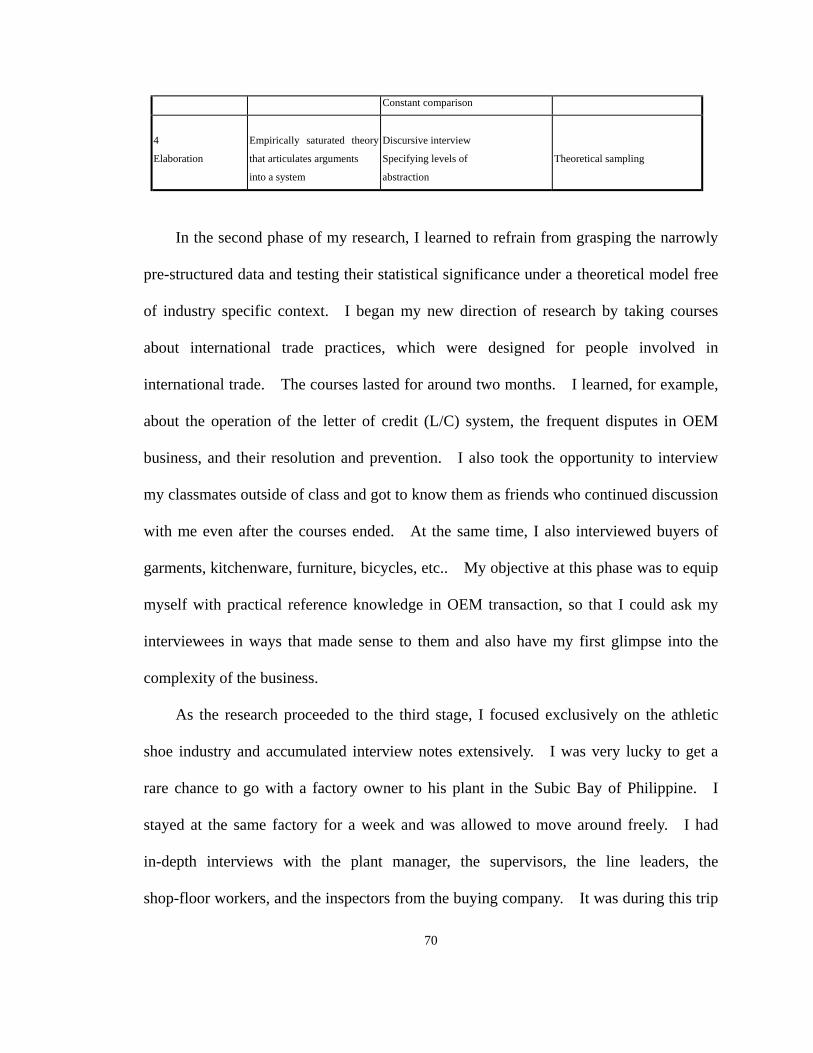

Table 2-2 Four Phases of the Research

Table 3-1 Geographical Distribution of Footwear Factories in Taiwan (1991)

Table 3-2 Structure of Plastic Shoe and Plastic Goods Industry

Table 3-3 The Structure of Japanese Footwear Exports (unit: million US $)

Table 3-4 Approved DFI and Capital Formation, selected years

Table 3-5 Export Sales and Unit Prices of Shoes from Taiwan by Year

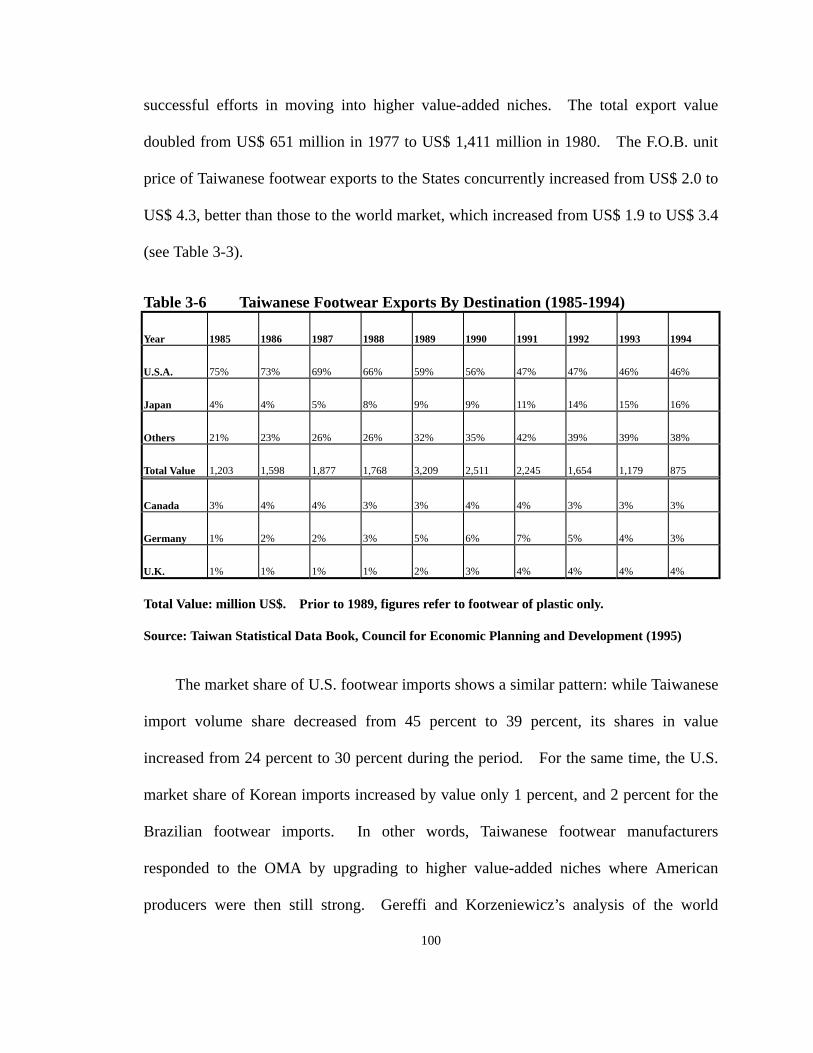

Table 3-6 Taiwanese Footwear Exports By Destination (1985-1994)

Table 4-1 Export Marketing Channels of Taiwanese Footwear

Table 4-2 L/C Payment in Total Export Trade from Taiwan, 1976-1992

Table 4-3 Average Size of Taiwanese Shoe Factories by Year

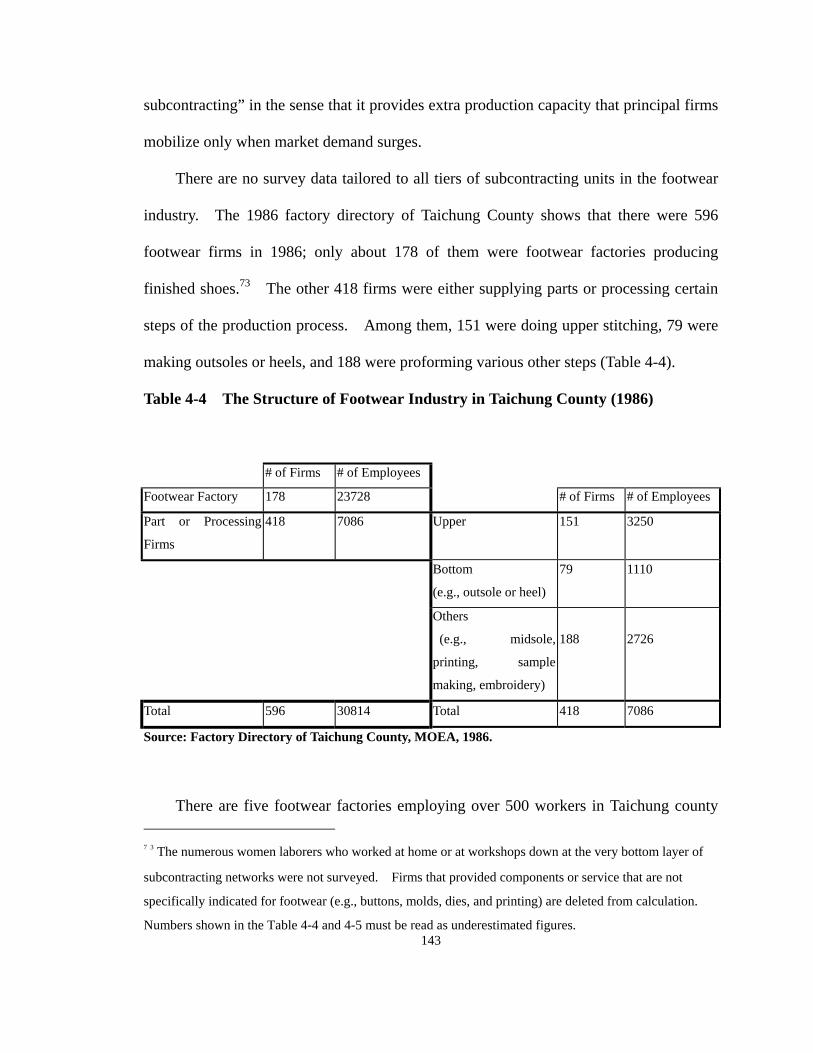

Table 4-4 The Structure of Footwear Industry in Taichung County (1986)

Table 4-5 Size Distribution of Footwear Firms in Taichung County

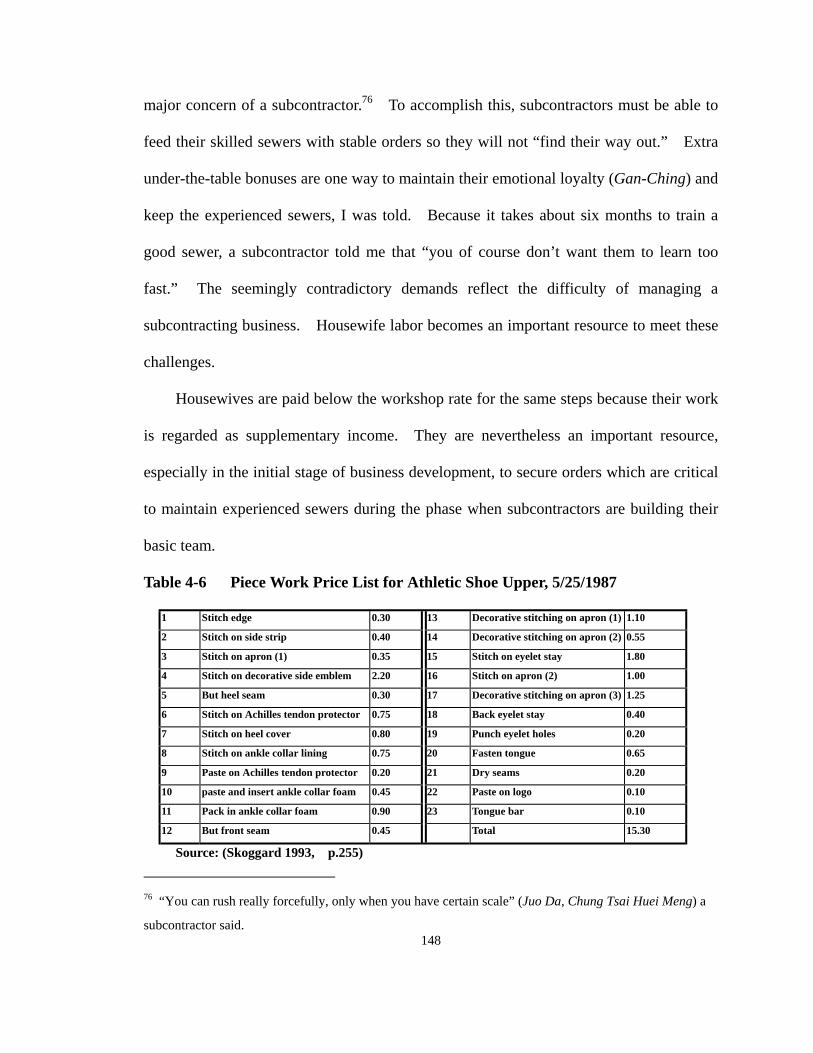

Table 4-6 Piece Work Price List for Athletic Shoe Upper, 5/25/1987

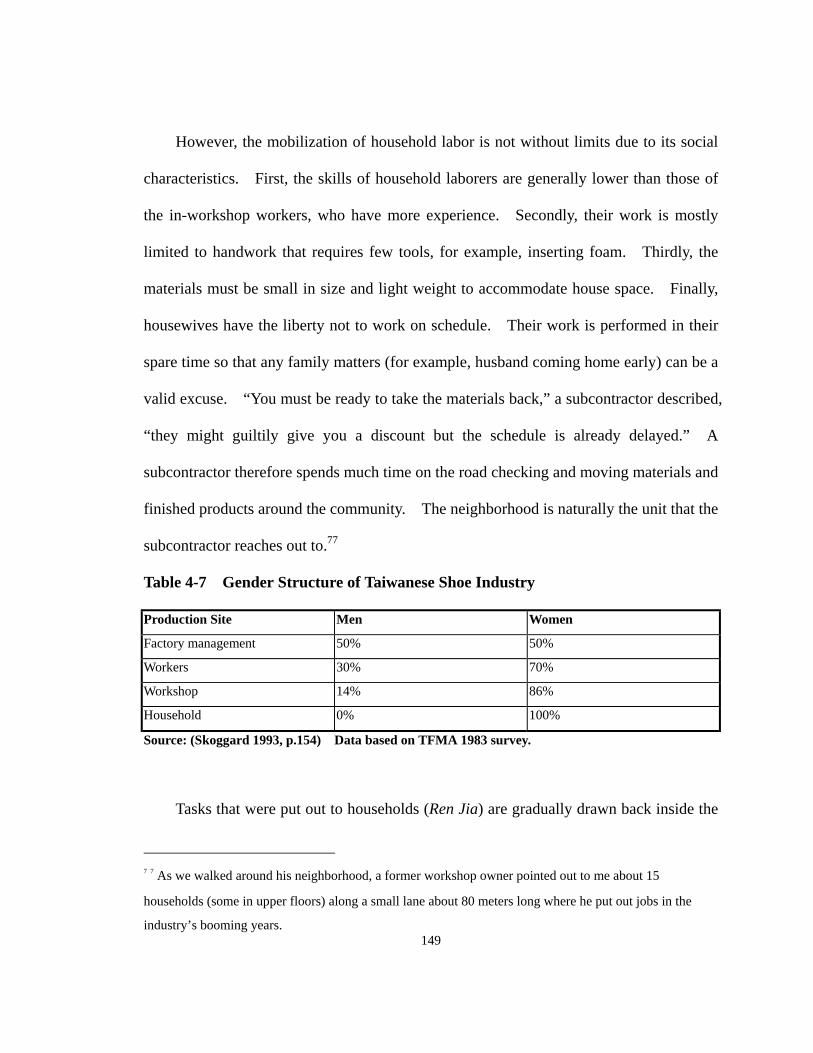

Table 4-7 Gender Structure of Taiwanese Shoe Industry

Table 5-1 The Causes and Consequences of Network Closure in the DSM

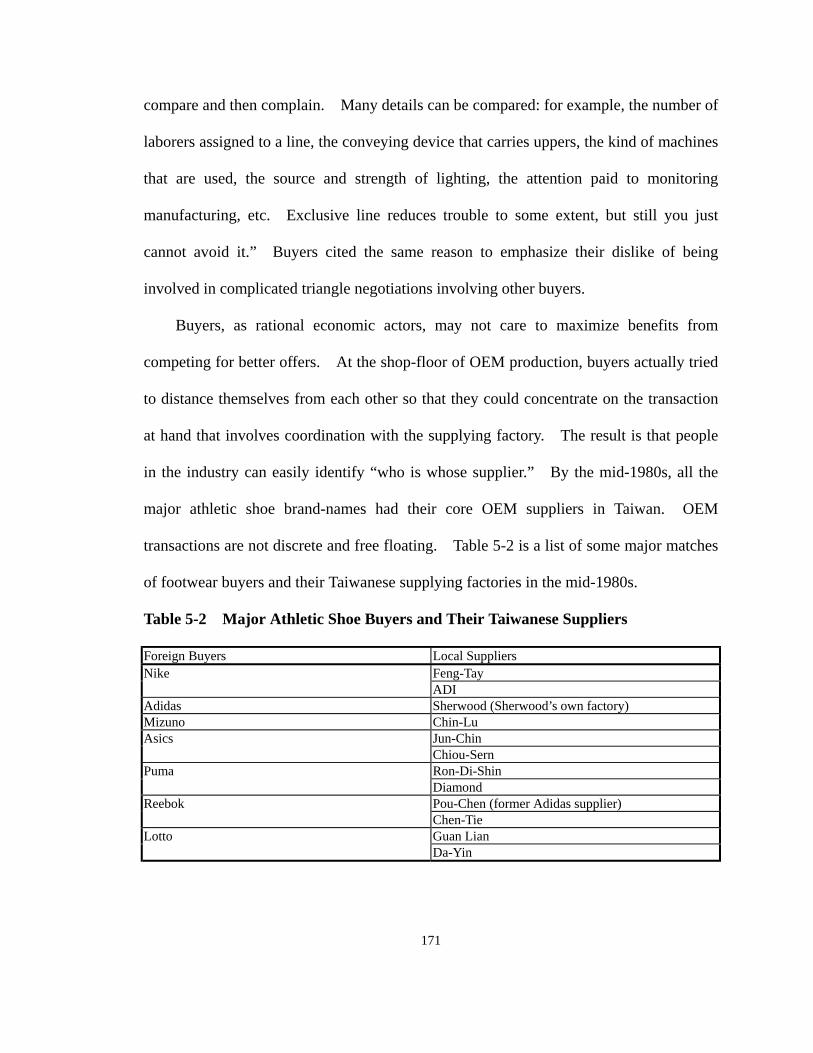

Table 5-2 Major Athletic Shoe Buyers and Their Taiwanese Suppliers

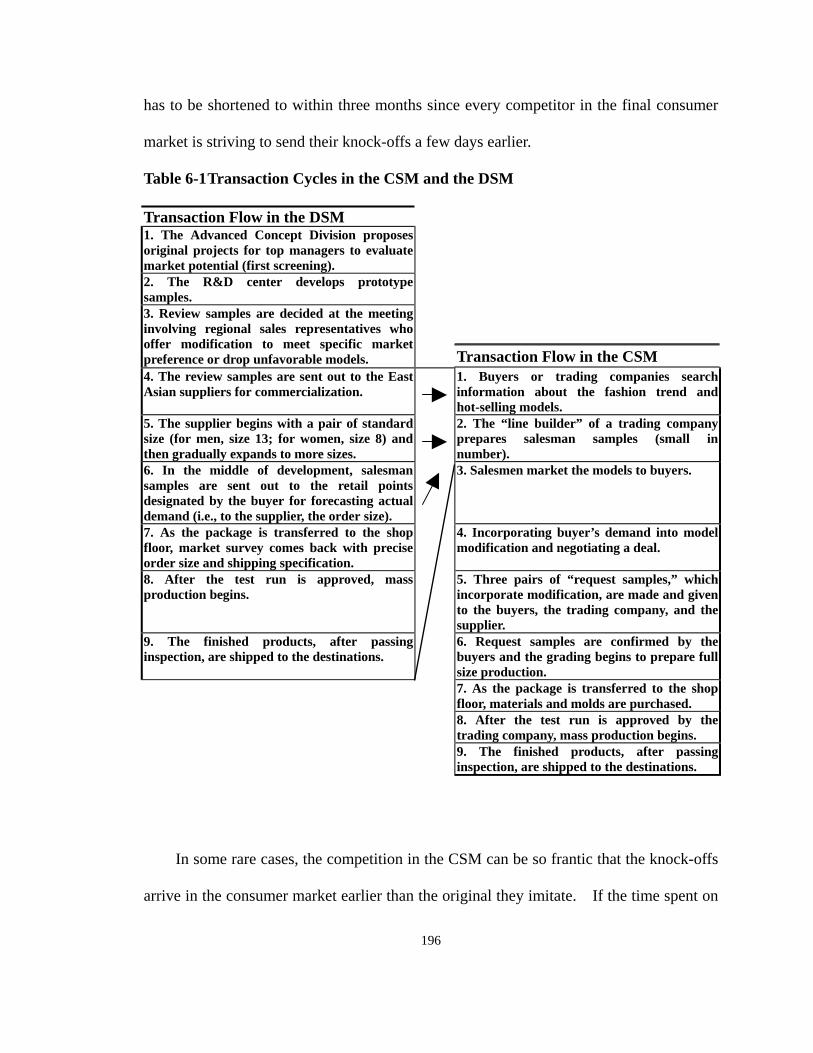

Table 6-1 Transaction Cycles in the CSM and the DSM

Table 6-2 Factory H’s Production Schedule for Late-March (an example)

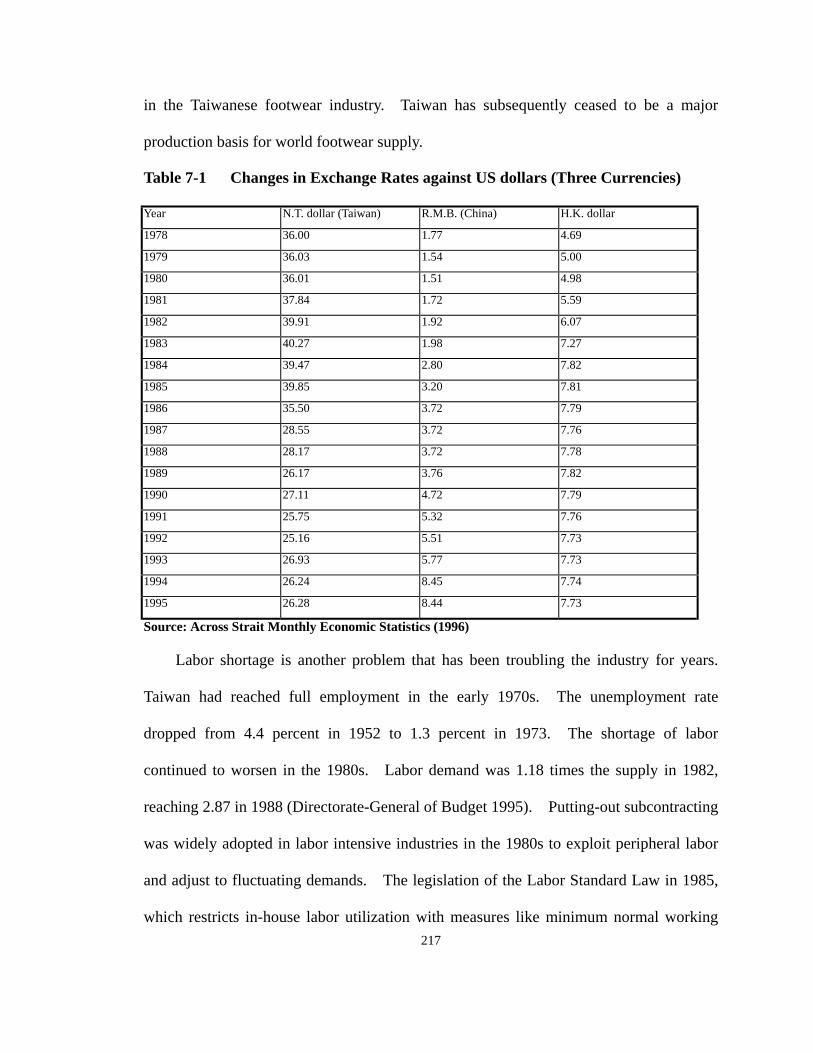

Table 7-1 Changes in Exchange Rates against US dollars (Three Currencies)

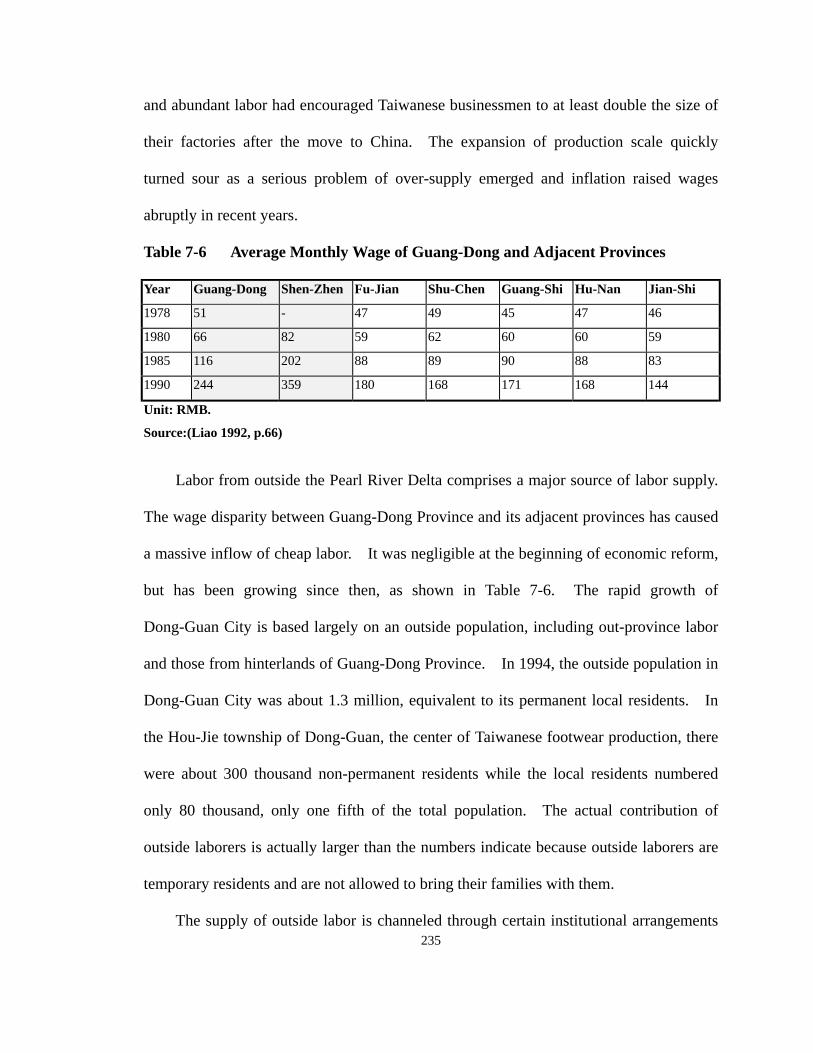

Table 7-2 Ratio of Exports and Imports to GDP: Guang-Dong and Whole China

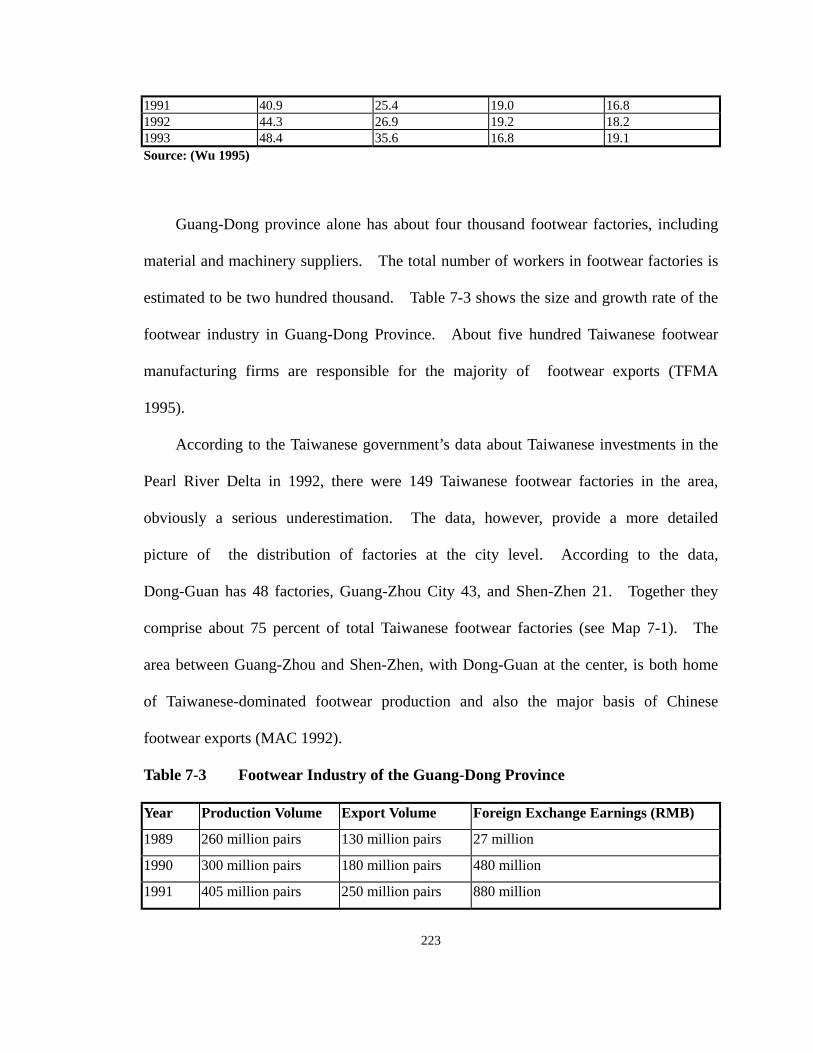

Table 7-3 Footwear Industry of Guang-Dong Province

Table 7-4 Basic Statistics of Dong-Guan City (1980-1993)

7 Table 7-5 Total Exports of Major Cities in Guang-Dong Province, China (1993)

Table 7-6 Average Monthly Wage of Guang-Dong and Adjacent Provinces

Table 8-1 The Operation of Taiwanese Footwear Factories in China

Table 8-2 The Export Value of Taiwanese Footwear and Machinery

Table 8-3 Production Volume of Taiwanese Synthetic Leather Industry

Table 8-4 The Regional Offices of Reebok’ Supplying Firms in China (1993)

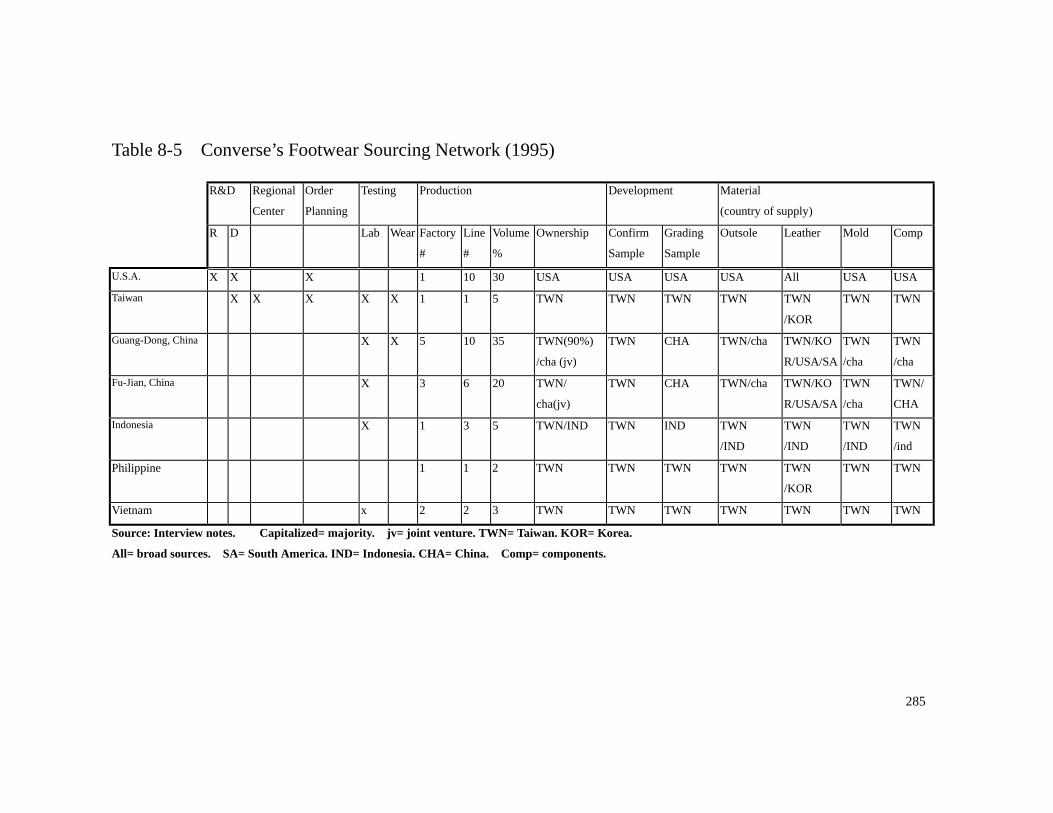

Table 8-5 Converse’s Footwear Sourcing Network (1995)

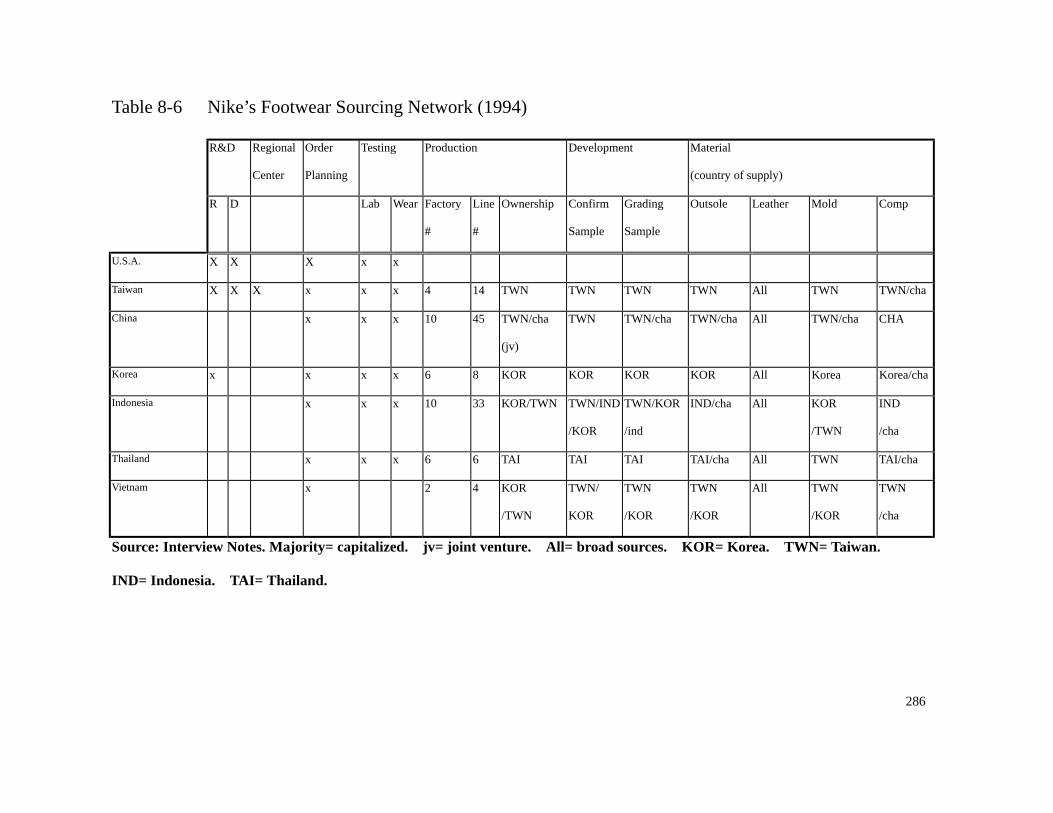

Table 8-6 Nike’s Footwear Sourcing Network (1994)

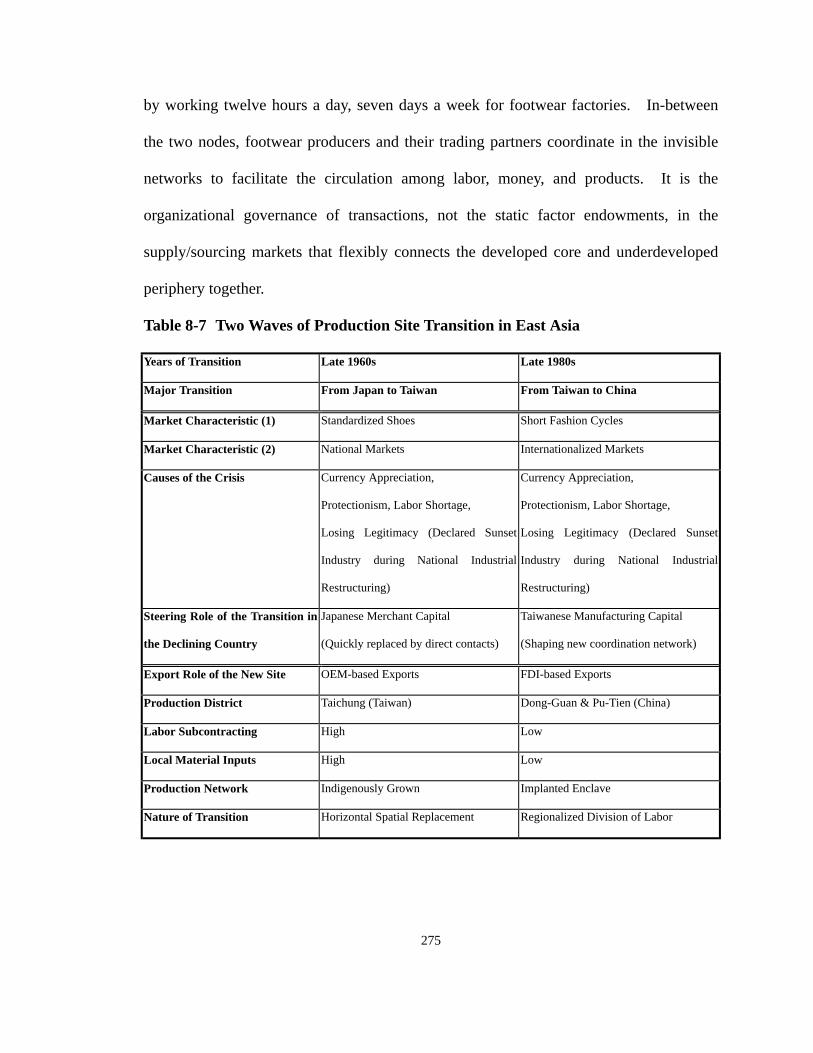

Table 8-7 Two Waves of Production Site Transition in East Asia

8

LIST OF FIGURES AND MAPS

Figure 2-1 The Nested Structure Underlying Economic Interactions

Figure 2-2 Export Roles in the Global Economy by Major Third World Regions

Figure 3-1 U.S. Import and Domestic Production of Nonrubber Footwear, 1968-1990

Figure 4-1 Shop-Floor Layout of a Taiwanese Footwear Factory

Figure 4-2 The Production Procedures of an Athletic Shoe

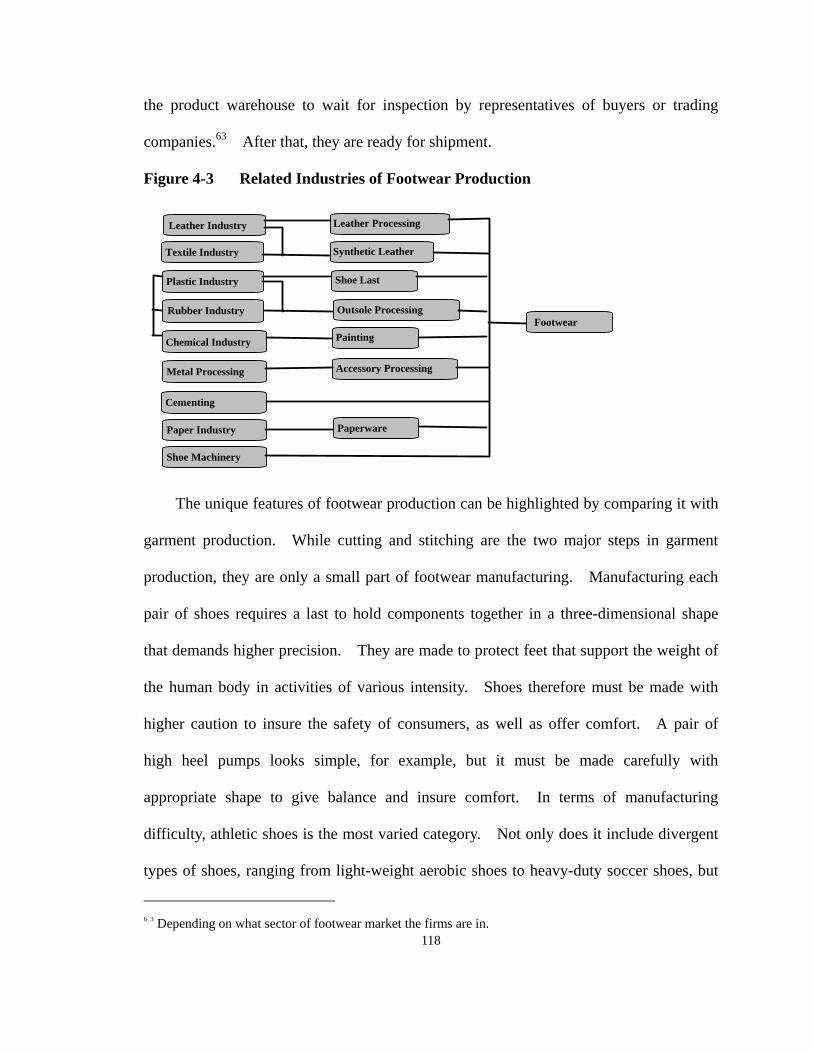

Figure 4-3 Related Industries of Footwear Production

Figure 4-4 A Schematic Flow of an OEM Transaction

Figure 4-5 The Structure of OEM Market Networks

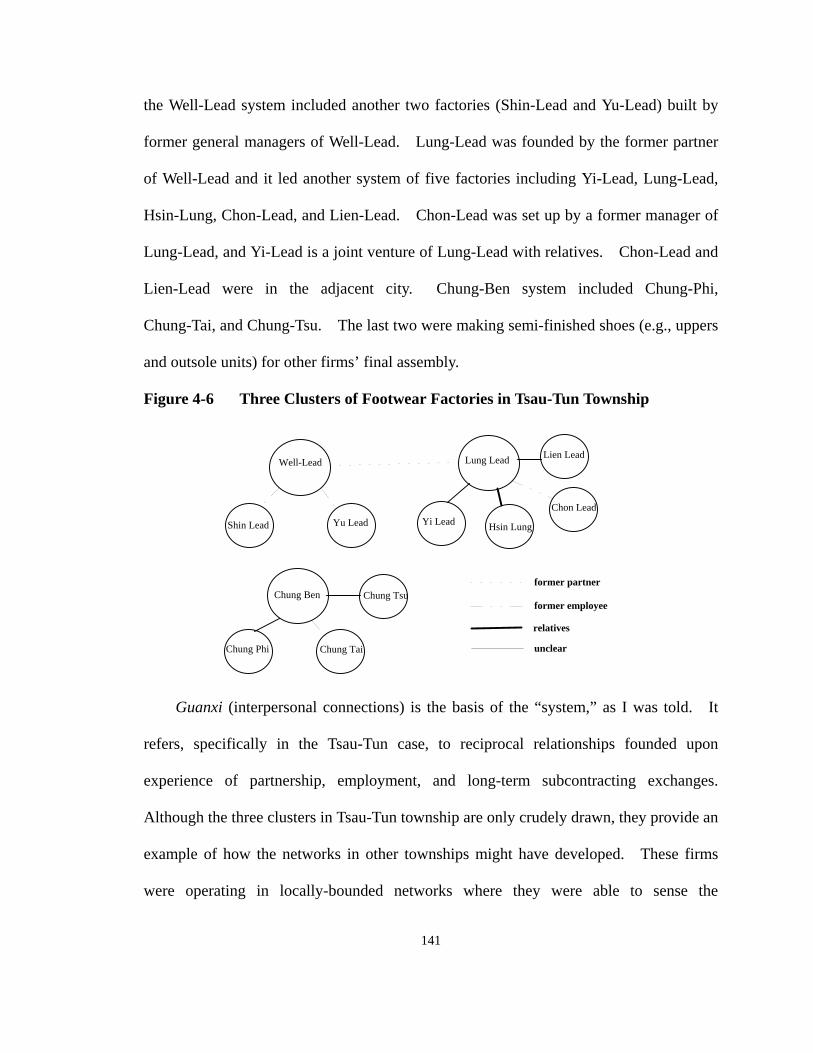

Figure 4-6 Three Clusters of Footwear Factories in Tsau-Tun Township

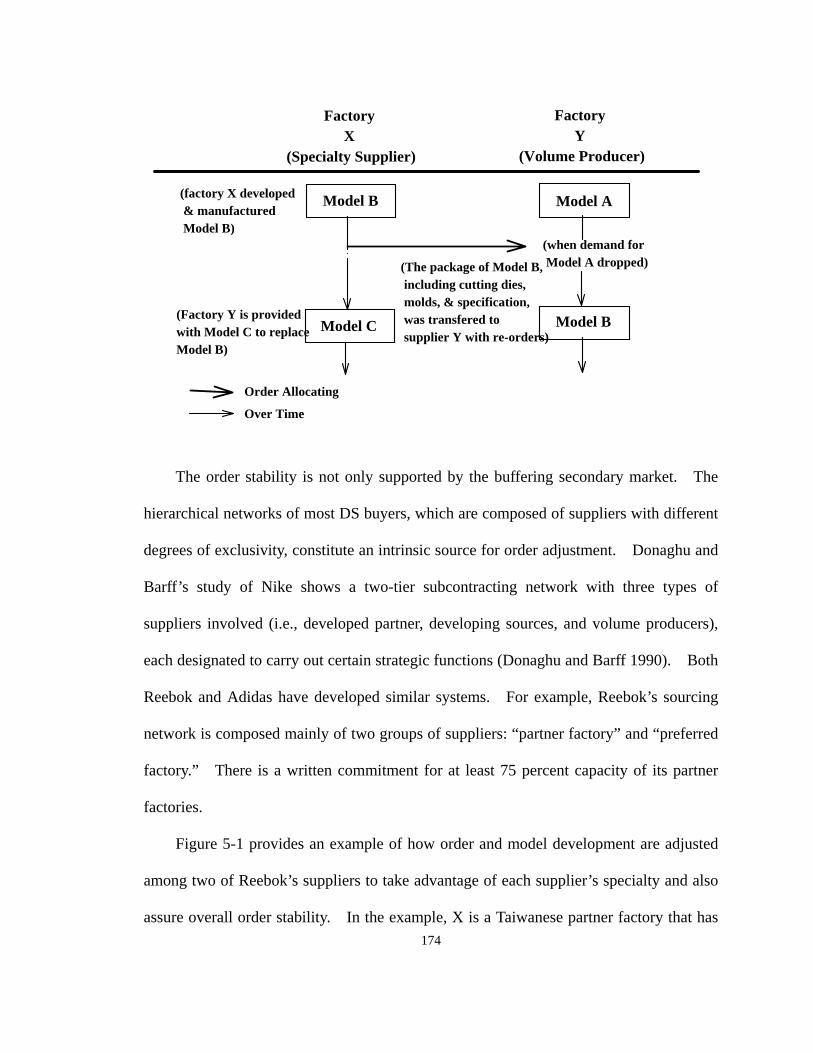

Figure 4-7 The Structure of Footwear Subcontracting Networks in Taiwan

Figure 5-1 Order Adjustment in Sourcing Network (An Example from Reebok)

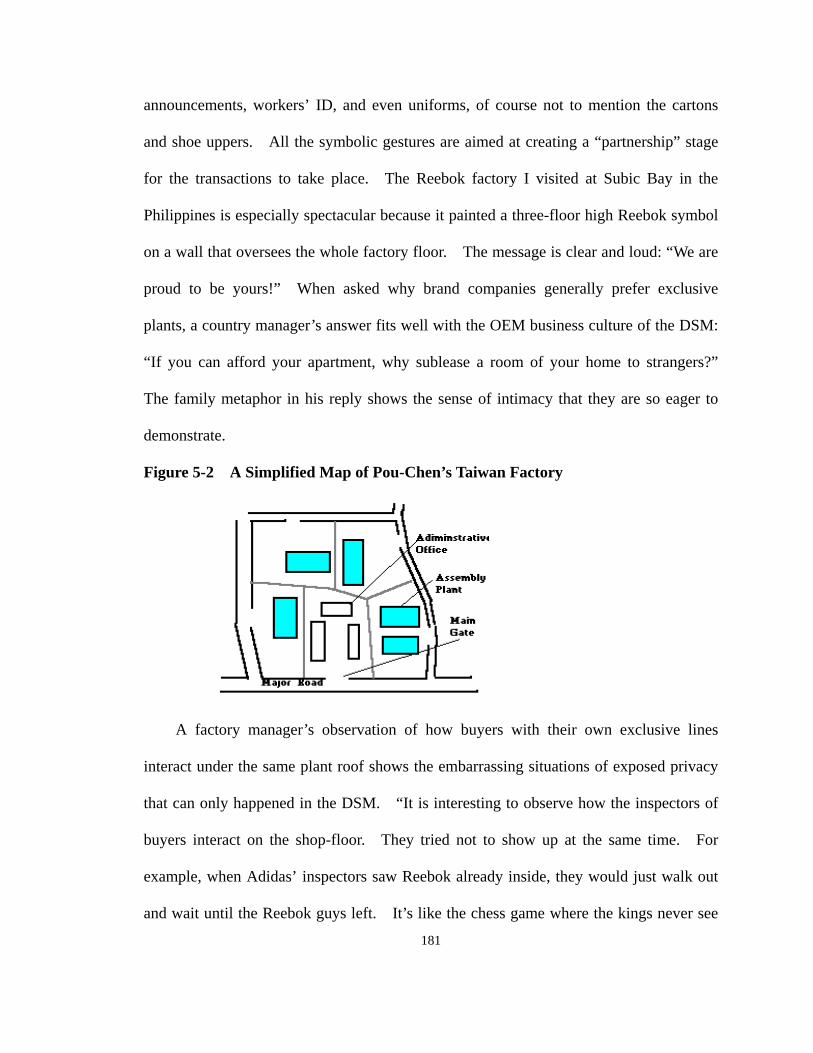

Figure 5-2 A Simplified Map of Pou-Chen’s Taiwan Factory

Figure 8-1 Regionalized Footwear Production/Sourcing Networks

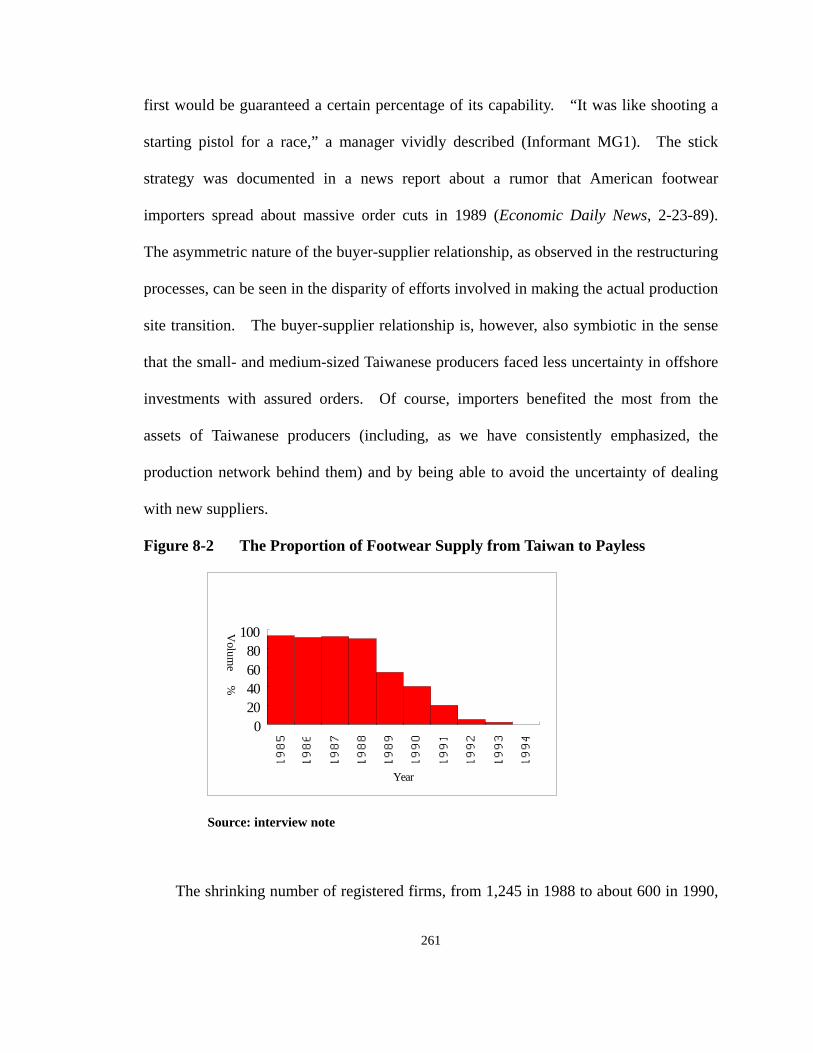

Figure 8-2 The Proportion of Footwear Supply from Taiwan to Payless

Map 1-1 Taiwan and its Neighbor Countries

Map 1-2 The Main Island of Taiwan

Map 7-1 Pearl River Delta and Dong-Guan City

9

PART I

CASE, THEORY, AND METHOD

10

Chapter 1 The Global Footwear Market and the Taiwanese Footwear Industry

We begin the thesis with a quick tour of the footwear industry over the last three

decades.1 We look both at the shifting global landscape of world footwear supply and

the development of the industry in Taiwan, a major supplying country. The subject is a

developing country’s labor-intensive manufacturing exports to the world market. The

story appears to be just another boring repetition about the mighty power of the

universalistic market’s invisible hand. Sociological curiosity however directs our

interest to the surprising twists and turns in the industry history. In the section about the

international market, we point to the empirical anomalies with which the price-making

market fails to cope. Sociology invites us to see markets as social constructions. The

formation and transformation of the Taiwanese footwear industry provide an excellent

opportunity to embed our quest for a sociological understanding in an empirically rich

context.

The World Footwear Market and the Fable of Economics

When I entered the field in 1993, the shoe industry of Taiwan was experiencing

turbulence after years of steady growth. A major exporting industry of the so called

“Taiwan Miracle” before the late 1980s had become negligible on the landscape. A

11

1 This chapter is designed to introduce the global and national contexts of Taiwanese footwear industry and

also highlight the questions that the thesis is intended to answer. Because of the intentions, much of the

descriptions in the chapter are not fully documented, but they will be empirically substantiated in the

subsequent chapters. I have also tried to avoid from framing my central concern too much in abstract

theoretical language. The main purpose of this chapter, as theory is concerned, is to highlight the

empirical sources of sociological theoretical interest.

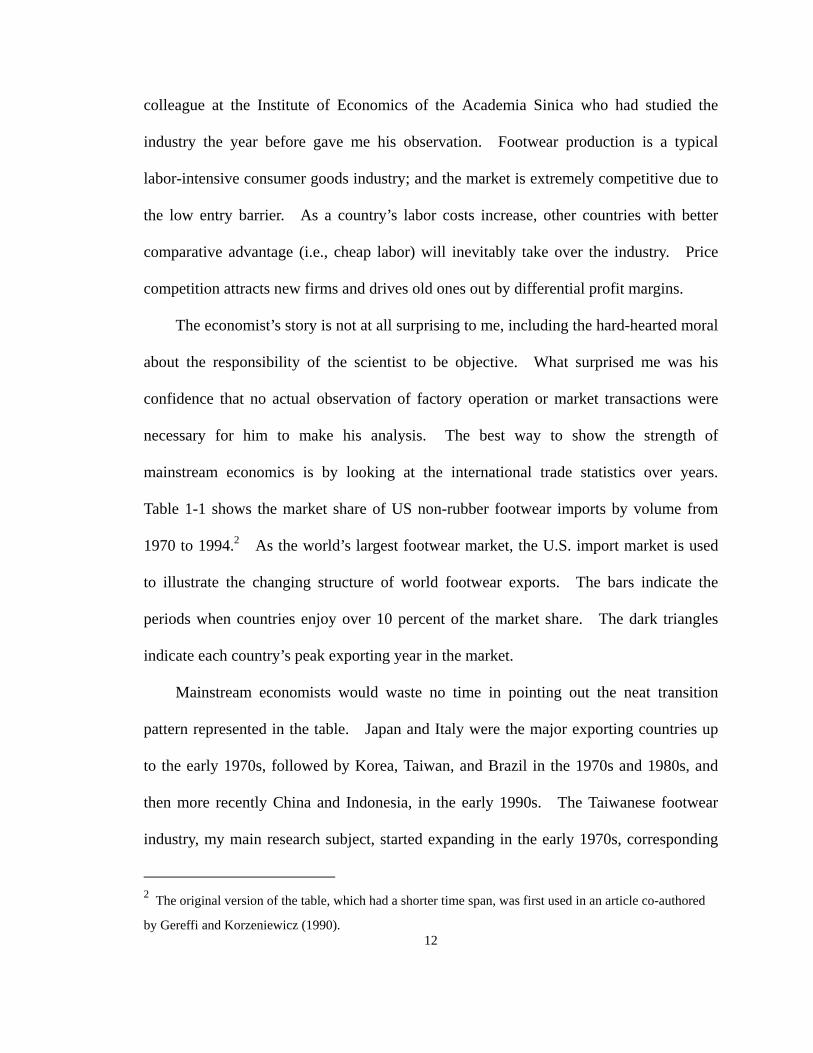

colleague at the Institute of Economics of the Academia Sinica who had studied the

industry the year before gave me his observation. Footwear production is a typical

labor-intensive consumer goods industry; and the market is extremely competitive due to

the low entry barrier. As a country’s labor costs increase, other countries with better

comparative advantage (i.e., cheap labor) will inevitably take over the industry. Price

competition attracts new firms and drives old ones out by differential profit margins.

The economist’s story is not at all surprising to me, including the hard-hearted moral

about the responsibility of the scientist to be objective. What surprised me was his

confidence that no actual observation of factory operation or market transactions were

necessary for him to make his analysis. The best way to show the strength of

mainstream economics is by looking at the international trade statistics over years.

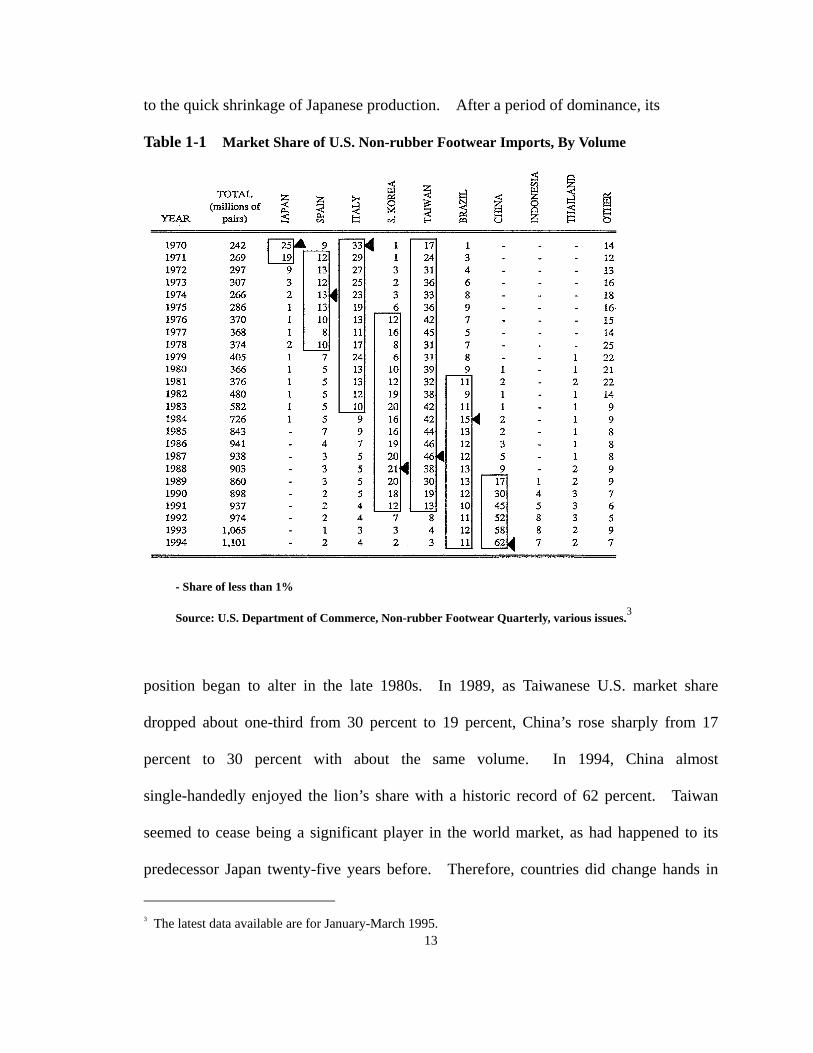

Table 1-1 shows the market share of US non-rubber footwear imports by volume from

1970 to 1994.2 As the world’s largest footwear market, the U.S. import market is used

to illustrate the changing structure of world footwear exports. The bars indicate the

periods when countries enjoy over 10 percent of the market share. The dark triangles

indicate each country’s peak exporting year in the market.

Mainstream economists would waste no time in pointing out the neat transition

pattern represented in the table. Japan and Italy were the major exporting countries up

to the early 1970s, followed by Korea, Taiwan, and Brazil in the 1970s and 1980s, and

then more recently China and Indonesia, in the early 1990s. The Taiwanese footwear

industry, my main research subject, started expanding in the early 1970s, corresponding

12

2 The original version of the table, which had a shorter time span, was first used in an article co-authored

by Gereffi and Korzeniewicz (1990).

to the quick shrinkage of Japanese production. After a period of dominance, its

Table 1-1 Market Share of U.S. Non-rubber Footwear Imports, By Volume

- Share of less than 1%

Source: U.S. Department of Commerce, Non-rubber Footwear Quarterly, various issues.3

position began to alter in the late 1980s. In 1989, as Taiwanese U.S. market share

dropped about one-third from 30 percent to 19 percent, China’s rose sharply from 17

percent to 30 percent with about the same volume. In 1994, China almost

single-handedly enjoyed the lion’s share with a historic record of 62 percent. Taiwan

seemed to cease being a significant player in the world market, as had happened to its

predecessor Japan twenty-five years before. Therefore, countries did change hands in

13

3 The latest data available are for January-March 1995.

sequence as the primary production site for the world footwear market, just as

comparative advantage theory would predict.

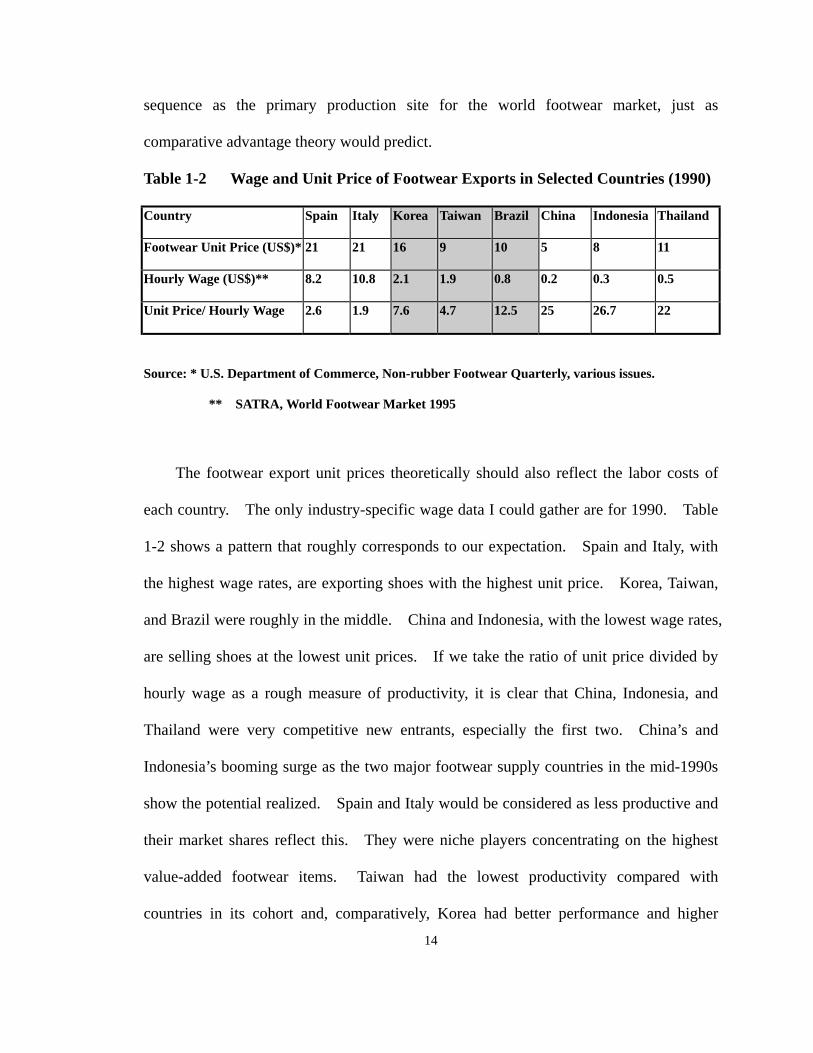

Table 1-2 Wage and Unit Price of Footwear Exports in Selected Countries (1990)

Country Spain Italy Korea Taiwan Brazil China Indonesia Thailand

Footwear Unit Price (US$)* 21 21 16 9 10 5 8 11

Hourly Wage (US$)** 8.2 10.8 2.1 1.9 0.8 0.2 0.3 0.5

Unit Price/ Hourly Wage 2.6 1.9 7.6 4.7 12.5 25 26.7 22

Source: * U.S. Department of Commerce, Non-rubber Footwear Quarterly, various issues.

** SATRA, World Footwear Market 1995

The footwear export unit prices theoretically should also reflect the labor costs of

each country. The only industry-specific wage data I could gather are for 1990. Table

1-2 shows a pattern that roughly corresponds to our expectation. Spain and Italy, with

the highest wage rates, are exporting shoes with the highest unit price. Korea, Taiwan,

and Brazil were roughly in the middle. China and Indonesia, with the lowest wage rates,

are selling shoes at the lowest unit prices. If we take the ratio of unit price divided by

hourly wage as a rough measure of productivity, it is clear that China, Indonesia, and

Thailand were very competitive new entrants, especially the first two. China’s and

Indonesia’s booming surge as the two major footwear supply countries in the mid-1990s

show the potential realized. Spain and Italy would be considered as less productive and

their market shares reflect this. They were niche players concentrating on the highest

value-added footwear items. Taiwan had the lowest productivity compared with

countries in its cohort and, comparatively, Korea had better performance and higher 14

productivity. This reflected the massive offshore investment of Taiwanese footwear

producers and government-assisted industrial rationalization in Korea as they responded

to an industrial crisis in 1990.

The transitions are manifested in different trajectories. Italy, Spain, and Brazil are

in the same trajectory, while Japan, Taiwan, Korea, and China are in another. Women

leather shoes is the major market niche of the first group. In 1993, Italy produced 452

million pairs of shoes, 313 million were leather and 166 million were for women. Spain

has a similar structure. Seventy-five percent of its 198 million pairs of shoes produced

in 1993 were leather. Among the leather shoes, 61 percent were for women. In terms

of export, 66 percent were leather shoes and 22 percent were textile shoes. Likewise,

Brazil’s 132 million pairs of shoe exports in 1991 included 89 percent of non-sports

leather shoes (SATRA 1995).

East Asian exports developed differently. The main item of East Asian footwear

exports had been sports shoes made of synthetic leather. As the industry upgraded,

sports shoes were increasingly made of real leather, but the category difference (i.e.,

sports shoes vs. dress shoes) still makes the two trajectories clearly recognizable.

Leather sports shoes comprised over 60 percent of footwear export value from Korea in

1992 (Footwear Industry Association in Korea 1993). In 1988, about 69 percent of the

leather sport shoes imported by the USA in volume came from Korea, and about 20

percent came from Taiwan. When the two countries dropped to 27 and 8 percent

respectively in 1992, Indonesia increased from less than one percent to 22 percent and

China 32 percent (Lim 1994: 570). Taiwan, different from Korea, had a long term

tradition of dress shoes with synthetic materials; athletic shoes gained increasing

15

importance only after the 1980s. In 1993, dress shoes, high heel, and boots together had

dropped to only eight percent of Taiwan’s exports, while sport shoes occupied 51.7

percent. The contrasting path is found elsewhere. Brazil had only about 1 percent of

sports shoes export in 1991. In the same year, only ten percent of Italy’s footwear

production were sports shoes.4

Of course, footwear exports from the countries are not completely segregated.

Some countries have a more diversified structure than others. Taiwan is a very good

case because it has been able to diversify into more categories, unlike Korea. Although

Taiwan started in the industry earlier, when diversified, it became a challenging

latecomer to Korean dominance in sports shoes. Because of its more diversified

structure, when dress shoes manufacturers were moved from Taiwan to China in the late

1980s, the Brazilian and Italian footwear industry began to feel the overwhelming threat

from the East Asia.

In other words, when the substitutability of products is low (e.g., not in the same

category), the co-variation between outputs of exporting countries declines, and as a

result, countries evolved in distinct ways. The best part of the economists’ story, which

they tout as about the “invisible hand,” ends about here.

Sociological curiosity provokes further questions however.

First of all, why did footwear exports from Taiwan come far earlier than in Korea

when they are in the same cohort? When Taiwan already enjoyed 17 percent of the US

market share in 1970, Korea was still at about 1 percent. And when Korea climbed to

12 percent in 1976, Taiwan’s share was 42 percent. Was it because that labor cost was

16

4 The exports figures based on function category are not available for Italy.

lower in Taiwan, especially considering the very low end shoes (e.g., slippers) they were

then producing? Evidence does not support this speculation. Taiwan’s GNP per capita

was US$ 140 in 1955, more than seventy percent above that of Korea. When the GNP

per capita of Korea reached US$ 150 in 1970, Taiwan moved up to US$ 312 (Levy 1988,

p.165). Comparative advantage provides no justification for the wide empirical

disparity between costs and performance at the stage of industry that was extremely labor

intensive. Socio-historic conditions must be taken seriously.

Another curious phenomenon is that two countries, Korea and Taiwan, dominated

the industry for almost two decades, strange given the long list of developing countries

waiting in line. In the athletic shoe market, Korea and Taiwan had over eighty percent

of the sports shoes market in their peak years of 1980s. In 1988, they together

controlled 90 percent of all leather athletic shoe imports to the USA. In 1987, they

contributed close to 70 percent of the US non-rubber footwear import market. While

Taiwan and Korea were losing their cost advantages in the late-1970s,5 not in the early

1990s, no other developing countries were able to seize the opportunity. It took another

ten years for the relocation to begin. The formation and transformation of a

labor-intensive industry involves more complex factors than just the marginal cost/profit

of maximizers in the competitive market.

In fact, with the second wave of transition inaugurated in the early 1990s, China’s 62

percent volume share in 1994 and 40 percent value share in 1993 show a further

concentration in the footwear supply market. Considering the ever-expanding US

(non-rubber) footwear import market, from 242 million pairs in 1970 when Taiwan took

17

5 Taiwan’s era of labor surplus came to an end early around 1968-1970 (Fei, Ranis and Kuo 1979).

over the position from Japan, to over 1 billion pairs in 1994, the increasing concentration

in footwear supply is even more dramatic than it appears. The lesson: the footwear

industry as the typical stepping stone for poor developing countries is not as big, or as

easily to step on, as economists would have us believe.

A recent industry survey of the Mexican footwear industry concludes that “the

optimism generated in the recent past soon became a spent force” and “the export

performance of the Mexican shoe industry must be judged as disappointing in that less

than ten percent of the output (22 million pairs) finds its way onto foreign market” (World

Footwear 1995). The article is in sharp contrast to an enthusiastic prediction made three

years ago about a “Mexican Footwear Revolution” (Kjelleren 1992). The expanding US

footwear import market has obviously not opened up as much as its size would suggest,

despite the aggressive tariff-reduction measures implemented by government-level

cooperation. The realities, which economists seem disciplined not to observe, urge us to

go beyond the factor endowment.6

“Why consistently East Asia?” A fruitful way of answering this question is to

examine closely the historical conjunctures of production site transition, partly because

they were also the times when opportunities for newcomers arose. With this approach, a

new set of questions logically follows. Who were the players involved in the transition

process? What conditions converged to trigger the transition? Were there two

different groups of buyers and suppliers, before and after the transition? How did the

18

6 In the model, economic units are too independent and egoistic to coordinate their actions; and for the

same reasons the price mechanism of the market will allocate them to their fittest positions according to

their cost structures. At the international level, the cost structure of firms could be bracketed and factor

endowment of nations stands out as the driving force (Krugman 1991).

new suppliers integrate various production factors? Did suppliers in the previous wave

give help (e.g., technical assistance) to firms in the new supplying country? Or, were

they involved in bitter competition for survival? Did buyers also change along with the

shift of production sites? Was the transition in the early 1990s when Taiwan was replaced

by China simply a repeat of the previous one in the late 1960s when Japan was leaving

the stage?

All these questions are related to an approach to understanding market dynamism

that steps away from the economist’s eternal (i.e., ahistorical) market. The aggregate

import-export data, which economists are keen to use, reach their limits. To explore

more deeply these questions, and to be better prepared to answer them, we must bring

both historical contingencies and actual firm behaviors back on stage. The global

bird’s-eye view of the shifting positions in the world footwear import/export structure

must now yield to a more concrete level of analysis that allows closer examination of

both history and actors in industry formation.

For that task, the story of Taiwanese footwear industry, with its longer span of

history, greater vitality and, most importantly, its perfect positioning in the intermediate

stage between Japan and China, is certainly worth examining. As we look closer at the

development of the industry in Taiwan, our questions can be re-phrased more specifically

and our quest for a sociological perspective can be embedded in rich empirical soil.

Taiwan and its Miracle Economy

Taiwan is situated in the Pacific Ocean about 100 miles from the southern coast of

the Chinese mainland. Located about midway between Korea and Japan to the north

19

and Hong Kong and Philippines to the south, Taiwan is at the geographical center

between the Northeast Asia and Southeast Asia. Shaped roughly like a tobacco leaf,

Taiwan is 245 miles long and 89.5 miles wide at its broadest point. The total area is

13,892 square miles, slightly larger than Maryland and Delaware combined. The

Central Mountain Range bisects Taiwan from north to south and about two-thirds of the

island is covered with forested peaks. Most of its 21 million population are

concentrated in the area composed of foothills, terraced flatlands, and coastal plains and

basins (see Map 1-1).

Table 1-3: General Features of Taiwanese Society and Economy

Selected Year 1960 1980 1994

Population (1,000 persons) 10,792 17,805 21,126

Exports (US$ billion) 0.2 19.8 93.0

Foreign Exchange Holdings 0.25 US$ billion (1965) 2.20 US$ billion 92.45 US$ billion

GNP (US$ billion) 1.7 41.4 244.2

GNP per capita (US$) 154 2344 11,604

Agriculture/GDP 28.5% 7.7% 3.6%

Industry/GDP 26.9% 45.7% 37.3%

Services/GDP 44.6% 46.6% 59.1%

Saving Rate* 17.8% 32.3% 26.5%

Distribution of Income** 4.4 (1974) 5.2 (1984) 5.4 (1993)

Illiteracy 27.1% 10.3% 6.0%

Unemployment Rate 4.0% 1.2% 1.6%

Average GNP Growth Rate 8.9% (1965-1994)

Area 13,900 miles2

* Gross National Saving/Gross National Product x 100 (%)

** Ratio of highest fifth’s (households) income to lowest fifth’s (households).

Source: Taiwan Statistical Data Book, Council for Economic Planning and Development (1995)

The economic growth of Taiwan has been spectacular, with an 8.9 percent average 20

growth rate from 1965 to 1994. With the world’s second highest population density at

2,422 people per square km of cultivated land and almost no natural resources, Taiwan

has successfully lifted its GNP from US$ 1.7 billion in 1960 to US$ 244 billion in 1994,

with foreign exchange holdings reaching over US$ 92 billion, second only to Japan.

The economic structure of Taiwan has experienced dramatic changes over the years.

The contribution of agriculture to GDP has decreased from 28.5 percent in 1960 to

merely 3.6 percent in 1994. The industrial sector’s contribution to GDP increased from

26.9 percent in 1960 to 47.1 percent in 1986; and after that, the success of

industrialization further stimulated the development of service sector to 59.1 percent in

1994. The speedy economic growth has not caused many of the problems created in

other developing countries. Income distribution has been amazingly equal. The ratio

of income for the top fifth of households to the bottom fifth was 5.4 in 1993, only a slight

increase from 4.4 in 1974. The unemployment rate has been very low since successful

industrialization and was 1.6 percent in 1994. The general features of Taiwanese

economy are listed in the Table 1-3. The economic success is measured not only by a

high growth rate, but also by the simultaneous achievement of equal income distribution,

and a low unemployment rate.

The Footwear Industry in the Industrialization of Taiwan

As one of the major export industries, the history of the footwear industry illustrates

the stages of the postwar economic development of Taiwan.

In 1949, the defeated Kuomintang (KMT) party was expelled from mainland China

and moved to Taiwan, with over two million refugees. Unemployment and inflation

21

were very serious problems7 and a massacre of Taiwanese civilians only two years

previous added to the social unrest. An ambitious land reform program was devised by

the ruling party to fostered social and political stability and increased agricultural

production. Taiwan’s import-substitution industrialization between 1953 and 1957 was

actually a first-aid measure to simultaneously preserve Taiwan’s scarce foreign exchange

and to produce essential consumer goods for self-sufficiency. This was the period of

after-war reconstruction.

Anticipating the end of American foreign aid, an economic reform program was put

in place in 1959, steering the economy toward export promotion. Taiwan’s first

export-processing zone (EPZ) was established in Kao-Hsiung in 1966, one year after the

withdrawal of aid, to attract foreign investment in labor-intensive industries. The

Taiwanese footwear industry began to develop at the same time, using mainly local

capital. It was one of the first waves of manufactured exports from Taiwan. Woven

slipper and sandals were the initial export categories.

The establishment of the Taiwanese Plastic Shoes Exporter’s Association (TPSEA)

in 1968 represents an important step in the formation of the industry. The 1973-74 oil

crisis hit Taiwan hard. Real GNP grew only 1.2 percent in 1974 and inflation climbed

to 47 percent, while exports declined in real terms by about 7 percent. The Taiwanese

government noticed the need for self-sufficiency in basic materials and intermediate

goods and adjusted its economy toward capital- and technology-intensive industries.

The Industrial Technology Research Institute was established in 1973 to assist industrial

22

7 The Taipei wholesale price index increased 260% in 1946, 360% in 1947 and 3500% in 1949 (Ho 1978, p.

104)

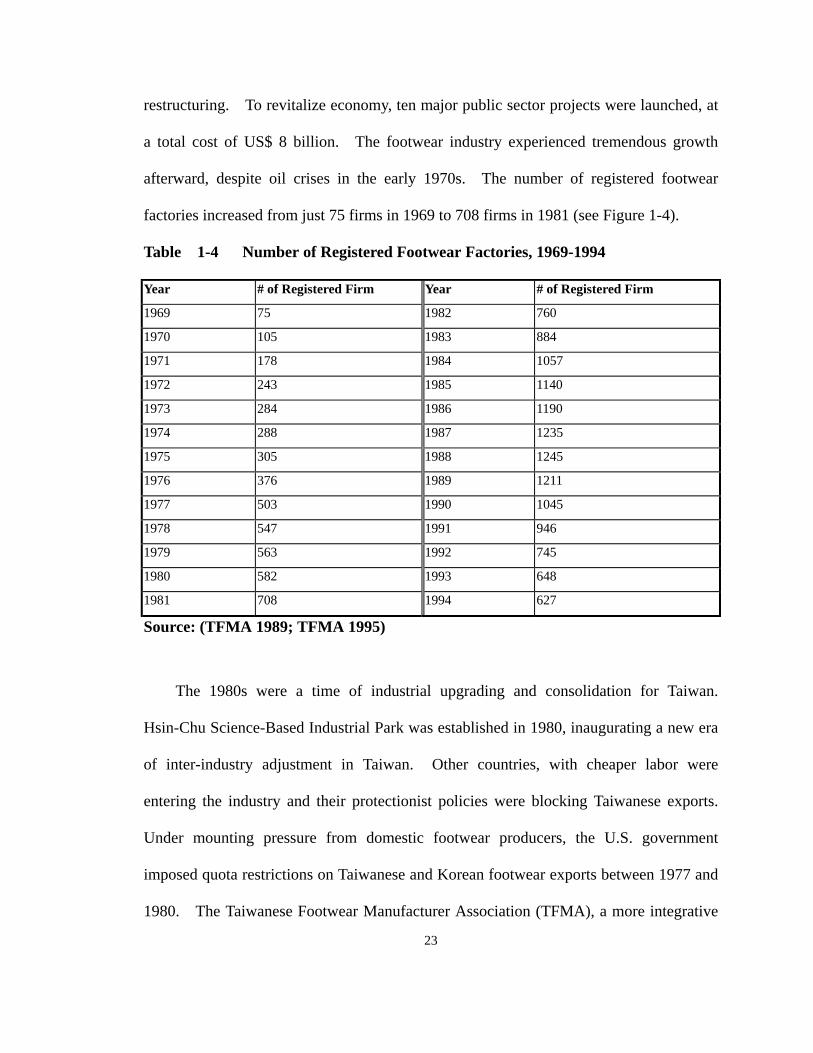

restructuring. To revitalize economy, ten major public sector projects were launched, at

a total cost of US$ 8 billion. The footwear industry experienced tremendous growth

afterward, despite oil crises in the early 1970s. The number of registered footwear

factories increased from just 75 firms in 1969 to 708 firms in 1981 (see Figure 1-4).

Table 1-4 Number of Registered Footwear Factories, 1969-1994

Year # of Registered Firm Year # of Registered Firm

1969 75 1982 760

1970 105 1983 884

1971 178 1984 1057

1972 243 1985 1140

1973 284 1986 1190

1974 288 1987 1235

1975 305 1988 1245

1976 376 1989 1211

1977 503 1990 1045

1978 547 1991 946

1979 563 1992 745

1980 582 1993 648

1981 708 1994 627

Source: (TFMA 1989; TFMA 1995)

The 1980s were a time of industrial upgrading and consolidation for Taiwan.

Hsin-Chu Science-Based Industrial Park was established in 1980, inaugurating a new era

of inter-industry adjustment in Taiwan. Other countries, with cheaper labor were

entering the industry and their protectionist policies were blocking Taiwanese exports.

Under mounting pressure from domestic footwear producers, the U.S. government

imposed quota restrictions on Taiwanese and Korean footwear exports between 1977 and

1980. The Taiwanese Footwear Manufacturer Association (TFMA), a more integrative

23

industrial association replacing TPSEA, was established in 1978 right after the

protectionism was taken place. Shocked by the quota, Taiwanese footwear producers

managed to upgrade and build even stronger ties with major footwear buyers.

Taiwan was the largest shoe supplier in 1986, and maintained this position until

1989. Footwear was the third largest export industry of Taiwan (Lin 1991, p.17). The

amazing success of the industry, given the difficult challenges over the years, was easily

forgotten amidst the rise of other industries such as machinery, telecommunication, and

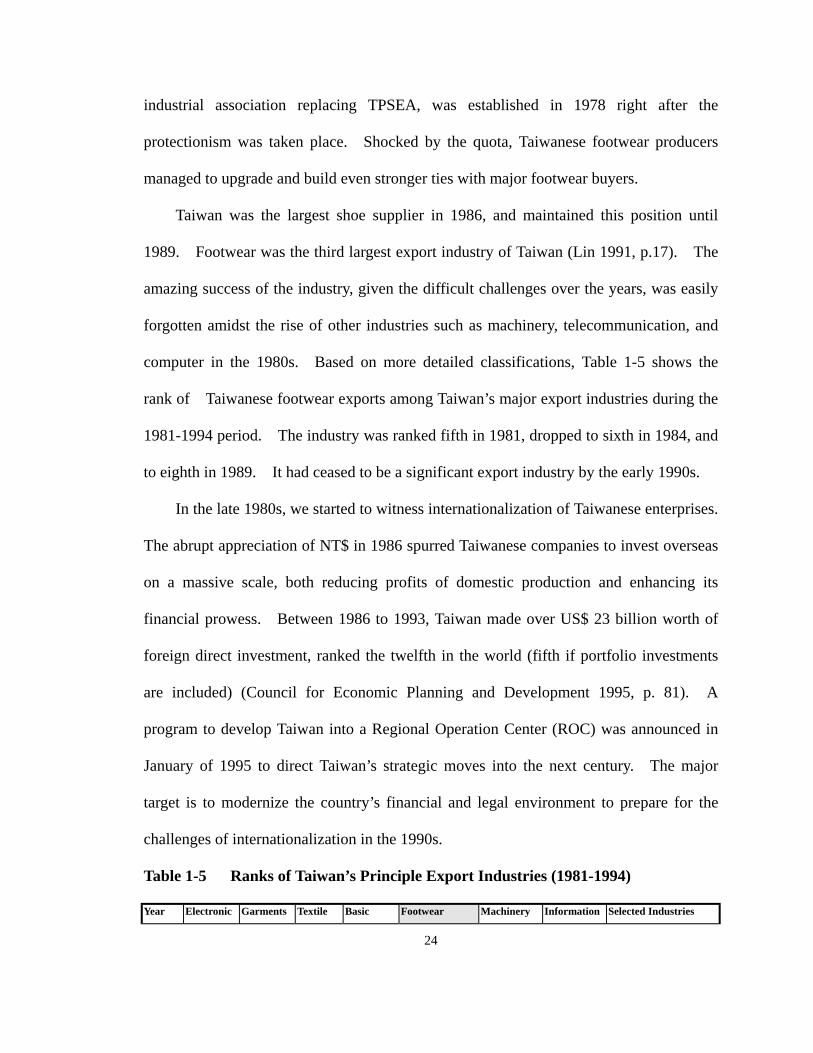

computer in the 1980s. Based on more detailed classifications, Table 1-5 shows the

rank of Taiwanese footwear exports among Taiwan’s major export industries during the

1981-1994 period. The industry was ranked fifth in 1981, dropped to sixth in 1984, and

to eighth in 1989. It had ceased to be a significant export industry by the early 1990s.

In the late 1980s, we started to witness internationalization of Taiwanese enterprises.

The abrupt appreciation of NT$ in 1986 spurred Taiwanese companies to invest overseas

on a massive scale, both reducing profits of domestic production and enhancing its

financial prowess. Between 1986 to 1993, Taiwan made over US$ 23 billion worth of

foreign direct investment, ranked the twelfth in the world (fifth if portfolio investments

are included) (Council for Economic Planning and Development 1995, p. 81). A

program to develop Taiwan into a Regional Operation Center (ROC) was announced in

January of 1995 to direct Taiwan’s strategic moves into the next century. The major

target is to modernize the country’s financial and legal environment to prepare for the

challenges of internationalization in the 1990s.

Table 1-5 Ranks of Taiwan’s Principle Export Industries (1981-1994)

Year Electronic Garments Textile Basic Footwear Machinery Information Selected Industries

24

Products Products Metals & Parts & Commun

1981 (1) (2) (3) (4) (5) 1.5 (6) - Toy & Sports G (7)

1982 (2) (1) (3) (4) (5) 1.5 (7) - Machinery (6)

1983 (1) (2) (3) (4) (5) 1.9 (6) - Toy & Sports G (7)

1984 (1) (2) (4) (5) (6) 2.3 (3) - Toy & Sports G (7)

1985 (2) (1) (3) (5) (6) 2.4 (4) (8) Toy & Sports G (7)

1986 (2) (3) (4) (6) (5) 3.1 (1) (8) Plastic Products (7)

1987 (2) (4) (3) (7) (6) 3.7 (1) (5) Toy & Sports G (8)

1988 (2) (6) (3) (5) (7) 3.9 (1) (4) Toy & Sports G (8)

1989 (2) (6) (3) (4) (8) 3.8 (1) (5) Plastic Products (7)

1990 (2) (8) (3) (4) (7) 3.5 (1) (5) Plastic Products (6)

1991 (3) (9) (2) (4) (8) 3.8 (1) (5) Plastic Products (6)

1992 (3) (10) (2) (4) (8) 3.7 (1) (5) Plastic Products (6)

1993 (2) (10) (3) (4) (9) 2.8 (1) (5) Plastic Products (6)

1994 (2) (9) (3) (4) (13) 1.7 (1) (5) Plastic Products (6)

Footwear and Parts column: billion US$.

Source: Taiwan Statistical Data Book, Council for Economic Planning and Development (1995)

The abrupt appreciation of the Taiwanese currency against the US dollar hit directly

the engine of exports. A labor shortage that had been haunting the industry, despite

flexible utilization of peripheral labor by the widespread putting-out system, hurt even

those firms which tried hard to upgrade into higher value-added niches. As the industry

moved toward the end of 1980s, a crisis was clearly in sight and the success story seemed

to be drawing to an end. The number of registered firms reached its peak in 1988 when

there were about 1245 registered firms. Subsequently, the industry started to decline,

falling to 627 firms in 1994. In just a few years, Taiwanese footwear producers lead the

first wave of offshore investment in post-war Taiwan, a challenge that both the Taiwanese

firms and the state had never before experienced. Years after being a backbone of

Taiwan’s postwar economic growth, the footwear industry became the forerunner of

Taiwan’s international investment in the 1990s.

25 Nine years after the first investment, the panic and frustration that once plagued

Taiwanese footwear producers were dissipated and a pattern of regional operation began

to emerge. The new structure is characterized by several features: 1) about 85 to 90

percent of footwear exports from China are now controlled by Taiwanese; 2) Chinese

state enterprises are actually discouraged from footwear exporting by Taiwanese

producers; 3) major footwear buyers, surprisingly especially those volume retailers who

are very sensitive to cost margin, remained in Taiwan; 4) Taiwan has become the world

center of footwear material and machinery supply; and 5) footwear sourcing transactions

now operate in a triangle system where orders are received, materials are procured, and

models are developed in Taiwan, productions are carried out in China, and finished goods

are shipped from Hong Kong.

The success story continues, as shown in the title of a journal report on the

Taiwanese footwear industry: “Another Sunrise of a Sunset Industry.” About seven

years ago, the Taiwanese official in charge of industrial development announced that shoe

manufacturing was a sunset industry. Years later, the current head of the Ministry of

Economic Affair, Bin-Quern Chian, on many occasions used the Taiwanese footwear

industry as a model of successful offshore investment. “The Made in Taiwan” era of the

industry is ending. But the industry has not died; it actually prospers. It is now shoes

“Made in China, the Philippines, Indonesia, or Vietnam by Taiwanese,” said Mr. Chian

before departing to Subic Bay for the opening ceremony of a Taiwanese-developed

industrial port in the Philippines.

The history of the industry parallels the stages of economic development of postwar

Taiwan. Footwear export was an important industry in the first wave of Taiwan’s export

growth in the late 1950s, when export promotion began. After a period of speedy

26

growth, it struggled to maintain momentum under severe competition and protectionism

in the late 1970s and early 1980s, and strove to reach its peak year in 1988 with nearly

US$ 4 billion of export value.8 However, its remarkable success under environmental

toughness was outshone by rising-star industries like machinery, information, and

tele-communication in the late 1980s (see Table 1-5). After a period of confusion and

frustration, it becomes clear that Taiwanese footwear producers have continued their

domination of the now regionally-operated footwear sourcing/ supplying networks.9

The Footwear Question: Taiwan’s Shifting Role in the International Market

The case of the Taiwanese footwear industry allows us to re-phrase the sociological

questions that we raised early in the chapter in a more specific context. Some countries,

such as Italy, are able to survive by making the highest value-added shoes for the world

market. The reasons why Italy has been able to continue its dominance in this niche

deserve careful examination. (Rabellotti 1995). The formation and transformation of

the Taiwanese footwear industry, which has been competing in the middle price-range,

are no less intriguing. Low wages alone do not explain success in the world market.

Despite low labor costs, closeness to the US market, and bilateral government

cooperation on tariff reduction, Mexican footwear exports have not lived up to that

expectation. The same question applies to the late development of the footwear industry

compared to Taiwan. Even though China opened its economy in the late 1970s and

Taiwan suffered labor shortages and protectionism, Taiwan still continued its dominance

8 This feature includes exports of both finished footwear and parts.

27

9 The detailed discussion will be presented in the chapters to follow.

in the world footwear market for over ten years. What are the barriers preventing

buyers shifting their orders to countries with far lower labor costs?

Based on the deductive model, we can always make the post de facto explanation

that the offshore investment of Taiwanese footwear producers reflects their declining

comparative advantage, and we could surely imagine a day when the Taiwanese are

completely replaced by the Chinese, who have direct contacts with Western buyers. The

question nevertheless remains: how do we explain the regional triangle manufacturing if

the footwear industry is understood only as labor-intensive and the market as only a

pricing mechanism? What are the assets Taiwanese producers withhold that allow them

to conduct direct investment in China, given the supposedly low entry-barrier in the

footwear industry? In other words, what are the barriers for fuller local participation in

China beyond simple labor inputs?

Although Taiwan has ceased to be a significant production base for the world

footwear market, and high-tech industries, like semiconductors, are driving the

Taiwanese economy toward a more advanced stage, a study that examines the formation

and transformation of the Taiwanese footwear industry is not simply a retrospective look

inspired by nostalgia. The exportation of footwear has been an industry representative

of Taiwan’s remarkable economic development. Even the industry’s offshore

investments in the 1990s are leading the way for other more advanced industries.

However, it is also a case that is most likely to be overlooked or misunderstood because

of its labor-intensiveness and severe competition. Without a clear understanding of the

historically-grounded and socially-embedded dynamism of Taiwanese footwear industry,

we would continue to examine even the more advanced industries through the simplistic

28

model of comparative advantage and its underlying theory of the universalistic market.

29

Chapter 2 Theory, Major Arguments, and Method

The thesis presents the result of sociological research on international trade,

specifically about the shifting role of Taiwan in the international footwear sourcing

networks. It is intended as an integrative research project that (1) combines the wisdom

of both developmental sociology and economic sociology, (2) explores a subject that has

rarely been touched in both fields, and (3) tries to push sociology into an area that has

been dominated by mainstream economics. Taiwanese footwear exports are chosen as

the case for the project because they represent a most-likely case of the competitive

market of mainstream economics in one of the most successful economies in the

developing world.10

This is not the first time that developmental sociology and other areas of sociology

have co-operated. In the 1980s, we witnessed the state-centered development studies

emerging concurrently with another stream in sociology to “bring the state back in” and

restore a historical sensibility traced back to our discipline’s classic tradition (Giddens

1981; Skocpol 1984; Evans 1985). Likewise, my current project would not be possible

without the research agenda represented in Gereffi’s framework of global commodity

chains (GCC) and the resurgence of economic sociology which climaxed in the

publication of The Handbook of Economic Sociology in 1994 (Swedberg 1990; Block

30

10 On the platform of developmental sociology, it examines the organizational features of the footwear

supply market in East Asia in order to shed new light on the development issue about the driving

mechanism of East Asian export-oriented industrialization. On the ground of economic sociology, the

thesis intends to illustrate the socially embedded conception of market by examining a most likely case of

the opposing mainstream free market and also pushes the economic sociology into the new terrain of the

international trade.

1990; Smelser and Swedberg1994).

This chapter describes the design of the research project. The first half discusses

the theoretical literature, the contending theories, and my alternative explanation. The

second half deals with methodological issues about how the research was conducted.

The fundamental theoretical statement I want to make in the thesis is that markets can be

more fruitfully analyzed as social constructions than seen as price mechanisms that

allocates resources without social coordination. I support this statement by

demonstrating how it can provide better answers to the anomalies in international trade

than those supplied by the price-mediated market.

The theoretical part of the chapter proceeds on two related theoretical contexts.

The context of developmental sociology creates a theoretical subject out of the Taiwanese

footwear industry. I point out the limits of current sociological approaches in filling the

theoretical void that mainstream economics leaves and explain how Gereffi’s GCC model

is providing a promising alternative which requires us to look at the market as socially

constructed. Economic sociology provides us with more detailed conceptual tools to

develop arguments regarding the social processes of market formation and the shifting

position of its constituent firms. The methodological section introduces the two major

methods I use in my research. My research experiences in conducting in-depth

interviews and participating in field observation are discussed. An introduction to the

phases of my research ends the chapter.

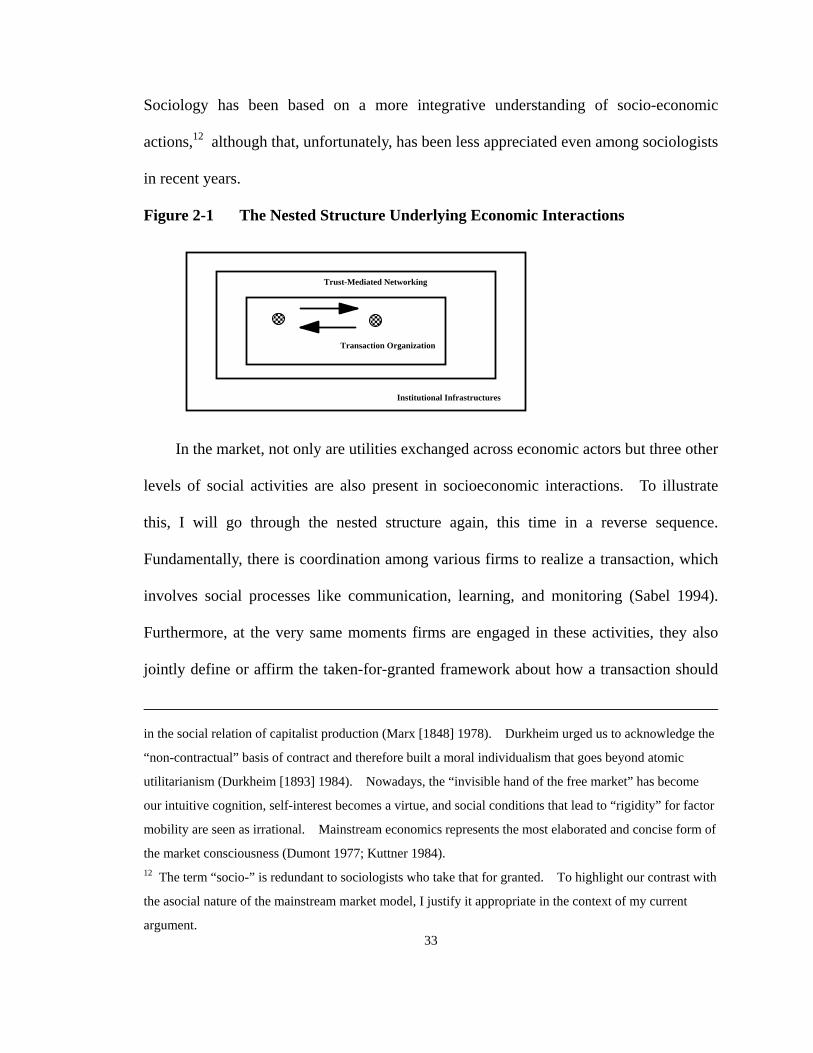

Economics vs. Sociology: Fundamental Statement

Most sociologists would agree that markets are social constructions. The social

31

factors that come into economic transactions can be conceived as three levels of a nested

structure. There is, at the very bottom, the institutional infrastructure of economic

transactions which involves exogenous sources of influence through organizations not

directly involved in transactions, such as industrial associations and government agencies.

Above that there are social networks among economic agents which accumulate and use

institutionalized resources as social capital in facilitating trust in transactions. Finally, at

the technical core of market, economic interactions are patterned behaviors with

recognizable features, which I will call “transaction organization” in the thesis. Firms in

an industry continue to grow because supporting institutions are in place, business

networks are maintained, and transactions are well coordinated. The thesis intends to

explain the formation and transformation of Taiwanese footwear industry by examining

closely the social construction of the international footwear sourcing market where they

reside.

This approach distinguishes my position clearly from the price-mediated market

model of mainstream economics I argue against in the thesis. My argument does not

deny the rational calculation of economic actors, much emphasized by the followers of

the economic model, but rather alleges its incompleteness. The weakness of the

price-mediated market model is disguised by the deductive nature of modern economics.

Reflection upon the historical origin and social consequences of the “self-regulating”

capitalist market have been central to our discipline since the early founders. 11

32

11 Weber studied historically the complex institutional infrastructures of Western capitalist economies and

the unintended consequences that negate individual freedom (Weber [1906-24] 1946). Marx unveiled the

hidden abode of the capitalist free market and struggled to restore the freedom of labor which is exploited

Sociology has been based on a more integrative understanding of socio-economic

actions,12 although that, unfortunately, has been less appreciated even among sociologists

in recent years.

Figure 2-1 The Nested Structure Underlying Economic Interactions

������������

������������

Transaction Organization

Institutional Infrastructures

Trust-Mediated Networking

In the market, not only are utilities exchanged across economic actors but three other

levels of social activities are also present in socioeconomic interactions. To illustrate

this, I will go through the nested structure again, this time in a reverse sequence.

Fundamentally, there is coordination among various firms to realize a transaction, which

involves social processes like communication, learning, and monitoring (Sabel 1994).

Furthermore, at the very same moments firms are engaged in these activities, they also

jointly define or affirm the taken-for-granted framework about how a transaction should

in the social relation of capitalist production (Marx [1848] 1978). Durkheim urged us to acknowledge the

“non-contractual” basis of contract and therefore built a moral individualism that goes beyond atomic

utilitarianism (Durkheim [1893] 1984). Nowadays, the “invisible hand of the free market” has become

our intuitive cognition, self-interest becomes a virtue, and social conditions that lead to “rigidity” for factor

mobility are seen as irrational. Mainstream economics represents the most elaborated and concise form of

the market consciousness (Dumont 1977; Kuttner 1984).

33

12 The term “socio-” is redundant to sociologists who take that for granted. To highlight our contrast with

the asocial nature of the mainstream market model, I justify it appropriate in the context of my current

argument.

be seen, what their relationships are, and what each party expects of the other. Finally,

the institutionalized environment of a transaction provides social capital to the residing

firms making possible future transactions.

A market is a “socially embedded” reality sui generis that cannot be reduced to

atomic individuals in competition.13 Once the multi-dimensional social underpinning of

economic action is taken into consideration, factors such as conventions, historical stage,

legitimization, coercion, norms, tacit knowledge, and patterned behaviors become

essential to our analysis of market formation. The following discussion will show why

this perspective is necessary to our research subject. We elaborate on the social

embeddedness later.

From Comparative Advantage to Commodity Chain

There have been various debates on international trade about the source of national

prosperity dating back at least to the eighteenth century between those who emphasized

international trade and those who stressed domestic agriculture (Smith [1776] 1976).

After the World War II, many economists optimistically believed selective policies based

on the import-substitution principle could bring balanced economic growth to developing

countries (Hirschman [1958] 1978). After the failure of the import-substitution policy

in Latin America in the early 1970s, dependency theory emerged arguing that increasing

34

13 A major function of concept is to distinguish. The concept of “embeddedness” was first raised by

Polanyi ([1944] 1957) in his study on the historical formation of the self-regulating market and its

empirical impossibility as manifested in the counter-movement to commodification of social fabrics .

Granovetter (1985) adopts the term to emphasize the profound social networking in economic transactions

which cannot be reduced to economic rationality.

participation in international trade simply traps developing countries in unequal

exchanges with core developed countries (Frank 1967; Amin [1973]1976 ). The issue

consequently shifted ground to criticisms of the “linear, Euro-centric, and ahistorical”

model of modernization theory. With certain adjustments, the dependent development

variant of the dependency group emerged in the late 1970s (Cardoso 1979; Evans 1979),

followed by a bargaining model that emphasizes interactions among the state, foreign

capital, and domestic capital (Gereffi 1983). The analysis of international trade shifted

its focus to the role of foreign capital and how the state in capital-receiving countries

could use it positively. The state-centered approach gained shape within this context.

The tremendous economic growth of the East Asian newly industrializing countries

(NICs), which relied heavily on export trade, in contrast to the worsening debt crisis in

Latin America, cast serious doubts on classic dependency theory (Barrett 1982) and

brought the free market model of mainstream economics back to center stage in the 1980s

(Balassa 1981). The state-centered theories quickly challenged the self-claimed triumph

of free market proponents in explaining East Asian industrialization (Deyo 1987; ;

Henderson 1987; Amsden 1989; Wade 1990; Deyo 1995). In one way or another,

criticisms of the model all point to the importance of state actions in facilitating economic

growth, whether by suppressing labor resistance (Deyo 1987), making the price wrong

(Amsden 1989), or strategic planning (Wade 1990). Another contrasting sociological

approach emphasizes a bottom-up perspective, studying the social process of labor

control, instead of state policies. From Deyo to Shieh’s more recent works, the

mechanism of labor control has been examined in great detail, covering the contributions

of networked production to efficiency, legitimacy, and mobility (Deyo 1989; Shieh 1992).

35

Those sociological theories raised solid doubts about the application of the free market

model to East Asian industrialization. However, none of the sociological approaches

have ever targeted international trade as such, the topic that made the resurgence of the

free market model possible.

Comparative Advantage Theory: Porter describes the comparative advantage

theory of economics as the “classic explanation” of industrial success in international

trade (Porter 1990, p.11). The theory can be traced back to Adam Smith, the founder of

modern economics, who emphasized the merit of international trade in increasing scale

economy and therefore specialization in the division of labor (Smith [1776] 1976).

Ricardo was the real founder of the theory, modifying Smith’s concept of absolute

advantage to the concept of comparative advantage, which fine-tunes the allocating

power of the price-mediated market to the marginal utility principle.14 In other words, a

country will specialize in the industry where its unit labor is more productive compared

to other countries (Ricardo [1817]1951). While Ricardo’s theory is based on

productivity, the popular version of comparative advantage developed by Heckscher and

Ohlin is based on “factor endowments” in which labor, land, capital, and natural

resources are specifically included (Ohlin 1935). The concept of “factor endowment”

36

14 In mercantilism, state emphasized trade gains in a zero-sum economic world of exchange, therefore

tariff restriction and quota were usually imposed to lessen import volume and hence increase national

capital accumulation. Adam Smith’s The Wealth of Nation argued in a opposite way emphasizing that

absolute advantage of countries in international trade will lead them to specialize in the production niche

that is most efficient in terms of resource allocation. Ricardo further extended Smith’s thesis. He argued

that even if a country is absolutely less efficient than its trading partners at everything, it still makes sense

for that country to specialize in producing that which it is relatively less inefficient, and to gain from the

superior relative efficiencies of its trading partners.

reflects two characteristics of the economic model: it focuses on the substantive inputs to

production and those factors are endogenously given. A more dynamic theory of

international trade is proposed by Vernon in his “product cycle” theory. The theory

argues that production will stay in the home market in the initial launch of a new product,

then moves overseas when foreign markets expand, and finally, as the technology

matures, foreign firms will take over production and the home market will become reliant

on foreign imports (Vernon 1966). In a case like footwear manufacturing, which has a

low technological entry barrier and a fully matured consumer market, Vernon’s theory

shares the same premise as other economic modes: the universalistic price-mediated

market.15

Our empirical investigation of the production site changes in the world footwear

market over the last twenty-five years and the development of the industry in Taiwan

shows many empirical anomalies for which comparative advantage theory fails to

account. If the price-mediated universalistic market and its application in comparative

advantage theory are sufficient to explain the transition in footwear production sites,

given the industry’s labor intensiveness and open competition: Why did Taiwan enter the

market earlier than Korea when its labor costs have been consistently higher? Why was

Taiwan able to maintain its position in the market through the 1980s, when it had lost its

labor advantage by the 1970s? Why has footwear supply to the world market been

concentrated in so few countries? Why did other developing countries, such as Mexico,

37

15 For simplicity, in the thesis, the term comparative advantage theory includes the product life cycle

theory, although I will use the more precise “price-mediated market” whenever possible. For more

comprehensive discussions on the comparative advantage theory see the edited book by Lipsey and Dobson

(1987).

with cheap labor costs, tariff reductions, and transportation convenience, fail to ascend in

the global market? What assets allow Taiwanese footwear producers to conduct

offshore investment while keeping original marketing networks in a regionalized

operation? To answer these questions satisfactorily, we need to study the footwear

export/sourcing market as a historically-contingent and socially-constructed reality.

With this general agenda in mind, now let us look at the current sociological alternatives

to the mainstream economic model.16

State-centered Theories: The state-centered approach to social development is a

broad category of theories involving different models of development research, all of

which emphasize the role of the state in actively creating competitive advantage for a

country. “Getting the prices wrong” shows their skepticism that the free market will

provide appropriate incentives to trigger growth of new and more value-added

industries.17 Amsden argues that distorting the market to give national firms investment

incentives is not enough. The successful developmental state also sets bench marks to

discipline firms learning to meet international standards (Amsden 1989). Wade gives

his solution to the controversy about whether the state leads or follows the market by

ascertaining whether state policies come before or after the investments in private sector

(Wade 1990).18 Evans’ recent work shows that a mix of autonomous state and

16 For more detailed discussion, please refer to Chapter 1. 17 The term was first phrased by Amsden. I see no reason that other proponents of the approach, like

Wade, would disagree.

38

18 In fact, recent studies of the early history of Taiwanese plastic industry show that its development

actually followed the expansion of its downstream industries, like footwear exports (Wang 1995; Chu

1995).

cooperative networks is able to embed the private sector as a critical ingredient for

industry growth (Evans 1995). In a recent report by the World Bank, East Asian

Miracle, a “market-friendly” view is advocated, which yields to states some policy space

in managing the market, a small but clear sign of the interventionist state’s achievement.

Although our case does reveal the weakness of the free market model, it also creates

difficulties for the state-centered approach. Researchers in the state-centered approach

devote their efforts to demonstrating the creation of factors endowments through state-led

non-market signals, but fall short in examining the market where profit-making firms

engage in their daily business. In a sense, restricted by the framework of the national

economy, the state-centered approach can be conceived as a dynamic model of factor

creation, which explains why it tends to focus only on the supply side of the market. A

direct result of this paradigm limitation is that the causal mechanism embedded in the

transnational economic linkages of an industry is seriously understudied. Ironically, the

East Asian model is mainly characterized by its heavy involvement in and reliance on

export trade. It seems only natural that the supporters of state-centered approach tend to

focus on those upstream, large-scale industries that provide materials mainly to the

downstream domestic producers actually involved in export trade.19 Similarly, the

state-centered approach also tends to provide many details on state policies and

state-capital interactions, but falls short in analyzing the firm activities in the market,

where success is measured. Because of this shortcoming, the effectiveness of state

39

19 Acknowledging this weakness, Wade defends that “by setting directions for the large-scale [upstream]

sector, the government influences the configuration of risks and profit opportunities for small-scale

[downstream] firms” (Wade 1990, p.306). Interestingly, a theory that intends to explain East Asian

economic growth places export sectors as exogenous to its research subject.

industrial policy is not fully explored but assumed, given the known performance of the

industry. As a result, the downstream, labor-intensive footwear exporting from Taiwan,

with a large number of firms, severe competition, and far less state intervention, becomes

a subject that the state-centered approach cedes to the price-mediated market approach of

economists, who claim that the state-centered approach does not know where foreign

revenues are actually earned.

Production-centered approach: Production-centered approach (Deyo 1989;

especially Shieh 1992) claims a bottom-up approach distinct from the state-centered

approach. It complements the weakness of state-centered approach by looking at the

very detailed processes of production organization in manufacturing exports. The

production-centered approach also goes beyond factor endowment and examines the

organizational capability of production networks in offering adjustments to market

demands. Although research prompted by the productin-centered approach provides a

valuable correction to the state-centered approach, its almost exclusive focus on the labor

process, especially the subcontracting networks, limits how much of the production

system it can observe. Production-centered approach is therefore an incomplete

framework because it fails to embed production in the wider organizational field of

transnational economic linkages, which then must reincorporate the marketing networks

of manufacturing exports. One obvious consequence of this shortcoming is that, while

production-centered approach correctly points to the function of subcontracting networks

in curtailing market uncertainty, the specific content of uncertainty is under-specified.

Without a balanced examination on the organization-environment fit, the causal

contribution of subcontracting arrangement to uncertainty absorption is not clear.

40

Without stretching networks to embrace the marketing end of the chain,

production-centered approach will always face the danger of being conceived as just

another dynamic theory of factor endowment in which the local production networks

represent an asset that is ultimately selected by the asocial free market on the

international level.

Global Commodity Chains (GCC): The anomalies in the economics’ asocial

market model leave a theoretical void neither state-centered approach nor

production-centered approach can fill satisfactorily. Gereffi’s GCC perspective offers

an integrated approach that fits exactly the empirical subject of my research and

overcomes the shortcomings of the two sociological approaches we discussed. The

concept of commodity chain was first proposed by Hopkin and Wallerstein in 1986 as an

analytical framework for studying the “network of labor and production process whose

end results in a finished commodity” (Hopkins and Wallerstein 1986). Gereffi redefines

the focus of the chain study from the narrow emphasis on production process to the

organizational features of a series of transactions throughout the chain. The broadened

focus allows him to expand the scope of the chain to incorporate the marketing activities

at the final retail market.

The immediate effect of the modification allows GCC to highlight a very

fundamental change in capitalism after 1980s toward a “globalized coordination

system”20 (Ross and Trachte 1990; Gereffi 1992). The new reality is characterized by

41

20 The term was first used by Gereffi in a draft prepared for a workshop on Changing Business Systems in

East Asia, Hong Kong, 11-14 July, 1995. “Global capitalism” is the term used by Ross and Trachte to

highlight a new stage of capitalism. Since the focus of my current discussion is not on that topic, I prefer

two fundamental features that relates directly to my research subject. The first feature is

the industrialization of the developing world, which has been a profound phenomenon

since the 1960s and now ceases to be a sufficient indicator of development.21 On the

demand side, there has been a substantial consolidation of power in the hands of

designers and retailers in the developed countries.22 There may not be much change in

the way footwear is produced over the decades, but if we take the whole GCC into

consideration, it becomes clear that what Gereffi calls a “buyer-driven commodity chain”

has been consolidated, whose impact on production is beyond the production-centered

approach’s narrow scope. A buyer-driven commodity chain, as opposed to a

“producer-driven commodity chain,” refers to industries in which large retailers,

brandnamed merchandisers, and trading companies play the pivotal role in setting up

decentralized production networks in a variety of exporting countries, typically located in

the Third World (Gereffi 1994 b).

The buyer-driven commodity chain provides a fundamental framework for my

research for the following reasons: (1) It offers a comprehensive analytical unit of export

transaction which encompasses both the production and marketing networks of footwear

exports from Taiwan; (2) it is a model based on international trade, instead of the

to use “globalized coordination system.” 21 In 1990, 34 percent of the GDP of East and Southeast Asia was in the manufacturing sector, compared to

26 percent for Latin America, 17 percent for South Asia, and only 11 percent for sub-Saharan Africa. The

manufacturing sector’s share of GDP in some developing nations, such as China (38 percent), Taiwan (34

percent), and South Korea (31 percent), was even higher than Japan’s manufacturing/GDP ratio of 29

percent (Gereffi 1995b, p.106).

42

22 Between 1991 and 2000, for example, the ten biggest retailers in the United States are predicted to

increase their share of the US retail market from 43 percent to nearly 60 percent (KSA, 1992).

internalized production system of MNCs often seen in the producer-driven commodity

chains; (3) the model provides solid ground for a sociological model of international

trade because the chain perspective emphasizes the inter-firm coordination networks

across adjacent sectors, not endogenously confined factors; and (4) GCC is nearly

equivalent to economic sociology’s concept of “organizational field” in the area of

international economy.23 It focuses on the institutional and organizational formation of

transactions in the industry-specific organizational field of commodity chains, taking

cultural conditions and state policies in the nodes of global networks into consideration

without collapsing into the limited frameworks of either the state-centered approach or

the producion-centered approach.

As a result of the above, the GCC approach regards the roles that firms in the

developing countries play in GCCs as a fundamental parameter of industry development.

I follow this approach, basing my research on an acknowledgement of the original

equipment manufacturing (OEM) nature of Taiwanese footwear exports. A transaction

is defined as OEM when the supplier has four characteristics in transaction: (1)

independent from the buyer in term of ownership; (2) without control over distribution

channels; (3) without a brand; and (4) produces goods according to the design offered by

the buyer or one who acts on behalf of the buyer. In a comparative study of the export

roles of developing countries, Gereffi concludes that the broad scope of export roles and

43

23 “Organizations are affected by the structure of relations of the inter-organizational system in which they are embedded, and these systems are in turn affected by the societal systems in which they are located, and these systems are in turn affected by the world system in which they are located. ... While we are busily attempting to raise our models and analytical frameworks to scale higher levels of complexity, some of our colleagues in social science have started with more encompassing units ... and appear to be building frameworks that increasingly stretch down to the level of organizations and inter-organizational systems. ... It appears that as we labor to examine the connections between organizations and larger social structures, we will be in good company.” (Scott 1992, p.177, in concluding a theoretical review)

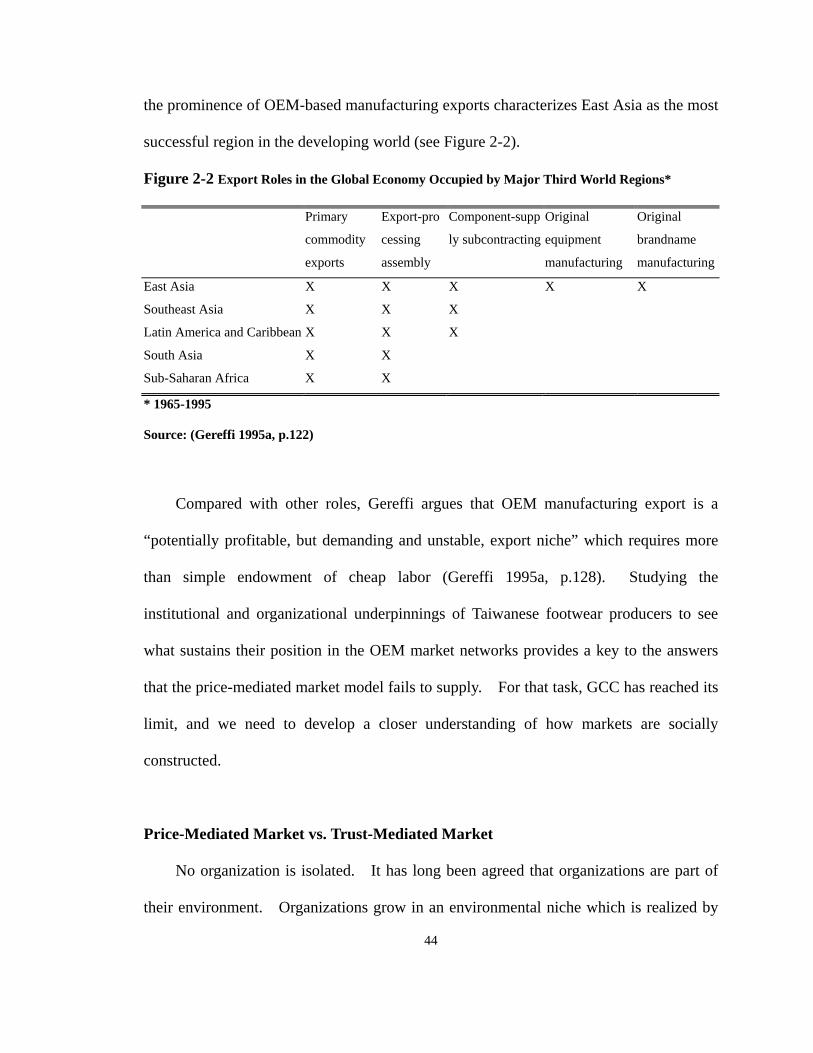

the prominence of OEM-based manufacturing exports characterizes East Asia as the most

successful region in the developing world (see Figure 2-2).

Figure 2-2 Export Roles in the Global Economy Occupied by Major Third World Regions*

Primary

commodity

exports

Export-pro

cessing

assembly

Component-supp

ly subcontracting

Original

equipment

manufacturing

Original

brandname

manufacturing

East Asia X X X X X

Southeast Asia X X X

Latin America and Caribbean X X X

South Asia X X

Sub-Saharan Africa X X

* 1965-1995

Source: (Gereffi 1995a, p.122)

Compared with other roles, Gereffi argues that OEM manufacturing export is a

“potentially profitable, but demanding and unstable, export niche” which requires more

than simple endowment of cheap labor (Gereffi 1995a, p.128). Studying the

institutional and organizational underpinnings of Taiwanese footwear producers to see

what sustains their position in the OEM market networks provides a key to the answers

that the price-mediated market model fails to supply. For that task, GCC has reached its

limit, and we need to develop a closer understanding of how markets are socially

constructed.

Price-Mediated Market vs. Trust-Mediated Market

No organization is isolated. It has long been agreed that organizations are part of

their environment. Organizations grow in an environmental niche which is realized by

44

their interaction with other organizations. They die out because they fail to mobilize

critical resources from their organizational environment. This view is compatible with

mainstream economics, except that the latter constructs a market model that makes the

social coordination among firms theoretically insignificant. According to economic

theory, in the capitalist economic sphere, competition characterizes the environment and