L'obituaire du chapitre de Saint-Materne à la cathédrale Saint ...

Upload

khangminh22Category

view

0download

0

December 29, 2003

Document of the World Bank

Report No. 25185-LCR

Saint Kitts and NevisOECS Fiscal Issues

Caribbean Country Management UnitPoverty Reduction and Economic Management UnitLatin America and the Caribbean Region

Report N

o. 25185-LCR

Saint Kitts and N

evis OEC

S Fiscal Issues

Policies to Achieve Fiscal Sustainability andImprove Efficiency and Equity of Public Expenditures

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

IOCR MDGs MIS MoF MoH MOW MTESP NHC NIA OECD OECS PAC PRGF PSIP PSIP oc PSIP PCC RGSM SEDU SELF SIGFIS SIGTAS SOEs SSMC sss UDC UK UNESCO VAT WAEMU WBI

Institutional and Organizational Capacity Review Millennium Development Goals Management information systems Ministry of Finance Ministry of Health Ministry of Communications, Works, Public Utilities and Posts Medium-Term Economic Strategy Paper National Housing Corporation Nevis Island Administration Organization for Economic Cooperation and Development Organization of Eastern Caribbean States Public Accounts Committee Poverty Reduction Growth Facility Public Sector Investment Program Public Sector Investment Program Operating Committee Public Sector Investment Program Project Cooperating Committee Regional Government Securities Market Small Enterprise Development Unit Student Education and Learning Fund Standardized Integrated Government Financial Information System Standardized Integrated Government Tax Administration System State-owned enterprises St. Kitts Sugar Manufacturing Company Social Security Scheme Urban Development Corporation United Kingdom United Nations Educational, Scientific, and Cultural Organization Value-added tax Western Africa Economic and Monetary Union World Bank Institute

Preface

This report was completed in June 2003 and reviews St. Kitts and Nevis public expenditures until the year 2002. The proposed policy recommendations reflect the situation o f the country at the time o f the completion of the report.

Acknowledgments

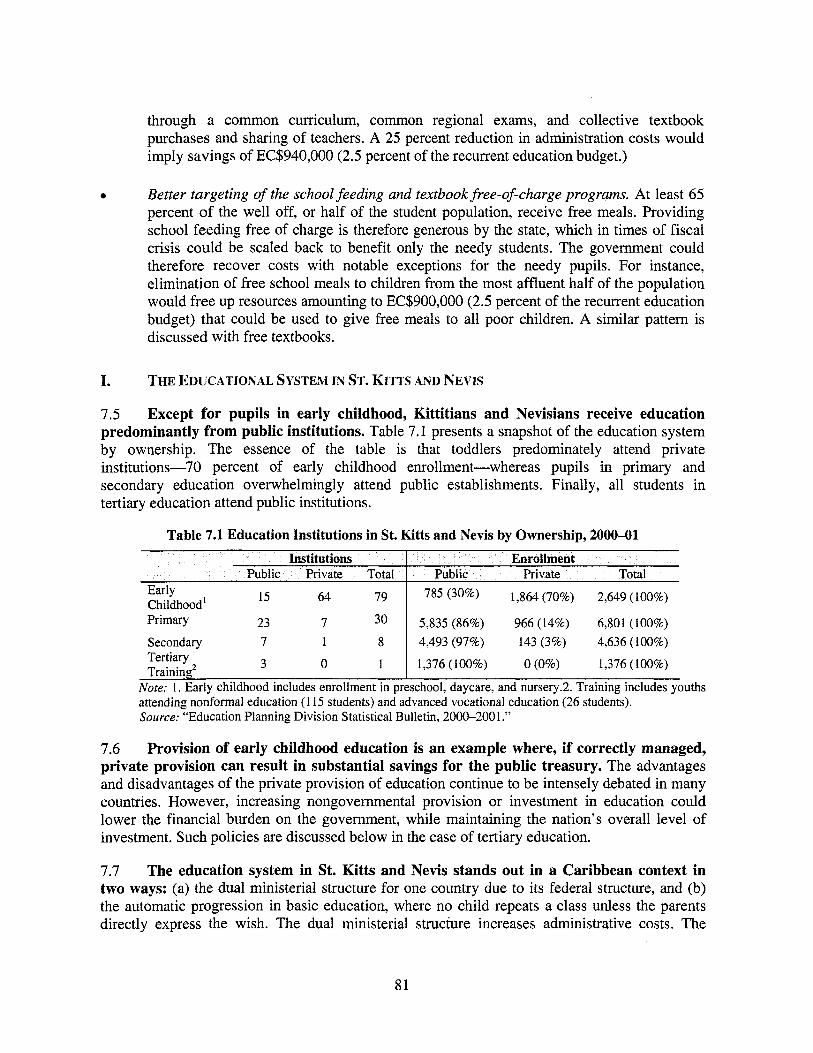

T h i s report i s based on the contributions o f a team consisting o f Lorraine Blank (social protection), Andreas Blom (education), Patrick Grady (public sector investment program and public sector employment and compensation), Ted Paterson (budget management), Helen Saxenian (health), and Claudia Sepdlveda (fiscal sustainability and fiscal and business cycles). As Task Manager, Claudia Sepdlveda was responsible for the overall preparation of the report. Shahrokh Fardoust and David Rosenblatt were peer reviewers.

The team would l i ke to thank Antonella Bassani and Mauricio Carrizosa for their helpful comments and their invaluable collaboration to improve this report. The report also benefited from the accomplished research assistance o f Laura dos Reis and Kevin Tomlinson and the excellent assistance of Anne Pillay.

The assistance, cooperation, and input o f many Government departments in St. Kitts and Nevis-too numerous to mention individually-is gratefully acknowledged. In particular, extensive assistance was received from the Budget and Planning Unit o f the Ministry o f Finance. The report also benefited from the assistance and cooperation o f the Eastern Caribbean Central Bank, the Caribbean Development Bank, and the International Monetary Fund. Without their help, preparation o f th is report would not have been possible.

Table of Contents

EXECUTIVE SUMMARY .............................................................................................................................. i 1 . I . I1 . I11 .

2 . I . I1 .

3 . I . I1 . I11 .

4 . I .

I1 . 5 . I .

I1 .

6 . I . I1 . I1 .

7 . I . I1 . I11 .

8 . I . I1

I11

FISCAL DEFICIT. PUBLIC DEBT. AND FISCAL SUSTAINABILITY ............................... 1 ST . KITTS AND NEVIS FISCAL PERF~RMANcE. 1990-2002 ............................................................. 2 DOES ST . KIPS AND NEVIS FACE A FISCAL SUSTAINABILITY PROBLEM? ..................................... 4 FISCAL CONSOLIDATION IN ST . KITTS AND NEVIS’S PUBLIC SECTOR .......................................... 11

FISCAL POLICY AND BUSINESS CYCLES ......................................................................... 17 TRENDS AND CYCLES IN ST . KIPS AND NEVIS FISCAL ACCOUNTS. 1980-2001 .......................... 18 THE STRUCTURAL BUDGET SURPLUS IN ST . KlTTS AND NEVIS .................................................... 23

BUDGET MANAGEMENT ....................................................................................................... 27 CONSTITUTIONAL AND LEGAL FRAMEWORK ................................................................................ 29 BUDGET PREPARATION. EXECUTION. AND MONITORING .............................................................. 30 BUDGET ACCOUNTABILITY ........................................................................................................... 37

THE PUBLIC SECTOR INVESTMENT PROGRAM ............................................................ 41 ST . KITTS AND NEVIS FEDERAL GOVERNMENT PSP: PREPARATION. EXECUTION. AND MONITORING .................................................................................................................................. 43 SIZE AND COMPOSITION OF THE NEVIS ISLAND ADMINISTRATION PSIP ...................................... 51

PUBLIC SECTOR EMPLOYMENT AND COMPENSATION ............................................. 53 RECENT TRENDS IN EMPLOYMENT AND COMPENSATION IN THE ST . KIPS AND NEVIS

RECENT TRENDS IN PUBLIC SECTOR EMPLOYMENT AND COMPENSATION IN THE NEVIS FEDERAL GOVERNMENT ................................................................................................................ 54

ISLAND ADMINISTRATION ............................................................................................................. 63

THE HEALTH SECTOR ........................................................................................................... 67 HEALTH OUTCOMES IN ST . K ITTS AND NEVIS ............................................................................... 68 THE HEALTH SYSTEM: COVERAGE AND DELIVERY ...................................................................... 72 USES OF HEALTH SPENDING IN ST . KIrlYrS AND NEVIS. 1995-2002 ............................................... 75

THE EDUCATION SECTOR .................................................................................................... 79 THE EDUCATIONAL SYSTEM IN ST . KITTS AND NEVIS .................................................................. 81 EDUCATION OUTCOMES IN ST . KITTS AND NEVIS ......................................................................... 82 USES OF EDUCATION EXPENDITURES IN ST . KITTS AND NEVIS. 1994-2002 ................................. 84

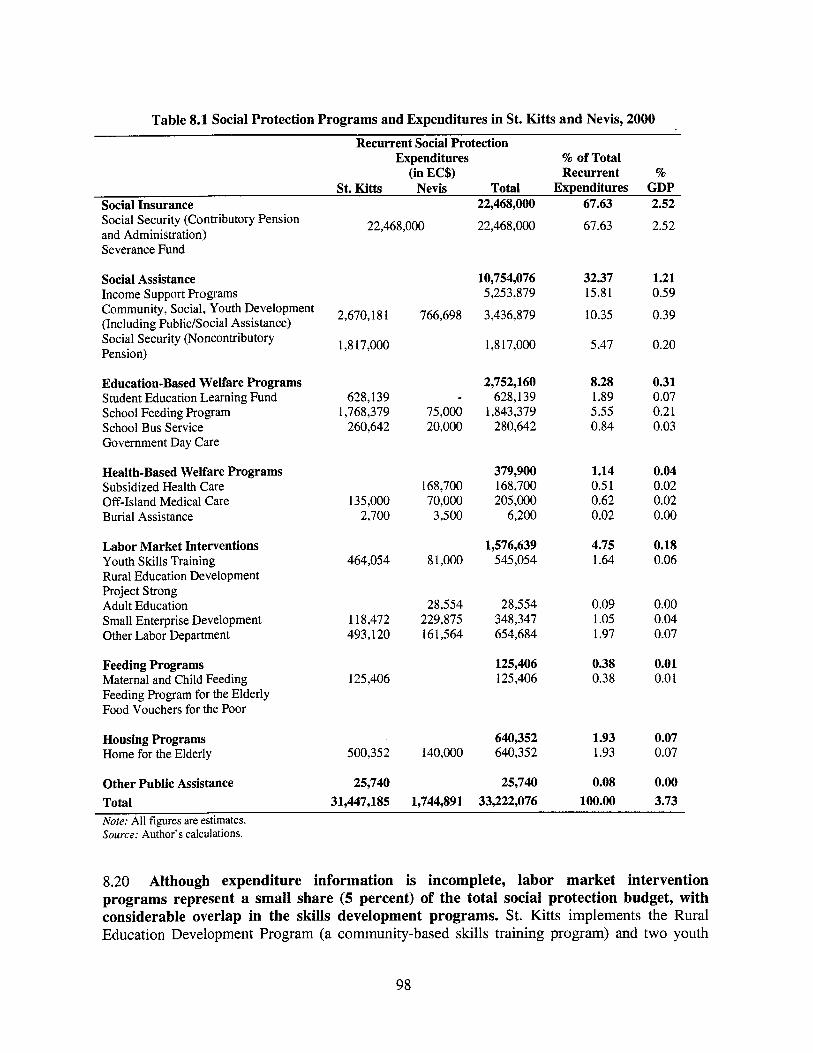

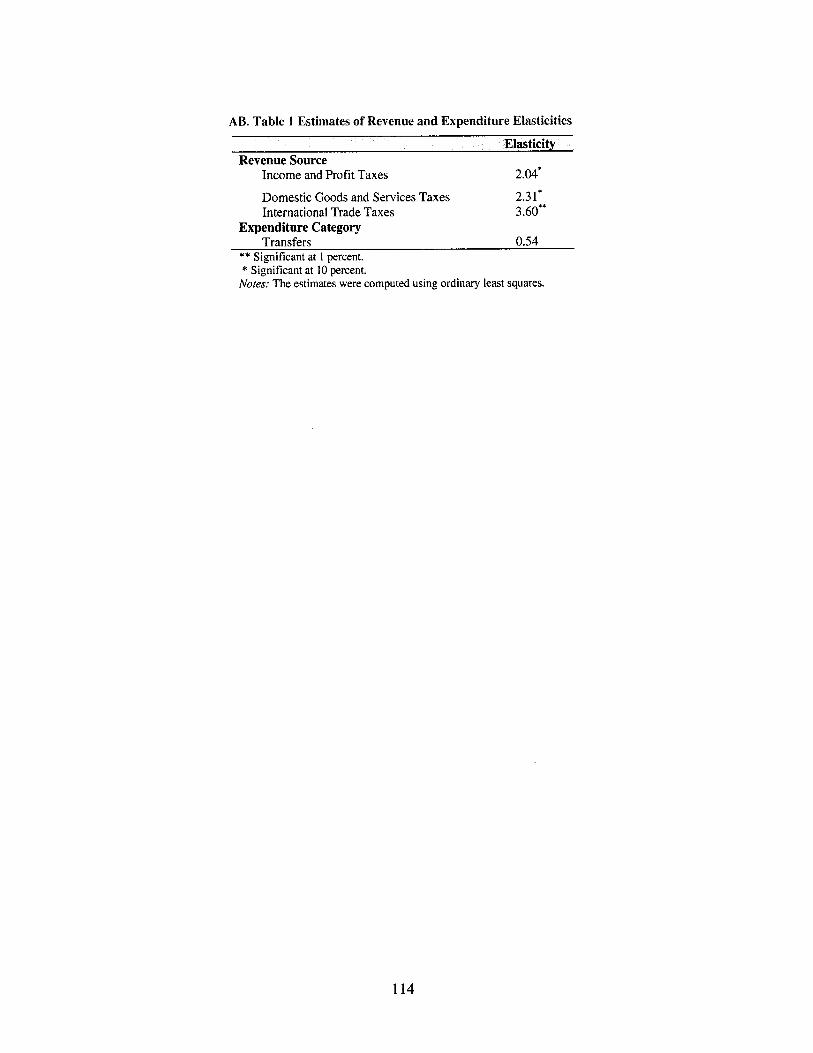

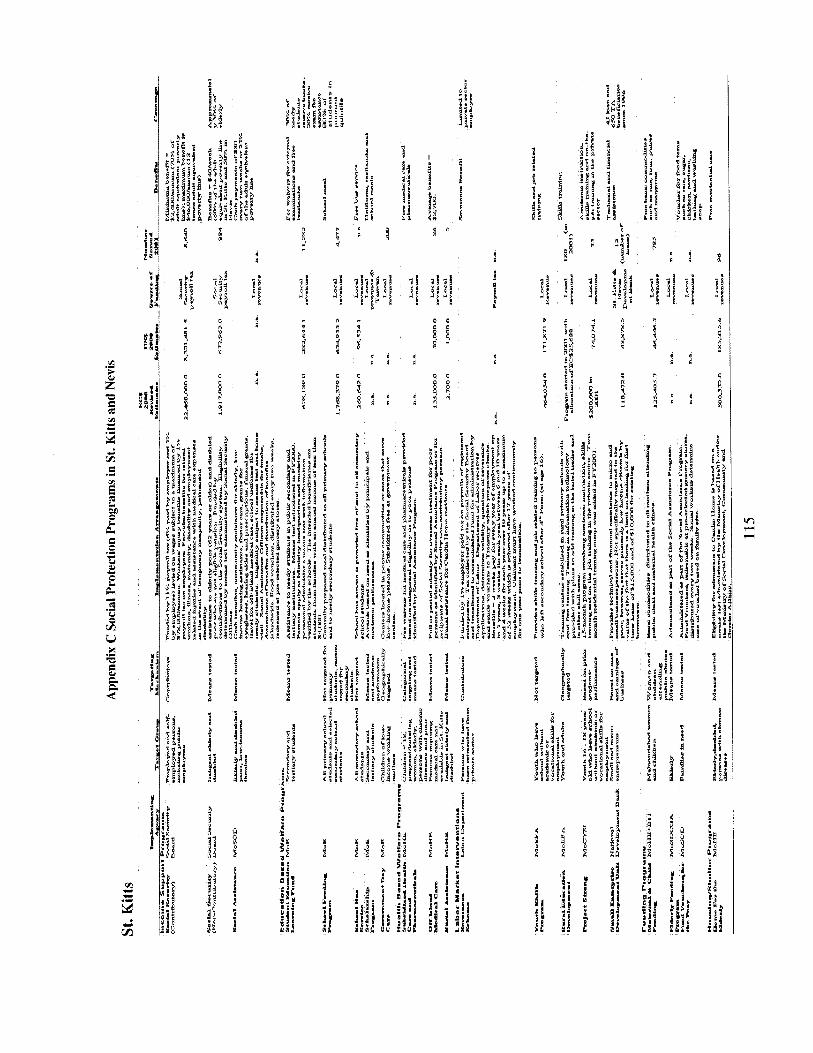

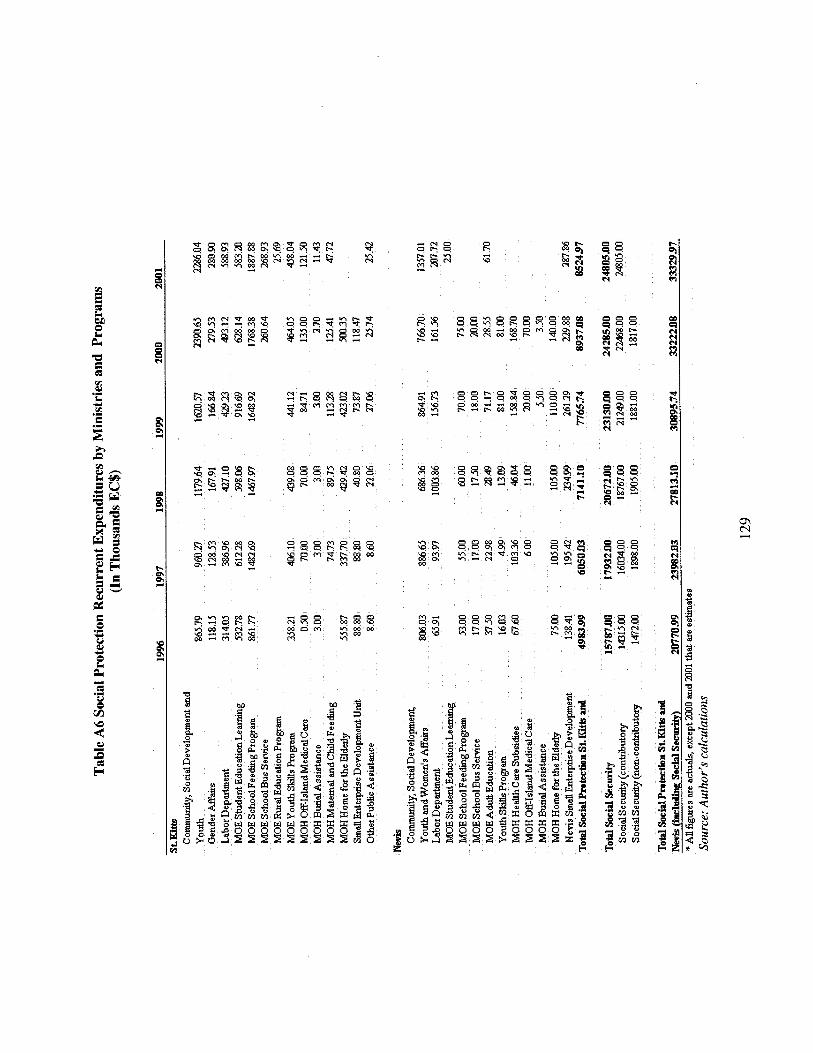

SOCIAL PROTECTION PROGRAMS .................................................................................... 93 ST . KITTS AND NEVIS SOCIAL PROTECTION STRATEGY AND PROGRAMS .................................... 95 COMPOSITION AND EVOLUTION OF SOCIAL PROTECTION SPENDING IN ST . KITTS AND

SOCIAL PROTECTION AND RISK MANAGEMENT IN ST . KITTS AND NEVIS ................................. 102 NEVIS. 1996-2001 ....................................................................................................................... 101

BIBLIOGRAPHY ..................................................................................................................................... 107

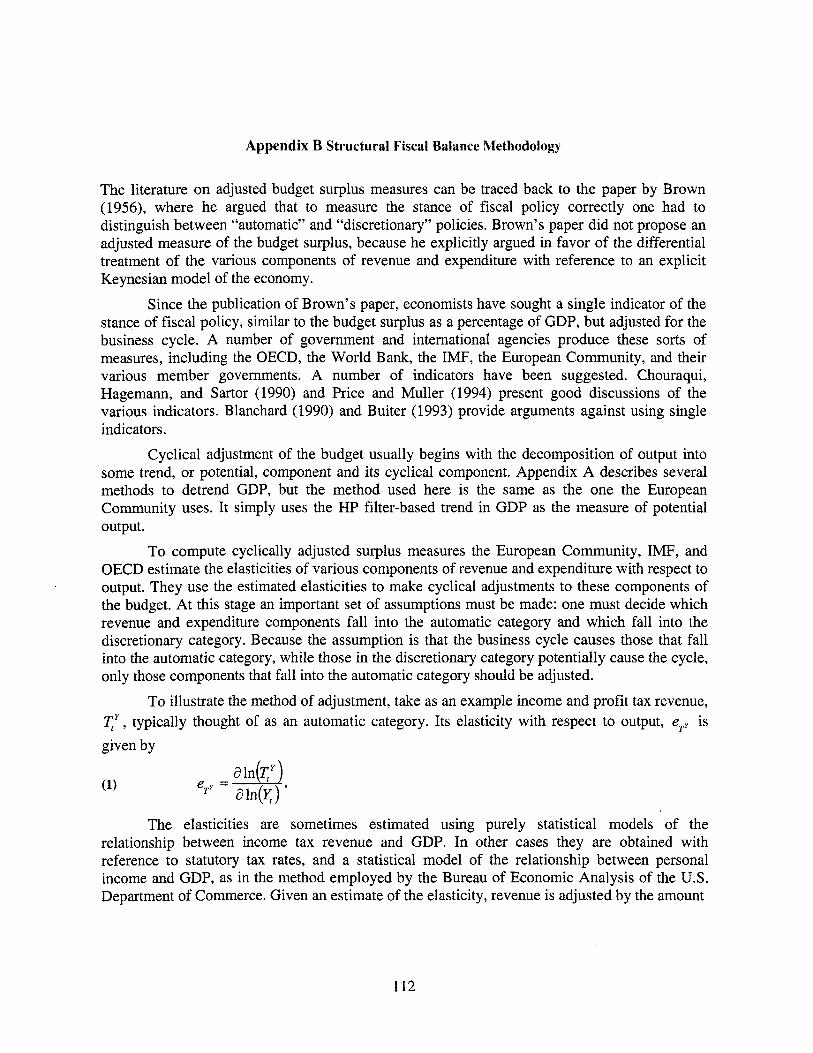

APPENDICES .......................................................................................................................................... 111 Appendix A The Hodrick-Prescott Detrending Procedure .......................................................... 111 Appendix B Structural Fiscal Balance Methodology ................................................................. 112

Appendix C Social Protection Programs in St . Kitts and Nevis .................................................. 1 15 ANNEXES .............................................................................................................................................. 117

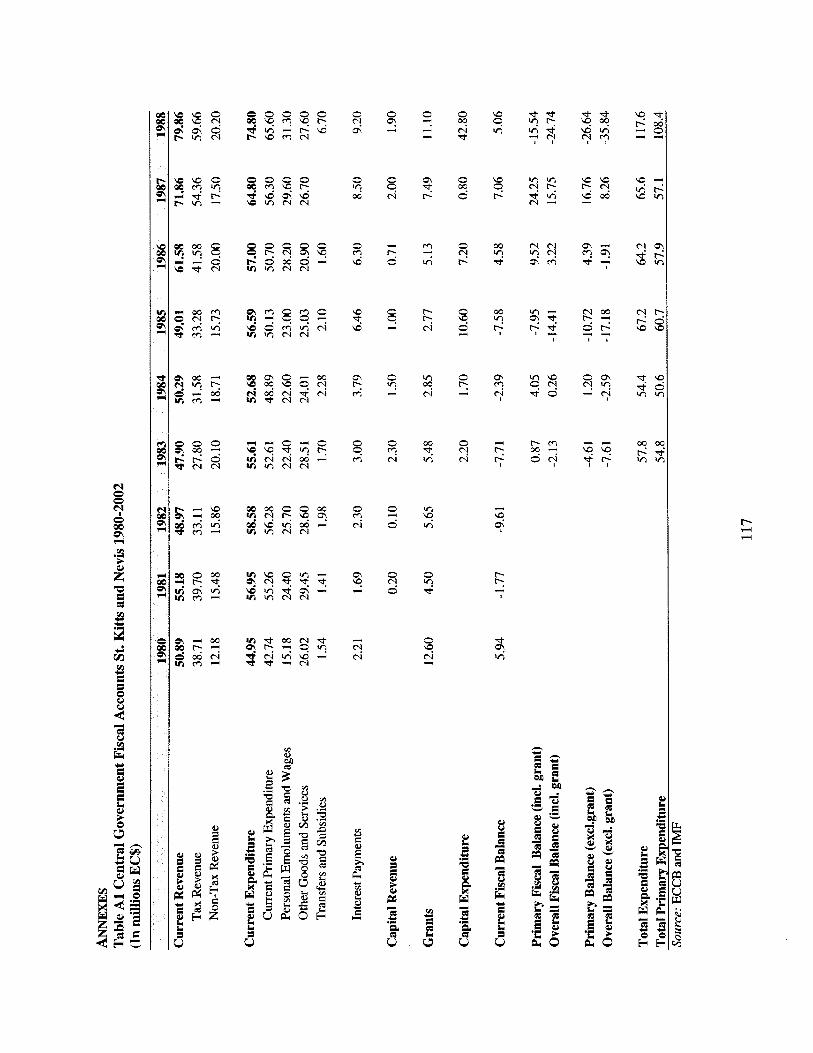

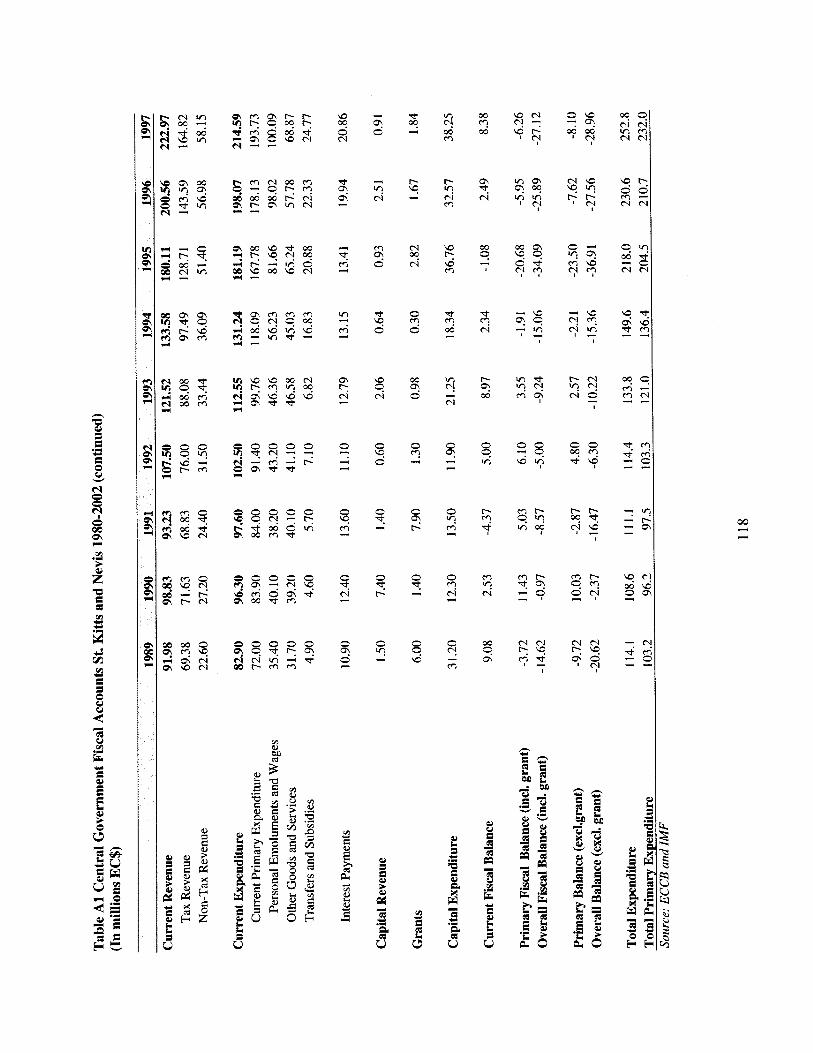

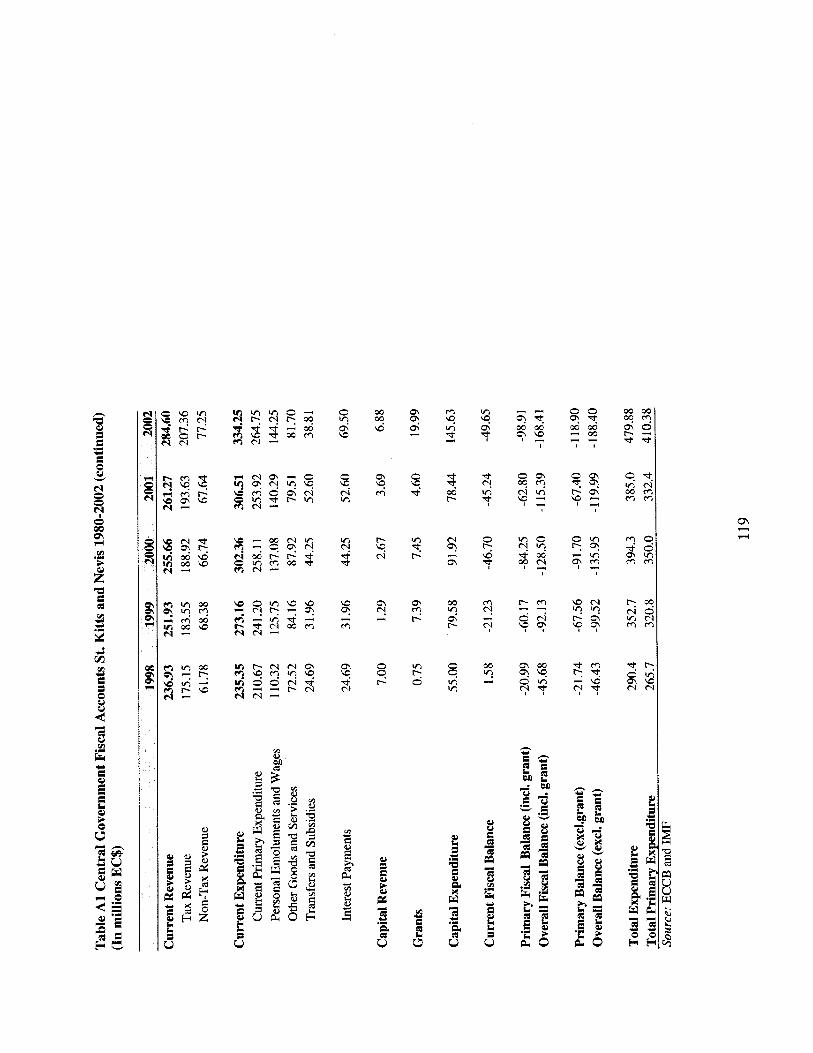

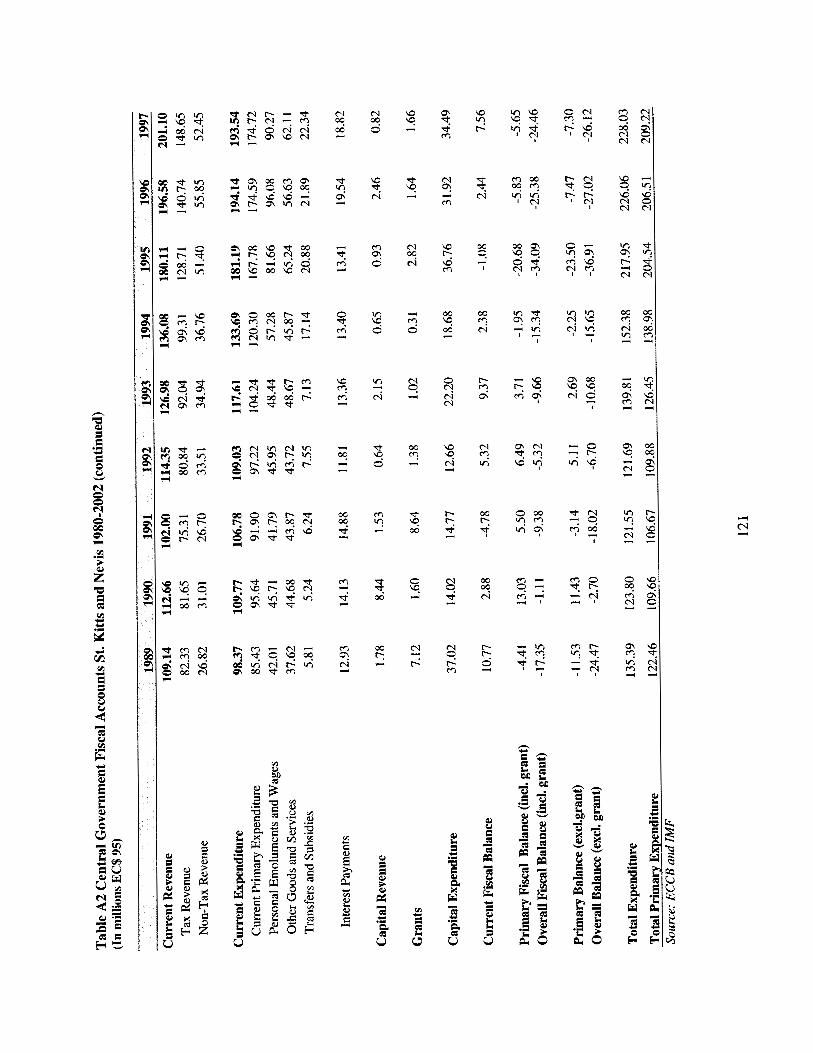

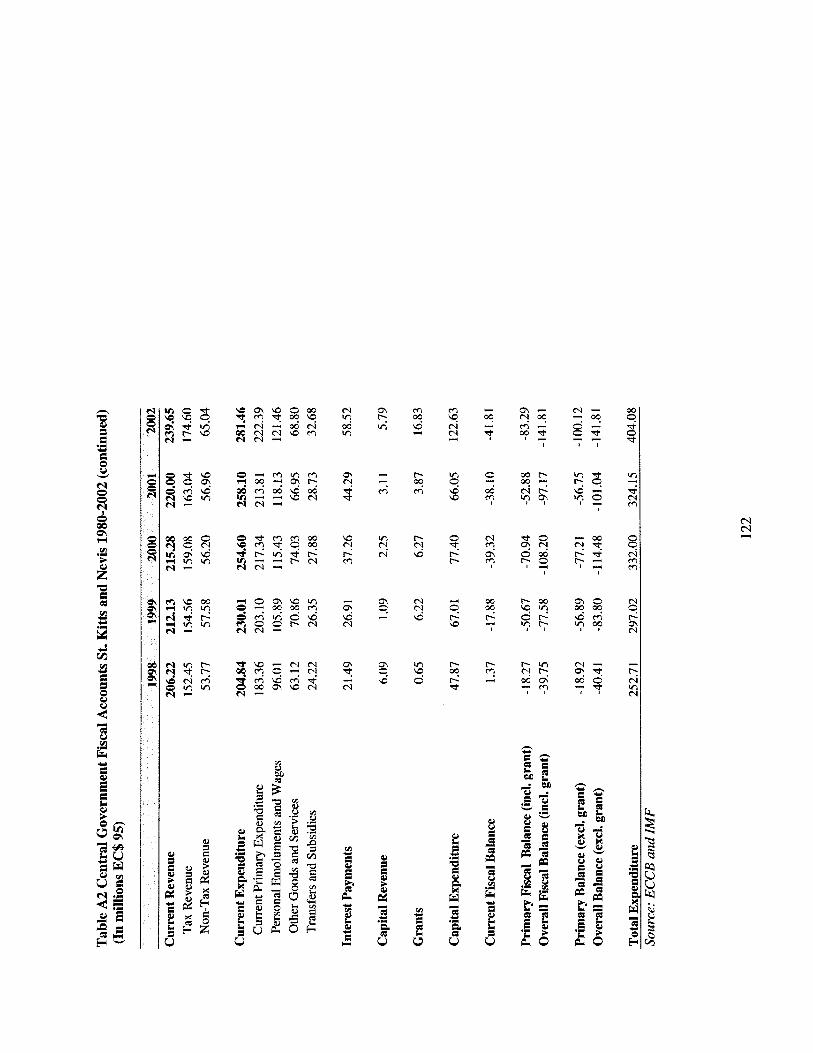

Table A1 Central Government Fiscal Acounts in St . Kitts and Nevis 1980-2002 (In millions EC$) .......................................................................................................... 120

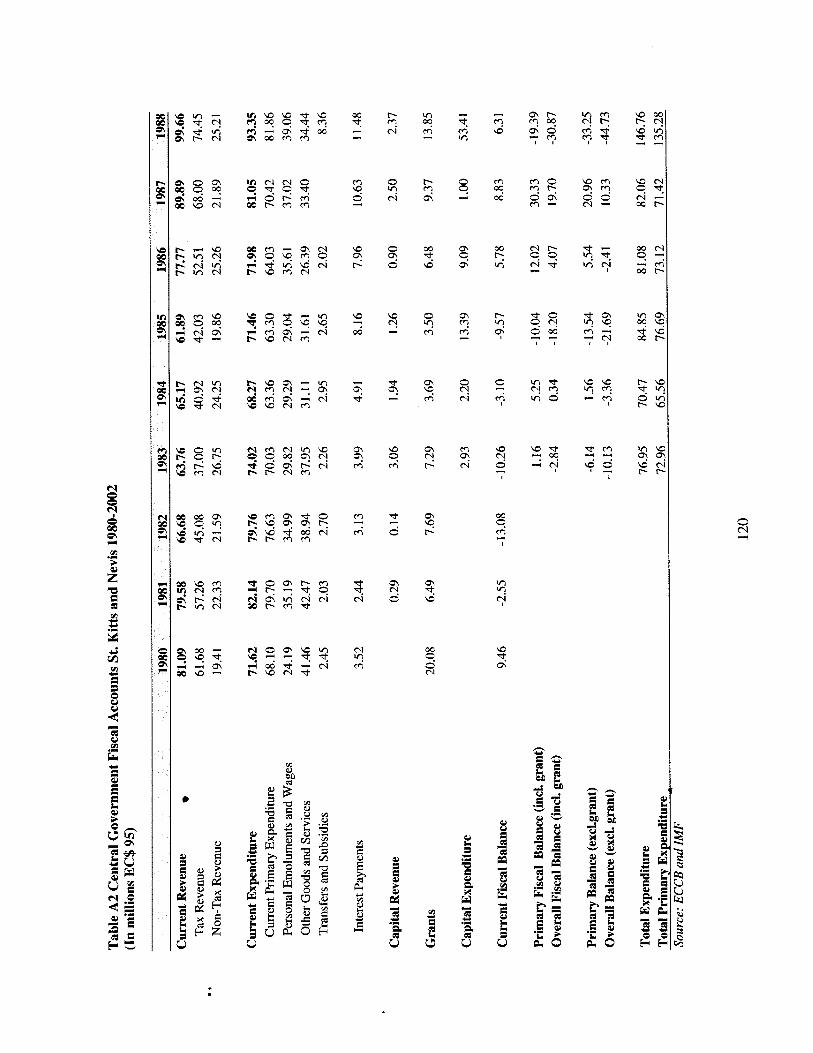

Table A2 Central Government Fiscal Acounts in St . Kitts and Nevis 1980- 2002 (In millions EC$ 95) ..................................................................................................... 123

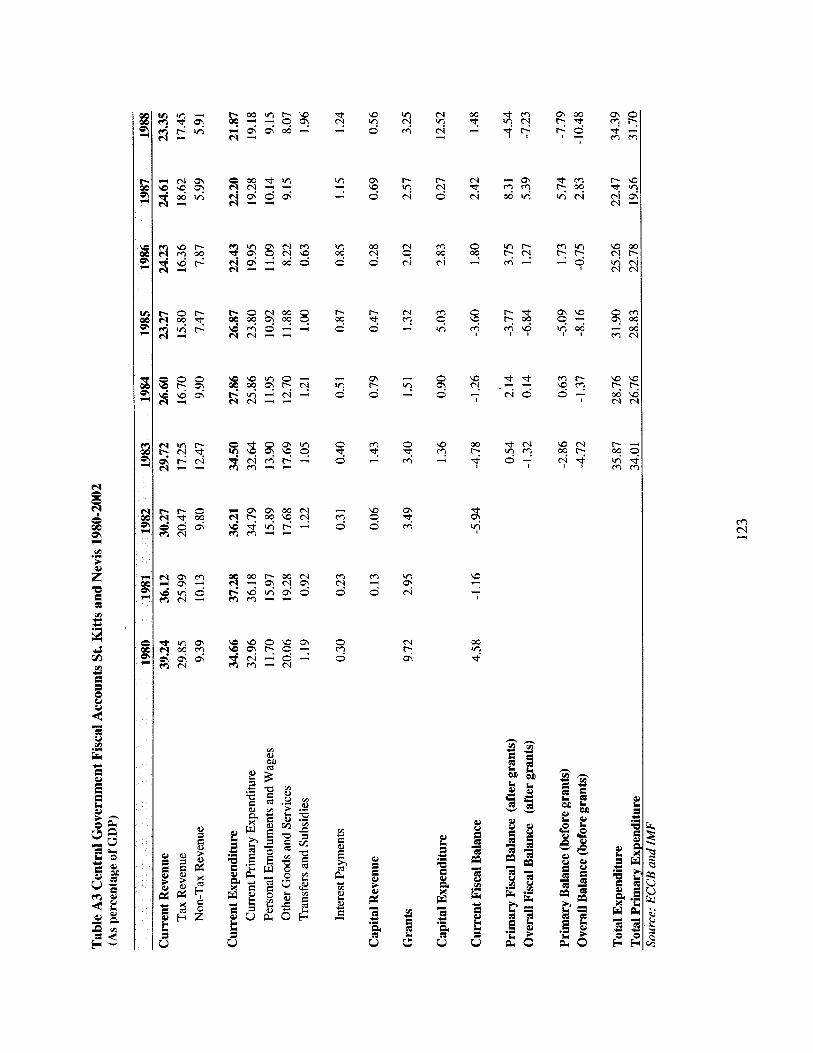

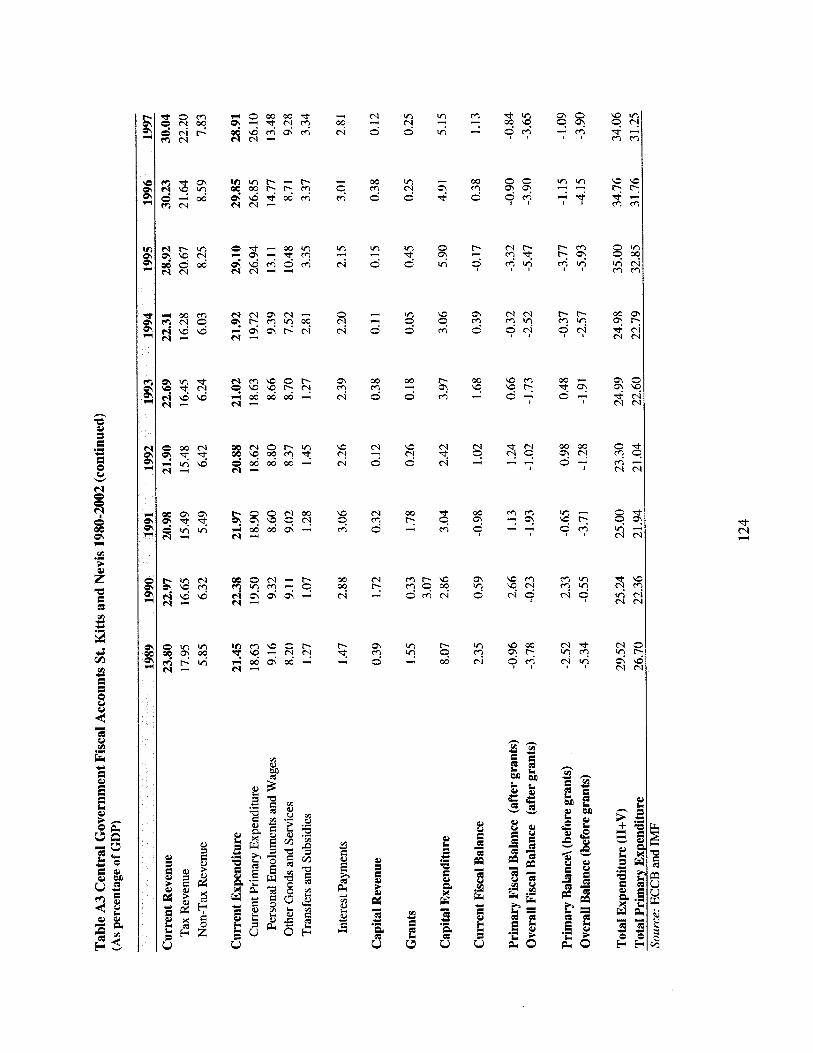

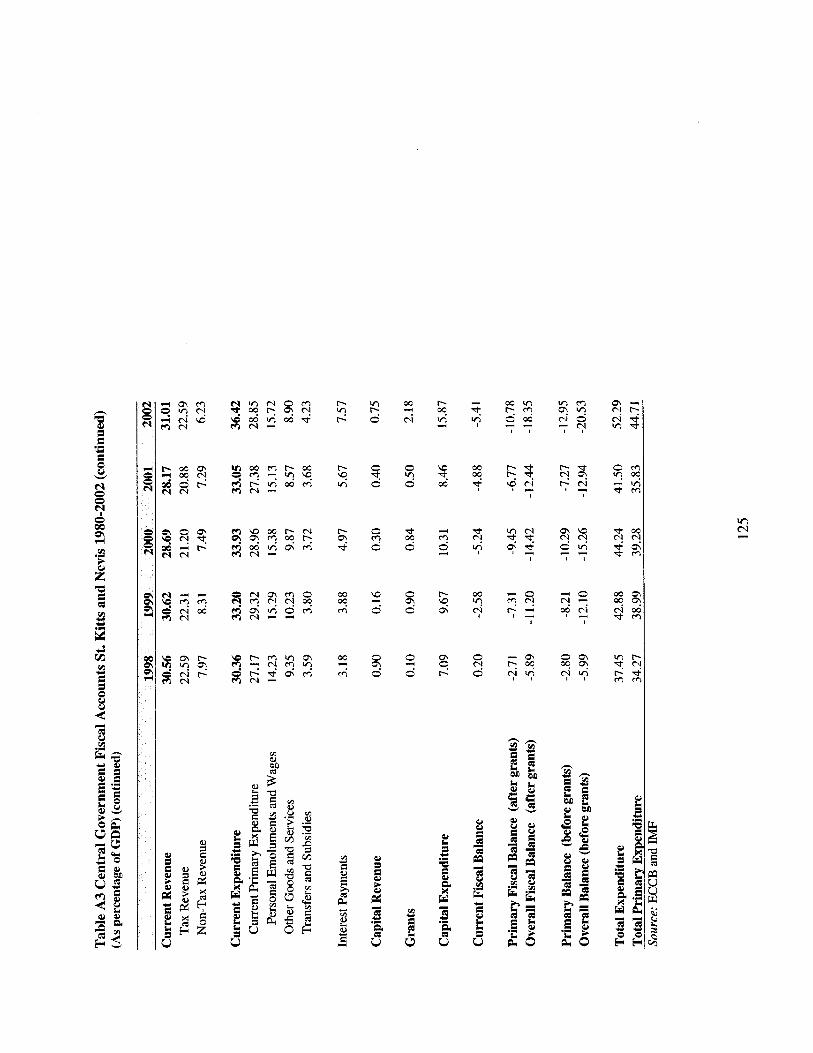

Table A3 Central Government Fiscal Acounts in St . Kitts and Nevis 1980-2002 (As percentage o f GDP) ............................................................................................... 126

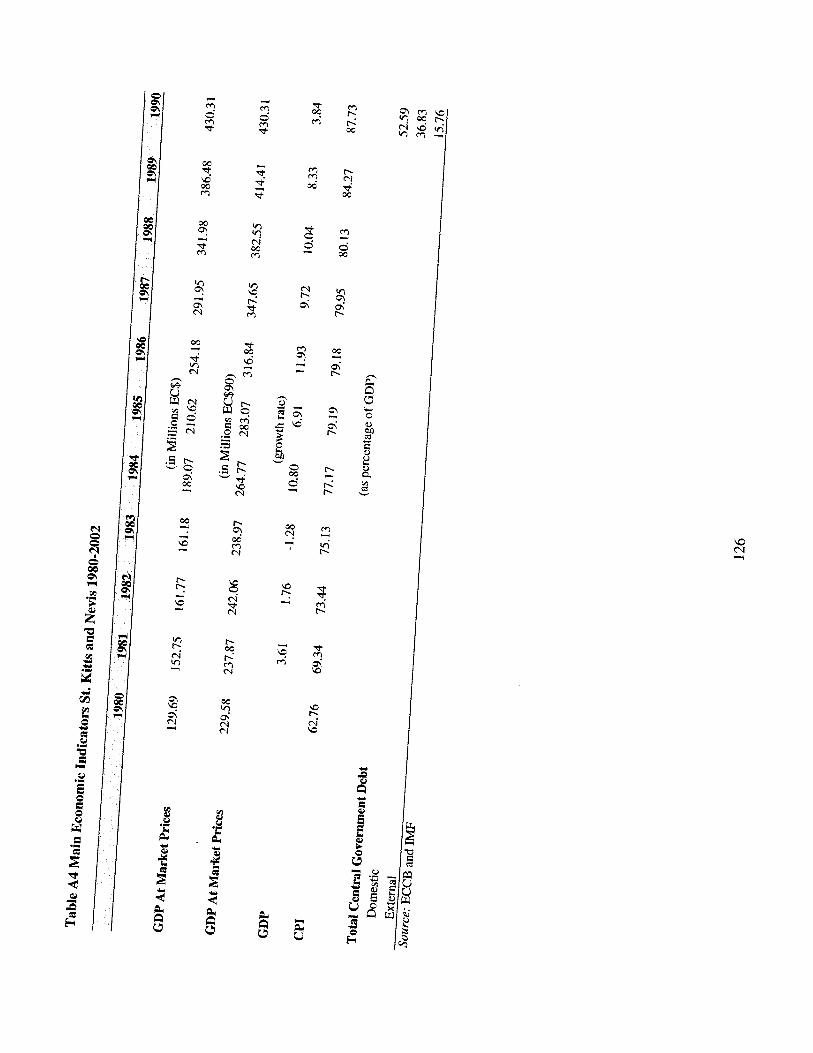

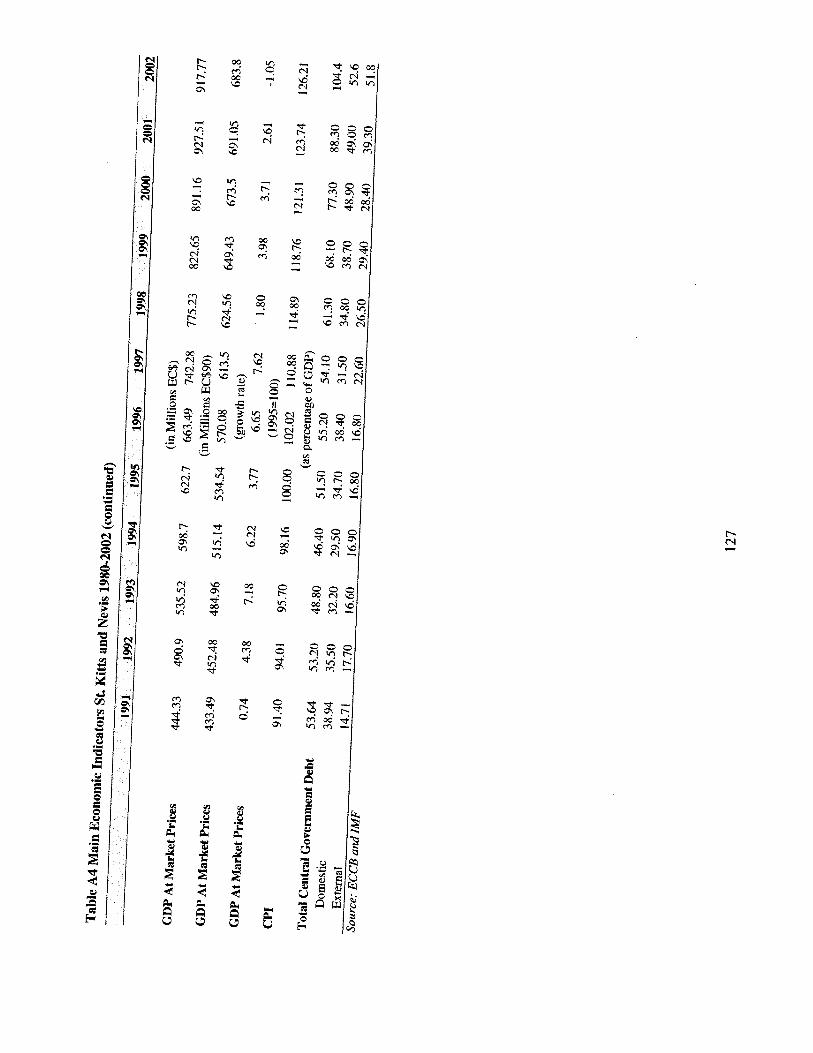

Table A4 Main Economic Indicators St . Kitts and Nevis 1980-2002 ......................................... 126

Table A6 Social Protection Recurrent Expenditures by Ministries and Programs Table A5 Operations o f Public Enterprises in St . Kitts and Nevis 1995-1998 ............................ 128

(In Thousands EC$) ..................................................................................................... 129

List of Tables

Table E.S. 1 Summary o f Policy Recommendations .............................................................................. xiv Table 1.1 Customs Revenue Forgone from Tax Concessions (as percentage o f GDP) .......................... 13 Table 2.1 Long-Term GDP. Central Government Revenue. and Expenditure Growth Rates.

1981-2002 ...................................................................................................................................... 20 Table 2.2 Cyclical Properties o f GDP. Central Government Revenue. and Expenditure. 1980-

2002 ............................................................................................................................................... 22 Table 3.1 Main Items Responsible for the Variance Between Actual and Budgeted Expenditures

in the Ministry of Finance and Planning. St . Kitts and Nevis. 1995-2000 (in millions EC$) ....... 35 Table 3.2 Ministries Consistently Over or Under Budget in St . Kitts and Nevis. 1995-2000

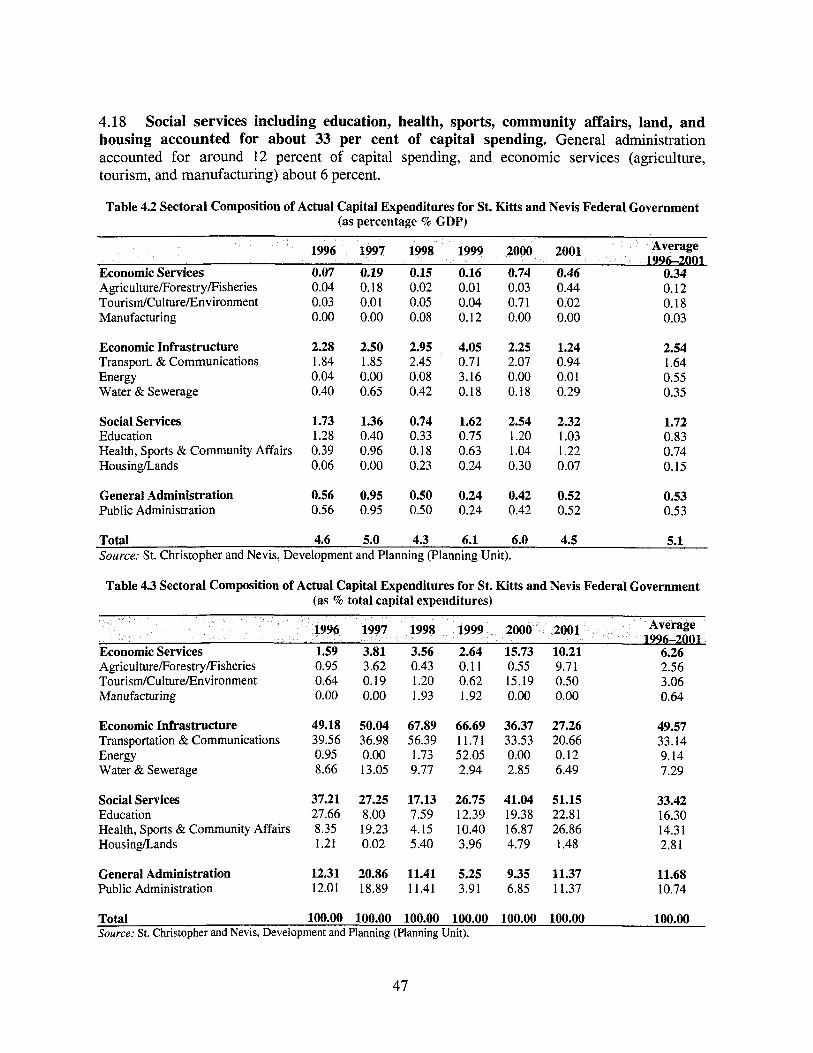

(average percentage) ...................................................................................................................... 36 Table 4.1 Medium-Term PSIF’ for St . Kitts and Nevis. 2001-06 (in thousands EC$) ........................... 44 Table 4.2 Sectoral Composition o f Actual Capital Expenditures for St . Kitts and Nevis Federal

Table 4.3 Sectoral Composition o f Actual Capital Expenditures for St . Kitts and Nevis Federal

Table 4.4 Source o f Financing o f St . Kitts and Nevis Federal Government Capital Expenditures

Table 4.5 Realization Rate o f St . Kitts and Nevis Federal Government Capital Expenditures.

Table 4.6 Realization Rate o f St . Kitts and Nevis Federal Government Capital Expenditures by Funding Source. 1994-2001 .......................................................................................................... 50

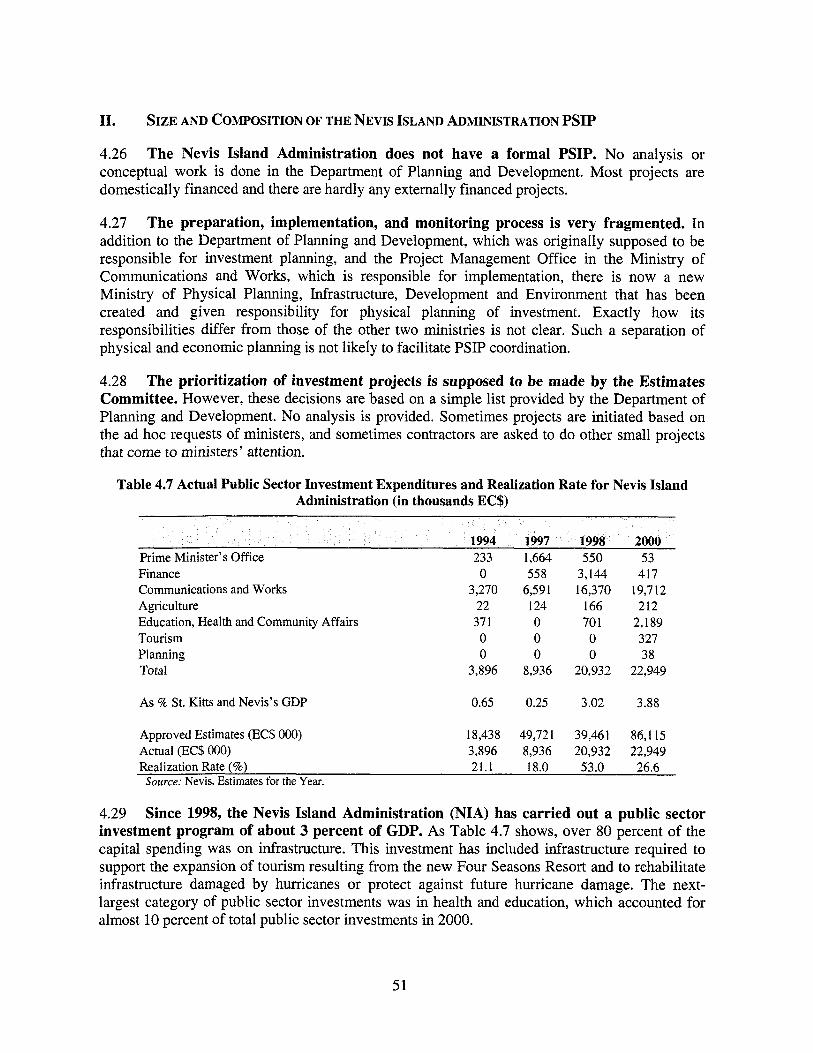

Table 4.7 Actual Public Sector Investment Expenditures and Realization Rate for Nevis Island Administration (in thousands EC$) ................................................................................................ 51

Table 5.1 Employment in the St . Kitts and Nevis Federal Government. 1995-2002 ............................. 55 Table 5.2 Distribution o f Established Positions by Ministry in the St . Kitts and Nevis Federal

Government. 2000-01 .................................................................................................................... 56 Table 5.3 St . Kitts and Nevis Federal Government Compensation. 1995-2002 .................................... 59 Table 5.4 Personal Emoluments and Wages by Ministry in the St . Kitts and Nevis Federal

Government (EC$) ......................................................................................................................... 60 Table 5.5 Public and Private Sector Wages in St . Kitts and Nevis. 2001 (EC$) .................................... 61 Table 5.6 Employment in Nevis Island Administration. 1995-2002 ..................................................... 63 Table 5.7 Established and Non-Established Positions. by Ministry. in the NIA. 2001-02 .................... 64 Table 5.8 Personal Emoluments and Wages in the NIA. 1997-2002 ..................................................... 65

Government (as percentage % GDP) ............................................................................................. 47

Government (as % total capital expenditures) ............................................................................... 47

(as % o f total capital spending) ...................................................................................................... 49

1 994-200 1 ...................................................................................................................................... 49

Table 6.1 Health Indicators in St . Kitts and Nevis Compared with Barbados. Jamaica. and other OECS Countries. 2000 .......................................................................................................... 69

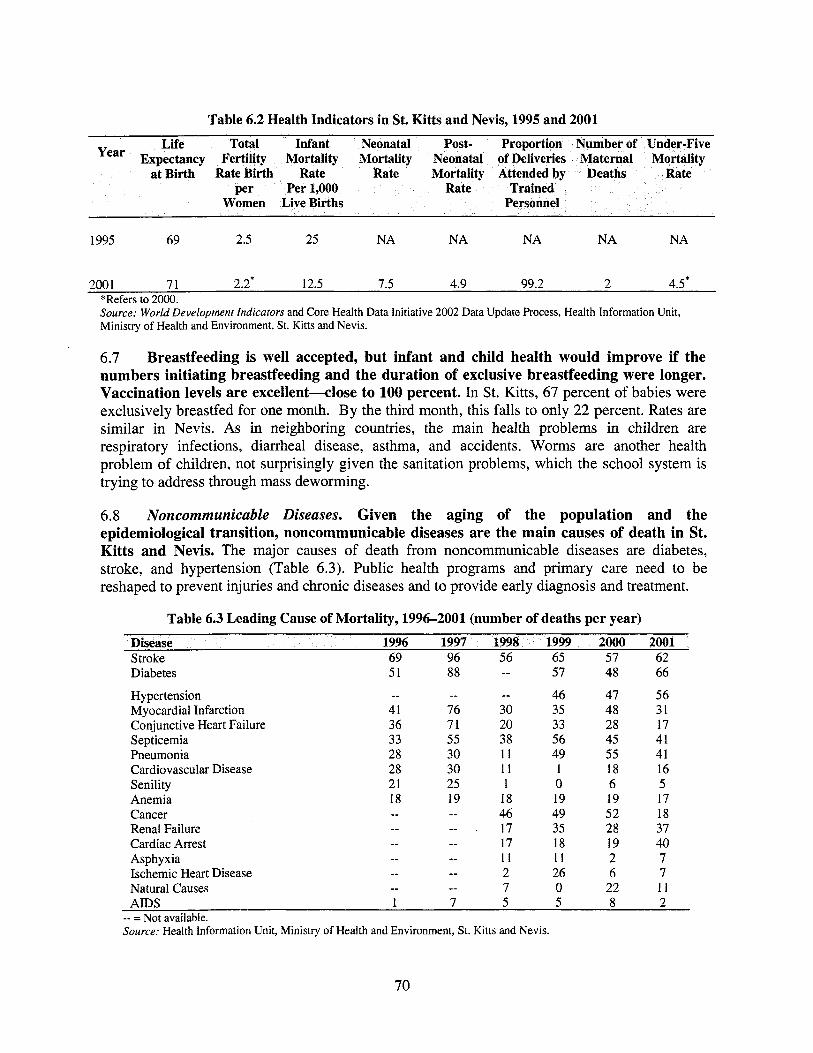

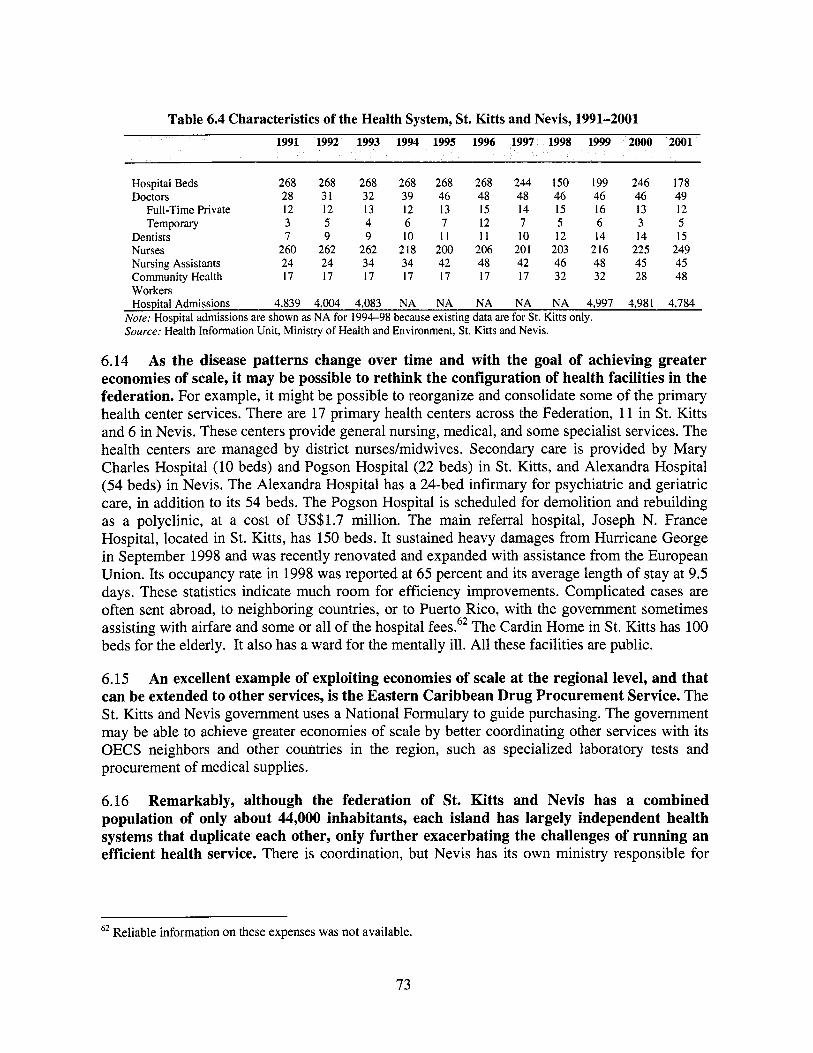

Table 6.2 Health Indicators in St . Kitts and Nevis. 1995 and 2001 ........................................................ 70 Table 6.3 Leading Cause of Mortality. 1996200 1 (number of deaths per year) .................................. 70 Table 6.4 Characteristics o f the Health System. St . Kitts and Nevis. 1991-2001 ................................. 73 Table 6.5 Uses of Health Facilities in St . Kitts and Nevis. 1999 (in percentage) .................................. 74 Table 6.6 Health Spending in St . Kitts and Nevis Compared to Barbados. Jamaica. and

other OECS countries. 2000 (as percentage) ................................................................................ 76 Table 6.7 Recurrent Health Spending in St . Kitts and Nevis. 1995-2002 (in EC $ 95) ........................ 77 Table 7.1 Education Institutions in St . Kitts and Nevis by Ownership. 2000-01 .................................. 81 Table 7.2 Distribution of Education Subsidies by Quintile. 1999 ......................................................... 88 Table 8.1 Social Protection Programs and Expenditures in St . Kitts and Nevis. 2000 .......................... 98 Table 8.2 Incidence of Poverty. Indigence. and Other Related Indicators. 1999 (percentage) ............ 102 Table 8.3 St . Kitts and Nevis Risk Indicators by Age Cohort. Existing Programs.

and Suggested Interventions ........................................................................................................ 103

List of Figures

Figure 1.1 St . Kitts and Nevis Central Government Fiscal Performance 1990-2002 (as % of

Figure 1.2 St . Kitts and Nevis Central Government Primary Expenditure, Interest Payment and

Figure 1.3 St . Kitts and Nevis Central Government Debt and Primary Surplus 1990-2002 (as % GDP) ............................................................................................................................................... 3

Figure 1.4 St . Kitts and Nevis Central Government Short-Term Fiscal Gap 1991-2002 (as % GDP) ............................................................................................................................................... 6

Figure 1.5 St . Kitts and Nevis Central Government Projected Short-Term Fiscal Gap 2003-2005 (as % GDP) ..................................................................................................................................... 7

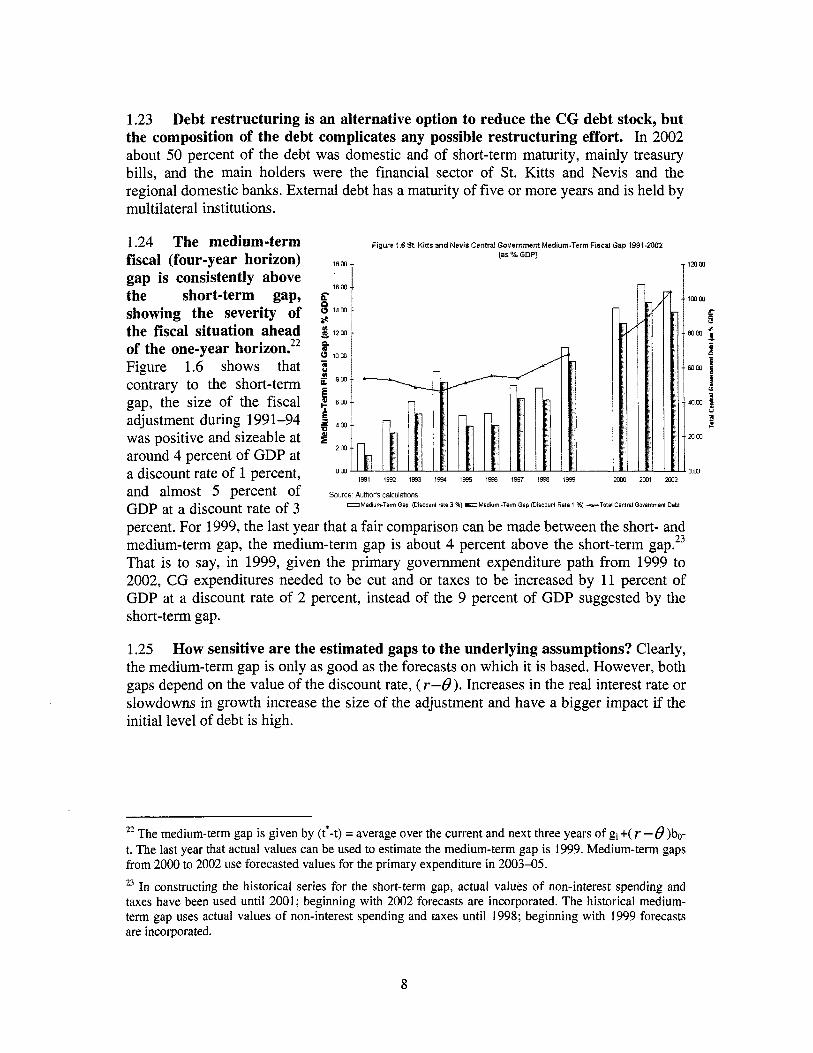

Figure 1.6 St . Kitts and Nevis Central Government Medium-Term Fiscal Gap 1991-2002 (as % GDP) ............................................................................................................................................... 8

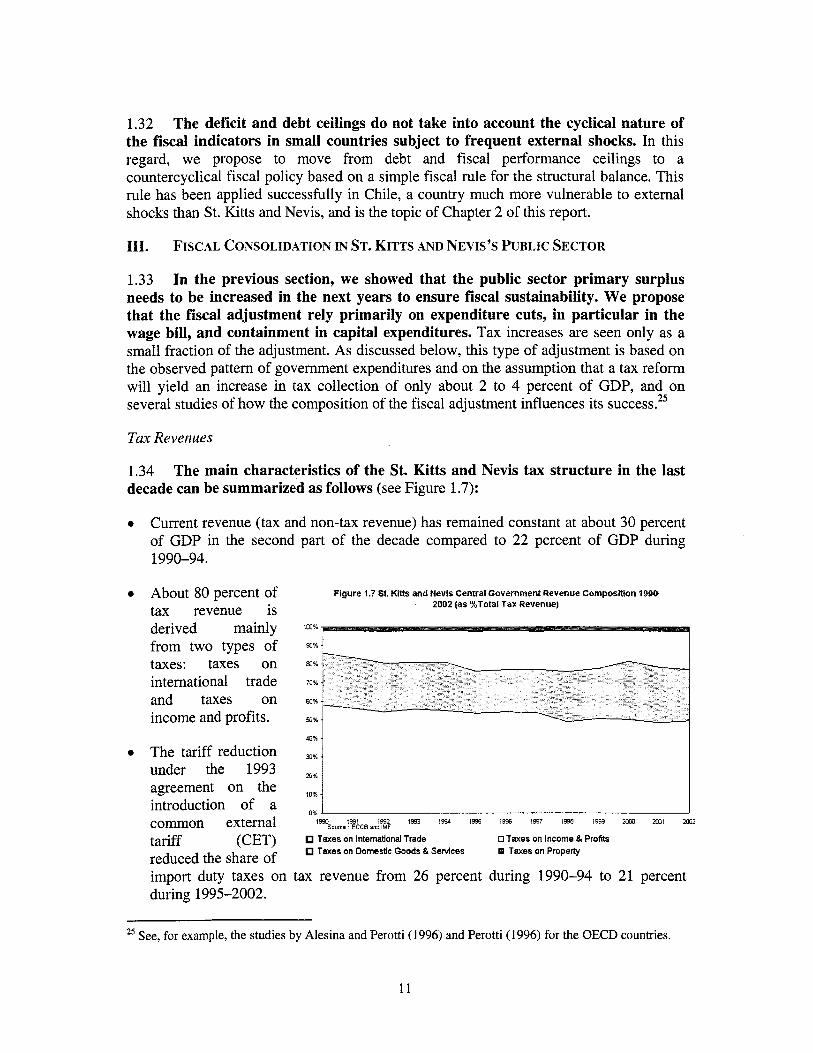

Figure 1.7 St . Kitts and Nevis Central Government Revenue Composition 1990-2002 (as % Total Tax Revenue) .............................................................................................................. 11

Figure 1.8 St . Kitts and Nevis Central Government Expenditure Composition 1990-2002 (as % of GDP) ............................................................................................................................... 14

Figure 1.9 St . Kitts and Nevis Central Government Expenditure Composition 1990-2002 (in millions EC$ 95) ....................................................................................................................... 15

Figure 2.1 St . Kitts and Nevis GDP, GDP Trend and Cyclical Component 1980-2002 ....................... 19 Figure 2.2 Fiscal Cyclical Adjustment in St . Kitts and Nevis 1983-2002 (as percentage of GDP) ....... 23 Figure 2.3 Cyclical Adjusted Primary, Overall, and Current Balance in St . Kitts and Nevis,

1983-2002 (as % GDP) ................................................................................................................ 24 Figure 3.1 St . Kitts and Nevis Government Structure ........................................................................... 29 Figure 3.2 The Budget Cycle in the St . Kitts and Nevis Federal Government ...................................... 32 Figure 3.3 Variance between Actual and Budgeted Recurrent Expenditures, Ministry of Finance

and all other Ministries St . Kitts and Nevis 1995-2000 (in percentage) ....................................... 34 Figure 3.4 Variance between Actual and Budgeted Recurrent Expenditures, Ministry of Works,

and all other Ministries St . Kitts and Nevis 1995-2000 (in percentage) ....................................... 35 Figure 5.1 Government Employment as Percentage of Population, 2001

(Selected Caribbean Countries) .................................................................................................... 56

GDP) ............................................................................................................................................... 2

Revenue 1990-2002 (as % of GDP) ................................................................................................ 3

Figure 5.2 Average Wage as a Percentage of GDP per capita. 2001

Figure 6.1 Share of Recurrent Health Expenditures in GDP. St . Kitts and Nevis 1995-2000

Figure 6.2 Share of Hospital Expenditures in Total Recurrent Health Expenditures. St . Kitts

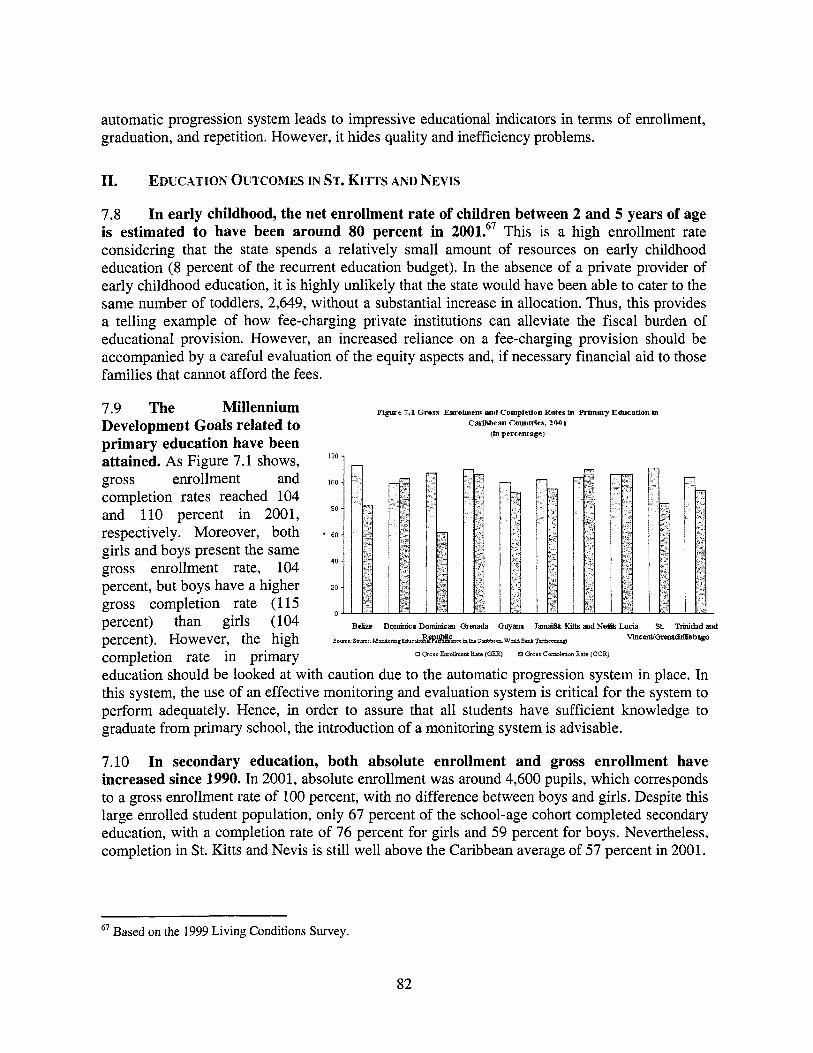

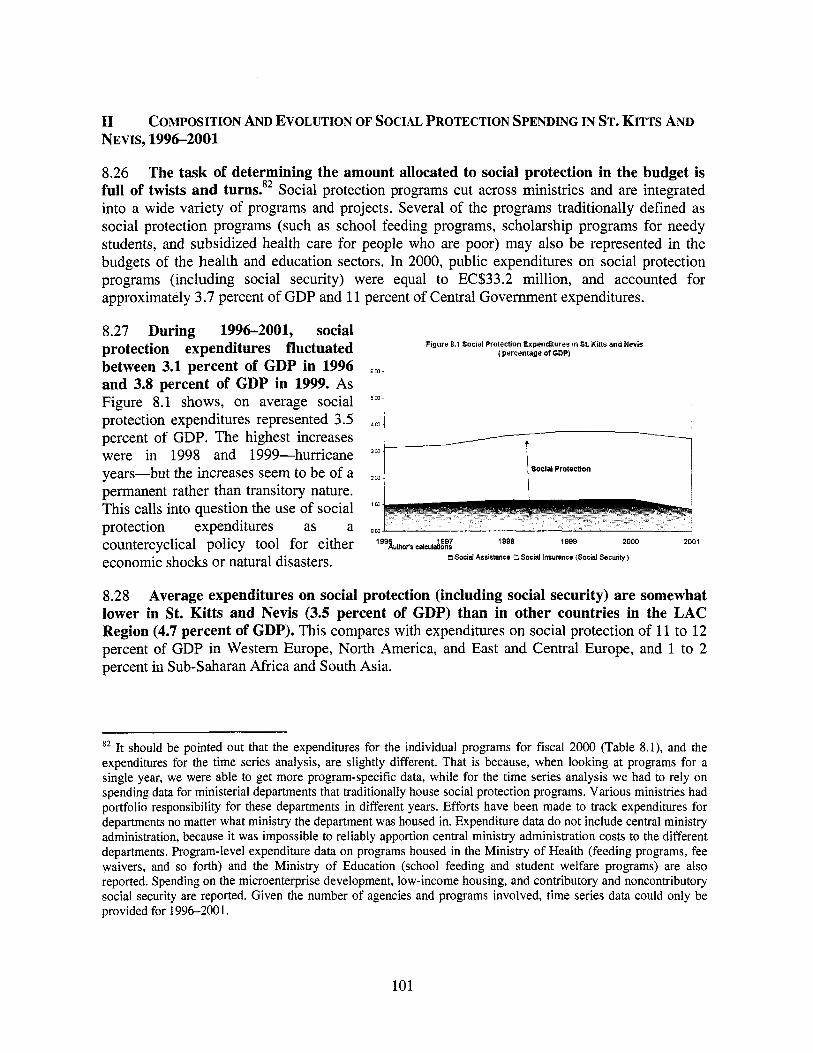

Figure 7.1 Gross Enrollment and Completion Rates in Primary Education in Caribbean Countries. 2001 (in percentage) ..................................................................................................... 82

Figure 7.2 Share of Education Expenditures in GDP. St . Kitts and Nevis 1994-2002 (as %) ............... 84 Figure 7.3 Education Expenditure in St . Kitts and Nevis 1994-2002 (millions of EC$ 95) .................. 84 Figure 7.4 Share of Recurrent Education Expenditures in Recurrent Expenditures.

St . Kitts and Nevis 1994-2002 (as %) ........................................................................................... 85 Figure 7.5 St . Kitts and Nevis Recurrent Education Expenditures by subsector 1996-2002

(as % Total) ................................................................................................................................... 85 Figure 7.6 Pupil-Teacher Ratio and Costs of Education in St . Kitts and Nevis. 2000 (in US$) ........... 89 Figure 7.7 Share of Trained Teachers in Primary and Secondary School. St . Kitts and Nevis.

1999 (in percentage) ...................................................................................................................... 91 Figure 8.1 Social Protection Expenditures in St . Kitts and Nevis (percentage of GDP) ..................... 101 Figure 8.2 Social Protection Expenditures in St . Kitts and Nevis (millions of EC$ 95) ..................... 102

(Selected Caribbean Countries) .................................................................................................... 61

(percentage) ................................................................................................................................... 76

and Nevis 1995-2002 (percentage) ............................................................................................... 77

List of Boxes

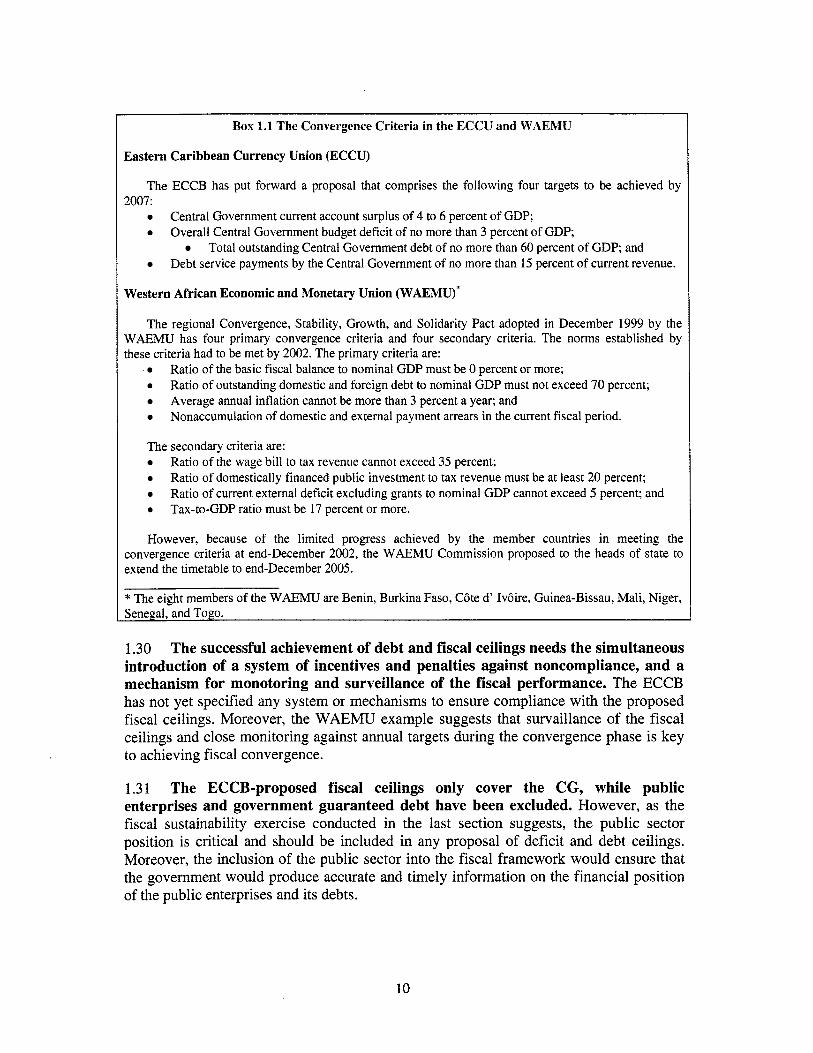

Box 1.1 The Convergence Criteria in the ECCU and WAEMU ........................................................... 10 Box 2.1 Chile’s Fiscal Rule ................................................................................................................... 26 Box 3.1 Financing Expenditures ‘Below the Line’. The Use of Advance and Deposits Accounts ...... 33 Box 4.1 Port Zante Cruise Ship dock .................................................................................................... 48 Box 5.1 Civi l Service Downsizing in Guyana ....................................................................................... 58 Box 6.1 Strengthening the National HIV/AIDS Program over 2003 to 2007: The St . Kitts and

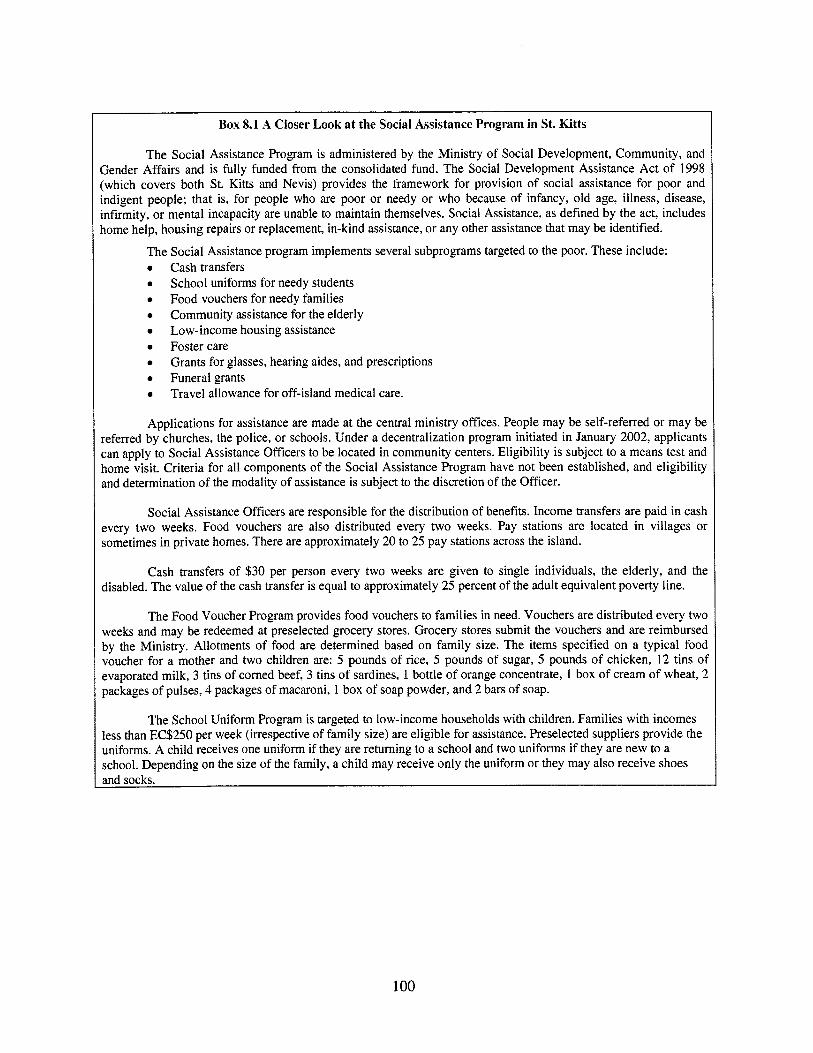

Nevis HIV/AIDS Prevention and Control Project ........................................................................ 72 Box 7.1 Financing of Tertiary Education in Latin America and the Caribbean .................................... 87 Box 8.1 A Closer Look at the Social Assistance Program in St . Kitts ................................................ 100

OECS FISCAL ISSUES: ST. KITTS AND NEVIS

EXPENDITURES POLICIES TO ACHIEVE FISCAL SUSTAINABILITY AND IMPROVE EFFICIENCY AND EQUITY OF PUBLIC

EXECUTIVE SUWIMARY

Overview

1. St. Kitts and Nevis is a two-island federation in the Eastern Caribbean with a combined population o f about 45,000 inhabitants (of whom 75 percent live in St. Kitts) and a per capita gross national income (GNI) o f US$ 6,980 in 2003 (World Bank Atlas Methodology, current US$). This small, open economy has traditionally depended on the production and export o f sugar. However, as a result o f declining trade preferences for sugar, in the last decade the structure o f the economy has shifted toward services, notably tourism. The economy i s highly vulnerable to exogenous shocks, such as hurricanes, which have inflicted substantial damage to the capital stock and reduced growth in recent years.

2. As a member o f the Eastern Caribbean Currency Union (ECCU), St. Kitts and Nevis shares a common central bank, the Eastern Caribbean Central Bank (ECCB), and a common currency, with the other five independent members o f the Organization o f Eastern Caribbean States (OECS) and three dependent territories (Anguilla, Montserrat and the British Virgin Islands).' Their currency i s the Eastern Caribbean (EC) dollar, which has been pegged to the U.S. dollar since 1976 at EC$2.70 per US$ I. The commitment to a fixed exchange rate and a prudent monetary policy under the ECCU umbrella has been a key element in maintaining an inflation rate close to international levels.

' The OECS consists o f six independent members: Antigua and Barbuda, Dominica, Grenada, St. Kitts and Nevis, St. Lucia, and St. Vincent and the Grenadines, in addition to three dependent territories of the United Kingdom, Montserrat (full member), Anguilla, and the British Virgin Islands (associate members).

3. Notwithstanding a common central bank and a common currency, St. Kitts and Nevis, like the other ECCU member countries, conducts fiscal policy independently. While limited progress has been made on a common fiscal policy in the region, the deterioration o f the ECCU fiscal position in the recent years, notably in Antigua, Dominica, and St. Kitts and Nevis, has reinitiated discussion among i ts members o f the need to coordinate fiscal policies.*

4. During 199G95, the St. Kitts and Nevis economy showed a strong growth performance, with a growth rate o f about 4.3 percent per year. However, since the mid- 1990s, economic growth in St. Kitts and Nevis slowed to 3.6 percent per year as a result o f exogenous shocks (declining trade preferences for sugar, hurricanes, the September 11 events, and the recent global economic slowdown), and declining productivity. Moreover, in 2002 the St. Kitts and Nevis economy contracted by 1.0 percent, the first economic contraction experienced by the country in almost 20 years. This slowdown and contraction have been accompanied by increasing fiscal deficits and rising public debt and debt service obligations. The medium term growth potential o f St. Kitts and Nevis i s in the range o f 3-4 percent, reflecting the completion o f most o f the major infrastructure projects, a pick up in the global economy inducing restoration o f tourism to it

* The communiqut of the Special Meeting of the OECS Authority, Castries, St. Lucia, September 28, 2001 alludes to the need to examine in the medium term public sector reform, aimed at increasing efficiency, and fiscal reform including matters related to revenue, expenditure, financing, and debt management, as well as common approaches to taxation and incentives to be applied to cruise shipping.

pre-September 2001 levels, and the near doubling o f the room capacity in the country as a result o f the opening of the 900- room Marriott Resort. Ma in exogenous risks to the medium term scenario are posed by a prolonged global recession, potential uncertainty engendered by Nevis’s plans to secede, a natural disaster such as a tropical storm or hurricane, and risks o f a drying up of the regional capital market fuelled by high fiscal deficit and debt ratios.

5. Despite high levels o f per capita incomes and good social service provision, poverty remains a persistent problem in St. Kitts and Nevis. The national 1999 survey data indicate that approximately one in three individuals are poor (that is, l iving below a locally defined poverty line). In St. Kitts 30.5 percent o f the population l ived below the poverty line, as did 32 percent in Nevis. Moreover, approximately 11 percent o f St. Kitts’s population and 17 percent o f Nevis’s population i s indigent; that is, they do not have sufficient resources to meet their basic dietary needs.3 Income insecurity/volatility at country and household levels as a result o f climatic and external economic shocks i s particularly pronounced in St. Kitts and Nevis, like in the rest o f the Caribbean, given i t s small size, limited economic diversification and high degree of openness, and i ts extreme vulnerability to hurricanes. The impact o f this extremely high volatility i s especially negative for the poor and near poor who may not be able to rely on savings or on the government’s social protection programs to smooth consumption during times o f hardship.

6. With respect to the Millennium Development Goals (MDGs), the primary education goal has been attained-primary education i s universal for boys and girls. I t i s likely that the goal o f eradicating extreme poverty and hunger w i l l be achieved; St. Kitts and Nevis i s estimated to have few habitants

l iving on less than US$ 1 per day. With respect to the health MDGs, the under5 mortality and HIV/AIDS goals are the most relevant to St. Kitts and Nevis. Malnutrition (defined as the prevalence o f underweight children), maternal mortality, and tropical diseases (other than dengue, which is endemic) are not major issues. The under-5 mortality rate in St. Kitts and Nevis dropped from an estimated 36 per 1,000 in 1990 to 24 per 1,000 in 2001. This i s a decline o f about 3.7 percent per year. The MDG target-a reduction o f two-thirds from 1990 to 2015- would require that the rate fall to about 12 per 1,000 by 20 15. According to trend projections, St. Kitts and Nevis wi l l not reach but w i l l come close to this MDG target, since the present trend would result in a rate o f 14 per 1,000 by 2015. The rate o f decline i s however likely to slow from 2001 to 2015, because as child mortality rates get lower, incremental declines get harder to achieve. I t i s difficult to assess the likelihood o f reaching the HIVIAIDS targets, because baseline data on HIV prevalence and incidence are poor. Adult HIV prevalence i s between 1.5 and 2 percent. The Government has launched a comprehensive HIV/AIDS prevention and control program with the support o f the World Bank with the objective o f reversing its spread.

7. To improve competitiveness, restore rapid economic growth, and ensure i ts medium-term sustainability in the context o f the currency union, the main challenges to the St. Kitts and Nevis government are to (a) tighten fiscal policy, notably through expenditure cuts; (b) increase the efficiency o f public investments and public service delivery; (c) strengthen regulation and efficiency o f public utilities and sea/air transport; and (d) promote education and skills development to prepare the population, notably the poor, to take advantage o f new opportunities in the global environment.

In 1999, the adult equivalent poverty and indigence lines were equal to EC$3,361 and EC$2,135 in St. Kitts, and EC$3,941 and EC$2,453 in Nevis.

We cannot estimate with certainty the share of the population living on less than US$1 per day because information i s unavailable regarding the purchasing power o f one U.S. dollar in St. Kitts and Nevis.

.. 11

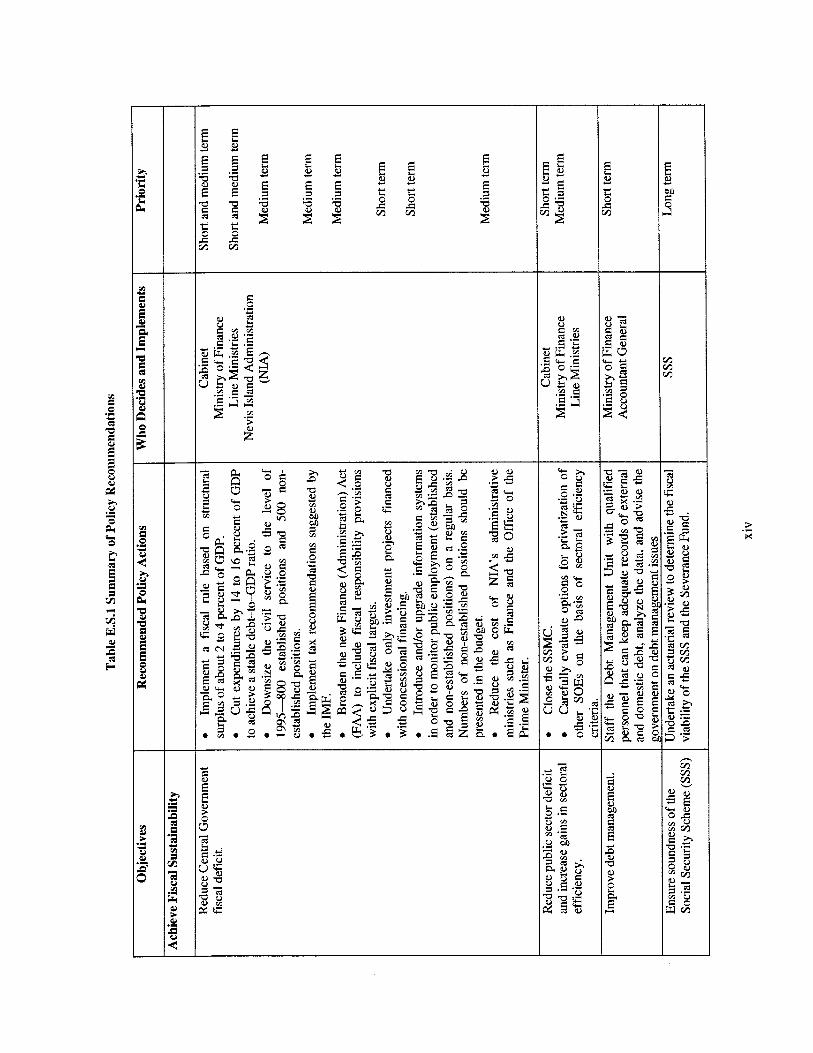

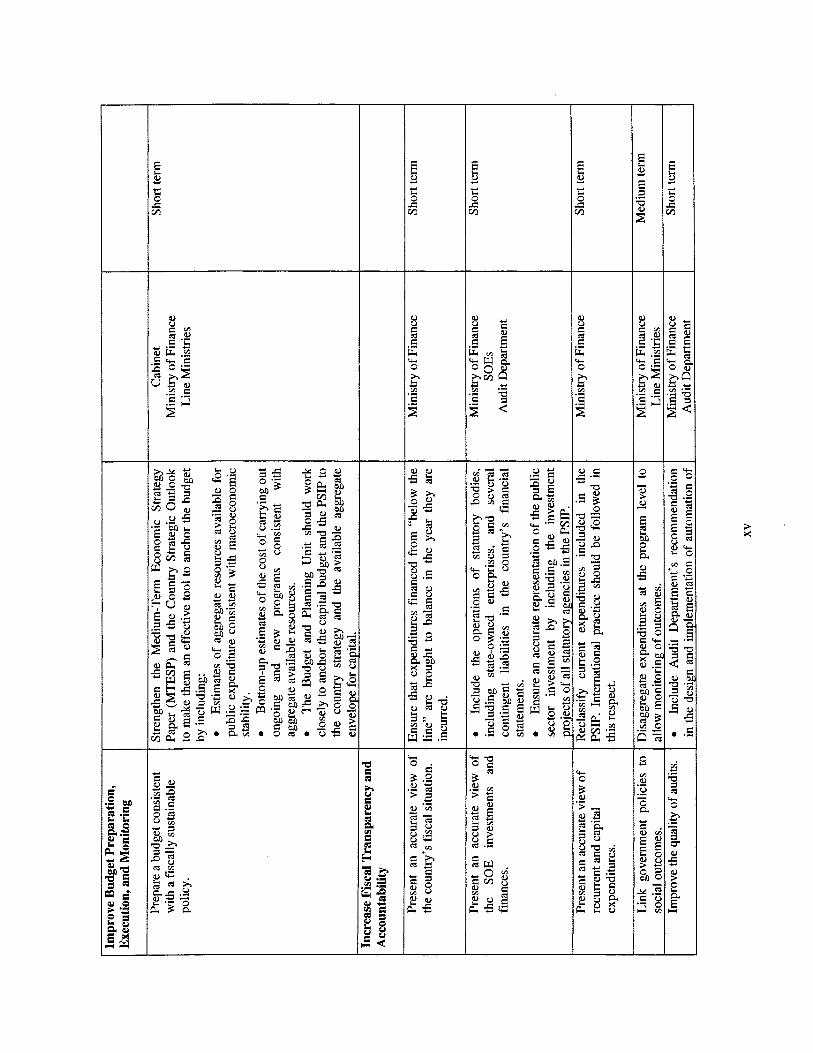

8. This report concludes that the fiscal deficit in St. Kitts and Nevis i s unsustainable and poses a risk to the stability o f the currency board arrangement. Most of the adjustment needed to achieve a sustainable fiscal policy w i l l have to come from expenditure cuts, in particular a reduction in the number o f established and non- established positions? containment o f capital expenditures to projects geared to growth and poverty reduction and funded largely by grants and concessional loans, and the closure o f the unprofitable St. Kitts Sugar Manufacturing Company (SSMC). A reduction in tax exemptions and discretionary concessions i s also essential, as i s a restructuring o f the revenue base through the introduction o f the value-added tax (VAT). While social indicators are good for a country at this level o f gross domestic product (GDP), there i s ample room for more efficient modalities o f education and health service delivery that can generate significant savings and improve effectiveness. In addition, the government should strive to ensure that i t s social programs, in particular social protection, are provided in a well-targeted and effective manner in order to provide more effective safety nets for the possible impact o f sugar sector restructuring, fiscal consolidation and the rationalization o f education and health service delivery, and continued vulnerability to external shocks. Specific recommendations on how to achieve fiscal sustainability,. improve social service delivery, and reform social protection are provided in the attached matrix. See Table E.S. I.

There are two types o f government positions in the St. Kitts and Nevis Federal Government: established and non-established. Employees in established positions are appointed by the Governor General upon formal request by the Public Service Commission, with the approval of the Establishment Division in the Prime Minister’s Office. Established positions are permanent positions listed in the budget, and their compensation i s classified as Personal Emoluments. Employees in non-established positions are hired directly by line ministries, their numbers are not presented in the budget, and only their wages are included as a line item.

9. The report i s organized as follows: Chapter 1 discusses fiscal sustainability in St. Kitts and Nevis and presents options for fiscal consolidation; Chapter 2 discusses the role o f the business cycle in the design o f fiscal policy by reviewing the cyclical components o f the fiscal accounts; Chapter 3 discusses the budget management system in place and i ts effect on budgetary outcomes. Chapter 4 examines the Public Sector Investment Program (PSIP); ,Chapter 5 discusses public sector employment and compensation; Chapters 6 and 7 examine public expenditures and outcomes in the education and health sectors; and Chapter 8, the final chapter, discusses social protection programs.

Fiscal Sustainability

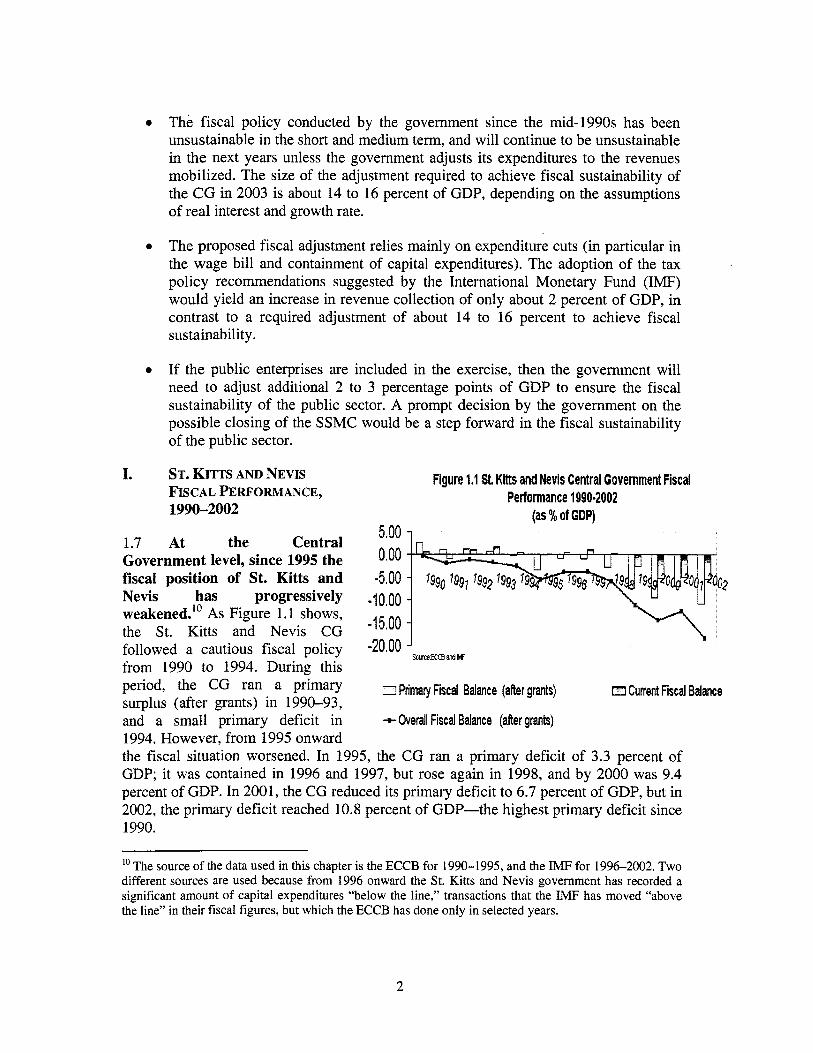

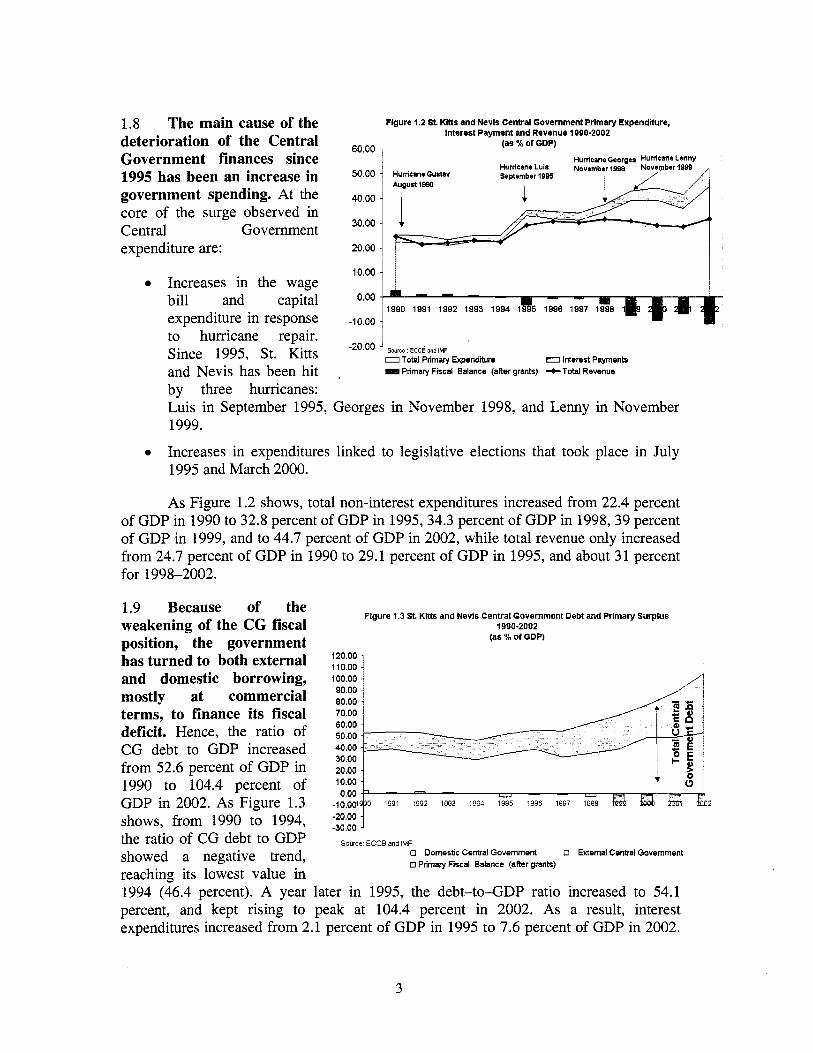

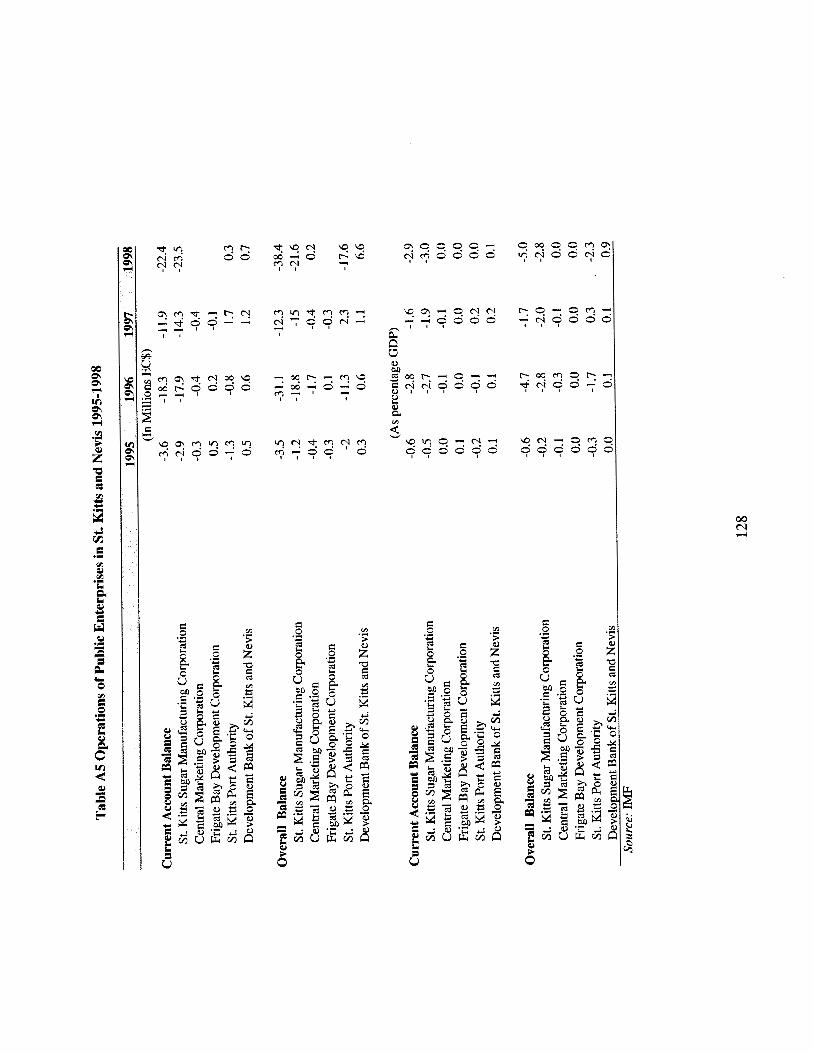

10. At the Central Government (CG) level, since 1995 the fiscal position o f St. Kitts and Nevis has weakened progressively (from a CG primary deficit of 3.3 percent in 1995 to 10.8 percent o f GDP in 2002). The main causes o f this deterioration have been increases in the wage bill and capital expenditure (to a degree in response to hurricane repair), and increases in expenditures linked to legislative elections that took place in 1995 and 2000. The government has relied on both external and domestic borrowing, mostly at commercial terms, to finance i t s fiscal deficit. As a result, the CG debt-to-GDP ratio increased from 5 1.5 percent o f GDP in 1995 to 104.4 percent o f GDP in 2002, and the interest expenditures increased from 2.1 percent o f GDP in 1995 to 7.6 percent o f GDP in 2002. The losses of public sector enterprises, notably the SSMC and the St. Christopher Air and Sea Ports Authority, put further pressure on the government deficit and public debt.

11. The short-term fiscal sustainability exercise (one year) shows that since 1995 the fiscal policy conducted by St. Kitts and Nevis (both the CG and the public sector) has been unsustainable. The short-term adjustment required to achieve fiscal sustainability o f the CG in 2003 i s about 14 to 16 percent o f GDP, depending on the assumptions o f real interest

... 111

and GDP growth rates. Since the CG guarantees the debt o f public enterprises, the government would need to adjust by additional 2 to 3 percentage points of GDP to ensure the fiscal sustainability o f the public sector.

12. This size o f adjustment is significant (equivalent to a primary surplus o f between 3 and 4 percent o f GDP), and it would be difficult to achieve it in the short-term, even with a major fiscal reform. The ECCB’s Monetary Council meeting that took place in February 2003 reconfirmed the agreed regional fiscal framework that includes ceilings on debt and fiscal performance of the CG (see Chapter 1, paragraph 1.28). The aim of the ECCB in setting these fiscal convergence criteria is to ensure long-run fiscal sustainability and the stability o f the currency union by limiting negative spillovers. Based on i ts fiscal ratios in 2002, the deadline for fiscal convergence (a four-year horizon) requires a fiscal adjustment higher than the one discussed above if the objective i s to meet the proposed 60 percent o f GDP ceiling, and wi l l require an even faster public sector reform and gearing up of the social protection programs.

13. Adoption o f the IMF tax policy recommendations would reduce the short-term fiscal gap only slightly. Hence, the fiscal adjustment would have to rely mainly on expenditure cuts, notably a reduction in the number o f established and non-established positions, containment of capital expenditures, and the closure o f the unprofitable SSMC. The increasing financial difficulties that the SSMC is facing are the result of a drop in productivity and the phasing out o f trade preferences. The report recommends that the government close the SSMC as soon as possible to avoid further deterioration o f an already unsustainable fiscal situation.

14. The sales o f government assets can be an option to soften the adjustment required to achieve fiscal sustainability. However, any privatization should not be driven by revenue considerations alone, but rather by the objective o f improving quality and efficiency and

increasing coverage, including establishing an adequate regulatory framework to ensure that public monopolies are not replaced by unregulated and inefficient private monopolies.

Fiscal Policy and the Business Cycle

15. Economic volatility tends to discourage long-term investments in physical and human capital, and thus leads to a lower growth potential. The poor segments o f the population are generally the most affected because they lack the means to protect themselves from adverse employment and income effects. Governments have a broad set o f instruments available to reduce aggregate volatility and i t s effects, one o f which i s fiscal policy. In developed economies, fiscal policy i s usually designed to stimulate output when the economy moves into recession and to contract output when an expansion takes place. A fiscal policy designed in this way leads to a strongly procyclical budget surplus (countercyclical fiscal policy).

16. The St. Kitts and Nevis GDP cyclical component shows no clear link to i ts major sources o f economic volatility, hurricanes, but several expansions and contractions are worth noticing. Between 1980 and 2002, St. Kitts and Nevis was hit by six hurricanes. In three out o f six hurricane years, St. Kitts and Nevis’s GDP decreased below i t s trend, and in the other three years increased above i t s trend. The deepest contraction took place in 1983, a year after the debt crisis and the greatest expansion in 1989, the year o f Hurricane Hugo.

17. All components o f the fiscal accounts are more volatile than GDP. The highest volatility i s for grants, capital expenditure; and capital revenue. Current expenditure, all i ts components, as well as capital expenditure are acyclical (that is, in good times or bad times the government does not increase or reduce its expenditures). This result i s similar to the one observed in Organization for Economic Cooperation and Development (OECD) countries, but not in developing countries. Current and tax revenue are procyclical (not

iv

surprising given that most taxes are in some way proportional to economic activity).

18. Finally, all measures o f fiscal balance such as primary, current, and overall balance are acyclical, that is, they do not co-move with the GDP cycle. In good times the government does not run a higher or lower fiscal surplus than its trend. This i s an interesting result and contrary to the empirical evidence for developing countries. However, most o f this evidence does not include small islands like St. Kitts and Nevis, in which the procyclicality o f tax revenues i s high enough and expenditures are acyclical.

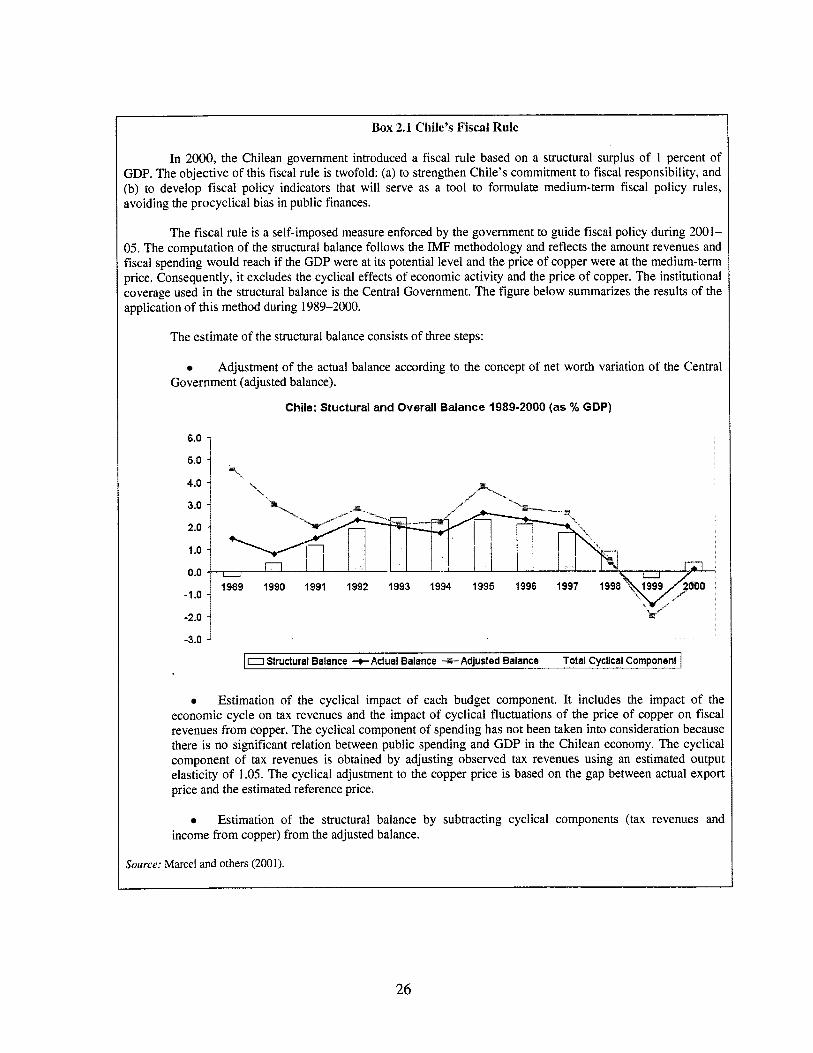

19. The cyclical adjustment to the government budget balances in St. Kitts and Nevis varies from -1.8 percent of GDP in 1983 and 2002 (recession years) to 1.9 percent o f GDP in 1989 (expansion year). For example, in 2002 the overall fiscal deficit after grants was 18.3 percent o f GDP, but factoring out the cyclical impact o f lower tax collection, the cyclically adjusted overall fiscal deficit was only 16.5 percent o f GDP. The St. Kitts and Nevis cyclical adjustment compared to other countries in the region i s in the low range. The cyclical adjustment in Chile i s between -4.0 and 2.5 percent o f GDP.

20. Once the cyclical effects are factored out, the country has run a structural primary, current, and overall deficit for most o f the 1990s. In 1994, the structural primary deficit was 0.5 percent o f GDP and kept increasing until it reached 8.9 percent o f GDP in 2002. The same pattern i s observed for the structural overall fiscal balance. Since 1993, the country has run a structural overall deficit that has increased until it reached 16.5 percent o f GDP in 2002. This confirms the conclusion that the business cycle has had little effect on the sharp deterioration o f St. Kitts and Nevis’s fiscal position.

21. Fiscal rules have two main objectives: (a) to enforce fiscal responsibility, and (b) to ensure a countercyclical fiscal policy. In this regard, St. Kitts and Nevis i s on the right path with an acyclical fiscal policy. However, in order to

move the country to a countercyclical fiscal policy we propose a fiscal rule based on a structural surplus o f about 2 to 4 percent o f GDP. This rule i s more austere than the Chilean fiscal rule o f a structural surplus o f 1 percent. However, considerations o f credibility and high GDP volatility in small islands would require that small countries like St. Kitts and Nevis adopt tighter fiscal rules. This fiscal rule implies a fiscal adjustment o f about 14 to 16 percent o f GDP, in line with the adjustment recommended to achieve fiscal sustainability.

22. However, successful implementation o f a fiscal rule based on a structural surplus w i l l require, as a first step, timely and reliable fiscal information. As discussed in the report, the current presentation o f the fiscal information does not follow international practices and presents a distorted picture o f the country’s fiscal situation.

Financial Management

23. St. Kitts and Nevis has introduced substantial changes to the budget structure and processes in the last few years, and its timely reporting is commendable. These changes, however, have not yet fully translated into improved resource allocation and effective expenditure controls, because o f the lack o f firm resource envelopes at the aggregate and ministry level underpinned by a medium-term economic strategy and ministries’ corporate plans nested in a consistent macroeconomic framework. Both the Strategic Country Outlook (a yearly document that presents the economic prospects o f the country for the next fiscal year) and the Medium-Term Economic Strategy Paper (MTESP, a four-year economic plan) last prepared for the Caribbean Group for Cooperation in Economic Development (CGCED) in June 2002, suffer from the same shortcomings: (a) top-down estimates o f aggregate resources available for public expenditure not always consistent with macroeconomic stability, (b) lack o f bottom-up estimates o f the cost o f carrying out ongoing and new programs, and (c) no attempt to reconcile the aggregate resources with the cost estimates

V

o f ongoing and new programs. Most o f the ministries’ corporate plans are out o f date or cannot provide a link among objectives, expenditure required, and outcomes.

24. The budget provides an accountant’s view o f government transactions rather than a presentation o f the government’s fiscal policy. The budget adheres to the traditional administrative, program, and economic structure format. However, this presentation i s insufficient to assess the fiscal position of the government and to follow up on key programs supposedly linked to policy priorities. The Ministry o f Finance does, however, have the capacity to present the budget by standard functional classification and i t i s recommended that it do so in fiscal year 2004.

25. Moreover, sizeable expenditures (mainly capital expenditures) have been financed from “below the line” using advances and deposit accounts without being brought to balance and reflected in the budget in the years in which they occur. Thus, the recurrent and overall balances, as well as other line items presented in the budget, do not represent an accurate picture o f the government’s fiscal situation. I t i s recommended that the government bring to balance all “below the line” accounts starting in 2003.

26. The debt management function i s the weakest component o f the financial management information system. Unti l 2002, the debt management function was split between a small unit in Finance, which uses the Commonwealth Secretariat Debt Recording and Management System (CS-DRMS) to maintain data on foreign debt, and the Accountant General’s Department, which handled domestic debt (mainly treasury bills). These units have now been merged and renamed the Debt and Investment Unit under the Accountant General. However, this new unit lacks qualified personnel to keep adequate records o f external and domestic debt to analyze the data and advise the government on debt management issues.

27. The Audit Department does a commendable job. Audit Reports are current for the federal government. Unlike in other OECS countries, reports in St. Kitts and Nevis no longer detail hundreds of oversights and minor transgressions, focusing instead on material findings. Also, the Audit Department continues a modest program o f value-for-money audits to supplement compliance audits. However, while in principle independent because o f authority specified in the Constitution, the Audit Department has no guaranteed operating budget or staffing complement, and must obtain approval from the Minister o f Finance via the annual Estimates process. Additional factors that have affected its efficacy are the automation o f critical financial management functions without adequate input from the Audit Department in the design and implementation stages, the nonfunctioning o f the Public Accounts Committee, and the lack of training for staff.

28. The financial statements o f St. Kitts and Nevis present a partial view o f government activities. Significant fiscal operations are excluded. The operations o f statutory bodies, including state-owned enterprises (SOEs), are not covered, and several contingent liabilities are not presented in the financial statements. Most o f the SOEs are significantly in arrears in the preparation o f their financial statements and the submission o f these for audit and for Parliament’s review. Although the Director o f Audit has the right to require submission o f SOE audit reports and to supplement them by further investigations if hehhe considers it necessary, he/she has not done so. Finally, following the last election, the members o f the Public Accounts Committee (PAC) were appointed in November 2000, but the Committee did not meet subsequently. The Committee did meet a few times during 1992-94, but took little action o f substance. Weak PACs are a common feature in the OECS countries, and the report presents recommendations to improve their functioning to become a vibrant component o f public financial oversight.

29. The formulation o f the budget receives inputs from the social partners, but this

v i

undoubtedly could be made more systematic. The recent agreement by OECS countries to establish National Economic Councils with public and private sector members may lead in this direction. However, the capacity o f the social partners-most o f which are small organizations-to go beyond their immediate concerns and address complex national policy issues remains limited.

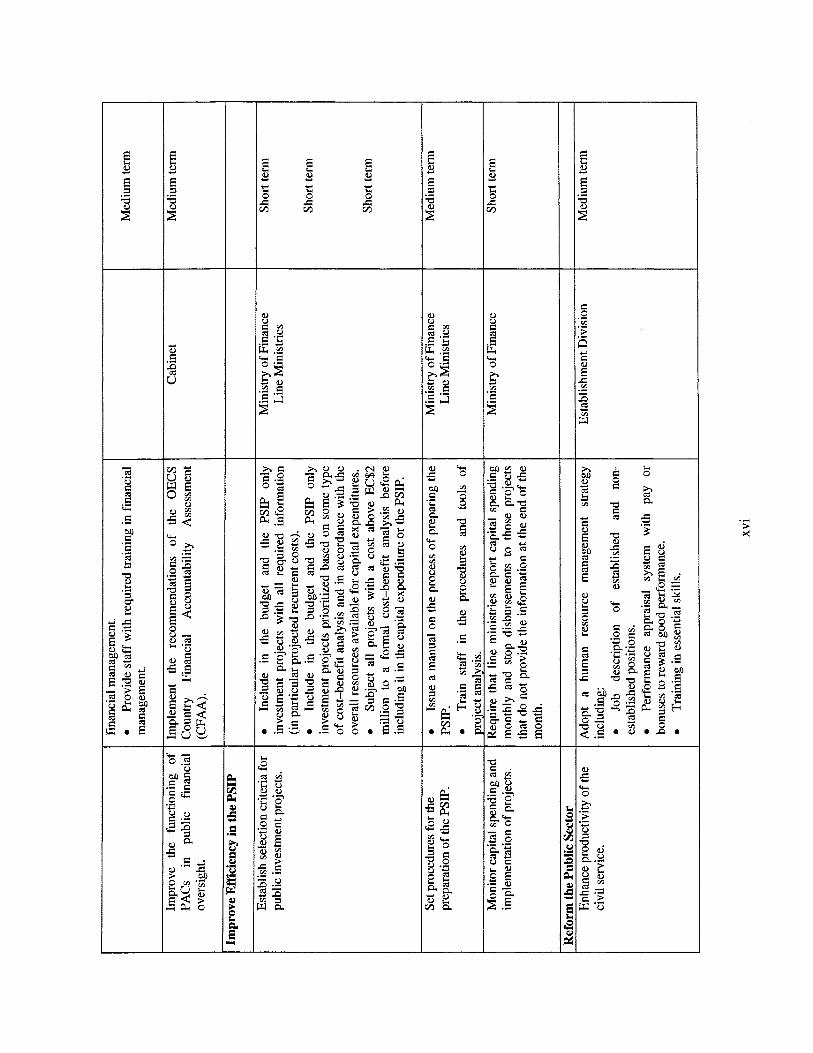

Public Sector Investment Program

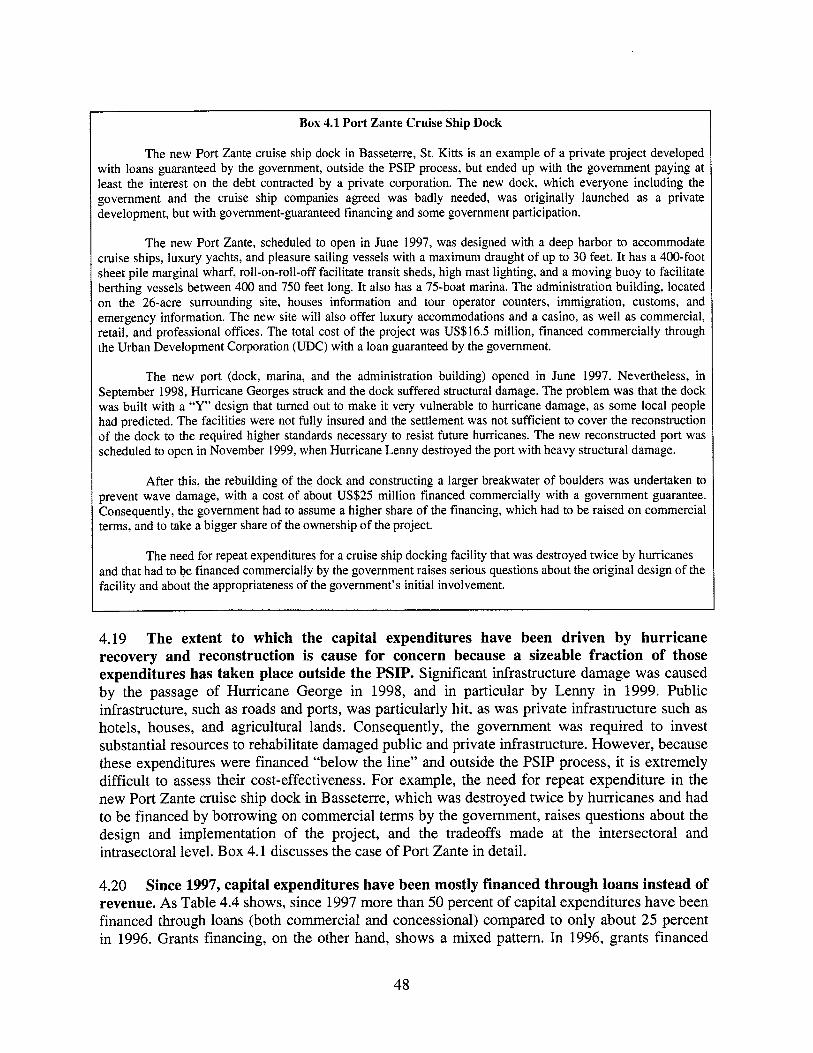

30. In St. Kitts and Nevis, on average, during 1995-2002, capital expenditures as a fraction o f GDP increased about three times compared to 1990-94, including “below the line” transactions not presented in the annual budget estimates. This increase in expenditures was mostly financed through loans (commercial and concessional) and is one of the main reasons behind the difficult fiscal position facing the government today. Although the damage caused by Hurricanes Luis in September 1995, Lenny in November 1998, and Georges in November 1999 explains part o f the increase in capital expenditures, a large portion was not hurricane related and i ts aim was not necessarily to stimulate growth or reduce poverty.

3 1. The public sector investment program of St. Kitts and Nevis does not include investment projects by statutory agencies, such as SOEs. This i s a serious gap because these investments can represent a sizeable portion o f the public sector investment program and can expose the government to serious fiscal liabilities. The government should ensure an accurate representation o f the public sector investment program by including in the PSIP the investment projects of all statutory agencies. Investment projects by private corporations but guaranteed by the government should be disclosed in the government’s financial statement as government liabilities.

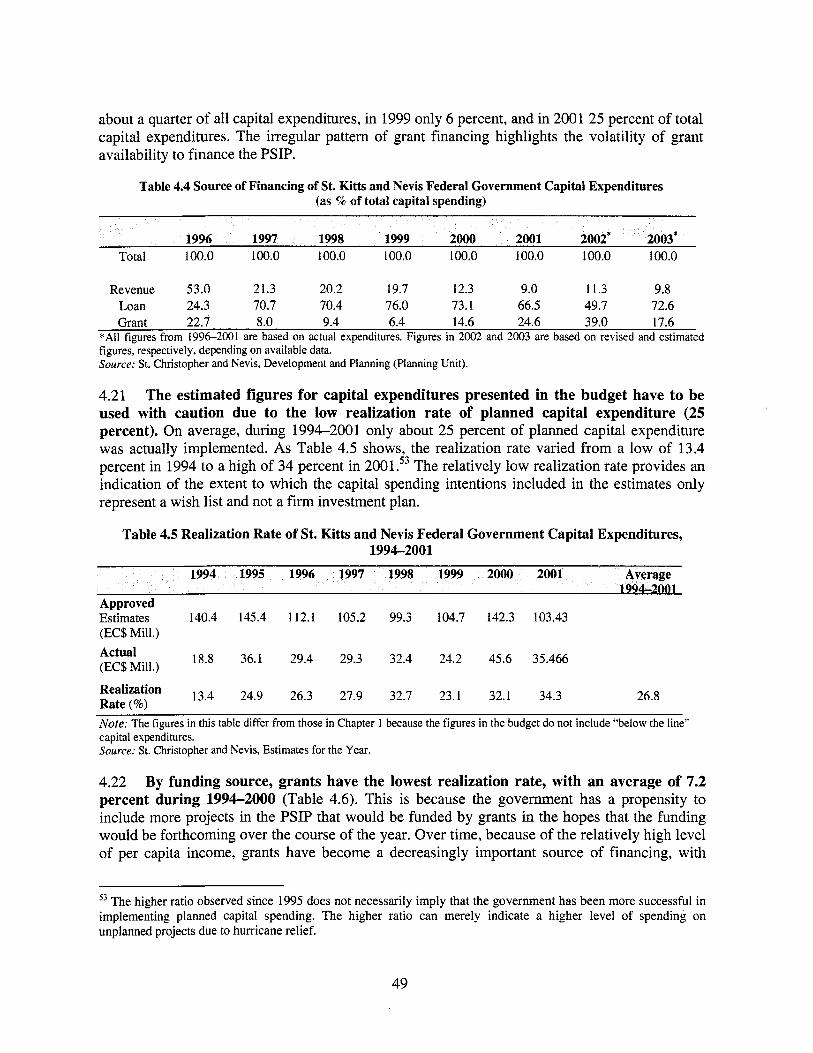

32. Although the PSIP i s prepared as a four-year rolling medium-term investment program, in practice the focus i s the one-year capital budget. The relatively low realization rate (about 25 percent) provides an indication o f the extent to

which the capital spending intentions included in the estimates do not represent a firm investment plan. N o cost-benefit analysis i s done by the line ministries to assess whether the projects proposed are cost-effective (with the exception o f those financed by external donors). Several investment projects included in the PSP and the capital budget should be classified as recurrent expenditures. Moreover, a significant amount o f the capital expenditures incurred by the government are recorded “below the line” and not captured in the PSIP.

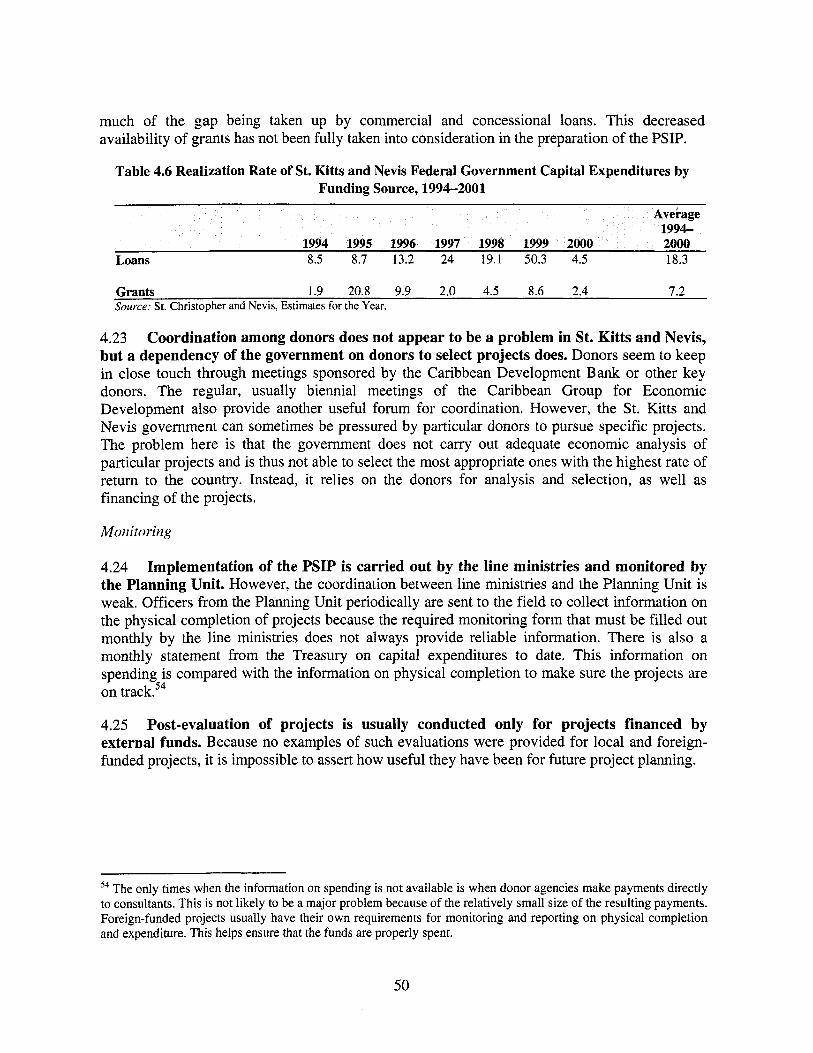

33. The implementation o f the PSIP i s carried out by the line ministries and monitored by the Planning Unit. However, the coordination among these agencies i s weak. Post-evaluation o f projects i s usually conducted only for projects financed by external funds. Because no examples o f such evaluations were provided for local and foreign-funded projects, it i s impossible to assert how useful they have been for future project planning.

Public Sector Compensation

34. Given the small size o f i t s economy and population, St. Kitts and Nevis has limited resources to carry out the whole range o f functions performed by any government. As several studies have shown, small countries tend to have bigger public administrations in response to the higher cost o f supplying public goods and the need to provide a stabilization role to ameliorate the effect of external shocks. However, in the case o f St. Kitts and Nevis the public administration i s too large and expensive for sound fiscal management.

35. The main finding o f this report i s that the high wage bill in the St. Kitts and Nevis Federal Government (1 5 percent o f GDP) i s employment driven rather than wage driven. During 1995- 2002, the number of established positions increased in total by 38 percent, and the number o f non-established positions in full-time equivalent basis increased in total by 124 percent. At the same time, government real wages decreased slightly. St. Kitts and Nevis’s ratio o f government employment to population

v i i

(1 4.2 percent) i s at least three times higher than that observed in other economies in the Caribbean. Although the federation structure o f the country and the fact that in St. Kitts and Nevis many public utilities are part o f the Central Government explains to some extent the high ratio, the main cause has been an increase in the numbers o f established and non- established positions since 1995.

36. In 2000, the Government ,imposed a freeze on new hiring and identified the wage bill as an area where cutbacks were needed as part o f a strategy o f fiscal consolidation. However, although the freeze has been implemented with some success for established employees, non- established employment head count has increased since 2000 in total by 31 percent, or 3.8 percent in full-time equivalent. In the short term, it i s critical that the government strengthens controls on non-established employment and reports i t in the estimates similar to the way i t reports established employment. Over the medium term, the downsizing in public service employment required to close the fiscal gap i s more than the 10 percent o f the current number o f employees foreseen by the government. Downsizing the civi l service to the levels o f 1995 by cutting 800 established positions and 500 non-established positions (head count) would reduce the wage bill by EC$42 million, or 5 percent o f GDP. The downsize w i l l have to be across all line ministries with National Security, Education, Health and Environment taking a significant cut because they represent about 70 percent o f all government employment.

37. The St. Kitts and Nevis government lacks a public sector human resource strategy. Job descriptions and performance appraisals, which are required to effectively manage personnel, do not exist even for established positions. N o systematic analysis o f training needs has been carried out. Training in essential skills i s deficient and there i s no training plan for individual employees to enable them to advance along their career paths. Training i s often offered in an unsystematic way, depending on the availability o f donor financing.

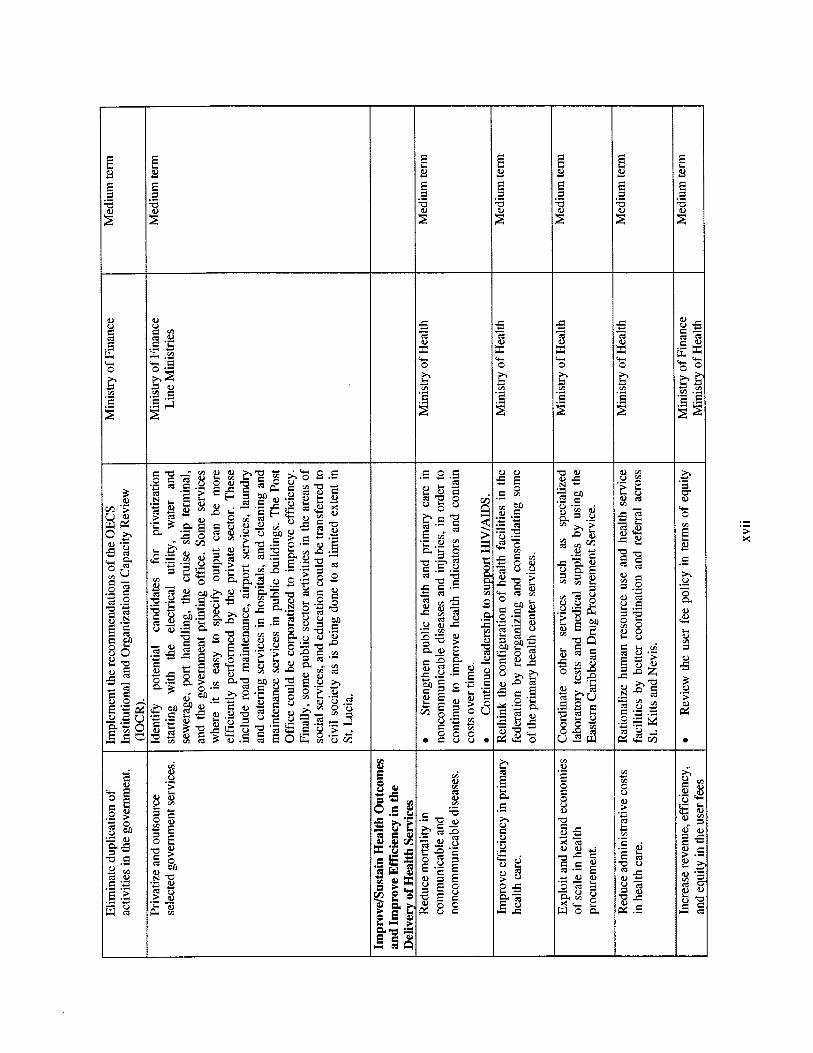

38. There is considerable scope for the government to divest some o f i ts functions to the private sector with the objective of improving quality and efficiency and increasing coverage. So far, only telecommunications has been privatized and garbage collection contracted out. The electrical utility, water and sewerage, port handling, the cruise ship terminal, and the government printing office could all be considered potential candidates for privatization. Some services where it i s easy to specify output can be more efficiently performed by the private sector. These include road maintenance, airport services, laundry and catering services in hospitals, and cleaning and maintenance services in public buildings. The Post Office could be corporatized to improve efficiency. Finally, some public sector activities in the areas of social services, and education could be transferred to nonprofit organizations, as is being done to a limited extent in St. Lucia.

39.The government has so far delayed the decision to downsize its c iv i l service and reform its public sector because i t hopes that the new Marriott Hotel, scheduled to operate at full capacity in September-October 2003, w i l l be able to absorb some o f the potential laid-off public servants, as well as some o f the workers that may lose their jobs if the sugar company (SSMC) i s closed down.

40. A public sector reform program would need to address the issue o f the existing fragmentation and duplication of work among ministries, departments, and agencies, leading to a diffusion o f responsibilities, and the possibility o f the government divesting some o f its functions to the private sector. The reform would need to be informed by a human resource management strategy, and a performance appraisal system should be established with pay or bonuses to reward good performance. I t would also need to be accompanied by the introduction and/or upgrade o f information systems in order to accurately cost i ts implications (pension and severance payments) and monitor public employment (established and non-established positions) on a regular basis.

v i i i

41. A Public Sector Reform Unit was recently established with the mandate to lead the process of public sector reform, which is directed at modernizing the public service. This w i l l include taking an inventory o f the human resource capacity of each ministry, identifying the relevant training to address any deficiencies discovered, and taking a critical look at the procedures and systems in use in the public service to make sure they have not become impediments to efficiency. I t i s encouraging that the government has established such a unit; however, i t i s not clear whether the unit w i l l be adequately funded and has the support of the Cabinet to carry out i ts mandate.

Health

42. The Federation of St. Kitts and Nevis has a health system with a strong primary health care focus. I t i s dominated by publicly financed and publicly provided health care. There are no private clinics or hospitals, but there are physicians in private practice. Public spending on health during 1995-2002 was about 3.3 percent o f GDP, on average. Public health spending in real terms grew for the same period at about 4.4 percent per year. Given the tight fiscal constraints, this growth i s unlikely to be maintained over the short to medium term. Moreover, wages absorb about 80 percent of all health spending in St. Kitts and 73 percent in Nevis. These figures are on the high side, and raise questions as to whether there i s sufficient allocation for pharmaceuticals, medical supplies, and maintenance of equipment and buildings. Capital expenditures in health are highly donor dependent, with a very large share from the European Community.

43. Public facilities appear to provide reasonably good coverage, with a good level o f consumer satisfaction. Nevertheless, the health system faces many challenges in the future. Most immediately, the public system i s facing strong budgetary pressures as part o f the overall fiscal crisis. St. Kitts and Nevis's small size and federation structure also pose many challenges to the administration of public health programs, such as (a) unexploited potential economies o f

scale, (b) duplication across islands o f planning and monitoring activities, (c) health services mostly publicly provided, (d) health financing m,ostly through general revenue, and (e) a high ratio o f nurses to physician. The health system also faces the challenge o f adapting to a changing disease profile, including the need to vigorously address HIV/AIDS. There i s coordination, but Nevis has its own ministry responsible for health, and its own chief secretary responsible for the administration o f local health services.

44. As the disease patterns change over time and with the goal o f achieving greater economies o f scale, i t may be possible to rethink the configuration o f health facilities in the federation, primarily by reorganizing and consolidating some o f the primary health center services. The government should also be able to achieve greater economies of scale by better coordinating health services with i ts OECS neighbors and other countries in the region, including specialized laboratory tests and procurement o f medical supplies, an excellent example o f exploiting economies o f scale at the regional level that can be extended to other services i s the Eastern Caribbean Drug Procurement Service.

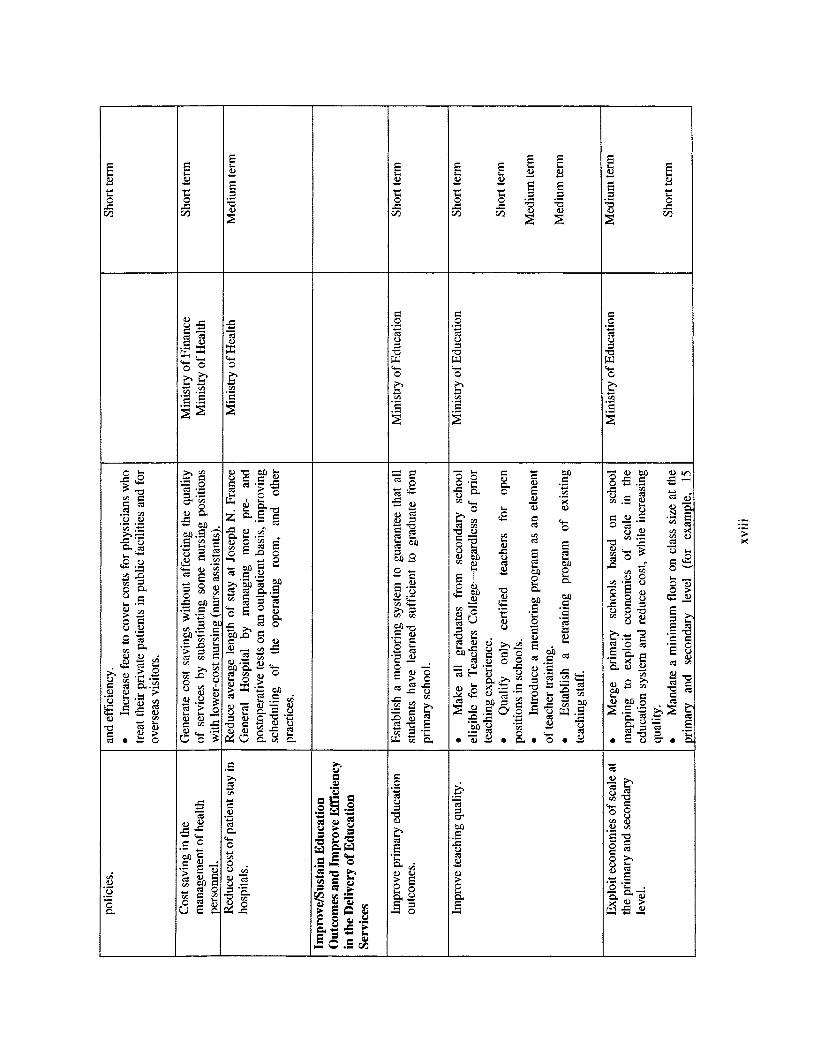

45. Public health financing i s mainly through the consolidated fund. Revenue from user fees is minor. User fees at public facilities amount to only about US$6 per capita per year, or 3 percent o f health recurrent spending in 2000. Facilities do not retain fees, so have little incentive to put effort into collection. Fees revert to the consolidated account. Furthermore, there are broad exemptions and fees are modest. While fees may seem low on a per service basis, user fees for a catastrophic health problem could put an unacceptably high burden on a poor household's financial situation, because the exemptions are not well targeted. The user fee policies would benefit from a review in terms o f equity and efficiency. The government should also consider how fees might be significantly increased to cover costs for physicians who treat their private patients in public facilities, and for overseas visitors.

ix

46. The government i s considering adopting a national health insurance system based on payroll taxes. Given that there is a general revenue-financed system in place, it i s not clear why it would make sense to add a payroll-tax system o f social insurance. The main motivation may be simply to find an additional source o f revenue for the health system. However, payroll tax systems have disadvantages. They are a tax on labor. In addition, given that many households are outside the formal sector, the system would not cover the full population. Working with the existing financing system, but finding ways to improve efficiency to ensure that the country i s getting better value for i t s money could be a better choice in the long run for such a small country. The main measures to improve efficiency over the short to medium term are (a) reorganizing and consolidating the primary health center services, (b) substituting nurses with nurse assistants where possible, and (c) increasing the reliance on well-targeted user fees for financing.

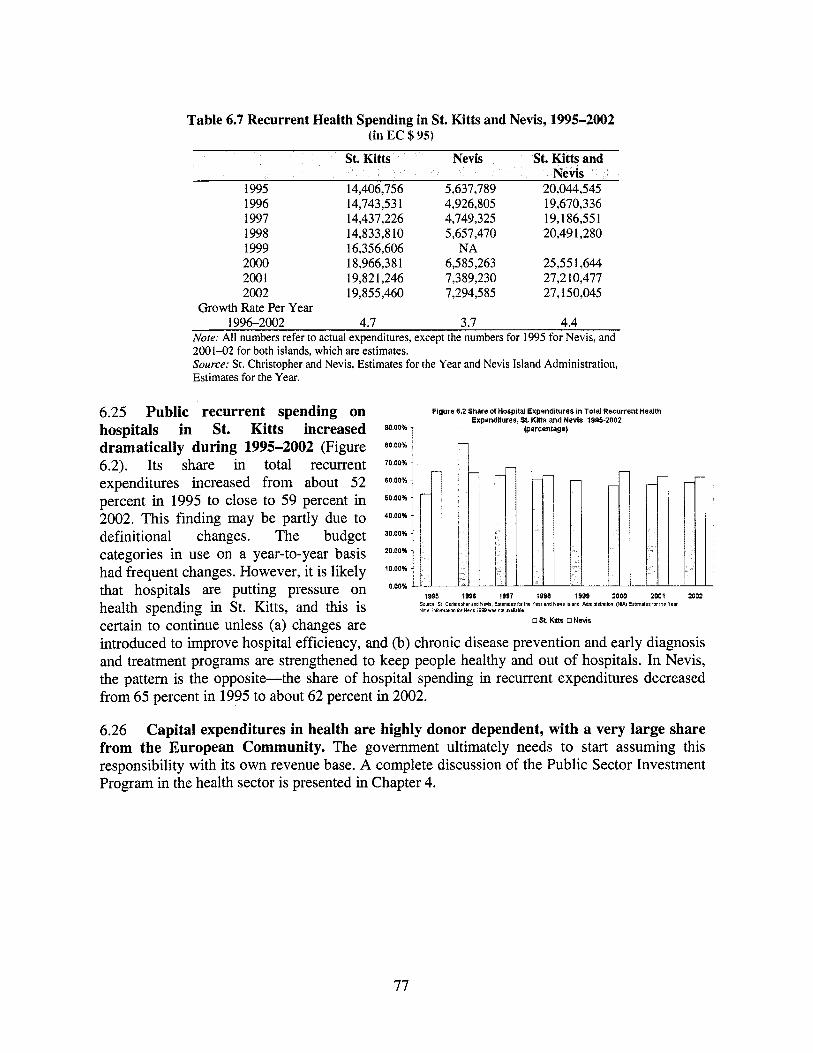

47. Public recurrent spending on hospitals in St. Kitts increased dramatically during 1995-2002. I t s share in total recurrent expenditures increased from about 52 percent in 1995 to close to 59 percent in 2002. This finding may be partly due to definitional changes. The budget categories in use on a year-to-year basis had frequent changes. However, i t i s likely that hospitals are putting pressure on health spending in St. Kitts, and this is certain to continue unless (a) changes are introduced to improve hospital efficiency, and (b) chronic disease prevention and early diagnosis and treatment programs are strengthened to keep people healthy and out o f hospitals.

Education

48. The close link between education and labor market earnings implies that the lack o f education is one o f the primary sources o f poverty in St. Kitts and Nevis. Data from the 1999 Survey o f Living Conditions indicate that 27 percent o f those with no education or a primary education are poor, while only 18 percent, 12 percent, and 5 percent are poor

among individuals with secondary, postsecondary, and university education, respectively. Hence, there are strong economic motives for the individual and the government to invest in education.

49. Education expenditures in St. Kitts and Nevis increased by about 40 percent in real terms between 1994 and 2000. However, this increase in public resources has not always been accompanied by an improvement in education outcomes, equity, and efficiency. The fiscal crisis that the country i s facing wi l l require a cut in expenditures for all sectors, but this should not preclude the government from completing the educational agenda by making better use o f the available resources and increasing the nongovernmental provision in education, for example, at the tertiary level.

50. Except for pupils in early childhood, Kittitians and Nevisians receive education predominantly from public institutions. The education system in St. Kitts and Nevis stands out in a Caribbean context in two ways: (a) the dual ministerial structure for one country due to i ts federal structure, and (b) the automatic progression in basic education, where no child repeats a class unless the parents directly express the wish. The dual ministerial structure increases administrative costs. The automatic progression system leads to impressive educational indicators in terms of enrollment, graduation, and repetition (with the millennium development goals related to primary education having been attained). However, it hides major quality and inefficiency problems. In this system, the use o f an effective monitoring and evaluation system is critical for the system to perform adequately.

51. During 1994-2001, on average, St. Kitts and Nevis spent about 5.2 percent o f GDP in recurrent and capital expenditures on education, with a rising trend toward the end o f the period. This compares with the average for Caribbean countries o f 6.6 percent of GDP and the Latin American average o f 4.1 percent of GDP.

52. Since the mid- 1990s, administration costs and tertiary education have taken an increasing

X

share o f recurrent education expenditures. Given the large fixed costs involved in education administration-for instance developing of exams, information systems, strategies, and curricula-it i s expected that smaller states allocate a higher share to administration.6 However, there are considerable savings to be gained from deeper within and cross-country cooperation, which, moreover, would stimulate quality improvements through international sharing o f best practices.

53. The share o f tertiary education in recurrent education expenditures increased from 14 percent in 1996 to 18 percent in 2002. In a Latin American context, this share i s below average, but so i s coverage o f tertiary education in St. Kitts and Nevis. The combination of limited access to tertiary education and a low cost- recovery ratio for tertiary education makes this budget line inequitable. Further, given that a nonnegligible share o f highly educated individuals migrates abroad, the public loses a corresponding share o f the returns to this public investment. I t i s recommended that fees be increased and regional cooperation between colleges be strengthened to ensure efficiency improvement through specialization.

54. The share o f secondary education expenditures in total recurrent education expenditures in the St. Kitts and Nevis Federal Government has decreased since the mid- 1990s. In the mid-l990s, 4 out o f each 10 education EC$ went to secondary education. At the start o f the new millennium, 3 out o f 10 reached this subsector. The adjustment reflects a serious squeezing o f nonsalary expenditures. The share o f recurrent expenditure to secondary education should not be allowed to fall further, and a reallocation o f recurrent expenditures to nonsalary expenditures at this level i s recommended.

The average cost of administration in other education systems in the Caribbean reaches 10 percent, twice the Latin American average of 5 percent.

55. The most important educational barriers for low-income families are limited access to, and inconsistent quality of, the education system. The School Feeding Program i s traditionally perceived as an expenditure line that benefits low-income students. However, in St. Kitts and Nevis at least 65 percent o f the well off, or half o f the student population, receive free meals. A similar pattern i s observed with free textbooks. The lack o f targeting for schoolbooks is especially worrisome given that 1 out o f 5 poor children has no textbook, while this happens for only 1 in 12 among children from the richest quintile. The government could hence either limit the School Feeding Program and textbook provision to low-income families only, or introduce fees for higher-income families.

56. Salaries are, by far, the largest spending item, taking up about 90 percent o f all recurrent education expenditures in 2000. At the secondary level, there i s especially reason for concern because the wage share in total secondary education spending increased from an already high 92 percent in 1996 to 99 percent in 2000. This leaves exceptionally little money to other crucially important learning inputs, such as writing paper, textbooks for poor students, and school maintenance. This skewed allocation o f expenditure toward salaries unnecessarily reduces the effectiveness o f public resources and results in inefficiently low learning. The main reason for the large share o f salaries in recurrent education expenditures i s the low pupil-teacher ratio. St. Kitts and Nevis spends the most per student per year in primary and secondary education among the Caribbean countries, US$860 and US$1,080, respectively. In primary and secondary education there are, on average, 18 and 13 pupils per teacher, respectively. The inefficiency involved in this poor teacher deployment is tremendous. I t i s recommended that these indicators be raised to the average Caribbean level, 25 and 18 pupils per teacher in primary and secondary education, respectively.

57. Quality o f instruction, and especially teacher qualification, i s key for increasing effectiveness o f learning. Teacher qualifications are inadequate in St. Kitts and Nevis. Only 56

xi

percent and 29 percent o f the teacher corps in primary and secondary education are adequately trained to perform their task. The lack o f qualifications i s a severe and long-term barrier for increased efficiency in the education sector. The inefficiency i s partially a result o f the rule o f admission at the teachers college that stipulates two years of teaching experience for eligibility. I t i s recommended that teachers be eligible for training before the commencement o f teaching.

Social Protection

58. Social protection programs in St. Kitts and Nevis emphasize risk-coping strategies; that is, programs to help households cope with the effects o f risk (especially poverty) rather than prevention and mitigation strategies. Moreover, the existing social protection programs are not well poised to respond to either significant economic downturns or natural disasters. Since the mid- 1990s, social protection expenditures in St. Kitts and Nevis have been on average about 3.5 percent o f GDP. Although below the average for the Latin American region (4.7 percent o f GDP), any effort to strengthen social protection cannot include costly new programs, given the difficult fiscal position that the St. Kitts and Nevis government is facing. Rather, what are required are improved targeting and distribution systems that can provide a safety net for possible retrenchment in the public sector and the sugar industry and that can be geared up quickly in the case o f external economic or climatic shocks.

59. The government o f St. Kitts and Nevis has adopted a social protection strategy designed to ensure access to health care and primary education and to expand access to secondary and tertiary ed~cat ion .~ The government also attempts to ensure that other programs and services (including income support, food, clothing, housing, and utilities) are available for the poor, This stated, the existing social protection strategy is not clearly articulated or well coordinated. There i s an array o f programs in both St. Kitts and Nevis, with little

’ Both as a federation and as separate island states.

coordination among programs within or between islands. With the exception o f the Social Security Program, programs are financed and administered separately by the two islands. Although the government has expressed its intent to better coordinate i t s social protection programs, it has yet to establish a mechanism to oversee the development o f an integrated social protection strategy and a rationalized set o f programs. The result i s that social protection priorities are not clearly identified, and fiscal prioritization o f programs i s lacking. This i s reflected in the budgetary process during which budgets are essentially determined by previous budget allocations and not in response to changing needs and priorities.

60. The large number o f programs, each with separate administrative systems and procedures, strain an already overburdened public sector. The lack o f coordinated efforts across ministries and departments has resulted in overlaps, duplication, inefficiencies, and administrative waste. To the degree to which they serve the elderly, Social and Public Assistance and noncontributory Social Security target the same group. Moreover, Social Security, the Social and Public Assistance programs, the Student Education and Learning Fund (SELF), and the Ministry o f Health all have different systems for identifying beneficiaries. This increases administrative costs and time costs for beneficiaries. There i s a need to strengthen the planning and executing capacity for these programs and to put in place mechanisms for their fiscal prioritization.

6 1. Several programs, including the school lunch program for primary students and a school bus service for secondary students, are not targeted and are provided cost-free irrespective of income. In St. Kitts, health care subsidies are targeted based on categorical criteria (children, elderly, disabled) rather than income. Reducing program leakage and introducing targeting o f school feeding and a few waivers for health services to the poor would considerably ease pressure on the budget. Divestment o f programs to private providers (profit or nonprofit) could also result in cost savings. However, much-

x i i

needed capacity building and institution strengthening, including development o f targeting, management information systems (MIS), and survey capacity, would add development and administrative costs. Expanding program coverage with provision o f benefits conditional on activities that promote human capital also come with their own investment costs. The net fiscal impact of the above reforms would need to be carefully assessed.

62. Effective planning w i l l require updated poverty and labor market information at regular intervals. Timely and reliable information on poor and vulnerable groups is essential for the design and implementation o f social safety net programs. The Caribbean Development Bank (CDB)-financed Poverty Assessment that was conducted in 1999 provided useful information; however, data on poverty and labor markets need to be collected on a regular basis.

63. Budgeting and management information systems also need to be strengthened. Several programs, including cash transfer and labor market programs, are not identified in the government’s budgets as separate programs. This limits effective planning and weakens fiscal accountability. Elevating social protection activities to program status would mean that expenditures, including expenditures by object code, could be easily tracked over time and evaluated with respect to program inputs and outcomes. In addition, management information systems need to be computerized.

64. Inadequate MIS systems and capacity constraints with respect to data collection, monitoring, and evaluation are common across the OECS. Regional initiatives to M I S development and monitoring and evaluation capacity building would address the human resource constraints in individual countries and would be more cost effective than developing systems on a country-by-country basis.

... X l l l

E .Y > s

> x .-

E

8 E Y

c CA

E b Y

5 c 2Y

o 0

9 9

2: 4 0 I

Y

2

U 0 3

E 3 8 Y Y

c Yl

> X

L k! Y il 0 c n

r P Y

5 8 L

4 3 z m Y

.- > x

E e, Y

E 5 8 Y

F v)

E 0 Ld .- Y

Y 8 rr G

Y m

E b Y

.3 G B

1

Y Q 0 m - x U 0

E ."

€ e, Y

E e, Y

i E 5

3 3 v3

M c M c 0

1. FISCAL DEFICIT, PUBLIC DEBT, AND FISCAL SUSTAINABILITY

1.1 St. Kitts and Nevis i s a two-island federation in the Eastern Caribbean with a combined population o f about 45,000 inhabitants (of whom 75 percent l ive in St. Kitts) and a GN1)of US$ 6,980 in 2003 (World Bank Atlas Methodology, current US$). The economy has traditionally depended on the production and export of sugar. However, in the last decade traditional economic activities such as agriculture have given way to a service-based economy.

1.2 St. Kitts and Nevis, as a member of the Eastern Caribbean Currency Union (ECCU), shares a common central bank, the Eastern Caribbean Central Bank (ECCB), and a common currency with the other five independent members o f the Organization of Eastern Caribbean States (OECS) and the two U.K. territories o f Anguilla and Montserrat.’ Their currency i s the Eastern Caribbean dollar, which has been pegged to the U.S. dollar since 1976 at EC$2.70 per US$1. The commitment to a fixed exchange rate and a prudent monetary policy under the ECCU umbrella has been a key element in maintaining an inflation rate close to international levels.

1.3 Notwithstanding a common central bank and a common currency, each member country conducts fiscal policy independently, and scant efforts have been made for a common fiscal policy in the region. Nevertheless, the deterioration o f the ECCU fiscal position in recent years, due mainly to the high fiscal deficits in Antigua, Dominica, and St. Kitts and Nevis, has reinitiated the discussion among i t s members o f the need to coordinate fiscal policies to ensure the stability o f the currency union.’

1.4 St. Kitts and Nevis’s fiscal position has deteriorated sharply since the mid-1990s. The main reasons for this deterioration are increases in the wage bill and capital expenditure in response to hurricane repair, a weakening of the finances of the state- owned St. Kitts Sugar Manufacturing Company (SSMC), increased expenditures linked to legislative elections that took place in July 1995 and March 2000, and increased debt service.

1.5 In light of the preceding discussion, the main objective o f th is chapter i s twofold: first, to evaluate the fiscal sustainability o f the St. Kitts and Nevis Central Government (CG) and public sector in the short and medium term, and second, to propose various options for the adjustment required to achieve fiscal sustainability.

1.6 The main findings and recommendations can be summarized as follows:

* The OECS consists o f six independent members: Antigua and Barbuda, Dominica, Grenada, St. Kitts and Nevis, St. Lucia, and St. Vincent and the Grenadines, and three dependent territories of the United Kingdom, Montserrat (full member), Anguilla, and the British Virgin Islands (associate members).

The communiqut of the Special Meeting of the OECS Authority, Castries, St. Lucia, September 28,2001 alludes to the need to examine in the medium term public sector reform, aimed at increasing efficiency, and fiscal reform including matters related to revenue, expenditure, financing, and debt management, as well as common approaches to taxation and incentives to be applied to cruise shipping.

0 The fiscal policy conducted by the government since the mid-1990s has been unsustainable in the short and medium term, and w i l l continue to be unsustainable in the next years unless the government adjusts i t s expenditures to the revenues mobilized. The size of the adjustment required to achieve fiscal sustainability o f the CG in 2003 i s about 14 to 16 percent of GDP, depending on the assumptions of real interest and growth rate.

0 The proposed fiscal adjustment relies mainly on expenditure cuts (in particular in the wage bill and containment o f capital expenditures). The adoption of the tax policy recommendations suggested by the International Monetary Fund (IMF) would yield an increase in revenue collection of only about 2 percent o f GDP, in contrast to a required adjustment o f about 14 to 16 percent to achieve fiscal sustainability .

0 If the public enterprises are included in the exercise, then the government w i l l need to adjust additional 2 to 3 percentage points o f GDP to ensure the fiscal sustainability o f the public sector. A prompt decision by the government on the possible closing o f the SSMC would be a step forward in the fiscal sustainability o f the public sector.

I. ST. KITTS AND NEVIS FISCAL PERFORMANCE, 1990-2002

Figure 1.1 St Kitts and Nevis Central Government Fiscal Performance 1990.2002

(as % of COP) 5.00 1.7 At the Central

Government level, since 1995 the 0.00 fiscal position of St. Kitts and -5.00 Nevis has progressively -10.00 weakened.” As Figure 1.1 shows, the St. Kitts and Nevis CG -15.00

Swce:ECCE and hF followed a cautious fiscal policy from 1990 to 1994. During this