Research Note - The Impact of Information Technology Investments and Diversification Strategies on...

11

MANAGEMENT SCIENCE Vol. 54, No. 1, January 2008, pp. 224–234 issn 0025-1909 eissn 1526-5501 08 5401 0224 inf orms ® doi 10.1287/mnsc.1070.0743 © 2008 INFORMS Research Note The Impact of Information Technology Investments and Diversification Strategies on Firm Performance Murali D. R. Chari School of Business and Economics, Indiana University South Bend, South Bend, Indiana 46634, [email protected] Sarv Devaraj Mendoza College of Business, University of Notre Dame, Notre Dame, Indiana 46556, [email protected] Parthiban David Division of Management, Price College of Business, University of Oklahoma, Norman, Oklahoma 73019, [email protected] A s companies continue to make large investments in information technology (IT), questions about how and in what contexts such investments pay off have gained importance. We develop a theoretical framework to explain how IT investments could pay off in the economically significant context of corporate diversification, and empirically find that the performance pay off to IT investments is greater for firms with greater levels of diversification. We also find that the performance payoff to IT investments is greater in related diversification than in unrelated diversification. Key words : information technology investments; business strategy; corporate diversification History : Accepted by Ramayya Krishnan, information systems; received November 18, 2004. This paper was with the authors 7 months for 3 revisions. Published online in Articles in Advance November 26, 2007. 1. Introduction Investment in information technology (IT) and impli- cations for firm performance are central issues in the IT payoff literature (see Melville et al. 2004 for a review). Although several studies have demonstrated payoffs to investing in IT (Anderson et al. 2006, Bharadwaj et al. 1999, Dos Santos et al. 1993, Hitt and Brynjolfsson 1996, Im et al. 2001, Mukhopadhyay et al. 1997), further research is needed to understand how and why these investments affect performance (Sambamurthy et al. 2003) and the contexts and con- ditions under which IT investment will have a bene- ficial impact (Clemons and Row 1991, Li and Ye 1999, Melville et al. 2004, Powell and Dent-Micallef 1997). We examine the performance impact of IT invest- ment in the context of corporate diversification, where firms own and operate businesses in multi- ple industries. Diversified corporations are significant consumers of IT investments (Dewan et al. 1998). Fur- thermore, these corporations are critical players in the economy accounting for a significant portion of eco- nomic activity in the United States and other countries (Montgomery 1994). 1 The question of whether IT in- vestments pay off in the context of corporate diversi- fication is therefore economically very significant. Our study contributes to the IT payoff literature in four ways. First, economic significance of IT invest- ments has long been a key motivation for studying IT payoffs (Brynjolfsson and Hitt 1996, Loveman 1994, Morrison 1997). Our study helps us understand the performance impact of IT investments in an econom- ically significant context that has not been studied in extant research. Second, authors have observed that “theoretical frameworks are yet to explain how and why these [IT] investments enhance firm per- formance” (Sambamurthy et al. 2003, p. 238). We address this call by developing a theoretical frame- work for IT payoff in the context of corporate diver- sification. Our framework draws from the literature on economies of scope and coordination and control 1 For example, 70% of the 500 largest firms in the United States are diversified, and the output of these largest 500 firms was equal to nearly three-fourths of the U.S. gross domestic product in 2005. 224

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Research Note - The Impact of Information Technology Investments and Diversification Strategies on...

MANAGEMENT SCIENCEVol. 54, No. 1, January 2008, pp. 224–234issn 0025-1909 �eissn 1526-5501 �08 �5401 �0224

informs ®

doi 10.1287/mnsc.1070.0743©2008 INFORMS

Research Note

The Impact of Information TechnologyInvestments and Diversification Strategies on

Firm Performance

Murali D. R. ChariSchool of Business and Economics, Indiana University South Bend, South Bend, Indiana 46634,

Sarv DevarajMendoza College of Business, University of Notre Dame, Notre Dame, Indiana 46556,

Parthiban DavidDivision of Management, Price College of Business, University of Oklahoma, Norman, Oklahoma 73019,

As companies continue to make large investments in information technology (IT), questions about how andin what contexts such investments pay off have gained importance. We develop a theoretical framework

to explain how IT investments could pay off in the economically significant context of corporate diversification,and empirically find that the performance pay off to IT investments is greater for firms with greater levels ofdiversification. We also find that the performance payoff to IT investments is greater in related diversificationthan in unrelated diversification.

Key words : information technology investments; business strategy; corporate diversificationHistory : Accepted by Ramayya Krishnan, information systems; received November 18, 2004. This paper waswith the authors 7 months for 3 revisions. Published online in Articles in Advance November 26, 2007.

1. IntroductionInvestment in information technology (IT) and impli-cations for firm performance are central issues in theIT payoff literature (see Melville et al. 2004 for areview). Although several studies have demonstratedpayoffs to investing in IT (Anderson et al. 2006,Bharadwaj et al. 1999, Dos Santos et al. 1993, Hittand Brynjolfsson 1996, Im et al. 2001, Mukhopadhyayet al. 1997), further research is needed to understandhow and why these investments affect performance(Sambamurthy et al. 2003) and the contexts and con-ditions under which IT investment will have a bene-ficial impact (Clemons and Row 1991, Li and Ye 1999,Melville et al. 2004, Powell and Dent-Micallef 1997).We examine the performance impact of IT invest-

ment in the context of corporate diversification,where firms own and operate businesses in multi-ple industries. Diversified corporations are significantconsumers of IT investments (Dewan et al. 1998). Fur-thermore, these corporations are critical players in theeconomy accounting for a significant portion of eco-nomic activity in the United States and other countries

(Montgomery 1994).1 The question of whether IT in-vestments pay off in the context of corporate diversi-fication is therefore economically very significant.Our study contributes to the IT payoff literature in

four ways. First, economic significance of IT invest-ments has long been a key motivation for studying ITpayoffs (Brynjolfsson and Hitt 1996, Loveman 1994,Morrison 1997). Our study helps us understand theperformance impact of IT investments in an econom-ically significant context that has not been studiedin extant research. Second, authors have observedthat “theoretical frameworks are yet to explain howand why these [IT] investments enhance firm per-formance” (Sambamurthy et al. 2003, p. 238). Weaddress this call by developing a theoretical frame-work for IT payoff in the context of corporate diver-sification. Our framework draws from the literatureon economies of scope and coordination and control

1 For example, 70% of the 500 largest firms in the United States arediversified, and the output of these largest 500 firms was equal tonearly three-fourths of the U.S. gross domestic product in 2005.

224

Chari, Devaraj, and David: Research Note: The Impact of IT Investments and Diversification StrategiesManagement Science 54(1), pp. 224–234, © 2008 INFORMS 225

to explain IT payoff in diversification as stemmingfrom two sources: (1) greater returns from sharing andtransferring IT assets across businesses, and (2) fromfacilitating coordination and control required to real-ize potential economies of scope in various assets andcapabilities.Third, the IT payoff literature has pointed out

that examining IT payoff without adequate fidelityhas contributed to conflicting results, which slowsdown cumulative knowledge building (Alpar andKim 1990, Brynjolfsson and Hitt 1996). Similarly, liter-ature reviews and meta-analysis of IT-payoff studieshave observed that conflicting and inconsistent find-ings are also attributable to alternative specificationsand measures used in different studies (Brynjolfssonand Hitt 1996, Kohli and Devaraj 2003, Mahmood andMann 2000). We control for a variety of knownextraneous influences on firm performance to ensuregreater fidelity in our analyses (Jarvenpaa et al. 1985),and perform extensive robustness checks using alter-native measures and specifications to enhance thecontribution of our findings to knowledge accumu-lation on IT payoffs. Fourth, our study contributesto the cross-fertilization of information systems (IS)research with research in other disciplines to addressquestions important to both IS scholars and those inother disciplines, as urged by authors studying IS asa reference discipline (Baskerville and Myers 2002).Specifically, our study brings together the IT payoffliterature and the strategic management literature toaddress the question of IT payoff in diversification.Our findings also contribute to the strategic manage-ment literature because the performance consequenceof IT investment in diversification has not been empir-ically tested in the extant strategy literature, eventhough strategy scholars have recognized the poten-tial role of IT for coordination within diversified firms(Hill and Jones 2007, Jones and Hill 1988).

2. Literature ReviewEarly IT payoff literature sought to establish a directlink between IT investment and performance, butdid not find consistent support for the relationship.The ensuing research has led to a growing consen-sus that competitive imitation and widespread ITadoption have rendered direct payoffs to IT invest-ment unlikely (Clemons and Row 1991, Vitale 1986).Instead, the emerging consensus in the literature isthat IT investment payoffs are contingent on the pres-ence of complementary factors or contexts (Clemonsand Row 1991, Powell and Dent-Micallef 1997, Weilland Aral 2006). Powell and Dent-Micallef (1997), forexample, showed that IT in itself did not enhanceperformance, but that it could improve performanceby leveraging complementary human and business

resources. Similarly, others have shown a positive per-formance impact for IT when it confers first-moveradvantages (Dos Santos and Peffers 1995) and when itis aligned with certain business strategies (Sabherwaland Chan 2001).We extend this line of research by studying the per-

formance impact of IT investment in the context ofcorporate diversification strategy. Corporate diversifi-cation strategy involves the pursuit of superior per-formance through the configuration and coordinationof activities across multiple businesses of a corpora-tion (Collis and Montgomery 1997). Economic ratio-nale for corporate diversification (also simply referredto as diversification) strategy exists when commonownership and operation of multiple businesses allowa diversified firm to achieve greater performance thanthat obtained by merely adding together the perfor-mance of these business had they been owned andoperated independently (Porter 1987). The superiorperformance in diversification strategy is expectedfrom economies of scope where a firm earns a greaterreturn on its investments by sharing and leveragingassets and capabilities resulting from its investmentsacross multiple businesses (Teece 1982). Gains fromeconomies of scope, however, will not be realized ifthe firm cannot effectively coordinate and control theinterbusiness dependencies and activities required forsharing and leveraging assets and capabilities, i.e.,implement the diversification strategy (Jones and Hill1988).The strategy literature describes two types of diver-

sification—related and unrelated. Related diversifi-cation involves operating businesses in industriesthat are related to each other and, therefore, offersopportunities to share operating assets and capabil-ities as well as financial resources. Unrelated diver-sification involves operating businesses in industriesnot related to each other and, consequently, presentsopportunities to share financial resources and a rela-tively limited set of opportunities to share operatingassets and capabilities (Jones and Hill 1988). Althoughrelated diversification offers the chance to share moreresources, implementing related diversification alsoinvolves greater coordination and control (Jones andHill 1988).Based on the coordination demands of diversifica-

tion strategies, Dewan et al. (1998) examined IT invest-ments in diversified firms and found that diversifiedfirms invested more in IT, with related diversifiersinvesting more than unrelated diversifiers. Combin-ing the Dewan et al. (1998) findings with studiesthat have explored a direct performance effect forIT investment (e.g., Bharadwaj et al. 1999) suggestsa mediation model for the performance impact ofIT in diversification, where diversification enhancesIT investment and this increased IT investment in

Chari, Devaraj, and David: Research Note: The Impact of IT Investments and Diversification Strategies226 Management Science 54(1), pp. 224–234, © 2008 INFORMS

turn enhances firm performance. However, as theevolving consensus in the IT payoff literature indi-cates, IT investment by itself is not likely to enhancefirm performance and, therefore, the relationshipbetween increased IT investment and firm perfor-mance also seems unlikely. In addition, a perfor-mance impact for IT investment in diversification isalso likely from sharing and transferring IT assetsacross businesses (Clemons and Row 1991), and thisperformance impact from economies of scope in ITinvestment is not captured by the mediation model.For these reasons, the mediation model is an unlikelyexplanation.2 However, given the significant role ofIT in facilitating coordination (Dewan et al. 1998) andthe opportunities for IT asset sharing in diversifiedfirms (Clemons and Row 1991), it is quite likely thata diversification strategy represents a complementarycontext that cocreates value for IT investment—valuethat can be empirically detected as a joint effect onfirm performance.Boal and Bryson (1987) present two related but dis-

tinct models to represent complementary relation-ships: (1) the familiar moderating effects model,where a direct relationship between one of the com-plementary variables and the outcome variable ismoderated by the other complementary variable (forexample, diversification moderating the relationshipbetween IT investment and performance), and (2) analternate interaction model, where the complemen-tary variables are expected to affect the outcome vari-able jointly and no direct effects are postulated. Wehave noted the evolving consensus in the IT pay-off literature that emphasizes the contextual natureof IT payoffs rather than direct performance effectsfor IT investment. There is a similar movement inthe strategy literature away from expecting a directperformance effect for diversification strategy, to amore nuanced position where the performance effectis expected to be contingent on developing coordi-nation and control capabilities required for imple-menting diversification strategy (Hill et al. 1992). Theevolving literatures in both IT payoff and diversifica-tion strategy are therefore consistent with the interac-tion model, where the focus is on the interaction effect(i.e., joint effect) between IT investment and diver-sification strategy, and no direct effect for either ITinvestment or diversification is postulated.

3. Hypothesis DevelopmentIn this section we develop our argument that ITinvestment will have a significant performance effectin diversification strategy from two sources. First,

2 We also tested the mediation model and did not find empiricalsupport for the model.

economies of scope from sharing IT assets and capa-bilities across businesses will lead to a greater returnon IT investment. Second, IT investment will have aperformance effect by enabling the coordination andcontrol of interbusiness dependencies and activitiesrequired to realize economies of scope from shar-ing various assets and capabilities, not just IT. Weapply these arguments to two aspects of diversifica-tion strategy: (1) the level of diversification (extent towhich a firm’s activities are spread across multiplebusinesses) and (2) the type of diversification (relatedversus unrelated diversification).

3.1. Greater Returns from Sharing andTransferring IT Assets and Capabilities

The main source of superior performance in diversi-fication is economies of scope. Although the focus ofextant diversification strategy literature has been oneconomies of scope from sharing research and devel-opment (R&D), marketing, and financial resources,given the large and growing size of IT investmentin firms,3 gains from sharing IT assets and capabil-ities in diversified firms are likely to be substantial.Clemons and Row (1991) discuss three avenues bywhich IT asset sharing can generate greater returnsfor IT investment in diversification strategy. First,Clemons and Row (1991) argue that using the sameIT asset to support the needs of multiple businessescan yield scale advantages in key IT resources. Tothe extent that activities of multiple businesses aresimilar, a diversified firm may be able to develop anIT system that can be utilized by its multiple busi-nesses. Clemons and Row (1991) provide the central-ized procurement system used by multiple businesseswithin Hewlett Packard as an example. A secondavenue to leverage IT investment across businessesis through the transfer of technologies across busi-nesses, where the IT capabilities or know-how devel-oped in one business is transferred and applied toanother business to create a new IT system (Clemonsand Row 1991). Such transfer of existing know-howallows the firm to create the new system faster andless expensively than if it were developed indepen-dently, thereby creating a greater return on its ITinvestment (Markides and Williamson 1994). Exploit-ing new uses for existing IT assets is the third avenuediscussed by Clemons and Row (1991) for generat-ing greater returns on IT investment in diversification.As an example, Amazon.com’s diversification into the

3 The U.S. Bureau of Economic Analysis reports that business (pri-vate nonresidential) investment in information processing and soft-ware has grown steadily over the years, exceeding investment inany other industrial equipment category, and accounting for a littleover 20% of all gross private domestic investment in the UnitedStates.

Chari, Devaraj, and David: Research Note: The Impact of IT Investments and Diversification StrategiesManagement Science 54(1), pp. 224–234, © 2008 INFORMS 227

e-commerce services business, through which Ama-zon offers its technological expertise to third partiessuch as Target and Toys RUs on a turnkey basis, hasopened a new avenue for the company to deployits sophisticated e-commerce systems and capabilities,and thereby increase returns on its original invest-ments in these technologies (Banham 2004). Becausegreater levels of diversification present opportunitiesfor sharing and transferring IT assets and capabili-ties across more businesses, the economies of scope inIT investment and the resulting performance impactfor IT investment are likely to be greater in more-diversified firms.The economies of scope in IT investment are also

likely to depend on the type of diversification. Becauseeconomies of scope in diversification arise from costsavings obtained when assets are shared betweenbusinesses or when assets developed in one busi-ness are deployed in another, the size of gains fromsharing and transferring an asset is a function of thecost of modifying it for use across the businesses(Teece 1982). The cost of modifying an asset canbe understood as imposing an efficiency loss associ-ated with deploying an asset developed in one busi-ness to another, and Montgomery and Wernerfelt(1988) show that efficiency losses are greater whenassets are deployed across unrelated industries thanwhen deployed across related industries. Montgomeryand Wernerfelt’s (1988) findings suggest that apply-ing IT assets to businesses in similar industries islikely to involve fewer modifications and, therefore,incur lower efficiency losses than applying them tobusinesses in dissimilar industries. Consequently, theeconomies of scope gains from sharing and trans-ferring IT assets and capabilities are likely to begreater in related diversification than in unrelateddiversification.

3.2. Payoff from Enabling Coordinationand Control

Although potential gains from sharing various assetsand capabilities including IT assets may be large,superior performance from diversification is not auto-matic, but will depend on the effective coordina-tion and control of interbusiness dependencies andactivities required to implement the strategy. Effec-tive coordination involves processing, sharing, andcommunicating information as needed across variousbusiness units, and control involves monitoring andevaluating performance to overcome agency conflicts(Jensen and Meckling 1992). Providing coordinationand control can be both complex and informationintensive (Hill and Hoskisson 1987). IT-enabled sys-tems such as ERP (enterprise resource planning),CRM (customer relationship management), and EAI(enterprise applications integration) can allow cor-porate managers to gain the necessary information

in a quick, reliable, and consistent format for deci-sion making (Hill and Jones 2007), and thereby helpunlock the potential performance advantages of di-versification (Jones and Hill 1988). Because greaterlevels of diversification increase the number of busi-nesses that need to be coordinated and controlled,the need for and, consequently, the benefits fromIT-enabled coordination and control are likely to begreater in firms with greater levels of diversification.The need for and the benefits from IT-enabled coor-

dination and control are also likely to depend onthe type of diversification. As Dewan et al. (1998)argued, coordination and control required to imple-ment related diversification, compared with unrelateddiversification, are much more complex and infor-mation-processing intensive, and therefore requiregreater reliance on IT-conferred capabilities. First,transferring and sharing operating assets and capa-bilities across related businesses requires coordinatingreciprocal interdependencies between the businesses,which are more complex and information-processingintensive than coordinating the pooled interdepen-dencies required to share financial resources (Hill andHoskisson 1987, Jones and Hill 1988, Thompson 1967).Second, implementing related diversification requiresmore complex control systems and, therefore, greaterreliance on IT than implementing unrelated diversi-fication. In related diversified firms, monitoring andevaluating performance is complex because of dif-ficulties in identifying, measuring, and rewardingthe relative contributions of interdependent businessunits; managers must therefore gather and processgreater amounts of information and do so more fre-quently to exercise effective control (Jones and Hill1988). In unrelated diversified firms, in the absenceof reciprocal interdependencies between businesses,corporate managers need only process informationspecific to each autonomous, unrelated division; man-agers can rely on periodically obtained objectivefinancial criteria that are tied to financial incentives toexercise effective control (Jones and Hill 1988).Consistent with this greater importance of IT-

conferred capabilities for coordinating and control-ling related diversification, Dewan et al. (1998) foundthat related diversified firms invested more on ITthan unrelated diversified firms. We argue that thegreater importance of IT in related diversification alsoreflects greater complementary value for IT invest-ments in related diversification. Complementaritiesamong factors arise when the value of one factor isenhanced by the presence of another factor (Baruaet al. 1996). As a complementary factor, IT invest-ment facilitates the development of sophisticatedinformation processing and coordination capabilitiescritical to unlocking the benefits of related diversi-fication, thereby contributing to firm performance.

Chari, Devaraj, and David: Research Note: The Impact of IT Investments and Diversification Strategies228 Management Science 54(1), pp. 224–234, © 2008 INFORMS

The lower complexity and information-processingneeds in unrelated diversification suggest that simplerinformation-processing mechanisms such as periodicmeetings and reviews may be quite effective for thetask, rendering IT-conferred coordination and controlcapabilities less important (Galbraith 1974). Conse-quently, IT investments are not likely to hold as higha complementary value in unrelated diversification asthey do in related diversification.

3.3. HypothesesIn summary, we have developed arguments that ITinvestment will have a performance effect in diver-sification strategy from two sources: (1) economiesof scope from sharing IT across multiple businesses,(2) enabling the coordination and control required torealize economies of scope in various assets, not justIT. These arguments are applied to two aspects ofdiversification strategy: (1) the level of diversificationand (2) the type of diversification.With regard to the level of diversification, we have

noted that firms with higher levels of diversificationhave opportunities for sharing IT assets and capabil-ities across more businesses and, therefore, are likelyto obtain a greater return on IT investment. Further-more, because more businesses need to be coordi-nated and controlled in more-diversified firms, thebenefits of IT-enabled coordination and control arealso likely to be greater in more-diversified firms. Forthese reasons, firms with higher levels of diversifica-tion are likely to obtain a greater performance impactfrom IT investment.

Hypothesis 1. The impact of IT investment on firmperformance will be greater for firms with greater levels ofdiversification.

With respect to the type of diversification, wehave noted that, because sharing and transferring ITassets and capabilities across related businesses, com-pared with unrelated businesses, are likely to involvelower efficiency losses, the economies of scope in ITinvestment are likely to be greater in related diver-sification than in unrelated diversification. Further-more, because coordination and control required inrelated diversification are much more complex andinformation-processing intensive, the need for andthe benefits from IT-enabled coordination and con-trol are likely to be greater in related diversificationthan in unrelated diversification. For these reasons,the performance impact of IT investment is likely tobe greater in related diversification than in unrelateddiversification.

Hypothesis 2. The impact of IT investment on firmperformance will be greater in related diversification thanin unrelated diversification.

4. Sample and Variables Used inthe Study

We followed prior research (Bharadwaj et al. 1999)and obtained IT investment data from annual IT sur-veys reported in the publication Information Week.Specifically, we use Information Week’s IW500 datafor 1997, the most recent year for which these dataare available. Data for other variables of interestwere also collected for the same year from varioussources. After excluding private firms and those forwhich data on other required variables could not beobtained, a total of 117 firms remained in the sample.The sample firms are comparable in size to the setof S&P 500 firms. Firms in the sample had averagesales of $9.42 billion, employed an average of 47�900employees, and obtained 22.3% of their sales from for-eign markets. In addition, about 65% of the firms werefrom the manufacturing sector and the rest were fromother sectors including retail, wholesale, transporta-tion, communication, and other services.

Firm performance, the dependent variable, was mea-sured as Tobin’s q (computed following Chung andPruitt 1994). Specifically, the measure was computedas a ratio of market value [(fiscal year-end marketvalue of equity) + (liquidating value of the firms’outstanding preferred stock) + (current liabilities) −(current assets) + (book value of inventories) +(long-term debt)] to book value of total assets.Tobin’s q incorporates a market-based measure offirm value, which is forward looking, risk adjusted,and less vulnerable to changes in accounting prac-tices and, hence, is considered appropriate for mea-suring the performance impact of IT investments(Bharadwaj et al. 1999). Tobin’s q has also been advo-cated as the appropriate measure for studying theperformance consequences of diversification strate-gies (Montgomery 1994, Montgomery and Wernerfelt1988). Montgomery (1994), for example, observes that,because marginal rents to diversification may befavorable even when average rents are not, averageaccounting returns may decline even when diversi-fication increases a firm’s economic value, which amarket-based measure such as Tobin’s q captures.Data for computing Tobin’s q were obtained fromCompustat.The two main independent variables in this

study are IT investment and diversification. FollowingBharadwaj et al. (1999), IT investment was measuredas the ratio of dollar investment in IT (obtained fromInformation Week) to sales (obtained from Compus-tat). Diversification was computed using an entropymeasure with data obtained from Compustat (Palepu1985). The entropy measure is widely used in thestrategy literature and was also the measure ofdiversification in Dewan et al. (1998). Details on theconstruction of the measure for related, unrelated and

Chari, Devaraj, and David: Research Note: The Impact of IT Investments and Diversification StrategiesManagement Science 54(1), pp. 224–234, © 2008 INFORMS 229

total diversification can be found in the study byDewan et al. (1998, pp. 230–231). Briefly, related diver-sification (RD) measures the extent of a firm’s opera-tions in different industries within the same two-digitStandard Industry Classification (SIC) code. Unrelateddiversification (UD) measures the extent of a firm’s op-erations in different two-digit SIC codes. Total diversi-fication (TD) measures the extent of a firm’s operationsin different industries, whether related or unrelated,and is equal to the sum of the two diversificationmeasures—RD and UD.We controlled for several industry-level variables

(industry capital intensity, market uncertainty, marketgrowth, industry concentration, and industry perfor-mance) and firm-level variables (firm size, capital struc-ture, R&D intensity, advertising intensity, and marketshare) that may affect firm performance to rule outalternative explanations and enhance the fidelity withwhich the relationships of interest are examined (Desset al. 1990, Jarvenpaa et al. 1985). The measures usedfor the industry-level and firm-level control variables,along with references to the prior research from whichthey were adopted, are listed in the appendix.

Capital intensity is an indicator of exit barriersand it has been argued that firms will assume therisks associated with sunk investments only whenthe promise of firm performance is high (Bettis 1981).Consequently, the association between capital intensityand performance is expected to be positive (Robinsand Wiersema 1995). Market uncertainty disruptsthe effectiveness of existing strategies and increasesthe information-processing requirements, thus, nega-tively impacting firm performance (Bergh 1998, Hill andHoskisson 1987). Market growth, on the other hand,

Table 1 Means, Standard Deviations, and Correlations

Variables Mean s.d. 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

1 Firm performance 1�47 0�802 Industry performance 2�78 1�35 0�423 Industry capital intensity 1�63 1�20 0�12 0�274 Industry concentration 40�60 16�30 0�11 0�08 −0�255 Market share 0�21 0�21 0�19 0�13 −0�21 0�506 Capital structure 0�66 0�44 −0�26 −0�05 0�34 −0�06 −0�037 R&D intensity 0�02 0�03 0�27 0�31 0�24 0�20 0�12 −0�148 Advertising intensity 0�01 0�02 0�31 0�29 −0�02 0�34 0�37 −0�08 0�139 Market uncertainty 1�01 0�01 −0�21 −0�07 −0�11 0�08 −0�02 −0�04 0�13 −0�11

10 Market growth 1�06 0�05 0�05 −0�02 −0�10 −0�07 −0�11 −0�28 0�28 −0�08 0�1611 Firm size 3�74 0�44 0�19 −0�01 −0�10 0�24 0�28 0�07 0�01 0�33 −0�09 −0�1012 Total diversification 0�46 0�49 0�05 0�11 −0�06 −0�02 0�05 −0�01 0�04 0�11 0�24 −0�09 0�0913 Related diversification 0�17 0�27 0�15 0�29 −0�07 0�07 0�12 0�10 0�16 0�06 0�16 −0�06 −0�02 0�6014 Unrelated diversification 0�29 0�39 −0�05 −0�07 −0�02 −0�07 −0�02 −0�08 −0�07 0�09 0�19 −0�08 0�13 0�83 0�0415 IT investment 0�02 0�02 0�28 0�29 0�14 0�13 0�02 0�13 0�15 −0�02 −0�19 0�07 −0�17 −0�05 0�14 −0�1616 IT ∗ TD 0�00 0�01 0�21 0�11 −0�13 −0�01 −0�07 −0�06 −0�06 −0�07 0�00 0�05 −0�03 −0�30 0�01 −0�38 0�0717 IT ∗RD 0�00 0�01 0�32 0�28 −0�07 0�00 −0�03 0�02 −0�07 −0�04 −0�04 0�02 −0�09 0�01 0�10 −0�06 0�55 0�6318 IT ∗UD 0�00 0�01 −0�14 −0�20 −0�06 −0�01 −0�05 −0�10 0�01 −0�03 0�04 0�04 0�07 −0�35 −0�11 −0�36 −0�57 0�39 −0�47

Notes. Correlations ±0�19 or larger are significant at p < 0�05 (two-tailed). Correlations ±0�24 or larger are significant at p < 0�01 (two-tailed). s.d., Standarddeviation.

IT ∗ TD is the interaction term for centered IT investment and centered total diversification.IT ∗RD is the interaction term for centered IT investment and centered related diversification.IT ∗UD is the interaction term for centered IT investment and centered unrelated diversification.

reduces competitive rivalry and, consequently, hasa positive impact on firm performance (Porter 1979).Industry concentration has been shown to have a neg-ative effect on firm performance in studies of IT invest-ment as well as diversification (Bharadwaj et al. 1999,Montgomery and Wernerfelt 1988). We include anadditional variable, industry performance, to control foraspects of the industry that are not captured by capitalintensity, market uncertainty, market growth, and concen-tration. Firm size is associated with economies of scaleand, hence, is expected to have a positive associationwith firm performance (Hitt et al. 1997). R&D intensityand advertisement intensity have been argued to indi-cate research and marketing capabilities, respectively,and have been shown to have a positive influenceon firm performance (Capon et al. 1990, Kotabe et al.2002). Firms often do not report R&D and advertis-ing expenses if these values are not deemed “mate-rial”; we followed prior research (see Bharadwaj et al.1999, p. 1016) and replaced missing values with zeros.In addition, we ran our analyses without these twovariables and found that our results did not change.Market share is argued to indicate market power andprovide scale benefits, and has been shown to havea positive impact on firm performance (Capon et al.1990). Similarly, prior work has empirically shownthat a firm’s capital structure (debt in particular) has anegative effect on firm performance (Hitt et al. 1997).

5. Analysis and ResultsTable 1 provides means, standard deviations, and cor-relations for the variables. The means and standarddeviations are in line with prior studies of diversifica-tion and those that use identical or similar measures

Chari, Devaraj, and David: Research Note: The Impact of IT Investments and Diversification Strategies230 Management Science 54(1), pp. 224–234, © 2008 INFORMS

for market uncertainty, market growth, and other controlvariables used in this study (Bergh 1998, Bharadwajet al. 1999, Hitt et al. 1997, Keats and Hitt 1988).To avoid multicollinearity problems that are likely

in regression models with interaction effects, we cen-tered the independent variables of interest as sug-gested by Aiken and West (1991). In addition, weran a battery of tests recommended by Hair et al.(1998), and Belsley et al. (1980) to examine if ourresults are affected by multicollinearity. Specifically,we examined the variance inflation factors (VIFs) andtolerance values, and conducted the two-stage processrecommended by Belsley et al. (1980). The VIFs werewell below the threshold value of 10 or greater, whichis indicative of multicollinearity (none of our VIFswere above 2.519), and the tolerance values were wellabove the suggested 0.10 or less threshold (our toler-ance values were 0.397 or greater), which is indica-tive of multicollinearity (Belsley et al. 1980, Hair et al.1998). The two-stage process recommended by Belsleyet al. (1980) also did not indicate that multicollinear-ity is a problem that affects our results. We also con-ducted tests to assess normality and constant varianceassumptions. The Kolomogorov-Smirnov test for nor-mality did not indicate deviations from normality,whereas White’s test for heteroscedascity supportedthe constant variance assumption.Our hypotheses pertain to the interaction effects,

i.e., the joint effects of IT investment (IT) and diver-sification (TD, RD, and UD) on firm performance �Q�.Our approach to testing interaction effects follows theprocedure outlined by Aiken and West (1991). Thepredicted value Q can be written as:

Q= B0 +B1IT+B2TD+B3IT TD+B4−n(controls)�

If B3 is zero, then we must conclude that the regres-sion of Q on IT is independent of the level of TD. IfB3 is significantly greater than zero, then we can con-clude that the regression of Q on IT depends on thelevel of TD. Our Hypothesis 1 predicts that B3 is sig-nificantly greater than zero. Using the two types ofdiversification, RD and UD, instead of total diversifi-cation, the above equation can be rewritten as followsand our Hypothesis 2 predicts that B4 will be greaterthan B5 in this disaggregated model.

Q = B0 +B1IT+B2RD+B3UD+B4IT RD+B5IT UD

+B6−n(controls)�

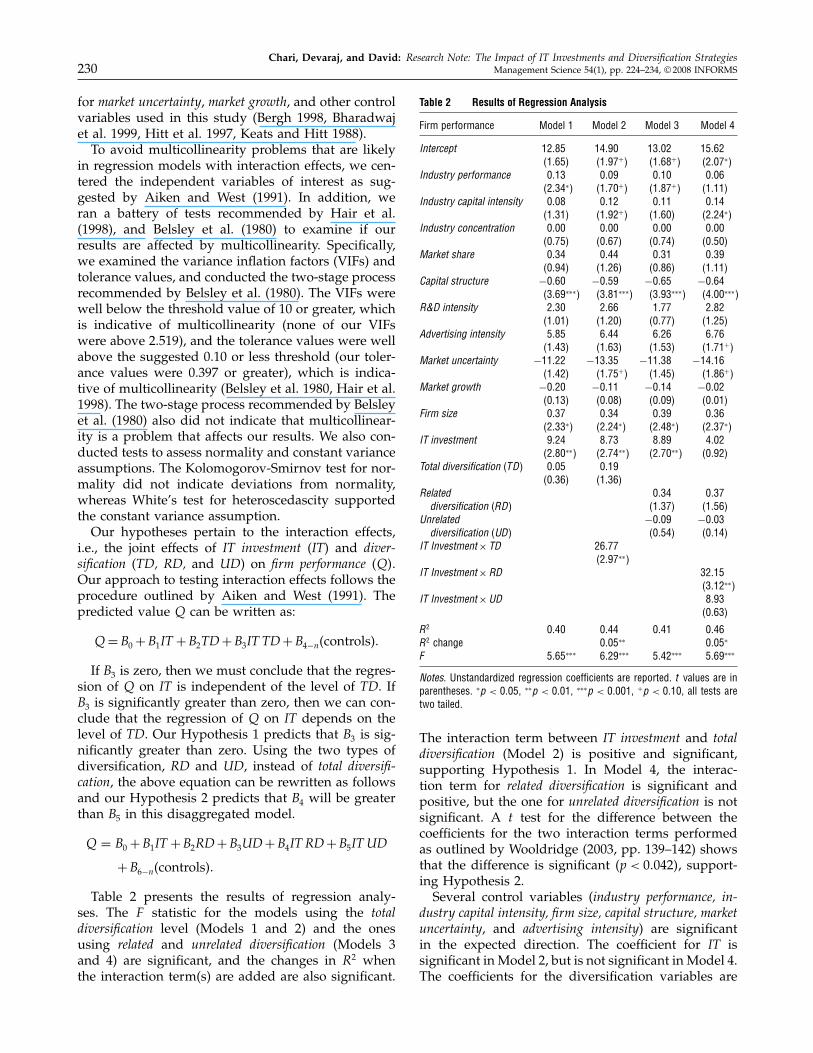

Table 2 presents the results of regression analy-ses. The F statistic for the models using the totaldiversification level (Models 1 and 2) and the onesusing related and unrelated diversification (Models 3and 4) are significant, and the changes in R2 whenthe interaction term(s) are added are also significant.

Table 2 Results of Regression Analysis

Firm performance Model 1 Model 2 Model 3 Model 4

Intercept 12�85 14�90 13�02 15�62�1�65� �1�97+� �1�68+� �2�07∗�

Industry performance 0�13 0�09 0�10 0�06�2�34∗� �1�70+� �1�87+� �1�11�

Industry capital intensity 0�08 0�12 0�11 0�14�1�31� �1�92+� �1�60� �2�24∗�

Industry concentration 0�00 0�00 0�00 0�00�0�75� �0�67� �0�74� �0�50�

Market share 0�34 0�44 0�31 0�39�0�94� �1�26� �0�86� �1�11�

Capital structure −0�60 −0�59 −0�65 −0�64�3�69∗∗∗� �3�81∗∗∗� �3�93∗∗∗� �4�00∗∗∗�

R&D intensity 2�30 2�66 1�77 2�82�1�01� �1�20� �0�77� �1�25�

Advertising intensity 5�85 6�44 6�26 6�76�1�43� �1�63� �1�53� �1�71+�

Market uncertainty −11�22 −13�35 −11�38 −14�16�1�42� �1�75+� �1�45� �1�86+�

Market growth −0�20 −0�11 −0�14 −0�02�0�13� �0�08� �0�09� �0�01�

Firm size 0�37 0�34 0�39 0�36�2�33∗� �2�24∗� �2�48∗� �2�37∗�

IT investment 9�24 8�73 8�89 4�02�2�80∗∗� �2�74∗∗� �2�70∗∗� �0�92�

Total diversification �TD� 0�05 0�19�0�36� �1�36�

Related 0�34 0�37diversification �RD� �1�37� �1�56�

Unrelated −0�09 −0�03diversification �UD� �0�54� �0�14�

IT Investment× TD 26�77�2�97∗∗�

IT Investment×RD 32�15�3�12∗∗�

IT Investment×UD 8�93�0�63�

R2 0�40 0�44 0�41 0�46R2 change 0�05∗∗ 0�05∗

F 5�65∗∗∗ 6�29∗∗∗ 5�42∗∗∗ 5�69∗∗∗

Notes. Unstandardized regression coefficients are reported. t values are inparentheses. ∗p < 0�05, ∗∗p < 0�01, ∗∗∗p < 0�001, +p < 0�10, all tests aretwo tailed.

The interaction term between IT investment and totaldiversification (Model 2) is positive and significant,supporting Hypothesis 1. In Model 4, the interac-tion term for related diversification is significant andpositive, but the one for unrelated diversification is notsignificant. A t test for the difference between thecoefficients for the two interaction terms performedas outlined by Wooldridge (2003, pp. 139–142) showsthat the difference is significant �p < 0�042�, support-ing Hypothesis 2.Several control variables (industry performance, in-

dustry capital intensity, firm size, capital structure, marketuncertainty, and advertising intensity) are significantin the expected direction. The coefficient for IT issignificant in Model 2, but is not significant in Model 4.The coefficients for the diversification variables are

Chari, Devaraj, and David: Research Note: The Impact of IT Investments and Diversification StrategiesManagement Science 54(1), pp. 224–234, © 2008 INFORMS 231

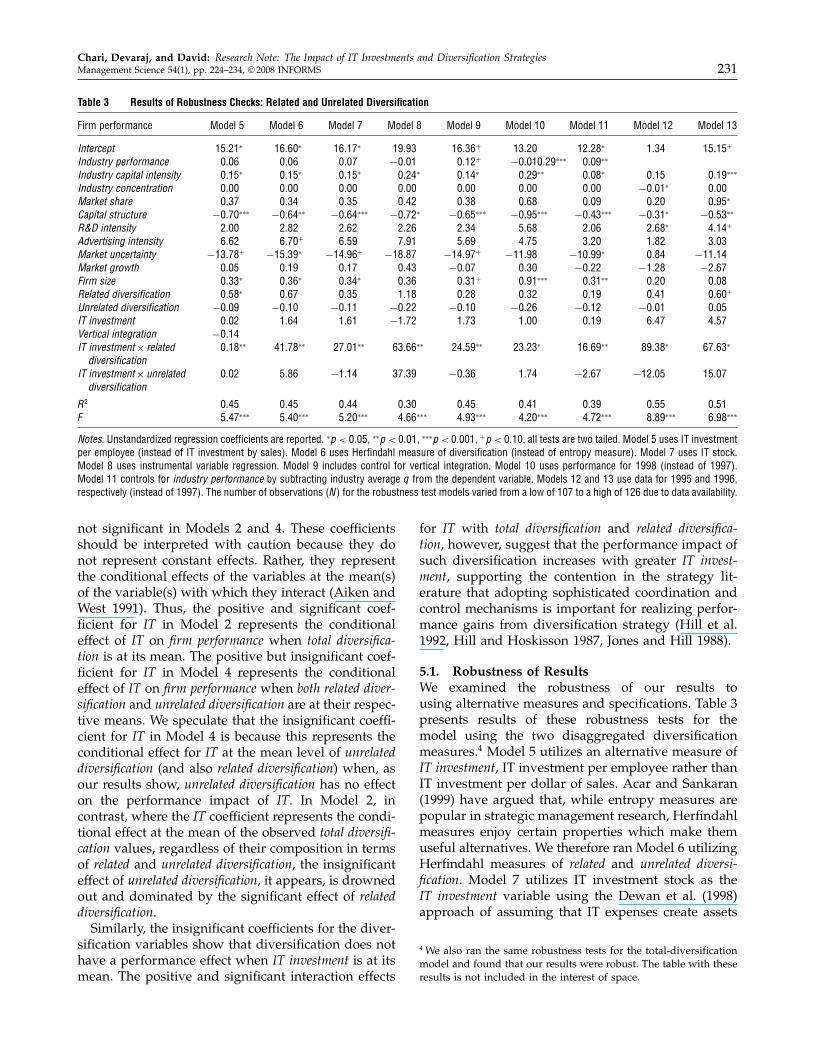

Table 3 Results of Robustness Checks: Related and Unrelated Diversification

Firm performance Model 5 Model 6 Model 7 Model 8 Model 9 Model 10 Model 11 Model 12 Model 13

Intercept 15�21∗ 16�60∗ 16�17∗ 19�93 16�36+ 13�20 12�28∗ 1�34 15�15+

Industry performance 0�06 0�06 0�07 −0�01 0�12+ −0�010�29∗∗∗ 0�09∗∗

Industry capital intensity 0�15∗ 0�15∗ 0�15∗ 0�24∗ 0�14∗ 0�29∗∗ 0�08∗ 0�15 0�19∗∗∗

Industry concentration 0�00 0�00 0�00 0�00 0�00 0�00 0�00 −0�01∗ 0�00Market share 0�37 0�34 0�35 0�42 0�38 0�68 0�09 0�20 0�95∗

Capital structure −0�70∗∗∗ −0�64∗∗ −0�64∗∗∗ −0�72∗ −0�65∗∗∗ −0�95∗∗∗ −0�43∗∗∗ −0�31∗ −0�53∗∗

R&D intensity 2�00 2�82 2�62 2�26 2�34 5�68 2�06 2�68∗ 4�14+

Advertising intensity 6�62 6�70+ 6�59 7�91 5�69 4�75 3�20 1�82 3�03Market uncertainty −13�78+ −15�39∗ −14�96+ −18�87 −14�97+ −11�98 −10�99∗ 0�84 −11�14Market growth 0�05 0�19 0�17 0�43 −0�07 0�30 −0�22 −1�28 −2�67Firm size 0�33∗ 0�36∗ 0�34∗ 0�36 0�31+ 0�91∗∗∗ 0�31∗∗ 0�20 0�08Related diversification 0�58∗ 0�67 0�35 1�18 0�28 0�32 0�19 0�41 0�60+

Unrelated diversification −0�09 −0�10 −0�11 −0�22 −0�10 −0�26 −0�12 −0�01 0�05IT investment 0�02 1�64 1�61 −1�72 1�73 1�00 0�19 6�47 4�57Vertical integration −0�14IT investment× related 0�18∗∗ 41�78∗∗ 27�01∗∗ 63�66∗∗ 24�59∗∗ 23�23∗ 16�69∗∗ 89�38∗ 67�63∗

diversificationIT investment× unrelated 0�02 5�86 −1�14 37�39 −0�36 1�74 −2�67 −12�05 15�07

diversification

R2 0�45 0�45 0�44 0�30 0�45 0�41 0�39 0�55 0�51F 5�47∗∗∗ 5�40∗∗∗ 5�20∗∗∗ 4�66∗∗∗ 4�93∗∗∗ 4�20∗∗∗ 4�72∗∗∗ 8�89∗∗∗ 6�98∗∗∗

Notes. Unstandardized regression coefficients are reported. ∗p < 0�05, ∗∗p < 0�01, ∗∗∗p < 0�001, +p < 0�10, all tests are two tailed. Model 5 uses IT investmentper employee (instead of IT investment by sales). Model 6 uses Herfindahl measure of diversification (instead of entropy measure). Model 7 uses IT stock.Model 8 uses instrumental variable regression. Model 9 includes control for vertical integration. Model 10 uses performance for 1998 (instead of 1997).Model 11 controls for industry performance by subtracting industry average q from the dependent variable. Models 12 and 13 use data for 1995 and 1996,respectively (instead of 1997). The number of observations �N� for the robustness test models varied from a low of 107 to a high of 126 due to data availability.

not significant in Models 2 and 4. These coefficientsshould be interpreted with caution because they donot represent constant effects. Rather, they representthe conditional effects of the variables at the mean(s)of the variable(s) with which they interact (Aiken andWest 1991). Thus, the positive and significant coef-ficient for IT in Model 2 represents the conditionaleffect of IT on firm performance when total diversifica-tion is at its mean. The positive but insignificant coef-ficient for IT in Model 4 represents the conditionaleffect of IT on firm performance when both related diver-sification and unrelated diversification are at their respec-tive means. We speculate that the insignificant coeffi-cient for IT in Model 4 is because this represents theconditional effect for IT at the mean level of unrelateddiversification (and also related diversification) when, asour results show, unrelated diversification has no effecton the performance impact of IT. In Model 2, incontrast, where the IT coefficient represents the condi-tional effect at the mean of the observed total diversifi-cation values, regardless of their composition in termsof related and unrelated diversification, the insignificanteffect of unrelated diversification, it appears, is drownedout and dominated by the significant effect of relateddiversification.Similarly, the insignificant coefficients for the diver-

sification variables show that diversification does nothave a performance effect when IT investment is at itsmean. The positive and significant interaction effects

for IT with total diversification and related diversifica-tion, however, suggest that the performance impact ofsuch diversification increases with greater IT invest-ment, supporting the contention in the strategy lit-erature that adopting sophisticated coordination andcontrol mechanisms is important for realizing perfor-mance gains from diversification strategy (Hill et al.1992, Hill and Hoskisson 1987, Jones and Hill 1988).

5.1. Robustness of ResultsWe examined the robustness of our results tousing alternative measures and specifications. Table 3presents results of these robustness tests for themodel using the two disaggregated diversificationmeasures.4 Model 5 utilizes an alternative measure ofIT investment, IT investment per employee rather thanIT investment per dollar of sales. Acar and Sankaran(1999) have argued that, while entropy measures arepopular in strategic management research, Herfindahlmeasures enjoy certain properties which make themuseful alternatives. We therefore ran Model 6 utilizingHerfindahl measures of related and unrelated diversi-fication. Model 7 utilizes IT investment stock as theIT investment variable using the Dewan et al. (1998)approach of assuming that IT expenses create assets

4 We also ran the same robustness tests for the total-diversificationmodel and found that our results were robust. The table with theseresults is not included in the interest of space.

Chari, Devaraj, and David: Research Note: The Impact of IT Investments and Diversification Strategies232 Management Science 54(1), pp. 224–234, © 2008 INFORMS

with a service life of three years and using IT invest-ment data for the three years 1995 through 1997 to cre-ate a proxy for IT investment stock. Model 8 reportsresults using an instrumental variable approach toaddress potential endogeneity/simultaneity of keyvariables. Following Lev and Sougiannis’s (1996)approach, we use the respective industry averagesto create instruments for IT investment and relatedand unrelated diversification. Wu-Hausman tests indi-cate that ordinary least-squares regression coefficientsare appropriate (Wooldridge 2003). Model 9 includes acontrol for vertical integration. Model 10 uses Tobin’s qfor 1998 instead of 1997 to examine lagged perfor-mance effects. Model 11 utilizes an alternative way tocontrol for industry performance; in this model we sub-tract the industry average Tobin’s q from the depen-dent variable and exclude the industry performancecontrol used in the other models. Models 12 and 13utilize data for the years 1995 and 1996, respectively,to examine the robustness of our results across time.The results for the robustness tests, including the sig-nificance of the interaction terms, are consistent withour original results, confirming the robustness of ourresults across these alternative models.

6. DiscussionIn this note, we examined the performance payoffto IT investment in the context of corporate diver-sification. We find that the performance impact ofIT investment is greater for firms with greater levelsof diversification. We also find that the performanceimpact of IT investment is greater in related diver-sification than in unrelated diversification, reflectingthe greater economies of scope for IT investment andthe greater importance of IT-enabled coordination andcontrol in related diversification. In fact, our resultsshow that the performance impact of IT investmentdid not increase with the level of unrelated diver-sification, suggesting that economies of scope for ITinvestment and complementary value from enablingcoordination and control in unrelated diversification,if present at all, may be negligible.Our findings hold implications for management

research and practice. Prior research has noted thatdiversified firms invest more in IT (Dewan et al. 1998).Our findings help infer when greater IT investmentin diversification is justified and can thereby guidemanagers in their IT investment decisions. IncreasingIT investment to accompany a firm’s overall diver-sification, our findings suggest, may be justified bythe greater performance impact of such investments.Our findings also suggest that the type of diversifica-tion pursued will be relevant in justifying increasedIT investment. Specifically, whereas greater IT invest-ment to accompany diversification across related busi-nesses can be justified by the greater performance

impact of IT, greater IT investment to accompanydiversification across unrelated businesses cannot besimilarly justified. To scholars and policy makersinterested in the economic impact of IT, our findings,together with the continued dominance of diversifiedfirms in the economy and the decline of unrelateddiversification among the largest U.S. firms (Daviset al. 1994), suggest that the overall economic impactof corporate IT investments is likely to be positive.Limitations of our study are as follows. First, our

measure of IT investment was based on budgets andnot actual spending. Although many prior studieshave used budgeted figures for investments, this is alimitation that future research could address. Second,although the measures of related diversification used inthis study have been used extensively, they rely onan SIC classification system, which may not indicateall of the ways in which businesses may be related(Markides and Williamson 1996). Finally, firms in thestudy were those for which IT investment data wereavailable from Information Week. Although a signifi-cant body of IT literature has been established usingthese data, generalizability of these findings to otherfirms is open to scrutiny.There are many useful directions for further re-

search. We discuss two of them here. First, furtherresearch could shed light on whether certain typesof IT systems provide better coordination capabil-ity in diversified firms than others. It would also beuseful to investigate whether sharing and transfer-ring certain types of IT assets across businesses cre-ates a greater performance effect than others. Second,there is growing interest in multipoint competition,where a diversified firm initiates action in one busi-ness to affect competitive outcomes in another busi-ness (Gimeno 1999). Multipoint competition requiressophisticated systems to supply information neces-sary to make decisions in one business based oncompetitive situations in another. It will be use-ful to study the information system profiles of suc-cessful multipoint competitors, as these firms couldoffer case studies of advanced information technologyuse in support of agility and entrepreneurial action(Sambamurthy et al. 2003) within diversified firms.

AcknowledgmentsThe authors thank the senior editor, associate editor, andthree anonymous reviewers for their constructive commentsduring the review process.

Appendix. Measures

Industry-Level Control VariablesIndustry performance = ∑

MBiPi, where MBi = averagemarket to book value for industry i and Pi = proportionof firm’s sales in industry i. Data source: Compustat. Priorstudies: Bharadwaj et al. (1999).

Chari, Devaraj, and David: Research Note: The Impact of IT Investments and Diversification StrategiesManagement Science 54(1), pp. 224–234, © 2008 INFORMS 233

Industry capital intensity = ∑CiPi, where Ci = average

capital intensity for industry i (measured as total assets/sales) and Pi = proportion of firm’s sales in industry i. Datasource: Compustat. Prior studies: Bharadwaj et al. (1999)and Capon et al. (1990).

Industry concentration=∑CR4iPi, where CR4i = four-firm

concentration ratio for industry i and Pi = proportion offirm’s sales in industry i. Data sources: Census Bureau andCompustat. Prior studies: Bharadwaj et al. (1999).

Market uncertainty = ∑UiPi, where Ui = volatility of

industry i’s sales and Pi = proportion of firm’s sales inindustry i. Volatility of industry sales was measured usingthe approach suggested by Bergh (1998) and Keats and Hitt(1988) using industry sales data for the five year period 1991to 1996. Data sources: Industry sales data from the CensusBureau and the Bureau of Economic Analysis; Proportion offirm sales in each industry from Compustat. Prior studies:Bergh (1998) and Keats and Hitt (1988).

Market growth = ∑GiPi, where Gi = industry i’s sales

growth and Pi = proportion of firm’s sales in industry i.Industry sales growth was measured using the approachsuggested by Bergh (1998) and Keats and Hitt (1988) usingindustry sales data for the five year period from 1991 to1996. Data sources and prior studies are the same as formarket uncertainty.

Firm-Level Control VariablesFirm size: Firm size is measured as log (sales).Market share=∑

MSiPi, where MSi =market share of thefirm in industry i and Pi = proportion of firm’s sales inindustry i. Data sources: Industry sales data from the Cen-sus Bureau; Firm sales in industry and proportion of firmsales in industry from Compustat. Prior studies: Bharadwajet al. (1999).

Capital structure: Measured as the ratio of total liabilitiesto sales. Data source: Compustat. Prior studies: Hitt et al.(1997).

R&D intensity: Measured as the ratio of R&D expen-ditures to sales. Data source: Compustat. Prior studies:Bharadwaj et al. (1999).

Advertising intensity: Measured as the ratio of advertisingexpenditures to sales. Data source: Compustat. Prior stud-ies: Bharadwaj et al. (1999).

ReferencesAcar, W., K. Sankaran. 1999. The myth of the unique decomposabil-

ity: Specializing the Herfindahl and entropy measures? Strate-gic Management J. 20(10) 969–975.

Aiken, L. S., S. G. West. 1991. Multiple Regression: Testing and Inter-preting Interactions. Sage Publications, Newbury Park, CA.

Alpar, P., M. Kim. 1990. A microeconomic approach to the measure-ment of information technology value. J. Management Inform.Systems 7(2) 55–69.

Anderson, M. C., R. D. Banker, S. Ravindran. 2006. Value impli-cations of investments in information technology. ManagementSci. 52(9) 1359–1376.

Banham, R. 2004. Amazon finally clicks. CFO 20(4) 20–25.Barua, A., C. H. S. Lee, A. B. Whinston. 1996. The calculus of reengi-

neering. Inform. Systems Res. 7(4) 409–428.Baskerville, R. L., M. D. Myers. 2002. Information systems as a ref-

erence discipline. MIS Quart. 26(1) 1–14.

Belsley, D. A., E. Kuh, R. E. Welsch. 1980. Regression Diagnostics:Identifying Influential Data and Sources of Collinearity. Wiley, NewYork.

Bergh, D. D. 1998. Product-market uncertainty, portfolio restruc-turing, and performance: An information-processing andresource-based view. J. Management 24(2) 135–155.

Bettis, R. A. 1981. Performance differences in related and unrelateddiversified firms. Strategic Management J. 2(4) 379–393.

Bharadwaj, A. S., S. G. Bharadwaj, B. R. Konsynski. 1999. Informa-tion technology effects on firm performance as measured byTobin’s q. Management Sci. 45(6) 1008–1024.

Boal, K. B., J. M. Bryson. 1987. Representation, testing, and policyimplications of planning processes. Strategic Management J. 8(3)211–231.

Brynjolfsson, E., L. Hitt. 1996. Paradox lost? Firm-level evidence onthe returns to information systems spending. Management Sci.42(4) 541–558.

Capon, N., J. U. Farley, S. Hoenig. 1990. Determinants of finan-cial performance: A meta-analysis. Management Sci. 36(10)1143–1159.

Chung, K. H., S. W. Pruitt. 1994. A simple approximation ofTobin’s q. Financial Management 23(3) 70–74.

Clemons, E. K., M. C. Row. 1991. Sustaining IT advantage: The roleof structural differences. MIS Quart. 15(3) 275–292.

Collis, D. J., C. A. Montgomery. 1997. Corporate Strategy: Resourcesand the Scope of the Firm. Irwin, Chicago.

Davis, G. F., K. A. Diekmann, C. H. Tinsley. 1994. The declineand fall of the conglomerate firm in the 1980s: The deinstitu-tionalization of an organizational form. Amer. Sociol. Rev. 59(4)547–570.

Dess, G. G., R. D. Ireland, M. A. Hitt. 1990. Industry effects andstrategic management research. J. Management 16(1) 7–27.

Dewan, S., S. C. Michael, C. Min. 1998. Firm characteristics andinvestments in information technology: Scale and scope effects.Inform. Systems Res. 9(3) 219–232.

Dos Santos, B. L., K. Peffers. 1995. Rewards to investors in inno-vative information technology applications: First movers andearly followers in ATMs. Organ. Sci. 6(3) 241–259.

Dos Santos, B. L., K. Peffers, D. C. Mauer. 1993. The impact of infor-mation technology investment announcements on the marketvalue of the firm. Inform. Systems Res. 4(1) 1–23.

Galbraith, J. R. 1974. Organization design: An information process-ing view. Interfaces 4(3) 28–36.

Gimeno, J. 1999. Reciprocal threats in multimarket rivalry: Stakingout “spheres of influence” in the U.S. airline industry. StrategicManagement J. 20(2) 101–128.

Hair, J. F., R. E. Anderson, R. L. Tatham, W. C. Black. 1998. Multi-variate Data Analysis. Prentice Hall, Upper Saddle River, NJ.

Hill, C. W. L., R. E. Hoskisson. 1987. Strategy and structure in themultiproduct firm. Acad. Management Rev. 12(2) 331–341.

Hill, C. W. L., G. R. Jones. 2007. Strategic Management Theory: AnIntegrated Approach. Houghton Mifflin, Boston.

Hill, C. W. L., M. A. Hitt, R. E. Hoskisson. 1992. Cooperative ver-sus competitive structures in related and unrelated diversifiedfirms. Organ. Sci. 3(4) 501–521.

Hitt, L. M., E. Brynjolfsson. 1996. Productivity, business profitabil-ity, and consumer surplus: Three different measures of infor-mation technology value. MIS Quart. 20(2) 121–142.

Hitt, M. A., R. E. Hoskisson, H. Kim. 1997. International diversifi-cation: Effects on innovation and firm performance in product-diversified firms. Acad. Management J. 40(4) 767–798.

Im, K. S., K. E. Dow, V. Grover. 2001. Research report: A reexami-nation of IT investment and the market value of the firm—Anevent study methodology. Inform. Systems Res. 12(1) 103–117.

Chari, Devaraj, and David: Research Note: The Impact of IT Investments and Diversification Strategies234 Management Science 54(1), pp. 224–234, © 2008 INFORMS

Jarvenpaa, S. L., G. W. Dickson, G. DeSanctis. 1985. Methodologicalissues in experimental IS research: Experiences and recommen-dations. MIS Quart. 9(2) 141–156.

Jensen, M. C., W. H. Meckling. 1992. Specific and general knowl-edge, and organizational structure. L. Werin, H. Wijkander,eds. Contract Economics. Blackwell, Oxford, UK, 251–274.

Jones, G. R., C. W. L. Hill. 1988. Transaction cost analysis ofstrategy-structure choice. Strategic Management J. 9(2) 159–172.

Keats, B. W., M. A. Hitt. 1988. A causal model of linkages amongenvironmental dimensions, macro organizational characteris-tics, and performance. Acad. Management J. 31(3) 570–598.

Kohli, R., S. Devaraj. 2003. Measuring information technology pay-off: A meta-analysis of structural variables in firm-level empir-ical research. Inform. Systems Res. 14(2) 127–145.

Kotabe, M., S. S. Srinivasan, P. S. Aulakh. 2002. Multinationality andfirm performance: The moderating role of R&D and marketingcapabilities. J. Internat. Bus. Stud. 33(1) 79–97.

Lev, B., T. Sougiannis. 1996. The capitalization, amortization, andvalue-relevance of R&D. J. Accounting Econom. 21(1) 107–138.

Li, M., L. R. Ye. 1999. Information technology and firm perfor-mance: Linking with environmental, strategic, and managerialcontexts. Inform. Management 35(1) 43–51.

Loveman, G. W. 1994. An assessment of the productivity impact ofinformation technologies. T. J. Allen, M. S. Scott Morton, eds.Information Technology and the Corporation of the 1990s: ResearchStudies. MIT Press, Cambridge, MA, 84–110.

Mahmood, M. A., G. J. Mann. 2000. Special issue: Impacts of infor-mation technology investment on organizational performance.J. Management Inform. Systems 17(1) 3–10.

Markides, C. C., P. J. Williamson. 1994. Related diversification, corecompetences and corporate performance. Strategic ManagementJ. 15(5) 149–165.

Markides, C. C., P. J. Williamson. 1996. Corporate diversificationand organizational structure: A resource-based view. Acad.Management J. 39(2) 340–367.

Melville, N., K. Kraemer, V. Gurbaxani. 2004. Review: Informa-tion technology and organizational performance: An integra-tive model of IT business value. MIS Quart. 28(2) 283–322.

Montgomery, C. A. 1994. Corporate diversification. J. Econom. Per-spectives 8(3) 163–178.

Montgomery, C. A., B. Wernerfelt. 1988. Diversification, Ricardianrents, and Tobin’s q. RAND J. Econom. 19(4) 623–632.

Morrison, C. J. 1997. Assessing the productivity of informationtechnology equipment in U.S. manufacturing industries. Rev.Econom. Statist. 79(3) 471–481.

Mukhopadhyay, T., S. Rajiv, K. Srinivasan. 1997. Information tech-nology impact on process output and quality. Management Sci.43(12) 1645–1659.

Palepu, K. 1985. Diversification strategy, profit performance, andthe entropy measure. Strategic Management J. 6(3) 239–255.

Porter, M. E. 1979. How competitive forces shape strategy. HarvardBus. Rev. 57(2) 137–145.

Porter, M. E. 1987. From competitive advantage to corporate strat-egy. Harvard Bus. Rev. 65(3) 43–59.

Powell, T. C., A. Dent-Micallef. 1997. Information technology ascompetitive advantage: The role of human, business, and tech-nology resources. Strategic Management J. 18(5) 375–405.

Robins, J., M. F. Wiersema. 1995. A resource-based approach to themultibusiness firm: Empirical analysis of portfolio interrela-tionships and corporate financial performance. Strategic Man-agement J. 16(4) 277–299.

Sabherwal, R., Y. E. Chan. 2001. Alignment between business andIS strategies: A study of prospectors, analyzers, and defenders.Inform. Systems Res. 12(1) 11–33.

Sambamurthy, V., A. Bharadwaj, V. Grover. 2003. Shaping agilitythrough digital options: Reconceptualizing the role of infor-mation technology in contemporary firms. MIS Quart. 27(2)237–263.

Teece, D. J. 1982. Towards an economic theory of the multiproductfirm. J. Econom. Behav. Organ. 3(1) 39–63.

Thompson, J. D. 1967. Organizations in Action. McGraw-Hill, NewYork.

Vitale, M. R. 1986. The growing risks of information systems suc-cess. MIS Quart. 10(4) 327–334.

Weill, P., S. Aral. 2006. Generating premium returns on your ITinvestments. Sloan Management Rev. 47(2) 39–48.

Wooldridge, J. M. 2003. Introductory Econometrics. South-Western,Mason, OH.