PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

21

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH Abstract This paper examines the opportunities of diversification across the European (specifically Eurozone’s) stock exchange markets by using three econometric approaches: short-run correlation, long-run correlation and co-integration in 200 securities randomly obtained from several of capital markets. In the last section the interest is shifted from the econometrics to the real market conditions examining a case study, where a moderate investor choose either the constructed portfolios or 10-year of maturity German bonds. Name: IOANNIS KORKOS Tutor: THEODOROS PANAGIOTIDIS SEPTEMBER 2013

Transcript of PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

Abstract

This paper examines the opportunities of diversification across the

European (specifically Eurozone’s) stock exchange markets by using

three econometric approaches: short-run correlation, long-run

correlation and co-integration in 200 securities randomly obtained from

several of capital markets. In the last section the interest is shifted from

the econometrics to the real market conditions examining a case study,

where a moderate investor choose either the constructed portfolios or

10-year of maturity German bonds.

Name: IOANNIS KORKOS

Tutor: THEODOROS PANAGIOTIDIS

SEPTEMBER 2013

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

2

TABLE OF CONTENTS

INTRODUCTION ............................................................................................ 3

LITERATURE REVIEW .................................................................................. 5

METHODOLOGY ............................................................................................ 6

RESULTS ........................................................................................................ 9

CONCLUSION ............................................................................................... 16

BIBLIOGRAPHY .......................................................................................... 18

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

3

INTRODUCTION

A portfolio that diminishes risk for various levels of returns is defined as an efficient portfolio.

Low risk acts like an incentive for a construction of a diversified portfolio. Apparently,

investors aim to achieve high returns and manage risk. This can be achieved by combining

financial objects with low correlation.

The greater the riskiness of each individual asset and the degree of dependence among the

equities, the greater the total risk of the portfolio. Whereas the number of equities included in

a portfolio rise, the portfolio variance decline so much is necessary to achieve negative or low

positive correlations but when the number become larger, the variance levels off.

Diversification can be achieved in three ways: by choosing stocks across countries, selecting

stocks across industries or picking stocks across both countries and industries. When

investing globally, an international diversified portfolio appears less risky in comparison with a

typical domestic portfolio. Offsetting can be crucial for the diversification: stocks doing better

in one market would probably offset the losses of the securities doing worse in another

country.

However, if the markets are highly correlated the advantages of diversification will be

eliminated. Correlation is notorious as a measure used for estimating the relations between

pairs of securities. The lower the correlation of the securities with their home market, the

greater the benefits of diversifying.

Yet, these gains require from the international markets not to move in a lockstep and often

depend on how foreign and domestic stocks move together. The optimization of this

technique can only be achieved by investing on emerging and frontier markets as

international diversification can offer more investment choices combined with low fluctuations

in returns. Usually, due to exposure in global crisis and contagion, international portfolio

diversification only reduces risk in the medium or long term.

Over the last two decades, the majority of the emerging economies appear to be highly

correlated with the European stock exchange markets. Whilst, capital flows are not

constrained and taking into consideration the globalized and integrated markets, correlation

between securities is expected to increase. It is often argued that one effect of globalization

in the capital markets are the increased correlations between stocks.

In periods of non-crisis, markets appear to have lower but still positive correlations with the

global benchmarks. Yet, in periods of economic stagnation securities seem to be more

associated than ever before, appearing higher correlations. Additionally, in periods of high

downward volatility or crisis securities seem to be more correlated with their benchmarks.

As empirical analysis has already showed, the benefit of diversification seems to sink in

phases of downturn, whilst correlation between equities increases to peak at 1 when the

market breaks down.

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

4

Traditionally, correlation and cointegration were used in order to achieve portfolio

diversification. In previous decades the most popular tool in portfolio construction used to be

the correlation coefficient: however the recent years, cointegration emerged as a more

efficient method.

Correlation coefficient (symbolized as ρ) refers to comovements in returns and asset prices.

Though, ρ is subject to significant fluctuations due to its short-term nature. Correlation always

lies between +1 and -1. The more positive (negative) the ρ the more synchronous (opposite)

the connection between two assets.

However, correlation is considered to be a static measure (valid only for I(0) variables), often

offering misleading results as it fails to take into account the dynamic relations among the

securities. That means that portfolios constructed based on ρ would probably require

rebalancing in the medium or long term (creating severe transaction costs), because there is

nothing to ensure that the relation between the assets will be tight for long.

Cointegration analysis refers to comovements in asset prices in a long-term basis. This

method is not being affected of short term variances. In addition cointegration is capable of

distinguishing the relation between two assets into short and long-term relation.

The main benefit of using cointegration is that allows access to the whole set of information

given by the financial variables. This method is capable to interpret the long run performance

of the time series and can be used to model the dynamics of a system in short and long-run

basis, while correlation lacks of being stable.

Cointegration and correlation seems to be related. Though, high (low) cointegration does not

imply high (low) correlation and conversely. Bearing in mind that the use of cointegration

does not crowd-out the correlation method as a short-run tool, we can use a combination of

these techniques: short-term correlation for stock selection and cointegration for the portfolio

optimization.

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

5

LITERATURE REVIEW

Plethora of bibliography has been written until now, referring to the techniques of

diversification. From a quite theoretical level of presenting the portfolio diversification benefits

and opportunities to a rather deep empirical analysis aiming to the construction of diversified

portfolios.

However, there is not a significant amount of academic literature developed on the three approaches of diversification simultaneously let alone about the European stock markets. Using data from African stock exchange markets, Alagidede, Panagiotidis and Zhang (2011) estimate the contemporaneous and the long-run correlation coefficients between the African markets as also cointegrtation to examine in what degree these markets are integrated.

Furthermore, Solnik (1995) presents the benefits of international diversification in the risk

reduction. For the period 1965-1974, Solnik demonstrates that through international

diversification risk can be reduced to half as the number of the stocks increases, compared to

the American stocks’ behavior.

In addition, Moss and Thuotte (2013) argue that African markets offer rather good

opportunities of diversification. Yet, these benefits can only be exist in a short-term basis. In

long-term more and more capital will be moved to exploit that opportunities that in the end

these benefits will evaporate.

Moreover, some papers work only on the long-run correlation estimator and its applications.

Albuquerque (2005) develops an alternative approach of choosing the optimal time interval

selection and alignment criteria for the nonparametric long-run correlation coefficients.

Kanas and Ioannidis (2010) are using the nonparametric correlation coefficient in order to

measure the statistical relation between spot and forward rate.

Regarding on cointegration, Alexander and Dimitriou (2002) offer two trading strategies

based on the concept of cointegration: the classic index tracking strategy and the long-short

market equity strategy. Similarly, Dunis and Ho (2005) use the same strategies in order to

build portfolios with European assets. Additionally, Alexander (1999) mobilizes cointegration

method in developing a model used for hedging activities worldwide.

Finally, Caldeira and Moura (2012) employ cointegration in order to locate the appropriate

stocks for the composition of a diversified portfolio from the Brazilian stock market.

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

6

METHODOLOGY

This project aims to examine which of the three methods: short-term correlation, long-term

(nonparametric) correlation and cointegration are more effective in the construction of a

diversified portfolio. By the term of diversified portfolio, is meant a portfolio that minimizes risk

(standard deviation or sigma) for various levels of returns.

First of all, daily close prices of 200 stocks from European stock exchange markets (Lisbon,

Paris, Berlin, Athens, Frankfurt, Milan, Amsterdam etc.) have been randomly obtained from

the yahoo financial website1 daily for 6 years, from the period January 2007 to December

2012. Missing observations were replaced with NA (not available) and close prices from all

the stock exchange markets were perfectly synchronized with the 1562 dates. In a true

trading environment distortions would have been created, if the closing prices were slightly

non-synchronous.

Secondly, daily returns of the 200 stocks were calculated2. Each portfolio constructed above

contains 40 equally weighted stocks. The advantage of this process is that by choosing the

European stock exchange markets, all the securities are denominated in a common currency,

the euro, staying away from exchange rate fluctuations.

This section is separated in three parts. The first part contains the methodology of estimating

the short-term correlation coefficient. Then, in the second part, the long-term correlation

coefficient is assessed. In the last part close prices time series are being cointegrated.

Short-term correlation

Correlation coefficient (symbolized as ρ) refers to comovements in returns and asset prices.

Though, ρ is subject to significant fluctuations. The main characteristic of this correlation is

the short-term behavior. The more frequent the fluctuations in the asset prices the more

frequent the variations in the correlation coefficient.

The time series of close prices of the stocks were imported in EVIEWS program and a table

with the correlation coefficients of all the pairs of stocks was exported in EXCEL. Then, ρ

were sorted from the most negative to positive, with every ρ corresponding to a pair of

stocks.

After that, stocks were sorted from these with the most negative ρ to these with the less

negative or positive ρ. Finally, five portfolios were constructed with 40 stocks each. The first

portfolio contains the stocks with the most negative ρ, whilst the fifth contains the stock with

the less negative or positive ρ.

The same procedure has been followed for the time series of the returns of the stocks. Five

portfolios were constructed too.

1 http://finance.yahoo.com/

2 ( Pt+1 – Pt)/ Pt

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

7

Finally, the close prices and the returns of each portfolio were calculated as also the average

return, the variance, the standard deviation, the skewness and the kurtosis.

Long-term correlation

Long-run correlation estimators are frequently used in economics (assessing the relations

between monetary and real variables) as also in finance (in the study of stock returns). Long-

run correlation is a non-parametric estimator, not appearing misspecification problems.

This part of the project is based on the article “Optimal Time Interval Selection in Long-Run

Correlation Estimation” (2005) written by Mr. Professor Pedro H. Albuquerque, Associate

Professor at the KEDGE Business School. Mr. Professor has developed a Long-Run

Correlation Estimator Code for EVIEWS3, this code calculates pairwise nonparametric long-

run correlation coefficients by using the optimal time interval selection and alignment criteria,

as described in "Optimal Time Interval Selection in Long-Run Correlation Estimation".

A similar process as in the sort-term correlation has been followed: long-term correlation

coefficients (symbolized as λ) have been gauged both for the close prices of the 200 stocks

and for the returns too. The contribution of Mr. Albuquerque at this point was crucial. Then

two tables were exported in EXCEL and the stocks have been sorted from the most negative

to less negative or positive.

Five portfolios were constructed with 40 stocks each for the close prices and the returns of

the stocks respectively: the first portfolios contain the stocks with the most negative λ, whilst

the fifths contain the stock with the less negative or positive λ.

At last average return, variance, standard deviation, skewness and kurtosis were estimated

after the construction of each portfolio based on the close prices and the returns.

Cointegration

The last decade, the method of cointegration has been a rather popular approach of

diversification among financial analysts and econometricians. They often use this method in

order to implement a long-short plan with would lead to the expected returns and low

correlation with the market.

Cointegration refers to comovement in asset prices and it is considered to be a great

statistical technique, allowing the application of simple estimation methods (OLS, maximum

likelihood) into non-stationary variables. That is the innovation of this method: the usage of

non-stationary data in comparison with other methods.

3 Source: http://www.pedrohalbuquerque.net/research.htm#codes . The Professor attempted to estimate the

long-run correlation coefficients for us, since we were doubtful whether the code is capable of managing so many data.

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

8

The time series of the close prices of the stocks have been imported in EVIEWS and tau-

statistics (symbolized as τ) were calculated for each pair of stocks manually using the Engle-

Granger cointegration test4 taking into account the ADF adjustment. Thus, a table has been

created in EXCEL containing the tau statistics.

Once again, stocks have been classified, this time from the most positive to negative and five

portfolios were constructed. Τhe first portfolio contains the stocks with the most positive τ,

whilst the fifth contains the stock with the less positive or negative τ.

Finally, the close prices of each portfolio were calculated as also the average return, the

variance, the standard deviation, the skewness and the kurtosis.

4 Engle, R.F. and C.W.J. Granger (1987), “Cointegration and Error-Correction:

Representation, Estimation, and Testing”, Econometrica 55

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

9

RESULTS

There are considered to be some basic statistics, describing the behavior of a portfolio.

These statistics are average return, variance and standard deviation. Yet, in this project

skewness and kurtosis have been also estimated.

The results of each method of diversification are presented above.

Short-run correlation

As already mentioned, in the short-term correlation two groups of portfolios were constructed.

One based on the close prices of the stocks and the other one based on stocks’ returns.

Here are the statistical measures, estimated on the close prices:

Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Portfolio 5

RETURN 0,1646 0,0328 0,1906 -0,0121 0,1241

VARIANCE 165,7219 80,2366 47,8006 14,6791 15,1004

STANDARD

DEVIATION

12,8733 8,9575 6,9138 3,8313 3,8859

SKEWNESS -0,3965 -0,8749 -0,8332 -0,7156 1,6663

KURTOSIS -0,1885 -0,1614 0,6224 0,2085 15,1250

To begin with, several fluctuations are noticed in the portfolios’ returns. The third one results

the highest return, when the forth one appears negative return. Quit high return also attains

the first portfolio.

Standard deviation (sigma), measures risk. In the first portfolio, which contains the stocks

with the more negative correlation, sigma is 12,873. Next, the sigma declines steadily to

reach 3,8 at the fourth and fifth portfolio.

Furthermore, the distribution of the first four portfolios appears slightly negative skewness.

This means that data spread out more to the left of the distribution. In the fifth portfolio

skewness appears to be positive and quite enough above zero: close prices spread more to

the right of the average mean.

Finally, kurtosis (sometimes referred as volatility of volatility) describes the trends of the

distribution. Since kurtosis in the first four portfolios is very close to zero, the distribution

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

10

approaches the normal distribution. In contrast with the fifth portfolio, where the distribution is

leptokurtic with higher peaks around the mean as also thick tails.

To continue with, now we present the table of the statistical measures assessed on portfolios

returns.

Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Portfolio 5

RETURN 0,0010 0,0011 0,0020 0,0008 0,0011

VARIANCE 0,0002 0,0002 0,0002 0,0002 0,0002

STANDARD

DEVIATION

0,0140 0,0127 0,0134 0,0143 0,0158

SKEWNESS 6,7103 1,4327 1,1610 0,3400 0,8775

KURTOSIS 116,2840 13,2800 19,1535 5,9526 12,9013

Portfolio returns range from 0,08% to 0,2%, not appearing negative returns. Standard

deviation fluctuates slightly from 1,27% in the second portfolio reaching 1,43% in the forth

portfolio and peaking at 15,8% in the fifth portfolio.

Moreover, skewness appears to be positive in all of the fifth portfolios. From very close to

zero in portfolios 4 and 5 to 6,71 in the first portfolio meaning that returns spread out more to

the right of the distribution. Finally, kurtosis being positive in all portfolios led to a leptokurtic

distribution.

Long-run correlation

Similarly, as mentioned in the methodology, in the long-run nonparametric correlation two

groups of portfolios were constructed. One based on the close prices of the stocks and the

other one based on stocks’ returns.

The statistical measures for the portfolios contain close prices are given in the table above:

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

11

Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Portfolio 5

RETURN 0,996 -0,374 -0,109 0,095 -0,086

VARIANCE 270,968 108,598 22,365 57,959 53,458

STANDARD

DEVIATION

16,461 10,421 4,729 7,613 7,312

SKEWNESS 0,580 0,462 0,909 -0,988 4,427

KURTOSIS -0,520 0,013 3,036 1,938 48,996

Portfolios based on the long-run correlation estimator appear to have positive as well as

negative returns. Return of the second portfolio slumps to -0,374 in contrast with the first

portfolio which achieve rather high return about 0,996. Standard deviation fluctuates from

16,46 in the first portfolio to decline at 4,73 in the fourth.

In addition, skewness of the portfolios is very close to zero approaching the normal

distribution, except of the fifth portfolio which appears high positive skewness with close

prices spread out more to the right of the average mean. Finally, all the portfolios except the

first one appear being leptokurtic from the second one very close to zero to the fifth one

having leptokurtic distribution with higher peaks around the mean.

The next table contain the statistical measures for the portfolios constructed based on the

returns of the stocks.

Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Portfolio 5

RETURN 0,0022 0,0007 0,0008 0,0012 0,0011

VARIANCE 0,0003 0,0001 0,0002 0,0002 0,0206

STANDARD

DEVIATION

0,0163 0,0119 0,0124 0,0155 0,1435

SKEWNESS 4,8260 -0,1165 1,6807 0,9344 1,7713

KURTOSIS 66,8428 4,0506 30,8187 9,1686 35,1816

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

12

Portfolio returns range between 0,07% of the second portfolio to 0,22% of the first portfolio.

The highest standard deviation appears in the first portfolio about 1,63% , when the second

portfolio seems to be the least risky of all.

Furthermore, the first portfolio appears positive skewness with the returns spread out the

right side of the distribution as also do the third, the forth and the fifth but more weakly. To

end up with kurtosis, all the portfolios have leptokurtic distribution with the first one having the

higher peaks around the mean.

Cointegration

Cointegration method has also followed in the methodology and with the Engle-Granger test:

five portfolios have been made based on the close prices. The results are presented above.

Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Portfolio 5

RETURN -0,355 0,016 0,051 0,499 0,384

VARIANCE 63,341 40,116 100,925 101,072 57,436

STANDARD

DEVIATION

7,961 6,336 10,049 10,057 7,581

SKEWNESS 1,265 -0,375 -0,918 0,094 -0,377

KURTOSIS 1,947 8,583 -0,091 -0,422 1,015

The first portfolio has negative returns in contrast with the other four appearing to have less

or more positive returns. Firstly, standard deviation swings from 7,96 in the first portfolio to

6,33 in the second, rising up at in the third and forth and decline at the fifth.

Finally, except of the first portfolio, all the other tend to approach a normal distribution, as

they have skewness very close to zero. The second portfolio appears to be the most

leptokurtic, with higher peaks concentrated around the mean.

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

13

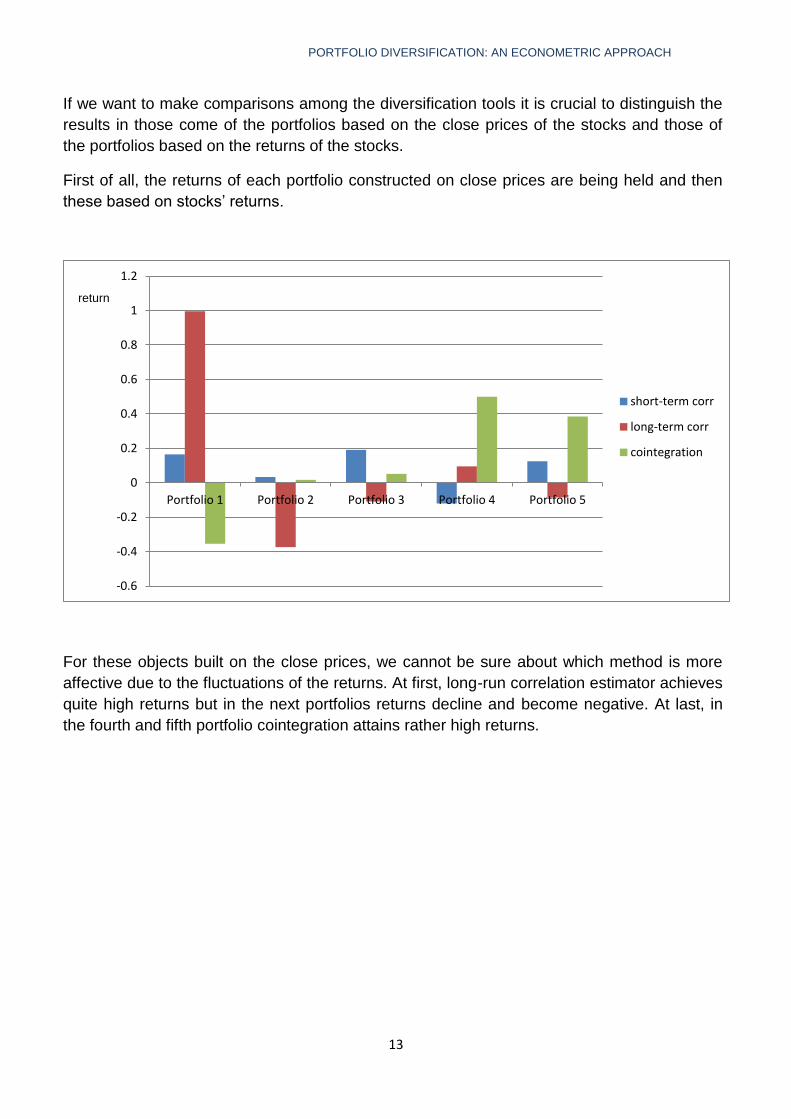

If we want to make comparisons among the diversification tools it is crucial to distinguish the

results in those come of the portfolios based on the close prices of the stocks and those of

the portfolios based on the returns of the stocks.

First of all, the returns of each portfolio constructed on close prices are being held and then

these based on stocks’ returns.

For these objects built on the close prices, we cannot be sure about which method is more

affective due to the fluctuations of the returns. At first, long-run correlation estimator achieves

quite high returns but in the next portfolios returns decline and become negative. At last, in

the fourth and fifth portfolio cointegration attains rather high returns.

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

1.2

Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Portfolio 5

short-term corr

long-term corr

cointegration

return

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

14

0

0,0005

0,001

0,0015

0,002

0,0025

Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Portfolio 5

short-term corr

long-term corr

To continue with portfolios made on stocks’ returns, long-term correlation appears to reach

higher returns, but only in the first portfolio, in the next two short-term correlation estimators

achieve relatively high returns. In the fifth one, the two methods reach the same return.

On the next diagram, standard deviations (symbolized as σ) are illustrated for the five

portfolios, based on the close prices, for each diversification method.

0

2

4

6

8

10

12

14

16

18

Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Portfolio 5

short-term corr

long-term corr

cointegration

standard

deviation

return

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

15

To begin with, long-run correlation seems to appear the highest σ to the first two portfolios

when cointegration attains quite high σ to the last three. Standard deviation based on short-

run correlation decline steadily to stabilize at the last two portfolios.

Then, the portfolios built according the stock returns appear standard deviations represented

above.

Standard deviation related to the short-run correlation estimator seems to be quite weak,

lower than 2% in the first four portfolios but in the fifth one, σ based on the long-run

correlation booms sharply.

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

Portfolio 1 Portfolio 2 Portfolio 3 Portfolio 4 Portfolio 5

short-term corr

long-term corr

standard

deviation

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

16

CONCLUSION

Researchers, financial analysts and econometricians argue that a monetary union, like the

Eurozone tends to diminish the gains of diversification mainly due to the stock market

integration. The tighter the relation between the European economies the weaker the benefits

of diversification. Frankel and Rose (1998) advocate that by the time a country enters in a

monetary union, the stock markets appear to be more correlated than ever before.

When examining the advantages of the diversification methods in the Eurozone’s stock

exchange markets we were doubtful about how adequate these benefits would be.

This argument lies on the method of calculating the Sharpe Ratio5. This ratio gives us the

excess return for each unit of risk in comparison with the risk free return. The greater the

Sharpe ratio the better deal with the risk.

Suppose we have an investor, who is neither risk-lover nor risk-averse, but moderate. He has

two options. The first one is to invest his money on the portfolios constructed above. The

second one is to invest his money on 10-year of maturity German bonds with return about

1,941.6

In the tables above the Sharp ratios for each method of diversification are being represented

as also for each portfolio, firstly for those based on the close prices and then for those based

on the returns.

Sharpe ratios Portfolio 1 Portfolio2 Portfolio 3 Portfolio 4 Portfolio 5

short-run correlation -0,138 -0,213 -0,253 -0,510 -0,468

long-run correllation -0,057 -0,222 -0,433 -0,242 -0,277

cointegration -0,288 -0,304 -0,188 -0,143 -0,205

5 Sharpe Ratio = (rp – rf)/σp , where rp is the return of the portfolio, rf the return of a risk free asset and σp the

standard deviation of the portfolio, known as risk. 6 Source http://gr.investing.com/rates-bonds/germany-10-year-bond-yield (visited on 4/9/2013).

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

17

In the two tables held above all the Sharpe ratios are negative. That means that the risk-less

equity would perform better than the portfolios built on the European stock exchange

markets.

In our case study, the investor would definitely choose to invest in the German bonds, as

their offer quite high returns (compared to our portfolios), for zero risk.

Diversifying across European stock exchange markets (especially in the Eurozone) does not

seem to be a very profitable process. Either short-run correlation or long-run correlation or

the cointegration does not offer sufficient investment opportunities. High returns can be

attained through the construction of the portfolios based on the close prices, but also the

quite high standard deviations cannot be ignored.

Globalization, market integration as also the common currency would apparently eliminate

any opportunities. Traditionally, during periods of economic and financial integration, markets

tend to reach extremely high (near to +1) correlations.

Investors seem to be possessed of confusion: one the one hand they want to reach high

returns and tend to look for secluded stock markets, which will not be related to the global

markets. On the other hand they are afraid of dispersing their money across regions.

Diversification can only benefit investors in a short term basis. Once a capital market

becomes notorious for offering quite high returns, capitals from other markets will flow

together in that market and in the long term any gain will evaporate. Then, investors will

search for a new effective capital market etc.

Sharpe ratios Portfolio 1 Portfolio2 Portfolio 3 Portfolio 4 Portfolio 5

short-run

correlation

-138,144 -152,825 -144,821 -135,648 -123,141

long-run

correllation

-118,753 -162,892 -156,575 -125,144 -13,514

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

18

BIBLIOGRAPHY

Adam, K., Jappelli, T., Menichini A., Padula M., & Pagano M. (2002). Analyse, Compare, and Apply

Alternative Indicators and Monitoring Methodologies to Measure the Evolution of Capital Market

Integration in the European Union, Centre for Studies in Economics and Finance (CSEF), Department

of Economics and Statistics, University of Salerno.

Alagidede, P., Panagiotidis, P., & Zhang X. (2011). Why a diversified portfolio should include African

assets, Applied Economics Letters, 18:14, 1333-1340.

Albuquerque, P. H. (2008). Optimal Time Interval Selection in Long-Run Correlation Estimation, Mimeo, Texas A&M International University, Laredo, TX. Alexander, C. (1999). Optimal Hedging using Co-integration, Philosophical Transactions of the Royal Society, London, Series A 357, pp. 2039-2058. Alexander, C. (1998). Volatility and Correlation: Measurement, Models and Applications, Risk Management and Analysis: Measuring and Modeling Financial Risk, Wileys. Alexander, C. (1999). Cointegration and correlation in energy markets, Managing Energy Price Risk, 2nd edition, Chapter 15, pp. 291-304. Risk Publications. Alexander, C., & Dimitriu, A. (2002). The Cointegration Alpha: Enhanced Index Tracking and Long-Short Equity Market Neutral Strategies, ISMA Discussion Papers in Financial 2002-08, ISMA Centre, University of Reading. Alexander, C., & Dimitriu, A. (2005). Indexing, cointegration and equity market regimes, International Journal of Finance and Economics, 10, 213–231. Alexander, C., Giblin I., & Weddington W. (2001). Cointegration and Asset Allocation: A New Active Hedge Fund Strategy, ISMA Center Discussion Papers in Finance 2001-03. Alexander, C. (1995) ‘Common volatility in the foreign exchange market’, Applied Financial Economics, 5, 1-10. Aslanidis, N., & Savva, C. (2011). Are there still portfolio diversification benefits in Eastern Europe? Aggregate versus sectoral stock market data, The Manchester School, Volume 79, Issue 6, pages 1323–1352. Benninga, S. (2008). Financial Modeling, The MIT Press, Cambridge, Chapters 10, 12, 33. Benninga, S. (2005). Principles of Finance with Excel, Oxford University Press, 2nd Edition, Chapters 10, 11, 12, 13. Brealey, R., & Myers, S. (2003). Principles of Corporate Finance, The MacGraw-Hill Companies, 7th edition, Chapters 4, 7, 8. Bugar G., & Maurer, R. (2002). International Portfolio Diversification for European Countries: The Viewpoint of Hungarian and German Investors, ASTIN BULLETIN, Vol. 32, No. 1, 2002, pp. 171-197. Caldeira, J., & Moura. G. (2012). Selection of a Portfolio of Pairs Based on Cointegration: The Brazilian Case, Economic Bulletin, 2 March 2012.

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

19

Chua, T. C., Lai, S., & Lewis K. (2010). Are the Gains from Foreign Diversification Diminishing? Assessing the Impact with Cross-listed Stocks, The National Bureau of Economic Research, NBER Working Paper No. 18627. Danthine, J., P., Giavazzi, F., & Thadden E. L. (2000). European Financial Markets After EMU: A First Assessment, The National Bureau of Economic Research, NBER Working Paper No 8044. Dunis, C., & Ho, R., (2005). Cointegration Portfolios of European Equities for Index Tracking and Market Neutral Strategies, Journal of Asset Management, Volume 6, Number 1, 1 June 2005 , pp. 33-52. Embrechts, P., McNeil, A., & Straumann, D. (1998). Correlation and Dependency in Risk Management: Properties and Pitfalls in ‘Risk Management: Value at Risk and Beyond, edited by M. A. H. Dempster, Cambridge University Press, pp. 176-237. Engle, R. F., &Granger, C. W. J. (1987). Cointegration and Error-Correction: Representation, Estimation, and Testing, Econometrica 55. Flavin, T., Hurley, M., & Rousseau, F. (2002). Explaining Stock Market Correlation: A Gravity Model Approach, The Manchester School, Volume 70, Issue S1, pages 87–106. Frankel, J. A., and. Rose, A. K. (1998). The endogeneity of the optimum currency area criteria, The Economic Journal 108, 1009-1025. Goetzmann, W., Li, L., & Rouwenhorst, G. (2001). Long-Term Global Market Correlations, The National Bureau of Economic Research, NBER Working Paper No. 8612. Hourvouliades, N. (2009). International Portfolio Diversification: Evidence from European Emerging Markets’, European Research Studies, Volume XII, Issue 4. Jorion, P. (1992). Portfolio Optimization in Practice, Financial Analysts Journal, Jan/Feb 1992, 48. Kanas, A., & Ioannidis, C. (2012). Revisiting the forward—spot relation: an application of the nonparametric long-run correlation coefficient, Journal of Economics and Finance, January 2012, Volume 36, Issue 1, pp 148-161. Lewis, K. (2012). Global Stock Market Linkages Reduce Potential for Diversification, Economic Letter: Insights from the Federal Reserve Bank of Dallas, Vol. 7, No. 2, February 2012. Marshall, C., & Siegel, M. (1996). Value-at-Risk: Implementing a Risk Measurement Standard’, 96-47, available at SSRN: http://dx.doi.org/10.2139/ssrn.1212.

McNeil, A., Frey, R., & Embrechts, P. (2005). Quantitative Risk Management: Concepts, Techniques and Tools, Chapter 7, pp. 283-351.

Moss, T., & Thuotte, R. (2013). Nowhere Left to Hide? Stock Market Correlation, Regional Diversification, and the Case for Investing in Africa, Working Paper 316, March 2013, the Center for Global Development.

Obstfeld, M. (1994). Risk-Taking, Global Diversification, and Growth, The American Economic Review, Vol. 84, No. 5, pp. 1310-1329.

Solnik, B. (1974). Why Not Diversify Internationally Rather Than Domestically, Financial Analysts Joumal, Vol. 30, No. 4.

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

20

Stangă, E., Anghel, F., & Avrigeanu, A. (2010). The Long – Short Strategy Based on Cointegration Concept, Romanian Economic and Business Review, Vol. 5, No. 1.

Tjostheim, D., & Hufthammer, K. (2013). Local Gaussian correlation: A new measure of dependence’, Journal of Econometrics, Volume 172, Issue 1, pp. 33–48.

PORTFOLIO DIVERSIFICATION: AN ECONOMETRIC APPROACH

21