Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm...

39

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? Carmona, Kahlil Marion H. De La Salle University, 2401 Taft Avenue, Manila, Philippines, E-mail: [email protected] Shi, Ailyn A. De La Salle University, 2401 Taft Avenue, Manila, Philippines, E-mail: [email protected] Tan, Alexis Georgette L. De La Salle University, 2401 Taft Avenue, Manila, Philippines, E-mail: [email protected] A common feature of the corporate sector of emerging markets like the Philippines is the prevalence of family-controlled conglomerates. This paper explores the effects of corporate diversification on firm value, particularly among family-controlled firms. Using firm-level data on 113 corporations that are listed in the Philippine Stock Exchange, we employ a generalized least squares random effects model to determine the effects of diversification behavior on firm value. We find that family owners play a significant role in moderating total diversification performance – said diversification tends to go beyond the optimal level, which reduces firm value. By further decomposing total diversification into its unrelated and related forms, we also find that most conglomerates are inclined to diversify to unrelated industries. With such findings, we assert that significant caution must be placed upon the use of unrelated corporate diversification among family firms due to the negative effects brought about by family entrenchment upon firm value. JEL Classification: G34, M14, G30 Keywords: Corporate Governance; Family Altruism; Diversification; Firm Value I. INTRODUCTION Family-controlled conglomerates are rapidly becoming the norm within the corporate sector, as can be gleaned from the literature. For instance, Shleifer and Vishny (1997) note that a lot of corporations around the world, including parts of Europe and East Asia, have controlling owners who may be the founders, themselves, or their offspring. In the Philippines, alone, Aquino (2003) asserts that influential families, such as the Aboitizes and Gokongweis, are the brains behind corporations that dominate the modern- day Philippine industry. Consistent with this is the finding of Claessens et al. (2000) that more than half of the local economy’s corporate assets are controlled by the country’s ten richest families. 1 In the case of the Philippine corporate sector, Figure 1.1 highlights the percentage of family ownership for Philippine Stock Exchange (PSE) firms from years 2008 to 2012, where controlling family ownership is seen to increase, albeit at a decreasing rate, throughout the five-year period. 1 Claessens and Fan (2003) have extensively delineated the unique ownership structure inherent in most Asian firms. A typical Asian corporation serves as the nexus for several more business groups, either public or private or both – all affiliated with a single family who holds most of the shares. This case is very much unlike companies in the Western region where shares are diffusely held. For a more substantial view on the case concerning firm ownership structures in several Asian countries, see Claessens et al. (2000). Figure 1.1. Family Ownership Families are theorized by the literature to be inclined towards entrenching themselves within the firm’s hierarchical structure due to psychological, rather than logical, reasons. The pressing need to maintain good family ties induces family owners to bequeath firm executive positions to kin (Karra et al., 2006). Furthermore, the welfare of the succeeding generations is accounted for through the creation of a succession plan involving the firm (Lien and Li, 2013). Thus, the nuances of diversification as a means of furthering family altruism and entrenchment have been widely explored. Aside from benefits pertaining to prolonged firm life and higher profits, it has been posited that the family legacy that is tied to the firm motivates such companies to diversify and, thus, attain improved firm value. However, it has also been 41.7205 41.721 41.7215 41.722 41.7225 41.723 41.7235 41.724 41.7245 41.725 41.7255 2008 2009 2010 2011 2012 Percentage of Family Ownership Year

Transcript of Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm...

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value?

Carmona, Kahlil Marion H. De La Salle University,

2401 Taft Avenue, Manila, Philippines, E-mail: [email protected]

Shi, Ailyn A. De La Salle University,

2401 Taft Avenue, Manila, Philippines, E-mail: [email protected]

Tan, Alexis Georgette L. De La Salle University,

2401 Taft Avenue, Manila, Philippines, E-mail: [email protected]

A common feature of the corporate sector of emerging markets like the Philippines is the prevalence of family-controlled conglomerates. This paper explores the effects of corporate diversification on firm value, particularly among family-controlled firms. Using firm-level data on 113 corporations that are listed in the Philippine Stock Exchange, we employ a generalized least squares random effects model to determine the effects of diversification behavior on firm value. We find that family owners play a significant role in moderating total diversification performance – said diversification tends to go beyond the optimal level, which reduces firm value. By further decomposing total diversification into its unrelated and related forms, we also find that most conglomerates are inclined to diversify to unrelated industries. With such findings, we assert that significant caution must be placed upon the use of unrelated corporate diversification among family firms due to the negative effects brought about by family entrenchment upon firm value. JEL Classification: G34, M14, G30 Keywords: Corporate Governance; Family Altruism; Diversification; Firm Value I. INTRODUCTION

Family-controlled conglomerates are rapidly becoming the norm within the corporate sector, as can be gleaned from the literature. For instance, Shleifer and Vishny (1997) note that a lot of corporations around the world, including parts of Europe and East Asia, have controlling owners who may be the founders, themselves, or their offspring. In the Philippines, alone, Aquino (2003) asserts that influential families, such as the Aboitizes and Gokongweis, are the brains behind corporations that dominate the modern-day Philippine industry. Consistent with this is the finding of Claessens et al. (2000) that more than half of the local economy’s corporate assets are controlled by the country’s ten richest families.1 In the case of the Philippine corporate sector, Figure 1.1 highlights the percentage of family ownership for Philippine Stock Exchange (PSE) firms from years 2008 to 2012, where controlling family ownership is seen to increase, albeit at a decreasing rate, throughout the five-year period.

1 Claessens and Fan (2003) have extensively delineated the unique ownership structure inherent in most Asian firms. A typical Asian corporation serves as the nexus for several more business groups, either public or private or both – all affiliated with a single family who holds most of the shares. This case is very much unlike companies in the Western region where shares are diffusely held. For a more substantial view on the case concerning firm ownership structures in several Asian countries, see Claessens et al. (2000).

Figure 1.1. Family Ownership

Families are theorized by the literature to be inclined

towards entrenching themselves within the firm’s hierarchical structure due to psychological, rather than logical, reasons. The pressing need to maintain good family ties induces family owners to bequeath firm executive positions to kin (Karra et al., 2006). Furthermore, the welfare of the succeeding generations is accounted for through the creation of a succession plan involving the firm (Lien and Li, 2013). Thus, the nuances of diversification as a means of furthering family altruism and entrenchment have been widely explored. Aside from benefits pertaining to prolonged firm life and higher profits, it has been posited that the family legacy that is tied to the firm motivates such companies to diversify and, thus, attain improved firm value. However, it has also been

41.7205 41.721

41.7215 41.722

41.7225 41.723

41.7235 41.724

41.7245 41.725

41.7255

2008 2009 2010 2011 2012

Perc

enta

ge o

f Fam

ily O

wner

ship

Year

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 2 suggested that over-diversification may generate counter-effects.

In developing economies, firm diversification tends to include a wide range of activities; i.e., firms extend their businesses to industries, which are not technologically related to their original core activities (Ungson, Steers, and Park, 1997). Scholars have tried to determine the optimal level of firm diversification where marginal cost is equal to marginal benefit. Despite the threats presented by over-diversification, many companies simply diversify beyond the optimal level; thus, destroying shareholders’ wealth (Martin and Sayrak, 2003).

In the Philippine context, where diversified family-based conglomerates dominate the corporate sector (Aquino, 2003), it has been noted that most of these firms started out in a particular core activity. For instance, the Ayala Corporation’s initial business revolves around land development. The Aboitiz Group started out as a shipping company, which used to transfer goods within the Visayas region. Henry Sy’s famous success story commenced from a small shoe store in Quiapo, Manila; said business prospered and soon became SM Investments Corporation. Other examples include San Miguel Corporation’s brewery and JG Summit Holdings’ cornstarch production.

Such firms have diversified into various activities – only some of which are related to the original core business. From their initial land business, the Ayala Corporation has since delved into financial (e.g. Bank of the Philippine Islands) and telecommunications services (i.e. Globe Telecoms). Nowadays, Aboitiz Group has power generation (e.g. Visayas Electric Company) and food production (i.e. Pilmico Foods Inc.). Even SM Prime Holdings has diversified into real estate development (i.e. SM Development Corporation) and financial services (e.g. Banco de Oro Unibank).

Accounts of further diversification pursuits in the local setting abound. Dumlao (2012) writes about JG Summit’s sale of P3.2 billion worth of shares. The company, thriving under the lead of the Gokongweis, has found the need to sell its company’s shares in order to diversify their investor base and, thus, be better suited to handle the increasing market demand. Aside from its engagement with the food, airline, property, banking, and petrochemical industries, the conglomerate is once again the focus of attention, as it also takes part in the gaming and tourism sectors.

Moreover, Aboitiz Equity Ventures, Inc. has been reported to venture into water distribution. Its other joint ventures will consist of the Mactan International Airport construction and the production of bio-methane fuel. It was reported that the company’s net income reached P6.8 billion in the first quarter of 2013 wherein the largest contribution can be traced back to the firm’s power sector (Austria, 2013).

Like other diversified conglomerates, San Miguel Corporation awaits the outcome of its diversification activities, such as the construction of the Tarlac-Pangasinan-La Union Expressway and the expansion of the Boracay Airport. Montealegre (2013) discloses that said conglomerate’s new businesses already account for 70% of the corporation’s P699 billion worth of revenues for 2013. Other business groups have also followed suit.

There are only a few studies on how the diversification phenomenon affects firm variables in the Philippines. Gutierrez and Rodriguez (2013) find evidence on the inclination of the largest locally-based conglomerates – most of which are family-controlled firms – to diversify to unrelated, as opposed to related, industries. However, the impact of unrelated or related diversification on firm value has not been accounted for in their study. Aquino (2003) investigates diversification effects on the value of Philippine firms and reports mixed results; however, his study did not account for family altruism effects on firm value. Thus, there is also a need to empirically substantiate the tenuous connection between firm value and family altruism, as characterized by higher controlling family ownership for firms.

The main theories of this study revolve around two equally corroborative presumptions. The first strand revolves around the agency theory as the foundation behind the firm agent’s motive to maximize his own preferences (Jensen and Meckling, 1976). Consequently, conflicting interests between the principal and the agent generate information asymmetry costs, which inhibit the growth of firm value. Family-dominated firms, on the other hand, are presumed to be free from agency problems – firm principals and agents, both of whom are posited to come from the same bloodline, are likely to exhibit converging interests towards the successful perpetuation of the family business (Amit and Villalonga, 2006). Such aligned motives indicate positive firm performance and firm value consequences. Conversely, increased family presence within the company signifies a higher incentive for the controlling family to expropriate and take advantage of minority shareholders, which, in turn, inhibits improvement of firm value (Amit and Villalonga, 2006; Morck and Yeung, 2003a). Extant empirical literature supports the effects of both sides of agency theory on firm performance and value in family-controlled firms.

The second strand posits the significance of family altruism on diversification motives of family-controlled firms. Because man is assumed to pursue goals that would maximize his own utility [agency theory], Lien and Li (2013) hypothesize that family firm owners find satisfaction in pursuing the welfare of their own kin. Hence, such firms tend to diversify, in order to strengthen the firm as the family legacy and to prevent feuds among successors through the

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 3 allocation of subsidiaries to each one of them. However, over-entrenchment through diversification tends to destroy firm value for these corporations. Nevertheless, Kachaner et al. (2012) note that family wealth is protected by diversification through the dilution of concentrated risk to a number of firm segments.

Empirical studies concerning family altruism, diversification, and firm value have been widely conducted for Western and East Asian countries. However, only a few have deigned to study the subject using Philippine-based conglomerates as basis.2 Karra et al. (2006) examine a Turkish firm and reports an initial positive relationship between family altruism and firm value; however, further family entrenchment causes firm value reductions. On the other hand, Saldaña (2001) and De Dios and Hutchcroft (2003) observe that business groups diversify to protect themselves against changing political and economic conditions. This spreads non-systematic risk for the firms because of capital diversification to non-related businesses. Anderson and Reeb (2003) also find better firm performance in family firms in the U.S., as opposed to non-family ones. Conversely, Lang and Stulz (1994) and Berger and Ofek (1995) find evidence that the market lowers the value of publicly traded diversified U.S. firms.

For East Asian firms, Chakrabarti et al. (2007) find that economies with developed institutional regulatory frameworks incur firm performance losses due to diversification, whereas those with underdeveloped regulatory frameworks benefit from diversification. Moreover, Aquino (2003) finds that diversification effects for Philippine firms behave in an inverted-U manner; that is, diversifying via subsidiaries or internal divisions appear to add firm value but any further diversification only reduces value.

In this study, empirical analysis is used to investigate the underlying effect of diversification, particularly that which is characterized by family control, on the overall firm value of Philippine publicly traded firms. Furthermore, total corporate diversification is decomposed into its unrelated and related forms, in order to determine which form better accounts for diversification performance in family-controlled firms. Although separation of ownership and control is a rarity in East Asian conglomerates (Claessens et al., 2000), we create a distinction between the two and refer to family firms as family-controlled. Control is distinguished from ownership by at least a 20% threshold of direct or indirect voting rights in the firm, as (i) said cutoff is sufficient to provide effective control in a firm (La Porta et al., 1999); (ii) most countries usually mandate a disclosure of ownership stakes from 10% to 20% (La Porta et al., 1999); and (iii) the International Accounting Standards Committee (IASC) labels a control 2 See Gutierrez and Rodriguez (2013), Aquino (2003), and Del Mundo et al. (2007).

minimum of 20% as ‘significant influence’ (Del Mundo et al., 2007). Therefore, we consider a conglomerate as family-controlled when members from a single family control for at least 20% of voting rights. Furthermore, by adopting the one-share-one-vote rule, which is common in East Asian countries (Claessens et al., 2000), we redefine a family-controlled firm as one wherein a single family owns at least 20% of the firm’s outstanding shares. On the other hand, we hesitate on making use of ‘ownership’ in this particular study since said terminology may imply full ownership of shares by a single family which, in this case, is impossible because the firms we deal with are publicly traded in the Philippine Stock Exchange (PSE).

To our knowledge, this is the first attempt on implementing a systematic study of the interaction between family altruism, diversification decisions, and firm value in the Philippine setting. Moreover, we further explore corporate diversification by decomposing it and analyzing the effects of its two forms upon firm value. We use annual firm-level data on 113 corporations that are listed in the Philippine Stock Exchange during the period 2008 to 2012. Through the necessary data obtained from annual reports filed with the PSE and SEC, we seek to investigate how corporate diversification, most particularly in family conglomerates, impacts firm value. Furthermore, we seek to uncover which type of diversification (unrelated or related) mostly accounts for total corporate diversification performance within the local setting. Also, we aim to identify principal-principal agency problems that may arise from differing motives between the controlling family and other block shareholders, such as banking institutions. Said principal-principal agency problems may arise depending on the depth of family entrenchment; as a shareholder, banks may support or refuse the diversification decisions of family-controlled firms in order to protect their investments in these corporations.

We believe that implications and recommendations arising from the results of this study can help improve corporate governance and aid investors in determining firm value based on the extent of diversification. Furthermore, for firms opting to diversify, this study will provide helpful information that enables them to zero-in on the trade-offs involved in diversification -- distributing diversified business interests among family members as a means of succession, in the face of potential loss of firm value. In the case of outsider block shareholders, the results of this study will help them assess whether or not it is wealth-maximizing to invest in a family-controlled corporation; thus, enabling them to pursue necessary and corrective measures to protect their shareholder value. Moreover, generalizations created in this study may contribute to current corporate literature and provide information as to how firms, which exhibit similar attributes to

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 4 that of Philippine companies, can further enhance their performance.

The rest of this paper is organized as follows: The next section describes the variables and related hypotheses in the framework of Philippine firm-level data, as well as the theory and relevant empirical studies supporting these. Section III discusses the data sample, proxy variables, the econometric models, and the estimation procedure used. Empirical results including summary statistics of variables are developed in Section IV. Lastly, significant findings, conclusions, and relevant recommendations are highlighted in Sections V, VI, and VII, respectively.

II. THEORIES, VARIABLES, AND HYPOTHESES DEVELOPMENT “The parent who leaves his son enormous wealth generally deadens the talents and synergies of the son.”

–Andrew Carnegie (1891)

Figure 2.1 provides a summary of the theoretical framework used in this study, which will be discussed in the succeeding paragraphs. Empirical findings from the literature will be used to substantiate this framework. Figure 2.1. Theoretical Framework

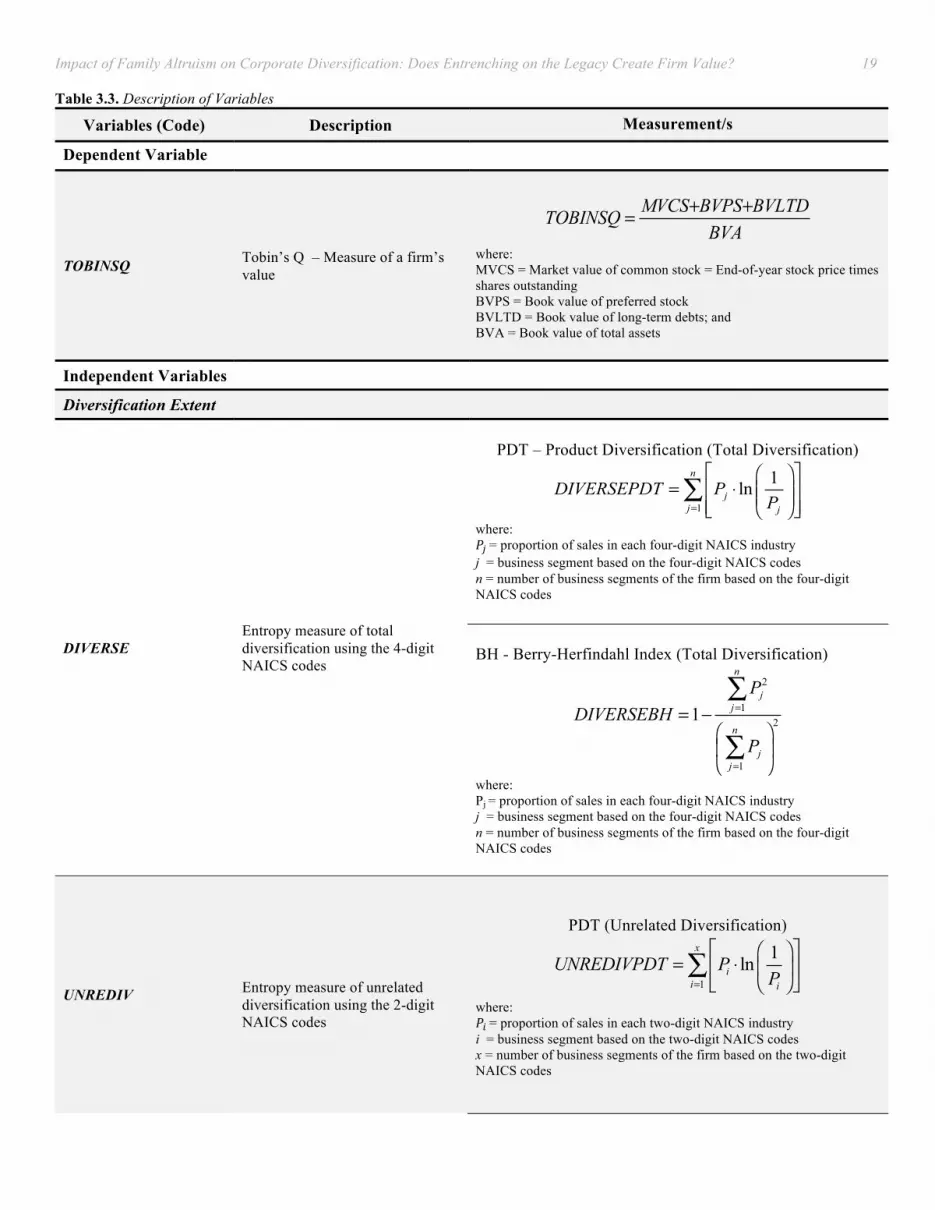

Dependent Variable Firm Value

The total economic value of the company, which is to be allocated to the firm’s shareholders, typically reflects firm value. Measures of firm value often revolve around market and book value pricings. While firm value may be captured

via mere equity or asset values, proxy measures are more commonly used in the literature. Zhan (2007) makes use of accounting measures, such as Return on Assets (ROA), as a proxy for firm value, whereas Berger and Ofek (1995) use Excess Value Added (EVA); however, the latter measure is a noisy proxy for firm value due to unreliability in computing for the weighted cost of capital. In this study, we use Tobin’s Q as a robust measure of firm value. Independent Variables Models A, B, and C: (Dependent Variable: Firm Value) Family Ownership and Control (Family Altruism) on Firm Value

The distinction between family ownership, control and management in family firms is murky, to say the least. This issue arose from the classic study of Berle and Means (1932) which finds that although ownership is widespread among minority shareholders in most U.S. firms, unwavering control still lies in the hands of managers. La Porta et al. (1999) deem this form of “managerialist” culture to be only applicable to large firms in rich countries. Their study contests this view by finding that there, indeed, exists separation of ownership and control in large firms, but the control lies instead in the hands of the shareholders. On the other hand, Claessens et al. (2000) find that ownership is rarely separable from control in East Asian firms. In particular, 60% of these firms are controlled by managers, which come from a single family owner.

Separation of ownership and control may not always be a result of the firm owner’s decision to pursue efficient capital formation3 or to extend firm or share rights to people outside his kinship group. For example, Padilla and Kreptul (2004) find that government interference may also cause such separation in power, in order to protect minority shareholders from the opportunistic behavior possibly exhibited by those in executive positions. Such regulations include taxation and/or rent controls – both of which reduce the incentive of owners to hold on to their rights (Padilla and Kreptul, 2004).

Furthermore, Westhead and Cowling (1996) emphasize the advantages of control and ownership separation by positing that giving control to an outsider CEO, who is not drawn from the kinship group owner of the firm, may bring about fresh ideas and technological advances and use resource networks to help the firm adapt to changes in external stimuli, which will improve firm performance and value. Hillier and

3 Owners may give control to managers outside his/her own family group, in order to allow for increased technical efficiency and skill, which only outsiders may possess (Westhead and Cowling, 1996).

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 5 McColgan (2005) further assert that such separation of power will limit the owner from practicing nepotism and appointing an inexperienced or unskilled kin to the position; thus, preventing the loss of value.

On the other hand, Westhead and Cowling (1996) argue that an outsider CEO may aim to maximize his utility function, instead of pursuing profit-maximization and value-enhancement strategies for the benefit of the firm. Furthermore, Zhu et al. (2010) find a decrease in firm performance in Chinese family-listed firms due to separation of ownership and cash flow rights. Agency costs caused by asymmetric information are also deemed to be negative consequences of such separation in power.

Using a sample of 634 family firms in seven Asian countries, Peng and Jiang (2010) find that the effect of family control on firm value significantly depends upon domestic legal and institutional regulations. In East Asia, particularly in Indonesia and Thailand, Claessens et al. (2000) find evidence of significant family control in more than half of the 2,980 sample firms. For the Philippines, they find that control is significant, with the 10 largest families controlling more than half of the country’s corporate assets. Specifically, by using a 10% control threshold, they report that 42% of Philippine firms are family-controlled. Moreover, they find separation of ownership and control to be low in the sample of Philippine firms, in large companies that are mostly dominated by families. Family Altruism

Consistent with agency theory, owners are assumed to be rational and profit-maximizing individuals who attempt to gain maximum economic benefits from their firms. However, another key assumption in the corporate literature is that, other than economic objectives, owners may also pursue non-economic motives that tend to benefit their family welfare (Karra et al., 2006). Consequently, owners may tend to pursue decisions that might not be optimal for the firm, yet consistent with their goal of maximizing their family’s well-being (Chrisman et al., 2004). As such, agency theory is deemed to be confining since it does not account for non-economic objectives, such as building family cohesion and giving employment to kin (Karra et al., 2006).

From an economic perspective, altruism is represented by a utility function that links the welfare of individuals (Schulze et al., 2003). Lubatkin et al. (2007) define altruism as a “self-other relationship”, which incorporates the interests of others into decision processes. Noe (2012) describes altruism as being “symmetric, limited and harsh” because its effects are too narrow and inclusive, and the consequences cannot be fully internalized by the recipient of such munificent behavior.

Schulze et al. (2003) emphasize the advantages of family altruism – owners extend benevolent behavior to their families, particularly to children, in such a way that families benefit from the munificent act. Moreover, altruism fosters commitment and consideration between parents and their offspring in such a way that the bond between them is sustained (Eshel et al., 1998; Schulze et al., 2003); through this, loyalty towards the family and firm is also established (Ward, 1997). As such, interests of both the parent and the child are aligned in matters concerning the firm – this limits information asymmetry (Karra et al., 2006), reduces agency costs and generates a family-oriented organizational culture that encourages risk-taking behavior, such as delving into international growth opportunities (Schulze et al., 2003). This allows for higher firm returns and increased firm production.

However, altruistic behavior existent within firms gives off a sense of collective ownership among family members which, in turn, creates a ‘self-reinforcing system of incentives’ that encourages members to be “selfless” to one another (Karra et al., 2006). Thus, families tend to appoint kin to firm positions; due to adverse selection or nepotistic behavior, disruptive ripples are generated by hiring inexperienced, unsatisfied or inefficient kin (Dyer, Jr., 2006; Karra et al., 2006; Astrachan et al., 2007). Moreover, this selfless act towards offspring incurs moral hazard losses through incentivizing the latter to manipulate the transfers of the parent in such a way that their own self-serving wants are catered (Lubatkin et al., 2007). This encourages the offspring to freeload (through the consumption of perks) or to shirk from their duties – both of which engender inefficiencies in firm governance and harm firm performance and value (Schulze et al., 2003; Lubatkin et al., 2007; Karra et al., 2006).

On the other hand, Stafford et al. (1999) theorize that families opt to bestow firm employment only upon relatives who are in good terms with the founding family, in order to promote business harmony and positive firm outcomes. Meanwhile, the exchange theory of Ingoldsby et al. (2004) is grounded upon self-interest. It asserts that participation in the family business lasts only for so long as the hired relative can provide economic and social benefits beyond the costs he or she incurs.

In a study concerning a renowned Turkish firm, Karra et al. (2006) find that reciprocated altruism has aligned the goals of the family and has reduced agency and monitoring costs towards heightened firm performance and value. However, as the business continued to expand, agency costs were aggravated due to the tendency of appointed family members to shirk. The effects of such free-riding behavior were magnified when the family-owner refused to sanction his kin. Moreover, the authors find that family altruism extends not only to immediate family members and distant kin, but

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 6 also to unrelated individuals who share the same ethnic culture as the owner. Thus, it can be posited that the effects of altruistic behavior made manifest by owners of family-controlled firms are even more extensive than initially supposed.

On the other hand, the family altruism and succession theory posits that family firm owners are highly incentivized to make prudent decisions that will enhance firm value. This is consistent with their objective of preserving the firm for the sake of succeeding generations. Consistent with this theory, Lien and Li (2013) find a positive relationship between family control and firm value prior to diversification.

However, Schulze et al. (2003) find evidence of an increase in agency costs due to negative altruism effects and a subsequent decline in firm performance using U.S. data. Using data on shipping firms in Norway and Sweden, Randoy and Jenssen (2003) find that the takeover of a CEO descendant causes a negative effect on firm performance, whereas descendant influence of the founder-Chairman contributes an improvement in firm value.4 Economic Entrenchment

Excessive family altruism and control imply

entrenchment of the family within the firm hierarchy. Morck et al. (2005) dub economic entrenchment as a phenomenon where controlling owners appear to possess political and institutional influence relative to their actual wealth. Shleifer and Vishny (1989), on the other hand, model entrenchment in terms of managerial investment – a phenomenon which occurs when the manager excessively invests in assets which are complementary to his personal skill. As such, the manager is made valuable to stockholders because of his unique skill contribution and, thus, entrenches himself within the firm in the process. Furthermore, Morck et al. (1998) define and measure family entrenchment in terms of family board ownership, whereas Tan (2009) links the concept to the reluctance of the incumbent CEO to vacate his position in favor of the heir apparent. Regardless, entrenchment stems from control manifested through a variety of mechanisms.

This firm-level entrenchment phenomenon inherent in family firms involves expanding existing lines of control. For instance, cross-shareholding, as defined by Ogishima and Kobayashi (2002), may take the form of unilateral or mutual shareholdings – the former implies a one-sided form of control

4 Randoy and Jenssen (2003) argue that descendant CEOs limit the firm from taking advantage of a competitive managerial labour market; thus, the firm fails to benefit from the skills and experience that can be offered by an outsider CEO in terms of strategy and decision-‐making. On the other hand, descendant Chairmen signify firm continuity and add firm value due to exhibited aligned interests with the objectives of the organization.

extension of Firm A over Firm B via ownership of shares, whereas the latter involves Firm A and Firm B strategically owning each other’s shares. Such a structure allows firms to extend control over another firm (Morck et al., 2005).

On the other hand, superior voting rights involve classes of stock which possess more votes per share than an ordinary common stock; thus, granting the holders superior voting rights, even if they own minimal equity in the firm (Morck et al., 2005). These allow the holder to command a majority of votes in a shareholders’ meeting and, thus, extend his control rights, even while accounting for only minimal ownership.

Moreover, control pyramids depict how magnification of control and wealth by firm owners intensifies through mere structures where the owners diversify and control listed companies, each of which controls several more, and so on. These structures allow a firm to control several more firms, which are collectively worth more than the family’s actual wealth; this is not possible through direct ownership alone. Morck et al. (2005) find that family members are usually appointed to key executive positions throughout the structure.

Consequently, it has been suggested that the aforementioned entrenchment channels and control mechanisms result to poor resource utilization because resources are typically diverted to the controlling family for their use. This implies inefficiencies in resource allocation, which increase value reduction. In a larger scale, economic entrenchment leads to what Morck et al. (2005) refer to as a “sub-optimal political economy equilibrium”, where capital allocation favors the elite families and may, thus, hamper the pace of innovation. Thus, the structure of the industry tips over – that is, entry barriers are erected and development of capital markets are stymied due to the political and corporate power exerted by the controlling families.

Furthermore, ill effects of entrenchment involve political rent-seeking, such as lobbying politicians and bribing judges, which a family firm might delve into due to lack of entrepreneurial skill or management talents of the family CEO (Morck and Yeung, 2003b; Chrisman et al., 2003). This particularly holds true for family firms, which are inherently reluctant to accept skilled outsiders, for fear of losing firm control. Thus, investments from a handful of these political elites may crowd out real investments (Chrisman et al., 2003) and innovation may be stifled if reliance upon the support of these lucrative politicians remains absolute.

Using the model of Stulz (1988), Claessens et al. (2002) illustrate a concave relationship between entrenchment and firm value – as managerial control and ownership increase, the negative consequences of entrenchment, which reduce firm value, overwhelm the positive benefits of managerial ownership. On the other hand, Morck et al. (1988)

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 7 report a non-monotonic relationship between entrenchment and firm value for U.S. firms – as entrenchment becomes more evident, firm value increases until the 5% level of ownership, declines sharply until the 25% level of ownership, then increases once more beyond said level. Morck et al. (1988) hypothesize that the increases in firm value may well represent convergence of principal-agent interests and/or the existence of high stocks of intangible assets in such firms5, whereas decreases in value reflect negative entrenchment effects, such as the pursuance of private interests by managers at the expense of minority shareholders.

Gomez-Mejia et al. (2001) study Spanish newspaper firms during the period 1966 to 1993 and report negative entrenchment consequences – that of better firm performances after the dismissal of a family CEO. Thus, Dyer, Jr. (2006) theorize that parent-owners are reluctant to monitor and discipline their kin executives due to altruism. Families tend to entrench their legacy within the firm and wait until firm performance is falling before initiating a change in leadership.6 As such, the unwillingness of family owners to monitor their agents implies adverse selection and shirking, which may impair firm value.

Hiller and McColgan (2005) find evidence in UK-listed companies that higher level of managerial control implies increased entrenchment, which diminishes firm value. Specifically, they report strong and positive responses in stock prices and a significant improvement in firm performance following the departure of a family CEO. Moreover, they find that shareholders accrue higher levels of cash flow streams after the departure of a family CEO and the replacement of a non-family member, which suggest the plausibility of expropriation taking effect prior to the replacement.

However, Burkart et al. (2003) show that entrenchment may reduce agency problems wherever legal protection of minority shareholders is weak. Because agency problems are severe as it is, the founding family must handle both ownership and management in order to avoid further information asymmetry consequences and agency costs. Shleifer and Vishny (1997) verify this in their survey of existing empirical literature by noting the significant role played by the legal environment upon firm structure. They find that in countries where legal protection of investors is not quite substantial, family firms and the entrenchment phenomenon abound which, in turn, protect minority shareholders against expropriation.

5 According to Morck et al. (1988), family firms with high firm value and which possess huge amounts of intangible assets require greater management ownership “to ensure proper management of said assets”. Hence, entrenchment and firm value may be positively correlated in the case of such firms. 6 This is in line with Karra et al.’s (2006) findings, which support the increase in agency costs brought about by excessive family altruism and entrenchment.

In East Asian firms, where entrenchment and concentration is found to be high, control is often magnified through the use of control pyramids and cross-shareholding among family firms, where the manager is usually related to the founding owner (Claessens et al., 2002). For a sample of publicly traded firms from eight East Asian countries, Claessens et al. (2002) find that entrenchment effects are negative – that is, increases in control rights by the largest shareholder cause a decline in firm value. In particular, the use of control mechanisms – cross-shareholding and control pyramids – leads to a negative, albeit insignificant, effect on firm value. Therefore, such mechanisms cannot be reliably attributed to value discounts within the region.

In this study, we define a controlling family as one that is composed of firm stockholders who share a common surname and whose total outstanding stockholdings in the firm equate to at least 20% (La Porta et al., 1999). Thus, we describe a family firm as one where there exists a single family who controls at least 20% of firm voting rights or owns at least 20% of outstanding stockholdings. Moreover, we formally define family altruism as the desire of a controlling family to extend its welfare to other family members and we characterize it as the extent of controlling ownership of a family within a firm.

We measure family control (FAMICON) as the total percentage of outstanding shares owned by members of a controlling family. Therefore, we hypothesize that: H1: Higher family control (FAMICON) will lead to higher firm value due to the inclination of family firm owners to make decisions that will contribute to improvements in firm value, in line with their objective to preserve the firm for succeeding generations. However, it can also lead to lower firm value due to negative altruism effects brought about by excessive family entrenchment within the firm. Diversification Decisions

The literature on corporate diversification is quite vast. As a strategy adopted in pursuit of corporate growth and enhanced firm value, diversification is a means by which a firm can expand its core business into other industries and increase profitability (Chandler, 1962; Hall, 1995). Matsusaka (2001) views diversification as a “match-and-search” process, wherein firms seek to invest in businesses that match their capabilities. In East Asia, where inefficient institutions are prevalent, diversification is typically identified in view of its capacity to internalize costs and functions for firms; thus, generating scope advantages and reducing corporate risk (Chakrabarti et al., 2007).

In this study, we adopt Ansoff’s (1957) general definition of corporate diversification as the process of

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 8 venturing into new markets with new products – the production of which may or may not be technologically related to the firm’s original core business. The subsidiary must, however, be connected to the parent firm (e.g. partial ownership of the subsidiary; affiliated with the parent).

Meanwhile, the classic Modigliani-Miller theory assumes that the market value of a firm is not dependent on the capital structure a firm employs, but on the risks underlying assets and on the firm’s earning power; thus, implying that in perfect capital markets, diversification is presumed to not be an influential determinant of firm value (Erdorf et al., 2012). However, the continued prevalence of firms operating in more than one industry cannot be explained by said theorem. Thus, Erdorf et al. (2012) provide reasons for firms’ diversification: Agency Theory

Agency problems are theorized to be rooted from the opportunistic behavior of the agent or management (Jensen and Meckling, 1976; Davis et al., 1997; Shleifer and Vishny, 1989). As such, agency theory predicts that firms diversify in order to maximize the agent’s utility at the expense of the firm’s shareholders – the principal (Fama and Jensen, 1983). Such firms are reported to diversify for the purposes of: (i) expanding power, prestige and level of entrenchment (Shleifer and Vishny, 1989; Jensen and Murphy, 1990; Jensen, 1986); (ii) improving a manager’s future career prospects (Aggarwal and Samwick, 2003); and (iii) reducing exposure of personal employment and individual portfolios to risk (Amihud and Lev, 1981). Thus, due to self-serving motives, the agent may tend to over-invest or over-diversify beyond the optimal level, which are posited to diminish firm value (Erdorf et al., 2012).

Aggarwal and Samwick (2003) use companies obtained from Standard & Poor’s dataset and find that diversification decisions are attributed to the marginal utility obtained by agents from diversifying; such decisions incur firm value reductions. Their results are consistent with that of Berger and Ofek (1995) and Lang and Stulz (1994), as both use U.S. firm-level data and find diminished firm value due to diversification. Internal Capital Markets

Internal capital markets, as defined by Maksimovic and Phillips (2013) and Erdorf et al. (2012), are mechanisms in which cash flows from a particular segment of a diversified firm can be used to internally subsidize another segment through firm resources. As such, resources used to finance segments are sourced internally, as opposed to funding by external financial instruments. Arguably, this method can be efficient if it eliminates costs created by financial constraints

in certain segments. However, Maksimovic and Phillips (2013) argue that inefficiency from using such markets may arise due to the rent-seeking behavior of the principal party; that is, the concentrated amount of capital may highly incentivize the owners or management to take advantage of opportunistic behaviors.

Rajan et al. (2000) use a sample of U.S. firms and find that greater diversification entails higher potential of misallocated capital due to “power struggles” existent between segments. Erdorf et al. (2012) further argue that over-investment in divisions with dire prospects may exacerbate inefficiency. However, Stein (1997) argues that executives may be able to efficiently allocate funding through business units through internal capital markets, given that they have insider information pertaining to each firm segment. Co-Insurance Effect Theory

Financial synergies, which occur when operations are

combined – as is the case in diversification where various industries or divisions function under one firm name – dilute the risk throughout the various segments and, thus, reduce the likelihood of insufficient debt service for a particular division. Kim and McConnell (1977) and Erdorf et al. (2012) point to Lewellen (1971) as the original proponent of this theory and explain how the latter argues that the imperfectly correlated earnings from two separate firms would “reduce the risk of default” when they merge. This motivates firms to diversify or to merge due to higher debt capacity potential. Using U.S. firm-level data, Kim and McConnell (1977) find that financial leverage was well-used by firms post-merging than the separate firms did before the merger. Family Altruism and Succession Theory

Lien and Li (2013) suggest that diversification helps to facilitate the process of inter-generational succession through fostering a set of subsidiaries that are self-sustaining. Family-controlled firms – in pursuit of their goal to maximize family well-being through effective management of the firm – tend to create succession plans that entail passing the firm down to the succeeding generations (Sharma et al., 2003), as soon as the current generation retires or steps down. This would motivate family firm owners to delve into diversification, in order to prevent competition and feuds among heirs, by allocating subsidiaries or divisions to each one of them, which would expand the family’s social network and pool of resources as well (Lien and Li, 2013).

Kachaner et al. (2012) note that executives of family-controlled businesses concentrate more on long-term investments to benefit the succeeding generations. Their study uses family firm-data from the U.S. and Europe and shows

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 9 that family businesses focus on resiliency rather than performance; that is, they tend to manage and improve on their downside, which enables them to avoid greater losses in times of crisis. They find that, in order to achieve resiliency, family-run firms exhibit surprising levels of diversification. Diversification is argued to be a key strategy to protect family wealth because if one sector is affected by the economy’s performance, businesses in other sectors can generate funds that can compensate for losses stemming from said sector.

However, such family altruistic behavior inclines family-managed firms to over-entrench themselves within various firm segments and, subsequently, destroy firm value (Lien and Li, 2013). Lien and Li (2013) verify this theory through their findings of a negative relationship between family-influenced diversification and firm value. Unrelated and Related Diversification

Markides (1995), Markides (1997), and Markides and Williamson (1996) classify diversification into two kinds: (i) unrelated or conglomerate diversification; and (ii) related or concentric diversification. The former refers to processes wherein the business branches out to subsidiaries whose products or industries are unrelated to the original business of the firm; conversely, the latter deals with related ones. Related diversification strategies may generate operational advantages for the family firm through the presence of synergies that may be captured through the creation of a portfolio of businesses that is ‘mutually reinforcing’ (Gomez-Mejia, 2007; Seth and Dastidar, 2009). On the other hand, unrelated diversification may reduce risk for the family due to investment in a variety of industries; reduction of risk implies higher operational efficiency and lower transactional costs for the firm (Amit and Wernerfelt, 1990). Thus, as Gomez-Mejia (2007) put so concisely, “related diversification offers scope economies, whereas unrelated diversification offers greater risk reduction.”

Chatterjee and Wernerfelt (1991) claim that firm resources are a focal determinant of the type of diversification strategy that a firm would invest in. If resources tend to be product-specific, then the firm would be constrained to related diversification; the converse holds true when resources are deemed to be flexible. On the other hand, Christensen and Montgomery (1981) suggest that market conditions also influence diversification and the type of strategy to be pursued. Specifically, in markets with ‘low-business opportunities’, firms would be constrained to pursuing related diversification due to lack of available markets to invest in. Moreover, Hall (1995) finds that a firm’s past performance affects its willingness to pursue diversification. Firms with below-par performance tend to diversify more, regardless of whether related or unrelated diversification is pursued, due to

the perception of such an activity as a solution to financial problems.

La Rocca and Stagliano (2012) find that unrelated diversification has a positive impact on firm value for a sample of 229 Italian firms. They attribute this to be a result of firm efficiencies which include lower risk and internalized capital markets. In contrast, Berger and Ofek (1995) find that unrelated diversification is associated with a larger value loss than related diversification for U.S. firm data. On the other hand, Markides and Williamson (1996) use the results of a survey of CEOs of U.S. firms and find that those that diversify towards related industries tend to be profitable, as long as they invest in strategic assets. Furthermore, using a sample of U.S. firms, Christensen and Montgomery (1981) find that related-constrained firms earn high returns and incur low risks because they are allowed to focus on capitalizing on their core strength and to operate within highly concentrated markets. On the other hand, they find that firms with unrelated diversification earn low returns and incur high risks due to firms’ inattention and entry into highly fragmented industries. Conversely, Marinelli (2011) studies U.S. firms and finds that related diversification is associated with lower firm performance, whereas unrelated diversification leads to enhanced firm performance.

In the Philippines, firms such as the Jollibee Food Group and the Sy Group engage in related diversification, whereas Ayala, Aboitiz, Metro Pacific, and the Andrew Tan Group engage in unrelated diversification. Moreover, there are companies, such as the Lopez Group of Companies, Gokongwei, San Miguel and DM Consunji Group, which prefer both diversification strategies (Gutierrez and Rodriguez, 2013).

Furthermore, Gutierrez and Rodriguez (2013) study the diversification strategies of the aforementioned firms and find that a majority of them pursue unrelated diversification, partly due to changes implemented by the government. These changes include, but are not limited to: (i) the deregulation of the Philippine telecommunication industry, which ushered in a flurry of foreign investments; and (ii) the privatization of the water utility business during the 1990s to the 2000s. Moreover, growth opportunities in the firms’ initial core businesses are found to be declining. Said findings imply that firms take into account the institutional context when determining the appropriate diversification strategy to pursue. Impact of Diversification Decisions on Firm Value

Theoretical suppositions argue that diversification can have both value-enhancing and value-reducing effects. Engaging in various lines of business within one firm can increase operational efficiency, whereas cross-subsidies involving misallocation of resources and the increased use of

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 10 such resources to fund unprofitable investments both reduce firm value (Berger and Ofek, 1995). Furthermore, higher business leverage (Lewellen, 1971) provides greater debt capacity to multi-segment firms. However, information asymmetry costs, which are highly prevalent in diversified firms due to wider dispersion of information, leads to lower firm profitability and value (Berger and Ofek, 1995).

Moreover, because the government collects taxes when income is positive but not when it is negative, Majd and Myers (1987) predict that diversified firms pay less tax than its individual segments would have paid separately, as long as one or more subsidiaries incur losses in some years; thus, diversified firms are said to have a tax advantage. However, Jensen (1986) suggests that the presence of increased cash flow in subsidiaries due to diversification induces managers to invest more in negative net present value projects. Meyer et al. (1992) further note that channeling resources into one or more failing subsidiaries generates value losses for multiunit firms.

Markides (1992) also suggests that overinvestment may diminish firm value. As pointed out by Aquino (2003), firm diversification depicts an inverted-U behavior, where diversifying and acquiring subsidiaries initially adds firm value but any further diversification hampers performance. Despite this, firms continue to diversify beyond the optimal level; thus, destroying firm value and shareholders’ wealth (Hoskisson et al., 1993; Martin and Sayrak, 2003; Tallman and Li, 1996).

The behavioral agency model developed by Wiseman and Gomez-Mejia (1998) further suggests that families are averse to losing their socio-emotional wealth (SEW) or the non-financial aspects of a firm, which include family identity and reputation and the perpetuation of the family dynasty. In line with this, Gomez-Mejia et al. (2007) find that family firms may prefer lower levels of diversification, in order to protect their current stock of socio-emotional wealth or value. This behavior implies that diversification may lead to firm value deterioration due to the following reasons (Gomez-Mejia et al., 2007):

(i) The complexity of the diversification process,

which involves delving into new territories using untried methods, may cause greater uncertainty and diminish SEW;

(ii) The necessity of using external financing and talent, which will introduce more external actors into the firm, may drive the firm’s modus operandi away from its objectives and diminish SEW; and

(iii) The inherent characteristic of family firms to exhibit strong inertia may engender resistance from family members when new markets and products are introduced; thus, SEW may diminish.

Empirical evidence on the relationship between firm diversification and firm value is inconclusive. For instance, in their seminal article, Lang and Stulz (1994) use a sample of U.S. firms and show that diversified firms have lower firm value, as opposed to non-diversified firms, although the reason behind said valuation difference has not been clearly explained. Berger and Ofek (1995) further investigate this result using U.S. firm-level data as well and report that inefficient diversification and overinvestment cause multi-segment firms to lose even more value. Denis et al. (2002) account for global diversification and find that firm value for U.S. firms is also reduced – attributing such reductions to agency conflicts and corporate governance problems. Furthermore, Graham et al. (2000) find that diversification reduces firm value due to investments in poorly performing subsidiaries.

For East Asian firms, particularly those operating in Indonesia, Thailand, Japan, Malaysia, South Korea and Singapore, Chakrabarti et al. (2007) note that the effects of diversification are contingent upon the institutional context of the economy. That is, for more developed economies, where the institutional framework is relatively more substantial, diversification leads to lower firm performance, whereas those with underdeveloped institutional environments benefit from diversification, albeit to some extent only. Diversification benefits are limited, however, particularly during the presence of economy-wide shocks (Montgomery, 1994).

On the other hand, Villalonga (2004) and Kuppuswamy and Villalonga (2010) find that diversification increases firm value due to efficiency in investment and to the ability of the firms to source external finances. Moreover, Hall (1995) finds that diversification does lead to increased firm performance, albeit insignificant, for U.S. firm data, and Matsusaka (2001) generates a model which highlights diversification as a value-maximizing strategy. Pandya and Rao (1998), however, report that, using U.S. firm data, low and averagely performing diversified firms do, indeed, exhibit higher firm performance and value than undiversified ones, yet best-performing diversified firms are found to earn lower returns than undiversified firms.

In this study, firm segments are classified according to the nature of each segment’s industry. While detailed segment information can easily be obtained from databases and firm reports, the 2007 North American Industry Classification System (NAICS) provides a streamlined and efficient classification method concerning firm-level industries. Thus, in this study, we consider a subsidiary as industrially-related to the original business if the first two-digits of its four-digit NAICS code are the same as that of the parent firm’s two-digit code; otherwise, it is unrelated.7 7 We make use of the NAICS, as opposed to the Philippine Standard Industrial Classification (PSIC) system, because the

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 11

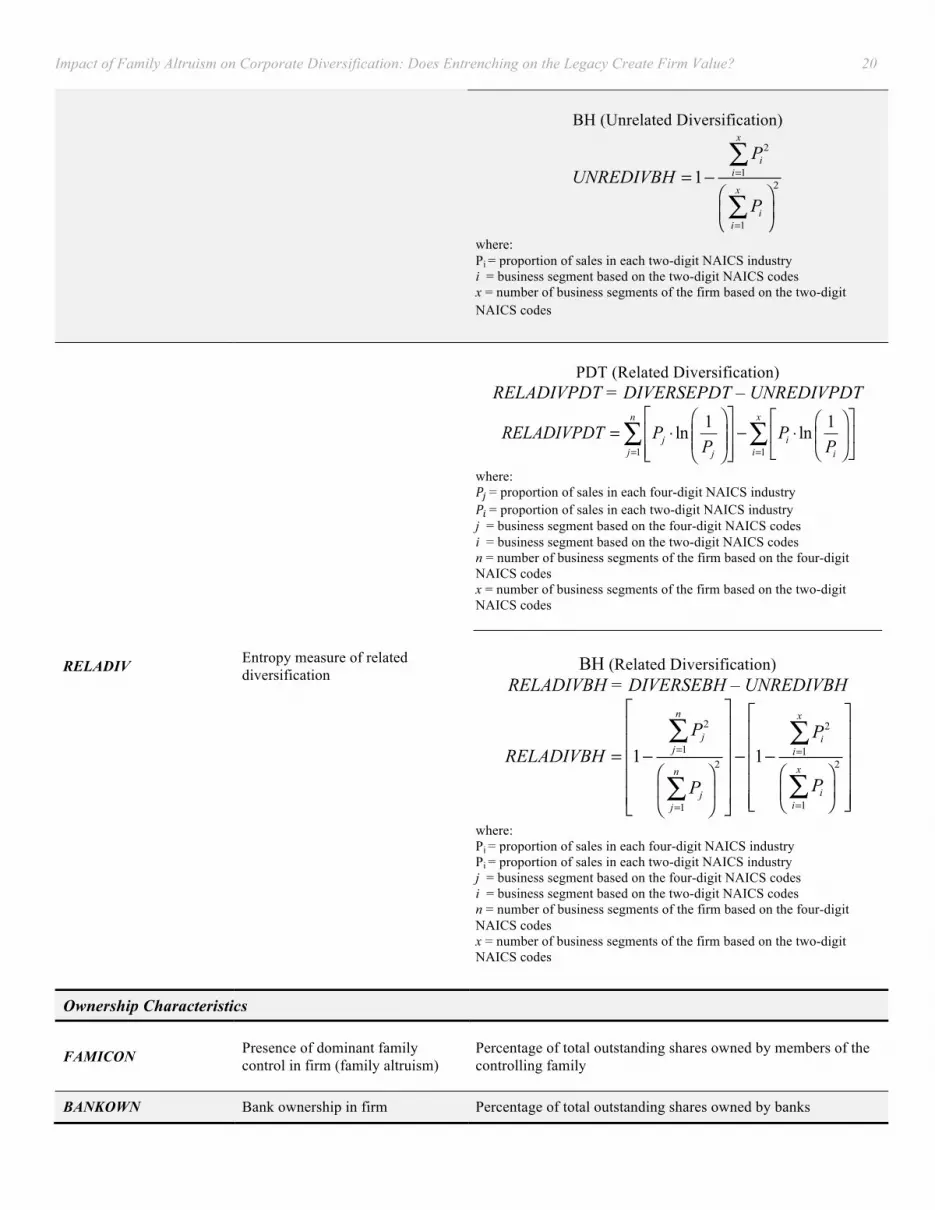

Various indices for measuring the extent of corporate diversification exist. In this study, we use the Entropy Index for Product Diversification (PDT) proposed by Hart (1971) and the Berry-Herfindahl index used by Montgomery (1982). Not only do both of these measures allow us to determine the extent of total corporate diversification pursued by a firm (DIVERSE), but they also enable us to decompose the extent with which a firm may pursue either unrelated (UNREDIV) or related (RELADIV) diversification.

Thus, we examine the relationship between diversification and firm value (TOBINSQ) and posit that: H2a: Higher total diversification (DIVERSE) will initially lead to higher firm value due to higher debt capacity and gains obtained from growth opportunities, but firms tend to over-diversify and eventually decrease firm value. This accounts for the inverted-U curve relationship (DIVERSE2) between firm value and the extent of total diversification. On the other hand, family firm members are highly inclined to over-entrench themselves within the firm through diversification for the sake of preserving family interests; hence, controlling family ownership will have a negative moderating effect on diversification performance (FAMICONDIVERSE negatively affects firm value). H2b: Growth opportunities inherent in industries outside the firm’s core business generate higher firm value for corporations that diversify to unrelated businesses (UNREDIV). However, firms eventually over-diversify and impair firm value. This phenomenon explains the presence of an inverted-U trend (UNREDIV2) between the extent of unrelated diversification and firm value. On the other hand, family firm owners, who seek to diversify to unrelated industries to prevent family members from competing within the same market, tend to over-entrench themselves within the firm. Such reckless behavior will cause family altruism to have a negative moderating effect on diversification performance (FAMICONUNREDIV negatively affects firm value). H2c: Conversely, related diversification (RELADIV) diminishes firm value by inhibiting the competitiveness of firms against those that are expanding their businesses to other growth-inducing industries. Family firm owners, however, are inclined to adopt more prudent measures to safeguard firm value against related diversification threats, in order to preserve the firm for succeeding generations. Hence, family altruism will have a positive

former is more universally recognized than the latter. Moreover, there exists no significant difference between the industry classification standards of the two.

moderating effect on firm value (FAMICONRELADIV positively affects firm value). On the other hand, no theory accounts for a curvilinear trend between firm value and related diversification. Bank Ownership on Firm Value

In recent years, the role and influence of banks has shifted from being mere creditors to corporate block holders. In the literature, various claims as to whether the presence of bank ownership can improve or impede firm value have surfaced. For example, Young et al. (2008) find evidence that institutional investors promote good corporate governance both in developed and developing economies. In contrast, Lin et al. (2009) posit that companies perform worse with bank ownership.

The decision of an investor or institution to participate in firm governance is, in fact, contingent upon the type of investment made. Le et al. (2006) observe that investors have different strategic preferences, depending on their investment choices. For example, mutual funds aim to maximize returns with efficient investments (i.e. low cost and short time); thus, investors are reluctant to participate in governance. Conversely, institutional investors, such as banks, have long-term investments and they are, therefore, willing to participate in corporate governance, in order to ensure that their investments gain profitable returns.

Moreover, the significant role played by institutional investors cannot be underestimated. Claessens and Fan (2003) argue that firms need to pay attention to the demands of such institutions, in order to enhance corporate governance. When agency problems are present, it is possible for the role of institutional investors to come into play, as their equity participation allows the firm to benefit from their established reputation; hence, enhancing the company’s credibility to its minor shareholders. In addition, even if Sarkar and Sarkar (2000) find no evidence that mutual funds are active in corporate governance, they were able to obtain information pertaining to a positive relationship between firm value and ownership by directors, foreigners, and lending institutions.

However, Gorton and Schmid (1996) argue that the Opposed Interests Hypothesis posits the existence of two kinds of conflicts-of-interest that may negatively affect firm value: First, the objectives of a bank shareholder may be in conflict with those of other shareholders. Such is the case when banks obtain information that can be used to their own benefit. Since banks can manage access to external capital, it may take advantage of the control it imposes over firms; thus, requiring firms to pay higher interest rates on loans. Secondly, conflicts-of-interest may arise due to proxy voting. Small blockholders, as compared to large non-bank blockholders, are less likely to prevent banks from engaging in activities that are

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 12 contrary to firm value maximization. Such conflict occurs when banks vote upon the shares of minor blockholders; hence, fulfilling bank interests rather than that of the firm’s.

The contradicting motives between bank and firm also affect the latter’s diversification decisions. Filatotchev and Toms (2006) observe that succession plans, which aim to entrench family control, tend to contradict the interests of other shareholders. In the event that a bank is active in corporate governance, the entrenchment and diversification motives of the controlling family will be minimized, so as to prevent value-reducing actions. However, empirical findings pertaining to effects of bank ownership on firm value are ambiguous. In their study of German banks and firms, Gorton and Schmid (1996) find that bank control varies from time to time. Evidence shows that during 1974, German bank ownership was exceedingly extensive such that banks already held the equity of firms. They also report that bank ownership positively affected firm performance and value. Conversely, in 1985, findings show that the power and extent of bank blockholdings have been reduced due to the development of security markets, although German bank ownership still enhanced the performance of firms.

Sarkar and Sarkar (2000) investigate the relationship between firm value and the extent of equity held by different types of blockholders (i.e. foreign, corporate, and financial holdings) for a sample of Indian firms. Their results show that financial institutions possessing low concentrations of equity holdings are passive; thus, there exists no significant relationship between the holdings of an institutional investor and firm value. Moreover, their findings are consistent with that of the German or Japanese bank-based form of governance wherein financial institutions start monitoring the company once they have considerable debt and equity holdings. This, in turn, results to improved firm value.

On the other hand, Lin et al. (2009) find that, in their study of Chinese-listed firms, bank ownership and investments weaken firm performance and value when the bank is a major shareholder. Moreover, Claessens and Fan (2003) review ownership structures and their effects on Asian markets including Japan, Indonesia, Thailand, Korea, and China. Their findings indicate that financing from internal markets often face misallocated capital issues due to agency problems. Likewise, external financial markets did not provide much discipline, as conflicts-of-interest continue to persist and rents brought by financial and political connections exist.

We define bank ownership as the act with which banks hold major portions of shares in a firm sufficient to merit voting power. We measure bank ownership (BANKOWN) as the percentage of outstanding shares owned by a bank. Thus, we hypothesize that:

H3: Higher bank ownership (BANKOWN) leads to a positive effect on firm value – firm value will improve due to the concern and interest exhibited by bank shareholders on firm performance. However, the Opposed Interests Hypothesis posits that increased levels of bank ownership leads to a decline in firm value due to conflicts-of-interest that may exist between bank shareholders and other blockholders. Hence, the relationship between bank ownership and firm value is ambiguous. Firm Size, Firm Age, and Nature of Industry on Firm Value Control variables deemed to possibly affect a firm’s diversification activities include firm age (FIRMAGE) and firm size (FRMSIZE). Similar to Lien and Li (2013), our measure of firm age is the number of firm-years since incorporation. On the other hand, firm size is an experience indicator gained by the firm from inception. Lien and Li (2013) use the scale of total capital measured as the sum of all long-term debt and equity to represent firm size. Alternatively, it is measured by Gomez-Mejia et al. (2007) as the natural logarithm of a firm’s total number of employees, and by Gomez-Mejia et al. (2003) as the natural logarithm of the average value of a firm’s sales. Market value of equity is another popular measure of firm size. In this study, we use market capitalization in its natural logarithmic form to account for firm size.

The quest for organizational immortality has long since garnered attention, yet literature has not tackled much of the subject. Firm age is widely posited to be positively-correlated with firm profitability and value due to firms’ tendency to learn as they age; through investing in R&D, hiring more labor and capital resources, and discovering a particular field of specialization, older firms enjoy higher profitability and value (Loderer and Waelchli, 2010). Another stream of research claims, however, that older firms are more prone to inertia and are less quick to adapt to changes in bureaucratic conditions; thus, incurring firm value losses (Majumdar, 1997). Therefore, the effect of firm age on firm performance is equivocal.

On the other hand, Gibrat’s Law of Proportionate Effects states that firm growth or firm performance, as the literature interchangeably uses, is independent from firm size. However, extant literature has disproved this law (Hall, 1987; Mansfield, 1962; Singh and Whittington, 1975). Larger firms are found to enjoy higher growth and firm value due to their ability to exploit scale economies and to easily access credit; possessing a broader pool of resources also allows them to benefit from increased production (Mansfield, 1962). However, small firms are also found to suffer less from agency problems and are more flexible in their organizational framework, which allows them to easily adapt to changing

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 13 conditions (Yang and Chen, 2009). Surviving smaller firms are also found to have higher growth rates than larger firms (Mansfield, 1962). Thus, the effect of firm size on firm performance is ambiguous.

Using the previously defined measures for firm age (FIRMAGE) and firm size (FRMSIZE), we hypothesize that: H4: Firm age (FIRMAGE) has an ambiguous effect on firm value. H5: Firm size (FRMSIZE) has an ambiguous effect on firm value.

Moreover, the food consumer and production industry has been continuously innovating and raking in sales increases. The continual increase in purchase expectations, which is brought about by the iterative development of consumer products, is expected to further boost profitability in the food industry. For instance, almost half of Pepsi Co.’s

2009 revenues were generated outside the U.S., and Unilever’s ice cream brands have consolidated sales revenues from almost 16 countries (Chatterjee et al., 2011); thus, contributing to increases in industry revenues and value. Furthermore, Pils (2009) asserts that businesses, whose specialization lies in the area of food and consumer services, are highly likely to gain firm value improvements through diversification, particularly to related industries. This is because diversification is theorized to maximize internal synergies by allowing the firm to fully utilize the potential of existing technologies and marketing systems that are prevalent in food-specializing businesses, nowadays. As such, we posit that: H6: Firms in the food consumer and production industry (CONSUMR) enjoy increased firm value.

Table 2.1 summarizes our hypotheses, in line with

the relevant theories that substantiate them.

Table 2.1. Summary of Hypotheses and A Priori Expectations

Variable Name Theory Justification

Family

Altruism and Succession

Theory

Agency Theory

Other Theories / Empirical

Results

Models A, B, and C (Dependent Variable: Firm Value – TOBINSQ)

FAMICON (+) (-) --

Family firms aim to preserve the firm for the sake of succeeding generations; hence, they will make decisions that will enhance firm value. However, agency theory posits that the excessive entrenchment of family members within the firm may induce these owners to expropriate from minority shareholders; hence, reducing firm value.

DIVERSE -- --

(+) Empirical Basis;

Co-Insurance Effect Theory

Diversification will initially increase firm value due to the ability of the firm to source external finances. The gains enjoyed by the firm from investing in growth opportunities outside the core industry also improve diversification performance (Villalonga, 2004). Moreover, financial synergies existent within various firm segments dilute risk across industries and increase the firm’s debt capacity.

DIVERSE2 -- (-)

(-) Empirical Basis

While diversification can have value-enhancing effects (firm expansion and growth), value-reducing consequences also result from increased tendencies of firm owners to over-diversify (Aquino, 2003). Moreover, the risks involved in the diversification process, as well as the necessity of introducing external talent and actors into the firm, may engender firm value. Likewise, self-serving motives may induce agents to eventually over-diversify and, consequently, expropriate minority shareholder wealth; thus, agency theory posits a negative curvilinear trend between diversification and firm value as well.

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 14

FAMICONDIVERSE (-) (-)

(-) Behavioral

Agency Model

Family control is manifested through family altruism, which, in turn, entrenches the family within the firm through the creation of succession plans for the next generation of family firm members. Because such family firms tend to over-entrench themselves by diversifying over the optimal level (Aquino, 2003; Martin and Sayrak, 2003), diversification performance is impaired. Likewise, agency theory posits that through over-entrenchment, excessive family control leads to expropriation of shareholder wealth at the behest of the self-serving agent. Thus, firm value deteriorates. Moreover, the behavioral agency model proposed by Wiseman and Gomez-Mejia (1998) theorizes that family firms exhibit strong resistance when new markets and products are introduced through diversification; the diversification process also proposes new and untried approaches, which the firm is not yet familiar with. Hence, it is very likely that firm value will diminish.

UNREDIV -- --

(+) Empirical Basis

Gutierrez and Rodriguez (2013) find unrelated diversification pursuits to be prevalent in the Philippine setting due to the abundance of growth opportunities outside a firm’s core industry. Moreover, Amit and Wernerfelt (1990) find that unrelated diversification pursuits reduce risk for the firm.

UNREDIV2 -- (-)

(-) Empirical Basis

Excessive investments and diversification towards unrelated industries may eventually erode firm value due to risks entailed whenever the firm delves into new industries and markets (Aquino, 2003). Moreover, eventual firm value deterioration is attributed to the likelihood of firm agents to over-entrench themselves within the firm, as manifested in over-diversification tendencies. This induces agents to expropriate from shareholders; thus, destroying firm value.

FAMICONUNREDIV (-) (-)

(-) Behavioral

Agency Model

Family firm owners seek to prevent family members from competing within the same market; thus, they diversify to unrelated industries. However, they tend to over-entrench themselves within the firm which, in turn, inclines them to expropriate from shareholders and to try new and untested diversification approaches (behavioral agency model). Thus, diversification performance is negatively moderated by the presence of family altruism.

RELADIV -- --

(-) Empirical Basis

Firms are reluctant to invest in segments that are aligned with the firm’s original industry because it inhibits their level of competitiveness against other firms, which are already expanding and raking in higher profits due to the gains harnessed from entering dynamic industries (Gutierrez and Rodriguez, 2013). Hence, firm value declines whenever firms are unable to compete.

Impact of Family Altruism on Corporate Diversification: Does Entrenching on the Legacy Create Firm Value? 15

RELADIV2 -- -- --

The relationship between firm value and the extent of related diversification is hypothesized to be linear. It does not follow the curvilinear supposition on total diversification because it is posited that related diversification does not significantly influence the extent of total diversification (Gutierrez and Rodriguez, 2013).

FAMICONRELADIV (+) -- --

Family firm owners, on the other hand, are theorized to be more watchful when firm value is inhibited due to repercussions brought about by lack of competitiveness that is posed by related diversification pursuits. Because they are more pressed to increase firm value due to family firm perpetuation purposes, they are asserted to find prudent ways to positively moderate the negative effects of related diversification on firm value.

BANKOWN (+) (+)

(-) Opposed Interests

Hypothesis

Banks, who have significant investments in the firm, seek to maximize returns by protecting firm value. As such, these institutions will oppose firm actions that will further entrench the family within the firm – such as over-diversification – which, in turn, will destroy firm value. Moreover, banks will ensure that shareholder wealth is not engendered by self-serving agents who seek to maximize personal utility; thus, effectively avoiding reductions in firm value. However, the Opposed Interests Hypothesis argues that higher levels of bank ownership may be detrimental to firm value due to conflicts-of-interest that may arise between bank shareholders and other blockholders.

FRMSIZE -- --

(+/-) Empirical Basis