RENEWABLE ENERGY - UNDP in Malaysia

48

M A L A Y S I A G E N E R A T I N G RENEWABLE ENERGY F R O M P A L M O I L W A S T E S

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of RENEWABLE ENERGY - UNDP in Malaysia

M A L A Y S I A G E N E R A T I N G

R E N E WA B L E E N E R G Y F R O M P A L M O I L W A S T E S

M A L A Y S I A G E N E R A T I N G

R E N E WA B L E E N E R G Y F R O M P A L M O I L W A S T E S

Generating Power 19-06-07 9/13/07 10:04 AM Page 1

Published by the United Nations Development Programme (UNDP), Malaysia.

© UNDP. All rights reserved.

First published August 2007.

ISBN 983-3904-01-3

United Nations Development ProgrammeWisma UN, Block C, Kompleks Pejabat Damansara,Jalan Dungun, Damansara Heights, 50490 Kuala Lumpur, Malaysia.www.undp.org.my

A catalogue record for this book is available from the Library of UNDP.

The contents may be freely reproduced for non-commercial purposes with attribution to thecopyright holders.Pictures and graphics are courtesy of PTM and UNDP.Maps are not authoritative on boundaries

Design: Thumb-Print Studio Sdn Bhd.

Generating Power 19-06-07 9/13/07 10:04 AM Page 2

Soaring energy prices are a reminder of the essential role that affordable energy plays in sustainable

economic growth and higher human development. Safeguarding energy supply, especially from clean

indigenous resources, has become more pressing than ever. Current patterns of energy generation

and use impact negatively on the environment at local, regional and global levels.

The degradation of our environment due to energy production from fossil fuels, have contributed to a

global reevaluation of energy use in all economic sectors. The need for sustainable energy use has become

more and more evident. As such, renewable energy is envisaged to become an increasing share of

Malaysia’s electricity generation. With abundant sources available, such as biomass and biogas, the palm

oil industry is likely to become ever more prominent in adopting renewable energy.

In 2002, the government of Malaysia initiated a project Biomass Power Generation and Cogeneration in

Palm Oil Industry (BIOGEN) to help promote the use of renewable energy, with support from the United

Nations Development Programme (UNDP), the Global Environment Facility (GEF) and the private sector.

The project’s primary objective is to develop and implement activities that will build stakeholders’ capacity

and facilitate the greater adoption of renewable energy system. It focuses on palm oil industries and the

use of waste material in generating electricity in the mills and selling it to the grid where possible. The

information presented in this publication provides an indication of the efforts being made and the related

policy implications.

This is the fourth of a new series of periodic publications that report on UNDP Malaysia’s work in its

energy and environment practice area. The large range of projects being undertaken in this portfolio is

designed to support Malaysia’s effort to achieve the Millennium Development Goal 7 (MDG7), of ensuring

environmental sustainability. The series of publications and updates on particular project may be accessed

through UNDP’s website, http://www.undp.org.my.

I would like to thank the GEF for cofunding this project and Ministry of Energy, Water and

Communications (MEWC) for implementing it with UNDP. I would also like to thank other institutional

participants and members of the Biogen team (page IX). Special thanks go to the Report Team for their

professionalism and good efforts in putting this publication together. I sincerely hope that it will be widely

read and will increase awareness of the critical importance of good environmental management on the use

of renewable energy.

iii

F o r e w o r d

Generating Power 19-06-07 9/13/07 10:04 AM Page 3

iv

The project has highlighted a number of important issues and some significant lessons

have been learnt. It is hoped that as the project move towards completion, these

experiences and the outcomes, in the form of policy development and the demonstration

models, will provide exemplars for further steps in renewable energy throughout Malaysia.

Richard Leete Ph.D

Resident Representative

United Nations Development Programme

Malaysia, Singapore & Brunei Darussalam

Generating Power 19-06-07 9/13/07 10:04 AM Page 4

C o n t e n t s

Foreword

Boxes, Tables, Figures and Map

Abbreviations and Acronyms

Glossary

Participants

Global Energy Production and ConsumptionWorld ScenarioExpanding demand for energySources of energyProblems posed by conventional fuelsBioenergy

Malaysia’s Energy ProfileEnergy policyConfiguring a Malaysian response to the global challenge

Palm Oil in the Global MarketThe uses and potential of palm oilPalm oil production and tradeOil palm industry and the environment

The Malaysian Palm Oil MarketModern commercial development

The Biogen ProjectProject strategyThe anticipated contribution of biomass to power generation

Implementing biomass power generation and cogenerationKey barriers to changeOperational uncertaintiesImmediate objectivesPlanned outputsFull scale modelKey achievementsChallenges

Lessons Learnt

Sources of Information PublicationsInternet

iii

vi

vii

viii

ix

1

9

12

15

17

29

31

Generating Power 19-06-07 9/13/07 10:04 AM Page 5

B o x e sBox 1 Renewables

Box 2 Uses of palm oil

T a b l e sTable 1 Selected renewables indicators for Southeast Asian countries, 2004

Table 2 Final energy demand by source, 2000-2010

Table 3 Status of SREP project, July 2006

Table 4 Area planted in oil palm by ownership, 2006

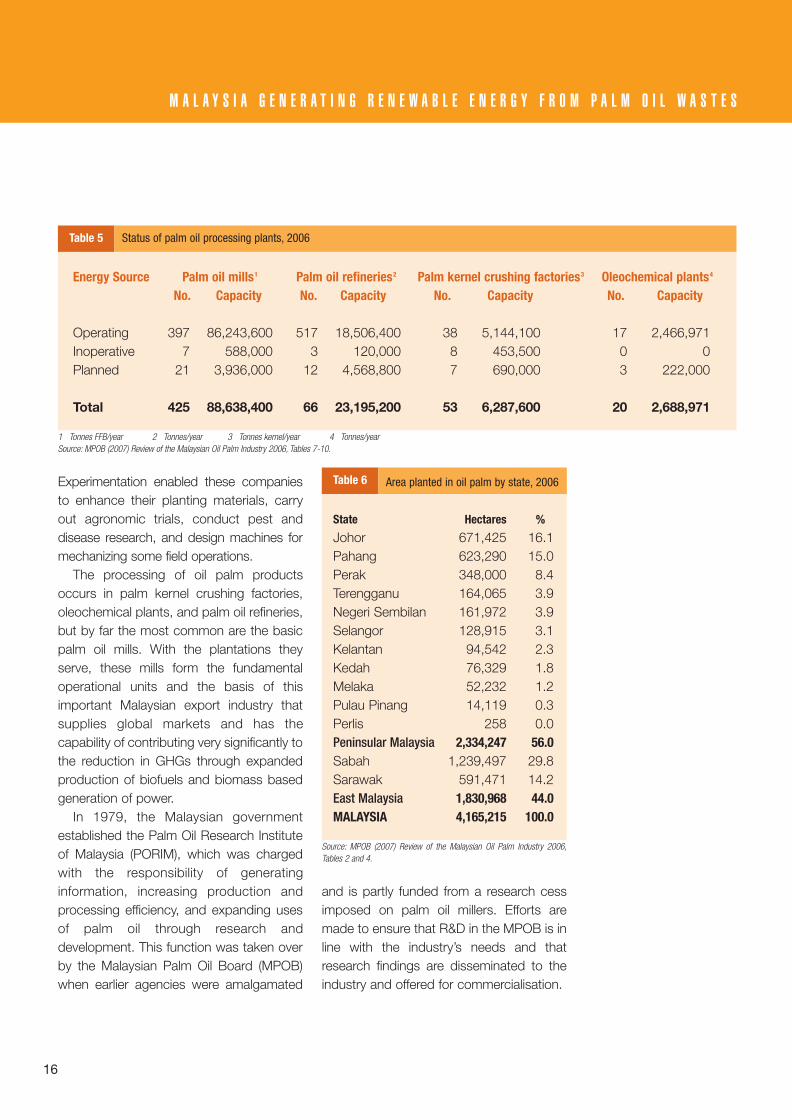

Table 5 Status of palm oil processing plants, 2006

Table 6 Area planted in oil palm by state, 2006

Table 7 Biomass resources potential, 2005

F i g u r e sFigure 1 Fuel share of world total primary energy supply, 2004

Figure 2 Global sectoral consumption of renewables, 2004

Figure 3 Biomass conversion paths

Figure 4 Global palm oil production and trade, 1961-2006

Figure 5 Average annual growth of palm oil versus other oils and fats, 1996-2006

Figure 6 Palm oil versus soy oil – global production and trade, 1996-2006

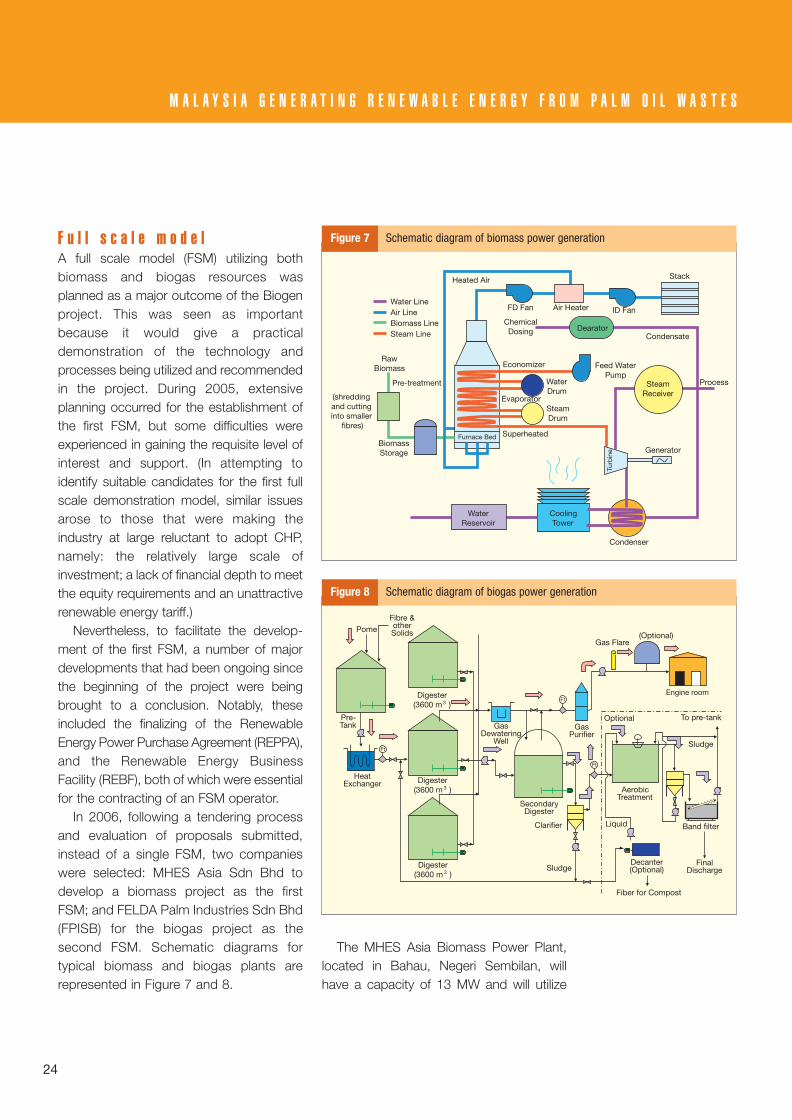

Figure 7 Schematic diagram of biomass power generation

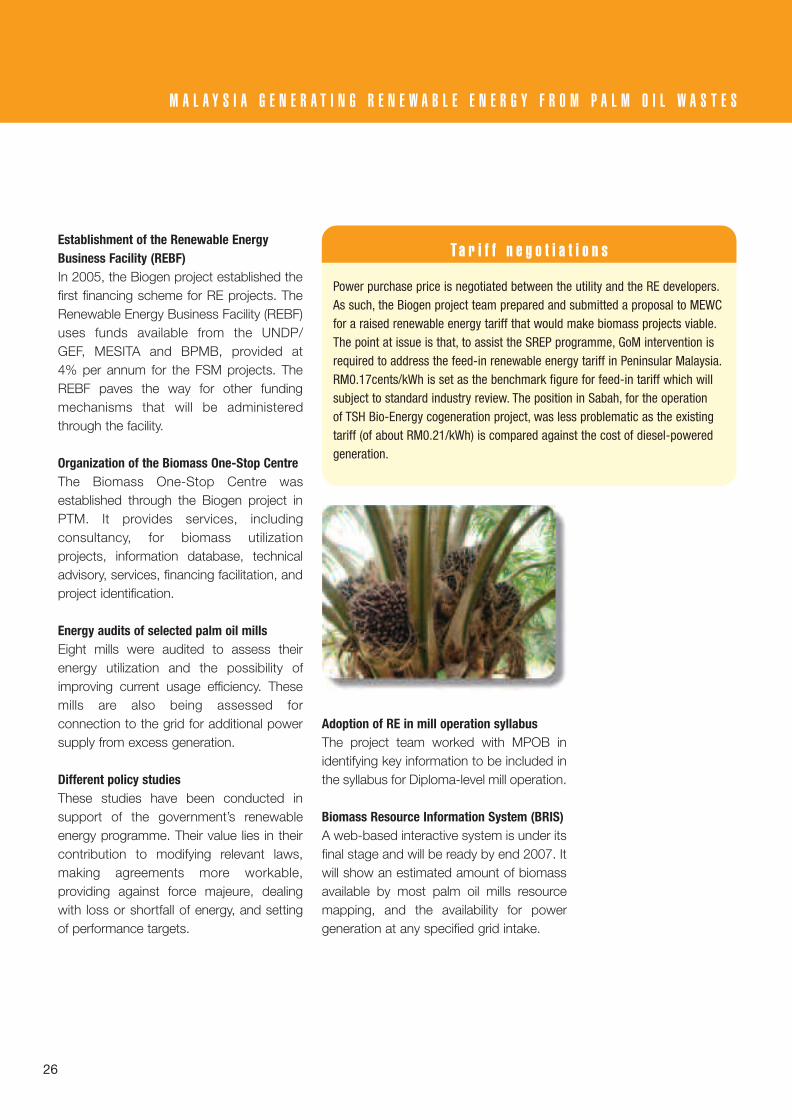

Figure 8 Schematic diagram of biogas power generation

M a pMap 1 Graphical representation of the palm oil processing plants, 2006

B o x e s , Ta b l e s , F i g u r e s a n d M a p

vi

Generating Power 19-06-07 9/13/07 10:04 AM Page 6

A b b r e v i a t i o n s a n d A c r o n y m s

vii

AAIBE Akaun Amanah Industri Bekalan Elektrik(MESITA)

APS Alternative Policy Scenario (of theInternational Energy Agency)

BPMB Bank Pembangunan Malaysia Berhad (new name for Bank Industri & Teknologi)

CDM Clean Development Mechanism (KyotoProtocol)

CHP Combined heat and power

EFB Empty fruit bunches

EPU Economic Planning Unit

FELCRA Federal Land Consolidation andRehabilitation Authority

FELDA Federal Land Development Authority

FFB Fresh fruit bunches

FSM Full scale model

GEF Global Environment Facility

GHG Greenhouse gas

GoM Government of Malaysia

Gt Gigatonnes

GWh Gigawatt hour

ha hectare

IEA International Energy Agency

kt kilotonne

KTAK Kementerian Tenaga, Air dan Kommunikasi(MEWC)

ktoe kilotonnes of oil equivalent

mb/d million barrels per day

mtoe million tonnes of oil equivalent

MEWC Ministry of Energy, Water andCommunications

MIEEIP Malaysian Industrial Energy EfficiencyImprovement Project

MNRE Ministry of Natural Resources andEnvironment

MPIC Ministry of Plantation Industries andCommodities

MPOB Malaysian Palm Oil Board

MPOC Malaysia Palm Oil Council

MW Megawatt

OECD Organisation for Economic Co-operation andDevelopment

OPEC Organization of the Petroleum ExportingCountries

POME Palm oil mill effluent

PORIM Palm Oil Research Institute of Malaysia

PTM Pusat Tenaga Malaysia (Malaysia EnergyCentre)

RE Renewable energy

REBF Renewable Energy Business Facility

REPPA Renewable energy power purchaseagreement

RISDA Rubber Industry Smallholders DevelopmentAuthority

RSPO Roundtable on Sustainable Palm Oil

SCORE Special Committee on Renewable Energy

SESB Sabah Electricity Sdn Bhd

SREP Small Renewable Energy Programme

TNB Tenaga Nasional Berhad

UNDP United Nations Development Programme

Generating Power 19-06-07 9/13/07 10:04 AM Page 7

viii

G l o s s a r y

anaerobic bacterial process without oxygen

bagasse residue of sugar cane crushing

baseload steady flow of power regardless of fluctuating demand

bioenergy energy produced from organic matter

Biogen codename of the project

carotenoids a compound that is a source of vitamin A

cogeneration production of electricity and thermal energy from a common fuel source

co-firing burning of secondary fuel (often renewable energy form) with primaryfossil-fuel in power plants

force majeure extraordinary, unforeseen event beyond the control of contracting parties

lignocellulosic woody biomass (timber, wood chips, straw, manure)

mesocarp fleshy part of the fruit between the skin and the kernel

oleochemical chemical derived from oils or fats

primary energy Energy embodied in natural resources before being converted to moreconvenient forms, such as electricity and gasoline

pyrolysis chemical decomposition of organic materials by heat in the absence ofoxygen

Generating Power 19-06-07 9/13/07 10:04 AM Page 8

ix

P a r t i c i p a n t s

I n s t i t u t i o n a l P a r t i c i p a n t sExecuting Agency Ministry of Energy, Water and Communications

Government of Malaysia

Implementing Agency Pusat Tenaga Malaysia

GEF Implementing Agency United Nations Development Programme

UNDP GEF Bangkok Regional Office

Donor Partners AAIBE, The Government of Malaysia

B i o g e n T e a mDr Anuar Abdul Rahman National Project Director

Ahmad Zairin Ismail Deputy Director

Dr. Sanjayan Velautham Chief Project Coordinator (effective May 2007)

Norasikin Ahmad Ludin Project Coordinator (until February 2007)

Ghazali Talib Programme Manager

Mohd Azwan Mohd Bakri Project Manager

Nor Azaliza Damiri Project Manager

Mohd Hairol Azlin Abdul Latif Project Manager

Mazlina Hashim Project Manager

Zaimul Khalil Project Manager

Mohd Hafiz Mohd Shuib Finance Officer (until February 2007)

Saharuddin Savee Finance Officer (effective Mar 2007)

Haniff Ngadi Technician

Generating Power 19-06-07 9/13/07 10:04 AM Page 9

R e p o r t T e a mDr. Sanjayan Velautham Chief Project Coordinator

Ghazali Talib Programme Manager

Professor Warwick Neville University of Auckland, Consultant

Asfaazam Kasbani UNDP Programme Manager

S t a k e h o l d e r sEconomic Planning Unit (EPU)

Ministry of Energy, Water and Communications (MEWC)

Ministry of Natural Resources and Environment (MNRE)

Malaysian Palm Oil Association (MPOA)

Palm Oil Millers Association (POMA)

Malaysian Palm Oil Board (MPOB)

Energy Commission

Bank Pembangunan Malaysia Berhad (BPMB)

Universities

P a r t i c i p a n t s

x

Generating Power 19-06-07 9/13/07 10:04 AM Page 10

W o r l d S c e n a r i oThe world is facing two energy relatedthreats:• lack of sustainable, secure and affordable

energy supplies; and • the environmental damage incurred in

producing and consuming ever-increasing amounts of energy.

In the first decade of the twenty-firstcentury, soaring energy prices anddestabilizing geopolitical events have beena reminder of the essential role thataffordable energy plays in economic growthand human development, and of thevulnerability of the global energy system tosupply disruption. Safeguarding energysupplies is an international priority, yetcurrent patterns of energy supply andconsumption themselves carry the threat ofirreversible environmental damage.

The need to curb growth in fossil energydemand, to increase geographic and fuelsupply diversity, and to mitigate climatedestabilizing emissions such as greenhouse

gases, is more pressing than ever. UnitedNations’ member countries have beguntaking initiatives on developing alternativeenergy scenarios and strategies aimed at a more sustainable and cleaner energyfuture. The Commission for SustainableDevelopment (UNCSD) for example,responsible for reviewing progress in theimplementation of Agenda 21 and the RioDeclaration on Environment and Develop-ment, discusses the use of renewableenergy in length and reaffirms commitmentsby member countries in adopting it wherepossible. UN Framework on Convention on Climate Change (UNFCCC), started in 1994, sets an overall framework forintergovernmental efforts to tackle thechallenge posed by climate change andrecognizes that the climate system is ashared resource whose stability can beaffected by industrial and other emissions ofcarbon dioxide and other greenhousegases. The use of renewable energy isfurther encouraged as the energy sector is

1

G L O B A L E N E R G Y P R O D U C T I O N A N D C O N S U M P T I O N

Generating Power 19-06-07 9/13/07 10:04 AM Page 1

2

the main culprit in GHG emissions. KyotoProtocol (started in 1997), strengthens theConvention by committing Annex I Partiesto individual, legally-binding targets to limitor reduce their greenhouse gas emissionsand the implementation of renewableenergy system remains as the most feasibleand popular options available.

For the G8 nations, the InternationalEnergy Agency (IEA) was requested toprepare a strategy in the form of anAlternative Policy Scenario (APS) thatproposes policies and measures for theconsideration of governments in order tosignificantly reduce the rate of increase inenergy demand and emissions. Theeconomic cost of these policies, putforward in 20061, would be more thanoutweighed by the economic benefits thatwould accrue from producing and usingenergy more efficiently.

With worldwide adoption of stricterenvironmental standards and guidelines forgreenhouse gas emissions, it is becomingclear that renewable energy systems will becredited for their inherent advantage inlowering emissions. These environmentalbenefits will contribute towards making thedelivered costs more palatable and arealready the driving force behind policyinitiatives in many more advanced countries.

Whether governments of OECD or non-OECD countries will adopt the AlternativePolicy Scenario or some elements of itremains to be seen: huge obstacles, rangingfrom powerful vested interests to publicindifference, will have to be overcome.Reconciling the goals of energy security andenvironmental protection requires strongand coordinated government action andpublic support.

Meanwhile, fossil fuel demand andgreenhouse gas emissions continue ontheir current unsustainable trajectories. Inthe following sections, the magnitude andimplications of these continuing trends aremore fully explored.

E x p a n d i n g d e m a n d f o re n e r g yBetween 2006 and 2030, unless strongand coordinated government action andpublic support significantly modify recenttrends, global primary energy demand isprojected to increase by just over half, or atan annual rate of 1.6%. Over 70% of thatincrease in demand will be from developingcountries, China alone accounting for nearly30%. This represents a significant shift inthe centre of gravity of global energydemand towards countries that areexperiencing faster economic (and oftenpopulation) growth than more advancedcountries such as those in the Organisationfor Economic Co-operation andDevelopment (OECD).

M A L A Y S I A G E N E R A T I N G R E N E W A B L E E N E R G Y F R O M P A L M O I L W A S T E S

1 International Energy Agency, World Energy Outlook 2006, Paris.

Generating Power 19-06-07 9/13/07 10:04 AM Page 2

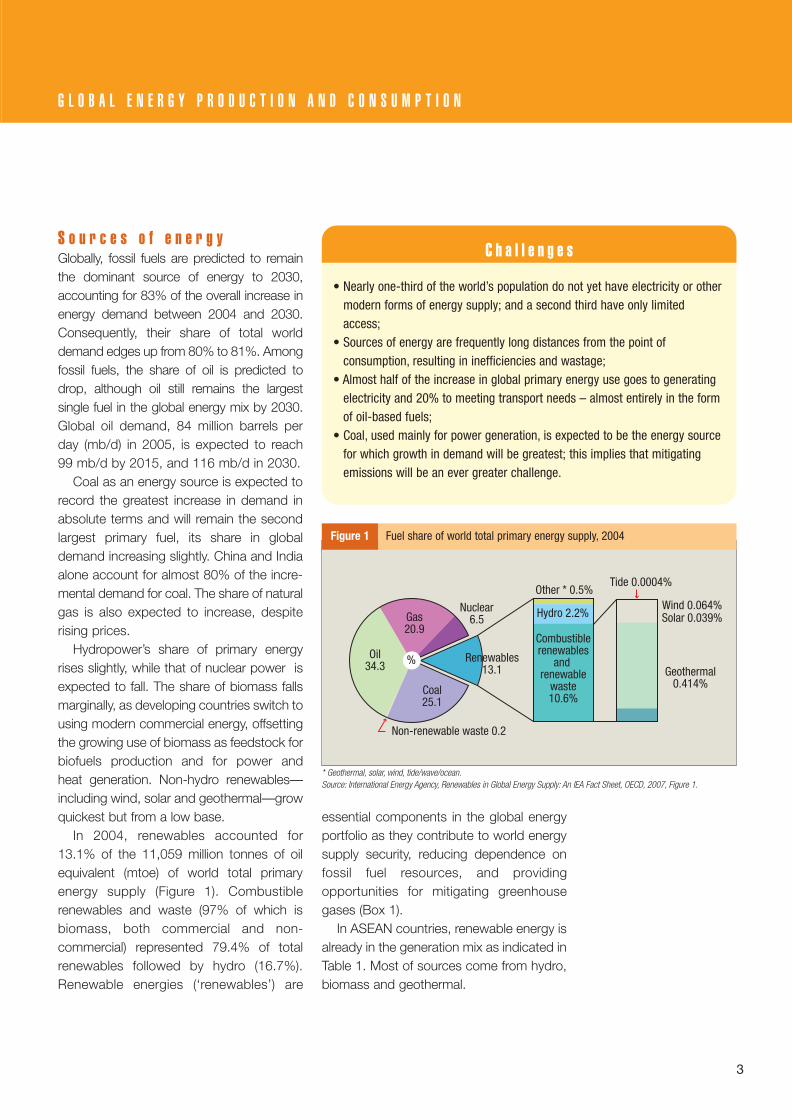

S o u r c e s o f e n e r g yGlobally, fossil fuels are predicted to remainthe dominant source of energy to 2030,accounting for 83% of the overall increase inenergy demand between 2004 and 2030.Consequently, their share of total worlddemand edges up from 80% to 81%. Amongfossil fuels, the share of oil is predicted todrop, although oil still remains the largestsingle fuel in the global energy mix by 2030.Global oil demand, 84 million barrels perday (mb/d) in 2005, is expected to reach99 mb/d by 2015, and 116 mb/d in 2030.

Coal as an energy source is expected torecord the greatest increase in demand inabsolute terms and will remain the secondlargest primary fuel, its share in globaldemand increasing slightly. China and Indiaalone account for almost 80% of the incre-mental demand for coal. The share of naturalgas is also expected to increase, despiterising prices.

Hydropower’s share of primary energyrises slightly, while that of nuclear power isexpected to fall. The share of biomass fallsmarginally, as developing countries switch tousing modern commercial energy, offsettingthe growing use of biomass as feedstock forbiofuels production and for power and heat generation. Non-hydro renewables—including wind, solar and geothermal—growquickest but from a low base.

In 2004, renewables accounted for13.1% of the 11,059 million tonnes of oilequivalent (mtoe) of world total primaryenergy supply (Figure 1). Combustiblerenewables and waste (97% of which isbiomass, both commercial and non-commercial) represented 79.4% of totalrenewables followed by hydro (16.7%).Renewable energies (‘renewables’) are

essential components in the global energyportfolio as they contribute to world energysupply security, reducing dependence onfossil fuel resources, and providingopportunities for mitigating greenhousegases (Box 1).

In ASEAN countries, renewable energy isalready in the generation mix as indicated inTable 1. Most of sources come from hydro,biomass and geothermal.

3

G L O B A L E N E R G Y P R O D U C T I O N A N D C O N S U M P T I O N

• Nearly one-third of the world’s population do not yet have electricity or othermodern forms of energy supply; and a second third have only limitedaccess;

• Sources of energy are frequently long distances from the point ofconsumption, resulting in inefficiencies and wastage;

• Almost half of the increase in global primary energy use goes to generatingelectricity and 20% to meeting transport needs – almost entirely in the formof oil-based fuels;

• Coal, used mainly for power generation, is expected to be the energy sourcefor which growth in demand will be greatest; this implies that mitigatingemissions will be an ever greater challenge.

C h a l l e n g e s

* Geothermal, solar, wind, tide/wave/ocean.Source: International Energy Agency, Renewables in Global Energy Supply: An IEA Fact Sheet, OECD, 2007, Figure 1.

Oil34.3

Gas20.9

%

Nuclear6.5

Other * 0.5%

Hydro 2.2%

Combustiblerenewables

and renewable

waste10.6%

Geothermal0.414%

Tide 0.0004%

Wind 0.064%Solar 0.039%

Coal25.1

Non-renewable waste 0.2

Renewables13.1

Figure 1 Fuel share of world total primary energy supply, 2004

Generating Power 19-06-07 9/13/07 10:04 AM Page 3

The principal constraint in advancingcommercial renewable energy over recentdecades has been cost-effectiveness. Withthe exception of large hydropower,combustible biomass and larger geo-thermal projects, the average costs ofrenewable energy are generally notcompetitive with wholesale electricity andfossil fuel prices.

P r o b l e m s p o s e d b yc o n v e n t i o n a l f u e l sEconomic and security issuesRising oil and gas demand, if unchecked,would accentuate the consuming countries’vulnerability to severe supply disruption andassociated price escalation. Most developedcountries and developing Asian countries arebecoming increasingly dependent on

4

M A L A Y S I A G E N E R A T I N G R E N E W A B L E E N E R G Y F R O M P A L M O I L W A S T E S

Solid biomass: Organic non-fossil material of biological origin that may be used as fuel for heat production or electricity generation.

Wood, wood waste and other solid waste: Purpose grown energy tree crops; woody materials generated by industrialprocesses (timber/paper industries in particular) or directly byforestry and agriculture (firewood, wood chips, bark, sawdust,shavings, chips, etc); wastes such as straw, rice husks, nut shells, poultry litter and crushed grape dregs.

Charcoal: Solid residue of the destructive distillation and pyrolysis of wood and other vegetal material.

Biogas: Gases composed principally of methane and carbon dioxide produced by anaerobic digestion of biomass and combusted to produce heat and/or power.

Liquid biofuels: Bio-based liquid fuel from biomass transformation, mainly used in transportation applications.

Municipal waste (renewables): Wastes produced by the residential, commercial, and public services sectors and

incinerated in specific installations to produce heat and/or power. The renewable energy portion is defined by the energy value ofcombusted biodegradable material, thus excluding any non-biodegradable waste.

Hydropower: Potential and kinetic energy of water converted into electricity in hydroelectric plants ranging in size from very smallto huge operations.

Geothermal energy: Energy emitted from within the earth’s crust, usually in the form of hot water or steam, exploited at suitablesites for electricity generation after transformation, or utilized directly as heat.

Solar Energy: Solar radiation exploited for hot water production and electricity generation. Passive solar energy for direct heating,cooling and lighting also contributes but is too difficult to measure and record in the data.

Wind energy: Kinetic energy of wind exploited for electricity generation by wind turbines.

Tide/Wave/Ocean energy: Mechanical energy derived from tidal movement, wave motion or ocean current, exploited for energygeneration.

Box 1 Renewables

Source of Information: International Energy Agency, Renewables in Global Energy Supply: An IEA Fact Sheet, OECD, 2007, Annex 1.

Generating Power 19-06-07 9/13/07 10:04 AM Page 4

5

G L O B A L E N E R G Y P R O D U C T I O N A N D C O N S U M P T I O N

imports as their indigenous production failsto keep pace with demand. Non-OPECproduction of conventional crude oil andnatural gas liquids is expected to peak byabout 2015. By 2030, OECD countries willbe importing two-thirds of their oil needscompared with 56% in 2005. A largeproportion of the additional imports willoriginate in the Middle East and betransported along lengthy and vulnerablemaritime routes. The concentration of oilproduction in a small group of countries with large reserves, notably the Middle EastOPEC members and Russia, will increasetheir market dominance and ability toimpose higher prices. An increasing shareof gas demand is also expected to be metby imports, via pipeline or in the form of liquidnatural gas shipped from distant suppliers.

Although most oil-importing economiesaround the world have continued to growstrongly, they would almost certainly havegrown even more rapidly had the price of oiland other forms of energy not increased.The longer prices remain high or rise further, the greater the threat to economic growth in all importing countries. Thegrowing insensitivity of oil demand to priceaccentuates the potential impact of a supplydisruption on international oil prices. Inparticular, the share of transport demand inglobal consumption is projected to rise, andas a result, oil demand can be expected tobecome less and less responsive tomovements in international crude oil prices.

Environmental issuesIf present production and consumptionpatterns continue, global energy related tocarbon dioxide (CO2) emissions will increaseby 14 gigatonnes (Gt), or 55%, to 40 Gt,

between 2004 and 2030, a rate of 1.7% peryear. Power generation contributes half ofthis increase in global emissions. Coalovertook oil in 2003 as the leadingcontributor to global energy related CO2

emissions and consolidates its positionthrough to 2030. Emissions are projected togrow slightly faster than primary energydemand, a reversal of the trend evidentsince 1980, because of the increase in the

A Share of total renewables in TPES.B Share of renewables excluding combustible renewables and waste.1 Total primary energy supply. 2 Million tonnes of oil equivalent.Source: International Energy Agency, Renewables in Global Energy Supply: An IEA Fact Sheet, OECD, 2007, Table 1.

Country/Continent Shares of Renewables in TPES1

Mtoe2

Brunei Darussalam 2.7 0.7 0.0Indonesia 174.0 30.8 3.8Malaysia 56.7 5.8 0.9Philippines 44.3 45.6 21.6Singapore 25.6 0.0 0.0Thailand 97.1 16.9 0.5Vietnam 50.2 50.2 3.0Asia 1,289.4 31.8 2.4World 11,058.6 13.1 2.7

TPES1 A%

B%

Table 1 Selected renewables indicators for Southeast Asian countries, 2004

Generating Power 19-06-07 9/13/07 10:04 AM Page 5

average carbon content of primary energyconsumption.

Developing countries account for overthree-quarters of the increase in global CO2

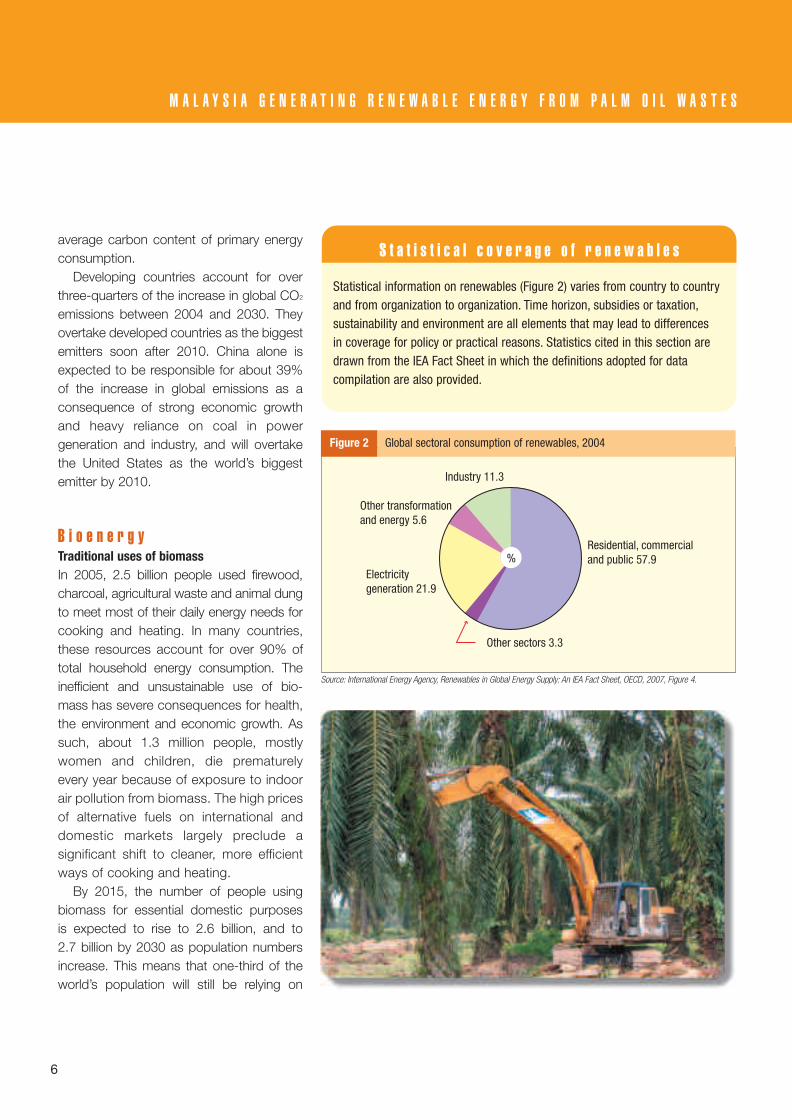

emissions between 2004 and 2030. Theyovertake developed countries as the biggestemitters soon after 2010. China alone isexpected to be responsible for about 39%of the increase in global emissions as aconsequence of strong economic growthand heavy reliance on coal in powergeneration and industry, and will overtakethe United States as the world’s biggestemitter by 2010.

B i o e n e r g yTraditional uses of biomassIn 2005, 2.5 billion people used firewood,charcoal, agricultural waste and animal dungto meet most of their daily energy needs forcooking and heating. In many countries,these resources account for over 90% oftotal household energy consumption. Theinefficient and unsustainable use of bio-mass has severe consequences for health,the environment and economic growth. Assuch, about 1.3 million people, mostlywomen and children, die prematurelyevery year because of exposure to indoorair pollution from biomass. The high pricesof alternative fuels on international anddomestic markets largely preclude asignificant shift to cleaner, more efficientways of cooking and heating.

By 2015, the number of people usingbiomass for essential domestic purposesis expected to rise to 2.6 billion, and to2.7 billion by 2030 as population numbersincrease. This means that one-third of theworld’s population will still be relying on

6

M A L A Y S I A G E N E R A T I N G R E N E W A B L E E N E R G Y F R O M P A L M O I L W A S T E S

Statistical information on renewables (Figure 2) varies from country to countryand from organization to organization. Time horizon, subsidies or taxation,sustainability and environment are all elements that may lead to differences in coverage for policy or practical reasons. Statistics cited in this section aredrawn from the IEA Fact Sheet in which the definitions adopted for datacompilation are also provided.

S t a t i s t i c a l c o v e r a g e o f r e n e w a b l e s

Source: International Energy Agency, Renewables in Global Energy Supply: An IEA Fact Sheet, OECD, 2007, Figure 4.

Industry 11.3

%

Other sectors 3.3

Residential, commercial and public 57.9

Other transformationand energy 5.6

Electricitygeneration 21.9

Figure 2 Global sectoral consumption of renewables, 2004

Generating Power 19-06-07 9/13/07 10:04 AM Page 6

biomass fuels, a share barely smaller thanin 2005.

Halving the number of households usingbiomass for cooking by 2015, arecommendation of the United NationsMillennium project, would involve 1.3 billionpeople switching to liquefied petroleum gasand other commercial fuels. This would nothave a significant impact on world oildemand and the equipment would cost lessthan US$1.5 billion per year. Vigorousconcerted government action, with supportfrom industrialised countries, would beneeded to achieve this target, together withincreased funding from both public andprivate sources. Policies would need toaddress barriers to access, affordability andsupply, and to form a central component ofbroader development strategies.

Modern forms and uses of biomassBiomass is attractive for use either as astand-alone fuel or in fuel blends, such asco-firing wood with coal, or mixing ethanolor biodiesel with conventional petroleumbased fuels. Anaerobic digestion has majorpotential in countries with ample resources.Electricity generated from biomass is basedon steam turbine technology. Many regionsof the world still have large untappedsupplies of biomass residues that could beconverted into competitively pricedelectricity using steam turbine power plants.

Biomass combustion for heat and poweris a fully mature technology. It offers both aneconomic fuel option and a ready disposalmechanism for agricultural, industrial andmunicipal wastes. However, the industryhas remained relatively stagnant eventhough demand for biomass (mainly wood)continues to grow in many developing

countries. One of the problems of biomassis that material directly combusted incooking stoves produces pollutants,leading to severe health and environmentalconsequences, although improved cookingstove programmes are alleviating some of these effects. A second issue is that burning biomass emits CO2, eventhough biomass combustion is generally

7

G L O B A L E N E R G Y P R O D U C T I O N A N D C O N S U M P T I O N

There are still 1.6 billion people in the world without electricity. To achieve theMillennium Development Goals relating to environmental degradation and useof solid fuels, this number would need to fall to less than one billion by 2015.

E n e r g y a n d t h e M i l l e n n i u m D e v e l o p m e n t G o a l s

Biomass resources include agricultural residues; animal manure; wood wastesfrom forestry and industry; municipal green wastes; sewage sludge; anddedicated energy crops such as short rotation (3-15 years) coppice(eucalyptus, poplar, willow), grasses, sugar crops (sugar cane, beet, sorghum),starch crops (corn, wheat) and oil crops (soy, sunflower, oilseed rape, iatropha,palm oil). Organic wastes and residues have been the main biomass sourcesso far, but energy crops are gaining in importance and market share. Residues,wastes, and begasse are primarily used for heat and power generation. Sugar,starch and oil crops are primarily used for fuel production.

B i o m a s s f e e d s t o c k a n d p r o c e s s e s

Generating Power 19-06-07 9/13/07 10:04 AM Page 7

considered to be ‘carbon-neutral’ becausecarbon is absorbed by plant material duringits growth, thus creating a carbon cycle.

Biomass can be burnt (or co-fired) toproduce electricity and steam in a CHPplant via a steam turbine in dedicatedpower plants. The typical size of theseplants is ten times smaller (less than 100MW) than coal fired plants because of thelimited availability of local feedstock andhigh transportation costs. Fossil energyconsumed for bio-power production usingforestry and agriculture products can be aslow as 2-5% of the final energy produced.Based on life-cycle assessment, net carbonemissions per unit of electricity can achievebelow 10% of the emissions from fossil fuelbased electricity.

BiofuelsBiofuels are expected to make a significantcontribution to meeting global roadtransport energy needs. They are estimatedto account for 4% of road fuel consumptionby 2030, up from 1% in 2005; under theIEA’s APS, consumption could be as highas 7%. The United States, European Unionand Brazil are likely to remain the leadingproducers and consumers of biofuels.Ethanol is expected to account for mostof the increase in biofuel use worldwide, as production costs are expected to fallfaster than those of biodiesel, the othermain biofuel.

Rising food demand, which competeswith biofuels for existing arable and pastureland, will constrain the potential for biofuelproduction using current technology. In2005, about 14 million hectares of land wereused for the production of biofuels, equal toabout 1% of the world’s available arable land.

This share is expected to rise to 2% by 2030,but if the policies of the APS are adopted,this would amount to 3.5%. The minimalamount of arable land needed in 2030 isequal to more than that of France and Spain,and under the APS would equate to all thearable land in the OECD countries.

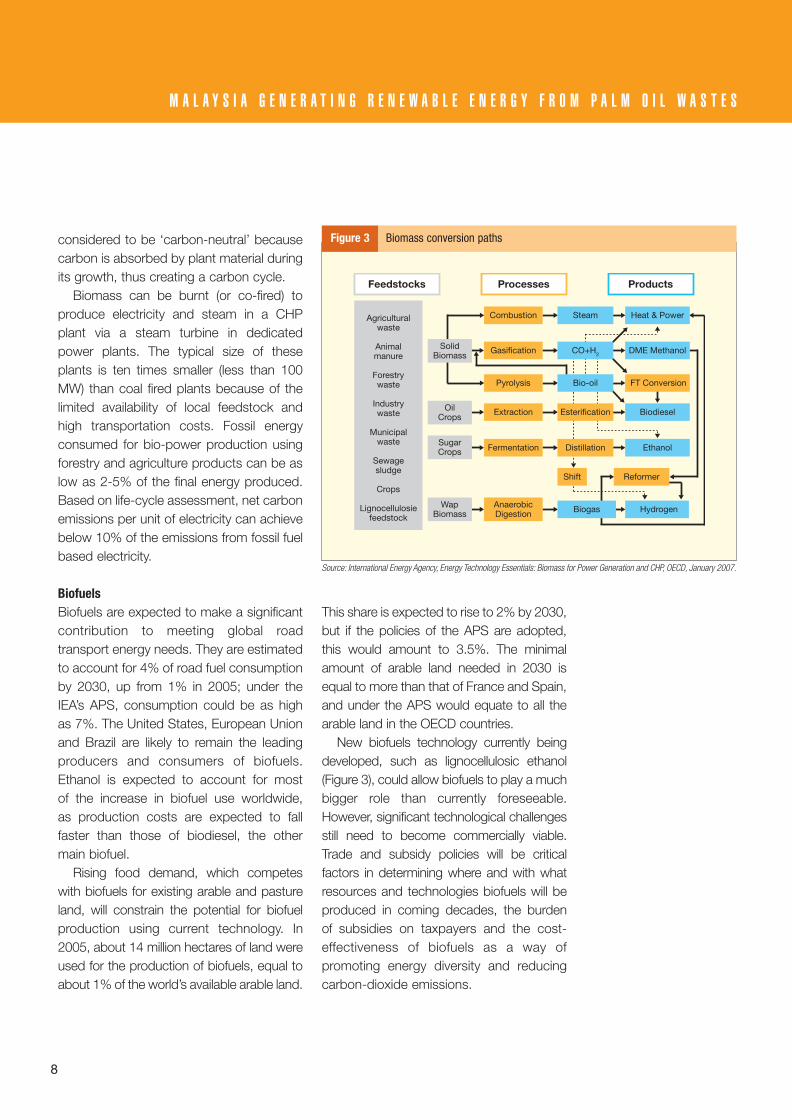

New biofuels technology currently beingdeveloped, such as lignocellulosic ethanol(Figure 3), could allow biofuels to play a muchbigger role than currently foreseeable.However, significant technological challengesstill need to become commercially viable.Trade and subsidy policies will be criticalfactors in determining where and with whatresources and technologies biofuels will beproduced in coming decades, the burden of subsidies on taxpayers and the cost-effectiveness of biofuels as a way ofpromoting energy diversity and reducingcarbon-dioxide emissions.

8

M A L A Y S I A G E N E R A T I N G R E N E W A B L E E N E R G Y F R O M P A L M O I L W A S T E S

Source: International Energy Agency, Energy Technology Essentials: Biomass for Power Generation and CHP, OECD, January 2007.

Feedstocks

Agriculturalwaste

Animalmanure

Forestrywaste

Industrywaste

Municipalwaste

Sewagesludge

Crops

Lignocellulosiefeedstock

Processes Products

SolidBiomass

Combustion Steam Heat & Power

DME Methanol

FT Conversion

Biodiesel

Ethanol

Reformer

Hydrogen

Bio-oil

Esterification

Distillation

CO+H2Gasification

Pyrolysis

Extraction

Fermentation

Biogas

Shift

AnaerobicDigestion

OilCrops

SugarCrops

WapBiomass

Figure 3 Biomass conversion paths

Generating Power 19-06-07 9/13/07 10:04 AM Page 8

9

M A L A Y S I A ’ S E N E R G Y P R O F I L E

E n e r g y p o l i c yThe crucial role of energy in achievingMalaysia’s development aspirations haslong been recognized, particularly in thecountry’s five-year plans. An early bench-mark was the establishment in 1974 ofPetroliam Nasional Berhad (PETRONAS) asthe national oil company responsible for theexploration, development, refining, andmarketing of Malaysia’s petroleum products.This development, of major significance tothe country’s economy, has been followedby the formulation of several importantpolicies reflecting the issues challengingthe government and the economy.

In keeping with the policies developedover the last four decades, the energysector is focused on ensuring a secure,reliable and cost-effective supply of energy,aimed at enhancing the competitivenessand resilience of the economy. The NinthMalaysia Plan 2006-2010 encouragesenergy efficiency, especially in transport,commercial and industrial sectors, and ingovernment buildings, and aims to diversifyfuel sources through greater utilization ofrenewable energy.

In Malaysia, the transport sector is thelargest consumer of energy accounting for40.5% of the total final commercial energydemand in 2005, followed by the industrialsector (38.6%) and the residential andcommercial sector (13.1%), all expected toincrease demand by over 6% during the2006-2010 period.

Electricity accounts for about 19% of thetotal final energy demand in Malaysia (Table 2). Reported electricity generationdoes not include electricity generateddirectly by industrial consumers for theirown use. In response to the Government of

Malaysia’s policy, the fuel mix for electricitygeneration is gradually being modified, withthe share of natural gas in particular being

Policy / Plan Broad Objectives1975 National introduced to ensure optimal use of petroleum petroleum policy resources, regulation of ownership and management of

the industry, and economic, social, and environmentalsafeguards in the exploitation of this valuable resource

1979 National formulated to achieve supply, utilization energy policy and environmental objectives

1980 National introduced to guard against over depletion policy exploitation of oil and gas

1981 Four fuel emphasis given to fuel diversification, designed to diversification policy avoid dependence on oil; aimed at placing increased

emphasis on gas, hydro and coal

2000 Renewable energy introduced in recognition of the potential of biomass,as the fifth fuel policy biogas and other renewable energy resources

2006 National designed to pave the way for extensive Biofuel Policy development of the biofuels industry

Seventh Malaysia Plan Emphasis on energy efficiency and on generation1996-2001, from renewable sources in an effort to reduce Eighth Malaysia Plan, the rapid depletion of other fuel sources2001-2005 and Ninth Malaysia Plan 2006-2010

Policies at a Glance

Generating Power 19-06-07 9/13/07 10:04 AM Page 9

10

M A L A Y S I A G E N E R A T I N G R E N E W A B L E E N E R G Y F R O M P A L M O I L W A S T E S

reduced to about 56% by 2010, and coalincreased substantially to 36.5% (from just8.8% in 2000).

Under the Ninth Malaysia Plan 2006-2010, it was estimated that demand forelectricity will reach 20,087 MW in 2010.Renewable energy is expected tocontribute 350 MW to the total energysupply by that time: about 300 MW of RE is expected to be generated and connectedto the grid in Peninsular Malaysia, and 50 MW to the grid in Sabah.

C o n f i g u r i n g a M a l a y s i a nr e s p o n s e t o t h e g l o b a lc h a l l e n g eThe increasing demand for fossil fuels,despite their proportional decline, poses amajor challenge for the Government ofMalaysia. Given the continuation of existingtrends, the power sector was forecast toincrease GHG emissions by 30% between1995 and 2005. The two other ongoingUNDP-GEF funded Malaysian IndustrialEnergy Efficiency Improvement Project(MIEEIP) and the Building Integrated

Photovoltaics (BIPV) are the manifestationof Malaysia’s commitment to reduce GHGemissions. The Biogen project aims tofurther mitigate these by progressivelyreplacing fossil fuels used in electricitygeneration mix with renewable energyresources, especially utilising wastes fromthe palm oil industry.

In 2001, in a significant step towardsencouraging and intensifying the utilisationof renewable energy (RE) in powergeneration, the Malaysian governmentlaunched the Small Renewable EnergyPower (SREP) programme. The objectivewas to encourage the private sector toundertake small power generation projectsusing renewable resources includingbiomass, biogas, municipal waste, solar,mini-hydro, and wind energy.

As recently as 2004, the programme wasnot progressing well due to the uncertaintyof long-term fuel supplies, long negotiationof the Renewable Energy Power PurchaseAgreement (REPPA) and difficulty insecuring loans to finance the projects.However, in 2005, the first grid connectedbiomass-based power plant in Malaysia,

Energy Source Petajoules Per cent of Total Average Annual Growth Rate (%)

Petroleum productsNatural gasElectricityCoal and cokeTotalPer capita consumption 2

1 Malaysia Plan 2 GigajoulesSource: Ninth Malaysia Plan 2006-2010.

820.0161.8220.441.5

1,243.7

52.9

1,023.1246.6310.052.0

1,631.7

62.2

1,372.9350.0420.075.0

2,217.9

76.5

65.913.017.73.4

100.0

62.715.119.03.2

100.0

61.915.818.93.4

100.0

4.58.87.14.65.6

3.3

6.17.36.37.66.3

4.2

2000 2005 2010 2000 2005 2010 8MP1 9MP2

Table 2 Final energy demand by source, 2000-2010

Generating Power 19-06-07 9/13/07 10:04 AM Page 10

11

M A L A Y S I A ’ S E N E R G Y P R O F I L E

TSH Bio-Energy Sdn Bhd, commencedoperations in Sabah which has an installedcapacity of 14 MW where 10MW is for thegrid-connection.

Under the SREP guidelines, maximumpower export capacity of a small RE plantfor sale to the grid is limited to 10 MW,although a plant’s overall capacity may belarger. The Special Committee on RE(SCORE), set up under the Ministry ofEnergy, Water and Communications,coordinates the implementation of theSREP applications and also formulatesgovernment’s strategy to intensify thedevelopment of RE as the country’s fifth fuelresource. A technical secretariat was alsoset up at the Energy Commission(Suruhanjaya Tenaga) to help facilitate theindustry’s participation in the programme.

The status of generating power fromrenewable energy sources is immense(Table 3), and by far the most easilyaccessible and cost-effective feed-stock isreadily available in the form of palm oilresidues. Traditionally palm oil mills haveutilized a proportion of this material togenerate the requisite heat and power forextracting oil from the fruit, but hugeadditional quantities of residues pose aserious disposal problem for the industry.Efficient methods of generating CHP tomeet operating requirements, plus asurplus of electricity utilizing the surplusrenewable residues for export to thenational grid, represents a double benefit forthe industry and for the country, whileassisting in the reduction of emissions fromfossil fuels. In addition, palm oil itself isalready being used on a small scale as abiofuel supplement to fossil fuels and moreefficient technologies are being developed

for this purpose. The palm oil industrytherefore has considerable potential forsupporting the economy through theprovision of renewable energy as well asthrough the traditional export of agriculturalcommodities.

Source: MEWC, 2006.

Broad

Category

Biomass

Landfill gas

Mini hydro

Total

– empty fruit bunches

– wood waste

– rice husks

– municipal waste

15

1

1

4

3

23

47

103.2

6.6

10.0

25.0

6.0

93.2

244.0

42.3

2.7

4.1

10.2

2.4

38.2

100.0

Specific type ofrenewable energy

Number ofprojects

Capacity (MW) forgrid connection

Contribution%

Table 3 Status of SREP project, July 2006

The first grid connected biomass based power plant in Malaysia startedcommercial operation early in 2005. TSH Bio-Energy Sdn Bhd, located in Tawau,Sabah, has an installed capacity of 14 MW and is contracted to sell 10MW toSabah Electricity Sdn Bhd (SESB) for 21 years. The cogeneration plant processespalm oil milling residues (mainly empty fruit branches) as fuel.

T h e f i r s t g r i d - c o n n e c t e d b i o m a s s p o w e r p l a n t

The Energy Commission (Suruhanjaya Tenaga) was established under theEnergy Commission Act 2001 to regulate the electricity supply and piped gassupply industries in Peninsular Malaysia and Sabah, whilst in Sarawak thestate Chief Electrical Inspectorate is the regulator of the electricity supplyindustry under the Electricity Ordinance of Sarawak. It acts as the SREPtechnical secretariat.

T h e E n e r g y C o m m i s s i o n

Generating Power 19-06-07 9/13/07 10:04 AM Page 11

T h e u s e s a n d p o t e n t i a l o fp a l m o i lPalm oil is the second most tradedvegetable oil crop in the world after soy, andover 90% of the world’s palm oil exports areproduced in Malaysia and Indonesia. Palm

oil is still mostly used as an ingredient in the manufacture and further processing of food products (Box 2), but many otheruses are becoming increasingly important.In the twenty-first century, concern forserious environmental issues is offering new

Palm oil can be used –As an edible oil:– a high quality cooking oil– a component of oil-based fats and margarine used in baking– an ingredient in wide range of cooking materials, dairy fat substitutes, milks and ice creams– a fat ingredient in animal feedAs an ingredient for non-edible uses:– soaps– biodegradable detergents– oleochemical products (fatty esters, fatty alcohol, fatty nitrogen compounds, glycerol)For non-edible applications:– drilling mud for the oil industry – metallic soaps for the manufacturing of– epoxidated oil as a plastifier and lubricating greases and metallic driers

sterilizer in the plastics industry (PVC) – fuels– gum – greases for lubrication and protection– candles – cold rolling presses in steel making– cosmetics – tinplate rolling– printing inks – acids to lubricate fibres in the textile industry

Box 2 Uses of palm oil

12

P A L M O I L I N T H E G L O B A L M A R K E T

Generating Power 19-06-07 9/13/07 10:04 AM Page 12

13

P A L M O I L I N T H E G L O B A L M A R K E T

opportunities for diversification of oil palmproducts. In particular, palm oil basedbiofuel provides a high quality supple-mentary fuel for blending with fossil fuelssuch as petroleum to help meet the growingrenewable energy demand emerging indeveloped countries, especially those of theEuropean Union. Nor is this the onlycontribution the industry can make torenewable energy: as noted earlier, residuebiomass from milling greatly exceeds thequantities required for heat and power tocarry out palm oil processing, and thesurplus residues can be utilized to generateelectricity for the national grid.

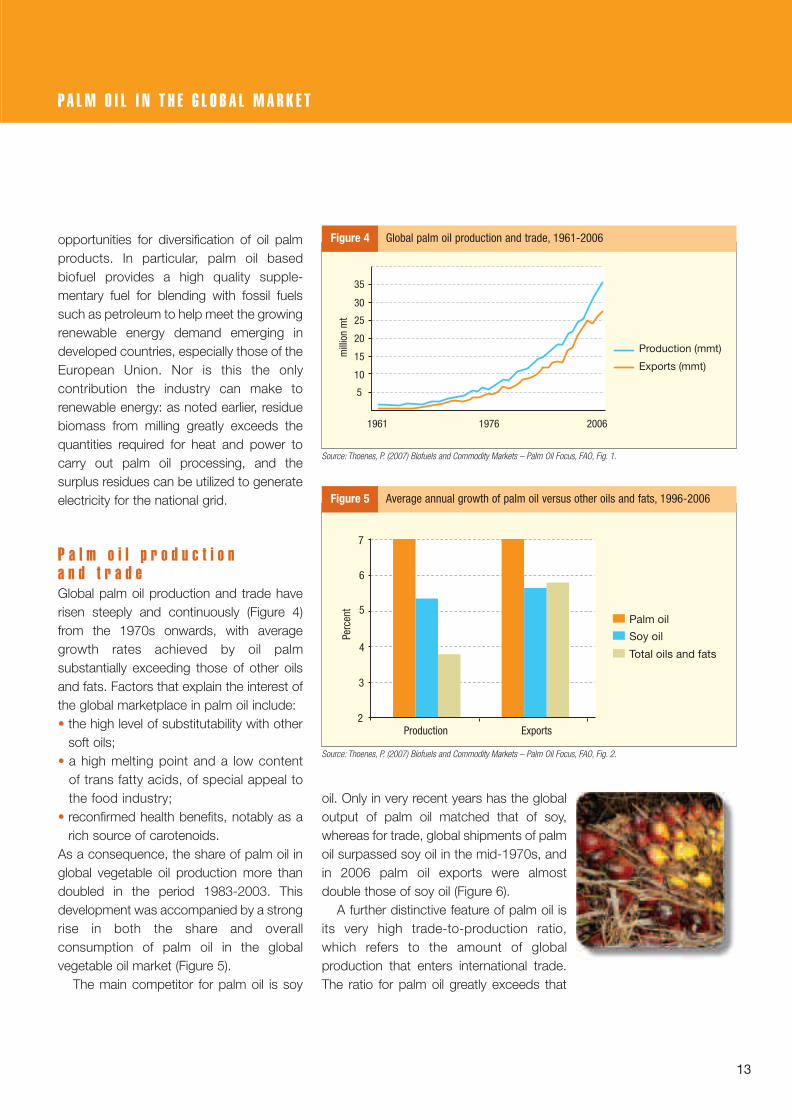

P a l m o i l p r o d u c t i o n a n d t r a d eGlobal palm oil production and trade haverisen steeply and continuously (Figure 4)from the 1970s onwards, with averagegrowth rates achieved by oil palmsubstantially exceeding those of other oilsand fats. Factors that explain the interest ofthe global marketplace in palm oil include:• the high level of substitutability with other

soft oils; • a high melting point and a low content

of trans fatty acids, of special appeal tothe food industry;

• reconfirmed health benefits, notably as arich source of carotenoids.

As a consequence, the share of palm oil inglobal vegetable oil production more thandoubled in the period 1983-2003. Thisdevelopment was accompanied by a strongrise in both the share and overallconsumption of palm oil in the globalvegetable oil market (Figure 5).

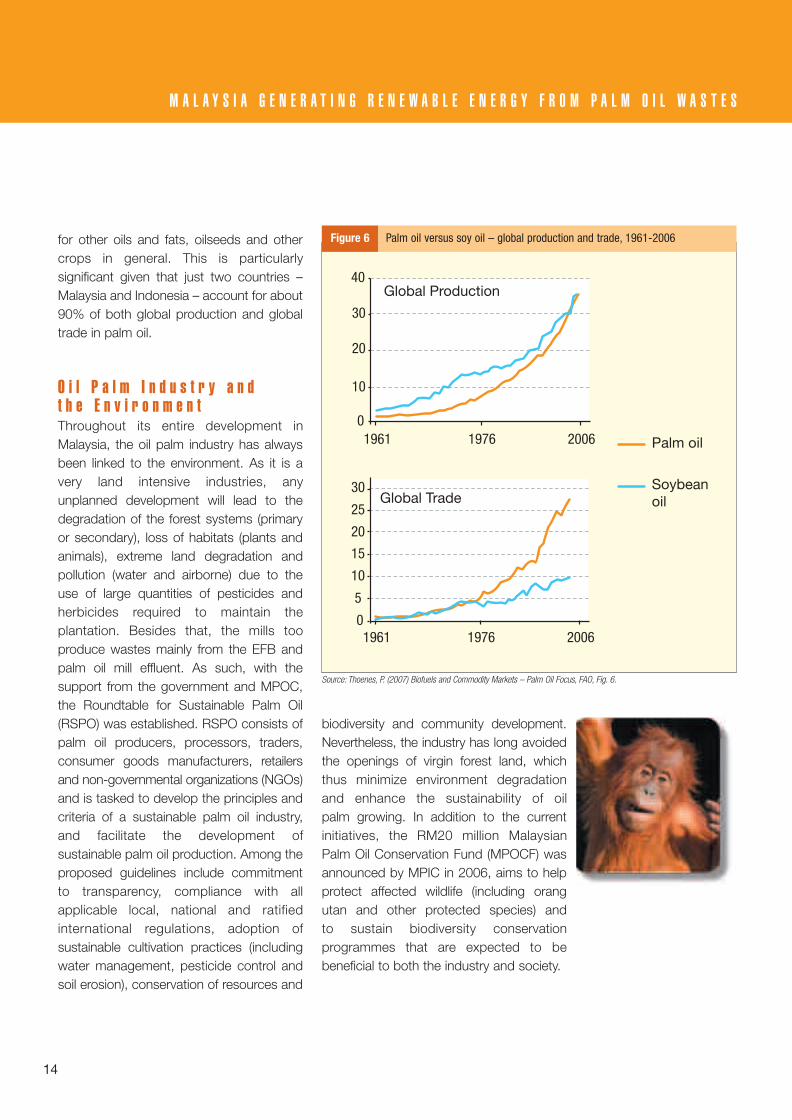

The main competitor for palm oil is soy

oil. Only in very recent years has the globaloutput of palm oil matched that of soy,whereas for trade, global shipments of palmoil surpassed soy oil in the mid-1970s, andin 2006 palm oil exports were almostdouble those of soy oil (Figure 6).

A further distinctive feature of palm oil isits very high trade-to-production ratio,which refers to the amount of globalproduction that enters international trade.The ratio for palm oil greatly exceeds that

Exports (mmt)

30

35

20

15

10

1961

mill

ion

mt

1976 2006

5

25

Production (mmt)

Source: Thoenes, P. (2007) Biofuels and Commodity Markets – Palm Oil Focus, FAO, Fig. 1.

Figure 4 Global palm oil production and trade, 1961-2006

Source: Thoenes, P. (2007) Biofuels and Commodity Markets – Palm Oil Focus, FAO, Fig. 2.

Production

Perc

ent

Exports

7

6

5

4

3

2

Palm oil

Soy oil

Total oils and fats

Figure 5 Average annual growth of palm oil versus other oils and fats, 1996-2006

Generating Power 19-06-07 9/13/07 10:04 AM Page 13

14

M A L A Y S I A G E N E R A T I N G R E N E W A B L E E N E R G Y F R O M P A L M O I L W A S T E S

for other oils and fats, oilseeds and othercrops in general. This is particularlysignificant given that just two countries –Malaysia and Indonesia – account for about90% of both global production and globaltrade in palm oil.

O i l P a l m I n d u s t r y a n d t h e E n v i r o n m e n tThroughout its entire development inMalaysia, the oil palm industry has alwaysbeen linked to the environment. As it is avery land intensive industries, anyunplanned development will lead to thedegradation of the forest systems (primaryor secondary), loss of habitats (plants andanimals), extreme land degradation andpollution (water and airborne) due to theuse of large quantities of pesticides andherbicides required to maintain theplantation. Besides that, the mills tooproduce wastes mainly from the EFB andpalm oil mill effluent. As such, with thesupport from the government and MPOC,the Roundtable for Sustainable Palm Oil(RSPO) was established. RSPO consists ofpalm oil producers, processors, traders,consumer goods manufacturers, retailersand non-governmental organizations (NGOs)and is tasked to develop the principles andcriteria of a sustainable palm oil industry,and facilitate the development ofsustainable palm oil production. Among theproposed guidelines include commitmentto transparency, compliance with allapplicable local, national and ratifiedinternational regulations, adoption ofsustainable cultivation practices (includingwater management, pesticide control andsoil erosion), conservation of resources and

biodiversity and community development.Nevertheless, the industry has long avoidedthe openings of virgin forest land, whichthus minimize environment degradation and enhance the sustainability of oil palm growing. In addition to the currentinitiatives, the RM20 million Malaysian Palm Oil Conservation Fund (MPOCF) wasannounced by MPIC in 2006, aims to helpprotect affected wildlife (including orangutan and other protected species) and to sustain biodiversity conservationprogrammes that are expected to bebeneficial to both the industry and society.

40

30

20

10

01961 1976 2006 Palm oil

Global Production

Soybean oil

30

20

15

10

01961 1976 2006

Global Trade

5

25

Source: Thoenes, P. (2007) Biofuels and Commodity Markets – Palm Oil Focus, FAO, Fig. 6.

Figure 6 Palm oil versus soy oil – global production and trade, 1961-2006

Generating Power 19-06-07 9/13/07 10:04 AM Page 14

15

T H E M A L A Y S I A N P A L M O I L M A R K E T

The oil palm is indigenous to West Africa,but the development of oil palm as aplantation crop started in Southeast Asia.Experimental planting began in PeninsularMalaysia in the late nineteenth century andthe first commercial oil palm estate wasestablished in Selangor in 1917. During the plantation development phase to about 1960, expansion was relatively slow reaching about 55,000 ha and,primarily because of processing difficulties,cultivation was not widely undertaken by smallholders. Large-scale expansioncommenced during the 1960s, mainly inresponse to the government’s diversifi-cation policy which aimed to reduce thedependence of the national economy onnatural rubber. Rubber prices werecontinuing to decline, there was mountingcompetition from synthetic rubber, and thedemand for edible oils was expanding.

M o d e r n c o m m e r c i a ld e v e l o p m e n t

Expansion of processing plant in the estatesector and the establishment of processingcooperatives, together provided the meansfor efficient processing of both plantationand smallholder palm oil production. TheFederal Land Development Authority(FELDA) was a key player in thegovernment’s implementation of itsdiversification and smallholder landsettlement policies and is still the largestproducer in the industry, owning over 16%of the total planted area (Table 4).

All states in Malaysia produce palm oilbut there is wide variation in the crop’sdistribution. Over 75% of total area plantedis located in just four states, Sabah, Johor,Pahang and Sarawak, each of which hasover half a million hectares under cultivation.Of the 4,165,215 ha planted in 2006,3,703,254 or 88.9% is classified as‘mature’ and in production (Table 5 and 6).

As a front runner in the development ofthe oil palm industry, Malaysia has had todevelop many of the agricultural andindustrial technologies required for the oilpalm industry to succeed, including asignificant R&D capability. For many decadesthis relied primarily on the ability of the largercompanies to carry out their own research.

In 2005, Malaysia’s totalland area had –• 59.5% under forest• 12.3% planted in

oil palm• 7.1% planted in other

agricultural crops

Source: MPOB (2007) Review of the Malaysian Oil Palm Industry 2006,Table 3.

Ownership

Private estatesFELDAFELCRARISDAState agenciesSmallholders

Total

2,476,135669,715159,78081,169

323,520454,896

4,165,215

59.416.13.82.07.8

10.9

100.0

Hectares %

Table 4Area planted in oil palm by ownership,2006

Generating Power 19-06-07 9/13/07 10:04 AM Page 15

16

M A L A Y S I A G E N E R A T I N G R E N E W A B L E E N E R G Y F R O M P A L M O I L W A S T E S

Experimentation enabled these companiesto enhance their planting materials, carry out agronomic trials, conduct pest anddisease research, and design machines formechanizing some field operations.

The processing of oil palm productsoccurs in palm kernel crushing factories,oleochemical plants, and palm oil refineries,but by far the most common are the basicpalm oil mills. With the plantations theyserve, these mills form the fundamentaloperational units and the basis of thisimportant Malaysian export industry thatsupplies global markets and has thecapability of contributing very significantly tothe reduction in GHGs through expandedproduction of biofuels and biomass basedgeneration of power.

In 1979, the Malaysian governmentestablished the Palm Oil Research Instituteof Malaysia (PORIM), which was chargedwith the responsibility of generatinginformation, increasing production andprocessing efficiency, and expanding usesof palm oil through research anddevelopment. This function was taken overby the Malaysian Palm Oil Board (MPOB)when earlier agencies were amalgamated

and is partly funded from a research cessimposed on palm oil millers. Efforts aremade to ensure that R&D in the MPOB is inline with the industry’s needs and thatresearch findings are disseminated to theindustry and offered for commercialisation.

Source: MPOB (2007) Review of the Malaysian Oil Palm Industry 2006,Tables 2 and 4.

State

JohorPahangPerakTerengganuNegeri SembilanSelangorKelantanKedahMelakaPulau PinangPerlisPeninsular MalaysiaSabahSarawakEast MalaysiaMALAYSIA

671,425623,290348,000164,065161,972128,91594,54276,32952,23214,119

2582,334,247

1,239,497591,4711,830,9684,165,215

16.115.08.43.93.93.12.31.81.20.30.0

56.029.814.244.0

100.0

Hectares %

Table 6 Area planted in oil palm by state, 2006

Energy Source

OperatingInoperativePlanned

Total

1 Tonnes FFB/year 2 Tonnes/year 3 Tonnes kernel/year 4 Tonnes/yearSource: MPOB (2007) Review of the Malaysian Oil Palm Industry 2006, Tables 7-10.

3977

21

425

86,243,600588,000

3,936,000

88,638,400

5173

12

66

18,506,400120,000

4,568,800

23,195,200

3887

53

5,144,100453,500690,000

6,287,600

1703

20

2,466,9710

222,000

2,688,971

Palm oil mills1

No. Capacity No. Capacity No. Capacity No. CapacityPalm oil refineries2 Palm kernel crushing factories3 Oleochemical plants4

Table 5 Status of palm oil processing plants, 2006

Generating Power 19-06-07 9/13/07 10:04 AM Page 16

17

T H E B I O G E N P R O J E C T

The Biogen project is jointly funded by theGovernment of Malaysia (GoM), the UnitedNations Development Programme (UNDP),the Global Environment Facility (GEF), andthe Malaysian private sector. Pusat TenagaMalaysia (PTM) is the implementing agencyunder the executing agency, the Ministry of Energy, Water and Communications(MEWC).

P r o j e c t s t r a t e g yThe Biogen project strategy involves anumber of activities and deliverables thataim to remove barriers to the utilisation ofcommercially viable biomass based powergeneration through CHP production in palmoil mills. The ultimate desired outcome is theimplementation of a demonstration schemeshowcasing a full scale model (FSM) ofbiomass based power generation with CHP in conjunction with a POME derivedbiogas system. While biomass utilisation

is well established, the project is intended to have a capacity building outcome,encouraging a substantial increase in bio-mass based power generation.

Central to the project strategy is theestablishment of an institutional awareness,responsibility and capacity within theGovernment of Malaysia as represented byMEWC, PTM and MPOB for identifying andremoving barriers to the implementation of

Sabah

TerengganuSOUTH CHINA SEA

Perlis

Kedah

Pulau Pinang

Selangor

N. Sembilan

Kuala Lumpur

Melaka

Johor

Pahang

Sarawak

Map 1 Graphical representation of the palm oil processing plants, 2006

The broad objective of the Biogen project is the reduction in the growth rate of greenhouse gas emissions from fossil fuel fired activities and from thedecomposition of unused biomass waste from palm oil mills (Map 1). This is to be achieved through the removal of the major barriers to the development of biomass based combined heat and power projects to supplant part of thecurrent fossil fuel electricity generation in Malaysia. Explicitly, the aim of theBiogen project is to reduce the growth rate of greenhouse gas emissions from fossil fired combustion processes by 3.8% by the end of 2008.

T h e B i o g e n p r o j e c t d e v e l o p m e n t o b j e c t i v e

Generating Power 19-06-07 9/13/07 10:04 AM Page 17

these measures in the Malaysian palm oilindustry. On the technical and businessside, capacity will be established forspecialist support and financial assistance.PTM, Bank Pembangunan Malaysia Bhd,and MPOB were designated as theagencies responsible for particular aspects,with the institutional focus located in PTMwhich has a coordinating role for the project.

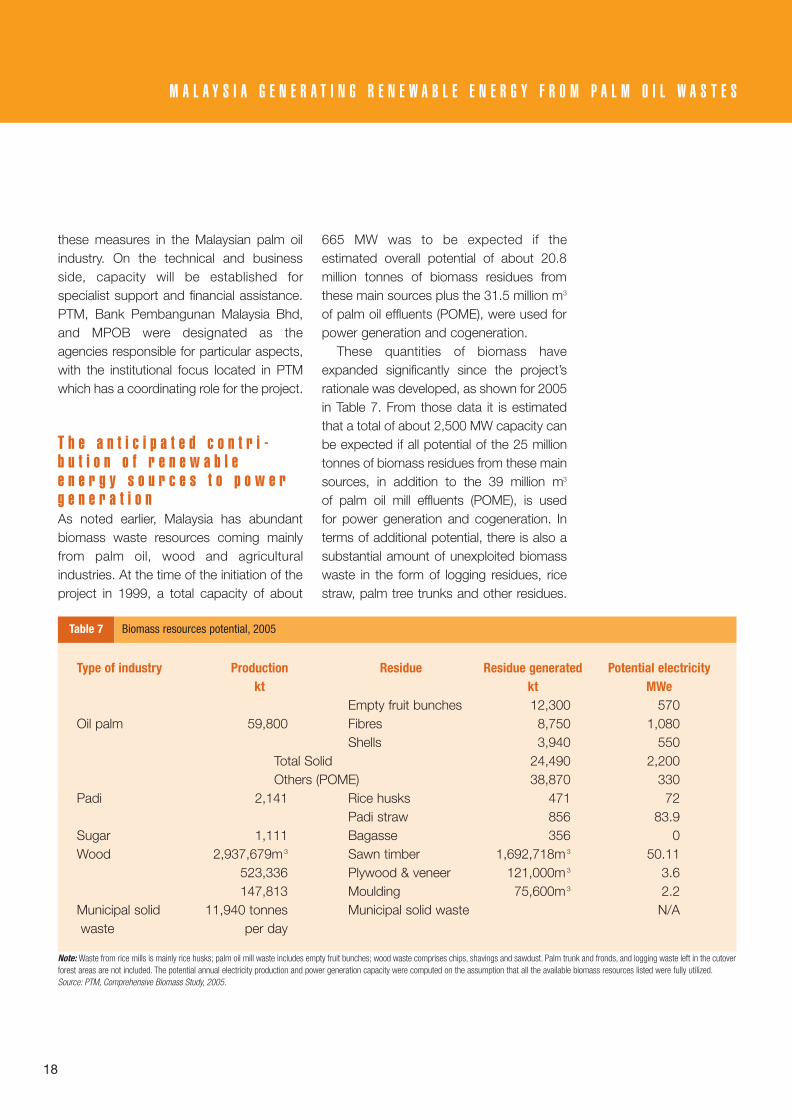

T h e a n t i c i p a t e d c o n t r i -b u t i o n o f r e n e w a b l ee n e r g y s o u r c e s t o p o w e rg e n e r a t i o nAs noted earlier, Malaysia has abundantbiomass waste resources coming mainlyfrom palm oil, wood and agriculturalindustries. At the time of the initiation of theproject in 1999, a total capacity of about

665 MW was to be expected if theestimated overall potential of about 20.8million tonnes of biomass residues fromthese main sources plus the 31.5 million m3

of palm oil effluents (POME), were used forpower generation and cogeneration.

These quantities of biomass haveexpanded significantly since the project’srationale was developed, as shown for 2005in Table 7. From those data it is estimatedthat a total of about 2,500 MW capacity canbe expected if all potential of the 25 milliontonnes of biomass residues from these mainsources, in addition to the 39 million m3

of palm oil mill effluents (POME), is used for power generation and cogeneration. Interms of additional potential, there is also asubstantial amount of unexploited biomasswaste in the form of logging residues, ricestraw, palm tree trunks and other residues.

Type of industry

Oil palm

Padi

SugarWood

Municipal solid waste

Note: Waste from rice mills is mainly rice husks; palm oil mill waste includes empty fruit bunches; wood waste comprises chips, shavings and sawdust. Palm trunk and fronds, and logging waste left in the cutoverforest areas are not included. The potential annual electricity production and power generation capacity were computed on the assumption that all the available biomass resources listed were fully utilized.Source: PTM, Comprehensive Biomass Study, 2005.

59,800

2,141

1,1112,937,679m 3

523,336147,813

11,940 tonnes per day

Total SolidOthers (POME)

Empty fruit bunchesFibresShells

Rice husksPadi strawBagasseSawn timberPlywood & veneerMouldingMunicipal solid waste

12,3008,7503,940

24,49038,870

471856356

1,692,718m 3

121,000m 3

75,600m 3

5701,080

5502,200

33072

83.90

50.113.62.2N/A

Productionkt

Residue Residue generated kt

Potential electricityMWe

Table 7 Biomass resources potential, 2005

18

M A L A Y S I A G E N E R A T I N G R E N E W A B L E E N E R G Y F R O M P A L M O I L W A S T E S

Generating Power 19-06-07 9/13/07 10:04 AM Page 18

19

T H E B I O G E N P R O J E C T

These additional biomass residues couldfurther supplement future biomass basedpower generation if required.

The palm oil industry accounts for thelargest biomass waste production inMalaysia, and since the 1960s, all palm oilmills have depended on their own biomasswastes for fuel, mainly the palm kernelshells and mesocarp fibres. Not only doespalm oil industry waste, including POME,represent the largest potential for biomassenergy utilisation in the country, but thisresource is readily available and in need ofan efficient and effective means of disposal.When the project was being planned, mostof these residues were disposed of throughincineration and dumping, with only a verysmall proportion being used by the mills in arather inefficient manner for their own heatand power requirements. However, thegovernment has banned the incineration ofbiomass waste (mainly empty fruit bunchesor EFB), and so the mills are obliged to findalternative means of disposing of theunutilized waste.

Other value-added uses of the wastehave been investigated with varyingdegrees of success, but commercialisationof these is not imminent. While palm oil millswith plantations can use their solid biomasswaste for mulching and soil conditioning orfertiliser, those without plantations areconsidering generating electricity that theycan sell to the national utility grid. Althoughpalm oil mills are aware of the potential ofbiogas generated from the biodegradationof POME, they are not currently utilising thisgas as there is no requirement to do so andthere is little local experience in handling it.

I m p l e m e n t i n g b i o m a s s a n db i o g a s s p o w e r g e n e r a t i o na n d c o g e n e r a t i o n Since the palm oil mills have abundantbiomass waste resources, their energysystems were designed to be cheap ratherthan efficient. Most of the existing biomasscombustion systems in Malaysia utilize lowefficiency low-pressure boilers where theoverall cogeneration efficiency is less than40%. An additional source of energy inpalm oil mills is the biogas produced in theanaerobic decomposition (for wastewatertreatment purposes) of palm oil mill effluent(POME). However, at that time, POMEderived biogas (mostly methane, CH4) was

• Palm oil millers• Local boiler manufacturers• Power equipment suppliers• Project developers• Local energy service industries• Engineering consulting firms• Financial and banking institutions• policy makers

B e n e f i c i a r i e s o f t h e p r o j e c t

Generating Power 19-06-07 9/13/07 10:04 AM Page 19

20

M A L A Y S I A G E N E R A T I N G R E N E W A B L E E N E R G Y F R O M P A L M O I L W A S T E S

not being recovered and used but allowedto dissipate into the atmosphere.

Commercially proven technologies wereavailable in the form of high-pressure boilersfor efficient production of power and heatfrom the biomass resources available. Dualfired boilers capable of burning either dieseloil or natural gas were identified as mostsuitable for burning palm oil waste sincethey could also facilitate the use of POMEderived biogas as a supplementary fuel.

K e y b a r r i e r s t o c h a n g eWhilst the concept of biomass based CHPgeneration for sale to the grid or otherconsumers is well accepted, lack ofexperience and a number of barriers havehindered its development.

Key barriers to the development of CHPgeneration in Malaysia that the project was attempting to overcome, included thefollowing:• Lack of information services to promote

biomass energy development and itsapplications, which includes,– a misconception that the technology is

unproven; – the belief that the industry lacks the

requisite technical ability; – the perception that use of biomass is

regressive in a modernizing industrialeconomy;

– a belief that investors view thegeneration and sale of electricity asmarginal to the core business of theindustry.

• Absence of a clear mechanism on re-newable energy technology developmentand applications despite the establishmentof a broad regulatory framework.

• Lack of accessible and favourablefinancing schemes because,– in the absence of supporting policies and

regulations it is difficult to gain fundingsupport from financial institutions;

– financing of projects based onrenewable energy technologies is anunfamiliar investment and perceived ashigh risk.

• Uncertain financial viability unlesssatisfactory pricing arrangements can be

Generating Power 19-06-07 9/13/07 10:04 AM Page 20

21

T H E B I O G E N P R O J E C T

reached, producing power for the utilitygrid would not be seen as an attractivebusiness venture;

• Lack of successful models to demon-strate viability as there were noprecedents beyond the inefficientbiomass fired CHP systems alreadyoperating in the palm oil and woodindustries;

O p e r a t i o n a l u n c e r t a i n t i e s• Biomass fuel supply relating to,

– reliability of the volume and quality ofEFBs;

– seasonal nature of palm oil millingoperations;

– absence of standard contractprocedures for the supply and pricingof EFBs.

• Minimum energy off-take that required,– to achieve an availability factor of 90%

to baseload allowing for maintenanceand forced outages.

• Efficiency of deployment of biomassbased energy technology required,– review of current practices for

incineration of excess biomass; – greater sophistication of operation and

manpower skills, interconnectionsafety, synchronization devices and themore rigorous demands of gridelectricity generation.

• Recovery of POME biogas for powergeneration lacked incentives althoughmillers were aware of the technology andthere were no restrictions on the releaseof biogas into the atmosphere.

• Purchase of electricity by the national utilitycompany and other REPPA issuesrequired the clarification and resolution.

I m m e d i a t e o b j e c t i v e s1. To provide adequate, affordable, accessible

and up-to-date information services,continuing education, and awarenessimprovement on the application ofrenewable energy resources to prospectiveRE developers, policy makers andtechnology suppliers.

2. To strengthen and formulate the policyand regulatory framework to encouragethe wide spread adoption of RE projects.

Generating Power 19-06-07 9/13/07 10:04 AM Page 21

22

M A L A Y S I A G E N E R A T I N G R E N E W A B L E E N E R G Y F R O M P A L M O I L W A S T E S

3. To encourage the implementation, thegovernment and financial community will provide financial assistance to the development of sustainable REfinancing.

4. To facilitate the effective demonstrationof the techno-economic viability, design,development, financing and sustainableoperation and maintenance of biomass-based and biogas-based, grid-connectedpower generation and cogenerationprojects.

5. To establish the potential and require-ments for the energy applications byproviding sufficient support to thetechnology suppliers.

P l a n n e d o u t p u t sThe project was designed to addressthe barriers in the development andimplementation of biomass-based, grid-connected power generation and CHPspecifically in the Malaysian palm oil industry.To achieve this objective the project wasorganised into five components, each withits own set of outputs that comprised theblueprint to be followed by the participatingagencies to achieve the objectives.

The major elements of each of thecomponents proceeded concurrently fromthe launching of the project at the beginningof 2002, with the objective of completingthe existing plans by early 2008. Whilst thisaccount has emphasised some key barriersand operational uncertainties, manyinitiatives were being undertaken that

supported and facilitated the immediateobjectives of the project culminating in thecontractual arrangements to set up the twofull scale demonstration models.

Component 1 Biomass information servicesand awareness enhancement Outputs~ Comprehensive biomass energy resource

inventory~ Biomass energy technologies and

technology application database~ Training courses on biomass energy

technology~ Integrated information dissemination

programme~ Biomass energy technology information

exchange service~ Renewable energy (RE) consultancy

service industry development~ Rating scheme for biomass based

companies

Generating Power 19-06-07 9/13/07 10:04 AM Page 22

23

T H E B I O G E N P R O J E C T

Component 2 Biomass policy studies andinstitutional capacity buildingOutputs~ Biomass policy document and analysis~ Biomass energy utilisation workshop series~ RE electricity generation policy~ RE electricity pricing~ Small RE project (SREP) strategy~ Clean Development Mechanism (CDM)

implementation in RE project~ RE electricity policy implementation

evaluation

Component 3 Financial assistance forrenewable energy projectsOutputs~ Training for financial institutions on

financing RE projects~ Establishment of RE fund~ Mechanism for the financing scheme~ Criteria for selecting fund applicants~ Arrangements for financial assistance for

RE projects~ Evaluation of RE projects financing

assistance programmes

Component 4 Demonstration schemesOutputs~ Biomass based power generation and

CHP demonstration programme~ Selection criteria for host demonstration

companies~ Suitable project demonstration sites~ Baseline data for three dimensional sites~ Specific demonstration programme

implementation requirements~ Installation and implementation of design/

plans for first demonstration site~ Financial and procurement assistance

arrangements for demonstration scheme

Component 5 Technology developmentOutputs~ Assessment of other uses of biomass

and biogas resources~ Evaluation of the energy utilization

performance of palm oil mills~ Training for palm oil mill plant engineers

and operators~ Financial assistance to local equipment

manufacturers ~ Assessment of capabilities of local steam

and power generation equipment~ Training on high efficiency designs and

production technologies The project has undertaken studies onBiomass Resource Assessment and, basedon the findings, the total potential forbiomass and biogas from palm oil millwastes was estimated, in 2005, to beapproximately 2,500 MW. Microanalysis oneight selected palm oil mills was carried outin terms of energy utilisation and thepotential for improving efficiency of currentusage. The mills have also been assessedfor the practical feasibility of feedingelectricity from excess power generationinto the national grid.

Generating Power 19-06-07 9/13/07 10:04 AM Page 23

24

M A L A Y S I A G E N E R A T I N G R E N E W A B L E E N E R G Y F R O M P A L M O I L W A S T E S

F u l l s c a l e m o d e lA full scale model (FSM) utilizing bothbiomass and biogas resources wasplanned as a major outcome of the Biogenproject. This was seen as importantbecause it would give a practicaldemonstration of the technology andprocesses being utilized and recommendedin the project. During 2005, extensiveplanning occurred for the establishment ofthe first FSM, but some difficulties wereexperienced in gaining the requisite level ofinterest and support. (In attempting toidentify suitable candidates for the first fullscale demonstration model, similar issuesarose to those that were making theindustry at large reluctant to adopt CHP,namely: the relatively large scale ofinvestment; a lack of financial depth to meetthe equity requirements and an unattractiverenewable energy tariff.)

Nevertheless, to facilitate the develop-ment of the first FSM, a number of majordevelopments that had been ongoing sincethe beginning of the project were beingbrought to a conclusion. Notably, theseincluded the finalizing of the RenewableEnergy Power Purchase Agreement (REPPA),and the Renewable Energy BusinessFacility (REBF), both of which were essentialfor the contracting of an FSM operator.

In 2006, following a tendering processand evaluation of proposals submitted,instead of a single FSM, two companieswere selected: MHES Asia Sdn Bhd todevelop a biomass project as the firstFSM; and FELDA Palm Industries Sdn Bhd(FPISB) for the biogas project as thesecond FSM. Schematic diagrams fortypical biomass and biogas plants arerepresented in Figure 7 and 8.

The MHES Asia Biomass Power Plant,located in Bahau, Negeri Sembilan, willhave a capacity of 13 MW and will utilize

Water LineAir LineBiomass LineSteam Line

RawBiomass

BiomassStorage

WaterReservoir

CoolingTower

Pre-treatment

(shredding and cutting into smaller

fibres)

Condenser

Generator

SteamReceiver

Process

Condensate

Stack

ID FanFD Fan Air Heater

Heated Air

DearatorChemicalDosing

Feed WaterPump

WaterDrum

SteamDrum

Evaporator

SuperheatedFurnace Bed

Economizer

Turb

ine

Figure 7 Schematic diagram of biomass power generation

PomeFibre &otherSolids

Pre-Tank

HeatExchanger

Digester(3600 m 3)3

Digester(3600 m 3)3

Digester(3600 m 3)3

GasDewatering

Well

SecondaryDigester

Clarifier

Sludge

Sludge

Decanter(Optional)

Fiber for Compost

FinalDischarge

Band filterLiquid

AerobicTreatment

Ft

Ft

Ft

To pre-tankGas

Purifier

Optional

(Optional)

Engine room

Gas Flare

Figure 8 Schematic diagram of biogas power generation

Generating Power 19-06-07 9/13/07 10:04 AM Page 24

25

T H E B I O G E N P R O J E C T

EFBs as fuel. The plant will sell 10MW ofelectricity to TNB for 21 years at the agreedREPPA price of between RM0.17/kWh to RM0.21/kWh. The power plant isscheduled for completion by early 2008.

The FPISB biogas project is to belocated in Serting Hilir palm oil mill, also inBahau, Negeri Sembilan, with theobjective of utilizing methane-rich POMEfor power generation. The plant will have apower generation capacity of 500 kW, withplans for expansion after the first few yearsof operation if agreed by the national utility.The project, still at the planning stage in2007, is estimated to reduce emissions by the equivalent of 45,000 tonnes of CO2 per year.

K e y a c h i e v e m e n t sThe finalization of the Renewable EnergyPower Purchase Agreement (REPPA) pro formaThis is the official document to be used bytransacting parties in processing loan

applications. Through the facilitation andinputs by the Biogen project, this outputhas been made possible with the closecoordination and cooperation of theGovernment of Malaysia through MEWC,PTM, ST, TNB, and other relevant agencies.The REPPA represents the preparednessfor commercialisation of renewable energypower.

REPPA is the legal document on the selling of electricity by renewable energyproject developers and the purchase of electricity by the national utilitycompanies (TNB/SESB). The rights and obligations of both parties cover thecommercial and technical aspects governing the project implementationapplicable throughout the lifetime of the agreement.

The Biogen project team was instrumental in reviewing the provisions ofthe agreement, customized for biomass power plants, and negotiating termswith the GoM, banking institutions and private sector stakeholders. Finaldetails of the agreement, relating mainly to tariff, were in process with theFSM participants in 2007.

R e n e w a b l e E n e r g y P o w e r P u r c h a s e A g r e e m e n t ( R E P P A )

Generating Power 19-06-07 9/13/07 10:04 AM Page 25

Establishment of the Renewable EnergyBusiness Facility (REBF)In 2005, the Biogen project established thefirst financing scheme for RE projects. TheRenewable Energy Business Facility (REBF)uses funds available from the UNDP/GEF, MESITA and BPMB, provided at 4% per annum for the FSM projects. TheREBF paves the way for other fundingmechanisms that will be administeredthrough the facility.

Organization of the Biomass One-Stop CentreThe Biomass One-Stop Centre wasestablished through the Biogen project inPTM. It provides services, includingconsultancy, for biomass utilizationprojects, information database, technicaladvisory, services, financing facilitation, andproject identification.

Energy audits of selected palm oil millsEight mills were audited to assess theirenergy utilization and the possibility ofimproving current usage efficiency. Thesemills are also being assessed forconnection to the grid for additional powersupply from excess generation.

Different policy studiesThese studies have been conducted insupport of the government’s renewableenergy programme. Their value lies in theircontribution to modifying relevant laws,making agreements more workable,providing against force majeure, dealingwith loss or shortfall of energy, and settingof performance targets.

Adoption of RE in mill operation syllabusThe project team worked with MPOB inidentifying key information to be included inthe syllabus for Diploma-level mill operation.

Biomass Resource Information System (BRIS)A web-based interactive system is under itsfinal stage and will be ready by end 2007. Itwill show an estimated amount of biomassavailable by most palm oil mills resourcemapping, and the availability for powergeneration at any specified grid intake.

26

M A L A Y S I A G E N E R A T I N G R E N E W A B L E E N E R G Y F R O M P A L M O I L W A S T E S