QUARTERLY UPDATE - Nedbank CIB Equity Research Portal

49

Please click here to view our Nedbank CIB disclaimer Adding optimism We adjust our growth expectations higher for 2021 and believe inflation is more likely to surprise on the downside rather than the upside. While fiscal challenges remain, the external tailwinds and the domestic rebound continues to provide a positive cyclical backdrop for local asset prices in general. While we remain neutral on the currency, we believe bonds provide value on a tactical basis. We also moved more equity sectors to Overweight from either Neutral or Underweight last quarter. Sector views and allocation: Overweight – Platinum group metals (unchanged from last quarter), telecommunications (unchanged), listed property (unchanged), media (unchanged) and apparel (from Underweight) Neutral – Food retail (unchanged) Underweight – Gold mining (unchanged) GDP growth – On the growth front, we expect GDP growth of 3.8% y/y in 2021 and 2.3% y/y in 2022. Monetary policy – We expect inflation of 3.9% in 2021 and 4.4% in 2022. We expect an unchanged repo rate this year. FX – We continue to hold a neutral view on the rand within the broad 15.00-16.00 range against the USD and are buyers of USD below 15.00. Fixed income – Both nominal bonds and ILBs provide value on a tactical basis, but elevated country risk premia limit upside over the medium term. We continue to favour short-dated ILBs relative to nominals – this upside is limited up to the 4y point. Thereafter, nominal bonds look more attractive given the higher real return. Telecoms and media – MTN’s FY20 results were a watershed moment, and in equal measure, revitalised and de-risked its investment case. Stickiness to data consumption will likely keep Vodacom SA data revenue in double-digit growth territory. Telkom’s 3Q update was characterised by meaningful FCF and net debt upgrades. We are very constructive on NPN/PRX going into CY 2021. We maintain our Overweight stance for the telecommunications sector. In media, we keep an Overweight rating on Naspers and move Prosus NA to Overweight. PGM equities – higher for longer: We remain bullish on the prospects for the PGM market. We expect the equities to rerate further, which could see more equity upside, even if there is a pullback in the basket price. Our top picks are NHM, IMP, RBP and SSW. Listed property – valuations and collection rates holding up: The property sector has returned +19.6% (vs +14.8% JSE All Share Index) since we upgraded to Overweight in December. We continue to see pockets of value within our coverage universe despite the recent rerating and operational headwinds facing the sector. We remain Overweight this sector. Our top picks are RES, NRP, FFA, EMI, VKE, MSP and RDF. Gold equities – running out of steam: We maintain our view that the gold equities will underperform the gold price, as company free cash flow and dividends could fall short of investor expectations over the next year. While we maintain an Underweight on the sector, our top picks within the sector are SSW and GFI. Retail equities – maintaining our positive view from a listed perspective: The agility, cash preservation, debt reduction and investment in value-creating strategies by listed SA retailers have supported our more positive view on the sector in recent months. Our top picks in food are SHP, SPP and WHL, while in apparel, our picks are MRP, PPH and TFG. ANALYST DETAILS Walter De Wet [email protected] +27726356268 Reezwana Sumad [email protected] +27112941753 Jones Gondo [email protected] +27115354050 Arnold Van Graan [email protected] +27112959361 Avinash Kalkapersad [email protected] +27115374181 Nthulleng Mphahlele [email protected] +27112947032 Preshendran Odayar [email protected] +27115374181 Neels Heyneke [email protected] +27115354041 Ridwaan Loonat [email protected] +27112943221 Saad Chothia [email protected] +27115374190 Ziyad Joosub [email protected] +27115374181 QUARTERLY UPDATE 2Q 2021 6 APRIL 2021

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of QUARTERLY UPDATE - Nedbank CIB Equity Research Portal

Please click here to view our Nedbank CIB disclaimer

Adding optimism

We adjust our growth expectations higher for 2021 and believe inflation is more likely to surprise on the downside rather than the upside. While fiscal challenges remain, the external tailwinds and the domestic rebound continues to provide a positive cyclical backdrop for local asset prices in general. While we remain neutral on the currency, we believe bonds provide value on a tactical basis. We also moved more equity sectors to Overweight from either Neutral or Underweight last quarter.

Sector views and allocation:

Overweight – Platinum group metals (unchanged from last quarter), telecommunications (unchanged), listed property (unchanged), media (unchanged) and apparel (from Underweight)

Neutral – Food retail (unchanged)

Underweight – Gold mining (unchanged)

GDP growth – On the growth front, we expect GDP growth of 3.8% y/y in 2021 and 2.3% y/y in 2022.

Monetary policy – We expect inflation of 3.9% in 2021 and 4.4% in 2022. We expect an unchanged repo rate this year.

FX – We continue to hold a neutral view on the rand within the broad 15.00-16.00 range against the USD and are buyers of USD below 15.00.

Fixed income – Both nominal bonds and ILBs provide value on a tactical basis, but elevated country risk premia limit upside over the medium term. We continue to favour short-dated ILBs relative to nominals – this upside is limited up to the 4y point. Thereafter, nominal bonds look more attractive given the higher real return.

Telecoms and media – MTN’s FY20 results were a watershed moment, and in equal measure, revitalised and de-risked its investment case. Stickiness to data consumption will likely keep Vodacom SA data revenue in double-digit growth territory. Telkom’s 3Q update was characterised by meaningful FCF and net debt upgrades. We are very constructive on NPN/PRX going into CY 2021. We maintain our Overweight stance for the telecommunications sector. In media, we keep an Overweight rating on Naspers and move Prosus NA to Overweight.

PGM equities – higher for longer: We remain bullish on the prospects for the PGM market. We expect the equities to rerate further, which could see more equity upside, even if there is a pullback in the basket price. Our top picks are NHM, IMP, RBP and SSW.

Listed property – valuations and collection rates holding up: The property sector has returned +19.6% (vs +14.8% JSE All Share Index) since we upgraded to Overweight in December. We continue to see pockets of value within our coverage universe despite the recent rerating and operational headwinds facing the sector. We remain Overweight this sector. Our top picks are RES, NRP, FFA, EMI, VKE, MSP and RDF.

Gold equities – running out of steam: We maintain our view that the gold equities will underperform the gold price, as company free cash flow and dividends could fall short of investor expectations over the next year. While we maintain an Underweight on the sector, our top picks within the sector are SSW and GFI.

Retail equities – maintaining our positive view from a listed perspective: The agility, cash preservation, debt reduction and investment in value-creating strategies by listed SA retailers have supported our more positive view on the sector in recent months. Our top picks in food are SHP, SPP and WHL, while in apparel, our picks are MRP, PPH and TFG.

ANALYST DETAILS

Walter De Wet

+27726356268

Reezwana Sumad

+27112941753

Jones Gondo

+27115354050

Arnold Van Graan

+27112959361

Avinash Kalkapersad

+27115374181

Nthulleng Mphahlele

+27112947032

Preshendran Odayar

+27115374181

Neels Heyneke

+27115354041

Ridwaan Loonat

+27112943221

Saad Chothia

+27115374190

Ziyad Joosub

+27115374181

QUARTERLY UPDATE 2Q 2021 2

6 APRIL 2021

QUARTERLY UPDATE

6 APRIL 2021 PAGE 2

Contents

Core macroeconomic views ........................................................................................ 3

Asset allocation and sector picks ................................................................................ 4

Sector views and sector performance ..................................................................... 4

Preference picks and selective bias within sectors ................................................. 4

Global Outlook: no structural shift higher in inflation just yet....................................... 5

Domestic growth – costs rising at slower pace ........................................................... 7

Costs of restrictions still rising but at a slower pace .................................................... 8

Monetary policy – we look for a delayed but muted hiking cycle ............................... 10

The SARB has been tolerant of negative real rates in the past ............................. 10

Fiscal policy bears some fruit, but we await the harvest ........................................... 12

Credit conditions are firmly negative, but borrowing window accommodative .......... 15

FX: Some strength, less predictable ......................................................................... 17

Fixed Income: country risk premia prevent outright bullishness................................ 19

SA Retail – Maintaining our positive view from a listed perspective ......................... 21

Share price performances and valuation ............................................................... 22

SA Property: Valuations and collection rates holding up .......................................... 24

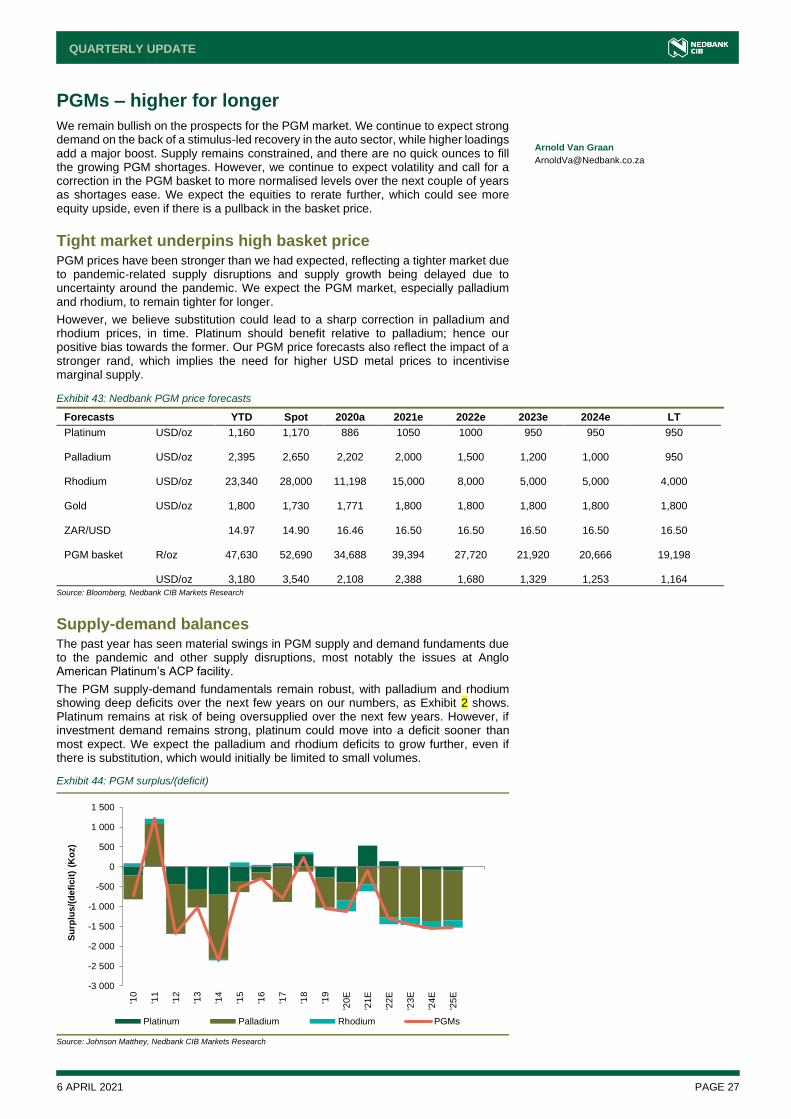

PGMs – Higher for Longer ........................................................................................ 27

Tight market underpins high basket price.............................................................. 27

Supply-demand balances ...................................................................................... 27

Supply ................................................................................................................... 28

Demand................................................................................................................. 28

PGM equity outlook ............................................................................................... 29

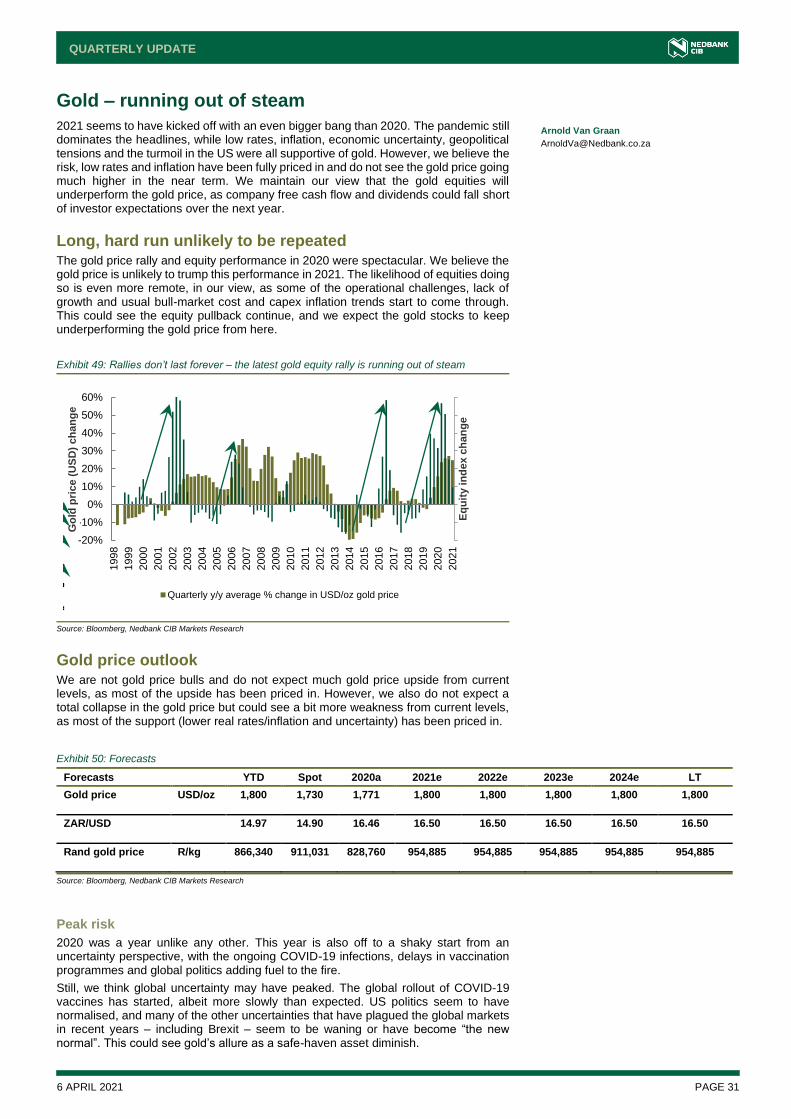

Gold - Running out of steam ..................................................................................... 31

Long hard run, unlikely to be repeated .................................................................. 31

Gold price outlook ................................................................................................. 31

Equities vs gold price ............................................................................................ 33

Valuations and fair values ..................................................................................... 33

Comp tables .......................................................................................................... 35

Telecommunications & Media ................................................................................... 36

MTN Group .......................................................................................................... 36

Vodacom Group .................................................................................................... 38

Telkom SA SOC .................................................................................................... 39

Naspers and Prosus .............................................................................................. 41

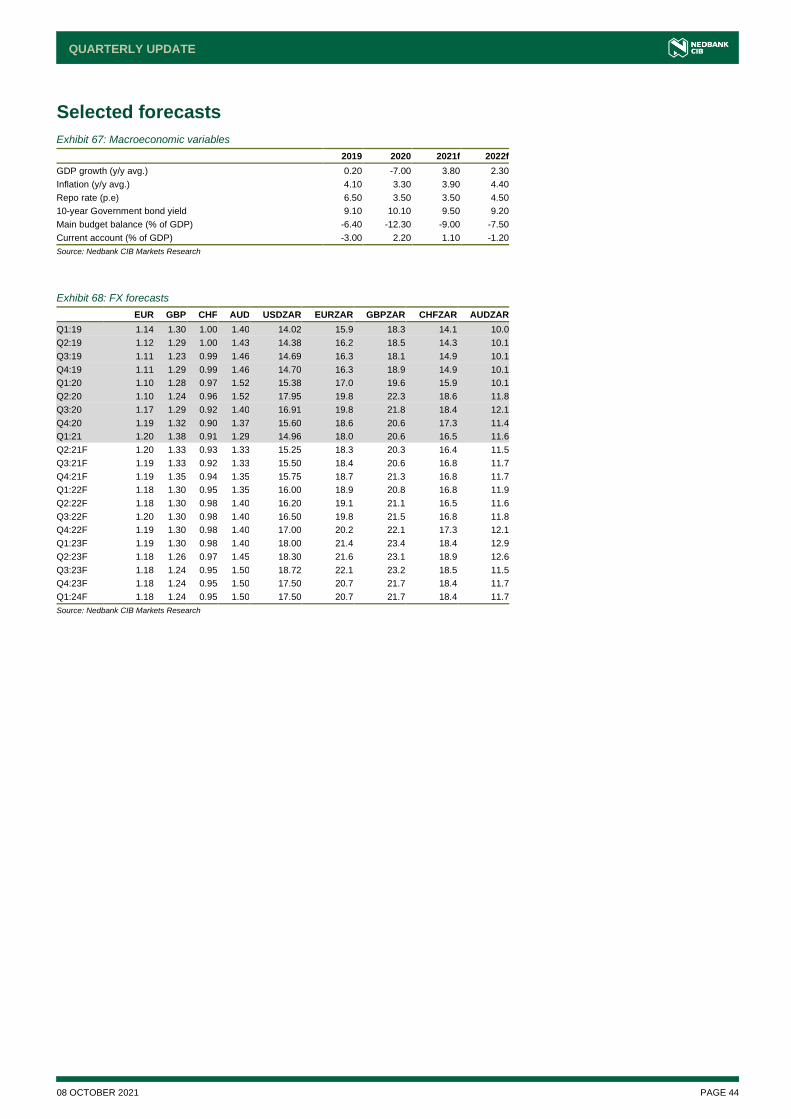

Selected forecasts .................................................................................................... 44

Contact details .......................................................................................................... 45

Disclaimer ................................................................................................................. 45

6 APRIL 2021 PAGE 3

QUARTERLY UPDATE

Core macroeconomic views

Exhibit 1: Summary of our core macroeconomic and market views

Growth We expect GDP growth of 3.8% y/y in 2021 and 2.3% y/y in 2022.

Currency

Our FX view since the start of the year remains unchanged – we hold a neutral view on the rand within the broad 15.00-16.00 range against the USD. We are buyers of USD on dips below 15.00. Should we have a bias, it is a strengthening bias for the rand against the USD – our fundamental indicators still suggest we should rather favour a slight strengthening bias as opposed to a weakening bias.

Inflation We expect it to average 3.2% in 1Q21 and 3.9% in 2021, vs the South African Reserve Bank’s (SARB’s) forecast of 4.3% for 2021. We forecast an average inflation rate of 4.4% in 2022.

SARB The SARB is likely to remain on hold at 3.5% for the remainder of 2021. We expect the SARB to raise the repo rate to 4.5% by the end of 2022.

Bond yields Our fair value estimate for the 10-year bond yield remains in the 9.00-9.50% range. We see our fair value estimate as a 6- to 12-month view.

Rating action

In 2020, both Fitch and Moody’s took negative rating actions on the SA sovereign, lowering their respective ratings by two notches over the calendar year to “BB-” and “Ba2”, respectively. Both agencies have maintained a “Negative” outlook. S&P affirmed its “BB/Stable” rating on SA after downgrading it in April 2020. We think S&P does not yet see SA as a “B+” credit (hence the “Stable” outlook), unlike Fitch. We think the National Treasury may have done enough to stave off a downgrade in 1H 2021, but this could still happen towards 1H 2022 if the implementation of the 2021 National Budget progresses too slowly or proceeds worse than anticipated (with regard to growth and fiscal stability trends). Debt affordability and the primary balance evolution will be core indicators to watch, with regard to fiscal slippage risks, at the 2021 MTBPS. SA’s debt-service costs are higher than similarly rated peers’ and if the trend does not reverse (on lower borrowing requirements) or if it should rise unexpectedly and peak above 25% of revenue, we think this could become a rating-downgrade trigger. In our view, the economic recovery remains tepid and the reform measures uncertain. The risks of slippage still outweigh stabilisation over the medium term.

Source: Nedbank CIB Markets Research

6 APRIL 2021 PAGE 4

QUARTERLY UPDATE

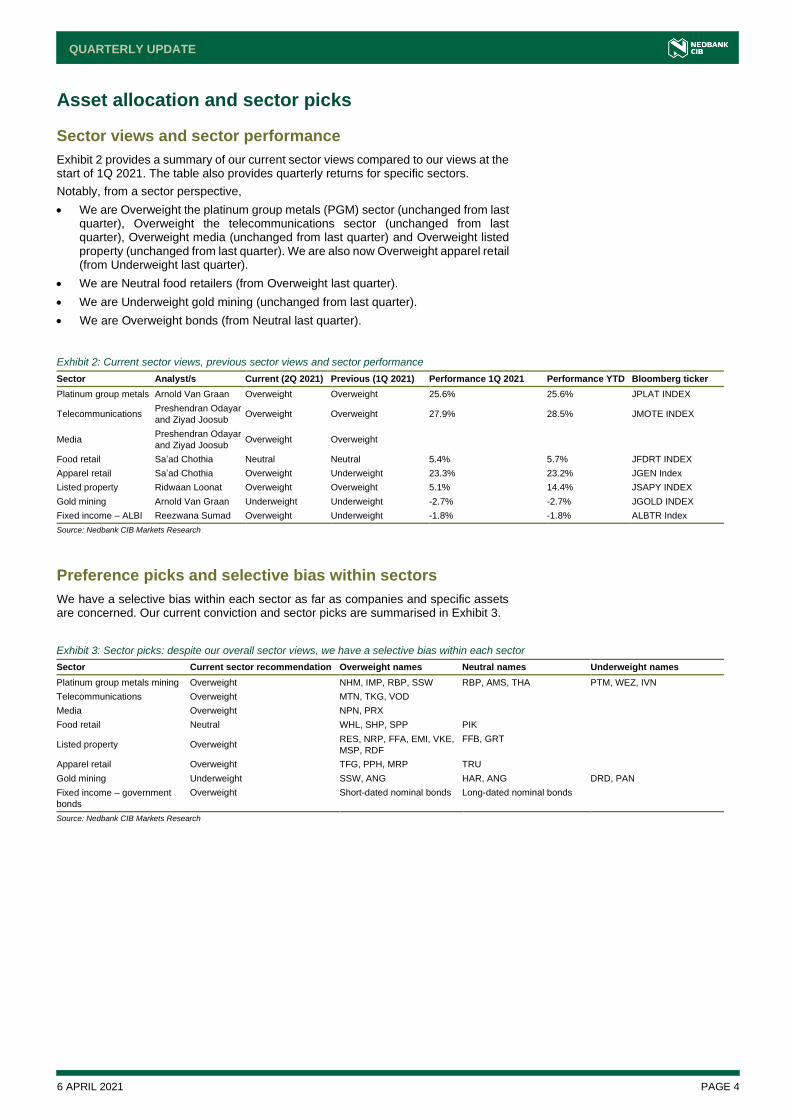

Asset allocation and sector picks

Sector views and sector performance

Exhibit 2 provides a summary of our current sector views compared to our views at the start of 1Q 2021. The table also provides quarterly returns for specific sectors.

Notably, from a sector perspective,

• We are Overweight the platinum group metals (PGM) sector (unchanged from last quarter), Overweight the telecommunications sector (unchanged from last quarter), Overweight media (unchanged from last quarter) and Overweight listed property (unchanged from last quarter). We are also now Overweight apparel retail (from Underweight last quarter).

• We are Neutral food retailers (from Overweight last quarter).

• We are Underweight gold mining (unchanged from last quarter).

• We are Overweight bonds (from Neutral last quarter).

Exhibit 2: Current sector views, previous sector views and sector performance

Sector Analyst/s Current (2Q 2021) Previous (1Q 2021) Performance 1Q 2021 Performance YTD Bloomberg ticker

Platinum group metals Arnold Van Graan Overweight Overweight 25.6% 25.6% JPLAT INDEX

Telecommunications Preshendran Odayar

and Ziyad Joosub Overweight Overweight 27.9% 28.5% JMOTE INDEX

Media Preshendran Odayar

and Ziyad Joosub Overweight Overweight

Food retail Sa’ad Chothia Neutral Neutral 5.4% 5.7% JFDRT INDEX

Apparel retail Sa’ad Chothia Overweight Underweight 23.3% 23.2% JGEN Index

Listed property Ridwaan Loonat Overweight Overweight 5.1% 14.4% JSAPY INDEX

Gold mining Arnold Van Graan Underweight Underweight -2.7% -2.7% JGOLD INDEX

Fixed income – ALBI Reezwana Sumad Overweight Underweight -1.8% -1.8% ALBTR Index

Source: Nedbank CIB Markets Research

Preference picks and selective bias within sectors

We have a selective bias within each sector as far as companies and specific assets are concerned. Our current conviction and sector picks are summarised in Exhibit 3.

Exhibit 3: Sector picks: despite our overall sector views, we have a selective bias within each sector

Sector Current sector recommendation Overweight names Neutral names Underweight names

Platinum group metals mining Overweight NHM, IMP, RBP, SSW RBP, AMS, THA PTM, WEZ, IVN

Telecommunications Overweight MTN, TKG, VOD

Media Overweight NPN, PRX

Food retail Neutral WHL, SHP, SPP PIK

Listed property Overweight RES, NRP, FFA, EMI, VKE,

MSP, RDF

FFB, GRT

Apparel retail Overweight TFG, PPH, MRP TRU

Gold mining Underweight SSW, ANG HAR, ANG DRD, PAN

Fixed income – government

bonds

Overweight Short-dated nominal bonds Long-dated nominal bonds

Source: Nedbank CIB Markets Research

6 APRIL 2021 PAGE 5

QUARTERLY UPDATE

Global outlook: no structural shift higher in inflation just yet

Since the 2008 GFC, monetary policy has changed dramatically. Prior to the GFC, central banks would tighten financial conditions at the first sign of consumer inflation; now it is official policy that the Fed will allow inflation to move above its target levels and target “average inflation”. The reason for this policy is, obviously, to make sure that deflationary “expectations” do not get a chance to become part of the social mood. The Fed has been buying inflation-linked bonds just to make sure the breakeven rate rises.

The market expects higher inflation over the next quarter because of base effects from the very low inflation numbers last year as the world went into lockdown. The more challenging question is not whether inflation will rise during 2Q21 but whether this higher inflation and nominal growth can be sustained beyond the second quarter.

We have been concerned about deflation over the past decade, and we do not believe it is time quite yet to change our view. The important word is “yet”, as we believe the foundation for the next inflationary cycle is being laid. The challenge is to try to figure out the route from the disinflationary forces that have been intact over the past 20 years to the much-anticipated inflation.

Lower highs since 2006

Since 2006, every high in inflation was lower both in the US and the EU, notwithstanding major expansion in the monetary base (Exhibit 4). It is now well known that all these QEs fuelled asset prices, as they compressed the bond term premium, but, unfortunately, this excess liquidity never made it into the real economy. The market expected inflation during QE1-QE3 after the GFC, after the G-20 bailout in early 2016 and then, obviously, with the latest monetary and fiscal stimulus. As 2Q21 unfolds, we would get more evidence as to whether this time would be different and excess liquidity will make it into the real economy.

There are differences between the stimulus packages from the bailouts in 2009-11 and again in 2016. The “helicopter money” in the form of COVID-19-related cheques and loan guarantee schemes did lead to an expansion in broad money, which is far more likely to create inflation that the expansion in the monetary base.

Diminishing return on debt likely to curb growth

But we remain sceptical whether the inflationary outlook will remain sustainable. Every time the QE sugar rush lost its effect over the past decade, the deflationary forces and the lack of growth returned. The single biggest reason for that, in our opinion, is the diminishing return of the extra debt added to the system, and this growing debt burden is now a major drag on economic growth.

The paradox of thrift adds to disinflation

The second reason why we believe economic growth and the inflation outlook will remain subdued comes from the “paradox of thrift”. If every entity in the economy saves, the economy will contract and disposable income will fall, making it very difficult to save yourself from this over-indebted situation. Hence, the government must become the major “dis-saver” in the economy, but this would lead to a crowding-out effect, and government spending has a very low multiplier. It is very clear from the flow

Neels Heyneke

We have been concerned about deflation over the past decade, and we do not believe it is time quite yet to change our view. The important word is “yet”, as we believe the foundation for the next inflationary cycle is being laid.

Exhibit 4: US 10y breakeven rate, inflation and EU Inflation

Source: Nedbank CIB Markets Research, Reuters, Bloomberg

6 APRIL 2021 PAGE 6

QUARTERLY UPDATE

of funds in Exhibit 5 that the US government has been the major force behind the economy since the Nasdaq crash. The US was very fortunate that demand for USD FX reserves funded the US government. Note how the savings from the rest of the world (ROW), the black dotted line, was rising during the commodity cycle.

In a bizarre way, the US does not decide its own savings rate; demand for FX reserves plays an important role. But foreign participation in the US bond market is declining, and the US must now supply or print its own savings. Everyone expects this major spending to materialise as soon as the lockdowns are over, but the corporate and household sector will have to save to fund government spending. The US can lure funds from overseas with higher real rates, which the asset markets, especially the stock market, will not be able to handle, or allow the currency to fall to a level where foreigners will participate. The Fed was very successful with the latter strategy over the past year.

There has also been a major change in social mood over the past decade as wages started to rise as a percentage of GDP, but the household savings rate has gone up from 0% to over 10% now. We believe this change in social mood is here to stay.

The second quarter is going to be very important in the sense that it would give us information on whether the world will be able to escape the low-growth environment of the past decade.

Exhibit 5: US flow of funds

Source: Nedbank CIB Markets Research, Reuters, Bloomberg

6 APRIL 2021 PAGE 7

QUARTERLY UPDATE

Domestic growth – costs rising at a slower pace

We expect growth of 3.8% y/y in 2021, up from our previous expectation of 2.5% y/y

We adjust our growth forecast higher. We now expect GDP to grow by 3.8% y/y in 2021 compared to 2.5% y/y previously (Exhibit 6). Our growth estimate is higher due to stronger external growth, with the IMF expecting world GDP to grow at 5.5% y/y in 2021 (up from 3.5% in December).

At the same time, we now expect gross fixed capital formation in 2021 to perform better than previously expected, by expanding 9.3% y/y, versus previous expectations of 6% y/y. This comes on the back of stronger global demand and commodity prices as well as a smaller government deficit than projected last year, which leaves more domestic savings for the private sector to invest. We expect household consumption expenditure to grow by 4.2% in 2021 following a contraction of -5.4% last year.

Consensus growth has moved higher to 3.5% y/y

The median Bloomberg consensus forecast for 2021 is currently at 3.5% y/y and, as such, we have moved from a below-consensus view to an above-consensus view on growth. At the end of December, the Bloomberg consensus expectation for 2021 growth was 3.8% y/y. In comparison to our view, in their latest updates, the SARB and the IMF in their January World Economic Outlook pin GDP growth at 3.8% and 2.8% y/y, respectively. The National Treasury (NT) forecast growth of 3.3% y/y for 2021 in the Budget in February.

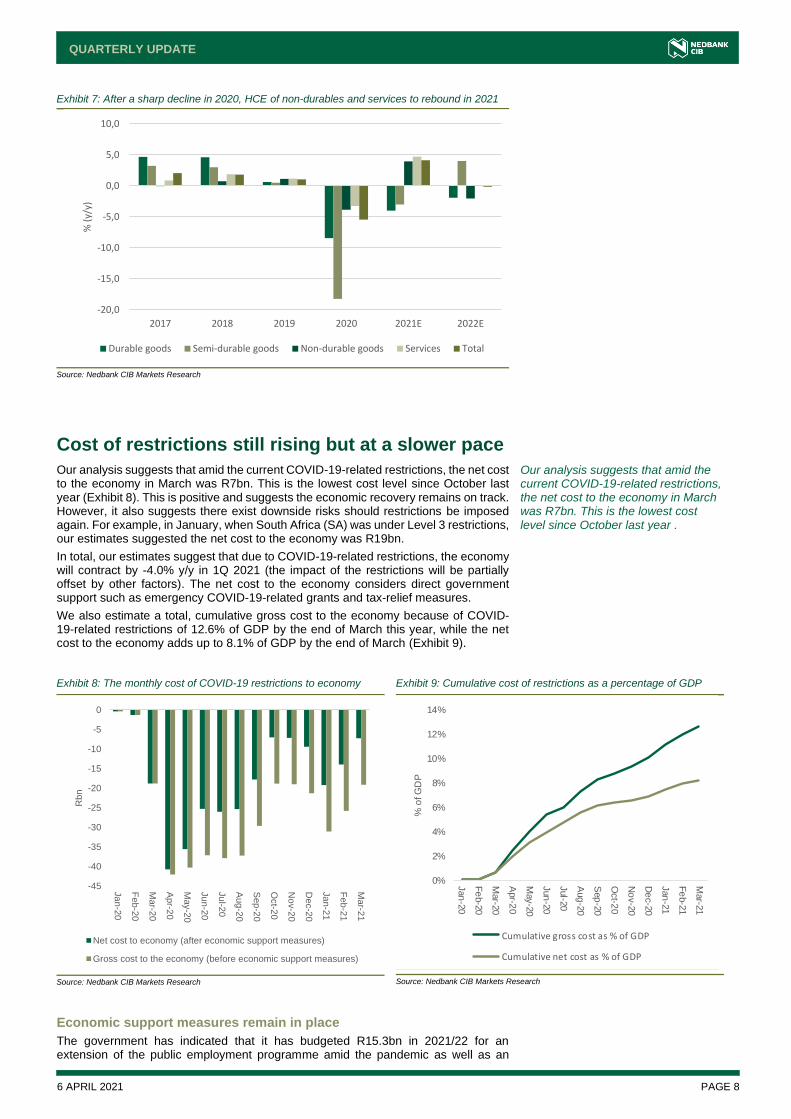

We expect HCE of non-durable goods and services to rebound

Household consumption expenditure (HCE) will likely remain weak, although we expect an expansion of 4.2% in 2021, this comes from a very low base in 2020. Consumption of durable and semi-durable goods would still contract, with only services and non-durable goods expected to expand, largely due to strong base effects from COVID-19-related restrictions in 2020 (Exhibit 7).

We adjust our growth forecast higher. We now expect GDP to grow by 3.8% y/y in 2021 compared to 2.5% y/y previously

Exhibit 6: South Africa GDP growth expectations for 2021

Source: Nedbank CIB Markets Research, SARB, IMF, National Treasury, Bloomberg

3,50%

3,80%

3,30%

2,80%

3,80%

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

3,50%

4,00%

Consensus SARB NT IMF Nedbank CIBMarkets Research

Walter de Wet, CFA

6 APRIL 2021 PAGE 8

QUARTERLY UPDATE

Cost of restrictions still rising but at a slower pace

Our analysis suggests that amid the current COVID-19-related restrictions, the net cost to the economy in March was R7bn. This is the lowest cost level since October last year (Exhibit 8). This is positive and suggests the economic recovery remains on track. However, it also suggests there exist downside risks should restrictions be imposed again. For example, in January, when South Africa (SA) was under Level 3 restrictions, our estimates suggested the net cost to the economy was R19bn.

In total, our estimates suggest that due to COVID-19-related restrictions, the economy will contract by -4.0% y/y in 1Q 2021 (the impact of the restrictions will be partially offset by other factors). The net cost to the economy considers direct government support such as emergency COVID-19-related grants and tax-relief measures.

We also estimate a total, cumulative gross cost to the economy because of COVID-19-related restrictions of 12.6% of GDP by the end of March this year, while the net cost to the economy adds up to 8.1% of GDP by the end of March (Exhibit 9).

Economic support measures remain in place

The government has indicated that it has budgeted R15.3bn in 2021/22 for an extension of the public employment programme amid the pandemic as well as an

Exhibit 7: After a sharp decline in 2020, HCE of non-durables and services to rebound in 2021

Source: Nedbank CIB Markets Research

Our analysis suggests that amid the current COVID-19-related restrictions, the net cost to the economy in March was R7bn. This is the lowest cost level since October last year .

Exhibit 8: The monthly cost of COVID-19 restrictions to economy

Source: Nedbank CIB Markets Research

Exhibit 9: Cumulative cost of restrictions as a percentage of GDP

Source: Nedbank CIB Markets Research

-20,0

-15,0

-10,0

-5,0

0,0

5,0

10,0

2017 2018 2019 2020 2021E 2022E

% (

y/y)

Durable goods Semi-durable goods Non-durable goods Services Total

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

Ja

n-2

0

Feb

-20

Mar-2

0

Apr-2

0

May-2

0

Ju

n-2

0

Ju

l-20

Aug

-20

Sep

-20

Oct-2

0

No

v-2

0

De

c-2

0

Ja

n-2

1

Feb

-21

Mar-2

1

Rbn

Net cost to economy (after economic support measures)

Gross cost to the economy (before economic support measures)

0%

2%

4%

6%

8%

10%

12%

14%

Jan

-20

Fe

b-2

0

Mar-2

0

Apr-2

0

May-2

0

Jun

-20

Jul-2

0

Aug

-20

Sep

-20

Oct-2

0

No

v-2

0

De

c-2

0

Jan

-21

Fe

b-2

1

Mar-2

1

% o

f G

DP

Cumulative gross cost as % of GDP

Cumulative net cost as % of GDP

6 APRIL 2021 PAGE 9

QUARTERLY UPDATE

extension of the COVID-19-related emergency grants. The NT has also indicated that the UIF is likely to pay out an additional R73.6bn this fiscal year via the TERF programme. As a result, we do not expect the majority of economic support measures to end in April but rather remain in place for most of the 2021/22 fiscal year. However, should the economic support measures be reduced downside risk to growth will emerge.

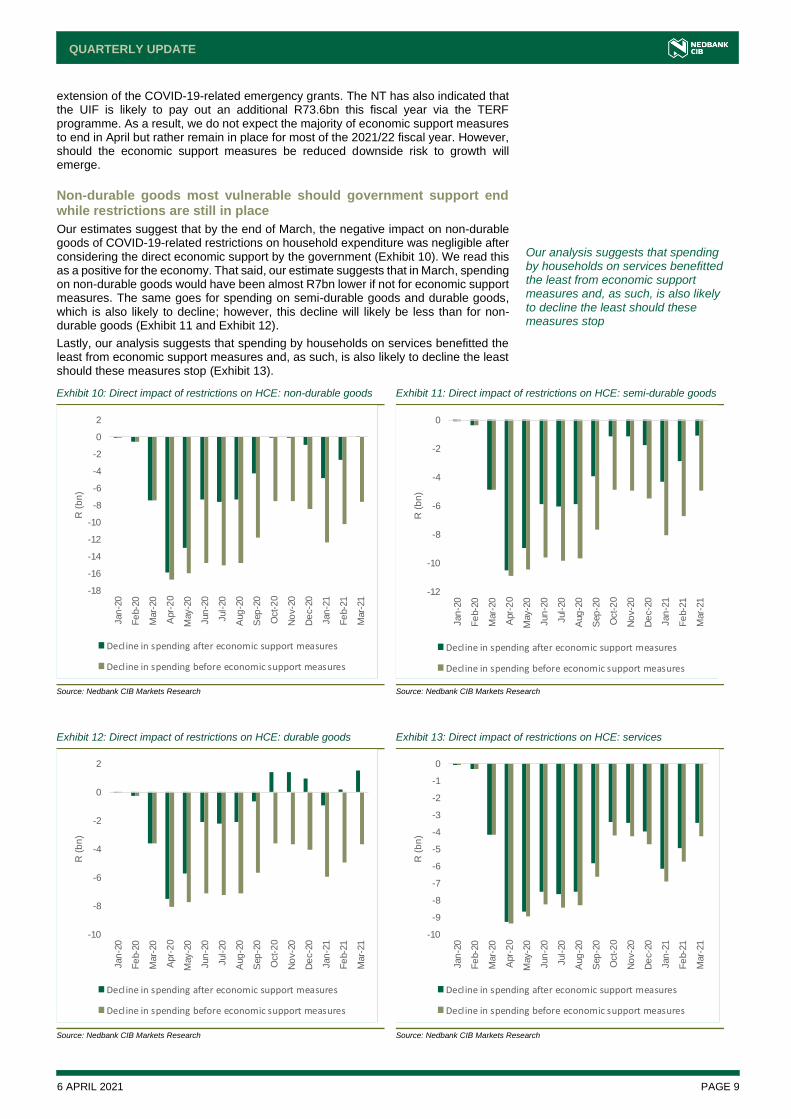

Non-durable goods most vulnerable should government support end while restrictions are still in place

Our estimates suggest that by the end of March, the negative impact on non-durable goods of COVID-19-related restrictions on household expenditure was negligible after considering the direct economic support by the government (Exhibit 10). We read this as a positive for the economy. That said, our estimate suggests that in March, spending on non-durable goods would have been almost R7bn lower if not for economic support measures. The same goes for spending on semi-durable goods and durable goods, which is also likely to decline; however, this decline will likely be less than for non-durable goods (Exhibit 11 and Exhibit 12).

Lastly, our analysis suggests that spending by households on services benefitted the least from economic support measures and, as such, is also likely to decline the least should these measures stop (Exhibit 13).

Our analysis suggests that spending by households on services benefitted the least from economic support measures and, as such, is also likely to decline the least should these measures stop

Exhibit 10: Direct impact of restrictions on HCE: non-durable goods

Source: Nedbank CIB Markets Research

Exhibit 11: Direct impact of restrictions on HCE: semi-durable goods

Source: Nedbank CIB Markets Research

Exhibit 12: Direct impact of restrictions on HCE: durable goods

Source: Nedbank CIB Markets Research

Exhibit 13: Direct impact of restrictions on HCE: services

Source: Nedbank CIB Markets Research

-18

-16

-14

-12

-10

-8

-6

-4

-2

0

2

Jan

-20

Fe

b-2

0

Mar-

20

Apr-

20

May-2

0

Jun

-20

Jul-

20

Aug

-20

Sep

-20

Oct-

20

No

v-2

0

De

c-2

0

Jan

-21

Fe

b-2

1

Mar-

21

R (

bn

)

Decline in spending after economic support measures

Decline in spending before economic support measures

-12

-10

-8

-6

-4

-2

0

Jan

-20

Fe

b-2

0

Mar-

20

Apr-

20

May-2

0

Jun

-20

Jul-

20

Aug

-20

Sep

-20

Oct-

20

No

v-2

0

De

c-2

0

Jan

-21

Fe

b-2

1

Mar-

21

R (

bn

)

Decline in spending after economic support measures

Decline in spending before economic support measures

-10

-8

-6

-4

-2

0

2

Jan

-20

Fe

b-2

0

Mar-

20

Apr-

20

May-2

0

Jun

-20

Jul-

20

Aug

-20

Sep

-20

Oct-

20

No

v-2

0

De

c-2

0

Jan

-21

Fe

b-2

1

Mar-

21

R (

bn

)

Decline in spending after economic support measures

Decline in spending before economic support measures

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

Jan

-20

Fe

b-2

0

Mar-

20

Apr-

20

May-2

0

Jun

-20

Jul-

20

Aug

-20

Sep

-20

Oct-

20

No

v-2

0

De

c-2

0

Jan

-21

Fe

b-2

1

Mar-

21

R (

bn

)

Decline in spending after economic support measures

Decline in spending before economic support measures

6 APRIL 2021 PAGE 10

QUARTERLY UPDATE

Monetary policy – we look for a delayed but muted hiking cycle

The SARB MPC turned decidedly hawkish in January 2021, and maintained this tone in March 2021, while keeping the repo rate flat at 3.50%. For the first time in almost a year, the MPC voted unanimously in March – we believe this signals a key shift in the MPC’s rhetoric and the end of the easing cycle. The lower inflation forecast for 2022-23 and fewer rate hikes (for 2021) signalled in the SARB’s QPM prevented a more hawkish stance by the SARB. The fact that the SARB now sees annual average inflation at or below its 4.5% target until 2023 could allow it to delay the hiking cycle into 2022, given the risks to the growth outlook over the medium term.

SARB maintains hawkish tone, but QPM hike profile marginally lower for 2021

The SARB MPC maintained its hawkish tone, and this was substantiated by a better economic outlook (and a smaller output gap), a faster global economic recovery and a general improvement in financial market conditions. However, it remains cognisant of the impact that the country’s electricity supply constraints will have on growth, along with weak public and private investment levels. New waves of COVID-19 infections and the uncertain nature of SA’s vaccination rollout programme pose additional risks to the growth outlook. The SARB’s inflation forecast was reduced for 2022 and 2023, which resulted in the QPM pushing out its forecast for hikes to the repo rate (albeit fractionally). The QPM now signals two hikes of 25bps each in 2021 (previously 2.44 hikes of 25bps each), but 3.8 and 4.5 hikes of the same magnitude for 2022 and 2023 (previously 3.4 and 3.9), respectively. In sum, the QPM reflects 10.3 hikes of 25bps each over the forecast period (compared to 9.72 in January).

In the absence of a sustained CPI breach above 4.5%, the SARB would be loath to begin normalising interest rates prematurely, as this risk undoing the relief it has provided to the economy, which would ultimately hurt growth further.

Exhibit 14: Real policy rates across the world

Source: Bloomberg, Nedbank CIB Markets Research

The SARB has been tolerant of negative real rates in the past The current real repo rate is 0.6%, while the expected repo rate for 2021 is -0.4% (based on our CPI forecast of 3.9%). SA has one of the highest real policy rates in the world (see Exhibit above), while it maintains its top spot with the highest real yield (10y) in the world. Monetary policy, therefore, remains supportive of the currency and inflation expectations, in our view. In 2008, despite the real repo rate declining to -1.69%, the SARB maintained its commitment to ease policy rates in order to safeguard economic growth after the crisis. From 2012 to 2013, the real repo rate averaged -0.56%, while the nominal repo rate remained broadly flat during this period

4,6

3,4

2,41,71,7

0,60,50,40,20,20,20,20,10,0

-0,2-0,3-0,3-0,5-0,5-0,6-0,6-0,6-0,8-0,8-0,9-1,0-1,0-1,2-1,2-1,2-1,3-1,4-1,5-1,8-1,8

-2,3-2,4-2,5-2,7-2,7-3,3

-5

-3

-1

1

3

5

7

Ch

ina

Tu

rke

y

Ind

on

es

ia

Th

ail

an

d

Mala

ys

ia

So

uth

Afr

ica

Ja

pa

n

Ire

lan

d

Mex

ico

Icela

nd

Ho

ng

Ko

ng

Co

lom

bia

Isra

el

Sp

ain

Taiw

an

Sw

itze

rla

nd

UK

Belg

ium

Po

rtu

ga

l

Fra

nc

e

Italy

Sin

ga

po

re

Au

str

ali

a

Can

ad

a

Fin

lan

d

Den

ma

rk

Ind

ia

New

Ze

ala

nd

Ru

ss

ia

Au

str

ia

Ge

rman

y

Sw

ed

en

US

Neth

erl

an

ds

Czec

h

Po

lan

d

Ch

ile

Bra

zil

Hu

ng

ary

Ph

ilip

pin

e

No

rwa

y

'Spot' real policy rate: nominal interest rate less inflation (current)

Reezwana Sumad

The QPM now signals two hikes of 25bps each in 2021 (previously 2.44 hikes of 25bps each), but 3.8 and 4.5 hikes of the same magnitude for 2022 and 2023 (previously 3.4 and 3.9), respectively.

6 APRIL 2021 PAGE 11

QUARTERLY UPDATE

as a result of heightened uncertainty as to when the Fed would begin hiking interest rates. The uncertain nature of the current pandemic warrants a similar response, in our view, until we are more certain about SA’s economic recovery. While several EM peers have begun to hike interest rates in 2021 (Brazil, Turkey, Russia, etc.), they do so out of necessity because inflation has risen well above their inflation targets. Barring a surprise and a sustained increase in inflation to 5%, we believe the SARB will keep the repo rate flat at 3.50% in 2021 and begin a gradual hiking cycle in 2022.

We expect inflation of 3.9% in 2021 and 4.5% in 2022

The SARB’s inflation forecast was revised 10bps higher (cumulatively) over the forecast period. However, this was mainly due to the +30bps revision to its 2021 inflation forecast (to 4.3%), as its forecasts for 2022 and 2023 fell 10bps each to 4.4% and 4.5%, respectively. The main reason for this shift is the upward revision to its oil price and electricity tariff assumptions for 2021. The SARB sees inflation breaching its 4.5% target for the next four quarters, before falling below 4.5% for the rest of the forecast period. Our own forecast reflects a more subdued inflation profile until 3Q22, when inflation is expected to rise above the SARB’s 4.5% target.

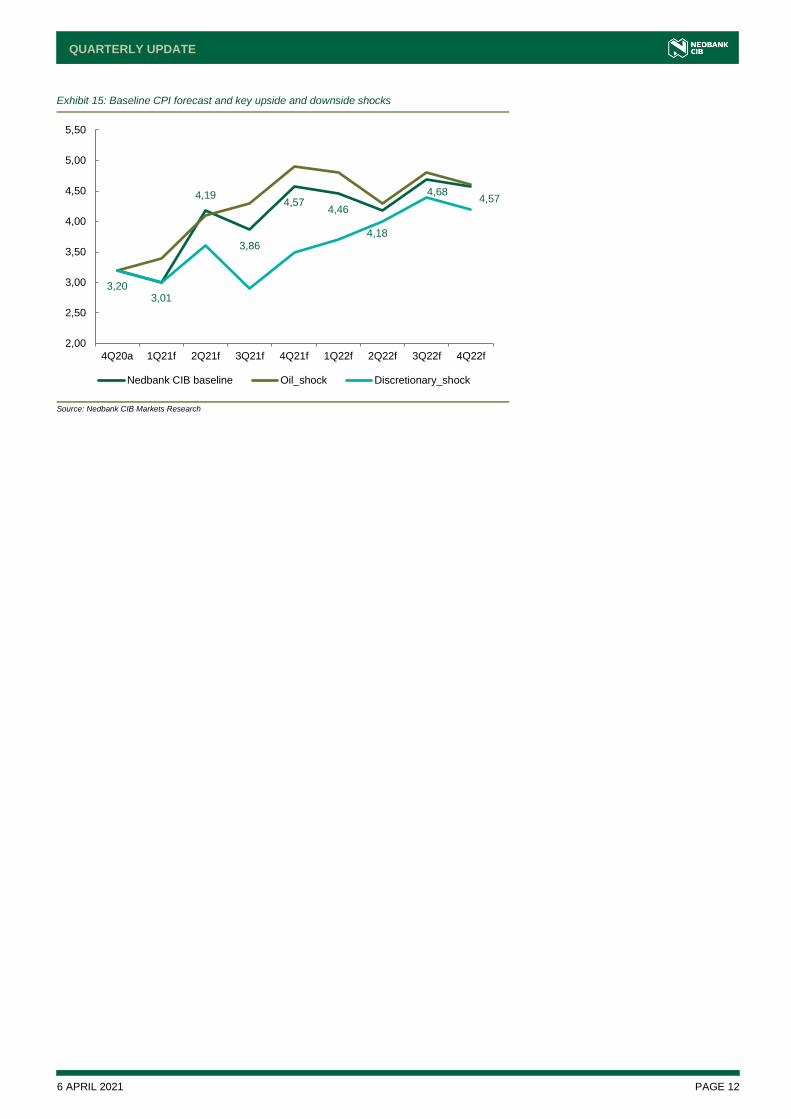

The balance of risks during a muted economic recovery

Exhibit 15 represents our baseline CPI forecasts over the next two years – we estimate average inflation rates of 3.9% in 2021 and 4.5% in 2022, up from 3.3% in 2020. Some of our assumptions underpinning these forecasts are as follows:

• A gradually weaker USDZAR, with an average exchange rate of R15.74 in 2021 and R17.70 in 2022

• An average Brent crude price of USD62/bbl in 2021 (and USD58/bbl in 2022) –while this is USD7/bbl higher than our forecast at the start of the year, it is partly offset by a sharp decline in medical aid and health inflation

• Average electricity price inflation of 13.5% in 2021 (and 11.8% in 2022) – this now accounts for the 15.6% Eskom tariff hike in April 2021

• A muted rental inflation trajectory (averaging 0.8% over the two-year period)

• Our model yields an average food inflation forecast of 5.2% in 2021 and 6.8% in 2022

We believe the main upside risks to our inflation forecast either stem from administered costs or are mainly exogenous in nature:

• A faster global economic recovery and increased demand for oil will likely manifest in a shock to international oil prices and SA fuel costs over the medium term. Alternatively, an oil shortage engineered by OPEC could also raise oil prices above our baseline assumption. An average oil price of USD70/bbl is used for the oil price shock in Exhibit 15.

Much like in 2020, a muted economic recovery in 2021 and 2022 would present material downside risks to our inflation forecast, as prices of discretionary goods and services are the worst affected by the lack of demand. Items such as restaurant prices, recreational and cultural goods and services, and miscellaneous goods and services could surprise to the downside, in our view.

The SARB sees inflation breaching its 4.5% target for the next four quarters, before falling below 4.5% for the rest of the forecast period. Our own forecast reflects a more subdued inflation profile until 3Q22, when inflation is expected to rise above the SARB’s 4.5% target.

6 APRIL 2021 PAGE 12

QUARTERLY UPDATE

Exhibit 15: Baseline CPI forecast and key upside and downside shocks

Source: Nedbank CIB Markets Research

3,203,01

4,19

3,86

4,574,46

4,18

4,684,57

2,00

2,50

3,00

3,50

4,00

4,50

5,00

5,50

4Q20a 1Q21f 2Q21f 3Q21f 4Q21f 1Q22f 2Q22f 3Q22f 4Q22f

Nedbank CIB baseline Oil_shock Discretionary_shock

6 APRIL 2021 PAGE 13

QUARTERLY UPDATE

Fiscal policy bears some fruit, but we await the harvest

Debt sustainability and financing the budget

• A combination of better global growth, local consumption and wage growth, and higher tax receipts from the mining sector boosts main budget revenue from 2020 to 2024 by R297bn compared to the 2020 MTBPS, along with real GDP growth. This, combined with new research detailing the negative impact of tax increases in a weak economy, prompted the government to cancel the implementation of its previously announced tax increases over the next four years.

• The government makes better spending decisions – consolidated expenditure has been revised lower by a cumulative R34bn until 2023/24: a material reduction to expenditure comes from the wage bill (-R144bn over the MTEF) and identifying and cutting out unnecessary government-funded programmes (-R163bn reduction over the MTEF). The fiscal framework reduces growth in the wage bill and the share of spending on wages, while sustaining real spending increases on capital payments, specifically for buildings and other fixed structures.

– The main budget deficit as a percentage of GDP is now projected at 6.5% for 2023/24 (vs 7.3% in the MTBPS). The deficit for 2021/22 is expected at 9% compared to 10.1% previously, while the 2022/23 forecast is 7.4% relative to the MTBPS estimate of 8.7%.

– While we forecast a primary budget deficit of 0.4% of GDP by 2023/24, implementation risk in the budget to achieve this outcome remains high.

– The newly announced pace of weekly bond issuance (of R6bn/week) will be sufficient to finance a budget deficit of R506bn in 2021/22, which is R23bn higher than what is actually needed to fund the deficit (of R483bn in the 2021 Budget). However, if the NT is unable to rein in expenditure as promised, the financing requirement would eventually rise.

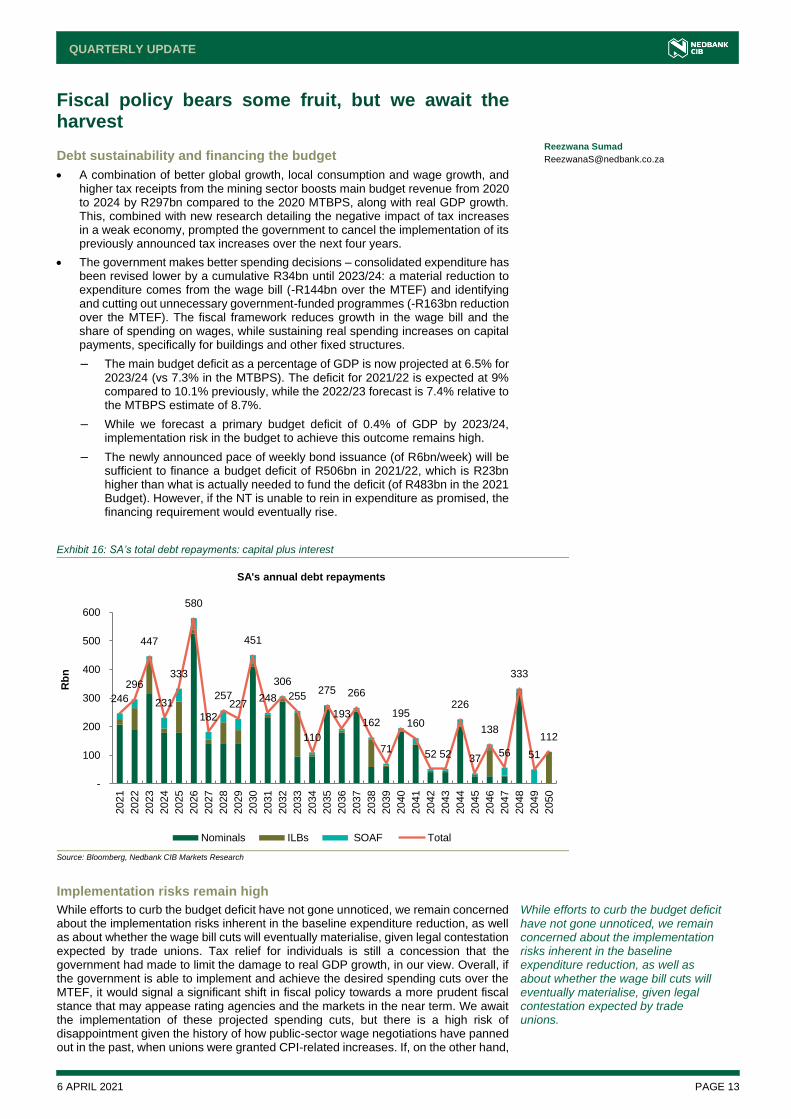

Exhibit 16: SA’s total debt repayments: capital plus interest

Source: Bloomberg, Nedbank CIB Markets Research

Implementation risks remain high

While efforts to curb the budget deficit have not gone unnoticed, we remain concerned about the implementation risks inherent in the baseline expenditure reduction, as well as about whether the wage bill cuts will eventually materialise, given legal contestation expected by trade unions. Tax relief for individuals is still a concession that the government had made to limit the damage to real GDP growth, in our view. Overall, if the government is able to implement and achieve the desired spending cuts over the MTEF, it would signal a significant shift in fiscal policy towards a more prudent fiscal stance that may appease rating agencies and the markets in the near term. We await the implementation of these projected spending cuts, but there is a high risk of disappointment given the history of how public-sector wage negotiations have panned out in the past, when unions were granted CPI-related increases. If, on the other hand,

246

296

447

231

333

580

182

257227

451

248

306

255

110

275

193

266

162

71

195160

52 52

226

37

138

56

333

51

112

-

100

200

300

400

500

600

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

2047

2048

2049

2050

Rb

n

SA's annual debt repayments

Nominals ILBs SOAF Total

Reezwana Sumad

While efforts to curb the budget deficit have not gone unnoticed, we remain concerned about the implementation risks inherent in the baseline expenditure reduction, as well as about whether the wage bill cuts will eventually materialise, given legal contestation expected by trade unions.

6 APRIL 2021 PAGE 14

QUARTERLY UPDATE

the government falls short of delivering a leaner expenditure profile over the MTEF, this threatens to derail debt projections, and raise the budget deficit over the MTEF. SA can ill afford such a development, particularly as the debt burden is unsustainably high already (Exhibit 17).

Exhibit 17: Debt-to-GDP ratio at risk of disappointing

Source: National Treasury, Nedbank CIB Markets Research

Exhibit 18: The government’s financing requirement (current = updated to include issuance reduction)

Rbn

2019/20a

Final

2020/21a

2021 Budget

2021/22e

2020 Budget 2021 Budget Current NCIB

Nominal bonds: 273.7 445.9 290.2 326.8 345.6 351.2

Issuance for the FYTD/year 204.4 230.4 233.9

Total non-comps 69.3 115.2 117.0

ILBs: 43.1 72.6 47.2 53.2 57.6 57.2

Total long-term market loans 316.8 518.5 337.4 380.0 403.2 408.4

Short-term loans and T-bills 36.1 97.1 48.0 9.0 9.0 9.0

Foreign loans 76.1 107.1 44.8 46.3 46.3 46.3

Extra issuance carried forward

Cash -1.8 -52.4 -0.3 112.6 112.6 112.6

TOTAL FINANCING

REQUIREMENT 427.3 670.3 429.9 547.9 571.1 576.3

(Less) redemptions -70.7 -66.9 -63.5 -65.3 -65.3 -65.3

Main budget deficit 356.6 603.4 366.4 482.6 505.8 511.0

FYTD = Fiscal year to date Source: National Treasury, Nedbank CIB Markets Research

45

50

55

60

65

70

75

80

85

90

95

%

Gross debt to GDP forecasts - evolution (% of GDP)

2017 Budget 2017 MTBPS 2018 Budget 2018 MTBPS

2019 Budget 2019 MTBPS 2020 Budget 2020 MTBPS

2021 Budget Nedbank CIB Actual

6 APRIL 2021 PAGE 15

QUARTERLY UPDATE

Credit conditions are firmly negative, but borrowing window is accommodative

Rating agencies are set to review SA in May 2021 – we expect no rating changes

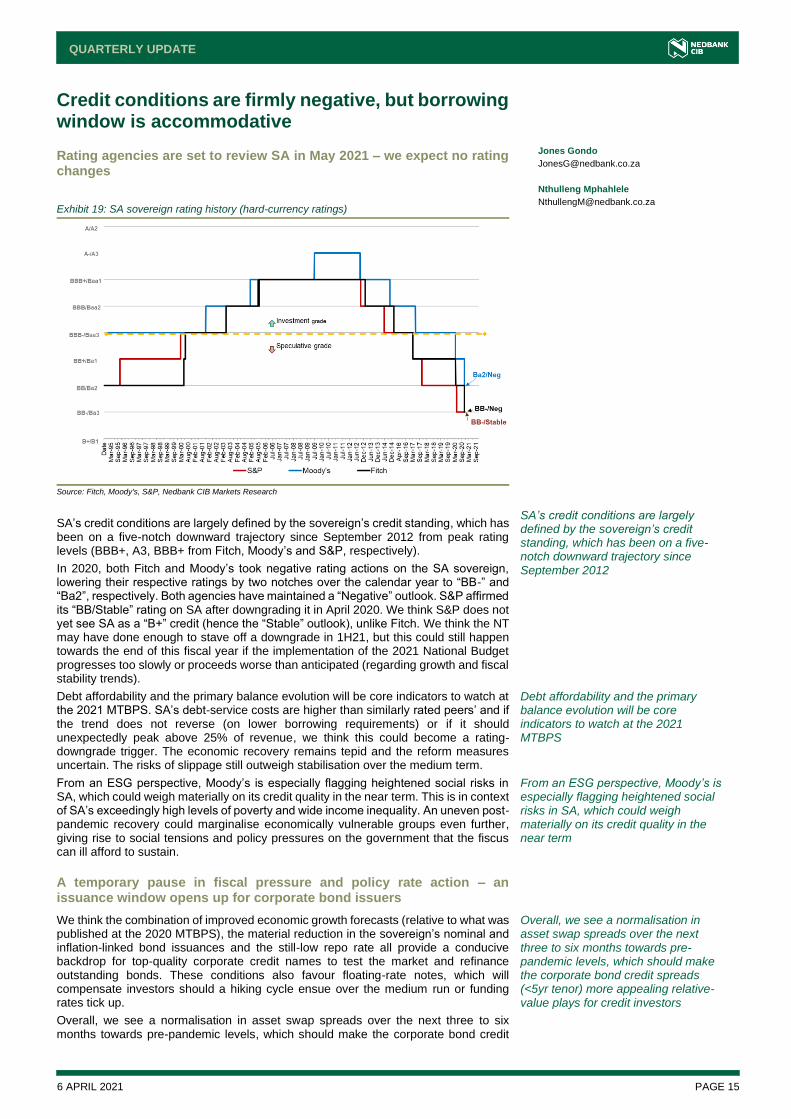

Exhibit 19: SA sovereign rating history (hard-currency ratings)

Source: Fitch, Moody's, S&P, Nedbank CIB Markets Research

SA’s credit conditions are largely defined by the sovereign’s credit standing, which has been on a five-notch downward trajectory since September 2012 from peak rating levels (BBB+, A3, BBB+ from Fitch, Moody’s and S&P, respectively).

In 2020, both Fitch and Moody’s took negative rating actions on the SA sovereign, lowering their respective ratings by two notches over the calendar year to “BB-” and “Ba2”, respectively. Both agencies have maintained a “Negative” outlook. S&P affirmed its “BB/Stable” rating on SA after downgrading it in April 2020. We think S&P does not yet see SA as a “B+” credit (hence the “Stable” outlook), unlike Fitch. We think the NT may have done enough to stave off a downgrade in 1H21, but this could still happen towards the end of this fiscal year if the implementation of the 2021 National Budget progresses too slowly or proceeds worse than anticipated (regarding growth and fiscal stability trends).

Debt affordability and the primary balance evolution will be core indicators to watch at the 2021 MTBPS. SA’s debt-service costs are higher than similarly rated peers’ and if the trend does not reverse (on lower borrowing requirements) or if it should unexpectedly peak above 25% of revenue, we think this could become a rating-downgrade trigger. The economic recovery remains tepid and the reform measures uncertain. The risks of slippage still outweigh stabilisation over the medium term.

From an ESG perspective, Moody’s is especially flagging heightened social risks in SA, which could weigh materially on its credit quality in the near term. This is in context of SA’s exceedingly high levels of poverty and wide income inequality. An uneven post-pandemic recovery could marginalise economically vulnerable groups even further, giving rise to social tensions and policy pressures on the government that the fiscus can ill afford to sustain.

A temporary pause in fiscal pressure and policy rate action – an issuance window opens up for corporate bond issuers

We think the combination of improved economic growth forecasts (relative to what was published at the 2020 MTBPS), the material reduction in the sovereign’s nominal and inflation-linked bond issuances and the still-low repo rate all provide a conducive backdrop for top-quality corporate credit names to test the market and refinance outstanding bonds. These conditions also favour floating-rate notes, which will compensate investors should a hiking cycle ensue over the medium run or funding rates tick up.

Overall, we see a normalisation in asset swap spreads over the next three to six months towards pre-pandemic levels, which should make the corporate bond credit

Jones Gondo

Nthulleng Mphahlele

SA’s credit conditions are largely defined by the sovereign’s credit standing, which has been on a five-notch downward trajectory since September 2012

Debt affordability and the primary balance evolution will be core indicators to watch at the 2021 MTBPS

From an ESG perspective, Moody’s is especially flagging heightened social risks in SA, which could weigh materially on its credit quality in the near term

Overall, we see a normalisation in asset swap spreads over the next three to six months towards pre-pandemic levels, which should make the corporate bond credit spreads (<5yr tenor) more appealing relative-value plays for credit investors

6 APRIL 2021 PAGE 16

QUARTERLY UPDATE

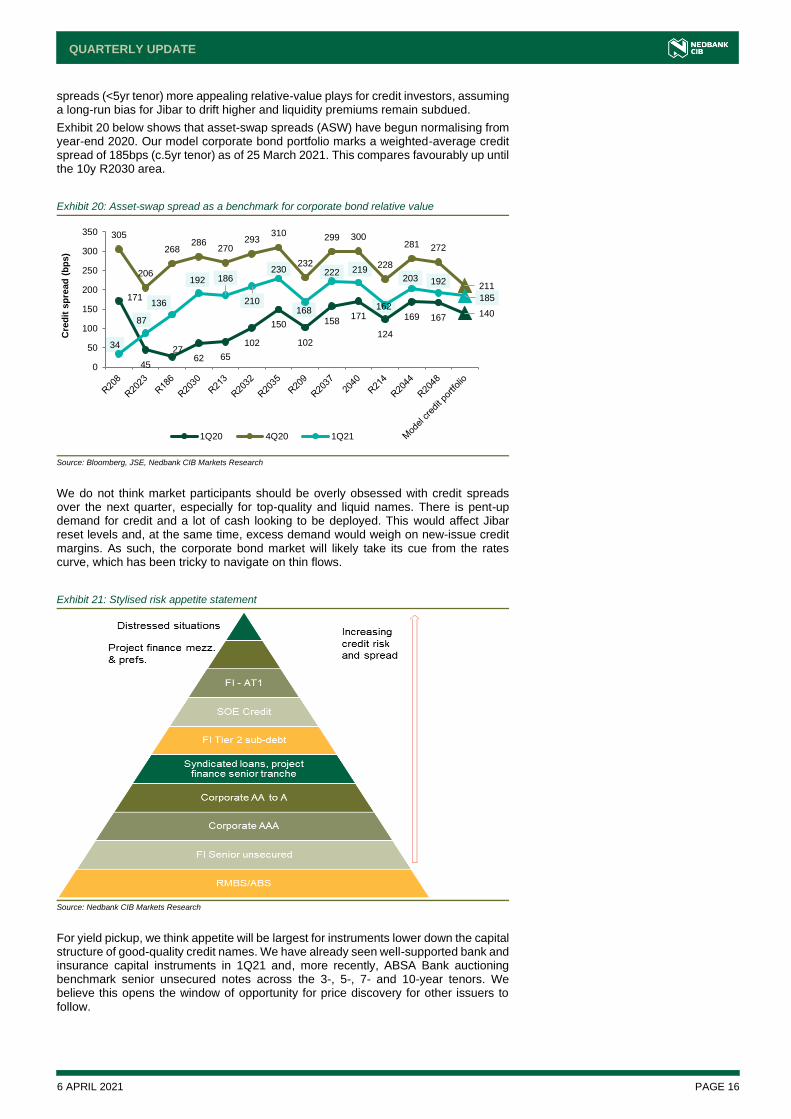

spreads (<5yr tenor) more appealing relative-value plays for credit investors, assuming a long-run bias for Jibar to drift higher and liquidity premiums remain subdued.

Exhibit 20 below shows that asset-swap spreads (ASW) have begun normalising from year-end 2020. Our model corporate bond portfolio marks a weighted-average credit spread of 185bps (c.5yr tenor) as of 25 March 2021. This compares favourably up until the 10y R2030 area.

Exhibit 20: Asset-swap spread as a benchmark for corporate bond relative value

Source: Bloomberg, JSE, Nedbank CIB Markets Research

We do not think market participants should be overly obsessed with credit spreads over the next quarter, especially for top-quality and liquid names. There is pent-up demand for credit and a lot of cash looking to be deployed. This would affect Jibar reset levels and, at the same time, excess demand would weigh on new-issue credit margins. As such, the corporate bond market will likely take its cue from the rates curve, which has been tricky to navigate on thin flows.

Exhibit 21: Stylised risk appetite statement

Source: Nedbank CIB Markets Research

For yield pickup, we think appetite will be largest for instruments lower down the capital structure of good-quality credit names. We have already seen well-supported bank and insurance capital instruments in 1Q21 and, more recently, ABSA Bank auctioning benchmark senior unsecured notes across the 3-, 5-, 7- and 10-year tenors. We believe this opens the window of opportunity for price discovery for other issuers to follow.

171

45

2762 65

102

150

102

158171

124

169 167 140

305

206

268286

270293

310

232

299 300

228

281 272

211

34

87

136

192 186

210

230

168

222 219

162

203 192

185

0

50

100

150

200

250

300

350

Cre

dit

sp

read

(b

ps)

1Q20 4Q20 1Q21

6 APRIL 2021 PAGE 17

QUARTERLY UPDATE

FX: some strength, less predictable

The rand has bounced between 14.50 and 15.50 since the start of the year. Price action counts for a lot, and the currency’s resilience suggests fundamentals still favour the rand.

For a moment, let’s move currency fundamentals aside

The rand just won’t give up. It has bounced back handsomely from close to the 15.50 level against the USD at the start of the week to the current level just below 14.80. Price action counts for a lot, and the currency’s resilience suggests fundamentals still favour the rand or, rather, they are stacked against the USD. From a domestic perspective, three obvious factors are in favour of the currency: (1) strong commodity prices, (2) a strong trade surplus (partly due to the high commodity prices) and (3) high real government bond yields.

But sometimes, it is worthwhile to take a step back, ignore currency fundamentals for a moment and look at what the statistics behind the price action tell us. We turn to our “extreme-peaks” model that we find useful in periods of extreme volatility to gauge where in the cycle the rand is.

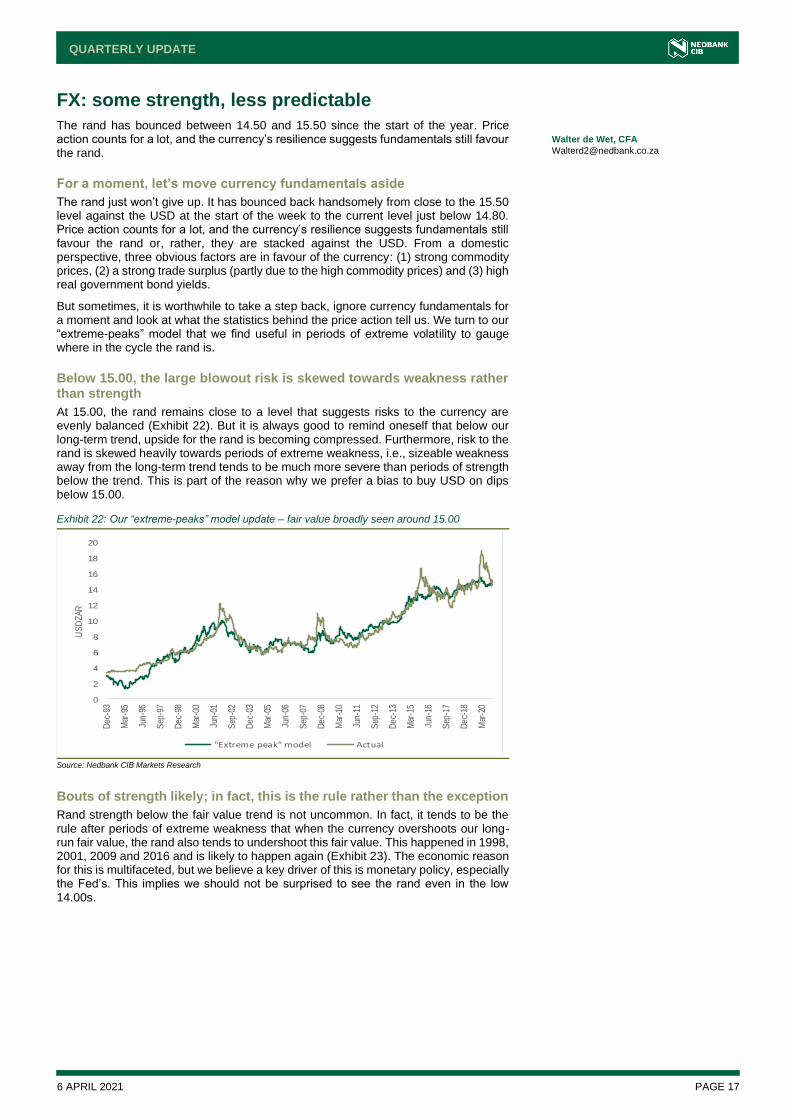

Below 15.00, the large blowout risk is skewed towards weakness rather than strength

At 15.00, the rand remains close to a level that suggests risks to the currency are evenly balanced (Exhibit 22). But it is always good to remind oneself that below our long-term trend, upside for the rand is becoming compressed. Furthermore, risk to the rand is skewed heavily towards periods of extreme weakness, i.e., sizeable weakness away from the long-term trend tends to be much more severe than periods of strength below the trend. This is part of the reason why we prefer a bias to buy USD on dips below 15.00.

Bouts of strength likely; in fact, this is the rule rather than the exception

Rand strength below the fair value trend is not uncommon. In fact, it tends to be the rule after periods of extreme weakness that when the currency overshoots our long-run fair value, the rand also tends to undershoot this fair value. This happened in 1998, 2001, 2009 and 2016 and is likely to happen again (Exhibit 23). The economic reason for this is multifaceted, but we believe a key driver of this is monetary policy, especially the Fed’s. This implies we should not be surprised to see the rand even in the low 14.00s.

Walter de Wet, CFA

Exhibit 22: Our “extreme-peaks” model update – fair value broadly seen around 15.00

Source: Nedbank CIB Markets Research

0

2

4

6

8

10

12

14

16

18

20

De

c-93

Mar

-95

Jun

-96

Sep

-97

De

c-98

Mar

-00

Jun

-01

Sep

-02

De

c-03

Mar

-05

Jun

-06

Sep

-07

De

c-08

Mar

-10

Jun

-11

Sep

-12

De

c-13

Mar

-15

Jun

-16

Sep

-17

De

c-18

Mar

-20

US

DZ

AR

"Extreme peak" model Actual

6 APRIL 2021 PAGE 18

QUARTERLY UPDATE

But the trend is less predictable and more volatile within a smaller band

Although currency strength below our fair value line is not uncommon following periods of extreme weakness, once the rand drops below our fair value trend, currency moves become more erratic within a smaller range, and the trend in direction becomes more random. Timing the market to buy USD, or sell rand for that matter, becomes more difficult; hence our preference for simply favouring a bias towards USD below 15.00 rather than getting “chopped up” in volatility.

Be patient; rinse and repeat

From a currency perspective, our view remains that if you are long rand, levels below 15.00 look attractive from a risk/return perspective, especially on a 12-month view. We remain cognisant that risk to the large rand blowouts is starting to get skewed against you below 15.00.

But history suggests one can be patient, too – there is likely to be more than one chance. We know the currency becomes more volatile in a smaller range, which means the rand is likely to provide more than one opportunity to buy USD below 15.00 for the time being. The weakness in the rand we experienced over the past few days and the accompanied pullback to below 15.00 are good examples, in our view.

For exporters, the opposite applies – there will be bouts of weakness in the near term to capitalise on – but don’t wait too long, as for now, rand weakness closer to 16.00 is likely to fade.

Exhibit 23: Deviation from model value – strength below fair value the rule, but trend more volatile

Source: Nedbank CIB Markets Research

-3.0

-1.5

0.0

1.5

3.0

4.5

De

c-9

3

De

c-9

4

De

c-9

5

De

c-9

6

De

c-9

7

De

c-9

8

De

c-9

9

De

c-0

0

De

c-0

1

De

c-0

2

De

c-0

3

De

c-0

4

De

c-0

5

De

c-0

6

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

De

c-1

3

De

c-1

4

De

c-1

5

De

c-1

6

De

c-1

7

De

c-1

8

De

c-1

9

De

c-2

0

US

DZ

AR

Actual minus fitted 1.5 st.dev 3 st.dev Mean

6 APRIL 2021 PAGE 19

QUARTERLY UPDATE

Fixed income: country risk premia prevent outright bullishness

Both nominal bonds and ILBs provide value on a tactical basis, but elevated country risk premia limit upside over the medium term. We continue to favour short-dated ILBs relative to nominals – this upside is limited up to the 4y point. Thereafter, nominal bonds look more attractive given the higher real return.

While our fair value has not changed, its composition has

A combination of higher US bond yields and lower credit risk premia has kept our fair value yields largely unchanged.

• We continue to maintain a fair value range for the R2030 of between 9.00% and 9.50%. This is made up of a US 10y yield of 1.50% (as the “risk-free” rate), a credit risk premium of 4.30% (to account for SA country-specific risk) and an inflation risk premium of 3.70% (the difference between long-run SA and US CPI).

• Our fair value range for the R2048 is 11.00-11.50%.

• We see our fair value estimate as a 6- to 12-month view. Long-dated bond yields have risen sharply as a result of the turmoil in Turkey recently, which means that yields are now attractive relative to our fair value. However, we remain cognisant of elevated country risk premia and the potential for fiscal slippage in the October MTBPS and, therefore, remain neutral long-duration bonds.

• A weaker-than-expected real GDP growth outcome may result in a delay in the SARB’s hiking cycle (into 2022). This is premised on our CPI estimates of 3.9% for 2021 and 4.5% for 2022. There is, therefore, potential for the curve to bull steepen into the 10y point.

Too much inflation risk and not enough credit risk…

Monetary policy and inflation: From 2006 to 2020, SA’s 5y average inflation rate fell consistently (Exhibit 24). SA CPI has essentially fallen to the SARB’s new 4.5% CPI target, and we believe it will remain anchored close to this target over the medium term.

Fiscal policy and debt: Tracking fiscal policy, debt levels and the sovereign credit rating in similar five-year intervals since 2006 yields very different results – the budget deficit trend (as a percentage of GDP) has trebled, while the debt-to-GDP ratio has doubled over this period. SA’s sovereign credit rating has fallen five notches during this period.

Exhibit 24: SA’s monetary and fiscal policy effectiveness (5-year averages)

CPI Budget balance (% of

GDP) Debt-to-GDP ratio Foreign currency credit rating

(S&P) - end of period

2006 - 2010 6.8 -1.72 29.53 BBB+

2011 - 2015 5.4 -4.66 42.09 BBB-

2016 - 2020 4.7 -5.3 56.24 BB-

Source: Bloomberg

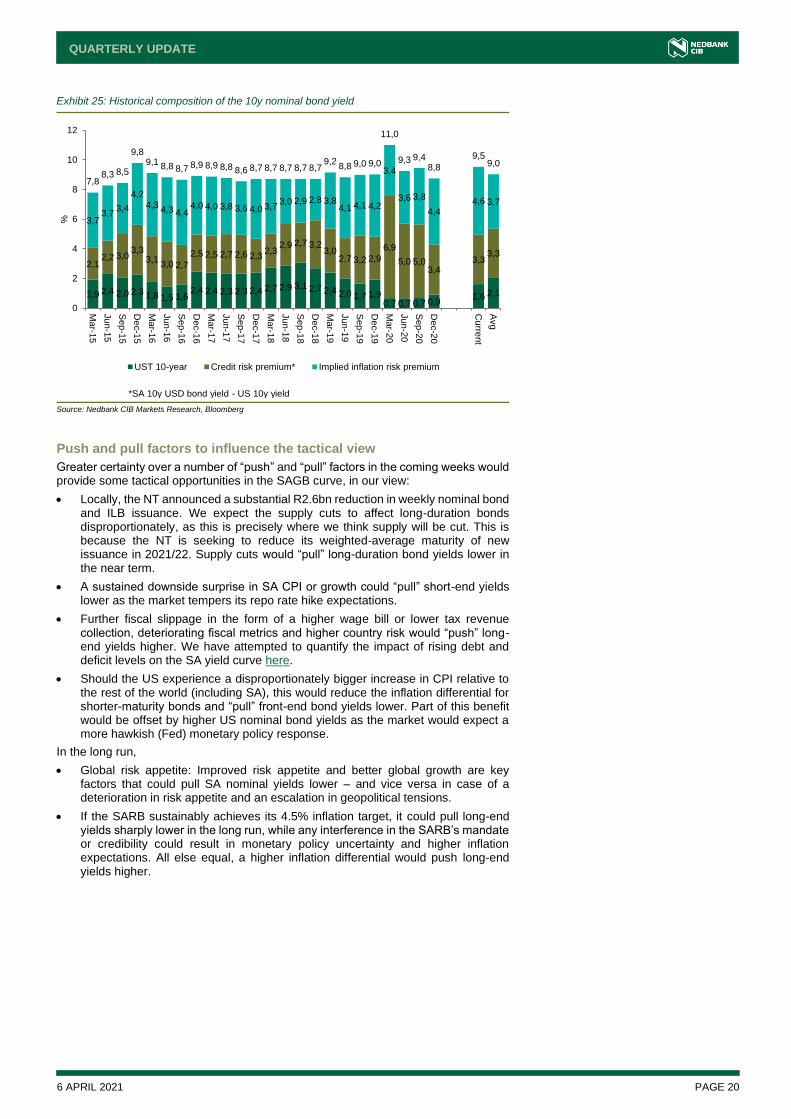

Yet, SA nominal bonds are currently pricing in high levels of inflation risk and a credit

risk premium that is on par with its long-run average (see Exhibit below). At the

current yield of 9.50%, the 10y benchmark bond is pricing in 330bps of credit risk and

460bps of inflation risk (i.e., SA CPI of 6.6%). The yield differential between SA’s 10y

USD bond and the US 10y bond is used to calculate the credit risk premium in the

chart below. Part of the reason behind high and rising levels of inflation risk

embedded in the 10y yield is possibly the expectation of fiscal risks starting to spill

over into inflation ultimately. This means the market is potentially starting to price in

higher inflation tolerance by the SARB in order to deflate the country’s rising debt

burden, notwithstanding a very credible SARB and low levels of current and surveyed

inflation.

Reezwana Sumad

Both nominal bonds and ILBs provide value on a tactical basis, but elevated country risk premia limit upside over the medium term.

This means the market is potentially

starting to price in higher inflation

tolerance by the SARB in order to

deflate the country’s rising debt

burden, notwithstanding a very

credible SARB and low levels of

current and surveyed inflation.

6 APRIL 2021 PAGE 20

QUARTERLY UPDATE

Exhibit 25: Historical composition of the 10y nominal bond yield

Source: Nedbank CIB Markets Research, Bloomberg

Push and pull factors to influence the tactical view

Greater certainty over a number of “push” and “pull” factors in the coming weeks would provide some tactical opportunities in the SAGB curve, in our view:

• Locally, the NT announced a substantial R2.6bn reduction in weekly nominal bond and ILB issuance. We expect the supply cuts to affect long-duration bonds disproportionately, as this is precisely where we think supply will be cut. This is because the NT is seeking to reduce its weighted-average maturity of new issuance in 2021/22. Supply cuts would “pull” long-duration bond yields lower in the near term.

• A sustained downside surprise in SA CPI or growth could “pull” short-end yields lower as the market tempers its repo rate hike expectations.

• Further fiscal slippage in the form of a higher wage bill or lower tax revenue collection, deteriorating fiscal metrics and higher country risk would “push” long-end yields higher. We have attempted to quantify the impact of rising debt and deficit levels on the SA yield curve here.

• Should the US experience a disproportionately bigger increase in CPI relative to the rest of the world (including SA), this would reduce the inflation differential for shorter-maturity bonds and “pull” front-end bond yields lower. Part of this benefit would be offset by higher US nominal bond yields as the market would expect a more hawkish (Fed) monetary policy response.

In the long run,

• Global risk appetite: Improved risk appetite and better global growth are key factors that could pull SA nominal yields lower – and vice versa in case of a deterioration in risk appetite and an escalation in geopolitical tensions.

• If the SARB sustainably achieves its 4.5% inflation target, it could pull long-end yields sharply lower in the long run, while any interference in the SARB’s mandate or credibility could result in monetary policy uncertainty and higher inflation expectations. All else equal, a higher inflation differential would push long-end yields higher.

1,9 2,4 2,0 2,3 1,8 1,5 1,62,4 2,4 2,3 2,3 2,4 2,7 2,9 3,1 2,7 2,4 2,0 1,7 1,9

0,7 0,7 0,7 0,91,6 2,1

2,12,2 3,0

3,33,1

3,0 2,7

2,5 2,5 2,7 2,6 2,32,3

2,9 2,7 3,23,0

2,7 3,2 2,9

6,9

5,0 5,03,4

3,33,3

3,73,7

3,4

4,24,3

4,3 4,44,0 4,0 3,8 3,6 4,0 3,7

3,0 2,9 2,8 3,84,1 4,1 4,2

3,4

3,6 3,8

4,44,6 3,7

7,88,3 8,5

9,89,1 8,8 8,7 8,9 8,9 8,8 8,6 8,7 8,7 8,7 8,7 8,7

9,28,8 9,0 9,0

11,0

9,3 9,48,8

9,59,0

0

2

4

6

8

10

12

Mar-1

5

Ju

n-1

5

Sep

-15

De

c-1

5

Mar-1

6

Ju

n-1

6

Sep

-16

De

c-1

6

Mar-1

7

Ju

n-1

7

Sep

-17

De

c-1

7

Mar-1

8

Ju

n-1

8

Sep

-18

De

c-1

8

Mar-1

9

Ju

n-1

9

Sep

-19

De

c-1

9

Mar-2

0

Ju

n-2

0

Sep

-20

De

c-2

0

Cu

rrent

Avg

%

UST 10-year Credit risk premium* Implied inflation risk premium

*SA 10y USD bond yield - US 10y yield

6 APRIL 2021 PAGE 21

QUARTERLY UPDATE

SA retail – maintaining our positive view from a listed perspective

SA has experienced rapid shifts in consumer spending patterns with visibly strong diverging trends that retailers have responded to quickly. The agility, cash preservation, debt reduction and investment in value-creating strategies by listed SA retailers have supported our more positive view on the sector in recent months. Our five upgrades since December 2020 (PPH, SPP, TFG and SHP all to Overweight, TRU to Neutral) have been followed by favourable share price movements with SA apparel players: +21.3% and SA food players: +19.5% since 1 December 2020. Although share prices have run, we think both the grocery and discretionary retail sectors are likely to generate strong earnings growth over the medium term (SA discretionary two-year CAGR FY21-23e: c.33% and SA food retail: 9.5%).

We still prefer SA discretionary retailers over food retailers, with our top picks in the sector remaining WHL, PPH and MRP, although in the food space, we still think SHP’s refreshed balance sheet, new Checkers strategy gaining momentum and slow exit out of unprofitable non-RSA geographies bode well for a strong earnings recovery for the business. Spar’s Polish recovery is the key catalyst for us in this business.

Exhibit 26: SA retail forecasts

SA apparel retail Rating CMP Target price Upside + DY

(%) FY20 DHEPS FY21e DHEPS FY22e DHEPS FY23e DHEPS 2-yr CAGR FY21-23e

The Foschini Group Overweight 119.0 128.0 7.5% 10.2 2.68 8.39 10.58 98.7%

Pepkor Holdings Overweight 15.6 18.0 15.3% 0.6 0.91 1.21 1.39 23.3%

Woolworths Holdings Overweight 47.6 55.0 15.6% 1.2 2.47 3.34 3.91 25.8%

Mr Price Group Overweight 180.3 200.0 11.0% 10.3 9.75 11.23 12.21 11.9%

Truworths Holdings Neutral 46.0 49.0 6.5% 4.1 4.50 4.84 4.97 5.1%

SA food retail Rating CMP Target price Upside + DY

(%) FY20 DHEPS FY21e DHEPS FY22e DHEPS FY23e DHEPS 2-yr CAGR FY21-23e

Shoprite Holdings Overweight 156.2 160.0 5.4% 7.11 8.45 9.53 10.14 9.6%

Pick n Pay Holdings Neutral 53.4 55.0 7.1% 2.77 2.46 2.93 3.21 14.2%

Spar Group Limited Overweight 193.7 212.0 14.1% 12.63 13.02 13.51 14.28 4.7%

Source: Bloomberg, Nedbank CIB Markets Research

Factors we think are likely to support this growth across discretionary retail: (1) a strong focus on value, casual and athleisure wear, (2) strong inventory management, lower risk of markdowns and more stable gross margins, (3) government assistance with the waiving of import duties on woven fabric, likely to benefit manufacturers and retailers, (4) e-commerce and (5) mid-market homeware, appliances and electronics.

Exhibit 27: Strong diverging trends from Oct to Dec suggesting that value players are likely to remain the key winners going into 2021; PPH, MRP, H&M were key outperformers

Exhibit 28: Recent trends showing mid-market retailers’ woes continuing into 2021, with weak growth reported by WHL and TRU

Source: Company data, Nedbank CIB Markets Research Source: Company data, Nedbank CIB Markets Research

-4,8

%

-4,2

%

2,4

%

-6,6

%-4,2

%

-7,4

%

0,0

%

-7,4

%

-8,2

%

-8,9

%

-2,0

%

-6,9

%

5,6

%

4,1

%

3,8

%

0,3

%

4,0

%

4,0

%

2,0

%

2,0

%

8,9

%

6,3

%

5,0

%

1,3

%

Total sales % ch LfL % ch Inflation Volume

WHL SA CGM TRU Africa

TFG Africa Apparel ex Jet MRP Apparel

H&M Pep/Ack

-12,4

%

-21,8

%

-6,3

%

-3,9

%

-8,3

%

-8,3

%

-11,0

% -7,0

%

-4,2

%

-6,9

%

-6,6

%

-8,3

% -3,1

%

-0,7

%

12,0

%

-0,4

%

-0,1

%

5,8

%

16,6

%

9,8

%

12,0

%

8,9

%

May/June July/Aug Sept/Oct/Nov Oct/Nov/Dec Jan/Feb

WHL SA FBH TRU Africa TFG Africa MRP Group Pep/Ackermans

Saad Chothia

6 APRIL 2021 PAGE 22

QUARTERLY UPDATE

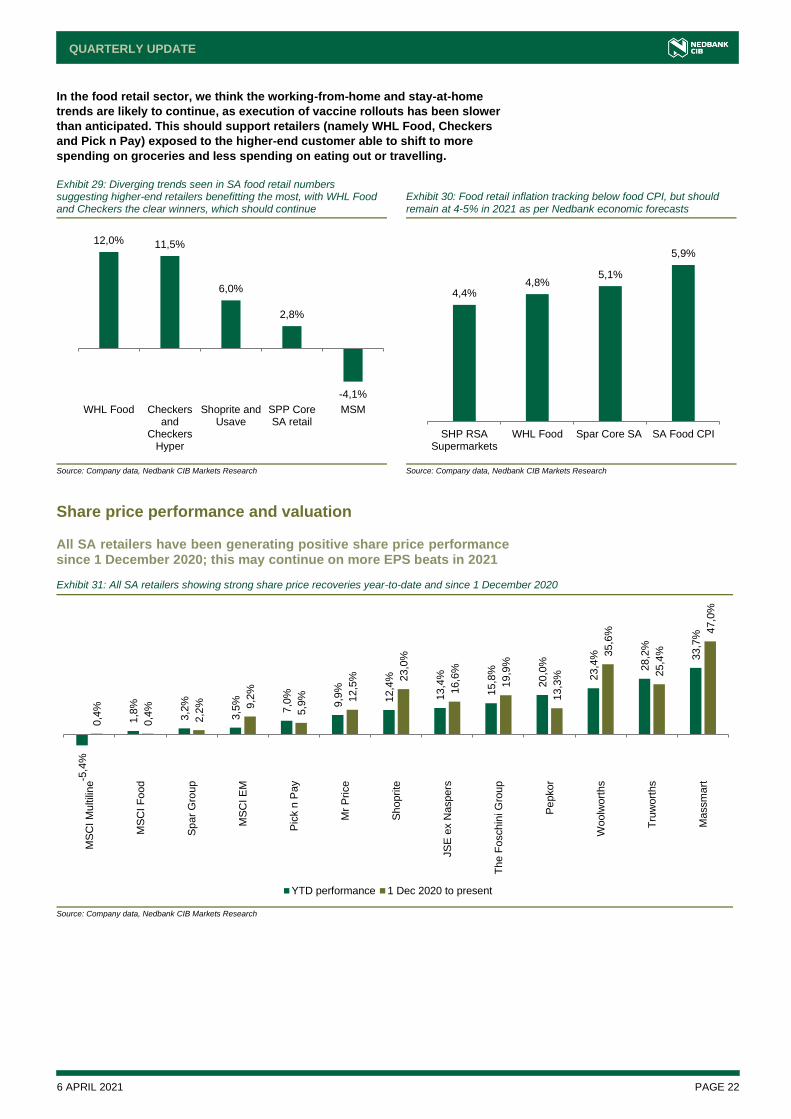

In the food retail sector, we think the working-from-home and stay-at-home

trends are likely to continue, as execution of vaccine rollouts has been slower

than anticipated. This should support retailers (namely WHL Food, Checkers

and Pick n Pay) exposed to the higher-end customer able to shift to more

spending on groceries and less spending on eating out or travelling.

Exhibit 29: Diverging trends seen in SA food retail numbers suggesting higher-end retailers benefitting the most, with WHL Food and Checkers the clear winners, which should continue

Exhibit 30: Food retail inflation tracking below food CPI, but should remain at 4-5% in 2021 as per Nedbank economic forecasts

Source: Company data, Nedbank CIB Markets Research Source: Company data, Nedbank CIB Markets Research

Share price performance and valuation

All SA retailers have been generating positive share price performance since 1 December 2020; this may continue on more EPS beats in 2021

Exhibit 31: All SA retailers showing strong share price recoveries year-to-date and since 1 December 2020

Source: Company data, Nedbank CIB Markets Research

12,0% 11,5%

6,0%

2,8%

-4,1%

WHL Food Checkersand

CheckersHyper

Shoprite andUsave

SPP CoreSA retail

MSM

4,4%4,8%

5,1%

5,9%

SHP RSASupermarkets

WHL Food Spar Core SA SA Food CPI

-5,4

%

1,8

%

3,2

%

3,5

%

7,0

%

9,9

%

12,4

%

13,4

%

15,8

%

20,0

%

23,4

%

28,2

%

33,7

%

0,4

%

0,4

%

2,2

% 9,2

%

5,9

% 12,5

% 23,0

%

16,6

%

19,9

%

13,3

%

35,6

%

25,4

%

47,0

%

MS

CI M

ultili

ne

MS

CI F

ood

Sp

ar

Gro

up

MS

CI E

M

Pic

k n

Pay

Mr

Price

Sh

oprite

JS

E e

x N

aspers

Th

e F

oschin

i G

roup

Pe

pkor

Woolw

ort

hs

Tru

wort

hs

Ma

ssm

art

YTD performance 1 Dec 2020 to present

6 APRIL 2021 PAGE 23

QUARTERLY UPDATE

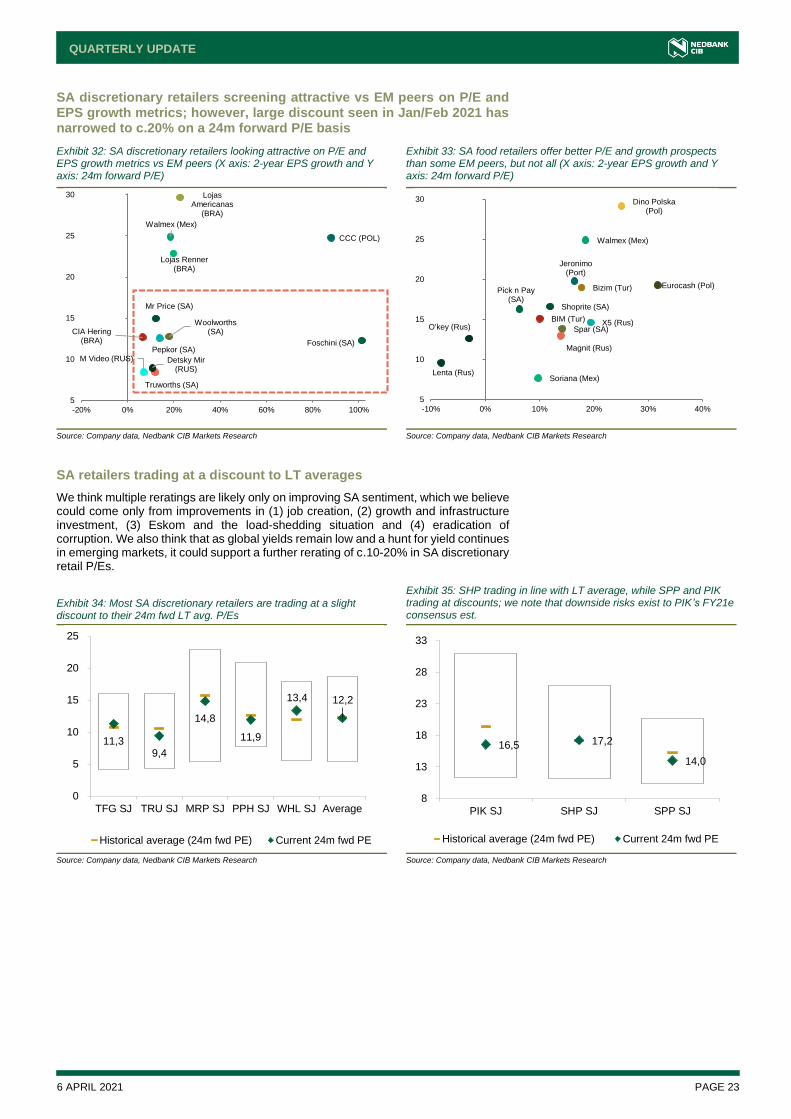

SA discretionary retailers screening attractive vs EM peers on P/E and EPS growth metrics; however, large discount seen in Jan/Feb 2021 has narrowed to c.20% on a 24m forward P/E basis

Exhibit 32: SA discretionary retailers looking attractive on P/E and EPS growth metrics vs EM peers (X axis: 2-year EPS growth and Y axis: 24m forward P/E)

Exhibit 33: SA food retailers offer better P/E and growth prospects than some EM peers, but not all (X axis: 2-year EPS growth and Y axis: 24m forward P/E)

Source: Company data, Nedbank CIB Markets Research Source: Company data, Nedbank CIB Markets Research

SA retailers trading at a discount to LT averages

We think multiple reratings are likely only on improving SA sentiment, which we believe could come only from improvements in (1) job creation, (2) growth and infrastructure investment, (3) Eskom and the load-shedding situation and (4) eradication of corruption. We also think that as global yields remain low and a hunt for yield continues in emerging markets, it could support a further rerating of c.10-20% in SA discretionary retail P/Es.

Exhibit 34: Most SA discretionary retailers are trading at a slight discount to their 24m fwd LT avg. P/Es

Exhibit 35: SHP trading in line with LT average, while SPP and PIK trading at discounts; we note that downside risks exist to PIK’s FY21e consensus est.

Source: Company data, Nedbank CIB Markets Research Source: Company data, Nedbank CIB Markets Research

Mr Price (SA)

Foschini (SA)

Woolworths (SA)

Pepkor (SA)

Truworths (SA)

Detsky Mir (RUS)

CCC (POL)

CIA Hering (BRA)

Walmex (Mex)

Lojas Renner (BRA)

Lojas Americanas

(BRA)

M Video (RUS)

5

10

15

20

25

30

-20% 0% 20% 40% 60% 80% 100%

Shoprite (SA)

Pick n Pay (SA)

Spar (SA)X5 (Rus)

Magnit (Rus)

Dino Polska (Pol)

O'key (Rus)

Lenta (Rus)

Eurocash (Pol)

Jeronimo (Port)

BIM (Tur)

Bizim (Tur)

Walmex (Mex)

Soriana (Mex)

5

10

15

20

25

30

-10% 0% 10% 20% 30% 40%

11,39,4

14,8

11,9

13,4 12,2

0

5

10

15

20

25

TFG SJ TRU SJ MRP SJ PPH SJ WHL SJ Average

Historical average (24m fwd PE) Current 24m fwd PE

16,5 17,2

14,0

8

13

18

23

28

33

PIK SJ SHP SJ SPP SJ

Historical average (24m fwd PE) Current 24m fwd PE

6 APRIL 2021 PAGE 24

QUARTERLY UPDATE

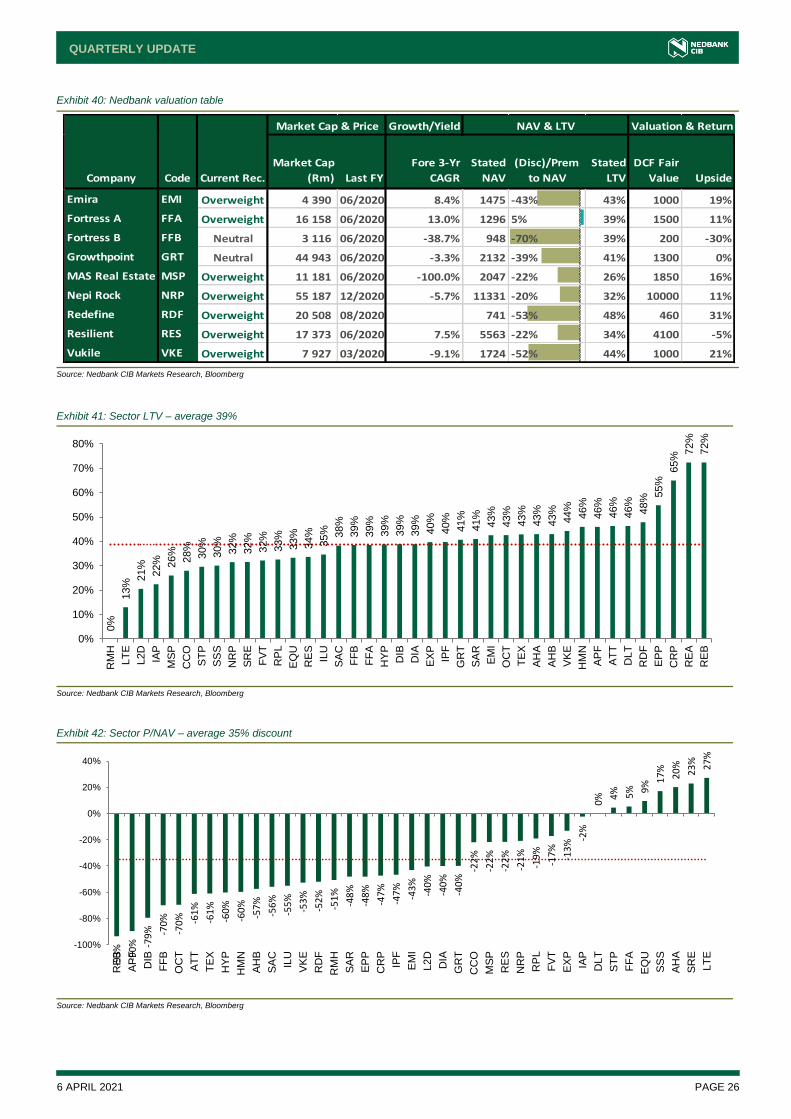

SA property: valuations and collection rates holding up

The property sector has returned +19.6% (vs +14.8% JSE All Share Index) since we upgraded to Overweight in December. We continue to see pockets of value within our coverage universe despite the recent rerating and operational headwinds facing the sector. We notice that the implied risk premium for the sector is beginning to normalise, currently printing at 5%. This is well below the 6.2% calculated in December, suggesting the market is assigning a lower risk metric to the sector as visibility improves.

The sector currently trades on a dividend yield of c.10.6% and at a 35% discount to NAV. This compares to an 11.8% yield and 50% discount in December. Below, we show that the SA property sector continues to trade at a discount to historical multiples while global peers have rerated to trade in line with their three-year averages.

Exhibit 36: Price to NAV – SA continues to trade at a discount, while global peers have rerated

Source: Nedbank CIB Markets Research, Bloomberg

A key risk to the sector amid the pandemic was the level of support landlords needed to provide to their tenants. While this remains ongoing (liquor, entertainment, restaurants, etc.), the quantum has reduced significantly. As can be seen in the chart below, rent relief (discounts and deferrals) at the peak of the pandemic averaged 80% of one month’s rent. However, the level of support provided has reduced, with landlords having more success in collecting rent. This bodes well for company earnings, given the low base.

Exhibit 37: Local rent relief as a percentage of company revenue

Source: Nedbank CIB Markets Research, company data

-0,12

-0,10

-0,08

-0,06

-0,04

-0,02

0,00

0,02

0,04

0,06

0

0,2

0,4

0,6

0,8

1

1,2

1,4

1,6

Japan Pan Asia HongKong

Europe Australia UK SA- AllProp

SA-SAPY

P/N

AV

3-Yr average Current Diff. (RHS)

19,3

%

17,5

%

17,5

%

16,5

%

13,8

%

12,6

%

12,6

%

12,0

%

11,4

%

11,0

%

8,9

%

8,3

%

5,9

%

5,5

%

0,0

%

8,2

%

9,2

%

9,5

%

10,4

%

2,9

%

6,3

%

2,4

%

5,3

%

2,7

%

0,4

%

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

1st period 2nd period

Ridwaan Loonat

6 APRIL 2021 PAGE 25

QUARTERLY UPDATE