PWB 2019-20: DRAFT BUDGET PARAMETERS - OECD

64

Organisation for Economic Co-operation and Development C(2018)98/REV1 For Official Use English - Or. English 4 July 2018 COUNCIL Council PWB 2019-20: DRAFT BUDGET PARAMETERS (Note by the Secretary-General) The document has been revised to take into account: • The release by INSEE of the end-June 2018 HCPI inflation index, used in the reference periods for calculating budget indexation; • The inclusion of the additional contribution from Lithuania in PWB 2019-20, given its intention to deposit its instrument of ratification to the OECD convention on 5 July 2018. JT03434341 This document, as well as any data and map included herein, are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of PWB 2019-20: DRAFT BUDGET PARAMETERS - OECD

Organisation for Economic Co-operation and Development

C(2018)98/REV1

For Official Use English - Or. English 4 July 2018

COUNCIL

Council PWB 2019-20: DRAFT BUDGET PARAMETERS

(Note by the Secretary-General) The document has been revised to take into account:

• The release by INSEE of the end-June 2018 HCPI inflation index, used in the reference periods for calculating budget indexation;

• The inclusion of the additional contribution from Lithuania in PWB 2019-20, given its intention to deposit its instrument of ratification to the OECD convention on 5 July 2018.

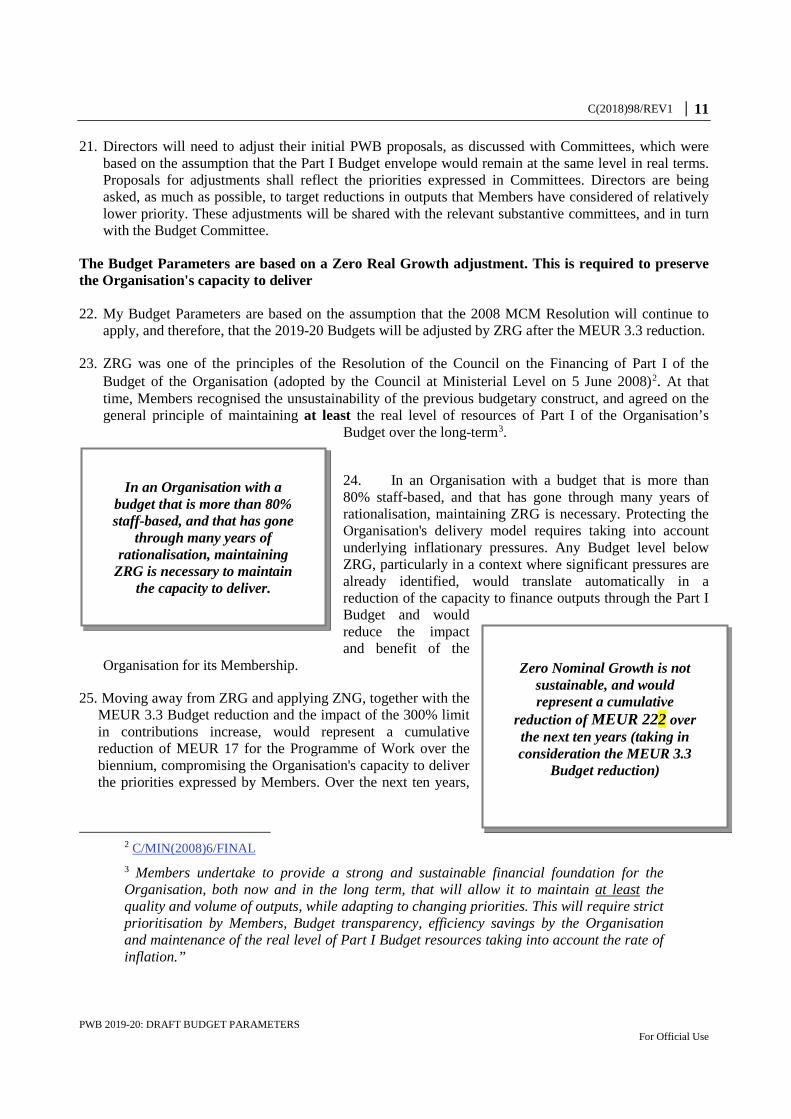

JT03434341

This document, as well as any data and map included herein, are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area.

2 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

TABLE OF CONTENTS

Purpose of the Secretary-General's Draft Budget Parameters ......................................................... 3

KEY FEATURES .................................................................................................................................. 4

1. Draft Budget Parameters - Considerations and Orientations ....................................................... 6

2. STRATEGIC PRIORITIES ........................................................................................................... 15

3. 2008-2018: Ten years of increased relevance and efficiency ....................................................... 19

3.1. Increased relevance and impact of the OECD ............................................................................ 19 3.2. A track record of efficiencies - V4M initiatives ......................................................................... 20 3.3. A streamlined corporate management layer ................................................................................ 22

4. FINANCIAL PARAMETERS FOR 2019-20 ................................................................................ 26

4.1. Reduction of the Budget Base and Allocation of the MEUR 3.3 Budget reduction ................... 26 4.2. 2019-20 level of the Budget ........................................................................................................ 29 4.3. The Accession of Lithuania and Colombia ................................................................................. 32 4.4. Level and Financing of the Central Priority Fund and Long-Term Reallocations ...................... 34 4.5. Part I financing and Budget envelope ......................................................................................... 34

5. PROPOSED REALLOCATIONS TO DELIVER ON PRIORITIES ........................................ 37

6. PART II PROGRAMMES ............................................................................................................. 40

7. PRE-ACCESSION BUDGETS ...................................................................................................... 41

8. ANNEX BUDGETS ......................................................................................................................... 42

8.1. Pensions ...................................................................................................................................... 42 8.2. Publications ................................................................................................................................. 42 8.3. Investments and Asset Replacement ........................................................................................... 43

9. VOLUNTARY CONTRIBUTIONS .............................................................................................. 44

10. CONCLUSION .............................................................................................................................. 45

ANNEX I: APPLICATION OF THE INFLATION MECHANISM TO THE PART I BUDGET46

ANNEX II: PART II PROGRAMMES: BUDGET APPROPRIATIONS OVER LAST BIENNIA .............................................................................................................................................. 48

ANNEX III: SUMMARY INFORMATION ON HORIZONTAL PROJECTS FOR PWB 2019-20 ........................................................................................................................................................... 49

Horizontal Project No. 1: Going Digital Phase II – Seizing Opportunities and Addressing Challenges .......................................................................................................................................... 49 Horizontal Project No. 2: Strategic Policies for Sustainable Infrastructure ....................................... 54 Horizontal Project No. 3: Building an OECD Housing Strategy ....................................................... 60

ANNEX IV: 2008-2018 Contributions by Member ......................................................................... 64

C(2018)98/REV1 │ 3

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

Purpose of the Secretary-General's Draft Budget Parameters

1. The Secretary-General's Draft Budget Parameters play a key role in the development of the OECD’s biennial Programme of Work and Budget (PWB). The Draft Budget Parameters provide:

• the main Budget assumptions underpinning the next biennium, and the estimated Part I Budget adjustments;

• the key orientations of the forthcoming Programme of Work; and • propose priority funding allocations.

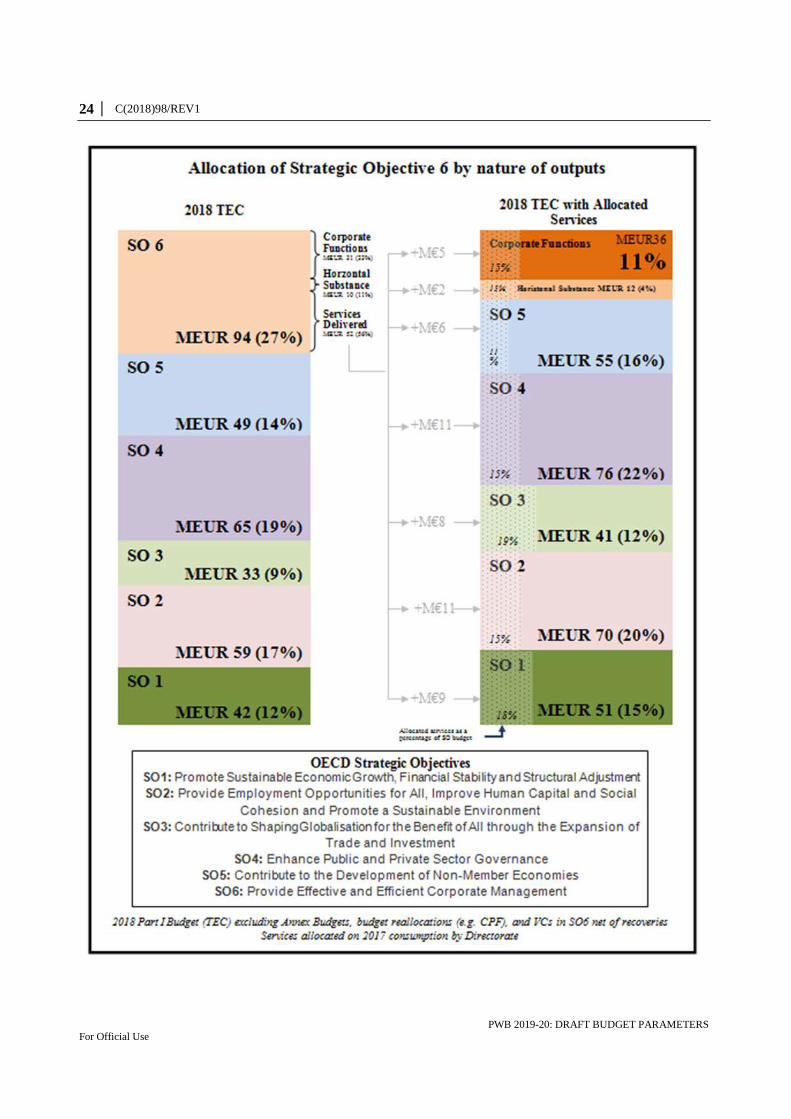

2. Members are invited to discuss the Draft Budget Parameters.

3. The Part I Budget base for 2019-20 has been adjusted in accordance with the recent Council Decision of the Council on the Level and Treatment of Assessed Contributions and Fixed Fees from Colombia, Costa Rica and Lithuania [C(2018)82/REV1]. It is also proposed to adjust the Part I Budget base in line with Zero Real Growth (ZRG), based on the 2008 Resolution of the Council on the Financing of Part I of the Budget of the Organisation (hereafter the 2008 MCM Resolution).1

4. In light of discussions in the Budget Committee on the Draft Budget Parameters and the Chair’s Progress Report, and consistent with the conclusions of the 2009 Council Working Party on Priorities [C(2009)111/REV1] the Council will be invited to take a decision on 12 July 2018.

5. In accordance with Financial Regulation 4 [C(2008)92/REV1], the Secretary-General will present his formal PWB submission in October.

1 C/MIN(2008)6/FINAL

4 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

KEY FEATURES

● The value of OECD deliverables to its Membership is far greater than the OECD Budget and Members’ contributions whether on an annual or cumulated basis. Its work creates opportunities for Members’ businesses and employees throughout the world, helps save billions of dollars for taxpayers, and boosts prospects for economic growth and well-being.

● Despite the agreement reached by Members in 2008, with a view to maintaining long-term, sustainable funding for the Organisation (Resolution of the Council on the Financing of Part I of the Budget of the Organisation [C/MIN(2008)6/FINAL] adopted by the Council at Ministerial Level on 5 June 2008),through the maintenance of the real level of Part I Budget resources taking into account the rate of inflation, Members have invited the Secretariat to absorb a MEUR 3.3 shortfall for the PWB 2019-20 [C(2018)82/REV1 Decision of the Council on the Level and Treatment of Assessed Contributions and Fixed Fees from Colombia, Costa Rica and Lithuania].

● Accordingly, my draft Budget Parameters for the PWB 2019-20 reflect the Members’ request to reduce the Budget Base by MEUR 3.3, which reduces the Organisation's Budget to a level below ZNG. This reduction will be distributed as follows:

o MEUR 1.45 reduction in Corporate Services (EXD); o MEUR 1.85 spread across all other Output Areas in line with the Medium-Term

Orientations provided by Members.

● This unanticipated reduction will require adjustments to outputs even though prioritisation exercises in Committees have indicated a significant level of unmet demand for outputs, and confirmed that all outputs endorsed by Committees are of high absolute priority. Therefore, outputs for which funding will be cancelled or decreased as a result of the reduction are outputs which had unequivocal Committee support.

● In addition, the Part I Budget needs to accommodate new annual recurring cost pressures of approximately MEUR 3.4, which include:

o The 2008 Part I Scale Rules capping real increases to any Member’s contribution to 300%. From 2020 on, this cap will affect two Members (Iceland and Luxembourg) for an estimated amount of KEUR 400 per year, which will have to be absorbed by the Secretariat, as per the 2008 Part I Scale Rules;

o The reinforcement of internal compliance functions, and of physical and data security; o The necessary replacement of class II assets (large equipment); and o The requirement to perform maintenance work to safeguard class III assets (buildings), for

which no funding is planned or available, given the previous decisions taken by Council with respect to reserves for this type of assets.

● The 2008 MCM Resolution is predicated on a commitment by Members to make resources available to the Organisation that, in turn, committed to realising efficiency savings, which it did, as outlined below.

“Members undertake to provide a strong and sustainable financial foundation for the Organisation, both now and in the long term, that will allow it to maintain at least the

C(2018)98/REV1 │ 5

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

quality and volume of outputs, while adapting to changing priorities. This will require strict prioritisation by Members, Budget transparency, efficiency savings by the Organisation and maintenance of the real level of Part I Budget resources taking into account the rate of inflation".

● While the 2008 MCM Resolution had no formal target for efficiency savings, the Secretariat has delivered significant results on this commitment with actual efficiencies amounting to MEUR 172 over the period 2008-18. On an annual basis, these efficiencies translate into 15.5% of the Organisation's annual Part I Budget in 2017. Over the next ten years, these past measures should continue to generate an estimated additional MEUR 310 of efficiency savings for Members.

● The 2008 MCM Resolution assumes an indexation of the Budget base by inflation (Zero Real growth, ZRG), to sustain outputs.

● Thus, in accordance with the terms of the 2008 MCM Resolution, the Budget is being prepared assuming the ZRG adjustment.

o However, it is important to note the negative impact that the 300% cap on Member contributions will have on the 2020 Budget (i.e. -0.2% impact, reducing the ZRG adjustment from 1.9% to 1.7%);

o The Part I Budget has been updated with regard to the forthcoming membership of Lithuania. Should Colombia deposit its instrument of accession in the course of the PWB process, the Part I Budget would be updated in accordance with the “Decision of the Council on the level of treatment of assessed contribution and fixed fees from Colombia, Costa Rica and Lithuania” [C(2018)82/REV1] dated 3 May 2018. However, this decision does not provide for the full coverage of recurring costs flowing from the accession of these countries. Additional Budgetary pressures are therefore expected.

o In that regard, I trust that Members will make best use of the flexibility provided by the fixed fee paid by new Members, during a phase-in period, to alleviate some of these pressures.

● Part II Budgets are being developed in parallel, according to their specific terms, and will be submitted to Council later in the year.

● Annex Budgets (Pensions, Investment and Publications) will be adjusted in accordance with relevant Council decisions, and should benefit from additional contributions provided by new Members.

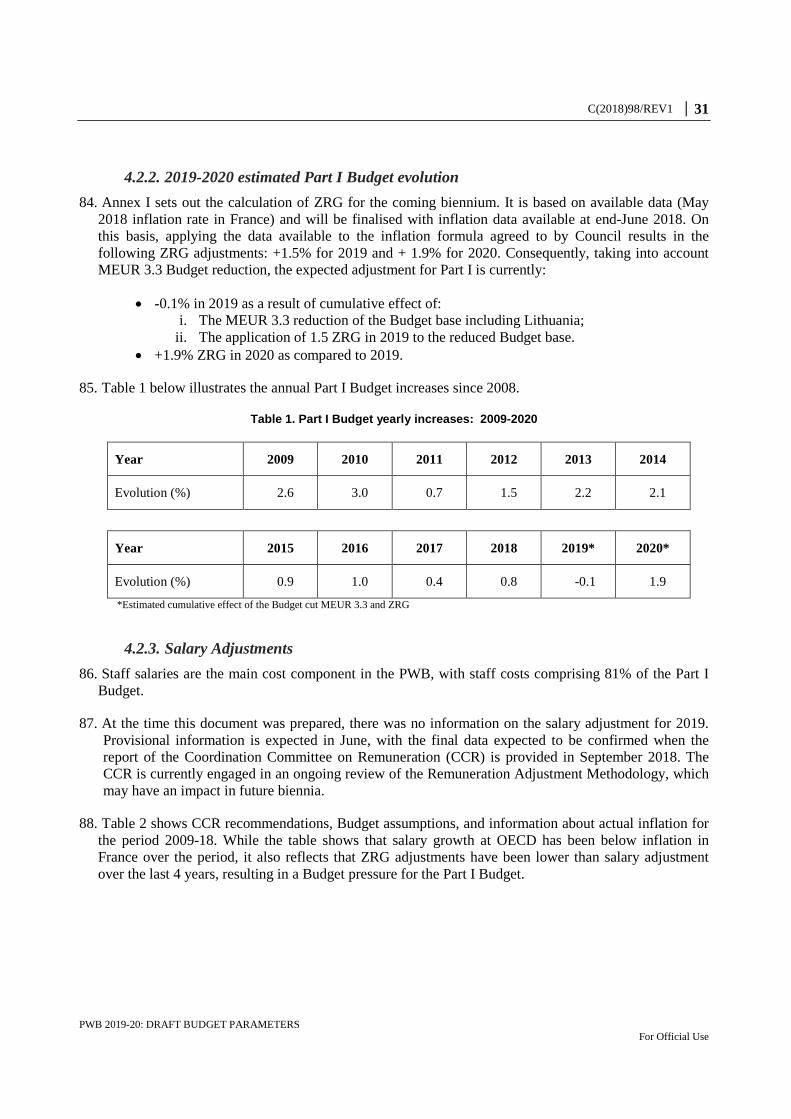

● The Secretariat will continue to: o seek efficiencies; o deliver Corporate Functions (management, control and compliance) efficiently and

effectively. Corporate functions currently represent 11% of the Part I Budget, following years of efficiency savings.

6 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

1. Draft Budget Parameters - Considerations and Orientations

Members continue to set high expectations for OECD outputs

6. There are increased demands by Members and Partners for targeted policy advice in the context of continued economic, social and environmental challenges and a concomitant need for effective national and international policy options to tackle diverse challenges including the productivity slowdown, growing inequalities, migration and climate change. The ongoing digitalisation of our economies and societies also calls for effective policy responses to leverage opportunities for businesses and citizens and tackle any risks, such as cybercrimes. Education, skills and other policies that promote opportunities for all should be a central part of the policy response to many of these challenges. The role of the Organisation is key, not only as a path-finder, but also to deliver options that advance important agendas in a complex international context.

7. My 21x21 agenda formed the basis for my mandate renewal. Through its implementation, and those of my annual Strategic Orientations, I continue to increase the relevance, inclusiveness and impact of the Organisation, building a “people-centred” growth narrative based on well-being.

8. The Organisation is also expected to continue to contribute to global agendas (SDGs, climate, etc.) and global fora, in particular the G7 and G20. Leveraging our standards on taxation, corporate governance, foreign bribery and Responsible Business Conduct (RBC), among others, is also key to the Organisation's goal of levelling the global playing field together with our work on trade, investment and competition. In this context, Members have affirmed their desire for continuous engagement with Key Partners and major emerging economies.

9. There continues to be sustained and urgent demands across policy sectors, as underscored by the 2018 Ministerial Council Meeting (MCM), my Strategic Orientations, the Ambassadors’ Informal

Convergence Paper, and PWB proposals from Committees.

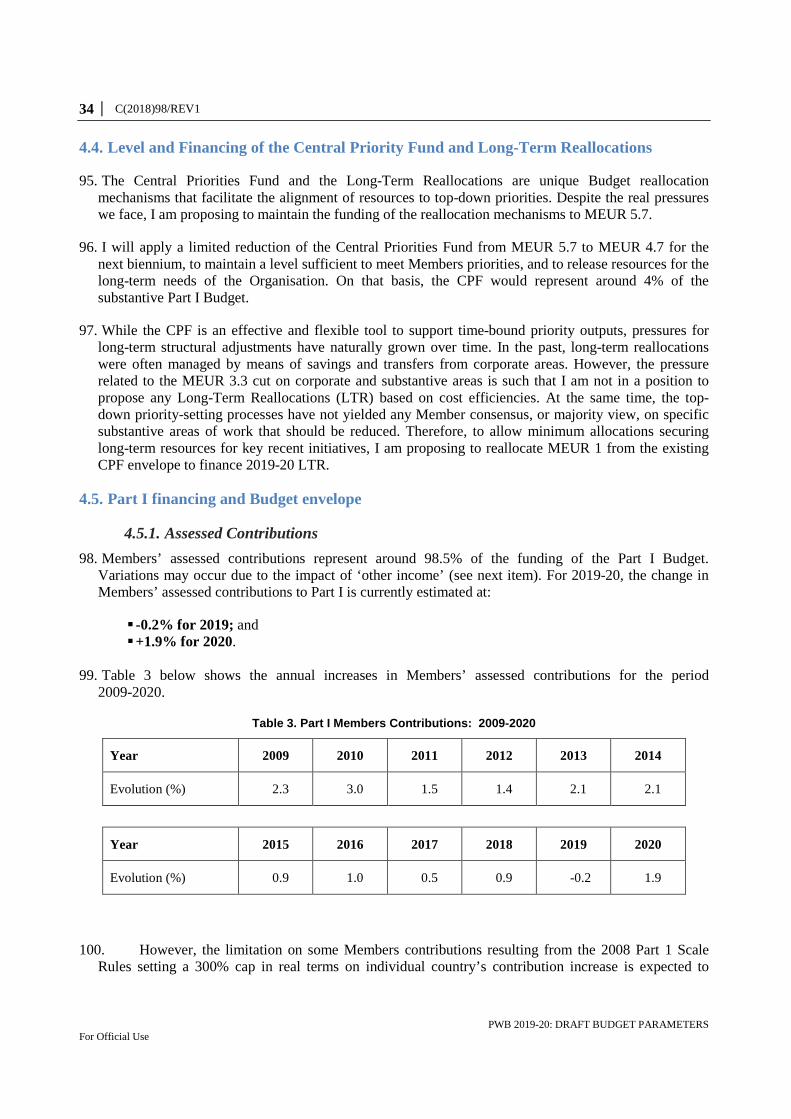

OECD delivers high value to its Members

10. Over the last 10 years, the OECD has saved its Members hundreds of times the Organisation’s annual Budget. Initiatives that have benefited Members include:

• New standards for information exchange that have played a key role in helping countries raise EUR 92 billion in increased revenues, of which EUR 66 billion accrued to Members, representing more than 330 times Members’ Part I assessed contributions;

• The OECD's Anti-Bribery Convention,

The OECD has saved taxpayers hundreds of times

the value of its annual Budget. New standards for

information exchange, for example, have played a key

role in helping countries raise EUR 92 billion in increased revenues, of which EUR 66 billion accrued to Members.

C(2018)98/REV1 │ 7

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

through which Parties collectively recovered at least USD 8 billion through foreign bribery enforcement actions between 2014, and mid-2017, i.e. nearly 35 times the OECD annual Budget.

11. On top of the above, the Organisation’s work allows its Members to make recurrent savings that amount to several times the value of its annual Budget, as evidenced by the following examples:

• The OECD’s Export Credit Agreement which contributes to save American taxpayers over USD 800 million per year (i.e. nearly 3.5 times the OECD’s annual Budget). Obviously, this is only a small part of the benefits accrued to the entire Membership.

• By working through the OECD’s Environment, Health and Safety Programme and agreeing on test methods and data quality standards, and by sharing the workload of chemical safety testing and assessments, Member governments and the industry save approximately EUR 150 million a year (i.e. equivalent to 75% of Members' Part I assessed contributions).

The Members' 2008 invitation to deliver additional efficiencies has been fully met by the Secretariat many times over.

12. The 2008 Resolution on the Financing of the Part I Budget, as agreed by Members, clearly enshrined the principle to preserve, at a minimum, the capacity of the Organisation to maintain the quality and quantity of its outputs through the Part I Budget, defined as at least Zero Real Growth.

13. In exchange for maintaining the level of outputs, the agreement included a concomitant commitment by the Organisation to deliver efficiencies. The Organisation has an impressive track record on continuously delivering additional efficiencies. Since 2008, major initiatives and reforms, along with the V4M project, not only increased the relevance of the Organisation, but also delivered tangible efficiencies amounting to 15.5 % of the 2017 Part I Budget (MEUR 31.1) on an annual basis.

14. Cumulative savings over the period of 2008-18 are estimated at MEUR 172.

• In addition to the savings realised, major reforms have contributed to improving the financial health of the Organisation, and will continue to generate additional savings. For example:

i. The decision to reduce the expatriation allowance to staff, as of 2012, and to transfer the resulting savings into the Post-Employment Healthcare Liability Reserve (PEHLR) will make it possible to match by 2046 the MEUR 400 projected liability. Thus, this cut in benefits, absorbed by staff, will allow to fully fund over time the PEHL liability.

ii. The Office Space Strategy, implemented in 2015, will continue to deliver savings over the coming 10 years. In total the Office Space business case estimates savings amounting to MEUR 36, of which nearly 9 have already materialised.

15. The 2008 MCM Resolution, was meant to provide a

Recurring efficiencies represent 15.5% of the annual 2017 Part I Budget, and have generated value to Members

that goes far beyond expected results.

Over the next ten years, these measures are expected to continue generating an

estimated additional MEUR 310 efficiency savings for

Members.

8 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

strong and sustainable financing for the OECD, and to rebalance Members’ contributions; it has been successful in achieving both goals. Unfortunately, the Resolution did not allow for each Member to cover their full cost and, therefore, a hybrid formula of “capacity to pay” and cost recovery remains in effect. This has resulted in a difference between the contributions paid by countries during the phase-in period, and the contributions they pay upon integrating at scale. It should be noted that, in 2008, Members had agreed to absorb any negative difference between the two sets of fees.

The uncertain and challenging context requires Members to provide the Organisation strong support

16. As I indicated at the Head of Delegations meeting on 16 February, preparation of the PWB 2019-20 is taking place in a very challenging financial context, characterised by complex and diverse constraints.

• Despite a strong signal from Members, initially expressed in the Ambassadors’ Informal Convergence Paper, where they reaffirmed the value of the OECD, and the many benefits flowing from its outputs, and where they expressed the collective view that Members wanted the OECD’s success to continue, recent decisions by Council, and the willingness of some Members to depart from the Resolution of the Council on the Financing of Part I of the Budget of the Organisation (adopted by the Council at Ministerial Level on 5 June 2008) have created uncertainty around the sustainability of the financing for the Organisation. It is worth reminding Members that a Resolution approved by Council is binding, and that abrogating it would require consensus among the Council.

• This precarity weakens the Organisation and jeopardises its ability to develop a programme of work that can meet Members’ ambitious expectations. It also risks undermining our capacity to attract and retain the talent necessary to deliver high-quality outputs that serve the interests of all Members. At this critical juncture, Member support is needed more than ever before, to safeguard the Organisation’s long-term success, at a particularly challenging moment for international co-operation.

The draft Budget Parameters integrate the requested MEUR 3.3 Budget reduction (1.6% of the Part I Budget) adding to already foreseen Budget pressures amounting to around MEUR 3.4 (1.7% of the Part I Budget)

17. Although the MEUR 3.3 Budget reduction represents a significant cut to the Part I resources of the Organisation, as well as a reversal of the intent of the 2008 MCM Resolution, I have taken this reduction into account for this proposal. Members should be aware that this reduction is ongoing.

Therefore, it has a compounded effect, which over ten years amounts to a cut of MEUR 36.

18. The resources of the Organisation will also suffer from the impact of the recent decision relating to the contributions of three New Members:

• This decision, while recognising additional recurrent costs resulting from the accession of new Members (adding the contribution at scale from new Members to the Budget), does not allow to cover systematically the full recurrent incremental costs for new Members that have relatively smaller economies.

A Budget cut of MEUR 3.3,

and pressures of MEUR 3.4, amount to MEUR 6.7, representing the equivalent of 3.3%

of the OECD’s Part I Budget

C(2018)98/REV1 │ 9

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

• Consequently, the Organisation will need to absorb additional pressures related to the accession of those countries.

19. In addition, significant cost increases need to be managed within the reduced Budget envelope. These pressures will amount to at least MEUR 3.4, and will need to be managed within the reduced Budget envelope. Addressing these pressures will require reviewing the level of services provided in certain areas, and will affect the Organisation's capacity to maintain sufficient funding for the future, thus reducing its ability to invest in transformative and innovative actions.

• The impact on some Members’ contributions resulting from the 2008 Part 1 Scale Rules setting a 300% cap in real terms on the increase of an individual country’s contribution. The agreement stated that any amount exceeding the 300% limit would have to be "absorbed in the Part I Budget of the Organisation" [C(2008)144/REV1, Appendix 4].

o Two countries will reach the 300% limit in 2020, resulting in an income reduction from assessed contributions of approximately KEUR 400 for the Organisation. Given the already severe impact of the MEUR 3.3 reduction on Part I resources, I am proposing that this additional pressure in 2020 be financed from the annual Part I savings resulting from the Office Space Strategy.

o As a result, the total effective amount of Members’ contributions in 2020 is expected to increase by 1.7% instead of the foreseen ZRG level of 1.9%.

• Implementation of new compliance functions. In line with my commitment to improve and keep the management of the Organisation at the leading edge among international organisations, the draft Budget will include a new Data Compliance Officer, an Ethics Officer as well as Whistle-blower functions. Their cost, KEUR 510, will have to be financed within the existing Budget.

• Increasing pressures on corporate service Budgets in 2019-20 to support OECD delivery of outputs and ensure a safe digital and physical work environment for staff and delegations as well as for visitors to the OECD. In the context of terrorist threats that have been particularly severe since the 2015 attacks in Paris, the Organisation has managed to increase security levels without calling on Members for additional funding.

• The table below provides the detailed estimates of the recurring pressures for the coming biennium.

10 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

• The environment for the Publications Annex Budget is increasingly challenging. PAC has, so-far, been successful in managing the financial impact of both the Council decision to make all OECD data “open, accessible and free” (2015) and the Council decision on financing the move to accruals (C(2016)149/REV1). On the income generation side, measures included a switch to a freemium business model, the launch of premium data services and the creation of the iLibrary Partnership Programme. On the cost side, new, lower-priced, contracts have been negotiated with suppliers while investments in digital publishing systems have been maintained. However, the pressure on the Budgets of subscribing institutions on the one hand, and increasing pressure for full open access to OECD content on the other are challenges that will need to be addressed in the coming biennium.

• There is also a risk that a 2019 salary adjustment (which has yet to be agreed by the Coordination Committee on Remuneration) will generate additional Budget pressures across Part I. This anticipated risk cannot be quantified at this early stage of the PWB process, and will have to be taken into account after the CCR recommendation is made, likely in the summer.

The Part I Budget reduction and emerging pressures will affect substantive outputs of “lesser priority” (as expressed by Members)

20. I am committed to continue delivering efficiencies, and the Secretariat will make every effort to limit the impact of Budget reductions and pressures on outputs. However, the requested reduction of MEUR 3.3 is already equivalent to an adjustment below ZNG, before taking into account the MEUR 3.4 pressures. It will thus inevitably affect some outputs. I am proposing to differentiate Budget cuts per output areas, taking into account the top-down priorities expressed through the Medium-Term Orientations Survey.

Identified Part I budget pressures KEUR % of Budget

Total identified pressures and Budget reduction -6 707 -3.3%

Budget Reduction -3 300 -1.6%

Decrease resulting from 2010-16 Members' contributions -3 300 -1.6%

Sub-Total Budget Pressures -3 407 -1.7%

Security and Assets Replacements -2 050 -1.0% Security enhancement (estimated for 2018) -400 -0.2%Replacement of Class III assets -1 300 -0.6%Digital security recurring pressure -350 -0.2%

Accounting and Compliance -1357 -0.7%Impact of the 300% limit rule to assessed contributions -400 -0.2%Ethics Officer -300 -0.1%Data Protection Officer -250 -0.1%New External auditors -60 0.0%OECD contribution to ISRP -130 -0.1%Part I and Publication contribution to finance the move to accruals -217 -0.1%

Salary LiabilitiesSalary increase NA

Budget reductions require cutting into

the funding of substantive outputs

C(2018)98/REV1 │ 11

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

21. Directors will need to adjust their initial PWB proposals, as discussed with Committees, which were based on the assumption that the Part I Budget envelope would remain at the same level in real terms. Proposals for adjustments shall reflect the priorities expressed in Committees. Directors are being asked, as much as possible, to target reductions in outputs that Members have considered of relatively lower priority. These adjustments will be shared with the relevant substantive committees, and in turn with the Budget Committee.

The Budget Parameters are based on a Zero Real Growth adjustment. This is required to preserve the Organisation's capacity to deliver

22. My Budget Parameters are based on the assumption that the 2008 MCM Resolution will continue to

apply, and therefore, that the 2019-20 Budgets will be adjusted by ZRG after the MEUR 3.3 reduction.

23. ZRG was one of the principles of the Resolution of the Council on the Financing of Part I of the Budget of the Organisation (adopted by the Council at Ministerial Level on 5 June 2008)2. At that time, Members recognised the unsustainability of the previous budgetary construct, and agreed on the general principle of maintaining at least the real level of resources of Part I of the Organisation’s

Budget over the long-term3.

24. In an Organisation with a budget that is more than 80% staff-based, and that has gone through many years of rationalisation, maintaining ZRG is necessary. Protecting the Organisation's delivery model requires taking into account underlying inflationary pressures. Any Budget level below ZRG, particularly in a context where significant pressures are already identified, would translate automatically in a reduction of the capacity to finance outputs through the Part I Budget and would reduce the impact and benefit of the

Organisation for its Membership.

25. Moving away from ZRG and applying ZNG, together with the MEUR 3.3 Budget reduction and the impact of the 300% limit in contributions increase, would represent a cumulative reduction of MEUR 17 for the Programme of Work over the biennium, compromising the Organisation's capacity to deliver the priorities expressed by Members. Over the next ten years,

2 C/MIN(2008)6/FINAL 3 Members undertake to provide a strong and sustainable financial foundation for the Organisation, both now and in the long term, that will allow it to maintain at least the quality and volume of outputs, while adapting to changing priorities. This will require strict prioritisation by Members, Budget transparency, efficiency savings by the Organisation and maintenance of the real level of Part I Budget resources taking into account the rate of inflation.”

In an Organisation with a budget that is more than 80% staff-based, and that has gone

through many years of rationalisation, maintaining

ZRG is necessary to maintain the capacity to deliver.

Zero Nominal Growth is not sustainable, and would represent a cumulative

reduction of MEUR 222 over the next ten years (taking in consideration the MEUR 3.3

Budget reduction)

12 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

the cumulative reduction would amount to MEUR 220, more than the 2018 Part I Budget.

Impact of budget pressures over 10 years (MEUR 3.3 reduction; ZNG increase; 300% rule on contributions)

26. There are signs of emerging inflation across many Members' economies. The provision for ZRG in a period where there is a clear risk of rising inflation will ensure that the Organisation can continue delivering and adapt to Members’ priorities.

The 2008 MCM Resolution Financing Agreement established a solid foundation among Members 27. The 2008 MCM Resolution provided that the assessed contributions of Members to the Part I Budget

be composed of two elements:

• a base fee of 30% of the Part I Budget to be shared equally among all Members. This provision mainly benefited large countries, in particular United States, Japan, Germany, United Kingdom, France, Italy and Spain. The base fee was phased-in to reach 30% over a 10 year period, ending in December 2018;

• a principal contribution, based on relative adjusted national income, for the remaining 70% of that Budget.

• As a result, the seven largest Members’ economies benefited from the 2008 MCM Resolution. Thus, their total share of assessed contributions went from 73.2% in 2008, down to 55.1% in 2018.

28. The compromise in the Resolution on the base fee, and the principal contribution was the result of a hard-reached compromise. Transition measures were necessary to smooth the impact for certain countries.

29. Since 2009, the U.S. percentage share of the Part I Budget has been decreasing steadily, given that the U.S. assessed contribution has only been increasing by a 0.3% yearly. This minimal 0.3% increase in the U.S. contribution will continue for several years, as long as the Budget increase remains higher than 0.3%. Provided ZRG continues to apply, the U.S. will get the full benefits of the 2008 MCM

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028Part I base 201.65Lithuania at scale 1.816Colombia at scale 2.644

206.11 209.2 213.17 216.37 219.62 222.91 226.25 229.64 233.08 236.58 240.13Cut from 2010-16 Members' contributions -3.3 -3.35 -3.41 -3.46 -3.52 -3.57 -3.62 -3.67 -3.72 -3.78 -3.84Cumulated cut from 2010-16 Members' contributions -3.35 -6.76 -10.22 -13.74 -17.31 -20.93 -24.6 -28.32 -32.1 -35.94Base for 2019 + ZRG 202.81 205.85 209.76 212.91 216.1 219.34 222.63 225.97 229.36 232.8 236.29ZNG (no increase) 202.81 202.81 202.81 202.81 202.81 202.81 202.81 202.81 202.81 202.81 202.81ZNG yearly -3.04 -6.95 -10.1 -13.29 -16.53 -19.82 -23.16 -26.55 -29.99 -33.48ZNG cumulated -3.04 -9.99 -20.09 -33.38 -49.91 -69.73 -92.89 -119.44 -149.43 -182.91300% cap -0.4 -0.4 -0.4 -0.4 -0.4 -0.4 -0.4 -0.4 -0.4300% cap cumulated 0.00 -0.4 -0.8 -1.2 -1.6 -2.0 -2.4 -2.8 -3.2 -3.6

Budget reduction+ZNG+300% cap -6.39 -10.76 -13.96 -17.21 -20.5 -23.84 -27.23 -30.67 -34.17 -37.72 (in %) -3.1% -5.0% -6.5% -7.8% -9.2% -10.5% -11.9% -13.2% -14.4% -15.7%Cut+ZNG+300% cap cumulated -6.39 -17.15 -31.11 -48.32 -68.82 -92.66 -119.89 -150.56 -184.73 -222.45

The seven largest Members’ economies benefited from the

2008 MCM Resolution. Indeed, their total share of assessed contributions went

from 73.2% in 2008, down to 55.1% in 2018.

C(2018)98/REV1 │ 13

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

Resolution and its estimated share of the Part I Budget will reach 17.8% in 2025 compared to 20.5% in 2018 and 25% in 2008.

High Budget reallocations amounting to MEUR 5.7, will allow alignment of the PWB with Members’ priorities

30. Beginning with the Medium Term Orientations Survey every two years, a clear continuing iterative process is in place to establish Members' priorities. From my Preliminary Views, to the Heads of Delegation progressive input and my Strategic Orientations, through the work of each individual Committee, and the consolidation of these ‘top-down’ and ‘bottom-up’ elements into a proposal which is reviewed twice by Members, the prioritisation of resources is established and refined over a period of 18 months before the start of each biennium.

31. Long-Term Reallocations have totalled MEUR 10.9 since 2009, and the Central Priorities Fund has been increased from an annual level of MEUR 3.1 in 2009, to the current MEUR 5.7 each year (for the 2017-18 biennium). For 2019-20, I am proposing:

• Time-bound reallocation proposals aligned with Members' priorities, through the Central Priorities Fund (CPF), of MEUR 4.7.

• Limited Long-Term Reallocations (LTR) of MEUR 1 aligned to ‘top-down’ priorities. Given the MEUR 3.3 cut in the Part I Budget envelope, it is not possible to propose reallocation from savings for this biennium. Therefore, LTRs will be funded by reducing the CPF envelope for the current biennium (2017-18).

32. The Secretary-General’s Allocation Fund will remain stable at MEUR 0.8, which is a decrease of 17% in real terms since it was fixed at this level in 2007.

Voluntary Contribution funding is expected to be in line with previous years, with moderate growth rate

33. Preliminary indications for voluntary contributions confirm our assumptions of a continued moderate growth of this source of financing.

OECD management practices shall remain at the leading edge

34. I reiterate my commitment to ensure effective and efficient financial, administrative, communications and management practices. In particular, my Budget proposal includes the reinforcement of certain compliance functions, and some ambitious measures to maintain the OECD at the leading edge among international organisations.

35. The Secretariat will continue the implementation and reinforcement of initiatives that are worth mentioning:

Overall, the mechanisms put in

place to allow flexibility in Budget

allocation and to meet Members’ priorities

have grown from 2.9% in 2009 to 6% in 2019-

20.

14 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

• In order to ensure a positive and productive workplace and to safeguard the reputation of the Organisation, the ethics framework has been strengthened. In this regard, 2017 was an important year, with the decisions to establish an ethics function and to develop a stand-alone whistle-blower protection policy. In the same area, the ethics training was rolled out for all OECD senior managers, an ethics intranet page was developed, and the ethics report will be issued annually instead of every two years to all staff and members.

• The risk management system, based on internationally recognised standards, drawing on the key principles of COSO’s Enterprise Risk Management is in the process of being reviewed and further strengthened notably with a view to making an explicit link between the objectives of the Programme of Work and Budget and risk identification.

• The governance framework in relation to personal data protection is being reinforced in order to align it with best standards and good practice, to demonstrate that the OECD has taken reasonable care in the treatment of personal data in case of personal data security breaches affecting the Organisation and its reputation and also to facilitate the continued receipt and transfer of personal data of European citizens, as well as grants from the EU to the OECD, by meeting the essential requirements of the EU legislation and the expectations of OECD’s Members, including European Members.

• In terms of transparency and disclosure of information, in addition to the above-mentioned annual ethics report, I decided in 2018 to make the full/detailed Internal Audit reports available to the full Membership, in addition to the summary Internal Audit reports. The Cour des Comptes has issued unqualified Financial Statements for the financial year 2017 -which represents 10 consecutive “clean” certifications in total- and the executive summaries of the External Auditor’s performance audit reports are released on the OECD website since 2017.

• Finally, thanks to the continued significant efforts made by management in 2018 to implement internal and external audit recommendations, the outstanding number of these recommendations is very limited and mostly due to the time needed for implementation.

Additional Budget from New Members

36. The Secretariat was informed by Lithuania that they intend to deposit their instrument of ratification to the OECD convention on 5 July 2018. Following C(2018)82/REV1 the proposed Part I Budget envelope thus includes an additional amount corresponding to the Part I scale estima ted contribution of MEUR 1.8 for Lithuania. The MEUR 1 annual fixed fee that will be paid in addition to the assessed contribution will be further discussed in the context of PWB for 2019-20. It is worth remembering that the assessed contribution of Lithuania will not cover its recurrent cost and therefore it is advisable to keep this additional MEUR 1 to bridge this gap. The planning assumption is that Members will agree to allocate sufficient amount of the fixed fees to cover as much as possible the recurring incremental costs arising from its accession. No additional amount for Colombia is included at this stage; should Colombia also deposit its instrument of accession to the OECD Convention in 2018, the Part I Budget would be adjusted later by its estimated contribution of MEUR 2.6 (and fixed fee of MEUR 1 to Annex budget).

Planning assumptions remain constant for around half of the Part II programmes

37. A similar Budget outlook is expected for around half of the Part II programmes, with the other Part II programmes subject to additional constraints (i.e. at, or close to, an unchanged Budget in nominal terms). Part II may face similar financial challenges and uncertainties as the Part I Budget.

C(2018)98/REV1 │ 15

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

2. STRATEGIC PRIORITIES

38. The OECD’s PWB 2019-20 reflects strong convergence between Members and the Secretariat on the Organisation’s priorities. In the coming biennium, we will take action to reinforce the global recovery and shape a more inclusive, people-centred and rules-based globalisation. We will not only continue to produce the best analysis and policy advice when needed, but also engage and defend multilateralism and the work of international institutions as a privileged channel for better outcomes among countries.

39. The identification of priorities is the result of a comprehensive and iterative consultation process with Members. The ‘top-down’ priorities emerge from: mandates emerging from the 2018 Ministerial Council Meeting (MCM), which are reflected in the MCM Chair’s Statement; the Ambassadors’ Informal Convergence Paper; my Strategic Orientations for 2018 [C/MIN(2018)1]; my '21 for 21' agenda; my Preliminary Views for the PWB 2019-20; the results of the Medium-term Orientations (MTO) Survey for 2019-20, which confirmed Members’ high levels of satisfaction with the allocation of Budget resources across the PWB [C(2017)115]; and my conversations with Leaders, Ministers and senior officials in OECD Member and Key Partner countries. Each Committee and Programme has translated these ‘top-down’ priorities into their own PWB proposals and integrated them with specific ‘bottom-up’ priorities identified and agreed for each policy area. The Organisation’s top priorities for the next biennium are to:

• Consolidate our core strengths and competitive advantages, including our evidenced-based and comparative policy work; data collection, measurement and analysis, and peer reviews, which are crucial to helping countries foster structural reforms and address social challenges. Our policy work will be expanded to support national reform implementation, following our work with Greece, Slovenia, Mexico and Hungary.

• Recalibrate our strategic approaches to communication to prioritise listening and engagement, and reflect on more effective ways to disseminate OECD data, analysis and outputs to key stakeholders.

• Continue developing a new growth narrative that tackles the root causes of inequality and puts people at the centre of economic policy. This includes taking forward our flagship Inclusive Growth Initiative by operationalising our fully-fledged Framework for Policy Action on Inclusive Growth, advancing our efforts to understand the Productivity-Inclusiveness Nexus, and strengthening the Business for Inclusive Growth Initiative. Across the house, we will give priority to the most vulnerable groups including youth, women, and children. Our new NAEC Innovation Lab – along with our ongoing strategic foresight and policy coherence work – will help us to develop a new economic narrative that delivers solid outcomes for growth and inclusion, a new social contract, and a new idealism.

• Move from evidence to action to tackle the main drivers of exclusion. This whole-of-OECD priority will identify concrete measures to: respond to wealth, income and spatial inequalities; deliver quality jobs, leveraging the new OECD Jobs Strategy; strengthen the links between our flagship work on education (PISA, PISA-D, PIAAC, global competence) and skills; cultivate patient-centred healthcare systems (PaRIS); facilitate the integration of migrants and refugees; bridge gender divides;

16 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

and foster equal opportunities for all, including in the digital world. These efforts will encompass the development of a coherent policy framework to support resilient, efficient and inclusive housing markets. They will also include the development of an integrated, multidisciplinary, and strategic OECD roadmap for sustainable infrastructure.

• Expand our work on the factors underpinning the growing ‘geography of discontent’, with a particular emphasis on making globalisation fairer and more transparent. This will involve taking forward the OECD’s game-changing contributions to global tax transparency through the Base Erosion and Profit Shifting (BEPS) Project and the Automatic Exchange of Information initiative, and ongoing work to address the tax challenges arising from the digital transformation.

• Advance efforts to restore citizen’s trust in the fairness and transparency of government and institutions, including at the multilateral level. In this respect, strengthening the impact and coherence of our comprehensive standards — covering, inter alia, tax, investment, anti-corruption and integrity, corporate governance, responsible business conduct, SME financing, state-owned enterprises, consumer policy, digital economy, and development finance — through the OECD’s Standard-Setting Review is critical to level the global playing field. To complement this work, we will seek to develop a more holistic approach to our anti-corruption and integrity work, including anti-bribery, standards and codes of conduct, conflicts of interest, whistle-blower protection, public procurement, open government and open data, and Responsible Business Conduct, guided by the OECD Strategic Approach to Combating Corruption and Promoting Integrity.

• Reflect on measures that can make the global system work better, harnessing the full range of international economic co-operation tools to make trade and investment policy free, fair and open. We will work to safeguard the rules-based international trade system by deepening the evidence base (through our work on Trade in Value-Added (TiVA), our Services Trade Restrictiveness Index, our Trade Facilitation Indicators, and our work on trade-distorting subsidies). On the investment side, we will refine our FDI Regulatory Restrictiveness Index, develop further the investment leg of global value chains (GVCs), and seek to support the integration of small-and medium-sized enterprises (SMEs) in GVCs. To complement these efforts, we will build the case for a forward-looking and evidence-based framework on SMEs.

• Continue our leadership of policy debates on emerging issues, while reinforcing our capacity to understand and address them. Advancing our work on the Going Digital horizontal project, including through the development of new international standards on blockchain, will be at the centre of these efforts.

• “Going national” on the work we do, and develop benchmarks and comparators that help move domestic agendas forward. Efforts to build the case for selective and strategic OECD enlargement, which will ultimately position the Organisation to serve all Members better, will continue.

• Marshall our multidisciplinary expertise to advance the global policy agenda, facilitate collective action and support the case for multilateralism. We will consolidate our proven track record of providing authoritative data, evidence and policy advice to advance the governance agendas of the G20 and G7, in line with the priorities of Argentina’s G20 Presidency and Canada’s G7 Presidency in 2018, and of Japan and France in 2019. Through strengthened collaboration with other international organisations ─ including the European Commission, WTO, ILO, FAO, WHO, IMF, World Bank, Financial Stability Board, the United Nations itself and its regional economic commissions and regional development banks ─ the OECD will seek to reduce overlap, harness synergies and ensure

C(2018)98/REV1 │ 17

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

consistency between our respective programmes of work. Given our growing engagement with the UN system, consolidating our UN office in New York will be of strategic importance.

• Sustain our efforts to ‘go global’ to enrich our understanding of shared challenges and ensure our work and advice is tailored to diverse contexts. A key component of this work will involve intensifying our engagement with Key Partners, Accession countries and prospective members (including Argentina, Brazil, Peru, Romania, Croatia and Bulgaria) to facilitate their adherence to more OECD bodies and legal instruments. Consolidating our regional programmes – covering Southeast Asia, the Middle East and North Africa, Latin America and the Caribbean, and Eurasia – and our country programmes with Kazakhstan, Morocco, Peru and Thailand will be critical for strengthening diversity, relying on the good work done across the house, including through the OECD Development Centre. We will also strive to coordinate better our support for non-Members and integrate more emerging and developing countries in our datasets, flagship publications and analysis.

• Continue supporting the implementation of ambitious global commitments, including the 2030 Agenda for Sustainable Development, the Addis Ababa Action Agenda, and the Paris Agreement. In particular, we will renew our focus on advancing implementation.

• Enhance further the quality and efficiency of the Organisation’s, management, administrative, communications and financial systems. This includes advancing our efforts to deliver V4M, implementing existing proposals on ethics and whistleblowing policy, continue to foster diversity and strive for gender equality across the house. The forthcoming independent evaluation will document the Organisation’s progress in these areas and will help guide future efforts.

• Ensure continuous improvements in the management and operations of the Organisation so that the OECD is recognised as being a leader in these fields. This includes:

o efforts to advance staff diversity and gender balance in our workforce;

o continuing to strengthen the evaluation functions;

o continuing value-for-money initiatives and related innovation;

o reinforcing audit and compliance functions;

o promotion of horizontal collaboration; and

o sustainment of our coherent and consistent communication efforts with staff and Members. This also include continuing our efforts to better communicate and explain the Budget, use of resources at the OECD and the added value delivered to our Membership.

40. Given the constraints for this PWB, the OECD will have to ensure that key corporate services provide the necessary support to maintain the Organisation’s capacity to deliver on the expected outputs. Corporate Services priorities will therefore focus primarily on:

• Maintaining a high level of security for people, data and operations; • Delivering additional savings, where possible, by adjusting levels of service, negotiating with

providers, and improving ways of working or processes;

• Delivering on key IT projects, and system renewals, and supporting the delivery of outputs;

• Continuing to deliver economies of scale, especially in HR and Finance, to accommodate the growing volumes of outputs with almost fixed levels of resources;

18 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

• Managing the moves required to accommodate the moderate staff growth, and make the best use of the OECD Boulogne Office Space; and

• Continuing to protect the assets of the Organisation. 41. Submissions for the Programme of Work and Budget for 2019-20 are at a very advanced stage of

development. In preparing their PWB proposals, Committees have been asked to fully incorporate the potential for capitalising on the Organisation’s unique ability to address cross-cutting, interlinked and complex policy challenges, as well as to apply strict prioritisation in their proposals, to allocate the Part I Budget to priorities.

C(2018)98/REV1 │ 19

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

3. 2008-2018: Ten years of increased relevance and efficiency

42. Over the last ten years, the relevance and impact of the Organisation has strongly increased for the benefit of all Members. In a context of constant and limited resources, this outcome reflects the Secretariat’s unwavering commitment to identifying and implementing efficiencies and savings, and applying best practices to the management of the Organisation.

3.1. Increased relevance and impact of the OECD

43. OECD products have proven over time to be relevant and useful for policymaking in Member and Partner countries. End-users have consistently provided feedback that OECD products are used extensively. All Output Results in 2015-16 were used by Members, either as a basis for policy change, or as a reference in policy discussions and studies. Overall, 98.2% were used by at least five Members, 74.1%, were used by at least one third of Members, and 36% were used by at least half of Members.

44. Over and above the extensive use by Members of OECD outputs to inform policy discussions, 76% of outputs were used as a basis for policy change. In total, Members indicated that there were 314 instances where 2015-16 OECD products were used as a basis for policy change. This is particularly impressive, given that policy reform cycles across all sectors in capitals are not necessarily synchronised with the OECD’s biennial work programme.

45. This reflects an upward trend in policy impact over time, from 2005, when around 30% of OECD outputs were rated by Members as having a high impact, to over 45% in 2015-16, with a peak of over 56% during the height of the global financial crisis.

Member Impact Ratings (2005-2016)

20 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

3.2. A track record of efficiencies - V4M initiatives

46. Since 2008, I have constantly promoted and embedded a culture of efficiency and cost consciousness in the Organisation. This has allowed, despite flat financing, for:

• an increase in the OECD’s value to its Members;

• the implementation of major reforms without requesting additional financing from Members; and

• additional funds allocated to substantive areas.

47. To reinforce further this culture of cost consciousness and ongoing improvement, I launched the whole-of-OECD Value for Money (V4M) Initiative. Since 2008, the OECD has delivered MEUR 172 in efficiencies:

• MEUR 125 by reducing staff benefits (reduction in staff allowances and temporary delays in applying the CCR salary increase recommendations) and actions to implement a thinner management structure over time;

• MEUR 26 thanks to the space rationalisation and the office space strategy; (reduction of rent cost per FTE and MEUR 9 one off effect in 2017, result of the positive outcome of negotiations on the early termination of the lease with the previous owner);

• MEUR 21 from other measures as documented in the V4M report and “The Book - Compendium of OECD Reference Documents”.

C(2018)98/REV1 │ 21

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

Table: Efficiencies delivered over 10 years

48. As a result, recurring efficiencies, representing 15.5% of the annual 2017 Part I Budget, have been generated constituting additional value to Members on top of the approved Budget. Over the next ten years, these measures implemented in the past will continue to avoid costs to Members estimated around MEUR 310.

49. The V4M Initiative has reinforced the Organisation’s capacity to generate significant measurable savings. In general these 'cost avoidance savings' relate to amounts that would have been spent to handle the same or increased volume / output. They cover a spectrum of savings including:

• cost reductions that do not lower the cost of products / services when compared against historical results, but rather minimise or avoid entirely the negative impact that a price increase would have caused;

• optimising the use of resources to increase output / capacity without increasing resource expenditure.

50. In summary, these savings have allowed the Organisation to do more within a flat Budget envelope, and increased the Organisation's capacity to deliver more and better quality outputs with increasing impact.

2009 2010 2011 2012 2013 2014 2015 2016 2017 One off 2017

Estimated 2018

CumulatedMEUR

Annual efficiency from the evolution in the average staff cost compared to 2009 - 4.8 5.3 7.0 10.7 10.9 11.0 17.3 19.4 19.4 105.8

Salary savings due to divergence from CCR recommendations since 2009 (real term) 0.9 - (0.3) 1.9 1.6 - 4.1

Contribution to PEHL funding (reduction of expatriation allowances)* 0.0 0.7 1.5 2.4 3.0 3.5 3.5 14.7

Effciencies from reduced staff benefits and managerial decisions on staff structure 0.9 4.8 5.0 8.9 13.0 12.4 13.4 20.3 22.9 0.0 22.9 124.5

Office space savings (including post 2017) 9.1 (0.2) 8.9

Efficiencies from Office space densification (office at KEUR 12) - 0.4 0.8 1.3 1.6 2.6 2.9 2.0 2.9 2.9 17.4

Efficiencies froms space rationalisation and the office space strategy 0.0 0.4 0.8 1.3 1.6 2.6 2.9 2.0 2.9 9.1 2.7 26.3

Etat d'urgence - Absorption of recurring Increased Security costs 0.8 0.6 0.4 1.8

Move to accruals (2017-2027) 0.2 0.2 0.4

Contribution to CIBRF (real term) 1.3 1.2 1.2 1.2 1.2 1.2 7.3 Latvia: difference between allocation and incremental recurring costs 0.9 0.9 1.8

Free data: estimated loss of income(delta programme) [C(2011)117/REV1] 2.4 2.4 2.4 2.4 9.6

Other Efficiency Measures 0.0 0.0 0.0 0.0 1.3 1.2 3.6 4.4 5.3 0.0 5.1 20.9

Total 0.9 5.2 5.8 10.2 15.9 16.2 19.9 26.8 31.1 9.1 30.6 171.7 Part I Budget (MEUR) 171.9 170.7 182.0 184.8 188.8 192.8 194.5 196.5 200.1 201.7 Part I Budget (MEUR) in 2017 value 193.2 186.3 197.3 197.2 197.3 197.2 197.3 197.3 200.1 Equivalent Part I budget without savings 194.1 191.5 203.0 207.5 213.1 213.5 217.2 224.0 231.1 9.1 232.3 Annual efficiency (%) 0.5% 2.8% 2.9% 5.2% 8.0% 8.2% 10.1% 13.6% 15.5% 15.2%

22 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

51. There are also many examples of improvement initiatives that may not immediately reduce costs, but provide benefits through improved process efficiency, employee productivity, improved quality and impact, improved competitiveness, etc. that over time often become cost savings. Some of the more emblematic of these initiatives include:

• ONE Secretariat and the introduction of the Way of Working Framework based on project management approaches are helping to increase not only the quality of what we produce but also staff productivity by harmonising the way OECD Outputs are produced, and by facilitating horizontal collaboration and knowledge sharing;

• improvements to the way we manage human resources that have helped to manage the mix

of skills and experience required for the efficient and effective delivery of the Programme of Work to achieve further reductions of staff costs per FTE;

• process improvements and the introduction of workflows for document clearance

processes; • clearer and more consistent guidance, and harmonised automated operational Budget

management across the Organisation; and • ONE for Members and Partners which is providing ‘Anytime, anywhere, any device’

access for delegates attending OECD meetings to meeting information and broadcast notifications through the OECD Network.

52. Efforts to drive internal efficiency are ongoing and spread across the Organisation, as evidenced by Directorates’ Biennial V4M Plans. The analysis of the progress achieved in the implementation of the 158 initiatives that were put in place over the two previous biennia indicates that approximately 44% of these are generating, or are expected to generate efficiencies for the Organisation by reducing the time and cost of producing OECD Outputs; and that these savings in time are being reinvested to increase the quality and impact of Outputs. Over 62% of the additional 63 V4M initiatives in the 2019-20 V4M Plans are expected to generate additional efficiencies.

3.3. A streamlined corporate management layer

53. It is a constant objective to develop the most efficient, streamlined and flexible management structure possible to allocate resources to substantive areas. The structure of our PWB does not allow for visibly demonstrating the efficiency of the management structure, since a significant part of resources and services delivering outputs are hosted under Output Group 6.3. Therefore I have asked our Executive Director to present a ‘fully allocated’ visual of 2017 costs of services provided by Output Group 6.3 to support the delivery of the Organisation’s outputs. The result is that after allocation of the services (e.g. office space, computers, conference rooms, and other services provided to Directorates), central functions only represent 11% of the OECD's total expenditures. This clearly demonstrates that the OECD operates with a streamlined and efficient management structure.

54. The below charts show current Budget allocations within Strategic Objective 6 by areas (Chart 1) and an estimate of how these allocations should be charged to outputs to present the full costs of outputs including services delivered by the corporate functions (Chart 2). For that purpose, the analysis distinguishes 3 main types of activities actually performed in output 6:

• services delivered;

C(2018)98/REV1 │ 23

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

• corporate functions (management, control, compliance); and • “horizontal substance”: some activities hosted in objective 6 relate strictly to substance (e.g.

SDD activity).

55. To improve communication in the future, and to facilitate the understanding of the OECD's Budget and financial flows, I strongly encourage that we consider how to present the Budget including a fully allocated view to Members for future PWBs.

• This will require a significant investment to adjust processes and systems; and

• at the same time, this will increase transparency and cost-consciousness, because:

i. Service providers are more accountable for the costs and quality of the services delivered; and

ii. internal clients are more sensitive to the costs they generate to the Organisation;

• Furthermore, this will also contribute to reinforcing the culture of client-service orientation within corporate areas.

56. The table below reflects the results of the simulation based on service consumption and show how corporate areas represent 11% of the total Part I Total estimated costs.

24 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

C(2018)98/REV1 │ 25

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

57. The limited weight of the corporate areas compared to the overall Organisation reflects:

• the high priority given to substantive areas, and

• the Organisation's efforts to maximise the value delivered to its Members.

58. Despite the Organisation's growth, and the concomitant increase in coordination required, staffing in corporate areas has remained relatively flat compared to the growth in substantive areas, thus representing a decreasing share of the Organisation's total staff.

CHART: STAFF Evolution

59. The pressure on corporate areas to deliver always more with less, together with the culture of efficiency and cost control, has allowed the redirection of any remaining funding to the substance, and to Members’ priorities, as reflected in the next section.

33%32%

31% 30% 30%29%

27%

26%25%

20%

22%

24%

26%

28%

30%

32%

34%

-

500

1,000

1,500

2,000

2,500

3,000

2009 2010 2011 2012 2013 2014 2015 2016 2017

FTE

Staff in Output Groups 6.1, 6.3, 6.4Staff in Substantive areas (PI + PII)% of staff in Output Groups 6.1, 6.3, 6.4

26 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

4. FINANCIAL PARAMETERS FOR 2019-20

60. In July 2018, in light of discussions in the Budget Committee, the Council will be invited to approve the level of the Part I Budget envelope for 2019-20. The below section describes the proposed financial parameters Members should take into consideration to inform their decision, namely:

• the measures put in place to manage the MEUR 3.3 reduction, and the MEUR 3,4 additional Budget pressures

• the need for at least ZRG adjustments on this reduced base Budget in line with the 2008 MCM Resolution in a context of potential salary pressures;

• the impact on recurring costs of the accession of Lithuania and the forthcoming impact for Colombia;

• the Budget Parameters for the PWB 2019-20, including:

i. the level of the Part I Budget, comprising:

1. Expected interest income

2. Level of other income

3. Calculation of ZRG

ii. the Central Priority Fund

iii. the Long-Term Reallocations 61. At the time this paper was prepared, neither final inflation data for the reference periods in respect of

the ZRG calculation, nor information about salary adjustments for 2019 and 2020, were available. Nonetheless, the data used in this paper are reasonable estimates and sufficiently robust to give Members a clear picture of the likely Budget level for the coming biennium. Adjustments will be made in September, when most final figures are available.

62. In the context of the discussion on new Members’ contributions, Members requested the Secretariat to implement a one-off Part I Budget reduction of MEUR 3.3.

63. This represents a substantial cut of 1.6% of the Part I Budget, thus setting the Budget base below ZNG level.

4.1. Reduction of the Budget Base and Allocation of the MEUR 3.3 Budget reduction

64. The reduction comes in an environment of ongoing cost-consciousness across the Organisation (see section on efficiency savings) which, through the V4M Project and other major reforms, continues to demonstrate the Secretariat’s awareness and determination to identify and implement efficiency measures. I have requested the Secretariat that the identified MEUR 3.4 additional pressures be absorbed within the existing resources. This represents a significant effort from Corporate Services.

C(2018)98/REV1 │ 27

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

65. This MEUR 3.3 Budget reduction follows a 1.25% across the board cut for the 2017-18 PWB. Even if this across the board reduction did not affect the overall Budget, since it was reallocated to finance Long-Term Reallocations, it required already in the last biennium a significant effort from Directors.

66. Considering the above mentioned elements, the MEUR 3.3 Part I Budget reduction cannot simply be managed through administrative efficiencies.

67. Despite my strong preference to preserve core financing for substantive Outputs, cutting Part I resources cannot rely solely on delivering new administrative efficiencies, and will have to impact the capacity of the Organisation to deliver outputs.

68. I propose to manage the Budget reduction by means of:

• MEUR 1.45 - Achieving new efficiencies in corporate services • MEUR 1.85 - Reducing available funding for other areas

Achieve new efficiencies in corporate services (1.45MEUR)

69. It is important to bear in mind that corporate functions, which, as I have indicated, are already experiencing significant additional cost pressures, exist to support and enable substantive outputs while ensuring the smooth running of the Organisation.

70. Cuts to corporate functions will require adjusting some parameters in the services delivered, and may have an impact on substantive outputs. However, the OECD will continue to work towards management excellence and will achieve efficiencies that focus on greening the OECD, ensuring the OECD is safe and secure, and increasing the accountability of corporate service delivery.

71. The details of Budget reductions to corporate functions will be provided to Budget Committee as part of the presentation on the draft preliminary PWBs for Strategic Objective 6.

Reduction in the Outputs to be delivered (1.85 MEUR)

72. Implementation of this Budget cut is an additional challenge for the Organisation to maintain its relevance in developing and promoting better policies.

• A simple across-the-board cut may have some superficial appeal as it has no regard for current areas of highest policy priority.

• Therefore, my strong view is that a targeted approach, taking into account Members’ priorities, for applying the Budget reductions will best protect Members’ interests and the Organisation's core work.

73. The task of identifying Budget reductions to substantive work is not easy. Members have given a clear message through the MTO Survey that every policy sector covered by the substantive programme of work is a high priority for a majority of Members. This was reinforced at the Heads of Delegation (HoDs) meeting on 16 February, where Members reiterated the value placed on OECD work. Conversely, there were no strong messages for reductions in the scope or breadth of the OECD’s sectoral coverage. However, some indications were given for the most supported areas of the Programme of Work. Even if I would have preferred a fully tailored approach to allocate the cuts on a restricted number of outputs, it is not realistic considering the overall general support provided by Members to all outputs. Therefore I propose to apply a middle ground approach whereby to introduce

28 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

some limited ponderation of the cuts per outputs based on Members’ indications for relative priorities from both the results of the MTO Survey and the HoDs discussion.

74. For all Output areas other than Corporate Services, I will apply a MEUR 1.85 Budget reduction and request Directors to identify the necessary Output cancellation and/or reduction to the following extent and principles :

a) no Budget Reduction for the Output Areas that garnered the largest number of ratings for an increase in resources in the MTO Survey (i.e. 1.3.1 - Digital Economy, 2.1.1 - Education, Economy and Society, 2.2.3 - Welfare and Social Inclusion);

b) a 2.5% cut representing 0.25 MEUR for the Output Areas that garnered the largest number of ratings for a decrease in resources in the MTO Survey (e.g. 3.1.3 - Trade and Domestic Policies, 3.2.2 - Agro-food, Trade and Development, 3.2.3 - Agriculture and Fisheries Sustainability, 4.1.3 - Corporate Governance, 4.2.2 - Finance, Insurance and Pensions);

c) a 1.5% percent reduction to all other Output Areas representing 1.6 MEUR

75. This reduction will necessarily impact the outputs discussed with the Committees in their preliminary PWBs. Therefore, Directors have submitted adjusted versions of their PWBs to their Committees. These adjusted versions will be presented to the Budget Committee during informal PWB presentations.

76. To give you some indication of the impact of the proposed reductions, there will be a need to cancel or reduce the scope of around 40 to 50 Intermediate Outputs. Our preliminary estimate is that a reduction in scope is likely for about 25% of these outputs, as alternative funding sources are unlikely to be available.

77. Based on the above assumptions, consolidated Budget reduction at Output Group level will be as follows:

C(2018)98/REV1 │ 29

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

Budget Reduction by Output Group in KEUR (Budget expressed in 2018 value before reallocation)

*Calculation for the budget reduction is based on 2019 base budget by output area before Long Term Reallocations, except for some areas that were not stabilised at the time the calculation was made and for which the budget reduction was calculated on 2018 base budget. ** The percentage variations compared to the initial assumptions are related to rounding in KEUR

4.2. 2019-20 level of the Budget

4.2.1. ZRG required to maintain the capacity to deliver 78. The 2008 MCM Resolution is intended to give the OECD “a strong and sustainable financial foundation

that will allow it to maintain at least the quality and volume of outputs, while adapting to changing priorities” [C/MIN(2008)6/FINAL].

79. The 2008 MCM Resolution called for:

• strict prioritisation by Members;

• Budget transparency;

• efficiencies; and

• a Zero Real Growth (ZRG) Part I Budget.

80. It acknowledged that the real Budget cuts experienced by the Organisation for more than a decade prior to 2008 were unsustainable and harmed OECD’s ability to deliver.

Base Budget Budget Reduction* %**

Total 201,650 (3,300) -1.6%

1.1 Economic Surveillance 20,640 (304) -1.5%

1.2 Industrial and Sectoral Policies 3,147 (46) -1.5%

1.3 Science and Technology Policies 6,712 (60) -0.9%

2.1 Human and Social Capital 3,900 (18) -0.5%

2.2 Employment Policies and Social Cohesion 6,020 (61) -1.0%

2.3 Environmental Sustainability 8,228 (121) -1.5%

2.4 Health System Performance 2,384 (35) -1.5%

3.1 International Trade 5,670 (101) -1.8%

3.2 Agriculture 7,353 (156) -2.1%

3.3 Taxation 6,518 (96) -1.5%

4.1 Business Climate 6,501 (110) -1.7%

4.2 Competition and Market Efficiency 5,169 (102) -2.0%

4.3 Public Sector Economics and Governance 7,071 (102) -1.4%

5.1 Development 6,389 (94) -1.5%

5.2 Global Relations 2,491 (37) -1.5%

6.1 Corporate Management 10,265 (150) -1.5%

6.2 Statistics 9,907 (138) -1.4%

6.3 Corporate Services 65,400 (1,445) -2.2%

6.4 Corporate Visibility 8,311 (123) -1.5%

CPF/LTR 5,700 SGAF 800 CIBRF 4,025 CIBRF funding by Annex budget (1,965) CIBRF funding by Reserve 1,015

30 │ C(2018)98/REV1

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

81. The ten-year phase-in period of the 2008 Resolution of the Council On the Financing of the Part I Budget of the Organisation, has been implemented as planned. Thus, 2019-20, will be the first biennium after the "phase-in period". The 2008 MCM Resolution provided for ZRG to be a ‘floor’. However, since 2008, the approved Budgets have not exceeded this floor and have remained flat (in real terms) despite the increased relevance and impact of the Organisation for its Members. In the context of a flat part I Budget in real terms, this high level of delivery was only possible through the continuous efforts of staff and management to deliver V4M initiatives on the one hand, and on the other hand, the support of donors, mostly Member countries who have provided their support to fund some areas of the Programme of Work through VCs (clearly recognising the value added, quality and relevance of OECD outputs). This source of financing currently represents around 36% of total expenditure in Part I and the early indications are that the moderate growth trend should continue in Part I and II.

82. My assumption is that once the reduction of MEUR 3.3 is applied to the Budget base, it will be adjusted by ZRG for the coming biennium. This is necessary to maintain the relevance and impact of the Organisation, and ensure that sufficient core Part I funding from assessed contributions is allocated to substantive outputs. It also respects fully the agreement among Members in the context of the 2008 Financial Reform.

83. In an Organisation where the predominant cost driver is staff costs (81% of Part I in 2017), and after many years of streamlining the staff structure (increasing the ratio of staff per manager from 14.2 in 2010 to 17.9 in 2017), ZRG for the Budget is necessary to avoid impact on the delivery of outputs. Also, most of the other expenditures are influenced by inflation and are already maintained at a low share of the Part I expenditure, which does not provide sufficient margin for a further reduction without impacting the outputs.

Chart 1. Evolution of the Structure of Part I Budget Expenditure (2009-2017 in real terms)

2017 Part I Budget Expenditure MEUR % Staff 154.1 81% Missions 6.1 3% Intellectual Services 15.5 8% Other expenditure 14.5 8% Total 190.3 100%

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013 2014 2015 2016 2017Staff Missions Intellectual Services Other expenditure

C(2018)98/REV1 │ 31

PWB 2019-20: DRAFT BUDGET PARAMETERS For Official Use

4.2.2. 2019-2020 estimated Part I Budget evolution 84. Annex I sets out the calculation of ZRG for the coming biennium. It is based on available data (May

2018 inflation rate in France) and will be finalised with inflation data available at end-June 2018. On this basis, applying the data available to the inflation formula agreed to by Council results in the following ZRG adjustments: +1.5% for 2019 and + 1.9% for 2020. Consequently, taking into account MEUR 3.3 Budget reduction, the expected adjustment for Part I is currently:

• -0.1% in 2019 as a result of cumulative effect of: i. The MEUR 3.3 reduction of the Budget base including Lithuania;

ii. The application of 1.5 ZRG in 2019 to the reduced Budget base. • +1.9% ZRG in 2020 as compared to 2019.

85. Table 1 below illustrates the annual Part I Budget increases since 2008.