PSA CHP 1 edited 2015

42

KAL 3023 PUBLIC SECTOR ACCOUNTING TOPIC 1: INTRODUCTION TO PUBLIC SECTOR FINANCIAL MANAGEMANT AND ACCOUNTING. SYED SOFFIAN/SOA/2013 1 11/03/22

Transcript of PSA CHP 1 edited 2015

KAL 3023 PUBLIC SECTOR ACCOUNTING TOPIC 1: INTRODUCTION TO PUBLIC SECTOR FINANCIAL MANAGEMANT AND ACCOUNTING.

SYED SOFFIAN/SOA/2013 111/03/22

SYED SOFFIAN/SOA/2013 211/03/22

Topic Outlines Introduction Definition of terminology Components of PS Features of PS Roles of public sector FM Activities and Framework Purposes of PSFM Objectives of Public Sector Acctg Characteristic of Public Sector Acctg Mgmt mechanism of the M’sian govt Comparison with Private Sector Roles of public sector accountant The users and uses of financial Report

Introduction

SYED SOFFIAN/SOA/2013 311/03/22

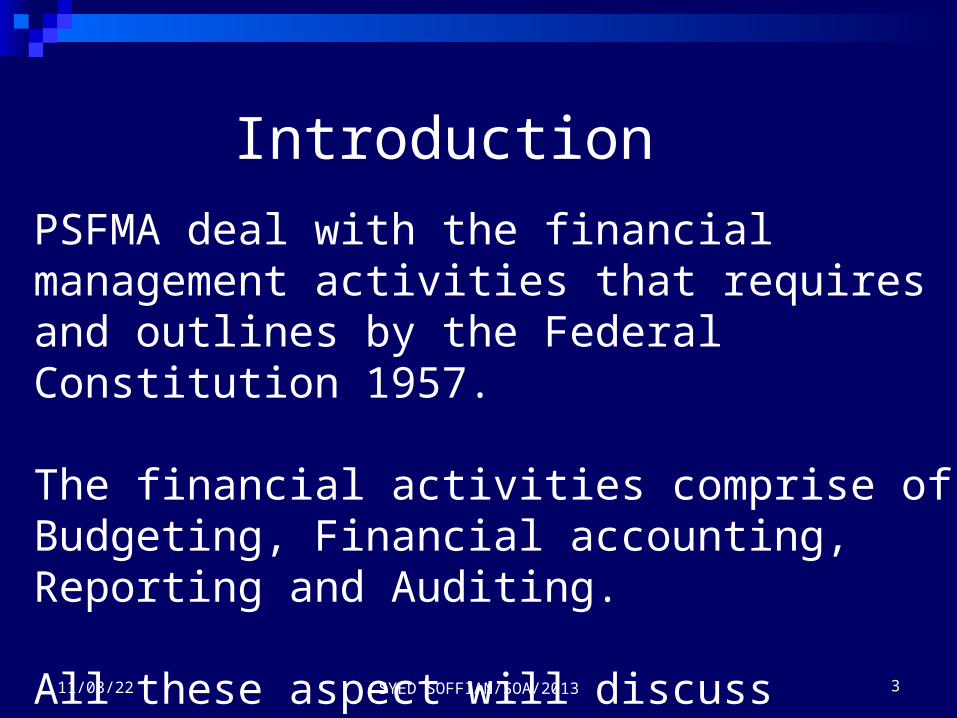

PSFMA deal with the financial management activities that requires and outlines by the Federal Constitution 1957.

The financial activities comprise of Budgeting, Financial accounting, Reporting and Auditing.

All these aspect will discuss thoroughly in the specific topic of this course.

Definition of Terminology

SYED SOFFIAN/SOA/2013 411/03/22

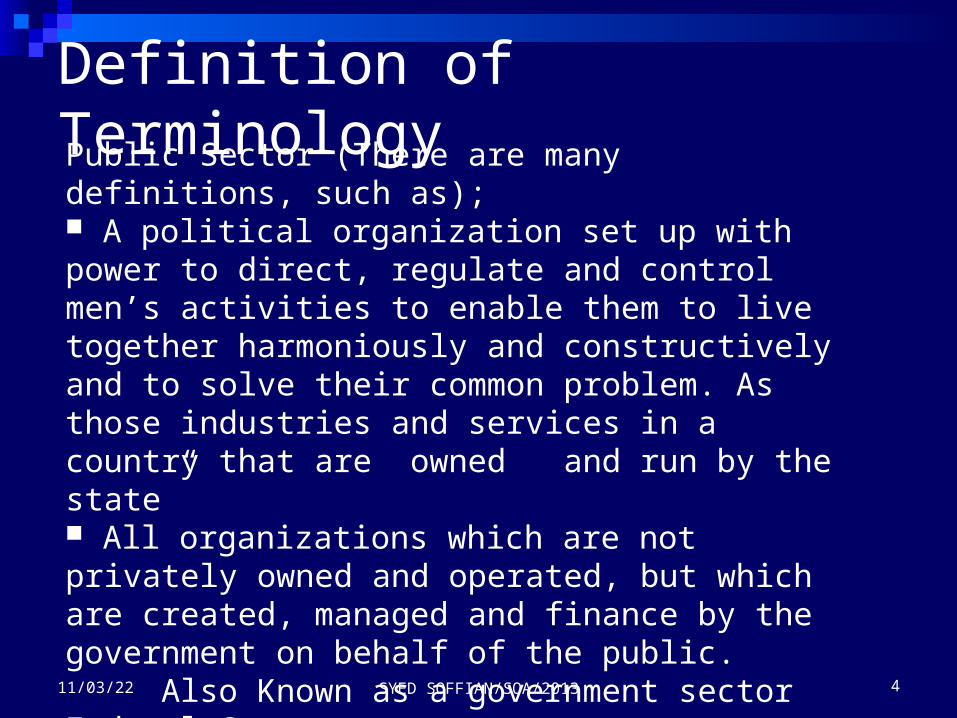

Public Sector (There are many definitions, such as); A political organization set up with power to direct, regulate and control men’s activities to enable them to live together harmoniously and constructively and to solve their common problem. As those industries and services in a country that are owned and run by the state” All organizations which are not privately owned and operated, but which are created, managed and finance by the government on behalf of the public. Also Known as a government sectorFederal GovernmentA government that operate at federal level and consists of Ministries, Departments, Units and Public enterprises

SYED SOFFIAN/SOA/2013 511/03/22

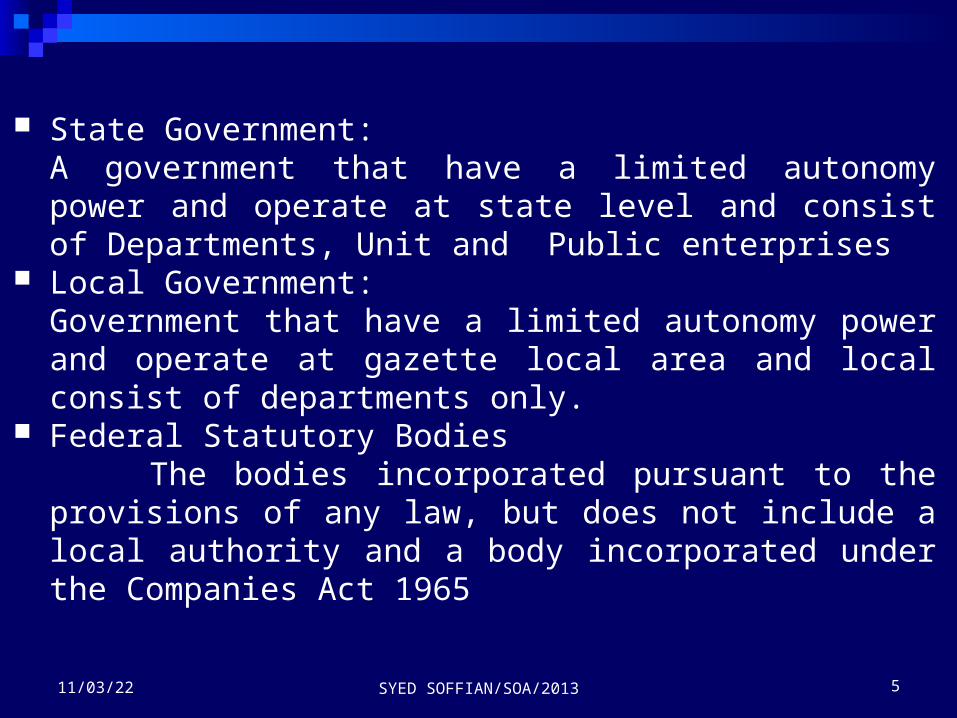

State Government:A government that have a limited autonomy power and operate at state level and consist of Departments, Unit and Public enterprises

Local Government:Government that have a limited autonomy power and operate at gazette local area and local consist of departments only.

Federal Statutory Bodies The bodies incorporated pursuant to the provisions of any law, but does not include a local authority and a body incorporated under the Companies Act 1965

SYED SOFFIAN/SOA/2013 611/03/22

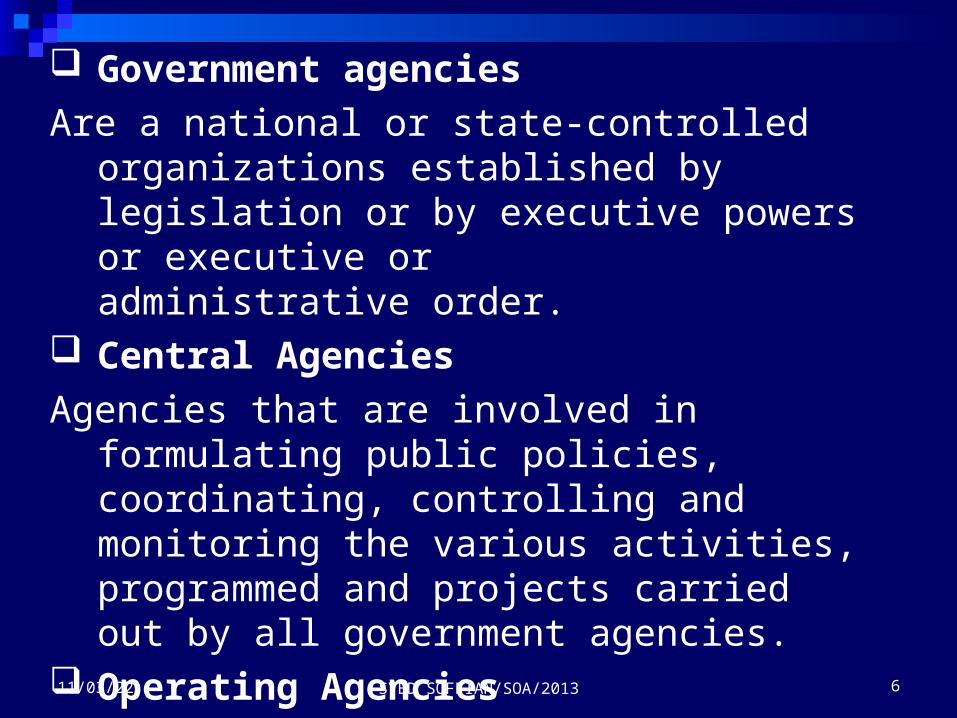

Government agenciesAre a national or state-controlled

organizations established by legislation or by executive powers or executive or administrative order.

Central AgenciesAgencies that are involved in

formulating public policies, coordinating, controlling and monitoring the various activities, programmed and projects carried out by all government agencies.

Operating Agencies The government agencies that are

responsible for planning and formulating and implementing certain specific government policies.

SYED SOFFIAN/SOA/2013 711/03/22

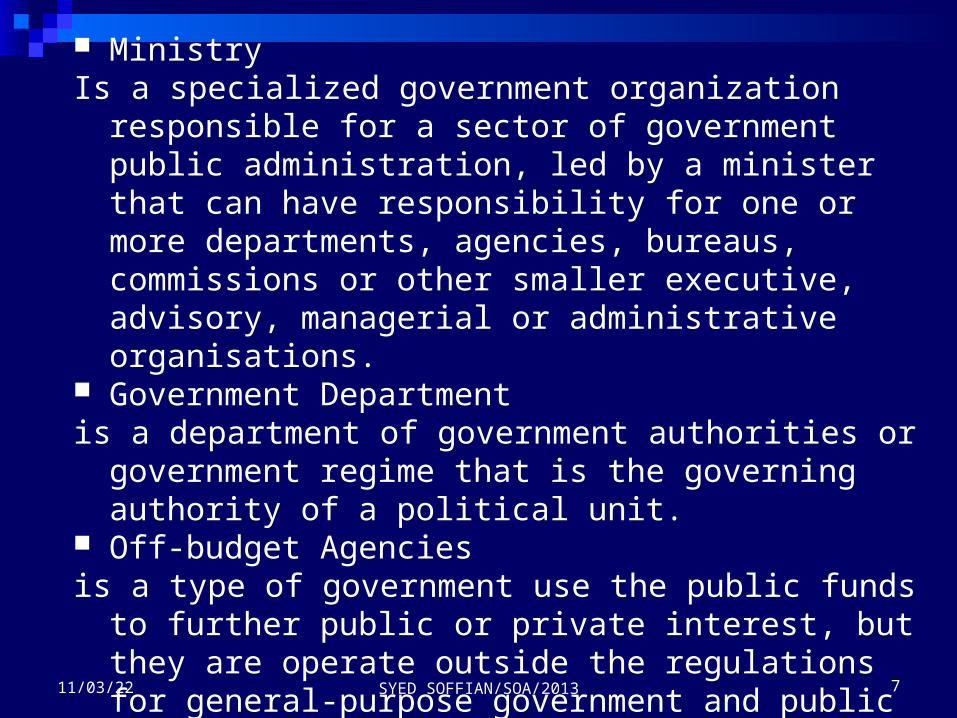

Ministry Is a specialized government organization responsible for a sector of government public administration, led by a minister that can have responsibility for one or more departments, agencies, bureaus, commissions or other smaller executive, advisory, managerial or administrative organisations.

Government Departmentis a department of government authorities or government regime that is the governing authority of a political unit.

Off-budget Agencies is a type of government use the public funds to further public or private interest, but they are operate outside the regulations for general-purpose government and public scrutiny and achieve self-funding by usually having taxation authority or fund themselves through fees for services rendered.

SYED SOFFIAN/SOA/2013 811/03/22

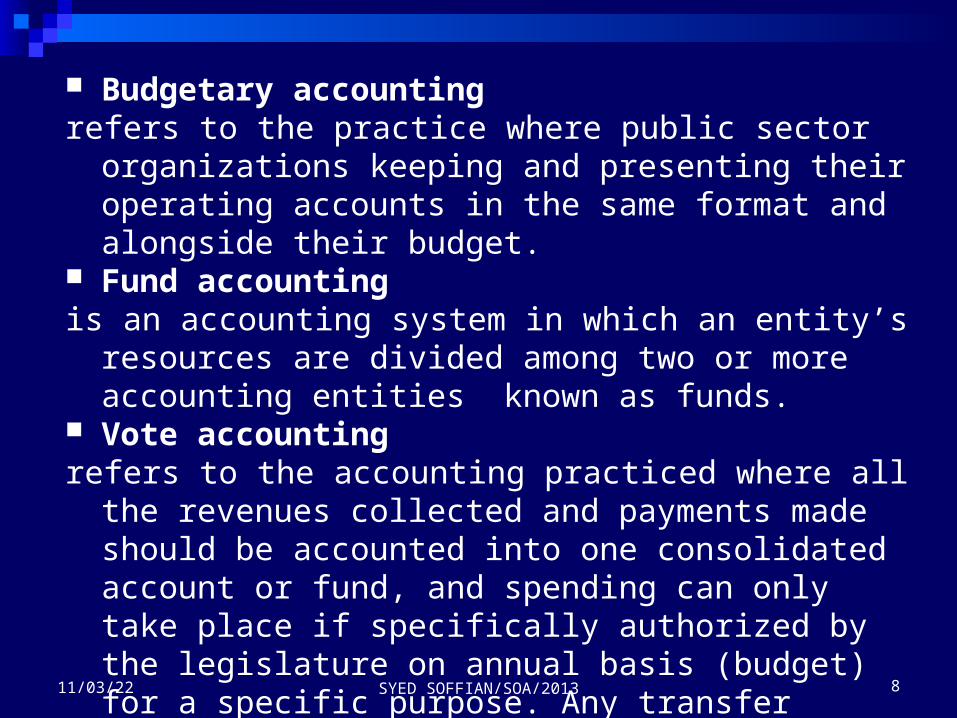

Budgetary accounting refers to the practice where public sector organizations keeping and presenting their operating accounts in the same format and alongside their budget.

Fund accounting is an accounting system in which an entity’s resources are divided among two or more accounting entities known as funds.

Vote accounting refers to the accounting practiced where all the revenues collected and payments made should be accounted into one consolidated account or fund, and spending can only take place if specifically authorized by the legislature on annual basis (budget) for a specific purpose. Any transfer between object of expenditure need to follow the virement procedure

SYED SOFFIAN/SOA/2013 911/03/22

Public sector financial management refers to the system by which financial

management resources are planned, directed and controlled to enable and influence the efficient and effective delivery of public service goals.

Public sector accounting is a process of identifying,

classifying, recording, summarizing, analyzing, reporting and interpreting government financial and data in the aggregate and detailed in accordance with regulations, accepted principles, concepts, conventions and standards

SYED SOFFIAN/SOA/2013 1011/03/22

Components of Public Sector Organization Federal Government (FG)State Government (SG)Local Government (LG)Public Enterprises (PE’s).

– SB– OBA– GLC– GLIC

SYED SOFFIAN/SOA/2013 1111/03/22

FEATURES OF PUBLIC SECTOR

SYED SOFFIAN/SOA/2013 1211/03/22

•Operate within a framework of public authorization and control• Plurality of objectives• Contributors of resources receive no direct interest• Varying accounting principles and practices• No individual shares of ownership

SYED SOFFIAN/SOA/2013 1311/03/22

ROLES OF PUBLIC SECTOR To enable a conducive and vibrant economic environment.

To facilitate growth and competitiveness of the industry and the Private Sector

To support the country manpower needs; and

To enhance the quality of life of Malaysian citizens.

SYED SOFFIAN/SOA/2013 1411/03/22

FINANCIAL MANAGEMENT ACTIVITIES AND FRAMEWORKS

Budgeting Financial AccountingFinancial reporting AuditingBased on constitutional Framework (refer part vii FC)

SYED SOFFIAN/SOA/2013 1511/03/22

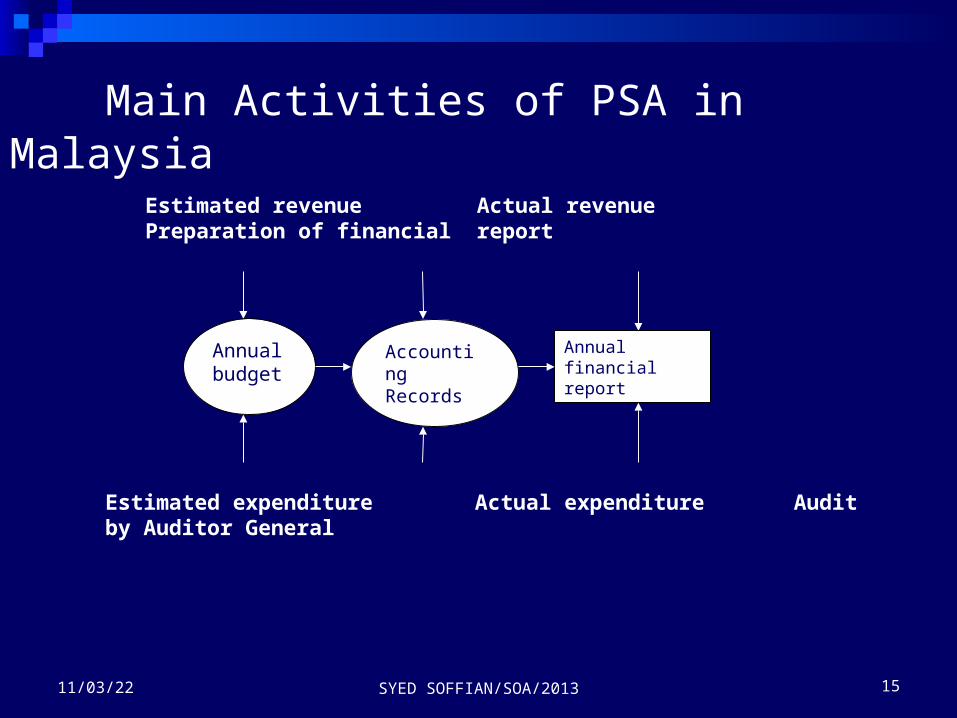

Main Activities of PSA in Malaysia

Estimated revenue Actual revenue Preparation of financial report

Annual budget

Accounting Records

Annual financial report

Estimated expenditure Actual expenditure Audit by Auditor General

SYED SOFFIAN/SOA/2013 1611/03/22

PURPOSES OF PSFM.To fulfill the legal requirement

– examples. Article 97 – 104 FC, FPA, AA, etc.

To achieve public Financial management accountability

– Financial (fiscal), management & programmed

THE IMPORTANCE OF FINANCIAL MANAGEMENT ADMINISTRATION

SYED SOFFIAN/SOA/2013 1711/03/22

To ensure the government has enough money for financing the program and activities and to achieve the state’s desired goal.

To ensure the public fund is managed in a proper manner by following the law, rules and procedures;

To avoid any misused of the fund and achieve efficiency in spending the public money.

Objectives of Public Sector Accounting

SYED SOFFIAN/SOA/2013 1811/03/22

To provide information necessary for efficient, effective and economical management an operation and of the resources entrusted to it

To provide information to enable managers

to report on the discharge of their responsibilities

to permit all public officials to report on the on the result of government operations and the use of public funds (accountability)

Characteristic of Public Sector Accounting

PSA will emphasis on:• Maintenance of books and all records properly.• Compliance with the related laws, rules and regulations. • Provides a comprehensive and accurate reports•Thus, accounting in public sector look at both the money and public property to account for as required by the Section 3, Financial Procedure Act 1957

7 Main Characteristics:1.Compliance with the requirements2. Budgetary Accounting3. Fund Accounting4. Vote accounting 5. Accounting basis 6. Coding system 7. Financial reporting SYED SOFFIAN/SOA/2013 1911/03/22

Fundamental in Public Sector Accounting

SYED SOFFIAN/SOA/2013 2011/03/22

1. Budgetary AccountingThe budget serves as a master blueprint for planning, control, and evaluation of governmental financial performance.

This is a system of accounting in which the reporting and budgeting system are integrated with financial transaction carrying with it budgetary implications right through the double entry process into the compilation of final accounts and gives a continuous update on how much of the budget remains unspent.

SYED SOFFIAN/SOA/2013 2111/03/22

2. Fund Accounting

Granof (1998). Fund Accounting is an accounting system in which an entity’s resources are divided among two or more accounting entities known as funds.Fund = Is accounting entity with self-balancing set of account for resources, and claim against them, that are segregated in accord with legal or contractual restrictions or to carry out specific activities.

Asset = Liabilities + Fund balance

4.Commitment Accounting Identifies and reserves funds for future payment obligation. Require to ensure that department anticipate their expenditures so as not to exceed appropriation ceilling

SYED SOFFIAN/SOA/2013 2311/03/22

5.Accrual Accounting Is a method of recording financial transactions in the period to which they are related. All assets owned by organization at the end of the period and all liabilities which exist at that point is also recognised in financial statement.

SYED SOFFIAN/SOA/2013 2411/03/22

6.Cash accounting Recognizes transaction and other events only when cash is received or paid. Financial statement prepare under cash basis provide readers with information about the sources of cash raised during the period, the purposes for which cash was used and cash balances at reporting date.

SYED SOFFIAN/SOA/2013 2511/03/22

Management mechanism of Malaysian Government

SYED SOFFIAN/SOA/2013 2611/03/22

Divide into various level:•Policy maker

– Parliament, ministries•Implementation

– Department, agencies•Watchdog agencies

– Auditor general, MACC, IIT, etc

The concept of Accountability and Stewardship

SYED SOFFIAN/SOA/2013 2711/03/22

Definition: Accountability - Responsibility to fulfill

obligation (Chamber’s 20th century Dictionary)

- Accountability is the obligation to give

answers and explanation concerning one’s

actions and performance, to those with a right

to require such answers and explanations.

-To be held responsible or to be required to account for proper stewardship of said resources

Stewardship Involves the administration,management and guardianship of resources,namely financial resources,provided by the public or taxpayer.

SYED SOFFIAN/SOA/2013 2811/03/22

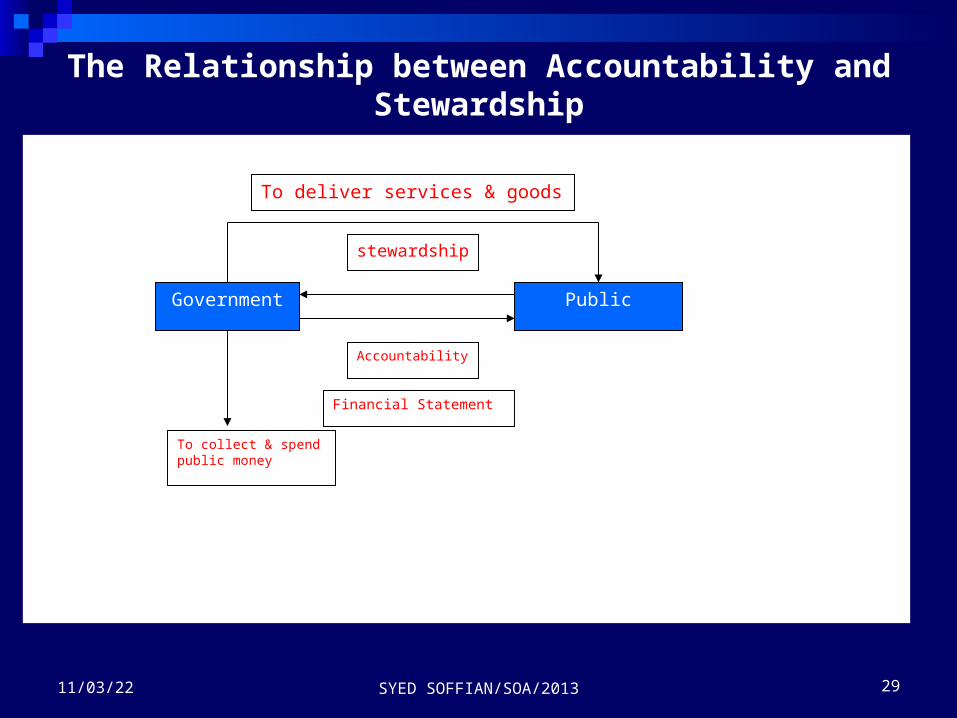

The Relationship between Accountability and Stewardship

SYED SOFFIAN/SOA/2013 2911/03/22

stewardship

Government Public

To deliver services & goods

Accountability

Financial Statement

To collect & spend public money

Accountability and public fund Control and management of public funds

are in the hands of the following:1) Parliament2) Treasury3) Agencies e.g. the ministries and

departments4) Auditor general5) Public accounts committee

SYED SOFFIAN/SOA/2013 3011/03/22

Cont..1) Parliament: Approves budget proposal- No expenditure can be incurred

without parliamentary approval- No tax can be levied without

necessary legal process- Parliament is the place where

accountability in govt. begins

SYED SOFFIAN/SOA/2013 3111/03/22

Cont..2) Treasury: Keeper of the public purse Examine expenditure proposals before presenting to parliament

Has the right to limit and suspend budget

3) Agencies: Controlling bodies of agencies are required to manage funds under their control in accordance with govt. policies, procedures and circulars

SYED SOFFIAN/SOA/2013 3211/03/22

Cont..4) Auditor general: Plays the role as the external auditor to govt.

To prepare audit reports for submission to parliament

Responsible to conduct:- Financial audit (compliance)- Performance audit (output and goals)

SYED SOFFIAN/SOA/2013 3311/03/22

Cont..5) Public accounts committee (PAC):

Responsible to examine the public account and the auditor general report if the account does not meet the proper accountability of public fund by public officials.

SYED SOFFIAN/SOA/2013 3411/03/22

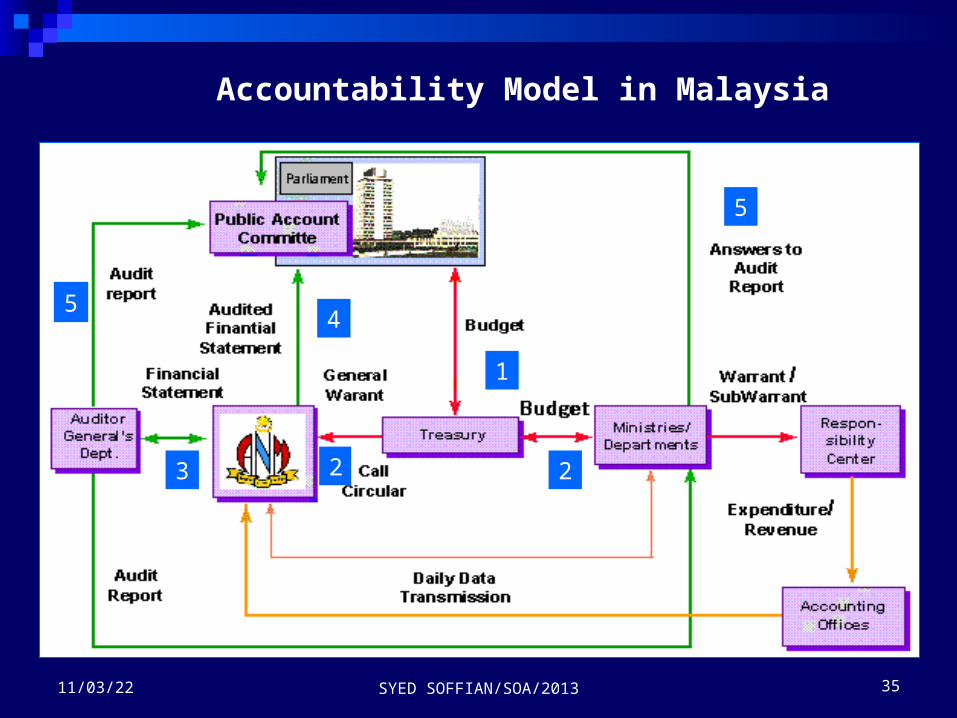

Accountability Model in Malaysia

SYED SOFFIAN/SOA/2013 3511/03/22

1

2

5

5

3

4

2

5

Explanation to Accountability Model

1) Budget prepare by treasury & table to the parliament for approval every year.

2) Approved budget will be distributed to all ministries & dept. by finance minister in the form of allocation warrant & also warrant to the accountant general office which serves as an authority for the AG office to utilise the consolidated fund required for expenditure

SYED SOFFIAN/SOA/2013 3611/03/22

Cont…3) By end of the year, AG office would prepare financial statement to be audited by the auditor general.

4) Audited financial statement will be table in parliament for approval as to discharge govt. accountability toward financial management.

5) Public account committee (PAC) is responsible to examine the public account & the auditor general report if the account doesn’t meet the proper accountability of public fund by public officials

SYED SOFFIAN/SOA/2013 3711/03/22

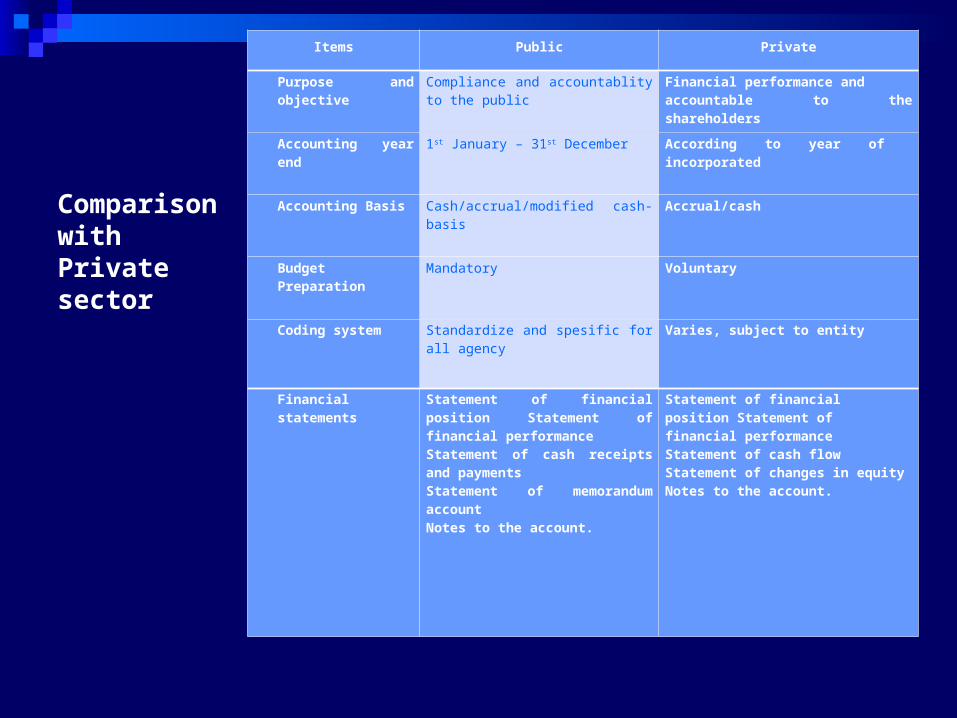

Comparison with Private sector

Items Public Private

Purpose and objective

Compliance and accountablity to the public

Financial performance andaccountable to the shareholders

Accounting year end

1st January – 31st December According to year of incorporated

Accounting Basis Cash/accrual/modified cash-basis

Accrual/cash

Budget Preparation

Mandatory Voluntary

Coding system Standardize and spesific for all agency

Varies, subject to entity

Financial statements

Statement of financial position Statement of financial performanceStatement of cash receipts and paymentsStatement of memorandum account Notes to the account.

Statement of financial position Statement of financial performanceStatement of cash flowStatement of changes in equityNotes to the account.

Roles of public sector accountants Play and important roles in enhancing:AccountabilityIntegrityEfficiency of both public money and property

ACW 420- Topic 1- ENGKU ISMAIL 201439

The Users of Public Sector Accounting Information External users:

Citizens/voters, tax payers, assembly man, analyst and mass media.

Internal users:Government (executives), legislation bodies and auditors.

SYED SOFFIAN/SOA/2013 4011/03/22

Conclusion

SYED SOFFIAN/SOA/2013 4111/03/22

Main activities for PSA are budget, accounting, reporting and auditing.Main Purposes to achieve accountability and fulfill the legalityBasic procedure and requirement need to refer and follow the Law requirement before accounting standardThe users of information include policy maker, parliament members and citizens.

THE END..

SYED SOFFIAN/SOA/2013 4211/03/22

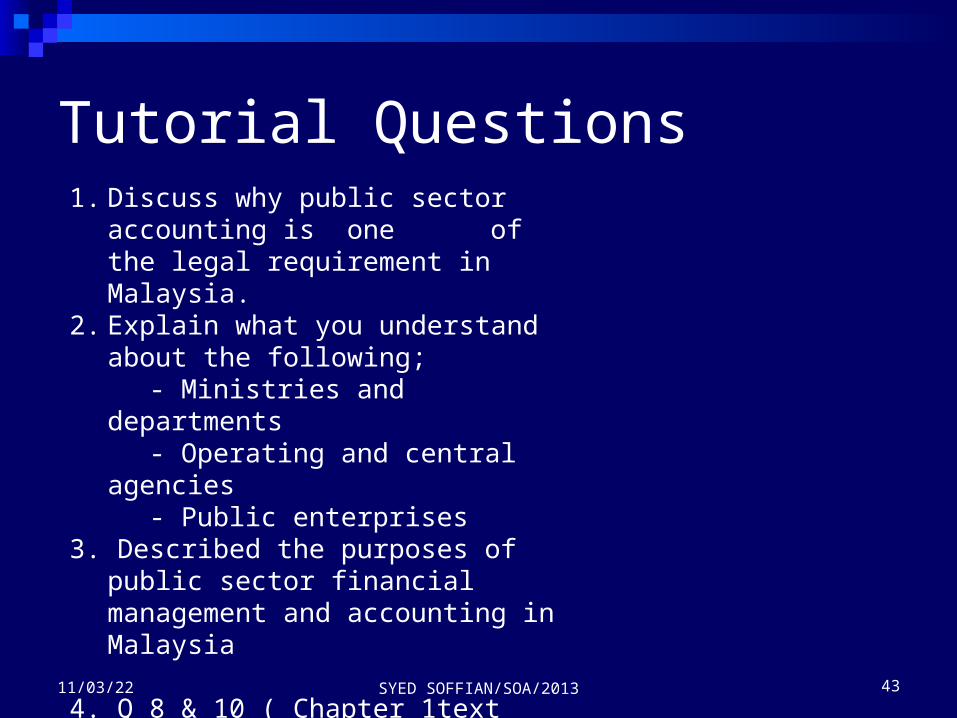

Tutorial Questions

SYED SOFFIAN/SOA/2013 4311/03/22

1. Discuss why public sector accounting is one of the legal requirement in Malaysia.

2. Explain what you understand about the following;

- Ministries and departments

- Operating and central agencies

- Public enterprises3. Described the purposes of

public sector financial management and accounting in Malaysia

4. Q 8 & 10 ( Chapter 1text book pg.20)

![Retell All [edited]](https://static.fdokumen.com/doc/165x107/631341535cba183dbf070426/retell-all-edited.jpg)