Project 1-5 combined

71

1 CHAPTER ONE INTRODUCTION 1.1 BACKGROUND TO THE STUDY According to Adeyemi (2006), the banking sector of any country is the engine of growth given its function of financial intermediation. Through this function, the banks facilitate capital formation, lubricate the production engine turbines and promote economic growth. The banking sector is also considered important as it is one of the few sectors in which the shareholders fund is only a small proportion of the liabilities of the enterprise. The volatile nature of this sector makes it a high risk environment which demands close monitoring to be able to perform effectively and efficiently (Owojori, Akintoye & Adidu, 2011). Credit Management can be viewed as written guidelines that set the terms and conditions for supplying goods on credit, customer qualification criteria, procedure for making collections, and steps to be taken in case of customer delinquency. Pandey (2004) submitted that credit is a marketing tool for expanding sales. Credit sales to customers however, must be well monitored because regardless of an organizations share of the market and demand for its products, if there are no measures put in place to regulate sales made to customers on credit, there could be problems especially those related to liquidity. Liquidity is cash, it is the ability of company to meet its financial obligations as when due. Liquidity ratios are used for liquidity management in every organization in the form of current ratio, quick ratio and Acid test ratio that greatly affect on performance of organization. Liquidity and its management determines to a great extent the growth and profitability of a firm. This is because either inadequate liquidity or excess liquidity may be harmful to the smooth running of the organization. This seeming controversy has attracted a lot of interest in the subject

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Project 1-5 combined

1

CHAPTER ONE

INTRODUCTION

1.1 BACKGROUND TO THE STUDY

According to Adeyemi (2006), the banking sector of any country is the engine of growth given

its function of financial intermediation. Through this function, the banks facilitate capital

formation, lubricate the production engine turbines and promote economic growth. The banking

sector is also considered important as it is one of the few sectors in which the shareholders fund

is only a small proportion of the liabilities of the enterprise. The volatile nature of this sector

makes it a high risk environment which demands close monitoring to be able to perform

effectively and efficiently (Owojori, Akintoye & Adidu, 2011).

Credit Management can be viewed as written guidelines that set the terms and

conditions for supplying goods on credit, customer qualification criteria, procedure for

making collections, and steps to be taken in case of customer delinquency. Pandey (2004)

submitted that credit is a marketing tool for expanding sales. Credit sales to customers however,

must be well monitored because regardless of an organizations share of the market and

demand for its products, if there are no measures put in place to regulate sales made to

customers on credit, there could be problems especially those related to liquidity.

Liquidity is cash, it is the ability of company to meet its financial obligations as when

due. Liquidity ratios are used for liquidity management in every organization in the form of

current ratio, quick ratio and Acid test ratio that greatly affect on performance of organization.

Liquidity and its management determines to a great extent the growth and profitability of a firm.

This is because either inadequate liquidity or excess liquidity may be harmful to the smooth

running of the organization. This seeming controversy has attracted a lot of interest in the subject

2

of liquidity management.(Egbide, Olubukunola & Uwalomwa, 2013).A company rich in fixed

assets may still be short of cash and therefore have difficulty in meeting current

obligations. Liquidity is the ability of the firm to convert assets into cash. It is also called

marketability or short-term solvency. The liquidity of a business firm is usually of particular

interest to its short-term creditors since the liquidity of the firm measures its ability to pay

those creditors. Several financial ratio measure the liquidity of the firm. Those ratios are the

current ratios, the quick ratio or acid test, net working capital, and the interval measure or

the burn rate. The impact of liquidity position in management of financial institution and other

economic unit have remained fascinating and intriguing, though very elusive in the process of in

investment analysis visa- visa bank port folio management.

The objective of this study is to empirically examine the impact of credit management and

liquidity position for Nigerian banking sector on its performance.

1.2 STATEMENT OF RESEARCH PROBLEM

The banking sector plays an important role in the economy of any nation. Every bank should be

able to keep an appropriate level of working capital. If the bank does not keep this level, it

affects performance (Bhunia & Brahma, 2011).Without cash, the bank will be in trouble and its

going concern will be in doubt.

Business analysts report that poor management is the main reason for business failure. It can be

argued that many banks in Nigeria went into liquidation because of poor credit management.

The inability of bank management to effectively address and manage credit has contributed to

the problem of bank failure.

3

This research aims at ascertaining the effect of credit management and liquidity position on bank

performance studying the credit management system of Nigerian banks and the various ways in

which they can be managed.

1.3 OBJECTIVES OF STUDY

The major aim of this research work is to evaluate the effect of credit management and liquidity

position on bank performance. The following are the specific objectives:

1.) To find out if credit management system allows for effective bank performance.

2.) To find out if there is a significant relationship between the liquidity and performance of

banks in Nigeria.

1.4 RESEARCH QUESTIONS

This research aims to provide answers to the following questions:

1.) Does credit management allow for effective bank performance?

2.) Is there a relationship between liquidity and performance?

1.5 RESEARCH HYPOTHESES

For this purpose of this study, the following hypothesis will be tested

Hypothesis 1

Ho - Credit management does not affect the performance of banks in Nigeria.

H1 – Credit management affects the performance of banks in Nigeria.

4

Hypothesis 2

H0 – There is no relationship between liquidity and bank performance.

H1 – There is a relationship between liquidity and bank performance.

1.6 SIGNIFICANCE OF STUDY

The significance of this study cannot be over emphasized especially now that the banking sector

is facing heat of Emefiele‟s banking reforms. Its significance among others is to add to the

general body of knowledge, enlighten the general public and shareholders on the effect of credit

management and liquidity position on performance of banks in Nigeria.

This study also seeks to explain to bank officials, what is involved in adoption of an efficient and

effective credit management.

This research work will be of great benefits to all stakeholders in the society. These people are:

Financial Analysts: This research will provide them with relevant areas from which liquidity of

firms can be analyzed. It will enlighten them on benefits of liquidity management ,its constraints

and limitations.

Bank Managers and Officials: This research will help enlighten bank performance about the

role and importance of credit management and help them understand how to effectively manage

credit.

Accountants and Auditors: This research could help provide accountants and auditors with

added knowledge on credit management as it could it be helpful when auditing and preparing

final accounts.

Researchers: This research work could be used by other people who wish to embark upon a

further research on the topic and related topics.

5

Investors: This research will provide them with what to look out for in companies financial

statements before deciding whether to invest or not. It will enlighten them on appropriate

financial ratios to use in detecting the liquidity level of companies.

Students: This research will help educate students on the concept of credit management and

liquidity and its components.

The General Public: This research could help educate the general public on credit management,

liquidity and bank performance.

1.7 SCOPE OF STUDY

The study will focus on the general impact of credit management and liquidity position on bank

performance, that is, how can credit management and liquidity position improve or reduce the

performance of banks.

Due to the amount of banks in Nigerian Stock Exchange, the research work was limited to the

fifteen listed banks in Nigeria. The above listed banks were chosen on the Nigerian Stock

Exchange due to ease of access of information.

1.8 LIMITATIONS OF STUDY

Time: Time constraints were one of the limitations encountered in the case of the study. The

time given for this research was too short due to the research work carried out during an

academic session, and the researcher did not have enough time to properly concentrate on this

particular study.

Finance: Finance was yet another problem that put a hold on the research work.

6

Lack of Facilities: Research facilities such as transportation make research easy and interesting.

But the researcher was not able to utilise this factor due to his distance from home and school.

Finally there was the problem of inadequate information and unavailable material or information

for the study.

1.9 SUMMARY OF RESEARCH METHODOLOGY

According to Business Dictionary (2012), it defined research methodology as the process used

to collect information and data for the purpose of making business decision. The methodology

may consist of publications, research works, journals and other online articles, and could

include both present and historical information that would be considered relevant to this study.

The research design of this strictly is strictly focused on the importance of credit management

and liquidity position on the Nigerian bank performance.

1.10 SOURCES OF DATA

There are two basic sources of data; primary and secondary data (Ojo 2005).Primary data refer

to data collected explicitly for a specific purpose .They are collected through the distribution of

questionnaires, coordination of interviews and direct observation and experiments.

Secondary data on the other hand, include government publications, syndicated services and

publications of international government (Ojo 2005). Others include articles, journals,

newspapers, magazines, internet and other published research works.

However, for the purpose of this research, the researcher made use of secondary data.

7

1.11 DEFINITION OF TERMS

For the purpose of this research the following words should be taken in order to enhance

understanding:

Credit Management: According to investorsword.com, credit management is a function

formed within a company to improve and control credit policies that will lead to an increase in

revenue and lower risk related to lending, reducing credit costs, extending more credit to

customers who they have assumed to have the capacity to repay back loans or grants to him, and

developing competitive credit terms and it is also called credit control.

Credit: According to mapsofworld.com, a credit is a legal contract where one party receives

wealth or resource from another party and promises to repay him on a future date along with

interest. In other words, a credit is an agreement of postponed or delayed payment of goods

bought or loan obtained and with the issuance of a credit, a debt is formed or created.

Liquidity Position: The liquidity position of a company is an ability to convert an asset into

cash quickly. The degree to which an asset or security can be bought or sold in the market

without affecting its price.

Liquidity Management: Liquidity management is the efficient control of current assets such as

stocks and converting it to cash in order to meet and pay current obligations of business, include

operating and financial expenses that are short term but maturing long term debt.

Bank: Bank can be defined as a financial house or a business responsible for keeping money for

individuals, make loans and offer other financial services or advice.

Credit Analysis: Credit analysis is concerned with the determination of the ability and

willingness of a borrower to repay a requested loan in accordance with the terms of the loan.

Credit Policy: It is a set of principles that a financial organization or business uses in deciding

8

who it will loan money to or give credit.

Risk: According to businessdictionary.com, it defined as risk a probability or threat for damage

to occur, injury, liability, loss or any other negative occurrence that is caused by external or

internal circumstances, and that may be avoided through intended action.

Credit Risk: Is the risk of loss due to a debtor‟s non-payment of a loan or other line of

credit (either the principal or interest).

Debt: According to investorswords.com, it defined debt as amount owed to a person or

organization for funds borrowed. Debt can be represented by a loan note, bond, mortgage

or other form stating repayment terms and, if applicable, interest requirements.

Profitability: This refers to the measure of returns on investment.

Financial Performance : Financial performance is the company‟s ability to generate new

resources from day to day operations over a given period of time.

Non–Performing loans: A sum of borrowed money upon which the debtor has not made

his or her scheduled payments for at least 90 days. A nonperforming loan is either in

default or close to being in default.

Performing loans: Loan on which payments of interests and principal are less than 90

days past due.

Obligor: A person or entity who is legally or contractually obliged to provide some

benefit or payment to another.

9

CHAPTER TWO

LITERATURE REVIEW

2.0 INTRODUCTION

In pursuance of this study “Credit Management and Liquidity Position on the performance of

banks”. This chapter aims at gathering some of the available information on this matter in order

to have an insight into what Credit management and Liquidity Position on the performance of

banks is all about.

Credit Management can be viewed as written guidelines that set the terms and conditions for

supplying goods on credit, customer qualification criteria, procedure for making collections, and

steps to be taken in case of customer delinquency. Pandey (2004) submitted that credit is a

marketing tool for expanding sales. Credit sales to customers however, must be well monitored

because regardless of an organizations share of the market and demand for its products, if there

are no measures put in place to regulate sales made to customers on credit, there could be

problems especially those related to liquidity. However, Liquidity is cash, it is the ability of

company to meet it financial obligations as when due. A company rich in fixed assets may still

be short of cash and therefore have difficulty in meeting current obligations. Liquidity is the

ability of the firm to convert assets into cash. It is also called marketability or short-term

solvency. The liquidity of a business firm is usually of particular interest to its short-term

creditors since the liquidity of the firm measures its ability to pay those creditors. Several

financial ratio measure the liquidity of the firm. Those ratios are the current ratios, the quick

ratio or acid test, net working capital, and the interval measure or the burn rate. The objective of

10

this study is to empirically examine the impact of credit management and liquidity position fo

Nigerian banking sector on its performance.

Pandy (2002) saw trade credit as a short term source of finance. He also said that, it is the credit

that a customer gets from a supplier of goods in the normal course of a business. Therefore, it is

mostly an informal arrangement between the supplier and the buyer as no legal documents are

signed. Pandy (2002), pointed out that trade credit may also take the form of bills payable. This

happens when the buyer signs a bill – a negotiable instrument to obtain trade credit of which in

his balance sheet, it appears as bills payable and it is said to be formal since a bill is a formal

acknowledgement of an obligation to repay an outstanding amount.

To supplier, any trade credit granted to a customer appears as account receivable, sundry debtors,

bills receivable depending on the one that is applicable.

The position of a company is an ability to convert an asset into cash quickly. The degree to

which an asset or security can be bought or sold in the market without affecting its price.

According to Anyanwu (1993) liquidity simply means the ability to convert an asset to cash with

minimum delay and minimum loss/cost. In the portfolio of listed banks, liquidity assets play a

very crucial role because banks operate largely with the funds borrowed from depositors in form

of demand and time deposits. These liquidity assets are the essential balance sheet items which

have the capacity to maintain the confidence of depositors which is the most valuable intangible

asset of the listed banking business (Spindt, 1980).

According to Nwankwo (1991), adequate liquidity enables a bank to meet three risks. First is the

funding risk – the ability to replace net outflows either through withdrawals of retail deposits or

nonrenewal of wholesale funds. Secondly, adequate liquidity is needed to enable the bank to

11

compensate for the non-receipt of inflow of funds if the borrower or borrowers fail to meet their

commitments. The third risk arises from calls to honour maturity obligations or from request for

funds from important customers.

Adequate enables the bank to find new funds to honour the maturity obligations such as a sudden

upsurge in borrowing under atomic or agreed lines of credit or to be able to undertake new

lending when desirable. For instance a request from a highly valued customer.

Adequate liquidity is also needed to avoid forced sale of asset at unfavourable market conditions

and at heavy loss. Adequate liquidity serves as vehicle for profitable operations especially to

sustain confidence of depositors in meeting short run obligations. Finally, adequate liquidity

guides against involuntary or non-voluntary borrowing from the regulatory authorities where

there is a serious liquidity crisis, the bank is placed at the mercy of the Central Bank, and hence

the control of its destiny may be handed over.

Having adequate or sufficient liquidity to meet all commitments at all times at normal market

rates of interest is indispensable for both large and small banks (Nwankwo, 1991). Liquidity is

the life blood of a banking setup. The ability of banks to meet their financial obligation is usually

measured by examining their balance sheet and relating same to its current assets to some or all

of their current liabilities. Fundamentally, a firm‟s liquidity rests not so much on its balance

sheet as on whether or not it is doing well and earning money. A strong balance sheet with a

large current ratio simply postpones liquidity problems for a short while if the firm is losing

money. Therefore, the complexity of devising an appropriate measure arises from the

uncertainties surrounding both size of the prospective needs for liquidity at any given time, and

the availability of sources of liquidity sufficient to meet them. There is also the impact of active

asset and liability management on liquidity management.

12

An accurate measurement of liquidity therefore requires going beyond the technical liquidity

indicated by the stock flow approach to an assessment of the stock of circumstances under which

a bank could come under pressure likely to affect worthiness in the market place. Liquidity can

be measured either as a stock at a point in time or as a flow over time. The most widely used is

the stock approach. One of these is the loan/deposit ratio which is the most popular and

commonly used measure in commercial banking.

According to Nwankwo (1991), under this measure, all bank loans are lumped together on the

basis that they are the most liquid of all bank assets. These are then compared with the total

deposit as a proxy for the liquidities that banks could be called upon honour. An increase in the

ratio indicates a less liquid position and vice versa.

2.1 CONCEPTUAL FRAMEWORK

Practically almost everything which has been written in the vast macro-economic literature has

some direct or remote connection with liquidity, this reflect its importance as a factor investment

decision and the concomitant effect on economic growth. A review of relevant literature is

ranged on the examination of related factors such as the conceptual framework review of

variable, current model and theories of the subject matter as incorporated into the wider scope of

banking.

Consequently the relationship between different parameters influencing the role liquidity

management is also examined under the conceptual framework. A review of related valuable

affecting the subject matters is looked into with eventual determination of which ones are more

relevant.

13

2.1.1 The Concept of Liquidity and Liquidity Management

Liquidity is the ability of a company to meet the short term obligations. It is the ability of the

company to convert its assets into cash. Short term, generally, signifies obligations which mature

within one accounting year. Short term also reflects the operating cycle: buying, manufacturing,

selling, and collecting.

Liquidity is a financial term that means the amount of capital that is available for investment.

Today, most of this capital is credit, not cash. Bank Liquidity simply means the ability of the

bank to maintain sufficient funds to pay for its maturing obligations. It is the bank‟s ability to

immediately meet cash, cheques, other withdrawals obligations and legitimate new loan demand

while abiding by existing reserve requirements. Nwaezeaku (2008) defined liquidity as the

degree of convertibility to cash or the ease with which any asset can be converted to cash (sold at

a fair market price).

Liquidity management therefore involves the strategic supply or withdrawal from the market or

circulation the amount of liquidity consistent with a desired level of short-term reserve money

without distorting the profit making ability and operations of the bank. It relies on the daily

assessment of the liquidity conditions in the banking system, so as to determine its liquidity

needs and thus the volume of liquidity to allot or withdraw from the market. The liquidity needs

of the banking system are usually defined by the sum of reserve requirements imposed on banks

by a monetary authority (CBN, 2012).

2.1.2 Liquidity and Business Decisions

Liquidity position could be understood by analysing the financial statements of a company.

Following financial items are required to understand the liquidity position of a company:

14

Current Assets

Current Liabilities

Liquidity position of a company can examined through financing decisions or investment

decisions. A company can finance its investment by different combination of current and long

term sources. In other words, a company can invest the money, raised through short term source

or long term sources, in the current assets or non-current assts. Some of the relevant business

strategies are as follows:

Financing the current assets by current sources

Financing the current assets by the long term sources

Financing non-current assets by the short term sources

Financing non-current assets by long term sources

2.1.3 Liquidity Position Indicators

There are several benefits from having an effective liquidity management strategy but there are

also some severe implications of misjudging the firms liquidity needs such as risk of bankruptcy

(Richards & Laughlin, 1980).

Generally current ratio, liquid ratio, absolute liquid ratio, debt-equity ratio, age of inventory, age

of debtors, age of creditors, cash to average daily cost of sales (in days),operating cash flow to

sales are very useful in ascertaining the short term debt paying ability or liquidity of a firm.

For measuring liquidity position, appropriate level of short term liquidity is required with whom

comparison can be made :

Liquidity position based on current ratios

Current Ratio

15

One of the most common and also the oldest measure of corporate liquidity is current ratio. It

was developed at the end of the 19th century in order to evaluate the credit-worthiness of the

companies (Beaver, 1966:71). In its simplicity it expresses the liquid resources available when

current liabilities are met and is calculated as follows:

Current Ratio = Current assets

Current liabilities

Maness & Zietlow (2005:27) has expressed that historically a current ratio of 2.0 has been a

norm, meaning that company has approximately twice as much current assets as coverage for

short term creditors. As the critique towards this measure often goes, it simplifies the protection

available for short-term creditors as not all the current assets are easily liquidated but can be tied

in the inventory.

Liquidity position based on quick ratio

Quick Ratio

Quick ratio or acid-test ratio is very similar to current ratio and solves the liquidation issues

mentioned above by excluding inventories from calculation:

Quick ratio (or acid-test ratio) = (Current assets-Inventory)

Current Liabilities

Usefulness of current and quick ratios for measuring working capital has been questioned

because of their static nature. As a balance sheet is a statement of stock instead of flows with the

result that ratios calculated from balance sheet accounts are liquidity stock measures at a certain

point in time. (Penman, 2007:725)

16

Liquidity position based on inventory to net working capital

Inventory to net working capital = Inventory

(Current assets - Current Liabilities)

A measure of the extent to which the firm's working capital is tied up in inventory.

Liquidity position based on working capital

Working capital plays an important role in firm‟s growth and profitability and is tightly

interlinked with the concept of liquidity. In its simplest and probably the most common form

working capital can be expressed as a difference between firm‟s current assets and current

liabilities. ( Larsson & Hammarlund, 2005:14).

Net Working Capital = Current Assets – Current Liabilities

Shin and Soenen have defined working capital as a “time lag between the expenditure for the

purchase of materials and the collection for the sale of the finished products” (Shin & Soenen,

1998). Working capital management (WCM) refers to a wider concept that covers both inventory

and work in progress and thereby combining elements of operations, production and financial

management.

Up to date several other measures are used in addition to current ratio and quick ratios. On the

other hand, even the importance of ratio analysis has been questioned and considered as a weak

tool for monitoring liquidity. According to Campbell, Johnson and Savoie‟s study (in Maness &

Zietlow 2005:32), monitoring of accounts receivables and good bank relations are valued over

the traditional ratio analysis among the financial managers. A common practice is to combine

several methods and use ratios as a part of liquidity management, but not rely solely on them.

(Maness & Zietlow, 2005:32)

17

There are several factors that need to be taken into consideration when doing ratio analysis.

Among the first conditions for ratio analysis is the good quality of accounting data which is a

natural premise since the analysis relies exclusively on financial statements (Beaver, 1966:99).

One of the earliest critiques towards ratios was concerned with the comparison among different

industries and groups of companies. As a response for that, several industry averages and means

have been developed ever since (Patricia, Harper & Eikner, 1999:96). Discussion around the

ratio analysis has been vivid and still ongoing and the latest studies remind the danger of using

benchmark values across the industries.

Huff, et al. (1999:104) found evidence of differences in liquidity ratios when different size of

companies compared. They put forward an argument that companies with little or no inventory

tend to have lower current ratios since their current assets are smaller. Another finding suggested

that current liabilities exceeded current assets, i.e. negative working capital balance, more often

among the small than larger companies (Huff et al. 1999:100-101). Smaller companies have

more extreme current ratio values (both very low and very high) than larger companies and

therefore the comparison of current ratios among larger companies is more meaningful since

there is likely to be less variation.

Also very common use of the ratios is the prediction of failure or financial distress. One of the

first studies about the bankruptcy prediction based on ratio analysis was conducted by Beaver in

1966 and his findings are still considered valid. He compared financial ratios of the companies

that went bankrupt with those that did not and found evidence that carefully conducted ratio

analysis can be a useful predictor of financial failure even five years prior to failure. As the

bankruptcy became more evident, the difference in ratios became also clearer, comparing to

surviving counterparts. (Beaver, 1966:102) The extent that Beaver used ratios in his analysis was

18

much higher than the aim of the current study. Focus is neither in the bankruptcy prediction but

on the differences in liquidity strategies and that is partly done by examining the use of liquidity

ratios. However, Beaver‟s findings hold 40 years later and well conducted ratio analysis is

considered a guiding tool to monitor liquidity and also financial performance and therefore ratio

analysis is very essential.

In summary, current and quick ratios have been traditionally most widely used tools monitoring

corporate liquidity. External users such as credit issuers have used them as measure for

evaluation companies credit-worthiness, whereas internal users have monitored how working

capital policy is executed inside the company. Usefulness of ratio analysis is questioned time to

time and one has to be careful when comparing companies across industries.

2.1.4 Concept of Credit Management

Credit (from Latin credere translation. "to believe") is the trust which allows one party to

provide resources to another party where that second party does not reimburse the first party

immediately (thereby generating a debt), but instead arranges either to repay or return those

resources (or other materials of equal value) at a later date. The resources provided may be

financial (e.g. granting a loan), or they may consist of goods or services (e.g. consumer credit).

Credit encompasses any form of deferred payment. Credit is extended by a creditor, also known

as a lender, to a debtor, also known as a borrower.

Credit does not necessarily require money. The credit concept can be applied in barter economies

as well, based on the direct exchange of goods and services. However, in modern societies, credit

is usually denominated by a unit of account. Unlike money, credit itself cannot act as a unit of

19

account. firms grant credit to their credit worthy customers, invariably we have accepted the

existence of debtors. In other words, granting of credit leads to creation of trade debts in business

which can be further classified into good debts, doubtful and bad debts. Management of debtors

is crucial in the management of working capital because poor management of trade debt can lead

to the provision of large sum of funds for bad and doubtful debts.

According to Pandey (2004), bad debt losses arise when the firm is unable to collect its accounts

receivable. The size of bad debt losses depends on the quality of accounts accepted by the firm.

In the words of Uchegbu (2001), it is wise to discourage bad debts and efforts should be made to

encourage discount more importantly cash discount. This is contrary under competitive business

environment were survival depends on the volume of turnover (sales) which in turn leads to trade

debt accumulation. Here debtors cannot be completely avoided it is therefore the work of the

management to initiate policies concerning credit sales so that they will survive in the business

environment they find themselves.

In the words of Donald and Penne (1987: 110), debtors or accounts receivable in a firm are

claims held against others in the operating circle. Trade debtors are further classified into trade

debtors and non-trade debtors. The amount which is owed by customers for goods and services

sold in the course of carrying on a business is termed trade debtors while on the other hand any

amount owed by customers arising from a variety of transitions that are oral or written promises

to pay other than goods at a later date is called non-trade debtors. Studies have shown that in the

period of boom (economic boom) customers tend to make cash purchases, pay their debts on

time and minimize the incidence of bad debts. On the other hand, the period of economic

recession is another situation. The uncertainty, which befalls the repayment of such debts, has

20

made the transactions to be based on customers‟ integrity, trust worthiness and his or her ability

to satisfy other conditionalities as placed by the selling organization.

2.1.5 Reasons for Granting Credit

Competition

Generally the higher the degree of competition, the more the credit granted by a firm (Pandey,

2004).

Company's bargaining power

If a company has a higher bargaining power vis-a-vis its buyers, it may grant no or less credit.

Marketing tool

Credit is used as a marketing tool, particularly when a new product is launched or which a

company wants to push its weak product.

Buyers requirements

In a number of business sectors buyers/dealers are "not able to operate without extending credit.

This is particularly so in the case of industrial products.

Buyers status

Large buyers demand easy credit terms because of buck purchases and higher bargaining power.

Some companies follow a policy of not giving much credit to small retailers since it is quite

difficult collect dues from them.

21

Relationship with dealers

According to Pandey (2004) companies sometimes extend credit to dealers to build long-term

relationship with them or to reward them for their loyalty.

Efficient credit sales management is necessary for achieving liquidity and profitability of a

company (Reddy and Kameswarri, 2004).

2.1.6 Efficient and Effective Credit Policy

According to Pandey (1993: 726), he opined that a firm's investments in receivables are effected

by some external factors such as the general economic conditions: - Industry norms, competitive

activities, political regulations and Technological change. But for effective management of trade

debt, firms should lay down guidelines and procedures for granting credit to individual‟s

customers and collecting the individual accounts.

Management naturally want to make efficient use of the available capital in the business and is

also interested in rapid turnover of accounts. Given the circumstance, a firm should formulate a

policy suitable for the firm and the commercial environment upon which credit sales will be

based. There are three major credit policy variables (factors) Rama Moorthy (1976:183) V12:

Credit Standards

According to Pandey (1993.726), credit standards are the criteria, which a firm follows in

selecting customers for the purpose of credit extension. He further reiterated that a firm may

have light

credit standards, that is, it may sell mostly on cash basis as may extend credit only to the most

reliable and financially strong customers. The implication of the above policy are many, for

22

instance, it will result to less bad debt losses and cost of credit administration. But such a firm

adopting the policy may not be able to expend sales. That is, the profit sacrificed on lost sales

may be more than the cost saved by the firm on the contrary, if credit standards are loose, the

firm may have large sales volume. But the firm will have to carry large receivables (debtors).

The cost of administering credit and bad debts losses will also increase, thus, the choice of

optimum credit standards involves a trade-off between incremental return and incremental cost.

Weston and Brigham (1986: 251), they enumerated the different types of cost associated with

credit sales. Such as:

(i) Cost of capital tied up in receivables (debtors),

(ii) Bad debts,

(iii) Higher investigation,

(iv) Collection cost.

According to Solomon and Pringle (1977: 201), they state that, the firm's credit policy will be

determined by the trade-off between opportunity cost and credit administration cost including

bad debts losses. In the words of Brain (1981), the objective of credit control is to strike a correct

balance between incremental return and incremental cost.

Credit Terms

These are stipulations under which the firm sells on credit to customers. They include: credit

period and cash discount.

Credit period refers to the length of time for which credit is extended to customers. Cash

Discount is a reduction in payment offered to customers to induce them to repay credit

23

obligations within a specified period of time, which will be less than the normal credit period. It

is usually expressed as a percentage of sales.

Collection Policy and Procedures

Collection policy is necessary for effective and efficient management of credit sales because

customers usually default in paying their debt as at when due, that is with reference to the terms

of credit. The collection policy aims at accelerating collection from slow-payers and thus

reducing incidence of Bad debts losses. Credit limit is the maximum amount of credit which the

firm will extend at a point of firm. Once the firm has taken a decision to extend credit to the

applicant, the amount and duration of the credit have to be decided. A collection policy should

ensure prompt and regular collection. Prompt collection is needed for fast turnover of working

capital, keeping collection costs and bad debts within limits and maintaining collection

efficiency. Regularity in collections keeps debtors alert, and they tend to pay their dues

promptly.

Some firms usually adopt a clear-sequence to collect the debt after the expiration of the normal

credit period granted to the customers; Firms may send a polite letter to the customers (as

reminder). A more severe letter will follow this afterwards. Other strategies may be the use of

telephones and personal visit by a company's representative. If all the above strategies fail, the

firm may resort to the use of collection agency and others such as legal action, etc. The result

will be a shift of loyalty and patronage to competitors and huge sales may be lost. However, a

situation where soft collection procedure is adopted, debtors may increase with profitability

being reduced. Hence, a fast and hard collection procedure is not desirable for a good firm to

survive.

24

2.1.7 Types of credit

There are many types of credit like trade credit , consumer credit, bank credit, commerce credit,

consumer credit, investment credit, international credit, public credit and estate. For the purpose

of this study, we shall be dealing with trade credit and consumer credit.

Trade credit

For companies in need of additional working capital, a trade credit can serve as a liquidity

reserve. This is a credit which is connected to one of the company‟s account. Usually the

company pays a yearly fee for the use of a trade credit and interest can be charged quarterly

(Larsson & Hammarlund 2005:130). What should be considered is that when interest is charged

quarterly it gives an interest on interest effect which can become very expensive for the

company.

Consumer credit

Consumer debt can be defined as „money, goods or services provided to an individual in lieu of

payment.‟ Common forms of consumer credit include credit cards, store cards, motor (auto)

finance, personal loans (installment loans), consumer lines of credit, retail loans (retail

installment loans) and mortgages. This is a broad definition of consumer credit and corresponds

with the Bank of England's definition of "Lending to individuals". Given the size and nature of

the mortgage market, many observers classify mortgage lending as a separate category of

personal borrowing, and consequently residential mortgages are excluded from some definitions

of consumer credit - such as the one adopted by the Federal Reserve in the US. Reference.

25

The cost of credit is the additional amount, over and above the amount borrowed, that the

borrower has to pay. It includes interest, arrangement fees and any other charges. Some costs are

mandatory, required by the lender as an integral part of the credit agreement. Other costs, such as

those for credit insurance, may be optional. The borrower chooses whether or not they are

included as part of the agreement.

Interest and other charges are presented in a variety of different ways, but under many legislative

regimes lenders are required to quote all mandatory charges in the form of an annual percentage

rate (APR). The goal of the APR calculation is to promote „truth in lending‟, to give potential

borrowers a clear measure of the true cost of borrowing and to allow a comparison to be made

between competing products. The APR is derived from the pattern of advances and repayments

made during the agreement. Optional charges are not included in the APR calculation. So if there

is a tick box on an application form asking if the consumer would like to take out payment

insurance, then insurance costs will not be included in the APR calculation.

2.1.8 The Five C's of Credit Management

In order to ensure effective credit management for bank performance Keplan (1998) noted the

use of “five C‟s of credit” to estimate the profitability of default in a formula known as the five

C's of credit when evaluating a credit application.

Character

26

The customer‟s willingness to settle his obligations when they are due has to be put into

consideration because it determines default rate.

Capacity

This is the ability of the customer to settle his financial obligations when they fall due. This is

determined by analyzing the firms operating cash flows.

Collateral

Most times, a firm may pledge an asset in the case of default. Such an asset has to be evaluated

to know its worth in case there was a default.

Conditions

A credit or financial manager should be able to assess the extent to which a customer‟s ability to

pay is likely to be affected by the prevailing economic decisions.

Capital

The financial reserve of a customer goes a long way to tell if he is able to meet his credit

obligation when they become due.

27

2.2 THEORITICAL FRAMEWORK

2.2.1 Theories of Liquidity and Liquidity Management

Liquid Asset Theory

This focuses on the asset side of the balance sheet and argues that banks must hold large amount

of liquid assets against possible demand or payment cushion of readily marketable short term

liquid assets against unforeseen circumstances. This approach is however very expensive in a

current world of dynamic money market (Ngwu, 2006:58)

Anticipated Income Theory

This theory holds that a bank‟s liquidity can be managed through the proper phasing and

structuring of the loan commitments made by a bank to the customers. Here the liquidity can be

planned if the scheduled loan payments by a customer are based on the future of the borrower.

According to Nzotta (2004) the theory emphasizes the earning potential and the credit worthiness

of a borrower as the ultimate guarantee for ensuring adequate liquidity. Nwankwo (1991) posits

that the theory points to the movement towards self-liquidating commitments by banks.

This theory has encouraged many listed banks to adopt a ladder effects in investment portfolio.

Shiftability Theory

This theory posits that a bank‟s liquidity is maintained if it holds assets that could be shifted or

sold to other lenders or investors for cash. This point of view contends that a bank‟s liquidity

could be enhanced if it always has assets to sell and provided the Central Bank and the discount

Market stands ready to purchase the asset offered for discount. Thus this theory recognizes and

28

contends that shiftability, marketability or transferability of a bank's assets is a basis for ensuring

liquidity. This theory further contends that highly marketable security held by a bank is an

excellent source of liquidity. Dodds (1982) contends that to ensure convertibility without delay

and appreciable loss, such assets must meet three requisites. Liability Management Theory

Liquidity management theory according to Dodds (1982) consists of the activities involved in

obtaining funds from depositors and other creditors (from the market especially) and determining

the appropriate mix of funds for a particularly bank. This point of view contends that liability

management must seek t answer the following questions:

- How do we obtain funds from depositors?

- How do we obtain funds from other creditors?

- What is the appropriate mix of the funds for any bank?

Management examines the activities involved in supplementing the liquidity needs of the bank

through the use of borrowed funds.

The liquidity management theory focuses on the liability side of bank balance sheet. This theory

contends that supplementary liquidity could be derived from the liabilities of a bank. According

to Nwankwo (1991) the theory argues that since banks can buy all the funds they need, there is

no need to store liquidity on the asset side (liquidity asset) of the balance sheet.

Liquidity theory has been subjected to critical review by various authors. The general consensus

is that during the period of distress, a bank may find it difficult to obtain the desired liquidity

since the confidence of the market may have seriously affected and credit worthiness would

invariably be lacking.

However, for a healthy bank, the liabilities (deposits, market funds and other creditors) constitute

an important source of liquidity.

29

Commercial Loan Theory

This theory has been subjected to various criticisms by Dodds (1982) and Nwankwo (1992).

From the various points of view, the major limitation is that the theory is inconsistent with the

demands of economic development especially for developing countries since it excludes long

term loans which are the engine of growth. The theory also emphasizes the maturity structure of

bank assets (loan and investments) and not necessarily the marketability or the shiftability of the

assets.

Also, the theory assumes that repayment from the self-liquidating assets of the bank would be

sufficient to provide for liquidity. This ignores the fact that seasonal deposit withdrawals and

meeting credit request could affect the liquidity position adversely. Moreover, the theory fails to

reflect in the normal stability of demand deposits in the liquidity consideration.

This obvious view may eventually impact on the liquidity position of the bank. Also the theory

assumes that repayment from the self-liquidating assets of a bank would be sufficient to provide

for liquidity.

This ignores the fact that seasonal deposit withdrawals and meeting credit request could affect

the liquidity position adversely.

Liability Management Theory

Advocate of liability management theory of liquidity of listed bank maintain that banks can meet

liquidity requirement by biding the marked for additional funds. This approach originally found

its strongest advocates in the large money market centers, the banks, and later develops the

negotiable type of certificate of deposit (CD) as a major money market instrument.

30

2.2.2 Theory of Credit

The word “credit” comes from the Latin word “credo” which means “I believe”. Hence, credit

is based upon belief, confidence, trust and faith. The loan is based upon the confidence of

borrower‟s future solvency and repayment. Hence, credit means ability to command the other‟s

capital in return for a promise to re-pay at some specified time in future. Besides, credit is the

combination of “ability to borrow” and “willingness to borrow”. Infact, credit is an

individual‟s borrowing capacity, often being considered as an “economic good” to be produced,

managed and marketed.

According to Vet (2012), he talked about the 3R principle of credit management which is:

Returns from an investment: The first R of credit

The returns from an investment, the first test of credit, have great significance to both creditor

and borrower. It requires that both borrower and lender are satisfied about the returns from credit

which cover the principal and interest. Furthermore, the basic question pertaining to returns

analysis is whether or not the use of credit generates adequate income and is most profitable use.

Thus, even though the use of credit may be profitable it should also be examined whether or not

it is the most profitable. Similarly, the examination of returns from an investment in terms of

generating adequate incomes to compensate for the contribution of family labour and

management as well as building owner‟s equity is also essential. Hence, overall profitability of a

farm business must be evaluated to assess the possibility of earning income from most profitable

enterprise to compensate the loss from another.

31

Thus, the problem of determining the most profitable use of capital is a part of decision making

and involves, (a) the selection of most profitable enterprises (product-product relationship), (b)

determining the most economical production techniques(factor-factor relationship), and (c)

determining the size of each enterprise (factor-product relationship).

Repayment capacity: The second R of credit

It should also be taken into consideration while extending/borrowing a loan. In fact, it is not only

sufficient for a loan to be productive rather it should also generate adequate returns so that loan

instalments can be repaid. It is quite possible that a loan may be productive but may not generate

adequate income after meeting the expenses to regularly pay the loan instalments.

The repaying capacity is the amount of money that a business would be able to spare from their

total earnings so as to repay the loan after meeting organization expenses. Ability to repay a loan

is influenced by the income generating capacity of the organization, off organization earnings,

the liquidity of the organization as reflected by the balance sheet and the cash flows on the

organization. Furthermore, the ability to repay may be influenced by numerous factors but

willingness to repay a loan is quite essential. In short run, the current assets must be able to repay

the current liabilities.

Risk bearing ability: The third R of credit

Risk bearing ability, the third R of credit, determines the quantum of credit which can be safely

used by the organization. It means the ability of borrower to withstand the unexpected low

incomes, unpredictable losses and expenses and to continue operations. It provides the “last line

of defence” in the use of credit. It is quite possible that a loan may be productive and may also

32

generate adequate repaying capacity but borrower may not be able to afford the shocks of

probable financial losses due to poor/inadequate risk-bearing ability. The assessment of risk

bearing ability is, therefore, essential since both returns and repayment capacity are based on

average estimates of production, prices and costs, which seldom hold true.

2.3 Financial Performance and Financial Institutions

Financial soundness is a situation where depositor‟s funds are safe in a stable banking system.

The financial soundness of a financial institution may be strong or unsatisfactory varying from

one bank to another (Bank of Uganda,2002).External factors such as deregulation, lack of

information among bank customers, homogeneity of the bank business and connections among

banks do cause bank failure.

Some useful measures of financial performance which is the alternative term as financial

soundness are Return on Equity (ROE) and Return on Assets(ROA).

2.3.2 RETURN ON EQUITY AND RETURN ON ASSETS

RETURN ON EQUITY

The amount of net income returned as a percentage of shareholders equity. Return on equity

measures a corporation's profitability by revealing how much profit a company generates with

the money shareholders have invested.

ROE is expressed as a percentage and calculated as:

Return on Equity = Net Income/Shareholder's Equity.

33

RETURN ON ASSETS

An indicator of how profitable a company is relative to its total assets. ROA gives an idea as to

how efficient management is at using its assets to generate earnings. It is calculated by dividing a

company's annual earnings by its total assets, sometimes this is referred to as "return on

investment". The higher the ROA number, the better, because the company is earning more

money on less investment.

ROA is expressed as a percentage and calculated as:

Return on Assets = Net Profit /Average Total Assets

34

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Introduction

This chapter presents the research design, method of study, subjects and instruments used the

procedure for the administration of the instrument and the data collection. It also discusses the

method of analysis, showing the various steps taken to ensure reliability and validity. This

chapter discloses the research methodology adopted for the project and contains the following

subheads: Research Design, Population of the study, Sample size and sampling technique, Data

gathering method, Actual field work or location of study, Data analysis method.

3.2 Research Design

Research design refers to the plan, structure and strategy used for the investigation in order to

obtain answer to research question (Blaikie, 2009). The research design used is cross sectional

design, it is appropriate when data are to be collected about a phenomenon at one or more points

in time to explore, describe or explain the interaction among variables (Asika, 1991)

Creswell (2014) also defined research design as types of inquiry within qualitative, quantitative

and mixed method approaches that provide specific directions for procedures in a research. This

research makes use of panel data methodology because it combines longitudinal and cross

sectional data. To analyze the panel data, the research uses Pearson‟s Product Moment

Correlation Coefficient and Regression analysis to test and prove the relevant hypothesis.

35

3.3 Population of Study

Asika (1991) described population as a census of all items or subjects that possess the

characteristics or that have knowledge of the phenomenon being studied. It is described as a set of

all participants that are eligible for the study. The population of the study in this research is the

entire listed banks in Nigerian Bank Industry.

Presently, on the Nigerian stock market, there are 15 banks listed under this category as at 28th

March, 2015 (Listed Banks: www.nse.com.ng, 2015). These will serve as the total population for

this study.

3.4 Sample Size and Sampling Technique

A sample is a part of the population and sampling is a procedure of drawing samples from a

population. This research work looked at the financial reports in banks listed on the Nigerian

Stock Exchange whose activities are going to have relevant impact on the economy due to their

method of operation.

Consequently, all the 15 banks listed on the Nigerian Stock Exchange were selected.

3.5 Data Gathering Method

This section answers the question to how data was collected. It outlines the: sources of data,

instruments of data collection, validity and reliability of instruments, and administration of

instruments.

36

3.5.1 Sources of Data

The data used in this research were obtained from sources the secondary sources. This data where

annual report from electronic database like www.nse.com.ng and africanfinancials.com

3.5.2 Instrument of Data Collection

This research made use of annual report from year 2010 to 2013 which will be employed to

gather necessary and relevant data. The technique will be used in order to reduce the problem

associated with data collection and to ensure that results from this are available. Apart from the

annual reports, data will also be collected from the following sources; financial summaries,

Journals and articles, Fact books, Internet sources.

3.5.3 Validity and Reliability of Instruments

(Izedonmi, 2005)Defines validity “as an indication of the extent to which a measure provides an

accurate representation of what one is trying to measure”. In testing the validity of the research

study, the researcher has ensured that the Static Regression Analysis (Panel Least Square

method) is used to run analysis to evaluate secondary data obtained from the bank‟s financial

statement.

Reliability tests aims at finding out if the measuring instrument will produce the same results or

outcomes when repeated over and over again. The use of only published audit annual reports of

the listed banks for this research justifies the validity of the source of data. These reports, so as to

37

ensure their reliability, are published so as to comply with statutory requirement, which carries

with penalty if information contained therein is found to be materially misleading for use.

3.6 Actual Field Work/ Location of Study

This research explores the link between credit management, liquidity position and bank

performance using secondary data. The data is collected from the Annual financial Statements of

the selected listed banks for the period of analysis 2010-2013. This research employs 15 banks

that geographically operate in Nigeria and are listed on the Nigeria stock exchange. The financial

statements provides information on the total asset, total equity, current assets, current liabilities,

profit after tax and other components used in this research.

This study concerns six variables: current ratio, non-performing loans, return on assets, return on

equity, total assets and total equity.

3.7 Method of Data Presentation

The analyzed results were presented based on the questions raised in the hypotheses formulated.

3.7.1 Methods of Data Analysis

The Pearson‟s Product Moment Correlation:

Correlation deals with the degree of relationship between two or more variables. Therefore, this

method was used to measure the degree of relationship between credit management, liquidity

position and performance.

38

Formula =

The Regression Analysis:

Regression analysis models are used to help us predict the value of one variable from one or

more other variables whose values can be predetermined. Therefore, regression analysis was

used to establish the relationship which exists between performance, liquidity and other variables

tested.

Formula = Y = f (x1, x2, x3 ...xn) + ( c1, c2)

This relationship is usually expressed as : y = mx + c

WHERE:

i. The dependent variable is denoted as y

ii. The independent variable is denoted as x1,x2,x3

iii. The control variable is denoted as c1, c2

Accounting ratios were also used in carrying out this research for effective comparison of the

variables.

All data collected were analyzed using SPSS 15.0 and E-views 5.0

3.8 Variable Description

3.8.1 Dependent Variable

For the purpose of this research, the dependent will be return on assets and return on equity.

39

RETURN ON EQUITY

The amount of net income returned as a percentage of shareholders equity. Return on equity

measures a corporation's profitability by revealing how much profit a company generates with

the money shareholders have invested.

ROE is expressed as a percentage and calculated as:

Return on Equity = Net Income/Shareholder's Equity.

RETURN ON ASSETS

An indicator of how profitable a company is relative to its total assets. ROA gives an idea as to

how efficient management is at using its assets to generate earnings. It is calculated by dividing a

company's annual earnings by its total assets, sometimes this is referred to as "return on

investment". The higher the ROA number, the better, because the company is earning more

money on less investment.

ROA is expressed as a percentage and calculated as:

Return on Assets = Net Profit /Average Total Assets

3.8.2 Independent Variables

For the purpose of this research, the independent variable will be current ratios and non

performing loans.

40

3.8.3 Control Variable

The control variable that will be used is the total assets and total equity.

3.8.4 Model Specification

As adapted from(W.Wongthatsanekorn, 2010). The research model for this research will be as

follows:

LROA = β0 + β1LNPL + β2LCR + β3LTA+ εit

LROE= β0 + β1LNPL + β2 LCR + β3LTE + εit

Where:

LROA measures the logged return on assets

LROE is measures the logged return on equity

LNPL is the logged non performing loans

LCR is the logged current ratio

LTA is the logged total assets

LTE is the logged total equity

Εit is the Error term

41

CHAPTER FOUR

DATA ANALYSIS AND PRESENTATION

This chapter will focus on the analysis and presentation of data obtained from the annual bank

reports of all listed banks in Nigeria. This empirical study is focused on a sample of 15 banks

with a period of 4 years from 2010-2013.The presentation of this chapter will be divided into

three parts. First, this chapter will be presenting a descriptive analysis as regards the relationship

between credit management, liquidity position and bank performance. Secondly, it presents the

correlation matrix analysis used in testing the hypothesis formulated. Thirdly it presents the

regression analysis used in testing the hypothesis formulated.

4.1 DATA PRESENTATION AND ANALYSIS

The presentation of data involved tables and figures which were used in the analysis of the

descriptive statistics, correlation analysis and regression analysis.

4.2 DATA ANALYSIS - PRELIMINARY

4.2.1 DESCRIPTIVE STATISTICS

Table 4.1 Descriptive Statistics (Summary of four years means and standard deviation

for the variables in testing all listed banks in Nigeria)

LNPL LCR LTA LTE LROA LROE Mean 23.81928 0.106237 27.04494 25.64064 -4.121170 -2.698624

Median 24.00222 0.106140 27.50804 25.64758 -4.166936 -2.312783

Maximum 25.43896 0.276115 28.80862 29.81932 -1.232029 0.090206

Minimum 21.41601 -0.320068 19.99265 18.72947 -7.824046 -9.210340

Std. Dev. 0.992423 0.089168 1.746731 1.599369 1.089081 1.721971

Skewness -0.642733 -1.938712 -2.403706 -0.935524 -0.347258 -2.395492

42

Kurtosis 2.798623 11.76209 9.552430 9.622725 5.350668 9.477867

Jarque-Bera 3.527028 191.2680 137.5949 98.66939 12.51665 135.2423

Probability 0.171441 0.000000 0.000000 0.000000 0.001914 0.000000

Sum 1190.964 5.311867 1352.247 1282.032 -206.0585 -134.9312

Sum Sq. Dev. 48.26032 0.389596 149.5025 125.3411 58.11876 145.2940

Observations 50 50 50 50 50 50

Source: E-views 5.0 descriptive output

Table 4.1 comprises of the descriptive statistics of both the dependent and independent variables

of the sample banks. It shows the mean, standard deviation, the minimum and maximum of the

variables used.

The results from the descriptive analysis were as follows:

1. The Mean is the average value of the series, gotten from an addition of the series and

dividing through by the number of observations in the series. From the Descriptive Analysis

table below, the mean for LNPL is 23.81928, LCR is 0.106237, LTA is 27.04494, LTE is

25.64064, LROA is -4.121170, and LROE is -2.698624.

2. The Median is the middle-value of the series arrived at when the values of the series are

prearranged in order from the minimum to the maximum values. The median determines the

centre of the distribution and it is less susceptible to outlier‟s effects than the mean. From the

table below, the median for LNPL is 24.00222, LCR is 0.106140, LTA is 27.50804, LTE is

25.64758, LROA is -4.166936, and LROE is -2.312783.

3. The Maximum and Minimum Statistics are the maximum and minimum values of the

series in the given sample. The maximum of LNPL is 25.43896,LCR is 0.276115 ,LTA is

28.80862,LTE is 29.81932,LROA is -1.2320209,LROE is 0.090206 while the minimums are

LNPL is 21.41601,LCR is -0.320068,LTA is 19.99265,LTE is 18.72947,LROA is -

7.824046,LROE is -9.210340.

43

4. The Standard Deviation is a measure of dispersion or spread in the series.

The Standard Deviation of the series from the table below for LNPL is 0.992423,LCR is

0.89168,LTA is 1.746731,LTE is 1.599369,LROA is 1.089081,LROE is 1.721971.

5. The Skewness is a measure of unevenness of the distribution of the series around its

mean. The skewness of a symmetric distribution, such as the normal distribution, is meant to be

zero. Positive skewness means that the distribution possesses a long right tail while a negative

skewness implies that the distribution possesses a long left tail. From the table above, it can be

seen that all the variable distributions are negative which then implies that they have long left

tails representing the negative Skewness of their distributions.

6. Kurtosis measures the Flatness or Peakedness of the distribution of the data. If the

kurtosis exceeds 3, the distribution is Leptokurtic (or peaked); if the kurtosis is less than 3, the

distribution is Platykurtic (or flat) relative to the normal. From the table, kurtosis exceeds three

in five of the variables which are LCR,LTA,LTE,LROA,LROE making them peaked but the

remaining one which is LNPL is less than three so it is relatively flat.

7. The Jarque-Bera is a test statistic for finding out whether the series is normally

distributed or not. The test statistic measures the difference of the skewness and kurtosis of the

series with those from the normal distribution.

The number of observations for the descriptive statistics is 50.

4.3 DATA ANALYSIS - ADVANCED

4.4 Data Diagnosis

Before correlation and regression can be carried out effectively certain assumptions must be put

in place such as normality, linearity and homoscedasticity, which must not be violated. These all

44

refer to various aspects of the distribution of scores and the nature of the underlying relationship

between the variables. These assumptions can be checked from the residuals scatter plots which

are generated as part of the multiple regression procedure. Residuals are the differences between

the obtained and the predicted dependent variable (OI) scores. The residuals scatter plots allow

you to check:

• Normality: the residuals should be normally distributed about the predicted OI scores;

• Linearity: the residuals should have a straight-line relationship with predicted OI scores;

• Homoscedasticity: the variance of the residuals about predicted OI scores should be the

same for all predicted scores.

One of the ways that these assumptions can be checked is by inspecting the residuals scatter plot

and the Normal Probability Plots of regression standardized residuals. The decision criteria is to

reject violation of the above assumptions which suggests no major deviations from normality if

in the Normal Probability Plot, points lie in a reasonably straight diagonal line from bottom left

to top right and in the Scatter plot of the standardized residuals, if the residuals are roughly

rectangularly distributed, with most of the scores concentrated in the centre (along the 0 point).

The presence of outliers can also be detected from the Scatter plot. Tabachnick and Fidell (2001)

define outliers as cases that have a standardised residual of more than 3.3 or less than –3.3. With

large samples, it is not uncommon to find a number of outlying residuals (Pallant, 2001).

4.4.1 Test for Normality

Normality is used to describe a symmetrical, bell-shaped curve, which has the greatest frequency

of scores in the middle, with smaller frequencies towards the extremes (Gravetter & Wallnau,

2000, cited in Pallant, 200, 1 p. 48).

45

Figure 4.1

Source: SPSS 15.0 Output (2015)

Figure 4.1 shows the frequency distribution of the series in the histogram. The histogram divides

the series range (the distance between the maximum and minimum values) into a number of

equal length intervals or bins and displays a count of the number of observations that fall into

Regression Standardized Residual

3210-1-2-3

Fre

qu

en

cy

20

15

10

5

0

Histogram

Dependent Variable: ROA

Mean =8.88E-16Std. Dev. =0.974

N =59

46

each bin. Normality is proved when the scores are reasonably normally distributed, that is, when

most scores are occurring in the center, tapering out towards the extremes.

4.4.2 Test for Linearity

The relationship between the two variables should be linear. This means that when you look at a

scatterplot of scores you should see a straight line (roughly0, not a curve (Pallant, 2001).

Observed Cum Prob

1.00.80.60.40.20.0

Exp

ecte

d C

um

Pro

b

1.0

0.8

0.6

0.4

0.2

0.0

Normal P-P Plot of Regression Standardized Residual

Dependent Variable: ROA

47

From above, there is no major deviation from normality, linearity and homoscedasticity as most

of the scores are located at the centre, that is, at zero point.

4.5 Correlation Analysis

Table 4.2 Correlation Analysis

Correlations

ROE ROA CR NPL TA TE

ROE Pearson Correlation 1 .183 .212 -.039 .093 .363(**)

Sig. (2-tailed) .163 .104 .775 .480 .005

N 60 60 60 57 60 59

ROA Pearson Correlation .183 1 .148 -.035 -.453(**) .309(*)

Sig. (2-tailed) .163 .259 .797 .000 .017

N 60 60 60 57 60 59

CR Pearson Correlation .212 .148 1 .142 -.127 .188

Sig. (2-tailed) .104 .259 .291 .332 .154

N 60 60 60 57 60 59

NPL Pearson Correlation -.039 -.035 .142 1 -.068 -.047

Sig. (2-tailed) .775 .797 .291 .616 .732

N 57 57 57 57 57 56

TA Pearson Correlation .093 -.453(**) -.127 -.068 1 .442(**)

Sig. (2-tailed) .480 .000 .332 .616 .000

N 60 60 60 57 60 59

TE Pearson Correlation .363(**) .309(*) .188 -.047 .442(**) 1

Sig. (2-tailed) .005 .017 .154 .732 .000

N 59 59 59 56 59 59

** Correlation is significant at the 0.01 level (2-tailed).

* Correlation is significant at the 0.05 level (2-tailed).

Source: SPSS 15.0 Output (2015)

Table 4.2 shows the significance, direction and strength of relationship between the dependent

variable (roe and roa) and the independent variables (non-performing loans and current ratio).

Direction of relationship: The correlation coefficient between total equity and return on equity

is positive (0.363), indicating a positive correlation between total equity and return on equity.

The lower the total equity, the lower the return on equity.

48

Also, the correlation coefficient between total asset and return on asset is negative (-0.453),

indicating a negative correlation between total asset and return on assets. The lower the total

asset, the higher the return on asset.

The correlation coefficient between total asset and total equity is positive (0.442), indicating a

positive correlation between total asset and total equity. The lower the total asset, the lower the

total equity.

The correlation coefficient between total equity and return on equity is positive (0.363),

indicating a positive correlation between total asset and return on equity. The lower the total

equity, the lower the return on equity.

Significance Level: The relationship between ROE and TE is 1%, the same goes for relationship

between ROA and TA, TA and TE. Likewise the relationship between ROA and TE is 5%.

Strength of the relationship: The sign in front of the R-value whether negative or positive

refers to the direction not the strength. The results suggests that there is a medium correlation

between total equity and return on equity (at 0.363), signifying an average relationship between

total equity and return on equity. This same assertion was true for the relationship between total

asset and return on assets (at -0.453). Similarly, the results suggest that there is a medium

correlation between total asset and total equity (at -0.442). This same assertion was true for the

relationship between total equity and return on assets (at 0.309), signifying a medium

relationship between the variables.

49

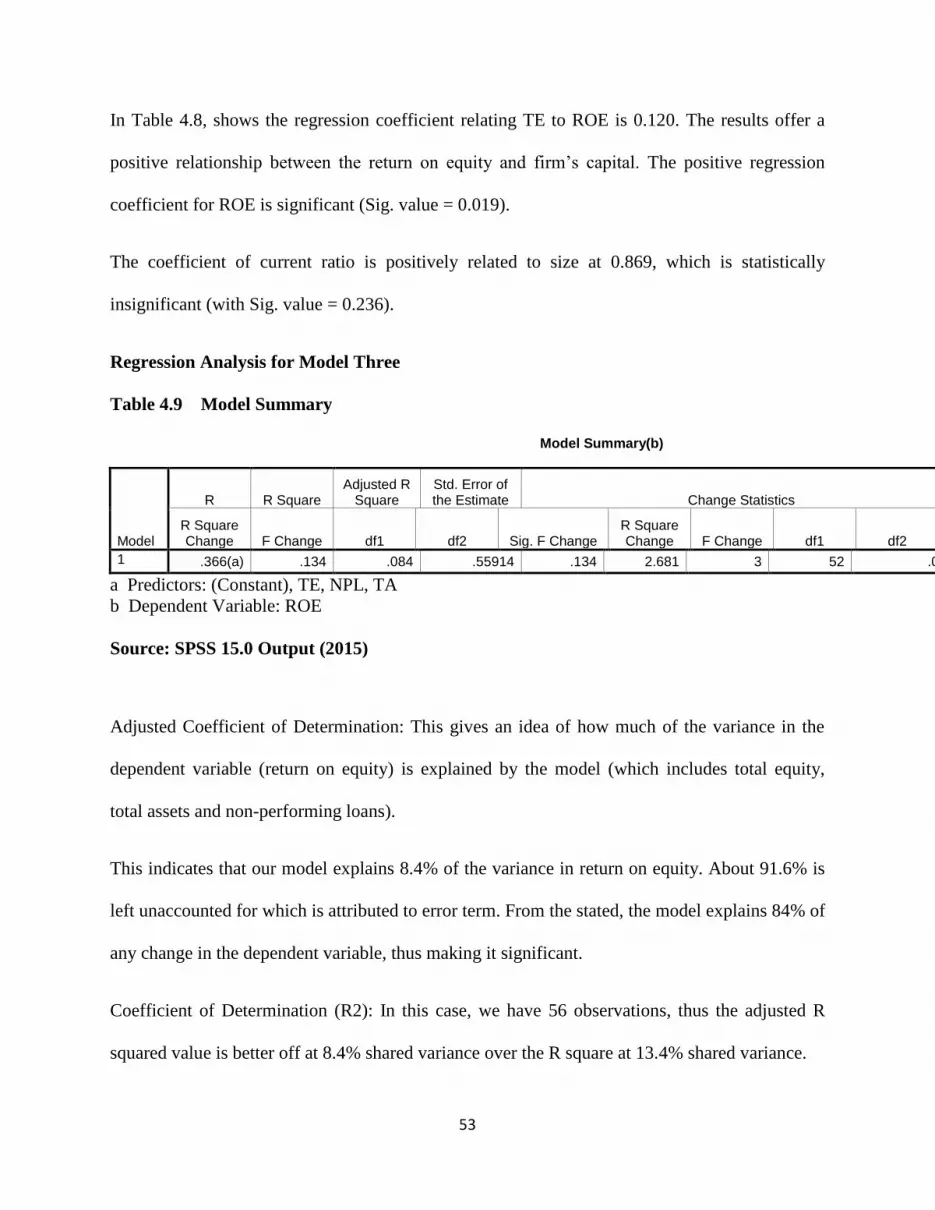

4.6 Regression Analysis

Regression Analysis seeks to explore the relationship between one continuous dependent

variable and a number of independent variables or predictors (usually continuous).

Regression Analysis for Model One

Table 4.3 Model Summary

Model Summary

Model

R R Square Adjusted R

Square Std. Error of the Estimate Change Statistics Durbin-Watson

R Square Change F Change df1 df2 Sig. F Change

R Square Change F Change df1 df2 Sig. F Change

1 .758(a) .574 .551 .03100 .574 24.746 3 55 .000 1.771

a Predictors: (Constant), TE, CR, TA

b Dependent Variable: ROA

Source: SPSS 15.0 Output (2015)

Adjusted Coefficient of Determination: This gives an idea of how much of the variance in the

dependent variable (return on equity) is explained by the model (which includes total equity,

current ratio and total assets).

This indicates that our model explains 55.1% of the variance in cash conversion cycle. About

44.9% is left unaccounted for which is attributed to error term. From the stated, the model

explains 55.1% of any change in the dependent variable, thus making it significant.