Professor Kratchman Finance 302

8

[Type text] Professor Kratchman Finance 302 February 22, 2012 Hansson Private Label, Inc.: A Case Study Through our analysis we have deemed that the proposed expansion of Hansson Private Label will benefit the company through added revenue, profit, and market share. The following are our findings to further explain our decision. The strategic implications of company’s expansion proposal are simple. First, increasing profits through expansion of production and of sales. Second and most important, is an increase in market share by driving both new customers and existing customers away from competitors. Also, an increase in production to drive the company’s growing market share. We feel that Gates’ projections are realistic for the company’s expansion. The projections are viable because they have an above 75% chance of returning a positive net present value (NPV) in addition to a solid internal rate of return (IRR) and would expand the relationships of the company with

Transcript of Professor Kratchman Finance 302

[Type text]

Professor Kratchman

Finance 302

February 22, 2012

Hansson Private Label, Inc.: A Case Study

Through our analysis we have deemed that the proposed

expansion of Hansson Private Label will benefit the company

through added revenue, profit, and market share. The

following are our findings to further explain our decision.

The strategic implications of company’s expansion

proposal are simple. First, increasing profits through

expansion of production and of sales. Second and most

important, is an increase in market share by driving both

new customers and existing customers away from competitors.

Also, an increase in production to drive the company’s

growing market share.

We feel that Gates’ projections are realistic for the

company’s expansion. The projections are viable because they

have an above 75% chance of returning a positive net present

value (NPV) in addition to a solid internal rate of return

(IRR) and would expand the relationships of the company with

[Type text]

its competitors and clients. A Sharpe ratio of 0.946 also

suggests a positive return in relationship to the added risk

assuming ours is higher than other projects’.

After our analysis of both the project and industry we

chose a WACC of 9.238%. This WACC value was chosen as it was

most in line with the market’s debt-to-value ratio. This

project would increase both capital structure and risk;

however according to the Sharpe ratio the increase in

capital structure justifies the risk.

Through our sensitivity analysis we have deemed the

selling price to be more sensitive to a change in net

present value than direct material costs. This was found via

a difference in slope. As for any long-term inflation rates,

we have deemed them negligible compared to Gates’

predictions as inflation affects the market and industry as

a whole and not just our company.

Based upon previous years’ income and market share for

HPL we decided upon a consistent 5% capacity increase until

it reached 85% in 2014. We see this as an appropriate

[Type text]

assumption due to the production reaching its maturity in

its sixth year.

In conclusion, through our extensive analysis we have

decided that it would be within the company’s best interest

to proceed with the investment and proposal. We would

maintain positive relationship and positive growth within

our respective market.

APPENDIX

[Type text]

HCL Ratios:

Filled out ratios

WACC calculation:

[Type text]

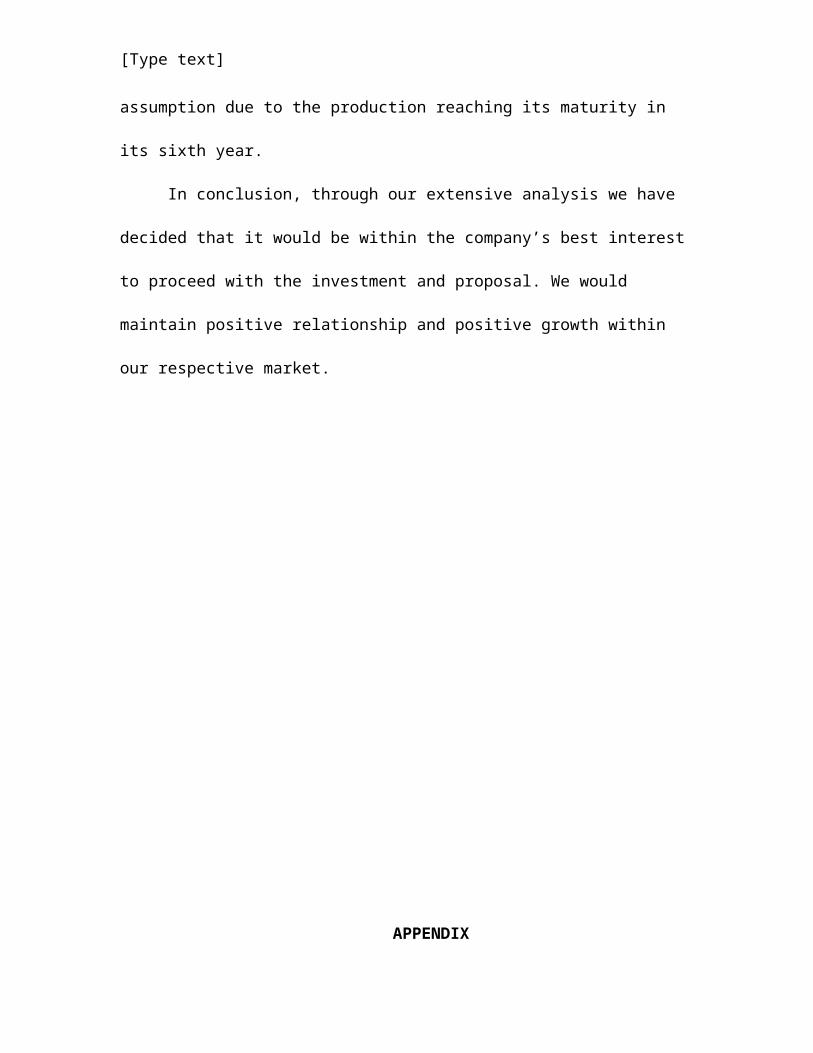

Debt to value is thrown off by Cathleen Sinclairs

debt to equity

Took out Cathleen Sinclair

Chose Wacc of 9.238 based on new debt to equity

ratio

[Type text]

Base Case:

Assumed capacity growth of 5% per year

o Based on previous revenues and projection of

more demand from customers

Worst:

Assumed units stayed consistent after year 4

[Type text]

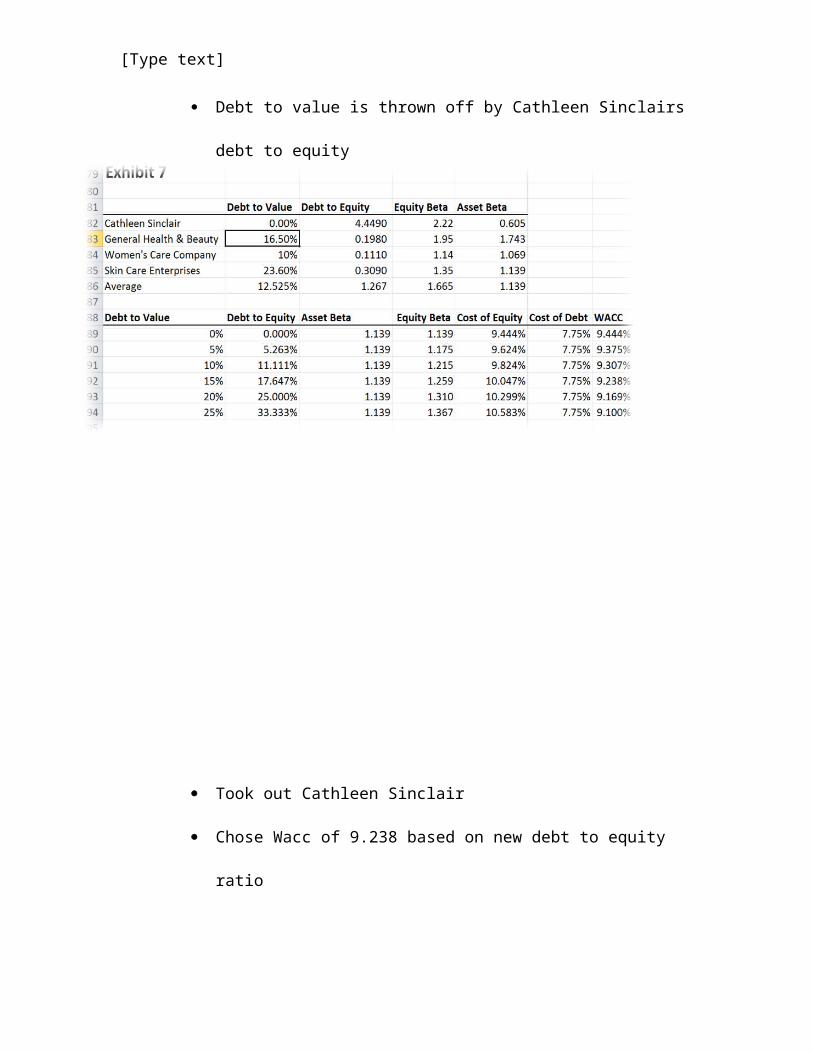

o Based on contract with customer ending

Best:

Assumed growth rate of 2%

o Assumed growth based average economic growth

Sensitivity analysis:

1 2 3 4 5 6 7 8 9

$(80,000,000.00)

$(60,000,000.00)

$(40,000,000.00)

$(20,000,000.00)

$-

$20,000,000.00

$40,000,000.00

$60,000,000.00

$80,000,000.00

$100,000,000.00

f(x) = 19605720.4357059 x − 91402171.192305

f(x) = 11318654.2228976 x − 49966840.1282637

f(x) = 385190.701910717 x + 4705376.40056312

Selling PriceLinear (Selling Price)Direct MaterialLinear (Direct Material)Capacity UtilizationLinear (Capacity Utilization)

[Type text]

Slope of lines suggest what variables are more

sensitive to NPV

o Selling price is most sensitive

o Capacity utilization is least sensitive