Principles of Accounting

11

Mandhu College Rahdhebai Hin’gun, Malé. Tel: +9603330055, Fax: +9603320603 COVER PAGE FOR WRITTEN ASSIGNMENTS Assignment Title: Principle of Accounting Assignment 1 Student Name(s)* Thoriq Ahmed Student ID(s) 6314 Module Name Principle of Accounting Module Code 0934 Course DOB2 Due Date * In case of group assignments write only the surname of all the members. Certification of Authorship Declaration: I/We declare that this is my/our own work and does not involve plagiarism or collusion. I/We have retained a copy of this assignment. I/We fully understand the penalties for submitting work which is wholly not my/our own.

-

Upload

mandhucollege -

Category

Documents

-

view

2 -

download

0

Transcript of Principles of Accounting

Mandhu College Rahdhebai Hin’gun, Malé. Tel: +9603330055, Fax: +9603320603

COVER PAGE FOR WRITTEN ASSIGNMENTS

Assignment Title: Principle of Accounting Assignment 1

Student Name(s)* Thoriq Ahmed

Student ID(s) 6314

Module Name Principle of Accounting

Module Code 0934

Course DOB2

Due Date

* In case of group assignments write only the surname of all the members.

Certification of Authorship

Declaration: I/We declare that this is my/our own work and does not involve plagiarism or collusion.

I/We have retained a copy of this assignment. I/We fully understand the penalties for submitting

work which is wholly not my/our own.

PRINCIPLES OF ACCOUNTING ASSIGNMENT 1 Thoriq Ahmed (DOB2) 6314

Page 2

PRINCIPLES OF ACCOUNTING ASSIGNMENT 1 Thoriq Ahmed (DOB2) 6314

Page 3

PRINCIPLES OF ACCOUNTING

ASSIGNMENT 1 THORIQ AHMED (DOB2)

6314

All The Answers are

highlighted in RED

color in Bold and

Italic

PRINCIPLES OF ACCOUNTING ASSIGNMENT 1 Thoriq Ahmed (DOB2) 6314

Page 4

PRINCIPLES OF ACCOUNTING

SEM 01

Assignment number 1

28.1 The plant and machinery cost account of a company is shown below. The company's policy is to

charge depreciation at 20% on the straight line basis, with proportionate depreciation in years of

acquisition and disposal.

PLANT AND MACHINERY – COST

20X5 $ 20X5 $

1 Jan Balance b/f 280,000 30 June Transfer disposal 14,000

1 Apr Cash 48,000 1 Sept Cash 36,000

31 Dec Balance c/f 350,000

364,000 364,000

What should be the depreciation charge for the year ended 31 December 20X5?

A $67,000

B $70,000

C $64,200

D $68,600 (2 marks)

28.2 Which of the following are correct?

1 The statement of financial position value of inventory should be as close as possible to net realizable

value.

2 The valuation of finished goods inventory must include production overheads.

3 Production overheads included in valuing inventory should be calculated by reference to the

company's normal level of production during the period.

4 In assessing net realizable value, inventory items must be considered separately, or in groups of similar

items, not by taking the inventory value as a whole.

A 1 and 2 only

B 3 and 4 only

C 1 and 3 only

D 2, 3 and 4 (2 marks)

PRINCIPLES OF ACCOUNTING ASSIGNMENT 1 Thoriq Ahmed (DOB2) 6314

Page 5

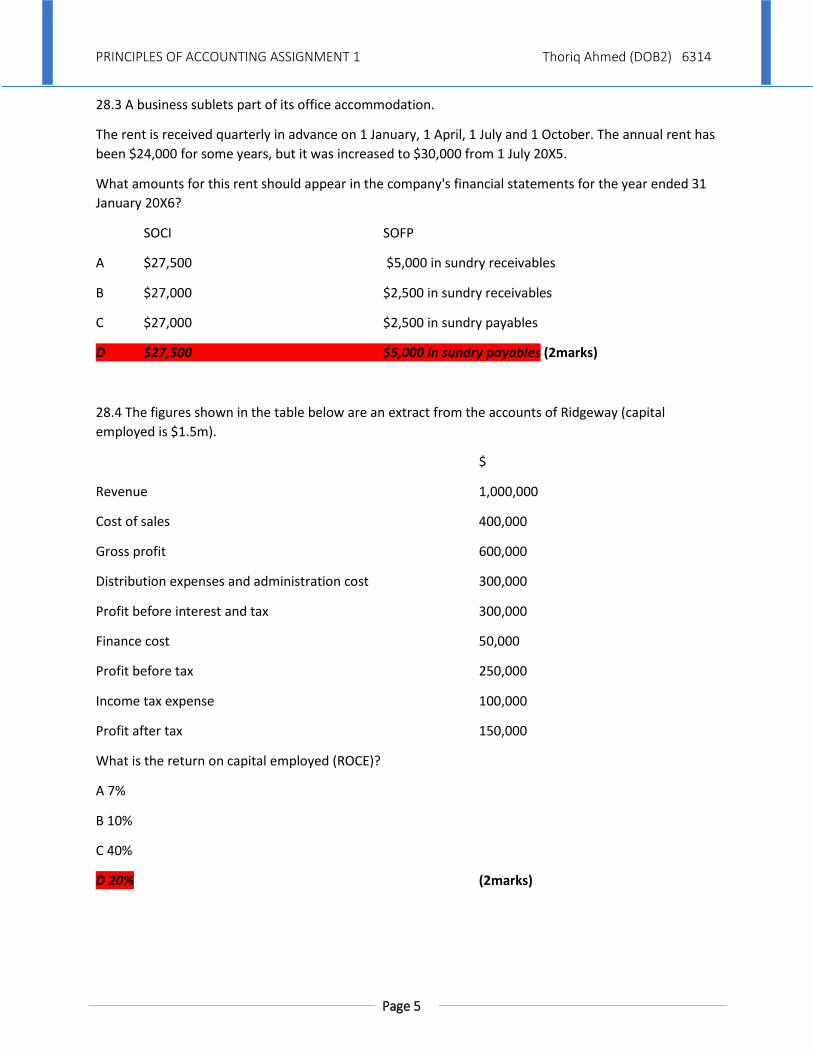

28.3 A business sublets part of its office accommodation.

The rent is received quarterly in advance on 1 January, 1 April, 1 July and 1 October. The annual rent has

been $24,000 for some years, but it was increased to $30,000 from 1 July 20X5.

What amounts for this rent should appear in the company's financial statements for the year ended 31

January 20X6?

SOCI SOFP

A $27,500 $5,000 in sundry receivables

B $27,000 $2,500 in sundry receivables

C $27,000 $2,500 in sundry payables

D $27,500 $5,000 in sundry payables (2marks)

28.4 The figures shown in the table below are an extract from the accounts of Ridgeway (capital

employed is $1.5m).

$

Revenue 1,000,000

Cost of sales 400,000

Gross profit 600,000

Distribution expenses and administration cost 300,000

Profit before interest and tax 300,000

Finance cost 50,000

Profit before tax 250,000

Income tax expense 100,000

Profit after tax 150,000

What is the return on capital employed (ROCE)?

A 7%

B 10%

C 40%

D 20% (2marks)

PRINCIPLES OF ACCOUNTING ASSIGNMENT 1 Thoriq Ahmed (DOB2) 6314

Page 6

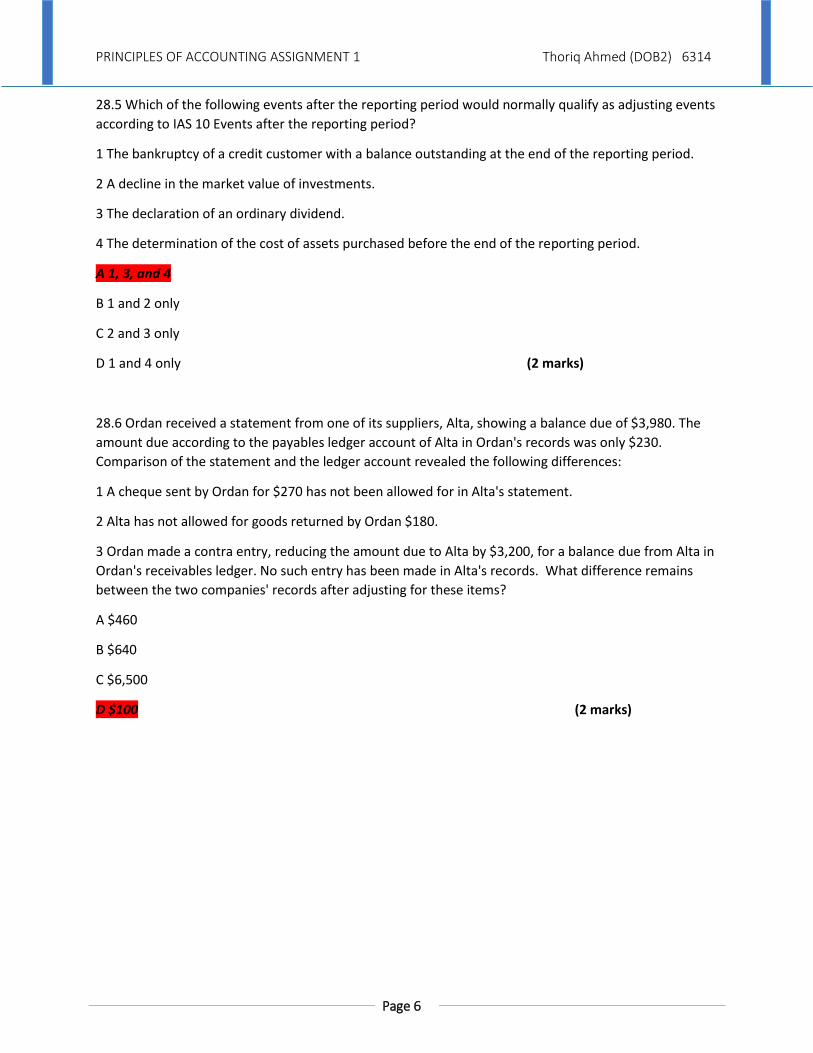

28.5 Which of the following events after the reporting period would normally qualify as adjusting events

according to IAS 10 Events after the reporting period?

1 The bankruptcy of a credit customer with a balance outstanding at the end of the reporting period.

2 A decline in the market value of investments.

3 The declaration of an ordinary dividend.

4 The determination of the cost of assets purchased before the end of the reporting period.

A 1, 3, and 4

B 1 and 2 only

C 2 and 3 only

D 1 and 4 only (2 marks)

28.6 Ordan received a statement from one of its suppliers, Alta, showing a balance due of $3,980. The

amount due according to the payables ledger account of Alta in Ordan's records was only $230.

Comparison of the statement and the ledger account revealed the following differences:

1 A cheque sent by Ordan for $270 has not been allowed for in Alta's statement.

2 Alta has not allowed for goods returned by Ordan $180.

3 Ordan made a contra entry, reducing the amount due to Alta by $3,200, for a balance due from Alta in

Ordan's receivables ledger. No such entry has been made in Alta's records. What difference remains

between the two companies' records after adjusting for these items?

A $460

B $640

C $6,500

D $100 (2 marks)

PRINCIPLES OF ACCOUNTING ASSIGNMENT 1 Thoriq Ahmed (DOB2) 6314

Page 7

28.7 A company's trial balance failed to agree, and a suspense account was opened for the difference.

Subsequent checking revealed that discounts allowed $13,000 had been credited to discounts received

account and an entry on the credit side of the cash book for the purchase of some machinery $18,000

had not been posted to the plant and machinery account.

Which two of the following journal entries would correct the errors?

Debit Credit

$ $

(1) Discounts allowed 13,000

Discounts received 13,000

(2) Discounts allowed 13,000

Discounts received 13,000

Suspense account 26,000

(3) Suspense account 26,000

Discounts allowed 13,000

Discounts received 13,000

(4) Plant and machinery 18,000

Suspense account 18,000

(5) Suspense account 18,000

Plant and machinery 18,000

A 1 and 4

B 2 and 5

C 2 and 4

D 3 and 5 (4 marks)

PRINCIPLES OF ACCOUNTING ASSIGNMENT 1 Thoriq Ahmed (DOB2) 6314

Page 8

28.8 At 1 January 20X5 a company had an allowance for receivables of $18,000 At 31 December 20X5

the company's trade receivables were $458,000.

It was decided:

(a) To write off debts totalling $28,000 as irrecoverable

(b) To adjust the allowance for receivables to the equivalent of 5% of the remaining receivables based

on past experience

What figure should appear in the company's statement of comprehensive income for the total of debts

written off as irrecoverable and the movement in the allowance for receivables for the year ended 31

December 20X5?

A $49,500

B $31,500

C $32,900

D $50,900 (2 marks)

PRINCIPLES OF ACCOUNTING ASSIGNMENT 1 Thoriq Ahmed (DOB2) 6314

Page 9

28.9The following payables ledger control account contains some errors. All goods are purchased on

credit.

PAYABLES LEDGER CONTROL ACCOUNT

$ $

Purchases 963,200 Opening balance 384,600

Discounts received 12,600 Purchases returns 17,400

Contras with amounts Cash paid to suppliers 988,400

receivable in receivables ledger 4,200

Closing balance 410,400

1,390,400 1,390,400

What should the closing balance be when the errors have been corrected?

A $325,200

B $350,400

C $358,800

D $376,800 (2 marks)

28.10 Which one of the following journal entries is required to record goods taken from inventory by the

owner of a business?

A Debit Drawings Credit Purchases

B Debit Sales Credit Drawings

C Debit Drawings Credit Inventory

D Debit Purchases Credit Drawings (2 marks)

PRINCIPLES OF ACCOUNTING ASSIGNMENT 1 Thoriq Ahmed (DOB2) 6314

Page 10

28.11 The following information is available about the transactions of Razil, a sole trader who does not

keep proper accounting records:

$

Opening inventory 77,000

Closing inventory 84,000

Purchases 763,000

Gross profit as a percentage of sales 30%

Based on this information, what is Razil's sales revenue for the year?

A $982,800

B $1,090,000

C $2,520,000

D $1,080,000 (2 marks)

28.16 Which of the following statements are correct?

1 All non-current assets must be depreciated.

2 If property accounted for in accordance with IAS 16 Property, plant and equipment is revalued, the

gain on revaluation is shown in the income statement.

3 If a tangible non-current asset is revalued, all tangible assets of the same class should be revalued.

4 In a company's published statement of financial position, tangible assets and intangible assets must be

shown separately.

A 1 and 2

B 2 and 3

C 3 and 4

D 1 and 4 (2 marks)

PRINCIPLES OF ACCOUNTING ASSIGNMENT 1 Thoriq Ahmed (DOB2) 6314

Page 11

28.12 The following bank reconciliation statement has been prepared by a trainee accountant at 31

December 20X5.

$

Balance per bank statement (overdrawn) 38,640

Add: lodgements not credited 19,270

57,910

Less: unpresentedcheques 14,260

Balance per cash book 43,650

What should the final cash book balance be when all the above items have been properly dealt with?

A $43,650 overdrawn

B $33,630 overdrawn

C $5,110 overdrawn

D $72,170 overdrawn (2 marks)

28.13 On 1 January 20X5 a company purchased some plant.

The invoice showed $

Cost of plant 48,000

Delivery to factory 400

One year warranty covering breakdown during 20X5 800

49,200

Modifications to the factory building costing $2,200 were necessary to enable the plant to be installed.

What amount should be capitalised for the plant in the company's records?

A $51,400

B $48,000

C $50,600

D $48,400 (2 marks)