Cryptography and Network Security Principles and Practice ...

Upload

khangminh22Category

view

0download

0

Board of StudiesThe Institute of Chartered Accountants of IndiaICAI Bhawan, A - 29, Sector - 62, Noida - 201 309 Phone : 0120 - 3045930E-mail : [email protected] : http://www.icai.org

ISBN 978-81-8441-871-2

October | 2020 | P2748 (Revised)

FOU

ND

ATION

COU

RSE - PRINCIPLES A

ND

PRACTICE OF ACCO

UN

TING

- MO

DU

LE -1

PAPER

1PAPER

1PAPER1

PAPER 1

BOARD OF STUDIES

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA (ICAI)

(SET UP BY AN ACT OF PARLIAMENT)

NEW DELHI

PRINCIPLESAND PRACTICEOF ACCOUNTING

MODULE - 1 OF 2

FOUNDATION COURSE

© The Institute of Chartered Accountants of India

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

This study material has been prepared by the faculty of the Board of Studies. The objective of the study material is to provide teaching material to the students to enable them to obtain knowledge in the subject. In case students need any clari�cations or have any suggestions to make for further improvement of the material contained herein, they may write to the Director of Studies.

All care has been taken to provide interpretations and discussions in a manner useful for the students. However, the study material has not been speci�cally discussed by the Council of the Institute or any of its Committees and the views expressed herein may not be taken to necessarily represent the views of the Council or any of its Committees.

Permission of the Institute is essential for reproduction of any portion of this material.

© THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA

All rights reserved. No part of this book may be reproduced, stored in a retrieval system, or transmitted, in any form, or by any means, electronic, mechanical, photocopying, recording, or otherwise, without prior permission, in writing, from the publisher.

Edition : July, 2017

First Revised : April, 2018

Reprint Edition : June, 2018

Updated Edition : February, 2019

Revised Edition : O ctober, 2020

Website : www.icai.org

E-mail : [email protected]

Department/ : Board of StudiesCommittee

ISBN No. : 978-81-8441-871-2

Price (All Modules) : ` 500/-

Published by : The Publication Department on behalf of The Institute of Chartered Accountants of India, ICAI Bhawan, Post Box No. 7100, Indraprastha Marg, New Delhi 110 002, India.

Printed by : Friends Digital Color Print Shop, Delhi November/2020/P2748 (Revised)

© The Institute of Chartered Accountants of India

BEFORE WE BEGIN …

SKILL REQUIREMENTS AT FOUNDATION LEVEL

The Board of Studies, ICAI has revised and updated the study material for Foundation (Entry Level Exam to the Chartered Accountancy Course). The contents have been designed and developed with an objective to synchronize the syllabus with the guidelines prescribed by IAESB (International Accounting Education Standards Board), IFAC (International Federation of Accountants), to instill and enhance the necessary pre-requisites for becoming a well-rounded, competent and globally competitive Accounting Professional.

The level of complexity of the study material is as per standards accorded by IAESB comprising an ideal mix of subjective and objective examination pattern to ensure discerning students get through and seek admission to the CA Course.

The paper of 'Principles and Practice of Accounting' at Foundation level concentrates on conceptual understanding of fundamentals of accounting. The objective of this paper is to develop an understanding of the basic concepts and principles of Accounting and apply the same in preparing �nancial statements of non-corporate entitie and simple problem solving.

This Study Material endeavouring towards accounting education, is committed to provide a framework for understanding accounting discipline and describing the fundamental accounting concepts and conventions of the basic accounting system. An attempt has been made to provide a solid foundation on which students can successfully build and enhance their studies.

KNOW YOUR SYLLABUS AND STUDY MATERIAL

The Study Material of Principles and Practice of Accounting has been designed having regard to the needs of home study and distance learning students. The Study Material has been divided into ten chapters, each addressing to a special aspect of accounting. Chapters 1 to 5 lay emphasis on bookkeeping aspect of accounting whereas chapter 7 deals with preparation of �nancial statements of sole proprietors. Chapter 6 covers accounting for special transactions like consignment, bills of exchange, sale of goods on approval basis, and average due date which are useful for di�erent business entities. Chapter 8 discusses accounting of partnership �rms and chapter 9 deals with �nancial statements of Not-for-pro�t organizations. Chapter 10 explains basic concepts of company accounts.

The study material has been bifurcated into two modules (Module I : Chapters 1 to 6 and Module II: Chapters 7 to 10) for easy handling and convenience of students. It is important to read the Study Material thoroughly and practice the questions for understanding the coverage of syllabus.

FRAMEWORK OF CHAPTERS – UNIFORM STRUCTURE COMPRISING OF SPECIFIC COMPONENTS

E�orts have been made to present each topic of the syllabus in a lucid manner. Care has been taken to present the chapters in a logical sequence to facilitate easy understanding by the

© The Institute of Chartered Accountants of India

students. Sincere e�orts have been undertaken to review and update the study material so that it re�ects the current position.

The content for each chapter/unit of the study Material has been structured in the following manner –

Components of each Chapter About the component

1 Learning Outcomes Learning outcomes which you need to demonstrate after learning each topic have been detailed in the �rst page of each chapter/unit. Demonstration of these learning outcomes would help you to achieve the desired level of technical competence.

2 Chapter/Unit Overview As the name suggests, the �ow chart/table/diagram given at the beginning of each chapter would give a broad outline of the contents covered in the chapter.

3 Content of each unit/ chapter The concepts and provisions of each topic is explained in student-friendly manner with the aid of Examples/ Illustrations/ Diagrams/Flow charts. These value additions would help you develop conceptual clarity and get a good grasp of the topic. Diagrams and Flow charts would help you understand the concept/application of topic in a better manner.

4 Illustrations involving conceptual understanding

Illustrations would help the students to understand the application of concepts. In e�ect, it would test understanding of concepts as well as ability to apply the concepts learnt in solving problems and addressing issues.

5 Summary A summary of the chapter is given at the end to help you revise what you have learnt. It would especially facilitate quick revision of the chapter the day before the examination.

6 Test Your Knowledge This section comprises of number of multiple choice questions, questions based on True and False statements, theoretical questions and practical questions which would help students to evaluate what they have understood after studying the chapter. The questions given in this section have also been supplemented with the answers to help the students in evaluating their solutions so that they can know where they have gone wrong.

We hope that these student-friendly features in the Study Material makes your learning process more enjoyable, enriches your knowledge and sharpens your application skills.

Happy Reading and Best Wishes!

© The Institute of Chartered Accountants of India

PAPER – 1 : PRINCIPLES AND PRACTICE OF ACCOUNTING

(One paper – Three hours – 100 Marks)

OBJECTIVE:

To develop an understanding of the basic concepts and principles of Accounting and apply the same in preparing �nancial statements and simple problem solving.

CONTENTS:

1. Theoretical Framework

(i) Meaning and Scope of accounting

(ii) Accounting Concepts, Principles and Conventions

(iii) Accounting terminology - Glossary

(iv) Capital and revenue expenditure, Capital and revenue receipts, Contingent assets and contingent liabilities

(v) Accounting Policies

(vi) Accounting as a Measurement Discipline – Valuation Principles, Accounting Estimates.

(vii) Accounting Standards – Concepts and Objectives.

(viii) Indian Accounting Standards – Concepts and Objectives.

2. Accounting Process

(i) Books of Accounts

(ii) Preparation of Trial Balance

(iii) Recti�cation of Errors.

3. Bank Reconciliation Statement

Introduction, reasons, preparation of bank reconciliation statement.

4. Inventories

Cost of inventory, Net realizable value, Basis and technique of inventory valuation and record keeping.

5. Concept and Accounting of Depreciation

Concepts, Methods of computation and accounting treatment of depreciation, Change in depreciation methods.

6. Accounting for Special Transactions

(i) Bills of exchange and promissory notes

Meaning of Bills of Exchange and Promissory Notes and their Accounting Treatment; Accommodation bills.

© The Institute of Chartered Accountants of India

(ii) Sale of goods on approval or return basis

Meaning of goods sent on approval or return basis and accounting treatment.

(iii) Consignments

Meaning and Features of consignment business, Di�erence between sale and consignment, Accounting treatments for consignment transactions and events in the books of consignor and consignee.

(iv) Average due Date

Meaning, Calculation of average due date in various situations.

(v) Account Current

Meaning of Account Current, Methods of preparing Account Current.

7. Final Accounts of Sole Proprietors

Elements of �nancial statements, Closing Adjustment Entries, Trading Account, Pro�t and Loss Account and Balance Sheet of Manufacturing and Non-manufacturing entities.

8. Partnership Accounts

(i) Final Accounts of Partnership Firms

(ii) Admission, Retirement and Death of a Partner including Treatment of Goodwill

(iii) Introduction to LLPs and Distinction of LLPs from Partnership.

9. Financial Statements of Not-for-Pro�t Organizations

Signi�cance of Receipt and Payment Account, Income and Expenditure Account and Balance Sheet, Di�erence between Pro�t and Loss Account and Income and Expenditure Account. Preparation of Receipt and Payment Account, Income and Expenditure Account and Balance Sheet.

10. Introduction to Company Accounts

(i) De�nition of shares and debentures

(ii) Issue of shares and debentures, forfeiture of shares, re-issue of forfeited shares

(iii) Statement of Pro�t and Loss and Balance Sheet as per Schedule III to the Companies Act, 2013.

© The Institute of Chartered Accountants of India

CONTENTS

MODULE 1 CHAPTER 1 : Theoretical FrameworkCHAPTER 2 : Accounting ProcessCHAPTER 3 : Bank Reconciliation Statement CHAPTER 4 : InventoriesCHAPTER 5 : Concept and Accounting of DepreciationCHAPTER 6 : Accounting for Special Transactions

MODULE 2CHAPTER 7 : Preparation of Final Accounts of Sole Proprietors CHAPTER 8 : Partnership AccountsCHAPTER 9 : Financial Statements of Not-For-Pro�t Organizations CHAPTER 10 : Company Accounts

© The Institute of Chartered Accountants of India

DETAILED CONTENTS : MODULE–1Pages

CHAPTER 1: THEORETICAL FRAMEWORK ...................................................................... 1.1–1.103

Unit 1: Meaning And Scope Of Accounting

Learning Outcomes ...................................................................................................................................................... 1.1

Unit overview.................................................................................................................................................................. 1.2

1.1 Introduction ................................................................................................................................................ 1.2

1.2 Meaning of Accounting ........................................................................................................................... 1.3

1.3 Evolution of Accounting as a Social Science ................................................................................... 1.6

1.4 Objectives of Accounting ....................................................................................................................... 1.7

1.5 Functions of Accounting ......................................................................................................................... 1.8

1.6 Book-Keeping ............................................................................................................................................. 1.8

1.7 Distinction Between Book-Keeping and Accounting ................................................................... 1.9

1.8 Sub-Fields of Accounting......................................................................................................................1.10

1.9 Users of Accounting Information .......................................................................................................1.10

1.10 Relationship of Accounting with other Disciplines .....................................................................1.11

1.11 Limitations of Accounting ....................................................................................................................1.14

1.12 Role of Accountant in the Society .....................................................................................................1.14

Summary ........................................................................................................................................................................1.18

Test Your Knowledge ..................................................................................................................................................1.19

Unit 2 : Accounting Concepts, Principles And Conventions

Learning Outcomes ....................................................................................................................................................1.22

Unit Overview ...............................................................................................................................................................1.23

2.1 Introduction ..............................................................................................................................................1.23

2.2 Accounting Concepts .............................................................................................................................1.24

2.3 Accounting Principles ............................................................................................................................1.24

2.4 Accounting Conventions ......................................................................................................................1.24

2.5 Concepts, Principles and Conventions - An Overview ...............................................................1.25

2.6 Fundamental Accounting Assumptions..........................................................................................1.35

2.7 Financial Statements ..............................................................................................................................1.35

Summary ........................................................................................................................................................................1.39

Test Your Knowledge ..................................................................................................................................................1.39

© The Institute of Chartered Accountants of India

Unit 3 : Accounting Terminology – Glossary

Learning Outcomes ...................................................................................................................................................1.43

Accounting Terminology - Glossary ..................................................................................................................... 1.43

Test Your Knowledge ................................................................................................................................................. 1.57

Unit 4 : Capital And Revenue Expenditures And Receipts

Learning Outcomes ...................................................................................................................................................1.58

Unit Overview ...............................................................................................................................................................1.58

4.1 Introduction ............................................................................................................................................. 1.58

4.2 Considerations in Determining Capital and Revenue Expenditures ................................... 1.59

4.3 Capital Expenditures and Revenue Expenditures....................................................................... 1.59

4.4 Capital Receipts and Revenue Receipts ......................................................................................... 1.61

Summary .......................................................................................................................................................................1.64

Test Your Knowledge .................................................................................................................................................1.64

Unit 5 : Contingent Assets And Contingent Liabilities

Learning Outcomes ...................................................................................................................................................1.66

Unit Overview ..............................................................................................................................................................1.66

5.1 Contingent Asset .................................................................................................................................... 1.66

5.2 Contingent Liabilities ............................................................................................................................ 1.67

5.3 Distinction Between Contingent Liabilities and Liabilities ..................................................... 1.67

5.4 Distinction Between Contingent Liabilities and Provisions .....................................................1.67

Test Your Knowledge ..................................................................................................................................................1.68

Unit 6 : Accounting Policies

Learning Outcomes ...................................................................................................................................................1.70

Unit Overview ...............................................................................................................................................................1.70

6.1 Meaning ..................................................................................................................................................... 1.70

6.2 Selection of Accounting Policies ....................................................................................................... 1.71

6.3 Change in Accounting Policies .......................................................................................................... 1.71

Summary .......................................................................................................................................................................1.72

Test Your Knowledge .................................................................................................................................................1.72

Unit 7 : Accounting As A Measurement Discipline – Valuation Principles, Accounting Estimates

Learning Outcomes ...................................................................................................................................................1.74

Unit Overview ..............................................................................................................................................................1.74

7.1 Meaning of Measurement ................................................................................................................... 1.75

© The Institute of Chartered Accountants of India

7.2 Objects or Events to be Measured ................................................................................................... 1.75

7.3 Standard or Scale of Measurement ...................................................................................................1.75

7.4 Dimension of Measurement Scale ................................................................................................... 1.76

7.5 Accounting as a Measurement Discipline ..................................................................................... 1.76

7.6 Valuation Principles ............................................................................................................................... 1.77

7.7 Measurement and Valuation .............................................................................................................. 1.80

7.8 Accounting Estimates ........................................................................................................................... 1.80

Summary ........................................................................................................................................................................1.81

Test Your Knowledge ..................................................................................................................................................1.81

Unit 8 : Accounting Standards

Learning Outcomes ....................................................................................................................................................1.84

Unit Overview ...............................................................................................................................................................1.84

8.1 Introduction of Accounting Standards ............................................................................................1.85

8.2 Objectives of Accounting Standards ................................................................................................1.85

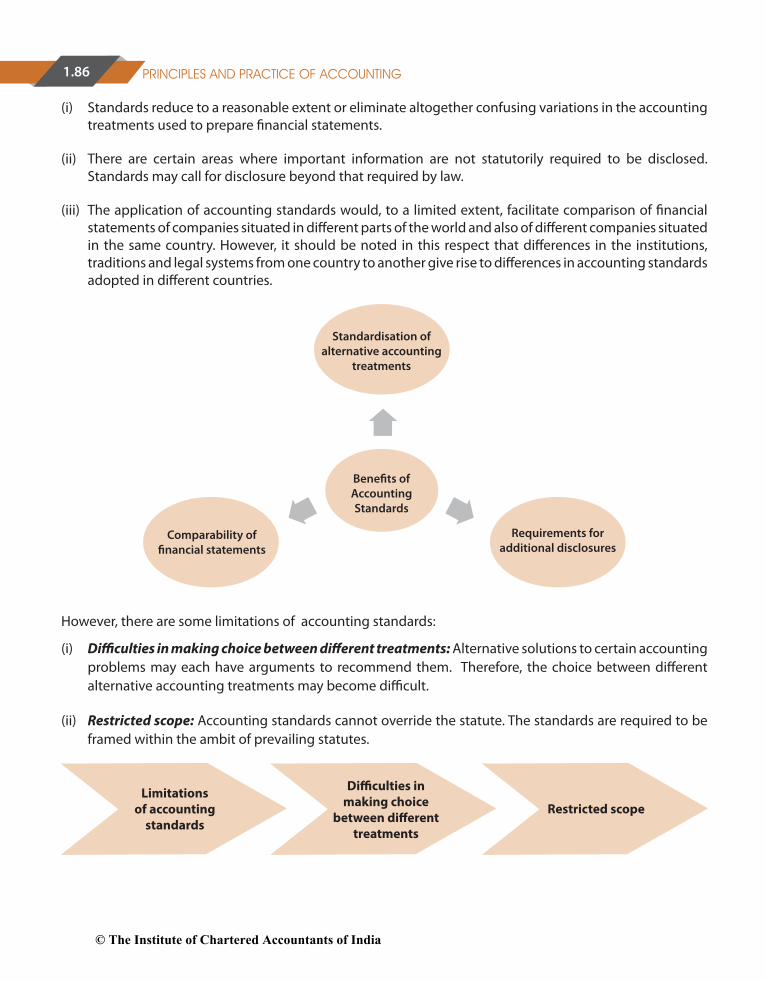

8.3 Bene�ts and Limitations of Accounting Standards .....................................................................1.85

8.4 Process of Formulation of Accounting Standards in India .......................................................1.87

8.5 List of Accounting Standards in India ..............................................................................................1.88

Test Your Knowledge ..................................................................................................................................................1.89

Unit 9 : Indian Accounting Standards

Learning Outcomes ....................................................................................................................................................1.91

Unit overview................................................................................................................................................................1.91

9.1 Need for Convergence towards Global Standards ......................................................................1.91

9.2 International Financial Reporting Standards as Global Standards ........................................1.92

9.3 Bene�ts of Convergence with IFRSS .................................................................................................1.93

9.4 Development in Indian Accounting Standards (Ind AS) ...........................................................1.93

9.5 List of IND AS .............................................................................................................................................1.94

Test Your Knowledge ..................................................................................................................................................1.95

True or False ..................................................................................................................................................................1.97

CHAPTER 2 : ACCOUNTING PROCESS ............................................................................. 2.1–2.121

Unit 1 : Basic Accounting Procedures - Journal Entries

Learning Outcomes ...................................................................................................................................................... 2.1

Unit overview.................................................................................................................................................................. 2.1

1.1 Double Entry System ................................................................................................................................ 2.2

© The Institute of Chartered Accountants of India

1.2 Advantages of Double Entry System .................................................................................................. 2.2

1.3 Account ......................................................................................................................................................... 2.2

1.4 Debit and Credit ......................................................................................................................................... 2.4

1.5 Transactions ................................................................................................................................................. 2.7

1.6 Accounting Equation Approach ........................................................................................................... 2.8

1.7 Traditional Approach..............................................................................................................................2.12

1.8 Modern Classi�cation of Accounts ....................................................................................................2.14

1.9 Journal .........................................................................................................................................................2.14

Summary ........................................................................................................................................................................2.24

Test Your Knowledge ..................................................................................................................................................2.24

Unit 2 : Ledgers

Learning Outcomes ....................................................................................................................................................2.32

Unit Overview ...............................................................................................................................................................2.32

2.1 Introduction ..............................................................................................................................................2.33

2.2 Specimen of Ledger Accounts ............................................................................................................2.33

2.3 Posting .........................................................................................................................................................2.33

2.4 Balancing an Account ............................................................................................................................2.33

Summary ........................................................................................................................................................................2.38

Test Your Knowledge ..................................................................................................................................................2.39

Unit 3 : Trial Balance

Learning Outcomes ...................................................................................................................................................2.43

Unit Overview ..............................................................................................................................................................2.43

3.1 Introduction ............................................................................................................................................. 2.43

3.2. Objectives of Preparing the Trial Balance ...................................................................................... 2.44

3.3 Limitations of Trial Balance ................................................................................................................. 2.45

3.4 Methods of Preparation of Trial Balance ........................................................................................ 2.45

3.5 Adjusted Trial Balance (Through Suspense Account) ................................................................ 2.49

3.6 Rules of Preparing the Trial Balance ................................................................................................. 2.49

Summary .......................................................................................................................................................................2.51

Test Your Knowledge ..................................................................................................................................................2.52

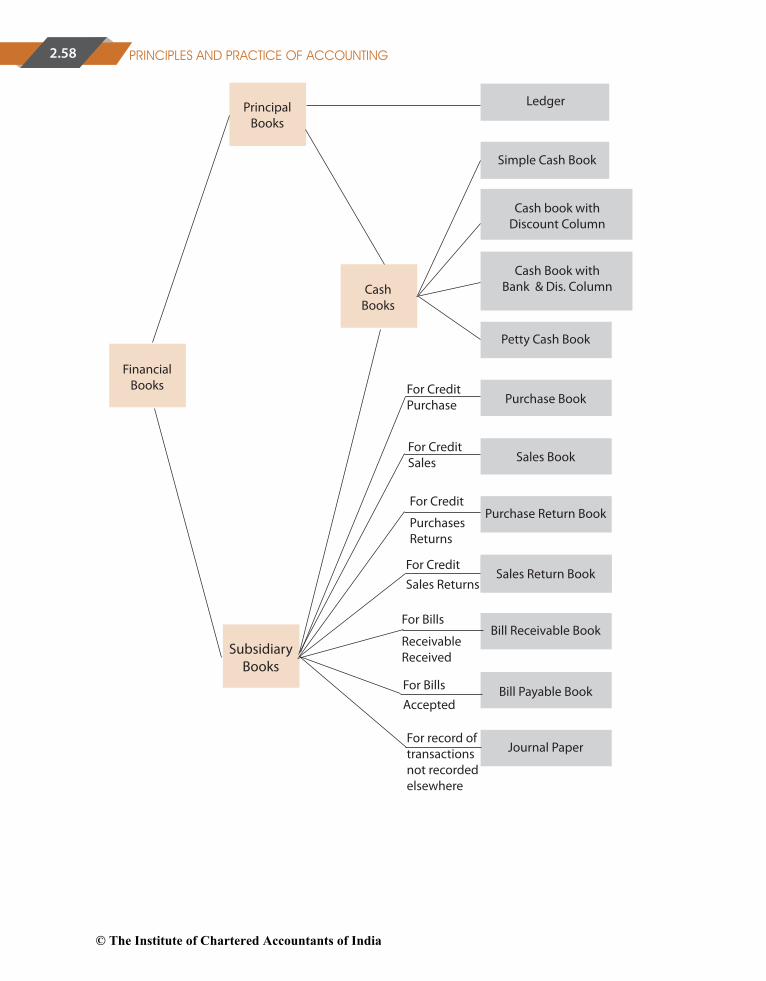

Unit 4 : Subsidiary Books

Learning Outcomes ...................................................................................................................................................2.56

Unit Overview ...............................................................................................................................................................2.56

© The Institute of Chartered Accountants of India

4.1 Introduction ............................................................................................................................................. 2.56

4.2 Distinction between Subsidiary Books and Principal books .................................................. 2.57

4.3 Purchases Book ....................................................................................................................................... 2.59

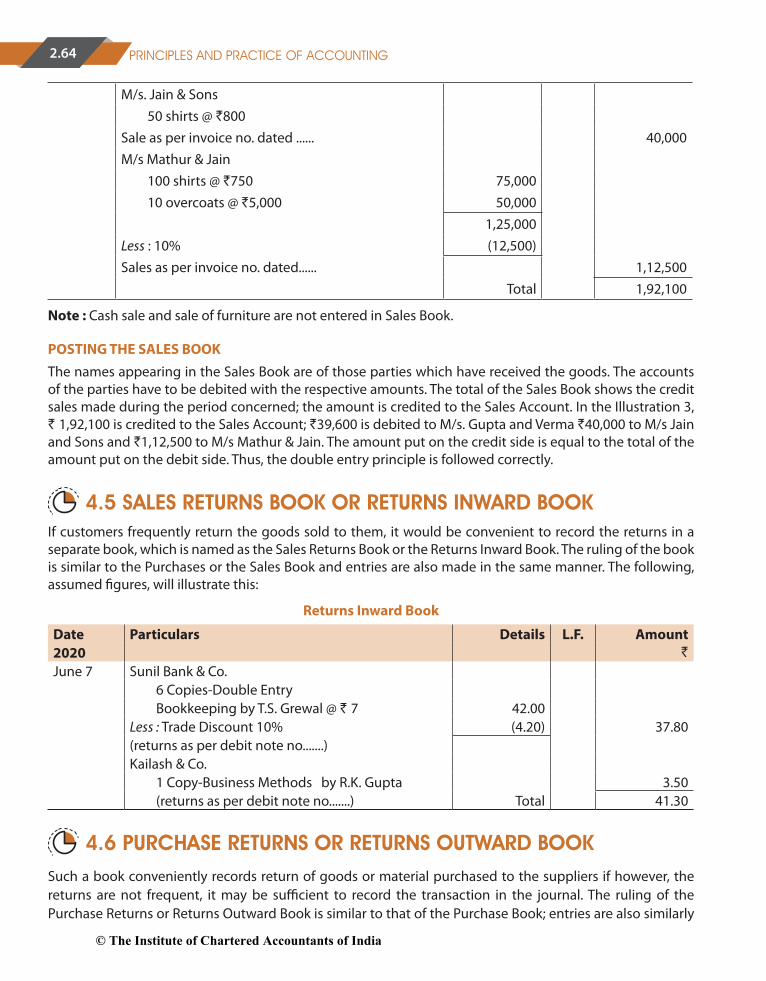

4.4 Sales Book ................................................................................................................................................. 2.64

4.5 Sales Returns Book or Returns Inward Book ................................................................................. 2.64

4.6 Purchase Returns or Returns Outward Book ................................................................................ 2.64

4.7 Importance of Journal .......................................................................................................................... 2.66

Summary .......................................................................................................................................................................2.68

Test Your Knowledge .................................................................................................................................................2.68

Unit 5 : Cash Book

Learning Outcomes ...................................................................................................................................................2.73

Unit Overview ...............................................................................................................................................................2.73

5.1 Cash Book - A Subsidiary Book and a Principal Book ................................................................ 2.74

5.2 Kinds of Cash Book ................................................................................................................................. 2.74

5.3 Posting the Cash Book Entries ........................................................................................................... 2.80

5.4 Petty Cash Book ...................................................................................................................................... 2.80

5.5 Entries for Sale Through Credit/Debit Cards ................................................................................. 2.83

Summary .......................................................................................................................................................................2.85

Test Your Knowledge .................................................................................................................................................2.86

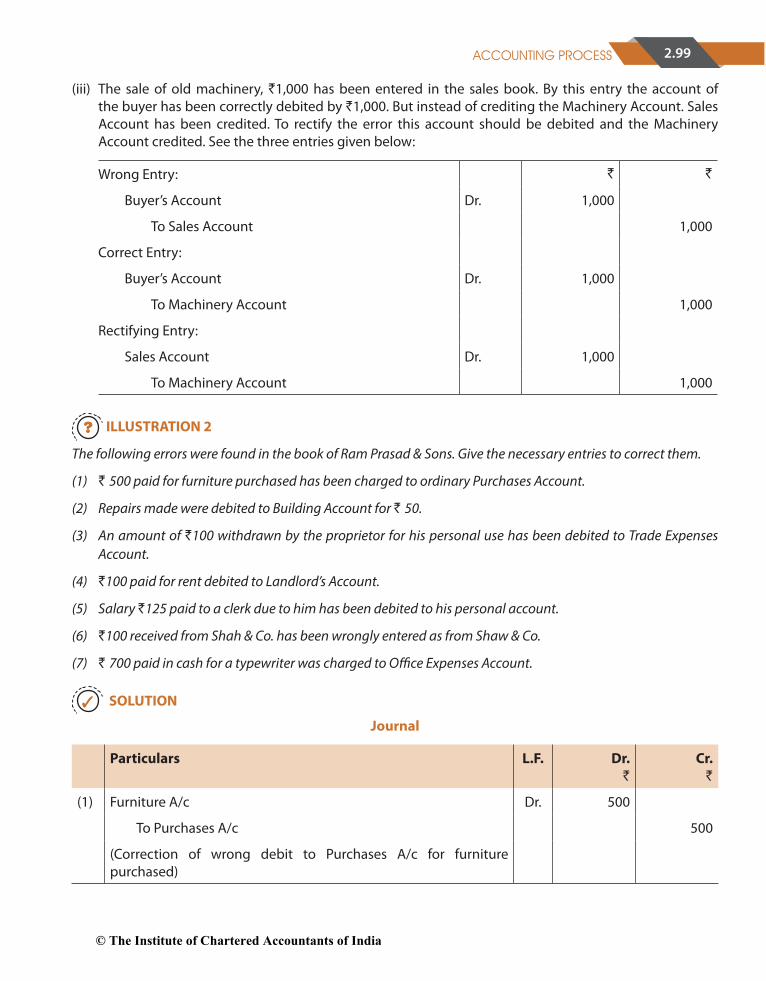

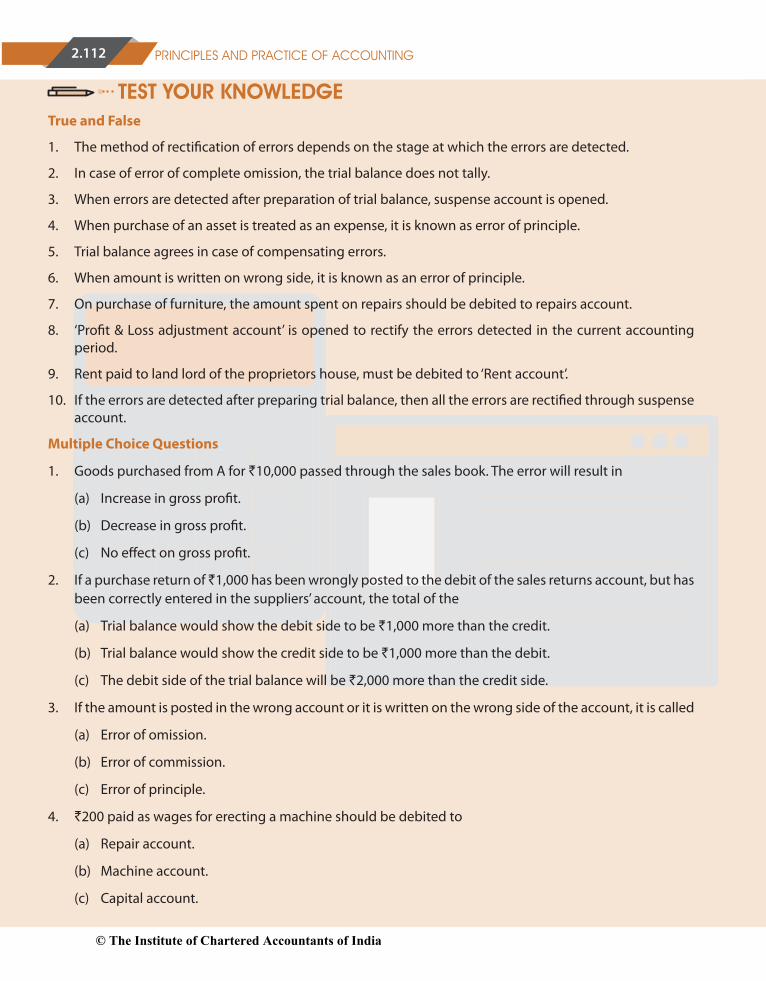

Unit 6: Recti�cation Of Errors

Learning Outcomes ...................................................................................................................................................2.90

Unit Overview ...............................................................................................................................................................2.90

6.1 Introduction ............................................................................................................................................. 2.90

6.2 Stages of Errors ........................................................................................................................................ 2.93

6.3 Types of Errors ......................................................................................................................................... 2.94

6.4 Steps to Locate Errors ........................................................................................................................... 2.95

6.5 Recti�cation of Errors ............................................................................................................................ 2.96

Summary .................................................................................................................................................................... 2.111

Test Your Knowledge .............................................................................................................................................. 2.112

CHAPTER 3: BANK RECONCILIATION STATEMENT ............................................................3.1–3.34

Learning Outcomes ..................................................................................................................................................... 3.1

Chapter Overview ......................................................................................................................................................... 3.1

1. Introduction ............................................................................................................................................... 3.2

© The Institute of Chartered Accountants of India

2. Bank Pass Book .......................................................................................................................................... 3.2

3. Bank Reconciliation Statement ........................................................................................................... 3.3

4. Importance of Bank Reconciliation Statement .............................................................................. 3.4

5. Procedure for Reconciling the Cash Book Balance with the Pass Book Balance.............. 3.12

6. Methods of Bank Reconciliation ....................................................................................................... 3.14

Summary .......................................................................................................................................................................3.26

Test Your Knowledge .................................................................................................................................................3.27

CHAPTER 4: INVENTORIES ..................................................................................................4.1–4.28

Learning Outcomes ..................................................................................................................................................... 4.1

Chapter Overview ......................................................................................................................................................... 4.1

1. Meaning ....................................................................................................................................................... 4.2

2. Inventory Valuation.................................................................................................................................. 4.3

3. Basis of Inventory Valuation ................................................................................................................. 4.4

4. Inventory Record Systems ..................................................................................................................... 4.5

5. Formulae/Methods to Determine Cost of Inventory .................................................................... 4.6

6. Inventories Taking .................................................................................................................................. 4.14

Summary .......................................................................................................................................................................4.19

Test Your Knowledge .................................................................................................................................................4.20

CHAPTER 5: CONCEPT AND ACCOUNTING OF DEPRECIATION .......................................5.1–5.30

Learning Outcomes ..................................................................................................................................................... 5.1

Chapter Overview ......................................................................................................................................................... 5.1

1. Introduction ............................................................................................................................................... 5.2

2. Factors in the Measurement of Depreciation ................................................................................. 5.4

3. Methods for Providing Depreciation ................................................................................................. 5.7

4. Pro�t or Loss on The Sale/Disposal of Property, Plant and Equipment ............................... 5.14

5. Change in the Method of Depreciation ..........................................................................................5.16

6. Revision of the Estimated Useful Life of Property, Plant and Equipment .......................... 5.18

7. Revaluation of Property, Plant and Equipment ........................................................................... 5.19

Summary .......................................................................................................................................................................5.20

Test Your Knowledge .................................................................................................................................................5.21

CHAPTER 6: ACCOUNTING FOR SPECIAL TRANSACTIONS ............................................ 6.1–6.122

© The Institute of Chartered Accountants of India

Unit 1: Bill Of Exchange And Promissory Notes

Learning Outcomes ...................................................................................................................................................... 6.1

Unit Overview ................................................................................................................................................................. 6.1

1.1 Bills of Exchange ........................................................................................................................................ 6.2

1.2 Promissory Notes ....................................................................................................................................... 6.3

1.3 Di�erences - Bill of Exchange and Promissory Note ..................................................................... 6.4

1.4 Record of Bills of Exchange and Promissory Notes ....................................................................... 6.5

1.5 Term of a Bill ................................................................................................................................................ 6.6

1.6 Expiry / Due Date of a Bill ....................................................................................................................... 6.6

1.7 Days of Grace .............................................................................................................................................. 6.6

1.8 Date of Maturity of Bill ............................................................................................................................. 6.6

1.9 Bill at Sight ................................................................................................................................................... 6.7

1.10 Bill after Date .............................................................................................................................................. 6.7

1.11 How to Calculate Due Date of a Bill .................................................................................................... 6.8

1.12 Noting Charges .......................................................................................................................................... 6.8

1.13 Renewal of Bill ............................................................................................................................................ 6.9

1.14 Retirement of Bills of Exchange & Rebate ......................................................................................... 6.9

1.15 Insolvency ..................................................................................................................................................6.15

1.16 Accommodation Bills .............................................................................................................................6.17

1.17 Bills of Collection .....................................................................................................................................6.23

1.18 Bills Receivable and Bills Payable Books ..........................................................................................6.24

Summary ........................................................................................................................................................................6.25

Test Your Knowledge ..................................................................................................................................................6.25

Unit 2 : Sale Of Goods On Approval Or Return Basis

Learning Outcomes ....................................................................................................................................................6.32

Unit Overview ...............................................................................................................................................................6.32

2.1 Introduction ..............................................................................................................................................6.32

2.2 Accounting Records................................................................................................................................6.33

Summary ........................................................................................................................................................................6.43

Test Your Knowledge ..................................................................................................................................................6.43

Unit 3 : Consignment

Learning Outcomes ...................................................................................................................................................6.49

Unit Overview ...............................................................................................................................................................6.49

3.1 Meaning of Consignment Account .................................................................................................. 6.50© The Institute of Chartered Accountants of India

3.2 Distinctions ................................................................................................................................................6.50

3.3 Accounting for Consignment Transactions and Events in the Books of the Consignor ................................................................................................................................................. 6.51

3.4 Valuation of Inventories ....................................................................................................................... 6.56

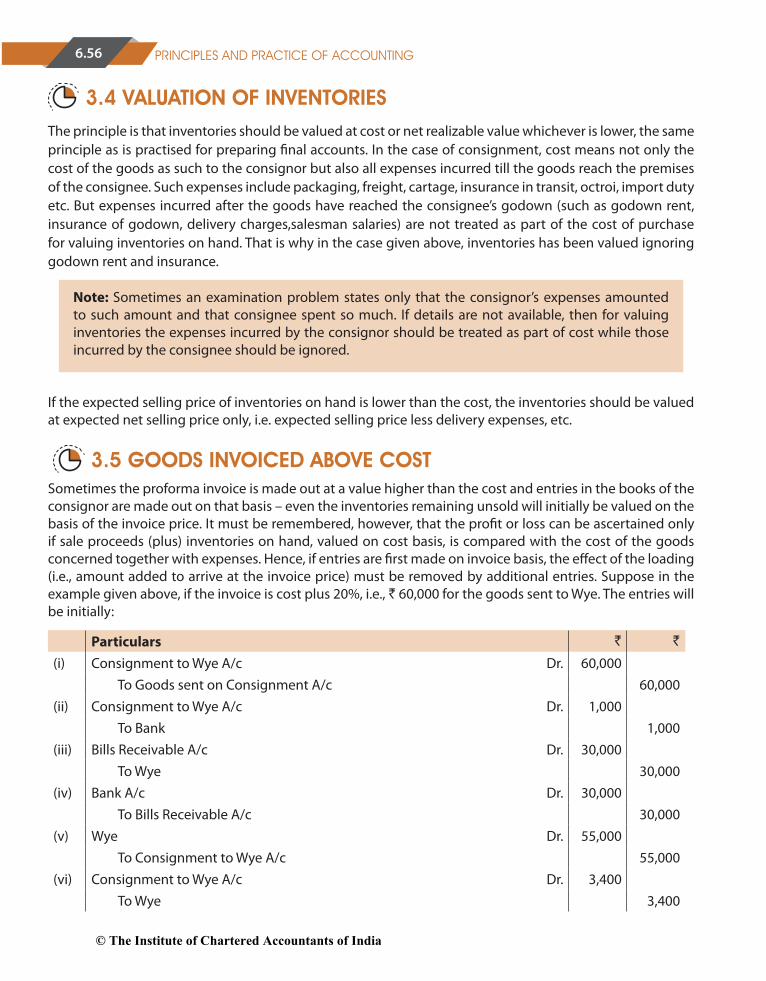

3.5 Goods Invoiced above Cost ................................................................................................................ 6.56

3.6 Normal Loss ...............................................................................................................................................6.59

3.7 Abnormal Loss ......................................................................................................................................... 6.59

3.8 Commission ...............................................................................................................................................6.60

3.9 Return of Goods from the Consignee ..............................................................................................6.61

3.10 Account Sales ........................................................................................................................................... 6.61

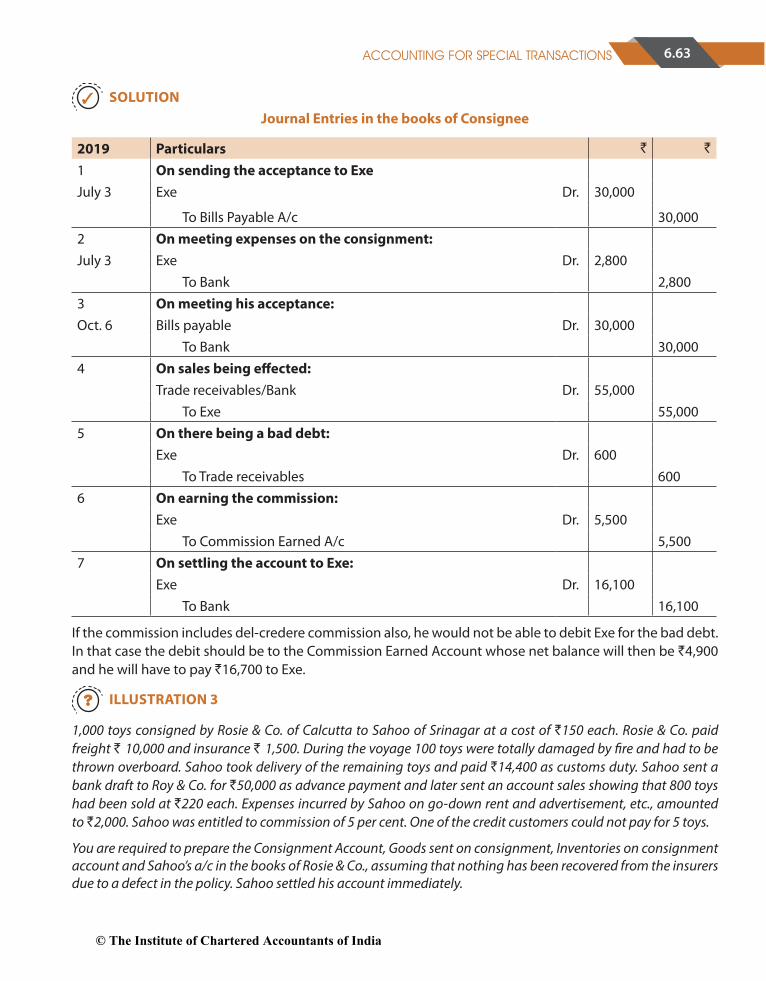

3.11 Accounting in the Books of the Consignee ....................................................................................6.62

3.12 Advance by the Consignee Vs Security against the Consignment ........................................6.67

Summary .......................................................................................................................................................................6.73

Test Your Knowledge ................................................................................................................................................. 6.74

Unit 4 : Average Due Date

Learning Outcomes ...................................................................................................................................................6.84

Unit Overview ...............................................................................................................................................................6.84

4.1 Introduction ............................................................................................................................................. 6.85

4.2 Concept of due date (Date of Maturity) ......................................................................................... 6.86

4.3 Types of Problems .................................................................................................................................. 6.88

Summary .................................................................................................................................................................... 6.102

Test Your Knowledge .............................................................................................................................................. 6.102

Unit 5 : Account Current

Learning Outcomes ................................................................................................................................................ 6.107

Unit Overview ........................................................................................................................................................... 6.107

5.1 Introduction .......................................................................................................................................... 6.107

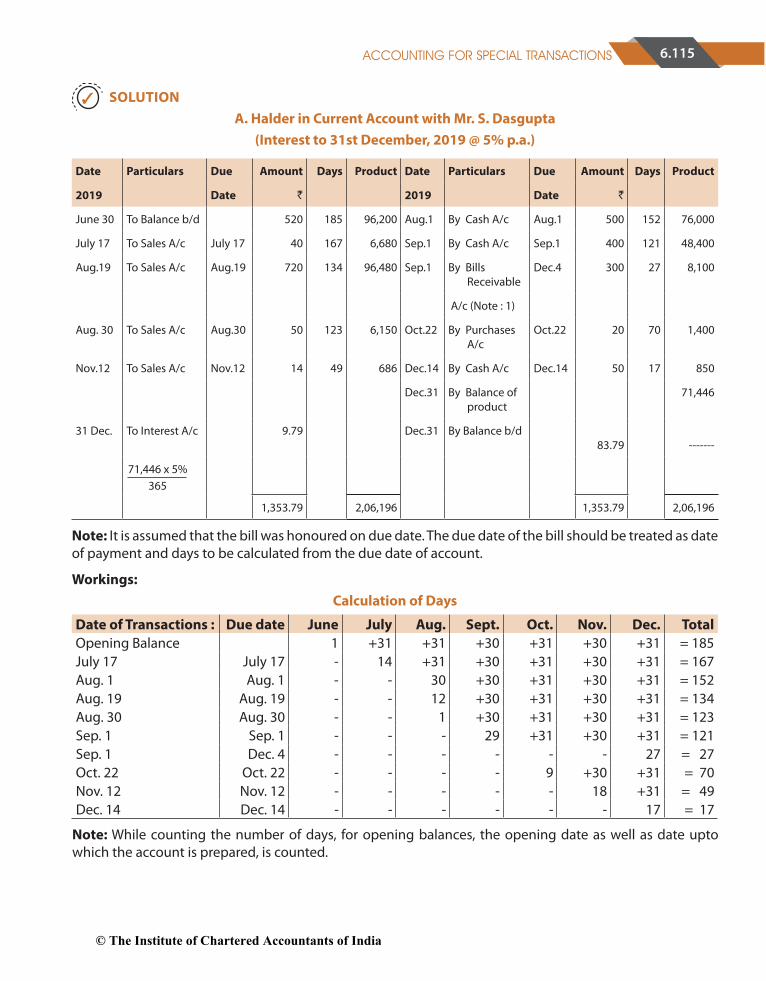

5.2 Preparation of Account Current ..................................................................................................... 6.108

Summary ..................................................................................................................................................................... 6.119

Test Your Knowledge ............................................................................................................................................... 6.119

© The Institute of Chartered Accountants of India

After studying this unit, you will be able to:

w Understand the meaning and signi�cance of accounting.

w Understand the meaning of book-keeping and the distinction of accounting with book-keeping.

w Appreciate the evolutionary process of accounting as a social science.

w Explain sub-�elds of accounting.

w Identify the various user groups for whom accounting information is to be generated.

w Understand the relationship of accounting with Economics, Statistics, Mathematics, Law and

Management.

w Explain the limitations of accounting.

w Appreciate the enlarged boundary of accounting profession and the areas where in a chartered

accountant plays an important role of rendering useful services to the society.

THEORETICAL FRAMEWORK

UNIT 1: MEANING AND SCOPE OF ACCOUNTING

LEARNING OUTCOMES

1CHAPTER

© The Institute of Chartered Accountants of India

© The Institute of Chartered Accountants of India

1.2 PRINCIPLES AND PRACTICE OF ACCOUNTING

1.1 INTRODUCTION Every individual performs some kind of economic activity. A salaried person gets salary and spends to buy provisions and clothing, for children’s education, construction of house, etc. A sports club formed by a group of individuals, a business run by an individual or a group of individuals, a local authority like Calcutta Municipal Corporation, Delhi Development Authority, Governments, either Central or State, all are carrying some kind of economic activities. Not necessarily all the economic activities are run for any individual bene�t; such economic activities may create social bene�t i.e. bene�t for the public, at large. Anyway such economic activities are performed through ‘transactions and events’. Transaction is used to mean ‘a business, performance of an act, an agreement’ while event is used to mean ‘a happening, as a consequence of transaction(s), a result.’

An individual invests `2,00,000 for running a stationery business. On 1st January, he purchases goods for ` 1,15,000 and sells for ` 1,47,000 during the month of January. He pays shop rent for the month ` 5,000 and �nds that still he has goods worth ` 15,000 in hand. The individual performs an economic activity. He carries on a few transactions and encounters with some events. Is it not logical that he will want to know the result of his activity?

UNIT OVERVIEW

Procedure of Accounting

Using the �nancial Information

Generating Financial Information

Recording

Input

Posting to ledger

Preparation of trial

balance

Preparation of �nal

accounts

Internal users• Board of Directors• Partners• Managers• Officers

External users• Investors• Lenders• Suppliers• Govt. agencies• Customers

Communicating Information to

users

Economic events and

transactions measured

in �nancial terms

Accounting Cycle Output

Identi�cation of transaction

Classifying Summarising Analyzing Interpreting Communicating

Recording of transactions in the books

of original entry

© The Institute of Chartered Accountants of India

© The Institute of Chartered Accountants of India

1.3THEORETICAL FRAMEWORK

We see that the individual, who runs the stationery business, earns a surplus of ` 42,000.

`

Goods sold 1,47,000Goods in hand 15,000

1,62,000Less : Goods purchased 1,15,000

Shop rent paid 5,000 (1,20,000)Surplus 42,000

Earning of ` 42,000 surplus is an event; also having the inventories in hand is another event, while purchase and sale of goods, investment of money and payment of rent are transactions.

Similarly, a municipal corporation got government grant ̀ 500 lakhs for adult education; it spent ̀ 250 lakhs for purchasing literacy kits, paid ` 200 lakhs to the tutors and is left with a balance of ` 50 lakhs. These are also transactions and events.

Similarly, the Central Government raised money through taxes, paid salaries to the employees, and spent on various developmental activities. Whenever receipts of the Government are more than expenses it has surplus, but if expenses are more than receipts it runs in de�cit. Here raising money through various sources can be termed as transaction and surplus or de�cit at the end of the accounting year can be termed as an event.

So, everybody wants to keep records of all transactions and events and to have adequate information about the economic activity as an aid to decision-making. Accounting discipline has been developed to serve this purpose as it deals with the measurement of economic activities involving in�ow and out�ow of economic resources, which helps to develop useful information for decision-making process.

Accounting has universal application for recording transactions and events and presenting suitable information to aid decision-making regarding any type of economic activity ranging from a family function to functions of the national government. But hereinafter we shall concentrate only on business activities and their accounting because the objective of this study material is to provide a basic understanding on accounting for business activities. Nevertheless, it will give adequate knowledge to think coherently of accounting as a �eld of study for universal application.

The growth of accounting discipline is closely associated with the development of the business world. Thus, to understand accounting as a �eld of study for universal application, it is best identi�ed with recording of business transactions and communication of �nancial information about business enterprise to facilitate decision-making. The aim of accounting is to meet the information needs of the rational and sound decision-makers, and thus, called the language of business.

1.2 MEANING OF ACCOUNTINGThe Committee on Terminology set up by the American Institute of Certi�ed Public Accountants formulated the following de�nition of accounting in 1961:

“Accounting is the art of recording, classifying, and summarising in a signi�cant manner and in terms of money, transactions and events which are, in part at least, of a �nancial character, and interpreting the result thereof.”

© The Institute of Chartered Accountants of India

© The Institute of Chartered Accountants of India

1.4 PRINCIPLES AND PRACTICE OF ACCOUNTING

As per this de�nition, accounting is simply an art of record keeping. The process of accounting starts by �rst identifying the events and transactions which are of �nancial character and then be recorded in the books of account. This recording is done in Journal or subsidiary books, also known as primary books. Every good record keeping system includes suitable classi�cation of transactions and events as well as their summarisation for ready reference. After the transactions and events are recorded, they are transferred to secondary books i.e. Ledger. In ledger, transactions and events are classi�ed in terms of income, expense, assets and liabilities according to their characteristics and summarised in pro�t and loss account and balance sheet. Essentially the transactions and events are to be measured in terms of money. Measurement in terms of money means measuring at the ruling currency of a country, for example, rupee in India, dollar in U.S.A. and like. The transactions and events must have at least in part, �nancial characteristics. The inauguration of a new branch of a bank is an event without having �nancial character, while the business disposed of by the branch is an event having �nancial character. Accounting also interprets the recorded, classi�ed and summarised transactions and events.

However, the above-mentioned de�nition does not re�ect the present day accounting function. The dimension of accounting is much broader than that described in the above de�nition. According to the above de�nition, accounting ends with interpretation of the results of the �nancial transactions and events but in the modern world with the diversi�cation of management and ownership, globalisation of business and society gaining more interest in the functioning of the enterprises, the importance of communicating the accounting results has increased and therefore, this requirement of communicating and motivating informed judgement has also become the part of accounting as de�ned in the widely accepted de�nition of accounting, given by the American Accounting Association in 1966 which treated accounting as:

“The process of identifying, measuring and communicating economic information to permit informed judgments and decisions by the users of accounts.”

In 1970, the Accounting Principles Board (APB) of American Institute of Certi�ed Public Accountants (AICPA) enumerated the functions of accounting as follows:

“The function of accounting is to provide quantitative information, primarily of �nancial nature, about economic entities, that is needed to be useful in making economic decisions.”

Thus, accounting may be de�ned as the process of recording, classifying, summarising, analysing and interpreting the �nancial transactions and communicating the results thereof to the persons interested in such information.

1.2.1 Procedural aspects of Accounting

On the basis of the above de�nitions, procedure of accounting can be basically divided into two parts:

(i) Generating �nancial information and

(ii) Using the �nancial information.

Generating Financial Information

1. Recording – This is the basic function of accounting. All business transactions of a �nancial character, as evidenced by some documents such as sales bill, pass book, salary slip etc. are recorded in the books of account. Recording is done in a book called “Journal.” This book may further be divided into several subsidiary books according to the nature and size of the business. Students will learn how to prepare journal and various subsidiary books in chapter 2.

2. Classifying – Classi�cation is concerned with the systematic analysis of the recorded data, with a view to group transactions or entries of one nature at one place so as to put information in compact

© The Institute of Chartered Accountants of India

© The Institute of Chartered Accountants of India

1.5THEORETICAL FRAMEWORK

and usable form. The book containing classi�ed information is called “Ledger”. This book contains on di�erent pages, individual account heads under which, all �nancial transactions of similar nature are collected. For example, there may be separate account heads for Salaries, Rent, Printing and Stationeries, Advertisement etc. All expenses under these heads, after being recorded in the Journal, will be classi�ed under separate heads in the Ledger. This will help in �nding out the total expenditure incurred under each of the above heads. Students will learn how to prepare ledger books in chapter 2.

3. Summarising – It is concerned with the preparation and presentation of the classi�ed data in a manner useful to the internal as well as the external users of �nancial statements. This process leads to the preparation of the �nancial statements.

4. Analysing – The term ‘Analysis’ means methodical classi�cation of the data given in the �nancial statements. The �gures given in the �nancial statements will not help anyone unless they are in a simpli�ed form. For example, all items relating to �xed assets are put at one place while all items relating to current assets are put at another place. It is concerned with the establishment of relationship between the items of the Pro�t and Loss Account and Balance Sheet i.e. it provides the basis for interpretation. Students will learn this aspect of �nancial statements in the later stages of the Chartered Accountancy Course.

5. Interpreting – This is the �nal function of accounting. It is concerned with explaining the meaning and signi�cance of the relationship as established by the analysis of accounting data. The recorded �nancial data is analysed and interpreted in a manner that will enable the end-users to make a meaningful judgement about the �nancial condition and pro�tability of the business operations. The �nancial statement should explain not only what had happened but also why it happened and what is likely to happen under speci�ed conditions.

6. Communicating – It is concerned with the transmission of summarised, analysed and interpreted information to the end-users to enable them to make rational decisions. This is done through preparation and distribution of accounting reports, which include besides the usual pro�t and loss account and the balance sheet, additional information in the form of accounting ratios, graphs, diagrams, fund �ow statements etc. Students will learn this aspect of �nancial statements in the later stages of the Chartered Accountancy Course.

The �rst two procedural stages of the process of generating �nancial information along with the preparation of trial balance are covered under book-keeping while the preparation of �nancial statements and its analysis, interpretation and also its communication to the various users are considered as accounting stages. Students will learn the term book-keeping and its distinction with accounting, in the coming topics of this unit.

Using the Financial Information

There are certain users of accounts. Earlier it was viewed that accounting is meant for the proprietor or owner of the business, but changing social relationships diluted the earlier thinking. It is now believed that besides the owner or the management of the business enterprise, users of accounts include the investors, employees, lenders, suppliers, customers, government and other agencies and the public at large. Accounting provides the art of presenting information systematically to the users of accounts. Accounting data is more useful if it stresses economic substance rather than technical form. Information is useless and meaningless unless it is relevant and material to a user’s decision. The information should also be free of any biases. The users should understand not only the �nancial results depicted by the accounting �gures, but also should be able to assess its reliability and compare it with information about alternative opportunities and the past experience. The owners or the management of the enterprise, commonly known as internal

© The Institute of Chartered Accountants of India

© The Institute of Chartered Accountants of India

1.6 PRINCIPLES AND PRACTICE OF ACCOUNTING

users, use the accounting information in an analytical manner to take the valuable decisions for the business. So the information served to them is presented in a manner di�erent to the information presented to the external users. Even the small details which can a�ect the internal working of the business are given in the management report while �nancial statements presented to the external users contains key information regarding assets, liabilities and capital which are summarised in a logical manner that helps them in their respective decision-making.

1.3 EVOLUTION OF ACCOUNTING AS A SOCIAL SCIENCEIn its oldest form, accounting aided the stewards to discharge their stewardship function. The wealthy men employed stewards to manage their property; the stewards in turn rendered an account periodically of their stewardship. This ‘Stewardship Accounting’ was the root of �nancial accounting system. The presently followed system of double-entry book-keeping has been developed only in the 15th Century. However, historians found records of debit and credit dating back to the 12th Century. Although double-entry system was followed, ‘stewardship accounting’ served the purpose of businessmen and wealthy persons at that time. In most of the countries, stewardship accounting was prevalent till the emergence of large-scale enterprises in the form of public limited companies.

In the second phase, the idea of �nancial accounting emerged with the concept of joint stock company and divorce of ownership from the management. To safeguard the interest of the shareholders and investors, disclosure of �nancial statements (mainly, pro�t and loss account and balance sheet) and other accounting information was moulded by law. Financial statements give periodic performance report by way of pro�t and loss account and �nancial position at the end of the period by way of Balance Sheet. It got the legal status due to changing relationships between the owners, economic entity and the managers. With the democratisation of society, the relationships between the enterprise on the one hand, the investors, employees, managers and governments on the other, have also undergone a sea-change. Also the prospective investors and other business contact groups want to know a lot about the business before entering into transactions. Thus, �nancial accounting emerged as an information system to identify, measure and communicate useful information for informed judgements and decisions by a broad group of users. In the third phase, accounting information was generated to aid management decision- making in particular. It contributed a lot to improve the quality of management decisions. This new dimension of accounting is called Management Accounting and it is the development of 20th Century only. It is pervasive enough to cover all spheres of management decisions.

Lastly, Social Responsibility Accounting is in the formative process, which aims at accounting for the social cost incurred by business as well as the social bene�t, created by it. It emerges from the growing social awareness about the undesirable by-products of economic activities. While earning pro�t, an enterprise incurs numerous social costs like pollution, using the resources of society like materials, land, labour etc. To compensate for this social cost, in today’s world, an enterprise is expected to generate some social bene�ts also like employment opportunities, recreation activities, more choice to customers at reasonable price, better quality products etc. Therefore it is demanded that the accounting system should produce a report measuring the social cost incurred and social bene�ts generated.

Social Science study man as a member of society; they concern about social processes and the results and consequences of social relationships. The usefulness of accounting to society as a whole is the fundamental criterion to treat it as a social science. Although individuals may bene�t from the availability of accounting information, the accounting system generates information for social good. It serves social purposes, it contributes for social progress; also it is being adapted to keep pace with social progress. So, accounting is treated as a social science.

© The Institute of Chartered Accountants of India

© The Institute of Chartered Accountants of India

1.7THEORETICAL FRAMEWORK

1.4 OBJECTIVES OF ACCOUNTINGThe objectives of accounting can be given as follows:

1. Systematic recording of transactions – Basic objective of accounting is to systematically record the �nancial aspects of business transactions i.e. book-keeping. These recorded transactions are later on classi�ed and summarized logically for the preparation of �nancial statements and for their analysis and interpretation.

2. Ascertainment of results of above recorded transactions – Accountant prepares pro�t and loss account to know the results of business operations for a particular period of time. If revenue exceed expenses then it is said that business is running pro�tably but if expenses exceed revenue then it can be said that business is running under loss. The pro�t and loss account helps the management and di�erent stakeholders in taking rational decisions. For example, if business is not proved to be remunerative or pro�table, the cause of such a state of a�air can be investigated by the management for taking remedial steps.

3. Ascertainment of the financial position of the business – Businessman is not only interested in knowing the results of the business in terms of pro�ts or loss for a particular period but is also anxious to know that what he owes (liability) to the outsiders and what he owns (assets) on a certain date. To know this, accountant prepares a �nancial position statement popularly known as Balance Sheet. The balance sheet is a statement of assets and liabilities of the business at a particular point of time and helps in ascertaining the �nancial health of the business.

4. Providing information to the users for rational decision-making – Accounting as a ‘language of business’ communicates the �nancial results of an enterprise to various stakeholders by means of �nancial statements. Accounting aims to meet the information needs of the decision-makers and helps them in rational decision-making.

5. To know the solvency position – By preparing the balance sheet, management not only reveals what is owned and owed by the enterprise, but also it gives the information regarding concern’s ability to meet its liabilities in the short run (liquidity position) and also in the long-run (solvency position) as and when they fall due.

An overview of objectives of accounting is depicted in the chart given below:

Systematic Recording of Transactions

Book-keeping: Journal, Leader and

Trial Balance

Ascertainment of Results

Manufacturing, Trading, Pro�t and

Loss Account

Ascertainment of Financial Position

Balance Sheet

Communicating Information to various Users

Financial Reports

Objectives of Accounting

© The Institute of Chartered Accountants of India

© The Institute of Chartered Accountants of India

1.8 PRINCIPLES AND PRACTICE OF ACCOUNTING

1.5 FUNCTIONS OF ACCOUNTINGThe main functions of accounting are as follows:(a) Measurement: Accounting measures past performance of the business entity and depicts its current

�nancial position.(b) Forecasting: Accounting helps in forecasting future performance and �nancial position of the

enterprise using past data and analysing trends.(c) Decision-making: Accounting provides relevant information to the users of accounts to aid rational

decision-making.(d) Comparison & Evaluation: Accounting assesses performance achieved in relation to targets and

discloses information regarding accounting policies and contingent liabilities which play an important role in predicting, comparing and evaluating the �nancial results.

(e) Control: Accounting also identi�es weaknesses of the operational system and provides feedbacks regarding e�ectiveness of measures adopted to check such weaknesses.

(f) Government Regulation and Taxation: Accounting provides necessary information to the government to exercise control on the entity as well as in collection of tax revenues.

1.6 BOOK-KEEPINGBook-keeping is an activity concerned with the recording of �nancial data relating to business operations in a signi�cant and orderly manner. It covers procedural aspects of accounting work and embraces record keeping function. Obviously, book-keeping procedures are governed by the end product, the �nancial statements. The term ‘�nancial statements’ means Pro�t and Loss Account, Balance Sheet and cash flowstatements including Schedules and Notes forming part of Accounts.

Book-keeping also requires suitable classi�cation of transactions and events. This is also determined with reference to the requirement of �nancial statements. A book-keeper may be responsible for keeping all the records of a business or only of a minor segment, such as position of the customers’ accounts in a departmental store. Accounting is based on a careful and e�cient book-keeping system.

The essential idea behind maintaining book-keeping records is to show correct position regarding each head of income and expenditure. A business may purchase goods on credit as well as in cash. When the goods are bought on credit, a record must be kept of the person to whom money is owed. The proprietor of the business may like to know, from time to time, what amount is due on credit purchase and to whom. If proper record is not maintained, it is not possible to get details of the transactions in regard to the incomes and expenses. At the end of the accounting period, the proprietor wants to know how much pro�t has been earned or loss has been incurred during the course of the period. For this lot of information is needed which can be gathered from a proper record of the transactions. Therefore, in book-keeping, the proper maintenance of books of account is indispensable for any business.

At this level, the major concern of the curriculum is with book-keeping and preparation of �nancial statements. It seems important to mention at this point that book-keeping and preparation of �nancial statements have legal implications also. Maintenance of books of accounts and the preparation of �nancial statements of a company are guided by the Companies Act, banks and insurance companies by special Acts governing these institutions and so on. However, for sole-proprietorship and partnership business, there is no speci�c legislation regarding maintenance of books of accounts and preparation of �nancial statements.

© The Institute of Chartered Accountants of India

© The Institute of Chartered Accountants of India

1.9THEORETICAL FRAMEWORK

1.6.1 Objectives of Book-keeping

1. Complete Recording of Transactions – It is concerned with complete and permanent record of all transactions in a systematic and logical manner to show its �nancial e�ect on the business.

2. Ascertainment of Financial Effect on the Business – It is concerned with the combined e�ect of all the transactions made during the accounting period upon the �nancial position of the business as a whole.

1.7 DISTINCTION BETWEEN BOOK-KEEPING AND ACCOUNTINGSome people mistake book-keeping and accounting to be synonymous terms, but in fact they are di�erent from each other. Accounting is a broad subject. It calls for a greater understanding of records obtained from book-keeping and an ability to analyse and interpret the information provided by book-keeping records. Book-keeping is the recording phase while accounting is concerned with the summarising phase of an accounting system. Book-keeping provides necessary data for accounting and accounting starts where book-keeping ends.

S. No. Book-keeping Accounting

1. It is a process concerned with recording of transactions.

It is a process concerned with summarising of the recorded transactions.

2. It constitutes as a base for accounting. It is considered as a language of the business.

3. Financial statements do not form part of this process.

Financial statements are prepared in this process on the basis of book-keeping records.

4. Managerial decisions cannot be taken with the help of these records.

Management takes decisions on the basis of these records.

5. There is no sub-�eld of book-keeping. It has several sub-�elds like �nancial accounting, management accounting etc.

6. Financial position of the business cannot be ascertained through book-keeping records.

Financial position of the business is ascertained on the basis of the accounting reports.

Relationship of Accounting and Book-keeping can be depicted in the following chart as

Accountancy

Accounting

Book Keeping

© The Institute of Chartered Accountants of India

© The Institute of Chartered Accountants of India

1.10 PRINCIPLES AND PRACTICE OF ACCOUNTING

1.8 SUB-FIELDS OF ACCOUNTINGThe various sub-�elds of accounting are: