Fundamental Accounting Principles Canadian Vol 2 Canadian ...

Upload

khangminh22Category

view

1download

0

1

Test Series: October, 2020

MOCK TEST PAPER

FOUNDATION COURSE

PAPER – 1: PRINCIPLES AND PRACTICE OF ACCOUNTING

ANSWERS

1. (a) 1 False- When shares are forfeited, the share capital account is debited with called up capital

of shares forfeited and the share forfeiture account is credited with amount received on shares

forfeited.

2. True - Discount at the time of retirement of a bill is a gain for the drawee and loss for the drawer.

3 False- Receipts and payments account is a classified summary of cash receipts and payments over a certain period together with cash and bank balances at the beginning and close of the period.

4 False- The right hand side of the equation includes cash twice- once as a part of current assets and another separately. The basic accounting equation is

Equity + Long Term Liabilities = Fixed Assets + Current Assets - Current Liabilities

5 False - According to Partnership Act, in the absence of any agreement to the contrary profits and losses are to be shared equally among partners.

6. False- Accrual concept implies accounting on ‘due’ or ‘accrual’ basis. Accrual basis of

accounting involves recognition of revenues and costs as and when they accrue irrespective

of actual receipts or payments.

(b) Journal Entries in the books of Symphony Bros.

Particulars Dr. Cr.

Amount (`) Amount (`)

(i) Salaries A/c 7,500

To Purchase A/c 7,500

(Being entry made for stock taken by employees)

(ii) Advertisement Expenses A/c 2,000

To Purchases A/c 2,000

(Being distribution of goods by the way of free samples)

(iii) Drawings A/c 1,400

To Petty Cash A/c 1,400

(Being the income tax of proprietor paid out of business money)

(iv) Purchase A/c 1,800

To Cash A/c 1,750

To Discount Received A/c 50

(Being the goods purchased from Naveen for ` 2,000 @ 10% trade discount and cash discount of ` 50)

© The Institute of Chartered Accountants of India

2

(c) Limitations which must be kept in mind while evaluating the Financial Statements are as follows:

• The factors which may be relevant in assessing the worth of the enterprise don’t find place in

the accounts as they cannot be measured in terms of money.

• Balance Sheet shows the position of the business on the day of its preparation and not on the

future date while the users of the accounts are interested in knowing the position of the

business in the near future and also in long run and not for the past date.

• Accounting ignores changes in some money factors like inflation etc.

• There are occasions when accounting principles conflict with each other.

• Certain accounting estimates depend on the sheer personal judgement of the accountant.

• Different accounting policies for the treatment of same item adds to the probability of

manipulations.

2. (a) Statement of Valuation of Stock on 30 th June, 2020

`

Value of stock as on 14th June, 2020 96,00,000

Add: Unsold stock out of the goods sent on consignment 4,80,000

Purchases during the period from 14th June, 2020 to 30th June, 2020

4,80,000

Goods in transit on 30th June, 2020 3,20,000

Cost of goods sent on approval basis (80% of ` 3,20,000) 2,56,000 15,36,000

1,11,36,000

Less: Cost of sales during the period from 14th June, 2020 to 30th June, 2020

Sales (` 27,20,000-` 3,20,000) 24,00,000

Less: Gross profit 1,92,000

22,08,000

Value of stock as on 30th June, 2020 89,28,000

Working Notes:

1. Calculation of normal sales: ` `

Actual sales 27,20,000

Less: Abnormal sales 2,40,000

Return of goods sent on approval 3,20,000 5,60,000

21,60,000

2. Calculation of gross profit:

Gross profit or normal sales

20/100 x ` 21,60,000

4,32,000

Less: Loss on sale of particular (abnormal) goods

(4,80,000 less 2,40,000)

2,40,000

Gross profit 1,92,000

© The Institute of Chartered Accountants of India

3

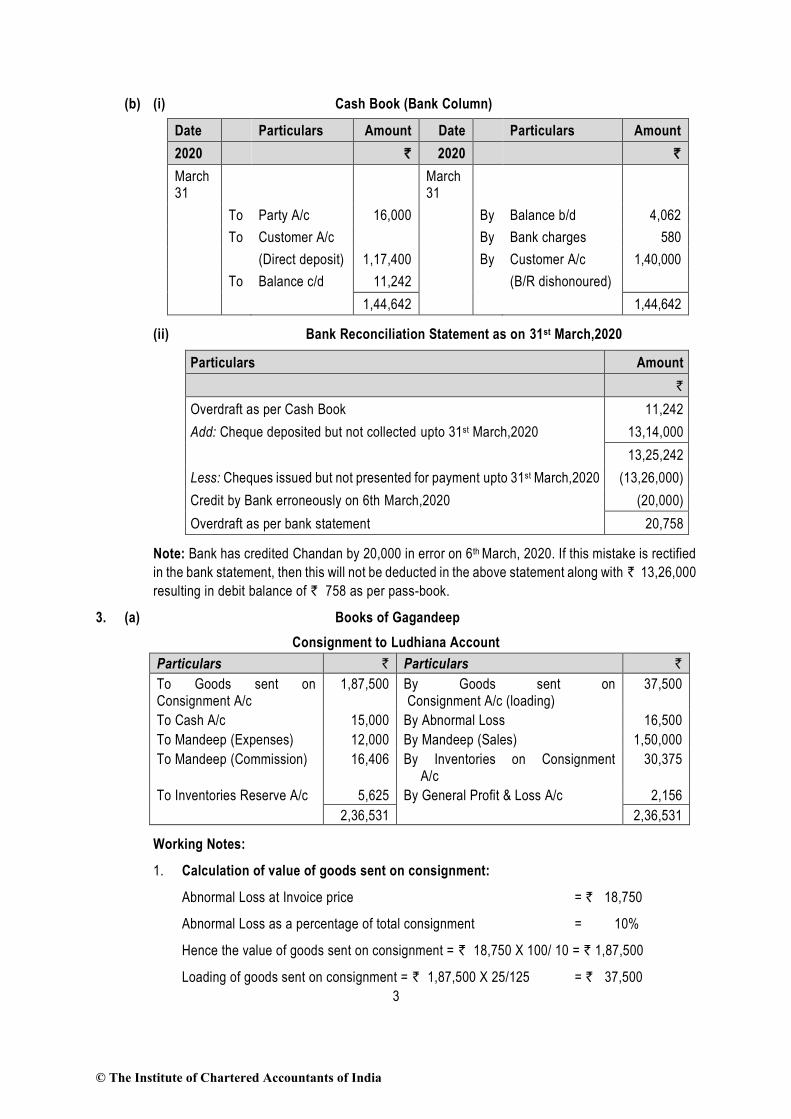

(b) (i) Cash Book (Bank Column)

Date Particulars Amount Date Particulars Amount

2020 ` 2020 `

March 31

March 31

To Party A/c 16,000 By Balance b/d 4,062

To Customer A/c By Bank charges 580

(Direct deposit) 1,17,400 By Customer A/c 1,40,000

To Balance c/d 11,242 (B/R dishonoured)

1,44,642 1,44,642

(ii) Bank Reconciliation Statement as on 31st March,2020

Particulars Amount

`

Overdraft as per Cash Book 11,242

Add: Cheque deposited but not collected upto 31st March,2020 13,14,000

13,25,242

Less: Cheques issued but not presented for payment upto 31st March,2020 (13,26,000)

Credit by Bank erroneously on 6th March,2020 (20,000)

Overdraft as per bank statement 20,758

Note: Bank has credited Chandan by 20,000 in error on 6th March, 2020. If this mistake is rectified

in the bank statement, then this will not be deducted in the above statement along with ` 13,26,000

resulting in debit balance of ` 758 as per pass-book.

3. (a) Books of Gagandeep

Consignment to Ludhiana Account

Particulars ` Particulars `

To Goods sent on Consignment A/c

1,87,500 By Goods sent on Consignment A/c (loading)

37,500

To Cash A/c 15,000 By Abnormal Loss 16,500

To Mandeep (Expenses) 12,000 By Mandeep (Sales) 1,50,000

To Mandeep (Commission) 16,406 By Inventories on Consignment A/c

30,375

To Inventories Reserve A/c 5,625 By General Profit & Loss A/c 2,156

2,36,531 2,36,531

Working Notes:

1. Calculation of value of goods sent on consignment:

Abnormal Loss at Invoice price = ` 18,750

Abnormal Loss as a percentage of total consignment = 10%

Hence the value of goods sent on consignment = ` 18,750 X 100/ 10 = ` 1,87,500

Loading of goods sent on consignment = ` 1,87,500 X 25/125 = ` 37,500

© The Institute of Chartered Accountants of India

4

2. Calculation of abnormal loss (10%):

Abnormal Loss at Invoice price = ` 18,750.

Abnormal Loss at cost = ` 18,750 X 100/125 = ` 15,000

Add: Proportionate expenses of Gagandeep (10 % of ` 15,000) = ` 1,500

` 16,500

3. Calculation of closing Inventories (15%):

Gagandeep’s Basic Invoice price of consignment= ` 1,87,500

Gagandeep’s expenses on consignment = ` 15,000

` 2,02,500

Value of closing Inventories = 15% of ` 2,02,500 = ` 30,375

Loading in closing Inventories = ` 37,500 x 15/100 = ` 5,625

Where ` 28,125 (15% of ` 1,87,500) is the basic invoice price of the goods sent on

consignment remaining unsold.

4. Calculation of commission:

Invoice price of the goods sold = 75% of ` 1,87,500 = ` 1,40,625

Excess of selling price over invoice price = ` 9,375 ( ` 1,50,000 - ` 1,40,625)

Total commission = 10% of ` 1,40,625 + 25% of ` 9,375

= ` 14,062.5 + ` 2,343.75

= ` 16,406

(b) In the books of Varun

Ankur in Account Current with Varun

(Interest to 31st March, 2020 @ 10% p.a)

Date Particulars Amount Days Product Date Particulars Amount Days Product

2020 ` ` 2020 ` `

Jan.1 To Balance b/d

2,500 90 2,25,000 Jan.24 By Promissor Varun Note (due date 27th April)

2,500 (27) (67500)

Jan. 11 To Sales 3,000 79 2,37,000 Feb. 1 By Purchases 5,000 58 2,90,000

Feb. 4 To Sales 4,100 55 2,25,500 Feb. 7 By Sales Return 500 52 26,000

Mar. 18 To Sales 4,600 13 59,800 Mar. 1 By Purchases 2,800 30 84,000

Mar. 31 To Interest 110 Mar. 23 By Purchases 2,000 8 16,000

Mar. 31 By Balance of Products 3,98,800

Mar. 31 By Bank 1,510

14,310 7,47,300 14,310 7,47,300

Working Note:

Calculation of interest: 𝟑,𝟗𝟖,𝟖𝟎𝟎

𝟑𝟔𝟓×

𝟏𝟎

𝟏𝟎𝟎= ` 110 (approx.)

© The Institute of Chartered Accountants of India

5

4. (a) Subscription for the year ended 31.3.2020

`

Subscription received during the year 11,25,000

Less: Subscription receivable on 1.4.2019 33,750

Less: Subscription received in advance on 31.3.2020 15,750 (49,500)

10,75,500

Add: Subscription receivable on 31.3.2020 49,500

Add: Subscription received in advance on 1.4.2019 27,000 76,500

Amount of Subscription appearing in Income & Expenditure Account 11,52,000

Sports material consumed during the year end 31.3.2020

`

Payment for Sports material 6,75000

Less: Amounts due for sports material on 1.4.2019 (2,02,500)

4,72,500

Add: Amounts due for sports material on 31.3.2020 2,92,500

Purchase of sports material 7,65,000

Sports material consumed:

Stock of sports material on 1.4.2019 2,25,000

Add: Purchase of sports material during the year 7,65,000

9,90,000

Less: Stock of sports material on 31.3.2020 (3,37,500)

Amount of Sports Material appearing in Income & Expenditure Account 6,52,500

(b) (i) Revaluation Account

` `

To Furniture 1,740 By Building 6,400

To Stock 2,140 By Sundry creditors 2,800

To Provision of doubtful debts (` 3,500 – ` 400)

3,100

By Investment 900

To Outstanding wages 3,120 ____

10,100 10,100

(ii) Partners' Capital Accounts

P Q R P Q R

` ` ` ` ` `

To Balance c/d

142,000 108,000 50,000 By Balance b/d 88,000 72,000 –

By Cash A/c – – 50,000

____

___

____

By Goodwill A/c

(Working Note)

54,000

36,000

142,000 108,000 50,000 142,000 108,000 50,000

© The Institute of Chartered Accountants of India

6

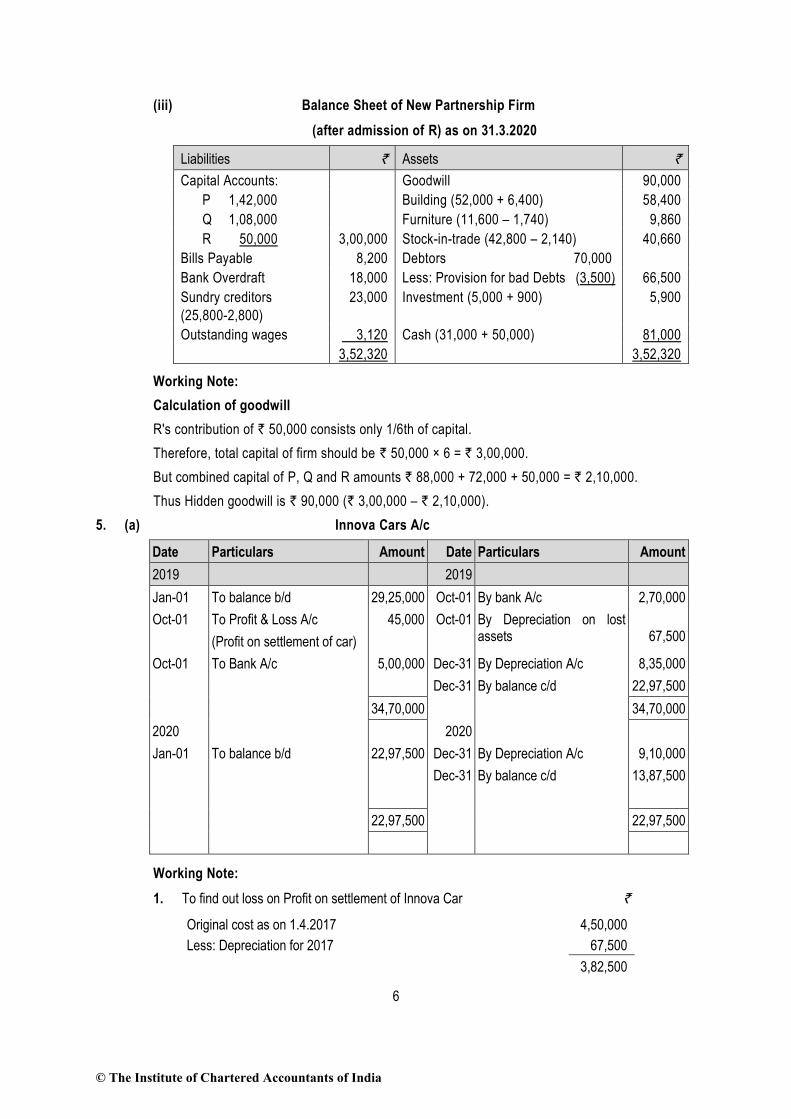

(iii) Balance Sheet of New Partnership Firm

(after admission of R) as on 31.3.2020

Liabilities ` Assets `

Capital Accounts: Goodwill 90,000

P 1,42,000 Building (52,000 + 6,400) 58,400

Q 1,08,000 Furniture (11,600 – 1,740) 9,860

R 50,000 3,00,000 Stock-in-trade (42,800 – 2,140) 40,660

Bills Payable 8,200 Debtors 70,000

Bank Overdraft 18,000 Less: Provision for bad Debts (3,500) 66,500

Sundry creditors

(25,800-2,800)

23,000 Investment (5,000 + 900) 5,900

Outstanding wages 3,120 Cash (31,000 + 50,000) 81,000

3,52,320 3,52,320

Working Note:

Calculation of goodwill

R's contribution of ` 50,000 consists only 1/6th of capital.

Therefore, total capital of firm should be ` 50,000 × 6 = ` 3,00,000.

But combined capital of P, Q and R amounts ` 88,000 + 72,000 + 50,000 = ` 2,10,000.

Thus Hidden goodwill is ` 90,000 (` 3,00,000 – ` 2,10,000).

5. (a) Innova Cars A/c

Date Particulars Amount Date Particulars Amount

2019 2019

Jan-01 To balance b/d 29,25,000 Oct-01 By bank A/c 2,70,000

Oct-01 To Profit & Loss A/c 45,000 Oct-01 By Depreciation on lost assets

67,500 (Profit on settlement of car)

Oct-01 To Bank A/c 5,00,000 Dec-31 By Depreciation A/c 8,35,000

Dec-31 By balance c/d 22,97,500

34,70,000 34,70,000

2020

2020

Jan-01 To balance b/d 22,97,500 Dec-31 By Depreciation A/c 9,10,000

Dec-31 By balance c/d 13,87,500

22,97,500 22,97,500

Working Note:

1. To find out loss on Profit on settlement of Innova Car `

Original cost as on 1.4.2017 4,50,000

Less: Depreciation for 2017 67,500

3,82,500

© The Institute of Chartered Accountants of India

7

Less: Depreciation for 2018 90,000

2,92,500

Less: Depreciation for 2019 (9 months) 67,500

2,25,000

Less: Amount received from Insurance company 2,70,000

45,000

(b) Trading and Profit and Loss Account of Mr. Sanjeev

for the year ended 31st March, 2020

.Dr. Cr.

Amount Amount

` ` ` `

To Opening stock 64,500 By Sales 4,27,150

To Purchases 3,062,00 Less: Sales return

5,150 4,22,000

Less: Purchases return 3,450 3,02,750 By Closing stock

To

To

To

Carriage inward

Wages

Gross profit c/d

2,250

23,430

2,79,070

80

100

80

100 ,0001,60 ̀ 2,50,000

6,72,000 6,72,000

To Salaries 45,100 By Gross profit b/d 2,79,070

To Rent 8,600 By Bad debts recovered

900

To Advertisement expenses 8,350

To Printing and stationery 2,500

To Bad debts 2,200

To Carriage outward 2,700

To Provision for doubtful debts

5% of ` 2,40,000 12,000

Less: Existing provision 6,400 5,600

To Provision for discount on debtors

2.5% of ` 2,28,000 5,700

Less: Existing provision 2,750 2,950

To Depreciation:

Plant and machinery 6,000

Furniture and fittings 2,050 8,050

To Office expenses 20,320

To Interest on loan 6,000

To Net profit

(Transferred to capital account)

1,67,600

_______

2,79,970 2,79,970

© The Institute of Chartered Accountants of India

8

Balance Sheet of Mr. Sanjeev as on 31st March, 2020

Amount Amount

Liabilities ` ` Assets ` `

Capital account 1,30,000 Plant and machinery 40,000

Add: Net profit 1,67,600 Less: Depreciation 6,000 34,000

2,97,600 Furniture and fittings 20,500

Less: Drawings 23,000 2,74,600 Less: Depreciation 2,050 18,450

Bank overdraft 1,60,000 Closing stock 2,50,000

Sundry creditors 95,000 Sundry debtors 2,40,000

Payable salaries 4,900 Less: Provision for doubtful debts 12,000

Provision for bad debts 5,700 2,22,300

Prepaid rent 600

Cash in hand 2,900

_______ Cash at bank 6,250

5,34,500 5,34,500

Working Note:

Rectification Entries

Particulars Dr. Cr.

Amount Amount

` `

(i) Returns inward account Dr. 5,150

Sales account Dr. 3,450

To Purchases account 5,150

To Returns outward account 3,450

(Being sales return and purchases return wrongly included in purchases and sales respectively, now rectified)

(ii) Drawings account Dr. 7,000

To Purchases account 7,000

(Being goods withdrawn for own consumption included in purchases, now rectified)

(iii) Plant and machinery account Dr. 900

To Wages account 900

(Being wages paid for installation of plant and machinery wrongly debited to wages, now rectified)

(iv) Advertisement expenses account Dr. 1,650

To Purchases account 1,650

(Being free samples distributed for publicity out of purchases, now rectified)

© The Institute of Chartered Accountants of India

9

6. (a)

Bank A/c Dr. 25,000

To Equity Share Application A/c 25,000

(Money received on application for 1,000 shares @ ` 25 per share)

Equity Share Application A/c Dr. 25,000

To Equity Share Capital A/c 25,000

(Transfer of application money on 1,000 shares to share capital)

Equity Share Allotment A/c Dr. 30,000

To Equity Share Capital A/c 30,000

(Amount due on the allotment of 1,000 shares @ ` 30 per share)

Bank A/c Dr. 30,000

To Equity Share Allotment A/c 30,000

(Allotment money received)

Equity Share First Call A/c Dr. 20,000

To Equity Share Capital A/c 20,000

(First call money due on 1,000 shares @ ` 20 per share)

Bank A/c Dr. 18,500

Calls-in-Arrears A/c Dr. 4,000

To Equity Share First Call A/c 20,000

To Calls-in-Advance A/c 2,500

(First call money received on 800 shares and calls-in-advance on 100 shares @ ` 25 per share)

(b) In the books of Aditya Company Ltd.

Journal Entries

Date Particulars Dr. Cr.

` `

(a) Bank A/c Dr. 45,00,000

To Debentures Application A/c 45,00,000

(Being the application money received on 10,000

debentures @ ` 450 each)

Debentures Application A/c Dr. 45,00,000

Discount on issue of Debentures A/c Dr. 5,00,000

To 9% Debentures A/c 50,00,000

(Being the issue of 10,000 9% Debentures @ 90% as per Board’s Resolution No….dated….)

(b) Fixed Assets A/c Dr. 20,00,000

To Vendor A/c 20,00,000

(Being the purchase of fixed assets from vendor)

Vendor A/c Dr. 20,00,000

Discount on Issue of Debentures A/c Dr. 5,00,000

To 9% Debentures A/c 25,00,000

© The Institute of Chartered Accountants of India

10

(Being the issue of debentures of ` 25,00,000 to vendor to satisfy his claim)

(c) Bank A/c Dr. 20,00,000

To Bank Loan A/c (See Note) 20,00,000

(Being a loan of ` 20,00,000 taken from bank by

issuing debentures of `25,00,000 as collateral security)

Note: No entry is made in the books of account of the company at the time of making issue of such

debentures. In the “Notes to Accounts” of Balance Sheet, the fact that the debentures being issued

as collateral security and outstanding are shown by a note under the liability secured.

(c) Distinction between Money Measurement concept and Matching concept

As per Money Measurement concept, only those transactions, which can be measured in terms

of money are recorded. Since money is the medium of exchange and the standard of economic

value, this concept requires that those transactions alone that are capable of being measured in

terms of money should be recorded in the books of accounts. Transactions and events that cannot

be expressed in terms of money are not recorded in the business books.

In Matching concept, all expenses matched with the revenue of that period should only be taken

into consideration. In the financial statements of the organization if any revenue is recognized then

expenses related to earn that revenue should also be recognized.

© The Institute of Chartered Accountants of India

Copyright © 2022 FDOKUMEN