Finance answer sheet Chapter 1 Financial and managerial accounting principles

30

Ch1 SE1 to SE4 CHAPTER 1—Solutions USES OF ACCOUNTING INFORMATION AND THE FINANCIAL STATEMENTS Chapter 1, SE 1. 1. g 6. i 2. f 7. d 3. b 8. a 4. c 9. j 5. e 10. h Chapter 1, SE 2. 1. b 4. b 2. c 5. a 3. a Chapter 1, SE 3. 1. a 4. c 2. c 5. a 3. b 6. c Chapter 1, SE 4. 1. Assets = $120,000 2. Stockholders' Equity = $ 72,000 3. Liabilities = $100,000

Transcript of Finance answer sheet Chapter 1 Financial and managerial accounting principles

Ch1 SE1 to SE4

CHAPTER 1—Solutions USES OF ACCOUNTING INFORMATION AND THE FINANCIAL STATEMENTS Chapter 1, SE 1. 1. g 6. i2. f 7. d3. b 8. a4. c 9. j5. e 10. h Chapter 1, SE 2.

1. b 4. b2. c 5. a3. a

Chapter 1, SE 3.

1. a 4. c2. c 5. a3. b 6. c Chapter 1, SE 4. 1. Assets = $120,000 2. Stockholders' Equity = $ 72,000 3. Liabilities = $100,000

Ch1 SE5 to SE 7

Chapter 1, SE 5.

1. Assets = Liabilitie+ Stockholders' Equity $240,000 = $90,000 + Stockholders' Equity $240,000 – $90,000 = $150,000

tockholders' Equity = $150,000 2. Assets = 0.2 Assets + $40,000

Assets – 0.2Assets = $40,000 0.8Assets = $40,000

Assets = $40,000 ¸ 0.8 Assets = $50,000

Liabilities = $50,000 x 0.2 = $10,000

Chapter 1, SE 6.

1. Beginning: $ 45,000 = Liabilities + $25,000 Liabilities = ### $ 45,000 = ### + $25,000

Change: + 30,000 ### $75,000 = ### + Stockholders' Equit

End:tockholders' Equity = ###2. Beginning: Assets = ### + $96,000

Assets = $146,000 $146,000 = ### + $96,000

Change: + 40,000 ### $186,000 = ### + Stockholders' Equit

End:tockholders' Equity = $166,000

Chapter 1, SE 7.

Net income = $108,000

Beginning of yearAssets = Liabilities +Stockholders' Equity

$280,000 = $120,000 + $160,000

During yearInvestment $ 40,000 Dividends 48,000

Net Income* 108,000

End of year $400,000 = $140,000 + $260,000

*( ### – ### ) – ### + $48,000 = $108,000

++

Ch1 SE8

Chapter 1, SE 8.

Global CompanyBalance SheetJune 30, 2009

Assets LiabilitiesCash ### Wages payable ###Accounts receivabl ###Building ### Stockholders' Equity

Common stock $24,000 Retained earnings ###Total stockholders' equity ###Total liabilities and

Total assets $29,400 stockholders' equity ###

*To balance

*+

Ch1 SE9

Chapter 1, SE 9.

Tarech CorporationIncome Statement

For the Year Ended December 31, 2010Revenue

Service revenue $4,800 Expenses

Total expenses ###Net income $2,350

Tarech CorporationStatement of Retained Earnings

For the Year Ended December 31, 2010Retained earnings, December 31, 2009 $ — Net income for the year ###Subtotal $2,350 Less dividends ###Retained earnings, December 31, 2010 $1,940

Tarech CorporationBalance Sheet

December 31, 2010Assets Liabilities

Cash $1,890 Accounts payable ###Other assets ###

Stockholders' EquityCommon stock ###Retained earnings ###Total stockholders' equity ###Total liabilities and

Total assets $2,890 stockholders' equity $2,890

Ch1 SE10 to E2

Chapter 1, SE 10.

Total assets:Beginning balance ###Ending balance ###Average total assets ($140,000 + $80,000) ÷ 2 ###

Net income ###

Return on Assets = Net Income

= $15,000

= ### or 13.6% Average Total Assets ###

Chapter 1, E 1.

1. The primary purpose of accounting is to provide decision makers with tcial information they need to make intelligent decisions. It is a valupline because of the usefulness of the information it generates.

2. Like managers of profit-seeking businesses, managers of government andfor-profit organizations must report to those who fund them, and they erate their organizations in a financially prudent way.

3. No. Not all economic events involve exchanges of value between a businand someone else. For example, when a customer places an order, it is economic event, but until the order is fulfilled, no exchange of valueplace.

4. Accounting treats sole proprietorships, partnerships, and corporationstities separate and apart from their owners because each form represenbusiness for which financial performance must be measured and reported

Chapter 1, E 2.

1. Expenses and dividends are the same in that they both reduce the retaiearnings component of stockholders' equity. They are different in thatpenses are also a component of net income, whereas dividends are a distion of assets to stockholders resulting from net income.

2. CVS and Southwest are comparable in that like all companies they have main goals: profitability and liquidity. How companies such as CVS anwest achieve these goals may make them incomparable in certain ways. Finstance, CVS is a retail (pharmacy and related) company, whereas Soutis a service (air transportation) company. CVS buys and leases retail whereas Southwest buys and leases aircraft.

3. GAAP differ from the laws of science in that they are not unchanging bare constantly evolving. They may change as business conditions changeas improved methods of accounting are introduced.

4. Unethical ways of accounting include recording and reporting business actions that did not occur or being dishonest in recording those that Financial statements are unethically prepared when they misrepresent apany's financial situation or contain false information.

Ch1 E3 to E5

Chapter 1, E 3.

1. a 5. k 9. g2. l 6. e 10. d3. c 7. b 11. f4. i 8. j 12. h

Chapter 1, E 4.

People who are interested in Gottlieb's financial statements are the folloManagementInvestors (stockholders in the company)CreditorsTax authoritiesRegulatorsLabor unionsCustomersEconomic planners

A partnership is a business that has two or more owners. A corporation is ness unit that has been granted a charter from the state and is legally seits owners (stockholders). A major advantage of the corporate form of busiover the partnership is that the stockholders' liability is limited to thestockholders' investments in the company, whereas the personal assets of pcan be called upon to pay the obligations of the partnership. Also, the trownership is easier with the corporation because the shares owned by a stoholder can be sold to another party. When ownership of a partnership changpartnership must be dissolved and another one formed.

Chapter 1, E 5.

1. This is not a business transaction because no economic exchange has taplace.

2. Yes, this is properly an expense of the business.3. Yes, this is properly an expense of the business.4. Yes, this is properly an expense of the business (assuming that Velu i

to repay the loan).

Ch1 E6 to E7

Chapter 1, E 6.

1. b 6. c2. c 7. b3. a 8. a4. a 9. c5. b 10. a

Chapter 1, E 7.

Company SalesUS.Chip 2,750,000 x 1.000 = ###Nanhai 5,000,000 x 0.130 = ###Tova ### x 0.009 = ###Holstein 3,500,000 x 1.470 = ###

Company AssetsUS.Chip 1,300,000 x 1.000 = ###Nanhai 2,800,000 x 0.130 = ###Tova ### x 0.009 = ###Holstein 3,900,000 x 1.470 = ###

Holstein is the largest in terms of sales and assets due to the high valu

Ch1 E8 to E9

Chapter 1, E 8.

1. Assets = Liabilities + Stockholders' Equity $380,000 = Liabilities + $155,000

Liabilities = ###2. Assets = Liabilities + Stockholders' Equity

Assets = ### + $79,500 Assets = ###

3. Assets = 1/3 Assets + $180,000 2/3 Assets = ###

Assets = ###Liabilities = 1/3 x ### = $90,000

4. Beginning: $310,000 = Liabilities + $150,000 Liabilities = ###

$310,000 = ### + $150,000 Change: + 45,000 ###

$355,000 = ### + Stockholders' EquityEnd: tockholders' Equity = ###

Chapter 1, E 9.

1. a. A 2. a. ISb. L b. BSc. A c. ISd. SE d. BSe. A e. ISf. L f. BSg. A g. RE

Ch1 E10

Chapter 1, E 10.

Uptime Services CompanyBalance Sheet

December 31, 2010Assets Liabilities

Cash ### Accounts payable ###Accounts receivable ###Supplies ### Stockholders' EquityBuilding ### Common stock ###Equipment ### Retained earnings ###

Total stockholders' equity ###Total liabilities and

Total assets ### stockholders' equity ###

Ch1 E11

Chapter 1, E 11.

Proviso CorporationIncome Statement

For the Year Ended December 31, 2009Revenue

Service revenue ###Expenses

Rent expense $2,400 Wages expense 16,680 Advertising expense 2,700 Utilities expense 1,800 Total expenses ###

Income before income taxes ###Income taxes expense ###Net income ###

Proviso CorporationStatement of Retained Earnings

For the Year Ended December 31, 2009Retained earnings, December 31, 2008 ###Net income for the year ###Subtotal ###Less dividends ###Retained earnings, December 31, 2009 ###

Proviso CorporationBalance Sheet

December 31, 2009Assets Liabilities

Cash ### Accounts payable ###Accounts receivable ###Supplies ### Stockholders' EquityLand ### Common stock $2,000

Retained earnings ###Total stockholders' equity ###Total liabilities and

Total assets ### stockholders' equity ###

Ch1 E12

Chapter 1, E 12.

1. Net income is: $13,250 Assets = Liabilities + Stockholders' Equity

End: $275,000 = ### + $124,500 Beginning: 180,000 = ### + 111,250 Net income $ 13,250

2. Net income is: $40,750 Change in Stockholders' Equity $13,250 + Dividends 27,500 Net income $40,750

3. Net loss is: $3,000 Change in Stockholders' Equity $13,250 – Stockholders' investments 16,250 Net loss ($ 3,000)

4. Net income is: $29,750 Change in Stockholders' Equity $13,250 + Dividends 29,000

$42,250 – Stockholders' investments 12,500 Net income $29,750

Ch1 E13, E14

Chapter 1, E 13.

Martin Service CorporationStatement of Cash Flows

For the Year Ended December 31, 2009Cash flows from operating activities

Net income ###Adjustments to reconcile net income to netcash flows from operating activities

(Increase) in accounts receivable ###Increase in accounts payable ### ###

Net cash flows from operating activities ###Cash flows from investing activities

Purchased equipment ###Net cash flows from investing activities ###

Cash flows from financing activitiesBorrowed from bank ###Paid dividends ###Net cash flows from financing activities ###

Net increase (decrease) in cash ###Cash at beginning of year ###Cash at end of year ###

Chapter 1, E 14.

Mrs. Kitty's Cookies, Inc.Statement of Retained Earnings

For the Year Ended January 31, 2010Retained earnings, January 31, 2009 $105,000 Net income for the year ###Subtotal $159,490 Less dividends ###Retained earnings, January 31, 2010 $159,490

Retained earnings represent the equity of the stockholders generated from income-producing activities of the business and kept for use in the busine

The board of directors of Mrs. Kitty's Cookies may have decided not to paydends because it wanted to use the funds for other purposes such as to finthe company's growth or pay off debt.

Ch1 E15 to E16

Chapter 1, E 15.

AICPA: American Institute of Certified Public AccountantsSEC: Securities and Exchange CommissionPCAOB: Public Company Accounting Oversight BoardGAAP: Generally accepted accounting principlesFASB: Financial Accounting Standards BoardIRS: Internal Revenue ServiceGASB: Governmental Accounting Standards BoardIASB: International Accounting Standards BoardIMA: Institute of Management AccountantsCPA: Certified public accountant

Chapter 1, E 16.

2010 2009Total assetsBeginning balance $480,000 $400,000 Ending balance $560,000 $480,000 Average total assets $520,000 $440,000

Net income $ 50,000 $ 48,000

Return on assets 9.62% 10.91%

Return on assets has decreased from 10.91 percent to 9.62 percent. The deccaused by the fast growth of the asset base that has not been matched by agrowth in net income.

2010 Return on AssetsNet Income = $50,000 = ### or 9.6%Average Total Assets ###

2009 Return on AssetsNet Income = $48,000 = ### or 10.9%Average Total Assets ###

Ch1 P1

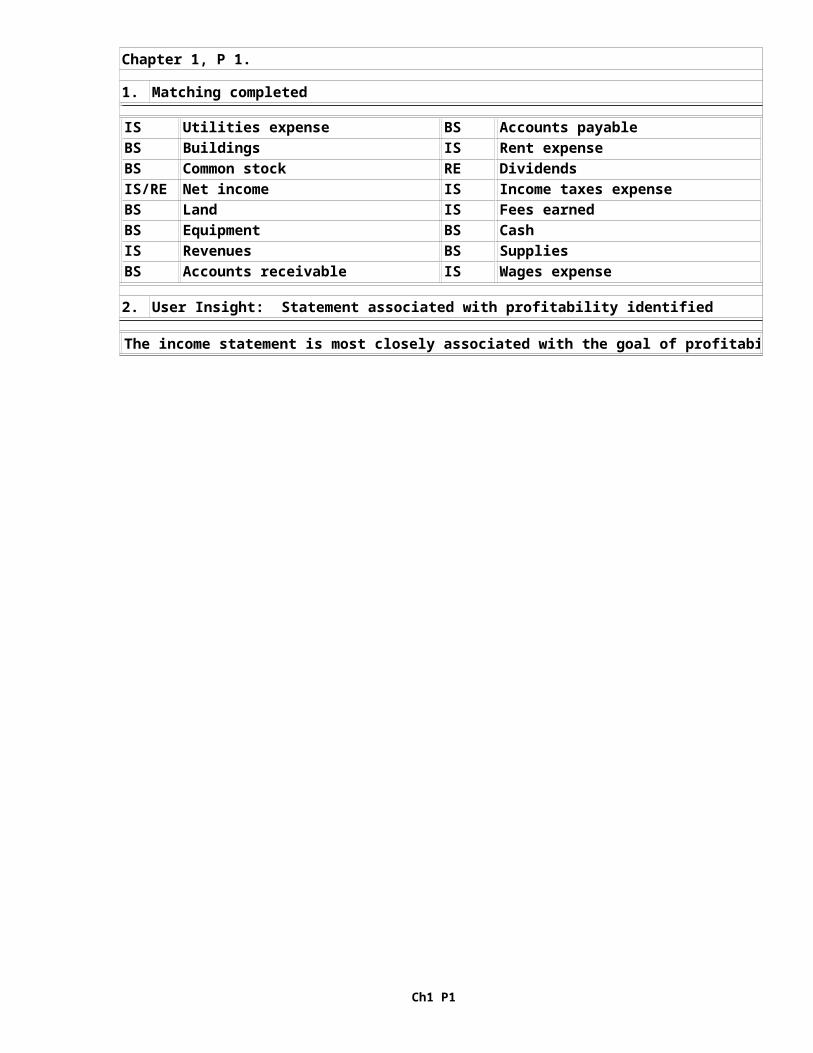

Chapter 1, P 1.

1. Matching completed

IS Utilities expense BS Accounts payableBS Buildings IS Rent expenseBS Common stock RE DividendsIS/RE Net income IS Income taxes expenseBS Land IS Fees earnedBS Equipment BS Cash IS Revenues BS SuppliesBS Accounts receivable IS Wages expense

2. User Insight: Statement associated with profitability identified

The income statement is most closely associated with the goal of profitabi

Ch1 P2

Chapter 1, P 2.

1. Financial statements completed

Set A Set B Set CIncome StatementRevenue $1,110 $ 6,800 (g) $240 Expenses 810 (a) ### 160 (m)Net income $ 300 (b) $ 1,600 (h) $ 80 Statement of Retained EarningsBeginning balance $2,900 ### $200 Net income 300 (c) ### 80 (n)Less dividends ### 1,000 (i) -- (o)Ending balance $3,000 $16,000 (j) $280 (p)Balance SheetTotal assets $6,600 (d) ### $580 (q)

Liabilities $1,600 ### $200 (r)Stockholders’ equity

Common stock ### ### 100 Retained earnings 3,000 (e) 16,000 (k) 280

Total liabilities and stockholders’ e $6,600 (f) $31,000 (l) $580

2. User Insight: Financial statement order explained

The income statement must be prepared first because the amount of net inconecessary to determine the ending balance of retained earnings. The statemretained earnings is prepared second because it provides the ending balanctained earnings for the balance sheet, which is prepared last.

Ch1 P3

Chapter 1, P 3.

1. Financial statements prepared

Landscape Design, Inc. Income Statement

For the Year Ended November 30, 2011Revenue

Design service revenue ###Expenses

Salaries expense $96,000 Marketing expense ###Office rent expense ###Supplies expense ###Total expenses ###

Income before income taxes ###Income taxes expense ###Net income ###

Landscape Design, Inc. Statement of Retained Earnings

For the Year Ended November 30, 20x8

Retained earnings, November 30, 20x7 ###Net income for the year ###Subtotal ###Less dividends ###Retained earnings, November 30, 20x8 ###

Landscape Design, Inc. Balance Sheet30-Nov-11

Assets LiabilitiesCash ### Accounts payable ###Accounts receivable ### Income taxes payable ###Supplies ### Salaries payable ###

Total liabilities ###

Stockholders' EquityCommon stock $15,000 Retained earnings ###Total stockholders' equity ###Total liabilities and

Total assets ### stockholders' equity ###

2. User Insight: Ability to pay bills evaluated

Ch1 P4

Chapter 1, P 4.

1. Financial statements preparedCollegiate Painters, Inc.

Income StatementFor the Year Ended September 30, 2010

RevenuePainting service revenue $78,800

ExpensesEquipment rental expense ###Marketing expense ###Salaries expense ###Supplies expense ###Truck rent expense ###Total expenses ###

Income before income taxes ###Income taxes expense ###Net income after taxes ###

Collegiate Painters, Inc.Statement of Retained Earnings

For the Year Ended September 30, 2010

Retained earnings, September 30, 20x6 ###Net income for the year ###Subtotal ###Less dividends ###Retained earnings, September 30, 20x7 ###

Collegiate Painters, Inc.Balance Sheet

September 30, 2010Assets Liabilities

Cash ### Accounts payable $10,500 Accounts receivable ### Income taxes payable ###Supplies ### Salaries payable ###Equipment ### Total liabilities $14,200

Stockholders' Equity

Ch1 P5

Chapter 1, P 5.

1. User Insight: Relationship of financial statementsThe income statement shows net income of $3,000 earned by the company a period of time. The amount of net income is necessary for the preparthe statement of retained earnings. The statement of retained earningsthe ending balance of $6,075. The ending balance of retained earnings in the stockholders' equity section of the balance sheet. The statemenflows explains the changes in the cash balance on the balance sheet duthe year.

2. User Insight: Liquidity and profitabilityThe income statement is most closely associated with the goal of profibecause it shows the earnings of the business. The cash flow statementmost closely associated with the goal of liquidity, because it shows tchanges in cash.

3. User Insight: Company's performance evaluatedThe company appears to be very profitable because it has earned $3,000income on revenues of $5,925. It has also paid dividends in the amount$2,400. However, the return on total assets (net income divided by totis only 5.56 percent, or $0.0556 on each dollar of assets invested. Mocompany might experience some challenges in its liquidity position in because it has liabilities of $13,350 and cash of only $6,525.

4. User Insight: Role of CPAWhen deciding whether to make a loan to a company, a banker evaluates company's ability to pay interest charges and repay the loan at the aptime. Accordingly, a banker studies the company's liquidity and cash fwell as its profitability. That information is represented in financiawhich are prepared by a company's management and can be falsified for sonal gain. To lend credibility to the financial statements, the bankequest an independent CPA audit. The audit would verify that the financments present the data fairly and conform to GAAP in all material resp

Ch1 P6

Chapter 1, P 6.

1. Financial statements completed

Set A Set B Set CIncome StatementRevenue ### ### $2,350 (m)Expenses 4,830 (a) ### (g) ###Net income ### $ 1,600 (h) $450 (n)Statement of Retained EarningsBeginning balance ### $15,400 $200 Net income 490 (b) 1,600 (i) 450 Less dividends 190 (c) ### 100 (o)Ending balance $2,100 (d) $16,000 $550 (p)Balance SheetTotal assets $2,700 (e) $26,000 (j) ###

Liabilities $400 (f) ### ###Stockholders’ equity

Common stock 200 ### 50 Retained earnings ### 16,000 (k) 550 (q)

Total liabilities and stockholders’ eq ### $26,000 (l) $1,900 (r)

2. User Insight: Financial statement order explained

The income statement must be prepared first because the amount of net inconecessary to determine the ending balance of retained earnings. The endingance of retained earnings is necessary for the preparation of the balance

Ch1 P7 (1)

Chapter 1, P 7.

1. Financial statements prepared

Dodge Realty, Inc. Income Statement

For the Year Ended December 31, 2011Revenue

Commission sales revenue ###Expenses

Commission sales expense ###Marketing expense ###Office rent expense ###Supplies expense ###Telephone and computer expenses ###Wages expense ###Total expenses ###

Income before income taxes ###Income taxes expense ###Net income $81,250

Dodge Realty, Inc.Statement of Retained Earnings

For the Year Ended December 31, 2011Retained earnings, December 31, 2010 ###Net income for the year ###Subtotal ###Less dividends ###Retained earnings, December 31, 2011 $76,550

Dodge Realty, Inc.Balance Sheet

December 31, 2011Assets Liabilities

Cash $65,750 Accounts payable ###Accounts receivable ### Income taxes payable ###Supplies 700 Salaries payable ###Equipment $59,900 Total liabilities ###

Stockholders' EquityCommon stock ###Retained earnings ###Total stockholders' equity ###Total liabilities and

Total assets ### stockholders' equity ###

Ch1 P7(2)

2. User Insight: Useful statement identified

The statement of cash flows is very useful in assessing whether a company'tions are generating sufficient funds to support expansion. The statement

Chapter 1, P 7. (Continued)

Ch1 P8(1)

Chapter 1, P 8.

1. Financial statements prepared

Creative Advertising, Inc.Income Statement

For the Year Ended January 31, 2010Revenue

Advertising service revenue ###Expenses

Equipment rental expense ###Marketing expense ###Salaries expense ###Supplies expense ###Office rent expense ###Total expenses ###

Income before income taxes $1,600 Income taxes expense 560 Net income ###

Creative Advertising, Inc.Statement of Retained Earnings

For the Year Ended January 31, 2010Retained earnings, January 31, 2009 $ — Net income for the year ###Subtotal ###Less dividends ###Retained earnings, January 31, 2010 ###

Creative Advertising, Inc.Balance Sheet

January 31, 2010Assets Liabilities

Cash ### Accounts payable $19,400 Accounts receivable ### Income taxes payable 560 Supplies 900 Salaries payable ###

Total liabilities ###Stockholders' Equity

Common stock ###Retained earnings ###Total stockholders' equity ###Total liabilities and

Total assets $27,300 stockholders' equity ###

Ch1 P8(2)

2. User Insight: Financial challenges identified

The company is challenged both in terms of profitability and liquidity. Pris low in that it has earned only $1,040 on revenues of $159,200. Liquidit

Chapter 1, P 8. (Continued)

Ch1 C1, C2

Chapter 1, C 1.

The three basic activities Costco will engage in to achieve its goals are activities (obtaining adequate funds or capital to operate its business), tivities (spending the capital it receives so that it will be productive),activities (running its business). Financing activities include obtaining owners and from creditors, such as banks and suppliers. They also include creditors and paying a return to the owners. Investing activities include buildings, equipment, and other long-lived resources needed in the operatibusiness and the sale of these resources when they are no longer needed bybusiness. Operating activities include selling merchandise and services totomers; employing managers and workers; buying, producing, and selling gooand services; and paying taxes to the government.

Costco's management is the group of people who have overall responsibilityerating the business and for meeting the company's profitability and liquiThe functions management must perform to fulfill its responsibility are obfinancial resources so the company can continue operating (financial managinvesting the financial resources of the business in productive assets thathe company's goals (asset management); developing and producing goods andservices (operations management); selling, advertising, and distributing gservices (marketing management); hiring, evaluating, and compensating empl(human resource management); and capturing, organizing, and communicating about all aspects of the company's operations (information management). Acing is covered by the last function.

Chapter 1, C 2.

Assets are economic resources owned by a business that are expected to benfuture operations. The people in an organization are not assets of the buscause they are not owned by the business. Businesses pay their employees operiodic basis (hourly, weekly, monthly, annually); they do not buy employSalaries, wages, and other costs associated with employment are consideredpenses and appear on the income statement.

Southwest Airlines considers its people to be its most important asset becthe costs of hiring, training, motivating, and compensating high-quality ewho will benefit future operations. Airlines depend on their ability to dekeep competent and motivated individuals. And their success in attracting taining high-quality employees depends on the opportunities and compensatithey provide.

Ch1 C3

Chapter 1, C 3.

Generally accepted accounting principles (GAAP) encompass the conventions,and procedures necessary to define accepted practice at a particular time.nancial statements are prepared in accordance with GAAP and audited by an pendent CPA, financial analysts will understand the significance of the amthe financial statements and will be able to assess a company's performancconfidence.

Some bodies that influence GAAP are as follows:

Public Company Accounting Oversight Board (PCAOB): Appoints the FASBto issue rules on accounting practice.

Financial Accounting Standards Board (FASB): The most important body thissues rules on accounting practice.

American Institute of Certified Public Accountants (AICPA): Influences ing practice through its senior technical committees.

Governmental Accounting Standards Board (GASB): Sets accounting standarfor government entities.

International Accounting Standards Board (IASB): Sets international accstandards.

Internal Revenue Service (IRS): Influences practice through rules for dincome tax liabilities.

Ch1 C4

Chapter 1, C 4.

1. Student A's assumption that an increase in total assets is equal to netfalse. It is true that net income results in an increase in assets, butother transactions. For example, investments by owners and loans from balso increase assets. Also, assets can be reduced by transactions that affect net income—for example, repayment of a loan.

Student B's assumption that the change in cash from one year to the nexequal to net income or loss is also false. All the examples cited abovecash but not net income. Moreover, revenue can be recorded before cash ceived, as when RIM bills a customer for services performed. And expenscan be recorded before cash is paid, as when RIM is billed by a supplieservices already received.

Student C is correct. To estimate net income from an examination of theance sheet, the change in retained earnings must be considered. Net inccreases retained earnings. So net income can be estimated by taking theence in retained earnings from one year to the next (there are no divid

2. Net income for 2008 was $1,293,867,000.

RIM, Retained Earnings, December 31, 2008 $1,653,094 Less RIM, Retained Earnings, December 31, 2007 359,227 Increase in RIM, Retained Earnings in 2008 $1,293,867 Plus dividends paid in 2008 — Net income in 2008 $1,293,867

* All numbers are in thousands.** Net income is approximate because there may be effects that are not bei

sidered at this point in the course.

*+

**+

Ch1 C5

Chapter 1, C 5.

1. The names CVS gives its four basic financial statements are as follows:Consolidated Statements of Operations (Income Statement)Consolidated Balance SheetsConsolidated Statements of Cash FlowsConsolidated Statements of Shareholders' Equity; includes data for reta

earnings

2. The accounting equation for CVS on December 31, 2008, is as follows:(in millions)

Assets = Liabilities + Stockholders' Equity $60,959.9 = $26,385.5 + $34,574.4

3. Total revenues of CVS for the year ended December 31, 2008 were $87,471million.

4. Yes. The company earned $3,212.1 million. This was an increase from net

dividends are distributions to owners.)

5. Yes, the company's cash and cash equivalents increased by $295.8 millionumber can be found toward the bottom of the statement of cash flows orcomputed by taking the difference of the cash and cash equivalents fromDecember 29, 2007 and December 31, 2008 balance sheets.

6. Cash flows from operating activities increased from 2007 to 2008. Cash used by investing activities were negative and greater in 2008 than in cash flows from financing activities increased from 2007 to 2008.

7. CVS was audited by Ernst & Young LLP. The auditor's report is importantcause it tells whether or not the company's financial statements and acpanying information are prepared in accordance with generally accepted counting principles. If this is so, then the reader of the financial stcan rely on them and analyze them. The auditor's report lends credibilifinancial statements.

ings of $2,637.0 million for the year ended December 29, 2007. (Note: Preference

Ch1 C6

Chapter 1, C 6.

1. With sales of $87,471.9 million and total assets of $60,959.9 million, Clarger than Southwest, which has revenues of $11,023 million and total a$14,308 million. Note that CVS generates 7.9 times as much sales on aboutimes the total assets of Southwest.

Neither assets nor revenues are better than the other to measure the sizcompany. Assets tell how large a company's resources are, and revenues thow well the company is able to generate revenue. Both are useful measurof a company's size.

2. CVS has net income (earnings) of $3,212.1 million, which is about 18 timthan Southwest's earnings of $178 million. CVS has had increasing net inover the three years, whereas Southwest's net income increased from 2006but then decreased greatly from 2007 to 2008.

3. In 2008, CVS had return on assets of 5.6 percent ($3,212.1 ÷ [($60,959$54,721.9) ÷ 2]), and Southwest had return on assets of 1.1 ($178 ÷ $16,772) ÷ 2]). By this measure, CVS is significantly more profitable Return on assets is a better measure than net income of the two companieprofitability because return on assets takes into account the relative scompanies.

4. CVS has cash and cash equivalents of $1,352.4 million compared to Southwcash and cash equivalents of $1,368 million. CVS's cash increased by $29million compared to the $845 million decrease by Southwest. CVS had cashfrom operating activities of $3,947.1 million compared with Southwest's used in operating activities of - $1,521 million. CVS has slightly less but by the measure of cash flows from operating activities, it has a lot

Ch1 C7

Chapter 1, C 7.

The ethical situations are presented for discussion purposes. Students arehave many different viewpoints.1. The alternative courses of action are to disclose or not to disclose t

ee's hourly rate. The information should not be disclosed because of idential nature.

2. The alternative courses of action are to ignore the inappropriate expeto report them to the home office. It might also be possible to discuswith the manager in private. This is a difficult situation because of bility of retribution. If the manager does not take appropriate remedithe accountant should report his actions—and be prepared to look for ajob.

3. The alternative courses of action are to accept the gift or to return a conflict of interest, the appropriate action would be to return the

4. This is a common problem faced by young accountants. The alternative cof action are to do the work and not report it, to do the work and reptalk to a superior as soon as the problem is recognized. The third altthe best because there may be some other reason that the job cannot bein the allotted time. Underreporting hours usually is not tolerated by

5. The alternative courses of action are to report or not to report the $Accountants must maintain their integrity, which means being honest. Tshould be reported; it would be illegal not to report it.

6. The courses of action are to disclose the investment or not to disclosvestment. A CPA must avoid even the appearance of a conflict of intereindependent, the CPA should disclose the investment and then sell the

Ch1 C8

Chapter 1, C 8.

Individual or Group Reason1. Management To evaluate the progress of the company in ach

ing profitability, liquidity, and other goa2. Stockholders To evaluate the success or failure of the comp

and to assess its future potential3. Creditors To evaluate the ability of the company to pay

current and future debts4. Potential stockholders To evaluate a possible investment in the compa

5. Internal Revenue Service To determine taxable income and federal tax liability

6. Securities and Exchange To determine whether the company has complied Commission with reporting regulations

7. Teamsters' union To justify demands for salary and benefit incr8. Consumers' group To collect data about employee work conditions

overseas facilities9. Economic adviser To make recommendations about the national

economy and policies related to the productconservation, and use of energy