Price stabilization using buffer stocks

22

1 PRICE STABILIZATION USING BUFFER STOCKS ∗ Iasson Karafyllis, George Athanasiou 1 and Stelios Kotsios Dept. of Economics, University of Athens, 8 Pesmazoglou Str., 10559, Athens, Greece Abstract The price stabilization problem is stated and solved for a mildly nonlinear cobweb model for a single commodity with stocks. It is shown that if the storage capacity for the particular commodity is sufficiently large then there exists a simple stabilization policy, such that the equilibrium price is a global attractor for the corresponding closed-loop system. JEL classification: C60; C61; C62; D40; L52 Keywords: Price Stabilization; Buffer Stocks; Cobweb Model 1. Introduction It is a well-known fact of economic reality that commodity prices are extremely volatile (Deaton and Laroque, 1992; Larson, Varangis and Yabuki, 1998; Osbourne, 2004). One of the instruments for price stabilization, which is found frequently in the economic literature, is the so-called buffer stock scheme. This instrument was implemented not only in developing countries but in the United States and Europe as well (He and Westerhoff, 2005, p. 2). For example, since the Second World War, the United States implemented buffer stock programs for various strategic materials and especially for oil (Nickols and Zeckhauser, 1977, p.p. 66-67). Jha and Srinivasan (2001) underline the importance of the operation of buffer stock programs for India. A retrospect in economic reality shows that the introduction of such programs, both in national and international level, faced difficulties with the funds that supported them (Larson, Varangis and Yabuki, 1998). The mechanism of a buffer stock program is to store a certain amount of the commodity in boom periods, when the price is low, and release a certain amount of the stored commodity in bust periods, when the price is high. Early theoretical work on the function of such programs include Keynes (1938), Kaldor (1939), Working (1949), Porter (1950) and Brennan (1958). We can discern many lines of research within the literature according to: i) who is conducting the stockpiling, ii) the policy rule, iii) the hypothesis about expectations and iv) the incidence of a speculative attack. The majority of the research is focused on the effect of government stockpiling on the stockpiling decision of risk-averse rational private agents with no market power (Wright and Williams, 1982b; Miranda and Helmberger, 1988; Wright and Williams, 1988; Newbery, 1989; Miranda and Glauber, 1993; Jha and Srinivasan, 1999; Jha and Srinivasan, 2001; Brennan, 2003). Under this framework, the stockpiling decision of the policy maker (the government or some international organization) can be conducted by following two rules: a “price band” (or “bandwidth”) rule or a “price peg” rule. There is also the possibility of implementing a mixture of these policy rules (Van Gronendaal and Vingerhoets, 1995, p. 260). When the policy maker follows the “price band” rule, the price is constrained in a predefined range (Miranda and Helmberger, 1988; Jha and Srinivasan, 1999; Jha and Srinivasan, 2001; Srinivasan and Jha, 2001; He and Westeroff, 2005). Whenever price hits the boundaries, the manager intervenes by increasing or decreasing the level of the stored commodity. In other words, the buffer stock agency provides a floor or incentive price to producers and a ceiling price to consumers. When the agency follows the “price peg” rule, it intervenes by augmenting or disposing stocks in order to keep the price as close as possible to a predefined target price path (Van Groenendaal and Vingerhoets, 1995). In other words, the manager adjusts his stocks so that the market price converges to the target price. The main methodology in order to derive the optimal private and government storage rules is the application of stochastic optimal control in a linear or non-linear setting. (Arzac, 1979; Teisberg, 1981; Wright and Williams, 1982a; Wright and Williams, 1982b; Newbery and Stiglitz, 1982; Wright and Williams, 1988; Jha and Srinivasan, 1999). Van Gronendaal and Vingerhoets (1995, p. 259) argue that we should search for buffer stock rules that are robust in a realistic setting. In order to support their argument they realized a comparison between the price behavior under an optimal buffer stock policy and the closed-loop price behavior under a buffer stock ∗ Research sponsored by the University of Athens contract 70/4/5026 1 Corresponding author. Granted by the State Scholarship Foundation. E-mail: [email protected]

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Price stabilization using buffer stocks

1

PRICE STABILIZATION USING BUFFER STOCKS∗

Iasson Karafyllis, George Athanasiou1 and Stelios KotsiosDept. of Economics, University of Athens,8 Pesmazoglou Str., 10559, Athens, Greece

AbstractThe price stabilization problem is stated and solved for a mildly nonlinear cobwebmodel for a single commodity with stocks. It is shown that if the storage capacity forthe particular commodity is sufficiently large then there exists a simple stabilizationpolicy, such that the equilibrium price is a global attractor for the correspondingclosed-loop system.

JEL classification: C60; C61; C62; D40; L52Keywords: Price Stabilization; Buffer Stocks; Cobweb Model

1. Introduction

It is a well-known fact of economic reality that commodity prices are extremely volatile (Deaton andLaroque, 1992; Larson, Varangis and Yabuki, 1998; Osbourne, 2004). One of the instruments for pricestabilization, which is found frequently in the economic literature, is the so-called buffer stock scheme. Thisinstrument was implemented not only in developing countries but in the United States and Europe as well (Heand Westerhoff, 2005, p. 2). For example, since the Second World War, the United States implemented bufferstock programs for various strategic materials and especially for oil (Nickols and Zeckhauser, 1977, p.p. 66-67).Jha and Srinivasan (2001) underline the importance of the operation of buffer stock programs for India. Aretrospect in economic reality shows that the introduction of such programs, both in national and internationallevel, faced difficulties with the funds that supported them (Larson, Varangis and Yabuki, 1998).

The mechanism of a buffer stock program is to store a certain amount of the commodity in boom periods,when the price is low, and release a certain amount of the stored commodity in bust periods, when the price ishigh. Early theoretical work on the function of such programs include Keynes (1938), Kaldor (1939), Working(1949), Porter (1950) and Brennan (1958). We can discern many lines of research within the literature accordingto: i) who is conducting the stockpiling, ii) the policy rule, iii) the hypothesis about expectations and iv) theincidence of a speculative attack. The majority of the research is focused on the effect of government stockpilingon the stockpiling decision of risk-averse rational private agents with no market power (Wright and Williams,1982b; Miranda and Helmberger, 1988; Wright and Williams, 1988; Newbery, 1989; Miranda and Glauber,1993; Jha and Srinivasan, 1999; Jha and Srinivasan, 2001; Brennan, 2003). Under this framework, thestockpiling decision of the policy maker (the government or some international organization) can be conductedby following two rules: a “price band” (or “bandwidth”) rule or a “price peg” rule. There is also the possibility ofimplementing a mixture of these policy rules (Van Gronendaal and Vingerhoets, 1995, p. 260). When the policymaker follows the “price band” rule, the price is constrained in a predefined range (Miranda and Helmberger,1988; Jha and Srinivasan, 1999; Jha and Srinivasan, 2001; Srinivasan and Jha, 2001; He and Westeroff, 2005).Whenever price hits the boundaries, the manager intervenes by increasing or decreasing the level of the storedcommodity. In other words, the buffer stock agency provides a floor or incentive price to producers and a ceilingprice to consumers. When the agency follows the “price peg” rule, it intervenes by augmenting or disposingstocks in order to keep the price as close as possible to a predefined target price path (Van Groenendaal andVingerhoets, 1995). In other words, the manager adjusts his stocks so that the market price converges to thetarget price.

The main methodology in order to derive the optimal private and government storage rules is the applicationof stochastic optimal control in a linear or non-linear setting. (Arzac, 1979; Teisberg, 1981; Wright andWilliams, 1982a; Wright and Williams, 1982b; Newbery and Stiglitz, 1982; Wright and Williams, 1988; Jha andSrinivasan, 1999). Van Gronendaal and Vingerhoets (1995, p. 259) argue that we should search for buffer stockrules that are robust in a realistic setting. In order to support their argument they realized a comparison betweenthe price behavior under an optimal buffer stock policy and the closed-loop price behavior under a buffer stock

∗ Research sponsored by the University of Athens contract 70/4/50261 Corresponding author. Granted by the State Scholarship Foundation. E-mail: [email protected]

2

feedback policy for a non-linear cocoa model, and they confirmed the mathematical fact that feedback control (incomparison with optimal control) provides robustness to modeling errors (Sontag, 1998).

However, some economists argue that in a liberalized economic environment, stockpiling as a tool to achieveprice stabilization, is costly (both for the private and the public sector) in comparison with other policy tools andshould be avoided (Jha and Srinivasan, 1999; Jha and Srinivasan, 2001; Srinivasan and Jha, 2001; Umali andDeininger, 2001; Dorosh and Shahabuddin, 2002; Brennan, 2003). They present the difficulties of operatingbuffer stock programs (e.g. crowding out private storage, lack of supporting funds, ineffectiveness inmaintaining price targets) and propose market oriented methods for price stabilization.

The goal of this paper is to address a quantitative analysis, in terms of control theory, of governmentstockpiling. Recent developments in mathematical control theory and dynamical systems theory for nonlinearsystems (existence of Lyapunov functions, e.g., Jiang and Wang, 2002; utilization of Lyapunov functions anddifference inequalities, e.g., Lakshmikantham and Trigiante, 2002; difference equations given through a system-theoretic framework, e.g., Sontag, 1998; attractor theory, e.g., Stuart and Humphries, 1998; nonlinear feedbackcontrol stabilization, e.g., Tsinias, Kotsios and Kalouptsidis, 1989; Tsinias, 1989), allow us to built more realisticeconomic models. We consider that the application of contemporary control techniques in non-linear dynamiceconomic models can provide us with the necessary policy tools for a better management of any economicsystem. More specifically, we analyze the price dynamics in a commodity market and the effects of governmentstorage on the behavior of the price. For the purpose of our analysis we develop a non-linear cobweb model,which describes sufficiently a commodity market, and we apply feedback control in the form of buffer stocks.Under this setting, we estimate the level of storage capacity that the government must have in order to achieveprice stabilization. In other words, we propose a “price peg” buffer stock policy that attempts to keep the totalsupply as close as possible to the equilibrium supply. We call this policy “Keep Supply at Equilibrium” (KSE)policy. This policy is in alignment with the argument of Newbery and Stiglitz (1981a, p. 20) that the emphasison prices has obscured the analysis and that it would be more logical to consider preserving mean supplyconstant. In addition, Makki et al. (2001, p. 127) argue that “buffer stocks is one of the principal means toreconcile the conflicting realities of unstable harvests and stable consumption”. Moreover, Krugman (2000)argues in favor of a buffer stock policy for the case of crude oil. In his own words: “… western governmentshave more than a billion barrels in reserve. Why not use those reserves to break the market corner, or at least tolimit its effectiveness?”. Finally, according to the Energy Secretary Samuel Bodman, “The Administration hasbeen clear that the Strategic Petroleum Reserve is a national security asset that can be used to protect Americanconsumers and our economy in the event of a major supply disruption, including natural disasters” (U.S.Department of Energy, August 2005). On this direction, the U.S. Department of Energy began (09/06/2005) asale of approximately 30 million barrels of crude oil, from the nation’s Strategic Petroleum Reserve, in order toenforce oil supplies in the aftermath of Hurricane Katrina (U.S. Department of Energy, September 2005).

The structure of this paper is as follows: in Section 2 a mildly nonlinear cobweb model is developed for asingle commodity with stocks and naïve expectations. The model is based on a piecewise linear S-shaped supplyfunction and takes into account the constraints which must be satisfied by the stored quantity of the commodityand the government intervention. In Section 3 the reader is introduced to the price stabilization problem and it isshown that if the storage capacity for the particular commodity is sufficiently large then the “Keep Supply atEquilibrium” (KSE) policy is successful (the equilibrium price is a global attractor for the corresponding closed-loop system). Numerical studies are also presented in Section 4, which test the success of the “Keep Supply atEquilibrium” (KSE) stabilization policy for certain cases. Finally the conclusions of the present work are givenin Section 5.

2. The Cobweb Model with Stocks

Let us denote by )(tP the price of a single commodity at period t , by )(tD the current consumption of thecommodity and by )1( +tS the current supply of the commodity.

We assume a linear strictly decreasing consumption demand function:

)()( tbPatD −= , 0, >ba (2.1)

In addition, following Hommes (1994), we assume an S-shaped monotonic piecewise linear supply functionof the private sector:

))1(()1( +=+ tPgtS e (2.2a)

3

{ }{ }dPcSPg +−= ;min;0max)( max , 0,, max >Sdc (2.2b)

where )1( +tP e is the expected price for the period 1+t and maxS is the highest supply level for thecommodity.

In order to introduce government stockpiling into our model we define two variables: )(tQ is a state variablewhich denotes the quantity of the commodity stored by the government at period t , and )(tG is the controlvariable (input) which denotes the quantity of the commodity released to the market by the government at period

1+t . When 0)( <tG then the government actually buys and stores )(tG commodity units at period 1+t .Furthermore, the quantity of the commodity stored by the government must satisfy the following differenceequation for all periods:

)()()1( tGtQtQ −=+ (2.3)

The rest analysis is straightforward. In a completely competitive market, the intertemporal market equilibrium isdescribed by the following material balance equation (Makki et al., 2001):

)()1()1( tGtStD ++=+ (2.4)

Finally, we assume, as a first approximation, the so-called naïve (or myopic) expectation about price:

)()1( tPtP e =+ (2.5)

which is met frequently in the literature.

Taking into account (2.1)-(2.5), the unique solution of (2.4) gives the following discrete-time control system:

( )))(()()1( 1 tPgtGabtP −−=+ − (2.6a)

)()()1( tGtQtQ −=+ (2.6b)

{ } )()())((;)(max max tQtGtPgQtQ ≤≤−− (2.6c)

where )1( +tP is the output of the system and 0max >Q denotes the storage capacity for the particularcommodity (for the derivation of (2.6c) see section A1 in the appendix). Simple inspection shows that if

maxmax SQa +> then the above evolution equation defines a control system with state space ],0[),0( maxQ×+∞(i.e., ],0[),0())(),(( maxQtQtP ×+∞∈ for all t ).

Proposition 2.1 (viability conditions): The inequalities maxmax SQa +> and adbc < are conditions for theviability of the commodity (for the derivation of the viability conditions see section A2 in the appendix).

Notice that the cobweb model (2.6) is nonlinear. The mildly nonlinear (piecewise linear) S-shaped supplyfunction given in (2.2 a,b) as well as the constraints satisfied by the stored quantity of the commodity and thegovernment intervention (see constraints (A1.1), (A1.2) and (A1.3) in section A of the appendix), explain thenonlinear character of the cobweb model (2.6). Clearly, a linear model cannot take into account such features,which are necessary for building a more realistic model.

Moreover, it should be emphasized that the control system (2.6) is a deterministic control system. However,in order to be able to capture uncertainties in the nominal model (2.6) as well as random perturbations we willalso consider system (2.6) under the presence of additive noise, that is, the “perturbed” system:

( )

{ } )()())((;)(max)()()1(

)())(()()1(

max

1

tQtGtPgQtQtGtQtQ

taAwtPgtGabtP

≤≤−−−=+

+−−=+ −

(2.7)

4

where the noise term )(tw satisfies 1)( ≤tw for all t and ( ))1,0[ maxmax1 QSaA +−∈ − denotes the amplitude

of the noise (for the derivation of the upper bound of the interval see section A3 in the appendix).

3. The Price Stabilization Problem

For the case with no government intervention ( 0)( ≡tG ) the corresponding dynamical system (2.6) is 1-dimensional (the state variable )(tQ is constant and irrelevant) and is given by the difference equation:

),0()(;))(()1( +∞∈=+ tPtPhtP (3.1)

where

+≥−+<<−+

≤=

−−

−−−

−−

1maxmax

1

1max

11

11

)()()())((:)(

dScPifSabdScPcdiftdPcab

cdPifabPh (3.2)

The dynamics of the system without government intervention were examined and the results are summarized inthe following table (the analysis is provided in section A4 of the appendix).

Table 1. Asymptotic behavior without government intervention

Cases Asymptotic behavior

1. dbbcadS

+−

>max and 11 <− db The equilibrium point dbcaPeq +

+= is globally asymptotically stable

2. dbbcadS

+−

≤maxThe equilibrium point )( max

1 SabPeq −= − is globally asymptotically stable

A. If b

bcadS −>max then a

period-2 solution is

121 PPP →→ where:

abP 11

−= and dc

badcabP ≤

−+=

22)(

B. If b

bcadSd

bcad −<≤

−max

a period-2 solution is

121 PPP →→ where:

abP 11

−= and dc

bSa

P ≤−

= max2

C. If d

bcadS −<max a period-2

solution is

121 PPP →→ where:

dSc

baSdcab

P max2

max1

)()( +≥

−++= and

dSc

bSa

P maxmax2

+<

−=

3. dbbcadS

+−

>max and 11 ≥− db

D. If 11 =− db there is an infinitenumber of non-trivial period-2solutions

121 PPP →→ where:

+

−

∈ −

dScab

bdbSad

dcP max1max

1 ;min,;max

arbitraryand 1

112 PcdabP −+= −−

We next state the tracking control problem for (2.6).

The tracking control problem for (2.6): Let 0>∗P the desired price. Is there a static feedback law (or pricestabilization policy):

))(),(()( tQtPφtG = (3.3)

5

such that the solution of the closed-loop system (2.6) with (3.1) satisfies ∗

+∞→= PtP

t)(lim for all initial conditions

],0[),0())0(),0(( maxQQP ×+∞∈ ?

Lemma 3.1 (Necessary Condition for solvability of the tracking control problem for (2.6)) If the trackingcontrol problem for (2.6) is solvable then the following condition must hold:

eqPP =∗

where eqP is the equilibrium price of the open-loop system (3.1) as defined in Table 1 by cases 1 and 2 .

Lemma 3.1(see section A5 in the appendix) indicates a major limitation imposed by the use of buffer stocks:the price dynamics can only have a unique accumulation point, which is no other than the equilibrium price. Thisimportant limitation may be used to explain the failure of buffer stock stabilization policies: if government triesto lead the commodity price to values different from the equilibrium values, the buffer stock stabilization policy(no matter how smart) will fail. On the same grounds, Van Gronendaal and Vingerhoets (1995; p. 259) argue that“the main lesson for buffer stock policy implementation should, however, not be that buffer stock agreements donot work, but that buffer stock intervention should not go against the general tendency of the market or, moreprecisely, the structural development in market prices”. Since the desired price must coincide with theequilibrium price, we may state next the price stabilization problem for (2.6).

The price stabilization problem for (2.6) is concerned with the existence of a static feedback law (or pricestabilization policy) given by (3.3) with 0),( =QPφ eq for all ],0[ maxQQ∈ , such that the equilibrium set

]},0[;),{( maxQQQPeq ∈ is a Global Attractor for the closed-loop system (2.6) with (3.3), i.e., eqtPtP =

+∞→)(lim

for all initial conditions ],0[),0())0(),0(( maxQQP ×+∞∈ . This problem is particularly interesting for the Case 3

described above, i.e., when dbbcadS

+−

>max and 11 ≥− db , since in this case the equilibrium set

]},0[;),{( maxQQQPeq ∈ is not a global attractor without government intervention, i.e., when 0)( ≡tG , asshown above.

Solution of the Price Stabilization Problem for (2.6):

We set:

{ }{ }max)(;))((max;)(min)( QtQtPgStQtG eq −−= (3.4)

where eqS is the equilibrium supply that corresponds to the equilibrium price bdcaPeq +

+= and ))(( tPg is the

estimated commodity supply for the period 1+t .

The feedback law described by (3.4) is particularly simple and attempts to bring the total quantity of theproduct available in the market at period 1+t (given by )()1( tGtS ++ ) as close as possible to the equilibriumsupply eqS . In order to specify this kind of policy we introduce the term “Keep Supply at Equilibrium” policy.According to what has been noted in the introduction, this policy corresponds indirectly to a “price peg” rulewhere the target price is the equilibrium price. Thus, if the government wants to stabilize the price of acommodity it must keep supply as close as possible to its equilibrium value.

Furthermore, formula (3.4) shows an important feature. For the implementation of the “Keep Supply atEquilibrium” (KSE) policy we need to know four things: the amount of the commodity stored )(tQ , the storagecapacity maxQ , the equilibrium supply eqS and the supply of the private sector ))(( tPg . Consequently, if thegovernment can estimate the supply of the private sector at any period it is not necessary to know the exactfunctional form of the function ))(( tPg .

The following proposition provides criteria for the success of the “Keep Supply at Equilibrium” (KSE) bufferstock policy.

6

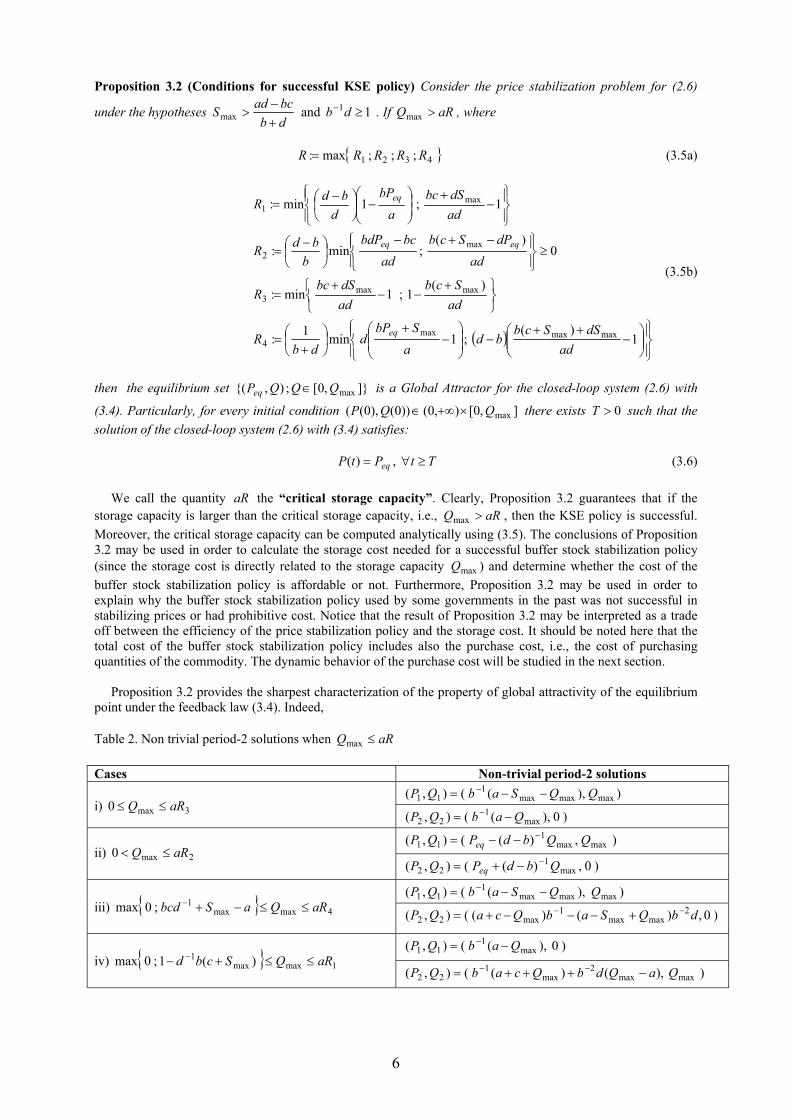

Proposition 3.2 (Conditions for successful KSE policy) Consider the price stabilization problem for (2.6)

under the hypotheses dbbcadS

+−

>max and 11 ≥− db . If aRQ >max , where

{ }4321 ;;;max: RRRRR = (3.5a)

( )

−

++−

−

+

+=

+

−−+

=

≥

−+−

−

=

−+

−

−

=

1)(

;1min1:

)(1;1min:

0)(

;min:

1;1min:

maxmaxmax4

maxmax3

max2

max1

addSScb

bda

SbPd

dbR

adScb

addSbc

R

addPScb

adbcbdP

bbdR

addSbc

abP

dbdR

eq

eqeq

eq

(3.5b)

then the equilibrium set ]},0[;),{( maxQQQPeq ∈ is a Global Attractor for the closed-loop system (2.6) with

(3.4). Particularly, for every initial condition ],0[),0())0(),0(( maxQQP ×+∞∈ there exists 0>T such that thesolution of the closed-loop system (2.6) with (3.4) satisfies:

eqPtP =)( , Tt ≥∀ (3.6)

We call the quantity aR the “critical storage capacity”. Clearly, Proposition 3.2 guarantees that if thestorage capacity is larger than the critical storage capacity, i.e., aRQ >max , then the KSE policy is successful.Moreover, the critical storage capacity can be computed analytically using (3.5). The conclusions of Proposition3.2 may be used in order to calculate the storage cost needed for a successful buffer stock stabilization policy(since the storage cost is directly related to the storage capacity maxQ ) and determine whether the cost of thebuffer stock stabilization policy is affordable or not. Furthermore, Proposition 3.2 may be used in order toexplain why the buffer stock stabilization policy used by some governments in the past was not successful instabilizing prices or had prohibitive cost. Notice that the result of Proposition 3.2 may be interpreted as a tradeoff between the efficiency of the price stabilization policy and the storage cost. It should be noted here that thetotal cost of the buffer stock stabilization policy includes also the purchase cost, i.e., the cost of purchasingquantities of the commodity. The dynamic behavior of the purchase cost will be studied in the next section.

Proposition 3.2 provides the sharpest characterization of the property of global attractivity of the equilibriumpoint under the feedback law (3.4). Indeed,

Table 2. Non trivial period-2 solutions when aRQ ≤max

Cases Non-trivial period-2 solutions)),((),( maxmaxmax

111 QQSabQP −−= −

i) 3max0 aRQ ≤≤)0),((),( max

122 QabQP −= −

),)((),( maxmax1

11 QQbdPQP eq−−−=

ii) 2max0 aRQ ≤<)0,)((),( max

122 QbdPQP eq

−−+=

)),((),( maxmaxmax1

11 QQSabQP −−= −

iii) { } 4maxmax1;0max aRQaSbcd ≤≤−+−

)0,)()((),( 2maxmax

1max22 dbQSabQcaQP −− +−−−+=

)0),((),( max1

11 QabQP −= −

iv) { } 1maxmax1 )(1;0max aRQScbd ≤≤+− −

)),()((),( maxmax2

max1

22 QaQdbQcabQP −+++= −−

7

In the above cases (where aRQ ≤max ), the control action given by the feedback law (3.4) is not able to cancelthe periodic orbits of the open-loop system. However, it can be verified that the total purchase cost over a cycle

for the period-2 solutions of the closed-loop system (2.6) with (3.4), given by ∑=

+2

1

)1()(t

tPtG is positive, i.e.,

the government increases its revenues by purchasing quantities of the commodity.

A final remark for the tracking control problem for (2.6) must be given. Lemma 3.1 showed a majorlimitation of the buffer stock stabilization policy. However, if government is allowed to change the tax rate ofthe commodity then the equilibrium price of the open-loop system (3.1) changes and can coincide with thedesired price ∗P . Then the KSE buffer stock policy may be used to stabilize the price dynamics. Thus weconclude that the tracking control problem for (2.6) is indeed solvable by making simultaneous use ofappropriate tax and buffer stock policies.

4. Numerical Investigations

In this section we present numerical investigations for the dynamic behavior of the commodity price under thefeedback law (3.4). We study the cobweb model developed in Section 2 for the following parameter values:

...10$/.)..(45.4;$/.)..(3

...20;...30

max

22

couScoudcoub

couccoua

===

==

(4.1)

where ... cou is an abbreviation of “units of commodity”. These parameter values ensure that the viabilityconditions for the commodity ( maxSa > and adbc < ) are satisfied.

It can be verified that the conditions dbbcadS

+−

>max and 11 ≥−db are satisfied and thus the equilibrium price

.../$7114.6 couPeq = is not a global attractor for the nominal system (2.6) without government intervention, i.e.,

for ...0max couQ = (see Section 2). The well-known phenomenon of the “hog cycles” (Hommes, 1998) appearsand in this case it was numerically verified that this period-2 solution attracts every solution starting from initialcondition that does not coincide with the equilibrium price (see Figure 2).

Proposition 3.2 guarantees that price stabilization by means of buffer stocks is feasible if the storage capabilitymaxQ exceeds aR , where the dimensionless constant R is determined by (3.5a,b). In this case we find:

001458.0=R

and thus the critical storage capability aR is:

...04374.0 couaR =

Notice that in this case the critical storage capability amounts to approximately only %45.0 of the equilibriumsupply ( ...8658.9 couSeq = ). We applied the feedback law (3.6b) with ...05.0max couQ = and the results areshown in Figure 1. As expected by Proposition 3.2, the equilibrium price is guaranteed to be the global attractorof this system.

We also considered the dynamic behavior of the price under the presence of noise. We applied the feedbacklaw (3.4) to the perturbed case (2.7) with noise amplitude 003.0=A . The results are shown in Figure 3. Forcomparison purposes in Figure 4 it is shown the dynamic behavior of the price under the presence of noise of thesame amplitude 003.0=A without government intervention, i.e., the solution of (2.7) with ...0max couQ = . It isevident that the price fluctuation is more intense (in terms of its variance) when the government does not apply abuffer stock stabilization policy.

8

6.4

6.5

6.6

6.7

6.8

6.9

7

7.1

0 20 40 60 80 100

t

P(t)

in $

Figure 1: Price Behavior for the nominal case (2.6) under the feedback law (3.4)

6.4

6.5

6.6

6.7

6.8

6.9

7

7.1

0 20 40 60 80 100

t

P(t)

in $

Figure 2: Price Behavior for the nominal case (2.6) without government intervention

9

6,4

6,5

6,6

6,7

6,8

6,9

7

7,1

0 20 40 60 80 100

t

P(t)

in $

Figure 3: Price Behavior for the perturbed case (2.7) under feedback control (3.4)

6,4

6,5

6,6

6,7

6,8

6,9

7

7,1

0 20 40 60 80 100

t

P(t)

in $

Figure 4: Price Behavior for the perturbed case (2.7) without government intervention

10

Next we study the total purchase cost of the commodity, defined by:

∑=

+=+t

i

iPiGtperiodtoupCostPurchaseTotal0

)1()(1

The quantity defined above means that the government spends ∑=

+−t

i

iPiG0

)1()( up to period 1+t in order to

achieve price stabilization (storage cost is not included). Clearly, if the total purchase cost up to period 1+t ispositive, then the government increases its revenues by purchasing quantities of the commodity. The totalpurchase cost up to period 1+t in general depends on the initial conditions )0(P and )0(Q . The evolution ofthe total purchase cost is crucial for the success of the buffer stock price stabilization policy. For example, if thetotal purchase cost decreases with time then the government has to increase its spending in order to achieve pricestabilization. On the other hand if the total purchase cost is bounded from below then the government has tospend a certain amount of money in order to achieve price stabilization. In Figure 5 it is shown the evolution ofthe total purchase cost for the nominal case (2.6) under the feedback law (3.4) with ...05.0max couQ = andinitial conditions .../$5.6)0( couP = , ...0)0( couQ = . It is clear that the total purchase cost is bounded frombelow. In Figure 6 it is shown the evolution of the total purchase cost for the perturbed case (2.7) with noiseamplitude 003.0=A under the feedback law (3.4) with ...05.0max couQ = and initial condition

.../$5.6)0( couP = , ...0)0( couQ = . The noise causes a very slow tendency of decrease for the total purchasecost.

-0,4

-0,35

-0,3

-0,25

-0,2

-0,15

-0,1

-0,05

0

0,05

0 20 40 60 80 100

t

Tota

l Cos

t in

$

Figure 5: Total Purchase Cost for the nominal case (2.6) under feedback control (3.4)

11

-0,45

-0,4

-0,35

-0,3

-0,25

-0,2

-0,15

-0,1

-0,05

0

0,05

0 100 200 300 400 500

t

Tota

l Cos

t in

$

Figure 6: Total Purchase Cost for the perturbed case (2.7) under feedback control (3.4)

Finally, the success of the “Keep Supply at Equilibrium” (KSE) price stabilization policy for morecomplicated price dynamics was investigated. We use the same cobweb model as previously but instead ofassuming the so-called naive (or myopic) expectation (2.5), we considered a linear backward-lookingexpectation with two lags (Collery 1955; Hommes 1998):

)1()1()()1( −−+=+ tPλtPλtP e (4.2)

where ℜ∈λ is a parameter determining the weights of the two past commodity prices. Taking into account(2.1)-(2.5), the unique solution of (2.4) gives the following discrete-time control system:

( )( )

( ){ } )()()1()1()(;)(max)()()1(

)1()1()()()1(

max

1

tQtGtPλtPλgQtQtGtQtQ

tPλtPλgtGabtP

≤≤−−+−−−=+

−−+−−=+ −

(4.3)

where g is the non-negative function defined by (2.2b). It should be emphasized that in the case of nogovernment intervention ( 0)( ≡tG ) the mildly nonlinear model (4.3) is capable of describing very complicatedprice dynamics.

In this case the “Keep Supply at Equilibrium” (KSE) price stabilization policy is described by the followingfeedback:

( ){ }{ }max)(;)1()1()(max;)(min)( QtQtPλtPλgStQtG eq −−−+−= (4.4)

where eqeq bPaS −= is the equilibrium supply that corresponds to the equilibrium price bdcaPeq +

+= and

( ))1()1()( −−+ tPλtPλg is the estimated commodity supply for the period 1+t . It is expected that if theparameter λ is sufficiently close to 1 (case of naive expectation) then the closed-loop system (4.3) with (4.4)will present the same characteristics as the case (2.6) with (3.4). Indeed, we investigated numerically the closed-loop system (4.3) with (4.4) under the same parameter values given in (4.1) and 1.1=λ . The equilibrium price

.../$7114.6 couPeq = is not a global attractor for the case of no government intervention and the well-knownphenomenon of “hog-cycles” appears (see Figure 7). It was found that there exists a critical storage capability

12

(which is greater than the critical storage capability predicted for the naive expectation ...04374.0 couaR = butstrictly less than ...06.0 cou ) such that if the storage capability maxQ is greater than the critical storagecapability then the “Keep Supply at Equilibrium” (KSE) buffer stock price stabilization policy described by (4.4)is successful. In Figure 8 it is shown the price dynamics for the closed-loop system (4.3) with (4.4) with

...06.0max couQ =

However, if the parameter λ is not close to 1 then the closed-loop system (4.3) with (4.4) has differentcharacteristics from the closed-loop system (2.6) with (3.4). Indeed, we studied the closed-loop system (4.3) with(4.4) under the same parameter values given in (4.1) and 2=λ . Again the equilibrium price

.../$7114.6 couPeq = is not a global attractor for the case of no government intervention and the well-known

phenomenon of “hog-cycles” appears once again. However, no matter how large the storage capability maxQ isselected the equilibrium price is not a global attractor and the period-2 solution persists. Thus in this case there isno critical storage capability and the KSE buffer stock price stabilization policy described by (4.4) is notsuccessful. In Figure 9 it is shown the persistent periodic solution for the closed-loop system (4.3) with (4.4) and

...10max couQ = . It should be emphasized that one of the points of the periodic cycle is actually the equilibriumprice but the second point is a significantly higher price. In Figure 10 it is shown the evolution of the totalpurchase cost for the closed-loop system (4.3) with (4.4) ...10max couQ = . It is evident that the governmentincreases its revenues by purchasing quantities of the commodity. This remarkable feature must not encouragethe reader since in this case the storage cost will be too high and a more detailed analysis is needed in order toinclude storage costs and possible noise terms.

The failure the KSE price stabilization policy described by (4.4) for the linear backward-looking expectationrule (4.2) with 2=λ indicates the need to study more complicated nonlinear models under more complicatedprice stabilization policies (possibly time-varying). The subject requires further research.

6,45

6,5

6,55

6,6

6,65

6,7

6,75

6,8

6,85

0 20 40 60 80 100

t

P(t)

in $

Figure 7: Price Dynamics for cobweb model (4.3) without government intervention

13

6

6,1

6,2

6,3

6,4

6,5

6,6

6,7

6,8

0 20 40 60 80 100

t

P(t)

in $

Figure 8: Price Dynamics for cobweb model (4.3) under feedback control (4.4)

6

6,5

7

7,5

8

8,5

9

9,5

10

10,5

0 20 40 60 80 100

t

P(t)

in $

Figure 9: Persistent Periodic Solution for cobweb model (4.3) with (4.4) and 2=λ

14

-5

0

5

10

15

20

25

0 20 40 60 80 100

t

Tota

l Cos

t in

$

Figure 10: Total Purchase Cost for cobweb model (4.3) with (4.4) and 2=λ

5. Conclusions

In the present work a mildly nonlinear cobweb model is developed for a single commodity with stocks andnaïve expectations. The model is based on a piecewise linear S-shaped supply function and takes into accountthe constraints which must be satisfied by the stored quantity of the commodity and the government intervention.For the particular model it is shown that if the storage capacity for the particular commodity is sufficiently large(greater than the critical storage capacity) then the “Keep Supply at Equilibrium” policy is successful (theequilibrium price is a global attractor for the corresponding closed-loop system). Moreover, formulae for thecomputation of the critical storage capacity are provided. The results indicate a trade off between the efficiencyof the price stabilization policy and the storage cost.

The main result of the present work (Proposition 3.2) may be used in order to calculate the storage costneeded for a successful buffer stock stabilization policy and determine whether the cost of the buffer stockstabilization policy is affordable or not. Furthermore, the results may be used in order to explain why the bufferstock stabilization policy used by some governments and international agencies in the past was not successful instabilizing prices or had prohibitive cost. Numerical studies are also presented, which test the success of the“Keep Supply at Equilibrium” (KSE) stabilization policy for certain cases.

Appendix

A1. Quantity constraints

We defined )(tQ as the quantity of the commodity stored by the government at period t , )(tG as thequantity of the commodity released to the market by the government at period 1+t and 0max >Q as the storagecapacity for the particular commodity. Consequently, the following intrinsic constraints must be satisfied for allperiods:

)()( tQtG ≤ and max)(0 QtQ ≤≤ for all t (A1.1)

15

i.e. the quantity of the commodity released by the government at period 1+t cannot exceed the quantity of thecommodity stored in period t and the quantity of the commodity stored at period t cannot exceed the storagecapacity ( maxQ ). Since the quantity of the commodity stored by the government at period 1+t cannot exceed

maxQ (the storage capacity), i.e., max)1( QtQ ≤+ , it follows from )()()1( tGtQtQ −=+ that the followingconstraint for the quantity of the commodity released to the market by the government at period 1+t must beobeyed:

)()( max tGQtQ ≤− for all t (A1.2)

The total quantity of the product available in the market at period 1+t is given by )()1( tGtS ++ and it must

be positive. Therefore because ))1(()1( +=+ tPgtS e , the following constraint must be obeyed in addition to theprevious constraints:

))1(()( +−≥ tPgtG e for all t (A1.3)

i.e. the government cannot buy a quantity that exceeds the quantity supplied by the private sector.

A2. Proposition 2.1 (Viability conditions)

Since the case 1)1( −=+ abtP is a consequence of a situation where the product is not supplied, in order toexclude the possibility of constant zero total supplied quantity of the product (when 0)( =tG for all t ) it suffices

to guarantee that ),(),( 1 QabQP −= , where ],0[ maxQQ∈ , is not an equilibrium point for the above dynamicalsystem for all t ; i.e., it suffices to have adbc < (A2.1).In order for 1−= abP not to be an equilibrium point, the following inequality must hold:

adbcabdcdPc <⇒>+−⇒>+− − 0)(0 1

The second viability condition is that the maximum of consumption demand must exceed the sum of themaximum supply, private and public i.e. maxmax SQa +> (A2.2).

If adbc < then a positive quantity of the product is available and the price is ( ))(1 PgGabP −−= − . Thisquantity is always positive if and only if maxmax SQa +> .

A3. Perturbation interval

According to Proposition 2.1 the second viability condition is maxmax SQa +> . Because the price must bealways positive (either in the nominal or the perturbed system) we must select an interval which satisfies thisconstraint. Thus, if we allow the noise term to satisfy the constraint 1)( ≤tw , then the maximum value ofaA cannot exceed the quantity maxmax QSa −− in order for the price to be positive.

A4. The dynamics of the model

We start from the closed-loop model (2.6) and then we analyze the dynamics of the open-loop model (3.2) byletting the control variable G to become zero.

It is convenient to introduce the dimensionless variables:

{ }{ }{ }{ }ctPdSQtQtautQtGtQatytPbatx

−−−==−= −−

)(;min;0max;)(;)(max;)(min)()()(;)1(:)(

maxmax

11 (A4.1)

16

and the dimensionless constants 0: 1 >= −dbr , 1:1 <=adbc

c , db

adbS

c <= max2 : , max

13 Qac −= . Thus the control

system (2.6) expressed in state space form and in dimensionless coordinates is given by the following discrete-time control system:

ℜ∈×+∞∈−=+

−−=+

)(,],0[),0())(),(())(),(),(()()1(

))(),(),(())((1)1(

3

2

21

tuctytxtutytxftyty

tutytxftxftx (A4.2)

where

{ }{ }{ }{ })(;;max;min:),,(;min;0max:)(

132

121

xfcyuyuyxfcxcrxf

−−=−=

Notice that 0)0,,(2 =yxf for all ],0[),0(),( 3cyx ×+∞∈ . There exists an equilibrium set for the case 0)( ≡tu(the so-called open-loop system) given by:

),(),( yxyx eq=

where ],0[ 3cy∈ is arbitrary and

−≤+−

−>+++

=rcccifrc

rcccifr

rcxeq

2212

2211

11

11

1 (A4.3)

The variable )(tu is directly related, by means of (A4.1), to the quantity of the commodity released to the marketby the government at period 1+t and is the control input of the system (i.e., )(tu can be manipulated in order toachieve a certain control objective).

The “perturbed” system that corresponds to system (A4.2) is:

ℜ∈×+∞∈−=+

+−−=+

)(,],0[),0())(),(())(),(),(()()1(

)())(),(),(())((1)1(

3

2

21

tuctytxtutytxftyty

tAwtutytxftxftx

For the case with no government intervention the corresponding dynamical system (A4.2) with 0)( ≡tu is 1-dimensional (the state variable )(ty is constant and irrelevant) and is given by the difference equation:

),0()(;))(()1( +∞∈=+ txtxhtx (A4.4)

where

+≥−+<<−+

≤=−=

212

2111

1

1

11

1)(1:)(

ccxifrcccxcifxrrc

cxifxfxh (A4.5)

17

We consider the following cases:

CASE 1: If rccc 221 1−>+ then 211 ccxc eq +<< (notice that 11 <c ) and consequently there exists an open

neighborhood around eqx where h is continuously differentiable (in fact linear). Thus local asymptotic stability

of the unique equilibrium point may be checked using linear theory, which demands 1)( <′ eqxh for local

asymptotic stability of the equilibrium point or equivalently:

1<r (A4.6)

However, it may be shown that the equilibrium point is globally asymptotically stable. We prove this fact byconsidering the Lyapunov function ( )2:)( eqxxxV −= . It is a matter of simple but tedious calculations to showthat, under hypothesis (A4.6), the following inequality holds:

)())(( xVxhV < , for all ),0( +∞∈x , eqxx ≠

which according to Corollary 3.3 in Jiang and Wang (2002), implies global asymptotic stability of theequilibrium point.

CASE 2: If rccc 221 1−≤+ then we notice that 21)( ccxh +≥ for all ),0( +∞∈x . Thus for every initialcondition ),0()0( +∞∈x we obtain:

eqxtx =)( for all 2≥t (A4.7)

Thus the equilibrium point rcxeq 21−= is a global attractor for system (A4.4). In fact, in this case thephenomenon of finite-time stability appears as (A4.7) shows (i.e., the equilibrium point is approached in finitetime).

CASE 3: If rccc 221 1−>+ and 1≥r the dynamics of the nominal system (A4.4) present the well-knownphenomenon of the “hog-cycles” as described in the literature. For the mildly nonlinear case (A4.4) the “hog-cycles” can be given explicitly:

Table 3. Asymptotic behavior of (A4.4 )

a) If 121 >+ cc a period-2 solution is 121 xxx →→ where:11 =x and 112 )1(1 ccrx ≤−−=

b) If 211 cc +≥ and 121 ≥+ rcc a period-2solution is

121 xxx →→ where:11 =x and 122 1 crcx ≤−=

c) If 121 <+ rcc a period-2 solution is: 121 xxx →→ where:

2122

11 )1(1 cccrcrx +≥+−−= and 2122 1 ccrcx +<−=d) If 1=r there is an infinite number of non-trivial period-2 solutions:

121 xxx →→ where:{ } { } arbitraryccccx );1min,1;max( 21211 +−∈ and

112 1 xcx −+=

18

Clearly, the existence of a non-trivial period-2 solution excludes the possibility of the existence of an equilibrium

point, which is a global attractor, i.e. the corresponding price equilibrium point r

rcxeq +

+=

11 1 is not a global

attractor.

A5. Proof of Lemma 3.1 (Necessary Condition for solvability of the tracking control problem)

By virtue of (A4.2) and continuity of the function 1f , it follows that the limit )))(),((),(),((lim 2 tytxφtytxft +∞→

exists and is given by:

)(1)))(),((),(),((lim 12∗∗

+∞→−−= xfxtytxφtytxf

t

The above equality implies that )(1))()1((lim 1∗∗

+∞→+−=−+ xfxtyty

t. If 0)(1 1 >+− ∗∗ xfx then we obtain

+∞=+∞→

)(lim tyt

, which contradicts the constraint ],0[)( 3cty ∈ . On the other hand, if 0)(1 1 <+− ∗∗ xfx then

we obtain −∞=+∞→

)(lim tyt

, which again contradicts the constraint ],0[)( 3cty ∈ . Thus we must necessarily have

0)(1 1 =+− ∗∗ xfx and consequently the desired price 0>∗x coincides with eqx , the unique equilibrium priceof the open-loop system (A4.4) defined by (A4.2). The proof is complete. <

A6. Proof of proposition 3.2

Following A4 we can transform proposition 3.2 as follows:

Consider the price stabilization problem for (A4.2) under the hypotheses rccc 221 1−>+ and 1≥r . If Rc >3 ,where

{ }4321 ;;;max: RRRRR = (A6.1)

{ } { }{ } { })1)(1(;)1(min)1(:;1;1min:

0;min)1(:;1;)1)(1(min:

22121

421213

2112211

1

−++−−++=−−−+=

≥−+−−=−+−−=−

−

rcccrrcxrrRccrccR

xcccxrRrccxrR

eq

eqeqeq

then the equilibrium set ]},0[;),{( 3cyyxeq ∈ is a Global Attractor for the closed-loop system (A4.2) with

))((1)( 1 txfxtu eq −−= . Particularly, for every initial condition ],0[),0())0(),0(( 3cyx ×+∞∈ there exists 0>T

such that the solution of the closed-loop system (A4.2) with ))((1)( 1 txfxtu eq −−= satisfies:

eqxtx =)( , Tt ≥∀ (A6.2)

Notice that

{ }{ }

−<++−≤+≤−++−

+−>+=−−−

−<+−−+−≤+≤−+−>++−−

=−−−−

−−−=−−

eq

eqeqeq

eq

eq

eq

eqeqeq

eq

eq

eqeq

xxfyifcxxfyxifxfxy

cxxfyifcxfxyxfy

xxfyifyxfcxxfyxifx

cxxfyifcyxfxfxyxfxf

xfxcyyxfxyxf

1)(01)(1)(1

1)())(1,,(

1)()(11)(1

1)()(1))(1,,()(1

)(1;max;min))(1,,(

1

311

313

12

11

31

3131

121

1312

19

+≥+<<+−

≤=

212

2111

1

1

0)(

ccxifrcccxcifxrrc

cxifxf

Making use of the above equalities in conjunction with hypotheses ],0[)( 3cty ∈ , rccc 221 1−>+ and 1≥r , itcan be shown that:

3

31

)1(

)()(1)1(

ctyand

tyctrxrctx

=+

−+−+=+ if })({:))(),(( 213

11 ccxycrxBtytx eq +<<−+=∈ − (A6.3)

3

32

)1(

)(1)1(

ctyand

tycrctx

=+

−+−=+ if }1{:))(),(( 23212 rccxyandccxBtytx eq −+−>+≥=∈ (A6.4)

0)1(

)(1)1(

=+

−=+

tyand

tytx if }10{:))(),(( 13 eqxyandcxBtytx −<≤<=∈ (A6.5)

0)1(

)()(1)1( 1

=+

−−+=+

tyand

tytrxrctx if }{:))(),(( 1

14 yrxxcBtytx eq−−<<=∈ (A6.6)

eqxtx =+ )1( if

∪×+∞=∈=

iiBcBtytx

4

135 \],0[),0())(),(( (A6.7)

Moreover, since rccc 221 1−>+ which directly implies 211 ccxc eq +<< (notice that 11 <c ), it follows thatthe following implications hold:

54321 ))1(),1(())(),(( BBBtytxBBtytx ∪∪∈++⇒∪∈ (A6.8)

52143 ))1(),1(())(),(( BBBtytxBBtytx ∪∪∈++⇒∪∈ (A6.9)

1,)())(),(( 0500 +≥∀=⇒∈ ttxtxBtytx eq (A6.10)

In order to show (A6.2) it suffices to show that for every initial condition ],0[),0())0(),0(( 3cyx ×+∞∈ thereexists 0≥T such that 5))(),(( BTyTx ∈ . The proof will be made by contradiction. Suppose on the contrary thatthere exists initial condition 5))0(),0(( Byx ∉ such that 5))(),(( Btytx ∉ for all 0≥t . Without loss of generalitywe may assume that 21))0(),0(( BByx ∪∈ (since if 43))0(),0(( BByx ∪∈ then by virtue of (A6.9) we wouldhave 21))1(),1(( BByx ∪∈ and then consider the solution with initial condition 21))1(),1(( BByx ∪∈ whichalso satisfies 5))(),(( Btytx ∉ for all 0≥t ). By virtue of implications (A6.8) and (A6.9) we must have:

21))(),(( BBtytx ∪∈ if t is even and 43))(),(( BBtytx ∪∈ if t is odd (A6.11)

Moreover, by virtue of (A6.3-7) we obtain:

0)( =ty if 1≥t is even and 3)( cty = if 1≥t is odd (A6.12)

By virtue of (A6.3-7), (A6.11-12) we must also have:

{ } )(;min 211

3 txxccrcxx eqeqeq ≤−++< − if 2≥t is even (A6.13)

20

Next we show that there exists 0>δ such that:

δ−≤+ )()2( txtx for all even integers 2≥t (A6.14)

Thus we obtain a contradiction, since (A6.13) in conjunction with (A6.14) and the fact that 1)( ≤tx for all 1≥twill give:

{ } δkkxxccrcx eqeq −≤+≤−++ − 1)22(;min 211

3 for all integers 1≥k

which cannot hold for { }eqeq xccrcδxδδk −+−−+≥ −−−−21

13

111 ;min1 .

Consequently, the rest part of proof is devoted to the determination of the constant 0>δ that satisfies(A6.14). For all 21)0),(( BBtx ∪∈ , it can be shown that:

CASE I: If ( ) 21131 )( cctxccxrx eqeq +<≤−++ − and eqxc −<13 then 31)2( ctx −=+

CASE II: If { })1(;min)()1( 131

2132 ccrcctxcrrxeq −++<<++ −− then 3

2 )1())(()2( crxtxrxtx eqeq +−−+=+

CASE III: If 21)( cctx +≥ and eqxc −<13 and 1213 −+≤ rccc then 31)2( ctx −=+

CASE IV: If 21)( cctx +≥ and )1()1(1 21

321 −++<<−+ − rcxrrcrcc eq then 32

21 )1(1)2( crrcrrctx +−+−+=+

CASE V: If none of the above holds then eqxtx =+ )2(

If CASE I is possible (i.e., if eqxc −<13 and 1213 −+< rccc ) then by virtue of the inequality 13 Rc > we must

necessarily have )1)(1( 13 eqxrc −−> − and consequently (A6.14) holds with

0)1())(1(: 11

31 >+−++= −− crcxr eqδ .

If CASE II is possible (i.e., if )( 13 cxrc eq −< and )()1( 2112

3 eqxccrrc −++< − ) then by virtue of the

inequality 23 Rc > we must necessarily have { }eqeq xcccxrc −+−−> 2113 ;min)1( and consequently (A6.14)

holds with { } 0)1(;min)1)(1()1(: 131

1213 >−−++−+−+−+= −eqeq xccrcxccrrcrδ .

If CASE III is possible (i.e., if eqxc −<13 and 1213 −+≤ rccc ) then by virtue of the inequality 33 Rc > we

must necessarily have 213 1 ccc −−> and consequently (A6.14) holds with 01: 321 >−++= cccδ .

If CASE IV is possible (i.e., if )1()1(1 21

321 −++<<−+ − rcxrrcrcc eq ) then by virtue of the inequality 43 Rc >

we must necessarily have )1()1)(1( 2211

3 −+++−> − rcccrrc and consequently (A6.14) holds with0)1)(1()1(: 2213 >−−−−++= rcccrcrδ .

If two or more cases are possible then the constant 0>δ that satisfies (A6.14) may be selected as the minimumof the corresponding constants given for each case. Thus property (A6.2) is proved.

Property (A6.2) implies that the −ω limit set of the bounded set ],0[]1,1[ 32 crc ×− is the equilibrium set],0[}{ 3cxeq × . Moreover, notice that for every initial condition ],0[),0())0(),0(( 3cyx ×+∞∈ we have

],0[]1,1[))1(),1(( 32 crcyx ×−∈ . By virtue of Definitions 1.7.1, 1.8.4 and Theorem 1.7.2 in Stuart andHumphries (1998), we conclude that the equilibrium set ],0[}{ 3cxeq × is a global attractor for the closed-loop

system (A4.2) with ))((1)( 1 txfxtu eq −−= . The proof is complete. <

21

References

Arzac, E. R., 1979. An Econometric Evaluation of Stabilization Policies for the U.S. Grain Market. WesternJournal of Agricultural Economics, 9-22.

Brennan, J. M., 1958. The supply of storage. The American Economic Review, 48, 50-72.Brennan, D., 2003. Price dynamics in the Bangladesh rice market: implications for public intervention.

Agricultural Economics, 29, 15-25.Collery, A., 1955. Expected price and the cobweb theorem. The Quarterly Journal of Economics, 69, 315-317.Deaton, A., Laroque, G., 1992. On the behavior of commodity prices. Review of Economic Studies, 59, 1-23.Dorosh, P., Shahabuddin, Q., 2002. Rice stabilization in Bangladesh: an analysis of policy options. Washington

DC: IFPRI, MSSD Discussion Paper 46.He, X. Z., Westerhoff, F. H., 2005. Commodity markets, price limiters and speculative price dynamics. Journal

of Economic Dynamics and Control, 29, 1577-1596.Hommes, C. H., 1994. Dynamics of the cobweb model with adaptive expectations and nonlinear supply and

demand. Journal of Economic Behavior and Organization, 24, 315-335.Hommes, C. H., 1998. On the Constistency of Backward-Looking Expectations: The Case of the Cobweb.

Journal of Economic Behavior and Organization, 33, 333-362.Jha, S., Srinivasan V. P., 1999. Grain price stabilization in India: evaluation of policy alternatives. Agricultural

Economics, 21, 93-108.Jha, S., Srinivasan, V. P., 2001. Food inventory policies under liberalized trade. International Journal of

Production Economics, 71, 21-29.Jiang, Z.P., Wang Y., 2002. A converse Lyapunov theorem for discrete-time systems with disturbances. Systems

and Control Letters, 45(1), 49-58.Kaldor, N., 1939. Speculation and economic stability. The Review of Economic Studies, 7, 1-27.Keynes, J. M., 1938. The policy of government storage of food-stuffs and raw materials. The Economic Journal,

48, 449-460.Krugman, P., 2000. A drop in the barrel ? The New York Times, 27/09/2000.Lakshmikantham, V., Trigiante D., 2002. Theory of difference equations. Numerical methods and applications.

2nd Edition, Marcel Dekker.Larson, D., Varangis, P., Yabuki, N., 1998. Commodity risk management and development. World Bank Policy

Research Working Paper No 1963.Makki, S., Tweeten, L., Miranda, M., 2001. Storage-trade interactions under uncertainty: Implications for food

security. Journal of Policy Modelling, 23, 127-140.Miranda, J. M., Glauber, W. J. ,1993. Estimation of dynamic nonlinear rational expectations models of primary

commodity markets with private and government stockholding. The Review of Economics and Statistics, 75,463-470.

Miranda, J. M., Helmberger, P., 1988. The effects of commodity price stabilization programs. The AmericanEconomic Review, 78, 46-58.

Newbery, M. D., Stiglitz, E. J., 1981a. The theory of commodity price stabilization. Oxford University Press.Newbery, M. D., Stiglitz, E. J., 1982. Optimal commodity stock-piling rules. Oxford Economic Papers, New

Series, 34, 403-427.Newbery, M. D., 1989. The theory of food price stabilization. The Economic Journal, 99, 1065-1082.Nickols, L. A., Zeckhauser, J. R., 1977. Stockpiling strategies and cartel prices. The Bell Journal of Economics,

8, 66-96.Osborne, T., 2004. Market news in commodity price theory: applications to the Ethiopian grain market. Review

of Economic Studies, 17, 133-164.Porter, R. S., 1950. Buffer Stocks and Economic Stability. Oxford Economic Papers, New Series, 2, 95-118.Sontag, E.D., 1998. Mathematical control theory. 2nd Edition, Springer-Verlag, New York.Srinivasan, V. P., Jha, S., 2001. Liberalized trade and domestic price stability: the case of rice and wheat in

India. Journal of Development Economics, 65, 417-441.Stuart, A.M., Humphries, A.R., 1998. Dynamical systems and numerical analysis. Cambridge University Press.Teisberg, J. T., 1981. A dynamic programming model of the U.S. strategic petroleum reserve. The Bell Journal

of Economics, 12, 526-546.Tsinias, J., Kotsios, S., Kalouptsidis, N., 1989. Topological dynamics of discrete-time systems. Proc. of MTNS,

Birkhauser, Basle, II, 1989, 457-463.Tsinias, J., 1989. Stabilizability of discrete-time nonlinear systems. IMA Journal of Mathematical Control and

Information, 1989, 135-150.U.S. Department of Energy. Office of Fossil Energy. August 2005. Available: www. fe.doe.gov/programs/reserves.htmlU.S. Department of Energy. Office of Fossil Energy. September 2005. Available:

www.fe.doe.gov/news/techlines/2005/tl_spr_drawdown2005_1.html

22

Umali-Deininger, D., Deininger, K., 2001. Towards greater food security for India’s poor: balancing governmentintervention and private competition. Agricultural Economics, 25, 321-335.

Van Groenendaal, W., Vingerhoets, J., 1995. Can International Commodity Agreements Work ?. Journal ofPolicy Modeling, 17, 257-278.

Working , H., 1949. The theory of price of storage. The American Economic Review, 39, 1254-1262.Wright, B., Williams, J., 1982a. The roles of public and private storage in managing oil import disruptions. The

Bell Journal of Economics, 13, 341-353.Wright, B., Williams, J., 1982b. The economic role of commodity storage. The Economic Journal, 92, 596-614.Wright, B., Williams, J., 1988. The incidence of market-stabilizing price support schemes. The Economic

Journal, 98, 1183-1198.