powerpoint on factors that contribute saving behavior among students of UiTM Malacca City campus

27

STUDY ON FACTORS THAT CONTRIBUTE SAVING BEHAVIOR AMONG STUDENTS OF UiTM MALACCA CITY CAMPUS PREPARED BY : NURDALINA BINTI ASMAWI 2012559583

Transcript of powerpoint on factors that contribute saving behavior among students of UiTM Malacca City campus

STUDY ON FACTORS THAT CONTRIBUTE SAVING BEHAVIOR AMONG STUDENTS OF UiTM MALACCA CITY CAMPUS

PREPARED BY :NURDALINA BINTI ASMAWI

2012559583

BACKGROUND OF THE STUDY According to Harrod (1939) and Domar (1946), the ability to save is depend on the speed of economic growth because high savings rate will drive up the rate of investment and consequently stimulates economic growth.

By referring the ethnic group in Malaysia, Malay citizen has highest percentage of bankruptcy cases for year 2012 follow by Chinese, Indian and Others. This situation is not a good sign for a developing country like Malaysia, since it might affects the economic performance of the country in the long term.

According to Ulkumen, Thomas, & Morwitz (2008) wrong prediction in spending may cause insufficient saving. While, lapses in self-control (Baumeister, 2002), 0ver emphasis on the present rather than the future (Lynch & Zauberman, 2006), or culture effects (Briley & Aker, 2006) also can be a factor that influence insufficient saving. Other than lack of saving awareness, Malaysians also poor in managing their financial that make them incurred into debts due to over use in credit card, lack of budgeting, overspending, inadequate shopping and lack of knowledge about money.

PROBLEM STATEMENT According to the Nellie Mae Annual report (2002) surprisingly, the Chinese students have the lowest level of financial skills even though Chinese were generally economically better than other ethnic groups. Indian students have the highest level and Malaysian students are in the average level.

According to Joo (2008) investigate that financial problems are the direct output of financial behavior like saving behavior, however, it is assumed that financial behavior by mediating with financial problems can influence financial satisfaction.

according to Masud (2004) and Sabri (2008) revealed that, university students are experiencing financial problems due to the lack of financial literacy. University students report having high debt, serious credit card usage, and high stress, as well as low financial satisfaction due to the lack of financial management skills (Holub, 2002; Nellie, 2002; Norvilitis et al., 2006; Norvilitis et al., 2003).

RESEARCH OBJECTIVE1) To examine the relationship between

financial literacy and saving behavior among students of UiTM Malacca city campus.

2) To analyze the relationship between parental socialization and saving behavior among students of UiTM Malacca city campus.

3) To investigate the relationship between

peer influence and saving behavior among students of UiTM Malacca city campus.

4) To determine the relationship of self-control and saving behavior among students of UiTM Malacca city campus.

RESEARCH QUESTION1) Does financial literacy affects saving

behavior among students of UiTM Malacca city campus?

2) Does parent socialization affect saving

behavior among students of UiTM Malacca city campus?

3) Does peer influence affects saving behavior

among students of UiTM Malacca city campus?

4) Does self-control affects saving behavior

among students of UiTM Malacca city campus?

THEORETICAL FRAMEWORK INDEPENDENT VARIABLES

DEPENDENT VARIABLE

Saving Behavior

Parental socialization

Peer influence

Self-control

Financial literacy

adapted from the framework developed by Lim et al.,(2011) and serve as the foundation of this study.

HYPOTHESESHYPOTHESIS 1H1: There is a relationship between financial literacy and saving behaviorH0: There is no relationship between financial literacy and saving behavior

HYPOTHESIS 2H1: There is a relationship between parental socialization and saving behaviorH0: There is no relationship between parental socialization and saving behaviorHYPOTHESIS 3H1: There is a relationship between peer influence and saving behaviorH0: There is no relationship between peer influence and saving behaviorHYPOTHESIS 4H1: There is a relationship between self-control and saving behaviorH0: There is no relationship between self-control and saving behavior

LITERATURE REVIEW

AUTHOR & YEAR VARIABLE EXPLANATION

Garman & Forgue (2006)

Financial literacy

financial knowledge is knowledge of facts, concepts, principles, and technological tools that is fundamental to being smart about money.

Webley & Nyhus (2006)

Parental Socializatio

n

The effect of parental influence to children’s saving, also found out that socialization of the importance of saving during childhood do influence the children economic behavior during adulthood.

AUTHOR & YEAR VARIABLE EXPLANATION

John (1999)

Peer Influence

Peers can be an additional source of financial socialization after parents that become a primary roles and direct source of financial practices.

prislin & wood(2005),webley & nyhus,

wood(2000),

bem(1972), wyer &

albarracin(2005)

Self-control

Influences such as social persuasion, perception of self-behavior and the motives or values that an individual holds will change an individual’s attitude from time to time

AUTHOR & YEAR VARIABLE EXPLANATION

Salikin, et al. (2012)

Saving behavior

The problems of doing saving in university life, such as the uncertain about where the money spent, or even about taking money from parents or others without permission for the spending that driven by their desires than their economic needs.

RESEARCH METHODOLOGY

RESEARCH DESIGN: Descriptive Study

POPULATION: Student of UiTM Malacca City Campus) - 200

SAMPLE SIZE: 200 respondents

(158/200)

SAMPLING TECHNIQUE: Simple random sampling- Non-Probability

DATA COLLECTION METHOD:

-Primary dataQuestionnaire -Secondary dataExternal sources

DATA ANALYSIS: SPSS version 20

SUMMARY OF RESPONDENT PROFILE

48%52%

GENDER

Male

Female

Figure 4.1: Percentage of Respondents based on Gender

Figure 4.1 shows that majority of the respondents are female (52%) while male (48%) represents the minority

3%

31%

61%

5%

Age

18 years old and below19 - 20 years old21 - 22 years old23 years old and above

Figure 4.2: Percentage of Respondents based on Age

Figure 4.2 shows that majority of the respondents fall into the age group of 21 to 22 years old (61%).

-Followed by the age group of 19 to 20 years old (31%) and 23 years old and above (5%). Meanwhile, there is only 3% of the respondents fall into the age group of18 years old and below.

Figure 4.3: Percentage of Respondents based on marital status

95%

5%

Marital status

Single

Married

Figure 4.3 demonstrates that almost all the respondents (95%) are single whereas only 5% of respondents are married.

Figure 4.4: Percentage of Respondents based on Course of Study

68%

32%

Course of study

Business

Non - Business

According to figure 4.4, the respondents who enrolled in business course (68%) are more than those who enrolled in non- business course (32%)

Figure 4.5: Percentage of Respondents based on Monthly Allowance Received from Parents

29%

42%

20%

3%6%

Monthly allowance received from parents

RM0 - RM200RM201 - RM500RM501 - RM800 RM801 - RM1000more than RM1000

Based on the chart above, most of the respondents receive allowance less than RM500 (42%) per month from their parents, followed by allowance received between RM0 – RM200 (29%) and RM501 – RM800 (20%).

-Result shows that only small portion of respondents receive substantial allowance from their parents more than RM1000 (6%) whereby only 3% of them fall into range of RM801 – RM1000.

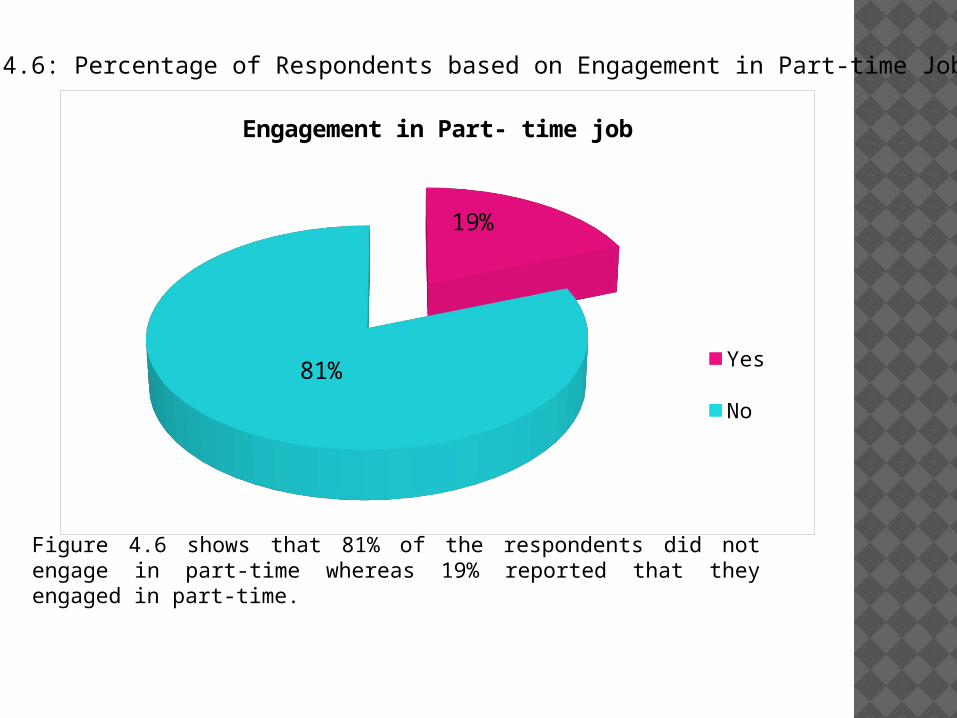

Figure 4.6: Percentage of Respondents based on Engagement in Part-time Job

19%

81%

Engagement in Part- time job

Yes

No

Figure 4.6 shows that 81% of the respondents did not engage in part-time whereas 19% reported that they engaged in part-time.

INTERNAL CONSISTENCY BY UMA SEKARAN AND BOUGIE

(2013)

RANGE OF INTERNAL CONSISTENCY RESULT

Less than 0.60 Poor

In the 0.70 range Acceptable

Over 0.80 Good

RELIABILITY TEST

Construct Cronbach's

Alpha

Number of

Items

relationshi

p

Financial

Literacy (IV1).833 5

Very good

Parental

Socialization

(IV2)

.705 4

good

Peer Influence

(IV3).709 5

good

Self-control

(IV4).744 4

good

Saving Behavior

(DV).779 5

good

DESCRIPTIVE ANALYSIS

N Minimum Maximum Mean Std. Deviation

MeanFIN 158 1.00 5.00 3.5000 .71016

MeanPAR 158 1.60 5.00 3.6924 .53923

MeanPEER 158 2.00 4.60 3.2797 .58165

MeanSELF 158 1.00 7.20 3.0342 .76590

MeanSAVING 158 2.20 5.00 3.7025 .61062

Valid N (listwise) 158

THE TABLE 4.1 SHOWS DESCRIPTIVE ANALYSIS OF FINANCIAL LITERACY, PARENTAL SOCIALIZATION, PEER INFLUENCE, AND SELF CONTROL (INDEPENDENT VARIABLES) AND SAVING BEHAVIOR (DEPENDENT VARIABLE). IN DESCRIPTIVE ANALYSIS, PARENTAL SOCIALIZATION HAS A HIGHEST MEAN WHICH IS 3.6924. IT INDICATES THAT PARENTAL SOCIALIZATION HAVE A STRONGEST INFLUENCE TOWARDS SAVING BEHAVIOR AMONG STUDENT OF UITM MALACCA CITY CAMPUS. MOREOVER, FINANCIAL LITERACY HAS A SECOND HIGHER WHICH IS 3.5000. IT INDICATES THAT FINANCIAL LITERACY HAS A STRONG INFLUENCE TOWARD SAVING BEHAVIOR AMONG STUDENT OF UITM MALACCA CITY CAMPUS. THUS, PEER INFLUENCE HAD MEAN WHICH IS 3.2797. IT INDICATES THAT FINANCIAL LITERACY HAS A STRONG INFLUENCE TOWARD SAVING BEHAVIOR AMONG STUDENT OF UITM MALACCA CITY CAMPUS. LASTLY SELF CONTROL HAD MEAN WHICH IS 3.0342. IT INDICATES THAT FINANCIAL LITERACY HAS A STRONG INFLUENCE TOWARD SAVING BEHAVIOR AMONG STUDENT OF UITM MALACCA CITY CAMPUS.

PEARSON CORRELATION ANALYSIS

Saving Behavior (DV)

Financial Literacy

(IV1)

Pearson Correlation .477**

Sig. (2-tailed) .000

Parental Socialization

(IV2)

Pearson Correlation .462**

Sig. (2-tailed) .000

Peer Influence (IV3)

Pearson Correlation .237**

Sig. (2-tailed) .003

Self Control (IV4)

Pearson Correlation .223**

Sig. (2-tailed) .004

Saving Behavior (DV)

Pearson Correlation 1

Sig. (2-tailed)

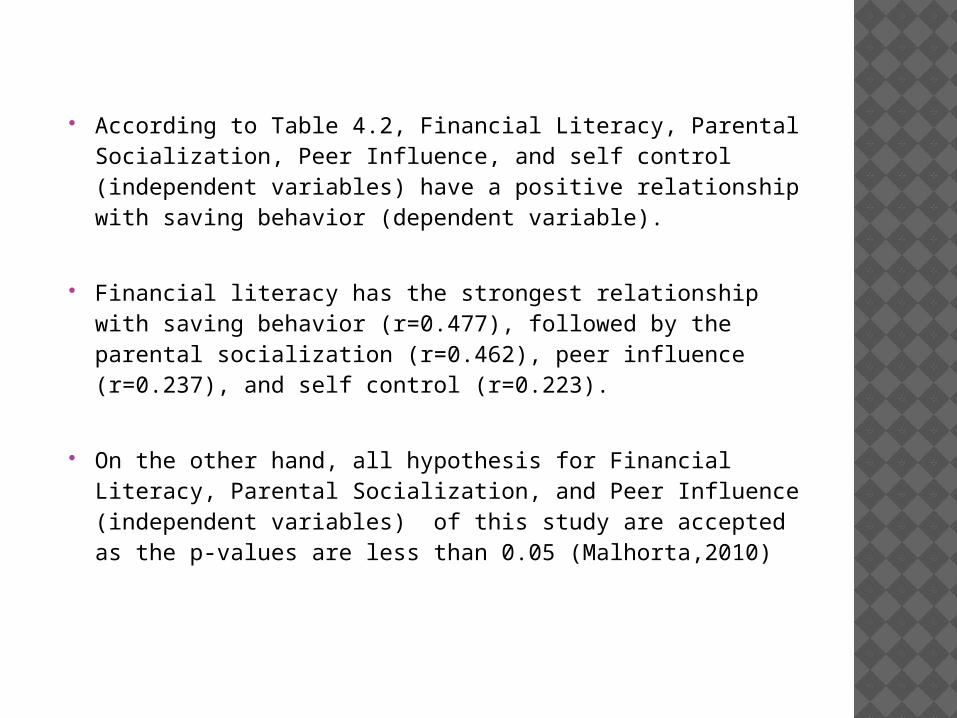

According to Table 4.2, Financial Literacy, Parental Socialization, Peer Influence, and self control (independent variables) have a positive relationship with saving behavior (dependent variable).

Financial literacy has the strongest relationship with saving behavior (r=0.477), followed by the parental socialization (r=0.462), peer influence (r=0.237), and self control (r=0.223).

On the other hand, all hypothesis for Financial Literacy, Parental Socialization, and Peer Influence (independent variables) of this study are accepted as the p-values are less than 0.05 (Malhorta,2010)

CONCLUSION

As a conclusion, all the four factors or independent variables of this research study affect on saving behavior among students of UiTM Malacca City campus

The result indicate that parental socialization is the most influential factors that contribute on saving behavior among students of UiTM Malacca City campus

From the finding, all the independent variables (financial literacy, parental socialization, peer influence, and self-control) have a positive and significant relationship with saving behavior

RECOMMENDATION

Provide a Telecommuting working style at PDB

Future studies should focus on workload or work stress and job satisfaction

Separate the staff category within the company to analyze specific category on job satisfaction

Study on relationship between political at workplace and job satisfaction

To extend study to find other factors that will lead towards job satisfaction at PDB

THANK YOU !