„Post-IBOR float legs“: ISDA Fallbacks - d-fine

23

„Post-IBOR float legs“: ISDA Fallbacks Digest of the mechanics Frankfurt, 20.09.2020

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of „Post-IBOR float legs“: ISDA Fallbacks - d-fine

„Post-IBOR float legs“:ISDA Fallbacks

Digest of the mechanics

Frankfurt, 20.09.2020

Agenda

0301 ISDA – Fallbacks: Introduction

0502 ISDA Fallbacks – Digest of the mechanics

1003 Discussion – Implementing the mechanics

1204 Appendix: Bloomberg Tickers

Note: The mechanics are presented as of 20.09.2020. Methodological changes by ISDA etc. should be followed carefully as thethe final publicaton of the amendments to the ISDA definitions is still outstanding.

Target Post-IBOR float legs and transtion paths– the two key points for legacy IBOR derivatives

This presentation covers the mechanics of the “Post-IBOR float leg” in plain vanilla swaps resulting from ISDA Fallback rules, pointing out various subtleties. It does not detail the transition path or other products.

Fallback triggered by (pre-)cessation events etc.

vs.

Active migration of legacy trades into deliberately chosen structures

Strategy to be chosen by institution

Transition paths

How do new standard market conventions look like?

How do the legs resulting from fallbackslook like?

How do conventions relate to each other (fallback to new products, derivatives to loans to MTNs etc.)?

Target Post-IBOR float leg

Legacy IBOR derivatives

ISDA Fallbacks© 2020 d-fine 3

ISDA – Fallbacks: Introduction

FOOD 4 THOUGHT: ISDA FALLBACKS

01

Introducing ISDA Benchmark Fallbacks in four basic points

The principle of the ISDA Benchmark Fallbacks is straightforward: one LIBOR fixing, one Fallback fixing. However, some subtleties of the mechanics need careful consideration.

ISDA Fallbacks

Cessation of an IBOR corrupts ISDA master agreement (MA) governed IBOR referencing trades.

ISDA will provide Fallback clauses in its 2006 ISDA definitions

via a supplement for new trades,

via a protocol for legacy trades.

What is provided by ISDA?

Every day Bloomberg publishes for none, one or several IBOR Fixing dates and all relevant tenors:

the Adjusted Reference Rate,

the Fallback Spread,

the “all-in” Fallback Rate.

What is the role of Bloomberg?

The Fallback Rate is the sum of:

Adjusted Reference Rate (ARR): RFRcompounded in-arrears over the respective IBOR tenor anchored by the IBOR Fixing date,

Fallback Spread: 5-year median ARR/ IBOR-basis, fixed prior to cessation.

What is the Fallback Rate?

Upon cessation of an IBOR, the floating rate option (FRO) referenced in the trade is replaced by a Fallback Rate.

Thereby interest rate periods, payment dates and fixing dates are kept, only the mechanics “under the hood” of the FRO in the ISDA MA are changed.

How do Fallback clauses work?

ISDA Fallbacks© 2020 d-fine 5

01.00 ISDA – Fallbacks: Introduction

ISDA Fallbacks – Digest of themechanics

FOOD 4 THOUGHT: ISDA FALLBACKS

02

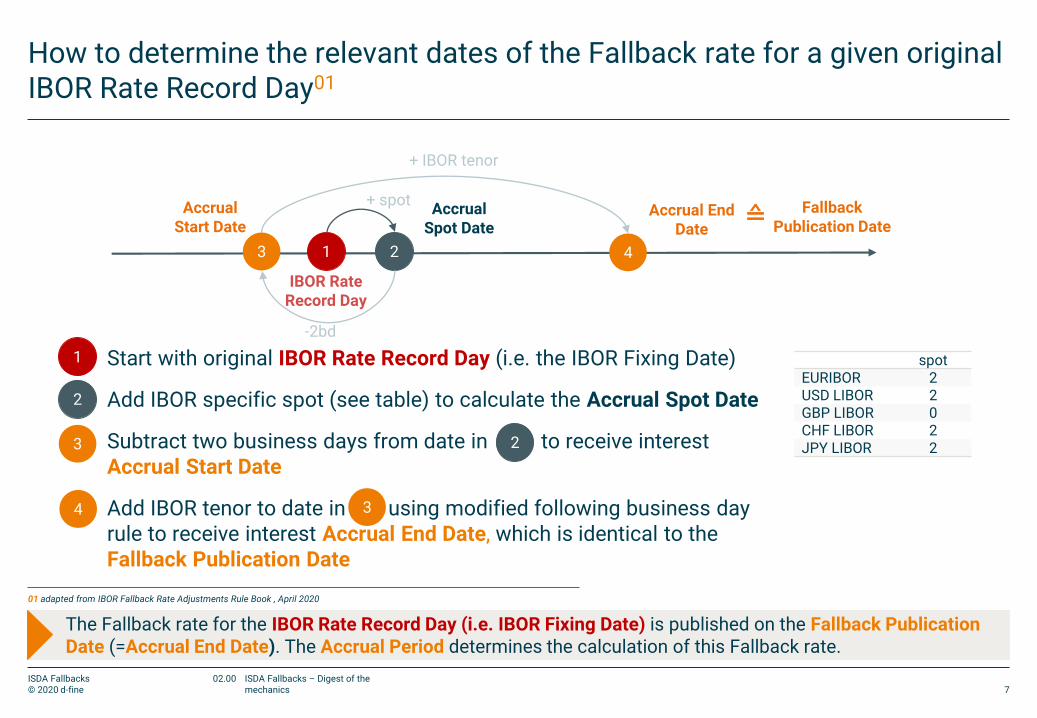

How to determine the relevant dates of the Fallback rate for a given original IBOR Rate Record Day01

The Fallback rate for the IBOR Rate Record Day (i.e. IBOR Fixing Date) is published on the Fallback Publication Date (=Accrual End Date). The Accrual Period determines the calculation of this Fallback rate.

1 23

spotEURIBOR 2USD LIBOR 2GBP LIBOR 0CHF LIBOR 2JPY LIBOR 2

1. Start with original IBOR Rate Record Day (i.e. the IBOR Fixing Date)

2. Add IBOR specific spot (see table) to calculate the Accrual Spot Date

3. Subtract two business days from date in to receive interest Accrual Start Date

4. Add IBOR tenor to date in using modified following business day rule to receive interest Accrual End Date, which is identical to the Fallback Publication Date

2

3

3

2

1

4

Accrual Start Date

Accrual End Date

4

FallbackPublication Date

≙Accrual Spot Date

01 adapted from IBOR Fallback Rate Adjustments Rule Book , April 2020

ISDA Fallbacks© 2020 d-fine 7

02.00 ISDA Fallbacks – Digest of the mechanics

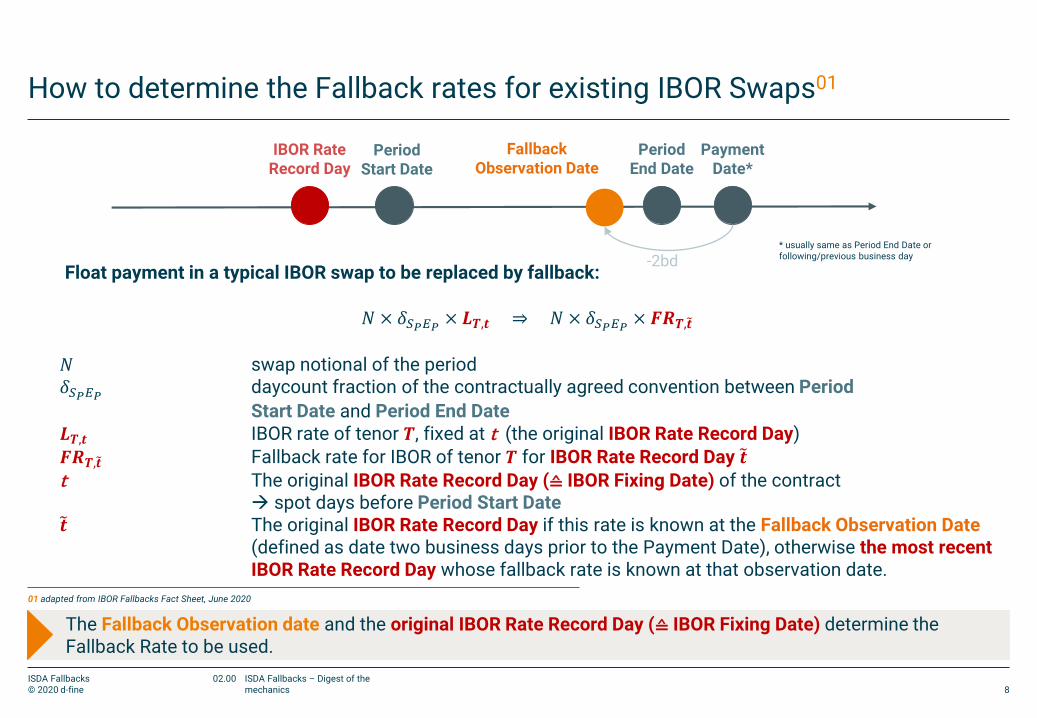

How to determine the Fallback rates for existing IBOR Swaps01

The Fallback Observation date and the original IBOR Rate Record Day (≙ IBOR Fixing Date) determine the Fallback Rate to be used.

Float payment in a typical IBOR swap to be replaced by fallback:

𝑁 × 𝛿𝑆𝑃𝐸𝑃 × 𝑳𝑻,𝒕 ⇒ 𝑁 × 𝛿𝑆𝑃𝐸𝑃 × 𝑭𝑹𝑻,𝒕

𝑁 swap notional of the period𝛿𝑆𝑃𝐸𝑃 daycount fraction of the contractually agreed convention between

and 𝑳𝑻,𝒕 IBOR rate of tenor 𝑻, fixed at t (the original IBOR Rate Record Day)𝑭𝑹𝑻,𝒕 Fallback rate for IBOR of tenor 𝑻 for IBOR Rate Record Day 𝒕

t The original IBOR Rate Record Day (≙ IBOR Fixing Date) of the contract spot days before

𝒕 The original IBOR Rate Record Day if this rate is known at the Fallback Observation Date (defined as date two business days prior to the Payment Date), otherwise the most recentIBOR Rate Record Day whose fallback rate is known at that observation date.

* usually same as Period End Date orfollowing/previous business day

FallbackObservation Date

01 adapted from IBOR Fallbacks Fact Sheet, June 2020

ISDA Fallbacks© 2020 d-fine 8

02.00 ISDA Fallbacks – Digest of the mechanics

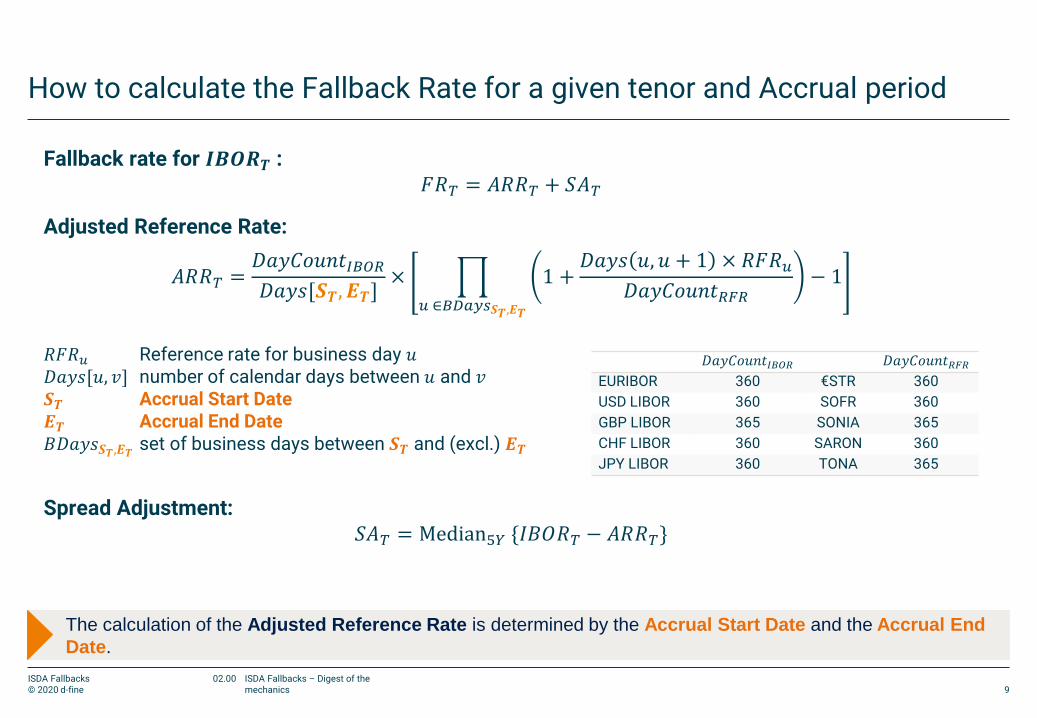

How to calculate the Fallback Rate for a given tenor and Accrual period

The calculation of the Adjusted Reference Rate is determined by the Accrual Start Date and the Accrual End

Date.

Fallback rate for 𝑰𝑩𝑶𝑹𝑻 :𝐹𝑅𝑇 = 𝐴𝑅𝑅𝑇 + 𝑆𝐴𝑇

Adjusted Reference Rate:

𝐴𝑅𝑅𝑇 =𝐷𝑎𝑦𝐶𝑜𝑢𝑛𝑡𝐼𝐵𝑂𝑅𝐷𝑎𝑦𝑠[𝑺𝑻, 𝑬𝑻]

× ෑ

𝑢 ∈𝐵𝐷𝑎𝑦𝑠𝑺𝑻,𝑬𝑻

1 +𝐷𝑎𝑦𝑠 𝑢, 𝑢 + 1 × 𝑅𝐹𝑅𝑢

𝐷𝑎𝑦𝐶𝑜𝑢𝑛𝑡𝑅𝐹𝑅− 1

𝑅𝐹𝑅𝑢 Reference rate for business day 𝑢𝐷𝑎𝑦𝑠[𝑢, 𝑣] number of calendar days between 𝑢 and 𝑣𝑺𝑻 Accrual Start Date𝑬𝑻 Accrual End Date𝐵𝐷𝑎𝑦𝑠𝑺𝑻,𝑬𝑻 set of business days between 𝑺𝑻 and (excl.) 𝑬𝑻

Spread Adjustment:𝑆𝐴𝑇 = Median5𝑌 {𝐼𝐵𝑂𝑅𝑇 − 𝐴𝑅𝑅𝑇}

𝐷𝑎𝑦𝐶𝑜𝑢𝑛𝑡𝐼𝐵𝑂𝑅 𝐷𝑎𝑦𝐶𝑜𝑢𝑛𝑡𝑅𝐹𝑅EURIBOR 360 €STR 360

USD LIBOR 360 SOFR 360

GBP LIBOR 365 SONIA 365

CHF LIBOR 360 SARON 360

JPY LIBOR 360 TONA 365

ISDA Fallbacks© 2020 d-fine 9

02.00 ISDA Fallbacks – Digest of the mechanics

Fallback publication details – example of what is published on a given fallback rate publication date

The fallback rates will have two dates associated with it

The Rate Record Day (Original IBOR fixing date)

Fallback rate publication date

It can happen that on a certain day no, one or several fallback rates (with different IBOR publication dates) are published

Example: IBOR rate is GBP LIBOR 1M. Bloomberg will publish:

No fallback rates on 12.05 since 12.04 is not a business day

One fallback rate on 13.05 with corresponding GBP LIBOR 1M reset date 15.04. (15.04. was the original IBOR Fixing date of the contract)

Two fallback rates on 11.05 with corresponding GBP LIBOR 1M reset dates 13.04 and 14.04 (choose the fixing whose associated date corresponds to the original IBOR fixing date of the contract)

ISDA Fallbacks© 2020 d-fine 10

02.00 ISDA Fallbacks – Digest of the mechanics

Discussion –Implementing the mechanics

FOOD 4 THOUGHT: ISDA FALLBACKS

03

Food for thought – points to consider when implementing ISDA Fallbacks front2back

A thorough discussion along the front2back chain is necessary. Note that the points above in no way claim completeness or comprehensiveness.

Fallback Rates as separate Indices?

Ability to apply fixings:

Identification of corresponding publication dates,

Triggering fixings at publication dates.

Life cycle events (e.g. partial term.)

Trade Life Cycle/ Cashflows

How to calculate forwards after the cessation event?

Integrate dedicated forward curves in curve universe (all-in?)? Implement full Fallback algorithm?

How to calculate accruals?

Fallbacks in complex models?

Valuation/ Curve building

Ability to feed and distribute several Fallback Rates (Rate reference day/ fixing) at a given day

Adjusted Reference Rate, Fallback Spread and all-in to be provided?

Irregular tenors to be provided centrally?

Market Data supply

Zero curve or spread curve setup?

Just OIS as risk factor? Separate “forward” and “discount” risk factors?

Realized vs. unrealized CFs (P&L)?

Basis risk to plain OIS leg

Spread in IR risk

Market Risk Measurement

ISDA Fallbacksfront2back

ISDA Fallbacks© 2020 d-fine 12

03.00 Discussion – Implementing the mechanics

Appendix

FOOD 4 THOUGHT: ISDA FALLBACKS

04

Bloomberg Tickersfor ISDA Fallback Rates

APPENDIX

04.01

Fallback rate data & tickers

Logic for GBP fallback tickers:

Index – BP0003M Index

Fallback Rate – FBP0003M Index

Fallback Spread – SBP0003M Index

Compounded RfR – SONIA3M Index

Bloomberg publishes compounded setting in arrears risk free rate, fallback spread adjustment and the all-in fallback rate (sum compounded risk free rate and fallback spread)

Overview of fallback rates for each index available at <FBAK> <GO> in Bloomberg Terminal

Example Quotes for GBP LIBOR on 08/06/20:

ISDA Fallbacks© 2020 d-fine 15

04.00 Appendix 04.01 Bloomberg Tickers for ISDA Fallback Rates

Other derivatives discussed by ISDA

APPENDIX

04.02

Derivatives in focus of ISDA aside the plain vanilla swap case

ISDA Fallback of legacy trades

Conventions for new products

The list is not exhaustive, only covering products in focus of ISDA.In particular exotic/structured IBOR derivatives need further attention.

FRAs

Swaps with period/tenor mismatch

Swaps with stubs

Swaps with early payment features

In-arrears swaps

Range Accruals

Cross Currency Swaps

CMS-products (ICE swap rate etc.)

Caps/Floors

Swaptions

ISDA Fallbacks© 2020 d-fine 17

04.00 Appendix 04.02 Other derivatives discussed by ISDA

d-fine and the Benchmark reform– selected references

APPENDIX

04.03

Overview on recent (and running) d-fine projects on the O/N- and IBOR-

transition

Implementation of the benchmark reform for interest rate in EUR for market and liquidity risk controllingLarge German banking

group

Pre-study on the impact and the need for action from international O/N-and IBOR-transitionGerman commercial bank

Training of the controlling (risk and finance) department concerning EONIA- and EURIBOR-transition/reform

German development

bank

Implementation of SOFR and €STR as indices and curves as well as introduction of a SOFR-linked FRNas new product

Large German commercial

bank

Support and advice in coping with EONIA/EURIBOR, SOFR/LIBOR etc. related need for actionSolution provider for

cooperative banks

Implementation of €STR and SOFR along the entire value chain (front2back)Large German commercial

bank

Support in the implementation of €STR and SOFR in settlement pricing and risk management and integration of ISDA fallbacks

Large CCP

ISDA Fallbacks© 2020 d-fine 19

04.00 Appendix 04.03 Selected references

Overview on recent (and running) d-fine projects on the O/N- and IBOR-

transition

Support in the planning, steering and delivery of the group-wide IBOR reform project, including setup of€STR FRN as new product and introduction of €STR/EURIBOR+ along the entire value chain (front2back)

Large German banking

group

Running support in the IBOR reform transformation project, including e.g. ECB “Dear CRO”-Letter and€STR/SOFR-curve implementation

German commercial bank

Support in the setup of €STR and SOFR curves in Front ArenaDutch asset manager

Support in the optimization of the FTP-models / FTP-framework, inter alia preparation of FTP in the post-

IBOR-world

European development

bank

Support in the bank-wide IBOR program, in particular introduction of €STR, SOFR and SONIA in

treasury and Risk (System Summit)German bank

Introduction of €STR curves and €STR products (System Front Arena)German bank

Introduction of RFR curves and RFR products (System SCD)Solution provider for

savings banks

ISDA Fallbacks© 2020 d-fine 20

04.00 Appendix 04.03 Selected references

Overview on recent (and running) d-fine projects on the O/N- and IBOR-

transition

Support of the project owner for the group-wide IBOR reform project

Consolidation and regular check/addition of the requirements as well as coordination of the completionof the several work streams

European development

bank

Support in the planning, steering and delivery of the group-wide IBOR reform project, including setup of RFR curves and products (System Summit and Algo) and establishment of impact analyses for switch and cessation events

Large Irish Bank

Support of the introduction of mortgages on SARON (daily compounding) in Quant-teamSwiss commercial bank

Extension of MoCA: introduction of the ESTR based valuation, scenarios and Value-at-RiskDeutsche development

bank

Planning of the introduction of SONIA-linked credit products

Adjustment of the interfaces from the bank‘s systems to Front ArenaGerman commercial bank

Production of ad-hoc analyses for the EONIA/ESTR transition (in RiskWatch)

Support during the NPP for several RFR related products, especially trials of new coupon structuresGerman commercial bank

Support in designing, implementing and testing new RFR curves and interest rate structures in WSSEuropean development

bank

ISDA Fallbacks© 2020 d-fine 21

04.00 Appendix 04.03 Selected references

Interested in further discussion?

Dr Sebastian SchneiderManagerTel +49 89 7908617-1308Mobile +49 162 2631540E-Mail [email protected]

Dr Hans Peter Waechter, CFA, FRMPartnerTel +49 89 7908617-488Mobile +49 162 2631356E-Mail [email protected]

Zürichd-fine AGBrandschenkestrasse 150CH-8002 Zü[email protected]

Wiend-fine Austria GmbHRiemergasse 14 Top 12A-1010 WienÖ[email protected]

Münchend-fine GmbHBavariafilmplatz 8D-82031 Grü[email protected]

Londond-fine Ltd6-7 Queen StreetLondon, EC4N 1SPUnited [email protected]

Frankfurtd-fine GmbHAn der Hauptwache 7D-60313 Frankfurt/[email protected]

Düsseldorfd-fine GmbHDreischeibenhaus D-40221 Dü[email protected]

Berlind-fine GmbHFriedrichstraße 68D-10117 [email protected]