Paula Johnson- Bacon - MPSC Electronic Docket Filings

165

August 5, 2021 Lisa Felice Executive Secretary Michigan Public Service Commission 7109 West Saginaw Highway Lansing, MI 48917 RE: In the matter of the application of DTE GAS COMPANY for authority to increase its rates, amend its rate schedules and rules governing the distribution and supply of natural gas, and for miscellaneous accounting authority MPSC Case No. U-20940 Dear Ms. Felice: Attached for electronic filing in the above captioned matter is DTE Gas Company’s Initial Brief along with a Proof of Service. Very truly yours, Paula Johnson-Bacon PJB/erb Attachments cc: Service List Paula Johnson-Bacon (313) 235-7052 [email protected] DTE Gas Company One Energy Plaza, 1635 WCB Detroit, MI 48226-1279

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Paula Johnson- Bacon - MPSC Electronic Docket Filings

August 5, 2021 Lisa Felice Executive Secretary Michigan Public Service Commission 7109 West Saginaw Highway Lansing, MI 48917 RE: In the matter of the application of DTE GAS COMPANY for authority to increase

its rates, amend its rate schedules and rules governing the distribution and supply of natural gas, and for miscellaneous accounting authority

MPSC Case No. U-20940 Dear Ms. Felice:

Attached for electronic filing in the above captioned matter is DTE Gas Company’s Initial Brief along with a Proof of Service.

Very truly yours,

Paula Johnson-Bacon PJB/erb Attachments cc: Service List

Paula Johnson-Bacon (313) 235-7052 [email protected]

DTE Gas Company One Energy Plaza, 1635 WCB Detroit, MI 48226-1279

STATE OF MICHIGAN

BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter of the application of ) DTE GAS COMPANY for authority to ) increase its rates, amend its rate ) Case No. U-20940 schedules and rules governing the ) distribution and supply of natural gas, ) and for miscellaneous accounting authority. ) )

DTE GAS COMPANY’S INITIAL BRIEF Dated: August 5, 2021

i

TABLE OF CONTENTS

I. INTRODUCTION ....................................................................................................... 1

II. HISTORY OF PROCEEDINGS ................................................................................. 4

III. JURISDICTION, STANDARD OF REVIEW AND RATE SETTING LAW. ......... 7

A. Jurisdiction and Standard of Review. ................................................................... 7

B. Ratemaking Principles Overview. ....................................................................... 10

IV. TEST YEAR. ............................................................................................................. 13

V. RATE BASE. ............................................................................................................. 14

A. Adjusted Total Rate Base .................................................................................... 14

B. Capital Expenditures. .......................................................................................... 14

1. Gas Delivery Plan (GDP) .................................................................................. 15

2. Routine Capital Spending ................................................................................. 16

a. Communications & Control - Meters ......................................................... 16

b. Service Renewals ......................................................................................... 19

c. Service Abandonments................................................................................ 20

d. New Market Attachments ........................................................................... 21

e. Service Alterations ...................................................................................... 22

f. Belle Isle Main Replacement ....................................................................... 24

g. System Reliability ........................................................................................ 24

h. Routine Transmission Plant........................................................................ 25

3. Gas Information Technology (IT) Spending .................................................... 27

4. Large Capital Projects. ..................................................................................... 32

a. TCARP ........................................................................................................ 33

b. Van Born ..................................................................................................... 34

c. Middlebelt Deration Project ....................................................................... 35

d. East Jefferson Project ................................................................................. 37

5. Contingency....................................................................................................... 38

C. Working Capital .................................................................................................. 44

VI. RATE OF RETURN .................................................................................................. 46

A. Capital Structure ................................................................................................. 46

ii

B. Debt Cost Rates. ................................................................................................... 51

1. Long-Term Debt. .............................................................................................. 51

2. Short-Term Debt. .............................................................................................. 51

C. Return on Common Equity. ................................................................................ 52

1. CAPM and ECAPM Estimates ........................................................................ 54

2. DCF Estimates .................................................................................................. 57

3. Risk Premium Estimate .................................................................................... 58

4. DTE Gas’s Return on Equity in Relation to Risk ............................................ 58

5. The Connection Between Equity and Capital Structure ................................. 60

6. Summary and Recommendations Regarding DTE Gas’s Cost of Equity. ...... 60

D. Other Cost Rates. ................................................................................................. 61

E. Overall Rate of Return. ....................................................................................... 61

VII. ADJUSTED NET OPERATING INCOME AND OTHER REVENUE-RELATED ISSUES. .................................................................................................. 61

A. Throughput .......................................................................................................... 62

1. Weather Normalization. ................................................................................... 62

2. Customer Usage. ............................................................................................... 63

3. Exelon Energy Company (Exelon) ................................................................... 65

4. Cost of Gas. ....................................................................................................... 65

5. End-Use Transportation (EUT)........................................................................ 65

B. Midstream Revenue ............................................................................................. 68

C. Other Operating Revenue ................................................................................... 69

D. Operating and Maintenance (O&M) Expenses .................................................. 70

1. Inflation ............................................................................................................. 71

2. Storage, Transmission, and Distribution O&M Expenses. ............................ 72

a. TCARP ........................................................................................................ 72

b. Transmission Integrity Management Program (TIMP) ............................ 73 c. Maximum Allowable Operating Pressure (MOAP) Records Remediation

…………………………………………………………………………….....74

d. Pipeline Safety Management System (PSMS) ............................................ 75

e. Meter Abnormal Operating Condition (AOC) Initiative .......................... 76

3. Customer Service O&M Expenses. .................................................................. 76

a. Meter Reading ............................................................................................. 77

iii

b. Customer Service Representatives (CSRs) ................................................. 78

c. Merchant Fees ............................................................................................. 79

4. Marketing, and Administrative and General O&M Expenses. ....................... 80

a. Injuries and Damages ................................................................................. 81

b. Rent Expense for Shared Assets and Related Information Technology(IT) O&M Costs .......................................................................................... 81

c. Contingency ................................................................................................. 96

5. Employee Benefits Expenses ........................................................................... 100

a. Pension. ...................................................................................................... 100

b. Other Post-Employment Benefit (OPEB) Expense. ................................. 102

c. Active Employee Benefits. ......................................................................... 103

d. Other Employee Benefit Costs. ................................................................. 106

6. Employee Compensation. ............................................................................... 108

E. Manufactured Gas Plant (MGP) Remediation Expenses ................................. 114

F. Uncollectible Expense ........................................................................................ 115

G. Lost And Unaccounted For (LAUF) and Company Use (CU) Gas, and Gas-In-Kind (GIK) ......................................................................................................... 116

H. Depreciation and Amortization ......................................................................... 118

I. Property and Other Taxes ................................................................................. 118

J. Income Tax Expenses ........................................................................................ 118

VIII. OTHER ISSUES. ..................................................................................................... 118

A. Revenue Decoupling Mechanism (RDM) .......................................................... 119

B. Infrastructure Recovery Mechanism (IRM) ..................................................... 120

1. Gas Renewal Program (GRP - combined MRP and MMO). ........................ 122

2. Meter Assembly Check Meter Move-out (MAC MMO) Program. ............... 122

3. Pipeline Integrity (PI) Program. .................................................................... 123

C. Leak Backlog ...................................................................................................... 126

D. Research and Development Cost Recovery....................................................... 126

E. Demand Response (DR) ..................................................................................... 129

F. Advanced Metering Infrastructure (AMI) Benefits Reporting ........................ 130

G. Accounting Requests .......................................................................................... 131

IX. REVENUE DEFICIENCY AND REQUESTED RATE RELIEF. ........................ 135

X. RATE DESIGN AND TARIFF REVISIONS. ........................................................ 135

iv

A. Allocation of Revenue Deficiency ...................................................................... 135

B. High-pressure and low-pressure distribution main plant, and volume-by-type studies ................................................................................................................. 139

C. Tariff Changes for All Customers ..................................................................... 140

D. Tariff Changes for Sales Rate Schedules .......................................................... 141

1. Revised IRM. ................................................................................................... 141

2. Low-Income Energy Assistance...................................................................... 142

E. Tariff Changes for EUT Service ........................................................................ 144

F. Tariff Changes for Off-System Storage and Transportation Service .............. 148

G. Proposed Monthly Customer Charges and Rate Schedule Economic Break-Even Points ......................................................................................................... 148

XI. REQUEST FOR RELIEF ....................................................................................... 149

1

I. INTRODUCTION

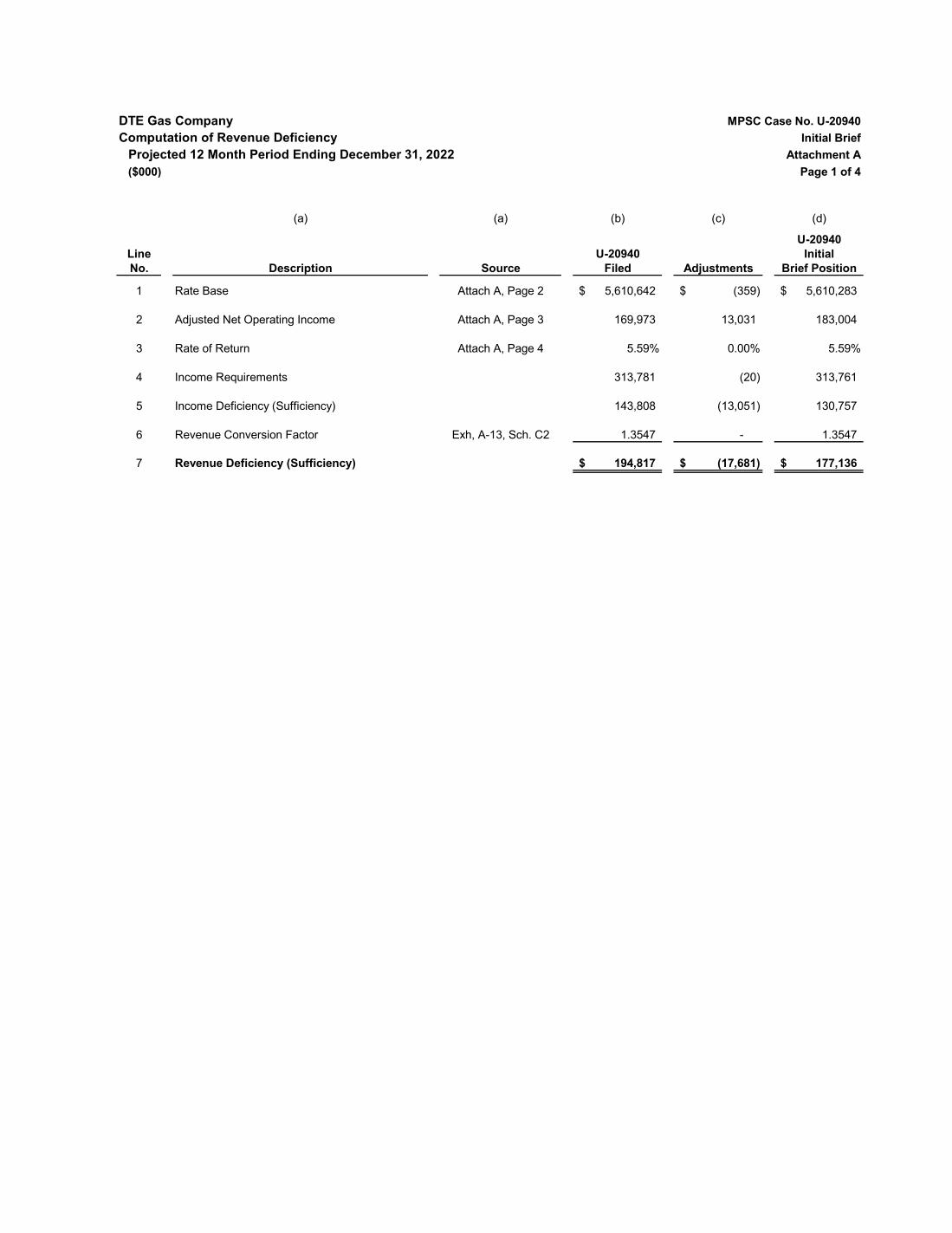

The filing of this case was driven by DTE Gas Company’s expected revenue shortfall of

$195 million for the Calendar year ended December 21, 2022. The real impact to customer rates

is about $157 million, since $38 million of this request will already have been recovered through

the Company’s existing Infrastructure Recovery Mechanism (“IRM”) surcharge that will terminate

when new base rates are established in this proceeding. Throughout the course of this case the

Company has agreed upon proposals or identified errors that have reduced its revenue deficiency

by $17.7 million to $177 million. The adjustments from its filed position are as follows:

Adjustments from Filed Position In millions1

Capital Expenditures O&M Service Renewal PPE / Vehicle Rental ($ 0.278) Uncollectible Expense ($ 2.4) Gas Information Technology ( 0.450) Transmission Right of way ( 2.0) TCARP Demand Charge ( 11.6) Shared Assets Customer Service ( 0.8) Shared Assets Other than

Customer Service ( 0.8)

Total Capital Expenditure Adj1 ($ 0.728) Total O&M Adjustments ($17.6)

DTE Gas filed its last application for rate relief on November 26, 2019. The Company

understands that the financial impacts of the Covid-19 pandemic are still lingering and was able to

delay filing a rate increase application in 2020 by controlling costs and implementing continuous

improvement to mitigate the impact of increasing operating costs. However, as we continue to

move forward, DTE Gas’s currently authorized rates will no longer be sufficient to provide the

level of safe and reliable service that the Company currently provides its customers.

1 Attachments A and B to this brief provide detailed calculations including tax impacts, half year convention and other resultant changes required to arrive at the final $17.7 million adjustment to the revenue requirement.

2

The Company has always had a positive economic impact on the communities it serves

and will continue to be a positive economic force during and after the pandemic by employing

over 1,800 employees, utilizing local contractors and vendors that also employ Michigan residents,

and continuing to pay millions of dollars in property taxes ($63 million in the 2019 historical test

year) to the cities and townships it serves. The rate relief requested in this case will allow the

Company to continue to provide economic support by sustaining employment and providing a

dependable revenue source to local communities. Additionally, although the low-income credit

proposals in this case do have an associated revenue increase, the increase in available credits will

provide added financial assistance to our most vulnerable customers.

The revenue request in this case is borne in large part out of a need to continue the

significant progress the Company has made in identifying and replacing its aging pipelines,

relocating customer meters from inside their homes to safer outside locations, create system

redundancies to improve reliability, increase security and resilience at gas facilities, reduce the

risk of catastrophic outages or damages, and enhance the Company’s safety programs. These

programs, and the resources required to support them, are necessary for the Company’s provision

of safe and reliable gas service now and into the future.

The Company has also presented a need for continued investment in its IT systems. The

investments made in this space are necessary to support all aspects of the Company’s operations

as well as general security and customer service programs. To create cost savings and efficiencies,

DTE Electric and DTE Gas share a substantial amount of IT resources. DTE Electric implements

these projects and DTE Gas pays DTE Electric for its proportionate share of the assets. Typically,

DTE Electric will receive approval in its general rate case for a particular level of Shared Asset IT

spending, which will flow through to DTE Gas’s next general rate case. This Shared Asset

3

reimbursement mechanism has been in place since the merger between MichCon and Detroit

Edison, and has been presented in DTE Gas’s prior rate cases at least since 2012. Due to the Covid-

19 pandemic and the electric company’s commitment to postpone its general rate case, the timing

of these asset approvals is out of sync. As a result, DTE Gas has presented evidence in this case to

support the increased Shared Asset charge resulting primarily from IT spending that will be

completed by DTE Electric for certain projects.

Inflation, primarily due to contracted wage increases and escalating contractor costs,

increased employee healthcare and benefit costs, and costs to comply with State and Federal

requirements are also driving the Company’s increased revenue requirement. These increased

costs, coupled with decreased sales due to energy waste reduction measures our customers are

implementing, lead to the rate relief requested in this case.

Last, as part of its rate structure, the Company is also requesting that the Commission

approve a well-balanced capital structure and sufficient return on equity to ensure that DTE Gas

maintains full access to capital at reasonable rates, terms, and conditions. Without solid financial

health, the Company’s cost of providing utility services to its customers could increase

significantly. The Company’s proposed return on equity of 10.25% is also necessary to ensure that

DTE Gas continues to be an attractive investment in the marketplace. Any decrease in the

Company’s capital structure will require a corresponding increase in return on equity to maintain

the Company’s financial health.

Each component of DTE Gas’s revenue requirement is supported by hundreds of pages of

testimony, 36 exhibits with multiple schedules, volumes of workpapers that were provided to Staff

and all intervenors at the outset of this case, and responses to more than 1,717 discovery requests

4

and 244 audit requests. The Company’s projected costs are reasonable and necessary as

contemplated by the laws governing utility rate setting and should be approved by the Commission.

II. HISTORY OF PROCEEDINGS

DTE Gas Company (DTE Gas or the Company) is presently serving its retail natural gas

transportation, storage and distribution customers under rates, terms and conditions established in

the Michigan Public Service Commission’s (MPSC or Commission) August 20, 2020 Order in

Case No. U-20642 that approved a settlement agreement related to general service rate relief and

other associated matters. On February 12, 2021, DTE Gas filed its Application (amended February

15, 2021), direct testimony, and exhibits with the Commission requesting to raise revenues by

approximately $195 million annually ($157 million net of the infrastructure surcharge that is

already reflected in rates). By February 24, 2021, DTE Gas published notice of its above request.

On March 11, 2021, a pre-hearing conference was held by Administrative Law Judge Sally

L. Wallace (the ALJ) who granted petitions to intervene filed by the Association of Businesses

Advocating Tariff Equity (ABATE); the Michigan Attorney General (AG); Citizens Utility Board

of Michigan (CUB); Dearborn Industrial Generation LLC (DIG); Detroit Thermal, LLC (Detroit

Thermal); Energy Michigan; Michigan Power Limited Partnership (MPLP); Residential Customer

Group (RCG); Retail Energy Supply Association (RESA); and Verso Corporation (Verso). Staff

also participated at the pre-hearing conference and a case schedule was established in accordance

with the March 4, 2021 Order in Case Nos. U-20940 and U-20962 (1T 8). On March 23, 2021,

the ALJ granted Vicinity Energy Grand Rapids, LLC’s (Vicinity Energy) petition to intervene out-

of-time.

DTE Gas sponsored the direct testimony and exhibits of 21 witnesses. Jennie Aud is DTE

Gas’s Director, Gas Control and Planning (qualifications and direct testimony at 5T 501–17); W.

5

Scott Bennett (who adopted the originally-filed testimony of Edward Solomon) is DTE Energy’s

Manager of Corporate Finance (qualifications and direct revised testimony at 5T 531–65); Daniel

Brudzynski is DTE Gas’s Vice President of Gas Sales and Supply (qualifications and revised direct

testimony at 5T579–619); Benjamin Burns is DTE’s Director of Electric Marketing and

Electrification (qualifications and direct testimony at 5T 643–49); Jaison Busby is DTE’s IT

Director of Power Supply, Energy Gas, and Enterprise Innovation (qualifications and revised

direct testimony at 5T 656-748); Henry Campbell is the Director of DTE’s Customer Care

Organization (qualifications and direct testimony at 5T 777–94); George Chapel is DTE Gas’s

Manager, Market Forecasting (qualifications and revised direct testimony at 5T 801-33); Michael

Cooper is DTE Energy Corporate Services LLC’s Director of Compensation, Benefits & Wellness

(qualifications and revised direct testimony at 5T 847–909); Henry Decker is DTE Gas’s Director,

Gas Sales and Marketing (qualifications and direct testimony at 5T 417–69): Mark C Johnson is

DTE Gas’s Director of Southeast Michigan Gas Operations (qualifications and revised direct

testimony at 5T 932–82); Tamara D. Johnson is DTE’s Director of Revenue Management and

Protection (RM&P) (qualifications and revised direct testimony at 5T 1000–1021); Robert Lee is

DTE Gas’s Manager of Environmental Management and Safety (qualifications and direct

testimony at 5T 1034–53); Habeeb Maroon is a Principal Financial Analyst in the Revenue

Requirements Department of DTE’s Regulatory Affairs organization (qualifications and direct

testimony at 5T 1056–85); Angie Pizzuti is DTE’s Vice President and Chief Customer Officer,

Customer Service (qualifications and direct testimony at 5T 1102–61); Alida Sandberg is DTE

Gas’s Director, Pipeline Safety and Regulatory Compliance (qualifications and direct revised

testimony at 5T 1175–1239); Rajan Telang is the Director, Regulatory Affairs for DTE Energy

(qualifications and revised direct testimony at 5T 1273–1315); Renee Tomina is DTE Gas’s

6

Director of Gas Operations (qualifications and revised direct testimony at 5T 1329–66); Theresa

Uzenski is the Manager of Regulatory Accounting for DTE Electric and DTE Gas (qualifications

and revised direct testimony at 5T 320–80); Kirk Vangilder is a Principal Financial Analyst for

Revenue Requirements in DTE’s Regulatory Affairs organization (qualifications and revised

direct testimony at 5T 1375–95); Dr. Bente Villadsen is a principal in The Brattle Group, which is

an economic, environmental and management consulting firm (qualifications and revised direct

testimony at 5T 1398–1500); and Sherri Wisniewski is DTE Energy’s Director of Tax Operations

(qualifications and direct testimony at 5T 1546–60);

On June 3, 2021, the Commission Staff, the and Intervenors filed their testimony, although

CUB, MPLP, RCG, RESA and Verso did not file any testimony. Staff sponsored Paul R. Ausum

(qualifications and direct testimony at 5T 1982–88);

On June 23, 2021, DTE Gas filed the rebuttal testimony and exhibits of witnesses Marisa

Ayala, DTE Gas’s Manager - Gas Operations (qualifications and rebuttal testimony at 5T 519–

28), Bennett (revised, 5T 566–76), Brudzynski (5T 620–40), Burns (5T 650–53), Busby (5T 749–

75), Campbell (5T 795–98), Chapel (5T 834–44 ), Cooper (5T 910–29), Decker (revised, 5T 470–

92), Mark C. Johnson (5T 983–98), Tamara D. Johnson (5T 1022–32 ), Maroun (5T 1086–99),

Pizzuti (5T 1162–72), Sandberg (revised, 5T 1240–71), Telang (5T01316–26), Tomina (revised,

5T 1367–72), Uzenski (5T 381–97), and Villadsen (5T 1501–43).

Cross-examination and binding-in of testimony was held on July 12 and 13, 2021. The

record consists of 2,131 pages of transcript and supporting exhibits.

7

III. JURISDICTION, STANDARD OF REVIEW AND RATE SETTING LAW.

A. Jurisdiction and Standard of Review.

The Commission has jurisdiction over this case pursuant to 1909 PA 106, as amended,

MCL 460.551 et seq.; 1919 PA 419, as amended, MCL 460.51 et seq.; 1939 PA 3, as amended,

MCL 460.1 et seq.; 1969 PA 306, as amended, MCL 24.201 et seq.; and the Commission’s Rules

of Practice and Procedure, as amended, 1999 AC, R 460.17101 et seq.

All Commission decisions must be authorized by law, and the Commission’s findings must

“be supported by competent, material and substantial evidence on the whole record.” Const 1963,

art 6, § 28. Substantial evidence is evidence “that a reasoning mind would accept as sufficient to

support a conclusion.” Monroe v State Employees’ Retirement Sys, 293 Mich App 594, 607; 809

NW2d 453 (2011). Expert testimony is “substantial” only if it is offered by a qualified expert who

has an informed and rational basis for his or her view, even if other experts disagree. Great Lakes

Steel v Public Service Comm, 130 Mich App 470, 481; 334 NW2d 321 (1983).

The preponderance of evidence standard applies in this proceeding. Aquilina v General

Motors Corp, 403 Mich 206, 210-211; 267 NW2d 923 (1978) (“The proof required in an

administrative proceeding…is the same as that required in a civil judicial proceeding: a

preponderance of the evidence.”). The preponderance of evidence standard is the lightest of all

evidentiary standards when compared to the heightened “clear and convincing” standard2 or the

“beyond a reasonable doubt” standard that is only applicable to criminal proceedings.3 The

“preponderance of the evidence” standard is generally defined as follows:

The greater weight of the evidence, not necessarily established by the greater number of witnesses testifying to a fact but by evidence that has the most convincing force; superior evidentiary weight that, though not sufficient to free the

2 In re Moss, 301 Mich App 76, 89-90; 836 NW2d 182 (2013). 3 Thangavelu v Dep’t of Licensing & Regulation, 149 Mich App 546, 554-555; 386 NW2d 584 (1986).

8

mind wholly from all reasonable doubt, is still sufficient to incline a fair and impartial mind to one side of the issue rather than the other. [Black’s Law Dictionary 1301 (9th ed 2009).] DTE Gas has the initial burden to prove its case by a preponderance of the evidence.

“[O]nce a utility has satisfied its initial burden of proof, another party ‘may challenge that evidence

and present evidence of unreasonableness.’ However, at that point, the other party has the burden

to demonstrate its position is correct.’” October 25, 2017 Order in Case No. U-18224, pp 14-15,

quoting January 11, 2010 Opinion and Order in Case Nos. U-15768 and U-15751, p 38. This

evidentiary standard also effectively bars last-minute criticisms of the Company’s evidentiary

presentation, as the Commission further explained:

The Commission finds that a delicate balance must be maintained concerning the burden of proof. The company has the burden of going forward and demonstrating that it has proposed just and reasonable rates. In this instance, Detroit Edison made that showing. The Staff in response may challenge that evidence and present evidence of unreasonableness. At that point, however, the Staff has the burden to demonstrate its position is correct. The company may then rebut the Staff’s criticisms of its case. The problem here is that the specific criticism that the company had not adequately explained itself came too late in the process for a fair determination on that issue, particularly given the evidence the company presented in support of its position. [January 11, 2010 Opinion and Order in Case Nos. U-15768 and U-15751, pp 37-38.] The Administrative Procedures Act (APA) precludes the Commission from making

decisions based on non-record materials. MCL 24.276 provides: “Evidence in a contested case . .

. shall be offered and made part of the record. Other factual information or evidence shall not be

considered in determination of the case except as permitted under [MCL 24.277] concerning

official notice of judicially cognizable facts and facts within the agency’s specialized expertise].”

Noncompliance with the APA is reversible error. In re Public Service Commission Guidelines for

Transactions Between Affiliates, 252 Mich App 254, 267; 652 NW2d 1 (2002).

9

The ability to take official notice is limited under applicable rules.4 See also Freed v Salas,

286 Mich App 300, 341; 780 NW2d 844 (2009), where the Court of Appeals affirmed the trial

court’s refusal to take judicial notice of a speed limit, explaining in part: “Given that the signage

and the traffic control order did not agree as to the speed limit for the area, the fact could not

reasonably be said to have been undisputed or capable of accurate and ready determination.”

The Commission recently explained that “because of the unforgiving time limits under

MCL 460.6a [which at that time had a 12-month deadline], official notice requests, especially

those that may generate controversy regarding the materiality or weight of the evidence proffered,

can rarely, if ever, be entertained after the close of the record” (December 11, 2015 Order in Case

No. U-17767, p 136, agreeing with ALJ’s denial of official notice request).

In Kar v Hogan, 399 Mich 529, 539; 251 NW2d 77 (1976), our Supreme Court explained

that “[t]he party alleging a fact to be true should suffer the consequences of a failure to prove the

truth of that allegation.” Thus, unproven allegations cannot stand in the place of evidence. Things

not proven must be taken as not existing, since a decision cannot be based upon conjecture. Star

4 Rule 428 of the Commission’s Rules of Practice and Procedure provides:

Except as otherwise provided by law, the commission and the presiding officer may take official notice of judicially cognizable facts and may take notice of general, technical, or scientific facts within the commission’s specialized knowledge. The commission or the presiding officer shall notify the parties at the earliest practicable time of any noticed fact that pertains to a materially disputed issue that is being adjudicated and, on timely request, the parties shall be given an opportunity before the final decision to dispute the fact or its materiality. The commission may use its expertise, technical competence, and specialized knowledge in the valuation of evidence presented to it.” [R 792.10428. Emphasis added.]

MRE 201(b) similarly provides: A judicially noticed fact must be one not subject to reasonable dispute in that it is either (1) generally known within the territorial jurisdiction of the trial court or (2) capable of accurate and ready determination by resort to sources whose accuracy cannot reasonably be questioned. (Emphasis added).

10

Steel v USF&G, 186 Mich App 475, 481; 465 NW2d 17 (1990); see also, Skinner v Square D Co,

445 Mich 153; 516 NW2d 475 (1994).

It is similarly well established that an agency decision may not be based on speculation.

Ludington Service Corp v Comm’r of Insurance, 444 Mich 481, 483, 494-97, 500-501, 507; 511

NW2d 661 (1994), amended 444 Mich 1240 (1994) (unanimously reversing agency decision that

exceeded the limits of the agency’s statutory authority, and that was based on speculation instead

of the required competent, material, and substantial evidence); In re Complaint of Pelland, 254

Mich App 675, 685-86; 658 NW2d 849 (2003); Battiste v Dep’t of Social Services, 154 Mich App

486, 492; 398 NW2d 447 (1986).

B. Ratemaking Principles Overview.

DTE Gas has constitutional protections against “takings” and confiscatory rates under the

Fifth Amendment to the U.S. Constitution, which is applicable to the states through the Fourteenth

Amendment. Similarly, Mich Const 1963, art 10, § 2 provides in part, “Private property shall not

be taken for public use without just compensation therefore being first made or secured in a manner

prescribed by law.” These constitutional protections have been recognized and applied to public

utility rates in well-established case law.5

The Michigan Supreme Court has provided further guidance that the Commission must use

in setting DTE Gas’s rates. Specifically, creating rates that recognize reductions in certain costs,

while ignoring the increase in other costs, violates the due process rights of utilities. The Court

5 See generally, Missouri ex rel Southwestern Bell Telephone Co v Public Service Comm of Missouri, 262 US 276; 43 S Ct 544; 67 L Ed 981 (1923); Federal Power Comm v Natural Gas Pipeline, 315 US 575; 62 S Ct 736; 86 L Ed 1037 (1942); Duquesne Light Co v Barasch, 488 US 299; 109 S Ct 609; 102 L Ed 2d 646 (1989). See also, Northern Michigan Water Co v Public Service Comm, 381 Mich 340; 161 NW2d 584 (1968); Consumers Power Co v Public Service Comm, 415 Mich 134; 327 NW2d 875 (1982); ABATE v Public Service Comm, 430 Mich 33; 420 NW2d 81 (1988).

11

cited with approval the conclusions of a circuit court judge granting an injunction against such

unlawful rates:

Certainly at first blush it would appear to anyone steeped in ‘due process’ considerations that it is grossly unfair to include certain items of decreased cost in rate determination while at the same time to exclude items of increased cost. [Michigan Consolidated Gas Company v Public Service Comm, 389 Mich 624, 633; 209 NW2d 210 (1973).] As a matter of fundamental ratemaking law, DTE Gas is entitled to a commensurate return

of and on its investment in providing utility service.6 It is axiomatic that utility rates are overall

rates. Federal Power Comm, supra, 320 US at 602; Michigan Bell Telephone Co v Public Service

Comm, 332 Mich 7, 37; 50 NW2d 826 (1952); MCL 460.6a(2)(b).

DTE Gas’s constitutional rights would be violated by a failure to acknowledge (and

establish rates based on) both decreasing and increasing costs. The United States Supreme Court,

in construing the Fifth Amendment mandates in conjunction with utility ratemaking, aptly

concluded:

Regulation may, consistently with the Constitution, limit stringently the return recovered on investment, for investors’ interests provide only one of the variables in the constitutional calculus of reasonableness (citations omitted). It is, however, plain that the ‘power to regulate is not a power to destroy,’ (citations omitted) and that maximum rates must be calculated for a regulated class in conformity with the pertinent constitutional limitations. Price control is “unconstitutional if arbitrary, discriminatory, or demonstrably irrelevant to the policy the legislature is free to adopt.” [Permian Basin Area Rate Cases, supra, 390 US at 769-770 (Emphasis added).]

The Commission has an obligation to facilitate DTE Gas’s financial health for the benefit

of its customers and shareholders. See, by way of example and not limitation, MCL 460.6a(2)(3);

6 See Bluefield Waterworks Improvement Co v Public Service Commission of West Virginia, 262 US 679, 690-694; 43 S Ct 675; 67 L Ed 1176 (1923); Federal Power Comm v Hope Natural Gas Co, 320 US 591, 603; 64 S Ct 281; 88 L Ed 333 (1944). See also Permian Basin Area Rate Cases, 390 US 747, 769-70; 88 S Ct 1344; 20 L Ed 2d 312 (1968); FPC v Memphis Light, Gas and Water Division, 411 US 458; 43 S Ct 1723; 36 L Ed 2d 426 (1973); General Telephone Co v Public Service Comm, 341 Mich 620; 67 NW2d 882 (1954); Michigan Consolidated Gas Co v Public Service Comm, 389 Mich 624; 209 NW2d 210 (1973).

12

Smith v Illinois Bell Telephone Co, 270 US 587, 591; 46 S Ct 408; 70 L Ed 747 (1926). Federal

Power Comm, supra, 320 US at 602; Michigan Bell Telephone Co, supra, 332 Mich at 37;

MichCon, supra, 389 Mich at 633; Michigan Bell Telephone Co v Engler, 257 F3d 587, 594-96

(CA 6, 2001). Furthermore, our Supreme Court has clearly stated that:

Statutes will be construed in the most beneficial way which their language will permit to prevent absurdity, hardship or injustice; to favor public convenience, and to oppose all prejudice to public interests. [Attorney General v Marx, 203 Mich 331, 335; 168 NW 1005 (1918).]

Under well-established ratemaking law, rates for utility service are set prospectively so that

the utility provides service and its customers receive service at established rates, which are based

on the estimated costs of providing that service, plus a reasonable return on the utility’s investment.

See ABATE v Public Service Comm, 208 Mich App 248, 257-258; 527 NW2d 533 (1994). This is

part of the “regulatory compact,” under which the utility dedicates its private property to serve the

public, and correspondingly receives a reasonable return on the value of its private property. In

Board of Public Utility Comm’rs v New York Telephone Co, 271 US 23; 46 S Ct 363; 70 L Ed 808

(1926), the United States Supreme Court explained that the just compensation safeguarded to the

utility by the Fourteenth Amendment is a reasonable return on the value of the property used at

the time that the property is being used for the public service. Rates that are not sufficient to yield

that present return are confiscatory. 271 US at 31. To the extent that the utility might have earned

sufficient revenue in the past, such past revenue cannot be used to sustain confiscatory rates in the

future. Id. at 32. Thus, it would be unconstitutional for the Commission to use hindsight or

otherwise base DTE Gas’s rates on past events.

The Michigan Supreme Court has recognized that the Commission has only limited

statutory authority, which does not include the authority to retroactively reduce rates. Michigan

Bell Telephone Co v Public Service Comm, 315 Mich 533, 347; 24 NW2d 200 (1946). A lawfully

13

established rate remains in force until altered by a subsequently established lawful rate. Id., at

544. A regulatory body cannot penalize a utility for collecting a rate during the period elapsing

between the date of the order prescribing the rate and the date of the subsequent order reducing it.

Id. at 543-44. Where the Commission establishes a reasonable rate in its legislative capacity, the

Commission cannot later, in its quasi-judicial capacity, find that the utility violated the law because

it charged that rate. Id. at 550-51.

The prohibition against retroactive ratemaking remains in effect and applies in this case so

that rates may only be set prospectively. “[T]he essential principal of the rule against retroactive

ratemaking is that when the estimates prove inaccurate and costs are higher or lower than predicted,

the previously set rates cannot be changed to correct for the error; the only step that the MPSC can

take is to prospectively revise rates in an effort to set more appropriate ones.” The Detroit Edison

Co v Public Service Comm, 416 Mich 510, 523; 331 NW2d 159 (1982) (opinion by Fitzgerald,

C.J.).

IV. TEST YEAR.

DTE Gas proposes a projected test year of January 1, 2022 through December 31, 2022

(5T 1282). Staff agrees (e.g., Exhibit S-1, Schedule A1) and there appears to be no disagreement

with respect to the projected test year among the parties.

Prior to 2008 PA 286, which allows utilities to use fully forecasted projected test years in

requesting rate relief,7 Commission policy called for the use of prior actual experience adjusted

for known and measurable changes. Notwithstanding the statutory authority to use a fully-

forecasted test period, DTE Gas used actual financial results from the historical test year ended

7 MCL 460.6a(1) relevantly states: “A utility may use projected costs and revenues for a future consecutive 12-month period in developing its requested rates and charges.”

14

December 31, 2019 as a starting point, and then normalized and adjusted those results for inflation

and other known and measurable changes, to arrive at a fully projected test year revenue deficiency

of approximately $195 million (5T 1281–82, 1385, 1394–95; Exhibit A-11, Schedule A1).8 In

other words, DTE Gas essentially utilized the Commission’s prior methodology, which produced

the equivalent of a fully-projected test year. This methodology is also reasonable in light of the

significant effects, and lingering uncertainties, from the COVID-19 pandemic (5T 1282).

V. RATE BASE.

A utility’s rate base consists of the net amount of capital invested in plant, plus the utility’s

working capital requirements. DTE Gas’s Total Rate Base for the projected test year is $5,610.6

million, which consists of $4,581.3 million of Net Utility Plant, and $1,029.3 million of Working

Capital (5T 1386; Exhibit A-12, Schedule B1).

A. Adjusted Total Rate Base

As discussed in Section II and Attachment A, page 2 of 4, the Rate Base adjustments the

Company is adopting pertain to 1) Service Renewal expenditures for personal protective

equipment and vehicle rentals arising from COVID safety requirements and 2) certain Gas

Information Technology projects. DTE Gas’s Total Rate Base as adjusted in this brief for the

projected period ending December 31, 2022 is reduced from $5,610.6 million to $5,610.3 million.

B. Capital Expenditures.

DTE Gas has made or will make approximately $1.5 billion of capital expenditures from

the end of the historical test year to the end of the projected test year (January 1, 2020 through

December 31, 2022). (Exhibit A-12, Schedule B5, line 28, columns (e) and (f)). These

8 DTE Gas’s $195 million Revenue Deficiency is based on a 13-month average Projected Rate Base of $5,611 million, Projected Net Operating Income (NOI) of $170 million, and an overall rate of return of 5.59%. The $5,611 million Total Rate Base is detailed on Exhibit A-12, Schedule B1. The $170 million NOI is developed on Exhibit A-13, Schedule C1. The 5.59% overall rate of return is set forth on Exhibit A-14, Schedule D1 (5T 1386).

15

expenditures should be approved because they are prudent investments in DTE Gas’s natural gas

system that are necessary for DTE Gas to maintain its safe and reliable system for distributing

natural gas to its customers. They are also integral parts of the Gas Delivery Plan (GDP), discussed

below (5T 1189, 1194).

The capital expenditure amount indicated above excludes new Infrastructure Recovery

Mechanism (IRM) expenditures beginning January 1, 2022 (5T 1194). DTE Gas proposes to

establish a new IRM surcharge beginning on January 1, 2022 to recover the incremental revenue

requirement associated with invested IRM capital, as further discussed in Sections VIII. B, and X.

D. 1 (5T 1194; Exhibit A-12, Schedule B5.5 Revised provides additional detail on DTE Gas’s 25

largest projects from January 2020 through December 2022 (5T 1179).

1. Gas Delivery Plan (GDP)

DTE Gas developed the GDP in accordance with the U-20642 settlement.9 The GDP is the

Company’s ten-year investment plan for its natural gas infrastructure (transmission, distribution,

and storage and compression assets). (Exhibit A-12, Schedule B5.6). It provides a roadmap for the

Company to continue to provide safe and reliable service to its 1.3 million customers, while

maintaining customer affordability in an environmentally responsible manner. The GDP is

intended to provide a clear and transparent ten-year framework setting forth: (1) the next decade

of natural gas capital investments planned by the Company, (2) how the Company plans to meet

the needs for natural gas supply and demand, and (3) how the Company will prioritize its pipeline

safety investments. The GDP should be viewed as a flexible working guide that will be updated in

response to new information and future events. It is also important to not view requests for

9 Paragraph 11 of the U-20642 settlement states: “DTE Gas will include a Natural Gas Delivery Plan in its next general rate case filing based on collaboration with and feedback from the MPSC Staff, which will provide the framework for the next ten years of investments in DTE Gas’s natural gas infrastructure.”

16

recovery in isolation, since they are part of a larger, deliberate long-term plan (5T 1188–91, 1290–

91).

A large portion of the risk mitigation capital expenditures in the GDP are prioritized to

address DTE Gas’s aging distribution and transmission pipeline infrastructure (5T 1188, 1291–

92). The capital safety and reliability projects identified in this case reflect the first three years of

the GDP (5T 1194).

2. Routine Capital Spending

Routine capital spending supports distribution, transmission, storage, and general plant

assets. DTE Gas has made or will make $712.3 million of routine capital expenditures from the

end of the historical test year to the end of the projected test year (December 31, 2019 through

December 31, 2022). (5T 583–84, 1196; Exhibit A-12, Schedule B5.1, line 6, columns (f) and (g),

with components reflected in lines 2 through 5). Mr. Brudzynski explained and supported the

routine capital expenditures required for distribution plant (5T 587–609), transmission plant (5T

610–13), storage plant (5T 613–15), and general plant (5T 615–19). Exhibit A-12, Schedule B5.5

Revised (DTE Gas Highest Cost Top 25 Capital projects), pages 3-14, provides project level detail

supporting the capital expenditures for the Gordie Howe International Bridge (GHIB), Howard

City System Supply, Southfield 24” Pipe Replacement, Myers Lake Community Expansion, Ferry

Rd Community Expansion, K-Line Pipe Replacement, Alpena West Branch Drain Line Lowering,

and Belle River/Columbus Valve Upgrade projects (5T 1196).

a. Communications & Control - Meters

Distribution includes Communications & Control – Meters. The Company supports $40.9

million of capital expenditures from January 1, 2020 through December 31, 2022 (illustrated in

Exhibit A-12, Schedule B5.1, page 2, line 10, columns (f) and (g)). The yearly average of $13.6

17

million is an increase of $1.3 million compared to the 5-year historical average, which was driven

primarily by additional meter purchases in 2020 (5T 600).

Staff took issue with the Company maintaining safety stock, inaccurately characterizing it

as “akin to contingency” (5T 1906). The Company disagrees. Witness Ayala explained that the

purpose of DTE Gas’s safety stock is to keep a sufficient supply of meters and modules on hand

to support unexpected field work and vendor shipping delays. Safety stock is planned and unique

for each meter depending on vendor lead time and the variability of usage. DTE Gas maintains

safety stock consisting of quantities (less than six months) required to meet business demand

variability, and to provide for any vendor delivery and shipping shortfalls. Recent experience with

vendor delays has demonstrated the importance of maintaining an ambient level of safety stock for

meters and modules, and it is critical to keeping customers’ gas flowing seamlessly (5T 522–23).

Staff’s concern also seems to be based on taking the word “contingency” out of context

from Mr. Brudzynski’s testimony. He more fully testified: “Carrying a certain level of inventory

contingency for unforeseen factors (weather, vendor delays, material shortages, etc.) called safety

stock, is a means to ensure an appropriate level of inventory is available during the year. At times

in the past, DTE Gas has experienced inventory shortages of available meters to timely perform

customer work” (5T 602). In contrast, a “contingency” is an undefined amount included in a

project that is above the best forecast for that project (5T 522).

Staff “concludes it is reasonable and prudent to only support purchases that cover the

company’s forecasted installations” (5T 1907). To the contrary, DTE Gas purchases meters for

non-forecasted installations and meter replacements that are driven by customer demand. The

Company always needs to have available stock to service customers. Therefore, it is reasonable

and prudent to purchase enough meters and modules to replenish safety stock. This is a standard

18

supply chain practice followed in all industries, especially in industries such as natural gas where

keeping energy flowing is critical to public health and safety (5T 523).

As Witness Ayala explained, Staff’s forecast represents only AMI/AMR first-time

installations, and does not include all other customer-requested work, Company-generated work,

and emergent meter work that is performed, which requires a new meter and module to be installed

(5T 523–26). See also Table 1 at 5T 524, which depicts the annual volume of new meters and

modules that are installed each year, based on a three-year average.

Staff “recommends a capital disallowance of $25,969 in 2020, $1,847,610 in 2021, and

$1,086,506 for AMI module purchases . . . [and a] capital disallowance of $765,785 in 2020,

$675,000 in 2021, and $1,086,206 in 2022 for AMR module purchase” (5T 1912). Staff further

“recommends a meter purchase disallowance of $1,286,634 in 2020, $7,728,000 in 2021, and

$6,824,125 in 2022. This amount removes the purchase cost associated with the Company’s

planned new installations, route maintenance, customer requested meter work, and ability to have

meter safety stock of 31,000 in 2021 and 2022” (5T 1916).

DTE Gas disagrees because, as discussed above, the proposed disallowances would limit

the number of modules and meters that it can supply for routine and non-forecasted field work.10

Staff’s proposals would also hinder the Company’s ability to serve customers in a timely fashion

and ensure their health and safety through uninterrupted service. Not having safety stock would

also lead to the above-described inefficiencies and additional logistical costs if a vender is late

with shipments (5T 527–28).

10 For every meter replacement there is a module replacement. It is imperative to have enough modules (AMI or AMR) for new meters. It is also necessary to have enough modules for other work. Approximately 10% of meter/module re-work orders (based on three years) occurs where a module is added or replaced on a meter, without a new meter installation (5T 527).

19

Staff’s proposed disallowance is also based on the inaccurate premise that “the Company

plans on purchasing more modules than they intend to install” (5T 1910). To the contrary, DTE

Gas only orders meters and modules that it plans to install in a given year and to replenish safety

stock if it has been used up. The Company follows a first-in, first-out (FIFO) approach to ensure

the use of the oldest inventory and to not hold stock longer than needed. It is critical for DTE Gas

to maintain inventory levels that allow the Company to run efficiently, ensure timely customer

service, and adhere to AGA and ASCM standards (5T 527–28).

Therefore, the Staff’s proposed meter and module disallowances should be rejected as

lacking in sound foundation, inconsistent with reasonable and prudent utility operations, and

contrary to the interests of reliability and customer safety.

b. Service Renewals

From January 1, 2020 through December 31, 2022, DTE Gas will have incurred $45.4

million of service renewal capital expenditures (5T 596; Exhibit A-12, Schedule B5.1, page 2, line

7, columns (f) and (g)). Three factors relating to COVID-19 caused an increase in service renewal

cost/unit from 2019 to 2020: (1) increased labor and labor-related overheads due to shifting

resources from O&M work to capital expenditure work, (2) increased personal protective

equipment (PPE) spend, and (3) vehicle rentals (5T 596–97).

AG witness Coppola took issue with the first factor, and calculated a proposed $6,657,000

disallowance by taking the increase in the labor and labor overheads unit cost from 2019 to 2020

($883 per unit, see Exhibit A-31, Schedule U1) and multiplying it by the forecasted units for 2020,

2021, and 2022 (5T 1648).

The Company disagrees with the AG’s recommended 2020 disallowance ($1,983,000). Mr.

Brudzynski explained that the COVID-19 pandemic caused an unprecedented economic disruption

in Michigan with the implementation of lockdowns, social distancing, and other health safety

20

measures as ordered by the Governor. As a result, many small commercial customers had to close

their businesses for extended periods of time or operate at severely curtailed capacity during 2020.

This unprecedented shutdown of large portions of the economy created uncertainty for many

companies in Michigan including DTE Gas. To mitigate some of this uncertainty, DTE Gas took

unprecedented one-time actions to re-prioritize resources from non-emergency O&M work to

capital, as previously discussed in discovery (see Exhibit A-31, Schedule U3). Shifting resources

was an efficient use of the labor force that otherwise would have been idle during unprecedented

times. Prioritizing capital work allowed DTE Gas to keep all employees gainfully employed and

productive during a period of uncertainty while completing work. Therefore, the Commission

should fully approve DTE Gas’s request for 2020 capital expenditures of $13,282,000 (5T 624).

The AG’s proposed $4,592,000 disallowance for 2021 and 2022 should also be rejected.

The shift in resources from O&M work to capital work was a one-time occurrence in 2020 in

response to the pandemic. The increased labor and labor overhead unit cost in 2020 from shifting

resources does not continue in 2021 and 2022. The increase in the labor and labor overhead unit

cost between 2019 and 2021 ($367 per unit) is due to normal costs of business including inflation,

and cost of living increases (Exhibit A-31, Schedule U2). Therefore, the AG’s proposed

disallowances for 2021 ($2,296,000) and 2022 ($2,296,000) should be rejected, and the

Commission should fully approve DTE Gas’s request for capital expenditures of $16,035,000 for

2021 and $16,096,000 for 2022 (5T 625).

c. Service Abandonments

From January 1, 2020 through December 31, 2022, DTE Gas will have incurred $17.3

million of service abandonment capital expenditures (5T 607; Exhibit A-12, Schedule B5.1, page

2, line 5, columns (f) and (g)). As with Service Renewals (discussed above), three factors relating

21

to COVID-19 increased DTE Gas’s service abandonments cost/unit from 2019 to 2020 (5T 607–

08).

Mr. Coppola again took issue with the first factor, and calculated a proposed $1,568,000

disallowance for 2020 by taking the increase in the labor and labor overheads unit cost from 2019

to 2020 ($834 per unit, see Exhibit A-31, Schedule U4) and multiplying it by the forecasted units

for 2020 (5T 1649).

The Company disagrees. As discussed above in the Service Renewals section, the shifting

of resources was an efficient use of DTE Gas’s labor force during the pandemic. Therefore, the

Commission should fully approve the Company’s request for capital expenditures of $4,943,000

for 2020 (5T 646).

d. New Market Attachments

From January 1, 2020 through December 31, 2022, DTE Gas will have incurred $205.1

million of new market attachments capital expenditures (Exhibit A-12, Schedule B5.1, page 2, line

13, columns (f) and (g)).

AG witness Coppola proposed disallowances of $10,901,000 for 2021, and $10,653,000

for 2022, based on his calculation of a lower cost per unit based on three-year average historical

costs plus 2% annual inflation (5T 1651).

The Company disagrees. Mr. Brudzynski explained that the AG’s calculations failed to

consider that contractor costs increased due to new blanket contracts (effective Q2 of 2020)

because DTE Gas’s previous contracts expired and new contracts were awarded. These new

contracts were evaluated through request for proposal process across vendors and based on

multiple performance criteria including safety, experience, resource capacity, and pricing so that

contracts were awarded to the best qualified vendors. The increased contractor costs result in

22

increases in New Markets work of approximately 10% in 2021 and 12% in 2022, compared to the

three-year average used by the AG (5T 626–27).

The AG’s calculations also failed to consider that the type or mix of attachments is

expected to change in 2021 and 2022 (fewer new home constructions that are typically on or near

a natural gas main and therefore are the least costly of attachments; 42% increase in attachment

requests requiring the extension of a main to provide service, and an increase in

EUT/Transportation New Customer Attachments), which increases the cost per attachment (5T

627).

e. Service Alterations

From January 1, 2020 through December 31, 2022, DTE Gas will have incurred $54.7

million of service alteration capital expenditures (5T 594; Exhibit A-12, Schedule B5.1, page 2,

line 6, columns (f) and (g)).

Staff recommended that service alterations capital expenditures be reduced to $7,191,336

in 2021, and $16,651,736 in 2022 (which would equal disallowances of $1,349,664 in 2021 and

$1,186,264 in 2022) reasoning that only a ‘fraction” of service alterations will require a cross-bore

inspection (5T 1836). A cross bore occurs when the service line intersects an existing underground

utility line during installation. With this new program, after a service alteration, the sewer line or

storm drain is inspected with a camera to ensure no intersection occurred. Any cross-bores that are

identified are remediated appropriately to ensure safe delivery of gas to customers (5T 595, 629).

Therefore, the Commission should fully approve the Company’s requested capital expenditures

for service alterations. Staff’s reasoning for their proposed disallowance is that only a ‘fraction”

of service alterations will require a cross-bore inspection (5T 1836).

The Company disagrees. Estimated costs for cross bore inspections were based on

negotiated contractual pricing and the Company’s forecasted volumes of service alterations

23

requiring cross bore inspections as required by the Company’s new safety procedure (Distribution

& Transmission procedures 4.6 - Identifying and protecting underground utilities, conduits and

structures) implemented in 4 January 1, 2021 (5T 629-630).

Staff’s calculations failed to consider increases in hard surface restoration and unit

complexity mix (5T 630). As Mr. Brudzynski explained, there has been an increasing trend for

hard surface restoration, which is driven by mains that are located under sidewalks or in roadways,

and by increased municipal permitting requirements. DTE Gas anticipates that 30% of the service

alterations completed in 2021 and 2022 will require hard surface restoration. Restoration costs will

also increase because restoration contracts were awarded in 2020 for the next three years starting

in 2021 (the average increase across contractors was 7% during restoration season and 17% for

backlog units to be completed after winter season construction). Changes in municipal permitting

requirements (outlining specifications for DTE Gas to follow in the restoration process) have also

led to increased costs (5T 628–29).

AG witness Coppola proposed disallowances of $2,372,000 for 2021, and $2,209,000 for

2022, based on his use of the cost per unit in 2020 (5T 1645). The AG’s calculations based on

2020 costs not only failed to consider the increases in hard surface restoration and unit complexity

mix discussed above, but also failed to consider that DTE Gas implemented the cross-bore safety

program on January 1, 2021 failing to address associated program costs incurred going forward.

A cross bore occurs when the service line intersects an existing underground utility line during

installation. With this new program, after a service alteration, the sewer line or storm drain is

inspected with a camera to ensure no intersection occurred. Any cross-bores that are identified are

remediated appropriately to ensure safe delivery of gas to customers (5T 595, 629). Therefore, the

24

Commission should fully approve the Company’s requested capital expenditures for service

alterations.

f. Belle Isle Main Replacement

In late November 2018, a contractor struck DTE Gas’s 4” 50 psig distribution main,

resulting in the total loss of gas service to the 20 customers on Belle Isle. In May of 2019, DTE

Gas implemented a long-term solution by installing 3400’ of 4” 6 distribution main via horizontal

directional drill (HDD) under the river. The solution cost approximately $2.5 million, $2.24

million of capital expenditure and $0.2 million of O&M. (5T 1233-34).

AG witness Coppola recommended that the Commission “remove the entire amount of

$2.4 million from rate base . . . [and] order the Company to permanently remove this amount from

rate base so that it is not included in future rate case filings” (5T 1653).

Witness Coppola’s recommendation is not appropriate as only $1.24 million has been

requested in this case. As Mr. Brudzynski explained, DTE Electric reimbursed DTE Gas $1.0

million of the $2.24 million total cost incurred (Exhibit A-31, Schedule U5). Adopting witness

Coppola’s recommendation would result in a $1.0 million disallowance of expenditures that are

not even being requested by the Company in this case (5T 631).

g. System Reliability

From January 1, 2020 through December 31, 2022, DTE Gas will have incurred $78.6

million of system reliability capital expenditures (5T 592; Exhibit A-12, Schedule B5.1, page 2,

line 8, columns (f) and (g)).

Staff proposed that the 2021 capital expenditure level be adjusted consistent with the 2020

capital expenditure level of $8,030,000 (which would be a $5,520,000 disallowance), reasoning

that “the Company provides no justification, support, or discussion to substantiate” increases in

capital costs related to regulator stations without take-off valves (5T 1834).

25

The Company disagrees. Mr. Brudzynski explained that Staff’s calculation apparently did

not consider the increase in projects from 2020 to 2021 (5T 632).

Staff further recommended that the Company should provide information related to the

cost drivers contributing to the increase in capital expenditures since the beginning of the program

for regulators stations without take-off valves in 2016 (5T 1835). Mr. Brudzynski responded by

listing process, design, and safety enhancements that have been implemented since the System

Reliability TOV program began in 2016. He further explained that the cost associated with TOV

program replacements depends on whether the regulator station is above or below grade. On

average, the recent enhancements result in cost increases of approximately $145,000 per below-

grade regulator installation, and approximately $58,000 per above-grade regulator installation.

This results in a total additional cost of $4,669,000 for TOV projects in 2021 (5T 633–36).11

Mr. Brudzynski further explained that the nature of the replacement work differs

significantly depending on whether the project is above or below grade. For 2021, the average

TOV project cost is $525,445 for above grade, and $107,963 for below grade. There is a

significantly higher percentage of below grade projects in 2021 compared to other years (10% in

2019; 16% in 2020; 37% in 2021; 13% in 2022), which results in a significantly higher average

cost per unit in 2021. Therefore, the Staff’s proposed $5,520,000 should not be adopted (5T 634–

35).

h. Routine Transmission Plant

From January 1, 2020 through December 31, 2022, DTE Gas will have incurred $50.3

million of routine transmission plant capital expenditures (5T 610–11; Exhibit A-12, Schedule

B5.1, page 1, line 3, columns (f) and (g)).

11 In response to Staff’s recommendation for further information (5T 1835), Mr. Brudzynski also provided additional detail regarding the remaining regulator station projects and a timeline for competition (5T 636).

26

AG witness Coppola recommended an $11.8 million disallowance for 2021 and 2022 for

eight soil-cover pipeline remediation projects, suggesting that the Company should explore and

evaluate alternatives (5T 1656).

The Company disagrees. Mr. Brudzynski explained that DTE Gas conducts pipeline

surveys per DTE Gas Standard 705. When an exposed pipe is identified, the Pipeline Integrity

Group ranks the exposure for risk using a relative model that considers various likelihood and

consequence factors. The remediation plan is to remediate the highest risk-ranked exposures. The

exposures in this case are ranked the highest. Prioritizing and permanently mitigating the highest

risk-ranked exposures ensures that DTE Gas provides customers with safe and reliable service.

Therefore, the AG’s proposed $11.8 million disallowance should not be adopted (5T 637–40).

In response to Mr. Coppola’s further suggestion that DTE Gas is replacing more pipeline

than necessary (5T 1630), Mr. Brudzynski explained that there are several reasons why the

replaced segment of pipeline is longer than the exposed or shallow segment. First, to avoid

significant impact to environmentally sensitive areas and connect the pipe in a non-sensitive area.

Second, the replacement plan must include considerations for pipe entry and exit space during

construction, as well as entry and exit angles that satisfy the minimum requirement of three feet of

cover at all below-grade locations on the new pipe. The increased length of the replacement pipe

due to the exit and entry bends also enables unrestricted access of in-line inspection tools during

pipeline assessments.

DTE Gas also uses alternative risk mitigation methods for pipeline restoration projects,

including adding soil cover and bank stabilization, subject to regulatory requirements and

effectiveness (5T 638–39).12 These alternatives are not suitable for the pipeline projects at issue

12 Pursuant to Michigan Gas Safety Standards, the minimum cover, in general, is 30” for a Class 1 location, and 36” for Class 2, 3, and 4 (5T 638).

27

because the projects are similar to other projects where governmental agencies denied permits

when alternative methods to add cover were proposed. The issue is that the pipelines are exposed

or extremely shallow perpendicular to the river at the original river/stream crossing location (low

point of the pipeline) due to natural scouring of the waterway at that location. Restoring cover by

adding soil and armoring structures on top of the pipeline to protect future exposure would

essentially create a weir on the river and fish passage issues. Governmental concerns resulted in

the denial of permitting for any remediation method other than pipeline replacement (5T 639–40).

3. Gas Information Technology (IT) Spending

Gas IT spending supports technology improvements necessary for DTE Gas to run its

business and provide workforce safety through cyber security programs, projects, and program

enhancements to improve systems reliability and added overall functionality. DTE Gas has made

or will make $28.2 million of IT capital expenditures from the end of the historical test year to the

end of the projected test year (December 31, 2019 through December 31, 2022). (5T 1198; Exhibit

A-12, Schedule B5, line 27, columns (e) and (f)). Exhibit A-12, Schedule B5.5 Revised (DTE Gas

Highest Cost Top 25 Capital Projects), pages 41-42, provides project level detail for the Field

Service Management (ClickSoft) and Picarro Leak Survey projects (5T 1199).

DTE Gas’s IT investment spending is part of the DTE IT Five-year Plan for 2021-2025,

which was filed on March 22, 2021 in Case No. U-20561 (5T 660–62, 1299). The IT Plan

categorizes IT projects into an IT Investment Portfolio, with IT Investment Categories (see the

matrix at 5T 662, 1301).

Witness Busby explained how the DTE enterprise IT capital investment planning process

occurs and how it tracks with the Five-Year IT Plan and that DTE Gas categorizes its IT spending

into five categories: Regulatory, Sustainment, Return to Health, IT Enhancements, and Strategic

Investments. He also provided extensive support, including approved business cases and updated

28

cost information for specific DTE Gas IT asset projects within each of these categories. In this

case, DTE Gas is requesting $28.2 million in capital expenditures for DTE Gas-specific IT projects

for the period 2020 through 2022. (Exhibit A-12, Schedule B5.4).

AG witness Coppola proposed $18.26 million of capital disallowances relating to six Gas

IT projects. The Company agrees with $450,000 of the AG’s recommendation related to the Field

Sketch Enhancement project, however, the Commission should reject $17.8 million of that

proposed disallowance, as discussed below.

ClickSoft Field Service Management

AG witness Coppola proposed a $6.8 million disallowance for capital expenditures for the

ClickSoft Field Service Management system, reasoning that “it is readily apparent that the

Company wants more current system with new features and exciting mobile phone connectivity,

although the current system is still functional and only six years old” (5T 1669).

The AG’s reasoning is incorrect. Mr. Busby explained that the current system is not six

years old; instead, it was initially implemented in 2007 (it was then known as Advantex). In 2014,

ASEA Brown Boveri (ABB) bought the Advantex software and rebranded it as Service Suite. The

vendor ABB has now deemed the application to be at the end of life. This poses many risks to

DTE Gas because ABB will no longer provide enhancements or defect remediations to this product

and will no longer invest in ensuring its stability. ABB will also no longer provide critical security

updates to ensure the software remains safe from new cyber threats. This increases the risk of

security vulnerabilities to DTE Gas’s infrastructure, which is an unacceptable risk (5T 683–85,

758–59).

Mr. Coppola also suggested that the Company did not provide business case justification

(5T 1668–69), but Mr. Busby explained in both his direct and rebuttal testimony that ABB is no

29

longer investing in product stability or security. If the system fails or is inaccessible due to a cyber-

attack, this would jeopardize the live field dispatch of gas operations employees who rely on the

dispatching and management system. From 2018-2020, unplanned outages caused an

approximately 56-hour field interruption during which the Company could not receive or send

dispatch to the field, including emergency gas leaks and outages. The Company must also perform

monthly planned outages to address performance and security-risk issues on the current end-of-

life system, which cost $10,000 to $15,000 per year. The investment is therefore justified to ensure

the timely scheduling and deployment of field resources, which will provide faster and more

efficient customer service (5T 684, 759).

Electronic Gas Management System (EGMS)

AG witness Coppola proposed a $3.3 million disallowance from 2019 to 2022 for the

Electronic Gas Management System (EGMS), claiming that “the Company failed to keep up with

vendor releases of system software updates and now finds itself in a situation where the vendor

can only provide limited support for the system” (5T 1671). He further suggested that “the

Commission should direct the Company to remove any disallowed amounts, previously

capitalized, from plant balances to avoid inclusion of these amounts in rate base in future rate

cases” (5T 1672).

The AG’s proposals should be rejected. Mr. Busby explained in both his direct and rebuttal

testimony that the EGMS application currently utilized by DTE Gas is now several versions behind

the standard version and is no longer supported. This project focuses on upgrading the application

to the current version (V 17.0) and security upgrades that will improve the Company’s ability to

mitigate security threats and associated vulnerability risk to nomination data on the EGMS system.

The AG’s assertion that the Company failed to manage the application is inaccurate. Decisions to

30

upgrade applications are frequently reviewed for priority, business value, and risk mitigation as

explained in the Company’s Five Year IT Plan. Through this process, the Company determined

that it is prudent to complete the necessary version upgrade at this time (5T 691, 760–61. See also

DTE Five Year IT Plan, section 4.B.ii, regarding asset lifecycles and refresh rates).

Mr. Coppola was similarly inaccurate in suggesting a concern that the “system will be

used by DTE Gathering Pipelines, an affiliate of DTE Gas” (5T 1671). There is a DTE Gas

Gathering software module within the EGMS system, but all expense-related information

presented in Mr. Busby’s testimony applies either to DTE Gas or the DTE Gas portion of a shared

asset (5T 761).

Gas IT Application Health

AG witness Coppola proposed that the Commission remove $3,977,000 from capital

expenditures from 2019 through 2022 for the Gas IT Application Health projects and direct the

Company to expense these costs in future years. He also proposed a $780,000 increase in O&M

for 2022. He reasoned that the description of the work “does not rise to the level of work that is

capitalizable under the Company’s accounting policy. These costs are routine operating and

maintenance costs, and they should be expenses each year” (5T 1673).

Mr. Busby disagreed, explaining that the investments should be capitalized under the

Company’s established accounting policy for IT costs. Upgrades and enhancements are capitalized

if it is probable that those expenditures will result in significant additional functionality, the

upgrade results in new software designs or a change to part of an existing software design, and a

materiality threshold of $10,000 for capitalizing upgrades and enhancements is met. In addition,

for the first 60 days following the in-service date of a software development project, the direct cost

of remediating all defects related to the originally planned design can be capitalized (5T 762). The

31

AG’s proposal to increase O&M to account for capital dollars should similarly be rejected as

inconsistent with the Company’s accounting policy (5T 762).

End of Life (EOL) Gas Device Program

AG witness Coppola proposed that the Commission remove $2,102,000 from 2019 to 2022

capital expenditures for the End of Life (EOL) Device Program, reasoning that the Company’s

end-of-life replacement cycle should be extended from five years to seven years (5T 1675)

The AG’s proposal should be rejected. Mr. Busby explained that the EOL Gas Device