ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE: EXPLORING THE EFFECTS OF PERFORMANCE MEASURES,...

30

Financial Accountability & Management, 26(4), November 2010, 0267-4424 ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE: EXPLORING THE EFFECTS OF PERFORMANCE MEASURES, PROCEDURAL JUSTICE AND INTERPERSONAL TRUST MAHFUD SHOLIHIN AND RICHARD PIKE ∗ INTRODUCTION Organisational commitment is widely recognised as an important factor positively influencing behaviour that is beneficial for organisations, such as employee effort, performance, attendance, and retention (for reviews, see for example, Mathieu and Zajac, 1990; Randall, 1990; and Meyer and Allen, 1997). Previous accounting studies have observed the significant role of organisational commitment in the effectiveness of management accounting and control systems. These studies suggest that organisational commitment reduces the propensity to create budgetary slack (Nouri, 1994; and Nouri and Parker, 1996), mediates the effect of budgetary participation on job performance (Nouri and Parker, 1998), and mitigates the negative effects of information asymmetry (Chong and Eggleton, 2007). This study explores whether, and if so how, the use of performance measures, procedural justice, 1 and interpersonal trust interact to affect the organisational commitment of senior police officers in one of the largest police forces in the United Kingdom. Examining the factors affecting organisational commitment in the police service is particularly relevant for research investigation as the policing function: Is a unique public service that relies on employee dedication in what is a turbulent, ambiguous and demanding role (Metcalfe and Dick, 2001; p. 401). Given that police agencies have themselves recognised difficulties in retention of trained police officers (Reiner, 1998), any ways by which organisational commitment can be enhanced is likely to improve retention rates. In the New Public Management (NPM) era, accounting ‘... is the dominant reference point for new style public service managers’ (Lapsley, 1999; p. 202) and ∗ The authors are respectively from the Accounting Department, Universitas Gadjah Mada, Indonesia; and the School of Management, Bradford University, UK. They wish to acknowledge the assistance of Andy Parr in data collection and to thank two anonymous referees for their helpful comments. Address for correspondence: Richard Pike, School of Management, Bradford University, Emm Lane, Bradford BD9 4JL, UK. e-mail: [email protected] C 2010 Blackwell Publishing Ltd, 9600 Garsington Road, Oxford OX4 2DQ, UK and 350 Main Street, Malden, MA, MA 02148, USA. 392

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE: EXPLORING THE EFFECTS OF PERFORMANCE MEASURES,...

Financial Accountability & Management, 26(4), November 2010, 0267-4424

ORGANISATIONAL COMMITMENT IN THE POLICESERVICE: EXPLORING THE EFFECTS OF

PERFORMANCE MEASURES, PROCEDURAL JUSTICEAND INTERPERSONAL TRUST

MAHFUD SHOLIHIN AND RICHARD PIKE∗

INTRODUCTION

Organisational commitment is widely recognised as an important factorpositively influencing behaviour that is beneficial for organisations, such asemployee effort, performance, attendance, and retention (for reviews, see forexample, Mathieu and Zajac, 1990; Randall, 1990; and Meyer and Allen, 1997).Previous accounting studies have observed the significant role of organisationalcommitment in the effectiveness of management accounting and control systems.These studies suggest that organisational commitment reduces the propensityto create budgetary slack (Nouri, 1994; and Nouri and Parker, 1996), mediatesthe effect of budgetary participation on job performance (Nouri and Parker,1998), and mitigates the negative effects of information asymmetry (Chong andEggleton, 2007).

This study explores whether, and if so how, the use of performance measures,procedural justice,1 and interpersonal trust interact to affect the organisationalcommitment of senior police officers in one of the largest police forces in theUnited Kingdom. Examining the factors affecting organisational commitmentin the police service is particularly relevant for research investigation as thepolicing function:

Is a unique public service that relies on employee dedication in what is a turbulent,ambiguous and demanding role (Metcalfe and Dick, 2001; p. 401).

Given that police agencies have themselves recognised difficulties in retentionof trained police officers (Reiner, 1998), any ways by which organisationalcommitment can be enhanced is likely to improve retention rates.

In the New Public Management (NPM) era, accounting ‘. . . is the dominantreference point for new style public service managers’ (Lapsley, 1999; p. 202) and

∗The authors are respectively from the Accounting Department, Universitas Gadjah Mada,Indonesia; and the School of Management, Bradford University, UK. They wish to acknowledgethe assistance of Andy Parr in data collection and to thank two anonymous referees for theirhelpful comments.

Address for correspondence: Richard Pike, School of Management, Bradford University,Emm Lane, Bradford BD9 4JL, UK.e-mail: [email protected]

C© 2010 Blackwell Publishing Ltd, 9600 Garsington Road,Oxford OX4 2DQ, UK and 350 Main Street, Malden, MA, MA 02148, USA. 392

ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE 393

has ‘. . . become increasingly salient as a control technology’ (Modell, 2004; p. 39).However, some (e.g., Mayston, 1985; Pollit, 1986; Ballantine et al., 1998; Kloot,1997; and Kloot and Martin, 2000) have been critical of seeking to improvepublic sector management through heavy reliance on financial performancemeasurement, and argue for a multidimensional approach to include non-financial measures (Modell, 2004). What is not clear is whether the use ofdifferent measures, such as financial or non-financial, in a police environmentyields different attitudinal and behavioural effects among police officers.

Early accounting studies on performance evaluation styles (e.g., Hopwood,1972; and Otley, 1978) suggest that the measures used to evaluate managerperformance influence attitudes and behaviour. However, subsequent studiestend to focus on the effects of only financial performance measures,2 with littleresearch attention being given to the use of non-financial performance measures.Moreover, most of the studies in this field draw on samples derived from privatesector organisations. This study seeks to address the gap in the literature byexamining the effects of the use of performance measures (whether financialor non-financial) within a police force in the UK. In particular, it explores howthese performance measures interact with procedural justice and interpersonaltrust to affect organisational commitment. Compared with most public sectororganisations the police service has received relatively little accounting researchattention (van Helden, 2005). Among the few accounting studies conductedin a police environment in the UK are Chatterton et al. (1996) and Collier(2001 and 2006). Chatterton et al. (1996) investigated the development ofmanagement accounting systems in the police service in England and Wales,Collier (2001) described the introduction of management accounting changethrough devolved financial management in a police force, and Collier (2006)explored the implementation of activity-based costing in the police service inEngland and Wales.

In this study, procedural justice is conceptualised as the judgements ofthe fairness of procedures used to evaluate employee performance and tocommunicate performance feedback. Procedural justice is important because ofits likely effect on organisational members’ attitudes (Hopwood, 1972; and Lindand Tyler, 1988) and organisational commitment (see for example, Colquittet al., 2001 for a review). Prior studies (e.g., Metcalfe and Dick, 2000 and2001; and Beck and Wilson, 2000) underscore the important influence ofjustice in enhancing organisational commitment within a police environment.As discussed later, some empirical studies (e.g., Beck and Wilson, 2000) suggestthat organisational commitment decreases with police officer tenure, in part dueto the negative work experiences and perceived lack of justice in procedures andinadequate management support. The importance of procedural justice in thepolice service is also recognised by the Home Office in the police performancemanagement framework (Home Office, 2004). Drawing on previous studieswhich found that the use of performance measures is associated with proceduraljustice (e.g., Hopwood, 1972; and Lau and Sholihin, 2005), and procedural justice

C© 2010 Blackwell Publishing Ltd

394 SHOLIHIN AND PIKE

is associated with organisational commitment (e.g., Magner and Welker, 1994;Magner et al., 1995; and Lau and Moser, 2008), we argue that proceduraljustice is a potential mediating variable on the relationship between performancemeasures employed and organisational commitment.

Interpersonal trust refers to:

subordinate’s trust or confidence in the superior’s motives and intentions with respectto matters relevant to the subordinate’s career and status in the organization (Read,1962; p. 8).

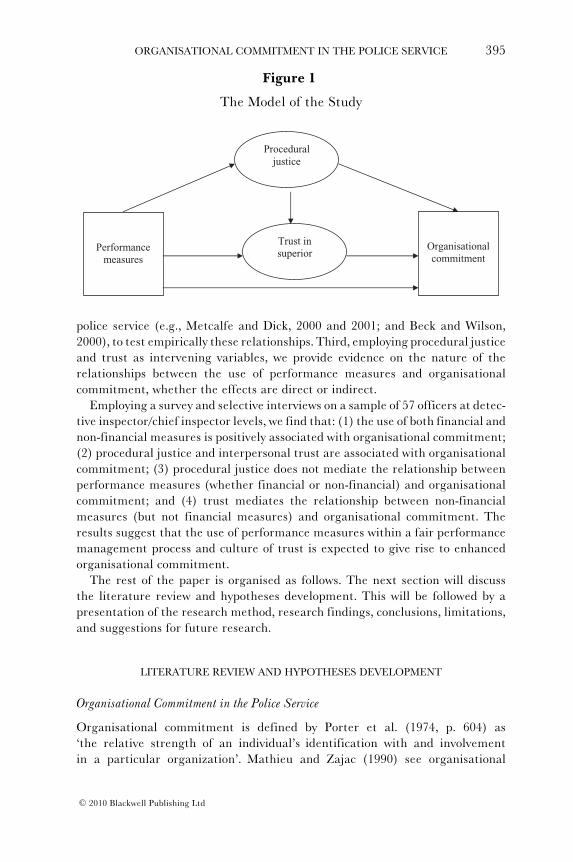

Interpersonal trust is viewed as an important contributor to organisationalperformance, particularly for organisations relying heavily on collaborative effort(Hartmann and Slapnicar, 2009). A police force is clearly such an organisation.The subordinate-supervisor trust relationship is particularly important as it leadsto improved communication and openness among organisation members (Read,1962), improves cooperation and mitigates agency problems (e.g., Jones, 1995),and enhances information exchange (e.g., Fisher et al., 2005). The extensiveliterature on trust suggests that it has an important effect on personality,interpersonal relationships, and cooperation within organisations (Lewicki et al.,1998); however, no prior study has examined whether interpersonal trust affectsthe organisational commitment among police officers. Trust is proposed as amediating variable because several accounting studies in the private sector (e.g.,Hopwood, 1972; Otley, 1978; Ross, 1994; and Lau and Sholihin, 2005) have founda significant relationship between performance measures and trust in supervisor;and trust was found to be associated with organisational commitment (e.g.,Albrecht and Travaglione, 2003; Nyhan, 1999; and Sholihin and Pike, 2009).Hence, our study hypothesises that both trust in supervisor and proceduraljustice are intervening variables which mediate the relationship between theuse of performance measures and organisational commitment of police officersas depicted in Figure 1.

The study contributes to the literature in three ways. First, it extendsthe literature on supervisory evaluative style which predominantly focuseson accounting (financial) performance measures (Lau and Sholihin, 2005) byexamining the effect of the use of financial and non-financial performancemeasures on the organisational commitment of police officers, and how theyinteract with procedural justice and interpersonal trust in this regard. This isconsistent with the suggestion made by, for example, Hartmann (2000) andOtley and Pollanen (2000). Hartmann (2000) advocates:

Based on RAPM (Reliance on Accounting Performance Measures) research specifichypotheses could be formulated about the usefulness of having multiple performanceindicators . . . about the effect of having non-financial or non-quantitative performancetargets . . . So far, both theory development and empirical evidence . . . are limited(p. 477).

Second, we move beyond the previous speculation regarding the effects ofprocedural justice and interpersonal trust on organisational commitment in the

C© 2010 Blackwell Publishing Ltd

ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE 395

Figure 1

The Model of the Study

Performance measures

Organisationalcommitment

Proceduraljustice

Trust in superior

police service (e.g., Metcalfe and Dick, 2000 and 2001; and Beck and Wilson,2000), to test empirically these relationships. Third, employing procedural justiceand trust as intervening variables, we provide evidence on the nature of therelationships between the use of performance measures and organisationalcommitment, whether the effects are direct or indirect.

Employing a survey and selective interviews on a sample of 57 officers at detec-tive inspector/chief inspector levels, we find that: (1) the use of both financial andnon-financial measures is positively associated with organisational commitment;(2) procedural justice and interpersonal trust are associated with organisationalcommitment; (3) procedural justice does not mediate the relationship betweenperformance measures (whether financial or non-financial) and organisationalcommitment; and (4) trust mediates the relationship between non-financialmeasures (but not financial measures) and organisational commitment. Theresults suggest that the use of performance measures within a fair performancemanagement process and culture of trust is expected to give rise to enhancedorganisational commitment.

The rest of the paper is organised as follows. The next section will discussthe literature review and hypotheses development. This will be followed by apresentation of the research method, research findings, conclusions, limitations,and suggestions for future research.

LITERATURE REVIEW AND HYPOTHESES DEVELOPMENT

Organisational Commitment in the Police Service

Organisational commitment is defined by Porter et al. (1974, p. 604) as‘the relative strength of an individual’s identification with and involvementin a particular organization’. Mathieu and Zajac (1990) see organisational

C© 2010 Blackwell Publishing Ltd

396 SHOLIHIN AND PIKE

commitment as the bond that links an individual to an organisation. Meyer et al.(1990) identify two types of organisational commitment: affective commitmentand continuance commitment. Affective commitment is characterised by a strongbelief in and acceptance of organisational goals and values and a willingnessto exert considerable effort on behalf of the organisation (Porter et al.,1974; and Angle and Perry, 1981); while continuance commitment refers tothe perceived costs associated with leaving the organisation, such as loss ofbenefits and seniority (Becker, 1960). Consistent with previous accountingstudies (e.g., Nouri and Parker, 1994, 1996 and 1998; and Chong and Eggleton,2007) we conceptualise organisational commitment as affective organisationalcommitment.

Reviews on organisational behaviour studies (see for example, Mathieu andZajac, 1990; Randall, 1990; and Meyer and Allen, 1997) find that organisationalcommitment is widely recognised as an important factor positively influencingbehaviour beneficial for organisations, such as employee effort and performance,attendance, and retention. Yet according to Metcalfe and Dick (2000 and2001) little research has been conducted in the UK police service on factorsassociated with organisational commitment. The earliest study of organisationalcommitment in the police force was conducted by van Maanen (1975) whoexamined the development trend of organisational commitment among USpolice recruits. Using a longitudinal study over a period of 30 months, the surveyfound that organisational commitment decreased with tenure and experience.However, compared to other public professions, such as public utility andhospital employees, the level of organisational commitment in the police servicewas significantly higher. Another relevant US study (Harr, 1997) employedfield observations and in-depth interviews with patrol officers, and found thatonly six percent of the patrol officers expressed a high level of organisationalcommitment. Low organisational commitment was found to be associatedwith occupational deviance, such as work avoidance, manipulation and deviantactivities against the organisation. A further study of US police officers conductedby Morris et al. (1999) found that organisational commitment is positivelyaffected by management support.

An Australian study by Beck and Wilson (2000) also found an inversecorrelation between organisational commitment and length of police officerservice. They speculated that the decrease in organisational commitment maybe due to the unique organisational characteristics in the police service whichflag a lack of ‘support, justice, and values’ giving rise to an ‘inventory of badexperiences’ (p. 132). Similar findings were reported by Lim and Teo (1998) ina study of police officers in Singapore.

In contrast to the above, UK studies conducted by Metcalfe and Dick(Metcalfe and Dick, 2000 and 2001; and Dick and Metcalfe, 2001) found thatorganisational commitment is positively correlated with rank seniority andtenure. Furthermore, they found that organisational commitment is affectedby management support and performance appraisal practice. The Dick and

C© 2010 Blackwell Publishing Ltd

ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE 397

Metcalfe (2001) study sought to compare the organisational commitment ofcivilian staff with police officers in a large police force in England, and toexamine whether managerial factors that affect organisational commitmentdiffer between the two groups. Dick and Metcalfe (2001) found the two groupspossessed similar levels of organisational commitment, although manageriallevel (officer rank) was positively associated with organisational commitmentfor uniform staff but not for civilian staff.

Overall, the organisational commitment studies among police officers suggestthat the UK context differs from other countries regarding tenure and organisa-tional commitment, but in all contexts organisational commitment is affected byvarious management and organisational factors. Our study will explore furthersome of these factors by examining whether organisational commitment ofdetective inspectors and detective chief inspectors is affected by the use ofperformance measures, procedural justice, and trust in superiors. It will alsocontrol for the effects of tenure.

Performance Measures and Organisational Commitment

The performance measurement literature in the private sector (e.g., Ittnerand Larcker, 1998; and Kaplan and Norton, 1992 and 1996) advocates the useof non-financial performance measures. This suggestion is mainly motivatedby the perceived loss of value relevance of traditional financial or accountingmeasures in understanding organisational performance (Johnson and Kaplan,1987; Lynch and Cross, 1991; and Ittner and Larcker, 1998). In the publicsector, as cited by Modell (2004), many accounting researchers (e.g., Mayston,1985; Pollit, 1986; Ballantine et al., 1998; Kloot, 1997; and Kloot and Martin,2000) have criticised attempts to improve public sector management perfor-mance by relying on financial measurement, and suggest that performancemeasurement in the public sector should be broadened to include non-financialaspects.

In the police service, both financial and non-financial measures are importantin managing police performance (Chatterton et al., 1996; and Home Office,2004). Studies conducted by Chatterton et al. (1996) and Collier (2001) foundthat following the introduction of the Financial Management Initiative in 1982,budgeting became the prevalent accounting form adopted by police forcesin the UK. With regard to non-financial measures, the practical guide toperformance management (Home Office, 2004) recognised the importance ofboth lead indicators (i.e. performance indicators which give an early signalof future performance against the force’s high-level performance outcomes)and lag indicators (i.e. indicators of past performance). For example, ‘timeto attend a burglary’ is a lead indicator and ‘the burglary detection rate’is the lag indicator. More recently, the practical guide to performancemanagement (Home Office, 2008) advocated that ‘everyone in the forceunderstands and acts upon the basic principles of performance management

C© 2010 Blackwell Publishing Ltd

398 SHOLIHIN AND PIKE

as relevant for their role’ (p.17). However, financial performance measuresand budget responsibility relate more to senior officers (Chatterton et al.,1996).

Prior studies in private sector firms (e.g., Lau and Sholihin, 2005) suggestthat the use of performance measures (either financial or non-financial) maybe positively associated with various functional attitudes and behaviour. Usinga sample of managers from Indonesian manufacturing companies, Lau andSholihin (2005) found that the use of performance measures is associated withprocedural fairness, interpersonal trust, and job satisfaction. Subramaniam andMia (2003) suggest that budget emphasis may be positively associated withorganisational commitment. In the private sector, they found a non-monotoniceffect of the interaction between budget emphasis and managers’ work-relatedvalues on organisational commitment. Lau and Moser (2008), using a sampleof managers from UK manufacturing organisations, found that the use ofnon-financial measures in evaluating subordinates’ performance is positivelyassociated with organisational commitment. Based on the results of studies inthe private sector we expect there will be a positive association between the useof performance measures (either financial or non-financial) and organisationalcommitment. However, such effect may be indirect via procedural justice andtrust, as will be discussed below.

Performance Measures, Procedural Justice, and Trust

The use of performance measures (whether financial or non-financial) in theprivate sector has been found to be associated with procedural justice andtrust (e.g., Hopwood, 1972; Otley, 1978; and Lau and Sholihin, 2005). Hopwood(1972) and Otley (1978) studied the effect of the use of financial measuresfor performance evaluation on subordinates’ attitudes and behaviour withinmanufacturing companies in the US and the UK, respectively. They founda positive relationship between the use of financial performance measures(budget constrained and profit conscious) on trust and procedural justice.A more recent study by Lau and Sholihin (2005), based on managers ofIndonesian manufacturing companies, found that the use of performancemeasures (either financial or non-financial) in evaluating managers is pos-itively associated with procedural justice and trust. Lau and Moser (2008),surveying managers of UK manufacturing companies, found that the use ofnon-financial measures is positively associated with procedural justice. Drawingon the above findings we therefore expect that the use of both financial andnon-financial performance measures in the police service will be positivelyassociated with procedural justice and trust in superiors. Thus we hypothesise thefollowing:

H1: The use of financial performance measures is positively associated withprocedural justice and trust.

C© 2010 Blackwell Publishing Ltd

ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE 399

H2: The use of non-financial performance measures is positively associatedwith procedural justice and trust.

Procedural Justice and Organisational Commitment

Procedural justice was first introduced as a term by Thibaut et al. (1974) withregard to the procedural effects on fairness judgments. The theory of proceduraljustice, developed in a legal setting by Thibaut and Walker (1978), deals primar-ily with the effects of process control in dispute resolution. Leventhal (1980) andLeventhal et al. (1980) extended its application to other allocation decisions,including decisions within organisational settings. Subsequent organisationalstudies found that procedural justice judgments played a major role in affectingorganisational behaviour such as organisational commitment (Lind and Tyler,1988; Colquitt et al., 2001; and Blader and Tyler, 2005). In this regard, Lind andTyler argue that:

To the extent that group procedures are fair, evaluation of the group and commitmentand loyalty to the group will increase (1988 p. 232).

A meta-analytic review of justice empirical studies by Colquitt et al. (2001)supports the positive association between procedural justice and organisationalcommitment. The empirical accounting literature also supports this relationship.Magner and Welker (1994) found procedural justice in budgetary resource allo-cation to be positively associated with organisational commitment and trust insuperiors among accounting department heads of American universities and col-leges. Magner et al. (1995) examined whether budgetary participation (a proxyof procedural fairness) interacts with budget favourability to affect subordinates’attitudes towards their superiors (trust) and their organisation (organisationalcommitment). They hypothesised that when subordinates’ received unfavourablebudgets, they would experience higher levels of trust towards their superiors andhigher degrees of organisational commitment when they had participated in thebudgetary process compared with those who had not participated. Using a sampleof international managers in private sector organisations they found significantinteraction between unfavourable budgets and budgetary participation affectingsubordinates’ trust in superiors and subordinates’ organisational commitment.Subordinates’ trust in their superior and organisational commitment werehigher in situations when they were allowed to participate in budget setting.Their findings support the argument that procedural fairness is an importantdeterminant of trust and organisational commitment. Using a sample ofmanagers from UK manufacturing organisations, Lau and Moser (2008) foundthat procedural justice is positively associated with organisational commitment.We therefore expect that procedural justice will be positively associated withorganisational commitment. Therefore we hypothesise:

H3: Procedural justice is positively associated with organisational commit-ment.

C© 2010 Blackwell Publishing Ltd

400 SHOLIHIN AND PIKE

Trust and Organisational Commitment

Zand (1997) defines trusting behaviour as a willingness to increase vulnerabilityto another person whose behaviour cannot be controlled in situations in which apotential benefit is much less than a potential loss if the other person abuses thevulnerability. Further, he suggests that trust between individuals will greatly in-crease their joint problem solving effectiveness, and increase their commitmentto each other and satisfaction with their work and their relationships. Trusttherefore has an important effect on interpersonal relationships, cooperation,and stability in social institutions and markets (Lewicki et al., 1998). Consistentwith previous accounting studies (e.g., Hopwood, 1972; Otley, 1978; Ross, 1994;and Lau and Sholihin, 2005), trust is conceptualised as interpersonal trust. Aspreviously mentioned, Read defines this as:

subordinate’s trust or confidence in the superior’s motives and intentions with respectto matters relevant to the subordinate’s career and status in the organization (1962,p.8).

Read (1962) further notes that trusting subordinates expect their intereststo be protected and promoted by their superiors, feel confident about dis-closing negative personal information, feel assured of full and frank infor-mation sharing, and are prepared to overlook apparent breaches of the trustrelationships.

Lau et al. (2008) argue that trust in supervisors may be associated withorganisational commitment because subordinates will tend to perceive theirorganisation through the supervisor’s actions. Using a sample of employees fromtwo public-sector organisations (with responsibilities for the administration ofpublicly funded library services, arts and theatres and land title), Albrecht andTravaglione (2003) found trust to be significantly associated with organisationalcommitment. Using 600 employees in three public organisations, Nyhan (1999)found that interpersonal trust is associated with organisational commitment. Asimilar finding was found by Sholihin and Pike (2009) using a sample of managersfrom private organisations with head offices in Europe and Africa. Given thisevidence, we hypothesise:

H4: Trust in superiors is positively associated with organisational commit-ment.

Procedural Justice and Trust

There is ample evidence to indicate that the implementation of proceduresperceived by subordinates as unjust is detrimental to the organisation’s interests(Greenberg, 1987; Friedland et al., 1973; Thibaut et al., 1974; and Kanferet al., 1997). Since the perception of unjust procedures can negatively affectorganisations, superiors are likely to maintain high procedural justice. Bymaintaining high procedural justice, it is expected that subordinates will havemore trust in superiors (Lind and Tyler, 1988).

C© 2010 Blackwell Publishing Ltd

ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE 401

Whitener et al. (1998) argue that a necessary foundation to increase trust ina supervisor is for the superior to engage in trustworthy behaviour. This implies(1) consistency across time and situations, which reflects the reliability andpredictability of actions; (2) integrity, which refers to the consistency betweena manager’s words and actions; (3) sharing and delegation of control, such asparticipation in decision making; (4) communication, that is, the informationshould be accurate, forthcoming, adequately explained, and open (exchangeideas freely); and (5) benevolence, that is, a sensitivity to subordinates’ needsand interests, and refraining from exploiting others for the benefit of one’s owninterests.

Previous studies in various settings reveal that procedural justice has apositive influence on trust (e.g., Alexander and Ruderman, 1987; Folger andKonovsky, 1989; and Konovsky and Pugh, 1994). Alexander and Ruderman(1987) investigate the relationship between fairness and various organisationaloutcomes using government employees at six US Federal installations. Theyfound that procedural justice significantly affects job satisfaction, evaluationof supervisor, conflict/harmony, trust in management, and turnover intention.Folger and Konovsky (1989) conducted a survey to examine the impact ofjustice on the decision of pay rises. Using samples of employees from afinancial services organisation they found that procedural justice positivelyaffects trust in supervisors and organisational commitment. Konovsky andPugh (1994) develop and empirically examine a social exchange model oforganizational citizenship behaviour. Using data from hospital employees andtheir supervisors, they found that procedural justice positively affects trust insupervisors.

Management accounting studies also found that procedural fairness affectstrust in superiors (Magner and Welker, 1994; Staley and Magner, 2006; Lauand Tan, 2006; and Lau et al., 2008). Magner and Welker (1994) found thatprocedural justice in budgetary resource allocation was positively associatedwith organisational commitment and trust in superiors. Staley and Magner(2006) develop and test a model based on social exchange theory on whetherprocedural and interactional budgetary fairness reduce managers’ propensity tocreate budgetary slack by way of enhancing managers’ trust in their immediatesupervisor. Drawing on a survey of US Federal government managers they foundthat procedural fairness positively affects trust in superiors. Surveying managersof manufacturing companies in Singapore, Lau and Tan (2006) found thatprocedural justice is positively associated with trust. In an Australian study ofhealth service managers Lau et al. (2008) found that procedural justice positivelyaffects trust.

Since previous studies overwhelmingly suggest that procedural jus-tice is positively associated with trust, the following hypothesis will betested:

H5: Procedural justice is positively associated with trust in superiors.

C© 2010 Blackwell Publishing Ltd

402 SHOLIHIN AND PIKE

RESEARCH METHOD

Data and Sample

Data for this study was gathered by means of a questionnaire survey3 sentto detective inspectors and detective chief inspectors, covering a range ofoperational and administrative roles, in a division of one of the largest PoliceForces in the United Kingdom (hereafter Force). Questionnaire findings weresupplemented by interview data. We focus on these managerial levels because,according to Butterfield et al. (2005), they are expected to take on more devolvedmanagement responsibility in the New Public Management era.

The interviews were conducted with four detective inspectors, selected fromrespondents who indicated willingness to participate further. Semi-structuredinterviews were performed, each lasting approximately one hour. The interviewquestions were developed in order to understand the survey findings better. Forexample, it explored further their understanding of the performance measuresused, the procedural justice perceptions, the interpersonal trust towards theimmediate supervisor, and how these issues affect their organisational commit-ment.

This combination of quantitative and qualitative approaches offered a morevalid, comprehensive and convincing picture of the research issues beinginvestigated (Creswell, 2003; and Modell, 2005). The quantitative approachpermits a statistical exploration of the research model, while the qualitativeapproach facilitates greater understanding of the findings and provides richermeanings in interpreting the quantitative results (Bryman and Bell, 2003).Creswell (2003) identifies three ways in which this mixed method of datacollection can be implemented: the sequential, concurrent, and transformativemixed methods. The sequential mixed method used in this study permits theresearcher to elaborate on or expand the findings of one method with anothermethod. The quantitative survey method, which drives the study, is conductedfirst in order to test the theoretical model, followed by the qualitative methoddesigned to offer a logical extension and resolve issues uncovered by the firstmethod through detailed interviews with four responding officers.

The survey was administered as follows. Working closely with a senior officerin the Force, a preliminary notification was circulated encouraging detectiveinspectors and detective chief inspectors to participate in the survey. Thesurvey instrument was distributed to 112 officers, together with an assuranceof confidentiality. Reminders were sent one, three and seven weeks after theoriginal mailing. The survey package and reminder letters were sent via e-mail.Respondents could return the completed questionnaires electronically by e-mailor send a hard copy version by post.

From 112 questionnaires distributed, 57 responses were received, representinga response rate of 51%. This is regarded as a particularly high response rate, giventhe recognised difficulties in accessing data within police institutions (Metcalfe

C© 2010 Blackwell Publishing Ltd

ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE 403

and Dick, 2000). Brodeur (1998) suggests that police force surveys typically enjoya response rate of 25–30%.

Non-response bias tests were conducted to examine whether there weresystematic differences between early and late responses. Responses were dividedinto two groups based on their dates of arrival. The test was performed by runningt-tests to compare the mean of responses for each variable between the twogroups. The results did not identify any systematic difference between early andlate responses.

Analysis of respondent characteristics reveals that, on average, they have beenworking in the Force for 22 years (ranging from 1–32 years), in their currentposition for 2.4 years (from 1–10 years), and been supervised by their currentsuperior for 1.5 years (from 1–5 years). Our preliminary analysis reveals thatthese demographic characteristics do not affect the responses.4

Variables and their Measurements5

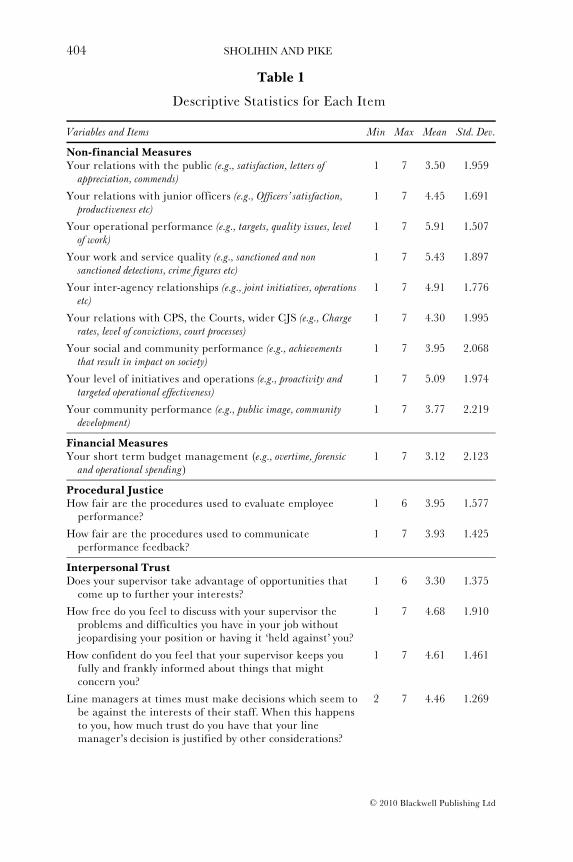

The use of performance measures. To measure this variable respondents wererequested to indicate how much importance they thought their supervisorsattach to certain performance measures when evaluating their performance,using a seven-point Likert scale, anchored 1 (no importance) and 7 (alwaysimportant) with 0 if not applicable.6 The performance categories used are basedon those of Ittner et al. (2003), which they consider to be important drivers oflong-term organisational success.7 However, following discussion with a policeinspector in the Force prior to finalising the questionnaire, they were adapted tomake the items more relevant to the officers responding. The nine non-financialmeasures identified are (1) relations with the public, (2) relations with juniorofficers, (3) operational performance, (4) work and service quality, (5) inter-agency relationships, (6) relations with the Crown Prosecution Service, Courts,and the wider Criminal Justice System, (7) social performance, (8) initiativesand operations, and (9) community performance. For financial measures we usea single category, i.e. short term budget management. The officers involved inthe survey have limited budget responsibility. This is specifically restricted tothe areas of overtime, travel, operations, and forensic.8 Further details of thequestionnaire are available in the Appendix.

Detailed descriptive statistics for each item of this variable and for othervariables are presented in Table 1. The table indicates that the most importantcategory used in their performance evaluation is ‘operational performance’ withan average score of 5.91. Other categories with scores above 5 are ‘work andservice quality’, and ‘level of initiatives and operations’. The least importantmeasure is ‘budget management’, with an average score of 3.12. This reinforcesthe point that there is limited budget responsibility at the level of officersurveyed, although the fact that it has one of the highest standard deviationsof the performance measures suggests that some officers have greater budgetresponsibility than others. In our further analysis we classified the ten categories

C© 2010 Blackwell Publishing Ltd

404 SHOLIHIN AND PIKE

Table 1

Descriptive Statistics for Each Item

Variables and Items Min Max Mean Std. Dev.

Non-financial MeasuresYour relations with the public (e.g., satisfaction, letters of

appreciation, commends)1 7 3.50 1.959

Your relations with junior officers (e.g., Officers’ satisfaction,productiveness etc)

1 7 4.45 1.691

Your operational performance (e.g., targets, quality issues, levelof work)

1 7 5.91 1.507

Your work and service quality (e.g., sanctioned and nonsanctioned detections, crime figures etc)

1 7 5.43 1.897

Your inter-agency relationships (e.g., joint initiatives, operationsetc)

1 7 4.91 1.776

Your relations with CPS, the Courts, wider CJS (e.g., Chargerates, level of convictions, court processes)

1 7 4.30 1.995

Your social and community performance (e.g., achievementsthat result in impact on society)

1 7 3.95 2.068

Your level of initiatives and operations (e.g., proactivity andtargeted operational effectiveness)

1 7 5.09 1.974

Your community performance (e.g., public image, communitydevelopment)

1 7 3.77 2.219

Financial MeasuresYour short term budget management (e.g., overtime, forensic

and operational spending)1 7 3.12 2.123

Procedural JusticeHow fair are the procedures used to evaluate employee

performance?1 6 3.95 1.577

How fair are the procedures used to communicateperformance feedback?

1 7 3.93 1.425

Interpersonal TrustDoes your supervisor take advantage of opportunities that

come up to further your interests?1 6 3.30 1.375

How free do you feel to discuss with your supervisor theproblems and difficulties you have in your job withoutjeopardising your position or having it ‘held against’ you?

1 7 4.68 1.910

How confident do you feel that your supervisor keeps youfully and frankly informed about things that mightconcern you?

1 7 4.61 1.461

Line managers at times must make decisions which seem tobe against the interests of their staff. When this happensto you, how much trust do you have that your linemanager’s decision is justified by other considerations?

2 7 4.46 1.269

C© 2010 Blackwell Publishing Ltd

ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE 405

Table 1 (Continued)

Variables and Items Min Max Mean Std. Dev.

Organisational CommitmentI am willing to put in a great deal of effort beyond that

normally expected4 7 6.21 0.709

I talk up this organisation to my friends as a greatorganisation to work for

2 7 5.09 1.461

I have found that my values and the organisation’s valuesare very similar

2 7 5.09 1.360

I would accept almost any type of job assignment in order tokeep working for this organisation

1 7 3.49 1.956

I am proud to tell others that I am part of this organisation 3 7 5.77 1.179

This organisation really inspires the very best in me in theway of job performance

1 7 3.89 1.644

I am extremely glad that I chose this organisation to workfor over others I was considering at the time I joined

2 7 5.68 1.365

For me this is the best of all possible organisations forwhich to work

1 7 4.16 1.801

I really care about the fate of this organisation 1 7 5.96 1.322

into financial measures (short term budget management) and non-financialmeasures (the other nine categories).

Procedural justice. This variable is measured using the instrument developedby McFarlin and Sweeney (1992) and has been employed in other accountingstudies (e.g., Lau and Sholihin, 2005; and Lau and Tan, 2006). Originally,this instrument consisted of four items. However, given that the pay andpromotion appraisal processes in the Force have little to do with attainingperformance targets, two items were deemed not relevant leaving two itemscovering fairness of procedures used by superiors to evaluate officer performanceand to communicate performance feedback.

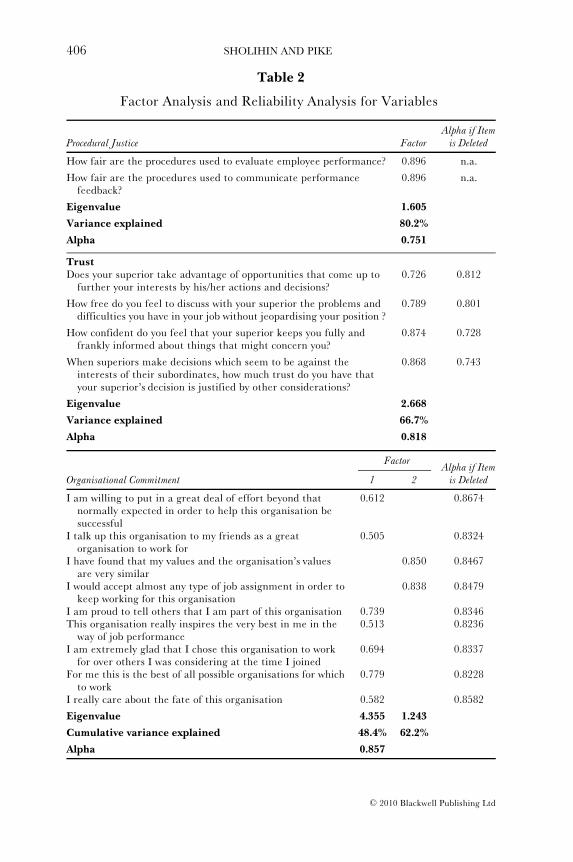

Table 1 shows that the means for the fairness of procedures used tocommunicate performance feedback and to evaluate officer performance are 3.93and 3.95, respectively. Factor analysis (see Table 2) extracted one factor withan eigenvalue greater than one (eigenvalue = 1.61; total variance explained =80.2%), while the Cronbach alpha coefficient (0.751) indicates acceptablereliability (Nunnaly, 1967).

Trust in superiors. This variable is measured using Read’s(1962) instrument whichhas been employed in other accounting studies (e.g., Otley, 1978; and Lau andSholihin, 2005). Table 1 indicates that the means of three items are above 4, indi-cating a reasonable level of interpersonal trust. However, the lower mean (3.30)for ‘Does your supervisor take advantage of opportunities that come up to furtheryour interests?’ indicates that the trust relationship is not altogether healthy.Factor analysis (see Table 2) for this variable reveals that only one factor with

C© 2010 Blackwell Publishing Ltd

406 SHOLIHIN AND PIKE

Table 2

Factor Analysis and Reliability Analysis for Variables

Alpha if ItemProcedural Justice Factor is Deleted

How fair are the procedures used to evaluate employee performance? 0.896 n.a.

How fair are the procedures used to communicate performancefeedback?

0.896 n.a.

Eigenvalue 1.605

Variance explained 80.2%

Alpha 0.751

TrustDoes your superior take advantage of opportunities that come up to

further your interests by his/her actions and decisions?0.726 0.812

How free do you feel to discuss with your superior the problems anddifficulties you have in your job without jeopardising your position ?

0.789 0.801

How confident do you feel that your superior keeps you fully andfrankly informed about things that might concern you?

0.874 0.728

When superiors make decisions which seem to be against theinterests of their subordinates, how much trust do you have thatyour superior’s decision is justified by other considerations?

0.868 0.743

Eigenvalue 2.668

Variance explained 66.7%

Alpha 0.818

FactorAlpha if Item

Organisational Commitment 1 2 is Deleted

I am willing to put in a great deal of effort beyond thatnormally expected in order to help this organisation besuccessful

0.612 0.8674

I talk up this organisation to my friends as a greatorganisation to work for

0.505 0.8324

I have found that my values and the organisation’s valuesare very similar

0.850 0.8467

I would accept almost any type of job assignment in order tokeep working for this organisation

0.838 0.8479

I am proud to tell others that I am part of this organisation 0.739 0.8346This organisation really inspires the very best in me in the

way of job performance0.513 0.8236

I am extremely glad that I chose this organisation to workfor over others I was considering at the time I joined

0.694 0.8337

For me this is the best of all possible organisations for whichto work

0.779 0.8228

I really care about the fate of this organisation 0.582 0.8582

Eigenvalue 4.355 1.243

Cumulative variance explained 48.4% 62.2%

Alpha 0.857

C© 2010 Blackwell Publishing Ltd

ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE 407

an eigenvalue value greater than 1 was extracted (eigenvalue = 2.67; totalvariance explained = 66.7%) and Cronbach’salpha coefficient for this instrumentis 0.818.

Organisational commitment. This variable measures the respondents’ attitudetoward their organisation (Magner et al., 1995) and is captured using the nine-item short-form scale from Mowday et al. (1979). Respondents were requiredto indicate their level of agreement on nine items on attitudes towards theirorganisation, using a seven-point Likert type scale ranging from 1 (stronglydisagree) to 7 (strongly agree). The highest score is 6.21 for the item ‘I amwilling to put in a great deal of effort beyond that normally expected’. However,the much lower mean (3.89) for ‘This organisation really inspires the very bestin me in the way of job performance’, suggests that many officers believe thatthey could perform better if they were more committed.

Table 2 shows that factor analysis of the nine items to measure this variablereveals two underlying factors but with one predominant factor (eigenvalue 4.4),accounting for 48.4% of the variance (only two item loads in factor 2). Thereliability (Cronbach alpha of 0.857) is acceptable. Consistent with previousstudies in management accounting (Chong and Eggleton, 2007; Lau et al., 2008;and Sholihin and Pike, 2009) we used all nine items.9

FINDINGS AND DISCUSSIONS

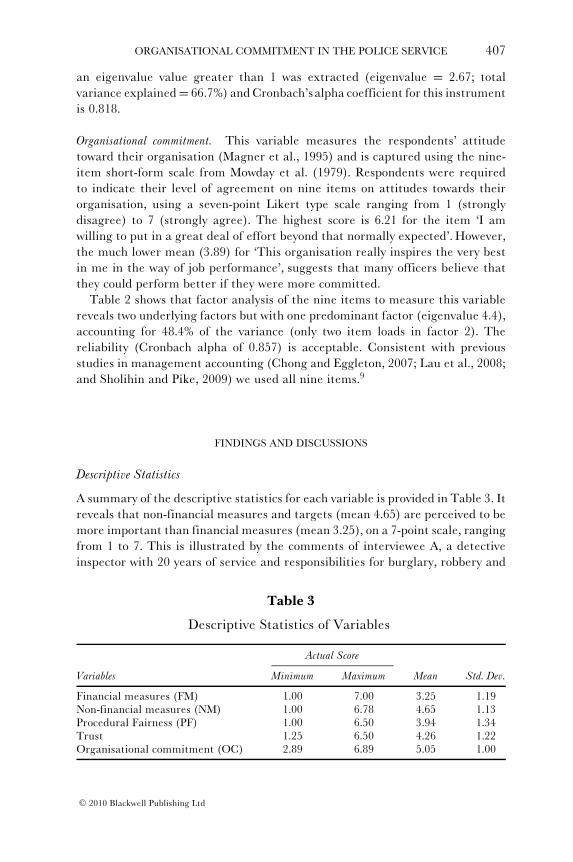

Descriptive Statistics

A summary of the descriptive statistics for each variable is provided in Table 3. Itreveals that non-financial measures and targets (mean 4.65) are perceived to bemore important than financial measures (mean 3.25), on a 7-point scale, rangingfrom 1 to 7. This is illustrated by the comments of interviewee A, a detectiveinspector with 20 years of service and responsibilities for burglary, robbery and

Table 3

Descriptive Statistics of Variables

Actual Score

Variables Minimum Maximum Mean Std. Dev.

Financial measures (FM) 1.00 7.00 3.25 1.19Non-financial measures (NM) 1.00 6.78 4.65 1.13Procedural Fairness (PF) 1.00 6.50 3.94 1.34Trust 1.25 6.50 4.26 1.22Organisational commitment (OC) 2.89 6.89 5.05 1.00

C© 2010 Blackwell Publishing Ltd

408 SHOLIHIN AND PIKE

vehicle theft detection:

My main responsibility is to achieve the detection rate in the area of the priority crimes,namely the burglaries, the robberies, and the theft of vehicles . . . and I do not have alot to do with budgets . . . the only one really I have access to is overtime.

Interviewee B, a detective inspector with 15 years of service, commented:

My main financial responsibility is to authorise expense claims and overtime. I havebeen told how many officers I have to deploy ‘on paper’ but do not control the actualnumbers that are deployed . . . . frequently team numbers are managed centrally to‘balance the books’, but less are provided than should be to reduce the cost of anofficer. This ‘tactic’ has evolved since devolved budgets were allocated to divisionalunits in the police, managed by ‘business managers’, civilian support staff along sidedivisional commanders.

The procedural justice variable has a mean of 3.94, implying that a largeproportion of the officers do not perceive the procedures used to evaluateperformance as fair. Given the importance placed on fairness in performanceevaluation in The Police Performance Management Guide (Home Office, 2004),one might have expected the rating to be higher. Part of the perceived problemwithin the police force is that the pay and promotion processes do not formallyconsider the levels of success in attaining performance measures. Interviewee Aobserved:

. . . I don’t think the way my job is evaluated will ever make any difference to whatreward I receive at the end of the day because of the way police regulations are theycan’t turn round . . . It doesn’t recognise what you’re doing . . .

Another respondent (interviewee C, a detective inspector with 22 years of policeservice) commented:

Strictly speaking . . . I would say that whether you have come in on target . . . it doesn’taffect the decision on pay or promotion.

However, another respondent (interviewee D, a detective inspector with 31 yearsof service responsible for shootings, stabbings and rape detection) argues:

I think it would be naive to think that performance measures aren’t taken into accountwhen officers go for promotion. Obviously the better performing candidates will beidentified and supported by their line managers for promotion but there is nothingwritten in policy to state so. Financial management does not factor at all in the processbut again if an officer was to waste huge resources it is unlikely he/she would besupported by their line managers.

In contrast to procedural fairness, we find that respondents’ trust in theirsuperiors and their commitment to their organisation are both relatively high(mean of 4.26 for trust, and 5.05 for organisational commitment). One inspector(interviewee A) described the loose linkage between performance targets andorganisation commitment as follows:

To me it’s more personal, I don’t like to do something and not do it by half. If I’mgiven something to do, I want to achieve it . . . . and I’ll feel a disappointment if I don’t

C© 2010 Blackwell Publishing Ltd

ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE 409

and therefore I’m fairly driven in achieving targets from my own point of view andI’ll drag everybody else along with me . . . and I think this job relies heavily on peoplelike myself to do that . . . . they know there’s a lot of committed individuals within thepolice service that want to do well. And it’s not just so they progress their own career,it’s just because they do feel about what they want to do . . . people having sort of aninner desire really to do well. Not necessarily for themselves, not necessarily to meettheir target but the fact that you know . . . for example, Mrs Smith has had her houseburgled and is now frightened to go to bed without the light on, on a night . . . So I seemyself as having more of an impact on trying to prevent those sort of issues happening.

Another respondent (interviewee D) explained his high levels of trust in hissuperior in terms of the clarity and transparency in communicating performancefeedback:

I don’t think there’s anything hidden there when I asked about the results ofPerformance Review . . . . . So the trust is there.

In summary, the descriptive statistics and interviews suggest that while theperceived procedural justice is relatively low, officers in the Force typicallyremain committed to the organisation’s goals and have healthy levels of trust intheir superiors.

Bivariate Analysis

Bivariate analysis was performed to explore associations between the variablesstudied. Table 4 reveals that both procedural justice and trust are positivelyassociated with organisational commitment (p < 0.05 and p < 0.01, respec-tively). The findings provide empirical support for the speculation of previousmanagement studies in a police context (e.g., Beck and Wilson, 2000) whichargue that the observed decreased organisational commitment may be becausethe work experiences of officers highlight ‘a lack of support, justice, andvalue’ (p. 132). The results also support the findings in organisational justicestudies (see for example, a meta analysis by Colquitt et al., 2001) as well asin management accounting studies in other environments (e.g., Magner and

Table 4

The Results of Correlation Analysis

FM NM PF Trust OC

FM 1NM 0.448∗∗ 1PF 0.057 0.98 1Trust 0.155 0.223 0.313∗ 1OC 0.313∗ 0.421∗∗ 0.334∗ 0.431∗∗ 1

Notes:∗∗Correlation is significant at the 0.01 level (2-tailed).∗Correlation is significant at the 0.05 level (2-tailed).

C© 2010 Blackwell Publishing Ltd

410 SHOLIHIN AND PIKE

Welker, 1994; Magner et al., 1995; and Lau and Moser, 2008). With regardto the positive association between trust and organisational commitment, theresult is consistent with Albrecht and Travaglione (2003) and Nyhan (1999) inthe public sector and Sholihin and Pike (2009) in the private sector.

The table also indicates that procedural justice is positively associated withtrust (p < 0.05). This is consistent with previous studies in other settings, such asgovernmental office employees (e.g., Alexander and Ruderman, 1987), hospitalemployees (e.g., Konovsky and Pugh, 1994), and manufacturing employees (e.g.,Folger and Konovsky, 1989). The findings also support previous accountingstudies in other environments (e.g., Magner and Welker, 1994; Staley andMagner, 2006; Lau and Tan, 2006; and Lau et al., 2008).

Further, Table 4 shows that the use of financial performance measures ispositively associated with organisational commitment (p < 0.05), although theresult is stronger for the use of non-financial measures (p < 0.01). The table, how-ever, shows no significant association between financial measures and proceduraljustice and trust. This also applies for the use of non-financial measures. Thesefindings differ from Lau and Sholihin’s (2005) study of manufacturing firmswhere both financial and non-financial performance measures were positivelyassociated with procedural justice and trust. One possible explanation couldbe the considerable difference in occupational culture between officers in apolice force and managers in private sector firms. Collier (2001) argues thatthe occupational culture of policing (the norms, values and beliefs held by policeofficers) affect all aspects of policing. These are reinforced by:

recruitment, training and socialization processes, embedded in the rank hierarchyand supported by rewards and sanctions . . . . They are firmly rooted in the notion ofconstabulary independence in which police officers are not employees but warrantholders (p. 472).

Overall, the results of the correlation analysis suggest that organisationalcommitment is enhanced where the performance evaluation and measurementprocedures for senior officers is perceived by them as fair in evaluatingperformance and communicating performance feedback, and fosters trust inthe subordinate-superior relationship. In addition, the results suggest thatprocedural fairness is an important determinant of interpersonal trust.

The correlation analysis does not provide initial support for hypothesisH1 (The use of financial performance measures is positively associated withprocedural justice and trust, and H2 (The use of non-financial performancemeasures is positively associated with procedural justice and trust). The results,however, provide initial support for H3 (Procedural justice is positively associatedwith organisational commitment), H4 (Trust in superiors is positively associatedwith organisational commitment), and H5 (Procedural justice is positivelyassociated with trust in superiors). In addition, the results of the bivariateanalysis also indicate that the effect of the use of financial and non-financialmeasures on organisational commitment is direct, as the use of measures,

C© 2010 Blackwell Publishing Ltd

ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE 411

either financial or non-financial, is not associated with procedural justice andtrust. In other words, procedural justice and trust do not appear to mediate therelationship between performance measures use and organisational commitment(see Baron and Kenny, 1986). In addition, the results of the bivariate analysissuggest that trust may mediate the relationship between procedural justice andorganisational commitment.

Baron and Kenny (1986) explain that a variable, such as trust, is said to havea mediating effect when the variable is correlated with the independent variable(procedural justice) as well as with the dependent variable (organisationalcommitment). They further argue that a variable may act as a full mediator orpartial mediator. Full mediation exists when the significant correlation betweenindependent and dependent variables ceases to remain significant followingintroduction of the proposed mediating variable in the model. Partial mediationarises when the mediating variable is included in the model and the relationshipbetween independent and dependent variable retains its significance. To ascer-tain the nature of the relationship of the variables studied, structural equationmodelling using a PLS approach is performed, as discussed below.

Structural Equation Model Analysis

A structural equation modelling approach is adopted because it offers the flex-ibility to model relationships among multiple predictor and criterion variables,constructs unobservable latent variables, models errors in measurement forobserved variables, and tests a priori theoretical and measurement assumptionsagainst empirical data (Chin, 1998a). In this study, a PLS approach is deemedmost appropriate because of the relatively small sample size.10

The PLS technique consists of both a measurement and structural model.The measurement model specifies the relationship between the manifest items(indicators) and latent variables (constructs) they represent. The structuralmodel identifies the relationships among constructs. PLS is therefore ableto assess the validity of constructs within the total model (Chenhall, 2005).The objective of the structural model using a PLS approach is to maximizethe variance explained by variables in the model using R-Square as thegoodness-of-fit measure (Chin and Newsted, 1999). The parameter estimationprocedure associated with covariance-based structural equation modeling isnot appropriate (Chin and Newsted, 1999; and Hulland, 1999). Rather, abootstrapping resampling procedure is used to estimate t-statistics for the PLSstructural path coefficient. Following standard practice in accounting studieswhich use PLS (e.g., Chenhall, 2005) this study uses a large bootstrap sampleof 500. This figure is chosen so that the data approximates normal distributionand leads to better estimates of test statistics as PLS does not required normaldistribution (Chin, 1998b; and Gefen et al., 2000).

In this study the relationships between latent variables (constructs) andtheir manifest items (indicators) are modeled as reflective indicators, whereby

C© 2010 Blackwell Publishing Ltd

412 SHOLIHIN AND PIKE

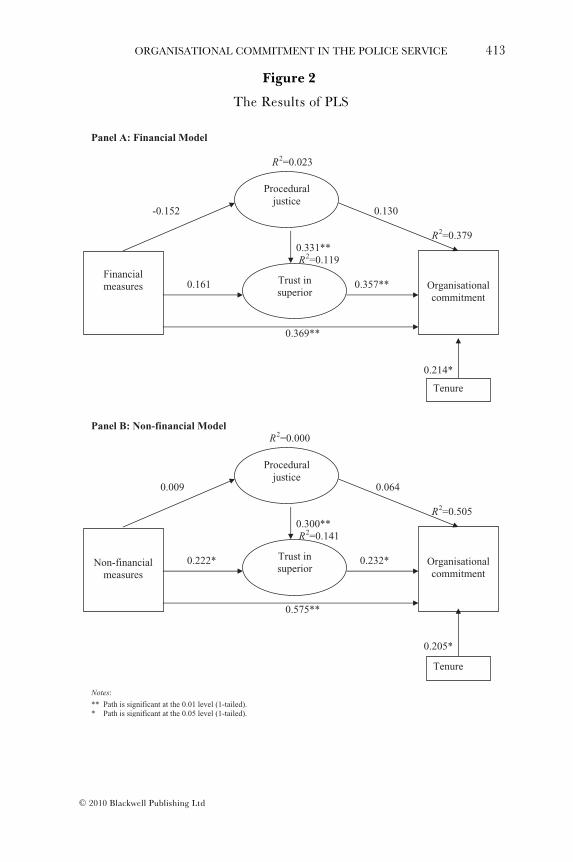

items for each construct are assumed to be correlated and measure the sameunderlying phenomenon (Gefen et al., 2000). Using this model, the individualitem reliability is assessed by examining the loading of measures with theirrespective construct.11 The measurement model reveals that all items loadon their respective construct above 0.5, except an item within organisationalcommitment construct. Hence the results of the PLS approach validate theresults of factor analysis previously performed.

Figure 2 presents the PLS results by controlling for the effect of tenure. Tenureis controlled as previous studies offer ambiguous results, where van Maanen(1975), Beck and Wilson (1997 and 2000), and Lim and Teo (1998) found thatorganisational commitment decreased with tenure, Metcalfe and Dick (2000and 2001), Dick and Metcalfe (2001) found that organisational commitmentincreased with tenure. The figure in Panel A shows the results of the structuralmodel of financial measures whilst Panel B shows the structural model for non-financial measures. Both models reveal that tenure is positively associated withorganisational commitment. The results therefore, are consistent with Metcalfeand Dick (2000 and 2001) and Dick and Metcalfe (2001) studies in the UK, butare contrary to the findings from other countries (e.g., van Maanen, 1975; Beckand Wilson, 1997 and 2000; and Lim and Teo, 1998).

Panel A shows that the use of financial measures is positively associated withorganisational commitment but not with procedural justice and trust, whichis consistent with results of bivariate analysis. This suggests that the effectof the use of financial measures on organisational commitment is direct, andis not mediated by procedural fairness and trust. Further, despite the strongsignificant zero-order correlation coefficient between procedural justice andorganisational commitment observed in Table 4, the structural model revealsthat the direct effect of procedural justice on organisational commitment is nolonger significant (see Figure 2 Panel A). Therefore, we conclude that trustfully mediates the relationship between procedural justice and organisationalcommitment. The findings suggest that the process of how procedural justiceaffects organisational commitment is that procedural justice enhances trustin superiors and then trust improves the level of organisational commitment.Finally, the R2 of 0.379 suggests that the use of financial measures, proceduralfairness, and trust combine to explain a reasonably large proportion of thevariation in organisational commitment.

Panel B of Figure 2 shows that the use of non-financial measures ispositively associated with organisational commitment and trust, but not withprocedural justice. This means procedural justice does not mediate therelationship between the use of non-financial measures and organisationalcommitment. The figure also indicates that trust is positively associatedwith organisational commitment. As with the financial model, there is nodirect effect of procedural justice on organisational commitment. Therefore,it can be concluded that the effect procedural justice has on organisationalcommitment is fully mediated by trust. However, the figure indicates that trust

C© 2010 Blackwell Publishing Ltd

ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE 413

Figure 2

The Results of PLS

Panel A: Financial Model

R2=0.023

-0.152 0.130

R2=0.3790.331**R2=0.119

0.161 0.357**

0.369**

0.214*

Financialmeasures Organisational

commitment

Proceduraljustice

Trust in superior

Tenure

Panel B: Non-financial Model R2=0.000

0.009 0.064

R2=0.5050.300**R2=0.141

0.222* 0.232*

0.575**

0.205*

** Path is significant at the 0.01 level (1-tailed).

Notes:

* Path is significant at the 0.05 level (1-tailed).

Non-financialmeasures

Organisationalcommitment

Proceduraljustice

Trust in superior

Tenure

C© 2010 Blackwell Publishing Ltd

414 SHOLIHIN AND PIKE

only partially mediates the relationship between non-financial measures andorganisational commitment because the association between non-financialmeasures and organisational commitment is still significant.

CONCLUSIONS

The purpose of this study is to examine whether, and if so how, the use of perfor-mance measures, procedural justice and trust interact to affect organisationalcommitment in the police service. Drawing on a sample of 57 inspecting levelofficers in one of the largest police forces in the UK, the results of descriptivestatistics indicate that the general level of organisational commitment ofdetective inspectors and detective chief inspectors is relatively high, with theperceived levels of interpersonal trust and procedural fairness somewhat lower.Further, using correlation analysis we find that the use of performance measures,whether financial or non-financial, is positively associated with organisationalcommitment. We also find that procedural justice is positively associated withtrust and these two variables are positively associated with organisationalcommitment.

The results suggest that among senior officers (inspectors and chief inspec-tors), greater reliance on performance measures within a fair performancemanagement process and a culture of trust between subordinate and superioris expected to give rise to enhanced organisational commitment. Although noprior public sector studies of this nature have been conducted, the findings areconsistent with previous accounting studies, such as Lau and Moser (2008)which found that the use of non-financial measures and procedural justiceare positively associated with organisational commitment. The results alsosupport the findings of studies on the importance of trust which found trust tohave an important effect on interpersonal relationships and cooperation withinorganisations (Lewicki et al., 1998). Our findings offer empirical support for thearguments, not empirically tested, of previous police studies (e.g., Metcalfe andDick, 2000 and 2001; and Beck and Wilson, 2000) on the importance of trustand procedural justice in raising commitment among police officers. Regardingprocedural justice, these findings within a specific policing context are consistentwith Lind and Tyler’s conclusion that:

. . . procedural justice is a remarkably potent determinant of affective reactions todecision making and that procedural justice has especially strong effects on attitudesabout institutions and authorities . . . we believe that attitudes toward the organization asa whole, including such things as organizational commitment, loyalty and work groupcohesiveness, are strongly affected by procedural justice judgment (1988, p. 179)(emphasis added).

Further analysis using structural equation modelling finds that proceduraljustice and trust do not mediate the relationship between the use of finan-cial measures and organisational commitment. In similar fashion, procedural

C© 2010 Blackwell Publishing Ltd

ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE 415

justice does not mediate the relationship between non-financial measures andorganisational commitment. However, trust is found to partially mediate theeffect of the use of non-financial measures and organisational commitment.This suggests that the greater subjectivity involved in measuring many non-financial performance measures demands a higher degree of interpersonal trustbetween officer and superior, and where this holds organisational commitmentis enhanced. Finally, we find that trust fully mediates the relationship betweenprocedural justice and organisational commitment.

Overall, the findings are consistent with previous studies in organisationaljustice that procedural justice positively affects trust and organisational com-mitment (Colquitt et al., 2001). An important finding is that in contrast to thestudies of Lau and Sholihin (2005) and Lau and Moser (2008) in the privatesector, we find that the use of performance measures (whether financial or non-financial) is not associated with procedural fairness. Lau and Sholihin (2005)found that the use of either financial or non-financial measures was positivelyassociated with procedural fairness, while Lau and Moser (2008) found the useof non-financial measures to be positively associated with procedural fairness.While it is tempting to interpret the difference in our findings in terms ofspecific public sector or police service characteristics, we would not wish to drawthis conclusion. Rather, we question whether the type of performance measureis really the determining issue. Extending the arguments of Hartmann andSlapnicar (2009), we speculate that fairness is associated with the characteristics orproperties of performance measures, such as the specificity, accuracy and degreeof participation in setting such measures, rather than the measures themselves.Hence, future study should examine such characteristics.

With regard to the association of tenure with organisational commitment, thisstudy supports the finding of Metcalfe and Dick (2001) that tenure of office ispositively associated with organisational commitment, in stark contrast to thefindings based on police services in the United States and Australia. This is anencouraging finding for the police service in the UK, and suggests that the workexperiences of police officers surveyed, supported by an environment and culture(such as the level of interpersonal trust and fairness of performance procedures),engender higher levels of organisational commitment.

From a practical perspective, the findings suggest that to enhance theorganisational commitment within a police force, those involved in the designand management of the performance measurement system should seek toimprove the perceived fairness of procedures for evaluation and feedback, and tofoster greater interpersonal trust in the subordinate-superior relationship. Theresults suggest that a fair procedure is an important component in increasinginterpersonal trust. Consequently, the police force should further develop thelevel of procedural justice in evaluating officers as recommended by the HomeOffice (2004). Given the relatively low levels of procedural fairness found amongmany of the officers surveyed, this is still in need of attention as it is clear thatsome officers perceive that the procedures used to evaluate their performance

C© 2010 Blackwell Publishing Ltd

416 SHOLIHIN AND PIKE

and communicate performance feedback are not fair. In this regard, Lind andTyler also suggest:

. . . organizational designers (should) look to procedural justice research for effectivemeans to enhance and maintain the quality of work life and the internal cohesiveness oforganizations. The research . . . shows that when procedures are fair, the organizationcan expect to see greater employee satisfaction, less conflict and more obedience toprocedures and decisions. These benefits can be realized at very little cost to theorganization – in fact, it is quite likely that the investment of organizational resourcesin the achievement of procedural justice would produce much greater benefit on thesedimensions at less cost than would most other changes in organizational policy orpractice (1988, p. 200–201) (parentheses added).

The above findings should be interpreted in the context of the study’slimitations. First, this study only relies on detective inspectors and chief detectiveinspectors. Future studies could expand the sample to include other rankswithin the police service. Other public sector organisations could also usefully beinvestigated. Secondly, this study relies on respondent perceptions, with all itslimitations. To partly counteract this limitation the survey was complementedby qualitative data using interviews with selected respondents. Future studiescould usefully adopt a more in-depth qualitative research approach to explorethe same issues. Finally, the finding that the use of performance measures isassociated with organisation commitment but not with procedural fairness andtrust are inconsistent with findings by Lau and Sholihin (2005) based on privatesector firms. Further research is called for to investigate whether this is peculiarto the police service, given its specific occupational culture, or equally applies toother public sector organisations.

NOTES

1 We use the terms procedural justice and procedural fairness interchangeably.2 This stream of study is also often termed as budget emphasis or Reliance on Accounting

Performance Measures study (for reviews see, for example, Hartmann, 2000; Otley andFakiolas, 2000; Vagneur and Peiperl, 2000; Noeverman et al., 2005; and Derfuss, 2009).

3 The survey instrument is available upon request from the authors.4 We split the respondents into two groups (below and above average for each demographic

factor, viz. (1) the length respondents had worked in the Force, (2) in their current position,and (3) been supervised by their current superior) and then ran t-tests to examine whetherthere was significantly different mean scores for each variable studied between the two groups.We find no significant difference for any of these variables.

5 The instruments were pilot tested using 15 MBA students of a UK university to seek feedbackon the clarity of contents and design of the instrument.

6 In the analysis, following Ittner et al. (2003), we converted 0 into 1.7 The original categories were: relations with customers, relations with employees, operational

performance, product and service quality, alliances with other organisations, relationswith suppliers, environmental performance, product and service innovations, communityperformance, and short term financial performance.

8 Operational issues refer to the requirement for additional patrols or pro-active investigationwork. An Inspector or Chief inspector can approve an operation targeting the problem withadditional resources. A budget is assigned to the operation and the officer controls it. Theyare performance managed and officers are held to account for costs incurred. The funds come

C© 2010 Blackwell Publishing Ltd

ORGANISATIONAL COMMITMENT IN THE POLICE SERVICE 417

from an operational budget that the Superintendent controls. Forensic enquiries go througha detective inspector to review and decide on the benefit/cost of sending the evidence to aforensic science laboratory. While the budget is controlled centrally at the Scientific SupportUnit, the detective inspector is required to check the feasibility of the submission producingrelevant evidence to the case.

9 In the main analysis similar results were found whether we used 7 or 9 items.10 For example, to employ AMOS it is more appropriate when the number of cases is above 200

(Bacon, 1997). With PLS we can use a small number of samples. Chin (1998b) argues that anadequate sample size for PLS is 10 times of the independent variables in the largest structuralequation. Since we have three independent variables in the largest structural equation, theminimum sample should be 30. Hence our current sample is adequate.

11 Whilst Hulland (1999) allows researchers to use a threshold of 0.4 loading to asses thereliability, to be consistent with the benchmark used in the factor analysis previouslyperformed, we use a threshold of 0.5.

REFERENCES

Albrecht, S. and A. Travaglione (2003), ‘Trust in Public-sector Senior Management’,The InternationalJournal of Human Resource Management, Vol. 14, pp. 76–92.

Alexander, S. and M. Ruderman (1987), ‘The Role of Procedural and Distributive Justice inOrganizational Behavior’, Social Justice Research, Vol. 1, pp. 177–98.

Angle, H.L. and J.L. Perry (1981), ‘An Empirical Assessment of Organizational Commitment andOrganizational Effectiveness’, Administrative Science Quarterly, Vol. 26, pp. 1–14.

Bacon, L.D. (1997), Using Amos for Structural Equation Modeling in Market Research (Lynd Bacon &Associates, Ltd. and SPSS Inc.).

Ballantine, J., S. Brignall and S. Modell (1998), ‘Performance Measurement and Management inPublic Health Services: A Comparison of U.K. and Swedish Practice’, Management AccountingResearch, Vol. 9, pp. 71–94.

Baron, R.M. and D.A. Kenny (1986), ‘The Moderator-Mediator Variable Distinction in SocialPsychological Research: Conceptual, Strategic and Statistical Considerations’, Journal ofPersonality and Social Psychology, Vol. 51, pp. 1173–82.

Beck, K. and C. Wilson (1997), ‘Police Officers Views on Cultivating Organizational Commitment:Implications for Police Managers’, Policing: An International Journal of Police Strategies &Management, Vol. 20, No. 1, pp. 175–95.

——— ——— (2000), ‘Development of Affective Organizational Commitment: A Cross-SequentialExamination of Change with Tenure’, Journal of Vocational Behavior, Vol. 56, pp. 114–36.

Becker, H. (1960), ‘Notes on the Concept of Commitment’, American Journal of Sociology, Vol. 66,pp. 32–42.

Blader, S.L. and T.R. Tyler (2005), ‘How Can Theories of Organizational Justice Explain theEffects of Fairness?’, in J. Greenberg and J.A. Colquitt (eds.), Handbook of Organizational Justice(Lawrence Erlbaum Associates, New Jersey).

Brodeur, P. (1998), ‘The Assessment of Police Performance’, in P. Brodeur (ed), How to RecognizeGood Policing (Sage, Thousand Oaks, CA).

Bryman, A. and E. Bell (2003), Business Research Methods (Oxford University Press, Oxford).Butterfield, R., C. Edwards and J. Woodall (2005), ‘The New Public Management and Managerial

Roles: The Case of the Police Sergeant’, British Journal of Management, Vol. 16, pp. 329–41.Chatterton, M.R., C. Humphrey and A.J. Watson (1996), On the Budgetary Beat: Investigation of the

Development of Management Accounting Systems in the Police Service in England and Wales (CIMAPublishing, London).

Chenhall, R.H. (2005), ‘Integrative Strategic Performance Measurement Systems, StrategicAlignment of Manufacturing, Learning and Strategic Outcomes: An Exploratory Study,’Accounting Organizations and Society, Vol. 30, pp. 395–422.

Chin, W.W. (1998a), ‘Issues and Opinion on Structural Equation Modeling’, MIS Quarterly, Vol. 22,pp. VII–XVI.

——— (1998b), ‘The Partial Least Squares Approach to Structural Equation Modeling’, inG.A. Marcoulides (ed.), Modern Methods for Business Research (Lawrence Erlbaum Associates,London).

C© 2010 Blackwell Publishing Ltd

418 SHOLIHIN AND PIKE

Chin, W.W. and P.R. Newsted (1999), ‘Structural Equation Modeling Analysis with Small SamplesUsing Partial Least Squares’, in R.H. Hoyle (ed.), Statistical Strategies for Small Sample Research(Sage Publication, Thousand Oak).

Chong, V.K. and I.R.C. Eggleton (2007), ‘The Impact of Reliance on Incentive-based Compen-sation Schemes, Information Asymmetry and Organisational Commitment on ManagerialPerformance’, Management Accounting Research, Vol. 18, pp. 312–42.