Opportunity Identification and Pursuit: Does an Entrepreneur’s Human Capital Matter

21

Opportunity Identification and Pursuit: Does an EntrepreneurÕs Human Capital Matter? Deniz Ucbasaran Paul Westhead Mike Wright ABSTRACT. Extending human capital approaches to entre- preneurship, an entrepreneurÕs ‘‘inputs’’ relating to their general (i.e. education and work experience) and entrepreneurship- specific human capital profile (i.e. business ownership experi- ence, managerial capabilities, entrepreneurial capabilities and technical capabilities) are presumed to be related to entrepre- neurial ‘‘outputs’’ in the form of business opportunity identifi- cation and pursuit. Valid and reliable independent variables were gathered from a stratified random sample of 588 owners of private firms. Ordered logit analysis was used to test several theoretically derived hypotheses. With regard to the number of business opportunities identified and pursued, entrepreneur- ship-specific rather than general human capital variables ‘‘explained’’ more of the variance. Entrepreneurs reporting higher information search intensity identified significantly more business opportunities, but they did not pursue markedly more or less opportunities. The use of publications as a source of information was positively associated with the probability of identifying more opportunities, while information emanating from personal, professional and business networks was not. Implications for practitioners and researchers are discussed. KEY WORDS: entrepreneurship-specific human capital, general human capital, information search, opportunity identification and pursuit JEL CLASSIFICATION: L26. 1. Introduction The human capital of individuals can shape their prospects (Becker, 1975, 1993). Links between entrepreneursÕ human capital profiles and out- comes relating to firm entry/exit and perfor- mance have been identified (Jovanovic, 1982; Bates, 1990; Cressy, 1996; Gimeno et al., 1997; Bosma et al., 2004). Currently, opportunity ori- ented conceptualisations of entrepreneurship are attracting attention (Shane and Venkataraman, 2000; Shane, 2003) but the human capital profiles of entrepreneurs who identify and pursue more business opportunities are not well understood (Busenitz et al., 2003). Shane (2003) argues that venture performance is determined by how effectively the entrepreneur deals with entrepre- neurial process activities relating to opportunity identification, evaluation and exploitation (Ardichvili et al., 2003). By solely focusing on venture performance, the effects of the various activities that lead to that performance may be confounded. There is, therefore, a need to disentangle the activities involved in the entre- preneurial process that can subsequently impact venture performance. Unfortunately, there is no conclusive evidence that suggests opportunity identification and pursuit influence venture out- comes. However, entrepreneurs who identify more opportunities may select to pursue better quality opportunities with greater wealth creating potential because they have more opportunities to choose from. Shepherd and DeTienne (2005) have detected a strong link between the number of opportunities identified and the innovativeness of those opportunities. The innovativeness of an opportunity may provide an indication of its ‘‘quality’’ (Fiet, 2002; Shane, 2000). Studies that focus solely on traditional firm performance outcomes do not provide an understanding of the relationship between entrepreneurÕs human capi- tal and the identification of opportunities that can create future venture wealth. Echoing the views of Venkataraman (1997), Gaglio and Katz (2001) argue that understand- ing the opportunity identification process Final version accepted on 17 October 2006. Deniz Ucbasaran, Paul Westhead and Mike Wright Nottingham University Business School Jubilee campus, Wollaton Road, Nottingham, NG8 1BB, UK E-mail: [email protected] Small Business Economics (2008) 30:153–173 Ó Springer 2007 DOI 10.1007/s11187-006-9020-3

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Opportunity Identification and Pursuit: Does an Entrepreneur’s Human Capital Matter

Opportunity Identification and Pursuit:

Does an Entrepreneur�s Human Capital

Matter?

Deniz UcbasaranPaul WestheadMike Wright

ABSTRACT. Extending human capital approaches to entre-

preneurship, an entrepreneur�s ‘‘inputs’’ relating to their general

(i.e. education and work experience) and entrepreneurship-

specific human capital profile (i.e. business ownership experi-

ence, managerial capabilities, entrepreneurial capabilities and

technical capabilities) are presumed to be related to entrepre-

neurial ‘‘outputs’’ in the form of business opportunity identifi-

cation and pursuit. Valid and reliable independent variables

were gathered from a stratified random sample of 588 owners of

private firms. Ordered logit analysis was used to test several

theoretically derived hypotheses. With regard to the number of

business opportunities identified and pursued, entrepreneur-

ship-specific rather than general human capital variables

‘‘explained’’ more of the variance. Entrepreneurs reporting

higher information search intensity identified significantly more

business opportunities, but they did not pursue markedly more

or less opportunities. The use of publications as a source of

information was positively associated with the probability of

identifying more opportunities, while information emanating

from personal, professional and business networks was not.

Implications for practitioners and researchers are discussed.

KEY WORDS: entrepreneurship-specific human capital,general human capital, information search, opportunityidentification and pursuit

JEL CLASSIFICATION: L26.

1. Introduction

The human capital of individuals can shape theirprospects (Becker, 1975, 1993). Links betweenentrepreneurs� human capital profiles and out-comes relating to firm entry/exit and perfor-mance have been identified (Jovanovic, 1982;

Bates, 1990; Cressy, 1996; Gimeno et al., 1997;Bosma et al., 2004). Currently, opportunity ori-ented conceptualisations of entrepreneurship areattracting attention (Shane and Venkataraman,2000; Shane, 2003) but the human capital profilesof entrepreneurs who identify and pursue morebusiness opportunities are not well understood(Busenitz et al., 2003). Shane (2003) argues thatventure performance is determined by howeffectively the entrepreneur deals with entrepre-neurial process activities relating to opportunityidentification, evaluation and exploitation(Ardichvili et al., 2003). By solely focusing onventure performance, the effects of the variousactivities that lead to that performance may beconfounded. There is, therefore, a need todisentangle the activities involved in the entre-preneurial process that can subsequently impactventure performance. Unfortunately, there is noconclusive evidence that suggests opportunityidentification and pursuit influence venture out-comes. However, entrepreneurs who identifymore opportunities may select to pursue betterquality opportunities with greater wealth creatingpotential because they have more opportunities tochoose from. Shepherd andDeTienne (2005) havedetected a strong link between the number ofopportunities identified and the innovativeness ofthose opportunities. The innovativeness of anopportunity may provide an indication of its‘‘quality’’ (Fiet, 2002; Shane, 2000). Studies thatfocus solely on traditional firm performanceoutcomes do not provide an understanding of therelationship between entrepreneur�s human capi-tal and the identification of opportunities that cancreate future venture wealth.

Echoing the views of Venkataraman (1997),Gaglio and Katz (2001) argue that understand-ing the opportunity identification process

Final version accepted on 17 October 2006.

Deniz Ucbasaran, Paul Westhead and Mike WrightNottingham University Business SchoolJubilee campus, Wollaton Road, Nottingham,NG8 1BB, UKE-mail: [email protected]

Small Business Economics (2008) 30:153–173 � Springer 2007DOI 10.1007/s11187-006-9020-3

represents a core question for the domain ofentrepreneurship research. Understanding therelationship between an entrepreneur�s humancapital profile and the opportunity identificationprocess is, therefore, an important theme thatwarrants additional research attention.Recently, several studies have empiricallyexplored the links between aspects of humancapital and opportunity identification (Davids-son and Honig, 2003; Arenius and DeClercq,2005; Arenius and Minnitti, 2005; Shepherd andDeTienne, 2005). These studies have enhancedour understanding of opportunity identificationand human capital but have focused on a nar-row array of human capital variables. They havealso generally solely explored responses fromstudents or nascent entrepreneurs, rather thanpractising entrepreneurs who in turn are heter-ogeneous regarding their experience of theentrepreneurial process (Westhead et al., 2005).Further, a number of these studies have failed tooperationalise the actual extent of opportunityidentification. Consequently, there is scantempirical evidence relating to the links betweenpracticing entrepreneurs� human capital profilesand their actual opportunity identification andpursuit activities. This research gap is the focusof this study, which seeks to make the followingcontributions.

First, a broader conceptualisation of an entre-preneur�s human capital is discussed. Previousstudies have focused mainly on education, workexperience, industry-specific experience and self-employment experience (Bates, 1990; Bruderlet al., 1992; Gimeno et al., 1997; Bosma et al.,2004). Growing interest in the psychologicalaspects of economics (Tversky and Kahneman,1974; Witt, 1998) suggests an entrepreneur�s cog-nitive characteristics also need to be considered(Alvarez and Busenitz, 2001; Ferrante, 2005;Markman et al., 2002). An entrepreneur�s humancapital relating to perceived capabilities (i.e. self-efficacy) are, therefore, considered in addition tothe widely used human capital indicators. Entre-preneurs can consciously invest in human capital.We also recognise that human capital may beaccumulated (e.g. work experience and entrepre-neurial experience) without any investment deci-sion being made. Learning-by-doing andexperientially acquired human capital is widely

recognised, and it is assumed that individualsactually learn from experience (Arrow, 1962;Jovanovic, 1982). Cognitive theorists, however,suggest this learning is not automatic. We extendthe existing literature by suggesting that the way inwhich human capital is acquired may be linked toopportunity identification and pursuit.

Second, a distinction is made between anentrepreneur�s general (i.e. education and workexperience) and entrepreneurship-specific humancapital profile (i.e. managerial capabilities,entrepreneurial capabilities, technical capabili-ties and business ownership experience). Whilethe distinction between general and specific hu-man capital is not new, we seek to provide in-sights into the relative importance of both generaland specific human capital with regard to thecontext of opportunity identification and pursuit.

Third, two outcomes from the entrepreneurialprocess are considered. Previous studies havegenerally focused on a single outcome. We rec-ognise that the human capital profiles leveragedto identify business opportunities may not be thesame as those required to pursue businessopportunities. The elements of an entrepreneur�shuman capital associated with opportunityidentification intensity (i.e. the number ofopportunities identified) are identified as well asthose associated with opportunity pursuitintensity (i.e. the number of identified opportu-nities pursued). In this study, opportunity pur-suit is defined as the commitment of time andresources into an opportunity for creating orpurchasing a business. Since, entrepreneurs maydecide to pursue only a subset of the opportu-nities they identify, this selection decision im-plies that pursued opportunities are perceived tobe of greater quality.

Fourth, we explore whether entrepreneurswho search for more information and utilizeparticular types of information, identify andpursue more business opportunities. Thisevidence will provide additional insights to thedebate surrounding whether opportunities areidentified as a result of information search, orthe alertness of the entrepreneur (Kaish andGilad, 1991; Fiet, 1996, 2002; Kirzner, 1997;Fiet et al., 2005). Human capital based consid-erations of opportunity identification and pur-suit emphasize the knowledge embodied within

154 Deniz Ucbasaran et al.

the entrepreneurs. In contrast, the informationsearch perspective suggests that opportunityidentification and pursuit may be enhanced byacquiring external information.

This article is structured as follows. In thenext section, a conceptual framework followinghuman capital theory is presented. A distinctionis made between general and entrepreneurship-specific human capital. Several hypotheses arethen derived. In the following section, the dataand research methodology are discussed.Results are then reported. Finally, conclusionsand implications for policy-makers, practitio-ners and researchers are discussed.

2. Conceptual underpinnings

2.1. Context

Human capital relates to a hierarchy of skillsand knowledge with varying degrees of trans-ferability (Castanias and Helfat, 1992). Scholarshave explored human capital ‘‘inputs’’ accumu-lated by entrepreneurs in relation to ‘‘outputs’’such as the decision to become self-employed,the size of the firm in which they have an equitystake (Bates, 1990; Otani, 1996), the survival ofthe firm (Gimeno et al., 1997; Bruderl et al.,1992) and the performance of the firm (Bosmaet al., 2004). Entrepreneurs with more (or higherquality) human capital ‘‘inputs’’ should reportsuperior ‘‘outputs’’ (Becker, 1975; Davidssonand Honig, 2003). In the context of entrepre-neurship, these ‘‘outputs’’ also relate to theidentification, pursuit and exploitation ofopportunities (Shane, 2003).

Debate still surrounds ‘‘if’’, ‘‘how’’ and‘‘why’’ human capital leads to monitored bene-fits. Empirical evidence relating to several con-texts, particularly education, supports the viewthat human capital is positively associated withfavourable outcomes such as higher earnings(Boylan, 1993) and productivity (Becker, 1975;Mincer, 1974). Education can be viewed as atype of credential that indicates a greater innateproductivity (Arrow, 1973; Spence, 1974). Amore sceptical view surrounding the value ofeducation has, however, been raised. Educationmay help an employer gauge an applicant�sintelligence, motivation and discipline, without

it directly affecting his/her actual productivity.Dore (1976) argues that education mattersbecause it confers status rather than the skills itimparts. This ‘‘dark side’’ of human capital1 isalso alluded to in relation to other aspects ofhuman capital. If human capital is acquiredthrough learning-by-doing, cognitive theoristssuggest biases in thinking may result. Experi-enced decision-makers can fall into mental ruts(Fiske and Taylor, 1991), and may fail to noticeand adapt to changes in the environment(Tversky and Kahneman, 1974). Decision-mak-ers may, therefore, not leverage their experienceand knowledge into superior performance.Consequently, the relationships between humancapital and entrepreneurial ‘‘outputs’’ (i.e.opportunity identification and pursuit) may notbe as obvious as initially assumed.

Becker (1993) has made a distinctionbetween general and specific human capital.General human capital relates to skills andknowledge that are easily transferable across avariety of economic settings. Conversely, spe-cific human capital relates to skills andknowledge that are less transferable and have anarrower scope of applicability (Gimeno et al.,1997). A number of studies have considered thegeneral and specific human capital profiles ofentrepreneurs (Bosma et al., 2004; Bruderlet al., 1992; Gimeno et al., 1997; Wiklund andShepherd, 2003). As earlier intimated, whilecognitive dimensions of entrepreneurship arereceiving increased attention, the cognitivecharacteristics of entrepreneurs have not beenexplicitly explored within a human capitalframework, with notable recent exceptions (e.g.Arenius and Minnitti, 2005; Ferrante, 2005). Inthis study, a broad conceptualisation of humancapital is presented to include widely useddimensions of human capital as well as cogni-tive dimensions.

In this study, an entrepreneur�s education andwork experience are regarded as surrogatemeasures of general human capital. Variablesrelating to prior business ownership experienceand self-perceived capabilities are considered assurrogate measures of entrepreneurship-specifichuman capital. The various human capitalvariables under consideration are discussed, inturn, below.

155Opportunity Identification and Pursuit: Does an Entrepreneur�s Human Capital Matter?

2.2. General human capital

2.2.1. EducationEducation is one of the most frequentlyexamined components of human capital. For-mal education is seen as providing the neces-sary cognitive skills to adapt to environmentalchanges (Hatch and Dyer, 2004). Education isa source of knowledge, skills, discipline, moti-vation and self-confidence (Cooper et al.,1994). Highly educated entrepreneurs may bebetter able to deal with complex problems.They may also leverage their knowledge andthe social contacts generated through theeducation system to acquire resources toidentify and exploit business opportunities(Shane, 2003; Arenius and DeClercq, 2005).On the other hand, formal education mayinculcate attitudes that are antithetical toentrepreneurship (Casson, 2003). Some studiessuggest that highly educated individuals aremore likely to establish new firms (Bates,1990), whilst other studies detect an inverserelationship between educational attainmentand firm formation (Storey, 1994). There isconsiderable debate as to the returns to entre-preneurship from being more or less highlyeducated (see Parker (2006) for a review).Recent evidence suggests that entrepreneurswho are more highly educated obtain a higherreturn to education than do employees (Parkerand van Praag, 2004; Van der Sluis et al.,2004). This would suggest that either morehighly educated entrepreneurs are moreadept at identifying opportunities and/or arebetter at realizing the returns from thoseopportunities. Currently, there is scant empir-ical evidence directly relating to the linksbetween an entrepreneur�s education attainmentand their ability to identify and pursue businessopportunities. Davidsson and Honig (2003),however, detected that nascent entrepreneurswith higher levels of education were more likelyto identify opportunities, but they were notmore likely to pursue identified opportunities.Arenius and DeClercq (2005) also found apositive relationship between education levelsand the likelihood of recognising opportunities.The latter findings need to be explored withreference to practicing entrepreneurs.

2.2.2. Work experienceWork experience is viewed as a key indicatorof general human capital (Castanias andHelfat, 2001). It can assist in the integrationand accumulation of new knowledge. Further,it can enable individuals to adapt to newsituations (Davidsson and Honig, 2003) andbecome more productive (Parker, 2006). Workexperience is associated with the ability tobecome self-employed and to start new firms(Bates, 1990; Gimeno et al., 1997). Severalindicators of work experience have beenoperationalised, which makes comparisonbetween studies difficult. Work experience hasfrequently been operationalised in terms of thenumber of years of work experience (Evansand Leighton, 1989; Bruderl et al., 1992). Thelatter indicator provides limited informationabout the nature of the skills and knowledgeacquired. Two alternative indicators of workexperience have been considered (Gimenoet al., 1997). First, the number of prior full-time jobs held measures the breadth ofdifferent experiences. Individuals with morethan one job setting exposure may acquire adiverse range of knowledge and skills.However, this may be subject to diminishingreturns (Mincer, 1974). Frequent job settingexposure may signal an individual with poorknowledge and skills. Second, the achievementlevel highlights the quality (or the nature) ofthe work experience acquired. Individuals whohave held a managerial position (or werepreviously self-employed) may be endowedwith superior levels of general human capital(Bates, 1990), which can be leveraged toidentify and pursue business opportunities.

2.3. Entrepreneurship-specific human capital

2.3.1. Business ownership experienceBusiness ownership has been long recognised asan important dimension of entrepreneurship(Hawley, 1907). Fama and Jensen (1983) arguethat classic entrepreneurial firms are those thatcombine residual risk bearers and decision-makers in the same individuals. Episodicknowledge of entrepreneurship can be acquiredthrough direct business ownership experience

156 Deniz Ucbasaran et al.

(Spender, 1996). This knowledge, which includesmanagerial experience, enhanced reputationand broader social and business networks(Shane and Khurana, 2003) can be leveragedto innovate new productive resource combi-nations (Parker, 2006), and to identify andpursue business opportunities. The latterbehaviour may be a function of an individual�scapacity to handle complex information andtheir prior knowledge (Shane, 2000). Westheadet al. (2005) detected that more experiencedentrepreneurs, particularly portfolio entrepre-neurs (i.e. those experienced entrepreneurswho own businesses simultaneously), hadmore diverse experiences and more resourcesthan inexperienced entrepreneurs. Experiencedentrepreneurs may have the ability to identifymore opportunities and leverage the resourcesrequired to pursue opportunities. Prior busi-ness ownership experience is viewed as anelement of entrepreneurship-specific humancapital (Gimeno et al., 1997; Chandler andHanks, 1998).

2.3.2. CapabilitiesTo ensure competitive advantage, firms mayneed to acquire, create and integrate resourcesinto dynamic capabilities (Teece et al., 1997).Some people have the ability to acquire,combine and co-ordinate the resources essen-tial for entrepreneurial activity (Erikson,2002). An individual�s cognition can beexplored with regard to self-assessed capabili-ties because they represent the core of anindividual�s self-efficacy belief (Delmar, 2000).The latter belief relates to the cognitiveresources and courses of action required toexercise control over events. Self-efficacyinfluences our courses of action, level of effort,how long we persevere, our resilience in theface of obstacles, adversity, or failure, andwhether our thoughts are self-hindering or self-aiding (Wood and Bandura, 1989; Markmanet al., 2002). Highly talented individuals oftenfail to leverage their skills because of deficits intheir self-efficacy (Wanberg et al., 1999).

Self-assessed capabilities are strongly associ-ated with more objective measures of capabilities(Gist, 1987). Individuals with more diverse capa-bilities may have the power to act in a broader

range of current and future circumstances(Loasby, 1998). Lazear (2004) suggests thatentrepreneurs need to be multi-skilled. Entrepre-neurs need to develop capabilities with regard toentrepreneurial, managerial and technical func-tional roles (Penrose, 1959).

3. Derivation of hypotheses

In this section, six hypotheses are derived withreference to the human capital perspective dis-cussed above.

3.1. Human capital and opportunity identification

An entrepreneur�s human capital profile,particularly prior knowledge (Shane, 2000;Shepherd and DeTienne, 2005) can beassociated with opportunity identification(Davidsson and Honig, 2003). From aninductive viewpoint, business opportunities areavailable in the environment and are waitingto be discovered. Kirzner�s (1973) ‘‘entrepre-neurial alertness’’ perspective suggests thatsome individuals have the ability to see whereproducts (or services) do not currently exist,or where they have unexpectedly emerged asbeing valuable. Conversely, from a deductiveviewpoint, imaginative entrepreneurs canleverage their experience, subjective under-standing and current information to identifyor create business opportunities (Witt, 1998).Irrespective of which viewpoint is taken,information and knowledge in some format isnecessary, but not sufficient, for the identifi-cation of a business opportunity. Entrepre-neurs with diverse human capital profiles mayleverage their wider knowledge and skills toidentify a greater number of opportunities. Ifopportunities are indeed circulating in theenvironment waiting to be discovered, indi-viduals with superior human capital may havegreater cognitive ability to be alert to oppor-tunities, knowledge of where to look for anopportunity, and/or knowledge of what anopportunity ‘‘looks like’’. Alternatively, ifopportunities are imagined or created, entre-preneurs with greater levels of human capitalmay have more ‘‘ingredients’’ to work with to

157Opportunity Identification and Pursuit: Does an Entrepreneur�s Human Capital Matter?

identify/create an opportunity. This discussionsuggests the following hypothesis:

H1 Entrepreneurs reporting higher levels ofhuman capital (i.e., general and entrepre-neurship-specific human capital) will identifymore business opportunities, in a given timeperiod.

3.2. Human capital and opportunity pursuit

Entrepreneurs do not exploit all the opportuni-ties they identify (Witt, 1998; Shane andVenkataraman, 2000). After identifying abusiness opportunity, an entrepreneur usuallyexpends time and resources evaluating the costsand benefits associated with exploiting theidentified opportunity. Opportunity pursuitrelates to the evaluation stage following theidentification of an opportunity that is reportedprior to potential exploitation. To the extentthat entrepreneurs pursue fewer opportunitiesthan they identify, this suggests that they per-ceive the former to be of higher quality. Anentrepreneur�s human capital may be leveragedto screen opportunities and select whichopportunities should be pursued. Entrepreneurswith superior human capital may draw upontheir knowledge to reject less viable opportuni-ties. Conversely, entrepreneurs with higher levelsof human capital may leverage their knowledgeto pursue perceived attractive opportunities(Davidsson and Honig, 2003).

An entrepreneur is only likely to pursue anopportunity, if the expected value of the returnfrom exploiting the identified opportunity exceedsthe opportunity cost of alternative activities.Individuals with more diverse human capitalprofiles may have higher expectations andthresholds for economic activity (Gimeno et al.,1997). Human capital may increase the expectedvalue from exploiting an opportunity. Further,individuals with superior levels of human capitalare likely to face less uncertainty surrounding thevalue to be gained from exploiting an opportunity(Shane and Khurana, 2003) since they have theskills and knowledge to effectively exploit theopportunity. Consequently, they may pursue alarger number of identified opportunities com-

pared with individuals with lower levels of humancapital. This discussion suggests the followinghypothesis:

H2 Entrepreneurs reporting higher levels ofhuman capital (i.e. general and entrepre-neurship-specific) will pursue more identifiedbusiness opportunities, in a given time period.

3.3. Distinguishing between general andentrepreneurship-specific human capital

Entrepreneurship-specific human capital may bemore important than general human capitalwith regard to opportunity identification andopportunity pursuit. An individual�s specifichuman capital can be associated with superioreconomic rents (Castanias and Helfat, 1992,2001; Hatch and Dyer, 2004). Entrepreneurship-specific human capital may represent a better‘‘guide’’ for entrepreneurs to identify opportu-nities than general human capital alone. Entre-preneurship-specific human capital can providean entrepreneur with the knowledge of where tolook for opportunities, as well as the ability toidentify an opportunity that might be ignored byentrepreneurs relying solely on their generalhuman capital.

With respect to opportunity pursuit, entre-preneurs with high levels of entrepreneurship-specific human capital may only be able toleverage this knowledge with regard to theentrepreneurial process. The opportunity costsassociated with pursing an opportunity are,therefore, likely to be lower for entrepreneurswith higher levels of entrepreneurship-specifichuman capital than those with higher levels ofgeneral human capital. This discussion suggeststhe following hypotheses:

H3a Entrepreneurship-specific human capital will‘‘explain’’ more of the variance in the numberof business opportunities identified, in a giventime period, than general human capital.

H3b Entrepreneurship-specific human capital will‘‘explain’’ more of the variance in the numberof business opportunities pursued, in a giventime period, than general human capital.

158 Deniz Ucbasaran et al.

3.4. Information search intensity

Why some people identify opportunities andothers do not may be related to the information(Kaish and Gilad, 1991; Fiet, 1996; Shane, 2000;Casson, 2003) and knowledge (i.e. the humancapital relating to prior information alreadypossessed) they possess (Venkataraman, 1997).If information facilitates the identification of anopportunity, individuals may choose to increasetheir access to opportunities by searching fornew/current information (Fiet, 1996; Shane,2003). In some instances, opportunities can beidentified when an entrepreneur combines priorinformation with new information. Entrepre-neurs differ with regard to their stocks of priorinformation (Shane, 2003). Prior informationcan direct attention, expectations and interpre-tations of market stimuli as well as the genera-tion of ideas (Gaglio, 1997). Experiencedentrepreneurs with specialist knowledge mayrestrict their scanning and concentrate theirinformation search within a more specificdomain based on routines (and informationsources) that worked well in the past (Cooperet al., 1994; Fiet, 2002). Some entrepreneurswith greater levels of human capital may beassociated with higher levels of alertness (Kirz-ner, 1997) and may not need to gather largeamounts of information to identify businessopportunities. By focusing on a smaller numberof diagnostic items of information, experiencedentrepreneurs can avoid information overload,which can degrade their decision-making capa-bilities (Jacoby et al., 2001). Nevertheless, for agiven level of prior information (i.e. specifichuman capital), entrepreneurs may be able toaccess opportunities by searching for up-to-dateinformation. This discussion suggests the fol-lowing hypothesis:

H4a Entrepreneurs reporting higher levels ofinformation search intensity will identifymore business opportunities, in a given timeperiod.

Some entrepreneurs collect and process infor-mation to make calculated judgements sur-rounding the feasibility and risks associatedwith the pursuit of an identified opportunity(Casson, 2003). The strengths, weaknesses,

opportunities and threats associated withpursuing the identified business ideas may beascertained by additional information collec-tion and processing. Further, the identifiedbusiness opportunity may only be pursued ifthe information suggests the opportunity isviable and/or valuable, that is, of higherquality than other identified opportunities thatare not pursued. Some entrepreneurs maychoose not to search for additional informa-tion. Entrepreneurs rely more extensively on anumber of decision-making short-cuts(i.e. heuristics) to a greater extent than non-entrepreneurs (Baron, 1998). In particular,entrepreneurs are associated more stronglywith the representativeness heuristic (Busenitzand Barney, 1997), which relates to the will-ingness to generalize from small samples thatdo not represent a population (Tversky andKahneman, 1974). Entrepreneurs exhibitingthis heuristic may be less likely to search forinformation. Despite the biased decision-making that may result from limited infor-mation search, the representativeness heuristiccan encourage an entrepreneur to pursue anopportunity (Busenitz and Barney, 1997).However, if too much time is spent acquiringinformation, the brief window of opportunityfor pursuing a venture idea may close.Extensive information search may preventsome entrepreneurs from pursing a businessopportunity. This may be desirable if theidentified business opportunity has a highprobability of failure. The above discussionsuggests the following hypothesis:

H4b Entrepreneurs reporting higher levels ofinformation search intensity will pursuefewer identified business opportunities, in agiven time period.

4. Data and research methodology

4.1. Sample, data collection and respondents

The sampling frame was constructed byobtaining sampling quotas for four broadindustrial categories (i.e. agriculture, forestryand fishing, production, construction and

159Opportunity Identification and Pursuit: Does an Entrepreneur�s Human Capital Matter?

services) and the eleven Government OfficialRegions from summary tables detailing thepopulation of businesses registered for Value-Added-Tax in Great Britain in 1999 (Office forNational Statistics, 1999). After excluding non-independent businesses, industry and standardregion sampling proportions were identified fora stratified random sample of private firms.

A stratified random sample of 4,324 inde-pendent private firms was drawn from a cleanedlist of business names purchased from Dun andBradstreet. A structured questionnaire wasmailed during September 2000 to a founder and/or principal owner. They were the key decision-maker and actively involved in the business aswell as knowledgeable about the firms activities(Campbell, 1955). The questionnaire surveyvalidated the status of each respondent. After athree-wave mailing (i.e. two reminders), 767valid questionnaires were obtained from a validsample of 4,307 private firms. The 18% validresponse rate compares favourably with similarstudies (Storey, 1994), which generally havemuch shorter and less detailed research instru-ments.

Respondents reported they were not thefounder and/or the principal owner, they hadonly inherited (an) established business(es) orwho filed missing information returns to any ofthe selected variables were excluded from anyfurther analysis. In total, 588 respondents pro-vided complete data for the selected variablesexplored.

Data were not gathered from multiplerespondents in each firm. However, strongpositive correlations were detected between theinformation gathered by the questionnaire andthe archival data provided by Dun and Brad-street relating to business age, employment sizeand legal status (i.e. Pearson correlation coeffi-cients ranged from 0.77 to 0.88). This evidencesuggests that the data collected from the keyinformants was reliable.

4.2. Sample representation

Chi-square and Mann–Whitney ‘‘U’’ tests didnot detect any significant response bias betweenthe valid respondents (n = 588) and non-respondents with regard to industry, standard

region, legal form, age of the business andemployment size at the 0.05 level. On these cri-teria, we have no cause to suspect that thesample of firms was not a representative sampleof the population of independent private firms.

4.3. Measures

The following measures relating to the depen-dent, independent and control variables wereoperationalised.

4.3.1. Dependent variablesConsistent with previous literature (Amabile,1990; Hills et al., 1997; Shepherd and DeTienne,2005), opportunity identification was opera-tionalised in terms of the number of opportunitiesidentified. A conservative definition of businessopportunities was selected. Respondents werepresented with a statement asking them, ‘‘howmany opportunities for creating or purchasing abusiness have you identified (‘spotted�) within thelast five years’’. They were presented with eightopportunity identification outcomes (i.e. 0, 1, 2,3, 4, 5, 6 to 10, or more than 10 opportunities).We detected that some categories had fewrespondents. The eight opportunity identifica-tion outcomes were collapsed into three broadercategories. The resulting categorization ensuredthat an acceptable number of respondentsbelonged to each category. Respondents whoreported that they had failed to identify anopportunity were allocated a value of ‘‘1’’, thosewho reported that they had identified one or twoopportunities were allocated a value of ‘‘2’’,whilst those who had identified three or moreopportunities were allocated a value of ‘‘3’’.

The number of opportunities pursued wasascertained. Respondents were presented with astatement asking ‘‘how many opportunities forcreating and purchasing a business have youpursued (i.e. committed time and resources to)within the last five years’’ (Hills et al., 1997). Asearlier intimated, this dependent variable doesnot relate to the exploitation of an opportunity,and it solely relates to the evaluation stage of theentrepreneurial process (Ardichvili et al., 2003;Shane, 2003). The perceived quality of anopportunity may be exhibited if an entrepreneurcommits time and resources to evaluating only a

160 Deniz Ucbasaran et al.

subset of identified opportunities. Respondentswere presented with eight opportunity pursuitoutcomes (i.e. 0, 1, 2, 3, 4, 5, 6 to 10, or morethan 10 opportunities). Some categories had fewrespondents. Consistent with the opportunityidentification variable, the eight opportunitypursuit outcomes were collapsed into threecategories. Respondents who reported that theyhad failed to pursue an identified opportunitywere allocated a value of ‘‘1’’, those whoreported that they had pursued one or twoopportunities were allocated a value of ‘‘2’’,whilst those who had pursued three or moreopportunities were allocated a value of ‘‘3’’.

4.3.2. Independent variablesTwo sets of general human capital variables werecollected with regard to education and workexperience. Consistent with previous studies(Bates, 1990; Bruderl et al., 1992; Honig, 2001;Van der Sluis et al., 2004), our education mea-sure relates to the years of education reported bythe respondents. Four dummy variables relatingto the respondents� highest level of educationwere also created for sensitivity analysis: (pre-university) technical qualification; undergraduatedegree; post-undergraduate professional qualifi-cation; and postgraduate degree. The compulsoryschool education variable was selected as thereference category.

The amount of work experience and the levelof attainment are important when constructing ameasure of work experience (Gimeno et al.,1997). The number of previous full-time jobs heldwas considered as a proxy for work experience.This variable was named number of organizationsworked for. To account for possible diminishingreturns (Mincer, 1974), the number of organiza-tions worked for squared was also operationa-lised. The level of managerial attainment wasascertained. Three dummy variables were calcu-lated on the basis of responses to the question‘‘what was your job status before starting yourfirst business?’’: ‘‘Manager or self-employed’’;‘‘professional’’ and ‘‘supervised others’’. The‘‘supervised no-one’’ variable was selected as thereference category.

Six entrepreneurship-specific human capitalvariables were collected. The level of businessownership experience was measured. Respon-

dents were asked to indicate the total number ofbusinesses in which they had prior minority ormajority business ownership, either as a businessfounder or a purchaser.

Respondents were presented with eightstatements relating to their perceived capabilities(Chandler and Hanks, 1998). An R-mode vari-max rotated principal components analysis(PCA) identified three components.2 Compo-nent 1 highlights the ‘‘entrepreneurial capability’’and relates to five statements focusing upon theidentification of opportunities. Further, com-ponent 2 highlights the ‘‘managerial capability’’.It relates to four statements focusing upon theability to manage and organize people and re-sources. Component 3 highlights the ‘‘technicalcapability’’ and relates to two statements focus-ing upon technical expertise. The standardizedand ortho-normalized component scores relatingto each of the three components were utilized asindependent variables.

Cooper et al.�s (1995) information searchintensity measure was operationalised. Eachrespondent was presented with 14 sources ofinformation. Respondents were asked to rateeach information source on a six point scaleranging from ‘‘did not use’’ which was allocated avalue of ‘‘0’’ to ‘‘very useful’’ which was allocateda value of ‘‘5’’. In contrast, the Cooper et al.,study only operationalised a four-point scale.Consistent with Cooper et al., only sources ofinformation that were used by at least 60% of therespondents were considered. Accordingly, eightout of the 14 sources were monitored (i.e. sup-pliers, employees, customers, friends, family,magazines/newspapers, trade publications andother business owners). Following Cooper et al.,a broad measure of information search intensitywas derived by summing the ratings for all eightinformation sources. This measure reflects thenumber of information sources used as well astheir relative usefulness.

While the latter measure provides a usefulindication of the level of information search, itdoes not distinguish between different types ofinformation sought. To provide a more robustanalysis of the role of information, two alter-native measures of information search wereconsidered. An R-mode PCA was used totransform and ortho-normalize the original

161Opportunity Identification and Pursuit: Does an Entrepreneur�s Human Capital Matter?

data relating to the 14 information sources.3

The PCA model is reported in Table II.Previous studies (Cooper et al., 1995) haveidentified two sources of information (i.e.professional/formal information versuspersonal/informal information), which may betoo broad. The PCA identified the followingfour distinct types of information sources:‘‘professional network’’ (i.e. consultants, banks,patents, national and local government sour-ces), ‘‘publications’’ (i.e. magazines and news-papers, trade publications and technicalliterature), ‘‘business network’’ (i.e. suppliers,employees and customers) and ‘‘personalnetwork’’ (i.e. other business owners, friendsand family). The standardized and ortho-normalized component scores relating to eachof the four components were utilized as inde-pendent variables. Second, the number ofinformation sources used was also selected asan indicator of information search.

4.3.3. Control variablesTen control variables were considered. Anentrepreneur�s age and gender have beenconsidered as dimensions of human capital(Cooper et al., 1994). To account for possiblenon-linearity and to avoid multicollinearity, theage of the respondent was measured in terms ofthe deviation from the mean age in years (i.e.49), and the age of the owner2 was measured interms of the deviation from the mean age2

(Aiken and West, 1991). A dummy variablewas created to capture the gender of respon-dents. Female entrepreneurs were allocated avalue of ‘‘0’’, whilst male entrepreneurs wereallocated a value of ‘‘1’’.

The entrepreneurial process may be shapedby external environmental conditions and theindustry entered may be a source of opportuni-ties (Shane, 2003). Six dichotomous variablesrelating to industry categories were measured.Each respondent was allocated to one of thefollowing broad six Standard Industrial Classi-fication (SIC) categories: agriculture, forestry,fishing, and mining and quarrying (SIC 0 & 2);manufacturing (SIC 3 & 4); distribution, hotels,catering and repairs (SIC 6); transport, storageand communication (SIC 7); financial interme-diaries, real estate, renting and business activi-

ties (SIC 8); and other services (SIC 9).Construction (SIC 5) was selected as the refer-ence category.

Opportunity identification and pursuit maybe shaped by the human capital of surroundingthe entrepreneur. There is increasing recognitionthat some entrepreneurs operate as part of ateam, with the team members representing animportant source of human capital (Ucbasaranet al., 2003). The human capital external to theentrepreneur was controlled for by the ‘‘numberof equity partners’’ in the surveyed business.

4.4. Validity

Convergent and discriminant validity was con-sidered by exploring the PCA component load-ings. The loadings ranged from 0.63 to 0.88 forthe ‘‘managerial capability’’, ‘‘entrepreneurialcapability’’ and ‘‘technical capability’’ compo-nents. Moreover, they ranged from 0.50 to 0.84for the ‘‘professional network’’, ‘‘publications’’,‘‘business network’’ and ‘‘personal network’’components. All component loadings were sta-tistically significant. Convergent validity wasapparent with regard to all the constructs. Also,the constructs appeared to exhibit discriminantvalidity insofar as each statement loading sig-nificantly on only one of the seven components.

4.5. Reliability

The Cronbach alphas for the ‘‘entrepreneurialcapability’’, ‘‘managerial capability’’ and ‘‘tech-nical capability’’ scales were 0.79, 0.85 and 0.67,respectively. The ‘‘professional network’’,‘‘publications’’, ‘‘business network’’ and ‘‘per-sonal network’’ scales had Cronbach�s alphascores of 0.78, 0.78, 0.67 and 0.70, respectively.The scales meet the recommended reliability level(Hair et al., 1995).

4.6. Endogeneity

The endogeneity issue needs to be considered inempirical research in the human capital area andhas received considerable attention where edu-cation is being considered. Biased regressioncoefficient estimates may be reported if endo-geneity is not considered. These biases result

162 Deniz Ucbasaran et al.

from omitted variables that affect both humancapital decisions and the outcome variable inquestion. Van der Sluis et al. (2004) highlighttwo potential sources of bias in the context ofeducation and entrepreneurial performance.First, unobserved individual characteristics suchas ability and motivation may influence both thelevel of education obtained and subsequententrepreneurial performance. Indeed, the theoryof signalling in education (Spence, 1974) rests onthe notion that educational investment is moreattractive to those with innate ability; a propo-sition which is understood by employers whothereby value it as a means of revealing asym-metric information. Second, as individuals maybase their decision to invest in education ontheir expected payoffs from the investment,education may be endogenous in a performance/outcome equation.

A number of solutions to alleviate endoge-neity problems have been presented (Hamiltonand Nickerson, 2003; Van der Sluis et al., 2004).Attempts are generally made to proxy forunobserved ability. Further, two-stage regres-sion procedures are selected that use instru-mental variables to make the endogeneityexogenous. Here, we attempt to control for therole of ability with reference to the selectedcapability measures (i.e. managerial, entrepre-neurial and technical capability). We acknowl-edge that the latter capability measures arebased on perceptions of capability, and thepotential problem of endogeneity may remain.Gist (1987), however, found a strong positivecorrelation between perceived and actual capa-bilities. To assess the extent to which endoge-neity might still be a problem, a Hausman testfor exogeneity (Hausman, 1978) was conducted.This test compares the coefficients from theoriginal regression with the coefficients from atwo stage least squares (2SLS) regression, whichinstruments the endogenous variables. A par-ent�s background has been regarded as a suitableinstrument for education (Blackburn andNeumark, 1993; Van der Sluis et al., 2004).Information was not collected relating to theeducation level of the parents. However, infor-mation relating to the occupation of the entre-preneurs� parent (i.e. main income earner) hadbeen gathered. Iyigun and Owen (1998) argue

that professionals (as opposed to entrepreneurs)accumulate their skills primarily by investing ineducation. Following this logic, we would expectentrepreneurs� parents who had a professionalbackground to report higher levels of education.To be an appropriate instrument we would wantthe parents� background to be correlated withthe entrepreneurs� education but uncorrelatedwith the dependent variables. The parentalbackground variable met these criteria.Accordingly, we instrumented years of educa-tion with whether the parent of the entrepreneurwas a professional in both the opportunityidentification and opportunity pursuit equa-tions. With reference to the Hausman test wefound no significant difference between the OLSbased and instrumental variable based coeffi-cients4 of education at the 0.1, 0.05, 0.01 levels.On this basis, we failed to reject exogeneity forthe instruments used. We concluded that edu-cation was exogenous in the opportunity iden-tification and opportunity pursuit equations.

The validity of the above analysis is based,among other factors, on the remainingindependent and control variables being exoge-nous. It is possible that other human capitalvariables may suffer from endogeneity. Thebusiness ownership experience variable, forexample, might suffer from endogeneity. Thelatter variable poses a different endogeneityproblem because it could have been acquiredsimultaneously with the identification of businessopportunities. To explore the extent to which thebusiness ownership experience variable wasendogenous; we sought to identify an appropri-ate instrument. Guided by the literature onhabitual (experienced) entrepreneurs (Westheadand Wright, 1998) we considered an entrepre-neur�s parental background. Evidence suggeststhat parental business ownership can have astrong impact on the decision to become anentrepreneur (Evans and Leighton, 1989; Bruderlet al., 1992), and this impact is particularlystrong for habitual entrepreneurs (Ucbasaranet al., 2006). A significant positive correlationbetween the respondent�s business ownershipexperience and whether one of their parents hadbeen a business owner was detected. It was,therefore, possible to instrument entrepreneur�sbusiness ownership experience with whether their

163Opportunity Identification and Pursuit: Does an Entrepreneur�s Human Capital Matter?

parents had been business owners. With refer-ence to the Hausman test, no significant differ-ence was detected between the OLS based andinstrumental variable based coefficients for busi-ness ownership experience at the 0.1, 0.05, 0.01levels. Moreover, the Hausman test relating toinstrumenting education and business ownershiptogether indicated that the instrumented coeffi-cients of education and business ownershipexperience (as described above) were not signifi-cantly different from the OLS coefficients at the0.1, 0.05 and 0.01 levels.

The Hausman tests suggest that the reportedanalyses relating to opportunity identificationand pursuit would not be seriously biased byendogeneity. For this reason, the followinganalysis relates to the earlier outlined orderedlogit procedure rather than the 2SLS. On a noteof caution, we acknowledge, that the detectedfinding that education and business ownershipexperience were exogenous, could have beeninfluenced by the quality of the instrumentsused. We have, however, sought to selectinstruments that have been guided by theory aswell as prior empirical evidence. A secondpotential concern is that we assumed that theremaining human capital variables were exoge-nous, and we considered instrumenting theremaining human capital variables. In addition,we do not know whether the information searchtook place before the 5 year opportunity iden-tification/pursuit window or during the 5 yearwindow. This may also cause an endogeneityproblem similar to that of business ownershipexperience discussed above. Unfortunately, weconfronted the same problem as Bosma et al.(2004) in their study of human capital andentrepreneurship. That is, we could not identifysuitable exogenous instrumental variables.

5. Results

Given the nature of the dependent variables,ordered logit and probit analysis were selected infavour of ordinary least squares regressionanalysis to test the hypotheses relating to thetwo dependent variables measured on ordinalscales (Greene, 1997). Because there was virtu-ally no difference between the results relating tothe ordered probit and logit analyses, only the

logit models are discussed. An analysis of thecorrelation matrix and the VIF scores suggestthat multicollinearity would not be a problemwithin the regression models (Hair et al., 1995).It should be noted that our data is cross-sectional in nature. Therefore, we are unable todraw causal inferences from the results discussedbelow.

5.1. Hypotheses relating to opportunityidentification

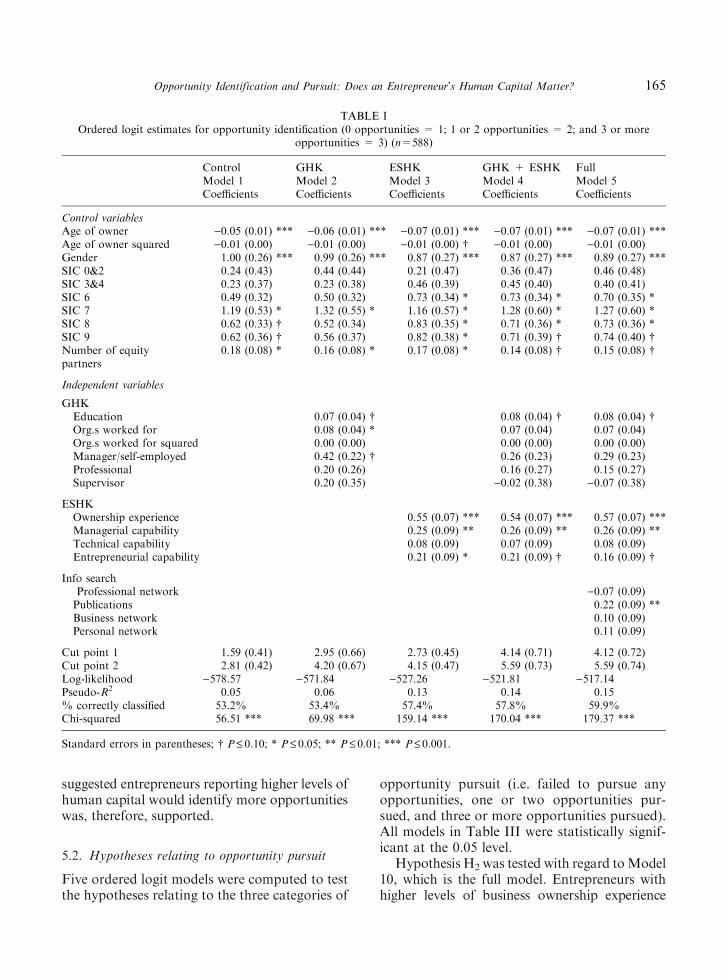

Five ordered logit models were computed to testthe hypotheses relating to the three categories ofopportunity identification (i.e. failed to identifyan opportunity, one or two opportunities iden-tified, and three or more opportunities identified).Model 1 in Table I is the ‘‘control model’’ andrelates solely to the control variables. Model 2includes the general human capital (GHK) andthe control variables. Model 3 includes theentrepreneurship-specific human capital (ESHK)variables and the control variables. Model 4includes the GHK, ESHK and the control vari-ables. Model 5 is the full model, which includesthe GHK, ESHK and control variables as well asthe information search variables. All models werestatistically significant at the 0.001 level.

Hypothesis H1 was tested in relation to Model5. Entrepreneurs with higher levels of education,work experience, business ownership experience,managerial capability and entrepreneurial capa-bility were significantly associated with anincreased probability of identifying more oppor-tunities (Table I). Though not reported inTable I, sensitivity analysis was conducted withreference to the education variable, to establish ifthe type of educationmattered. The latter analysisrevealed that those respondents who reported apostgraduate degree as their highest level of edu-cation were weakly associated with an increasedprobability of identifying more opportunitiesrelative to those who had only received compul-sory school education (P<0.089). The other‘‘types’’ of education were not found to besignificantly associated with opportunity identifi-cation. The inclusion of the human capital vari-ables (i.e. GHK and ESHK) made a significantcontribution over and above the control model(DR2 = 0.09, P<0.001). Hypothesis H1 that

164 Deniz Ucbasaran et al.

suggested entrepreneurs reporting higher levels ofhuman capital would identify more opportunitieswas, therefore, supported.

5.2. Hypotheses relating to opportunity pursuit

Five ordered logit models were computed to testthe hypotheses relating to the three categories of

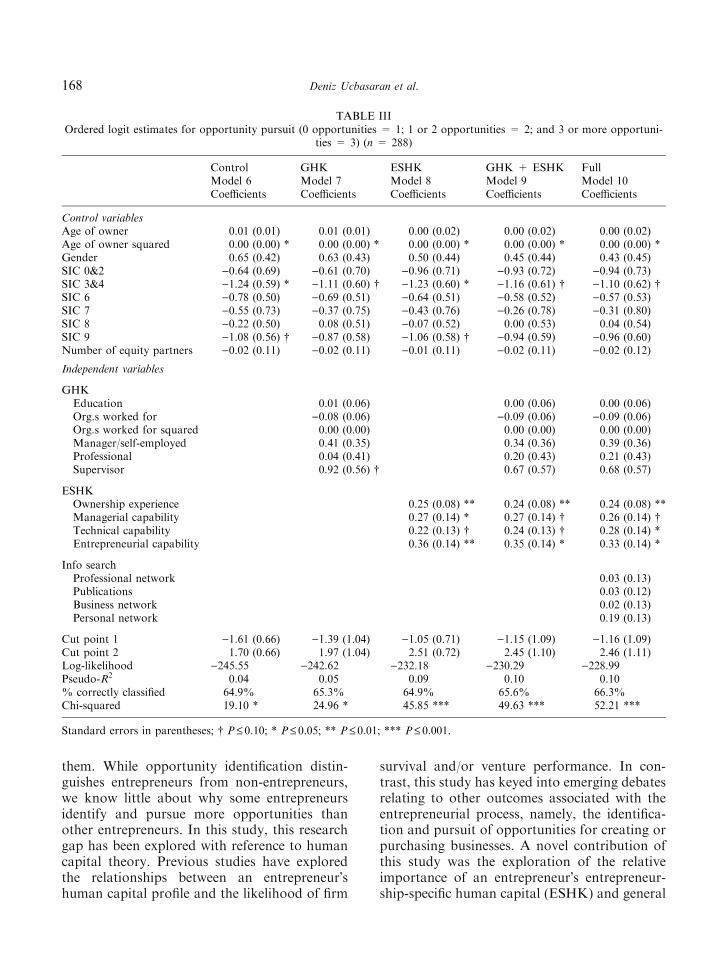

opportunity pursuit (i.e. failed to pursue anyopportunities, one or two opportunities pur-sued, and three or more opportunities pursued).All models in Table III were statistically signif-icant at the 0.05 level.

Hypothesis H2 was tested with regard toModel10, which is the full model. Entrepreneurs withhigher levels of business ownership experience

TABLE IOrdered logit estimates for opportunity identification (0 opportunities = 1; 1 or 2 opportunities = 2; and 3 or more

opportunities = 3) (n=588)

ControlModel 1

GHKModel 2

ESHKModel 3

GHK + ESHKModel 4

FullModel 5

Coefficients Coefficients Coefficients Coefficients Coefficients

Control variablesAge of owner )0.05 (0.01) *** )0.06 (0.01) *** )0.07 (0.01) *** )0.07 (0.01) *** )0.07 (0.01) ***Age of owner squared )0.01 (0.00) )0.01 (0.00) )0.01 (0.00) � )0.01 (0.00) )0.01 (0.00)Gender 1.00 (0.26) *** 0.99 (0.26) *** 0.87 (0.27) *** 0.87 (0.27) *** 0.89 (0.27) ***SIC 0&2 0.24 (0.43) 0.44 (0.44) 0.21 (0.47) 0.36 (0.47) 0.46 (0.48)SIC 3&4 0.23 (0.37) 0.23 (0.38) 0.46 (0.39) 0.45 (0.40) 0.40 (0.41)SIC 6 0.49 (0.32) 0.50 (0.32) 0.73 (0.34) * 0.73 (0.34) * 0.70 (0.35) *SIC 7 1.19 (0.53) * 1.32 (0.55) * 1.16 (0.57) * 1.28 (0.60) * 1.27 (0.60) *SIC 8 0.62 (0.33) � 0.52 (0.34) 0.83 (0.35) * 0.71 (0.36) * 0.73 (0.36) *SIC 9 0.62 (0.36) � 0.56 (0.37) 0.82 (0.38) * 0.71 (0.39) � 0.74 (0.40) �Number of equitypartners

0.18 (0.08) * 0.16 (0.08) * 0.17 (0.08) * 0.14 (0.08) � 0.15 (0.08) �

Independent variables

GHKEducation 0.07 (0.04) � 0.08 (0.04) � 0.08 (0.04) �Org.s worked for 0.08 (0.04) * 0.07 (0.04) 0.07 (0.04)Org.s worked for squared 0.00 (0.00) 0.00 (0.00) 0.00 (0.00)Manager/self-employed 0.42 (0.22) � 0.26 (0.23) 0.29 (0.23)Professional 0.20 (0.26) 0.16 (0.27) 0.15 (0.27)Supervisor 0.20 (0.35) )0.02 (0.38) )0.07 (0.38)

ESHKOwnership experience 0.55 (0.07) *** 0.54 (0.07) *** 0.57 (0.07) ***Managerial capability 0.25 (0.09) ** 0.26 (0.09) ** 0.26 (0.09) **Technical capability 0.08 (0.09) 0.07 (0.09) 0.08 (0.09)Entrepreneurial capability 0.21 (0.09) * 0.21 (0.09) � 0.16 (0.09) �

Info searchProfessional network )0.07 (0.09)Publications 0.22 (0.09) **Business network 0.10 (0.09)Personal network 0.11 (0.09)

Cut point 1 1.59 (0.41) 2.95 (0.66) 2.73 (0.45) 4.14 (0.71) 4.12 (0.72)Cut point 2 2.81 (0.42) 4.20 (0.67) 4.15 (0.47) 5.59 (0.73) 5.59 (0.74)Log-likelihood )578.57 )571.84 )527.26 )521.81 )517.14Pseudo-R2 0.05 0.06 0.13 0.14 0.15% correctly classified 53.2% 53.4% 57.4% 57.8% 59.9%Chi-squared 56.51 *** 69.98 *** 159.14 *** 170.04 *** 179.37 ***

Standard errors in parentheses; � P £ 0.10; * P £ 0.05; ** P £ 0.01; *** P£ 0.001.

165Opportunity Identification and Pursuit: Does an Entrepreneur�s Human Capital Matter?

and managerial, technical and entrepreneurialcapabilities were associated with an increasedprobability of pursuing more opportunities. Onlyfour out of the ten human capital variables weresignificant. The inclusion of the human capitalvariables (i.e. GHK and ESHK) made a signifi-cant contribution over and above the controlmodel (DR2 = 0.06, P<0.001). Hypothesis H2

is, therefore, supported.

5.3. Hypotheses relating to general versus specifichuman capital

To test hypothesis H3a, we compared thecontribution of the ESHK variables and thenGHK variables over and above that‘‘explained’’ by the sum of the control vari-ables. Further, we examined the magnitude ofthe relationship between the respective humancapital variables and the dependent variableby exploring the probability effects. Theinclusion of the GHK variables made a sig-nificant contribution above and above thecontrol model (DR2 = 0.01, P<0.001). TheGHK variables also made a significant con-tribution above and above the control andESHK variables (DR2 = 0.01, P<0.001). Theinclusion of the GHK variables enhanced themodel. However, a larger improvement inmodel fit was associated with the inclusion ofthe ESHK variables. The inclusion of theESHK variables made a significant contribu-tion above and above the control variables(DR2 = 0.08, P<0.001), and above andbeyond the control and GHK variables(DR2 = 0.08, P<0.001). These findingssupport hypothesis H3a.

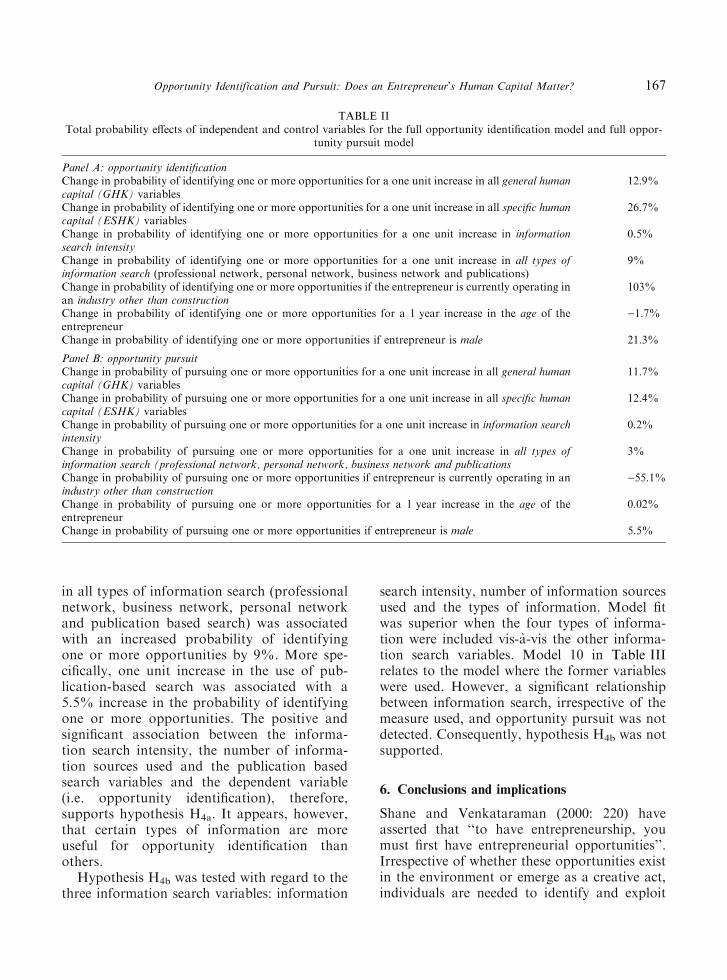

Examination of the probability effects of theGHK and ESHK variables also provides supportfor hypothesis H3a. ESHK variables had strongerrelationships with the number of opportunitiesidentified than the GHK variables. Panel A inTable II shows that a one unit increase in each ofthe GHK variables together, was associated withan increased probability of an entrepreneuridentifying one or more opportunities by 12.9%.However, one unit increase in each of the ESHKvariables together, was associated with an in-creased probability of an entrepreneur identify-ing one or more opportunities by 26.7%. This

evidence provides additional support forhypothesis H3a.

The methodology employed to test hypothesisH3a was used to test hypothesis H3b. Theinclusion of the GHK variables did not make asignificant contribution over and above thecontrol model (DR2 = 0.01). Conversely, theinclusion of the ESHK variables made a signif-icant contribution over and above the controlvariables (DR2 = 0.05, P<0.001). These find-ings support hypothesis H3b.

The probability effects of the GHK andESHK variables were also examined. Thoughnone of the GHK variables were significant,Panel B in Table II shows that a one unitincrease in each of the GHK variables jointlywas associated with an increased probability ofan entrepreneur pursuing one or more oppor-tunities by only 11.7%. However, a one unitincrease in each of the ESHK variables jointlywas associated with an increased probability ofan entrepreneur pursuing one or more oppor-tunities by 12.4%. Although the difference in theprobability effects of the joint GHK and ESHKvariables does not seem great, in conjunc-tion with the earlier evidence relating to changesin model fit and the significance of individ-ual variables, there is some support forhypothesis H3b.

5.4. Hypotheses relating to information search

Hypothesis H4a was tested using multipleinformation search variables. The model pro-ducing the best overall fit is reported in Model5 of Table I. Although not reported inTable III, entrepreneurs who reported higherlevels of information search intensity (i.e.based on Cooper et al.�s (1995) measure) andthose who used more information sourceswere significantly associated with an increasedprobability of identifying more businessopportunities. Model 5 shows that only pub-lication-based information search was signifi-cantly associated with opportunityidentification. Information search based onpersonal, professional and business networkswere not significantly associated withincreased opportunity identification. Panel Ain Table II illustrates that a one unit increase

166 Deniz Ucbasaran et al.

in all types of information search (professionalnetwork, business network, personal networkand publication based search) was associatedwith an increased probability of identifyingone or more opportunities by 9%. More spe-cifically, one unit increase in the use of pub-lication-based search was associated with a5.5% increase in the probability of identifyingone or more opportunities. The positive andsignificant association between the informa-tion search intensity, the number of informa-tion sources used and the publication basedsearch variables and the dependent variable(i.e. opportunity identification), therefore,supports hypothesis H4a. It appears, however,that certain types of information are moreuseful for opportunity identification thanothers.

Hypothesis H4b was tested with regard to thethree information search variables: information

search intensity, number of information sourcesused and the types of information. Model fitwas superior when the four types of informa-tion were included vis-a-vis the other informa-tion search variables. Model 10 in Table IIIrelates to the model where the former variableswere used. However, a significant relationshipbetween information search, irrespective of themeasure used, and opportunity pursuit was notdetected. Consequently, hypothesis H4b was notsupported.

6. Conclusions and implications

Shane and Venkataraman (2000: 220) haveasserted that ‘‘to have entrepreneurship, youmust first have entrepreneurial opportunities’’.Irrespective of whether these opportunities existin the environment or emerge as a creative act,individuals are needed to identify and exploit

TABLE IITotal probability effects of independent and control variables for the full opportunity identification model and full oppor-

tunity pursuit model

Panel A: opportunity identificationChange in probability of identifying one or more opportunities for a one unit increase in all general humancapital (GHK) variables

12.9%

Change in probability of identifying one or more opportunities for a one unit increase in all specific humancapital (ESHK) variables

26.7%

Change in probability of identifying one or more opportunities for a one unit increase in informationsearch intensity

0.5%

Change in probability of identifying one or more opportunities for a one unit increase in all types ofinformation search (professional network, personal network, business network and publications)

9%

Change in probability of identifying one or more opportunities if the entrepreneur is currently operating inan industry other than construction

103%

Change in probability of identifying one or more opportunities for a 1 year increase in the age of theentrepreneur

)1.7%

Change in probability of identifying one or more opportunities if entrepreneur is male 21.3%

Panel B: opportunity pursuitChange in probability of pursuing one or more opportunities for a one unit increase in all general humancapital (GHK) variables

11.7%

Change in probability of pursuing one or more opportunities for a one unit increase in all specific humancapital (ESHK) variables

12.4%

Change in probability of pursuing one or more opportunities for a one unit increase in information searchintensity

0.2%

Change in probability of pursuing one or more opportunities for a one unit increase in all types ofinformation search (professional network, personal network, business network and publications

3%

Change in probability of pursuing one or more opportunities if entrepreneur is currently operating in anindustry other than construction

)55.1%

Change in probability of pursuing one or more opportunities for a 1 year increase in the age of theentrepreneur

0.02%

Change in probability of pursuing one or more opportunities if entrepreneur is male 5.5%

167Opportunity Identification and Pursuit: Does an Entrepreneur�s Human Capital Matter?

them. While opportunity identification distin-guishes entrepreneurs from non-entrepreneurs,we know little about why some entrepreneursidentify and pursue more opportunities thanother entrepreneurs. In this study, this researchgap has been explored with reference to humancapital theory. Previous studies have exploredthe relationships between an entrepreneur�shuman capital profile and the likelihood of firm

survival and/or venture performance. In con-trast, this study has keyed into emerging debatesrelating to other outcomes associated with theentrepreneurial process, namely, the identifica-tion and pursuit of opportunities for creating orpurchasing businesses. A novel contribution ofthis study was the exploration of the relativeimportance of an entrepreneur�s entrepreneur-ship-specific human capital (ESHK) and general

TABLE IIIOrdered logit estimates for opportunity pursuit (0 opportunities = 1; 1 or 2 opportunities = 2; and 3 or more opportuni-

ties = 3) (n = 288)

ControlModel 6

GHKModel 7

ESHKModel 8

GHK + ESHKModel 9

FullModel 10

Coefficients Coefficients Coefficients Coefficients Coefficients

Control variablesAge of owner 0.01 (0.01) 0.01 (0.01) 0.00 (0.02) 0.00 (0.02) 0.00 (0.02)Age of owner squared 0.00 (0.00) * 0.00 (0.00) * 0.00 (0.00) * 0.00 (0.00) * 0.00 (0.00) *Gender 0.65 (0.42) 0.63 (0.43) 0.50 (0.44) 0.45 (0.44) 0.43 (0.45)SIC 0&2 )0.64 (0.69) )0.61 (0.70) )0.96 (0.71) )0.93 (0.72) )0.94 (0.73)SIC 3&4 )1.24 (0.59) * )1.11 (0.60) � )1.23 (0.60) * )1.16 (0.61) � )1.10 (0.62) �SIC 6 )0.78 (0.50) )0.69 (0.51) )0.64 (0.51) )0.58 (0.52) )0.57 (0.53)SIC 7 )0.55 (0.73) )0.37 (0.75) )0.43 (0.76) )0.26 (0.78) )0.31 (0.80)SIC 8 )0.22 (0.50) 0.08 (0.51) )0.07 (0.52) 0.00 (0.53) 0.04 (0.54)SIC 9 )1.08 (0.56) � )0.87 (0.58) )1.06 (0.58) � )0.94 (0.59) )0.96 (0.60)Number of equity partners )0.02 (0.11) )0.02 (0.11) )0.01 (0.11) )0.02 (0.11) )0.02 (0.12)

Independent variables

GHKEducation 0.01 (0.06) 0.00 (0.06) 0.00 (0.06)Org.s worked for )0.08 (0.06) )0.09 (0.06) )0.09 (0.06)Org.s worked for squared 0.00 (0.00) 0.00 (0.00) 0.00 (0.00)Manager/self-employed 0.41 (0.35) 0.34 (0.36) 0.39 (0.36)Professional 0.04 (0.41) 0.20 (0.43) 0.21 (0.43)Supervisor 0.92 (0.56) � 0.67 (0.57) 0.68 (0.57)

ESHKOwnership experience 0.25 (0.08) ** 0.24 (0.08) ** 0.24 (0.08) **Managerial capability 0.27 (0.14) * 0.27 (0.14) � 0.26 (0.14) �Technical capability 0.22 (0.13) � 0.24 (0.13) � 0.28 (0.14) *Entrepreneurial capability 0.36 (0.14) ** 0.35 (0.14) * 0.33 (0.14) *

Info searchProfessional network 0.03 (0.13)Publications 0.03 (0.12)Business network 0.02 (0.13)Personal network 0.19 (0.13)

Cut point 1 )1.61 (0.66) )1.39 (1.04) )1.05 (0.71) )1.15 (1.09) )1.16 (1.09)Cut point 2 1.70 (0.66) 1.97 (1.04) 2.51 (0.72) 2.45 (1.10) 2.46 (1.11)Log-likelihood )245.55 )242.62 )232.18 )230.29 )228.99Pseudo-R2 0.04 0.05 0.09 0.10 0.10% correctly classified 64.9% 65.3% 64.9% 65.6% 66.3%Chi-squared 19.10 * 24.96 * 45.85 *** 49.63 *** 52.21 ***

Standard errors in parentheses; � P £ 0.10; * P £ 0.05; ** P £ 0.01; *** P£ 0.001.

168 Deniz Ucbasaran et al.

human capital (GHK) profile in understandingthe extent of opportunity identification andpursuit, especially with respect to the incorpo-ration of prior business ownership experience.The study also explored whether the humancapital profile ‘‘inputs’’ associated with moreopportunity identification ‘‘outputs’’ weredifferent to those associated with more oppor-tunity pursuit ‘‘outputs’’. Finally, the study hassought to contribute to the emerging debate onthe role of information search in opportunityidentification. Below, we reflect on our findingsand discuss their implications for researchersand practitioners.

Relative to the ESHK variables, the GHKvariables had lower ‘‘explanatory’’ power withregard to both opportunity identification andpursuit. In fact, none of the GHK variableswere significantly associated with opportunitypursuit, while only one GHK variable wasassociated with opportunity identification.Entrepreneurs reporting higher levels of edu-cation reported a higher probability of iden-tifying more opportunities. Education can actas a source of both knowledge and motivation(Cooper et al., 1994), the two essential ingre-dients for opportunity identification (Shane,2003). It is important to note that education isoften endogenous in models of entrepreneurialperformance (Van der Sluis et al., 2004). Testssuggested that the presented results were notbiased by endogeneity. This may be becausethe study did not focus on the traditionalmeasures of entrepreneurial performancerelating to venture performance outcomes. Itmay, however, be because weak instrumentsinfluenced the endogeneity tests conducted.The limitations associated with the presentedcross-sectional data and the potential endo-geneity problems resulting from this areacknowledged.

Several ESHK variables were significantlyassociated with both a higher probability ofidentifying more opportunities and pursuingmore opportunities. These were business own-ership experience and managerial and entrepre-neurial capabilities. It appears that many of theskills needed to identify opportunities are alsothose needed for later stages in the entrepre-neurial process. These latter dimensions of hu-

man capital may be important in terms ofproviding access to knowledge and they mayheighten the confidence of the entrepreneur. Theperceived capabilities of entrepreneurs are anelement of their self-efficacy (Delmar, 2000).This self-efficacy has a strong impact on will-ingness to act and overcome obstacles (Woodand Bandura, 1989) and exploit opportunities(Markman et al., 2002).

Managerial capabilities were significantlyassociated with a higher probability of bothidentifying and pursuing more opportunities.These capabilities may also allow entrepreneursto see means-ends relationships (Gaglio andKatz, 2001) more clearly than those withoutthem. Ardichvili et al. (2003) made an importantdistinction between an idea and an opportunity.Entrepreneurs with higher levels of managerialcapability may be better able to convert an ideainto an opportunity.

Despite the above similarities between thehuman capital profiles needed for opportunityidentification and pursuit, there were a numberof differences. Most notably, technical capabil-ities were not significantly associated withopportunity identification but they were associ-ated with more pursued opportunities. Techni-cal knowledge may reduce the risks and costsassociated with the exploitation of an opportu-nity. This may encourage entrepreneurs withgreater technical skills to pursue an opportunity.

Entrepreneurial, managerial and technicalcapabilities (Penrose, 1959) are needed in theentrepreneurial process though to varyingdegrees. To address barriers to opportunityidentification and pursuit, some entrepreneursmay circumvent their own human capital defi-ciencies by attracting entrepreneurial teammembers with complementary human capitalprofiles. Indeed, entrepreneurs operating as partof a larger entrepreneurial team were associatedwith a higher probability of identifying moreopportunities.

This study provides novel findings relating tothe relationships between an entrepreneur�sinformation search behaviour and their oppor-tunity identification behaviour. A distinctionwas made between an entrepreneur�s priorinformation (i.e. knowledge) as embodied intheir human capital profile compared with their

169Opportunity Identification and Pursuit: Does an Entrepreneur�s Human Capital Matter?

current information exhibited by reportedinformation search behaviour. Entrepreneursreporting higher levels of information searchintensity (based on Cooper et al., 1995 measure)and those who utilized more information sour-ces were significantly more likely to identifymore opportunities. The literature distinguishesbetween different types of information (Kaishand Gilad, 1991). Further, certain types ofinformation may be more useful in the oppor-tunity identification process than other types(Fiet, 2002). This study highlighted that entre-preneurs used the following four broad sourcesof information; their professional network, theirbusiness network, their personal network andpublications. Fiet (2002) theorised that specificinformation would be more valuable than gen-eral information in the public domain. It isinteresting to note, therefore, that while infor-mation emanating from the entrepreneur�s per-sonal, professional and business networks wasnot significantly associated with opportunityidentification, information from publicationswas. Interviewing repeat entrepreneurs, Fietet al. (2004) show that these entrepreneurs doindeed use general information (e.g. publica-tions). However, they argue that it is the inter-action between specific and general informationthat is likely to yield the most beneficial resultsin terms of identifying valuable opportunities.Our evidence suggests that certain types ofinformation (i.e. publications-based) was posi-tively associated with more opportunities iden-tified, in a given period. Additional research iswarranted to explore the relationship betweenthe type of information used and the nature ofthe opportunity identified (e.g. wealth creatingpotential, innovativeness etc.). Future studiesmay also consider whether entrepreneurs scanthe informational environment with no partic-ular opportunity in mind (Kaish and Gilad,1991), or whether they systematically search forinformation and/or opportunities (Fiet, 2002).

The quality of the opportunities identifiedand subsequently rejected or pursued by entre-preneurs were not explored (Chandler andHanks, 1994; Fiet, 2002), representing a limita-tion of this study. We focus on the quantityrather than quality of opportunities identifiedand pursued. Future research might usefully

explore the relationships between entrepreneurs�GHK and ESHK profiles and their propensityto identify and pursue opportunities with sig-nificant wealth creating potential. A relateduseful exercise may be to explore the relation-ship between opportunity identification/pursuitstrategies and venture performance, althoughlinking the two aspects directly may pose oper-ational issues. A case for focusing upon theopportunity rather than the firm or the entre-preneur as the unit of academic analysis maybear some theoretical as well as empirical fruitto guide future research.

Two key factors have been singled out asimportant drivers of entrepreneurial activity(Reynolds et al., 2002); the existence of entre-preneurial opportunities and individuals whoare able to recognise and act on these opportu-nities. This study focused on the latter. Externalenvironmental conditions may also be associ-ated with the identification of opportunities. Theavailability of entrepreneurial opportunities canbe influenced by the industry context, oftenresulting from technological, industrial andsocietal changes (Eckhardt and Shane, 2003).Further, the various components of humancapital may have differential effects under vari-ous industry conditions (Bosma et al., 2004;Honig, 2001). In this study, external environ-mental conditions were controlled for with re-gard to the main industrial sector where theentrepreneur had positioned the surveyed firm.While the evidence presented in Tables I and IIIsuggest that industry conditions matter, addi-tional studies are warranted that utilize moresophisticated measures relating to externalenvironmental conditions.

Our findings provide insights to assist calls toconsider the entrepreneur (or the entrepreneur-ial team) rather than solely the firm as the unitof analysis through all stages of the entrepre-neurial process (Westhead et al., 2005). Thisstudy suggests a need to recognise that somehuman capital skills required for opportunityidentification differ from those required foropportunity pursuit. Presented evidence sug-gests that entrepreneurs leverage their ESHK toa greater extent than their GHK to identify andpursue opportunities. Policy to address attitu-dinal, resource and operational barriers to the

170 Deniz Ucbasaran et al.