mm - World Bank Documents & Reports

136

; i i G O _ ~H H_ >s ~~ zu z 4 A~~~~~~~~~~~~~~~~~~~~~~~~~~~~ =z.-4- ~~~~44A ~ ~ ~ ~ ~ P ?Tho <., m~. . )s* 7 4 4o''<--#r 42~~~~~~~~~~~~~~ U - , A- -> -a t444 - _ _.**** dd- _ P -4d .. ,,,-__~- .>. - _ _ j ,.... C ~~- = -~~~~ ~~~. -, .J- wr,ys, mm~ ~ ~~~~~~ ;- ^ *~~~~~ _ - ' 4 ' ' - _ ' ' 4 .~ _ -_ __ =A Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized closure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized closure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of mm - World Bank Documents & Reports

; i i G

O _ ~H H_

>s ~~ zu z 4

A~~~~~~~~~~~~~~~~~~~~~~~~~~~~

=z.-4-~~~~44A ~ ~ ~ ~ ~ P

?Tho <., m~. . )s* 7 4 4o''<--#r

42~~~~~~~~~~~~~~ U - , A- -> -a t444 - _ _.**** dd- _ P -4d .. ,,,-__~- .>. - _

_ j ,.... C ~~- =

-~~~~ ~~~. -, .J- wr,ys,

mm~ ~ ~~~~~~ ;- ^ *~~~~~ _ - ' 4 ' '

- _ ' ' 4 .~ _

-_ __ =A

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

.~~~~~~~~~~~~~ D ;h . ..... -.... *..... ... .. . . ... .... ... .... .:: <.. :Fi. .. ..... ..... ..... .... ..... ... ...... ..... .... .......... ... .. ... ... i. ... ... ... .. . :, ..........-.....

... ~~~~~~~~~~~~~~~~~~~~~~..... ..... ..... ..... ..... ... ... ... . .... . . .... ..... ....... ..... ..... ..... ..... ... ... ...... ..

.............. .. . . . . . . . . . . . . . . . . . ... ..... ..... . .. ..... ..... ... . . . . . . . . . . . . . . . . . . . . . . . . . . ... ... ......... . . . . . . . . . . . . . . . . . . . . . . . ........... ............

,i, V,ji,i'i iji;t :..: ; s,:z,j

........................ ................. ..... ..... .. ..... .... ..... ..... ... ......... . .............................. ..... ...... ..... .... ..... .... ...... ...... .... ... . ... ... . ................ ...... .. .

i 3i -. C z - 83'; - {- -D- f i- % ! ." , .. , _, , .R .', -, if. _, ... , el'. f'..".2 F

The International Finance Corporation (IFC), a multilateral institution, was established in 1956 with

a mandate to foster economic growth by promoting private sector investment in its developing mein-

ber countries. TFC is a member of the World Bank Group, which also indudes the International Bank

for Reconstruction and Development (IBRD), the International Development Association (IDA), and

the Multilateral Investment Guarantee Agency (MIGA). Although IFC's activities are closely coordi-

natcd with, and complement, the overall development objectives of the other World Bank Group

institutions, IFC is legally and financially independent, with its own Articles of Agreement, share-

holders, financial structure, management, and staff.

IFC combines the characteristics of a multilateral development bank and a private merchant bank. Its

share capital is provided by its 147 developed and developing member countries, which collectively

determine its policies and activities. IFC's profitability, strong shareholder support, and substantial

paid-in capital base have allowed it to raise most of the funds for its lending activities through its

triple-A rated bond issues in the international financial markets. Equity investments are financed

from the capital base and retained earnings.

In its project financing role IFC provides loans and makes equity investments. Unlike most multilate-

ral institutions, IFC does not require government guarantees for its financing. Like a private financial

institution, the Corporation prices its finance and services in line with the market and seeks profitable

returns. IFC shares full project risks with its partners.

IFC's experience in doing business in developing countries as well as its risk-management skills and

thorough project appraisals all contribute to the success of the private sector projects it supports.

These qualities also enable IFC to play an important catalytic role in mobilizing additional project

fiuding from other investors and lenders, either in the form of cofinancing or through loan syndica-

tions, the underwriting of debt and securities issues, and guarantees. In addition to project finance

and resource mobilization, IFC offers a full array of advisory services and technical assistance, helping

private businesses in the developing world to increase their chances of success and advising govern-

ments on creating an environmenit that encourages private investment.

In its 36 years of operation, IFC has provided nearly $11 billion in financing for more than 1,000

companies in 98 developing countries. Today IFC is the largest source of direct financing for private

sector projects in developing countries. IFC has a vital role to play in helping developing countries to

make the transition to open, market-oriented economies and to build strong private sectors. As more

and more developing countries adopt market-based policies, demand for IFC's services-loans,

equity investments, resource mobilization, and advice-continues to grow.

T AB LE OF CON T ENT S

LETTER TO THE BOARD OF GOVERNORS 1

THE YEAR IN REVIEW 2

PRIVATE INVESTMENT ISSUES 6

The Climate for Private Investment 6

Privatization 11

REPORT ON OPERATIONS 17

Project Financing 17

Resource Mobilization 18

Risk-Management Services 20

Advisory Services and Technical Assistance 21

REGIONAL REPORTS 25

Sub-Saharan Africa 25

Asia 35

Europe 44

Latin America and the Caribbean 53

Middle East and North Africa 65

MANAGEMENT AND ORGANIZATION 71

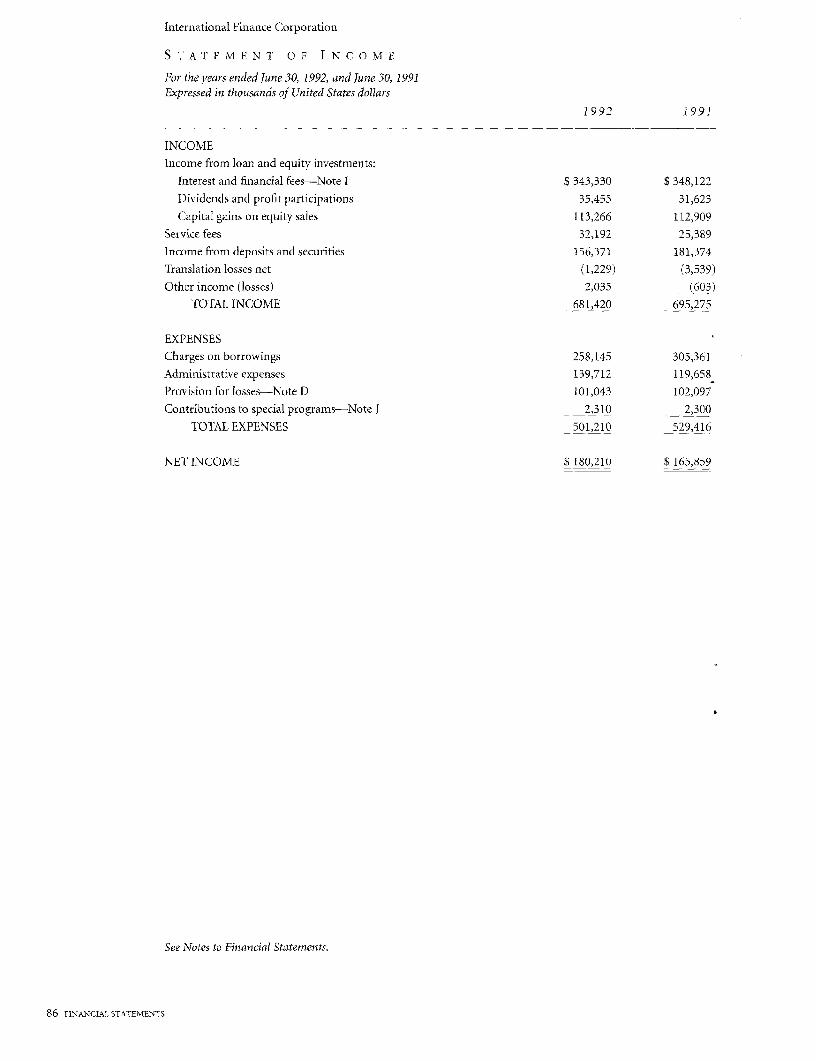

FINANCIAL REVIEW 81

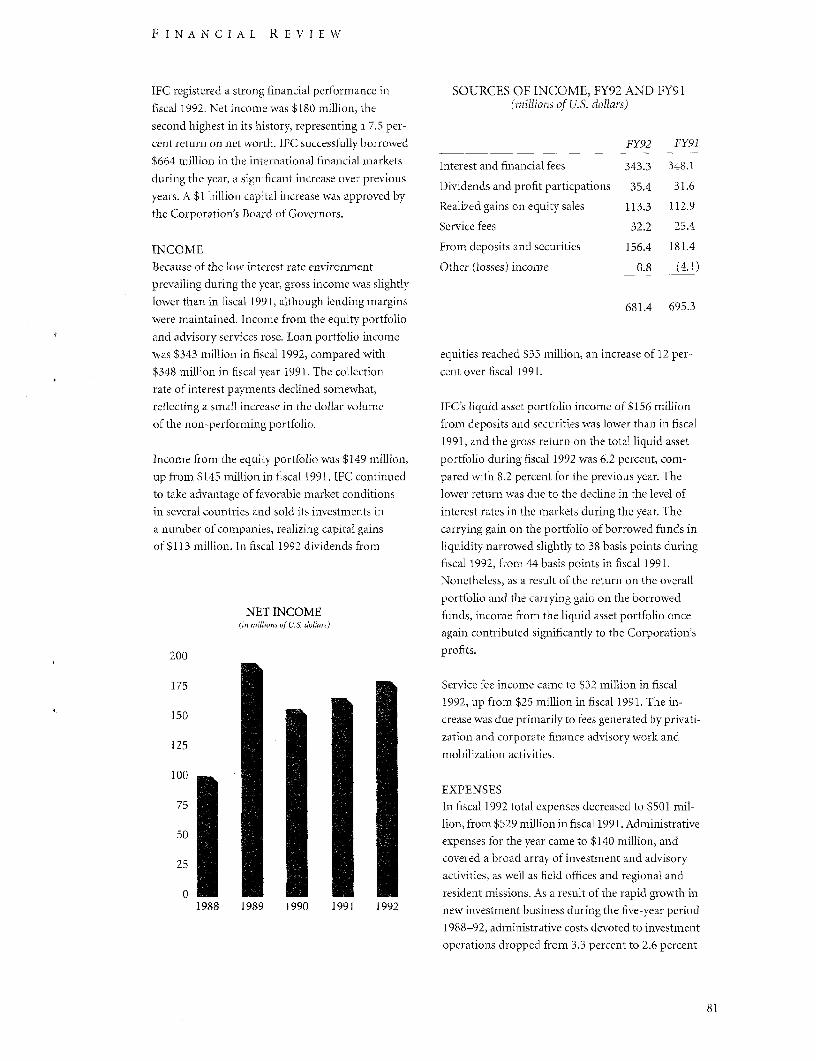

Income 81

Expenses 81

Capital and Retained Earnings 82

Funding Management 82

Financial Statements 85

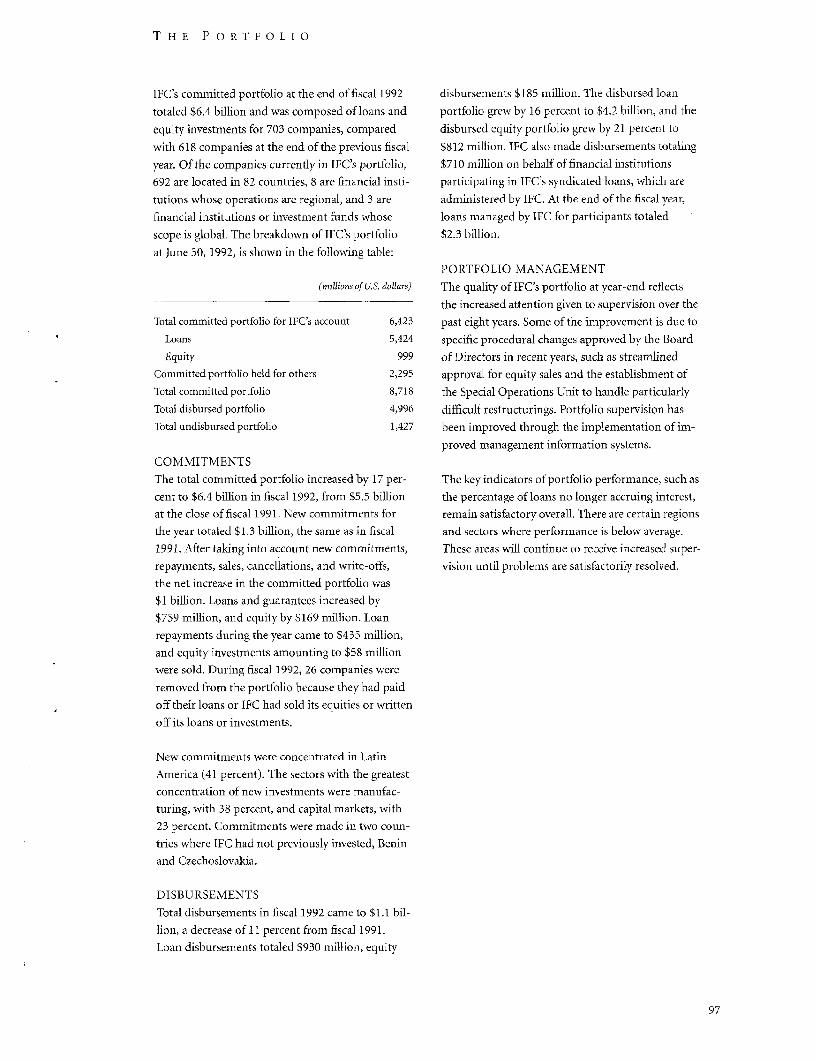

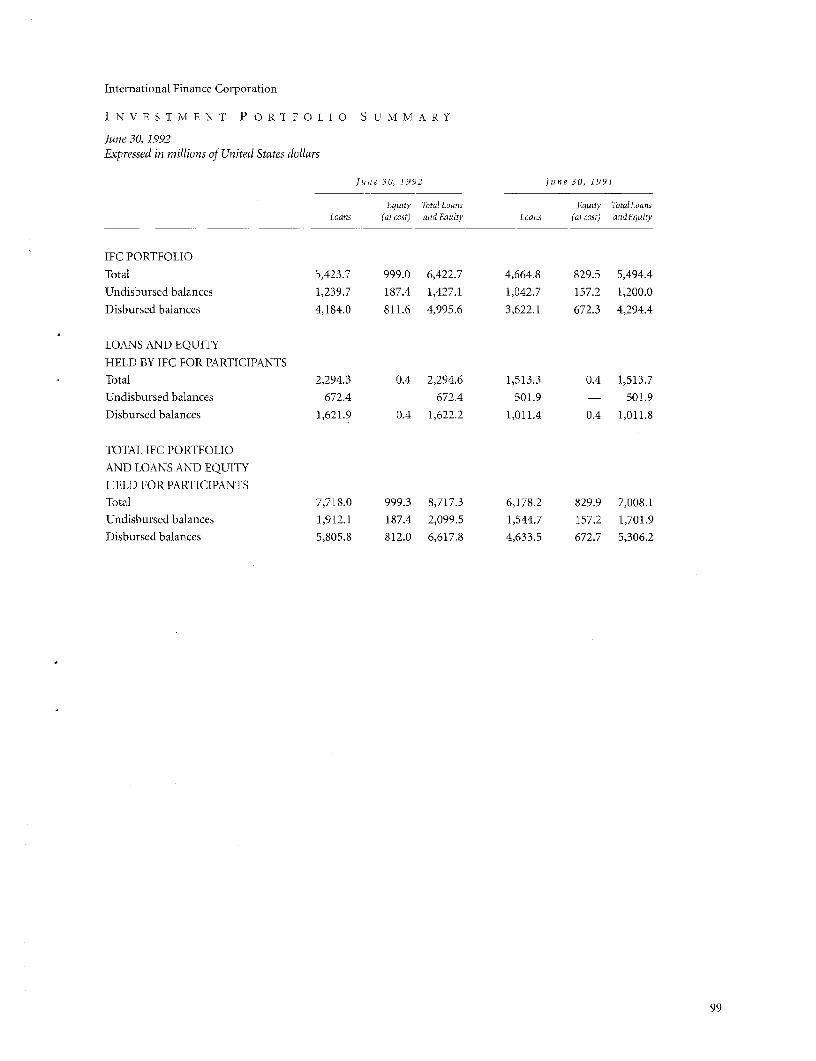

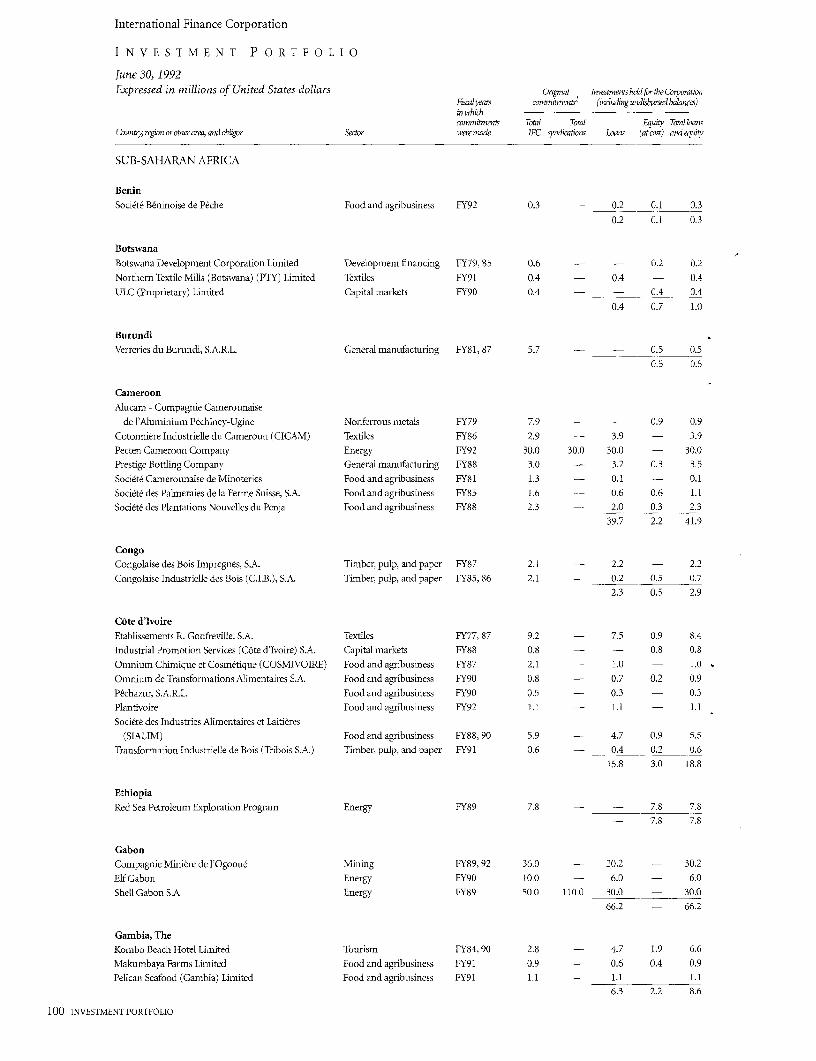

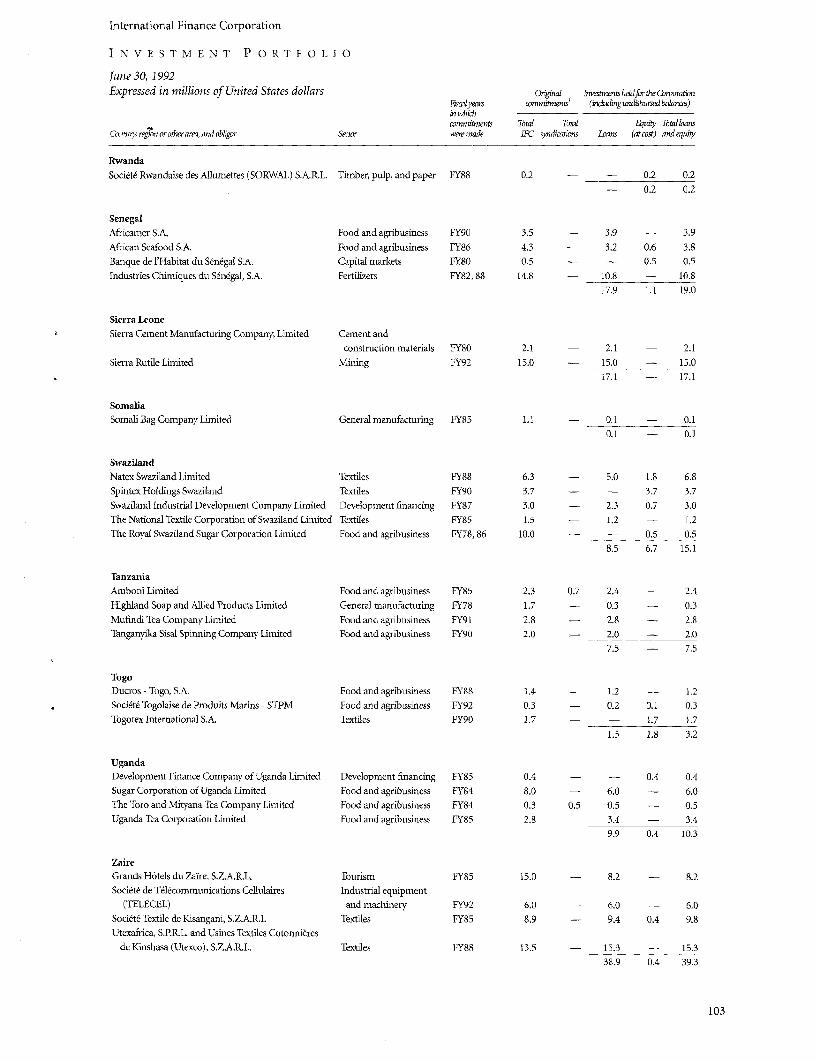

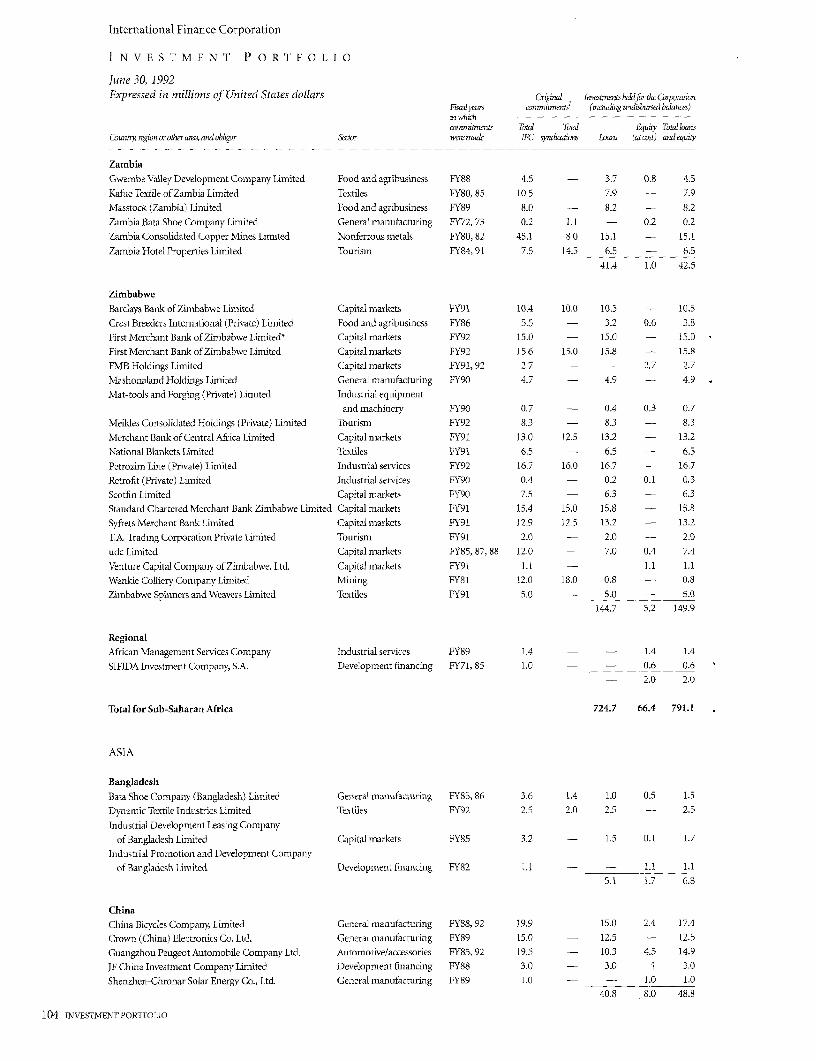

THE PORTFOLIO 97

Commitments 97

Disbursements 97

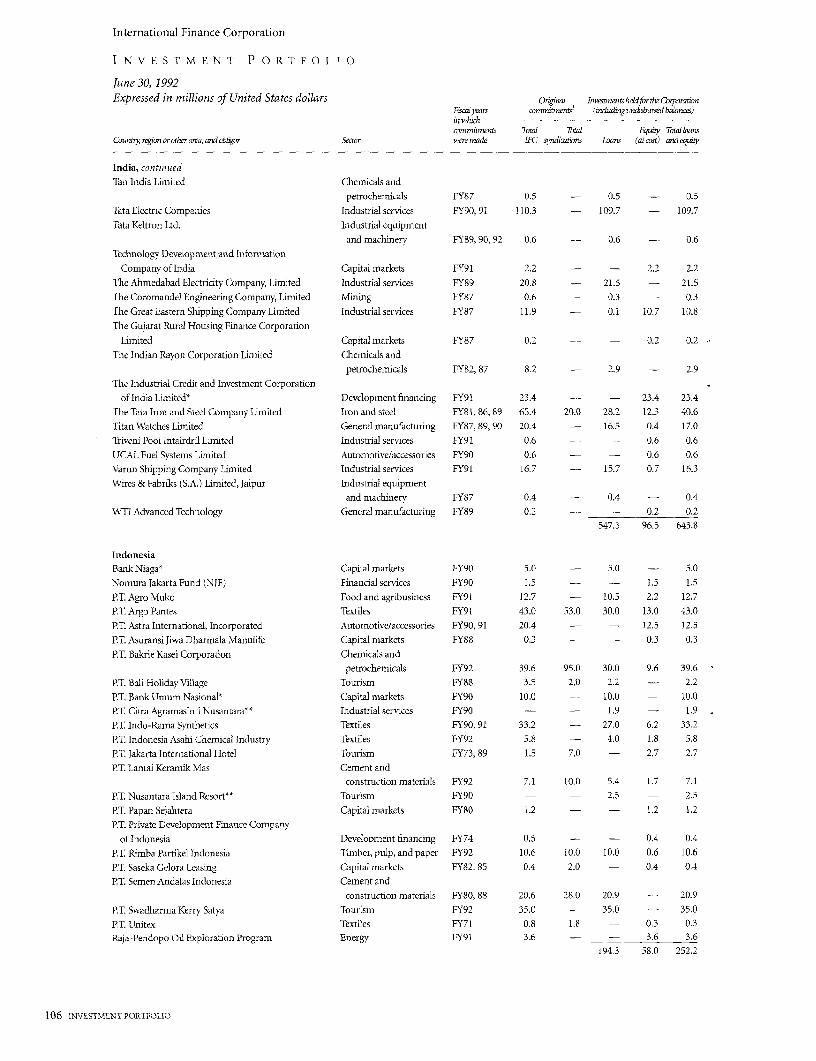

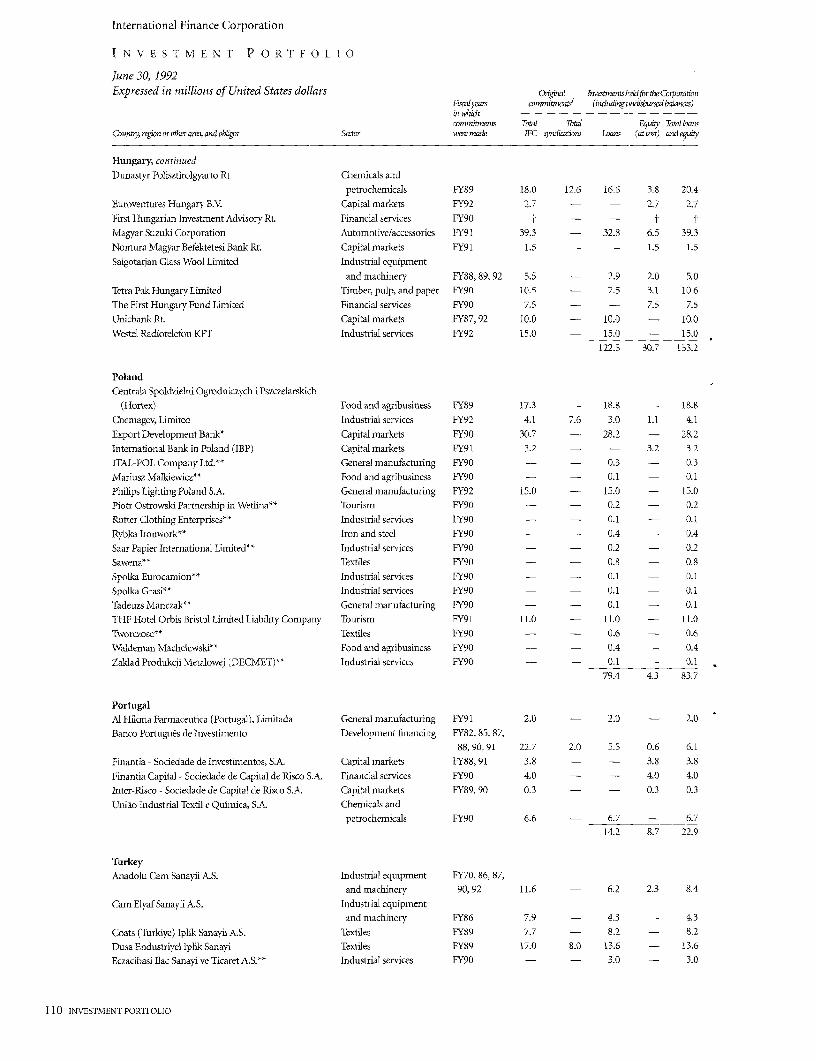

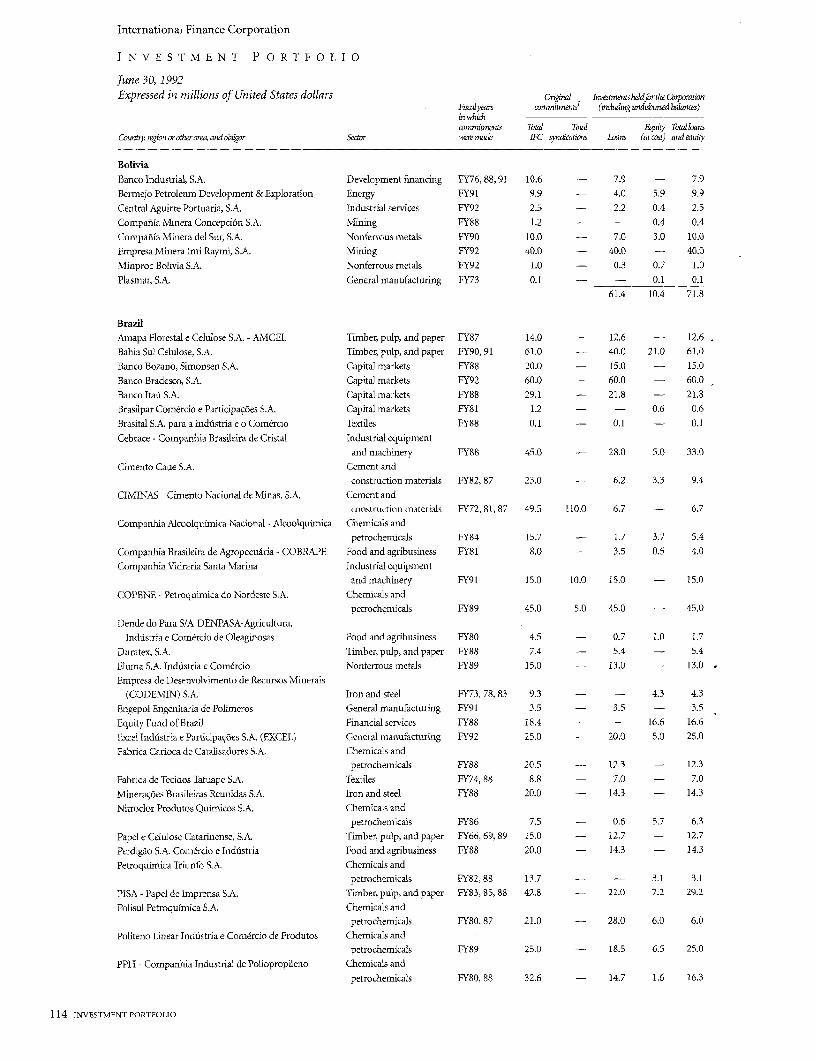

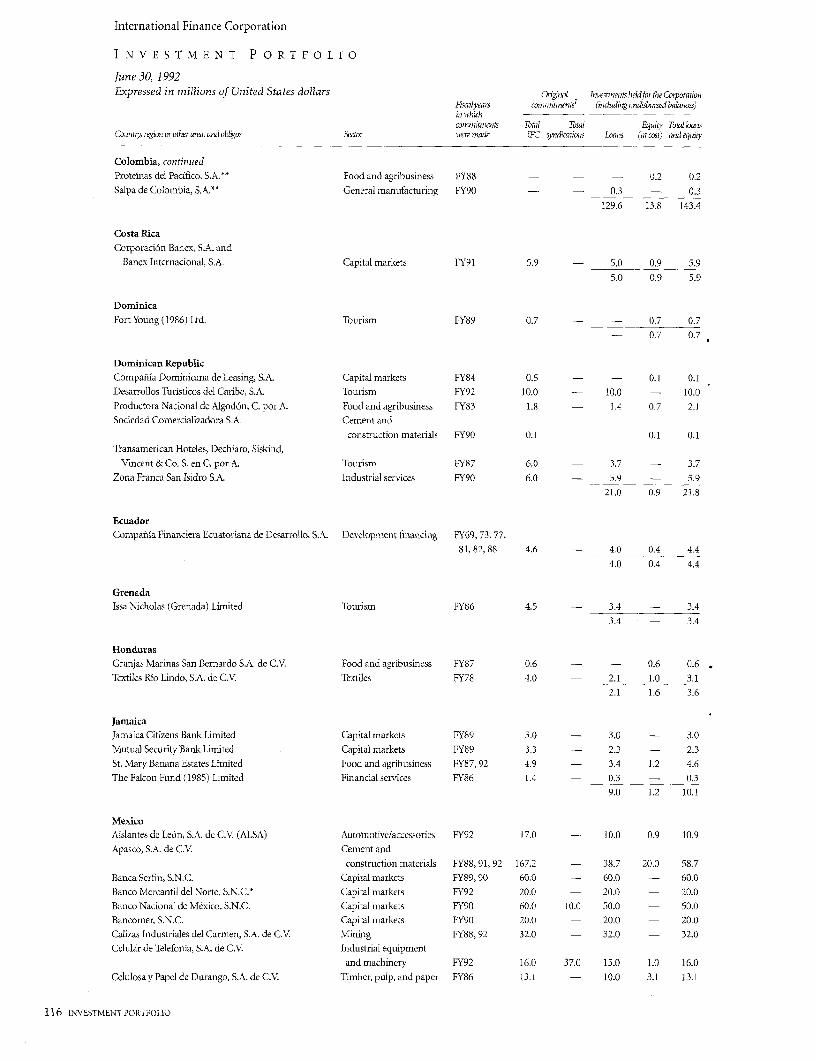

IPortfolio Management 97IFC's Investment Portfolio at June 30, 1992 99

Statement of Cumulative Commitments 121

APPENDIXES

Governors and Alternates 122

Directors and Alternates and Their V4oting Power 124

IFC Management 125

Acronyms, Abbreviations, Notes,

and Definitions 128

August 6, 1992

TO THE BOARD OF GOVERNORS,

The Board of Directors of the International Finance Corporation has had this Annual Report for the fiscal

year ending June 30, 1992, prepared in accordance with the By-Laws of the Corporation. Mr. Lewis T. Preston,

President of the Corporation and Chairman of the Board of Directors, has submitted this Report, together with

the accompaniying audited financial statements, to the Board of Governors.

The Directors are pleased to report that, in fiscal 1992, IFC continued to expand its project financing

operations and advisory activities in its developing member countries, while further strengthening its financial

position.

4%4' 'A b q ; 4j, i,.

'.4X

IFC's Boardof D,rectors, i. -

Januiary 14, 1992

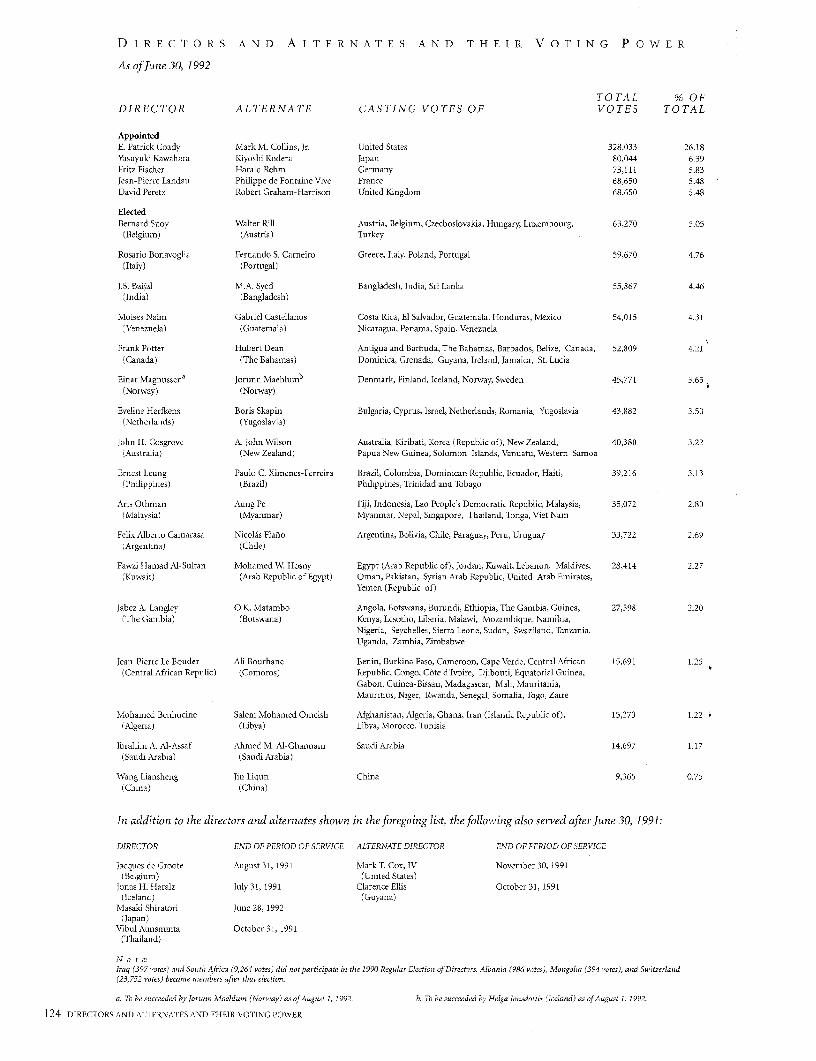

DIRECTORS ALTERNATES

Ibrahim A. Al-Assaf Ahmed M. Al-ChannamFawzi Hamad Al-Sultan Mohamed W. HosnyAris Othman Aung PeJ.S. Baijal M.A. SyedMohamed Benhocine Salem Mohamed OmeishRosario Bonavoglia Fernando S. CarneiroFelix Alberto Camarasa Nicolas FlantoE. Patrick Coady Mark M. Collins, Jr.John H. Cosgrove A. John WilsonFritz Fischer Harald RehmEveline Herfkens Boris SkapinYasuyuki Kawahara Kivoshi KoderaJean-Pier re Landau Philippe de Fontaine ViveJabez A. Langley O.K. MatamboJean-Pierre Le Bouder Ali BourhancErnest Leung Paulo C. Ximenes-FerreiraJorunn Maehlum Helga JonsdottirMoises Naim Gabriel CastellanosDavid Pcretz Robert Graham-Harrison

iFCs Board Frank Potter Hubert Deanof Directors, Bernard Snoy W\alter Rill

August 6, 1992 WTang Liansheng Jin Liqun

T HE Y E A R IN R E V I E W

4 ~~~~~~~~~~voting power required for approval of future capital

.U. ̂ - . t . t t; increases and charter amendments.

ICX Cooperation between the IBRD and I FC has been

t3- I g i f000; -1 < _ : i; strengthened to achieve greater complementarity in

their support of private sector development. IFC hasbcgun to work with the IBRD on assessments of the

privatc sector in about 20 countries. 'these studies are

fewis T Prestor,mw^_ left to rigt: iW intended to deepen the World Bank Group's under-Lewis T Preston,uPresident of the standing of obstacles to private sector cLevelopment in

VAdrld R3an1k individual member countries and to serve as the basisGrouip, and

Sir Wtillianm Ryic for future assistance strategies. tFC andi the IBRD areEx ec utive Vice also coordinating their operations and sectoral work.

President of IEC

The Corporation achieved its k-ey objectives in its

Fiscal 1992 was a year of challenge and change for investment operations in fiscal 1992. The volume of

IFC. Demand for the Corporation's finance and ad- project financing approved increased over the previ-

visory services continued to increase as countries ous fiscal year, as expected. IFC approved $1.8 billion

throughout the developing world persevered with in financing for its own account for 167 projects,

free-market reforms. Albania, Bulgaria, Equatorial compared with $1.5 billion for 152 projects in fiscal

Guinea, the Lao People's Democratic Republic, and 1991. Equity and quasi-equity investments, which

Switzerland joined the Corporation during the year, represented 21 percent of total financing approved

and Comoros joined shortly after the close of the for IFC's own account, were increased in accordance

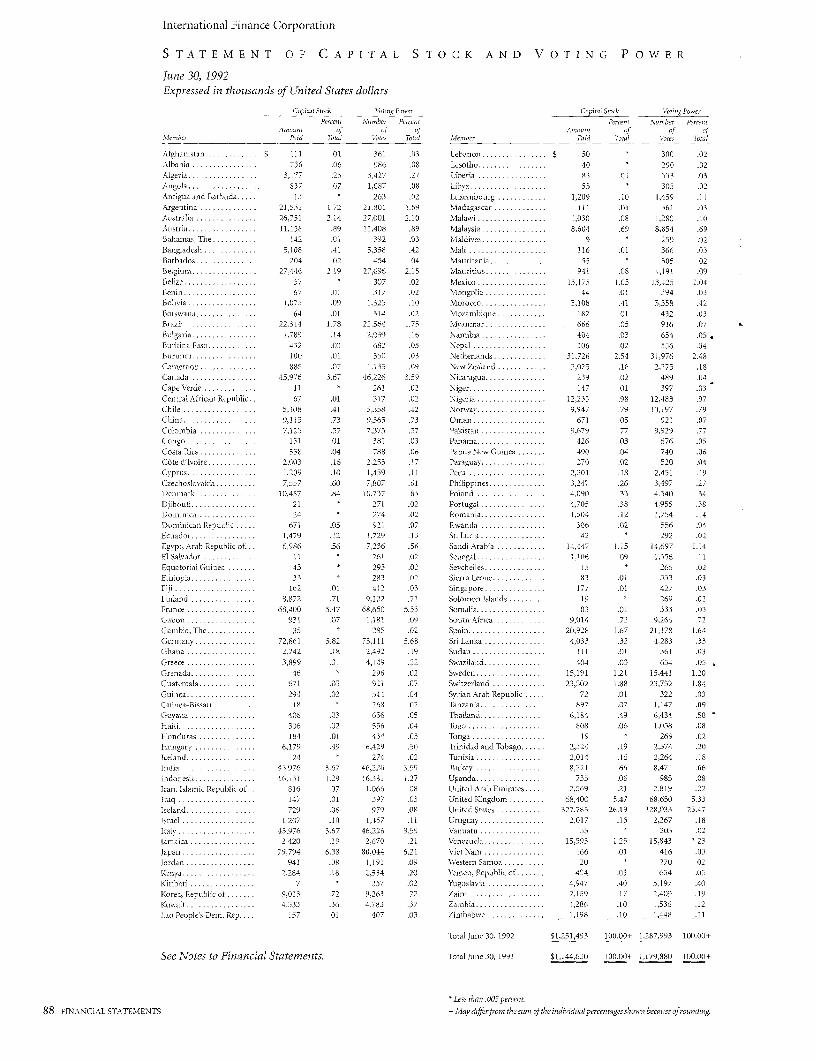

fiscal year, bringing IFC's membership to 147 coun- with the Corporation's goal of helping companies

tries. Fourteeni of the 15 former Soviet republics had in developing countries to decrease their reliance on

applied for membership by year-end. debt financing.

The capital increase recommended by the Board of It was another record year for IFC's mobilization

Directors at the end of fiscal 1991 was approved by activities. The Corporation approved $1.4 billion

the Board of Governors on May 4, 1992. IFC's autho- in syndicated loans and the underwriting of securi-

rized capital has thus been increased from $1.3 bil- ties issues and investnenit funds. In adlition, IFC

lion to $2.3 billion. The $1 billion increase was attracted funds from other investors and lenders in

intended to enable IFC to increase new investment the form of cofinancing. Projects approved by IFC

approvals in all regions by 1O percent a year until had total investment costs of $12 billion; this means

1998, bringing annual approvals to about S4 billion other sources provided nearly S6 in project

by the end of the decade. With the accession to mem- finance for every $1 approved by IFC.

bership of the fornmer Soviet republics, this rate of

growth will probably be increased to 12-15 percent. IFC offered clients a broader range of financial

products and services, helping them to gain access to

To accommodate the memberships of the former sophisticated risk management techniques, such as

Soviet republics, the Board of Directors approved currency and interest rate swaps and commodities-

a resolution on June 18, 1992, recommending a hedging facilities, that would not normally be avail-

$150 million selective capital increase. Of this able to companies in developing cooFtTies. Nine

amount, $132 million will be allocated to the new projects involving hedging instruments were

members, and the balance will be available to approved, of which thrce were for companies in

accommodate future requests for shares. IFC's Board sub-Saharan Africa.

of Governors is expected to approve the resolution

before the end of the calendar year. The Directors Through financial intermediaries, the Corporation

also recommended that the Corporation's Articles was able to provide financing and financial products

of Agreement be amended to increase the total to small and medium-sized companies. Eight projects

2 THE YEAR IN REVIEW

HIGHLIGHTS OF THE YEAR

OPERATIONAL RESULTS

New prolects approved 167

Total financing, including syndications and underwriting $3.2 billion

Financing for IFC's own account $1.8 billion

Total project costs $12.0 billion

Disbursed loan and equity portfolio for IFC's own account, at June 30, 1992 $5.0 billion

RESOURCES AND INCOME

Net income $180.2 million

Paid-in capital $1.3 billion

Retained earnings $1.1 billion

Borrowings for the year $724 million

involving credit and guarantee lines and risk- IFC's disbursed portfolio grewby 16 percent over the

management facilities, totaling $150 million, year. At year-end, the disbursed portfolio included

were approved. One of these, an innovative multi- loans and investments of $5 billion, compared with

product agency credit line extended to a leading $4.3 billion at June 30, 1991.

Mexican bank, will makie a range of financial prod-

ucts available to small and medium-sized companies Demand for the Corporation's advisory services and

in Mexico. technical assistance grew substantially during the

fiscal year. IFC launched a program of technical

An increasingly important activity is the introduc- assistance in the republics of the former Soviet

tion of sound companies in IFC's developing mem- Union, designing and implementing Russia's first

ber countries to the international financial markets. privatization, which involved the auction of 2,000

In fiscal 1992 IFC was a co-lead manager of seven small-scale enterprises in Nizhny Novgorod. It

international securities issues by companies in Asia, stepped up its advisory activities in connection with

Europe, and Latin America, and two investment privatization and corporate restructuring, working

funds in Latin America. on assignments in Asia, Europe, and Latin America

during the year. It also worked on 30 assignments

Projects approved by IFC in fiscal 1992 were in a involving the provision of technical assistance in

broad range of sectors, including financial services, capital market development.

tourism, mining, petrochemicals, power, oil and gas

exploration, agribusiness, and general manufactur- The Corporation again achieved a strong financial

ing. Funding was approved for a number of newly performance. Net income was $180 million, repre-privatized companies in Eastern and Central Europe. senting a return of 7.5 percent on the Corporation's

In an effort to encourage private investment in infra- net worth. Although income from IFC's loan port-

structure, FC approved financing for infrastrLucture folio decreased slightly because of the decline in

proJects in Africa, Asia, Europe, and Latin America. interest rates, income from the equity portfolio

It also approved two projects in Latin America that increased. Capital gains from sales of equity invest-

will have significant environmental benefits. ments reached $113 million, the same as in fiscal

1991. Service fee income incr-eased by 28 percent,

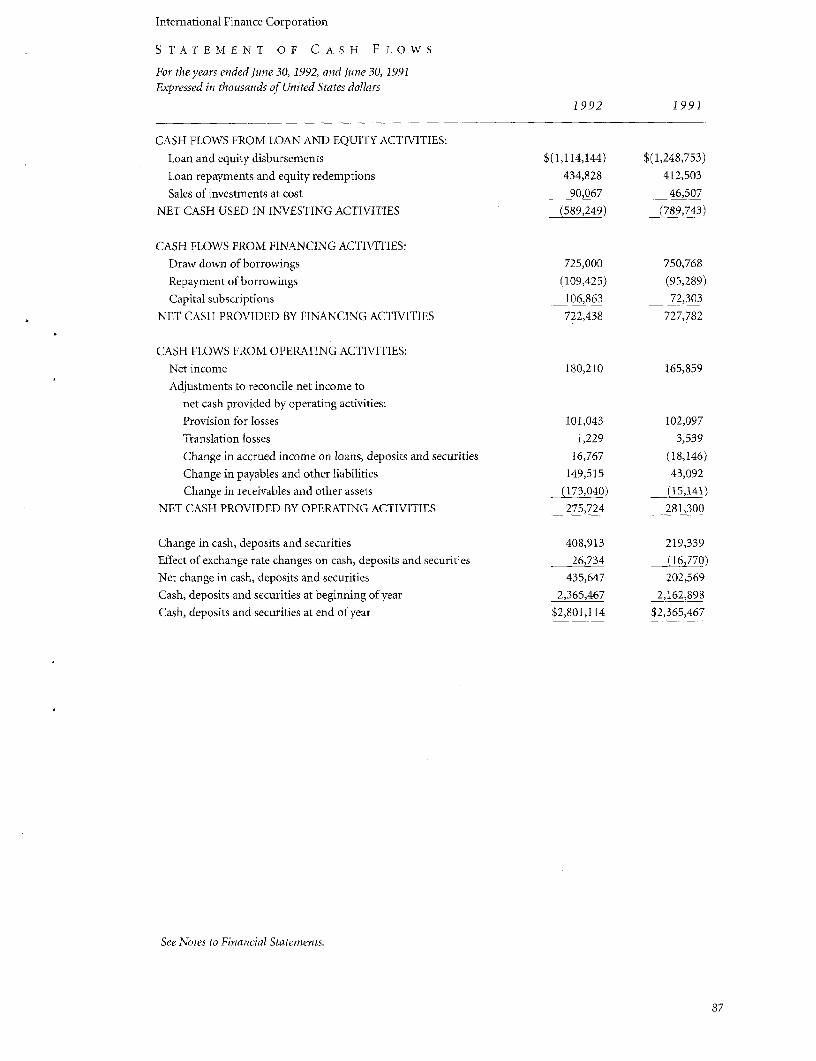

New commitments during the year totaled from $25 million in fiscal 1991 to S32 million in fiscal

$1.3 billion. With disbursements of $1.1 billion, 1992.

3

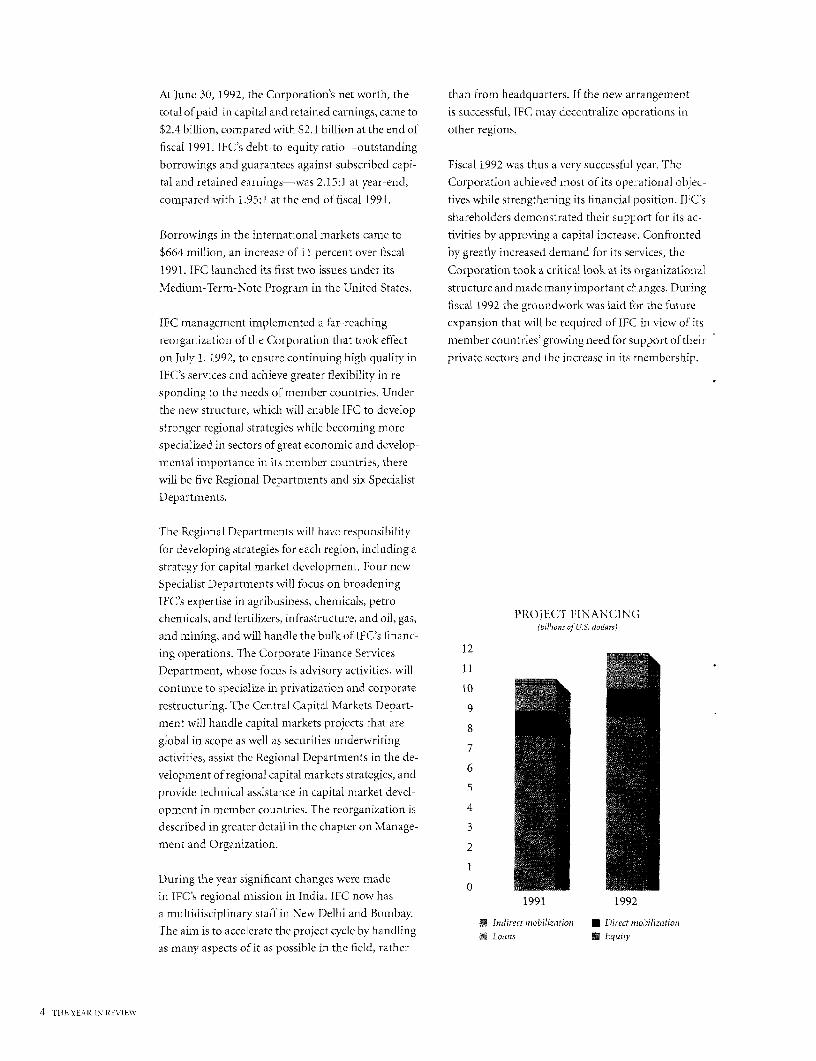

At June 30, 1992, the Corporation's net worth, the than from headquarters. If the new arrangement

total of paid- in capital and retai ned earniings, came to is successful, TFC mnay decentralize operations in

$2.4 billion, compared with $2.1 billion at the end of other regions.

fiscal 1991. IFC's debt-to-equity ratio-outstanding

borrowings and guarantees against subscribed capi- Fiscal 1992 was thus a very successful year. The

tal and retained earnings-was 2.15:1 at year-end, Corporatiorn achieved most of its oper-ational objec-

compared with 1.95:1 at the end of fiscal 1991. tives while strengthening its financial position. IFC's

shareholders demonstrated their supFort for its ac-

Borrowings in the international markets came to tivities by approving a capital increase. Confronted

$664 million, an increase of 11 percent over fiscal by greatly increased demand for its services, the

1991. IFC launched its first two issues under its Corporation took a critical look at its organizational

Medium-Term-Note Program in the United States. structure and made manyimportant ckanges. During

fiscal 1992 the groundwork was laid for the future

IFC management implemented a far-reaching expansion that will be required of IFC in view of its

reorganizationi of the Corporation that took effect memiiber counitries>growing need for sLpport of their

on July 1, 1992, to ensure continuing high quality in private scctors and the increase in its rnembership.

IFC's services and achieve greater flexibility in re-

sponding to the needs of member countries. Under

the new structure, which will enable IFC to develop

stronger regional strategies while becoming more

specialized in sectors of great economic and develop-

mental importance in its member countries, there

will be five Regional Departments and six Specialist

Departments.

The Regional Departments will have responsibility

for developing strategies for each region, including a

strategy for capital market development. Four new

Specialist Departments will focus on broadening

IFC's expertise in agribusiness, chemicals, petro-chemicals, and fertilizers, infrastructure, and oil, gas, PRO JECT FINANCING

w 1 ~~~~~~~~~~(billions of U.S. dXoSllos)

and mining, and will handle the bulk of IFC's financ-

ing operations. The Corporate Finance Services 12

Department, whose focus is advisory activities, will 11

continue to specialize in privatization and corporate 10

restructuring. The Central Capital Markets Depart- 9

ment will handle capital markets projects that are 8

global in scope as well as securities underwriting 7

activities, assist the Regional Departments in the de-

velopment of regional capital markets strategies, and 6

provide technical assistance in capital market devel- 5

opment in member countries. The reorganization is 4

described in greater detail in the chapter on Manage- 3

ment and Organization. 2

1During the year significant changes were made

in tFC's regional mission in India. IFC now has 1991 1992

a multidisciplinary staff in New Delhi and Bombay. rnibilizatiot U Direcriobitization

The aim is to accelerate the project cycle by handling 1 Loatis 1 Equity

as many aspects of it as possible in the field, rather

4 ma YEAR [N REVIEaW

THE PAST TEN YEARS(mnillions of U.S. dollars)

FISCAL YEAR 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992

OPERATIONS

Investment ApprovalsNumber ofprojects 57 62 75 85 92 95 92 122 152 167

Total financing 917 700 938 1,164 914 1,270 1,710 2,201 2,846 3,227Financing forIFC's own account 425 396 611 710 790 1,039 1,292 1,505 1,540 1,774

UTnderwriting andsyndications 492 305 328 454 124 231 418 695 1,306 1,452

Total project costs 2,994 2,482 2,788 3,588 4,343 5,010 9,698 9,490 10,683 12,000

Committed PortfolioNO i 67cr offirins 341 349 366 377 409 454 468 495 618 703

Total committedportfolio 3,005 3,245 3,318 3,441 3,795 4,270 4,968 5,884 7,008 8,718

For IFC's ownaccount 1,882 1,990 2,116 2,387 2,756 3,374 4,045 4,752 5,494 6,423

Held for others 1,123 1,255 1,202 1,054 1,039 896 923 1,132 1,514 2,295

RESOURCES AND INCOME

CapitalizationBorrowings 536 583 825 1,223 1,581 2,047 2,255 3,580 4,130 5,114Paid-in capital 544 544 546 602 722 850 948 1,072 1,145 1,251Retained earnings 204 230 258 284 338 438 633 792 958 1,138

EarningsNet income 23.0 26.3 28.3 25.4 53.8 100.6 196.5 157.0 165.9 180.2

5

P R I VA T E I N V E S T ME N T I S S U E S

T H E C L I M A T E F O R P R I VA T E I N V E S T M E N T

GLOBAL INVESTMENT TRENDS enterprises, resulted in some positive growth in per

Economic growth rates in the leading industrialized capita incomes, after a prolonged period of falling

countries continued to be modest in 1991. Real incomes.

growth, which had falleni to 2.6 percent in 1990,

weakened further in 1991, averaging only 1.2 per- Elsewhere in the developing world, the impact of

cent. Recession persisted in the United States and the difficult conditions of 1990 continued to be felt

the United Kingdom, and growth slowed in France, in 1991. Tfhe aftcrmath of the Gulf crisis, including

Germany, and Japan. Excluding Eastern Europe, the U.N. embargo of Iraq, continued to affect

where economic activity contracted, the average several countries in the Middle East; per capita

economic growth rate for the developing countries income in the region as a whole declined. Despite

was significantly higher than that of the industrial economic liberalization programs, growth also

countries, although still fairly modest, at 3.4 percent. slowed in the South Asian countries. There was a

However, because of the economic slowdowin in the large drop in measured output in Eastern Europe

industrialized countries, demand and prices for and the former Soviet republics. The trading

commodities, which account for an important share regimes that once linked the former COMECON

of exports from developing countries, remained low, countries have collapsed, and the progress of

and investment prospects continued to be uncertain. programs to create market economies and to

Average per capita income in the developing coun- liquidate inefficient enterprises and privatize other

tries fell slightly for the second year in a row, enterprises has been relatively slow in many of

these countries. Prudent economic policies in sub-

The pattern of growth in the developing world wvas Saharan Africa led to sustained growtlh in a few

decidedly mixed. In East Asia, export-oriented countries, but, overall, per capita incomnes in the

countries continued to expand vigorously, despite region declined because of difficult economic

slower growth in many customer nations. In several conditions resulting from political instability,

larger countries in Latin America, economic reforms, severe drought conditions in southern Africa, and

including the widespread privatization of state weak commodity prices.

GROSS DOMESTIC PRODUCT, 1989-1991

1 9 89 1 990 1 991

Real Real Real Real Real RealGDP per capita GDP per capita GDO' per capita

GDP GDP GDP'

Seven major OECD countries 3.3 2.6 2.6 2.0 1.2 0.7

Developing countries 2.9 0.9 1.9 (0.6) 1.9 (0.2)

Sub-Saharan Africa 3.1 (0.2) 0.9 (2.1) 2.3 (1.0)

East Asia 5.6 3.8 6.7 4.6 7.1 5.6

South Asia 4.8 2.5 4.8 2.6 3.6 1.5

Latin America 1.2 (0.8) (0.1) (2.3) 2.6 0.6

Middle Fast and North Africa 2.5 (0.5) 1.0 0.5 (1.9) (4.6)

CentralandEasternEurope' 0.7 0.0 (8.7) (3.7) (14.1) (14.2)

'Not including the former Soviet Union N o t e: Parentheses denotenegative nunsbe's. S o u r c e iBRD.

6 THE CLIMATE FOR PRI'VATE INVESTMENT

NET FOREIGN DIRECT INVESTMENT FLOWS TO DEVELOPING COUNTRIES,1985-91(milkions of U.S. dollars)

10,000

8,750

7,500

6,250

5,000

3,750

2,500

1,250

-1,250

1985 1986 1987 1988 1989 1990 1991

* Sub-SaharanAfrica * Europe V- South Asia

Rn Middle East and North Africa 7 Latin A merica and the Caribbean i East Asia

Economic sluggishness in many industrial and greater developmenital imipact, sinice it tends to be

developing countries in 1991 was matched by a concentrated in countries that are liberalizing their

slowdown in the growth of international trade. In economies and seeking doser links with international

1991 the rate of trade growth declined for the third markets.

straight year. However, although the volume of world

trade expanded by only 3 percent, the smallest gain Foreign direct investment (FDI) has been growing

since 1983, trade, particularly among developing rapidly, and, although unevenly spread, is now an

couintries, contiinued to expand more rapidly than important source of development financing in many

output. Trade trends again demonstrated clearly the countries. In 1990 FDI accounted for more than 10

increasing importance of manufactured exports to the percent of private investment in developing countries,

growth prospects of developing countries, which have compared with an average of about 6 percent during

increased their share of markets in the European the period 1978-88. FDI accounted for almost one-

Community, Japan, and the United States, from 2.4 third of net long-term resource flows to the develop-

percent in 1980 to well over 3 percent today. Manu- ing world in 1991, a proportion thal has doubled

factured goods now account for over half of total since 1985.

shipments from developing countries to these

markets. Governments throughout the developing world

recognize the increasing importance of private

FOREIGN DIRECT INVESTMENT investment-particularly FDI-both in overall capitalSince 1986, new private investment in developing formation and in gaining access to technology,

countries has grown from 10 percenit to nearly 12 maniagerial expertise, and internationial distributioni

percent of GDP in 1991-the highest level since the channels. This recognition, as well as the scarcity of

early 1970s. However, in the 1970s much invcstment alternative sources of funding and the poor perfor-

was made in response to widespread protectionist mance of state enterprises, are the driving forces

policies and was therefore inefficient on an interna- behind the movement toward private sector develop-

tional scale; today private investment is likely to have a ment seen throughout the developing world.

7

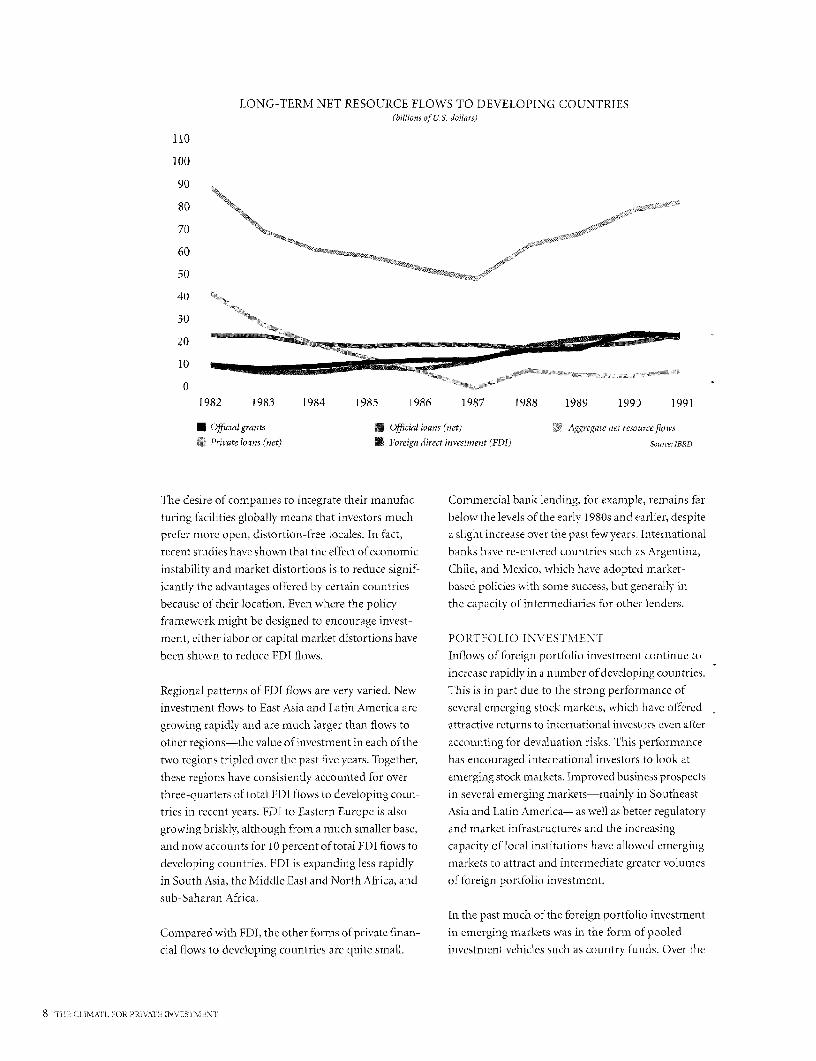

LONG-TERM NET RESOURCE FLOWS TO DEVELOPING COUNTRIES(billions of U.S. dollars)

110

100

90

80 -5 --- gg

70 ~-

60, ,

50

40

30

20

10

01982 1983 1984 1985 1986 1987 1988 1989 199) 1991

i Officialgrants a Official loans (net) Aggregate net resourceflowvs

ff Private loans (net) U Foreign direct investment (FDI) So.rce: IBRD

'fhe desire of companies to integrate their manufac- Commercial bank lending, for example, remains farturing facilities globally means that investors much below the levels of the earlv 1980s and earlier, despiteprefer more open, distortion-free locales. In fact, a slight increase over the past few years. International

recent studies have shown that the effect of economic banks have re-entered countries such as Argentiina,instability and market distortions is to reduce signif- Chile, and Mexico, which have adopted market-icantly the advantages offered by ccrtain countries based policies with some success, but generally inbecause of their location. Even where the policy the capacity of intermediaries for other lenders.framework might be designed to encourage invest-

ment, either labor or capital market distortions have PORTFOLIO INVESTMENTbeen shown to reduce FDI flows. Inflows offoreigin portfolio investment continue to

increase rapidly in a number of developing countries.Regional patterns of FDI flows are very varied. New This is in part due to the strong perfornance ofinvestment flows to East Asia and Latin America are several emerging stock markets, which have offeredgrowing rapidly and are much larger than flows to attractive returns to international investors even afterother regions-the value of investment in each ofthe accounting for devaluation risks. This performancetwo regions tripled over the past five years. Together, has encouiraged interniationial investors to look atthese regions have consistently accounted for over emerging stock markets. Improved business prospectsthree-quarters of total FDI flows to developing coun- in sevcral emerging markets-mainly in Southeasttries in recent years. FDI to Eastern Europe is also Asia and Latin America-as well as better regulatorygrowing briskly, although from a much smaller base, and market infrastructures and the increasingand now accounts for 10 percent oftotal FDI flows to capacity of local institLtLionis have allowed emergingdeveloping countr-ies. FDI is expanding less rapidly markets to attract and intermediate greater volumesin South Asia, the Middle East and North Africa, and of foreign portfolio investment.

sub-Saharan Africa.

In the past much of the foreign portfolio investment

Compared with FDI, the other forms of private finan- in emerging markets was in the form of pooledcial flows to developing coLntries are quite small. investment vehicles such as country funds. Over the

8 mc CLIMAI tE cR PR1\'XIE OVE5YME\xN

PERCENTAGE CHANGE IN STOCK MARKET INDEXESFOR SELECTED EMERGING AND DEVELOPED MARKETS

July 1, 1991-June 30, 1992

COLOMBIA

ARGENlINA

PAKISTAN

INDIA

PHILIPPINES

CHILE

MEXICO

MSCI EUROPE

VENEZUELA

U.S. (S&P 500'

THAILAND

JORDAN

MALAYSIA

BRAZIL

PORTUGAL

IFC COMfPOSITE

GREECE

INDONESIA

TAIWAN (CHINA)

MSCI JAPAN

KOREA

NIGERIA

TURKEY

ZIMBABWE

-80 -60 -40 -20 0 20 40 60 80 100 120 140 160 180 200 220 240

X Emergingmarkets E Developed markets 3 Index of 20 emerging markets

Nose: Chanes are measured sU.S. Iotar terms Souerce For er-eepgg martent, FC P-erging Markets Data Ease; t o. ether sta- k m,arkets MSCI Perspective.

past two or three years there has been a marked The existence of active securities markets in develop-

trend, especially in the more advanced developing ing countries and growing access to international

coountries of Southeast Asia and Latiin Aimerica, for mnarkets have already helped to ease the difficulty

companies to access foreign portfolio investment companies in these countries have had in raising

directly by issuing securities in the international long-term financing for capital expenditures and

markets. Now that companies in developing expansion. In 1991 alone, over 1,000 companies in

countries are gaining access to equity-based the 20 largest emerging markets raised an estimated

instruments such as American Depositary Receipts $18.2 billion through new share offerings-this

and Global Depositary Receipts, some of the figure is equivalent to nearly three-quarters of total

practical constraints faced by international inves- FDI flows to the entire developing world that year.

tors buying emerging markets equities are being

overcome. INVESTMENT PROSPECTS

For developing countries to experience rapid eco-

The importance of poI-tfoJio investiment in ermerg- nomic expansion, growth in the industrial countries

ing markets is expected to grow during this decade will have to improve. The prospects for the near term

as more companies source foreign capital by either are only moderately encouraging. A modest recovery

making their issues abroad or, where domestic has begun in the United States early in 1992, and

markets are well developed, selling locally listed growth is expected to improve somewhat in France,

shares to foreign investors. The entry of foreign Germany, and the United Kingdom. Of the larger

securities firms in domestic markets as intermediar- industrial economies, only Japan's is expected to

ies is likely to prove helpful in channeling foreign grow more slowly in 1992 than in 1991. Overall,

portfolio investment. The abilities of such companies the growth of the industrial countries is projected

to bring issuers and investors together across to increase to only 1.8 percent in 1992, but to rise

national boundaries would benefit both inter- somewhat in 1993, and long-term real interest rates

national investors and domestic companies. are likely to remain high.

9

Even a weak recovery, however, is likely to stimulate

growth in developing countries. And, although real

commodity prices are likely to remain relatively low

for some years, they are expected to increase slightly,

In addition, debt-service ratios have been declining

in highly indebted middle-income countries, as

interest rates fall in the United States and Japan.

These factors, along with successful stabilization

and reform programs in several developing coun-

tries, should result in slightly higher rates of growvth

in 1992. The overall rate of growth in developing

countries (excluding Eastern Europe) is expected

to increase from 3.4 percent in real terms in 1991,

to 4.3 percent in 1992, with somewhat faster growth

in the years beyond.

East Asia, where growth rates are expected to remain

high, offers encouraging investment prospects.

Economic recovery in Latin America, after the

so-called "lost decade" of the 1980s, should con-

tinue, as a number of countries pursue market-

oriented policies. Growth should increase in the

Middle East and North Africa because of reconstruc-

tion efforts and, more important, because of market

reforms in several countries. Future growth in South

Asia remains a question, although there has been

significant and encouraging liberalization in India

and Pakistan. Many countries in sub-Saharan Africa

have also begun economic reform programs but, on

the whole, prospects for that region remain difficult.

Certainly the growth prospects of developing coun-

tries will improve if barriers to trade are reduced.

Positive resolutionl of the remaining problems in

the Uruguay Round of GATT negotiations is vitally

important to the expansion of exports from develop-

ing countries, particularly manufactured exports.

If agreement can be reached on several non-tariff

barriers to trade (for example, the Multifiber

Arrangemeint, agricultural subsidies and quotas,

antidumping regulations, "voluntary" export

restraints), the climate could be improved for sub-

stantially increasing exports from developing coun-

tries to the industrial countries.

10 rHE CLIMATE FOR PRIVATE INVESTMENT

P R I VA T I Z A T I O N

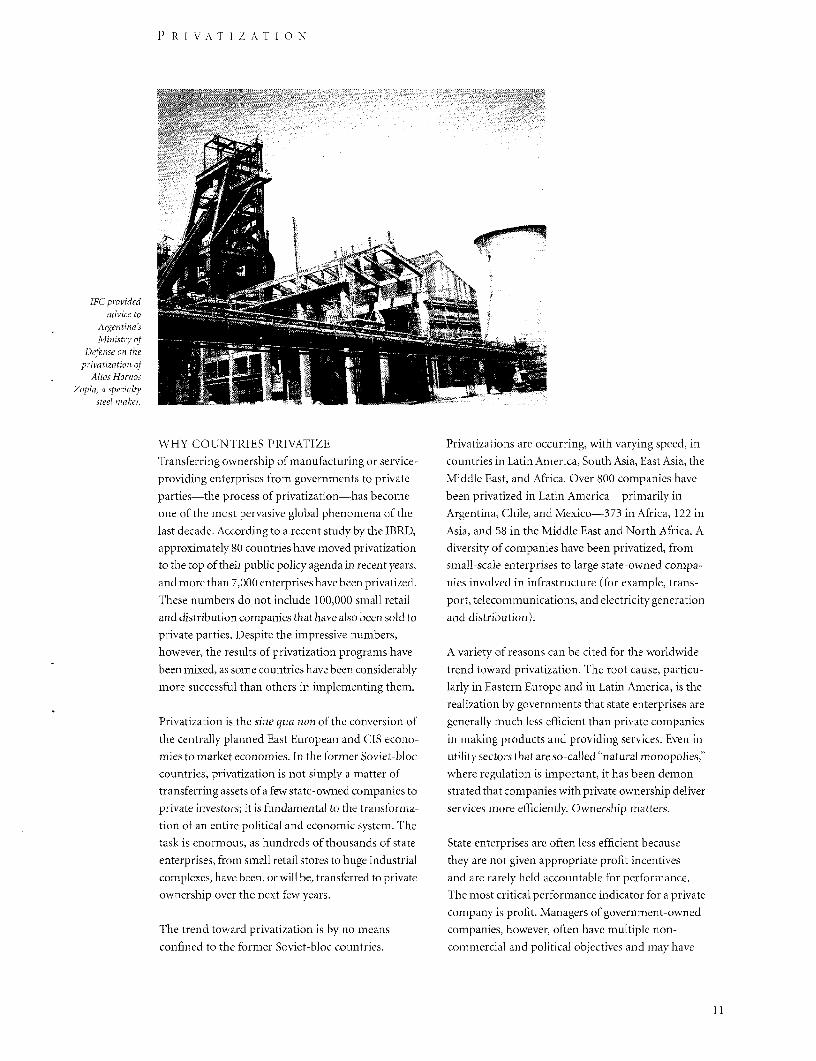

IFCprovided

a vile 0Q_fifi!;;

Argemintia's

Mitlistry of-

Defense on thePrivatization ofi :

Altos HorizosZopla, c specialty - -

WHY COUNTRIES PRIVATIZE Privatizations are occurring, with varying speed, in

Transferring ownership of manufacturing or service- countries in Latin America, South Asia, East Asia, the

providing enterprises from governments to private Middle East, and Africa. Over 800 companies have

parties-the process of privatization-has become been privatized in Latin America-primarily in

one of the most pervasive global phenomena of the Argentina, Chile, and Mexico-373 in Africa, 122 in

last decade. According to a recent study by the IBRD, Asia, and 58 in the Middle East and North Africa. A

approximately 80 countries have moved privatization diversity of companies have been privatized, from

to the top of their public policy agenda in recent years, small-scale enterprises to large state-owned compa-

and more than 7,000 enterprises have been privatized. nies involved in infrastructure (for example, trans-

These numbers do not include 100,000 small retail port, telecommunications, and electricity generation

and distribution companies that have also been sold to and distribution).

private parties. Despite the impressive numbers,

however, the results of privatization programs have A variety of reasons can be cited for the worldwide

been mixed, as some countries have been considerably trend toward privatization. The root cause, particu-

more successful than others in implementing them. larly in Eastern Europe and in Latin America, is the

realization by governments that state enterprises are

Privatization is the sine qua }lon of the conversion of generally much less efficient than private companies

the centrally plannled East Furopean and CIS econo- in makinig products and providing services. Even in

mies to market economies. In the former Soviet-bloc utility sectors that are so-callcd "natural monopolies,"

countries, privatization is not simply a matter of where regulation is important, it has been demon

transferring assets of a few state-owned companies to stratedthat companies with private ownership deliver

private investors; it is fu ndamiiental to the transforma- services more efficiently. Ownership matters.

tion of an entire political and cconomic system. The

task is enormous, as hundreds of thousands of state State enterprises are often less efficient because

enterprises, from small retail stores to huge industrial they are not given appropriate profit incentives

complexes, have been, or will be, transferred to private and are rarely held accountable for performnanice.

ownership over the next few years. The most critical performance indicator for a private

company is profit. Managers of government-owned

The trend toward privatization is by no means companies, however, often have multiple non-

confined to the former Soviet-bloc countries. conmmercial and political objectives and may have

11

restricted decision-mrnaking powers. They may, for is part of a program of economic reforms intended to

example, be expected to increase employment, produce a more open economy. It does little good, in

irrespective of the cost or efficiency of doing so. terms of economic efficiency, for a government to

Or they may be required to sell goods at artificially sell an enterprise and then provide continuing pro-

low prices. Consequently, it is difficult to hold these tection or subsidies to the new private owners. Com-

managers accountable for financial results or failures petition is an essential discipline. WAhere competitive

to improve efficiency. They can always provide plau- conditions exist, experience shows that privatization

sible explanations for unprofitable operations, and can yield significant benefits.

there is usually no effective penalty for financial

failure. At best, there is little incentive to risk changes IFC'S ROLE

that might improve operations. At worst, the lack IFC's role in the area of privatization has been grow-

of accountability and of transparent performance ing rapidly over the past few years as part of a World

criteria may encourage corruption. Bank GTroup effort to foster private sector activity

in developing member countries. While other inter-

State enterprises may also undermine competition in national institutions offer advisory assistance on

the marketplace. They face no credible bankruptcy macroeconomic or privatization policy issues, IFC

th reat, as experieence sh ows that govern ments usually ha1s focused no1 the i miplementation of model priva ti-

bail them out when losses multiply. Frequently, zation transactions. IFC has been able to make a

where government-owned companies compete in valuable contribution to the implementation of the

markets with private firms, the former survive only privatization process, either by advising govern-

because governments have been willing to provide ments and enterprises on the process, or by investing

protection or subsidies or both. in the newly privatized companies.

The increased financial burden put on government IFC's assistance may be provided in either the sale or

budgets by state enterprises also helps to explain the the purchase of privatized enterprises. IFC may ad-

growingprivatizaliorn mnovemenit. External financinig vise sellers on1 strUcturinig, negotiatinig, and imple-

of losses or of the capital needed for necessary invest- menting specific privatization transactions. Or it

ment programs has become more difficult for many may act as an adviser and investor in the acquisition

governments. The largest source of finance for devel- of state-owned properties and help buyers raise some

oping countries in the 1970s, commercial bank lend- of the financing needed by the privatized companies.

ing to governments, has practically disappeared. IFC's special character as an international institu-

Given this situation, the transfer of companies to the tion, as well as its background in project financing

private sector eliminates a persistent drain on gov- and its experienced staff, all contribute greatly to its

ernment resources. Some countries, notably Chile ability to provide understanding, credibility, and

and Mexico, have found that privatizations can resttl transparency in the privatization process.

in substantial, though temporary, cash flows that can

be used to fund other activities. IFC has a close relationship with its member country

governments, which are all IFC shareholders and are

As a result of these changes over the past decacle, represenrted on its Board of Directors. In additioni,

there are few policymakers who doubt that free IFC has extensive knowledge of, and contact with,

competitive markets and a prominent role for private many major industrial groups in the world, and has

enterprise are essential components of a successful an established record as a useful business partner and

economic development strategy. commercially motivated investor. These factors help

IFC to play an "honest broker" role between govern-

Privatization is not an end in itsclf, however. Rather, ments and investors, and may also increase the pub-

the goal is development of a competitive private lic's confidence and acceptance-an essential

sector. Under private ownership, management ingredient for successful privatizations.

incenitive structures change markedly, leading to snore

focused, profit-seeking behavior. These motivations In providing assistance, IFC is ablc to make in-depth

can lead to greater efficiency, provided privatization operational and strategic assessments. tt has in-house

12 PRIVATIZATION

technical, financial, legal, and economic staff, many To date, IFC has been involved in more than 40

of whom had experience at senior levels in their in- privatization assignments in either an advisory or an

dustries or professions before joining IFC, and who investment capacity. Although IFC's privatization

are accustomed to working in countries around the activities date back to 1986, most of its assignments

world. With its experience and resources, IFC can have been undertaken since 1990 when it established

take wider developmenital concerns into account its Corporate Finanice Services Department, which

when working on a privatization-for example, the assists clients with corporate restructuring and

effect on employment, investment needs, and future privatization. Reflecting recent developments in

operating conditions. Eastern Europe, a number of IFC's advisory assign-

ments have been in that rcgion (Czechoslovakia,

IFC's approach to privatization is tailored to Poland, and Russia), but IFC has also been active in

circumstances in individual countries. In countries Argentina, the Philippines, Portugal, and Morocco,

where privatization is just beginning, or is being and its privatization activities have been regionally

attempted on a mass scale, IFC's aim is to help dispersed.

creale model privatization transaictions. In carrying

out some of the first privatizations in a particular- IFC also seeks opportunities to help private compa-

country, IFC addresses and resolves problems nies to negotiate the purchase of, and obtain financing

that could also hamper later privatizations. In some for, the rehabilitation of state-owned firms. The

countries, IFC's contribution can add the most value Corporation has participated in 20 privatization

by focusing on the first privatizations of large, transactions through its investment activities. These

complex state enterprises. In other countries, IFC's projects have ranged in size from less than $5 million

assistance has been instrumental in starting the to over $190 million. In addition to providing its own

privatization process in other ways appropriate to funding, IFC has sought to mobilize as much external

the circumstanices, such as an auction of small finanlcial participation as possible. In this fiscal year,

enterprises in Russia. half of the privatization projects approved by IFC's

management have been in Eastern Europe, and somc

In countries where privatization programs are fully of these are quite large. Smaller IFC investment

developed and are being implemented, typically projects in Eastern Europe have included the

in Latin America and Asia, IFC focuses its activities privatization of a lighting products firm in Poland and

on particularly difficult state enterprises whose a banking enterprise in Czechoslovakia. Elsewhere,

successful privatization has the potential to create projects have ranged from a number- of small

substantial added value and significant economic privatizations in Africa, primarily of financial

benefits. institutions and of textiles, wood-processing, and

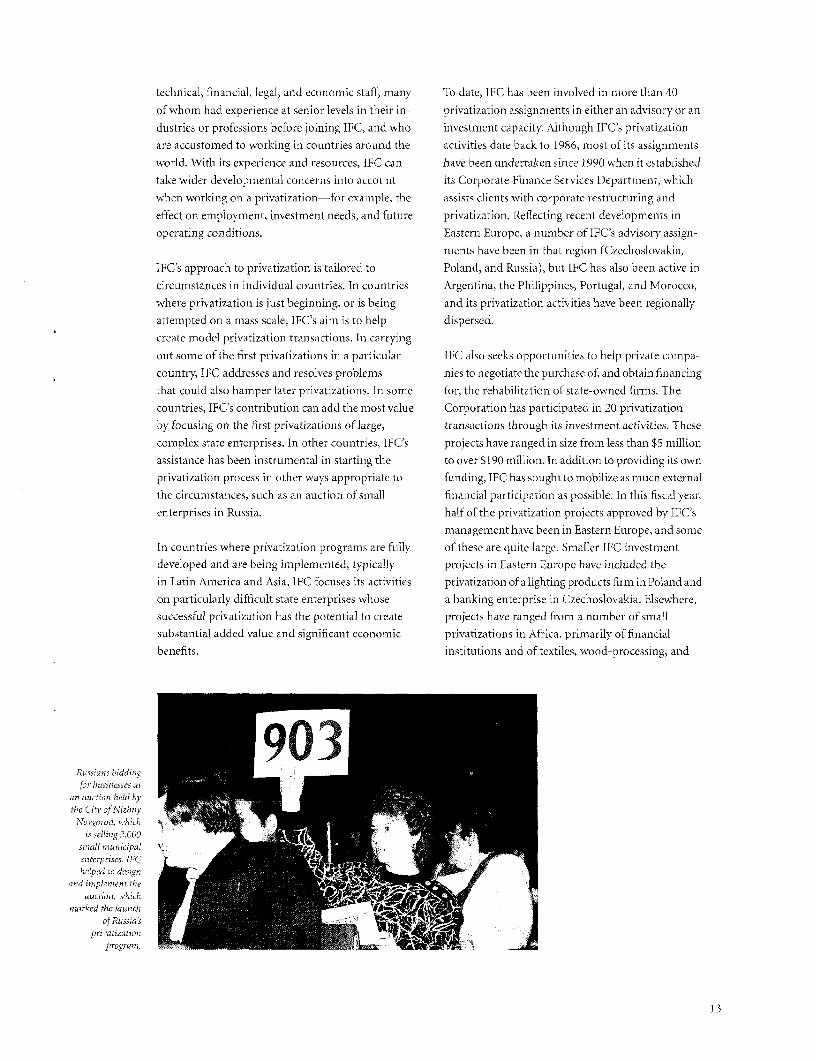

9 3Russi ddin,.

fee /1auction held by_di7e Citv o(.Nizlr y

Novgorod, 4whT!is sellitlg 2,000 , f{('. _ j , ; _

stulall nicipal'

hc[lped to design i,,jand imvpleetit the _

aun ctia ii, wh;chtriark-ed the lawill_Z i7chT4@i

privatizat.ion % g Z 1

13

pharmaceutical companies, to large projects focusing first on completing smaller or simpler asset

in telecommunications (Chile) and mining and sales. Such sales allow the opportuni-y to demon-

metals (Venezuela). strate early success and to avoid costly learning mis-

takes. The experience acquired can then be applied in

SOME OBSERVATIONS progressively larger or more complex: transactions.

IFC's privatization work has given the Corporation

practical experience and some insights into the In addition to policy and process issues at the macro-

process-what works and what doesn't-and what economic level, privatization raises n amerous issues

features are present in successful privatization at the transaction level, for example: (1) how a com-

programs. pany should be sold (by auction, public offer, or ne-

gotiated sale); (2) to whom it should be sold (to

It goes almost without saying that privatization ben- foreigners, the public, the workers, local groups);

efits from a positive macroeconomic framework that (3) whether a company should be restructured prior

makes investment attractive. Typically a positive to sale; (4) how it should be offcred for sale (with

frarnework is designed to foster competitive and free or without liabilities, with or without labor obliga-

markets, and encourage private initiative. Specific tions); and (5) what is an adequate sale price. An-

aspects of such a framework include fiscal discipline, swers to these questions usually need to be worked

liberal trade policies, realistic and stable exchange out in recognition of the enterprise's circumstances,

rates, and freedom from price controls and other the governmernt's objectives, and practical realities.

measures that inhibit competition. Countries with Case-by-case solutions, although time-consuming,

successful privatization programs have often recog- are hard to avoid. 'T'he effort required makes privati-

nized the positive role foreign direct investment can zation one of the most administratively complex

play, and have provided inducements and legal assur- challenges governments face in efforts to develop

ances to foreign investors. The participation of domes- market-oriented economies. The scale of the prob-

tic investors is even nmore importanit, and privatization lem of transformation in Central Europe and in the

programs can serve as a catalyst to broaden public former Soviet republics is particularly daunting.

participation in local capital markets. Supporting privatization in its member countries is

one of IFC's top priorities for the 1990s.

An essential element in a successful privatization

program is strong public support. Information

campaigns to increase public understanding of the

process and its objectives are important. In this

regard, the decisionmaking process must be shown

to be transparent and fair.

Finally, governments need to be prepared to over-

come bureaucratic and political resistance to privati-

zation. Action requires strong and sustained political

will, Privatization has succeeded where policy deci-

sions and coordination are centralized in a strong,

motivated, and competent government team held

accountable for speed and transparency.

A host of practical problems arise in the sale proccss.

Among other things, there is a need to reconcile the

interests of directly affected groups, sort out legal

problems, and work out bidding procedures. Some

of these problems cannot he seen clearly until the

process is well under way. For this reason, it can be

useful to conduct a privatization program in stages,

14 PRIVATIZATION

PRIVATIZATION OF A LARGE INDUSTRIAL ENTERPRISE: SKODA PILSEN

Skoda Pilsen, one of Czechoslovakia's largest industrial enterprises, is being restructured and privatized as part of

the Government of Czechoslovakia's program of economic reform. The company is located in and around the city of

Pilsen. Tt has nearly 40,000 employees and annual sales of roughly $2 billion, calculated at international prices. Its

18 operating divisions mnani ufacture everythingfrom castings andforgings to trolleys and loco motives, fromn machine

tools and steel rolling mills to turbines and nuclear reactors. Over the past year, lEC has provided assistance with the

restructuring of some of Skoda's operations-in particular, it advised Skoda on the establishment of two joint ventures

with foreign partners.

Skoda is a microcosmti of the probleems, issues, and opportunities confronting the economies of Eastern Europe.

Like many other industrial enterprises, it is operating in an environment undergoing a radical transformation, as

Czechoslovakia movesfrom a command to afree-mnarket economy. Stripped of its traditional markets, Skoda is being

forced to confront its ownl inefficiencies in produiction, management, and marketing.

IFC's work consisted of two phases. Duiring the first phase, IrC sent a 21 -person team-financial analysts, engineers,

industry specialists, and consultants to Pilsen to conduct a strategic review of the company, division by division,

identifying Skoda's strengths and weaknesses and making recommendations to Skoda's management. The teamn found

that Skoda's strengths and weaknesses were typical of comnpanies throughout Eastern Europe. In itsfavor, Skoda had

a strong industrial tradition, excellent engineerinlg and technical skills, low labor costs, existing engineering and

manufacturing capacity, and access to East European markets. However, it also had a number of problems that need-

ed to be addressed. Skoda had traditionally operated as a production unit rather than a business enterprise and had

little experience with international competition. Its equipment andproduction operations needed to be changed, and

new business and marketing methods were required.

The second phase of lFC's advisory work involved the establishment of two new joinit ventures, onefor the power

generation operations of Skoda Pilsen and its affiliate, Skoda Praha, and the other for Skoda's locomotive manufac-

turing operations. IFC helped Skoda solicit interestfrom a wide range of international investor groups, all of which

were considered to have the capacity to assist in solving the company's management, mnarketing. andfinancinig

problems. After selection of a short-list, negotiations were conducted, which led to a sale agreement. The agreement

provided not onlyfor theppurchase price but alsofor other commitments regarding investment, employment, training,

management assistance, and technology transfer.

Skoda selected Siemens AG of Germany as its partnerfor both of thejoint ventures and signed ouitline agreements

before the end of 1991. Skoda and Siemens have set up working groups to complete detailed preparations, business

plans, and agreementsfor the formation of the joint ventures.

15

PRIVATIZAI'ION OF SMALL-SCALE ENTERPRISES IN NIZHNY NOVGOF.OD

IFC played the leading role in helping Russia launch its first privatization program. It designed and implemented

the country's first mass privatization of small-scale enterprises, in the city of Nizhny Novgorod (formerlyv Gorky), the

capital of the Nizhny Novgorod region. This city, which has apopulation of 1.45 million, wasfounded in 1221, at theconfluence of the Volga and Oka rivers in the heart of European Russia. It was Russia's main trade and commercial

center before the 1917 Revolution. Until September 1991 it was a closed city with restricted access to outsiders.

The Nizhny Novgorod mass privatization involves the auctioning of 2,000 retail shops, food stores, and communal

facilities owned by the city. Its design was based on the requirements of Russia's privatization law ana regulations, the

city'sparticular needs, and the experiences of IFC and others involved in privatizationt in Poland and Czechoslovakia.

To expedite the process, IFC, working under the World Bank Technical Assistance Program, assemb.ed an interna-

tional team of experts. Staff and consultants were brought to Nizhny Novgorodfrom Poland, auctioneers and imple-

menters of small-scale privalization from Czechoslovakia, and lawyersfrom Sweden and the United States. Russian

officials went to Czechoslovakia to watch the auctioning of municipal property in Prague.

The auctions began in March. In designing the program, IFC emphasized speed, efficiency, and trarsparency. All

Russian citizens were allowed to participate, and incentivies were offered to shop employees. Transfer of control was

almost irmmediate-the new owners took over twa days after the auction. Auctions are now held weekly and are

attended by hundreds of local citizens, as well as officials from other regions and cities. Despite initiail misgivings by

members of the workers' collectives about the program, many of the premises sold have been bought by the collectives.

Incentives offered to the collectives include a 3opercentdiscount on the saleprice and a one-year installmentpayment

program. About 75 percent of the enterprises'former employees have been re-hired by ithe new owners; part of the

auction proceeds go to a fund to help workers affected by the privatizations.

The Nizhny Novgorod privatization model is being adopted bv cities throughout Russia. IFC has been asked to

prepare a manual for the Ministry of Privatization on how to privatize small-scale municipal enterprises, based

on the Nizhny Novgorod experience.

PRIVATIZATION OF AlTOS HORNOS ZAPLA IN ARGENTINA

IFC was the adviser to theArgentineMinistryofDefense in theprivatization ofthesteel companyAltos Hornos Zapla

(AHZ), thefirst successfillprivatization of the Fabricaciones Militares Defense Ministry holdings in Argentina. AHZ

is a steel mill located itn Palpala, Province of Jujuy, approximately 1,000 miles northwest of Buenos Aires. The steel

mill, which is capable of producing specialty and high-quality steels, was experiencing significant losses at the time

the privati2ation process started, and suffering from low productivity and substantial operational inefficiencies.

IFC designed and implemetnted a privatization strategyforAIIZ that wouldfulfill the Government's objectives of

removing a loss-makingfirm from the budget and ensuring that the mill continued to operate. Moreover, the priva-

tization had to be implemented in a relatively short time. IFCpromoted the mill to interested parties in Asia, Europe,

and South America with experience in steel manufacture.

Theformulafor evaluating the bids gave weight not only to theprice offered, but also to the number ofjemployees that

would be retained and the amount of investment the buyer was prepared to make. On March 31, 1992, the Ministry

of Defense awarded AHZ to a consortium including an Argentine engineeringfirm and a French specialty-steel-

maker; the mill was transferred to its new owners on July 1, 1992. IFC is the privatization adviserfor ECA, another

company owned by the Ministry of Defense. The valuation of ECA has been completed, and the privatization strategy

is beingfinalized.

1 6 PRIVATIZAI ION

R F P () R T O N 0 P F R A T I O N S

l'he Corporation approved a total of $3.2 billion The amount of financing approved for IFC's own

in financing for 167 new projects during fiscal account increased for most regions, with the biggest

1992, compared with $2.9 billion in financing for increase in the Middle East and North Africa.

152 projects in fiscal 1991. Of the total approved,

$1.8 billion is for IFC's own account. The remaining Seventy-nine of the projects approved in fiscal 1992,

$1.4 billion will be mobilized through loan syndica- representing $780 million in financing, were located

tions and securities underwriting; it was a record in countries with per capita incomes of $830 or less.

year for the Corporation's mobilization activities. Loans and investments approved for projects in the

In addition, private placements by IFC of securities poorest countries accounted for 47 percent of the

of client companies came to $27.5 million. The total number of projects and 45 percent of the financing

costs of the projects approved in fiscal 1992 are approved for IFC's owvn account.

estimated at $12 billion. IFC's advisory operations

also increascd in fiscal 1992, particularly in connec- SEC'1'ORAL BREAKDOWN OF PROJECTS

tion with privatizations, as a number of developing The Corporation approved financing for projects

countries around the world began making the tran- in a broad range of sectors in fiscal 1992, in-

sition to market economies. cluding financial services, tourism, mining,

petrochemicals, electricity, oil and gas exploration,

PROJECTr FINANCING telecommunications, agribusiness, and general

Financinig approved by IFC for its own account imanufacturinig.

in fiscal 1992 includes loans of $1.2 billion;

guarantees, swaps, and standby arrangements IC achieved its objective of increasing its support

of $251 million; and equity and quasi-equity for capital market development in its member coun-

investments of $375 million. The average size of tries. Loans and investments for a broad variety of

IFC's investments was $11 million. All of IFC's financial institutions-for example, conmmercial

loans were made at market rates, with maturities and investment banks, leasing companies, discount

ranging from four to fifteen years, and grace periods houses, insurance companies, and venture capital

of onie to nine years. Interest rates ranged from funds-accounted for 17 percent of financinig ap-

100 to 300 basis points over six-month LIBOR proved for the Corporation's own account.

for variable loans or the swap-based equivalents

for fixed-rate loans.

FY92 APPROVAI.S BY SECTORAs in previous years, IFC offered loans denominated (miOllons of Us. dollars)

in the ma jor international currencies, at either fixed Timnber, pulp, and paper Cenent and$133 construction materials

or variable rates, at the client's choice; 93 percent $134

of the loans appr-oved during fiscal 1992 wcre Food and agribusiness

denominated in U.S. dollars. tumam,fucoring,Textiles ~ ~ ~ ~ ~~~atomotive

Policy and regulatory changes affecting exchange T industrialeuipmnent

rates and securities markets in several niember ,2u 4

countries made it possible for- IFC to achieve one

of its objectives for fiscal 1992-increasing its equity X396

and quasi-equity investments. Total equity and

quasi-equity financing approved accounted for Capital

21 percent of the volume of financing approved for marketendevelopment

the Corporation's account. Chemicals' fnancepetrochemicals, financial servicesfertilizers a445

GEOGRAPHIC DISTRIBUTION OF PROJECTS $624Mning, nonferrous

Consistent with its goal of achieving geographical Touirism, other services Mnetals, iron, steel

diversity in its project financing activities, IFC $574 $486

approved projects in 51 countries in fiscal 1992. Total $3,227

17

Funding was approved for a number of newly priva- industrialized countries have introduced exemptions

tized companies in Eastern and Central Europe, in- from country-risk provisioning requirements for

cluding the first commercial bank to be privatized participations in IFC's loans. Since initiating its

in Czechoslovakia. Two projects approved in Latin syndications program in the 1960s, IFC has placed

America have important environmenltal implica- over $4.6 billion in loan participationis with 319

tions: a reforestation project in Ecuador and a credit finiancial institutions; it cLurrently admninisters for

line to a bank in Argentina to finance the conversion the account of its participants a loan portfolio of

of buses to compresscd natural gas. IFC also ap- over $2 billion. Of the total volume of syndicated

proved financing for a number of infrastructure loans approved in fiscal 1992, 42 percent will go to

projects, promoting private sector participation in borrowers in Latin America, followec. by 26 percent

industries that were once the preserve of the state. to Asia, 15 percent to Europe, 11 percent to sub-

These projects include a toll road in Mexico; tele- Saharan Africa, and 6 percent to the Middle East

communications companies in Costa Rica, Hungary, and North Africa.

Jamaica, and Romania; an oil pipeline in Zimbabwe;

and power generation and transmission in India. The largest syndications approved and processed

during the year included loans to Cornpanlia de

RESOURCE MOBILIZATION Tel6fonos de Chile, for a telephone expansion projectMobilizing funds from other investors and lenders in Chile ($113 million); Ashanti Goldfields Corpora-

for projects is one of IFC's essential functions. In tion (Ghana), Ltd., for a gold-mine expansion

fiscal 1992, as in fiscal 1991, for every $1 of project project ($110 million); Metor S.A., for the Jose

financing approved by IFC for its own account, methanol project in VTenezuela ($100 million);

other investors and lenders provided $6-either P.T. Bakrie Kasei Corporation, for a terephthalic

directly, through the Corporation's loan syndica- acid plant in Indonesia ($95 million); Pilipinas Shell

tions or underwriting of investment funds and Petroleum Corporation, for a new refinery in thesecurities issues, or indirectly, in the form of Philippines ($85 million); a group of four commer-

cofinancing. cial Moroccan banks ($70 million); Bahia Sul

Celulosc S.A., for a pulp and paper plant in BrazilSYNDICATIONS ($60 million); Ram Dis Ticaret A.S., part of Turkey's

Fiscal 1992 was another record year for IFC's Koc Group ($55 million); and P.T. Swadharma Kerry

syndications program. The volume of loan syndica- Satya in Indonesia, for the construction of the

tions approved by the Board of Directors reached Shangri-La Jakarta Hotel ($51 million).

$1.4 billion for 39 projects, up from the previous

year's record figures of $1.3 billion for 33 projects. Continuing the pattern of recent years, the largest

'the volume of syndicated loan signings was at a participants in IFC loans signed in fiscal 1992 wererecord level of $913 million. A total of 67 banks from European banks (82 percent by volume). Asian

22 countries participated in IFC loans during the banks took 16 percent, and North American banks

year, taking an aggregate of 190 individual loan 2 percent. While the preponderance of European

participations. banks remains strong, it is one of IFC's objectives

to broaden the geographical distribution of partici-

IFC's ability to mobilize commercial hank resources pants in its loans.

through its participation mechanism is an important

factor in its success in financing projects in the SECURI'I ES UNDERWRITING

developing world including many countries where In fiscal 1989 IFC created the International Securities

banks are still reluctant to increase their direct loan Division (ISD) within the Capital Markets Depart-exposure. While participants share fully in the ment to mobilize funds for private sector companies

commercial risks of projects, historically they have in developing countries in the international capital

also enjoyed the advantages, particularly as regards markets through pooled investment vehicles such

country and transfer risks, that IFC has always as "country funds" that invest in emerging stockderived from its status as a multilateral development markets, and through international securities issues.

institution. Banking regulators in a number of IFC's assistance takes the form of structuring,

18 REPORT ON OPERATIONS

LOAN S YN DI CAT IO NS SIGN ED IN F IS CAL 1 9 9 2

REGIONAL BREAKDOWN

BORROWERS PARTICIPATING BANKS

Latin America and Caribbean ($365.0 million) U Europe ($745.0 million)

C Asia ($267.0 million) U Asia ($148.5 million)

* Europe ($135.5 million) W North America ($14.5 million)

* Middle East and North Africa ($81.0 million) U Other ($5.0 million)

Sub-Saharan Africa ($64.5 million)

PARTICIPANTS IN IFC SYNDICATIONS

ABN-AMRO Bank NV Credit Suisse Nederlandse FinancieringsArab Banking Corporation B.S.C. The Dai-Ichi Kangyo Bank, Ltd. Maatschappij voorAsian Banking Corporation Den Danske Bank A/S Ontwikkelingslanden N.V. (FMO)

Asian Finance & Investment Deutsche Bank AG The Nippon Credit Bank, Ltd.Corporation Ltd. Die Erste bsterreichische Spar-Casse- NMB Postbank Groep N.V.

ASLK-CGER Bank Bank NordbankenBanco Exterior de Espafna Dresdner Bank AG The Norinchukin BankBank of Ireland Ecobank Transnational Incorporated Oversea-Chinese Banking

The Bank of Tokyo, Ltd. Girozentrale und Bank der Corporation Ltd.

Banque et Caisse d'Epargne de l'Etat osterreichischen Sparkassen AG Raiffeisen Zentralbank 0sterrcich AGLuxembourg Hanil International Finance Ltd. Saehan Merchant Banking

Banque Francaise du Commerce Hill Samuel Bank Ltd. Corporation

Exterieur The Hongkong & Shanghai Banking Soci6te Generale

Banque Indosuez Corporation Ltd. Standard Chartered Bank PLC

Banque Internationale a Luxembourg The Industrial Bank of Japan, Ltd. Sddwestdeutsche LandesbankSA KKBC International Ltd. Girozentrale

Banque Nationale de Paris Korea International Merchant Bank The Sumitomo Trust and Banking

Banque Sudameris Korea Long Term Credit Bank Company, Ltd.Banque Worms Korean Frcnch Banking Corporation Swiss Bank Corporation

Barclays Bank plc Kredietbank NV Swiss VolksbankBayeriscde Landesbank Girozenitrale The Long-Term Credit Bank of Japani, Tat Lee Bank Ltd.Bayerische Vereinsbank AG Ltd. Union de Banques Arabes et

Berliner Bank AG Malayan Banking Berhad Francaises-UBAFThe Commercial Bank of Korea Ltd. Manufacturers Hanover Trust Union Bank of Finland Ltd.

Commerzbank AG Company Union Bank of SwitzerlandCooperatieve Centrale Raiffeisen- The Mitsubishi Bank, Limited Westdeutsche Landesbank

Boerenleenbank BA (Rabobank The Mitsubishi Trust and Banking Girozentrale

Nederland) Corporation Z-Landerbank, Bank Austria AG

Credit Lyonnais Morgan Guaranty Trust CompanyCredit National of New York

19

PROJECT APPROVALS BY REGION, FY92 AND FY91

F Y 9 2 F Y9 1Financing Financing

Total for IFC's Total for IFC'sNumber finlancinig' own account Numiber finanLcing owTI acccurnt

(in millions of US. dollars] IOl-Ons oj US doU. rs)

Sub- Saharan Africa 50 441 284 42 319 194Asia 34 813 456 39 1,178 534

Europe 23 465 233 15 292 189Latin America and the Caribbean 45 1,253 607 43- 886 502Middle East and North Africa 15 25 174 8 64 64W\Torldwide2 - - - 3 108 58Total 167 3,227 1,774 152 2,846 1,540

1. Dollar asnoan: refers to totaldfnaocing approvedfor IFC', account, loan syndications, and vnderwritng.

2. Multicountry Loan Facilities and Comnmoonwealth Equity Fond.

underwriting, and placing securities, and IFC always issues accounted for $553 million, debt issues for

acts as co-lead manager, working in partnership with $357 million, and country funds for $95 million.

leading financial institutions; to date it has worked Among the pioneering issues in which IFC was

closely with more than 25 international investment involved during the year were a $228 million global

and commercial banks, which have served as lead equity issue by the Mexican company Vitro, one of

managers. IFC is involved in country and other fund the first Latin American companies to access the

instruments principally when they are among the international equity markets; a $53 million issue

first few in a given country or region, or if they open by Corinion, the first international equiity offering

up a new international capital market. Similarly, lFC by a Venezuelan company; a $72 million initial

typically is involved in an emerging markets corpo- public offering by Grupo Posadas, a medium-sized

rate issue if it is the first of its type for an IFC client, Mexican company; a $208 million revenue bond

or if it opens Lip a new interniational capital market issue for the Mexico City-Toluca Toll Road, Mexico's

for the client. IFC does not engage in secondary first private sector revenue bond issue; a $50 million

market-making or trading activities. floating rate note issue for Interbank, the first issue

of its kind by a private Turkish bank; and the

The emphasis of IFC's securities activities in fiscal $52 million Latin America Capital Fund, which is

1992 shifted from counitry funds, which are now a the region's first fund specializinig in stocks ofssmaller

well-established product, to the underwriting of companies.

international corporate issues. Many cormpanies in

developing countries experiencing economic growth RISK -MANAG EM INT S ERVI CES

find that their financiing needs have increased signif- The Corporation is helping conspanies in developing

icantly. Some of these companies are attempting to countries to gain access to derivative products that

fill a significant portion of their financing needs by would otherwise be unavailable to theni. Since fiscal

issuing securities in the international capital mar- 1990, when IFC executed its first swaps on behalf

kets. Many foreign institutional investors, because of clients, demand by companies in developing

of their positive experience with country funds, are countries for services and products related to finan-

increasingly willing to purchase securities issues by cial risk management has grown significantly. Swaps

the companies in wvhich the funds invest, particularlv and other derivative products (options snd forward

if the securities can be traded easily and efficiently in contracts) enable companies to manage commodity,

the international capital markets. foreign exchange, and interest rate risks by allowing

them to better match the denominations and interest

In fiscal 1992 IFC acted as a joint- or co-lead manag- rates of their assets and liabilities and minimize the

er for nine securities issues totaling $1 billion; equity negative impact that mismatches can have on income.

20 REPORT ON OPERATIONS

In fiscal 1992 IFC extended its internmediationl activ- of non-hanik finanicial institutions, the use of vouch-

ities to cover hedging instruments for commodity ers and mutual funds for privatizing state enterpris-

exposures as well as for currencies. It provided clients es, and the development of leasing legislation.

with a variety of risk-management services, includ-

ing advice on hedging strategies and the creation IFC has set up trust funds with the European

of hedging facilities to intermediate the execution Community and the bilateral agencies of several

of swaps and options over a specified time period, countries (Canada, Finland, India, Italy, Japan, the

direct intermediation of swaps, and mobilization of Netherlands, Norway, Sweden, Switzerland, and

swap coun1terparties in the interniational financial the United States) to finance activities related to

markets through guarantees or credit enhancement. the development of bankable new projects and the

IFC approved nine projects involving the provision rehabilitation of projects in difficulty. During

of hedging instruments to companies in sub-Saharan fiscal 1992 the Corporation financed 25 technical

Africa, Europe, Latin America, and the Middle East. assistance projects in 19 countries, including feasibil-

Through these projects, IFC will help clients hedge a ity studies, technology transfer, sector analyses,

total notional prinicipal amrLouIlt of $900 million and pilot operations, and set up a new trust fund

equivalent. with the European Community to finance tech-

nical assistancc in Asia. IFC has also made arrange-

ADVISORY SERVICES AND TECHNICAL ments with donor countries enabling it to increase

ASSISTANCE technical assistance in Eastern and Central Europe

In the past five years, demand for IFC's advisory and the CIS.

services has grown, particLdarly in connection with

privatizations and corporate restructurings. During The Corporation's Technical Advisory Service,

fiscal 1992 the Corporation received 30 advisory established in fiscal 1991, provided advice on

mandates, over one-third of which related to privati- projects in the agro-industry; cement, petro-

zations. In addition, it was developing proposals for chemicals, and oil exploration and development

another 10 potential assignments. sectors to businesses and governments in Europe

and Latin America.Demand for advisory services is concentrated in

Latin America and Eastern Europe, where the

Corporation advises both governments and enter-prises in its member countries on privatizations LOAN AND INVESTMENT APPROVALS,

FY88-FY92and corporate restructur-ings. During fiscal 1992 (millions of U.S. dollors)

in Argentina, for example, IFC acted as financial 3,500

adviser to the Ministry of Defense in the sale of a steel

manufacturer; it also completed a valuation of two 3,000

of Brazil's leading producers of petrochemicals. IFC

acted as financial adviser in the privatization of 2,500

enterprises in Czechoslovakia, Poland, and other 2,000

Central European countries. A pilot privatization 2,0

program involving the auction of small-scale 1,500

enterprises in Nizhny Novgorod, Russia, proved

very successful, and Russiani officials plan to use 1,000

it as a model for privatizations in other cities.

During the year, IFC worked on 30 technical assis-

tance projects related to capital market development. 1988 1989 1990 1991 1992

Two of these were regional in scope; the others were

located in 21 countries. IFC provided advice on Loan

matters such as securities market regulations, the re- Equity7i Syndiranxons and underwritingstructuring of commercial banks and establishment

21

The Foreign Investment Advisory Service (FIAS),

which is operated jointly by TFC, the IBRD, and

MIGA, provides advice to member countries on

attracting foreign direct investment. In fiscal 1992

FIAS completed 24 advisory assignments in 21

countries and one assignment in Central Europe.

FIAS's activities are described on p. 74.

IFC's operations are complemented by facilities that

help small-scale entrepreneurs develop business

proposals and raise financing for projects-the

Africa Project Development Facility, the Business

Advisory Service for the Caribbean and Central

America, the Polish Business Advisory Service,

and the South Pacific Project Facility. IFC helped

to establish these facilities, and is the executing

agency for all of them.

22 REPORT ON OPERATIONS

SE LE CTED CO RPO RATE SEC URIT IE S IS SUES

UN DE RWRI TTEN BY IF C IN F ISCAL 1 99 2

4GRMN INTERBANK A.S.

UJ.S.S50XDO.OOFloating Rale Notes Dlue 191)7

7.111=1 fl"~~~~~~~~~~~~~~~~~~~~~~~~~~r

L($ APASCO, S.A. de C.V.