Mental accounting and cause related marketing strategies

12

ORIGINAL ARTICLE Mental accounting and cause related marketing strategies Ilaria Baghi & Enrico Rubaltelli & Marcello Tedeschi Received: 22 April 2010 / Accepted: 3 August 2010 / Published online: 11 August 2010 # Springer-Verlag 2010 Abstract The aim of the present study is to verify if people’ s perception of cause related marketing (CRM) strategies is influenced by the mental accounting format used to present the price of the product and the amount of money donated to the social cause. However, such an effect is conditional on the type of product used for the campaign as the mental accounting is only expected to enhance the consumers’ perception of CRM programs supported by hedonic products and not their perception of programs supported by utilitarian products. In Experiment 1, results show that only for hedonic products an integrated mental accounting induces people to perceive the CRM program more positively than a separated one. In Experiment 2, the integrated mental accounting reduces people’ s guilt about the purchase of hedonic products, therefore explaining why this manipulation has a different impact on hedonic and utilitarian products. Keywords Cause related marketing . Mental accounting . Consumer behavior . Product type 1 Introduction In recent years, more and more companies all around the world are associating their products to some sort of charitable projects. Pringle and Thompson (1999) motivate Int Rev Public Nonprofit Mark (2010) 7:145–156 DOI 10.1007/s12208-010-0055-4 I. Baghi (*) : M. Tedeschi Department of Social, Cognitive, and Quantitative Sciences, University of Modena and Reggio Emilia, Viale Allegri, 9, 42100 Reggio Emilia, Italy e-mail: [email protected] M. Tedeschi e-mail: [email protected] E. Rubaltelli Department of Developmental and Socialization Psychology, University of Padova, Via Venezia 8, 35131 Padova, Italy e-mail: [email protected]

Transcript of Mental accounting and cause related marketing strategies

ORIGINAL ARTICLE

Mental accounting and cause relatedmarketing strategies

Ilaria Baghi & Enrico Rubaltelli & Marcello Tedeschi

Received: 22 April 2010 /Accepted: 3 August 2010 /Published online: 11 August 2010# Springer-Verlag 2010

Abstract The aim of the present study is to verify if people’s perception of causerelated marketing (CRM) strategies is influenced by the mental accounting formatused to present the price of the product and the amount of money donated to thesocial cause. However, such an effect is conditional on the type of product used forthe campaign as the mental accounting is only expected to enhance the consumers’perception of CRM programs supported by hedonic products and not theirperception of programs supported by utilitarian products. In Experiment 1, resultsshow that only for hedonic products an integrated mental accounting induces peopleto perceive the CRM program more positively than a separated one. In Experiment2, the integrated mental accounting reduces people’s guilt about the purchase ofhedonic products, therefore explaining why this manipulation has a different impacton hedonic and utilitarian products.

Keywords Cause related marketing . Mental accounting . Consumer behavior .

Product type

1 Introduction

In recent years, more and more companies all around the world are associating theirproducts to some sort of charitable projects. Pringle and Thompson (1999) motivate

Int Rev Public Nonprofit Mark (2010) 7:145–156DOI 10.1007/s12208-010-0055-4

I. Baghi (*) :M. TedeschiDepartment of Social, Cognitive, and Quantitative Sciences, University of Modena and ReggioEmilia, Viale Allegri, 9, 42100 Reggio Emilia, Italye-mail: [email protected]

M. Tedeschie-mail: [email protected]

E. RubaltelliDepartment of Developmental and Socialization Psychology, University of Padova, Via Venezia 8,35131 Padova, Italye-mail: [email protected]

this trend suggesting that adopting a cause can give a brand or a product a credo or abelief system and result in a significantly improved consumer perception andpurchase intention. Doing so, companies aim to create a positive brand image and toincrease market shares. Such a strategy has been defined “cause related marketing”(CRM; Varadarajan and Menon 1988), that is the process of formulating andimplementing marketing activities that are characterized by an offer from the firm tocontribute a specified amount to a designated cause when consumers engage inrevenue-providing exchanges that satisfy organizational and individual objectives.

This kind of marketing activity is a way to link products with a sociallyresponsible program following a strategy, which is ultimately directed to strength thepositive and emotional image of the product itself and to increase its market shares(Varadarajan and Menon 1988). In this sense many studies demonstrated that CRMstrategies may lead to favorable attitudes toward the socially responsible brand andits products (Brown and Dacin 1997; Ross et al. 1992; Webb et al. 2000) andinfluence purchase intention (Sen and Morwitz 1996).

Previous research showed that CRM is more effective when the social cause isassociated with an hedonic product rather than an utilitarian one (Strahilevitz 1999;Strahilevitz and Meyers 1998). Strahilevitz (1999) suggested that such a resultshould depend on the guilt that consumers feel when buying a product that has noutilitarian value (see also Dhar and Wertenbroch 2000). Therefore, knowing that bypurchasing an hedonic product they are also helping to raise money in support of asocial cause increases the consumers willingness to buy it. In turn, that makes theCRM program more effective.

In the present paper, the aim is to show that the difference found between hedonicand utilitarian products is conditional to the way the price of the product and theamount donated to the social cause are presented. There are two different ways inwhich the price of CRM products can be expressed. One way is to segregate theprice of the product from the amount donated to the social cause (segregated mentalaccount: e.g., Mp3 player Brand X: $160.00+$8.00 which will be donated tosupport medical research). This format has the advantage to state explicitly whichamount of money will be donated to the social cause. However, it may also inducepeople to think that it is a surcharge to the regular price of the product and that theyare asked to pay for the donation. A second way is to combine these two amounts ofmoney and present a single price (integrated mental account: e.g., Mp3 player BrandX: $168.00 of which 5% is donated to support medical research). This format makesless clear which amount of money will be donated to the social cause since theconsumer is asked to calculate it. On the other hand, in such a condition it looks likethe company is actually giving away part of its revenues in order to support thesocial cause and the consumer should not be induced to think that he/she is asked topay any surcharge.

Coherently with the above reasoning, the past literature on mental accounting(Thaler 1985; 1999) suggests that the second solution (single price) should alwaysbe perceived as more attractive and should also induce the consumers to perceive thesocial cause more positively. Such a conclusion is based on the hedonic framingexplanation of mental accounting, which suggests that people feel less sad whenpresented with a single loss than with several smaller losses that add up to the samevalue of the single one (Thaler and Johnson 1990). Thaler (1999) suggested that the

146 I. Baghi et al.

hedonic framing explanation is only valuable to describe how people react todifferent presentations of the same events, whereas they seem unable to actually editthe way information are presented in order to maximize their hedonistic reactions.However, subsequent studies showed that, despite the general inability to integratelosses, contextual variables may help people to do so (Bonini and Rumiati 2002;Kim 2006). For instance, Kim (2006) was able to show particular conditions inwhich the integration-of-losses prevails on the segregation. This author suggestedthat the salience of the information plays an important role in leading people tosegregate or integrate two different payments. In a broader sense, salience is thedegree to which a stimulus stands out in a situation (Augoustinos et al. 1995). Inother words, how information facilitates or hampers people’s way to process it hasan influence on their decision-making (Darke and Chung 2005; Heath et al. 1995).For example, if segregation of a payment has a visually salient surcharge then peopleshould see it as a separate entity and the segregated prices should induce a lessfavorable opinion. On the contrary, if the surcharge is not visually salient peopleshould pay less attention to it and not consider it as a separate entity (Kim 2006).These results are coherent with our hypothesis that the mental accounting formatshould play a role in the consumers’ perception of CRM programs. The segregatedformat should make the donation look as a visually salient surcharge reducingpeople’s support for the CRM strategy.

Recent research on price partitioning showed that presenting a price partitioned ina set of mandatory charges can either increase or decrease people’s preference for aproduct (Bertini and Wathieu 2008). In fact, price partitioning can be useful when ithelps to direct consumer’s selective attention to secondary attributes that would beoverlooked when they are presented through an all-inclusive price format (similar towhat it is called here integrated mental accounting). However, as Bertini andWathieu suggested, if the secondary attribute made more visible by the pricepartitioning is mediocre, firms should be better off using an all-inclusive format. Theintent of the present study is to apply this reasoning to CRM strategies since thedonation to the social cause is not an attribute that can improve the consumers’experience with the product (differently, for example, from the in-flight entertainmentused by Bertini and Wathieu 2008, Experiment 1). Therefore, even from the point ofview of price partitioning the integrated format should be more effective than theseparated one when presented with a CRM campaign. Once again, the hypothesiswould be that consumers should have a positive attitude toward a brand that supports asocial cause. However, such attitude should be more positive when the price isintegrated since when presented with the separate mental accounting consumers canfocus their attention on a sum of money that they are paying for a feature of theproduct that they are not going to experience.

Moreover, the hypothesis is to find an interaction between the mental accounting(price format) and the type of product associated with the CRM campaign. Inparticular, a difference between integrated and segregated mental accounts shouldonly be found for the hedonic products and not for the utilitarian ones as for thehedonic products the integrated mental account, compared with the segregated one,should help to reduce the sense of guilt as well as to avoid the inference that there issome sort of surcharge to the regular price of a product that is not fulfilling anyinstrumental goal.

Mental accounting and cause related marketing strategies 147

In addition, a CRM program associated with an utilitarian product should not beperceived more positively when the mental accounting is integrated rather thansegregated. This is because people do not feel guilty about buying an utilitarian productthat is fulfilling an instrumental goal therefore the integrated mental accounting shouldnot contribute to make consumers feeling better about their purchase.

In other words, the focus of interest lies in showing that the effectiveness of aCRM program does not simply depend on the type of product it is associated with(as suggested by previous research; see Strahilevitz 1999) nor it depends just on theformat used to communicate how much money is donated to the social cause.

In detail, the hypotheses are the following:

H1: The type of mental accounting should influence people’s ratings ofattractiveness of the cause related program when the presented with ahedonistic product. No influence is expected for utilitarian goods.

H2: The type of mental accounting should also influence people feelings towardthe social cause when the cause related product has a hedonistic nature. Noinfluence is expected for utilitarian goods.

H3: Mental accounting should influence people perceived usefulness of the CRMprogram when they are presented with hedonistic products. No influence isexpected for utilitarian goods.

H4: Mental accounting should influence people trust in the CRM program whenthe cause related product has a hedonistic nature. No influence is expected forutilitarian goods.

2 Experiment 1

2.1 Method

Participants One-hundred and two university students (44% males; mean age22 years) took part in the study. They were presented with either the integratedmental accounting format or the separated one.

Materials and procedure Each participant was presented with four hypotheticalscenarios describing products involved in a CRM program. The four products werethe following: Mp3 player, digital camera, microwave oven, and laser printer. Thefirst two products were supposed to be hedonic whereas the other two weresupposed to be utilitarian. To check for the hedonic and pleasure-driven nature of theproducts participants were asked to rate them on the following two dimensions:pleasant/unpleasant and satisfactory/unsatisfactory. Participants answered using7-point scales ranging from 1 (respectively: “very unpleasant” and “veryunsatisfactory”) to 7 (respectively: “very pleasant” and “very satisfactory”).

The price of the cause related products was manipulated accordingly with the twodifferent mental accounting formats: separated (e.g. Mp3 player €160.00+€8.00, the€8.00 are donated to support medical research) and integrated (e.g. Mp3 player€168.00, 5% of the price is donated to support medical research). Each participantsaw the four cause related products with the same mental accounting format (either

148 I. Baghi et al.

four CRM products presented using an integrated mental accounting or four CRMproducts presented using a separated mental accounting).

There were four dependent variable. Each of them was tested with a separatequestion. The first question asked to rate “how attractive or unattractive do you findthe product?” on a 9-point scale ranging from −4 (“very unattractive”) to+4 (“veryattractive”). The second question asked the participants to state “how strong a feelingdo you have toward the social cause supported by the product?” on a 9-point scaleranging from 0 (“not strong at all”) to 8 (“very strong”). In the third questionparticipants had to judge how useful they perceived to be the support given by theproduct to the social cause on a 9-point scale ranging from 0 (“not useful at all”) to8 (“very useful”). Finally, in the last question they were asked to rate “how confidentare you about the good use of the money collected selling the product?” on a 9-pointscale ranging from 0 (“not confident at all”) to 8 (“very confident”).

The experimental design was 2 (mental accounting) x 4 (products) with the lastfactor within subjects.

2.2 Results

The first analysis assessed the manipulation check, therefore it was tested whetherparticipants perceived the hedonic versus utilitarian nature of the four productsaccordingly with our expectations. The ratings on the pleasant/unpleasant andsatisfactory/unsatisfactory scales showed that the manipulation of the products typologywas perceived as expected. Results showed that participants judged the hedonicproducts (Mp3 player and digital camera) significantly more pleasant and satisfying thenthe utilitarian ones (laser printer and microwave oven). Contrast effects showed thatparticipants judged the Mp3 player more pleasant (Mp=5.73) and satisfying (Ms=5.44)than the utilitarian products: respectively F(1, 101)=92.77; μ2=.32; p<.01 and F(1,101)=19.04; μ2=..09; p<.01 for the comparisons with the laser printer (Mp=4.52 andMs=4.95) and F(1, 101)=68.64; μ2=.26; p<.01 and F(1, 101)=16.80; μ2=.07; p<.01for the comparisons with the microwave oven (Mp=4.68 and Ms=4.93).

Similarly, the digital camera (Mp=5.77 and Ms=5.73) induced higher pleasureand satisfaction than the two utilitarian products: respectively F(1, 101)=61.85;μ2=.24; p<.01 and F(1, 101)=45.97; μ2=.19; p<.01 for the comparisons with thelaser printer and F(1, 101)=76.72; μ2=.28; p<.01 and F(1, 101)=43.09; μ2=.18;p<.01 for the comparisons with the microwave oven.

At this point the attention can be turned to the question presented to measureparticipants’ perception of the CRM programs described using either one or the othermental accounting format. Analyses of variance showed that the hypothesizedinteractions between the condition (integrated versus separated mental accounting)and the type of product (hedonic versus utilitarian) were significant for all the fourdependent measures: respectively, F(1, 101)=16.96; μ2= .14; p< .01 forattractiveness; F(1, 101)=16.23; μ2=.14; p<.01 for strength of the feeling; F(1,101)=24.08; μ2=.19; p<.01 for usefulness of the contribution to the social cause;F (1, 101)=28.14; μ2=.22; p<.01 for confidence in the good use of money.

Across all the dependent measures the CRM campaign associated with the Mp3player was judged more positively when using the integrated mental accounting

Mental accounting and cause related marketing strategies 149

format then the segregated one (always p<.01; see Table 1 for the mean ratings). Thesame pattern of results was found for the CRM campaign associated with the digitalcamera (always p<.02 or lower).

No significant difference between the two mental accounting formats was foundon any of the dependent variables when the CRM campaigns were associated withthe utilitarian products (see Table 2).

2.3 Discussion

The results of Experiment 1 supported the hypothesis about the effect that the mentalaccounting has on the consumers’ perception of a CRM program. Reesults foundsupport for the interaction between the mental accounting factor and the type ofproduct. As expected, the manipulation of the mental accounting format waseffective only when the CRM program was associated with the hedonic products andallowed to significantly improve the perception of this marketing strategy when themental accounting was integrated rather than separated. On the other hand, when theCRM program was associated with the utilitarian products no significant differencebetween the two mental accounting conditions were found.

The main result of Experiment 1 is to show that a CRM strategy is not necessarilymore effective when it is associated with hedonic products, as previous findings wouldsuggest (see Strahilevitz 1999). Indeed, note that, coherently with these findings,previous studies found a difference between hedonic and utilitarian products since theywere using an integrated mental accounting format rather than a segregated one.Otherwise, on the basis of the present findings, no difference would have been found.

3 Experiment 2

In Experiment 1, the aim is to show that the advantage of a CRM program applied toan hedonic product is limited to the use of a particular format to communicate thefraction of the price that is donated to the social cause. Past research (Strahilevitz

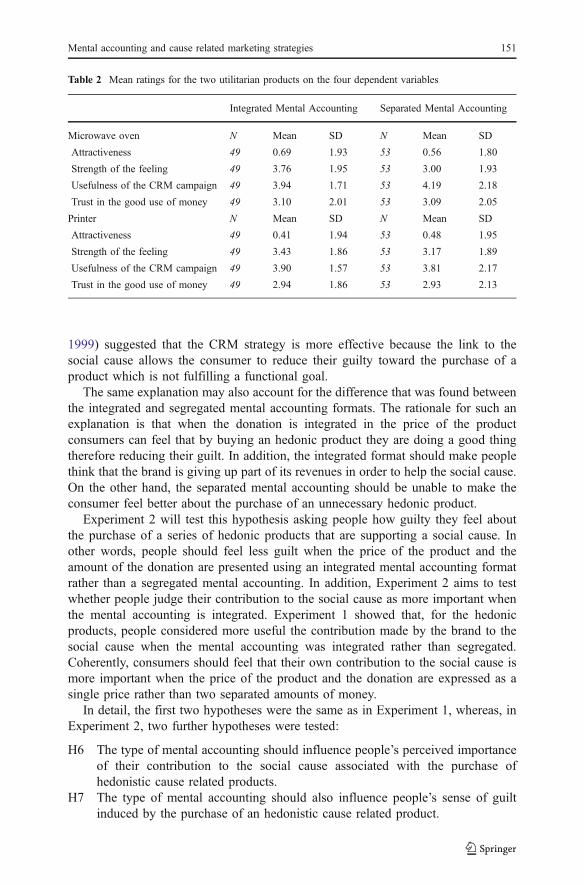

Table 1 Mean ratings for the two hedonic products on the four dependent variables

Integrated Mental Accounting Separated Mental Accounting

Mp3 player N Mean SD N Mean SD

Attractiveness 49 2.51 1.89 53 .74 1.82

Strength of the feeling 49 5.43 2.43 53 3.63 1.98

Usefulness of the CRM campaign 49 5.88 1.90 53 4.56 2.18

Trust in the good use of money 49 5.08 2.57 53 3.31 2.26

Digital camera N Mean SD N Mean SD

Attractiveness 49 2.10 1.81 53 1.04 1.73

Strength of the feeling 49 5.20 2.15 53 3.72 1.96

Usefulness of the CRM campaign 49 5.31 1.99 53 4.37 2.10

Trust in the good use of money 49 4.82 2.36 53 3.22 2.20

150 I. Baghi et al.

1999) suggested that the CRM strategy is more effective because the link to thesocial cause allows the consumer to reduce their guilty toward the purchase of aproduct which is not fulfilling a functional goal.

The same explanation may also account for the difference that was found betweenthe integrated and segregated mental accounting formats. The rationale for such anexplanation is that when the donation is integrated in the price of the productconsumers can feel that by buying an hedonic product they are doing a good thingtherefore reducing their guilt. In addition, the integrated format should make peoplethink that the brand is giving up part of its revenues in order to help the social cause.On the other hand, the separated mental accounting should be unable to make theconsumer feel better about the purchase of an unnecessary hedonic product.

Experiment 2 will test this hypothesis asking people how guilty they feel aboutthe purchase of a series of hedonic products that are supporting a social cause. Inother words, people should feel less guilt when the price of the product and theamount of the donation are presented using an integrated mental accounting formatrather than a segregated mental accounting. In addition, Experiment 2 aims to testwhether people judge their contribution to the social cause as more important whenthe mental accounting is integrated. Experiment 1 showed that, for the hedonicproducts, people considered more useful the contribution made by the brand to thesocial cause when the mental accounting was integrated rather than segregated.Coherently, consumers should feel that their own contribution to the social cause ismore important when the price of the product and the donation are expressed as asingle price rather than two separated amounts of money.

In detail, the first two hypotheses were the same as in Experiment 1, whereas, inExperiment 2, two further hypotheses were tested:

H6 The type of mental accounting should influence people’s perceived importanceof their contribution to the social cause associated with the purchase ofhedonistic cause related products.

H7 The type of mental accounting should also influence people’s sense of guiltinduced by the purchase of an hedonistic cause related product.

Table 2 Mean ratings for the two utilitarian products on the four dependent variables

Integrated Mental Accounting Separated Mental Accounting

Microwave oven N Mean SD N Mean SD

Attractiveness 49 0.69 1.93 53 0.56 1.80

Strength of the feeling 49 3.76 1.95 53 3.00 1.93

Usefulness of the CRM campaign 49 3.94 1.71 53 4.19 2.18

Trust in the good use of money 49 3.10 2.01 53 3.09 2.05

Printer N Mean SD N Mean SD

Attractiveness 49 0.41 1.94 53 0.48 1.95

Strength of the feeling 49 3.43 1.86 53 3.17 1.89

Usefulness of the CRM campaign 49 3.90 1.57 53 3.81 2.17

Trust in the good use of money 49 2.94 1.86 53 2.93 2.13

Mental accounting and cause related marketing strategies 151

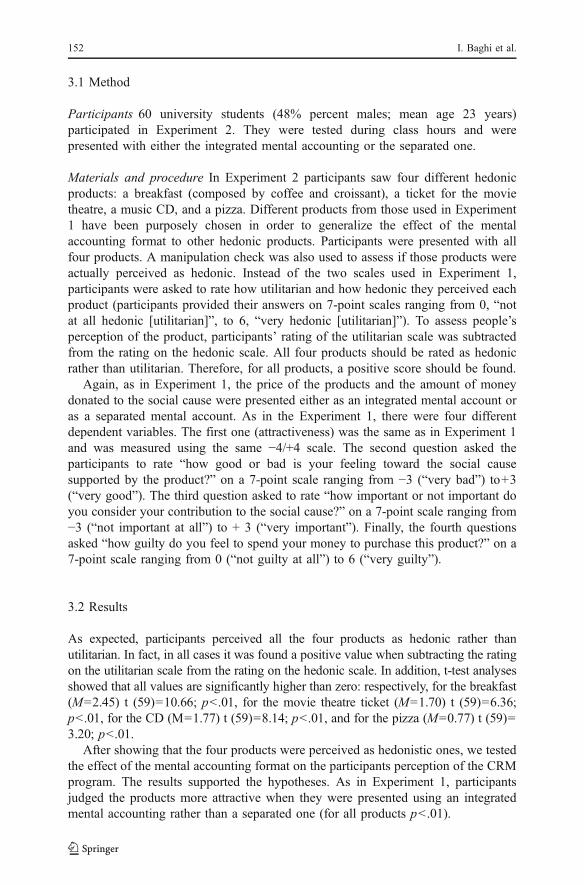

3.1 Method

Participants 60 university students (48% percent males; mean age 23 years)participated in Experiment 2. They were tested during class hours and werepresented with either the integrated mental accounting or the separated one.

Materials and procedure In Experiment 2 participants saw four different hedonicproducts: a breakfast (composed by coffee and croissant), a ticket for the movietheatre, a music CD, and a pizza. Different products from those used in Experiment1 have been purposely chosen in order to generalize the effect of the mentalaccounting format to other hedonic products. Participants were presented with allfour products. A manipulation check was also used to assess if those products wereactually perceived as hedonic. Instead of the two scales used in Experiment 1,participants were asked to rate how utilitarian and how hedonic they perceived eachproduct (participants provided their answers on 7-point scales ranging from 0, “notat all hedonic [utilitarian]”, to 6, “very hedonic [utilitarian]”). To assess people’sperception of the product, participants’ rating of the utilitarian scale was subtractedfrom the rating on the hedonic scale. All four products should be rated as hedonicrather than utilitarian. Therefore, for all products, a positive score should be found.

Again, as in Experiment 1, the price of the products and the amount of moneydonated to the social cause were presented either as an integrated mental account oras a separated mental account. As in the Experiment 1, there were four differentdependent variables. The first one (attractiveness) was the same as in Experiment 1and was measured using the same −4/+4 scale. The second question asked theparticipants to rate “how good or bad is your feeling toward the social causesupported by the product?” on a 7-point scale ranging from −3 (“very bad”) to+3(“very good”). The third question asked to rate “how important or not important doyou consider your contribution to the social cause?” on a 7-point scale ranging from−3 (“not important at all”) to + 3 (“very important”). Finally, the fourth questionsasked “how guilty do you feel to spend your money to purchase this product?” on a7-point scale ranging from 0 (“not guilty at all”) to 6 (“very guilty”).

3.2 Results

As expected, participants perceived all the four products as hedonic rather thanutilitarian. In fact, in all cases it was found a positive value when subtracting the ratingon the utilitarian scale from the rating on the hedonic scale. In addition, t-test analysesshowed that all values are significantly higher than zero: respectively, for the breakfast(M=2.45) t (59)=10.66; p<.01, for the movie theatre ticket (M=1.70) t (59)=6.36;p<.01, for the CD (M=1.77) t (59)=8.14; p<.01, and for the pizza (M=0.77) t (59)=3.20; p<.01.

After showing that the four products were perceived as hedonistic ones, we testedthe effect of the mental accounting format on the participants perception of the CRMprogram. The results supported the hypotheses. As in Experiment 1, participantsjudged the products more attractive when they were presented using an integratedmental accounting rather than a separated one (for all products p<.01).

152 I. Baghi et al.

In addition, the integrated mental accounting induced the participants toexperience a better feeling than the separated mental accounting: respectively,t (58)=5.98; p<.01 for the breakfast, t (58)=3.46; p<.02 for the movie theater ticket,t (58)=4.22; p<.01 for the CD, and t (58)=4.48; p<.01 for the pizza (see Table 3 forthe mean ratings).

When asked to rate how important was their contribution to the social cause,participants provided a higher rating if the price of the product and the donation tothe social cause were integrated in a single value than expressed as separate entities:respectively, t (58)=5.62; p<.01 for the breakfast, t (58)=4.39; p<.01 for the movietheater ticket, t (58)=2,71; p<.01 for the CD, and t (58)=3.65; p<.01 for the pizza.

Finally, supporting the explanation based on the reduction of the guilt when themental accounting is integrated, participants felt more contrition buying an hedonicproduct when the product-social cause association was presented as two separatecosts rather than a single price: respectively, t (58)= −5.63; p<.01 for the breakfast,t (58)= −3.06; p<.01 for the movie theater ticket, t (58)= −4.65; p<.01 for the CD,and t (58)= −4.24; p<.01 for the pizza.

3.3 Discussion

Experiment 2 supported our hypotheses and showed that people purchasing an hedonicproduct experience a lower level of guilty in the integrated mental accounting conditionthan in the separated mental accounting condition. Furthermore, results show thatparticipants perceive their contribution to the social cause as more important when themental accounting is integrated rather than separated. These findings suggest that the

Table 3 Mean ratings for the affective reactions, importance of the participant’s contribution and thefeeling of guilt

Integrated MentalAccounting

Separated MentalAccounting

Affective reactions N Mean SD N Mean SD

Breakfast 32 2.44 .72 28 .50 1.67

CD 32 1.69 1.36 28 .54 1.20

Movie theater ticket 32 1.62 1.56 28 .11 1.17

Pizza 32 1.94 1.08 28 .64 1.62

Importance of the participant’s contribution N Mean SD N Mean SD

Breakfast 32 2.34 .87 28 .57 1.53

CD 32 1.75 1.37 28 .25 1.27

Movie theater ticket 32 1.59 1.64 28 .50 1.45

Pizza 32 1.81 1.47 28 .54 1.20

Feeling of guilt N Mean SD N Mean SD

Breakfast 32 .78 .79 28 2.21 1.17

CD 32 1.00 1.32 28 1.93 .98

Movie theater ticket 32 .84 .68 28 2.14 1.41

Pizza 32 .56 .62 28 1.68 1.34

Mental accounting and cause related marketing strategies 153

contribution to the social causes is not always perceived in the same way, that is,integrating or separating the donation from the price of a specific cause related productcould exert an influence on individuals’ belief about the importance of their support tosocial issue. Companies can use the donation formula as a tools available to them toincrease people’s involvement and contribution to a specific social problem.

The present findings shed light on the hypothesis that the mental accounting has asignificant impact on consumers’ perception of a CRM program. The results are alsoconsistent with recent literature on price partitioning suggesting that directingconsumers’ attention toward a secondary attribute may either improve or reducepeople’s preference for the product (Bertini and Wathieu 2008). In particular, theproduct looks worse if the secondary attribute is mediocre or if it is simply related tothe image of the brand and not to the actual experience people have with the product.

4 General discussion

The purpose of the present paper was to show that cause related marketing (CRM) isinfluenced by the mental accounting format used to present the price of the productand the amount of money donated to the social cause: integrated format (the price ofthe product and the amount of the donation are expressed as a single value) versusseparated format (the price of the product and the amount of the donation areexpressed as separate values). Moreover, the paper aimed to show that the mentalaccounting influence on the perception of cause related marketing programs ismediated by the product typology: hedonistic goods versus utilitarian ones.

Experiment 1 showed that the manipulation of the mental accounting format had aneffect when people were presented with hedonic products but not when they werepresented with utilitarian products. Moreover, when the mental accounting format isseparated there is a much smaller difference, if any, between hedonic and utilitarianproducts supporting a social cause. Therefore, the mental accounting format plays asignificant role in shaping the previous findings suggesting that the association betweena social cause and a specific brand is more effective when the product is hedonic ratherthan utilitarian (see Strahilevitz 1999). In other words, this means that to build aneffective CRM strategy is not sufficient to choose the right product typology but it isfundamental to take into consideration psychological factors like the mental accounts(Thaler 1985; 1999). Otherwise, even the choice of an hedonic product could lead to avery small increase in the effectiveness of this marketing strategy.

Overall, these findings suggest that a CRM strategy that is built giving the properconsideration to psychological factors can not only improve the brand image, andhopefully increase the amount of money raised by the social cause, but also make thepurchasing experience more gratifying thanks to a reduction of the sense of guilt feltby the consumers when they are buying an hedonic product. By way of an integratedmental accounting it is possible to communicate the brand social involvement as acore attribute of the product (the donation is embodied into the price) and not as asecondary attribute (the donation is presented as a separated cost) that is not addinganything to the consumer experience with the product.

Every company trying to maximize the positive effects of such a marketingstrategy, both in terms of corporate image and actual support to the social cause,

154 I. Baghi et al.

should apply it to products that are not perceived as goal oriented and present itusing an integrated mental accounting. Such a solution seems to help the consumerto perceive a stronger association between the product and the social cause and toenrich the purchase experience with a social value that is able to soothe the negativeemotions, such as the sense of guilt, induced by spending money to buy a frivolousand pleasure oriented product.

Not only the purchase experience, but also the perceived social value of the brandcan be improved by a cause related marketing program that communicates its socialinvolvement as a core attribute of the product (the donation is embodied into theprice) and not as an added and occasional element (the donation is presented as aseparated cost). In this perspective, the way in which a separated format detaches thedonation from the price of the product could implicitly suggest to the consumers thatthe cause related campaign is a temporal sort of social “promotion” and not a realand permanent philanthropic mission of the brand. Otherwise, the integration of thecharity into the value of the product may evoke a lasting sense of responsibility orconcern for the problems and injustices of the society.

However, it is noteworthy that the strategy of communication presented in thepresent work may lead to undesirable results and negative implications for both theconsumers and the companies if applied in the wrong way. On many occasions CRMprograms require the consumer to pay a somewhat higher price in order to allow thecompany to cope with increased costs (e.g., advertising of the campaign or changesto make the product more exclusive). Despite, the potentially good intentions of aCRM strategy, someone might find ethically questionable to use an integrated mentalaccount when the consumer is required to pay more than the regular price sinceExperiment 1 revealed that people have a more positive perception of the socialcause when the donation is integrated into the price of the product. Such a use of thestrategy advocated in the present work would lure, somewhat unethically, theconsumers toward a more expensive product even though they were not willing topay the additional cost.

On the other hand, a company may make a strategic decision to give up some ofits revenues in order to improve its corporate image helping the social cause withoutasking this contribution to the consumers. In such a case, to use a separated mentalaccounting could be a way to show the actual amount of money that the company isgiving up in favor of the social cause. However, such a strategy is likely to backfireinducing the consumers to think that the donation is collected using their moneyinstead of those of the company.

In conclusion, the findings of the present study have important managerialimplications. First of all, marketing practitioners must consider that if they want topromote social causes with their products, they need to make strategic decisionscarefully. They should taken into account both cognitive factors (e.g., people’s wayof processing information about the costs of the donation) and emotional ones (e.g.,sense of guilt) in order to communicate, effectively, their genuine interest forbeneficial social actions. Also in the selection of the product typology, they shouldconsider the emotional factors linked to the purchase experience that induceconsumers to comply with a social aim. The chance to donate some money in favorof a social cause is not desirable in itself. Companies should present it together witha good that is hedonistic and not goal oriented. Moreover, in cause-related marketing

Mental accounting and cause related marketing strategies 155

initiatives, it is not enough to stress the social aim. The hedonistic nature of aproduct and the format of the contribution should also be emphasized. Consumersshould believe that the philanthropic aim will lead to solve the trade-off between thehedonistic satisfaction and the sense of guilt.

References

Augoustinos M, Walker I, Donaghue N (1995) Social Cognition: An Integrated Introduction. SageFoundation, London

Bertini M, Wathieu L (2008) Attention Arousal Through Price Partitioning. Market Sci 27(2):236–246Bonini N, Rumiati R (2002) Acceptance of a Price Discount: The Role of the Semantic Relatedness

Between Purchases and the Comparative Price Format. J Behav Decis Making 15(3):203–220Brown TJ, Dacin PA (1997) The Company and the Product: Corporate Association and Consumer Product

Responses. J Market 61(1):68–84Darke PR, Chung CMY (2005) Effects of Pricing and Promotion on Consumer Perceptions: It Depends on

How You Frame It. J Retailing 81(1):35–47Dhar R, Wertenbroch K (2000) Consumer Choice Between Hedonic and Utilitarian Goods. J Market Res

37(1):60–71Heath TB, Chatterjee S, France KR (1995) Mental Accounting and Changes in Price: The Frame

Dependence of Reference Dependence. J Cons Res 22(1):90–97Kim HM (2006) The Effect of Salience on Mental Accounting: How Integration Versus Segregation of

Payment Influences Purchase Decisions. J Behav Decis Making 19(4):381–391Pringle H, Thompson M (1999) Brand Spirit. Wiley, West SussexRoss JK, Patterson LT, Stutts MA (1992) Consumer Perceptions of Organizations That Use Cause-Related

Marketing. J Acad Market Sci 20(1):93–97Sen S, Morwitz VG (1996) Consumer reactions to a provider’s position on social issues. J Consum

Psychol 5(1):27–48Strahilevitz M (1999) The Effect of Product Type and Donation Magnitude on Willingness to Pay More

for a Charity-Linked Brand. J Consu Psychol 8(3):215–241Strahilevitz MA, Meyers JG (1998) Donation to Charity as Purchase Incentive: How Well They Work

May Depend on What You Are Trying to Sell. J Consum Res 24(4):434–446Thaler RH (1985) Mental Accounting and Consumer Choice. Market Sci 4(3):199–214Thaler RH (1999) Mental Accounting Matters. J Behav Decis Making 12(3):183–206Thaler RH, Johnson EJ (1990) Gambling with the house money and trying to break even: The effects of

prior outcomes on risky choice. Manag Sci 36:643–660Varadarajan PR, Menon A (1988) Cause-Related Marketing: A Coalignment of Marketing Strategy and

Corporate Philanthropy. J Market 52(3):58–74Webb DJ, Green CL, Brashear TG (2000) Development and Validation of Scales to Measure Attitudes

Influencing Monetary Donations to Charitable Organizations. J Acad Market Sci 28(2):299–309

156 I. Baghi et al.