MATERIALS - HKEXnews

271

MATERIALS BRING A PROSPEROUS LIFE Annual Report 2013 China National Materials Company Limited A joint stock company incorporated in the People’s Republic of China with limited liability ( Stock Code: 01893 )

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of MATERIALS - HKEXnews

Chin

a Nation

al Materials

Com

pan

y Limited

China National MaterialsCompany Limited

2013 An

nu

al Rep

ort

MATERIALSBRING A PROSPEROUS LIFE

Annual Report 2013

China National MaterialsCompany Limited

A joint stock company incorporated in the People’s Republic of China with limited liability

(Stock Code: 01893)

1Annual Report 2013

CONTENTS

CORPORATE INFORMATION 2

CORPORATE PROFILE 4

CORPORATE STRUCTURE 5

FINANCIAL SUMMARY 6

BUSINESS SUMMARY 7

CHAIRMAN’S STATEMENT 8

MANAGEMENT DISCUSSION AND ANALYSIS 11

BIOGRAPHY OF DIRECTORS,

SUPERVISORS AND SENIOR

MANAGEMENT 25

DIRECTORS’ REPORT 33

SUPERVISORY COMMITTEE’S REPORT 47

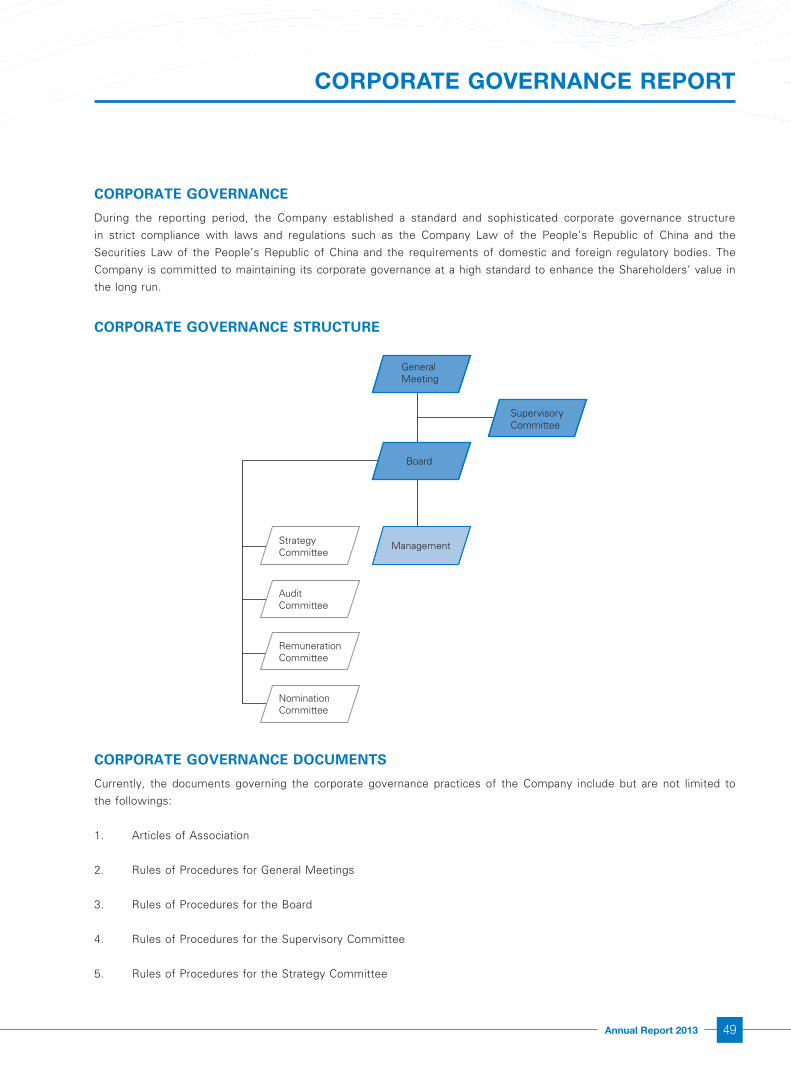

CORPORATE GOVERNANCE REPORT 49

INDEPENDENT AUDITOR’S REPORT 63

CONSOLIDATED STATEMENT OF

PROFIT OR LOSS 65

CONSOLIDATED STATEMENT OF PROFIT OR

LOSS AND OTHER COMPREHENSIVE INCOME 66

CONSOLIDATED STATEMENT OF

FINANCIAL POSITION 67

CONSOLIDATED STATEMENT OF

CHANGES IN EQUITY 69

CONSOLIDATED STATEMENT OF

CASH FLOWS 72

NOTES TO THE CONSOLIDATED

FINANCIAL STATEMENTS 75

DEFINITIONS 265

China National Materials Company Limited2

CORPORATE INFORMATION

As at 31 December 2013

DIRECTORSExecutive Directors1

LIU Zhijiang (Chairman)LI Xinhua (Vice-chairman)

Non-executive Directors2

YU Shiliang

ZHANG Hai

LI Jianlun

YU Guobo

TANG Baoqi

Independent Non-executive Directors2

LEUNG Chong Shun

LU Zhengfei

WANG Shimin

ZHOU Zude

SupervisorsXU Weibing (Chairman)ZHANG Renjie

WANG Jianguo

WANG Yingcai3

QU Xiaoli

STRATEGY COMMITTEE4

LIU Zhijiang (Chairman)YU Shiliang

LI Xinhua

ZHANG Hai

LI Jianlun

YU Guobo

ZHOU Zude

AUDIT COMMITTEELU Zhengfei (Chairman)WANG Shimin

YU Shiliang5

REMUNERATION COMMITTEEWANG Shimin (Chairman)6

LEUNG Chong Shun

LU Zhengfei

NOMINATION COMMITTEELIU Zhijiang (Chairman)7

WANG Shimin8

ZHOU Zude

1 On 5 February 2013, Mr. LIU Zhijiang was re-designated from a non-executive Director to an executive Director of the Company

and was appointed as the Chairman of the Board; Mr. LI Xinhua was appointed as the Vice-chairman of the Board; Mr. YU

Shiliang was re-designated from an executive Director to a non-executive Director. Please refer to the announcement of the

Company dated 5 February 2013 for details.2 On 30 July 2013, Mr. LI Jianlun and Mr. YU Guobo were appointed as non-executive Directors of the Company, and Mr.

SHI Chungui ceased to be an independent non-executive Director of the Company. Please refer to the announcement of the

Company dated 30 July 2013 for details.3 On 30 July 2013, Mr. YU Xingmin ceased to be a Supervisor of the Company, and Mr. WANG Yingcai was appointed as a Super-

visor of the Company. Please refer to the announcement of the Company dated 30 July 2013 for details.4 On 5 February 2013, Mr. LIU Zhijiang was appointed as the Chairman of the Strategy Committee in place of Mr. YU Shiliang. On

30 July 2013, Mr. ZHANG Hai, Mr. LI Jianlun and Mr. YU Guobo were appointed as members of the Strategy Committee.5 On 5 February 2013, Mr. YU Shiliang was appointed as a member of the Audit Committee in place of Mr. LIU Zhijiang.6 On 30 July 2013, Mr. WANG Shimin was appointed as the Chairman of the Remuneration Committee in place of Mr. SHI

Chungui.7 On 5 February 2013, Mr. LIU Zhijiang was appointed as the Chairman of the Nomination Committee, and Mr. YU Shiliang ceased

to be a member of the Nomination Committee.8 On 30 July 2013, Mr. WANG Shimin was appointed as a member of the Nomination Committee in place of Mr. SHI Chungui.

3Annual Report 2013

CORPORATE INFORMATION

As at 31 December 2013

SECRETARY TO THE BOARDGU Chao

JOINT COMPANY SECRETARIESGU Chao

YU Leung Fai (HKICPA, AICPA)

AUTHORISED REPRESENTATIVESLIU Zhijiang1

YU Leung Fai (HKICPA, AICPA)

REGISTERED OFFICE AND PLACE OF BUSINESS11 Beishuncheng Street

Xizhimennei

Xicheng District

Beijing 100035, the PRC

PLACE OF BUSINESS IN HONG KONG7th Floor, Hong Kong Trade Centre

161-167 Des Voeux Road Central

Hong Kong

LEGAL ADVISORSDLA Piper (as to Hong Kong law)Jia Yuan Law Firm (as to PRC law)

AUDITORSHong Kong auditor

SHINEWING (HK) CPA Limited

PRC auditor

ShineWing Certified Public Accountant LLP

HONG KONG H SHARE REGISTRAR AND TRANSFER OFFICEComputershare Hong Kong Investor Services Limited

17M Floor, Hopewell Centre

183 Queen’s Road East

Wanchai, Hong Kong

STOCK CODE01893

COMPANY WEBSITEhttp://www.sinoma-ltd.cn

INVESTOR CONTACTTel: (8610)8222 9925

Fax: (8610)8222 8800

E-mail: [email protected]

1 On 5 February 2013, Mr. LIU Zhijiang was appointed as the authorised representative of the Company in place of Mr. Yu Shiliang.

China National Materials Company Limited4

CORPORATE PROFILE

China National Materials Company Limited is a joint stock company approved by the State-owned Assets Supervision and

Administration Commission of the State Council and established jointly by China National Materials Group Corporation

Ltd. and other promoters. The Company was incorporated on 31 July 2007 and was listed on the Main Board of the

Hong Kong Stock Exchange on 20 December 2007.

The Company is mainly engaged in cement equipment and engineering services, cement and high-tech materials

businesses. The Company possesses series of core technologies such as glass fiber, composite materials, synthetic

crystals, advanced ceramics and new dry process cement technology, with pioneering research and development

capabilities, strong implementation capability for commercialisation of innovative technologies, successful mergers and

acquisitions experience and unique business model.

The Company is the largest provider of cement equipment and engineering services globally and is a leading producer of

non-metal materials in the PRC. The Company is the only enterprise in the non-metal materials industry in the PRC with

a business model that integrates research and development, industrial design, equipment manufacturing, engineering and

construction services and production.

The Company is committed to maintaining sustainable development for the long term and continuously creates value for

all our stakeholders including Shareholders, customers, employees and the society. The Company upholds our positioning

as an innovative, international and value-added enterprise. We strive to become the leading provider of technology, core

equipment and engineering and system integration services in the global cement engineering industry and to become a

prominent developer and provider of non-metal materials and related products globally.

5Annual Report 2013

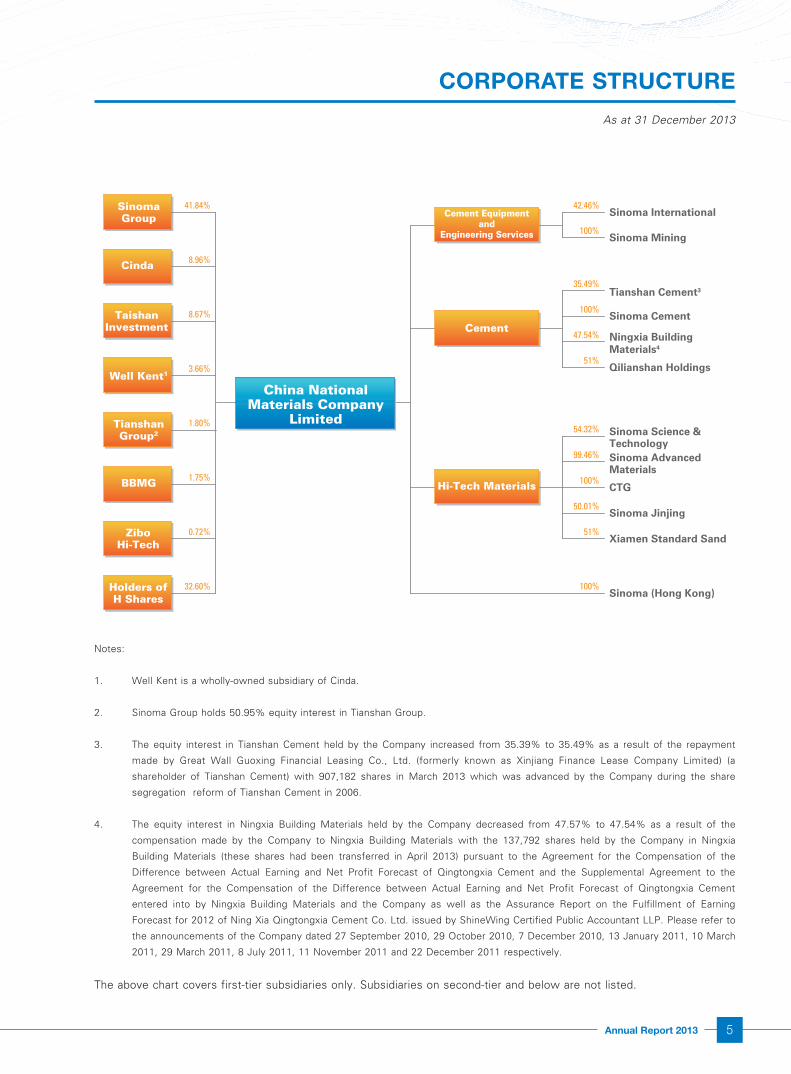

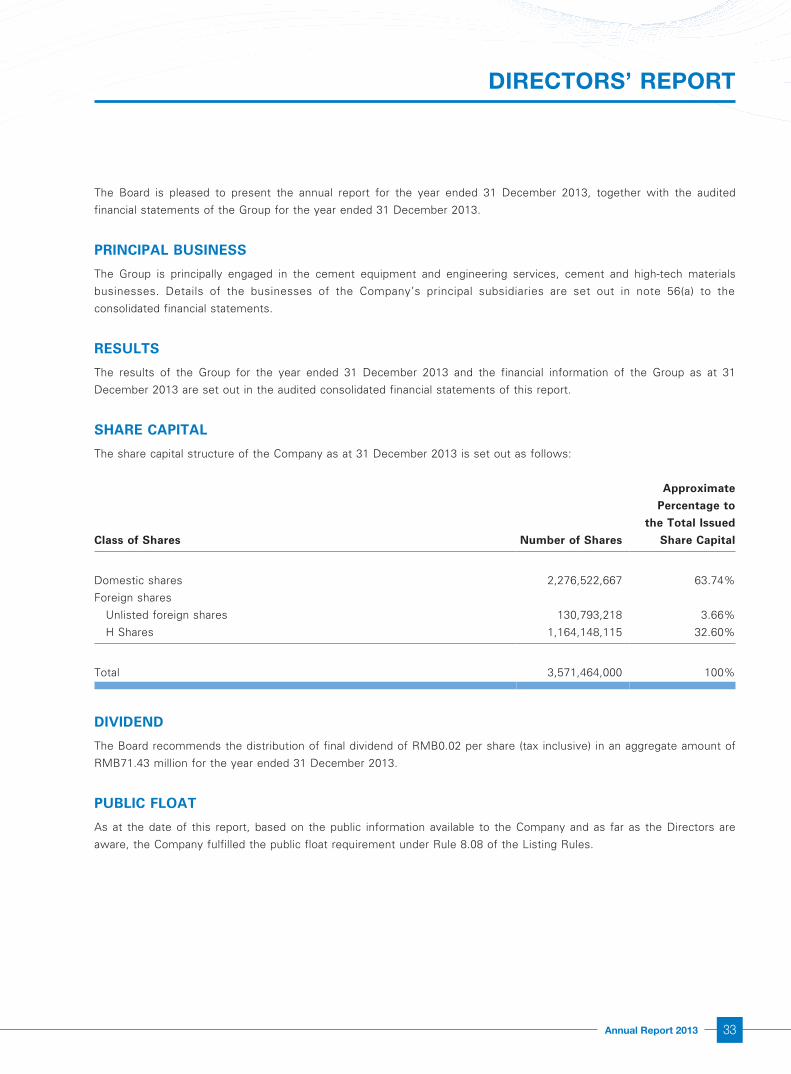

CORPORATE STRUCTURE

As at 31 December 2013

41.84%

8.96%

8.67%

3.66%

32.60%

1.80%

1.75%

0.72%

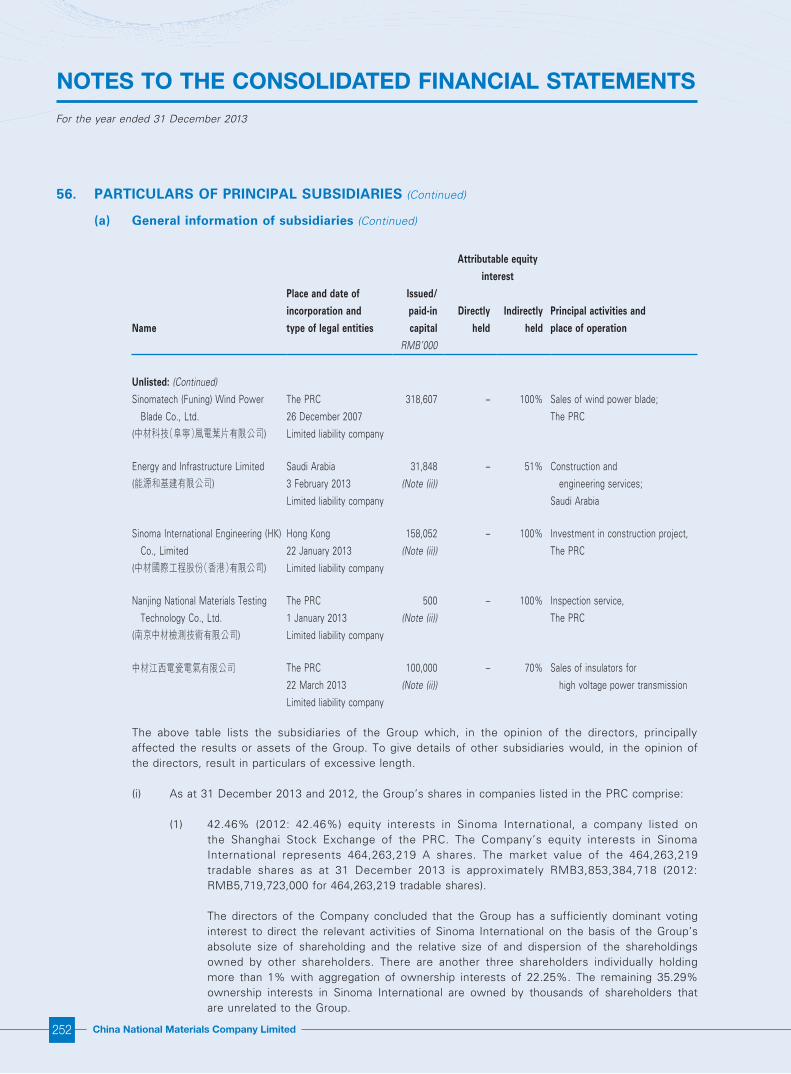

42.46%Sinoma International

Sinoma Mining

Tianshan Cement3

Sinoma Cement

Ningxia BuildingMaterials4

Qilianshan Holdings

Sinoma Science &TechnologySinoma AdvancedMaterials

CTG

Sinoma Jinjing

Xiamen Standard Sand

Sinoma (Hong Kong)

100%

35.49%

100%

100%

47.54%

51%

54.32%

50.01%

99.46%

100%

51%

SinomaGroup

Cinda

TaishanInvestment

Well Kent1

TianshanGroup2

BBMG

ZiboHi-Tech

Holders ofH Shares

China NationalMaterials Company

Limited

Cement Equipmentand

Engineering Services

Cement

Hi-Tech Materials

Notes:

1. Well Kent is a wholly-owned subsidiary of Cinda.

2. Sinoma Group holds 50.95% equity interest in Tianshan Group.

3. The equity interest in Tianshan Cement held by the Company increased from 35.39% to 35.49% as a result of the repayment

made by Great Wall Guoxing Financial Leasing Co., Ltd. (formerly known as Xinjiang Finance Lease Company Limited) (a

shareholder of Tianshan Cement) with 907,182 shares in March 2013 which was advanced by the Company during the share

segregation reform of Tianshan Cement in 2006.

4. The equity interest in Ningxia Building Materials held by the Company decreased from 47.57% to 47.54% as a result of the

compensation made by the Company to Ningxia Building Materials with the 137,792 shares held by the Company in Ningxia

Building Materials (these shares had been transferred in April 2013) pursuant to the Agreement for the Compensation of the

Difference between Actual Earning and Net Profit Forecast of Qingtongxia Cement and the Supplemental Agreement to the

Agreement for the Compensation of the Difference between Actual Earning and Net Profit Forecast of Qingtongxia Cement

entered into by Ningxia Building Materials and the Company as well as the Assurance Report on the Fulfillment of Earning

Forecast for 2012 of Ning Xia Qingtongxia Cement Co. Ltd. issued by ShineWing Certified Public Accountant LLP. Please refer to

the announcements of the Company dated 27 September 2010, 29 October 2010, 7 December 2010, 13 January 2011, 10 March

2011, 29 March 2011, 8 July 2011, 11 November 2011 and 22 December 2011 respectively.

The above chart covers first-tier subsidiaries only. Subsidiaries on second-tier and below are not listed.

China National Materials Company Limited6

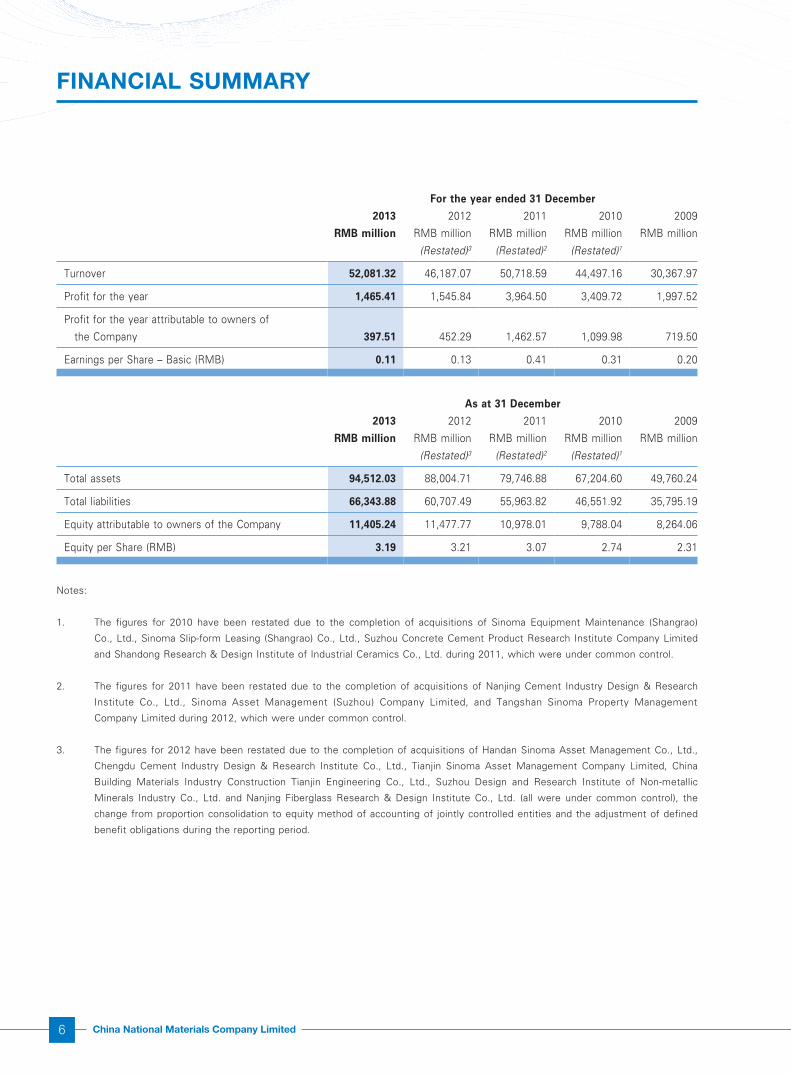

FINANCIAL SUMMARY

For the year ended 31 December

2013 2012 2011 2010 2009

RMB million RMB million RMB million RMB million RMB million

(Restated)3 (Restated)2 (Restated)1

Turnover 52,081.32 46,187.07 50,718.59 44,497.16 30,367.97

Profit for the year 1,465.41 1,545.84 3,964.50 3,409.72 1,997.52

Profit for the year attributable to owners of

the Company 397.51 452.29 1,462.57 1,099.98 719.50

Earnings per Share – Basic (RMB) 0.11 0.13 0.41 0.31 0.20

As at 31 December

2013 2012 2011 2010 2009

RMB million RMB million RMB million RMB million RMB million

(Restated)3 (Restated)2 (Restated)1

Total assets 94,512.03 88,004.71 79,746.88 67,204.60 49,760.24

Total liabilities 66,343.88 60,707.49 55,963.82 46,551.92 35,795.19

Equity attributable to owners of the Company 11,405.24 11,477.77 10,978.01 9,788.04 8,264.06

Equity per Share (RMB) 3.19 3.21 3.07 2.74 2.31

Notes:

1. The figures for 2010 have been restated due to the completion of acquisitions of Sinoma Equipment Maintenance (Shangrao)

Co., Ltd., Sinoma Slip-form Leasing (Shangrao) Co., Ltd., Suzhou Concrete Cement Product Research Institute Company Limited

and Shandong Research & Design Institute of Industrial Ceramics Co., Ltd. during 2011, which were under common control.

2. The figures for 2011 have been restated due to the completion of acquisitions of Nanjing Cement Industry Design & Research

Institute Co., Ltd., Sinoma Asset Management (Suzhou) Company Limited, and Tangshan Sinoma Property Management

Company Limited during 2012, which were under common control.

3. The figures for 2012 have been restated due to the completion of acquisitions of Handan Sinoma Asset Management Co., Ltd.,

Chengdu Cement Industry Design & Research Institute Co., Ltd., Tianjin Sinoma Asset Management Company Limited, China

Building Materials Industry Construction Tianjin Engineering Co., Ltd., Suzhou Design and Research Institute of Non-metallic

Minerals Industry Co., Ltd. and Nanjing Fiberglass Research & Design Institute Co., Ltd. (all were under common control), the

change from proportion consolidation to equity method of accounting of jointly controlled entities and the adjustment of defined

benefit obligations during the reporting period.

7Annual Report 2013

BUSINESS SUMMARY

Cement Equipment And Engineering Services

2013 2012 Change (%)

Amount of new order intakes (RMB million) 34,212 30,832 10.96

Amount of backlog (RMB million) - as at 31 December 56,742 55,187 2.82

Cement

2013 2012 Change (%)

Sales volume of cement (‘000 tonnes) 74,700 63,020 18.53

Sales volume of clinker (‘000 tonnes) 10,030 8,800 13.98

High-tech Materials

2013 2012 Change (%)

Sales volume of glass fiber and products (‘000 tonnes) 448 442 1.36

Sales volume of fan blades for wind power generators (set) 1,816 1,267 43.33

Sales volume of solar-energy fused silica crucibles (unit) 37,300 32,265 15.61

Sales volume of natural gas cylinders (unit) 254,471 205,318 23.94

China National Materials Company Limited8

CHAIRMAN’S STATEMENT

Dear Shareholders,

On behalf of the Board, I present to you the annual report and results of the Company for 2013, and to report to you on

the development focus of the Company for 2014.

In 2013, despite the slow recovery in the global economy, the aftermath of the global financial crisis persisted, leading to

stagnant international trade and greater pressure from trade protectionism. Affected by several factors such as excessive

production capacity and insufficient effective demand (especially shrinking overseas demand), the PRC economy was

faced with greater downward pressure. Responding to the complicated external environment and increasingly intensified

market competition, the Company aggressively exploited new market and proactively adjusted industrial structure,

meanwhile strived to increase revenue and efficiency and reduce expenses and costs, so as to effectively curb the

decline in profits and continuously strengthen its market competitiveness. During the reporting period, turnover of the

Group was RMB52,081.32 million, representing a year-on-year increase of 12.76%. Profit for the year was RMB1,465.41

million, representing a year-on-year decrease of 5.20%. Profit for the year attributable to owners of the Company was

RMB397.51 million, representing a year-on-year decrease of 12.11%. Earnings per share of the Company amounted to

RMB0.11.

CEMENT EQUIPMENT AND ENGINEERING SERVICES

Facing the significant decline in the fixed asset investments in domestic cement industry and the complicated and

volatile environment of the international market, the segment aggressively explored the overseas markets by leveraging

on its market competitive strength and advantages in the industry, with the amount of new order intakes for the year

amounting to RMB34.2 billion, representing a year-on-year increase of 11%, of which the amount of new order intakes

from the overseas markets amounted to RMB23.3 billion, representing a year-on-year increase of 68%. As at 31

December 2013, the amount of backlog of the segment amounted to RMB56.7 billion, laying a solid foundation for the

sustainable and healthy development of the segment in future.

CEMENT

The segment managed to overcome the dual adverse impacts of slowdown in the domestic economy and excessive

production capacity in the cement industry, and reinforced marketing efforts to continuously increase its market share,

achieving a year-on-year growth of 18% in the sales volume of cement and clinker. While maintaining its advantages

in the regional market, the segment enhanced benchmark comparison management, continuously improved operation

management and reduced production costs, resulting in a year-on-year decrease of 10% in the cost for each tonne of

cement. Responding to the excessive production capacity in cement industry, the segment accelerated the phase-out of

backward production capacity and technology upgrade of the existing production lines, so as to adjust its development

pace at the right time and to the right extent. As at the end of 2013, the production capacity of cement amounted to

105.88 million tonnes. The segment continued to extend its industrial chain, with the production capacity of commercial

concrete amounting to 32.65 million cubic meters. The scale of the cement and commercial concrete business

maintained stable growth.

9Annual Report 2013

CHAIRMAN’S STATEMENT

HIGH-TECH MATERIALS

Due to the impact of shrinking overseas demand, trade protection, excessive production capacity and weak domestic

demand, the major product markets of the segment remained sluggish with difficulties in product sales and payment

collection. In light of the unfavorable environment, the segment proactively expanded market coverage by forging alliance

with strategic partners and adopting flexible sales strategies, meanwhile strived to strengthen its competitiveness by

enhancing management capability, constantly reducing costs and optimizing process and workflows. The wind power fan

blade business proactively developed new products, focusing on development of large-size fan blades to increase the

added value of products, resulting in an increase of 3 percentage points in gross profit margin of products. The segment

stepped up efforts to explore the domestic and overseas markets in the CNG cylinder business, with the sales volume

increasing by 28% over the same period of last year. In addition to its efforts to enhance market promotion in the LNG

cylinder business, the segment continued to improve product quality and production scale. The Company constantly

adjusted its product mix and strengthened management on the coordinated development of sales and production in the

glass fiber and products business, achieving a production-to-sales ratio of 103% during the reporting period.

PROSPECTS

In 2014, despite the overall slow recovery in the global economy, the path to recovery will remain very bumpy, and

competition in the international market will become more intensified. The slowdown trend in overseas demand growth

will not be obviously improved. Although the long-term prospect of the PRC economy is positive, the foundation for

recovery is not very solid, thus the government will deepen reform and seek growth while maintaining stabilization.

The market competition will get intensified, and efforts will be made to deepen structural adjustment. The increase

in the costs of production essentials and the constraints in the resource and environment will constantly increase the

pressure in cost. The benefits and temporary setbacks brought by reform will impose far-reaching impact on the future

development of the Company. Seizing the opportunities brought by deepening of reform, structural adjustment as well

as promotion of urbanization and the development of the central and western regions, the Company will continuously

optimize enterprise structure and resource allocation, enhance basic management, strengthen technology innovation

and new product R&D and accelerate technology reform on existing industries and product upgrade, so as to enhance

the market competitiveness of its products. Adhering to the industry development concept of “innovation orientation,

quality and efficiency and sustainable development”, the Company will shift its focus from scale expansion to quality and

efficiency. In an effort to further deepen the strategy of “overseas expansion”, the Company will continuously increase

the share of overseas assets and businesses, step up efforts in exploring the international market, facilitate the transition

from domestic-oriented operation to internationalized operation and make continuous efforts to innovate its business

model, so as to improve the influence of the SINOMA brand and its capability for technology innovation. By enhancing its

capability in strategic leading, the Company will allocate quality assets to the high-end of the industrial chain and value

chain, and proactively promote the extension of industrial chain into the professional and high-end market. Furthermore,

the Company will strive to reduce costs and increase efficiency, allocate funds reasonably, reduce financing costs and

improve capital utilization, so as to maintain stable growth of the business.

CEMENT EQUIPMENT AND ENGINEERING SERVICES

The cement equipment and engineering services segment will continue to explore the international market, in an effort to

continuously increase its market share in Asia and Africa and strengthen the exploration of the cement engineering EPC

market focusing on states and regions including India, Russia and South America. The segment will proactively explore

the domestic market in energy conservation and environmental protection and technology reform of cement enterprises.

While maintaining its competitive edge in the cement engineering service market, the segment will continue to perfect

and innovate its business model, improve product and service quality, and facilitate the diversified development in the

China National Materials Company Limited10

CHAIRMAN’S STATEMENT

related industries. The segment will actively develop the business of diversified engineering services, increase the share

of spare parts and post-service businesses, and vigorously promote the business of co-disposal of waste, sludge and

urban garbage by cement kiln. The segment will further strengthen its efforts in the R&D of equipments, accelerating

the expansion of the equipment manufacturing business into the mining, metallurgical, chemical and power industries.

CEMENT

The release of the “State Council’s Guidelines on Addressing Severe Overcapacity Contradiction” and the “Notice

on Curbing the Blind Expansion of Industries with Serious Overcapacity jointly issued by National Development and

Reform Commission and the Ministry of Industry and Information Technology”, and the increasing efforts by the local

governments in eliminating backward production capacities and closing over-polluted enterprises, will help to promote the

positive development of cement industry. The segment will seize the opportunities brought to the industry by the State’s

economic policy to strengthen construction of new urbanization and the renovation of squatter settlements as well as the

State Council’s decision to further expedite railway construction in the central and western regions to vigorously enhance

its influence and control over the market and continuously improve its profitability. In light of market layout, the segment

will deepen benchmark comparison management, speed up technology reform and upgrade on existing production lines,

promote energy conservation and emission reduction, reduce production costs and proactively promote the expansion of

the business of co-disposal of industrial waste materials and urban garbage by cement kiln. Leveraging on the favourable

policies provided by the State for “overseas expansion”, the segment will speed up its investments in overseas markets.

HIGH-TECH MATERIALS

In light of the domestic and international economic environment and the market changes, the high-tech materials

segment will continue to deepen strategy implementation and target management, strengthen innovation in various

key factors such as management, technology and business model, enhance control on product quality and production

process, in an effort to cut costs, reduce inventories and trade receivables and improve operating efficiency of assets.

The segment will adjust its production and sales strategies in a timely manner, with an aim to maintain its leading

position in the wind power fan blade and natural gas cylinder industries. The wind power fan blade business will

continue to step up efforts in new product development and increase the proportion of production and sale of large-

size fan blades, striving to maintain a higher gross profit margin of the products and promote the implementation of

internationalization strategy on a timely basis. Tapping on the favourable market opportunities, the natural gas cylinder

business will speed up the establishment of sales channels and seek for more strategic partners. Efforts will be made

to further standardize the management on the production lines of the solar-energy fused silica crucibles and other high-

tech materials, so as to enhance qualified product rate. The glass fiber and products business will continue to reduce

production costs and adjust products mix, in an effort to improve product competitiveness.

On behalf of the Board, I would like to express my heartfelt gratitude to all the shareholders, investors and customers for

your long-term support to the Company and also thank the management and all staff of the Company for their dedication

and hard work for the Group.

LIU Zhijiang

Chairman of the Board

28 March 2014

11Annual Report 2013

MANAGEMENT DISCUSSION AND ANALYSIS

BUSINESS REVIEW

Overview

The Company, being the largest cement equipment and engineering services provider in the world, as well as a leading

producer of non-metal materials in China, is principally engaged in three business segments, namely, cement equipment

and engineering services, cement and high-tech materials.

CEMENT EQUIPMENT AND ENGINEERING SERVICES

Industry Review

During the reporting period, the global economy in general showed a trend of slow recovery. There were still many

uncertainties about the future development, and competition in the international market became more intensified.

Although an overall recovery trend in the international cement project construction market was still missing, some

regional markets had shown active performance. The long term prospect of the domestic economy was positive, but

the foundation for a stabilized market with steady growth was not solid enough. Affected by excessive production

capacity, the additional cement and clinker production capacity in China recorded a growth of 94.3 million tonnes in 2013,

representing a significant decline as compared to that of 2012. The fixed asset investments in domestic cement industry

completed in 2013 amounted to RMB132.86 billion, representing a year-on-year decrease of 3.70%. The number of new

production lines in domestic cement industry was dropping rapidly year by year.

Business Review

Continuously enhancing exploitation of the international market to maintain its market shares

During the reporting period, the Company enhanced adjustment in operating strategy, shifting market exploration from

focusing on both the domestic and international markets to focusing on the international market with the domestic

market as supplement. The Company aggressively expanded overseas sales channels and made full use of the influence

of its brand name, in an effort to further explore the potential markets such as the Middle East, Southeast Asia, South

America, Europe and Africa. The amount of overseas new order intakes for the year amounted to RMB23.259 billion,

representing a year-on-year increase of 67.66%. The amount of new EPC order intakes from the international market

ranked first in terms of market share for the sixth consecutive years.

Achieving overall smooth progress in projects under construction and further improving contract

performance capability

The Company always took it as a priority to strengthen its contract performance capability and improve service

quality, and achieved remarkable results. During the reporting period, a total of twelve EPC projects have received

Final Acceptance Certificate (FAC) and eleven EPC projects have received Provisional Acceptance Certificate (PAC), in

which, the EPC project of phase II cement production line with 5,300t/d of the Silemani Cement Plant (SCP) in Iraq was

honored the “Overseas Construction Project Luban Award” by the China Construction Industry Association. Despite

many unfavorable factors, and with advanced preparation and careful planning, the EPC project of HCC5,000t/d cement

production line in Saudi Arabia was eventually completed as scheduled and was honored the “Special Contribution

Award” by the Saudi Arabia government. The excellent performance of overseas contracts helped to promote the

establishment of company brand and offered great support to boost our market competitive strength.

China National Materials Company Limited12

MANAGEMENT DISCUSSION AND ANALYSIS

Enhancing cooperation to improve international operation capability

During the reporting period, the Company forged alliance with some world-known enterprises such as Lafarge to

cooperate with these companies in establishment of international brand, financing, management, talent cultivation,

technology innovation and industry complementary development, global resource allocation and international market

exploration. Focusing on improvement of the core tache of the industrial chain and achieving global resource allocation

by channeling investments overseas, the Company successfully acquired LNVT, a cement equipment and engineering

company in India, so as to realize local operation and promote exploration of the Indian market, enhancing the export and

brand influence of our cement equipment business in the Indian market.

Making new R&D achievements and continuously enhancing technical competitiveness

The Company further improved the enterprise-centered and market-oriented R&D system supported by industry,

academy and research. Strengthening collaborative innovations and conducting R&D to meet the demands of industrial

development, it has gained the R&D and manufacturing capabilities in the fields of integrated sludge disposal as well

as waste gasification technology and equipment; meanwhile, it also further accelerated the transformation of scientific

research results and effectively promoted the development of the industry. The TRMR60.4 raw materials vertical roller

mill with the largest production per hour, a product manufactured by the Company in China, passed the new product

assessment organized by China Building Materials Federation and filled the domestic blank of single raw materials

vertical roller mill with a production of 6000 to 7000 tonnes per day to support cement clinker production lines. The

crushing and grinding equipment have entered the metallurgical and mining markets.

CEMENT

Industry Review

During the reporting period, the domestic cement industry started to show a rebound trend. Although the industry

witnessed a sluggish situation in the first half of the year, it benefited from investment in fixed assets and the rapid

development of the real estate industry in the second half as well as the increasing downstream demands and recorded

an annual total production of cement of 2.42 billion tonnes, representing a year-on-year increase of 9.3%. As regards

supply, as China enhanced policy control over the cement industry and other industries with excessive production

capacity, and local governments stepped up their efforts to eliminate backward production capacity and shut down

enterprises with emissions beyond the standards, the excessive growth of production capacity was effectively curbed,

new production capacity in China further declined and the oversupply situation was mitigated. The profitability of the

industry was improved as evidenced by the whole industry’s annual profit of RMB76.6 billion, or a year-on-year increase

of 16.4%.

Business Review

Implementing prudent development strategy to respond to industry overcapacity

Facing the industry-wide overcapacity situation, the segment maintained a prudent development momentum, controlled

the investment and construction rate of new cement and commercial concrete mixing station projects, accelerated the

elimination of backward production capacity, and increased the technical transformation and optimization and upgrade

of existing production lines. During the reporting period, the production capacity of cement and commercial concrete

reached 105.88 million tonnes and 32.65 million cubic meters respectively.

13Annual Report 2013

MANAGEMENT DISCUSSION AND ANALYSIS

Optimizing the operation capability of the segment and continuing to enhance the competitive advantage

Focusing on operational optimization, this segment continuously carried out management optimization and technical

innovations for the existing production lines, improved the performance indicators of the production lines, and constantly

reduced the product manufacturing costs of the segment. During the reporting period, the costs per tonne of cement

fell by 10% as compared to the previous year, and standard coal consumption per tonne of clinker fell by 0.8 kilogram

as compared to the previous year. As the product costs continued to decline, the competitive advantage of the segment

was enhanced. As the overall environment of the industry became positive, the segment recorded a significant growth

as compared to the previous year.

Continuing to implement the strategy of energy conservation and emission reduction and fulfilling

corporate social responsibility

The segment was always committed to energy conservation and emission reduction of cement production lines, and

continued to earnestly fulfill corporate social responsibility. During the reporting period, the segment invested in the

construction of waste heat power generation capacity of 55.5MW, the installed capacity totaled 348.5MW, and the

accumulated power generation for the year reached 1,528.488 million kwh, reducing 1.3718 million tonnes of carbon

dioxide emission; in accordance with the new standards concerning nitrogen oxides emissions from the cement industry

issued by the Ministry of Environmental Protection of the People’s Republic of China, the segment continued to build

supportive denitrification systems for cement clinker production lines. So far, over 50% of the production lines have run

the denitrification systems.

HIGH-TECH MATERIALS

Industry Review

During the reporting period, the global economy recorded slow recovery. Except for the wind power fan blade industry

which presented a rebound trend, the other industries were exposed to sluggish markets and intensifying competitions.

The wind power fan blade industry witnessed overall improvement as the State Grid launched several projects to

promote wind power grid integration, which continuously optimized the layout of wind power development and mitigated

the “abandoning wind power” scenario to some extent. In 2013, the newly installed capacity of China’s wind power

industry amounted to approximately 16.1GW, representing a year-on-year increase of 24%. The CNG cylinder industry

was exposed to intensifying market competitions at home and abroad, and the demand for natural gas at the domestic

market dropped due to the increase of price; as regards the overseas markets, while the new cylinder factories in

China, India and other countries commenced production, the demands from the traditional consumption countries

(Pakistan, Thailand, Uzbekistan, etc.) dropped significantly due to policies and gas prices, resulting in increasingly heated

competitions. The situation of the domestic and overseas markets of the glass fiber industry was more severe and

complicated than 2012 as the growth rate of domestic economy slowed down and the downstream enterprises of the

glass fibre composite materials industry chain faced overall depression. 2013 was the most depressed year for electronic

yarn and electronic glass fabrics in the history. The glass roving, yarn and electronic glass fabric products recorded

industry-wide loss; as regards the overseas markets, the U.S. and Japan markets remained relatively stable, but their

growth was limited; the consumption volume of glass fibers in Middle East was similar to that of 2012 and only half of

that of 2008; the Indian market remained subdued; Europe was still at low ebb. The solar-energy fused silica crucibles

industry picked up slightly, but has not got completely out of the trouble.

China National Materials Company Limited14

MANAGEMENT DISCUSSION AND ANALYSIS

Business Review

Strengthening technical innovations and driving quality improvement and cost control

During the reporting period, leveraging on the advantages of sophisticated R&D platform and the super R&D team, the

high-tech materials segment continuously strengthened technical innovations, kept optimizing the production process,

improved labor productivity, improved product performance and cut down overall costs. In particular, the average sales

costs of wind power fan blades decreased by 10.80% while the gross margin increased by 3.17 percentage points as

compared with the previous year respectively. The average sales costs of CNG cylinders decreased by 1.12% while the

gross margin increased by 3.14 percentage points as compared with the previous year respectively.

Enhancing the management of inventory and accounts receivable and improving efficiency of fund application

During the reporting period, the high-tech materials segment continuously strengthened the management of the

enterprise’s inventory and accounts receivable, tried to reduce the proportions of inventory and accounts receivable to

income, cut down the funds taken up and reduced operational risks. The proportion of inventory to turnover dropped by

5 percentage points while the proportion of accounts receivable to turnover dropped by 3 percentage points.

Optimizing customer management and developing the market in a comprehensive way

During the reporting period, the high-tech materials segment continued to optimize customer management by

implementing classified management of customers. While retaining old customers, the segment continuously explored

new customers. Each key product has realized customer diversification, thus avoiding the risks due to a single customer

and increasing the market share at the same time. The production and sales volume of wind power fan blades continued

to lead the domestic market. The sales volume of cylinder also achieved relatively big growth.

15Annual Report 2013

MANAGEMENT DISCUSSION AND ANALYSIS

FINANCIAL REVIEW

Year ended

31 December

2013

Year ended

31 December

2012 Change

RMB million RMB million RMB million %

(Restated)

Turnover 52,081.32 46,187.07 5,894.25 12.76

Cost of sales (42,069.19) (37,829.05) (4,240.14) 11.21

Gross profit 10,012.13 8,358.02 1,654.11 19.79

Other gains 1,391.84 1,452.56 (60.72) (4.18)

Selling and marketing expenses (1,822.56) (1,553.64) (268.92) 17.31

Administrative expenses (5,450.37) (4,651.29) (799.08) 17.18

Exchange (loss) gain (85.26) 1.69 (86.95) (5,144.97)

Other expenses (53.32) (31.81) (21.51) 67.62

Operating profit 3,992.46 3,575.53 416.93 11.66

Interest income 139.25 170.09 (30.84) (18.13)

Finance costs (1,961.95) (1,683.51) (278.44) 16.54

Share of results of associates 66.35 7.37 58.98 800.27

Share of results of joint ventures (27.27) (10.67) (16.60) 155.58

Profit before tax 2,208.84 2,058.80 150.04 7.29

Income tax expense (743.43) (512.96) (230.47) 44.93

Profit for the year 1,465.41 1,545.84 (80.43) (5.20)

Profit for the year attributable to:

Owners of the Company 397.51 452.29 (54.78) (12.11)

Non-controlling interests 1,067.90 1,093.55 (25.65) (2.35)

Dividends 71.43 107.14

Results Performance

During the reporting period, profit before tax of the Group was RMB2,208.84 million, representing a year-on-year increase

of 7.29%. Profit for the year attributable to owners of the Company was RMB397.51 million, representing a year-on-year

decrease of 12.11%. Earnings per share of the Company was RMB0.11.

Consolidated Operating Results

The financial information for the segments presented below is before elimination of inter-segment transactions and

before unallocated expenses.

Turnover

Turnover of the Group in 2013 was RMB52,081.32 million, representing an increase of 12.76% as compared with

RMB46,187.07 million in 2012. The increase was mainly due to the increase in the turnover of the cement segment.

In particular, turnover of the cement equipment and engineering services segment, cement segment and high-tech

materials segment decreased by RMB316.77 million, increased by RMB3,906.87 million and increased by RMB807.26

million, respectively.

China National Materials Company Limited16

MANAGEMENT DISCUSSION AND ANALYSIS

Cost of Sales

Cost of sales of the Group in 2013 was RMB42,069.19 million, representing an increase of 11.21% as compared with

RMB37,829.05 million in 2012. The increase was mainly due to the increase in product sales volume of the cement

segment. In particular, cost of sales of the cement equipment and engineering services segment, cement segment

and high-tech materials segment increased by RMB150.74 million, increased by RMB2,043.69 million and increased by

RMB680.95 million, respectively.

Gross Profit and Gross Margin

Gross profit of the Group in 2013 was RMB10,012.13 million, representing an increase of 19.79% as compared with

RMB8,358.02 million in 2012. In particular, gross profit of the cement equipment and engineering services segment,

cement segment and high-tech materials segment decreased by RMB467.51 million, increased by RMB1,863.18 million

and increased by RMB126.31 million, respectively.

Gross margin of the Group in 2013 was 19.22%, representing an increase of 1.12 percentage points as compared with

18.10% in 2012.

Other Gains

Other gains of the Group in 2013 were RMB1,391.84 million, representing a decrease of 4.18% as compared with

RMB1,452.56 million in 2012 which was mainly due to the decrease in gains from disposal of long-term equities.

Selling and Marketing Expenses

Selling and marketing expenses of the Group in 2013 were RMB1,822.56 million, representing an increase of 17.31% as

compared with RMB1,553.64 million in 2012. The increase was mainly due to the increase in product sales volume of

the cement segment. In particular, selling and marketing expenses of the cement equipment and engineering services

segment, cement segment and high-tech materials segment increased by RMB13.97 million, increased by RMB217.51

million and increased by RMB37.45 million, respectively.

Administrative Expenses

Administrative expenses of the Group in 2013 were RMB5,450.37 million, representing an increase of 17.18% as

compared with RMB4,651.29 million in 2012. The increase was mainly due to the significant increase in impairment loss

recognised in respect of assets. In particular, administrative expenses of the cement equipment and engineering services

segment, cement segment and high-tech materials segment increased by RMB279.16 million, increased by RMB520.15

million and increased by RMB12.89 million, respectively.

Exchange (Loss) Gain

Exchange loss of the Group in 2013 was RMB85.26 million, representing a decrease of 5,144.97% as compared with the

exchange gain of RMB1.69 million in 2012. The decrease was mainly due to the large amount of deposits denominated

in foreign currency held by the Group and the appreciation of the RMB during the period.

Other Expenses

Other expenses of the Group in 2013 were RMB53.32 million, representing an increase of 67.62% as compared with

RMB31.81 million in 2012. The increase was mainly due to the increase in loss from the disposal of fixed assets.

17Annual Report 2013

MANAGEMENT DISCUSSION AND ANALYSIS

Operating Profit and Operating Profit Margin

Operating profit of the Group in 2013 was RMB3,992.46 million, representing an increase of 11.66% as compared with

RMB3,575.53 million in 2012. In particular, operating profit of the cement equipment and engineering services segment,

cement segment and high-tech materials segment decreased by RMB761.25 million, increased by RMB1,175.64 million

and decreased by RMB139.98 million, respectively.

Operating profit margin in 2013 was 7.67%, representing a decrease of 0.07 percentage point as compared with 7.74%

in 2012.

Interest Income

Interest income of the Group in 2013 was RMB139.25 million, representing a decrease of 18.13% as compared with

RMB170.09 million in 2012.

Finance Costs

Finance costs of the Group in 2013 were RMB1,961.95 million, representing an increase of 16.54% as compared with

RMB1,683.51 million in 2012. The increase was mainly due to the expansion of the scale of financing.

Share of Results of Associates

Share of results of associates of the Group in 2013 was RMB66.35 million, representing an increase of 800.27% as

compared with RMB7.37 million in 2012. The increase was mainly due to the increase of the results of some associates

and the disposal of some loss-making associates during the period.

Share of Results of Joint Ventures

Share of results of joint ventures of the Group in 2013 was a loss of RMB27.27 million, representing an increase of

155.58% as compared with a loss of RMB10.67 million in 2012. The increase was mainly due to the increase of losses

made by some joint ventures during the period.

Income Tax Expense

Income tax expense of the Group in 2013 was RMB743.43 million, representing an increase of 44.93% as compared

with RMB512.96 million in 2012, mainly due to the significant growth in the result of the cement segment during the

period as compared with the corresponding period of last year.

Profit for the Year Attributable to Non-controlling Interests

Profit for the year attributable to non-controlling interests of the Group in 2013 was RMB1,067.90 million, representing a

decrease of 2.35% as compared with RMB1,093.55 million in 2012.

Profit for the Year Attributable to Owners of the Company

Based on the above, profit for the year attributable to owners of the Company in 2013 was RMB397.51 million,

representing a decrease of 12.11% as compared with RMB452.29 million in 2012.

Segment Results

The financial information for each segment presented below is before elimination of inter-segment transaction and before

unallocated expenses.

China National Materials Company Limited18

MANAGEMENT DISCUSSION AND ANALYSIS

Cement Equipment and Engineering Services

2013 2012 Change

RMB million RMB million %

(Restated)

Turnover 22,668.36 22,985.13 (1.38)

Cost of sales 19,611.94 19,461.20 0.77

Gross profit 3,056.42 3,523.93 (13.27)

Selling and marketing expenses 190.81 176.84 7.90

Administrative expenses 2,380.65 2,101.49 13.28

Segment results 541.09 1,302.34 (58.45)

Turnover

Turnover of the cement equipment and engineering services segment in 2013 was RMB22,668.36 million, representing

a decrease of 1.38% as compared with RMB22,985.13 million in 2012. The decrease was mainly due to the significant

decrease in sales revenue of trading.

Cost of Sales

Cost of sales of the cement equipment and engineering services segment in 2013 was RMB19,611.94 million,

representing an increase of 0.77% as compared with RMB19,461.20 million in 2012, mainly due to the increase in

business volume of the main businesses.

Gross Profit and Gross Margin

Gross profit of the cement equipment and engineering services segment in 2013 was RMB3,056.42 million, representing

a decrease of 13.27% as compared with RMB3,523.93 million in 2012. Gross margin of the cement equipment and

engineering services segment decreased by 1.85 percentage points from 15.33% in 2012 to 13.48% in 2013. The

decrease was mainly attributable to the decrease in contract price due to severe market competition.

Selling and Marketing Expenses

Selling and marketing expenses of the cement equipment and engineering services segment in 2013 were RMB190.81

million, representing an increase of 7.90% as compared with RMB176.84 million in 2012, mainly due to the increase in

labor costs.

Administrative Expenses

Administrative expenses of the cement equipment and engineering services segment in 2013 were RMB2,380.65 million,

representing an increase of 13.28% as compared with RMB2,101.49 million in 2012. The increase was mainly due to the

significant increase in impairment loss.

Segment Results

Based on the above, results of the cement equipment and engineering services segment in 2013 were RMB541.09

million, representing a decrease of 58.45% as compared with RMB1,302.34 million in 2012.

19Annual Report 2013

MANAGEMENT DISCUSSION AND ANALYSIS

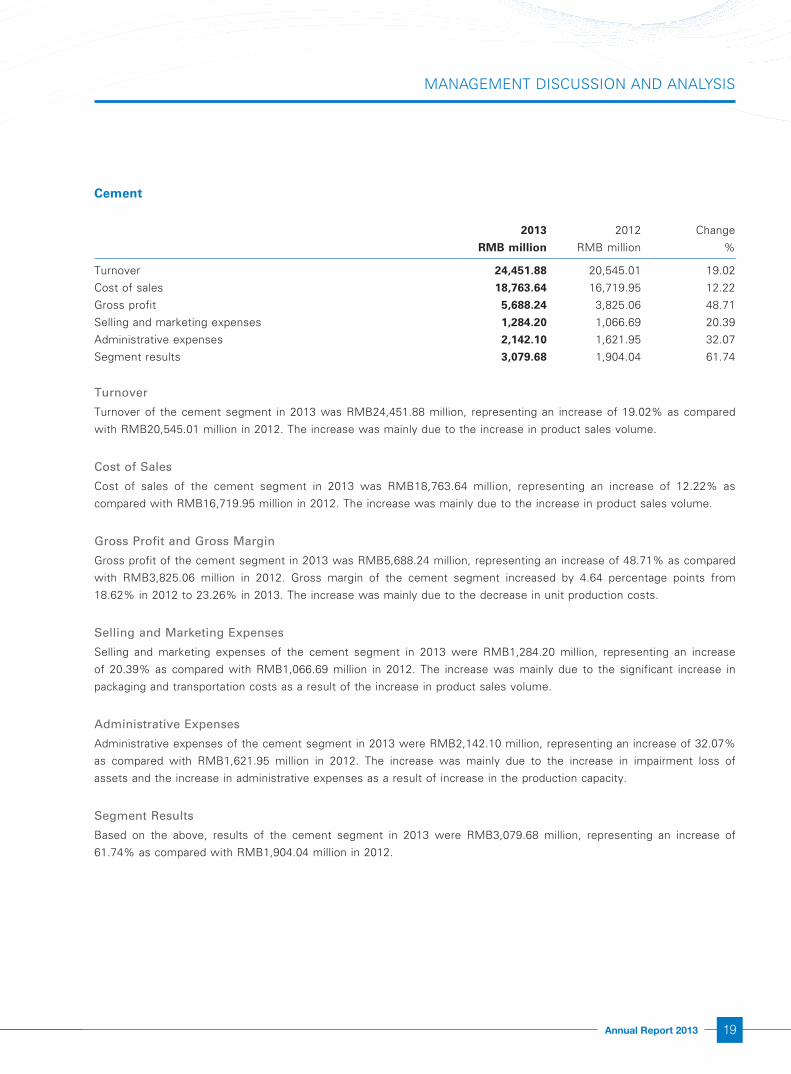

Cement

2013 2012 Change

RMB million RMB million %

Turnover 24,451.88 20,545.01 19.02

Cost of sales 18,763.64 16,719.95 12.22

Gross profit 5,688.24 3,825.06 48.71

Selling and marketing expenses 1,284.20 1,066.69 20.39

Administrative expenses 2,142.10 1,621.95 32.07

Segment results 3,079.68 1,904.04 61.74

Turnover

Turnover of the cement segment in 2013 was RMB24,451.88 million, representing an increase of 19.02% as compared

with RMB20,545.01 million in 2012. The increase was mainly due to the increase in product sales volume.

Cost of Sales

Cost of sales of the cement segment in 2013 was RMB18,763.64 million, representing an increase of 12.22% as

compared with RMB16,719.95 million in 2012. The increase was mainly due to the increase in product sales volume.

Gross Profit and Gross Margin

Gross profit of the cement segment in 2013 was RMB5,688.24 million, representing an increase of 48.71% as compared

with RMB3,825.06 million in 2012. Gross margin of the cement segment increased by 4.64 percentage points from

18.62% in 2012 to 23.26% in 2013. The increase was mainly due to the decrease in unit production costs.

Selling and Marketing Expenses

Selling and marketing expenses of the cement segment in 2013 were RMB1,284.20 million, representing an increase

of 20.39% as compared with RMB1,066.69 million in 2012. The increase was mainly due to the significant increase in

packaging and transportation costs as a result of the increase in product sales volume.

Administrative Expenses

Administrative expenses of the cement segment in 2013 were RMB2,142.10 million, representing an increase of 32.07%

as compared with RMB1,621.95 million in 2012. The increase was mainly due to the increase in impairment loss of

assets and the increase in administrative expenses as a result of increase in the production capacity.

Segment Results

Based on the above, results of the cement segment in 2013 were RMB3,079.68 million, representing an increase of

61.74% as compared with RMB1,904.04 million in 2012.

China National Materials Company Limited20

MANAGEMENT DISCUSSION AND ANALYSIS

High-tech Materials

2013 2012 Change

RMB million RMB million %

(Restated)

Turnover 6,802.69 5,995.43 13.46

Cost of sales 5,341.12 4,660.17 14.61

Gross profit 1,461.57 1,335.26 9.46

Selling and marketing expenses 347.56 310.11 12.08

Administrative expenses 868.56 855.67 1.51

Segment results 589.04 729.02 (19.20)

Turnover

Turnover of the high-tech materials segment in 2013 was RMB6,802.69 million, representing an increase of 13.46% as

compared with RMB5,995.43 million in 2012. The increase was mainly due to the increase in sales volume of the major

products.

Cost of Sales

Cost of sales of the high-tech materials segment in 2013 was RMB5,341.12 million, representing an increase of 14.61%

as compared with RMB4,660.17 million in 2012. The increase was mainly due to the increase in sales volume of the

major products.

Gross Profit and Gross Margin

Gross profit of the high-tech materials segment in 2013 was RMB1,461.57 million, representing an increase of 9.46%

as compared with RMB1,335.26 million in 2012. Gross margin of the high-tech materials segment decreased by 0.78

percentage point from 22.27% in 2012 to 21.49% in 2013. The decrease was mainly due to the decrease in the gross

margin of the fiberglass products.

Selling and Marketing Expenses

Selling and marketing expenses of the high-tech materials segment in 2013 were RMB347.56 million, representing an

increase of 12.08% as compared with RMB310.11 million in 2012. The increase was mainly due to the increase of the

transportation costs.

Administrative Expenses

Administrative expenses of the high-tech materials segment in 2013 were RMB868.56 million, representing an increase

of 1.51% as compared with RMB855.67 million in 2012.

Segment Results

Based on the above, results of the high-tech materials segment in 2013 were RMB589.04 million, representing a

decrease of 19.20% as compared with RMB729.02 million in 2012.

21Annual Report 2013

MANAGEMENT DISCUSSION AND ANALYSIS

Liquidity and Capital Resources

Cash flows:

2013 2012

RMB million RMB million

(Restated)

Net cash from operating activities 496.93 1,592.36

Net cash used in investing activities (2,891.54) (5,743.77)

Net cash from financing activities 474.48 3,103.93

Cash and cash equivalents at the end of the year 7,270.06 9,235.27

Net cash from operating activities

Net cash from operating activities decreased from RMB1,592.36 million in 2012 to RMB496.93 million in 2013. The

decrease was mainly due to the increase in trade and other receivables.

Net cash used in investing activities

Net cash used in investing activities decreased from RMB5,743.77 million in 2012 to RMB2,891.54 million in 2013. The

decrease was mainly due to the decrease in the investment in fixed assets.

Net cash from financing activities

Net cash from financing activities decreased from RMB3,103.93 million in 2012 to RMB474.48 million in 2013. The

decrease was mainly due to the decrease in equity finance on a year-on-year basis.

Working Capital

As at 31 December 2013, the Group’s cash and cash equivalents amounted to RMB7,270.06 million (2012: RMB9,235.27

million). Unutilised bank credit facilities amounted to RMB30,125.71 million (2012: RMB31,172.86 million). The current

ratio (calculated by dividing the total current assets by the total current liabilities) of the Group as at 31 December 2013

decreased to 82.28% (2012: 88.18%).

The Group monitors its capital status on the basis of the net debt ratio which is calculated as net debt divided by total

capital. Net debt is calculated as the total amount of interest-bearing debts (including current and non-current borrowings,

short-term financing bills, medium-term notes and corporate bonds as shown in the consolidated statement of financial

position) less restricted bank balances and bank balances and cash. As at 31 December 2013, the net debt ratio of the

Group was 94.74% (2012: 80.46%).

With stable cash inflow from daily operating activities as well as existing unutilised bank credit facilities, the Group has

sufficient financing resources for its future expansion.

China National Materials Company Limited22

MANAGEMENT DISCUSSION AND ANALYSIS

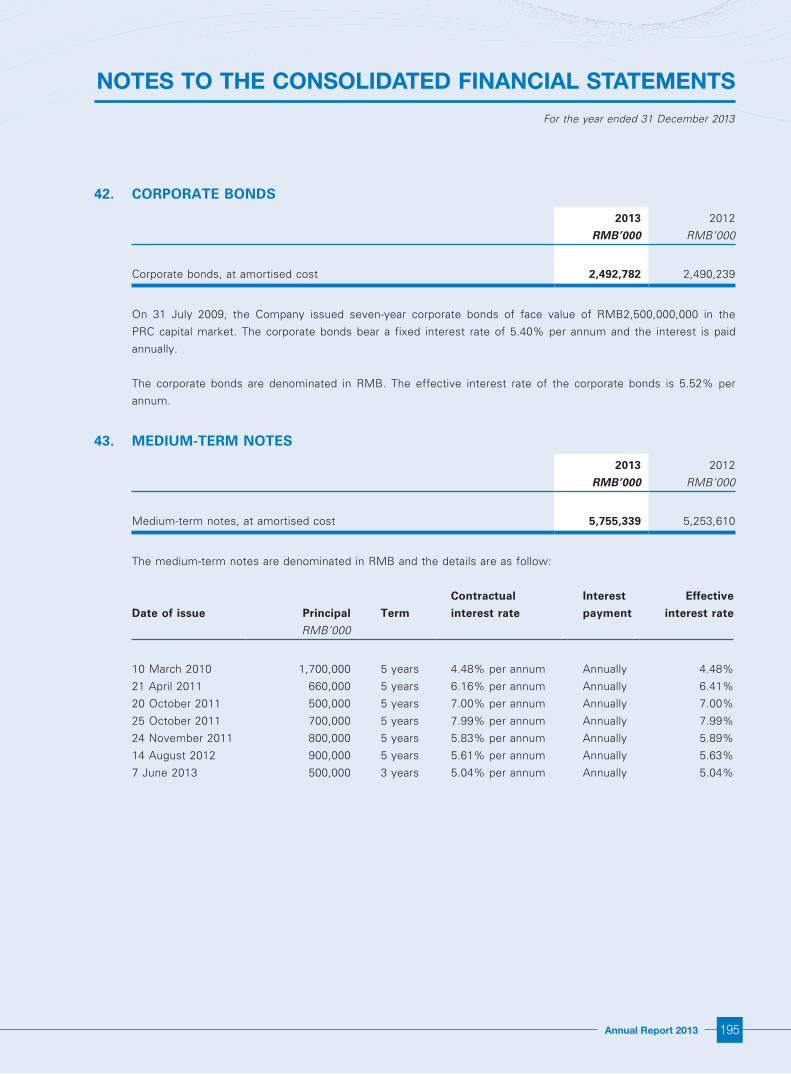

Borrowings

As at 31 December 2013, the balance of the Group’s borrowings amounted to RMB35,337.37 million.

31 December

2013

31 December

2012

RMB million RMB million

(Restated)

Short-term borrowings and long-term borrowings due within one year 16,257.82 15,749.45

Short-term financing bills 2,900.00 400.00

Long-term borrowings, net of portions due within one year 7,931.43 9,280.60

Corporate bonds 2,492.78 2,490.24

Medium-term notes 5,755.34 5,253.61

Total borrowings 35,337.37 33,173.90

Net Current Liabilities

As at 31 December 2013, the net current liabilities of the Group was approximately RMB8,587.84 million, representing an

increase of RMB3,629.52 million as compared with the net current liabilities of RMB4,958.32 million as at 31 December

2012. The increase was mainly due to the increase in the short-term borrowings, short-term financing bills and trade and

other payables.

Inventory Analysis

As at 31 December 2013, the inventory of the Group was approximately RMB8,773.28 million, representing an increase

of RMB379.93 million as compared with RMB8,393.35 million as at 31 December 2012. The inventory turnover days

decreased from 78.63 days in 2012 to 73.45 days in 2013.

Trade Receivables

As at 31 December 2013, the Group’s trade receivables was approximately RMB12,497.38 million, representing an

increase of RMB2,125.83 million as compared with the trade receivables of RMB10,371.55 million as at 31 December

2012. In 2013, the average turnover days of trade receivables of the Group increased by 5.17 days from 73.87 days in

2012 to 79.04 days in 2013, which was due to the longer turnover day of the receivables of the commercial concrete

products and the increase in its sales volume.

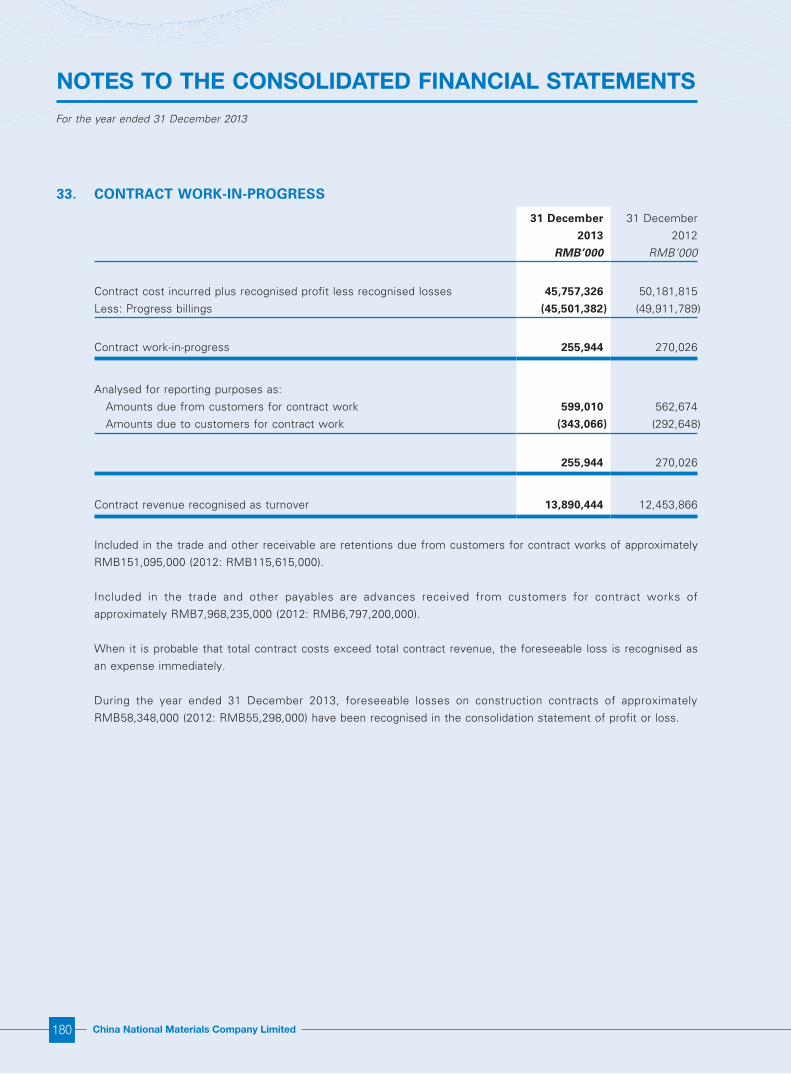

Contract Work-in-Progress

As at 31 December 2013, the Group’s contract work-in-progress was approximately RMB255.94 million (as at 31

December 2012: RMB270.03 million).

Pledge of Assets

The Group’s property, plant and equipment, and prepaid lease payments with carrying values of RMB1,079.59 million

and RMB49.33 million respectively as at 31 December 2013 were pledged as security (31 December 2012: RMB3,305.17

million and RMB107.38 million respectively).

23Annual Report 2013

MANAGEMENT DISCUSSION AND ANALYSIS

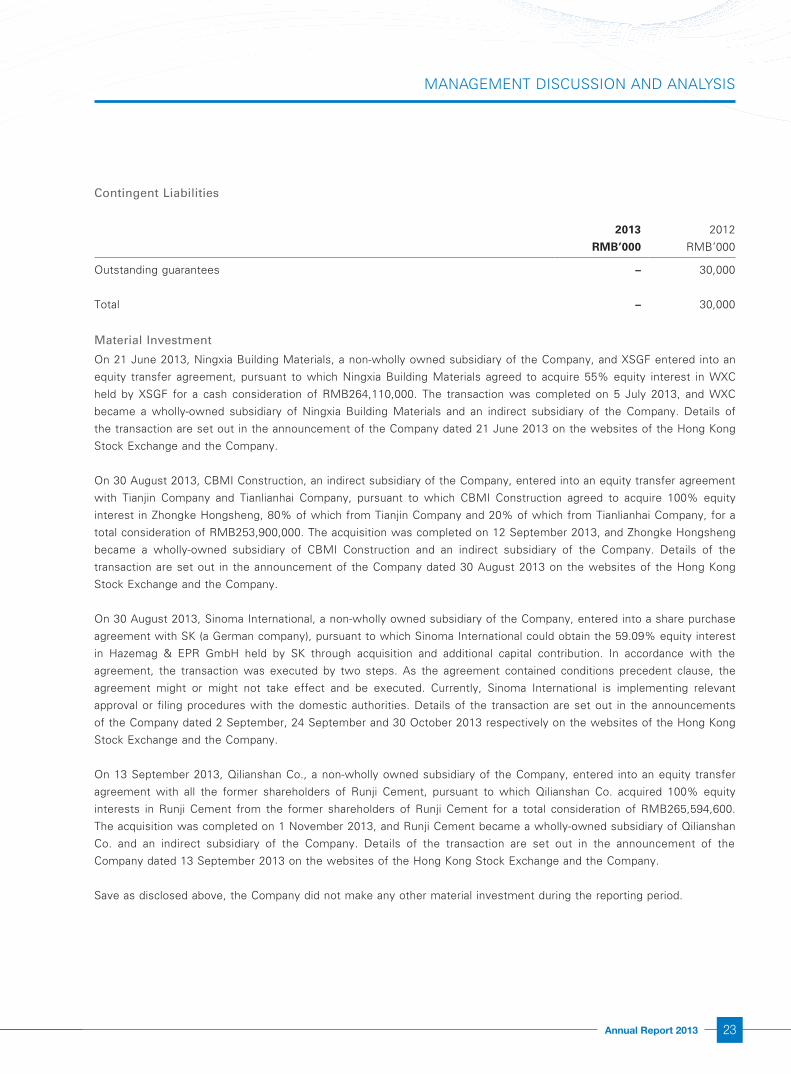

Contingent Liabilities

2013 2012

RMB’000 RMB’000

Outstanding guarantees – 30,000

Total – 30,000

Material Investment

On 21 June 2013, Ningxia Building Materials, a non-wholly owned subsidiary of the Company, and XSGF entered into an

equity transfer agreement, pursuant to which Ningxia Building Materials agreed to acquire 55% equity interest in WXC

held by XSGF for a cash consideration of RMB264,110,000. The transaction was completed on 5 July 2013, and WXC

became a wholly-owned subsidiary of Ningxia Building Materials and an indirect subsidiary of the Company. Details of

the transaction are set out in the announcement of the Company dated 21 June 2013 on the websites of the Hong Kong

Stock Exchange and the Company.

On 30 August 2013, CBMI Construction, an indirect subsidiary of the Company, entered into an equity transfer agreement

with Tianjin Company and Tianlianhai Company, pursuant to which CBMI Construction agreed to acquire 100% equity

interest in Zhongke Hongsheng, 80% of which from Tianjin Company and 20% of which from Tianlianhai Company, for a

total consideration of RMB253,900,000. The acquisition was completed on 12 September 2013, and Zhongke Hongsheng

became a wholly-owned subsidiary of CBMI Construction and an indirect subsidiary of the Company. Details of the

transaction are set out in the announcement of the Company dated 30 August 2013 on the websites of the Hong Kong

Stock Exchange and the Company.

On 30 August 2013, Sinoma International, a non-wholly owned subsidiary of the Company, entered into a share purchase

agreement with SK (a German company), pursuant to which Sinoma International could obtain the 59.09% equity interest

in Hazemag & EPR GmbH held by SK through acquisition and additional capital contribution. In accordance with the

agreement, the transaction was executed by two steps. As the agreement contained conditions precedent clause, the

agreement might or might not take effect and be executed. Currently, Sinoma International is implementing relevant

approval or filing procedures with the domestic authorities. Details of the transaction are set out in the announcements

of the Company dated 2 September, 24 September and 30 October 2013 respectively on the websites of the Hong Kong

Stock Exchange and the Company.

On 13 September 2013, Qilianshan Co., a non-wholly owned subsidiary of the Company, entered into an equity transfer

agreement with all the former shareholders of Runji Cement, pursuant to which Qilianshan Co. acquired 100% equity

interests in Runji Cement from the former shareholders of Runji Cement for a total consideration of RMB265,594,600.

The acquisition was completed on 1 November 2013, and Runji Cement became a wholly-owned subsidiary of Qilianshan

Co. and an indirect subsidiary of the Company. Details of the transaction are set out in the announcement of the

Company dated 13 September 2013 on the websites of the Hong Kong Stock Exchange and the Company.

Save as disclosed above, the Company did not make any other material investment during the reporting period.

China National Materials Company Limited24

MANAGEMENT DISCUSSION AND ANALYSIS

Material Acquisitions and Disposals of Assets

Save the relevant acquisitions as disclosed in the above section headed “Material Investment”, the Company did not

have any material acquisition or disposal of assets in respect of its subsidiaries and associates during the reporting

period.

Market Risks

The Company is exposed to various types of market risks in the normal course of its business, including contract risk,

foreign exchange risk, interest risk and raw materials and energy price risk.

Contract Risks

The international business accounts for a larger proportion in the Company’s cement equipment and engineering services

businesses, with a long construction period. Furthermore, in respect of the overseas contracts, under the impacts of

uncontrollable factors such as the global environment and political and economic conditions of the place of contract

performance, certain projects may have the risks of being deferred, modified or terminated.

During the reporting period, the Company further enhanced the management of contract risks, standardized contract

terms of new order intakes and improved the execution ability of contracts. The Company cleared out the contracts at

hand and had carried out risk prevention plan. For the projects under construction, the Company enhanced assessment

of the default in payment of project owners, paid close attention to the project owners’ credit status, and conduct

periodic settlement for projects in time. For delay and suspension in the construction of the related projects, the

Company actively communicated with the project owners to avoid losses. The Company will continue to strengthen the

above measures in the future to effectively address the contract risks.

Foreign Exchange Risks

The Group conducts its domestic business primarily in RMB, which is also its functional currency. However, overseas

engineering projects and export of products are denominated in foreign currencies, primarily US dollars and Euro.

Therefore, the Group bears the risks of fluctuations of exchange rate to a certain extent.

Interest Rate Risks

The Group raises borrowings to support general corporate purposes, including capital expenditures and working capital

needs. The interest rate of the borrowings is subject to adjustment by its lenders in accordance with changes of the

regulations of the People’s Bank of China. Therefore, the Group bears the risks arising from the fluctuations in the

interest rate of the borrowings.

Raw Materials and Energy Price Risks

The Company mainly consumes raw materials and energy resources, such as steel, coal, electricity and natural gas, the

price fluctuation of which has a significant impact on the cost of the Company.

25Annual Report 2013

BIOGRAPHY OF DIRECTORS, SUPERVISORS AND SENIOR MANAGEMENT

EXECUTIVE DIRECTORS

LIU Zhijiang, aged 56, has been an executive Director and chairman of the Board since February 2013. Prior to that,

Mr. Liu served as a non-executive Director from July 2007 to February 2013. He has over 30 years of experience in the

PRC non-metal materials industry and served a number of key positions in Tianjin Cement Industry Design & Research

Institute from August 1982 to May 2005, such as deputy head and head of the institute. He served as a deputy general

manager of the Parent from May 2005 to May 2009; a director and general manager of the Parent from May 2009 to

January 2013, and has been appointed as the chairman of the Parent since January 2013. Mr. Liu has been serving

as a director of two A share-listed companies, namely Sinoma International and Tianshan Cement, since April 2006

and January 2014, respectively, and served as the chairman of the board of Sinoma International from April 2006 to

December 2009. Mr. Liu is entitled to a special government allowance provided by the State Council. He was awarded as

Provincial Young and Middle Aged Expert with Important Contribution (省部級有重要貢獻的中青年專家), China Engineering

Design Master and was included in the first group of national candidates for the New Century Hundred-Thousand-

Ten Thousand Talents Project (新世紀百千萬人才工程國家級人選). Mr. Liu also serves various positions such as the

vice president of China Building Materials Federation (中國建築材料聯合會) and the president of China Building Material

Construction Association (中國建材工程建設協會). Mr. Liu graduated from South China University of Technology (華南理工大學) in July 1982, majoring in binding materials. He is a professorate senior engineer.

LI Xinhua, aged 49, is an executive Director and president of the Company and has been the vice chairman of the Board

since February 2013. He served as a vice president of the Company from July 2007 to October 2009. He has been

serving as an executive Director since December 2009; vice chairman of the Board from December 2009 to May 2011,

and president of the Company since January 2011. Mr. Li has over 25 years of experience in the non-metal materials

industry. Mr. Li has served various key positions, such as vice president and president in Beijing FRP Research and

Design Institute (北京玻璃鋼研究設計院), currently a subsidiary of the Parent, from August 1985 to March 2002. Mr. Li

was the chairman of the board of Sinoma Science & Technology, an A share-listed company, from May 2003 to May

2013, and served as the president of Sinoma Science & Technology from October 2009 to August 2010. Mr. Li has been

serving as a director of the Parent since January 2013 and has served as a general manager of the Parent since February

2013. From May 2011 to October 2012, he served as a director of BBMG Corporation. He has also been serving as

director of four listed companies, namely, Sinoma Science & Technology, Qilianshan Co., Sinoma International and

Ningxia Building Materials, since May 2003, June 2011, July 2011 and December 2011, respectively, and as a director of

Sinoma Finance since April 2013. Mr. Li is a National Young and Middle Aged Expert with Important Contribution (國家有突出貢獻的中青年專家) and is entitled to a special government allowance provided by the State Council. Mr. Li currently

serves as the vice president of China Building Materials Federation (中國建築材料聯合會), the vice president of Chinese

Society for Composite Material (中國複合材料學會), and the vice chairman of Chinese Ceramic Society (中國硅酸鹽學會).

Mr. Li graduated with a bachelor’s degree in chemistry from Shandong Institute of Building Materials (山東建材學院) in

July 1985. He is a professorate senior engineer.

China National Materials Company Limited26

BIOGRAPHY OF DIRECTORS, SUPERVISORS AND SENIOR MANAGEMENT

NON-EXECUTIVE DIRECTORS

YU Shiliang, aged 59, re-designated as a non-executive Director since February 2013. Mr. Yu served as an executive

Director and president of the Company from July 2007 to March 2009, and then was re-designated as a non-executive

Director and ceased to be the president of the Company since March 2009. From May 2011 to September 2012, he

served as the vice chairman of the Board, and was appointed as an executive Director and chairman of the Board from

September 2012 to February 2013. Mr. Yu has worked over 30 years in the non-metal materials industry. Mr. Yu has

held various positions in State Bureau of Building Materials Industry Xianyang Research & Design Institute of Ceramics

(國家建材局咸陽陶瓷研究設計院), such as the deputy head and head of the institute from July 1980 to April 1995 and

served as the head of State Building Materials Bureau Synthetic Crystals Research Institute (國家建材局人工晶體研究所), currently a subsidiary of the Parent, from April 1995 to April 1997. Mr. Yu served as the general manager of the

Parent from April 1997 to October 2000 and served as the deputy general manager of the Parent from October 2002 to

November 2007 and has been serving as the vice chairman of the board of the Parent since May 2009. Mr. Yu served

as a director of Sinoma Science & Technology, a listed company, from December 2001 to December 2004 and has been

serving as its director since March 2008, as a director of BBMG Corporation, a listed company, since October 2012 and

as a director of Sinoma Finance since April 2013. Mr. Yu was entitled to a special government allowance provided by the

State Council. In 2006, he was awarded the fifth National Outstanding Entrepreneur in Innovation. Mr. Yu was elected

as the representative to the 16th and 17th National People’s Congress of Chinese Communist Party. He graduated

from Nanjing University of Technology (南京工業大學) in August 1978, majoring in ceramics. He is a professorate senior

engineer.

ZHANG Hai, aged 55, is a non-executive Director. Mr. Zhang has been serving as the deputy general manager of the

Parent since January 1996, and the secretary to the board of the Parent since May 2009. Mr. Zhang served various

positions in different departments of the State Bureau of Building Materials Industry from August 1982 to January 1996,

including a technician in the Beijing FRP Research and Design Institute (北京玻璃鋼研究所), the principal staff member,

the deputy division head, the division head of the personnel department and the director of the office of the Party

leadership group. Equipped with over 30 years of experience in the PRC non-metal materials industry, Mr. Zhang is

entitled to a special government allowance provided by the State Council. Mr. Zhang graduated with a doctoral degree

in economics from Wuhan University of Technology (武漢理工大學) in December 2007. He is a professorate senior

engineer.

LI Jianlun, aged 56, has been a non-executive Director since July 2013. Mr. Li has served as the vice general manager

of the Parent since April 1997 and as the director of the China Construction Materials and Geological Prospecting Center

(中國建築材料工業地質勘查中心), currently a subsidiary body of the Parent, since September 2007. Mr. Li had served in

China Construction Materials and Geological Prospecting Center at several positions such as the division head of the

personnel division, the division head of the planning division, and the assistant to director from July 1982 to April 1997,

served as the director of our predecessor, China National Non-Metallic Materials Corporation from February 2002 to July

2007 and also served as the director of Tianshan Cement from October 2005 to December 2011. Mr. Li graduated from

the Department of Economics and Management of Hebei Geological Institute with a bachelor’s degree in August 1982.

Mr. Li is a senior economist.

27Annual Report 2013

BIOGRAPHY OF DIRECTORS, SUPERVISORS AND SENIOR MANAGEMENT

YU Guobo, aged 57, has been a non-executive Director since July 2013. Mr. Yu has served as the vice general manager

of the Parent since November 1998. Mr. Yu had served in Shandong Industrial Ceramics Research and Design Institute

(山東工業陶瓷研究設計院) at several positions such as engineer, vice director and director of research office, vice head

and head of the institute from January 1982 to November 1997, and during this period, Mr. Yu was accredited at Italian

WELKO Company as the engineer from October 1988 to October 1989. Mr. Yu had served as the vice general manager

of China Inorganic Materials Technology Industrial Company (中國無機材料科技實業公司) from November 1996 to

November 1998. Mr. Yu graduated from Wuhan University of Technology (武漢理工大學) with a doctor’s degree majoring

in information management in December 2007. Mr. Yu is a professorate senior engineer and is entitled to a special

government allowance provided by the State Council.

TANG Baoqi, aged 54, is a non-executive Director. Mr. Tang has over 30 years of experience in the banking industry and

financial industry. Mr. Tang served in various departments in the headquarters of China Construction Bank from August

1983 to June 1999, including the transportation division in the second investment department, the non-industrial division

in the investment department, the reserve loan division in the second credit department, the electrical, mechanical and

textile division in the credit department and in the planning and finance division in the business department. Mr. Tang

served in the debt management department of China Cinda Asset Management Co., Ltd. from June 1999 to February

2000. Mr. Tang served as the general manager in asset management department of Well Kent International Investment

Company Limited from February 2000 to April 2006. From April 2006 to April 2011, Mr. Tang has served as the chief

financial officer of Well Kent International Investment Company Limited. Since April 2011, Mr. Tang has served as the

vice president of Well Kent International Investment Company Limited. Mr. Tang graduated with a bachelor’s degree in

economics from the Infrastructure Finance and Credit Faculty of Hubei Institute of Finance and Economics (湖北財經學院)

in August 1983. He is also qualified as a senior economist.

INDEPENDENT NON-EXECUTIVE DIRECTORS

LEUNG Chong Shun, aged 48, is an independent non-executive Director. Mr. Leung has been serving as an independent

non-executive director of Lijun International Pharmaceutical (Holding) Co., Ltd (利君國際醫藥(控股)有限公司) since

October 2005 and an independent non-executive director of China Communications Construction Company Ltd. (中國交通建設股份有限公司) since January 2011, and served as an independent non-executive director of China Metal Recycling

(Holdings) Limited from May 2009 to August 2013. Mr. Leung is a partner of Woo Kwan, Lee & Lo. (胡關李羅律師行), a

reputable law firm based in Hong Kong. Mr. Leung became a practicing lawyer since 1991. Mr. Leung graduated from

the University of Hong Kong in November 1988 where he obtained a bachelor’s degree of Laws with honours and is

qualified as a solicitor in both Hong Kong and England.

LU Zhengfei, aged 50, is an independent non-executive Director. Mr. Lu is currently an associate dean, a professor and

a supervisor of doctoral students with Guanghua School of Management of the Peking University (北京大學光華管理學院). He is also a consultant to the China Accounting Standards Committee of the Ministry of Finance of the PRC (財政部會計準則委員會), an executive director and academic committee member of the Accounting Society of China (中國會計學會), an executive member of the Standing Committee of the China Audit Society (中國審計學會), and a guest

editor of Accounting Research (《會計研究》) and Audit Research (《審計研究》). Mr. Lu has over 20 years of experience in

the accounting industry and therefore has gained extensive operational and managerial experience as well as profound

knowledge of this field. Mr. Lu served as an independent non-executive director of PICC Property and Casualty Company

Limited (中國人民財產保險股份有限公司) from February 2004 to January 2011 and has been serving as an independent

supervisor of such company since January 2011. Mr. Lu has been an independent non-executive director of Sinotrans

Limited (中國外運股份有限公司) since September 2004, an independent non-executive director of Sino Biopharmaceutical

Limited (中國生物制藥有限公司) since November 2005, an independent non-executive director of Lian Life Insurance

China National Materials Company Limited28

BIOGRAPHY OF DIRECTORS, SUPERVISORS AND SENIOR MANAGEMENT

Company, Ltd (利安人壽保險股份有限公司) since May 2011, an independent non-executive director of Mit Automobile

Service Co., Ltd. (an unlisted company) since February 2012 and an independent non-executive director of Bank of China

Limited since July 2013. Mr. Lu was selected as one of the “Top 100 Talents Program (百人工程)” in social science

theories in Beijing in 2001 and one of the “New Century Excellent Scholarship Program (新世紀優秀人才支持計劃)”