Market Update 2014 27th Edition September 2014 Edited by Katie Hughes Toys & Games

52

Market Update 2014 27th Edition September 2014 Edited by Katie Hughes ISBN 978-1-78304-211-1 Toys & Games

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Market Update 2014 27th Edition September 2014 Edited by Katie Hughes Toys & Games

Market Update 2014

27th Edition September 2014Edited by Katie Hughes

ISBN 978-1-78304-211-1

Toys & Games

In today’s competitive business environment, knowledge and understanding of yourmarketplace is essential. With over 30 years’ experience producing highly respectedoff-the-shelf publications, Key Note has built a reputation as the number one sourceof UK market information. Below are just a few of the comments our business partnersand clients have made on Key Note’s range of reports.

“The test of any marketing strategy and plan lies in the quality of information used, upon whichmarketing judgments and decisions are based. Quality is the key word here. The Key Notereports are an excellent source of such quality information, covering a wide variety of productsectors.”

The Chartered Institute of Marketing

“I regard Key Note as the number one provider of UK market research. The way Key Notecontent is packaged and presented is appealing and easy to understand and therefore a mustfor my taught course students. Its products are complemented by remarkably high levels ofcustomer service.”

University of Cambridge, Judge Business School

“Key Note is one of the most dynamic and intuitive products the department subscribes to. Ithas also remained one of the most-used services for a number of years. The combination ofmarket reports, linked to real company data, within one product, is particularly useful. Theconstant investment and desire to improve the service sets it aside from a number of otherorganisations and I look forward to working with them for many years to come.”

Jack Mears, Knowledge and Information Partner, Department for Business,Innovation and Skills

“Key Note is the Swiss Army knife of report platforms, incorporating both consumer and B2Bresearch (not to mention Companies House data). It therefore has a comprehensive line-up oftitles, all of which are frequently updated. I like the fact that the analysis within the reports isbased on ‘hard data’, through a combination of in-house and external sources. As a result, usingKey Note is a great way to keep up-to-speed on a variety of markets, sectors, products andbrands and it’s a great tool to have on hand for new business and strategy development.”

Jim Clark, Head of Insight, IPA

Toys & Games Foreword

© Key Note Ltd 2014

Contents

Introduction & Definition 1

REPORT COVERAGE....................................................................................................................1

MARKET SECTORS.......................................................................................................................1

1. Executive Summary 2

2. What’s KEY in the Market? 3

KEY DRIVERS.................................................................................................................................3

MARKET TRENDS.........................................................................................................................3

Child Population.............................................................................................................................3

Table 2.1: UK Child Population by Age (000), 2009-2013......................................................4

Number of Live Births...................................................................................................................4

Table 2.2: Number of Live Births and Total Fertility Rates in England and Wales(000 and number), 2009-2013.....................................................................................................5

Figure 2.1: Number of Live Births and Total Fertility Rates in England and Wales(000), 2009-2013.............................................................................................................................5

Household Activity.........................................................................................................................6

Table 2.3: People in Households by Type of Household and Combined EconomicActivity Status of Household Members in the UK (000), April to June 2009-2013...........6

Tablets vs. Traditional Toys..........................................................................................................8

Hamleys’ Top 10 List 2014............................................................................................................9

’Pocket-Money’ Toy Volume Fall................................................................................................9Trends in Distribution.................................................................................................................10

ECONOMIC TRENDS..................................................................................................................10

Table 2.4: UK Economic Trends (000, £m, million and £), 2009-2013................................11

KEY CURRENT ISSUES...............................................................................................................13

HOW ROBUST IS THE MARKET?...........................................................................................13

3. Market Size, Segmentation & Forecasts 15

MARKET SIZE & SEGMENTATION.........................................................................................15

The Total Market.........................................................................................................................15

Table 3.1: The Total UK Market for Traditional Toys and Games by Value(£m at rsp), 2009-2013.................................................................................................................15

Toys & Games Contents

© Key Note Ltd 2014

Figure 3.1: The Total UK Market for Traditional Toys and Games by Value(£m at rsp), 2009-2013.................................................................................................................15

Market Sectors..............................................................................................................................16

Table 3.2: The Total UK Market for Traditional Toys and Games by Product Sectorby Value (£m at rsp), 2013..........................................................................................................16

Figure 3.2: The Total UK Market for Traditional Toys and Games by Product Sectorby Value (£m at rsp), 2013..........................................................................................................17

Infant/Pre-School Toys and Games...........................................................................................17

Activity Toys..................................................................................................................................17

Dolls................................................................................................................................................18

Games and Puzzles......................................................................................................................18

Outdoor and Sports Toys and Games......................................................................................19

Vehicles..........................................................................................................................................19

Action Toys....................................................................................................................................19

Electronic Toys..............................................................................................................................19

Plush Toys......................................................................................................................................20

Other Products..............................................................................................................................20

MARKET POSITION....................................................................................................................20

The UK............................................................................................................................................20

Table 3.3: Consumer Expenditure on Games, Toys and Hobbies and Total DomesticExpenditure in the UK (£m), 2009-2013..................................................................................21

OVERSEAS TRADE......................................................................................................................21

General Overview........................................................................................................................21

Table 3.4: UK Trade Balance of Toys and Games by Value (£m), 2009-2013...................22

Figure 3.3: UK Trade Balance of Toys and Games by Value (£m), 2009-2013..................22

Exports............................................................................................................................................23

Table 3.5: UK Exports of Toys and Games by Value (£000 and %), 2012 and 2013.......23

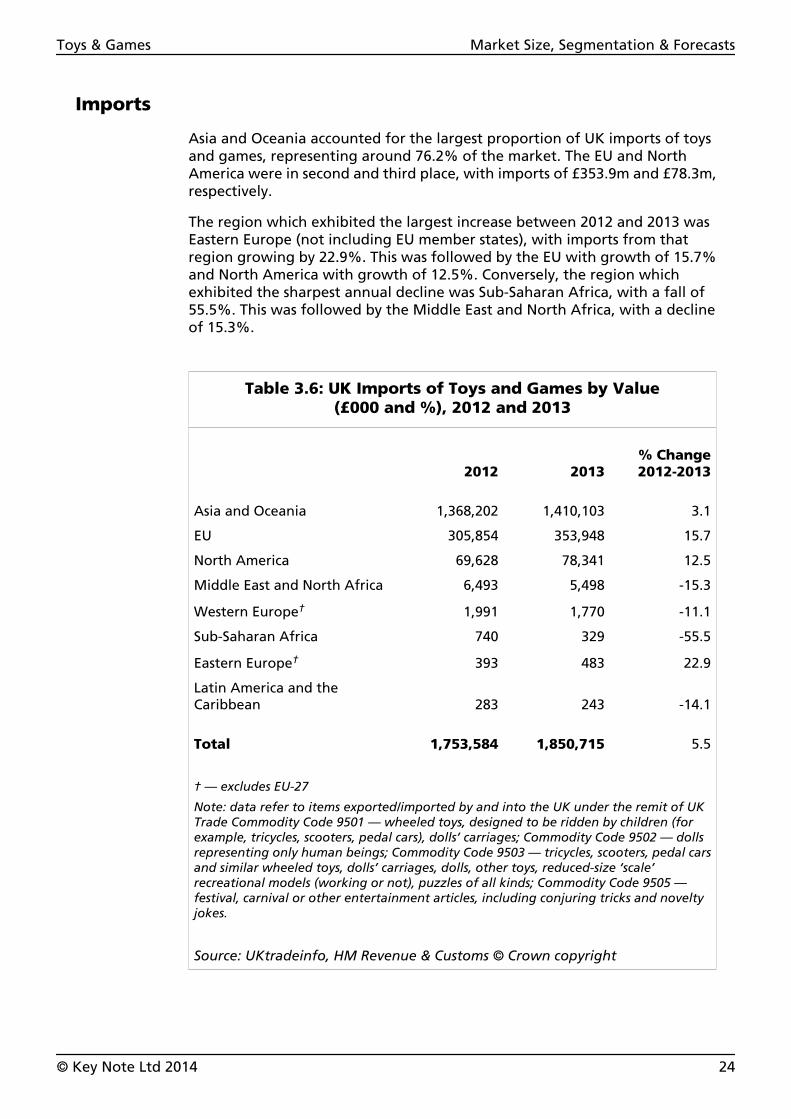

Imports...........................................................................................................................................24

Table 3.6: UK Imports of Toys and Games by Value (£000 and %), 2012 and 2013.......24

FORECASTS..................................................................................................................................25

Future Trends................................................................................................................................25

Forecast Economic Trends..........................................................................................................25

Table 3.7: Forecast Economic Trends (000, %, million), 2014-2018...................................26

Toy Renting...................................................................................................................................26

Upcoming Toy Merchandising Opportunities........................................................................27

Forecast Total Market.................................................................................................................27

Table 3.8: The Forecast Total UK Market for Traditional Toys and Games by Value(£m at rsp), 2014-2018.................................................................................................................27

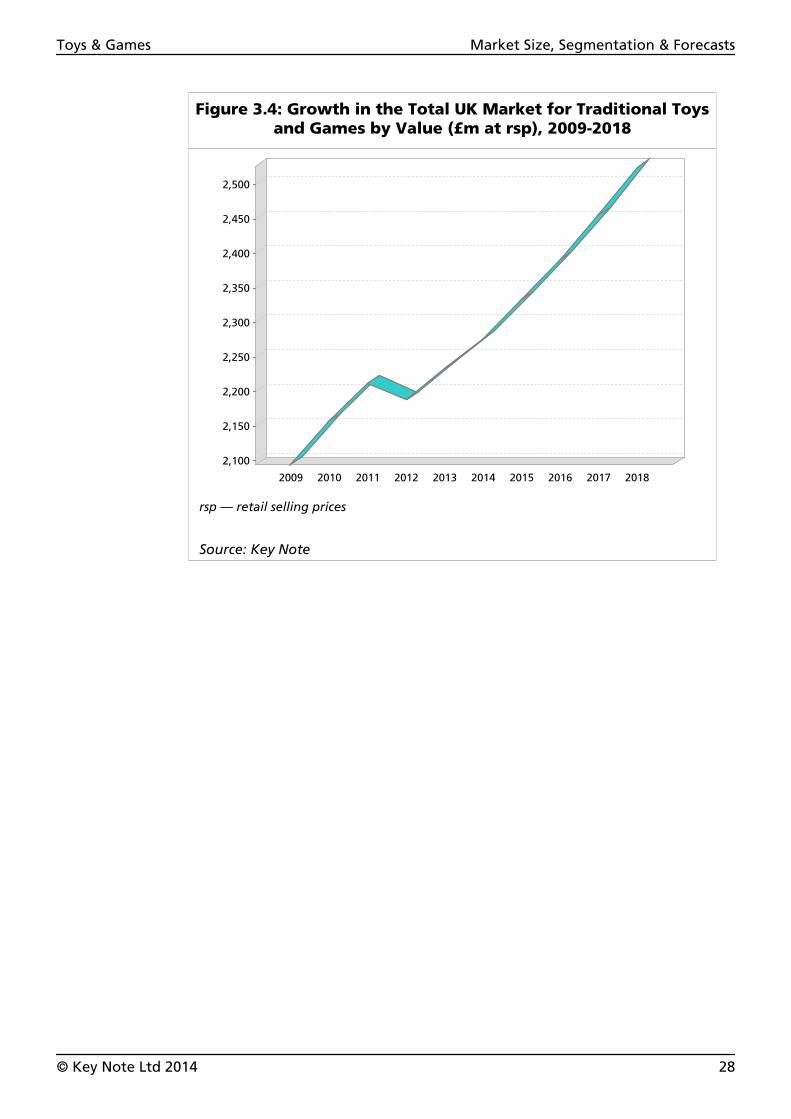

MARKET GROWTH....................................................................................................................27

Figure 3.4: Growth in the Total UK Market for Traditional Toys and Games by Value(£m at rsp), 2009-2018.................................................................................................................28

Toys & Games Contents

© Key Note Ltd 2014

4. Strengths, Weaknesses, Opportunities & Threats 29

STRENGTHS..................................................................................................................................29

WEAKNESSES..............................................................................................................................29

OPPORTUNITIES.........................................................................................................................30

THREATS.......................................................................................................................................31

5. PESTEL 32

POLITICAL ....................................................................................................................................32

Counterfeit Toys...........................................................................................................................32

ECONOMIC .................................................................................................................................32

Improving Economy Boosts Toys and Games Sales...............................................................32

SOCIAL .........................................................................................................................................33

Gender Stereotypes.....................................................................................................................33

TECHNOLOGICAL ......................................................................................................................33

New Generation of Video Gaming Consoles..........................................................................33

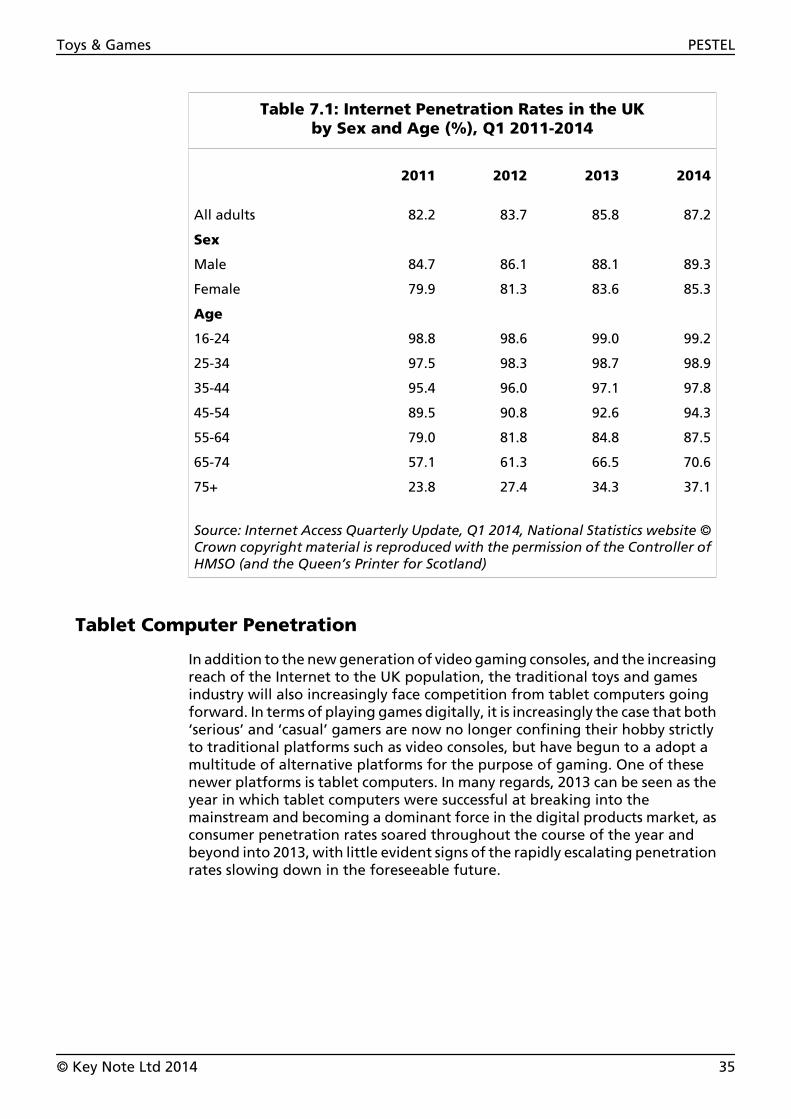

Internet Access in the UK...........................................................................................................34

Table 7.1: Internet Penetration Rates in the UK by Sex and Age (%), Q12011-2014......................................................................................................................................35

Tablet Computer Penetration...................................................................................................35

ENVIRONMENTAL ....................................................................................................................36

Going Green With Eco-Friendly Toys.......................................................................................36

LEGISLATIVE ...............................................................................................................................37

General Legislation......................................................................................................................37

New Toy Safety Directive............................................................................................................37

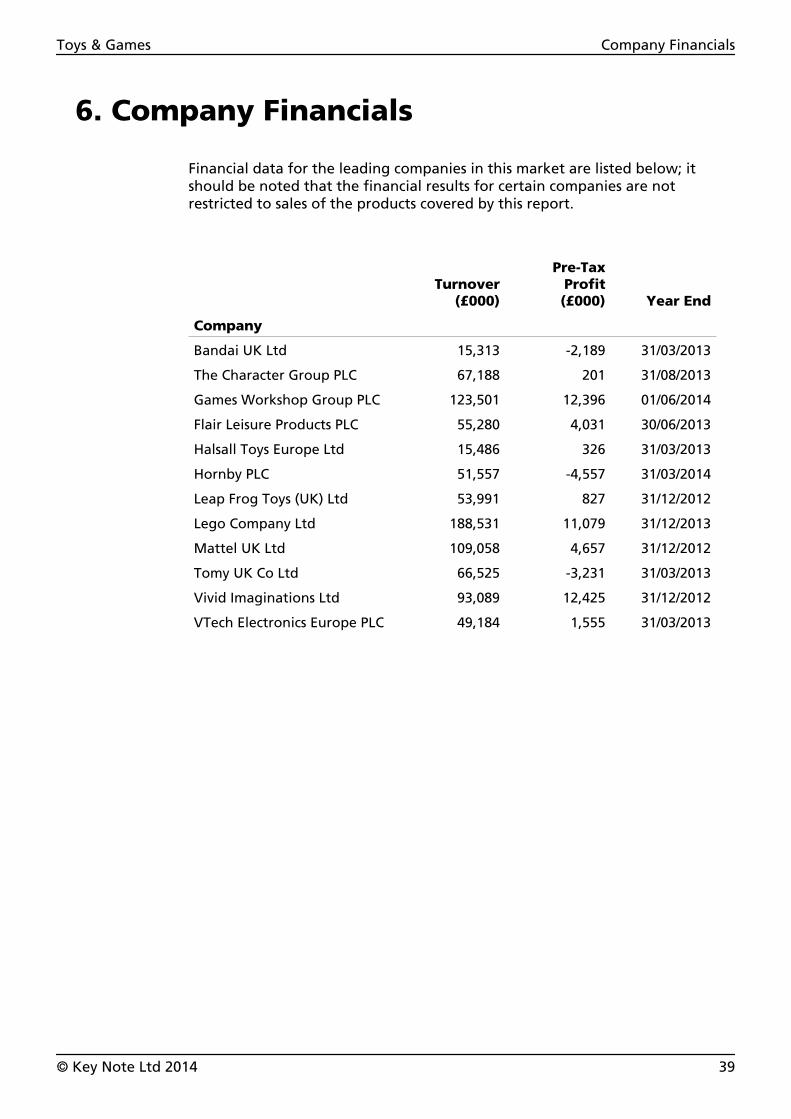

6. Company Financials 39

7. Further Sources 40

Publications.................................................................................................................................40

Government Publications ......................................................................................................40

Key Note Research 41

The Key Note Range of Reports 42

Toys & Games Contents

© Key Note Ltd 2014

Introduction & Definition

REPORT COVERAGE

This Key Note Market Update analyses and evaluates the UK market fortraditional toys and games. The scope of products covered by this report focusspecifically on toys and games targeted towards those aged under 14, but mayalso include some that are bought and used by adults. It should be noted thatdespite this report not explicitly covering electronic products such as video,personal computer (PC), and console games and systems, toys and games whichcontain an electronic element that target the under-14s age group have beenincluded. In addition, such items may be discussed, where relevant, in relationto their competition to the traditional toys and games market.

MARKET SECTORS

This Key Note Market Update predominantly focuses on the traditional toysand games market, which has been sub-categorised into the following sectorsfor the purposes of more thorough analysis:

• action toys — e.g. action figures, wrestling toys, toy guns, etc.

• activity toys — e.g. building and construction sets, and arts and crafts

• dolls

• electronic toys — e.g. educational computers and electronic learning aids(ELAs)

• games and puzzles — e.g. board games, jigsaws and other puzzle games

• infant/pre-school toys and games — e.g. toys targeting children aged 5 andunder

• outdoor and sports toys and games — e.g. outdoor playsets, swings,playhouses, trampolines and climbing frames

• plush toys — e.g. stuffed toys and teddy bears

• vehicles — e.g. toy cars, trains and planes

• other products — e.g. dressing-up clothes and pocket-money novelties, etc.

Toys & Games Introduction & Definition

© Key Note Ltd 2014 1

1. Executive Summary

Key Note estimates that between 2009 and 2013, the overall value of the UKmarket for traditional toys and games grew by 6.6%, although growth in themarket has failed to maintain consistency, with a decline of 1.1% in 2012 forinstance. These fluctuations between growth and decline are, in part, a resultof the economic downturn, with growth continuing to remain unstablefollowing the recession of 2008/2009.

The UK market for toys and games is also suffering from underinvestment innew product development (NPD) across Europe, in addition to the decliningpresence of high-street toy retailers, such as Modelzone and the Early LearningCentre (ELC). Downwards pressure has also been put on the market by theinflux of discount and value toy retailers, particularly online retailers such asAmazon.com, which are able to offer prices beneath those seen at traditionaltoy retailers.

Figures from National Statistics suggest a continuing consumer base for toysand games, with the number of children aged 14 and under in the UKcontinuing to exhibit signs of growth between 2009 and 2013, with furtherincreases forecast in the future. However, despite these trends, fears have beenraised about the enduring appeal of digital and electronic products, which areincreasingly taking up a greater share of children’s time at the expense ofplaying with traditional toys. In order to combat this, toymakers have investedconsiderable sums of money in developing new hybrid game-toy products, suchas the popular console playset game Skylanders, which is now thought to beworth in excess of $1bn. In addition, the ascent of digital and electronic gamingcontent has in some cases spurned successful traditional toy and game productlines, perhaps most notably the Angry Birds franchise.

These new trends, in addition to the improving economic fortunes of the UKand increases in new product development (NPD), are anticipated to lift thevalue of sales for toys and games in the UK in 2014 and onwards, withnoticeably stronger growth coming from online retailing distributors, mostlikely at the expense of sales in-store.

Key Note forecasts that the UK market for toys and games will grow at anaverage annualised pace of between 1.9% and 2.8% between 2014 and 2018,with the value of the market rising by 10.9% over the forecast period as awhole.

Toys & Games Executive Summary

© Key Note Ltd 2014 2

2. What’s KEY in the Market?

KEY DRIVERS

• The toys and games industry in the UK and around the world sawsubstantially reduced new product development (NPD) in the aftermath ofthe 2008/2009 recession. However, in the midst of improving global economicfortunes, investment in the development of the industry is expected toincrease in coming years, offering a considerable boost to the market.

• Toys and games remain extremely popular forms of gift-giving, meaning themarket is most profitable during peak seasons, notably Christmas. Themarket currently looks forward to Christmas 2014 with optimism as consumerexpenditure on gift-giving is expected to rise year-on-year.

• An improving economic outlook in the UK will make consumers more willingthan in previous years to spend money on toys and games.

• Increasingly, the importance of electronic and digital innovations isbecoming more prevalent in the toys and games industry, as the market looksto cope with increasing competition from items such as smartphones andtablet computers, which are taking up an ever greater proportion ofchildren’s spare time.

• Healthy population growth in the under-14s age group will contribute to asteadily growing consumer base for the foreseeable future.

• Character licensing provides new opportunities for product sales, and canprove particularly popular as new television programmes and films arereleased. Most significantly in the future, the industry will look forward tothe upcoming new Star Wars film trilogy, which is anticipated to boost toysales for the franchise.

MARKET TRENDS

Child Population

According to figures from National Statistics, the population of children in theUK aged 14 and under grew at a relatively steady year-on-year rate between2009 and 2013, rising by 2.3% overall and reaching a projected figure of11.3 million at the end of the 5-year review period.

Toys & Games What’s KEY in the Market?

© Key Note Ltd 2014 3

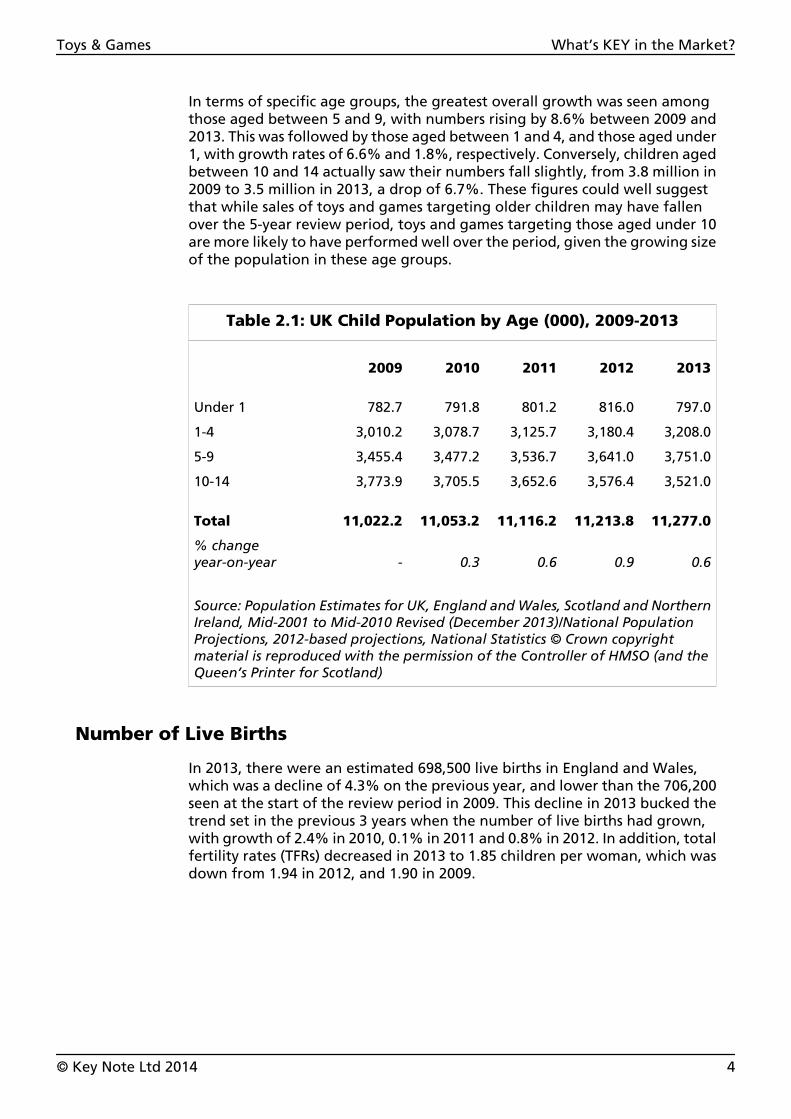

In terms of specific age groups, the greatest overall growth was seen amongthose aged between 5 and 9, with numbers rising by 8.6% between 2009 and2013. This was followed by those aged between 1 and 4, and those aged under1, with growth rates of 6.6% and 1.8%, respectively. Conversely, children agedbetween 10 and 14 actually saw their numbers fall slightly, from 3.8 million in2009 to 3.5 million in 2013, a drop of 6.7%. These figures could well suggestthat while sales of toys and games targeting older children may have fallenover the 5-year review period, toys and games targeting those aged under 10are more likely to have performed well over the period, given the growing sizeof the population in these age groups.

Table 2.1: UK Child Population by Age (000), 2009-2013

2009 2010 2011 2012 2013

Under 1 782.7 791.8 801.2 816.0 797.0

1-4 3,010.2 3,078.7 3,125.7 3,180.4 3,208.0

5-9 3,455.4 3,477.2 3,536.7 3,641.0 3,751.0

10-14 3,773.9 3,705.5 3,652.6 3,576.4 3,521.0

Total 11,022.2 11,053.2 11,116.2 11,213.8 11,277.0

% changeyear-on-year - 0.3 0.6 0.9 0.6

Source: Population Estimates for UK, England and Wales, Scotland and NorthernIreland, Mid-2001 to Mid-2010 Revised (December 2013)/National PopulationProjections, 2012-based projections, National Statistics © Crown copyrightmaterial is reproduced with the permission of the Controller of HMSO (and theQueen’s Printer for Scotland)

Number of Live Births

In 2013, there were an estimated 698,500 live births in England and Wales,which was a decline of 4.3% on the previous year, and lower than the 706,200seen at the start of the review period in 2009. This decline in 2013 bucked thetrend set in the previous 3 years when the number of live births had grown,with growth of 2.4% in 2010, 0.1% in 2011 and 0.8% in 2012. In addition, totalfertility rates (TFRs) decreased in 2013 to 1.85 children per woman, which wasdown from 1.94 in 2012, and 1.90 in 2009.

Toys & Games What’s KEY in the Market?

© Key Note Ltd 2014 4

Table 2.2: Number of Live Births and Total Fertility Ratesin England and Wales (000 and number), 2009-2013

2009 2010 2011 2012 2013

Live births (000) 706.2 723.2 723.9 729.7 698.5

% changeyear-on-year - 2.4 0.1 0.8 -4.3

Total fertility rate† 1.90 1.94 1.93 1.94 1.85

† — the average number of live children that a group of women would bear if theyexperienced the age-specific fertility rates of the calendar year in question throughouttheir childbearing lifespan

Source: Birth Summary Tables, England and Wales, 2013, National Statistics ©Crown copyright material is reproduced with the permission of the Controller ofHMSO (and the Queen’s Printer for Scotland)

Figure 2.1: Number of Live Births and Total Fertility Ratesin England and Wales (000), 2009-2013

2009 2010 2011 2012 2013697.5

700.0

702.5

705.0

707.5

710.0

712.5

715.0

717.5

720.0

722.5

725.0

727.5

730.0

Source: Birth Summary Tables, England and Wales, 2013, National Statistics ©Crown copyright material is reproduced with the permission of the Controllerof HMSO (and the Queen’s Printer for Scotland)/Key Note

Toys & Games What’s KEY in the Market?

© Key Note Ltd 2014 5

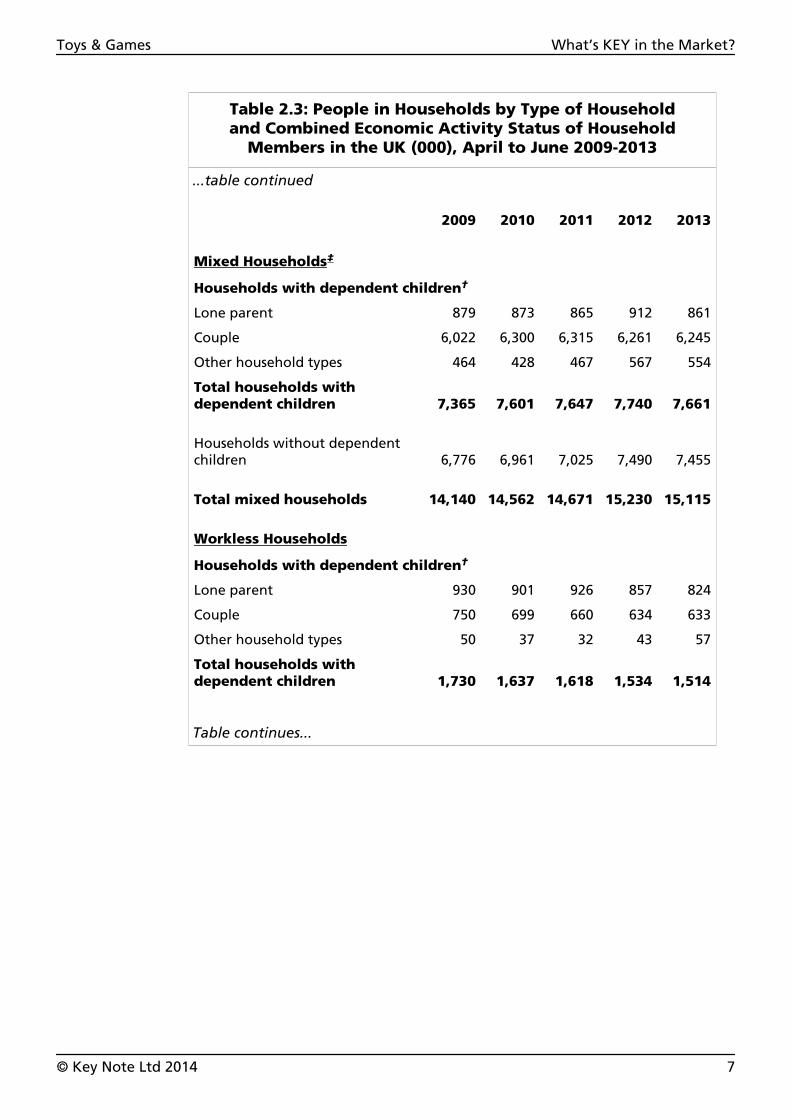

Household Activity

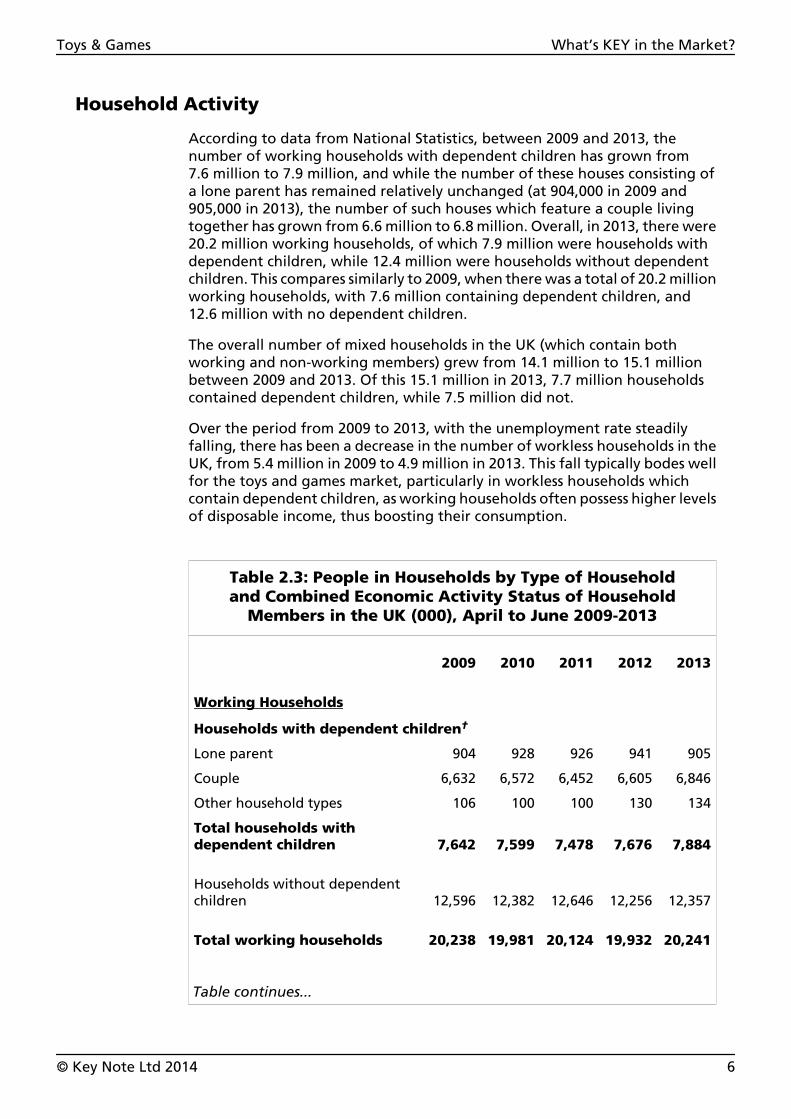

According to data from National Statistics, between 2009 and 2013, thenumber of working households with dependent children has grown from7.6 million to 7.9 million, and while the number of these houses consisting ofa lone parent has remained relatively unchanged (at 904,000 in 2009 and905,000 in 2013), the number of such houses which feature a couple livingtogether has grown from 6.6 million to 6.8 million. Overall, in 2013, there were20.2 million working households, of which 7.9 million were households withdependent children, while 12.4 million were households without dependentchildren. This compares similarly to 2009, when there was a total of 20.2 millionworking households, with 7.6 million containing dependent children, and12.6 million with no dependent children.

The overall number of mixed households in the UK (which contain bothworking and non-working members) grew from 14.1 million to 15.1 millionbetween 2009 and 2013. Of this 15.1 million in 2013, 7.7 million householdscontained dependent children, while 7.5 million did not.

Over the period from 2009 to 2013, with the unemployment rate steadilyfalling, there has been a decrease in the number of workless households in theUK, from 5.4 million in 2009 to 4.9 million in 2013. This fall typically bodes wellfor the toys and games market, particularly in workless households whichcontain dependent children, as working households often possess higher levelsof disposable income, thus boosting their consumption.

Table 2.3: People in Households by Type of Householdand Combined Economic Activity Status of Household

Members in the UK (000), April to June 2009-2013

2009 2010 2011 2012 2013

Working Households

Households with dependent children†

Lone parent 904 928 926 941 905

Couple 6,632 6,572 6,452 6,605 6,846

Other household types 106 100 100 130 134

Total households withdependent children 7,642 7,599 7,478 7,676 7,884

Households without dependentchildren 12,596 12,382 12,646 12,256 12,357

Total working households 20,238 19,981 20,124 19,932 20,241

Table continues...

Toys & Games What’s KEY in the Market?

© Key Note Ltd 2014 6

Table 2.3: People in Households by Type of Householdand Combined Economic Activity Status of Household

Members in the UK (000), April to June 2009-2013

...table continued

2009 2010 2011 2012 2013

Mixed Households‡

Households with dependent children†

Lone parent 879 873 865 912 861

Couple 6,022 6,300 6,315 6,261 6,245

Other household types 464 428 467 567 554

Total households withdependent children 7,365 7,601 7,647 7,740 7,661

Households without dependentchildren 6,776 6,961 7,025 7,490 7,455

Total mixed households 14,140 14,562 14,671 15,230 15,115

Workless Households

Households with dependent children†

Lone parent 930 901 926 857 824

Couple 750 699 660 634 633

Other household types 50 37 32 43 57

Total households withdependent children 1,730 1,637 1,618 1,534 1,514

Table continues...

Toys & Games What’s KEY in the Market?

© Key Note Ltd 2014 7

Table 2.3: People in Households by Type of Householdand Combined Economic Activity Status of Household

Members in the UK (000), April to June 2009-2013

...table continued

2009 2010 2011 2012 2013

Households without dependentchildren 3,655 3,781 3,738 3,489 3,378

Total workless households 5,385 5,418 5,356 5,023 4,892

Total households 39,763 39,962 40,151 40,186 40,248

† — dependent children refers to children aged under 16 and those aged 16 to 18 yearsold who are never married and in full-time education

‡ — mixed households contain both working and workless members

Note: totals may not sum due to rounding at source.

Source: Working and Workless Households, 2013, National Statistics © Crowncopyright material is reproduced with the permission of the Controller of HMSO(and the Queen’s Printer for Scotland)

Tablets vs. Traditional Toys

The substantial boom in the sale of tablet computers in recent years,particularly since 2010, has had a considerable impact on NPD and recent trendswithin the toys and games market, with both Leap Frog and VTech releasingtheir third generation of tablet computers for children during 2013. In someregards, this trend has negatively impacted on potential sales in the traditionaltoys and games market, with the widespread availability of mobile phones,smartphones and tablet computers causing a surge in mobile gaming in recentyears — a trend which is now consuming a greater proportion of children’splaying time, often at the expense of playing time with traditional toys andgames.

This rising popularity of tablets and other digital products has had theknock-on effect of encouraging toy manufacturers to expand their repertoireto include app (application) development, for instance Mattel’s developmentof its app range for the Hot Wheels franchise, and Hasbro’s decision to acquiremobile games company Backflip in order to enhance its range of mobile gamesbased on the toy firm’s biggest and most successful brands. At the same timea number of gaming app developers, including those behind the hugelysuccessful Angry Birds, have expanded in the opposite direction, using theirdigital success to launch their own range of traditional toy and gamingproducts, such as plush toys and board games, etc.

Toys & Games What’s KEY in the Market?

© Key Note Ltd 2014 8

Overall, there has been an evident trend by children in favour of increasinglydigital and electronic toys. This was confirmed by the NPD Group’s Evolutionof Play Report which has revealed that in recent years, sales of traditional toysand games have suffered at the hands of electronic goods, most notably tabletcomputers. In its predictive list of the top selling toys and games for Christmas2014, Hamleys has anticipated that this trend is likely to continue, with the vastmajority of products on its list containing at least some element of digital/electronic content (see below).

Hamleys’ Top 10 List 2014

Owing to the fact that the toys and games market in the UK is highlydependent on seasonal sales, most notably around the Christmas period, keyplayers look closely at the trends evident in the market in the run-up to thesales rush, with the aim of benefitting from sales of products which are provingpopular. As such, many toy manufacturers and stores traditionally hold eventsin June or July to showcase the products they believe will be most popularahead of Christmas; in June 2014, retailer Hamleys revealed its prediction as towhich toys would be the most popular in the run-up to Christmas 2014, withthe vast majority of items being tech-based. The top ten included:

1. My Friend Cayla (£75)

2. Doh Vinci Style and Store Vanity design kit (£25)

3. Kidizoom SWmart Watch (£50)

4. Barbie Colour Change Bag (£40)

5. Teksta T-Rex (£59.99)

6. Leapfrog LeapTV (£135)

7. Transformers Chomp & Stomp robot (£115)

8. BoomCo Rapid Madness blaster (£65)

9. Ice Skating Anna & Elsa from Frozen (£30)

10. Xeno toy (£100).

’Pocket-Money’ Toy Volume Fall

It is thought that in 2013, the volume of ‘impulse purchase’ toys priced under£5 witnessed a substantial decline. The market for such products, oftendescribed as the ‘pocket money sector’, represents around half of all toys sold,in terms of volume sales. It is believed that such toys are typically bought eitherby children, using their own allowances, or sometimes by parents who give into pestering from their children while on shopping trips. Is it expected thatwhile such purchases by children will have remained static throughout the year,purchases by parents are anticipated to have fallen, as consumers reigned inspending in the midst of the UK’s continuing recovery from the economicdownturn.

Toys & Games What’s KEY in the Market?

© Key Note Ltd 2014 9

Trends in Distribution

Toys and games can be distributed in a number of ways, ranging from onlinesellers to supermarkets and specialist shops. Although traditional, high-streetretailers including The Entertainer, Mothercare, The Disney Store, the EarlyLearning Centre (ELC) and Toys ‘R’ Us continue to possess a substantial shareof the market in terms of distribution, such stores have suffered in recent yearsas a result of increased competition among alternative distributors, such assupermarkets, discount stores and online retailers, including Amazon, eBayand Play.com; many of these distributors are able to provide a considerablerange of toys and games at prices cheaper than those witnessed in high-streetstores. Of particular note is supermarkets, which have increasingly devoted agreater amount of shelf space to non-food lines, including children’s toys andgames — a trend particularly evident during peak seasons such as Christmas.Overall, an obvious trend exists in which consumers are increasingly opting topurchase toys and game products via online means; however, at least for theforeseeable future, tangible in-store sales of such products will continue tocommand a substantial share of overall sales.

ECONOMIC TRENDS

According to data released by National Statistics, the population of the UKcontinued to rise at a healthy annual rate of between 0.6% and 0.8% between2009 and 2013, to reach a projected 64.1 million. This trend was assisted by theUK’s relatively high birth rate and ageing population, in addition to positivelevels of net migration. The growing population should, in theory, result in anoverall boost in consumer spending, which in turn will benefit the widereconomy, including the UK market for toys and games. In particular, the UK’srelatively high birth rate will result in a steady and consistent number ofchildren in the UK, which would be a positive development for the prospect ofthe UK’s toys and games market.

Despite the UK’s economic performance following on from the 2008/2009recession being somewhat inconsistent, recently the country has begun toexhibit more positive signs of stabilisation and growth. In 2013, the UK grewat an annualised pace of 1.7%, with the country anticipated to be thefastest-growing economy in the Group of 7 (G7) nations in 2014. Although thisis a positive development for the UK, it should be remembered that grossdomestic product (GDP) was only able to match its pre-recession peak in thelatter half of 2014.

The 2008/2009 recession and subsequent economic difficulties caused anoticeable fall in the level of inflation in the country, with the UK brieflyentering a deflationary period in 2009, with prices dropping by 0.5%year-on-year. Actions by the Bank of England (BoE), including droppinginterest rates to a historic low of 0.5% and launching a quantitative easing (QE)program worth £375bn, helped to push inflation to a peak of 5.2% in 2011;this steadily fell to 3.2% in 2012 and 3% in 2013. Inflation, as measured by theconsumer price index (CPI), fell to 2% in December 2013, in line with the BoE’starget, and as of July 2014 was at 1.6%.

Toys & Games What’s KEY in the Market?

© Key Note Ltd 2014 10

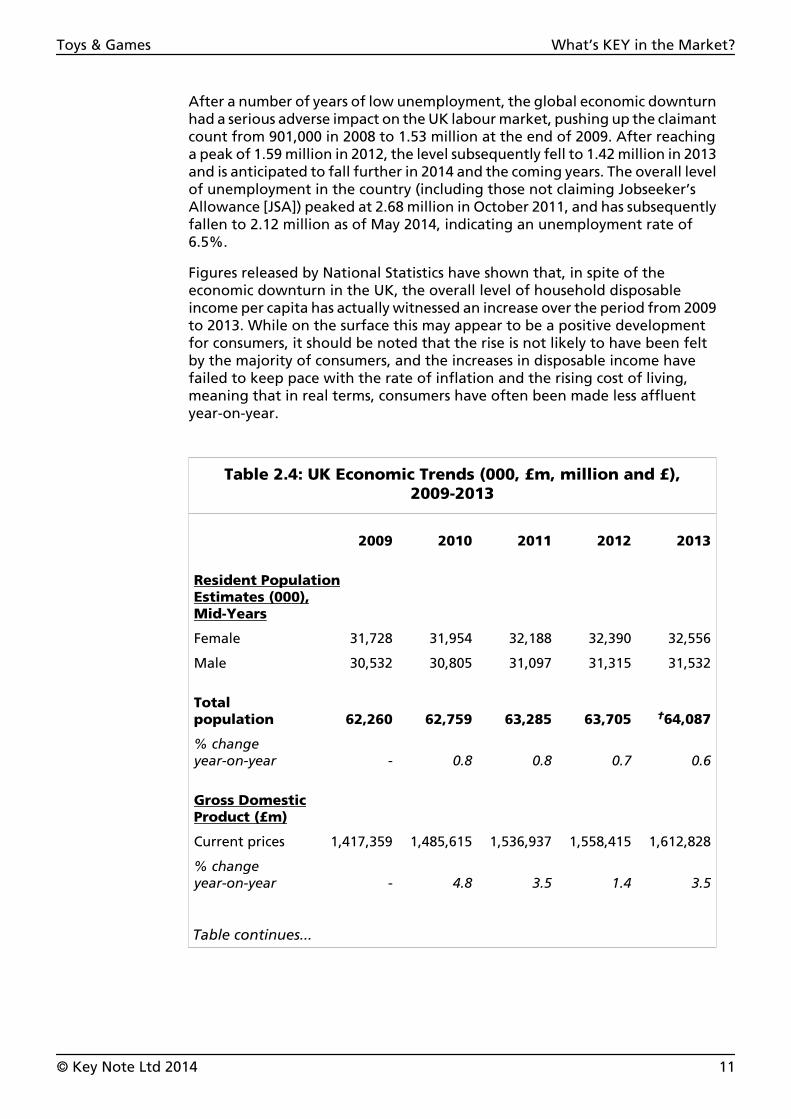

After a number of years of low unemployment, the global economic downturnhad a serious adverse impact on the UK labour market, pushing up the claimantcount from 901,000 in 2008 to 1.53 million at the end of 2009. After reachinga peak of 1.59 million in 2012, the level subsequently fell to 1.42 million in 2013and is anticipated to fall further in 2014 and the coming years. The overall levelof unemployment in the country (including those not claiming Jobseeker’sAllowance [JSA]) peaked at 2.68 million in October 2011, and has subsequentlyfallen to 2.12 million as of May 2014, indicating an unemployment rate of6.5%.

Figures released by National Statistics have shown that, in spite of theeconomic downturn in the UK, the overall level of household disposableincome per capita has actually witnessed an increase over the period from 2009to 2013. While on the surface this may appear to be a positive developmentfor consumers, it should be noted that the rise is not likely to have been feltby the majority of consumers, and the increases in disposable income havefailed to keep pace with the rate of inflation and the rising cost of living,meaning that in real terms, consumers have often been made less affluentyear-on-year.

Table 2.4: UK Economic Trends (000, £m, million and £),2009-2013

2009 2010 2011 2012 2013

Resident PopulationEstimates (000),Mid-Years

Female 31,728 31,954 32,188 32,390 32,556

Male 30,532 30,805 31,097 31,315 31,532

Totalpopulation 62,260 62,759 63,285 63,705 †64,087

% changeyear-on-year - 0.8 0.8 0.7 0.6

Gross DomesticProduct (£m)

Current prices 1,417,359 1,485,615 1,536,937 1,558,415 1,612,828

% changeyear-on-year - 4.8 3.5 1.4 3.5

Table continues...

Toys & Games What’s KEY in the Market?

© Key Note Ltd 2014 11

Table 2.4: UK Economic Trends (000, £m, million and £),2009-2013

...table continued

2009 2010 2011 2012 2013

Annualchain-linked GDP 1,461,361 1,485,616 1,502,216 1,506,388 1,532,652

% changeyear-on-year - 1.7 1.1 0.3 1.7

Rate of Inflation (%)

Inflation -0.5 4.6 5.2 3.2 3.0

Percentage pointchangeyear-on-year - 5.1 0.6 -2.0 -0.2

Actual Number ofUnemployed Personsin the UK (million)

Actual number ofclaimants 1.53 1.50 1.53 1.59 1.42

% changeyear-on-year - -2.0 2.0 3.9 -10.7

Household DisposableIncome Per Capita (£)

Householddisposable income 15,443 16,058 16,371 16,830 17,058

% changeyear-on-year - 4.0 1.9 2.8 1.4

† — does not sum due to rounding at source

GDP — gross domestic product

Note: inflation is at retail price index (RPI); inflation data shown are annual averagechanges; claimant count measures the number of people claiming Jobseeker’s Allowance.

Source: Population Estimates for UK, England and Wales, Scotland and NorthernIreland, Mid-2001 to Mid-2010 Revised, December 2013/National PopulationProjections, 2012-based projections/United Kingdom Economic Accounts Q12014, published June 2014/Consumer Price Inflation, July 2014/Labour MarketStatistics, August 2014, National Statistics website © Crown copyright material isreproduced with the permission of the Controller of HMSO (and the Queen’sPrinter for Scotland)

Toys & Games What’s KEY in the Market?

© Key Note Ltd 2014 12

KEY CURRENT ISSUES

The UK market for traditional toys and games is forecast by Key Note to havegrown by 2.1% in value in 2013 despite a number of hurdles. One of the keycurrent issues facing the market is the enduring threat posed from counterfeitproducts, with the existence of such items providing a cheaper alternative togenuine goods, and therefore damaging industry-wide sales figures. Inaddition, and more recently, the market for traditional toys and games hascome under increasing pressure from electronic/digital devices. The uptake ofproducts such as smartphones and tablet computers has soared in recent years,with a significant proportion of children now owning multiple such devicesand subsequently spending increasingly greater amounts of their leisure timeusing these products as opposed to playing with traditional toys and games.

In order to counter this problem, many toys and games manufacturers areadding digital content to their products in order to address the threat fromsmartphones and tablet computers, with retailer Hamleys predicting that themajority of the most popular children’s toys and games in the run-up toChristmas 2014 will contain at least an element of digital content. In additionto devices such as smartphones and tablet computers, the toys and gamesmarket is currently competing against the video gaming industry, particularlyin light of the recent launch of the eighth-generation of gaming consoles,which are expected to hinder sales in the traditional toys and games market.Presently, the toys and games industry is witnessing a growing trend of ‘toyrenting’, and looking forward, the market will be hotly anticipating, as ever,the new release of blockbuster films such as the upcoming new Star Warstrilogy, with the release of such films and television shows typicallyencouraging a boost in sales of toys and games associated with such franchises.

HOW ROBUST IS THE MARKET?

Recent years have seen the volume and value sales of toys and games fluctuateconsiderably, particularly in response to the 2008/2009 recession and aperceived lack of NPD, a feature especially prevalent within the Europeanmarketplace. Although the UK economic recovery has gathered noticeablemomentum during the latter part of 2013 and 2014, consumer spending hasremained subdued as expenditure on discretionary items, such as toys andgames, has been either frozen or reduced in line with pressures on householdbudgets.

Increasingly, children are beginning to mature at a much younger age thanpreviously, with the uptake of electronic and digital products commencing ata much earlier stage than ever before. Additionally, and partly owing to thistrend, children are now more wired towards the latest crazes and fashions,thereby forcing toys and games manufacturers into producing ever-greaterinnovations and modern products in order to maintain competitiveness in asaturated marketplace. Consequently there has been an apparent move awayfrom traditional toys, for instance toy vehicles, collectibles and plush toys, withsales in each of these categories suffering as a result over the past few years.

Toys & Games What’s KEY in the Market?

© Key Note Ltd 2014 13

Despite economic difficulties and evolving trends in the industry, the overallmarket for toys and games in the UK can be considered relatively robust. Atpresent, and looking forward, the demand for toys and games is forecast toremain stable, particularly as many parents appreciate the developmental andeducational added value that such products can provide for their children. TheUK’s recent return to economic normalcy is likely to drive growth in the future,with NPD activity also expected to witness growth in the coming years. As withprevious years, the UK’s positive birth rate is forecast to contribute towards acontinual increase in the potential consumer base for toys and games.

Toys & Games What’s KEY in the Market?

© Key Note Ltd 2014 14

3. Market Size, Segmentation & Forecasts

MARKET SIZE & SEGMENTATION

The Total Market

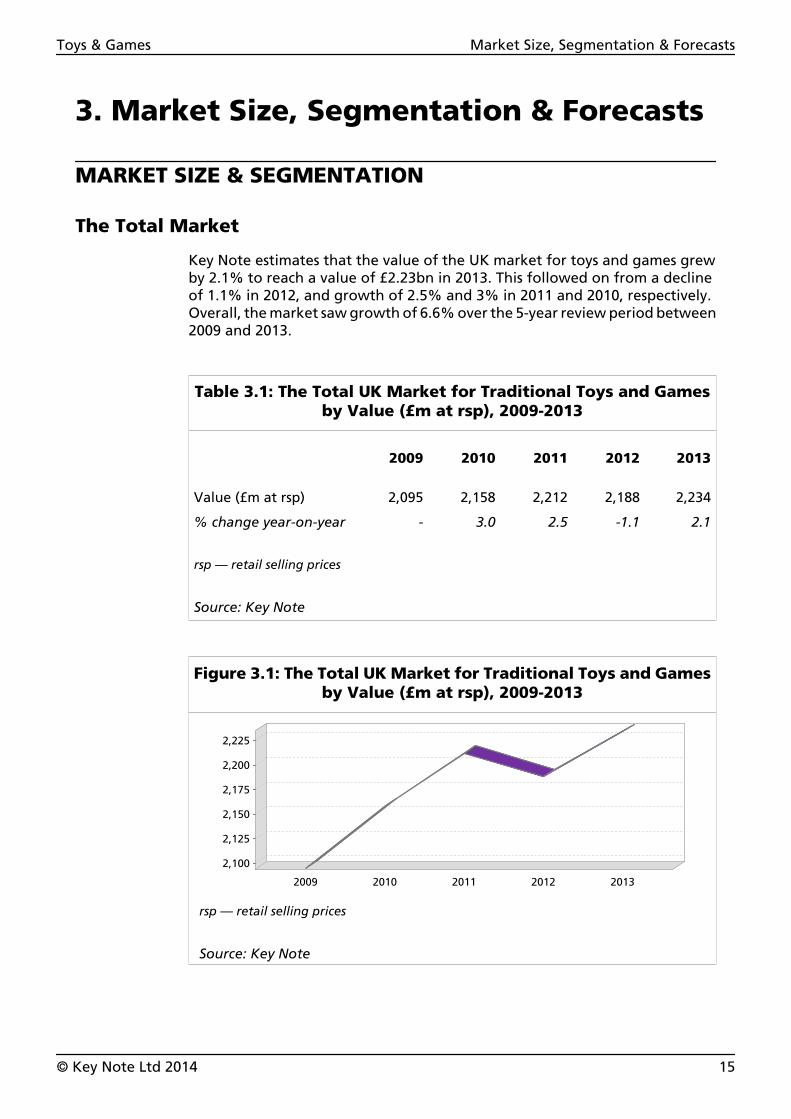

Key Note estimates that the value of the UK market for toys and games grewby 2.1% to reach a value of £2.23bn in 2013. This followed on from a declineof 1.1% in 2012, and growth of 2.5% and 3% in 2011 and 2010, respectively.Overall, the market saw growth of 6.6% over the 5-year review period between2009 and 2013.

Table 3.1: The Total UK Market for Traditional Toys and Gamesby Value (£m at rsp), 2009-2013

2009 2010 2011 2012 2013

Value (£m at rsp) 2,095 2,158 2,212 2,188 2,234

% change year-on-year - 3.0 2.5 -1.1 2.1

rsp — retail selling prices

Source: Key Note

Figure 3.1: The Total UK Market for Traditional Toys and Gamesby Value (£m at rsp), 2009-2013

2009 2010 2011 2012 2013

2,100

2,125

2,150

2,175

2,200

2,225

rsp — retail selling prices

Source: Key Note

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 15

Market Sectors

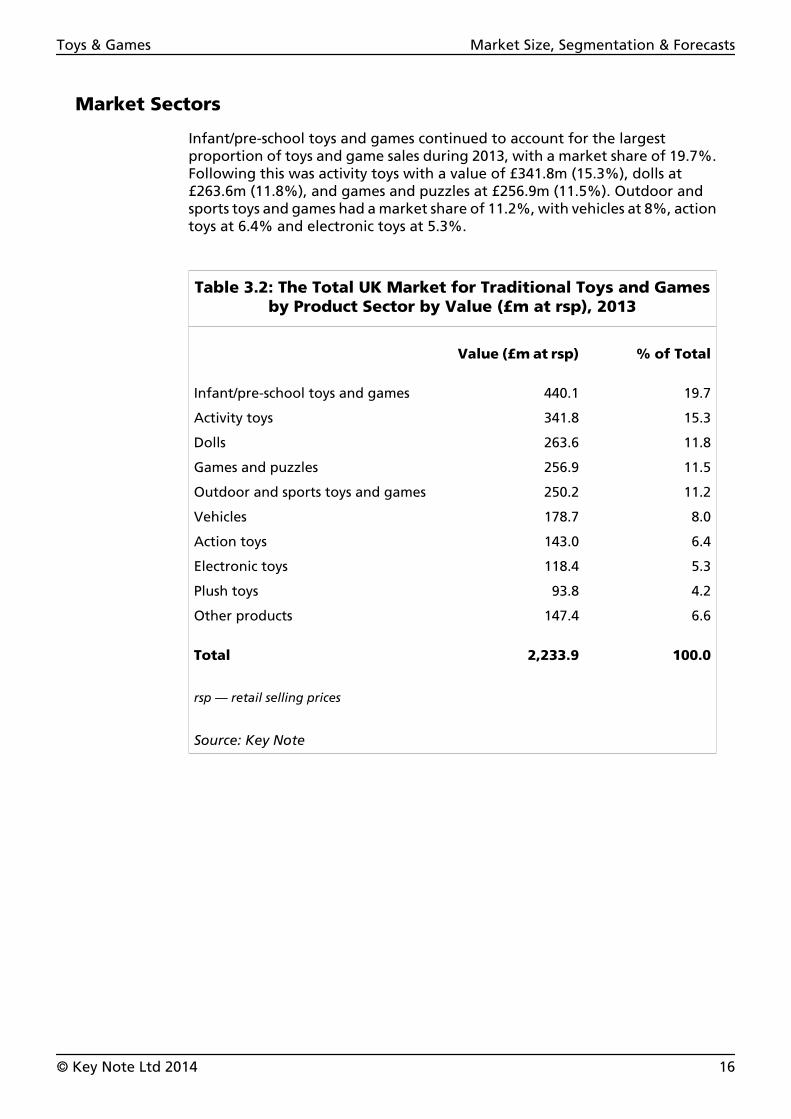

Infant/pre-school toys and games continued to account for the largestproportion of toys and game sales during 2013, with a market share of 19.7%.Following this was activity toys with a value of £341.8m (15.3%), dolls at£263.6m (11.8%), and games and puzzles at £256.9m (11.5%). Outdoor andsports toys and games had a market share of 11.2%, with vehicles at 8%, actiontoys at 6.4% and electronic toys at 5.3%.

Table 3.2: The Total UK Market for Traditional Toys and Gamesby Product Sector by Value (£m at rsp), 2013

Value (£m at rsp) % of Total

Infant/pre-school toys and games 440.1 19.7

Activity toys 341.8 15.3

Dolls 263.6 11.8

Games and puzzles 256.9 11.5

Outdoor and sports toys and games 250.2 11.2

Vehicles 178.7 8.0

Action toys 143.0 6.4

Electronic toys 118.4 5.3

Plush toys 93.8 4.2

Other products 147.4 6.6

Total 2,233.9 100.0

rsp — retail selling prices

Source: Key Note

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 16

Figure 3.2: The Total UK Market for Traditional Toys and Gamesby Product Sector by Value (£m at rsp), 2013

Infant/pre-school

Activity toys

DollsGam

es and puzzles

Outdoor and sports

Vehicles

Action toys

Electronic toys

Plush toys

Other

0

50

100

150

200

250

300

350

400

450

rsp — retail selling prices

Source: Key Note

Infant/Pre-School Toys and Games

In 2013, infant/pre-school toys and games continued to account for the largestshare of the overall UK market for toys and games, with a market value of£440.1m, representing 19.7% of the total. Sales in this particular sectorobserved an increase of 2.8% over the course of 2013.

The infant/pre-school toys and games market is primarily targeted towardschildren aged 2 and under, and is saturated with well-known brands such asTOMY, Fisher-Price Sidney and PlaySkool. In addition to these establishedbrands, other pre-school licences also maintain a considerable presence withinthe sector, including leading brands such as Peppa Pig and Thomas & Friends.

Activity Toys

In 2013, Key Note estimates that retail sales of activity toys amounted to£341.8m, representing 15.3% of the total UK toys and games market.

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 17

The activity toys sector includes items such as building and construction sets,and arts and crafts. The arts and crafts category of this sector is the largestsubsector and can include items such as jewellery making sets, with popularbrands including Aqua Beads, Hama and Grafix; cookery sets, such as thoseproduced by Kitchen Craft and Cooksmart; and arts and painting sets, andmodelling and play putty sets. Licenced entertainment brands, includingDisney, Peppa Pig and Thomas & Friends, also feature heavily.

Danish brand Lego dominates the building sets subsector of the market, whileconstruction toy sets produced by K’NEX also remain popular. The success oflicensed entertainment products also remains important for this subsector,with franchises such as Harry Potter, Star Wars and Toy Story assisting to drivesales in recent years.

Dolls

Key Note estimates that total sales of dolls stood at a value of £263.6m in 2013,thereby representing 11.8% of the overall market.

Although this sector of the market has been dominated by leading doll brandBarbie, from Mattel, for a number of years, Barbie products have begun to losemarket share of late, with the brand facing stiff competition from alternativedoll ranges, such as Monsters High and Bratz. This area of the market continuesto benefit considerably from new product innovation and add-on products,such as accessories and clothing, which are often bought as separate items afterthe purchase of an initial doll. Additionally, many of the major brands, forinstance Barbie and the Cabbage Patch Kids, have continued to remain popularamong doll collectors, with some products now commanding high prices if theyare seen as collectibles.

Games and Puzzles

In 2013, Key Note estimates that the value of the games and puzzles marketwas worth £256.9m, representing 11.5% of the overall market.

This particular sector of the market includes products such as board games,puzzles, jigsaws and party games. Growth within this sector has been drivensomewhat by the desire among consumers to purchase less-expensive indoorgames, such as games and puzzles, rather than expensive days out orhigher-priced items. A number of board game manufacturers have utilised thepopularity of digital/console games in order to enhance their own products,for instance, Mattel’s launch of Knock on Wood, an Angry Birds-themed boardgame. Conversely, the popularity of technology has also allowed for a greaternumber of board games in this sector which utilise technology, such as DVDs,to come into existence, such as the Scene It? range of games.

Another trend that has emerged in this sector is ‘retro’ packaging, with anumber of well-known, classic board games, including Monopoly, nowavailable in old-fashioned boxes in order to appeal to both adults and children.

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 18

Outdoor and Sports Toys and Games

Key Note estimates that the value of sales of outdoor and sports toys andgames reached £250.2m in 2013, representing 11.2% of the overall market.

This subsector of the market includes products such as trampolines, skates andskateboards, scooters, swing sets, footballs and other various ball and racketgames. Popular brands within this subsector include Swingball and ChadValley, which produce a variety of games sets for children for particular sports,such as cricket and football. In addition, wheeled toys have remained popularin past years, particularly scooters, following an influx of a range of licensedscooters from popular children’s franchises, including Disney, Peppa Pig andFireman Sam.

Vehicles

Key Note estimates that retail sales of toy vehicles reached a value of £178.7min 2013, representing 8% of the total toys and games market.

Some of the major brands within the toy vehicle sector include Hot Wheels andMatchbox, both of which are produced by Mattel, and Scalextric from Hornby.Recent advances in technology and new product development (NPD) haveallowed manufacturers of such toys to incorporate the popularity of mobiledevices into their products, with a number of toy vehicles now available thatcan be controlled via the iPhone. In addition to this, the release of popularDisney films Cars and Cars 2 is expected to have sparked an interest in toyvehicles, and as such, a range of the films’ characters in the form of toy vehicleshave been released onto the market.

Action Toys

Key Note estimates that the value of sales for action toys reached £143m in2013, representing 6.4% of the overall UK market for toys and games.

For a number of years, growth in this sector of the market has principally beendriven by associated film releases, for instance the Transformers, G.I. Joe andStar Wars franchises, all of which have served to boost the sector and sparkedthe development and release of new action toy product lines. One of the mostpopular brands of action toys in the UK is Star Wars, which is anticipated to befurther boosted in line with the upcoming release of the new trilogy of StarWars films, starting in 2015. Other popular movie titles which have bolsteredthis sector of the market include Spiderman, Batman, Iron Man, Thor andTheAvengers.

Electronic Toys

Key Note estimates that sales of electronic toys in the UK stood at £118.4m in2013, thereby representing 5.3% of the overall toys and games market.

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 19

The increasing popularity of tablet and other electronic devices in recent years,particularly since 2010, has been reflected in increased NPD activity in thissector, with market leaders VTech and Leap Frog both introducing theirthird-generation (3G) tablet computers for children during 2013. Anotherrecent development within the electronic toys sector has been ‘apptivity’products, such as steering wheels, for instance, which can be connected to theiPhone for playing downloadable games.

Plush Toys

Key Note estimates that retail sales of plush toys reached £93.8m in 2013,accounting for 4.2% of total toys and games sales in the UK.

Sales of plush toys witnessed a decline in 2013, mainly as a result of increasingcompetition from alternative toys such as digital products, with a far greateramount of NPD focusing on electronic gadgets or hybrid digital-physicalproducts.

Major brands dominating this sector of the market include items such as BeanieBabies and Pillow Pets. Demand for such products usually peaks depending oncurrent trends, with many lines quickly coming into and going out of fashionin quick succession, such as Go Go Hamsters in the UK.

The market is also strengthened to a certain extent by the enduring popularityof specialised stores within the sector, such as Build-A-Bear Workshops, whichwere founded in the US in 1997 and expanded in the UK after The BearWorkshop was purchased from Hamleys in 2006.

Other Products

Other products within the toys and games market include dressing-up clothesand pocket-money novelties, which are typically inexpensive. Key Noteestimates that sales of other products reached £147.4m in 2013, accounting for6.6% of the total toys and games market in the UK.

MARKET POSITION

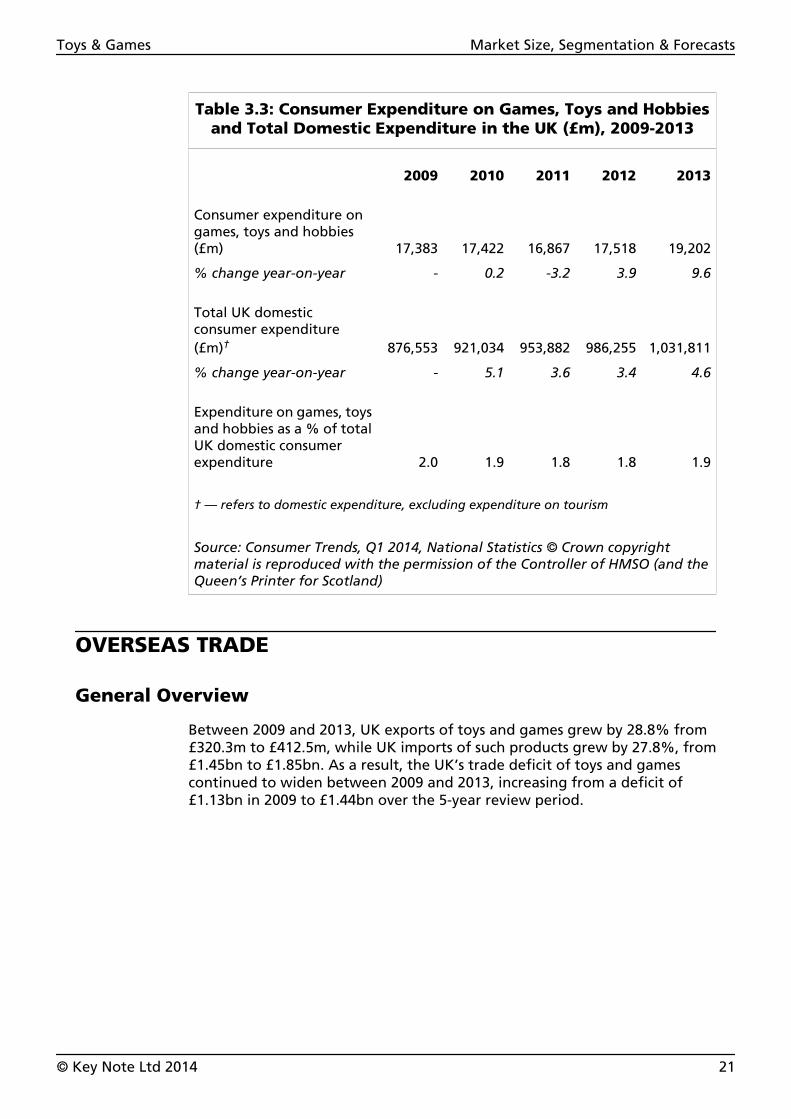

The UK

According to figures from National Statistics, consumer expenditure on games,toys and hobbies grew by 9.6% in 2013 to reach a value of £19.2bn, which wasan increase of 10.5% over the 5-year review period between 2009 and 2013.This meant that in 2013, consumer expenditure on games, toys and hobbiesrepresented 1.9% of total UK domestic consumer expenditure, which wasdown from a share of 2% in 2009.

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 20

Table 3.3: Consumer Expenditure on Games, Toys and Hobbiesand Total Domestic Expenditure in the UK (£m), 2009-2013

2009 2010 2011 2012 2013

Consumer expenditure ongames, toys and hobbies(£m) 17,383 17,422 16,867 17,518 19,202

% change year-on-year - 0.2 -3.2 3.9 9.6

Total UK domesticconsumer expenditure(£m)† 876,553 921,034 953,882 986,255 1,031,811

% change year-on-year - 5.1 3.6 3.4 4.6

Expenditure on games, toysand hobbies as a % of totalUK domestic consumerexpenditure 2.0 1.9 1.8 1.8 1.9

† — refers to domestic expenditure, excluding expenditure on tourism

Source: Consumer Trends, Q1 2014, National Statistics © Crown copyrightmaterial is reproduced with the permission of the Controller of HMSO (and theQueen’s Printer for Scotland)

OVERSEAS TRADE

General Overview

Between 2009 and 2013, UK exports of toys and games grew by 28.8% from£320.3m to £412.5m, while UK imports of such products grew by 27.8%, from£1.45bn to £1.85bn. As a result, the UK’s trade deficit of toys and gamescontinued to widen between 2009 and 2013, increasing from a deficit of£1.13bn in 2009 to £1.44bn over the 5-year review period.

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 21

Table 3.4: UK Trade Balance of Toys and Games by Value(£m), 2009-2013

2009 2010 2011 2012 2013

Exports 320.3 342.7 372.8 374.4 412.5

Less imports 1,448.4 1,816.7 1,687.7 1,753.6 1,850.7

Trade balance -1,128.1 -1,474.0 -1,314.9 -1,379.2 -1,438.2

Note: data refer to items exported/imported by and into the UK under the remit of UKTrade Commodity Code 9501 — wheeled toys, designed to be ridden by children (forexample, tricycles, scooters, pedal cars), dolls’ carriages; Commodity Code 9502 — dollsrepresenting only human beings; Commodity Code 9503 — tricycles, scooters, pedal carsand similar wheeled toys, dolls’ carriages, dolls, other toys, reduced-size ‘scale’recreational models (working or not), puzzles of all kinds; Commodity Code 9505 —festival, carnival or other entertainment articles, including conjuring tricks and noveltyjokes.

Source: UKtradeinfo, HM Revenue & Customs © Crown copyright

Figure 3.3: UK Trade Balance of Toys and Gamesby Value (£m), 2009-2013

Exports

Imports

Trade balance

20092010

20112012

2013

-1,000

-500

0

500

1,000

1,500

Note: data refer to items exported/imported by and into the UK under the remit of UKTrade Commodity Code 9501 — wheeled toys, designed to be ridden by children (forexample, tricycles, scooters, pedal cars), dolls’ carriages; Commodity Code 9502 — dollsrepresenting only human beings; Commodity Code 9503 — tricycles, scooters, pedal carsand similar wheeled toys, dolls’ carriages, dolls, other toys, reduced-size ‘scale’recreational models (working or not), puzzles of all kinds; Commodity Code 9505 —festival, carnival or other entertainment articles, including conjuring tricks and noveltyjokes.

Source: UKtradeinfo, HM Revenue & Customs © Crown copyright/Key Note

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 22

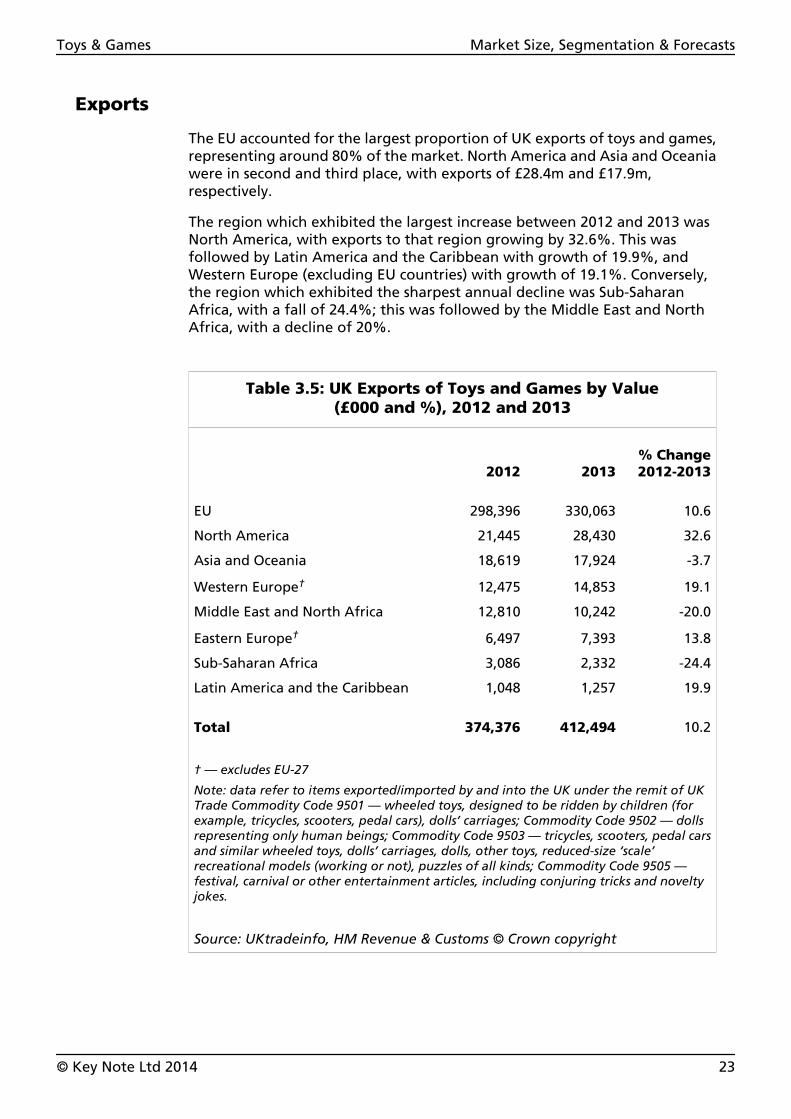

Exports

The EU accounted for the largest proportion of UK exports of toys and games,representing around 80% of the market. North America and Asia and Oceaniawere in second and third place, with exports of £28.4m and £17.9m,respectively.

The region which exhibited the largest increase between 2012 and 2013 wasNorth America, with exports to that region growing by 32.6%. This wasfollowed by Latin America and the Caribbean with growth of 19.9%, andWestern Europe (excluding EU countries) with growth of 19.1%. Conversely,the region which exhibited the sharpest annual decline was Sub-SaharanAfrica, with a fall of 24.4%; this was followed by the Middle East and NorthAfrica, with a decline of 20%.

Table 3.5: UK Exports of Toys and Games by Value(£000 and %), 2012 and 2013

2012 2013% Change2012-2013

EU 298,396 330,063 10.6

North America 21,445 28,430 32.6

Asia and Oceania 18,619 17,924 -3.7

Western Europe† 12,475 14,853 19.1

Middle East and North Africa 12,810 10,242 -20.0

Eastern Europe† 6,497 7,393 13.8

Sub-Saharan Africa 3,086 2,332 -24.4

Latin America and the Caribbean 1,048 1,257 19.9

Total 374,376 412,494 10.2

† — excludes EU-27

Note: data refer to items exported/imported by and into the UK under the remit of UKTrade Commodity Code 9501 — wheeled toys, designed to be ridden by children (forexample, tricycles, scooters, pedal cars), dolls’ carriages; Commodity Code 9502 — dollsrepresenting only human beings; Commodity Code 9503 — tricycles, scooters, pedal carsand similar wheeled toys, dolls’ carriages, dolls, other toys, reduced-size ‘scale’recreational models (working or not), puzzles of all kinds; Commodity Code 9505 —festival, carnival or other entertainment articles, including conjuring tricks and noveltyjokes.

Source: UKtradeinfo, HM Revenue & Customs © Crown copyright

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 23

Imports

Asia and Oceania accounted for the largest proportion of UK imports of toysand games, representing around 76.2% of the market. The EU and NorthAmerica were in second and third place, with imports of £353.9m and £78.3m,respectively.

The region which exhibited the largest increase between 2012 and 2013 wasEastern Europe (not including EU member states), with imports from thatregion growing by 22.9%. This was followed by the EU with growth of 15.7%and North America with growth of 12.5%. Conversely, the region whichexhibited the sharpest annual decline was Sub-Saharan Africa, with a fall of55.5%. This was followed by the Middle East and North Africa, with a declineof 15.3%.

Table 3.6: UK Imports of Toys and Games by Value(£000 and %), 2012 and 2013

2012 2013% Change2012-2013

Asia and Oceania 1,368,202 1,410,103 3.1

EU 305,854 353,948 15.7

North America 69,628 78,341 12.5

Middle East and North Africa 6,493 5,498 -15.3

Western Europe† 1,991 1,770 -11.1

Sub-Saharan Africa 740 329 -55.5

Eastern Europe† 393 483 22.9

Latin America and theCaribbean 283 243 -14.1

Total 1,753,584 1,850,715 5.5

† — excludes EU-27

Note: data refer to items exported/imported by and into the UK under the remit of UKTrade Commodity Code 9501 — wheeled toys, designed to be ridden by children (forexample, tricycles, scooters, pedal cars), dolls’ carriages; Commodity Code 9502 — dollsrepresenting only human beings; Commodity Code 9503 — tricycles, scooters, pedal carsand similar wheeled toys, dolls’ carriages, dolls, other toys, reduced-size ‘scale’recreational models (working or not), puzzles of all kinds; Commodity Code 9505 —festival, carnival or other entertainment articles, including conjuring tricks and noveltyjokes.

Source: UKtradeinfo, HM Revenue & Customs © Crown copyright

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 24

FORECASTS

Future Trends

Forecast Economic Trends

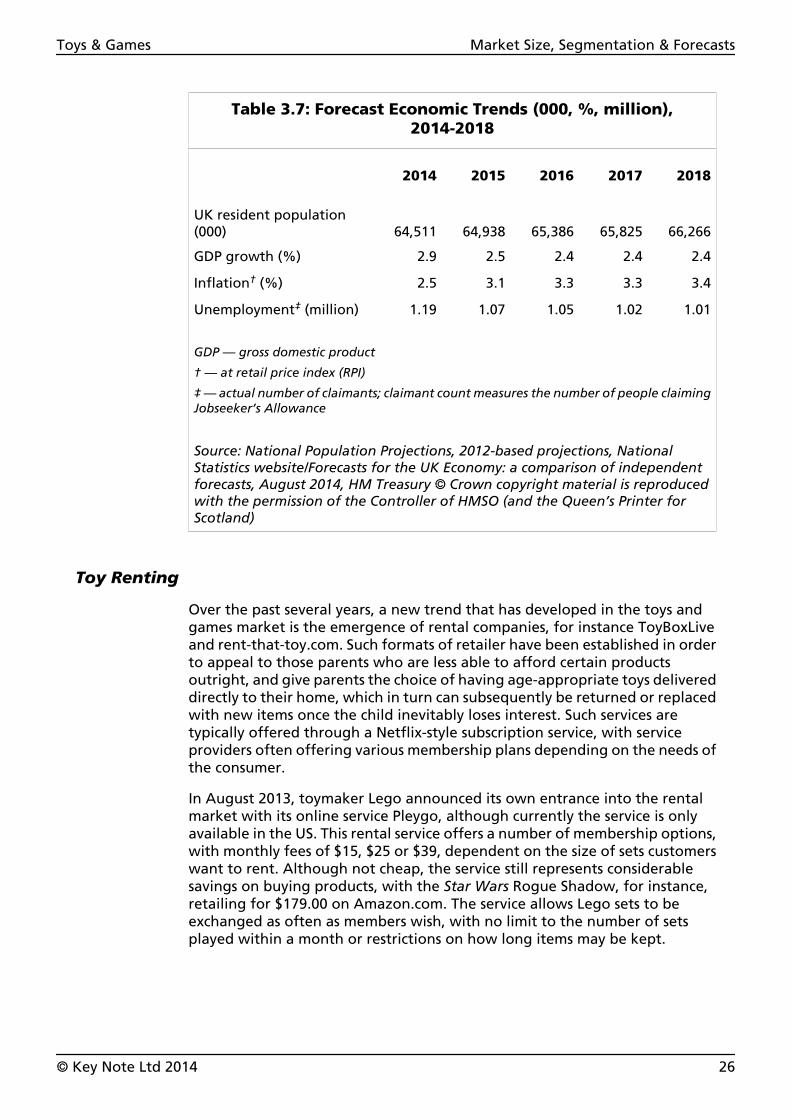

Estimates from National Statistics predict that the total population of the UKwill rise from 64.5 million in 2014 to 66.3 million in 2018, representing a rise of2.7% over the 5-year period. This rise is likely to be attributable to the UK’shigher birth than death rate, in addition to a continual positive net migrationlevel and ageing population for the foreseeable future. The growingpopulation should, in theory, result in an overall boost in consumer spending,which in turn will benefit the wider economy, including the UK market for toysand games.

Forecast figures from the UK Treasury indicate an expected gross domesticproduct (GDP) growth rate of 2.9% in 2014, 2.5% in 2015 and 2.4% thereafterto the end of the review period. While this anticipated growth is positive forthe economy, it should be noted that these levels remain beneath those seenprior to the economic downturn, and that, therefore, recovery is not yet fullyentrenched. This may be attributable, in part, to tight public-sector fiscalconsolidation, in addition to lingering concerns in the Eurozone, which servesas the UK’s most vital trading partner. Nevertheless, in spite of theless-than-impressive forecast growth figures, it is anticipated that the UK willbe the fastest-growing economy in the Group of 7 (G7) nations in 2014, andone of the better-performing countries in Europe.

The most recent economic data indicated that inflation, as measured by theretail prices index (RPI), will average 2.5% in 2014, which remains above theBank of England’s (BoE’s) target rate of 2%. From 2014 onwards, inflation isanticipated to edge upwards, to reach 3.4% by 2018.

The next few years will witness a steady decline in the level of unemploymentin the UK, largely as a result of strong forecast growth in private-sectoremployment. The unemployment rate, as measured by the number ofclaimants of Jobseeker’s Allowance, is anticipated to fall from 1.19 million in2014 to 1.01 million in 2018.

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 25

Table 3.7: Forecast Economic Trends (000, %, million),2014-2018

2014 2015 2016 2017 2018

UK resident population(000) 64,511 64,938 65,386 65,825 66,266

GDP growth (%) 2.9 2.5 2.4 2.4 2.4

Inflation† (%) 2.5 3.1 3.3 3.3 3.4

Unemployment‡ (million) 1.19 1.07 1.05 1.02 1.01

GDP — gross domestic product

† — at retail price index (RPI)

‡ — actual number of claimants; claimant count measures the number of people claimingJobseeker’s Allowance

Source: National Population Projections, 2012-based projections, NationalStatistics website/Forecasts for the UK Economy: a comparison of independentforecasts, August 2014, HM Treasury © Crown copyright material is reproducedwith the permission of the Controller of HMSO (and the Queen’s Printer forScotland)

Toy Renting

Over the past several years, a new trend that has developed in the toys andgames market is the emergence of rental companies, for instance ToyBoxLiveand rent-that-toy.com. Such formats of retailer have been established in orderto appeal to those parents who are less able to afford certain productsoutright, and give parents the choice of having age-appropriate toys delivereddirectly to their home, which in turn can subsequently be returned or replacedwith new items once the child inevitably loses interest. Such services aretypically offered through a Netflix-style subscription service, with serviceproviders often offering various membership plans depending on the needs ofthe consumer.

In August 2013, toymaker Lego announced its own entrance into the rentalmarket with its online service Pleygo, although currently the service is onlyavailable in the US. This rental service offers a number of membership options,with monthly fees of $15, $25 or $39, dependent on the size of sets customerswant to rent. Although not cheap, the service still represents considerablesavings on buying products, with the Star Wars Rogue Shadow, for instance,retailing for $179.00 on Amazon.com. The service allows Lego sets to beexchanged as often as members wish, with no limit to the number of setsplayed within a month or restrictions on how long items may be kept.

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 26

Upcoming Toy Merchandising Opportunities

In addition to seasonal peaks and various ‘trend crazes’, the market for toysand games is also highly dependent on the success of alternative industries,perhaps noticeably the film industry. Many toys and games product rangeshave been launched on the back of successful film franchises, such as HarryPotter, Star Wars, Lord of the Rings, etc. Looking forward, following on fromthe 2012 decision by The Walt Disney Company to purchase Lucasfilm, the toysand games market will be eagerly anticipating the arrival of the new sequeltrilogy of Star Wars films, set to be first released in 2015, which is forecast toencourage a considerable range of associated toys and games onto the market.The industry has also been boosted in recent years by the new Hobbit films,the third and final of which is due to be released in December 2014. Otherupcoming blockbusters which are due to boost the toys and games industryinclude new instalments from The Hunger Games and Jurassic Park, amongothers.

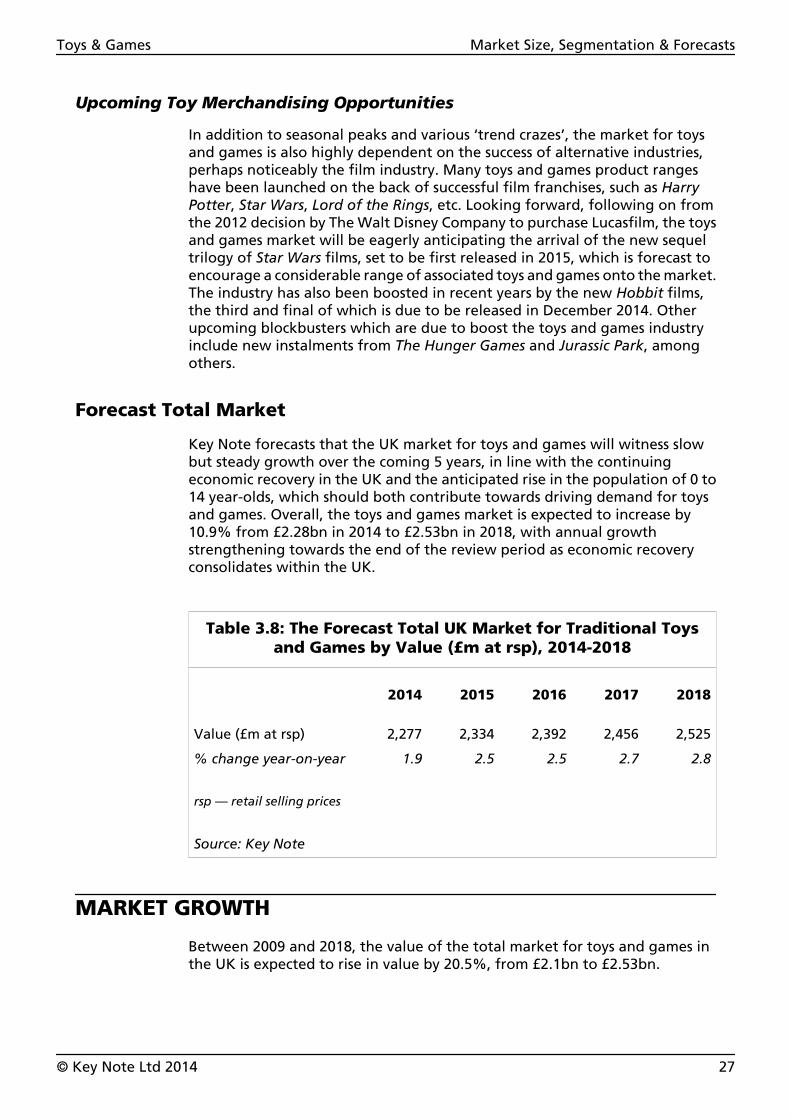

Forecast Total Market

Key Note forecasts that the UK market for toys and games will witness slowbut steady growth over the coming 5 years, in line with the continuingeconomic recovery in the UK and the anticipated rise in the population of 0 to14 year-olds, which should both contribute towards driving demand for toysand games. Overall, the toys and games market is expected to increase by10.9% from £2.28bn in 2014 to £2.53bn in 2018, with annual growthstrengthening towards the end of the review period as economic recoveryconsolidates within the UK.

Table 3.8: The Forecast Total UK Market for Traditional Toysand Games by Value (£m at rsp), 2014-2018

2014 2015 2016 2017 2018

Value (£m at rsp) 2,277 2,334 2,392 2,456 2,525

% change year-on-year 1.9 2.5 2.5 2.7 2.8

rsp — retail selling prices

Source: Key Note

MARKET GROWTH

Between 2009 and 2018, the value of the total market for toys and games inthe UK is expected to rise in value by 20.5%, from £2.1bn to £2.53bn.

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 27

Figure 3.4: Growth in the Total UK Market for Traditional Toysand Games by Value (£m at rsp), 2009-2018

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

2,100

2,150

2,200

2,250

2,300

2,350

2,400

2,450

2,500

rsp — retail selling prices

Source: Key Note

Toys & Games Market Size, Segmentation & Forecasts

© Key Note Ltd 2014 28

4. Strengths, Weaknesses, Opportunities &Threats

STRENGTHS

• One of the key characteristics of the toys and games market is the high levelof new product development (NPD), which means there is a considerableamount of consumer choice.

• In addition to NPD, the industry is also highly dependent on new and evolvingtrends, which tend to appear and disappear from the market at a very fastpace; parents are often keen to ensure their children are given the mostpopular toys of the moment, thus serving to boost sales.

• Toys and games remain popular gift items, meaning that the market is mostprofitably during peak seasonal periods, such as Christmas, in addition toother celebrations/festivities.

• The importance of toys and games to children’s development has beenenhanced by campaigns such as ‘Make Time 2 Play’ by the British Toy & HobbyAssociation (BTHA), thereby consolidating sales for items which are perceivedto offer educational and developmental benefits.

• Toys and games are widely available across a broad spectrum of pricing levels,meaning that a considerable choice of toys and games are available to thevast majority of consumers, regardless of socio-economic background.

• The toys and games market is boosted significantly by hobby-makers andcollectors, who often drive sales in the market, with special collectors’ itemsand limited-edition items performing particularly well consideringconsumers’ willingness to spend greater sums of money.

• The rising proportion of couples waiting until they are older and morefinancially stable before starting a family means that, in theory, the averagehousehold with young children now has a greater amount of disposableincome to spend on toys and games.

• The majority of children have — and constantly expand upon — a largecollection of toys and games, with parents willing to spend money on a rangeof different products for their kids.

WEAKNESSES

• The UK toys and games industry is highly saturated and extremelycompetitive, with a substantial multitude of products on the market; thisoften makes it difficult for small- to medium-sized enterprises (SMEs) to gaina meaningful foothold in the industry.

Toys & Games Strengths, Weaknesses, Opportunities & Threats

© Key Note Ltd 2014 29

• As the market is heavily dependent on new trends, products and toy rangescan enter and leave the marketplace very quickly, sometimes resulting in theover-production of items which will eventually never sell.

• The expansion of supermarkets and online retailers, for instance Amazon andPlay.com, into the toys and games market has had a negative impact onhigh-street retailers of toys and games, many of which have found itincreasingly hard to compete with the lower-cost models of the supermarketsand online retailers.

• Additionally, the influx of value toy retailers, such as supermarkets andonline retailers, has put downwards pressure on the value of the market.

• There is a strong second-hand marketplace for toys and games, with onlineauction site eBay particularly popular among consumers, which in turndilutes the potential value of primary retail sales.

• New product launches, which can often be expensive, carry a high risk in thecrowded marketplace.

OPPORTUNITIES

• Character licensing opportunities provide new opportunities for productdevelopment, and can prove particularly popular as new programmes andfilms are released (e.g. the upcoming Star Wars sequel trilogy).

• New trends, for instance girls’ construction sets and strategy-based boardgames, have provided new opportunities for toys and games developers andmanufacturers of late.

• In recent years there has been substantial growth in the size and scope ofchildren’s media — particularly children’s television — and this has assistedin driving licensing and promotional opportunities within this particularsector of the toys and games market.

• New electronic and digital innovations are providing an increasingly greaterlevel of interactivity and sophistication, a trend which is particularlyprevalent in the educational and learning sector of the market.

• The rising penetration of the Internet, portable hand-held devices and socialmedia in the UK has assisted in facilitating greater promotional campaigns,product launches and marketing activity in recent years.

• The increasing popularity of certain mobile gaming titles has provided newopportunities for toy manufacturers to develop physical toy ranges tocompliment the franchise. For instance, Angry Birds toys and games haverecently been introduced onto the market to take advantage of the game’shuge digital appeal.

• The UK’s birth rate remains healthy, and looks set to remain so for theforeseeable future. As such, the potential consumer base for toys and gamesin the UK looks set to grow in the coming years.

Toys & Games Strengths, Weaknesses, Opportunities & Threats

© Key Note Ltd 2014 30

THREATS

• The competition posed by the rapid ascent of mobile gaming and onlinegaming in recent years has had a severe impact on the toys and gamesmarket, with many developers and manufacturers forced to diversify intothese sectors themselves.

• The recent release of the eighth generation of video gaming consoles hasthe potential to attract consumer spending away from spending ontraditional toys and games.

• Children’s toys and games are subject to an increasing multitude oflegislation and safety protocols, which can demand a substantial level ofinvestment on the part of manufacturers in order to ensure compliance.Additionally, product recalls can often result in negative press for toy brandsand their manufacturers.

• Children are increasingly maturing at an earlier age than previousgenerations, and as a result, their time spent playing with toys and games isdecreasing when compared to older generations.

Toys & Games Strengths, Weaknesses, Opportunities & Threats

© Key Note Ltd 2014 31

5. PESTEL

POLITICAL

Counterfeit Toys

In was revealed by the European Commission (EC) in August 2013 thatthroughout 2012, an estimated €19.5m worth of counterfeit toys (at domesticvalue, had such toys been genuine) were seized by EU customs and bordercontrol agencies. Toys (excluding games/electronic games) accounted for 4.1%of all seizures throughout the year. However, the figures published by theCommission are thought only to represent a small fraction of the total valueof counterfeit good distributed across EU member states, as many items aresuccessful in evading detection by authorities. The substantial trade incounterfeit goods can potentially have severe consequences for end users, withmany items failing to adhere to the strict safety and manufacturing standardsenforced on the genuine industry.

Globally, moves have been made in order to stem the flow of counterfeit toys,with the International Standards Organization (ISO) announcing in September2012 that it had established a new standard aimed at making it easier to locatecounterfeit products across the globe. It is anticipated that the new standard,the ISO 12931:2012, will make it easier to provide reliable evidence to identifygenuine products by specifying performance requirements for authenticationtools, such as holograms, taggants and marks. The new standards will apply toboth toy products and/or their packaging.

ECONOMIC

Improving Economy Boosts Toys and Games Sales

The UK economy finally emerged from recession in January 2010, putting anend to 6 months of quarterly contractions. Nevertheless, growth remainedpatchy and inconsistent. Although the UK appears to have finally pulled outof recession, levels of economic growth have remained below those recordedpre-recession, with data showing that the UK economy grew by 1.7% in 2013at annual chain-linked gross domestic product (GDP), but that the total GDPonly surpassed its pre-recession peak in the latter half of 2014. The UK isanticipated to be the best-performing economy in the Group of 7 (G7) nationsin 2014, and one of the better performing countries in Europe.

In addition to GDP growth, as of June 2014 inflation was at 1.6%, which iscomfortably beneath the Bank of England’s (BoE’s) target rate of 2%, andunemployment continues to fall year-on-year. These positive economicindicators represent optimism for the future of the toys of games industry, assuch trends will see household disposable incomes increase, which in turnshould encourage higher consumer expenditure, including in the toys andgames market.

Toys & Games PESTEL

© Key Note Ltd 2014 32

SOCIAL

Gender Stereotypes

In response to perceived gender stereotyping regarding the manufacture andsale of toys and games in the UK, the industry has been challenged on itsperpetuation of the issue in terms of toy development and marketing tochildren in recent years. Campaign groups including Let Toys Be Toys andPinkstinks have emerged, challenging the practice of gender-stereotyped shopdisplays and the segregation of boys’ and girls’ items in stores. Of notice, recentcampaigns by Pinkstinks have challenged a global toy range distributed by theEarly Learning Centre (ELC), which included a girls’ pink edition featuringmermaids and a blue edition for boys showing boats. In addition, the grouphas also scrutinised toy ranges aimed at girls which include pink vacuumcleaners and lilac ironing boards; and recently spearheaded a campaign onsocial media sites Twitter and Facebook after which supermarket retailerSainsbury’s was forced to remove gender-specific labelling from an own-brandtoy line which featured doctors’ outfits tagged for boys and nurse andbeautician outfits for girls.

Although marketing based on gender has been a key feature of the toys andgames industry for the past several years, historically, this has not always beenthe case. For instance, according to an article published by the New YorkTimes in 2012, advertising based on gender was found to have been relativelyabsent during the 1970s, with close to 70% of advertising bearing nocorrelation to gender. However, by 1995, gender-specific advertising of toyshad become a distinct element within the industry, with the majority of toysnow carrying some form of gender labelling, either explicitly or subtly, i.e.through colour.

TECHNOLOGICAL

New Generation of Video Gaming Consoles