Market Overview

16

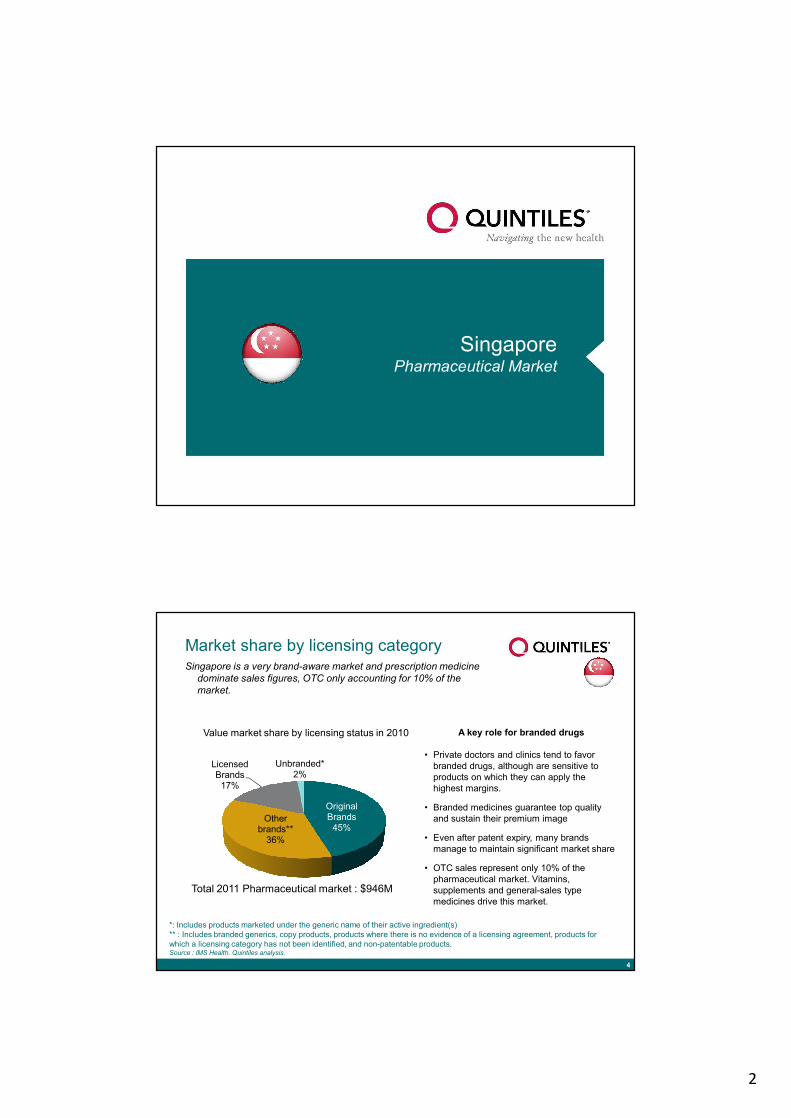

1 Pharmaceutical Market Overview – Singapore, Malaysia and Indonesia Successful Market Entry Strategy for ASEAN 5 December 2012 Fredrik Nyberg, Senior Director Quintiles Consulting Market Overview Key comparables for Singapore, Malaysia and Indonesia 2 Malaysia Population 29M Nominal GDP $247B Health expenditure per capita $677 Physicians per 10,000 population 9.4 Singapore Population : 5.3M Nominal GDP : $266B Health expenditure per capita : $2086 Physicians per 10,000 population : 18.3 Indonesia Population 250M Nominal GDP $835B Health expenditure per capita $99 Physicians per 10,000 population 2.9 All $ are US$. Sources : Population and GDP : CIA (2011); Health expenditure per capita are WHO (2009), total health expenditure are Espicom 2009

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Market Overview

1

Pharmaceutical Market Overview – Singapore, Malaysia

and Indonesia

Successful Market Entry Strategy for ASEAN

5 December 2012

Fredrik Nyberg, Senior Director Quintiles

Consulting

Market OverviewKey comparables for Singapore, Malaysia and Indonesia

2

Malaysia

Population29M

Nominal GDP$247B

Health expenditure per capita

$677Physicians per

10,000 population9.4

Malaysia

Population29M

Nominal GDP$247B

Health expenditure per capita

$677Physicians per

10,000 population9.4

SingaporePopulation : 5.3M

Nominal GDP : $266BHealth expenditure per capita : $2086

Physicians per 10,000 population : 18.3

SingaporePopulation : 5.3M

Nominal GDP : $266BHealth expenditure per capita : $2086

Physicians per 10,000 population : 18.3

Indonesia

Population250M

Nominal GDP$835B

Health expenditure per capita

$99Physicians per

10,000 population2.9

Indonesia

Population250M

Nominal GDP$835B

Health expenditure per capita

$99Physicians per

10,000 population2.9

All $ are US$. Sources : Population and GDP : CIA (2011); Health expenditure per capita are WHO (2009), total health expenditure are Espicom 2009

2

SingaporePharmaceutical Market

Original Brands

45%Other

brands**36%

Licensed Brands

17%

Unbranded*2%

Market share by licensing categorySingapore is a very brand-aware market and prescription medicine

dominate sales figures, OTC only accounting for 10% of the market.

4

*: Includes products marketed under the generic name of their active ingredient(s)** : Includes branded generics, copy products, products where there is no evidence of a licensing agreement, products for which a licensing category has not been identified, and non-patentable products.Source : IMS Health. Quintiles analysis.

A key role for branded drugs

• Private doctors and clinics tend to favor branded drugs, although are sensitive to products on which they can apply the highest margins.

• Branded medicines guarantee top quality and sustain their premium image

• Even after patent expiry, many brands manage to maintain significant market share

• OTC sales represent only 10% of the pharmaceutical market. Vitamins, supplements and general-sales type medicines drive this market.

Value market share by licensing status in 2010

Total 2011 Pharmaceutical market : $946M

3

Key buyersLeading hospital groups, independent clinics and pharmacy chains

can be considered the three key target groups in Singapore

5

Leading private hospital group: Parkway Pantai (IHH Group)• 55% market share of medical

tourists coming to SGP• 4 major hospitals• Medical centers and clinics, health

screening facilities, radiology facilities, laboratories

• 3,400 beds & 1,200 accredited medical specialists

Public hospital purchase drugs through tendering processes managed by SingHealth and NHG

HealthCare Professionals (HCP) Hospitals Retail Pharmacies

Neither TCM stores nor retail chain sell much prescription

drugsSource : MOH Medical Directory, Nielsen (drug store numbers, 2010), Parkway website. IMS. Quintiles analysis

304

126

10343

Traditional Medical Stores

Clinics

Dentists

Opticians Optometrists

TCM practionners

Doctors

3365

1705

2371

2671

10600

• Most clinics dispense medicine • Clinics and hospitals dispense the vast majority of prescription drugs• Most clinics are independent, although groups such as Healthway have

many clinics

Three chains hold 85% of the retail pharmacy market, focusing on OTC and

consumer goods

Physicians per 10,000 population : 18.3

Key Suppliers

• Singapore is a logistics hub, with over 25 productions sites. Seven plants are set to open over 2010-2013, most of them dedicated to biologics.

• Leading MNCs present in Singapore include :

• Regional leaders are also present and have significant market share, such as

• 3 players dominate pharmaceutical distribution, each of them operating in their own niche:

Singapore is a destination of choice because it :1. Is centrally located, business-friendly environment and financial incentives2. Welcomes the testing and the introduction of innovative medical treatments3. Is home to a number of regional KOLs4. Private healthcare plays a dominant role5. Leads regional harmonization efforts on regulatory aspects

Singapore attract many MNC’s that see Singapore as a gateway to the rest of Asia-Pacific

6

4

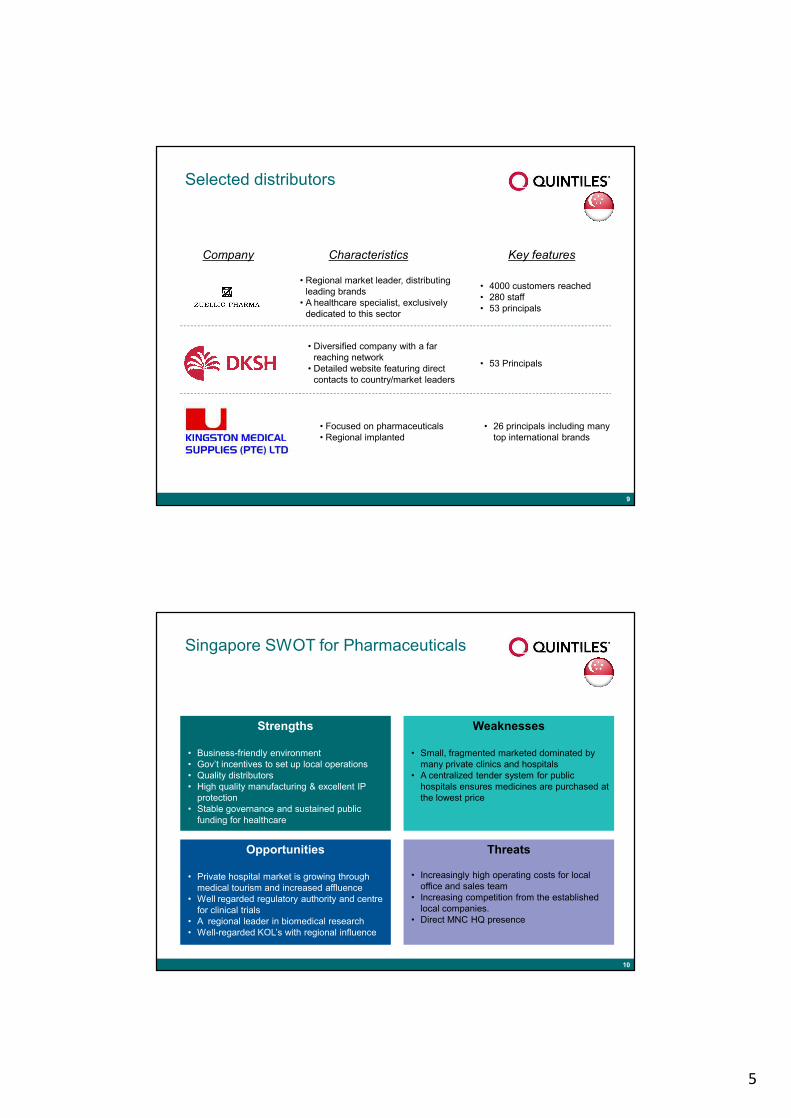

Pharmaceutical distribution channels & market sharePrivate doctors and private hospitals dominate pharmaceutical sales

in value and should be targeted in priority

7

Manufacturers

Marketing Agents*

Public Hospitals & Specialty centers

Private practitioners

& clinics

SingHealth GPO

Private Hospitals

Retail Pharmacies

Patients

Drugstores / Other retail

outlets

* Many distributors are also marketing agentsSources: IMS Health. Quintiles analysis.

30% 34%9%

8% 19%

2010Market Share

Distributors*

Pharmaceuticals sales forecast

8

Market Drivers

• Population ageing and increasing chronic diseases

• Launch and uptake of new innovative drugs

• Private sector usage of branded pharmaceuticals

• Increased government financial support and screening campaigns

• High costs of living and stagnant wages

• Price pressure imposed by central tender processes for public hospitals

Source: IMS Health & Quintiles Analysis

0

200

400

600

800

1000

1200

1400

2010 2011 2012 2013 2014 2015

946 998 1063 1135 1213 1299

Sales in M US$

CAGR6.5%

21%

17%

13%12%7%

7%

30%

2015 market share by therapeutic class

Oncology & immunomodulatorsCardiovascularMetabolicAntiinfectiveCNSRespiratoryOther classes

Market Restraints

5

Selected distributors

9

CharacteristicsCompany Key features

• 26 principals including many top international brands

• Focused on pharmaceuticals• Regional implanted

• Regional market leader, distributing leading brands

• A healthcare specialist, exclusively dedicated to this sector

• 4000 customers reached• 280 staff• 53 principals

• Diversified company with a far reaching network

• Detailed website featuring direct contacts to country/market leaders

• 53 Principals

Singapore SWOT for Pharmaceuticals

10

Strengths

• Business-friendly environment• Gov’t incentives to set up local operations• Quality distributors• High quality manufacturing & excellent IP

protection• Stable governance and sustained public

funding for healthcare

Weaknesses

• Small, fragmented marketed dominated by many private clinics and hospitals

• A centralized tender system for public hospitals ensures medicines are purchased at the lowest price

Opportunities

• Private hospital market is growing through medical tourism and increased affluence

• Well regarded regulatory authority and centre for clinical trials

• A regional leader in biomedical research • Well-regarded KOL’s with regional influence

Threats

• Increasingly high operating costs for local office and sales team

• Increasing competition from the established local companies.

• Direct MNC HQ presence

6

• Understand the market dynamics• Ask end-users to recommend the

best distributors• Take time to meet and evaluate

potential distribution partners• Provide training and sales/marketing

support early

Key market entry challenges & strategies

11

ComplianceMarket & Pricing strategy

MarketAccess

Partner Selection

Market Entry

Clinical Support

Drug registration

Local contacts Regulatory approval

Sustained growth

Supplier / Distributor / End-user interactions

Market Entry

• Shortcut regulatory process with Abridged Route

• Use distributor to make regulatory submission

• Prioritize dispensing GP’s

• Anticipate lower prices in Government tender process

• View Singapore entry as a stepping stone to the region

• Enable high-level interactions between top South Korean clinicians and Singaporean KOL’s

• Singaporean KOL support could facilitate entry into other markets

MalaysiaPharmaceutical Market

7

Market share by licensing category

Value market share by licensing status in 2010

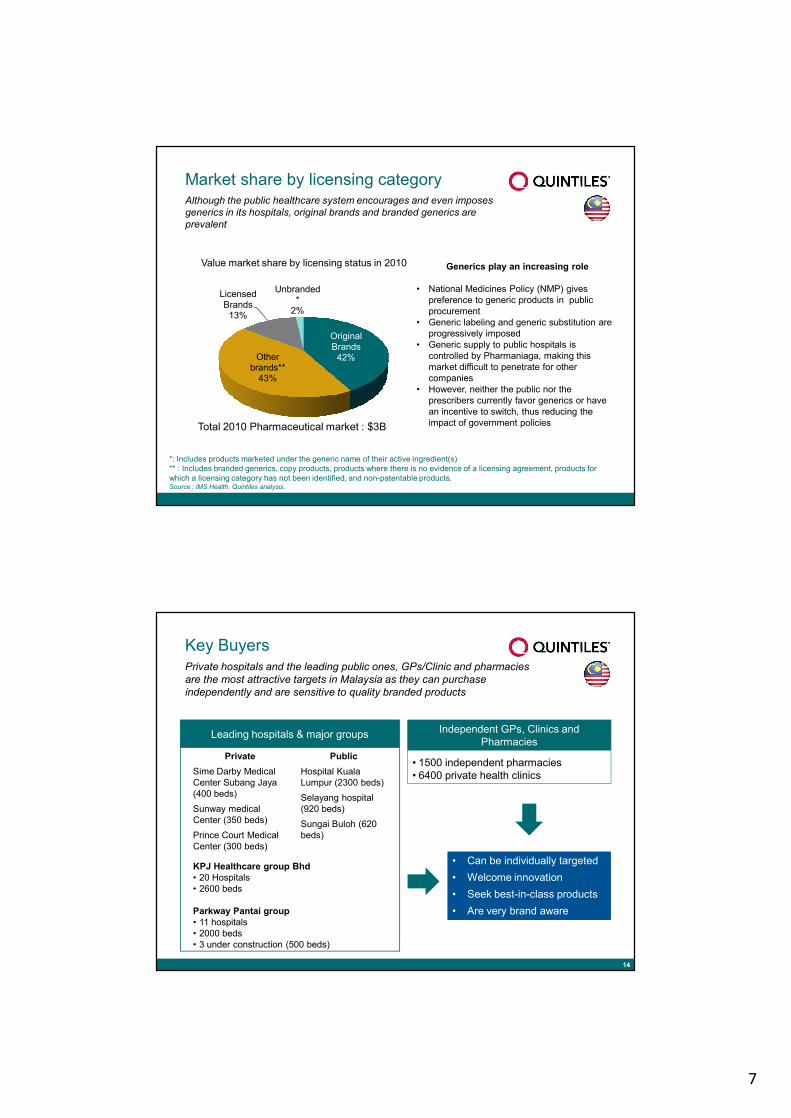

Although the public healthcare system encourages and even imposes generics in its hospitals, original brands and branded generics are prevalent

Original Brands

42%Other brands**

43%

Licensed Brands

13%

Unbranded*

2%

*: Includes products marketed under the generic name of their active ingredient(s)** : Includes branded generics, copy products, products where there is no evidence of a licensing agreement, products for which a licensing category has not been identified, and non-patentable products.Source : IMS Health. Quintiles analysis.

Generics play an increasing role

• National Medicines Policy (NMP) gives preference to generic products in public procurement

• Generic labeling and generic substitution are progressively imposed

• Generic supply to public hospitals is controlled by Pharmaniaga, making this market difficult to penetrate for other companies

• However, neither the public nor the prescribers currently favor generics or have an incentive to switch, thus reducing the impact of government policiesTotal 2010 Pharmaceutical market : $3B

Key BuyersPrivate hospitals and the leading public ones, GPs/Clinic and pharmacies are the most attractive targets in Malaysia as they can purchase independently and are sensitive to quality branded products

14

Leading hospitals & major groups Independent GPs, Clinics and Pharmacies

• 1500 independent pharmacies• 6400 private health clinics

KPJ Healthcare group Bhd• 20 Hospitals• 2600 beds

Parkway Pantai group• 11 hospitals• 2000 beds• 3 under construction (500 beds)

• Can be individually targeted• Welcome innovation• Seek best-in-class products• Are very brand aware

PrivateSime Darby Medical Center Subang Jaya (400 beds)Sunway medical Center (350 beds)Prince Court Medical Center (300 beds)

PublicHospital Kuala Lumpur (2300 beds)Selayang hospital (920 beds)Sungai Buloh (620 beds)

8

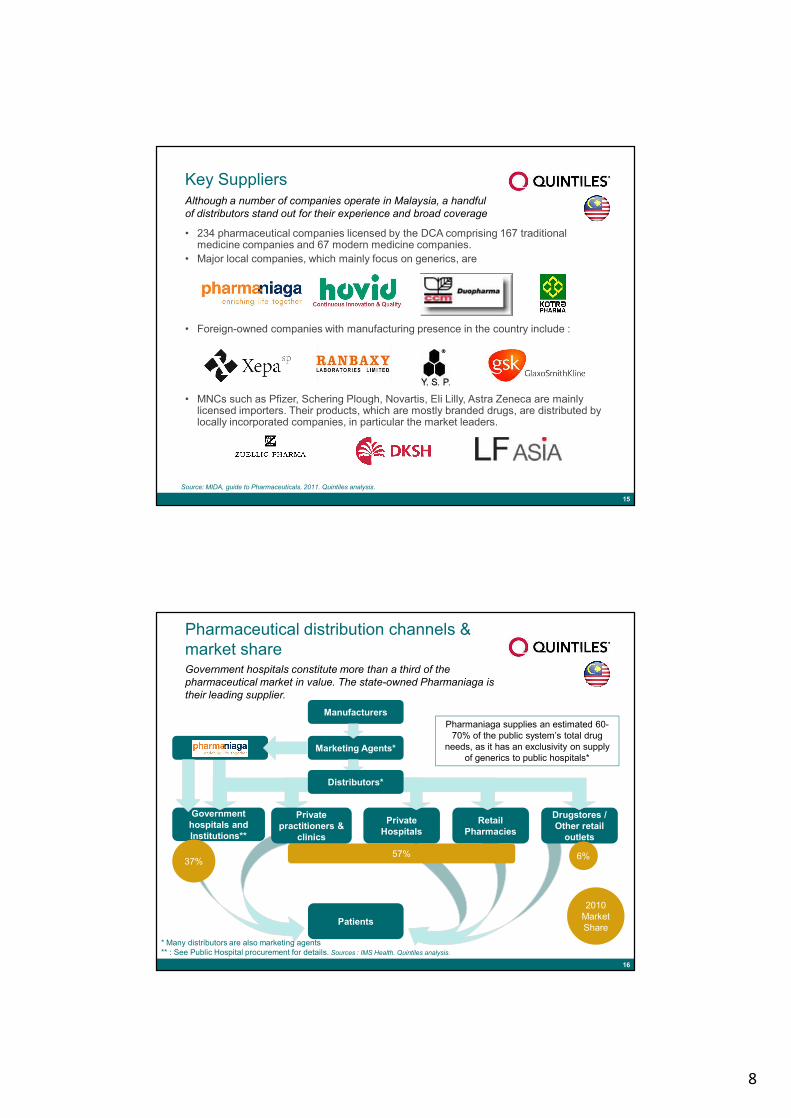

Key Suppliers

• 234 pharmaceutical companies licensed by the DCA comprising 167 traditional medicine companies and 67 modern medicine companies.

• Major local companies, which mainly focus on generics, are

• Foreign-owned companies with manufacturing presence in the country include :

• MNCs such as Pfizer, Schering Plough, Novartis, Eli Lilly, Astra Zeneca are mainly licensed importers. Their products, which are mostly branded drugs, are distributed by locally incorporated companies, in particular the market leaders.

Although a number of companies operate in Malaysia, a handful of distributors stand out for their experience and broad coverage

15

Source: MIDA, guide to Pharmaceuticals, 2011. Quintiles analysis.

Pharmaceutical distribution channels & market shareGovernment hospitals constitute more than a third of the pharmaceutical market in value. The state-owned Pharmaniaga is their leading supplier.

16

Manufacturers

Marketing Agents*

Government hospitals and Institutions**

Private Hospitals

Retail Pharmacies

Patients

Drugstores / Other retail

outlets

6%

2010Market Share

Distributors*

37%57%

Private practitioners &

clinics

Pharmaniaga supplies an estimated 60-70% of the public system’s total drug

needs, as it has an exclusivity on supply of generics to public hospitals*

* Many distributors are also marketing agents** : See Public Hospital procurement for details. Sources : IMS Health. Quintiles analysis.

9

11%

14%

15%

17%8%

6%

29%

Oncology & immunomodulatorsCardiovascularGI & MetabolicAntiinfectiveCNSRespiratoryOther classes

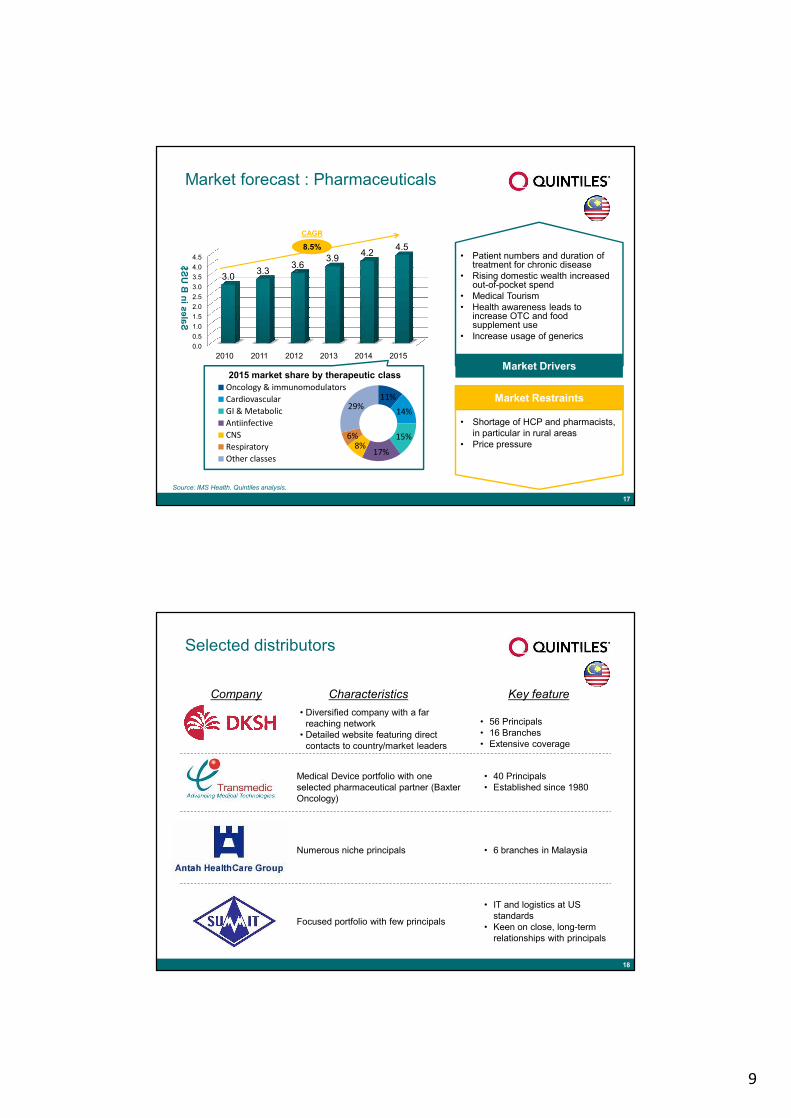

Market forecast : Pharmaceuticals

17

Market Drivers

Market Restraints

• Patient numbers and duration of treatment for chronic disease

• Rising domestic wealth increased out-of-pocket spend

• Medical Tourism• Health awareness leads to

increase OTC and food supplement use

• Increase usage of generics

• Shortage of HCP and pharmacists, in particular in rural areas

• Price pressure

Source: IMS Health. Quintiles analysis.

0.00.51.01.52.02.53.03.54.04.5

2010 2011 2012 2013 2014 2015

3.0 3.3 3.63.9 4.2 4.5

CAGR

8.5%

Sales in B US$

2015 market share by therapeutic class

Selected distributors

18

Antah Healthcare Numerous niche principals

CharacteristicsCompany

Tbc…

Key feature

• 6 branches in Malaysia

Focused portfolio with few principals

• IT and logistics at US standards

• Keen on close, long-term relationships with principals

• 56 Principals• 16 Branches• Extensive coverage

Transmedic Medical Device portfolio with one selected pharmaceutical partner (Baxter Oncology)

• 40 Principals• Established since 1980

• Diversified company with a far reaching network

• Detailed website featuring direct contacts to country/market leaders

10

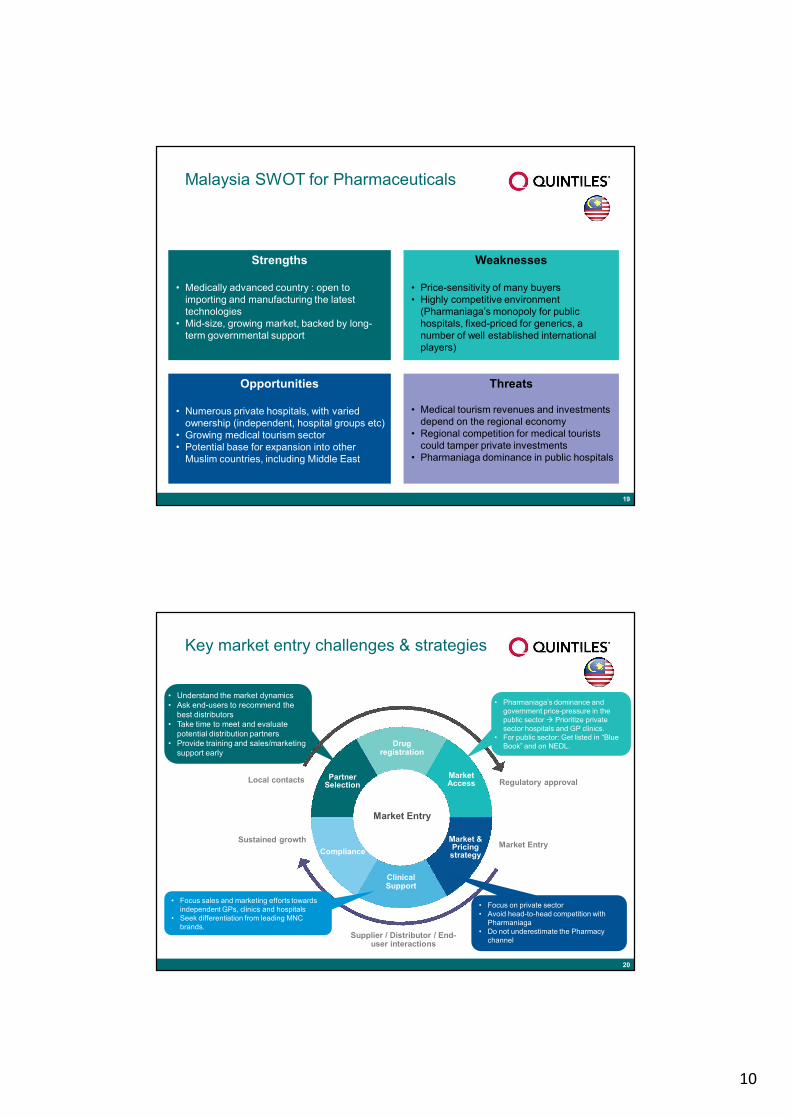

Malaysia SWOT for Pharmaceuticals

19

Strengths

• Medically advanced country : open to importing and manufacturing the latest technologies

• Mid-size, growing market, backed by long-term governmental support

Weaknesses

• Price-sensitivity of many buyers• Highly competitive environment

(Pharmaniaga’s monopoly for public hospitals, fixed-priced for generics, a number of well established international players)

Opportunities

• Numerous private hospitals, with varied ownership (independent, hospital groups etc)

• Growing medical tourism sector• Potential base for expansion into other

Muslim countries, including Middle East

Threats

• Medical tourism revenues and investments depend on the regional economy

• Regional competition for medical tourists could tamper private investments

• Pharmaniaga dominance in public hospitals

• Understand the market dynamics• Ask end-users to recommend the

best distributors• Take time to meet and evaluate

potential distribution partners• Provide training and sales/marketing

support early

Key market entry challenges & strategies

20

ComplianceMarket & Pricing strategy

MarketAccess

Partner Selection

Market Entry

Clinical Support

Drug registration

Local contacts Regulatory approval

Sustained growth

Supplier / Distributor / End-user interactions

Market Entry

• Pharmaniaga’s dominance and government price-pressure in the public sector à Prioritize private sector hospitals and GP clinics.

• For public sector: Get listed in “Blue Book” and on NEDL.

• Focus on private sector• Avoid head-to-head competition with

Pharmaniaga• Do not underestimate the Pharmacy

channel

• Focus sales and marketing efforts towards independent GPs, clinics and hospitals

• Seek differentiation from leading MNC brands.

11

IndonesiaPharmaceutical Market

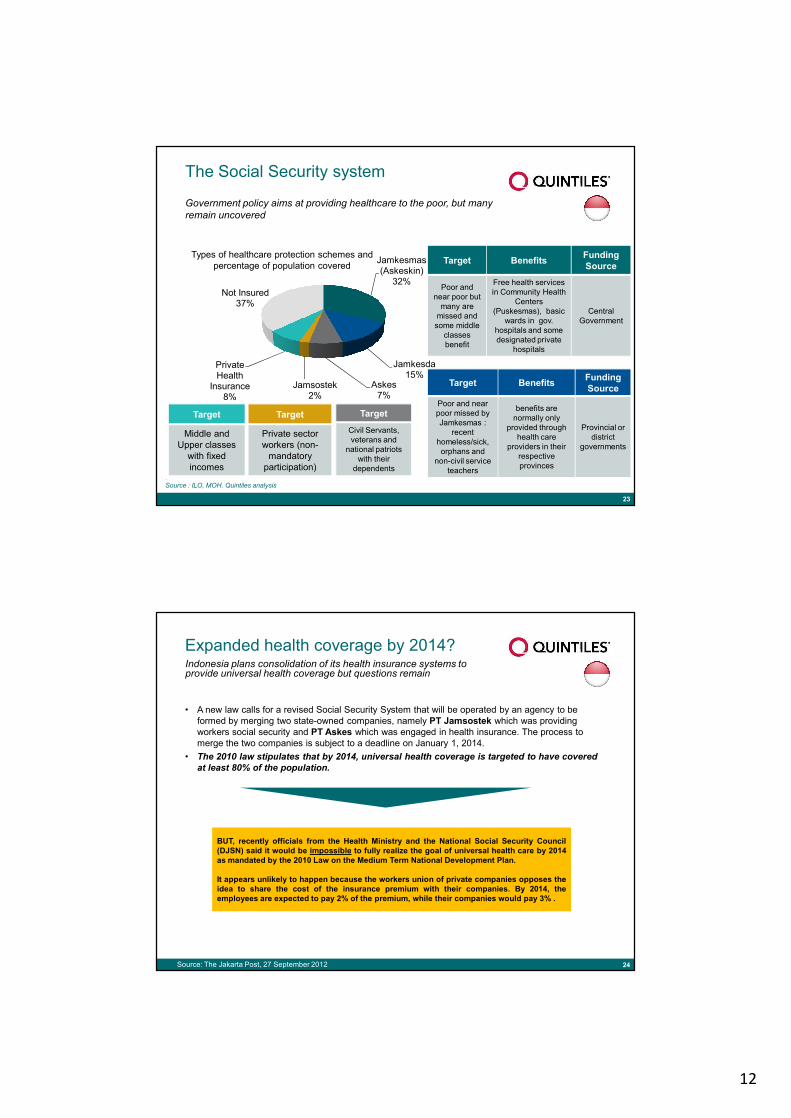

Market share by licensing category

A key role for OTC

• The OTC market represented 40% of the Indonesian pharmaceutical market.

• Local companies hold more than 80% of the OTC market

• Over 75% of total OTC sales are done in market stalls (warungs), grocery stores, supermarkets and minimarkets and not in the traditional retail pharmacy, drugstore and hospital channels.

• Modern herbal medicine brands are growing fast• Lack of IP-protection means even protector

originator brands may be made available by local companies

Most drugs sold in Indonesia are either branded generics or do not belong to a defined category. OTC medication accounts for 40% of the pharmaceuticals market

22

Value market share by licensing status in 2009

Original Brands

4%

Unbranded generics*

11%Licensed Brands

3%

Other Products**

82%

*: Includes products marketed under the generic name of their active ingredient(s)** : Includes branded generics, copy products, products where there is no evidence of a licensing agreement, products for which a licensing category has not been identified, and non-patentable products.Source : IMS Health & Quintiles analysis

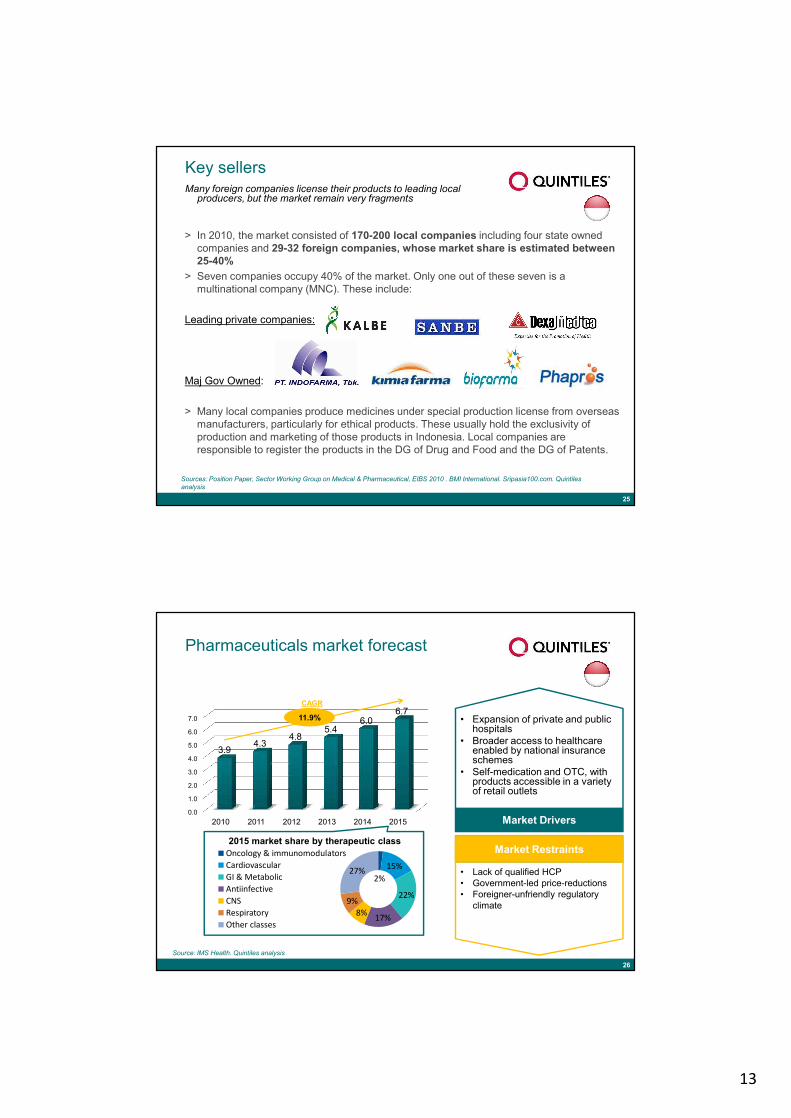

12

Jamkesmas (Askeskin)

32%

Jamkesda 15%

Askes7%

Jamsostek2%

Private Health

Insurance8%

Not Insured37%

The Social Security system

Government policy aims at providing healthcare to the poor, but many remain uncovered

23

Target Benefits FundingSource

Poor and near poor but

many are missed and

some middle classes benefit

Free health services in Community Health

Centers (Puskesmas), basic

wards in gov. hospitals and some designated private

hospitals

Central Government

Target Benefits FundingSource

Poor and near poor missed by Jamkesmas :

recent homeless/sick, orphans and

non-civil service teachers

benefits are normally only

provided through health care

providers in their respective provinces

Provincial or district

governments

. Source : ILO, MOH. Quintiles analysis

Target

Civil Servants, veterans and

national patriots with their

dependents

Target

Middle and Upper classes

with fixed incomes

Target

Private sector workers (non-

mandatory participation)

Types of healthcare protection schemes and percentage of population covered

Expanded health coverage by 2014?

• A new law calls for a revised Social Security System that will be operated by an agency to be formed by merging two state-owned companies, namely PT Jamsostek which was providing workers social security and PT Askes which was engaged in health insurance. The process to merge the two companies is subject to a deadline on January 1, 2014.

• The 2010 law stipulates that by 2014, universal health coverage is targeted to have covered at least 80% of the population.

Indonesia plans consolidation of its health insurance systems to provide universal health coverage but questions remain

24Source: The Jakarta Post, 27 September 2012

BUT, recently officials from the Health Ministry and the National Social Security Council(DJSN) said it would be impossible to fully realize the goal of universal health care by 2014as mandated by the 2010 Law on the Medium Term National Development Plan.

It appears unlikely to happen because the workers union of private companies opposes theidea to share the cost of the insurance premium with their companies. By 2014, theemployees are expected to pay 2% of the premium, while their companies would pay 3% .

13

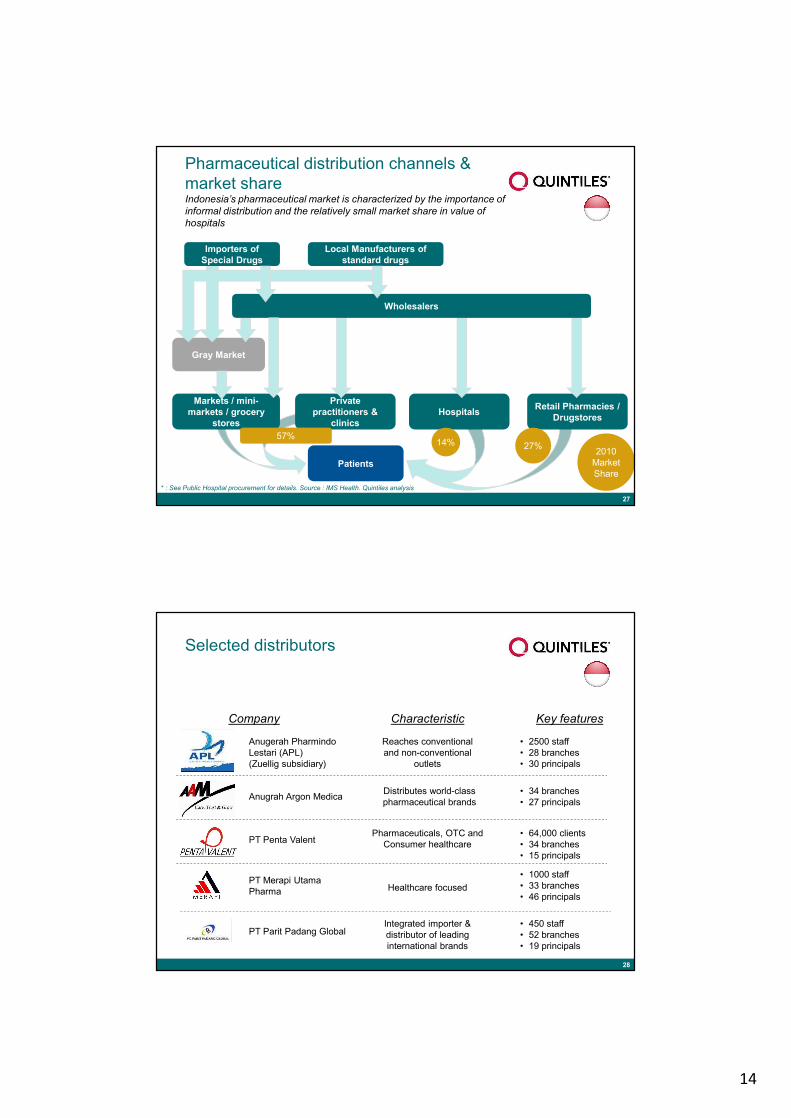

Key sellers

> In 2010, the market consisted of 170-200 local companies including four state owned companies and 29-32 foreign companies, whose market share is estimated between 25-40%

> Seven companies occupy 40% of the market. Only one out of these seven is a multinational company (MNC). These include:

Leading private companies:

Maj Gov Owned:

> Many local companies produce medicines under special production license from overseas manufacturers, particularly for ethical products. These usually hold the exclusivity of production and marketing of those products in Indonesia. Local companies are responsible to register the products in the DG of Drug and Food and the DG of Patents.

Many foreign companies license their products to leading local producers, but the market remain very fragments

25

Sources: Position Paper, Sector Working Group on Medical & Pharmaceutical, EIBS 2010 . BMI International. Sripasia100.com. Quintiles analysis

2%15%

22%

17%8%9%

27%

Oncology & immunomodulatorsCardiovascularGI & MetabolicAntiinfectiveCNSRespiratoryOther classes

Pharmaceuticals market forecast

26

Source: IMS Health. Quintiles analysis

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2010 2011 2012 2013 2014 2015

3.94.3

4.85.4

6.06.7

CAGR

11.9%

Market Drivers

• Expansion of private and public hospitals

• Broader access to healthcare enabled by national insurance schemes

• Self-medication and OTC, with products accessible in a variety of retail outlets

• Lack of qualified HCP• Government-led price-reductions• Foreigner-unfriendly regulatory

climate

Market Restraints2015 market share by therapeutic class

14

Pharmaceutical distribution channels & market shareIndonesia’s pharmaceutical market is characterized by the importance of informal distribution and the relatively small market share in value of hospitals

27

Local Manufacturers of standard drugs

Gray Market

* : See Public Hospital procurement for details. Source : IMS Health. Quintiles analysis

6%Private

practitioners & clinics

Importers of Special Drugs

Patients

Hospitals Retail Pharmacies / Drugstores

Wholesalers

Markets / mini-markets / grocery

stores

27% 2010Market Share

57%14%

Selected distributors

28

Reaches conventional and non-conventional

outlets

Characteristic

Distributes world-class pharmaceutical brands

• 2500 staff• 28 branches• 30 principals

Key features

• 34 branches• 27 principals

PT Parit Padang Global

Anugerah PharmindoLestari (APL) (Zuellig subsidiary)

Anugrah Argon Medica

Healthcare focused• 1000 staff• 33 branches• 46 principals

PT Merapi UtamaPharma

Pharmaceuticals, OTC and Consumer healthcare

• 64,000 clients• 34 branches• 15 principals

Integrated importer & distributor of leading international brands

• 450 staff• 52 branches• 19 principals

PT Penta Valent

Company

15

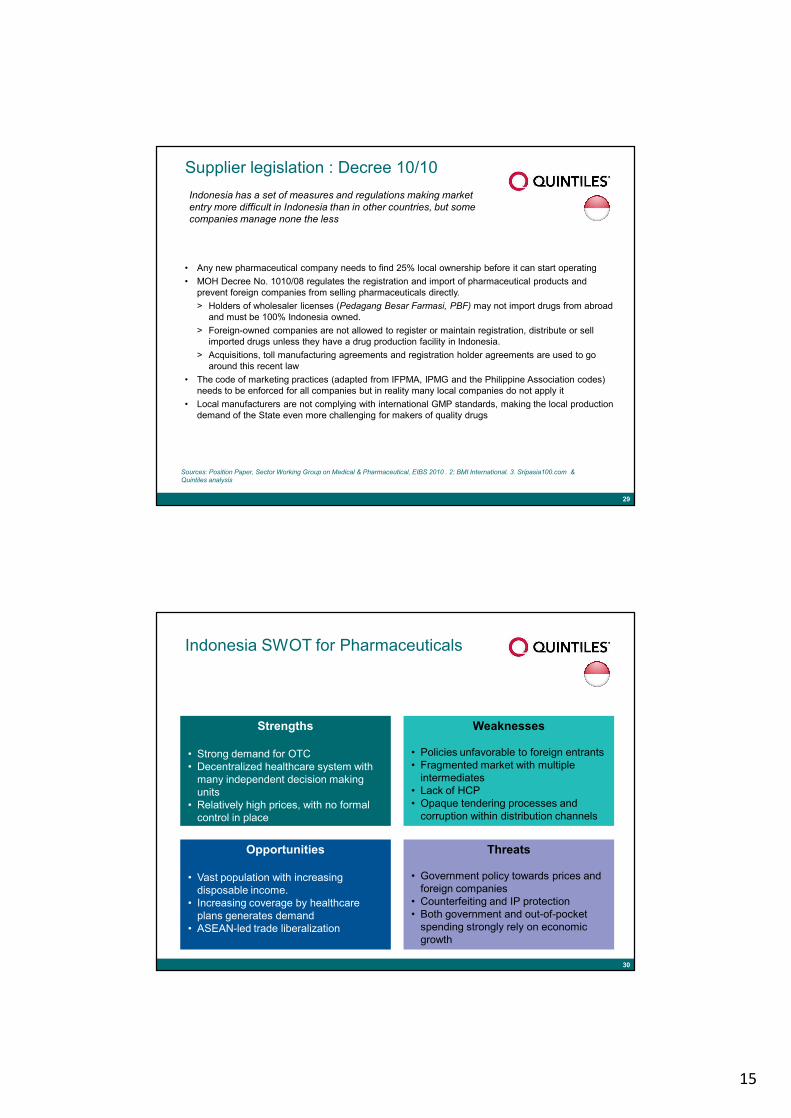

Supplier legislation : Decree 10/10

• Any new pharmaceutical company needs to find 25% local ownership before it can start operating• MOH Decree No. 1010/08 regulates the registration and import of pharmaceutical products and

prevent foreign companies from selling pharmaceuticals directly. > Holders of wholesaler licenses (Pedagang Besar Farmasi, PBF) may not import drugs from abroad

and must be 100% Indonesia owned.> Foreign-owned companies are not allowed to register or maintain registration, distribute or sell

imported drugs unless they have a drug production facility in Indonesia.> Acquisitions, toll manufacturing agreements and registration holder agreements are used to go

around this recent law• The code of marketing practices (adapted from IFPMA, IPMG and the Philippine Association codes)

needs to be enforced for all companies but in reality many local companies do not apply it• Local manufacturers are not complying with international GMP standards, making the local production

demand of the State even more challenging for makers of quality drugs

Indonesia has a set of measures and regulations making market entry more difficult in Indonesia than in other countries, but some companies manage none the less

29

Sources: Position Paper, Sector Working Group on Medical & Pharmaceutical, EIBS 2010 . 2: BMI International. 3. Sripasia100.com & Quintiles analysis

Indonesia SWOT for Pharmaceuticals

30

Strengths

• Strong demand for OTC• Decentralized healthcare system with

many independent decision making units

• Relatively high prices, with no formal control in place

Weaknesses

• Policies unfavorable to foreign entrants• Fragmented market with multiple

intermediates• Lack of HCP• Opaque tendering processes and

corruption within distribution channels

Opportunities

• Vast population with increasing disposable income.

• Increasing coverage by healthcare plans generates demand

• ASEAN-led trade liberalization

Threats

• Government policy towards prices and foreign companies

• Counterfeiting and IP protection• Both government and out-of-pocket

spending strongly rely on economic growth

16

Keys to Success in Indonesia

Ø Given the importance of self-medication and the reduced role of GPs direct to consumer advertising may be effective

Ø Distribution channels must cover the unconventional outlets for drugs (markets, grocery stores, mini markets).

Ø Partnership with pharmacy chains and franchise could be win-win situations to increase market share

Ø Flexibility when dealing with hospitals, and capacity to meet unexpected/urgent demands will enable to gain market share

31

32

Quintiles East Asia Pte Ltd79, Science Park Drive, #06-08,CINTECH IV, Science Park One,Singapore 118264

Contact details:

[email protected], Regulatory Strategy+ 65 6602 1254

[email protected] Director Consulting Asia+ 65 6602 1175