Zinc Market Overview - Nexa Resources - Investor Relations

32

October, 2018 Vazante Mine Zinc Market Overview Nexa Investor Meeting

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Zinc Market Overview - Nexa Resources - Investor Relations

October, 2018

Vazante Mine

Zinc Market OverviewNexa Investor Meeting

DEMAND AND ZINC APPLICATIONS

SUPPLY

HOW WE GOT HERE?

PRESENTATION CONTENT

OTHER SUPPLY SOURCES

SUBSTITUTION TREATS AND NEW APPLICATIONS

DEMAND AND ZINC APPLICATIONS

SUPPLY

PRESENTATION CONTENT

OTHER SUPPLY SOURCES

SUBSTITUTION TREATS AND NEW APPLICATIONS

Glencore

China

Mines

MODEST SUPPLY INCREASES IN THE LAST CYCLE AND PRODUCTION CURTAILMENTS IN 2015, DRASTICALLY REDUCED CONCENTRATE STOCKS, TAKING IT TO CRITICAL LOW LEVELS IN DAYS OF CONSUMPTION

ZINC CONCENTRATE STOCKS (Mt)

The consequent constraints on concentrate supplies has depleted stocks of zinc concentrate.

4757 60 53

28 26

0

20

40

60

2

0

1

3

2,0

2012 2013

1,5 2,1

2014

1,9

2015

1,0

2016

0,9

2017

8,2

2017

12,912,8

2012 2013 2014

4,9

20162015

4,7

13,0 13,112,1 13,0

8,48,2

4,6 4,7

8,1

4,9 4,8

7,4 8,2

-8%

ROWChina

Zn Conc stocks - days of requirement Zn Conc stocks (Mt)

GLOBAL ZINC CONCENTRATE OUTPUT (Mt)

Sources: Wood Mackenzie Long Term Outlook Q2

Century and Lesheen (two of the world’s biggest mines) closed its operations as their reserves depleted

Chinese environmental protection program started in 2014, forcing out-of-specifications operations to shut down

In the end of 2015, Glencore announced the reduction of 500kt in its mine operations due to poor price conditions

4

A LACK OF ZINC CONCENTRATE AND METAL LED TO LOW LEVEL OF STOCKS AND A RAPID INCREASE OF METAL PRICES SINCE END OF 2015

1.946 1.909

2.164

1.928

2.095

2.703

2012 2013 2014 2015 2016 2017

GLOBAL REFINED ZINC MARKET BALANCE (Mt) ZINC LME PRICES (USD/t)

20132012 20172015

13,713,2

20162014

12,5 12,912,7 13,2 13,7 13,8 13,6 13,514,1 14,4

-0,3 -0,2 -0,4 -0,1 -0,5 -0,9

Supply Demand

GLOBAL ZINC STOCKS (Mt)

113103

88 8570

46

2.13

2.71

2014

2.42

0.691.22

0.31 0.43

2012

2.56

0.930.24

2013

2.52

1.54

0.08

2.55

0.460.20

2015

0.15

2016

0.180.07

2017

3.95 3.733.30 3.21

1.79

Zn stocks - days of requirement

SHFEZn implied stocks (Mt)

LME

Sources: Wood Mackenzie Long Term Outlook Q2; Bloomberg 5

FOR THE SECOND TIME SINCE 80´S ZINC MARKET IS FACING TIGHTNESS BOTH IN CONCENTRATE AND METAL

0

1.000

2.000

3.000

4.000

0

5.000

10.000

15.000

2007 2012 201620142011 20132009 2018e1998 200520041994 200820031999 20101997 20011996 200019951984 199319921990 2002 200619871985 1988 20171989 19911986 2015

+13 +106 -181 -125 -2 +19 +76 +270 +406 +584 +87 -337 -218 +10 -25 +26-23 +353 +394 +280 -112 -480

-659-258 +320

+1.103

+1.088

+513-254

-219 -434-90 -494 -915 -710

SUPPLY

DEMAND

FORECAST

LME $2017

980 1.086905 780 778 797 872

1.1431.549

2.133 2.2201.883

1.665 1.675 1.6522.005

2.3992.680 2.568

2.088

1.4291.171

1.491

2.595

3.683

4.1963.942

3.723

3.289 3.199

2.705

1.790

1.080

56 62 50 42 42 43 48 63 86 117 115 90 79 78 74 73 67 82 94 102 91 72 47 37 49 94 116 123 113 103 88 85 70 46 27

199019871984 2018e19971985 19911986 20171988 1992 1993 1994

1.675

20071995 200019961989 1999 2001 2002 2003 2004 20122005 20162006 2008 2009 2010 2011 2013 2014 2015

1.649

1998

Stock impliedLME $ 2017 Days of consumptionForecast

FLY UP

1989 vs 1987 = +97%

FLY UP

2006 vs 2004 = +193%

FLY UP

2018 as of March vs 2016 = +60%

LOW LEVEL OF METAL STOCKS CRITICAL LEVEL OF METAL STOCKSCRITICAL LEVEL OF CONCENTRATE STOCKS ( ~30 DAYS OF REQUIREMENT)

2008/2009 CRISIS

CRITICAL LEVEL OF METAL STOCKSCRITICAL LEVEL OF CONCENTRATE STOCKS ( ~29 DAYS OF REQUIREMENT)

SYNCHRONIZED GLOBAL GROWTHSources: Wood Mackenzie Long Term Outlook Q2; Nexa Forecast 6

GIVEN THE HISTORICAL PRICE BEHAVIOR, CRITICAL LEVEL OF STOCKS IN DAYS OF CONSUMPTION SHOULD SUPPORT HIGH LME PRICES, HOWEVER…

14.713.5

2017 2018

14.4 14.0

-0.9 -0.7

46Stocks in days of consumption 27

272

jan

325

fev mar abr mai jun jul ago set

254 249

364345

331

288

251

+114-113

Stocks LME

Stocks SHFE

Supply

Demand

Global Refined Zinc Balance (Mt) Zinc total metal stocks (kt)

2018 - Forecast

1.8Implied stocks (Mt) 1.1

7Sources: Wood Mackenzie Long Term Outlook Q2; Nexa Forecast; LME

Inflow of metal in LME and SHFE warehouses

Even with the metal influx in March, the official stocks drawdown trend continued during the year

…AFTER REACHING 10-YEAR HIGH IN THE BEGINNING OF THE YEAR, ZINC LME PRICE PLUMMED REACHING 2-YEAR LOW IN SEPTEMBER

1,000

0

2,000

3,000

4,000

3,618

2012

LME

(USD

/t) 2,095

1,946

2,164

1,909

2013 2014

1,928

2015 2016

2,703

2,287

2017

3,007

2018*

1,331YTD

Source: Bloomberg 8

February 16th

September 17th

* As of October 9th

Low

High

Price, jan 2016 = 100

Zn

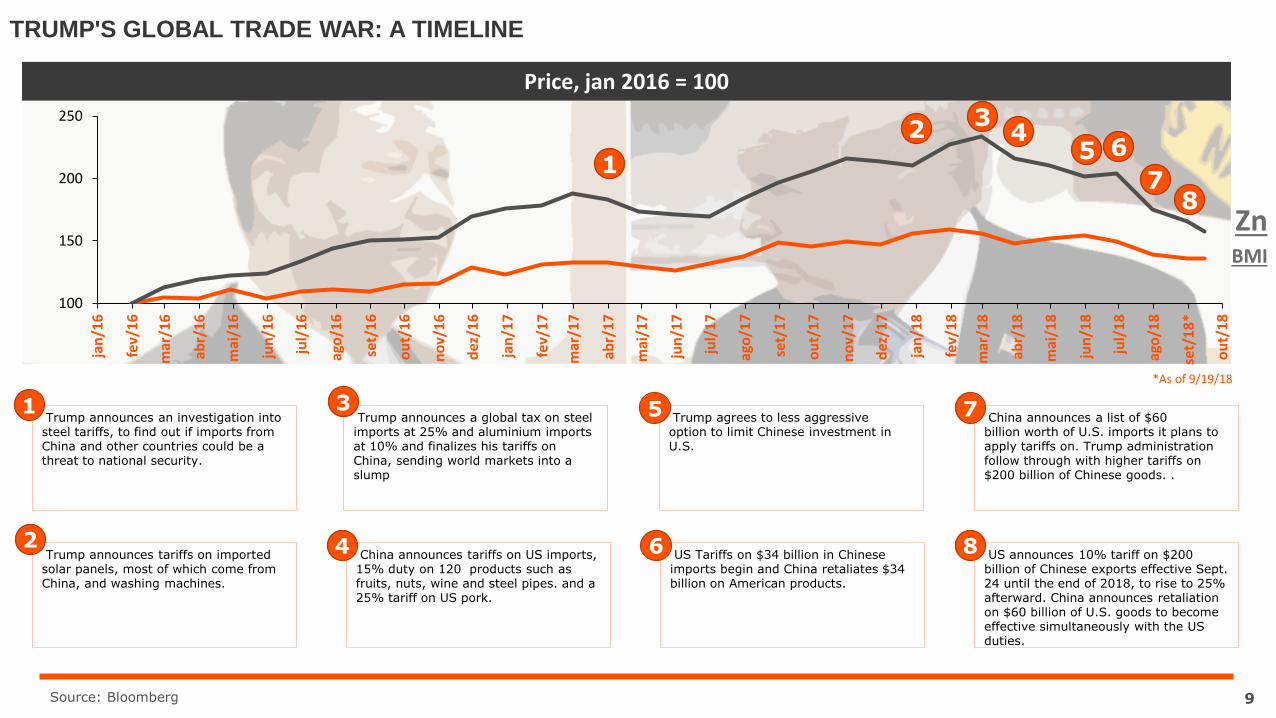

TRUMP'S GLOBAL TRADE WAR: A TIMELINE

Trump announces an investigation into steel tariffs, to find out if imports from China and other countries could be a threat to national security.

1

Trump announces tariffs on imported solar panels, most of which come from China, and washing machines.

2

Trump announces a global tax on steel imports at 25% and aluminium imports at 10% and finalizes his tariffs on China, sending world markets into a slump

3

China announces tariffs on US imports, 15% duty on 120 products such as fruits, nuts, wine and steel pipes. and a 25% tariff on US pork.

4

Source: Bloomberg 9

100

150

200

250ja

n/1

6

set/

17

mar

/16

jul/

16

ago

/16

fev/

16

abr/

16

ago

/18

set/

18

*

mai

/16

jul/

17

jun

/16

set/

16

no

v/1

7

mai

/17

ou

t/1

6

mar

/18

mar

/17

dez

/17

ou

t/1

7

dez

/16

abr/

17

jan

/18

fev/

17

jun

/17

no

v/1

6

mai

/18

jan

/17

fev/

18

abr/

18

jun

/18

jul/

18

ou

t/1

8

ago

/17

1

23

45 6

78

*As of 9/19/18

BMI

Trump agrees to less aggressive option to limit Chinese investment in U.S.

5

US Tariffs on $34 billion in Chinese imports begin and China retaliates $34 billion on American products.

6

China announces a list of $60 billion worth of U.S. imports it plans to apply tariffs on. Trump administration follow through with higher tariffs on $200 billion of Chinese goods. .

7

US announces 10% tariff on $200 billion of Chinese exports effective Sept. 24 until the end of 2018, to rise to 25% afterward. China announces retaliation on $60 billion of U.S. goods to become effective simultaneously with the US duties.

8

SUPPLY

HOW WE GOT HERE?

PRESENTATION CONTENT

OTHER SUPPLY SOURCES

SUBSTITUTION TREATS AND NEW APPLICATIONS

ZINC HAS MANY FINAL USES, BUT THE MAJOR PART OF ITS END-USE IS CONSTRUCTION AND INFRASTRUCTURE

CONSTRUCTION &

INFRASTRUCTURE

9,5 Mt

(66%)

AUTOMOTIVE &

INDUSTRIAL MACHINERY

4.0 Mt

(28%)

AGRIBUSINESS

& OTHERS

0.07 Mt

(0.5%)

CONSUMER GOODS

0.8 Mt

(5.5%)

Sources: Wood Mackenzie Long Term Outlook Q2 11

IN RECENT YEARS, GLOBAL SYNCRONIZED GROWTH IS FOSTERING STABLE DEMAND INCREASE

Sources: FMI, LCA, Wood Mackenzie Long Term Outlook Q2

SYNCHRONIZED GLOBAL ECONOMY GROWTH HISTORICAL DEMAND GROWTH

EmergingDevelopedChina

15%

48.2%(6.92Mt)

60%

25.3%(3.63Mt)

25%

26.5%(3.8Mt)

% of Zn

Demand

% of Global

GDP

Global Growth (% YoY)

3,7

5,6

3,6

2011

5,2

3,7

3,53,8

6,8

3,4

2012

13,7

3,8

6,0

3,6

12,7

3,5

2013

6,3

3,6

2014

6,5

3,7

2015

3,7

2016

6,9

3,6

2017

3,6

12,5 13,2 13,8 14,1 14,4

2,4%

China EmergingDevelopedRefined zinc demand (Mt)

+ 1,900 kt

CHINA

DEVELOPED

EMERGING

+ 1,709 kt

-169 kt

+372 kt

12

GLOBAL DEMAND - REFINED ZINC

Developed economies demand is still expected to grow ~200kt in the 19-23

cycle

India is growing above 7% a year, with good potential zinc demand. On the

other hand, Brazil and Russia are underperforming among the EMs.

Metal demand in China should come from initiatives championed by the

president such as povertyalleviation which will result in slum clearance and open up new land for

residential construction in rural areas.

6.924 7.166 7.399 7.589 7.783 8.021 8.261

3.634 3.650 3.702 3.734 3.746 3.780 3.8063.804 3.866 3.896 3.946 4.032 4.149 4.270

20222019 202120182017 2020 2023

14.362 14.682 14.997 15.268 15.561 15.950 16.338+2,2%

Emerging Advanced China

+ 1,656 kt

CHINA

DEVELOPED

EMERGING

+ 1,095 kt

+156 kt

+404 kt

GLOBAL(kt)

Sources: Wood Mackenzie Long Term Outlook Q2; Nexa Forecast 13

DEMAND AND ZINC APPLICATION

HOW WE GOT HERE?

PRESENTATION CONTENT

OTHER SUPPLY SOURCES

SUBSTITUTION TREATS AND NEW APPLICATIONS

USA

• 10th in reserves: 6Mt

• 9th in production: 351kt

PERU

• 4rd in reserves: 16Mt

• 2nd in production: 1,387kt

• 7th in reserves: 12Mt

• 5th in production: 746kt

CANADA

• 3th in reserves: 20Mt

• 6th in production: 730kt

MEXICO

• 11th in reserves: 4.8Mt

• 7th in production: 485kt

BOLIVIA

• 13th in reserves: 3.6Mt

• 11th in production: 252kt

SWEDEN

• 5th in reserves: 13Mt

• 8th in production: 383kt

KAZAKHSTAN

• 8th in reserves: 9Mt

• 4th in production: 844kt

INDIA

• 6th in reserves: 12.6Mt

• 1st in production: 5,052kt

CHINA

• 1st in reserves: 28Mt

• 3rd in production: 848kt

AUSTRALIA

ZINC

World Total Reserves: 195Mt

TOP 10: 148Mt (76%)

ROW: 47Mt

TOP 10 COUNTRIES OF ZINC PRODUCTION AND RESERVES

Sources: Wood Mackenzie Long Term Outlook Q2; SNL

• 18th in reserves: 2.2Mt

• 12th in production: 158kt

BRAZIL

• 2nd in reserves: 24Mt

• 10th in production: 276kt

RUSSIA

15

MINE SUPPLY IS FORECAST TO GROW BY CLOSE TO 3.3% PER YEAR OVER THE PERIOD 2018-2023, CONCENTRATE STOCKS ARE FORECAST TO REMAIN AT LOW LEVELS UNTIL 2019-20

MINE PRODUCTION EVOLUTION (kt)

14.009

16.477

1.451 1.830

1.558

Production 2023Brownfield/Increases

Closures/Reduction

Production 2018 Greenfield

531

China

+3%

Sources: Wood Mackenzie Long Term Outlook Q2; Nexa Forecast 16

CHINA HAS ITS OWN STANDARD TO CLASSIFY ZINC MINES AND COMPARED TO ROW, MOST OF OUTPUT COMES FROM SMALL/MEDIUM MINES

TINY / SMALL>1 <10 ktpy of Zinc

MEDIUM>10 <50 ktpy of Zinc

LARGE>50 ktpy of Zinc

> 1000 ktpa ore mined300-1,000 ktpa ore minedSmall 30-300 / Tiny <30 ktpa ore mined

~700 mines 78 mines 13 mines

• Owners of mines are appointed by government• No tailing dam• Milling: some mine use same concentrator• Inadequate safety and environmental standard• Production is very price sensitive

• Medium and big companies• Some mines have tailing dam others

share/rent from big mines• More integrated with smelters• Short/medium term mining plan

• Bigger and listed companies• Tailing dam• Medium/long term mining plan• Higher level of automation • Concern regarding safety and environmental

standards

2,246 kt46%MINE production

1,581 kt32% 1,062 kt22%

Sources: Wood Mackenzie Long Term Outlook Q2; SMM 17

THE FIRST ROUND OF DEEP DIVE ANALYSIS OF CHINESE ZINC MINING LED US TO TO BE ABLE TO CRITICIZE/ANALYZE DATA AND INFORMATION

CHINA CONCENTRATE PRODUCTION (Zn kt)

? ?

CHINA MINING - 1st ROUND

?

1

CRITICIZE/ANALYZE DATA AND INFORMATION – CONSIDERED IN OUR

PRICE MODEL 2

Sources: Wood Mackenzie Long Term Outlook Q2; Nexa Analysis 18

4.1205.463

6.1245.051 676931

Concentrate Metal Demand

Imported

Domestic Production

6.139

4.8545.936

6.924

Imported 1.121

MetalConcentrate Demand

Domestic Production

6755.9756.611

CHINA MARKET BALANCE (kt) CHINA MARKET BALANCE (kt)

20172017

4.3005.850

6.630

Domestic Production

1.210

Concentrate

5.510 750

Metal Demand

Imported

6.600

CHINA MARKET BALANCE (kt)

2017

4.2005.900

6.800

Concentrate

6756.575

Metal Demand

Imported

Domestic Production

CHINA MARKET BALANCE (kt)

2017

?

CONSULTANCY COMPANIES HAVE DIFFERENT NUMBERS REGARDING CHINESE MINE PRODUCTION

Sources: Wood Mackenzie Long Term Outlook Q2; Antaike, CRU, SMM 19

AFTER TWO ROUNDS OF CHINA MINING DEEP DIVE, NEXA’S BASE CASE SCENARIO FOR NEXT CYCLE CONSIDERS THAT CHINA WILL ADD ~100Kt PER YEAR

2.932 3.139 3.163 3.1883.702

4.2454.588 4.738 4.901 4.768 4.695 4.854 5.053 5.159 5.250 5.378 5.481 5.584

-1.000

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

20132006 200920082007 2010 20122011 2014 2015 20202016 2017 2018 2019 2021 2022 2023

6%

7%0% 2%

Increm. Prod. (kt)

Y/Y (%)

343 208 24 25 514 543 343 150 163 -133 -73 159 199 106 92 128 130 103

13.2% 7.1% 0.8% 0.8% 16.1% 14.7% 8.1% 3.3% 3.4% -2.7% -1.5% 3.4% 4.1% 2.1% 1.8% 2.4% 1.9% 1.9%

BASE CASE

Sources: Wood Mackenzie Long Term Outlook Q2; Nexa Forecast 20

REACHING THE 8TH YEAR OF DEFICIT IN 2019, THE ZINC MARKET WILL NEED TO RESUPPLY ITS LOW STOCKS LEVELS

16,338

13,972

15,56115,891

14,93514,682

2023

15,48215,268

2022

15,95016,381 16,616

14,997

20212018 2019 2020

-710-62

+214+330

+431 +278Supply

Demand

REFINED ZINC BALANCE FORECAST (kt)

IMPLIED

STOCKS (kt) 1,083 1,021 1,235 1,565 1,996 2,274

STOCKS IN DAYS OF CONSUMPTION WILL REACH

CRITICAL LEVEL IN 2019

AFTER A LONG PERIOD OF DEFICIT, ZINC MARKET BALANCE WILL TURN TO SURPLUS, HOWEVER, THAT WON’T BE

ENOUGH TO RISE THE STOCKS TO HIGH LEVELS

STOCKS IN DAYS OF

CONSUMPTION (kt)27 25 30 37 45 51

Sources: Wood Mackenzie Long Term Outlook Q2; Nexa Forecast 21

DEMAND AND ZINC APPLICATIONS

SUPPLY

HOW WE GOT HERE?

PRESENTATION CONTENT

SUBSTITUTION TREATS AND NEW APPLICATIONS

Zn Concentrate~ 50-55% Zn

Other Sources

Secondary~ 15 – 25% zn

(EAF dust, oxides, low Zn content, etc)

Worldwide, the zinc production from secondary is around10% from total production.

In Juiz de Fora smelter, Nexa has about 20-24%of total production of metallic zinc fromsecondary sources.

Tailings~4-8% Zn*

Utilization of residue from zinc tailings in the beneficiation plantto produce Zn concentrate• New Century Resources has started the tailings flotation activities required

to produce zinc concentrate at its mine in Queensland, Australia.• Woodlawn Project - Blend of underground ore and reclaimed tailings

Main Source 90% 10%

MINERAL EXTRACTION FROM MINES IS NOT THE ONLY SOURCE FOR ZINC METAL PRODUCTION

Mining from underground or/and open pit mines

LME (-) TC

Sources: Wood Mackenzie Long Term Outlook Q2 23

5,5

6,0

6,5

7,0

7,5

8,0

8,5

9,0

9,5

10,0

10,5

11,0

11,5

12,0

12,5

13,0

2000 2005 2010 2015

GLOBAL USAGE OF SECONDARY FEED (% of TOTAL FEED)

ZINC CONTENT IN E.A.F. DUST (KTON)GLOBAL CAPACITY

1.257 kton.

Steel Prod.

364.000

7.100

1.400

Zinc Content

1.583.000

EAF Dust

EAF Steel

EAF technology represents 19% of global

steel production…

87%

…that generates 2% of EAF Dust as

residue……with 22% of Zinc

content.

SINCE 2000 THE ROLE OF SECONDARIES IN FEEDING THE WORLD’S PRIMARY ZINC SMELTERS IS GROWING, HOWEVER IS LIMITED BY AVAILABILITY

Sources: Wood Mackenzie Long Term Outlook Q2; Nexa Forecast 24

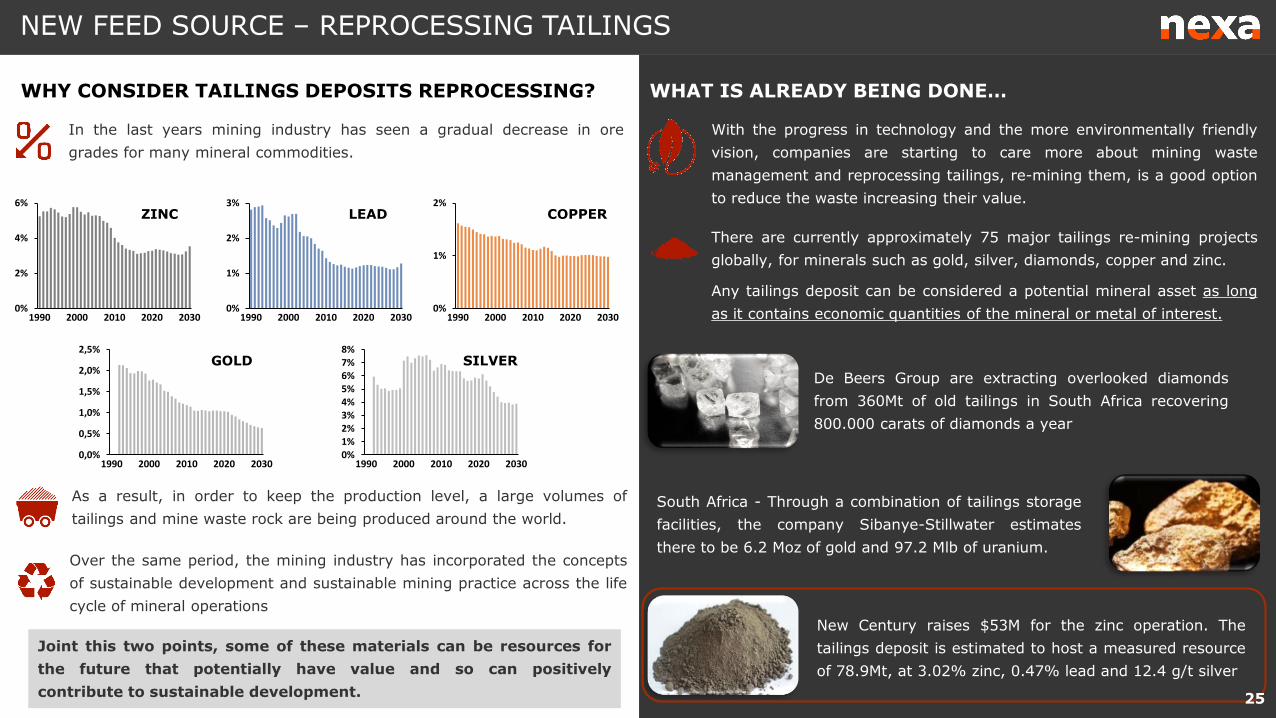

WHAT IS ALREADY BEING DONE…

With the progress in technology and the more environmentally friendly

vision, companies are starting to care more about mining waste

management and reprocessing tailings, re-mining them, is a good option

to reduce the waste increasing their value.

There are currently approximately 75 major tailings re-mining projects

globally, for minerals such as gold, silver, diamonds, copper and zinc.

Any tailings deposit can be considered a potential mineral asset as long

as it contains economic quantities of the mineral or metal of interest.

De Beers Group are extracting overlooked diamonds

from 360Mt of old tailings in South Africa recovering

800.000 carats of diamonds a year

South Africa - Through a combination of tailings storage

facilities, the company Sibanye-Stillwater estimates

there to be 6.2 Moz of gold and 97.2 Mlb of uranium.

New Century raises $53M for the zinc operation. The

tailings deposit is estimated to host a measured resource

of 78.9Mt, at 3.02% zinc, 0.47% lead and 12.4 g/t silver

WHY CONSIDER TAILINGS DEPOSITS REPROCESSING?

In the last years mining industry has seen a gradual decrease in ore

grades for many mineral commodities.

Over the same period, the mining industry has incorporated the concepts

of sustainable development and sustainable mining practice across the life

cycle of mineral operations

Joint this two points, some of these materials can be resources for

the future that potentially have value and so can positively

contribute to sustainable development.

0%

2%

4%

6%

1990 20202000 203020100%

1%

2%

3%

1990 2000 20202010 20300%

1%

2%

1990 2030202020102000

ZINC LEAD COPPER

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

1990 203020102000 20200%1%2%3%4%5%6%7%8%

1990 2000 2010 2020 2030

GOLD SILVER

As a result, in order to keep the production level, a large volumes of

tailings and mine waste rock are being produced around the world.

NEW FEED SOURCE – REPROCESSING TAILINGS

25

DEMAND AND ZINC APPLICATIONS

SUPPLY

HOW WE GOT HERE?

PRESENTATION CONTENT

OTHER SUPPLY SOURCES

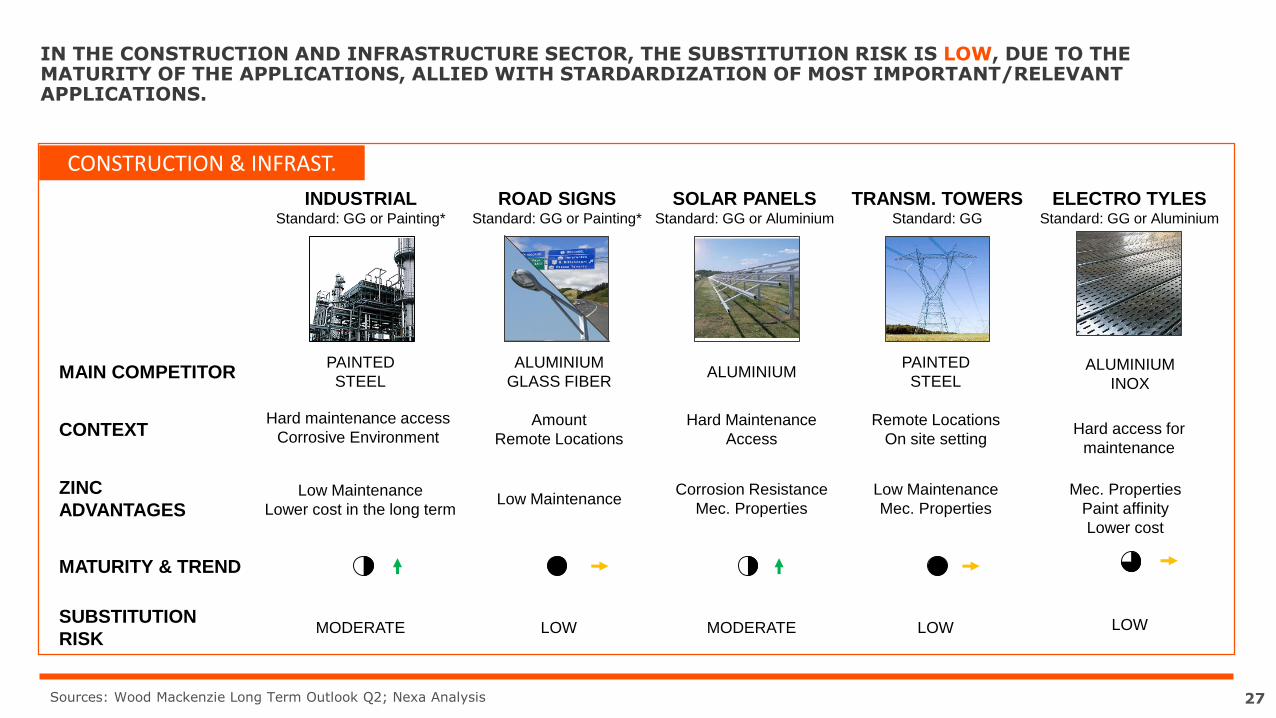

IN THE CONSTRUCTION AND INFRASTRUCTURE SECTOR, THE SUBSTITUTION RISK IS LOW, DUE TO THE MATURITY OF THE APPLICATIONS, ALLIED WITH STARDARDIZATION OF MOST IMPORTANT/RELEVANT APPLICATIONS.

MAIN COMPETITOR

SUBSTITUTION

RISK

ZINC

ADVANTAGES

CONTEXT

INDUSTRIALStandard: GG or Painting*

MODERATE

PAINTED

STEEL

Low Maintenance

Lower cost in the long term

Hard maintenance access

Corrosive Environment

ROAD SIGNSStandard: GG or Painting*

TRANSM. TOWERSStandard: GG

SOLAR PANELSStandard: GG or Aluminium

ALUMINIUM

GLASS FIBERALUMINIUM

PAINTED

STEEL

LOW MODERATE LOW

Corrosion Resistance

Mec. Properties

Low Maintenance

Mec. Properties

Amount

Remote Locations

Hard Maintenance

Access

Remote Locations

On site setting

MATURITY & TREND

Low Maintenance

CONSTRUCTION & INFRAST.

ELECTRO TYLESStandard: GG or Aluminium

ALUMINIUM

INOX

LOW

Hard access for

maintenance

Mec. Properties

Paint affinity

Lower cost

Sources: Wood Mackenzie Long Term Outlook Q2; Nexa Analysis 27

FOR NON STANDARDIZED APPLICATIONS, THE RISKS OF SUBSTITUTION ARE MODERATE TO LOW, DUE TO ZINC’S ADVANTAGES IN THE LONG TERM AND LOW IMPACT IN TOTAL CONSTRUCTION COST.

GALVANIZING THE STEEL STRUCTURE REPRESENTS ONLY ABOUT 1% OF TOTAL CONSTRUCTION COST

ROOF TILES STORAGE BUILDING FACADES

CONCRETE

Al

Corten

Inox

Al

Low Cost

Fast Setting

Aesthetics

Mec. Resistance

Thermal Comfort

Low Cost

LOW MODERATE MODERATE

Construction time

Sustainability

Recyclability

Galvalume

(45% Zn)

Mec. Proprieties

Paint affinity

Lower cost

SILOS LSF

Al

Inox

Hard access for

maintenance

MODERATE

Mec. Properties

Lower Cost

Al

Wood Frame

Sustainability

No waste

LOW

Mec. Properties

Corrosion Resist.

MAIN COMPETITOR

SUBSTITUTION

RISK

ZINC

ADVANTAGES

CONTEXT

MATURITY & TREND

CONSTRUCTION & INFRAST.

DOOR HANDLE

LOW

Al

Inox

Mec. Properties

Lower Cost

Cost

Sources: Wood Mackenzie Long Term Outlook Q2; Nexa Analysis 28

FOR THE AUTOMOTIVE MARKET, THE SUBSTITUTION RISK IN AUTO BODY PARTS IS LOW, DUE TO STEEL INDUSTRY EFFORTS TO REDUCE WEIGHT AND THE SUBSTITUTION COSTS IN THE INDUSTRY AND SUPPLY CHAIN.

FOR THE DIE CASTING INTERNAL PARTS, MOST OF THE SUBSTITUTION HAS ALREADY HAPPENED.

AUTO BODY PARTS INTERNAL PARTS

ALUMINIUMALUMINIUM

Weight

Reduction

LOW LOW

Injection Cost

Mec. PropertiesMec. Properties

Weight

Reduction

MAIN COMPETITOR

SUBSTITUTION

RISK

ZINC

ADVANTAGES

CONTEXT

USAGE / MATURITY

Zinc and Aluminium Die-Castings in Automobiles (# parts per auto)

AUTOMOTIVE864

857

845837 833 831

820815

807

789

750

775

800

825

850

875

20

14

20

16

20

11

20

10

20

13

20

17

20

12

20

15

20

18

20

19

20

22

20

20

20

21

20

23

20

24

20

25

-33 kg per vehicle

Steel consumption in Light Commercial Vehicles

(kg/year)

Sources: Wood Mackenzie Long Term Outlook Q2; Nexa Analysis 29

THE GALVANIZING MARKET MATURITY IS DIFFERENT IN EACH PART OF THE WORLD. EMERGING COUNTRIES STILL HAVE A LOT OF BASIC APPLICATIONS TO DEVELOP, INCREASING ZINC DEMAND.

GALVANIZING DIFFERENT DEVELOPMENT STAGES: GROWING MARKETS PERFORMING MARKETS DEVELOPED MARKETS

1 2 3Start up

Simple products

Start serial production

Industry Products

Mass Production

Products Standard

Architecture

Advanced products

Developed serial products

GROWING PERFORMANCE DEVELOPED

Per Capita Zn Consumption: LATAM 1,3 kg/hab, Asia 2,2 kg/hab, US 3,4 kg/hab and Europe 3,4 kg/hab.

PERU COLOMBIA BRAZIL MEXICO CHILEMALAYSIA, INDONESIA

AND VIETNAM INDIA CHINA JAPAN USA EU

Sources: IZA; Nexa Analysis 30

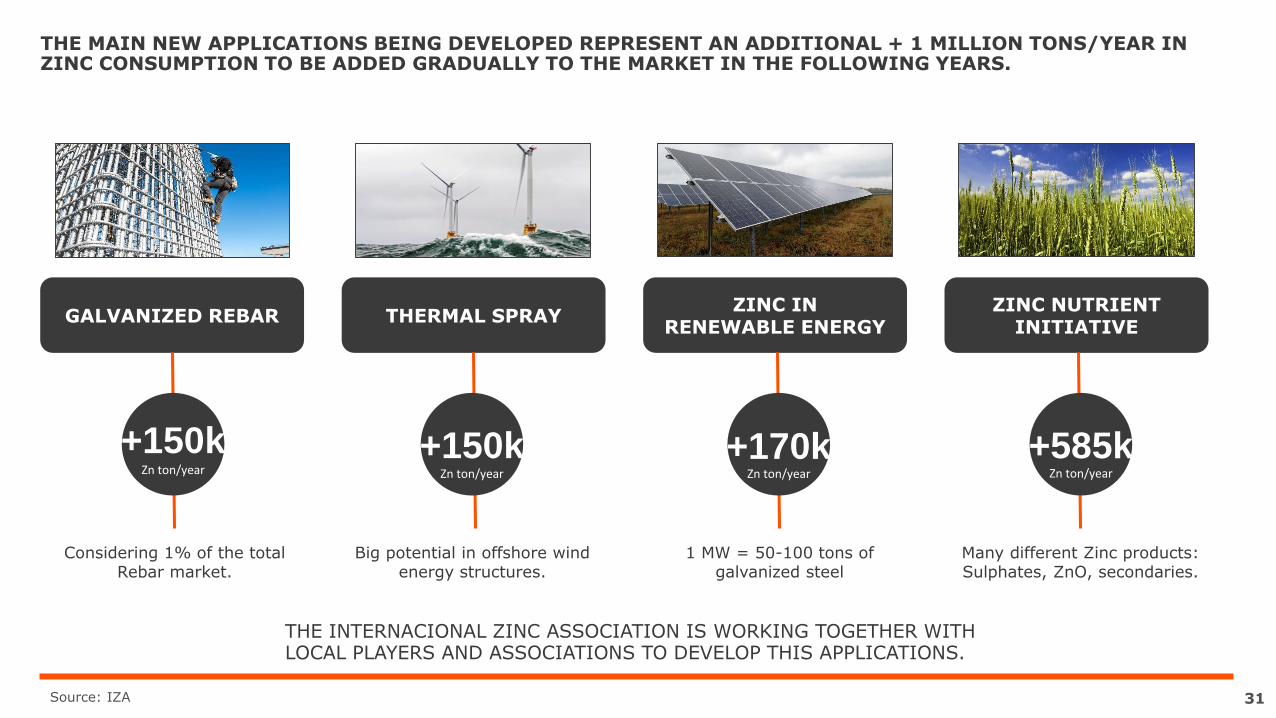

THE MAIN NEW APPLICATIONS BEING DEVELOPED REPRESENT AN ADDITIONAL + 1 MILLION TONS/YEAR IN ZINC CONSUMPTION TO BE ADDED GRADUALLY TO THE MARKET IN THE FOLLOWING YEARS.

GALVANIZED REBAR THERMAL SPRAYZINC IN

RENEWABLE ENERGYZINC NUTRIENT

INITIATIVE

+150kZn ton/year

Big potential in offshore wind energy structures.

Considering 1% of the total Rebar market.

1 MW = 50-100 tons of galvanized steel

Many different Zinc products: Sulphates, ZnO, secondaries.

Zn ton/year

+150k +10kZn ton/year

+170kZn ton/year

+585k

THE INTERNACIONAL ZINC ASSOCIATION IS WORKING TOGETHER WITH LOCAL PLAYERS AND ASSOCIATIONS TO DEVELOP THIS APPLICATIONS.

Source: IZA 31

October, 2018

Vazante Mine

Zinc Market OverviewNexa Investor Meeting