Bond Market overview - VCBS

151

BÁO CÁO TRIỂN VỌNG 2020 VCBS RESEARCH DEPARTMENT Nov.2020 OUTLOOK 2021

-

Upload

khangminh22 -

Category

Documents

-

view

6 -

download

0

Transcript of Bond Market overview - VCBS

BÁO CÁO TRIỂN VỌNG 2020

VCBS RESEARCH DEPARTMENT

Nov.2020

OUTLOOK 2021

MACROECONOMY

FIXED INCOME MARKET

EQUITY MARKET

INDUSTRY AND STOCK PICKS

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

WORLD SITUATION- CORRUPTION GROWTH DUE TO THE PANDEMIC

3

Estimated GDP growth in 2020

>6%

3 – 6%

0 – 3%

-3 – 0%

< -3%

Không có dữ liệu GDP Growth in 2019

Source: IMF, VCBS compile

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

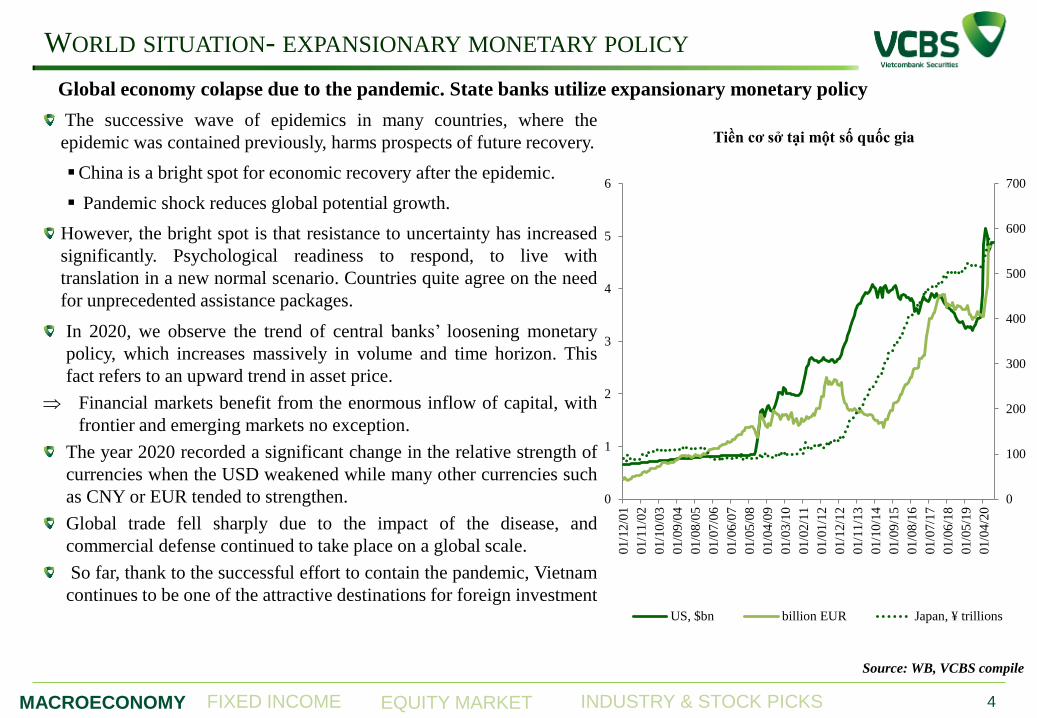

The successive wave of epidemics in many countries, where the

epidemic was contained previously, harms prospects of future recovery.

China is a bright spot for economic recovery after the epidemic.

Pandemic shock reduces global potential growth.

However, the bright spot is that resistance to uncertainty has increased

significantly. Psychological readiness to respond, to live with

translation in a new normal scenario. Countries quite agree on the need

for unprecedented assistance packages.

In 2020, we observe the trend of central banks’ loosening monetary

policy, which increases massively in volume and time horizon. This

fact refers to an upward trend in asset price.

Financial markets benefit from the enormous inflow of capital, with

frontier and emerging markets no exception.

The year 2020 recorded a significant change in the relative strength of

currencies when the USD weakened while many other currencies such

as CNY or EUR tended to strengthen.

Global trade fell sharply due to the impact of the disease, and

commercial defense continued to take place on a global scale.

So far, thank to the successful effort to contain the pandemic, Vietnam

continues to be one of the attractive destinations for foreign investment

WORLD SITUATION- EXPANSIONARY MONETARY POLICY

4

Source: WB, VCBS compile

Global economy colapse due to the pandemic. State banks utilize expansionary monetary policy

0

100

200

300

400

500

600

700

0

1

2

3

4

5

6

01/1

2/0

1

01/1

1/0

2

01/1

0/0

3

01/0

9/0

4

01/0

8/0

5

01/0

7/0

6

01/0

6/0

7

01/0

5/0

8

01/0

4/0

9

01/0

3/1

0

01/0

2/1

1

01/0

1/1

2

01/1

2/1

2

01/1

1/1

3

01/1

0/1

4

01/0

9/1

5

01/0

8/1

6

01/0

7/1

7

01/0

6/1

8

01/0

5/1

9

01/0

4/2

0

Tiền cơ sở tại một số quốc gia

US, $bn billion EUR Japan, ¥ trillions

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

Growth in Q4 is forecast to reach 4% - 5% due to gradual growth drivers with a post-epidemic recovery. GDP growth in 2020 is expected

to reach 2.73% - 3.06%.

In 2020, GDP in 2021 shall increase by about 6.5% -7.0% based on the contributions of the following components:

We expect consumer demand to grow significantly from the low level of 2020. Retail sales of goods will continue to recover after

disease control efforts have proven effective, with the "new normal" regime, which helps consumer demand rebound even demand

in non-essential consumer goods.

The processing and manufacturing industry remains an important indicator of the health of the manufacturing industry, which

contributes a lot to GDP, showing signs of a positive recovery after the epidemic has been contained.

Along with that, the successful maintenance of macroeconomic stability and the consistent policy of the government in attracting the

influx of capital flows from China, contributing to promoting investment from both public sectors. private. In particular, we draw

attention to infrastructure investment activities not only in traditional economic centers but also in many surrounding satellite cities

such as Long An, Vung Tau, Dong Nai,… in the South or Hai Phong, Quang Ninh, Thanh Hoa… in the North. These are considered

to promote private investment, creating the foundation for sustainable growth of the economy.

ECONOMIC STATUS QUO 2020- OUTLOOK 2021

5

Source: CEIC, GSO, VCBS compile

GDP growth in 2021 shall reach 6,5% - 7,0%

2,8%-3,1%

6,50%-7%

0%

1%

2%

3%

4%

5%

6%

7%

8%

2013 2014 2015 2016 2017 2018 2019 E2020 E2021

GDP growth

Inflation 3,1% -

3,4%

Deposit rates tick down

50 bps

GDP growth

6,5%-7,0%

Exchange rate ±0.5%

CPI

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

OUTLOOK 2021: ADAPT TO DEVELOP

6

Governments shows consistence in policies to create favorable conditions to attract in inflows.

Preparation means of production: chuẩn bị

về tư liệu sản xuất cơ bản: soil, water,

electricity, infrastructure.

Human resource: especially the quality of

higher education, college and vocational

training

Invest in infrastructure in a number of key

areas, including cities in critical economic

regions in the Southern and Northern

regions.

Prerequisite for development: disease is

contained; smooth coordination of fiscal

and monetary policy; Utilize public

investment to promote private investment.

=> FDI inflows continue to be expected to

be an important source to promote

economic growth in the coming years.

0

5

10

15

20

25

2015 2016 2017 2018 2019 10T.2020

Vốn đầu tư trực tiếp FDI (tỷ USD)

FDI đăng ký (ytd) FDI giải ngân (ytd)

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

STABILITY - INFLATION

7

Source: CEIC, GSO, VCBS compile

Favorable movements will be maintained in 2021.

-2%

0%

2%

4%

6%

8%

-0.5%

0.0%

0.5%

1.0%

1.5%

01

/15

04

/15

07

/15

10

/15

01

/16

04

/16

07

/16

10

/16

01

/17

04

/17

07

/17

10

/17

01

/18

04

/18

07

/18

10

/18

01

/19

04

/19

07

/19

10

/19

01

/20

04

/20

07

/20

10

/20

01

/21

04

/21

07

/21

10

/21

CPI

CPI (mom) CPI (yoy)

VCBS assesses that 2021 will recognize many favorable factors:

The government will not increase the base salary for 2021.

Although consumer demand is still recovering well, but not strong

enough to create upward pressure on inflation.

Food and foodstuff groups: the price movements of rice and pork:

Vietnam, with the strength of agriculture, can be completely proactive

and control the supply. In addition, the re-herds and import of pig

breeds are also promoted.

Monetary policy is operated flexibly, minimizing impacts.

Prices of public goods, electricity, water under the Government's

control.

However, there are certain factors that put upward pressure on inflation:

Domestic consumption demand recorded a significant improvement in

the non-essential consumption group.

Oil prices depended on the world oil prices; however, oil prices are

unlikely to rise sharply amid global supply chain disruption.

Due to negative impacts from natural disasters, the demand for civil

and repair materials may increase.

The medical group can also record increased pressure according to

global needs, increasing need for treatment due to prevention.

The inflation rate in 2021 is forecasted to be less than 4%. Specifically,

VCBS forecast that inflation will increase by 3.1% - 3.4%.

Foodstuff

Grains

Outdoor

eating

Housing, water,

eletricity, gas

and other fuels

Transport Furniture,

household

equipment and maintenance

Clothing and

footwear

Education

Health

Entertainment

Beverage and

tobacco

Miscellanous

goods and

services

Communication

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

Exchange rates are expected to have stable movements:

The supply of foreign currency is quite abundant in the context of: (1) Capital

flows of direct and indirect investment and remittances are quite positive; (2)

Trade balance is forecasted to continue a large surplus.

The trend of loosening monetary policy of central banks in the world, cash flow

still looks to bright macroeconomic stability like Vietnam.

Uncertainty is still happening around the world, but investors have become

accustomed to the fact that uncertainties always exist and adapt to these events.

The State Bank still shows a flexible and consistent policy to support and

stabilize the macro-economy in general and exchange rates in particular.

Uncertainty as well as world movements are still a big question mark for the

market, thus, exchange rates may be under certain pressure around volatile events.

The exchange rate will fluctuate in a tight band of 0.5% for the whole year

2021.

STABILITY – EXCHANGE RATES

8

Source: CEIC, Bloomberg, SBV, VCBS compile

Exchange rates will remain stable in 2021.

0

20

40

60

80

100

120

2012 2013 2014 2015 2016 2017 2018 2019 2020E

Exchange reserve (USDbn)

85

87

89

91

93

95

97

99

101

103

105

01/18 04/18 07/18 10/18 01/19 04/19 07/19 10/19 01/20 04/20 07/20 10/20

DXY

20,000

20,400

20,800

21,200

21,600

22,000

22,400

22,800

23,200

23,600

24,000

24,400

03/15 11/15 07/16 03/17 11/17 07/18 03/19 11/19 07/20

Exchange rate USD/VND

Reference exchange rate Ceiling exchange rate

Floor exchange rate VCB spot bid exchange rate

VCB spot offer exchange rate

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

STABILITY – DEPOSIT AND LENDING RATES

9

Source: GSO, VCBS compile

Credit growth

The orientation of the State Bank towards commercial banks will continue to be

remained, focusing on quality instead of increasing outstanding loans.

Therefore, credit growth is expected to increase lower than 2016-2017, and

nearly equivalent to 2018-2019.

Accordingly, credit will focus on credit institutions with good asset, and will be

less for credit institutions that have not finished handling outstanding debts.

Deposit rates

We expect deposit rates may decrease further, then stabilize at the low levels:

Central banks over the world are expected to maintain loosening monetary

policy for a long time.

The central bank's direction is to reduce interest rates and spend resources to

deal with bad debts. Accordingly, VCBS will observe management actions,

especially the Circular amending Circular 01.

The increasing trend of deposit rates in the previous years mainly came from

mobilizing to adapt safety ratios, attracting customers, and having sources for

credit loans. By 2021, under the management of the State Bank, with credit will

focus on quality, thus, the trend of increasing interest rates is unlikely to return.

Risks: Upward pressure on deposit rates may appear at the end of the year,

when banks promote lending activities, as well as businesses and residents tend

to withdraw money from the system. However, VCBS believes that this

pressure, if any, will not be large, credit for the whole year is forecast to

increase by 11-12%, lower than the 2016-2017 period.

Lending rates

The target of reducing lending interest rates (for the whole year) to support growth

can be achieved thanks to the following factors:

Foreign investment cash flow creates favorable conditions for liquidity

The decreasing deposit rates is basic for the downward trend on lending rates.

Deposit rates are forecasted to decrease by 50 points and then stabilize on the

low levels. Lending rates may decrease by 30-50 points.

4%

9%

14%

19%

24%

29%

34%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 E2020 E2021

Credit growth

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

7.50

8.00

Deposit rates (Unit: %)

HĐ 1 tháng HĐ 3 tháng HĐ 6 tháng HĐ trên 12 tháng

MACROECONOMY

FIXED INCOME MARKET

EQUITY MARKET

INDUSTRY AND STOCK PICKS

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

GOVERNMENT BOND MARKET- STATUS QUO 2020

11

Source: HNX, VCBS compile

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

Oct

07

- O

ct 1

1

Oct

21

- O

ct 2

5

Oct

28

- N

ov

01

No

v 1

1 -

No

v 1

5

No

v 2

5 -

No

v 2

9

Dec

09

- D

ec 1

3

Jan

06

- J

an 1

0

Jan

20

- J

an 2

4

Feb

10

- F

eb 1

4

Feb

24

- F

eb 2

8

Mar

09

- M

ar 1

3

Mar

23

- M

ar 2

7

Ap

r 0

6 -

Ap

r 1

0

Ap

r 2

0 -

Ap

r 2

4

May

04

- M

ay 0

8

May

18

- M

ay 2

2

Jun

01

- J

un

05

Jun

15

- J

un

19

Jun

29

- J

ul

03

Jul

13

- J

ul

17

Jul

27

- J

ul

31

Au

g 1

0 -

Au

g 1

4

Au

g 2

4 -

Au

g 2

8

Sep

07

-

Sep

11

Sep

21

-

Sep

25

Oct

05

-

Oct

09

Oct

19

-

Oct

23

No

v 0

2 -

No

v 0

6

Volume (VND bn) Winning rates Auction results

Volume 5Y 7Y 10Y 15Y 20Y 30Y

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

01

/19

02

/19

03

/19

04

/19

05

/19

06

/19

07

/19

08

/19

09

/19

10

/19

11

/19

12

/19

01

/20

02

/20

03

/20

04

/20

05

/20

06

/20

07

/20

08

/20

09

/20

10

/20

Primary market

KBNN NHCSXH NHPT

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

01

/16

04

/16

07

/16

10

/16

01

/17

04

/17

07

/17

10

/17

01

/18

04

/18

07

/18

10

/18

01

/19

04

/19

07

/19

10

/19

01

/20

04

/20

07

/20

10

/20

Bond yields

2Y 3Y 5Y 7Y 10Y 15Y

After being under strong and rapidly increasing pressure at the end of Q1.2020, the

downtrend dominated the Government bond market.

The reasons for the increase in bond yields at the end of Q1: (1) Exchange rate

was under pressure; Along with that, (2) Interbank interest rates slightly increased

and (3) Market members were more cautious in the context of complicated Covid-

19 translation, affecting most of the manufacturing and business sectors.

The reasons explain the downward trend in bond yields later on: (1) Interbank

interest rates maintained at a record low level, indicating a surplus of liquidity in

the banking system, (2) Demand for investment in Risk-free assets continue to

increase in the context of existing uncertainties (3) Psychology of market

members is getting more confident as the Government's measures in the

implementation of dual goals are drastic and effective. (4) Recent legal

documents and draft sub-law documents refer to a closer inspection, which aims

at more sustainable development of other fixed-income product, recently

considered to be a replacement product to government bond.

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

In 2020, SBV cut rates three times. In the context of abundant liquidity due to slow credit growth, interbank record a downward force and

even reach a record-breaking low level.

OUTLOOK FOR INTERBANK MARKET

12

Source: NHNN. Bloomberg, VCBS compile

In the context of (1) ample liquidity, (2) stable exchange rates, (3) direct and indirect investment flows that continue to rush to the

Vietnamese market, we expect interbank interest rates to stabilize on the current low threshold.

However, interest rates may slightly tick up for some times due to: (1) seasonal factors, (2) credit growth rebounds, (3) deposits of the

State Treasury in the system Commercial banks as well as the progress of disbursement of public investment capital.

Besides, the interbank interest rate depends heavily on the management as well as the direction of the State Bank in the open market

through repo and treasury bills, which should be considered to be a factor.

Thus, market factors supporting the interbank interest rate level can remain at a low level, but still under upward pressure around

certain times.

Interbank rate settle at a record-breaking low level.

0.0%

2.0%

4.0%

6.0%

01

/16

03

/16

05

/16

07

/16

09

/16

11

/16

01

/17

03

/17

05

/17

07

/17

09

/17

11

/17

01

/18

03

/18

05

/18

07

/18

09

/18

11

/18

01

/19

03

/19

05

/19

07

/19

09

/19

11

/19

01

/20

03

/20

05

/20

07

/20

09

/20

11

/20

ON 1W 2W 1M

Interbank market Trước 16/3 12/5 1/10

Refinancing rate 6,00% 5,00% 4,50% 4,00%

Rediscounting rate 4,00% 3,50% 3,00% 2,50%

OMO rates 4,00% 3,50% 3,00% 2,50%

Ceiling rates time deposits < 1M 0,80% 0,50% 0,20% 0,20%

Ceiling rates time deposits 1-6M 5,00% 4,75% 4,25% 4,00%

Ceiling rates for short-term loan in prioity sector 6,00% 5,50% 5,00% 4,50%

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

GOVERNMENT BOND MARKET-– OUTLOOK 2021

13

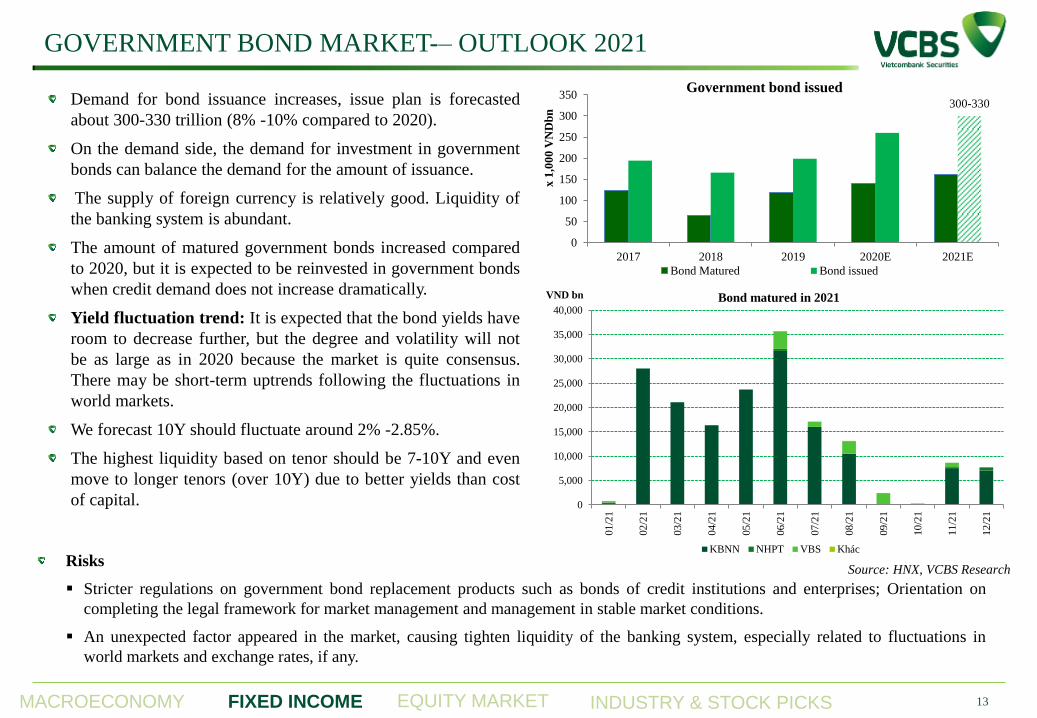

Demand for bond issuance increases, issue plan is forecasted

about 300-330 trillion (8% -10% compared to 2020).

On the demand side, the demand for investment in government

bonds can balance the demand for the amount of issuance.

The supply of foreign currency is relatively good. Liquidity of

the banking system is abundant.

The amount of matured government bonds increased compared

to 2020, but it is expected to be reinvested in government bonds

when credit demand does not increase dramatically.

Yield fluctuation trend: It is expected that the bond yields have

room to decrease further, but the degree and volatility will not

be as large as in 2020 because the market is quite consensus.

There may be short-term uptrends following the fluctuations in

world markets.

We forecast 10Y should fluctuate around 2% -2.85%.

The highest liquidity based on tenor should be 7-10Y and even

move to longer tenors (over 10Y) due to better yields than cost

of capital.

Source: HNX, VCBS Research

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

01

/21

02

/21

03

/21

04

/21

05

/21

06

/21

07

/21

08

/21

09

/21

10

/21

11

/21

12

/21

VND bn Bond matured in 2021

KBNN NHPT VBS Khác

300-330

0

50

100

150

200

250

300

350

2017 2018 2019 2020E 2021E

x 1

,00

0 V

ND

bn

Government bond issued

Bond Matured Bond issued

Risks

Stricter regulations on government bond replacement products such as bonds of credit institutions and enterprises; Orientation on

completing the legal framework for market management and management in stable market conditions.

An unexpected factor appeared in the market, causing tighten liquidity of the banking system, especially related to fluctuations in

world markets and exchange rates, if any.

MACROECONOMY EQUITY MARKET NGÀNH VÀ DOANH NGHIỆP TRIỂN VỌNG FIXED INCOME

BOND MARKET –2020

14

DIVERSIFICATION INTO CORPORATE BONDS

Source: HNX, VCBS

80,254

141,340 181,093

248,024 256,223

312,205

244,221

157,547

197,769 228,699

25,000

28,707

34,412

48,047

42,769

97,413

115,416

146,039

296,713 303,800

0

100,000

200,000

300,000

400,000

500,000

600,000Issued bond

Gov Bond Gov-Backed Bond Muni Bond Corp Bond

8.0% 9.7%

12.2% 14.3%

16.2%

27.3% 27.6% 27.9% 26.9% 27.9% 3.3% 2.0%

2.7% 2.5%

3.4%

5.3% 6.2% 7.9% 11.3%

14.4%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%Outstanding bond/GDP

Gov Bond Gov-Backed Bond Muni Bond Corp Bond

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

BOND MARKET – Primary market

15

Source: HNX, VCBS

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Jan 1

9

Feb

19

Mar

19

Apr

19

May

19

Jun

19

Jul

19

Aug

19

Sep

19

Oct

19

Nov

19

Dec

19

Jan 2

0

Feb

20

Mar

20

Apr

20

May

20

Jun

20

Jul

20

Aug

20

Sep

20

Oct

20

Primary market

ST VBSP VDB

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

Oct

07

- O

ct 1

1

Oct

21

- O

ct 2

5

Oct

28

- N

ov

01

No

v 1

1 -

No

v 1

5

No

v 2

5 -

No

v 2

9

Dec

09

- D

ec 1

3

Jan

06

- J

an 1

0

Jan

20

- J

an 2

4

Feb

10

- F

eb 1

4

Feb

24

- F

eb 2

8

Mar

09

- M

ar 1

3

Mar

23

- M

ar 2

7

Ap

r 0

6 -

Ap

r 1

0

Ap

r 2

0 -

Ap

r 2

4

May

04

- M

ay 0

8

May

18

- M

ay 2

2

Jun

01

- J

un

05

Jun

15

- J

un

19

Jun

29

- J

ul

03

Jul

13

- J

ul

17

Jul

27

- J

ul

31

Au

g 1

0 -

Au

g 1

4

Au

g 2

4 -

Au

g 2

8

Sep

07

-

Sep

11

Sep

21

-

Sep

25

Oct

05

-

Oct

09

Oct

19

-

Oct

23

No

v 0

2 -

No

v 0

6

Vol (VND bn) Wininng rates GB Auction results

Volume 5Y 7Y 10Y

15Y 20Y 30Y

5.05 5.75

8.7

13.03 12.41

13.45 13.67

3

5

7

9

11

13

15

Average issued tenors

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

20000.0

40000.0

60000.0

80000.0

100000.0

120000.0

140000.0

160000.0

5Y 7Y 10Y 15Y 20Y 30Y

Goverment bond issuance 10M.2020

Offering volume Winning volume

Winning-to-offering ratio Issuing plan

Banks Other

financial

institutions

Government bond‟s holders

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

BOND MARKET – Secondary market

16

Source: HNX, Bloomberg, VCBS

DOWANWARD FORCE IS EXPECTED TO DOMINATE BOND MARKET

0.0%

2.0%

4.0%

6.0%

01

/16

03

/16

05

/16

07

/16

09

/16

11

/16

01

/17

03

/17

05

/17

07

/17

09

/17

11

/17

01

/18

03

/18

05

/18

07

/18

09

/18

11

/18

01

/19

03

/19

05

/19

07

/19

09

/19

11

/19

01

/20

03

/20

05

/20

07

/20

09

/20

11

/20

ON 1W 2W 1M

Interbank rates

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

01

/16

04

/16

07

/16

10

/16

01

/17

04

/17

07

/17

10

/17

01

/18

04

/18

07

/18

10

/18

01

/19

04

/19

07

/19

10

/19

01

/20

04

/20

07

/20

10

/20

Bond Yields

2Y 3Y 5Y 7Y 10Y 15Y

0.0

1.0

2.0

3.0

4.0

1Y 2Y 3Y 5Y 7Y 10Y 15Y

Yield Curve

6/30/2020 9/30/2020

10/30/2020

1,429

789 270 422

-222

1,681

-275 -465

624

-655

1,209 963

2,121

1,445

2,933

48 720

2,870

1,721

907

2,240

-553 -672 37

938

-1,712 -1,880

1,254 1,768

2,269

43

-485

1,177

255

01

/18

04

/18

07

/18

10

/18

01

/19

04

/19

07

/19

10

/19

01

/20

04

/20

07

/20

10

/20

Foreign investors in the secondary market

Net position (Unit: bn.VND)0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Outright

<3 3-5 5-7 7-10 > 10Y

1,668

3,642 3,655

6,354

8,962

8,756 7,977 7,861

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

0

300

600

900

1,200

1,500

1,800

2,100

2,400

VN

D b

n

x1

,00

0 V

ND

bn

Total volume (left side) Average daily volume (right side)

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

GOVERNMENT BOND MARKET – 2021 OUTLOOK

17

Volume of bond issuance is forecasted about VND 300-

330 trillion (+8%-10% yoy).

The investment demand for Government bonds can

completely balance the amount of forecasted bond

issuance.

Liquidity of the banking system, if seasonal effects are

excluded, is likely to be abundant.

Bond yields have room to decrease, however, the

volatility may appear more in 2021.

The highest liquidity based on tenors should be 7-10Y

tenors (and >10Y tenor).

Risks: An unexpected factor appeared in the market,

causing the operator to tighten the liquidity of the

banking system.

KEY FACTORS

Liquidity on interbank market.

SBV’s regulating policy

Disbursement for infrastructure speed up

Trend of higher asset prices in the world.

Sentiment over macro-economics foundation.

Source: HNX, VCBS Research

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Jan-2

1

Feb

-21

Mar

-21

Apr-

21

May

-21

Jun

-21

Jul-

21

Aug

-21

Sep

-21

Oct

-21

Nov

-21

Dec

-21

VND Billion Matured Bonds in 2021

ST VDB VBSP Other

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

CORPORATE BOND MARKET – 3Q. 2020 RECAP

18

Real estate

Banks

Electricity,

Water

Securities

Construction

Other

financial

instutions Others

Issued bonds by industry

25,000

28,707

34,412

48,047

42,769

97,413

115,416

146,039

296,713 303,800

0

100,000

200,000

300,000

400,000

500,000

600,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 9M.2020

Issued bond

Gov Bond Gov-Backed Bond Muni Bond Corp Bond

Decree 81/2020 / ND-CP effect from September 2020 has significantly reduced the amount of issued bonds issued in the last month

of the third quarter. However, the previous period saw the large amount of issued bonds.

On July 28, HNX issued Document No. 384/QD-SGDHN on the Regulation on operation of the Website corporate bond

information.

The SBV is drafting a Circular on purchase and sale of notes, treasury bills, certificates of deposit, bonds issued by other credit

institutions, foreign bank branches. In which, valuable papers can be purchased with tenor less than 12 months in secondary

market.

Source: Fiinpro, HNX, VCBS compiles

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

CORPORATE BOND MARKET – 3Q. 2020 RECAP

Volume

(VNDbn)

Average

tenors

Average

yields

HDBank 19,527 8.5 7.5%

Sovico 18.000 3 10.5%

Masan 14,085 3 9.5%

VIB 13.500 3 5.7%

Vinhomes 12.000 2.5 9.5%

Volume

(VNDbn)

Average

tenors

Average

yields

Phat Dat Corporation 510 1 13.0%

Centre of international

relation & investment 50 1 13.0%

IDJ 229 3 13.0%

Nam La Hydro power 100 3.5 13.0%

Trinh Gia Nguyen

Telecommunications 1,400 1 12.5%

0

1

2

3

4

5

6

7

8

Electricity,

Water

Banks Real estate Construction Securities Other

financialinstutions

Others

Average tenors

Average

0%

2%

4%

6%

8%

10%

12%

14%

Other

financialinstutions

Construction Real estate Electricity,

Water

Others Securities Banks

Average yields

Average

Table. Top 5 companies issue the largest volume of bonds Table. Top 5 companies issue the highest yield of bonds

Source: Fiinpro, HNX, VCBS compiles

MACROECONOMY

FIXED INCOME MARKET

EQUITY MARKET

INDUSTRY AND STOCK PICKS

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

STOCK MARKET HIGHLIGHTS IN 2020

21

Source: Bloomberg, VCBS

80

88

96

104

112

120

128

136

144

400

450

500

550

600

650

700

750

800

850

900

950

1,000

1,050

1,100

1,150

VN Index HNX Index

VN Index -4,6% HNX Index +31,4%

GDP Q1.2020

+3,82% yoy

The US - China

signed trade

agreement

Phase 1 China imposed

lockdown 3 cities in

Hubei province

Oil prices

plummeted

because Russia

and OPEC did not

reach an

agreement

WTI crude oil prices

delivered in May closed

at negative prices

The WHO declares Covid-

19 as a global pandemic

Vietnam airlines are

allowed to increase

their domestic flight

frequency by 2.5 times

SBV lowered the

executive interest

rate for the second

time this year

The Chinese

National Assembly

passed the National

Security Law in

Hong Kong

New developments

appeared in the US-

China trade war

GDP Q2.2020

+0,36% yoy

FED announced new

inflation approach

EVFTA is in

effect

SBV lowered the

executive interest rate

for the third time this

year

GDP Q3.2020

+2,62% yoy

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

STOCK MARKET HIGHLIGHTS IN 2020

Source: Fiinpro, Bloomberg, VCBS

Q1.2020 witnessed the largest drop of VN Index since

August 2001 as Covid-19 became a pandemic. Due to the

decrease of the majority of sectors, the benchmark index

declined by 24.9%, with the most affected sectors

including aviation, travel & entertainment. However,

thanks to the success in disease control and the timely

social distancing period, the uptrend dominated during Q2

and Q3. Bullish index along with improving liquidity

indicated the optimism of investors about the long-term

economic outlook. As most of the world has not been able

to effectively contain the pandemic, many developed

countries have to face shutdowns, Vietnam’s market

occupied the spotlight as an outperforming economy.

In the last quarter, VN Index suddenly surpassed 970

points, erasing the decline in first half of 2020 during the

announcement of listed companies’ Q3 business results in

October 2020. The gain was led by the banking sector and

several other large-cap stocks such as VNM, HPG, MSN,

etc. However, at the beginning of November, the lack of

supportive information and profit-realizing pressure

caused VN Index to fluctuate around 940 points.

4

0

100

200

300

400

500

600

700

800

400

500

600

700

800

900

1,000

1,100

Volume VN Index

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

MSN HPG CTG VNM GVR SAB BID VHM VIC GAS

Top contribution to VN Index in 2020

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

RELATIVE VALUATIONS OF VIETNAM’S STOCK MARKET IN 2020

Source: Fiinpro, Bloomberg, VCBS

0

5

10

15

20

25

30

35

40

45 Sectors‟ P/E in Vietnam

15.95

11.07

28.88

23.05 20.71

2.05 1.74 1.39 1.43 1.43

0

5

10

15

20

25

30

35

VN Index IDX Composite Index FTSE Bursa Malaysia

EMAS Index

PSE All shares Index SET Index

Vietnam Indonesia Malaysia Phillipines Thailand

Average P/E & P/B in ASEAN markets

P/E

P/B

5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Sectors' P/B in Vietnam

2019

2020

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

-40,000

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

40,000

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20

Foreign sector transaction volume (HSX, HNX & Upcom) (VND thousand billion)

Giá trị mua

Giá trị bán

Giá trị ròng

FOREIGN INVESTORS’ HIGHLIGHTS IN 2020

24

Source: Fiinpro

-4,000,000

-2,000,000

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

VHM PLX PGD MWG PHR VJC VRE VIC HPG MSN

Foreign sector net buy/(sell) (VND million) Due to the impact of economic distress from the

Covid-19 pandemic, foreign investors net sold

since February 2020, among which the most

aggressive selling periods were Q1, August and

October. Up until Nov 10th, net selling value of

foreign investors was VND 11,554 billion in all

three exchanges (namely HSX, HNX and

UpCom).

The most noticeable put-through transaction in

2020 belongs to the deal of VHM’s shares in

June with total value reaching VND 15,000

billion. On the other hand, VRE, VIC, MSN and

HPG were the most net-sold shares.

BRENT CRUDE OIL

25

Daily Weekly Monthly Quaterly Yearly YTD

-1.29% 7.85% -3.79% -4.60% -35.14% -38.79%

Price changes (as at November 06th, 2020)

• In 2020, Brent crude oil’s price fell below USD 20 per

barrel at times.

• The movement of global oil prices in 2020 is relatively

unstable, and we have seen many factors affecting oil

prices, from geopolitical fluctuations, advances in

science and technology or policy shifting of countries in

the world, especially crude oil producing countries. But

the strongest impact on oil price movements is still the

Covid-19 epidemic.

• Prestigious financial institutions in the world have

released many different forecasts for oil prices.

Specifically, International Monetary Fund predicts that

global oil price in 2021 will be in the range of USD 40-

50 per barrel, equivalent to half of the USD 80 per

barrel price that Saudi Arabia needs to achieve the

balance of its state budget.

• Meanwhile, the bank of Morgan Stanley forecasts that

Brent oil price will reach USD 50.00 per barrel in

1H.2021 thanks to a weak dollar and accelerating

inflation, while WTI oil prices will reach USD 47.50

per barrel in Q3.2021.

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

US

D/b

arr

el

Oil prices 2020

Source: Bloomberg, VCBS

NATURAL RUBBER

26

Daily Weekly Monthly Quaterly Yearly YTD

-2.29% -2.17% 10.11% 29.65% 13.12% 5.79%

Price changes (as at November 06th, 2020)

• In 2020, natural rubber price witnessed a new record:

Price reached the highest level in years on October 29th,

2020 after a Reuters poll showed that China's economy

in 2021 would recover strongly from the recession

caused by the Covid-19 pandemic.

• According to the Association of Natural Rubber

Producing Countries (ANRPC), in 2020, natural rubber

production will face difficulties due to epidemics,

which will limit labor force in the industry and make

transportation more difficult. The world’s natural rubber

production has decreased by 8.70% in the first 8 months

of 2020, reaching 7.778 million tons, and is expected to

decrease by 3.00% more in the remaining 4 months of

2020 and Q1.2021.

• However, ANRPC forecasts that the trend of rising

rubber prices will continue to exist in the coming

months, mainly due to the recovery of China's

manufacturing sector, amid an increase in car sales in

India and the prospect of a new economic stimulus

program in the U.S.. September was the first month the

automobile industry recovered almost globally, after a

long period of decline caused by the Covid-19

epidemic.

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

180.00

200.00

US

D/k

g

Rubber prices 2020

Source: Bloomberg, VCBS

STEEL

27

Daily Weekly Monthly Quaterly Yearly YTD

0.00% 3.33% 7.86% 10.49% 2.97% 4.42%

Price changes (as at November 06th, 2020)

• China’s spot steel prices have recovered towards the

end of 2020. In 2020, steel prices have fallen below

CNY 520.00 per ton at times due to the impact of trade

war tensions as well as signals of China’s decelerating

economic growth due to the effects of Covid-19

pandemic.

• Sales volume recovered in Q2.2020, due to higher

demand from real estate sector. Compared with the 14%

decrease over the same period in Q1.2020, 1 percentage

point lower than the same period in Q2.2020 can be

considered an impressive sign of recovery.

• Meanwhile, iron ore prices in 2020 and the following

years are forecast to decline due to more abundant

supply but lower demand.

• The World Steel Association (Worldsteel) forecasts that

global steel demand will decrease by 6.40% in 2020 due

to the negative impact of the Covid-19 epidemic, but

will gradually recover in 2021.

• According to Worldsteel’s experts, there is a possibility

that the decline in steel demand in most countries will

not be as serious as the situation of the global economy,

as Covid-19 has more serious effects on industries with

less usage steel, like consumption and services.

However, in many developed economies, steel demand

has not fully recovered since the 2008 financial crisis

and still remained low.

480.00

500.00

520.00

540.00

560.00

580.00

600.00

CN

Y/T

on

Chinese steel spot price 2020

Source: Bloomberg, VCBS

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

MSCI FRONTIER MARKET 100 INDEX RAISING VIETNAMESE

STOCKS’ WEIGHT

28

Source: Bloomberg, VCBS

As Kuwait has been upgraded to Emerging Market since

November 2020, MSCI also announced the new weight of the

constituents in MSCI Frontier Market 100. In particular, MSCI

Frontier Market 100 index will be restructured in 5 stages to

exclude Kuwait’s stocks from the index, from November 2020 to

November 2021.

After the first restructuring phase in November 2020, the weight of

Vietnamese stocks in MSCI Frontier Market 100 Index will

increase to 15.76% from the current 12.65%. We estimates that the

ETF Ishare MSCI Frontier Market 100 ETF will net buy about

VND 280 billion after the restructuring phase in November 2020

allocated to 28 Vietnamese stocks, with PDR and KDC being

newly added stocks.

Source: MSCI

Ticker

Current

Weight

(%)

Expected

Weight post-

phase 1 (%)

Expected

Value post-

phase 1

(USD)

Expected Net

Buy post-phase 1

(USD)

Expected Net Buy

post-phase 1

(VND)

1 VRE 0.47 0.58 2,274,680 421,272 9,794,567,424

2 VNM 2.06 2.55 10,033,295 1,911,947 44,452,758,336

3 VJC 0.45 0.55 2,177,885 403,107 9,372,230,266

4 VIC 2.1 2.55 10,033,295 1,777,391 41,324,345,751

5 VHM 1.45 1.78 7,017,630 1,312,620 30,518,421,498

6 VHC 0.1 0.12 483,974 76,353 1,775,206,904

7 VGC 0.16 0.20 774,359 154,201 3,585,173,534

8 VCB 0.83 1.02 4,016,988 736,366 17,120,502,517

9 TCH 0.1 0.12 483,974 102,596 2,385,367,814

10 STB 0.17 0.21 822,757 165,881 3,856,738,638

11 SSI 0.18 0.22 871,154 178,665 4,153,950,119

12 SHB 0.19 0.23 919,552 172,643 4,013,955,580

13 SBT 0.11 0.15 590,194 163,805 3,808,473,533

14 SAB 0.31 0.38 1,500,321 273,226 6,352,502,290

15 PVS 0.09 0.11 435,577 80,261 1,866,077,681

16 POW 0.12 0.15 580,769 100,996 2,348,156,167

17 PLX 0.14 0.17 677,564 120,467 2,800,867,124

18 NVL 0.39 0.48 1,887,501 371,421 8,635,533,392

19 MSN 1.07 1.32 5,178,527 984,823 22,897,132,843

20 KBC 0.08 0.10 387,180 62,804 1,460,188,957

21 HPG 1.29 1.59 6,243,271 1,165,985 27,109,151,419

22 HDB 0.26 0.32 1,258,334 217,097 5,047,507,979

23 GEX 0.15 0.18 725,962 154,940 3,602,362,968

24 GAS 0.13 0.16 629,167 115,805 2,692,457,036

25 BVH 0.08 0.10 387,180 72,216 1,679,015,865

26 BID 0.17 0.21 822,757 143,946 3,346,735,240

27 PDR 0 0.10 393,463 393,463 9,148,004,415

28 KDC 0 0.10 393,463 393,463 9,148,004,415

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

DERIVATIVE MARKET HIGHLIGHTS IN 2020

29

Source: Fiinpro, Bloomberg, VCBS

• After the sell-off in March, VN30 Index had an impressive recovery momentum, by the end of October 2020, the index had

increased by 54.00% compared to the lowest point of 600. During the highly volatile period in Q2 and Q3, the derivative

market was driven by speculators. However, from the end of Q3 until now, VN30 recovered strongly to 900 points with

positive cash flow returning to the underlying stock market and liquidity in the derivative market shrinking.

• As of now, the underlying index has increased 1.80% YTD while VN30F1M has increased by 2.50%. Market liquidity also

improved significantly compared to 2019’s, namely the average total trading volume per session reached more than 161,600

contracts (up by 90% compared to that in 2019) and the total average transaction by session reached VND12,700 billion

(67% higher than that in 2019). The average number of open interests (OI) per session also reached more than 23,500

contracts, which was an increase of 17.50% compared to that in 2019.

• Besides VN30 futures, Covered Warrants (CW) market also recorded many impressive milestones. The total number of CWs

on the market currently is 107, based on 21 underlying stocks. However, CW market is still one-way long market, only

allowing call options to be listed.

400.00

500.00

600.00

700.00

800.00

900.00

1,000.00

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

01/08/2020 02/08/2020 03/08/2020 04/08/2020 05/08/2020 06/08/2020 07/08/2020 08/08/2020 09/08/2020 10/08/2020

Khối lượng GD Vị thế mở VN30 VN30F1M

VIETNAM‟S

STOCK MARKET

OUTLOOK IN 2021

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

In 2021, we expect the Vietnam’s stock market outlook and market

size to achieve a certain growth compared to 2020’s but the growth

rate will somewhat be limited, due to the fact that most supportive

factors in 2020 are forecast to not improve but even weaken in

2021. Some key takeaways are as follows:

The peaks of benchmark indices in 2021 are projected to

increase by about 8-15% compared to those at the end of

2020, and will be greatly affected by the recovery rate of the

Vietnam’s economy in the context of the "new normal” in

Vietnam and the development of the Covid-19 pandemic

globally.

VN Index tends to move around a higher "base", but the

fluctuation range (the difference between the year's highest

and lowest) will be around 120-150 points and not as large as

in 2020, while HNX Index is projected to fluctuate in a

range of ~ 20 points.

Average trading volume in 2021 continued to improve

compared to that in 2020, reaching an average of 400-410

million shares per session on all three exchanges,

equivalent to an increase of about 5% yoy.

Trading value is expected to increase by about 8.00%

corresponding to an average trading value per session of

about VND 6,900-7,000 billion on all three exchanges.

STOCK MARKET’S OUTLOOK IN 2021

31

PROJECTIONS OF BENCHMARK INDICES

Source: Fireant, VCBS

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

PUBLIC INVESTMENT PLAN AND DISBURSEMENT IN 2021

15

Investing in new projects in 2021 will not be easy

Limited resources: Public investment in 2021 will slightly increase compared to the disbursement plan in 2020, at VND

477,300 billion (+ 1.4% yoy). However, according to the statistics of the Ministry of Planning and Investment, the capital

demands from ministries and provinces are 682,000 billion VND.

The gap time between submitting and approving mid-term public investment plans for the period 2021-2025 is

interpolated with 2021’s investment plan. 2021 is the first year of the five-year socio-economic development plan as well

as the first year of the mid-term public investment plan for the period of 2021-2025, but it is only until July 2021 that the

mid-term plan is officially approved.

With (1) limited funding and (2) late approval of the investment plan, highly prioritized investments for 2021 will be

transitional projects and those completing in 2021, focusing on projects that have been approved between 2016 and 2020,

major infrastructure projects, etc. Newly submitted projects will be delayed in the context of unapproved 2021-2025

public investment plan and the negative effects of Covid-19 on the economy.

No. Project Total Investment

(bil VND) Contractors

1 Nha Trang - Cam Lam 7,615 Bidding in progress.

2 Cam Lam - Vinh Hao 13,600 Bidding in progress.

3 Mai Son – Route 45 12,111 Bidding in progress.

4 Vinh Hao – Phan Thiet 11,183 Bidding in progress.

5 Phan Thiet – Dau Giay 14,356 Bidding in progress.

Transitional projects to be implemented in 2021*

Long Thanh Airport Phase 1

Total Investment (bil VND) 109,200

Expected completion 2025

Cost structure (bil VND) Clearance: 18.500

Construction: 90.700

Progress Clearance: 2,500 ha

Key project 2021*

*Source: VCBS

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

EVFTA – TARIFF CUT COMMITMENTS BETWEEN EU & VN

33

(Source: VCCI, VCBS)

Product Instant Effect Guideline

Machinery and

equipment 61% of tariff remove to 0% Remaining tariff remove to

Car and

Automobile

equipment

- Cars (over 2500 cm3 running diesel,

over 3000 cm3 running in cylinders)

will reduce tax to 0% after 9 years

- Other types of cars are subject to a 10-

year tax reduction commitment

- Auto spare parts are removed tax

import after 7 years

- Regular computers and computers

over 150 cm3 have import tax of 0%

after 10 years and 7 years

Alcohol beverage

- Wine and spirits will be exempt from

import tax after 7 years

- The schedule for tax elimination for

beer is 10 years

Fresh/Frozen

Meat

- Import tax on frozen pork will be 0%

after 7 years; Import duties on other

types of pork will be 0% after 9 years

- Chicken will be exempt from import

tax after 10 years

- Beef will be exempted from import tax

after 3 years

Medical drugs 71% of tariff remove to 0% The rest will be eliminated from tariffs

on a 5 to 7 year schedule

Chemical 70% of tariff remove to 0% The rest will be eliminated tariffs on a

maximum 7-year schedule

Texile and shoe

material 80% of tariff remove to 0%

The rest will be eliminated tariffs on a 3

to 5 year schedule

Milk and milk

product

44% of tariff is remove to

0%, some would take up to

3 years

The rest will be eliminated tariffs on a

5-year schedule

Oil and Gasoline Import duties will be cleared after 10

years

Product Instant Effect Guideline

Texiles 42.5% of tariff remove to

0% 3 - 7 years

Shoe Some tariff is remove to

0% 4 – 8 years

Yarn

Some industrial and

garment yarn remove to

0%

Remove to 0% within 4 years

Catfish/Seafood Tariff on seafood reduce to

0%

Catfish tariff reduce from 9% to 0%

in 3 years

Drugs and

Medical

Equipment

All Tariff remove to 0%

Electronic device

and equipment 74% of tariff remove to 0%

Other tariff reduce to 0% within 6

years

Agriculture

product

Raw agriculture product

tariff remove to 0%, apply

quota on rice export

Processed product tariff is reduce to

0% within 4 to 8 years

Processed food

and Frozen meat Most tariff remove to 0%

Poultry fillet, exotic organs remove

to 0% in 8 years

Car

Industrial, Specialized

vehicles tariff remove to

0%

Tariff remove from 10% to 0%

within 4 – 8 years, depend on engine

capacity

Motorbike Tariff on motorbike < 250

cm3 remove to 0%

Tariff on motorbike >250 cm3,

electrical bike remove to 0% within

4 to 6 years

Chemical and

material

Most tariff is remove to

0%

Remaining tariff remove 0% to 4

years

Woods and

Wooden product 74% of tariff remove to 0%

Remaining tariff remove to 0% after

4 years

EU TARIFF CUT COMMITMENTS VIETNAM TARIFF CUT COMMITMENTS

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME

In the context of similar level of risk vs. opportunity, we believe that investment opportunities in 2021 will lean to basic industries

serving as essential inputs for the economic growth in Vietnam ("back to basics") for the time to come:

The shift of global supply chains, the industrialization (and digitization) of the domestic economy and the urbanization process in

Vietnam will all require essential inputs such as Electricity (both electricity transmitting and producing); Basic construction

materials (cement, steel, wood, stone); and Agricultural products. These sectors also benefit from the government's public

investment in building new infrastructure projects and upgrading existent infrastructures, as well as the overall recovery of the

domestic demand.

Another noteworthy group is companies that support the increase of trade between Vietnam and other partners thanks to the free

trade agreements signed recently and in the near future, typically seaport & logistics sectors. These companies also supports the

shift of manufacturing chains from China to other countries with more competitive labor costs, which includes Vietnam.

Although it seems contrary to the investment opinion that we outline above, we also want to emphasize on companies which

introduce and apply new technologies to its day-to-day business operations. The application of advanced technologies in

business, including the "digitization" of Vietnam’s economy, is inevitable and irreversible. Therefore, even though changes from

old to new always bring about risks, the potential positive outcomes, which are the improvements of productivity, business

performance and resource usage efficiency, still outweigh the risks caused by the transition process.

And lastly, we also want to include companies with their “specific catalysts“, i.e. seeking foreign strategic partners,

conducting M&A, IPOs, listing new shares and moving listed shares to other stock exchanges, etc.

SOME NOTEWORTHY INVESTMENT HINTS IN 2021

34

“A BIRD IN THE HAND IS WORTH TWO IN THE BUSH” So far, 2020 has witnessed many ups and downs of the global economy as well as major

stock markets in the world due to the impacts of Covid-19 pandemic. We believe that

what happened in the world in 2020 still potentially leaves over many negative

consequences and risks in 2021.

On the other hand, Vietnam's macro-economy remained stable, highlighted by

optimistic economic growth and inflation and exchange rates under control. Moreover,

low interest rates globally, with Vietnam being no exception, open up many

investment opportunities in industry-leading companies which are also the main

driving force behind the growth of Vietnam's stock market in the long run.

MACROECONOMY

FIXED INCOME MARKET

EQUITY MARKET

INDUSTRY AND STOCK PICKS

STOCK PICKS

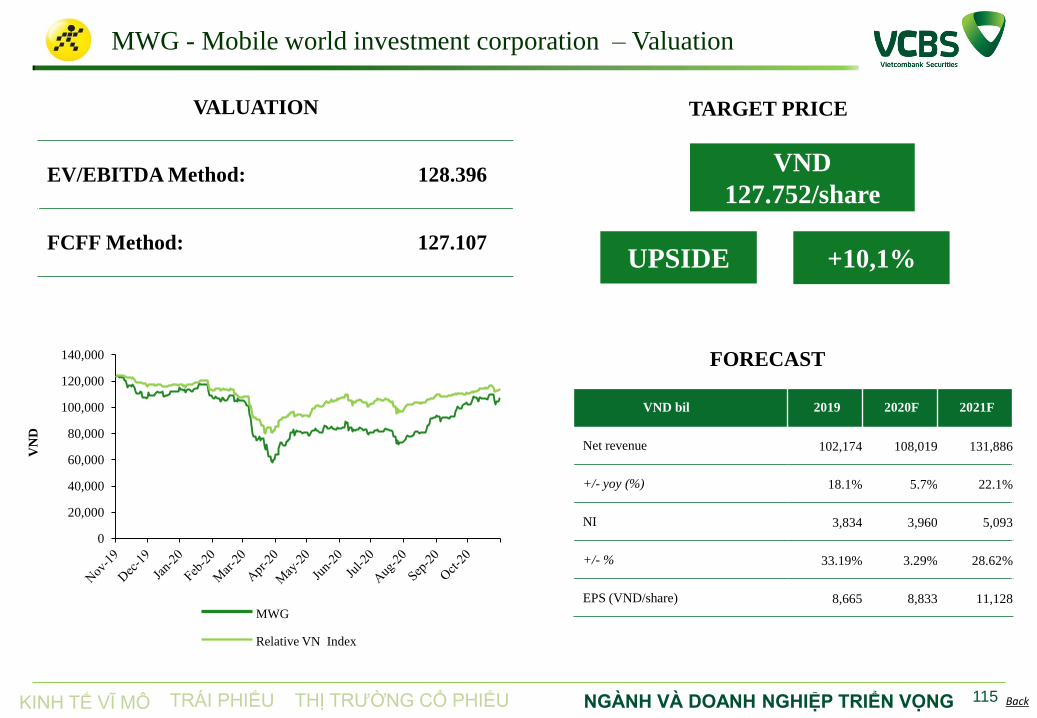

36

• ACB MBB TPB BANKS

• VHM REAL ESTATE

• ACV GMD AVIATION -

SEAPORTS

• HPG PTB CONSTRUCTION MATERIALS

• PC1 ENERGY

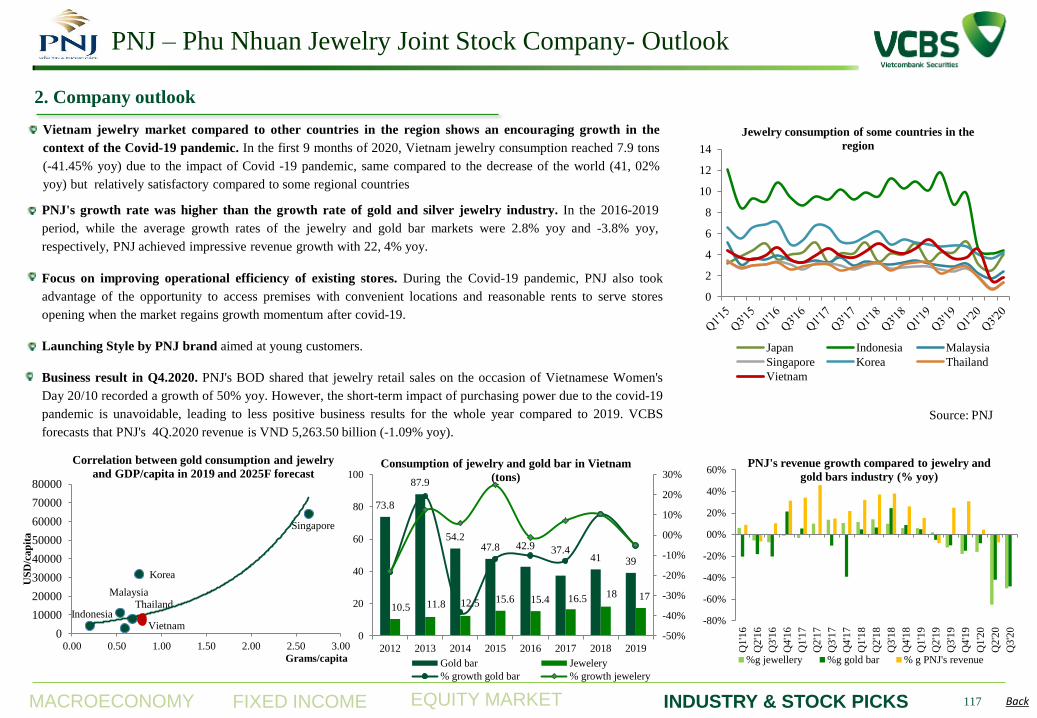

• MWG PNJ RETAIL

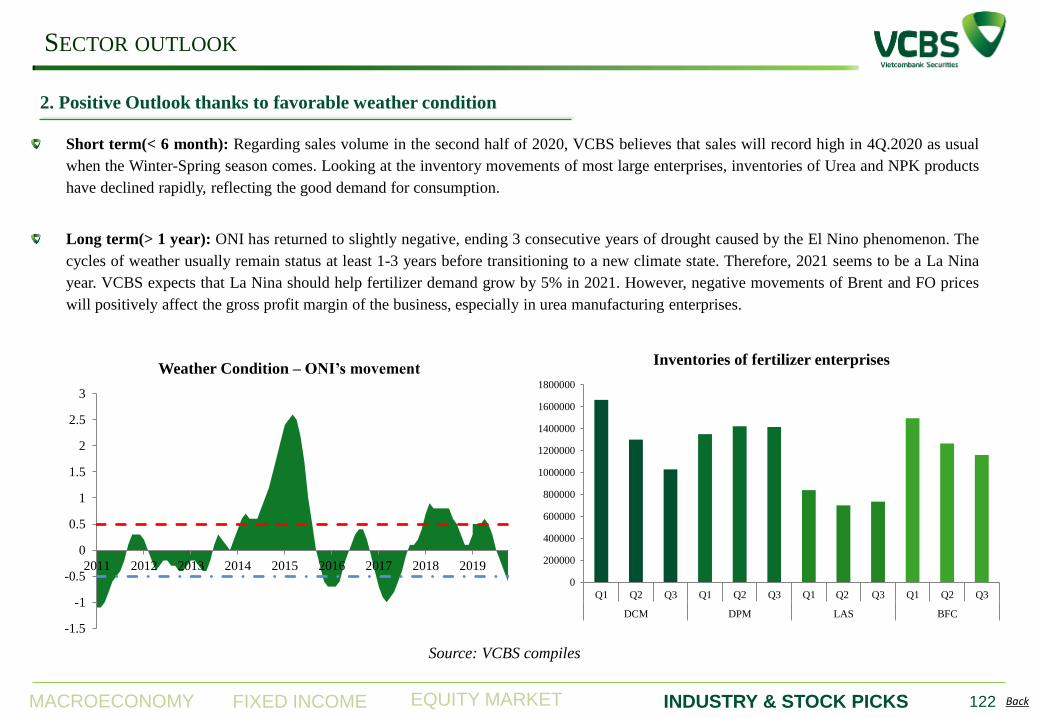

• DCM FERTILIZERS

• STK TEXTILES

• DGC PLC FPT BWE OTHERS

BANKING

SECTOR

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

BANKING SECTOR – UPDATE

38

Source: SBV, Banks, VCBS sumary

Credit growth is slower than previous years but showing signs of

speeding again:

- Expected to be less than 10% for the whole of 2020.

- 9M.2020: credit growth from corporate bonds contributed 25% of

growth and credit growth from large corporate customers contributed

about 60% of the growth.

SBV has loosened “room” for credit growth for many banks:

- With the purpose of stimulating credit growth to support economic

growth, SBV has loosened the credit growth room for banks that meet

2 factors: (1) financial health, (2) capability of growth.

- Banks are given higher rooms: TCB, HDB, VPB, TPB, VIB, MBB

Credit growth is expected to recover and reach about 11-12% in

2021.

6.09%

0.0%

5.0%

10.0%

15.0%

20.0%

T1 T2 T3 T4 T5 T6 T7 T8 T9 T10 T11 T12

Credit growth ytd

2015 2016 20172018 2019 2020

-11% -1% 9% 19%

EIB

CTG

BID

STB

VCB

TCB

ACB

MBB

LPB

VIB

HDB

VPB

SHB

TPB

9M.2020 Credit growth

Customer loans Corporate bonds

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

BANKING SECTOR – UPDATE

39

Retail credit was slower in 9M.2020, however, it is still the segment many banks prioritize:

‐ Retail loans has low Weighted Risk when calculating CAR (depending on collateral or 80% if no real estate collateral)

‐ Retail loans improve loan yield and reduce concentration risk.

‐ Potential to increase retail credit proportion remains as Vietnam's proportion of retail loans is still lower than that of developed countries

and people's lifestyles are changing towards more debt acceptance. However, this segment will face a higher level of competition as more

and more banks switch focus to retail.

22.8%

25.7%

34.7%

39.7%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

Propotion of Retail credit

40% 40%

44%

48%

36%

38%

40%

42%

44%

46%

48%

50%

Viet Nam ASEAN-3 China US

Proportion of retail banking loans in 2019

Source: SBV, Banks, Bloomberg, VCBS sumary

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

BANKING SECTOR – UPDATE

40

Deposit from customers increased by 6.1% in 8M.2020. The average listed

deposit rate has decreased by 100 - 120 bps from the beginning of 2019

depending on the term.

Banks' cost of funds recorded a rapid decline in Q3.2020.

There has not been enough pressure to make deposit rates rise again:

- There has been no liquidity risk coming from bad debt.

- Less pressure on indicators: (1) credit growth partly based on corporate bonds

reduces the pressure on LDR as the numerator only takes into account loans to

customers; (2) not paying cash dividend according to SBV’s directive causing

CAR to increase; (3) pressure on the ratio of short-term capital for medium and

long-term loans was reduced slightly when SBV delayed the deadline of lowering

the ceiling rate.

- Liquidity pressure from credit growth is not expected to appear in 2020 and may

not appear until the end of 2021.

Lending rate is adjusted to decrease but at a slower pace than listed deposit

interest rate:

- Banks balance the impact of lowering deposit rates and lending rates on NIM.

- Corporate customers enjoy more preferences on lending rate reduction and debt

structure than individuals. In addition, new loans will have lower interest rates

than current outstanding loans.

NIM is expected to remain at 2020 level in 2021.

3.00

4.00

5.00

6.00

7.00

8.00

Average deposit rates (Unit: %)

D.R (1 month) D.R (3 months)

D.R (6 months) D.R (above 12 months)

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

VC

B

TC

B

MB

B

CT

G

TP

B

VIB

AC

B

BID

ST

B

HD

B

EIB

LP

B

VP

B

SG

B

KL

B

NA

B

VB

B

BV

B

SH

B

NV

B

BA

B

CASA ratio and Cost of funds

CASA 2019 CASA Q3.2020 Cost of fund Q3.2020

Source: SBV, Banks, VCBS sumary

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

7.50%

8.00%

8.50%

9.00%

9.50%

10.00%

10.50%

11.00%

Loans to customers's yield recorded on financial

statement

Banking system Banks listed on HOSE and HNX

Group of dynamic banks*

BANKING SECTOR – UPDATE

41

Note: banks can use different methods of statistic when announcing the amount

of restructured loans

NPLs and risk assets ratio increased from above 3% at the end of 2019 to 4.5% in Q3.2020 according to SBV data.

Many banks recorded recovery of restructured loans:

- Many banks recorded no increase in restructured loans in Q3.2020. In addition, yields recorded on customer loans recovered strongly in

some banks with good asset quality. The main reason comes from the fact that part of the restructured customers now has cash flows to

pay interests and even principals.

- With many customers recovering their production and business activities, the expected amount of restructured loans turning into bad

debts when Circular 01 expires is low.

*: ACB, MBB, HDB, TCB, TPB, VIB, VPB

NPL ratio

2019

NPL ratio

Q3.2020

Restructured loans

Under Cir.01/

Customer loans

Update time

ACB 0,54% 0,83% 3,20% 2020 Sep

CTG 1,16% 1,87% 0,90% 2020 Sep

EIB 1,17% 2,46% 6,00% 2020 May

HDB 1,36% 1,83% 4,50% 2020 Sep

MBB 1,16% 1,50% 3,20% 2020 Sep

TCB 1,33% 0,60% 3,07% 2020 Sep

TPB 1,29% 1,79% 7,40% 2020 Sep

VCB 0,79% 1,01% 1,34% 2020 Sep

VIB 1,96% 2,14% 0,40% 2020 June

VPB 3,42% 3,65% 10,50% 2020 Sep

Banking system 2,00% T7.2020

Banking system 3,90% 2020 Sep

Source: SBV, Banks, VCBS sumary

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

BANKING SECTOR – UPDATE

42

Free transfers have gradually become the trend among the group of

dynamic banks: Increasing transaction fees can help banks increase their

Non interest income, however the fee exemption combined with other

forms of customer experience enhancement helps banks attract regular

customers, thus reducing capital costs as CASA increases and gaining

deposits. In addition, attracting individual customers is also helpful for

increasing credit when this is the target customer group of many banks.

Decree 81/2020/ND-CP affects the bond retail-distribution activities of

some banks:

- Private placement: bond is locked for 1 year and now requires at least 6

months between 2 consecutive bond issuances. In addition, open-ended

bond investment funds are not allowed to buy bonds issued from private

placement.

- Public offering: higher requirement on issuers and the underwriter

cannot control demand.

Source: SBV, Banks, VCBS sumary

0%

50%

100%

150%

200%

0

500

1,000

1,500

2,000

2,500

2016 2017 2018 2019 9T.2020

Mil

lio

n t

ran

sact

ion

s

Number of money transfer transaction

Number of transaction yoy growth

0%

20%

40%

60%

80%

100%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

2016 2017 2018 2019 9T.2020

VN

D t

rill

ion

Money transfer transaction value

Transaction value yoy growth

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

BANKING SECTOR – 2021 FORECAST

43

8%

9%

10%

11%

12%

13%

14%

15%

16%

TCB EIB HDB VPB ACB TPB MBB VIB VCB CTG BID LPB

Capital adequacy ratio - CAR 2019

Bank groups:

- Large banks (AGR, VCB, BID, CTG): continue to be under pressure to reduce lending rates when SBV doesn’t changed their monetary

policy.

- Dynamic banks (ACB, MBB, TCB, VPB, VIB, TPB): has higher credit growth due to better sources of capital (higher equity source from

retain earning) and smaller scale. In addition, the pressure to lower deposit rate is lower than the large banks, leading to a positive growth

in total income.

Circular 01 expected to expire in 2021, when Covid-19 pandemic ends since many countries can mass produce preventive vaccines.

- With good signs of recovery in restructured loans, an increase in bad debt coming from restructured customers is expected to account for

0.5 - 1% of total loan balance and there will be a strong variation between banks depending on asset quality.

- Impact on provision expense will spread gradually in 2021 and 2022 because outstanding loan still has a 360-day deferred payment process

from the new repayment term to switch from group 1 debt to group 5 debt.

Source: SBV, Banks, VCBS sumary

9.2% 9.2% 9.8% 9.6% 9.5%

10.4% 10.6% 10.7% 10.7% 10.7%

08%

09%

10%

11%

12%

CAR ratio of the group of banks that applies

Circular 41 (Basel II)

State owned banks Joint stock commercial Banks

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

2020 BANKING STOCKS RECOMENDATION

44

9T.2020

indicators Total Asset Total Equity EBT NIM ROE NPL LLCR Asset quality Earning outlook Recommendation

Unit VND billion VND billion VND billion % % % %

ACB 418,748 32,919 6,411 3.54% 22.11% 0.83% 117% High Increasing Buy

BAB 112,042 8,194 522.087 1.95% 8.14% 0.81% 124% No rating No forecast No recommendation

BID 1,467,806 81,441 7,062 2.45% 10.68% 1.97% 87% Average Increasing Outperform

BVB 54,561 3,840 138 2.10% 4.46% 2.98% 48% No rating No forecast No recommendation

CTG 1,261,204 83,322 10,364 2.84% 13.70% 1.87% 84% Average Stable Outperform

EIB 151,274 16,597 1103.612 2.20% 5.29% 2.46% 50% Low Stable No recommendation

HDB 273,290 23,885 4,381 5.10% 19.52% 1.83% 64% Average Increasing Outperform

KLB 55,592 3,907 144.573 1.82% -0.12% 6.63% 17% No rating No forecast No recommendation

LPB 211,978 13,765 1741.441 3.18% 12.81% 1.64% 73% No rating Stable Hold

MBB 427,175 48,254 8,134 4.93% 18.44% 1.50% 119% Average Increasing Buy

NAB 119,474 6,113 388 2.46% 11.04% 2.28% 38% No rating No forecast No recommendation

NVB 74,335 4,283 29 2.14% 1.05% 1.80% 65% Low No forecast Underperform

SGB 22,700 3,672 177 3.28% 2.55% 2.14% 40% No rating Stable No recommendation

SHB 401,926 23,876 2607.122 2.64% 12.93% 2.47% 57% Low Increasing Hold

STB 485,213 28,205 2325.693 2.47% 8.65% 2.14% 74% No rating No forecast No recommendation

TCB 401,462 70,608 10,711 4.85% 17.23% 0.60% 148% Average Increasing Outperform

TPB 193,461 15,438 3,024 4.02% 25.26% 1.79% 92% Average Increasing Buy

VBB 82,270 5,303 374 0.99% 7.98% 2.03% 54% No rating No forecast No recommendation

VCB 1,188,572 93,576 15,965 2.99% 19.41% 1.01% 215% High Increasing Outperform

VIB 213,086 16,552 4,025 3.95% 27.93% 2.14% 48% High Increasing Hold

VPB 413,892 49,726 9,398 8.57% 21.81% 3.65% 48% Low Stable Hold

Source: SBV, Banks, VCBS sumary

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

ASIA COMMERCIAL BANK (ACB) – OVERVIEW

45

Main business activities:

ACB is a joint stock commercial bank with a dynamic business model and

high risk management capabilities. The bank focuses most of its business

activities in the retail customer segment, with real estate collateral for

loans mainly. ACB's asset quality is well controlled with low NPLs ratio.

Shareholder structure:

Including 30% owned by foreign funds, 7% owned by Tran Hung Huy

(Chairman of the Board of Directors) and family members, the rest are

other shareholders.

Business results:

In 9M.2020, ACB recorded EBT of VND 6,411 billion (+15.3% yoy).

Positive growth rate was achieved thanks to good growth in net interest

income as well as non-interest income.

7% 6%

4%

5%

5%

3%

7% 63%

Share holder structure

Dragon Financial Holdings Limited

Vietnam Enterprise Investments Limited

First Burns Investments Limited

Sather Gate Investments Limited

Whistler Investments Limited

Asia Reach Investments Limited

Tran Hung Huy and familiy members

Others

Subsidiary Sector Charter capital

Ownership 2019 EBT

(VND billion) (VND billion)

ACBS Securities 1500 100% Na

ACBA Asset management 340 100% 7

ACBL Finance lease 300 100% 12

ACBC Fund management 50 100% 1

7,563

11,439

14,033

16,097

12,966

1,667 2,656

6,389 7,516

6,411

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2016 2017 2018 2019 Q3.2020V

ND

bil

lio

n

TOI and EBT

TOI EBT

Source: SBV, ACB, VCBS sumary

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back 46

INVESTMENT CATALYSTS

Credit growth of 10.7% after 9M.2020: in 2019 ACB has CAR of 11.7%, belonging to the group with optimal capital adequacy ratio to keep

balance between credit growth and target profit. We expect ACB will continue to be assigned a higher credit growth target than the industry

average in the coming years.

Potential for good growth in non-interest income:

⁃ ACB owns a portfolio of government bonds of VND 61,632 billion, bond yield recorded at 5.0% in Q3.2020. The recorded yield was much

higher than the government bond interest rate in the market at 1-2%. Thus, ACB can record an abnormal profit from investment securities if the

bank sells some of these government bonds.

⁃ According to the bank's expectation, ACB could sign an exclusive Bancassurance contract in 2020. With its position as one of the banks with the

highest insurance sales in the system and the negotiation process took place very thoroughly, we expect that ACB could get a higher upfront fee

than peer average.

ASIA COMMERCIAL BANK (ACB)

0

50

100

150

200

250

300

350

400

2017 2018 2019 Q3.2020

VN

D t

rill

ion

Loans and deposit

Net loan Customer deposit & valuable paper

3.6% 3.6% 3.6% 3.8% 3.7% 3.3%

3.7%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

NIM

NIM Int earning asset yield Cost of fund

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Q1.2019 Q3.2019 Q1.2020 Q3.2020

VN

D b

illi

on

ACB's government bond outstanding

Government bond outstanding

Yield recorded

Source: SBV, ACB, VCBS sumary

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back 47

INVESTMENT CATALYSTS

Good asset quality with high quality assets:

⁃ ACB focuses on lending to high-income individual customers. The bank recorded the

lowest Credit cost / Outstanding balance ratio in the industry.

⁃ The collaterals for ACB's loans are mainly real estate with clear legal status and stable

market value in the long term. In case customers cannot pay their debts, the debt

recovery process of ACB is relatively favorable with recovery rate among the highest in

the industry.

Stable profitability helps BVPS continue to grow at an expected rate of 25% in 2020

and 26% in 2021.

High possibility of entering the VN-30 index basket in the restructuring period of

July 2021 after listing in HOSE.

ASIA COMMERCIAL BANK (ACB)

23.2%

45.5%

46.7%

49.4%

0% 20% 40% 60% 80% 100%

2017

2018

2019

9T.2020

Total income structure

Operating expense Provision expense EBT

0.7% 0.7% 0.7%

0.5% 0.7% 0.7%

0.8%

0.3%

0.5%

0.7%

0.9%

1.1%

1.3%

NPL

Net NPL ratio Overdue loan ratio

52 148 79

369

1,765

1,428

0

500

1,000

1,500

2,000

2014 2015 2016 2017 2018 2019

VN

D b

illi

on

Recovery of loans previously

written-off

Bad debt write off

Recovery of loans previously written-off

2%

52%

102%

152%

202%

0

500

1000

1500

2000

2500

3000

2016 2017 2018 2019 9T.2020

VN

D b

illi

on

Provision expense

Provision expense LLCR

Source: SBV, ACB, VCBS sumary

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back 48

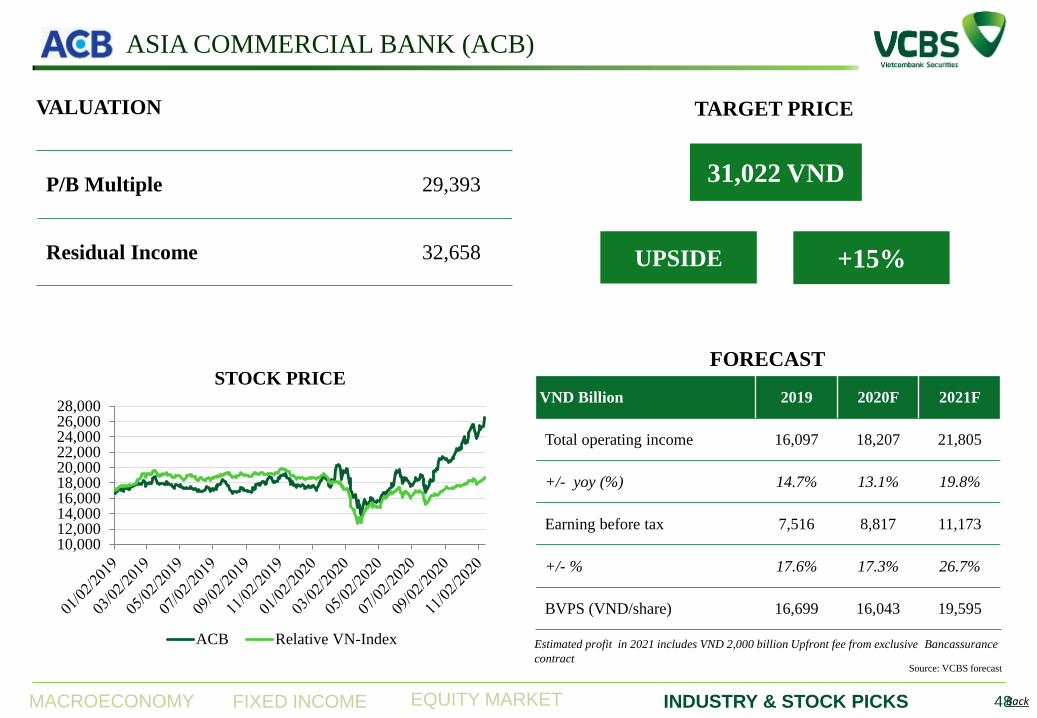

P/B Multiple 29,393

Residual Income 32,658

FORECAST

VALUATION

31,022 VND

TARGET PRICE

+15% UPSIDE

ASIA COMMERCIAL BANK (ACB)

10,00012,00014,00016,00018,00020,00022,00024,00026,00028,000

STOCK PRICE

ACB Relative VN-Index Estimated profit in 2021 includes VND 2,000 billion Upfront fee from exclusive Bancassurance

contract

VND Billion 2019 2020F 2021F

Total operating income 16,097 18,207 21,805

+/- yoy (%) 14.7% 13.1% 19.8%

Earning before tax 7,516 8,817 11,173

+/- % 17.6% 17.3% 26.7%

BVPS (VND/share) 16,699 16,043 19,595

Source: VCBS forecast

MACROECONOMY EQUITY MARKET INDUSTRY & STOCK PICKS FIXED INCOME Back

MILITARY COMMERCIAL JOINT STOCK BANK (MBB)

49

Main business activities

MBB is a joint stock commercial bank with a dynamic business

model, including many subsidiaries operating in the banking and

finance sector. MBB has special advantages thanks to standing in

the Army group.

Shareholder structure

Including 14% owned by Viettel, 9% owned by SCIC, 23% foreign

owned, the rest are other shareholders.

Business results

In 9M.2020, MBB recorded EBT of VND 8,134 billion (+ 6.8%

yoy). The Bank recorded positive growth in total income and has

made a conservative provision for outstanding loans affected by

Covid-19 since Q1.2020.

14%

9%

7%

7%

4% 3%

54%

Share holder structure

Viettel

SCIC

Vietnam Helicopter

Corporation