Management practices in Australasian ethical investment products: a Role for regulation?

17

Electronic copy available at: http://ssrn.com/abstract=1742577 Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment * Correspondence to: Matthew Haigh, Toulouse Business School, 31068 Toulouse Cedex 7, France. E-mail: [email protected] Business Strategy and the Environment Bus. Strat. Env. 19, 147–163 (2010) Published online 14 February 2008 in Wiley InterScience (www.interscience.wiley.com) DOI: 10.1002/bse.613 Management Practices in Australasian Ethical Investment Products: A Role for Regulation? Matthew Haigh 1 * and James Guthrie 2 1 Toulouse Business School, Toulouse, France 2 Discipline of Accounting, School of Business, Faculty of Economics and Business, University of Sydney, Australia ABSTRACT This paper adds to the literatures on socially responsible investment (SRI), investment management, regulation of financial services and social accounting by providing a compre- hensive survey of investment methods used in SRI products and regulated social reporting in financial services. Australian and New Zealand regulations require issuers of self- declarative SRI products to provide details on methods used in portfolio construction. Regulators’ objectives to standardize the reporting of portfolio construction and thus improve its comparability were identified by examination of parliamentary debates and other public reports. Portfolio construction styles of 86 SRI products managed by 63 finan- cial institutions in Australia and New Zealand were chosen for analysis. Statistical analysis was conducted to identify associations between styles, construction methods and assess- ment techniques over a four-year period: 2004–2007. These aspects were further examined in 18 case studies. Over the period, diversity and intensity of construction methods had increased both within and between investment managers. The non-standard nature of management consultation used in SRI products, marketing needs to distinguish rather than standardize investment methods and the types of information thought relevant to clients did not reconcile easily with the types of information required by regulation. The more recent products in the sample tended to reference market indexes in portfolio construction, separate social considerations from financial considerations and delegate qualitative assess- ments of invested companies. Consumer policy implications arise from questions bearing on the integrity of information attached to investment products and the effective monitor- ing of delegated investment processes. Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment. Received 11 October 2007; revised 14 December 2007; accepted 17 December 2007 Keywords: ethical investment; financial service regulation; social reporting; socially responsible investment; SRI; sustainable development

-

Upload

curtinsarawak -

Category

Documents

-

view

4 -

download

0

Transcript of Management practices in Australasian ethical investment products: a Role for regulation?

Electronic copy available at: http://ssrn.com/abstract=1742577

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment

* Correspondence to: Matthew Haigh, Toulouse Business School, 31068 Toulouse Cedex 7, France. E-mail: [email protected]

Business Strategy and the EnvironmentBus. Strat. Env. 19, 147–163 (2010)Published online 14 February 2008 in Wiley InterScience(www.interscience.wiley.com) DOI: 10.1002/bse.613

Management Practices in Australasian Ethical Investment Products: A Role for Regulation?

Matthew Haigh1* and James Guthrie2

1 Toulouse Business School, Toulouse, France2 Discipline of Accounting, School of Business, Faculty of Economics and Business,

University of Sydney, Australia

ABSTRACTThis paper adds to the literatures on socially responsible investment (SRI), investment management, regulation of fi nancial services and social accounting by providing a compre-hensive survey of investment methods used in SRI products and regulated social reporting in fi nancial services. Australian and New Zealand regulations require issuers of self- declarative SRI products to provide details on methods used in portfolio construction. Regulators’ objectives to standardize the reporting of portfolio construction and thus improve its comparability were identifi ed by examination of parliamentary debates and other public reports. Portfolio construction styles of 86 SRI products managed by 63 fi nan-cial institutions in Australia and New Zealand were chosen for analysis. Statistical analysis was conducted to identify associations between styles, construction methods and assess-ment techniques over a four-year period: 2004–2007. These aspects were further examined in 18 case studies. Over the period, diversity and intensity of construction methods had increased both within and between investment managers. The non-standard nature of management consultation used in SRI products, marketing needs to distinguish rather than standardize investment methods and the types of information thought relevant to clients did not reconcile easily with the types of information required by regulation. The more recent products in the sample tended to reference market indexes in portfolio construction, separate social considerations from fi nancial considerations and delegate qualitative assess-ments of invested companies. Consumer policy implications arise from questions bearing on the integrity of information attached to investment products and the effective monitor-ing of delegated investment processes. Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment.

Received 11 October 2007; revised 14 December 2007; accepted 17 December 2007

Keywords: ethical investment; fi nancial service regulation; social reporting; socially responsible investment; SRI; sustainable

development

Electronic copy available at: http://ssrn.com/abstract=1742577

148 M. Haigh and J. Guthrie

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

Introduction

AUSTRALIAN AND NEW ZEALAND REGULATIONS REQUIRE ISSUERS OF INVESTMENT PRODUCTS WITH PUBLIC

social mandates to provide information to consumers on portfolio construction processes. This paper

documents the styles and methods of socially responsible portfolio construction in these two countries.

The results are viewed in light of the objective of regulation to standardize the reporting of portfolio

construction and so improve comparability for retail investors and members of pension funds. Regulators’ objec-

tives were identifi ed by examination of parliamentary debates, Bills, explanatory memoranda attached to Acts and

submissions to Senate hearings. A survey identifi ed the diversity of investment styles and portfolio construction

methods in Australasian socially responsible investment (SRI) products in 2004 (when the regulations were

introduced) and in 2007.

A proliferation of reported methods, styles and investment biases over the four-year period of study had led to

certain diffi culties for product issuers. From a consumer perspective, there was little basis to compare portfolio

construction methods in 2004 and again in 2007. Case studies identifi ed reporters’ motivations and attitudes

toward the regulation, suggesting that diversity of construction method remains an important marketing tool.

Older investments tended to report integration of social and economic considerations in portfolio construction.

More recent products tended to use market indexes to design portfolios, separate social considerations from fi nan-

cial considerations and delegate qualitative assessments of companies, with little corollary disclosure of monitoring

of agents. A general tendency was augmentation of questionnaire-based assessments of invested companies with

direct consultation of management and with publicly available information.

The paper adds to the literature on SRI by providing a replicable survey of investment methods in a distinct

jurisdictional region and geographical market. A contribution to the literature on fi nancial service regulation is an

assessment of regulatory policy affecting an important segment of fi nancial services: managed investments and

pension schemes. A contribution is made to the literature on social and environmental reporting in the paper’s

critique of the focus of reporting regulation on reported claims rather than a focus on monitoring processes of

actual investment management.

The paper is organized into fi ve further sections, as follows. The following section provides a background to

regulation of certain types of information disclosure attaching to investment products. The next section outlines

research on SRI, fi nding hitherto unanswered calls for research on the regulation of social reporting. The fourth

section justifi es the research methods, namely, a series of case studies and an analysis of the portfolio construction

of Australasian investment products holding public social mandates. The fi fth section presents the results and a

fi nal section refl ects on their signifi cance in light of regulators’ objectives, drawing some policy implications.

Regulation of Information Attached to Managed Investment Products

Recent fi nancial service regulation in Australia, New Zealand, the United Kingdom and the Netherlands has

required managers of retail investment products to disclose how and whether they deploy ‘social considerations’

in portfolio construction. Such initiatives are in keeping with the main aim of regulation of conduct of business

of fi nancial services: ‘to establish rules and guidelines about appropriate behaviour and business practices in

dealing with customers’ (Edwards and Wolfe, 2005, p. 49). Regulatory initiatives have been accompanied by the

increasingly popular style of investment management known variously and self-declaratively as ‘ethical’, ‘socially

responsible’ and ‘sustainable’. Portfolio construction methods of socially responsible managed investment have

relatively recently moved away from the type of tailored portfolio construction popular in the 1980s and 1990s,

which took into account normatively undesirable and desirable types of investment (Ali et al., 2003). Recent prac-

tice has been noted as representing a style indistinguishable from conventional portfolio construction processes

(Bauer et al., 2004; Haigh, 2006a), a shift that has been associated with a tendency to consult management of

individual companies, capital market participants such as brokers and custodians, and regulators themselves as

the primary methods of having regard to pre-defi ned qualitative investment criteria. This latter approach has

Management Practices in Australasian Ethical Investment Products: A Role for Regulation? 149

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

replaced to an extent the previous tendency of selection and divestment of individual companies based on qualita-

tive assessments (Amalric, 2004; Statman, 2000).

Table 1 shows market share of retail socially responsible products in the US, Europe and Australia, as at 2002.

Although market share is low, the persistence and potential growth of SRI has attracted the attention of non-

governmental groups seeking avenues for their agendas, a phenomenon that has not gone unnoticed by

legislators.

Consumer protection in relation to fi nancial investments has increasingly concerned legislators since the early

1990s (Grahl, 2006). Such concerns are of particular relevance in Australia. Employers of Australian waged

workers make statutory minimum payments to pension funds on behalf of their employees. The ability of employ-

ees to choose their own pension fund was enacted into Australian law in June 2004. Accordingly, legislators have

paid increasing attention to information that fi nancial institutions attach to investment products marketed at retail

consumers (see Richardson, 2002). Australia’s program of regulatory reform of its fi nancial services culminated

in the Australian Financial Services Reform Act (Cth) 2001. Effective from March 2004 (with reporting guidelines

issued December 2003), the Act modifi es the Corporations Act (Cth) 2001 (referred to hereafter as the Corpora-

tions Act), which governs Australian fi nancial services. Inter alia, the Corporations Act has been modifi ed to require

managers to describe the bases of investment policies in a product disclosure statement. A PDS is required to be

attached to any product ‘with an investment component’ offered to retail clients (Financial Services Reform Bill

2001) and should consist of information that a ‘person would reasonably require for the purpose of making

a decision, as a retail client, whether to acquire the fi nancial product’ (ASIC, 2001). The regulations pertain to

products offered by managed investment funds (mutual funds), pension funds, and investment life and general

insurers.

The background to Australia’s regulatory reform program is found in Australian Commonwealth Senate Hear-

ings, submissions to Joint Committees and speeches in the federal House of Representatives. In June 1996, the

Australian Federal Treasurer commissioned an inquiry into the Australian fi nancial system. Inter alia, the inquiry

was charged with recommending a regulatory structure for the Australian fi nancial services sector. The inquiry

produced the Wallis report, which eventually led to the Corporate Law Economic Reform Program, resulting in

major amendments to the Corporations Act, including those inserted by the Financial Services Reform Act. On

22 August 2001, Senator Murray of the Australian Democrats spoke to the Australian Senate on the Financial

Services Reform Bill 2001, describing the stimulus to the legislation:

The Wallis report recommended the introduction of a single licensing regime for all fi nancial sales, advice

and dealing, and the creation of a consistent and comparable product disclosure framework . . . The general

aim of the Bill is to provide . . . uniform disclosure obligations for all fi nancial products provided to retail

clients (Hansard, 2001a, p. 26 315).

In the same speech, Senator Murray drew the parliament’s attention to a supplementary report to the Bill. The

report had questioned the integrity of some of the claims attached to SRI products:

[T]he Democrats are alert to . . . exaggerated claims . . . made about fi nancial products, and that is why we think

some legislative attention is necessary (Hansard, 2001a, pp. 26 316–26 317).

Europe US AustraliaDec 2001 Sep 2002 Sep 2002

Billion EUR USD AUDSRI FUM 14.4 15.7 2.1Total FUM 3600.0 6059.0 721.3Percentage FUM 0.4 0.2 0.3

Table 1. Comparative market share of public social investment mandatesSource: Haigh and Hazelton (2004). SRI: socially responsible investment. FUM: funds under management.

150 M. Haigh and J. Guthrie

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

Concerns of legislators toward the integrity of information supplied to retail investors can also be found in the

Australian House of Representatives Standing Committee on Environment and Heritage meeting held in Decem-

ber 2002 on the matter of labour employment in the environment sector. Inter alia, committee members discussed

the lack of established standards of information reporting systems employed in the fi nancial sector, particularly

by issuers of products branded as ‘socially responsible’ and ‘ethical’ (Hansard, 2002).

In a Joint Statutory Committee on Corporations and Securities meeting to discuss the Financial Services Reform

Bill 2001, held 14 June 2001, submissions were heard from representatives of Australia’s Ethical Investment

Association and two social managed funds, Glebe Asset Management Ltd and Westpac Investment Management

Ltd (subsequently merged into the BT Group). The Joint Committee disclosed that proposed amendments to the

Bill that would require disclosures of ‘social considerations’ deployed in portfolios were due to the action of the

Australian Conservation Foundation (ACF) (Hansard, 2001b). Namely, the ACF had lobbied the Australian govern-

ment using the document of Kerr and Zubevich (2002) on several occasions over 2000–01. This document

asked the government to require fi nancial institutions to report on whether they employed environmental

considerations.

The ACF was again represented at the fi rst public hearing into the provisions of the Financial Services Reform

Bill 2001, constituted in the Joint Statutory Committee on Corporations and Securities (Hansard, 2001c). In the

last item heard on that day (27 April 2001), Mr Michael Kerr, one of the co-authors of Kerr and Zubevich (2002),

submitted a proposal for an amendment to the Financial Services Reform Act. The wording of the proposal was

extracted from the amendment and Regulation to the British Pensions Act 1995 (mentioned above). Other than

the addition of ‘labour standards’ (the result of a late amendment submitted by Senator Stephen Conroy of the

Australian Labor Party), the Parliament adopted Mr Kerr’s proposed amendment verbatim. Sections 1013D and

1013DA of the Corporations Act retain the proposal that the disclosures apply to investment life insurance products,

managed investment products and pension products. A proposal to include the required information in product

disclosure statements, rather than in a separate statement of investment principles, was also accepted.

Plausible reasons for the virtually unaltered adoption of the amendment are an appeal made by Mr Kerr relating

to the expected growth of social investment (an expectation not realized to date: see Table 1), member choice of

pension funds for Australian waged workers1 and perhaps the political sensitivity of various organizations cited as

supporting the ACF proposal, including that of the ACF itself. (Organizations named as supporting the proposal

included state governmental Environment Protection Authorities, The Australian Democrats (former political

party) and the Australian banking corporation Westpac Bank Ltd (Hansard, 2001c).) Section 1013DA charges the

regulator, the Australian Securities and Investment Commission, with issuance and monitoring of compliance to

reporting ‘guidelines’ (mandatory) pertaining to Section 1013D. Issued in December 2003, the guidelines (ASIC,

2003) require reporters to follow the following sequence:

(1) a general description regarding the extent to which labour standards, environmental, social and ethical con-

siderations are taken into account, and a statement if not. If (1) is positive,

(2) identifi cation of such considerations;

(3) extent of variance of application between asset classes;

(4) identifi cation of the entity responsible for selecting and implementing such considerations and the degree to

which reliance is placed on information provided by others;

(5) application methods and a statement if there are no predefi ned methods. If (5) is positive,

(6) weighting system used;

(7) retention and realization policies;

(8) methods used to monitor adherence to the methodology, and a statement if otherwise.

A similar requirement in New Zealand (Section 60, NZ Superannuation and Retirement Income Act 2001)

requires guardians of pension funds and issuers of investment products to develop and comply with a Statement

of Investment Policies, Standards and Procedures that sets out investment policy and investment performance

measures.

1 Member choice of pension fund for Australian employees is contained in the Choice of Superannuation Funds (Consumer Protection) Bill, tabled in the Australian Parliament in 1998 and ratifi ed by the Senate in July 2004.

Management Practices in Australasian Ethical Investment Products: A Role for Regulation? 151

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

Prior Literature

Socially responsible managed investment has attracted performance analyses, event studies, behavioural analyses

and some sociological attention. More than 30 studies provide functional descriptions of portfolio construction in

support of a research objective that would ascertain whether deployment of extra-fi nancial considerations might

produce economic returns signifi cantly different to those earned by conventional managed investment portfolios

(see Ali and Gold, 2002a, 2002b; Banz, 1981; Bauer et al., 2004, 2005, 2007; Cummings, 2000; DiBartolomeo

and Kurtz, 1999; Diltz, 1995; Gold and Ali, 2002; Hamilton et al., 1993; King and Lenox, 2001; Kreander, 2001;

Kreander et al., 2002; Statman, 2000). Others have sought to identify whether events such as the economic

embargo imposed on South Africa in the 1970s produced above-average economic performance in portfolios that

had excluded affected companies (see Freedman and Jaggi, 1988; Freedman and Stagliano, 1991; Grossman and

Sharpe, 1986; Paul and Aquila, 1988; Shane and Spicer, 1983). To this end, decision-usefulness studies have sought

to identify extra-fi nancial factors used in investment selection and investment divestment policy (see Buzby, 1974;

Buzby and Falk, 1979; Epstein and Freedman, 1994; Hutton et al., 1998; Noci, 1995; Rockness and Williams,

1988; Ryall and Riley, 1996; Stone, unpublished Ph.D. dissertation; Spiller, 1999, 2000). For example, Perks et al. (1992) examined the investment policies and practices of a sample of UK-based ‘ethical’ unit trusts, seeking to

establish the extent to which corporate annual reports provided useful information.

Another group of studies has concentrated on cognitive aspects of decision making and behavioural motivations

of retail investors faced with ‘qualitative information’ such as selected environmental and social issues connected

with the operations of investments (see Anand and Cowton, 1993; Beal and Goyen, 1998a, 1998b; Belkaoui, 1980;

Haigh, 2007; Irvine, 1987; Lewis, 2001; Lewis and Cullis, 1990; Lewis and Mackenzie, 2000; Lewis et al., 1998;

Mackenzie, unpublished Ph.D. thesis; Mackenzie and Lewis, 1999; Milne and Chan, 1999; Rikhardsson and

Holm, 2006; Rivoli, 1995; Webley et al., 2001; Winnett and Lewis, 2000). Generally, this body of work, much of

it consisting of experimental studies of actual and hypothetical investors, would lend support to the behavioural

strand in institutional fi nance, challenging the mean-variance theorem of neoclassical economics (also see Statman,

1999; Thaler, 1980, 1999, 2000). Related to the ‘performance studies’ and the ‘behavioural studies’ groups is

another focus, which has sought to identify demographic features of individuals attracted to this style of investment

(see Friedman and Miles, 2001; Tippet, 2002; Tippet and Leung, 2001; Woodward, 2000).

Comprehensive surveys of portfolio construction and reporting practices associated with SRI have been few.

Despite evidence of associations between consumers’ investment intentions and social reports attached to invest-

ment products (Haigh, 2007; Lewis, 2001), and calls for work examining the integrity of information attached to

SRI products (Michelson et al., 2004; Ryall and Riley, 1996; Schoenenberger, 1994; Schrader, 2006), studies

examining concrete links between claims and practice are restricted to those by Berger (2004) and Mathieu

(2000).

The social and environmental accounting literature has tended to direct attention to social reporting practices

of fi rms (see Guthrie and Parker, 1990; Adams, 2002; O’Dwyer, 2002) rather than those of institutional investors.

The absence of research on SRI in this fi eld is not necessarily suggestive of insuffi cient interest. Until now, the

social accounting literature has tended to focus on motivations of reporters issuing information on a voluntary

basis (Owen et al., 2001) rather than on regulation of extra-fi nancial reporting by companies and fi nancial institu-

tions. An ideological critique of regulated reporting of environmental information is found in the work of Gibson

(1996). Legal comment on SRI can be found in the work of Moodie and Ramsay (2003), Richardson (2002) and

Whincop (2003). With respect to the attention of trustees and investment managers paid to extra-fi nancial consid-

erations in portfolio construction, discussion has tended to favour a wide interpretation of fi duciary responsibility

of trustees and investment managers.

Work from critical theorists has suggested that the SRI style possibly serves as a manifestation of institutional

legitimacy (Owen, 1990, contra Bruyn, 1987; Schwartz, 2003) and the political economy (Cullis et al., 1992; Frank-

furter et al., 1997; Grahl, 2006; Haigh and Hazelton, 2004; Haigh, 2006b; Harte et al., 1991; Lewis et al., 1998;

Mackenzie, unpublished Ph.D. thesis; O’Rourke, 2003; Paul and Aquila, 1988). Others have commented on

political advantages of social reporting for institutional investors (Haigh, 2006c; Harte et al., 1991; Owen, 1990;

Owen et al., 2001). Gray and Jenkins (1993) argue that accountabilities of public reporters can switch between

152 M. Haigh and J. Guthrie

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

various modes, including managerial, professional, probity, political, public and personal. Two of those categoriza-

tions bear relevance in examination of the attitudes of SRI reporters. Managerial accountability requires an agent

to account for its decision-making outcomes and the means and procedural rules used to arrive at those outcomes.

The Australian reporting regulations were intended to address managerial accountability of investment managers.

Probity accountability is discharged when an SRI manager (product issuer, to use the parlance of the regulations)

complies with regulatory requirements.

Research Method

Portfolio construction styles of 86 SRI products managed by 63 fi nancial institutions in Australia and New Zealand

were identifi ed in May 2007 and examined for relevant associations. Construction styles of 69 products of the

sample in 2007 were identifi ed in March 2004, which allowed comparison.

Identifi cation of construction methods was informed by the Australian study of Bauer et al. (2004) and the

classifi catory disclosure headings used in the Australian regulatory guidelines. A popular technique used to assess

companies is known as engagement; this involves consultation of management of invested companies and/or use

of voting rights on matters relating to environmental, social and corporate governance risks. Two further construc-

tion methodologies in wide use are security screening and indexing. The former takes two forms: ‘negative’ exclu-

sionary security screens used to guide the exclusion of potential investments and the divestment of current

investments by reference to predefi ned qualitative criteria; ‘positive’ inclusionary security screens used to identify

potential investments and the maintenance of current investments. Indexing approaches tend towards two forms:

in one, investment selection and portfolio weighting is guided by conformance of portfolio weightings to stock

market sectors in combination with qualitative ranking of companies in each sector. This style has been referred

to as ‘best of sector’. A variant is informed by conventional stock market indexes that have been tailored for envi-

ronmental and social considerations. An example is the Dow Jones Sustainable Group Indexes, which are tailored

from the Dow Jones Indexes.

A series of case studies was conducted to gain an understanding of the various methodologies employed, how

methodologies were developed and to what extent methodologies were taken into consideration during investment

decisions, and in the process identifying perceptions of managers towards regulation of information disclosures.

The case studies used 19 semi-structured interviews conducted in November and December of 2004 with senior

investment managers, social investment consultants, representatives of research houses, industry associations and

regulatory bodies. The choice of interviewees was informed by their organizations’ prominence in SRI. Organiza-

tions represented 95 per cent of the Australian retail market for public SRI products at the time of interview. With

the exception of properties and investment companies, all managers had allocated over 75 per cent of their funds

under management to equities, with the remainder allocated to cash and fi xed interest securities, no part of which

had been screened for social considerations. (Private investment mandates were not sampled as the reporting

regulations are directed to public mandates attached to retail products.) On most occasions, arrangements were

made to speak to the fi rst point of written contact, which included heads of investor relations departments,

company secretaries, business development managers and chief investment offi cers. All interviewees were involved

directly in the production of the product disclosure statement (PDS), the document containing relevant disclosures

for the purposes of the regulations. While most interviews were conducted in the head offi ces of employer orga-

nizations, in three cases an agreement was made to conduct interviews at an investment industry fair2. The sources

of information on construction methods discussed in the interviews were the PDS, the management discussion

and analysis section contained in members’ reports, ‘stand-alone’ sustainability/social reports issued on an occa-

sional or regular basis and reports posted to corporate Internet websites. Interviewees confi rmed that these report-

ing points capture all written reports on social, environmental and governance issues considered in portfolio

construction.

2 Interview questions were sent to interviewees prior to interview. Access to organizations was granted on the express understanding that the results would be published anonymously. Interested readers can access interview notes and recordings on request.

Management Practices in Australasian Ethical Investment Products: A Role for Regulation? 153

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

Interviewees were asked to describe historical (pre-2004) and current (2004) methods used to deploy non-

fi nancial considerations in portfolio construction. Data obtained in 2004 were combined with data obtained in

2007, allowing a longitudinal analysis of methodologies. The analysis represents a qualitative variant of the

approach followed by Bauer et al. (2004).

Results

This section uses two sub-sections to show the investment methods and regulatory policy outcomes. The fi rst

presents an analysis of investment styles, methods and investment assessment measures used in Australasian

investment products in 2004 and in 2007. Descriptive results are presented fi rst, followed by tests of association.

The sub-section that follows enriches the statistical results by providing interview quotations emerging from dis-

cussions on (a) the requirements to disclose portfolio construction methods and (b) construction methods used

in SRI products.

Portfolio Construction Styles Used in Socially Responsible Investments

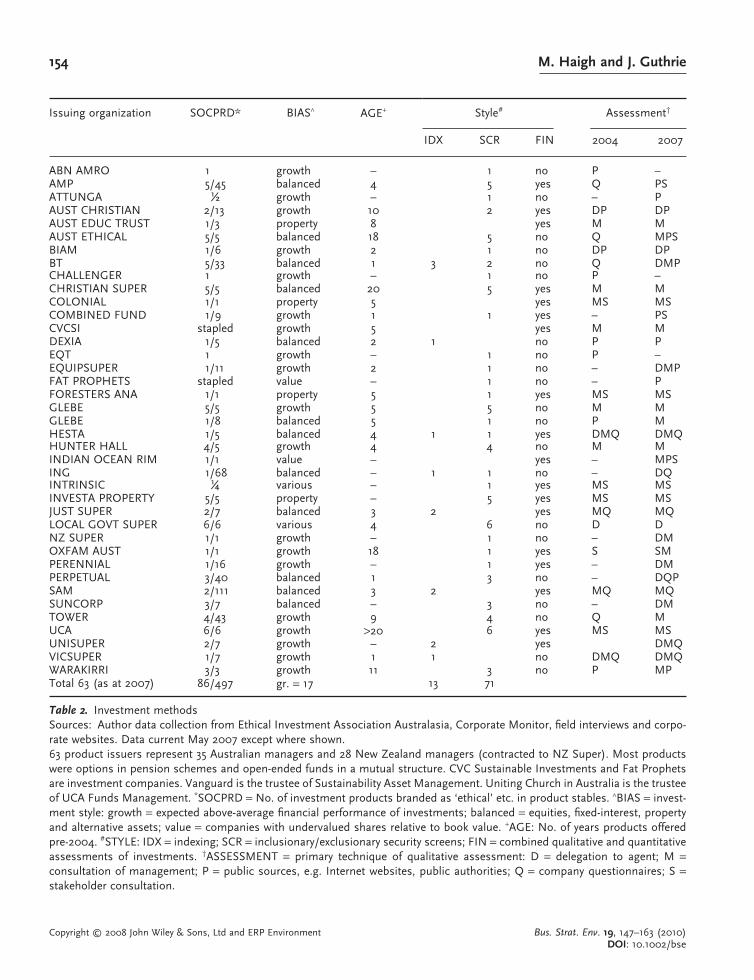

In May 2006, a sample of 86 self-declarative SRI products, representing 63 investment managers, was constructed.

This sample was matched to a sample constructed in March 2004, the process yielding 69 products where man-

agement styles in both years could be compared. The sample of managers from 2007 represented all Australian

managers (35) offering public social mandates attached to retail investment products, and one New Zealand public

sector pension fund. The NZ fund had contracted its portfolio management to 28 investment managers. Table 2

profi les the products in the sample.

The ‘SOCPRD’ column in Table 2 gives socially responsible products offered relative to total numbers of invest-

ment products (wholesale and retail) in investment houses. Investment styles followed are shown in the ‘BIAS’

column. Where a number of products were offered by a single manager the approach shown is that which is

common to all, and is otherwise shown as ‘Various’. Categories of construction style are those used by Bauer et al. (2004, 2005, 2007) and follow industry practice. The ‘AGE’ column indicates the period of time (years) man-

agers had offered socially responsible products prior to the advent of the reporting regulation, March 2004. ‘AGE’

data are given for comparison purposes and to identify relations with investment styles. Investment styles are

shown either as an indexing approach, under which portfolio composition is modelled on main stock market

indexes, or a security screening approach, under which portfolio construction is guided by approaches that select/

refrain from investments conforming/not conforming to pre-defi ned extra-fi nancial criteria. The FIN column

indicates whether managers had reported attempts to combine qualitative and quantitative assessment criteria (as

required by the Australian reporting guidelines). The two extreme right columns in Table 2 give the most com-

monly used techniques to make qualitative assessments of investments and potential investments.

The descriptive results are presented fi rst. Sixty-four products (55.0 per cent) of the sample represent the single

SRI product offered by the fi nancial institution at the time of study. Seventeen (20.0 per cent) SRI products were

offered alongside four or more SRI products from a single manager. The most common investment bias in the

SRI product sample is growth (47.5 per cent). The most popular construction style is screening (72 products or

84.0 per cent). Of 86 SRI products, 70 products (81.4 per cent) were constructed using only security screens, 10

(11.6 per cent) by reference to indexes, two used both and four used neither. Indexing (13 products) was adopted

mainly by managers holding relatively large and diverse product stables. Indexing is associated with newer SRI

products. One in two managers (18) showed attempts to combine qualitative and quantitative assessments of

investments.

Turning to assessment techniques, fi ve techniques were used to assess qualitative aspects of investments: ques-

tionnaires, stakeholder consultation, management consultation, publicly available information and delegation of

assessments to agents. Adoption of four of these techniques increased signifi cantly between 2004 and 2007. Most

of the increases are accounted for by new product launches. Use of management consultation increased from 51.0

per cent in 2004 to 83.0 per cent in 2007 (71 products). Use of public sources of information increased from 12.0

to 35.0 per cent (30 products), as stakeholder consultation increased from 21.7 to 31.0 per cent (27 products) in

154 M. Haigh and J. Guthrie

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

Issuing organization SOCPRD* BIAS^ AGE+ Style# Assessment†

IDX SCR FIN 2004 2007

ABN AMRO 1 growth – 1 no P –AMP 5/45 balanced 4 5 yes Q PSATTUNGA ½ growth – 1 no – PAUST CHRISTIAN 2/13 growth 10 2 yes DP DPAUST EDUC TRUST 1/3 property 8 yes M MAUST ETHICAL 5/5 balanced 18 5 no Q MPSBIAM 1/6 growth 2 1 no DP DPBT 5/33 balanced 1 3 2 no Q DMPCHALLENGER 1 growth – 1 no P –CHRISTIAN SUPER 5/5 balanced 20 5 yes M MCOLONIAL 1/1 property 5 yes MS MSCOMBINED FUND 1/9 growth 1 1 yes – PSCVCSI stapled growth 5 yes M MDEXIA 1/5 balanced 2 1 no P PEQT 1 growth – 1 no P –EQUIPSUPER 1/11 growth 2 1 no – DMPFAT PROPHETS stapled value – 1 no – PFORESTERS ANA 1/1 property 5 1 yes MS MSGLEBE 5/5 growth 5 5 no M MGLEBE 1/8 balanced 5 1 no P MHESTA 1/5 balanced 4 1 1 yes DMQ DMQHUNTER HALL 4/5 growth 4 4 no M MINDIAN OCEAN RIM 1/1 value – yes – MPSING 1/68 balanced – 1 1 no – DQINTRINSIC ¼ various – 1 yes MS MSINVESTA PROPERTY 5/5 property – 5 yes MS MSJUST SUPER 2/7 balanced 3 2 yes MQ MQLOCAL GOVT SUPER 6/6 various 4 6 no D DNZ SUPER 1/1 growth – 1 no – DMOXFAM AUST 1/1 growth 18 1 yes S SMPERENNIAL 1/16 growth – 1 yes – DMPERPETUAL 3/40 balanced 1 3 no – DQPSAM 2/111 balanced 3 2 yes MQ MQSUNCORP 3/7 balanced – 3 no – DMTOWER 4/43 growth 9 4 no Q MUCA 6/6 growth >20 6 yes MS MSUNISUPER 2/7 growth – 2 yes DMQVICSUPER 1/7 growth 1 1 no DMQ DMQWARAKIRRI 3/3 growth 11 3 no P MPTotal 63 (as at 2007) 86/497 gr. = 17 13 71

Table 2. Investment methodsSources: Author data collection from Ethical Investment Association Australasia, Corporate Monitor, fi eld interviews and corpo-rate websites. Data current May 2007 except where shown.63 product issuers represent 35 Australian managers and 28 New Zealand managers (contracted to NZ Super). Most products were options in pension schemes and open-ended funds in a mutual structure. CVC Sustainable Investments and Fat Prophets are investment companies. Vanguard is the trustee of Sustainability Asset Management. Uniting Church in Australia is the trustee of UCA Funds Management. *SOCPRD = No. of investment products branded as ‘ethical’ etc. in product stables. ^BIAS = invest-ment style: growth = expected above-average fi nancial performance of investments; balanced = equities, fi xed-interest, property and alternative assets; value = companies with undervalued shares relative to book value. +AGE: No. of years products offered pre-2004. #STYLE: IDX = indexing; SCR = inclusionary/exclusionary security screens; FIN = combined qualitative and quantitative assessments of investments. †ASSESSMENT = primary technique of qualitative assessment: D = delegation to agent; M = consultation of management; P = public sources, e.g. Internet websites, public authorities; Q = company questionnaires; S = stakeholder consultation.

Management Practices in Australasian Ethical Investment Products: A Role for Regulation? 155

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

the same period. Use of questionnaires to assess companies decreased, however, from 42.0 per cent in 2004 to

17.0 per cent (15 products) in 2007. This movement is accounted for by three managers ceasing use of question-

naires and another four managers taking up the method. Delegation of qualitative assessment of investments

increased from 12.0 per cent in 2004 to 30.2 per cent (26 products) in 2007; all of this increase is accounted for

by new product launches. The frequency of use of combinations of assessment methods (instead of merely one

method used) increased from 2004 to 2007: from 31.8 to 67.4 per cent. Table 3 gives combinations of assessment

methods used in both years.

Table 3 shows that 11 combinations of corporate assessment methods were used in 2007, compared with four

combinations in 2004. The most popular combination in both years is management and stakeholder consultation

(12.5 per cent in both). The largest change is increased use of publicly available information, such as reports made

available on corporate and government websites. Twenty-six of 33 (78.7 per cent) new assessment combinations

in 2007 used publicly available information to assess qualitative aspects of portfolio investments.

To examine the relevance of the regulators’ assumption that investment methods used in SRI products can be

meaningfully compared, relations were identifi ed between investment approaches, portfolio construction methods

used and techniques used to assess qualitative characteristics of investments. The examination used a series of

non-parametric tests for the purpose3. Table 4 gives the results of tests of association. If the results do not reject

the null, the results might be taken as suggestive evidence that various process and styles of construction of SRI

products provide little bases of comparison. Three tests are used:

• combination of fi nancial and qualitative factors in portfolio construction and age of products;

• combination of fi nancial and qualitative factors used in portfolio construction and portfolio construction methods

(indexing and screening);

• portfolio construction methods and qualitative assessment techniques (questionnaires, stakeholder consultation,

management consultation, publicly available information, delegation of assessments to agents). This test was

conducted with 2004 data and again with 2007 data.

Combinations 2004 2007

DMQ 2 3DP 2 2MQ 2 2MS 5 5DM 3DMP 2DQ 1DQP 1MP 1MPS 2PS 2SM 1Total 11 25Mode* M = 5 (45.4%) M = 18 (72.0%)

Table 3. Combinations of investment screening styles* Mode is treated as an appropriate measure of central tendency for nominal variables.

3 Parametric testing such as matched pairs signed ranks could not be used because the data in the various categories were not continuous and did not exhibit the qualities that would be required for stronger parametric analysis (see Dowdy et al., 2004; Hair et al., 1998; Tabachnik and Fidell, 2001). Although the data set was of insuffi cient size (100 observations are considered as suffi cient by Gibbons and Chakraborti (1992, p. 121)), the chi-square was chosen as a measure of association technique as other suitable non-parametric tests of inference (e.g., eta statistic) require variables containing ordinal data.

156 M. Haigh and J. Guthrie

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

Age of product and fi nancial integration

FI_No FI_Yes

Chi-square 38.7 26.563Df 28 24Sig. 0.085 0.325Cramer’s V 0.734 0.722

Indexing and fi nancial integration

FI_No FI_Yes

Chi-square 4.000 4.000Df 1 1Sig. 0.046 0.046Cramer’s V 1.000 1.000

Screening and fi nancial integration

FI_No FI_Yes

Chi-square 76.000 33.000Df 20 9Sig. 0.000 0.000Cramer’s V 1.000 1.000

Indexing and assessment technique: 2004

Qstnre Public Engage Stkhldr Delegate

Chi-square 10.000 NA 4.000 – NADf 4 – 1 – –Sig. 0.040 – 0.046 – –Cramer’s V 1.000 NA 1.000 – NA

Indexing and assessment technique: 2007

Qstnre Public Engage Stkhldr Delegate

Chi-square 6.000 2.000 12.000 – 10.000Df 1 1 4 – 4Sig. 0.014 0.157 0.017 – 0.000Cramer’s V 1.000 1.000 1.000 – 1.000

Screening and assessment technique: 2004

Qstnre Public Engage Stkhldr Delegate

Chi-square 10.000 14.000 4.000 10.000 8.000Df 6 4 1 4 4Sig. 0.125 0.007 0.046 0.040 0.092Cramer’s V 1.000 1.000 1.000 1.000 1.000

Screening and assessment technique: 2007

Qstnre Public Engage Stkhldr Delegate

Chi-square 3.000 25.667 60.000 16.000 33.000Df 1 9 20 4 12Sig. 0.083 0.002 0.000 0.003 0.001Cramer’s V 1.000 0.882 1.000 1.000 1.000

Table 4. Results of tests of association

Management Practices in Australasian Ethical Investment Products: A Role for Regulation? 157

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

Financial Integration and Age of ProductsTable 4 gives a signifi cant association between managers who do not combine fi nancial and qualitative assessments

of investments, and age of products, giving X2 = 38.7, positive Cramer’s V = 0.734, signifi cant at the 0.085 level.

This result implies weakly that ‘social considerations’ attaching to older products (namely, those offered prior to

2004) tend not to reference fi nancial considerations.

Financial Integration and Portfolio Construction MethodsAssociation with indexing is not signifi cant, while association with screening is highly signifi cant. The presence

of fi nancial integration and screening is strongly and positively associated, X2 = 33.0, Cramer’s V at unity, signifi -

cant at the 0.000 level. Abstention from fi nancial integration, and screening, is strongly and positively associated,

X2 = 76.0, Cramer’s V at unity, signifi cant at the 0.000 level. These contrary results point to diversity of method

in screening approaches.

Portfolio Construction Methods and Qualitative Assessment Techniques in 2004 and 2007Indexing. Association of indexing and qualitative assessments in 2004 is not signifi cant. In 2007, indexing was

associated signifi cantly with two of fi ve assessment techniques. Management consultation (‘Engage’, Table 4) is

weakly and positively associated, X2 = 12.0, Cramer’s V at unity, signifi cant at the 0.17 level. Indexing and delega-

tion gives X2 = 10.0, Cramer’s V at unity, signifi cant at the 0.04 level. These results suggest a modest change in

the types of qualitative assessment in indexing managers. In 2004, indexing is not associated with qualitative

assessments of investments. In 2007, indexing managers had made greater use of management consultation.

Screening. Association of screening and qualitative assessments in both years is signifi cant, as expected. In 2004,

association of screening with public information gives X2 = 14.0, Cramer’s V at unity, signifi cant at the 0.007 level.

Association of the former variable with stakeholder consultation gives X2 = 10.0, Cramer’s V at unity, signifi cant

at the 0.04 level.

Style shifts occurring between 2004 and 2007 are stronger associations with public information and stakeholder

consultation, a signifi cant association with management consultation and a signifi cant association with delegation.

Screening and public information in 2007 gives X2 = 25.6, Cramer’s V at 0.882, signifi cant at the 0.002 level.

Association with stakeholder consultation gives X2 = 16.0, Cramer’s V at unity, signifi cant at the 0.003 level.

Screening and management consultation is strongly associated in 2007, X2 = 60.0, Cramer’s V at unity, signifi cant

at the 0.000 level.

Screening and delegation is also strong, giving X2 = 33.0, Cramer’s V at unity, signifi cant at the 0.001 level.

These results suggest an increased reliance, over the relevant period, on multiple methods of qualitative assess-

ment techniques, including increased use of management consultation. Screening managers tended not to delegate

qualitative assessment of investment in 2004, while this had become more common in 2007.

Other tests show signifi cant associations between screening and indexing construction methods, X2 = 30.4,

signifi cant at the 0.000 level. (The latter combination is known at the ‘ethical overlay’ method. It entails re-weight-

ing of portfolios rather than divestment of stocks.) Screening and management consultation, signifi cant at X2 =

30.4, α = 0.000 level, indicates that the presence of screening is associated with the tendency to actively assess

companies using data gained from personal consultation. In contrast, association between indexing and manage-

ment consultation was insignifi cant at X2 = 1.75, α = 0.4. The latter result lends support to the conclusions drawn

from the tests presented above, viz., indexing approaches are not associated with management consultation. (Sig-

nifi cant exceptions to the screening/no engagement combination can be found. For example, Sustainability Asset

Management (‘SAM’, Table 2) uses an indexing style derived from the Dow Jones Group of Indexes in combina-

tion with extensive direct consultation.)

Generally, the statistical analysis suggests wide diversity and intensity of investment style, methods and qualita-

tive assessment techniques. Over the 2004–07 period, management consultation and the use of publicly available

information as assessment techniques increased in popularity. The latter information source might be associated

with recent proliferation of stand-alone corporate social responsibility information made widely available in elec-

tronic format, in Australia and elsewhere (Adams and Frost, 2004; Guthrie et al., 2007; Serrano-Cinca et al., 2007).

Wider use of information sources was made by all types of investment manager.

158 M. Haigh and J. Guthrie

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

Investment approaches (growth, value, index etc.), portfolio construction styles and assessment methods

are unrelated in 2004 and in 2007. More recent products exhibited a tendency to reference market indexes

in portfolio construction, to separate social considerations from fi nancial considerations and to delegate qualitative

assessments of companies. The fi ndings would support the econometric studies of Bauer et al. (2004, 2007),

which suggest that SRI in Australia, Canada and Europe has moved from an earlier distinct management

style (1986–late 1990s) to one more homogeneous with those of conventional managed investments. It is

plausible to posit that such an observed diversity of styles, methods and assessments might create diffi culties

for product issuers. Examination of this possibility is the focus of the next section, which presents the case

studies.

Perceptions of Reporters Toward Regulated Reporting

Views and attitudes of capital market players should provide important insights into what investment funds

are trying to achieve in their investment methods, compared with objectives of their reporting. No attempt was

made to disentangle social and environmental reporting from social and environmental practice. The case studies

sought to inform two sets of questions: the processes by which investment managers selected and applied social

considerations in portfolio construction, and practitioners’ receptions of reporting legislation. The latter set is

presented fi rst.

Reception of Regulatory Requirements to Report Management MethodsThe interview extracts given in this section suggest that regulatory requirements pertaining to SRI products in

Australia and New Zealand have generally been received negatively by investment managers. The interview extracts

were drawn from both dedicated SRI managers who only offer socially tailored products, and general managers

who offer SRI products as part of wide product stables. Many interviewees objected to the level of required detail,

arguing that retail investors would consider such disclosures irrelevant. The principal of a consultancy providing

qualitative assessments of companies clarifi ed:

The reporting guidelines are asking providers of investment products to disclose how they’re differentiating

their process. However, socially responsible investment funds are extensively marketed more over their dif-

ferentiation of outcome than their process.

A principal of another consultancy used by several Australian investment managers explained that the reporting

management processes was unimportant to managers because it was considered unimportant to investors.

At the end of the day, you’re looking for differentiation of outcome, not so much the process. If a manager

uses a negative screen you’re not really concerned about what they’re doing, it’s the outcome, and people are

refl ecting behaviour in an outcome.

This attitude was supported by other interviewees (investment managers), with comments given such as the fol-

lowing: ‘Ultimately, the test is the returns earned’ and ‘Methodologies are just that, methodologies, it’s the outcome

that counts’.

Generally, outcomes and processes of direct consultation were considered unsuitable for the PDS. The following

comments explain preferences of some managers for direct consultation over questionnaire-based evaluation of

operations: ‘It’s sort of moving on in our understanding of companies’ and ‘Building the relationship means that

you can try to infl uence change before it gets to the annual general meeting, and having to stand up and em barrass

them in front of their other investors’.

That the use of various assessment methods typically changed between reporting periods was also considered

by some to bring diffi culties to periodic disclosure. The following two extracts illustrate: ‘If you have something

that’s in the PDS and it becomes out of date, then you have to redo it, and so that’s a problem’; ‘Anything that is

grey will go to the board for approval. We face a dilemma with fi nding how to describe that in the PDS’.

Management Practices in Australasian Ethical Investment Products: A Role for Regulation? 159

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

One interviewee was reluctant to report on the value of engagement and other assessment techniques for SRI

products for fear of carrying the implication that the investment house’s conventionally constructed investment

products were in some way defi cient.

If we’re out there saying ‘Invest in our socially responsible fund, it will perform better because in the longer-

term the companies are more sustainable and face less litigation against them’, then the question that people

will use against us is ‘Well, why isn’t your whole process and your mainstream funds run that way too?’.

All interviewees considered that disclosure of portfolio stocks was important. The following interview extract

illustrates.

I mean you talk about it [reports of SRI methods] all you want, but ultimately the test for an investor is answered

by the questions ‘Who does this fund invest in?’ and ‘Are they investing in companies that I think they should

or shouldn’t be?’.

Insights into Management Methods Used in SRI ProductsThis section illuminates the results of the analysis of portfolio construction styles presented above. The previous

section indicated a proliferation of styles, assessment techniques and investment biases. The following interview

extract illustrates the variety of techniques used by one manager.

We will look at stakeholder reactions to company activities and practices, media reports around those issues,

look across a range of public databases, track information on legal compliance on matters such as environ-

mental regulations and legislation, equal opportunity and anti-discrimination legislation, workplace safety

legislation, and the attention of corporate regulators. This research provides the basis for engagement of

extended dialogue with companies.

Economic and qualitative assessments of companies were kept distinct by some managers. One interviewee

explained the distinction with the following comment: ‘The fi nancial assessment process is quite segregated. The

investment managers run a quant process over the stocks that are given to us by our social screening agency’.

Others made explicit attempts to integrate economic and qualitative assessments. One interviewee described invest-

ment processes in its organization as commencing with exclusion of selected industrial sectors such as uranium

mining and alcohol manufacturing, then the following.

We look at companies from sustainability perspective and corporate social responsibility perspectives. For our

investment purposes, what we expect is high levels of corporate social responsibility for those industries that

are less aligned with sustainability. Those who are in high-sustainability companies, we believe they have

higher growth profi les. Similarly, we incorporate corporate social responsibility as part of the risk premiums.

The lower the risk, the more value there is in the company. Through the fi nancial assessment, we get a

positive bias for those who are higher in sustainability and those who are better in CSR [corporate social

responsibility].

Information disclosures of that fund were deliberately kept simple: ‘What we talk about [in the PDS] is that our

corporate social responsibility is based on a system of “bang, bang, bang and therefore that is used when deciding

whether or not to invest from an environment, social, whatever perspective, and that’s how we decide what invest-

ment”. Anything else just becomes too complicated’.

Several interviewees augmented management consultation and questionnaires with information gained from

public third parties and corporate Internet websites. Others used networks of environmental and social non-

governmental groups. Interviewees who had offered social investment products prior to 2004 tended to use

screening approaches as their main construction method in 2007. They also tended to have direct access to well

developed networks, including, for example, the Australian Conservation Foundation, Greenpeace chapters, The

160 M. Haigh and J. Guthrie

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

Wilderness Society and Community Aid Abroad. By contrast, indexing managers at earlier stages of product life

cycles tended to look to the government, as put by one interviewee, ‘to move the agenda forward’.

Discussion

The material above illustrates that a sample of managers have found it diffi cult to outline construction styles and

qualitative assessment processes succinctly for the purposes of a PDS summary. The statistical analysis and inter-

view extracts illustrate that processes followed in social portfolio construction are fl uid and dynamic, vary over

time and between individual companies, products and issuers and, often, are undocumented. The reporting

requirements, in contrast, imply that management processes are static and have been (or should be) documented

inside investment fi rms and scrutinized by investment committees. Such a signifi cant gap between regulators’

objectives and managerial practice might account for the perceptions of interviewees that the form, if not the

intent, of the legislation is inappropriate.

Several policy implications arise from the form of the regulated reporting. One, the dynamic nature of portfolio

design and construction of SRIs does not lend itself immediately to description in product disclosure statements.

Reporting, as Gibson (1996) argues in the context of the reporting of pollution allowances, is not the problem.

The evidence we have presented suggests that the monitoring of qualitative research delegated to agent fi rms has

been lax. If this is the general case, and the wide size of our sample suggests that this might be so in Australia,

the monitoring of delegated parts of the investment function is a matter for regulatory policy setting. Managers

who had delegated SRI assessment in entirety to agents tended to exhibit relatively superfi cial understanding of

how social responsibility might be represented in portfolios, considering that effective reporting of such was ulti-

mately a matter of legality. Some interviewees in this group considered the regulations to represent a kind of public

imprimatur over the use of social considerations in managed investment portfolios, and as such a precursor of

government-provided fi nancial advantages.

Two, given the extensive discussion period leading up to the regulations, a wide sample of reporters perceive

the regulations as a compliance burden and cost impost. Interviewees considered that retail investors and members

of pension funds are interested more in economic outcomes than portfolio construction. This perception perhaps

explains a generally less than enthusiastic response to the reporting mandate. A corollary is that regulation of

product information cannot be expected to automatically promote clarity of disclosure and hence comparability.

The regulations were issued to promote integrity of investment reporting and practice in SRI products. Legislators

have asserted that the regulation provides for a basic level of consumer protection yet have allowed reporters to

decide the content and format of disclosures. An observed increased reliance of product issuers on qualitative

information in the public domain suggests that regulators’ attention should shift from disclosure of method to

the integrity of information attached to investment products.

Finally, the demonstrated diversity of investment methods suggests that markets for SRI products do not just

happen. SRI markets are created for various reasons, including market opportunism, isomorphism, founding

legacies and pressures from customers, members and invested companies. These origins shape the appropriate

form of accountability to be discharged, which in turn is likely to impact on the extensiveness, quality and quantity

of reporting. Our examination suggests that the form and content of disclosures informing on the construction of

SRI products, prior to regulation, refl ected diversity of origin, purpose and method. Regulated standardized report-

ing can be expected to detract from a plurality of interests (Gray and Jenkins, 1993). How this might bring

benefi ts for retail investors is unclear.

Acknowledgements

The collaborative partner (Australian Council of Super Investors) has 27 major pension funds as its members. Their members manage AUD$55billion for benefi ciaries that represent 75 per cent of the Australian work force. The authors acknowledge the fi nancial assistance of ACSI that made possible the research presented in this paper and the support of the Macquarie Univer-sity External Collaborative Research Grants Scheme. The authors acknowledge participants at the European Accounting

Management Practices in Australasian Ethical Investment Products: A Role for Regulation? 161

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

Association Congress, Lisbon 2007. The assistance of Fiona Crawford of the University of Sydney and of staff members of Macquarie Graduate School of Management in the primary research and early editing is appreciated.

Regulation and Industry Codes

Association of Superannuation Funds of Australia Ltd, ASFA BP 17 Guidelines for Fund Trustees, Sydney.

ASX Corporate Governance Council, Principles of Good Corporate Governance and Best Practice Recommenda-

tions, Sydney.

Australian Investment and Financial Services Association, Corporate Governance: a Guide for Fund Managers and

Corporations (Blue Book), Sydney.

Australian Investment and Financial Services Association, Shareholder Activism among Fund Managers: Policy

and Practice, Sydney.

Australian Investment and Financial Services Association, Guidance Note 14.00: Socially Responsible Investment

Disclosure, Sydney.

Australian Securities and Investments Commission (ASIC) (2001), PS 168 Disclosure: Product Disclosure State-

ments (and Other Disclosure Obligations), ASIC, Canberra.

Australian Securities and Investments Commission (ASIC) (2003), Section 1013DA Disclosure Guidelines, ASIC,

Canberra.

Corporations Act 2001(Cth) 2001, Commonwealth of Australia, Canberra.

Financial Services Reform Bill 2001, Explanatory Memorandum, Commonwealth of Australia, Canberra.

New Zealand Superannuation and Retirement Income Act 2001.

Statutory Instrument 1999 (No. 1849), The Occupational Pension Schemes (Investment and Assignment, Forfei-

ture, Bankruptcy etc.) Amendment Regulations 1999, Her Majesty’s Stationery Offi ce, London.

Statutory Instrument 2001 (No. 3649), The Financial Services and Markets Act 2000 (Consequential Amendments

and Repeals) Order 2001, Her Majesty’s Stationery Offi ce, London.

References

Adams CA. 2002. Internal organisational factors infl uencing corporate social and ethical reporting: beyond current theorising. Accounting, Auditing and Accountability Journal 15(2): 223–250.

Adams CA, Frost G. 2004. The Development of Corporate Web-Sites and Implications for Ethical, Social and Environmental Reporting Through These Media, research monograph. Institute of Chartered Accountants of Scotland: Edinburgh.

Ali PU, Gold M. 2002a. Investing for good: the cost of ethical investment. Companies and Securities Law Journal 20(5): 307–309.

Ali PU, Gold M. 2002b. An Appraisal of Socially Responsible Investment and Implications for Trustees and Other Investment Fiduciaries, Centre for

Corporate Law and Securities Regulation, The University of Melbourne.

Ali PU, Stapledon G, Gold M. 2003. Corporate Governance and Investment Fiduciaries. Lawbook: Sydney.

Amalric F. 2004. Shareholder Activism as Information Sharing, Working Paper 04/04, CCRS Working Paper Series, Centre for Corporate

Responsibility and Sustainability, University of Zurich.

Anand P, Cowton CJ. 1993. The ethical investor: dimensions of investment behavior. Journal of Economic Psychology 14: 377–385.

Australian Securities and Investments Commission (ASIC). 2001. PS 168 Disclosure: Product Disclosure Statements (and other Disclosure Obliga-tions). ASIC: Canberra.

Australian Securities and Investments Commission (ASIC). 2003. Section 1013DA Disclosure Guidelines. ASIC: Canberra.

Banz RW. 1981. The relationship between return and market value of common stocks. Journal of Financial Economics 9(1): 3–18.

Bauer R, Derwell J, Otten R. 2007. Canadian ethical mutual funds: performance and investment style in a multifactor framework. Journal of Business Ethics 70(2): 111–124.

Bauer R, Koedijk K, Otten R. 2005. International evidence on ethical mutual fund performance and investment style. Journal of Banking and Finance 29: 1751–1767.

Bauer R, Otten R, Rad AT. 2004. Ethical Investing in Australia: is There a Financial Penalty? working paper, University of Maastricht.

Beal D, Goyen M. 1998a. Are Ethical Investors Real? The Investment Research Guide to Socially Responsible Investing, The Colloquium on

Socially Responsible Investing, Plano, TX.

Beal D, Goyen M. 1998b. ‘Putting your money where your mouth is’: a profi le of ethical investors. Financial Services Review 7(2): 129–143.

Belkaoui A. 1980. The impact of socio-economic accounting statements on the investment decision: an empirical study. Accounting, Organiza-tions and Society 5(3): 2632–2683.

162 M. Haigh and J. Guthrie

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

Berger C. 2004. Disclosure of Ethical Considerations in Investment Product Disclosure Statements. Australian Conservation Foundation: Carlton,

Victoria.

Bruyn ST. 1987. The Field of Social Investment. Cambridge University Press: London.

Buzby S. 1974. The nature of adequate disclosure. Journal of Accountancy 137(4): 38–50.

Buzby S, Falk H. 1979. Demand for social responsibility information by university investors. The Accounting Review 54(1): 23–37.

Cullis JG, Lewis A, Winnett A. 1992. Paying to be good? UK ethical investments. Kyklos 45: 3–23.

Cummings LS. 2000. The fi nancial performance of ethical funds: an Australian perspective. Journal of Business Ethics 25(1): 79–92.

DiBartolomeo D, Kurtz L. 1999. Managing Risk Exposures of Socially Screened Portfolios, Northfi eld working paper, Northfi eld University.

Diltz JD. 1995. Does social screening affect portfolio performance? Journal of Investing Spring: 64–69.

Dowdy S, Wearden S, Chilko D. 2004. Statistics for Research, 3rd edn. John Wiley & Sons: Hoboken, NJ.

Edwards J, Wolfe S. 2005. Compliance: a review. Journal of Financial Regulation and Compliance 13(1): 48–59.

Epstein MJ, Freedman M. 1994. Social disclosure and the individual investor. Accounting, Auditing and Accountability Journal 7(4): 94–109.

Frankfurter GM, Haughen B, McGoun E, Salandro D, Herb P. 1997. Pushing the epsilon to the abyss: post-modern fi nance. International Review of Financial Analysis 6(2): 133–177.

Freedman M, Jaggi M. 1988. An analysis of the association between pollution disclosure and economic performance. Accounting, Auditing and Accountability Journal 1(2): 43–58.

Freedman M, Stagliano AJ. 1991. Differences in social-cost disclosures: a market test of investor reactions. Accounting, Auditing and Account-ability Journal 4(1): 68–83.

Friedman AL, Miles S. 2001. SRI and corporate social and environmental reporting in the UK: an exploratory study. The British Accounting Review 33(4): 523–548.

Gibbins JD, Chakraborti S. 1992. Nonparametric Statistical Inference. 3rd Edition, Marcel Dekker: New York.

Gibson K. 1996. The problem with reporting pollution allowances: reporting is not the problem. Critical Perspectives on Accounting 7(6):

655–665.

Gold M, Ali PU. 2002. Analysing the cost of ethical investment. Journal of the Securities Institute of Australia 3: 9–14.

Grahl J. 2006. Financial integration in the EU: policy issues and proposals. Critical Perspectives on Accounting 17: 253–267.

Gray A, Jenkins W. 1993. Codes of accountability in the new public sector. Accounting, Auditing and Accountability Journal 6(3): 52–67.

Grossman B, Sharpe W. 1986. Financial implications of South Africa divestment. Financial Analysts Journal 42(4): 15–31.

Guthrie J, Cugensan S, Ward L. In press. Industry specifi c social and environmental reporting: the Australian food and beverage industry.

Accounting Forum.

Guthrie J, Parker LD. 1990. Corporate social disclosure practice: a comparative international analysis. Advances in Public Interest Accounting 3:

159–175.

Haigh M. 2006a. Camoufl age play: making moral claims in managed investments. Accounting Forum 30(3): 267–283.

Haigh M. 2006b. Social investment: subjectivism, sublation and the moral elevation of success. Critical Perspectives on Accounting 17(8):

989–1005.

Haigh M. 2006c. Managed investments, managed disclosures: fi nancial services reform in practice. Accounting, Auditing and Accountability Journal 19(2): 186–204.

Haigh M. 2007. What counts in social managed investments: evidence from an international survey. Advances in Public Interest Accounting 13:

35–62.

Haigh M, Hazelton J. 2004. Financial markets: a tool for social responsibility? Journal of Business Ethics 52(1): 59–71.

Hair JE Jr, Anderson RE, Tatham RL, Black WC. 1998. Multivariate Data Analysis, 5th edn. Prentice-Hall, Englewood Cliffs, NJ.

Hamilton S, Jo H, Statman M. 1993. Doing well while doing good? The investment performance of socially responsible mutual funds. Finan-cial Analysts Journal Nov./Dec.: 62–66.

Hansard. 2001a. Proceedings of the Senate, 22 August 2001, Debate No. 11. Australian Parliamentary Library: Canberra; 26 315–26 317. www.

aph.gov.au/hansard/senate/dailys/ds220801.pdf [17 August 2004].

Hansard. 2001b. Proceedings of the Joint Statutory Committee on Corporations and Securities, 14 June 2001, CS 245-250. Australian Parlia-

mentary Library: Canberra. www.aph.gov.au/hansard/joint/commttee/j4982.pdf [17 August 2004].

Hansard. 2001c. Proceedings of the Joint Statutory Committee on Corporations and Securities, 27 April 2001. Australian Parliamentary Library:

Canberra; 1–52. www.aph.gov.au/hansard/joint/commttee/j4808.pdf [17 August 2004].

Hansard. 2002. Proceedings of the House of Representatives Standing Committee on Environment and Heritage, Public Hearing 12 December

2002, EH 56-59. Australian Parliamentary Library: Canberra. www.aph.gov.au/hansard/reps/commttee/R5977.pdf [17 August 2004].

Harte G, Lewis L, Owen DL. 1991. Ethical investment and the corporate reporting function. Critical Perspectives on Accounting 2(3): 227–254.

Hutton RB, d’Antonio L, Johnsen T. 1998. Socially responsible investing: growing issues and new opportunities. Business and Society 37(3):

281–296.

Irvine WB. 1987. The ethics of investing. Journal of Business Ethics 6(3): 233–242.

Kerr M, Zubevich K. 2002. Where is Your Superannuation Money Going? An Environmental Perspective. Australian Conservation Foundation:

Melbourne.

King A, Lenox M. 2001. Does it really pay to be green? An empirical study of fi rm environmental and fi nancial performance. The Journal of Industrial Ecology 5(1): 105–116.

Kreander N. 2001. An Analysis of European Ethical Funds, Occasional Research Paper 33. Certifi ed Accountants Educational Trust: London.

Kreander N, Gray RH, Power DM, Sinclair CD. 2002. The fi nancial performance of European ethical funds 1996–1998. Journal of Accounting and Finance 1: 3–22.

Management Practices in Australasian Ethical Investment Products: A Role for Regulation? 163

Copyright © 2008 John Wiley & Sons, Ltd and ERP Environment Bus. Strat. Env. 19, 147–163 (2010) DOI: 10.1002/bse

Lewis A. 2001. A focus group study of the motivation to invest: ‘ethical/green’ and ‘ordinary’ investors compared. The Journal of Socio-Economics 30(4): 331–341.

Lewis A, Cullis J. 1990. Ethical investments: preferences and morality. The Journal of Behavioral Economics 19(4): 395–411.

Lewis A, Mackenzie C. 2000. Support for investor activism among UK ethical investors. Journal of Business Ethics 24(3): 215–222.

Lewis A, Webley P, Winnett A, Mackenzie C. 1998. Morals and markets: some theoretical and policy implications of ethical investment. In

Choice and Public Policy, Taylor-Gooby P (ed.). Macmillan: London; pp. 164–182.

Mackenzie C, Lewis A. 1999. Morals and markets: the case of ethical investing. Business Ethics Quarterly 9(3): 439–452.

Mathieu E. 2000. Response of UK Pension Funds to the Social Investment Disclosure Regulations. UK Social Investment Forum: London.

Michelson G, Wailes N, van der Laan S, Frost G. 2004. Ethical investment processes and outcomes. Journal of Business Ethics 52(1): 1–10.

Milne MJ, Chan CC. 1999. Narrative corporate social disclosures: how much of a difference do they make to investment decision-making?

British Accounting Review 31: 439–457.

Moodie G, Ramsay I. 2003. Managed Investment Schemes: an Industry Report. Centre for Corporate Law and Securities Regulation, The Uni-

versity of Melbourne.

Noci G. 1995. Supporting decision-making for recycling-based investments. Business Strategy and the Environment 4(2): 62–72.

O’Dwyer B. 2002. Conceptions of corporate social responsibility: the nature of managerial capture. Accounting, Auditing and Accountability Journal 16(4): 523–557.

O’Rourke A. 2003. The message and methods of ethical investment. Journal of Cleaner Production 11(6): 683–693.

Owen DL. 1990. Towards a theory of social investment: a review essay. Accounting, Organizations and Society 15(3): 249–265.

Owen DL, Swift T, Hunt K. 2001. Questioning the role of stakeholder engagement in social and ethical accounting, auditing and reporting.

Accounting Forum 25(1): 264–282.

Paul K, Aquila DA. 1988. Political consequences of ethical investing: the case of South Africa. Journal of Business Ethics 7: 691–697.

Perks RW, Rawlinson DH, Ingram L. 1992. An exploration of ethical investment in the UK. British Accounting Review 24: 43–65.

Richardson BJ. 2002. Ethical investment and the Commonwealth’s Financial Services Reform Act 2001. National Environmental Law Review

2: 47–60.

Rikhardsson P, Holm C. 2006. The effect of environmental information on investment allocation decisions – an experimental study. Business Strategy and the Environment in press.

Rivoli P. 1995. Ethical aspects of investor behavior. Journal of Business Ethics 14: 265–277.

Rockness J, Williams PF. 1988. A descriptive study of social responsibility mutual funds. Accounting, Organizations and Society 13(4):

397–411.

Ryall C, Riley S. 1996. Appraisal of the selection criteria used in green investment funds. Business Strategy and the Environment 5(4): 231–

241.

Schoenenberger N. 1994. A case study of ethical/green/environmental funds, corporate governance and stakeholder management. Business Strategy and the Environment 3(3): 22–26.

Schrader U. 2006. Ignorant advice – customer advisory service for ethical investment funds. Business Strategy and the Environment 15(3):

200–214.

Schwartz MS. 2003. The ‘ethics’ of ethical investing. Journal of Business Ethics 43: 195–213.

Serrano-Cinca C, Fuertes-Callén Y, Gutiérrez-Nieto B. 2007. Internet reporting in microfi nance institutions. Proceedings of the European

Accounting Association 30th Annual Congress, Lisbon.

Shane PB, Spicer BH. 1983. Market response to environmental information produced outside the fi rm. The Accounting Review 58(3): 521–

539.

Spiller R. 1999. Creating an ethical inventory. New Zealand Management 46(1): 52–54.

Spiller R. 2000. Ethical business and investment: a model for business and society. Journal of Business Ethics 27(1/2): 149–160.

Statman M. 1999. Behavioral fi nance: past battles and future engagements. Financial Analysts Journal 55(6): 18–27.

Statman M. 2000. Socially responsible mutual funds. Financial Analysts Journal 56(3): 30–39.