Main project

72

CHAPTER ONE 1.0 Introduction This chapter represents the following subtopics of chapter one in the following order; background to the study, statement of the problem, research objectives , research questions, significance of the study, research limitations, scope of the study and conceptual framework. It is the section that lays the section of the foundation of the study. 1.1 Background to the study Exchange rate exposure is becoming an increasingly important issue in international financial management. Exchange rate fluctuations are a major source of risk for multinational corporations. To mitigate exchange rate uncertainty, it has been claimed that hedging; not only financial hedging, but also operational hedging can protect companies from unexpected movements of exchange rates (Allayannis, Ihrig, and Weston (2000)). Corporate hedging refers to the use of off-balance-sheet instruments and on-balance-sheet strategy (Nance (1993)). Firms that are exposed to exchange rate risk can actively reduce currency risk by two ways. On the one hand, firms can hedge exchange rate risk by financial hedging, entering into derivatives contracts, such as forwards, futures or 1

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Main project

CHAPTER ONE

1.0 Introduction

This chapter represents the following subtopics of chapter one in

the following order; background to the study, statement of the

problem, research objectives , research questions, significance of

the study, research limitations, scope of the study and conceptual

framework. It is the section that lays the section of the

foundation of the study.

1.1 Background to the study

Exchange rate exposure is becoming an increasingly important issue

in international financial management. Exchange rate fluctuations

are a major source of risk for multinational corporations. To

mitigate exchange rate uncertainty, it has been claimed that

hedging; not only financial hedging, but also operational hedging

can protect companies from unexpected movements of exchange rates

(Allayannis, Ihrig, and Weston (2000)). Corporate hedging refers to

the use of off-balance-sheet instruments and on-balance-sheet

strategy (Nance (1993)). Firms that are exposed to exchange rate

risk can actively reduce currency risk by two ways. On the one

hand, firms can hedge exchange rate risk by financial hedging,

entering into derivatives contracts, such as forwards, futures or

1

options. The hedging with these off-balance-sheet contracts has a

negative effect on exchange rate exposure. On the other hand, firms

can reduce their exposure through on-balance-sheet hedging. Firms

can move factories to its sales markets and as a result revenues

and expenses are incurred in the same currency. This is also called

operational hedging, which has a negative effect on exchange rate

exposure.

1.1.1 What Is Foreign Exchange Rate Exposure

The exchange rate is the price of one country’s currency in terms

of another currency and it is one of the most important prices in

the open economy. It is a well-known fact that after the breakdown

of the Bretton Woods System of fixed exchange rates in 1973,

exchange rate volatility has increased dramatically and

unpredictably. For example, exchange rates are typically four times

as volatile as interest rates and ten times as volatile as

inflation rates.

It is widely believed that exchange rate movements should affect

the value of a firm. A multinational corporation (MNC) with

subsidiaries in foreign locations, an exporter or importer

concentrating on international trade or even a firm that has no

direct international activities will be affected by the exchange

rate fluctuations.

2

The general concept of exchange rate exposure refers to the degree

to which a company is affected by exchange rate changes. A number

of theoretical papers have investigated the possible sources of

exchange rate exposure. For example, Dumas (1978), Adler and Dumas

(1980), and Hodder (1982) have defined economic exposure to

exchange rate movements as the regression coefficient of the real

value of a firm on the exchange rate across states of nature. As

Adler and Dumas (1984) point out, from the viewpoint of U.S.

investors, exposure is the regression coefficient or, if there are

many currencies, the vector of partial regression coefficients,

when an asset’s dollar price is regressed on exchange rates. From

the viewpoint of the firm and its managers, exposure is a

statistical quantity rather than a (projected) accounting number.

The regression coefficient concept of exposure provides a single

comprehensive measure that summarizes the sensitivity of the whole

firm, to all the various ways in which exchange rate changes can

affect it. Once exposure is so measured it can, for purposes of

managerial control, be decomposed into distinct components. The

decomposition can produce the counterparts of translation and

transaction exposure as part of the total exposure. Neither parts

should be ignored or hedged alone

3

Based on the impact of exchange rate changes on a firm, there are

mainly two types of exchange rate exposure – accounting exposure,

and transaction exposure

Accounting exposure, also known as translation exposure, refers to

the changes in income statement items and the book value of balance

sheet assets and liabilities that are caused by an exchange rate

change. More specifically, it arises from the need, for the purpose

of reporting and consolidation, to convert the financial statements

of foreign operations from the local currencies involved to the

home currency.

Transaction exposure results from transactions that give rise to

known, contractually binding future foreign-currency-denominated

cash inflows or outflow. Since the transaction will result in a

future foreign currency cash inflow or outflow, any change in the

exchange rate between the time the transaction is entered into and

the time it is settled in cash will lead to a change in the

domestic currency amount of cash inflow or outflow.

1.1.2 Corporate Hedging

Corporate hedging refers to the use of off-balance-sheet

instruments such as forwards, futures, swaps and options to reduce

the volatility of firm value (Nance (1993)).

4

Managing foreign exchange exposure is now an important aspect of

corporate risk management.

Hedging a particular currency exposure means establishing an

offsetting currency position such that whatever is lost or gained

on the original currency exposure is exactly offset by a

corresponding foreign currency gain or loss on the currency

Exchange rate exposure is becoming an increasingly important issue

in international financial management. Exchange rate fluctuations

are a major source of risk for multinational corporations. To

mitigate exchange rate uncertainty, it has been claimed that

hedging, not only financial hedging, but also operational hedging

can protect companies from unexpected movements of exchange rates

(Allayannis, Ihrig, and Weston (2000)).

Firms that are exposed to exchange rate risk can actively reduce

currency risk by two ways. On the one hand, firms can hedge

exchange rate risk by financial hedging, entering into derivatives

contracts, such as forwards, futures or options. The hedging with

these off-balance-sheet contracts has a negative effect on exchange

rate exposure. On the other hand, firms can reduce their exposure

through on-balance-sheet hedging. Firms can move factories to its

sales markets and as a result revenues and expenses are incurred in

the same currency. This is also called operational hedging, which

has a negative effect on exchange rate exposure.5

According to the classic Modigliani and Miller theory, financial

risk management is irrelevant to the firm. Investors can hedge on

their own by holding well-diversified portfolios. Optimal hedging

theories, however, suggest that a firm’s hedging activities affect

the extent to which the firm is exposed to exchange rate movements.

In a world of market imperfections, firms have incentives to employ

derivative instruments to hedge against exchange rate risk.

Extensive use of derivatives as hedging instruments should diminish

a firm’s exposure.

.

1.2 Problem statement

Previous researches have tried to uncover the impact of financial

derivatives’ use on exchange rate exposure by using a series of

variables that existing studies find to be important in explaining

a firm’s hedging policy to proxy for financial hedging. For

example, He and Ng (1998) relate the exchange rate exposure to the

level of its export ratio and variables that are proxies for its

hedging needs. For the past few decades, the effectiveness of

currency hedging has been studied by a number of papers providing

empirical results of both US and European countries. In addition to

Allayannis and Ofek’s (2001) study indicating that the use of

foreign currency derivatives can significantly reduce the exchange

rate exposure of US firms, jong, Ligterink and Macrae (2002) take a6

look at Dutch firms. They found that financial hedging by using

derivative has no significant effects on the exchange exposure,

which is in contrast to their hypothesis. In line with theory, they

find that exchange rate exposure is significantly reduced through

operational hedging by producing in factories abroad. Nydahl (2001)

has also studied the Swedish firms and found that the foreign

exchange exposure is negatively related to the use of currency

derivatives

These abovementioned results are only applied to the US and

European countries, few studies thus far have examined the hedging

effects of firms in African countries.

Kenya has witnessed local companies operating in various

countries. Furthermore there are extraordinary high portion of MNCs

that are significantly exposed to exchange rate risk. In this light

the researcher will seek to answer the question, does hedging

effectively reduce these exchange rate exposures? In this study, we

will examine the hedging effectiveness on companies trading in the

stock exchange.

While most studies have examined firms’ financial hedging, few

studies have examined firms’ operational hedging. Diversifying

operations in different countries is a very important way to

eliminate exchange rate risk. However, it is difficult to measure

operational hedging. Jong, Ligterink and Macrae (2002) gather the7

operational hedging information through a tailor-made questionnaire

by asking the firms directly to indicate what percentage of total

exposure the firm hedges through its operation. They find that

operational hedging has significant negative effect on exchange

rate exposure for a sample of Dutch firms. Allayannis, Ihrig, and

Weston (2000) develop several measures of geographic dispersion

that proxy for the use of operational hedging strategies, they find

that geographic dispersion through the location of subsidiaries

across multiple countries or regions does not reduce exchange rate

exposure.

This study will aim at investigating both financial and operational

hedging in the risk management strategies of multinational

corporations.

Moreover, as the use of the foreign currency derivatives for

financial hedging has grown dramatically in the past two decades, I

take a further step to examine the determinants of the use of

derivatives.

While these tests reveal the factors that prompt corporations to

hedge, they do not answer the question of what determines the

extent of hedging.

1.3 General objectives

8

To investigate the various financial and operating hedging

strategies and / or tools on foreign exchange rate exposure and how

such strategies impact on firms’ value.

Specific objectives of this study.

1. To examine the effectiveness of financial hedging on exchange

rate exposure.

2. To determine the effect of operating hedging on exchange rate

exposure.

3. To determine how each strategy contributes to the risk

management of eliminating exchange rate exposure and improving

firm value.

4. To examine the effectiveness of derivatives use on firm market

value.

1.4 Empirical Questions of This Study

1. Can financial hedging reduce the exchange rate exposure of

multinational corporations and what determines the use of

foreign currency derivatives by corporations?

2. Can operational hedging reduce the exchange rate exposure of

multinational corporations and what determines the use of

foreign currency derivatives by corporations?

3. Do exchange rate movements affect firm value? Is exchange rate

exposure significant for the multinational corporations?

4. Does hedging affect firms’ market value?9

1.5 Justification of the study

While there are an increasing number of studies providing evidence

that firms that hedge fit the profile of one theory or another, no

study have addressed the question of whether there is a direct

relation between hedging and firm value. The study will try to find

out which hedging strategies that a firm can use to increase its

value.

Empirical examination of hedging theories has been difficult. Many

previous papers have been unable to uncover the impact of financial

derivatives’ use on exchange rate exposure due to unavailability of

data on hedging instruments. Most of the earlier studies used

survey data to examine why firms use derivatives. For example,

Nancy, Smith and Smithson (1993) use survey data to compare

characteristics of firms that actively hedge with those that do

not.

IFRS 7 requires firms to disclose information on financial

instruments with off-balance sheet risk (e.g., futures, forwards,

options and swaps) with effect from January 1 2009. With the

availability of derivative data, the effect of the use of

derivatives on foreign exchange exposure can be easily examined

using a sample of Kenya multinationals. I will use detailed

10

derivative data to examine whether firms use foreign currency

derivatives for hedging or for speculative purposes.

1.6 Significance of the research.

The study will have the following benefits which will justify why

it need to be undertaken.

Multinationals corporations; There has been a sharp increase in

foreign investment in Kenya. Multi-national and transnational

corporations are playing increasingly important roles in Kenyan

business. The researches will benefits companies quoted in the NSE

with subsidiaries in foreign countries.

Firms that have foreign involvement; Kenyan corporate units are

also engaging in a much wider range of cross border transactions

with different countries and products. Kenyan firms have also been

more active in raising financial resources abroad. All these

developments combine to give a boost to cross-currency cash flows,

involving different currencies and different countries. The

corporate enterprises in India are increasingly alive to the need

for organised fund management and for the application of innovative

hedging techniques for protecting themselves against attendant

risks. Derivatives are the tools that facilitate trading in risk.11

Importers and exporters will understand the effect of international

dynamics on the local economy

The foreign exchange market is still evolving and corporate

enterprises are going through the movements in transition from a

passive to an active role in risk management. There is no organized

information available on how the corporate enterprises in India are

facing this challenge. It is in this context that a review of the

perceptions and concerns of the corporates, in relation to

derivatives and of their initiatives in tuning the organisational

set up to acquire and adopt the requisite skills in risk

management, assumes significance. Appropriate policy and other

measures can then be taken to accelerate the process of further

development of foreign exchange market and also upgrade foreign

exchange risk management (FERM) with higher professionalism and

increased effectiveness.

The liberalisation of the kenyan economy started in 1991.Demand and

supply conditions now govern the exchange rates in our foreign

exchange market. A fast developing economy has to cope with a

multitude of changes, ranging from individual and institutional

preferences to changes in technology, in economic policies, in

regulations etc. Besides, there are changes arising from external

trade and capital account interactions. These generate a variety of

risks, which have to be managed.12

1.7 Scope of the study

The study may not be wholly relied upon in determining similar

cases in the future as factors triggering the foreign exchange

reactions changes from time to time.

-Secondly, other factors that affect the stock market have not been

included and their effect on this study is therefore not

established empirically. As such an element of error cannot be

ruled out.

-The study is based on estimates and forecasts which may have a

significant variation from the actual results.

13

CHAPTER TWO

2.0 Literature review

A number of empirical researches have examined the question of how

firms deal with the foreign exchange risk. Usually, firms utilize

two different ways to hedge the exchange rate risk. One is a

financial hedge through financial market instruments, such as

exchange rate derivatives or foreign currency debt, and the other

is an operational hedge through the operational setup of the

exporting firm. To effectively manage long-term exchange rate

risks, firms should built operational hedging strategies in

addition to widely used financial hedging strategies. Most studies

focus on currency hedging1. These studies analyze the relationship

between operational hedging and financial hedging and show the

14

effectiveness of both strategies by conducting empirical analysis

based on firms' stock return

2.1 Operational hedging

Real options are referred to as operational hedging mechanisms in

the operations management literature. Operational hedging has been

studied in a variety of fields - operations management, finance,

strategy and international business. In all fields, operational

hedging is discussed in conjunction with financial hedging, and

mostly analyzed in a multinational context. The existence of risks

that can only be managed operationally (Triantis 2000) means that

operational hedging constitutes an important part of firm-level risk

management programs: Empirical investigations (Allayannis et al.

2001, Pantzalis et al. 2001) clearly demonstrate that firms do use

operational hedges in managing their risks.

The finance literature has used the term “operational hedging” in

the last decade with increasing frequency. It is always discussed in

conjunction with its financial counterpart, financial hedging. In

the finance literature, operational hedging is the course of action

that hedges the firm’s risk exposure by means of non-financial

instruments, particularly through operational activities.

15

2.12 Operational hedging strategies.

Similar to the operations management literature, operational

flexibility is the major operational hedging strategy discussed in

the finance literature. Finance research underlines the value-

enhancing capability of this kind of flexibility by referring to

its real option features. Even in a risk-neutral setting, creating

real option features in an existing investment increases value by

providing flexibility in the decision-making process. Since most of

the papers are in the context of multinational corporations,

operational flexibility in the form of switching production or

sourcing locations is the most prevalent type of operational

hedging strategy.

In addition to operational flexibility, geographical

diversification is discussed as another operational hedging

strategy in a multinational context. Geographical diversification

is aligning the costs and revenues of a firm so that they are

exposed to the same risks. Domestic firms selling to foreign

markets can ensure that their production costs and sales revenues

are exposed to the same exchange rate uncertainties by opening a

production facility in these markets. As in the case of operational

flexibility, firms reduce their downside exposures to exchange rate

risks by eliminating the negative effect of appreciated local16

currency (in the form of higher production costs). However,

different from operational flexibility, firms also sacrifice the

gains in the upside by forgoing the positive effect of depreciated

currency (in the form of lower production costs). Therefore,

geographical diversification reduces the total variability of cash

flows.

Chowdry and Howe (1999) consider opening a production facility in a

foreign market as the operational hedging strategy of multinational

firms without differentiating between geographical diversification

and operational flexibility. They analyze the conditions under

which firms engage in financial and operational hedging strategies

with respect to exchange rate and demand risks. They state that by

having plants in several countries, multinationals can align their

costs and revenues besides shifting production among these

locations. They argue that the facility location decision is

considered to be an operational hedging strategy only when firms

are concerned with the variability of their operating profits.

Hommel (2003) considers geographical diversification and

operational flexibility in the form of a real switching option as

two separate operational hedging strategies. He investigates the

incentives of firms to hedge currency risk with financial and

operational (there, “operative”) means in a multinational context.

The hedging motivation is introduced through a minimum profit17

constraint such that firms have incentives to hedge their payoffs

to satisfy this constraint. He argues that operational flexibility

is employed as a hedging device when the exchange rate and demand

volatility are sufficiently large (in that case the minimum profit

constraint is violated); otherwise it serves as a value driver to

enhance expected profits.

These papers emphasize that because operational flexibility can be

used for a purely value-enhancement motive, it is considered to be

an operational hedging strategy only when there is a risk hedging

motive for employing it. Generally speaking, operational actions

are considered to be operational hedges if they are taken in order

to reduce a risk measure of concern. In particular, if firms care

about downside risk (e.g. having a minimum profit constraint),

then operational hedges mitigate risk through a reduction in the

downside exposure.

If variance of the payoffs is the risk measure under consideration

(e.g. having a convex tax schedule), then operational hedges

mitigate risk through a reduction in variance.

In empirical research in risk management, operational hedging

strategies are always studied in conjunction with financial

derivatives in an exchange rate or commodity setting. Geographical

diversification and operational flexibility are the operational

hedging strategies implemented through different operational18

decisions. This field mainly investigates the substitutability or

complementarities of operational and financial hedging instruments

and tests whether firms use risk management activities under

different risk management motives.

Fok et al. (1997) consider locating production facilities in major

foreign markets to minimize foreign exchange rate exposure, and

choosing a technology to minimize exposure to commodity price risk

to be production-originated hedging instruments of multinational

firms. Although the term “operational hedging” is not used, the

former is simply geographical diversification whereas the latter is

similar to a product differentiation strategy (Miller 1998), which

is a type of operational flexibility.

In a multinational context, Allayannis et al. (2001) proxy the

operational hedging of multinationals by the level of geographic

dispersion (the location of subsidiaries across multiple countries

or regions) without differentiating between geographical

diversification and operational flexibility. They investigate both

financial and operational exchange rate risk management strategies

of firms, and demonstrate how much each strategy contributes to the

overall goal of mitigating risk and improving shareholder value.

In a similar framework, Doukas and Padmanabhan (2002) consider the

intangible assets of firms to be operational hedging devices with

respect to political risks. The authors argue that by having high19

levels of intangible assets, firms can compensate the loss due to

the political interruption of a host government using their other

assets (for example, in other countries). Observe that high levels

of intangible assets provide flexibility in terms of shifting

resources among countries or businesses; this is another form of

operational flexibility.

In a commodity setting, Petersen and Thiagarajan (2000) focus on

gold mining firms. These firms, by adjusting their mining strategies

as a function of gold price, create cost structures that positively

correlate with the price of gold. Operational flexibility, created

by the ability to adjust cost structures, is their operational

hedging strategy, and creates a natural hedge against gold price

exposure.

Carter et al. (2003) define operational hedging strategies as a

combination of production and marketing strategies across the firm’s

operating units developed to manage long-term exposures. Other than

geographical diversification, they discuss real option type

operational hedging strategies such as shifting sourcing or

production, exploiting growth-options, having pricing flexibility

and abandoning foreign markets. Observe that all of these strategies

are again types of operational flexibility.

In the international business literature, Pantzalis et al. (2001)

define operational hedging as the firm’s operational decisions20

(related to marketing, production, sourcing, plant location,

treasury) that are best suited to managing the exchange rate

exposure on the firm’s competitive position across markets. Without

using the term “geographical diversification,” they consider the

shifting of production to offset price changes with local cost

changes to be an operational hedging strategy. As another

operational hedging strategy, they describe the operational

flexibility of multinationals in the form of shifting production and

transferring resources within their network.

Research in the strategy field provides a more comprehensive and

complete discussion of diversification and operational flexibility

from different perspectives. Diversification is defined as having

different lines of business through mergers and joint ventures

(Wang and Lim 2003), of which geographical diversification is one

type.

Kogut (1985) analyzes diversification and operational flexibility

as risk management tools of multinationals. He examines how

operational flexibility and diversification change the risk

profiles of firms. He argues that an operational decision (the

sourcing policy in this case) can create three different types of

risk profile: speculative, hedged and flexible. The speculative

profile is betting on one site mainly to benefit from economies of

scale in operations. By matching the exchange rate exposure on the21

cost side with that on the profit side, the firm can create a

hedged risk profile. This approach corresponds to the geographical

diversification strategy discussed in the finance literature.

Finally, a flexible risk profile created through operational

flexibility permits the firm to exploit uncertainties by creating

real options. Operational flexibility creates both arbitrage

(exploitation of differences between markets such as production

switching) and leverage (enhancing strategic position such as

increased bargaining power in negotiations with local governments)

opportunities for multinationals.

Miller (1998) says that strategic hedges, which he defines as real

options, can be used to hedge corporate downside risk. He discusses

operational flexibility and diversification as strategic hedges:

Similar to operational flexibility, diversification is claimed to

have real option benefits. In particular, diversification into new

product or geographic markets has an option value through creating

growth options (Kogut 1991, Kogut and Kulatilaka 1994). Other than

aligning costs and revenues, by opening a production facility in a

foreign country, firms can exploit being in that market by the cost

effectiveness of launching new products in the same market. Under

operational flexibility, Miller lists developing in-house capacity

to produce inputs when a firm has negative exposure to input

prices, vertical integration of a key supplier when the firm faces22

the price risk of a non-commodity input, reducing the price

elasticity of demand through product differentiation, and

increasing customer brand loyalty and switching costs when the firm

faces price competition.

2.2 Financial hedging

Financial approach involves the usage of various financial

instruments, such as forward or futures contracts, options, and

swaps. The goal of financial hedging is to increase value by

minimizing the variance of the net cash flows. Financial

instruments are considered to be an appropriate tool for minimizing

the risk from near-term exposures that have predetermined future

cash flows and can be relatively easily quantified (Srinivasulu

1981, Lessard 1986, Bodnar et al. 1995). The potential of the

financial instruments to manage operating exposure to exchange rate

changes is limited due to the broader scope of exposure, its longer

time horizon and existing uncertainty in the underlying cash flows

in addition to the exchange rate uncertainty. The elements of

operating exposure affect all parts of the company and therefore

cannot be exclusively look upon as a financial phenomenon. For

example, financial means become irrelevant hedging mechanisms when

changes in the exchange rates alter the competitive position of the

company or results in loss of various business opportunities.23

According to the risk management literature, management of the

operating exposure should be based on the strategic coordination of

the activities in company’s financial and operational areas. The

strategic financial approach to the management of the operating

exposure is based on the proper choice of the financing base and

may involve the choice of alternative credit lines in different

currencies or even in different countries

CHAPTER THREE

3.0 RESEARCH METHODOLOGY

3.1 Introduction

This chapter will cover in details the different methods that the

researcher will use to carry out the research and acquire data, the

target population for the study, sample and sampling procedure and

design, description of research instruments, description of data

collection procedure and tools to be used in data analysis.

24

3.2 Research Design

This study adopts a descriptive research design. This is a method

of collecting data by interviewing or administering a questionnaire

to sample of individuals (Orodho, 2003). In order to archive the

objectives of the study, the questionnaires were designed with the

intention of answering the research questions. Descriptive research

design is systematic, empirical inquiry into which the researcher

does not have direct control of independent valuables as their

manifestation have already occurred or because they reflecting the

state of happenings and qualify the obtained findings through the

use of qualitative analysis (Mugenda And Mugenda 1999). It means

considering such basic questions as what, how, when, when and where

about a given phenomenon.

3.3 Target Population

The target population is the financial managers and treasury

managers of selected companies listed in the NSE. The Nairobi

stock exchange has 58 companies listed (CMA annual report2011).

Such companies are distributed across the following industry

portfolios or segments;

Agricultural

Automobiles and accessories

Banking 25

Commercial and services

Construction and allied

Energy and petroleum

Insurance

investment

Manufacturing and allied

Telecommunication and technology

Due to the specialized nature of this study, and how it relates to

a specific market segment, the study selected such companies that

have foreign subsidiaries, engage on export and import or are

concentrating on international trade. As such the population

covered two department of the companies analysed below.

Table 1 population size

Department No of

companies

% of companies

Finance

department

58 50%

Treasury

department

58 50%

Total 116 100%

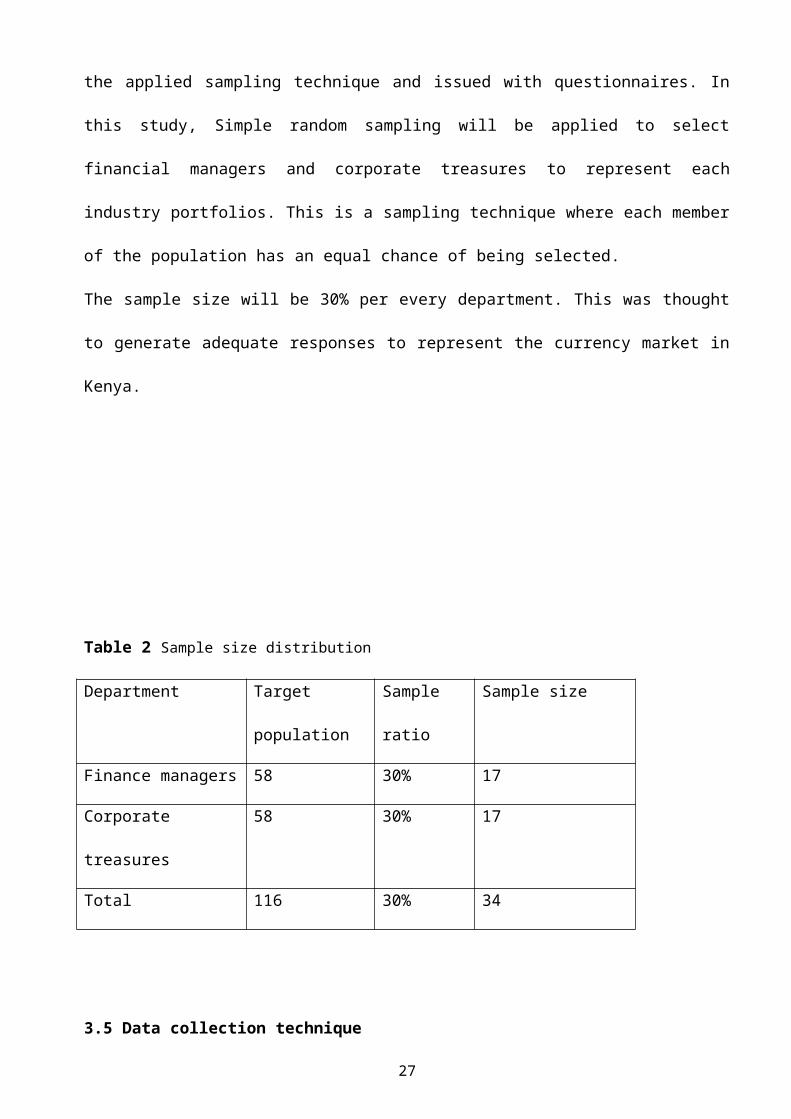

3.4 Sample and sampling procedure

This represented the number of respondent that will be selected by

26

the applied sampling technique and issued with questionnaires. In

this study, Simple random sampling will be applied to select

financial managers and corporate treasures to represent each

industry portfolios. This is a sampling technique where each member

of the population has an equal chance of being selected.

The sample size will be 30% per every department. This was thought

to generate adequate responses to represent the currency market in

Kenya.

Table 2 Sample size distribution

Department Target

population

Sample

ratio

Sample size

Finance managers 58 30% 17

Corporate

treasures

58 30% 17

Total 116 30% 34

3.5 Data collection technique

27

The method of data collection will be done using both primary and

secondary data. Primary data will be collected by use of

questionnaires. Operational hedging information will be gathered

through tailor-made questionnaires by asking the firm directly to

indicate what percentage of total exposure the firm hedges through

it operations.

Secondary data will be collected from the following sources; -The

companies published financial statements which give information on

financial instruments with off-balance-sheet risk. This will help

to estimate exposure for the period from 2009 to 2011, the

historical data on the exchange rates of the Kenya shilling against

the dollar will be obtained from: www.exchange-

rates.org/ history /KES/ USD /G . The rates of the Kenya shilling to the

dollar were obtained for the same period. Data regarding individual

firms’ stock prices, market index as measured by 20-share NSE Index

are obtained from NSE database. Exchange rate and trade volume data

to construct trade-weighted exchange rate will be obtained from

IFS.

3.5.1 Data collection Instruments

This comprise of questionnaires being the main instruments of use.

The questionnaires were sent to corporate treasurers and financial

managers to source data on firms’ hedging policies and their use of28

derivatives. The vast majority of questions in the survey were of

the open ended and close ended variety. The survey was designed in

this way to maximize the response rate while eliciting the

information of greatest interest. The main part of the

questionnaires required firms to indicate whether they hedged and

if so whether they used derivatives instruments for hedging. There

was also a section requiring firms to provide their motives for

hedging.

To examine the determinants of derivative use, i employ a series of

financial valuables which are obtained from Worldscope database.

3.6 Data Analysis

For this exploratory and descriptive study, composite standard

deviation, frequency distribution, tables and graphs are used. The

mean values are used to resolve the research questions. The most

positive and most negative responses are also discussed.

Data collected was coded and analyzed. This process involved coding

of all responses, which were then fed into a computer and analyzed

using the standard statistical package for social sciences (SPSS).

Descriptive statistical techniques were applied to the data.

29

This involved reducing the accumulated data into a manageable size

by looking at mean, averages, percentages and patterns that the

data had produced. This involved applying statistical and

descriptive techniques to the data and exploring various

relationships. It also involved viewing for consistent results that

could be interpreted and linked to answer the research questions.

This analysis was able to generate adequate results on the research

questions leading to conclusive results. The results are presented

in form of tables, figures and graphs in the next chapter.

CHAPTER FOUR

4.0 PRESENTATION OF THE FINDINGS AND INTERPRETATION

4.1 INTRODUCTION

The results of the data analysis and the findings are presented in

this chapter. The presentation is inform of graphs, and tables.

Fourty questionnaires were administered through emails that were

30

sent out to finance managers and corporate treasurers who were

expected to answer and elaborate on their knowledge of foreign

exchange exposure and how they hedge the exchange rate risks. The

responders were called and asked to fill out the questionnaires and

email them back with the answers. Persuasion by phone calls was

used to encourage all responders to answer the questions and return

the results to the researcher. Out of the 40 dealers questioned, 40

responded. This gave a response rate of 100% on the questionnaires

administered. The data collected was coded and analyzed. The

analysis involved the use of frequencies, percentages and mean

scores.

4.2 Data presentation and analysis of the Findings

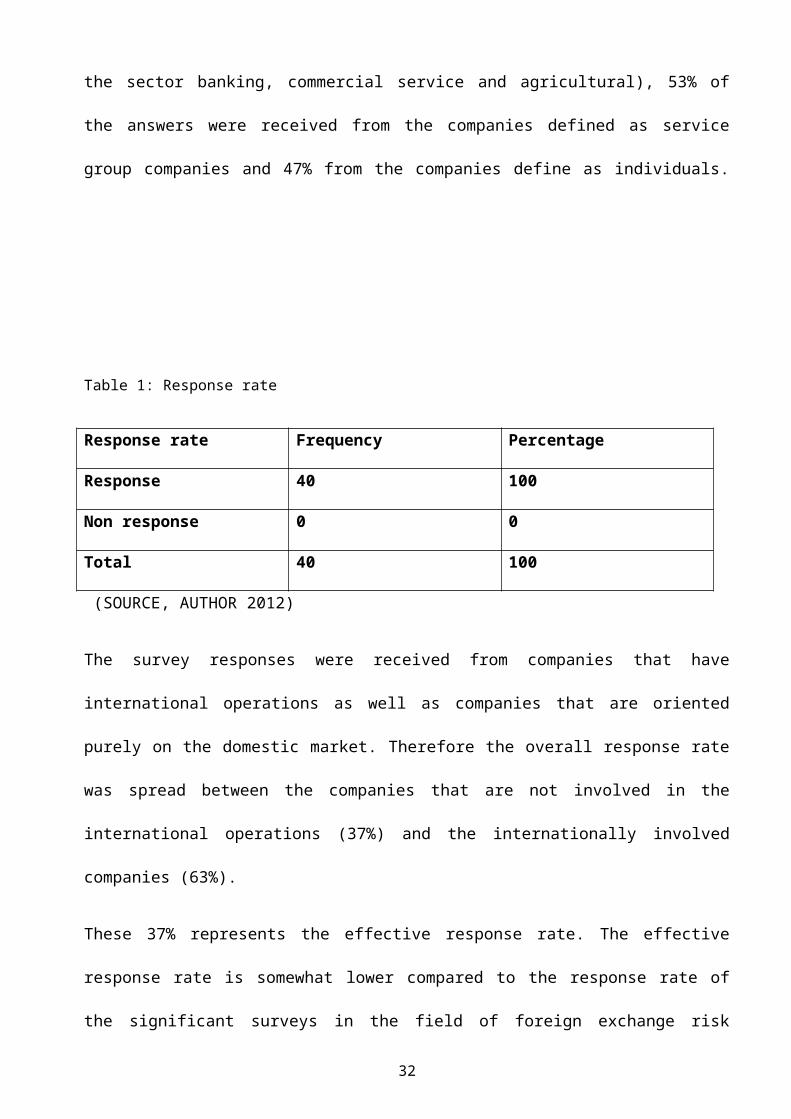

4.2.1 Response rate

The achieved response rate of the survey from the angle of the

whole target population, the economic sectors and groups of

industrial and service companies is reported in table 1 below. 40

companies have chosen to take part in the survey and an overall

response rate of 100% was achieved. The answers were received from

companies that represent all 10 economic sectors included in the

research. Response rate for each sector varied from a minimum of

30.8% (for the sector “manufacturing”), to maximum of 53.7% (for

31

the sector banking, commercial service and agricultural), 53% of

the answers were received from the companies defined as service

group companies and 47% from the companies define as individuals.

Table 1: Response rate

Response rate Frequency Percentage

Response 40 100

Non response 0 0

Total 40 100

(SOURCE, AUTHOR 2012)

The survey responses were received from companies that have

international operations as well as companies that are oriented

purely on the domestic market. Therefore the overall response rate

was spread between the companies that are not involved in the

international operations (37%) and the internationally involved

companies (63%).

These 37% represents the effective response rate. The effective

response rate is somewhat lower compared to the response rate of

the significant surveys in the field of foreign exchange risk

32

management. However the 40 companies that were contacted for the

purpose of the survey included both companies that are and are not

involved into international activities and only those companies

that have international operations are of interests to this study.

Excluding not internationally involve companies from the target

group would significantly improve the effective response rate.

Otherwise, the number of the responding companies tat are

internationally involve is significant for conducting statistical

calculations an generalizing the results of the survey. Therefore

we conclude that the survey response is quite satisfactory.

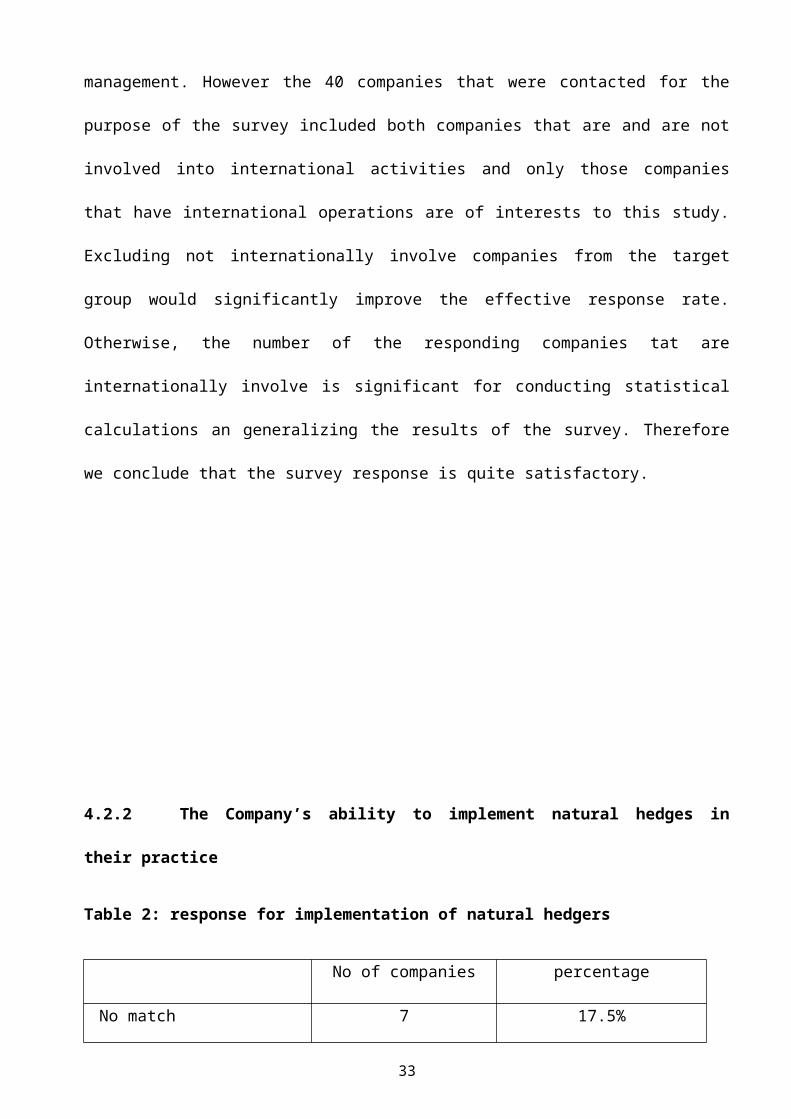

4.2.2 The Company’s ability to implement natural hedges in

their practice

Table 2: response for implementation of natural hedgers

No of companies percentage

No match 7 17.5%

33

Relatively low match 5 12.5%

Match to some degree 15 37.5%

Relatively high match 9 22.5%

Complete match 4 10%

40 100%

Figure 1; implementation of natural hedgers

The majority of the companies (37.6%) have a certain match between

currencies in which their operating revenues and costs are

denominated. And overall 87.1 % of the companies have at least some

match in the currencies since only 12.9% of the companies answered

that they have no match in the currencies at all. This 12.9% is

probably equal to that group of companies that have production or

sourcing in the country with one particular currency.

34

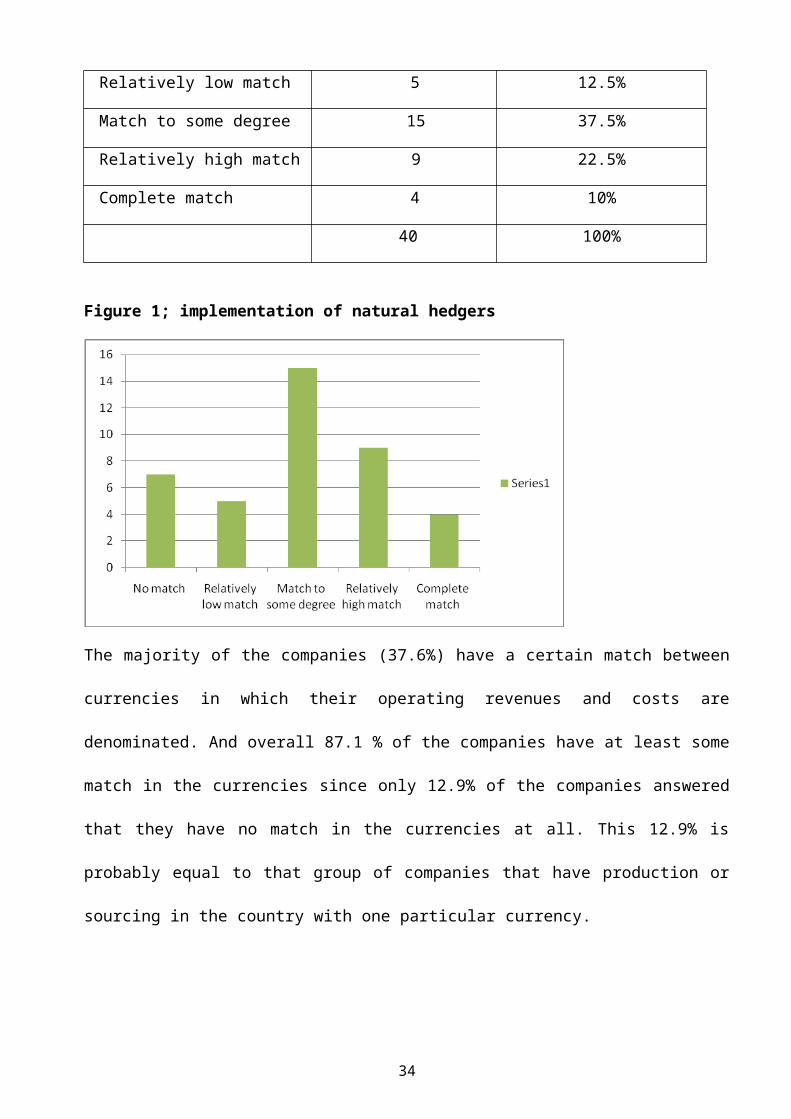

4.2.3 Number of foreign subsidiaries

Table 3: Number of foreign subsidiariesThe table reports the results of survey question 5: How many foreign

subsidiaries does your company have? The answers were received as ordinal

numerals from 0 to 50 with the max”more than 50”29. In the table

the answers are presented in the defined intervals. The number and

the percentage of the companies for each interval are calculated

Figure2: number of subsidiaries

35

N Percentage

0 3 7.5%

1-5 8 20%

6-10 12 30%

11-20 11 27.5%

21-30 6 15%

Total 40 100%

Almost 35% of the companies do not have foreign subsidiaries abroad

indicating that a “physical” presence in foreign countries is not a

necessary condition for the companies to be involved in

international activities. The majority of the companies (45.7%),

however, have between 1 and 5 subsidiaries abroad. About 58% of the

companies have from 1 to 10 subsidiaries abroad. On average the

companies have 3.4 subsidiaries abroad.

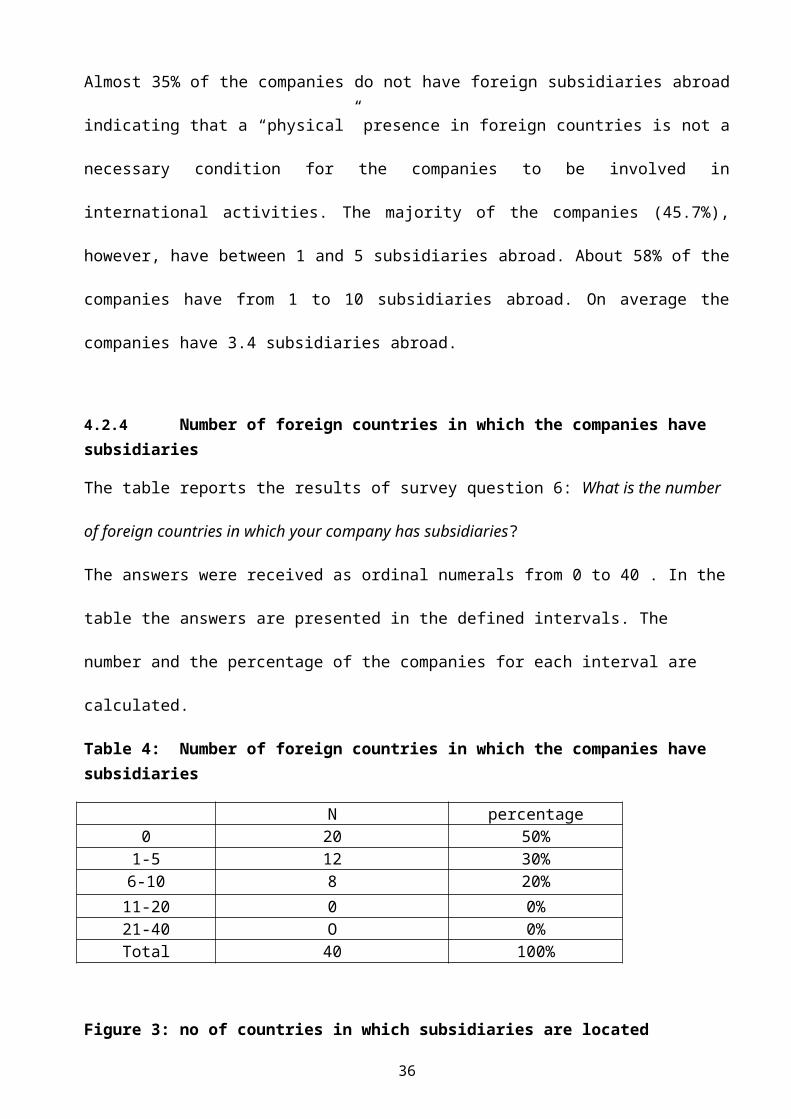

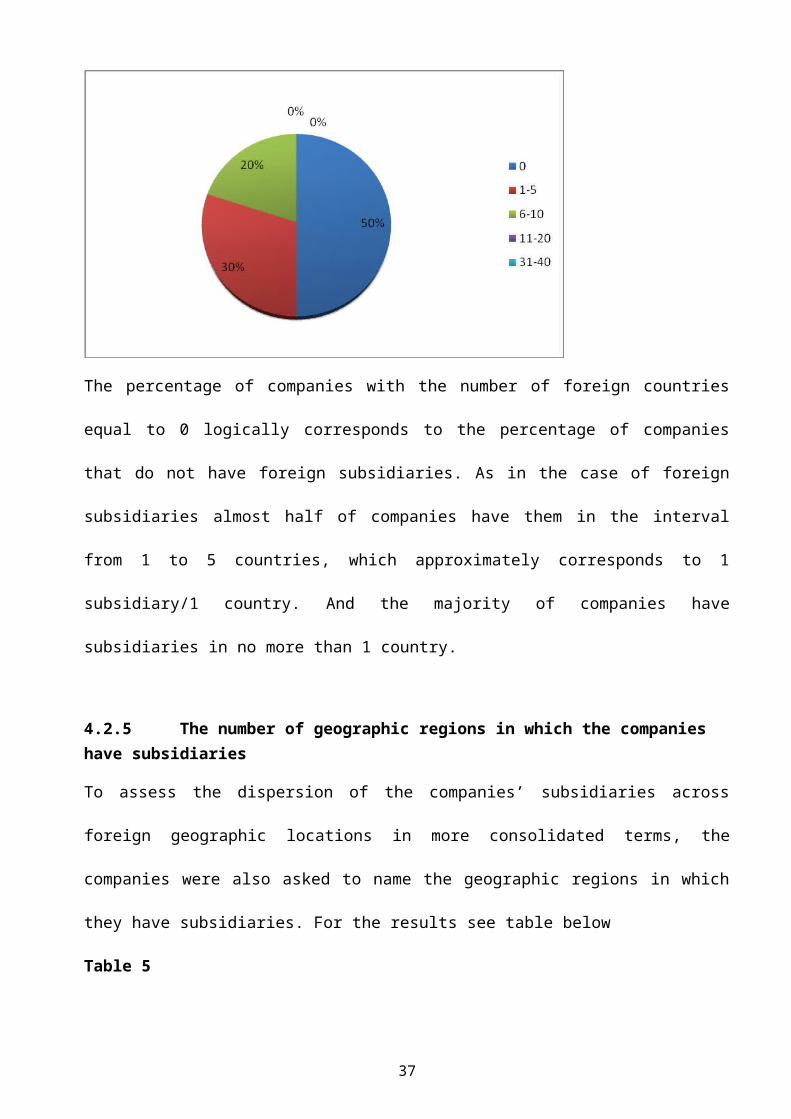

4.2.4 Number of foreign countries in which the companies have subsidiaries

The table reports the results of survey question 6: What is the number

of foreign countries in which your company has subsidiaries?

The answers were received as ordinal numerals from 0 to 40 . In the

table the answers are presented in the defined intervals. The

number and the percentage of the companies for each interval are

calculated.

Table 4: Number of foreign countries in which the companies have subsidiaries

Figure 3: no of countries in which subsidiaries are located

36

N percentage0 20 50%

1-5 12 30%6-10 8 20%11-20 0 0%21-40 O 0%Total 40 100%

The percentage of companies with the number of foreign countries

equal to 0 logically corresponds to the percentage of companies

that do not have foreign subsidiaries. As in the case of foreign

subsidiaries almost half of companies have them in the interval

from 1 to 5 countries, which approximately corresponds to 1

subsidiary/1 country. And the majority of companies have

subsidiaries in no more than 1 country.

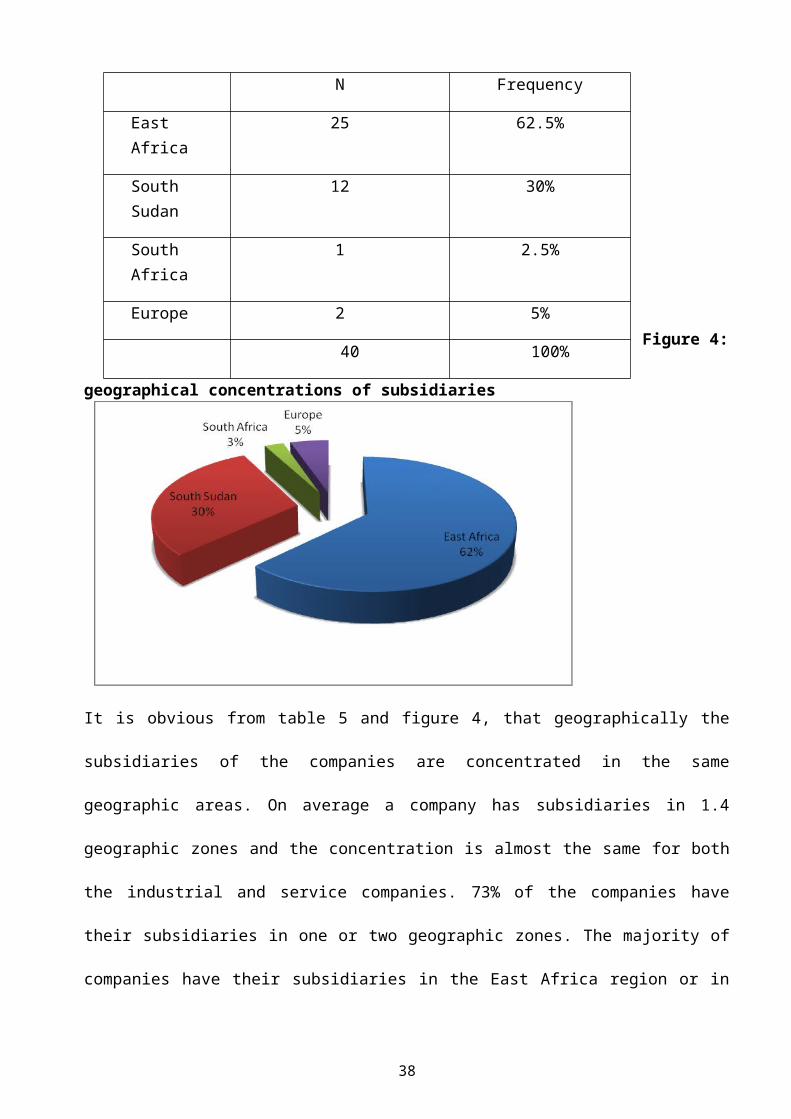

4.2.5 The number of geographic regions in which the companies have subsidiaries

To assess the dispersion of the companies’ subsidiaries across

foreign geographic locations in more consolidated terms, the

companies were also asked to name the geographic regions in which

they have subsidiaries. For the results see table below

Table 5

37

Figure 4:

geographical concentrations of subsidiaries

It is obvious from table 5 and figure 4, that geographically the

subsidiaries of the companies are concentrated in the same

geographic areas. On average a company has subsidiaries in 1.4

geographic zones and the concentration is almost the same for both

the industrial and service companies. 73% of the companies have

their subsidiaries in one or two geographic zones. The majority of

companies have their subsidiaries in the East Africa region or in

38

N Frequency

East Africa

25 62.5%

South Sudan

12 30%

South Africa

1 2.5%

Europe 2 5%

40 100%

south Sudan. The third most popular location is the US and Canada

followed by the South Africa.

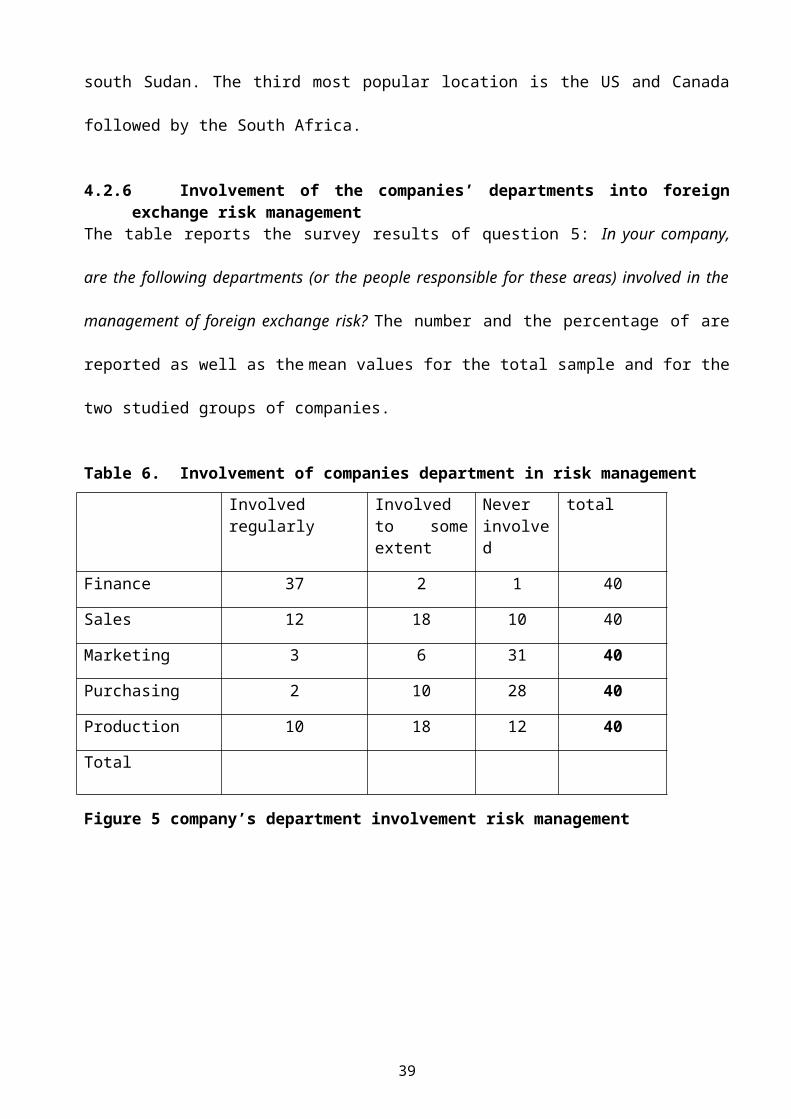

4.2.6 Involvement of the companies’ departments into foreignexchange risk management

The table reports the survey results of question 5: In your company,

are the following departments (or the people responsible for these areas) involved in the

management of foreign exchange risk? The number and the percentage of are

reported as well as the mean values for the total sample and for the

two studied groups of companies.

Table 6. Involvement of companies department in risk management

Figure 5 company’s department involvement risk management

39

Involvedregularly

Involvedto someextent

Neverinvolved

total

Finance 37 2 1 40

Sales 12 18 10 40

Marketing 3 6 31 40

Purchasing 2 10 28 40

Production 10 18 12 40

Total

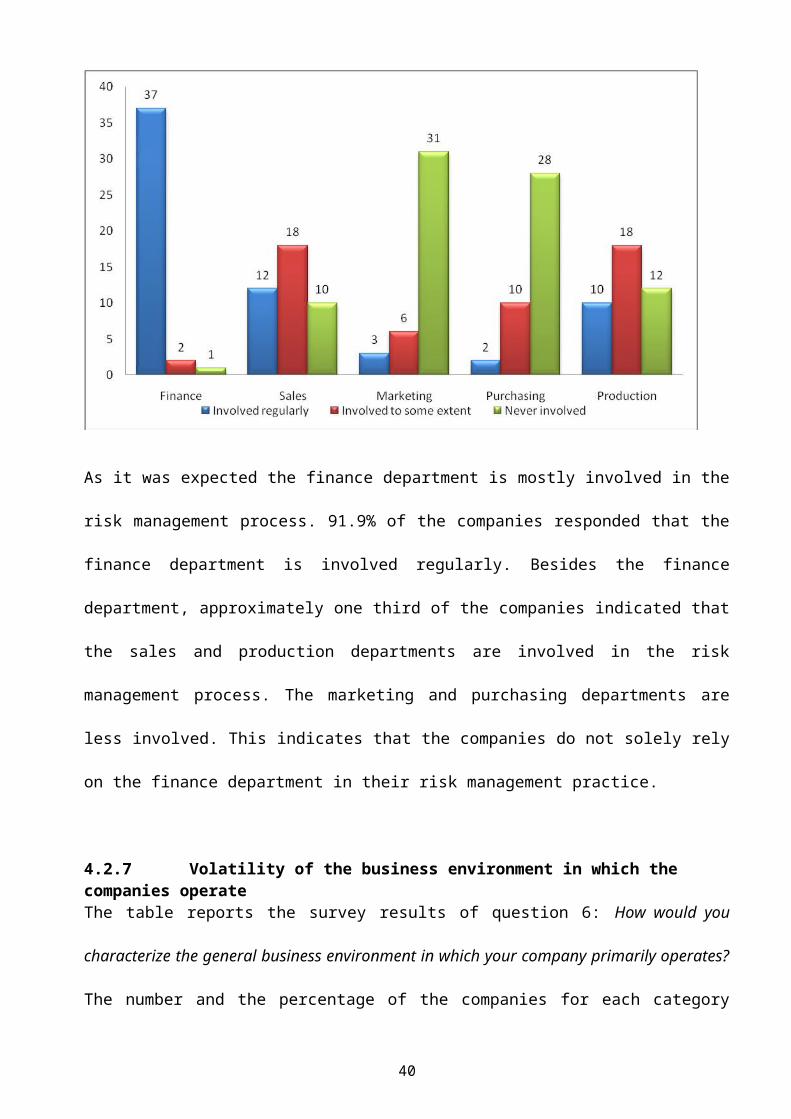

As it was expected the finance department is mostly involved in the

risk management process. 91.9% of the companies responded that the

finance department is involved regularly. Besides the finance

department, approximately one third of the companies indicated that

the sales and production departments are involved in the risk

management process. The marketing and purchasing departments are

less involved. This indicates that the companies do not solely rely

on the finance department in their risk management practice.

4.2.7 Volatility of the business environment in which the companies operate The table reports the survey results of question 6: How would you

characterize the general business environment in which your company primarily operates?

The number and the percentage of the companies for each category

40

are reported as well as the mean values for the total sample and for

the two studied groups of companies

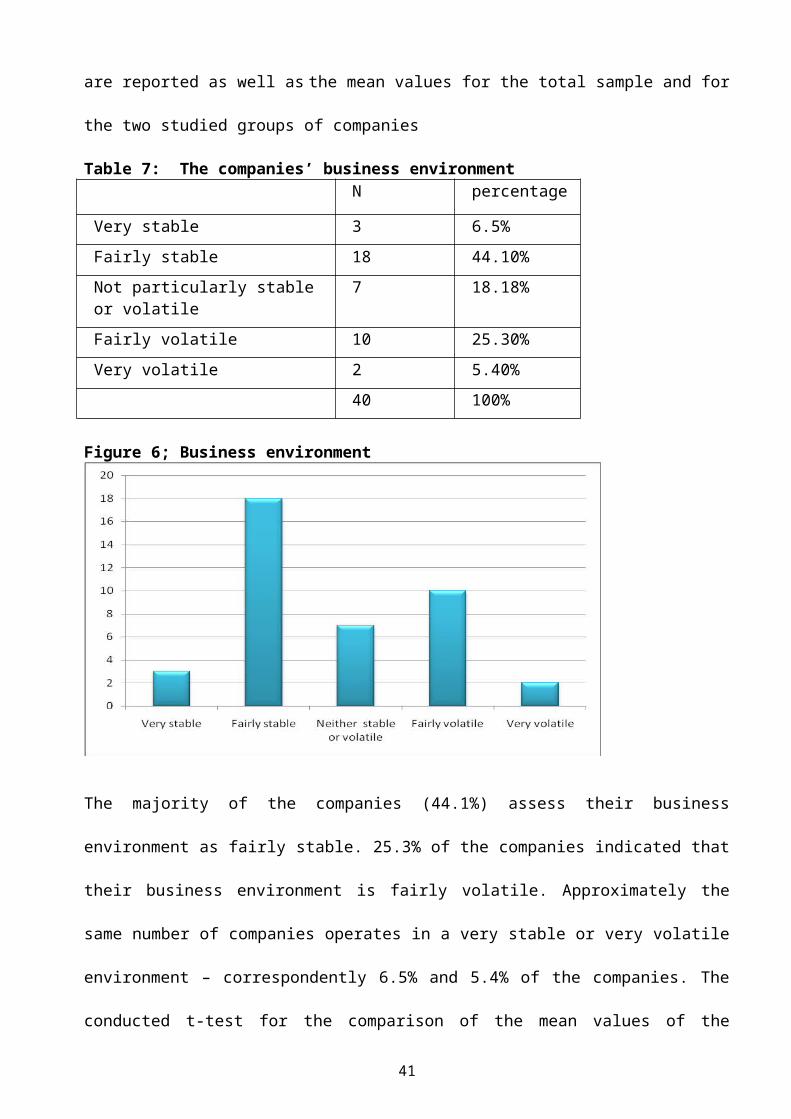

Table 7: The companies’ business environment N percentage

Very stable 3 6.5%Fairly stable 18 44.10%Not particularly stable or volatile

7 18.18%

Fairly volatile 10 25.30%Very volatile 2 5.40%

40 100%

Figure 6; Business environment

The majority of the companies (44.1%) assess their business

environment as fairly stable. 25.3% of the companies indicated that

their business environment is fairly volatile. Approximately the

same number of companies operates in a very stable or very volatile

environment – correspondently 6.5% and 5.4% of the companies. The

conducted t-test for the comparison of the mean values of the

41

indicator for the industrial and service groups showed that there

is statistically significant difference, though at a 10% level.

Thus, on average the industrials on average operate in more stable

environment than the service companies.

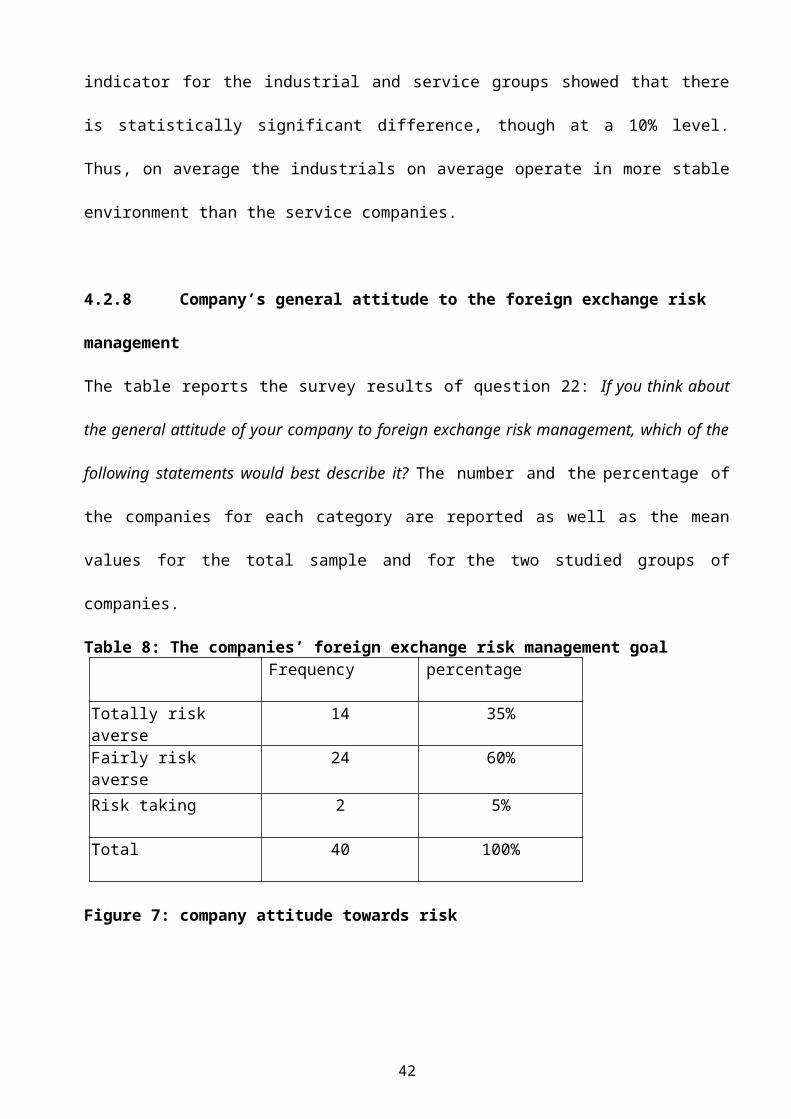

4.2.8 Company’s general attitude to the foreign exchange risk

management

The table reports the survey results of question 22: If you think about

the general attitude of your company to foreign exchange risk management, which of the

following statements would best describe it? The number and the percentage of

the companies for each category are reported as well as the mean

values for the total sample and for the two studied groups of

companies.

Table 8: The companies’ foreign exchange risk management goalFrequency percentage

Totally risk averse

14 35%

Fairly risk averse

24 60%

Risk taking 2 5%

Total 40 100%

Figure 7: company attitude towards risk

42

34.4% of the companies stated that their only task is to minimize

the negative impact of exchange rate fluctuations. Only 5.4% of the

companies indicated that they are risk taking and therefore they

are constantly seeking additional return from the risk management

activities

4.3 Financial hedging strategy

The second part of the survey was mostly concerned with specific

potential and actual financial hedging strategies on exchange rate

exposure management of the companies. The questions in the section

were asked in order to determine the various tools for financial

hedging and the impact of financial hedging strategies for the

companies. The results of the survey for these questions are

presented in the following tables.

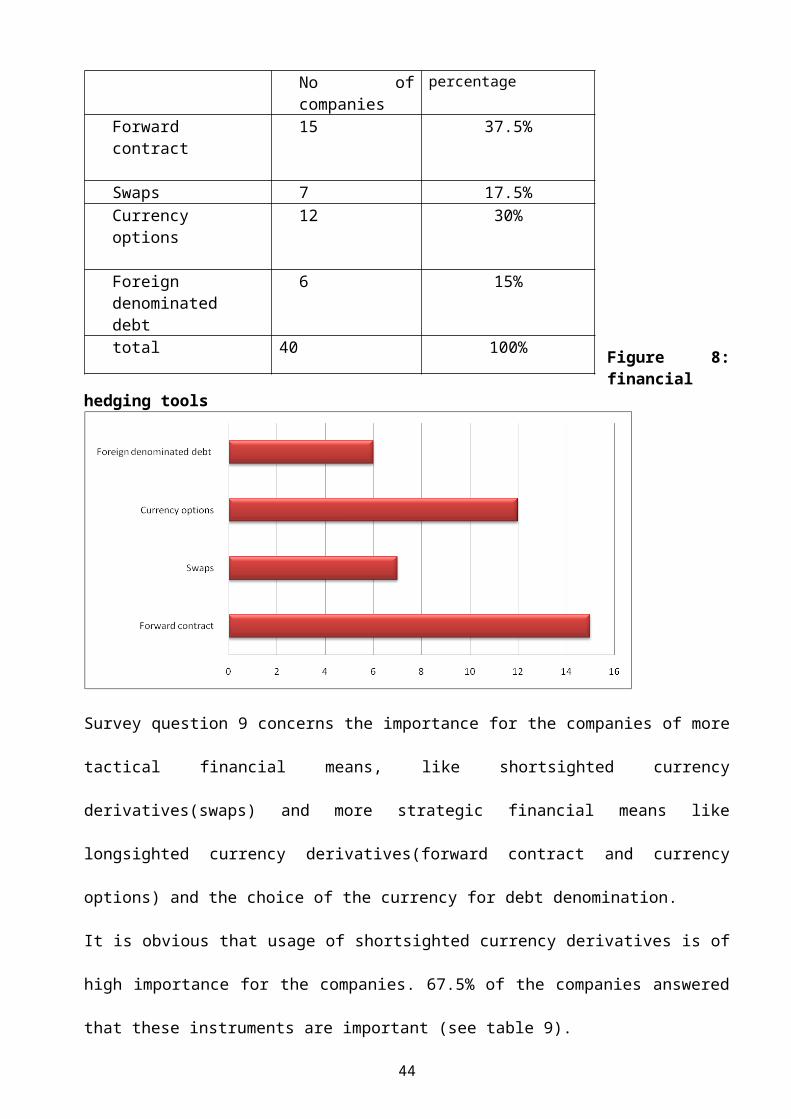

4.3.1 Derivatives used by the firm for financial hedging

Table 9: Types of derivatives used

43

Figure 8:financial

hedging tools

Survey question 9 concerns the importance for the companies of more

tactical financial means, like shortsighted currency

derivatives(swaps) and more strategic financial means like

longsighted currency derivatives(forward contract and currency

options) and the choice of the currency for debt denomination.

It is obvious that usage of shortsighted currency derivatives is of

high importance for the companies. 67.5% of the companies answered

that these instruments are important (see table 9).

44

No ofcompanies

percentage

Forwardcontract

15 37.5%

Swaps 7 17.5%Currencyoptions

12 30%

Foreigndenominateddebt

6 15%

total 40 100%

On the second place ranked after its importance for the companies

to manage their foreign exchange risk is the choice of swaps. For

30% of companies this tool is at least somewhat important.

So, we can see that most of the companies would choose tactical

financial instruments when managing foreign exchange exposure. In

the case when they will need to apply a more strategically oriented

approach they would rather choose longsighted currency derivatives

instead of foreign debt.

4.3.2 The impact of shortsighted currency derivatives (Forwardcontracts, options)

Table 10

Impact 1

Strongly Agree

2Agree

3Disagree

4StronglyDisagree

5Can’t

Tell

To reduce corporate taxliability

8 24 6 1 1

Lowers the probability of firmencountering financial distress.

17 20 3 0 0

Derivatives reduces volatilityin accounting earnings

13 25 1 0 1

Reduced volatility in cash flowsand earnings in imperfect market

12 26 2 0 0

Increase firms market price inthe presence of agency betweenshareholders and bondholders

8 20 5 4 3

Protect against downside riskand allow upside appreciation

17 19 4 0 0

45

Generate profit by trading inthe financial markets

4 22 8 0 6

frequency 69 156 29 4 11

percentage 25.65 57.99

10.78 1.49 4.09

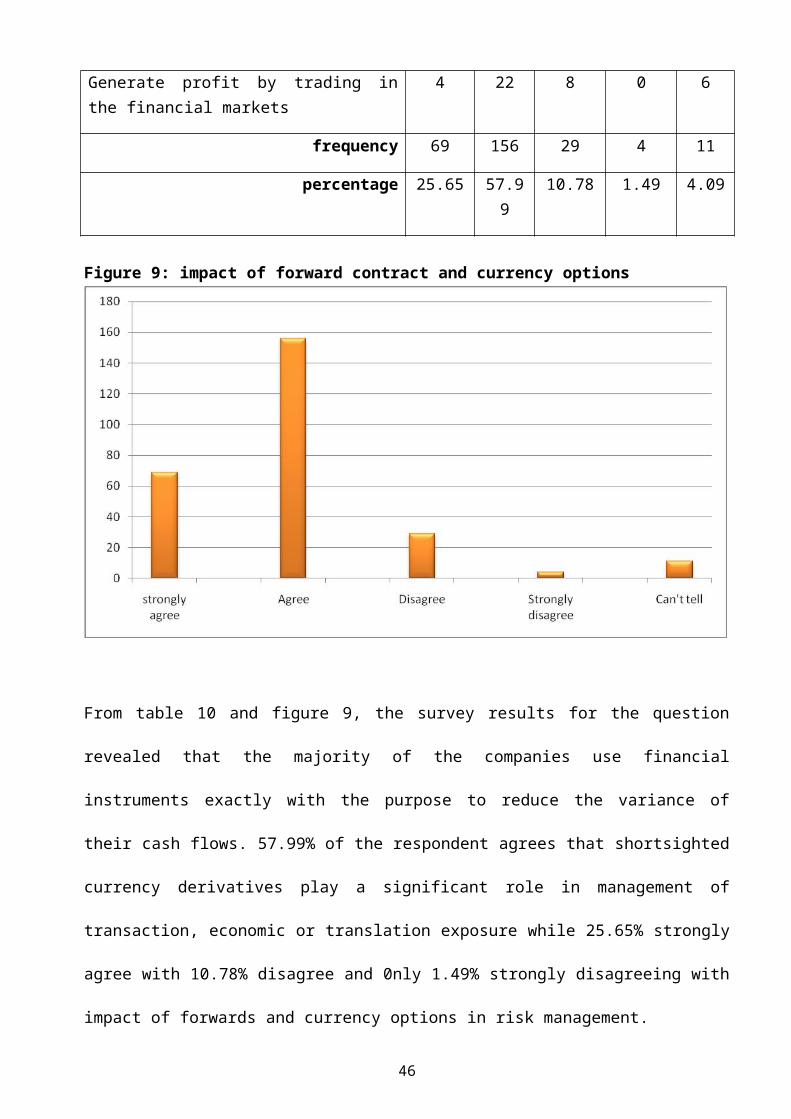

Figure 9: impact of forward contract and currency options

From table 10 and figure 9, the survey results for the question

revealed that the majority of the companies use financial

instruments exactly with the purpose to reduce the variance of

their cash flows. 57.99% of the respondent agrees that shortsighted

currency derivatives play a significant role in management of

transaction, economic or translation exposure while 25.65% strongly

agree with 10.78% disagree and 0nly 1.49% strongly disagreeing with

impact of forwards and currency options in risk management.

46

4.3.3 Impact of use of longsighted currency derivatives(swaps) as hedging tools

Table 11: impact of swaps

1 2 3 4 5

Minimize the costs of foreignconversion while protecting againstexchange rate risk.

21 15 2 1 1

Minimise risk & maximise certaintyof revenue & costs & activelymanage risks in order to makeprofit contribution

18 21 1 0 0

Increase firm value in the presenceof financial distress costs

21 14 2 2 1

reduced volatility in interest rate 19 17 1 0 0

reduce financial distress costs 21 15 2 1 1

Give companies a better match between liabilities and revenue

19 17 1 0 3

Ensures certainty of receipt of 17 22 1 0 0

47

foreign monies

To achieve better lending rates 25 15 0 0 0

Frequency 161 136 10 4 6

Percentage 50.79

42.90 3.15 1.26 1.89

Figure10: impact of using swaps

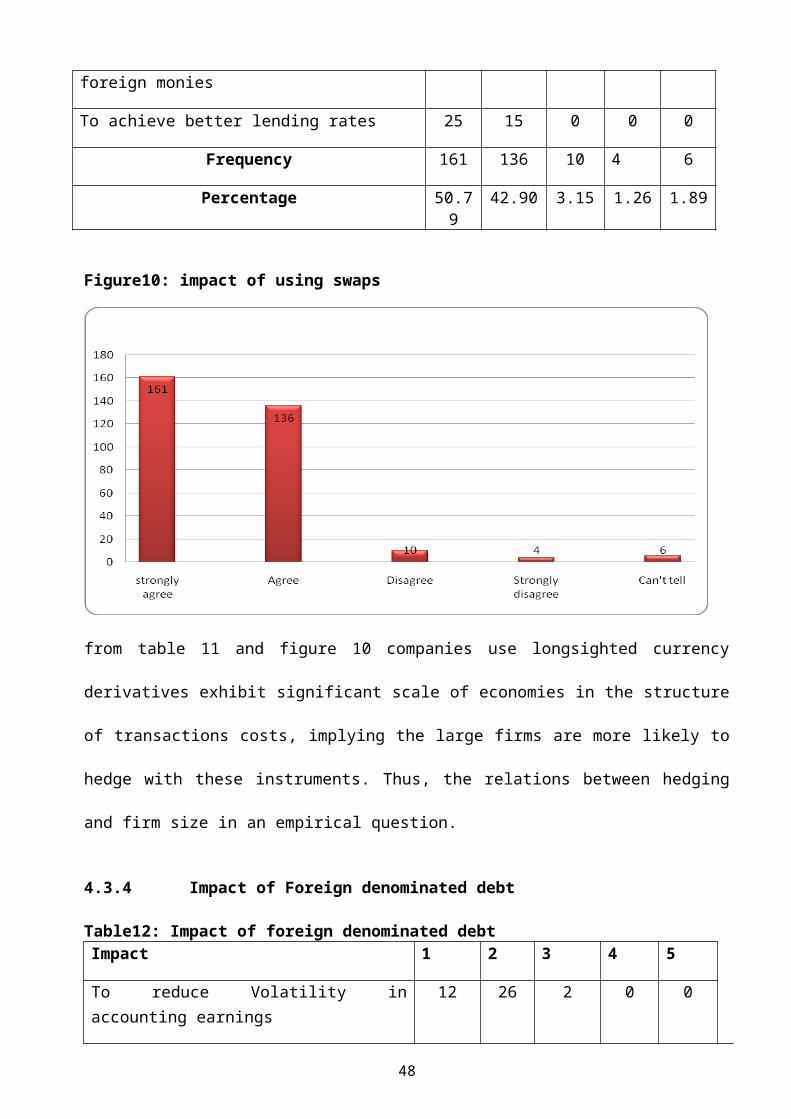

from table 11 and figure 10 companies use longsighted currency

derivatives exhibit significant scale of economies in the structure

of transactions costs, implying the large firms are more likely to

hedge with these instruments. Thus, the relations between hedging

and firm size in an empirical question.

4.3.4 Impact of Foreign denominated debt

Table12: Impact of foreign denominated debtImpact 1 2 3 4 5

To reduce Volatility inaccounting earnings

12 26 2 0 0

48

Volatility in cash flows 10 19 7 2 2

Generate additional returns andenhance the profitability of thetreasury activity.

12 17 8 2 1

Reduce funding costs/ make thebest use of borrowingopportunities

17 20 3 0 0

Financial price risk hedging 14 18 6 2 0

To hedge translation exposure 17 18 6 2 0

To hedge transaction exposure 13 22 3 0 2

Frequency 95 140 34 6 5

Percentage 33.93%

50% 12.14%

2.14%

1.79%

Figure 11: Impact of foreign denominated debt

Table 12 and figure 11 findings shows that debt denominated in

foreign currency are used to reduce the probability that a firm

encounters financial distress by reducing the variability of firm

49

value, and thereby reduces the expected costs of financial

distress.

4.4 OPERATIONAL HEDGING

4.4.1 Operating hedging strategies in use

Table 13; we use the following operational means as hedging tools

Strategies N percentage

Geographical location 12 30%

Alternative Pricing 8 20%

Timing & choice of new market &market segments

7 17.5%

Choice of alternative inputsourcing locations

4 10%

Planning and production mix. 9 22.5%

Total 40 100%

Figure12: Operational hedging strategies

50

30% of the companies stated that they had entered a new foreign

market where they did not have any sales and operations before.

This provides evidence that when resorting to operational hedging

techniques in the form of various real actions the companies are

primarily oriented on getting advantages through exchange rate

changes.

The change of product mix was the second most popular strategy

(22.5%) adopted as a response to exchange rate changes. The last

important operational instrument chosen was the timing and choice

of new market segments (10).

The degree of the importance of such operational instruments as

market choice, the choice of sourcing and production locations is

similar for the companies.

51

4.4.1 The impact of operational approach to exchange rate risksexposure

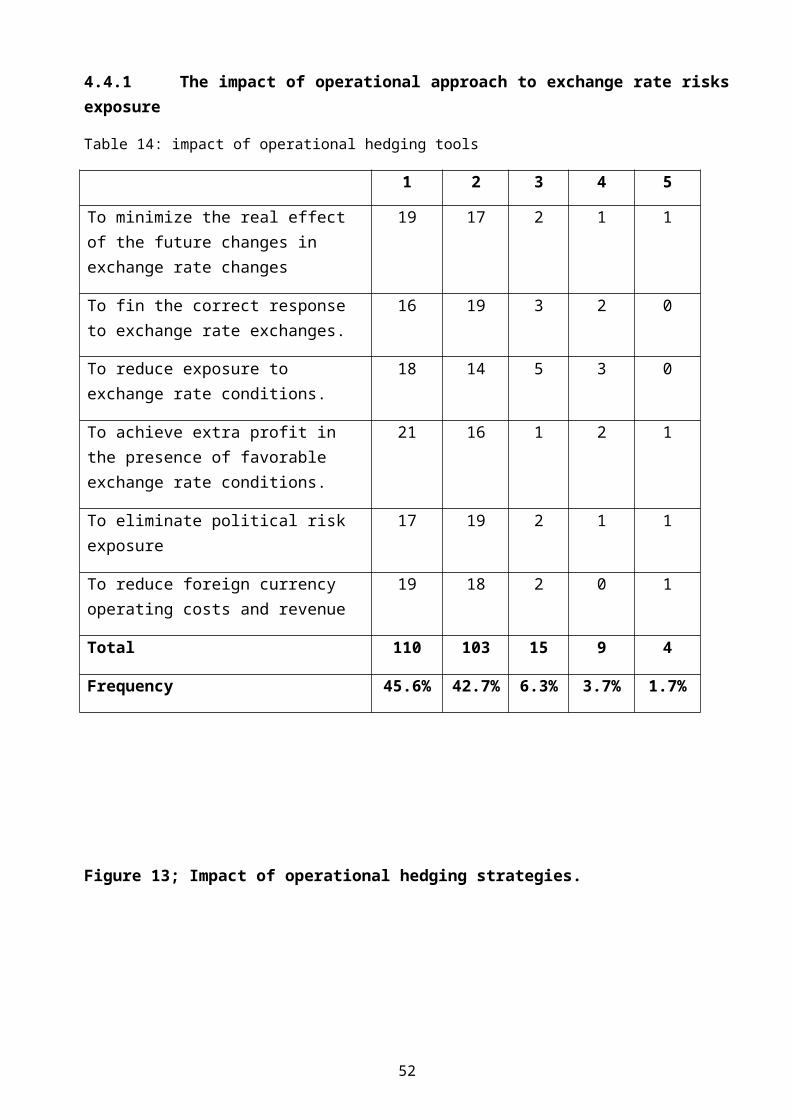

Table 14: impact of operational hedging tools

1 2 3 4 5

To minimize the real effect of the future changes in exchange rate changes

19 17 2 1 1

To fin the correct response to exchange rate exchanges.

16 19 3 2 0

To reduce exposure to exchange rate conditions.

18 14 5 3 0

To achieve extra profit in the presence of favorable exchange rate conditions.

21 16 1 2 1

To eliminate political risk exposure

17 19 2 1 1

To reduce foreign currency operating costs and revenue

19 18 2 0 1

Total 110 103 15 9 4

Frequency 45.6% 42.7% 6.3% 3.7% 1.7%

Figure 13; Impact of operational hedging strategies.

52

Table 14 and figure 13 findings shows that majority of the above

are likely impact of operational hedging strategy. 45.6% and 42.7%

strongly agree that operating strategies minimses volatility on

cash flow by minimizing the real effect of the future company

exposure to exchange risks.

4.4.2 The importance of operational meansThe table report survey results of question 14: in order to manage

the impact of exchange rate fluctuations on your company’s

operating cash flows or competitive position, how important are the

following operational means for your company?

1 2 3 4 5

Product mix choice 18 4 11 6 1

Market choice 14 6 8 9 3

Production locations 16 4 10 8 2

Pricing strategy 10 3 5 14 8

53

Frequency 58 17 34 37 14

Percentage 32.25% 10.63% 21.25% 23.13% 8.75%

Figure 14 Importance 0f operational means

From the table 15 and figure 14 it shows that the above operational

means were commonly used to manage the impact of exchange rate

fluctuations on operating cash flows or competitive position. The

degree of the importance of such operational instruments as market

choice, the choice of sourcing and production locations is similar

for the companies. These instruments are relatively unimportant for

the companies’ sine on average the importance of usage of these

instruments was placed between the “neither important nor

important” and the “somewhat unimportant” categories. It is

interesting to notice, that the choice of sourcing locations and54

the production location was not as important for the companies as

one would assume, since three is a wide spread assumption that

companies will always look for “cheaper” sourcing or production

locations. Furthermore, the industrial companies’ choice of

sourcing locations was slightly more important that it was for the

service companies.

4.5 Effectiveness of hedging strategies on firm’s value

The survey results for the previous questions indicate that in

general the companies tend to name various financial hedging means

as more important than operational means. However, from those

results it is difficult to conclude something concrete about the

importance between financial and operational means. For this

purpose the companies were directly asked to define the importance

between the financial and operational means for their management of

the operating foreign exchange exposure.

4.5.1 Relative importance of financial or operational means.

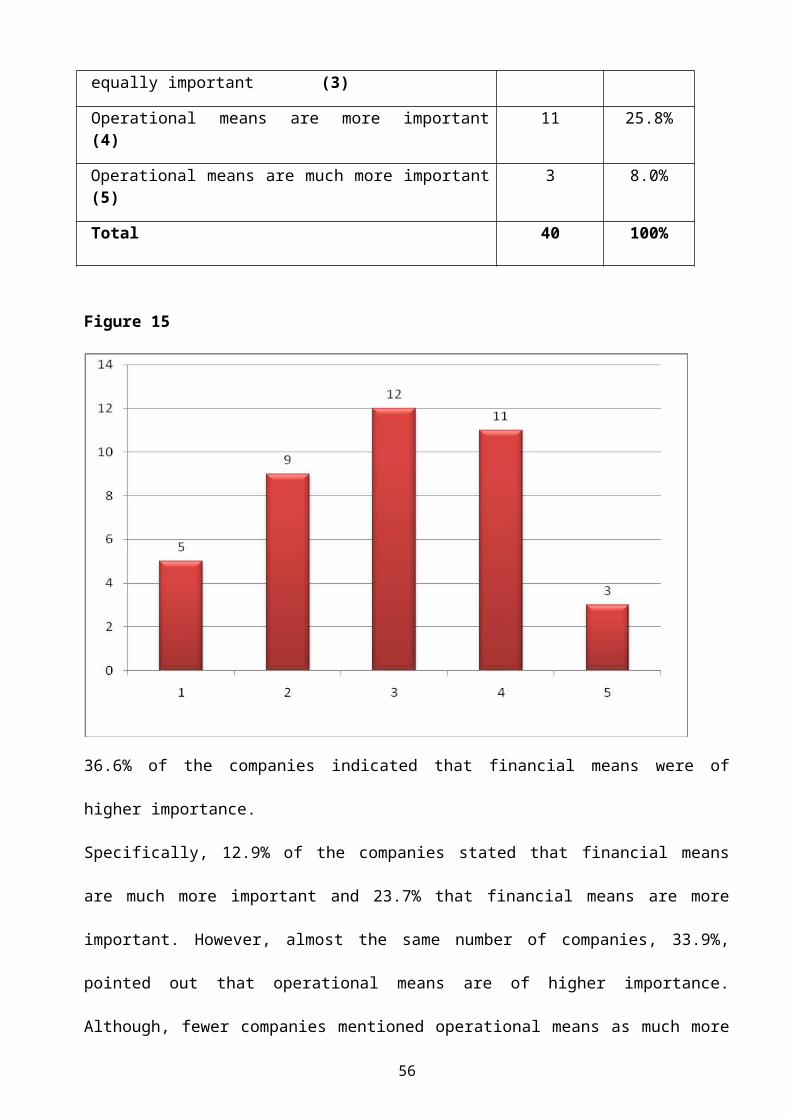

Table 16 importance of financial or operational hedging strategy

Frequency Percentage

Financial means are much more important(1)

5 12.9%

Financial means are more important(2)

9 23.7%

Financial and operational means are 12 29.6%

55

equally important (3)

Operational means are more important(4)

11 25.8%

Operational means are much more important(5)

3 8.0%

Total 40 100%

Figure 15

36.6% of the companies indicated that financial means were of

higher importance.

Specifically, 12.9% of the companies stated that financial means

are much more important and 23.7% that financial means are more

important. However, almost the same number of companies, 33.9%,

pointed out that operational means are of higher importance.

Although, fewer companies mentioned operational means as much more

56

important compared to the number of companies that mentioned

financial means as much more important. Despite the fact that the

majority of the companies were inclined to pick one of the risk

management approaches, financial or operational, the most

interesting results was that the most frequently chosen category

was category 3 “financial and operational means are equally

important”. Thus the results of the survey provide a clear

indication that both financial and operational means are at the

same level of importance for the companies.

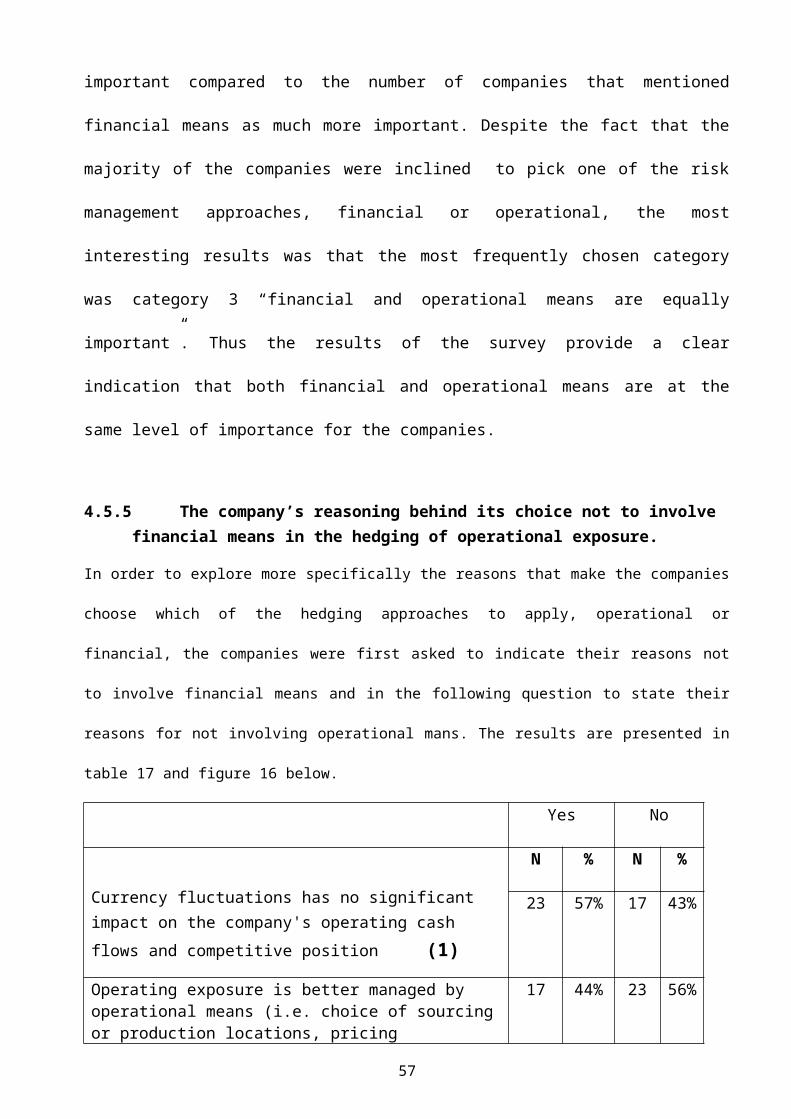

4.5.5 The company’s reasoning behind its choice not to involve financial means in the hedging of operational exposure.

In order to explore more specifically the reasons that make the companies

choose which of the hedging approaches to apply, operational or

financial, the companies were first asked to indicate their reasons not

to involve financial means and in the following question to state their

reasons for not involving operational mans. The results are presented in

table 17 and figure 16 below.

Yes No

Currency fluctuations has no significant impact on the company's operating cash flows and competitive position (1)

N % N %

23 57% 17 43%

Operating exposure is better managed by operational means (i.e. choice of sourcingor production locations, pricing

17 44% 23 56%

57

strategy etc) (2)Operating exposure cannot be quantified properly in order to be hedged by financial means (3)

14 35% 26 65%

The cost of hedging by financial means aretoo high (4)

15 38% 25 62%

Lack of knowledge and expertise of operating exposure (5)

8 19% 32 81%

The management of the company believes that in the long run positive and negative exchange rate changes cancel each other out. (6)

14 35% 26 65%

The proper financial instruments are not available on the market. (7)

5 13% 35 87%

Figure16

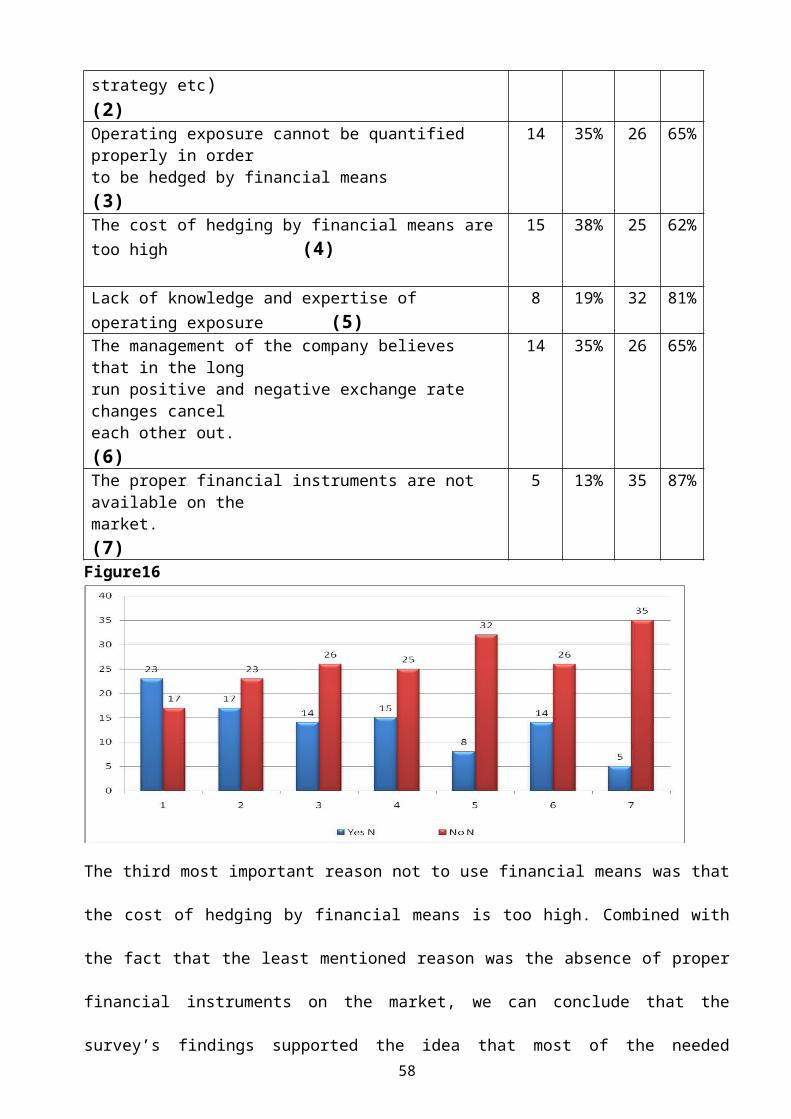

The third most important reason not to use financial means was that

the cost of hedging by financial means is too high. Combined with

the fact that the least mentioned reason was the absence of proper

financial instruments on the market, we can conclude that the

survey’s findings supported the idea that most of the needed58

financial instruments can be found on the market but in some cases,

especially in the long run, their usage will be very costly for the

companies.

As in the case of financial means, when the influence of exchange

rate changes on the company’s operating cash flows is

insignificant, the company’s does no resort to risk management

actions. That is why the reason was chosen as the primary reason by

companies. (See table 18 below)

Table 18: the company’s reasoning behind its choice not to involve

operational means in the hedging operating exposure.

Yes No

Currency fluctuations has no significant impact on the company's operating cash flows and competitive position (1)

N % N %

21 51% 19 49%

Operating exposure is better managed by operational means (i.e. choice of sourcingor production locations, pricingstrategy etc) (2)

19 49% 21 51%

The cost of hedging by financial means aretoo high (3)

14 35% 26 65%

Operational exposure cannot be quantified properly in order to hedge by financial means. (4)

13 34% 27 66%

The management of the company believes that in the long run positive and negative exchange rate changes cancel each other out.

11 28% 29 72%

59

(5)Lack of knowledge and expertise of operating exposure (6)

8 21% 32 79%

Figure 17

Again, the evidence was found that in the case when companies chose

not to use operational means the first explanation would be that

the exposure could be better managed by financial means. Based

solely on the results of question 16 and 17, we cannot affirm if

the companies consider the financial and operational hedging

options as complements or substitutes to each other.

60

CHAPTER FIVE

5.0 SUMMARY OF MAJOR FINDINGS, CONCLUSIONS AND RECOMMEDATIONS.

5.1 IntroductionIn this chapter, the findings of the study are given. The chapter

is arranged as follows: introduction, summary of major findings,

answers to rsearch questions, recommendations, limitations and

suggested area of further research.

5.2 summary of major findings.

5.3 Conclusions

The present study complements the existing risk management

literature by providing empirical evidence on the strategic foreign

exchange risk management practice by companies quoted in the

Nairobi Stock Exchange. The empirical data obtained from the

conducted survey supports the fact that interactions between

operational and financial strategies are seen as being complements

to each other. One third of the responding companies’ directly

stated that operational or financial means are equally important in

the management of foreign exchange operating exposure.61

Further more, the companies indicated that the second most

important reason for not involving financial means into the risk

management of operating exposure is that the exposure can be

managed by the means of various operational strategies. Operational

flexibility was named as the most popular operational hedging

strategy used by the companies. When it comes to the adoption by

the companies various real actions as a response to foreign

exchange rate fluctuations, the majority of the companies consider

a shift of supplier to foreign locations where it became cheaper to

source due to exchange rate changes.

Among the company specific factors that explain the importance and

application of financial and operational hedging approaches the

measures of multinationality and foreign exposure are undoubtedly

significant as explanatory factors for the importance and

application of hedging strategies. Besides these measures, on the

aggregate level the measures of profitability and growth

opportunities, the company’s risk objective and the involvement of

the operational and financial department in the risk management

process are also significant factors in explaining the importance

of operational hedges and the size of the company, its capital

structure and the involvement of he operational and financial

departments are important as an explanation of the importance of

financial means.62

As in the case of the importance of financial and operational

approaches, the measures of multinationality and foreign exchange

exposure are also the most significant factors that explain the

companies’ actual and potential involvement in real action

strategies and the usage of shortsighted and longsighted financial

means. Risk management objectives and involvement of both financial

and operational departments were important factors in explaining

the actual real options strategies adopted by the companies as a

response t exchange rate changes. Additionally, the presented

growth opportunities are explanatory factors for the possible real

options strategies undertaken by the companies and company’s size

is significant for explaining the usage of shortsighted financial

means.

5.4 Suggestion for further research.

The research looked at only companies’ listed in the Nairobi stock

Exchange. Further research is also desirable that can provide

comparable empirical study on small and medium sized companies

which are not quoted. Analysis on ales aggregate level, like an

analysis of companies from the same industry would be advantageous

and a study with follow-up interviews or case study on the topic

would also be relevant.

63

5.5 Limitation of study

There are some limitations to the presented research. Despite the

attempt design objective and precise questions one can argue about

a certain degree of subjectivity in some of the survey questions.

This is one of the possible reasons that some of the regression

results were not robust when the regressions were estimated on the

restricted sample of companies. Generally, the limitations of the

research do not make the results less valuable for the desion

making process. However, the results should be interpreted with a

certain degree of prudence.

List of references

Aabo, T. and Simkins B.J., 2005, “Interaction between real options

and financial hedging: fact or fiction in managerial decision-

making”, Review of Financial Economics 14, pp.

353 – 369.

Adler, M. and Dumas, B., 1984, “Exposure to currency risk:

definition and measurement”. Financial Management, 13(2), pp. 41-

50.

Aggarwal, R. and Soenen, L., 1989, “Managing persistent real

changes in currency values: the roles of multinational operating

64

strategies”, Columbia Journal of World Business, vol. 24, 3, pp.

60-67

Allayannis, G., Ihrig, J. and Weston, J.P., 2001, “Exchange-Rate

Hedging: Financial versus Operational Strategies”, AEA Papers and

Proceedings, may, pp. 391 – 395.

Allen, L. and Pantzalis, C., 1996. “Valuation of the operating

flexibility of multinational

corporations”. Journal of International Business Studies, 27, pp.

633–653.

Andersen, T.M., Dalim, B., Linderoth, H., 2006, ”The Danish

Economy, An International Perspective”, 2nd Edition, DJOF

Publishing Copenhagen.

Bartram, S., Dufey, G. and Frenkel, M.R., 2005, “A primer on the

exposure of nonfinancial corporations to foreign exchange rate

risks”. Journal of Multinational Financial Management 15, pp. 394-

413.

Belk, P.A. and Edelshain D. J., 1997, “Foreign Exchange Rate

Management – The Paradox”. Managerial Finance 23, pp. 5-24.

Belk, P.A. and Glaum, M., 1990, “The Management of Foreign Exchange

Risk in UK

Multinationsl: An Empirical Investigation”, Accounting and Business

Research, 21,81, pp. 3-13

65

Bodnar, G.M. and Gentry, W.M., 1993, “Exchange rate exposure and

industry characteristics: evidence from Canada, Japan and the USA”.

Journal of International Money and Finance 12, pp. 29-45.

Bodnar, G.M., Hayt, G.S. and Marston, R.C., 1998. Wharton Survey of

Financial Risk Management by US Non-Financial Firms. Financial

Management 27, pp. 70-91.

Booth, L. and Rotenberg, W., 1990, “Assessing Foreign Exchange

Exposure: Theory and Application Using Canadian Firms” Journal of

International Financial Management and Accounting 2, 1, pp. 1 – 22.

Bradley, K. and Moles, P., 2002, “Managing Strategic Exchange Rate

Exposures: Evidence from UK firms”. Managerial Finance 28, pp. 28 -

41

Capel, J., 1997, “A Real Options Approach to Economic Exposure

Management”. Journal of International Financial Management and

Accounting 8, 2, pp. 87-113.

Carter, D. A., Pantzalis, C. and Simkins, B., 2003, “Asymmetric

exposure to foreign exchange risk: Financial and real options

hedges implemented by U.S. multinational corporations”. Proceedings

from the 7th Annual International Conference on Real

Options: Theory Meets Practice. Washington, D.C.

Choi, J.J. and Kim, Y.C., 2003, “The Asian exposure of U.S. firms:

Operational and risk 68 Management Strategies”. Pacific-Basin

Finance Journal 11, pp. 121-138.66

Chowdhry, B. abd Howe, J.T.B., 1999, “Corporate risk management for

multinational corporations: financial and operational hedging

policies”. European Finance Review 2, pp. 229-246

Driouchi, T., Battisti, G. and Bennett, D., 2006, “Downsize Risk

Implications of Multinationality and Real options” Proceedings from

the 10th Annual International Conference on Real Options: Theory

Meets Practice, New-York City, USA, June 14-17

Faseruk, A. and Mishara, D.R., 2008, “An examination of US dollar

risk management by Canadian non-financial firms”. Management

Research News, vol. 31, 8, pp. 570-581

Flood, E. and Lessard, D.R., 1986, “On the measurement of

operating exposure to exchange rates: conceptual approach ”.

Financial management, spring, pp. 25-36.

Froot, K. A., Scharfstein, D. S. and Stein, J. C., 1993. “Risk

Management: Coordinating Corporate Investment and Financing

Policies”. The Journal of Finance 48, 5, pp. 1629- 1658

Froot, K.A., Scharfstein, D. S. and Stein, J.C., 1994. “A framework

for Risk Management”. Harvard Business Review, nov.-dec., pp. 91 –

102.

Géczy, C., Minton, B. A., Schrand, C., 1997, “Why Firms Use

Currency Derivatives.”

The Journal of Finance, 52, 4, September , p. 1323-1354.

67

Glaum, M., 1990, “Strategic Management of Exchange Rate Risks”.

Long Range

Planning 23, 4, pp. 65 – 72.

Hakkarainen, A., Joseph, N., Kasanen, E. and Puttonen, V., 1998.

“The Foreign Exchange Exposure Management Practices of Finnish

Industrial Firms” Journal of International Financial Management and

Accounting 9, 1, pp. 34 – 57.

Hair, J., Babin, B., Money, A. and Samouel, P., ”Essentials on

Business Research Methods”. Wiley, US., 2003.

Hau, H., 1999, “Comment on “ Corporate risk management for

multinational corporations: financial and operational hedging

policies”, European Finance Review 2, pp. 247-249

Hollensen, S., 2007, “Global marketing: a decision-oriented

approach”, N.Y., Prentice Hall/Financial times, 714 p.

Hommel, U., 2003, ”Financial versus operative hedging of currency

risk”. Global Finance Journal 14, pp. 1-18

Joseph, N.L., 2000, “The choice of hedging techniques and the

characteristics of UK industrial firms”. Journal of Multinational

Financial Management 10, pp. 161-184.

Kato,I. and Uctum, M., 2008, “Choice of exchange rate regime and

currency zones”. International Review of Economics and Finance, 17,

pp. 436 – 456.

68

Kogut, B. and Kulatilaka, N., 1994, “Operating Flexibility, Global

Manufacturing, and the Option Value of a Multinational Network”.

Management Science 40, 1, pp. 123-139.

Kuhn, J., 2007, Corporate Risk Management and Hedging Practice by

Medium-sized Companies in Denmark”, Master thesis, Aarhus School of

Business.69

Lessard, D.R. 1986, “Financial and Global Competition” in

Completion in Global industries, ed. M.Porter, Harvard Business

Press, Boston, Massachusetts

Loderer, C. and Pichler, K., 2000, “Firms, do you know your

currency risk exposure? Survey results”. Journal of Empirical

Finance, 7, pp. 317 – 344.

Marshall, A. P., 2000, “Foreign Exchange Rate Management in UK,

USA and Asia Pacific multinational companies”. Journal of

Multinational Financial Management 10, pp. 185 – 211.

Martin, A. D. and Mauer, L. J., 2003, “Transaction versus economic

exposure: which has greater cash flow consequences?” International

Review of Economics and Finance 12, pp. 437 – 449.

Mello, A. S., Parsons, J.E. and Triantis, A. J., 1995, “An

Integrated Model of multinational flexibility and financial

hedging”. Journal of International Economics 39, pp. 27-51.

Miller, K. D., 1998, “Economic exposure and integrated risk

management”, Strategic Management Journal, 19, 5, 497-514 pp.69

Moffett, M.H. and Karlsen, J. K., 1994, “Managing Foreign Exchange

Rate Exposure”. Journal of International Financial Management and

Accounting 5, 2, pp. 157 – 175.

Nance, D. R., Smith, C. W., Smithson, C. W., 1993, “On the

Determinants of Corporate Hedging”. The Journal of Finance, 48, 1,

March, p. 267-284

Pantzalis, C., Simkins, B.J. and Laux, P.A., 2001, “Operational

Hedges and the Foreign Exchange Exposure of U.S. Multinational

Corporations”. Journal of International Business Studies, 32, 4,

pp. 793 – 812.

Rangan, S., 1998. Do Multinationals operate Flexibly? Theory and