MacArthur - Roadshow Presentation - Final - 130917

56

Investors Presentation For Debenture Offering CP All Public Company Limited 17 September 2013

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of MacArthur - Roadshow Presentation - Final - 130917

Investors Presentation

For Debenture Offering

CP All Public Company Limited

17 September 2013

Disclaimer

This presentation contains some information from other sources, that CPALL does not make any representations

regarding the use, validity, accuracy, or reliability of, or the results of the use of information, data but not limited to,

all text, and images (“the Content”) on this presentation. Some content may contain forward-looking statements,

that based on management’s view upon the information currently available to us. These statement are subject to

certain risks and uncertainties that could cause the actual results materially differed from what had been previously

stated.

The Content and the Forward-looking statements state within this presentation only as the date they made. CPALL

undertakes no responsibility on the change after that date stated herein.

The material set forth herein is for informational purposes only. It should not be construed, as an offer of securities for

sale.

2

Agenda

• The Company

• Financial Performance

• The Acquisition of MAKRO

• The Offering

Appendix

• Financial Statements

• Industry Outlook

3

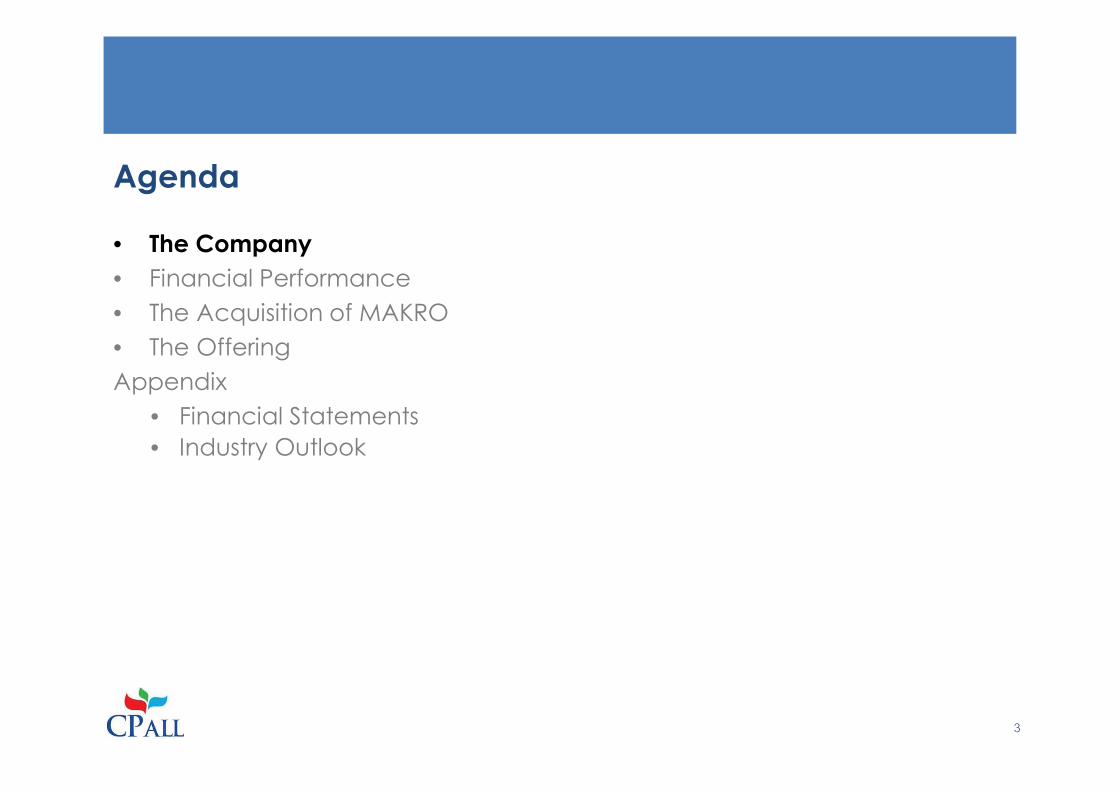

CPALL at a Glance

The Company

Dominant Brand Image

• Opened the first store in 1990 as the 1st CVS in Thailand

• Have extensive store network throughout the country

• Ranked no.1 market share of CVS chain format in Thailand

• Act as the biggest distribution channel/gaining highest market share in many categories e.g. pasteurized milk, confectionery, soft drink, etc.

Leverage ExtensiveNetwork

• Offer more products and services e.g.

• Bill payment services (“Counter Service”), managing 12 million transactions monthly

• Books and magazines (“Book Smile”)

• Launch new product lines e.g.

• Freshly baked bakery and freshly brewed coffee (“Kudsan”)

• Health & beauty products (“eXta”)

Concrete Business Platform

• Manage highly efficiency distribution centers and own 5 main DCs : 2 in the Greater Bangkok, 1 in the south (Suratthani),1 in the northeastern (KhonKaen), 1 in the north (Lampoon). The new DC in the Central (Samut Sakhon) is scheduled to open in 2014.

• Gain full support from wholly-owned subsidiaries e.g. CPRAM, RTL and Suksapiwat (retailing vocational school)

4

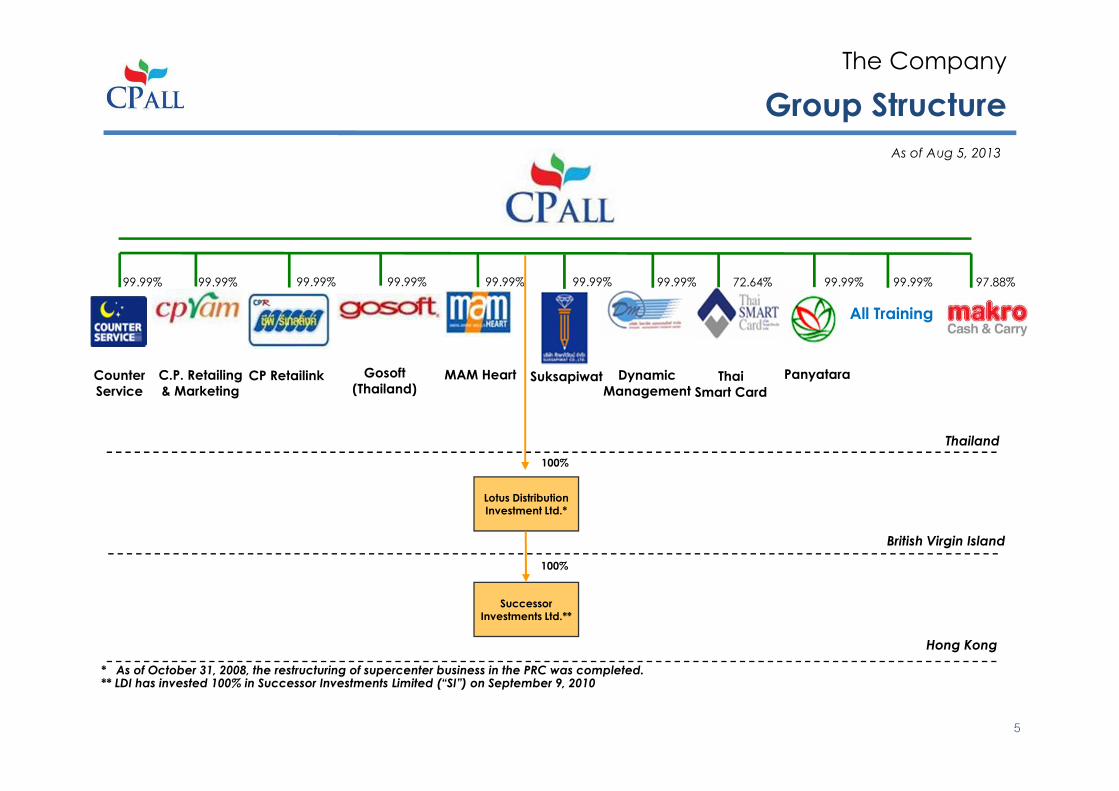

Group Structure

The Company

As of Aug 5, 2013

C.P. Retailing

& Marketing

Thailand

British Virgin Island

Lotus Distribution Investment Ltd.*

100%

* As of October 31, 2008, the restructuring of supercenter business in the PRC was completed.** LDI has invested 100% in Successor Investments Limited (“SI”) on September 9, 2010

Successor Investments Ltd.**

Hong Kong

100%

Counter

ServiceThai

Smart Card

CP Retailink Gosoft

(Thailand)MAM Heart

99.99% 99.99% 99.99% 99.99% 99.99% 99.99%

Dynamic

Management

99.99%

Suksapiwat

72.64%

Panyatara

99.99%

All Training

99.99% 97.88%

5

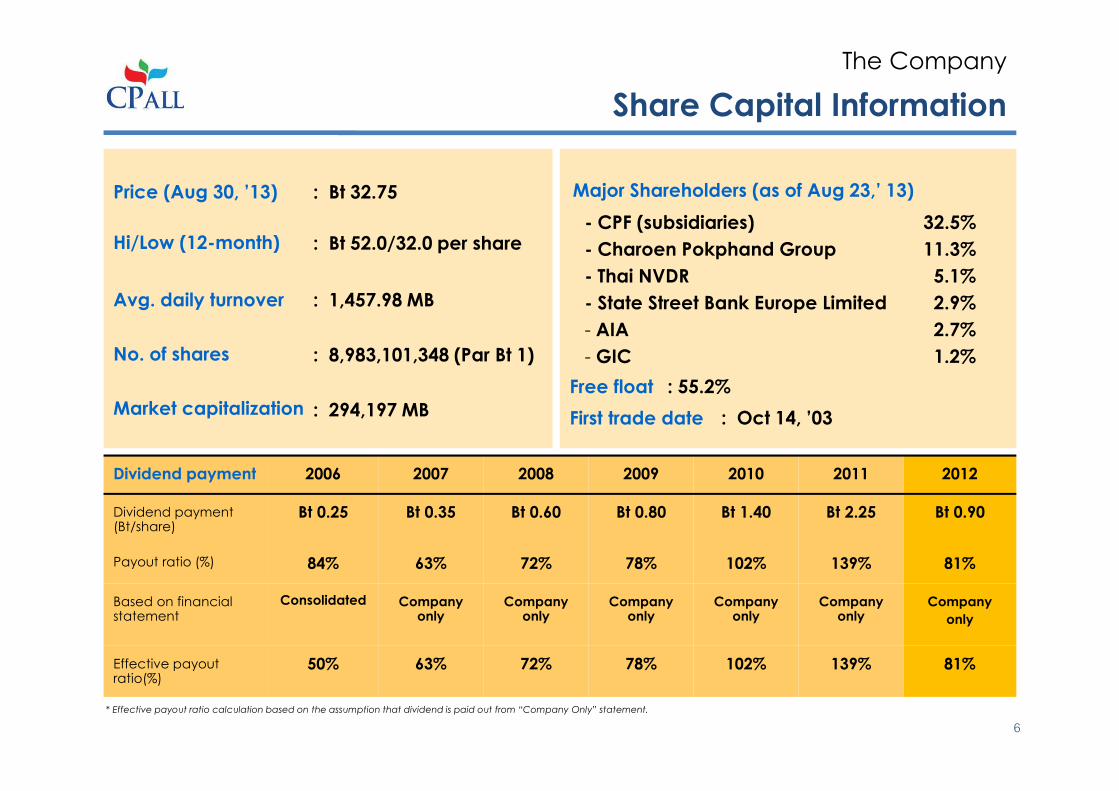

: Bt 32.75

: Bt 52.0/32.0 per share

: 1,457.98 MB

: 8,983,101,348 (Par Bt 1)

: 294,197 MB

Price (Aug 30, ’13)

Hi/Low (12-month)

Avg. daily turnover

No. of shares

Market capitalization

Major Shareholders (as of Aug 23,’ 13)

* Effective payout ratio calculation based on the assumption that dividend is paid out from “Company Only” statement.

Dividend payment 2006 2007 2008 2009 2010 2011 2012

Dividend payment (Bt/share)

Bt 0.25 Bt 0.35 Bt 0.60 Bt 0.80 Bt 1.40 Bt 2.25 Bt 0.90

Payout ratio (%) 84% 63% 72% 78% 102% 139% 81%

Based on financial statement

Consolidated Company only

Company only

Company only

Company only

Company only

Company

only

Effective payout ratio(%)

50% 63% 72% 78% 102% 139% 81%

: Oct 14, ’03First trade date

Free float : 55.2%

- CPF (subsidiaries) 32.5%

- Charoen Pokphand Group 11.3%

- Thai NVDR 5.1%

- State Street Bank Europe Limited 2.9%

- AIA 2.7%

- GIC 1.2%

Share Capital Information

6

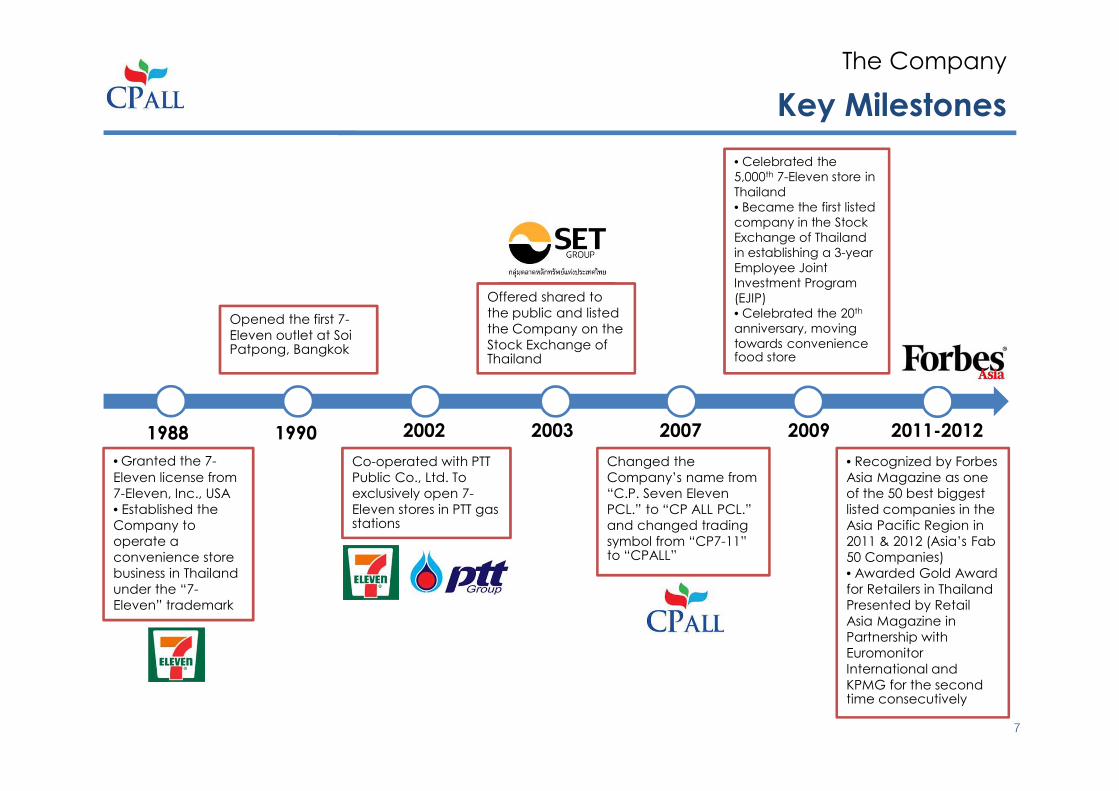

The Company

Key Milestones

The Company

1988 1990 2002 2003 2007 2009 2011-2012

• Granted the 7-

Eleven license from

7-Eleven, Inc., USA

• Established the

Company to

operate a

convenience store

business in Thailand

under the “7-

Eleven” trademark

Opened the first 7-

Eleven outlet at SoiPatpong, Bangkok

Co-operated with PTT

Public Co., Ltd. To

exclusively open 7-

Eleven stores in PTT gas stations

Offered shared to

the public and listed

the Company on the

Stock Exchange of Thailand

Changed the

Company’s name from

“C.P. Seven Eleven

PCL.” to “CP ALL PCL.”

and changed trading

symbol from “CP7-11” to “CPALL”

• Celebrated the

5,000th 7-Eleven store in

Thailand

• Became the first listed

company in the Stock

Exchange of Thailand

in establishing a 3-year

Employee Joint

Investment Program

(EJIP)

• Celebrated the 20th

anniversary, moving

towards convenience food store

• Recognized by Forbes

Asia Magazine as one

of the 50 best biggest

listed companies in the

Asia Pacific Region in

2011 & 2012 (Asia’s Fab

50 Companies)

• Awarded Gold Award

for Retailers in Thailand

Presented by Retail

Asia Magazine in

Partnership with

Euromonitor

International and

KPMG for the second time consecutively

7

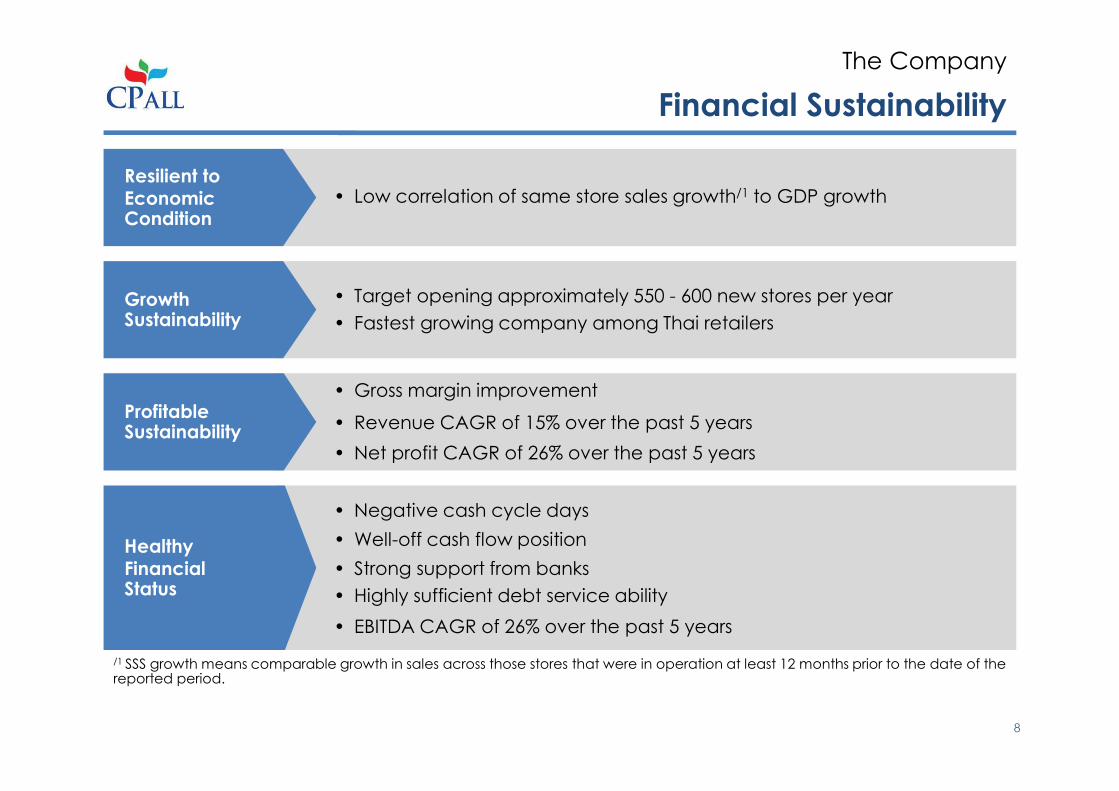

Financial Sustainability

The Company

• Low correlation of same store sales growth/1 to GDP growth

• Target opening approximately 550 - 600 new stores per year

• Fastest growing company among Thai retailers

• Gross margin improvement

• Revenue CAGR of 15% over the past 5 years

• Net profit CAGR of 26% over the past 5 years

• Negative cash cycle days

• Well-off cash flow position

• Strong support from banks

• Highly sufficient debt service ability

• EBITDA CAGR of 26% over the past 5 years

Resilient to EconomicCondition

Growth Sustainability

Profitable Sustainability

HealthyFinancial Status

/1 SSS growth means comparable growth in sales across those stores that were in operation at least 12 months prior to the date of the reported period.

8

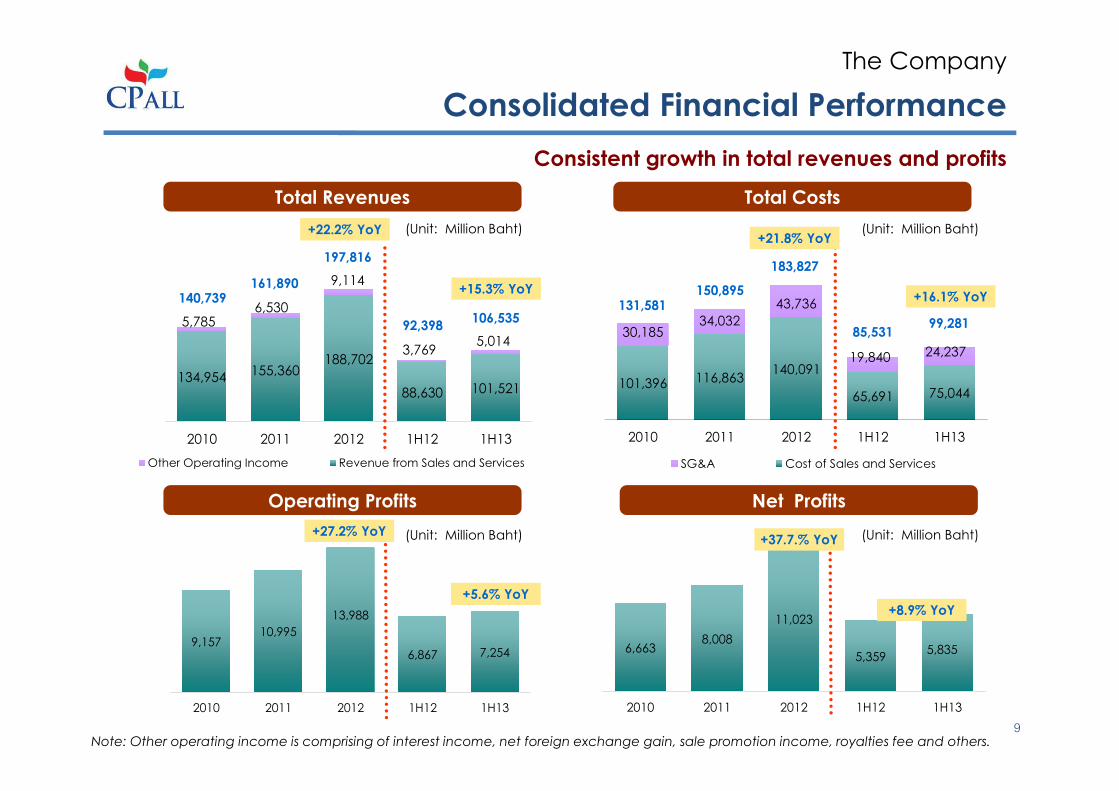

9,15710,995

13,988

6,867 7,254

2010 2011 2012 1H12 1H13

6,6638,008

11,023

5,3595,835

2010 2011 2012 1H12 1H13

134,954155,360

188,702

88,630 101,521

5,7856,530

9,114

3,7695,014

2010 2011 2012 1H12 1H13

Other Operating Income Revenue from Sales and Services

101,396 116,863140,091

65,691 75,044

30,18534,032

43,736

19,840 24,237

2010 2011 2012 1H12 1H13

SG&A Cost of Sales and Services

(Unit: Million Baht) (Unit: Million Baht)

(Unit: Million Baht) (Unit: Million Baht)

+8.9% YoY

+16.1% YoY150,895

140,739161,890 +15.3% YoY

131,581

+5.6% YoY

92,39885,531

197,816183,827

106,535 99,281

+22.2% YoY

+37.7.% YoY+27.2% YoY

+21.8% YoY

Consolidated Financial Performance

The Company

9Note: Other operating income is comprising of interest income, net foreign exchange gain, sale promotion income, royalties fee and others.

Net ProfitsOperating Profits

Total Revenues Total Costs

Consistent growth in total revenues and profits

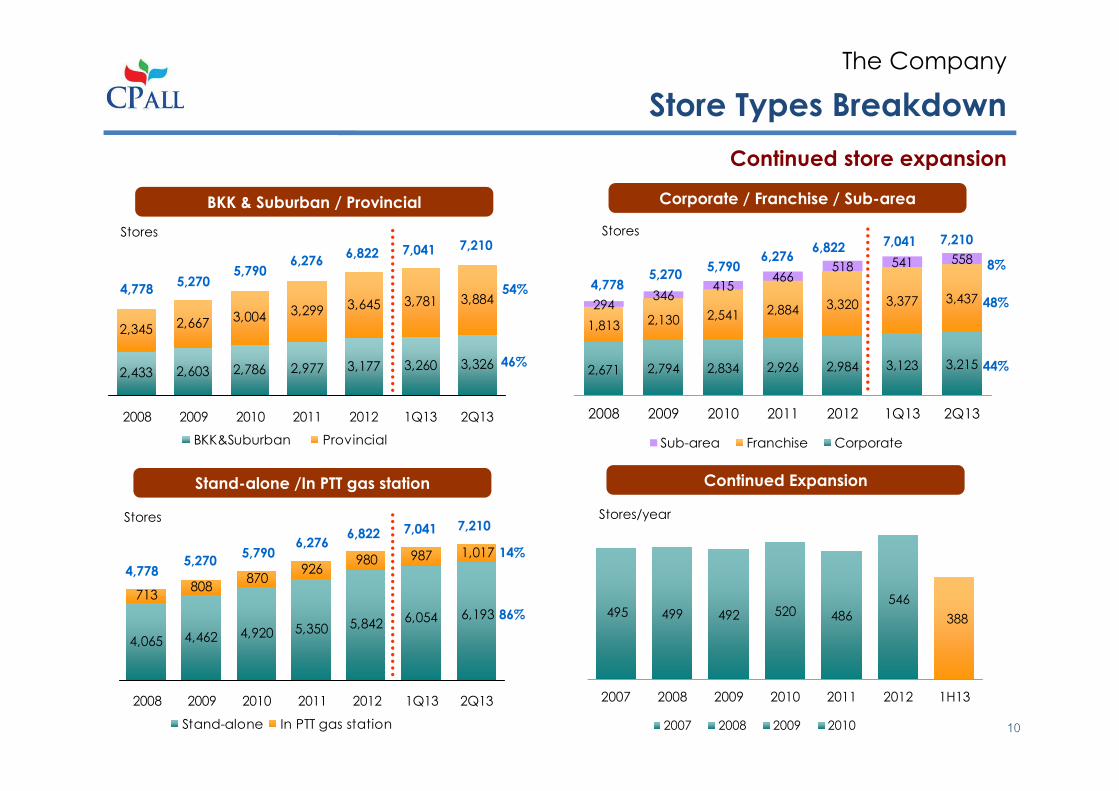

Store Types Breakdown

The Company

4,462 4,920 5,350 5,842

808870

926980 987

6,1936,054

4,065

1,017

713

2008 2009 2010 2011 2012 1Q13 2Q13

Stand-alone In PTT gas station

Stores

4,7785,270

5,7906,276

14%

86%

6,822

2,433 2,603 2,786 2,977 3,177 3,260 3,326

2,345 2,667 3,004 3,299 3,645 3,781 3,884

2008 2009 2010 2011 2012 1Q13 2Q13

BKK&Suburban Provincial

BKK & Suburban / Provincial

Stores

54%

46%2,671 2,794 2,834 2,926 2,984 3,123 3,215

1,813 2,130 2,541 2,884 3,320 3,377 3,437294346

415466

518 541 558

2008 2009 2010 2011 2012 1Q13 2Q13

Sub-area Franchise Corporate

Corporate / Franchise / Sub-area

Stores

44%

48%

8%

Stand-alone /In PTT gas station

7,041 7,210

4,7785,270

5,7906,276

6,822 7,041 7,210

4,7785,270

5,7906,276

6,822 7,041 7,210

495 499 492 520 486

546

388

2007 2008 2009 2010 2011 2012 1H13

2007 2008 2009 2010

Continued Expansion

Stores/year

10

Continued store expansion

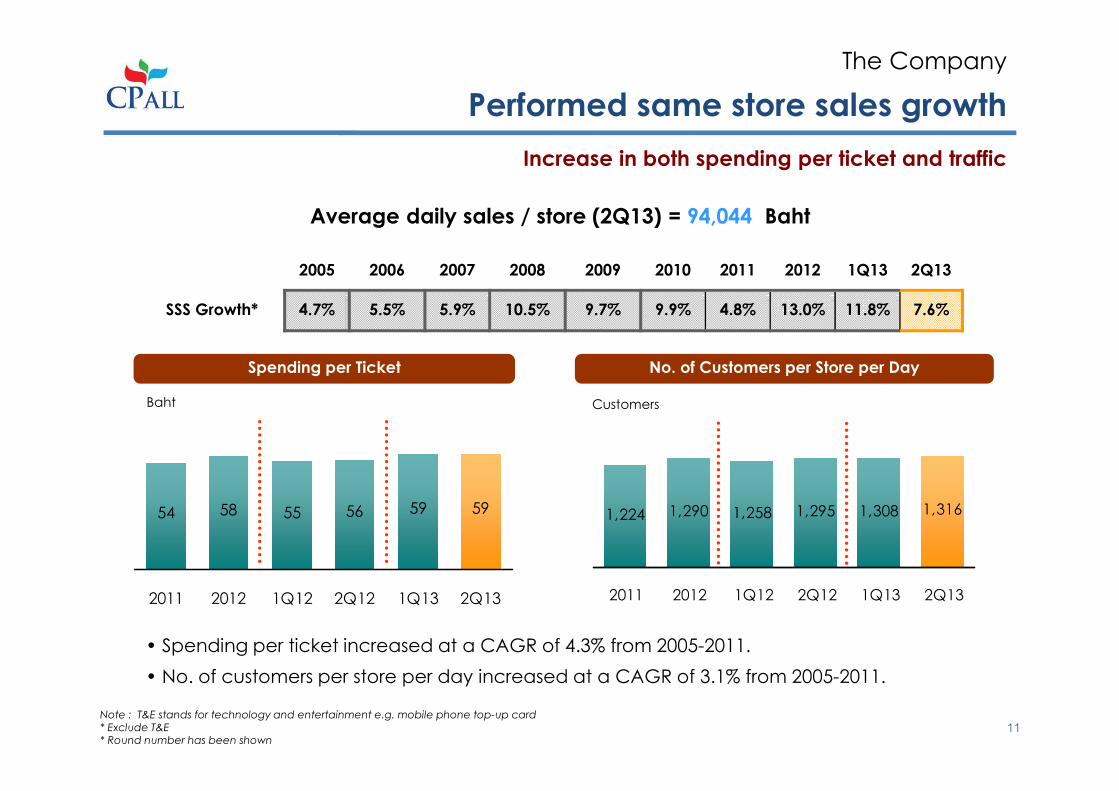

Performed same store sales growth

The Company

54 58 55 56 59 59

2011 2012 1Q12 2Q12 1Q13 2Q13

1,224 1,290 1,258 1,295 1,308 1,316

2011 2012 1Q12 2Q12 1Q13 2Q13

Note : T&E stands for technology and entertainment e.g. mobile phone top-up card* Exclude T&E* Round number has been shown

Average daily sales / store (2Q13) = 94,044 Baht

2005 2006 2007 2008 2009 2010 2011 2012 1Q13 2Q13

SSS Growth* 4.7% 5.5% 5.9% 10.5% 9.7% 9.9% 4.8% 13.0% 11.8% 7.6%

Baht Customers

• Spending per ticket increased at a CAGR of 4.3% from 2005-2011.

• No. of customers per store per day increased at a CAGR of 3.1% from 2005-2011.

Spending per Ticket No. of Customers per Store per Day

Increase in both spending per ticket and traffic

11

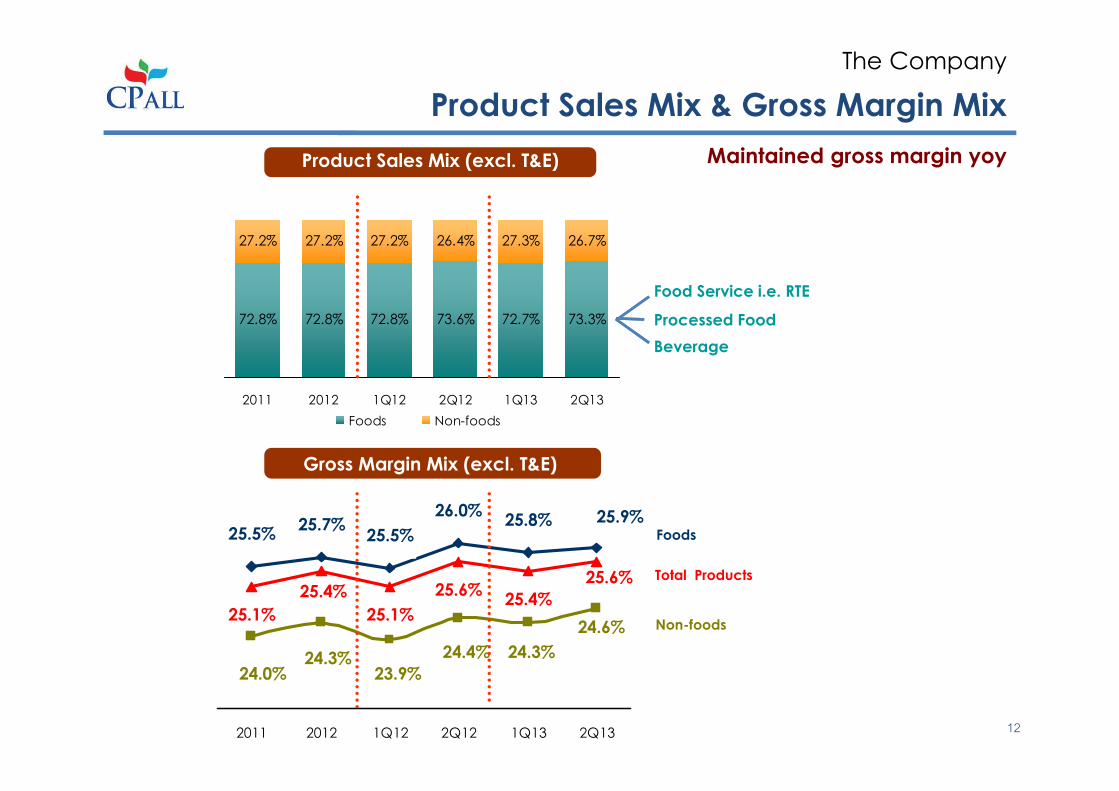

Product Sales Mix & Gross Margin Mix

The Company

Maintained gross margin yoy

72.8% 72.8% 72.8% 73.6% 72.7% 73.3%

27.2% 27.2% 27.2% 26.4% 27.3% 26.7%

2011 2012 1Q12 2Q12 1Q13 2Q13

Foods Non-foods

25.9%25.8%26.0%

25.5%25.7%

25.5%

24.6%

23.9%

24.4% 24.3%

24.0%24.3%

25.4%25.6%

25.1%

25.4%

25.1%

25.6%

2011 2012 1Q12 2Q12 1Q13 2Q13

Total Products

Non-foods

Foods

Product Sales Mix (excl. T&E)

Gross Margin Mix (excl. T&E)

Food Service i.e. RTE

Processed Food

Beverage

12

Product Strategy

The Company

13

• Strengthen CP ALL’s position as a ‘Convenience Food Store’ (CFS)

• Product differentiation - have supporting facilities to strengthen our position as a

convenience food store esp. Ready to eat items

CP Foods, the sister company, help supply frozen food and chilled food products i.e. package sausages, bolognas, burgers, etc.

CPRAM (100% own), manufactures frozen food, chilled food, and bakery products i.e. Dim Sum, Chinese bun, rice burgers, bakery etc.

Other services

The Company

14

• Financial services – install ATMs and provide in-store bill payments service

ATM: partner with all commercial banks to offer more than 6,000 ATM services at the stores

Counter Services ( 100% own ): provide financial payment services of more than 10 million transactions/month, with over 300 venders i.e. utilities, credit cards, telecom, transportation, entertainment, etc.

Supporting Facilities

• Maintenance service

Retaillink ( 100% own ): import equipment and provide service maintenance, becoming one of the largest company with over 1,000 mechanical staffs.

• Educational service

Suksapiwat ( 100% own ), be the first to offer work-based learning program in Thailand. This helps secure manpower to support growth for 7-Eleven stores.

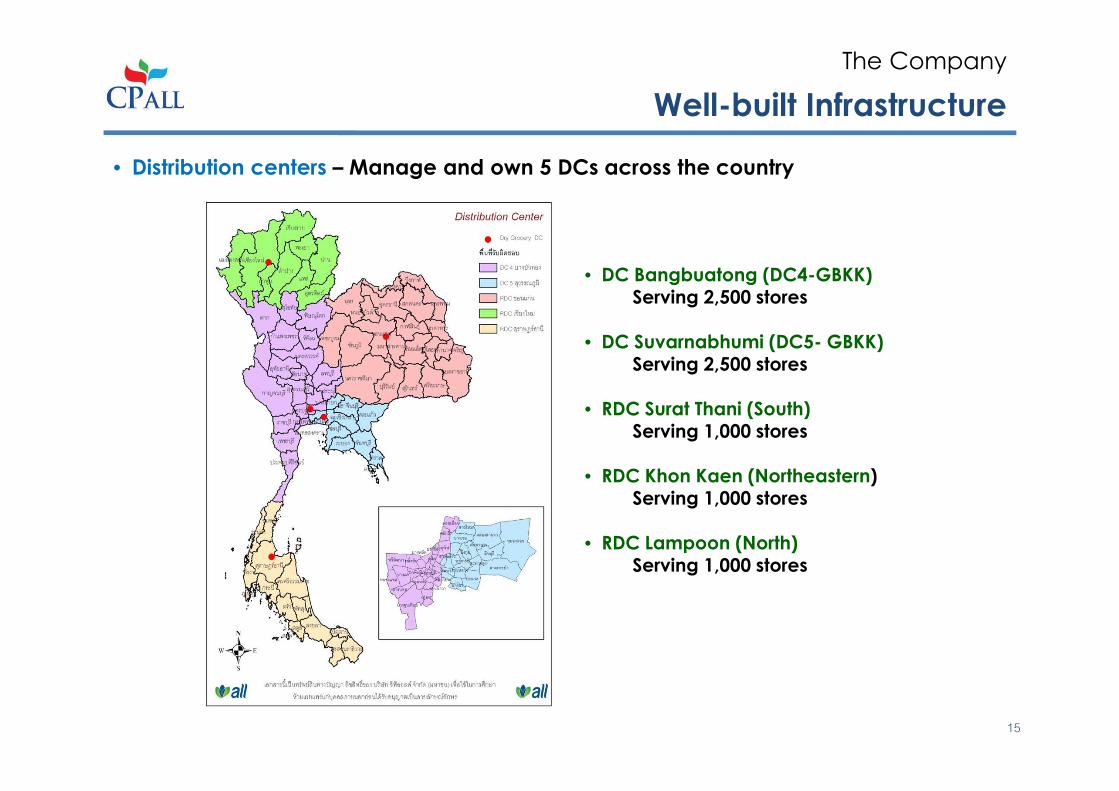

Well-built Infrastructure

The Company

15

• Distribution centers – Manage and own 5 DCs across the country

• DC Bangbuatong (DC4-GBKK) Serving 2,500 stores

• DC Suvarnabhumi (DC5- GBKK)Serving 2,500 stores

• RDC Surat Thani (South)Serving 1,000 stores

• RDC Khon Kaen (Northeastern)Serving 1,000 stores

• RDC Lampoon (North)Serving 1,000 stores

Operational Strategy

The Company

Stamp “ Love Thailand” PromotionFood & Drink Promotion

Promotional campaign

7-Eleven.

26 Apr – 25 May 1326 Jul – 25 Nov 13

Promotional campaign

7-Eleven.

More than 200 food & drink items were offered at a special price

Customers get a stamp valued of Baht 1 for every Baht 50 purchase or more stamps from a wide range of product items participating the campaign which can be used for cash discount or exchanged for a

premium gift.

New stamp promotion for 2013 has already launched under “Love Thailand” theme

16

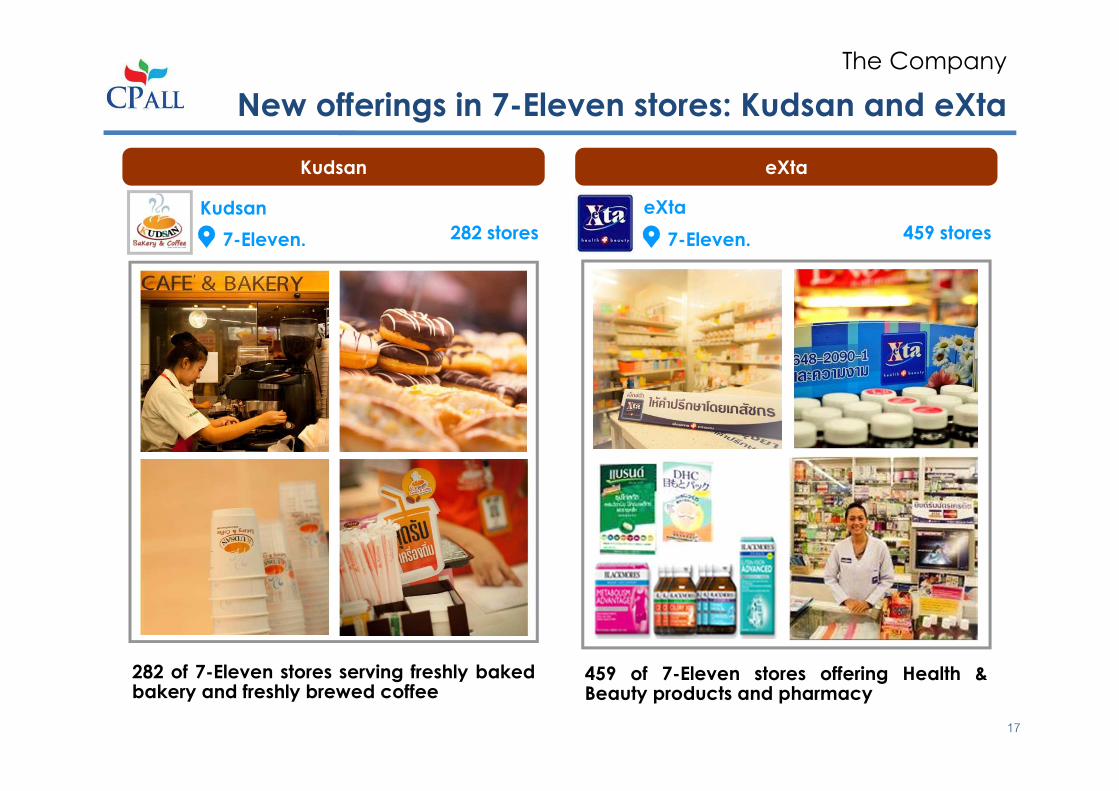

New offerings in 7-Eleven stores: Kudsan and eXta

The Company

282 of 7-Eleven stores serving freshly baked bakery and freshly brewed coffee

Kudsan

Kudsan

282 stores

eXta

eXta

459 stores

459 of 7-Eleven stores offering Health & Beauty products and pharmacy

7-Eleven. 7-Eleven.

17

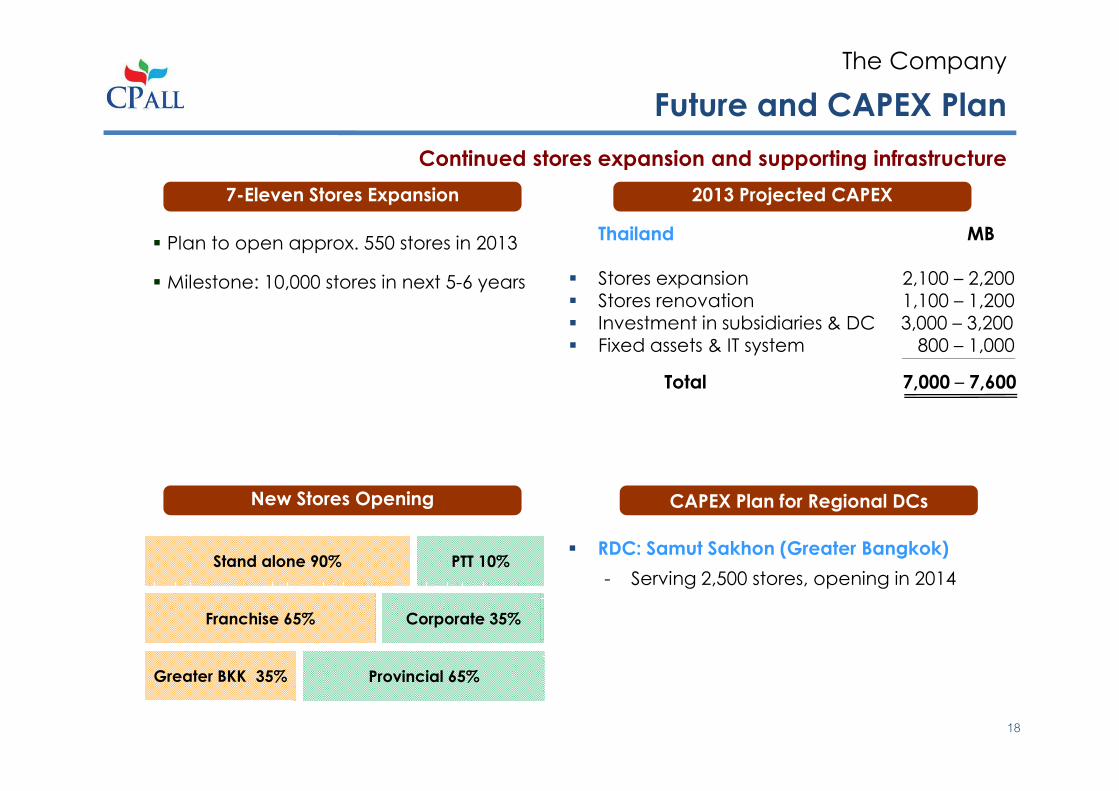

Future and CAPEX Plan

The Company

Continued stores expansion and supporting infrastructure

7-Eleven Stores Expansion 2013 Projected CAPEX

CAPEX Plan for Regional DCsNew Stores Opening

Thailand MB

� Stores expansion 2,100 – 2,200� Stores renovation 1,100 – 1,200� Investment in subsidiaries & DC 3,000 – 3,200� Fixed assets & IT system 800 – 1,000

Total 7,000 – 7,600

� Plan to open approx. 550 stores in 2013

� Milestone: 10,000 stores in next 5-6 years

Stand alone 90% PTT 10%

Franchise 65% Corporate 35%

Greater BKK 35% Provincial 65%

� RDC: Samut Sakhon (Greater Bangkok)

- Serving 2,500 stores, opening in 2014

18

Agenda

• The Company

• Financial Performance

• The Acquisition of MAKRO

• The Offering

Appendix

• Financial Statements

• Industry Outlook

19

Financial Highlight

Financial Performance

Units: MB Q2-12 Q2-13 %Chg 1H12 1H13 %Chg

Company Only

Total Revenue 47,368 53,149 +12.2% 91,268 105,187 +15.3%

Net Profit 2,703 2,829 +4.7% 5,152 5,747 +11.5%

Consolidated

Total Revenue 47,731 53,633 +12.4% 92,398 106,535 +15.3%

Net Profit 2,602 2,649 +1.8% 5,359 5,835 +8.9%

Company Only 2007 2008 2009 2010 2011 2012

Total Revenue 81,807 98,108 115,285 138,092 159,226 194,695

Net Profit 2,504 3,740 4,597 6,143 7,274 9,982

20

4.7% 4.9%5.6%

6.2%5.5%

6.0%4.9%

2010 2011 2012 1Q12 2Q12 1Q13 2Q13

8.7% 8.8% 8.8%

9.8%

8.7%9.1%

7.9%

2010 2011 2012 1Q12 2Q12 1Q13 2Q13

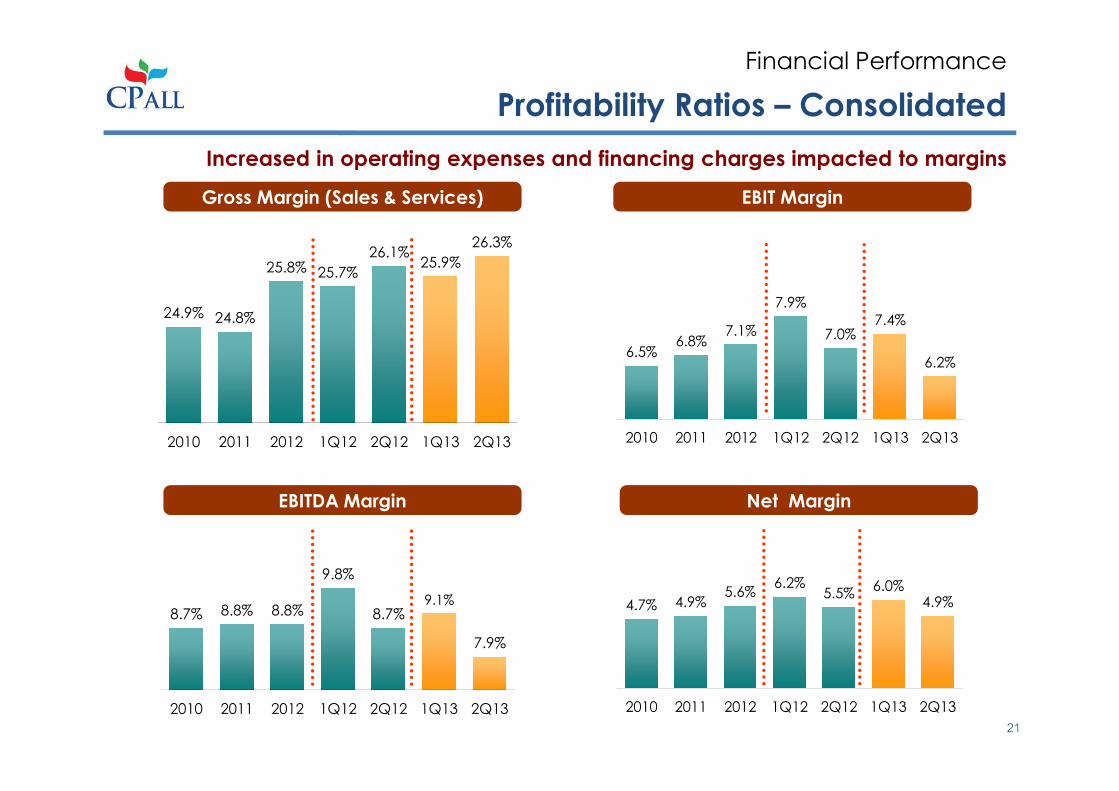

Profitability Ratios – Consolidated

Financial Performance

Gross Margin (Sales & Services) EBIT Margin

Net MarginEBITDA Margin

24.9% 24.8%

25.8% 25.7%

26.1%25.9%

26.3%

2010 2011 2012 1Q12 2Q12 1Q13 2Q13

6.5%6.8%

7.1%

7.9%

7.0%7.4%

6.2%

2010 2011 2012 1Q12 2Q12 1Q13 2Q13

Increased in operating expenses and financing charges impacted to margins

21

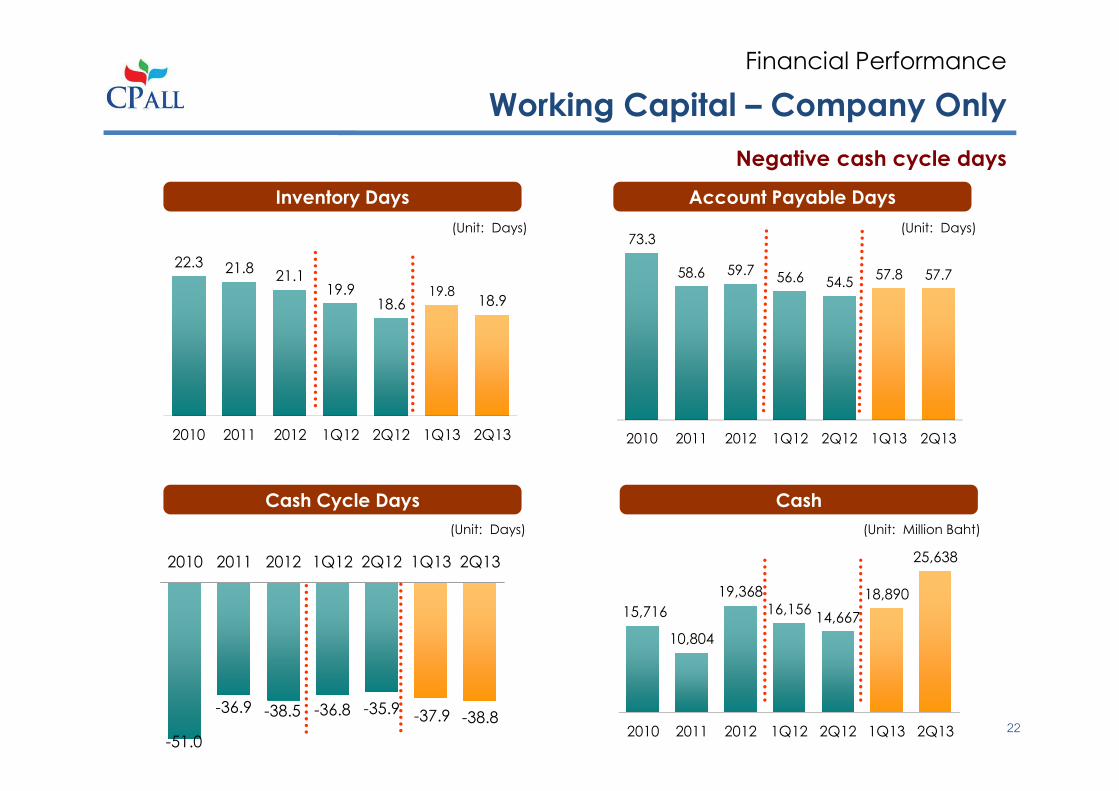

Working Capital – Company Only

Financial Performance

Inventory Days Account Payable Days

CashCash Cycle Days

Negative cash cycle days

73.3

58.6 59.756.6 54.5

57.8 57.7

2010 2011 2012 1Q12 2Q12 1Q13 2Q13

22.3 21.821.1

19.918.6

19.818.9

2010 2011 2012 1Q12 2Q12 1Q13 2Q13

(Unit: Days) (Unit: Days)

-51.0

-36.9 -38.5 -36.8 -35.9 -37.9 -38.8

2010 2011 2012 1Q12 2Q12 1Q13 2Q13

15,716

10,804

19,368

16,15614,667

18,890

25,638

2010 2011 2012 1Q12 2Q12 1Q13 2Q13

(Unit: Days) (Unit: Million Baht)

22

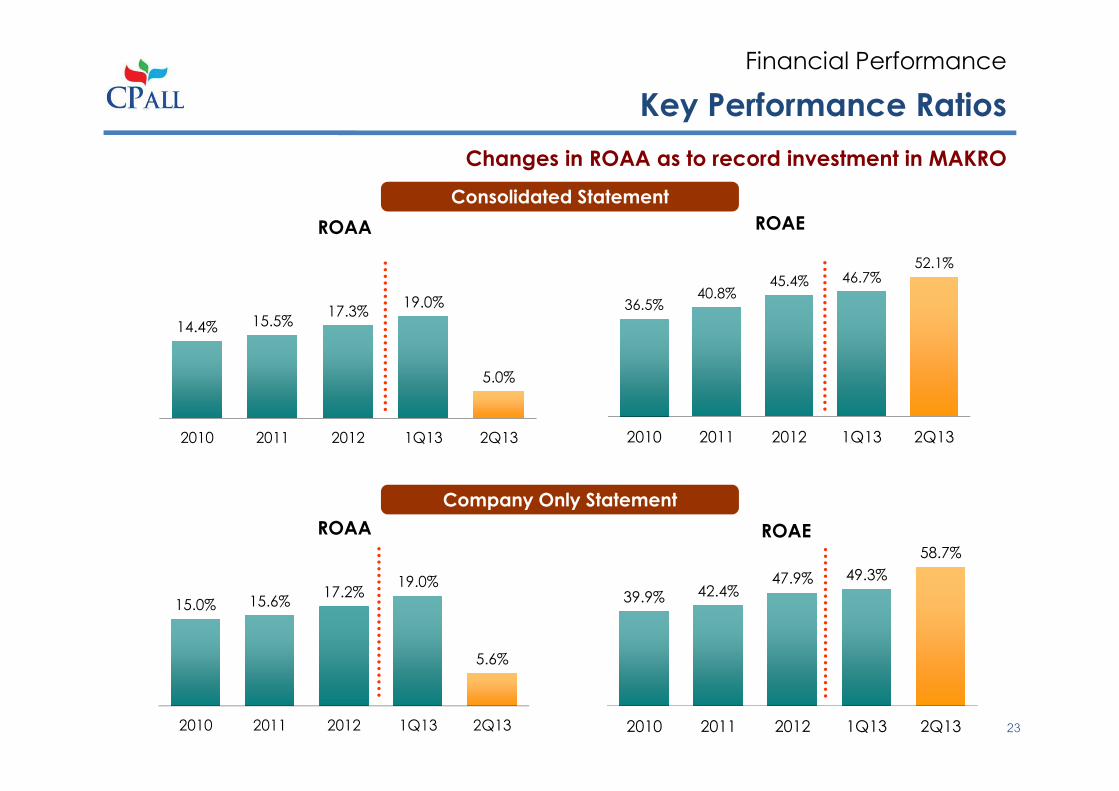

Key Performance Ratios

Financial Performance

Consolidated Statement

Company Only Statement

Changes in ROAA as to record investment in MAKRO

39.9% 42.4%47.9% 49.3%

58.7%

2010 2011 2012 1Q13 2Q13

36.5%40.8%

45.4% 46.7%52.1%

2010 2011 2012 1Q13 2Q13

15.0% 15.6%17.2%

19.0%

5.6%

2010 2011 2012 1Q13 2Q13

14.4% 15.5%17.3%

19.0%

5.0%

2010 2011 2012 1Q13 2Q13

ROAA ROAE

ROAA ROAE

23

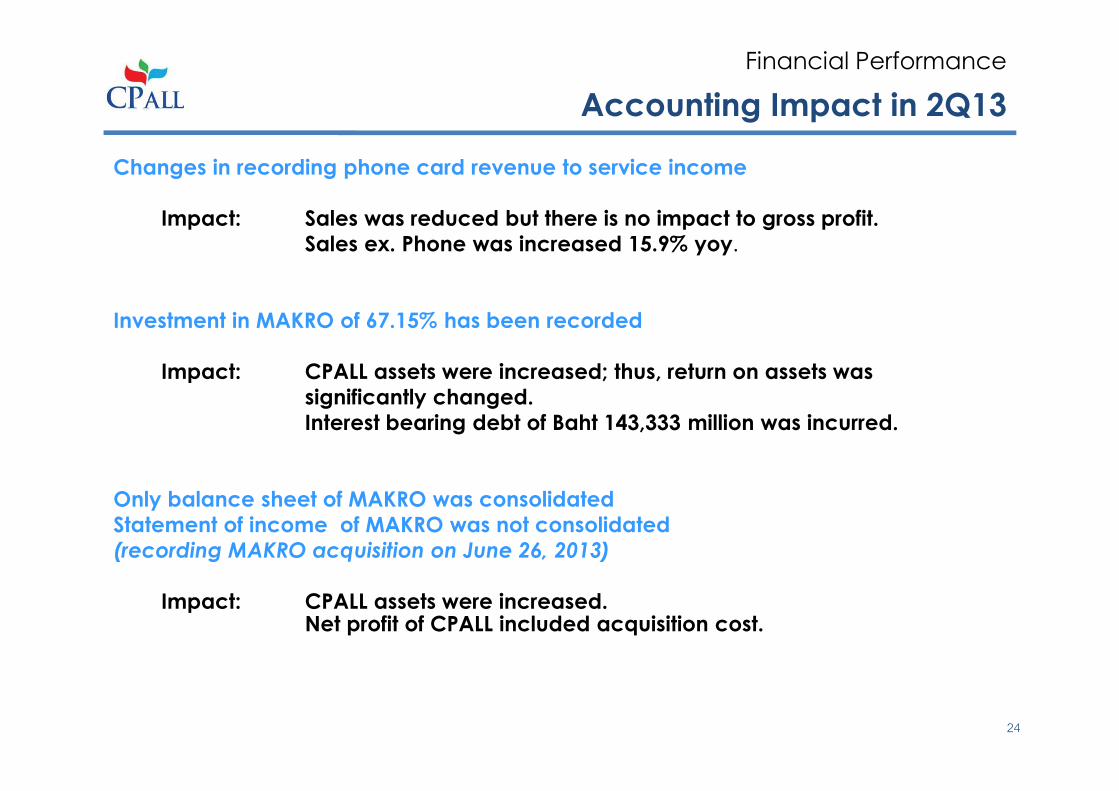

Accounting Impact in 2Q13

Financial Performance

Changes in recording phone card revenue to service income

Impact: Sales was reduced but there is no impact to gross profit.

Sales ex. Phone was increased 15.9% yoy.

Investment in MAKRO of 67.15% has been recorded

Impact: CPALL assets were increased; thus, return on assets was

significantly changed.

Interest bearing debt of Baht 143,333 million was incurred.

Only balance sheet of MAKRO was consolidated

Statement of income of MAKRO was not consolidated

(recording MAKRO acquisition on June 26, 2013)

Impact: CPALL assets were increased.Net profit of CPALL included acquisition cost.

24

Agenda

• The Company

• Financial Performance

• The Acquisition of MAKRO

• The Offering

Appendix

• Financial Statements

• Industry Outlook

25

Transaction Overview

The Acquisition of MAKRO

Transaction Structure

CPALL to acquire MAKRO in 2 steps

• Initial Acquisition: Acquire shares of

1) Siam Makro PCL (“MAKRO”)

2) Siam Makro Holdings Co., Ltd. and

3) OHT Co., Ltd. resulting in a total shareholding,

both direct and indirect, in MAKRO of approx.64.35% including MAKRO’s

Brand, IP and IT

• Tender Offer: Subsequently trigger mandatory tender offer for remaining shares

Transaction Size THB 188,880 mm for total equity value

Tender Offer Price THB 787 per share

Acquisition Funding Debt financing and internal cash flow

Conditions Precedent CPALL’s EGM’s approval with 75% supporting votes

Timeline CPALL’s EGM on 12 Jun 2013

• Initial acquisition after CPALL’s EGM approval in June 26, 2013

• T/O period in 28 Jul – 5 Aug 2013

• Completion in August 8, 2013

As of August 5, 2013, which was the last tender offer date, CPALL

successfully finished acquiring 97.88% shares of MAKRO

26

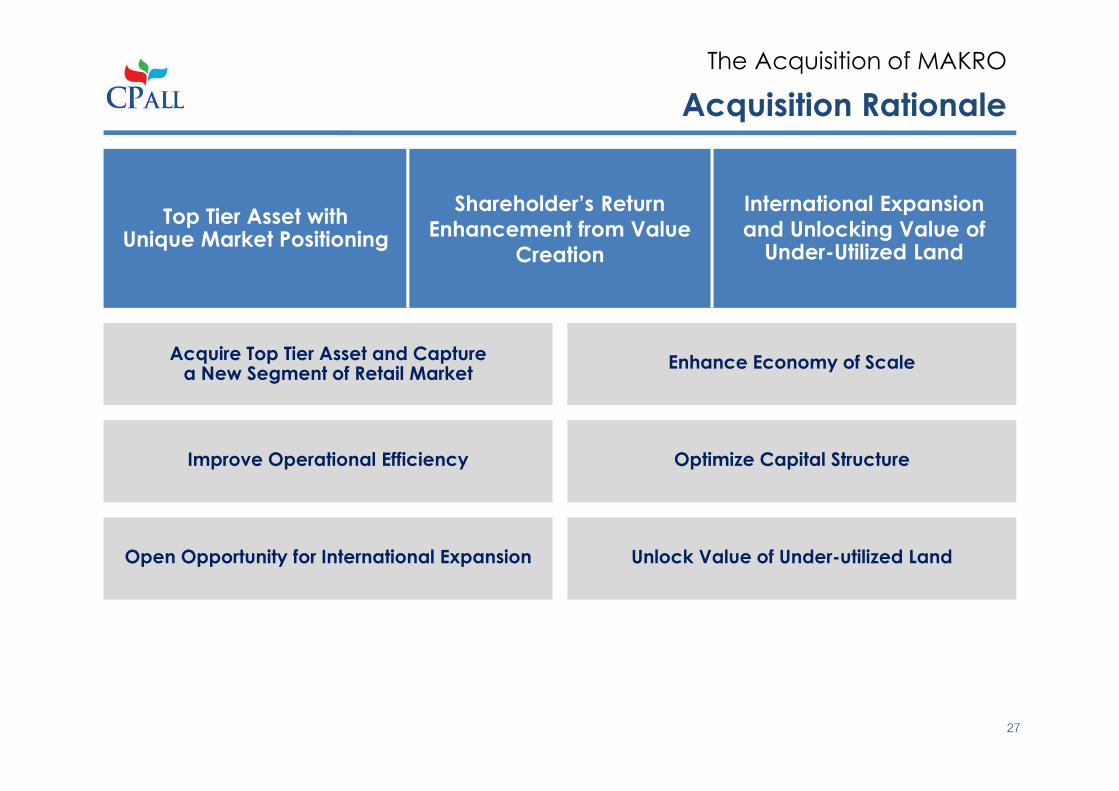

Acquisition Rationale

The Acquisition of MAKRO

Top Tier Asset with Unique Market Positioning

Shareholder’s Return

Enhancement from Value

Creation

International Expansion

and Unlocking Value ofUnder-Utilized Land

Acquire Top Tier Asset and Capturea New Segment of Retail Market

Improve Operational Efficiency

Open Opportunity for International Expansion

Enhance Economy of Scale

Optimize Capital Structure

Unlock Value of Under-utilized Land

27

7,0658,515

10,266

12,195

6,744

9.0%

9.6%

10.3%10.6% 10.7%

8%

9%

10%

11%

5,000

7,000

9,000

11,000

13,000

2009 2010 2011 2012 1H13

Gross Profit (THB mm) Gross Margin

Acquisition Rationale

The Acquisition of MAKRO

28

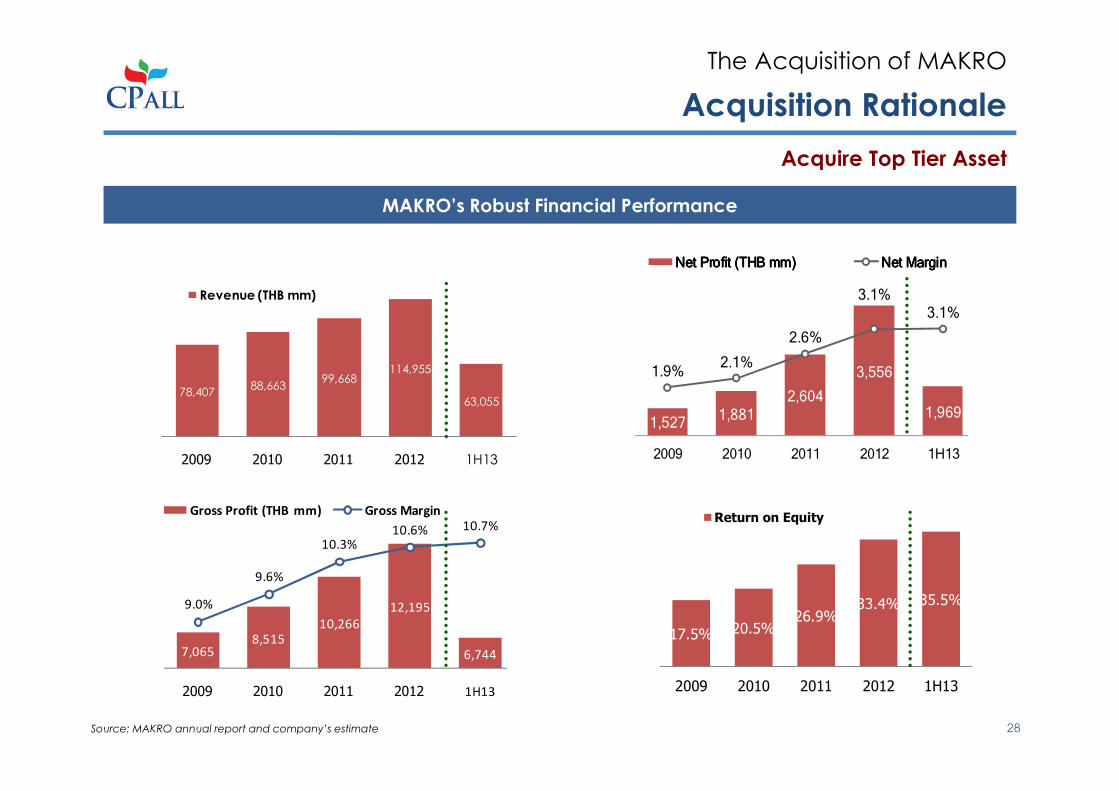

Acquire Top Tier Asset

MAKRO’s Robust Financial Performance

1,5271,881

2,604

3,556

1,969

1.9%2.1%

2.6%

3.1%3.1%

1%

2%

3%

4%

1,000

2,000

3,000

4,000

2009 2010 2011 2012 1H13

Net Profit (THB mm)Net Profit (THB mm)Net Profit (THB mm)Net Profit (THB mm) Net MarginNet MarginNet MarginNet Margin

Source: MAKRO annual report and company’s estimate

78,40788,663

99,668114,955

63,055

2009 2010 2011 2012 1H13

Revenue (THB mm)

17.5% 20.5%26.9%

33.4% 35.5%

2009 2010 2011 2012 1H13

Return on Equity

Acquisition Rationale

The Acquisition of MAKRO

29

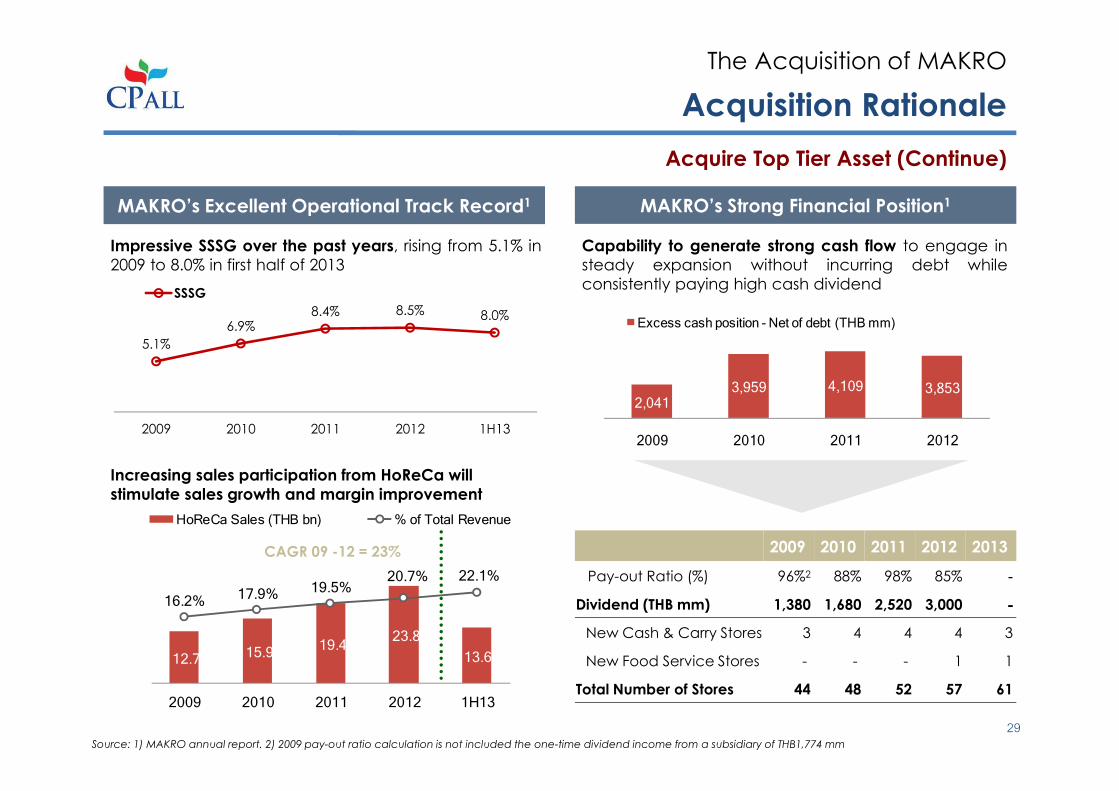

Acquire Top Tier Asset (Continue)

MAKRO’s Excellent Operational Track Record1

Impressive SSSG over the past years, rising from 5.1% in

2009 to 8.0% in first half of 2013

Increasing sales participation from HoReCa will

stimulate sales growth and margin improvement

12.7 15.9 19.4

23.8

13.6

16.2%17.9% 19.5%

20.7% 22.1%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

-

5.0

10.0

15.0

20.0

25.0

2009 2010 2011 2012 1H13

HoReCa Sales (THB bn) % of Total Revenue

CAGR 09 -12 = 23%

MAKRO’s Strong Financial Position1

Capability to generate strong cash flow to engage in

steady expansion without incurring debt while

consistently paying high cash dividend

2,0413,959 4,109 3,853

2009 2010 2011 2012

Excess cash position - Net of debt (THB mm)

2009 2010 2011 2012 2013

Pay-out Ratio (%) 96%2 88% 98% 85% -

Dividend (THB mm) 1,380 1,680 2,520 3,000 ----

New Cash & Carry Stores 3 4 4 4 3

New Food Service Stores - - - 1 1

Total Number of Stores 44 48 52 57 61

Source: 1) MAKRO annual report. 2) 2009 pay-out ratio calculation is not included the one-time dividend income from a subsidiary of THB1,774 mm

5.1%

6.9%8.4% 8.5% 8.0%

2009 2010 2011 2012 1H13

SSSG

Acquisition Rationale

The Acquisition of MAKRO

30

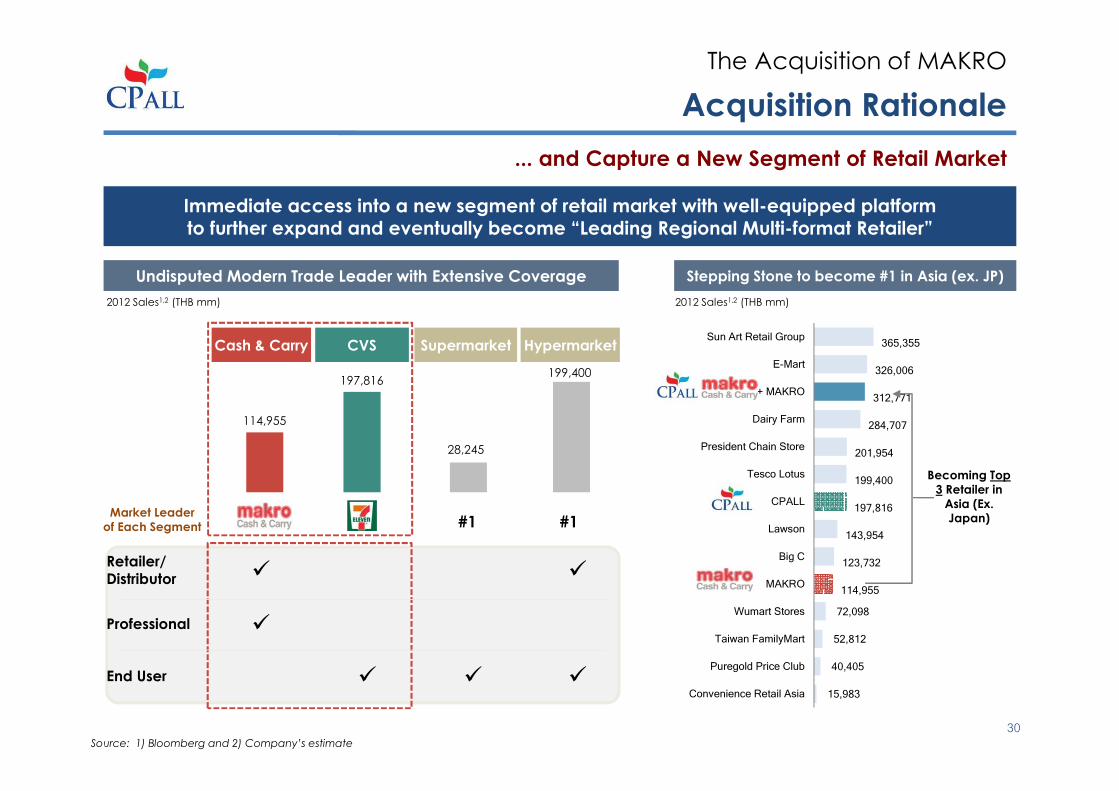

... and Capture a New Segment of Retail Market

Retailer/Distributor � �

Professional �

End User � � �

Source: 1) Bloomberg and 2) Company’s estimate

Undisputed Modern Trade Leader with Extensive Coverage Stepping Stone to become #1 in Asia (ex. JP)

2012 Sales1,2 (THB mm)

HypermarketSupermarket

Market Leader

of Each Segment

199,400

28,245

Cash & Carry

114,955

CVS

197,816

#1 #1

15,983

40,405

52,812

72,098

114,955

123,732

143,954

197,816

199,400

201,954

284,707

312,771

326,006

365,355

Convenience Retail Asia

Puregold Price Club

Taiwan FamilyMart

Wumart Stores

MAKRO

Big C

Lawson

CPALL

Tesco Lotus

President Chain Store

Dairy Farm

CPALL + MAKRO

E-Mart

Sun Art Retail Group

Becoming Top

3 Retailer in

Asia (Ex. Japan)

Immediate access into a new segment of retail market with well-equipped platformto further expand and eventually become “Leading Regional Multi-format Retailer”

2012 Sales1,2 (THB mm)

Acquisition Rationale

The Acquisition of MAKRO

31

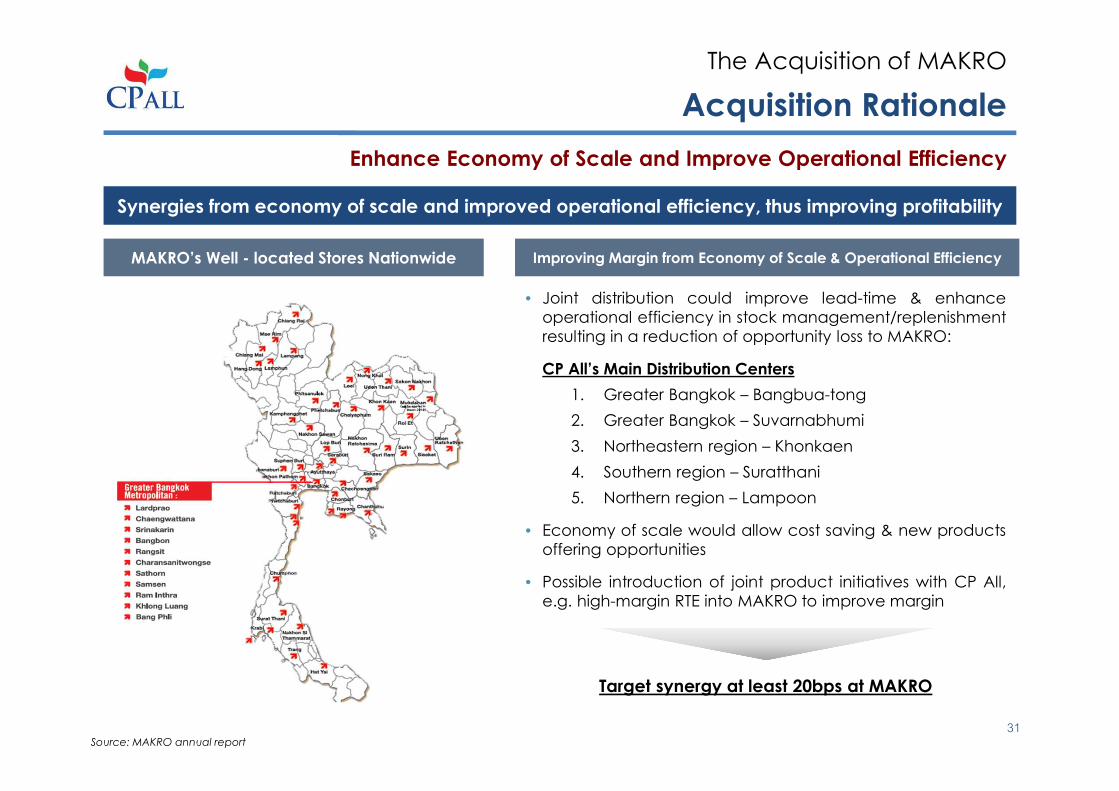

Enhance Economy of Scale and Improve Operational Efficiency

Synergies from economy of scale and improved operational efficiency, thus improving profitability

• Joint distribution could improve lead-time & enhance

operational efficiency in stock management/replenishment

resulting in a reduction of opportunity loss to MAKRO:

CP All’s Main Distribution Centers

1. Greater Bangkok – Bangbua-tong

2. Greater Bangkok – Suvarnabhumi

3. Northeastern region – Khonkaen

4. Southern region – Suratthani

5. Northern region – Lampoon

• Economy of scale would allow cost saving & new products

offering opportunities

• Possible introduction of joint product initiatives with CP All,

e.g. high-margin RTE into MAKRO to improve margin

MAKRO’s Well - located Stores Nationwide Improving Margin from Economy of Scale & Operational Efficiency

Source: MAKRO annual report

Target synergy at least 20bps at MAKRO

Acquisition Rationale

The Acquisition of MAKRO

32

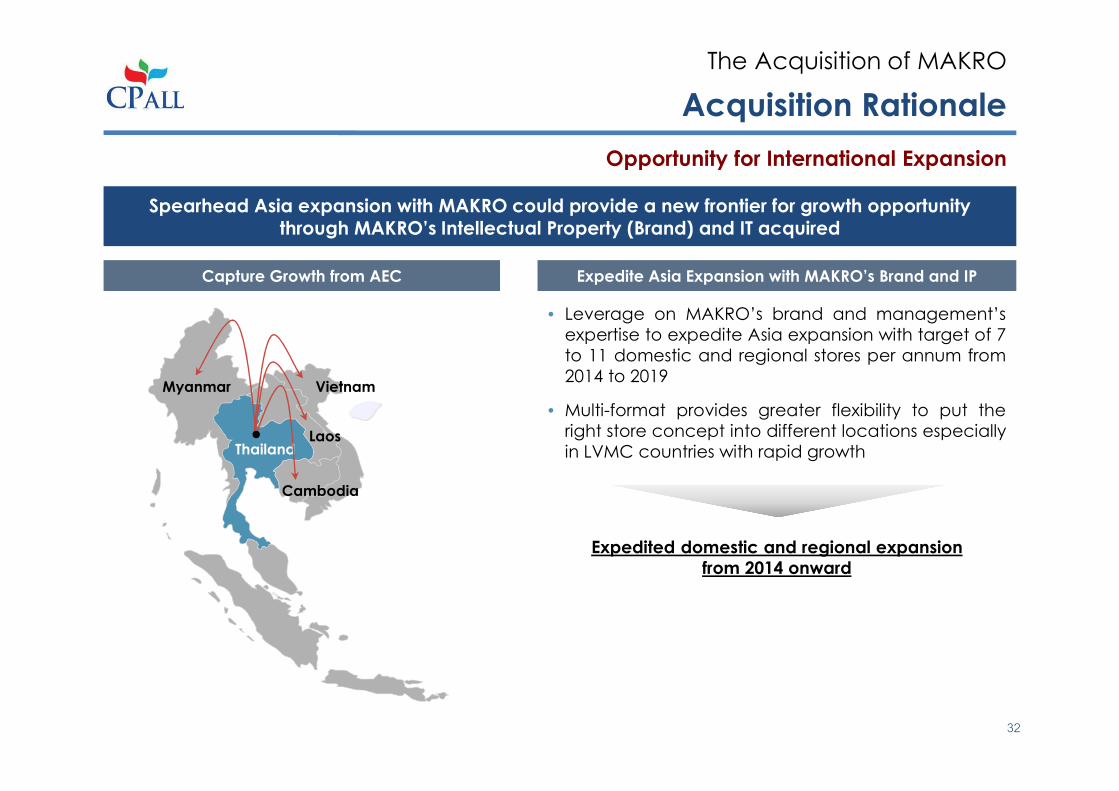

Opportunity for International Expansion

Spearhead Asia expansion with MAKRO could provide a new frontier for growth opportunity through MAKRO’s Intellectual Property (Brand) and IT acquired

• Leverage on MAKRO’s brand and management’s

expertise to expedite Asia expansion with target of 7

to 11 domestic and regional stores per annum from

2014 to 2019

• Multi-format provides greater flexibility to put the

right store concept into different locations especially

in LVMC countries with rapid growth

Expedited domestic and regional expansion

from 2014 onward

Myanmar

LaosThailand

Cambodia

Vietnam

Capture Growth from AEC Expedite Asia Expansion with MAKRO’s Brand and IP

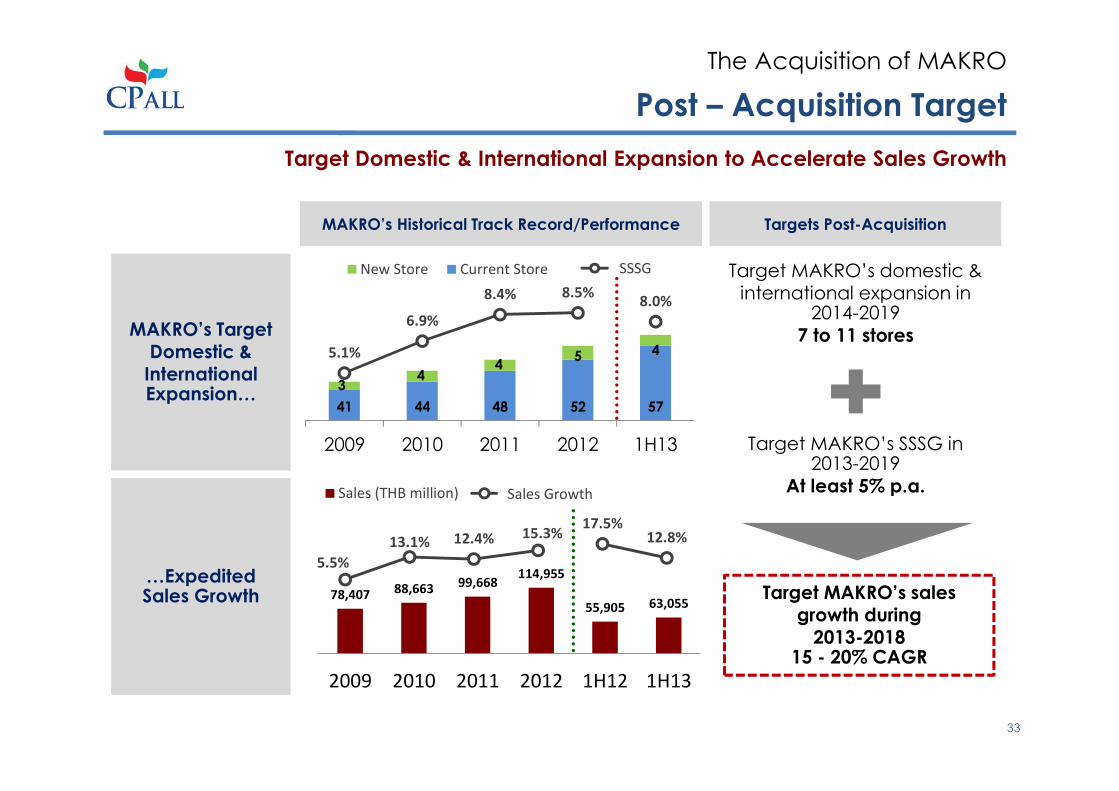

5.1%

6.9%

8.4% 8.5%8.0%

2012

78,407 88,663 99,668114,955

55,905 63,055

2009 2010 2011 2012 1H12 1H13

Sales (THB million)

5.5%

13.1% 12.4% 15.3%17.5%

12.8%

1H13

41 44 48 52 57

34

45 4

2009 2010 2011 2012 1H13

New Store Current Store

Post – Acquisition Target

The Acquisition of MAKRO

MAKRO’s TargetDomestic & InternationalExpansion…

…ExpeditedSales Growth

MAKRO’s Historical Track Record/Performance Targets Post-Acquisition

Target MAKRO’s domestic &international expansion in

2014-2019

7 to 11 stores

Target MAKRO’s SSSG in2013-2019

At least 5% p.a.

Target MAKRO’s salesgrowth during 2013-2018

15 - 20% CAGR

33

Target Domestic & International Expansion to Accelerate Sales Growth

Sales Growth

SSSG

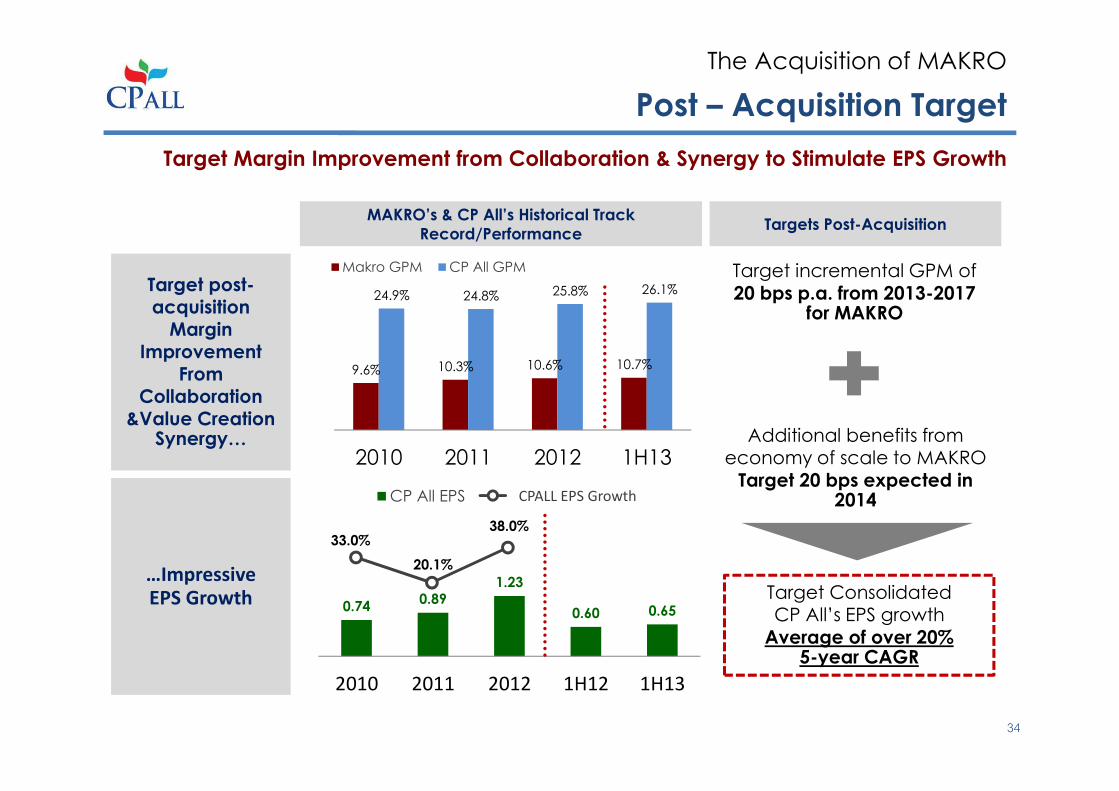

9.6% 10.3% 10.6% 10.7%

24.9% 24.8% 25.8% 26.1%

2010 2011 2012 1H13

Makro GPM CP All GPM

Post – Acquisition Target

The Acquisition of MAKRO

Target post-acquisition Margin

ImprovementFrom

Collaboration &Value Creation

Synergy…

…Impressive EPS Growth

Target incremental GPM of

20 bps p.a. from 2013-2017 for MAKRO

Additional benefits fromeconomy of scale to MAKRO

Target 20 bps expected in 2014

Target ConsolidatedCP All’s EPS growth

Average of over 20%5-year CAGR

34

Target Margin Improvement from Collaboration & Synergy to Stimulate EPS Growth

MAKRO’s & CP All’s Historical Track

Record/PerformanceTargets Post-Acquisition

0.740.89

1.23

0.60 0.65

2010 2011 2012 1H12 1H13

CP All EPS

33.0%

20.1%

38.0%

1H13CPALL EPS Growth

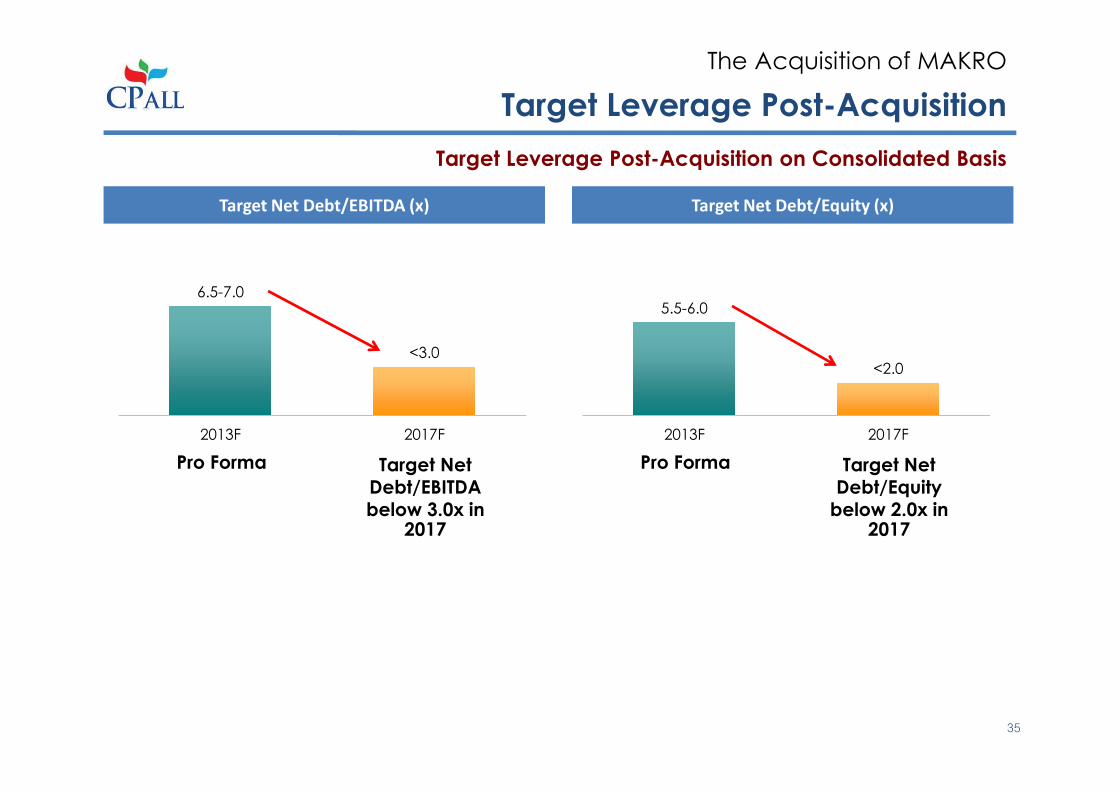

Target Leverage Post-Acquisition

The Acquisition of MAKRO

Target Leverage Post-Acquisition on Consolidated Basis

35

Target Net Debt/EBITDA (x) Target Net Debt/Equity (x)

6.5-7.0

<3.0

2013F 2017F

5.5-6.0

<2.0

2013F 2017F

Pro Forma Target Net Debt/EBITDA below 3.0x in

2017

Pro Forma Target Net Debt/Equity below 2.0x in

2017

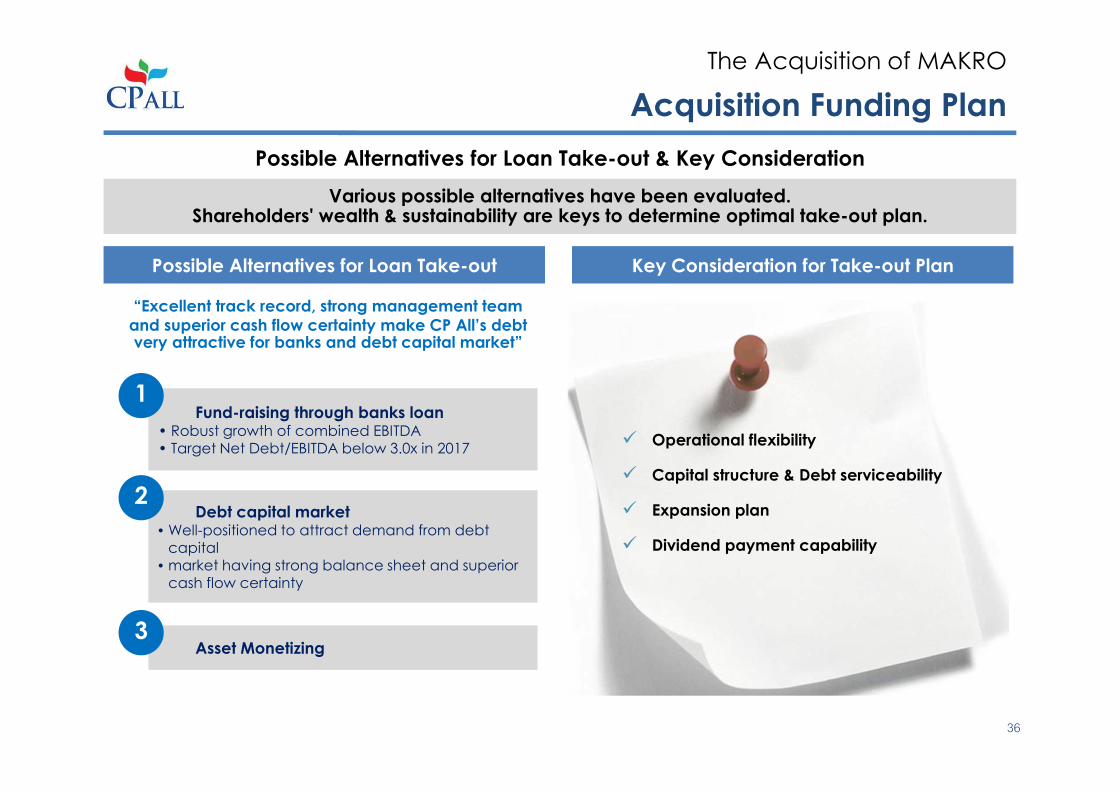

Acquisition Funding Plan

The Acquisition of MAKRO

Various possible alternatives have been evaluated. Shareholders' wealth & sustainability are keys to determine optimal take-out plan.

Possible Alternatives for Loan Take-out & Key Consideration

Possible Alternatives for Loan Take-out Key Consideration for Take-out Plan

“Excellent track record, strong management team

and superior cash flow certainty make CP All’s debt very attractive for banks and debt capital market”

Fund-raising through banks loan • Robust growth of combined EBITDA• Target Net Debt/EBITDA below 3.0x in 2017

1

Debt capital market • Well-positioned to attract demand from debt

capital• market having strong balance sheet and superior

cash flow certainty

2

Asset Monetizing3

36

� Operational flexibility

� Capital structure & Debt serviceability

� Expansion plan

� Dividend payment capability

Agenda

• The Company

• Financial Performance

• The Acquisition of MAKRO

• The Offering

Appendix

• Financial Statements

• Industry Outlook

37

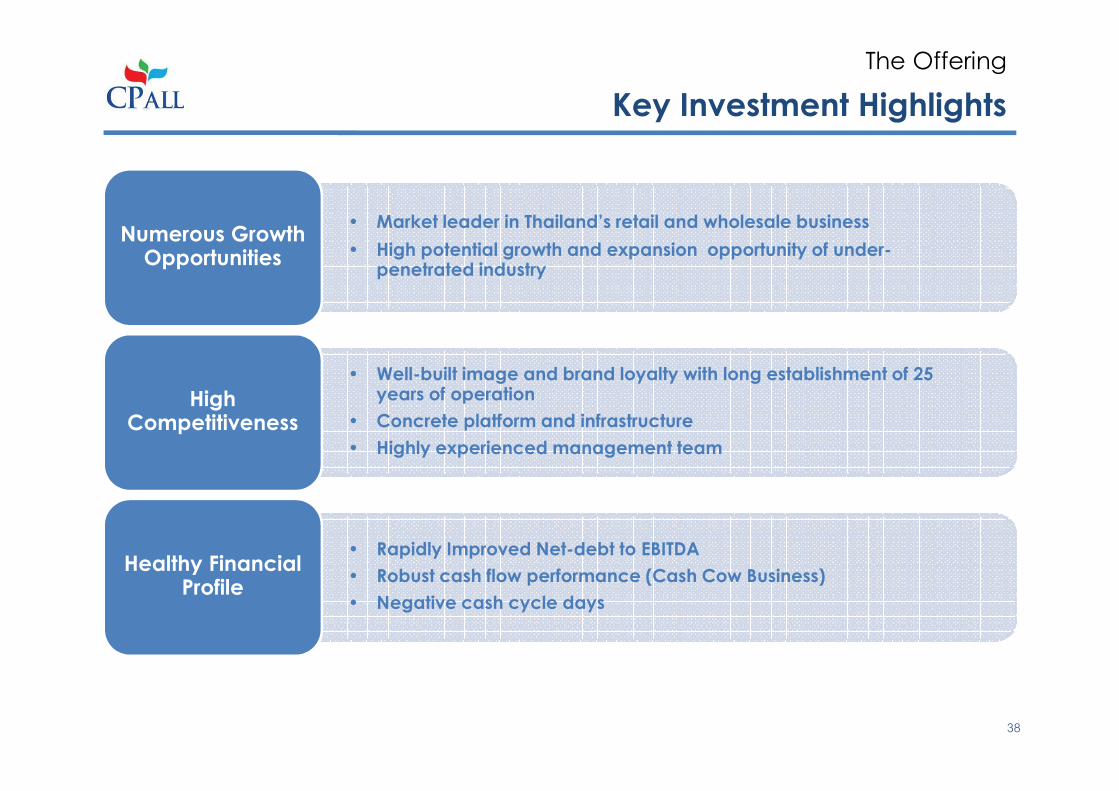

Key Investment Highlights

The Offering

• Market leader in Thailand’s retail and wholesale business

• High potential growth and expansion opportunity of under-penetrated industry

Numerous Growth Opportunities

• Well-built image and brand loyalty with long establishment of 25 years of operation

• Concrete platform and infrastructure

• Highly experienced management team

High Competitiveness

• Rapidly Improved Net-debt to EBITDA

• Robust cash flow performance (Cash Cow Business)

• Negative cash cycle days

Healthy Financial Profile

38

Summary of the Offering

The Offering

Issuer CP All Public Company Limited (“CPALL”)

Joint Lead Arrangers

Bangkok Bank Public Company Limited (“BBL”)

Krung Thai Bank Public Company Limited (“KTB”)

The Siam Commercial Bank Public Company Limited (“SCB”)

The Hongkong and Shanghai Banking Corporation Limited (“HSBC”)

Standard Chartered Bank (Thai) Public Company Limited (“SCBT”)

Type of Debentures THB Unsubordinated and Secured Debentures

Security MAKRO shares

Company Rating A+(tha) by Fitch Ratings (Thailand) Limited

Issue Rating A+(tha) by Fitch Ratings (Thailand) Limited

Placement Methodology Public Offering Private Placement

Target InvestorsRetail Investors

(excluding co-operatives)

Institutional and HNW Investors

(excluding individual investors)

Tenor (Bullet Payment) 3, 5, 7, and 10 years 3, 5, 7, and 10 years

Registrar BBL

Debentureholders’ Representative SCB

Coupon Payment Semi-Annually

Use of Proceeds Debt Repayment and/or Business Operation

39

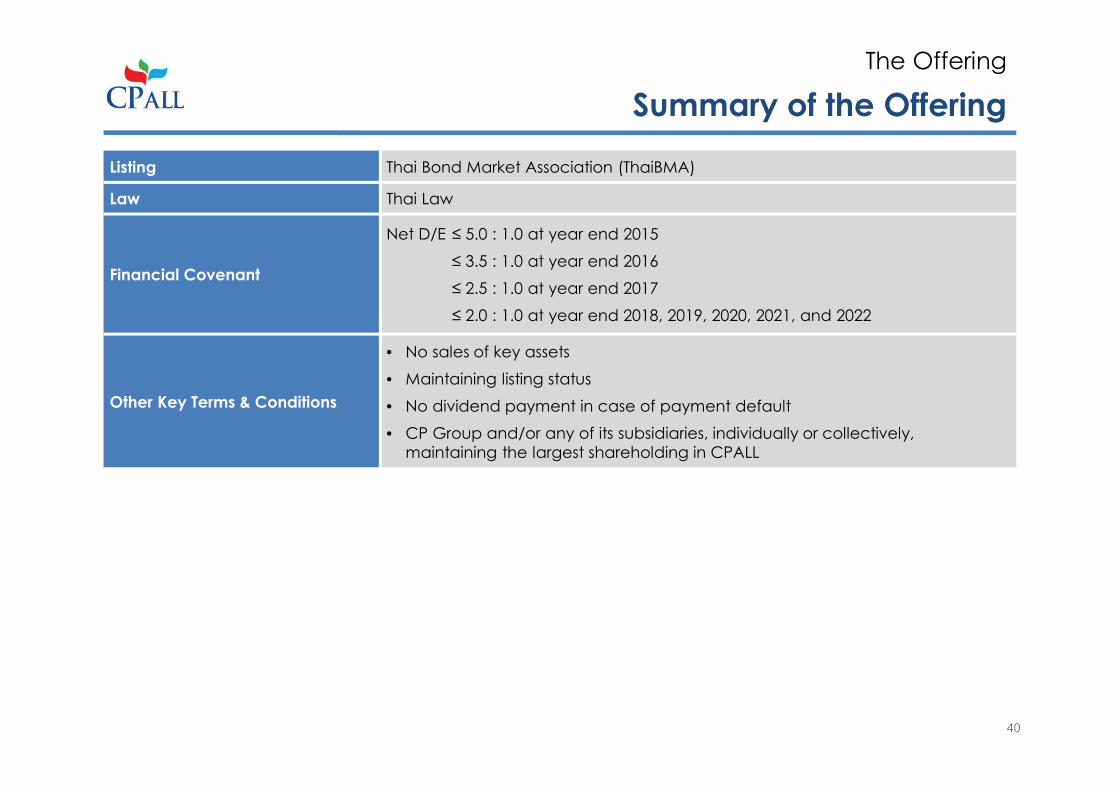

Summary of the Offering

The Offering

Listing Thai Bond Market Association (ThaiBMA)

Law Thai Law

Financial Covenant

Net D/E ≤ 5.0 : 1.0 at year end 2015

≤ 3.5 : 1.0 at year end 2016

≤ 2.5 : 1.0 at year end 2017

≤ 2.0 : 1.0 at year end 2018, 2019, 2020, 2021, and 2022

Other Key Terms & Conditions

• No sales of key assets

• Maintaining listing status

• No dividend payment in case of payment default

• CP Group and/or any of its subsidiaries, individually or collectively,

maintaining the largest shareholding in CPALL

40

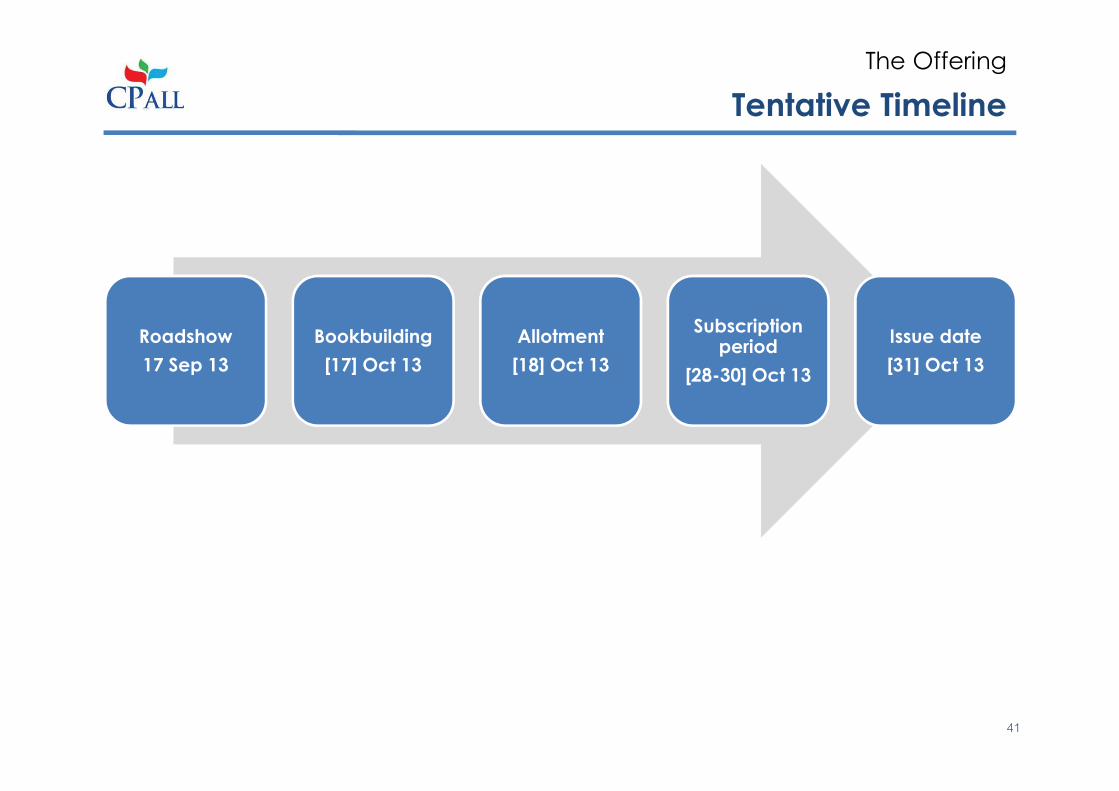

Tentative Timeline

The Offering

Roadshow

17 Sep 13

Bookbuilding

[17] Oct 13

Allotment

[18] Oct 13

Subscription period

[28-30] Oct 13

Issue date

[31] Oct 13

41

Agenda

• The Company

• Financial Performance

• The Acquisition of MAKRO

• The Offering

Appendix

• Summary of Financial Statements

• Industry Outlook

42

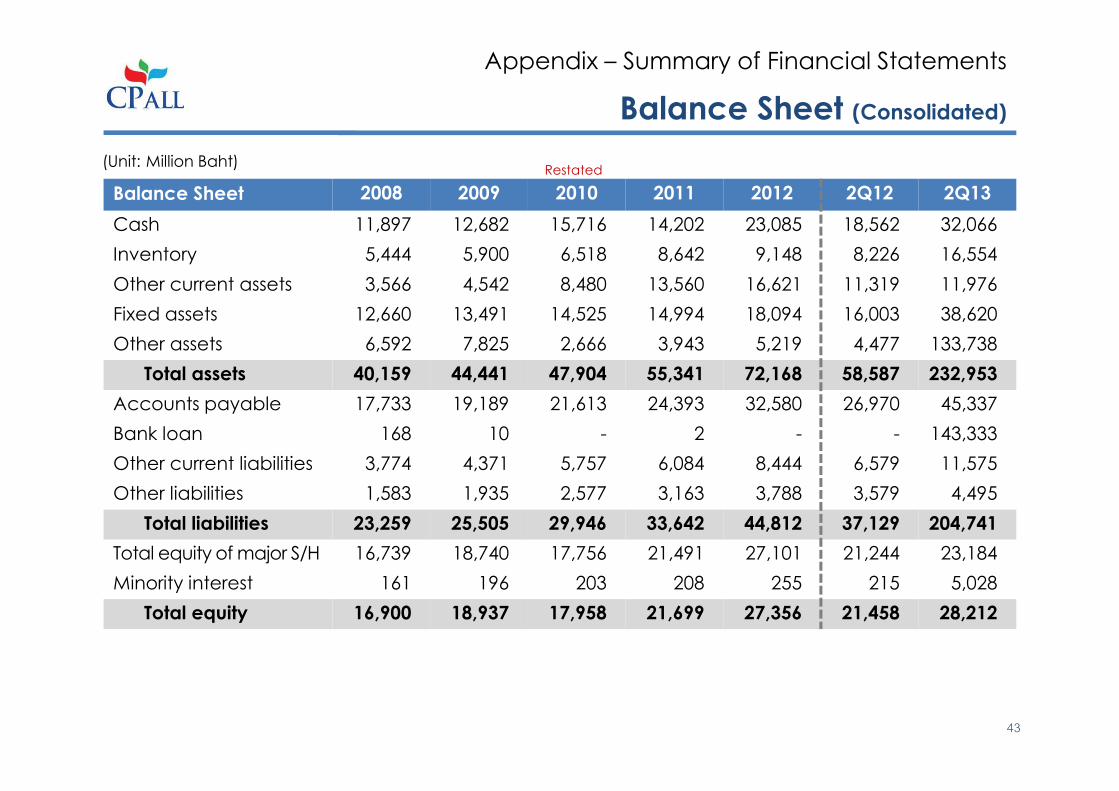

Balance Sheet 2008 2009 2010 2011 2012 2Q12 2Q13

Cash 11,897 12,682 15,716 14,202 23,085 18,562 32,066

Inventory 5,444 5,900 6,518 8,642 9,148 8,226 16,554

Other current assets 3,566 4,542 8,480 13,560 16,621 11,319 11,976

Fixed assets 12,660 13,491 14,525 14,994 18,094 16,003 38,620

Other assets 6,592 7,825 2,666 3,943 5,219 4,477 133,738

Total assets 40,159 44,441 47,904 55,341 72,168 58,587 232,953

Accounts payable 17,733 19,189 21,613 24,393 32,580 26,970 45,337

Bank loan 168 10 - 2 - - 143,333

Other current liabilities 3,774 4,371 5,757 6,084 8,444 6,579 11,575

Other liabilities 1,583 1,935 2,577 3,163 3,788 3,579 4,495

Total liabilities 23,259 25,505 29,946 33,642 44,812 37,129 204,741

Total equity of major S/H 16,739 18,740 17,756 21,491 27,101 21,244 23,184

Minority interest 161 196 203 208 255 215 5,028

Total equity 16,900 18,937 17,958 21,699 27,356 21,458 28,212

Balance Sheet (Consolidated)

Appendix – Summary of Financial Statements

(Unit: Million Baht)Restated

43

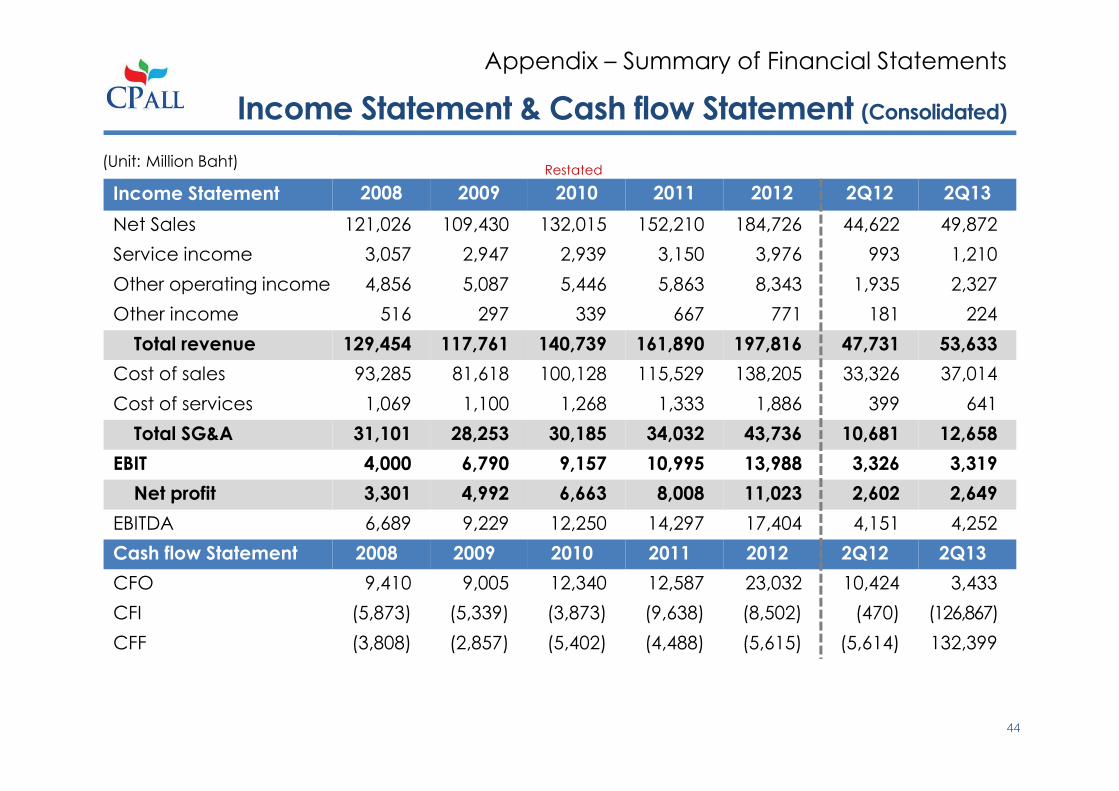

Income Statement & Cash flow Statement (Consolidated)

Appendix – Summary of Financial Statements

Income Statement 2008 2009 2010 2011 2012 2Q12 2Q13

Net Sales 121,026 109,430 132,015 152,210 184,726 44,622 49,872

Service income 3,057 2,947 2,939 3,150 3,976 993 1,210

Other operating income 4,856 5,087 5,446 5,863 8,343 1,935 2,327

Other income 516 297 339 667 771 181 224

Total revenue 129,454 117,761 140,739 161,890 197,816 47,731 53,633

Cost of sales 93,285 81,618 100,128 115,529 138,205 33,326 37,014

Cost of services 1,069 1,100 1,268 1,333 1,886 399 641

Total SG&A 31,101 28,253 30,185 34,032 43,736 10,681 12,658

EBIT 4,000 6,790 9,157 10,995 13,988 3,326 3,319

Net profit 3,301 4,992 6,663 8,008 11,023 2,602 2,649

EBITDA 6,689 9,229 12,250 14,297 17,404 4,151 4,252

Cash flow Statement 2008 2009 2010 2011 2012 2Q12 2Q13

CFO 9,410 9,005 12,340 12,587 23,032 10,424 3,433

CFI (5,873) (5,339) (3,873) (9,638) (8,502) (470) (126,867)

CFF (3,808) (2,857) (5,402) (4,488) (5,615) (5,614) 132,399

Restated

44

(Unit: Million Baht)

Balance Sheet (Company Only)

Appendix – Summary of Financial Statements

Balance Sheet 2008 2009 2010 2011 2012 2Q12 2Q13

Cash 8,866 9,496 12,180 10,804 19,368 14,667 25,638

Inventory 4,940 5,470 6,019 7,901 8,286 7,529 7,996

Other current assets 2,540 4,346 4,247 8,780 12,644 7,377 5,892

Fixed assets 9,317 10,269 11,428 11,743 13,711 12,469 15,767

Other assets 7,961 9,010 9,355 10,674 11,840 11,032 148,378

Total assets 33,624 38,591 43,229 49,902 65,849 53,074 203,671

Accounts payable 12,611 15,123 17,482 20,005 25,740 22,253 25,039

Bank loan - - - - - - 141,228

Other current liabilities 6,487 6,681 7,606 8,461 13,517 9,473 12,913

Other liabilities 1,396 1,757 2,381 2,895 3,420 3,278 3,655

Total liabilities 20,495 23,560 27,469 31,361 42,677 35,004 182,836

Total equity of major S/H 13,129 15,031 15,760 18,541 23,172 18,070 20,835

Minority interest - - - - - - -

Total equity 13,129 15,031 15,760 18,541 23,172 53,074 20,835

Restated

45

(Unit: Million Baht)

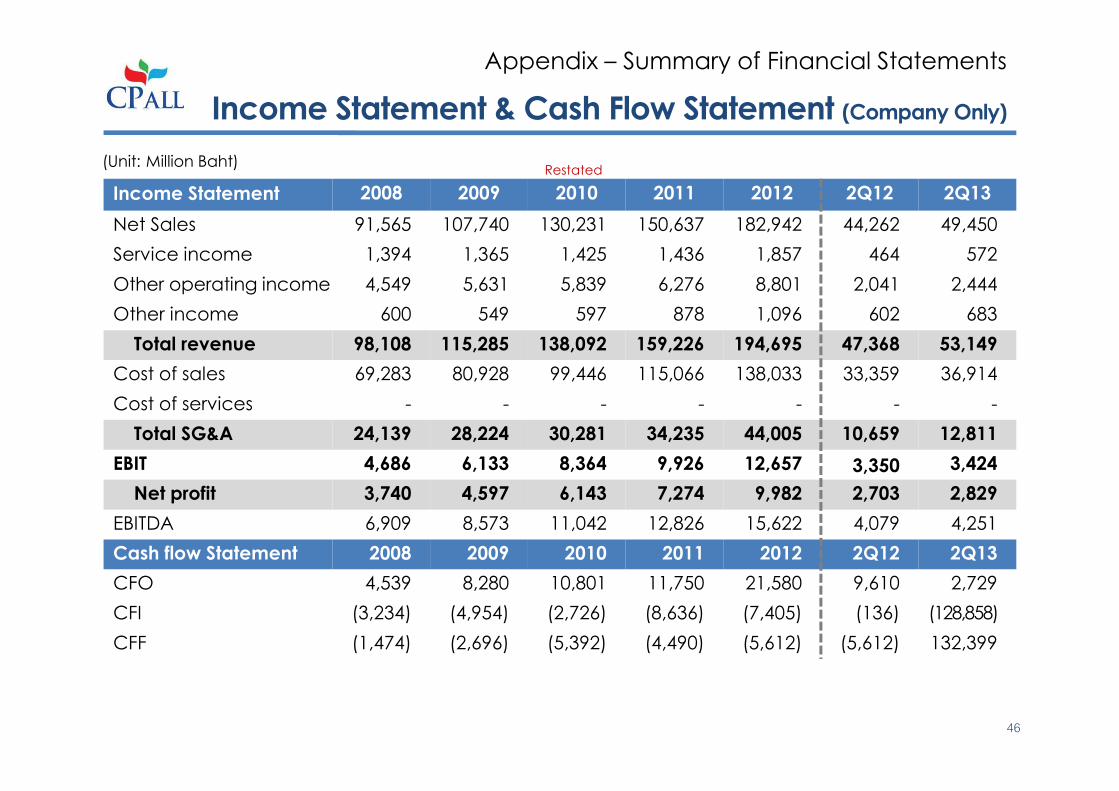

Income Statement & Cash Flow Statement (Company Only)

Appendix – Summary of Financial Statements

Income Statement 2008 2009 2010 2011 2012 2Q12 2Q13

Net Sales 91,565 107,740 130,231 150,637 182,942 44,262 49,450

Service income 1,394 1,365 1,425 1,436 1,857 464 572

Other operating income 4,549 5,631 5,839 6,276 8,801 2,041 2,444

Other income 600 549 597 878 1,096 602 683

Total revenue 98,108 115,285 138,092 159,226 194,695 47,368 53,149

Cost of sales 69,283 80,928 99,446 115,066 138,033 33,359 36,914

Cost of services - - - - - - -

Total SG&A 24,139 28,224 30,281 34,235 44,005 10,659 12,811

EBIT 4,686 6,133 8,364 9,926 12,657 3,350 3,424

Net profit 3,740 4,597 6,143 7,274 9,982 2,703 2,829

EBITDA 6,909 8,573 11,042 12,826 15,622 4,079 4,251

Cash flow Statement 2008 2009 2010 2011 2012 2Q12 2Q13

CFO 4,539 8,280 10,801 11,750 21,580 9,610 2,729

CFI (3,234) (4,954) (2,726) (8,636) (7,405) (136) (128,858)

CFF (1,474) (2,696) (5,392) (4,490) (5,612) (5,612) 132,399

Restated

46

(Unit: Million Baht)

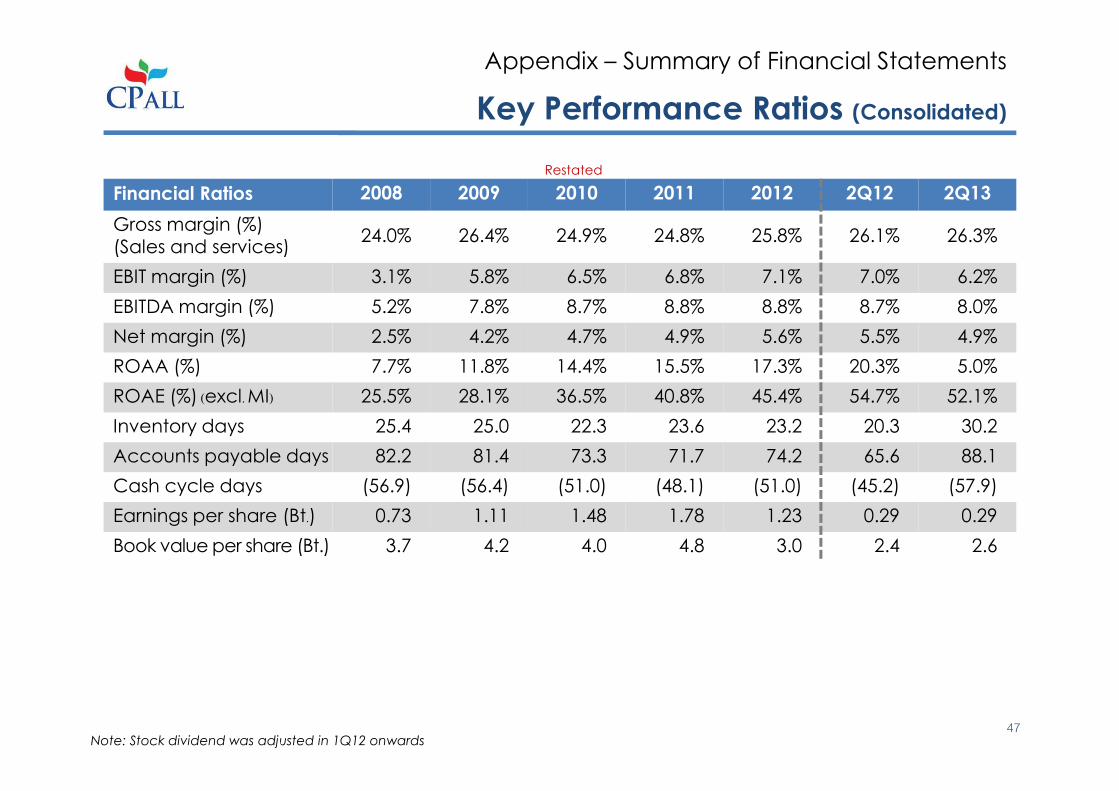

Financial Ratios 2008 2009 2010 2011 2012 2Q12 2Q13

Gross margin (%)(Sales and services)

24.0% 26.4% 24.9% 24.8% 25.8% 26.1% 26.3%

EBIT margin (%) 3.1% 5.8% 6.5% 6.8% 7.1% 7.0% 6.2%

EBITDA margin (%) 5.2% 7.8% 8.7% 8.8% 8.8% 8.7% 8.0%

Net margin (%) 2.5% 4.2% 4.7% 4.9% 5.6% 5.5% 4.9%

ROAA (%) 7.7% 11.8% 14.4% 15.5% 17.3% 20.3% 5.0%

ROAE (%) (excl. MI) 25.5% 28.1% 36.5% 40.8% 45.4% 54.7% 52.1%

Inventory days 25.4 25.0 22.3 23.6 23.2 20.3 30.2

Accounts payable days 82.2 81.4 73.3 71.7 74.2 65.6 88.1

Cash cycle days (56.9) (56.4) (51.0) (48.1) (51.0) (45.2) (57.9)

Earnings per share (Bt.) 0.73 1.11 1.48 1.78 1.23 0.29 0.29

Book value per share (Bt.) 3.7 4.2 4.0 4.8 3.0 2.4 2.6

Key Performance Ratios (Consolidated)

Appendix – Summary of Financial Statements

Restated

Note: Stock dividend was adjusted in 1Q12 onwards47

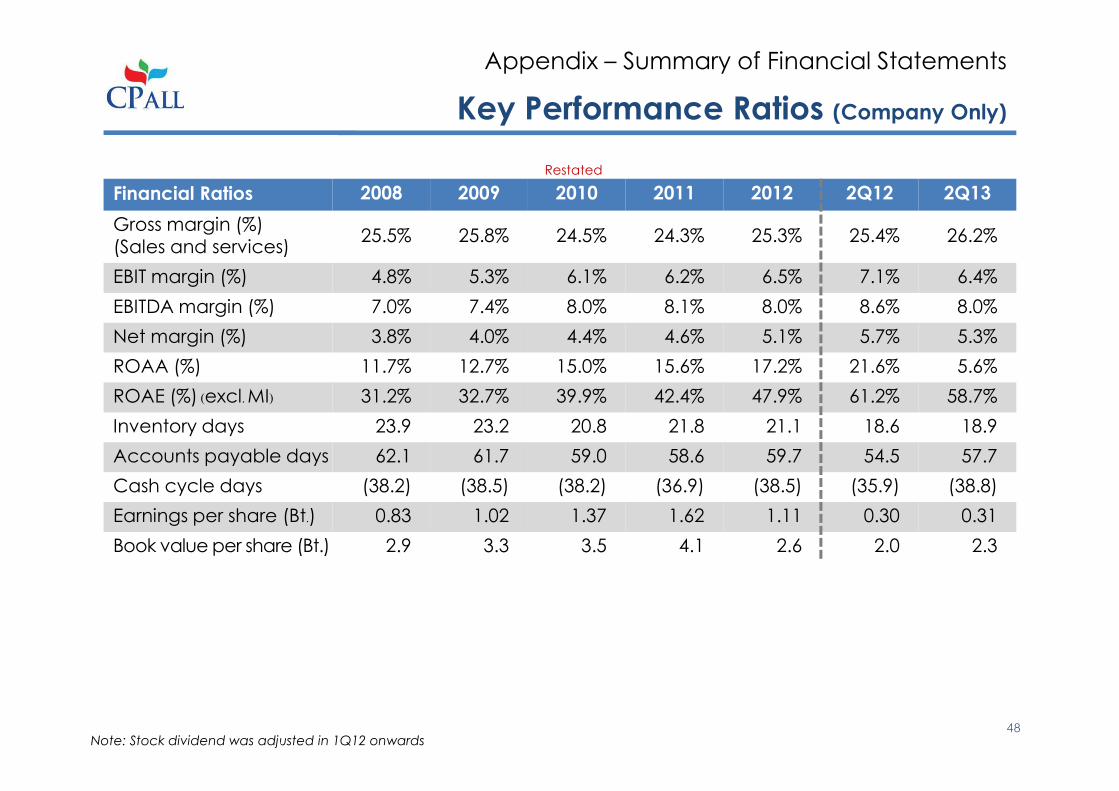

Financial Ratios 2008 2009 2010 2011 2012 2Q12 2Q13

Gross margin (%)(Sales and services)

25.5% 25.8% 24.5% 24.3% 25.3% 25.4% 26.2%

EBIT margin (%) 4.8% 5.3% 6.1% 6.2% 6.5% 7.1% 6.4%

EBITDA margin (%) 7.0% 7.4% 8.0% 8.1% 8.0% 8.6% 8.0%

Net margin (%) 3.8% 4.0% 4.4% 4.6% 5.1% 5.7% 5.3%

ROAA (%) 11.7% 12.7% 15.0% 15.6% 17.2% 21.6% 5.6%

ROAE (%) (excl. MI) 31.2% 32.7% 39.9% 42.4% 47.9% 61.2% 58.7%

Inventory days 23.9 23.2 20.8 21.8 21.1 18.6 18.9

Accounts payable days 62.1 61.7 59.0 58.6 59.7 54.5 57.7

Cash cycle days (38.2) (38.5) (38.2) (36.9) (38.5) (35.9) (38.8)

Earnings per share (Bt.) 0.83 1.02 1.37 1.62 1.11 0.30 0.31

Book value per share (Bt.) 2.9 3.3 3.5 4.1 2.6 2.0 2.3

Key Performance Ratios (Company Only)

Appendix – Summary of Financial Statements

Restated

Note: Stock dividend was adjusted in 1Q12 onwards48

Agenda

• The Company

• Financial Performance

• The Acquisition of MAKRO

• The Offering

Appendix

• Summary of Financial Statements

• Industry Outlook

49

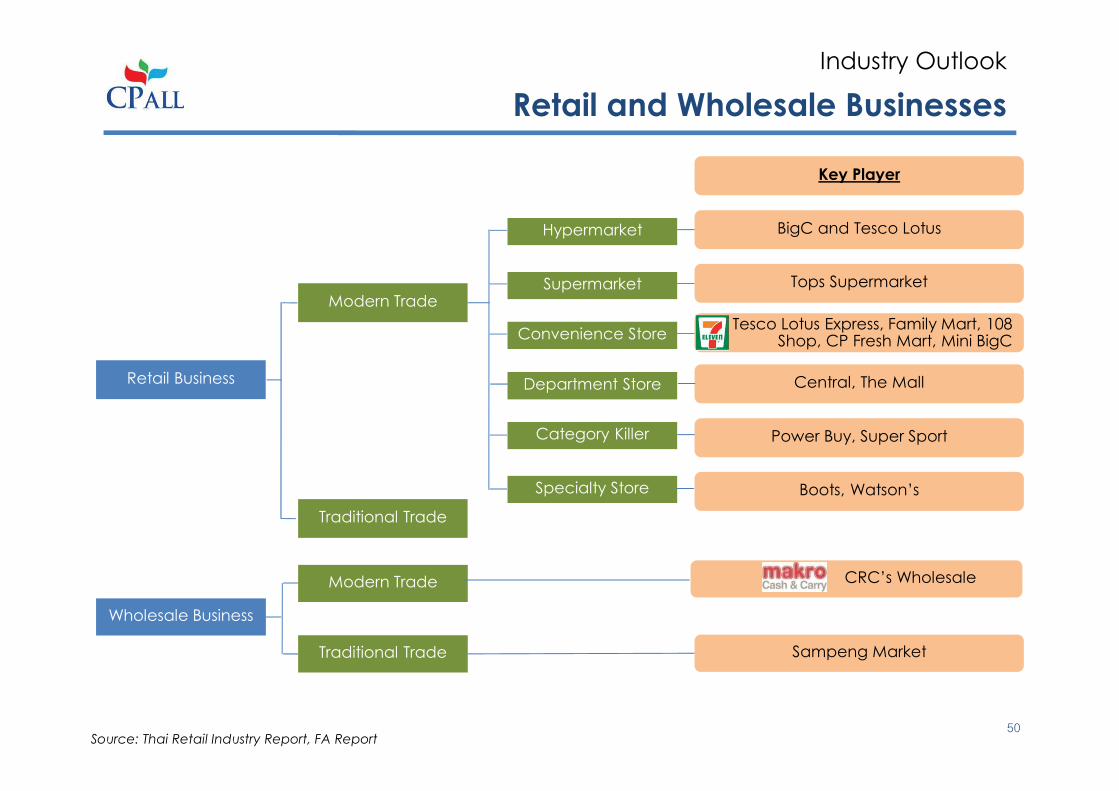

Retail and Wholesale Businesses

Industry Outlook

Retail Business

Traditional Trade

Modern Trade

Hypermarket

Supermarket

Convenience Store

Department Store

Category Killer

Specialty Store

BigC and Tesco Lotus

Tops Supermarket

Tesco Lotus Express, Family Mart, 108 Shop, CP Fresh Mart, Mini BigC

Central, The Mall

Power Buy, Super Sport

Boots, Watson’s

Key Player

Wholesale Business

Modern Trade

Traditional Trade

CRC’s Wholesale

Sampeng Market

Source: Thai Retail Industry Report, FA Report50

Retail Business in Thailand

Industry Outlook

6.9%

-0.7%

11.7%

3.8% 6.4%

5.8%3.4%

4.6% 4.8% 5.6%

2008 2009 2010 2011 2012

GDP Growth Retail Sales Growth

1,235,695

54

1,1

55

52

2,5

11

48

5,6

72

45

4,0

79

41

4,5

21

37

9,9

73

34

5,2

69

34

0,9

16

34

0,4

79

The highest 10’s GPP* Per Capita in 2011 (Baht per annum)

Source: Euromonitor, NESDB

Source: NESDB

*GPP = Gross Provincial Product

9%

7%

5% 1%1%

1%

Others

76%

Retailing Brand Shares 2012

Source: Euromonitor,

• Retail industry was a core contributor to Thai’s

economy and was resilient to economic cycle

• A number of Thai consumers prefer shopping at

the most convenient location. As a result, retailing

operators were attempting to respond to this

demand by having more shops expansion

• The giant retailers were gearing up for this

strategy. 7-Eleven by CP All PCL will continue to

be a leading player in this area

• While market saturation could be seen in Bangkok

and metropolitan area, the expansion will also

start to penetrate provincial and rural areas

Thailand GDP Growth VS Retail Sale Growth

51

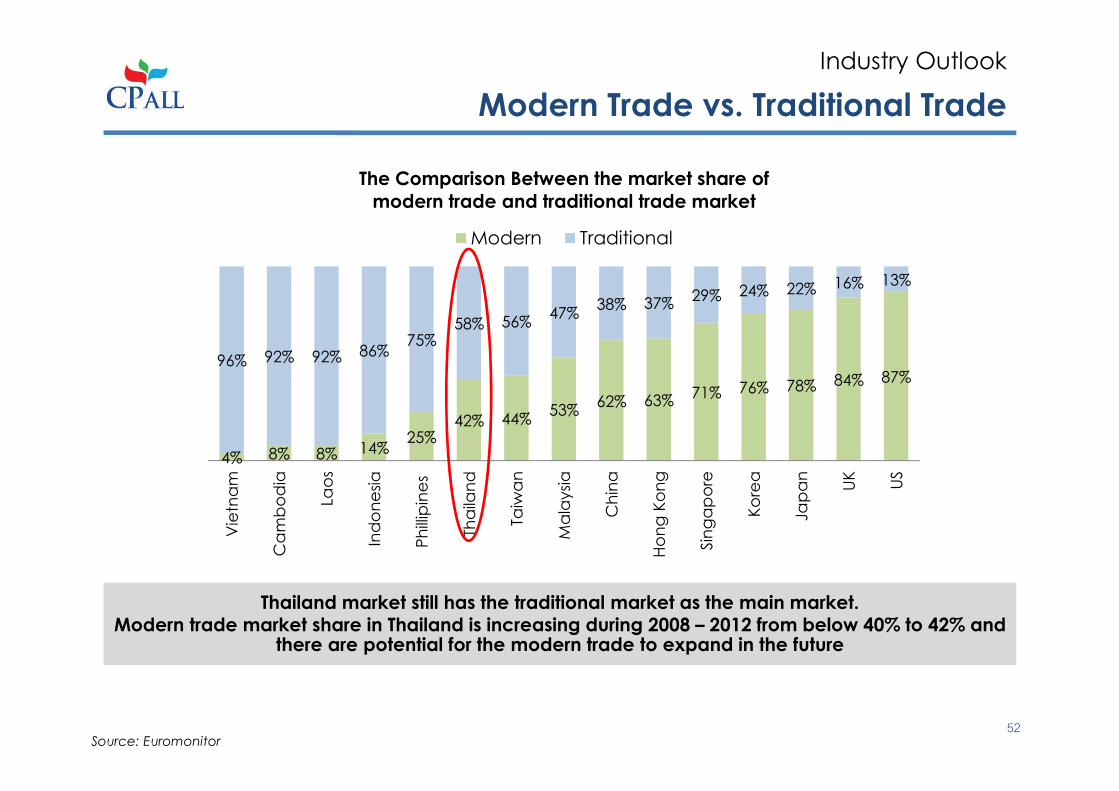

Modern Trade vs. Traditional Trade

Industry Outlook

4% 8% 8% 14%25%

42% 44%53%

62% 63%71% 76% 78% 84% 87%

96% 92% 92% 86%75%

58% 56%47%

38% 37%29% 24% 22% 16% 13%

Vie

tna

m

Ca

mb

od

ia

Lao

s

Ind

on

esi

a

Ph

illip

ine

s

Tha

ilan

d

Taiw

an

Ma

laysi

a

Ch

ina

Ho

ng

Ko

ng

Sin

ga

po

re

Ko

rea

Ja

pa

n

UK

US

The Comparison Between the market share of

modern trade and traditional trade market

Modern Traditional

Thailand market still has the traditional market as the main market.Modern trade market share in Thailand is increasing during 2008 – 2012 from below 40% to 42% and

there are potential for the modern trade to expand in the future

Source: Euromonitor52

South Korea

3 8

113

5

234

283

Hypermarket Supermarket Convenience store

Thailand

Developed Asia

Thai Retail Trade

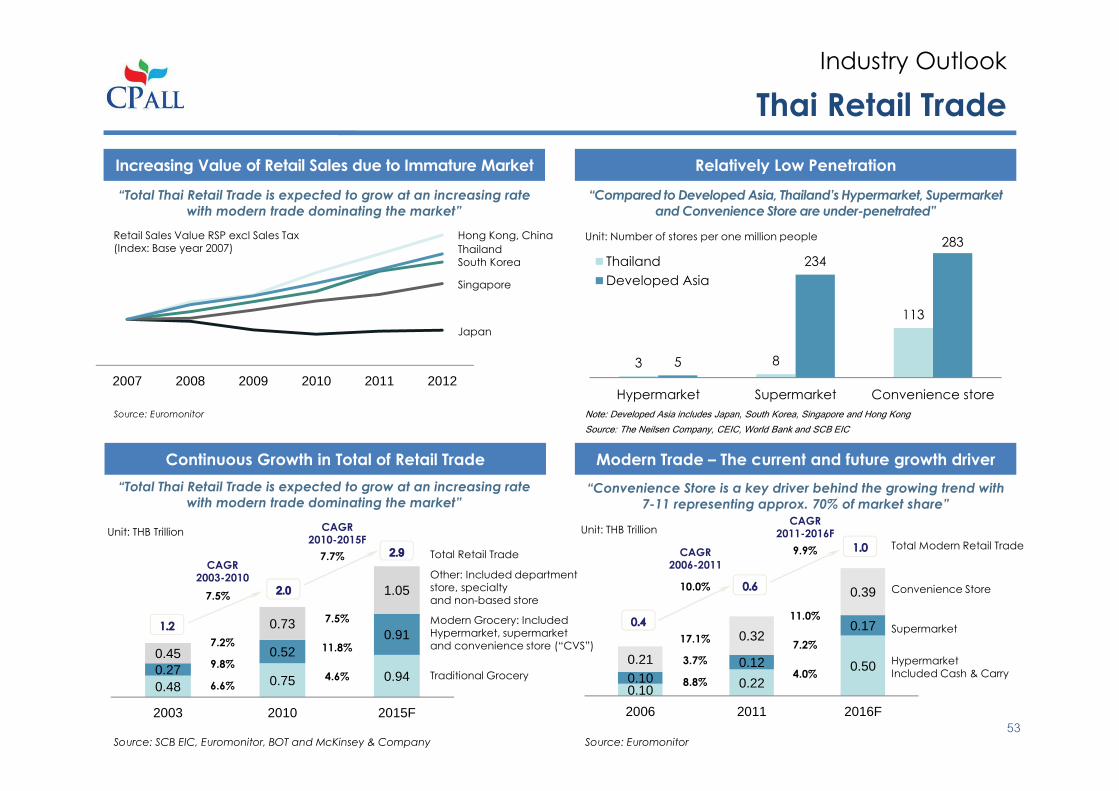

Industry Outlook

2007 2008 2009 2010 2011 2012

Increasing Value of Retail Sales due to Immature Market

Note: Developed Asia includes Japan, South Korea, Singapore and Hong Kong

Source: The Neilsen Company, CEIC, World Bank and SCB EIC

Relatively Low Penetration

“Total Thai Retail Trade is expected to grow at an increasing rate

with modern trade dominating the market”

“Compared to Developed Asia, Thailand’s Hypermarket, Supermarket

and Convenience Store are under-penetrated”

Unit: Number of stores per one million people Retail Sales Value RSP excl Sales Tax(Index: Base year 2007)

Source: Euromonitor

Japan

Singapore

Thailand

Hong Kong, China

Continuous Growth in Total of Retail Trade

Source: Euromonitor

Modern Trade – The current and future growth driver

“Total Thai Retail Trade is expected to grow at an increasing rate

with modern trade dominating the market” “Convenience Store is a key driver behind the growing trend with

7-11 representing approx. 70% of market share”

Source: SCB EIC, Euromonitor, BOT and McKinsey & Company

0.48 0.75 0.940.270.52

0.910.45

0.73

1.05

2003 2010 2015F

CAGR 2003-2010

CAGR 2010-2015F

6.6%

9.8%

7.2%

4.6%

11.8%

7.5%

Total Retail Trade

Other: Included department store, specialtyand non-based store

Modern Grocery: Included Hypermarket, supermarketand convenience store (“CVS”)

Traditional Grocery

7.5%

7.7%

Unit: THB Trillion

0.10 0.220.50

0.100.12

0.17

0.21

0.32

0.39

2006 2011 2016F

Total Modern Retail Trade

Convenience Store

Supermarket

HypermarketIncluded Cash & Carry

CAGR 2006-2011

CAGR 2011-2016F

10.0%

9.9%

8.8%

3.7%

17.1%

4.0%

7.2%

11.0%

Unit: THB Trillion

53

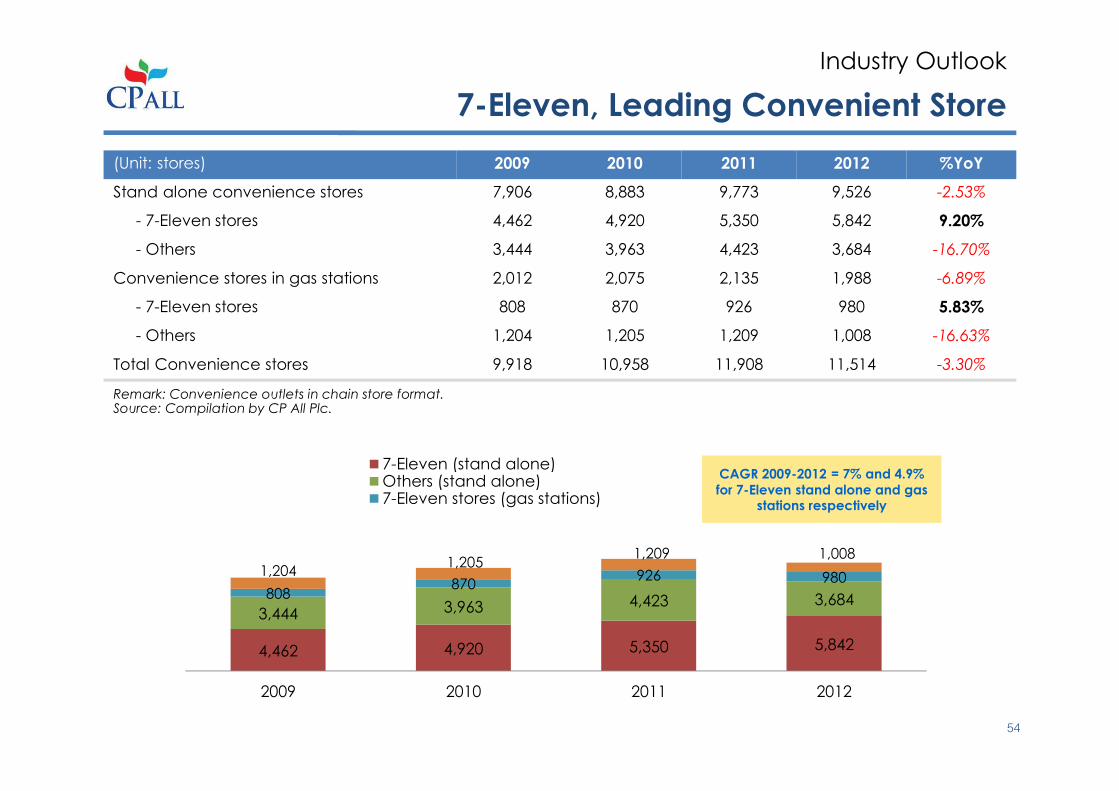

7-Eleven, Leading Convenient Store

Industry Outlook

(Unit: stores) 2009 2010 2011 2012 %YoY

Stand alone convenience stores 7,906 8,883 9,773 9,526 -2.53%

- 7-Eleven stores 4,462 4,920 5,350 5,842 9.20%

- Others 3,444 3,963 4,423 3,684 -16.70%

Convenience stores in gas stations 2,012 2,075 2,135 1,988 -6.89%

- 7-Eleven stores 808 870 926 980 5.83%

- Others 1,204 1,205 1,209 1,008 -16.63%

Total Convenience stores 9,918 10,958 11,908 11,514 -3.30%

4,462 4,920 5,350 5,842

3,444 3,963 4,423 3,684808870

926 9801,2041,205

1,209 1,008

2009 2010 2011 2012

7-Eleven (stand alone)Others (stand alone)7-Eleven stores (gas stations)

Remark: Convenience outlets in chain store format.Source: Compilation by CP All Plc.

CAGR 2009-2012 = 7% and 4.9%

for 7-Eleven stand alone and gas stations respectively

54

Q&A

THANK YOU