Local finance guide - Parkinson's UK

64

Local finance guide A guide for all volunteers with responsibility for local group financial activity

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Local finance guide - Parkinson's UK

LocalfinanceguideA guide for all volunteers with

responsibility for local group

financial activity

Local Finance Guide EA 03022017.pdf 1 09/02/2017 16:07:12

1

Introduction

We hope this guide will be a useful and accessible tool for all local finance volunteers in the local group network. It has been revised to include the latest information as of January 2017. Throughout the guide we refer to branch treasurers and support group finance contacts as local finance volunteers, and we refer to branches and support groups as local groups. The guide covers the policies and procedures required of local groups to make sure Parkinson’s UK meets the legal requirements of the Charity Commission, Office of the Scottish Charity Regulator, accounting standards, Company Law and HM Revenue & Customs etc. These policies and procedures will also enable your local group to meet the Parkinson’s UK Local Group Rules (available at parkinsons.org.uk/localgroupresources). We hope this approach helps every local finance volunteer, whatever their level of experience, to gain a clear understanding of their responsibilities. Some local finance volunteers come from an accounting or bookkeeping background, and may already be familiar with some of the guidance we give, for example around keeping a cashbook. If you do have an accounting or bookkeeping background, please take note of the Parkinson’s UK guidance we provide, but do whatever works for you. This guide is available on our website, along with other documents and resources for volunteers with responsibility for local group financial activity: parkinsons.org.uk/treasurers You can get copies of all the documents and templates that we refer to in this guide either on the website above or from your local staff contact. Don’t forget, the Local Networks Finance team is always more than happy to hear from you if you have any queries about your role and your responsibilities. Email [email protected]

Call 020 7932 1324 At Parkinson’s UK we strive to be a charity that listens to, and properly involves and consults, people affected by Parkinson’s. We’re committed to listening to the needs and views of those using our services. Your views are important in helping us to improve the quality of services that we offer. We welcome your feedback, whether positive or negative. Email [email protected] Call the Head of Involvement and Inclusion on 020 7963 3901 Write to the Head of Involvement and Inclusion at Parkinson’s UK, 215 Vauxhall Bridge Road, London SW1V 1EJ

Local Finance Guide EA 03022017.pdf 2 09/02/2017 16:07:12

2

1.Local finance volunteers and local groups 3 1A Local finance volunteers 3 1B Managing the charity’s funds 5 1C Parkinson’s Links: for everyone, everywhere 6 2.Getting started 8 2A Current accounts 8 This includes information about opening a bank account, signatories, interest and the importance of retaining documents. 2B Deposit accounts 11 2C Support groups and sub groups 12 2D Depositing funds with UK office 13 2E Use of funds 13 3.Up and running: the essentials 15 3A Keeping track of money 15 This includes information about keeping a cashbook and how to record income and expenditure. There is also information about banking income, what to do when you receive gifts, making payments, VAT advice and related party transactions. 3B Transfers between your accounts 32 3C Moving funds between your local group and UK office 33 3D Petty cash 36 3E Bank reconciliation 38 This section will instruct you on how to perform a bank reconciliation but also the importance of doing it for fraud prevention and details of our whistleblowing procedure if you have concerns. 3F Reporting 40 4.Up and running: more important information 41 4A Restricted funds 41 4B Legacies and in memoriam donations 44 4C Gift Aid 45 4D Trading 47 4E Paying volunteer expenses 48 4F Equipment 49 4G Events 51 5.Monitoring and reviewing 54 5A Retaining documents 54 5B Preparing a budget 55 5C Reserves 56 5D Annual Financial Return (AFR) 57 6.Handing over: making it easy 60 7.Closing a local group 61

Local Finance Guide EA 03022017.pdf 3 09/02/2017 16:07:12

3

1. Local finance volunteers and local groups

1A Local finance volunteers Local finance volunteers are volunteers who are responsible for the financial activity in a local group. It is a great opportunity to contribute to the work of Parkinson’s UK if you have experience of, or are interested in, bookkeeping. It is essential for making sure our local groups run successfully and continue to benefit people affected by Parkinson’s in their area. Throughout this guide we refer to branch treasurers and support group finance contacts as local finance volunteers. The following information covers a wide range of eventualities, so at first it may look daunting. But don’t worry – everything will be explained clearly. And remember that the Local Networks Finance team is here to support you if you have any questions or queries. Purpose of the role 1. To record your local group’s financial activity accurately.

2. To keep both your local group and UK office informed of your local group’s

financial position in line with reporting requirements. 3. To provide guidance to the local group on internal control and financial

procedures. Key tasks and responsibilities As a volunteer responsible for local group finances, you must:

ensure financial transactions are handled safely and accurate records are kept

if required, maintain a local bank account(s) in the charity’s name, making

sure all income is banked upon receipt

record all local group assets, making sure arrangements exist for their safekeeping

complete and return Annual Financial Return (AFR) forms in line with the requirements set by the Local Networks Finance team and present the submitted AFR to your local group annually

make sure all volunteer expense claims are paid in line with the charity’s

Volunteer Expenses Policy

make sure there is a smooth handover to the next finance volunteer of all documents and money, including this guide

attend all meetings, as far as is practicable, and prepare an up-to-date financial report for each one, ensuring it is checked and signed by another lead volunteer if your local group is a branch

advise your local group on financial policies, internal controls and appropriate use of funds

make sure financial decisions are agreed by lead volunteers and recorded

Local Finance Guide EA 03022017.pdf 4 09/02/2017 16:07:12

4

Qualities, skills and experience There is no requirement to have any previous financial or accounting experience, although you will find the role easier if you have previous cashbook and spreadsheet experience. You may find it helpful to use a computer if you have access to one, because our electronic cashbook template (available on the website at parkinsons.org.uk/treasurers) will make your role easier. But this is not mandatory. Practicalities of the role Volunteer Support Contact: Your volunteer co-ordinator and Local Networks

Finance team.

Location: Your local group.

Anticipated length of role: Minimum one year, and no longer than six consecutive years.

Anticipated time contribution:

This will vary depending on the size of your local group. In general, we advise you to allow up to two or three hours per week, keeping your cashbook up-to-date and checking that your bank reconciliation is correct. At certain times of the year you may need to give more time. For example, when you are preparing a budget for your local group, or when completing your local group’s Annual Financial Return at the end of the year. The organisation’s financial year runs from January to December.

Training provision

Your volunteer co-ordinator will give an induction to the role and the charity and ask you to complete the online volunteer induction modules.

Familiarise yourself with this guide – we hope it covers everything you need to know.

There are a number of resources available at parkinsons.org.uk/treasurers or by request if you don’t have online access.

All local finance volunteers will be invited to a training session by their volunteer co-ordinator. This may not be straight away, but the guide will help you until you can attend a session near you.

Your volunteer co-ordinator and the Local Networks Finance team will provide guidance and support.

In most cases, the previous finance volunteer will be on hand to help with the handover process.

Volunteer expenses Expenses incurred in your volunteer role should be reimbursed by your group in line with the Volunteer Expenses Policy.

Local Finance Guide EA 03022017.pdf 5 09/02/2017 16:07:12

5

Regulated activities and criminal record check requirements

All local finance volunteers must be a member of the charity.

You’ll need to supply your volunteer co-ordinator with two references. They can give you more information about what references are appropriate.

Parkinson’s UK does not involve volunteers in regulated activities and therefore

does not require volunteers to undertake a criminal record check.

When becoming an account signatory, banks perform a credit check.

You cannot be a financial volunteer in a local group if you are declared bankrupt. This information must be disclosed to your volunteer co-ordinator as part of the recruitment and selection process. For more information on the election process, please refer to the Local Group Rules.

For support or advice on volunteering please email [email protected] or call 020 7963 9328. You can also ask for a copy of a specific role description if required.

Data Protection

Under the Data Protection Act 1998, Parkinson’s UK has legal obligations whenever we handle personal data. This includes someone’s name, address, email address, telephone number and date of birth. Under the Act, we need to make sure the information we keep about people is good quality, relevant, up to date, protected and secure.

As a local finance volunteer, you may have access to people’s personal details, eg membership lists stating if someone is eligible for Gift Aid. For this reason, local finance volunteers must sign a confidentiality agreement, which you can get from your local staff contact. For more information about data protection, please see the Local Group Directory at parkinsons.org.uk/localgroupresources

1B Managing the charity’s funds It is important to remember that it is not solely the responsibility of local finance volunteers to make financial decisions on behalf of a local group. In the case of branches, financial decisions must be made by the committee (including the treasurer) and formally minuted. In the case of any other local groups, financial decisions should still be made by the consensus of the lead volunteers and recorded- an email is sufficient. When you become a finance volunteer, you take on a custodial role and are responsible for the safekeeping of the charity’s local funds. These funds must only be used to support the aims and objectives of the charity and for activities within the guidelines provided for local groups. You will find it useful to familiarise yourself with the Local Group Directory and the core components of Parkinson’s Links to help inform decisions on good use of funds. Internal control Internal control provides reasonable assurance that the aims of the charity will be met, that our financial reporting is reliable and that we are compliant with all applicable laws and regulations.

Local Finance Guide EA 03022017.pdf 6 09/02/2017 16:07:12

6

The internal control for local groups relates to the rules, policies and processes that provide the limits within which a local group can operate and that a finance volunteer should adhere to. These limits are required to ensure the charity’s resources are directed, monitored and measured correctly. Internal control is important in preventing and detecting fraud and protecting the organisation’s resources, including our reputation. They also help us to protect our volunteers. There are a number of key internal controls a local finance volunteer must remember and apply and they will all be explained in this guide.

1C Parkinson’s Links: for everyone, everywhere People affected by Parkinson’s have told us what support they need locally to help them feel in control of life with the condition. Parkinson’s Links is a framework to help our local groups, volunteers and staff to determine local priorities – by mapping what is available and working together to fill the most urgent gaps. This means everyone can access core opportunities and services to empower them to take control. Parkinson’s Links works by:

signposting people to existing activities and services

working in partnership with other organisations

delivering a service or activity ourselves through staff or volunteers In every case, we will encourage and support people to make the connections they want to make, in the most convenient ways for them. Parkinson’s Links Support and activities The table below lists the support that people affected by Parkinson’s have told us they want to see in their local area. Together these make up the core components of Parkinson’s Links. To ensure that we use charity money in the most effective way, we have also agreed who should benefit from this support. This is also shown below:

Area of support Who is this support for?

People with Parkinson’s

Carers Others

Mutual support, ie the opportunity to share experiences with people in a similar situation

Information, advice and signposting to further help

Befriending

Exercise

Therapeutic activity

Self-management

Social activity

Financial assistance (local grant funding)

Listening to views, feedback and needs

Local Finance Guide EA 03022017.pdf 7 09/02/2017 16:07:12

7

People have also told us that they expect there to be a number of different activities happening in their local area. These include:

campaigning

access to information about, and opportunities to participate in, current research projects

marketing activity

fundraising Parkinson’s Links and local groups Parkinson’s UK staff, local groups, local volunteers and other organisations are all involved in providing access to Parkinson’s Links. Local groups are already an important part of enabling access to Parkinson’s Links. They do this through:

providing friendship, support and activities that people affected by Parkinson’s have told us they need to stay in control

working in partnership with other organisations to provide this support

signposting people affected by Parkinson’s to the information, support and services available

Helping people to access Parkinson’s Links We know that currently not everyone across the UK is able to find the information, support and services that they need. So local groups, volunteers and staff will work together to make sure that we are providing access to Parkinson’s Links for everyone affected by Parkinson’s locally. We do not expect our current local group volunteers to take on any additional work or responsibility unless they want to, and we will work together locally to decide the best way to make Parkinson’s Links available. The Board of Trustees has agreed that our priority now is to focus on providing access to Parkinson’s Links locally. This will build on the great things that local groups are doing, and support all of our volunteers to do what they want to do. We have already identified some gaps between our ambition to make Parkinson’s Links available and what people currently have access to. We will work with local groups and volunteers to see how we can best fill these gaps, and to develop tools and resources to support access to Parkinson’s Links across the UK. Local Development Teams Local Development Teams are being set up to look at how to increase access to Parkinson’s Links within local areas. Each local area will have a Local Development Team of volunteers, people with Parkinson’s and local staff. This team will compare what people affected by Parkinson’s have told us they need within their local area with what is actually available – including support and activities provided by other organisations. This will help them to identify the gaps in access to Parkinson’s Links and make decisions about how these can be filled. The Local Development Team’s role doesn’t stop there – they’ll need to oversee the development work to fill these gaps and make sure they improve access to what people have said they need.

Local Finance Guide EA 03022017.pdf 8 09/02/2017 16:07:12

8

2. Getting started

2A Current accounts As soon as a local group begins to receive funds and make payments, it is important that all funds raised are held in an account in the charity’s name. Any money not held in an account in the charity’s name leaves the charity, and the individuals concerned, open to allegations of fraud. Choosing a bank The charity’s funds are not covered by the Financial Services Compensation Scheme, so we wouldn’t receive compensation in the event that your chosen bank fails. Therefore, you must choose your bank from the approved list, which you can get from the Local Networks Finance team. Consider issues such as convenience, reliability and services offered. This information should be available to you locally. Whichever bank you eventually choose must be agreed by your lead volunteers. Account type Parkinson’s UK is a charity and a limited company. You must notify your bank of this, and open an account that is relevant for an incorporated body. Some charity, community or club and association accounts will not be applicable.

Local groups must not have any credit or debit cards associated with their account. All payments should be made by cheque or through dual authorisation internet banking. Local groups must not have, apply for or use, an overdraft or loan. If your local group might become in financial difficulty, please contact your volunteer co-ordinator. Authorisation from UK office To request a bank approval letter in order to open an account in the name of the charity, please contact your volunteer co-ordinator, providing the names of the signatories and the address of your chosen bank. The Local Networks Finance team will then send a letter out to you as soon as possible, signed by the Chief Executive. Completing account application forms You need to complete bank account application forms from the point of view of the whole charity, as local groups are part of the charity and a legal entity of Parkinson’s UK. Forms provided by banks can be difficult to use, so contact the Local Networks Finance team if you have any questions or need any clarification. You should then provide details specific to your local group when asked to provide correspondence details or anything relating to your local group’s bank account activity locally. It is important that you complete the forms using the charity’s national details, as follows. Account name The operating name of the charity is Parkinson’s UK. However, the legally registered name remains Parkinson’s Disease Society of the United Kingdom.

Local Finance Guide EA 03022017.pdf 9 09/02/2017 16:07:12

9

Therefore, your local bank account name must be:

Your bank should accept cheques payable to either Parkinson’s UK or Parkinson’s Disease Society. If your bank has any objections, please contact us for a letter of authorisation. Important information you may be asked Registered Name: Parkinson’s Disease Society of the United

Kingdom Operating Name: Parkinson’s UK Registered Address: 215 Vauxhall Bridge Road, London

SW1V 1EJ Legal Status: Charity & Company limited by

Guarantee Company no.: 00948776 Charity no. (England and Wales): 258197 Charity no. (Scotland): SCO37554 Business commenced 26/02/1969 Country of registration: UK Nature of business: Providing information and support to people

affected by Parkinson’s Number of trustees: 11 2015 annual turnover: £31.5m No: of people employed 485

This information is accurate as of January 2017. For up-to-date figures, please either view the Parkinson’s UK Annual report and accounts, available at parkinsons.org.uk/annualreport, or see the Parkinson’s UK page on the Charity Commission website. Signatories A signatory is a person authorised to issue instructions on your local group’s bank account. Local finance volunteers must give signatories a copy of the guidance regarding their responsibilities and make sure they are aware of the constraints and the rules surrounding the use of funds, internal controls and the Volunteer Expenses Policy. All new signatories from December 2016 are required to provide a reference to their local volunteer co-ordinator. Local groups must have a minimum of three signatories on each account, one of which is the lead finance volunteer. Your bank mandate must state that your account requires two signatories to authorise any payment. However, we recommend having at least four signatories. This is helpful if you have signatories who are ill, on holiday or away – you should still have signatories available to make payments. There are also constraints signatories must know about:

Signatories must not sign a cheque payable to themselves or a related party.

Parkinson’s Disease Society of the UK ………………… Group

Local Finance Guide EA 03022017.pdf 10 09/02/2017 16:07:12

10

If signatories are related, they must not sign the same cheque.

Signatories must never sign a blank or partially completed cheque.

Lead volunteers should approve all expenditure, and financial decisions must be recorded.

All signatories must verify the documentation associated with the payment before signing.

A signatory must be a member of Parkinson’s UK and listed as a member of their local group. It is important to keep the signatories listed on your account up-to-date and in line with the rules and guidance on who can be a signatory. This helps to ensure you have valid signatories available to authorise payments. If the local group wishes to make any changes to the account these should be agreed by lead volunteers and recorded, and you should let your local staff contact know. You will need to complete the relevant form from your bank and it may require two of the current signatories to approve the change. It’s therefore a good idea to take a blank mandate change form (available from your bank) with you to your AGM, so that new signatories can be added as soon as possible. Banks will require identification for new signatories and may perform credit checks – make sure new signatories are aware of this. Bank mandate The bank mandate is the formal instruction to the bank which, amongst other details, lists the signing arrangements for operating the account. The bank mandate will include a list of the signatories authorised to issue instructions. If the local group wishes to make any changes to the account, these should be agreed by the lead volunteers and recorded. A copy of all bank mandates should remain with the group’s financial records. Internet banking You may be asked if you are interested in using an online banking facility. We must follow the Charity Commission guidelines to protect volunteers and the charity’s funds, so this is only be allowed in the following instances:

1. If it’s possible to open a dual authorisation online account. With such a system, one user can log on and initiate a transaction but a second user must then log on to authorise it from a pending transactions screen.

This provides similar control to having two signatures on a cheque but can be speedier and more convenient as the two users do not need to be at the same computer or available at the same time. Internet banking should be secure provided individuals do not divulge their security details to each other, or anyone else.

Most banks provide dual authorisation systems but there may be a transaction cost for this. Local groups should ask their bank for details of similar products.

Don’t forget: Every financial decision must be agreed by your lead volunteers and recorded.

Local Finance Guide EA 03022017.pdf 11 09/02/2017 16:07:12

11

To maintain the security over electronic bank accounts these basic precautions should be in place:

After each transaction, a print-out should be taken (or an archive kept) showing details of the transaction.

Print outs (or an archive independent of the bank’s online archive) of statements should be retained as part of the accounting records – it’s often possible to receive physical paper statements alongside an online account.

Make sure all PCs are up to date with anti-virus, spyware and firewall software (the bank may suggest a specific programme for protection).

Keep all the password(s) and PIN(s) secret.

2. If you can get ‘read only’ access to view bank statements or recent transactions,

but are not able to make payments (some ‘read only’ accounts will allow you to move funds between two accounts held by your local group). This will help you keep your records up to date without having to wait for paper bank statements. This may not be explicitly offered, but when setting up a new user for internet banking, you can state that their payment and transfer limit is ‘0’, preventing the user from performing any transactions.

Interest Some bank accounts will pay a level of interest on their funds, and this will be added periodically. So if you hold a passbook account you will need to get this updated to reflect the interest received. It is important to record this income under the right heading in the cashbook. As interest will appear on your bank statement, you will need to add it to your cashbook in order to reconcile your cashbook with your bank statement. Any funds deposited centrally with UK office will earn interest, but we will account for that centrally and can provide you with a statement of funds held on request. Retaining documents Keep a copy of the bank mandate (and any updates to this) and all bank statements in a safe place. You should keep the bank mandate for the lifetime of your group, and bank statements for six years and the current financial year. When a statement arrives, make sure that it follows on from the last one you received. If not, request the missing statement from your bank as soon as possible.

2B Deposit accounts There are three main reasons for opening a deposit/additional account: 1. Extra income from interest earned.

2. If your local group is building funds for a particular project or purchase, for

example exercise equipment to be used at the group meeting, you may find it helpful to hold this in a separate account.

3. Similarly, some local finance volunteers like to hold a separate account for restricted funds.

Local Finance Guide EA 03022017.pdf 12 09/02/2017 16:07:12

12

If you have or require a deposit account, consider whether the funds held locally are being put to the best use for people affected by Parkinson’s. For more information, see section 5C Reserves on page 56.

If opening or holding a deposit account, remember to do the following:

Make sure the bank is aware that, as a registered charity, we are not liable for tax and this should not be deducted from any interest paid.

If your deposit account has a passbook, make sure that this is updated regularly. In particular, make sure that any interest due is recorded in the passbook at the year end, so that this figure can be recorded on the Annual Financial Return forms.

Familiarise yourself with section 3B Transfers between your accounts on page 32.

If the local group’s current and deposit accounts are held at the same branch, it often makes it easier to transfer money quickly between the two accounts. Achieving favourable interest rates Deposit accounts can be a valuable source of extra income, but currently the returns are very low. Local groups must not put money away on fixed-term, notice period or limited access deposits. All local groups can lodge funds with UK office in a centrally

held fund in their name, receiving a highly competitive rate of interest. For more

information, see section 2D Depositing funds with UK office on page 13. Investing funds Our Investment Committee, made up of trustees and financial experts, is responsible for assisting the Board of Trustees in ensuring that the charity’s funds are not put at risk. They meet to discuss major economic changes, and have decided that the charity should restrict its investments to banks with the highest credit ratings and/or with high levels of UK government ownership. For up-to-date information on this, please contact the Local Networks Finance team.

The Investment Committee also carefully manages our centralised banking and portfolio of investments to ensure that the charity’s funds are both secure and working to achieve the best rate of return. Investing the charity’s funds at a local level (in stocks, shares, investments etc) is both risky and unlikely to result in a high rate of return.

Therefore, local groups must not invest funds in anything other than with a bank from the approved list which you can get from the Local Networks Finance team. Shares No local group should hold or purchase shares. If you are gifted shares please contact the Local Networks Finance team immediately to arrange their sale.

2C Support groups and sub groups

Support groups

The Board of Trustees set a limit on the level of funds that support groups can hold locally. The amount held locally must not exceed £2,000 (as at December 2016).

Local Finance Guide EA 03022017.pdf 13 09/02/2017 16:07:12

13

Any excess money must be forwarded to UK office, with two options:

Transfer any excess funds towards centrally funded local activities.

Deposit any excess funds in an account held centrally on your group’s behalf.

Sub groups Where a branch has a sub group (the setting up of which is subject to the approval of the country director or England manager), the finance volunteer of the parent group is responsible for the funds held and used by the sub group. This includes the responsibility for:

accurately recording all financial activity

keeping both the parent group and UK office informed of the sub group’s financial position

providing guidance to the sub group on internal control procedures Sub groups must not have their own bank account.

2D Depositing funds with UK office It is possible to deposit funds with UK office which can be transferred back to you at any time, in any amount, and statements are available on request. Benefits of depositing funds centrally include:

Interest – we are able to offer a highly competitive interest rate (currently 0.5% – contact the Local Networks Finance team for an up-to-date rate).

Security – the charity’s funds are not covered by the Financial Services Compensation Scheme, so it is essential that our funds are secure and our Investment Committee ensures that all central funds are held in safe banks.

Send in a cheque made payable to Parkinson’s UK, letting us know that you would like us to hold these funds for your local group. To request these funds be transferred back to your local group, please send your request to the Local Networks Finance team. Payments are made weekly, so a transfer back to your local group’s authorised charity account shouldn’t take long. Support groups will need to provide a bank statement to confirm that a requested transfer will not cause them to exceed the limit they can hold locally. 2E Use of funds As a charity there are restrictions on what sort of things we can and can’t use money given to us to fund. In local groups, the appropriate use of funds is the responsibility of all lead volunteers, not just the finance volunteer, but they can advise on this. It is essential to remember that all funds held by Parkinson’s UK have been accepted with the understanding that they will be used to help people affected by Parkinson’s, and to further the charity’s aims and objectives. As such, it is important to consider whether your local group is spending its funds in the most appropriate and beneficial way.

Local Finance Guide EA 03022017.pdf 14 09/02/2017 16:07:12

14

Any expenditure planned by your local group should be reviewed in light of the following documents:

Local Group Rules.

Local Group Directory.

The Memorandum and Articles of Association for the charity – legal document

defining the charity’s area and scope of operation.

This guide.

Your local group should also consider if the expenditure will help the charity meet our goals, as set out in section 1C Parkinson’s Links: for everyone, everywhere on page 6, particularly in helping to provide access to the components of Parkinson’s Links. If you or your local group is uncertain whether expenditure is appropriate, please contact your volunteer co-ordinator or the Local Networks Finance team. Inappropriate use of funds See the following table for a number of commonly discussed uses of funds that are considered inappropriate. Please note, this is not an exhaustive list.

Staff Local groups must not employ staff, including, but not limited to, Parkinson’s nurses. Donations to

other charities Making donations to other charities is not permissible. However, this is distinct from groups making payments to other charities in return for goods and services, such as paying to use a hall to hold a meeting. NHS or

statutory services

Local groups must not make donations to the NHS or Parkinson’s nurses directly. Responsibility for negotiating and ensuring terms of nurse services rests with the Service Improvement Programme Manager, so please forward all enquiries to UK office. Local groups should not be paying for statutory services either. Research not

via national office

Local groups must not commission research or donate directly to a research team. All the research that Parkinson’s UK supports must go through our rigorous review process under the terms of our membership to the Association of Medical Research Charities (AMRC) before funds can be awarded. If you wish to transfer an amount to research, you can, via UK office. If your local group would like to support a specific project you can do this for transfers in excess of £2,000. Please contact the Research team for more information at [email protected] Investments Local groups must not have investments of any kind.

Buildings, vehicles etc

Local groups must not purchase buildings, vehicles, caravans, holiday homes etc.

Local Finance Guide EA 03022017.pdf 15 09/02/2017 16:07:12

15

Charging for local group activities Currently there is no guidance around charging for local group activities. Your local group may decide to charge for local group activities, but this must not exceed what is reasonable to cover the costs. Consider if it is a good use of funds to charge nothing for activities – consider subsidies. You should only subsidise costs for people with Parkinson’s and their carers, whether they are members or not. However, your decision to provide a subsidy may be influenced by how many people are accessing an activity provided by your group and how much the group can afford to subsidise so that this is equitable.

Purchases Some local groups may make purchases for their group, eg a PA system or exercise equipment for group meetings or a marquee for events. It is important that anything over a £100 is entered into your asset register, you can find more information about this in section 4F Equipment on page 49.

3. Up and running: the essentials

3A Keeping track of money It is essential to keep an accurate and up-to-date cashbook to record all income and expenditure, whether by cheque, cash or transfer. It is essential to meet the regulations for charity and company accounting and will make your role easier.

You cannot rely on bank statements for this information. Although they will show dates and amounts, there is no breakdown of the amounts banked or paid, they do not record the purpose and they do not account for petty cash transactions. Keeping a detailed cashbook ensures that all income and expenditure is recorded and accounted for.

Using the cashbook template provided will mean that we are much better placed to assist you, both in getting started and with problem solving. It will also make the Annual Financial Return process easier for you. An electronic version (which is an Excel workbook) is available on the website at parkinsons.org.uk/treasurers. You can also request this by email from the Local Networks Finance team. It will automatically fill in a summary financial report for the year to date financial position of your local group, which can be printed off to provide a convenient report for updating your local group’s lead volunteers. It will also calculate the adjusted balance based on uncleared expenditure and income, easing the bank reconciliation process. If you have experience in accounting or bookkeeping, you may already have software that you prefer to use. As long as you adhere to Parkinson’s UK reporting guideline requirements in section 3F Reporting on page 40, you can use whatever works best for you to keep your cashbook.

Local Finance Guide EA 03022017.pdf 16 09/02/2017 16:07:12

16

Keeping a cashbook by hand If you prefer to keep a cashbook by hand, you can request a paper version from the Local Networks Finance team, but do remember that this will make it harder to look up information. You must also manually check that all amounts have been entered and totalled correctly.

Our electronic cashbook will total automatically and carry forward figures. To check totals by hand requires a process called ‘cross casting’ which is detailed on page 23. Keep in mind that you will also be required to produce summary reports of financial activity, and this will be time consuming if you’re working by hand. For a branch, we advise that you feed back at all committee meetings. We try to make the cashbook as easy to use as possible, both electronically and by hand, but if you wish to suggest changes or add more detail to the template, please contact the Local Networks Finance team. Do I need more than one cashbook? The instructions in this guide are based on using one main cashbook (with separate income and expenditure sheets) covering all bank accounts and petty cash. This is our recommended method of keeping a cashbook as it simplifies the reporting process, but other options you may wish to consider include:

keeping a cashbook for bank account(s) held, and a separate petty cashbook

keeping one cashbook for unrestricted funds and one for restricted funds

keeping one cashbook for all bank accounts and petty cash

some combination of the above

If you use one cashbook and have multiple accounts, you will need to monitor each account’s balance to make sure you have sufficient funds available. Recording income If a donor requests a receipt for their donation, we are legally required to provide one. Receipt books are available at most stationary stores. Please ensure these are used, as they contain all legal information required.

Downloading Open Office If you don’t have Microsoft Office (Excel, Word etc) but would like to use our electronic templates you can download a suite of software called Open Office for free. Open Office will enable you to use our templates fully and hopefully make your life easier. Visit www.openoffice.org In order to download the Open Office spreadsheet software, Calc (their version of Excel), you have to download the whole suite (including equivalents for Word, PowerPoint, Access etc). You will then be able to use our combined cashbooks and reports template. If you have any concerns at all with installing this software please contact the Local Networks Finance team who will be able to help.

Local Finance Guide EA 03022017.pdf 17 09/02/2017 16:07:12

17

It is also necessary to keep documentation that comes in with anything you receive to help you identify it later. Examples of documents worth keeping are:

signed cash tally sheets

letters stating the donation be used for a specific purpose

remittance advice

receipts

In the template cashbook provided (see example in Fig 1), you should record the following:

Date you receive the cash/cheque.

Name of donor and/or details of event associated with the income, or internal document reference number.

Paying-in slip reference number.

Whether the amount has cleared the bank (reflected on your bank statement).

Whether the income has been restricted for a specific activity by the donor.

Income amount under the relevant heading(s). When using the electronic version the Total column will populate automatically.

Fig 1 Sample income cash sheet (the ‘Income breakdown’ section of this cashbook

has been shortened for ease of illustration)

As you can see, keeping a cashbook allows you to record information relatively simply. On the left you record all identifying details, and on the right you provide a breakdown of where the money has come from by putting it under the relevant heading.

The cashbook should record each item you have received separately. For example, in Fig 1, you would not combine on one line John Smith’s general donation and the collection, even if they were paid in on the same day. You may also get one cheque for two different purposes (commonly, a subscription for the local group with an additional donation). In this case, the separate amounts should be entered under the relevant headings in the right-hand income breakdown. The column titled ‘Total’ should add these together.

Identifying details Income breakdown

Local Finance Guide EA 03022017.pdf 18 09/02/2017 16:07:12

18

Cleared bank income Once your bank statements arrive, cross-reference the amounts on the statement with your cashbook. Update the ‘Cleared bank’ column with a ‘Y’ for any items that appear on your bank statement. This will be essential for your bank reconciliation. In Fig 1, May’s statement has arrived showing the £50 has cleared the bank, so there is now a ‘Y’ in the ‘Cleared bank’ column. In the electronic version of the cashbook this cleared entry no longer appears in the ‘Outstanding items’ column. However, we haven’t received June’s statement yet, so it is unknown whether the subsequent two amounts have cleared the bank or not. If keeping a cashbook by hand, there is no need to enter an ‘N’ here, simply mark off with a ‘Y’ or a tick when the item does clear the bank. In the electronic version of the cashbook the income and outstanding items feed into the bank reconciliation of the financial report page. Restricted income It is a legal requirement to record whether income is restricted. For more information, see section 4A Restricted funds on page 41. Income – Cashbook Advice Below is a breakdown of the different headings on the income sheet of our cashbook, along with a description of what would be classified under each heading. We have also included the row number these correspond to on the Annual Financial Return (AFR).

Cashbook title AFR Row

Description and examples

Transfer from deposit/petty cash account

N/A Any money moved out of the deposit account, or the return of a cash float.

Money received for forwarding to UK Office

1 Any donations received by your local group for use by UK office eg membership for Parkinson’s UK or funds raised by individuals where they want the money to go to UK office (for research etc).

Membership collected locally for group

2 Membership of your local group.

Local group membership and donations received from UK office

Membership and donations

3a All membership and donations received via UK office (excluding legacies and Gift Aid); including the return of donations in Gift Aid submissions.

Gift Aid 3b Any Gift Aid tax claimed by UK office and returned to your local group. This is listed in your quarterly donation reports.

Grants 4 Any grants received by your local group directly, eg Big Lottery or your local authority.

Local Finance Guide EA 03022017.pdf 19 09/02/2017 16:07:12

19

Legacies received directly By local group

5 If you directly receive a legacy, please contact the Local Networks team at [email protected] to arrange to forward it back to UK office. If there is an exceptional circumstance where the legacy is banked locally, please list here.

Legacies received via UK Office

6 Legacies paid to your local group via UK office.

General donations 7 Donations or gifts given directly to your local group, including income from Trusts, individuals and companies (eg donations from individuals or organisations not related to events or other fundraising activities).

Fundraising 8 Any event that is held to raise funds (eg collections, raffles, sponsored walks/ runs/ sky dives, auctions of goods, concerts, quiz nights, tea afternoons, cake sales, jumble sales, fairs etc). Please remember to record all income and expenditure from fundraising separately; do not just record net proceeds in income.

In memoriam donations and funeral collections

9 Donations given by friends and family in memory of a person who has died. Note: if it has been requested that the money raised is to be passed to UK office, this should be included under the heading ‘Any money received for forwarding to UK office’ (AFR row 1). If you receive in memoriam donations that were paid directly to UK office, these will be paid back to the group in the quarterly payment run and should be under the heading ‘Local group membership and donations received from UK office – Membership and donations’ (AFR row 3a).

Group activities

Social activities/ meetings

10a Income collected from attendees for local group meetings eg refreshments.

Exercise activities

10b Income collected from attendees for exercise or therapeutic activities.

Therapeutic activities

10c

Holiday/outings 10d Income collected for holidays or outings eg a trip to the seaside, theatre.

Interest on bank balances 11 Any interest earned on bank accounts or other deposits held by your local group.

Transfers from other Parkinson’s UK groups

12 To ensure we do not double count, please list any money you receive from other Parkinson’s UK local groups here.

Local Finance Guide EA 03022017.pdf 20 09/02/2017 16:07:12

20

Other items 13 Any other income you cannot categorise elsewhere. Please make a note of high-value income, as details need to be provided on the Annual Financial Return.

Sale of purchased items inc. Parkinson’s UK Sales Ltd items

14 This includes the money received from selling any items purchased from Parkinson’s UK Sales, eg Christmas cards, T- shirts.

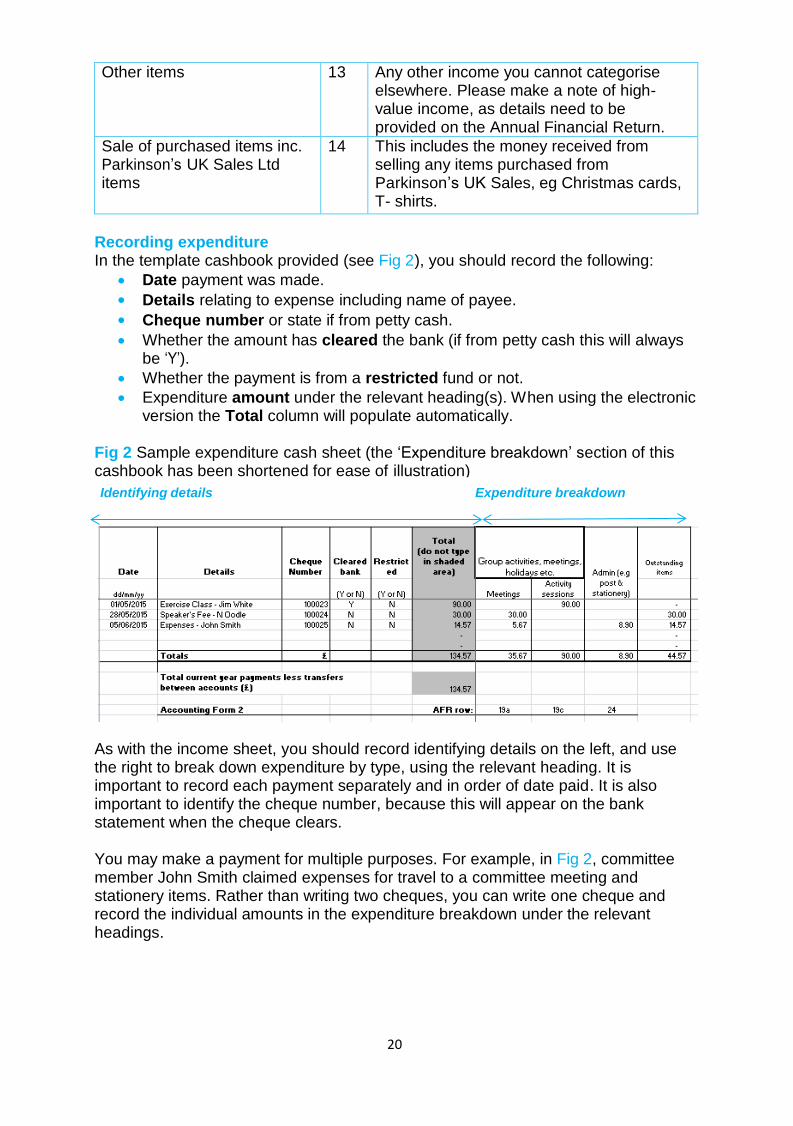

Recording expenditure In the template cashbook provided (see Fig 2), you should record the following:

Date payment was made.

Details relating to expense including name of payee.

Cheque number or state if from petty cash.

Whether the amount has cleared the bank (if from petty cash this will always be ‘Y’).

Whether the payment is from a restricted fund or not.

Expenditure amount under the relevant heading(s). When using the electronic version the Total column will populate automatically.

Fig 2 Sample expenditure cash sheet (the ‘Expenditure breakdown’ section of this cashbook has been shortened for ease of illustration)

As with the income sheet, you should record identifying details on the left, and use the right to break down expenditure by type, using the relevant heading. It is important to record each payment separately and in order of date paid. It is also important to identify the cheque number, because this will appear on the bank statement when the cheque clears. You may make a payment for multiple purposes. For example, in Fig 2, committee member John Smith claimed expenses for travel to a committee meeting and stationery items. Rather than writing two cheques, you can write one cheque and record the individual amounts in the expenditure breakdown under the relevant headings.

Identifying details Expenditure breakdown

Local Finance Guide EA 03022017.pdf 21 09/02/2017 16:07:12

21

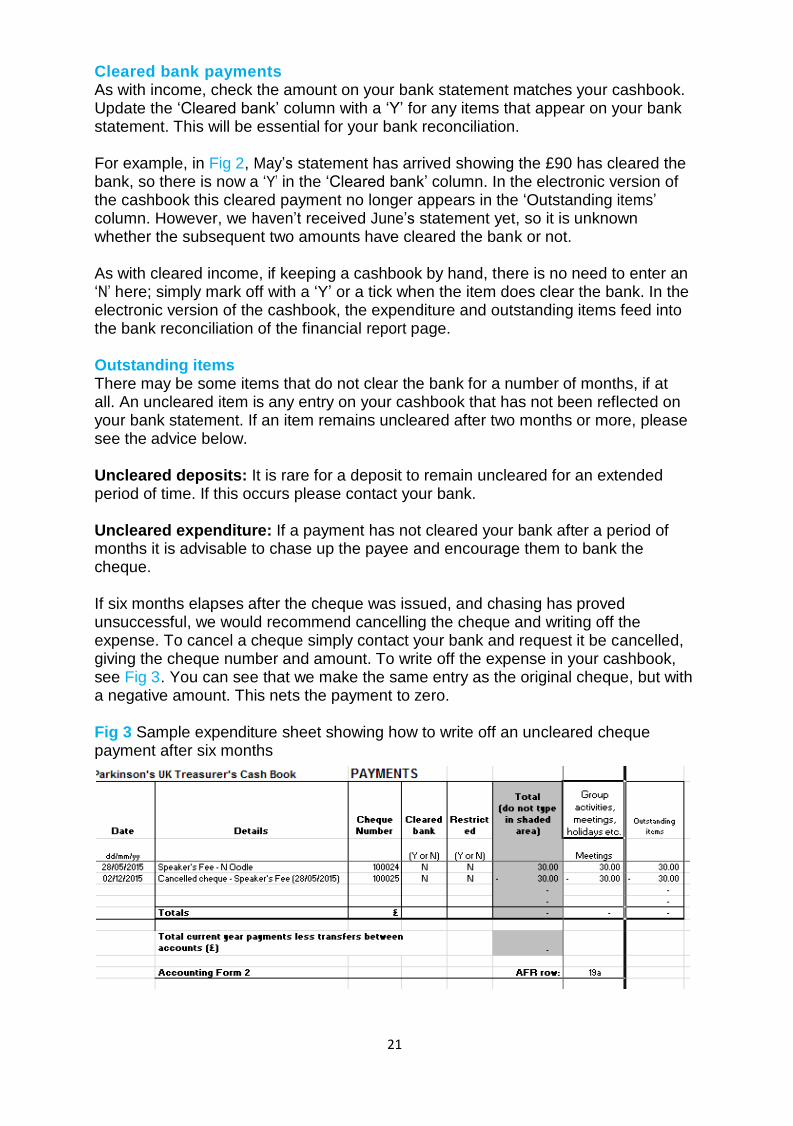

Cleared bank payments As with income, check the amount on your bank statement matches your cashbook. Update the ‘Cleared bank’ column with a ‘Y’ for any items that appear on your bank statement. This will be essential for your bank reconciliation. For example, in Fig 2, May’s statement has arrived showing the £90 has cleared the bank, so there is now a ‘Y’ in the ‘Cleared bank’ column. In the electronic version of the cashbook this cleared payment no longer appears in the ‘Outstanding items’ column. However, we haven’t received June’s statement yet, so it is unknown whether the subsequent two amounts have cleared the bank or not. As with cleared income, if keeping a cashbook by hand, there is no need to enter an ‘N’ here; simply mark off with a ‘Y’ or a tick when the item does clear the bank. In the electronic version of the cashbook, the expenditure and outstanding items feed into the bank reconciliation of the financial report page. Outstanding items There may be some items that do not clear the bank for a number of months, if at all. An uncleared item is any entry on your cashbook that has not been reflected on your bank statement. If an item remains uncleared after two months or more, please see the advice below.

Uncleared deposits: It is rare for a deposit to remain uncleared for an extended period of time. If this occurs please contact your bank.

Uncleared expenditure: If a payment has not cleared your bank after a period of months it is advisable to chase up the payee and encourage them to bank the cheque. If six months elapses after the cheque was issued, and chasing has proved unsuccessful, we would recommend cancelling the cheque and writing off the expense. To cancel a cheque simply contact your bank and request it be cancelled, giving the cheque number and amount. To write off the expense in your cashbook, see Fig 3. You can see that we make the same entry as the original cheque, but with a negative amount. This nets the payment to zero. Fig 3 Sample expenditure sheet showing how to write off an uncleared cheque payment after six months

Local Finance Guide EA 03022017.pdf 22 09/02/2017 16:07:12

22

Expenditure – Cashbook Advice This is a breakdown of the different headings on the expenditure sheet of our cashbook, along with a description of what would be classified under each heading. We have also included the row number these correspond to on the Annual Financial Return (AFR).

Cashbook title AFR Row

Description and examples

Transfer to deposit/petty cash account

N/A Any money moved into the deposit account, or drawn down for petty cash or a cash float.

Money forwarded to UK office

15a Any donations received at your local group that are not intended for local group use and have been passed to UK office (eg a donation from an individual for research given to your local group must be forwarded to UK office). Note: this should correspond with the Income heading ‘Money received for forwarding to UK office’ (AFR row 1).

Donations sent to UK office for Gift Aid reclaim

15b Any local group cheque sent to UK office with the intention of claiming Gift Aid, eg donations that you are submitting to claim Gift Aid. When returned to your local group this will be included under the Income heading ‘Local group membership and donations received from UK office – Membership and donations’ (AFR row 3a).

Group transfers to UK office

Research 16a Transfers made by your local group for research.

Improving services

16b Transfers made by your local group for service improvement, eg campaigning, Parkinson’s nurse grants and training bursaries

Within our region/country

16c Transfers made by your local group for local activities.

Other 16d Transfers made by your local group to be used where the need is greatest, or monies sent to UK office to be held on behalf of your local group.

Payments to other voluntary Organisations

17 Donations to other voluntary organisations or charities should not be made, but payments for services rendered are acceptable. For example, paying a charity representative’s speaker’s fee is allowed, but would be categorised under the heading ‘Group activities – social activities/meetings’ (AFR row 22a)

Local Finance Guide EA 03022017.pdf 23 09/02/2017 16:07:12

23

Fundraising 18 Any costs incurred in the running of fundraising events (eg venue hire, entertainment, volunteer expenses relating to a fundraising activity etc). Remember to record all income and expenditure from fundraising separately; do not just record net proceeds in income.

Campaigning 19 Any costs incurred while undertaking campaigning activity, eg travel expenses to local CCG meeting on behalf of local group.

Marketing 20 Any costs incurred while undertaking marketing activity, eg leaflet printing.

Research activity 21 Any costs incurred while providing research activity, eg research talk.

Group activities

Social activities/ meetings

22a Any costs incurred by holding local group meetings, eg venue hire, refreshments, speakers’ fees, transport etc.

Exercise activities

22b Any costs incurred by holding exercise or therapeutic activity, eg instructor fees, venue hire etc.

Therapeutic activities

22c

Holidays/outings

22d Any costs incurred in providing holidays or outings, eg transport, entry fees etc.

Support for Individuals

23 Any equipment that will provide support, or specifically purchased for individuals, eg walking frames; any activities that provides a break for a carer (providing a relief from their responsibilities) or a supportive environment, eg Crossroads scheme; any other individual support related costs, eg cost of a taxi. We will be providing further guidance around this.

Admin (eg stationery and postage

24 Any expenses for postage, newsletters etc required to run your local group.

Group governance (committee meetings and related volunteer expenses)

25 Any expenses incurred in running the committee or leading the local group eg mileage, meeting refreshments.

Transfer to other Parkinson’s UK local groups

26 To ensure we do not double count, please list any payments to other Parkinson’s UK local groups here.

Other items 27 This is where you should note the purchases or any other expenditure you cannot categorise elsewhere, eg branch equipment, computer for committee.

Cost of purchasing items for resale

28 This includes any items purchased from Parkinson’s UK Sales, eg Christmas cards, T-shirts.

Local Finance Guide EA 03022017.pdf 24 09/02/2017 16:07:13

24

Restricted expenditure It is a legal requirement to record whether expenditure is from a restricted fund. For more information, see section 4A Restricted funds on page 41.

Cross casting

Cross casting is a method of checking that any addition is correct, either in your cashbook or anywhere else you may be totalling different columns (eg on cash tally sheets). It’s relatively simple, so don’t be put off by the name. You only really need to do this if you are keeping your cashbook by hand.

With regards to your cashbook, this process should always be completed when you finish an income or expenditure sheet, but can be done periodically as required. In order to check that the figures and addition have been entered correctly, all we need to do is check that the totals of the income breakdown section are the same as the overall ‘Total’ column.

Fig 4 Cross casting

To do this, check that the addition in the Total column is correct (see black arrow).

Next, add up the totals for each heading in the income breakdown (see red arrow) and check that it is the same as the overall Total. In the above example, we are checking:

If these two amounts don’t equal each other, check that for each row the figure in the Total column is the total of the individual items in the income breakdown for that row eg for ‘S Price’ 5.00 + 15.00 = 20.00. Secondly, check that the totals for each column/heading in the income breakdown are correct (see cyan arrow).

If you are starting a new sheet in your cashbook, once you have confirmed that your total figures are correct, you can enter these at the top of the next sheet. In this way, the totals from whichever sheet you are currently working with will always give your totals for the year. Conversely, you may wish to start a new sheet on a monthly basis, keeping the totals for each month separate.

50.00

=

+

20.00 5.00 + 65.00 + 98.76

+

98.76

Local Finance Guide EA 03022017.pdf 25 09/02/2017 16:07:13

25

Closing a cashbook off for a year

It is important to close off your cashbook at the end of a year, and begin a new one for the year ahead. To do so, you need to perform a successful bank reconciliation as at 31 December, calculating the total of any uncleared expenditure or income. If your bank statement lists transactions after 31 December, these items of income or expenditure must still be listed as uncleared for the year end bank reconciliation. Your signed year end bank reconciliation, which can be found in the cashbook, and the AFR should be kept in the group’s financial records, filed under the relevant year. Uncleared bank items at the year end When starting a cashbook for a new year, the opening cashbook balance will account for any items uncleared at the year end. Usually, uncleared items will be reflected on the first statement of the year, allowing you to reconcile your bank statement with your cashbook.

If any uncleared items from the previous year are not reflected on your first statement your cashbook will not balance with your bank statement by this amount. As soon as the payment does clear this will rectify itself and you will be ready for the year.

You will find it helpful to keep an up-to-date list of any individual items of expenditure or income which were uncleared at the year end because these items should not be re-entered into your cashbook when they appear on your bank statement.

If an item is uncleared for more than six months, see Outstanding items on page 21. Starting a new year You must open a new cashbook at the start of each new calendar year, and you will require an opening ‘Start of year’ cashbook balance. If you use either the paper or electronic version of our template this will be your ‘Cashbook balance at 31 December’ (Financial report - D) from your bank reconciliation for the prior year.

If you are using our cashbook templates for the first time we have set up a few templates to help you establish your opening cashbook balance.

If you are using the electronic version of our cashbook, simply complete the ‘Start of year’ sheet of the electronic combined cashbook and report. This adjusts your bank and cash balances for your reconciling items.

If you are using a paper template, simply complete the ‘Start of year’ section on the ‘Parkinson’s UK bank reconciliation’.

The ‘Start of year’ section duplicates your year-end bank reconciliation from the previous year, and will provide you with an opening cashbook balance for the year. The most common error made is using a bank balance from your bank statement as your ‘Start of year figure’.

Local Finance Guide EA 03022017.pdf 26 09/02/2017 16:07:13

26

Banking income (cheques/cash/electronic transfer/CAF vouchers)

It is important to bank cash and cheques as soon as possible because this will ensure that all monies are secure. It will give the donor peace of mind and increase the chances of the funds clearing successfully. If your local group has a high level of activity you should bank as frequently as possible. It is good practice to bank at least on a weekly basis.

Cheques

It is important to verify that cheques have been filled in correctly when you receive them. You must never attempt to amend this information yourself, because changes to cheques can only be made by the donor. When collecting cheques, you may wish to write a short note on the back to help you identify who gave it to you and why. This will not affect your ability to cash the cheques but it will be helpful when you are putting the information into your cashbook before banking the money. Cash It is important to bank all cash you receive as soon as possible. Do not use any cash received to make payments as if it were petty cash. It is important to record income gross, not with expenditure already deducted. Banks will be able to provide cash bags to make the paying in process more simple. Paying in at the Post Office You can deposit money and cheques into most major bank accounts at the counter in most Post Offices. This may be convenient if you don’t have a branch of your bank near you. Please check with your local Post Office about this service.

Electronic transfer Donors may wish to make a donation to your local group using an electronic bank transfer. You will need to provide your sort code, account number and, in some instances, which bank you hold your account with. As this is potentially sensitive information it is advisable only to provide this to individuals or organisations you are familiar with.

The donor will be prompted to provide a reference for the payment, and this should appear on your bank statement. To help you identify what the funds are and where/who they came from, we would recommend that the donor includes their name and any other information you would find helpful.

CAF vouchers The Charities Aid Foundation (CAF) is used by some donors to make donations. The donor will put money they want to donate into a CAF account and CAF will add Gift Aid to this. The donor can then pay those funds to a charity by sending them a voucher, single payment or standing order. Other organisations that operate with a similar process to CAF include KKL, Charities Trust and Stewardship.

Local Finance Guide EA 03022017.pdf 27 09/02/2017 16:07:13

27

CAF vouchers cannot be presented at your bank. Send the vouchers to the Supporter Services team at UK office to be processed; the funds will be returned to your local group in the relevant quarterly payment run. Please fill in the charity name and number (258197 and SCO37554) before sending to UK office for processing. Attach a note clearly stating the name of your local group and that the funds should be returned to your local group.

The income relating to vouchers should be entered into your cashbook when you receive the funds in your quarterly payment run.

Paying-in slips Many banks will provide you with a paying in book, which is a collection of numerically sequenced paying in slips. When you make a deposit, the paying in slip number should be reflected on your bank statement. Please use this book if you have one, because it will enable you to make notes on the stubs, and easily identify deposits on your bank statement.

Other banks provide blank paying in slips, and will only include the date and amount of deposit on your bank statement. In this instance, we strongly advise keeping a record of the date and amount at the time of deposit to help you identify amounts on your bank statements later. You should keep all paying in books, stubs and receipts. Card payments Local groups must not accept credit or debit card payments. If you receive enquiries from donors about making payments by card, please direct them to our website at parkinsons.org.uk where they can make donations online. They can also donate by calling our Supporter Services team on 0800 138 6593. If they would like the donation to go to your local group please ask them to state this at the point of donation.

Major gifts A major gift is funding from a charitable trust or government organisation, or a gift of £1,000 or more from an individual. You can claim Gift Aid on individual donations as long as they haven’t given the gift from their own personal or family charitable trust, or if it is a culmination of money raised for an event. For more information, see section 4C Gift Aid on page 45.

Don’t forget Amounts received by CAF voucher already have Gift Aid claimed on them, so no further claim can be made against donations of this kind. Also, these vouchers must only ever be considered as a donation (which may include sponsorship or in memoriam donations), and cannot be accepted in exchange for goods or a service. For example, they must not be accepted to cover:

any kind of raffle ticket

entry to an event

any other payment for which the donor receives a benefit

If you are in any doubt about whether a voucher can be accepted for a particular use, please contact the Local Networks Finance team for clarification.

Local Finance Guide EA 03022017.pdf 28 09/02/2017 16:07:13

28

The Major Gifts team are happy to advise you on any part of your major gifts fundraising – they are experienced in handling relationships with major donors, and can work with you to help generate more donations. What to do when you get a major gift If you receive a major gift make sure you keep copies of all correspondence, including a copy of the cheque if there is one. Having the paperwork available will be really useful in the case of any queries in the future. Don’t forget to thank the donor. There are several ways to do this:

In person, if they handed the donation to you personally, or you see them soon afterwards.

A phone call is a quick way to let the donor know their donation has arrived.

A thank you letter is almost always needed. Most organisations will require an official receipt, and a thank you letter can act as one if it mentions the gift amount.

Organisations (charitable trusts and government organisations) A charitable trust is a charity that is set up as a funding organisation, to fund the work of other charities. Government organisations such as local councils or the Big Lottery Fund (including Awards for All) can also give grants. Many organisations give funds towards specific projects that you do (such as exercise classes). If they have given towards a specific project, this is ‘restricted income’ and can only be used for that purpose. For more information, see section 4A Restricted funds on page 41. If the funds are not used for the right purpose then the funder has the right to ask for the money back. Funding from any government organisation is classified as a ‘grant’ and needs to be recorded as a grant in your records and in your Annual Financial Return. Sometimes other funders (like charitable trusts) call their funding a grant, but only funding from government organisations is classified as a grant in this way. Unfortunately, we cannot claim Gift Aid on any funding from a charitable trust or organisation. Building the relationship and reporting back to the donor One of the best ways to help secure funding in the future is to build a good relationship with a major donor, whether this is an individual donor or an organisation. One very good way to do this is to report back after funds have been used. This is a requirement for most organisations that give funds, so it is a good idea to keep records of the project or activity as it happens, to make this easier. Always include information about the difference the project has made to the lives of people affected by Parkinson’s, and it’s always nice to include a quote or two from people who have directly benefited. If you need any help you can contact the Major Gifts team by emailing [email protected] – they will be happy to support you.

Local Finance Guide EA 03022017.pdf 29 09/02/2017 16:07:13

29

Gifted items Your local group may be gifted an item, such as an antique, to be sold to raise funds. These items are gifted to Parkinson’s UK on the understanding that that proceeds from their sale will be used to support people affected by Parkinson’s in pursuit of our vision. It’s important to ensure that the best possible outcome is achieved from selling gifted items.

What to do when you receive a gifted item? When your group received a gifted item or donation, this should be shared with your committee at the next meeting or with the groups other lead volunteers at the next available opportunity. This, and the agreed course of action for sale or raffle of the item, should be minuted or recorded.

If approached by a donor before being gifted an item, groups should advise the donor to sell items themselves and donate the money to the group. If the donor doesn’t wasn’t to do this, your group should define the donor’s expectations regarding the value of the gift and what will happen to it (eg whether it is to be sold, raffled etc) before they receive the items.

If your group believes the gift to be worth over £100, you should seek reputable advice regarding the value of the items and the most effective way to achieve the best return. If there is a significant discrepancy between this valuation and the donor’s expectations you may want to go back to the donor to explain this and confirm whether they are happy to proceed on this basis.

Ensure to record any financial transactions/income arising from sale of item. The Local Networks team will be able to help if you are unsure – contact them at [email protected].

Thanking donors With any donation or gifted item, it is courteous to thank the donor, no matter what the size. It is good practice to write to them rather than email them, and to do so on Parkinson’s UK headed paper.

Making payments Outward payments should be made by cheque or electronic transfer. All cheques must be signed by two signatories, and any payments online must be authorised by signatories using a dual authorisation banking system. Where dual authorisation internet banking is not available, we require local groups to make payments by cheque.

Local groups must not set up Direct Debits, or have credit, debit, fuel or store cards related to their local group’s account.

Invoices and receipts When paying a bill, always ask for an invoice and attach the receipt. Record the cheque number and date paid on the invoice/receipt, as this enables you to match up your bank statement, cheque book and payment documents.

All payments must be evidenced by documentation, such as an expenses form with receipts attached or an invoice with a receipt. Wherever possible, reserve payments until goods or services have been delivered.

Local Finance Guide EA 03022017.pdf 30 09/02/2017 16:07:13

30

In circumstances where it is impossible to get a receipt (eg a toll charge) a note should be created to attach as documentation, listing the details of the expenditure. This absence of a receipt should be shared with your lead volunteers. Payments should have been agreed by lead volunteers in advance of expense anyway.

Writing a cheque Banks recommend a few basic precautions when writing cheques:

Write the cheque in pen.

Write the payee’s name as fully as possible, avoiding abbreviations (to avoid alterations or misinterpretations).

Start writing as close to the left-hand side of the cheque as possible to avoid anything being added.

Similarly, strike through any blank spaces once you have finished to avoid anything being added.

If a cheque is reported missing, always stop the cheque at the bank before issuing a replacement. Some banks may charge for this.

Cheque books should always be kept in a secure location.

Make sure that signatories are aware of their duties and responsibilities and are familiar with the guidance before signing cheques. What if a supplier won’t accept a cheque? This situation is generally avoidable if you plan ahead. Check with the supplier or venue if they accept cheque payments before you order or book anything. If they do not, you should ideally look for an alternative supplier or venue, because there is no ideal alternative to paying by cheque.

If you can’t pay by cheque and cannot find another supplier or venue, your lead volunteers will need to approve a course of action. For example, withdrawing cash from the local group account. This will need to be organised in advance as two signatories will be required to authorise this and you will need to make a trip to the bank. You should consider and mitigate any risk involved here as a local group, especially any potential risk to the member carrying the cash.

If a member offers to pay the expense and then make a claim through expenses, your lead volunteers should make sure they are aware of the exact amount involved and ask them to make sure that they will not incur any fees or suffer any hardship because of this. If agreed by your lead volunteers, you should then ensure the member is reimbursed as quickly as possible.

Please consider the implications these options place on our volunteers –first in terms of our exposure to theft or fraud, and second in terms of the burden placed on the out-of-pocket volunteer. Always ensure all documentation and receipts are retained and recorded in the normal manner.

VAT advice Parkinson’s UK is not VAT registered, so we cannot reclaim any VAT that we pay. However, there are a number of items where local groups may be entitled to a VAT exemption. These include:

advertising and any associated artwork

aids and equipment for those affected by Parkinson’s

Local Finance Guide EA 03022017.pdf 31 09/02/2017 16:07:13

31

In order to claim our exemption from VAT, we need to give the supplier a certificate detailing the goods being purchased and the relevant section of the VAT legislation that applies: this must be provided prior to payment. VAT certificates should be signed by the Director of Finance, IT and Performance.

If you think that something you are buying might come into one of the categories above, please contact the Local Networks Finance team for a VAT exemption certificate.

To provide you with more information on what may be included in each category we have included below excerpts from the guidance provided by HM Revenue & Customs on their website. You can find out more by visiting the website at www.hmrc.gov.uk/vat

Category HMRC explanation Example

Advertising and any associated artwork

“Your charity can advertise VAT-free in any medium that communicates with the public, such as a newspaper or television, providing the advert is placed on someone else's time or space. ... The VAT relief does not cover costs for advertising in your own media - for example in your charity’s own magazine, on your own website, or on your own T-shirts etc.”

Advertisement in local newspaper for local group meetings/activities

Equipment “If your charity is purchasing certain goods and services to make available to disabled people for their personal or domestic use they can be zero-rated.”

Weighted cutlery, laser canes for a specified individual.

Related party transactions All lead volunteers must declare and record any direct or indirect financial interest they may have in any contract for goods or services entered into by your local group, or in the sale or disposal of any asset. A member having such an interest must refrain from voting on any matter concerning that contract.

Related parties include:

members of the same family or household or related person

any business partner

where the member has a participating interest

If such a transaction occurs, the decision agreed by your local group must be recorded and include the following details:

The name of the transacting related party.

The relationship between the related party and Parkinson’s UK.

A description of the related party transaction with Parkinson’s UK.

The amount of the transaction and any outstanding balances.

If you are unsure, discuss with your local staff contact.

Local Finance Guide EA 03022017.pdf 32 09/02/2017 16:07:13

32

3B Transfers between your accounts

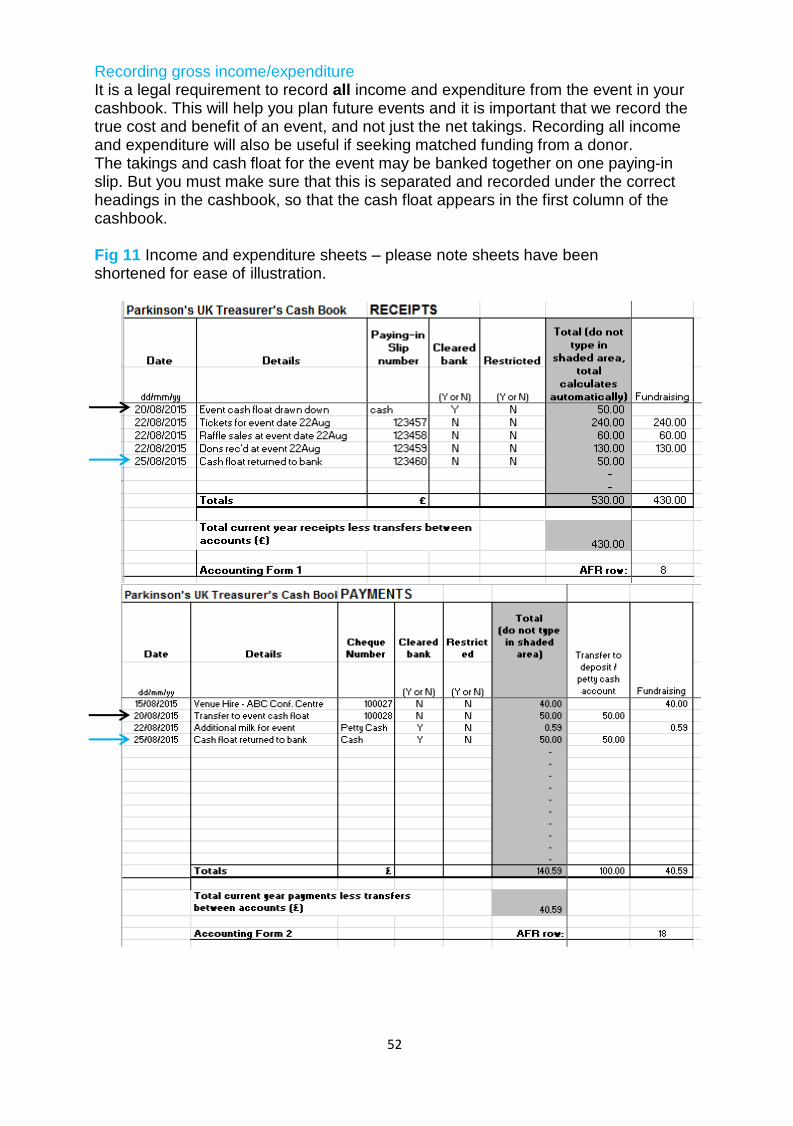

As a charity we must ensure that we accurately record our income and expenditure. In the case of transfers between your local group’s own accounts, it is important these are not counted as income or expenditure as they are an internal movement within the local group. The same logic applies to transfers to petty cash. To make sure all transactions are recorded we have provided columns in the cashbook to record movements between your local group’s own accounts (including petty cash). This is the first column after the ‘Total’ column, and does not feed into the financial report, nor is there a corresponding Annual Financial Return (AFR) row number as this information is not required. Recording a transfer Fig 5 Income and expenditure sheets demonstrating transfer between accounts – please note sheets have been shortened for ease of illustration.

In Fig 5 there is a transfer of £500 from the Current to the Deposit account – recording this in both the income and expenditure sheets will ensure that we have a record of this transfer, and that we can reconcile our bank statements with our cashbook.

In the electronic version of the cashbook, there is an adjusted total at the bottom of each sheet. The ‘Total current year payments less transfers between accounts’ (highlighted by an arrow) is the total that carries through to the financial report as total income/expenditure.

Local Finance Guide EA 03022017.pdf 33 09/02/2017 16:07:13

33