events organized in qatar - india-qatar year of culture 2019

Upload

khangminh22Category

view

0download

0

In this issue

Islamic Capital Markets Briefs ................ 1

Islamic Ratings Briefs ................................ 9

IFN Reports ................................................11

Encore Calls for More Variety in Europe ........................................................13

Islamic Finance in Europe .......................15

Islamic Financial Services in Italy ..........18

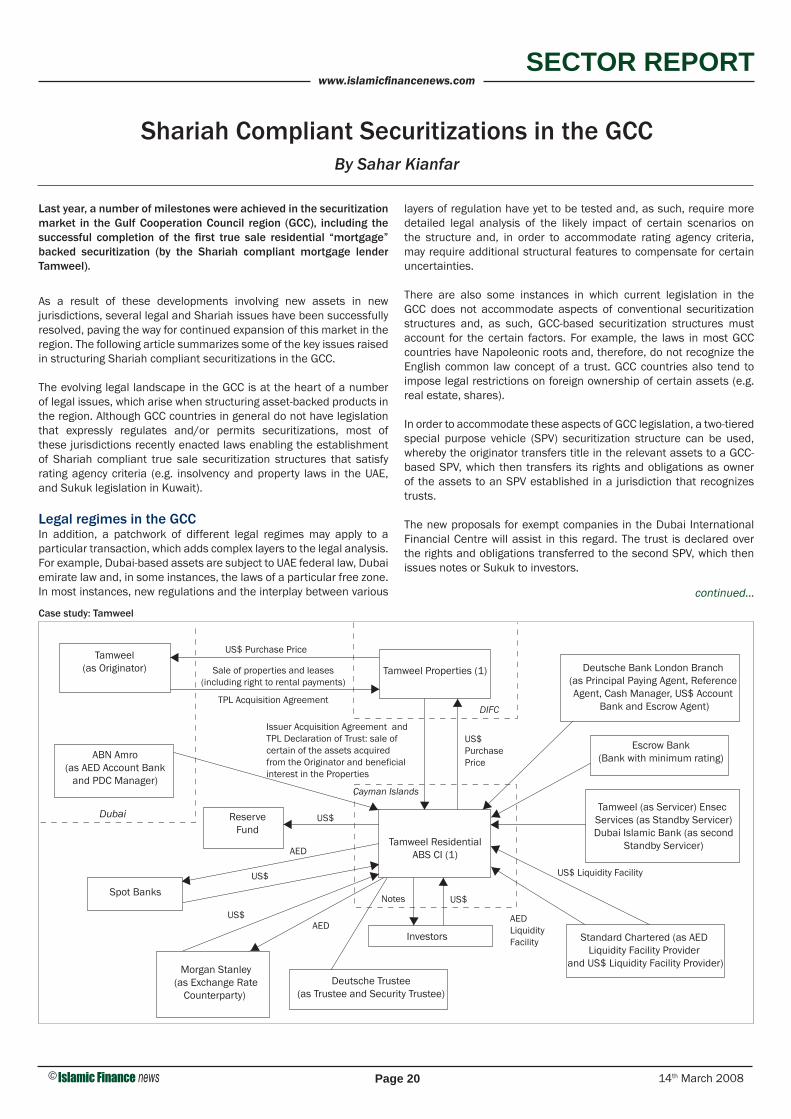

Shariah Compliant Securitizations in the GCC ..................................................20

IMF on Islamic Banks: Build Skyscrapers, Not the Titanic ...........................................22

Emerging Markets Buck the Trend ........23

Meet the Head ..........................................24M A Majeed, The Institute of Islamic Banking & Finance

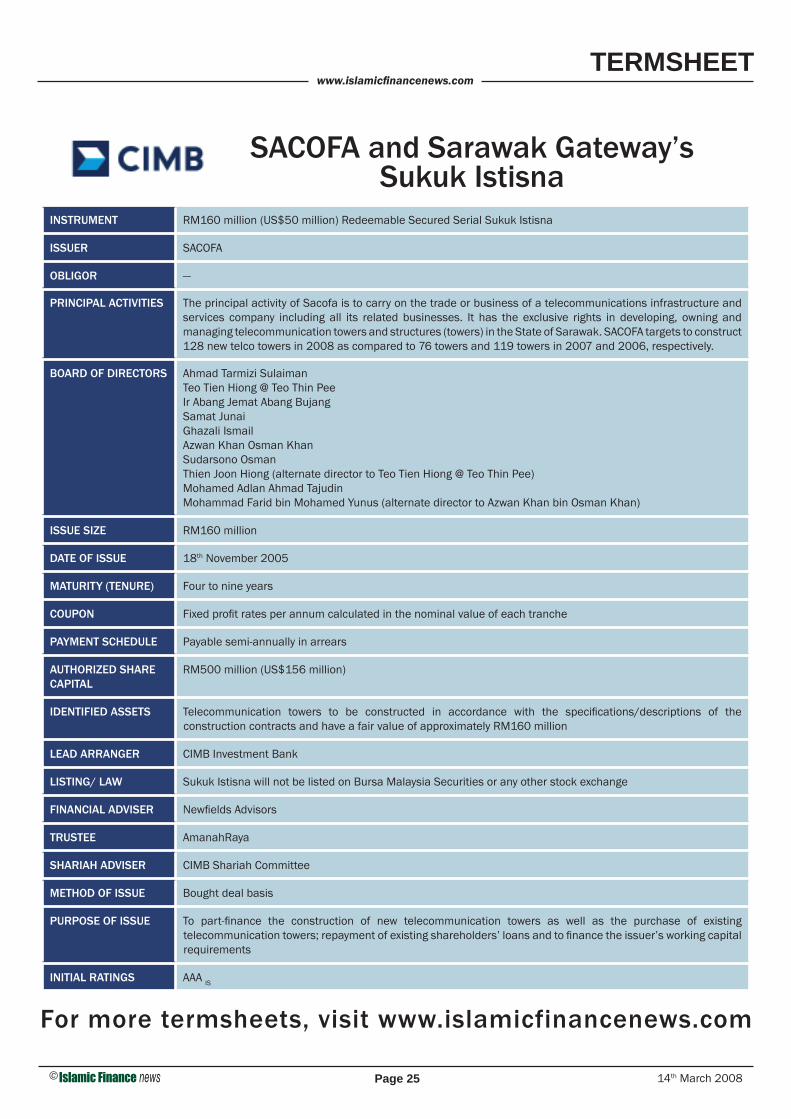

Termsheet ..................................................25SACOFA and Sarawak Gateway’s Sukuk Istisna

Takaful News Briefs..................................26

Takaful Report ..........................................27Takaful Products in Trinidad and Tobago

Moves .........................................................28

Deal Tracker ..............................................29

Islamic Funds Tables ................................30

Dow Jones Islamic Indexes .....................31

Malaysian Sukuk Update .........................32

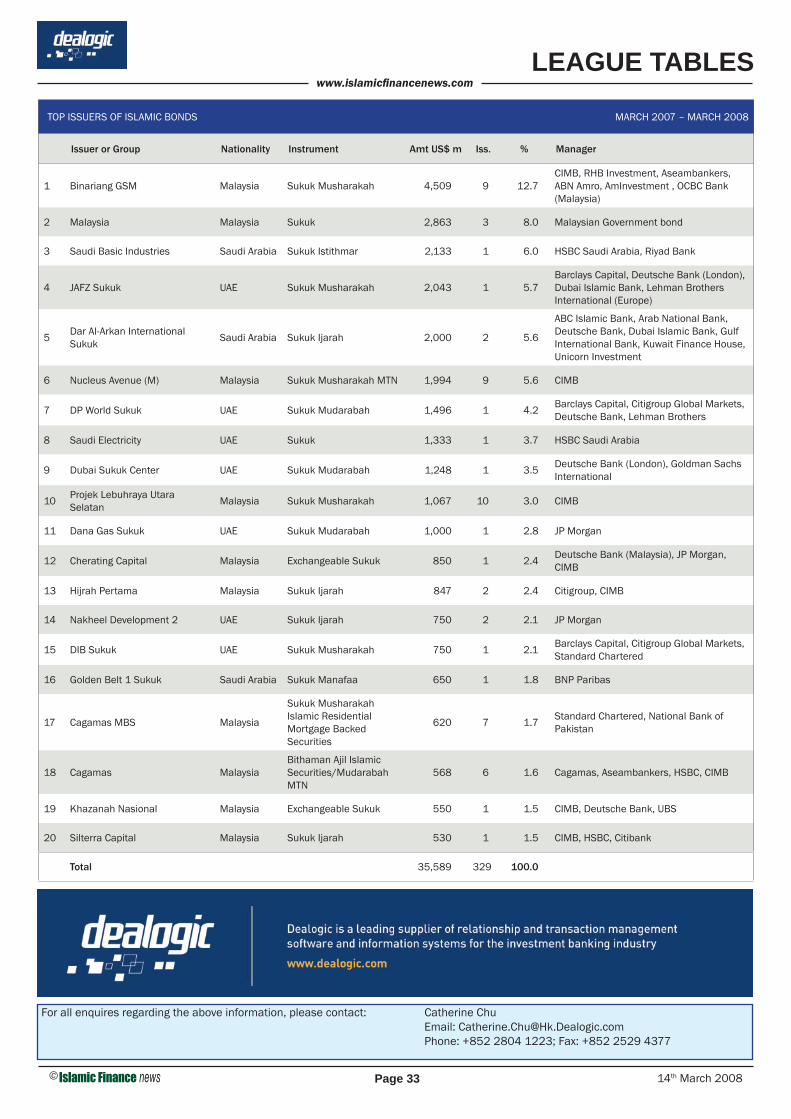

Islamic League Tables .............................33

Events Diary...............................................36

Subscriptions Form ..................................37

Country Index ............................................37

Company Index .........................................37

Vol. 5, Issue 10 14th March 2008

T h e W o r l d ’ s G l o b a l I s l a m i c F i n a n c e N e w s P r o v i d e r

UKPositive vibe from budget announcementsAlthough no fi nality has been reached on the issuance of the UK sovereign Sukuk, the British government through the 2008 Budget Report gave assurance that it will continue to study the feasibility of the issuance.

In the report, Chancellor of the Exchequer Alistair Darling points out it will be premature for the government to make an announcement on the outcome of the feasibility study, especially given the range of issues being considered.

An update of the work program, including a response to the recently closed public consultation, will be provided in the summer.

Darling also announced measures to further support Islamic fi nance in the UK. The government aims to provide relief from stamp

duty land tax (SDLT) for alternative fi nance investment bonds.

It will also amend legislation to treat these instruments as loan capital for stamp duty and stamp duty reserve tax purposes, and modify legislation that will allow corporation and income tax rules on these instruments to be amended in the future, should that prove necessary.

The proposals received the thumbs up from those within the Islamic fi nance industry.

They say the announcement will further escalate London’s aspiration to be a global hub for Islamic fi nance

(Also see IFN Reports on page 12)

SOUTH AFRICANewGold, Absa Capital’s fi rst Shariah ETFSouth African investment bank Absa Capital’s NewGold exchange-traded fund (ETF) has been certifi ed Shariah compliant, a fi rst for a South African ETF.

“Demand for Shariah investments is escalating in South Africa,” says Vladimir Nedeljkovic, head of ETFs and index products at Absa Capital. “There is an estimated ZAR1.8 billion (US$231 million) of annual investible assets held by Muslim investors and this represents a signifi cant niche target market. There is defi nitely an opportunity for

more Shariah instruments to come to market including structured products.”

NewGold ETF is the largest in South Africa with ZAR6.4 billion (US$820 million) assets under management, which have increased more than four times since the beginning of 2007.

Absa also plans to launch an ETF tracking the FTSE/JSE Shariah All-Share Index, but no agreement has been reached as yet. Absa Capital is an affi liate of UK investment bank, Barclays Capital.

QATARJapan banks focus on Islamic funds Japanese banks have been focusing on Islamic funds, recognizing the country can play the role of a gateway internationally in a regional market from Asia to strengthen

inter-regional linkages between Asia and the Gulf, said Tadashi Maeda, director-general of Japan’s energy and natural resources fi nance department.

www.islamicfi nancenews.comNEWS BRIEFS

Page 2 14th March 2008©

TAIWANMega International gets regulator’s OKTaiwan’s Financial Supervisory Commission has approved Mega International Commercial Bank’s application to set up a representative offi ce in Abu Dhabi and a branch in Macau.

The bank, a unit of Mega Financial Holding, will be the fi rst Taiwanese bank to operate in the UAE, the commission said. After the establishment of the Abu Dhabi offi ce, Mega International will close its representative offi ce in Bahrain, the commission said without providing a time frame.

Formerly known as International Commercial Bank of China, the bank assumed its current name after merging with Chiao Tung Bank in 2006.

UAEShuaa set to start Saudi operationsDubai-based Shuaa Capital has won fi nal approval to begin operations in Saudi Arabia to set up a SAR150 million (US$40 million) brokerage fi rm. The investment bank will own 60% in Shuaa Capital Saudi Arabia, based in Riyadh, it said.

“Our Saudi Arabian operations, together with our regional presence across the GCC and Arab world, will expand our ability to offer clients advanced fi nancial services, both locally and internationally,” CEO Iyad Duwaiji said.

Omar Al Jaroudi will head up the Saudi unit, which will offer brokerage, asset management and investment banking services.

BAHRAINSeychelles license for BMIBahrain-based BankMuscat International (BMI) has received a license from the Central Bank of Seychelles to set up an offshore banking venture.

BMI will manage BMI Offshore Bank, a joint venture with locally incorporated Nouvobanq, the largest bank in Seychelles.

BMI Offshore Bank will engage in offshore banking and private banking services and provide access to trust and investment services. The new venture is expected to be operational by the third quarter.

QATARQNB investment armQatar National Bank (QNB) has reached an advanced stage in obtaining the necessary approvals to establish QNB Capital, which will have a capital of US$150 million. It will be set up at the Qatar Financial Centre.

The bank is fi nalizing all related work with regard to the legal and structural form of the company. QNB Capital will provide investment banking services, advisory and structured fi nance and direct investments. These will be independent of regular commercial activities.

QATARUNB to set up Qatar branchUnion National Bank has received approval from the Qatar Financial Centre Regulatory Authority to set up a branch in the Qatar Financial Centre (QFC).

The branch’s permitted activities would include accepting deposits and providing and arranging of credit facilities within the QFC to wholesale customers.

UNB is the fi rst bank from the UAE to achieve this status.

UAEShariah banking software launchedInfosys Technologies has launched the latest version of its Financial Universal Banking Solution banking software, which includes a component for Islamic banking. The Indian software company said that version 10 of its system will meet Shariah requirements concerning the payment of interest.

MALAYSIAWestports Sukuk oversubscribedWestports Malaysia’s initial issuance of RM445 million (US$139 million) of the RM800 million (US$250.32 million) Sukuk Musharakah medium-term notes (MTN) program has been oversubscribed by an average of 6.3 times based on the original size of RM345 million (US$107.94 million), said OSK Holdings (OSK).

Due to overwhelming demand, the book building process and scheduled to close on the 4th March was completed on the 29th

February.

OSK said the proceeds would be used to refi nance Westports’ existing bank borrowings, fi nance the construction of a new container terminal and acquisition of machineries and equipment.

MALAYSIAA leg up for Islamic fi nance The rising oil price will give Islamic fi nance a leg up to grow beyond 20% this year, thus promoting liquidity and funds from countries in the Middle East. There will also be a slight impact on the subprime market.

With technology and international standards together with greater awareness and knowledge, Islamic fi nance could be further expanded to create more products acceptable internationally. Once the global standardization has been achieved, Islamic fi nance will take a larger share of the market, said Majid Dawood, CEO of Yasaar, an independent global Shariah consultancy.

At present, Asian Islamic fi nancial services are highly concentrated in Malaysia with focus on banking assets, Sukuk issuance, asset management and Takaful assets. Malaysia accounts for 76% of the banking assets in Asian Islamic fi nancial services, 95.5% of Sukuk issuance in Asia and 83% of Takaful assets in Asia.

(Also see IFN Reports on page 11)

www.islamicfi nancenews.comNEWS BRIEFS

Page 3© 14th March 2008

www.maplesandcalder.com

Contact Tahir Jawed at +971 4 360 4070 or e-mail: [email protected]

Offshore expertisewith a local presence.

The world's leading offshore law firm and the first to establish an office in the Middle East. Maples offers clients around the Middle East an unparalleled range of Cayman Islands and British Virgin Islands legal services, including advising on offshore Islamic finance structures such as sukuk transactions, investment funds, trusts and securitisations.

UAEDIB, MAG ink home loan dealDubai Islamic Bank (DIB) has agreed to provide Shariah compliant home loans for about AED2 billion (US$544.7 million) worth of properties developed by MAG Group Property Development (MAG).

Under the deal, DIB will offer fi nance to buyers of properties in three of MAG’s current projects in prominent developments in Dubai: MAG 226 in Jumeirah Village; MAG 228B in phase three of International City; and MAG 218 at Dubai Marina.

UKHalal fi nance growing in popularityIslamic compliant fi nance products are not just popular with Muslims, but also people of other religious faiths, observed Junaid Bhatti, Islamic fi nance expert and director of Ballencrieff House.

“There are three main factors driving the growth of Shariah compliant fi nance in the European markets — Muslim customers, non-Muslims looking for ethical fi nance and fi nally, the governments themselves,” he explained.

With over 50,000 UK Islamic fi nance customers and a worldwide industry growth rate of between 15% and 20%, the products are growing in popularity, Junaid said.

QATARQatar Islamic to sell shares from TuesdayQatar Islamic Bank, will sell 17.9 million shares to existing shareholders at QAR70 (US$19.25) apiece as part of a plan to boost capital by 10%.

The shares will be on offer from the 18th March to 31st, the Doha-based bank said.

Qatar Islamic is also studying expansion into Egypt and Turkey as well as Indonesia and Brunei through its Asian Finance Bank unit. Qatar Islamic owns 70% of Kuala Lumpur- based Asian Finance.

KUWAITNBK unveils Thahabi Ijarah IVNational Bank of Kuwait (NBK) has launched its Thahabi Ijara Fund IV to meet the needs of its Thahabi customers for low-risk investments that generate a consistent monthly income, said NBK’s assistant gen-eral manager, consumer banking group, Abdullah Al Najran Al Tuwaijri.

“Thahabi Ijara Fund IV represents the continuation of NBK’s strategy to provide its valued clients with best-in-class investment products, and follows in the footsteps of NBK’s previous and successful Ijarah fund launches,” he said.

The three-week offer period commenced on the 9th March. The minimum expected income for the Thahabi Ijara IV Fund will be fi xed after the end of the investment period.

BAHRAINPorta Reef-BIsB fi nancing dealInvestors with intention to seek market residential units can now access competitive fi nancing options through a new partnership between Porta Reef and Bahrain Islamic Bank (BIsB). Porta Reef is a US$90 million project being undertaken by Abu Dhabi Investment House.

The agreement states that BIsB will offer fi nancing packages to buyers who wish to purchase one of the 150 residential units on sale at the Porta Reef development.

The partnership is the fi rst such agreement between Porta Reef and a fi nancial provider, and is intended to increase accessibility for Porta Reef’s niche target market.

BAHRAINSukuk market set to cross US$100 billion The global market for Sukuk more than doubled last year to exceed US$60 billion, and is on track to top the symbolic US$100 billion mark in the next few years, concluded Standard & Poor’s (S&P) in its latest report.

“We expect Sukuk growth to remain on the same impressive trajectory, fueled by huge investment and fi nancing needs, notably in countries of the Gulf and Asia,” said S&P credit analyst, Mohamed Damak.

He added Sukuk is set to continue providing issuers with non-bank alternatives to longer-term funding and their growth has been slowed in the past six months by unfavorable credit market conditions.

To date, S&P rates 22 Sukuk, the bulk of which are Ijarah or Musharakah and carry credit enhancements.

www.islamicfi nancenews.comNEWS BRIEFS

Page 4 14th March 2008©

www.IslamicFinanceTraining.com

FOR MORE INFORMATION, contact: Andrew Tebbutt Tel: 603 2143 8100;

Email: [email protected]

CALENDAR 2008

Risk Management, Basel II & Islamic Banking Regulation

17 – 19 March, KUALA LUMPUR

Refresher Day: Principles of Islamic Finance & Investment

23 March, DUBAI

Sukuk & Islamic Capital Markets: Product & Documentation

24 – 26 March, DUBAI

Introduction to Islamic Finance & Banking7 – 9 April, SINGAPORE

Islamic Financial Markets, Treasury & Derivatives

20 – 22 April, BAHRAIN

Islamic Financial Markets, Treasury & Derivatives

13 – 15 May, SINGAPORE

Islamic Financial Engineering & New Product Development18 – 21 May, DUBAI

Refresher Day: Principles of Islamic Finance & Investment

2 June, LONDON

Sukuk & Islamic Capital Markets: Product & Documentation

3 – 5 June, LONDON

presents

QATARCentral Bank sells certifi cates of depositQatar Central Bank has completed its fi rst auction of certifi cates of deposit (CDs) as part of Qatar’s attempts to soak up excess liquidity and help tackle infl ation.

The country has the highest infl ation in the region, at 13.74% in the last quarter of 2007. The central bank sold QAR1 billion (US$275 million) worth of 91-day CDs at a coupon rate of 3%.

BAHRAINBankers probe fi nance issuesAbout 60 senior bankers from Bahrain, the GCC, Malaysia and Indonesia took part in a two-day seminar on corporate governance issues in Islamic fi nance, co-organized by the Islamic Financial Services Board (IFSB), the World Bank corporate governance departments and the Global Corporate Governance Forum. The event was hosted by the Central Bank of Bahrain.

“IFSB has drafted a series of principles on Islamic fi nance and this event was designed to raise awareness of these issues,” said Eugene Spiro, global corporate governance forum senior projects offi cer.

UAEDIB announces 40% cash dividend Shareholders of Dubai Islamic Bank (DIB) have approved distribution of 40% cash dividend and 15% bonus at their annual general meeting. The bank’s fi nancial results for the year ended the 31st December 2007 were approved at the meeting.

In 2007, DIB reported AED2.5 billion (US$680 million) in net profi t, an increase of 60% compared to AED1.56 billion (US$420 million) in 2006. In addition, the assembly reviewed the Director’s Report and Annual Report of the Fatwa and Shariah Supervisory Board.

UAEDIC denies Citi requested fundsDubai International Capital (DIC) has denied the rumor that Citigroup had approached it for funds.

“We have not been privy to any non-public information about the company, neither has Citi approached DIC for a capital raise,” DIC said in a statement. This followed DIC CEO Sami Al-Ansari’s comment that it would take a lot more money to rescue Citigroup, which since November has raised about US$30 billion of capital from Abu Dhabi, Kuwait and Saudi Arabia’s Prince Alwaleed.

QATARQNB Al Islami’s Vehicle Lease productQatar National Bank Al Islami (QNB Al Islami) has launched its Vehicle Lease (Ijarah Al Markabat). This product will allow the bank to fi nance both new and used vehicles at competitive profi t rates.

Under the scheme, QNB Al Islamic will fi rst buy the vehicle then lease it out to the client, who will buy or obtain the vehicle at the end of the lease period.

QNB Al Islami also utilizes this formula to fi nance constructive projects. Last year, the bank developed the “lease ending in ownership”, which allows customers to have their various construction projects fi nanced with competitive prices.

www.islamicfi nancenews.comNEWS BRIEFS

Page 5© 14th March 2008

MALAYSIAKFH and unit win Islamic fi nance awardsKuwait Finance House (KFH) and its subsidiary Kuwait Finance House Malaysia (KFHM) bagged awards for “Best Overall Islamic Bank”, “Most Innovative Islamic Bank” and “Best Islamic Bank in Kuwait” at the 2007 Islamic Finance news Awards ceremony held last Thursday.

Meanwhile, CIMB Islamic Bank CEO Badlisyah Abdul Ghani picked up the award for “Best Individual Islamic Banker”, a recognition given to outstanding individuals in the banking sector.

Khazanah Nasional won for “Cross-Border Deal of the Year” and “Equity Deal of the Year” following its Cherating Capital exchangeable Sukuk transaction.

Bank Negara Malaysia was named the “Best Central Bank in Promoting Islamic Finance” while Malayan Banking was recognized for “Malaysian Deal of the Year”.

UAESleeping giant awakensIslamic real estate fi nancing has been likened to a sleeping giant about to awaken with international multi-billion dollar deals set to make new records this year, according to leading fi nance industry watchers.

The burgeoning economies of the Gulf Cooperation Council (GCC) along with Asia-Pacifi c are the driving forces, said Irina Awote, director of the Real Estate Finance and Investment Conference, which is scheduled to take place in May.

Moody’s Investors Service noted that one of the main areas of growth is expected to be Islamic real estate investment trusts, or REITs, aided by the tremendous concentration of high net worth individuals and family businesses with a collective wealth in the GCC alone estimated to be over US$1.3 trillion.

BAHRAINBahrain Bay land parcels taken upBahrain Bay, the US$2.5 billion landmark waterfront community located in the heart of Manama, has sold 60% of its land parcels to international and regional developers and investors.

The development has attracted investments from leading local and regional fi rms such as Al Baraka Group, the Bahrain-based Global Islamic Bank, as well as Salhia Real Estate, the leading Kuwaiti property developer.

In addition, Guidance Financial Group, the international Shariah compliant fi nancial services group, recently committed to developing a Shariah-based boutique hotel within Bahrain Bay.

DENMARKBanks to comply with Shariah Three local banks in the Jutland region of Denmark have agreed to offer mortgage loans that comply with Islamic laws, it was reported Wednesday. To meet the requirements, the Danish banks have created what resembles a leasing agreement for Muslims in the area.

The three banks — Sparekassen Farsø, Sparekassen Vendsyssel and Sparekassen Hobro — with cooperation of a fourth (Den Jyske Sparekasse) created a company to handle the new Amanah Kredit mortgages.

Niels Mogaard, director of Amanah, said the arrangements were already in use, especially in the city of Aalborg.

www.islamicfi nancenews.comNEWS BRIEFS

Page 6 14th March 2008©

UAEA&O adviser to US$1.2 billion MudarabahAllen & Overy (A&O) advised Emirates Islamic Bank and Emirates Bank International on a US$1.2 billion dual currency Mudarabah facility for Limitless, a landmark transaction signifying confi dence in the region’s real estate sector, said A&O senior associate, Shehzaad Sacranie.

She said the syndicate proves there is a continued appetite for investment in the real estate sector and a growing interest in Shariah compliant fi nancings.

The proceeds of this transaction will be used to fund landmark real estate projects being developed by Limitless in Russia, Saudi Arabia, India, Jordan, Vietnam and Malaysia and in the UAE.

UAEAmlak to fund growth through SukukAmlak plans to raise AED6 billion (US$1.63 billion) in Sukuk and loans this year to fi nance growth, said CEO Arif Al Harmi.

“We are looking at raising AED6 billion through various schemes this year. We will be tapping different markets and investors. We are looking at medium- to long-term funding,” explained Arif, adding that Amlak is seeking a banking license from the UAE Central Bank in order to access customer deposits.

“We are moving ahead with our plans, whether we get the banking license or not. Our plans will not be affected by with this.”

BAHRAINFinancing facility arranged for SBGGulf International Bank, Arab Bank, Calyon Credit Agricole CIB and Emirates Bank International have made an arrangement of a SAR3.2 billion (US$854.4 million) Islamic contracting facility for the Saudi Binladin Group (SBG). The four banks acted as lead arrangers.

The transaction, which comprises a Murabahah facility, letters of credit facility and guarantee issuing facilities, will be used by the Saudi borrower to fi nance the construction of a housing project for the King Abdullah University of Science & Technology.

KUWAIT KFH seeks Morocco, Algeria propertiesKuwait Finance House (KFH) is increasing its investments in real estate and wants to acquire properties in Morocco and Algeria, said KFH managing director, Bader Al-Mukhaizeem.

KFH recently won a license this month to start Sukuk Company, a venture for trading Islamic bonds.

MIDDLE EASTComplementary new business modelsThe pure commercial-banking model in Islamic banking in the GCC is being complemented by developed forms of more specialized Shariah compliant fi nancial intermediation, said Moody’s in a report.

Maturing operating environments and imperfect risk positioning tend to weigh on Islamic banks’ risk profi les and ultimately on their stand-alone credit ratings, the report said.

The commercial-banking business model, dominated by both the corporate and retail business lines, is now being enhanced by the emergence of two new activities.

While Shariah compliant investment banking has grown as a successful way to manage alternative Islamic asset classes, specialized fi nancial institutions focusing on mortgage, housing and consumer banking have been providing fi nancing solutions to households facing unprecedented needs, said Anouar Hassoune, a Moody’s analyst who wrote the report.

QATARQIB profi ts soarQatar Islamic Bank (QIB) has recorded full-year profi ts of QAR1.25 billion (US$3.45 million) in 2007, compared to QAR1 billion (US$2.84 million) in 2006, indicating a year-on-year growth of 25.2%. The bank’s board of directors has recommended the distribution of cash dividend of 20%, or QAR2 (US$0.55) per share and 50% bonus shares.

It has also recommended a further capital increase via a rights issue amounting to 20% to be fl oated in two stages during 2008 and 2009 (10% at each stage) to strengthen QIB’s fi nancial position to meet the requirements of its expansion and execution of its strategic plans.

During this fi nancial year the depositors’ share of the profi ts reached QAR343 million (US$94.31 million), an increase of 33% over the previous year, and QIB’s total assets reached QAR21.3 billion (US$5.86 billion) as compared to QAR14.9 billion (US$4.1 billion) in 2006, recording an increase of QAR6.4 billion (US$1.76 billion) at a growth rate of 43%.

CONFERENCESPRIVATE EQUITY INTERNATIONAL

THE PEI ISLAMIC ALTERNATIVE ASSETS FORUM:LONDON 200820-21 May 2008, London

A PRIVATE EQUITY INTERNATIONAL CONFERENCE

Private Equity International is delighted to announce the second running of its Islamic Alternative Assets Forum.

With a programme that delivers in-depth analysis of how Shariah-compliant alternative investment capital is raised, managed, deployed and realised, it is the only event of its kind and is designed expressly for practitioners like you.

Key themes will include:

• Understanding Shariah supervisory boards and the decision making process• The use of Sukuk within private equity – Islamic bonds?• Anatomy of an investor – Shariah compliance versus returns• Fundraising – sources of capital• Impact of the credit markets on Islamic finance investors• Shariah compliant fund structuring

“Islamic investing in alternative assets is set to grow dramatically. PEI’s conference brought together the leading international players – as speakers and delegates – for a serious, informed discussion of the key issues in this area. The tight focus on alternative assets lent extra credibility and resonance to the forum.”- Dr Humayon Dar, Chairman, BMB Islamic

Learn more and register today at:www.peimedia.com/if08

www.islamicfi nancenews.comNEWS BRIEFS

Page 7© 14th March 2008

PAKISTANUBL Fund investing overseasUBL Fund Managers, Pakistan’s leading asset management company in the private sector, has ventured abroad to capitalize on global investment potential globally.

United Composite Islamic Fund, a balanced Shariah compliant fund that gave a calendar year return of 18% to its investors in 2007, will be the fi rst UBL fund to offer exposure in overseas markets. A portion of the fund’s assets has been invested in regional Shariah compliant equity funds that are being managed by globally recognized investment managers.

OMANBourse expecting three IPOsThe Muscat Securities Market (MSM) expects three companies — one of them an industrial fi rm — to sell shares in initial public offerings this year and list them on the region’s best-performing bourse, said chairman Abdullah bin Salim al Salmi on Tuesday.

Oman’s benchmark is up more than 16% this year, making it the best performer in the Gulf Arab region. It surged almost 62% last year.

BAHRAINABC closes Murabahah dealABC Islamic Bank has closed the senior phase of a US$100 million three-year syndicated revolving Murabahah fi nancing facility for a Kuwaiti real estate services company. This is the debut syndication for Munshaat Real Estate Projects Company and the funds will be used to fi nance development of prime properties in the Holy Haram area in Makkah and Madinah in Saudi Arabia.

Athman Investment Company, Kuwait, is the fi nancial adviser for Munshaat, a Shariah compliant company.

Prior to general syndication, BNP Paribas, Emirates Bank International, and Saudi British Bank joined the facility as mandated lead arrangers at the senior stage.

UAEGulf Bank profi t up 23%Gulf Bank reported a record net profi t of US$477.8 million for 2007. This marked an increase of 23% over the previous year’s results, with earnings per share rising nearly 23% to 44.7 US cents.

Total assets increased by more than 25%, surpassing US$18.5 billion for the fi rst time.

JORDAN/SYRIAJordan Islamic Bank setting up in SyriaJordan Islamic Bank will open a branch in Syria, said vice-chairman and general manager Musa Shihadeh. Speaking on the sidelines of a conference on Islamic banking in Syria, Musa underlined the importance of Jordanian-Syrian cooperation in the banking sector, in particular.

Jordan has 23 banks, two of which are Islamic banks. Islamic banks account for around 15% of the banking business in the kingdom.

Commercial Bank of Kuwait (CBK) is seeking to buy 70% of Yemen Gulf Bank. CEO of CBK Jamal al-Mutawa said the head of the Yemeni bank had approved a US$30 million investment to be made jointly by CBK and the World Bank’s commercial lending arm.

The deal would increase Yemen Gulf Bank’s capital to US$30.19 million.

CBK seeks 70% stakeKUWAIT

80327 IceBreaker IFN[E2]8.ai 2/15/08 9:01:15 PM

www.islamicfi nancenews.comNEWS BRIEFS

Page 8 14th March 2008©

UAENational Bonds sales grew 109%The sales of Dubai-based National Bonds Corporation, which takes care of the UAE’s Shariah compliant national savings scheme, grew 109% to AED180 million (US$49 million) last month from AED86 million (US$23.42 million) a year ago, according to a company statement.

It said sales in February represented a 29% growth from AED140 million (US$38.13 million), a development which CEO Mohammad Qasim Al Ali said indicates that a “savings culture” is becoming popular in the UAE.

Last year, the company disbursed an annual profi t of 6.03% to investors.

UKBLME latest to join FLA divisionThe Finance and Leasing Association (FLA) announced that the Bank of London and The Middle East (BLME) has become the latest business to join its asset fi nance division, making the fi rst Islamic bank to become a full member of the association.

“We are pleased to be a full member of the FLA, which for many years has provided a strong platform for UK leasing businesses. Our membership is testimonial to the increasing demand for Islamic fi nancial products in the UK as well as our commitment to providing innovative lease fi nancing solutions in the UK. We look forward to a long lasting working relationship,” said Humphrey Percy, CEO of BLME.

BAHRAINIIB’s net income up by 56% Bahrain-based International Investment Bank’s (IIB) net income rose US$21.1 million last year, up 56.3% from the US$13.5 million recorded in 2006. Chairman Saeed Abdul Jalil Mohammad Al Fahim said the numbers refl ect the continued growth of IIB’s business and its ability to effectively develop and offer a diverse range of attractive investment opportunities.

Total income increased by 39.4% to US$34.3 million from US$24.6 million, mainly from investment banking fees that increased by 33.3% to US$22.8 million from US$17.1 million in 2006, generated from the structuring, underwriting and the placement of new investments.

SAUDI ARABIAMMG to launch IPO in MaySaudi Arabian contractor Mohammed al-Mojil Group (MMG) will stage an initial public offering (IPO) of 30% of its shares in May. The IPO, held over nine days, will open on the 3rd May.

A portion of the shares will be set aside for institutional investors. MMG specializes in onshore and offshore oil and gas and petrochemicals projects in the kingdom.

HSBC Saudi Arabia has been appointed fi nancial adviser and lead manager for the IPO.

UAEChallenges for Gulf’s private banksMargin pressures, eroding prices and rapid product commoditization are some challenges faced by foreign players looking to enter the Gulf’s increasingly competitive private banking industry, according to global management consultant Boston Consulting Group (BCG).

In its report on global wealth management and private banking, BCG said global wealth grew by 7.5% in 2006 to US$97.9 trillion and it expects assets under management to continue their steady rise.

Foreign players face additional challenges, such as growing competition from Islamic banks, In terms of assets, Islamic banking represents 15% to 20% of local retail banking markets in the GCC.

Many conventional banks in the region are converting to Islamic banks, and some global players have established Islamic windows to meet increased demand from the public and private sectors. Islamic banks are more profi table than conventional banks because their funding costs are generally lower as a result of government subsidies, the report said.

QATARQNB sets up fi nance companyQatar National Bank (QNB) is setting up an Islamic fi nancial services company with Kuwaiti partners. Qatar’s largest lender by market value will own 30% of Kuwaiti-Qatari Company for Ijara Investment, amounting to KWD24 million (US$88 million).

The new fi rm will offer Islamic fi nance services across the Gulf Arab region.

R e g i s t r a t i o n I s F r e e - L i m i t e d S e a t s A v a i l a b l e

V i s i t w w w . s a m a m e d i a . n e t a n d c l i c k o n “ R e g i s t e r t o a t t e n d ”

The Diplomat Radisson SAS - Kingdom of BahrainMarch 18 - 19, 2008

Organized &Managed By

Bronze SponsorPlatinum Sponsor s

Strategic Finance Publication Partner

Strategic Information Partner

Online Media Partner

BNP PARIBAS

www.samamedia.net

www.islamicfi nancenews.comRATINGS NEWS

Page 9© 14th March 2008

MALAYSIANo immediate impact from KLK bondsRAM Ratings has stated that Kuala Lumpur Kepong’s (KLK) proposed US$300 million nominal value fi ve-year Unsecured Guaranteed Exchangeable Bonds via KLK Capital Resources have no immediate impact on the AA2/P1 ratings of the group’s existing RM500 million (US$157.86 million) Sukuk Ijarah Commercial Paper/Medium-Term Notes Programme (2007/2011).

RAM Ratings believes that the group’s fi nancial profi le would still be within levels that commensurate with its AA2/P1 ratings and that the issuer of the proposed Exchangeable Bonds will have the option of increasing the issued amount by another US$100 million in the event of an over-allotment.

MALAYSIAAA-IS for Stratavest Sukuk MARC has assigned the rating of AA-IS to independent power producer Stratavest’s RM120 million (US$37.68 million) nominal value Sukuk Ijarah. Proceeds from the issuance of the Sukuk Ijarah will be utilized largely to fi nance the purchase and/or early redemption of Stratavest’s outstanding Al-Bai’ Bithaman Ajil (ABBA) bonds and to fi nance advances of RM31.3 million (US$9.83 million) to Stratavest’s shareholder, Eden.

The outlook on the rating is stable.

MALAYSIAAAA for IBK debt facilityRAM Ratings has assigned an AAA rating to Industrial Bank of Korea’s (IBK) proposed RM3 billion (US$9.42 million) Multi-Currency Conventional and/or Islamic Medium-Term Notes program, with a stable outlook.

The rating is anchored by IBK’s strategic role as a specialized policy bank that has been entrusted to provide impetus to the growth and development of small and medium-sized enterprises.

MALAYSIANPE notes on rating watchRAM Ratings has placed the respective AA3 and A1(s) ratings of New Pantai Expressway’s (NPE) RM490 million (US$153.8 million) Senior Bai’ Bithaman Ajil Notes (2003/2013) and RM250 million (US$78.47 million) Junior Bai’ Bithaman Ajil Notes (2003/2016) on rating watch, with a negative outlook.

The rating watch is triggered by the longer-than-expected completion of a refi nancing exercise, which had been intended to fully repay the Senior and Junior Notes by the 31st December 2007.

MALAYSIAMARC maintains Emas Kiara IndustriesMARC continues to maintain its AID/MARC-2ID ratings on Emas Kiara Industries’ (EKI) RM80 million (US$24.97 million) Partially Underwritten Murabahah Notes Issuance Facility/ Islamic Medium-Term Notes Issuance Facility (MUNIF/IMTN) on MARCWatch Developing where they were placed since the 10th December 2007.

The rating action follows slower-than-anticipated progress on EKI’s acquisition of a 51% stake in Carimin. EKI has extended the timeline for submission to the authorities in respect of the proposed acquisition for a further three months that commenced on the 26th February.

EKI is conducting due diligence for the proposed acquisition.

QATARSovereign credit ratings affi rmedStandard & Poor’s (S&P) has affi rmed its ‘AA-/A-1+’ sovereign credit ratings on Qatar as the result of its strong fi scal surpluses, substantial external liquidity, healthy economic prospects and high per capita income. The outlook is stable.

“The ratings remain constrained, however, primarily by the geopolitical risks facing sovereigns in the Gulf region, and capacity and institutional constraints which are higher than for other AA-rated sovereigns,” said S&P credit analyst, Luc Marchand.

MALAYSIAMARC reaffi rms Sapura EnergyMARC has reaffi rmed the long-term rating of Sapura Energy’s (SE) RM140 million (US$43.71 million) Al Bai’ Bithaman Ajil Islamic Debt Securities (BaIDS) at AID, with a stable outlook.

The reaffi rmed rating refl ects SE’s moderate business profi le as an oil and gas service provider with sustained operating track record evidenced by its ability to renew/obtain new contracts from its major customers.

Although revenue has been on an overall uptrend since 2003, SE’s fi nancial metrics have been somewhat tempered by fl uctuating profi tability and tight cash fl ow position as a result of stiff competition from other players with a larger asset base.

MALAYSIASACOFA’s Sukuk Istisna reaffi rmedMARC has reaffi rmed the ratings of SACOFA and its special purpose subsidiary, Sarawak Gateway’s RM160 million (US$50.51 million) Sukuk Istisna and RM240 million (US$50.51 million) Sukuk Ijarah at AAAIS.

The negative outlook on the ratings has been maintained.

(Also see Termsheet on page 25)

UAEDIB’s Sukuk trust certs assigned AStandard & Poor’s has assigned its A preliminary rating to Dubai Islamic Bank’s (DIB) US dollar fl oating-rate Sukuk trust certifi cates due 2012.

The transaction involves a special-purpose company incorporated in accordance with the laws of the Cayman Islands, DIB Sukuk, issuing rated ‘Musharakah sharikat melk’ Sukuk trust certifi cates. The proceeds of the Sukuk will be ultimately used for general funding purposes of DIB, which will sell a given percentage of a pool of assets to the issuer.

www.islamicfi nancenews.comRATINGS NEWS

Page 10 14th March 2008©

MALAYSIAMoody’s, Fitch maintain ratingCredit rating agencies Fitch and Moody’s on Monday maintained their sovereign ratings on Malaysia even as investors offl oaded local stocks and currency because of heightened uncertainty after the recent elections.

Investors are worried about a possible shift in government policy amid speculation that Prime Minister Abdullah Ahmad Badawi could be pressured to resign. But Fitch and Moody’s said Malaysia’s economy was still on a sound footing.

The government’s improving fi scal position supported Malaysia’s rating, said Franklin Poon, a director with Fitch. Fitch has an A- long term foreign currency rating with a positive outlook and an A+ long-term local currency rating with a stable outlook.

Moody’s has a long-term foreign and local currency bond rating of A3 with a stable outlook for Malaysia. Standard & Poor’s had earlier said there was no change to Malaysia’s sovereign rating, and has ‘A-/A-2’ foreign currency and ‘A+/A-1’ local currency ratings on the country.

MALAYSIAKrisAssets bonds reaffi rmedRAM Ratings has reaffi rmed the AAA(bg) rating of KrisAssets Holdings’ (KrisAssets) RM200 million (US$63.37 million) nominal value Bank-Guaranteed Bonds (BG Bonds), with a stable outlook. The rating mirrors the credit strength of the guarantor bank, i.e. Public Bank, the general bank ratings of which were reaffi rmed by RAM Ratings at AAA/P1, with a stable outlook, in May 2007. The bank guarantee from Public Bank enhances the credit profi le of the BG Bonds beyond KrisAssets’ stand-alone credit risk.

KrisAssets is a subsidiary and property-investment arm of IGB Corporation with two subsidiaries, i.e. Mid Valley City and Mid Valley Capital. Mid Valley City owns and operates Mid Valley Megamall.

THIS TIME LAST YEAR• First National Bank of Bostwana became the fi rst

conventional bank in Botswana to introduce an Islamic banking unit.

• Bank Negara Malaysia governor Dr Zeti Akhtar Aziz called for Islamic fi nancial institutions to expand their reach to untapped markets.

• The General Council for Islamic Banks and Financial Institutions proposed the set-up of a mega Islamic bank to fund large projects in Muslim countries.

• The Sharjah Electricity and Water Authority closed its nine-year Sukuk Ijarah at US$350 million. The Sukuk was lead arranged and underwritten by ABC Islamic Bank, Gulf International Bank, Kuwait Finance House and the Sharjah Islamic Bank.

• The Dubai Financial Services Authority signed a cooperation agreement with the New Zealand Securities Commission.

• Project fi nancing for the 288 meter Bishopsgate Tower — London’s tallest building — was sold at £200 million (US$391.4 million) to Islamic investment fi rm Arab Investment.

• The International Islamic Trade Finance Corporation commenced business with a start-up capital of US$3 billion.

• The Sharaf Group, along with Protea Hospitality Corporation of South Africa, launched Sharaf Protea Hotels Middle East to manage Shariah compliant hotels and furnished apartments.

• OCBC Bank’s Islamic banking income increased by 16% to RM52 million (US$14.8 million) as at the 31st December 2006.

• Dubai Islamic Bank’s Islamic home fi nance facility attracted applications worth PKR5.5 billion (US$90.6 million).

MALAYSIATenaga Nasional reaffi rmedMARC has reaffi rmed Tenaga Nasional’s (TN) issuer rating of AA+ and rated the utility’s Islamic debt facilities for its RM2 billion (US$6.31 million) Al-Bai’ Bithaman Ajil Bonds AA+ID and RM1.5 billion (US$4.73 million) Murabahah Commercial Papers and Murabahah Medium-Term Notes MARC-1ID/AA+ID.

The rating fi rm rated TN’s RM1 billion (US$3.16 million) Al-Bai Bithaman Ajil Notes Issuance Facility AA+ID.

The developing outlook on the ratings refl ects uncertainty as to the timing and magnitude of a potential revision on gas prices, given the increased likelihood of a near-term gas price revision, and the credit implications of an upward revision in prices on TN’s fi nancial profi le.

MALAYSIARating watch on SDE liftedRAM Ratings has lifted the Rating Watch (with a negative outlook) on Senai-Desaru Expressway (SDE) while simultaneously reaffi rming the AA3 rating of the company’s RM1.46 billion (US$462.55 million) nominal value Bai Bithaman Ajil Islamic Debt Securities (2005/2024).

Nonetheless, the outlook on the rating remains negative.

www.islamicfi nancenews.comIFN REPORTS

Page 11© 14th March 2008

Islamic fi nance can only catch up with its conventional partner once the industry has a standardized Shariah compliant fi nancial rules that cuts across the globe, said Majeed Dawood, CEO of Yasaar, an independent Islamic fi nance consultancy.

He said coupled with current technology and standard of innovations, Islamic fi nance will be able to capture a larger share of the market in no time. Dawood added that the scholars are already working toward achieving core standardization.

“When we have a standard rule, a product can be introduced all over the world with only minor amendments to accommodate each country’s jurisdiction and tax laws,” Majeed told reporters after speaking at the luncheon briefi ng on Islamic fi nance in Asia organized by index provider FTSE Group.

Majeed, however, could not set a timeframe on when the industry can expect such standardization due to mounting challenges posed by the different interpretations of the scholars representing Islam’s four different sects.

“It’s going to take time. Institutions like AAOIFI (Accounting and Auditing Organization for Islamic Financial Institutions) and IFSB (Islamic Finance Services Board) are already in place to close the gaps. These two (organizations) are already creating a level playing fi eld across the board.

“I must stress that we are referring to a 40-year-old industry as compared to a 700-year-old one (conventional fi nance). We will get there… of course, it will not take us 600 years but the standardization will come.”

Majeed also expressed confi dence that the Islamic fi nance market will grow much higher than the 20% projected by most analysts. “With the high liquidity and escalating oil prices, the industry can easily surpass the 20% growth expectation.”

“There was a slight setback last year with the announcement that 85% of the GCC Sukuk was non-Shariah compliant. We saw a lot of people pulling back on their Sukuk products.

“But now that scholars have settled that issue, we should expect more Sukuk to be introduced in the second quarter. That would further boost the industry up a few notches.”

In his presentation at the luncheon, Majid said Asia was experiencing a boom in Islamic fi nancial services at a growth rate in excess of 20% per annum.

At present, Asian fi nancial services are highly concentrated in Malaysia with focus on banking assets, Sukuk issuance, asset management and Takaful.

He added that in the Malaysian market, wholesale Islamic fi nancial services under the corporate loans segment had grown 14.1 times compared with 2.9 times for the conventional banking system while trade fi nance expanded 32.5 times against 5.3 times and corporate fi xed deposit grew 17 times compared with 2.3 times.

By Arfa’eza A Aziz

Standardization the way to goASIA/GLOBAL

In Malaysia’s equity market, about 85% of the stocks listed on the Exchange are Shariah compliant. So, when Malaysian stocks plunged 9.5% last Monday following the dismal performance of the Barisan Nasional (BN, or National Front) government in last week’s general elections, players in the Islamic fi nance industry were wary of the future.

Although stocks rebounded the next day, some observers believe the development will leave a lingering effect on the near-term outlook for the market.

However, CIMB Islamic Bank CEO Badlisyah Abdul Ghani said the dip — Malaysia’s lowest in seven years — was an expected reaction to the elections, which saw the BN lose control of fi ve states (out of 13) to the opposition coalition, Barisan Alternatif.

“The stocks picked up today (11th March). It’s a typical reaction due to the current development in Malaysia’s political scenario. I believe the election results showed the level of maturity that Malaysia has achieved,” said Badlisyah, when Islamic Finance news spoke with him at the Islamic Funds Asia meet in Kuala Lumpur on Tuesday.

He stressed that there was no reason to believe that the political stability and strength of the Malaysian government has been greatly affected.

“The levels of confi dence are still intact. We must remember that the federal government is being ruled by the BN, which won 140 (parliament) seats; only eight seats short of the two-thirds majority. It does not face any risk in running the country. From the business point of view, that’s comforting,” he said.

As to whether foreign investments would be affected, Badlisyah said such fear should not exist. “Like I said earlier, the federal government is the government that will take charge of the major economic policies.”

Concurring with Badlisyah was Bank Islam’s senior economist, Azrul Azwar. “The results showed that democracy is alive in Malaysia. Foreign investors who place democratic principles very highly will be keener to come to Malaysia.”

Azrul believed that the market reaction would not have been so negative if not for the current global fi nancial uncertainty due to the subprime woes. He pointed out that most Asian markets sank on Monday, with Tokyo’s market falling to a 2½-year low.

He said investors should view the situation positively. “It’s a great time to buy now that the price is low.”

Despite these brave statements, international markets continue to be wary. On Wednesday, Standard & Poor’s Equity Research reduced its weighting on Malaysia to underweight from marketweight, citing higher risk to earnings outlooks following the election results.

Lorraine Tan, vice-president of S&P Equity Research, Asia, said that the infrastructure sector is likely to be hurt. She believed a number of the special economic zone projects that the federal government favors may be put on hold.

Market dip has no lingering effectMALAYSIA

www.islamicfi nancenews.comIFN REPORTS

Page 12 14th March 2008©

“Boring”, “subdued” and “a damp squib”. Those were some of the reactions by the British press and commentators to the UK 2008 Budget Report presented by Alistair Darling, Chancellor of the Exchequer, on Wednesday.

Indeed, free press thrives in the UK. But more importantly, the budget is assurance that the Islamic fi nance industry will continue to thrive in the country hailed as Europe’s gateway to Islamic fi nance.

Darling took the UK government a step closer to issuing its fi rst sovereign Sukuk, stating that the government will continue to examine the feasibility of such an issuance and, in the Finance Bill 2008, take legal powers to facilitate any future sovereign issuance, as well as provide a full response to the recently closed public consultation on Sukuk issuance in the summer.

It is obvious that the government refused to take the bait reeled by opposition parties, the Conservatives and the Liberal Democrats who have deliberately sought to play up the so-called religious and tax implications of the issuance of a UK sovereign Sukuk.

Darling’s announcement relating to Islamic fi nance includes proposals to:

• legislate, following consultation, in the Finance Bill 2009 to provide relief from stamp duty land tax (SDLT) for Sukuk (referred to as alternative fi nance investment bonds);

• amend the law to classify Sukuk as tax-exempt loan capital for stamp duty and stamp duty reserve tax (SDRT);

• adjust legislation to allow existing corporation tax and income tax rules on Islamic fi nance arrangements (referred to as alternative fi nance arrangements) to be amended by regulation and work with the UK banking regulator (the Financial Services Authority) and stakeholders to clarify the regulatory treatment of Sukuk.

One of the industry players who hailed the announcements was John Challoner, tax partner at law fi rm Norton Rose. “For the last few years, HMRC (Her Majesty’s Revenue and Customs) has been receptive to representations made for the tax treatment of Islamic fi nance to be no more onerous than conventional fi nance. Last year saw legislation which permits UK companies to issue Sukuk.

“The legislation, however, did not extend to removing the SDLT charges which would make Sukuk uneconomic where the assets underlying the bonds are UK land and buildings. It has now been announced that, subject to consultation, the legislation will be amended to remove these charges,” said Challoner.

His colleague, senior associate Davide Barzilai, added that the tax aspects, coupled with the restated intention to issue a Government Sukuk, will give the UK an Islamic fi nance initiative.

Meanwhile, Islamic fi nance consultant Junaid Bhatti welcomed the government’s continued support for halal fi nance.

“Promoting ethical fi nancial conduct is at the core of Islamic principles. The chancellor is working to create a level playing fi eld for British Muslims who want to run their fi nancial affairs in accordance with their

religious ethics,” said the director of Ballencrieff House, an Islamic fi nance consultancy.

“Right now, the capitalist economies are suffering severe liquidity shortages due to the global credit crunch. These economic problems are a result of irresponsible lending and the gambling of customers’ money by non-ethical fi nancial institutions. Islamic fi nance is the perfect antidote to this because it forces banks to act more responsibly and with greater transparency.

“It does this by shifting a greater amount of risk away from customers and back to the banks, and through an insistence that all transactions must be supported by tangible assets.”

Although Darling fell short of setting a date for an inaugural sovereign Sukuk, Junaid believes the budget lays the foundations for the UK government to issue a sovereign Sukuk (Islamic bond) within the next year.

“Several measures have been announced for this historic project. The main changes will be the introduction of changes to the stamp duty regulations to ensure that Sukuk will be given the same tax treatment as conventional bonds,” he said.

Junaid thinks the report is also a boon to foreign investments in the UK. “Offi cial support for Islamic fi nance, through the issuance of Sukuk by a western government, will send a powerful signal to Muslims in the UK and abroad… The move will also encourage more Muslims from the oil-rich Middle East to invest more of their funds in one of the UK’s four (recently-authorized) Islamic banks.”

The UK is home to some two million Muslims and its Islamic banks have more than 30,000 customers across the country. Since 2003, the Islamic mortgage market has grown to over GBP500 million (US$1.01 billion) — an increase of about 50% in the last year alone.

In Budget 2006, the government announced its commitment to work with the fi nancial sector to establish a high-level group, with senior representatives from across the fi nancial sector, to develop and support a new strategy to promote London as the leading international fi nancial center. The Islamic Finance Experts Group was established as a result.

Budget 2007 introduced new measures for Sukuk, enabling them to be issued, held and traded in the same way as corporate bonds. This is expected to increase primary issuance in the UK, and there is also a growing secondary Sukuk market in London.

HMRC issued guidance alongside Budget 2007 on the treatment of Musharakah, a common structure used for Islamic mortgages; and Takaful products, to provide more clarity and encourage growth in these markets.

On the 6th April 2007, the FSA introduced new protections in the housing market for consumers wanting to buy their homes in a way that complies with Shariah law through a home purchase plan.

By Arfa’eza A Aziz

New Darling of Islamic fi nanceUK

www.islamicfi nancenews.comINTERVIEW

Page 13© 14th March 2008

At the recent Islamic Funds Asia meet (which ended on Wednesday) in Kuala Lumpur, John A Sandwick boldly told the audience why he’ll be voting for Barack Obama, US Senator for Illinois who’s gunning to become the fi rst black leader of the Free World.

“We need to put some wisdom in the White House,” quipped the managing director of Geneva-based Encore Management.

As frank as he is in expressing his political inclination, Sandwick adopts the same attitude when he gives talks on Islamic fi nance. Speaking to Islamic Finance news on the industry’s development in Europe, the well-known expert in Islamic assets management did not mince his words. Sandwick said Swiss banks will suffer “swift and brutal” consequences if they don’t establish a legitimate base for Islamic assets management in the country.

He also expressed concerns over the limited Islamic fi nancial and investment products in the continent, adding that too much focus is being given on private equity, which is often just “venture capital in disguise”. While private equity is good for any economy, but there are limits, he stressed.

In the interview, he also spoke on the challenges that Europe faces in building its Islamic funds and investment market. Below are his takes on the industry.

The UK is shaping up to be the Islamic fi nance capital for Europe. What are the main reasons for that? What does it have that other European countries don’t?Clearly, the most important element of successful Islamic fi nancing of any kind is a legal and regulatory framework that accepts that not all distributions of cash are subject to withholding taxes. The UK has made substantial progress in recognizing that a lot of Islamic investing is not equity investing in the conventional western sense according to tax regulators, and permitted distributions without withholding tax. This alone is the biggest single step any European or in fact any government can make to support Islamic banking and fi nance.

The tax authorities in countries like France, Germany and Switzerland have been slow to acknowledge there are alternative treatments of cash distributions, capital structures and the like when it comes to Islamic investing. We believe this will ultimately change, especially as the stakes get higher. Remember, the oil exporting states of the GCC have about US$38 trillion in total revenue during the next 20 years, of which Morgan Stanley estimates only 10% can be deployed into domestic economy investments. Where will the 90% go? They will go to international capital markets and direct investing.

As Islamic investing becomes increasingly common among sovereign wealth funds within the GCC, you will see an automatic adjustment by European — and indeed many non-European — governments to Islamic structures and tax treatment.

What do other countries need to do to catch up with the UK? How long will it take to see them on par?Some governments will take a long time to adjust. France, in particular, has a very dedicated commitment to the secular treatment of all government affairs. They might ask: Why should tax treatment of Islamic investing be any different from conventional investing?

In fact, I think that each government in Europe has already looked into these issues, and is already considering how and when to implement policies to support and encourage Islamic investments and fi nance.

Why have other countries been slow to allow full-fl edged Islamic banks and fi nancial institutions as opposed to the UK, which now has allowed four full-fl edged Islamic banks?I wouldn’t criticize their slow behavior, I would encourage their more rapid absorption of the new technologies and policies required to encourage Islamic banking. You know that governments everywhere take slow, measured steps on all banking regulatory matters, and Islamic banking is no exception to this rule.

London is leading the pack simply because it has: (a) a long tradition of fi nancial market innovation; and (b) much deeper ties to the international communities that host most of today’s Islamic banking professionals, meaning Dubai, Bahrain, Kuala Lumpur and other locals.

Switzerland holds potential in tapping the growing investors’ base from the Middle East. Do you think it is doing enough to take Islamic fi nance to a higher level? What needs to be done there?In general, there appears to be an overwhelming paralysis in Switzerland to the Islamic asset management industry. Not a single Swiss bank, or foreign bank in Switzerland, seems to be making any solid, concerted approach to Islamic wealth management. This is strange as there is (a) a gigantic pool of perhaps US$200 billion in Muslim-owned funds in the Swiss banking system, and (b) nearly every Swiss bank has opened for business in Dubai, Manama and/or Doha. What is the cause of this paralysis?

It could be that after the demise of Bank Noriba (sponsored by UBS), there seems to be fear or reputation risk in the event of another failure. Further, I myself have actually heard senior Swiss bankers say they think Islamic banking is a fad, eventually to disappear after the industry’s fi rst major scandal.

I have heard other Swiss banking leaders say they don’t understand or they fear the heterogeneous nature of fatwa (religious edict) and fear issuing a product with one fatwa that won’t be accepted by the majority of their clients.

In my opinion, the Swiss must get moving now to establish a legitimate base of Islamic assets management before it is too late. Can you imagine what will happen if Singapore, Dubai or any other proposed center of Islamic assets management begins to eat into the Swiss market share in the Gulf states and Saudi Arabia? The consequences could be swift and brutal if the Swiss banks don’t respond, and that could be very soon.

Encore Calls for More Variety in EuropeBy Arfa’eza A Aziz

continued...

www.islamicfi nancenews.comINTERVIEW

Page 14 14th March 2008©

Encore Calls for More Variety in Europe (continued...)

What are the other major challenges does Europe face in developing the Islamic fi nance market? How can these challenges be overcome?Wholesale Islamic banking, meaning corporate fi nance, treasury, capital markets and similar services, are the easiest parts of the Islamic banking package to absorb because here, the regulatory involvement is relatively easy and limited.

Retail banking is the most diffi cult as it involves massive regulatory interference, just as retail banking requires everywhere. I think right now, most European governments are taking a ‘wait-and-see’ approach toward retail Islamic banking, observing the experience of the UK fi rst before they make any formal entries into this area.

What has been Europe’s best achievement in Islamic fi nance so far? I applaud the establishment of so many Islamic investment houses in London. It will stimulate even further growth in the industry throughout Europe. Unfortunately, there are far too many Islamic private equity ventures in London; often, they are really only venture capital disguised as and with the more conservative name of private equity. And, while so many businesses were established, we still see very few actual products or announcements from the majority of them.

It is hard to say they have achieved much more other than physical presence, of course part of which is a more diffi cult regulatory environment outside of the UK. I’ll hold my opinion for the time being on the word ‘achievement’ and wait for something more concrete before I bestow that honor.

East Asia and the US have expressed interest in setting up a global Islamic fi nance hub. What plus points does Europe have over the other non-Muslim majority jurisdictions?You are interviewing me as I am here in Kuala Lumpur attending Islamic Funds Asia, where yesterday (the 10th March) I was teaching a master class on Islamic assets management to eager and very professional Malaysian and Singapore bankers.

Without a doubt, East Asia is very far ahead in the legitimatization of the Islamic banking industry, and I mean that on a worldwide basis. The industry here is very professional and they are both serving client needs and making money. In fact, Europe and the US simply have to emulate the success of Islamic banking in countries like Malaysia to achieve the same results. Europe, of course, is home to many devout Muslims, not all of whom are skeptics or cynical about Islamic banking. Given meaningful alternatives that match conventional banking in all respects, this will cause the vast majority of European and American Muslims to choose this alternative.

There is a dearth of Islamic fi nance experts even in Malaysia and the Middle East, which are considered leaders of the industry. Do you think the shortage of such experts is one of the main reasons

Europe’s Islamic fi nance development is slow? If so, how do you think the problem can be overcome?Yes, I got a smile with that last question. I speak at Islamic banking conferences all over the world and am often surprised to hear the length of service an individual has in the industry. Many of them proudly proclaim they have been ‘Islamic bankers’ for six or 12 months! But, that’s really not a barrier. Good banking is good banking, regardless of one’s faith, and in fact, other than learning the basics of Islamic banking, any good banker can become an expert Islamic banker in short order. It is in fact only a matter of time before Islamic banking is fully legitimized worldwide. I don’t see a single element of Islamic banking that would prevent this. Its adaptability to all commercial and regulatory environments is very high.

Do you think Islamic wealth management in Europe can ever catch up with its conventional partner?Yes, of course, in the long term, it can and it will. Even in Germany, we are seeing some pension funds looking at offering their Muslim employees an Islamic retirement fund alternative. But the biggest complaint is the huge lack of products. As mentioned above, the Islamic banking units of so many Arab and European banking entities are falling all over themselves to create more private equity, which is often just venture capital in disguise.

Of course, private equity is good for any economy, but there are limits. Someone somewhere must create, manage and distribute world-class Islamic mutual funds of all kinds. The gigantic empty space in terms of Islamic products is what fi rst needs to be fi lled. Only then can Islamic wealth management become a serious alternative to conventional asset management. We at Encore are working on that right now, with a soon-to-be established Bahrain-based fully dedicated Islamic mutual funds company.

How do you view Islamic fi nance in Europe in the next fi ve years? What are the changes you want to see?My predictive powers are poor, as are everyone else’s. I can’t tell you exactly where we will be in Europe, but I can tell you that we at Encore are trying to become a catalyst for change. Europe needs Islamic banking. Europe needs Islamic assets management. Of that, there is no doubt.

Translating that need into a reality is the diffi cult part. When will the French central bank, for example, permit what will perhaps be the most successful Islamic retail banking enterprise in all of Europe? It’s hard to say. Eventually they will, as eventually all European banking and regulatory bodies will absorb and adapt their own versions of an Islamic banking environment.

Unlike the opinion of one Swiss banker, as I stated earlier, the Islamic banking industry is not going to disappear with the fi rst scandal or meltdown. It is here to stay.

Next Forum Question

In your view, what is hampering the growth of Islamic fi nance in the west?

If you would like to air your views on the next Islamic Finance Forum Question, please email your response of between 50 and 300 words to Christina Morgan, Forum Editor, at: [email protected] before Wednesday, 19th March 2008.

www.islamicfi nancenews.comCOUNTRY REPORT

Page 15© 14th March 2008

Islam all too often resonates negatively in Europe, with much non-Muslim public opinion uncomfortable with Islamic culture and values. Secular and Christian opinion is at best suspicious of Shariah law, and indeed often antagonistic.

The notion of wanting to apply Shariah principles to banking and fi nance is treated with skepticism, if not outright hostility, especially as there is no concept of Christian or Jewish banking, even if there are some parallels between Shariah fi nancial principles and the teaching of the Old Testament.

Yet, Islamic fi nance is thriving in Europe, and many major European banks perceive it as a profi table opportunity to generate new business rather than as a threat to existing business. Although Islam is sometimes viewed as prescriptive and concerned with restricting choice, Islamic fi nance is about widening choice, and in particular about providing alternatives to interest-based fi nance. The aim is to develop fi nancial products that are seen as ethical and within the realm of socially responsible investment.

Much of the focus is on Shariah compliant asset management, with a section on liquidity management without the use of conventional instruments such as treasury bills, and an extensive discussion of the structuring of Islamic Sukuk securities.

In the banking fi eld, the development of Islamic retail banking in Europe is reviewed, with a further section devoted to Shariah compliant wealth management and private banking. Prospects for Islamic investment banking are also considered as well as the European experience of Shariah compliant fund management.

Finally, future prospects for Islamic banking and fi nance in Europe are assessed, notably the provision of Shariah compliant services for continental European Muslims, and the possible implications of Turkey’s accession to the European Union (EU) will be examined, although there the fortunes of Islamic fi nance have been rather mixed.

The Islamic fi nancial activities of major European banks will become apparent from the discussion, as will the Islamic fi nance operations of some of the Arab banks with subsidiaries and branches in Europe.

The achievements of the European-based, exclusively-Islamic banks will also be reviewed, notably those of Islamic Bank of Britain (IBB) and the European Islamic Investment Bank (EIIB).

Islamic fi nance has become a key dimension of the relationship between Arab banks and their European counterparties. While the Arab banks imported most of their conventional fi nancial products from Europe in the past, now European banks are importing Shariah compliant products from the Arab world, not only for their overseas Arab clients, but more signifi cantly for the growing Muslim population of Europe. Thanks to the emergence of Islamic banking, knowledge transfers in fi nance have become a two-way process rather than simply a one-sided affair. European banks have as much to learn from the Arab world as the latter have from Europe as interdependence replaces dependence.

Role of Islamic fi nance in Euro-Arab banking relationsThe increasing spread of Shariah compliant fi nance, and the dynamism of the economies where it is important, is making the Euro-Arab fi nancial relationship more a partnership of equals in the 21st century. In contrast to much of the 19th and 20th centuries, the Arab economies underperformed those of Europe, and one explanation for this underperformance was the development of a fi nancial system in the region based on riba that was never fully accepted, given its inherent confl ict with Islamic values. Fortunately now pious Muslims have a real choice, as Shariah compliant products have been developed over the last three decades to serve most of their fi nancial needs, and these products are at least as effi cient as their conventional counterparts.

The UK has been the gateway for Islamic fi nance to enter Europe, partly refl ecting the role of London as the leading international fi nancial center, but also as a consequence of the exposure of leading British banks to the Arab and wider Islamic world and their knowledge of these markets. It was the Arab joint-venture banks that fi rst brought Islamic fi nance to London in the early 1980s as Islamic banks in the Gulf found that re-depositing on a Murabahah basis could be an effective tool for liquidity management, with the mark-ups generated from trading activity on the London Metal Exchange.

Islamic Finance in EuropeBy Prof Rodney Wilson

continued...

“The UK has been the gateway for Islamic fi nance to enter Europe, partly refl ecting the role of London as the leading international fi nancial center, but also as a consequence of the exposure of leading British banks to the Arab and wider Islamic world and their knowledge of these markets”

www.islamicfi nancenews.comCOUNTRY REPORT

Page 16 14th March 2008©

Islamic Finance in Europe (continued...)

The UK has also hosted the fi rst Islamic retail bank in Europe, the IBB which started operations in September 2004, and the EIIB, which opened for business in 2006. The leading conventional banks have also become involved in serving the local retail market for Islamic fi nancial services, notably HSBC and Lloyds TSB, both of which provide Islamic deposit facilities and housing fi nance using Shariah compliant structures.

It is of course internationally that European banks have made the greatest contribution to Islamic fi nance with Barclays Capital partnering Dubai Islamic Bank (DIB) for the world’s largest Sukuk issuances; Standard Chartered making a notable contribution to Islamic fi nance through its networks in the Gulf, Pakistan and Malaysia; Deutsche Bank in pioneering capital protected funds in the Gulf, and UBS in developing Shariah compliant wealth management services to name just some examples. The operations of these major European banks will be also reviewed here.

Early Islamic trade fi nance operationsIt was the involvement of European banks in the Gulf that fi rst resulted in them encountering demands for Islamic fi nance. These date back over 80 years, as it was in the 1920s that the Eastern Bank, the predecessor of StanChart, was informed by the ruler of Bahrain that the bank’s proposed branch on the island would only be allowed if it avoided all interest-based transactions. At the same time, the National Handelsbank of the Netherlands, the predecessor of ABN Amro, was allowed to establish itself in Jeddah to provide money-changing services for pilgrims from Dutch Indonesia, the condition being that it avoided all interest-based transactions.

For the next 50 years, most of the European banks involved in the Muslim world carried out their business using interest, as indeed did their local counterparts, within fi nancial systems where governments believed religion had no role to play. By the late 1970s, however, the perceptions of European bankers were starting to change, largely as a result of the emergence of Islamic banks in the Gulf, with DIB the fi rst to be established in 1974, followed by Kuwait Finance House (KFH) in 1977, and the Bahrain Islamic Banks in 1978.

All these banks were extensively involved in Shariah compliant trade fi nance, especially of imports from Europe, using a structure known as Murabahah, whereby an Islamic bank would purchase an imported good on behalf of a client, and then resell the good to the importer for deferred payments covering the costs of the purchase plus a mark-up representing the bank’s profi t. As the bank was involved in a real trading transaction which involved ownership risks, this justifi ed its profi t, unlike interest on a conventional loan where there was only the credit risk of default.

As the payments by the Islamic banks would be made to the European exporter’s bank, those bankers involved started to learn about Islamic fi nance. In a conventional trading transaction usually the exporter’s bank would demand a letter of credit from an importer’s bank that would guarantee the payment.

With Murabahah, however, as it is an Islamic bank, and not the import distributor or agent who is making the payment, letters of credit are arguably unnecessary, as well-regulated banks are less likely to default than individual corporate clients. This potentially lowered the

costs of trade fi nancing, but European banks acting on behalf of their exporting clients were only prepared to wave the requirement for their Shariah compliant counterparties to provide letters of credit if they were satisfi ed that these Islamic banks could meet their payments obligations. To be confi dent in the timely payment of receivables, European banks needed to fi nd out more about Islamic banking and understand how Islamic fi nancing techniques worked.

Although Islamic banking and fi nancial services have been offered from Europe for almost three decades in many respects, the industry is still in its infancy. Much of the business activity has been focused on Shariah compliant institutions from the Gulf and high net worth Muslim investors, but this has resulted in activity being somewhat cyclical and linked to oil market developments.

The impact on Europe’s resident Muslim population has been marginal, and mostly confi ned to the UK, even though France and Germany have much larger Muslim populations, with that of France exceeding fi ve million. The Gulf and wider Muslim world is likely to continue to generate substantial Islamic fi nance business for London as an international fi nancial center and Europe’s leading investment banks and asset managers, but the longer-term prospects are more likely to be shaped by developments within Europe and further EU enlargements.

Prospects for Islamic fi nance in EuropeThere are two major issues, the fi rst being whether retail Islamic banking services can be provided for continental Europe’s Muslim population and if this is desirable. Second, there is the issue of EU enlargement to encompass countries and regions with long established Muslim populations in the Balkans, and Turkey, the most populous state in Europe, with over 72 million Muslims.

Although the EU functions as a single market, banking and fi nancial regulation is devolved to member states. In the UK, the Financial Services Authority has played a pro-active role with respect to Islamic banking and fi nance and been broadly supportive, but that has not been the position elsewhere in Europe, where central banks and other regulatory authorities have shown little interest.

There is also a negative perception of Shariah, especially among right-wing and nationalist politicians, which potentially inhibits the spread of Islamic banking and fi nance. What is not always appreciated is that Shariah compliance in fi nance is a choice, and not about the imposition of Shariah on those, including Muslims, who want to lead secular lives and manage their fi nancial affairs in a conventional manner.

continued...

“There is also a negative perception of Shariah, especially among right-wing and nationalist politicians, which potentially inhibits the spread of Islamic banking and fi nance”

www.islamicfi nancenews.comCOUNTRY REPORT

Page 17© 14th March 2008

Islamic Finance in Europe (continued...)

Some critics assert that Islamic fi nance is simply another facet of segregation and places Muslim banking in a ghetto, but those who rebut this argument point out, as shown earlier, that many leading European banks are now heavily involved in Islamic fi nance. There is certainly potential to develop more Shariah compliant savings and fi nancing products for Europe’s Muslim community, as well as distribute Takaful insurance which remains in its infancy in Europe, despite the involvement of fi rms such as Allianz and Prudential in the Takaful industry in the Gulf. At present, the worldwide value of Takaful premiums amounts to US$1.7 billion, but less than 1% of this is spent in Europe.

The greatest potential for Islamic fi nance in Europe is undoubtedly in Turkey, where Islamic banking has been established since the 1980s although it remains on the fringes of the fi nancial system, accounting for less than 5% of deposits. Opinions on its merits are politicized as already indicated.