Literature review

38

CHAPTER I1 REVIEW OF LITERATURE

Transcript of Literature review

CHAPTER I1

REVIEW OF LITERATURE

CHAPTER I1

REVIEW OF LITERATURE

INTRODUCTION

Marketing by service industries are yet to gain momentum, especially when it

comes to marketing by comniercial banks. In India, the liberalization of the financial

sector has impelled all the players to redefine what business they are in and

strategically think how to stay ahead in the existing business. Marketing orientation of

banks is imperative for survival and success.

EARLIER STUDIES

Marketing of financial services by banks is under active and extensive

discussion among academicians and bank personnel. Survey and research have been

conducted both by academic researchers and practitioners on the various aspects of

services marketing in general and financial services marketing by banks in particular

both in India as well as abroad.

Sewice Marketing

A study by George William R and Hiran C Barksdale (1974) on the marketing

activities in the service firms discovered that services marketing is generally on the

low ebb. Service firms tend. to be less marketing oriented; less likely to have

marketing mix activities car:ried out in the marketing department; less likely to

perform analysis in the area of service product; more likely to undertake advertising

internally rather than go to specialized advertising agencies; less likely to have overall

sales plan; less likely to develop sales training programmes; less likely to utilize the

55

-- Review of Literature

services of marketing cons~iltants and marketing research firms; and less likely to

spend much on marketing, as a percentage of gross sales.'

Study by Bessom, Richard M and Donald W Jackson Jr (1975) of 400 service

and marketing firms revealed that service firms are less likely to have marketing

departments, to make use of sales planning and training, and to employ marketing

professionals like consultants, advertising firms and market research agencies.'

James F Devlin (2000) studied as to how attempts can be made to add value

when offering services exhibiting increased complexity, intangibility and

impalpability in the eyes of most consumers. It was found that the features and quality

of the core service provided are judged by managers to be more important in adding

value to more complex services; as are organizational factors such as image and

reputation. In addition, price i:j perceived to be significantly more important in adding

value to more simple, rather than complex, offerings.3

Characteristics of Services

Anne M Smith (1990) studied way the four distinguishing characteristics of

services-intangibility, inseparability, heterogeneity and perishability affect clients'

perceptions of quality service from banks. The study revealed that intensifying

competition and increasing customer expectations have created a climate where

'quality' is considered to be a major strategic variable for improving customer

satisfaction and thus the profitability of financial service providers.4

Financial Services Marketing

Sankaran M (1999) studied the measures that would help domestic players in

financial services sector to improve their competitive efficiency, and thereby to

56 Review of Literature

reduce the transaction costs. The study found that the specific set of sources of

sustainable competitive adv,mtage relevant for Financial Service Industry are: a)

product and process innovations, b) brand equity, c) positive influences of

'Communication Goods', d) corporate culture, e) experience effects, f) scale effects,

and g) information technolog!/. 5

Trevor Watkins (1989) while studying the current state of the financial

services industry worldwide identified four major trends: (1) the trend towards

financial conglomeration; (2) globalization (3) information technology in bank

marketing; and (4) new approaches to financial services marketing. These trends, it

was concluded, will affect the marketing of banks and other financial services in the

1990s.~

Marisa Maio Mackay (2001) examined whether differences exist between

service and product markets, which warrant different marketing practices by applying

ten existing consumer based measures of brand equity to a financial services market.

The results found that most rneasures were convergent and correlated highly with

market share in the predicted direction, where market share was used as an indicator

of brand equity. Brand recall and familiarity, however, were found to be the best

estimators of brand equity in the financial services market.'

Bank Marketing

In Berry, Kehoe and Lindgreen's study (1980) it has been found that most

frustrating aspects of bank marketing were a) lack of management support, b) lack of

interdepartmental cooperation c) crisis management d) government intrusion e)

advertising and media

57

--- Review of Literature

T G Nair (1992) in his study depicts the growth and expansion of Financial

Services industry in India. Banks in order to overcome the competition from other

agencies are providing s wide range of services. Public sector Canara Bank observed

the year 1984 as 'Year of Marketing' to create among the staff an awareness of the

need for customer satisfaction. The findings stress greater need for a change in the

attitude, especially in the case of the counter clerks, field staff and sales force of the

bank, towards the cu~ tomers .~

Customer Needs

Geiger's ( 1 975) study was to establish the needs of customers. Social structure

of the bank's customers and the image that the customers had of the banks were

studied along with customers judgment of the range of services that the banks had to

offer, the effectiveness of various advertising and other sales promoting measures,

and the custon~ers' will to save and other habit. Findings indicate that satisfied

customers are more pos~tively !minded than those who are critical of what their banks

have to offer them."

The study by Syed Asad Akbar (1990) revealed the need for a more customer-

oriented approach to bank marketing, and more emphasis on improved marketing

strategies. Stressing the need for a 'Plan Oriented Marketing', suggestions were made

that new product development should be done on an on going basis and schemes

which have failed to take off should be reviewed and if necessary modified or

dropped."

5 8

-- Review of Literature

Lewis and Birmingham (1991), studied the needs, attitudes and behaviour of

youth market for financial services and found the youth market not homogenous in

terms of needs and behaviou:r.I2

Boyd er ( ~ i ( 1 994) conducted a study on consumer choice criteria in financial

institution selection in U SA and found that reputation and interest rates

(loans/savings) more important than friendliness of employees, modern facilities and

drive - in - service. I3

Rajagopla Nair ( 1 994) in his study on rural bank marketing found that security

and liquidity are the major pre-requisites for deposits by rural customers and that

interest rate on deposits is not at all a criterion for rural bank depositors to deposit

their savings with commercial banks.14

Huu Phuong Ta and Kiir Yin Har (2000) studied bank selection preferences of

undergraduates in Singapore. In the study, nine criteria for bank selection decision

and five banks were identified, and the decision problem structured into a three-level

hierarchy using the Analytic Hierarchy Process. The findings indicate that

undergraduates place high emphasis on the pricing and product dimensions of bank

service^.'^

Products

National Institute of Bank Management's study on deposit mobilization

(1969) concluded that mobilization of resources is one important facet of the various

services performed by banks. Banks should classify depositors into segments and take

intensive measures to market their services to them. They should design suitable

schemes to mobilize the savings and attract them through suitable media of publicity.

59 Review of Literature

The various techniques of banks are essentially based on the principles of mobility,

flexibility, convenience, reduction of cash drain, automatic facilities and special

inducements. More personalized service to achieve deposit mobilization at branches.I6

Place

In Rossier's study (1973) suggests that banks should not open a branch

without first analyzing market potential and determining the expenditure required to

obtain a sufficient market share. The risk in expansion is not so much one of opening

unprofitable branches, but rather of allocating scarce resources of managerial talent,

qualified personnel and capital to marginal projects.'7

A study by Meidan (1976) revealed that about 90 percent of the respondents

banked at the branch nearest to their home place or place of work. Convenience, in

terms of location, was also found to be the single most important factor for selecting a

branch."

Ron Laursen and Ron McTavish (1994) in their research found that workplace

banking - the provision of banking services to company employees at their place of

work - was attractive to employers and employees and that they utilized the services

19 to a great extent.

People

Peter W Turnbull ( 1 982) places the branch bank manager in a central position

in the business in respect of the marketing efficiency of the banks at the local level.

The study identified three reasons which underlie the lack of marketing orientation:

motivation, ability and time. and says that banks need to move quickly to ensure that

branch bank mangers can speedlly meet the challenge. It was suggested that managers

60

-- Review of Literature

be given knowledge inputs on the principles of marketing and develop in them the

commitment to implementing the principles in practice.20

Promotion

A study conducted by Preston et a1 (1978) indicates that there is no significant

difference between the retention rates of premium-attracted and of,non-premium

offered deposit accounts. Consequently, the conclusion is that customers attracted by

a free premium were just as loyal as those customers attracted by a lower -price

banking service premium.2'

Dr.Chidambaram (1994) studied the promotional mix available to bankers for

the marketing of services such as direct marketing, public relations, social banking

and customer meets. The study concludes that a good promotional mix is one that a)

that takes into account the objectives of the bank and lays emphasis on those services

which are of current significance, b) reaches various customer segments very

effectively, c) creates a desire to seek out the services offered, d ) builds a positive

image for the bank, and e) strike a balance between cost and e f f e c t i ~ e n e s s . ~ ~

F G Crane (1990) using a case study analysis, found that corporate advertising

should be an integral component of the marketing communications program of a

financial services institution and recommends that managers need to pay more

attention to successfully integrate corporate advertising integrated with product

advertising.23

6 1 --- Review of Literature

Advertising

In Raybum's study (1978) it was suggested that the purpose of the advertising

and promotional functions is to create demand for the bank's services and to build and

maintain goodwill towards the organization.24

Subba Rao (1982) conducted a study to find out the influence of different

media of advertisement and different forms of personal selling on the deposit

mobilization of commercial banks both in urban and rural areas. The study suggested

that the medium of English News papers need not be used widely as its impact is very

little on urban customers and it is almost negligible on rural depositors. Personal

selling or direct contact has been suggested as the best method, :since it educates the

potential rural customers into the bargain.2"

Singh J D (1983) in his study examined the trends in bank advertising in the

seventies in India. The study revealed that the bank advertisements were created

seemingly for the sake of advertising rather than for creating the market or serving the

customer satisfactorily. There is lack of professionalism in bark advertising and

marketing. Suggestions were made to give stress on 'positioning the bank' rather than

on selling the products afier identification and prediction of customer requirements.2"

Image Building

K m Vysya Bank (1989) undertook a study on the image of the bank. The

study disclosed that the success of bank marketing depends on building a bank image

in the minds of the customers. In a market where product competition does not exist,

it is the bank image that will survive.27

62 ---- Review of Literature

Leonard and Spencer (1991) studied the importance of bank image as a

competitive strategy for increasing customer traffic flow. Preference for banks

amongst students as provider of financial services; greater c'onfidence in large-

medium -sized banks, importance of courtesy by personnel, competitive deposit rates

and loan availability were the key findings,28

Henry A Laskey, Bruce Seaton and J A F Nicholls (1992) evaluated the

effectiveness of alternate forms of bank advertising, the alternative forms of which

differ in terms of main message strategy and overall method of presentation

(structure). The study exarn~ned the relative effects of verbal only advertisements

compared to those that combine both pictures and words. The differences between

informational and transfonnaticrnal strategies were also studied, by including both

male and female models while studying transformational strategies. Results suggest

that advertisements. whlcli include both verbal and pictorial components were

superior and informational strategy is more effective for bank advertising than a

transformational strategy.'"

Marketing Communication

Andersen P.H (200 1) studied marketing communication using three classical

rhetorical elements, ancl found communication process as developing an

understanding of the communicator's intentions and qualities (ethos) and the

communication climate (pathos). both o i which are necessary for engaging in

constructive dialogues with customers (logos). On this basis, the study outlined a

model for integrating practiccs of marketing communication with relationship

63 Review of Literature

building and illustrated the model using a case study from a Danish bank as a

reflective d e ~ i c e . ~ ' '

Marketing Techniques

Research on Marketing techniques by Hussain, Farhat Dr (1987) found that in

particular, the banks should apply marketing techniques in the following areas: i)

Identifying the present and future needs of the market for services both for deposits

and lending, ii) Selecting the markets the banks want to serve and identifying the

needs of the target group, iii) Setting up of targets for existing services and

introducing new services, iv) P'zrsuading customers to use the services at the profit to

the bank, v) Deciding best locations for new branches, and vi) Expanding

internationally."

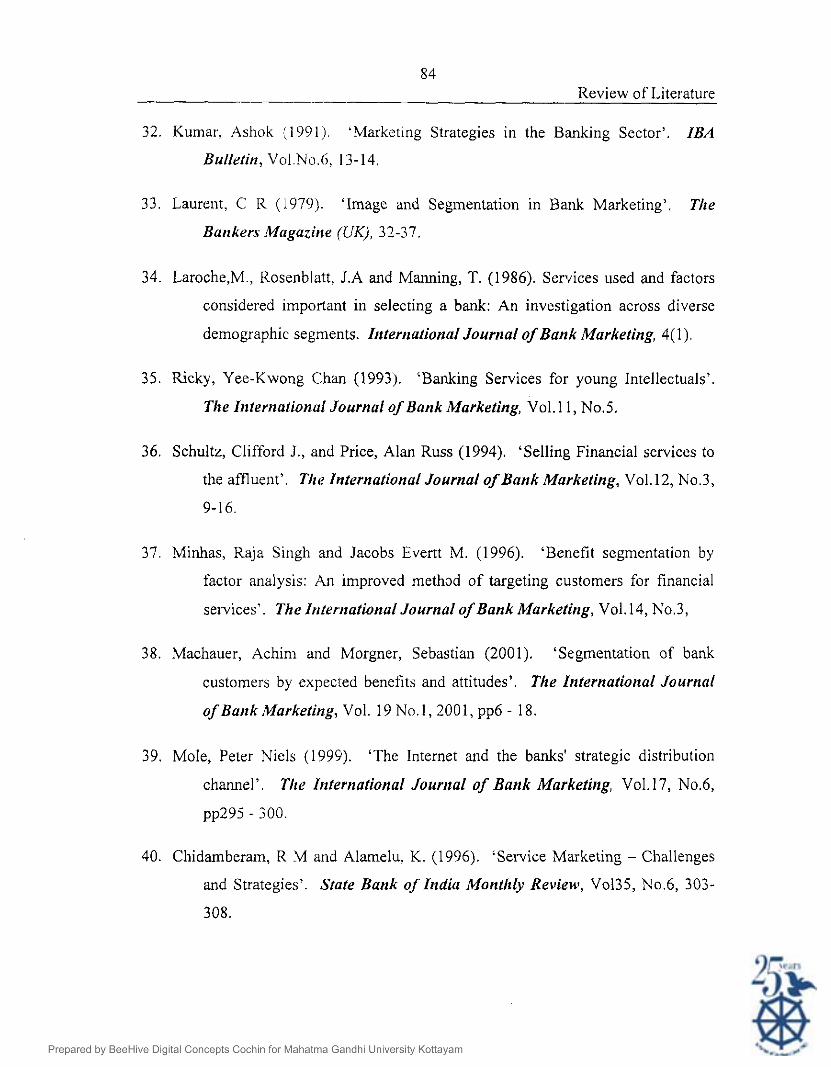

Ashok Kumar (1991) made an attempt to review and assess the extent of

application of marketing concepts and techniques in the banking sector. It has been

recommended that while folmulating marketing strategy, a bank should focus

attention on consumer sovereignty, on the attitude, responsiveness and personal skills

of their staff, on revitalizing the marketing department, on top management support to

the marketing department, and on participation of marketing personnel in key bank

decisions. Efforts should be made by the banks to understand and estimate the attitude

and perceptions of their customers as accurately as possible to enable them to plan the

market segments and design service offerings to suit their customer^.^'

64

-- Review of Literature

Market Segmentation

The real need of market segmentation was investigated by Laurent (1979)

employing a factor analysis centered around five banks that differed from each other

on seven main attributes: friendliness, quality of service, community spirit,

modernness of facilities, convenience, range of services and ownership. The main

findings revealed that on thc basis of pcrceptions of the overall image of the five

banks relative to each other, there existed three distinct market segments:

convenience, service, and staff friendliness -oriented segments.33

Laroche, Rosenblatt k Manning ( 1 986) studied diverse denlographic segments

to find the services used and factors considered important in selecting a bank. Key

findings included importance of location convenience, speed of service, competence

and friendliness of bank persontlel.34

Ricky Yee-Kwong Chan (1993) conducted a study on the banking behaviour

of college students that confirmed several findings from western countries like

limited banking demand of students, popularity of split banking in account ownership,

price consciousness of students, and importance of locational convenience and on-

campus promotion. Suggests th,at in order to turn this segment into a lucrative one,

bankers need to adopt a long-tern1 perspective and place more emphasis on service

quality and promoting tht: concept of "one-stop banking".3"

In a study by Clifford .I Schultz and Russ Alan Prince (1994) the factors that

predict the successful sale of financial services to affluent investors were gone into,

by collecting data using a nc\v set of scales that measure traits, selling strategies, and

65 Review of Literature

compliance gaining tactics. Results suggest that effective relationship managers to sell

the services of financial service institutions to various; geographically diverse,

affluent investors 11sc these tactics called .in~otainment'.~"

Raj Singh Minhas arid Everett M Jacobs (1996) used benefit segmentation by

factor analysis group customers in relation to their particular attitudes and behaviour

instead of geographic, demographic, socio-economic, and psychological

characteristics to segment the market for financial services. The study identified eight

benefits, in order of their popularity as personal service, investment, limited banking,

accessible cash, cash card, advice, money management, and full banking.37

Achim Machauer and Sebastian Morgner (2001) studied the use of

segmentation by demographic factors in bank marketing and found that the

correlation of such factors with the needs of customers is often weak. Finding is that

segmentation by expected benefits and attitudes could enhance a bank's ability to

address the conflict between individual service and cost-saving standardi~ation.'~

Niels Peter Mols (19951) in his study found that the bank customers may be

divided into an Internet banking segment and a Branch banking segment and that the

former is growing and thc latter is declining, necessitating the development of

technology in bank

Technology

In their study 'Services Marketing - Challenges and Strategies',

Dr.Chidambaram and b1s.K. /\.lameleu (1996) suggested that banks should become

technology friendly By investing in technology a bank can carve a niche for itself.

Well-furnished preinises are a must for the satisfaction of both employees and

66 Review of Literature

customers. Professionalized. well-trained and motivated employees will improve the

marketability of a bank.'"

Gaston Leblanc (1 990) studied customer motivations towar~is the use and non-

use of an Automated Teller Machine (ATM) customers of a financial institution. An

analysis of results baseti on dcmographic variables revealed significant differences

between users and nonusers in terms of education only. Results also show that

convenient accessibility of a financial institution and avoidance of waiting lines is the

principal reasons for using the automated teller.41

Robert Rugimbana and Philip Iversen's study (1994) was to determine the

association between consumer ATM usage patterns and their perceptions of ATM

attributes by identifying those variables that distinguish users and non-users. The

results based on a survey of 630 retail banking consumers from two separate

Australian banking institutions suggest that successful marketing strategies must

focus on the most important attributes of ATMs as well as identify different user

groups and develop strategies to maximize their patronage.42

Mathew Joseph, Cindy McClure and Beatriz Joseph (1999) explored the use of

technology in the de1iver.y of banking services as it is being employed to reduce costs

and eliminate uncertainties. Results indicated that consumers have perceptual

problems with some aspects of electronic banking.43

Mark R Nclson (1999) studied the trends and patterns surrounding the

interface between the market~ng and information services functions within the

financial services industry It was found that many banks lack alignment or

integration between thelr marketing and information services f~~nctions. In~proving

67 Review of Literature

this cross-functional interfa1:e may lead to more effective use of information

technology to support the marketing f~tnction in many banks.44

The study by Ali Yakhlef (2001) found that as more and more of the

transaction processing load is taken over by technology, banks are concentrating on

strengthening their marketing approach and re-inventing their business model.

Traditional bank branches, with an infrastructure supporting transaction processing,

were being transformcd into an open-space interface within which bank experts

engage intimately with their customers, delivering specialized, advisory services with

more focus on retail banking.4"

Retail Banking

Bill Stephenson and Julia Kiely (1991) researched into the key issues facing

banks in order to become better at selling in the personal banking market. The results

indicate that the radical change in management style, training, nlotivation and

recognition of branch sales personnel is called for. Developing a true sales culture

requires major alterations to management structure and style, and is most likely to be

successfUlly achieved by 'top-down' target setting based on corporate business

objective^.^^

James F Devlin (1995) studied the developments in the distribution of retail

banking services in the UK, using the case study of First Direct, a subsidiary of

Midland Bank that successfully introduced telephone-banking service. It was found

that in an increasingly competitive and dcregulated environment, superior distribution

strategies concerned with how to conlmunicate with, and deliver products to the

68 Review of Literature

consumer could provide institutions with significant competitive advantage in the

marketplace."

Study by I-iughes (1969) had revealed that banks used different benchmarks

for measuring the degree of success of a branch marketing strategy - dollar volume of

deposits, market share of deposits, the number of depositors arid the share of the

depositors.'*

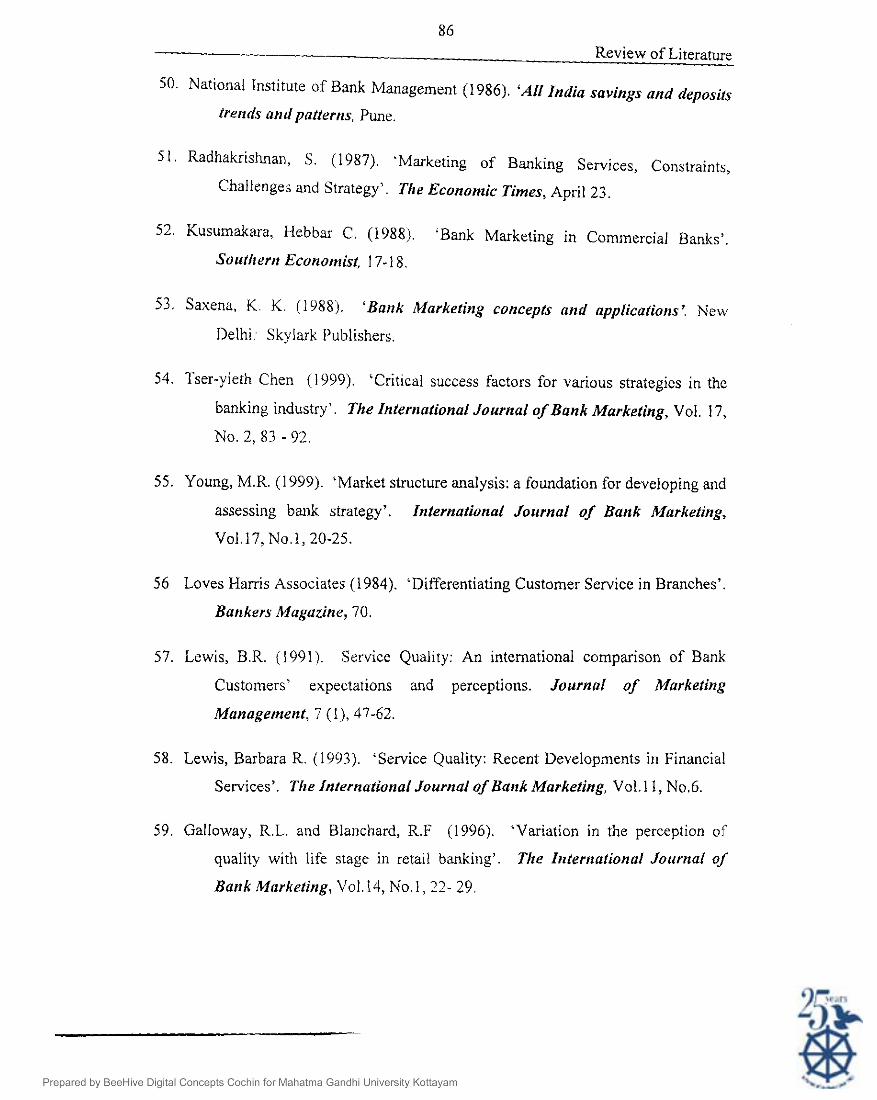

Ravisankar 'T S (1985) in a study on 'Marketing Strategies and Planning for

Business Growth in Banks' says that the marketing plan for banking services should

be supported by appropriate marketing strategies. He suggests that marketing strategy

for banks must be oriented towards customers-current and potential.49

NIBM (1986) conducted a large-scale survey to study the behaviour of

households and to develop appropriate marketing strategies for deposit mobilization

and found that banking is largely a habit of literate Indians. Majority of the non-bank

savers is illiterates. The level of awareness of bank deposit schemes is quite low

among rural non-bank savers. The study stresses the need for adopting appropriate

marketing strategies to penetrate ~ntapped market for

Radhakrishnan ( 1 987) conducted a study on 'Marketing of Banking Services,

Constraints, Challenges and Strategy' and found that mixed banking, complaints from

customers about bank char.ges, competition from Non-banking financial companies

and growing investment consciousness of the public are some of the impediments to

bank marketing. It is suggested that the Branch Manager can design appropriate

69 -- Review of Literature

marketing strategy tllrough identification of customer needs and service efficiency

with appropriate differentiation by understanding customer behaviour."

Kusumakara 'Iebbar (1988) studied marketing strategies of banks aimed at

inculcating the habit of thrifl among the people. The suggestion is that keeping the

rural branchcs open on Surrdays can augment savings. Direct marketing is also

suggested to reduce waiting time and enhance customer satisfaction. Rude behaviour

of the employees, suspicious looks of the staff, vague knowledge of the products,

undynamic promotional methods etc., may hamper the banking business in rural

areas."

Saxena (1988) has in his study found that it was a mistaken belief that every

other instrument of saving available in the market competes with: bank deposits. As

each saving instrument aims at satisfying one or the other motive for saving and is

different in nature, instruments of one group are not likely to affect others. The study

concludes that banks should adopt aggressive marketing strategies to identify new

potential customers in order to maintain their share in the savings of the household

sector. 53

Tser-yieth Chen (1 999) aj~plied the Critical Success Factor (CSF) approach to

identify the appropriate CSFs underlying the strategies employed in banks. The result

of a factor analysis suggcstcd four con~posite CSFs: bank operation management

ability, developing bank trademarks ability. bank marketing ability, and financial

market management ability s4

Young (1999) utilizing perceptual mapping to assist in analyzing market

structure and in developing strategies, tried to examine how consumers perceive

70 Review of Literature

alternative banks 011 important attributes. It was found that market structure analysis

could assist the bank 111 identifying potential opportunities in differentiation and in

assessing the viability of lo\\. cost as a competitive

Quality of Service

Lovis Harris Associates (1984) conducted a national consumer survey to

determine what characteristics are most important in bank selection in UK. It revealed

that the quality of customer service was one of the three top issues and the consumers

ranked the quality of their bank relationships as even more important than the fees

charged for services '' In the study by Lewis ( 1 991), an international comparison of bank customer's

expectations and perceptions of service quality were made. It was found that in spite

of the existence of very high expectations of service quality and high perception of

service received, gaps did exist."

Barbara R Lcwis (1993) studied the service quality initiatives in financial

services to find the determinants and measurement of quality. Attention was also

given to research applications, which focus on management, employee and customer

perspectives. The findings emphasizes the need for an integrated approach to scrvice

quality and the development of service quality measurement tools.58

Galloway and Blanchard (1996) studied the retail customer perceptions of

those factors which determine service quality and whether or not life stage affects

perceptions of quality. The study proposes a model based on the three dimensions of

process/outco~~~e, subjectrvei ob.jectlve and soft~hard.~'

71

--- Review of Literature

Worcester (1997) in his study found that banking in Britain has suffered a

crisis of identity in recent years due to falling standards of service. The study suggests

that marketing and image research studies should be given the same attention as the

monthly financial figures, should be treated with the same respect and should feed

into strategic decision making. The study identified five areas of activity for financial

institutions to focus, namely: strategic direction; legal threats to survival; capital

management; succession; and protection and promotion of the corporate reputation.6o

Customer Service

La Londe, Cooper and Noordewier (1988) found customer service as a

separate mix of elements and sees the logistics function as being subsumed within the

customer service activity. The result of this study shows the relative importance of

customer service contrasted with other elements of the marketing mix including

advertising, prornotio~~, and sales effort. Most respondents rated customer service

ahead of advertising. promotion and sales effort in terms of importance and ranked

third behind product and price '' The study by Biswas N 13hattacharpa (1991) concludes that to succeed in a

liberalized and deregulated market scenario bankers have to stress the maxim of

marketing that customers come first. Marketing management should cover the entire

organization and strategy rnust combine the various structures and functions of an

organization to deliver satisfaction to the customer on an ongoing basis. 'Cross

culture Marketing' will require the induction of skills and infusion of marketing

knowledge through training and development. Since only satisfied employees can

72 Review of Literature

give satisfactory customer service, strategic human resource management will be very

important."

Robert Johnston's !1997) study found that certain actions, such as increasing

the speed of processing information and customers, are likely lo have an important

affect in tenns of delighting customers. However other activities, such as improving

the reliability of equipment, will lessen dissatisfaction rather than delight customers.

Suggests that it is more important to ensure that the dissatisfiers are dealt with before

the satisfiers and emphasizes the need for genuine commitment and attentiveness by

front-line staff.63

Dan Sarel and Howard Mannorstein (1998) examined the effects of perceived

employee action and customer prior experience, on reactions to service delays by

conducting a field study of customers experiencing actual delays in a major retail

bank. The findings indicate that events and actions taking place prior to, during and

after the delay, affect consumer response. 64

The key insights of a multi- year, multi -sector stream of research on customer

service by Parasuraman suggest that the scope of marketing should be broadened to

include the delivery of customer service as an integral component and that a judicious

blending of conventional marketing and superior customer service is the best recipe

55 for sustained market success.

Eapen Varghese (2001) in his study attempted to assess the customer service

rendered by commercial banks in Kerala. I t was found that there is no difference

between the services rendered by public sector banks and private sector banks.66

73 Review of Literature

Quick Service

Kamath (1979) conducted a study on the marketing of bank service and

customer service with special reference to the customers of the branches of Syndicate

Bank in Bombay City. The study concluded that quick and better services offered by

a bank would be thc most important variable in attracting and retaining a bank

customer. Price and I'lacc nlixelj have less relevance in the marketing mix of banking

products and ~erv ices . '~

Ranade M P (1985) in his study on 'Marketing of deposits and allied services

to non-resident -customers opinion' concluded that quick service is the major factor

influencing a Non Resident Indian's (NRI) selection of a bank. Existing deposit

schemes alone does not satisfy the ~ ~ 1 s . ~ '

Customer Satisfaction

Luiz Moutinho and Douglas T Brownlie (1989) explored the nature and

direction of the satisfactions that are delivered to consumers of bank services. I t was

revealed that respondents had high levels of satisfaction with regard to the location

and accessibility of branches and ATMs, and acceptance of the current levels of

banking fees; but expressed some caution in their evaluation of new and improved

service. 69

A study by Rosenberg and Czpeil (1984) claims that it is between five to ten

times as expensive to win a ne\v customer than i t is to retain an existing one.'"

Research by Susan Fournier and David Glen Mick (1999) revealed that

customer satisfaction is an active, dynamic process that evolves over time and should

74 Review of Literature

not be considered only fr0n.l the perspective of a single transaction. Findings suggest

that the (dis) satisfaction of other relevant household members often contribute to an

individual customer's (dis) ~atisfaction.~'

Customer Loyalty

Gerrard and Cunningham (2000) has developed a model of bank switching

that contained six switchi:ng incidents. The study also investigated if certain

demographic characteristics of Singapore's graduates could be used to distinguish

those who have switched ba:nks from their counterparts. The results showed that the

types of incident that most often influenced bank switching were 'inconvenience',

followed by 'service failures' and 'pricing'. The demographic characteristics that

were subject to testing, namely gender, age, salary and racial group, showed no

significant differences '' Relationship Marketing

Jain, Pinson& Malhotra (1987) studied the customer loyalty in retail banking

and found that customer loyalty is a useful construct. Economic rationale swayed

bank non-loyal segment whereas the bank loyal segment placed greater emphasis on

human aspects of b a ~ l k l n ~ . ~ ~

Meidan and bloutinho (1988) conducted an attitudinal research on bank

customer perceptions and loyalty. The key findings were that banks should develop

ATM usage; financial institutions should review basic banking services and that

customer loyalty is a function of more than one ~ar iable . '~

Bhattacharya and Ghose (1989) studied the nature of marketing of banking

services in the 90s, given the challenges confronting the commercial banking. The

75 Review of Literature

study revealed that the 90s saw an aggressive marketing approach in rural and semi-

urban sectors anticipating. identifying, reciprocating and satisfying customers' needs

effectively, efficiently and profitably and thereby improve .the banker customer

r e l a t i o n ~ h i ~ . ' ~

Reichheld and Sasser (1990) in their study observed a cross-industry trend and

have found sales and profirs per account rise along with the longevity of the

relationship. And therefore i t is suggested that organizations should attempt to

improve their customer retention efforts.76

The study by Jean Perien, Pierre Fillatrault and Line Ricard (1992) identified

the major problen~s raised by the implementation of an effective relationship

approach. Competitive pressures as well as the search for fee based incomes; mainly

derived from cross selling, have forced commercial financial institutions to redefine

their marketing strategies and I:O focus on 'relationship marketing'. From this critical

analysis, it is concluded that relationship banking is a major corporate issue, not the

sole responsibility of front-line people nlarketing and strategic issues are merging7'

Christine Ennew (1996) examined the extent to which participation in the

banking relationship occurs and the implications of this for quality of service. It was

found that the development of effective customer relationships is the key element of

marketing strategies in the service sector. The ability of an organization to develop

and maintain a relationship with its customers will be dependent on their willingness

to participate. For participation to be worthwhile, customers must perceive that i t

yields benefits that are greater than those which accrue from n ~ n - ~ a r t i c i ~ a t i o n . ~ ~

76 Review of Literature

The study by James Barnes and Darrin Howlett (1998) offer a consumer-

focused approach to defining the principles of relationship marketing, and examine

the conditions under which service marketers can expect to form relationship with

their customers. The research reveals that the affective dimensions of the service

encounter best predict quality relationships.79

Dwayne Gremler, Kevin Gwinner and Stephen Brown (2001), using the four

dimensions of interpersonal. bonds viz., trust, care, rapport, and familiarity, found that

as a customer's trust increases in a specific employee or employees, positive word of

mouth (WOM) cotnrnunical.ion about the organization also increases. Such a trust is a

consequence ot' three other interpersonal relationship dimensions: a personal

connection between employees and customers, care displayed by employees, and

employee familiarity with c ~ s t o r n e r s . ~ ~

Internal Marketing

Research by Singh (1985) on Bank Marketing found that a good number of

banks in India had taken steps to make use of internal marketing for purposes of

raising the customer service consciousness, and business mindedness on the part of

their employees.8'

The study by Scott Kelley (1 990) considered the customer orientation of the

customer contact personnel in four banks and found that specifically the relationships

between employee motivation, satisfaction, and role clarity are all directly related to

customer orientation. However when these variables are considered together,

motivation and role clarity appear to have the greatest impact on the customer

orientation of employees.n2

77 Review of Literature

A pilot study in internal marketing by Helman and Payne (1992) suggested that

formalized internal marketing programmes are still fairly rare. Other findings were:

Internal marketing is generally not a discrete activity, but is implicit in quality

initiatives. customer :service programmes and broader business strategies.

* Internal Marketing comprises structured activities accompanied by a range of

less formal ud hoc initiatives

Communication is critical to successful internal marketing.

Internal n-rarketing performs a critical role in competitive differentiation.

Internal Marketing has an important role to play in reducing conflict between

the functional areas ofthe organization.

Internal Marketing is ;an experiential process, leading employees to form their

own conclusions.

Internal marketing is evolutionary: it involves the s l o ~ f erosion of barriers

between departments ;md functions. It has an important role in helping with

the balancing of' marketing and operations.

Internal Marketing is used to facilitate a spirit of innovation.

Internal marketing is more successful when there is commitment at the highest

level, when all employees cooperate, and an open management style

prevai~s.83

The empirical study on internal service encounter satisfaction by Dwayne

Gremler, Mary Jo Bitner arid Kenneth Evans (1995) by using the critical incident

methodology found that internal customers are similar to external customers in that,

7 8

- Review of Literature

with a few interesting differences, the same types of events and behaviours

distinguish satisfactory and dissatisfactory incidents in both internal and external

encounters. Introducing the concept of the 'internal service encounter', i t was found

that an internal custon~er's (i.e. employee's) satisfaction with a service firm could be

significantly influenced by service encounters experienced with internal service

providers.84

Christo Boshoff and Madele Tait (1996) studied the internal marketing

concept based on the belief that a firm's intemal market'employees can be motivated

to strive for customer consciousness, market orientation and sales mindedness through

the application of accepted. external marketing approaches and principles. This study

reveals that these objectives could be achieved by marketing, among others, the

service firm's goals, objectives and values to frontline employees.85

Study by Donald J Shemweli and Ugur Yavas(1998), found that establishing a

sales culture is very important to a bank's success. The study recommends strategies

to increase sales per employee, improve cross selling to high-value customers, and

enable banks to focus on solving customer needs to the mutual benefit of both parties.

It requires providing consistently excellent service quality and sales and customer

interaction training for all boundary-spanning employees.s6

The study by Adrian Sargeant and Saadia Asif (1998) was to explore the

relevance of the concept of internal marketing to the financial service arena and the

extent to which it may be possible to utilize internal marketing as a means of reducing

the service gaps. The research found no evidence that internal marketing as a concept

is as yet fully understood by management, either at the junior, or more senior levels,

79 Review of Literature

within each organization and that there is a clear need to adopt a more strategic

perspective on internal inarlceting activity to reduce the senice gaps and to compete

effectively in a market increasingly driven by the quality of the service demanded?'

Mark Durkin and I-Iadyn Bennet (1999) conducted research among employees

of a large retail bank and found three different types of employee commitment

(internalized commitment, identification commitment and compliance commitment).

It was found that high levels of internalized commitment are essential for the

successful implementation of the emerging relationship marketing strategy.

Employees show unexpectedly low levels of internalized commitment, coupled with

higher than expected levels a f compliance commitment. Combined with respondents

low intention to leave, the case bank seems to have many employees who, while

reluctant to leave, seem at hest unable, and at worst unwilling to embrace new change

initiatives and who consequently show low levels of identification with the values of

the organization."

Research by Lindgreen and Crawford (1999) suggests that for employee

empowerment to work there has to be investment in proper customer focused staff

training to enhance such different skills as industry knowledge, customer service

communications, presentation and t e a m ~ o r k . ~ "

Need for Study

Almost all studies reviewed above highlight that significant studies have been

made in various parts of the world on the pivotal role of various aspects of marketing

of financial services. However, there is a dearth of research studies conducted to

80 Review of Literature

evaluate the marketing strategies of financial services by commercial banks,

especially in the context of financial sector reforms, which has brought paradigm shift

in the way financial services are marketed by commercial barks. In this context, a

systematic study taking the premier bank of Kerala - State Bank of Travancore - as a

case study assumes relevance and deserves deeper academic attention

8 1 Review of Literature

REFERENCES

1. William, George K and B'arksdale, Hiran C. (1974). 'Marketing Activities in the

Service Industries'. .lourrial of Marketing, 65-70.

2. Bessom, Richard M., and Donald, Jackson Jr. D. (1975). 'Service Retailing A

strategic Marketing Approach'. Journal of Retailing, 75-84.

F 3. Delvin, James F (2000). 'Adding value to retail financial services'. Tlze

International .Jo~rrtzal of Bank Marketing, Vol.18. No. 5 , 222 - p232

4. Smith, Anne M (1990). 'Quality Aspects of Services Marketing'. Marketing

Ifztelligertce & Planrring, Vo1.8, No.6

5. Sankaran M (1999). 'Creating and Sustaining competitive advantage of

Financial Service Industry in India'. Indian Management, 83-89.

6. Watkins, Trevor (1989). 'Bank Marketing: Current Issues, Trends and

Developments'. Marketing Intelligence & Planning, Vo1.7, No.9

7. Mackay, Maio Marisa (2001). 'Application of brand equity measures in service

markets'. Jo~trrzal of Services Marketing, Vo1.15, No.3,2 10-221.

8. Berry L.L., Kehoc W.J.. and Lindgreen, J.H, Jr. (1980). 'How Bank Marketers

View Their Jobs'. Tlze Bnnkers'Magazine (USA), Vo1.163, No.6 35-40.

9. Nair T G (1992). 'Ncw dimensions in Marketing'. Financialfipress, 7.

10. Geiger, H (1975). 'Standard Surveys for Analysing Local Bank Competition'.

In 'The Use of Market Research in Financial Fields', ESOMAR, 85-95.

11 . Akbar, Syed Asad (1990). 'Bank Marketing - Some Issues'. JOB MNR, Vo1.4

No. 12,20-22.

82

-- Review of Literature

12. Lewis, B.R and Birmingham, G.H (1991). The youth Market for financial

services. International Jourtzal ofBank Marketing, 9(2), 3-1 1.

13. Boyd, W.L., Leonard, M and White, C. (1994). Custonler preferences for

Financ~al Serv~ces: An analysis'. International Journal of Bank

Marketing, 12(1), 0- 15.

14. Rajagopala Nair (1994). 'Rural Bank Marketing in Kerala'. Unpublished

Doctoral Dissertation, University of Kerala.

15. Huu Phuong Ta; Kar Yin Har (2000). 'A study of bank selection decisions in

Singapore using the Analytical Hierarchy Process'. The International

Journal of Bank Marketing, Vol. 18 No. 4, 170 - 180.

16. National Institute of Bank Management (1969). 'Deposit Mobilisntion'.

Bombay.

17. Rossier J.A. (1973). 'The Coming Crisis in Bank Management'. Tlze Bankers'

Magazine, 7-9 and 53-57.

18. Meidan A (1976). 'Branch Manager's Attitude on Bank Objectives and

Operations'. Procee'dings of the European Academy of' Advanced Research

in Marketing Conference, France: Insend, 215-228.

19. Laursen, Ron, McTavish, Ron (1994). 'Is Workplace Banking Feasible?' Tlze

International Journal ofBarlk Marketing, Vo1.12 No.2, 3 - 14.

20. Turnbull, Peter h. (198:2). 'The Role of the Branch Bank Manager in the

Marketing of Bank Services'. Europemz Journal of Marketing, Vol. 16 No.

3, 31 - 36.

21. Preston R.H, Dwyer I:.II and Rudelius 91978). 'The Effectiveness of Bank

Premiums'. Journal of Marketing, Vo1.42, No.3, pp 91-96.

83 Review of Literature

22. Chidambram R M. (1994). 'Promotional Mix for Bank Marketing'. IBA Bulletin, Vol. 16, No.3, 24-26.

23. Crane, F.G. (1990). 'The need for Corporate Advertising in the Financial

Services Industry: a Case Study Illustration'. JourrtaI of Services

Marketing, Vo1.4, No.2, 1990.

24. Rayb~~rn L.G (1978). 'Cost Standards for Bank Advertising'. The Bankers'

Magazine (USA). 'Vo1.161, No.4, 33-38.

25. Subba Rao, P. (1982). 'Commercial banks and deposit mobilization - A survey'.

Prujnan, Vol XI, Mo.3.

26. Singh, J. D. (1983). 'Bank advertising in India -1971-1980'. Prajnan, Vol XI],

No.4.

27. Karur Vysya Bank Ltd. (1989). 'Study on the image ofthe Bank'

28. Leonard, M and Spencer, A. (1991). The Importance of Image as a Competitive

Strategy: An exploratory study in Commercial Banks. International

Journal ofBunk Marketing, 9 (4), 25-29.

29. Laskey, Henry A., Seaton, Bruce and Nichools, J.A.F. (1992). 'Strategy and

Structure in Hank Advertising: An Empirical Test'. Tlte Internatiotral

Journal of Bank Marketing, Vol. 10 No. 3.

30. Andersen, P.H. (2001:1. 'Relationship developmenr and marketing

communication: an integrative model'. Tlte Journal of Business and

Industrial Marketing, Vo1.16, No.3, 167-1 83.

31. Hussain, Farhat Dr (1987). 'Public Sector Commercial Bunking in India - Developntenl - Conslraints - Recent trends'. New Delhi: Deep & Deep

publications.

84 Review of Literature

32. Kumar, Ashok ( 1 99 1 :I. 'Marketing Strategies in the Banking Sector'. IBA

Bulletin, Vol.No.6. 13-14.

33. Laurent, C R (1979). 'Image and Segmentation in Bank Marketing'. Tlze

Bankers Magazine (UK), 32-37.

34. Laroche,M., Rosenblatt, J.A and Manning, T. (1986). Services used and factors

considered important in selecting a bank: An investigation across diverse

demographic segments. InterrzationaI Journal of Bank Marketing, 4(1).

35. Ricky, Yee-Kwong Chan (1993). 'Banking Services for young Intellectuals'.

Tlze International Journal of Bank Marketing, Vol.11, No.5.

36. Schultz, Clifford J., and Price, Alan Russ (1994). 'Selling Financial services to

the affluent'. Tlre International Journal of Bank Marketing, Vol. 12, No.3,

9-16.

37. Minhas, Raja Sirlgh and Jacobs Evertt M. (1996). 'Benefit segmentation by

factor analysis: An improved method of targeting customers for financial

services'. Tlze International Journal of Bank Marketing, Vo1.14, No.3,

38. Machauer, Achinl and Morgner, Sebastian (2001). 'Segmentation of bank

customers by expected benefits and attitudes'. The International Journal

of Bank Marketing, Vol. 19 No.1, 2001, pp6 - 18.

39. Mole, Peter Niels (1994). 'The Internet and the banks' strategic distribution

channel'. Tlze International Journal of Bank Marketing, Vo1.17, No.6,

pp295 - 300.

40. Chidamberam, R M and Alamelu, K. (1996). 'Service Marketing - Challenges

and Strategies'. State Bank of Indict Monthly Review, Vo135, No.6, 303-

308.

85 Review of Literature

4 1 . Leblanc, Gaston ( 1990). 'Customer Motivations: Use and Non-use of Automated

Banking'. The I~rternational Journal of Bank Marketing, Vo1.8, No. 4.

42. Rugimbana, Robert and Iversen, Philip (1994). 'Perceived Attributes of A'TMs

and Their Markcting Implications'. Tlze International Journal of Bank

Marketing, Vol. 12, No. 2, 30 - 35.

43. Joseph, Mathew, McClure, Cindy and Joseph, Beatriz (1999). 'Service quality in

the banking sector: the impact of technology on service delivery'. The

International Journal ofBank Marketing, Vol. 17, No. 4, 182 - 193.

44. Nelson, Mark R. (1999). 'Bank marketing and information technology: a

historical analysis of the post-1970 period'. The International Journal of

Bank Marketing, Vo1.17, No.6, 265 - p274.

45. Yakhlef, Ali (200 I). 'Does the Internet compete with or complement bricks-and-

mortar bank branches?' International Journal of Retail & Distribution

Management, Vo1.29, No.6, 272 - p28 1.

46. Stephenson, Bill and Kiely, Julia (1991). 'Success in selling - The current

challenge in Banking'. Tlze International Journal of Bank Marketing,

Vo1.9, No.2.

47. Devlin, James I:. (1995). 'Technology and innovation in retail banking

distribution '. The International Journal of Bank Marketing, Vo1.13, No.4,

19 - 25.

48 Hughes, G D. (1 969). ' Tlre Boston Five Cents Savings Bank'. Research Paper,

Graduate School of Business, Harvard University, Boston.

49. Ravisankar T S (1985). 'IMarketing Strategies and Planning for Business Growth

in Banks'. SBZ Motrllrly Review, Vo1.16, No.2, 27-32.

86 -- Review of Literature

50. National Institute of Bank Management (1986). 'AN India savings and deposits

trends and patterns, Pune.

51. Radhakrishnal~, S. (1987). 'Marketing of Banking Services, Constraints,

Challenges and Strategy'. The Economic Times, April 23.

52. Kusumakara, tlebbar C. (1988). 'Bank Marketing in Commercial Banks'.

So~rfhern Econon~ist, 17-1 8.

53. Saxena, K . K . (1988). 'Bank Marketing concepts and applications'. New

Delhi: Skylark I'ublishers.

54. Tser-yieth Chen (1999). 'Critical success factors for various strategies in the

banking industry'. The International Journal ofBank Marketing, Vol. 17,

N O . 2. 8 3 - 92.

55. Young, M.R. (1999). 'Market structure analysis: a foundation for developing and

assessing bank strategy'. International Journal of Bank Marketing,

V01.17, No.1, 20-25.

56 Loves Harris Associates (1984). 'Differentiating Customer Service in Branches'.

Bankers Magudne, 70.

57. Lewis, B.R. (1991). Service Quality: An international comparison of Bank

Customers' expectations and perceptions. Journal of Marketing

Management, 7 (1). 4'7-62.

58. Lewis, Barbara R. (1993). 'Service Quality: Recent Developments in Financial

Services'. The International Journal of Bank Marketing, Vol.1 I, No.6.

59. Galloway, R.L. and Blanchard, R.F (1996). 'Variation in the perception of

quality with life stage in retail banking'. Tlre Itztert~ational Joi~rnal of

Bank Marketing, Vo1.14, No.l,22- 29.

87 -. Review of Literature

60. Worcester, R.M (1997). 'Managing the image of your bank: the glue that binds'.

The It~ternutior~al Journal of Bank Marketing, Vol. 15, No. 5, 146 - 152.

61. La, Londe B.J., (Zooper, M.C., and Noordewier, T.G. (1988). 'Customer Service:

A management perspective'. Council ofLogistics Management.

62. Bhattacharya, Biswas N. (1991). 'Marketing Management and Innovations in the

light of Liberalisation'. Prajnan, NIBM, Vo1.20, No.4,419-428.

63. Johnston, Robert (1997). 'Identifying the critical determinants of service quality

in retail banking: importance and effect'. Tlze International Journal of

Bank Marketing, Vo1.15, No. 3, 1997,pplll - 116.

64. Sarel, Dan and Marmorstein, Howard (1998). 'Managing the delayed service

encounter: the role of employee action and customer prior experience'.

Journal of Services Marketing, Vol.12, No. 3 , 195 - 208.

65. Parasuraman, A. (2000). 'Superior Customer Service and Marketing Excellence:

'Two sides of the same success Coin'. Vikalpa, Indian Institute of

Management, Ahmedabad, Vol.25 No.3.

66. Varghese, Eapen (2001). 'Marketing of Bank Services', Unpublished Doctoral

Thesis, Department of Commerce, University of Kerala.

67. Kamath, K M. (1979). 'Marketing of Banking services with special reference

to branches in Bombay of Syndicate Bank Customer service'. BMP thesis,

NIBM, Pune.

68. Ranade, M.P. (1985). 'Marketing of deposits and allied services to non-

residents'. BbIP thesis, NIBM, Pune.

69. Moutinho, Luiz and Brownlie, Douglas T. (1989). 'Customer Satisfaction with

Bank Services: A Multidimensional Space Analysis'. The International

Journal of Bank Marketing, Vo1.7, 1989.

8 8 -- Review of Literature

70. Rosenberg. L. I. and Czepiel, J.A. (1984). 'A marketing approach to customer

retention'. Joctrnal of Consumer Marketing, Vol 1, 1984, pp 45-5 1.

71. Fournier, Susan and bilick, Glen David (1999). 'Rediscovering Satisfaction'.

Journal of Marketing, 63, 5-23.

72. Gerrard, P . . Cunningham, J.B. (2000). "The bank switching behaviour of

Singapore's graduates '. Journal of Financial Services Marketing, Vo1.5,

No.2, 118-112(11).

73. Jain, A.K., Pinson,C., imd Malhotra,N.K. (1987). 'Customer loyaltjJ as a

construct in the marketing of bank services'. International Journal of Bank

marketing, 5(.3), I98'7,pp 49-72.

74. Meidan, A., and bloutinho, L (1988). Bank customers' perceptions and loyalty:

An attitudinal research. European Marketing Academy Proceedings, 472-

493.

75. Bhattacharya, Biswas N, and Ghose, B.K. (1989). Paper presented at flae

sikteetltf~ International Marketing Congress. New Delhi, 4-7.

76. Reichheld, F., and Sasser, W.E. Jr. ( I 990). 'Zero defections: Quality comes to

service'. Harvard Business Review, 105-1 1 1.

77. Perrien, Jean, Fillatrault, Pierre and Ricard, Line (1992). 'Relationship

Marketing and Commercial banking: A critical Analysis'. Tlre

International Jolotrrtial of Bank Marketi~tg, Vol.10, No.7.

78. Ennew, Christine 'I' (1996). 'Good and bad customers: the benefits of

participating in the banking relationship'. Tlte International Journal of

Bank Marketing, Voi. 14, No.2, 5 - 13.

89

-- Review of Literature

79. Barnes, Jaines G. and Howlett, Darrin M. (1988). .Predictors of equity in

relationships between financial services providers and retail customers'.

The Journczl oJ'Bank Marketing, Vo1.16, No. I . 1 5-23.

80. Gremler, Dwayne I)., Gwinner, Kevin P. and Brown, Stephen W. (2001).

'Generating positive word-of-mouth communication through customer-

employee relationships'. International Journal of Service Industry

Management, Vol. 12, No.l,44- p59.

81. Singh, J D. (1985). 'Bank Marketing in India'. International Journal of Bank

Marketing, 3(2), 1985,48-63.

82. Kelley, Scott W. (1990). 'Customer Orientation of Bank employees and culture'.

The International Journal of Bank Marketing, Vo1.8, No.6.

83. Helman, D., and Payne, A. (1992). Internal Marketing: Mytlt versus realify.

Cranfield School of Evlanagement Working Paper, Cranfield, SWP 5192.

84. Gremler, Dwayne D., Bitner, Jo Mary, Evans, Kenneth R. (1 995). 'The internal

service encounter'. Logistics Information Management, Vo1.8, No.4, 28 - p34.

85. Boshoff, Christo and Tait, Madele (1996). 'Quality perception in the Financial

services sector The potential impact of Internal Marketing'. International

Journal of Service Industry Management, Vo1.7, No.5,5-3 1.

86. Shemwell, Donald I., and Yavas, Ugur (1998). 'Seven best practices for creating

a sales culture: transitioning from an internally-focused, transaction-oriented

culture to a customer-focused, sales- oriented culture'. Tlte International

Journal of Bank Marketing, Vol. 16, No. 7,293 - p298.

90 Review of Literature

87. Sargeant, Adrian Asif, Saadia (1998). 'The strategic application of internal

marketing - an investigation of UK banking'. Tlze Internatio~zal Journal of

Bank Marketing, Vo1.16, No.2,66 -- p79.

88. Durkin, Mark and Bennet, Hadyn (1999). 'Employee con~n~itment in retail

banking: identifying and exploring hidden dangers'. Tlze International

Joiirnal of Bank Marketing, Vo1.17, No.3, 124-137.

89. Lindgreen, i\., and Crawford, I. (1999). 'Implementing, Monitoring and

Measuring a Programme of Relationship Marketing'. Marketing

Intelligence and Planning, Vo1.17, No.5,235.