The Immense Accumulation of Spectacles: Crisis Capitalism or Crisis Exceptionalism

Upload

independentCategory

view

1download

0

Finance 499: Undergraduate Research

Title: 2008 Subprime crisis

Opening-Aftermath of the crisis

The financial crisis that was brought into the limelight in

2008 was claimed to be the second worst crisis after the

1932 Great Depression. Lehman Brothers, the fourth largest

investment bank in the United States, was declared bankrupt,

and the government had to face the accusations of

encouraging “moral hazard” and bail out various institutions

that were considered as “too big to fail,” such as AIG.

Housing prices tanked and foreclosures rates went up

significantly. Consumers lost their confidence, credit

markets were frozen, banks were not willing to lend to each

other and the whole financial market and economic activities

were essentially brought to a halt. The Dow Jones

Industrial Average index fell from 14,000 points to 6,600 by

March 2009. The unemployment rate ratcheted up to 10.1% by

October 2009, the highest rate since 1983i. As of the time

this paper is written, the rate is hovering around 7.7%.

1

Despite the fall in unemployment, many skeptics opined that

it was primarily due to the increase in discouraged workers

or those who give up looking for a job. To increase

employment, the US real GDP has to increase. Typically after

a recession, the economy will grow at a rate of 4.2% per

annum, but after this recession, the US economy has been

growing at a rate of 2.2%. The 2008 financial crisis has

still its imprints, and it remains to be seen whether the US

can come out of the recession and start growing.

Overview of investigation:

What caused the crisis and who is to blame? The paper aims

to seek the answers to the two questions. The paper will

delineate that “intelligence hazard” and avaricious culture

in the banking industry, i.e. excessive risk exposure in

pursuit of higher returns and utilization of flawed

financial models/ standard ratings, the corrosive

relationships that have developed between the government and

Wall street, and the incompetence of the Federal Reserve

were the reasons that contributed to the financial meltdown.

2

The mechanism on how it happened:ii

In a traditional sense, a bank (lender) would conduct due

diligence before it lent money to a house buyer (borrower),

because the lender would have a stake in the loan, and a bad

debt did not reflect well on a lender’s financial

performance/balance sheet. The establishment of Fannie Mae

and Freddie Mae and the redlining regulation, however, gave

rise to a financial activity called securitization. Under

securitization, instead of getting the interest and partial

principal payment from the borrower over time, the lender

could now sell the right of the payment to an investment

bank, in return for a fee. In other words, the lender

transferred the risk of default to another buyer, the

investment bank. Since the lender did not need to bear the

default risk anymore but can get paid for the loan that it

made, it had less incentive to conduct due diligence on the

borrower’s ability to pay back what he borrowed. Lender

started to make loans to a homebuyer who had shady credit

score, or the subprime borrower. The investment bank which

3

bought the right of payment from the lender set up a special

entity for the collective right to get the payment, packaged

it into tranches called the CDO, and issued shares, called

the Mortgage backed securities (MBS) to the general public

who wanted high returns for their investment, and earned

handsomely for the selling of shares.

Government intervention in the housing market (as discussed

in the section “a brief look into the history) kept housing

prices high and thus everyone thought it was a good idea to

buy a house as an asset. The frenzy of borrowing and

securitization began.

To prevent exposure to credit risk, or the default on

interest and or principal payments by mortgage holders, the

investment bank bought a form of insurance, or CDS, from an

insurer, such as most notably, AIG. The bank would pay an

insurance premium to AIG to insure against credit risk. In

exchange, AIG promised to pay the investment bank if it

turned out that the borrower did default.

4

In the era of rising house prices, the structure looked

profitable and risk free. Everyone in the mortgage food

chain stood to benefit as long as the home buyer didn’t

default.

Housing prices began to decline in 2006 and increasing

defaults and foreclosures have caused banks to run out of

money and the inability of AIG to pay its promised payment

saw Lehman Brothers to declare bankruptcy and Bears Stern

and Merrill Lynch to be bought at pennies. The United States

was thus sent into a period of recession.

A brief look into the history: How banks came up with the

idea of securitization

To fully grasp the scenario of the financial crisis, I found

it important to go back to the 1930s to talk about the

establishment of Fannie and Freddie Mae. During that time,

the United States had just come out from the Great

Depression, and in 1939, President Franklin D. Roosevelt and

5

congress passed a bill to establish Fannie Mae to expand the

secondary mortgage market by securitizing mortgages in the

form of Mortgage backed securities. Fannie Mie and Freddie

Mae gave the implicit guarantee that they would buy the

mortgages from the lenders and thus enabled lenders to

provide more long term mortgages. The initial motivation

for securtization was to increase liquidity to the mortgage

market. The increased house prices and the guarantee

subsequently brazened the Wall Street risk takers for

extensive securitization. Here you are talking about

current day right? Not the period immediately post Great

Depression.

Fannie and Freddie were not( in the early stages of the

housing price run up) buying up subprime loans.

It is a recipe for disasters. In 2003, Fannie and Freddie

became the biggest mortgage companies in the United States,

holding mortgages for about 31million households, with

amount totaled up to 5.4 trillion dollars (70% of the

mortgage market).iii With these two companies acting as the

big brothers of the real estate, increasingly, the

6

requirements to buy a house became loose, and banks were

taking more risks in making risky house loans.

Originally it was nonbank lenders that were making risky

loans, not Fannie and Freddie which had higher standards for

securitization.

The continued government intervention in real estate through

Fannie and Freddie by injecting capital also created a

housing bubble that kept propping up housing prices without

the break to return to a “balance point.” When it started to

in 2006, the bubble burst.

The banking system: Why banks could not recover from shock

Banks faced bankruptcy during the financial crisis due to

the following main reasons: Intelligence hazard and Wall

Street’s greed. Banks took too much risks with models that

were flawed (were the models flawed or was it the data that

the models were using to estimate VAR, etc flawed?), such as

7

the Value at Risk model (VAR), which justified higher

leverage for higher earnings (Are you saying that the

earnings that were estimated using these models ended up

being too ooptimistic?) and underestimated correlation and

volatility, thus were lacking of equity buffer. The use of

RAROC on tranches too enabled high leverage without taking

into account the default of tranches, which although were

given AAA ratings, worked like a Ponzi scheme.

Wall Street’s greed also contributed to banks being too

short funded with an extreme duration gap , and thus a big

decrease in the value of the assets during the meltdown

Explain better. Greed too led to the misleading and

blatantly wrong ratings from the rating agencies. Avarice

was at play and rationale failed to stop the frenzy.

Banks have been using VAR to

calculate the equity buffer, or the

capital that a bank needed to withstand a change in the

maximum interest rate (the change was denoted in basis

8

VAR=( -D.V.n. √N. σ)/ (1+r)

D: duration, V: value,

n: Standard deviation,

points). Under the international regulation, to be in the

99% percentile, or to sustain only a 1% chance of bankruptcy

the next business days, for 10 days, a bank must adjust the

standard deviation, or n, to 2.33, and N, to 10, and then

come up with the VAR as an equity buffer.

VAR had not been a reliable modeliv. UBS, reported 50 VAR

exceptions for 2008 and 29 for 2007. At the 99% confidence

level chosen, there should have only been about 2.5

exceptions per year. Credit Suisse experienced 25 and nine

VAR exceptions in 2008 and 2007, respectively, also at 99%

confidence level. The model might be a decent one to use

during a calm financial period and gave banks lots of

earnings due to the low equity required, but the model

proved to be disastrous for banks in 2008, a period of wild

volatility. So isn’t this saying that the data they were

using to estimate VAR values came from periods with adverse

events that were not sizable?

9

One of the shortcomings of the model was that it calculated

the equity buffer solely by looking at past events. The

financial instruments and derivatives that were the

culprits, such as the CDOs and CDS, were new creations of

Wall Street, and thus there was no historical data available

on the behaviors of these instruments. Lacking of this

crucial information meant that banks were not able to

capture the correlation of the movements of the different

assets. It turned out that the correlation between the

various asset classes was remarkably high, and together with

the high volatility in interest rate in the year 2008, the

risk exposure of banks went up a notch. VAR of banks went

up accordingly by a significant amount, but it was too

sudden and too late for banks to have enough equity buffer.

Banks were distressed.

At this point, it is worth mentioning that the decrease in

bank’s asset value, apart from banks were being too short

funded, was exacerbated by the default of the mortgages

(assets). Banks were using the Risk-adjusted return on

10

capital (RAROC) framework to calculate the profitability of

its tranches, which were rated AAA by rating agencies, and

the scenario backfired.

RAROC was introduced in the 1970s by Bankers Trust. It

enabled banks to compete with commercial papers due to fewer

capital requirements (unclear-I don’t understand the

connection to commercial paper are you saying the model was

first used to evaluate RAROC on commercial paper which is a

short term debt instrument issued by credit worthy firms)

but should only be used to make loans to good standing

borrowers since RAROC did not take into account default

risk. The era of Great Moderation in the 1980s saw the

volatility index (VIX) and overall risk go down. There was

a sense of complacency in the market, and banks started to

take on more risks by upping their leverage. RAROC thus

began to be used and seemed to cause no major problems.

Using RAROC and VAR, the two flawed models to evaluate risky

and new instruments, have enabled banks to lever up. Banks’

11

leverage ratio was able to go up to a dangerous level. The

financial crisis saw Freddie Mae leveraged 40 to 1, while

Bears Stern was 33 to 1, which means it had only $3 equity

for every $100 asset. Intelligence hazard implied that Wall

Street used the models knowing the potential risk but did

not stop due to high returns.

Aside from not having enough equity as buffer, greed led to

banks’ great loss on their asset value. It has been a

tradition for banks to be the maturity intermediary, and in

the years leading to the financial crisis, banks had been

actively borrowing short term monies (deposit, or liability)

to fund long term assets due to the prospect of great money

earning potential in the mortgage market. The duration gap

increased and the extreme short funding situation put banks

at high risk of losing asset value when interest rate

increases.

When LDL < ADA , an increase in

the interest rate would force a bank to pay higher interest

12

Duration Gap, ΔV: (LDL/1+rL)-(ADA/1+rA) * Δrf

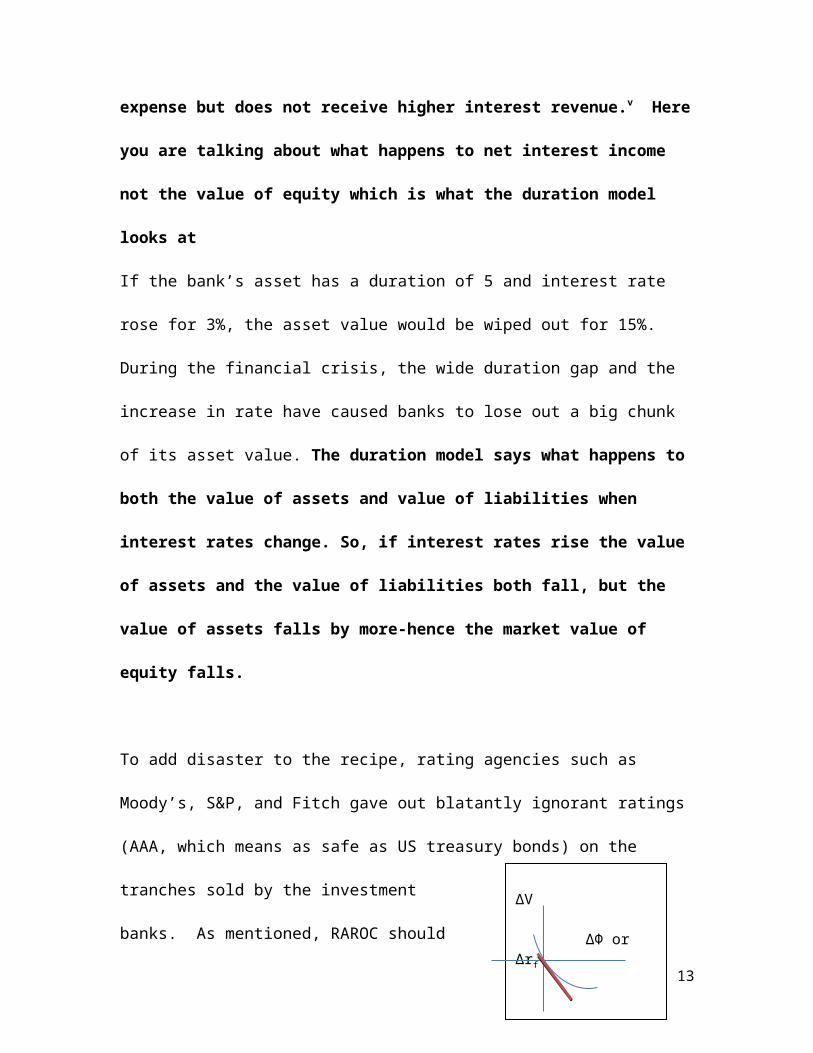

expense but does not receive higher interest revenue.v Here

you are talking about what happens to net interest income

not the value of equity which is what the duration model

looks at

If the bank’s asset has a duration of 5 and interest rate

rose for 3%, the asset value would be wiped out for 15%.

During the financial crisis, the wide duration gap and the

increase in rate have caused banks to lose out a big chunk

of its asset value. The duration model says what happens to

both the value of assets and value of liabilities when

interest rates change. So, if interest rates rise the value

of assets and the value of liabilities both fall, but the

value of assets falls by more-hence the market value of

equity falls.

To add disaster to the recipe, rating agencies such as

Moody’s, S&P, and Fitch gave out blatantly ignorant ratings

(AAA, which means as safe as US treasury bonds) on the

tranches sold by the investment

banks. As mentioned, RAROC should

13

ΔV ΔΦ or Δrf

only be used when evaluating an asset that will not default.

The rating agencies had a conflict of interest, because they

were given a huge fee by the bank to evaluate the tranches.

Tranches turned out to be not AAA and borrowers default and

credit risk increases. Banks did not anticipate the fall in

the value of loan and eventually have its asset wiped out.

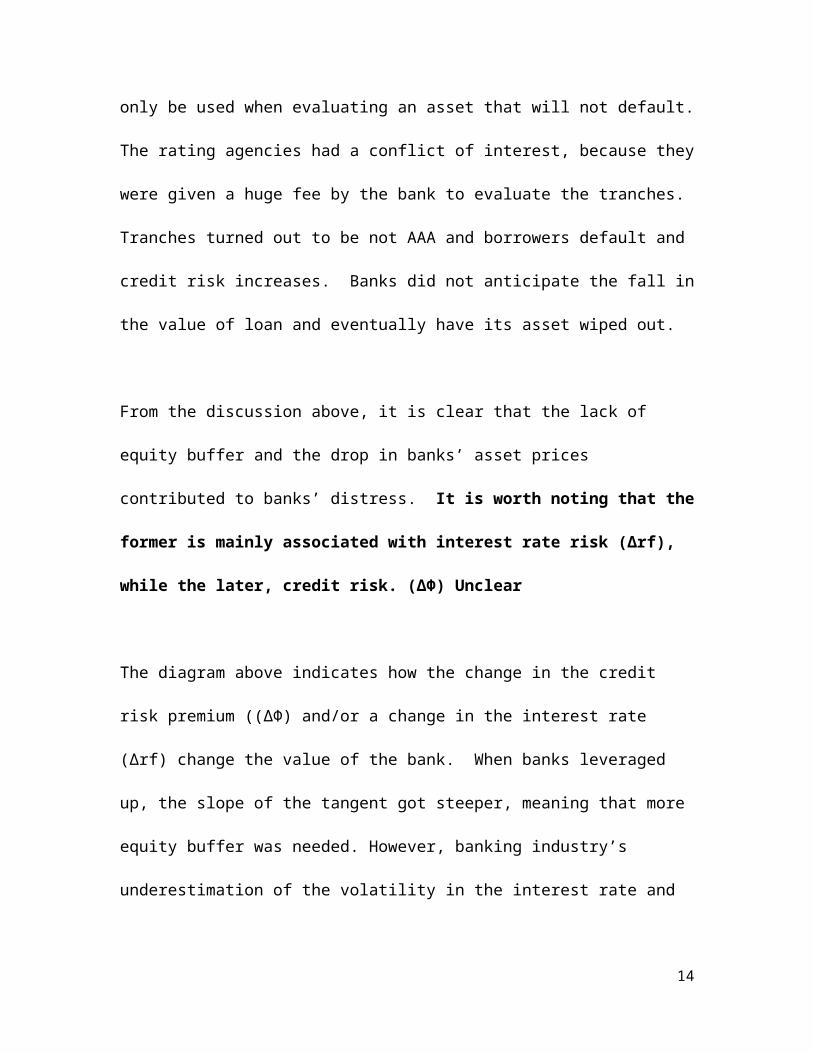

From the discussion above, it is clear that the lack of

equity buffer and the drop in banks’ asset prices

contributed to banks’ distress. It is worth noting that the

former is mainly associated with interest rate risk (Δrf),

while the later, credit risk. (ΔΦ) Unclear

The diagram above indicates how the change in the credit

risk premium ((ΔΦ) and/or a change in the interest rate

(Δrf) change the value of the bank. When banks leveraged

up, the slope of the tangent got steeper, meaning that more

equity buffer was needed. However, banking industry’s

underestimation of the volatility in the interest rate and

14

the complacency to use RAROC has caused them to belly up

within days during 2008, a period of rare volatility.

Banks should be able to hedge against interest rate risk in

the futures market. However, they failed to hedge. Banks

should also be able to hedge against credit risk by getting

CDS. It would work provided that the counterparty is

solvent. Unfortunately, in 2008, the counterparty was AIG,

which was not able to fulfill their promise for payments

until the government bailed it out.

The banking industry’s serious of overdependence of

financial models that were at flawed, constant ignorance of

potential risks in pursuit of higher returns, and standard

rating agencies’ collusion for profitable ratings culminated

in the 2008 financial crisis.

Government deregulation and Failure of the FED: what

completed the risky game

15

Government’s deregulation and the corrosive relationships

between Washington and Wall Street was the reason that the

aforementioned problems in the baking industry were

tolerated and further helped in building up the crisis.

Washington started out as being a strict regulator. As part

of the new deal, President Franklin D. Roosevelt passed the

Glass Steagall Act in 1933 to disallow banks with customer

deposits from engaging in investment banking activities.

The regulatory policies at that time were biased toward

control and protection rather than open markets and

competition. It was Glass-Steagall that prevented the banks

from using insured depositories to underwrite private

securities and dump them on their own customers. From 1933

to 1999, there were very few large bank failures comparable

to the panic of 2008. The law worked exactly as intended.

In April 1998, Travelers and Citicorp were trying to merge,

and Sanford Weil found loopholes within the act and join

with powerful forces to overturn the act. In 1999,

16

Democrats led by President Bill Clinton repealed Glass-

Steagall at the behest of the big banks. The Gramm-Leach-

Bliley Act was enacted by congress, effectively undid many

of the provisions of the Glass Steagall Act of 1933,

resulted in large part deregulation and easy lending

policies. Once again, banks originated fraudulent loans and

once again they sold them to their customers in the form of

securities.

Aside from the repeal of Glass Steagall as a milestone of

government’s deregulation, the government has also been

deregulating in many other areas.vi For example, In May

1998, congress blocked the bill by the Commodity Futures

Trading Commission (CFTC) for regulation, thereby giving

more freedom to the derivatives market and became the basis

for massive speculation. Then in 2004, the Securities and

Exchange Commission (SEC) adopted a voluntary regulation

scheme for investment banks that enabled them to incur much

higher levels of debt, and loosen capital reserve

requirements based on their internal “risk assessment

17

models.” In 2006, a law was passed and handcuffed the SEC

from properly regulating the private credit rating

companies, paving way for rampant collusion to give out AAA

ratings and incorrectly assessment of the quality of

mortgage backed securities.

WHAT drove deregulation? Robert Weissman, the lead author of

the report, "Sold Out: How Wall Street and Washington

Betrayed America," captured it succinctly. "Congress and

the Executive Branch responded to the legal bribes from the

financial sector, rolling back common-sense standards,

barring honest regulators from issuing rules to address

emerging problems and trashing enforcement efforts. The

progressive erosion of regulatory restraining walls led to a

flood of bad loans, and a tsunami of bad bets based on those

bad loans.” Wasn’t deregulation also a product of academic

thinking that the invisible hand of the markets does the

best in allocating capital, that the market should police

itself?

18

Thus, granted that the United States is labeled as a

democratic country, one almost always does not realize that

it is not so much as democratic as a dictated, because

important decisions always are decided by a few individuals’

who contributed big campaign money.

The financial sector invested more than $5 billion in

political influence purchasing in Washington over the past

decade, with as many as 3,000 lobbyists winning deregulation

and other policy decisions that led directly to the current

financial collapse. It is equivalent to having 5 lobbyists

for each and every one of the congressman. One of the most

prominent of which is the Financial Services Roundtable

which was set up in 2000 and represents 100 of the largest

integrated financial services companies and whose members

are the CEOs of the 100 largest financial services

companies.

Having a comfortable relationship with the government, and

thus the lack of regulation, has not only enabled Wall

Street to cover its underlying problematic structure, as

19

mentioned in the section “The banking system,” but also

enabled the powerful banks to take power into their own

hands to create risky and complicated derivatives, such as

the collateralized debt obligations (CDO) and credit default

swaps (CDS) that led to massive speculative and ridiculous

risk exposure. See “The mechanism on how it happened” to

understand the unsustainability of the derivatives.

There was also a culture of cronyism in Washington that

could facilitate business dealings with regulatory approval.

The financial sector buttressed its political strength by

placing Wall Street expatriates in top regulatory positions,

including the post of Treasury Secretary held by two former

Goldman Sachs chairs, Robert Rubin and Henry Paulson. Henry

Paulson was in the position from 2006-2009 under President

George W. Bush, and he was one of the main proponents for

deregulation and for increasing leverage when he was the CEO

of Goldman Sachs. His relationship with Wall Street was

subsequently called into question when Goldman Sachs turned

out to be the biggest beneficiary from the AIG bailout, and

20

it was paid 100 cents on a dollar for the CDS that it

purchased when Paulson was the CEO.

Apart from having a too close relationship with Wall Street,

the government was to blame for having Alan Greenspan served

as the Federal Reserve chairman from 1987-2006. vii

Greenspan was instrumental in perpetuating the mortgage

market crisis by fueling the bubble with different policies

and statements. On February 23, 2004, Greenspan gave a

speech extolling the virtues of floating rate mortgages,

saying “many homeowners might have saved tens of thousands

of dollars had they held adjustable-rate mortgages….the

traditional fixed rate mortgages may be an expensive way of

financing a home.” In the subsequent two years, interest

rates quadrupled from 1 percent to 4.5 percent.

One of the most important features for the bubble was the

practice of mortgage equity withdrawal, or the “housing

ATM,” which enableed homeowners to routinely extract some

21

portion of their home equity to spend. On November 13, 2002,

Greenspan explained: “besides sustaining the demand for new

construction, mortgage markets have also been a powerful

stabilizing force over the past two years of economic

distress by facilitating the extraction of some of the

equity that homeowners had built up over the years.”

Greenspan was a serial bubble-blower. His term saw the

market crash of 1987, the Savings and Loan crisis, the

crash of the Russian ruble and Long Term Capital Management,

the 2000 tech bubble, the supposed Y2K disaster, and last

but not least, the credit bubble and real estate crisis of

2008. Prior to Greenspan's arrival, excluding the brief

mania for commodities and precious metals in late '79 and

early '80, the U.S. had been bubble-free for over 50 years.

Conclusion:

From the discussions above, “intelligence hazard” and

avaricious culture in the banking industry, i.e. excessive

risk exposure in pursuit of higher returns and utilization

22

of flawed financial models/ standard ratings, the corrosive

relationships that have developed between the government and

Wall Street, and the incompetence of the Federal Reserve

were the reasons that contributed to the financial meltdown

The meltdown has totally ruined the financial industry. The

TARP fund was mandated to be received by major banks, and

thus, blurred public’s ability in differentiating between

good and bad banks.

The crisis’s impact can still be felt today with

unemployment rate still is up at 7.7% and GDP growth below

the normal rate.

it remains to be seen when the United States can be back on

track for growth again. “Greed is good,” as popularized by

Gordon Gekko, turned out not to be so good after all.

23

References:

24

i 2008, September. "Financial crisis of 2007–2008 - Wikipedia, the free encyclopedia." Wikipedia, the free encyclopedia. N.p., n.d. Web. 5 Apr. 2013. <http://en.wikipedia.org/wiki/Financial_crisis_of_2007%E2%80%932008#US_stock_market>.

ii "Mortgage-Backed Securities I ." Mortgage-Backed Securities I . N.p., n.d. Web. 30 Aug.2007. <https://www.youtube.com/watch?v=oosYQHq2hwE>.

iii Viet-Nam, 1968 LBJ was dealing with, and bear much of the risk of loss implicitly. I do not like GSE&. "Another bailout that will cost the tax payers billions of dollars, post one | Fort Wayne Politics." Fort Wayne Politics. N.p., n.d. Web. 5 Apr. 2013. <http://fortwaynepolitics.com/2008/09/another-bailout-that-will-cost-the-tax-payers-billions-of-dollars-post-one/>.

iv Triana, Pablo. "VaR: The number that killed us." Futures: Stock, Commodity, Options, and Forex Strategies for the Serious Trader. N.p., n.d. Web. 5 Apr. 2013. <http://www.futuresmag.com/2010/12/01/var-the-number-that-killed-us?t=technology&page=2>.

v Hess, Alan. Finance 423, Banking Coursepack. Seattle: Foster School of Business, 2012. Print.

vi "What Drove Deregulation." zFacts on Controversial Topics. N.p., n.d. Web. 5 Apr. 2013. <http://zfacts.com/node/341>.

vii Fleckenstein, William A., and Frederick Sheehan. Greenspan's bubbles: the age of ignorance at the Federal Reserve. New York: McGraw-Hill, 2008. Print.

-before Freddie and fannie were the lead (required strong background checks), untiltheir reputation was hurt and bankers found way to structure the whole MBS market (that the world was flushed with cash was another extra carrot)> 2001 9/11 wanna customers to spend,2002 bush encouraged minority homeowers

Lier loans, home prices go up, people more money to spend, retail sales up, furtherpropped by Fed’s low interest rates

Copyright © 2022 FDOKUMEN